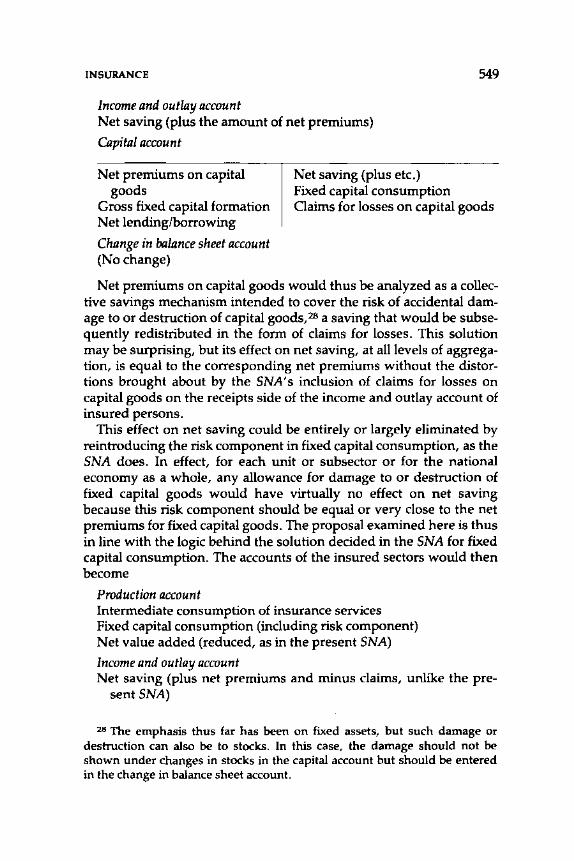

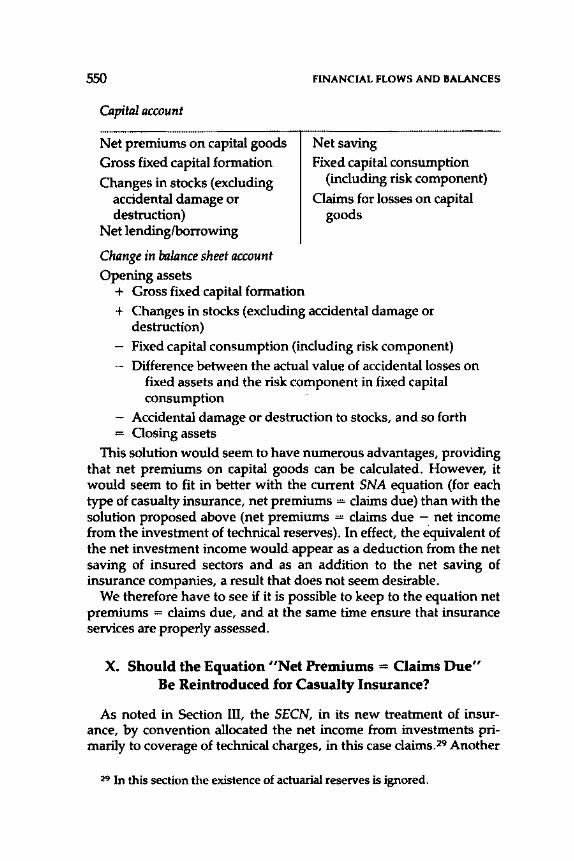

theimf's statistical systems - imf elibrary - international

TRANSCRIPT

THEIMF'S STATISTICAL

SYSTEMS in Context of Revision of the United Nations'

A System of National Accounts

As of May 1,1991, while this book was in press, the IMF's Bureau of Statistics became the Statistics Department of the Fund. Consequently, all references to the Bureau of Statistics herein should be understood to refer to the Statistics Department.

THEIMF'S STATISTICAL

SYSTEMS in Context of Revision of the United Nations'

A System of National Accounts

Statistics Department

Edited by Vicente Galbis

International Monetary Fund Washington, D.C. • 1991

© 1991 International Monetary Fund Reprinted May 1995

Library of Congress Cataloging-in-Publication Data

The IMP's statistical systems in context of revision of the United Nations' A system of national accounts I Statistics Department; edited by Vicente Galbis

p. em. "A selection of papers presented at three expert group meetings

sponsored by the Fund in 1987-88" -Foreword. Includes bibliographical references. ISBN 1-55775-159-5 1. National income-Accounting. I. Galbis, Vicente, 1942-

ll. International Monetary Fund. Statistics Dept. lll. International Monetary Fund. HC79.15144 1991 339.3'2'015195- dc20 91-2489

Both this book's cover and its interior were designed by the IMF Graphics Section.

The following symbols have been used throughout this book:

to indicate that data are not available;

CIP

to indicate that the figure is zero or less than half the final digit shown, or that the item does not exist;

Between years or months (e.g., 1991-92 or January-June) to indicate the years or months covered, including the beginning and ending years or months;

Between years (e.g., 1991/92) to indicate a crop or fiscal (financial) year.

"Billion" means a thousand million.

Details may not add to totals shown because of rounding.

The term "country," as used in this book, does not in all cases refer to a territorial entity that is a state as understood by international law and practice; the term also covers some territorial entities that are not states but for which statistical data are maintained and provided internationally on a separate and independent basis.

Price: US$35.00 Address orders to:

External Relations Department, Publication Services International Monetary Fund, Washington D.C. 20431, U.S.A.

Telephone: (202) 623-7430 Telefax: (202) 623-7201 Cable: Interfund

internet: publications @imf.org

recycled paper

Foreword

T HE INTERNATIONAL MONETARY FUND has always attached considerable importance to the development of appropriate meth

odologies in its work in balance of payments, government finance, and monetary statistics. The Fund's contribution to the development of international statistics also takes other forms, including a system of statistical communications with member countries, technical assistance to member countries on statistical matters, cooperation in these matters with other international organizations, and compilation of its own statistical publications.

The role of the IMF within the international statistical community has allowed the Fund to participate actively in the ongoing revision of the United Nations' A System of National Accounts (SNA), last revised in 1968. The work on revision of the SNA may be seen as part of the Fund's commitment to achieve a greater degree of coordination in the statistical field with other international agencies. The Fund has also begun to revise the fourth edition of its Balance of Payments Manual, issued in 1977, and to refine further its methodology for monetary statistics, based on the draft of A Guide to Money and Banking Statistics. A Manual on Government Finance Statistics was published by the Fund in 1986. The Fund hopes that these efforts will not only lead to methodological improvements and a greater consistency in national statistics but will also promote harmonization of these statistical systems among themselves and with the SNA.

This volume contains a selection of papers presented at three expert group meetings sponsored by the Fund in 1987-88 for the revision of the SNA. These meetings dealt with issues in the balance of payments, government finance, and monetary statistics and were part of a sequence of expert group meetings organized by the interested international organizations to oversee the revision process. The papers place the Fund's statistical methodologies in the context of revision of the SNA and explain the contr;bution that the Fund has made, and can make, to the process of harmonization.

Although the papers represent the views of individual contributors

v

vi FOREWORD

and not necessarily those of their respective institutions, I trust that they will be of interest to those whose task it is to compile macroeconomic statistics and to develop new ideas to cope with the challenges of the interrelation, simplification, and evolution of these statistics.

MICHEL CAMDESSUS

Managing Director International Monetary Fund

Preface

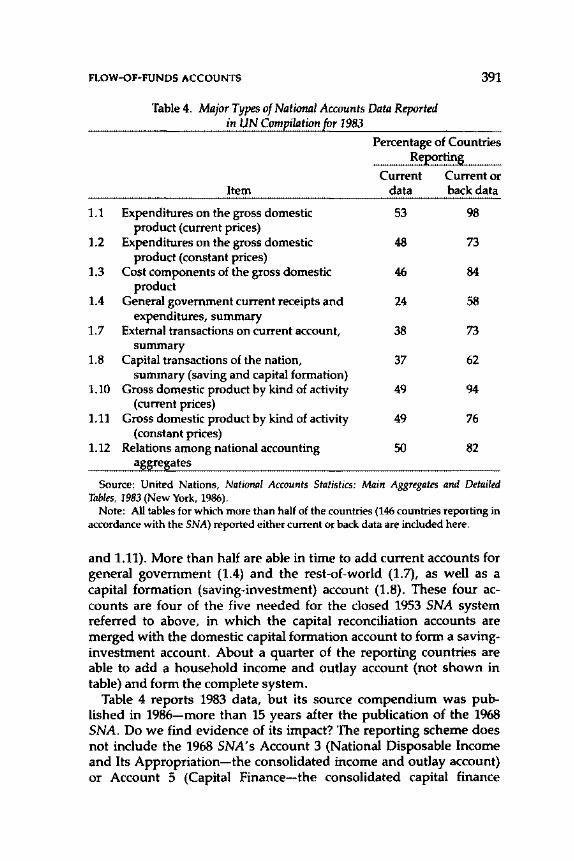

A T ITS TWENTY-FIRST session in 1981 the Statistical Commission of the United Nations discussed proposals for improvement of the

United Nations' A System of National Accounts (SNA), last published in 1968. Following this, an Expert Group Meeting on the Review and Development of the SNA, held in New York in March 1982, recommended that a long-term review of the SNA be undertaken to produce a revised SNA. To assist in this process, the Intersecretariat Working Group on National Accounts-a group comprising representatives of the UN, the Organization for Economic Cooperation and Development (OECD), the European Community (EC), the World Bank, the IMF and the five UN Regional Economic Commissionswas established. The main goals set for the revision of the SNA were to simplify the 1968 SNA so that it will be more directly relevant to the needs of member countries; to resolve methodological issues and internal inconsistencies noted since publication of the 1968 SNA; and to harmonize the SNA as much as possible with related statistical systems, especially the Fund's systems and methodologies relating to balance of payments, government finance, and monetary statistics.

The revision process has centered on a series of meetings of expert groups composed of national experts and the members of the Intersecretariat Working Group. In 1987 and 1988 the Fund sponsored three of these expert group meetings. They dealt with external sector transactions (March 23-April2, 1987), public sector accounts Oanuary 25-29, 1988), and financial flows and balances (September 6-15, 1988).

This volume contains a selection of the papers prepared for the expert group meetings sponsored by the Fund. The structure of the volume has three parts, corresponding to the issues discussed at each of the three meetings. In all, 32 papers are presented, most of them short. A brief introduction has been provided by the editor. Some of the papers have been modified for publication, with certain material, especially annexes and appendices, deleted to simplify and shorten the presentation or to avoid unnecessary repetition. The papers have

vii

viii PREFACE

not been revi<:ed, however, to reflect discussion during the expert group meetings. Thus, the contents of this volume should in no way pre-empt or prejudice the views expressed by participants at those meetings, the conclusions and recommendations of the meetings, or the solutions that may eventually prevail in achieving harmony between the revised SNA and the Fund's statistical methodologies. Rather, I would hope that these papers are viewed as research material that is interesting for its analytical approaches to some longstanding issues, and to new methodological issues in the field of economic statistics. The papers therefore represent solely the views of the authors and not the official views of the Fund or of other organizations.

Finally, I would like to thank the contributors to this volume not only for preparing the papers but also for their cooperation with the editor in the thankless task of streamlining the presentation by deleting some material, as noted above; this made it possible to publish the papers in a single volume without reducing their substance. I would also like to thank James McEuen of the Fund's External Relations Department for painstakingly reviewing the draft papers and for making many useful editorial suggestions at various stages of production of this volume.

JoHN B. McLENAGHAN

Director Statistics Department

International Monetary Fund

Contents

Foreword Michel Camdessus • v

Preface John B. McLenaghan • vii

Introduction Vicente Galbis • xiii

- PART I-

EXTERNAL SECTOR TRANSACTIONS

1. Residents of an Economy Arie C. Bouter • 3

2. Treatment of International Organizations Gerard G. Raymond • 20

3. Change of Ownership and Time of Recording in the National Accounts

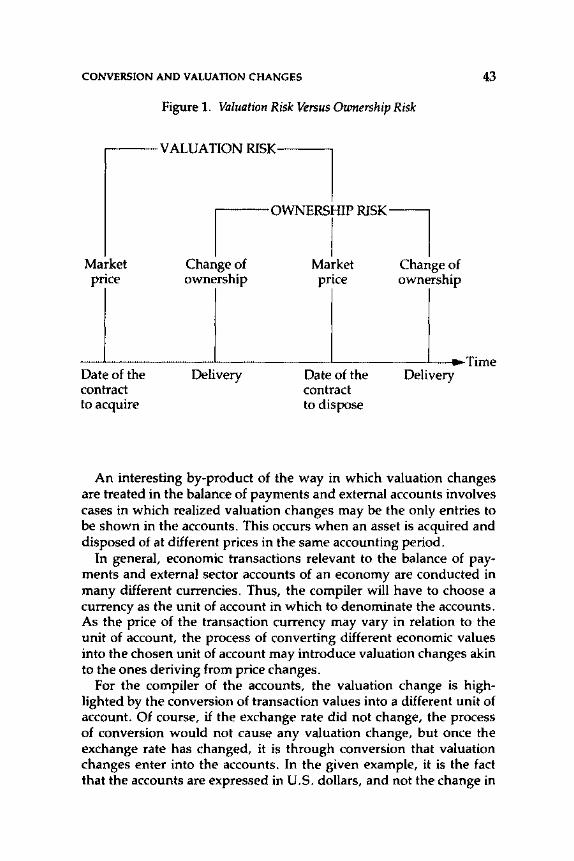

Robert McColl • 26

4. Conversion of Balance of Payments Transactions as a Source of Valuation Changes: Problems,

Principles, and Practical Solutions Pierre Luigi Parcu • 41

ix

X CONTENTS

5. Currency Conversion in a Multiple Exchange Rate System Marianne Schulze-Ghattas • 51

6. Treatment of Exchange Rate Differentials in the National Accounts

Jan van Tongeren • 63

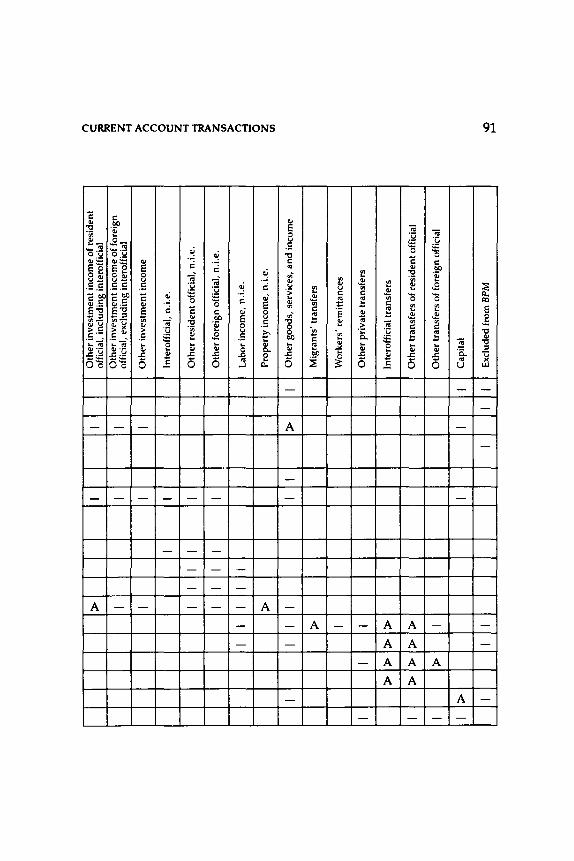

7. Harmonization of the Classification of External Current Account Transactions

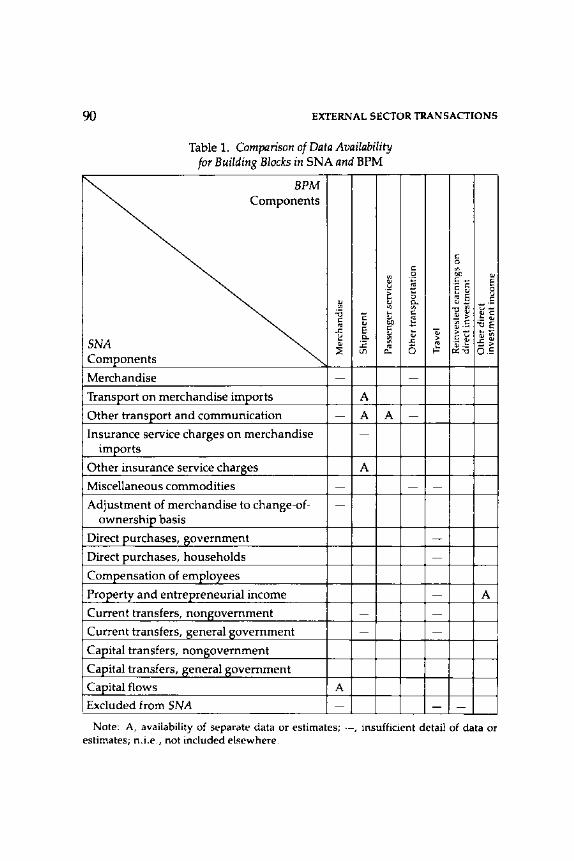

Arie C. Bouter and Jan van Tongeren • 85

8. Proposed Treatment of Reinvested Earnings on Direct Investment

Geoffrey J. Robertson • 106

9. Classification of International Transactions in Services, Income, and Unrequited Current Transfers

Arie C. Bouter • 119

10. Measurement of a Nation's Terms of Trade Effect and Real National Disposable Income

Within a National Accounting Framework Mick Silver and Khashayar Mahdavy • 123

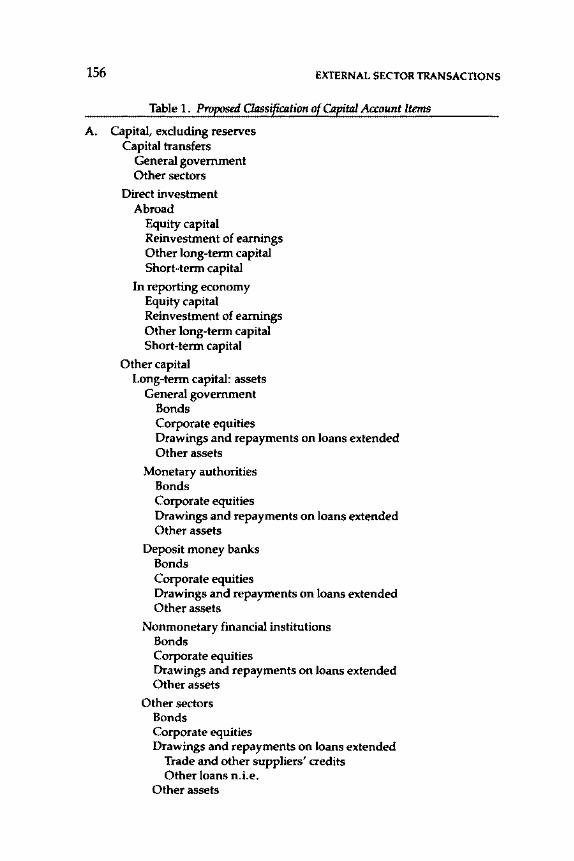

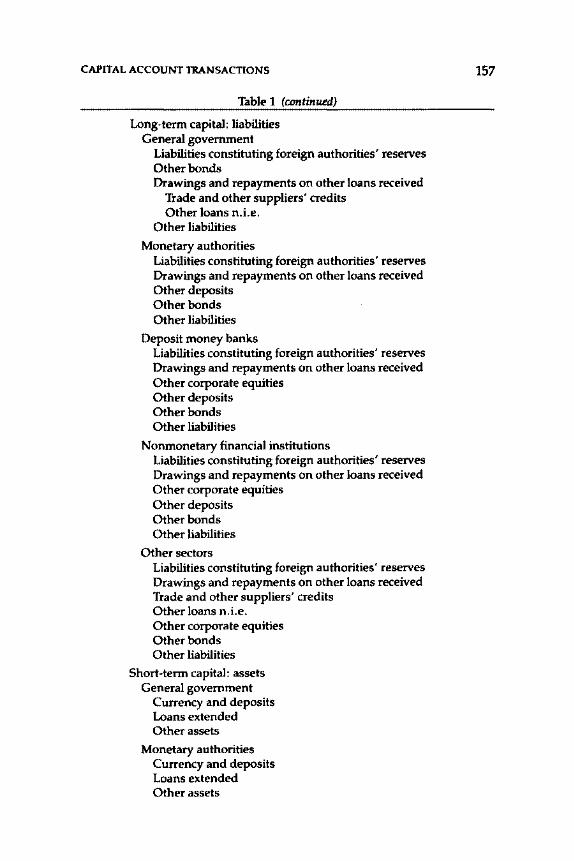

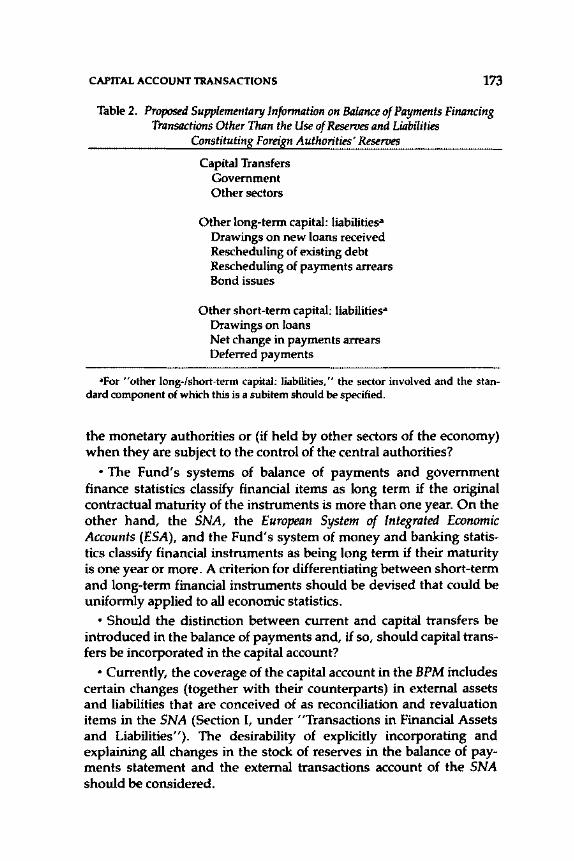

11. Classification of Capital Account Transactions Mahinder S. Gill• 154

12. Classification of Corporate Enterprises D. Keith McAlister • 175

13. New Financial Instruments and the Balance of Payments George H. Hoezoo • 181

14. Classification of Transactions in Zero-Coupon Bonds, Junk Bonds, and Indexed Bonds

in the Balance of Payments Robert McColl• 195

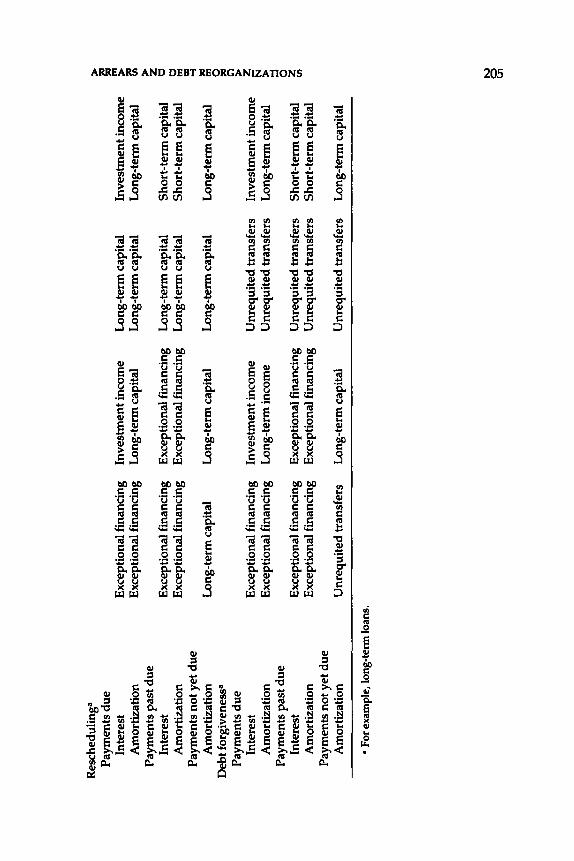

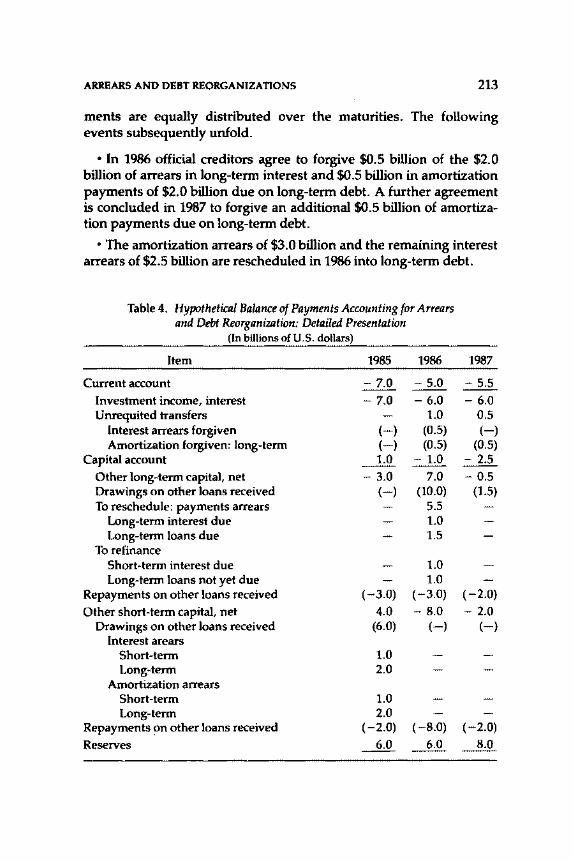

15. Some Issues in the Balance of Payments Presentation of Arrears and Debt Reorganization

John E. Thornton • 201

CONTENTS

-PART II-

PUBLIC SECTOR ACCOUNTS

16. A Discussion of Public Sector Accounts Jonathan Levin, Jan van Tongeren,

Brian Newson, and Derek Blades • 217

17. An Example of Progress in Delineating Relationships Between Government Finance Statistics and National Accounts Concepts

Jonathan Levin and Jan van Tongeren • 276

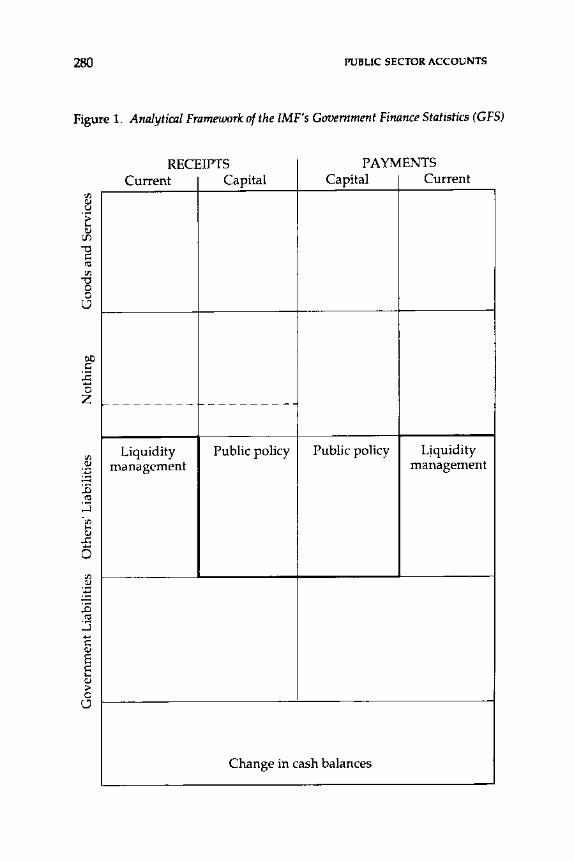

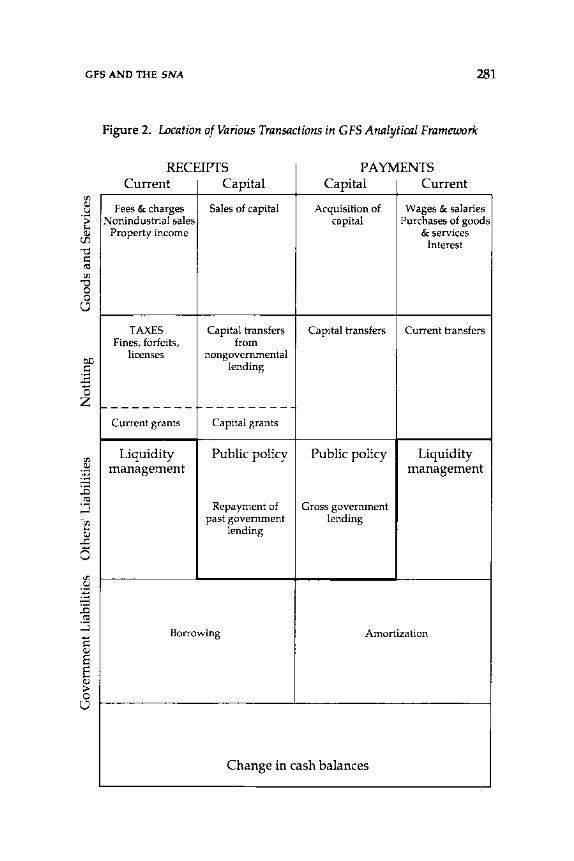

18. Overall Relationships Between the IMF' s Government Finance Statistics and A System of National Accounts

Jonathan Levin • 278

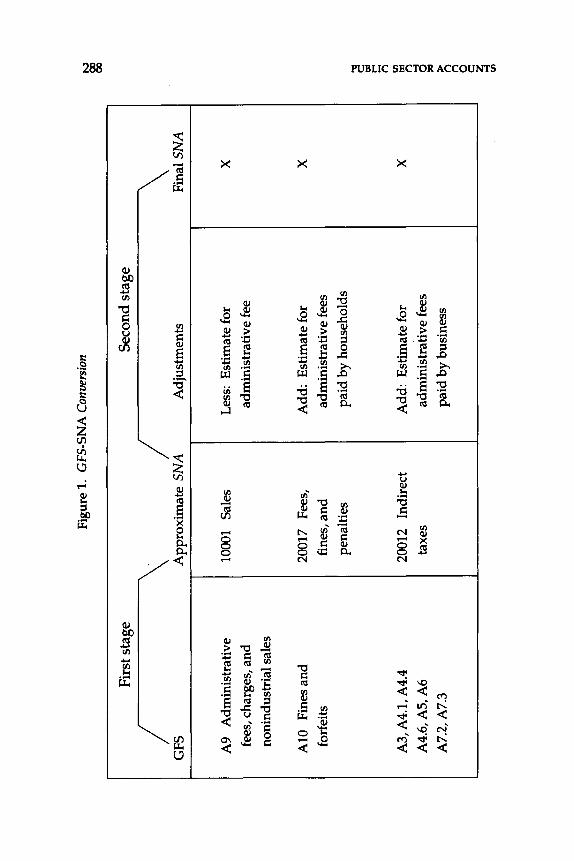

19. Derivation of System of National Accounts Value from Government Finance Statistics Data

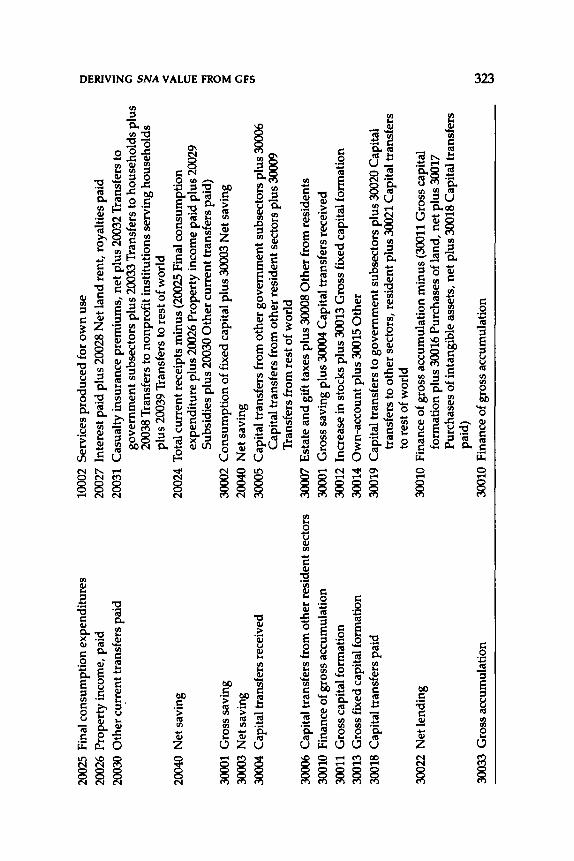

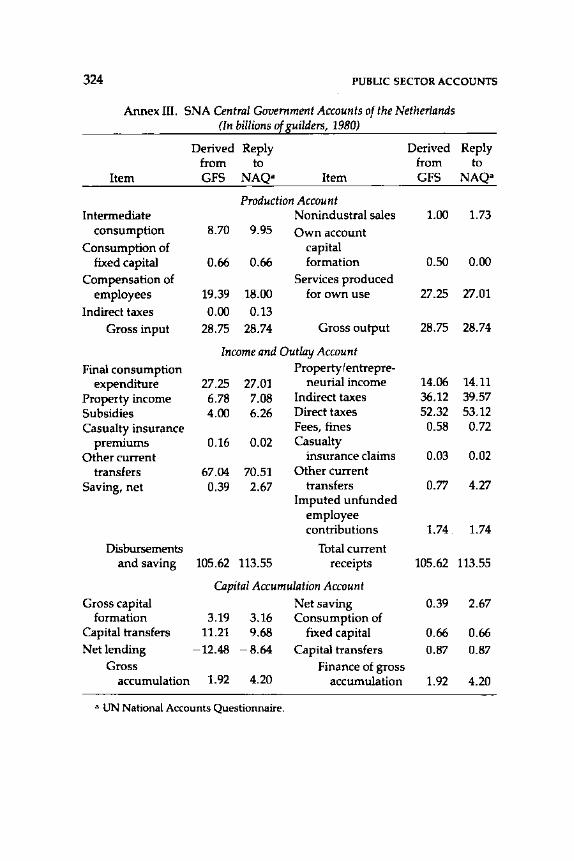

Jan van Tongeren and Irene Tsao • 286

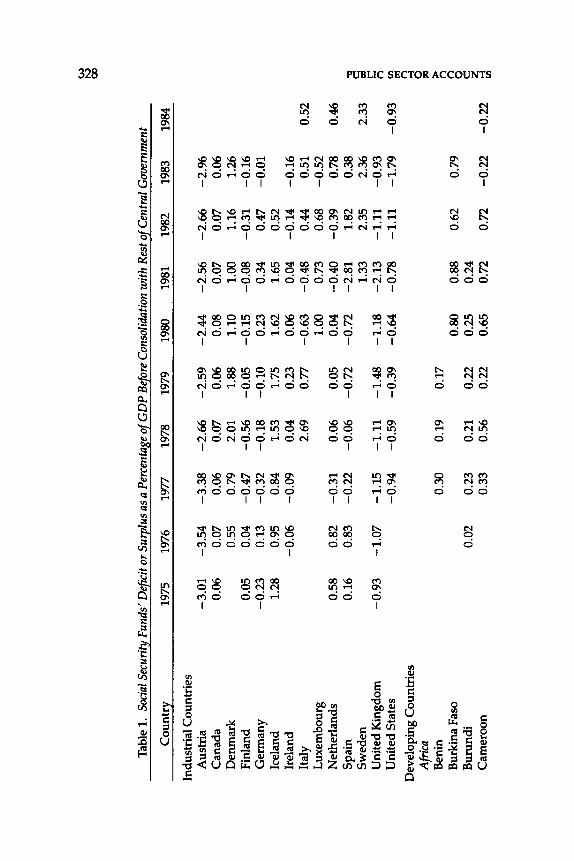

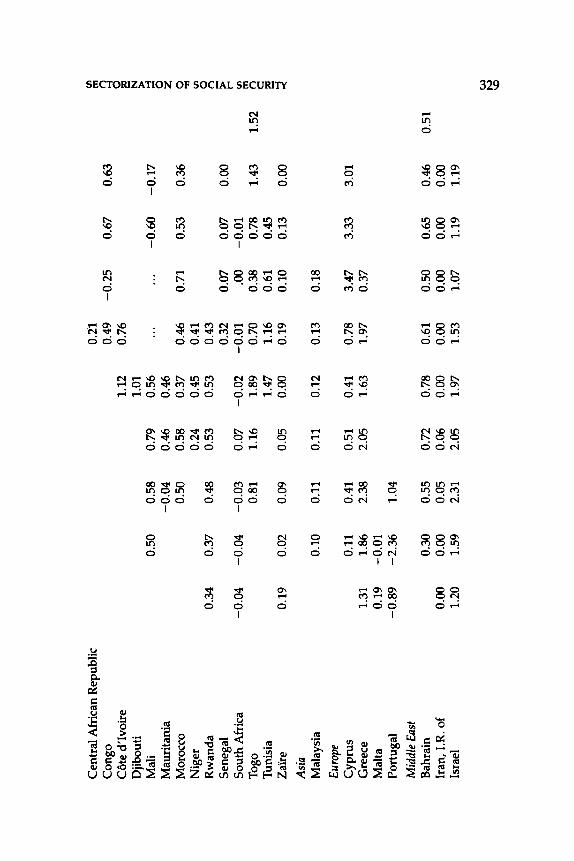

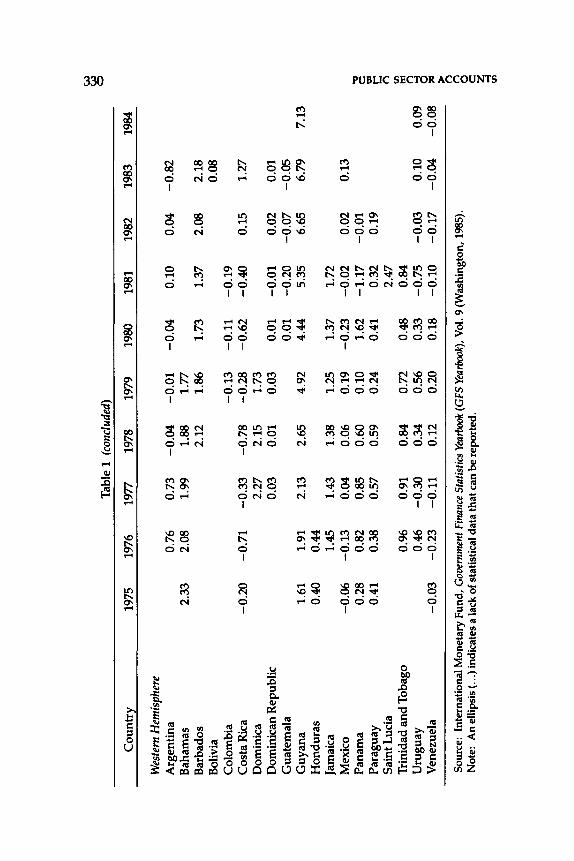

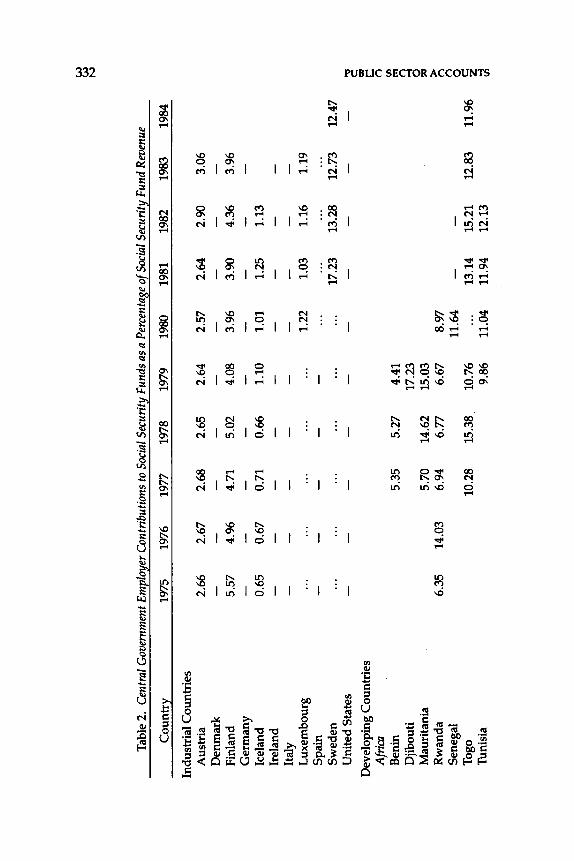

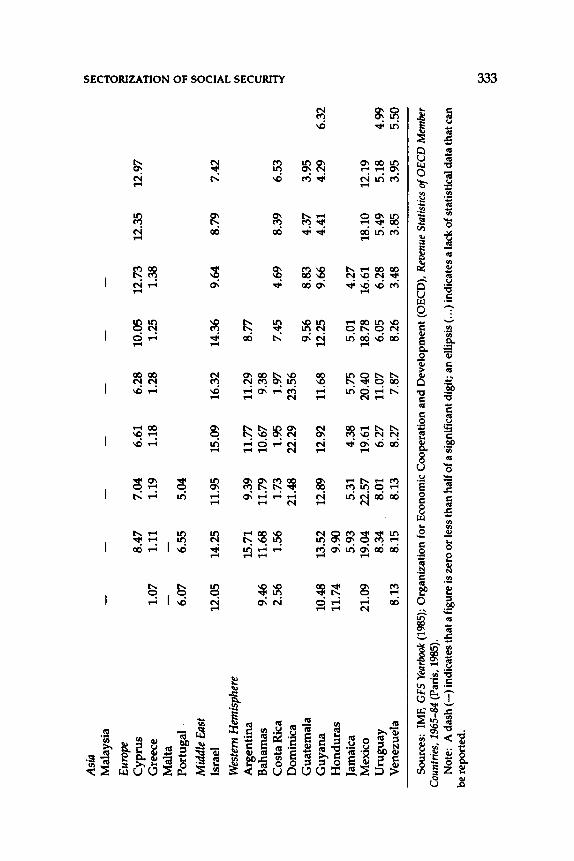

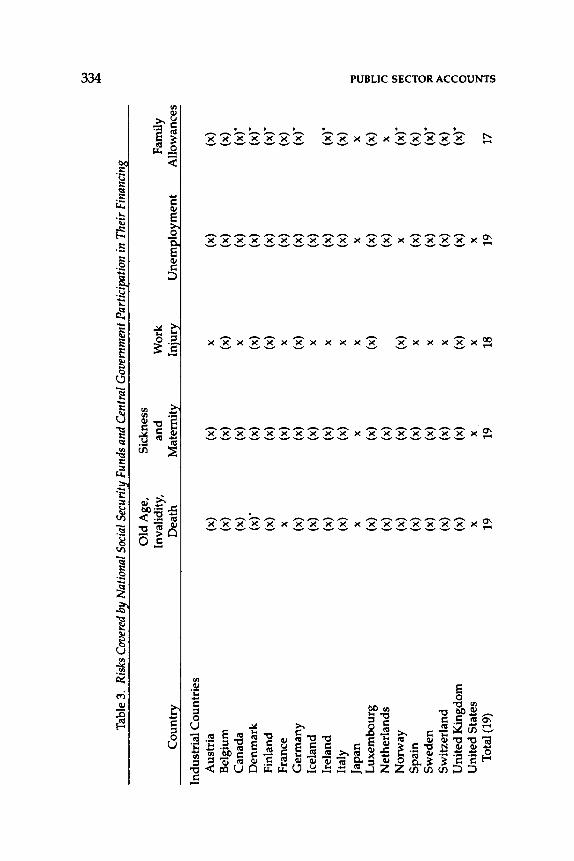

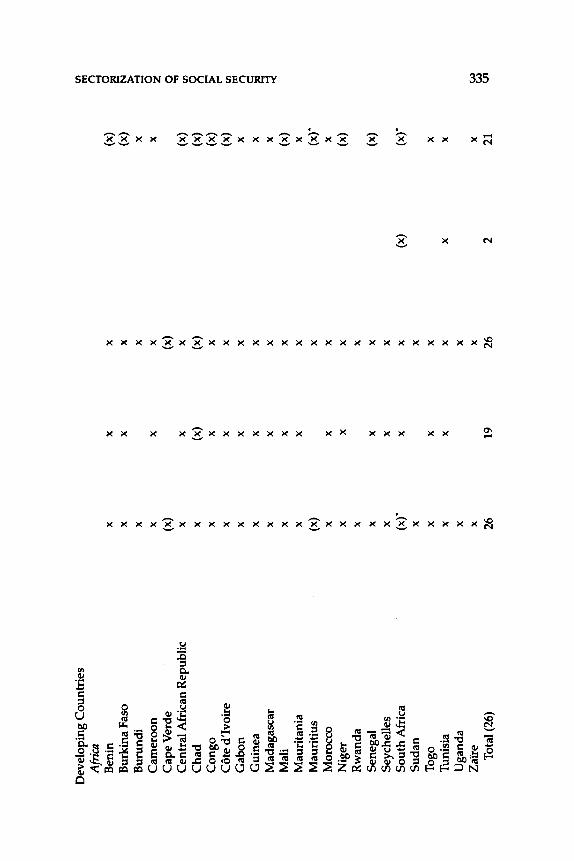

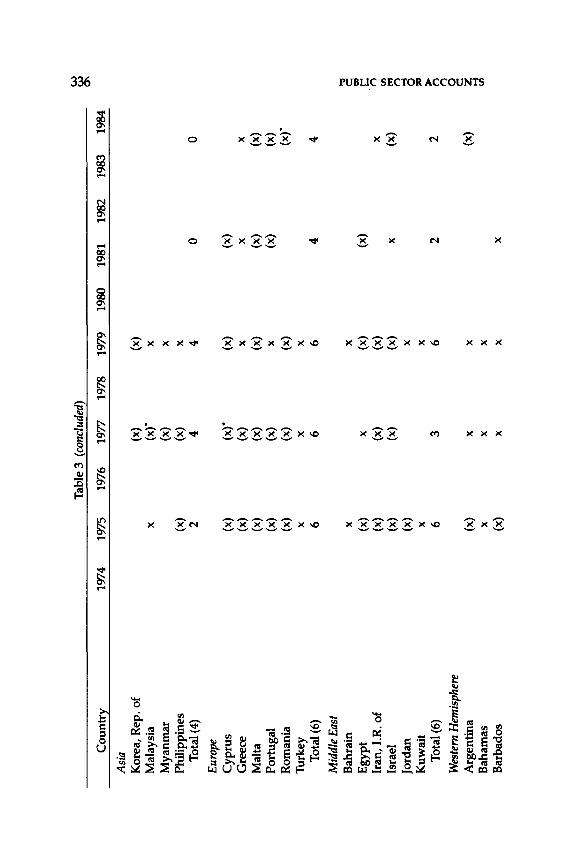

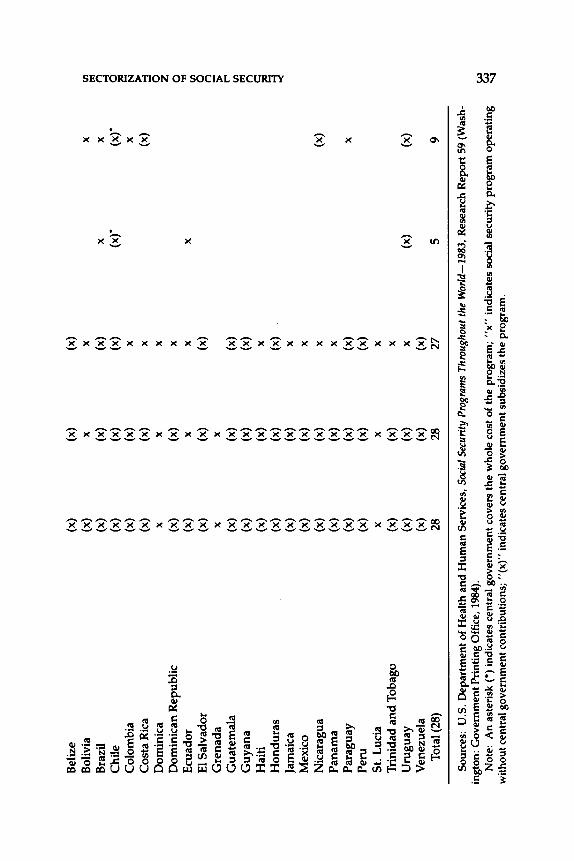

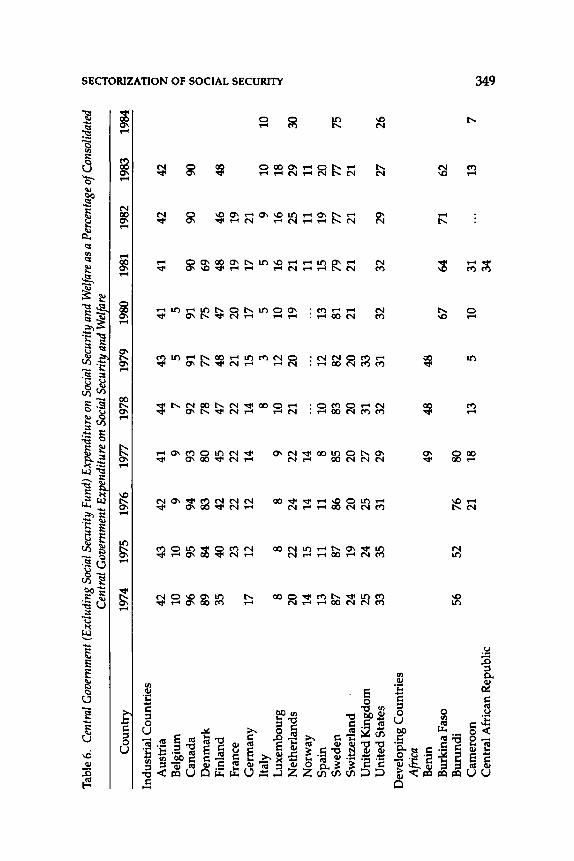

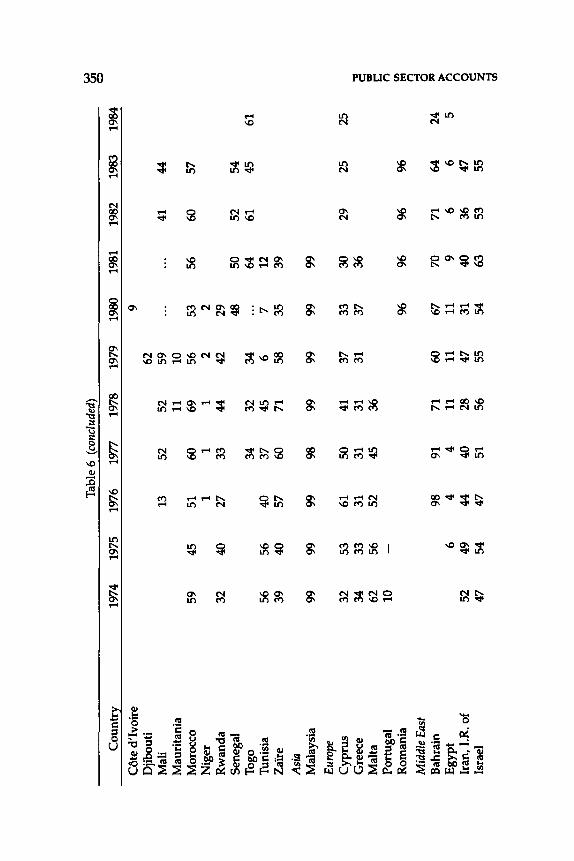

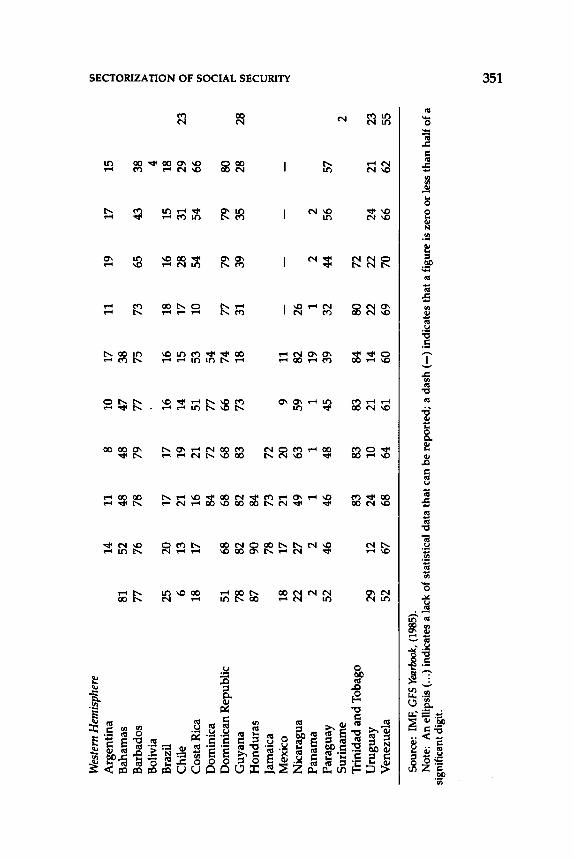

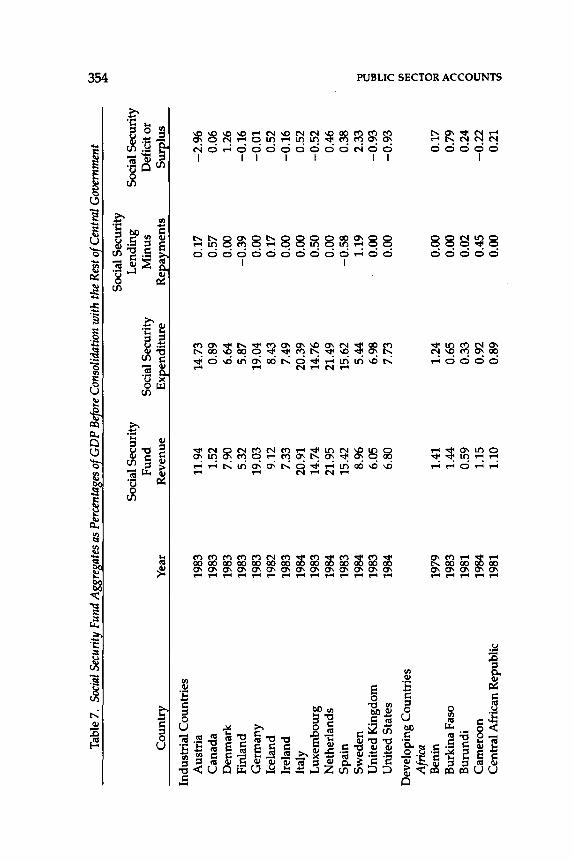

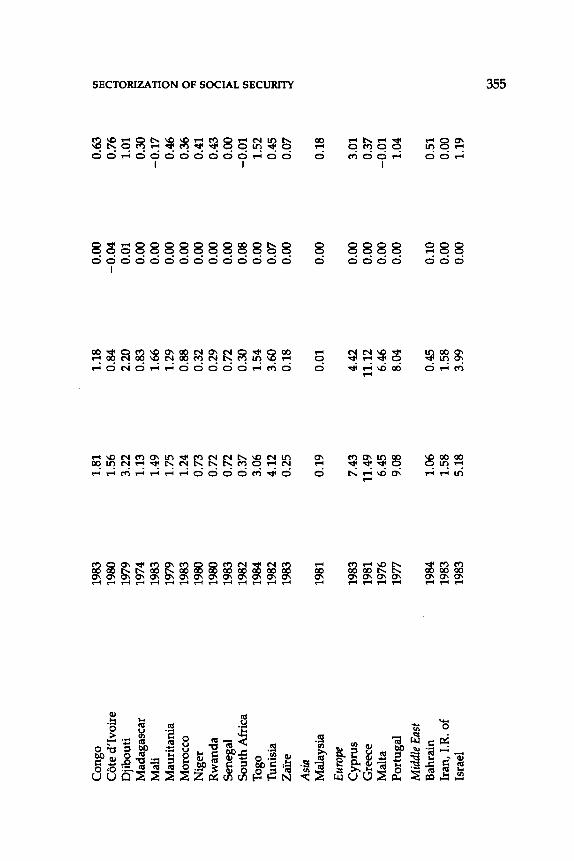

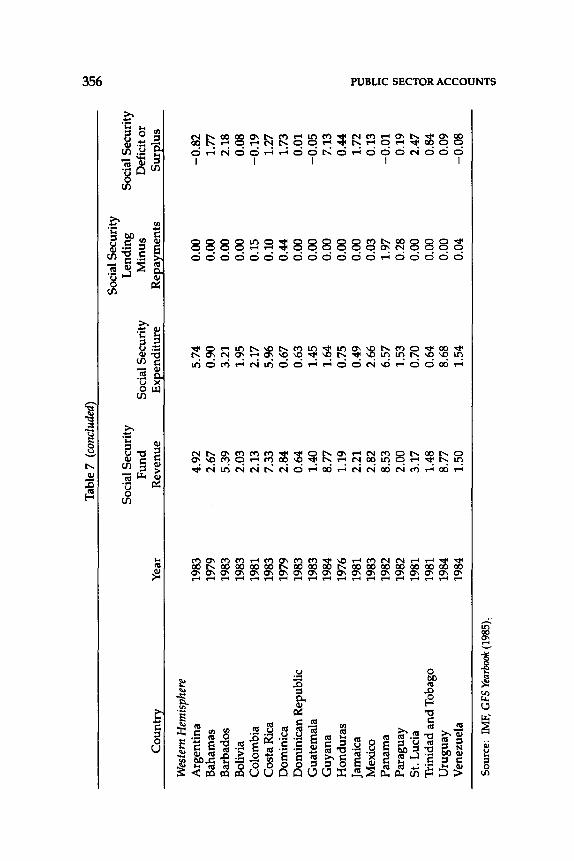

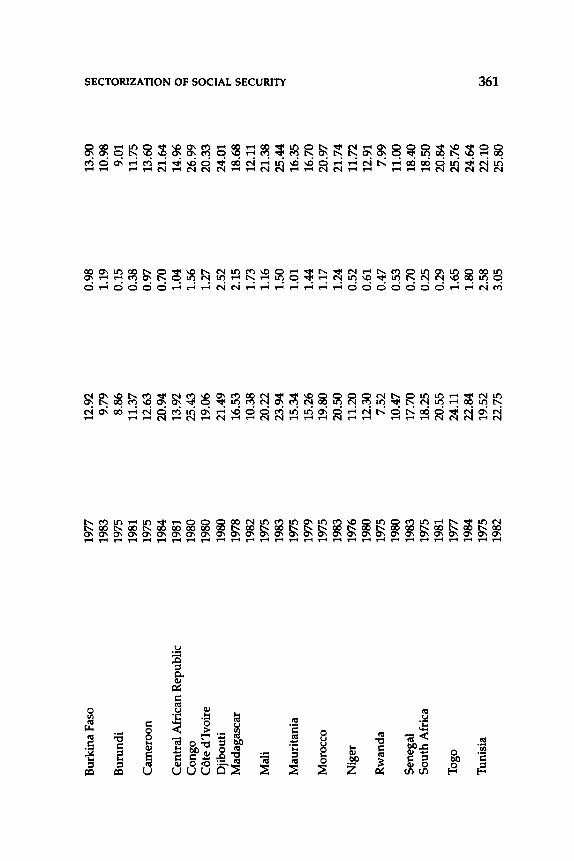

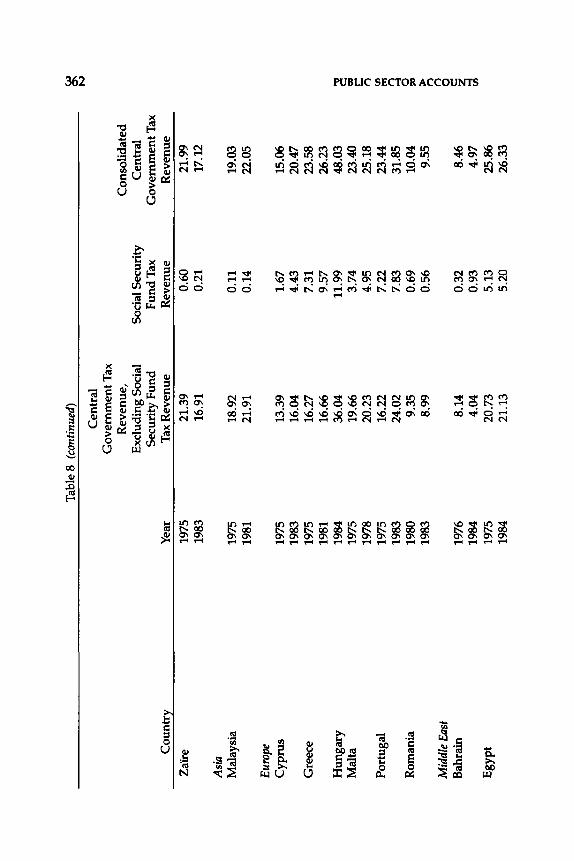

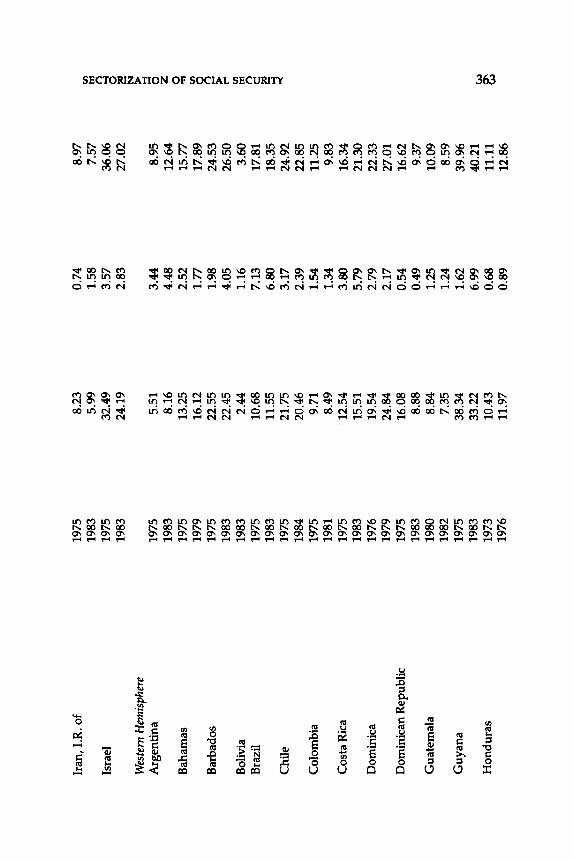

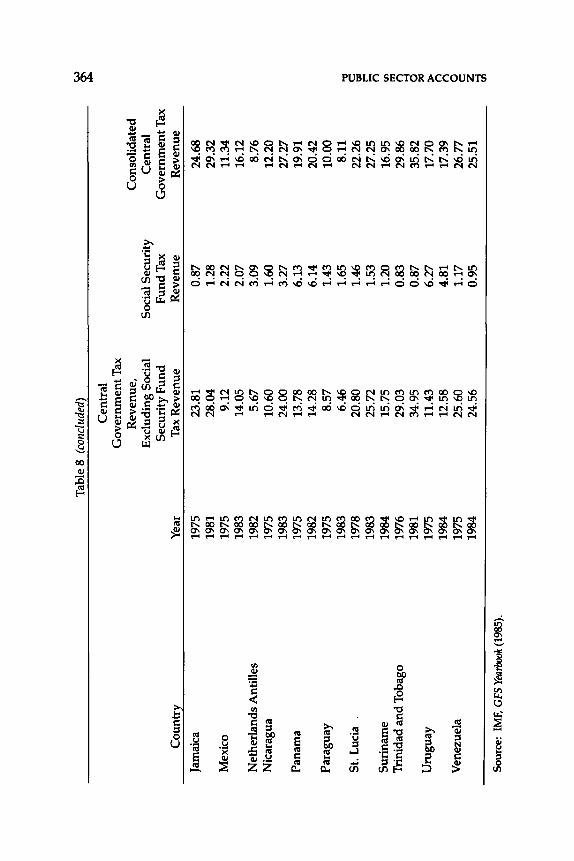

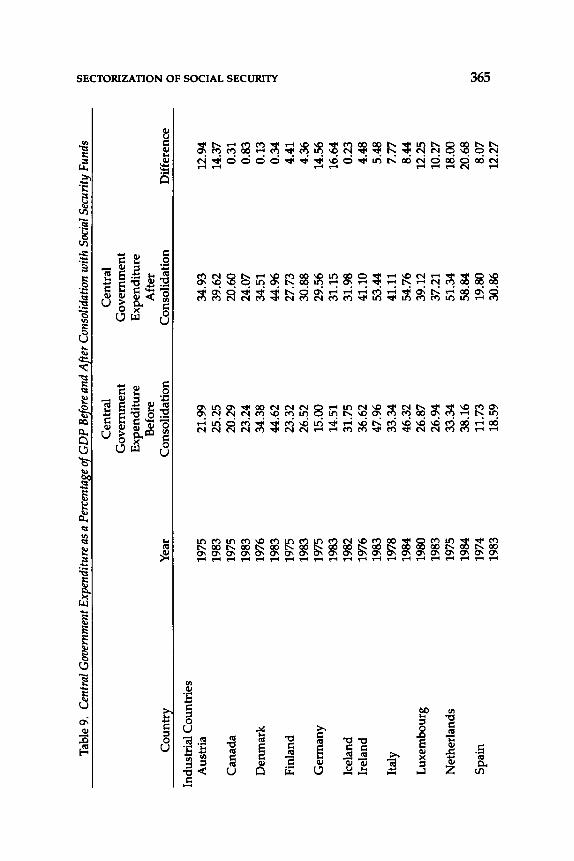

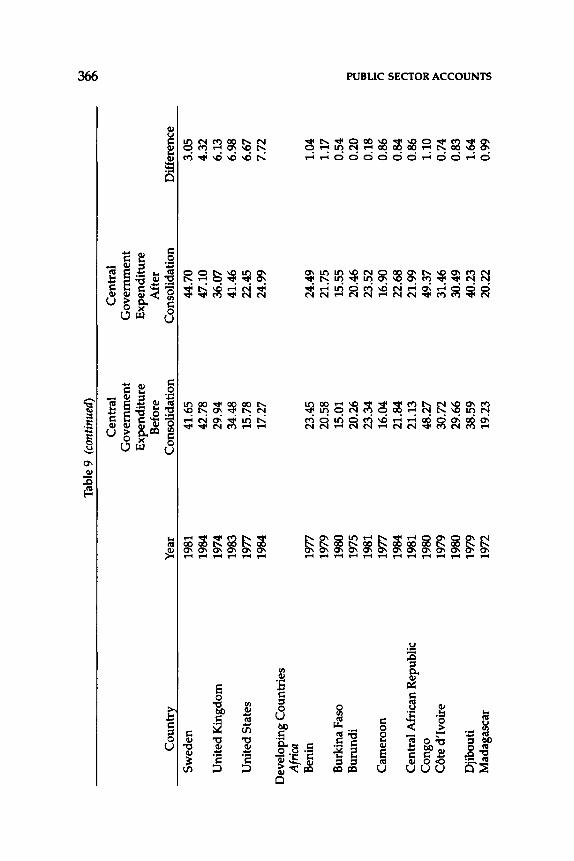

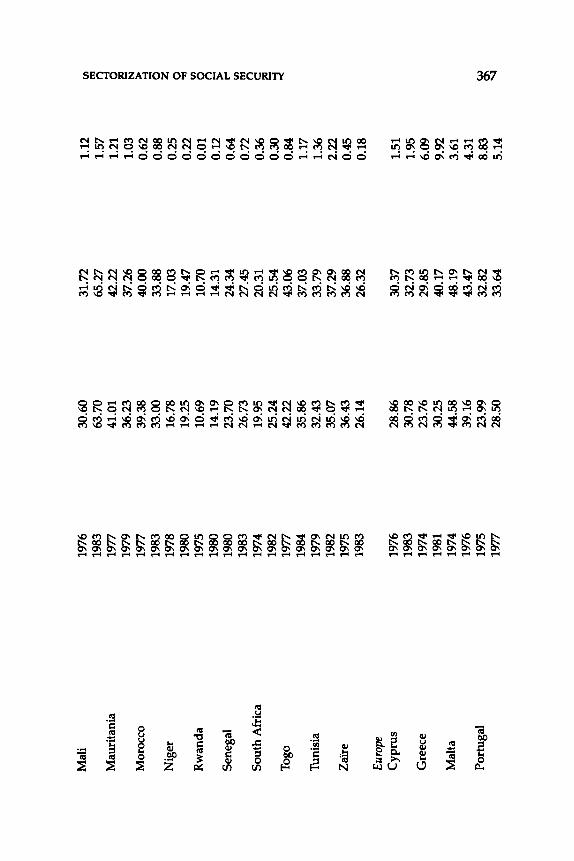

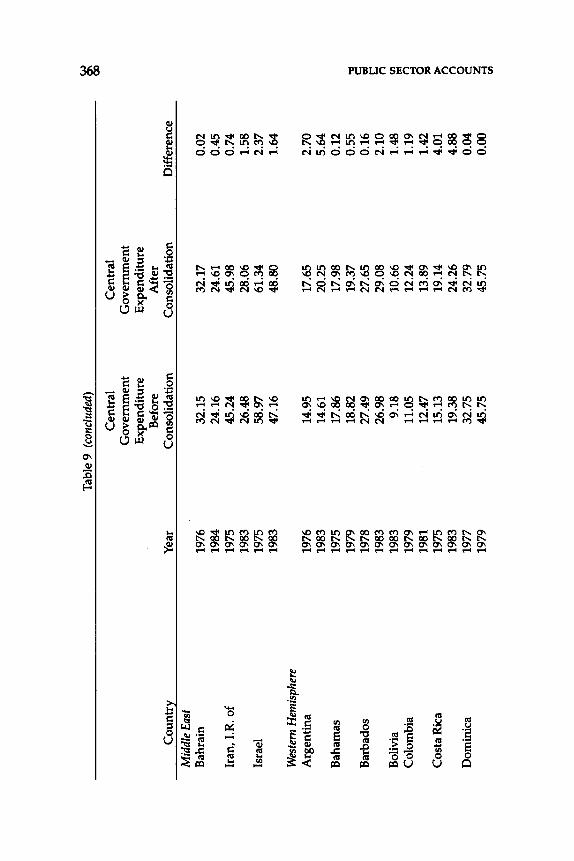

20. Sectorization of Social Security Funds Teresa Villacres • 325

-PART III

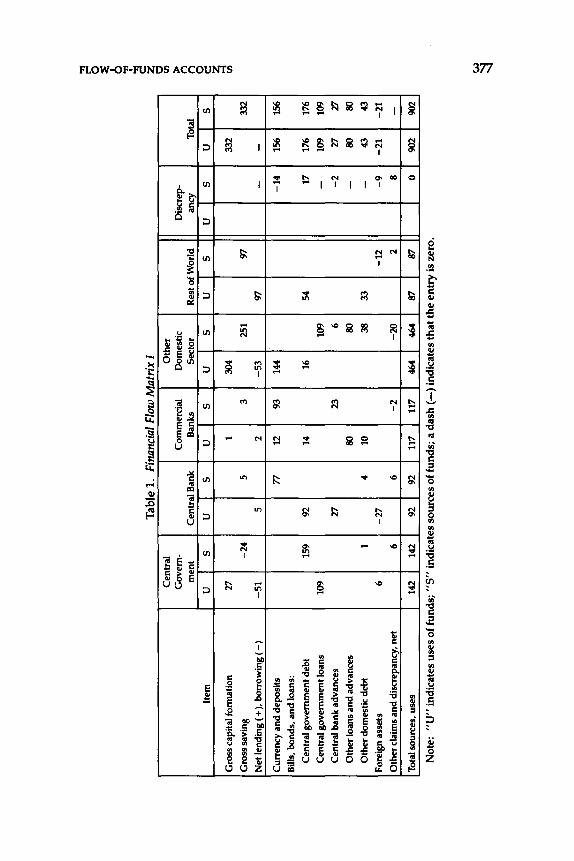

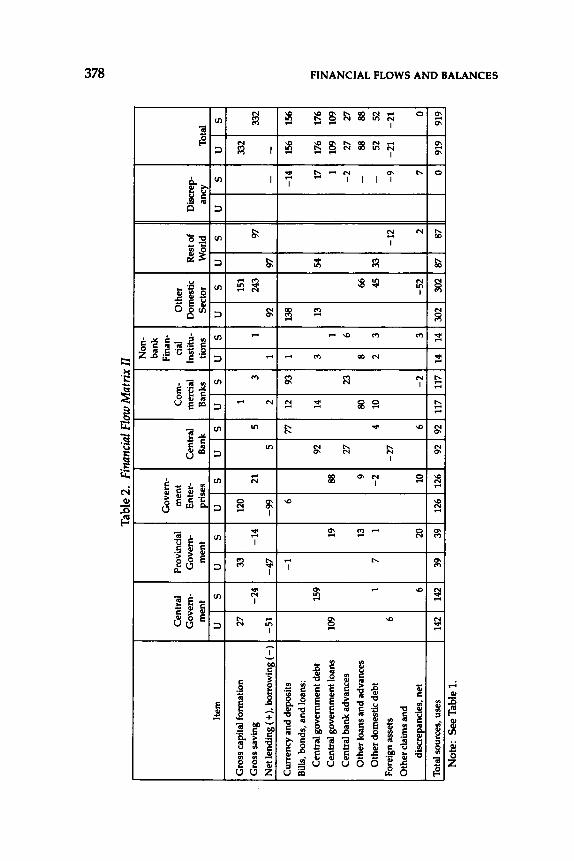

FINANCIAL FLOWS AND BALANCES

21. Flow-of-Funds Accounts, A System of National Accounts, and Developing Countries

John C. Dawson • 375

22. The Financial Sector Edward W. Saunders • 413

23. Monetary Concepts and Definitions Emmanuel 0. Kumah • 427

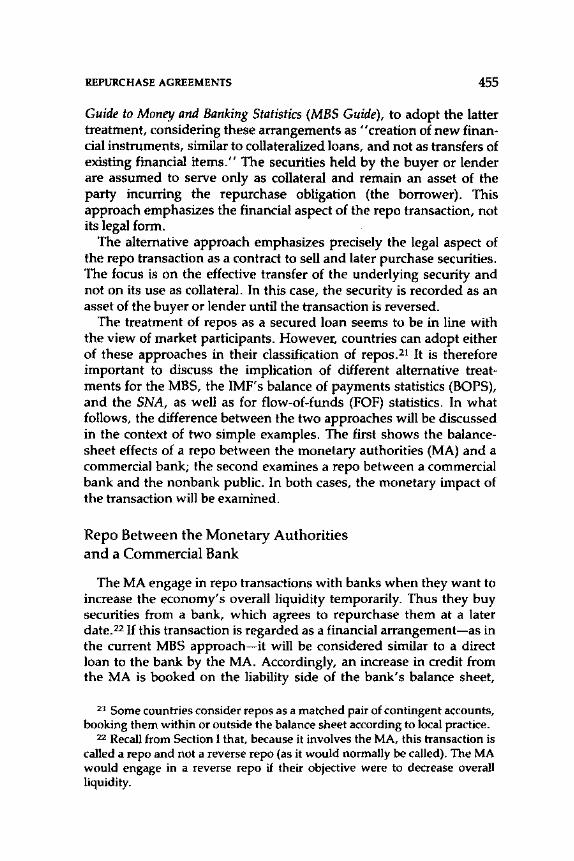

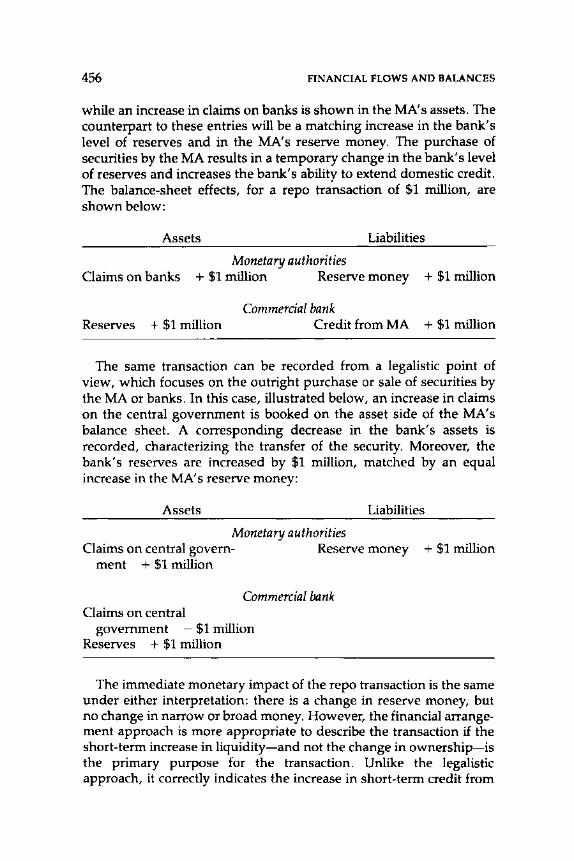

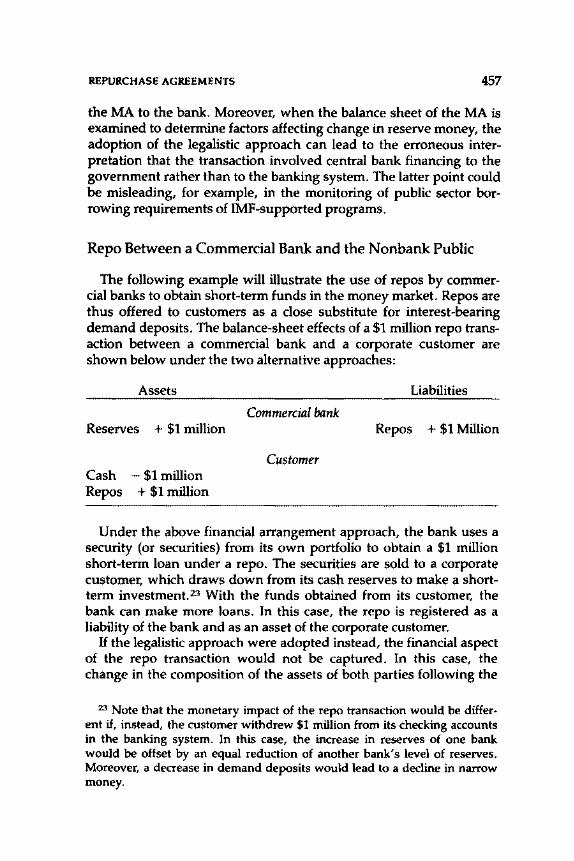

24. Repurchase Agreements and Financial Analysis Marta Castello-Branco • 442

25. Recording of Financial and Operational Leases and of Income on Zero- and Low-Coupon Bonds

Balance of Payments Division, IMF Bureau of Statistics • 460

xi

xii

26. Financial Leasing Brian Newson • 467

CONTENTS

27. Treatment of Deep-Discounted and Index-Linked Bonds in the National Accounts

Brian Newson and Soren Brodersen • 483

28. Principles of Valuation and Reconciliation Items in the IMF' s Money and Banking Statistics

and A System of National Accounts Keith G. Dublin • 505

29. Treatment of Output in the Banking Industry Abul Siddique • 520

30. A Further Look at the Treatment of Insurance in A System of National Accounts

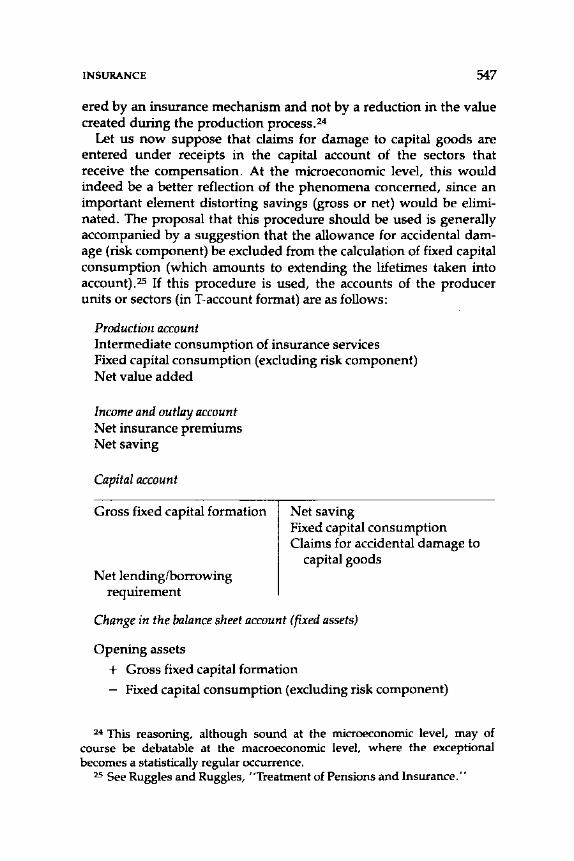

Andre Vanoli • 530

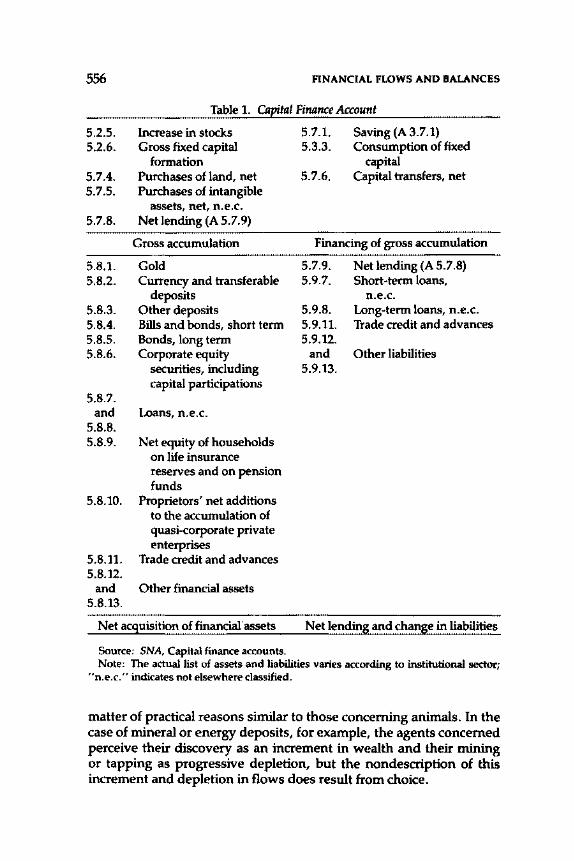

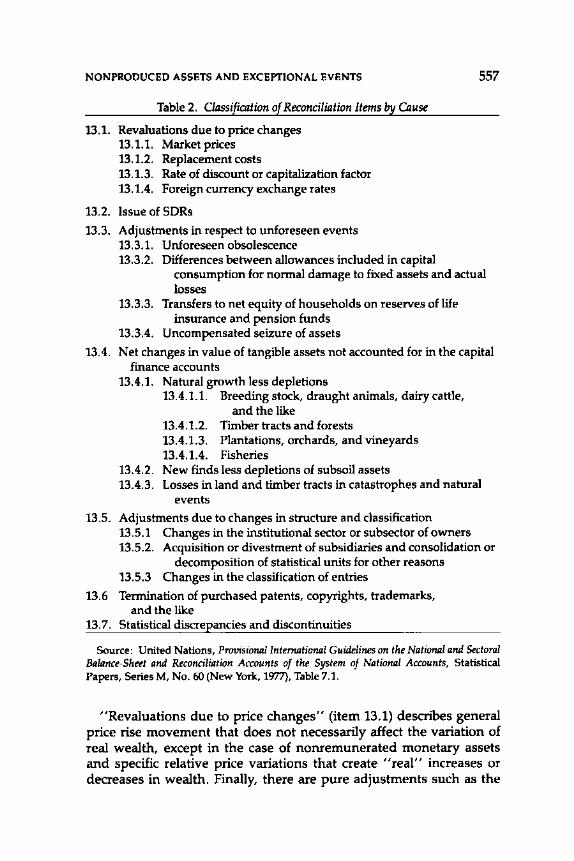

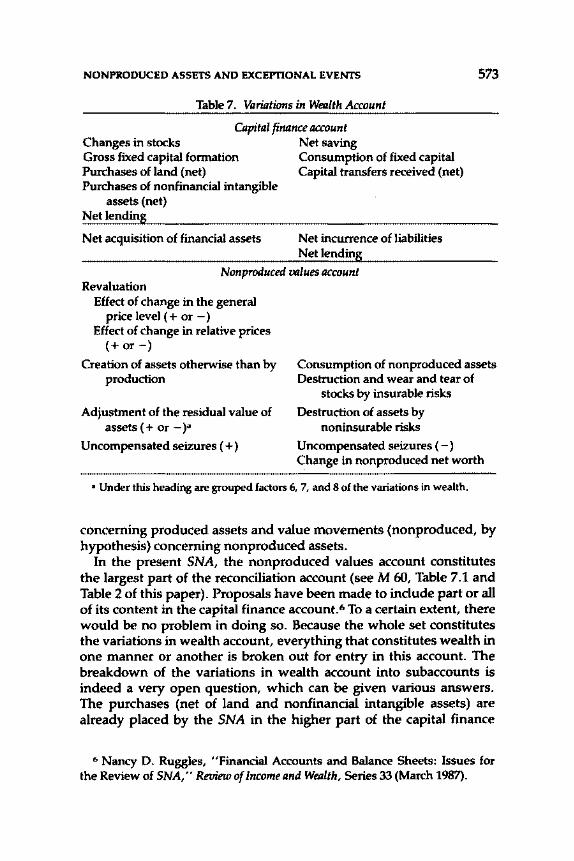

31. How to Treat Nonproduced Assets and Exceptional Events in the National Accounts? Considerations

on the Variations in Wealth Accounting Jean-Paul Milot, Pierre Teillet, and Andre Vanoli • 554

32. Fixed Capital Formation by Owner and User Heinrich Lutze[ • 590

Contributors • 595

Abbreviations • 597

Introduction

VICENTE GALBIS

T HREE BROAD GOALS have been set for the revision of the United Nations' A System of National Accounts (SNA). 1 First, it is generally

recognized that there is scope for a simplification of the system of accounts to make it more directly relevant for the purposes of compilation and the needs of users. Many countries have encountered difficulties in the implementation of some aspects of the 1968 (current) version of the SNA and in preparing current data for the national accounts. In addition, the continued expansion of the framework of the SNA through "Guidelines" and "Handbooks," which complement the basic SNA document (known as the "Blue Book"), makes it advisable to take a fresh and comprehensive look at the entire system. In this context, a particular emphasis is planned to be given to the special concerns of the developing countries. Second, a need has been felt to take into account several relatively important methodological developments that have occurred since the publication of the 1968 SNA and that are not reflected in the current basic framework. These developments suggest that improvements in the methodological and analytical bases of the SNA are possible. Third, there is a need for harmonization of the SNA with related systems of macroeconomic accounts, among them the systems developed by the IMF relating to compilation of its balance of payments statistics (BOPS), government finance statistics (GFS), and money and banking statistics (MBS).

The three goals are closely interrelated. Simplification of the SNA is

1 United Nations, Department of Economic and Social Affairs, Statistical Office of the United Nations (UNSO), A System of National Accounts, Studies in Methods, Series F, No. 2, Rev. 3 (New York, 1968). Hereafter in this volume, referred to without full bibliographic citation (see the list of abbreviations at the back of the volume).

xiii

xiv INTRODUCTION

necessarily linked with methodological improvements, especially those that encompass concepts that direct attention to the broader aspects of the measurement of economic activity. In turn, methodological improvements, as well as practical advances in the measurement process, are often the basis for the harmonization of the various systems of macroeconomic accounts. For these reasons, all of the expert group meetings for the revision of the SNA had these three purposes in mind, although with different degrees of emphasis depending on the subject under discussion.2

The three expert group meetings for the revision of the SNA sponsored by the IMF in 1987 and 1988 placed particular emphasis on methodological improvements bearing on the harmonization issue. This was particularly appropriate because the Fund's main statistical systems-the BOPS, the GFS, and the MBS-cover in detail three of the broad macroeconomic sectors that are encompassed in the SNA. Data corresponding to these systems form part of the principal statistical publication of the Fund, International Financial Statistics (IFS), and of its other statistical publications.J The principal focus of the papers included in this volume-originally presented as background papers for the discussions of the expert group meetings-is on harmonization. The objective of harmonization is broad consistency between these specialized statistical systems and the SNA on major methodological issues, including the appropriate sectorization, classification of transactions, and type of data. The development of the Fund's statistical methodologies and systems, while taking into account the overall structure and framework of the SNA, initially arose out of pragmatic responses to various challenges faced in the respective statistical areas, in different IMF departments, and over different

2 Eight expert group meetings were held on specific topics, as follows: SNA Structure (Geneva, June 1986), Prices and Quantity Comparisons (Luxembourg, November 1986), External Transactions (Washington, March-April 1987), Household Sector Accounts (Aorence, August-September 1987), Public Sector Accounts (Washington, January 1988), Production Accounts and Input-Output Tables (Vienna, March 1988), Financial Aows and Balances (Washington, September 1988), and Reconciliation of SNA/MPS [Material Product System] Standards on National Accounting (Moscow, December 1989). In addition, there have been several meetings on SNA Coordination to discuss preliminary drafts of the revised SNA.

3 In addition, the IMF collects and publishes data on other subjects such as exchange rates, Fund transactions, international liquidity, interest rates, prices, and output and employment in IFS, and on international trade by partner country in Direction of Trade Statistics (DOTS).

INTRODUCTION XV

periods. 4 For this reason, as well as for complex issues of substance, there are a number of outstanding issues, of both form and method, for the process of harmonization. The papers included in this volume have served, as much as anything, to direct the efforts of the groups of experts in their deliberations on outstanding methodological issues with a view to bringing about the desired harmonization.s They have also provided a basis for a discussion of methodological adaptations and innovations for possible incorporation in the SNA as well as in the revised Fund methodologies.

The IMF's Balance of Payments Manual (BPM) incorporates a conceptual framework relating the balance of payments to the external sector accounts of the SNA (BPM, Chapter 2, Section 6, paragraphs 44-51, and Appendix C). Although in principle the relationship between the two systems of accounts is clear-cut, the BPM (Appendix C) notes that there are many practical problems that are substantial enough to discourage the task of harmonization. Fortunately, however, this pessimistic view has been superseded by recent developments; for instance, a more recent examination of this issue suggests that "these two systems are consistent and interrelated. " 6 A harmonized presentation is planned to be provided in the revised SNA, as well as in the fifth edition of the BPM; harmonization issues will also be taken into account in the Balance of Payments Compilation Guide, which is being prepared by the Fund's Bureau of Statistics (now the Statistics Department). 7 The essays in this volume should serve to illustrate many of the outstanding issues on which substantial progress in this area has been made.

The Fund's A Manual on Government Finance Statistics (GFSM) discusses in detail the relationships between the GFS and the govern-

4 The IMF's Balance of Payments Manual (BPM), first issued in 1948, was last revised in 1977 (the fourth edition). A Manual on Government Finance Statistics (GFSM) was issued in draft in 1974 and was published in 1986. An internal Fund document in draft, A Guide to Money and Banking Statistics in International Financilll Statistics (MBS Guide), was produced in 1984.

s The reports of the expert group meetings are being used to guide the authors charged with drafting the revised SNA.

6 The World Bank, International Monetary Fund, Bank for International Settlements (BIS), and Organization for Economic Cooperation and Development (OECD), External Debt: Definitions, Statistical Coverage and Methodology (Paris, 1988), p. 17.

7 It is planned that the Balance of Payments Compilation Guide will also serve as a "Handbook of National Accounting on External Sector Transactions," to be published by UNSO.

xvi INTRODUCTION

ment sector of the SNA.B To facilitate the compilation of national accounts for the government sector of the SNA from the GFS, the GFSM presents detailed "bridge tables" between the two data systems. 9 This is possible because the underlying building blocks included in both systems should in principle agree. The main differences between the two systems are that the SNA records transactions on an accrual basis, has three separate but interrelated accounts, and classifies taxes and subsidies according to whether or not they are incurred in the course of production. The GFSM, on the other hand, provides for the presentation of accounts on a cash basis, organized into a single balanced account; taxes are classified by their base. Many of these differences and suggested ways of harmonization are discussed in the essays included in the present volume.

Although the current draft of A Guide to Money and Bankmg Statistics in International Financial Statistics (MBS Guide) does not contain a separate section on the relationships between the MBS and the SNA, many references are made in the text, as appropriate, to these relationships. The essays in this volume further elucidate these relationships and suggest that both the revised SNA and the draft MBS Guide, which is also planned for revision, will develop explicit principles for their harmonization.

The basic interrelationships between the Fund's main statistical systems and the SNA are clearly perceived from the perspective of the flow-of-funds (FOF) accounts, which may be viewed as a component of the broader SNA. The FOF accounts contain a closed system of financial flows among transactors by type of financial transaction and also connect financial flows to the overall surpluses (net savings) and deficits (net borrowing) resulting from the sectoral (nonfinancial) production, income, and outlay accounts of the SNA.1o Furthermore, by a coordinated approach to the sectorization of the SNA and the FOF accounts, it can be shown that the Fund's main statistical systems correspond to three macrosectors into which the economy may be disaggregate at the first level of disaggregation of the SNA, including as a component the FOF accounts (that is, the government, financial, and rest-of-world sectors; the remaining macrosectors comprise, in essence, households and corporations). This reinforces the interest in

8 GFSM (1986, Chapter 5). 9 Similar tables are included in UNSO, Handbook of National Accounting,

Public Sector Accounts, Studies in Methods, Series F, No. 50 (New York, 1988). 10 The FOF system, like the broader SNA, is a closed (self-contained) sys

tem of accounts in the sense that it can in the aggregate be specified as a complete set of equations.

INTRODUCTION xvii

the harmonization of these systems (see Chapter 21 in this volume). The benefits of relating the Fund's main systems to the SNA should be seen in eliminating unnecessary discrepancies, as well as duplicative efforts in compiling statistics. In fact, the Fund's statistical systems should be able to provide much of the data required for the construction of the SNA and related FOF accounts; data for the SNA, BOPS, and GFS are largely in the form of flows and, therefore, comparable in principle. Although the MBS data are mainly stock data, financial flow data can be derived from stock data by adjusting changes in stock data to eliminate elements of revaluation changes and other reconciliation factors.

A main challenge, therefore-and the one addressed by the papers in this volume-is to harmonize as much as possible the sectoral information from the SNA (and FOF) with the corresponding sectors covered by the IMF's main statistical systems. Successful efforts in the harmonization process will be of great benefit to compilers and users of macroeconomic statistics.

I. External Sector Transactions

The first six papers in Part I of this volume deal with some general methodological principles in compilation of statistics on the external sector of the SNA and the balance of payments.

The crucial concept of the residents of an economy-a concept needed to distinguish external (rest-of-world) from domestic transactions-is the subject of the papers by Bouter and Raymond. Bouter (Chapter 1) presents a comprehensive review of the residency criteria given in the SNA and the BPM; he shows that, although the main concepts regarding the territory of an economy and the "center of economic interest" of a given entity remain valid, some supplementary rules of thumb are required to pin down the criteria in special cases-for example, when the entity changes territory, especially when it does so frequently, and when it remains permanently outside the territory of any national economy. He goes on to specify in some detail the entities that are to be considered residents of an economy. Broad economic groups are examined for this purpose: the general government, private nonprofit bodies serving individuals, enterprises, and international organizations. The specific issues raised by the treatment of the last of these are discussed in greater detail by Raymond (Chapter 2). After reviewing the criteria in the SNA and the BPM, Raymond advocates a more refined definition of an international organization as one whose authority derives directly from the

xviii INTRODUCTION

authority of its member countries and that has a sovereign status (that is, the laws and regulations of the country or countries in which it is located do not apply to it). However, the decision to treat an entity as an international organization for statistical purposes can only be made on a case-by-case basis. International organizations are not considered residents of any national economy; each is treated as a separate economy. The only resident entity of an economy comprising an international organization is that organization itself.

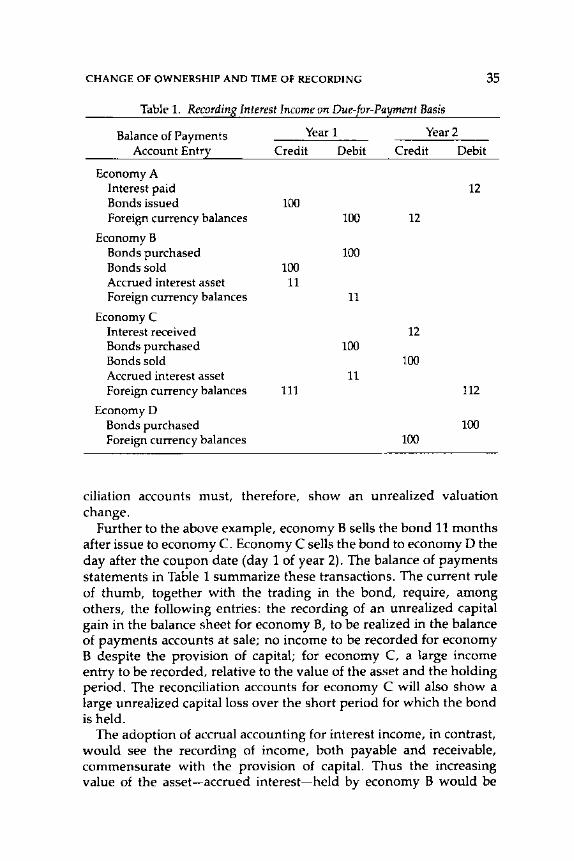

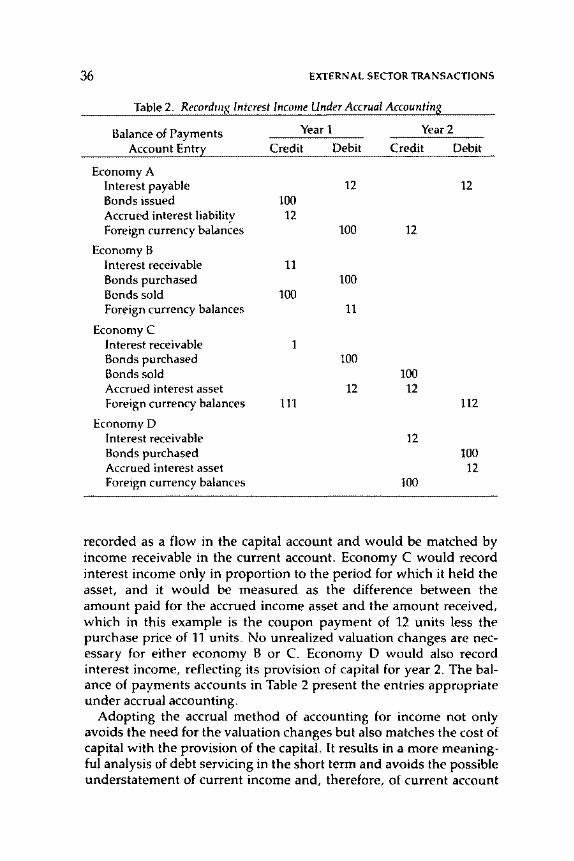

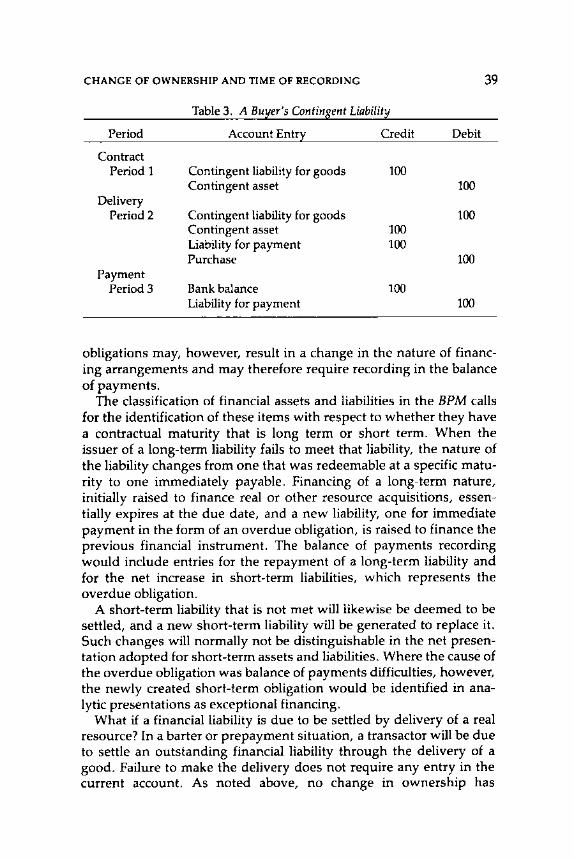

The change-of-ownership principle, which is used to determine whether a transaction has in fact taken place, and the time for recording a transaction are discussed by McColl (Chapter 3). He first points out that ownership is presumed to be identical to legal ownership except in three cases: when legal ownership cannot be granted, as in the case of illegal transactions; when the transactions are between two transactors that are part of the same legal entity; and when the resource is provided under a financing arrangement (including financial leasing) that transfers economic control and most of the risks of ownership of the asset to another party without transferring legal ownership. Other proper accounting requirements are that the two sides to a transaction must be recorded simultaneously by the two transactors and that the time of recording must have economic significance (that is, it must refer to the change of control or ownership over economic resources). McColl concludes that the only accounting framework to meet these criteria is accrual accounting, whereas cash accounting recognizes only one transaction-payment-that may not be concomitant with the transfer of economic control and o~nership. He goes on to apply accrual accounting methods to the recording of transactions between affiliate companies, financial leases, interest income (particularly in the case of deep-discounted bonds), and overdue obligations.

Issues of conversion and exchange rate differentials in balance of payments statistics and the SNA are the focus of the papers by Parcu, Schulze-Ghattas, and van Tongeren. The conversion of transactions denominated in different currencies into a common valuation currency is the specific subject discussed by Parcu (Chapter 4). This is a subject of considerable interest-and controversy-in recording external transactions in the SNA and the balance of payments because the increased variability of exchange rates since the introduction of the floating exchange rate system has made the problem of conversion more difficult. The analogy between valuation changes resulting from price changes and those stemming from exchange rate changes clarifies the nature of the analytical problem for statistical recording. The general recommendation has been to choose for conversion the

INTRODUCTION xix

exchange rate prevailing at the date of the contract. Unfortunately, the practical applicability of this principle is severely limited by lack of adequate statistical information. For this reason, in practice, transaction values are usually converted into the unit of account at an average rate for the period in which the transaction occurs. Parcu suggests that this practice inevitably distorts the statistics and makes them less reliable, the more so the wider the fluctuations in exchange rates. The difficulties for statistical recording are even more severe in countries with a multiple exchange rate system-as discussed by SchulzeGhattas (Chapter 5). In principle, two possible methods of conversion may be applied in the presence of multiple rates: conversion of each individual transaction at the exchange rate at which it was effected, or conversion of all transactions at a unitary conversion rate. The latter method has the merit that it ensures the recording of the taxes or subsidies that are implicit in a multiple exchange rate system. The main practical problem, however, is the determination of the appropriate unitary conversion rate. A reasonable proxy may be a weighted average of the different exchange rates observed in a multiple exchange rate system, the weights being the shares of the transactions effected at each particular rate.

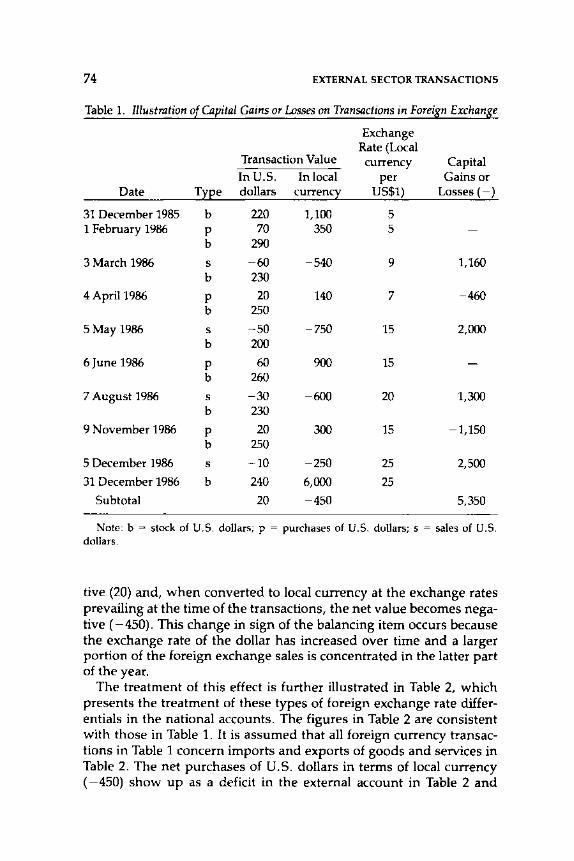

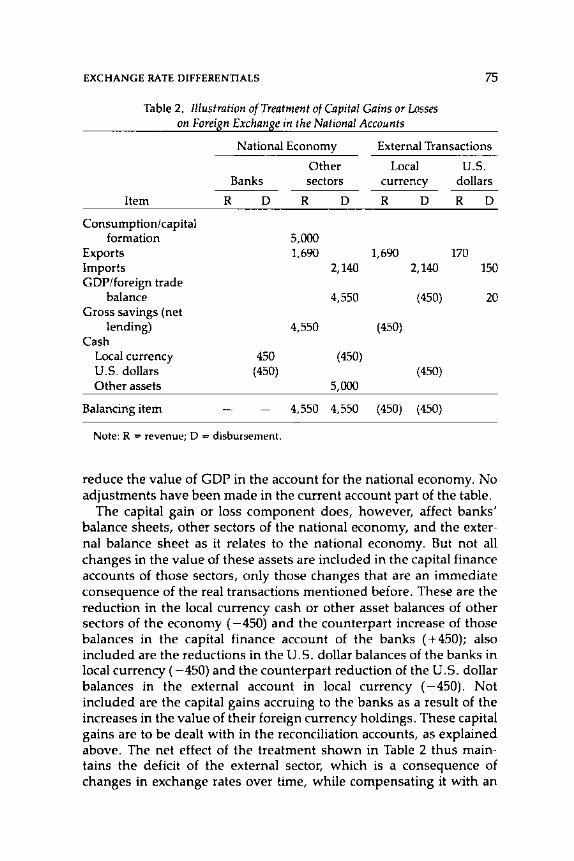

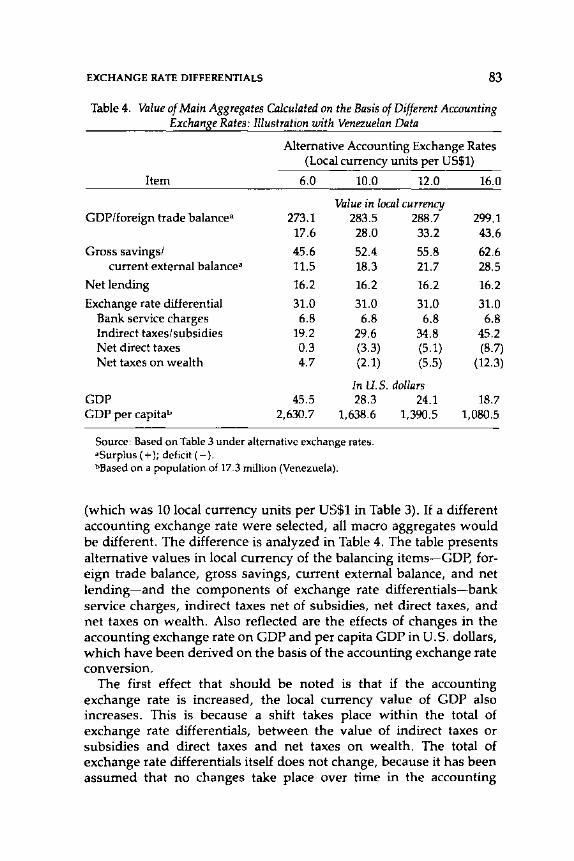

A different set of issues on the treatment of exchange rate differentials is raised by van Tongeren (Chapter 6). Focusing not only on the external accounts but also on other sectors of the national accounts and on the effects on gross domestic product (GOP) and its components, he proposes a distinction between three components of exchange rate differentials: bank service charges, capital gains or losses, and taxes or subsidies. His conclusions are in line with those of Schulze-Ghattas in that a unitary exchange rate is proposed in circumstances of multiple exchange rate regimes that generate taxes or subsidies. However, van Tongeren suggests that no adjustments are indicated for changes in exchange rates over time, with the valuation of purchases and sales of foreign currency being recorded at their actual exchange rates. Revenues derived from those changes should be treated as capital gains or losses and included in the revaluation account.

The nine remaining papers in Part I deal with the classification of transactions in both the external sector of the SNA and the balance of payments, and taken together they cover both current and capital account transactions as well as new financial instruments. In their joint paper, Bouter and van Tongeren (Chapter 7) focus on the harmonization of current account transactions between the SNA and the balance of payments. They first identify outstanding issues for harmonization by reference to the characteristics of the standard compo-

XX INTRODUCTION

nents of the current account in the SNA and the BPM and the relationships between them. Next, they discuss the results of a survey of the practices of selected countries, issue by issue, pointing out the differences between the SNA and the BPM components and, where necessary, suggesting modifications of the components that would result in a closer harmonization of the two systems. The main outstanding issues identified are that the SNA deviates in some respects from the change-of-ownership principle, whereas the BPM is consistent in its application; that reinvested earnings of direct-investment enterprises that have foreign branches or subsidiaries are not included in the SNA, but are included in the BPM; that imports are valued on a c.i.f. (cost, insurance, freight) basis in the SNA and on an f.o.b. (free on board) basis in the BPM; that monetary and nonmonetary gold are treated differently in the two systems; that the SNA has a separate identification of labor and property income received by factors of production, but the BPM does not; and that the SNA requires various imputations for insurance transactions that are not made in the BPM. In Chapter 8, Robertson discusses the need to include reinvested earnings of direct-investment enterprises in the SNA-as is already done in the BPM-exemplifying very well one of the harmonization issues raised by Bouter and van Tongeren.

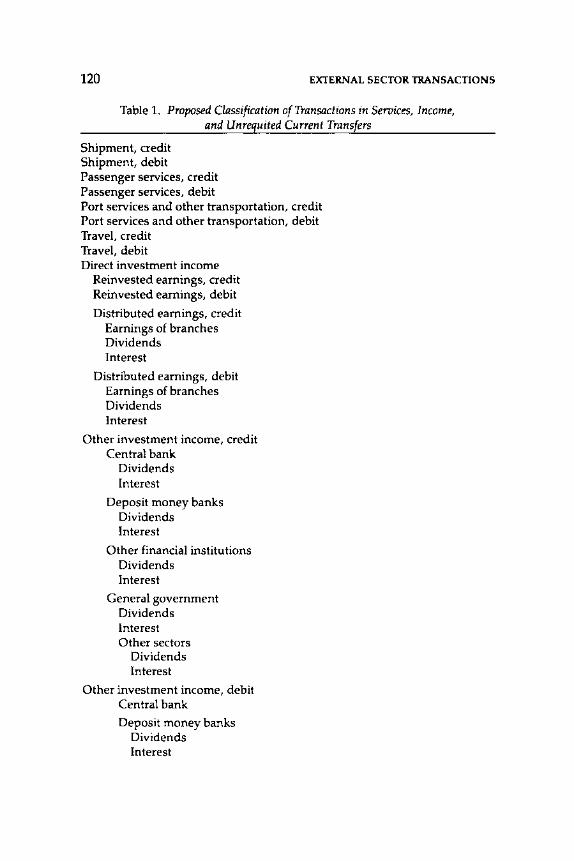

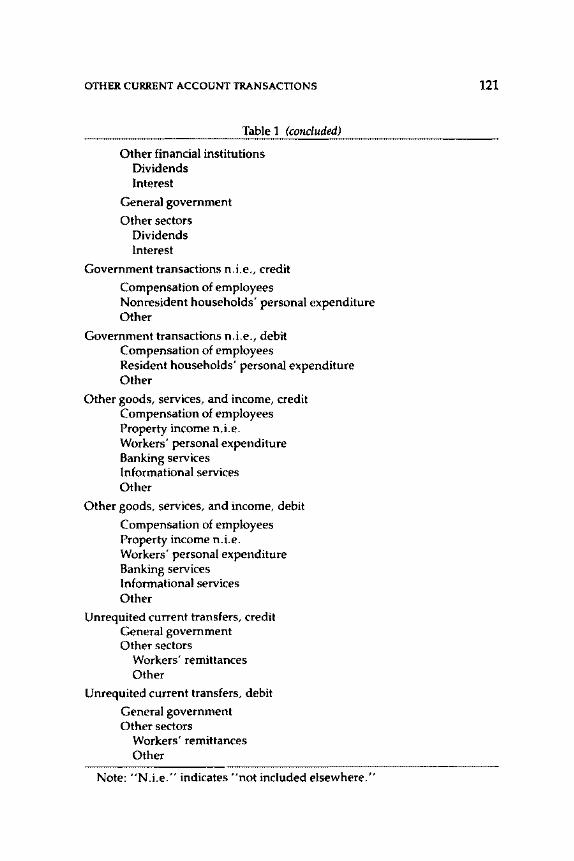

In a separate paper on the treatment of services, income, and unrequited transfers (Chapter 9), Bouter proposes a revised classification of the standard components for these current account items (42 in the BPM), taking into account the need to make improvements without substantially increasing the number of components and the desirable harmonization of the underlying transactions between the BPM and the SNA. One of his main proposals is to separate investment income into interest income and dividends, a breakdown indispensable for compiling debt service ratios.

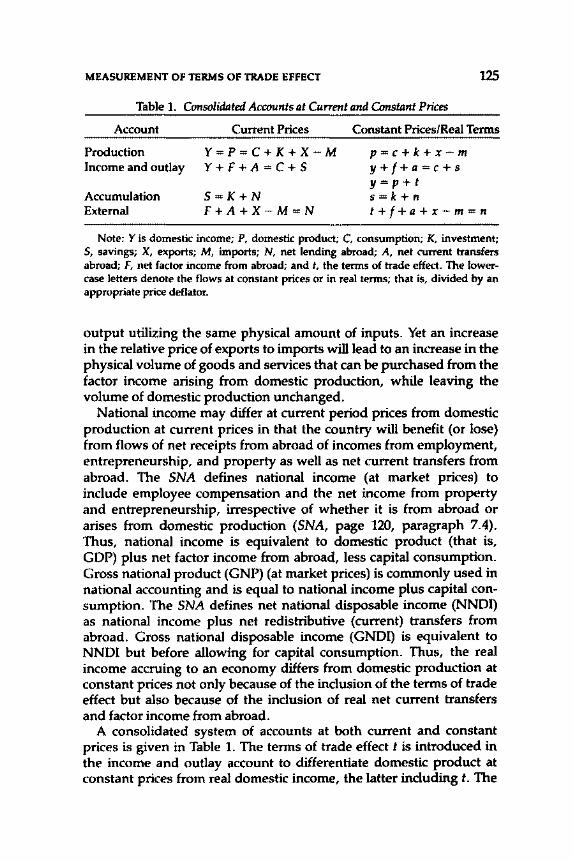

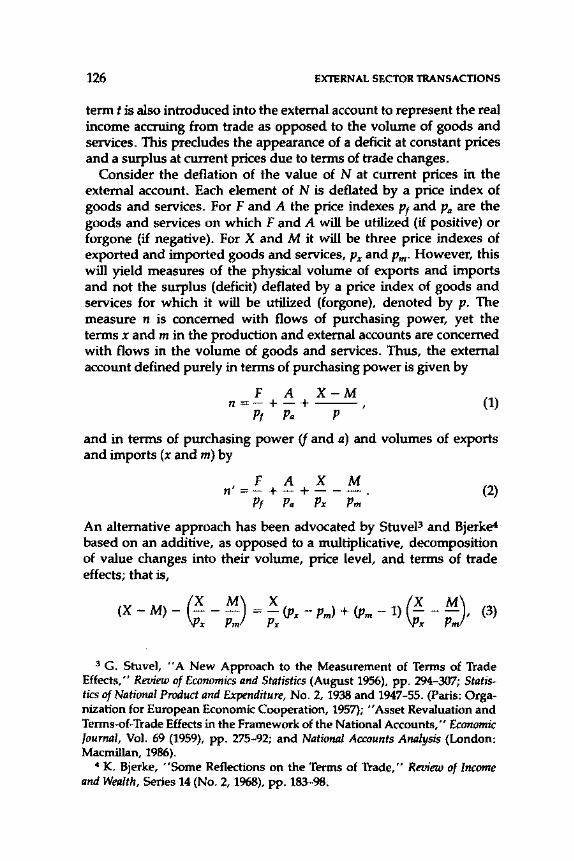

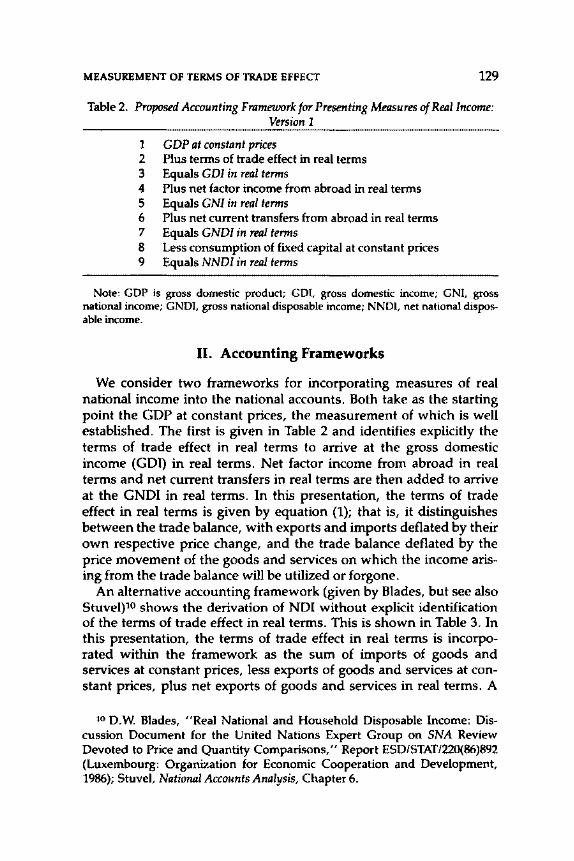

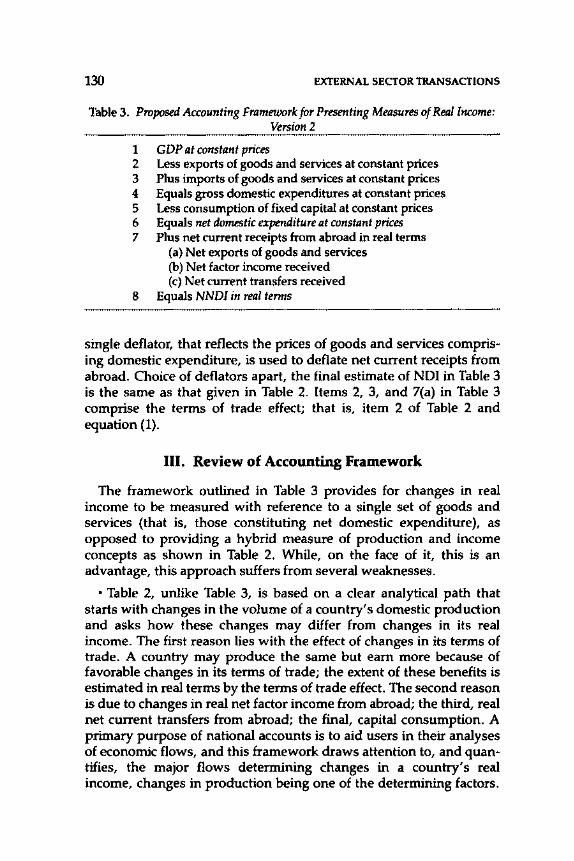

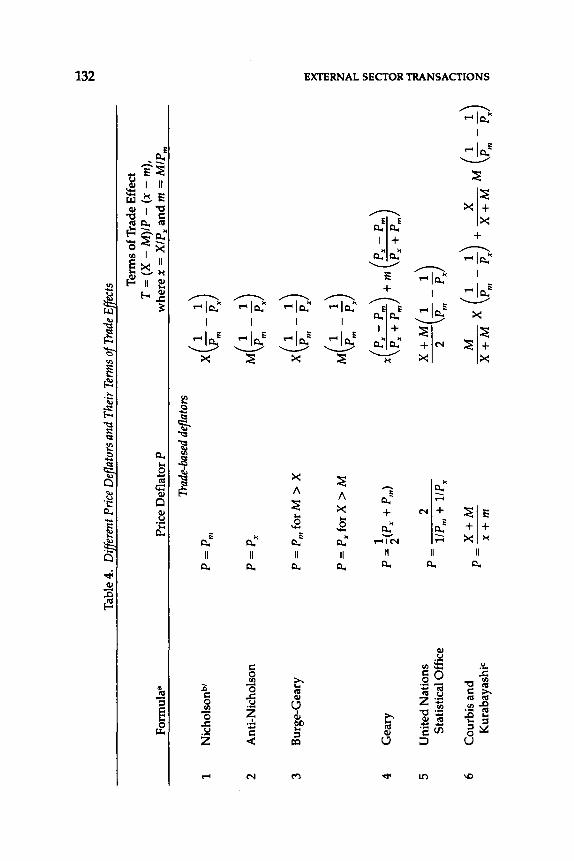

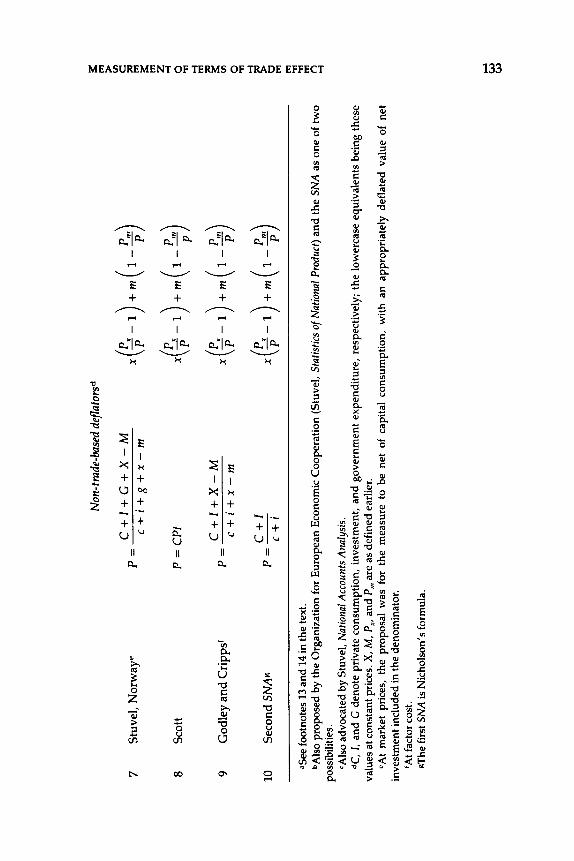

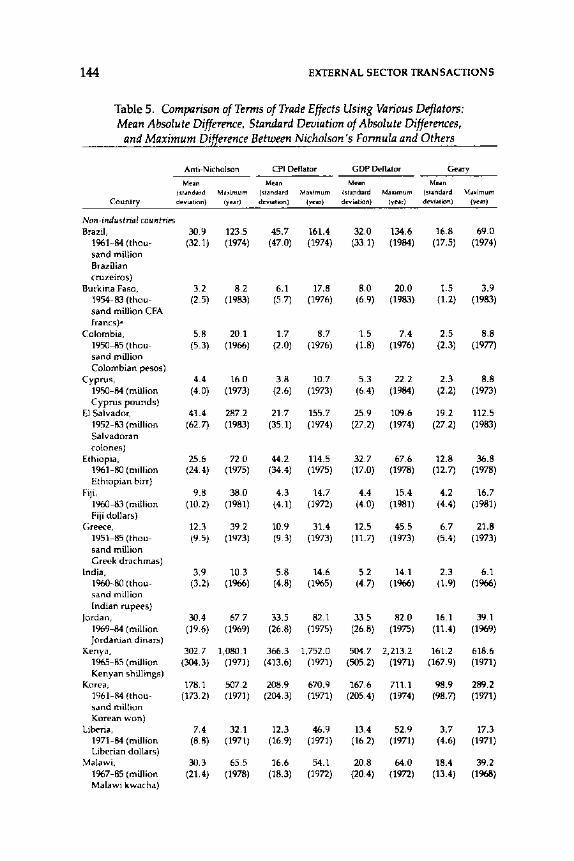

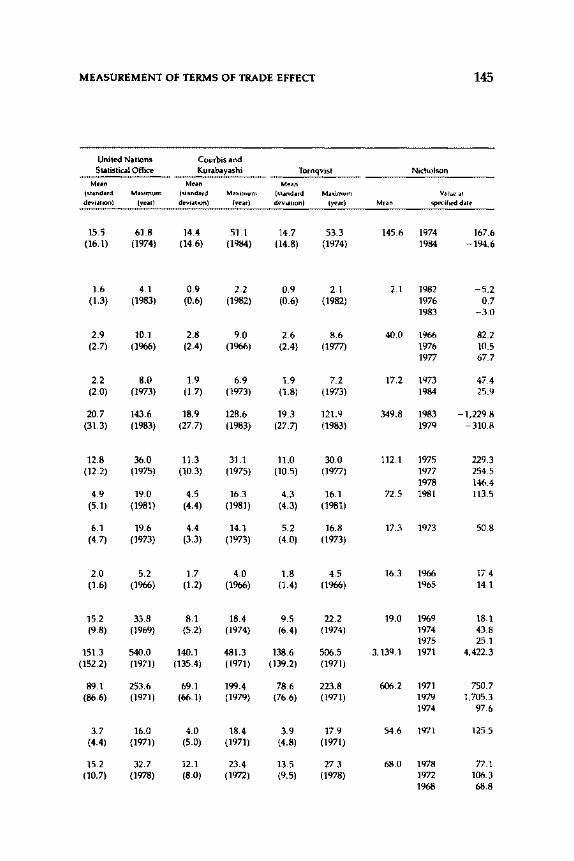

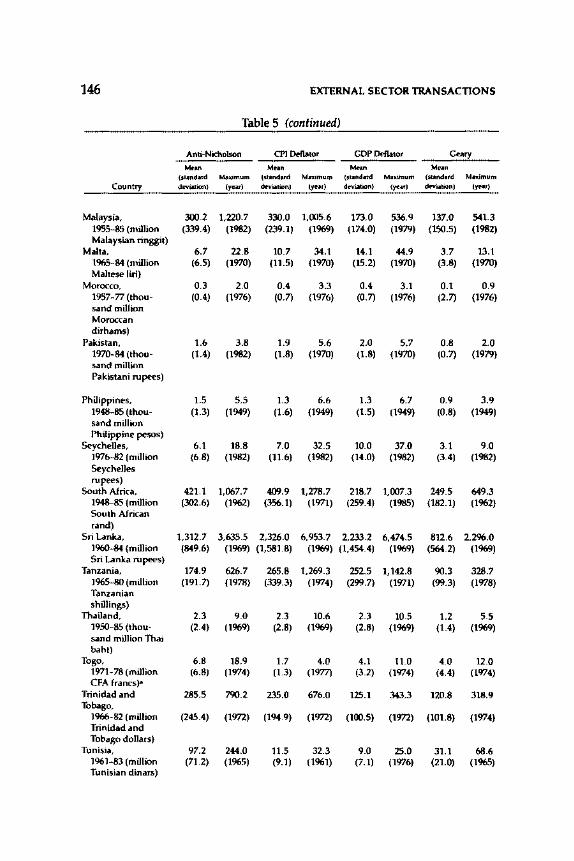

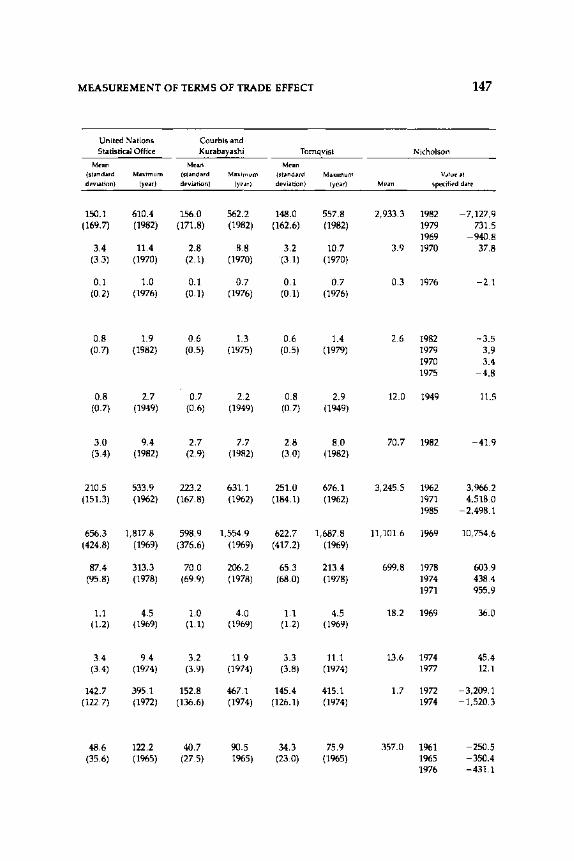

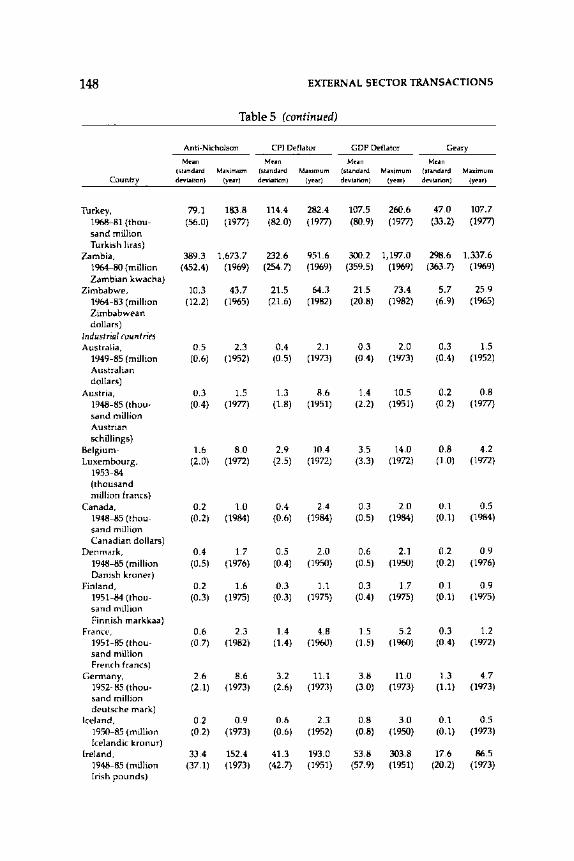

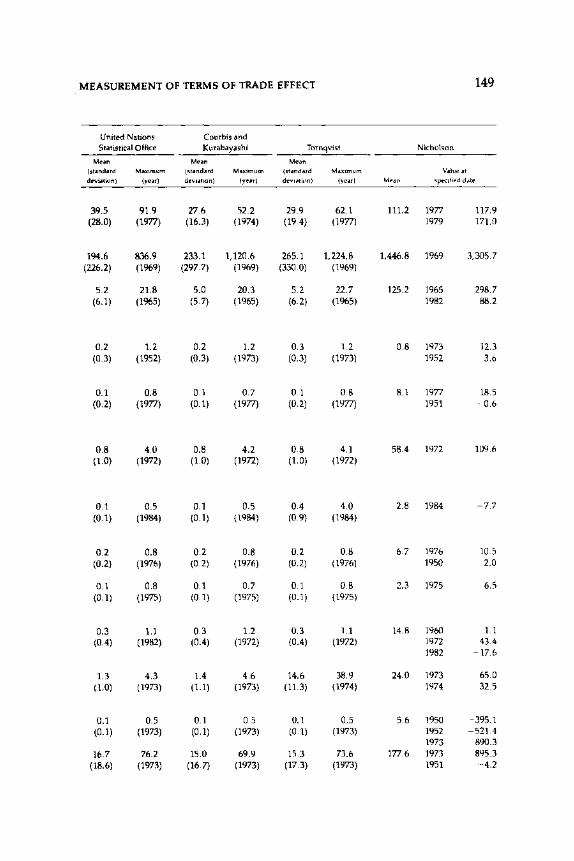

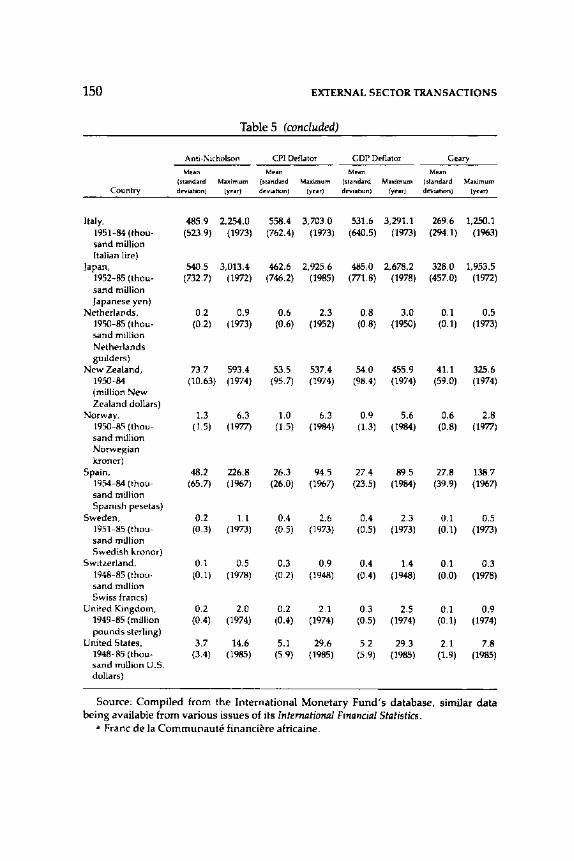

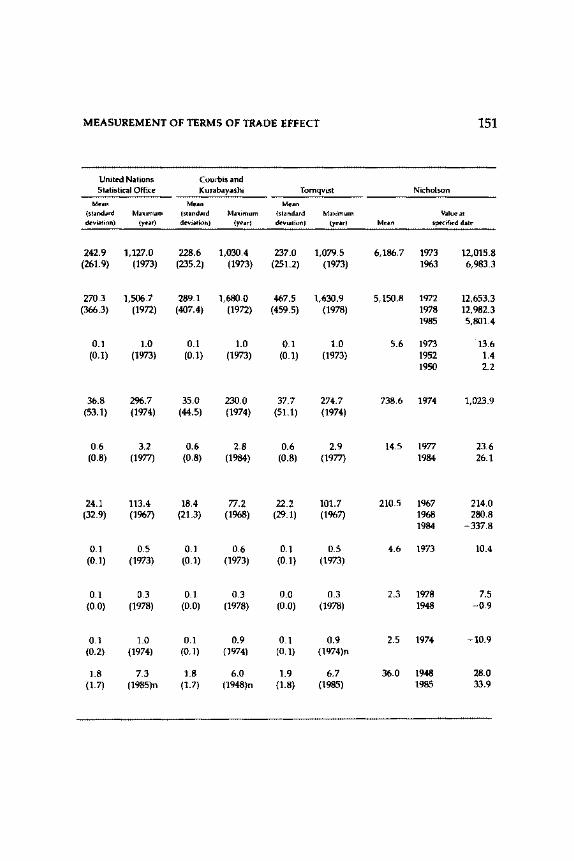

In contrast to the other papers, Silver and Mahdavy (Chapter 10) focus on a specific statistical issue related to the current account-the measurement of the terms of trade in real terms-and its implication for the measurement of real national disposable income. They show that the measurement of real values is dependent on the price indices on which the terms of trade are based and that the results are therefore subjective. The diverse implications of different price deflators for the terms of trade effect are shown.

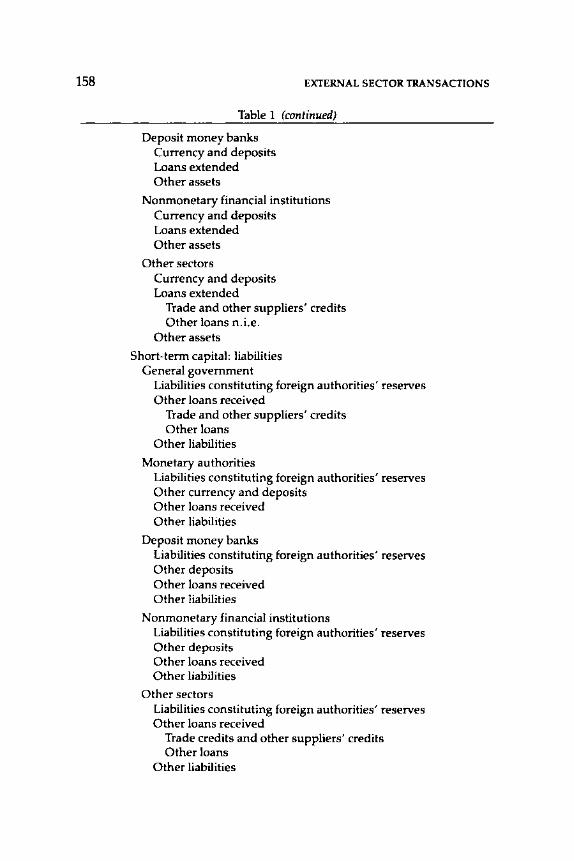

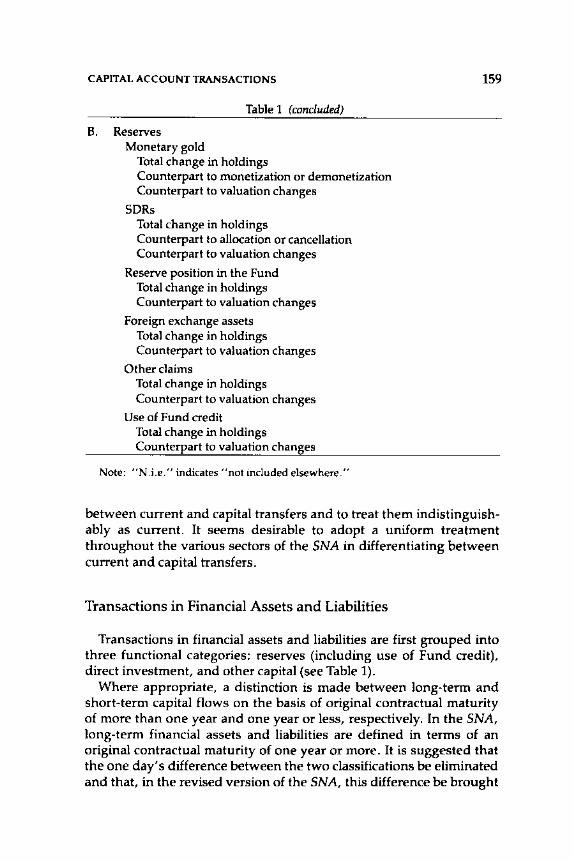

The paper by Gill (Chapter 11) turns to the general classification of capital account transactions and reviews the criteria for compilation of this complex part of the balance of payments. The author concludes that a substantial modification of the structure of the capital account would be required to serve the IMF' s analytical and operational

INTRODUCTION xxi

needs, to harmonize the balance of payments with the rest-of-world sector of the SNA, and to promote harmonization between the Fund's systems for balance of payments, government finance, and money and banking statistics, among other purposes. One of the amendments proposed by Gill is to distinguish between current and capital transfers in the balance of payments, as is currently done in the SNA. Another amendment would consist in merging portfolio investment, currently a separate item, into other (nonreserve and nondirect investment) capital movements and to distinguish the relevant capital flows in terms of the domestic sector of the creditor or the debtor instead of following an instrument-by-instrument approach. This revision would facilitate reconciliation with related bodies of economic statistics, provide better material for a variety of economic analyses, and facilitate the link between stock and flow data. In the new order, the current classifications of capital movements-by long term and short term and by financial instrument-would be relegated to secondary distinctions. This shift would recognize the lesser roles now played by these concepts, as secondary markets make the longshort distinction less relevant and the differences between instruments blur as a result of financial innovations. It is, however, proposed that the sectorization follow the functional approach of the GFSM and the draft MBS Guide, instead of the institutional approach espoused in the SNA.

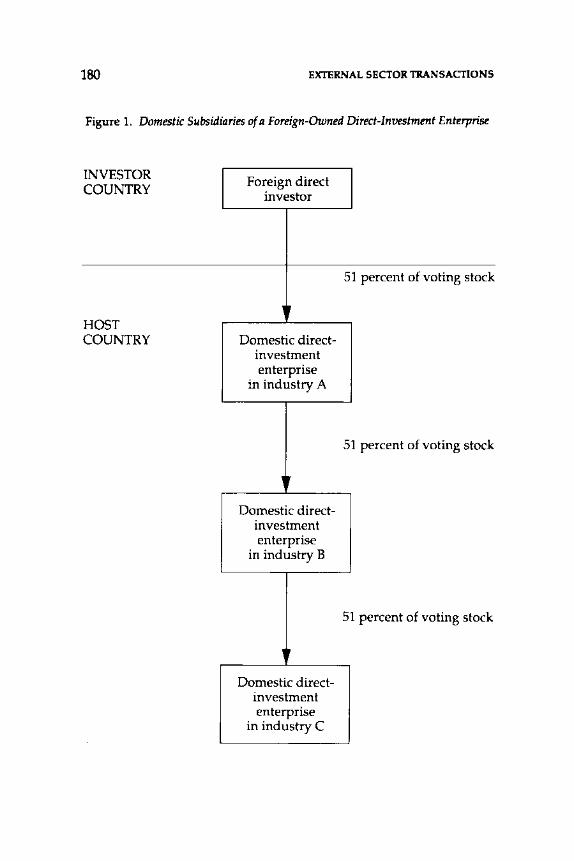

The paper by McAlister on the classification of corporate enterprises (Chapter 12) deals with criteria for distinguishing between resident-owned and foreign-owned enterprises, particularly in relation to the definition of direct investment, a separate component of the capital account. Specifically, the paper examines the notion of foreign ownership with reference to the concept of direct investment as currently formulated in the BPM.

The papers by Hoezoo, McColl, and Thornton elaborate on the proposed reclassification of the capital account of the balance of payments suggested by Gill. Hoezoo (Chapter 13) reviews the treatment of new financial instruments in the balance of payments-including note issuance facilities, swaps, options and futures, and Eurobondsand shows that their classification can be handled within the methodological guidelines provided by the current BPM. The issues arising from the securitization of debt and off-balance-sheet transactions and debt capitalization are also discussed and suggestions made for their treatment within the parameters of the BPM. A more specific discussion of the treatment of zero-coupon bonds, junk bonds, and indexed bonds in the balance of payments is provided by McColl (Chapter 14). His main conclusion in this respect is the same as that of

xxii INTRODUCTION

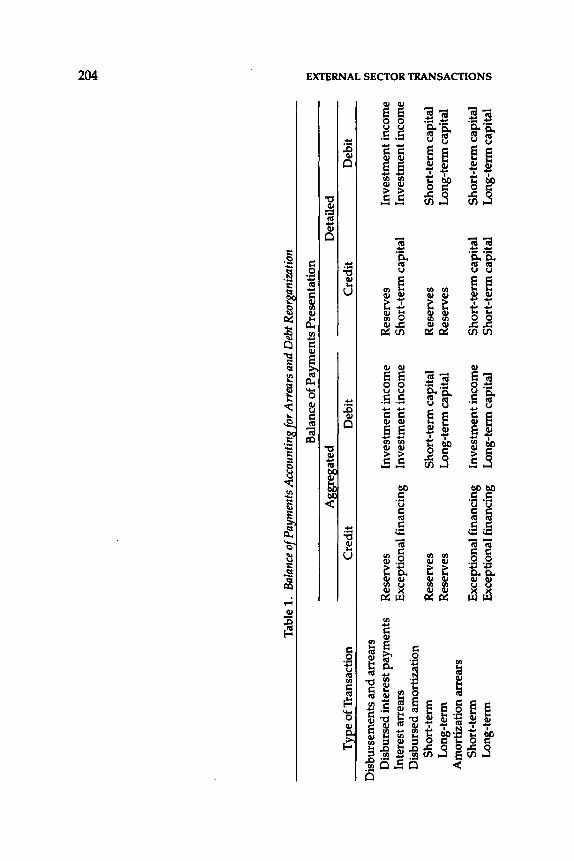

Hoezoo: that all of these bonds, although very different from each other and different from standard bonds, do not exhibit any features for which the BPM does not already contain appropriate recommendations for proper classification. Finally, Thornton (Chapter 15) provides a framework for the presentation of arrears and debt reorganization in the balance of payments. Building on the general methodology of the BPM to this effect, he shows that a proper treatment requires the use of accrual rather than cash accounting to allow for the identification of arrears and debt reorganization transactions. This new treatment requires an increase in the detail given in the accounts beyond the current list of standard components in order to identify these transactions, which constitute part of the II exceptional financing'' of the balance of payments recorded ''below the line.''

II. Public Sector Accounts

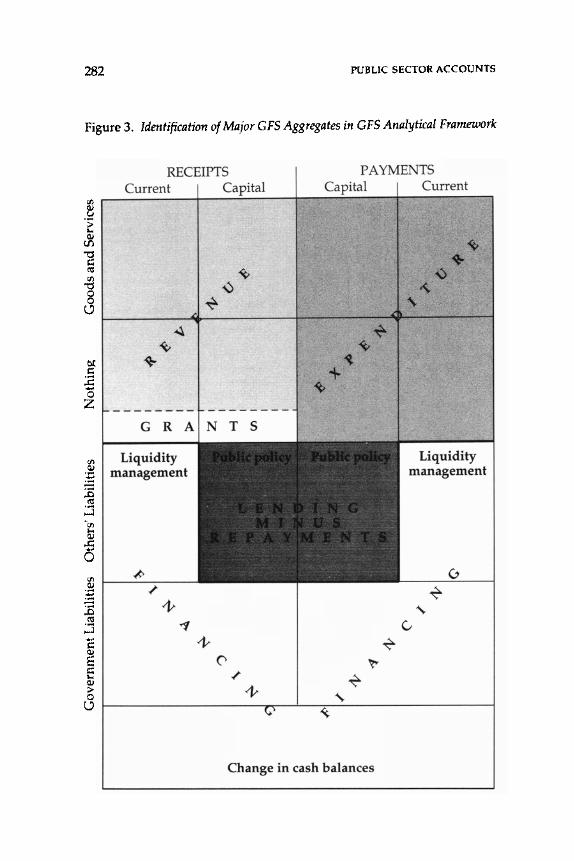

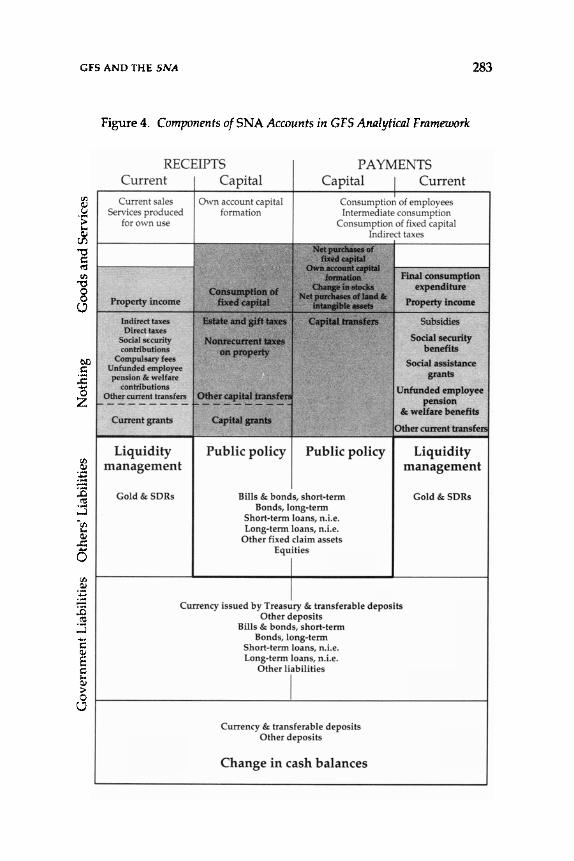

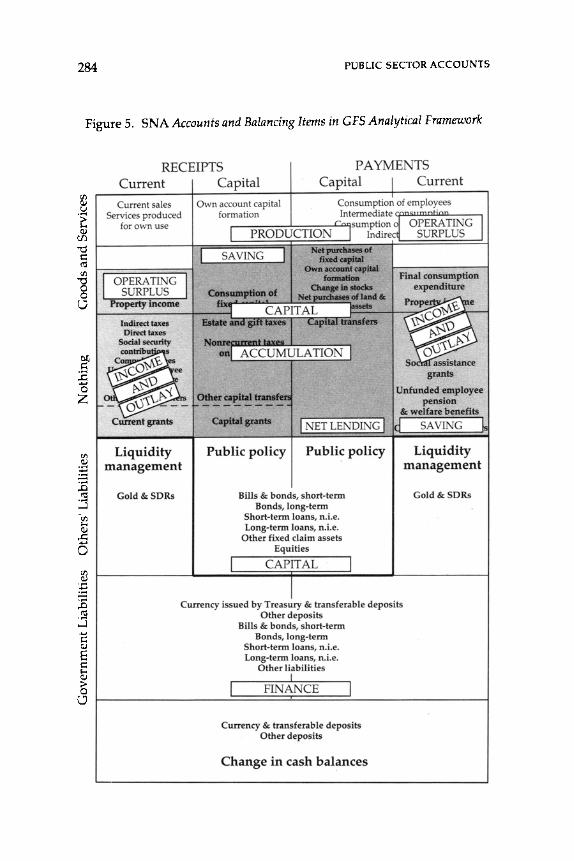

Part II of the volume contains five papers that are quite different in size and content but cover most of the issues of harmonization between the government sector of the SNA and the GFSM. The first paper (Chapter 16)-the result of efforts by staff members of four international agencies-reviews most of the outstanding harmonization issues in this field; it served as a basic discussion paper and an annotated agenda for the Expert Group Meeting on Public Sector Accounts held in January 1988. The other papers address specific issues included in the group's agenda.

The discussion paper begins with an examination of the different objectives served by the government sector of the SNA and the GFSM and concludes that, although further harmonization would be useful, it is unlikely that either system can be entirely replaced by the other. The GFS is a system directly derived from government accounting records needed for operational purposes, and is largely a cash-based system. The SNA, on the other hand, requires the government sector to be treated symmetrically with other sectors of the economy and uses accrual accounting. In addition, there are many minor conceptual differences between the two systems, as well as data discrepancies arising from different compilation procedures.

The discussion paper deals next with the coverage of transactors, with special emphasis on borderline issues between the government sector and other institutional sectors and within subsectors of the government sector. Among the most difficult external borderline issues are those concerning the treatment of government departmental enterprises and ancillary enterprises as belonging to either the

INTRODUCTION xxiii

enterprise sector or the general government; the attribution of community production of capital goods to the sector responsible for their upkeep; the rerouting of central and commercial banking activities performed by government to the financial sector, a practice supported by both the GFSM and the draft MBS Guide but not indicated by the SNA; the attribution of government employees' pension funds and welfare schemes to either the financial sector or the government; the assignment of nonprofit institutions to various institutional sectors; and the appropriate classification of supranational authorities and other international organizations. The main intrasectoral issues concern the classification of central, state, local, and other government levels; and the treatment of social security funds, which are consolidated with the corresponding level of government in the GFSM but constitute a separate subsector in the SNA.

Another section of Chapter 16 deals with various issues in the registration of transactions, including the choice of accrual versus cash accounting, procedures for consolidation of the accounts, gross versus net recording of entries, and imputations and rerouting. The analytical framework of the government accounts, focusing in particular on the distinction between current and capital accounts, and the definitions of government saving and overall deficit or surplus are discussed next. The final section of the paper deals with selected classification issues, including the treatment of taxes, social security contributions, fees, property income, indexation payments, and the functions of government.

A concise historical account of the main efforts to date on the harmonization between the GFSM and the SNA, with special attention to the "bridge tables" between the two systems and the further links sought through joint country questionnaires, is provided in the joint paper by Levin and van Tongeren (Chapter 17).

The overall relationships between the GFSM and the SNA are the subject of the next paper, Chapter 18, by Levin. Apart from the rerouting of some government monetary authority and deposittaking functions to the financial sector in the GFSM, there are some other major differences between the two systems, namely (1) the classification of government lending together with expenditures "above the line" in the GFSM, while government lending is "below the line" (that is, in the finance account) in the public sector accounts of the SNA, mainly because of the need for symmetry with the treatment of other sectors; (2) the consolidation of social security funds in the GFSM with the level of government at which they operate, while the SNA groups all social security funds into a single subsector of the government; (3) the cash basis of GFS data, in contrast to the accrual

xxiv INTRODUCTION

basis of .the SNA, which covers some transactions not reflected in cash payments as well as some imputations.

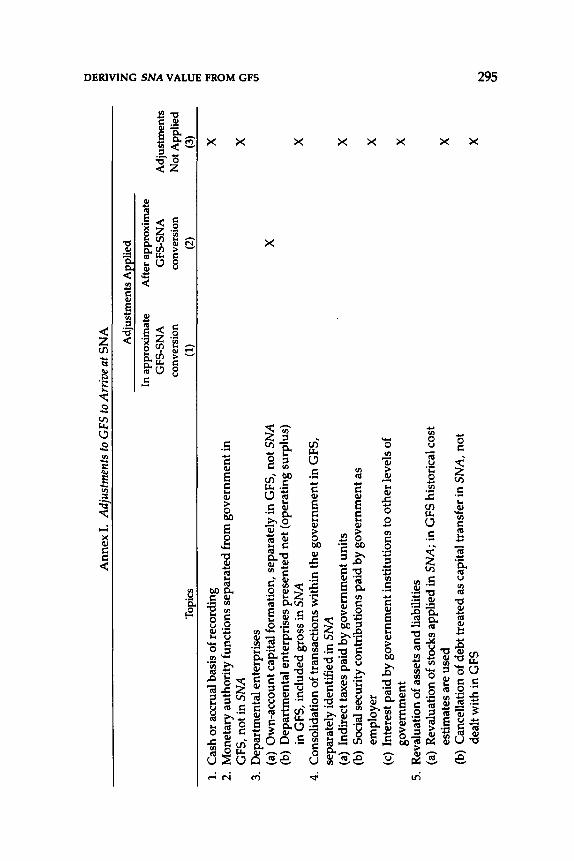

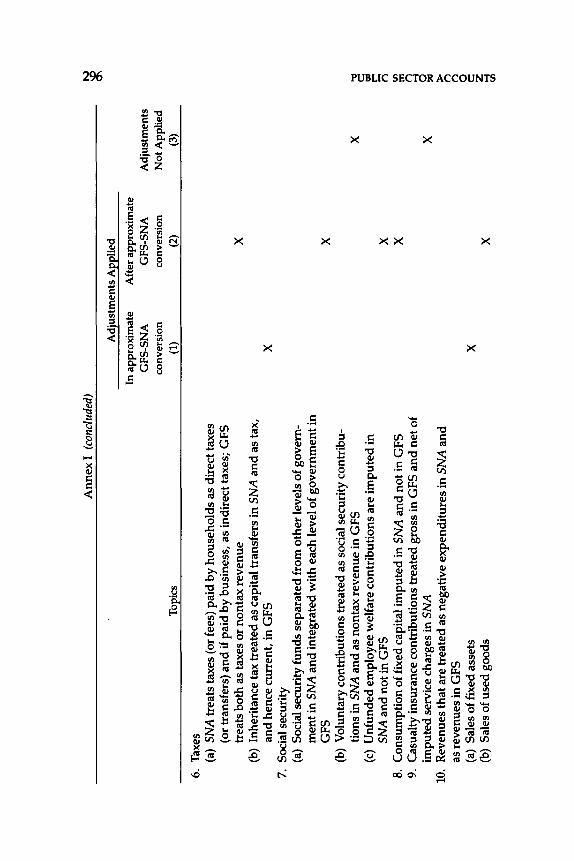

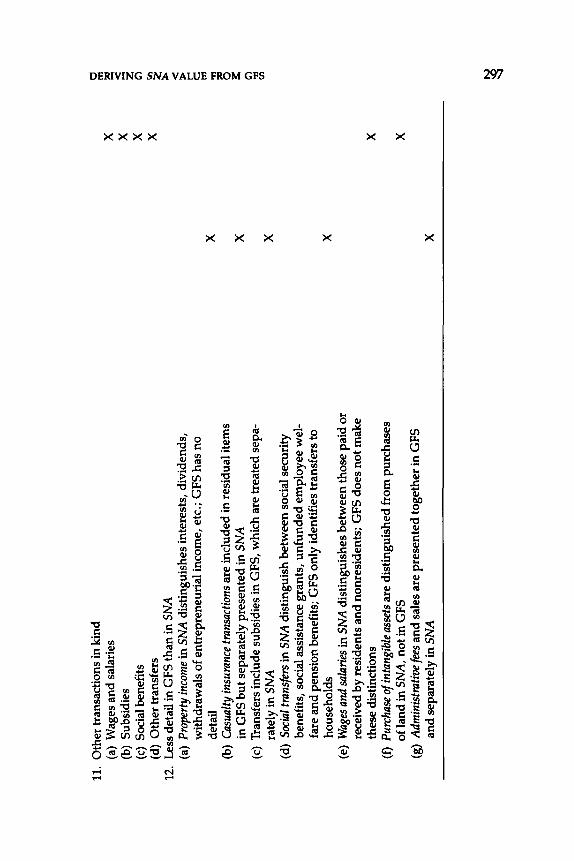

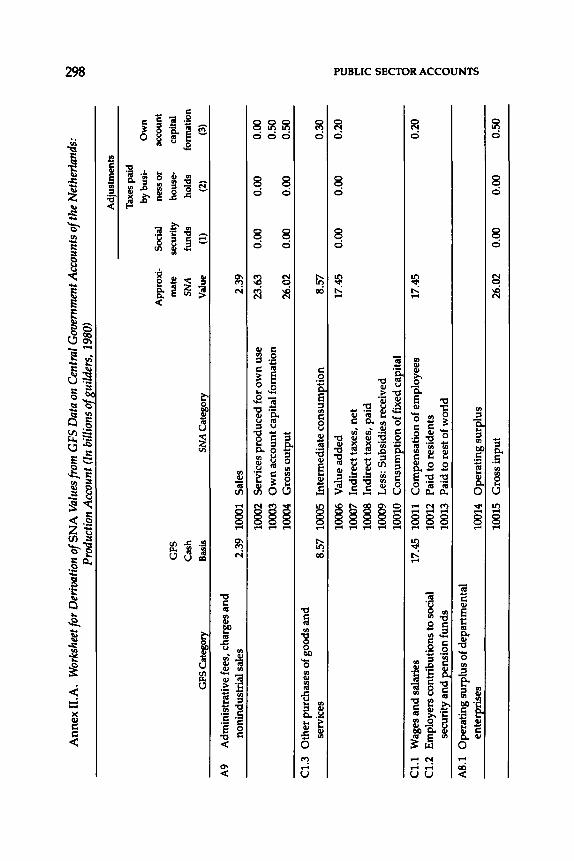

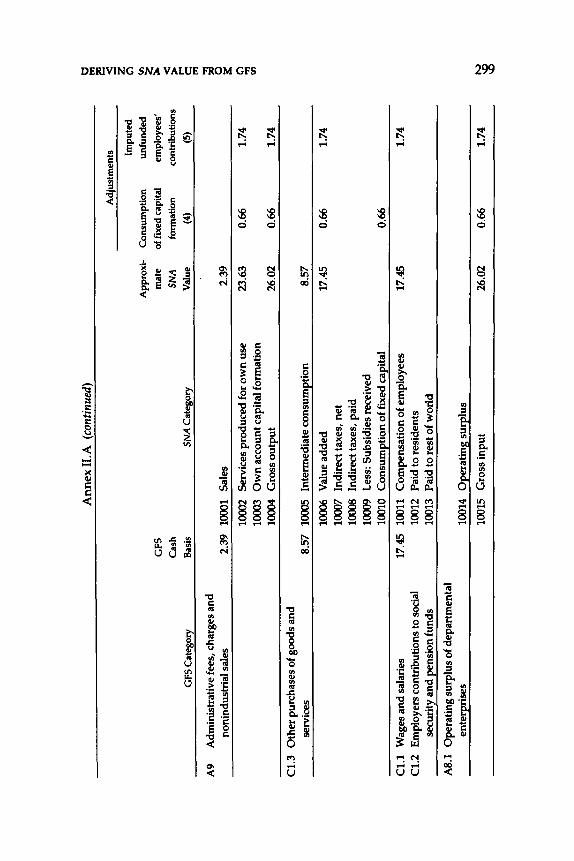

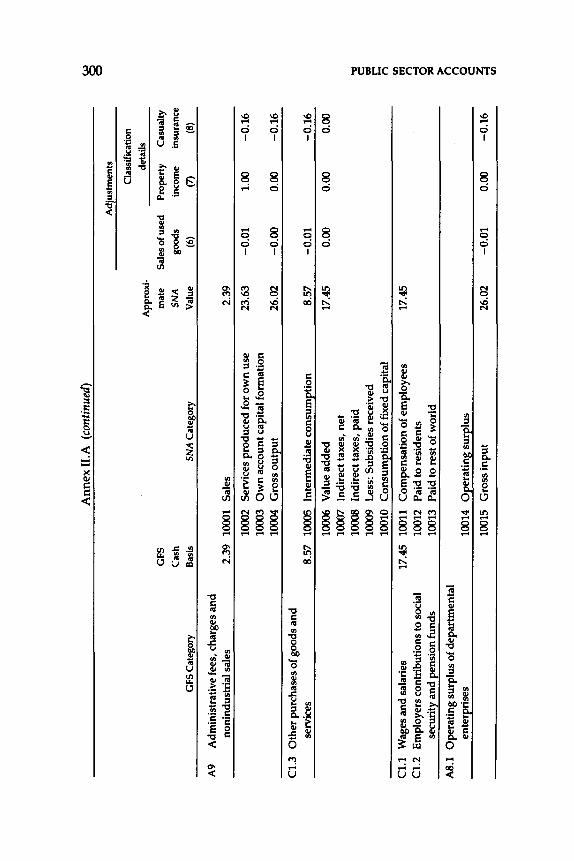

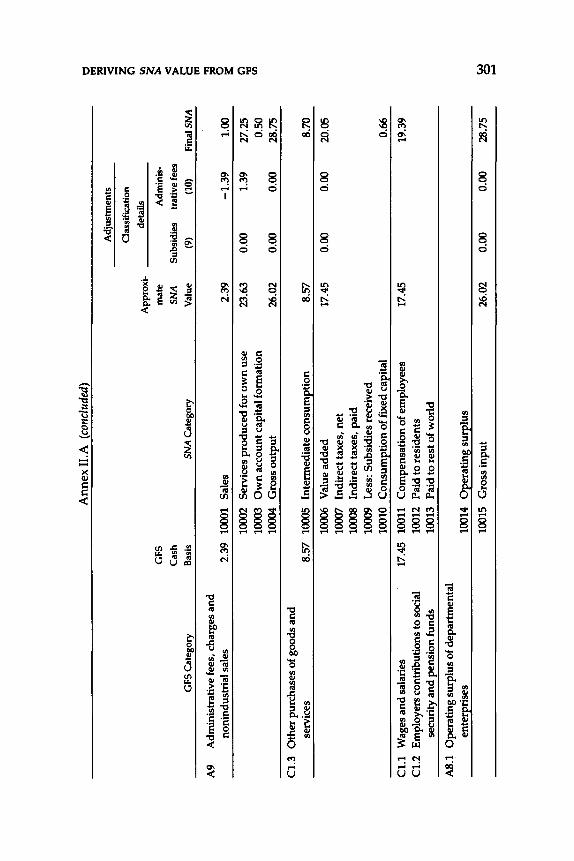

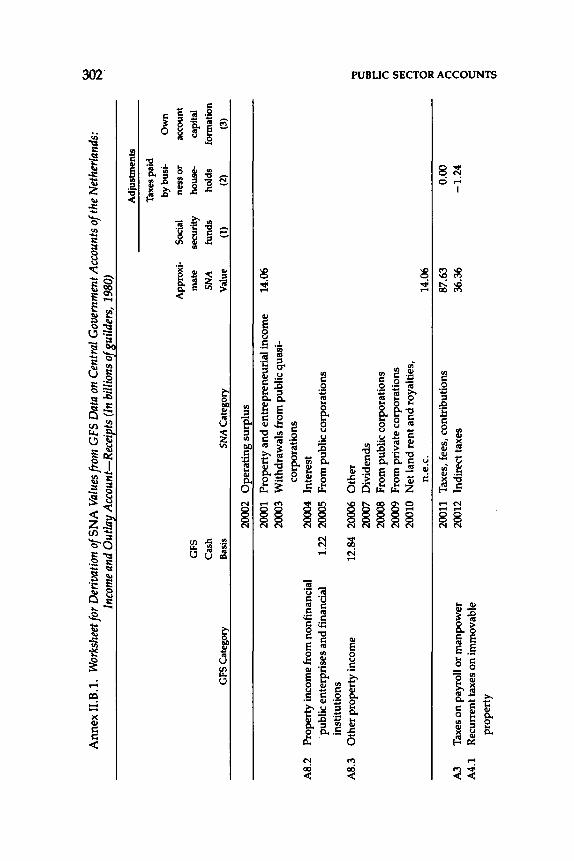

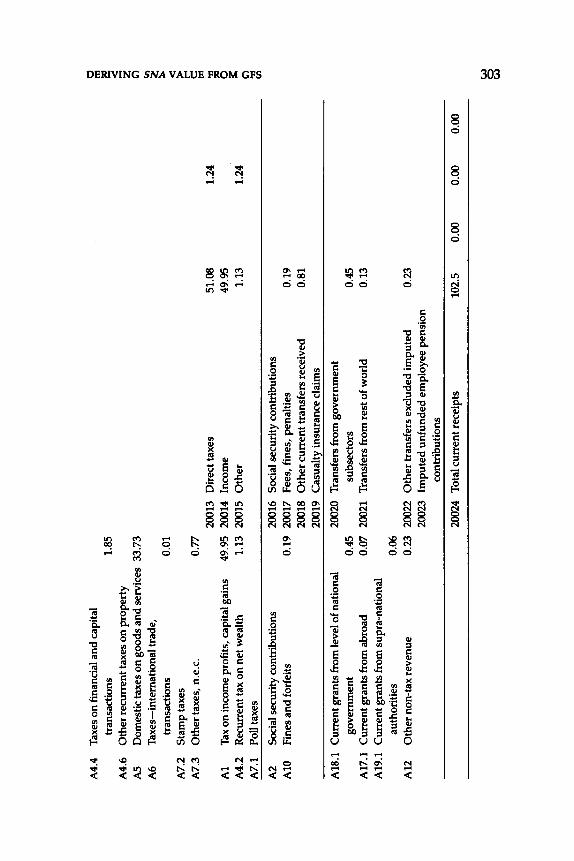

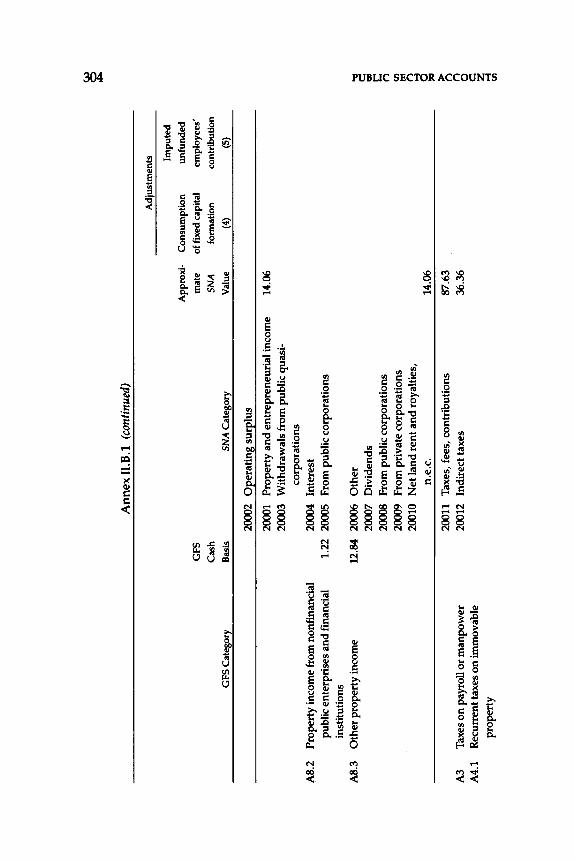

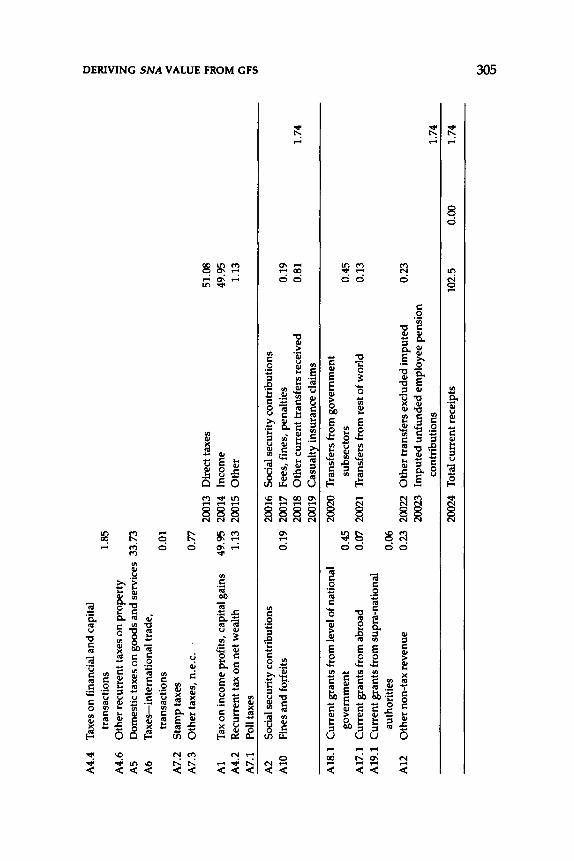

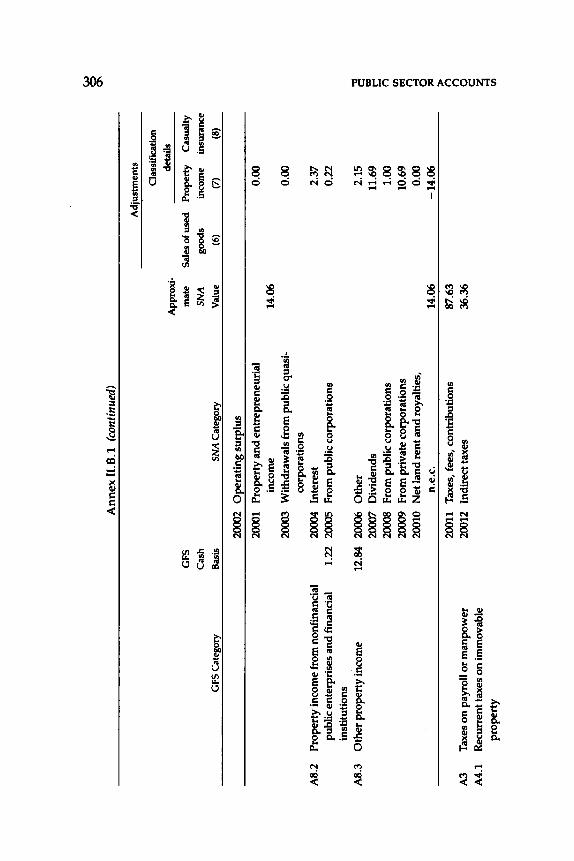

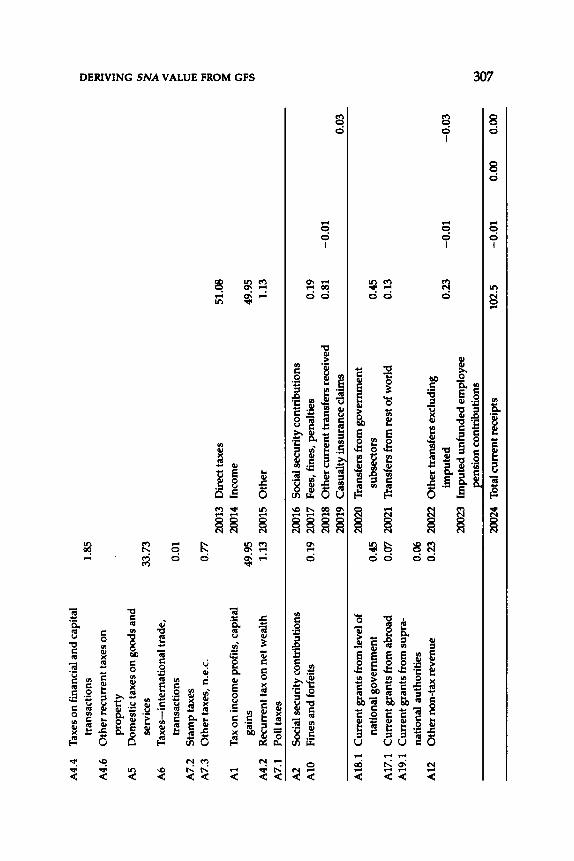

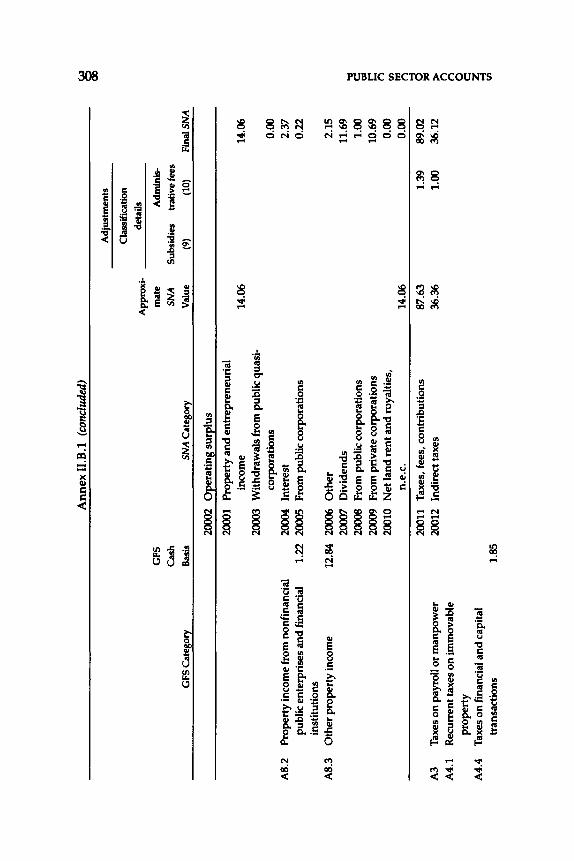

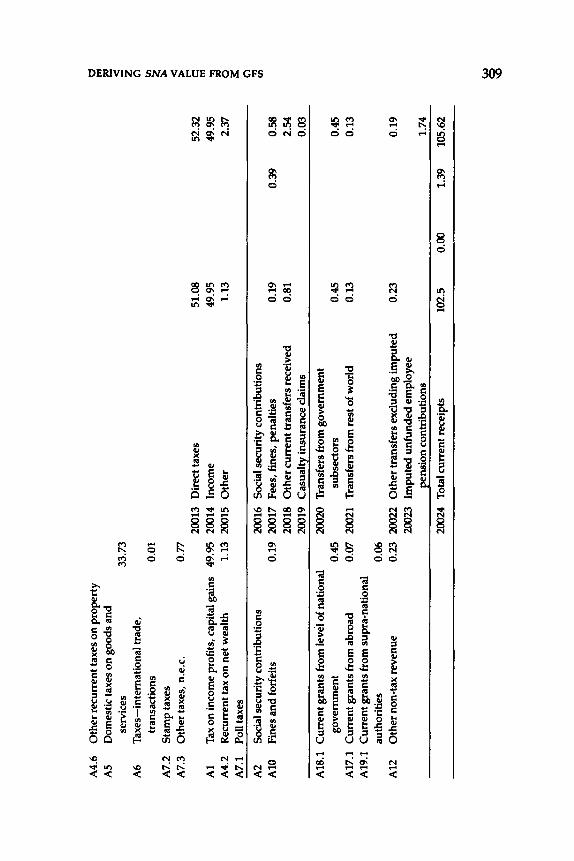

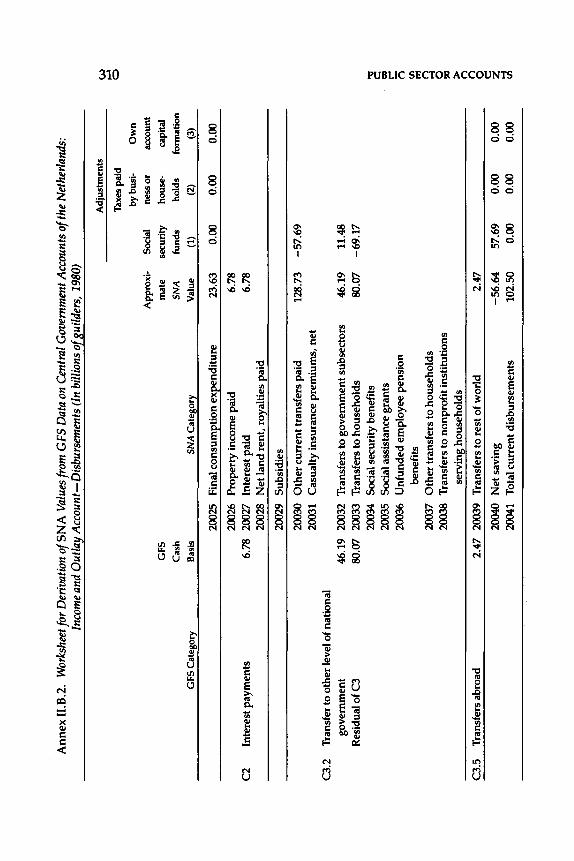

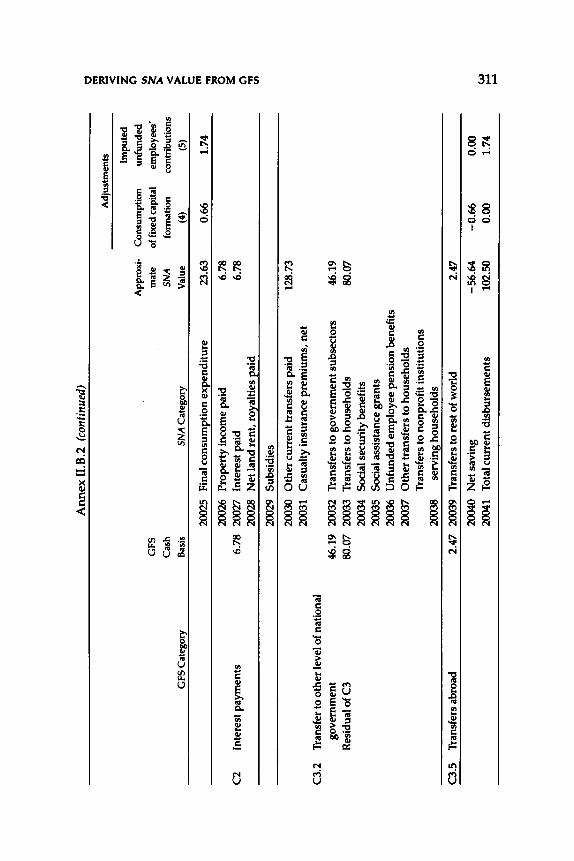

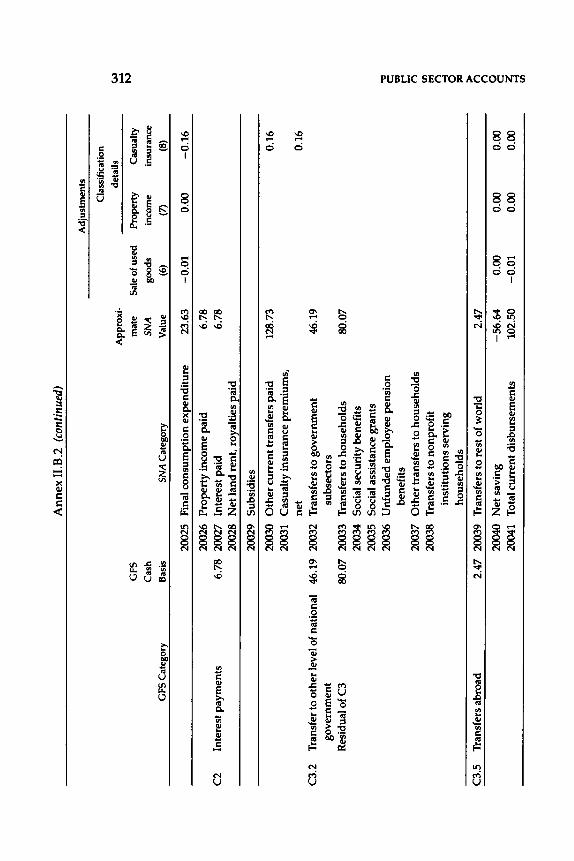

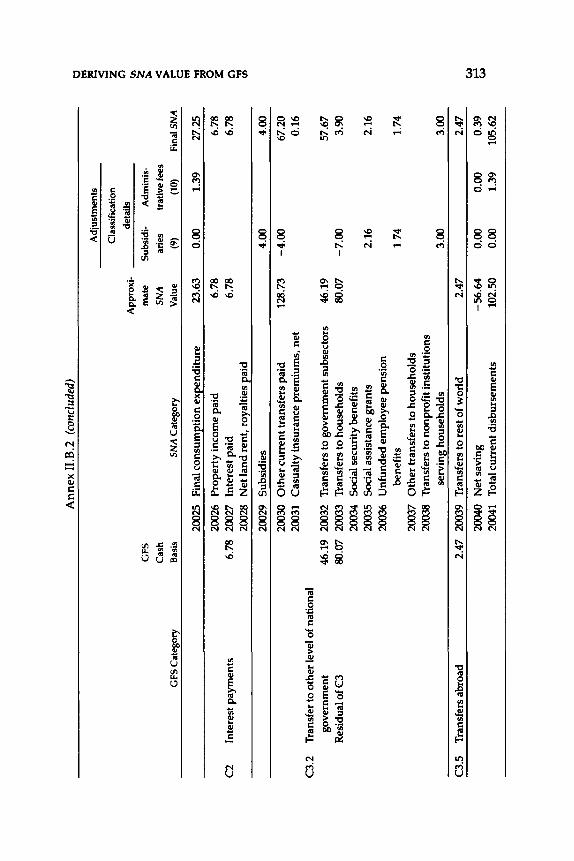

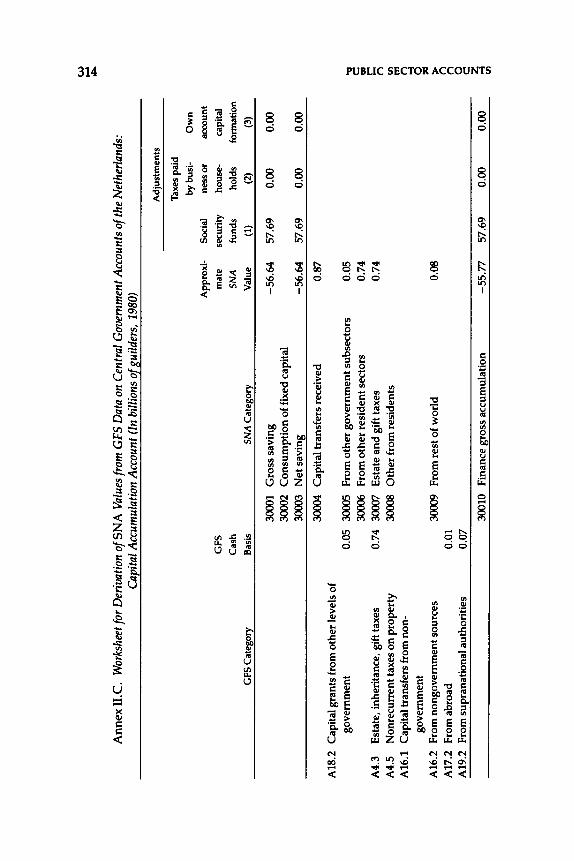

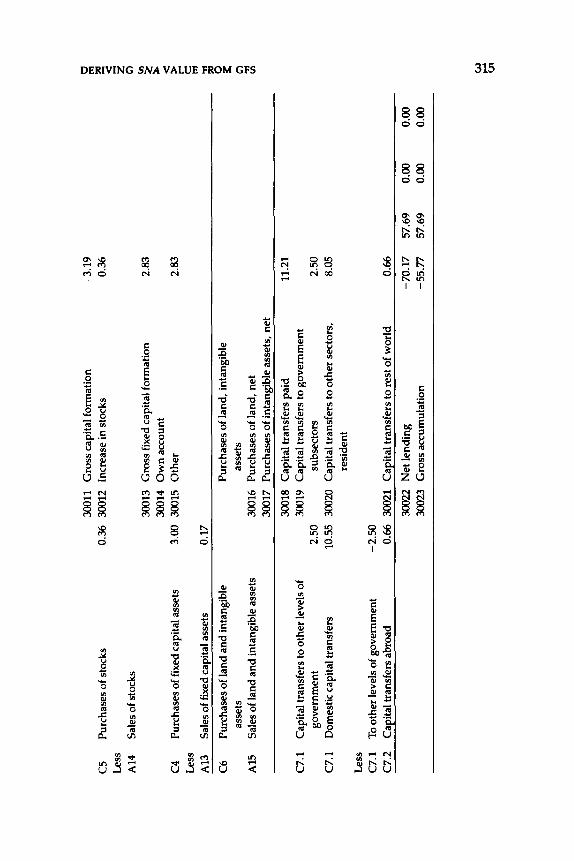

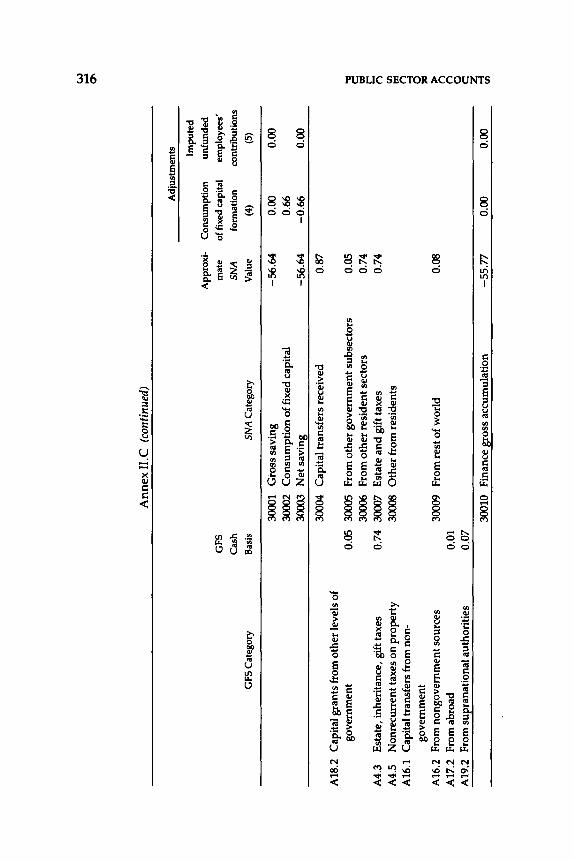

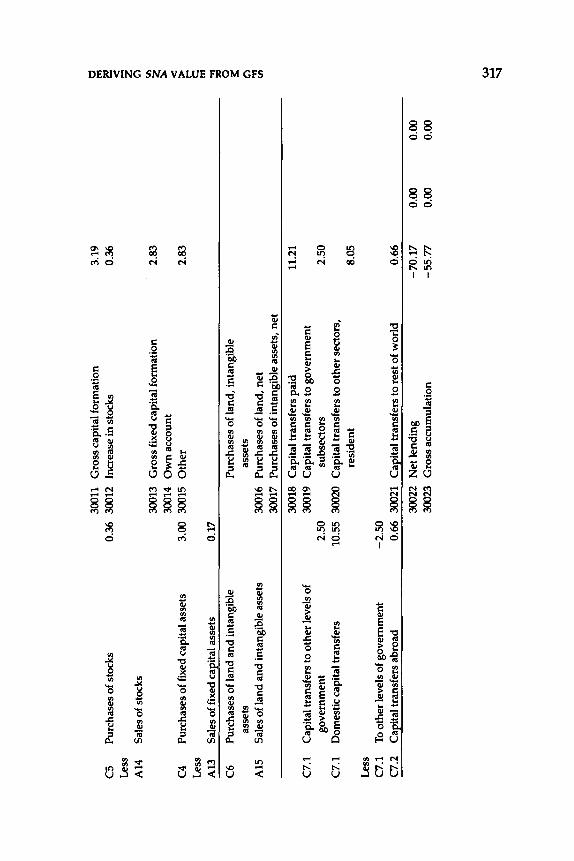

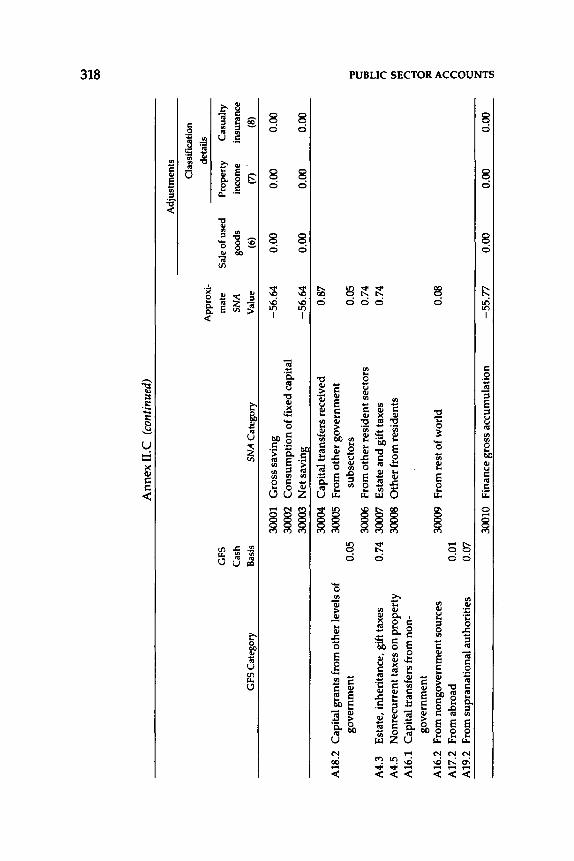

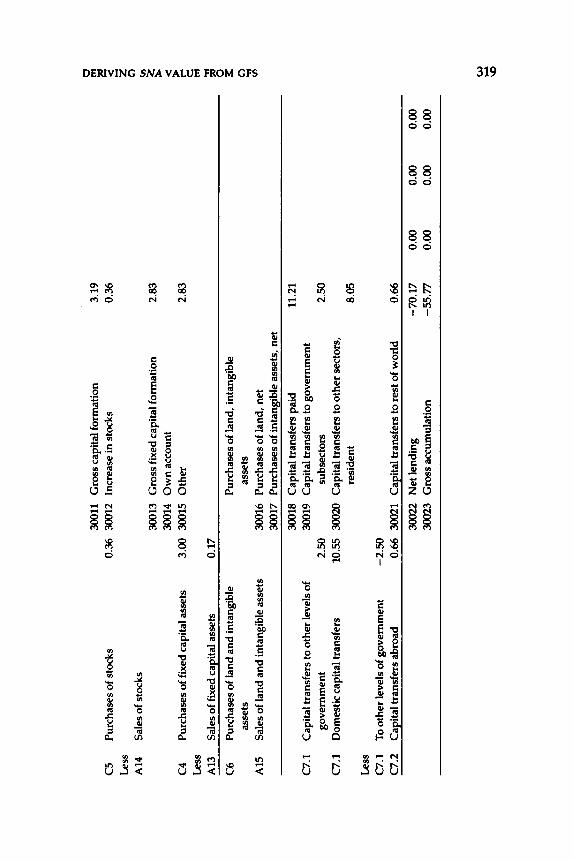

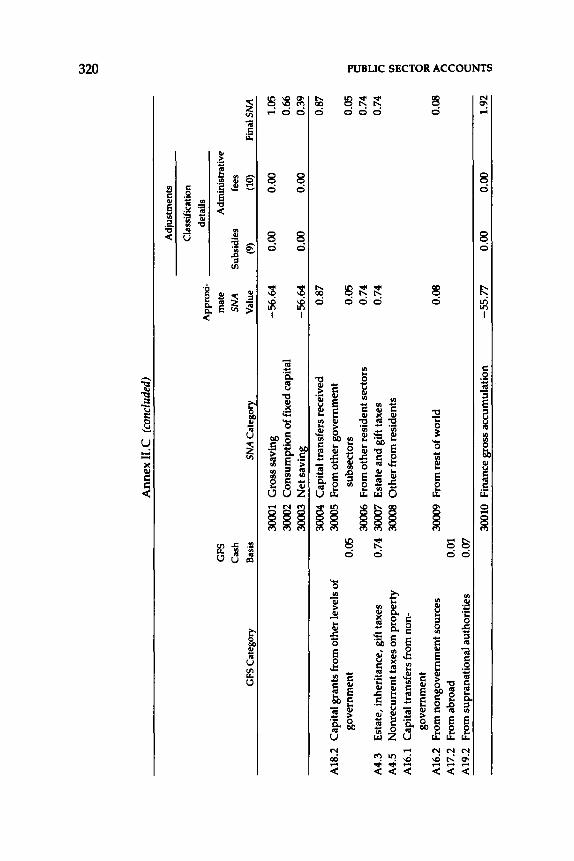

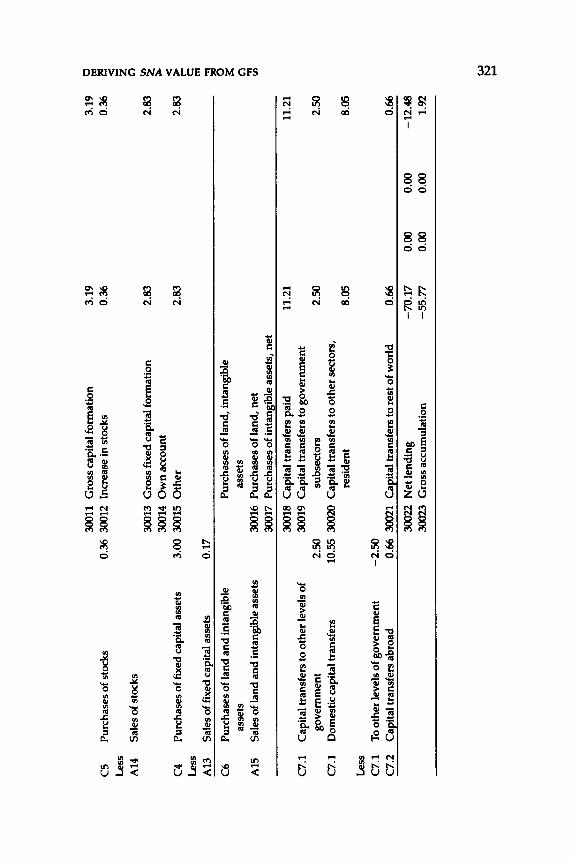

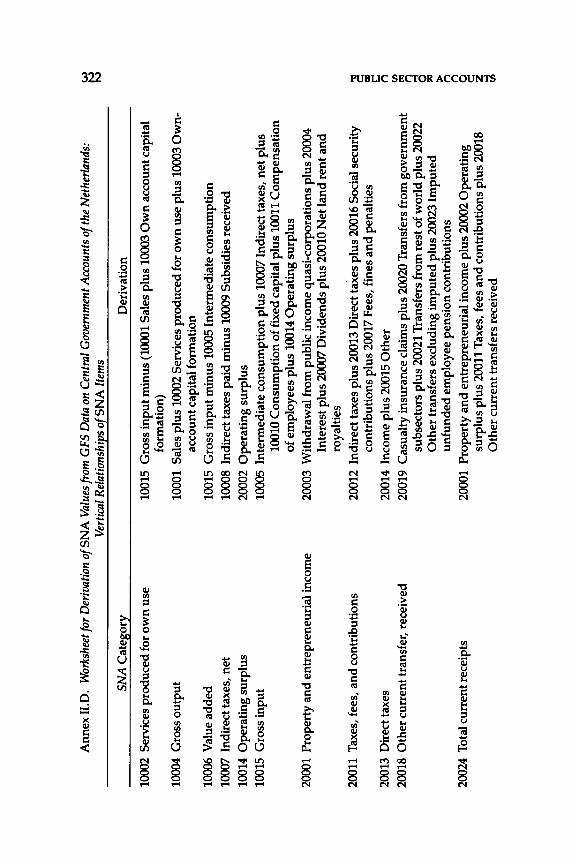

The paper by van Tongeren and Tsao (Chapter 19) on the derivation of SNA value from GFS data is important for the harmonization issue because it shows how GFS data can be adjusted to obtain estimates of the public sector accounts of the SNA.

The differences of treatment of the sectorization of social security funds between the GFSM and the SNA continue to be a matter of controversy. Villacres (Chapter 20) discusses this issue in light of comprehensive statistics on the operations of such funds in different countries and concludes that both classifications are useful. A separate compilation of statistics on social security funds, as in the SNA, may serve to examine, among other things, the financial health of these institutions. At the same time, because national social security funds have reached significant proportions in many countries, their consolidation with central government data, as in the GFSM, can provide a more comprehensive view of the influence of central government policies on the economy.

III. Financial Flows and Balances

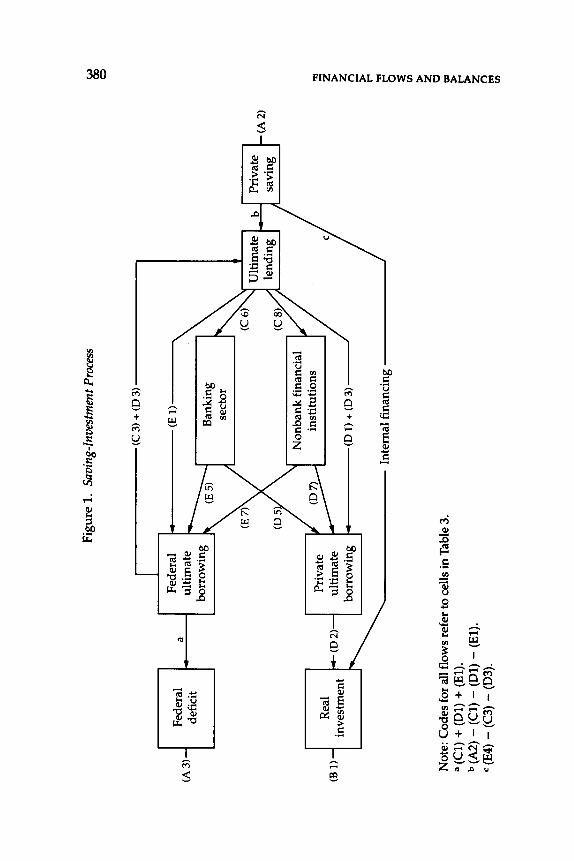

The papers in Part III of the volume cover much ground on the relationships between the Fund's MBS and the SNA. 11 Dawson sets the stage for the analysis of these relationships by means of presenting an overview (Chapter 21) of the financial accounts of the SNA and a useful analytical framework for the study of the relationship between the FOF, conceived as an element of the SNA, and other SNA elements. As noted earlier, Dawson shows, by an appropriate sectorization of the economy, that the three main statistical systems of the Fund provide most of the information needed to compile a simplified but useful FOF accounts and to relate these accounts to other elements of the SNA. This finding reinforces the interest in the harmonization among all these interrelated statistical systems, and therefore between the MBS and the SNA.

The appropriate sectorization of the financial sector is the specific

11 The term MBS is used here to describe the Fund's system of money and banking statistics and the methodology associated with that system as currently practiced by the IMF staff. This practice does not necessarily coincide in all cases with the draft MBS Guide (not available to the public), which in some respects has been superseded by developments in financial instruments and innovations.

INTRODUCTION XXV

subject of the paper by Saunders (Chapter 22), who discusses the precise coverage of the MBS and contrasts it with that of the fin<mcial sector of the SNA. A primary difference is the inclusion, in the central bank subsector of the MBS, of financial activities encompassing monetary authority functions carried out by government, whereas such functions are retained in the government sector of the SNA. This rerouting is done to identify certain key financial aggregates. Other differences relate to the subsectorization of the accounts within the financial sector. In both cases a harmonization is contemplated in the revision of the SNA and the draft MBS Guide.

Kumah (Chapter 23) describes the evolution of monetary concepts and definitions and shows the shift of emphasis, from narrow definitions of money to broader monetary aggregates, that has taken place in many countries over the years. This has reflected both the relatively faster growth of other financial intermediaries in relation to deposit money banks and the development of new financial instruments-by both bank and nonbank financial intermediariesthat are close substitutes for money.

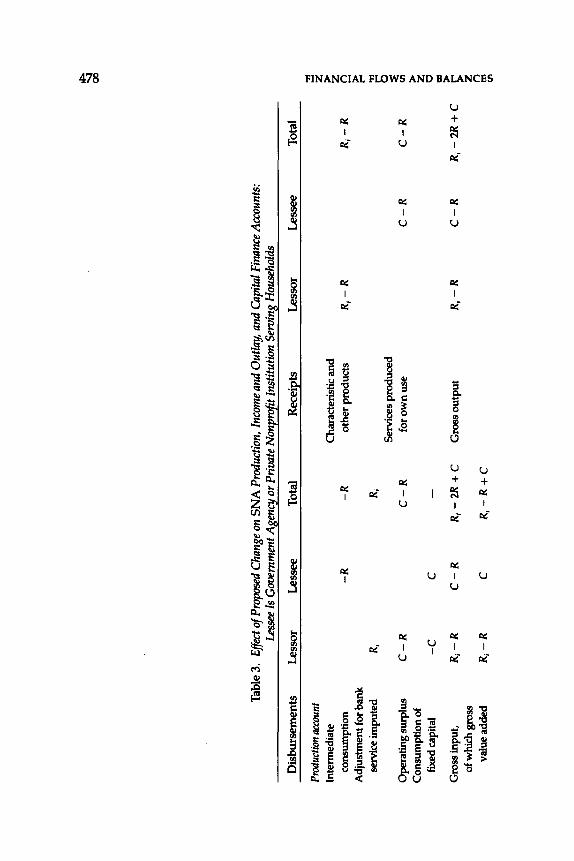

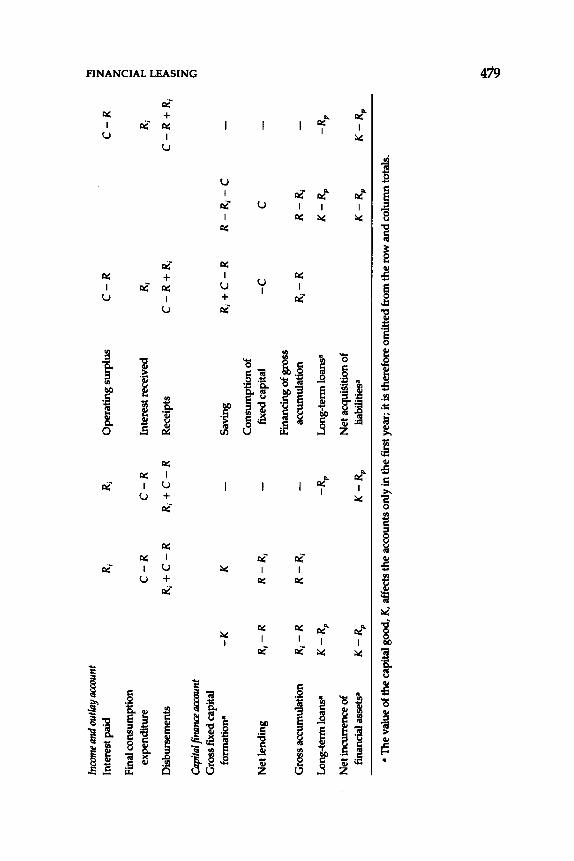

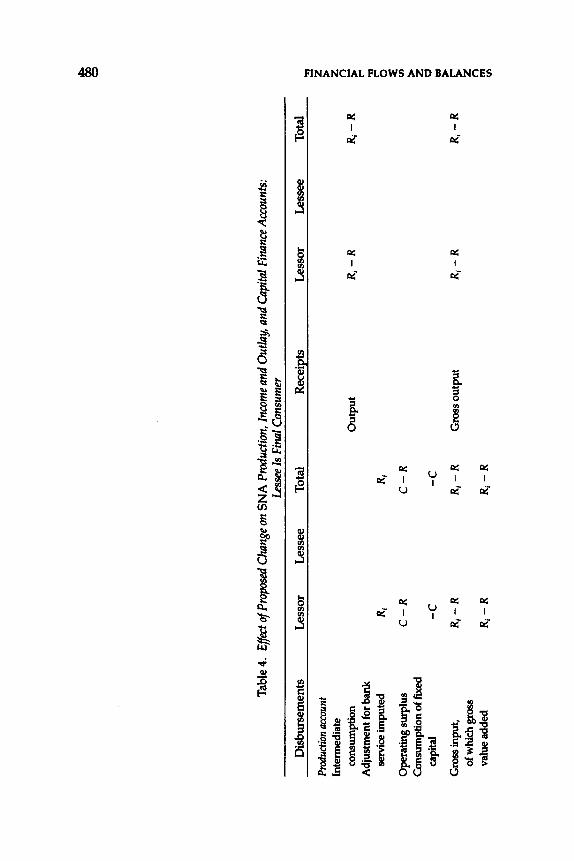

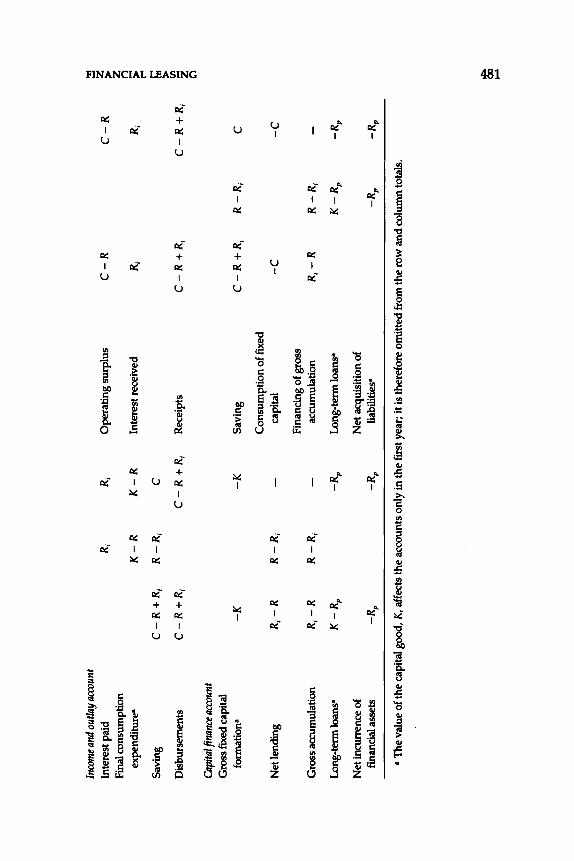

The statistical treatment of selected new financial instruments is examined in four papers that deal respectively with repurchase agreements (by Castello-Branco), financial leases and zero- and lowcoupon bonds (by the Balance of Payments Division of the IMF' s Bureau of Statistics), deep-discounted and indexed bonds (by Newson and Brodersen), and financial leases (by Newson); the last three overlap to some extent. Repurchase agreements ("repos") involve the sale of a financial asset or group of assets, with the agreement to reverse the transaction at some specified date in the future. Castello-Branco (Chapter 24) proposes that repos be treated in the SNA as a new financial instrument, similar to a collateralized loan, following the current practice in the MBS. However, this treatment would not be consistent with that in the BPM, which treats repos as a direct transfer of ownership of the underlying securities.

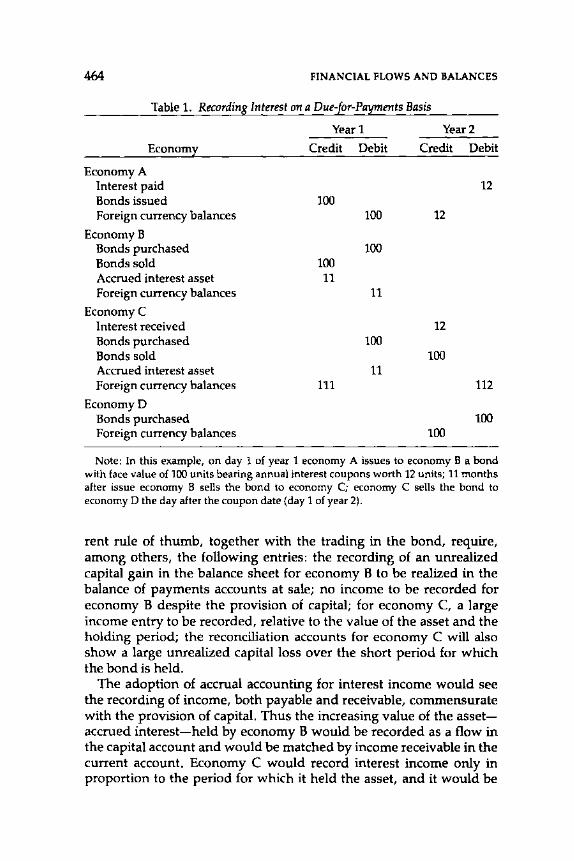

The treatment of leases has long been a subject of controversy because of the wide variety of legal and financial arrangements covered under this instrument, but in general a distinction is made between financial and operational leases. As pointed out in the paper by the Balance of Payments Division (Chapter 25), the BPM defines a financial lease as an arrangement that provides for the recovery by the lessor of all (or substantially all) of the cost of the goods, together with carrying charges. The BPM also indicates that, in practice, a recovery of three fourths of the cost of the goods together with the carrying charges is taken as evidence that a change in ownership from lessor to lessee is intended. All other leases that do not meet these

xxvi INTRODUCTION

requirements are considered to be operational leases implying that the legal owner retains control over the assets. In financial leasing, by contrast, such control passes effectively to the lessee, who for statistical purposes becomes the owner. In this way the "ownership concept" is broadened for financial leases to encompass an element of control over the assets. However, Newson (Chapter 26) suggests new qualitative rather than quantitative criteria to differentiate between the two types of leases.

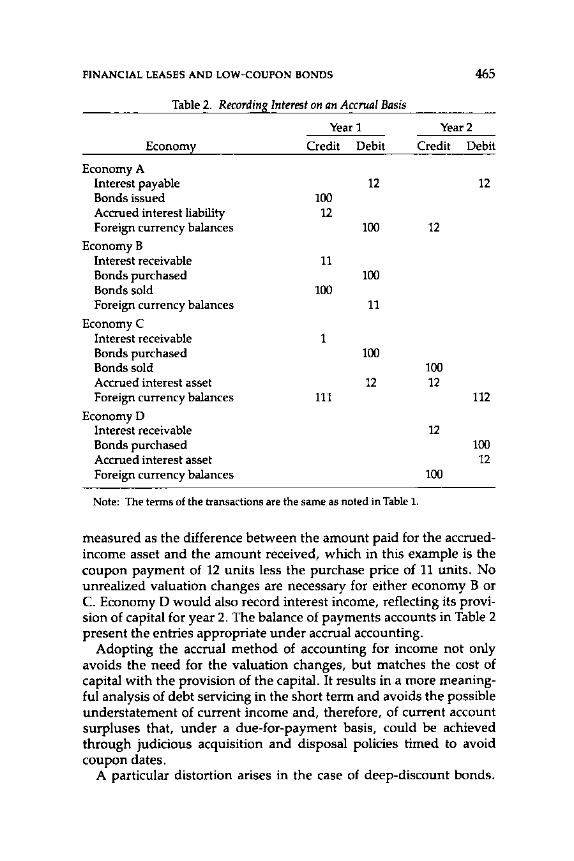

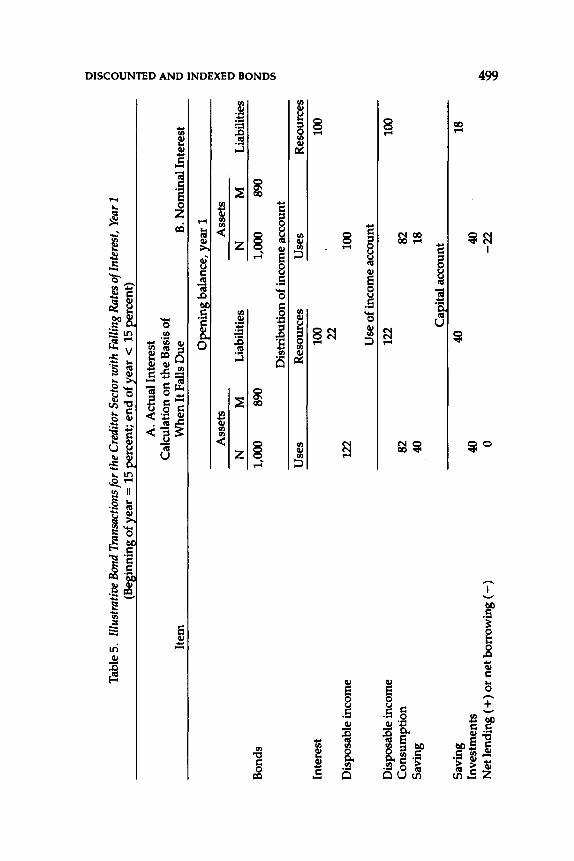

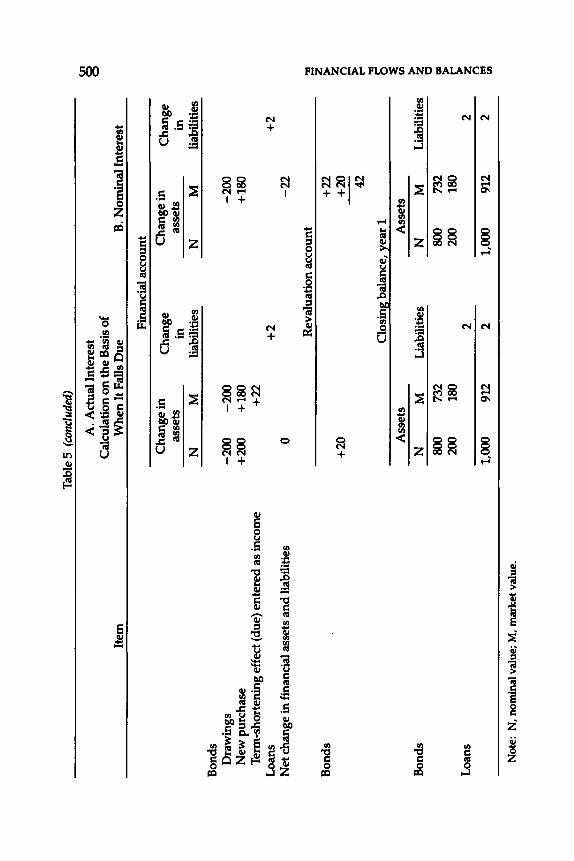

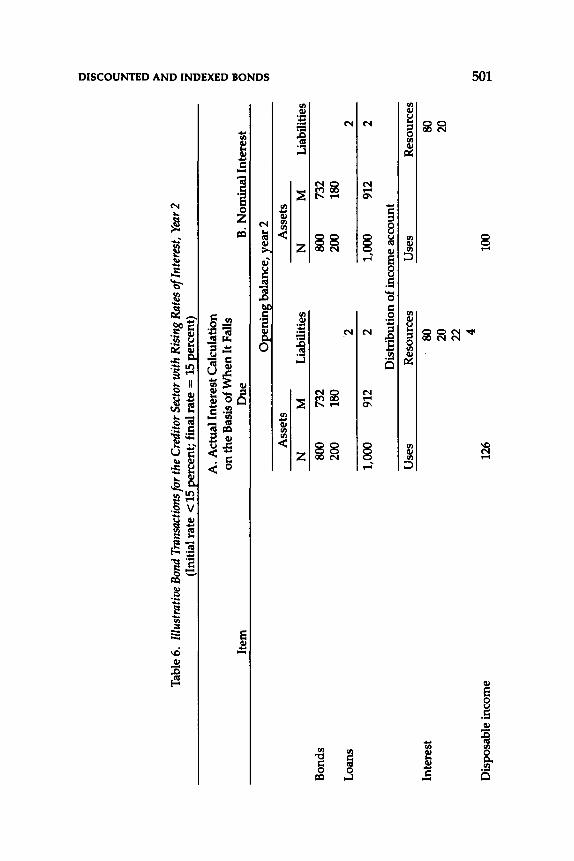

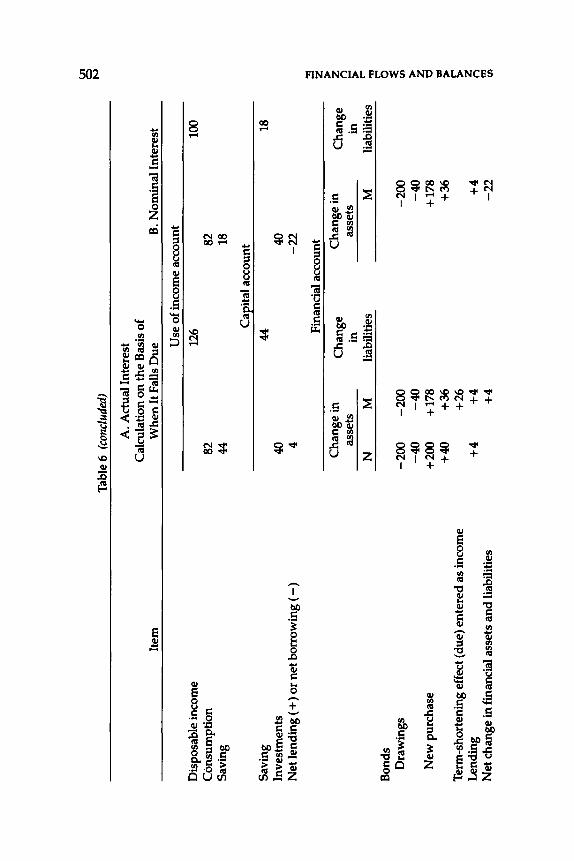

With respect to the recording of income on zero- and low-coupon bonds, the accrual method of accounting is proposed by the Balance of Payments Division; this method results in interest being imputed periodically over the life of the debt while the value of the principal reflects the increasing debt associated with accumulating interest. By contrast, cash accounting would attribute all interest (or capital gain) to the last period. However, there are other problems that affect classification-for instance, the difficulty of distinguishing interest from capital gain when bonds issued at deep discount, as in the case of low- or zero-coupon bonds, are traded in secondary markets or when indexing contracts are involved. A method to deal with these issues is presented in the paper by Newson and Brodersen (Chapter 27).

The principles of valuation and reconciliation in the MBS and the SNA are discussed by Dublin (Chapter 28). Changes in balance sheets over time include not only all transactions that have taken place during the period but also nontransaction items such as changes in the valuation of assets and liabilities (revaluation), changes in classification, and errors and omissions in the recording of transactions. All these nontransaction items are collectively assigned to the reconciliation accounts in the SNA. The valuation principles for recording transaction and nontransaction flows, as they apply to financial instruments, are now similar for both the SNA and the MBS, emphasizing the symmetrical treatment of assets and liabilities. Short-term instruments are recorded at book value, long-term domestic currency assets and liabilities at market prices, and foreign currency assets and liabilities at the prevailing exchange rate. The practices for the derivation of transaction flows from balance-sheet positions in the absence of direct transactions data are also illustrated.

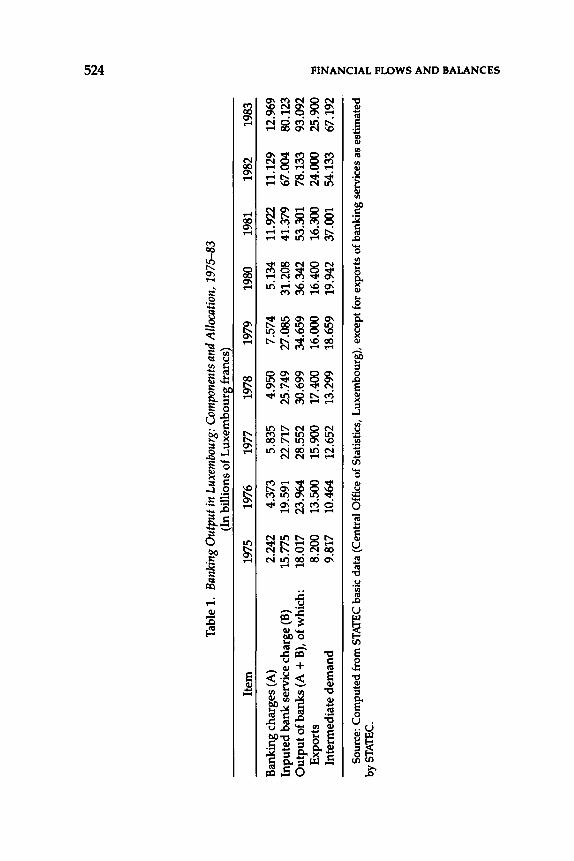

A miscellaneous group of papers, dealing with some of the most difficult and controversial issues raised on money and banking statistics, completes this volume. Both Siddique and Vanoli deal with the treatment of financial intermediaries from the point of view of their contribution to output and incpme in the SNA. Siddique (Chapter 29) discusses the issue of the treatment of output in the banking industry,

INTRODUCTION xxvii

comparing current SNA practice with some proposals for change. Alternative methods of deriving banking output are reviewed, and an illustration from data for Luxembourg is provided. As opposed to the current practice in the SNA of allocating banking services to depositors only, the paper proposes allocating such services to both borrowers and depositors, highlighting thereby the intermediation function of the banking industry. Siddique also addresses an important issue concerning the allocation of imputed banking services between intermediate and final demand-in contrast to the present SNA, which allocates all imputed bank service charges to intermediate demand. Moreover, although Siddique's paper refers to "banks," its analysis applies equally well to all other financial intermediaries except for insurance entities, for whom a specific treatment is necessary. The appropriate treatment of insurance in the SNA is the subject of Vanoli's paper (Chapter 30), which proposes that insurance services should be defined as gross premiums earned, plus net investment income, less technical charges, the last of these being computed as the claims due plus the changes in technical reserves.

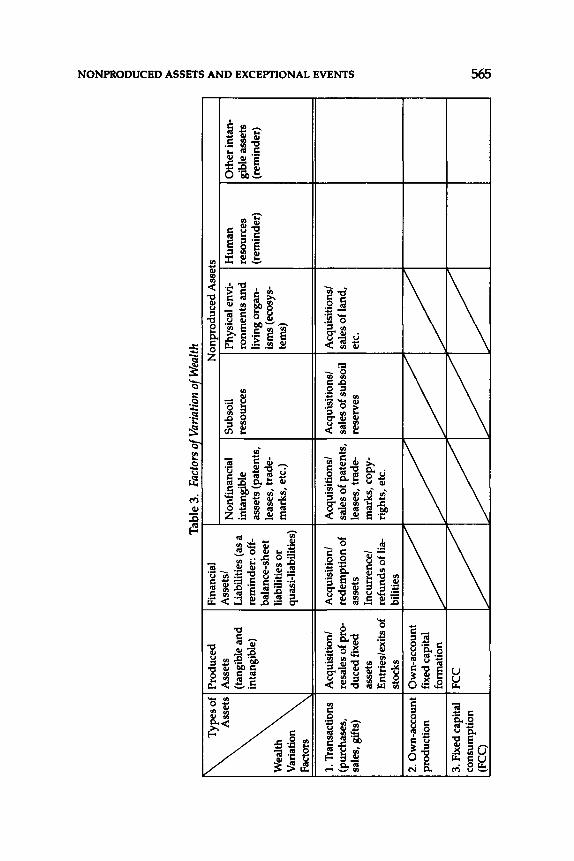

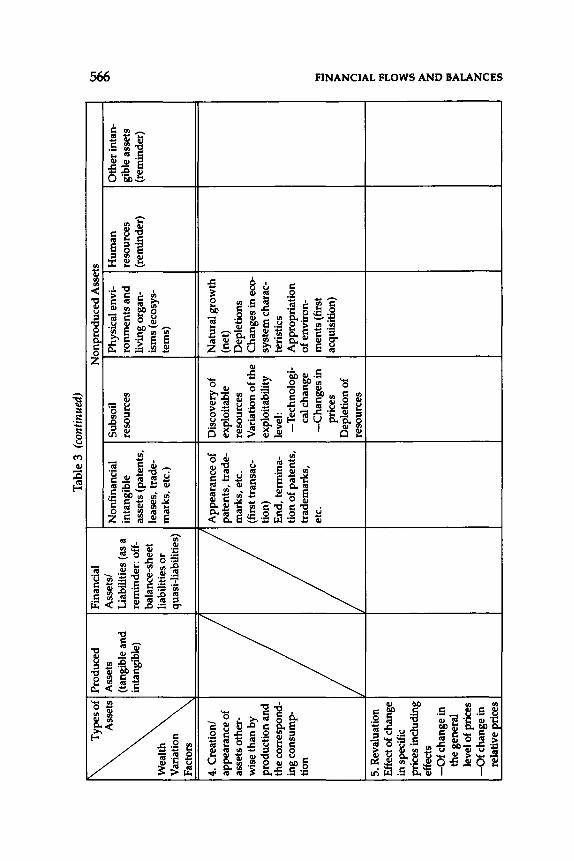

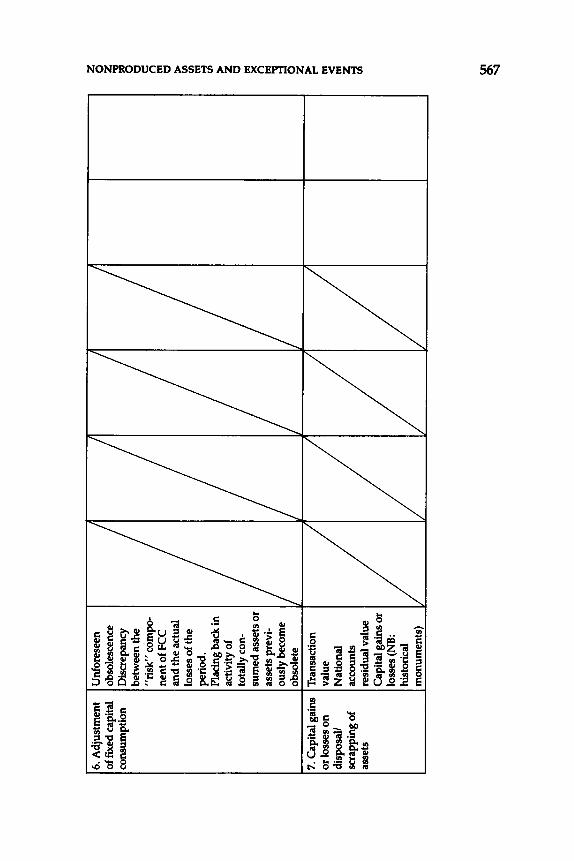

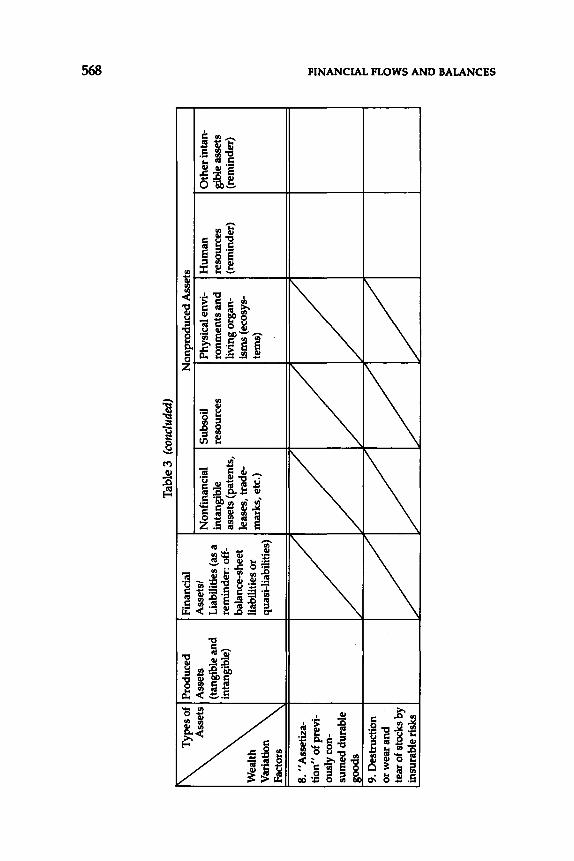

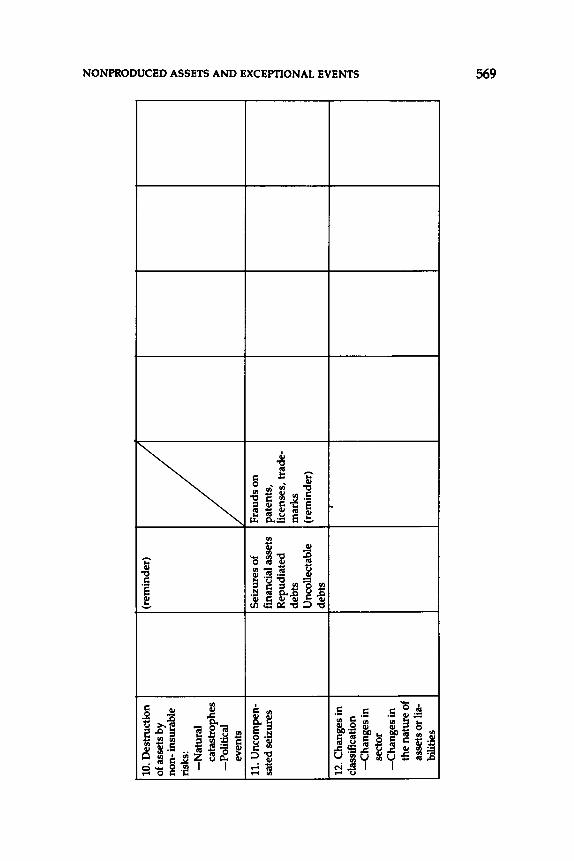

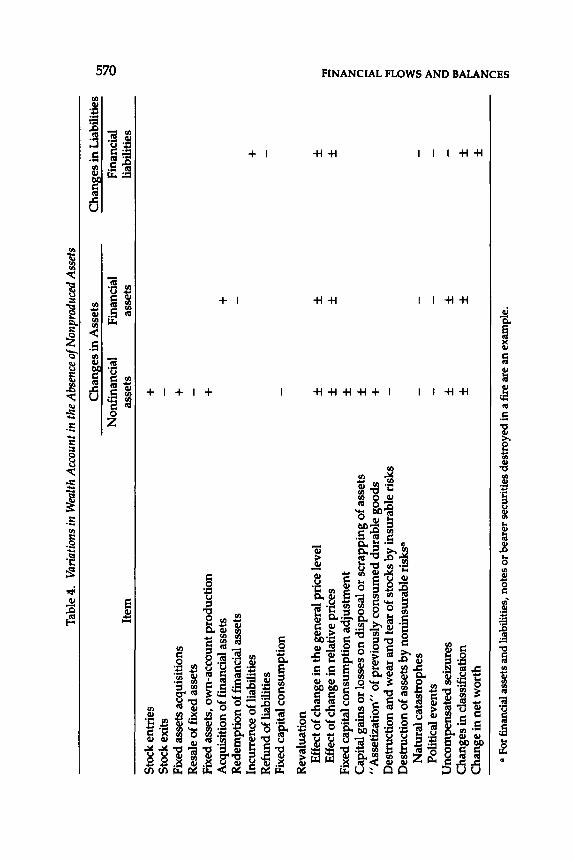

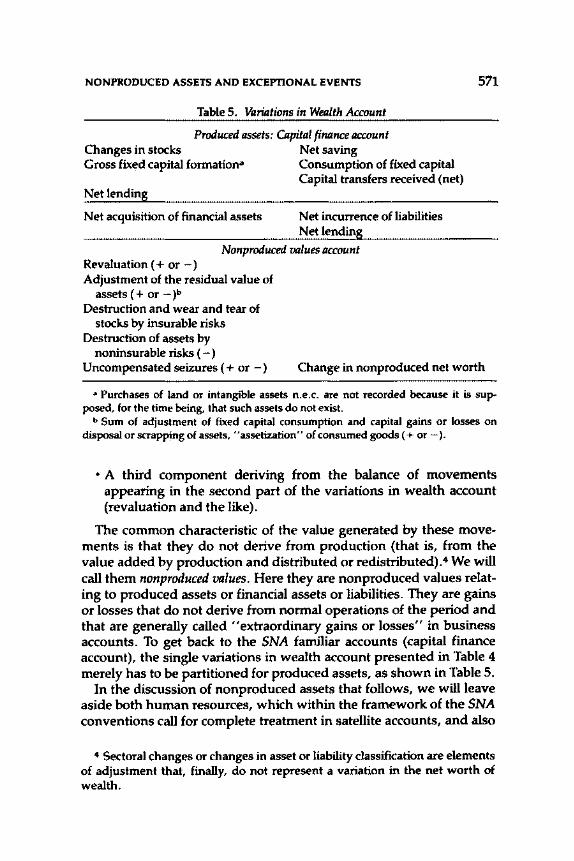

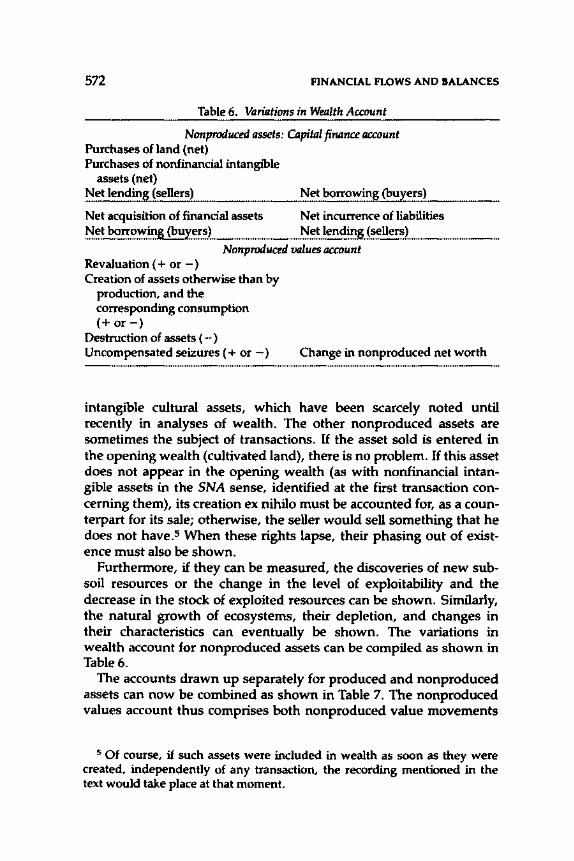

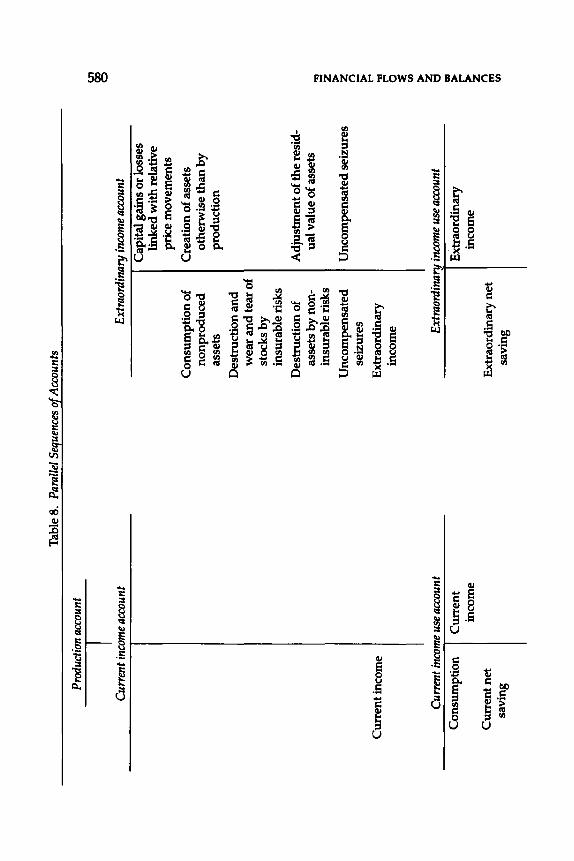

General insights into broader concepts of the SNA that help clarify the relationships between flows and stocks are provided in the papers by Milot, Teillet, and Vanoli and by Liitzel. Understanding of these relationships is needed to relate the real sector SNA flows to the balance sheets, which necessarily comprise both real and financial assets in the same account. Milot, Teillet, and Vanoli (Chapter 31) provide an analysis of various factors, besides real and financial transactions, that explain variations in wealth, including nonproduced assets, such as land, forests, and rivers, and exceptional events, such as earthquakes.

Liitzel' s paper on the treatment of fixed capital formation by owner and user (Chapter 32}, deals with the issue of allocating fixed capital formation (or fixed assets) to investing sectors (producers). The conclusion that emerges is that whether the owner or the user concept should be applied for recording fixed capital formation by investors should depend on the intended purpose of the data. Thus, although preference should be given to the ownership concept in the SNA, the user concept should also be included as an additional recording devise in some cases. An application is suggested to the issue of recording financial leasing, which, as noted earlier, has gained considerable importance. Liitzel's principles suggest that the revised SNA should consider financial leasing as an acquisition of a fixed asset on long-term credit. The relevant commodity should therefore be shown as part of the fixed capital of the borrower, who would be treated for statistical purposes as an owner.

Part I

EXTERNAL SECTOR

TRANSACTIONS

1

Residents of an Economy

ARIE C. BoUTER

I N CONNECTION with the forthcoming revision of the United Nations' A System of National Accounts (SNA), a question has arisen

about whether the definition of the residents of an economy,1 given in the 1968 version of the SNA and in the 1977 edition of the IMF's Balance of Payments Manual (BPM) can continue to serve as the basis for compiling national accounts and balance of payments statistics that provide the users of these statistics-the central authorities of the compiling economy and the international organizations-the information they need for policy purposes. That question is discussed in Section I of this chapter. The concept underlying the definition given there is virtually the same as that underlying the definition of residents in the 1968 version of the SNA. Therefore, measures of gross domestic product (GOP) and gross national product (GNP) based on the definition given in Section I should be similar, if not the same, as those based on the 1968 definition of the residents of an economy. The continuity of the existing time series would thus be maintained.

The residency status of the general government, individuals, private nonprofit bodies serving individuals, and enterprises of an econ-

1 In this paper, an "economy" refers to a sovereign state, a part of a sovereign state, a combination of two or more sovereign states, or an international organization. In this context an international organization is defined as an organization that derives its authority from the central authorities in its member countries, who have relinquished part of their authority. Except for an economy that is an international organization, the "residents of an economy" comprise the general government, individuals, private nonprofit bodies serving households, and enterprises. The residents of an economy that is an international organization do not comprise individuals, private nonprofit bodies serving households, and enterprises; in such an economy, the role of the international organization is comparable to that of the general government in other economies.

3

4 EXTERNAL SECTOR TRANSACTIONS

omy is discussed in Sections II through V; the residency status of international organizations, which are not considered to be residents of any national economy, including the economy in which they are located or conduct their affairs, is discussed in Section VI. Brief conclusions are given in Section VII.

I. Policy Needs of the Authorities

The government of an economy sets policy and makes the laws and regulations that apply to it. These laws and regulations affect, in principle, all entities-those physically or legally present in that economy ("residents"), as well as those physically or legally present in the rest of the world ("nonresidents").2 The enforcement of these laws and regulations as they affect residents differs considerably, however, from their enforcement with respect to nonresidents. For residents of the given economy, enforcement of the laws and regulations is straightforward because it derives from the government's authority in that economy. In contrast, because the government of the given economy lacks the authority to enforce its laws and regulations in the rest of the world, enforcement of· those laws and regulations with respect to nonresidents is not practicable. If at all, enforcement on nonresidents comes about only when the government of the given economy can exert pressure on entities in the rest of the world through affiliated entities in the given economy. Moreover, nonresidents are, more than anything else, subject to the possibly contradictory policies of the authorities in the rest of world and, therefore, may not be able to comply with the laws and regulations of the given economy. Thus, it appears that for statistical, analytical, and policy purposes the residents of a given economy can best be defined in terms of their presence in the territory of that economy-the home economy. In this context, the territory of an economy is defined to include its territorial seas and air space, as well as those international

2 For example, a potential exporter of a commodity in the rest of the world is affected by the laws and regulations of a given economy when the residents of that economy decide not to import that commodity in light of the laws and regulations of the economy. A transaction that takes place notwithstanding those laws and regulations is an illegal transaction for the importing economy. For the exporting economy, however, it is a legal transaction that should be recorded in the national accounts and balance of payments statistics of both economies, despite the fact that the transaction is illegal for the importing economy. Failure to record the transaction in the importing economy has caused imbalances in the global accounts.

RESIDENTS OF AN ECONOMY 5

waters beyond its territorial seas and the international air space beyond its territorial air space over which the economy has or claims to have exclusive jurisdiction.

The strict application of this concept of residence to a given entity that temporarily enters or leaves the territory of a given economy would affect the classification of the transactions of that entity during that time and would require the recording, both in the national accounts and in the balance of payments, of the two successive changes in the international investment position that result from that entity's temporary change of residence. This change in recording would be particularly bothersome in extreme situations-for example, when an individual leaves the territory of the home economy for a one-day vacation, or when an enterprise installs equipment in the territory of an economy other than the home economy. If a vacationing individual continued to be a resident of the home economy, that individual's expenditures on goods and services for use during his vacation should be classified under travel (direct purchases abroad). If, however, a vacationing individual temporarily became a resident of the host economy, these same expenditures should be classified under private unrequited transfers (other capital transfers by private sector, denoting a change in net worth). Similarly, for an enterprise installing equipment in the territory of an economy other than the home economy, the recording and classification of the various transactions would depend on the residency status of that enterprise. For example, any payment for wages to residents of the host economy would be recorded as labor income, and the proceeds from the installation services should be recorded as services (miscellaneous commodities) if the enterprise continued to be a resident of the home economy. The net proceeds from the installation services (gross proceeds from the installation services minus payments for wages), however, should be recorded as investment income (entrepreneurial income) if the enterprise temporarily became a resident of the host economy.

In addition, the strict application of that concept of residence would require the recording, both in the national accounts and in the balance of payments, of the two successive changes in the international investment position that result from an entity's temporary absence from the home economy. An entity's claims on and liabilities to other residents of the home economy would, for one day, become that economy's foreign liabilities and claims, whereas an entity's claims on and liabilities to residents of the rest of the world would become, again for one day, the rest of the world's domestic liabilities and assets. Thus, if an entity were defined in terms of its presence in the

6 EXTERNAL SECTOR TRANSACTIONS

territory of an economy, a good deal of information would be required to implement the existing accounting rules.

In view of these considerations, it appears that there would seem to be justification for defining the residents of an economy as the entities that may be expected to consume goods and services, participate in production, or engage in other economic activities in the territory of an economy on other than a temporary basis. Under this approach, however, questions would arise about the length of time an entity can remain outside the territory of the home economy and about the activities in which it can engage during that time without the entity undergoing a change in its residency status.

Obviously, the longer an entity stays outside the territory of the home economy and the more an entity is integrated in the economy where it is temporarily located (the host economy), the more reason there is for treating that entity as a resident of the host economy. Entities whose stay in the territory of a host economy is brief and whose integration in the host economy is tenuous-as in the examples cited above-should not be considered residents of that economy during that period. In contrast, entities whose stay in the territory of the host economy is indefinite and whose integration in the host. economy is substantial should clearly be considered residents of that economy.

An approach to determining residency that is based on the length of stay and on the degree of integration in the host economy, however, cannot be adopted. For one thing, ranking of entities according to these criteria is not a feasible undertaking. Furthermore, even if such ranking were made, it would still be a matter of judgment to decide exactly how long and for what purpose an entity would have to be in the territory of the host economy to become a resident; that is, where the borderline between residents and nonresidents should be drawn. Therefore, a supplementary rule of thumb for determining the residency status of entities that temporarily remain outside the home economy would seem to be needed. Moreover, because little information on the activities of entities that temporarily remain outside the territory of the home economy is commonly available, there would seem to be justification for expressing that rule in terms of a period of time during which an entity can remain outside the territory of its home economy without undergoing a change in its residency status.

Because the introduction of such a rule would affect both the compilation and the analytical usefulness of the data, it is important that the rule represent the best possible trade-off between these two aspects. Therefore, such a rule might be that entities entering the

RESIDENTS OF AN ECONOMY 7

territory of an economy for less than one year would not become residents of that economy, and that entities leaving the territory of an economy for less than one year would continue to be residents of that economy.

The one-year time span of an entity's presence in a given economy as the basis for identifying resident and nonresident entities is not in itself sacrosanct. One could argue for a period longer than one year. What is important is that, from a statistical and analytical standpoint, an objective criterion rather than a vague reference to some concept of ''center of economic interest'' be adopted for demarcating resident and nonresident entities. Although the length of the period to be used for identifying resident and nonresident entities could certainly be a point for discussion in any reappraisal of the existing guidelines on residence, consideration of maintaining continuity in the time series would favor retention of the present one-year rule.

Under this approach, however, a problem of principle would arise for entities that, after a point in time, remain permanently outside the territory of any national economy (that is, in international waters or air space) or that move frequently between the territories of two or more economies, thus posing a problem similar to that of entities remaining permanently in international waters or air space. As a matter of principle, such an entity should be attributed to a single economy on the basis of that entity's being subject to the laws, regulations, and protection of that economy. But because information for such attribution is generally not available, still another supplementary rule of thumb to deal with both of these cases would have to be provided. Such a rule might suggest that until the time an entity that is physically or legally present in more than one national territory during the course of a year, or outside any national territory, has established residency elsewhere, it continues to be a resident of the economy of which it was a resident before it left its territory. In this connection, it should be recognized that failure to attribute an entity to any economy has caused asymmetries in the global accounts.

The analytical and statistical considerations discussed in this section point to the need for formulation of guidelines on residence such as those described in Sections II-VI.

II. General Government

The general government agencies that are residents of an economy include all departments, establishments, and bodies of its central, state, and local governments located in its territory and the embas-

8 EXTERNAL SECTOR TRANSACTIONS

sies, consulates, military establishments, and other entities of its general government located elsewhere.

The general government of an economy comprises all agencies of the public authorities not classified elsewhere:

• Government departments, offices, and other bodies, whether covered in ordinary or extraordinary budgets or in extra budgetary funds, that engage in administration, defense, and regulation of the public order, promotion of economic growth and welfare and technological development, provision of education, health, cultural, recreational, and other social and community services free of charge or at sales prices that do not fully cover their costs of production

• Other nonprofit organizations serving individuals or business enterprises that are wholly, or mainly, financed and controlled by the public authorities and nonprofit organizations primarily serving government bodies themselves

• Social security arrangements for large sections of the community imposed, controlled, or financed by the government, including voluntary social security arrangements for certain sections of the community and pension funds that are considered to be part of the public social security schemes

• Unincorporated government enterprises that mainly produce goods and services for the government itself or that primarily sell goods and services to the public, but that operate on a small scale

• Public saving and lending bodies that are financially integrated with a government or that lack the authority to acquire financial assets or incur liabilities in the capital market.

Because embassies, consulates, military establishments, and other entities of a general government are subject mainly to the laws and regulations of the economy they represent, they are considered to be residents of that economy and not of the economy in which they are physically located.

III. Individuals

In this section a general concept of residence for individuals is proposed and a classification of individuals whose stay in a given economy is to be considered temporary is drawn. Implications of the general definition are then discussed.

RESIDENTS OF AN ECONOMY 9

General Definition

The concept of residence adopted for individuals is designed to encompass all persons who may be expected to stay in the territory of a given economy on other than a temporary basis, including residents who leave the territory of that economy for whatever period of time but do not establish residency elsewhere. For individuals other than government employees and employees of international organizations, a temporary basis is defined to be a period of less than one year. Because they are subject mainly to the laws and regulations of that economy, government employees are always considered to be residents of the country employing them. In a somewhat analogous manner, employees of international organizations are always considered to be residents of the economy in which either the headquarters or the regional offices of their employer are physically located.

For purposes of the application of this definition, the following types of individual are considered to be in a given economy on a temporary basis:

• Visitors (tourists)-that is, persons in the given economy for less than one year, specifically for reasons of recreation or holiday, medical care, religious observances, family matters, participation in international sports events and conferences or other meetings, and study tours or other student programs

• Crew members of vessels, aircraft, or other types of mobile equipment who do not live in the given economy but are stopping off or laying over there

• Commercial and business travelers who are to be in the given economy for less than one year and employees of nonresident enterprises who have come to the economy for less than one year to perform a given task, such as installing machinery or equipment purchased from their employer

• Seasonal workers-that is, persons who are, and will be, in the given economy explicitly for the purpose of seasonal employment only-and other workers hired by resident entities for less than one year

• Official diplomatic and consular representatives, members of the armed forces, and other government personnel of a foreign economy (together with their dependents), regardless of the length of stay in the given economy

• Employees of international organizations (together with their dependents) who are outside the economy in which their

10 EXTERNAL SECTOR TRANSACTIONS

employer is physically located, regardless of the length of stay in the given economy; employees in the regional offices of such organizations would be considered residents of the economy in which the regional office is located

• Border workers-that is, persons who cross the border between two economies daily (or slightly less frequently, but regularly) because they work in the given economy but have their abode in another economy.

Special Implications of the Definition of an Individual

Some clarification might be helpful with regard to the residence of government personnel. It is suggested that all government personnel (together with their dependents) who are outside the home economy should be treated uniformly. In particular, this means that technical assistance personnel should be treated as nonresidents of the host economy.

Technical assistance personnel are employees of the donor government who are either hired specifically for the technical assistance assignment or are existing employees reassigned to provide technical assistance. The salaries (and allowances) of these personnel are paid by the donor government, although some local costs may be borne by the recipient economy. Most assignments of this kind would be, perhaps, for 18 months to two years, although some assignments could extend for many years. The donor economy considers these employees as its residents and considers that it has "stationed" these employees in the recipient economy. If, however, a donor country gave a cash grant to a recipient economy, which uses the funds to hire a foreign expert, the situation would be different. In that case, the foreign expert would be considered to be a resident of the recipient economy, according to the general rule of residence.

The determination of residence according to an individual's length of stay in an economy would mean that the following individuals would be deemed to be residents of the economy where they are staying: workers, including expatriate businessmen, who expect to be in the economy for one year or more; illegal aliens; and refugees.

Workers Who Expect to Be in a Given Economy for One Year or More

It is suggested that all individuals who enter the territory of a given economy with the intention of staying there for at least one year should

RESIDENTS OF AN ECONOMY 11

be treated as residents of that economy, with the exception of employees of foreign governments and of international organizations that are physically located in another economy. Residents of the given economy would, therefore, include all long-term workers, no matter the circumstances in which they are accommodated, the ties they maintain with their countries of origin, or the level of salaries they earn.

It has also been suggested by some analysts that nationals of an economy who work on contract in another economy for varying periods (so-called migrant workers or guest-workers) be regarded as residents of the home economy regardless of their length of stay abroad. It has been argued that these workers have employment contracts (sometimes renewable) typically of one to two years in duration and that they invariably return to their home country when their contracts have expired. Often, during their period of employment abroad, the guest-workers leave their families behind in their home countries. The argument is made that these workers continue to have their economic association with their home countries. For this reason, some analysts would suggest that they be considered residents of their home economies rather than of the host economies. The argument against this line of reasoning is that, with the exception of government employees and employees of international organizations, the same thinking could be applied to all other categories of individuals-including students who are domiciled abroad for varying lengths of time, depending on the duration of their study programs. It would not seem appropriate to single out the category of migrant workers or guest-workers as an exception to the general rules of residence. Furthermore, as pointed out in Section I, for statistical purposes one needs an objective yardstick, preferably with reference to some observable characteristic such as length of stay, to distinguish between resident and nonresident entities.

Illegal Aliens and Refugees

Because the length of stay of illegal aliens and refugees in a given economy is often indeterminate and there is no other economy to which their residence can be more meaningfully assigned, it is suggested that these individuals should be treated as residents of the economy where they are staying.

Individuals who are permanently moving from one economy to another-for example, some members of ships' crews and international travelers-also have to be assigned to an economy. The definition of residence given above accommodates these individuals by

12 EXTERNAL SECTOR TRANSACTIONS

assigning them to the economy where they had established residence before moving from one economy to another.

lV. Private Nonprofit Bodies Serving Individuals

All private nonprofit bodies classed as serving individuals are resident economic entities of the economy in whose territory the bodies are located or conduct their affairs. Such bodies are not entirely, or mainly, financed and controlled by organs of general government, and they furnish educational, health, cultural, recreational, and other social and community services to individuals either free of charge or at sales prices that do not fully cover the costs of production.

V. Enterprises

As in Section III, here a general definition is proposed and then qualified.

General Definition

Resident enterprises of a given economy are the actual or notional units that engage in (1) production of goods and services on the territory of that economy, (2) transactions in land located within the territory of that economy, or (3) transactions in leases, rights, concessions, patents, copyrights, and similar nonfinancial intangible assets issued by the government of that economy.

Special Implications of the Definition of an Enterprise

The definition of a resident enterprise holds special implications for transactions in land and nonfinancial intangible assets, the breakup of single legal entities, mobile equipment, enterprises engaged in installation of machinery or equipment, agents of enterprises, and leased goods. These implications are explored in the following paragraphs.

Transactions in Land and Nonfinancial Intangible Assets

Unlike other real assets used in the production of goods and services, land can be used in such production only in the territory of the economy where it is located. Nonfinancial intangible assets, such as

RESIDENTS OF AN ECONOMY 13