conquering cash flow - cfo perspective

TRANSCRIPT

Conquering Cash FlowTHE COMPLETE GUIDE TO SMALL BUSINESS

CASH FLOW MANAGEMENT

By Rob Stephens, CPA

$

Conquering Cash Flow The Complete Guide to Small Business Cash Flow Management By Rob Stephens

CFO Perspective, LLC PO Box 14439 Spokane Valley, WA 99214 509.202.4652 cfoperspective.com

©2020 CFO Perspective, LLC

All rights reserved. No part of this book may be reproduced in any manner without prior permission from CFO Perspective, LLC.

DISCLAIMER

THIS BOOK CANNOT AND DOES NOT CONTAIN LEGAL, TAX, PERSONAL FINANCIAL PLANNING, OR INVESTMENT ADVICE. The legal, tax, personal financial planning, or investment information is provided for general informational and educational purposes only and is not a substitute for professional advice. The use of or reliance on any information contained in this book is solely at your own risk. ACCORDINGLY, BEFORE TAKING ANY ACTIONS BASED ON SUCH INFORMATION, WE ENCOURAGE YOU TO CONSULT WITH THE APPROPRIATE PROFESSIONALS. CFO Perspective, LLC assumes no responsibility for errors or omissions in the contents of the book. We do not provide any legal, tax, personal financial planning, or investment advice.

Cover Design by Nick Schaffert

Table of Contents Chapter 1: The Importance of Cash Flow ................................................ 1

Chapter 2: Profit Is Not Cash Flow........................................................... 4

Chapter 3: The Cash Conversion Cycle .................................................... 7

Chapter 4: The Three Tanks of Cash ....................................................... 12

Chapter 5: Keeping an Eye on Cash Flow .............................................. 14

Chapter 6: Historical Cash Flow Statements ......................................... 19

Chapter 7: Working Capital and Cash Conversion Metrics .................. 22

Chapter 8: Working Capital, EBITDA, and Free Cash Flow .................. 25

Chapter 9: Creating and Using a Cash Flow Projection ........................ 33

Chapter 10: Tips on Monitoring Cash ..................................................... 38

Chapter 11: Sources of Funds ................................................................. 41

Chapter 12: Loans .................................................................................... 44

Chapter 13: Other Types of Debt ........................................................... 49

Chapter 14: Equity ................................................................................... 52

Chapter 15: Everything In Between ....................................................... 55

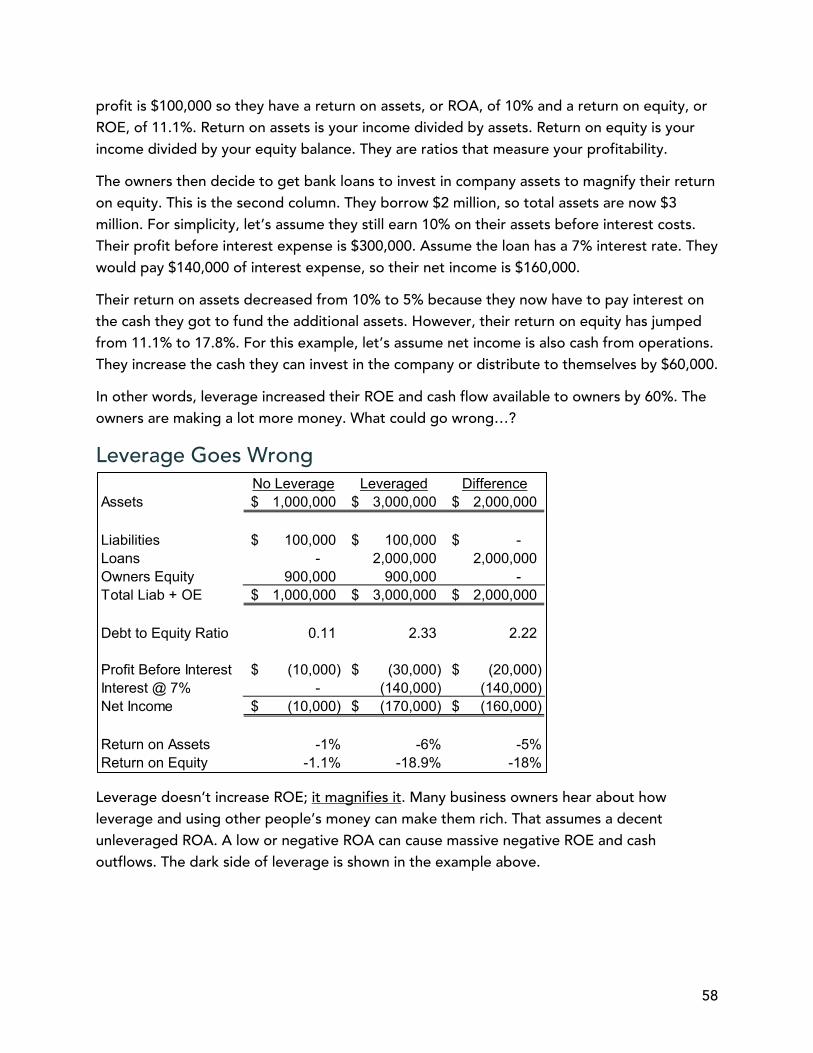

Chapter 16: Managing Debt and Equity ................................................ 57

Chapter 17: The Art of Managing Cash Flows....................................... 62

Chapter 18: Managing Excess Cash ....................................................... 67

Chapter 19: Cash and Growth ................................................................ 73

Chapter 20: Surviving a Cash Crunch ..................................................... 77

Chapter 21: A Final Word on Cash Flow ................................................ 79

Appendix A: Glossary .............................................................................. 80

1

Chapter 1: The Importance of Cash Flow “Never take your eyes off the cash flow because it’s the lifeblood of business.”

- Richard Branson

It’s difficult to overemphasize the importance of cash flow to a small business. Fluctuating cash flows are a huge source of stress for small business owners.

A study by QuickBooks revealed shocking statistics about cash flow issues for small business owners:

• 69% of small business owners have been kept up at night by concerns about cash flow.

• More than half of U.S. businesses have lost $10,000 or more by foregoing a project or sales specifically due to issues created by insufficient cash flow.

• 61% of small businesses regularly struggle with cash flow.

How important is cash flow management to the success of your business? A U.S. Bank study found that 82% of small businesses fail because of poor cash flow management skills or poor understanding of cash flow.

Managing cash flow was one of my primary roles as the CFO of multiple small and medium-sized businesses. I’ve had to learn how to manage cash flow in the good times and the bad. This guide is a collection of tips and techniques to reduce your stress and increase your cash flow.

This guide will help you conquer your cash flow by:

• Helping you get your hands around your current and projected cash flows • Providing methods to increase cash flow and reduce dips in cash flow • Identifying critical sources of cash for your business

The Goal of Cash Flow Management Now that we grasp its importance, let’s look at what we want to accomplish by managing cash. At a high level, managing cash is the art of holding enough cash—but no more than enough. It’s a balance between:

1. Having enough cash to meet needs and capture opportunities 2. Minimizing the reduction of earnings caused by holding cash

You want enough cash for expenses like paying employees and vendors or making loan payments. You also want cash available to reinvest in your company, to grow, or to buy other companies. Owners may have a minimum amount of cash they need to be distributed to them from the company.

At the same time, cash sitting in your bank account doesn’t earn very much. It’s one of your lowest-yielding assets. You need to put it to work in your business to earn higher returns.

2

When you don’t have opportunities to invest cash for higher returns in your business, you need to consider paying it out to owners.

What Exactly Is Cash Flow? We can’t talk about cash flow until we first agree on what it is. Cash flow is the amount of money flowing into and out of a business.

That’s all it is. Pretty simple, huh? Yet small business owners are often confused about one major thing regarding cash flow: Cash flow is NOT the same as profit.

Profit is an accounting concept of revenues (a.k.a. income) reduced by expenses. There are all sorts of rules about when you have revenue or when you have an expense. In fact, the last major accounting standard update on revenue was 700 pages long!

Here’s the problem: you can’t pay your bills with profits. Vendors only take real money. Your company’s profit is a good measure of performance, but it’s not the only thing to watch. 54% of all companies filing for bankruptcy experienced record sales in the weeks before they filed.

Let me explain a few terms I will use throughout this guide so you’re clear on what I mean by each.

• Cash: Cash is money you receive from any payment source. It could be via debit card or credit card payments from your customers. In other words, it’s anything that’s deposited into your bank account that makes the balance go up.

• Cash inflows and cash outflows: A cash inflow is cash that you receive, usually from your customers. A cash outflow is money that you paid or transferred to someone else. The main example is when you pay suppliers or other vendors.

• Revenue and expense: These are components of your profit according to accounting rules. These may cause a simultaneous cash inflow or outflow, but not always. For example, you may record revenue from a sale but not collect the cash from the customer until weeks later. I’ll explain this more in a later chapter.

• Net cash flow or net income: Anytime you see the word “net” in the world of finance, it means that one number was subtracted from another to get to a “net” result. For example, net cash flow is calculated as your cash inflows minus your cash outflows. Revenue minus expense equals net income.

Now that you understand a few basic terms, I want to sho you how easy it is to calculate your cash flow: grab a bank statement and subtract your ending account balance from your starting account balance. If it’s a positive number, you had positive cash flow. If it’s a negative number, you had negative cash flow.

You’ve got this! This guide will make you even better at cash flow management.

3

You also have access to free resources to help you implement what you learn in this book. They are at the Conquering Cash Flow Resources page at https://cfoperspective.com/ccfr. The site has the following resources:

• Cash flow projection templates • Training videos • Supplemental guide to cash metrics

I’ll explain the largest misunderstanding small businesses have about profits and cash flow in the next chapter.

4

Chapter 2: Profit Is Not Cash Flow “One of the earliest lessons I learned in business was that balance sheets and income statements are fiction. Cash flow is reality.” - Chris Chocola

Here’s the first formula in this book: Profits ≠ Cash Flow

It’s simple but very important. Profits do not equal cash flow. In other words, having high profits does not mean you have high cash flow.

A growth strategy to increase profits often leads to a decrease in cash, at least in the short term. This is why high-growth companies are so prone to bankruptcy. I explain growth and cash flow management later in this book.

Cash vs. Accrual Accounting Let me explain cash vs. accrual accounting so you can better understand how accounting profits are different than cash flows.

You may have seen in Quickbooks or whatever accounting program you use that you can run your financial statements using the cash or accrual basis. Accrual basis is an alternative reality that accountants live in to more accurately record profitability. It takes a little getting used to, so I’ll compare cash and accrual basis accounting.

In cash basis accounting, revenues are recorded when you receive cash from the sale, and expenses are recorded when you pay money.

In accrual accounting, revenues are recorded when they are earned. The Financial Accounting Standards Board, or FASB, recently released a 700-page set of rules for when this occurs. I won’t bore you with the details. It’s generally when you’ve done some work or sold a product and the person owes you money.

If they pay you right away, your cash revenue and your accrual revenue are recorded on the same day. However, what if you sell them something in May, but they don’t pay you until July? In accrual accounting, you earned the money in May, so the revenue is recorded in May. The amount they owe you is called an account receivable. The balance on that account receivable is zeroed out when they pay you. In cash accounting, you don’t record the revenue until June, when you receive the cash.

Now for expenses. In accrual accounting, product costs are expensed when you sell the product. Your inventory balance on your balance sheet is the cost of buying and producing items you haven’t sold yet. In cash accounting, you would have expensed those costs when you paid for them. All your other expenses are generally expensed when you owe them.

5

Let’s say you bought office supplies in May and paid for them in June. In accrual accounting, you expense them in May, when you owe money to the supplier. In cash accounting, you would expense them in June, when you paid the supplier. In accrual accounting, you would have an account payable for the amount you owe the supply company from the time you recorded the expense until you paid the supply company.

Large expenses are spread over time. Fixed assets are things like equipment and buildings. Their costs are expensed over the months they are expected to be used by you. Spreading out the costs is called depreciating them. Each month’s cost is that month’s depreciation expense.

Good Profit but Bad Cash Flow OK, sorry for the accounting lesson; time to wake up!

Here’s an example of how profits can look OK while cash is on a roller coaster. Let’s say you made 100 T-shirts at a total cost of $800 and sold them for $1,000. Congrats! You just made a $200 profit! In accrual accounting, the revenue, cost, and profit are all recorded at the same time.

Now let’s assume you paid for the cost of goods when you ordered them. Your invoices to customers said their payment was due in 30 days. Your cash flow for your first month during production is negative $800. The following month, you receive the payments from your customers, so your cash flow spikes up to $1,000.

That dip followed by a spike may not be a problem for a small amount, but if you had a shot at a $2 million profit opportunity, could you find $8 million to pay for the cost of goods to capture it?

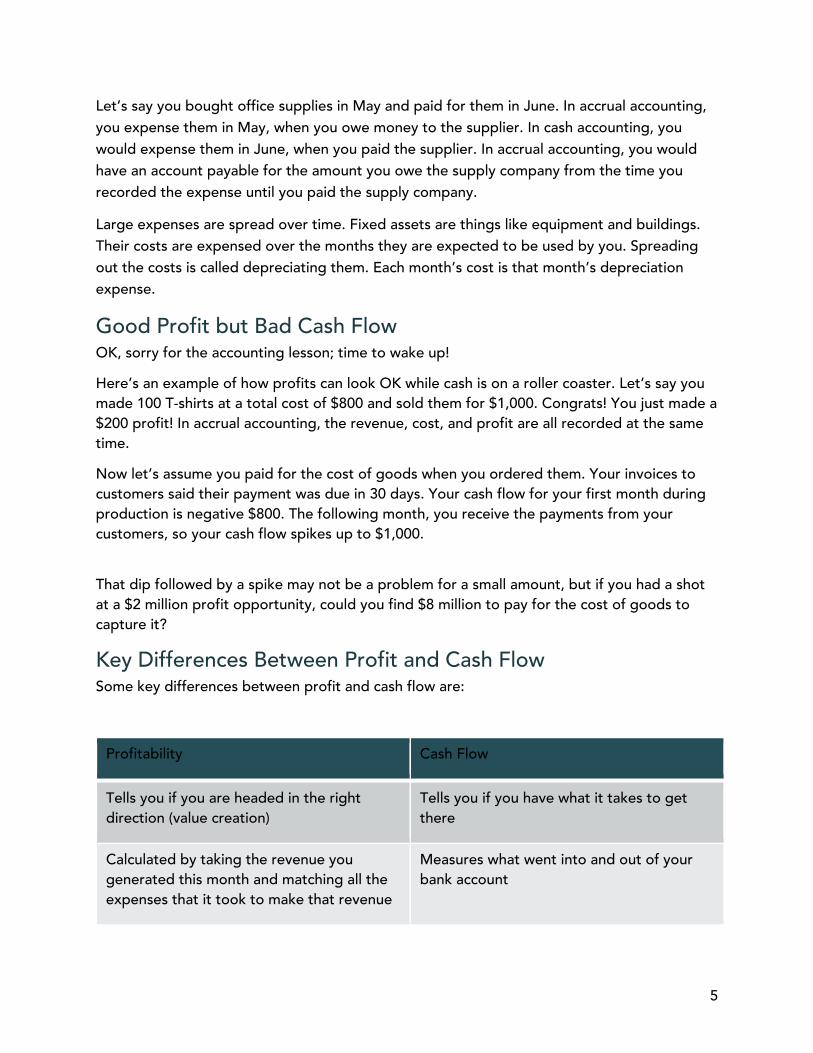

Key Differences Between Profit and Cash Flow Some key differences between profit and cash flow are:

Profitability Cash Flow

Tells you if you are headed in the right direction (value creation)

Tells you if you have what it takes to get there

Calculated by taking the revenue you generated this month and matching all the expenses that it took to make that revenue

Measures what went into and out of your bank account

6

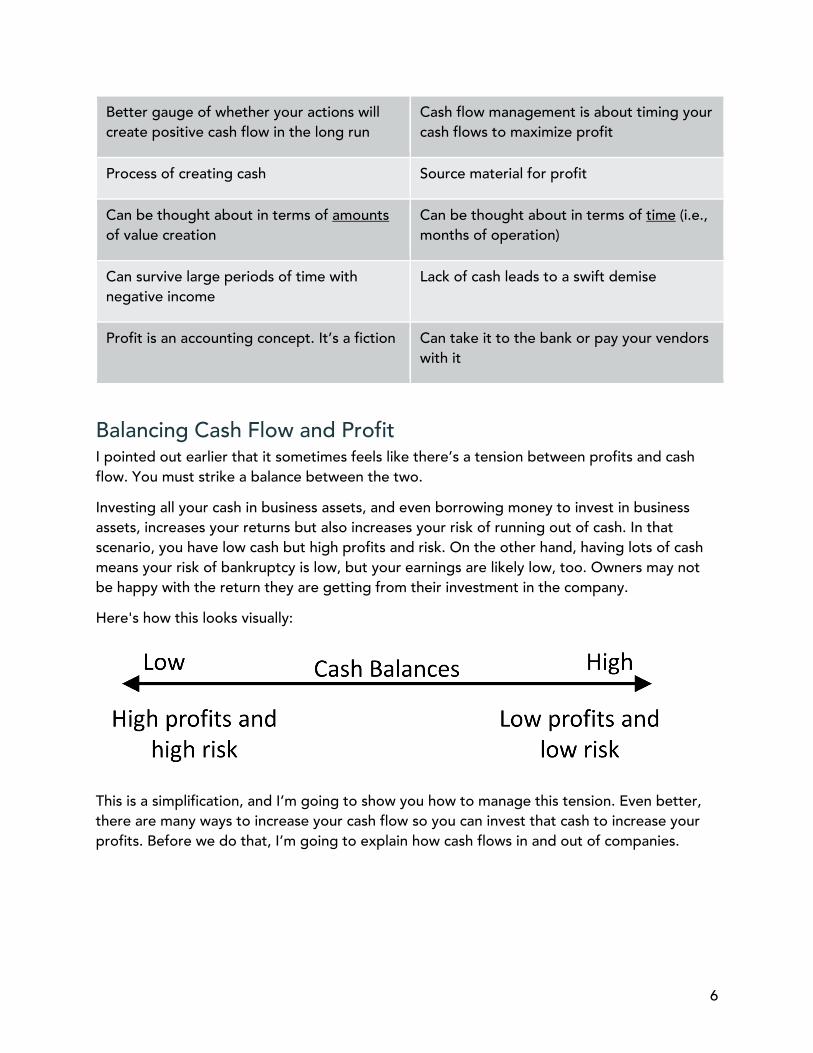

Better gauge of whether your actions will create positive cash flow in the long run

Cash flow management is about timing your cash flows to maximize profit

Process of creating cash Source material for profit

Can be thought about in terms of amounts of value creation

Can be thought about in terms of time (i.e., months of operation)

Can survive large periods of time with negative income

Lack of cash leads to a swift demise

Profit is an accounting concept. It’s a fiction Can take it to the bank or pay your vendors with it

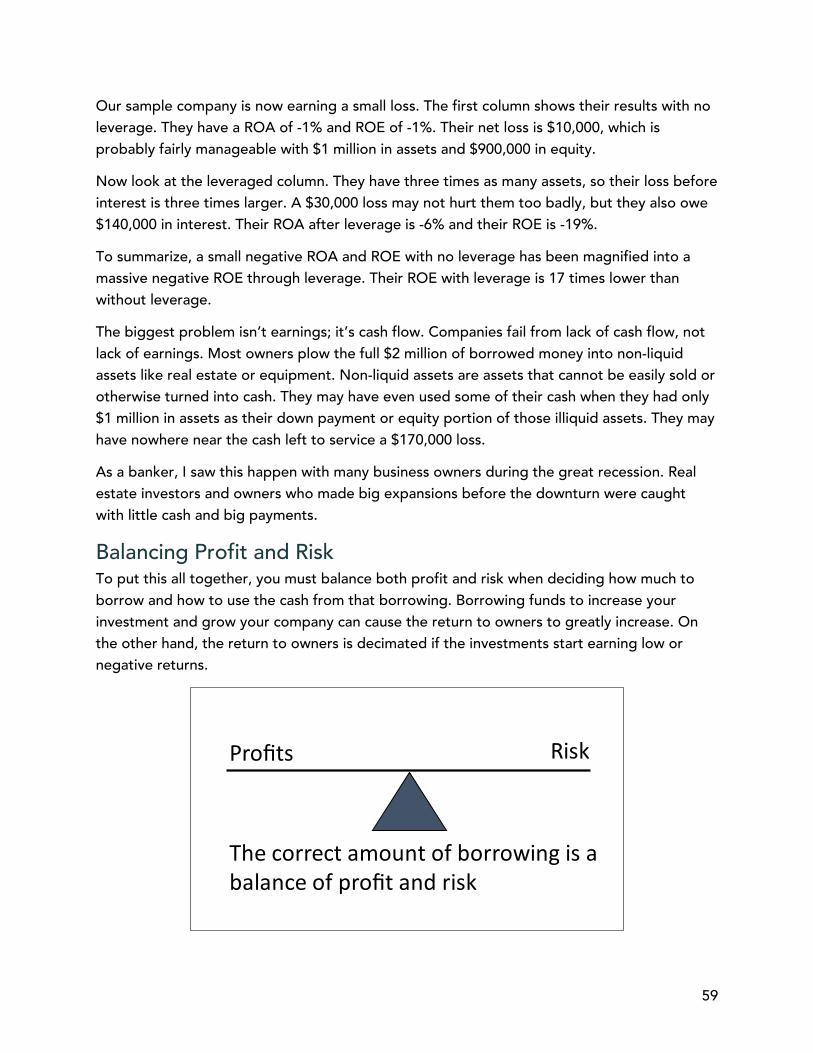

Balancing Cash Flow and Profit I pointed out earlier that it sometimes feels like there’s a tension between profits and cash flow. You must strike a balance between the two.

Investing all your cash in business assets, and even borrowing money to invest in business assets, increases your returns but also increases your risk of running out of cash. In that scenario, you have low cash but high profits and risk. On the other hand, having lots of cash means your risk of bankruptcy is low, but your earnings are likely low, too. Owners may not be happy with the return they are getting from their investment in the company.

Here's how this looks visually:

This is a simplification, and I’m going to show you how to manage this tension. Even better, there are many ways to increase your cash flow so you can invest that cash to increase your profits. Before we do that, I’m going to explain how cash flows in and out of companies.

7

Chapter 3: The Cash Conversion Cycle "Success works as a cycle—growth and contraction, balancing and unbalancing—all while you're encountering hurdles that get higher and higher over time.” - Julien Smith

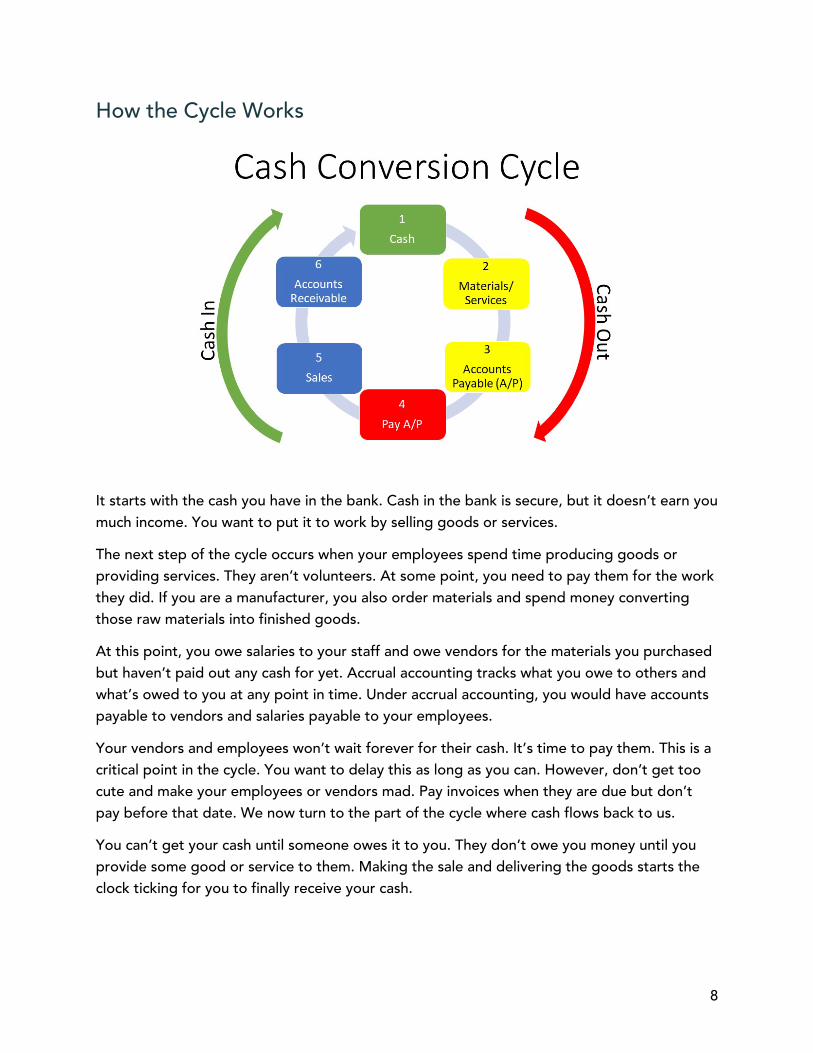

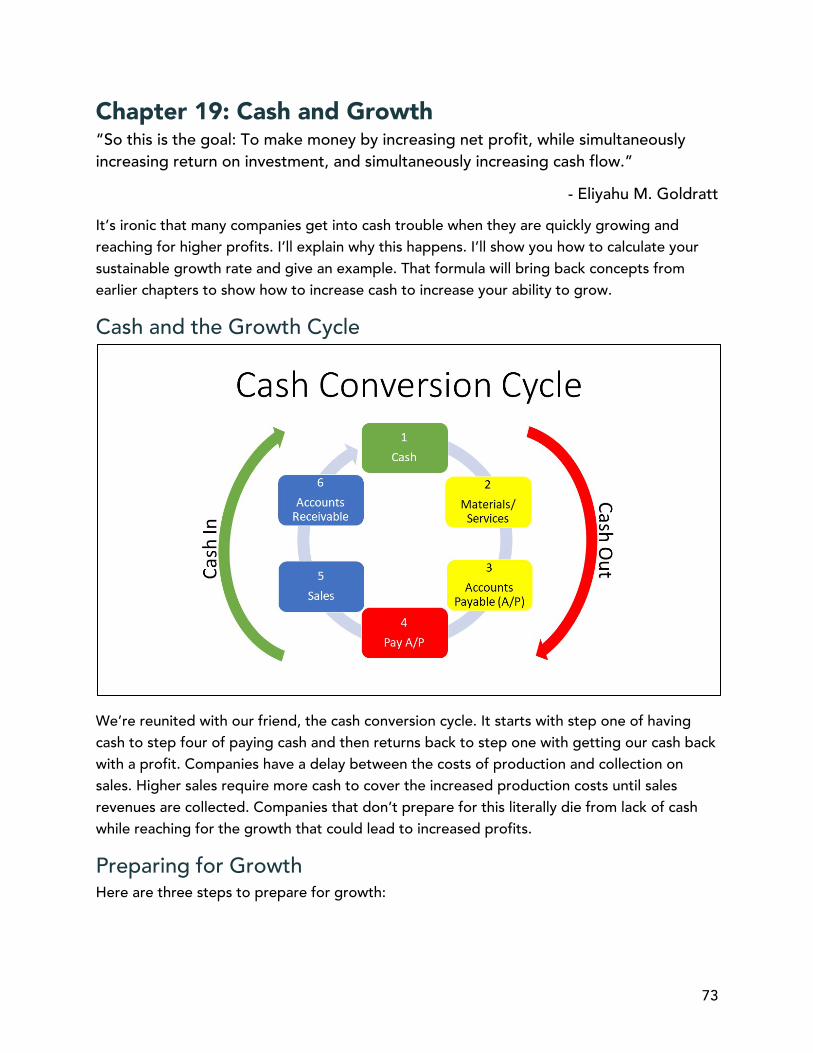

Your business is a constant cycle of cash being invested and then received back, hopefully with a profit. This cycle is called the cash conversion cycle. Knowing how it works allows you to have less cash lost to the cycle. Most importantly, you’ll have cash available when you need it.

The cash conversion cycle of drawing in cash and releasing cash is like drawing in a breath and releasing it. A runner breathes more quickly the faster they go. Top athletes have trained their bodies to get the most power from that oxygen. Cash is the oxygen of your business. You’ll receive a higher return on your cash by speeding up your cash conversion cycle.

I’ll show you how the cycle works and why it causes cash to go down for a while when you reach for growth. Your cash conversion cycle may need to be supplemented with other cash sources that I’ll explain. Understanding the cash conversion cycle allows you to avoid cash crunches and capture opportunities.

I’ll also explain how to calculate your cash conversion cycle. For those of you who aren’t math fans, fear not. I’ve created a cash conversion cycle calculator that you can get at the resources page (https://cfoperspective.com/ccfr) for this book. The resources page also has videos that explain how to use the calculator and how to decrease your cash conversion cycle.

8

How the Cycle Works

It starts with the cash you have in the bank. Cash in the bank is secure, but it doesn’t earn you much income. You want to put it to work by selling goods or services.

The next step of the cycle occurs when your employees spend time producing goods or providing services. They aren’t volunteers. At some point, you need to pay them for the work they did. If you are a manufacturer, you also order materials and spend money converting those raw materials into finished goods.

At this point, you owe salaries to your staff and owe vendors for the materials you purchased but haven’t paid out any cash for yet. Accrual accounting tracks what you owe to others and what’s owed to you at any point in time. Under accrual accounting, you would have accounts payable to vendors and salaries payable to your employees.

Your vendors and employees won’t wait forever for their cash. It’s time to pay them. This is a critical point in the cycle. You want to delay this as long as you can. However, don’t get too cute and make your employees or vendors mad. Pay invoices when they are due but don’t pay before that date. We now turn to the part of the cycle where cash flows back to us.

You can’t get your cash until someone owes it to you. They don’t owe you money until you provide some good or service to them. Making the sale and delivering the goods starts the clock ticking for you to finally receive your cash.

9

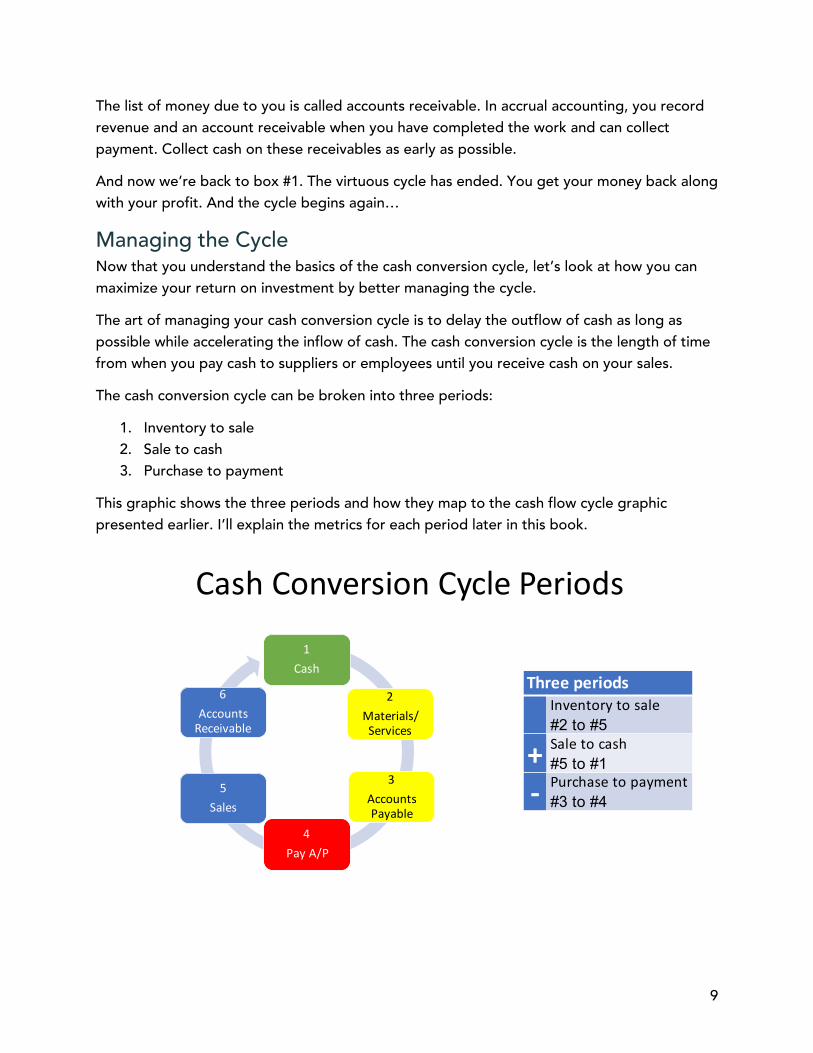

The list of money due to you is called accounts receivable. In accrual accounting, you record revenue and an account receivable when you have completed the work and can collect payment. Collect cash on these receivables as early as possible.

And now we’re back to box #1. The virtuous cycle has ended. You get your money back along with your profit. And the cycle begins again…

Managing the Cycle Now that you understand the basics of the cash conversion cycle, let’s look at how you can maximize your return on investment by better managing the cycle.

The art of managing your cash conversion cycle is to delay the outflow of cash as long as possible while accelerating the inflow of cash. The cash conversion cycle is the length of time from when you pay cash to suppliers or employees until you receive cash on your sales.

The cash conversion cycle can be broken into three periods:

1. Inventory to sale 2. Sale to cash 3. Purchase to payment

This graphic shows the three periods and how they map to the cash flow cycle graphic presented earlier. I’ll explain the metrics for each period later in this book.

1Cash

2 Materials/Services

3Accounts Payable

4Pay A/P

5Sales

6Accounts

Receivable

Cash Conversion Cycle Periods

Three periodsInventory to sale#2 to #5

+ Sale to cash#5 to #1

- Purchase to payment#3 to #4

10

Imagine a distributor who buys inventory on January 1 and pays for it on January 15th. They take the product and put it in their warehouse, where it sits until they sell it on April 1st. They collect cash from the buyer 60 days later, on May 31st.

Let’s break that down into the three cash conversion periods:

• Period 1 of inventory to sale is January 1 – April 1 or 90 days • Period 2 of sale to cash is April 1 – May 31 or 60 days • Period 3 of purchase to payment is January 1 – January 15 or 14 days

The total cash collection cycle in this example is 137 days.

They spent their cash on January 15th and didn’t get it back until May 31st. That’s 137 days. They lost that cash for over a third of the year!

Shortening the Cycle The shorter the cash conversion cycle, the more cash you have to capture opportunities, make investments, or pay critical bills.

Some ways to shorten the cycle include:

• Sending invoices as early as possible • Providing incentives for quick payment • Contacting your past-due customers and asking when they expect to pay you • Factoring • Not paying vendors until the due date • Negotiating payment plans with vendors

Let’s go back to our distributor example and make some changes:

• They now don’t pay their vendor until the invoice is due on January 31st. That shortens their cash conversion cycle by 16 days.

• They buy smaller quantities of inventory but order more frequently. They may pay more in shipping or lose quantity discounts, but tying up cash in inventory also has costs. Storage facilities have costs. Ordering in smaller batches may also reduce spoilage and obsolescence of inventory. Our example distributor reduces their inventory, so it only sits in the warehouse for half the time. That reduces their cash conversion cycle by 45 days.

• They invoice immediately upon shipment and clearly state that payment is due in 30 days. They call on customers who are late until those customers are trained to make timely payments. This decreases their cash conversion cycle by 30 days.

Putting this all together, we’ve reduced the cash conversion cycle by 91 days. It’s gone from 137 days to 46 days—a 66% decrease.

11

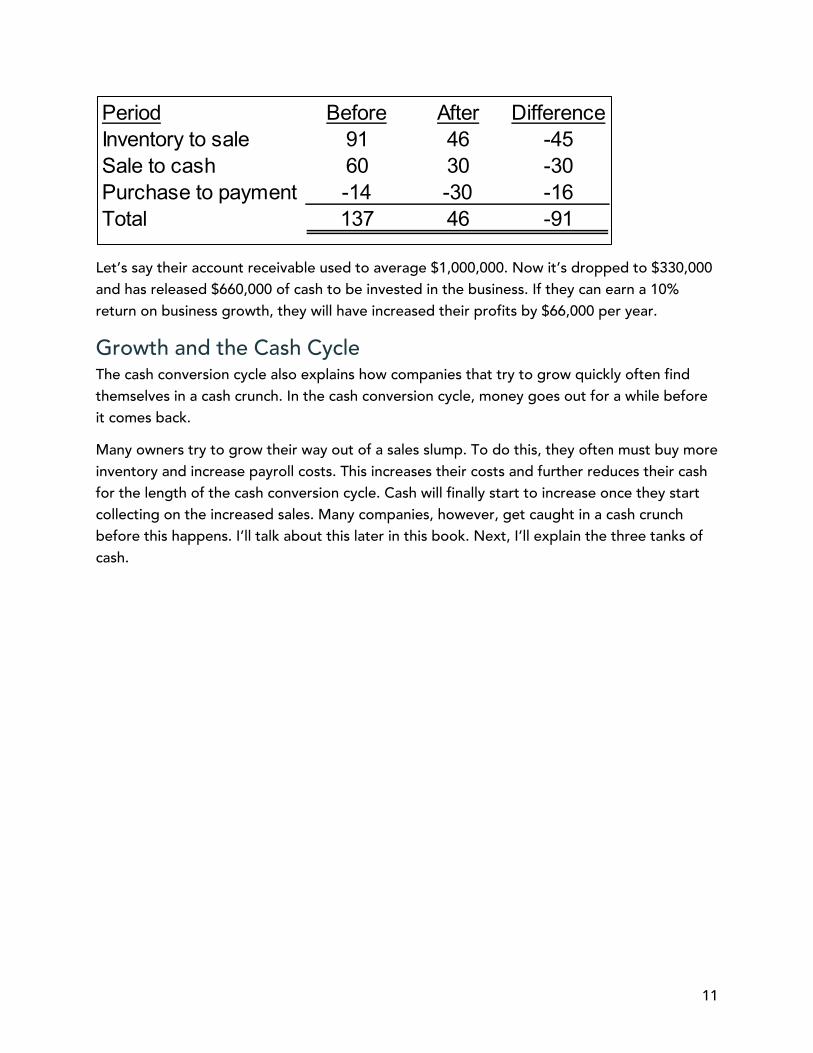

Let’s say their account receivable used to average $1,000,000. Now it’s dropped to $330,000 and has released $660,000 of cash to be invested in the business. If they can earn a 10% return on business growth, they will have increased their profits by $66,000 per year.

Growth and the Cash Cycle The cash conversion cycle also explains how companies that try to grow quickly often find themselves in a cash crunch. In the cash conversion cycle, money goes out for a while before it comes back.

Many owners try to grow their way out of a sales slump. To do this, they often must buy more inventory and increase payroll costs. This increases their costs and further reduces their cash for the length of the cash conversion cycle. Cash will finally start to increase once they start collecting on the increased sales. Many companies, however, get caught in a cash crunch before this happens. I’ll talk about this later in this book. Next, I’ll explain the three tanks of cash.

Period Before After DifferenceInventory to sale 91 46 -45Sale to cash 60 30 -30Purchase to payment -14 -30 -16Total 137 46 -91

12

Chapter 4: The Three Tanks of Cash “Cash, though, is to a business as oxygen is to an individual: never thought about when it is present, the only thing in mind when it is absent.” - Warren Buffett

The cash conversion cycle explains operating cash inflows and outflows. As we saw in the growth scenario, you need investment and financing cash flows to support and balance your operating cash flows. Let’s look at how all three types of cash flows fit together.

Think of managing your company’s cash as coordinating three tanks of liquid. In fact, a company’s access to cash is often referred to as its “liquidity.”

There are three main sources and uses of cash. Think of each as a tank of cash:

• Investments: The investing tank is the amount of money your current and potential owners have available to invest in the company.

• Operations: The operations tank is your business’s checking account. The amount of cash in the tank rises and falls with the cash conversion cycle.

• Financing: The financing tank is the money you can borrow from banks, friends, and family.

A business starts when the owners transfer their liquid cash to the operations tank. The business spends this cash for operations, reducing the tank.

13

Soon, the business produces a return on the cash, which starts to fill the tank back up. Successful businesses have so much cash coming into the tank that they can flow it back to the owners or make bigger investments for growth.

Once lenders are confident that you can keep your operations tank filled, they are willing to allow you to tap into their tank of funds when you need it. Now the owners’ tank isn’t the only spare tank of cash available when you need cash for growth or a big investment.

A cash crunch happens when the operations tank is draining and the owners have already drained everything they had in their investment tank. Lenders get concerned they won’t get their money back from the company, so they shut off their pipeline of cash to the company. I was a bank CFO during the Great Recession and saw companies get into this cash crunch situation.

Ironically, what often caused the cash crunches were good economic times. Owners saw lots of opportunities to make profits in their companies. They drained all their personal cash reserves into the company. At the same time, they borrowed all they could and made big investments.

Everything worked as long as the economy allowed the operations tank to refill with cash quickly. However, the economy repeatedly goes up and then goes down. When it goes down, the operations tank fills much more slowly. With no reserves in the investment tank and no more access to the borrowing tank, the operations tank went down the expense drain.

The next few chapters will explain how to monitor cash so you always know how much cash is in the tanks.

14

Chapter 5: Keeping an Eye on Cash Flow “Entrepreneurs believe that profit is what matters most in a new enterprise. But profit is secondary. Cash flow matters most.” - Peter Drucker

The quote above shows that businesses can forget how important it is to monitor cash flow. Monitoring your cash flow is not difficult. However, you must commit to no longer being too buried in the details of the business to check if you have enough cash for the road ahead.

Cash flow mistakes can cause missed opportunities and stress. Worst case scenario, they could be fatal to the company. Below are some classic mistakes made by small businesses:

• Not monitoring cash flow • Watching historical cash flow but not projecting cash flows • Thinking you can spend cash if there is money in the bank • Letting receivables go months past due • Not starting with enough cash • Not keeping a cash cushion • Overspending • Not saving enough cash to pay taxes

Do any of these mistakes sound distressingly familiar? You’re not alone if you’ve struggled with managing your company’s cash. Knowing these errors is half the battle. The tips and techniques in the next few chapters will help you become a master of cash flow management.

You can monitor your cash flows from three perspectives:

• Historical cash flows • Cash metrics • Forward-looking cash flow projections

Let’s dig deeper into each.

Historical Cash Flows Looking at historical cash flow patterns can help you better understand your business. This allows you to make better decisions about how to manage cash in the present. Most business accounting software systems have reports that show your historical cash flows. Sometimes the report is called a “statement of cash flows.”

The accounting and auditing rules define a standard format for a formal statement of cash flows. This format has three main sections:

• Cash flows from operations: Typical large cash flows in this section are cash receipts from customer sales and cash payments to suppliers and other vendors. It also

15

includes tax payments. A healthy company has positive cash flow from operations.

• Cash flows from investing: This includes cash flows caused by the purchase or sale of equipment, land, buildings, furniture, or investments.

• Cash flows from financing: Financing cash flows arise from cash receipts from owners investing in the company or cash paid out in dividends. It also includes cash from borrowings and cash payments on those loans.

One of the first things to look at on a statement of cash flows is the total net cash flow of each of those sections. You want your cash flow from operations to be positive to buy equipment or other assets (an investing activity). You may need cash for loan payments (a financing activity). You ultimately want cash to pay the owners (a financing activity). You need to find financing sources of cash if your cash flow from operations is running negative.

Your accounting software may not show cash flows in this format, or it may have reports in other formats. One of the best historical reports is a list of your cash inflows and outflows by month. This will show if you have “seasonal” cash flows, which is also called “seasonality.” Seasonality just means that your cash flows have a consistent pattern of rising and falling. Later, I’ll show you how to smooth out seasonal cash flows by changing the timing of cash flows. Lines of credit, which we’ll cover in the Sources of Funds section, are also an excellent option for businesses with seasonality.

Farmers have months of negative cash flow as they grow their crops. This is followed by a spike of cash inflows at harvest. Nonprofits have a spike in cash inflows at year-end or after a major fundraising event. These businesses learn how to manage their cash flow seasonality.

It’s good to learn if your business has cash flow patterns within a month. For example, you may have higher cash inflows on certain days of the month. You likely have a significant cash outflow on payroll days. One of my main jobs as the CFO of a small company was to make sure we had cash ready for payroll days. You can occasionally bounce a check to a vendor but you should never, ever blow a paycheck. This guide will help you never make that mistake.

Cash Metrics Cash metrics are ratios of your cash flows over time or your cash balances at a point in time. The amount that’s a good ratio for your company is unique to each industry. The most useful analysis to do with these ratios is to compare your ratios to companies like yours or compare your ratios over time to spot trends. Here are some common ratios for small businesses:

Cash Flow Margin Ratio Definition: Cash flow from operations divided by sales

This is a crucial ratio that tells you how much cash you are currently generating for every dollar in sales. A higher ratio is better.

16

Current Ratio Definition: Current assets divided by current liabilities

Current assets and liabilities are items on your balance sheet that will usually be received or paid in cash in the next year. If the ratio is greater than one, your balance sheet is expected to produce positive cash flow. If the ratio’s less than one, you will need additional cash to pay your liabilities that come due in a year. A higher ratio means you are less likely to run into cash flow problems. Of course, there are all sorts of cash flows that arise from things not on the balance sheet, so this ratio is good but doesn’t tell the whole story.

Current Liability Coverage Ratio Definition: Net cash from operations divided by current liabilities

Liabilities can be paid by cash on hand (measured by the current ratio) and by cash generated from operations, which this ratio measures. Like the current ratio, higher is better.

Quick Ratio (AKA Acid Test Ratio) Definition: Current assets (minus inventory, prepaid expenses, and supplies) divided by current liabilities

This ratio removes some assets and is a tougher test of your cash flows than the current ratio. Like the current ratio, higher is better from a cash flow perspective.

Burn Rate Definition: Number of days the company can operate using only the cash on hand

This is a crucial ratio for startup companies who have no inflows or not enough to fund their growth. Many high-tech startups closely monitor this metric. This metric tells you roughly how long you can survive until you need to raise more funds (for example, from venture capital or from current owners).

Forward-Looking Cash Flow Projections A cash flow projection is the most important financial report for your business, yet so many businesses miss out on its benefits. Your forecast doesn’t have to be complicated or fancy. It just needs to give you an estimate of when your cash inflows and outflows will occur. Pick a time frame that you think you can reasonably, roughly predict (for example, one month, three months, or one year). One option is to have a more detailed projection for the next 1-3

17

months and then a rougher projection for the following 4-12 months. I’ll go into more detail in the next chapter on how to build and use a cash flow projection.

There are numerous benefits of a cash flow projection. They go well beyond the survival of your company or the ability to have the cash available to capture an opportunity when it arises. Here are some of these benefits.

• Early identification of potential low (or negative) cash balances: The more time you have to make adjustments, the more adjustment options you have. A projection lets you know when you need to speed up cash collection or slow down payments to avoid a cash crunch. For example, there may be times when you have enough cash to quickly pay invoices to capture discounts. Other times, you may need to delay payment.

• Your bank, investors, or other stakeholders need it: One of your sources for cash may be investors or banks. They will want assurance that your company has enough cash for operations and to pay them back. The very act of having a cash flow projection shows your business management skills and builds credibility with them.

• Operations coordination: The timing of when to hire staff, make significant purchases, and distribute cash to owners can all be modeled to make sure your strategy is feasible. You may find that you need to adjust the timing or amounts of some of your strategies. Not having a projection might cause you to make decisions or promises that you can’t fulfill.

• Identify cash “leaks”: It’s easy for small things that suck cash out of your business to go unnoticed in daily operations. Reviewing the cash flow projection can show:

o lags between sales and cash receipt for those sales o lags between the purchase of inventory and cash receipt on sales of that

inventory o opportunities to stretch out one set of payments to prioritize another set of

payments.

• Identify the need to get a loan or a capital infusion: The projection may say that operational cash flows will not be enough to fund opportunities for investment and growth. This means you may need additional cash from lenders or owners.

• Avoid tax penalties: It’s not uncommon for bankers to see companies that are making sales but don’t have enough cash to pay the taxes on those sales. Don’t mess with the IRS. Be ready to pay your taxes on time to avoid unnecessary penalties.

• You’re more ready for big cash outflows: Taxes aren’t the only payment you don’t want to miss. Preparing the schedule helps you identify big cash outflows like payroll

18

payments for which you may need some time to gather cash.

• Match cash outflows to the seasonality of inflows: Many businesses have a pattern of high cash inflows during certain months of the year and low cash inflows during other parts. At the same time, their expenses may be evenly spread throughout the year. This causes months with positive cash flow and other months with negative cash flow. The projection makes sure you have enough cash built up to cover those lean months.

• Plan out ownership equity distributions: A good cash flow projection for your company allows you to plan your equity distributions. This helps with your personal financial planning.

• Capture Opportunities: Your projection tells you when you will be able to make major investments like equipment purchases. This lets you know when you can start looking for deals on these investments. If you know that good deals often regularly occur during a certain part of the year, you can adjust your cash flows to be ready to capture those deals.

The next three chapters will go into more detail about your historical cash flow statement, metrics, and cash flow projections.

19

Chapter 6: Historical Cash Flow Statements “Many small businesses would rather face an angry barbarian horde than tackle their cash flow statement.” -Nicole Fende

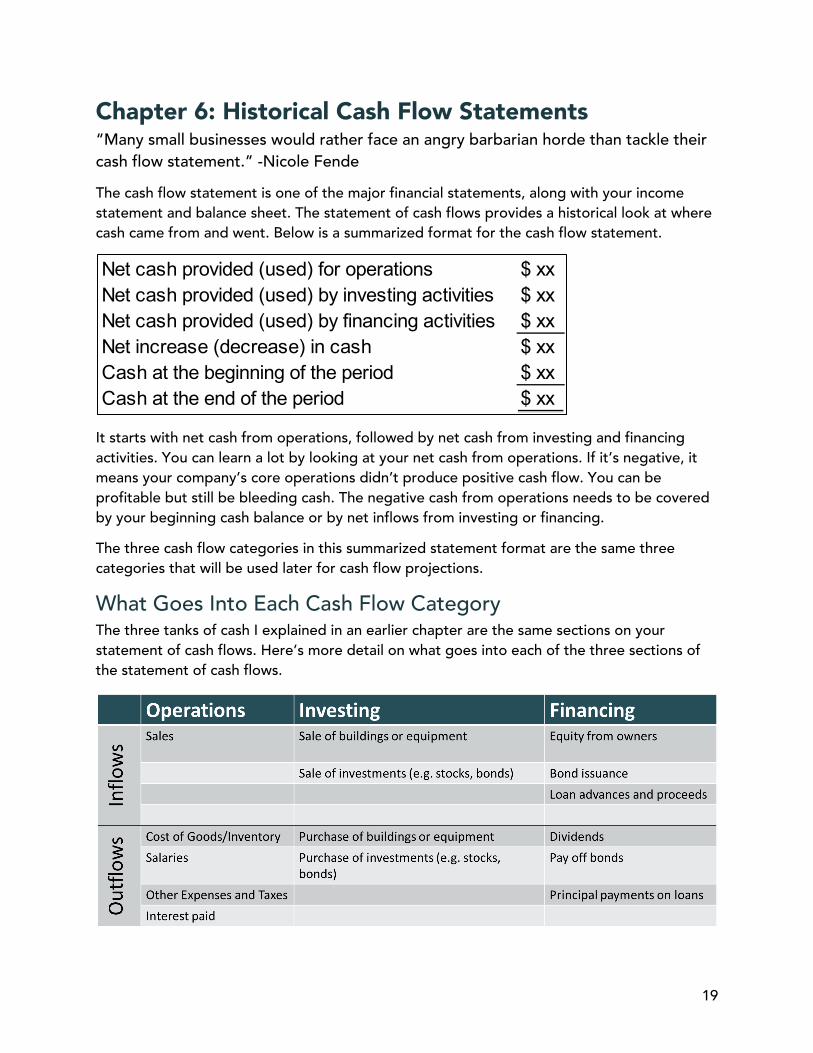

The cash flow statement is one of the major financial statements, along with your income statement and balance sheet. The statement of cash flows provides a historical look at where cash came from and went. Below is a summarized format for the cash flow statement.

It starts with net cash from operations, followed by net cash from investing and financing activities. You can learn a lot by looking at your net cash from operations. If it’s negative, it means your company’s core operations didn’t produce positive cash flow. You can be profitable but still be bleeding cash. The negative cash from operations needs to be covered by your beginning cash balance or by net inflows from investing or financing.

The three cash flow categories in this summarized statement format are the same three categories that will be used later for cash flow projections.

What Goes Into Each Cash Flow Category The three tanks of cash I explained in an earlier chapter are the same sections on your statement of cash flows. Here’s more detail on what goes into each of the three sections of the statement of cash flows.

Net cash provided (used) for operations $ xxNet cash provided (used) by investing activities $ xxNet cash provided (used) by financing activities $ xxNet increase (decrease) in cash $ xxCash at the beginning of the period $ xxCash at the end of the period $ xx

20

Operational cash inflows are sales. Outflows are most of the expenses on the income statement, also known as the profit and loss statement.

Investing cash flows come from buildings and equipment. Investments like stocks and bonds are also investment cash flows.

Financing cash flows include loans, debt, and equity cash flows.

The statement of cash flows tells you whether your sales produced enough cash to cover your operating expenses or whether you needed other sources of cash. You can learn a company’s sources of funds, whether they are investing enough to replace their fixed assets, and how much cash the owners received.

The income statement shows a company’s profitability, but the cash flow statement gives you further insights into how your company achieved those profits. You can also learn the warning signals that cash flow is becoming a problem, even if your company is showing profits.

What You Might Miss The statement of cash flows provides some basic information, but you may miss some important things you need to know to manage cash. One way to see this is by trending cash flows over time.

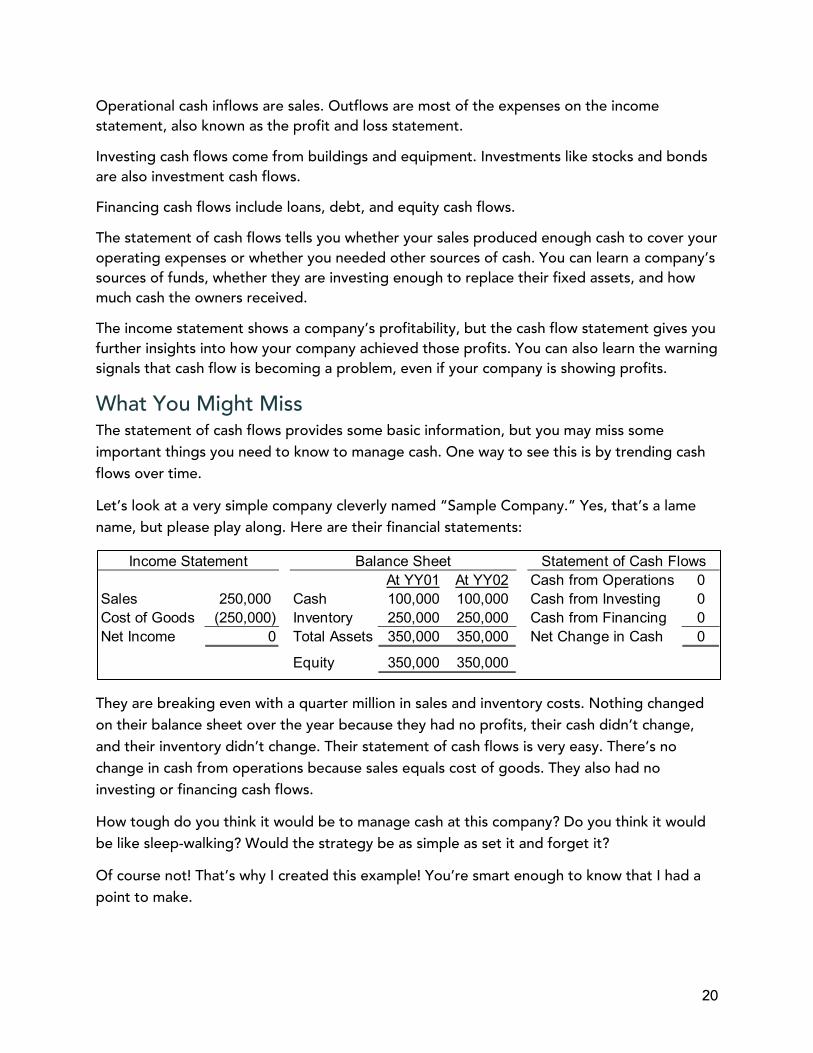

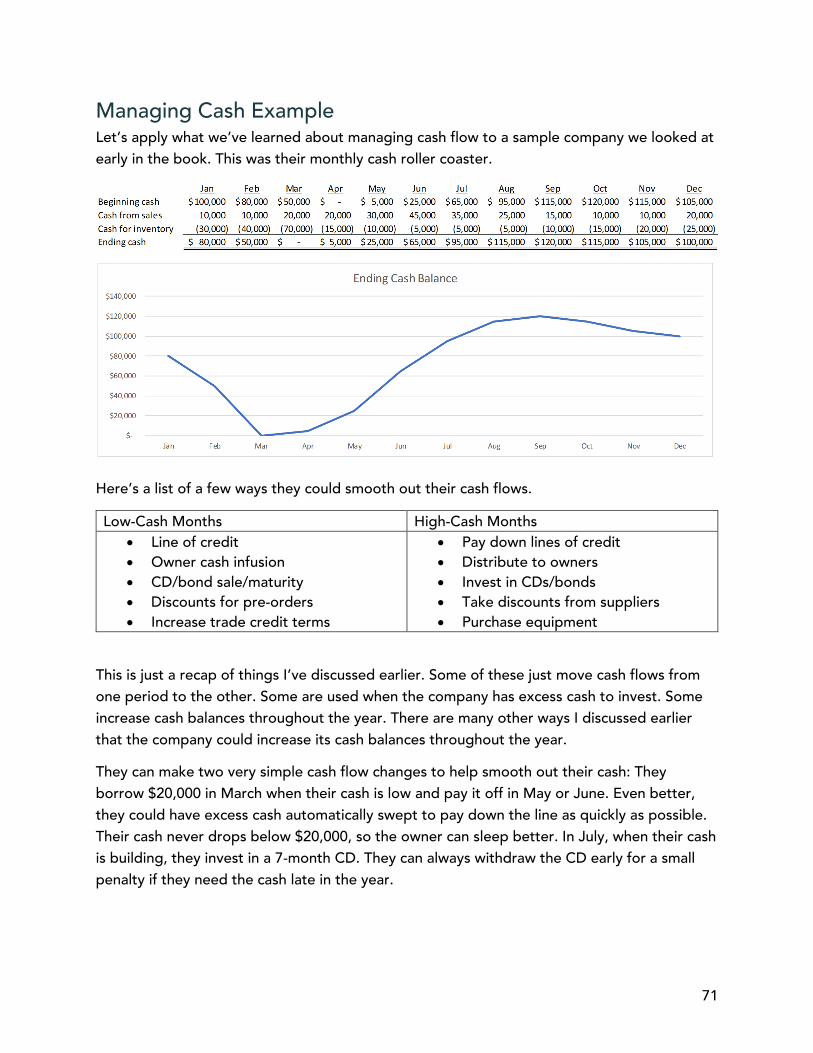

Let’s look at a very simple company cleverly named “Sample Company.” Yes, that’s a lame name, but please play along. Here are their financial statements:

They are breaking even with a quarter million in sales and inventory costs. Nothing changed on their balance sheet over the year because they had no profits, their cash didn’t change, and their inventory didn’t change. Their statement of cash flows is very easy. There’s no change in cash from operations because sales equals cost of goods. They also had no investing or financing cash flows.

How tough do you think it would be to manage cash at this company? Do you think it would be like sleep-walking? Would the strategy be as simple as set it and forget it?

Of course not! That’s why I created this example! You’re smart enough to know that I had a point to make.

At YY01 At YY02 Cash from Operations 0Sales 250,000 Cash 100,000 100,000 Cash from Investing 0Cost of Goods (250,000) Inventory 250,000 250,000 Cash from Financing 0Net Income 0 Total Assets 350,000 350,000 Net Change in Cash 0

Equity 350,000 350,000

Balance SheetIncome Statement Statement of Cash Flows

21

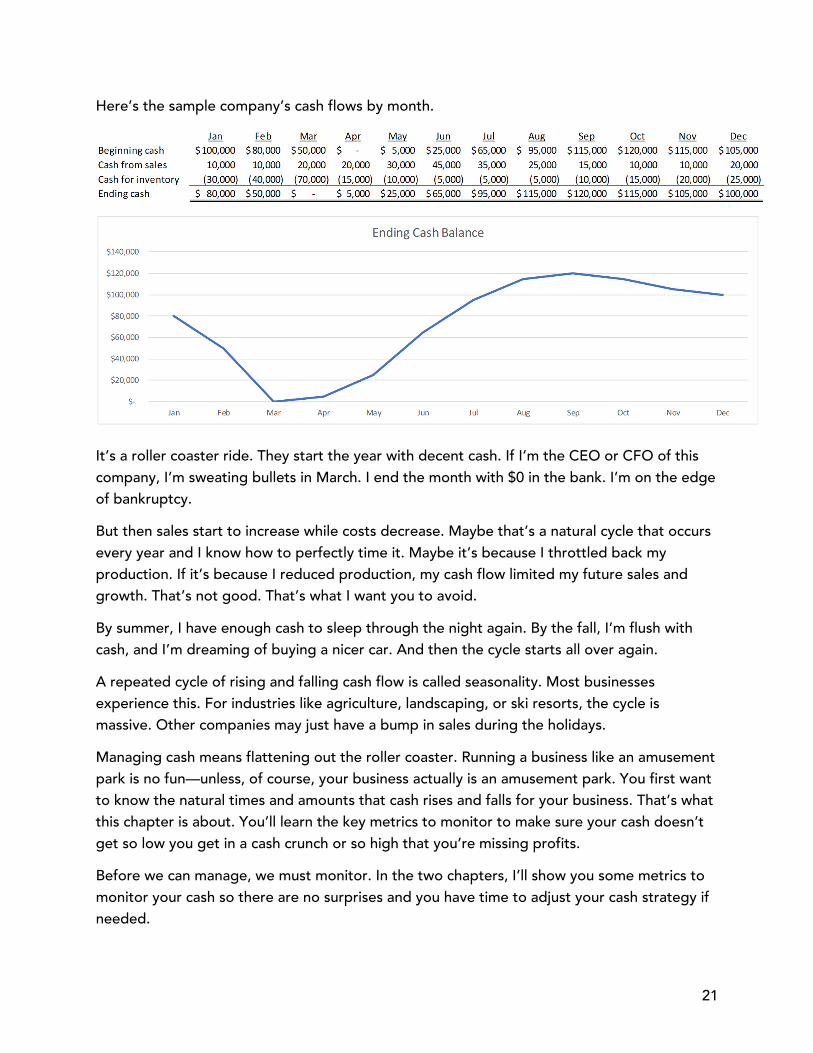

Here’s the sample company’s cash flows by month.

It’s a roller coaster ride. They start the year with decent cash. If I’m the CEO or CFO of this company, I’m sweating bullets in March. I end the month with $0 in the bank. I’m on the edge of bankruptcy.

But then sales start to increase while costs decrease. Maybe that’s a natural cycle that occurs every year and I know how to perfectly time it. Maybe it’s because I throttled back my production. If it’s because I reduced production, my cash flow limited my future sales and growth. That’s not good. That’s what I want you to avoid.

By summer, I have enough cash to sleep through the night again. By the fall, I’m flush with cash, and I’m dreaming of buying a nicer car. And then the cycle starts all over again.

A repeated cycle of rising and falling cash flow is called seasonality. Most businesses experience this. For industries like agriculture, landscaping, or ski resorts, the cycle is massive. Other companies may just have a bump in sales during the holidays.

Managing cash means flattening out the roller coaster. Running a business like an amusement park is no fun—unless, of course, your business actually is an amusement park. You first want to know the natural times and amounts that cash rises and falls for your business. That’s what this chapter is about. You’ll learn the key metrics to monitor to make sure your cash doesn’t get so low you get in a cash crunch or so high that you’re missing profits.

Before we can manage, we must monitor. In the two chapters, I’ll show you some metrics to monitor your cash so there are no surprises and you have time to adjust your cash strategy if needed.

22

Chapter 7: Working Capital and Cash Conversion Metrics “Money is always eager and ready to work for anyone who is ready to employ it.”

- Idowu Koyenikan

This is the first of two chapters on metrics to monitor your cash. We’ll focus on the cash conversion cycle metrics in this chapter. Remember, you have access to free resources at the Conquering Cash Flow Resources page at https://cfoperspective.com/ccfr. One of those resources is a guide for the metrics in these chapters.

The resources page also includes a tool to calculate your cash conversion metrics. You can also use it to model how much your cash and profit might increase by reducing your cash cycle. This will be very helpful for you with those metrics. I’ll explain more about the tool and show examples later in this chapter.

The cash conversion cycle is like your company breathing in and releasing out cash. It releases cash in the cycle and then draws it back in again at the end of the cycle. Your business will turn a little blue if it’s a long time between breaths of cash. You can speed up the cycle by tracking and improving its three periods.

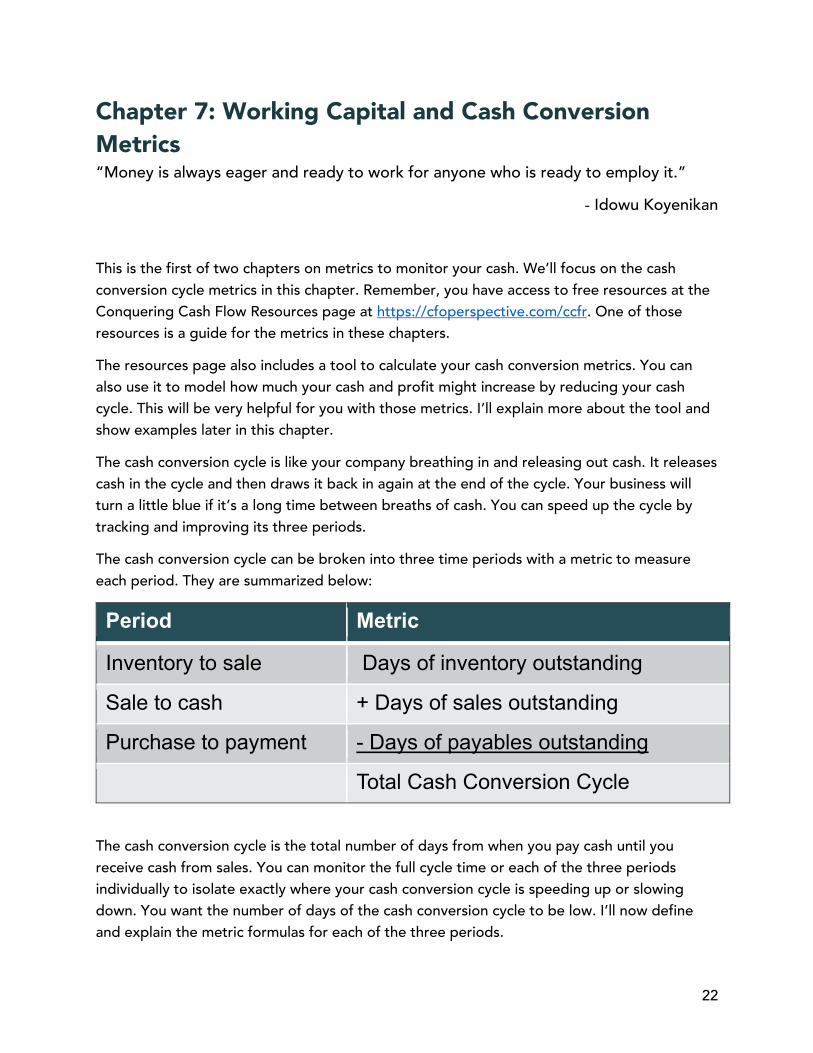

The cash conversion cycle can be broken into three time periods with a metric to measure each period. They are summarized below:

Period Metric

Inventory to sale Days of inventory outstanding

Sale to cash + Days of sales outstanding

Purchase to payment - Days of payables outstanding

Total Cash Conversion Cycle

The cash conversion cycle is the total number of days from when you pay cash until you receive cash from sales. You can monitor the full cycle time or each of the three periods individually to isolate exactly where your cash conversion cycle is speeding up or slowing down. You want the number of days of the cash conversion cycle to be low. I’ll now define and explain the metric formulas for each of the three periods.

23

Days of Inventory Outstanding (DIO) Formula: Average inventory / (cost of goods sold/365)

The days of inventory outstanding is the average number of days it takes to sell inventory.

The last part of the formula (cost of goods sold/365) is your average daily cost of goods, assuming you’re using the cost of goods over a year. I explain how to calculate your average inventory in the metrics PDF.

A lower number is generally better.

Days Sales Outstanding (DSO)

Formula: Average receivables / (net sales/365)

The days sales outstanding is the number of days it takes to collect cash from sales.

The last part of the formula (net sales/365) is your average daily sales amount. Divide your current or average accounts receivable balance by your daily sales to calculate the number of days it takes to collect cash from sales. Net sales are your sales minus any returns or uncollectable sales.

Once again, lower numbers are better.

Days Payable Outstanding (DPO)

Formula: (Average payables + average accrued liabilities) / (cost of goods sold/365)

The days payable outstanding is the number of days from the purchase of materials or labor until you pay cash for them.

The last part of the formula (cost of goods sold/365) is the average daily cost of goods.

Higher is better for this metric, but you don’t want this metric to be so high that you anger your vendors and employees.

Turnover Ratios You can also express those previous formulas as turnover ratios. A turnover ratio measures how many times per year you complete each stage of the cycle. It may be easier for you to understand the number of days in the cycle, rather than a turnover ratio. However, the

24

turnover ratios may be used in industry stats you receive or reports you get, so I’ll explain them.

These ratios are another way to measure your cash efficiency. Being efficient with your cash means two things. First, you use as little of your cash as possible to create a return on that cash. Second, the cash you invest is returned to you as quickly as possible. Both types of efficiency increase your cash balances.

For example, your inventory turnover ratio is your cost of goods divided by the average inventory balance during the period of those costs. I list the other formulas in the metrics PDF on the resources page at cfoperspective.com/ccfr.

25

Chapter 8: Working Capital, EBITDA, and Free Cash Flow “If you don’t collect any metrics, you are flying blind. If you collect and focus on too many, they may be obstructing your field of view” - Scott Graffius

That last chapter on metrics was so much fun that I created this sequel chapter on metrics. We’ll cover EBITDA and free cash flow, which are broad measures of how much cash your company produces. I’ll also explain the debt service coverage ratio, which is used by bankers when deciding whether to grant a loan to your company, and the cash burn rate.

Working Capital Working capital can be measured two ways.

1. Net working capital is calculated as your current assets minus your current liabilities. 2. The current ratio is your current assets divided by your current liabilities.

They are simple formulas but immediately lead to the question: “What’s a ‘current’ asset and a ‘current’ liability?” Assets are things you own or have rights to. Examples include cash, inventory, and accounts receivable. Liabilities are things you owe, like payments to your vendors or lenders. Assets and liabilities are listed on your balance sheet.

The word “current” means the asset will be converted into cash within a year or the liability will be paid within a year. “Noncurrent” assets and liabilities are all other assets and liabilities. Many accountants create balance sheets grouped into current and noncurrent sections. This type of balance sheet is called a classified balance sheet.

These metrics are a rough estimate of whether you will receive enough cash in the next year to pay what you owe in the next year. That’s why the current ratio is used by lenders to determine whether you are financially healthy enough to receive a loan.

For both formulas, a higher number is better.

The next page has a sample calculation of net working capital and the capital ratio.

26

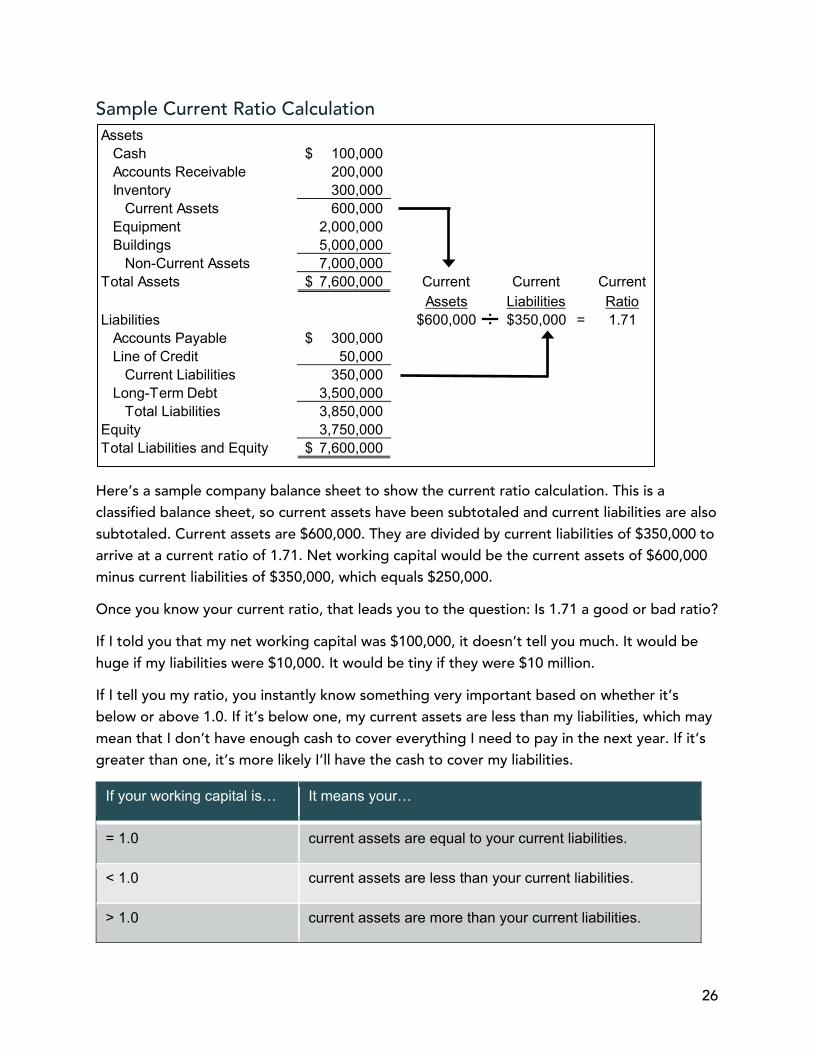

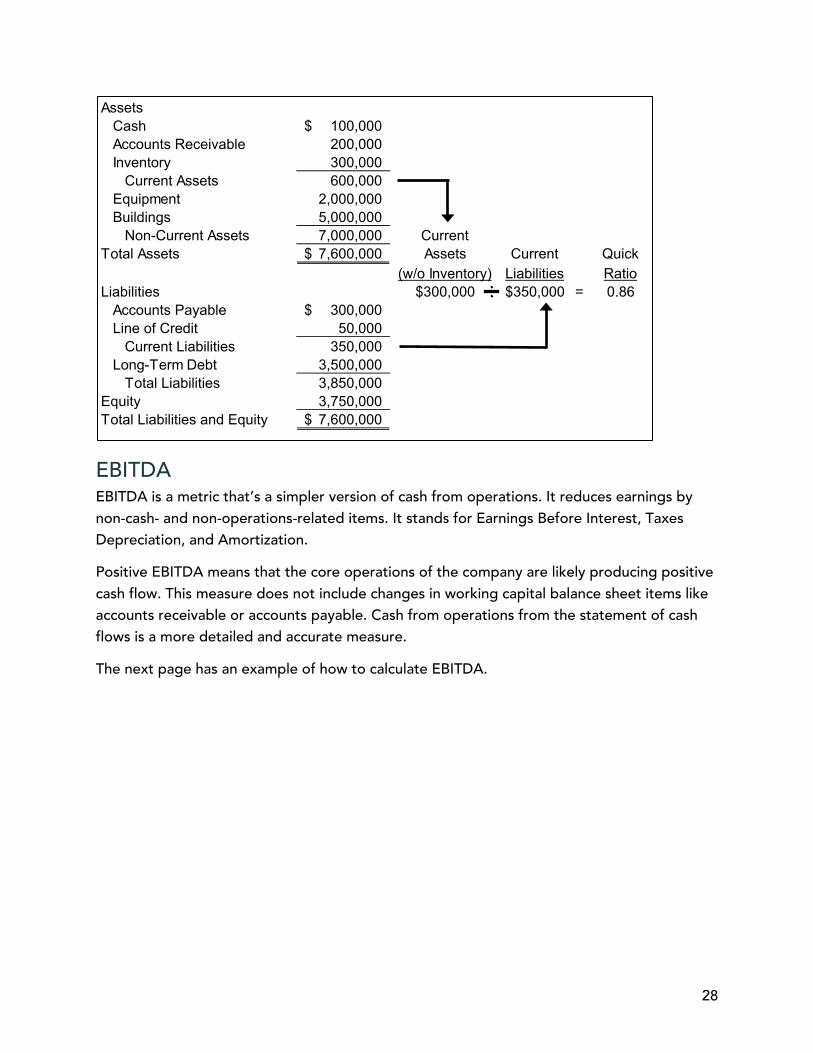

Sample Current Ratio Calculation

Here’s a sample company balance sheet to show the current ratio calculation. This is a classified balance sheet, so current assets have been subtotaled and current liabilities are also subtotaled. Current assets are $600,000. They are divided by current liabilities of $350,000 to arrive at a current ratio of 1.71. Net working capital would be the current assets of $600,000 minus current liabilities of $350,000, which equals $250,000.

Once you know your current ratio, that leads you to the question: Is 1.71 a good or bad ratio?

If I told you that my net working capital was $100,000, it doesn’t tell you much. It would be huge if my liabilities were $10,000. It would be tiny if they were $10 million.

If I tell you my ratio, you instantly know something very important based on whether it’s below or above 1.0. If it’s below one, my current assets are less than my liabilities, which may mean that I don’t have enough cash to cover everything I need to pay in the next year. If it’s greater than one, it’s more likely I’ll have the cash to cover my liabilities.

If your working capital is… It means your…

= 1.0 current assets are equal to your current liabilities.

< 1.0 current assets are less than your current liabilities.

> 1.0 current assets are more than your current liabilities.

AssetsCash 100,000$ Accounts Receivable 200,000 Inventory 300,000

Current Assets 600,000 Equipment 2,000,000 Buildings 5,000,000

Non-Current Assets 7,000,000 Total Assets 7,600,000$ Current Current Current

Assets Liabilities RatioLiabilities $600,000 $350,000 = 1.71

Accounts Payable 300,000$ Line of Credit 50,000

Current Liabilities 350,000 Long-Term Debt 3,500,000

Total Liabilities 3,850,000 Equity 3,750,000 Total Liabilities and Equity 7,600,000$

27

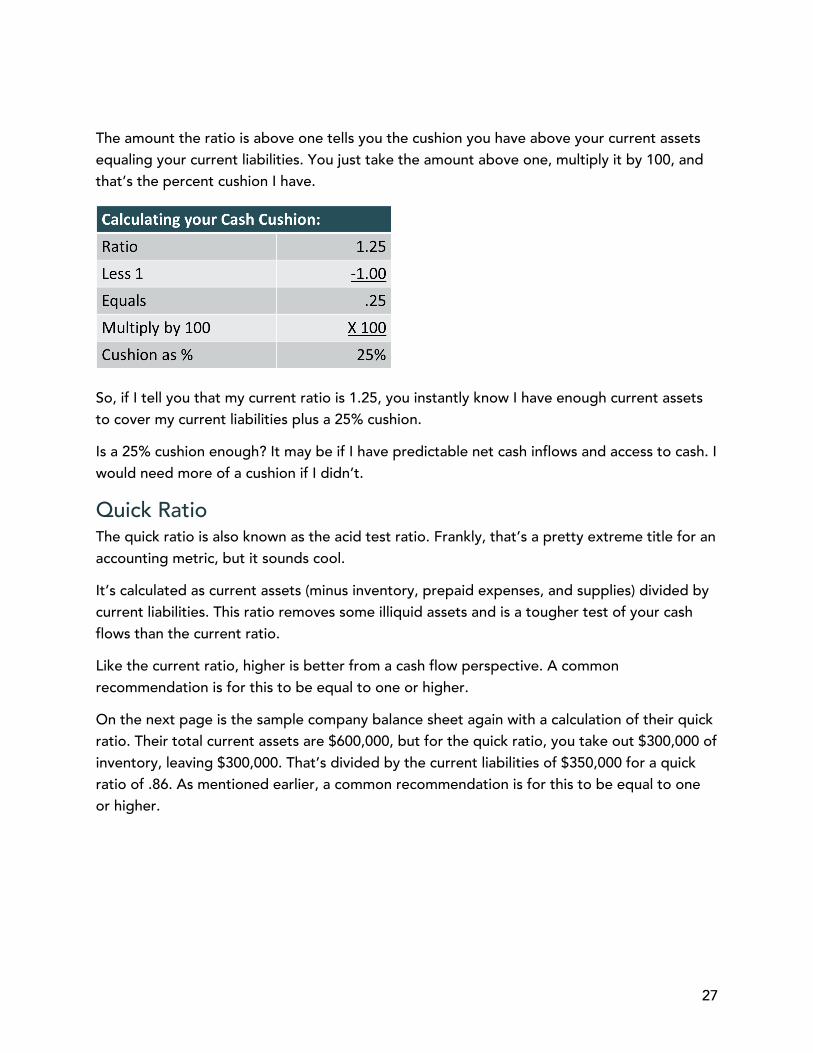

The amount the ratio is above one tells you the cushion you have above your current assets equaling your current liabilities. You just take the amount above one, multiply it by 100, and that’s the percent cushion I have.

So, if I tell you that my current ratio is 1.25, you instantly know I have enough current assets to cover my current liabilities plus a 25% cushion.

Is a 25% cushion enough? It may be if I have predictable net cash inflows and access to cash. I would need more of a cushion if I didn’t.

Quick Ratio The quick ratio is also known as the acid test ratio. Frankly, that’s a pretty extreme title for an accounting metric, but it sounds cool.

It’s calculated as current assets (minus inventory, prepaid expenses, and supplies) divided by current liabilities. This ratio removes some illiquid assets and is a tougher test of your cash flows than the current ratio.

Like the current ratio, higher is better from a cash flow perspective. A common recommendation is for this to be equal to one or higher.

On the next page is the sample company balance sheet again with a calculation of their quick ratio. Their total current assets are $600,000, but for the quick ratio, you take out $300,000 of inventory, leaving $300,000. That’s divided by the current liabilities of $350,000 for a quick ratio of .86. As mentioned earlier, a common recommendation is for this to be equal to one or higher.

28

EBITDA EBITDA is a metric that’s a simpler version of cash from operations. It reduces earnings by non-cash- and non-operations-related items. It stands for Earnings Before Interest, Taxes Depreciation, and Amortization.

Positive EBITDA means that the core operations of the company are likely producing positive cash flow. This measure does not include changes in working capital balance sheet items like accounts receivable or accounts payable. Cash from operations from the statement of cash flows is a more detailed and accurate measure.

The next page has an example of how to calculate EBITDA.

AssetsCash 100,000$ Accounts Receivable 200,000 Inventory 300,000

Current Assets 600,000 Equipment 2,000,000 Buildings 5,000,000

Non-Current Assets 7,000,000 CurrentTotal Assets 7,600,000$ Assets Current Quick

(w/o Inventory) Liabilities RatioLiabilities $300,000 $350,000 = 0.86

Accounts Payable 300,000$ Line of Credit 50,000

Current Liabilities 350,000 Long-Term Debt 3,500,000

Total Liabilities 3,850,000 Equity 3,750,000 Total Liabilities and Equity 7,600,000$

29

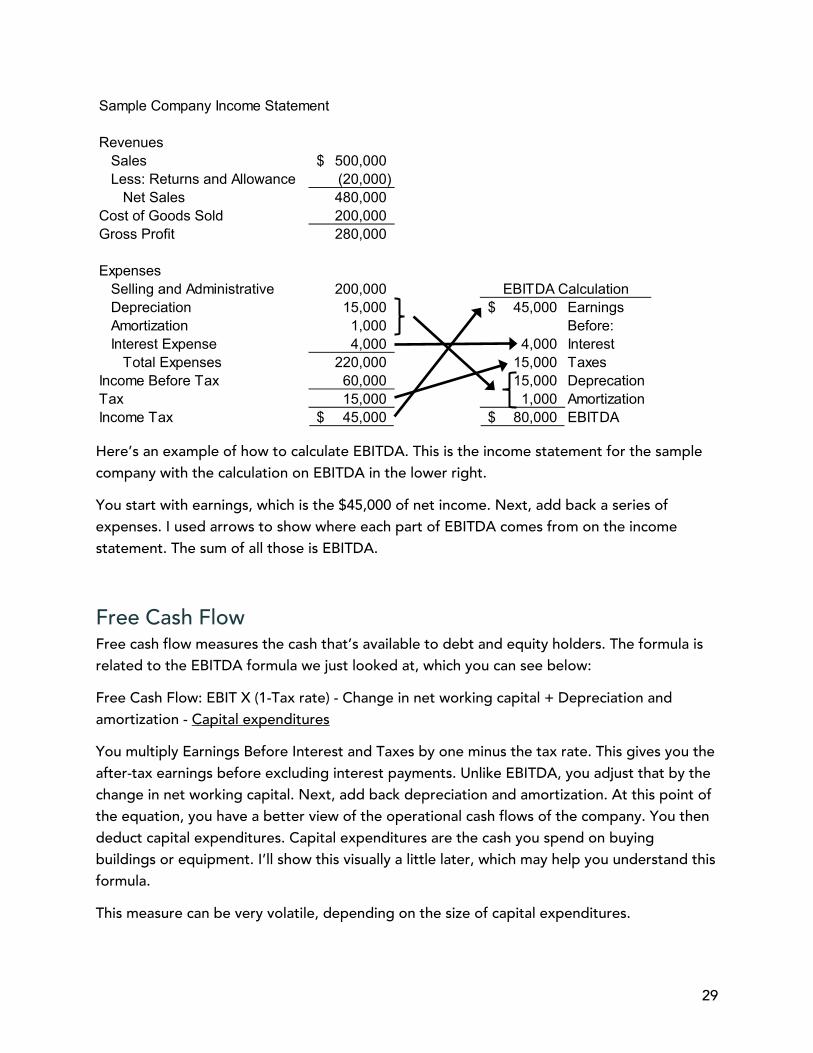

Here’s an example of how to calculate EBITDA. This is the income statement for the sample company with the calculation on EBITDA in the lower right.

You start with earnings, which is the $45,000 of net income. Next, add back a series of expenses. I used arrows to show where each part of EBITDA comes from on the income statement. The sum of all those is EBITDA.

Free Cash Flow Free cash flow measures the cash that’s available to debt and equity holders. The formula is related to the EBITDA formula we just looked at, which you can see below:

Free Cash Flow: EBIT X (1-Tax rate) - Change in net working capital + Depreciation and amortization - Capital expenditures

You multiply Earnings Before Interest and Taxes by one minus the tax rate. This gives you the after-tax earnings before excluding interest payments. Unlike EBITDA, you adjust that by the change in net working capital. Next, add back depreciation and amortization. At this point of the equation, you have a better view of the operational cash flows of the company. You then deduct capital expenditures. Capital expenditures are the cash you spend on buying buildings or equipment. I’ll show this visually a little later, which may help you understand this formula.

This measure can be very volatile, depending on the size of capital expenditures.

Sample Company Income Statement

RevenuesSales 500,000$ Less: Returns and Allowance (20,000)

Net Sales 480,000 Cost of Goods Sold 200,000 Gross Profit 280,000

ExpensesSelling and Administrative 200,000 Depreciation 15,000 45,000$ EarningsAmortization 1,000 Before:Interest Expense 4,000 4,000 Interest

Total Expenses 220,000 15,000 TaxesIncome Before Tax 60,000 15,000 DeprecationTax 15,000 1,000 AmortizationIncome Tax 45,000$ 80,000$ EBITDA

EBITDA Calculation

30

Free Cash Flow to Equity Free cash flow to equity measures the cash that’s available to the owners and investors in a company. So, unlike free cash flow, this looks at cash after cash flows from debt. Here’s the formula:

Free Cash Flow to Equity: Net profit + Depreciation - Change in net working capital - Capital expenditures + Net new debt

A company that creates free cash is more valuable. This free cash can be distributed to owners, or they can get their cash from selling the company.

The more free cash flow, the more valuable the company. The more valuable the company, the higher the selling price of the company. The higher the selling price of the company, the more cash the investors get when they sell their ownership.

Free cash flow to equity is net profit plus depreciation, minus the change in working capital, minus capital expenditures, plus net new debt. If you were to think in terms of the accounting statement of cash flows, it’s like the change in net cash excluding equity cash flows. Once again, this measure can be very volatile, depending on the size of capital expenditures.

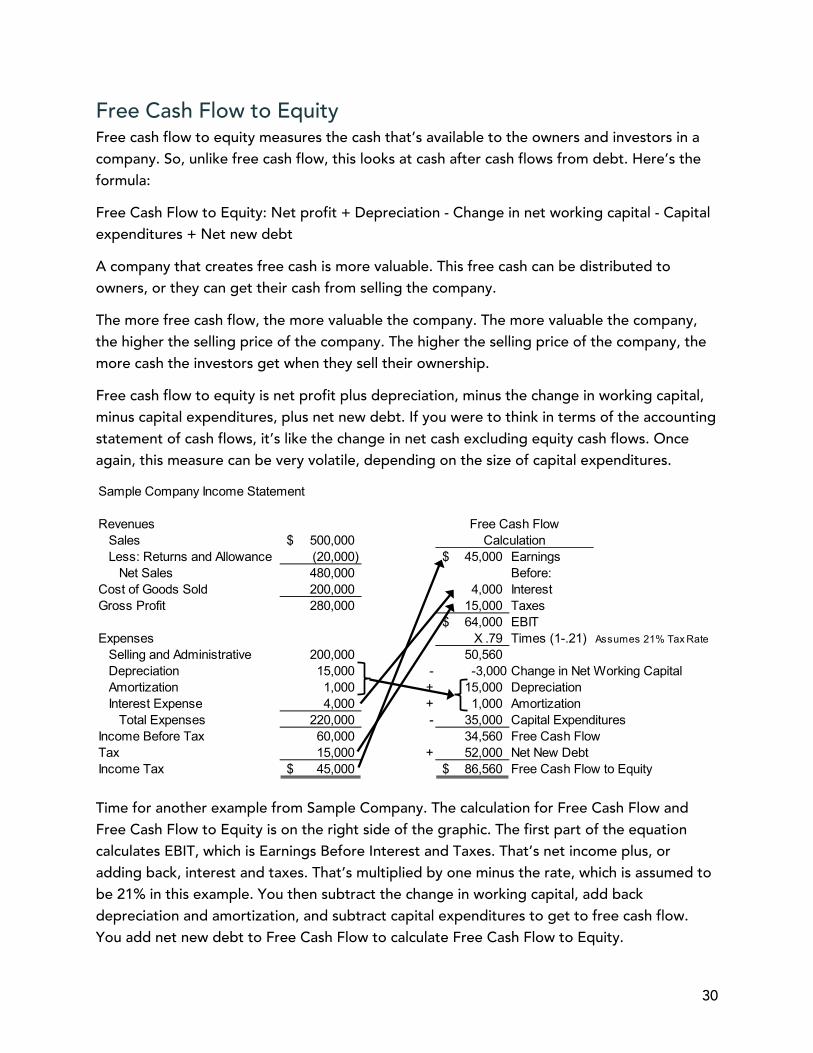

Time for another example from Sample Company. The calculation for Free Cash Flow and Free Cash Flow to Equity is on the right side of the graphic. The first part of the equation calculates EBIT, which is Earnings Before Interest and Taxes. That’s net income plus, or adding back, interest and taxes. That’s multiplied by one minus the rate, which is assumed to be 21% in this example. You then subtract the change in working capital, add back depreciation and amortization, and subtract capital expenditures to get to free cash flow. You add net new debt to Free Cash Flow to calculate Free Cash Flow to Equity.

Sample Company Income Statement

RevenuesSales 500,000$ Less: Returns and Allowance (20,000) 45,000$ Earnings

Net Sales 480,000 Before:Cost of Goods Sold 200,000 4,000 InterestGross Profit 280,000 15,000 Taxes

64,000$ EBITExpenses X .79 Times (1-.21) Assumes 21% Tax Rate

Selling and Administrative 200,000 50,560 Depreciation 15,000 - -3,000 Change in Net Working CapitalAmortization 1,000 + 15,000 DepreciationInterest Expense 4,000 + 1,000 Amortization

Total Expenses 220,000 - 35,000 Capital ExpendituresIncome Before Tax 60,000 34,560 Free Cash FlowTax 15,000 + 52,000 Net New DebtIncome Tax 45,000$ 86,560$ Free Cash Flow to Equity

CalculationFree Cash Flow

31

Debt service coverage ratio (“DSCR”) OK, hang tight, because we’re down to our last three metrics.

The debt service coverage ratio is a type of debt-to-income ratio that’s used for business loans. It’s calculated as cash flow by debt payments. The cash flow number used is usually EBITDA.

Lenders will calculate it based on the business’s financials but will also compute the global debt service coverage ratio, which combines the business financials with the owner’s financials. The owner’s financial health can be a strength or liability to the company.

At the banks I worked at, lenders were looking for a ratio of 1.25 or higher. This is consistent with industry norms and Small Business Administration (SBA) loans. A ratio of one means EBITDA equals debt service. The minimum ratio of 1.25 adds a .25 or 25% cushion.

The debt service coverage ratio measures your cash flow and ability to pay. When lenders assess the risk of their loan portfolio, they break losses into two components: the probability of default and the severity of default. This ratio measures the probability of default, which is how likely the borrower will not be able to meet their contractual debt service obligations.

Cash flow margin ratio Once you know your cash flow from operations, you can calculate your cash flow margin ratio. This is your cash flow from operations divided by your sales.

This tells you how much actual net cash you’re earning on your sales. A higher ratio is better, of course.

You can use this ratio to quickly estimate future operating cash flows if you know your sales. Multiply your projected sales by the cash flow margin and—voila!—you have estimated your projected cash flow from operations. I provide a sample of how to do this in the Metrics PDF.

Burn rate The burn rate is the amount of cash you spend over a period of time. It’s usually measured monthly. You can estimate your burn rate by calculating your change in cash during a past period divided by the number of months in that period. You can also use the projected change in cash from your cash projection divided by the number of months in the projection.

This metric tells you roughly how long you can survive until you need to raise more funds (for example, from venture capital or from current owners). This is a crucial metric for startup companies who have no inflows or not enough to fund their growth. I worked in public accounting in Seattle, and startups I audited closely monitored this metric. At startups, this is like a countdown timer that ticks very loudly.

32

For example, let’s say your burn rate is $10,000 per month and you have $50,000 of cash. $50,000 divided by $10,000 is five, so you have five months until you need to find more cash or you run out of money.

Whew! That was a lot of ratios! Sorry for all the math. Understanding these ratios helps you know how lenders calculate whether to give you a loan. The metrics provide the pulse rate for the lifeblood of cash in your business. However, the most powerful cash management tool is a cash flow projection. I explain how to use one in the next chapter.

33

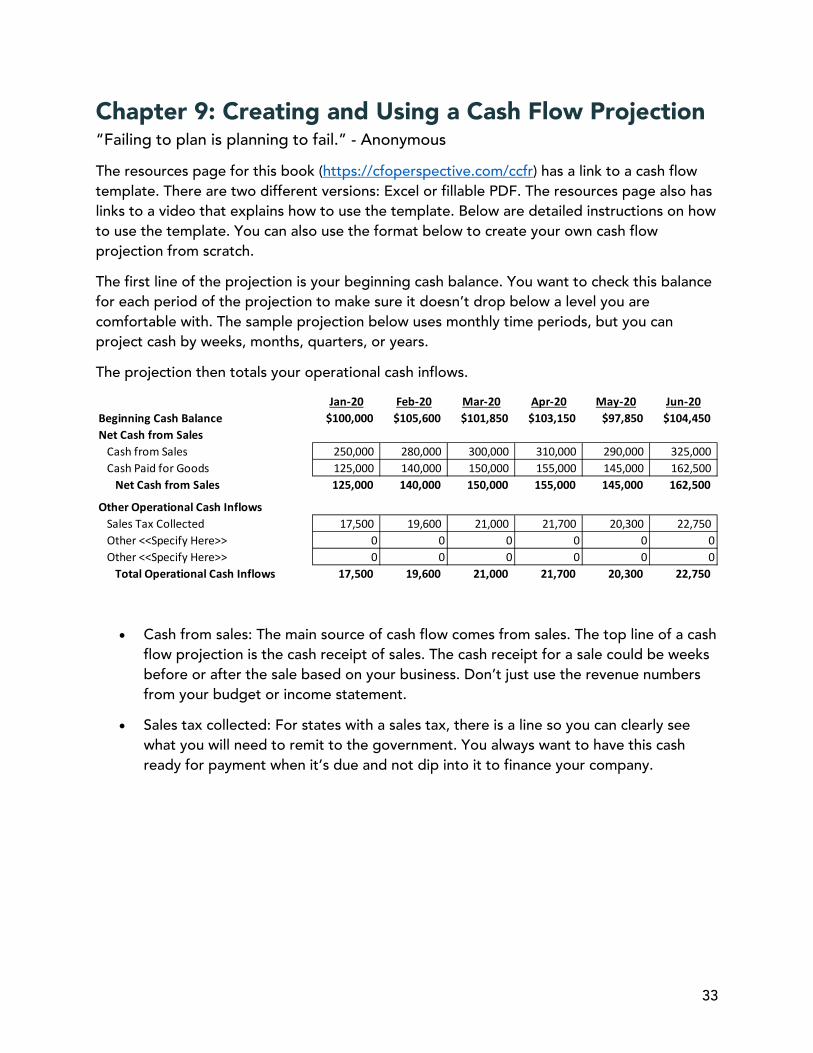

Chapter 9: Creating and Using a Cash Flow Projection “Failing to plan is planning to fail.” - Anonymous

The resources page for this book (https://cfoperspective.com/ccfr) has a link to a cash flow template. There are two different versions: Excel or fillable PDF. The resources page also has links to a video that explains how to use the template. Below are detailed instructions on how to use the template. You can also use the format below to create your own cash flow projection from scratch.

The first line of the projection is your beginning cash balance. You want to check this balance for each period of the projection to make sure it doesn’t drop below a level you are comfortable with. The sample projection below uses monthly time periods, but you can project cash by weeks, months, quarters, or years.

The projection then totals your operational cash inflows.

• Cash from sales: The main source of cash flow comes from sales. The top line of a cash flow projection is the cash receipt of sales. The cash receipt for a sale could be weeks before or after the sale based on your business. Don’t just use the revenue numbers from your budget or income statement.

• Sales tax collected: For states with a sales tax, there is a line so you can clearly see what you will need to remit to the government. You always want to have this cash ready for payment when it’s due and not dip into it to finance your company.

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20Beginning Cash Balance $100,000 $105,600 $101,850 $103,150 $97,850 $104,450Net Cash from Sales

Cash from Sales 250,000 280,000 300,000 310,000 290,000 325,000 Cash Paid for Goods 125,000 140,000 150,000 155,000 145,000 162,500

Net Cash from Sales 125,000 140,000 150,000 155,000 145,000 162,500

Other Operational Cash InflowsSales Tax Collected 17,500 19,600 21,000 21,700 20,300 22,750 Other <<Specify Here>> 0 0 0 0 0 0Other <<Specify Here>> 0 0 0 0 0 0

Total Operational Cash Inflows 17,500 19,600 21,000 21,700 20,300 22,750

34

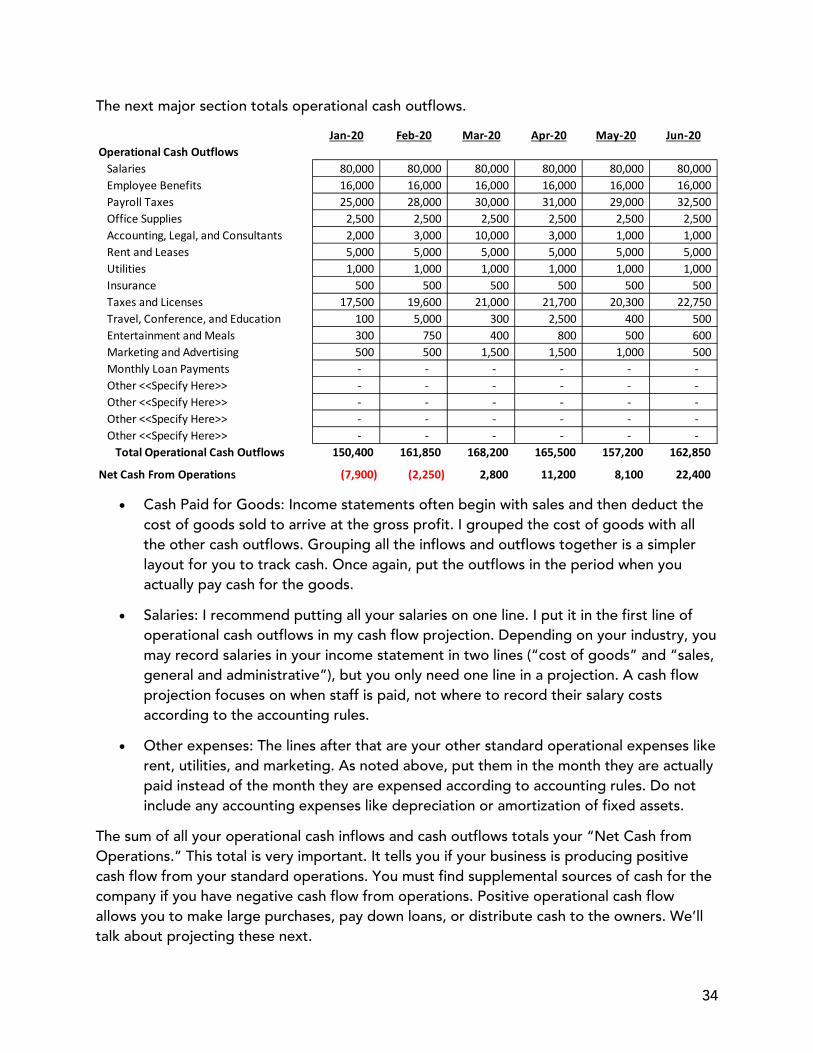

The next major section totals operational cash outflows.

• Cash Paid for Goods: Income statements often begin with sales and then deduct the

cost of goods sold to arrive at the gross profit. I grouped the cost of goods with all the other cash outflows. Grouping all the inflows and outflows together is a simpler layout for you to track cash. Once again, put the outflows in the period when you actually pay cash for the goods.

• Salaries: I recommend putting all your salaries on one line. I put it in the first line of operational cash outflows in my cash flow projection. Depending on your industry, you may record salaries in your income statement in two lines (“cost of goods” and “sales, general and administrative”), but you only need one line in a projection. A cash flow projection focuses on when staff is paid, not where to record their salary costs according to the accounting rules.

• Other expenses: The lines after that are your other standard operational expenses like rent, utilities, and marketing. As noted above, put them in the month they are actually paid instead of the month they are expensed according to accounting rules. Do not include any accounting expenses like depreciation or amortization of fixed assets.

The sum of all your operational cash inflows and cash outflows totals your “Net Cash from Operations.” This total is very important. It tells you if your business is producing positive cash flow from your standard operations. You must find supplemental sources of cash for the company if you have negative cash flow from operations. Positive operational cash flow allows you to make large purchases, pay down loans, or distribute cash to the owners. We’ll talk about projecting these next.

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20Operational Cash Outflows

Salaries 80,000 80,000 80,000 80,000 80,000 80,000 Employee Benefits 16,000 16,000 16,000 16,000 16,000 16,000 Payroll Taxes 25,000 28,000 30,000 31,000 29,000 32,500 Office Supplies 2,500 2,500 2,500 2,500 2,500 2,500 Accounting, Legal, and Consultants 2,000 3,000 10,000 3,000 1,000 1,000 Rent and Leases 5,000 5,000 5,000 5,000 5,000 5,000 Utilities 1,000 1,000 1,000 1,000 1,000 1,000 Insurance 500 500 500 500 500 500 Taxes and Licenses 17,500 19,600 21,000 21,700 20,300 22,750 Travel, Conference, and Education 100 5,000 300 2,500 400 500 Entertainment and Meals 300 750 400 800 500 600 Marketing and Advertising 500 500 1,500 1,500 1,000 500 Monthly Loan Payments - - - - - - Other <<Specify Here>> - - - - - - Other <<Specify Here>> - - - - - - Other <<Specify Here>> - - - - - - Other <<Specify Here>> - - - - - -

Total Operational Cash Outflows 150,400 161,850 168,200 165,500 157,200 162,850

Net Cash From Operations (7,900) (2,250) 2,800 11,200 8,100 22,400

35

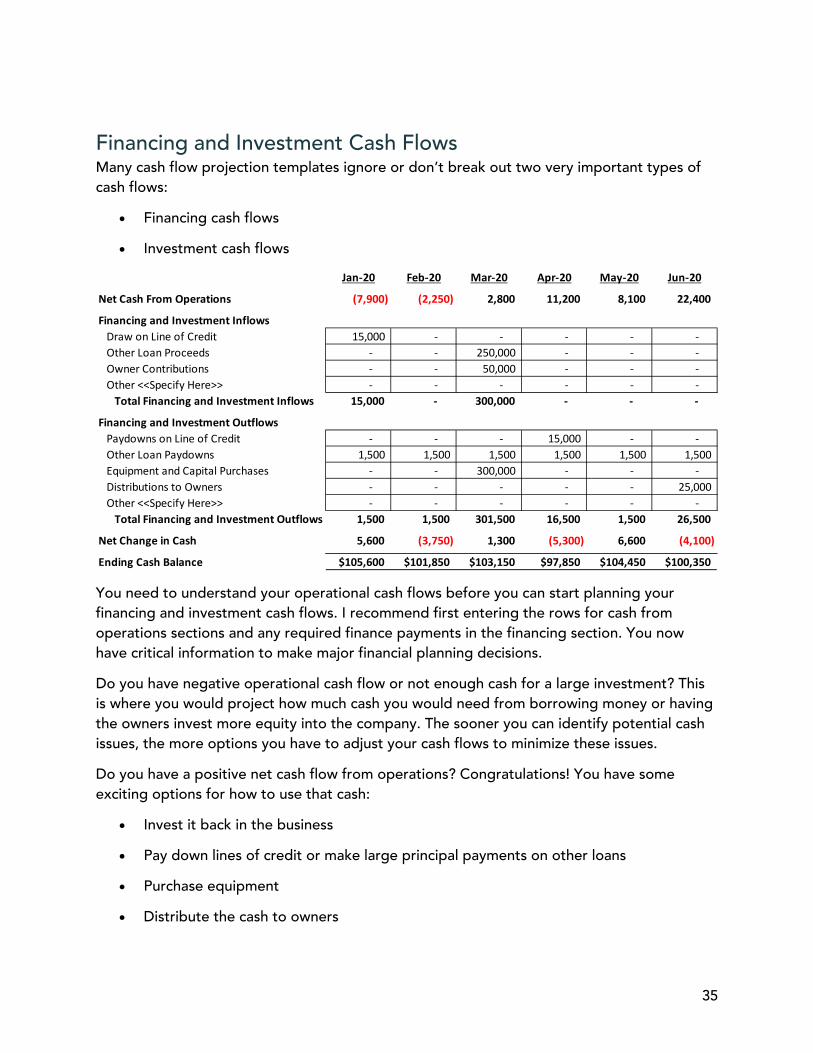

Financing and Investment Cash Flows Many cash flow projection templates ignore or don’t break out two very important types of cash flows:

• Financing cash flows

• Investment cash flows

You need to understand your operational cash flows before you can start planning your financing and investment cash flows. I recommend first entering the rows for cash from operations sections and any required finance payments in the financing section. You now have critical information to make major financial planning decisions.

Do you have negative operational cash flow or not enough cash for a large investment? This is where you would project how much cash you would need from borrowing money or having the owners invest more equity into the company. The sooner you can identify potential cash issues, the more options you have to adjust your cash flows to minimize these issues.

Do you have a positive net cash flow from operations? Congratulations! You have some exciting options for how to use that cash:

• Invest it back in the business

• Pay down lines of credit or make large principal payments on other loans

• Purchase equipment

• Distribute the cash to owners

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20

Net Cash From Operations (7,900) (2,250) 2,800 11,200 8,100 22,400

Financing and Investment InflowsDraw on Line of Credit 15,000 - - - - - Other Loan Proceeds - - 250,000 - - - Owner Contributions - - 50,000 - - - Other <<Specify Here>> - - - - - -

Total Financing and Investment Inflows 15,000 - 300,000 - - -

Financing and Investment OutflowsPaydowns on Line of Credit - - - 15,000 - - Other Loan Paydowns 1,500 1,500 1,500 1,500 1,500 1,500 Equipment and Capital Purchases - - 300,000 - - - Distributions to Owners - - - - - 25,000 Other <<Specify Here>> - - - - - -

Total Financing and Investment Outflows 1,500 1,500 301,500 16,500 1,500 26,500

Net Change in Cash 5,600 (3,750) 1,300 (5,300) 6,600 (4,100)

Ending Cash Balance $105,600 $101,850 $103,150 $97,850 $104,450 $100,350

36

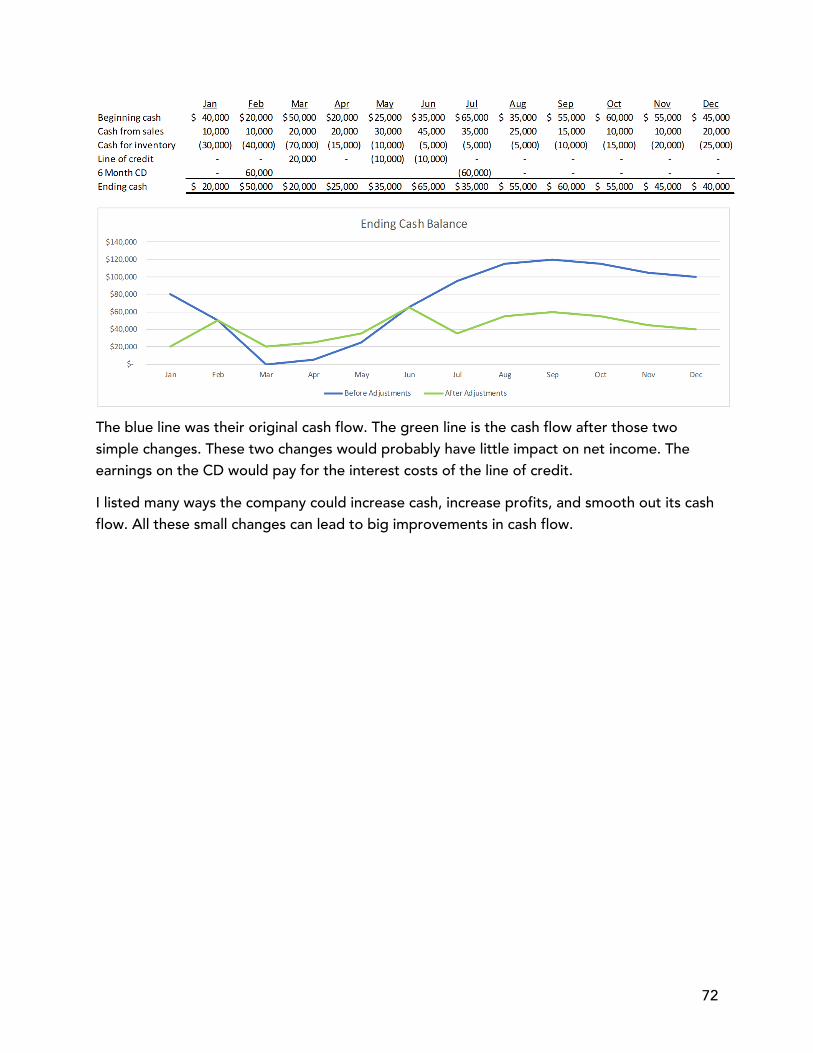

In the sample projection, the owner contributed $50,000 to the company and the company borrowed $250,000 to purchase $300,000 of equipment. This will allow them to continue or even accelerate growth. The company is producing enough cash in the projection by the sixth month for the owner to distribute $25,000 back to themselves.

The sample projection shows how positive cash flow can be invested back into the company for growth to enhance future returns to the owners. The projection helps identify that possibility so you can capture it. In addition to investing for a future return to owners, cash was also distributed for the personal cash needs of the owner. Cash flow planning for a small business must be done in the context of the personal financial planning of the owners.

The key takeaway is that the power of a projection isn’t tapped if you just enter your best guess of all the items and accept the results. Take the time to think through the possibilities and options. Running multiple scenarios both reduces risk and increases reward. I’ll talk more about this at the end of the chapter.

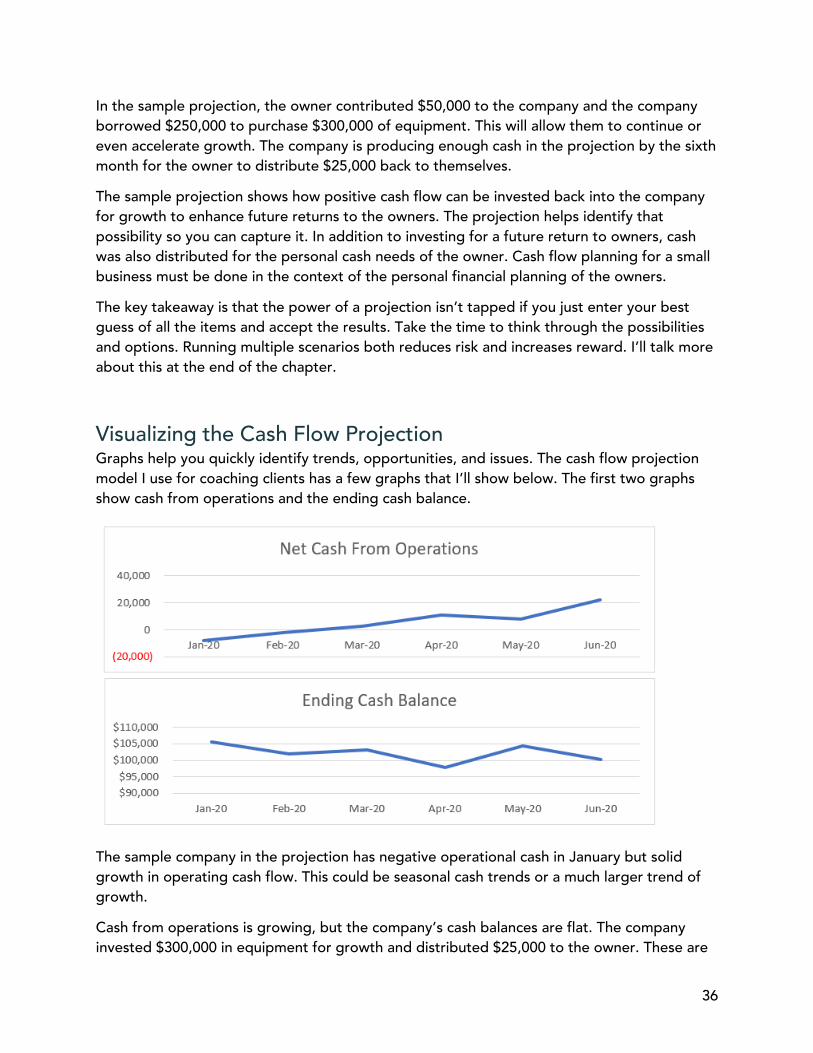

Visualizing the Cash Flow Projection Graphs help you quickly identify trends, opportunities, and issues. The cash flow projection model I use for coaching clients has a few graphs that I’ll show below. The first two graphs show cash from operations and the ending cash balance.

The sample company in the projection has negative operational cash in January but solid growth in operating cash flow. This could be seasonal cash trends or a much larger trend of growth.

Cash from operations is growing, but the company’s cash balances are flat. The company invested $300,000 in equipment for growth and distributed $25,000 to the owner. These are

37

financing and investment cash flows that aren’t included in the operating cash flows of the first graph.

Cash in the bank provides a margin of safety for the company. On the other hand, cash is a very low-yielding asset for your company and can often be invested back into the company for higher future returns. Modeling different combinations of investing or distributing cash allows you to achieve the optimal balance of risk and reward.

Additional Scenarios Provide More Insights Congratulations! If you followed all these steps, you now have a very powerful cash flow projection for your business. The insights you gained from this projection will help you avoid the stress caused by a lack of cash.

Even more exciting, you may have excess cash that you can use to grow your business or distribute to yourself.

Now that you have a baseline projection, you can learn so much more by exploring other scenarios. For example:

• Do you have enough cash to hire staff or buy equipment sooner than you projected in your baseline? Run a scenario to see how much sales and cash flow would increase by investing in staff or equipment sooner.

• What if there was an event that caused cash collections from sales to fall below your projection? Do you have enough cash cushion to weather it? Run a scenario with your best guess of the potential drop in cash. If your cash runs dangerously low, you can adjust other cash flows to plan how you would deal with this situation.

You can save your baseline as a document and then create each of these scenarios and save them with other names. The power of the cash flow projection is in the thought you put into it to contemplate threats and capture opportunities.

You may wonder exactly how to change the timing or amount of cash flows. I’ll show you that in the next chapter.

38

Chapter 10: Tips on Monitoring Cash “We were always focused on our profit and loss statement. But cash flow was not a regularly discussed topic. It was as if we were driving along, watching only the speedometer, when in fact we were running out of gas.” - Michael Dell

How often should you monitor cash?

Imagine you drove your car without ever checking the gas gauge. Some of you may do this. You never think about how much gas you have until the gas light comes on. That works as long as there is a gas station nearby whenever the light comes on.

I live in the western United States. Sometimes it’s a long distance between gas stations. On some routes I drive, there are signs that say “next services 50 miles” or “next services 90 miles.” If your light came on 20 miles after that sign and you have 70 miles to go until the next station, you have a problem.

Monitoring Methods Let’s translate this analogy to managing cash. Monitoring metrics is like watching your gas gauge or low gas warning light. Cash flow projections are like using a map app to know how long until the next gas station.

If you have low cash balances and uncertain cash flows, you will need to frequently monitor cash metrics. This is like constantly monitoring your gas gauge. You have little room for error, which in the analogy is running out of gas/cash. Run frequent cash flow projections for short periods of time. Early in my career, I worked for a company that went bankrupt. They ran cash projections once or twice a week that showed weekly cash flows for the next few months. Longer cash flow projections may not be helpful if you have very uncertain cash flows.

If you have high cash balances with frequent and predictable cash flows, then you can monitor your cash more like a person who only thinks about filling up when the gas light comes on. You can monitor cash metrics less frequently. You want some way for a warning to trigger when your cash balances are high or getting low. You still want to run long-term cash flow projections for planning purposes. Even in this scenario, you may decide to manage your cash more aggressively, in which case you need to monitor your metrics and run projections more frequently. I’ll explain what I mean by managing cash aggressively later in the book.

The long stretches of road between gas stations are like companies that have infrequent but adequate cash flows. I used to work at a community bank that made loans to farmers. These farmers had a big inflow of cash at harvest, followed by months of expenses of planting and raising crops. They would submit their annual farm budgets, which were cash projections. The

39

bank would monitor the farmers' expenses compared to the budget. Those whose expenses strayed above budget needed to come into the bank so we could see if they needed a larger line of credit and whether they would break even on their crop. Companies with infrequent cash flows need to run longer-term projections and monitor their metrics to make sure they are staying on track with the projection.

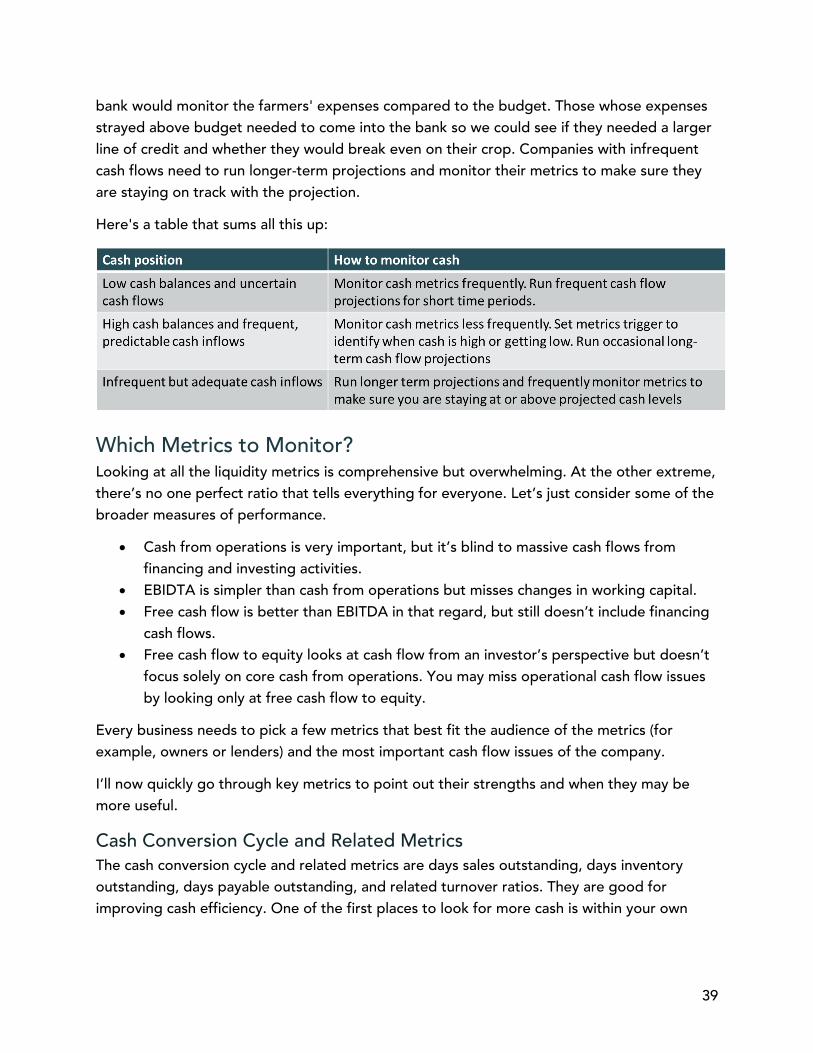

Here's a table that sums all this up:

Which Metrics to Monitor? Looking at all the liquidity metrics is comprehensive but overwhelming. At the other extreme, there’s no one perfect ratio that tells everything for everyone. Let’s just consider some of the broader measures of performance.

• Cash from operations is very important, but it’s blind to massive cash flows from financing and investing activities.

• EBIDTA is simpler than cash from operations but misses changes in working capital. • Free cash flow is better than EBITDA in that regard, but still doesn’t include financing

cash flows. • Free cash flow to equity looks at cash flow from an investor’s perspective but doesn’t

focus solely on core cash from operations. You may miss operational cash flow issues by looking only at free cash flow to equity.

Every business needs to pick a few metrics that best fit the audience of the metrics (for example, owners or lenders) and the most important cash flow issues of the company.

I’ll now quickly go through key metrics to point out their strengths and when they may be more useful.

Cash Conversion Cycle and Related Metrics The cash conversion cycle and related metrics are days sales outstanding, days inventory outstanding, days payable outstanding, and related turnover ratios. They are good for improving cash efficiency. One of the first places to look for more cash is within your own

40

operations. Use these metrics to improve how quickly you can collect on accounts receivable, managing inventory, or scheduling payments to vendors.

Current Ratio Net working capital, current ratio, and quick ratio are simple ways to roughly assess whether you have enough cash for the next year. Making a cash projection is much better but you can use this for a quick check, especially when you have high and consistent cash inflows.

EBITDA and Free Cash Flow EBITDA and free cash flow are good simple estimates of your cash from operations. They may be easier for you to measure on a frequent basis than your cash from operations from a cash flow statement.

Free Cash Flow to Equity Free cash flow to equity is more useful for planning distributions or cash investments from owners.

Debt Service Coverage Ratio (DSCR) The debt service coverage ratio or DSCR will be used by lenders, so monitor this when you are preparing to get loans or have loans outstanding.

Burn Rate The burn rate is very useful for early-stage companies with few sales but big expenses. It’s also important for fast-growing companies. Finally, companies with net negative cash flow and the possibility of bankruptcy should use this to estimate how long they have until they have to declare bankruptcy.

41

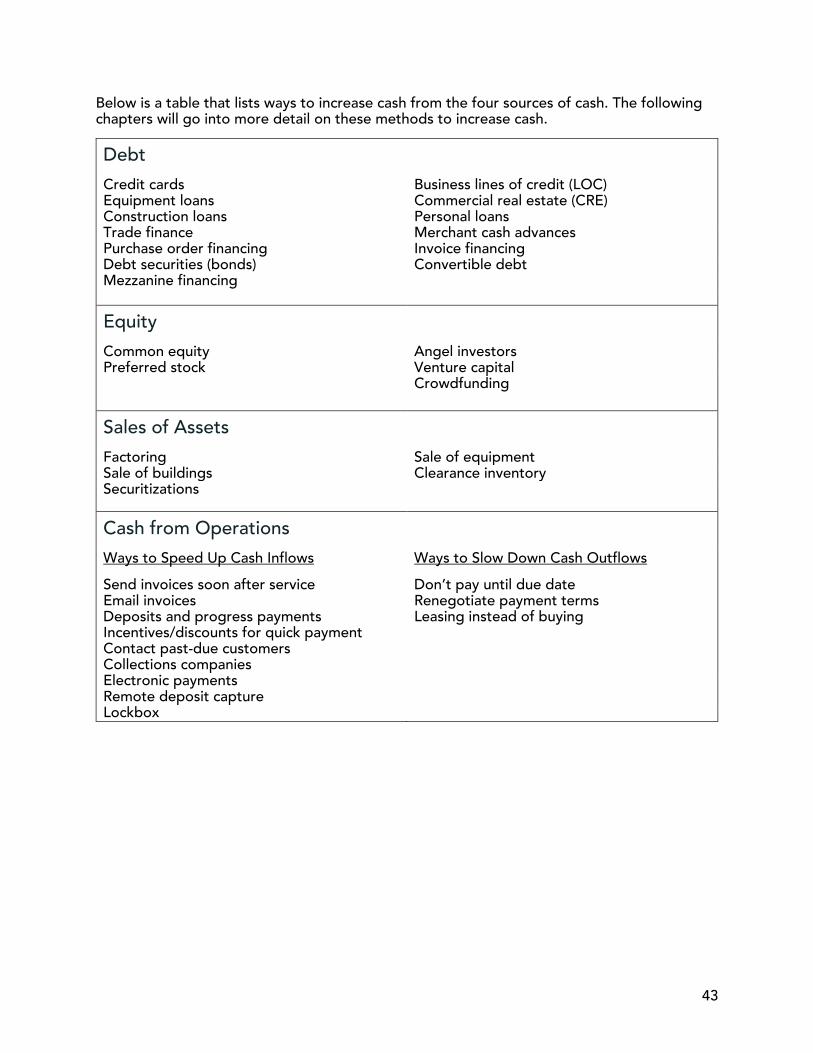

Chapter 11: Sources of Funds “It takes money to make money.” - Anonymous

The quote above seems to ring true when a large investment is needed before revenues and cash inflows come from that investment. Examples of these investments are:

• Equipment • Inventory • Buildings • Software

There are four major types of sources of funds:

Net Cash from Operations I covered cash from operations in the chapter on the cash conversion cycle. That section covered how your company produces cash and why it’s important for that cash engine to be efficient. Later in this book, I’ll explain ways to speed up the cycle and to increase your cash.

We then covered ways to measure and monitor cash flow. Most of those metrics measured how well you produce cash from operations. Assessing your past cash flow metrics also gives you a starting point to measure your progress from implementing the strategies we’ll go through later in this book.

Asset Sales You can receive cash in exchange for selling things your business owns. The use of factoring that was mentioned earlier in the guide could be thought of as an asset sale. The sales of any investments, land, buildings, or equipment can bring you cash. Selling excess or obsolete inventory at low prices is another way to generate cash.

Borrowing Loans to the company can come from banks, family, friends, or your own pocket. Loans are an agreement that requires payment back of the amount of the loan (called the “principal” of the loan) and interest. The next chapter will talk about different types of loans. There are also many other types of debt, such as trade finance or merchant advances, which will be covered in the chapter after that.

Equity Ownership Equity is the value of the company. Owners of the company have rights to a share of that equity. For example, if you owned 10% of a company that was sold, then you would be paid 10% of the value of your company. One of the ways to gain equity rights is by providing cash to the company to receive a share of the equity. That’s

42

where the terms “shareholders” and “shares of stock” come from. I have a chapter on equity where I’ll discuss things like angel investors and venture capital.

Debt and equity are listed above as if they are two distinct buckets, but the range of funding is actually closer to a spectrum between debt and equity. There is a chapter that looks at these types of funding that fall between pure loans and equity. Examples of these include convertible debt, preferred stock, and some types of crowdfunding.