preparation of financial statements

TRANSCRIPT

PREPARATION OF FINANCIAL STATEMENTS

PREPARED FOR: MS. KIM OANH VU

PREPARED BY: AN DUC KIEN

STUDENT NO: F06-066

CLASS: F06B

SUBMISSION DEADLINE: 14th November,

Table of ContentsINTRODUCTION..................................................1

CHAPTER 1: HOW INFORMATION NEEDS OF DIFFERENT USER GROUPS VARY. 2CHAPTER 2: PREPARATION OF FINANCIAL STATEMENTS.................3CHAPTER 3: INCOMPLETE RECORDS..................................7CHAPTER 4: FINANCIAL STATEMENT PUBLICATION BY A PARTNERSHIP FIRM..............................................................11CHAPTER 5: CONSOLIDATION OF ACCOUNTS..........................15CONCLUSION...................................................19

References....................................................19

INTRODUCTIONA financial statement (or financial report) is a formal record ofthe financial activities of a business, person, or other entity(Anon., n.d.). Financial statement record all the financialactivity of business during a period of time. Financialinformation is presented in a structured manner and in a formeasy to understand.

Balance sheet: represent the value of company’s assets,liabilities and equity

Income statement or profit and loss report: reportscompany‘s income, expenses and profit during a period oftime

Giving the exact financial information is essential to decisionmaking of different groups of user. To do that, it require acareful analysis from the financial data. This report will helpreader to understand how to prepare a financial statement forsole trader and partnership through the example of Nguyen Luucompany and EdLu Ltd.

CHAPTER 1: HOW INFORMATION NEEDS OF DIFFERENTUSER GROUPS VARY

Different user groups have different requirement for the information from the financial statement of a business. Businesses need to know that in order to provide the right information for them. User groups could be divided in two types: external and internal group (Anon., 2013).

1. Internal groupa. Managers and Owners: they need information in order to

measure the company performance and plan theappropriate strategy for the company. The manager andowner need information from financial report fordecision making. For owners, they use the informationfrom financial statement to analyze the profitabilityof their investment and decide to keep investing in thecompany or not.

b. Employees: They also use information from financialstatement to assess profitability of company in orderto make sure the security of the job and their futurein the company. Employee needs of information alsoinclude performance bonuses, commissions, revenuesharing or simply want to know the financial standingof their employer.

2. External group:a. Creditors: this users need information in order to

consider: Should we lend them our money? The mostcommon user in this group is bank. When a company wantto borrow money from the bank, the bank usually look inthe financial statement of company, specifically the

Page | 2

debt section in order to assess the ability to repay ofthe company.

b. Investors: Investors use information in order toconsider the financial strength of a company. Thiswould help them to make investment decisions.

c. Government: base on the financial statement of acompany, the government can determine the exact amountof tax that the company have to pay, line with thecompany financial strength.

d. Customers: Customer are interested to judge theprofitability of the business for assess the ability ofthe company to survive so that they are supplied. Withstrong financial background also relate to qualityproducts and the innovation of products.

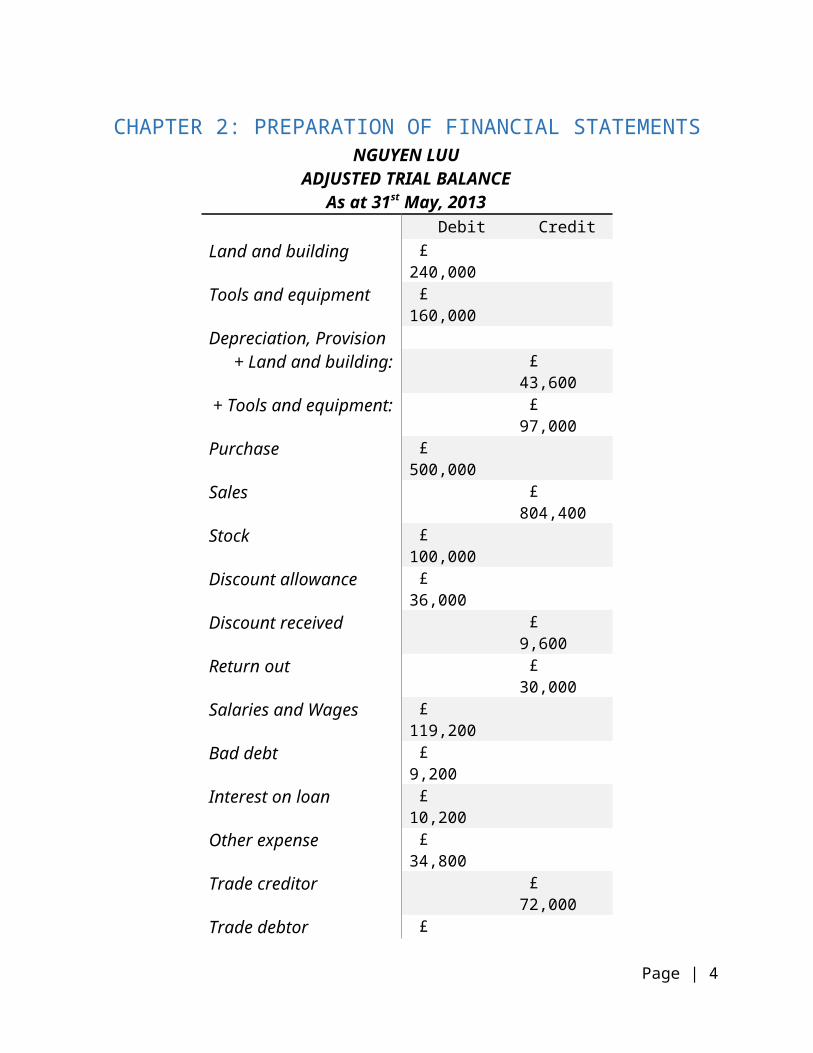

CHAPTER 2: PREPARATION OF FINANCIAL STATEMENTSNGUYEN LUU

ADJUSTED TRIAL BALANCEAs at 31st May, 2013

Debit Credit Land and building £

240,000 Tools and equipment £

160,000 Depreciation, Provision

+ Land and building: £ 43,600

+ Tools and equipment: £ 97,000

Purchase £ 500,000

Sales £ 804,400

Stock £ 100,000

Discount allowance £ 36,000

Discount received £ 9,600

Return out £ 30,000

Salaries and Wages £ 119,200

Bad debt £ 9,200

Interest on loan £ 10,200

Other expense £ 34,800

Trade creditor £ 72,000

Trade debtor £

Page | 4

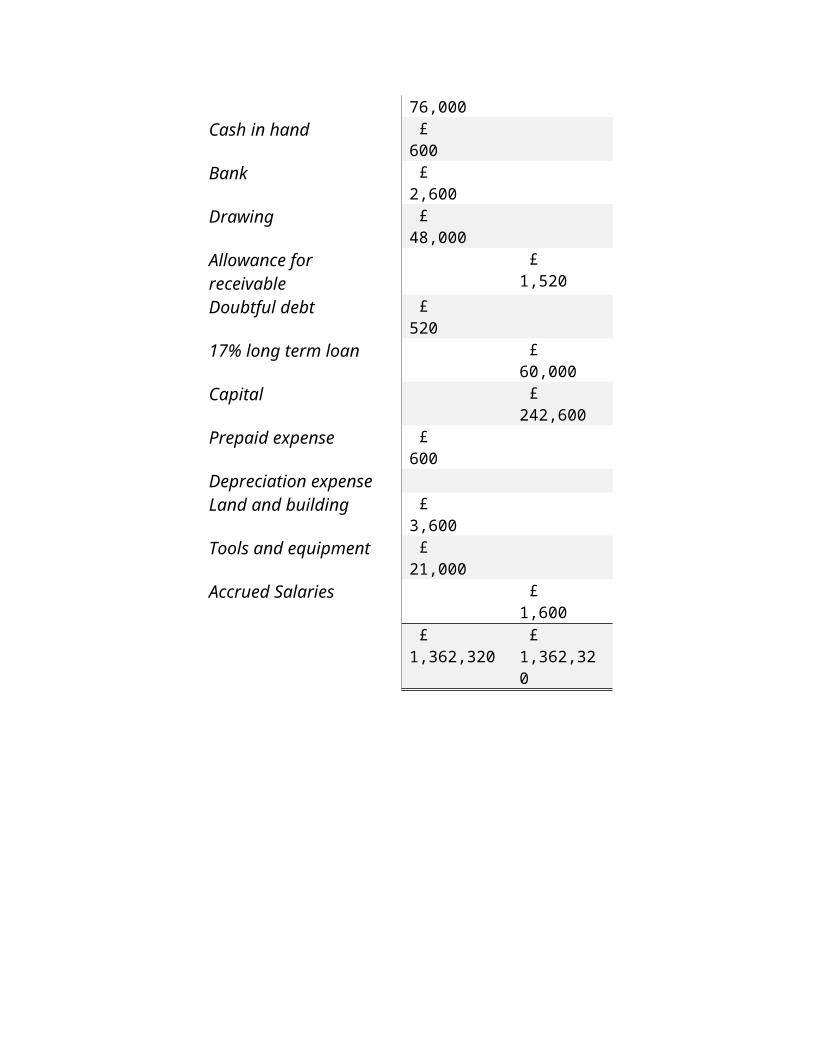

76,000 Cash in hand £

600 Bank £

2,600 Drawing £

48,000 Allowance for receivable

£ 1,520

Doubtful debt £ 520

17% long term loan £ 60,000

Capital £ 242,600

Prepaid expense £ 600

Depreciation expenseLand and building £

3,600 Tools and equipment £

21,000 Accrued Salaries £

1,600 £ 1,362,320

£ 1,362,320

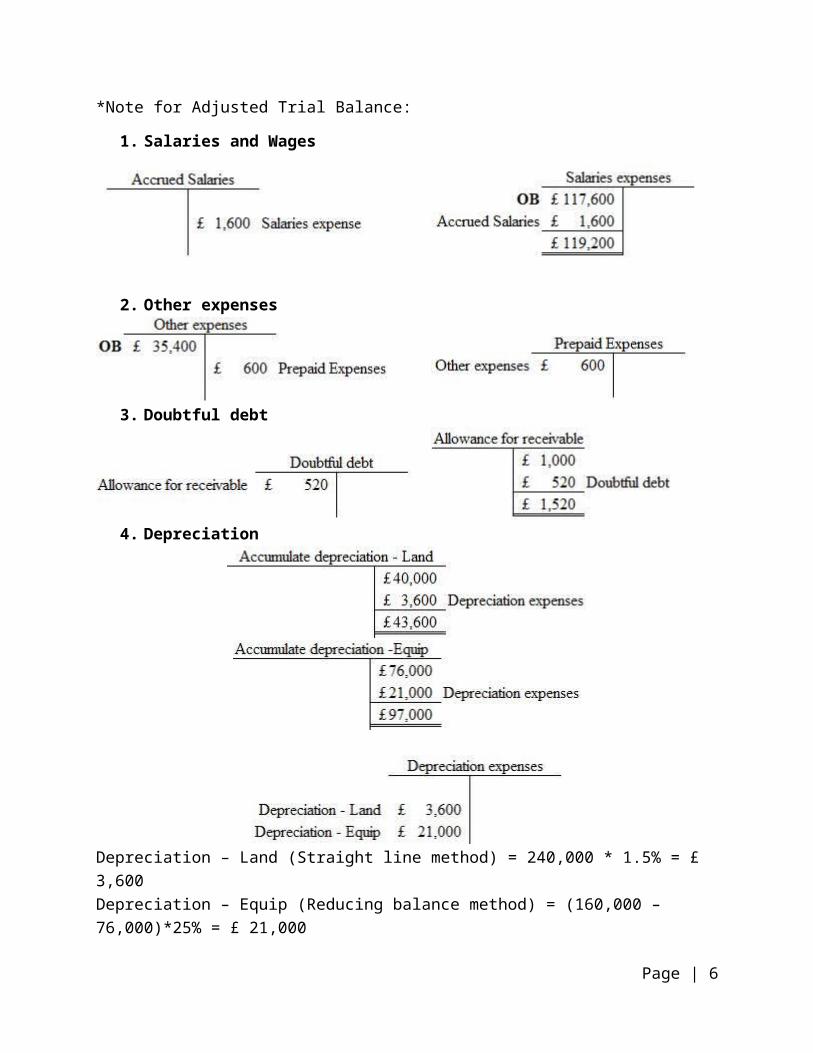

*Note for Adjusted Trial Balance:

1. Salaries and Wages

2. Other expenses

3. Doubtful debt

4. Depreciation

Depreciation – Land (Straight line method) = 240,000 * 1.5% = £ 3,600Depreciation – Equip (Reducing balance method) = (160,000 – 76,000)*25% = £ 21,000

Page | 6

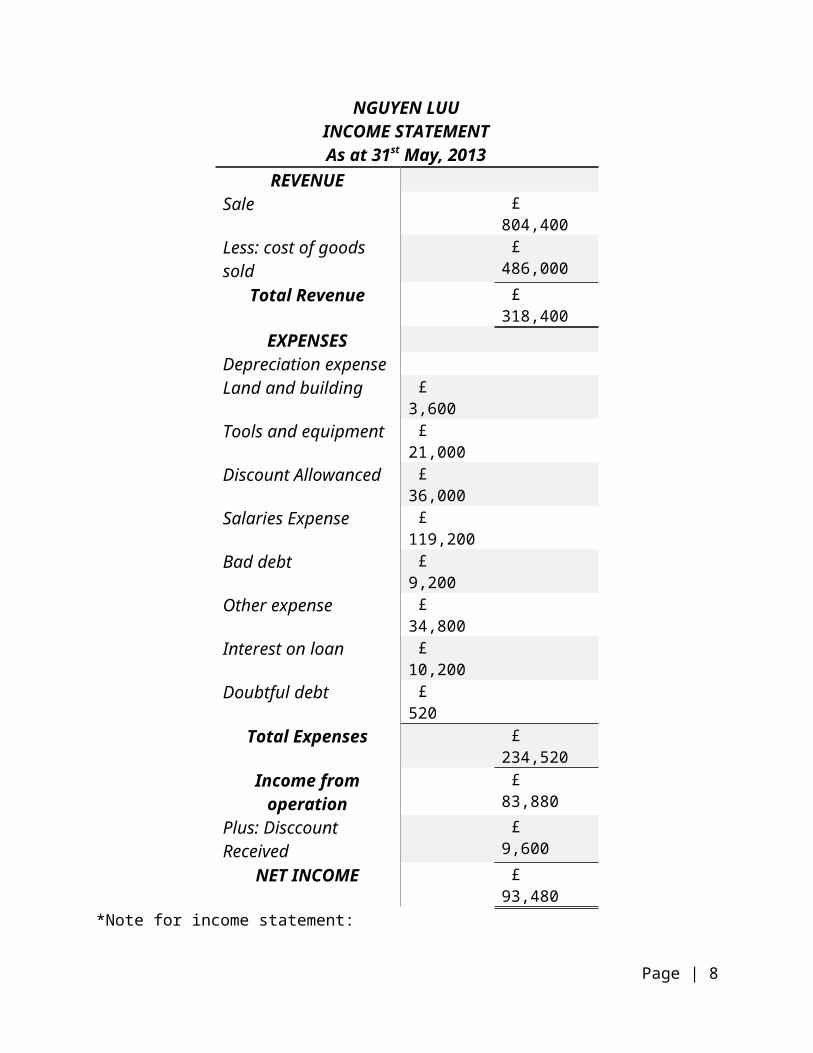

NGUYEN LUUINCOME STATEMENTAs at 31st May, 2013

REVENUESale £

804,400 Less: cost of goods sold

£ 486,000

Total Revenue £ 318,400

EXPENSESDepreciation expenseLand and building £

3,600 Tools and equipment £

21,000 Discount Allowanced £

36,000 Salaries Expense £

119,200 Bad debt £

9,200 Other expense £

34,800 Interest on loan £

10,200 Doubtful debt £

520 Total Expenses £

234,520 Income from

operation £ 83,880

Plus: Disccount Received

£ 9,600

NET INCOME £ 93,480

*Note for income statement:

Page | 8

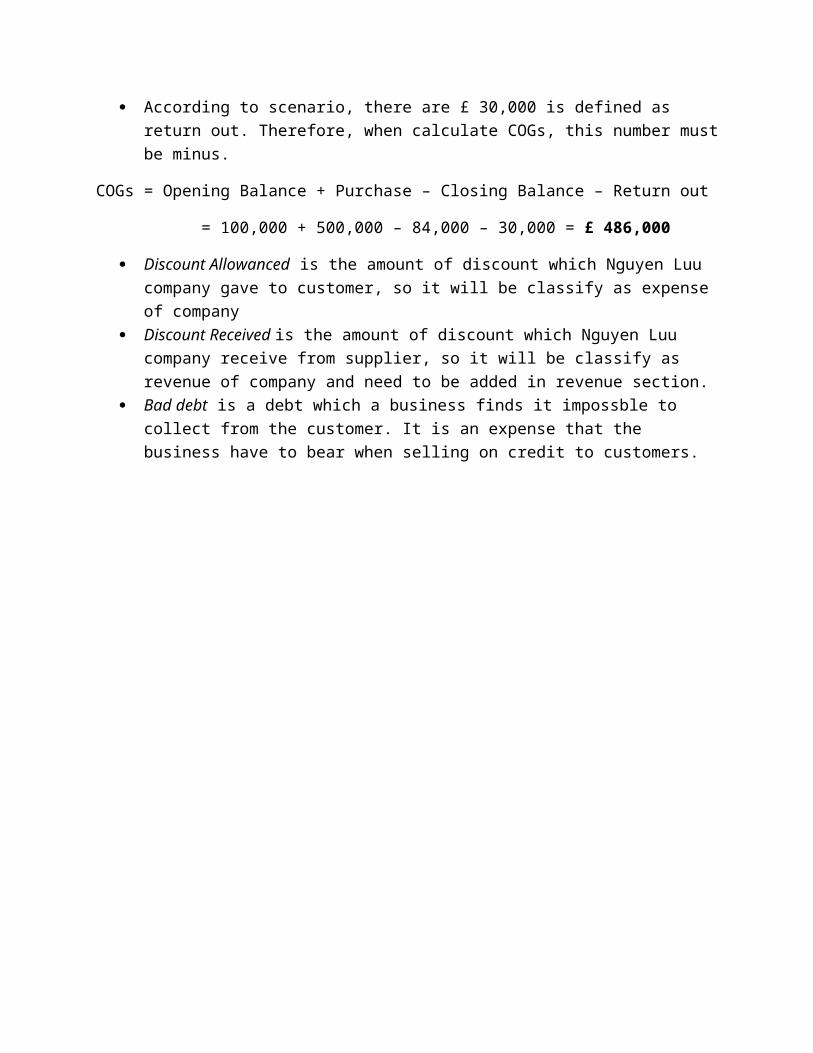

According to scenario, there are £ 30,000 is defined as return out. Therefore, when calculate COGs, this number mustbe minus.

COGs = Opening Balance + Purchase – Closing Balance – Return out

= 100,000 + 500,000 – 84,000 – 30,000 = £ 486,000

Discount Allowanced is the amount of discount which Nguyen Luu company gave to customer, so it will be classify as expense of company

Discount Received is the amount of discount which Nguyen Luu company receive from supplier, so it will be classify as revenue of company and need to be added in revenue section.

Bad debt is a debt which a business finds it impossble to collect from the customer. It is an expense that the business have to bear when selling on credit to customers.

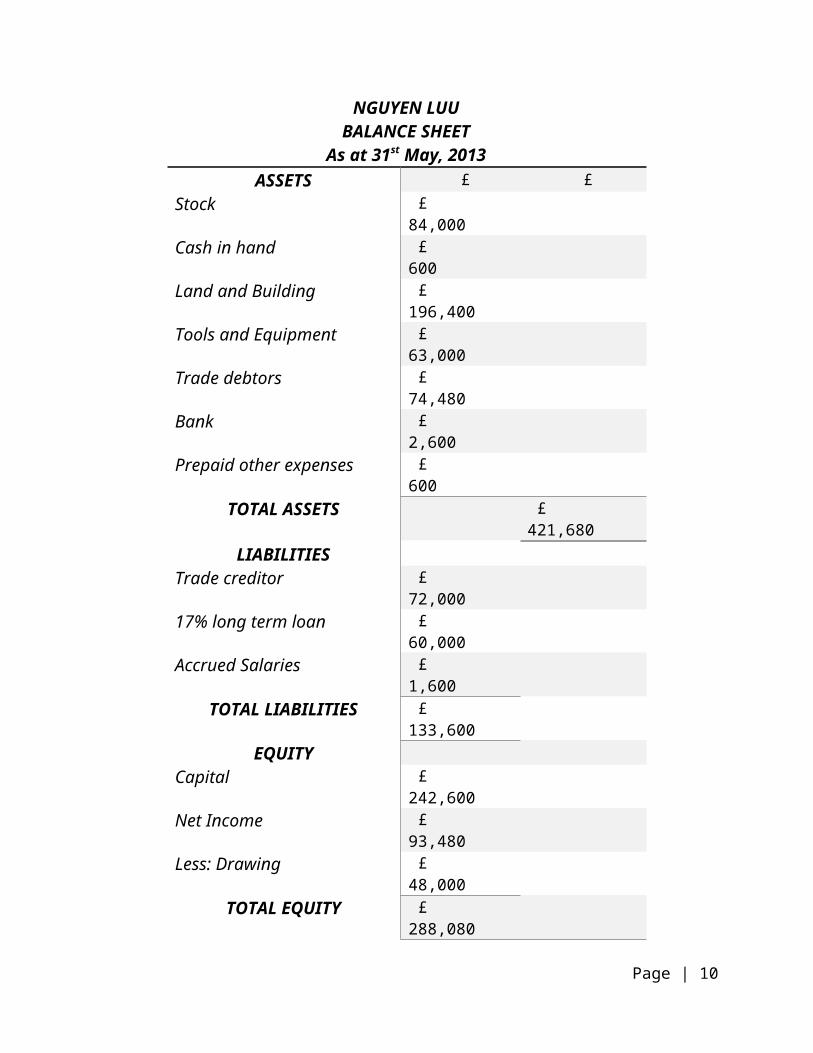

NGUYEN LUUBALANCE SHEET

As at 31st May, 2013ASSETS £ £

Stock £ 84,000

Cash in hand £ 600

Land and Building £ 196,400

Tools and Equipment £ 63,000

Trade debtors £ 74,480

Bank £ 2,600

Prepaid other expenses £ 600

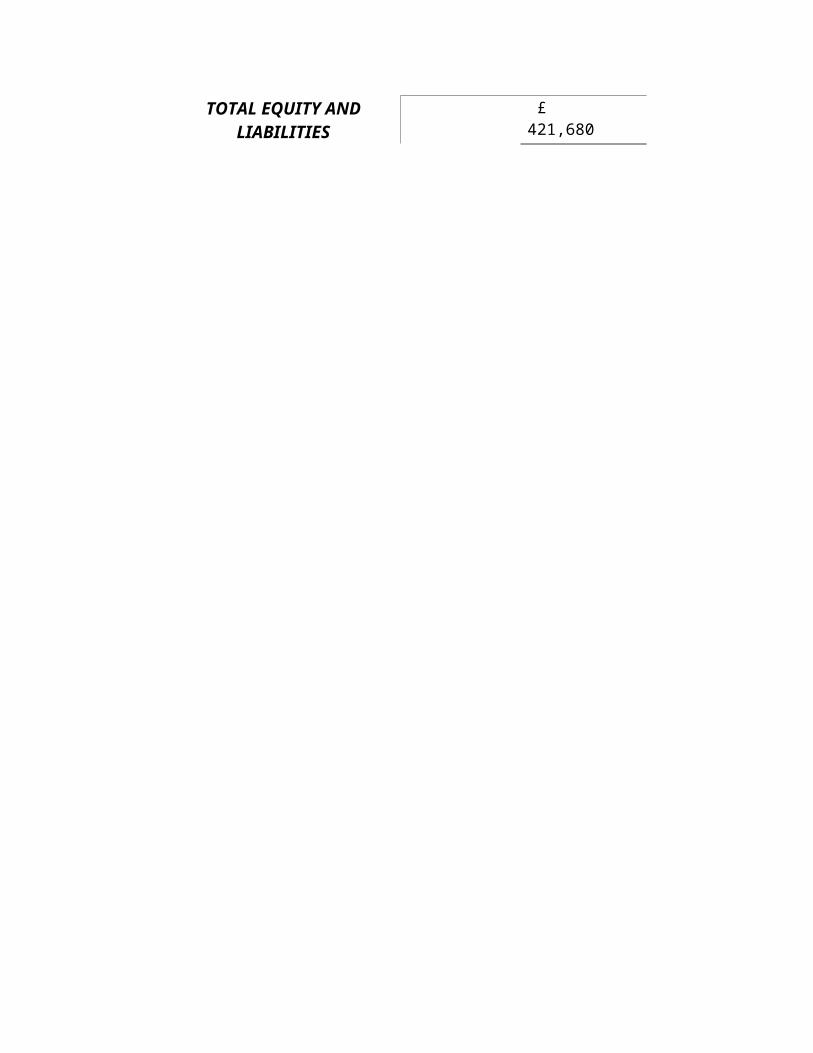

TOTAL ASSETS £ 421,680

LIABILITIESTrade creditor £

72,000 17% long term loan £

60,000 Accrued Salaries £

1,600 TOTAL LIABILITIES £

133,600 EQUITY

Capital £ 242,600

Net Income £ 93,480

Less: Drawing £ 48,000

TOTAL EQUITY £ 288,080

Page | 10

TOTAL EQUITY ANDLIABILITIES

£ 421,680

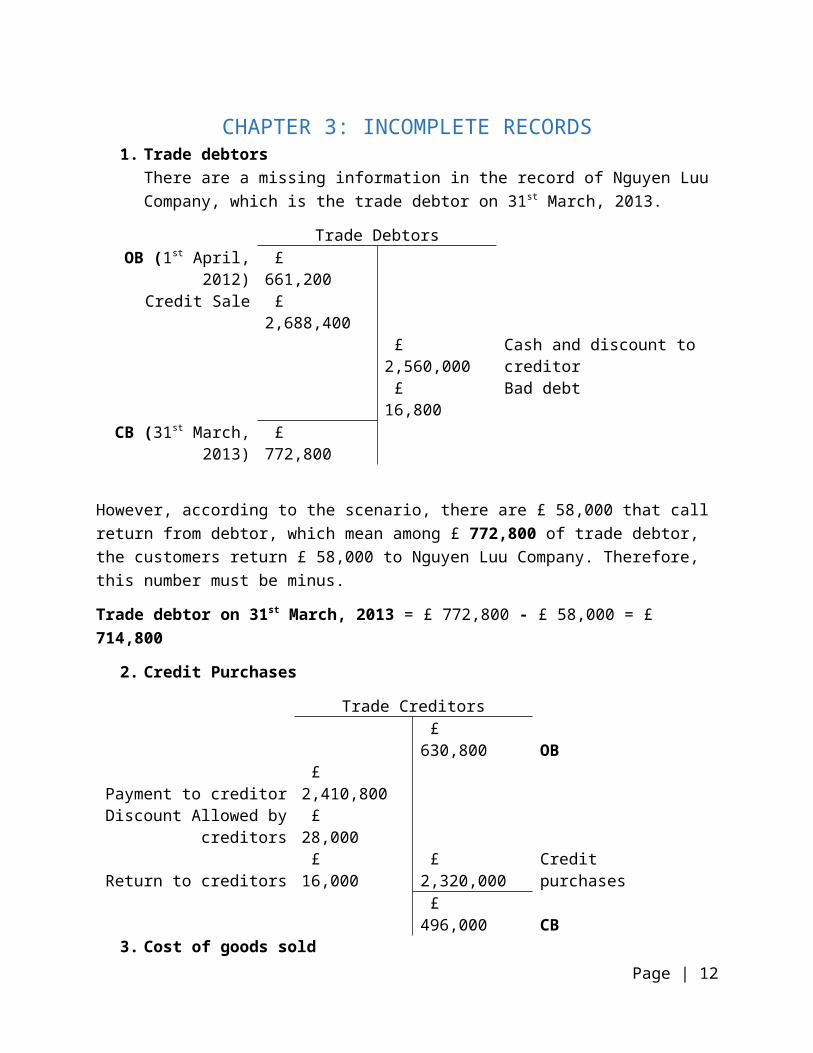

CHAPTER 3: INCOMPLETE RECORDS1. Trade debtors

There are a missing information in the record of Nguyen Luu Company, which is the trade debtor on 31st March, 2013.

Trade DebtorsOB (1st April,

2012) £ 661,200

Credit Sale £ 2,688,400

£ 2,560,000

Cash and discount to creditor

£ 16,800

Bad debt

CB (31st March,2013)

£ 772,800

However, according to the scenario, there are £ 58,000 that call return from debtor, which mean among £ 772,800 of trade debtor, the customers return £ 58,000 to Nguyen Luu Company. Therefore, this number must be minus.

Trade debtor on 31st March, 2013 = £ 772,800 - £ 58,000 = £ 714,800

2. Credit Purchases

Trade Creditors

£ 630,800 OB

Payment to creditor £ 2,410,800

Discount Allowed bycreditors

£ 28,000

Return to creditors £ 16,000

£ 2,320,000

Credit purchases

£ 496,000 CB

3. Cost of goods soldPage | 12

COGS = Opening stock balance + Purchase – Closing stock balance – Return to creditors

= 321,600 + 41,200 + 2,320,000 – 444,800 – 15,000

= £ 2,222,000

4. Fixed Assets Depreciation

Fixed Assets

OB £ 464,400

Machinery acquired bycheque

£ 127,200

£ 110,000 Depreciation

£ 591,600

Less: CB £ 481,600

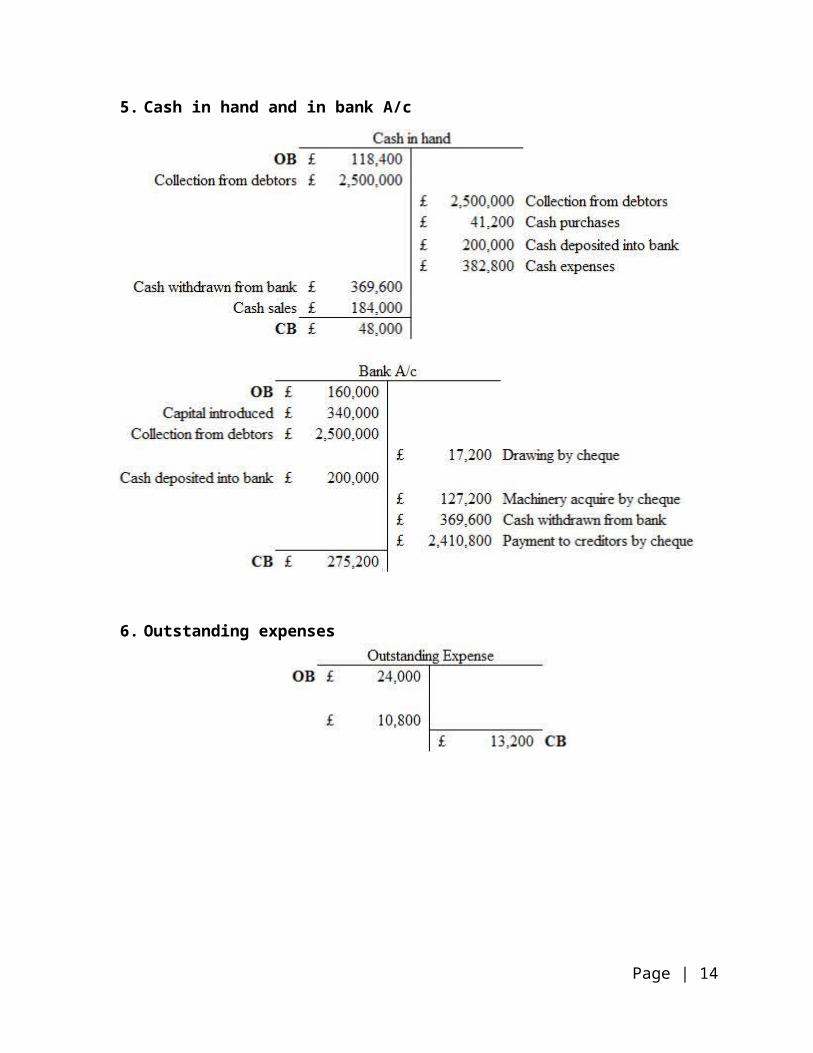

5. Cash in hand and in bank A/c

6. Outstanding expenses

Page | 14

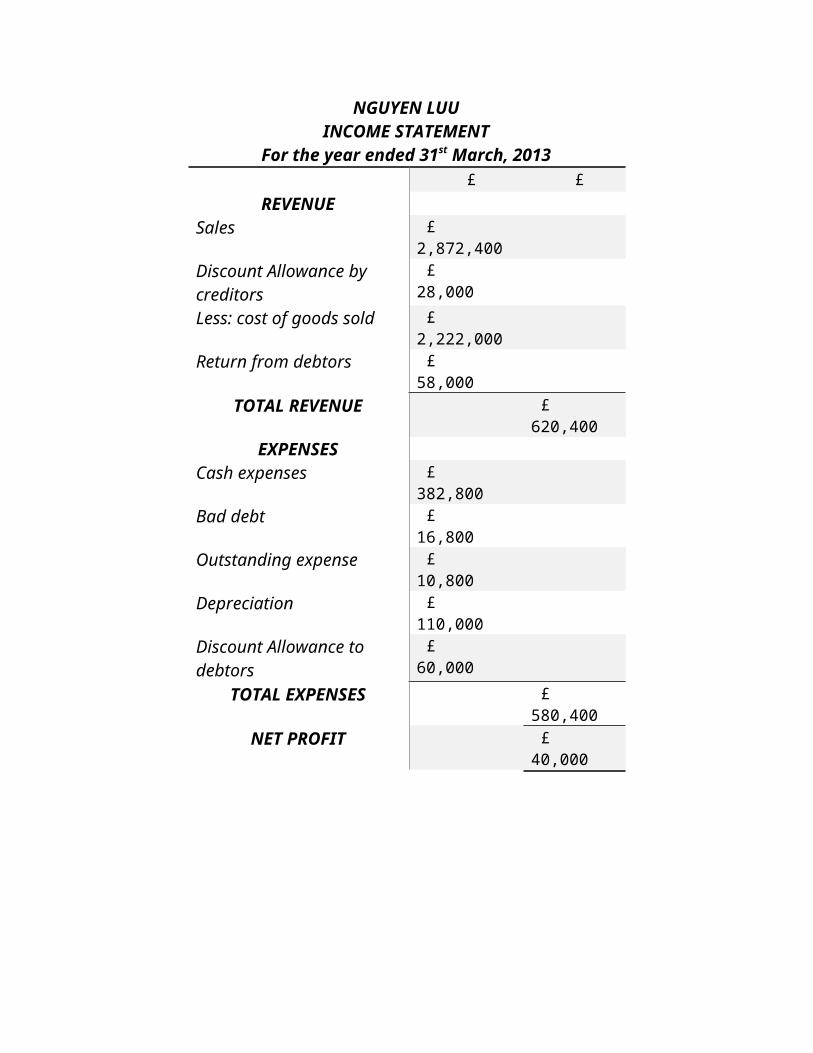

NGUYEN LUUINCOME STATEMENT

For the year ended 31st March, 2013 £ £

REVENUESales £

2,872,400 Discount Allowance by creditors

£ 28,000

Less: cost of goods sold £ 2,222,000

Return from debtors £ 58,000

TOTAL REVENUE £ 620,400

EXPENSESCash expenses £

382,800 Bad debt £

16,800 Outstanding expense £

10,800 Depreciation £

110,000 Discount Allowance to debtors

£ 60,000

TOTAL EXPENSES £ 580,400

NET PROFIT £ 40,000

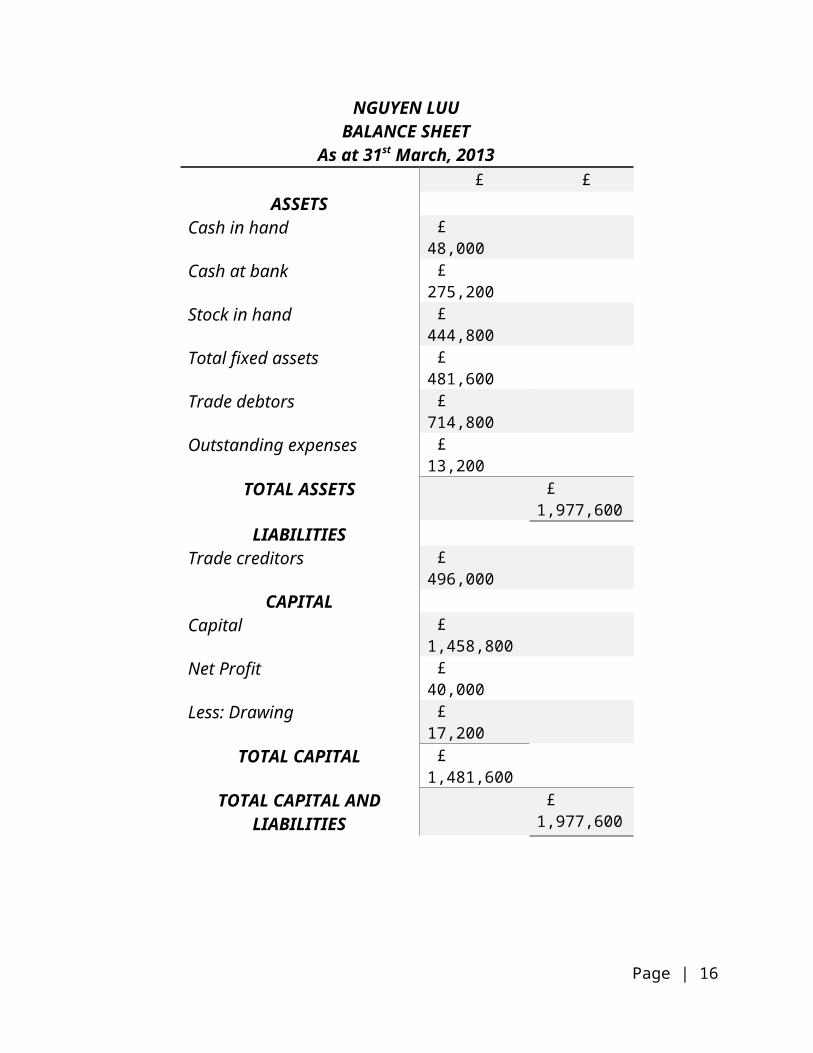

NGUYEN LUUBALANCE SHEET

As at 31st March, 2013 £ £

ASSETSCash in hand £

48,000 Cash at bank £

275,200 Stock in hand £

444,800 Total fixed assets £

481,600 Trade debtors £

714,800 Outstanding expenses £

13,200

TOTAL ASSETS £ 1,977,600

LIABILITIESTrade creditors £

496,000 CAPITAL

Capital £ 1,458,800

Net Profit £ 40,000

Less: Drawing £ 17,200

TOTAL CAPITAL £ 1,481,600

TOTAL CAPITAL ANDLIABILITIES

£ 1,977,600

Page | 16

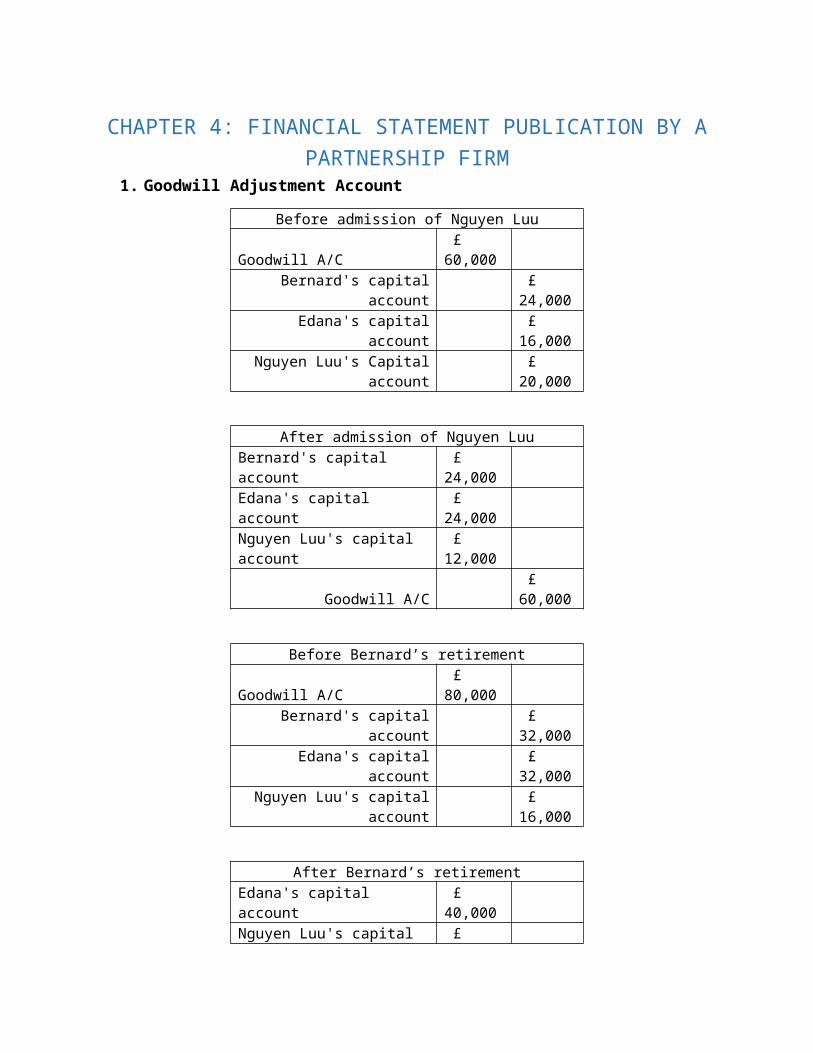

CHAPTER 4: FINANCIAL STATEMENT PUBLICATION BY APARTNERSHIP FIRM

1. Goodwill Adjustment Account

Before admission of Nguyen Luu

Goodwill A/C £ 60,000

Bernard's capitalaccount

£ 24,000

Edana's capitalaccount

£ 16,000

Nguyen Luu's Capitalaccount

£ 20,000

After admission of Nguyen LuuBernard's capital account

£ 24,000

Edana's capital account

£ 24,000

Nguyen Luu's capital account

£ 12,000

Goodwill A/C £ 60,000

Before Bernard’s retirement

Goodwill A/C £ 80,000

Bernard's capitalaccount

£ 32,000

Edana's capitalaccount

£ 32,000

Nguyen Luu's capitalaccount

£ 16,000

After Bernard’s retirementEdana's capital account

£ 40,000

Nguyen Luu's capital £

account 40,000

Goodwill A/C £ 80,000

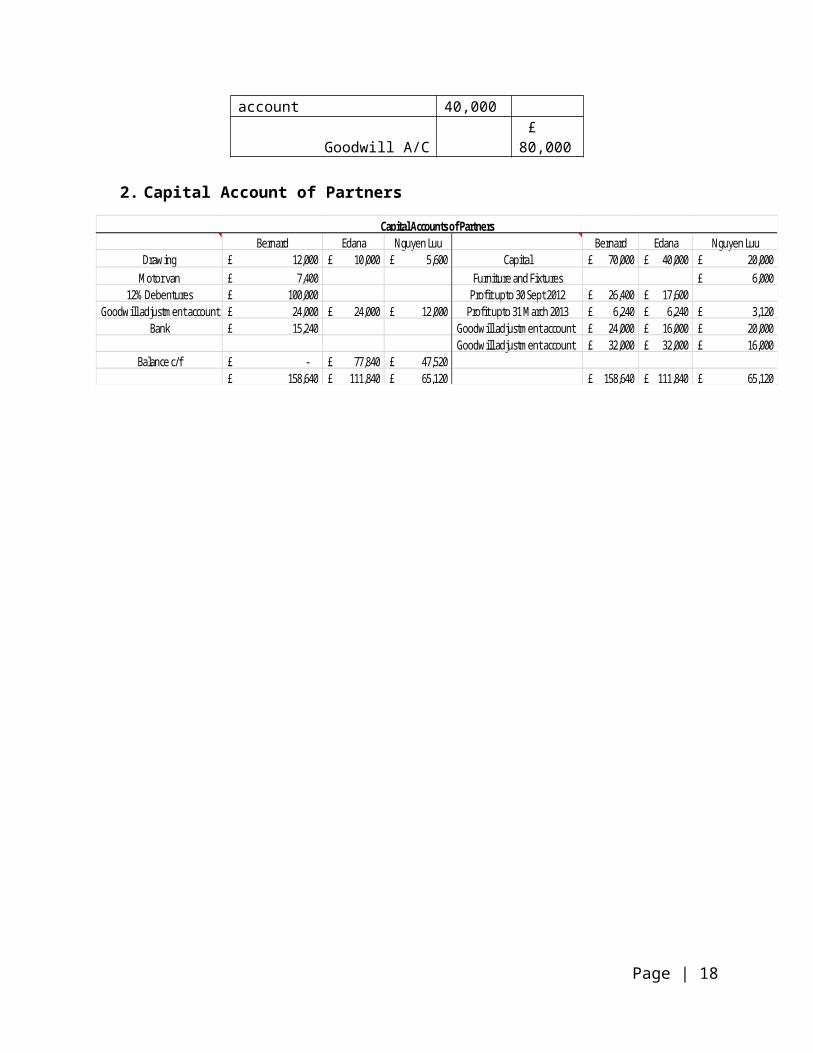

2. Capital Account of Partners

Bernard Edana Nguyen Luu Bernard Edana Nguyen LuuDrawing 12,000£ 10,000£ 5,600£ Capital 70,000£ 40,000£ 20,000£ M otor van 7,400£ Furniture and Fixtures 6,000£

12% Debentures 100,000£ Profit upto 30 Sept 2012 26,400£ 17,600£ Goodwill adjustm ent account 24,000£ 24,000£ 12,000£ Profit upto 31 M arch 2013 6,240£ 6,240£ 3,120£

Bank 15,240£ Goodwill adjustm ent account 24,000£ 16,000£ 20,000£ Goodwill adjustm ent account 32,000£ 32,000£ 16,000£

Balance c/f -£ 77,840£ 47,520£ 158,640£ 111,840£ 65,120£ 158,640£ 111,840£ 65,120£

Capital Accounts of Partners

Page | 18

*Notes:

The balance c/f of Bernard must equal to 0 because he retire, so the remaining in bank account of Bernard will equal to total assets of Bernard minus total amount of Bernard’s withdraw

Bernard’s bank account = 158,640 – (12,000 +7,400 + 100,000 + 24,000) = £ 15,240

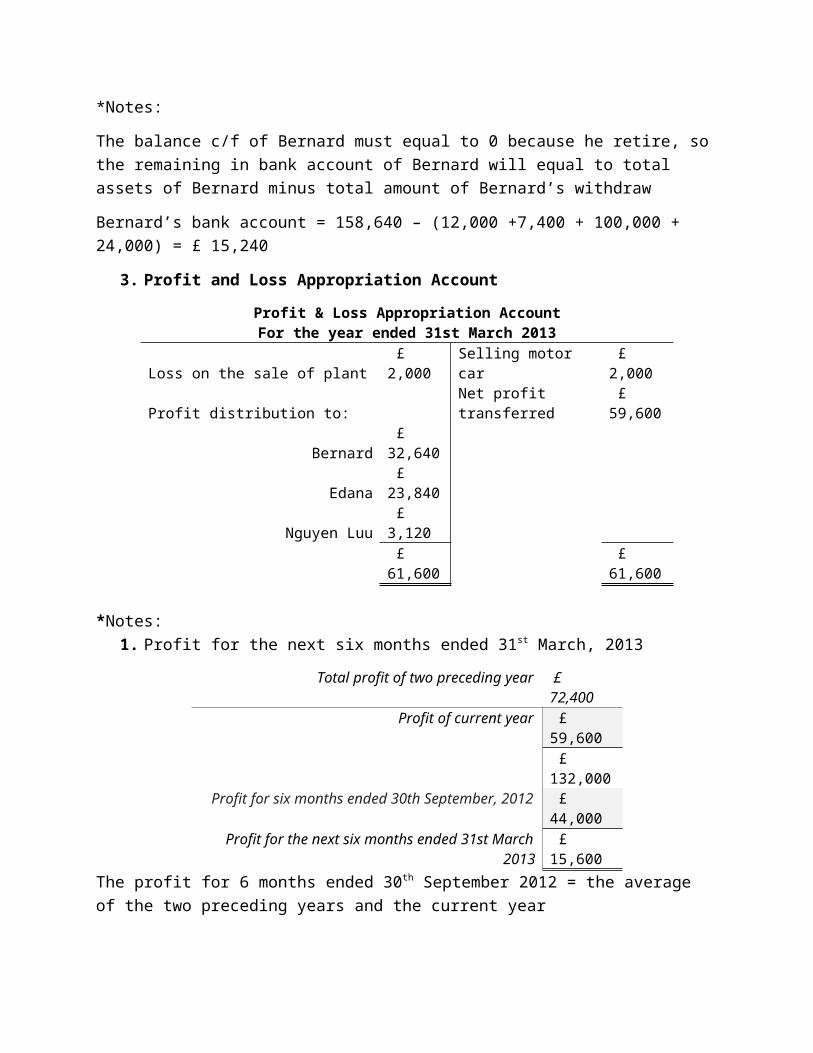

3. Profit and Loss Appropriation Account

Profit & Loss Appropriation AccountFor the year ended 31st March 2013

Loss on the sale of plant £ 2,000

Selling motor car

£ 2,000

Profit distribution to:Net profit transferred

£ 59,600

Bernard £ 32,640

Edana £ 23,840

Nguyen Luu £ 3,120 £ 61,600

£ 61,600

*Notes:1. Profit for the next six months ended 31st March, 2013

Total profit of two preceding year £ 72,400

Profit of current year £ 59,600 £ 132,000

Profit for six months ended 30th September, 2012 £ 44,000

Profit for the next six months ended 31st March2013

£ 15,600

The profit for 6 months ended 30th September 2012 = the average of the two preceding years and the current year

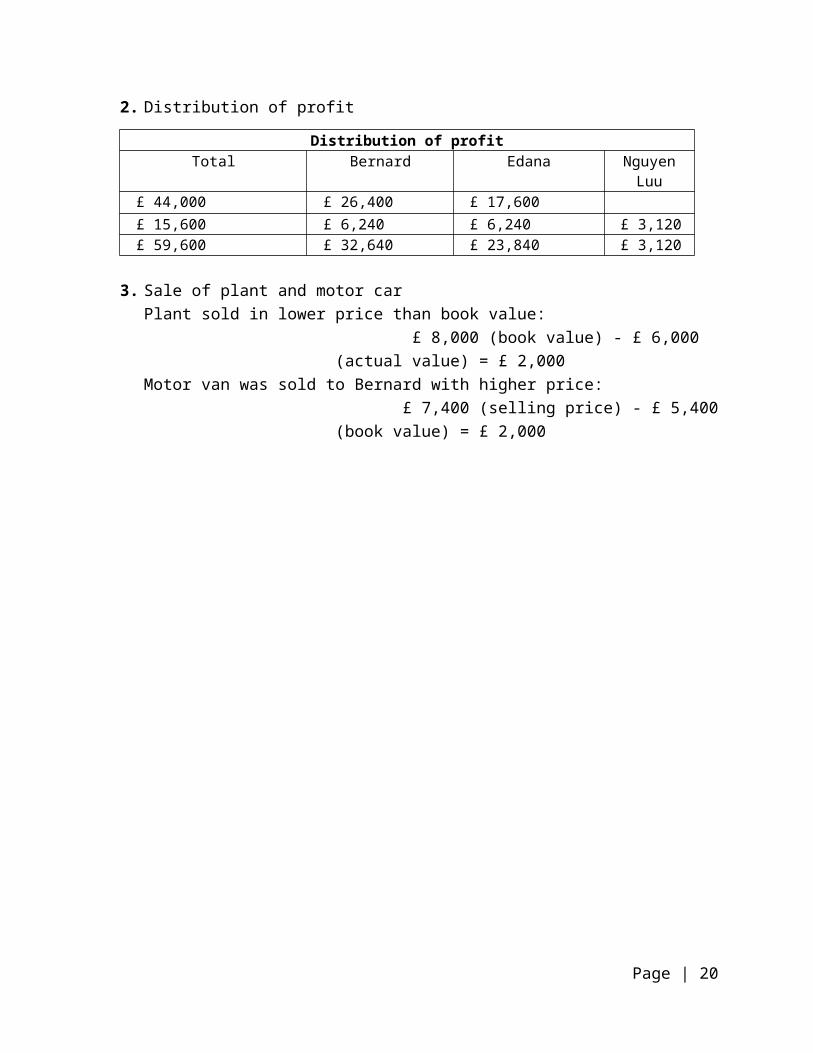

2. Distribution of profit

Distribution of profitTotal Bernard Edana Nguyen

Luu £ 44,000 £ 26,400 £ 17,600 £ 15,600 £ 6,240 £ 6,240 £ 3,120 £ 59,600 £ 32,640 £ 23,840 £ 3,120

3. Sale of plant and motor carPlant sold in lower price than book value:

£ 8,000 (book value) - £ 6,000 (actual value) = £ 2,000

Motor van was sold to Bernard with higher price: £ 7,400 (selling price) - £ 5,400(book value) = £ 2,000

Page | 20

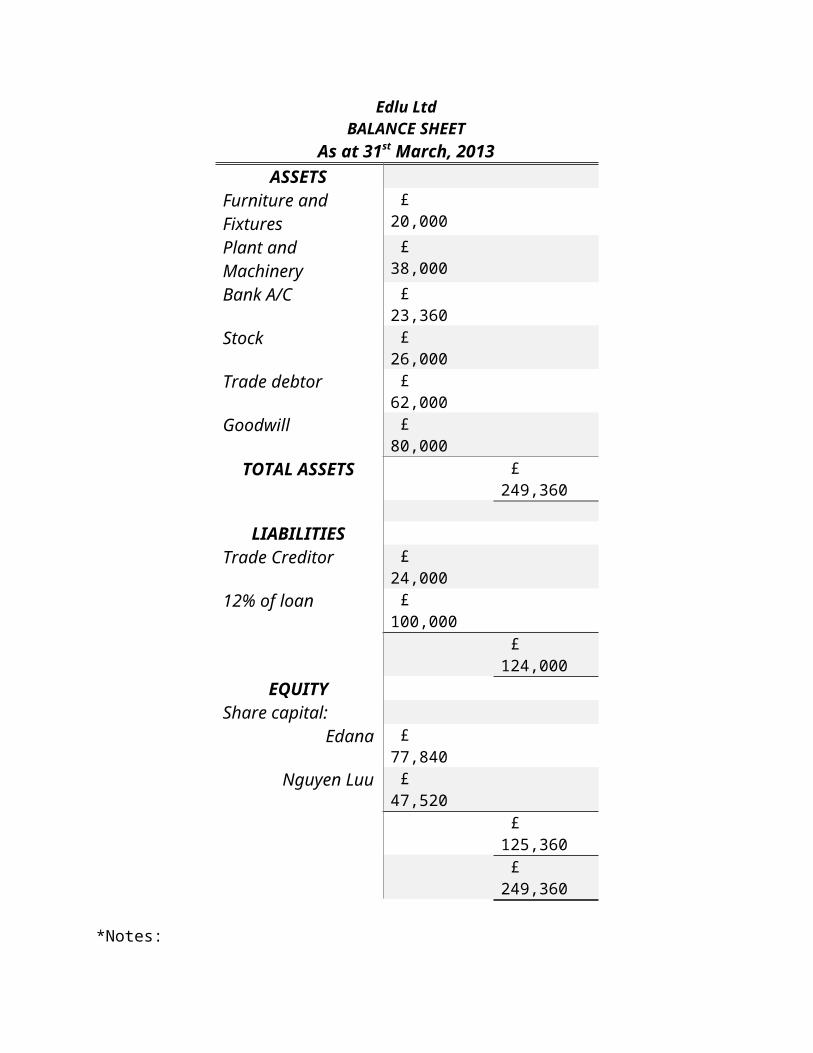

Edlu LtdBALANCE SHEET

As at 31st March, 2013ASSETS

Furniture and Fixtures

£ 20,000

Plant and Machinery

£ 38,000

Bank A/C £ 23,360

Stock £ 26,000

Trade debtor £ 62,000

Goodwill £ 80,000

TOTAL ASSETS £ 249,360

LIABILITIESTrade Creditor £

24,000 12% of loan £

100,000 £

124,000 EQUITY

Share capital:Edana £

77,840 Nguyen Luu £

47,520 £

125,360 £ 249,360

*Notes:

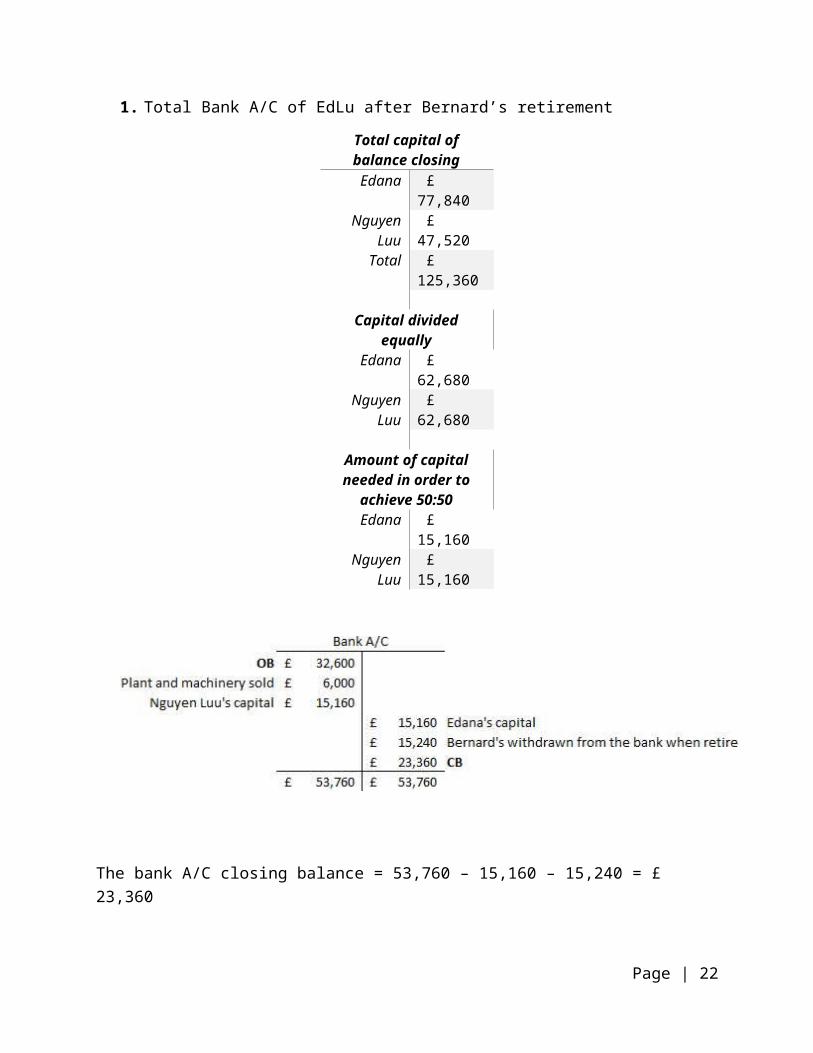

1. Total Bank A/C of EdLu after Bernard’s retirement

Total capital ofbalance closingEdana £

77,840 Nguyen

Luu £ 47,520

Total £ 125,360

Capital dividedequally

Edana £ 62,680

NguyenLuu

£ 62,680

Amount of capitalneeded in order to

achieve 50:50Edana £

15,160 Nguyen

Luu £ 15,160

The bank A/C closing balance = 53,760 – 15,160 – 15,240 = £ 23,360

Page | 22

CHAPTER 5: CONSOLIDATION OF ACCOUNTSEdLu LTD

Consolidated Statement of Comprehensive IncomeFor the year ended 31st March, 2013

£’000 Revenue (Note 2) £

1,060,000 Cost of sales (Note 3) £

557,600 Gross profit £

502,400 Distribution cost £

59,200 Administrative expenses £

77,000 Finance cost £

4,200 Profit before tax £

362,000 Income tax expense £

123,800 Profit for the year £

238,200

Other comprehensive incomeGain on revaluation of land £

7,000 Loss on fair value of equity financial asset investment

£ 1,800 £ 5,200

Total comprehensive income £ 243,400

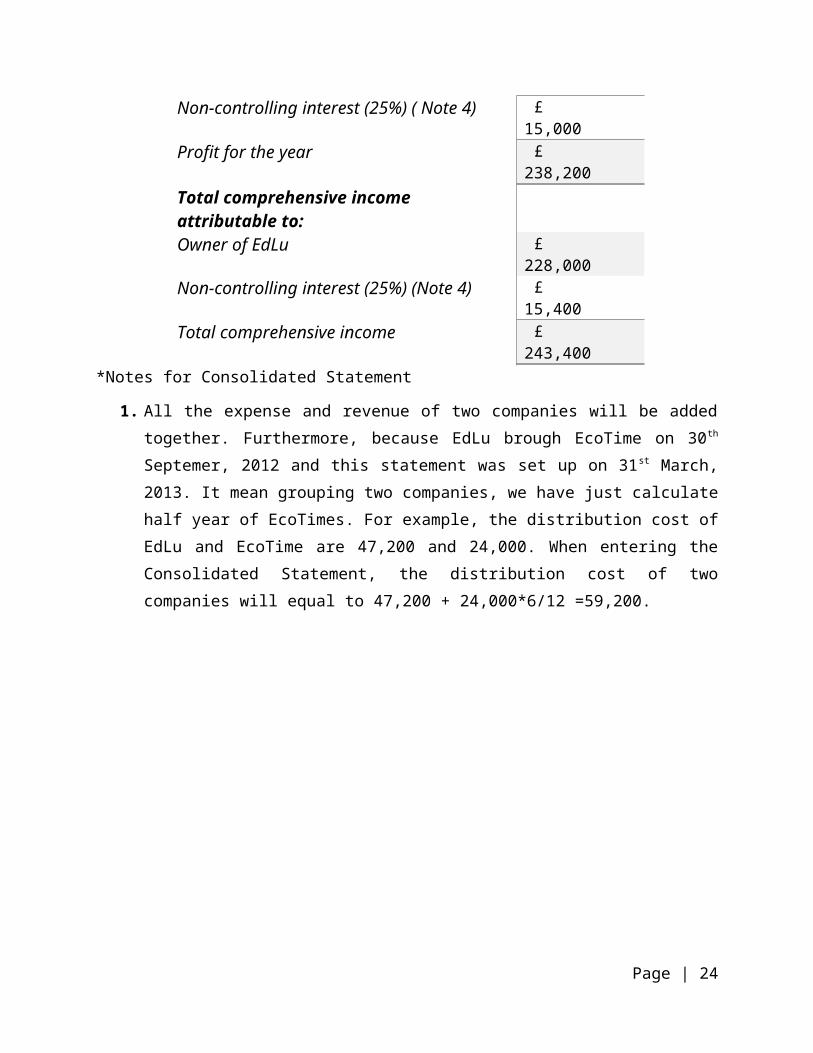

Profit attribute to:Owner of EdLu £

223,200

Non-controlling interest (25%) ( Note 4) £ 15,000

Profit for the year £ 238,200

Total comprehensive income attributable to:Owner of EdLu £

228,000 Non-controlling interest (25%) (Note 4) £

15,400 Total comprehensive income £

243,400 *Notes for Consolidated Statement

1. All the expense and revenue of two companies will be addedtogether. Furthermore, because EdLu brough EcoTime on 30th

Septemer, 2012 and this statement was set up on 31st March,2013. It mean grouping two companies, we have just calculatehalf year of EcoTimes. For example, the distribution cost ofEdLu and EcoTime are 47,200 and 24,000. When entering theConsolidated Statement, the distribution cost of twocompanies will equal to 47,200 + 24,000*6/12 =59,200.

Page | 24

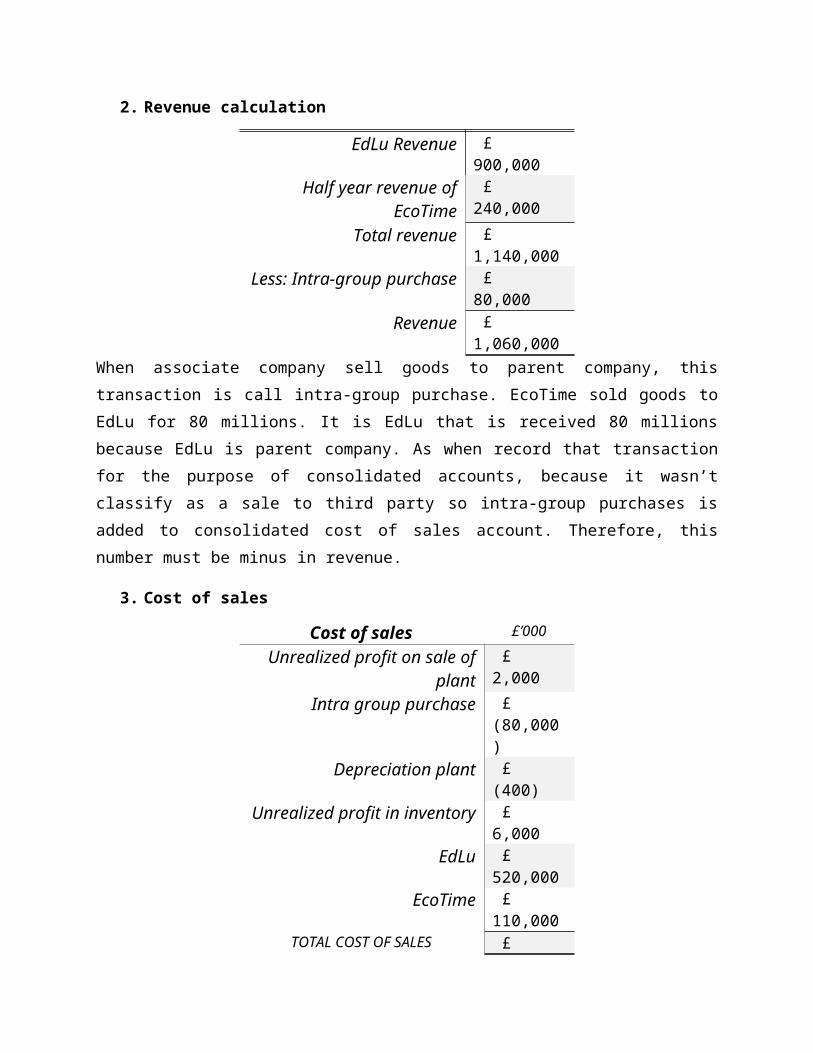

2. Revenue calculation

EdLu Revenue £ 900,000

Half year revenue ofEcoTime

£ 240,000

Total revenue £ 1,140,000

Less: Intra-group purchase £ 80,000

Revenue £ 1,060,000

When associate company sell goods to parent company, thistransaction is call intra-group purchase. EcoTime sold goods toEdLu for 80 millions. It is EdLu that is received 80 millionsbecause EdLu is parent company. As when record that transactionfor the purpose of consolidated accounts, because it wasn’tclassify as a sale to third party so intra-group purchases isadded to consolidated cost of sales account. Therefore, thisnumber must be minus in revenue.

3. Cost of sales

Cost of sales £’000

Unrealized profit on sale ofplant

£ 2,000

Intra group purchase £ (80,000)

Depreciation plant £ (400)

Unrealized profit in inventory £ 6,000

EdLu £ 520,000

EcoTime £ 110,000

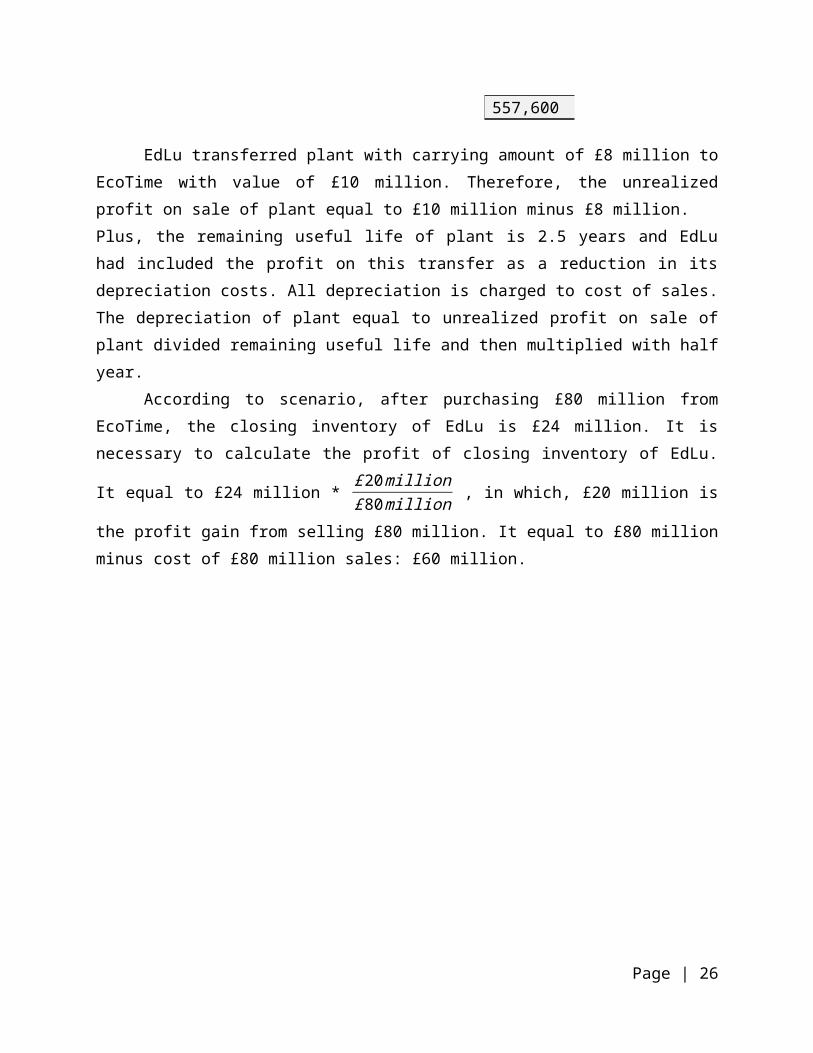

TOTAL COST OF SALES £

557,600

EdLu transferred plant with carrying amount of £8 million toEcoTime with value of £10 million. Therefore, the unrealizedprofit on sale of plant equal to £10 million minus £8 million.Plus, the remaining useful life of plant is 2.5 years and EdLuhad included the profit on this transfer as a reduction in itsdepreciation costs. All depreciation is charged to cost of sales.The depreciation of plant equal to unrealized profit on sale ofplant divided remaining useful life and then multiplied with halfyear.

According to scenario, after purchasing £80 million fromEcoTime, the closing inventory of EdLu is £24 million. It isnecessary to calculate the profit of closing inventory of EdLu.

It equal to £24 million * £20million£80million , in which, £20 million is

the profit gain from selling £80 million. It equal to £80 millionminus cost of £80 million sales: £60 million.

Page | 26

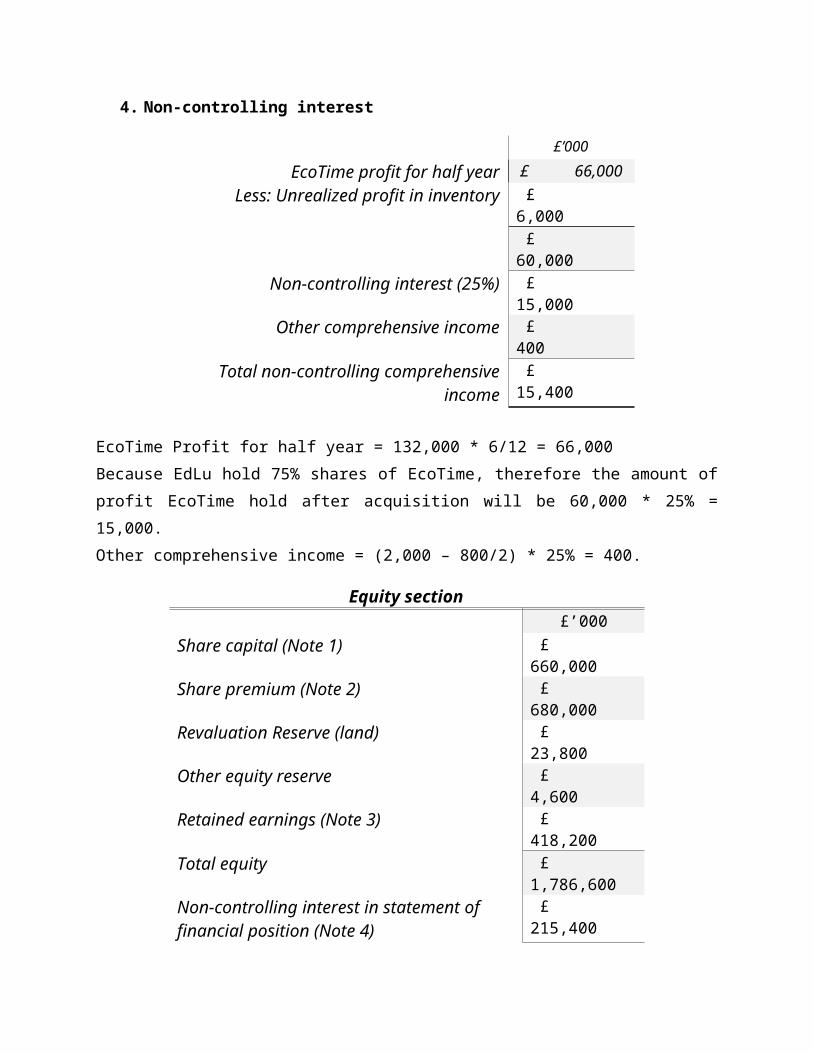

4. Non-controlling interest

£’000EcoTime profit for half year £ 66,000

Less: Unrealized profit in inventory £ 6,000 £ 60,000

Non-controlling interest (25%) £ 15,000

Other comprehensive income £ 400

Total non-controlling comprehensiveincome

£ 15,400

EcoTime Profit for half year = 132,000 * 6/12 = 66,000Because EdLu hold 75% shares of EcoTime, therefore the amount ofprofit EcoTime hold after acquisition will be 60,000 * 25% =15,000.Other comprehensive income = (2,000 – 800/2) * 25% = 400.

Equity section£’000

Share capital (Note 1) £ 660,000

Share premium (Note 2) £ 680,000

Revaluation Reserve (land) £ 23,800

Other equity reserve £ 4,600

Retained earnings (Note 3) £ 418,200

Total equity £ 1,786,600

Non-controlling interest in statement of financial position (Note 4)

£ 215,400

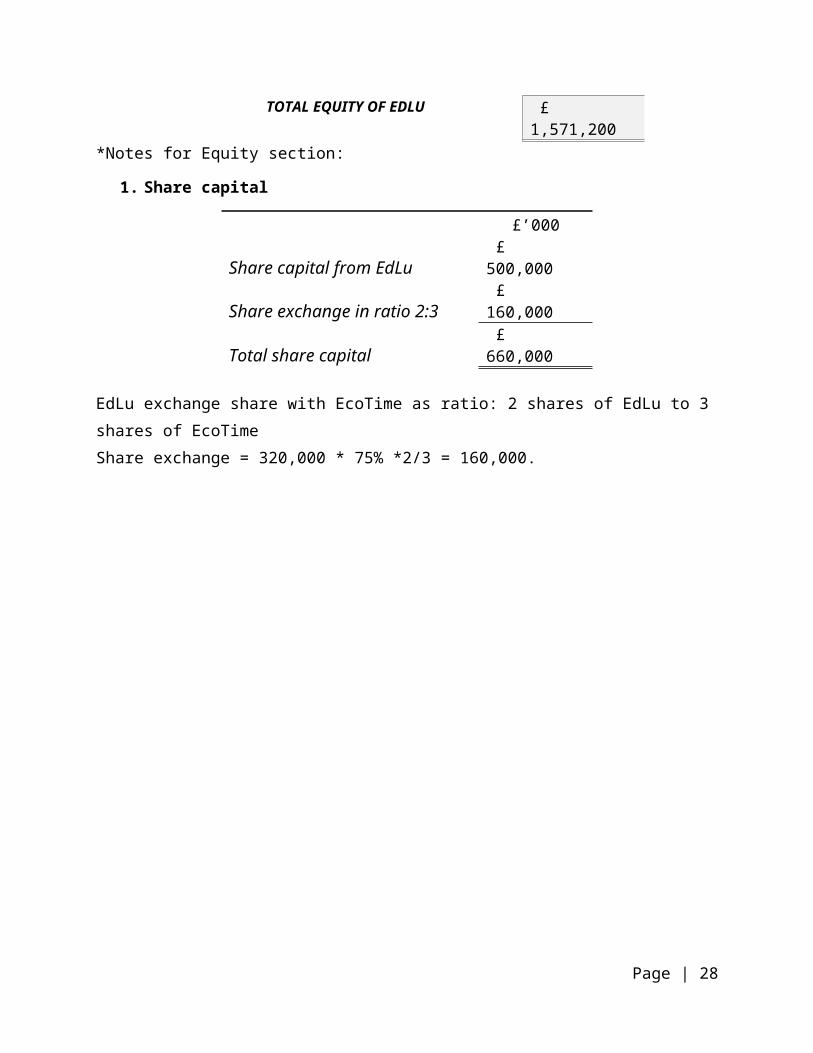

TOTAL EQUITY OF EDLU £ 1,571,200

*Notes for Equity section:

1. Share capital

£’000

Share capital from EdLu £ 500,000

Share exchange in ratio 2:3 £ 160,000

Total share capital £ 660,000

EdLu exchange share with EcoTime as ratio: 2 shares of EdLu to 3 shares of EcoTimeShare exchange = 320,000 * 75% *2/3 = 160,000.

Page | 28

2. Share Premium = EdLu share premium before buy EcoTime + Share exchange in ratio 2:3 * price in excess of share nominal value

= 200,000 + 160,000*3 = £ 680,0003. Retained Earnings

£’000Retained earnings of EdLu as at 1 April 2012

£ 180,000

Profit attribute to owner of EdLu £ 238,200

Total £ 418,200

4. Non-controlling interest in statement of financial position

£’000

Share preminum at 31st March 2013 £ 200,000

Non-controlling interest in total comprehensive income

£ 15,400 £ 215,400

CONCLUSIONIn conclusion, this report had provided a detail way to make

financial statement in different cases. From the incompleterecord of Nguyen Luu, researcher have prepared the financialstatements, and from that Nguyen Luu, owner of the company canclearly see the profit and loss of his company for the year ended31st March, 2013 and the value of his company’s assets,liabilities and equity. The researcher also handle the financialstatement of a partnership firm, including Goodwill AdjustmentAccount; Capital Accounts of three owners: Bernard, Edana andNguyen Luu; Profit and Loss Appropriation Account and finally,the balance sheet of EdLu Ltd, a company set up by Nguyen Luu andEdana after Bernard retire. Researcher also prepare consolidationaccount when EdLu Ltd purchased 75% of equity shares of anothercompany, EcoTimes.

ReferencesAnon., 2013. Users of Financial Statements. [Online] Available at: http://finance.mapsofworld.com/financial-report/statement/users.html[Accessed 14 November 2014].

Anon., n.d. Presentation of Financial Statements. [Online] Available at: http://www.iasplus.com/en/standards/ias/ias1[Accessed 14 November 2014].

Page | 30