regional decentralization and fiscal incentives: federalism, chinese style

TRANSCRIPT

Regional Decentralization and Fiscal Incentives:

Federalism, Chinese Style1

Hehui JinDepartment of Economics

Stanford University

Yingyi QianDepartment of Economics

University of Maryland

and

Barry R. WeingastHoover Institution and

Department of Political ScienceStanford University

January 2000

Abstract

The theory of market-preserving federalism stresses the importance of decentralization andincentives of government on market development. Using a panel data set, we investigate thecentral-provincial relationship during China's reform process. [In comparison with the pre-reformperiod,] we find much stronger correlations between local government budgetary revenue collectionand its budgetary expenditure under the implementation of "fiscal contracting system." *comparedwith the pre-reform period.* We also find that more fiscal decentralization and stronger fiscalincentives — the latter measured in terms of higher (ex ante) marginal local *budgetary* revenueretention rate — implies faster development of non-state enterprises and more reform in state-ownedenterprises, while the Party's control over appointment has opposite effects. However, the Party'scontrol is effective in restricting local government's investment but ineffective in curbing local creditexpansion, suggesting that the Party's control had played some, but limited, role in helpingmacroeconomic stability. We also compare federalism, Chinese style, to federalism, Russian style.

1 We would like to thank Roger Gordon, Yasheng Huang, John McMillan, Peter Murrell, Gerard Roland,Andrei Shleifer, Heng-fu Zou, and the participants at the Fifth Nobel Symposium in Economics for helpfulcomments and discussions and the Center for Research on Economic Development and Policy Reform at Stanfordfor financial support.

1

I. Introduction

Reforming the government is a crucial component of both the transition from a planned

to a market economy and economic development. Creating thriving markets in these

economies typically require transforming a highly centralized and interventionist

government into one that complements the market and fosters decentralized economic

activities. Democracy, separation of powers, and the rule of law are among the

important institutions that allow citizens to hold the government accountable for its

economic actions and to secure markets from arbitrary state intrusion. Yet in many

countries, these institutions are incomplete or absent altogether, raising questions about

how these states can improve their governance structures. In this paper, we study

federalism as an alternative approach. By devolving power from the central to local

levels, federalism may help implement a limited yet effective government.

Traditional theories of federalism emphasize allocative benefits of

decentralization in public goods and services. There are two related ideas. First,

according to Hayek's (1945) idea on the use of knowledge in society, local

governments have better access to local information, which allows them to provide

public goods and services more efficiently than the national government. Second,

Tiebout (1956) introduced the inter-jurisdictional competition dimension and argued

2

that such a competition provides a sorting mechanism to better match public goods and

services with consumers' preferences. Drawing on these ideas, Musgrave (1959) and

Oates (1972) built a theory of fiscal federalism, stressing among other things the

appropriate assignment of taxes and expenditures to the various levels of government

to improve welfare. They also suggested that inappropriate decentralization may

induce a range of allocative distortions, regional inequality, and fiscal instability.

Extending the traditional theory, the recent theory of "market-preserving

federalism" emphasizes additional benefits of decentralization, which appear to be

especially important for transition and developing economies (McKinnon, 1997; Qian

and Roland, 1998; Qian and Weingast, 1997; Weingast, 1995; and Wildasin, 1997).

[Paralleling several other recent studies of public incentives under federalism, these

works stress:] the importance of decentralization of authority and the incentives of

governments [( Buchanan and Brennan, 1980; Epple and Zelenitz, 1981; Inman 1988;

and Inman and Rubinfeld, 1997)]. This theory focuses on how the inter-governmental

relationship affects the government's behavior toward business enterprises and market

development. The issue of aligning government incentives with promoting markets is

especially acute for transition economies just emerging from central planning. In these

countries, as in developing countries generally, economic development depends

crucially on whether the government plays the role of the "grabbing hand" or that of the

3

"helping hand" vis-a-vis business enterprises (Shleifer and Vishny 1999). The theory

of market-preserving federalism suggests how and when federalism can serve as a

means of limiting the grabbing hand and encouraging the helping hand of governments

in these countries.

Lacking democracy, the rule of law, and other constitutional constraints on the

national government, China's transition to markets has long been associated with the

devolution of authority from the central to local governments (Montinola, Qian, and

Weingast, 1995; Chang and Wang, 1998; Oi 1999, Xu and Zhuang, 1998). Using a

provincial data set from 1982 to 1992, we study empirically the emergence of the

Chinese style of federalism from the perspective of market-preserving federalism. As

far as we know, we are the first to include in the data the ex ante marginal rates of local

revenue retention. *Data on the ex ante, or promised, sharing schemes are indeed much

harder to come by. Yet* [Although this data is difficult to obtain,] we think it is the

right variable for studying the effects of incentives on the margin[. I]n contrast, the

more readily available data on the ex post ratios of revenue retention over collection

only measures the average realized revenue retention.

Our first major finding concerns the change of fiscal incentives facing local

governments. In examining the implementation of the "fiscal contracting system"

between the central and provincial governments, we find that the discrepancy between

4

ex ante contracts and ex post implementation declined over time and was *not too big*

[relatively small] on average. The implementation of the fiscal contracting system has

immediate implications on the fiscal incentives faced by local governments. We find,

on average, a strong correlation between ex post provincial budgetary revenue

collection and expenditure in post-reform period, about four times as large in the

magnitute as before the reform. Our finding also reveals a substantial reduction in the

ratchet effect after the reform as compared to the pre-reform period. [Put simply, in the

pre-reform period, the central government reacted to higher local revenues this year by

requiring higher remittances next year; in the post-reform period, this ratchet effect is

far smaller.]

Our second major finding concerns the effects of fiscal decentralization, fiscal

incentives, and the Party's control over local government official appointment[s] on

provincial economic development and reform. We find that, across provinces and over

time, more fiscal decentralization and stronger fiscal incentives — the latter measured

in terms of higher (ex ante) marginal local revenue retention rate — positively affect

the development of non-state enterprises in terms of the growth of rural or total non-

state enterprise employment. {YQ: I removed a “they” here and replaced it with my

guess at the appropriate antecedent. If I’m wrong, please fix:} In addition, more fiscal

decentralization and stronger fiscal incentives *they* also induce more reforms in state-

5

owned enterprises in terms of the increased shares of contract workers in the total state

employment and bonuses in total employee wages. On the other hand, we find that the

Party's control over personnel has the opposite effect: closer integration of provincial

officials with the central government — indexed by their career background vis-a-vis

the central government — entails slower development of non-state enterprises and less

reform in state enterprises.

Although the Party's control plays a negative role in promoting provincial

economic development and reform, {YQ: is this accurate?:} [following Huang (1996)]

we find some evidence suggesting that it may have helped macroeconomic stability.

Specifically, stronger association of provincial officials with the central government

implies a more restricted expansion of local government-driven investment that [many]

viewed as a source of macroeconomic instability during the period we study. [We also

show that] the Party's control is ineffective in curtailing the expansion of bank credit,

another source of macroeconomic instability. This [instability] constitutes a main

reason for the later monetary reform.

We compare Federalism, Chinese style, with Federalism, Russian style. Recent

studies of Russia's transition stress the problematic role of the government in reform.

Shleifer (1997) and Frye and Shleifer (1997), for example, provide evidence that local

governments in Russia have been playing the role of "grabbing hands" that retard

6

private business development. Zhuravskaya (2000) finds that the existing revenue

sharing schemes between the Russian regional and local governments provide the latter

with no fiscal incentives to increase their tax base: increases in local government

revenues were almost entirely exacted by the regional government. It is the lack of

fiscal incentives that explains why local government is predetory on private businesses.

This contrast in incentives faced by local governments presents a partial

explanation for the different performances of the Chinese and Russian reforms.

Interestingly, Russia has done more than China in terms of privatization of state-owned

enterprises and liberalization of markets. But apparently it has failed to provide local

governments with good incentives to pursue local prosperity. Our perspective suggests

the critical importance of government incentives for successful reform. Liberalization

and privatization without altering government incentives are insufficient to produce

meaningful economic reform.

To our knowledge, there are only few empirical studies on the effects of fiscal

federalism on economic and government performance. Using the data from both the

U.S. states and the world, Oates (1985) tested Brennan and Buchanan's (1980)

hypothesis that the size of the public sector should vary inversely with the extent of

fiscal decentralization and only found very weak supporting evidence. Huther and Shah

(1998) assembled a sample of 80 nations to examine the relationship between fiscal

7

decentralization and a series of measures of economic and political performance (such

as debt-to-GDP ratio, quality of government, and political freedom). In nearly every

case, they found a significant and positive correlation between increased fiscal

decentralization and improved performance. We will review several recent studies on

China's fiscal federalism later.

The remainder of the paper is organized as follows. Section II describes the

central-local relationship during China's reform. Section III develops our theoretical

perspective. Section IV describes the data and the construction of variables. Section

V presents evidence on the implementation of the fiscal contracting system and the

resulting fiscal incentives for local governments. Section VI presents evidence on the

effects of fiscal decentralization, fiscal incentives, and the Party's control over

personnel. Our conclusions follow.

II. Regional Decentralization and Fiscal Contracting during China's Reform

A. Regional Decentralization during the Reform

8

China's government administration (and its fiscal system) has five levels: (1)

central; (2) provincial; (3) prefecture; (4) county; and (5) township.2 We refer to all

subnational governments as local governments in this paper in general, but in the

empirical sections we refer to provincial governments as local governments.

2 Below the township level, the village is an informal level of government. A municipality can be one of thelevels of a province, prefecture, or county; most municipalities are at the prefecture level.

Since 1979, devolution of economic authority from the central to local

governments has been a critical component of [Chinese] reform. Because of the legacy

of central planning, the government had comprehensive control over the economy.

Therefore, devolution of government authority from the central to local levels is a much

broader issue than fiscal affairs. First, local governments supervise about three quarters

of the state industrial firms[, as measured by] *with regard to* output; they also have

a major responsibility for state fixed investments. Second, local governments assume

primary authority to regulate the local economy, such as licensing, defining the scope

and role of non-state firms, coordinating urban development plans, and even resolving

business disputes. Third, local governments provide an array of local public goods,

9

such as schools, health care, culture, police, as well as infrastructure and other support

for economic development. For example, they play an important role in attracting

foreign investment into their localities.

Before the reform, the shares of local government expenditure in total

government expenditure were 46% for 1971-75 and 50% for 1976-80. After the

reform, the shares were 51% for 1981-85 and 60% for 1986-90. Only a few countries,

such as Switzerland and the United States, have a share of local government spending

as total government spending above 40 percent. On average, the share for

industrialized countries is 34 percent and, for developing countries, 22 percent (World

Bank, 1996). Therefore, by this measurement of decentralization alone, China has

always been very decentralized as compared to other countries.

However, the share of local government expenditures itself does not capture the

important aspects of reform and decentralization in China. Prior to the reforms, local

governments had no authority over the structure of local expenditures. After the

reforms, local governments acquired authority over expenditures within a broad set of

guidelines set by the central government. In particular, ministries at the central level

could no longer issue mandatory spending targets for provinces. Provinces also gained

the authority to decide on the fiscal arrangements with the sub-provincial governments

within the provinces (Oksenberg and Tong, 1991). Given that the local government has

10

the authority over its spending structure, the higher the share of local spending in total

government spending, the more the fiscal decentralization.

Despite decentralization in the fiscal and economic spheres, China [remains]

*has been, and still is,* under the one-party political system. The essential channel of

the Communist Party's control is its continued monopolistic political power over the

appointment and dismissal of government officials. In particular, the central

government, through the Party, selects top provincial officials. In terms of the

allocation of authority over appointing and dismissing local government officials, there

is no fundamental change before and after the reform.

[Nonetheless, the central government has used its appointment powers

differently since the initiation of reform.] *However,* Local government officials

appointed by the central government are far from homogeneous. [Local government

officials vary considerably in a range of characteristics, both cross-regional and over

time.] Some *of them* [officials] have deeper roots in their localities because they are

promoted from within the provinces. Others are more loyal to the central government

because they serve concurrently in the central government or because they are

transferred from the central government ministries or Party apparatus. {rewrote this

sent:} Not only does the effective influence of the central government over provincial

11

government policy vary with the characteristics of local government officials, but

provincial government officials' local knowledge and networks also differ.

B. The Fiscal Contracting System

China's decentralization involved more than just the devolution of government

authority. It also involved changes concerning how revenue is divided between central

and local governments through a major institutional innovation called the "fiscal

contracting system" (caizheng chengbao zhi) introduced between 1980 and 1993.

Government revenue in China falls into two categories: budgetary funds and

extra-budgetary funds.3 Budgetary funds include major taxes and some surcharges.

Up to 1994, all budgetary revenues except custom's duties were collected by local

governments and shared upward with the central government. In 1980, reforms put into

place the fiscal contracting system, which is also known by its nickname "eating from

separate kitchens" (fenzao chifan). This system represents a dramatic departure from

the previous system of "unified revenue collection and unified spending" (tongshou

tongzhi), or what is known as "eating from one big pot" (chi daguofan). The previous

system provided few incentives for the local governments to collect revenues or

3 The third category is off-budget funds (also known as "self-raised funds"), which include surcharges, userfees, and other types of fees. Because they are not recorded, we cannot include them in the research.

12

develop their local economies. The new system altered the vertical relationships

between the central and provincial governments. The local governments not only had

the authority over local expenditures, more importantly, they also entered long-term

fiscal contracts (typically five years) with the central government. [Two rationales

underlie] the new fiscal contracting system: [it was] intended [first] to guarantee the

central government a certain flow of revenue from local governments; *on the one hand

and* [and second] to provide local governments with incentives to build up local

economies and their revenue base on the other.

Under the fiscal contracting system, the central and provincial revenue and

expenditures were determined in three steps (Wong, 1997). First, central fixed revenue

was defined to include custom's duties, direct tax or profit remittance from the central

government supervised state-owned enterprises (SOEs), and some other taxes. All

other revenue falls under the heading "local revenue."

Second, the local revenue was divided between the central and provincial

governments according to pre-determined sharing schemes. These schemes evolved

through three phases. The first phase ran from 1980 to 1984, the second from 1985 to

1987 (transitional), and the third from 1988 to 1993. These sharing schemes vary

across provinces and over time. For example, between 1980 and 1987, Guangdong

province would remit a fixed amount per year, and between 1988 and 1993, it would

13

remit an amount that increased by a fixed 9 percent per year. Guizhou province would

receive subsidies which increased by a fixed 10 percent per year. On the other hand,

Jiangsu province would remit a fixed share of revenue to the central government. Over

time, many provincial governments retained 100 percent of the total local revenue at

the margin, which effectively made them residual claimants.

Third, after the division of local revenue according to the sharing schemes, some

extra remittance and transfer payments took place between the central government and

the provinces. For example, the central government sometimes "borrowed" from the

provinces. It also made additional transfer payments (not specified in the sharing

schemes) to provinces, which generally fell into two categories: earmarked subsidies

(zhuanxiang butie), the most important one is price subsidies for urban residents

compensating them for food price increases, and matching grants (peitao buokuan),

such as funds for highway building. {I rewrote this sent:} Of course, the larger this type

of ex post redistribution, the less important the pre-determined revenue sharing

schemes.

The second revenue category, [called] extra-budgetary funds, consists of tax

surcharges and user fees levied by central and local government's agencies, as well as

earnings from {YQ: is this all SOEs or just those under the local government’s

jurisdiction?:}SOEs. The extra-budgetary revenue emerged in the 1950s but only

14

became institutionalized after the reform. Unlike the budgetary local revenues, the

extra-budgetary local revenues are not subject to sharing with the central government,

although the latter may impose taxes on them. In 1978, total extra-budgetary revenue

was about 10 percent of the GDP while total budgetary revenue was about 31 percent.

In 1993, the extra-budgetary revenue was up to 16 percent of the GDP and the

budgetary revenue was down to 16 percent of the GDP (Statistical Yearbook of China,

1995). While about three-quarters of the extra-budgetary funds are retained earnings

by SOEs and by their supervisory government agencies at the central and local levels,

at least 30 percent of the extra-budgetary funds are used for government expenditures

to supplement the budgetary funds (Fan, 1996).

III. Transition to Markets and the Theory of Market-Preserving Federalism

A fundamental issue in transition economies (and, to a large extent, developing

economies) is reorienting the role of government from one that commands and controls

the economy to one that fosters decentralized markets. However, private initiatives and

market development will not emerge automatically unless the government stops playing

the "grabbing hand." On the other hand, they will flourish faster if the government

plays the "helping hand." Whether the government plays one role or the other depends

15

on the institutional constraints [it faces.] *imposed upon the government.* In mature

market economies, the rule of law, separation of powers, and democracy are all

important institutions to make the government accountable. In many transition or

developing countries, in contrast, these liberal mechanisms are incomplete or absent

altogether. Federalism, with the vertical division of power within the government, is

an alternative to provide the credible limits on government behavior.

Not just any form of federalism will do (Parikh and Weingast, 1997). In

particular, federalism needs to be structured to insure local government authority and

proper incentives. Building on many previous contributions (e.g., Buchanan and

Brennan, 1980; Epple and Zelenitz, 1981; Inman 1988; and Inman and Rubinfeld,

1997), the theory of market-preserving federalism stresses the appropriate institutional

arrangement of government decentralization and its effects on market development

(McKinnon, 1997; Qian and Roland, 1998; Qian and Weingast, 1997; Weingast, 1995;

and Wildasin, 1997). In the Chinese context and during the period we study, the major

development event is the fast growth of "non-state enterprises," which include both

private and "collective" enterprises, the latter are in effect local government enterprises.

At the same time, reforms were also carried out inside state enterprises without

privatization. These reforms include the introduction of bonuses to supplement fixed

16

wages to enhance the incentives of employees and the increased number of workers

hired on the term rather than permanent basis.

How does market-preserving federalism contribute to the market development?

The benefit from decentralization of authority is first due to the nature of dispersed

knowledge in the economy as Hayek stressed. Decentralization of government

authority makes better use of local information possessed by local governments. In

contrast, centralization of government authority is costly because information

transmission from local to central government is often distorted and incomplete.

Second, the case of decentralization also rests on the differences among people at the

central and local levels. Local government officials who have long worked in the

locality have more local knowledge about the environment and have better local

networks than the officials who were previously working at the central government.

Local government officials may also have different objectives from the central

government officials. For example, central government officials are far more concerned

about ideology than local government officials. Third, decentralization induces inter-

jurisdictional competition. Under centralization, the central government has monopoly

power of economic regulation. Under decenralization with goods and factor mobility,

competition rewards local governments friendly to markets as factors of production

17

move to their regions, while punishes heavily interventionist local governments which

lose factors of production.

Our first hypothesis is that the more decentralization of authority to local

governments, the faster the growth of the non-state sector and the more reform in state-

owned enterprises in the local economy. {YQ: I don’t follow that this next sent means:

it’s incomplete:} The converse is also true, the closer association of local government

officials with the central government.

But decentralization of authority *would be* [is] meaningless if the central

government takes away all *the* revenue [generated by] *that* local governments

*generate.* Conversely, the larger the marginal fraction of revenues a local government

is allowed to keep, the stronger the local government's incentives to increase its

revenue base, which in turn depends on local economic prosperity. This implies that

strong links between local expenditures and local revenue help align the interests of

local governments to local market development. Note that such links require limits on

inter-governmental fiscal transfers, in two directions — limits on central government

exactions from lower governments and limits on the central government's creation of

a soft budget constraint in the form of subsidies to fiscally imprudent local

governments.

18

Our second hypothesis is that the higher the marginal proportion of revenue

retained by the local governments, the faster the growth of the non-state sector and the

more reform in state-owned enterprises. Because onerous restrictions on enterprises

reduce their revenue, lower governments facing stronger fiscal incentives are likely to

impose fewer economic restrictions on and give more support for non-state enterprises.

Stronger fiscal incentives may lead local governments to restructure the state-owned

enterprises under their supervision, becuase poorly performing SOEs increase their

financial burden.

Although the market-preserving federalism theory stresses the important benefits

of decentralization, it does not consider a complete decentralization desirable. There

are certain areas, such as the supply of national public goods, where the authority needs

to be centralized. Decentralization of authority in monetary policy, for example, will

result in inflation, because it creates a free-rider's problem as each region would get the

full benefit of inflation but only bear a partial cost. In a mature federal system, the

federal government has a clear responsibility for the supply of national public goods.

In China, such a federal authority is absent. For example, China continued to rely on

an old institution — the Party control — to achieve the macroeconomic stability. Our

third hypothesis is that the Party's control over personnel appointment helps maintain

macroeconomic stability.

19

[To determine whether these hypotheses hold in practice requires empirical

data.] *These hypotheses need to be tested because the claimed effects do not always

come out naturally.* Decentralization may be ineffective, or worse, it may be

counterproductive because local governments use their newly acquired authority to

protect and exploit the local economy rather than expanding it. Provincial governments

may fail to respond to incentives. Or these incentives may result in more corruption

rather than more development. Finally, the Party control over appointment may not be

effective at all in maintaining macroeconomic stabilility because of the bureaucratic

delay or the crudeness of the instrument.

Although it extends the traditional theory of fiscal federalism, the theory of

market-preserving federalism differs from the former in important ways. One major

difference concerns the role of revenue transfers between the central and local

governments. While arguing for the benefits of decentralization of expenditure,

traditional fiscal federalism usually does not consider regional self-finance (i.e.,

requiring that local governments rely on their own tax revenue to finance their

expenditures) desirable because of possible allocative distortions under decentralized

revenue collection. This approach is often used to rationalize sizeable transfers from

the central to local governments in order to address vertical imbalances. *fill the gap

between decentralized expenditure and centralized revenue collection.* In contrast, the

20

theory of market-preserving federalism stresses the importance of governments'

incentives. For that purpose, it emphasizes the potential benefit of linking local

governments' revenue collection with their expenditure. {I reversed the clauses in this

sent and broke it in two:} This is especially important for economies *that just step out

of* [emerging from] the shadow of central planning. The pervasive revenue

redistribution in these economies destroyed both local governments' positive incentives

and their financial discipline.

IV. Data and Variables

In most of our empirical work, we use a panel data set of 29 provinces after the reform

from 1982 to 1992.4 For the purposes of comparison, we also use pre-reform

provincial revenue and expenditure data from the period from 1970 to 1979. We

obtained most of our data from the State Statistical Bureau (1997), supplemented by

data from various sources of official government publications at the national,

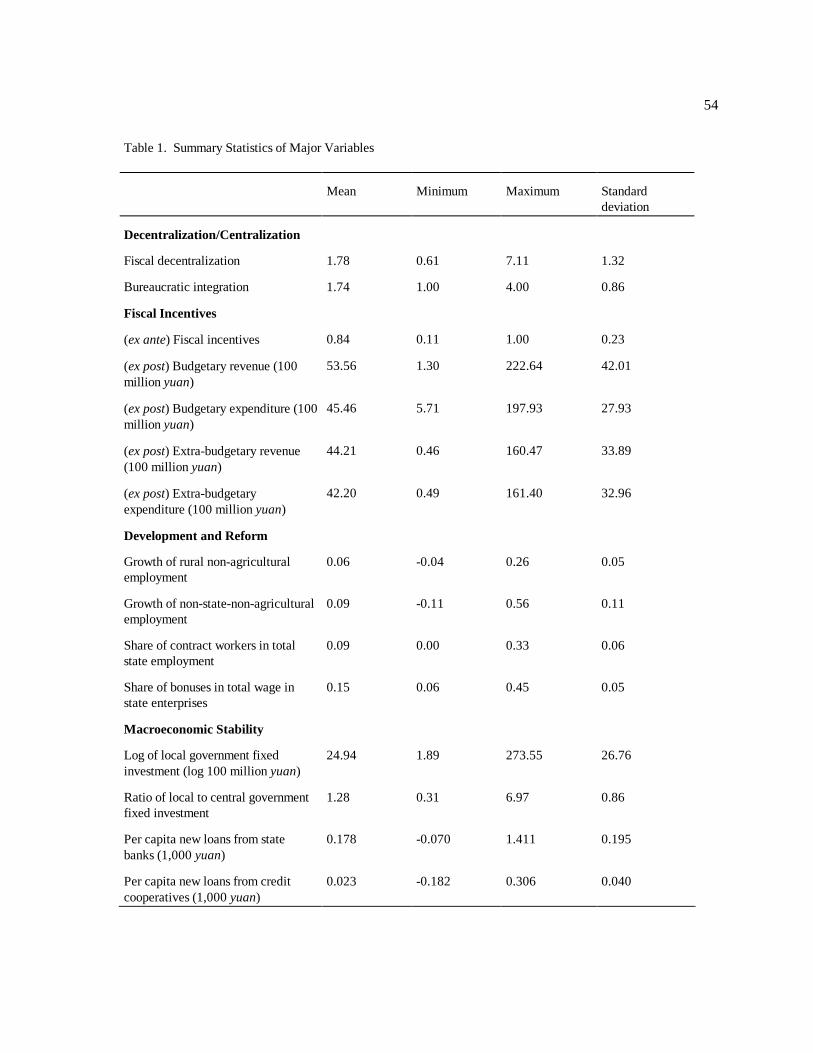

provincial, and municipality levels. Table 1 presents summary statistics of the variables

defined below.

21

[Insert Table 1 here]

A. Variables for Regional Decentralization

We use two variables to measure the degree of decentralization. We first

consider the fiscal aspect of decentralization in terms of budgetary expenditure. The

measure of fiscal decentralization is the ratio of provincial government spending (per

capita) to central government spending (per capita) as in Zhang and Zou (1998). Under

the assumption that local government has the authority over its expenditure, the higher

the ratio, the more the fiscal decentralization. This is the most common measure for

fiscal decentralization used in the literature.

4 The data excludes Tibet.

We make one adjustment to the fiscal expenditure data because the original data

has an inconsistency: *problem:* price subsidies were netted out from revenue and

expenditure before 1986 but added *back* to both revenue and expenditure

after[ward.] *1986.* Most of the price subsidies are the central government's

earmarked transfers to local governments (Wong, 1997). To make the data consistent

22

throughout the sample period, we exclude the price subsidies from the government

expenditure data after 1986. Because explicit provincial data on their price subsidy

expenditures are unavailable, we use the following method to estimate them. First, we

apply the central and local shares of price subsidies nationwide (Hofman, 1993) to

calculate the total local expenditures of the price subsidies for each year. Because the

price subsidies are exclusively for urban residents and they are provided more or less

uniformly across provinces, we then use the provincial share of urban residency in the

country to allocate price subsidies to each province. Figure 1 presents the sample

average of local government budgetary expenditure in total government budgetary

expenditure over time.

[Insert Figure 1 here]

The second variable we use for decentralization or centralization relates to

personnel appointment. Because top provincial officials are not elected but are

appointed by the central government and the Communist Party, it is important to see

how this political control process affects the economic behavior of local governments

and performance of local economy. Constructed by Huang (1996), this variable

concerns characteristics of top provincial officials in their relationship with the central

government. The index, called bureaucratic integration, is based on the career

background of the provincial Party Secretaries. [The indexed] for a provincial Party

23

Secretary [was] *the* scored *is* 1 if he/she was promoted from within the same

province; 2 if he/she was moved to the current post from another province; 3 if he/she

served in the central government before his/her current appointment; and 4 if he/she

concurrently holds a post in the central government (such as a Politburo seat).

This variable measures the degree of "closeness" of top provincial officials with

the central government: The higher the score, the closer is the top provincial officials

to the central government. {YQ: why does the last part of the sentence hold? I made

a guess:} A lower score provincial official is more likely to have better local

information and local connections, and moreover, they are more [likely to be]

committed to [fostering] *the* local prosperity. In contrast, a higher score provincial

official is more likely to have poor local information and local connections, but better

central government connections and more loyal to central government's objectives.

Figure 2 plots the average of bureaucratic integration across provinces over time.

[Insert Figure 2 here]

B. Variables for Fiscal Incentives

[Our] fiscal decentralization measure *by the ratios of local to central

government expenditure* does not capture the [marginal] fiscal incentives facing local

governments. *at the margin.* To examine the ex post fiscal incentives, we look at

24

realized provincial budgetary revenue and budgetary expenditure separately. As

explained in section II, provincial budgetary revenue is the revenue generated in the

province, excluding those revenues designated as the central government's fixed

revenue. On the other hand, provincial budgetary expenditure is the actual provincial

government spending, after contractual obligations are fulfilled and renegotiation takes

place. We also consider provincial extra-budgetary revenue and extra-budgetary

expenditure. Although *there is* no sharing arrangement *through fiscal contracts on*

[cover] extra-budgetary revenue, *between the central and provincial government, there

is no reason for us to believe a priori that* the central government *will not take away

any* [might extract a portion of these] funds.5 *from local extra-budgetary revenue.

Therefore, these two variables can take different values.*

{I rewrote this sent:}We also measure (ex ante) fiscal incentives, defined as the

(ex ante) marginal retention rate of local revenue collection by provincial governments,

*which was contained in* [as determined by] the fiscal contracts between the central

and provincial governments. In contrast to the ratio of local to central government

5 All provincial budgetary and extra-budgetary data are consolidated figures within a province.

25

expenditure, the fiscal incentive variable measures how local governments are rewarded

(or punished) at the margin from an increase (or decrease) in local revenue collection.

The fiscal contracting system was implemented between 1980 and 1993.

However, data for 1980 and 1981 are incomplete. Data for 1993 is distortionary due

to the anticipation of a major change in the fiscal system in 1994. For example, one

provision of the 1994 reform, announced in the fourth quarter of 1993, compensated

local governments based on their 1993 figures of local expenditure. This provision

gave an incentive for local governments to inflate the local expenditure figures toward

the year end. We exclude 1993 and use only the data from 1982 to 1992.6 {YQ:

moved this to FN6}*We collected the information about provincial marginal retention

rates in the fiscal contracts from Chen (1988), Oksenberg and Tong (1991), and Bahl

and Wallich (1992). In cases where there are several marginal retention rates for

6 We collected the information about provincial marginal retention rates in the fiscal contracts from Chen(1988), Oksenberg and Tong (1991), and Bahl and Wallich (1992). In cases where there are several marginalretention rates for different revenue brackets, we use the rate for the highest revenue bracket because the datareveals that all the provinces in fact ended up with that bracket. Furthermore, we use the 1992 data with caution,because in that year four provinces were selected for the experiment of a new tax system to be implementednationwide in 1994. Therefore, these provinces were not officially on the fiscal contracting system any more. Dropping off these four data points has little effect on our results.

26

different revenue brackets, we use the rate for the highest revenue bracket because the

data reveals that all the provinces in fact ended up with that bracket.*

The provincial marginal revenue retention rates involve one complication.

Starting in 1986, several large cities became fiscally independent from [their]

provinces, *where they are located,* directly contracting with the central government

(they are known as "separately plan listed cities"). We have tried to incorporate the

information on these city contracts into the provincial contracts by constructing an

average provincial marginal retention rate using city revenue and provincial revenue

(excluding the relevant city) as weights.7 Figure 3 plots the average of the provincial

marginal revenue retention rates and the share of provinces with 100 percent marginal

retention rates.

[Insert Figure 3 here]

C. Variables for Local Economic Performance

The non-state sector in urban and, especially, rural areas is widely regarded as

the engine of China's growth. We use two variables to measure the development

reflecting the entry and expansion of non-state enterprises: growth of rural enterprise

7 The incorporated information on "separately plan listed cities" include Wuhan (1986-92) in Hubei;Chongqing (1986-92) in Sichuan; Shenyang (1988-92) in Heilongjiang; Ningbo (1988-92) in Zhejiang; andQingdao (1991-92) in Shandong. Information sources are the provincial and city statistical yearbooks.

27

employment, which covers all non-agricultural activities in the rural areas, and growth

of non-state non-agricultural employment, which includes both urban and rural non-

state industry and services.

We study the reform within the state sector by examining two variables: the

changes in the share of contract workers in total state employment and in the share of

bonuses in total state employee wages. Prior to 1992, China did not privatize any state

enterprise. *But the* [Nonetheless] state-owned enterprises *still* underwent modest

reforms. For example, they changed their employment practices by hiring workers on

a contractual basis rather than giving them permanent positions. They also increasingly

used bonuses as a form of payment in addition to fixed salary. Both reforms were

intended to improve workers' incentives.8

Local governments in China have the control over local fixed investments. We

use the log of local government fixed investment to indicate the level of local

government investment activities and the ratio of local to central government fixed

8 Groves et al. (1994) used the similar variables as the measurements of state-owned enterprise reform inChina, and their data came from the enterprise level survey in four provinces.

28

investment to measure the relative weight of the local government’s role in investment

relative to the central government in a province.

During the period spanned by our data, the state banking system was

decentralized to a large degree, and local governments had enormous influence over

credit policy. We use two variables as measures of local credit expansion: per capita

new loans from state banks and per capita new loans from credit cooperatives. The

provincial governments have direct influence over state bank branches in their

provinces, but their influence on credit cooperatives are only indirect because these

cooperatives are supervised by county governments.

V. The Fiscal Incentives for Local Governments

We assess the implementation of the fiscal contracting system by first comparing the

actual provincial expenditure with the revenue retention amount implied by the ex ante

fiscal contracts. This allows us to estimate the extent of ex post readjustment of

revenue remittance and subsidies beyond the contracts. High ex ante marginal retention

rates together with small ex post readjustments *would support the claim* [show] that

29

the implementation of the fiscal contracting system *is responsible for* [creates] the

ex post strong link between revenue and expenditure.

*With* the [data] *information* on fiscal contracts *, we can* [allows us to]

examine the deviation of actual implementation of the fiscal contract from the promised

one. Fiscal readjustment (ex post) *is a* measure[s]*ment of* the difference between

actual provincial expenditure and "pre-defined" revenue retention, as indicated in the

fiscal contracts.9 A negative value of fiscal readjustment means that the province

spends less than the contractual provision would entail. We interpret the first case to

be the one in which the province ex post remitted extra revenue to the central

government, for example, *when it was* [if it were] forced to "lend" revenue to the

central government. These cases represent the central government's "predation." *On

the other hand,* A positive value of fiscal readjustment indicates that the province ex

post received extra subsidies from the central government, a signal of the "soft budget

constraint" (Kornai, 1986).10 For any given year, we use the average of this variable

9 Again, the data is adjusted for price subsidies after 1986: local portions of price subsidies are excluded fromlocal expenditure. They were earmarked central government transfers and were determined solely by the numberof urban residents anyway.

10 We make a few qualifications regarding the interpretation of the variable fiscal readjustment. First, weimplicitly assume that each province has a balanced budget each year without carry-overs from the previous yearor savings into the next year. This is basically true. Second, because our information about the fiscal contractsis limited to fixed subsidies/remittances and marginal retention rates, we have to omit other pre-defined transfersor transfers based on exogenous criteria such as natural disaster relief. However, such transfers are notsignificant. Third, because we look at net transfers (i.e., expenditure minus revenue retention), it is possible thattwo way transfers are high but net transfers are low. Despite these limitations, this variable provides useful

30

across provinces weighted by provincial expenditure to measure the average deviation

of implemented fiscal contracts from the promised ones.

information on the significance of ex post readjustment of fiscal revenue retention.

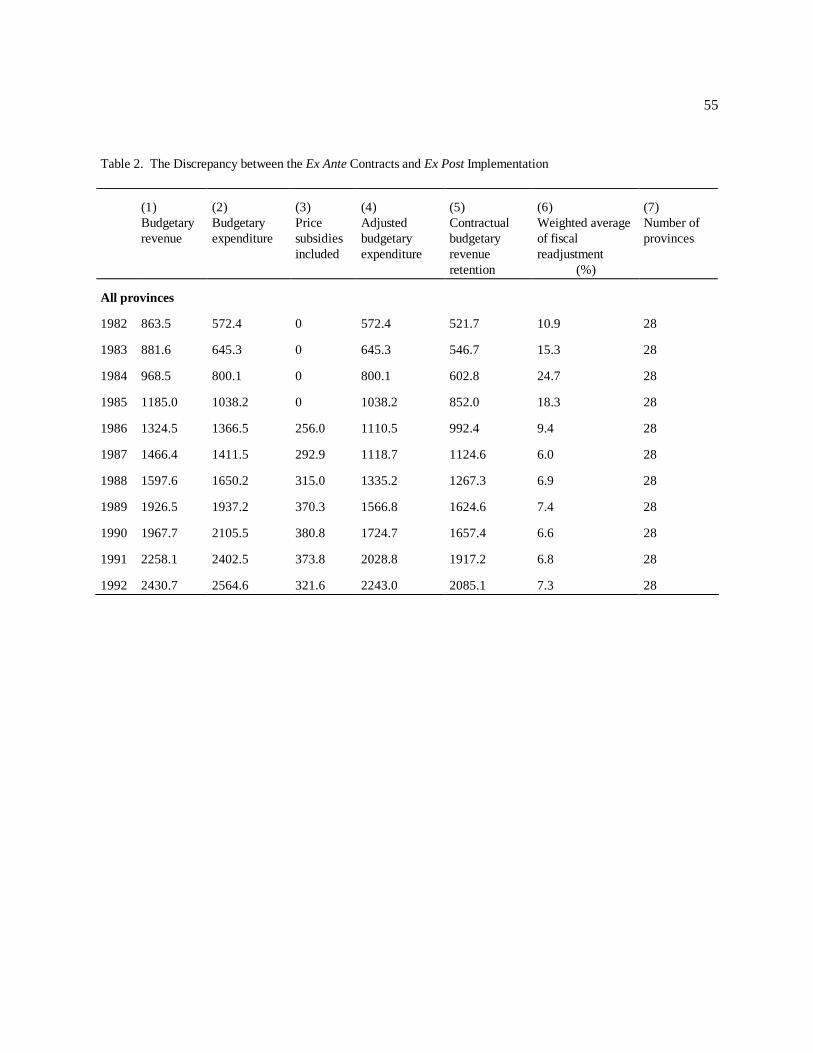

{YQ: I broke this sentence in two:}Consider Table 2, which reports in column

(6) the weighted average of the fiscal readjustment across provinces between 1982 and

1992, as measured by the absolute difference between actual expenditure and

contractual revenue retention divided by expenditure. The data display a declining trend

over time. After 1986, this variable fell below 8 percent. This evidence suggests that

the extent of ex post readjustments have become more limited over time. Further, after

1986, they have been relatively limited in scope. On average, actual provincial

expenditures correspond reasonably well to their contractual revenue retention. Of

course, we do not expect an exact correspondence due to ex post adjustments to

exogenous events that occur during the year, such as natural disasters.

[Insert Table 2 here]

31

Next we divide the provinces into two categories: extra remittance provinces,

defined as those whose expenditure fall short of pre-defined revenue; and extra subsidy

recipient provinces, defined as those whose expenditure exceed pre-defined revenue.

Examining the two groups separately, we find that there are generally fewer extra

revenue remitting provinces (see column (7), first panel of Table 3) than extra

subsidized provinces (see column (7), second panel of Table 3). This indicates that the

ex post extra transfers from the center to provinces (i.e., the problem of soft budget

constraints) is quantitatively more significant than extra transfers from the provinces

to the center.11

[Insert Table 3 here]

Because of the potential [for] *problem of* central government predation, the

phenomena of extra remitting provinces is of special interest. If the central government

behaved in a predatory fashion — for example, if it consistently forced the more

successful provinces to remit significant amount of additional revenue — the magnitude

of this figure would be significant. The results in the first panel of Table 3 suggest that

these additional remittances are small. After the difficult year of 1989, only one-third

11 This may also due to the fact that we were unable to account for some earmarked subsidies.

32

of the provinces remitted additional money, and the average amounted to a relatively

small portion of their expenditure, under four percent.

Table 3 also reveals two aspects of a sudden increase in extra remittances from

provinces to the central government in 1989. First, the average quantity of extra

remittances increased to 7.67 percent of expenditures (see column (6), first panel).

Second, the number of provinces making the extra remittances jumped to 19 out of 28

(see column (7), first panel). The Table also shows a decrease in extra subsidies from

the central to local governments as compared with other years, before and after

(columns (6) and (7), second panel).

The changes in 1989 are not surprising. In that year, conservatives in the

government temporarily gained power after the Tiananmen Square incident, causing a

temporary setback in reform. Importantly, Table 3 reveals two aspects of this setback.

First, this change was relatively short lived: after 1989, the fiscal data return to their

previous trend. Second, the absolute amount was modest. Although many more

provinces were subject to additional remittances in 1989, remittances averaged less

than eight percent of expenditures. Indeed, these data support the common anecdotal

evidence in the literature that the setback in reform after Tiananmen Square was

temporary. By the early 1990s, the number of provinces with extra remittances were

small, as was the average magnitude of the extra remittance.

33

What is the role of the fiscal contracting system in providing fiscal incentives for

local governments? We provide evidence showing that *implementation of* the fiscal

contracting system has improved fiscal incentives by providing a stronger link between

provincial marginal revenue collection and marginal expenditure. To that end, we look

at the correlations between provincial ex post realized revenue and expenditure. We

run the following fixed effect model:

(5.1) Xit = ai + ?t + ßYit + µit,

where Xit is province i’s expenditure in year t, Yit is province i’ revenue in year t, the

a i's are provincial fixed effects, ?t's are the year dummies, and µit's are the disturbance

terms. These tests are designed to *tell us how closely* examine the link [between]

*are* local expenditures *to* and local revenues, after controlling for provincial

inherent characteristics and nationwide changes over time.

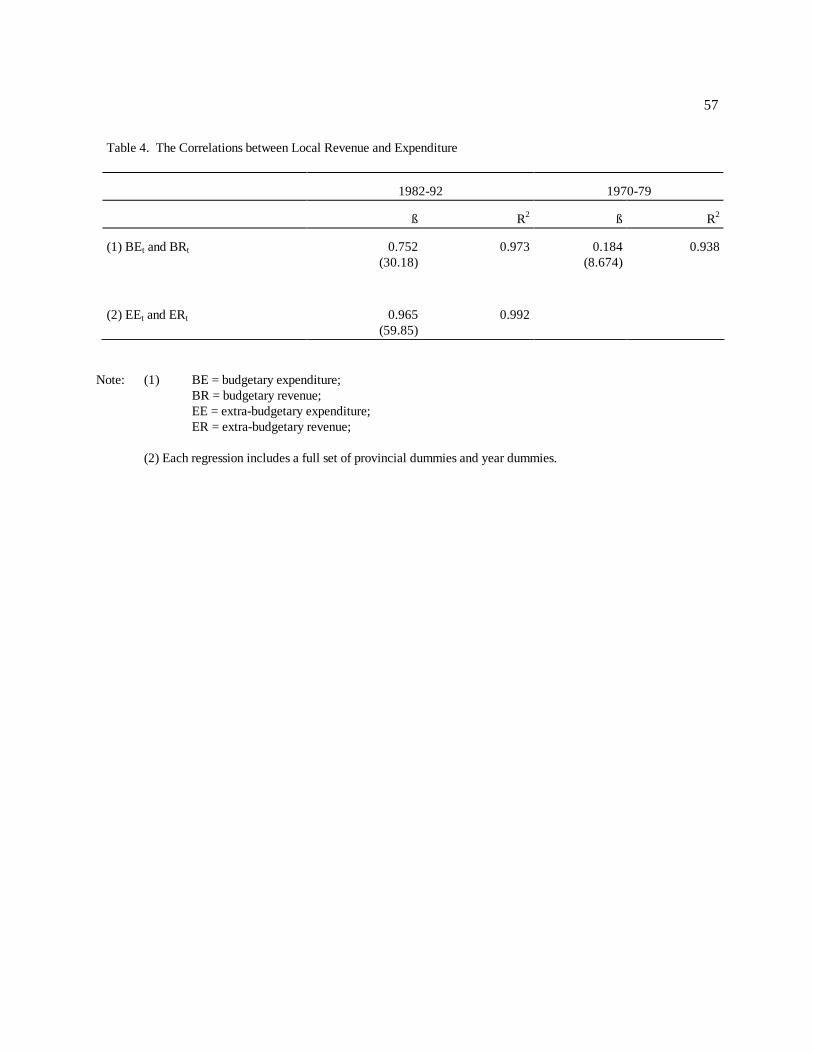

Table 4 reports the results. For data from 1982 to 1992, row (1) shows a

coefficient of 0.752 on provincial budgetary revenue in its budgetary expenditure

equation; and row (2) shows an even larger coefficient for the extra-budgetary

expenditure equation (0.965). These results *mean* [imply] that, on average, a one

yuan increase in provincial budgetary revenue results in about three-quarters yuan of

34

provincial budgetary expenditure. Further, the relationship becomes almost one to one

for extra-budgetary revenue and expenditure. Taken together, the results demonstrate

that the fiscal system in China's reform has produced, on average, a strong link between

local expenditure and local revenue generation. *As a result, the* Provinces in China

[therefore] tend to be "self financing" at the margin. This translates into strong fiscal

incentives for local governments to pursue local prosperity in order to increase their

own revenue base.12

[Insert Table 4 here]

To put the above results in perspective, we compare them with the results from

pre-reform China. Using data on pre-reform China from 1970 to 1979, row (1) of

Table 4 reveals a very small coefficient on provincial budgetary revenue in the

budgetary expenditure equation, 0.184 before the reform as compared to 0.752 after the

reform. [These results show that,] prior to economic reform, the central government

extracted revenue from high revenue provinces while subsidizing low revenue

provinces. [Indeed,] a coefficient of 0.184 indicates that, prior to the reforms, the

central government, on average, extracted over 80 percent of any increase in local

revenues. This figure fell dramatically after the reform, indicating that the central

12 Using the three year data of 1983, 1987, and 1990 individually, Knight and Li (1999) also found that thecorrelations between local extra-budgetary revenue and expenditure were generally higher than those betweenlocal budgetary revenue and expenditure, and the latter increased over time.

35

government, on average, extracts less than twenty-five percent of any increase in local

revenues.

A comparison of our findings with similar investigations of post-transition Russia

is revealing. Zhuravskaya (2000) examined the fiscal incentives of city governments in

the region-city fiscal relationship in post-reform Russia, showing a pattern which she

interpreted as predation. Using the data of 35 cities for the period 1992-1997 and by

regressing the change in "shared revenues" between local and regional governments on

the change of "own revenue," she finds that the coefficient is -0.90. She interprets this

result as evidence that increases in a city's revenue are almost entirely offset by

decreases in shared revenues from the region to the city. Exaction of this magnitude

destroys cities' fiscal incentives to increase their tax base. These results stand in sharp

contrast with the post-reform China. In a separate regression we find that in China, any

increase in extra-budgetary revenue (corresponds to "own revenue" in Russia) does not

have this kind of negative effect on the change of budgetary expenditure (corresponds

to "shared revenue" in Russia). The coefficient is actually positive, which in part

reflects the fact that budgetary and extra-budgetary revenues have similar tax bases.

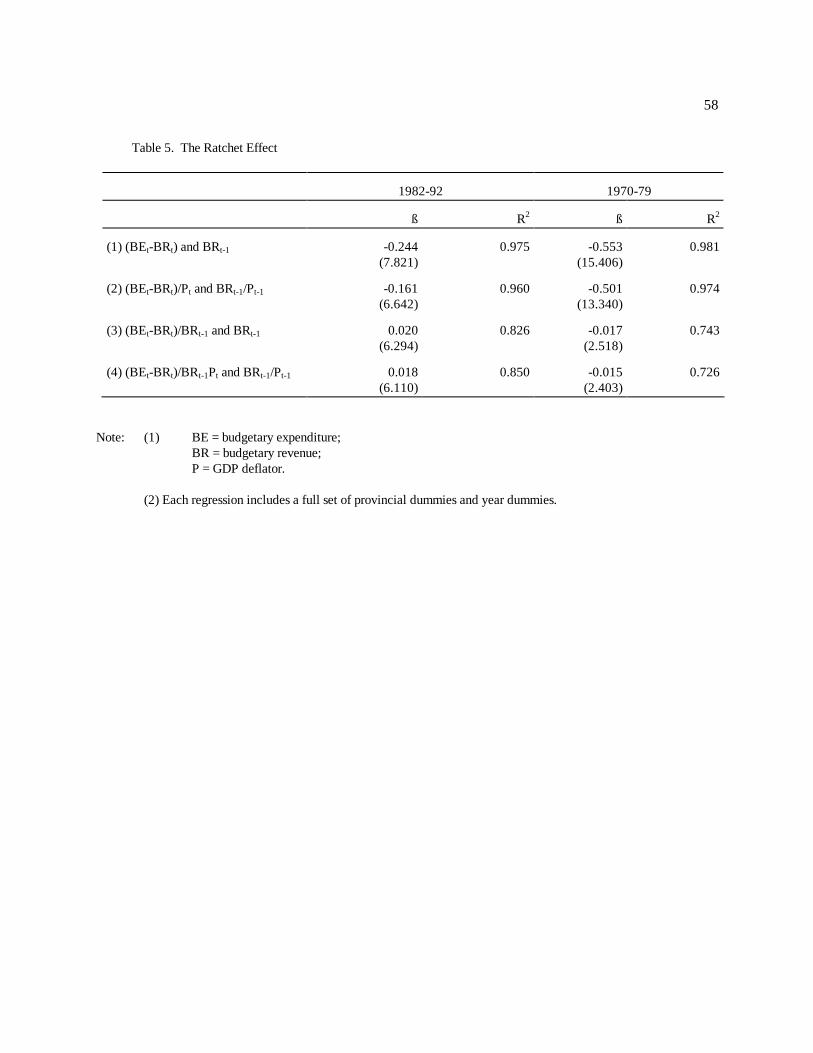

We next investigate an aspect of dynamic incentives, that is, the possibility of

a "ratchet effect" over time. The ratchet effect occurs when higher revenue collection

this year leads to a higher revenue remittance or fewer subsidies in the future

36

(Weitzman, 1980). [For example to what extent do revisions in the fiscal contract exact

recent fiscal gains?] We study this problem by regressing the difference between

budgetary expenditure and revenue (i.e., "subsidies" or negative "revenue remittance")

on the previous year's budgetary revenue to see the ratchet effect for the remittance

level. We also regress the difference as a proportion of budgetary revenue on the

previous year's budgetary revenue to see the ratchet effect for the remittance rate. The

ratchet effect implies a negative coefficient from these regressions, and the larger the

absolute number, the greater the effect.

{YQ: don’t we want to say here that, when we hold constant for inflation, the

effect is even smaller, .16?} Row (1) of Table 5 shows a modest ratchet effect for the

level after the reform, and row (2) shows that this effect survives inflation adjustment,

although becomes somewhat smaller. For every one yuan increase in provincial

revenue in the current year, the province will face, on average, a 0.24 yuan increase of

remittance to the central government in the next year. {YQ: what does this sent mean?

It seems to contradict the above. Please explain:}However, rows (3) and (4) show that

there is no ratchet effect for the rate. These results imply that, on average, the level of

remittance to the central government increased modestly over time from provinces

experiencing economic growth, but not the rate.

[Insert Table 5 here]

37

[In contrast, our investigation of the ratchet effect prior to the reforms reveals

(see row (1) of Table 5) a very strong ratchet effect before the reform: a one yuan

increase in this year's provincial revenue results in a 0.55 yuan reduction in next year's

subsidies (or, an increase in the next year's revenue remittance). In comparison, at

0.24, the ratchet effect after the reform halved from the pre-reform value. Moreover,

there was also a ratchet effect for the rate: row (3) shows that a 100 million yuan of

revenue increase in the previous year led to 1.7 percentage points increase of the rate

of remittance. This ratchet effect on the rate disappeared after the reform. Therefore,

provinces' concerns about increased future obligations from current increase of revenue

collection abated after the reform.

VI. The Effects of Regional Decentralization and Fiscal Incentives

In investigating the effects of regional decentralization and fiscal incentives [on the

local economy], we focus on three variables: fiscal decentralization (as measured by

the ratio of local to central spending), bureaucratic integration (as measured by the

career background of local government officials vis-a-vis the central government), and

ex ante fiscal incentives (as measured by the ex ante marginal local retention rate in the

38

fiscal contract). To our knowledge, we are the first to use the last variable as well as

the combination of the three in an econometric study of China's reform.

Specifically, we investigate the following model:

(6.1) Xit = ai + ßt + d'Zit + s 'Wit + uit.

In equation (6.1), Xit is a vector of variables measuring local economic performance in

a province. The ai's represent the provincial specific effects, which we assume are

constant for each province, implying that our specification is a fixed effect model. The

ßt's are the annual dummies, which are intended to capture the effects of nationwide

macroeconomic fluctuation. Zit is a vector of variables measuring fiscal

decentralization, bureaucratic integration, and fiscal incentives. Wit is a vector of

control variables. The uit's are the disturbance terms. Our fixed effect model implies

that any correlations between X and Z cannot be attributed to inherent provincial

characteristics.

Development and Reform

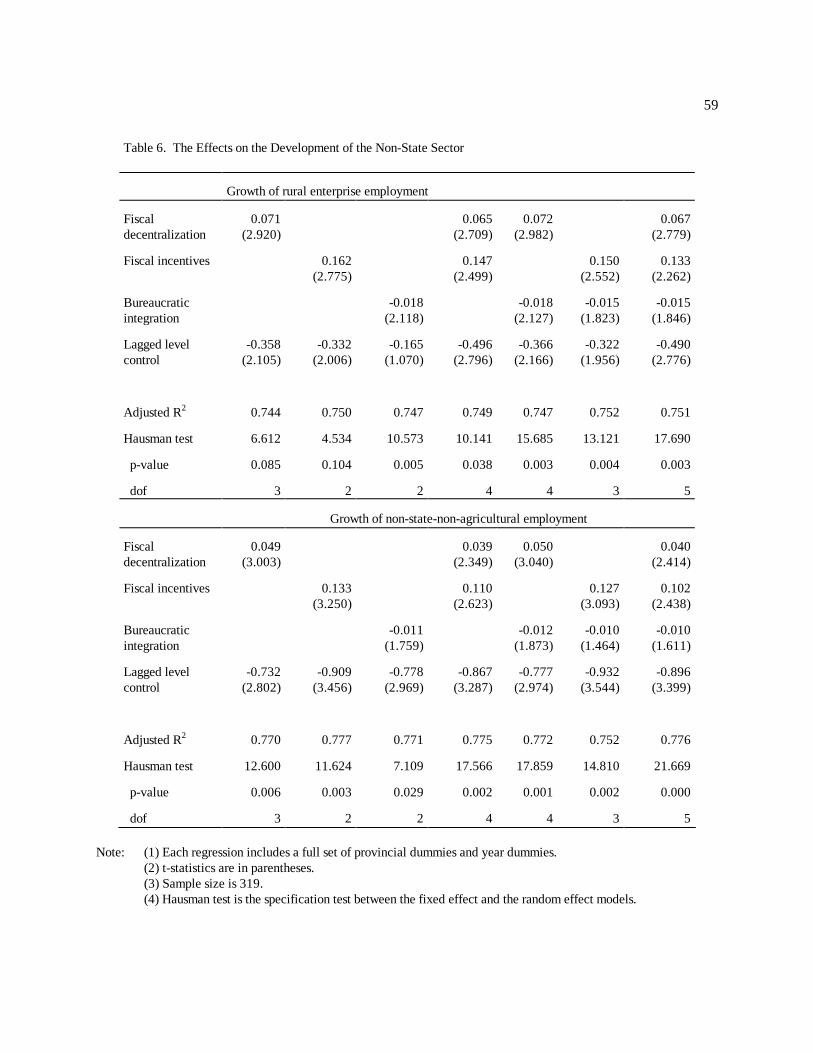

Our first task is to test the first and second hypotheses. Table 6 presents our

results on the effects of fiscal decentralization, fiscal incentives, and bureaucratic

39

integration on the development of non-state enterprises. The dependent variable in the

first panel of Table 6 is the growth of rural enterprise employment, a narrower measure

of non-state sector development; the dependent variable in the second panel is the

growth of non-state-non-agricultural employment in both urban and rural areas, a

broader measure. In these regressions, the control variables in W include the lagged

level variables, which are the share of rural enterprise employment in rural labor force

and the share of non-state-non-agricultural employment in total labor force respectively.

The two panels give similar results. First, the level variables have negative

coefficients, which is expected. In a model in which a "convergence" tendency exists,

"frontier" can be pushed outward by the increase of "effort," which is determined by

regional decentralization and fiscal incentives. Given regional decentralization and

fiscal incentives, the higher the previous level of industrialization, the harder it is to

grow faster. Second, both the single variable and multivariable regressions reveal that

fiscal decentralization have positive effects on the development of non-state

enterprises.13 Third, fiscal incentives have positive and significant effects on the

development of non-state enterprises; these effects remain significant even after

13 A previous study by Zhang and Zou (1998) reported a negative and significant effect of fiscaldecentralization on provincial growth during China's reform. We found that such negative effect would disappearand actually would turn into a positve effect if the set of annual dummy variables is included in their regressions. This suggests that their findings perhaps resulted from the failure to filter out economy-wide cyclic effects.

40

controlling for fiscal decentralization. This implies that fiscal decentralization alone is

not enough to explain the growth of the non-state sector, fiscal incentives have

additional explanatory power. Quantitatively, if the marginal revenue retention rate in

a province increases by 10 percentage points, then the growth rate of non-state

enterprises in that province would increase by 1.33 percentage points, when it is

measured for rural area only; and 1.02 percentage points, when measured for both rural

and urban areas. Finally, bureaucratic integration has a negative effect on developing

non-state enterprises. If the degree of bureaucratic association with the central

government moves up by one unit (say if the current provincial Party secretary who was

previously promoted from within the province is now replaced by someone who is

moved from another province), then the growth rate of non-state enterprises in the

province would be reduced by 1.5 percentage points for rural area and by 1.0

percentage points for both rural and urban areas respectively.

[Insert Table 6 here]

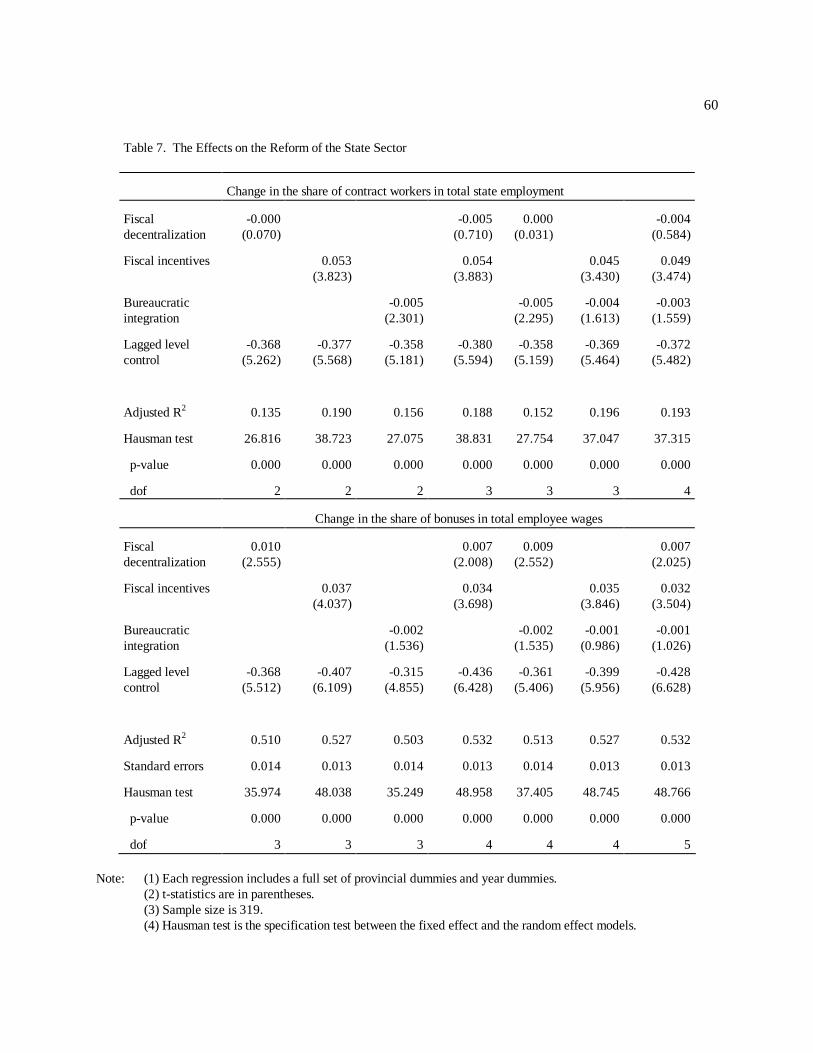

We carry out a similar exercise for the reform of state-owned enterprises. The

first panel of Table 7 reports our results on the change of the share of contract workers

in total state employment and the second panel on the change in the share of bonuses

in total employee wages. Again, the level control variables -- the share of contract

workers and the share of bonuses -- have negative coefficients, which mean that the

41

higher the [initial] shares, *to start with,* the more difficult it is to increase the shares

further. [The degree of] fiscal decentralization has significant effects on the change of

the share of bonuses in total employee wages, but not on the change of the share of

contract workers in total state employment. However, fiscal incentives have positive

effects for both reform measurements. Stronger fiscal incentives foster reform by

increasing the share of contract workers relative to permanent workers and the share

of bonuses in total employee wages. These effects remain significant after controlling

for fiscal decentralization. A 10 percentage point increase in the marginal revenue

retention rate in a province leads to a 0.49 percentage point increase in the share of

contract workers and a 0.32 percentage point increase in the share of bonuses.

In contrast to permanent workers, who are under the traditional socialist labor

conditions of "iron rice bowls," contract workers do not have tenure and are more likely

subject to market conditions. More contract workers relative to permanent workers

mean that enterprises are better restructured to market orientation. Bonuses, as

compared to fixed wages, represent a compensation form that is more closely linked

to workers performance, a higher share of bonuses in total employee wages implies

enterprise workers are better motivated. Finally, we find negative effects of

bureaucratic integration on the reforms in both measures. The effect is significant for

the share of contract workers, but not for the share of bonuses.

42

[Insert Table 7 here]

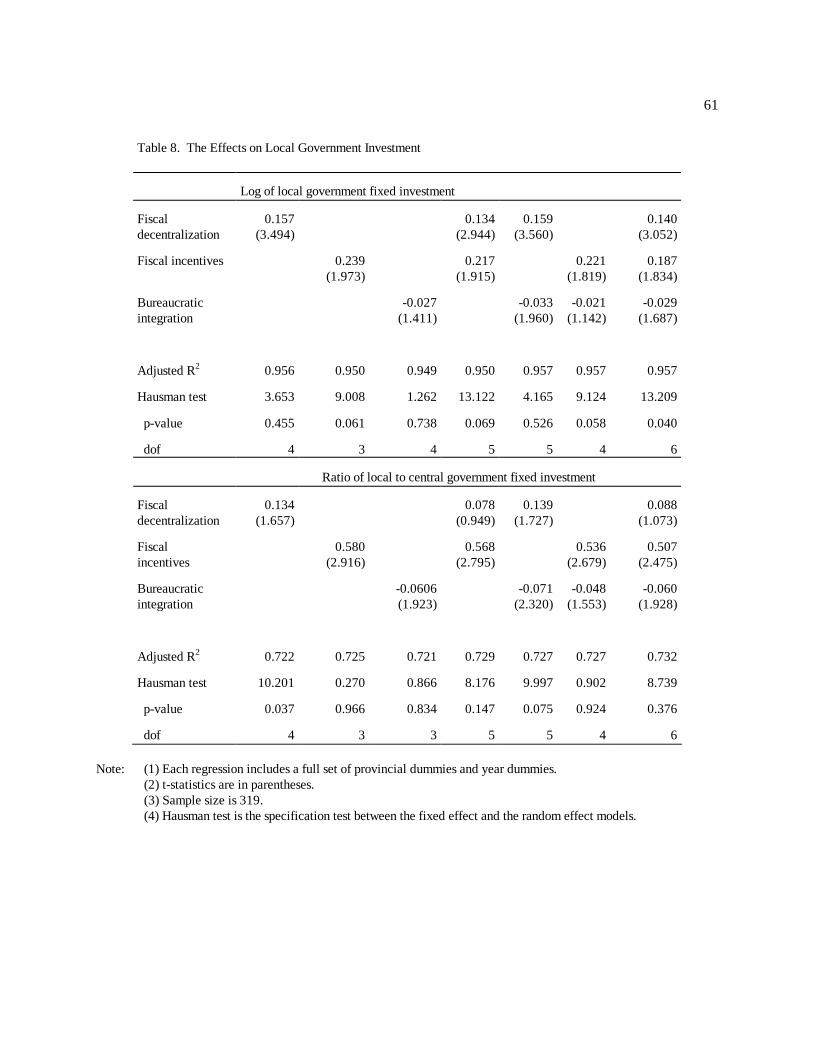

Macroeconomic Stability

We have demonstrated that Party control over personnel has a negative effect on

development and reform. [We now turn to our third hypothesis concerning whether]

*does the* Party control play[s a] positive role [in] helping macroeconomic stability.

*Our next task is to test our third hypothesis.* We examine two aspects related to

macroeconomic stability, one on real side and the other on financial side. Consider the

real side: during this period, excessive local government fixed investment was often

considered an importance source of macroeconomic instability and inflation. We

examine the relationship between bureaucratic integration and local government's fixed

investment and report the results in Table 8. Although we found that more fiscal

incentives are associated with higher local government investment, we also found that

more bureaucratic integration is associated with lower local government fixed

investment. Here local government investment is measured by both the level of local

government fixed investment and by the ratio of local to central government fixed

43

investment. These effects remain even after controlling for fiscal decentralization. This

suggests that Party control does play a role in maintaining macroeconomic stability.14

14 Huang (1996) also obtained the result on the effect of bureaucratic integration in curbing local governmentinvestment in a different regression without the fixed effect and without controlling for fiscal decentralization andfiscal incentives.

[Insert Table 8 here]

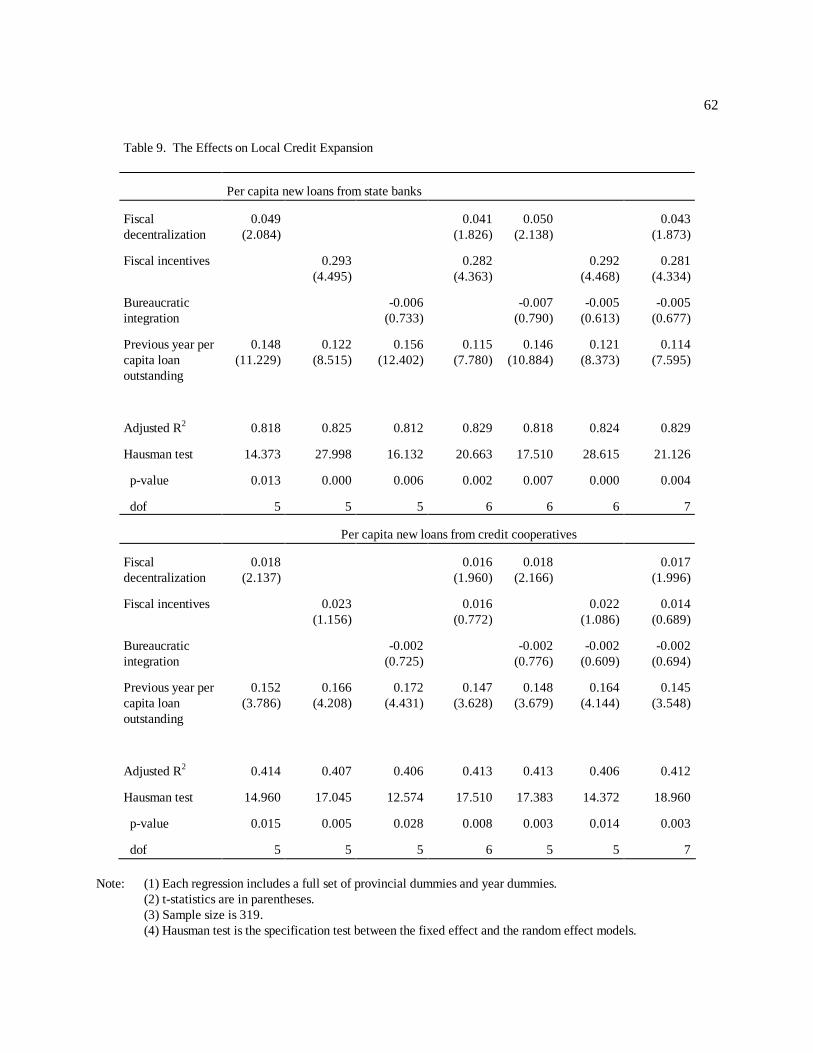

On the financial side, we examine the relationship between bureaucratic

integration and local credit expansion (see Table 9). In China and during the period,

all the credit sources were controlled by government, especially by local governments.

Local governments had have influences on credit expansion from two types of financial

institutions: state banks and credit cooperatives. The provincial governments had direct

influence over state bank branches in their provinces, but not directly over credit

cooperatives {YQ:is this correct:}(which the county governments controlled). We

found that fiscal decentralization has a positive effect on credit expansion from both

sources, but fiscal incentives only have significant effects on the access to loans from

the state banks, not from credit cooperatives. This provides some evidence that

44

stronger fiscal incentives for local governments were associated with more local

government's access to credit from the sources that they have direct control over. On

the other hand, unlike its effect on local government investment, bureaucratic

integration has no significant effect on local credit expansion from either source. This

suggests that the Party control is not effective in controlling local governments' access

to credit. To the extent that credit expansion is a major source of inflation, the Party's

control has not achieved that objective. This is perhaps an important reason for the

monetary reform in 1994.

[Insert Table 9 here]

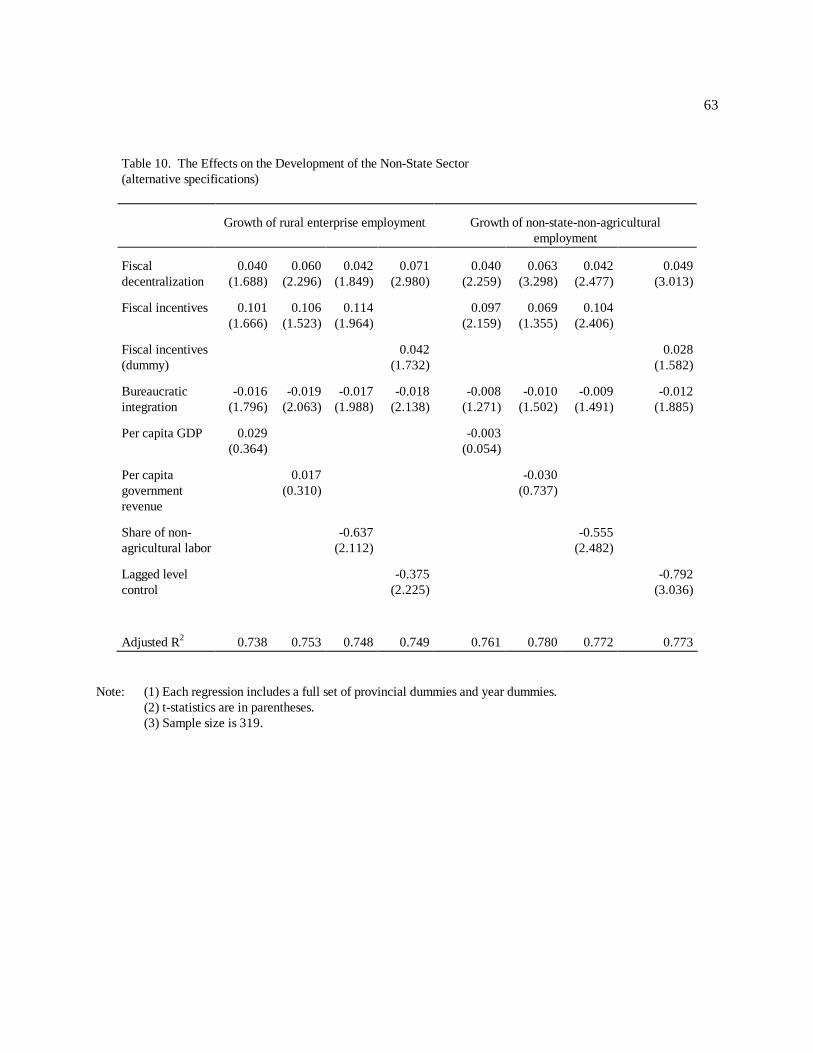

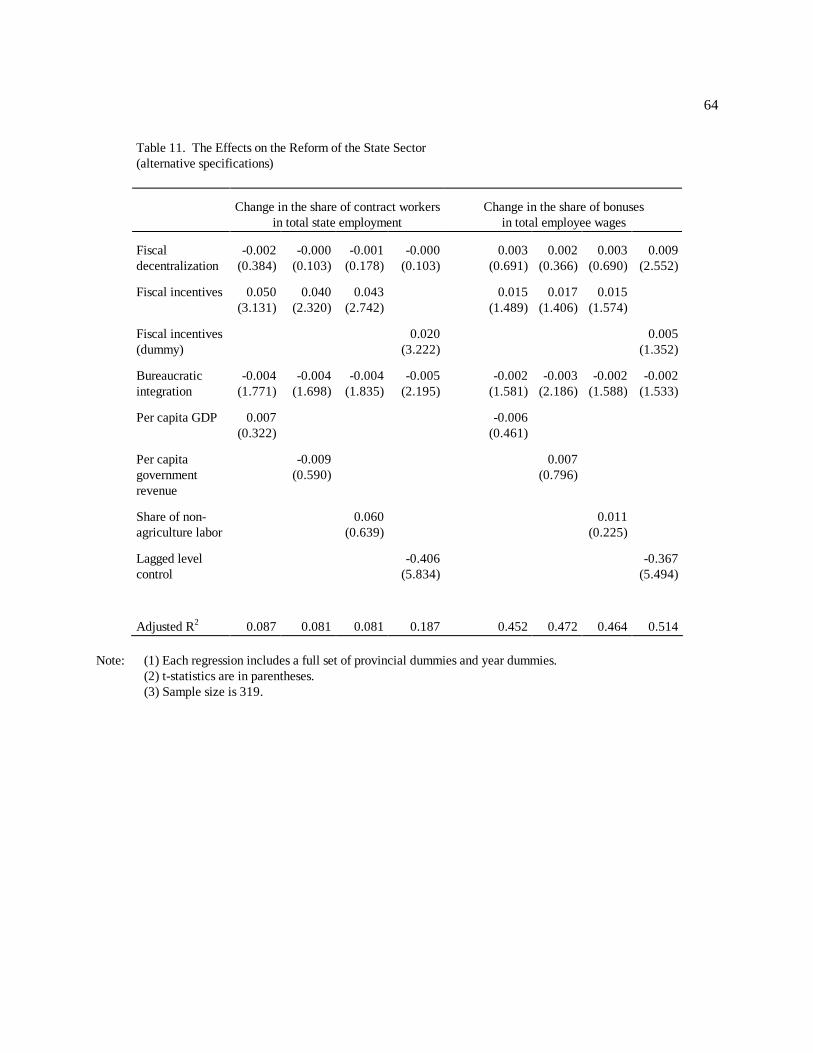

Robustness

To check the robustness of our estimations, we consider several alternative

specifications. First, in addition to the fixed effect models, we also estimated the

random effect models and tested for the validity of the two specifications. We report

the Hausman test results at the bottom of Tables 6-9, which favor the fixed effect model

over the random effect model in almost all cases. As noted by Hsiao (1986), the

random effect models are no longer valid when the provincial specific effects are

correlated with the other independent variables. {What does “in the later” mean in this

sent?:}This is certainly the case in our models as we show, in the later, that both the

45

marginal incentives and bureaucratic integration depend on provincial specific

conditions which are captured in provincial fixed effects. This is why the random effect

model is rejected in almost all the cases.

Second, we have also run parallel regressions replacing the fiscal incentive

variable with a qualitative variable that takes value 1 if the marginal retention rate is

100 percent and 0 otherwise. This intends to test the impacts of the possible

error-in-variable problem in the measurement of the marginal retention rates. The

results are reported in the last columns of Tables 10 and 11. The magnitudes and

significance of the all our estimated coefficients remain unchanged except for the non-

agricultural employment equation in which the coefficient of fiscal incentive turns out

positive but insignificant, indicating that there may exist some error-in-variable

problem. But clearly, the problem is not serious enough to distort our qualitative

results.

[Insert Tables 10 and 11 here]

Third, to see if our estimations are sensitive to our choice of control variables in

the estimations of the development and reform equations, we have replaced the control

variable with alternative variables representing the level of economic development,

such as per capita GDP, per capita government revenue, and the share of non-

agriculture labor force in the total labor force. We want to make sure that our results

46

are not sensitive to the correlation between our independent variables (i.e., marginal

retention rates and bureaucratic integration) and the level of economic development.

The first three columns of Tables 10 and 11 present the estimation results using these

alternative control variables. All the results indicate that our estimates are quite robust.

The qualitative results concerning the positive effects of fiscal decentralization and

fiscal incentives and the negative effects of bureaucratic integration have been

preserved in almost all cases.

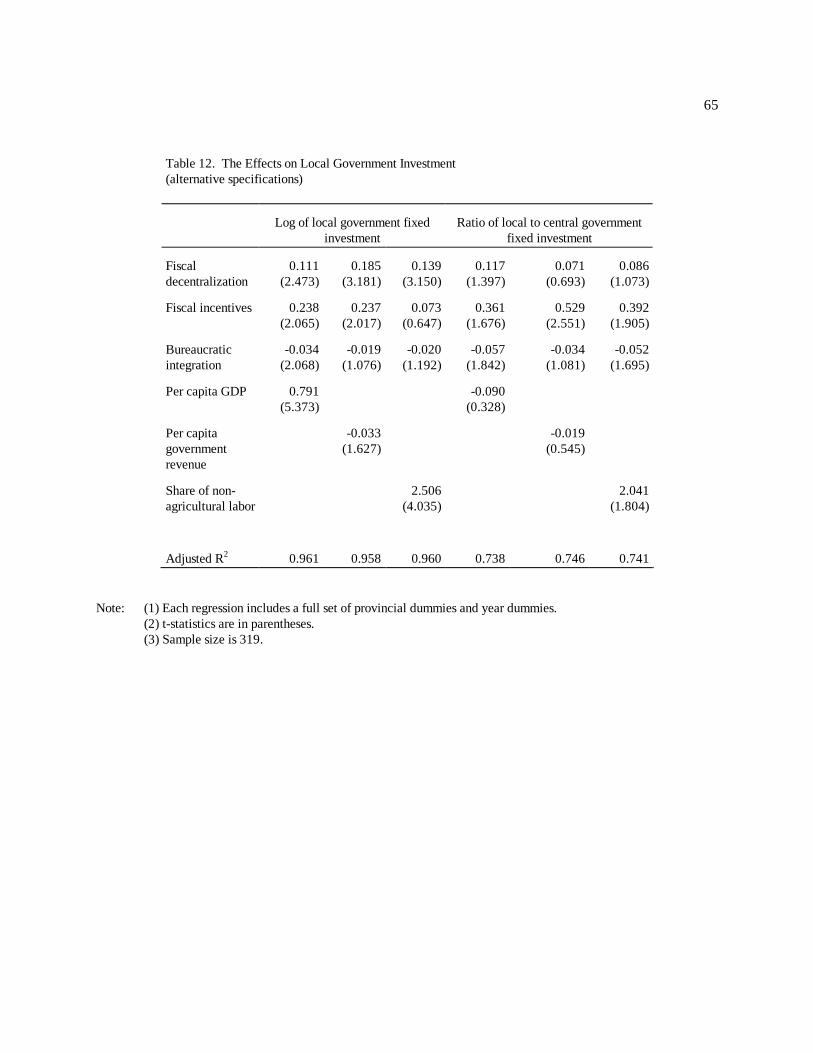

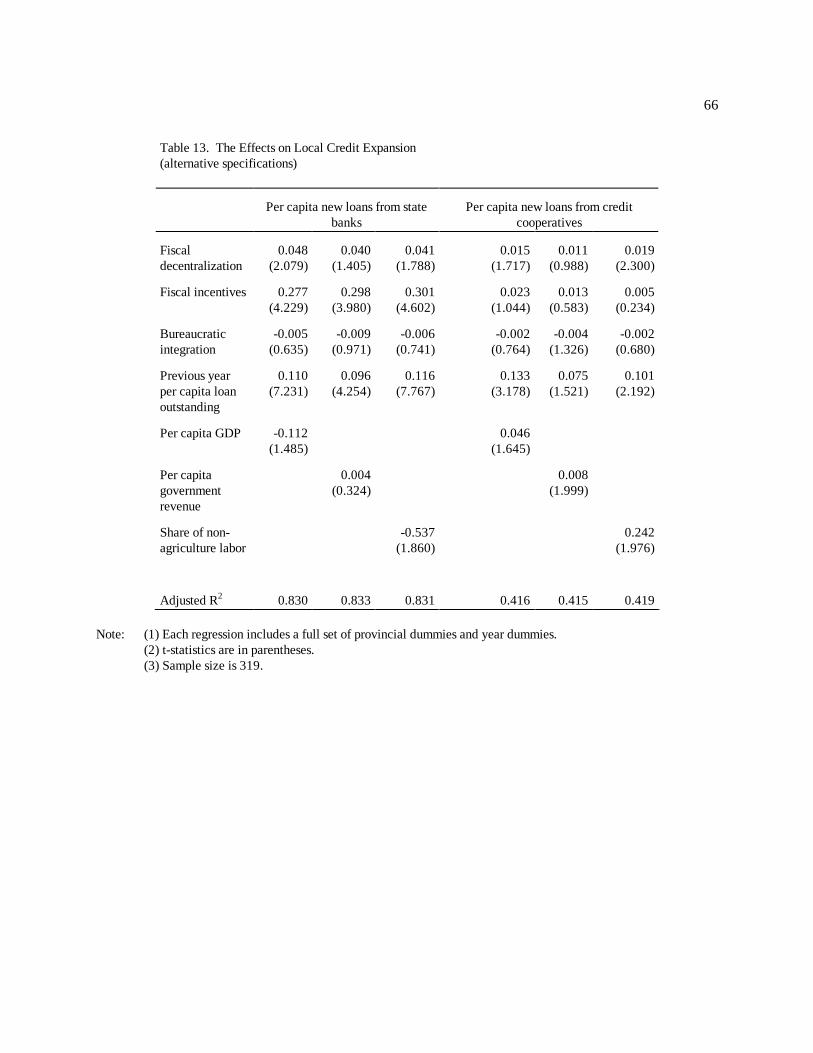

For the equations of macroeconomic stability, we have also estimated the models

with alternative control variables for the level of development. Again the all of our

qualitative results hold unchanged, as shown in Tables 12 and 13.

[Insert Tables 12 and 13 here]

The Endogeneity Problem Related to Marginal Retention Rates and Bureaucratic

Integration

In this subsection we turn to the possible endogeneity problem. The marginal

retention rates are treated as a largely predetermined variable in our model, since the

fiscal contracts are determined every 3-5 years and remain rather stable during the

intervals. {YQ: I rewrote this sent:}Still, one may argue that the choice of marginal

retention rates depended on certain characteristics that also influenced the dependent

47

variables. However, we argue that, since the contracts are fixed for several years, the

characteristics which were considered in the choice of marginal retention rates are often

those long-term factors which do not subject to year to year changes. These factors are

more or less stable, and therefore can be largely captured by our provincial fixed

effects.

Generally speaking, the marginal retention rates are not based on current income

levels. We found that, even in simple regressions, they are not correlated with per

capita real GDP. {YQ: I rewrote the next three sent’s:}In particular, richer provinces

were not systematically more likely to get higher or lower incentives. Even when the

sample is restricted to revenue surplus provinces, there is no significant correlation

between marginal retention rates and per capita GDP. Nor is the marginal retention rate

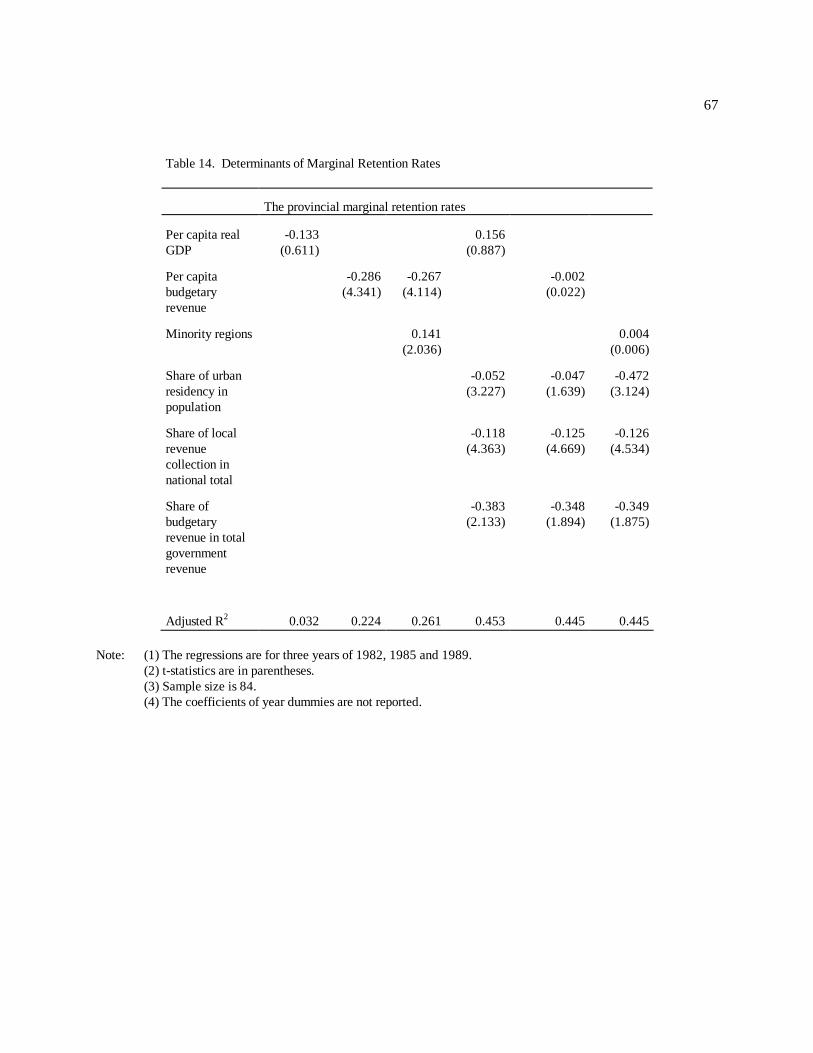

determined randomly. The result in Table 14 show that they are negatively correlated

with the level of per capita budgetary revenues. The positive correlation holds after

controlling for bureaucratic integration, minorities regions and budgetary revenue

shares in total government revenues, but fails to hold after controlling for the share of

urban residency in total population. Higher marginal retention rates are given to

minority regions. But minority dummy becomes insignificant when urban residency or

per capita budgetary revenue is included. A quite robust result is that marginal rates

are negatively correlated with urban residency and the importance of the province in

48

generating budgetary revenues for the center (as measured by the shares of the

provincial budgetary revenue in national totals). Both factors are more or less stable

in the short run.

[Insert Table 14 here]

Because top provincial bureaucrats, once appointed, usually remain in office for

at least 5 years, the variable of bureaucratic integration remains relatively stable for

each province, displaying perhaps two or three discrete jumps during our sample period

of 11 years. As Huang (1996) explained, this variable is constructed primarily on the

basis of the career background of provincial officials that is based on their past

performance history; only the coding of the concurrent centralists refers to their

contemporaneous status. These facts enable us to treat [bureaucratic integration] as

predetermined. But unlike the marginal retention rates, the bureaucratic integration is

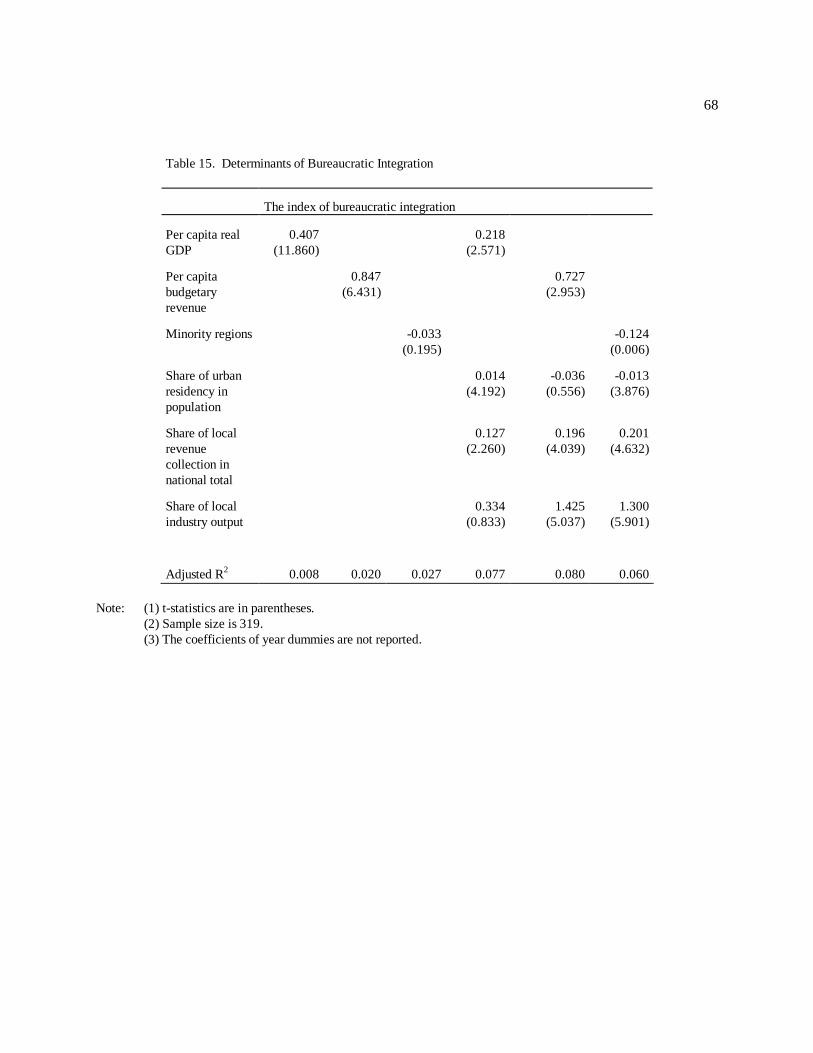

found positively correlated with per capita GDP [(see Table 15)]. Richer provinces are

more bureaucratically integrated than poorer provinces. It is also positively correlated

with per capita budgetary revenues, the share of urban residency in total population, the

share of state industry in the province. No evidence shows that minority regions are

either less or more integrated.

[Insert Table 15 here]

49

Since both the marginal retention rates and bureaucratic integration remain stable

in most of the years, we only have to consider its endogenous determination when they

display discrete jumps. This suggests that the same variables lagged one year are good

candidates for instruments. With these instruments we have run two stage regressions

for all the equations and found all of them yield the similar results as we obtained

before. These results indicate that the endogeneity problem is not serious in our models.

[Insert Table 16 here]

In summary, we found evidence showing that more fiscal decentralization and

stronger fiscal incentives are associated with the faster development of non-state

enterprises and in reform of state enterprises in China. We also found evidence that

greater bureaucratic integration, reflecting the Communist Party’s control over

personnel, has the opposite effect. On the crucial issue of development and reform, the

fiscal contracting system seems to play a major positive role. Although Party control

generally is not favorable to development and reform, it seems to have some role in

maintaining macroeconomic stability through restricting local government investment,

but not through restricting credit expansion.

Some of our above results parallel recent studies for Russia. Using a (ex post)

binary proxy for fiscal incentives rather than the (ex ante) marginal retention rate here,

Zhuravskaya (2000) found in Russia cities stronger fiscal incentives have positive

50

effects on private business formation, the shares of local public spending on education

and health care, and the outcome of local public goods provision as measured in terms

of reducing infant mortality rates and the percentages of school children who have to

go to evening schools to compensate for the lack of education provided by the local

governments. Freinkman and Yossifov (1998) used the share of local governments

total revenue in the consolidated regional budgetary revenue as a measure of fiscal

decentralization within a region. They found that fiscal decentralization increases the

share of expenditures on education in regional government budget, increases regional

industrial output growth, but it also increases regional budget deficits.

VII. Conclusions

Building on the theory of market-preserving federalism, this paper studies the changing

central-local relationship in China and its impact on market development. Many

anecdotes suggest the importance of decentralization and government incentives in the

previous studies on China's reforms (for example, Montinola, Qian, and Weingast,

1995). The econometric results in this paper provide some systematic evidence on the

importance of decentralization and incentives. We find that fiscal decentralization and

51

fiscal incentives are generally conducive to local economic development. In contrast,

Communist Party control over personnel is not so conducive, despite its contributions

to macroeconomic stability.

Relying on the traditional theory of fiscal federalism, some economists criticize

China's decentralization and provincial "self-financing" on three grounds. First, some

argue decentralization and fiscal contracting seemed to create a variety of

microeconomic distortions (Wong, 1992). For example, decentralization may have

induced local governments into over-investment, duplication, regional market

protectionism, and more local bureaucratic interventions. Second, decentralization and

fiscal contracting seemed to have increased regional inequality due to the constraints

on revenue redistribution by the central government (Wong, 1991). Third, the fiscal

contracting system also greatly reduced the central government's ability to conduct

fiscal policy because it surrendered fiscal instruments and received fewer tax revenues

(Bahl and Wallace, 1992).

{YQ: I moved this sent to a new paragraph. We have to explain why we

conclude this and why the traditional fiscal federalism perspective is wrong.}}Focusing

on incentives of government, our results show that some of these criticisms of China's

decentralization and fiscal reform need to be qualified or even reconsidered.

52