‘european monetary integration and the public-private money divide: can post-crisis reforms...

TRANSCRIPT

Paperpreparedforthe3rdWorkshopinInternationalStudiesoftheEuropean

InternationalStudiesAssociation(EISA),Tübingen,6-8April2016;WorkshopR:

“Livingthe‘NewNormal’:Post-crisisPoliticsofMoney,DebtandTime”.

Thisisafirstdraft,pleasedonotcite!

EuropeanMonetaryIntegrationandthePublic-PrivateMoney

Divide:CanPost-CrisisReformsHarmonizePrivateMoneyCreation

intheEurozone?

SteffenMurau

CityUniversityLondon

NorthamptonSquare

London,EC1V0HB

UnitedKingdom

Abstract

Basedontheconceptual frameworkof the ‘MoneyView’, thispaperarguesthatEuropean

monetaryintegrationuntiltheEurocrisishasonlyfocusedonharmonizingpublicmoneyon

a supranational levelwhileneglectingprivatecreditmoneycreation.Theprivately issued

credit money supply in the European Monetary Union (EMU) is made up of both bank

deposits and ‘shadow money’ forms (e.g. money market fund shares and repurchase

agreements). The paper discusses if the institutional evolution and the political reform

projects after the crisis lead to an upload of the frameworks for private credit money

creationonaEuropeanlevel.Ontheonehand,thepapertakesintoaccounttheECB’srole

incompensatingtheunwillingnessofEuropeanbankstocontinueintra-EMUcross-border

lending by tolerating and supporting TARGET 2 balances. On the other the hand, it

addressestheBankingUnionreforms.Thepaperfindsthatwithregardtobankdepositsas

‘traditional’ private credit money, a spill-over is taking place that by and large leads to

monetary integration further down the monetary hierarchy and seems to establish the

public-private partnership for deposit creation on a European level. Finally, the paper

definesanavenueforfurtherresearchonthecreationandregulationofshadowmoneyin

theEMU.

.

Keywords:EuropeanMonetaryUnion,EuropeanCentralBank,BankingUnion,

Eurocrisis,TargetII,PrivateMoney.

Wordcount:8.780

2

1.Introduction

This paper adopts a ‘Money View’ perspective to provide an analysis and

interpretationofrecenteventsintheEuropeanMonetaryUnion(EMU).TheMoney

View is an institutionalist framework for the analysis of monetary and financial

systems. A key concept of theMoney View is to regard themonetary systems as

hierarchical:Differentlayersofpublicandprivatemonetaryinstruments,issuedby

different financial institutions,co-existnext toeachother(Mehrling2011,2015a).

The contemporarymoney supply is thusmadeupof three typesof creditmoney:

liabilities issued by central banks (central bank deposits and currency), liabilities

issuedbycommercialbanks(deposits)and liabilities issuedbynon-bankfinancial

institutions that trade at par to the former, termed ‘shadowmoney’ (e.g. money

marketfundsharesandrepurchaseagreements)(cf.Pozsar2014).

Matthias Matthijs and Mark Blyth begin their 2015 edited volume ‘The

FutureoftheEuro’withthefollowingstatement:“Whatwetermtheeuroexperienceshows how unfinished institutional design of the euro led to overall economic

divergenceacross theEurozone, rather than the convergence thatEU leadershad

anticipated at Masstricht in the early 1990s” (Matthijs and Blyth 2012: 2). This

paper concurs with the assessment that the EMU’s architecture is unfinished.

However,astheMoneyViewperspectivewillyield,itisnotsomuchunfinisheddue

toa lackofpoliticalor fiscalunion, as traditionally argued. Instead, themonetary

unionthatwascreatedbytheTreatyofMaastrichtin1992isinitselfincompleteas

ithasmerelyuploadedthetoplevelofthemonetaryhierarchytoaEuropeanlevel.

The creation of money forms further down the hierarchy, i.e. bank deposits and

shadowmoney,remainedlargelynationallyorganised.

Basedonthisnotion,thispaperaskswhetherpost-crisisreformsoftheEMU

areabletoharmonizeprivatemoneycreationintheEurozone.Theanalysisfocuses

on bank deposits as the traditional form of privately issued credit money and

postpones the study of shadow money to future research. It discusses the

institutional evolution of the European Central Bank (ECB) with regard to cross-

border deposit flows in the EMU aswell as the political project of establishing a

Banking Union. The study suggests that despite drawbacks in the Banking Union

project, there is a neofunctionalist spill-over going on that establishes the public-

privatepartnershipfordepositcreationonaEuropeanlevel.

Thepaperisorganizedasfollows.Section2presentssomekeyaspectsofthe

MoneyViewasaconceptuallensforscholarshipinInternationalPoliticalEconomy

(IPE)thatseekstostudythepoliticaleconomyofmonetaryandfinancialsystems.

Section3appliesthoseconceptsonthehistoryofEuropeanmonetaryandfinancial

integrationuptotheoutbreakoftheEurocrisis;itfindsthatonlythetoplayerofthe

hierarchyofmoneyhadbeenintegratedsofar.Section4discussestheimpactofthe

EurocrisisasabankingcrisisandstudiestheinstitutionaldevelopmentoftheECB

aswellasthepoliticalprojectofBankingUnion.Section5concludesandspellsout

theavenueforfurtherresearch.

3

2.The‘MoneyView’asaConceptualLensforIPE

The ‘Money View’ is an institutionalist conceptual framework for the analysis of

creditmoney systems. Common sense among central bankers in the late 19th and

early 20th century, yet ousted after theWorldWars, the Money View has gained

momentumafterthe2007-9FinancialCrisis.Ithasbeenusede.g.toanalyzeshadow

bankingand the institutional evolutionof theFederalReserve (cf.Mehrling2011,

2013;Pozsar2014).Inthis,theMoneyViewstandsincontrasttothemodel-based,

ahistoricalapproachofneo-classicaleconomicsasittakesinstitutionsseriouslyand

focuses on the actual ‘financial plumbing’ of the ‘real world’. Methodically,

argumentsoftheMoneyViewarebasedontheanalysisofbalancesheetdynamics.

Inthis,theMoneyViewtakestheproverbialassessmentofMinsky(1986)seriously,

accordingtowhichmoneycreationisnothingbutamerebalancesheetoperation.

FollowingMehrling (2015a), this sectionpresents threeanalytical concepts

ofaMoneyViewperspectivethatareparticularlyusefulforinstitutionalistanalyzes

in IPE:moneycreationasa swapof IOUs, thehierarchyofmoneyand thepublic-

private money hybridity. As a fourth dimension specific to the EMU, the section

introducesthedistinctionbetweennationalandsupranationalmoneycreation.

Money creation as a swap of IOUs: The Money View is an expression ofwhatSchumpeter (1954:686)callsa ‘credit theoryofmoney’, according towhich

money in its essence is circulating debt. The underlying notion of the monetary

system is that of a payment system (Mehrling 2011) or an accounting system of

exchange (Arnon 2011: 152ff). Payment occurs via tradable debt claims (‘inside

money’) that are transferred in between the accounts of the participating

institutions.Thisfollowstheaccountingrulesofdouble-entrybookkeeping.Hence,

the formallyaccurateway thatallows representing thedynamics in thepayments

systemandgoesrighttotheheartofthematterisananalysisofbalancesheets.

In such a creditmoney system,money creation takes placewhen financial

institutions,inexchangeforalong-termIOUowedtothem,createashort-termIOU

that can be traded on secondarymarkets against commodities, services or other

financial instruments. The most common example is when banks issue loans by

creatingdeposits.Theloanconstitutesanassetofthebank,asitisalong-termIOU

owedtothebank;thedeposit,asashort-termIOUowedbythebank,isthebank’sliability. In terms of balance sheet mechanics, when a bank hands out a loan, it

expandsitsbalancesheetonbothsidesandswapsIOUsofdifferentmaturities.The

short-termmaturities,insofarastheyaretradableonasecondarymarket,function

asmoney that can be used by the receiver of the loan. Assuming that regulatory

restrictionsareabsent,moneycreationcanthusliterallyoccuroutofnothing:

Borrower Bank

+Money +Loan +Loan +Money

(short-termIOU) (long-termIOU) (long-termIOU) (short-termIOU)

4

Moneycreation,fromaMoneyViewperspective,isthusthe‘byproduct’ofgranting

credit(McMillan2014:6).Empirically, thecontemporaryfinancialsystemhastwo

mainchannelsofcreditmoneycreation:Ontheonehand,commercialbanksissue

deposits in the traditional banking system. In the shadowbanking system, on the

other hand, various non-bank financial institutions – conceptually understood as

shadowbanks–createshort-termIOUsthatfunctionas‘shadowmoney’.

Ifcreditmoneycreatedtodayisapromisetopaycreditmoneytomorrow,we

seemtobeapproachinglogicaldifficulties.Whatisthepaymentofultimatemoney

supposedtobe?Atraditionalargumentisthatitmustbeamoneyformwith‘actual

value’.Thisiswhyuntilthe20thcentury,themajorityofmonetarytheorists,which

ultimatelyadheredtoa‘monetarytheoryofcredit’,believedthatitwasnotpossible

to decouple monetary systems from a scarce commodity such as gold (cf. Arnon

2011).Acounter-argumentcomesfromMitchell-Innes(1914),oneofthe‘founders’

ofamoderncredittheoryofmoney,whopostulatesthatweonlyneedthehighest

moneyasan‘idea’–asa‘unitofaccount’.“Theeye”,heargues,“hasneverseen,nor

thehandtouchedadollar.Allthatwecantouchorseeisapromisetopayorsatisfy

adebtdueforanamountcalledadollar”(Mitchell-Innes1914:155).

TheHierarchy ofMoney:Themonetary system as a payments systems isfundamentally hierarchical (Minsky 1986). The idea of hierarchy refers to the

differentformsofcreditmoneywithinadomesticpaymentssystemandthevarious

institutionsissuingthemastheirliabilities.Moneyformshigherupinthehierarchy

aresafer,moreacceptablefromademandsideandofmorestablevalue,yetscarcer

andmoreexclusive to supply;money forms furtherdown thehierarchyaremore

‘elastic’tocreateandmoreaccessiblefromthesupplyside,butarelessacceptable

fromademandsideandhaveahigherriskofbreakingawayfrompar.Thereason

forthis is thatparclearance– i.e.keepingupaone-to-oneexchangeratebetween

variouscreditmoney formsatdifferentpositionswithinthehierarchyofmoney–

cannotbe taken forgranted.Parclearanceneeds tobeactivelyestablished,either

politicallybythecentralbankorviamarketforces(cf.Mehrling2015a).

Figure1–basedonMehrling (2012)–highlights this idea in the formofa

‘MonetaryPyramid’.Onthetopisanactualorafictionalunitofaccount–e.g.gold

ordollar,respectively.Belowthisarearangeofinstitutionsissuingdebtclaimsas

insidemoney.TheIOUsissuedbythecentralbankarehigherrankingthanthoseof

thecommercialbankingsystem,whichinturnarehigherrankingthanthoseofthe

shadowbanking system.Money creation as a swapof IOUs involves transcending

thedifferentlayersofthehierarchy.Withinthehierarchy,thevariousIOUsimplya

promisetopaythehigher-rankingformofmoney.Themoneyformsituatedatthe

topisthefinalmeansofsettlingpayment(cf.Pozsar2014:7-8).Inthis,thereisno

cleardividinglinebetweenmoneyandcredit.Dependingontheissuinginstitution’s

positioninthehierarchy,acreditmoneyformwilllooklikemoneyifheldasasset

on the institution’s balance sheet or credit if held as liability on the institution’s

balance sheet (cf. Mehrling 2012). The money forms further up in the hierarchy

5

haveahigher‘moneyness’,i.e.theyappearasmoneytoagreaternumberofactors,

whilethe‘creditness’ofmoneyincreasesfurtherdownthehierarchy:

Figure1–TheHierarchyofMoney(conceptually)

Public-privatemoney hybridity:Money that is created as a byproduct ofcredit intermediationcanbeissuedbothbypublicandbyprivateinstitutions.The

money supply in general is thus a hybrid of public and private money forms. In

normaltimes,publicandprivatemoneyformstradeatparwitheachother,which

makesthemappearsimilarandconcealsinherentdifferences.FromaMoneyView

perspective,real-worldmonetarysystemsarethussituatedinbetweenidealizations

thatseethemoneysupply–beit inadescriptiveoranormativesense–aseither

purelypublic(cf.Knapp1905)orpurelyprivate(cf.Menger1892;vonHayek1976).

The actual delineation between public and private money forms is historically

contingentandcanshiftovertime.

Figure 2—based on Pozsar (2014: 15)—shows the ‘Money Matrix’ as a

heuristic tool to systematize the public-private divide of creditmoney forms. The

leftcolumndisplaystwodifferentcategoriesofpubliccreditmoney:Themoney-like

liabilities of a public institution, typically a modern-type central bank or the

treasury,arepurepublicmoney.Private-publicmoney are themoney-like liabilitiesofprivateinstitutionsthathavepublicliquidityandsolvencybackstopsandcantap

public institutions’ balance sheets via the discount window or deposit insurance.

Thus,apublic-privatepartnershipformoneycreationisinplace,inwhichthepublic

authorities also assume competences for regulating and supervising the private

issuing institutions. The right column displays two different categories of private

credit money: The money-like liabilities of private institutions that do not have

tradeatquasi-par

tradeatpar

CentralBank’s

IOUs

BankingSystem’s

IOUs

ShadowBanking

System’sIOUs

‘Moneyness’

ofIOUs

‘Creditness’ofIO

Us

Scarcity E

lasticity

QuantityofIOUs

UNITOFACCOUNT

6

access to backstops on a public balance sheet are public-privatemoney if issuedagainstpublicassets,andpurelyprivatemoneyifissuedagainstprivateassets.

PublicCreditMoneyForms PrivateCreditMoneyForms

(1)PurePublicMoney

• Issuedbyapublicinstitution(e.g.centralbankortreasury)

PublicInst.

Anyassets PurePublic

Money

(3)Public-privateMoney

• Issuedbyaprivateinstitution• Publicassetsascollateral

PrivateInst.

Publicassets Public-private

Money

(2)Private-publicMoney

• Issuedbyaprivateinstitution• Backstoppedatpublicinstitution

PrivateInst.

Anyassets Private-public

Money

PublicBackstops

(4)PurePrivateMoney

• Issuedbyaprivateinstitution• Privateassetsascollateral

PrivateInst.

Privateassets Pure-Private

Money

Figure2–TheMoneyMatrix(conceptually)

National vs supranational level:When considering the creation of publiccreditmoney,itplaysaroleonwhichhorizontallayerwithinapoliticalsystemthe

respectivepublicauthoritiesaresituated. InmodernWestern liberaldemocracies,

the nation state has typically assumed this responsibility (Helleiner 2003). In the

caseofaregional integrationprojectsuchas theEU,however, theresponsibilities

maybespreadacrossdifferentlayerswithinamulti-levelgovernancesystem.Purepublic money may be issued by national or supranational central banks ortreasuries.Privatepublicmoneymayhave liquidityandsolvencybackstopson thebalance sheets of national or supranational public institutions, and national or

supranationalbodiesmayassumeresponsibilitiesforregulationandsupervision.

Inaddition,similarconcernsaboutthenationalorsupranationallevelapply

to private credit money. On the one hand, public-privateand pure privatemoney,although they are not publicly backstopped, are created on money and capital

markets that may be national or supranational with regard to their scope and

regulation.Ontheotherhand, in thecaseofpublic-privatemoney, itplaysarole ifthepubliccollateralthatisusedisthatofanationalorasupranationalinstitution.

7

3.EuropeanMonetaryIntegration(1957-2009)

This sectionwill apply the conceptual insightsof theMoneyViewaspresented in

Section2ontheEMUbeforetheEurocrisis,whichbegantounfold in2009. Itwill

study in terms of the Money Matrix how the processes of European monetary

unification had an impact on various forms of public and private credit money

withinEurope.Inthis,itwilldiscussthefirsttwowavesofmonetaryandfinancial

integration (1957-1980 and 1985-2005). As to be demonstrated, only the key

centralbankmoney forms—currencyaswellascentralbankdeposits—were fully

integrated on a supranational level. Commercial bank deposits remained in an

ambiguouspositionbetweennationalandsupranationalregulatorycompetences.In

addition,newformsof‘shadowmoney’emergedintheprivatecreditmoneyrealm.

ThesetupoftheMoneyMatrixintypicalEuropeanstatesbeforetheprocess

ofmonetaryintegrationcanbeimaginedasdepictedinFigure3,whichincorporates

the ‘traditional’moneysupply inthemid-20thcentury.Liabilities issuedbycentral

banks,i.e.currencyandcentralbankdeposits,arepurepublicmoneyandsituatedatthetopofthemonetaryhierarchy.Theyweredenominatedinvariousnationalunits

of account. Deposits as liabilities issued by commercial banks are private-publicmoneyinsofarastheyfallunderthedepositinsurancelimit,andpureprivatemoneyiftheyareuninsured(cf.Pozsar2014:13-17).1

Public Credit Money Forms Private Credit Money Forms

(1) Pure Public Money NATIONAL: Central Bank liabilities • Currency (Notes, Coins) • Central bank deposits

(3) Public-private Money

(2) Private-public Money

NATIONAL: Commercial bank liabilities • Insured bank deposits

(4) Pure Private Money

NATIONAL: Commercial bank liabilites • Uninsured bank deposits

Figure3–TheMoneyMatrix(empirically,mid-20thcentury)

1 Pozsar(2014)alsoregardsshort-termbondsissuedbytheTreasury,insofarastheytradeatpar

to central bank liabilities, as a form of pure publicmoney. For the perspective adopted in thispaper,thisaspectisleftaside.

8

European monetary integration prior to the International Financial Crisis

2007-9andtheEurocrisis(from2009)hasoccurredintwomajorwavesthatfirst

ledtoestablishingtheEuropeanMonetarySystem(EMS),andthenintroducedthe

euroasasinglecurrency(Valiante2016:28-37):

Thefirstwavedatesbackto1957andbeganwiththeTreatyofRome,which

foundedtheEuropeanCommunityandinprincipleallowedfreecapitalmovement

insofaras itwasnecessarytomakethesinglemarket function.Thiswasthebasis

fortwoCapitalDirectivesof1960and1963thatopenedupcross-borderflowsfor

somebankingtransactionsbutnotthefinancialmarketingeneral.The1966Segré

Report called for further financial integration and the establishment of a joint

securitiesmarket.With theBrettonWoodsSystemgraduallycollapsing in the late

1960sandearly1970s,agroupofexpertsunderthechairmanshipofPierreWerner

wasgiven themandate to inquire into thepossibilityof establishinganEconomic

and Monetary Union in the European Community. The Werner Report of 1970

proposedtorealizeEconomicandMonetaryUnioninstages,butpostponedastrict

timetable. Instead, it fostered the establishment of a single currency bank (the

‘Snake in the tunnel’). After the Nixon shock and the failure of the Snake, the

EuropeanMonetary System (EMS)was established in 1979, whichwas based on

fixedbutadjustableexchangeratesandtheintroductionoftheEuropeanCurrency

Unit (Valiante2016:29-31).Asasystemof fixedexchangerates, theEMSkeptall

formsofpublicandprivatecreditmoneynationalbutonlycoordinatedfluctuations

oftheinner-Europeanexchangerate.

The second wave of financial integration started with the 1985 EC White

Paper on Completing the Internal Market (or ‘Single Market Programme’), which

madethepointthatasinglefinancialmarkethadtobebasedonfreemovementof

capital and financial services. The 1987 Single European Act reaffirmed that the

single market should be completed by the end of 1992. In 1988, the European

Council returned to the ideas of theWernerReport and restated the ‘objective of

progressive realization of economic and monetary union’. In 1989, the Delors

Reportwaspublished,writtenbyacommitteeinchargeofproposingtangiblesteps

towardsmonetaryunion,whichconsidereditasnecessaryformonetaryunionthat

currenciesaremadeirreversiblyconvertibleandthatbankingandfinancialmarkets

are fully integrated. 2 The plan for Economic and Monetary Union was then

implementedinthreephases:complete freedomofcapital transactionandgreater

governmental and central bank coordination from 1990; economic policy

convergence and lauch of the European Monetary Institute from 1994; and the

introductionoftheeuroinlinewiththeestablishmentoftheEuropeanCentralBank

(ECB) conducting a single monetary policy as head of the European System of

Central Banks (ESCB) in 1999. The detailed architectural design of the European

Monetary Union (EMU) had been decided upon in the 1992 Maastricht Treaty,

whichhadtailoredtheStabilityandGrowthPact(Valiante2016:31-34).

2 The call for full integration of banking and financial markets is the origin of today’s call for

BankingandCapitalMarketUnion.

9

Asaconsequenceofthesecondwaveofmonetaryandfinancialintegration,

the regulatory competences for the public and private credit money forms were

spreadacrossdifferentlayersofthemulti-levelgovernancesystem.Thus,howwere

the key credit money forms situated within the Money Matrix and the national-

supranationaldivide?

Central bank liabilities:The foundation of the EuropeanMonetary Unionwiththeintroductionoftheeuroasasinglecurrencyandtheestablishmentofthe

ECB as an independent EU institution situated at the top of a federal system of

National Central Banksmade the realm of purepublicmoney supranational. Bothcurrencyand centralbankdepositswereputunder the controlECB, although the

executionofmanypolicies is stilldoneby theNationalCentralBanks (NCBs).For

those member states participating in EMU, the euro replaced various national

currenciesastheunitofaccountatthetopofthemonetaryhierarchy.

Commercial bank liabilities:Bank deposits as commercial bank liabilitiesare created by banks as private institutions, but public authorities provide an

institutionalframeworkthatamountstoanelaboratepublic-privatepartnershipfor

deposit creation. It is made up of four dimensions: liquidity backstops, solvency

backstops,bankregulationandbanksupervision(cf.Section2,alsoseeBundesbank

2014).Whilst therealmofpurepublicmoneyatthetopof themonetaryhierarchywasput under full supranational control, theprivate-publicmoney realmwasnot,giventhatnotallofthefourdimensionsweretransferredtotheEUlevel:

First, the liquidity backstops were in principle made supranational as the

ECB became responsible for the discountwindow.With the ECB in charge of the

EMU’smonetarypolicy,ithasreceiveddiscretionovertheshort-terminterestrate

atwhichbankscanborrowcentralbankdeposits.Whiletheactualimplementation

of those policies may still be conducted by the National Central Banks, they are

subjecttodirectivescomingfromtheECB.However,NationalCentralBanksstillare

in the position to give Emergency Liquidity Assistance to their national banks at

theirowndiscretion;theECBinthisregardonlyhasvetopowers.

Second,thesolvencybackstopsforbankswerenotunifiedonasupranational

levelas thedeposit insuranceschemesremainedentirelyunder thecontrolof the

EMUmemberstates.Thus,solvencyriskwasnotpooledonaEuropeanlevel,butthe

nationalinsurancesystemsremainedinplace,which—asof2007—notonlyvaried

from country to country with regard to their perceived credibility, but also had

differentactualquantitativelevelsofdepositinsurance.

Third, the competences for the regulation of commercial banks—i.e. the

determination and enforcement of general rules for the banking industry (cf. De

Larosièreetal.2009:13)—werespreadacrossnational,Europeanandinternational

levels. The main example for the impact of international financial governance

processesonbankingregulationbeforetheEurocrisisaretheBaselAccords(BaselI

of 1988 and Basel II of 2004), which provided international guidelines for bank

10

capitalrequirements.BaselIIwastranslatedintonationallawsofEUMemberStates

via theEUDirectives2006/48/EGand2006/49/EG (cf. Goldbach2015). Still, the

national levelscontinuedtobe themost importantand influential frameworks for

bank regulation and reflected various national particularities and historical

experiences(cf.Busch2009).

Fourth, the supervision of commercial banks—i.e. the “process designed to

oversee financial institutions in order to ensure that rules and standards are

properly applied” (De Larosière et al. 2009: 13)—remained largely national. The

national competent authorities had a focus on micro-prudential supervision of

individualbanksbutneglectedtransnationalandmacroprudentialrisks(ibid:10).

Shadow money forms: Financial globalization, the development ofeurodollarmarkets and the rise of the shadowbanking system roughly coincided

withthesecondwaveofEuropeanmonetaryandfinancialintegration.Inthecourse

ofthisprocess,newformsofprivatecreditmoneysubstitutesdevelopedthattrade

at par to the traditionalmoney supply and thus found their way into theMoney

Matrix.3While this is particularly true for theUnited States,which are situated at

thecentreoftheglobalfinancialsystem,italsohadanimpactonEurope.Following

Ricks(2016),amongtheprivatecreditmoneyformsthatemergedintherunupto

the2007-9FinancialCrisis,aremoneymarketfundshares,repurchaseagreements

(‘repos’), asset-backed commercial papers, and eurodollars. To a certain extent,

theseshadowmoneyformsalsoaffecttheeuroarea,eitherbecausetheyarecreated

domestically or have a transnational scope and are thusmeaningful for the EMU

financialsystem(cf.Bakk-Simonetal.2012,Gabor2013,Bundesbank2014).

Shadow money forms, as private money substitutes, naturally occupy the

‘private credit money’ realm and are either public-private or pure-privatemoney,dependingonthecollateralagainstwhichtheyareissued.IntheEMU,whilesome

country-specificandsupranationalregulationsareinplace,theydonothavepublic

backstops(Bundesbank2014:17).Yet, in2008,publicbackstopswereestablished

bytheFederalReserveandtheU.S.Treasurytobackstopmoneymarketfundshares

andreposintheUnitedStates.Thosebackstopsarestillinplacetodayintheformof

implicitguarantees.Bothshadowmoneyformsthuswereshiftedfromtheprivate

to the public credit money realm and effectively became private-public money(Murau 2016). It may be argued that the Federal Reserve backstops also affect

shadow money in the EMU, e.g. due to the liquidity swap lines that the Fed

establishedwiththesixmajorcentralbankin2007(cf.Mehrling2015b,McDowell

2012).4

3 Foratheoreticaldescriptionontheriseofnewformsofprivatecreditmoneysubstitutesdueto

financialinnovationintimesofanexpandingleveragecycle,seeMinsky(1986),.4 DevelopingasystematicunderstandingoftheroleofshadowmoneyintheEMUandhowprivate

creditmoney creation in theU.S. as the centre of the global financial systemhas transnational

effectsonEuropewillbeaconceptualkeychallengeslyingaheadforthisresearchproject.

11

Figure 4 synthesizes the findings that the above discussion of the various

layers within the EMU’s monetary hierarchy has generated. It demonstrates that

despitetheintroductionofthesinglecurrency,Europeanmonetaryintegrationhas

remained incompletebecause thecreationof creditmoney forms furtherdown in

thehierarchywasnotorganizedonaEuropeanlevel.Ontheonehand,thisrefersto

bank deposits as the ‘traditional’ privately issued creditmoney form, forwhich a

public-privatepartnershipisinplace,yetwithbackstopsandresponsibilitiesspread

acrossnationalandsupranational jurisdictions.Ontheotherhand,shadowmoney

forms—primarily money market fund shares and repurchase agreements—have

emergedwithevenmorediffuseregulatoryresponsibilites.

Public Credit Money Forms Private Credit Money Forms

(1) Pure Public Money Supranational: Central Bank liabilities • Currency (Notes, Coins) • Central bank deposits

(3) Public-private Money

Diffuse responsibilities: Shadow money • issued against public debt

(2) Private-public Money

Between national + supranational: Commercial bank liabilities • Insured bank deposits

(4) Pure Private Money

Between national + supranational: Commercial bank liabilites • Uninsured bank deposits

Diffuse responsibilities: Shadow money • issued against private debt

Figure4–TheMoneyMatrix(empirically,pre-2009)

According to a dominant narrative, the EMU’s architecture is incomplete

because there is only monetary and not fiscal union. The notion that it is not

possible tohavea functioningmonetaryunionwithouta fiscalunionmayormay

not be true. Still, the present analysis suggests that itmisses an important point:

ThereisnotevenapropermonetaryunionintheEMU.AMoneyViewperspective—

whichregardsthemonetarysystemashierarchicalandasapublic-privatehybrid—

suggeststhatonlytheformsofpurepublicmoneyattheverytopofthehierarchyofmoneywereuploadedonUnionlevel.Themoneyformsfurtherdownthehierarchy,

whichfunctionallyandquantitativelyareamuchmoreimportantpartofthegeneral

moneysupply,havenotbeenintegrated.

12

4.InstitutionalevolutionsincetheEurocrisis

This section will focus on commercial bank deposits as the second layer in the

EMU’s hierarchy of money and discuss the institutional evolution that has been

initiated by the Eurocrisis. As a starting point, it will take the account of the

monetaryhierarchywithintheEMUasithaddevelopedduringthesecondwaveof

monetary and financial integration. Themain question to be asked iswhether an

uploadofthepublic-privatepartnershipontheEuropeanlevelhastakenplaceoris

currentlyunderway.Toanswerthisquestion,boththeinstitutionaldevelopmentsof

theECBandthepoliticalprojectofestablishingBankingUnionwillbelookedat.The

sectionwill first recall somekeyaspectsof theEurocrisis as abanking crisis that

mutatedintoasovereigndebtcrisis.Afterwards,itwilldiscussboththeinstitutional

developmentsoftheECBandthepoliticalprojectofestablishingBankingUnion.

4.1TheEurocrisisasabankingcrisis

Inthewakeofthe2007-9FinancialCrisis,severestrainsmanifestedthemselvesin

theEMUandtriggeredwhatbecameknownastheEurocrisis.Mostprominently,the

Eurocrisisbecameassociatedwithasovereigndebtcrisisduetodramaticincreases

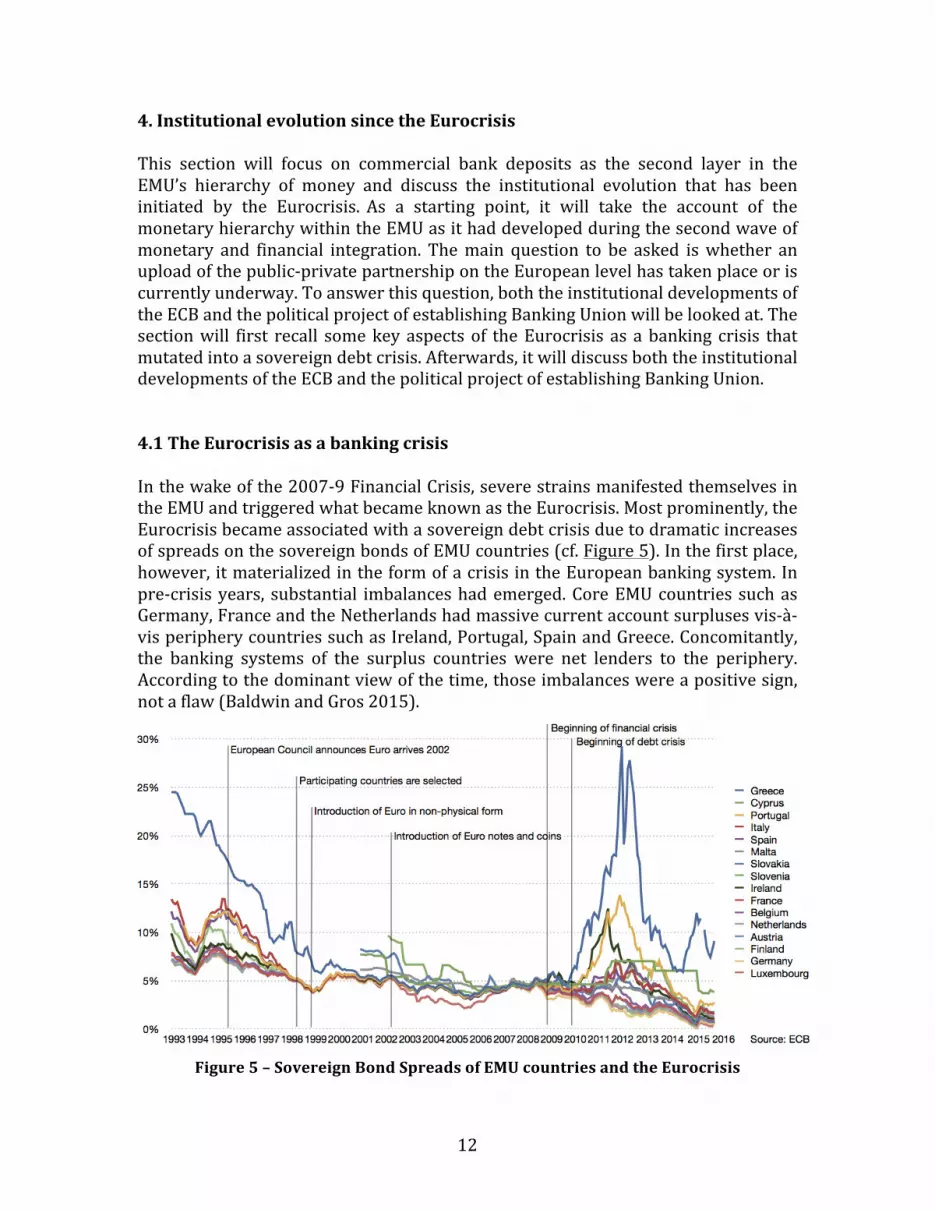

ofspreadsonthesovereignbondsofEMUcountries(cf.Figure5).Inthefirstplace,

however,itmaterializedintheformofacrisisintheEuropeanbankingsystem.In

pre-crisisyears, substantial imbalanceshademerged.CoreEMUcountries suchas

Germany,FranceandtheNetherlandshadmassivecurrentaccountsurplusesvis-à-

visperipherycountriessuchasIreland,Portugal,SpainandGreece.Concomitantly,

the banking systems of the surplus countries were net lenders to the periphery.

Accordingtothedominantviewofthetime,thoseimbalanceswereapositivesign,

notaflaw(BaldwinandGros2015).

Figure5–SovereignBondSpreadsofEMUcountriesandtheEurocrisis

13

With the outbreak of the Eurocrisis, cross-country lending activities of

European banks came to a halt. It became obvious that, due to the absence of

supranational structures forprivatemoney,eurodenominatedbankdepositsheld

in deficit countries were different from those in surplus countries. Figure 6—

adopted from Gros (2012)—visualizes what happened with intra-European

financial flows during the Eurocrisis. In 2010, the initially free flows of deposits

throughtheeuroareastoppedandconcentratedontheNortherncountries,which

wereperceivedasasafehaven.Thesuddenstopoffinancialflowshadasubstantial

negative impact onbothbanks and governments in theperipheral countrieswith

currentaccountdeficits.Thebankingcrisisspilled-overintoasovereigndebtcrisis:

Low growth rates lead to rising government deficits and increasing public ratios,

andanumberofgovernmentshadtotakeonsomeoftheirbankingsystem’sdebts

ontheirbalancesheets(BaldwinandGros2015).

Figure6–BankLiquidityFlowsintheEMU,beforeandduringtheEurocrisis

In reaction to theEurocrisis,nationalgovernments,EU institutionsand the

ECBadoptedarangeofdifferentemergencyinterventions.Inthebankingcrisis,the

maincrisisresponseswereconductedbytheECBwithstandardandnon-standard

measures.With sovereigndebtbecoming thepressing issue, theECB launched its

SecuritiesMarketProgramme(SMP)in2010andin2012itssuccessor,theOutright

Monetary Transactions (OMT) programme, following the announcement of ECB

PresidentDraghi“todowhateverittakes”topreservetheeuro(McBrideandAlessi

2015, Draghi 2012). On a political level, the European Financial Stability Facility

(EFSF) and the European Financial Stabilisation Mechanism (EFSM) were

established, later succeed by European Stability Mechanism (ESM), and reforms

suchastheEuropeanSemester,theSixpackandtheEuro-Plus-Packintroduced.

The next sections will concentrate on two particular aspects of post-crisis

institutionalevolution.First,itwillbediscussedhowtheECBtookonthefunctionof

backstoppingcross-borderflowsintheEMUviatheTARGET2system.Second,the

projectofBankingUnionwillbelookedatwhich—ifsuccessful—willestablishthe

public-privateframeworkfordepositcreationonaEuropeanlevel.

14

4.2TheECBasbackstopforcross-borderdepositflows

When the cross-border flows of deposits across the EMU came to a halt, the ECB

developedintothecoreinstitutionoftheEuropeanbankingsystemthatconstantly

providesliquidityandincentivisescross-borderfinancialflows.Figure7—adopted

fromGros (2012)—visualises this function that theECB started to exercise in the

crisis:TheECBseeks todirect the funds thatareconcentrated in the ‘overflowed’

Northbacktothe‘driedout’South.

Figure7–ImpactoftheECBonBankLiquidityFlowstocombattheEurocrisis

Before the Eurocrisis, the current account deficits in the EMU had been

financedbytheprivatebankingsystem.Thebankingsystemsofthedeficitcountries

took out loans from the banking systems of the surplus countries and received

privatelycreateddepositsinstead:

Figure8–PrivateLendingwithinEMU(pre-crisis)

IntheEurocrisis,thismechanismceasedtowork.Banksofsurpluscountrieswere

no longerwilling to lend tobanksofdeficit countries as they feareda collapse of

those banks or even the bankruptcy of the deficit country,whichprobablywould

havesweptawayitsdomesticbankingsystem.

Banking

System

of

Deficit

Country

(e.g.Greece)

Loan

Eurodeposits

Banking

System

of

Surplus

Country

(e.g.Germany)

15

Atthispointinthecrisis,euro-denominateddepositswithintheEurosystem

were close to breaking par. Effectively, a Greek euro deposit was no longer

equivalent to a German euro deposit. Par, however, was sustained during the

Eurocrisis,despitetheunwillingnessofsurplusbanksto lendtodeficitbanks.The

reasonisthattheEurosystemsteppedinandtheECBadopteditsroleasthemain

conduitforcross-bordercapitalflows(Gros2012):Surplusbanksstartedlendingto

theirrespectivesurpluscentralbank;deficitbanksborrowedfromtheirrespective

central bank. The necessary cross-border transactions then were conducted

between both central banks: This manifested itself in the form of TARGET 2

balances(Figure9).

Figure9–PubliclendingwithinEMUviaTARGETIIbalances(post-crisis)

TARGET 2—the Trans-European Automated Real-time Gross Settlement

Express Transfer System—is the Eurosystems internal payment and settlement

system. Whittaker (2016: 1) explains that it is a necessary feature within the

Eurosystemtoclearcross-borderpaymentsthatnationalcentralbanks(NCBs)can

borrowfromeachotherviaTARGET2:“IfadepositismovedfromaGreekbanktoa

German bank, for instance, the Greek bank makes up for its lost deposit by

Banking

System

of

Deficit

Country

(e.g.Greece)

Banking

System

of

Surplus

Country

(e.g.Germany)

EuropeanSystemofCentralBanks

TARGETII

‘Borrowing’

TARGETII

‘Lending’

Deficit

Central

Bank

Surplus

Central

Bank

EuropeanCentralBank

16

borrowingmorefromitsNCB(theBankofGreece,BoG);thecurrentaccountofthe

GermanbankatitsNCB(theBundesbank)iscredited;andtheBundesbankacquires

a claim on the BoG. The accumulation of these debts between the NCBs are the

Target2 balances”. As Sinn and Wollmershäuser (2012: 468-469) put it in their

seminalpublicationonTARGET2balances,thesurplusesanddeficitsinTARGET2

“basically have to be understood as classical balance-of-payments surpluses and

deficitsasknownfromfixed-exchange-ratesystems.”TARGET2thusmirrorsintra-

EMUcrossborderflowsinthedepositsystem.

Figure 10—adopted from Whittaker (2016)—depicts the aggregated

TARGET2liabilitiesofItaly,Spain,PortugalandGreecefrom2008to2016.

Figure10–TARGET2liabilitiesofItaly,Spain,PortugalandGreece(2008-2016)

The chart indicates the extent towhich theEurosystemhasprovided elasticity to

the banking systems of deficit countries. As to Sinn and Wollmershäuser (2012:

469), the ECB “tolerated and actively supported voluminousmoney creation and

lendinginthecoreoftheEurozone”.Thus,moneycreationthat inpre-crisistimes

occurred on the private balance sheets of European banks was shifted up in the

hierarchyofmoneytopublicbalancesheets.

17

4.3BankingUnion

The primary political response to the distortions in the banking system that

occurred in the context of the Eurocrisis is the project of establishing a Banking

Union. In this,EUpolicy-makersre-address issues thathadbeenraisedalready in

theDelorsReportof1989.ThekeypublicationlayingouttheEU’sstrategytowards

harmonizingtheEuropeanbankingsystemsaftertheEurocrisisarethreehigh-level

reports,namelytheDeLarosièreReportonFinancialSupervision(DeLarosièreet

al.2009), theFourPresidents’Report ‘TowardaGenuineEconomicandMonetary

Union’(VanRompuyetal.2012)aswellastheFivePresidents’Report‘Completing

Europe’s Economic and Monetary Union’ (Juncker et al. 2015). Valiante (2016)

framesthisasthethirdwaveofmonetaryandfinancialintegration.

TheDeLarosièreReportcalledforthecompletionoftheSingleRulebookfor

bank regulationanda joint architecture forbank supervision (DeLarosière2009,

Valiante 2016: 38). The introduction of a Banking Union has primarily been

suggestedintheFourPresidents’Report.TheReportcallsfor“theestablishmentof

an effective Single Supervisory Mechanism (SSM) for the banking sector and the

entryintoforceoftheCapitalRequirementRegulationandDirective(CRR/CRDIV)”

as well as for an “[a]greement on the harmonization of national resolution and

deposit guarantee frameworks, ensuring appropriate funding from the financial

industry”(cf.VanRompuyetal.2012).TheFivePresidents’Reportre-emphasizes

the need of a ‘Banking Union’, in conjunction with the introduction of a ‘Capital

MarketsUnion’,toachievea‘FinancialUnion’(Junckeretal.2015:4-5).

Alreadyon17April2012,sixmonthsbeforetheFourPresident’sReportwas

published,IMFManagingDirectorChristineLagardehadineffectcalledpubliclyfor

a European Banking Unionwhen she stated: “In the euro zone, a single financial

market cannot rely on legal and institutional frameworks that operate on an

asymmetric national basis. To break the feedback loop between sovereigns and

banks,weneedmorerisksharingacrossbordersinthebankingsystem.Inthenear

term, a pan-euro area facility that has the capacity to take direct stakes in banks

would help. Looking further ahead, monetary union needs to be supported by

strongerfinancialintegrationwhichouranalysissuggestsbeintheformofunified

supervision, a single bank resolution authority with a common backstop, and a

singledepositinsurancefund“(Lagarde2012).

ThemaindrivingforceforBankingUnion,asreferredtoinpublicdocuments,

istobreakthestrongconnectionbetweensovereignsandbanks(Lagarde2012;Van

Rompuyetal.2012).Atthesametime,establishingaEuropeanBankingUnion—if

successful—impliesanuploadofthepublic-privateframeworkfordepositcreation

to a European level. An effective Banking Union would bring along a unified

supranational organization of those elements of the public-private framework,

which had not been fully integrated prior to the Eurocrisis, namely solvency

backstops,bankregulationandbanksupervision.

18

Solvency backstop: Establishing a joint solvency backstop for commercialbanksinadditiontotheexistingliquiditybackstoptakesplaceintwomainways.On

theonehand,nationaldeposit insurance levelshavebeen fullyharmonized forall

EU countries at an amount 100.000 EUR. This has been implemented via an EU

DirectiveofMarch2009(Directive2009/14/EC)andwasreachedon31December

2010. It was seen as a first step towards establishing a single European Deposit

InsuranceScheme(EDIS),asproposedintheFivePresidents’Report(Junckeretal.

2015:11).ThisaspectofBankingUnion,however,hasbeen themostcontestedso

far, especially because Germany is substantially opposed to it. Therefore, it is far

fromcertainthatthepoliticalclimatewillallowthatasingledepositinsurancefund

isgoingtobeestablishedanytimesoon(Strupczewski2015).

On the other hand, the European regime for recovery and resolution of

commercialbanksestablishedaEuropeanbackstopforsystemicallyrelevantbanks

thatfacebankruptcy.Theideaoftherecoveryandresolutionregime—inlinewith

theguidelinesagreeduponattheG20SummitofPittsburghin2009—isthatlarge

banks corporations should be able to become bankrupt whilst the systemically

relevantpartsoftheirbusinesscontinuetofunction.Thisistoavoidthe‘toobigto

fail’problemwhichbecamemanifestinthe2007-9FinancialCrisis.Inthisrecovery

and resolution is supposed to remain fiscally neutral. Thus, the recovery and

resolutionregimeseekstoestablishasolvencybackstopthatispubliclyorganized,

yetprivately funded.Thishasbeen implemented in theEUvia theBankRecovery

andResolutionDirective(BRRD)thatwaspassedinDecember2013. Itprovidesa

common framework for all EU countries of how to dealwith troubled banks. For

EMUMember States, the BRRD has established the Single ResolutionMechansim

(SRM).TheSRMcentralisesthedecision-makingprocessforbankresolutionatthe

Single Resolution Board (SRB) and creates a Single Resolution Fund (SRF) that

directlycoversallsignificantinstitutionsandcross-borderbanks(cf.PWC2014).

Bank regulation:Harmonizing European bank regulation has occurred intwomajorsteps.Ontheonehand,theSingleRulebook,whichhadbeenbroughtup

bytheDeLarosièreReport,shouldconceptualizeaunifiedframeworkforregulating

the EU’s financial sector. In particular, the banking system was to become more

resilient, transparent and more efficient. To this end, the European Banking

Authority (EBA) was established in 2011 with the mandate to develop binding

technicalstandardsandguidelinesfortheSingleRulebook(EBA2016).

Ontheonehand,theBaselIIIAccordsforbanks’capitalrequirementshave

been translated into EU law via the Capital Requirements Directive IV (CRD IV),

whichwas formally published in June 2013. It contains the Capital Requirements

Directive (2013/36/EU) (CRD), which is to be implemented into national law, as

well as the Capital Requirements Regulation (575/2013) (CRR), which directly

appliestobanksandfinancialfirmsintheEU.Amongothers,CRDIVenhancesthe

requirements for thequality andquantityof thebanks’ equity, new requirements

forliquidityandleverage,newlawsforcounterpartyrisk,andnewmacroprudential

standards(BankofEngland2016).

19

Bank supervision:Bank supervision has been harmonized on a Europeanlevelbyestablishing theSingleSupervisoryMechanism(SSM)basedon theSingle

Rulebook.Within the SSM, the ECB and national competent authorities (NCAs) of

participating Member States have harmonized their responsibilities for bank

supervision according to a single rulebook. In this, the ECB directly supervises

banks thatarecategorisedas ‘significant’,whileNCAssupervisebanksconsidered

‘lesssignificant’.TheSSMofficiallyenteredintooperationinNovember2014(ECB

2014:4).IntheFourPresidents’Report,withregardtotheSSM,itwasperceivedas

“crucial that the ECB is equipped with a strong supervisory toolkit, and that the

ECB’s ultimate responsibility for banking supervision is coupled with adequate

controlpowers(VanRompuyetal.2012:6).

5.Conclusionandnextresearchsteps

Thequestionthispaperhassoughttoaddresswaswhetherpost-crisisreformsand

institutionaldevelopmentscanharmonizeprivatemoneycreationintheEurozone.

TheanalysisproceededfromaMoneyViewperspective,accordingtowhich

themoneysupplyismadeupofdifferent,hierarchicallystructuredIOUsthattrade

atpartoeachotherandcanbeissuedbypublicorprivateinstitutions.Inthis,the

conceptuallensonmoneystandsincontrasttotheviewthatpublicauthoritiesare

able to control the money supply. Money creation is seen as a phenomenon

endogenous to the financial system. The lending activities of financial institutions

cannot be fully regulated by public authorities. Financial innovation will always

makeitpossibletodevelopmoneysubstitutesoutsideofthegovernmentcontrolled

monetaryrealm.Therefore,themoneysupplyismadeupofcentralbankliabilities,

depositsas‘traditional’bankmoneyaswellas‘shadow’moneyformsissuedbynon-

bankfinancialinstitutions.

Ashasbeenarguedinthepresentanalysis,inthesecondwaveofEuropean

monetaryandfinancialintegration,onlythetoplevelinthehierarchyofmoneyhas

been integratedonasupranational levelasonlycentralbank liabilitieshavebeen

trulyEuropeanized.Allothermoneyforms,whichareissuedonprivateinstitutions’

balance sheets, were only integrated to an incomplete extent. The Eurocrisis has

demonstratedthedeficienciesofthesystem,asbankslargelystoppedcross-border

lendingandappliednationalrationalesagain.Thiswasevidenceforthefactthatthe

public-private framework for deposit creation had remained mainly nationally

organisedandarobustEMU-widebankingsystemwasabsent.

TheprojectofBankingUnionthathasbeenontheagendaforthepastyears

inprincipleaddressestheshort-comingswithregardtodepositcreation.TheFive

Presidents’ Report argues—verymuch in linewith aMoney View perspective on

EMU—that “[a]s thevastmajorityofmoney isbankdeposits,money canonlybe

trulysingle if confidence in thesafetyofbankdeposits is thesame irrespectiveof

the Member State in which a bank operates” (Juncker et al. 2015: 11). Banking

20

Unionthusseeks touploadthepublic-private framework fordepositcreationtoa

Europeanlevel.Inadditiontothesupranationalliquiditybackstop,asupranational

solvency backstop for banks as well as supranational bank regulation and

supervisionaretobeestablished.However,thepoliticalprocessofcreatingBanking

Unionhasproventobeslowanduncertain.WhiletheSingleResolutionMechanism

and the Single Supervisory Authority are in place today, the plan for a European

DepositInsuranceMechanismhasrecededintothedistance.

Inthemeantime,theECBhasmadearemarkableinstitutionaldevelopment

and has de facto taken on new responsibilities. During the crisis, it covered the

unwillingness of the European banking system for cross-border lending. By

tolerating increasing TARGET 2 balances, the Eurosystem effectively allowed

compensating the collapse of privatemoney creationwith publicmoney creation.

From a Money View perspective, this may be interpreted as a shift of money

creationfromtheprivatetothepublicrealm.

Thepresentanalysis thussuggests tocautiouslyrespondto thequestionof

this paper with a Yes. Banking Union appears to be a typical EU-style functional

spill-over: Integration in one policy field works well for a while until a crisis

emerges that creates a perceived need for further integration of a neighbouring

policyfield(cf.Haas1958).Itseemsthattheprivate-publicframeworkfordeposit

creation is slowlybeinguploadedon aEuropean level.Wherepolitical actionhas

beenabsent,sloworineffective,theECBhassteppedin.Still,theeffectivenessofthe

actual political measures is a major concern. It remains to be seen if the reform

stepsthathavebeenannouncedorweretakenwillproveviableandsufficientinthe

future.

However,thispaper’sanalysisofpost-crisisdevelopmentshasonlyfocused

onthe ‘traditional’moneysupply.Asanextstepintheresearchprocess, itwillbe

necessarytoaddresstheuseofprivatemoneysubstituteswithintheEMU.TheU.S.

basedshadowbankingsystembringsforthanumberofsystemicallyprivatecredit

money forms (Ricks 2016) that for institutional investors play the role of cash.

“Money beginswhereM2 ends”, says Pozsar (2015). To understand the extent to

whichthoseU.S.specific,yetinherentlytransnational,phenomenacanbetranslated

toEuropeandplaya role in theeuroareawill require furtherempirical analysis.

StudyingtheEuropeanshadowmoneysupplywillcomplementtheaboveanalysisof

privatecreditmoneycreation in theEMUanddeliveramorecompletepictureon

thequestion if therealmofprivatecreditmoney isbeingharmonized in thepost-

crisisEMU.

Understanding the role of private creditmoney in the EMU is particularly

relevant as there is a chance that endogenous institutional developments in the

market-based credit system could be able to overcome the structural national

separationwithin theEMU’sdepositbankingsystemifpoliticalmeasures fail. It is

thus possible that new financial structures emerge next to the fragmented EMU-

banking system that are actually supranational in nature. The recent analysis of

21

Valiante(2016)suggestsanunderstandingthatinstitutionalevolutionshouldgoin

thisdirection,asheidentifiesfortheEMUan“overrelianceonitsbankingsystem”

(ibid: xiii). He consequently endorses the Commission’s push towards a Capital

Market Union. This would certainly have an effect on private money creation

beyond the commercial banking system and eventually imply a harmonization of

shadowmoneycreationonaEuropeanlevel.

Following from the above, Figure11presents apreliminary accountof the

MoneyMatrixasithasdevelopedinthepost-crisisEMU:

Public Credit Money Forms Private Credit Money Forms

(1) Pure Public Money Supranational: Central Bank liabilities • Currency (Notes, Coins) • Central bank deposits

(3) Public-private Money

Diffuse responsibilities: Shadow money • issued against public debt

(2) Private-public Money

Towards supranational: Commercial bank liabilities • Insured bank deposits

(4) Pure Private Money

Towards supranational: Commercial bank liabilites • Uninsured bank deposits

Diffuse responsibilities: Shadow money • issued against private debt

Figure11–TheMoneyMatrix(empirically,post-crisis)

As this table indicates, the future of private money creation in the European

MonetaryUnionremainsanopenquestionanddeservesfurtherresearch.

22

References

Allen,Franklinetal.(eds.)(2013)Political,FiscalandBankingUnioninthe

Eurozone?,EuropeanUniversityInstitute(Florence,Italy)andWhartonFinancial

InstitutionsCenter,UniversityofPennsylvania(Philadelphia,USA).

Arnon,Arie(2011)MonetaryTheoryandPolicyfromHumeandSmithtoWicksell.Money,Credit,andtheEconomy,Cambridge:CambridgeUniversityPress.

Bakk-Simon,Kláraetal.(2012)ShadowBankingintheEuroArea.AnOverview,EuropeanCentralBank,OccasionalPaperSeriesNo133.

Baldwin,RichardandGros,Daniel(2015)WhatCausedtheEurozoneCrisis?,CentreforEuropeanPolicyStudies,CEPSCommentary,Brussels,27November2015.

Belke,A.H.andGros,D.,BankingUnionasaShockAbsorber(April15,2015).Ruhr

EconomicPaperNo.548.http://ssrn.com/abstract=2618397

Bindseil,Ulrich(2014)MonetaryPolicyOperationsandtheFinancialSystem

Bundesbank(2014)TheShadowBankingSystemintheEuroArea.OverviewandMonetaryPolicyImplications,DeutscheBundesbank,MonthlyReportMarch2014.

Busch,Andreas(2009)BankingRegulationandGlobalization,OxfordandNewYork:OxfordUniversityPress.

DeLarosière,Jacquesetal.(2009)ReportoftheHigh-LevelGrouponFinancialSupervisionintheEU(“DeLarosièreReport”),EuropeanCommission,Brussels,25February2009.

Draghi,Mario(2012)StatementofECBOutrightMonetaryTransactions,Bloomberg,6September2012,http://www.bloomberg.com/news/articles/2012-09-

06/draghi-s-statement-on-ecb-outright-monetary-transactions-text(accessed2

April2016).

EuropeanBankingAuthority(2016)TheSingleRulebook,http://www.eba.europa.eu/regulation-and-policy/single-rulebook(accessed2April2016).

EuropeanCentralBank(2014)GuidetoBankingSupervision,EuropeanCentralBank,FrankfurtamMain,November2014.

EuropeanCentralBank(2015),“Theroleofthecentralbankbalancesheetin

monetarypolicy”,EconomicBulletin,Issue42015.Gabor,Daniela(2013)ShadowInterconnectedness.ThePoliticalEconomyof(European)ShadowBanking,UWEBristol,WorkingPaper.

Goldbach,Roman(2015)GlobalGovernanceandRegulatoryFailure.ThePoliticalEconomyofBanking,Houndsmill:PalgraveMacmillan.

Gros,Daniel(2012),TheEuroCrisis.FiscalorFinancial,PresentationatCentreforMonetaryEconomics(CME),Oslo,June2012,http://www.bi.edu/cmeFiles/2012

%2006%20Seminar%20med%20Daniel%20Gros.pdf(accessed1April2016)

Gros,Daniel(2013),PrinciplesofaTwo-TierEuropeanDeposit(Re-)InsuranceSystem,CEPSPolicyBrief,http://www.ceps.eu/publications/principles-two-tier-european-deposit-re-insurance-system(accessed2April2016)

Haas,Ernst(1958)TheUnitingofEurope,Stanford:StanfordUniversityPress.Hayek,FriedrichAugustvon(1976[1990])DenationalisationofMoney-TheArgumentRefined.AnAnalysisoftheTheoryandPracticeofConcurrentCurrencies,London:TheInstituteofEconomicAffairs.

23

Helleiner,Eric(2003)TheMakingofNationalMoney.TerritorialCurrenciesinHistoricalPerspective,IthacaandLondon:CornellUniversityPress.

Juncker,Jean-Claudeetal.(2015)CompletingEurope’sEconomicandMonetaryUnion(“FivePresidents’Report”),EuropeanCommission,Brussels,June2015.

Knapp,GeorgFriedrich(1905)StaatlicheTheoriedesGeldes,Leipzig:Duncker&Humblot.

Lagarde,Christine(2012)OpeningRemarkstotheIMF-CFPRoundtableontheFutureofFinancialRegulation,InternationalMonetaryFund,Speech,WashingtonD.C.,17April2012.

Lamfalussy,Alexandreetal.(2001)FinalReportoftheCommitteeofWiseMenontheRegulationofEuropeanSecuritiesMarkets(“LamfalussyReport”),Brussels,15February2001.

Matthijs,MatthiasandBlyth,Mark(2015)TheFutureoftheEuro,OxfordandNewYork:OxfordUniversityPress.

McBride,JamesandAlessi,Christopher(2015)TheRoleoftheEuropeanCentralBank,CouncilonForeignRelations,CFRBackgrounders,9July2015,http://www.cfr.org/europe/role-european-central-bank/p28989(accessed

2April2016)

McDowell,Daniel(2012)'TheUSas'SovereignInternationalLast-ResortLender'.

TheFed'sCurrencySwapProgrammeduringtheGreatPanicof2007-09',NewPoliticalEconomy17(2),pp.157-178.

McMillan,Jonathan(2014)TheEndofBanking.Money,Credit,andtheDigitalRevolution,Zero/OneEconomicsGmbH.

Mehrling,Perry(2011)TheNewLombardStreet.HowtheFedBecametheDealerofLastResort,PrincetonandOxford:PrincetonUniversityPress.

Mehrling,Perry(2012)'TheInherentHierarchyofMoney',in:LanceTaylor,Armon

Rezai,andThomasMichl(ed.)SocialFairnessandEconomics.EconomicEssaysintheSpiritofDuncanFoley,OxonandNewYork:Routledge,pp.394-404.

Mehrling,Perry(2013)'FinancialGlobalizationandtheFutureoftheFed',in:

ToshiakiHirai,MariaCristinaMarcuzzo,andPerryMehrling(ed.)KeynesianReflections.EffectiveDemand,Money,Finance,andPoliciesintheCrisis,OxfordUniversityPress,pp.268-285.

Mehrling,PerryG.(2015a)WhyIsMoneyDifficult?,BarnardCollegeofColumbiaUniversity,Blog.

Mehrling,Perry(2015b)ElasticityandDisciplineintheGlobalSwapNetwork,InstituteforNewEconomicThinking,WorkingPaper.

Menger,Carl(1892)'OntheOriginsofMoney',EconomicJournal2(6),pp.239-255.Minsky,HymanP.(1986)StabilizinganUnstableEconomy,NewHavenandLondon:YaleUniversityPress.

Mitchell-Innes,Alfred(1914)'TheCreditTheoryofMoney',TheBankingLawJournal31,pp.151-168.

Moloney,N.(2014),“EuropeanBankingUnion:assessingitsrisksandresilience.”,

CommonMarketLawReview,51(6).pp.1609-1670

Moore,BasilJ.(1988)HorizontalistsandVerticalists.TheMacroeconomicsofCreditMoney,Cambridge:CambridgeUniversityPress.

24

Murau,Steffen(2016)‘ShadowMoneyandthePublicMoneySupply:TheImpactof

the2007-9FinancialCrisisontheMonetarySystem’,ConferencePaper,

presentedatthe57thAnnualMeetingoftheInternationalStudiesAssociation,

Atlanta(Georgia).

Pozsar,Zoltan(2014)ShadowBanking.TheMoneyView,OfficeofFinancialResearch,WorkingPaper.

PriceWaterhouseCoopers(2014)EUBankRecoveryandResolutionDirective.‘TriumphorTragedy?’,PwCEuropeanFinancialSystemRegulation,January2014.

Schumpeter,JosephAlois(1954[2006])HistoryofEconomicAnalysis,NewYork:OxfordUniversityPress.

Sinn,Hans-WernerandWollmershäuser,Timo(2012)'TargetLoans,Current

AccountBalancesandCapitalFlows.TheECB'sRescueFacility',InternationalTaxandPublicFinance19(4),pp.468-508.

Strupczewski,Jan(2015)‘EUDepositInsurance’VanishesfromEULeaders’DraftConclusions,Reuters,18December2015,http://uk.reuters.com/article/us-eurozone-banks-deposits-idUKKBN0U11LV20151218(accessed2April2016)

TheEconomist(2015)TheLaunchofEuro-styleQE,22January2015,http://www.economist.com/blogs/freeexchange/2015/01/ecb-makes-its-mind-

up(accessed2April2016)

Valiante,Diego(2012),“Lastcallforabankingunionintheeuroarea”,Applied

EconomicsQuarterly,Vol.58,No.2,pp.153–170

Valiante,Diego(2015),“Bankingunioninasinglecurrencyarea:evidenceon

financialfragmentation”,inJournalofFinancialEconomicPolicy,Vol.7Iss:3,

pp.251–274,earlierversionasaCEPSWorkingDocument(2014),n.388,

February.

VanRompuy,Hermanetal.(2012)TowardsaGenuineEconomicandMonetaryUnion(“FourPresidents’Report”),EuropeanCouncil,Brussels,5December2012.

Whittaker,John(2016)EurosystemDebtsDoMatter,LancasterUniversityManagementSchool,WorkingPaper,1February2016.