money creation - wur

TRANSCRIPT

• Who does make money and who is making money out of it?

Money creation

You remember these guys?

2

Monetary misconceptions

• Money doesn’t make you happy. Or does it?

• Money is the ‘mud of the earth’ and it is the root of all evil

• Pecunia non olet………..

• A world without money would be a better world. Which is true..

• …….if you are fond of extreme poverty

• …….if you dislike economic freedom

• …….or both

• Money is an essential precondition for economic freedom in an advanced society

3

Content: above all a lot of questions!

• What is money? (wrap up)

• Who creates money and why?

• Is the production of money very profitable?

• What kind of reform is possible, if necessary?

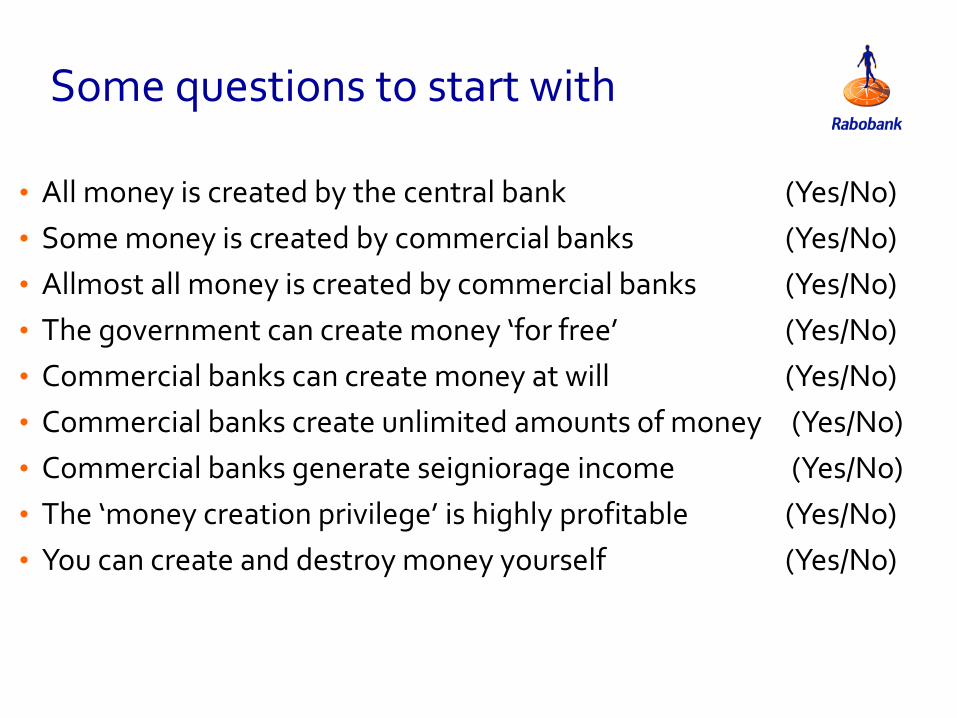

Some questions to start with

• All money is created by the central bank (Yes/No)

• Some money is created by commercial banks (Yes/No)

• Allmost all money is created by commercial banks (Yes/No)

• The government can create money ‘for free’ (Yes/No)

• Commercial banks can create money at will (Yes/No)

• Commercial banks create unlimited amounts of money (Yes/No)

• Commercial banks generate seigniorage income (Yes/No)

• The ‘money creation privilege’ is highly profitable (Yes/No)

• You can create and destroy money yourself (Yes/No)

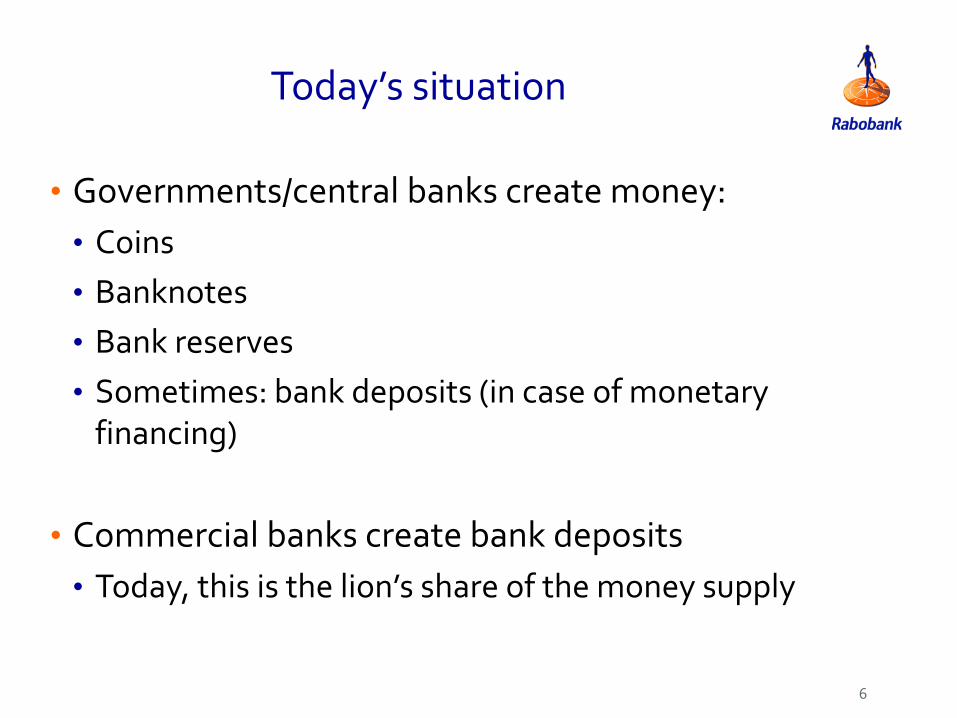

Today’s situation

• Governments/central banks create money:

• Coins

• Banknotes

• Bank reserves

• Sometimes: bank deposits (in case of monetary financing)

• Commercial banks create bank deposits

• Today, this is the lion’s share of the money supply

6

The Dutch money supply(source: DNB, based on ECB-data, Oct. 2017)

7

Commercials banks

Central bank and

governments

Position 1: governments should decide on the money supply

8

• Do you agree?

• Why?

• Who created money in the past?

• During the early coining of gold and silver, private parties decided on the amount of coins in circulation!

• Question: why did governments monopolize money creation?

Sound money?

9

Sound money!

10

Is money creation still profitable today?Yes it is. Enter seigniorage!

11

• Seigniorage (in Dutch: geldscheppingswinst) : the income earned by the entity that produces the money and that is the first to bring it into circulation.

• Example: the production of a € 100 banknote costs € 0.01 per note. Which means that its production is very profitable (to be precise € 99,99 pro note) for the first issuer.In this example: the central bank/government

• Printing banknotes (both by public and private entities) is potentially highly profitable and therefore a dangerous thing

• The production of bank money is of a different order…….

12

“History is largely inflation engineered by government”

“The source and root of all monetary evil …..[is] the government monopoly on the issue and control of money”

Friedrich A. Hayek (Nobel prize economics, 1974, 1978)

Is money creation by the government a bad thing?

13

• Not by definition. The creation of money by the government is a form of taxation and taxation is a legal form of fund raising of governments.

• Especially in countries with weak institutions seigniorage may be an essential part of the funding of the government budget. Absolutely no problem with that.

• The danger is that in countries with weak institutions and lack of effective parliamentary control it may be very dangerous.

• Germany 1923, Zimbabwe 2008, Venezuela 2018, Turkey 2019?

“A Government can live for a long time, even the German Government or the Russian Government, by printing paper money.”

What is raised by printing notes is just as much taken from the public as is a beer-duty or an income-tax. What a government spend the public pay for. There is no such thing as an uncovered deficit.’

John Maynard Keynes, A Tract on Monetary reform (1924)

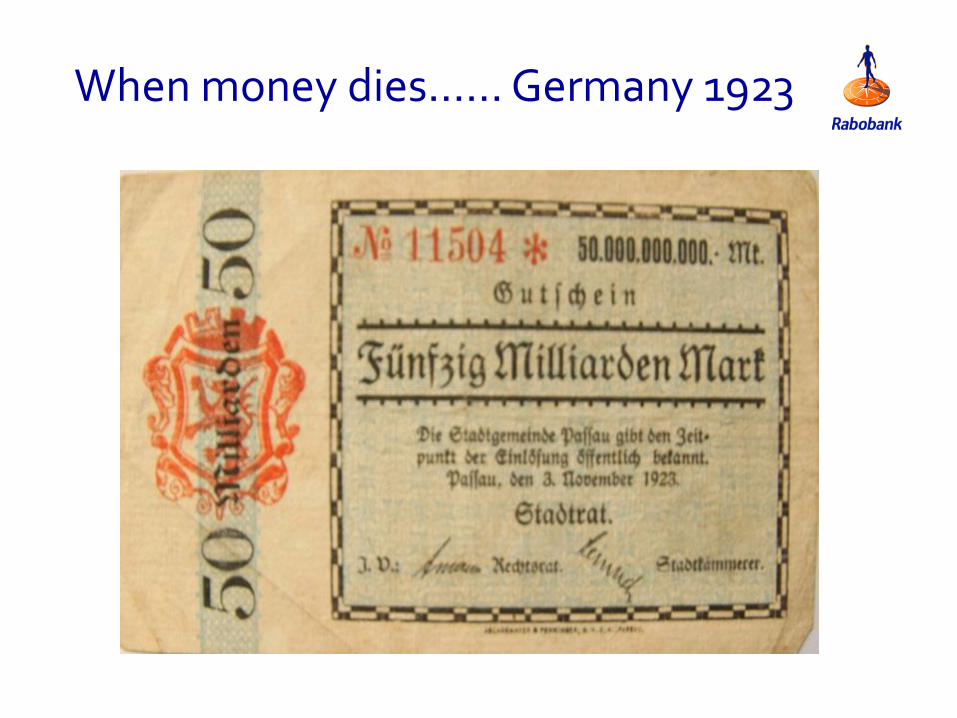

The road to hyperinflation

When money dies…… Germany 1923

15

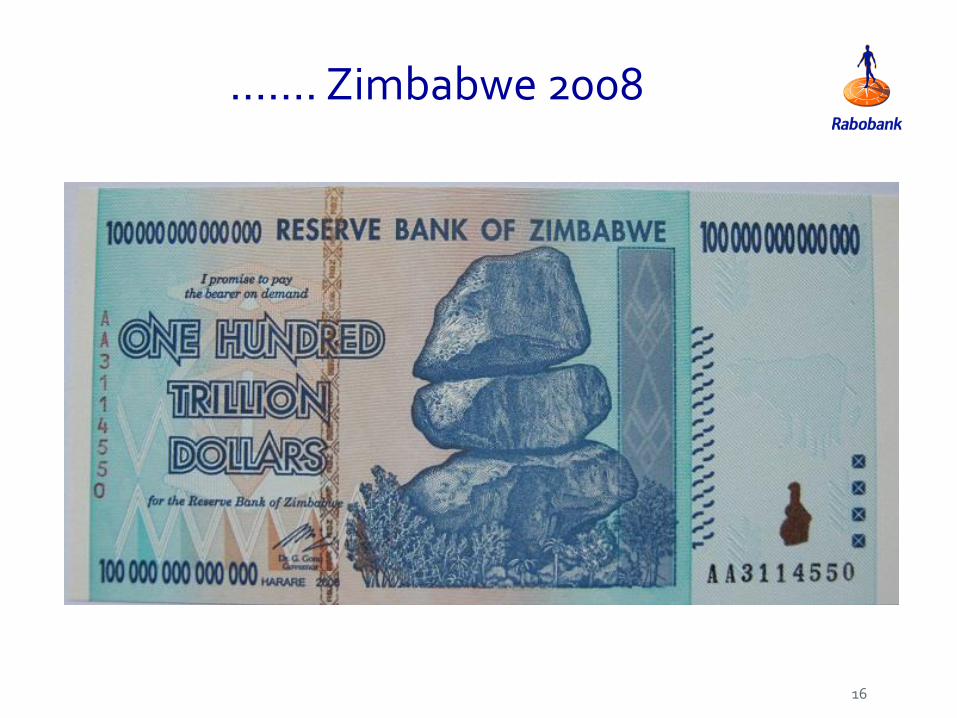

……. Zimbabwe 2008

16

The ugly face of hyperinflation(national currency/USD, index)

17

1

10

100

1000

10000

100000

1000000

10000000

100000000

1E+09

1E+10

1E+11

1E+12

1E+13

1E+14

1E+15

t=1 t=2 t=3 t=4 t=5 t=6

Germany Turkey Venezuela Zimbabwe

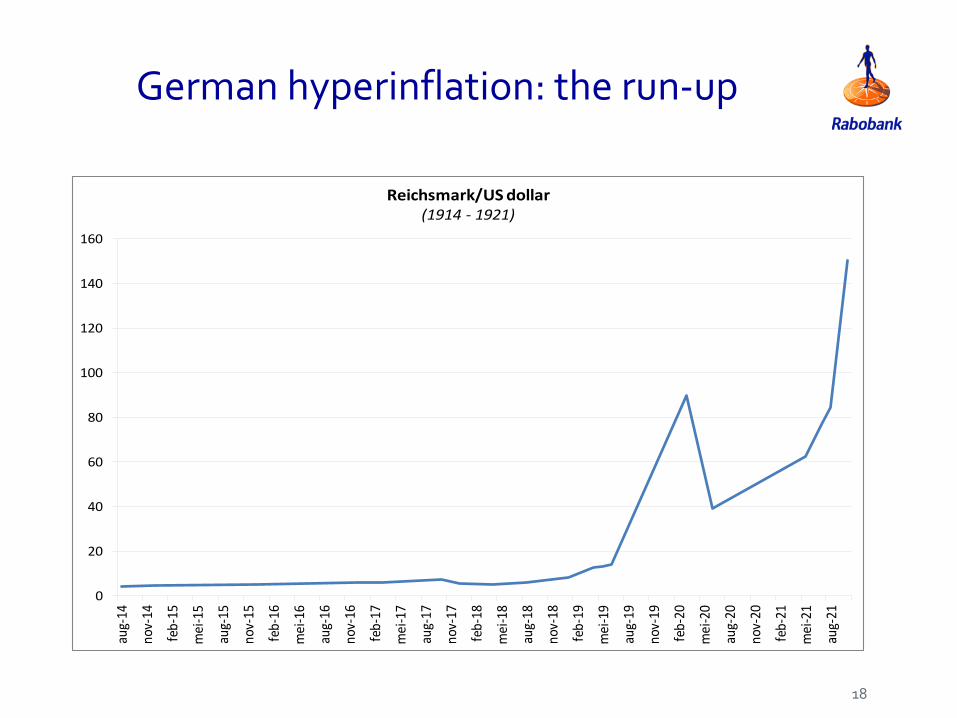

German hyperinflation: the run-up

18

0

20

40

60

80

100

120

140

160

aug-

14

nov-

14

feb-

15

mei

-15

aug-

15

nov-

15

feb-

16

mei

-16

aug-

16

nov-

16

feb-

17

mei

-17

aug-

17

nov-

17

feb-

18

mei

-18

aug-

18

nov-

18

feb-

19

mei

-19

aug-

19

nov-

19

feb-

20

mei

-20

aug-

20

nov-

20

feb-

21

mei

-21

aug-

21

Reichsmark/US dollar(1914 - 1921)

When money died

19

1

10

100

1000

10000

100000

1000000

10000000

100000000

1E+09

1E+10

1E+11

1E+12

1E+13

jan

-19

mrt

-19

mei

-19

jul-

19

sep

-19

nov

-19

jan

-20

mrt

-20

mei

-20

jul-

20

sep

-20

no

v-2

0

jan

-21

mrt

-21

mei

-21

jul-

21

sep

-21

no

v-2

1

jan

-22

mrt

-22

mei

-22

jul-

22

sep

-22

nov

-22

jan

-23

mrt

-23

mei

-23

jul-

23

sep

-23

no

v-2

3

Reichsmark/US dollar(1914 - 1923, logaritmische schaal)

Vrije Universiteit Amsterdam

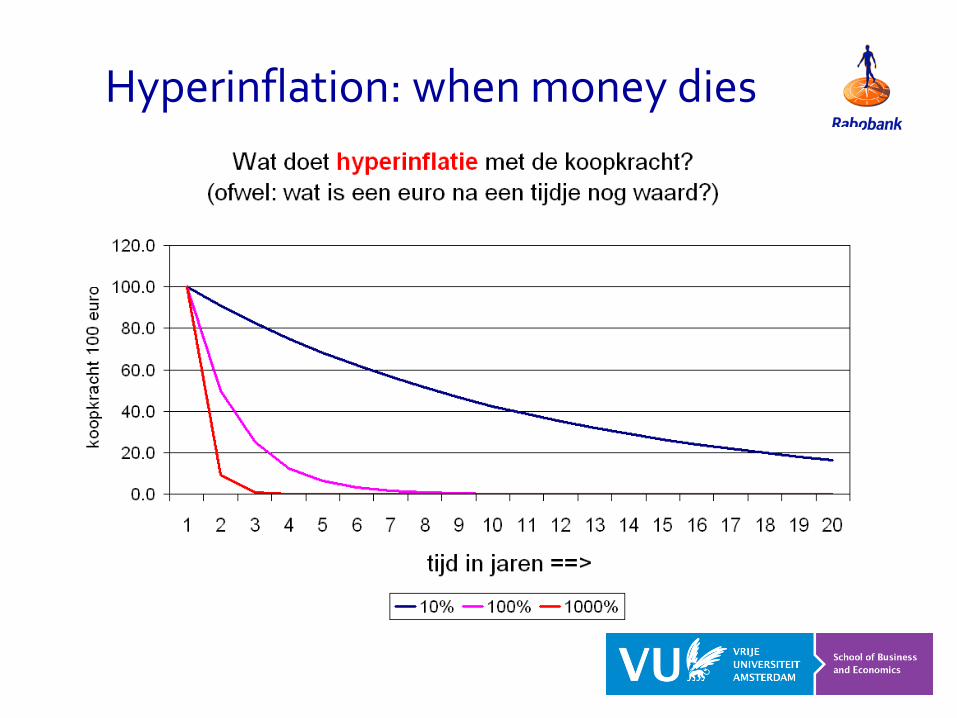

Hyperinflation: when money dies

Vrije Universiteit Amsterdam

Hungary (1946) > 900.000.000.000.000.000.000.000.000%

Greece (1944) > 30.000.000.000%

Germany (1923) > 20.000.000.000%

Venezuela (2018) > 1.000.000.000%

Zimbabwe (2008) > 66.000%

Poland (1923) 51.699%

Russia (1990) 13.535%

Nicaragua (1987) 13.110%

Peru (1990) 7.482%

Brazil (1990) 2.948%

Source: Reinhart & Rogoff, This time is different, 2010, 182 -187

The highest hyperinflations

Is money creation profitable?How about banks? And their clients?

22

• Banks don’t earn seigniorage: the money created by commercial banks is not owned by the bank but by their clients. And the clients are the first to bring it into circulation.

• But clients don’t earn seigniorage either. This is because against the newly created bank deposits (owned by the clients) stand newly created debt (owned by the banks).

• Money creation by the banks does not change net wealth or debt positions

• What changes is the degree of liquidity!

23

24

“Banks coin illiquid assets into liquidity”

Milton Friedman, Nobel prize economics, 1976

25

Money creation: governments and banks compared

26

Money creation by: Governments Commercial banks

Seigniorage income Yes No

Free funding Yes Yes

Automatic brakes No Yes

‘out of thin air’ Yes No

Initiative of moneycreation

With the government With the banks and/or their clients

Note that seigniorage income is a form of taxation

In Europe monetary financing of public spending is explicitly forbidden by law.

27

• It is part of Treaty, article 123.1

• This reflects the German trauma of 1923, when hyperinflation effectively eliminated the middle class and paved the way for fascism.

• Germany would rather kill the euro than accept a government monopoly on money creation!

• Keep this in the back of your mind, we will come back to this later……

Monetary financing of government spending

Increase in governmentspending, financed bythe central bank

Money comesdirectly in circulation andeconomic activitywill increase

Money lands in bank accounts of companies andemployee, involvedin public projects (M1 increases)

Money is spendand/or saved

Monetary base increases, bank reserves larger

Banks can lendmore money , which will resultin increase of M1

Helicopter Money

Government hands out money to citizens as a present, financed bythe central bank

Money lands in bank accounts of thepeople that receivethis present

Money is spendand/or saved

Monetary base increases, bank reserves larger

Banks can lendmore money , which will resultin increase of M1

Can money creation by commercial banks also run out of hand?

30

• Yes, it can. Banks can extend too much credit, buy to many securities……

• But supervisors have all instruments available to regulate it!

• Central banks regulate the size and costs of bank liquidity

• Banking supervisors demand minimum levels of solvency and liquidity ratios

• Competition authorities prevent dominant market positions

What seems to be the most stable situation?

31

• Governments: no, or little seigniorage by money creation

• Central banks: regulate market liquidity

• Bank supervisors: close monitoring of banking ratios

• Commercial banks: creating liquidity for their clients

• Central banks: ex-post monitoring of monetary aggregates and, if necessary, adapting market conditions

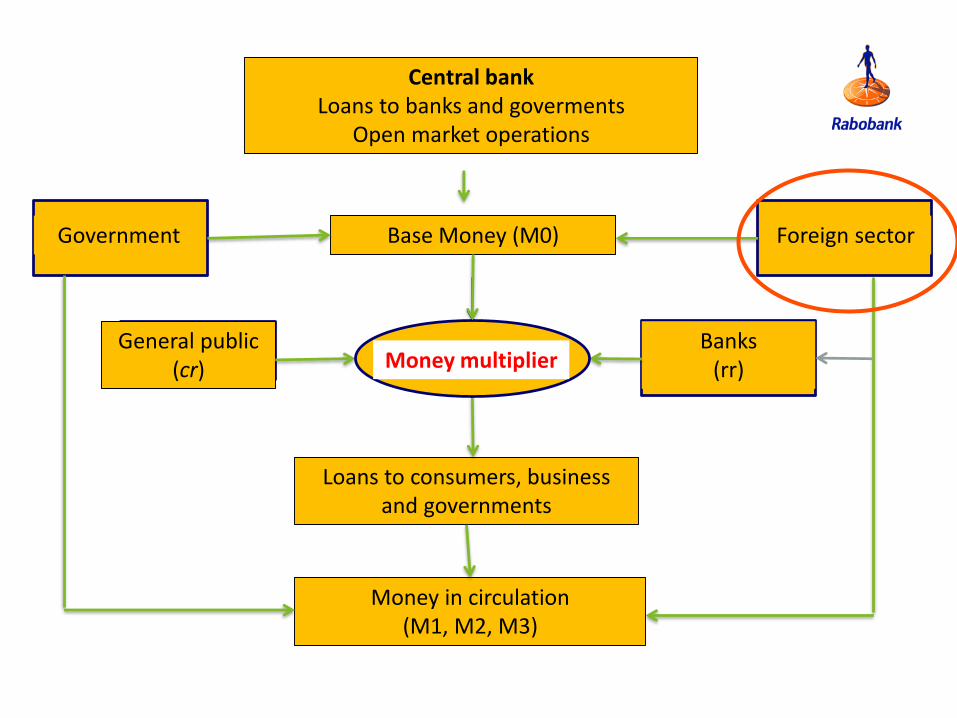

Central bankLoans to banks and goverments

Open market operations

Base Money (M0)

Loans to consumers, business and governments

Money in circulation(M1, M2, M3)

Government Foreign sector

General public(cr)

Banks(rr)Money multiplier

What are the problems with this system?

33

Banks are vulnerable for bank runs

Banks have a privilege in the shape of ‘free funding’

Bank may make mistakes in their lending decisions

People make take up too much debt

Supervisors may be too lax and/or make mistakes

The system may be procyclical

What are the problems with this system?

34

Banks are vulnerable for bank runsThis is a serious item, which only the central bank can solve

Banks have a privilege in the shape of ‘free funding’If this is the case, it can be easily solved by paying interest on payment accounts

Bank may make mistakes in their lending decisions and/or people make take up too much debt. Yes, they usually do

Supervisors may be too lax and/or make mistakes. Yes, but they’ve learned a lot

The system may be procyclical. Yes, but supervisors have many way to prevent this to happen

Reform proposals

35

• There are several proposals, viz.

1. The Chicago Plan (100% money) (Fisher, 1935)1. Make payment systems a public function, executed by a public

institution (basically the same proposal)

2. Digital cash

3. Denationalization of money (Hayek, 1975)

• We will focus on ad 1) and give some brief thoughts on ad 2). I will not go into ad 3), but you can always ask…..

The questions to be asked are….

36

• Which problems are solved?

• Are any new problems created?

• What is thee added value?

• What is the essence of these proposals?

• Is it possible?

• Which has already happened?

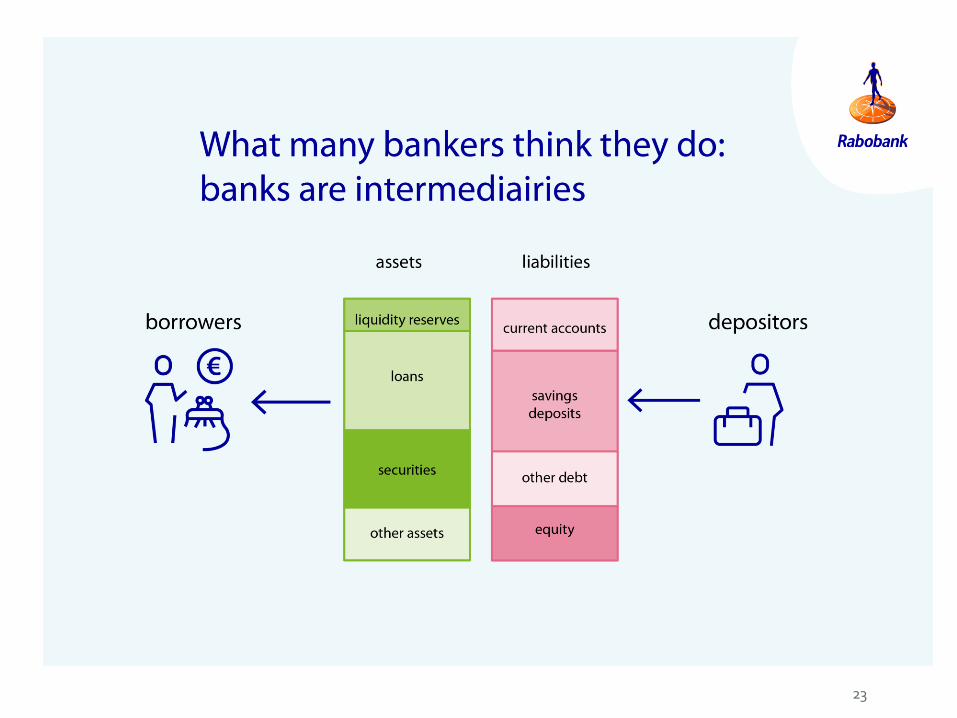

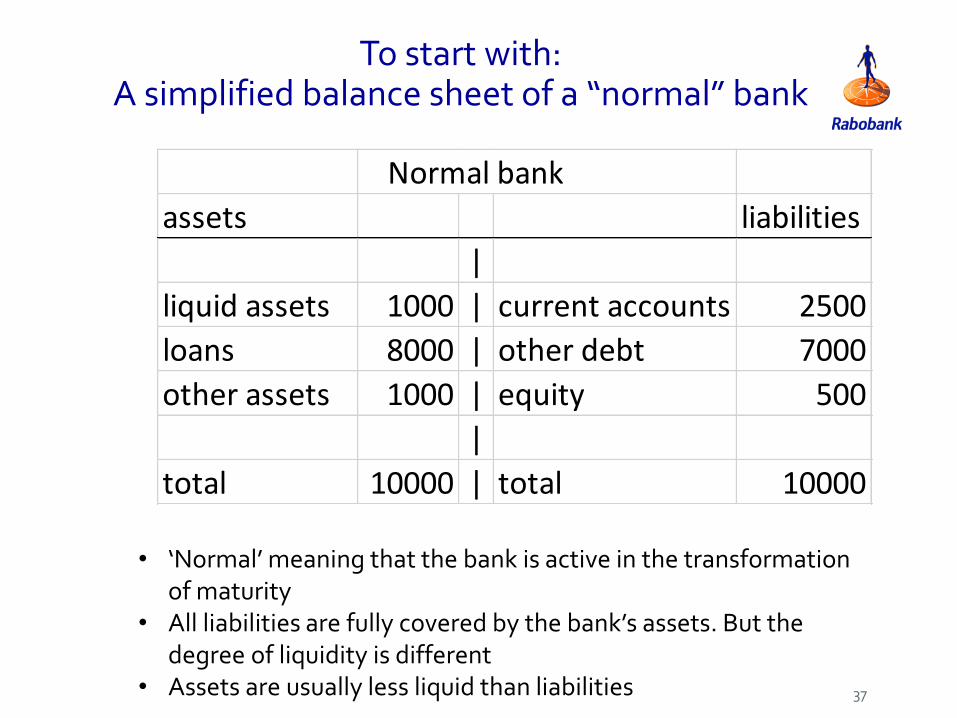

To start with:A simplified balance sheet of a “normal” bank

37

Normal bank

assets liabilities

|

liquid assets 1000 | current accounts 2500

loans 8000 | other debt 7000

other assets 1000 | equity 500

|

total 10000 | total 10000

• ‘Normal’ meaning that the bank is active in the transformation of maturity

• All liabilities are fully covered by the bank’s assets. But the degree of liquidity is different

• Assets are usually less liquid than liabilities

Full reserve banking

Making banks safer……

• Based on the so-called Chicago Plan (1930s)

• International movement “full reserve money”

• Modernizing money (UK), Ons Geld, SFL (NL), Vollgeld (SWI)

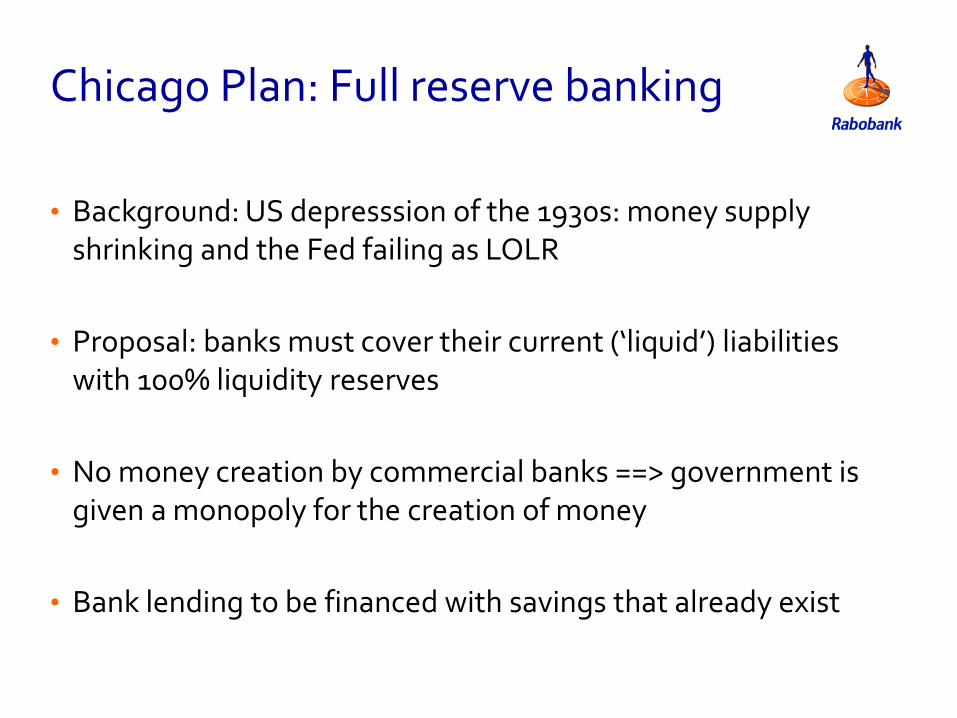

Chicago Plan: Full reserve banking

• Background: US depresssion of the 1930s: money supplyshrinking and the Fed failing as LOLR

• Proposal: banks must cover their current (‘liquid’) liabilitieswith 100% liquidity reserves

• No money creation by commercial banks ==> government is given a monopoly for the creation of money

• Bank lending to be financed with savings that already exist

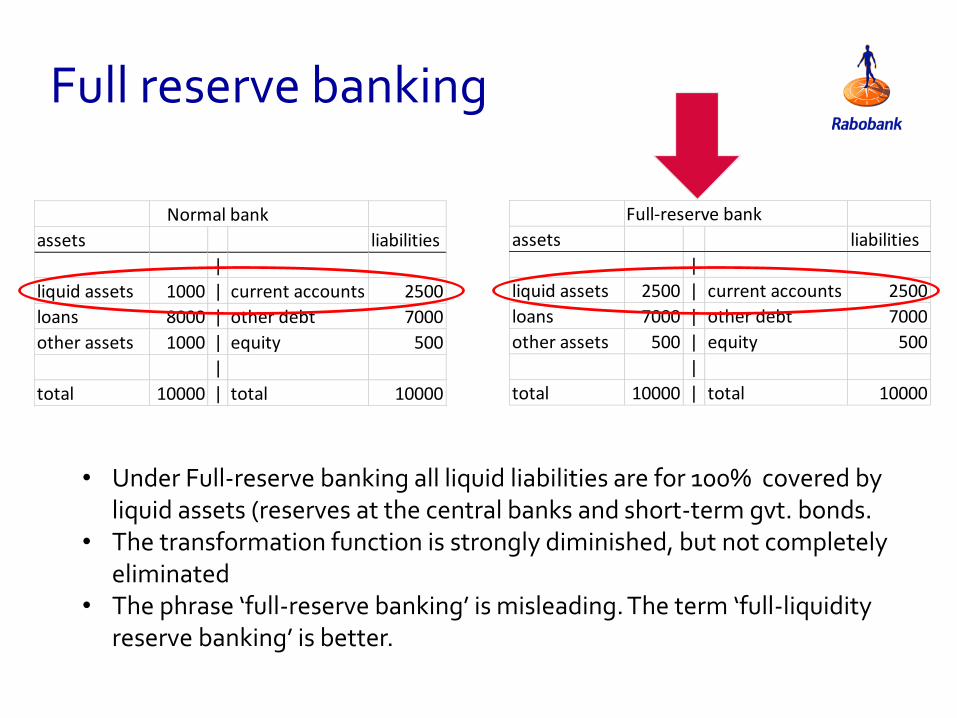

Full reserve banking

Normal bank

assets liabilities

|

liquid assets 1000 | current accounts 2500

loans 8000 | other debt 7000

other assets 1000 | equity 500

|

total 10000 | total 10000

Full-reserve bank

assets liabilities

|

liquid assets 2500 | current accounts 2500

loans 7000 | other debt 7000

other assets 500 | equity 500

|

total 10000 | total 10000

• Under Full-reserve banking all liquid liabilities are for 100% covered by liquid assets (reserves at the central banks and short-term gvt. bonds.

• The transformation function is strongly diminished, but not completely eliminated

• The phrase ‘full-reserve banking’ is misleading. The term ‘full-liquidity reserve banking’ is better.

Effects of full reserve banking

• Probability of a bank run (almost) fully eliminated, as liquidity risk forindividual banks becomes much smaller. This is an important positive factor.

• Savers are forced to hold their savings in depositi with a longer maturity. Liquid savings should be held on an non-interest current account. Otherwisethe plan doesn’t work.

• All banks become secundary banks, just intermediation of existing money

• Banks lose a source of income, ==> holding a bank account becomes muchmore expensive

• Financial innovations should be eliminated, as near-monies may underminethe system

Effects of full reserve banking (2)

• The government gets a monopoly on money creation. Open questions are:

• Can the government create the right amount of liquidity on the right time, the right place, and in the right amount

• Remember the large potential ways to create and/or destroy liquidity

• How can the government forecast the ex-ante right amount of money? Notice the importance of cross-border transactions.

• Government monopoly on money creation may be dangerous (see earlier)

• Banks become more stable because some risks are shifted back todepositors

42

Central bankLoans to banks and goverments

Open market operations

Base Money (M0)

Loans to consumers, business and governments

Money in circulation(M1, M2, M3)

Government Foreign sector

General public(cr)

Banks(rr)Money multiplier

Effects of full reserve banking (3)

• The international dimension is completely overlooked

• Cross-border flows have a potential major, but completely unpredictable influence on

• The monetary base

• The liquidity position of banks

• The amount of money in circulation

• The whole idea that anyone can predict the ex-ante money supply is completely flawed.

• And cross-border flows are huge, especially for a small country like NL

44

Effects of full reserve banking (4)

• The consequences of full-reserve banking are highly uncertain

• To make it work and give it a chance there are three options:

1. It is introduced on a pan-EMU level (meaning the EU Treaty should be rewritten)

2. Cross-border flow within EMU are forbidden, which means partly dismantling the Internal Market

3. The Netherlands would have to leave EMU and, as a consequence, the EU

• My prediction: this is not going to fly

45

Other options

• The positive effect of the Chicago Plan can for a large extent be realized within the existing framework

• Some issues are already being addressed by the regulatory framework of BIS-3, which introduces new criteria such as the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR)

• If you think that banks benefit too much form money creation force them to pay interest on payment accounts.

• If you want make the payment systems safer force banks to have collateral ready to increase their liquidity position if the circumstances deteriorate

46

Digital cash• Digital cash: a digital variety of the bank note

• Everybody gets a bank account at the central bank

• Positive: everybody has a safe haven for his or her money

• Negative: a bank run is made much easier. Even a spark can trigger one meaning the central bank should massively intervene to support banks

• Impact on stability potentially strongly negative. Therefore, most central banks are against this.

47

An ‘in-between’ solution: the deposit bank

• A deposit bank offers payment accounts that are fully covered by reserves at the central bank

• This means that a full-reserve bank is created in the current system

• Questions:

• What is the earning model?

• Why would this be more attractive than holding a normal bank account

• Even this bank would have (operational) risk which must be ensured

• DNB has blocked this bank by refusing a banking licence. Good decision?

48

Conclusions

• Personally, I think that full-reserve banking is not a good idea.

• It had never been tested in practice

• Its economic consequences are uncertain

• Against the positive effects are a lot of negatives (such as massive monetary financing by the government)

• Most of the positive effects can be realised within the existing framework

• Even if you think that it is a good idea: it is not possible to introduce this on the national level within the EU

• The costs of exiting the E(M)U are huge. The are dwarfing any positive effect from full-reserve banking.

• A deposit bank may be reconsidered, although I have my doubt that it will work

49

50

51

• Any questions?

Thank you

Lees onze publicaties op: https://economie.rabobank.com