for inflation - imf elibrary

TRANSCRIPT

Adjustment of Taxable Profits

for Inflation

GEORGE E. LENT*

INANCIAL STATEMENTS based on historical costs increasingly departfrom current values during an inflationary period and have distorting

effects on the measurement of business profits. For this reason, periods ofrapid inflation, especially following a major war or economic crisis, havebeen met in some countries by measures for the revaluation of businessaccounts for purposes of reports to shareholders and the determination oftaxable income.

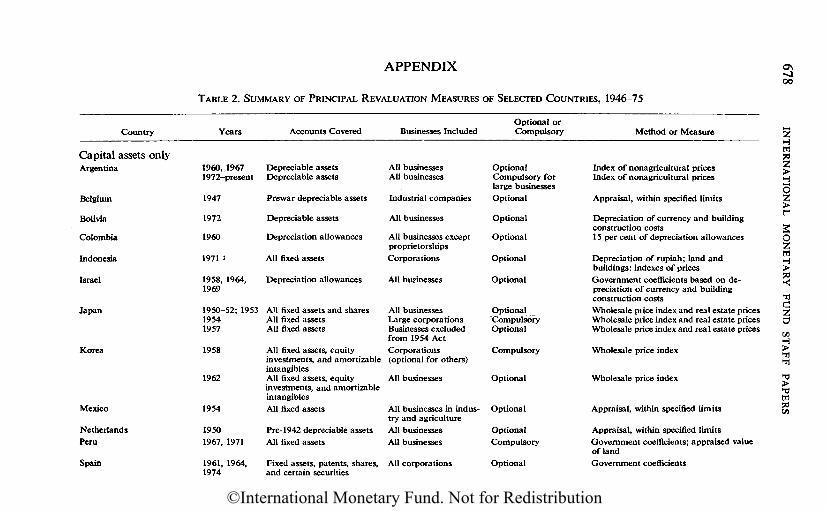

The inflationary aftermath of World War II was accompanied by revalu-ation measures in a number of major industrial countries, including Aus-tria, Belgium, France, the Federal Republic of Germany, Italy, Japan,and the Netherlands.1 But such provisions did not gain acceptance inCanada, the United Kingdom, the United States, or the Scandinaviancountries. Inflation-ridden Latin American countries also recognized thatfor tax and other purposes there was a need for revaluing business assetsand, in some cases, liabilities. These countries include Argentina, Bolivia,Brazil, Chile, Mexico, Peru, and Uruguay. In Asia, Korea and Indonesia,as well as Japan, have authorized similar techniques. Argentina, Austria,Colombia, and Israel have provided for the adjustment of depreciationallowances without, however, requiring a restatement of balance sheetaccounts.

This paper reviews the principles of accounting for inflation, includingthe accounting techniques that have been proposed, and describes theirapplication to the taxation of business profits in some 20 countries for

*Mr. Lent, Senior Advisor in the Fiscal Affairs Department, has been on the fac-ulties of the University of North Carolina and Dartmouth College. He has served asan assistant director of the tax analysis staff, U. S. Treasury Department, and asConsultant to the Organization of American States.! For a survey of earlier history, see Taxation and Research Committee, Associ

tion of Certified and Corporate Accountants, Accounting for Inflation (London,1952), pp. 99-144.

641

F

©International Monetary Fund. Not for Redistribution

642 INTERNATIONAL MONETARY FUND STAFF PAPERS

which information is available. This is followed by an analysis of theprobable effects of such measures on the economy, equity, and taxadministration. Possible alternatives are also examined.

I. Alternative Approaches to Adjustment

Although there is a diversity of views in the accounting profession onhow price level adjustments should be reflected in financial accounts,there are two main currents of thought on the principles underlying suchadjustments.2 One approach is based on the replacement cost principle,according to which only nonmonetary assets would be valued at their cur-rent replacement cost. The other view is based on what may be character-ized as the revalorization principle, which calls for the adjustment of allbalance sheet items by a general price index. It should be noted that reval-ued accounts would not necessarily replace conventional financial state-ments based on historical cost, but would supplement them, in reports toshareholders and the revenue service. In some countries, however,revaluation is reflected in accounts under provisions of company law.

REPLACEMENT COST APPROACH

Revaluation of business assets at replacement cost is concerned princi-pally with the adjustment of nonmonetary assets, such as inventories,land, and depreciable equipment and structures. From the standpoint oftaxation, its implications for depreciation allowances and inventories areof the greatest importance.

Depreciable assets

There is general agreement that the purpose of depreciation accountingis to allocate the cost of a depreciable asset over its useful life in a system-atic and rational manner.3 The income tax laws generally provide for"reasonable" allowances based on acquisition costs less estimated salvagevalue. Guidelines to the useful lives of various categories of depreciableassets are usually provided, and the method of allocating costs over time

2 For good overviews see Patrick R. A. Kirkman, Accounting Under InflationaryConditions (London, 1974) and R. S. Gynther, Accounting for Price-LevelChanges: Theory and Procedures (New York, 1966).

3 "Depreciation accounting is a system of accounting which aims to distribute thecost or other basic value of tangible capital assets . . . over the estimated useful lifeof the unit (which may be a group of assets), in a systematic and rational manner.It is a process of allocation, not of valuation." American Institute of CertifiedPublic Accountants, Accounting Terminology Bulletin, No. 1 (New York, 1953).

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 643

is usually prescribed, whether on a straight-line, declining balance, orother basis.

During an inflationary period it is clear that the market value (orreplacement cost) of depreciable assets progressively departs from theirbook value and that fixed annual allowances based on the cost of assetsacquired in prior years tend to enhance business profits. It is claimed bysome that conventional depreciation methods do not fulfill one of theirbasic functions of accounting for the replacement of plant and equipment.From the point of view of tax policy, it is alleged that the taxation of earn-ings that does not allow for replacement of assets diverts to the govern-ment funds that are necessary to maintain intact the capital of a business—that is, it is a tax on capital.

The most commonly accepted solution to this problem is the revalua-tion of depreciable assets, such as buildings, plant, and equipment,through appraisal or by the use of an index of construction costs. Therevaluation increment is credited to a special reserve account, and currentdepreciation allowances are based on the appreciated book values. Thedifference between depreciation based on original cost and on replace-ment cost is thereby excluded from taxable profits where such revaluationis authorized under the income tax laws.

The revaluation of nonmonetary assets for reporting purposes hasgained wide acceptance by the accounting profession in a number ofcountries, although there is no agreement on the particular measuresemployed by businesses.4 Support for this practice in the United Stateswas given in 1964 by a committee of the American Accounting Associa-tion, which recommended that current cost be adopted immediately as thebasis for valuation of land, buildings, and equipment wherever the differ-ences between current and historical costs are significant and the avail-able measures of current cost are sufficiently objective.5

This view is consistent with the economic concept of income thatunderlies the national income accounts. In measuring net national product,an allowance must be made for the consumption of capital that will keepcapital intact. While various interpretations have been given to the con-cept of "keeping capital intact" in estimating net capital formation, it restson the condition that the stock of capital will be able to maintain its cur-

4 For an earlier survey of business practice, see E. Gary Brown, Effects of Taxa-tion: Depreciation Adjustments for Price Changes (Graduate School of BusinessAdministration, Harvard University, 1952; reprinted by Maxwell Reprint Company,Elmsford, New York, 1970).

5 Accounting Review, Vol. 39 (July 1964), p. 698. The majority of the membersof another committee recommended the use of replacement cost for inventories asthe best of several alternative methods.

©International Monetary Fund. Not for Redistribution

644 INTERNATIONAL MONETARY FUND STAFF PAPERS

rent rate of production for the future.6 This implies a measure of capitalconsumption based on current values of capital stock rather than on itshistorical costs. Universal failure to provide for such an adjustment innational income accounts results in the overstatement of net nationalproduct. Similarly, failure to provide for the tax free recovery of capitalinvestment at less than current value overstates taxable income and mayresult in a tax on capital.

Inventories

Although investment in inventories is subject to gains and losses arisingfrom price changes, replacement of these inventories is on a much shortertime cycle than fixed assets. However, so-called inventory profits (andlosses) may be considerable, depending on the relative importance ofinventories to total business assets, their rate of turnover, and the rate ofchange in prices. In reckoning business profits and inventory investmentin the national income accounts, such inventory gains and losses aregenerally eliminated (for example, the inventory valuation adjustment inU. S. accounts).

The conventional method of charging materials to cost of goods sold isthe first-in, first-out method (FIFO). According to this method, cost ofgoods sold is equal to the book value of inventories at the beginning of theaccounting period, plus purchases and less the book value (the lower ofcost or market value) of goods at the end of the period. During an infla-tionary period, these historical costs charged to sales are generally lessthan their market value at the time of sale. The appreciation in the valueof the asset carried therefore creates a so-called inventory profit, or wind-fall gain, which is subject to ordinary income tax.

The replacement cost approach to the elimination of inventory profitscalls for the valuation of opening and closing inventories at currentmarket (or net realizable) value; purchases, including cost of manufac-turing during the year charged to cost of goods sold, must also be adjustedto their average replacement cost. Other methods include the base stockmethod, which eliminates inventory profits related to a basic quantity ofstock necessary for business operations.

6 For a thorough analysis of the principles involved in measuring net capital for-mation under constant prices, see Edward F. Denispn, "Theoretical Aspects of Quali-ty Change, Capital Consumption, and Net Capital Formation," in Problems ofCapital Formation: Concepts, Measurement, and Controlling Factors, NationalBureau of Economic Research, Studies in Income and Wealth, Vol. 19 (PrincetonUniversity Press, 1957), pp. 215-61. The principles and techniques of adjusting forprice changes are presented in Allan H. Young, "Alternative Estimates of CorporateDepreciation and Profits: Parts I and II," Survey of Current Business, Vol. 48(April 1968, pp. 17-28; May 1968, pp. 16-28).

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 645

The last-in, first-out method (LIFO) also substantially reduces theeffect of price changes on profits. This follows the principle of chargingfirst to sales the cost of the most recently acquired goods. In this way, thegap between the current replacement price and the historical cost of goodssold in an inflationary situation is narrowed and inventory profits are min-imized. This technique is used in the United States, where it was firstaccepted for tax purposes in 1938, but it has gained acceptance in fewother countries. It should be noted that LIFO inventories are carried onthe books at their earliest acquired costs and that in an inflationary situa-tion their book value is greatly understated. In this respect LIFO does notconform to the principle of reflecting current values on financial state-ments that is advocated by proponents of price level accounting.

REVALORIZATION APPROACH

In contrast to the replacement cost principle, revalorization, or pricelevel accounting, provides for the conversion of historical cost financialstatements to monetary units of constant purchasing power. Revaloriza-tion differs in two essential respects from the concepts underlying replace-ment cost: (1) it adjusts all items of the balance sheet—assets and liabili-ties—for changes in the value of money, and (2) it employs a standardindex of changes in the general price level rather than special indices (orappraisal) for particular balance sheet items.7

These models make a distinction between so-called monetary and non-monetary items in the balance sheet. Monetary items are assets and liabili-ties, the amounts of which are fixed by contract or statute; they includecash and accounts and notes receivable, as well as short-term and long-term liabilities. Holders of monetary assets lose purchasing power duringan inflationary period, whereas debtors gain by a reduction in the realvalue of obligations payable. In converting from historical cost accountsto current purchasing power statements, monetary items remainunchanged at the current balance sheet date. This is because they repre-sent cash or the contractual amount of claims due and claims payable.However, as gains and losses tend to arise from changes in the general

7 For authoritative statements by the accounting profession in the United Statesand the United Kingdom on the principles involved, see Accounting PrinciplesBoard, American Institute of Certified Public Accountants, Financial StatementsRestated for General Price Level Changes (New York, 1969); and AccountingStandards Steering Committee, The Institute of Chartered Accountants in Englandand Wales, Accounting for Changes in the Purchasing Power of Money, ProvisionalStatement of Standard Accounting Practice No. 7 (London, May 1974). Theaccounting institutes of Scotland and Ireland joined with the institute of Englandand Wales in supporting similar rules before the Inflation Accounting Committee.

©International Monetary Fund. Not for Redistribution

646 INTERNATIONAL MONETARY FUND STAFF PAPERS

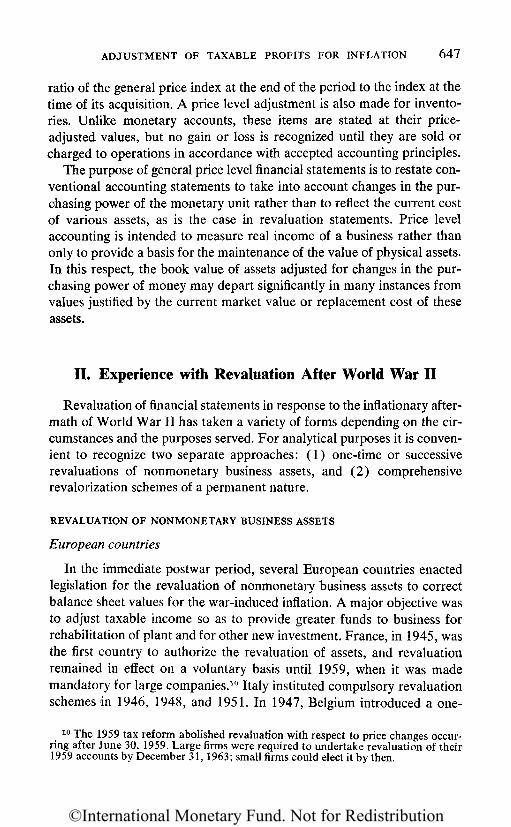

price level, monetary assets and liabilities appearing in financial state-ments of prior periods are restated in monetary units of constant purchas-ing power by multiplying each item by the ratio of the current generalprice index to the index of the earlier period. The net effect of the priceadjustment on monetary assets and liabilities is recognized as a gain orloss for the accounting period.8

The effect of price level adjustments on monetary assets and liabilitiesmay be illustrated by the following example, which assumes a 40 per centincrease in the price level over a year:

January 1 December 31 Price AdjustmentCash and accounts

receivable 60,000 75,000 -27,000Short-term

liabilities 30,000 40,000 +14,000Long-term

liabilities 100,000 100,000 +40,000Net gain +27,000

The loss in purchasing power of 13,000 on a short-term monetaryaccount is more than offset by the gain of 40,000 in long-term obligations,leaving a net gain of 27,000 which is charged to the profit and lossaccount.9 While accountants differ on the treatment of gains on long-termliabilities, the British and U. S. accounting associations are in agreementin treating them as part of profits before taxation.

Nonmonetary items such as land, buildings, machinery, and equipmentare restated in the current year's balance sheet at a value adjusted forchanges in the general purchasing power of the monetary unit since thetime they were acquired; that is, each separate item is adjusted by the

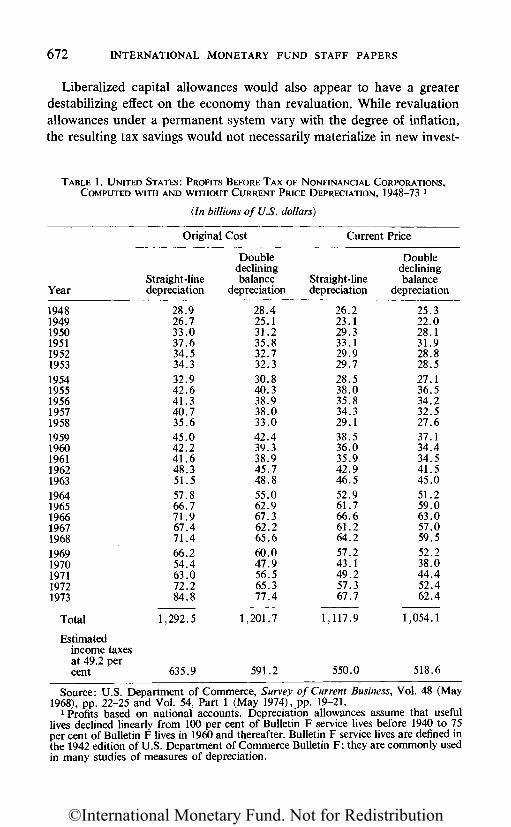

8 A question may arise over the validity of adjusting the value of fixed incomeinstruments (the rate of interest on which already reflects the rate of inflation). If,for example, the interest rate is 15 per cent, of which 10 percentage points compen-sate for an anticipated decline in purchasing power, it might be argued that theholder is already compensated for inflation. However, if the entire 15 per cent inter-est is taxable at, say, 50 per cent, the 7.5 per cent yield after tax would be negative.It is necessary, therefore, to index the principal amount to avoid taxation of capital.For example, a $1,000 debenture carrying 15 per cent interest would be revalued at$900, so as to protect the investor against taxation of the $100 loss in capital; taxwould be limited to $25, and the nominal yield after tax would be 12.5 per cent—equivalent to a real rate of return of 2.5 per cent. The borrower's interest cost of$150 would be offset by a real gain of $100 on the debt; if deductible at a tax rateof 50 per cent, the real cost would be equivalent to the $25 yield of the investor,that is, 2.5 per cent. See Vito Tanzi, "Inflation, Indexation, and Interest IncomeTaxation" (unpublished, International Monetary Fund, February 14,1975).

9 The loss in cash and accounts receivable is calculated at 40 per cent of 60,000,or 24,000, plus 40 per cent of one half of the year's increase, assuming that theincrease has taken place evenly through the year. A similar computation is made forthe increase in liabilities.

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 647

ratio of the general price index at the end of the period to the index at thetime of its acquisition. A price level adjustment is also made for invento-ries. Unlike monetary accounts, these items are stated at their price-adjusted values, but no gain or loss is recognized until they are sold orcharged to operations in accordance with accepted accounting principles.

The purpose of general price level financial statements is to restate con-ventional accounting statements to take into account changes in the pur-chasing power of the monetary unit rather than to reflect the current costof various assets, as is the case in revaluation statements. Price levelaccounting is intended to measure real income of a business rather thanonly to provide a basis for the maintenance of the value of physical assets.In this respect, the book value of assets adjusted for changes in the pur-chasing power of money may depart significantly in many instances fromvalues justified by the current market value or replacement cost of theseassets.

II. Experience with Revaluation After World War II

Revaluation of financial statements in response to the inflationary after-math of World War II has taken a variety of forms depending on the cir-cumstances and the purposes served. For analytical purposes it is conven-ient to recognize two separate approaches: (1) one-time or successiverevaluations of nonmonetary business assets, and (2) comprehensiverevalorization schemes of a permanent nature.

REVALUATION OF NONMONETARY BUSINESS ASSETS

European countries

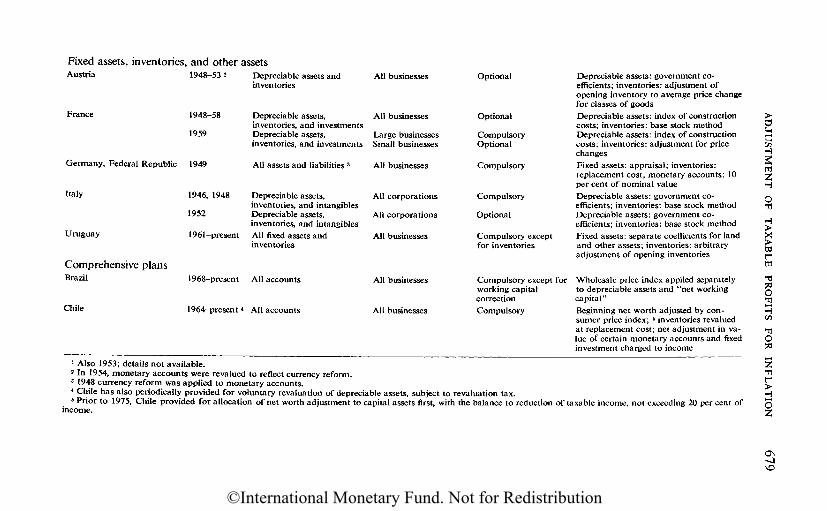

In the immediate postwar period, several European countries enactedlegislation for the revaluation of nonmonetary business assets to correctbalance sheet values for the war-induced inflation. A major objective wasto adjust taxable income so as to provide greater funds to business forrehabilitation of plant and for other new investment. France, in 1945, wasthe first country to authorize the revaluation of assets, and revaluationremained in effect on a voluntary basis until 1959, when it was mademandatory for large companies.10 Italy instituted compulsory revaluationschemes in 1946, 1948, and 1951. In 1947, Belgium introduced a one-

10 The 1959 tax reform abolished revaluation with respect to price changes occur-ring after June 30, 1959. Large firms were required to undertake revaluation of their1959 accounts by December 31, 1963; small firms could elect it by then.

©International Monetary Fund. Not for Redistribution

648 INTERNATIONAL MONETARY FUND STAFF PAPERS

time voluntary plan substantially limited to industrial assets acquiredprior to World War II. Austria enacted legislation annually from 1947 to1954 that provided for revaluation of inventories as well as of depreci-able assets; this culminated in the 1954 plan for revaluation of monetaryaccounts as well. Following its currency reform of 1948, the FederalRepublic of Germany enacted a revaluation plan in 1949 that also tookinto account the effect of the new deutsche mark on monetary assetsand liabilities. In 1950, the Netherlands introduced a voluntary revalua-tion scheme similar to that of Belgium. Spain's first revaluation planwas not instituted until 1961; this was followed by similar schemes in1964 and 1974.

Scope of revaluation. In Austria, Belgium, France, the Federal Repub-lic of Germany, and the Netherlands, all business firms were covered bythe revaluation laws, while in Italy and Spain only corporations wereaffected. Although the need for balance sheet conformity and improve-ment of investment and other decisions based on financial statementswould seem to call for mandatory schemes, especially for larger compa-nies, the majority of schemes adopted were optional. Revaluation wasmandatory only in the Federal Republic of Germany and Italy (exceptin 1952), and for the final provision in France (1959), when companieswith a turnover exceeding 5 million francs were required to revaluetheir financial statements. In Italy, the linking of revaluation withattempts to improve accounting and to reduce tax evasion was a strongargument for compulsion.

Only in Austria and the Federal Republic of Germany was revaluationapplied to all balance sheet items (assets and liabilities), because of theneed to correct monetary accounts for the new currency. In Italy andFrance, the revaluation measures embraced inventories as well as fixedassets; Italy also covered licenses and patents, and France covered securi-ties, receivables, and liabilities in foreign currency. Spain's law includedpatents, receivables, certain securities, and payables in foreign currency.Spain also provided for the revaluation of assets and liabilities previouslyexcluded from the balance sheet, Belgium and the Netherlands limitedrevaluation substantially to fixed assets acquired before World War II;Belgium further restricted it to industrial plant and equipment. An addi-tional feature of the optional schemes was that the decision to revalue andthe degree of revaluation, within statutory limits, could be decided on anasset-by-asset basis. In Spain, however, a decision to revalue applied toall eligible assets.

Several countries recognized that inflation would be advantageous tofirms that financed the purchase of assets with loans. Belgium, for exam-

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 649

pie, limited the degree of revaluation allowed when this type of financingwas important.11 In France and Spain, full revaluation was permitted inorder to reflect current values in the balance sheet, and a higher tax wasplaced on the revaluation reserve from loan-financed assets.

Techniques of adjustment. Most of the European schemes represented aresponse to what was thought to be a limited period of exceptional infla-tion. The revaluations have therefore been one-time affairs or have takenplace at discrete intervals. This is seen most clearly in Belgium, the Fed-eral Republic of Germany, and the Netherlands. In Italy, the adjustmentprocess spanned a longer period, but there was no attempt at a continuouscorrection for inflation. Spain has also revalued periodically. Of the coun-tries surveyed, France comes the nearest to a system of continual adjust-ment to a relatively long period of inflation, with measures in force from1945 to 1959. Revaluation below the maximum allowed in any particularyear could be made up in subsequent years.12

Revaluation provisions differed in their adjustment for depreciationthat was previously allowed. Clearly, the tax advantage of future depre-ciation is greater, the less the revalued asset is reduced by previouslyclaimed depreciation. The general rule is to adjust depreciation reservesby the relevant price coefficient for each year's depreciation. Futuredepreciation allowances are thus limited to the replacement cost, lessrevalued depreciation, or to the remaining useful life of the asset. Onedeparture from this rule was the option given by Austria to increasedepreciation allowances or to revalue pre-1946 assets still in use even ifthey were fully depreciated.13

In Belgium, the Netherlands, and the Federal Republic of Germany,revaluation was not linked to any price index but was based on estimatedreplacement cost within certain limits. Belgium allowed revaluation ofassets by the lower of their estimated current value and two and a halftimes their book value on August 31, 1939, reduced by the degree ofphysical depreciation. The Netherlands limited revaluation to double the1949 book value of machinery and short-lived buildings (ten years orless) and ratios declining with the life of buildings beyond ten years. Inthe Federal Republic of Germany, replacement value was estimated bythe individual firm, with declarations for a postwar capital levy providingsome curb on the values submitted. All machinery and equipment had to

11E. B. Nortcliffe, "Revaluation of Assets in Belgium," Accountant (LondonApril 23, 1949), pp. 323-26.

12 Harvard University Law School, World Tax Series, Taxation in France (Com-merce Clearing House, Chicago, 1966), p. 325.

13Felix Kollritsch, "Austria's Answer to Inflationary Profits and Taxation"Accounting Review, Vol. 36 (July 1961), pp. 439-45.

©International Monetary Fund. Not for Redistribution

650 INTERNATIONAL MONETARY FUND STAFF PAPERS

be valued at a minimum of one third of replacement cost, to which wasadded the remaining two thirds, weighted according to the proportion ofthe remaining life of the asset.14

In other European countries, depreciable assets were revalued by coef-ficients issued by the government. These were related to the year ofacquisition and applied to the original cost of the asset; a correspondingadjustment was made for each year's depreciation. The French coeffi-cients were based on the wholesale prices of construction materials,lumber, and steel. In Austria, Spain, and Italy, fixed assets were revaluedby coefficients that reflected increases in the wholesale price level.

Different laws limiting the taxation of inventory profits have been inforce in France since 1939.15 Between 1952 and 1959, the law wasdesigned to exempt from tax the inventory profits on basic minimumstocks of a permanent investment character. An inventory valuationaccount could be set up so as to exclude inventory profits from tax; ifprices declined, the difference in value was restored to taxable income.The 1959 tax reform replaced the base stock method by a deduction fromtaxable income of increases in value of all inventories attributable to priceincreases of 10 per cent or more.16

The revaluation law in the Federal Republic of Germany provided forinventories to be valued at the lower of their replacement costs on Au-gust 31, 1948 or August 31, 1949. The Government later enacted a lawthat allowed inventory valuation deductions on essentially the samebasis as the post-1959 French system. Italy, in 1951, authorized valua-tion profits on "permanent stock," considered essential to the normaloperation of a firm, to be deducted from taxable profits.17

Austria's inventory adjustment best conformed to price level account-ing. Although initially (1947) legislation provided for an arbitrary dou-bling of beginning inventories, by 1951 the additional deduction was basedon 90 per cent of the difference between average unit costs of beginning

14 For assets fully depreciated in the books but still in use, the proportion ofreplacement value taken was lower. M. Peter Holzer and Hanns-Martin Schonfeld,"The German Solution of the Postwar Price Level Problem," Accounting Review,Vol.38 (April 1963), p. 379.

15 M. Peter Holzer and Hanns-Martin Schonfeld, "The French Approach to thePost-War Price Level Problem," Accounting Review, Vol. 38 (April 1963),pp. 384-87.

16 Since 1948, France also permitted deductible inventory reserves to takeaccount of fluctuations in prices of specified basic raw materials acquired in worldmarkets; in 1959, this provision was extended to materials purchased in national ter-ritory. See Harvard University Law School, Taxation in France (cited in footnote12), pp. 315-22.

17 Harvard University Law School, World Tax Series, Taxation in Italy (Com-merce Clearing House, Chicago, 1964), Paragraph 6/5.1, p. 383.

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 651

and closing inventories for different classes of goods, reduced by factorsbased on turnover.18

Treatment of revaluation surplus. Of these European countries, onlyFrance and Spain enacted a supplementary tax on income or on therevaluation surplus arising from the write-up in the book value of assets.During the years 1945-48, French firms choosing to revalue wererequired to pay profits tax at 28 per cent rather than at the standard 25per cent. This differential rate was replaced in 1949 by a 5 per cent taxlimited to the revaluation gain from assets financed by loans. With theintroduction in 1959 of the compulsory measure, a 3 per cent tax wasimposed on the reserves resulting from revaluation of depreciable assets,and a 6 per cent tax was placed on reserves for the maintenance of basestock inventories. Spain's 1961 revaluation law levied three different ratesof tax on the revaluation gain: a simple revaluation tax of 1.5 per cent, 8per cent on assets financed by loans, and 3 per cent on assets not pre-viously entered in the accounts. In 1964, these rates were reduced to 0.15per cent, 4 per cent, and 1.5 per cent, respectively. The 1974 legislationdid not carry a tax.

Several countries placed constraints on the distribution of revaluationgains. Such gains simply reflected write-ups on the books of the enter-prise, distribution of which would be inconsistent with a major purpose ofthe related tax benefits to finance plant rehabilitation and other newinvestment.

Asian countries

Several Asian countries have also provided for the revaluation of assetsfor tax and other purposes; these countries include Indonesia, Japan, andKorea.19 The Japanese revaluations, initiated in 1950, were dictated bythe postwar inflation that distorted financial accounts and taxable incomein the face of urgent needs to rehabilitate plant.20 The other countries

18 Kollritsch, op. cit., p. 443.19 Israel granted additional depreciation allowances for machinery and buildings

following the currency devaluations in 1954, 1962, and 1967. The supplementaryallowance for assets purchased with foreign exchange was based on the differencebetween the old and new exchange rates. For domestically financed assets, a loweramount was given, depending on the date the asset was acquired.

20 The initial measure largely followed the recommendations by the Shoup reporton the Japanese tax system: Report on Japanese Taxation by the Shoup Mission,General Headquarters, Supreme Commander for the Allied Powers (Tokyo, Sep-tember 1949), Vol. II, p. 126. An excellent analysis of this experience is given bySidney Davidson and Yasukichi Yasuba, "Asset Revaluation and Income Taxationin Japan," National Tax Journal, Vol. 13 (March 1960), p. 46.

©International Monetary Fund. Not for Redistribution

652 INTERNATIONAL MONETARY FUND STAFF PAPERS

have revalued more recently. Korea enacted legislation for the revaluationof assets in 1958 and 1962, in response to a 60 per cent annual rate ofinflation prior to the initial measure. Indonesia provided for revaluationof fixed assets following major inflationary episodes in 1953 and 1971.The latter was preceded by more than a hundred-fold price increasebeginning in 1965.

Scope of revaluation. With the exception of the 1954 Japanese revalua-tion and the 1958 measure in Korea, the schemes in these countries wereoptional.21 The 1954 Japanese revaluation remained optional for smallfirms, and the 1958 Korean measure was optional for sole proprietors.Indonesia restricted revaluation to corporations.

The measures enacted in these countries generally applied to a range ofassets similar to those of the postwar European revaluations, with theexception of inventories. Indonesia restricted revaluation to fixed assets(land, buildings, and machinery) that were acquired between 1960 and1970. Korea included some intangible assets and shares as well as fixedassets, while the Japanese measures referred to all fixed assets and up to1953 to shares. The pre-1954 Japanese acts provided for selectiverevaluation of individual assets and categories of assets (for example,land) up to the limits prescribed by the index.

Techniques of adjustment. None of these countries has provided for acontinuous adjustment for inflation. Indonesia's two postwar revaluationswere separated by 18 years, while in Japan and Korea successive meas-ures reflected the lack of impact of the initial acts as well as continuedinflation. Japan's 1950 law had only limited response, and it was extendedin 1951 to take account of conditions generated by the Korean conflict; itwas amended again in 1953 and a new act was introduced in 1954. In1957 the 1954 legislation was extended to firms previously excluded.

Japan's and Korea's revaluations were linked explicitly to movementsin price indices. The technique employed in these countries for deprecia-ble assets was to apply the increase in the wholesale price index from theyear of acquisition to the depreciated cost of the asset, following thedeclining balance method. Separate indices of land values were used.Indonesia provided for the revaluation of the original cost of plant andequipment and each year's depreciation by means of government-issuedcoefficients. These coefficients were based on the depreciation of the Indo-nesian rupiah's exchange rate with the U. S. dollar, reflecting the fact that

21 Despite the compulsory nature of the 1958 Act in Korea, there was widespreadfailure to comply. See Samuel S. O. Lee, "Korean Accounting Revaluation Laws."Accounting Review, Vol. 40 (July 1965), p. 624.

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 653

virtually all machinery and equipment were imported. The coefficients forbuildings and land were calculated on the cost of construction and theestimated value of land.

Treatment of revaluation surplus. Following the recommendations ofthe Shoup Mission, Japan in 1950 levied a 6 per cent tax on the revalua-tion gain, payable over three years; this was re-enacted in 1951. The pro-visions of the tax were eased in subsequent amendments; the 1953amendment extended the payment period to five years, and the 1954 lawcut the tax to 3 per cent, exempting the amount by which the compulsoryrevaluation exceeded that allowable under the 1951 Act, Indonesiaimposed a seemingly heavy tax of 10 per cent of the revaluation gain,payable in eight quarterly installments; in addition, a capital tax of 10per cent had to be paid at the time of capitalization. In 1958, Korealevied a 1 per cent revaluation tax, which was halved in the 1962 revalua-tion.

Latin American countries

Since 1942, ten Latin American countries have adopted revaluationschemes for business income tax purposes: Argentina, Bolivia, Brazil,Chile, Colombia, Ecuador, Mexico, Paraguay, Peru, and Uruguay.22

While all ten schemes originated in inflationary situations, those of Bolivia(1972) and Mexico (1954) were directly related to currency devalua-tions that followed a period of rising prices.23 Generally, these schemeswere introduced for the purpose of adjusting depreciation allowances toreplacement values. The early revaluation provisions of both Brazil andChile, however, were intended to adjust capital values for excess profitstax purposes and were later extended to the business income tax. Uru-guay's provision for the revaluation of assets accompanied the introduc-tion of its income tax in 1961, but it also applied to the excess profits tax,which was modified at the same time.

Partial systems, calling for the restatement of asset values (Argentina,Bolivia, Mexico, Peru, and Uruguay), will be treated apart from those ofBrazil and Chile, which evolved into permanent revalorization systems of

22 For a comprehensive survey and analysis, see Arturo E. Lisdero and Luis E.Outeiral, Contabilidad e Inflation: El ajuste integral, Los revaluos legales, contablese impositivos (Cordoba and Buenos Aires, 1973). Argentina's plans through 1957are described in Enrique J. Reig, El Impuesto a los Reditos, 5th edition (BuenosAires, 1970).

23 Bolivia's 1972 revaluation decree was followed by a new income tax law of1973, which authorizes a new revaluation when reductions in the exchange rate orincreases in prices reach 15 per cent of the level on December 31, 1971 (DecreeLaw No. 11154 of 1973).

©International Monetary Fund. Not for Redistribution

654 INTERNATIONAL MONETARY FUND STAFF PAPERS

a more comprehensive character. Except for Argentina's 1971 law andUruguay's legislation, the plans of these countries provided for a one-time revaluation of fixed assets. Uruguay's scheme extends to items otherthan fixed assets, but it is less comprehensive than that of either Brazilor Chile. Colombia's 1960 scheme provided for price level adjustmentsto depreciation allowances, rather than for revaluation of assets. Cor-porations and limited share partnerships were permitted to credit annual-ly to this reserve an additional 15 per cent of the cost of machineryand equipment acquired prior to the 1957 currency devaluation, withinspecified limits.

Coverage. The revaluation plans of Argentina, Bolivia, Peru, and Uru-guay are of general application to all enterprises, while Mexico's legisla-tion was limited to firms engaged in industrial, agricultural, and fishingactivities. All firms covered by the law in Peru and Uruguay are requiredto revalue fixed assets; Argentina's provision is mandatory for only largefirms. Bolivia's provisions appear to be optional, as were Mexico's.Argentina, Bolivia, and Mexico limited revaluation to depreciable assets,Peru covered land as well, while Uruguay provides for adjustments to thevalue of depreciable assets, land, and inventory (inventory revaluation isoptional).

Techniques. Different policies have been followed with regard to boththe indices or measures of revaluation for tax purposes and the limitswithin which they operate. Uruguay, for example, issues maximum andminimum coefficients of price changes from past years (based on generalchanges in replacement value) that are applied to the original cost of theasset, depending on its year of acquisition; depreciation corresponding tothe useful life spent is also revalued. Different coefficients based on cost ofconstruction and land values are applied to real estate. Argentina's priceadjustments have also been based on coefficients issued by the Govern-ment. In its 1972 decree, Bolivia distinguished between domestic andimported capital goods, the former being increased by 20 per cent and thelatter by 60 per cent, slightly less than the extent of the devaluation.Peru's 1971 decree provided for a 55 per cent increase in the Decem-ber 31, 1967 values established by the predecessor Act of 1967, andsmaller adjustments for assets acquired in 1968 and 1969; correspondingadjustments were made for accumulated depreciation. Mexico, on theother hand, authorized taxpayers to increase the book value of theirassets (unless fully depreciated) on the basis of an appraisal but not bymore than 40 per cent of the book value on April 19, 1954. Additional

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 655

depreciation based on this adjustment was deductible only for the 15 percent distributable profits tax and not for the schedular taxes.

Of these countries, only Uruguay has authorized adjustment of inven-tory costs. Initially, opening inventories were revalued at replacementcost, and the excess over cost was excluded from taxable income. Sincethen, various prescribed percentages of opening inventories have beendeductible, provided the amount did not exceed taxable income.

Special reserves and^r evaluation tax. Since 1960, Argentina has levieda tax ranging from 3 to 10 per cent of one half the increase in book valueof the assets, depending on the size of the increment; this tax is deductiblefor income tax purposes. The revaluation reserve arising from the 1967and 1971 revaluations of assets in Peru was subject to a 10 per cent tax.Bolivia imposed a tax of 5 per cent on the 1972 revaluation gain trans-ferred to a special reserve; a 5 per cent tax was also authorized under itspermanent legislation of 1973. Mexico's reserve was subject to the samerules as those governing its special 10 per cent reinvestment reserve; theamount could be capitalized and was subject to the distributable profitstax only when the company redeemed its shares or was liquidated.Although Uruguay does not impose a special tax on the revaluationreserve, the higher valuation is subject to its net wealth taxes.

COMPREHENSIVE REVALORIZATION SCHEMES—BRAZIL AND CHILE

The profit adjustment schemes of Brazil and Chile have graduallyevolved after years of experimentation with partial adjustment plans.24 InBrazil, the legal provisions and administrative regulations governing thereadjustment mechanisms are continually being modified. Chile, until1974, has had a fairly stable permanent adjustment system, but ithas been complicated by successive partial revaluations.

The techniques employed by these two countries have some fundamen-tal similarities. Both systems are based on the concept that income isequivalent to the increase of a firm's net worth in real terms and that thetax law should take into account the effects of inflation on all items thatenter into the determination of net worth—both assets and liabilities.However, neither system conforms to the revalorization model advancedby the British and U. S. accounting professions.

24 For a more detailed history and analysis of these plans, see Milka Casanegra-Jantscher, "Taxing Business Profits During Inflation: The Latin American Experi-ence" (unpublished, International Monetary Fund, April 16, 1975; forthcoming inInternational Tax Journal).

©International Monetary Fund. Not for Redistribution

656 INTERNATIONAL MONETARY FUND STAFF PAPERS

Chilean system

Chile's scheme for the annual adjustment of profits derives from a pro-vision enacted in 1959,25 which established an optional system of networth revaluation available to all taxpayers subject to business incometaxes. As part of the income tax reform enacted in 1964, this provisionwas modified in some respects and made mandatory.26 The system hasbeen based on the annual adjustment of net worth for changes in the con-sumer price level. Until 1975, the total amount of adjustment available toa taxpayer was determined by multiplying the net worth at the beginningof the year by the relative change in the consumer price index during theyear. This amount was apportioned first to revaluation of fixed assets, byapplying to their net value the same relative change in the consumer priceindex; any balance remaining could be deducted directly from that year'sprofits, but it could not exceed 20 per cent of such profits.

New legislation, effective in 1975, repealed the 20 per cent limitationand made sweeping changes in the revaluation scheme.27 The full amountof the net worth adjustment is now deducted directly from taxableincome. Compensating adjustments, however, must be made to taxableincome for changes in the value of certain assets and liabilities. The lawcalls for revaluation of the following accounts: (1) beginning-of-yearfixed assets, equity investment, patents, and copyrights; (2) inventory atreplacement cost; (3) index-linked monetary accounts; and (4) mone-tary accounts in foreign currencies. Operating results for the taxable yearwould reflect the revalued accounts in accordance with accepted account-ing principles—for example, depreciation and inventory accounting.Although there is no precedent for taxing unrealized revaluationincreases in fixed assets at income tax rates, this effect is mitigated by thenet worth adjustment. Moreover, the new law was accompanied by one ofChile's periodic revaluations, which largely nullified its effect for 1975.

The normal operation of the Chilean permanent profits adjustmentscheme has been subject to periodic provisions for the revaluation ofassets. The main object of these revaluations has been to escape from thelimitations of the permanent system by allowing full revaluation of fixedassets and inventory, generally up to replacement values. Although a spe-cial tax is imposed on the resulting reserves, many taxpayers have takenadvantage of the revaluation provisions. Chile has thus combined the fea-tures of both replacement value and revalorization of financial statementsin a way that distorts equity and complicates administration.

25 Law No. 13305 of April 4, 1959. A revised plan was made effective in 1975.26 Ley de Impuesto a la Renta (Law No. 15564), February 14, 1964.27 Decree Law No. 822, December 31, 1974.

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 657

Brazilian system

The Brazilian profits adjustment system shares many features with theChilean scheme but conforms better to the revalorization system advo-cated by the accounting profession.28 It is composed of two parts: therevaluation of fixed assets and the revaluation of working capital. The firstof these is mandatory; the second is optional. A third component, which isclosely related to these two, is the treatment of income and expenses con-nected to index-linked claims.

Brazil provided for revaluation of fixed assets for many years, but until1964 its use was limited to financial statements and to the valuation ofcapital for purposes of the excess profits tax. Taxpayers were thenallowed to write off the amount of the revaluation of depreciable assetsagainst taxable income. This amount was treated separately at first as anew investment with the same useful life as the original asset, but since1974 it may be amortized over the balance of the useful life of the asset.Revaluation is based on the index used to adjust indexed treasury bonds,an index which reflects changes in the wholesale price level.

The second component of the Brazilian profits adjustment scheme isthe revaluation of so-called working capital by the same price index. Thisprovision was introduced in 1964 for purposes of computing the excessprofits tax,29 but in 1968 this system was modified and made applicable tothe business profits tax. Working capital is defined as the differencebetween equity capital and the net book value of fixed assets. Liabilitiesexclude all debt expressed in foreign currency, or subject to indexation,that is related directly to the acquisition of fixed assets. The resultingadjustment in each year is considered as the amount necessary to preserveworking capital intact. If the amount is negative, taxpayers may opt forthe adjustment and deduct this amount from their taxable profits.

An important complement of the Brazilian adjustment scheme is thehandling of amounts received or paid as "monetary correction"—that is,payments (excluding interest) derived from transactions subject to index-ation. The indexed component of loans paid or received by enterprises istreated in a special account. If the total amounts paid exceed thosereceived, the difference may be deducted from profits; if the total amountsreceived exceed those paid out, the difference is now (since 1974) treatedas taxable income.

28 The law in effect through 1974 was amended by Decree Law No. 1338, Ar-ticle 14, July 23, 1974, effective January 1, 1975. See also regulations announcedon October 15, 1974, Portaria 544.

29 The excess profits tax was repealed in 1966.

©International Monetary Fund. Not for Redistribution

658 INTERNATIONAL MONETARY FUND STAFF PAPERS

III. Evaluation of Price Level Adjustments

Too little is known about the experience with the various plansdescribed above to state with any confidence what effects they have hadon new investment, economic stability, resource allocation, the distribu-tion of the tax burden, administration and compliance, or indeed, govern-ment revenue. Any such analysis must therefore rest largely on theoreticalgrounds and find support from whatever fragmentary information is avail-able.

ALLOCATIVE EFFECTS

It seems clear that the tax benefits of partial revaluation plans vary withthe composition of business assets and the degree of inflation.Capital-intensive industries with long-lived assets stand to gain most fromthe introduction of such a scheme, first, because their fixed assets gener-ally comprise the largest share of total assets, and, second, because of agenerally older age distribution of plant and machinery, the replacementcost of which has risen the most (although subject to depreciation alreadyaccrued). Industries with heavy inventory investment may also realizesubstantial benefits, depending on the extent of the price rise in particularcommodities. This distribution of tax benefits is consistent with the objec-tive of partial revaluation measures to provide funds for investment.Although the timing of the tax savings may not coincide with a replace-ment program, except for inventories, greater cash flow is made availablefor additional new investment, repayment of debt, and other corporatepurposes that strengthen the company's financial position.

Some indication of the relative benefits implicit in partial revaluationplans is provided by an analysis of the 1971 balance sheets of 137 corpo-rations trading on the London market.30 As expected, financial companiesincluding those in banking and insurance were not affected because theyowned little or no depreciable assets or inventories. Of the remaining 124companies, 55 would have received the greatest benefits from revaluationof inventories; these included the tobacco manufacturing, general engi-neering, merchandising, textile, and food processing industries. Slightlyfewer companies (49) would have had the largest benefits from revalua-tion of their plant and equipment accounts, although many of these wouldhave also benefited greatly from the elimination of inventory profits.

30 R. S. Cutler and C. A. Westwick, "The Impact of Inflation Accounting on theStock Market," Accountancy, Vol. 83 (March 1973), pp. 15-24. While relativelyfew companies were covered, they accounted for about 75 per cent of total stockmarket values in 1971.

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 659

These industries were concentrated in shipping, oil, building materials,and hotels.

The effects on income of the revalorization plan supported by the Brit-ish accounting profession were distributed somewhat differently, espe-cially because of the offsetting gain on long-term debt. Of the 137 compa-nies in the sample, such inflation accounting would have reduced thereported earnings by about 75 per cent, with reductions up to 200 percent (one company having a considerably higher reduction). The greatestrelative decreases in reported earnings were in electrical manufacturing,shipping, automobiles, textiles, and engineering, with average reductionsranging from 60 to 174 per cent. On the other hand, price level adjust-ment had relatively little effect on merchandising and banking, but itappreciably increased earnings of breweries, hotels, and insurance andreal estate companies because of their relatively large liabilities.

Similar estimates for selected corporations in the United States havebeen made by Davidson and Weil.31 Using procedures that conform gen-erally to those recommended by the APB Statement No. 3,32 they calcu-late the effect of price level adjustments on net income in 1973 bothbefore and including the gain or loss on monetary items for 60 majorindustrial companies and 24 utilities. Adjusted net income before the gainor loss on monetary accounts of industrial companies shows reductionsranging from 7 to 90 per cent of reported income, with a median reduc-tion of about one third. The median reduction for public utilities in 1973is about 25 per cent.

Inclusion of monetary accounts produces a much wider divergence ofprice-adjusted income from reported income for industrials, ranging froma reduction of 82 per cent to an increase of 76 per cent. The medianchange for the 60 companies, however, is very slight, amounting to areduction of 5 per cent. As could be expected because of their heavy debtstructure, the price-adjusted income of every public utility was increased,in several cases by 100 per cent or more. The median increase was abouttwo thirds.

ECONOMIC STABILITY AND GROWTH

All plans for the revaluation of depreciable assets and inventoriesunder inflationary conditions have the effect of reducing business taxable

31 Sidney Davidson and Roman L. Weil, "Inflation Accounting: What Will Gen-eral Price Level Adjusted Income Statements Show?" Financial Analysts Journal,Vol. 31 (January/February 1975), pp. 27-31, 70-84; "Inflation Accounting: PublicUtilities," Financial Analysts Journal, Vol. 31 (May/June 1975), pp. 30-34, 62.

32 Accounting Principles Board Statement No. 3, Financial Statements Restatedfor General Price-Level Changes (1969).

©International Monetary Fund. Not for Redistribution

660 INTERNATIONAL MONETARY FUND STAFF PAPERS

income, and (unless offset by tax on revaluation gains) of reducing busi-ness taxes. This results in greater internally generated funds at the dis-posal of the business. The magnitude of the impact depends, of course, onthe particular form of the revaluation, the rate of increase in prices, andthe level of business income tax rates. In an inflationary situation theincreased cash flow tends to stimulate greater investment and therebyintensifies demand pressures. If the inflation is accompanied by high inter-est costs, the larger internal funds reduce dependency on the capitalmarket and better enable capital investment programs to be carried out.The reduction in tax revenue, however, may require the government toincrease its borrowing and thereby sustain high interest rates that militateagainst investment in other sectors of the economy—housing, for example—unless corrective action is taken to increase revenues or to reduceexpenditures. It may fairly be concluded then that indexation of corporateprofits based on the revaluation principle adds to inflationary pressures.

Because of the offsetting effect on taxable income of the indexation ofbusiness liabilities, revalorization would result in mixed effects, dependingon the composition of assets and capital structure of different businesses.On balance, there would be relatively little effect on revenues and, conse-quently, on inflationary pressures. Public utilities for example, wouldsuffer higher taxes because of their heavy debt structure.

The longer-range effects of revaluation would depend largely on thetrend of prices. If economic pressures and structural changes result in acontinuation of past inflationary influences, permanent schemes for reval-uation of assets would provide continuing tax relief to business. Unlessoffset by higher tax rates or by arbitrary limits on the tax benefits, this taxreduction would lower the cost of capital and would increase investment,with the result that a larger share of the gross national product would gointo capital formation. The increase in productive capacity could helpbreak supply bottlenecks and thus help contain price increases in certainindustries. The adoption of a comprehensive revalorization plan, how-ever, would temper such a trend, depending on the proportion of businessdebt to revalued assets.

PRICING POLICY

If revalued financial statements were utilized for business planning pur-poses, the economic effects outlined above probably would be reinforcedby upward price adjustments. Replacement costs would be factored intothe pricing policies of producers, with the result that administered priceswould often follow more closely changes in the market value of invento-ries and plant and machinery. The extent to which supplemental revalua-

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 661

tion statements now prepared by corporations enter into pricing policy isnot known, but their general acceptance for tax purposes probably wouldlend greater support and interest in their use as a management tool in thisrespect.33 The more revaluation is embedded in internal costing systems,the more it is likely to enter into pricing, depending on the freedom of dis-cretionary action.

EFFECT ON CAPITAL MARKET

The acceptance by investors of financial statements based on price leveladjustments would enable a more realistic appraisal to be made ofchanges in company earnings over an inflationary period. If reportedearnings were deflated for higher replacement costs, they would tend to bereflected in lower share prices. Similarly, revalorization plans would havediverse effects, depending on whether or not price-adjusted earnings werereduced. Lower reported earnings would at the same time cool investors'expectations for dividends and better enable management to justifygreater retention of funds for new investment. Indeed, it could be arguedthat dividends would not be covered by earnings in many cases.34

While revaluations have been undertaken in a number of industrialcountries, no special analysis appears to have been made of the stockmarket reaction except in Japan, where, as described below, specialrequirements governing capitalization are believed to have had a dampen-ing effect. The degree to which investors may discount share prices for theeffect of permanent inflation accounting on reported earnings seemshighly conjectural. In speculating about the probable effect of the pro-posed British revalorization system on the stock market, Cutler and West-wick concluded that the most likely outcome would be a fall in prices ofsome company shares and a rise in others, depending on the direction ofshift in earnings, with little or no general decline in prices.35

An important issue arises over requirements governing the capitaliza-tion of the revaluation reserve by the issuance of capital stock. Such capi-talization has been justified under voluntary schemes as an obligation ofthe taxpayer to retain rather than to distribute corporate assets, consistentwith the purpose of revaluation to finance new capital investment. InJapan, however, a larger capital stock account combined with lowerreported earnings was believed to depress stock market values and makestock financing more difficult because it compounded the reduction in theratios of both earnings and dividends to capital. This proved to be a very

33 See Brown (cited in footnote 4), p. 48.34 See Cutler and Westwick, op. cit. About eight companies are shown to have

made dividends that were not covered by price-adjusted earnings for the year™ Ibid.,?. 11.

©International Monetary Fund. Not for Redistribution

662 INTERNATIONAL MONETARY FUND STAFF PAPERS

controversial provision of the Japanese voluntary revaluation schemesand was resolved only by a compromise in the 1954 Act that limiteddividends to 15 per cent of capital unless at least 30 per cent of therevaluation reserve was capitalized.3^

TAXATION OF REVALUATION GAINS

The taxation of revaluation gains may substantially nullify the incometax benefits of asset revaluation and its economic consequences outlinedabove. The rate of tax, if any, and the provision for its payment thusrequire a delicate balancing of equity and economic considerations if vol-untary revaluation is to gain wide acceptance. Except for Bolivia, France,Japan, Korea, and Peru, mandatory plans have not been accompanied bytax on revaluation gains, and the tax has been reduced under successivevoluntary plans in other countries.37

Credit restrictions during inflation generally impair business liquidityand impose constraints on the financing of investment in current, as wellas in fixed, assets. While business cash flow may be enhanced by thereduction of tax liabilities attributable to higher depreciation on revaluedassets, even a moderate tax on revaluation gains, especially if real estate iscovered, may offset income tax savings. For this reason payment of therevaluation tax is sometimes spread over several years.38 Calculations forJapan show that there was a net tax benefit from revaluation of deprecia-ble assets over their useful life, assuming a 10 per cent discount rate,although the benefit was very small for assets with a useful life of 50 yearsand more.39 At lower discount rates the savings would be greater.40

A revaluation levy, therefore, may greatly restrict the benefits to theeconomy that are sought through revaluation of assets, especially if thereis little or no income tax benefit, as for real estate and certain other assets.Such levies in France may partly explain why only about 12 per cent of allbusinesses and 32 per cent of corporations assessed on the basis of actualincome elected the plan.41 In Japan, the results were also disappointing.

36 Davidson and Yasuba (cited in footnote 20), p. 57.37 Higher book values are also subject to net wealth taxes in several countries—

for example, Argentina, Chile, Peru, and Uruguay. Property tax also applied torevalued assets in Japan, and a capital levy, payable over 30 years, was applied inthe Federal Republic of Germany.

38 Japan initially spread payment of its 6 per cent levy over three years and laterover five years. Indonesia's 10 per cent tax was payable in two years.

39 Davidson and Yasuba, op. cit., p. 53.40 For a mathematical analysis of the revenue effects of a revaluation tax under

different conditions, see Armando P. Ribas, "Effects of a Tax on Revaluation ofAssets" (unpublished, International Monetary Fund, December 11,1974).

41 Foreign Tax Policies and Economic Growth, Report of a conference held atThe Brookings Institution, December 5-7, 1963, published by the National Bureauof Economic Research (Columbia University Press, 1966), p. 310.

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 663

Following the 1951 extension of the 1950 Act, only about 22 per cent ofeligible juridical persons revalued, although they accounted for about 72per cent of the potential amount of revaluation that could be claimed.42

Indonesia's 10 per cent levy exacted an even higher price for revaluation,and its law expired after two years without any corporation electing itsprovisions.

EQUITY ISSUES

Substantial differences in the nature of the plans, their conceptual basis,and their application make it difficult to draw any general conclusionsabout the equity of adjusting taxable profits for inflation. However, assuch schemes are limited to price adjustment of business profits, theyclearly favor one class of taxpayer over others for which no comparablerelief may be provided. Moreover, the distribution of the tax benefitsamong different businesses may raise serious questions of discrimination.One aspect of this that needs to be considered is the price index that isemployed.

Discrimination between business and nonbusiness taxpayers

However well it can be rationalized by accounting principles and eco-nomic theory, the revaluation of assets for tax purposes confers a specialbenefit on most business firms that mitigates the effects of inflation ontheir tax burden. Without comparable adjustments for other classes ofincome, it results in a redistribution of income taxes among differentincome sources. This can be seen most clearly for fixed incomes based oninterest, annuities, and pensions, the purchasing power of which is alsodiminished by inflation. If, however, there is provision for the indexationof debt instruments, as in Brazil and Chile, such discrimination is some-what lessened.43

The case for discrimination against wage and salary income is lessclear. If the level of wages and salaries parallels the rising general pricelevel, personal income taxes increase more than proportionately undergraduated rates and fixed family allowances and thus increasingly impingeon the cost of living. Unless income tax adjustments corresponding withthose provided for businesses are made, a question of tax equity arises,even though the tax relief is provided on entirely different grounds. Pricelevel adjustments of personal income taxes by indexation of family allow-

42 Davidson and Yasuba, op. cit., pp. 50-51.43 For a survey of Brazil's experience, see Jack D. Guenther, " 'Indexing' Versus

Discretionary Action—Brazil's Fight Against Inflation," Finance and Development,Vol. 12 (September 1975), pp. 24-29.

©International Monetary Fund. Not for Redistribution

664 INTERNATIONAL MONETARY FUND STAFF PAPERS

ances and tax brackets, as has been done in a number of countries,redresses the imbalances in the distribution of the tax burden that wouldotherwise arise.44

Discrimination among businesses

Not all revaluation schemes have included all businesses but have beenlimited to corporations or to certain types of industry. While for reasonsof compliance cost and minimal benefits not all businesses may wish toavail themselves of the provision, denial of its possible advantages createsinequities. On the other hand, there is less reason to make revaluationmandatory for all businesses, most of which are small private firms. Com-pulsory legislation has sometimes been limited to larger corporations (forexample, in Argentina, France, and Japan), but in most countries it hasbeen mandatory for all corporations (for example, in Brazil, Chile, theFederal Republic of Germany, Italy, Korea (first plan), Peru, and Uru-guay). In some countries revaluation provisions were optional for unin-corporated businesses.

Any partial revaluation scheme that is limited to the indexation of par-ticular assets is bound to discriminate between different businesses,depending on the composition of their total assets. Failure to index liabili-ties, also, so as to give effect to the reduction in purchasing power ofmoney, understates increases in net worth over the taxable year andthereby understates real net incomes. Companies with a heavy debt struc-ture payable in local currency therefore enjoy a relatively greater tax bene-fit than those with small debt.45 Similarly, if monetary assets are notindexed, earnings are overstated in terms of changes in their purchasingpower.

For these reasons, comprehensive revalorization plans that adjust theassets and liabilities of all businesses for changes in the value of moneybest serve equity for tax and other purposes.46 The theoretical basis forthis view is supported by the accounting profession. The permanentindexation schemes of Brazil and Chile come closest to realizing this goal,but the adjustment of net working capital is optional in Brazil.

44 See Amalio Humberto Petrei, "Inflation Adjustment Schemes Under the Per-sonal Income Tax," Staff Papers, Vol. 22 (July 1975), pp. 539-64; Fiscal AffairsDepartment, "Adjustment of Taxation for Inflation" (unpublished, InternationalMonetary Fund, May 23, 1975).

45 This fact was recognized by France and Spain in imposing a heavier revalua-tion tax on assets financed by debt.

46 While Edwards and Bell agree that such a system would tend to make theincome tax more equitable, they are of the opinion that business policy decisionscan be based only on balance sheet adjustments for particular price changes. SeeEdgar O. Edwards and Philip W. Bell, The Theory and Measurement of BusinessIncome (University of California Press, 1961), pp. 16-28.

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 665

Within the context of partial revaluation plans, different techniques foradjusting depreciation to current replacement cost during an inflationaryperiod also have widely varying effects on different businesses, dependingon the age composition of their depreciable assets. In the introduction ofthe plan, the theoretically correct principle calls for revaluation of assetsby price coefficients based on their year of acquisition; a correspondingadjustment should be made for revaluing accumulated depreciationallowances.47 This is the method most commonly employed in one-timerevaluations; succeeding revaluations would reflect price changes from theprevious revalued base.

Other plans (for example, Bolivia's) simply adjust uniformly the bookvalue of all depreciable assets in use at a specified date (and not writtenoff) by an index of change in prices (or decline in the exchange rate)since that date. If prices have been rising, this procedure fails to write upthe value of assets acquired before that date to their current values anddiscriminates against companies with an older age distribution of assets.The revaluation of depreciation allowances, as in Colombia and Israel,has a similar result.

Some firms may be unable to realize the tax benefit of an increase indepreciation allowances because it cannot be absorbed by income. Thissituation may develop in slow growth industries with heavy investment infixed assets and low profit margins. Extended loss carry-over provisionsmay improve this condition, although the present value of the deductionwould be reduced.

Revaluation gains and taxation

As has been noted, some countries have imposed a special tax on thewrite up in book value. As this capital gain is attributable to inflation, abasic question arises as to whether it should be taxed, especially if it is notrealized. From an economic point of view, these gains do not reflect realincome, and their taxation would appear to be inconsistent with the prin-ciples of replacement cost accepted by the government for tax and finan-cial accounting purposes.

From an equity point of view, however, taxation of the gains on assetsmay find some support in compensating for the benefit that is implicit inthe failure to adjust liabilities for inflation. If the revaluation is elective,the tax may be regarded as a charge for the privilege of revaluing. This isespecially true if the new value establishes a fresh basis for capital gains

47 If the declining value depreciation method is employed, current depreciationallowances are computed on the net value of assets after revaluation of the cost ofthe asset and the depreciation previously claimed.

©International Monetary Fund. Not for Redistribution

666 INTERNATIONAL MONETARY FUND STAFF PAPERS

tax purposes.48 On the other hand, when revaluation gains arise fromrevalorization of monetary as well as nonmonetary accounts, their taxa-tion would not seem to be justified.

As has been seen, the level of the revaluation tax is quite arbitrary andhas varied from a nominal rate in Korea and Spain to as high as 10 percent in Indonesia and Peru. There is no relevant criterion other than astandard rate of the capital gains tax itself, which may be so punitive as todefeat the purpose of revaluation. The appropriate rate of tax, if any, andits period of payment must therefore be guided by a proper balance ofeconomic and equity considerations. The 6 per cent rate adopted byJapan was determined after a careful examination of the liquidity positionof Japanese companies and their ability to meet payments without jeop-ardizing new investment.

The choice of an index

Equity considerations are important in the selection of a price index orother measures employed for the adjustment of balance sheet accounts toinflation. The index chosen should, of course, be consistent with theintended objectives of the revaluation. For this reason it is important todistinguish between adjustments to current value under the replacementcost approach and purchasing power indices under revalorization schemes.

Replacement cost. If replacement cost is accepted as a valid basis ofaccounting for current depreciation and inventories, it is necessary toraise a basic question of what is to be replaced.49 Because of technologicalimprovements, machinery and equipment are rarely replaced with identi-cal assets but rather with assets of greater productivity.50 Therefore, useof replacement cost of existing machinery and equipment would generallyprovide greater allowances than necessary to maintain the current level ofoutput in the future, and the tax benefits would be unnecessarilyenhanced. Varying rates of technological improvement in different indus-tries would be a source of inter-industry discrimination.

One-time revaluations may be based on company appraisal of themarket value of assets for their replacement cost (as in Belgium, theNetherlands, and the Federal Republic of Germany), but a permanentplan should be based on more objective measures, such as coefficients

48 In countries where corporations and other businesses are subject to net wealthtaxes, there would be less justification for a revaluation levy.

49 As is pointed out in Section IV, economists and accountants are by no meansagreed that provision of funds for replacement is the proper function of deprecia-tion accounting.

50 Indeed, the assets of a business may not be replaced at all, if business decisionsdictate. For example, certain equipment may be leased rather than owned.

©International Monetary Fund. Not for Redistribution

ADJUSTMENT OF TAXABLE PROFITS FOR INFLATION 667

that reflect changes in market values. This would, in principle, requirethe use of special indices related to average price increases experiencedfor different categories of assets: buildings, machinery and equipment,land, and inventories of particular materials. Unless official coefficientsare prescribed, tax avoidance will be invited and administration mademore difficult. The unavailability of appropriate indices in many coun-tries has made it necessary to resort to proxies that may not reflectaccurately changes in market prices of different categories of assets.When most of the capital equipment is imported, an adjustment basedon depreciation in the value of the currency may be appropriate (as inBolivia and Indonesia), but this would not be suitable for domestic andproduction costs. In the absence of an index of domestic constructioncosts, it may be necessary to employ a wholesale price index of non-agricultural goods (as in Argentina). Indexation of the value of realestate, when included, raises special problems either because such anindex is rarely computed or, if it is, because wide variation in the appre-ciation of land values in different areas make any single measureunacceptable for all companies.

REVALORIZATION

In accounting for the effect on profits of general changes in purchasingpower, it would be desirable to employ a very broad index of pricechanges, such as the GNP deflator. Yet very few countries have developeda reasonably accurate deflator, and all but these few would be forced toemploy a second-best index. Indeed, neither Brazil nor Chile employs thisbroad measure in its comprehensive revalorization scheme; instead, Braziluses a wholesale price index and Chile uses the consumer price index.

The question inevitably arises as to how accurately either wholesaleprice or retail pri^e indices reflect changes in general purchasing power.They are known to have serious weaknesses, especially in developingcountries, depending on the accuracy of reported prices, the properweighting of commodities and services consumed throughout the country,and the statistical bias of the computation. Even so, their uniform applica-tion to all businesses would distort taxable profits less than no revaloriza-tion at all. Efforts to revalorize accounting statements for tax purposesneed not await the perfection of a deflator, provided the available toolsare not seriously inaccurate.

ADMINISTRATION AND COMPLIANCE

Any major departure from conventional accounting principles is boundto increase the problem of compliance and administration of an income

©International Monetary Fund. Not for Redistribution

668 INTERNATIONAL MONETARY FUND STAFF PAPERS

tax. This is especially true of revaluation schemes which superimpose newtechniques on existing standards for the determination of taxable incomeand which frequently require the observance of related rules governingdistribution and capitalization of revaluation gains. The effective use ofrevaluation provisions therefore rests largely on the quality of theaccounts that are maintained in the country. Recognition of this fact isseen in the adoption of elective schemes in most countries and, wheremandatory, their limitation to corporations or large businesses. Whileother considerations have influenced the election of revaluation, account-ing requirements undoubtedly played a major role in the relatively lowproportion of small businesses that opted for the provisions in France andJapan, the only countries for which there are relevant data. On the otherhand, it is reported that the 1947 revaluation in Belgium was carried outvery smoothly and that virtually every eligible firm took advantage of it.51

Different plans, of course, vary in their complexity, depending on thescope of assets and other accounts covered, on the frequency of revalua-tion, and on related provisions, such as taxation of revaluation gains andrestrictions on their distribution. One-time plans limited to the revaluationof fixed assets pose fewer problems than continuing plans.

Comprehensive revalorization schemes instituted by Brazil and Chilecompound the problems of compliance as well as administration. This isespecially true when there are introduced refinements related to the natureof debt obligations (as in Brazil) and limitations on benefits (as inChile). Periodic modifications of the law to meet changing conditions andtechnical refinements have a cumulative effect on the burden of compli-ance and administration.

The indexation of inventories presents special problems of enforcementbecause of the greater opportunities for evasion. It is especially difficult toascertain the various components of inventories and to be certain that theappropriate price index has been applied. While the base stock inventorymethod has gained acceptance in European countries, it does not lenditself to businesses with highly diversified goods and high turnover (forexample, department stores). The LIFO inventory method substantiallyeliminates inventory profits and is not difficult to apply once it is estab-lished.

Revalorization introduces further complications in the harmonizationof income taxes within a common market area such as the European Eco-nomic Community, as well as in adjusting to double taxation relief forbranches and subsidiaries in countries without a comparable system.

51 See Accounting for Inflation (cited in footnote 1), p. 109.