a study on cash flow analysis of nestle

TRANSCRIPT

PROJECT REPORT

On

A STUDY ON CASH FLOW ANALYSIS OF NESTLE

INDIA LTD.

BY

ABHISHEK S

(1NH19MBA03)

Submitted to

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE OF ENGINEERING,

OUTER RING ROAD, MARATHALLI,

BENGALURU

In partial fulfilment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

MR SANTOSH KUMAR

ASSISTANT PROFESSOR

2019 - 2021

CERTIFICATE

This is to certify that ABHISHEK S bearing USN 1NH19MBA03, is a bonafide

student of Master of Business Administration course of the Institute 2019-21,

autonomous program, affiliated to Visvesvaraya Technological University,

Belgaum. The project report on “A STUDY ON CASH FLOW ANALYSIS OF

NESTLE INDIA LTD.” is prepared by her under the guidance of Prof Santosh

Kumar in partial fulfilment of requirements for the award of the degree of Master

of Business Administration of Visvesvaraya Technological University, Belgaum

Karnataka.

Signature of Internal Guide Signature of HOD Signature of principal

Name of the Examiners with affiliation Signature with date

1. External Examiner

2. Internal Examiner

DECLARATION

I, ABHISHEK S hereby declare that the project report on “A STUDY ON CASH FLOW

ANALYSIS OF NESTLE INDIA LTD.” with reference to “ NESTLE INDIA LTD. ” prepared by

me under the guidance of Prof. SANTOSH KUMAR, faculty of M.B.A Department, New Horizon

College of Engineering.

I also declare that this project report is towards the partial fulfilment of the university

regulations for the award of the degree of Master of Business Administration by Visvesvaraya

Technological University, Belgaum.

I have undergone an industry project for a period of Twelve weeks. I further declare that this

report is based on the original study undertaken by me and has not been submitted for the award

of a degree/diploma from any other University / Institution.

Signature of Student

Place:

Date:

ACKNOWLEDGEMENT

The successful completion of the project would not have been possible without

the guidance and support of many people

I am thankful to my internal guide Prof Santosh Kumar, for his/her constant

support and inspiration throughout the project and invaluable suggestions,

guidance and also for providing valuable information.

Finally, I express my gratitude towards my parents and family for their

continuous support during the study.

ABHISHEK S

1NH19MBA03

5

Date : 15th July 2021

PROJECT WORK CERTIFICATE

This is to inform that Mr. ABHISHEK S bearing USN 1NH19MBA03 has successfully

completed freelance project work under the guidance of Prof. SANTOSH KUMAR

We found his extremely inquisitive and hard working. He has demonstrated active interest

in learning and was also willing to put in his best efforts. His performance on task assigned

was highly appreciated.

His association with me was very fruitful and I wish him best luck for his career ahead.

Sincerely,

(Internal Guide)

6

TABLE OF CONTENTS

SL. NUMBER CONTENTS PAGE NUMBERS

1

Executive summary

07

2

Chapter 1- Theoretical Background of The

Study

8-16

3

Chapter 2- Industry Profile &

Company Profile

17-27

4

Chapter 3- Research Methodology

28-32

5

Chapter 4- Data Analysis and Interpretation

33-72

6

Chapter 5 - Summary of Findings,

Suggestion and Conclusion

73-75

7

Bibliography

76

8

Annexure

7

EXECUTIVE SUMMARY:

Cash flow is the money that comes in and goes out of a company. It is the generation of income and the

payment of expenses. Cash inflows result from either the generation of revenue through the selling of

goods and services, money borrowed, or money earned through investments.

If more cash is coming into the company than leaving the company, you are experiencing positive cash

flow. But if more cash is leaving the company than coming into the company, then you are experiencing

negative cash flow. Keep in mind that just because you are experiencing negative cash flow for the

moment doesn't mean you are going to suffer a loss, because cash flow is dynamic. Cash flow is reported

on the company's cash flow statement, which is also called a statement of cash receipts and disbursements.

Cash flow statement helps to identify the sources from where cash inflows have arisen within a

particular period and also shows the various activities where in the cash was utilized.

Cash flow statement is significant to management for proper cash planning and maintaining a

proper matching between cash inflows and outflows.

Cash flow statement shows efficiency of a firm in generating cash inflows from its regular

operations.

Cash flow statement reports the amount of cash used during the period in various long-term

investing activities, such as purchase of fixed assets.

Nestlé India Limited is the Indian subsidiary of Nestle which is a Swiss multinational company. The

company is headquartered in Gurgaon, Haryana. The company's products

include food, beverages, chocolate, and confectioneries.

The company was incorporated on 28 March 1959 and was promoted by Nestle Alimentana S.A. via a

subsidiary, Nestle Holdings Ltd. As of 2020, the parent company Nestle owns 62.76% of Nestle India. The

company has 9 production facilities in various locations across India.

In the light of all above, I have undertaken a project on “A Study on Cash-flow analysis of NESTLE

INDIA LIMITED”. This is an effort to make an analysis and comparison on food processing sector

companies like nestle, Parle and heritage. I am undertaking a study based on cash flow analysis and ratio

analysis of the company through financial statements of the companies.

8

CHAPTER 1

THEORETICAL BACKGROUND OF THE STUDY

INTRODUCTION

Every big and small firms performs cash transactions. Cash transaction refers to cash inflows and

outflows. Cash inflows and outflows help to review success, failure of a firm and its ability to meet

maturing debts. Such review and evaluation are possible if the statement of cash flow is prepared.

Accounting standard Board (ASB) at international level in 1996 suggested every firm to publish the

statement of cash flow along with the final accounts. Since then the statement of cash flow is getting more

recognition than funds flow statement.

The statement that shows cash inflows and outflows of a firm for a specified period is called the cash flow

statement. Cash flow statement demonstrates where the cash has come during the period and what the firm

has done with the available cash. Therefore, cash flow statement shows a picture of cash movement

occurred in and out from a firm during a year in a summarized form. Cash flow statement gives a picture

of sources and applications of cash of a firm for a year.

DEFINITION:

“Cash Flow is the money that comes in and goes out of a company. It is the generation of income and the

payment of expenses. Cash inflows result from either the generation of revenue through the selling of

goods and services, money borrowed, or money earned through investments.”

If more cash is coming into the company than leaving the company, you are experiencing positive cash

flow. But if more cash is leaving the company than coming into the company, then you are experiencing

negative cash flow. Keep in mind that just because you are experiencing negative cash flow for the

moment doesn't mean you are going to suffer a loss, because cash flow is dynamic. Cash flow is reported

on the company’s cash flow statement, which is also called a statement of cash receipts and disbursements.

The cash flow statement was previously known as the flow of Cash statement. The cash flow statement

reflects a firm's liquidity.

The balance sheet is a snapshot of a firm's financial resources and obligations at a single point in time, and

the income statement summarizes a firm's financial transactions over an interval of time. These two

financial statements reflect the accrual basis accounting used by firms to match revenues with the expenses

associated with generating those revenues. The cash flow statement includes only inflows and outflows of

cash and cash equivalents; it excludes transactions that do not directly affect cash receipts and payments.

These non-cash transactions include depreciation or write-offs on bad debts or credit losses to name a few.

The cash flow statement is a cash basis report on three types of financial activities: operating activities,

investing activities, and financing activities. Non-cash activities are usually reported in footnotes.

9

Important definitions As per Accounting Standard -3 (revised)

‘Cash’ comprises cash in hand and demand deposits with banks.

‘Cash equivalents’ are short term highly liquid investments that are readily convertible into known amount

of cash and which are subject to an insignificant risk of changes in value. Examples of cash equivalents are

a) Treasury Bills

b) Commercial papers

c) Investment funds

d) Free Saving Account.

STRUCTURE OF CASH FLOW STATEMENT: The cash flow statement is distinct from the income

statement and balance sheet because it does not include the amount of future incoming and outgoing cash

that has been recorded on credit. Therefore, cash is not the same as net income which, on the income

statement and balance sheet, includes cash sales and sales made on credit.

Cash flow activities

The cash flow statement is partitioned into three segments, namely:

1. Cash flow resulting from operating activities;

2. Cash flow resulting from investing activities;

3. Cash flow resulting from financing activities.

The money coming into the business is called cash inflow, and money going out from the business is

called cash outflow.

Operating activities

Operating activities include the production, sales and delivery of the company's product as well as

collecting payment from its customers. This could include purchasing raw materials, building inventory,

advertising, and shipping the product.

Under IAS 7, operating cash flows include:

a. Receipts from the sale of goods or services

b. Receipts for the sale of loans, debt or equity instruments in a trading portfolio

c. Interest received on loans

d. Payments to suppliers for goods and services

e. Payments to employees or on behalf of employees

f. Interest payments (alternatively, this can be reported under financing activities in IAS 7)

g. Buying Merchandise

Items which are added back to [or subtracted from, as appropriate] the net income figure (which is found

on the Income Statement) to arrive at cash flows from operations generally include:

Depreciation (loss of tangible asset value over time)

10

Deferred tax

Amortization (loss of intangible asset value over time)

Any gains or losses associated with the sale of a non-current asset, because associated cash flows

do not belong in the operating section (unrealized gains/losses are also added back from the income

statement).

Dividends received

Revenue received from certain investing activities

Investing activities

These are the acquisition and disposal of long term assets such as land, building, plant machinery etc and

other investments not included in cash equivalents. Cash flow from investing activities represents the

extent to which expenditure has been made for resources intended to generate future income and cash

flows.

Examples of investing activities are

Purchase or Sale of an asset (assets can be land, building, equipment, marketable securities, etc.)

Loans made to suppliers or received from customers

Payments related to mergers and acquisition. Financing activities

Financing activities

Include the inflow of cash from investors such as banks and shareholders, as well as the outflow of cash to

shareholders as dividends as the company generates income. Other activities which impact the long-term

liabilities and equity of the company are also listed in the financing activities section of the cash flow

statement.

Under IAS 7,

a) Payments of dividends

b) Payments for repurchase of company shares

c) For non-profit organizations, receipts of donor-restricted cash that is limited to long-term purposes

Items under the financing activities section include:

a. Dividends paid

b. Sale or repurchase of the company's stock

c. Net borrowings

d. Payment of dividend tax

e. Repayment of debt principal, including capital leases.

11

CASH FLOW FROM OPERATING ACTIVITIES

Cash flows from operating activities can be calculated by two methods

a) Direct method b) Indirect method

a) Direct Method

The direct method for creating a cash flow statement reports major classes of gross cash receipts and

payments. Under IAS 7, dividends received may be reported under operating activities or under investing

activities. If taxes paid are directly linked to operating activities, they are reported under operating

activities; if the taxes are directly linked to investing activities or financing activities, they are reported

under investing or financing activities. Generally Accepted Accounting Principles (GAAP) vary from

International Financial Reporting Standards in that under GAAP rules, dividends received from a

company's investing activities is reported as an "operating activity," not an "investing activity.”

b) Indirect Method

The indirect method uses net-income as a starting point, makes adjustments for all transactions for non-

cash items, then adjusts from all cash-based transactions. An increase in an asset account is subtracted

from net income, and an increase in a liability account is added back to net income. This method converts

accrual-basis net income (or loss) into cash flow by using a series of additions and deductions.

1. Decrease in non-cash current assets are added to net income

2. Increase in non-cash current asset are subtracted from net income

3. Increase in current liabilities are added to net income

4. Decrease in current liabilities are subtracted from net income

5. Expenses with no cash outflows are added back to net income (depreciation and/or amortization expense

are the only operating items that have no effect on cash flows in the period)

6. Revenues with no cash inflows are subtracted from net income

7. Non-operating losses are added back to net income

8. Non-operating gains are subtracted from net income.

Rules (financing activities)

Finding the Cash Flows from Financing Activities is much more intuitive and needs little explanation.

Generally, the things to account for are financing activities:

a. Include as outflows, reductions of long term notes payable (as would represent the cash repayment of

debt on the balance sheet)

b. Or as inflows, the issuance of new notes payable

c. Include as outflows, all dividends paid by the entity to outside parties

d. Or as inflows, dividend payments received from outside parties

e. Include as outflows, the purchase of notes stocks or bonds

12

f. Or as inflows, the receipt of payments on such financing vehicles.

In the case of more advanced accounting situations, such as when dealing with subsidiaries, the accountant

must

a. Exclude intra-company dividend payments.

b. Exclude intra-company bond interest.

Main Difference between Direct and Indirect Method of SCF

The main difference between the direct method and the indirect method of presenting the statement of cash

flows (SCF) involves the cash flows from operating activities. (There are no differences in the cash flows

from investing activities and/or the cash flows from financing activities.)

EXAMPLE OF DIRECT METHOD

I. Cash Flow from Operating Activities (Direct Method/ Indirect Method)

II. Cash Flow from Investing Activities

III. Cash Flow from Financing Activities

Classification by activities provides information that allows users to assess the impact of those

activities on the financial position of the enterprise. This information also helps in evaluating the inter -

relationships between these activities.

Cash Flows from Operating Activities

Cash Flows from operating Activities are primarily derived from the Principal Revenue-producing

activities of the enterprise.

There are 2 methods of preparing the Cash Flows from Operating Activities:-

Direct Method

Indirect Method

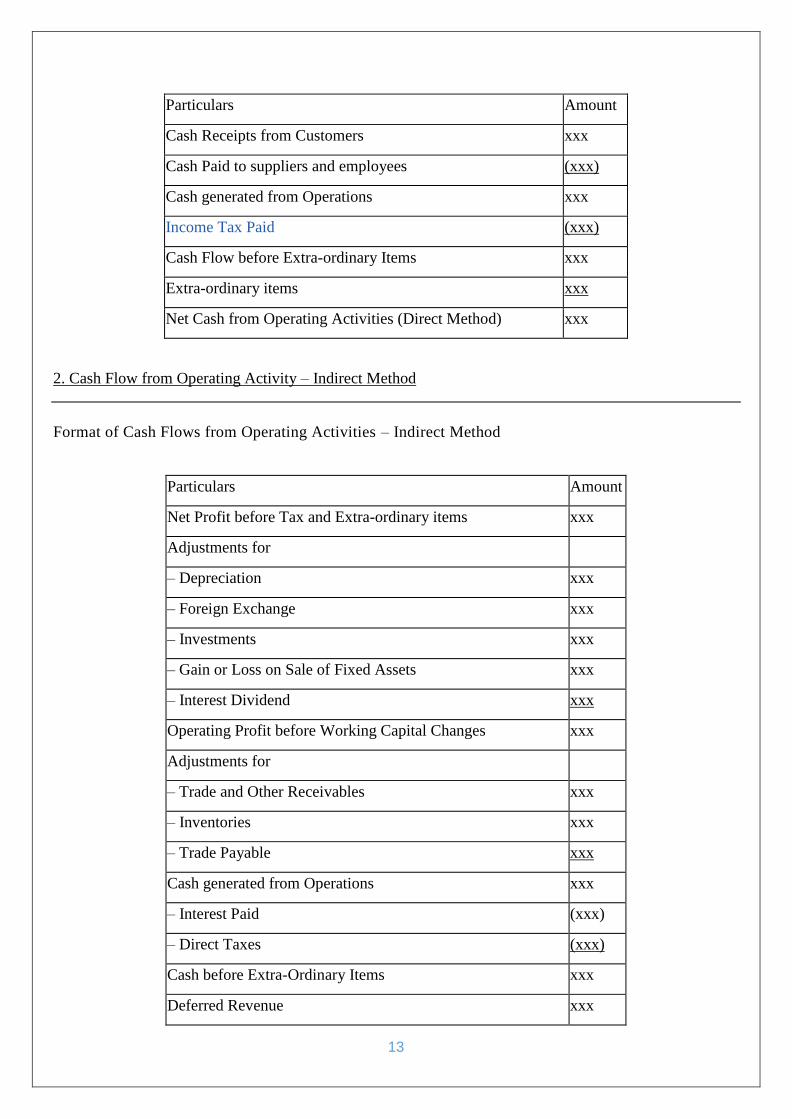

1. Cash Flow from Operating Activity- Direct Method

Format for Computation of Cash Flows from Operating Activities as per Direct Method

13

Particulars Amount

Cash Receipts from Customers xxx

Cash Paid to suppliers and employees (xxx)

Cash generated from Operations xxx

Income Tax Paid (xxx)

Cash Flow before Extra-ordinary Items xxx

Extra-ordinary items xxx

Net Cash from Operating Activities (Direct Method) xxx

2. Cash Flow from Operating Activity – Indirect Method

Format of Cash Flows from Operating Activities – Indirect Method

Particulars Amount

Net Profit before Tax and Extra-ordinary items xxx

Adjustments for

– Depreciation xxx

– Foreign Exchange xxx

– Investments xxx

– Gain or Loss on Sale of Fixed Assets xxx

– Interest Dividend xxx

Operating Profit before Working Capital Changes xxx

Adjustments for

– Trade and Other Receivables xxx

– Inventories xxx

– Trade Payable xxx

Cash generated from Operations xxx

– Interest Paid (xxx)

– Direct Taxes (xxx)

Cash before Extra-Ordinary Items xxx

Deferred Revenue xxx

14

Net Cash Flow from Operating Activities (Indirect Method) xxx

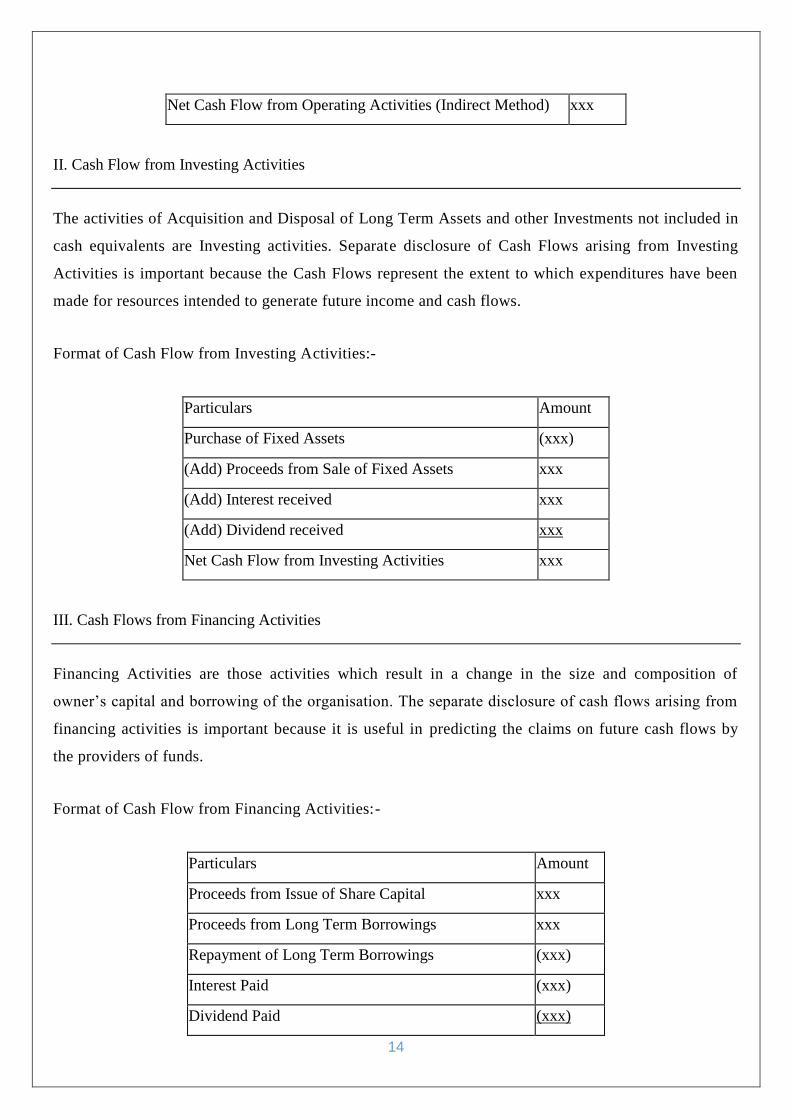

II. Cash Flow from Investing Activities

The activities of Acquisition and Disposal of Long Term Assets and other Investments not included in

cash equivalents are Investing activities. Separate disclosure of Cash Flows arising from Investing

Activities is important because the Cash Flows represent the extent to which expenditures have been

made for resources intended to generate future income and cash flows.

Format of Cash Flow from Investing Activities:-

Particulars Amount

Purchase of Fixed Assets (xxx)

(Add) Proceeds from Sale of Fixed Assets xxx

(Add) Interest received xxx

(Add) Dividend received xxx

Net Cash Flow from Investing Activities xxx

III. Cash Flows from Financing Activities

Financing Activities are those activities which result in a change in the size and composition of

owner’s capital and borrowing of the organisation. The separate disclosure of cash flows arising from

financing activities is important because it is useful in predicting the claims on future cash flows by

the providers of funds.

Format of Cash Flow from Financing Activities:-

Particulars Amount

Proceeds from Issue of Share Capital xxx

Proceeds from Long Term Borrowings xxx

Repayment of Long Term Borrowings (xxx)

Interest Paid (xxx)

Dividend Paid (xxx)

15

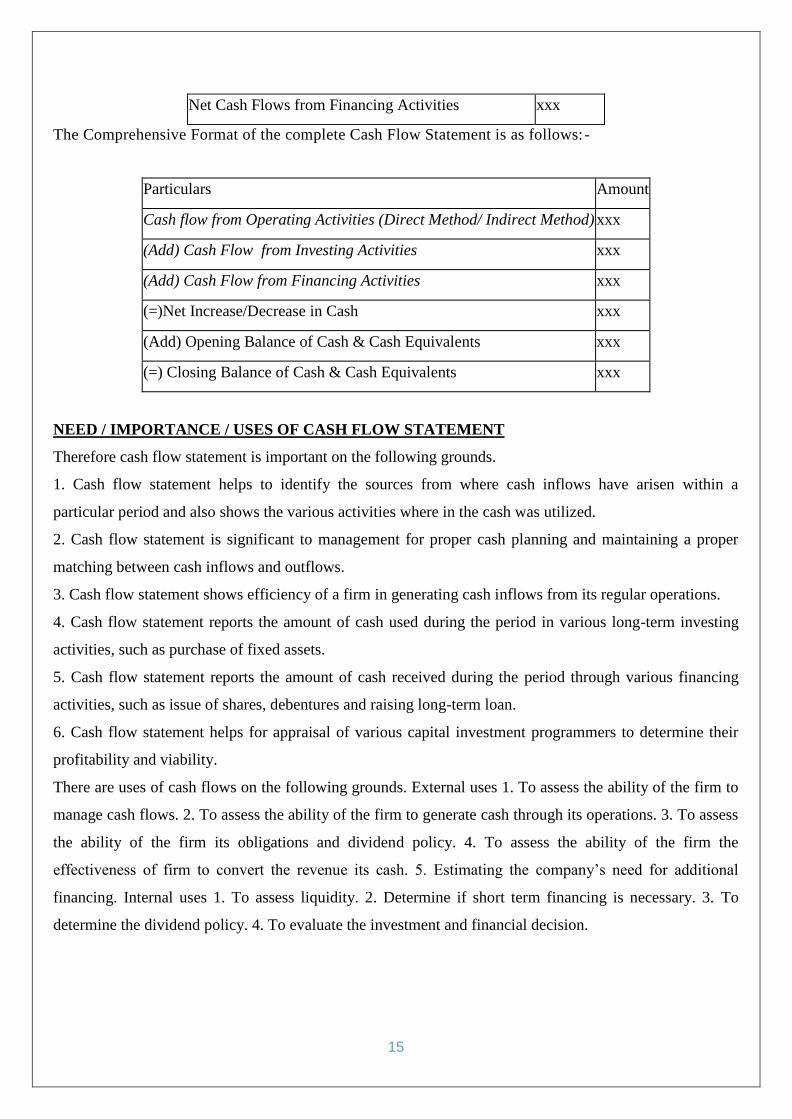

Net Cash Flows from Financing Activities xxx

The Comprehensive Format of the complete Cash Flow Statement is as follows:-

Particulars Amount

Cash flow from Operating Activities (Direct Method/ Indirect Method) xxx

(Add) Cash Flow from Investing Activities xxx

(Add) Cash Flow from Financing Activities xxx

(=)Net Increase/Decrease in Cash xxx

(Add) Opening Balance of Cash & Cash Equivalents xxx

(=) Closing Balance of Cash & Cash Equivalents xxx

NEED / IMPORTANCE / USES OF CASH FLOW STATEMENT

Therefore cash flow statement is important on the following grounds.

1. Cash flow statement helps to identify the sources from where cash inflows have arisen within a

particular period and also shows the various activities where in the cash was utilized.

2. Cash flow statement is significant to management for proper cash planning and maintaining a proper

matching between cash inflows and outflows.

3. Cash flow statement shows efficiency of a firm in generating cash inflows from its regular operations.

4. Cash flow statement reports the amount of cash used during the period in various long-term investing

activities, such as purchase of fixed assets.

5. Cash flow statement reports the amount of cash received during the period through various financing

activities, such as issue of shares, debentures and raising long-term loan.

6. Cash flow statement helps for appraisal of various capital investment programmers to determine their

profitability and viability.

There are uses of cash flows on the following grounds. External uses 1. To assess the ability of the firm to

manage cash flows. 2. To assess the ability of the firm to generate cash through its operations. 3. To assess

the ability of the firm its obligations and dividend policy. 4. To assess the ability of the firm the

effectiveness of firm to convert the revenue its cash. 5. Estimating the company’s need for additional

financing. Internal uses 1. To assess liquidity. 2. Determine if short term financing is necessary. 3. To

determine the dividend policy. 4. To evaluate the investment and financial decision.

16

OBJECTIVES OF CASH FLOW STATEMENT

To find the liquidity position of the Nestle. For the availability cash and utilization of the cash by

the organization.

It will help find to assess the company's ability to generate positive cash flows in the future

To assess its ability to meet its obligations to service loans, pay dividends etc.

To assess the effect on its finances of major transactions in the year.

To study the firms liquidity.

To learn about how company manage its cash & become such well recognized profitable industry

& if there is any problem arise then what steps taken by company.

17

CHAPTER 2

INDUSTRY PROFILE

Food processing sector is indispensable for the overall development of an economy as it provides a vital

linkage and synergy between the agriculture and industry. It helps to diversify and commercialise farming;

enhance income of farmers; create markets for export of agro foods as well as generate greater

employment opportunities. Through the presence of such industries, a wider range of food products could

be sold and distributed to the distant locations.

The term 'food processing' is mainly defined as a process of value addition to the agricultural or

horticultural produce by various methods like grading, sorting and packaging. In other words, it is a

technique of manufacturing and preserving food substances in an effective manner with a view to enhance

their shelf life; improve quality as well as make them functionally more useful. It covers spectrum of

products from sub-sectors comprising agriculture, horticulture, plantation, animal husbandry and fisheries.

Food processing industry is one of the largest industry in India and is ranked 5th in terms of production,

consumption and export. Earlier, food processing was largely confined to the food preservation, packaging

and transportation, which mainly involved salting, curdling, drying, pickling, etc. However, over the years,

with emerging new markets and technologies, the sector has widened its scope. It has started producing

many new items like ready-to-eat food, beverages, processed and frozen fruit and vegetable products,

marine and meat products, etc. It also includes establishment of post-harvest infrastructure for processing

of various food items like cold storage facilities, food parks, packaging centres, value added centres,

irradiation facilities and modernised abattoir.

Major Areas The sector comprises of the following major areas

Fruits & Vegetables Beverages, Juices, Concentrates, Pulps, Slices, Frozen & Dehydrated products,

Wine Potato Wafers/Chips etc.

Fisheries Frozen & Canned products mainly in fresh form

Meat & Poultry Frozen and packed mainly in fresh form, Egg Powder

Milk & Dairy Whole Milk Powder, Skimmed milk powder, Condensed milk, Ice cream, Butter and

Ghee

Grain and Cereals Flour, Bakeries, Biscuits, Starch Glucose, Cornflakes, Malted Foods, Vermicelli,

Pasta Foods, Beer and Malt extracts, Grain based Alcohol.

Consumer Industry Chocolates, Confectionery, Soft/Aerated Beverages/Drinks

Plantation Tea, coffee, cashew, cocoa, coconut etc

18

HISTORY OF FOOD PROCESSING

GLOBAL FOOD PROCESSING INDUSTRY

The Global Processed Food Industry is valued at US $ 3.2 trillion and accounts for over 3/4th of global

food sales. Despite the large size of the industry, only 6% of the processed food is traded the world over as

compared to bulk agricultural commodities where 16% of produce is traded. Growth of the sector has been

the highest in developed economies, especially across Western Europe, North America, Japan and

Australia. USA is the single largest consumer of processed food and accounts for 31% of global sales. The

food processing sector has seen substantial growth in developing economies with increase in GDP, per

capita income and the resultant changes in lifestyle. Organized retailing and availability of better

processing technologies too have contributed to the accelerated growth of the sector.

FOOD PROCESSING INDUSTRY IN INDIA

The Indian food processing industry stands at $135 billion and is estimated to grow with a CAGR of 10

per cent to reach $200 billion by 2015. The food processing industry contributed 7% to India‘s GDP. The

industry employs around 13 million workers directly and about 35 million indirectly.

The industry is segmented into sectors namely, milk and allied products (dairy), meat and poultry, seafood,

bakery and confectionery, fruit and vegetables, grain, pulses and oilseeds (staple) products, alcoholic and

non-alcoholic products (beverages), and packaged foods. The classification is not distinct as many

processed products overlap different segments.

India ranks No. 1 in the world in production of Milk (Fresh, whole, buffalo), Pulses, Ginger, Chick Peas,

Bananas Guavas, Papayas and Mangoes. Further, India ranks No. 2 in the world in production of Rice,

Wheat, Potatoes, Garlic, Cashew Nuts, Groundnuts, Dry Onion, Green Peas, Pumpkins, Gourds, and

cauliflowers. With the huge production base India can easily become the leading food supplier to the world

and at the same time serving its vast growing domestic market with over a billion people.

Key growth drivers of Food Processing Sector in India

Increasing spending on health and nutritional foods.

Increasing number of nuclear families and working women

Changing lifestyle

Functional foods, fresh or processed foods

Organized retail and private label penetration

Changing demographics and rising disposable incomes

Key opportunities in Food Processing Sector

Processable varieties of crop

Contract farming

19

Investments in infrastructure through Public Private partnership (PPP) 17

Mega Food parks

Logistics and cold chain infrastructure

Food safety Management Systems

Machinery and packaging

COMPANY PROFILE

Nestle India Limited is the Indian subsidiary of Nestle which is a Swiss multinational company. The

company is headquartered in Gurgaon, Haryana. The company's products

include food, beverages, chocolate, and confectioneries.

The company was incorporated on 28 March 1959 and was promoted by Nestle Alimentana S.A. via a

subsidiary, Nestle Holdings Ltd. As of 2020, the parent company Nestle owns 62.76% of Nestle India. The

company has 9 production facilities in various locations across India.

Mission Statement

Nestle is...

...the world's leading nutrition, health and Wellness Company. mission of "Good Food, Good Life" is to

provide consumers with the best tasting, most nutritious choices in a wide range of food and beverage

categories and eating occasions, from morning to night.

20

Vision and values

To be a leading, competitive, Nutrition, Health and Wellness Company delivering improved

shareholder value by being a preferred corporate citizen, preferred employer, preferred supplier

selling preferred products.

SWOT ANALYSIS

STRENGTHS

The company enjoy good support of parent company Nestle S.A. which is a nutrition, health and wellness

company headquartered in Vevey, Waadt, Switzerland. The company's product portfolio includes baby

foods, bottled water, cereals, chocolate and confectionery, coffee, culinary products, chilled and frozen

foods, dairy products, drinks, nutritional products, ice-cream, cooking aid products, pet care products,

sports nutrition products, weight management and pharmaceutical products.

The company has strong brands like Nescafe, milkmaid, kit Kat, etc. and the company is known for

product innovation. Under the dynamic leadership of the current Chairman and Managing Director Mr.

Suresh Narayanan Nestlé India is doing extremely well and in fact the company is even open to strategic

acquisition for faster growth. More importantly brand under his stewardship Maggi attained over 60

percent market share and almost reached the pre-crisis level in value sales volume.

Nestle have a century old presence in India when Nestlé Anglo Swiss Condensed Milk Company (Export)

Limited imported and sold the finished products in the Indian market The company has been an associate

in India's growth and has a very unique association of confidence and commitment with the people of

India. The Companies have provided direct and indirect employment to over one million people including

farmers, suppliers of packaging materials and other.

Nestle India, achieved a major landmark in the financial year 2017 as the first listed food company to

cross Rs10,000 crore in sales in India. Also, the good financial performance in first quarter of the current

financial year leads to good show in share prices of Nestlé India in National Stock Exchange and Bombay

Stock Exchange.

WEAKNESSES

Nestle India was caught off the guard as the company was totally ignorant and were ill prepared to

manage the regulator’s call on Maggi ban and more importantly the responses to Maggi ban were very

brief and not adequately culture-sensitive. Heavy dependence on milk products and nutrition, the largest

category that contributes nearly 47.6% to the company's top line is another major weakness of the

21

company.

OPPORTUNITIES

The company have excellent potential for growth in confectionery and beverage segment. The Company

have a global portfolio of about 2,000 brands including bestselling brands like Aero, Cerelac, Chocapic,

Nescafe, Boost, Kit Kat, Crunch, S. Pellegrino, Perrier, Nido, La Laitiere, Carnation, Milo, Nestea,

Nesquik, Dreyer’s, Movenpick and Alpo, Beneful. But in India they are operating with a truncated

portfolio of just 20 brands. So, the company can capitalise on the product and brand strength of the parent

company.

THREATS

The company is facing stiff competition from new entrants like Ferrero India and Patanjali Products.

Raising cost of input is another threat is a common problem faced by most of the companies in Fast

Moving Consumer Goods sector. Maggi ban negative publicity is probably the major threat for the

company and if the issue have not been raised, the company would have reached Rs. 10,000 crore mark a

couple of years ago.

HISTORY

Nestle India is one of the largest players in India's Fast-moving consumer goods segment and has a long

history in the country.

Nestlé India Limited was incorporated at New Delhi on 28 March 1959 and was promoted by Nestle

Alimentana S.A. via a wholly owned subsidiary, Nestle Holdings Ltd., Nassau, Bahama Islands.

The company built their first production facility in 1961 at Mogo, in the Indian state of Punjab.

Nestlé's second plant was set up at Choladi in Tamil Nadu, the plant was built primarily to process the

tea grown in the area.

In 1989, the company established a factory at Nanjangud in Karnataka.

The company entered the confectionery business in 1990 by introducing Nestlé premium chocolate.

In 1991, they started the production of soya based products through a joint venture with the BM

Khaitan group.

In the year 1995 and 1997 Nestlé established two facilities in Goa at Ponda and Bicholim respectively.

In April 2000 they entered the liquid milk and iced tea markets.

2006 marked the year when the company set up its 7th factory at Pantnagar in Uttarakhand.

The company opened another plant in Karnataka in 2011 bringing up its total plants in India to eight.

In October 2020, Nestle India announced investment of Rs. 2,600 crores for a new plant

at Sanand in Gujarat

22

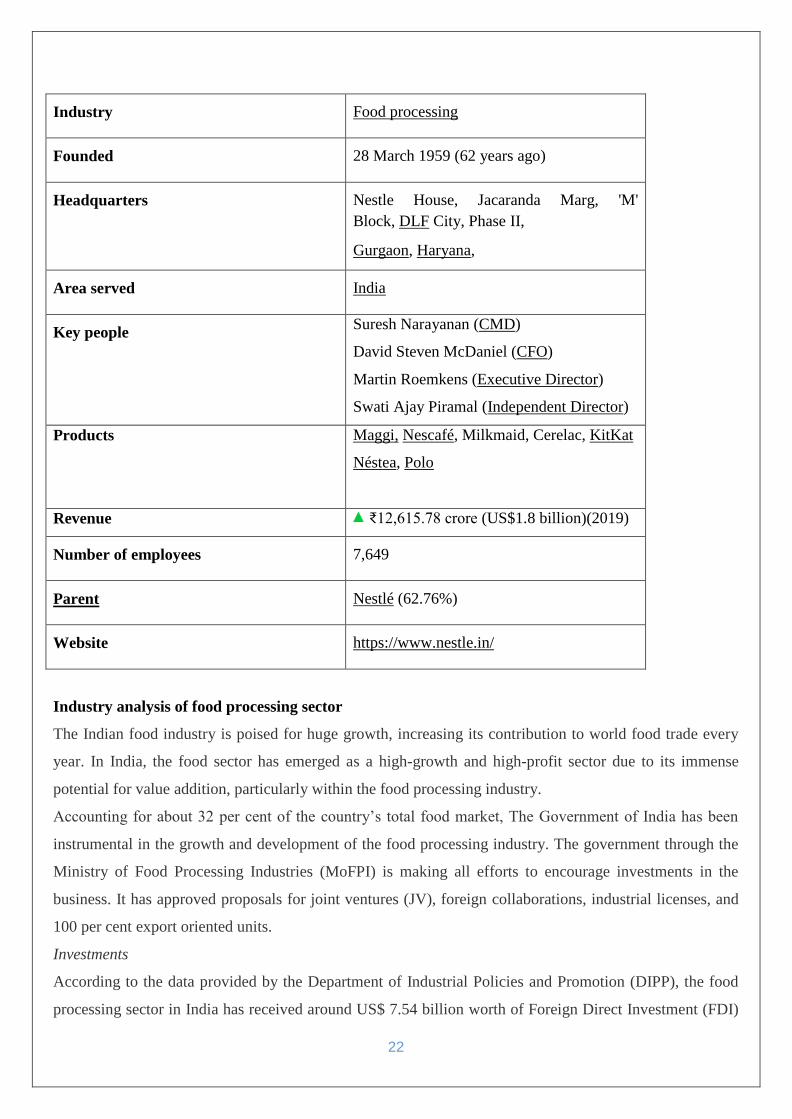

Industry Food processing

Founded 28 March 1959 (62 years ago)

Headquarters Nestle House, Jacaranda Marg, 'M'

Block, DLF City, Phase II,

Gurgaon, Haryana,

Area served India

Key people Suresh Narayanan (CMD)

David Steven McDaniel (CFO)

Martin Roemkens (Executive Director)

Swati Ajay Piramal (Independent Director)

Products Maggi, Nescafé, Milkmaid, Cerelac, KitKat

Néstea, Polo

Revenue ₹12,615.78 crore (US$1.8 billion)(2019)

Number of employees 7,649

Parent Nestlé (62.76%)

Website https://www.nestle.in/

Industry analysis of food processing sector

The Indian food industry is poised for huge growth, increasing its contribution to world food trade every

year. In India, the food sector has emerged as a high-growth and high-profit sector due to its immense

potential for value addition, particularly within the food processing industry.

Accounting for about 32 per cent of the country’s total food market, The Government of India has been

instrumental in the growth and development of the food processing industry. The government through the

Ministry of Food Processing Industries (MoFPI) is making all efforts to encourage investments in the

business. It has approved proposals for joint ventures (JV), foreign collaborations, industrial licenses, and

100 per cent export oriented units.

Investments

According to the data provided by the Department of Industrial Policies and Promotion (DIPP), the food

processing sector in India has received around US$ 7.54 billion worth of Foreign Direct Investment (FDI)

23

during the period April 2000-March 2017. The Confederation of Indian Industry (CII) estimates that the

food processing sectors have the potential to attract as much as US$ 33 billion of investment over the next

10 years and also to generate employment of nine million person-days.

Some of the major investments in this sector in the recent past are:

Global e-commerce giant, Amazon is planning to enter the Indian food retailing sector by investing

US$ 515 million in the next five years, as per Mr Harsimrat Kaur Badal, Minister of Food

Processing Industries, Government of India.

Parle Agro Pvt Ltd is launching Frooti Fizz, a succession of the original Mango Frooti, which will

be retailed across 1.2 million outlets in the country as it targets increasing its annual revenue from

Rs 2800 crore (US$ 0.42 billion) to Rs 5000 crore (US$ 0.75 billion) by 2018.

US-based food company Cargill Inc, aims to double its branded consumer business in India by

2020, by doubling its retail reach to about 800,000 outlets and increase market share to become

national leader in the sunflower oil category which will help the company be among the top three

leading brands in India.

Mad Over Donuts (MoD), outlined plans of expanding its operations in India by opening nine new

MOD stores by March 2017.

Danone SA plans to focus on nutrition business in India, its fastest growing market in South Asia,

by launching 10 new products in 2017, and aiming to double its revenue in India by 2020.

Uber Technologies Inc plans to launch UberEATS, its food delivery service to India, with

investments made across multiple cities and regions.

Government Initiatives

Some of the major initiatives taken by the Government of India to improve the food processing sector in

India are as follows:

The Government of India aims to boost growth in the food processing sector by leveraging reforms

such as 100 per cent Foreign direct investment (FDI) in marketing of food products and various

incentives at central and state government level along with a strong focus on supply chain

infrastructure.

In Union Budget 2017-18, the Government of India has set up a dairy processing infra fund worth

Rs 8,000 crore (US$ 1.2 billion).

The Government of India has relaxed foreign direct investment (FDI) norms for the sector,

allowing up to 100 per cent FDI in food product e-commerce through automatic route.

24

The Food Safety and Standards Authority of India (FSSAI) plans to invest around Rs 482 crore

(US$ 72.3 million) to strengthen the food testing infrastructure in India, by upgrading 59 existing

food testing laboratories and setting up 62 new mobile testing labs across the country.

The Indian Council for Fertilizer and Nutrient Research (ICFNR) will adopt international best

practices for research in fertiliser sector, which will enable farmers to get good quality fertilisers at

affordable rates and thereby achieve food security for the common man.

The Ministry of Food Processing Industries announced a scheme for Human Resource

Development (HRD) in the food processing sector. The HRD scheme is being implemented

through State Governments under the National Mission on Food Processing. The scheme has the

following four components:

o Creation of infrastructure facilities for degree/diploma courses in food processing sector

o Entrepreneurship Development Programme (EDP)

o Food Processing Training Centres (FPTC)

o Training at recognised institutions at State/National level

PARLE

Parle Products Private Limited is an Indian food products company. It owns the

famous biscuit brand Parle-G. In 2019, it had a 7% share of the global biscuit market, growing to 50% by

of 2020. As of 2020, as per Nielsen, it is the largest selling biscuit brand in the world.

HISTORY

Parle Products company was founded in 1929 in British India by the Chauhan family of Vile Parle,

Bombay. Parle began manufacturing biscuits in 1939. In 1947, when India became independent, the

company launched an ad campaign showcasing its Gluco biscuits as an Indian alternative to the British

biscuits.[5] The Parle brand became well known in India following the success of products such as

the Parle-G biscuits and cold beverages like Gold Spot, Thums Up and Frooti.

The original Parle company was split into three separate companies, owned by the different factions of the

original Chauhan family, with a majority of it owned by Parle Agro products:[6]

25

Parle Products (1950s), led by Vijay, Sharad and Raj Chauhan (owner of the brands Parle-G, 20-20,

Magix, Milkshakti, Melody, Mango Bite, Poppins, Londonderry, Kismi Toffee Bar, Monaco and

KrackJack).

Parle Agro (1960s), led by Prakash Chauhan and his daughters Schauna, Alisha and Nadia (owner of

the brands such as Frooti and Appy).

Parle Bisleri (1970s), led by Ramesh Chauhan, his wife Zainab Chauhan and their daughter Jayanti

Chauhan.

Type Private limited

Traded as Unlisted

Industry Food

Founded 1929

Founder Chauhan family

Headquarters Vile Parle (East),

Mumbai, Maharashtra,

India

Products Parle-G, 20-20 Cookies, Happy Happy,

Hide & Seek, Krackjack, Magix Creme,

Milano, Monaco

Owner Vijay Chauhan, Sharad Chauhan & Raj

Chauhan

Number of employees 50,500

Website www.parleproducts.com

26

HERITAGE

Heritage Foods Limited (commonly known as Heritage Foods) is one of the largest private

sector dairy enterprises in Southern India.

HISTORY

The Heritage Group was founded in 1992 by Telugu Desam Party Chief and former Chief Minister of

Andhra Pradesh Shri Nara Chandrababu Naidu, with three-business divisions viz., Dairy, Retail and Agri

under its flagship Company Heritage Foods Limited (HFL), one infrastructure subsidiary - Heritage Infra

Developers Limited and other associate Companies viz., Heritage Finlease Limited, Heritage International

Limited and Heritage Agro Marine Private Limited. The annual turnover has crossed $200 million USD

during FY 2008'09.

Heritage’s milk products have market presence in Telangana, Andhra Pradesh, Karnataka, Kerala, Tamil

Nadu, Maharashtra, Delhi, Rajasthan and Punjab. It has retail stores across Bangalore, Chennai,

Hyderabad and Visakhapatnam. Integrated agri operations are in Chittoor and Medak Districts and these

are backbone to retail operations.

Type Public limited company (BSE)

Industry Dairy and Agribusiness

Founded 1992

Founder Nara Chandrababu Naidu

Headquarters Hyderabad, Telangana, India

Key people Nara Brahmani (Executive Director)

Sambasiva Rao (President)

27

Revenue US$300 million (in 2014 -15)

Owner Nara family

Number of employees 3000+

Website www.heritagefoods.in

28

CHAPTER 3

RESEARCH METHODOLOGY

Literature survey

This chapter looks at the concept of cash flow statement as given by other authors and researchers with

importance to accountability, profit measurement, solvency, ambiguity, and disclosure and their specific

relevance for proper financial management of commercial company .one of the aim and objectives of this

dissertation was to review conceptual though and theoretical framework related to cash flow analysis.

Developing a critical review of cash flow literature and any related issues help the researcher, manager and

any potential reader to better understand the subject and also provide a framework for data analysis.

Governance as stated in the UK charity commission standard for good governance code is “the systems

and processes concerned with ensuring the overall direction, effectiveness, supervision and accountability

of an organization.”

This chapter begins with a clarified concept of cash flow as stated by the Financial Accounting Standard

Board (FASB) and also develop and update and utility of cash flow when managing commercial activities.

How the better knowledge on that topic helps in business decision making nowadays.

Expansion of the reporting standard

The Financial Accounting Standards Board (FASB) introduced Statement of Financial Accounting

Standards No. 95 which is the Statement of Cash Flows in November 1987. The requirement of

FASB 95 regarding a full set of financial statements classified cash flow as the fourth required financial

statement (along with a balance sheet, income statement, and statement of retained earnings). This

statement established standards for cash flow reporting, and dated out the Accounting Principles Board

(APB) Opinion No. 19, Reporting Changes in Financial Position. In March 1971, the APB Opinion No.19

gave chances to enterprises to report cash flow information in a statement of changes in financial position

commonly called a funds statement. During that time, there was no formal or universally accepted

definition to catalogue each statement even though the term “funds” was not sufficiently defined (Alves et

al 2008). Every single industry however had different funds constitution to others since the statement

referred to changes in funds. The term funds referred sometimes to cash for some company meanwhile

some used cash and short term investment and some used quick asset, some used working capital. The

relevance and the valuation of funds statement has been recognized in most company but the lack of

consistency in format and focus from one firm to another was responsible of the main reason that the

FASB obviously took up the matter and with extensive commentary from accountants and any other

interested parties, adopted the standards espoused in FASB 95.it effectively took place in 1988 had not

encouraged use of the world “funds” because it had been stated with so much (Alves et al 2008).

29

A cash flow statement is an important indicator of financial health because it is possible for a company to

show profits while not having enough cash to sustain operations. It is a financial report that shows to the

user the source of a company's cash and how it was spent over a specific period of time. A cash flow

statement counters the ambiguity regarding a company's solvency that various accrual accounting

measures create. It also categorizes the sources and uses of cash to provide the reader with an

understanding of the amount of cash a company generates and uses in its operations, as opposed to the

amount of cash provided by sources outside the company, such as borrowed funds or funds from

stockholders. The cash flow statement also tells the reader how much money was spent for items that do

not appear on the income statement, such as loan repayments, long-term asset purchases, and payment of

cash dividends (Ryan 2007).

Requirements for cash flow statement

Thornton (2008) indicated that FASB 95 requires a statement of cash flows to classify cash receipts and

cash payments in accordance with the prescribe format whether they start from operating activities,

investing activities, or financing activities. The provisions given by FASB are as follows on the

presentation of cash flow statement are:

A. it provides that the cash flows statement should be prepared under either direct or indirect method and

provides examples of how to use each method when preparing statements. b. It also provides that under the

core concept, cash is stated as “cash and cash equivalents”. while cash is the most liquid assets within the

asset portion of a company’s balance sheet including currency and bank deposit, in the other hand cash

equivalents are asset that are ready to be converted into cash such as money market holding, short term

government bond, bills, marketable securities and commercial paper. Other sources of investments such as

stocks, bonds, futures contracts, and so forth are not considered cash.

Cash and profitability concepts

Cash

Cash is one of the most important aspects of running any large or small business. It is one of the single

most important reasons why many businesses fail regardless of how good the business is. The physical

aspect of cash can be any currency, coins on hand, bank balances, negotiable money and so forth.

Managing cash flow therefore is vitally important in the soft running, survival and success of a business

(Atrill P. 2004).

The use of some examples has illustrated how cash flow can make the difference between success and

failure. The meaning of failure in this case is insolvency that is, the company is unable to pay its debts.

The term bankrupt is sometimes used to describe that situation, even though it is only individual who can

be declared bankrupt. But sometimes both terms can be confusing.

30

Significance of cash flow

There is a significant importance of cash flow to a business. Cash flow as defined above is the inflow and

outflow of cash or liquidized finances. The following are some advantages of inward and outward flow of

cash.

a) Income Assurance: The biggest importance of cash flow is that the business organization tends to have

an assured income irrespective of the outside economic condition. Many business corporations have a very

well balanced and uniform inward and outward cash flow.

b) Ensures Timely Payment: The uniform and assured cash flow, in both the directions, ensures two

principal payments, namely, the salaries of employees are paid on time and installments of all loans are

made on time. This safeguards the trust of employees and upholds the credit rating.

c) Return Ratio: The analysis of cash flow ensures that the business is not investing finances in the wrong

avenues, and investments already made are paying off well. This ratio is often termed as return over asset

ratio.

d) Keeps You Out of Debt: The timely cash inflow plays a very instrumental role in keeping you out of

debt, as a timely inflow of cash prevents you from taking small loans.

e) Saves Unnecessary Expenditure: The use of inward and outward cash flow prevents all unnecessary

expenditure such as piled up interest, late payment charges, etc.

f) Timely Investments: As the inflow and outflow of cash is on time, you are left with adequate free and

liquid finances, which you may invest in time bound instruments and securities.

g) Good cash flow practices ensure smooth operation of the company when accrued revenue is still sitting

in accounts receivable. Often an increase in sales does not automatically mean an increase in cash flow at

least not right away. for instance, a company with £3 million annual revenue and 30day gap days between

the day of payment and the day of sales is likely to be more cash rich than the company with£5 million in

sales and a 3 days float. By using cash flow forecasting practices, the company can anticipate when they

are most likely to be cash flush and when they are most likely to be cash-strapped so that they can plan

their capital purchase.

h) Effective cash flow management is vital to every organization; it is an important aspect when planning

business functioning. Earning income is (or should be ) one the main focus of company objectives. It can

be profitable in and of itself. Cash shortages result in increased cost, such as interest charges on loans, late

payment penalties, and loss of vendors discount for paying bill promptly. Cash flow improvements can

eliminate these costs and create the opportunity for more favorable payment terms on some type of

payments. A better understanding of cash flow management can be benefit to many organization with a

comprehensive guide for:

i) Identifying and understanding organization’s cash flow characteristics, strengths and weaknesses

31

j) Improving cash flow through implementing relevant strategies.

k) Improving overall performance by using cash flow.

Limitations of the cash flow statement

Some of the limitations of the cash flow statement are as follows:

As the enterprise shifts from strictly cash basis, enters into credit transactions as well takes into account

prepared and accrued items, the net income no doubt would generally represent an increase in working

capital. Yet equating net income in cash flow for such enterprise would be inaccurate and misleading since

a number of noncash items affects the net income of the firm.

Cash flow is part of working capital. The volume of cost flowing in any part of the system and the speed at

which it flows determines the amount of capital. Tied up sometimes in any segment of the enterprise or

business. At any given time cash flow analysis used in connection with ratio analysis provided a barometer

for measuring the aforesaid change and financing problem of the business much more manageable

There are two methods of preparing cash flow statement:

1) DIRECT METHOD

2) INDIRECT METHOD

Sometimes it can be possible that due to the of wrong method the accurate cash the company cannot make

proper cash planning.

Data of collection

Primary data: not applicable

Secondary data:

Secondary data has been collected from

Websites

journals

Research design & methodology

Research design is blue print of data collection, measurement & analysis of data. It indicate both structure

of problem & plan of investigation used to obtain empirical evidence on those relationship .There are

generally three types of research design which are as follows.

1 Exploratory studies

2. Descriptive studies

3. Causal studies

For the research design I have selected DESCRIPTIVRE STUDIES because as cash flow analysis is topic

in which there must detail description of all transaction are required to study so that we get idea how cash

is collect from various sources & utilized in organization. Further while doing in depth study we get

complete picture of process that follow in organization. Significant of study Aim of work help to reach

32

destination by problems arises in the way work become more efficient if purpose for doing work is clear.

Scope Statement of Cash Flows

1. Consolidated cash flow is a financial statement that presents information about the company's cash

receipts and disbursements during the accounting period.

2. The purpose of cash flow statement is to provide information on sources and uses of cash and cash

equivalents during the period of accounting and cash reconciliation at the beginning of the period with

cash at the end of the period plus the cash equivalent balances.

3. The general form of the cash flow statement shows cash receipts and disbursements are divided into

three categories, namely: cash flow from operating activities, cash flows from investing activities and cash

flows arising from financing activities.

33

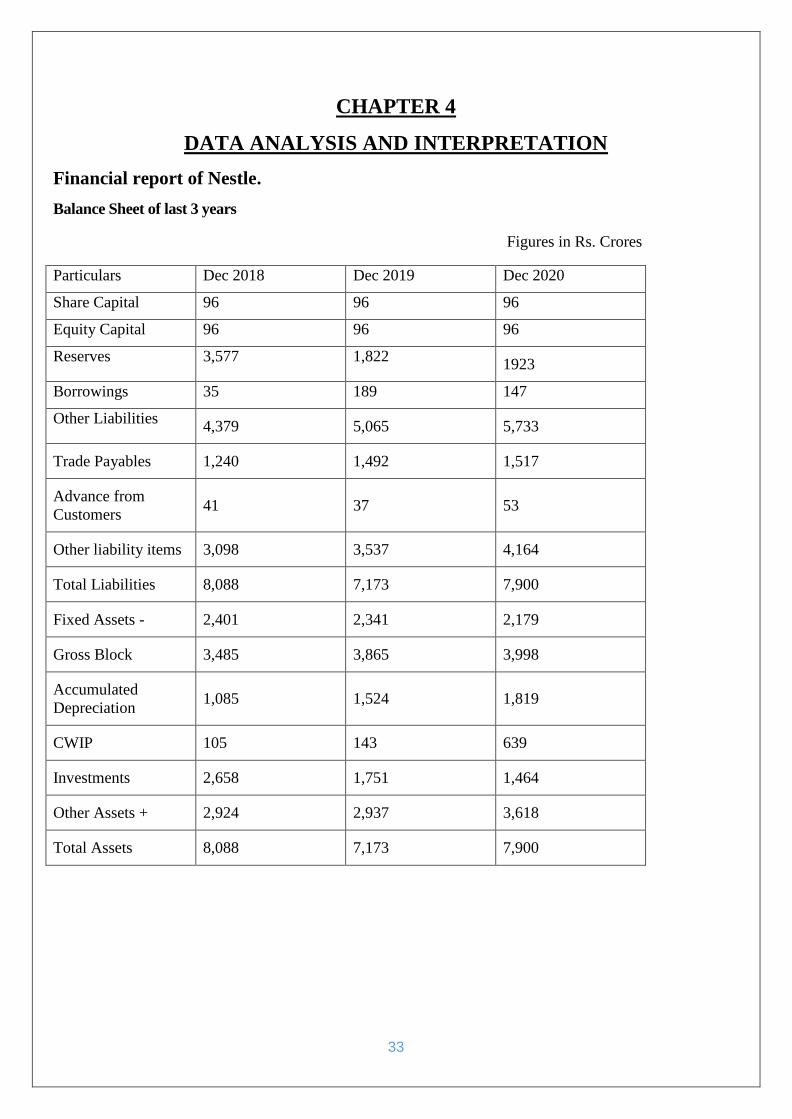

CHAPTER 4

DATA ANALYSIS AND INTERPRETATION

Financial report of Nestle.

Balance Sheet of last 3 years

Figures in Rs. Crores

Particulars Dec 2018 Dec 2019 Dec 2020

Share Capital 96 96 96

Equity Capital 96 96 96

Reserves 3,577 1,822 1923

Borrowings 35 189 147

Other Liabilities 4,379 5,065 5,733

Trade Payables 1,240 1,492 1,517

Advance from

Customers 41 37 53

Other liability items 3,098 3,537 4,164

Total Liabilities 8,088 7,173 7,900

Fixed Assets - 2,401 2,341 2,179

Gross Block 3,485 3,865 3,998

Accumulated

Depreciation 1,085 1,524 1,819

CWIP 105 143 639

Investments 2,658 1,751 1,464

Other Assets + 2,924 2,937 3,618

Total Assets 8,088 7,173 7,900

34

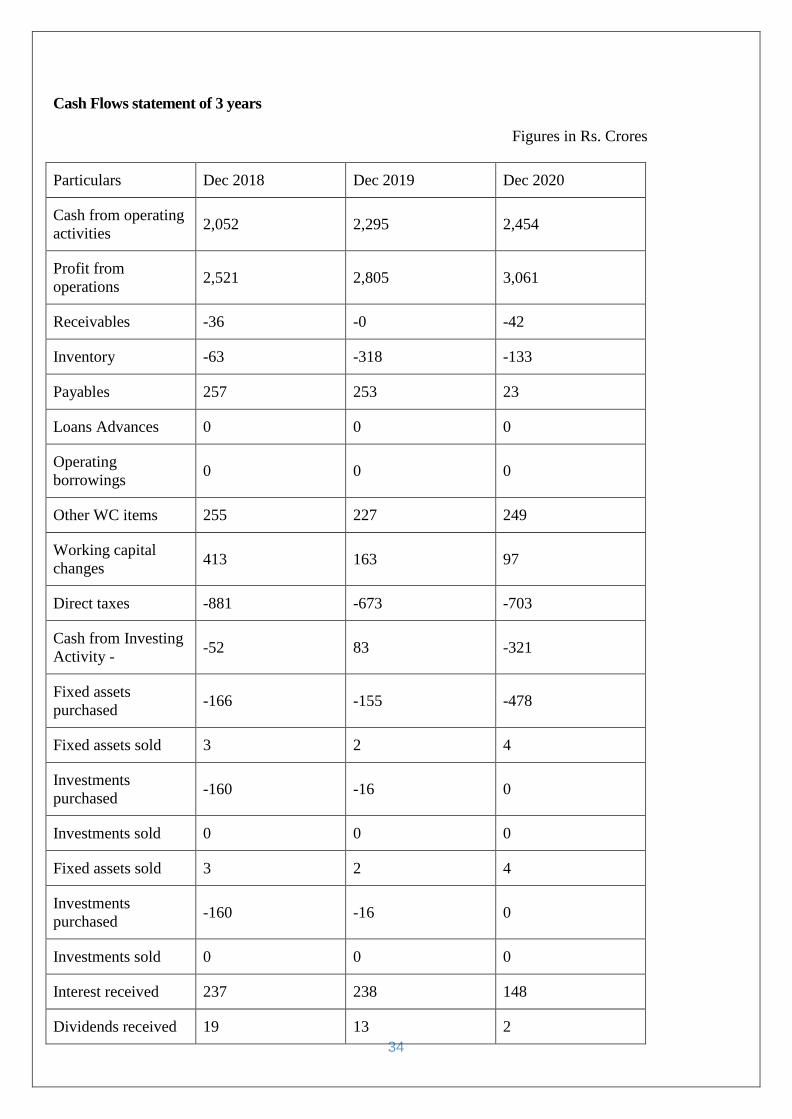

Cash Flows statement of 3 years

Figures in Rs. Crores

Particulars Dec 2018 Dec 2019 Dec 2020

Cash from operating

activities 2,052 2,295 2,454

Profit from

operations 2,521 2,805 3,061

Receivables -36 -0 -42

Inventory -63 -318 -133

Payables 257 253 23

Loans Advances 0 0 0

Operating

borrowings 0 0 0

Other WC items 255 227 249

Working capital

changes 413 163 97

Direct taxes -881 -673 -703

Cash from Investing

Activity - -52 83 -321

Fixed assets

purchased -166 -155 -478

Fixed assets sold 3 2 4

Investments

purchased -160 -16 0

Investments sold 0 0 0

Fixed assets sold 3 2 4

Investments

purchased -160 -16 0

Investments sold 0 0 0

Interest received 237 238 148

Dividends received 19 13 2

35

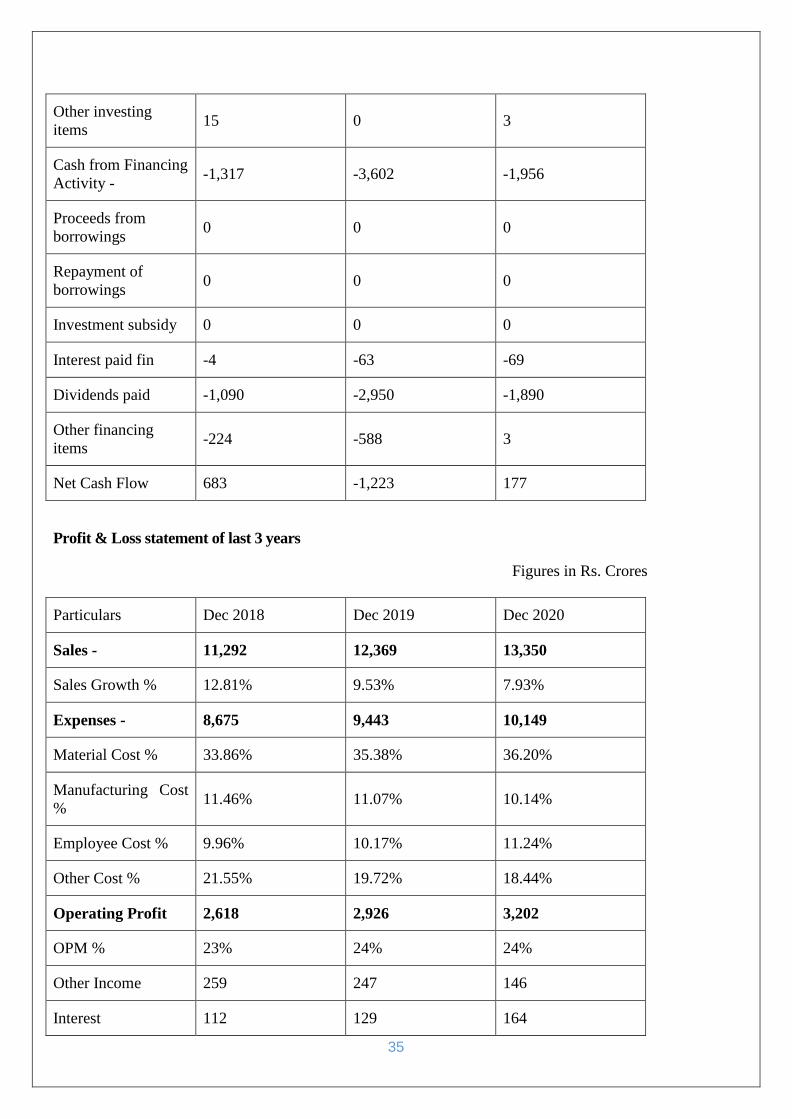

Other investing

items 15 0 3

Cash from Financing

Activity - -1,317 -3,602 -1,956

Proceeds from

borrowings 0 0 0

Repayment of

borrowings 0 0 0

Investment subsidy 0 0 0

Interest paid fin -4 -63 -69

Dividends paid -1,090 -2,950 -1,890

Other financing

items -224 -588 3

Net Cash Flow 683 -1,223 177

Profit & Loss statement of last 3 years

Figures in Rs. Crores

Particulars Dec 2018 Dec 2019 Dec 2020

Sales - 11,292 12,369 13,350

Sales Growth % 12.81% 9.53% 7.93%

Expenses - 8,675 9,443 10,149

Material Cost % 33.86% 35.38% 36.20%

Manufacturing Cost

% 11.46% 11.07% 10.14%

Employee Cost % 9.96% 10.17% 11.24%

Other Cost % 21.55% 19.72% 18.44%

Operating Profit 2,618 2,926 3,202

OPM % 23% 24% 24%

Other Income 259 247 146

Interest 112 129 164

36

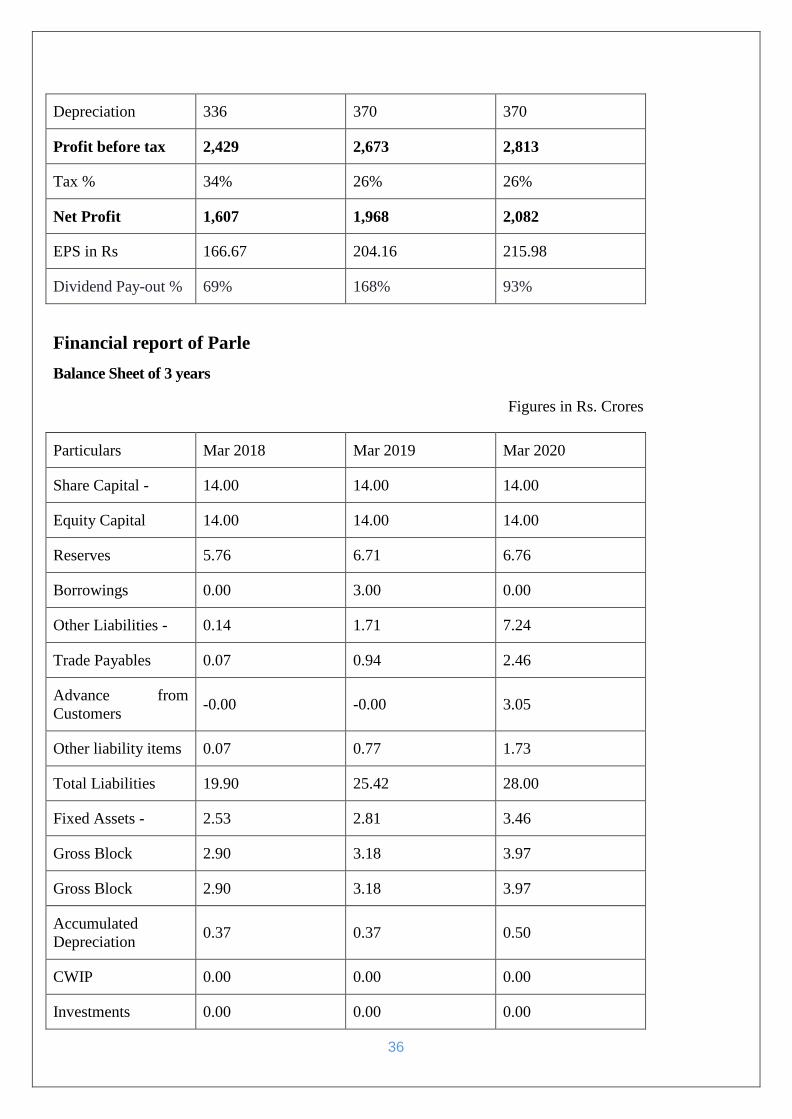

Depreciation 336 370 370

Profit before tax 2,429 2,673 2,813

Tax % 34% 26% 26%

Net Profit 1,607 1,968 2,082

EPS in Rs 166.67 204.16 215.98

Dividend Pay-out % 69% 168% 93%

Financial report of Parle

Balance Sheet of 3 years

Figures in Rs. Crores

Particulars Mar 2018 Mar 2019 Mar 2020

Share Capital - 14.00 14.00 14.00

Equity Capital 14.00 14.00 14.00

Reserves 5.76 6.71 6.76

Borrowings 0.00 3.00 0.00

Other Liabilities - 0.14 1.71 7.24

Trade Payables 0.07 0.94 2.46

Advance from

Customers -0.00 -0.00 3.05

Other liability items 0.07 0.77 1.73

Total Liabilities 19.90 25.42 28.00

Fixed Assets - 2.53 2.81 3.46

Gross Block 2.90 3.18 3.97

Gross Block 2.90 3.18 3.97

Accumulated

Depreciation 0.37 0.37 0.50

CWIP 0.00 0.00 0.00

Investments 0.00 0.00 0.00

37

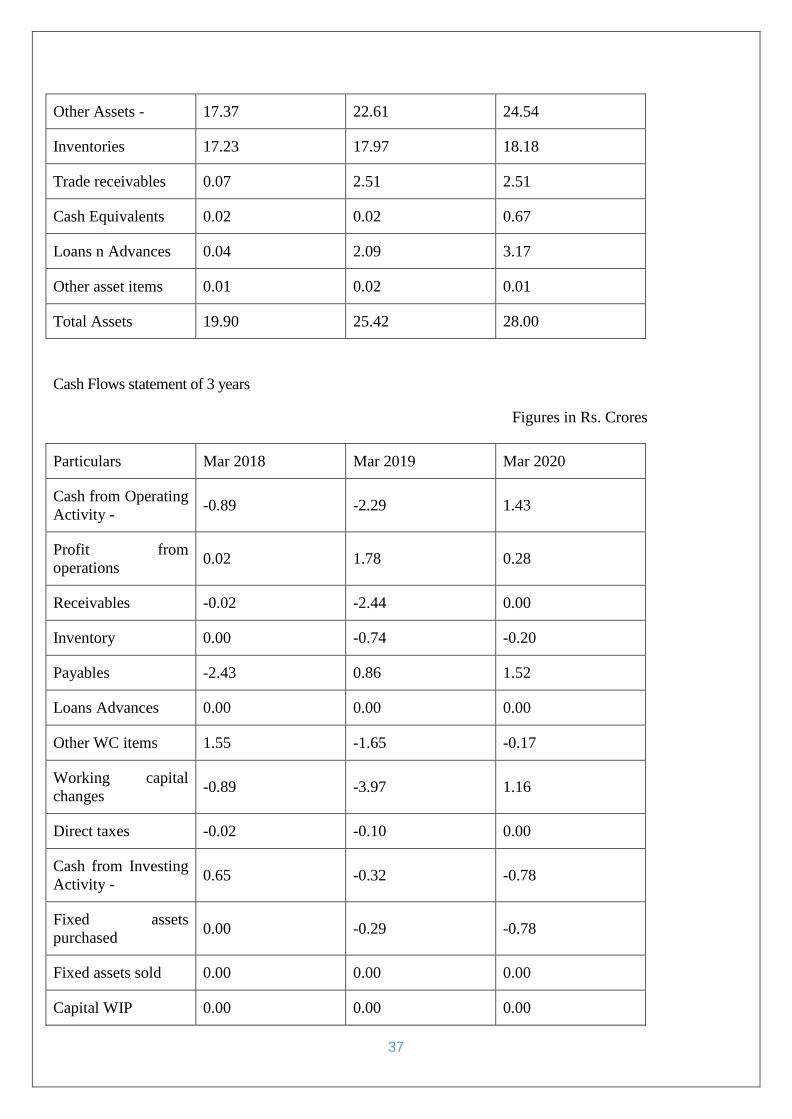

Other Assets - 17.37 22.61 24.54

Inventories 17.23 17.97 18.18

Trade receivables 0.07 2.51 2.51

Cash Equivalents 0.02 0.02 0.67

Loans n Advances 0.04 2.09 3.17

Other asset items 0.01 0.02 0.01

Total Assets 19.90 25.42 28.00

Cash Flows statement of 3 years

Figures in Rs. Crores

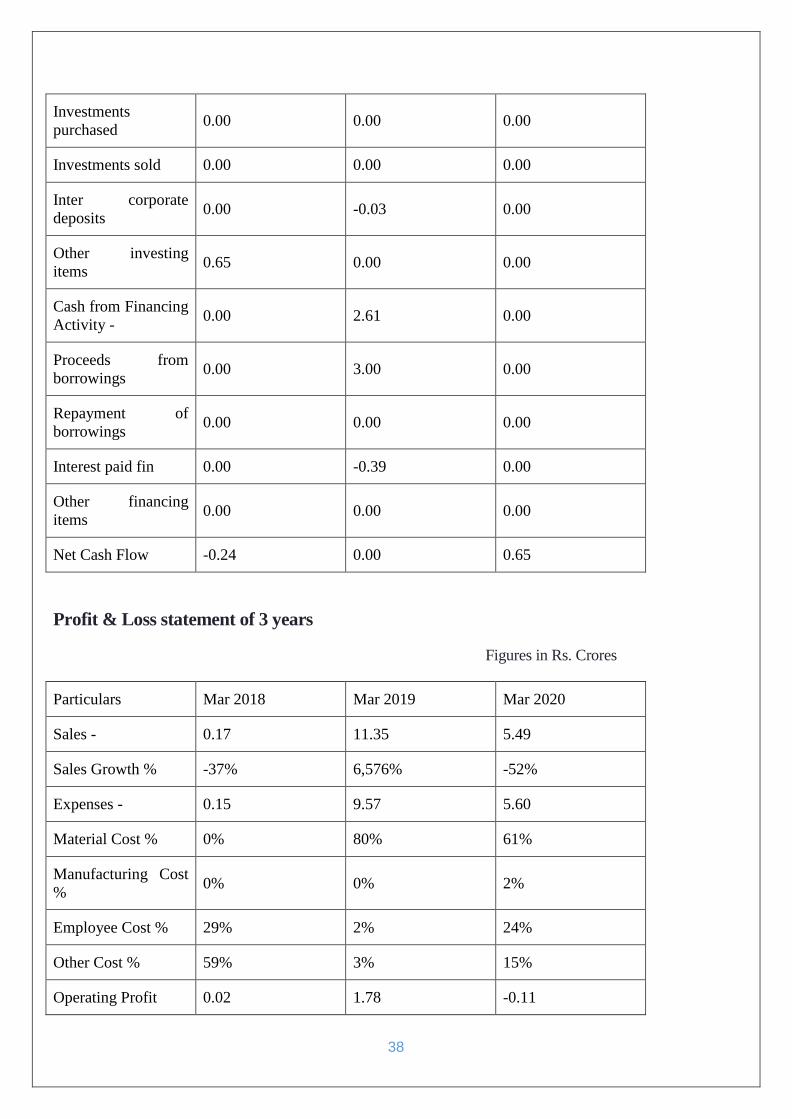

Particulars Mar 2018 Mar 2019 Mar 2020

Cash from Operating

Activity - -0.89 -2.29 1.43

Profit from

operations 0.02 1.78 0.28

Receivables -0.02 -2.44 0.00

Inventory 0.00 -0.74 -0.20

Payables -2.43 0.86 1.52

Loans Advances 0.00 0.00 0.00

Other WC items 1.55 -1.65 -0.17

Working capital

changes -0.89 -3.97 1.16

Direct taxes -0.02 -0.10 0.00

Cash from Investing

Activity - 0.65 -0.32 -0.78

Fixed assets

purchased 0.00 -0.29 -0.78

Fixed assets sold 0.00 0.00 0.00

Capital WIP 0.00 0.00 0.00

38

Investments

purchased 0.00 0.00 0.00

Investments sold 0.00 0.00 0.00

Inter corporate

deposits 0.00 -0.03 0.00

Other investing

items 0.65 0.00 0.00

Cash from Financing

Activity - 0.00 2.61 0.00

Proceeds from

borrowings 0.00 3.00 0.00

Repayment of

borrowings 0.00 0.00 0.00

Interest paid fin 0.00 -0.39 0.00

Other financing

items 0.00 0.00 0.00

Net Cash Flow -0.24 0.00 0.65

Profit & Loss statement of 3 years

Figures in Rs. Crores

Particulars Mar 2018 Mar 2019 Mar 2020

Sales - 0.17 11.35 5.49

Sales Growth % -37% 6,576% -52%

Expenses - 0.15 9.57 5.60

Material Cost % 0% 80% 61%

Manufacturing Cost

% 0% 0% 2%

Employee Cost % 29% 2% 24%

Other Cost % 59% 3% 15%

Operating Profit 0.02 1.78 -0.11

39

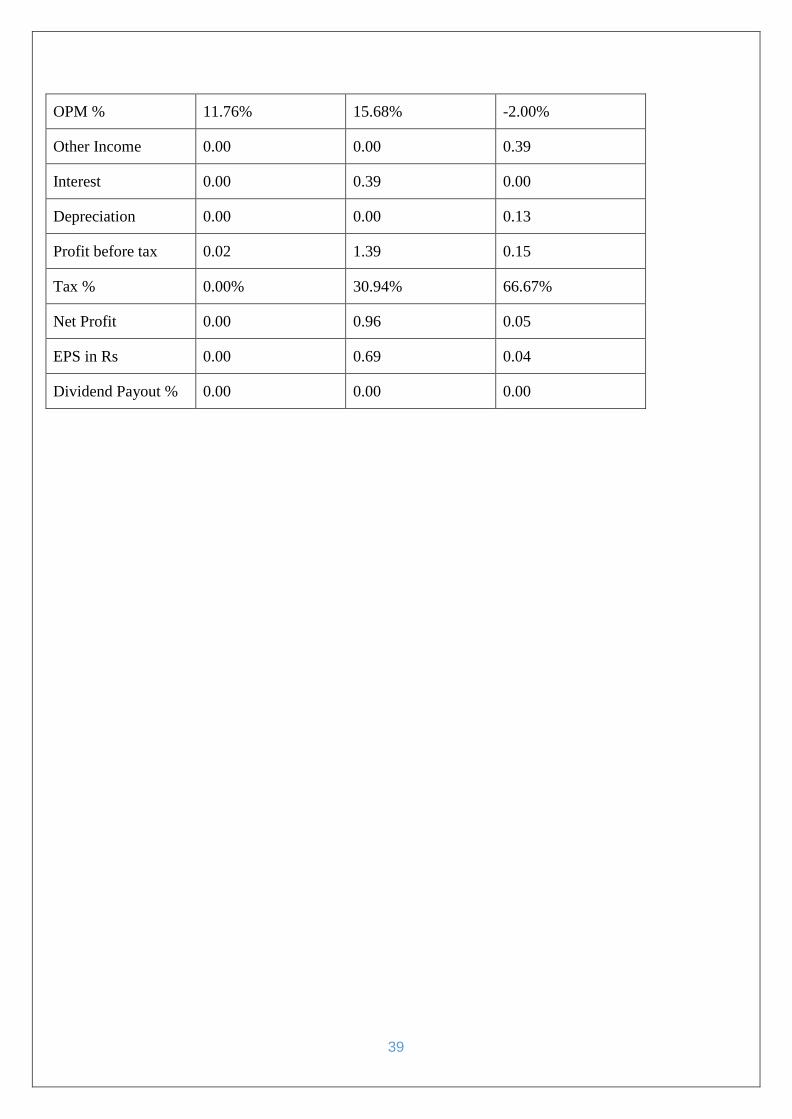

OPM % 11.76% 15.68% -2.00%

Other Income 0.00 0.00 0.39

Interest 0.00 0.39 0.00

Depreciation 0.00 0.00 0.13

Profit before tax 0.02 1.39 0.15

Tax % 0.00% 30.94% 66.67%

Net Profit 0.00 0.96 0.05

EPS in Rs 0.00 0.69 0.04

Dividend Payout % 0.00 0.00 0.00

40

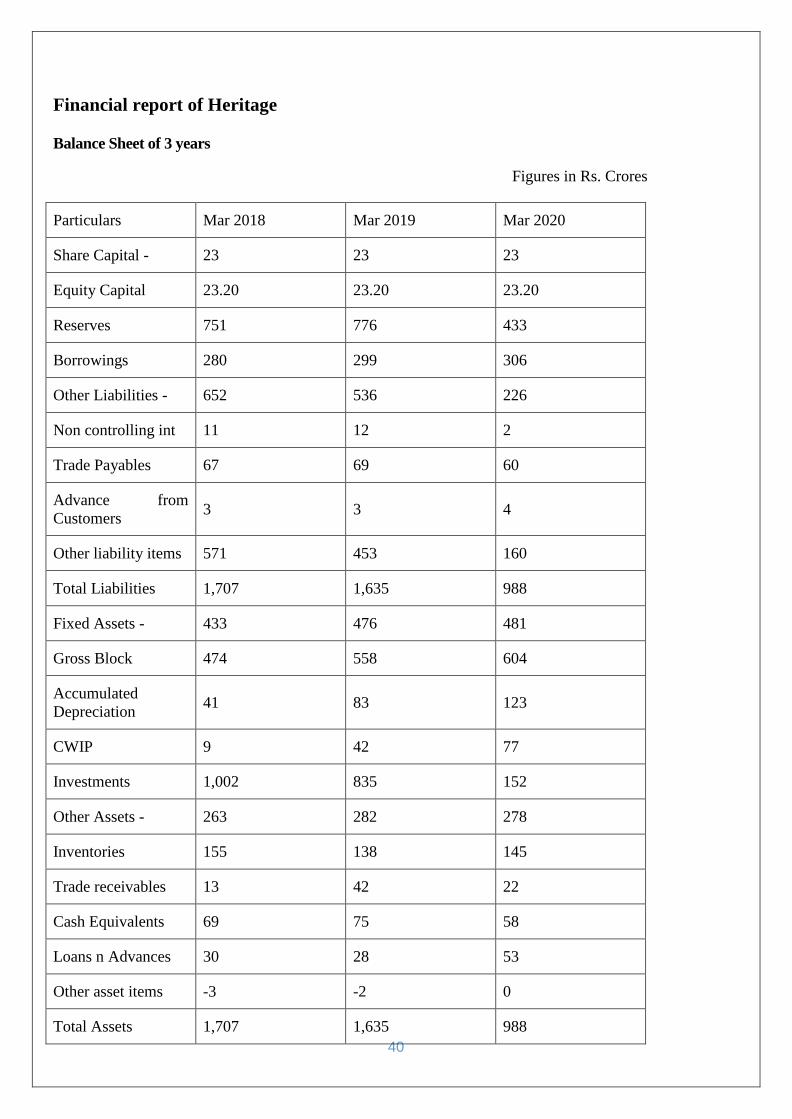

Financial report of Heritage

Balance Sheet of 3 years

Figures in Rs. Crores

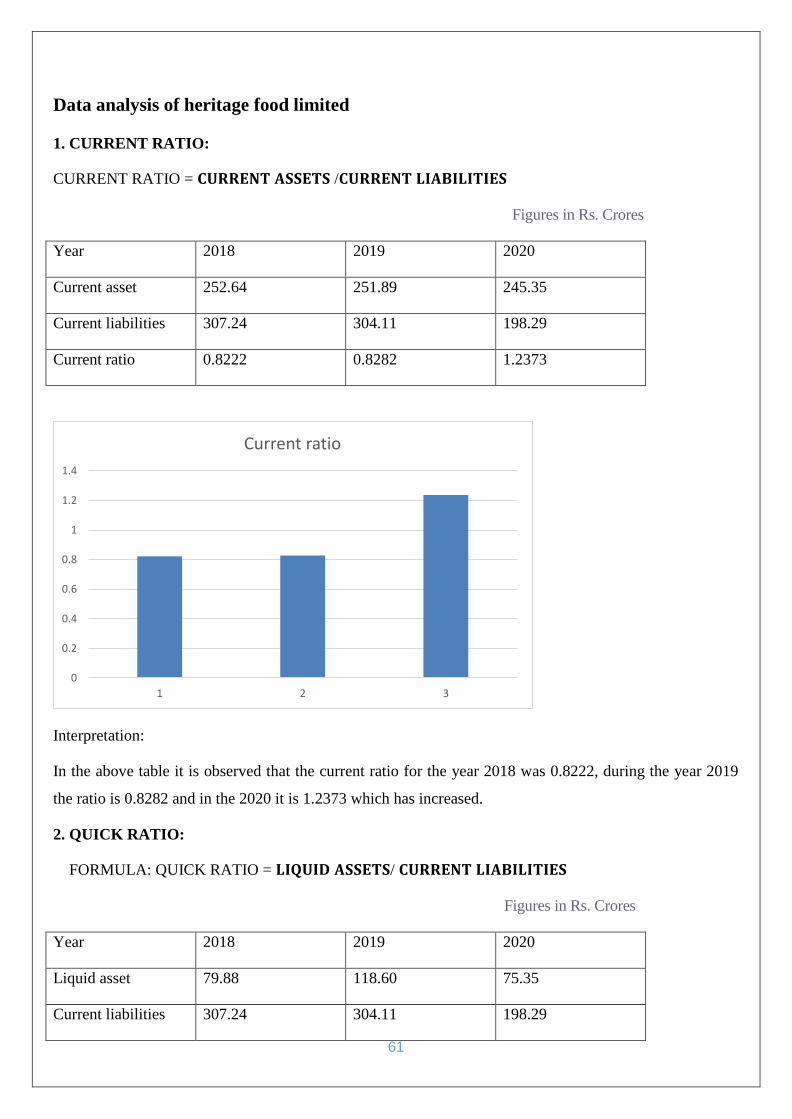

Particulars Mar 2018 Mar 2019 Mar 2020

Share Capital - 23 23 23

Equity Capital 23.20 23.20 23.20

Reserves 751 776 433

Borrowings 280 299 306

Other Liabilities - 652 536 226

Non controlling int 11 12 2

Trade Payables 67 69 60

Advance from

Customers 3 3 4

Other liability items 571 453 160

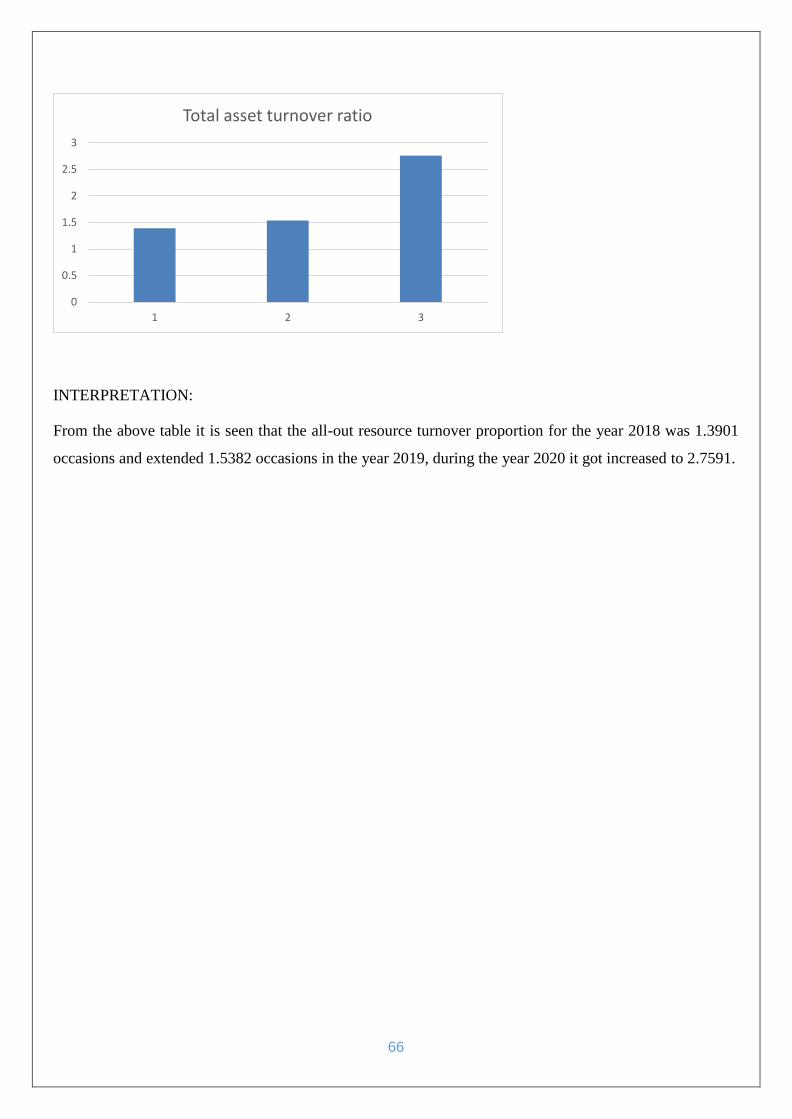

Total Liabilities 1,707 1,635 988

Fixed Assets - 433 476 481

Gross Block 474 558 604

Accumulated

Depreciation 41 83 123

CWIP 9 42 77

Investments 1,002 835 152

Other Assets - 263 282 278

Inventories 155 138 145

Trade receivables 13 42 22

Cash Equivalents 69 75 58

Loans n Advances 30 28 53

Other asset items -3 -2 0

Total Assets 1,707 1,635 988

41

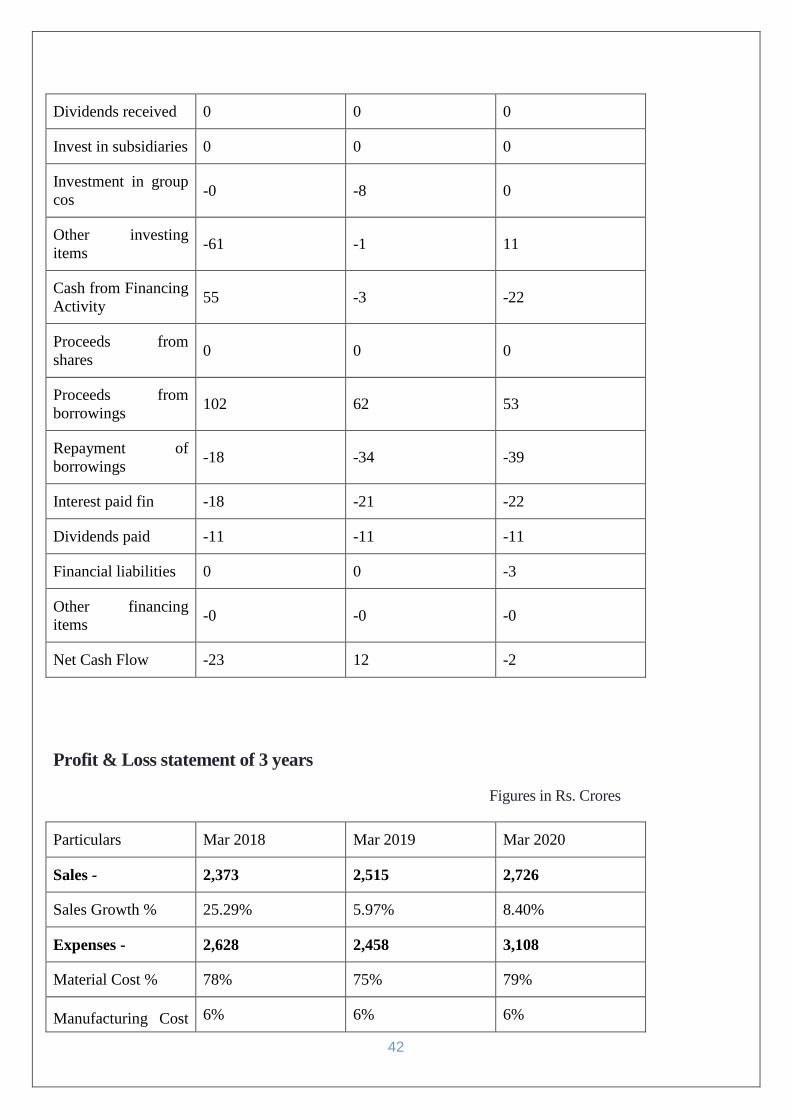

Cash Flow statement of 3 years

Figures in Rs. Crores

Particulars Mar 2018 Mar 2019 Mar 2020

Cash from Operating

Activity 121 148 117

Profit from

operations 138 195 134

Receivables 2 -31 20

Inventory 15 16 -6

Payables -4 4 -9

Loans Advances 0 1 -1

Other WC items -1 1 -1

Working capital

changes 11 -8 3

Direct taxes -29 -38 -19

Other operating

items 0 0 0

Exceptional CF

items 1 -1 -1

Cash from Investing

Activity -200 -133 -97

Fixed assets

purchased -144 -127 -112

Fixed assets sold 4 3 4

Investments

purchased 0 0 0

Investments sold 0 0 0

Investment income 0 0 0

Interest received 1 1 1

42

Dividends received 0 0 0

Invest in subsidiaries 0 0 0

Investment in group

cos -0 -8 0

Other investing

items -61 -1 11

Cash from Financing

Activity 55 -3 -22

Proceeds from

shares 0 0 0

Proceeds from

borrowings 102 62 53

Repayment of

borrowings -18 -34 -39

Interest paid fin -18 -21 -22

Dividends paid -11 -11 -11

Financial liabilities 0 0 -3

Other financing

items -0 -0 -0

Net Cash Flow -23 12 -2

Profit & Loss statement of 3 years

Figures in Rs. Crores

Particulars Mar 2018 Mar 2019 Mar 2020

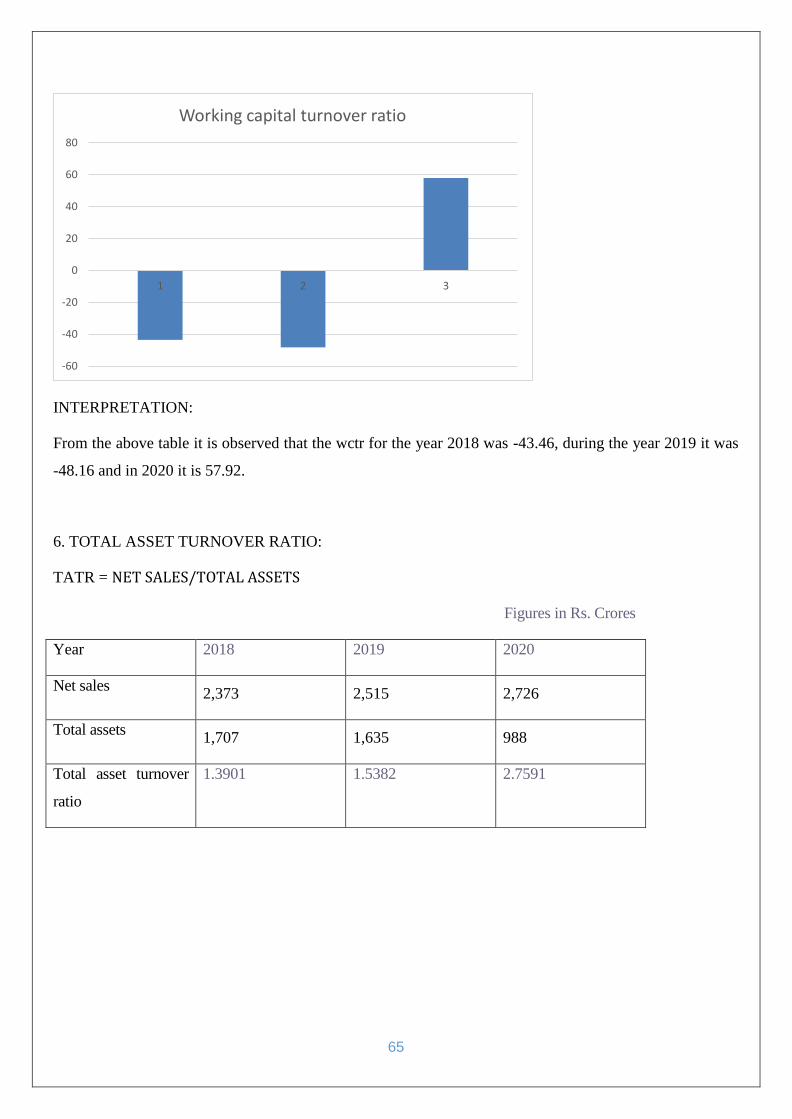

Sales - 2,373 2,515 2,726

Sales Growth % 25.29% 5.97% 8.40%

Expenses - 2,628 2,458 3,108

Material Cost % 78% 75% 79%

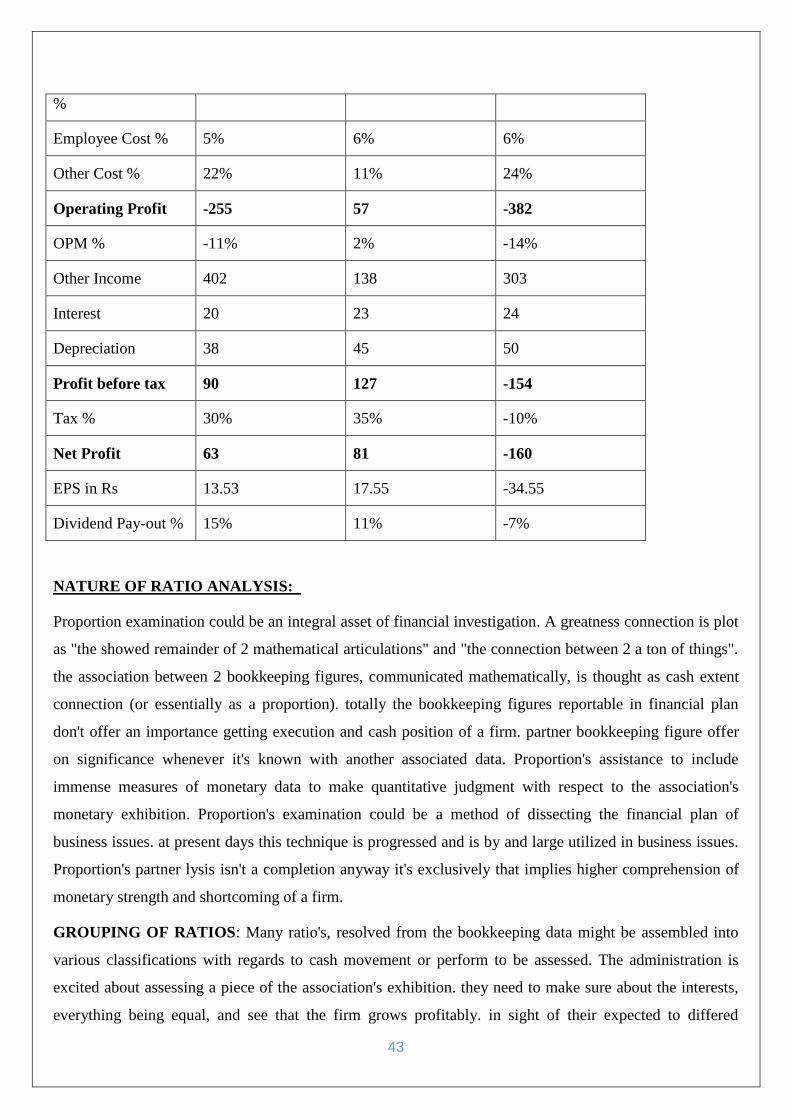

Manufacturing Cost 6% 6% 6%

43

%

Employee Cost % 5% 6% 6%

Other Cost % 22% 11% 24%

Operating Profit -255 57 -382

OPM % -11% 2% -14%

Other Income 402 138 303

Interest 20 23 24

Depreciation 38 45 50

Profit before tax 90 127 -154

Tax % 30% 35% -10%

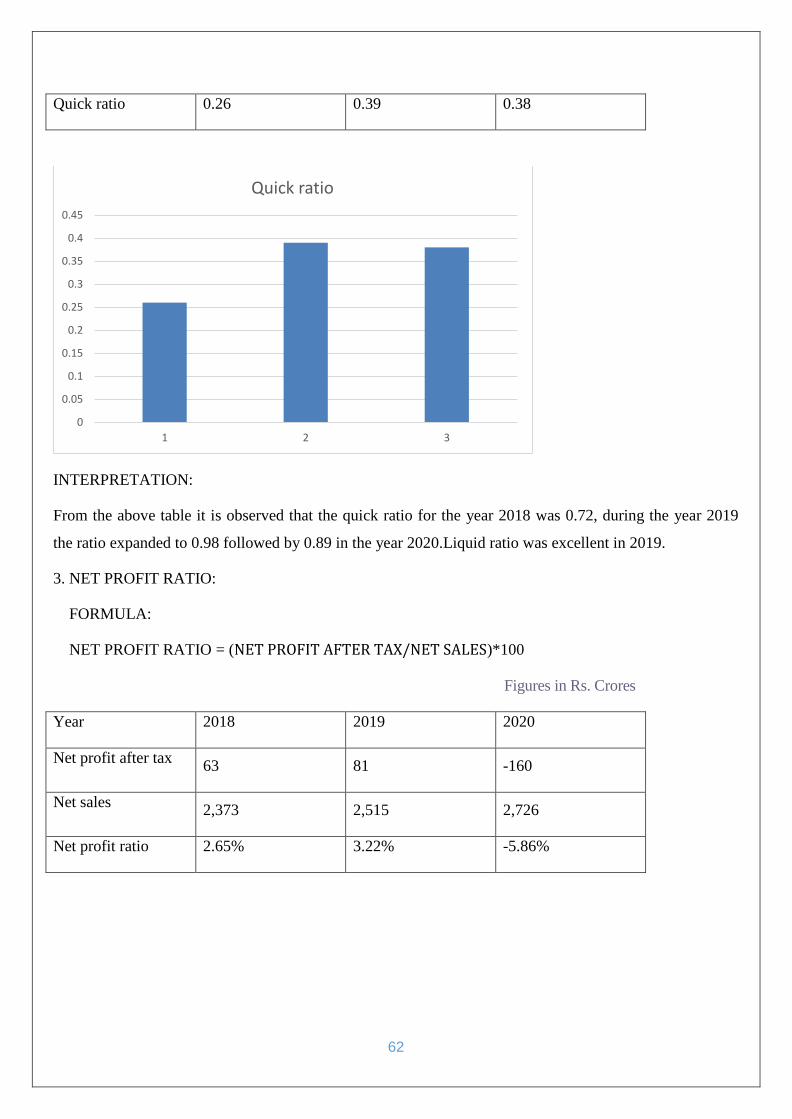

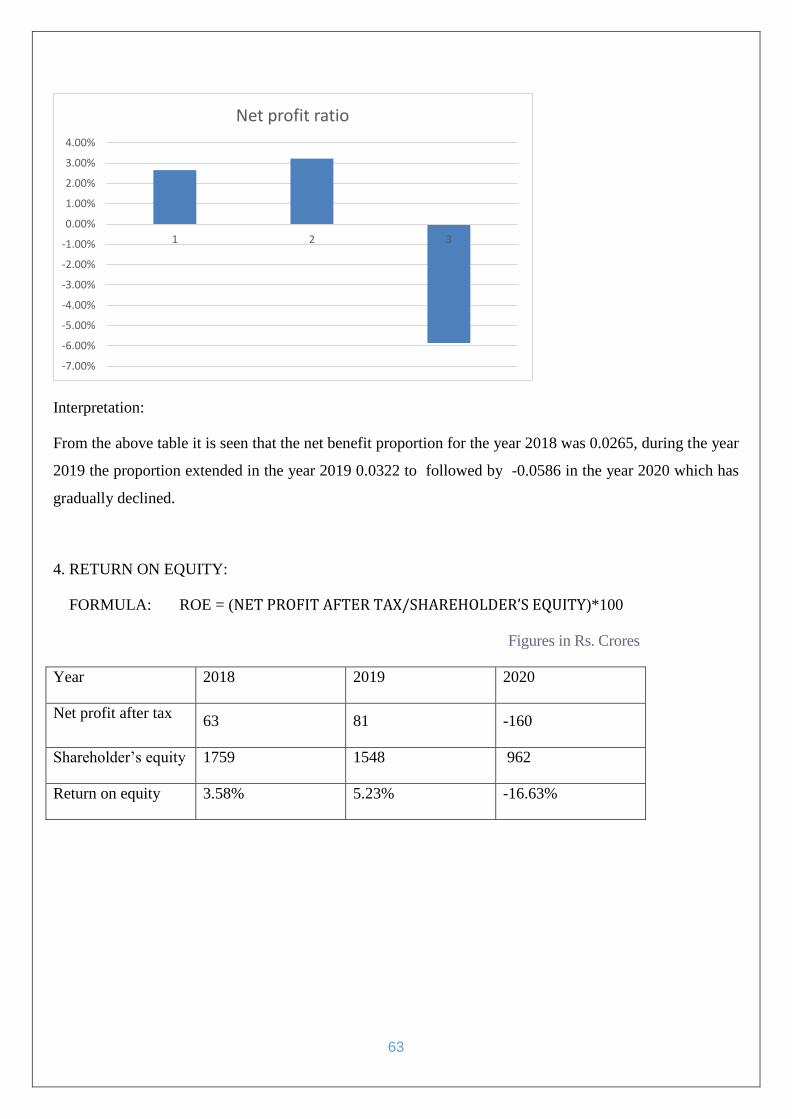

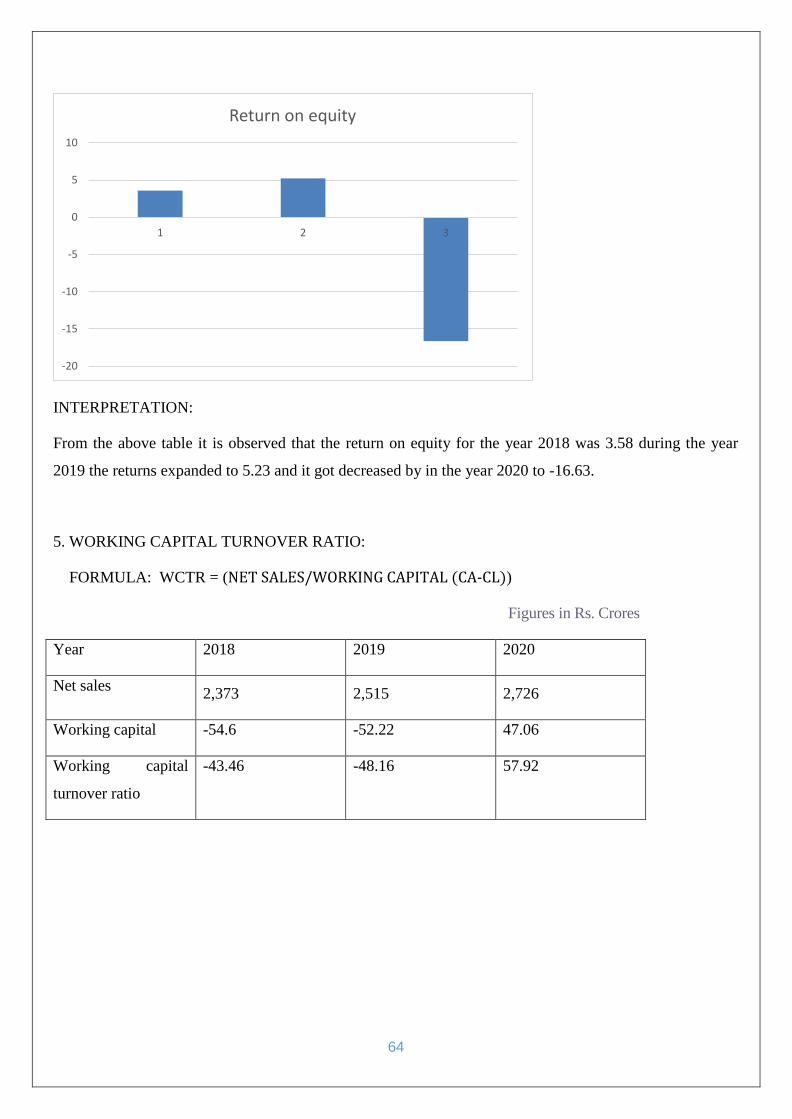

Net Profit 63 81 -160

EPS in Rs 13.53 17.55 -34.55

Dividend Pay-out % 15% 11% -7%

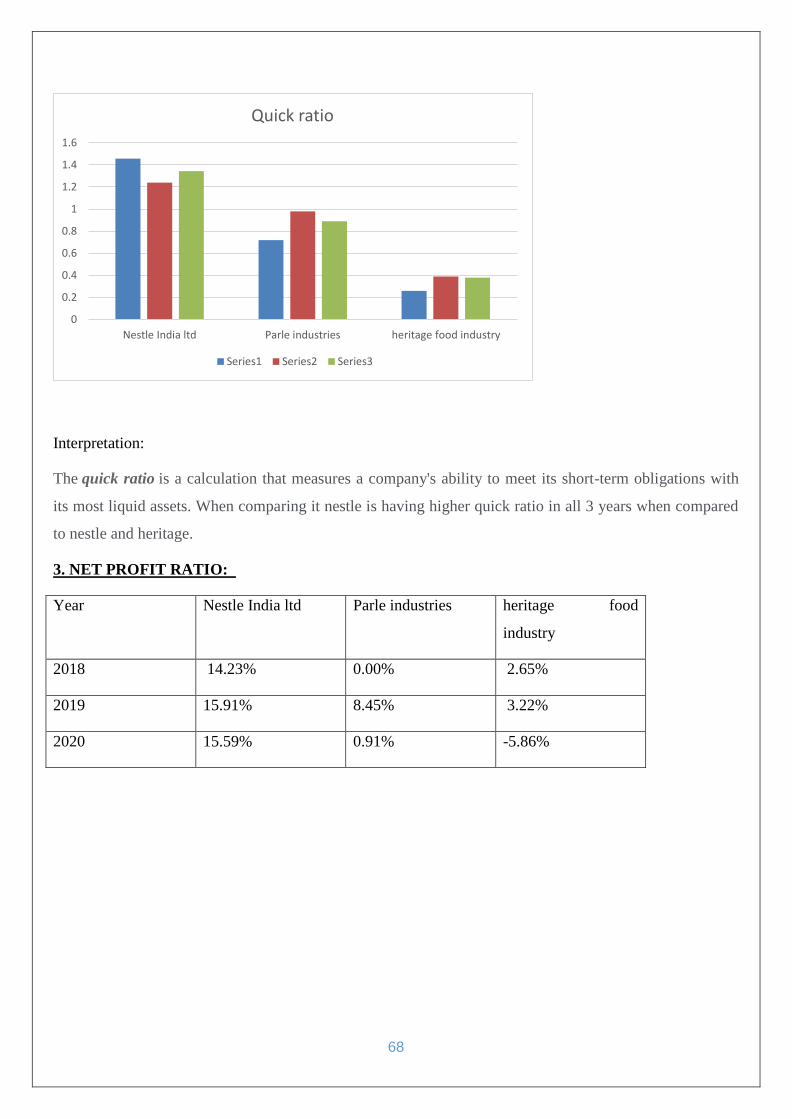

NATURE OF RATIO ANALYSIS:

Proportion examination could be an integral asset of financial investigation. A greatness connection is plot

as "the showed remainder of 2 mathematical articulations" and "the connection between 2 a ton of things".

the association between 2 bookkeeping figures, communicated mathematically, is thought as cash extent

connection (or essentially as a proportion). totally the bookkeeping figures reportable in financial plan

don't offer an importance getting execution and cash position of a firm. partner bookkeeping figure offer

on significance whenever it's known with another associated data. Proportion's assistance to include

immense measures of monetary data to make quantitative judgment with respect to the association's

monetary exhibition. Proportion's examination could be a method of dissecting the financial plan of

business issues. at present days this technique is progressed and is by and large utilized in business issues.

Proportion's partner lysis isn't a completion anyway it's exclusively that implies higher comprehension of

monetary strength and shortcoming of a firm.

GROUPING OF RATIOS: Many ratio's, resolved from the bookkeeping data might be assembled into

various classifications with regards to cash movement or perform to be assessed. The administration is

excited about assessing a piece of the association's exhibition. they need to make sure about the interests,

everything being equal, and see that the firm grows profitably. in sight of their expected to differed

44

employments of ratio's, proportions square measure coordinated into following four imperative

classifications:

1. Liquidity proportion's

2. Leverage proportion's

3. profit proportion's

4. Activity proportion's

LIQUIDITY RATIOS: Liquidity proportions live the association's ability to satisfy its present

commitments as and after they become due. They show whether the firm pays its short-run assets or not.

Liquidity proportions build up a connection among cash and distinctive current resources for current

commitments gives a quick live of liquidity. A firm should ensure that it doesn't devastations from

nonattendance of liquidity and besides that it doesn't have further liquidity. a substantial degree of liquidity

is to boot horrendous, idle resources secure nothing. The most notable liquidity greatness relations are:

1) Current proportion

2) Fast extent connection

3) Money greatness connection

1. CURRENT RATIO: It is liquidity proportion's that gauges an organization's capacity to pay criminal

responsibility. The extent connection is particularly acclimated offer an arrangement of the organization's

capacity to take care of its short-run liabilities (obligation and payables) with its short-run resources

(money, stock, receivables). It shows the openness of current resources in rupees for each one rupee of

current risk.

2. FAST RATIO: Speedy extent connection, in like manner known as evaluation size connection, develops

a connection between quick, or fluid, resources and current liabilities. Partner in addition to is fluid in the

event that it could be brought back to life into cash without a moment's delay or modest as of now while

not misfortune significant. cash is that the most fluid in addition to and various resources that square

measure saw as similarly fluid. Inventories square measure saw as less fluid. the quick size connection is

got wind by separating resources by current liabilities.

3. MONEY RATIO: Money extent connection build up connection among cash and current resources. It

shows the degree of cash in current resources. it's determined by separating cash by current liablities.

4. INFLUENCE RATIOS: Leverage greatness connection show the assets gave by the since quite a while

ago run lenders and short-run leasers. The since quite a while ago run leasers like debenture holders, cash

foundations and so forth on various hand momentary loan bosses like investors and providers of crude

45

materials, square measure a great deal of included with respect to the association's present obligation

paying capacity. There should be a suitable combination of Debt and proprietor's value in money the

company's resources. Influence size relations square measure determined from record item decides the

proportion of obligation in absolute money.

The most notable impact extent relations are:

1) Total obligation proportion

2) Debt value extent connection

3) Interest inclusion greatness connection

4) Proprietary greatness connection

1. TOTAL DEBT RATIO: A few obligation proportions may scrounge deal to explore the since quite a

while ago run monetary state of a firm. The firm can be engaged with knowing the degree of the fixed

costs obligation inside the capital structure. It might, consequently, figure obligation greatness connection

by isolating all out complete obligation by capital utilized on internet resources. All out obligation can

exemplify short and since quite a while ago run borrowings from cash foundations, debentures/protections,

installment arrangements for getting equipment's, bank borrowings, public stores and the other fixed costs

advance. Capital utilized can exemplify all out obligation web esteem.

2. DEBT EQUITY RATIO: The all-out obligation value extent connection gives the sign of the capital

structure and shrinks the organization is additional sharp about borrowings (obligation) or speculators

capital (equity)to reserves quality and movement. Lower the obligation value size connection, higher the

quantity of insurances. An obligation value extent connection of 2:1 is enumerable deals. The obligation

incorporates of all present moment in addition as longstanding time and value contains total assets and

inclination capital and deferred liabilities.

3. INTERSEST COVERAGE RATIO: The interest inclusion extent connection or the time interest got

used to check the organizations' obligation association ability. The premium inclusion greatness

connection is devastated by partitioning profit before interest and costs by interest charges. The interest

inclusion extent connection shows the events the interest charges unit lined by reserves that customarily

exist for their installment. we'll compute the premium inclusion greatness connection as profit before

deterioration, interest and duties isolated by interest.

4. PROPRITERY RATIO: Proprietary magnitude relation shows the link between shareholders fund to

total quality of the priority the shareholders fund is equity share capital, and distributed capital, reserve and

overflow, accumulated loss. got to be deducted from this total the complete quality denotes the complete

reserve of the priority. The magnitude relation is of nice implication to creditors since it permits them to

46

fund out the magnitude relation of shareholders’ funds at intervals the entire investment of trade.

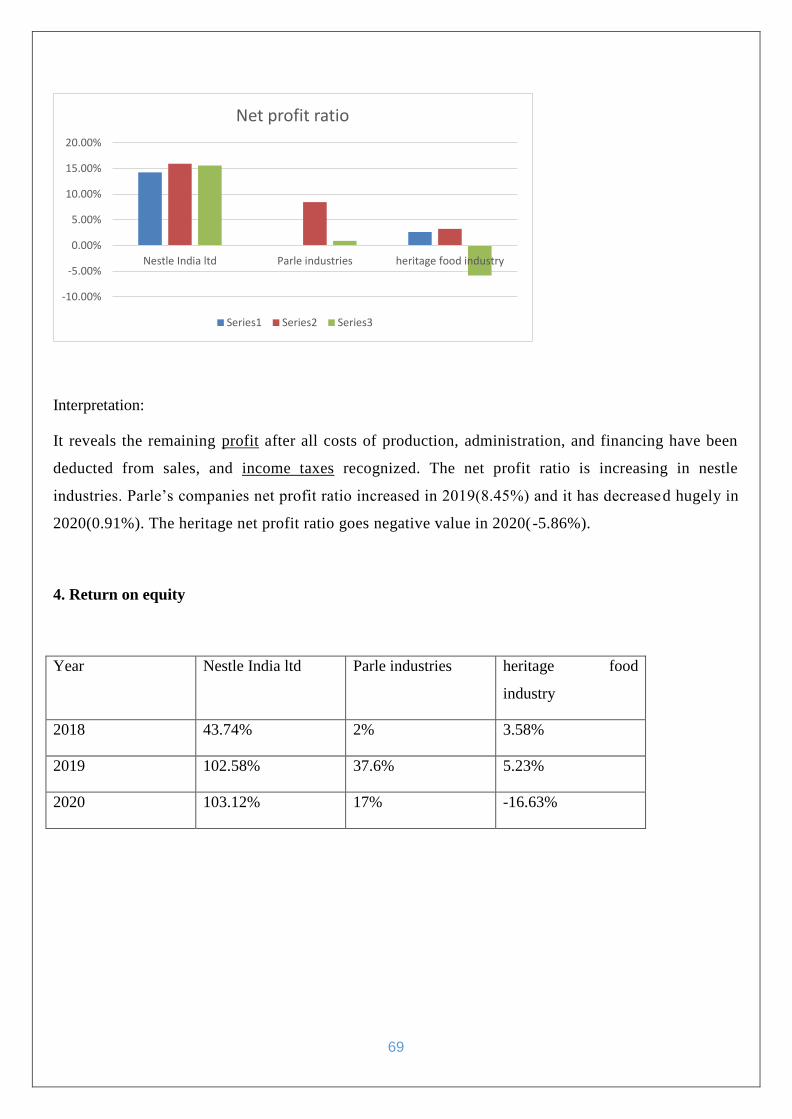

5. PROFITABILITY RATIOS: Gain magnitude relation live overall performance and effectiveness of the

firm. The Management of the firm is after all wanting to live its operational efficiency. The efficiency of a

firm and its ability to substantiate adequate returns to its shareholders depends ultimately on the profits

earned by it. Creditors ought to be compelled to urge interest and compensation of principal usually.

Proprietors starvation to induce a required rate of come on their investment. The most common gain

quantitative relations are:

1) lucre magnitude relation

2) profits magnitude relation

3) Earnings per share magnitude relation

4) come on shareholder’s fund magnitude relation

5) operational profit

1. LUCRE RATIO:

First gain magnitude relation in relative to sales is that the lucre margins the lucre margin reflects. The

efficiency thereupon the management product every unit of product. This magnitude relation determines

the everyday unfold between the worth of merchandise oversubscribed and conjointly the sales revenue. A

high magnitude relation is that the image of fine management. A margin of profit magnitude relation might

upsurge thanks to any of following elements: higher sales prices price of merchandise oversubscribed

extraordinary consistent, lower price of merchandise oversubscribed, sales price remaining constant. an

occasional lucre margin might replicate higher price of merchandise oversubscribed because of inability to

urge raw materials at constructive terms, inefficient utilization of plant and machinery resulting in higher

price of production or because of fall in costs in market. This magnitude relation shows the sting left at

intervals the wake of meeting producing costs. It measures the effectiveness of production moreover as

rating.

2. PROFITS RATIO:

Net profit magnitude relation (NP ratio) communicates the link between profits once taxes and sales. This

magnitude relation could also be a live of the gain profits is found out once taking into thought the

operational and non-operating product of incomes and expenses. The magnitude relation indicates what

portion of financial gain is left for the householders in any case expenses square measure met. This

magnitude relation the earning left for shareholders as a proportion of financial gain. It measures overall

efficiency of production, management, selling, financing, rating and tax management.

47

3. OPERATING RATIO:

This magnitude relation communicates the link between operational profit and sales. it's functioned out by

dividing operational profit by financial gain. With the assistance of this magnitude relation, one can opt for

the chief efficiency which may not be reflected at intervals the profits magnitude relation.

4. EARNING PER SHARE:

The company profit per share (EPS) magnitude relation enable uSSs. to measure earnings in connexion

every share on issue. This magnitude relation is importance as a result of as a capitalist space unit your

owner in associate company every share is reflective of this EPS demonstrates what proportion every offer

you own has procured (or) will earn if we've got a bent to square measure relating prospective EPS.

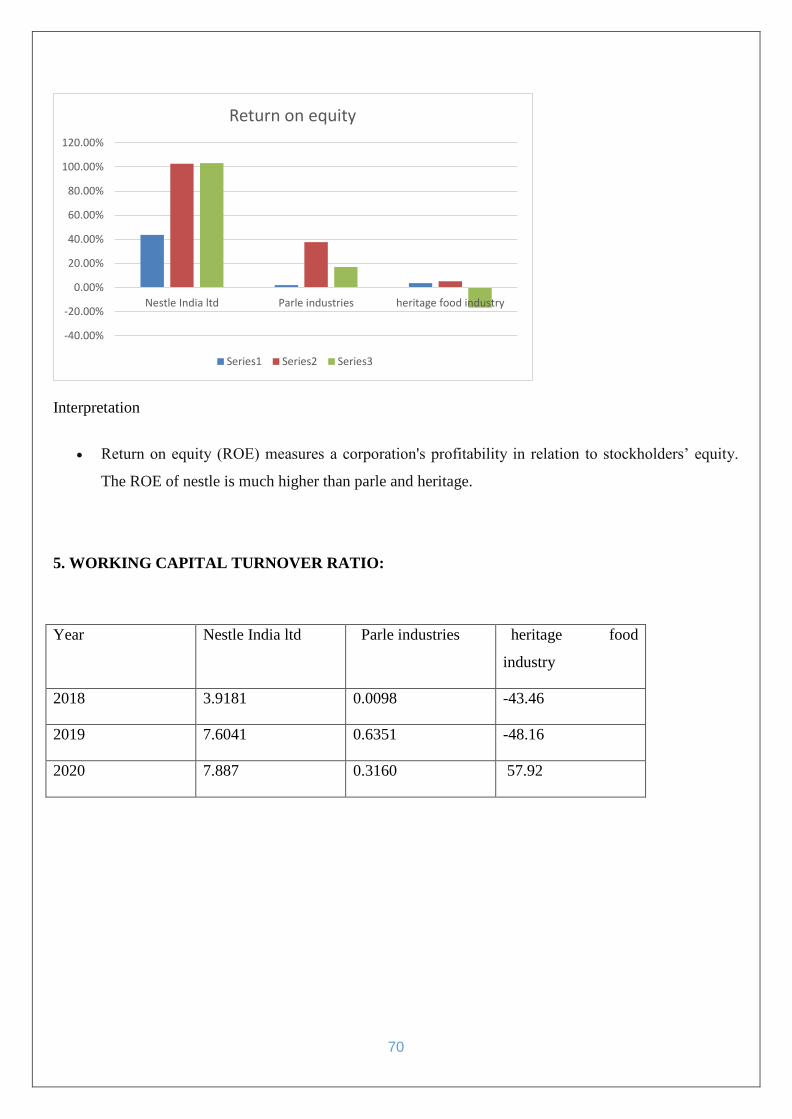

5. COME ON SHAREHOLDERS INVESTMENT RATIO:

Profit for investors' venture greatness connection could likewise be a live of by and large addition of the

exchange and is figured by isolating web acquire once revenue and duty by normal investors' value. it's

generally named as gone ahead all out value (ROTE) size connection and are accessible back on total

assets extent connection. The size connection is frequently communicated in extent.

6. DIVIDEND PAYOUT RATIO: Dividend pay-out magnitude relation discloses what portion of this

earnings the company is paying to its stockholders at intervals the fashion of dividend and what portion the

company is cultivation back at intervals the trade for growth in future. it's computed by dividing the

dividend per share by the earnings per share (EPS) for a selected quantity.

7. ACTIVITY MAGNITUDE RELATION OR TURNOVER RATIO: Movement extent connection are

included anyway quickly the resources of the firm are dealt with these proportions absolute connection

between the level of deals and interest in various resources inventories, resources, mounted resources, and

so on Action proportions are locked in to check the intensity with that the firm oversees and endeavor its

resources. the higher administration of furthermore, and hence the bigger amount of deals. These

proportions are otherwise called flip over proportions because of they show the speed with that resources

are reawakened into deals.

The most common turnover magnitude relations are:

1) Debtors turnover ratio

2) Credit turnover magnitude relation

3) assets turnover magnitude relation

4) Total plus turnover magnitude relation

5) Inventory turnover magnitude relation

48

1. DEBTORS TURNOVER RATIO: The assets turnover magnitude relation, additionally called the

debtor’s turnover magnitude relation, is Associate in Nursing potency magnitude relation that estimates

however expeditiously an organization is utilizing its assets. The assets turnover magnitude relation

measures the number of times over a given amount that an organization collects its average assets.

2. CREDIT TURNOVER RATIO: The indebtedness turnover magnitude relation, otherwise known as the

liability’s turnover or the creditors turnover magnitude relation, may be a liquidity magnitude relation that

measures what number times an organization

Pays its creditors over Associate in Nursing accounting amount. The accounts owed turnover magnitude

relation may be a live of short liquidity, with the next owed turnover magnitude relation being a lot of

favourable.

3. ASSETS TURNOVER RATIO: The assets turnover magnitude relation is additionally brought up as

income to assets. It indicates a company’s effectiveness in utilizing its assets. The assets turnover

magnitude relation is calculated as follows: internet annual sales divided by the common quantity of assets

throughout the same 12-month amount.

4. TOTAL PLUS TURNOVER RATIO: The plus turnover magnitude relation may be a potency

magnitude relation that measures a company's ability to come up with sales from its assets by scrutiny

income with average total assets. At the tip of the day, this magnitude relation shows however

expeditiously an organization will utilize its assets to come up with sales.

5. INVENTORY TURNOVER RATIO: The inventory turnover magnitude relation is Associate in nursing

potency magnitude relation that shows however effectively inventory is managed by scrutiny value of

products sold-out with average inventory for an amount. This measures what number times average

inventory is "turned" or sold-out throughout an amount.

49

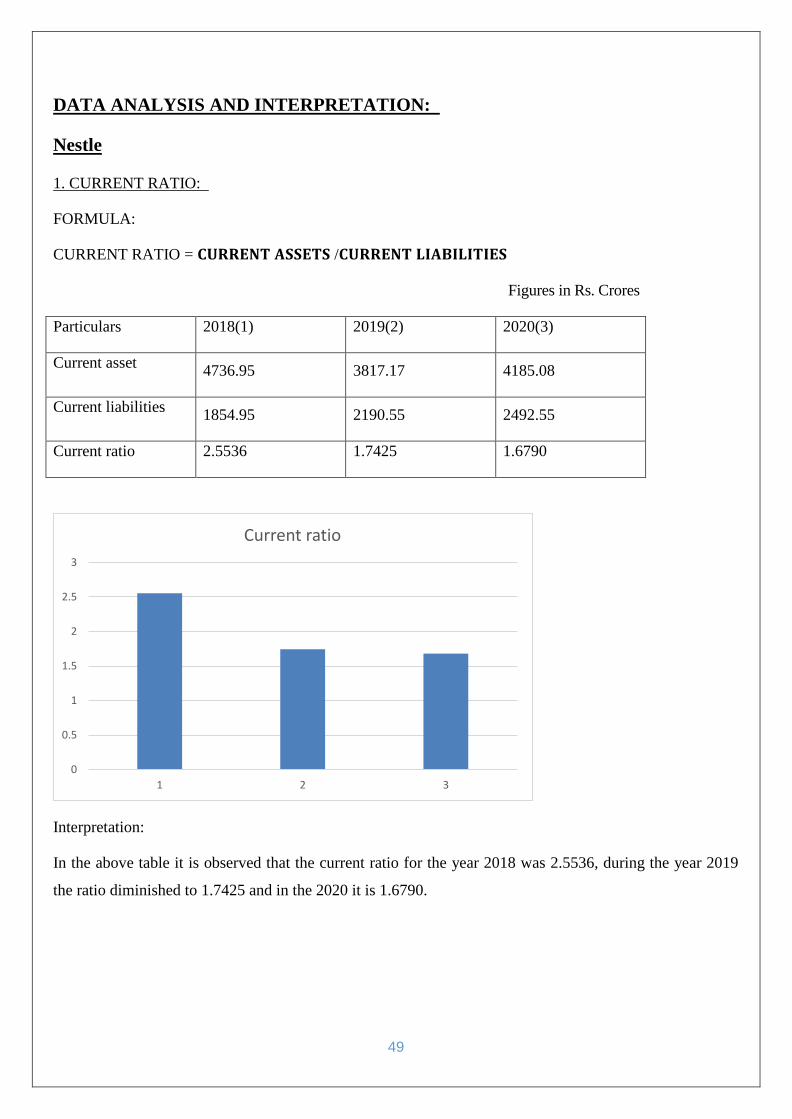

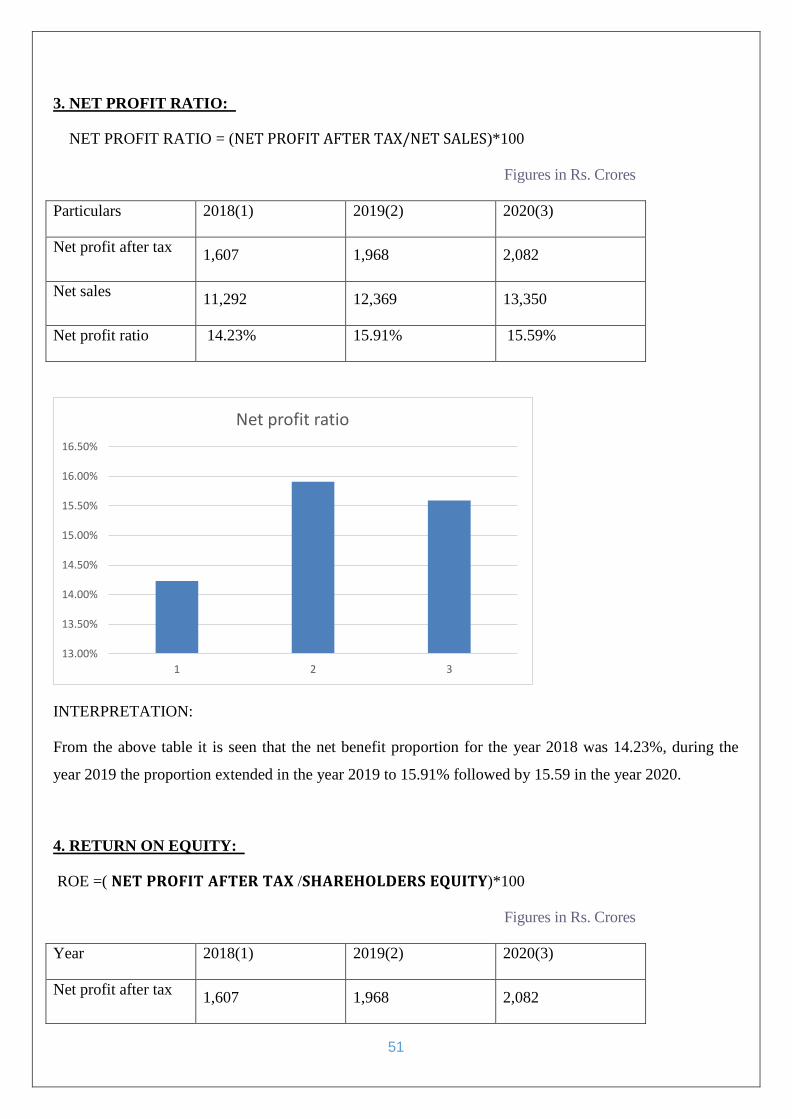

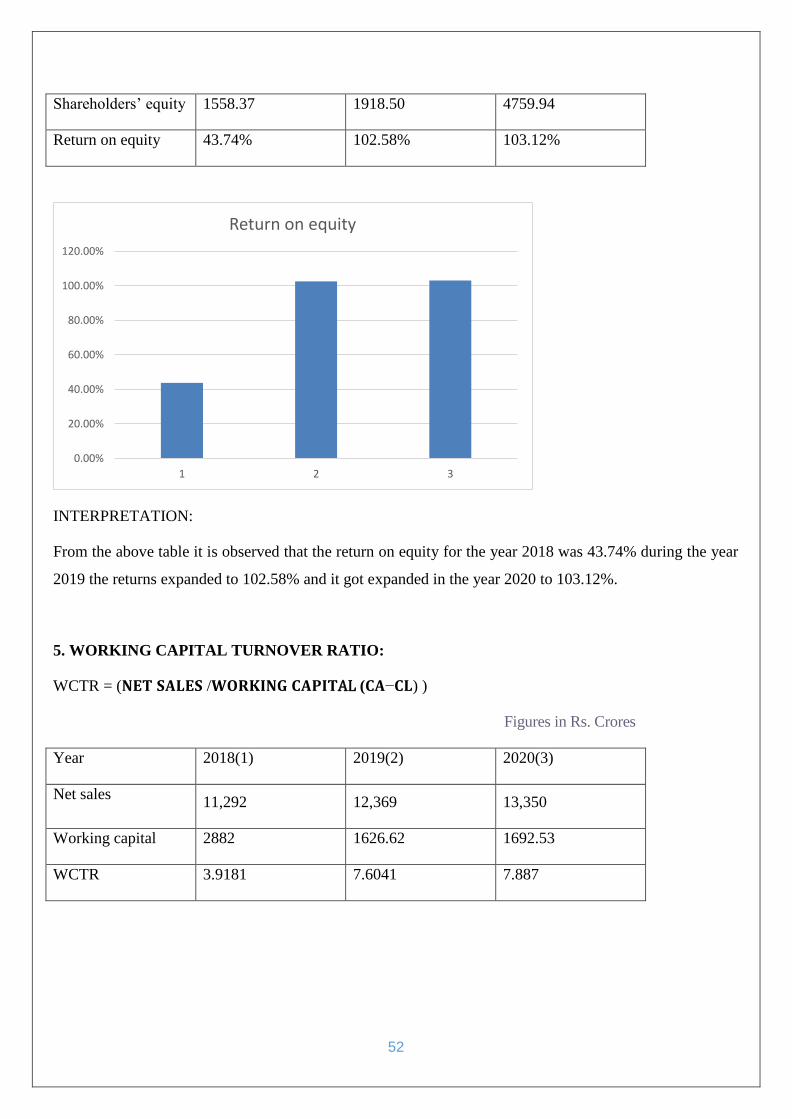

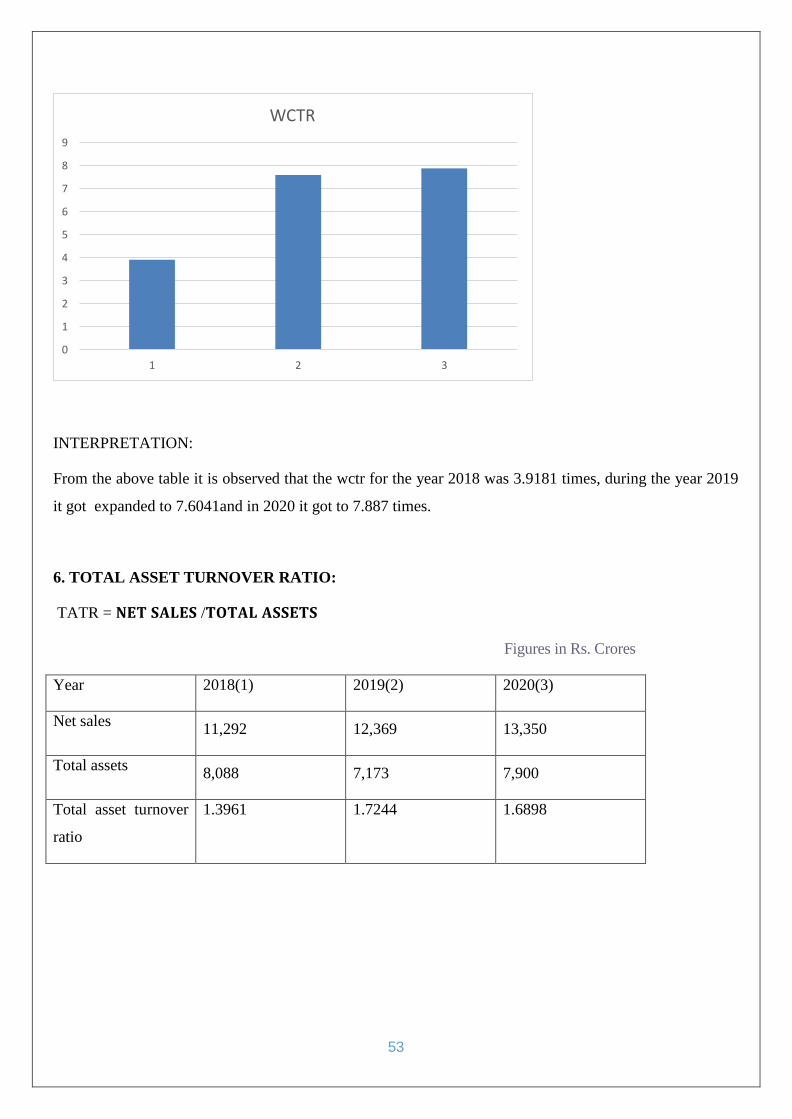

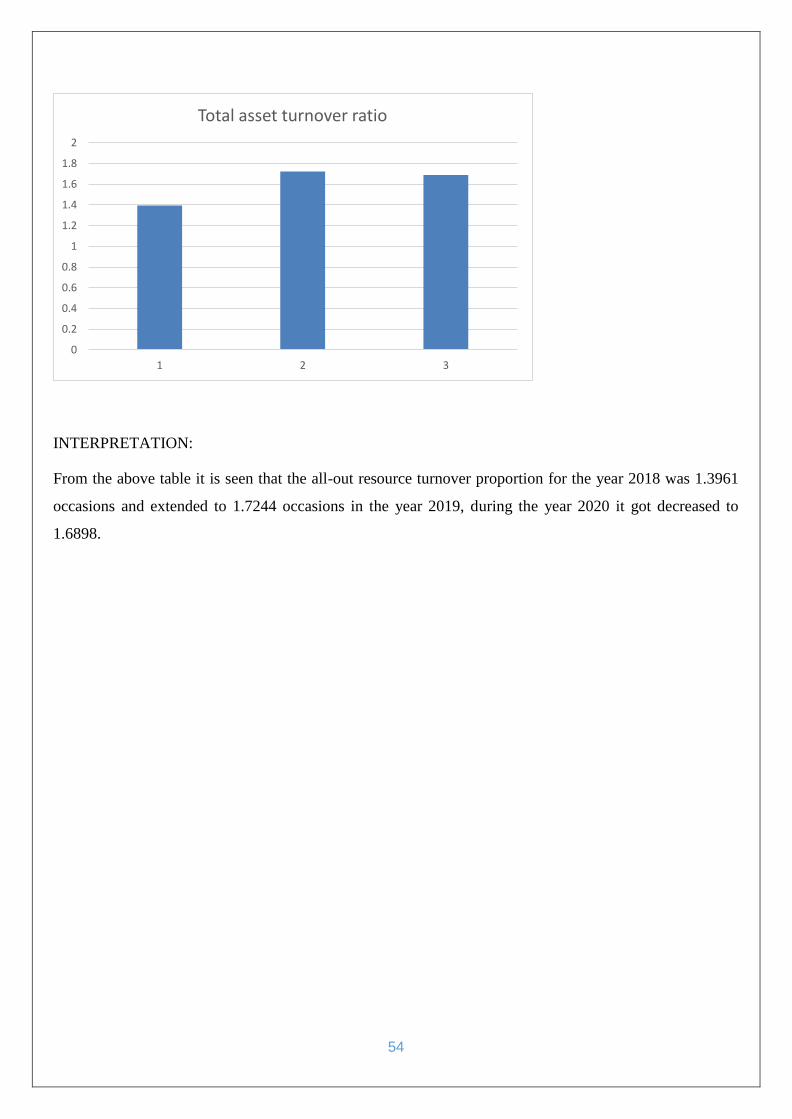

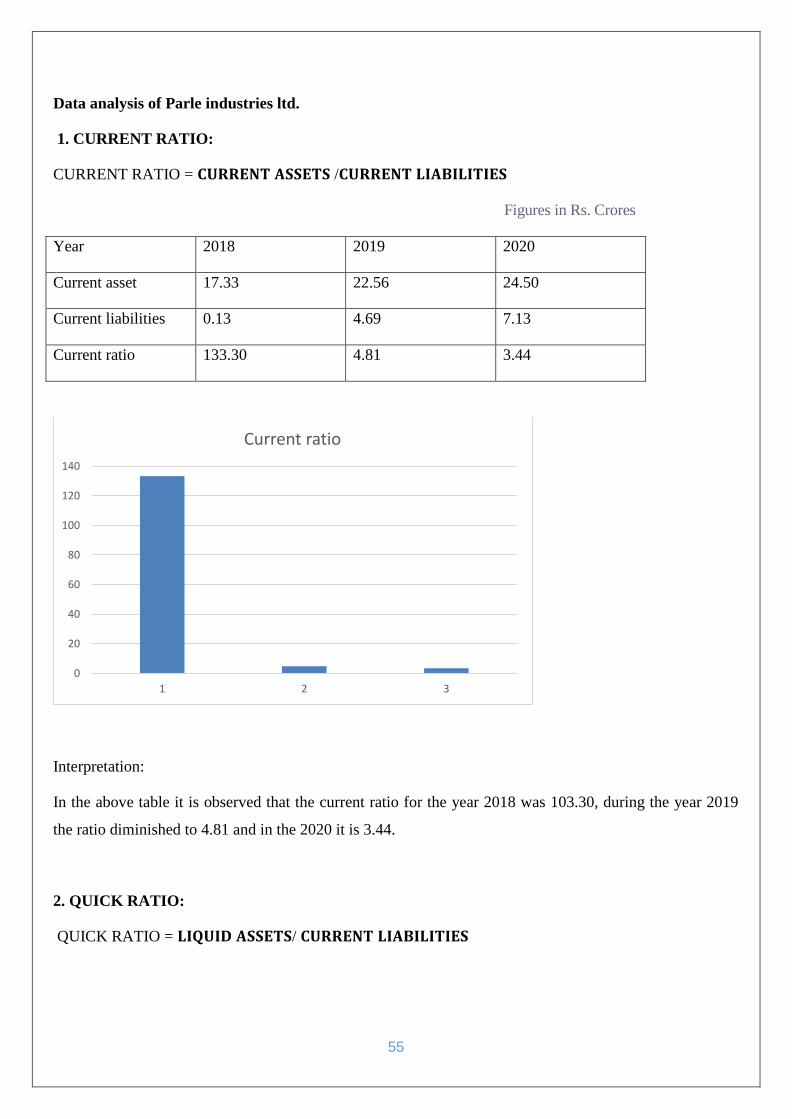

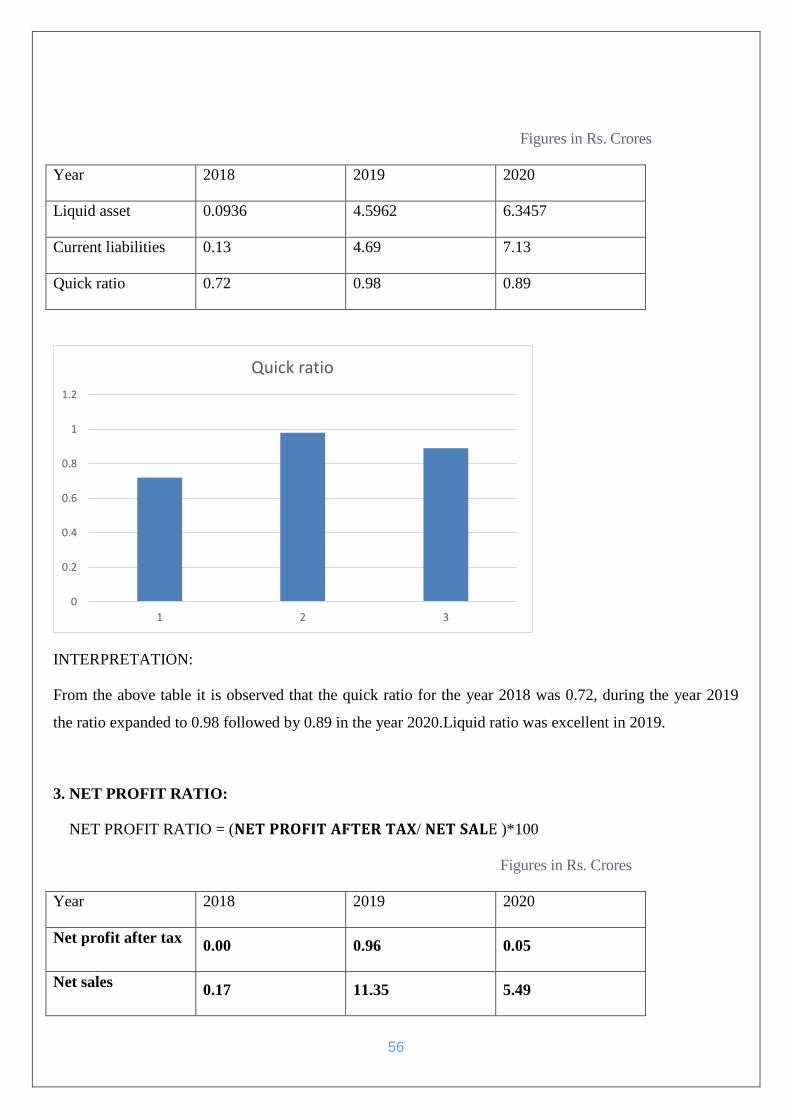

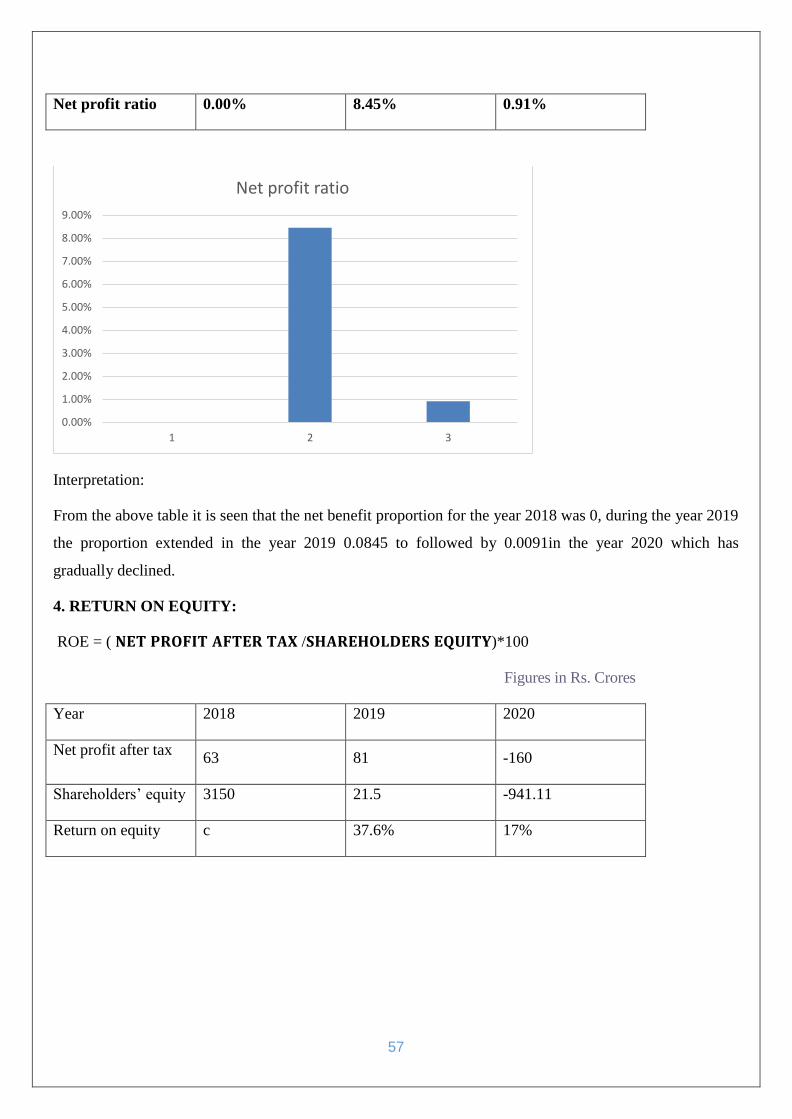

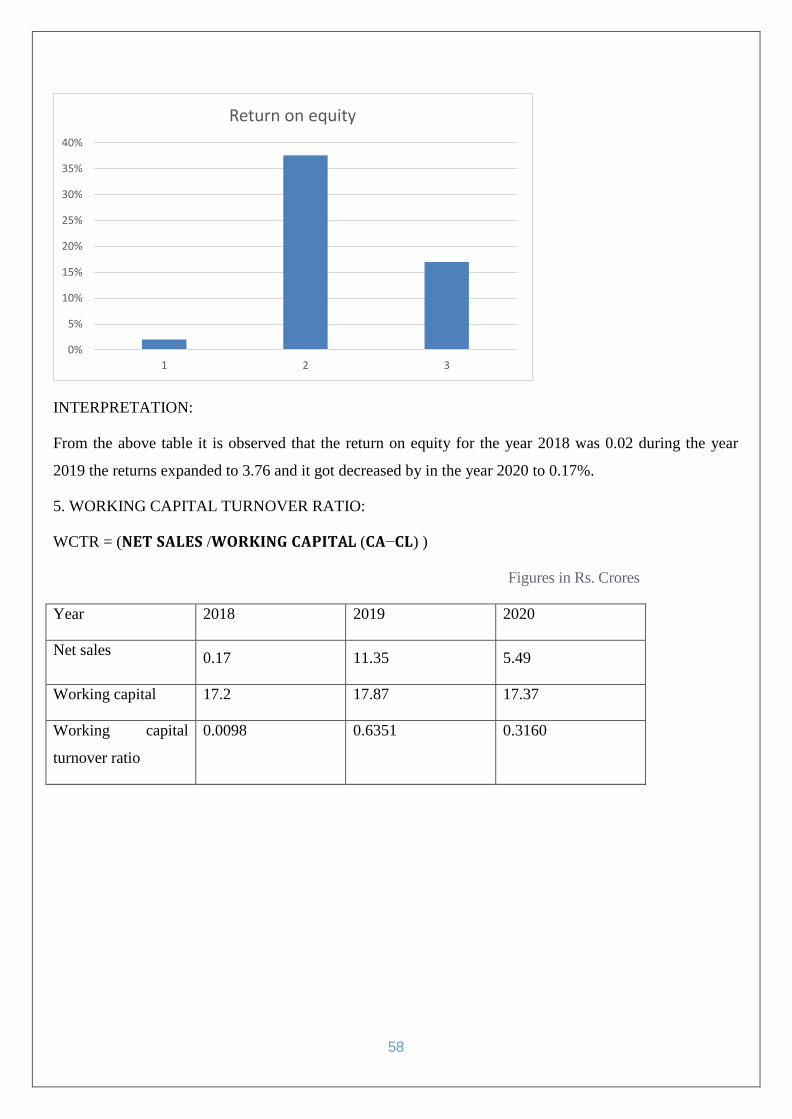

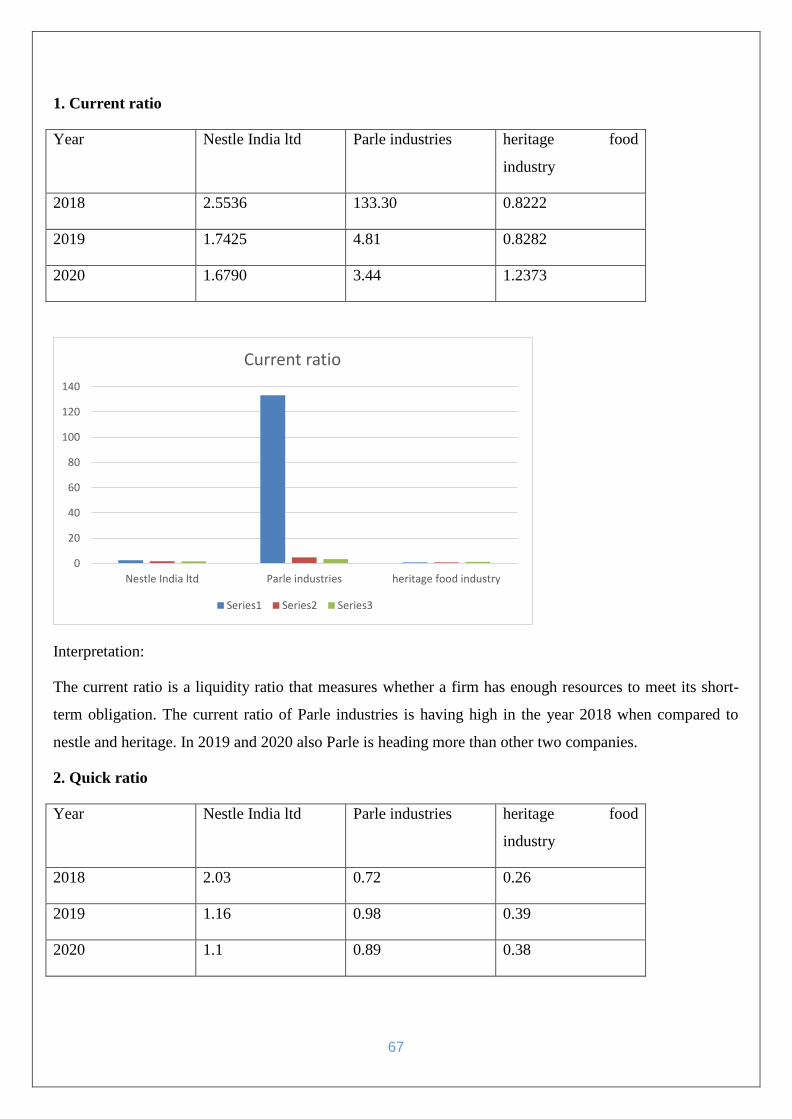

DATA ANALYSIS AND INTERPRETATION:

Nestle

1. CURRENT RATIO:

FORMULA:

CURRENT RATIO = 𝐂𝐔𝐑𝐑𝐄𝐍𝐓 𝐀𝐒𝐒𝐄𝐓𝐒 /𝐂𝐔𝐑𝐑𝐄𝐍𝐓 𝐋𝐈𝐀𝐁𝐈𝐋𝐈𝐓𝐈𝐄𝐒

Figures in Rs. Crores

Particulars 2018(1) 2019(2) 2020(3)

Current asset 4736.95 3817.17 4185.08