in the middle east and north africa - imf elibrary

TRANSCRIPT

in theMiddle EastandNorth Africa

g

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

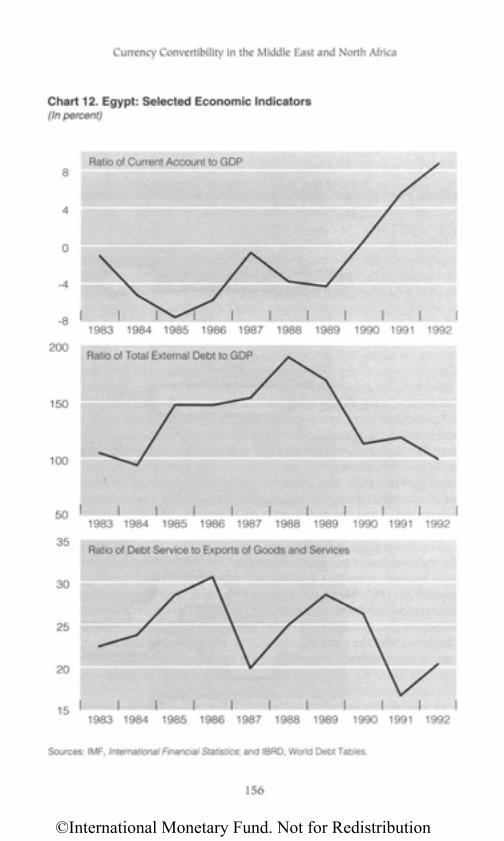

CurrencyConvertibilityin theMiddle EastandNorth Africaeditors

Manuel GuitianSaleh M. Nsouli

International Monetary Fund

Washington • 1996

Papers presented at a seminarheld in Marrakesh, Morocco,December 16-18, 1993

©International Monetary Fund. Not for Redistribution

© 1996 International Monetary Fund

Cover design by IMF Graphics Section

Cataloging-in-Publication Data

Currency convertibility in the Middle East and North Africa / editors ManuelGuitian, Saleh M. Nsouli. — Washington, D.C. : International Monetary Fund,1996

p. cm.

"Papers presented at a seminar held in Marrakesh, Morocco, December 16-18,1993."

ISBN 1-55775-564-7

1. Currency convertibility — Middle East. 2. Currency convertibility —Africa, North 3. Foreign exchange — Middle East. 4. Foreign exchange —Africa, North. I. Guitian, Manuel. II. Nsouli, Saleh M.HG3968.2.C97 1996

Price: $19.50

Address orders to:International Monetary Fund, Publication Services

700 19th Street, N.W., Washington D.C. 20431, U.S.A.Telephone: (202) 623-7430

Telefax: (202) 623-7201Internet: [email protected]

©International Monetary Fund. Not for Redistribution

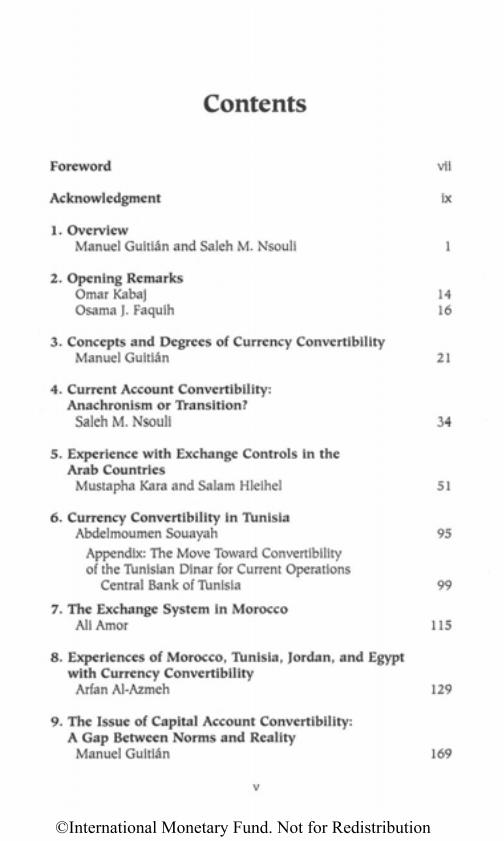

Contents

Foreword vii

Acknowledgment ix

1. OverviewManuel Guitian and Saleh M. Nsouli 1

2. Opening RemarksOmar Kabaj 14Osama J. Faquih 16

3. Concepts and Degrees of Currency ConvertibilityManuel Guitian 21

4. Current Account Convertibility:Anachronism or Transition?

Saleh M. Nsouli 34

5. Experience with Exchange Controls in theArab Countries

Mustapha Kara and Salam Hleihel 51

6. Currency Convertibility in TunisiaAbdelmoumen Souayah 95

Appendix: The Move Toward Convertibilityof the Tunisian Dinar for Current Operations

Central Bank of Tunisia 99

7. The Exchange System in MoroccoAli Amor 115

8. Experiences of Morocco, Tunisia, Jordan, and Egyptwith Currency Convertibility

Arfan Al-Azmeh 129

9. The Issue of Capital Account Convertibility:A Gap Between Norms and Reality

Manuel Guitian 169

V

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

Foreword

Promoting currency covertibility, mainly as it relates to external currentaccount transactions, has been at the heart of the International

Monetary Fund's mandate since its foundation. As financial markets havegrown and become more globalized, the size and impact of capital move-ments have increased in importance. This was recognized in the 1995communique of the Interim Committee of the IMF's Board ofGovernors, which underscored the benefits of increased freedom of cap-ital movements and emphasized the importance of firm economic policiesto reduce the volatility of capital movements. The Committee encour-aged the Fund to pay increased attention to issues relating to capitalaccount transactions. Consequently, the Fund's advice on convertibilityhas expanded in line with developments in world economic conditions.

The seminar on Currency Covertibility in the Middle East and NorthAfrica that took place in Marrakesh at the end of 1993 coincidedwith the increased momentum toward establishing current account con-vertibility in the region. Most notably, Morocco and Tunisia, followingthe successful implementation of adjustment programs, had accepted theobligations relating to the provisions on current account convertibilityunder the Fund's Articles of Agreement. Lebanon and Jordan followedsuit. Many other countries in the region, which have different degrees ofcurrency convertibility, are moving in the direction of accepting theobligations.

The seminar helped focus the attention of the many participants fromthe region on the benefits and conditions for adopting and sustainingconvertibility. The papers published in this volume attest to the effortsthat these countries are making and to the issues that they must confrontin moving to full convertibility.

vii

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

This volume will contribute to clarifying the issues and reformsinvolved as the Middle East and North African countries establish bothcurrent and capital account convertibility, thereby further integratingtheir economies into the globalized world economy.

MICHEL CAMDESSUS

Managing DirectorInternational Monetary Fund

viii

©International Monetary Fund. Not for Redistribution

Acknowledgment

The papers that are reproduced in this book were presented at the con-ference on Currency Convertibility in the Middle East and North

Africa at the end of 1993. They covered a wide range of general theoret-ical issues and provided empirical information on the progress that thecountries in the region were making in establishing the convertibility oftheir currencies. The seminar came at an appropriate time, shortly fol-lowing Morocco's and Tunisia's introduction of convertibility for currentaccount transactions and as other countries in the region were moving inthat direction.

We would like to thank our colleagues in the Middle EasternDepartment and the Monetary and Exchange Affairs Department of theInternational Monetary Fund (IMF) for their encouragement and sup-port in the preparation of this book. Since the original papers werepresented in different languages (English, Arabic, and French), we wantto express our appreciation to our colleagues in the IMF's Bureau ofLanguage Services, who assisted in the translation into English of thosepapers that were originally in Arabic and French. We would also like tothank Janet Bungay of the African Department, who undertook extensiveediting of the some of the translated papers. Ilse-Marie Fayad providedexcellent research support, and Maureen Burke unstinting assistance inprocessing the various drafts of the manuscript. Particular thanks go toJuanita Roushdy of the External Relations Department for her thoroughediting of the final draft manuscript and for coordinating the publicationof the book.

We are also grateful to the authors, who reviewed the edited and, insome cases, the translated versions of their papers. The papers represent

ix

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

the personal views of the authors and reproduce the data and informationprovided by the authors at the time of the conference. The affiliations andposition of the authors are those that were in effect when the conferencetook place.

We hope that these papers will provide useful insights to other coun-tries inside and outside the region on the issues involved as they lay thefoundation for establishing the convertibility of their currencies in anincreasingly globalized world economy.

MANUEL GUITIAN AND SALEH M. NSOULI

X

©International Monetary Fund. Not for Redistribution

OverviewManuel Guitian and Saleh M. Nsouli

Currency convertibility—defined in the broadest sense as the right toconvert freely and without limit a currency into any other at the pre-

vailing exchange rate—is the linchpin of today's globalized world econ-omy. To assess the importance of convertibility, it is only necessary topoint out that a system of well-managed convertible national currenciesimparts to the international arena advantages analogous to those result-ing from the introduction of money in a national economy, most notably,the elimination of barter (and the need for coincidence of needs) as abasis for international trade and the provision of an instrument for the de-velopment of financial markets.

It is not, therefore, surprising that the founding fathers of the Inter-national Monetary Fund (IMF) saw the promotion of convertibility—al-beit limited mainly to current account transactions—as central to theFund's mandate under Article VIII of the Articles of Agreement. Yet theIMF's limited concept of convertibility has become increasingly anachro-nistic in today's globalized world economy, where current and capital ac-count transactions are at the very least equally important. The logical nextstep was taken at the last meeting of the Interim Committee of the Boardof Governors of the International Monetary Fund. The Committee, in itscommunique of October 8,1995, "stressed that increased freedom of cap-ital movements and globalized markets bring significant benefits to allcountries (p. 2)." It underscored the importance of a "consistent imple-mentation of firm economic policies . . . to help reduce the volatility ofcapital movements," and encouraged the Fund "to pay increased attentionto capital account issues and the soundness of financial systems. . . .(p. 2)"

1

d

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

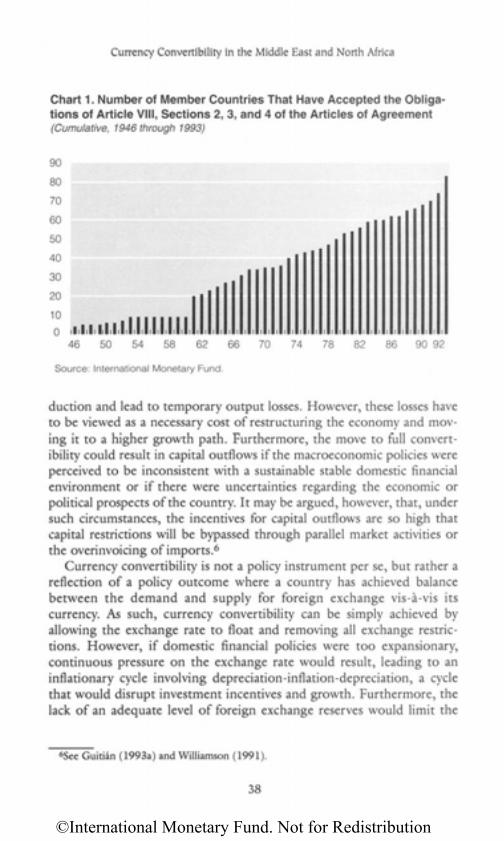

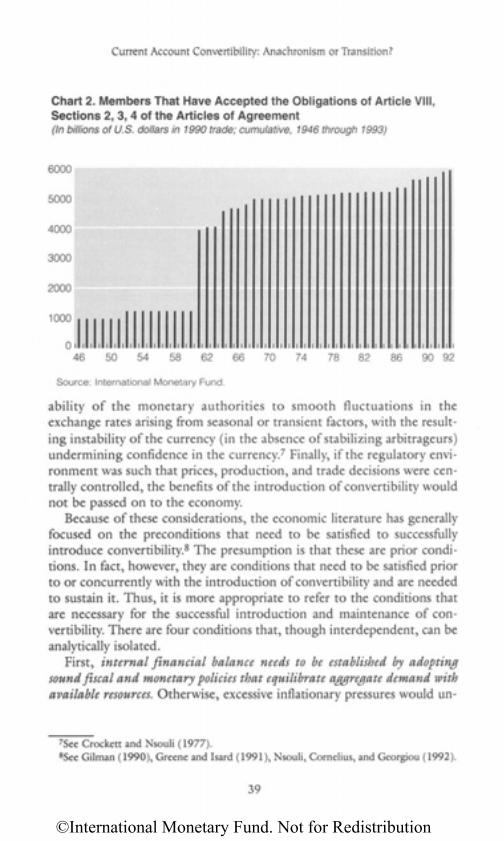

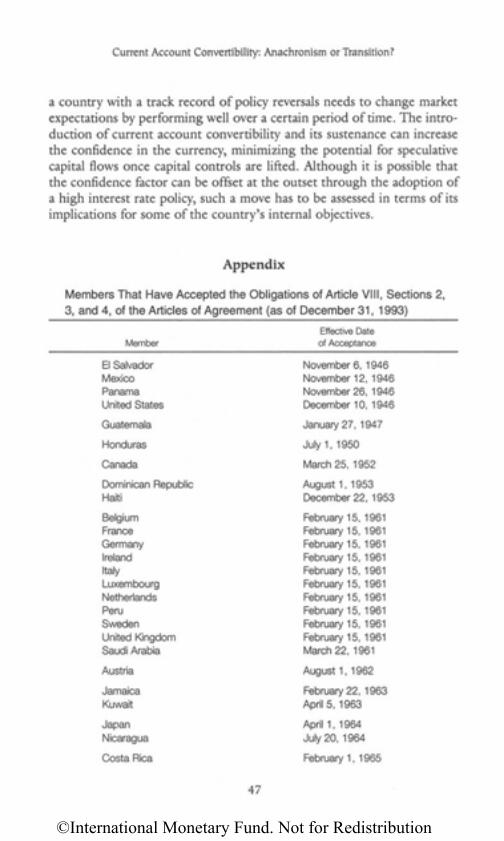

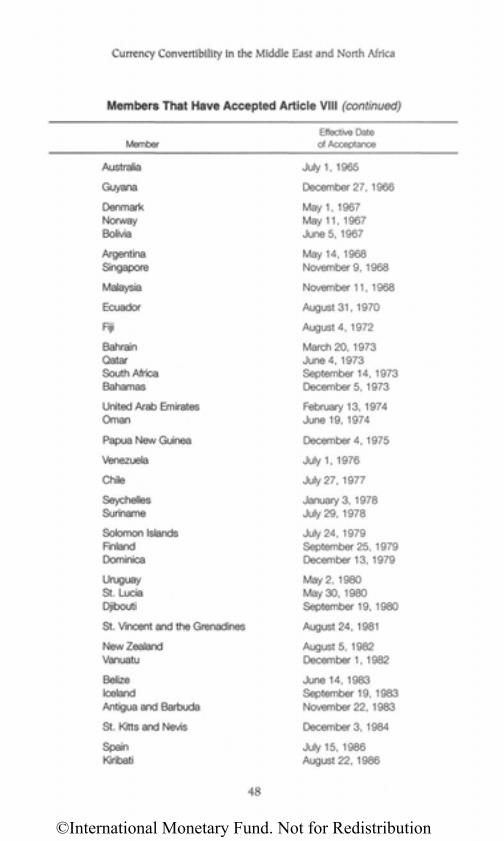

The Fund has made significant progress in its original mandate to en-courage members to establish current account convertibility, under Arti-cle VIII, Sections 2, 3, and 4 of the Articles of Agreement. As of Octo-ber 10, 1995, 109 member countries out of a total membership of 180had accepted the obligations under Article VIII. During the twenty yearsfollowing the establishment of the Fund, 1946-65, only 27 countries ac-cepted those obligations. The pace picked up during the following twentyyears, 1966-85, but only marginally, with 33 additional countries accept-ing those obligations. It is only over the last eleven years, 1986-96 (as ofMay 21, 1996), that the pace accelerated significantly, with an additional55 countries accepting those obligations. Interestingly, only 6 countriesin the Middle East had accepted those obligations (Saudi Arabia, Kuwait,Bahrain, Qatar, the United Arab Emirates, and Oman) through 1974,while no North African country had. Remarkably, there was a hiatus untilJanuary 1993, when Tunisia and Morocco accepted those obligations,becoming the first North African countries to do so. Lebanon followedsuit in September 1993, with Jordan being the latest country in the re-gion to accept in February 1995. Many countries, however, both in theMiddle East and North Africa, as well as in the rest of the world, haveachieved in an economic sense de facto current account convertibility,with only some technical issues hindering them from complying with theobligations under Article VIII. Furthermore, many countries that haveaccepted the obligations under Article VIII, as well as many of those thathave not, do have to varying degrees capital account convertibility.

Themes of the Seminar

The seminar in Marrakesh, organized by the Arab Monetary Fund incollaboration with the Government of the Kingdom of Morocco and theInternational Monetary Fund, focused on both the theoretical aspectsand empirical issues relating to the introduction of currency convertibil-ity. It came on the heels of the above-mentioned establishment of currentaccount convertibility in Morocco and Tunisia, an accomplishment thatboth countries considered as evidence of the success of their adjustmentand reform efforts.

The seminar gathered a wide array of government officials and aca-demicians from the Middle East and North Africa. The papers presentedcovered a number of theoretical questions that contrasted the experienceof a number of Middle Eastern and North African countries in movingtoward convertibility, and provided detailed case studies of Morocco'sand Tunisia's efforts to establish current account convertibility. Both of

2

©International Monetary Fund. Not for Redistribution

Overview

the speakers who delivered opening remarks—Omar Kabbaj, Morocco'sMinister Delegate to the Prime Minister Responsible for Economic In-centives, and Osama Faquih, Director General and Chairman of theBoard of the Arab Monetary Fund—stressed the importance of convert-ibility for fostering trade and financial linkages among the Arab coun-tries and with the rest of the world, for promoting investment andgrowth, and for enhancing regional economic cooperation. Kabbajpointed to the lessons that could be drawn from the Moroccan experi-ence, while Faquih highlighted the achievements of both Morocco andTunisia in establishing current account convertibility and noted theprogress that Egypt, Jordan, and Mauritania had made toward that ob-jective in recent years. They both encouraged the participants to focuson the theoretical aspects of the move to convertibility and the empiri-cal experience of the region.

Against this background, there were a number of questions that wereaddressed at the seminar:

• What are the various concepts and degrees of convertibility?• What are the costs and benefits of convertibility?• What are the policy preconditions for the successful establishment

and the conditions for sustaining currency convertibility?• What are the considerations involved in the sequencing of policies

and the speed with which convertibility can be introduced?• Should current account convertibility be established before moving

to full convertibility?• What is the status of exchange restrictions in Arab countries, and

what progress has been made in eliminating them?• What have been the specific experiences of Tunisia, Morocco,

Egypt, and Jordan in moving toward convertibility?• In a more general vein, how has the financial code of conduct with

regard to convertibility established nearly five decades ago in theBretton Woods Conference changed?

Concepts and Degrees of Convertibility

Manuel Guitian set the stage for the discussion by reviewing the vari-ous concepts and degrees of convertibility. He provided a broad currentdefinition of the concept of convertibility, namely, as the right to convertfreely a national currency into any other currency. In this context, he differentiated between soft convertibility, which involves a market-deter-mined exchange rate system, and hard convertibility, which involves a

3

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

fixed exchange rate system. He noted that, in today's world of flexibleexchange arrangements, it was soft convertibility that prevailed. He ex-plained that the move from hard to soft convertibility, associated with theabandonment of the Bretton Woods par value regime, was fostered bythe latter's very success in promoting the integration of nationaleconomies into the world system, which heightened the difficulties en-countered by countries to live within the constraints imposed by the con-sequent interdependence.

Guitian underscored that few currencies adhered to the above defini-tion of full convertibility. He noted that there were limitations or re-strictions that resulted in different degrees of convertibility. He examinedthe degree of convertibility from three angles. First, from the standpointof holders, he differentiated between external and internal convertibility.The former refers to the right of foreign holders of currency to converttheir balances into foreign exchange, while the latter refers to the rightof domestic holders of currency to convert their balances into foreign ex-change. Second, from the standpoint of the purpose, Guitian pointed outthat the degree of convertibility was circumscribed by the nature of thetransaction—with current and capital account convertibility being thetraditional distinction. Third, from a geographical standpoint, the differ-entiation could be made between regional and global convertibility.

Convertibility, in a fundamental sense, was affected by restrictionsother than those on exchange transactions, particularly those on importsof goods and services and of capital exports, Guitian explained. For in-stance, a currency that is convertible because there are no exchange re-strictions could be made practically inconvertible through trade and cap-ital controls. He argued that the interconnections between financial andreal transactions provided the basis for the distinction of real or com-modity convertibility (prevailing when there are no exchange and tradecontrols) and financial convertibility (requiring only the absence of ex-change controls).

Guitian noted that the degree of convertibility in the IMF is assessedby three standards: the currency's usability (the purpose), its exchange-ability (into other currencies), and its exchange value (hard or soft con-vertibility). He explained that the first two standards are conceptuallysubject to well-defined boundaries. A currency can be used either for allpurposes or not at all. Similarly, a currency can be exchanged either forall currencies without limit or for none. The degree of convertibility canbe defined as involving gradations within these boundaries. However, asfar as exchange value is concerned, the standard of relativity is different,with the degree of currency convertibility depending on the extent orscale of oscillations in its exchange value. In this context, Guitian noted

4

©International Monetary Fund. Not for Redistribution

Overview

that the focus of convertibility in the IMF's Articles of Agreement on cur-rent account transactions reflected the original concern with restoring thefree flow of international trade in goods and services that had been dis-rupted by World War II.

Preconditions, Sequencing, and Speed

Saleh Nsouli focused on the preconditions to convertibility, the bene-fits and costs associated with the establishment of convertibility, the considerations behind the appropriate speed at which convertibility can beintroduced, and the issues involved in sequencing the reforms to meet thepreconditions.

He explained that currency convertibility was not a policy instrumentper se, but rather a reflection of a policy outcome where a country hadachieved balance between the demand for and supply of foreign ex-change vis-a-vis its currency. As such, currency convertibility could besimply achieved by allowing the exchange rate to float and removing allexchange restrictions. However, if domestic financial policies were tooexpansionary, continuous pressure would then be exerted on the ex-change rate, leading to an inflationary cycle involving depreciation-infla-tion-depreciation—a cycle that would disrupt investment incentives andgrowth. Furthermore, the lack of adequate foreign exchange reserveswould limit the ability of the monetary authorities to smooth fluctua-tions in the exchange rates arising from seasonal or transient factors,with the resulting instability of the currency (in the absence of stabiliz-ing arbitrageurs) undermining confidence in the currency. Finally, if theregulatory environment was such that prices, production, and trade de-cisions were controlled centrally, the benefits of the introduction of con-vertibility would not be passed on to the economy. In this light, henoted that four preconditions needed to be met, namely, achieving in-ternal financial balance through sound fiscal and monetary policies;achieving external financial balance through an appropriate exchangerate; building up adequate international reserves; and liberalizing theincentives system.

The speed with which convertibility is introduced and the sequencingof its introduction were critical to ensure that it generates beneficial ef-fects for the economy, Nsouli explained. He noted that the successfuladoption of convertibility involved a comprehensive set of both macro-economic and structural reforms to achieve financial balance and alloca-tive efficiency. It was, therefore, synonymous with successful adjustment.He argued that the distinction between the fast and gradual approaches

5

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

to adjustment was somewhat overdrawn. In practice, the speed of adjust-ment—and the concomitant introduction of convertibility—would de-pend on the specific circumstances of each country but could be definedtheoretically as being the optimal adjustment trajectory that will maxi-mize the country's inter temporal welfare function, with an appropriatesocial discount rate, subject to various financial and structural constraints.

With regard to sequencing, he gave high priority to macroeconomicpolicies designed to align aggregate demand with available resources. Buthe emphasized the need to take into account the compatibility of struc-tural reforms with the re-establishment of macroeconomic stability; thecomplementarity of policies in determining the timing of their introduc-tion; the lead time involved in the preparation and the implementation ofpolicies; the gestation period for the reforms to yield results; and the dis-tribution effects to avoid social tensions that would derail the reforms.

Within the above framework, he examined three different approachesto convertibility: front-loaded, preannouncement, and by-product. Ingeneral, he considered that the first approach to convertibility, where theestablishment of convertibility had to lead policy decision making, im-plied a low social discount rate and a binding external financial constraint,with sequencing being governed by the need for rapidly adjusting macro-economic policies and introducing complementary structural measuresup front. In the process, the compatibility, lead time, gestation, and dis-tribution considerations would be constrained. The preannouncementapproach, which involved setting a specific date for eliminating currentaccount restrictions, subordinated all objectives and policies to theachievement of convertibility and implied a higher social discount ratethan the front-loaded approach, with less of an external financial con-straint. It was less binding in terms of macroeconomic compatibility,complementarity, lead time, and gestation considerations, as well as dis-tribution effects. Finally, under the by-product approach, Nsouli ex-plained, convertibility was not an objective of economic policy per se. Itwas, therefore, consistent with either a high or a low social rate of dis-count, with the pace of adjustment and reforms proceeding either slowlyor quickly. The availability of financing would, of course, be an importantconsideration, but issues relating to compatibility, complementarity, leadtime, gestation, and distribution were likely to dominate the process.

Nsouli concluded that, while current account convertibility in today'sworld could be viewed as an anachronism in the sense that it deprived thecountry of the full benefits of convertibility, many countries had movedgradually to establish current account and, subsequently, capital accountconvertibility. In terms of the framework discussed, the establishment ofcurrent account convertibility as a transitional step toward achieving full

6

©International Monetary Fund. Not for Redistribution

Overview

convertibility would seem consistent with the "revealed" optimal adjust-ment path that would maximize a country's welfare function.

Reviewing the Arab Experience

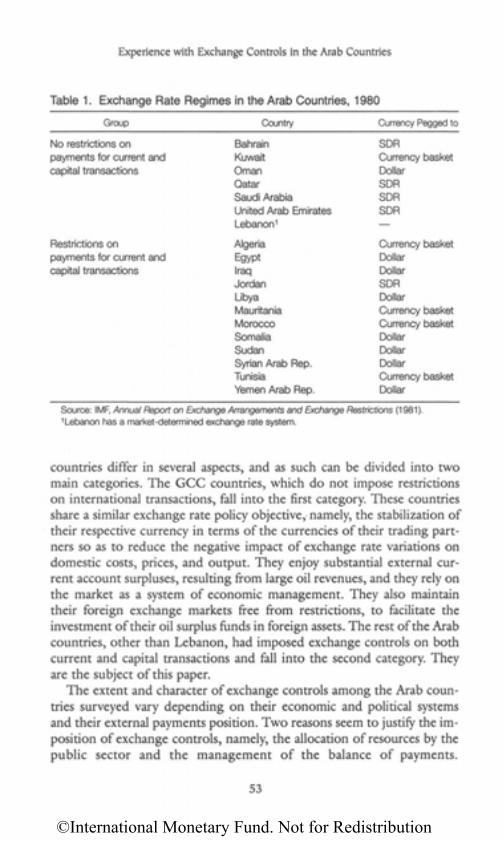

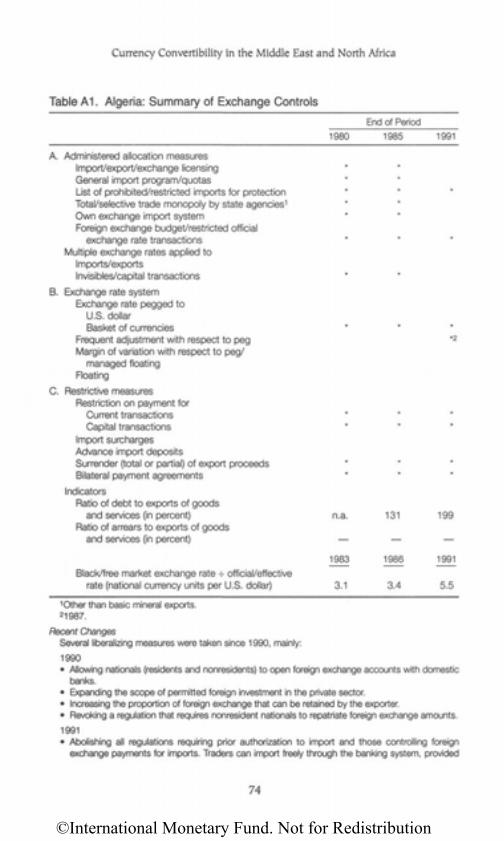

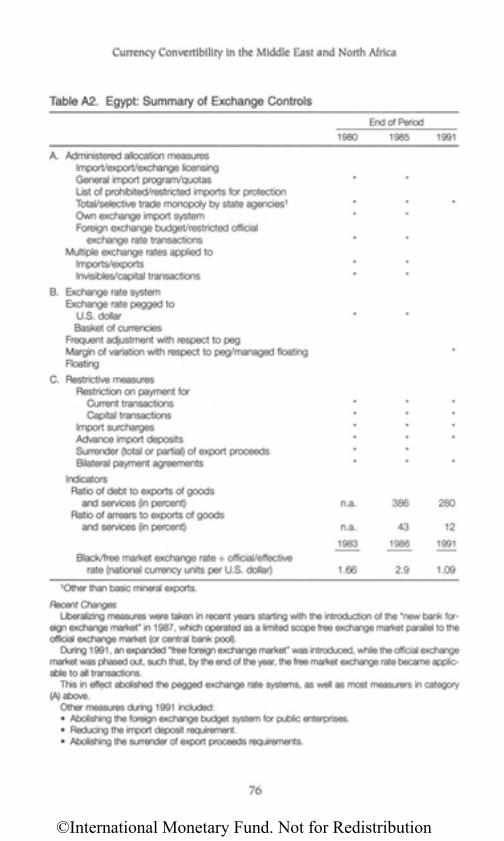

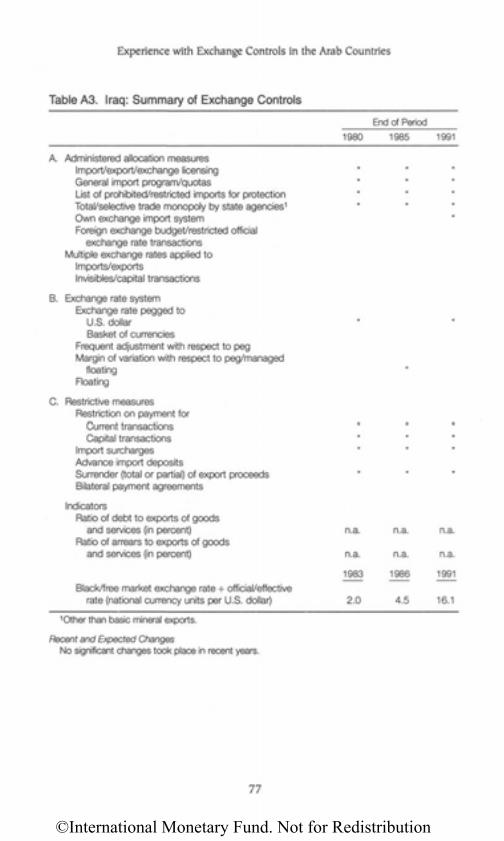

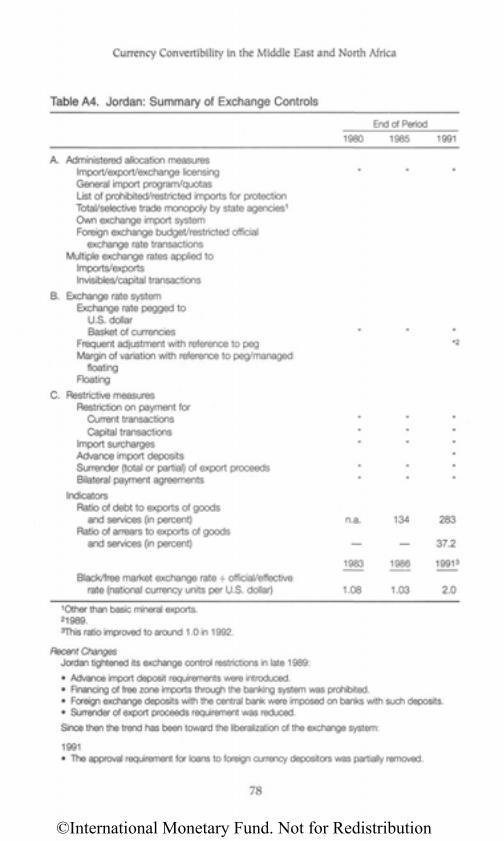

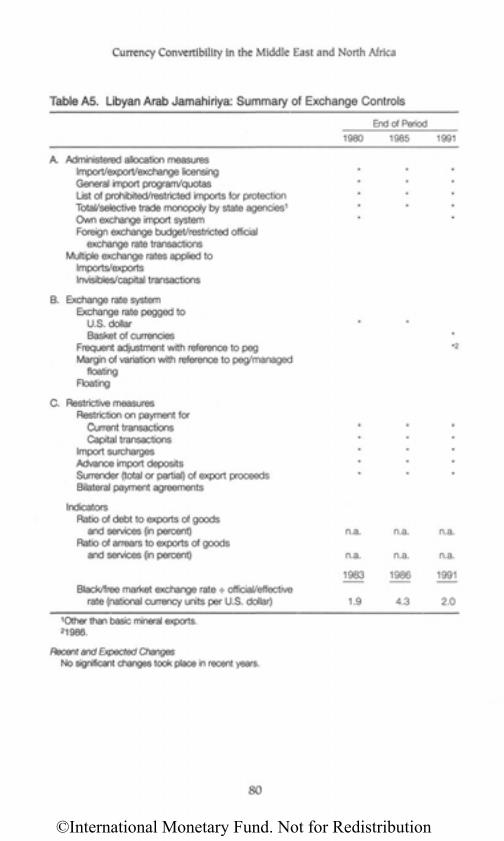

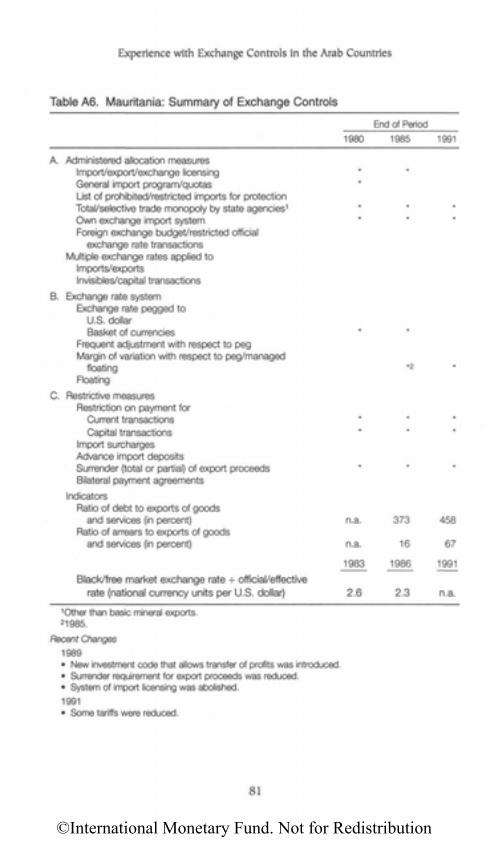

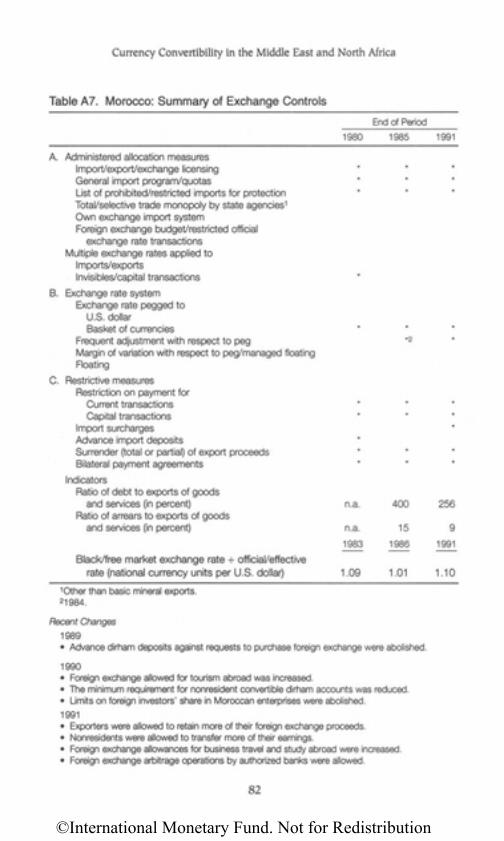

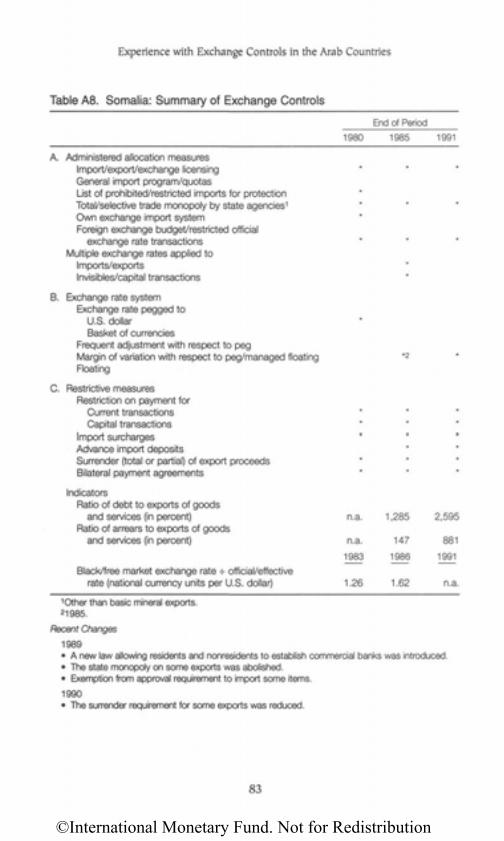

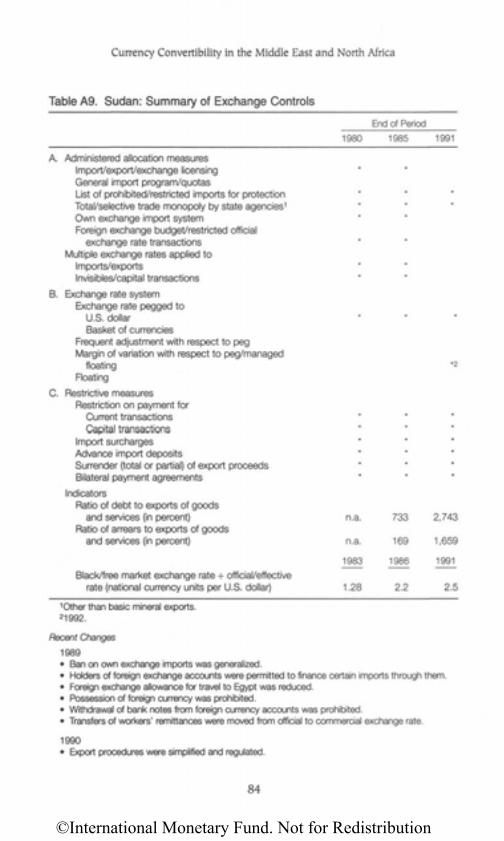

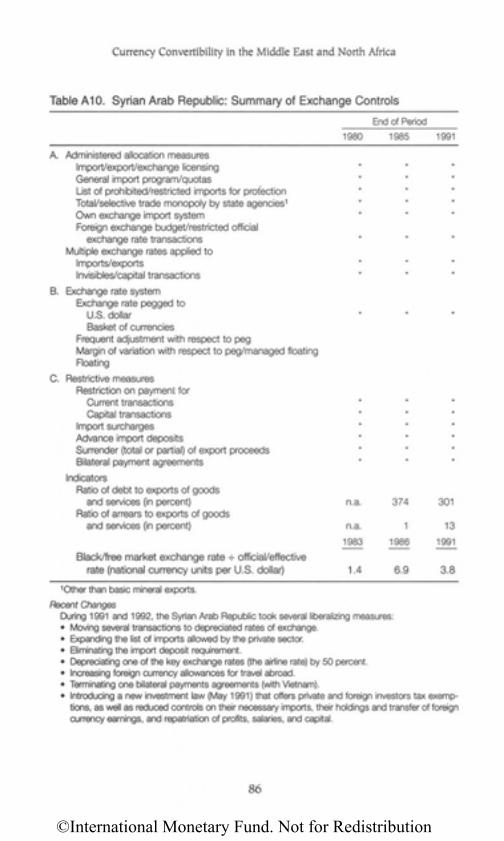

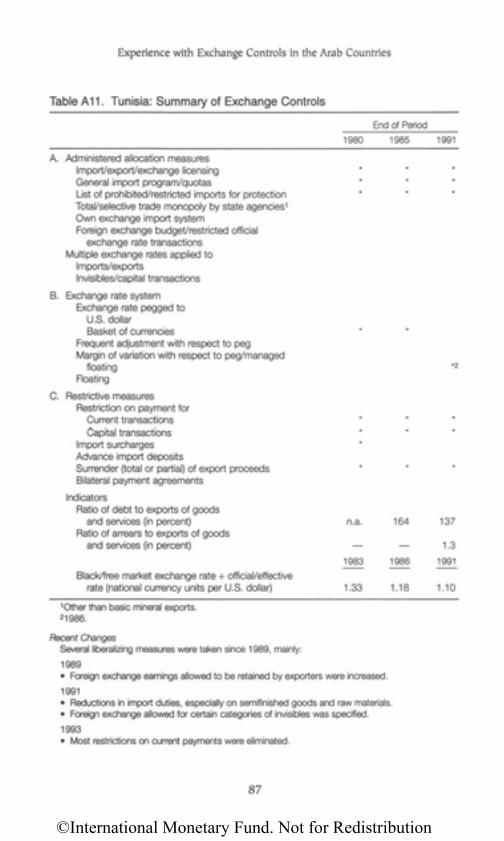

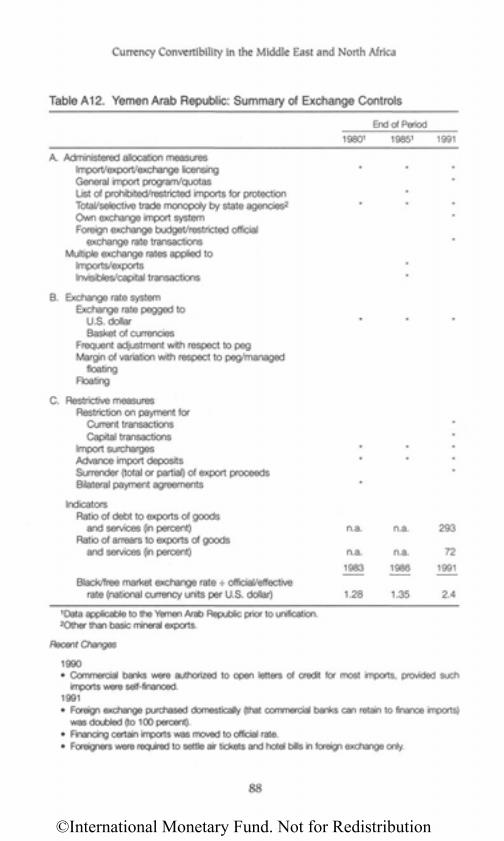

Moustapha Kara and Salam Hleihel focused on the reforms in the 12Arab countries with exchange restrictions on current or capital transac-tions, or both (Algeria, Egypt, Iraq, Jordan, Socialist People's LibyanArab Jamahiriya, Mauritania, Morocco, Somalia, Sudan, Syrian Arab Re-public, Tunisia, and the Republic of Yemen), underscoring that 8 otherArab countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, UnitedArab Emirates, and Lebanon) had no restrictions. They explained that thereforms of the exchange systems in most of the 12 countries had gainedmomentum in the 1980s.

Kara and Hleihel broke down the 12 Arab countries surveyed into twogroups. Group A was characterized as a set of countries that had or hadhad a dominant public sector and a centrally planned economy, andwhere the government exercised strict control over the volume and allo-cation of foreign exchange. The group comprised Algeria, Egypt, Iraq,Socialist People's Libyan Arab Jamahiriya, Somalia, Sudan, and the Syr-ian Arab Republic. In these countries, exchange controls were part of thesystem of economic management. Group B was defined as consisting ofcountries with market-oriented economies and whose main reason for ex-change controls was the management of the balance of payments. Thesewere Jordan, Mauritania, Morocco, Tunisia, and the Republic of Yemen.In these countries, exchange controls aimed at limiting the balance ofpayments pressures and supporting the exchange rate.

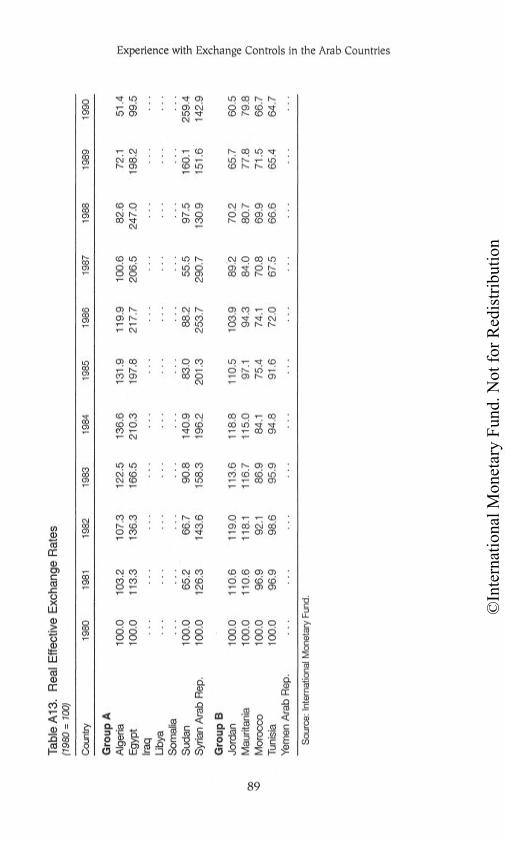

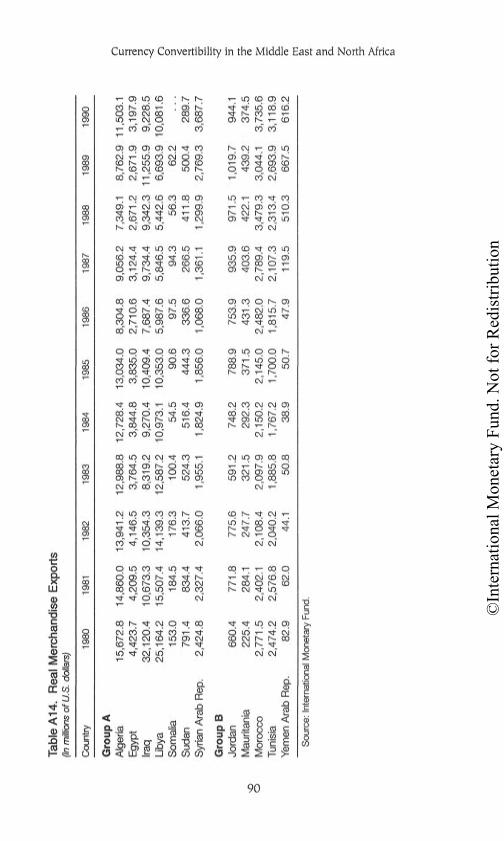

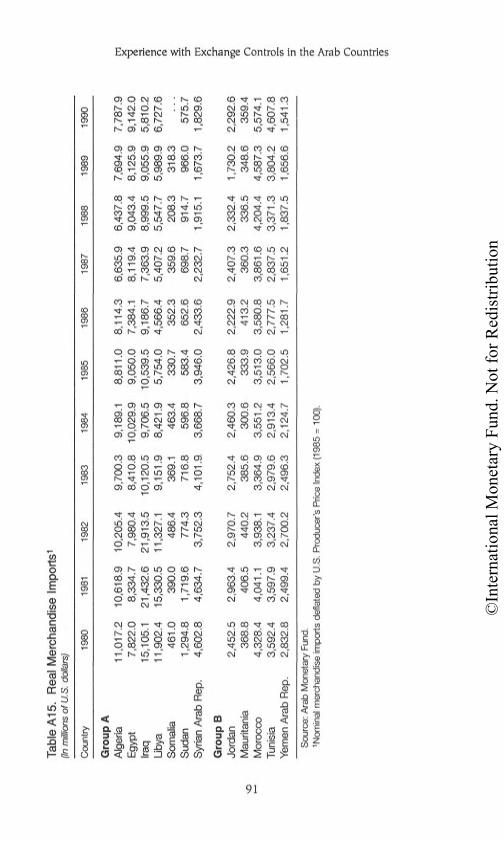

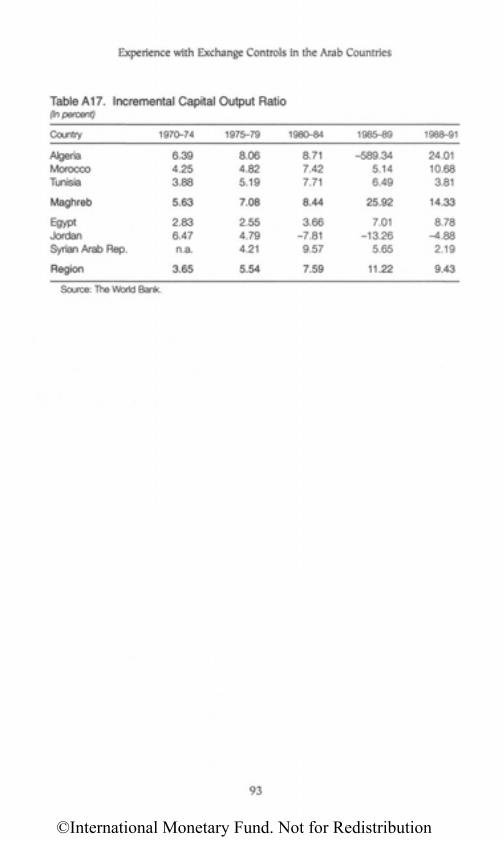

Kara and Hleihel noted that countries in Group A suffered fromhigher distortions than those in Group B. Countries in Group A had gen-erally experienced during the 1980s a more pronounced real effective ap-preciation of their currencies, a greater diversion of domestic resourcesfrom the traded to the nontraded sectors, a more disappointing exportperformance, a wider divergence between official and parallel market ex-change rates, a more acute diversion of foreign exchange to parallel mar-kets, and a higher volume of capital flight. For both groups, howevergrowth performance had been disappointing during the 1980s, as com-pared with the previous decade, and efficiency, as measured by the incre-mental capital output ratio, had remained low.

Countries in group A had pursued the transition to liberalized ex-change systems since 1980 in stages rather than in one step, Kara andHleihel explained. By 1991, Egypt had virtually fully liberalized its ex-

7

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

change regime and unified its exchange rate. In Sudan, although a uni-fied foreign exchange market was introduced in 1992, the exchange ratehad not been sufficiently flexible and exchange controls had remained inplace, with the result that activity on the parallel market had continued toreflect the pressures on external resources. In spite of periods of progressin re-establishing external financial balance and reducing exchange con-trols, Somalia had continued to experience divergences between the offi-cial and parallel market exchange rates throughout the 1980s. In Algeria,efforts to liberalize exchange restrictions remained constrained to a cer-tain degree in 1992 by external sector difficulties. The Syrian Arab Re-public, which had reduced exchange restrictions somewhat by 1992, con-tinued to have multiple exchange rates. Iraq and the Socialist People'sLibyan Arab Jamahiriya were singled out as the only two countries thatdid not undertake significant exchange reforms. By contrast, considerableprogress in reducing exchange restrictions in group B had been achieved.Both Morocco and Tunisia had made major strides in liberalizing theirexchange controls, particularly for current account transactions, in thecontext of comprehensive adjustment programs. Similarly, Mauritaniaand Jordan had moved forward. The Republic of Yemen's exchange sys-tem, however, had become more restrictive.

Specific Case Studies: Tunisia, Morocco,Egypt, and Jordan

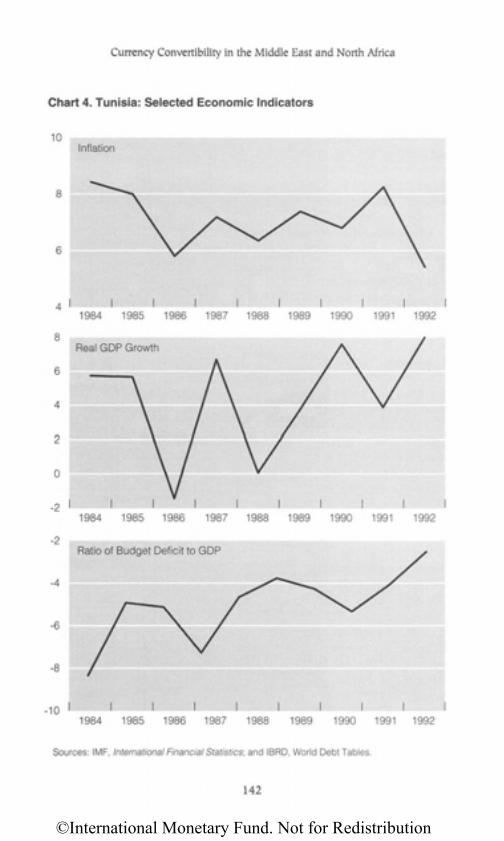

Three studies focused in greater depth on Tunisia, Morocco, Egypt,and Jordan. Abdelmoumen Souayah reviewed Tunisia's experience indecontrolling its exchange system, while Ali Amor traced that ofMorocco. Arfan Al-Azmeh provided a comparative study of the fourcountries.

Souayah placed the move to convertibility in Tunisia in the context ofthe overall reorientation of the country's economic and financial poli-cies. He considered that the revival of interest in a liberal economy inTunisia had followed the failure of the socialist system of development.This revival coincided with the external payments crisis that facedTunisia in 1986, and which had prompted the government to launch aprogram aimed at economic rehabilitation and consolidation. Under theprogram, progress in liberalizing and restructuring the economy hadbeen made in a number of areas, notably the import system, the taxstructure, and the financial system. The pursuit of sound budgetary,monetary, and exchange rate policies had helped reduce inflation andstrengthen the external sector position. This had enabled Tunisia to lib-

8

©International Monetary Fund. Not for Redistribution

Overview

eralize exchange restrictions for current account transactions at the endof 1992 and accept in January 1993 the obligations under Article VIII.Souayah foresaw the next phases toward the establishment of full con-vertibility, with the expected establishment in 1994 of a foreign ex-change market and the continued pursuit of coherent macroeconomicpolicies.

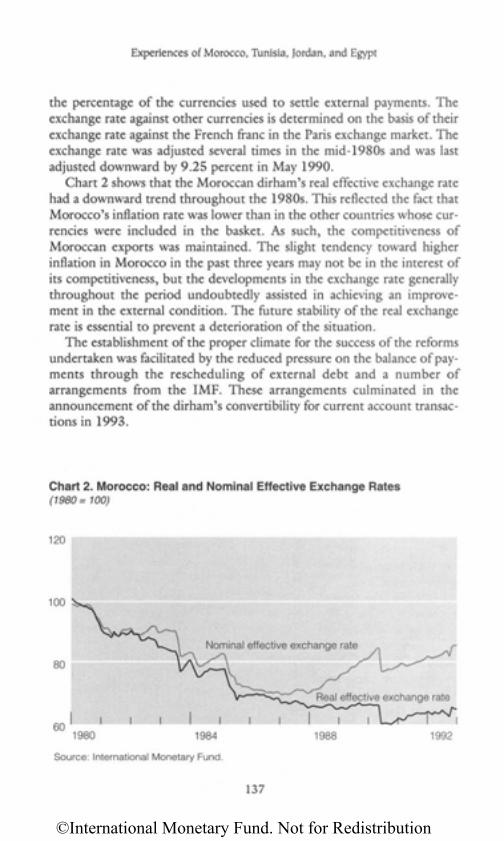

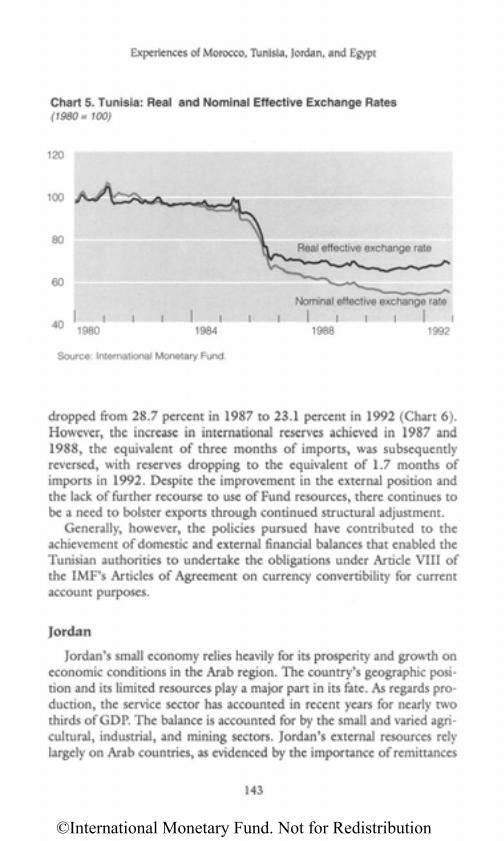

Amor traced exchange controls in Morocco to the colonial era, as partof a strategy to promote the Moroccan economy's integration intoFrance's metropolitan economic system. Upon independence, such con-trols were viewed as a means of promoting development. In analyzing de-velopments during the 1970s, he reached the conclusion that the ex-change restrictions had contributed to stifling economic activity andworsening the financial imbalances. Accordingly, the government had de-cided in 1983 to liberalize and open up the economy in the context ofsuccessive structural adjustment programs. A gradual approach to liberal-izing exchange controls had been chosen to allow the banking system toadapt to the new environment and to avoid "jeopardizing the fabric ofthe domestic economic system." Amor saw considerable positive resultsfrom the liberalization measures implemented, including those on ex-change controls. He considered the shift in the structure of imports to-ward capital and semifinished goods as a positive development associatedwith increased investment. Exports had also increased and been diversi-fied, while tourism receipts had expanded. Both remittances and foreigdirect investment had risen sharply. The improvement in the external sec-tor position had contributed to a reduction in the debt-service burdenand the buildup in foreign exchange reserves. At the same time, real GDPgrowth had averaged 3.5 percent a year during 1983-92. Looking ahead,he, like Souayah, foresaw the move to full convertibility and the estab-lishment of a foreign exchange market.

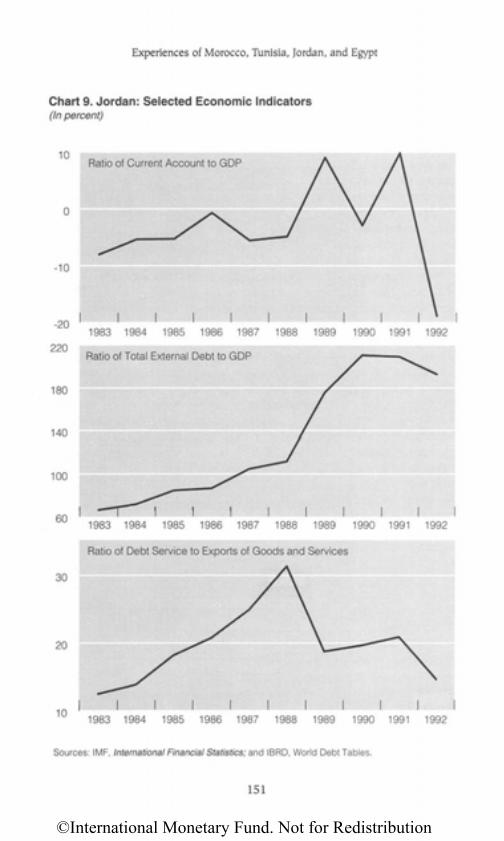

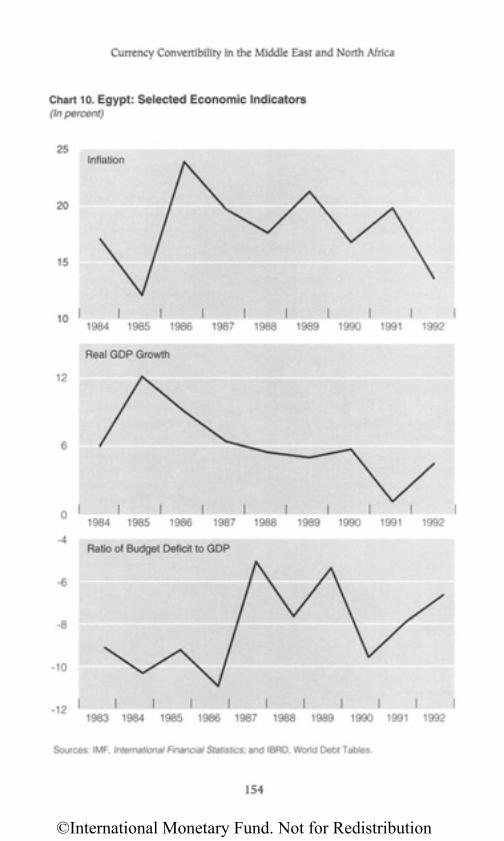

In a comparative study, Arfan Al-Azmeh reviewed the progress madeby Morocco, Tunisia, Jordan, and Egypt in meeting the four major pre-conditions for establishing convertibility. He considered that Morocco,which had made significant strides in reducing its budget deficit, main-taining a realistic exchange rate, building up its foreign exchange re-serves, and substantially decontrolling the incentives system, had satisfiedall four preconditions. However, it needed to remain vigilant in avoidinga resurgence of inflationary pressures and safeguarding its competitive-ness. While Tunisia had also met the preconditions, he considered thatthe progress made had been less than that achieved by Morocco andcalled for completing promptly the envisaged reforms in the secondphase. With regard to Egypt and Jordan, Al-Azmeh explained that theyhad hastened to virtually eliminate the exchange restrictions on current

9

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

transactions as soon as external balance had been re-established and for-eign exchange reserves built up, but that both domestic financial man-agement efforts and structural reforms needed to be pursued.

Al-Azmeh noted a number of similarities and differences in the ap-proaches of these countries to establishing convertibility. First, all fourcountries had embarked on the liberalization of their exchange systems inthe context of comprehensive adjustment and reform programs. Second,the progress in exchange liberalization took place at different rates. In Mo-rocco, the pace was gradual and in tandem with that of trade liberalization.In Egypt, it had also been phased in between 1987 and 1991 in conjunc-tion with the progress made in the reform process. By contrast, in Tunisia,it had been concentrated in the final years of the 1986-92 reform pro-gram. In Jordan, the rapidity with which the move toward convertibilityhad progressed had reflected the limited degree of restrictions already inplace. Third, the timing of the announcement of convertibility had dif-fered. In Morocco, it was announced as an objective a year before it wasachieved, while in Tunisia it was announced at the same time it was im-plemented. In Egypt and Jordan, no announcement had been made (as ofthe end of 1993) as there remained some technical obstacles to officiallyaccepting the obligations under Article VIII. Overall, Al-Azmeh consid-ered that the experience of these four countries showed that convertibil-ity, rather than representing invariably the culmination of adjustment andreform programs, could be viewed as an integral part of the adjustmentand reform process, complementing and reinforcing it.

Capital Account Convertibility

In presenting the last paper at the seminar, Guitian made a strong casefor an up-front move to full convertibility as a means of leading financialpolicies and economic reforms, thereby turning the tables on thepreconditions for establishing convertibility. He stressed that economiclogic advocates the dismantling of capital controls; developments in theworld economy make them undesirable and ineffective; and a strong casecan be made in support of a rapid and decisive liberalization of capitaltransactions. All these conditions underpin strongly a code of conductthat eschews resort to capital controls as an acceptable course of actionfor economic policy.

Guitian argued that, with the growing predominance of capitalmovements in international transactions, the international financial codeof conduct focusing on current account convertibility that was estab-lished nearly five decades ago in the Bretton Woods Conference had be-

10

©International Monetary Fund. Not for Redistribution

Overview

come outdated. He explained that there were normative benefits to bederived from updating the code of conduct to include full convertibilitywith the benefits deriving mainly from the provision of faster and clearersignals when inconsistencies arose between national and internationalconsiderations of events. He emphasized that controls could only serve apalliatives to temporarily contain, but not to eliminate, the underlyingpressures, and that, in any event, capital controls could be circumvented.

The case for capital controls, Guitian explained, was based on the im-portance of meeting the necessary preconditions before moving to exter-nal financial liberalization, such as achieving a sustainable fiscal positiona realistic exchange rate, as well as a well-functioning liberal domestic financial system. He feared, however, that waiting to fully meet such pre-conditions to liberalize capital movements could foster the maintenanceof capital controls. He considered that opening the capital account with-out fully meeting the preconditions would exert pressures to adoptquickly the necessary policies to bring about balance and stability to theeconomy. Nonetheless, he cautioned that, while capital account liberal-ization could be undertaken in less-than-optimal domestic economicconditions, it should not be undertaken under circumstances so far fromoptimality that the credibility of the decision to open the economy to in-ternational financial transactions would be so impaired that it could notbe sustained. In this regard, Guitian dismissed the notion that the open-ing of the current account should precede the liberalization of the capi-tal account, arguing that there did not seem to be any a priori reason whythe two accounts could not be opened up simultaneously.

Regarding the speed of liberalization, Guitian acknowledged thatthere was no single, categorical answer but leaned in the direction of fastliberalization. He felt that there was no guarantee that the leeway to ad-just to confront competition in a gradual approach would be, in effect,used, but rather that the tendency of operators would be to continue ex-ploiting the opportunities of a closed or partially closed economy. If agradual opening were to encourage delays in adjustment, he consideredthat its costs would not fall below those resulting from a fast liberaliza-tion. By contrast, a rapid opening of the economy would provide quicklyto economic agents the transparent signals that would generate gains inefficiency and attract international resource flows.

Conclusions

A number of general conclusions can be drawn from the seminar, al-though authors differed in their emphasis. First, currency convertibility is

11

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

critical to help integrate the Middle East and North Africa into the glob-alized world economy. Apart from the systemic benefits, there are bene-fits to be derived in each country in terms of the resulting allocative effi-ciency, the necessary macroeconomic discipline, the increasedproductivity and competitiveness, the attraction of foreign direct invest-ment, and the importation of technological know-how. The downsiderisks were viewed particularly in terms of the potential for temporary pro-duction dislocations and disruptive capital flows.

Second, the establishment of currency convertibility is part of an over-all adjustment and reform process. The case studies of Tunisia and Mo-rocco, which assumed the obligations under Article VIII in early 1993,and the comparative study with Egypt and Jordan, which had only defacto achieved convertibility by the time of the seminar, illustrated clearlyhow convertibility had progressed in the context of the adjustment andreform programs that these countries had implemented.

Third, the achievement of domestic and external balances, the buildupof reserves, and the liberalization of the incentives system are importantpreconditions for the establishment and the sustenance of convertibility.The theoretical underpinnings of meeting those preconditions were ana-lyzed, and the case studies showed the progress that various Middle East-ern and North African countries had made in this regard. While most au-thors considered that convertibility should follow the establishment ofthe preconditions, at least one author put forward the possibility that theintroduction of convertibility could prompt the authorities to moverapidly to satisfy those preconditions.

Fourth, current account convertibility can be viewed as a transitionalphase toward the establishment of full convertibility. Most participantswere of the view that a gradual approach would minimize the costs andmaximize the benefits of establishing convertibility. The theoreticalframework for analyzing the optimal speed of introducing convertibility,as part of the overall adjustment process, suggested that it was difficultempirically to qualify a process as fast or gradual. Certainly, the casestudies pointed to the "revealed preferences" of the countries consideredto proceed in a phased and gradual manner. The point, however, wasmade that too gradual an approach could result in perpetuatingrestrictions and inefficiencies, while the benefits of full convertibilitycould be reaped earlier if it were introduced rapidly and supported bythe necessary policies.

Fifth, the progress toward officially establishing convertibility in theMiddle East and North Africa needs to be accelerated. Only eight coun-tries in the region had accepted the obligations under Article VIII by thetime of the seminar, and only two additional ones have accepted those

12

©International Monetary Fund. Not for Redistribution

Overview

obligations since then. While a number of other countries in the regionhave already de facto virtually full convertibility, some minor restrictionsstill impede them from assuming the obligations under Article VIII anddeprive them of the benefits of the signaling effect of the irreversibility ofassuming such obligations. Still, some other countries in the region re-main far from satisfying the preconditions and need to implement the ad-justment policies and structural reforms needed to lay the foundation forestablishing convertibility.

13

©International Monetary Fund. Not for Redistribution

Opening Remarks

Omar Kabbaj*

It is an honor and a genuine pleasure for me to deliver the openingremarks today for this seminar on currency convertibility. I wish, first ofall, to welcome you to Marrakesh, a city with a rich cultural heritage anda wealth of tourist attractions. I also wish to thank the authorities of theArab Monetary Fund and the International Monetary Fund for choosingto hold this seminar in the Kingdom of Morocco. In addition, I wouldlike to express our appreciation to Mr. Osama Faquih, Director Generaland Chairman of the Board of the Arab Monetary Fund, who has hon-ored us by attending and participating personally in this important event,and to congratulate him on his election as President of the IslamicDevelopment Bank. Furthermore, I wish to extend greetings to thesenior officials from the participating countries. Their presence demon-strates the interest and importance that the Arab countries' monetaryauthorities accord to the topics to be discussed during this seminar.

While I will leave to the distinguished experts participating in this con-ference the comprehensive discussion and analysis of the various theoret-ical and practical issues related to currency convertibility, I wish, never-theless, to share with you a few key ideas on the matter, and some lessonsin this regard that can be drawn from the Moroccan experience.

Convertibility represents a far-reaching instrument to facilitate inte-gration into the global economy. The worldwide adoption of marketeconomies, the development of world trade, and the increasing mobility

*Minister Delegate to the Prime Minister, Responsible for Economic Incentives,Kingdom of Morocco.

14

g

©International Monetary Fund. Not for Redistribution

Opening Remarks

of capital flows have led to the globalization of the international econo-my and exchange system. In these circumstances, domestic economiescannot play a role in this process and benefit fully from its advantagesunless they introduce the necessary instruments and mechanisms, includ-ing the establishment of the convertibility of their currencies, therebyeliminating all exchange restrictions. Convertibility is also necessary fordomestic economies to achieve an optimal allocation of their resources.

While structural reforms are designed to eliminate sectoral distortionsand to strengthen the rules of the market, they will remain limited inscope if they are not supported by currency convertibility. Indeed, con-vertibility makes it possible for economic transactors to choose freelybetween the domestic market and external markets and promotes priceformation through the free interplay of market forces, which is conduciveto the efficient allocation of resources and the stimulation of competi-tiveness within an economy.

With respect to the Arab world, I must stress the important role thatconvertibility can play in enhancing cooperation among the countries,especially in the commercial, economic, and financial spheres. There is nodoubt that the spread of convertibility within the Arab world can open upnew prospects for the economies through the development of inter-Arabinvestment flows, increased trade among Arab countries, and theenhancement of complementarity in production structures.

It is important to emphasize that convertibility should not be limitedpurely to international current account operations. Rather, it should beintroduced gradually to encompass capital account transactions andshould be accompanied by the establishment of a foreign exchange mar-ket. In my view, full convertibility should be the final objective, support-ed by the required structural reforms and a viable macroeconomicframework.

You will certainly have the opportunity during the seminar to learnmore about the Moroccan experience with convertibility. Let me stress,however, a number of issues related to that experience that I consider ascrucial. The introduction of convertibility in Morocco is the crowningachievement of an economic restructuring and adjustment process thatbegan in 1983. This effort has led to clear progress in correcting domes-tic and external imbalances, liberalizing the economy, notably throughthe development of market mechanisms and the promotion of private ini-tiative, and opening up the Moroccan economy to the outside world.Based on these achievements, Morocco was able, effective January 1993,to introduce the convertibility of the dirham for international currentaccount operations and to end the cycle of rescheduling by resuming reg-ular payments for its external debt service.

15

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

The latter two actions were taken in a particularly unfavorable inter-national environment and in the midst of a two-year drought. The econ-omy, however, had become sufficiently robust and, thus, able to enterinto a new phase of integration into the world economy. At the sametime, an appropriate fiscal and monetary stance was maintained and fur-ther structural reforms were pursued. Capital inflows have continued, theexternal current account deficit has been held to acceptable levels, andnet international reserves are growing. We can, therefore, say that, near-ly one year after its introduction, the impact of convertibility onMorocco's economy has proved to be largely positive. We have clearedthe hurdle of introducing convertibility, while avoiding many of thepotential risks inherent in such an operation.

The widening of the scope of convertibility was pursued in 1993, par-ticularly with the liberalization of access to external financing for eco-nomic operators and the authorization for exporters and Moroccansresiding abroad to hold convertible foreign exchange accounts. Weintend to persevere in this direction and to establish a foreign exchangemarket. This task is already listed among the priorities set by theGovernment of His Majesty, the King, as recently described before theHouse of Representatives within the framework of the government'sprogram.

Before closing, I would like to suggest that the eminent experts fromthe international organizations and representatives of the Arab countries'monetary authorities participating in this seminar provide greater enlight-enment on two factors I consider current and of great interest in con-ducting financial policy. I refer, first, to an analysis of the relationshipbetween convertibility and the modernization of financial systems and thedevelopment of capital markets, and, second, to an examination of theimpact of convertibility on both direct and portfolio foreign investment.Given the significance of the topics to be discussed and the caliber of thespeakers, I feel certain that the deliberations will be rich and extremelyuseful for policymakers in the Arab world.

Osama J. Faquih*

I am delighted to welcome you to this historical and beautiful city ofMarrakesh, well known for its deeply rooted Arab and Islamic back-ground. I am pleased to inaugurate with you today this important and

* Director General and Chairman of the Board, Arab Monetary Fund.

16

©International Monetary Fund. Not for Redistribution

Opening Remarks

specialized seminar on currency convertibility, which has been placedunder the auspices of the Moroccan Ministry of Finance and jointly spon-sored by the Institute of the International Monetary Fund (IMF) and theArab Monetary Fund's Economic Policy Institute.

The seminar has been designed to address a number of substantiveissues that are both theoretically and empirically related to economicadjustment. In that context, it aims at providing an opportunity for ageneral review of the adjustment efforts in certain Arab countries and aclose assessment of the experiences of Morocco and Tunisia, whichannounced at the beginning of this year the establishment of currentaccount convertibility of their national currencies. Both are considered tobe pioneers in that area.

As many of the papers before you emphasize, currency convertibilityhad been one of the central concepts that the founding fathers of theBretton Woods system had intensively debated and sought to codify inthe wake of World War II. It constituted a key pillar underlying efforts toestablish a multilateral system of payments in respect of current transac-tions among nations and to eliminate foreign exchange restrictions thatimpede the growth of international trade. As a matter of fact, Article VIIIof the IMF's Articles of Agreement sets out in detail the rules and behav-ior to be observed by countries that accept the obligations of itsprovisions.

Five decades have elapsed since then, and the benefits of convertibili-ty for the promotion of free international trade, allocative efficiency, com-petitiveness, savings and investment flows have been clearly establishedand the risks for an individual country well identified. Yet, until recentlymany nations around the world, including some Arab countries, havebeen unable to establish convertibility.

It is against such a background that the Arab Monetary Fund (AMF)and the IMF, which is in charge of surveillance over exchange arrange-ments worldwide, have joined in organizing this seminar. They have invit-ed a distinguished group of eminently qualified experts, practitioners,academicians, and Arab officials to meet and exchange ideas and views onthe various notions of convertibility, the benefits and risks associated withthe concept, the conditions for its successful application, and its role instructural economic adjustment and growth.

The importance that the AMF attaches to currency convertibility is amirror image of the high priority accorded to its action program for eco-nomic stabilization and structural adjustment in Arab countries.Alongside this pursuit, the AMF program currently seeks to foster link-ages among Arab economies; to actively contribute to efforts aimed atmobilizing savings and resources and their channeling into productive

17

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

investments; to enhance the technical capabilities of the staff of officialArab monetary, banking, and financial agencies; and to promote closercooperation with regional and international financial institutions.

Indeed, the early 1980s witnessed a heightened international interestin macroeconomic adjustment policies and their implications. That peri-od was characterized by a rapid deterioration of domestic and externalfinancial imbalances, a dramatic increase of indebtedness and debt servicand poor economic growth performance in many developing nations.These included several Arab countries that courageously initiated andimplemented, at painful costs, comprehensive adjustment programs.

Interest in the adjustment process was not restricted only to indebtedArab countries confronting fiscal and external deficits. In fact, the Araboil producing countries have also realized in the past few years the impor-tance and urgency of timely adjustment in the face of declining terms oftrade associated with falling oil prices. As a result, these countries volun-tarily proceeded to rationalize government budgets and adopted prudentmonetary policies as part of their strategy to contain inflationary pres-sures. They concomitantly sought to diversify the sources of their rev-enues and to actively promote non-oil industries and exports. Reflectingthese endeavors, macroeconomic adjustment efforts and structuralreform programs in many Arab countries began to bear fruit.

In Morocco, substantial progress was achieved as policies pursued con-tributed to the resumption of growth, the diversification of the produc-tive and export base, the containment of inflation, and a considerablestrengthening of the external sector position. These achievementsenabled the country to announce the establishment of current accountconvertibility of the dirham. In this context, I should like to address aspecial tribute to His Majesty King Hassan II and the wise MoroccanGovernment, who should be fully credited for steering the economy ofMorocco in the right direction.

In this connection, a particular word of appreciation is due to HisExcellency Mohamed Barrada, former Minister of Finance, for his relent-less efforts and resolute determination in carrying out over a number ofyears a series of macroeconomic adjustment and reform programs. Theseaimed at enabling Morocco to enter a new era of increased self-reliance.There is no doubt in my mind that his successor, Professor MohamedSaghu, who has contributed significantly to the design and elaboration ofthose programs before assuming his current post, will seek to consolidatethe progress achieved by staying the course. I therefore wish him everysuccess in this pursuit.

In Tunisia, the adjustment efforts deployed and reform programsimplemented during the past eight years have been met with equal suc-

18

©International Monetary Fund. Not for Redistribution

Opening Remarks

cess. The policies pursued have led to the revitalization of economic activ-ity, the reduction in the rate of inflation, and the strengthening in theexternal sector position. These achievements enabled Tunisia to establishthe convertibility of the dinar of current account transactions at thebeginning of 1993.

In Egypt, a multiphase reform program was initiated in 1987. Itsimplementation has yielded a number of positive economic develop-ments, including an improvement in the government's financial positionand a strengthening in the balance of payments and international reservepositions. During 1991, the Egyptian authorities canceled the system ofmultiple exchange rates and floated the national currency. Many restric-tions on external trade and exchange were removed, paving the way forfull liberalization of the exchange system. The authorities are currentlyactively engaged in further action in that direction, while concurrentlyendeavoring to expedite the reform, restructuring, and privatization ofpublic sector enterprises.

Since 1989, Jordan has embarked on a major macroeconomic adjust-ment program and geared its policies toward restoring domestic andexternal financial balance. Notwithstanding the detrimental repercussionsof the 1990-91 crisis in the region, Jordan continued its adjustment ef-forts, which included, inter alia, the reduction of exchange restrictions,thereby putting the country close to achieving convertibility of theJordanian dinar for current account transactions.

In Mauritania, the authorities started in 1985 to implement successiveadjustment programs, which included several policy measures aimed atliberalizing the trade and exchange system. In that connection, a series ofactions were taken to review, simplify, and reduce custom tariffs. Importlicensing was dismantled, and some flexibility was introduced in theexchange rate system.

In a number of other Arab countries facing domestic and external dif-ficulties and imbalances, the authorities have been responding to the sit-uation by adopting, in varying degrees, adjustment policies and measures.Broadly, these aim at restoring financial balance, reforming the price sys-tem, and promoting greater private sector participation in economicactivity and growth. The results achieved by these countries are encour-aging. They provide scope for hope and optimism in the willingness andability of the authorities to maintain the adjustment momentum withinthe framework of comprehensive programs geared toward moving theireconomies to the path of sustainable growth, strengthening their balanceof payments position, and improving their creditworthiness.

As you all know, the world economy is becoming increasingly interde-pendent and globalized. In view of this, the ability of developing

19

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

20

nations—including Arab countries—to successfully safeguard the hard-won fruits of their comprehensive economic adjustment programs andfar-reaching liberalization of their trade and payment systems criticallydepends on the openness of markets in industrial countries and theremoval of barriers to international trade and payment restrictions.However, it is to be feared that, as a result of growing protectionist ten-dencies, the expected benefits from the grouping of industrial countriesinto gigantic regional economic and trading blocs might be limited tomember states only. If so, this would constitute a serious blow to theadjustment process in developing countries, which have made majorstrides in the past few years. Indeed, developing countries have complet-ed at a socially painful cost the requisite wide-ranging structural reformsand have thus succeeded in raising the level of the production of com-petitive exportables. Such countries, however, are set to face considerabledifficulties in marketing their exports. It, thus, becomes evident that, if itis incumbent upon developing countries facing imbalances to take timelycorrective action, then industrial countries—both old and new—shouldat the same time expedite the removal of obstacles to the flows of trade.More important, it is the responsibility of industrial countries to endeav-or to establish a more liberal, open, and equitable international econom-ic and trading system. The revitalization of their own economies and theprovision of adequate financial support on appropriate terms remain keyfactors for the success of economic adjustment and growth in developingcountries.

Once again, I would like to welcome you and to reiterate my thanksand appreciation to the officials of the Moroccan Ministry of Finance forhosting this seminar and for the excellent facilities and arrangements theyhave put in place. Special thanks are due to the International MonetaryFund for its instrumental cooperation in the organization and conduct ofthis seminar and for the valuable papers prepared by its staff. I would alsolike to thank the participants for their attendance and willingness to sharewith us and among themselves their knowledge, experience, and views onthe various aspects and issues of the seminar's central theme.

©International Monetary Fund. Not for Redistribution

Concepts and Degrees of CurrencyConvertibility

Manuel Guitian*

Currency convertibility has always been a fundamental notion in inter-national economic relations. Yet, since the abandonment of the

Bretton Woods par value regime, a remarkable degree of silence has untilrecently surrounded the subject. Possibly this silence is related to theadvent and prevalence of flexible exchange rate arrangements that fol-lowed the Bretton Woods order. The reason could be that, in theory,flexible exchange rates would make exchange and other restrictionsunnecessary or redundant; and, therefore, under such exchange ratearrangements currencies would be convertible by definition, so to speak.But as is often the case, what can be expected in principle does not alwaysmaterialize in practice; exchange, payments, and other internationalrestrictions have continued to prevail in the period of flexible exchangerates and, therefore, questions of currency convertibility have remainedopen.

Recently, though, the silence has been broken and numerous writingson the subject of convertibility have begun to appear. Two different setsof factors account for the renewed interest. One has been the widespread

* Director, Monetary and Exchange Affairs Department, International Monetary Fund.The views expressed in the paper are those of the author and should not be attributed tothe International Monetary Fund. For the preparation of the paper, I have relied extensiv-ely on the work on convertibility of several of my colleagues or ex-colleagues in the Fund.I would like to mention, in particular, Gold (1971), Polak (1991), Gilman (1990), Greeneand Isard (1991), and Mathieson and Rojas-Suarez (1993).

21

g

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

process of reform currently under way in the ex-collectivist economies ofcentral and eastern Europe, as well as of the former Soviet Union, thatbegan in the late 1980s. The other has been the process of domesticfinancial sector deregulation and capital market liberalization that eitherde jure or de facto has been carried out during the last decade in theindustrial world at large and in many developing countries.

From the standpoint of the societies in transition from central plan-ning to a market-based system of economic organization, the issue of cur-rency convertibility has become important in that it constitutes a keycomponent of their reform efforts. In this context, it has been pointedout that the concept of convertibility transcends the boundaries of a nar-row monetary question and that it embodies central elements of the strat-egy to transform economic regimes radically and comprehensively.

Developments in domestic financial markets in industrial economiesand in many developing countries and the consequent globalization ofinternational capital markets, in turn, have also stimulated interest in cur-rency convertibility issues. The interest here has focused on the degree,rather than the concept, of convertibility. In this regard, the issuesbrought to the fore have been those concerning currency convertibilityfor capital account transactions, more commonly referred to as capitalaccount convertibility.1

This paper discusses the concept of convertibility in its various modal-ities and degrees. Convertibility, like other related economic concepts,such as liquidity and restrictiveness, is not always amenable to precise def-initions and, therefore, it is worth stating explicitly what it entails, itsscope, which is not invariant in time or in economic usage.

Concept of Convertibility

Traditionally, that is, until early in this century, convertibility generallyreferred to the right to unrestrictedly convert a currency into gold at agiven rate of exchange. This right was an essential component in the func-tioning of the gold standard that prevailed at the end of the nineteenthand the beginning of the twentieth centuries. In this sense, no currency isconvertible today. At present, gold no longer plays a significant monetaryrole and therefore convertibility into it is no longer a relevant concept.Instead, convertibility now refers to the right to convert freely a nationalcurrency at the going exchange rate into any other currency. Clearly, the

1See Mathieson and Rojas-Suarez (1993) and Guitian (1992a).

22

©International Monetary Fund. Not for Redistribution

Concepts and Degrees of Currency Convertibility

going exchange rate can be either fixed or flexible, in principle, and con-vertibility is a concept that would apply to a currency under either regime.Yet, as hinted in the introduction, the strength of the concept of convert-ibility is not invariant with regard to the existing exchange system.

To the extent that flexibility in exchange rates replaces the need forrestrictions on exchange transactions, it is clear that such flexibility andcurrency convertibility go hand in hand. Deviations between the twoconcepts arise whenever a flexible exchange rate coexists with exchangerestrictions, as is often the case in practice. In theory, though, flexibleexchange rates render such restrictions (and international reserves)unnecessary, or in any event less necessary than otherwise. Convertibilityin this context is a corollary of exchange rate flexibility. A soft concept ofconvertibility, therefore, would be embodied in the ability to engage inunrestricted exchange of currencies at market-determined exchange rates.

Most discussions of convertibility, however, do not envisage such anunconstrained notion. In fact, the general understanding of convertibili-ty is rather the right to engage in unrestricted exchange of currencies ata given exchange rate. This is a hard concept of convertibility and the oneassociated with fixed exchange regimes. To the extent, though, thatexchange restrictions accompany fixed exchange rate systems, the scopeof convertibility is thereby limited.

So far, the discussion has been conducted on the basis that convertibili-ty is a financial, a currency, concept. And it has been argued that the con-cept depends on the nature of the exchange regime, both in terms of theexchange rate system and of the presence or absence of exchange restric-tions. But even when exchange restrictions do not exist, convertibility in afundamental sense is very much affected by restrictions other than those onexchange transactions. This is particularly true with controls on the under-lying transactions, such as those on imports of goods and services and ofcapital exports. That is to say, a currency that is convertible at a givenexchange rate (the hard concept discussed above), because there are noexchange restrictions, can be made practically inconvertible through tradeand capital controls. These interconnections between financial and realtransactions are the basis for the distinction between real or commodityconvertibility (prevailing when there are no exchange and trade controls)and financial convertibility (requiring only absence of exchange controls).

Degrees of Convertibility

Apart from the various definitions of convertibility just discussed,there are a number of other meanings given to the term that, rather than

23

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

reflect additional variations of the concept itself, represent differences indegree. These degrees are derived from various perspectives from whichthe question of convertibility of a currency can be examined. The mostcommon angles have been (a) the holders of the currency balances;(b) the purposes for which convertibility is sought; and (c) the geo-graphical scope of convertibility.

From the standpoint of the holders of currency balances, distinctionshave been made between external convertibility and internal convertibil-ity. External convertibility typically refers to extending to foreign holdersof currency the right to convert their balances into foreign exchange.This form of restricted convertibility becomes relevant in settings wherepromotion of foreign capital inflows is a relevant consideration. Moregenerally, external convertibility will provide incentives for foreigners toengage in economic transactions in the countries that provide this freedom to their currency. Internal convertibility, in turn, typically relates tothe right given to domestic (resident) holders of currency to convert theirbalances into foreign exchange. This modality of restricted convertibility,although it is not inconsistent with the promotion of foreign investment,focuses more on other aspects of an economy's performance. Apart fromproviding incentives to residents to hold domestic cash balances, internalconvertibility exposes domestic economic policies to external competi-tion. As such, it poses risks to the policymaker, but it also contributes tomaking domestic policies internationally competitive. These two forms ofrestricted convertibility are also often referred to as nonresident versusresident convertibility.

From the standpoint of the purposes for which convertibility issought, the criterion to define its scope is the nature of the transactionfor which the foreign exchange is required. The traditional distinctionhere is between current account convertibility and capital account con-vertibility. Current account convertibility is the most common conceptand is defined as the right to convert currency balances into foreign ex-change for making payments for goods and services, or more general-ly, for payments related to current transactions. This is the degree ofconvertibility sought by the Bretton Woods par value regime. During itsexistence, participating countries undertook a commitment to establishfor their currencies convertibility at a fixed exchange rate for paymentsin foreign exchange in respect of current international transactions andtransfers. Capital account convertibility refers to the unrestricted right ofcurrency holders to convert their balances into foreign exchange forpayments in respect of capital transactions and transfers. This type ofconvertibility has been less widespread in practice than the one on cur-rent account. Nevertheless, recent liberalization of capital markets and

24

©International Monetary Fund. Not for Redistribution

Concepts and Degrees of Currency Convertibility

financial sector deregulation trends have developed throughout theworld economy and de jure or de facto capital account convertibility hasbecome more common. In the particular context of the EuropeanMonetary System (EMS), virtually all its participants have lifted capitalcontrols, thereby ensuring capital account convertibility for their cur-rencies. In connection with the variety of incentives that each type ofconvertibility confers, it is clear that current account convertibility (likeinternal convertibility) stresses the competitiveness of an economy, whilecapital account convertibility (like external convertibility) emphasizes aneconomy's ability to attract foreign capital. There are, of course, over-laps in the effects of each type of convertibility, but they do not invali-date the distinction.

From the standpoint of geographical scope, a distinction can be madebetween regional convertibility and global convertibility. Regional con-vertibility denotes the right to convert domestic currencies into the cur-rencies of a given number of countries in a region. This was obtained, forexample, when the participating countries of the European PaymentsUnion (EPU) made their currencies reciprocally convertible but did notextend convertibility to the United States or other countries. More gen-erally, even currencies with broader convertibility typically limit it, forpractical purposes, to the main currencies in the system, that is, those inwhich international transactions are denominated. In the EMS, of course,participating currencies (until recently) exhibited hard convertibilityamong themselves and soft convertibility for outside currencies. Globalconvertibility, in turn, confers the right to currency holders to converttheir balances into any foreign currency. As already noted, convertibilityis only relevant or necessary in relation to the main international curren-cies. As with languages, ability to speak a few of the major ones doesensure capacity for universal communication.

Convertibility in the IMF

In the IMF, there are three essential aspects of the concept ofconvertibility that are traditionally stressed: the usability of a currency, itsexchangeability, and its exchange value. These are the key standards forthe measurement of the convertibility of a currency. From thisstandpoint, a currency would be deemed to be fully convertible if it canbe used for all purposes without restrictions of a financial, or moreprecisely, a currency character; it can be exchanged for any other currencywithout limitations of a financial (or currency) nature; and it can be used

25

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

or exchanged at a given rate of exchange, be it a par value, central rate,official rate, or some legal exchange rate.

Then, if these three standards are not satisfied, totally or in part, thecurrency in question will fall short of complete convertibility, that is, of afull direct or financial convertibility. Since each of the standards can bemet to a varying extent, it is clear that convertibility will also exhibitdiverse degrees. A currency may be partly usable, that is, usable for somepurposes but not for others, or partly exchangeable and therefore, itsstanding on the convertibility axis cannot be described as either convert-ible or inconvertible.

An analogous relativity arises in connection with the third standard,that is, the currency exchange value, which was the basis for the distinc-tion made earlier between hard and soft convertibility. On the assumptionof unlimited usability and exchangeability, the robustness of the conceptof convertibility will depend on the currency's exchange value. In theextreme, that is, when this exchange value is determined by a freely fluc-tuating exchange rate, in a narrow sense, the currency will fulfill the threestandards and therefore may be considered convertible. But this inter-pretation sets no boundary or constraint on the exchange value of thecurrency. In contrast, the other two standards exhibit well-definedbounds, at least conceptually. A currency can be used either without lim-its, that is, for all purposes, or not at all, that is, for no purpose, or morerealistically, for only a few purposes; these two extremes confine the scopeof relativity of convertibility on this scale. In turn, a currency can beexchanged either for all currencies without limit or for none; here again,this dimension of convertibility is bound by these two outer frontiers. Butas far as exchange value is concerned, the scope of relativity is of a differ-ent nature: there is the possibility of defining convertibility on this scaleas meaning that a currency is usable and exchangeable either at a givenrate of exchange or at any rate of exchange. The former definition guar-antees, so to speak, the currency's exchange value, but the latter offers nosuch guarantee. Clearly, the usefulness of the concept of currency con-vertibility when its exchange value can oscillate without limits is veryreduced, if it exists at all. Currencies can, of course, have varying degreesof convertibility in terms of the standard of their exchange value, whichwill depend on the particular exchange rate regime in place. The essentialissue on this front revolves around where the exchange risk falls. Does theissuer of the currency or do its holders bear such risk? Hard convertibili-ty allocates the risk to the issuer of the currency; soft convertibility pass-es it on to the holders of the currency balances.

The definition of convertibility in the Fund's Articles of Agreementreflected the concern in the membership with restoring the free flows of

26

©International Monetary Fund. Not for Redistribution

Concepts and Degrees of Currency Convertibility

international trade in goods and services that had been disrupted byWorld War II. This concern meant that the commitment in the area ofconvertibility that members undertook extended only to current transac-tions. This commitment is reflected in the Articles of Agreement asfollows:

Subject to the provisions of Article VII, Section 3(b) and Article XIV,Section 2, no member shall, without the approval of the Fund, imposerestrictions on the making of payments and transfers for current interna-tional transactions. (Article VIII, Section 2(a); italics added.)

The reference to Article VII, Section 3(b) concerns an authorizationthat the Fund can provide to members to limit the freedom of exchangeoperations in a currency that has been declared scarce. This scarcity clausewas included in the Articles of Agreement to provide a constraint onunduly persistent balance of payments surpluses. As succinctly put in theKeynes Plan for an International Clearing Union,

. . . a country finding itself in a creditor position against the rest of the woas a whole should enter into an arrangement not to allow this credit balancso long as it chooses to hold it, to exercise a contractionist pressure againstworld economy. . . (Horsefield's italics).2

The concern was with regard to symmetry, that is, with rules thatwould apply to both members with persistent deficits or surpluses in theirbalance of payments. But it also arose, in substance, with the need toavoid contractionist pressures on world trade, as made clear in the abovequotation.

The second proviso, the reference to Article XIV, Section 2, refers totransitional arrangements that members are permitted to maintain untiltheir balance of payments positions allow them to fulfill their convertibil-ity commitment. The proviso states:

A member . . . may . . . maintain and adapt to changing circumstances therestrictions on payments and transfers for current international transactionsthat were in effect on the date on which it became a member. (Article XIV,Section 2)

A third proviso of importance in the context of the Fund's concept ofconvertibility relates to the definition of the meaning and scope of pay-ments for current international transactions, which include

2See Horsefield (1969, Vol. III, p. 5, para. 10). This volume contains the various pro-posals put forth by a number of countries for an institution like the Fund. These includedthe quoted Keynes Plan, a U.S. proposal for an International Stabilization Fund (the WhitePlan), a French Plan on international monetary relations, and a Canadian Plan for anInternational Exchange Union.

21

©International Monetary Fund. Not for Redistribution

Currency Convertibility in the Middle East and North Africa

(1) all payments due in connection with foreign trade, other current busi-ness, including services, and normal short-term banking and creditfacilities;

(2) payments due as interest on loans and as net income from other invest-ments;

(3) payments of moderate amount for amortization of loans or for depre-ciation of direct investments; and

(4) moderate remittances for family living expenses.

The Fund may, after consultation with the members concerned, determinewhether certain specific transactions are to be considered current transac-tions or capital transactions. (Article XXX)

Some of these categories are viewed, from an economic standpoint, ascapital transactions. To a large extent, though, their inclusion reflectedconcern with encouraging sound development in current account trans-actions. These transactions typically require normality in the use andrepayment of short-term banking and credit facilities and payments ofregular loan amortization as well as allowance for depreciation of directinvestment.