financial analysis lecture 2 cash flow statement and cash flow analysis

TRANSCRIPT

Financial Analysis

Lecture 2

Cash Flow Statement and Cash

Flow Analysis

Tatjana Mavrenko, BA SBS

CF Statement

Helps assess a company’ s

historical ability to generate cash

that can be invested in additional

assets or distributed to its capital

providers

CF Statement

Company’ s cash receipts and

cash payments during an

accounting period, showing how

these cash flows link the ending

cash balance to the beginning

balance shown in the company’ s

balance sheet

CF Statement

The cash-based information in CF

statement contrasts with the

accrual-based information from the

income statement

CF Statement

A reconciliation between reported

income and Cash Flows from

operating activities provides info:

when, where, and how company is

able to generate cash from its

operation

CF Statement

- Does the company generate enough cash

from its operations to pay for its new

investments, or relying on new debt to

finance them?

- Does the Company pay dividends to

common stockholders using cash generated

from operations, from selling assets, or

from issuing debt?

CF Statement

Classifies all cash flows as being

provided by (or used for):

- Operating

- Investing, or

- Financing activities

(IFRS, IAS Nr.7, U.S.GAAP FAS Nr.95)

CF Statement

Operating activities: •Company’s day-to-day activities that create

revenues (selling inventory, providing services)

•Cash inflows: sales, collection of accounts

receivable

•Cash outflows: cash payment for inventory,

salaries, taxes, other operating expenses, paying

to account payable

CF Statement

Investing activities: •Purchasing and selling investments (property,

plant, equipment, intangible assets, other long-

term assets, long-term and short-term

investments in equity and debt issued by other

companies (not cash equivalents and not dealing

and trading securities).

•Cash inflows: sale of long-term assets

•Cash outflows: payment for purchase of long-

term assets

CF Statement

Financing activities: •Obtaining or repaying capital (equity or long-

term debt). 2 primary sources: shareholders and

creditors

•Cash inflows: cash receipts from issuing stock

or bonds, from borrowing

•Cash outflows: payments to repurchase stock,

pay dividends, repay bonds and other

borrowings.

•NOTE: Account payable = operation activities

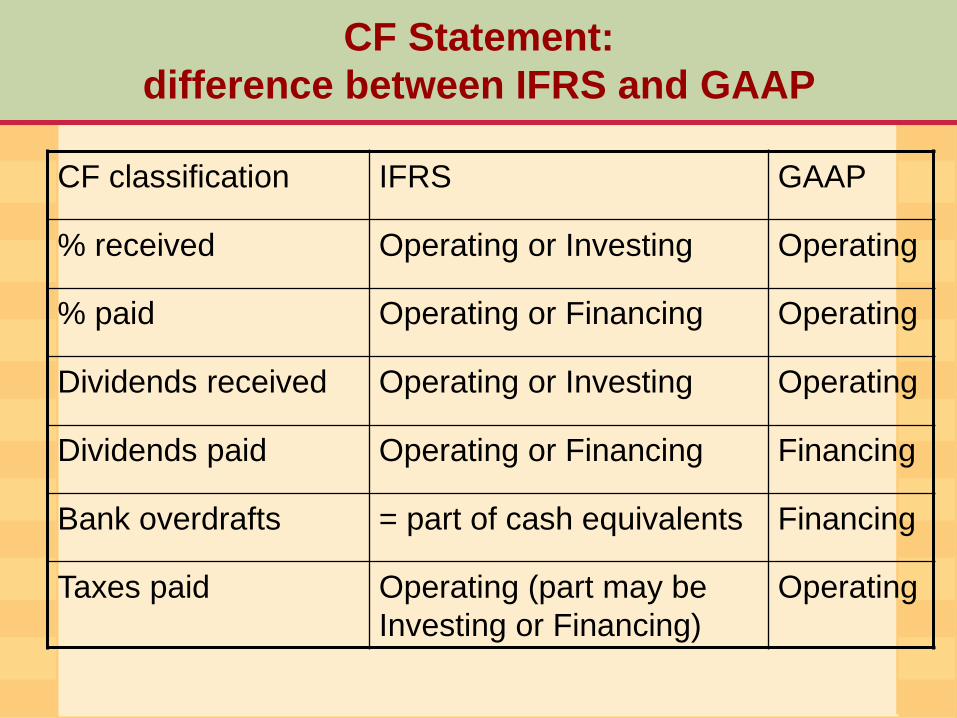

CF Statement:

difference between IFRS and GAAP

CF classification IFRS GAAP

% received Operating or Investing Operating

% paid Operating or Financing Operating

Dividends received Operating or Investing Operating

Dividends paid Operating or Financing Financing

Bank overdrafts = part of cash equivalents Financing

Taxes paid Operating (part may be

Investing or Financing)

Operating

CF Statement

Has 2 major presentation formats:

- Indirect

- Direct

CF Statement

Indirect:

How cash flow from operations can

be obtained from reported net

income as the result of a series of

adjustments (non-cash, non-

operating)

CF Statement

Direct:

specific cash inflows and outflows

that result in reported cash flow

from operating activities.

Eliminates any impact of accruals

CF Statement

IFRS: Direct or Indirect, Direct is encouraged

(Tax cash flows must be separately

disclosed in SF statement)

CF Statement

GAAP: Direct or Indirect, Direct is encouraged.

If Direct – a reconciliation of net

income and operating cash flow must

also be provided.

Interest and taxes paid must be

disclosed in footnotes if not presented

on the CF statement

CF Statement

See example (excel)

CF Statement Analysis

Useful information for

understanding a company’s

business and earnings and for

predicting its future cash flows

Evaluation of the sources and uses of cash

-Evaluate where the major sources

and uses of CF are between

operating, investing, and financing

activities

-Evaluate the primary determinants

of operating, investing, and

financing CFs

Evaluation of the sources and uses of cash

-Major sources of cash vary with

company’ s stage of growth:

-Mature company: over long term

should generate cash from its

operating activities

-New or growing company:

operating CF may be negative for

some period of time

-CF is used for investments

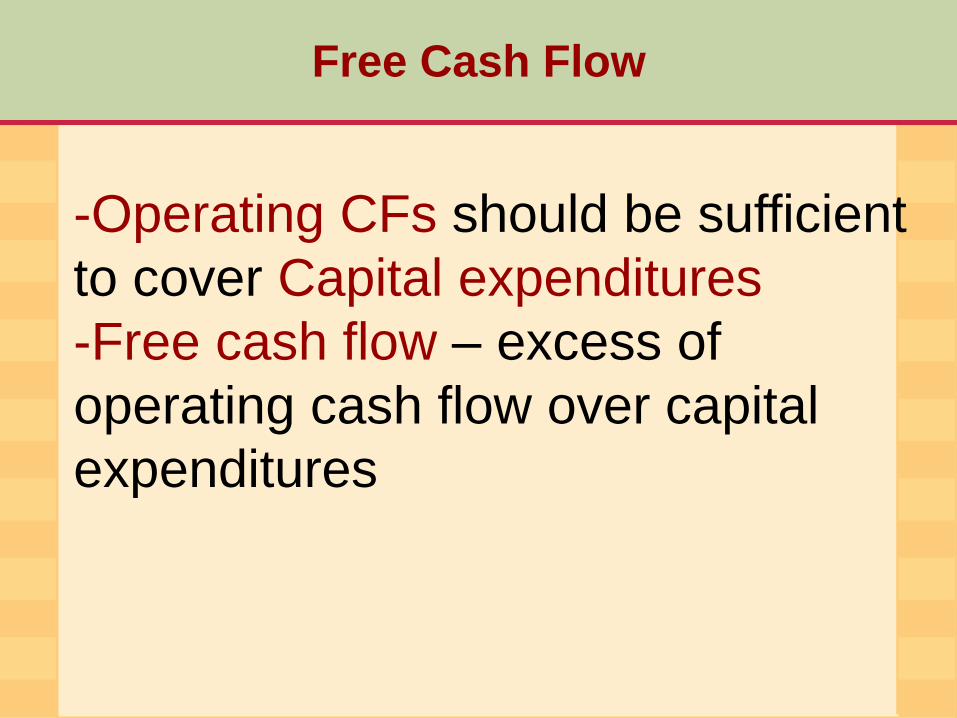

Free Cash Flow

-Operating CFs should be sufficient

to cover Capital expenditures

-Free cash flow – excess of

operating cash flow over capital

expenditures

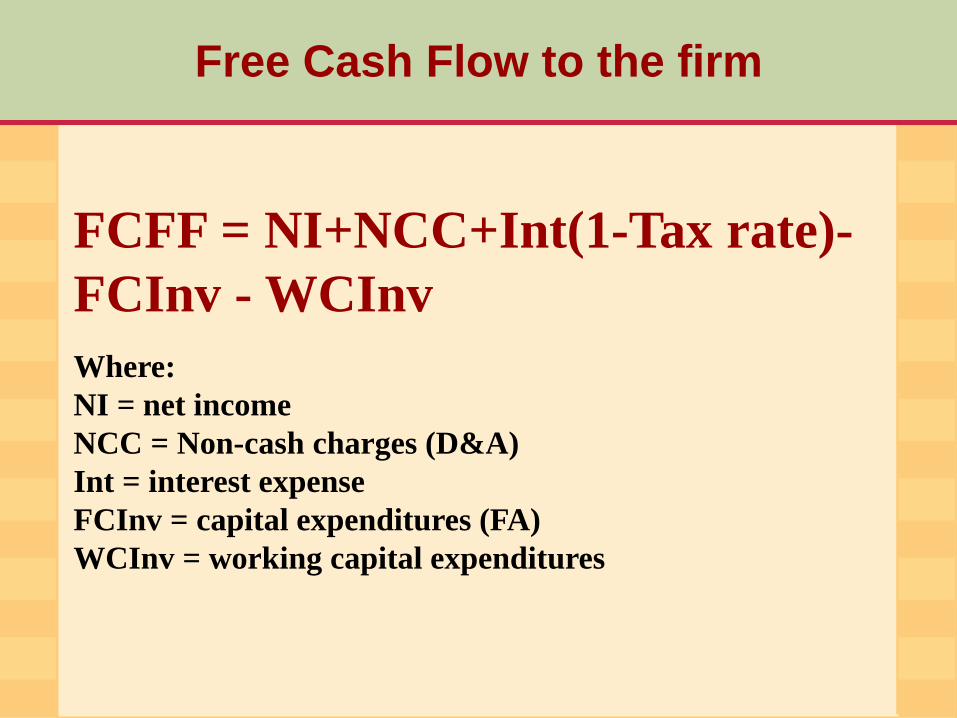

Free Cash Flow to the firm

FCFF = NI+NCC+Int(1-Tax rate)-

FCInv - WCInv

Where:

NI = net income

NCC = Non-cash charges (D&A)

Int = interest expense

FCInv = capital expenditures (FA)

WCInv = working capital expenditures

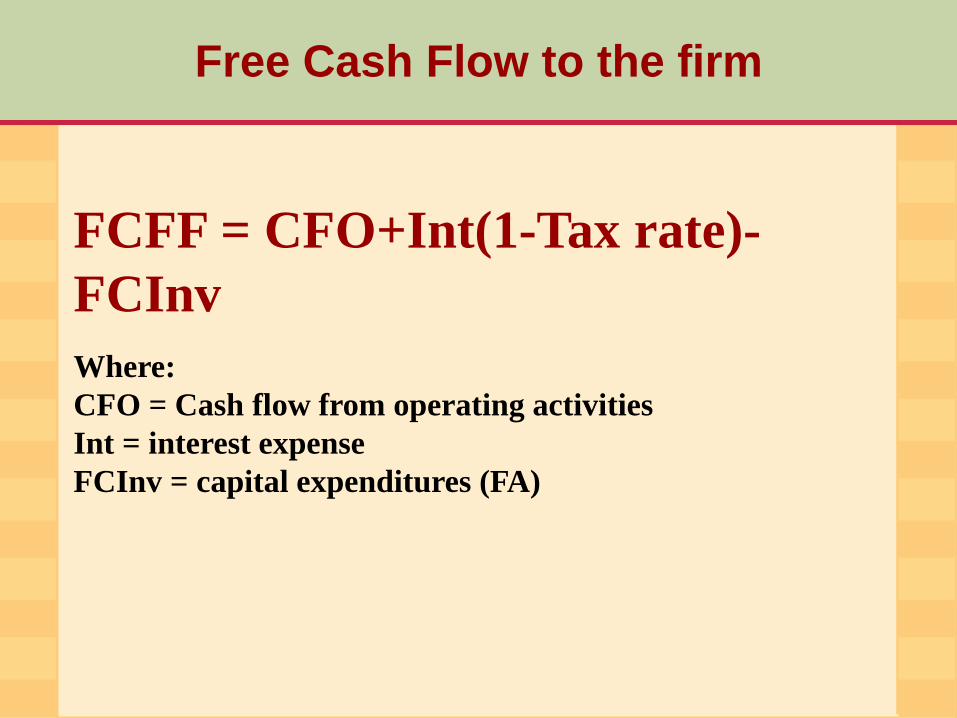

Free Cash Flow to the firm

FCFF = CFO+Int(1-Tax rate)-

FCInv

Where:

CFO = Cash flow from operating activities

Int = interest expense

FCInv = capital expenditures (FA)

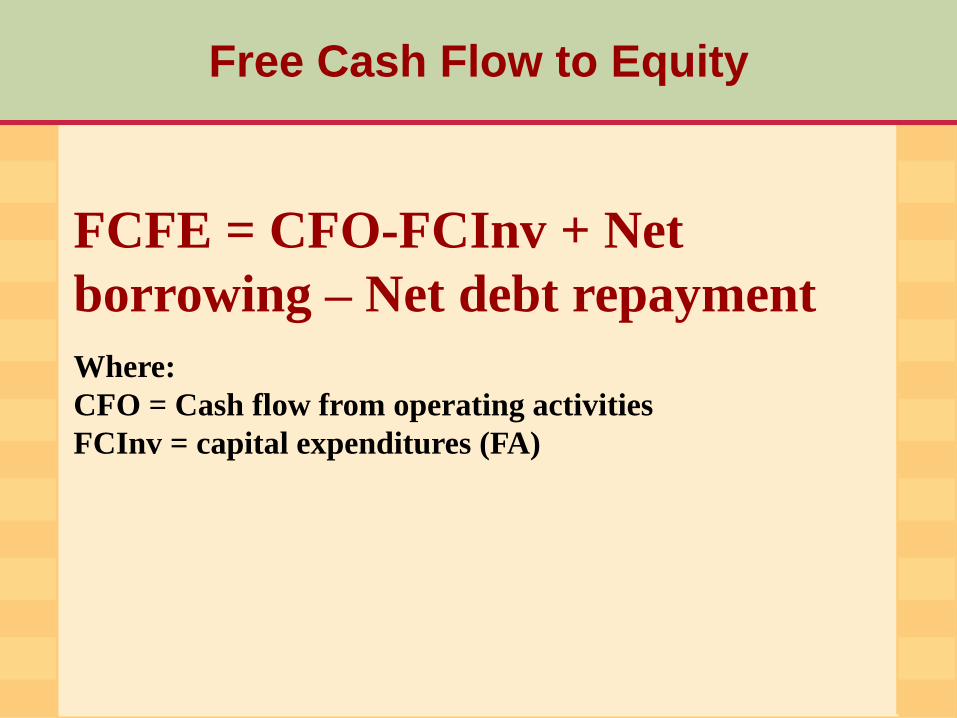

Free Cash Flow to Equity

FCFE = CFO-FCInv + Net

borrowing – Net debt repayment

Where:

CFO = Cash flow from operating activities

FCInv = capital expenditures (FA)

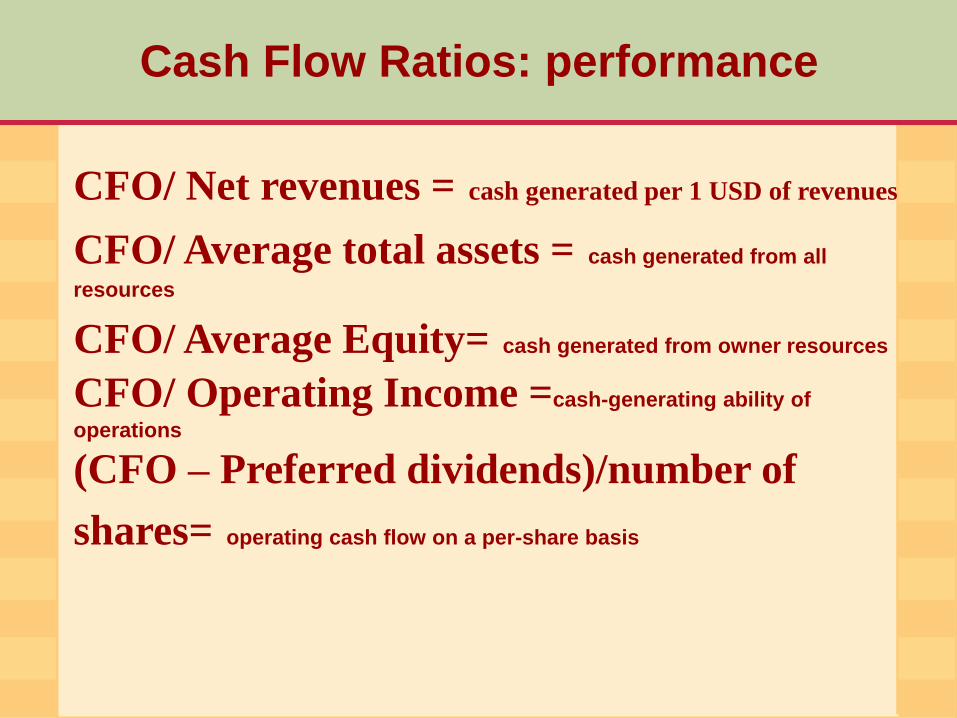

Cash Flow Ratios: performance

CFO/ Net revenues = cash generated per 1 USD of revenues

CFO/ Average total assets = cash generated from all

resources

CFO/ Average Equity= cash generated from owner resources

CFO/ Operating Income =cash-generating ability of

operations

(CFO – Preferred dividends)/number of

shares= operating cash flow on a per-share basis

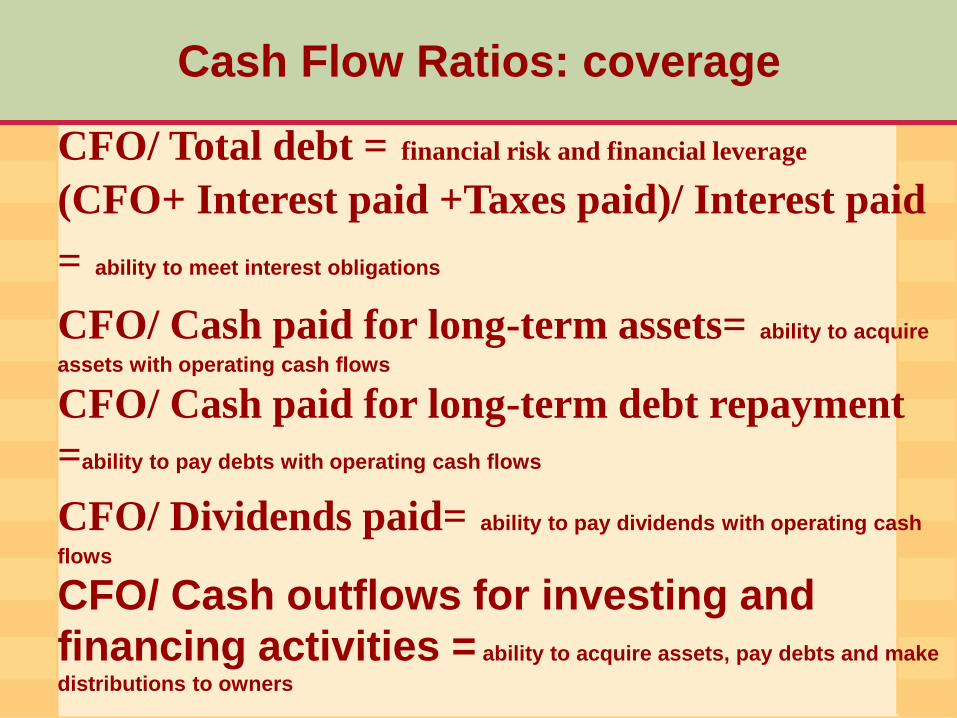

Cash Flow Ratios: coverage

CFO/ Total debt = financial risk and financial leverage

(CFO+ Interest paid +Taxes paid)/ Interest paid

= ability to meet interest obligations

CFO/ Cash paid for long-term assets= ability to acquire

assets with operating cash flows

CFO/ Cash paid for long-term debt repayment

=ability to pay debts with operating cash flows

CFO/ Dividends paid= ability to pay dividends with operating cash

flows

CFO/ Cash outflows for investing and

financing activities = ability to acquire assets, pay debts and make

distributions to owners