annual report & financial statements 2016

TRANSCRIPT

ANNUAL REPORT& FINANCIALSTATEMENTS2016

Defined Contribution

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

Trustees and Professional Advisors 04

About the Fund 05

Key Highlights

Fund Structures

07

07

Chairman’s Report 10

Secretary’s Report

Trustees’ Profile

18

24

Statement on Corporate Governance 27

Statement of Trustees’ Responsibilities

Report of the Board of Trustees

34

33

Report of the Independent Auditor 35

Financial Statements

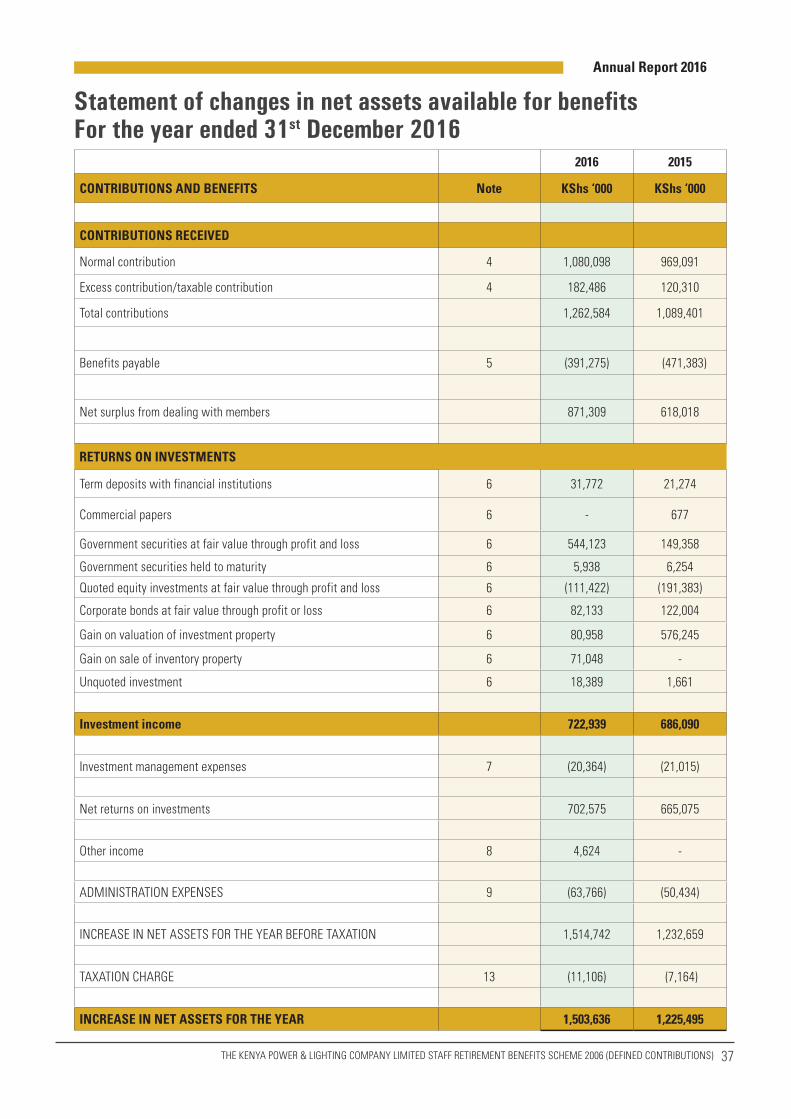

• Statement of Changes in Net Assets Available for Benefits 37

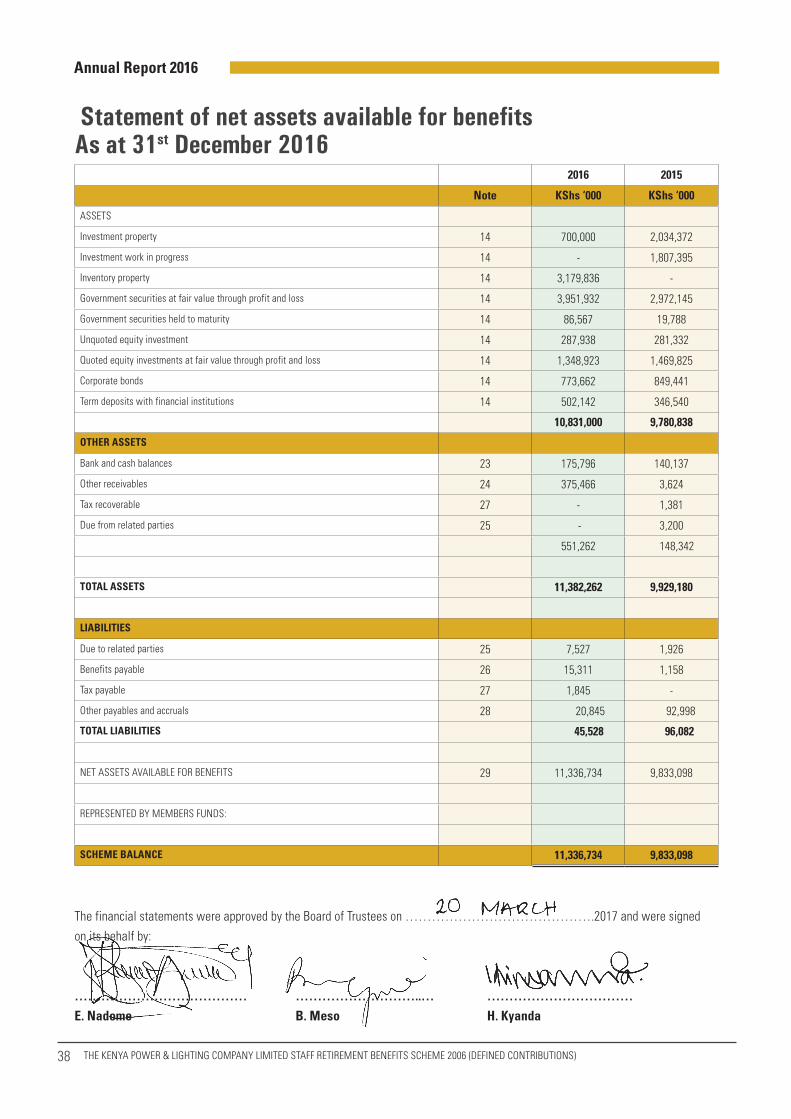

• Statement of Net Assets Available for Benefits 38

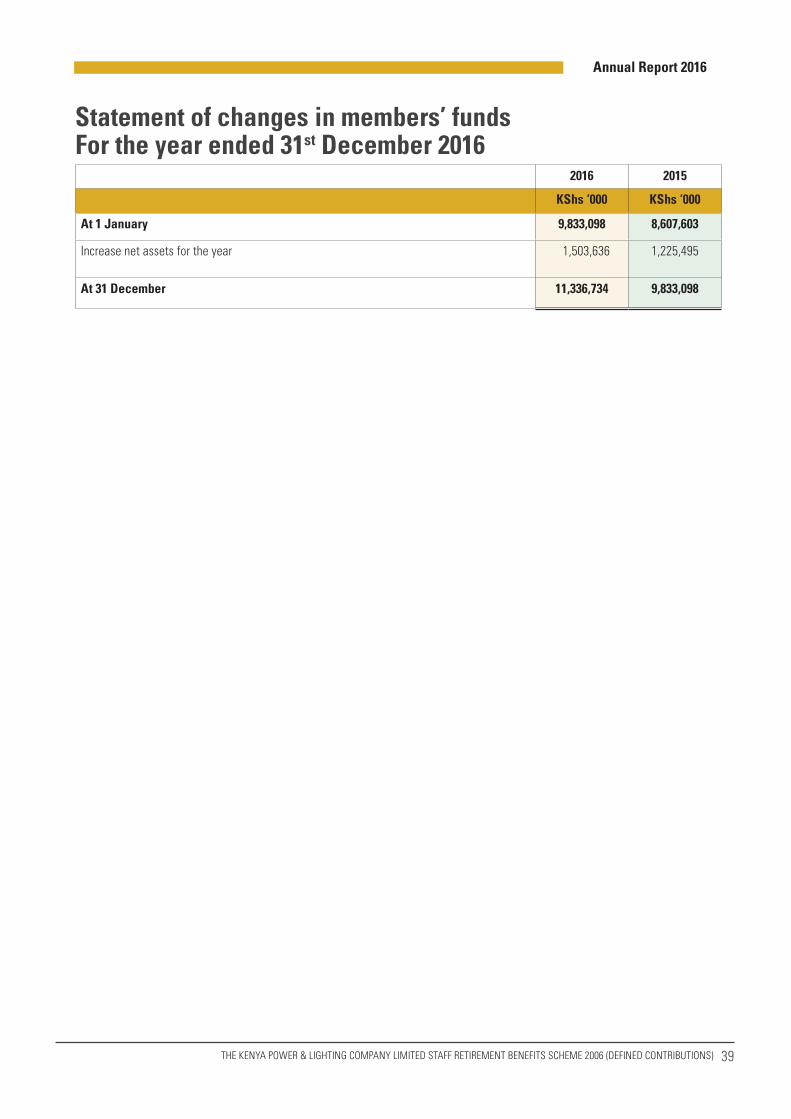

• Statement of Changes in Member’s Funds 39

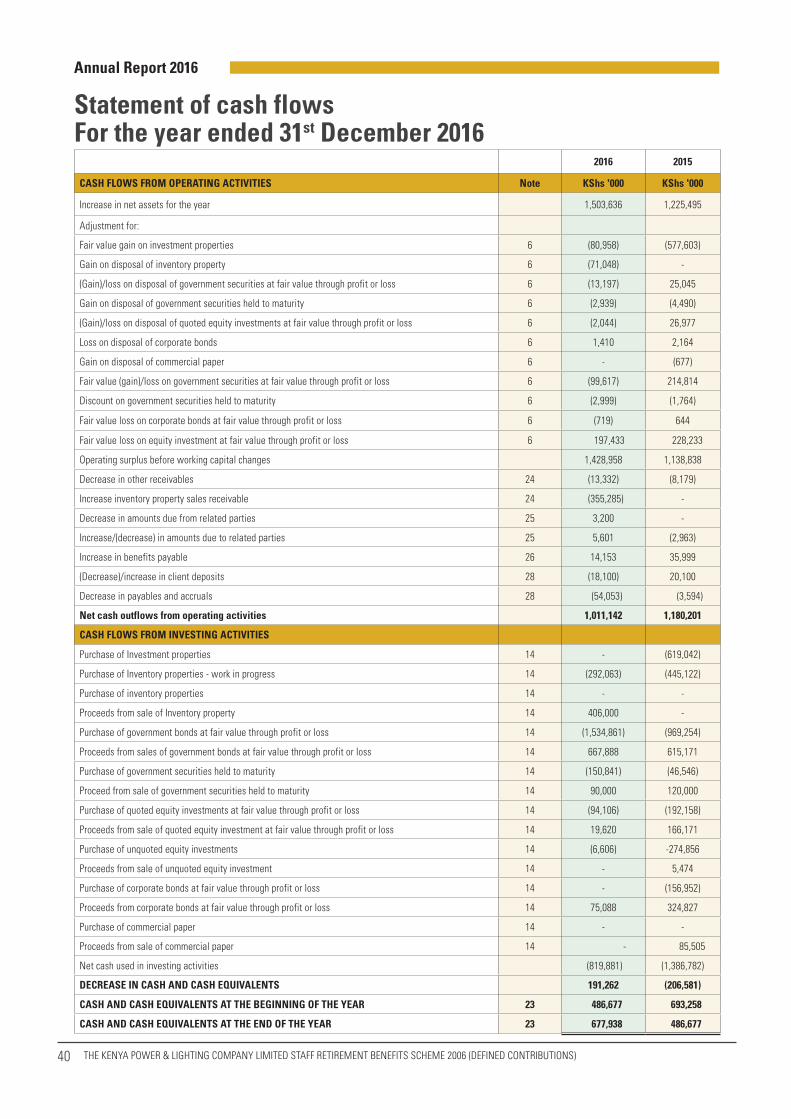

• Statement of Cash Flows 40

• Notes to the Financial Statements 41-80

CONTENTS

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

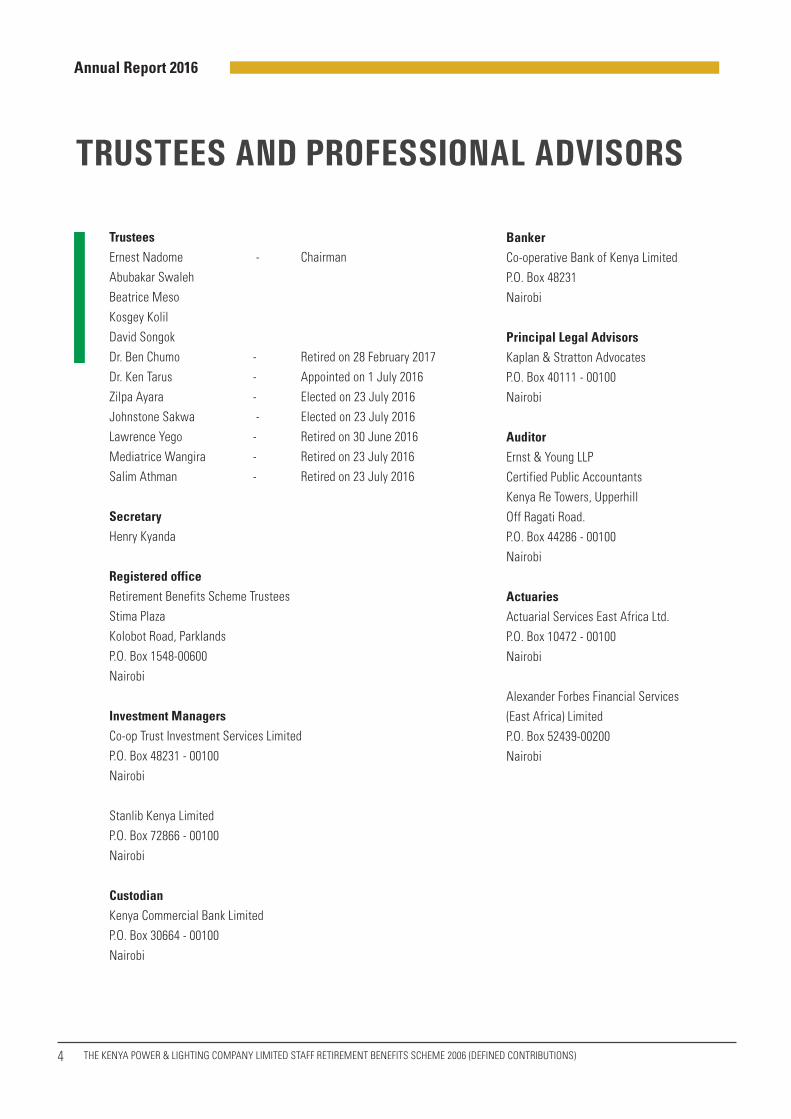

TRUSTEES AND PROFESSIONAL ADVISORS

TrusteesErnest Nadome - Chairman Abubakar Swaleh Beatrice Meso Kosgey KolilDavid Songok Dr. Ben Chumo - Retired on 28 February 2017Dr. Ken Tarus - Appointed on 1 July 2016Zilpa Ayara - Elected on 23 July 2016Johnstone Sakwa - Elected on 23 July 2016Lawrence Yego - Retired on 30 June 2016 Mediatrice Wangira - Retired on 23 July 2016 Salim Athman - Retired on 23 July 2016

SecretaryHenry Kyanda

Registered officeRetirement Benefits Scheme TrusteesStima PlazaKolobot Road, ParklandsP.O. Box 1548-00600Nairobi

Investment ManagersCo-op Trust Investment Services LimitedP.O. Box 48231 - 00100Nairobi

Stanlib Kenya LimitedP.O. Box 72866 - 00100Nairobi

CustodianKenya Commercial Bank LimitedP.O. Box 30664 - 00100 Nairobi

BankerCo-operative Bank of Kenya LimitedP.O. Box 48231Nairobi

Principal Legal AdvisorsKaplan & Stratton AdvocatesP.O. Box 40111 - 00100Nairobi

AuditorErnst & Young LLPCertified Public AccountantsKenya Re Towers, UpperhillOff Ragati Road.P.O. Box 44286 - 00100Nairobi

ActuariesActuarial Services East Africa Ltd.P.O. Box 10472 - 00100Nairobi

Alexander Forbes Financial Services(East Africa) LimitedP.O. Box 52439-00200Nairobi

4

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

The Kenya Power & Lighting Company Limited, Staff Retirement Benefits Scheme 2006 (“the Fund”) was established by a Trust Deed and started operations on

1 July 2006. The Fund was formed for the employees of the Kenya Power & Lighting Company Limited (“Kenya Power”) as a result of the closure of Kenya Power’s Defined Benefit Scheme (“DB Fund”). The Fund is governed by a Trust Deed and Rules which have been approved by the Retirement Benefits Authority (RBA).

The main purpose of the Fund is the provision of retirement benefits to the members upon attainment of the retirement age of sixty years, and where applicable, benefits for the dependants of deceased members. The Fund is approved by Kenya Revenue Authority as a retirement benefits scheme for the purposes of the Income Tax (Retirement Benefits) Rule No. 4 and is treated as an ‘exempt registered scheme’ for the purposes of that Act (1st Schedule 14). However, income generated from contributions in excess of the KShs 20,000 per month per member statutory limit is subject to tax.

ABOUT KENYAPOWER PENSION FUND

5

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

VISION

To be the best-in-class occupational scheme inwhole of Africa.

MISSION

To deliver value and quality of life in retirement to our members.

CORE VALUES

• Integrity• Accountability• Courteous service• Stewardship

Fund BenefitsThe Fund is a Defined Contributions Scheme. Upon retirement a member receives 1/3 of his benefits as a lumpsum and an annuity for life of such an amount as shall be then purchased by 2/3 of his/her benefits according to immediate annuity rates applicable at the time of purchase from an insurance company selected by the member.

MembersThe members of the Fund comprises of active in service employees of the sponsors and deferred members. The current sponsors include Kenya Power and Lighting Company Limited, Kenya Electricity Transmission Company Limited and Kenya Nuclear Power Board. Eligible members are permanent and pensionable employees.

SECRETARIAT

Board ofTrustees

Members(In service members,

defered members

Custodian Auditors

FundManagers

Actuary

THE FUND STRUCTURE

6

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

SECRETARIAT

Board ofTrustees

Members(In service members,

defered members

Custodian Auditors

FundManagers

Actuary

THE FUND STRUCTURE

KEY HIGHLIGHTS

26.8%

12.9%13.5%

7.5% 7.0%

0%

5%

10%

15%

20%

25%

30%

2012 2013 2014 2015 2016

% R

etur

n on

Inve

stm

ents

Year

Return on Investments

1,705.1 1,567.5

1,881.1

1,225.5

1,503.6

0

500

1,000

1,500

2,000

2012 2013 2014 2015 2016

Amou

ntKS

hs. M

illio

ns

Year

Increase in Net Assets

5.16 6.73 8.61 9.83 11.34

0

5

10

15

2012 2013 2014 2015 2016

Fund

Val

ue(K

Shs.

Billi

ons)

Year

Fund Growth

6,117 6,087

6,394

6,792

7,180

6,0006,2006,4006,6006,8007,0007,200

2012 2013 2014 2015 2016

Tota

l Num

ber

Year

Membership Growth

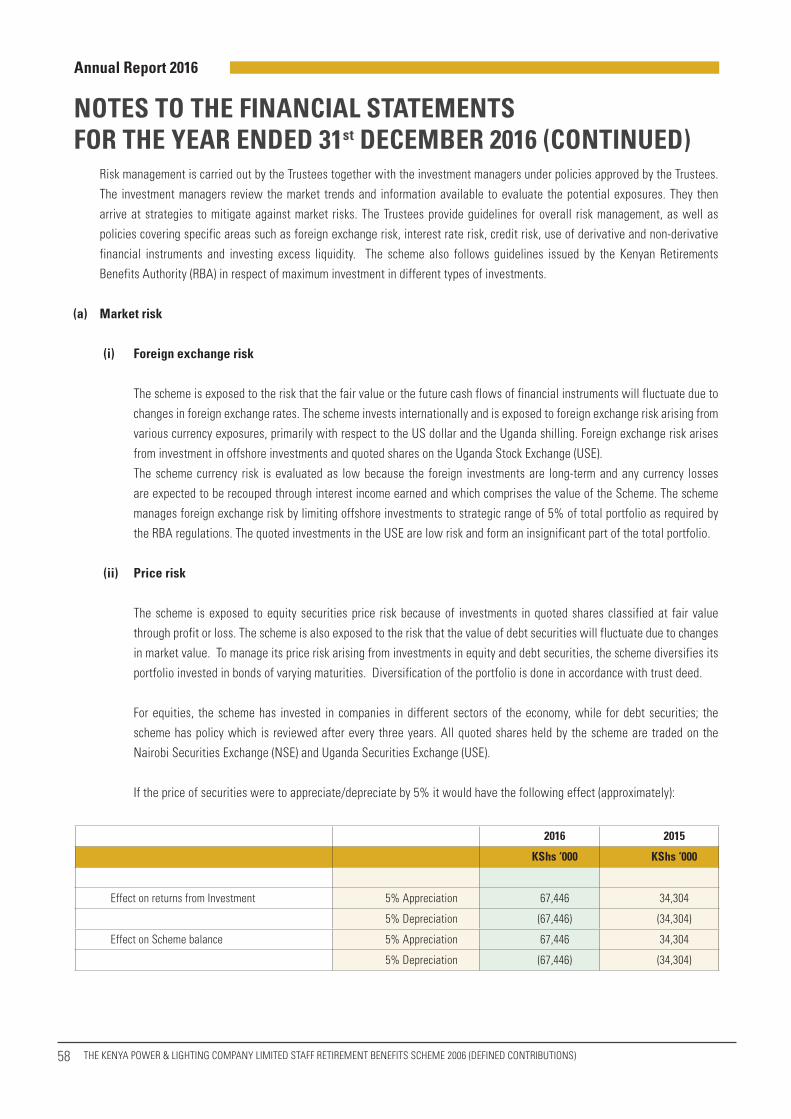

The Fund’s objective is to achieve a superior return on investment through development and management of a diversified

portfolio that also mitigates against investment risks. The gross return on investment for 2016 was 7%. (2015: 7.5%). The

performance was weighed down by volatility in the capital markets that adversely affected the performance of the equity

asset class.

Key Highlights

7

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

KEY HIGHLIGHTS

26.8%

12.9%13.5%

7.5% 7.0%

0%

5%

10%

15%

20%

25%

30%

2012 2013 2014 2015 2016

% R

etur

n on

Inve

stm

ents

Year

Return on Investments

1,705.1 1,567.5

1,881.1

1,225.5

1,503.6

0

500

1,000

1,500

2,000

2012 2013 2014 2015 2016

Amou

ntKS

hs. M

illio

ns

Year

Increase in Net Assets

5.16 6.73 8.61 9.83 11.34

0

5

10

15

2012 2013 2014 2015 2016

Fund

Val

ue(K

Shs.

Billi

ons)

Year

Fund Growth

6,117 6,087

6,394

6,792

7,180

6,0006,2006,4006,6006,8007,0007,200

2012 2013 2014 2015 2016

Tota

l Num

ber

Year

Membership Growth

0.00%

0.50%

1.00%

1.50%

2012 2013 2014 2015 2016

0.43

%

0.57

%

0.45

%

0.51

%

0.56

%

Year

Admin. Expenses

KEY HIGHLIGHTS

26.8%

12.9%13.5%

7.5% 7.0%

0%

5%

10%

15%

20%

25%

30%

2012 2013 2014 2015 2016

% R

etur

n on

Inve

stm

ents

Year

Return on Investments

1,705.1 1,567.5

1,881.1

1,225.5

1,503.6

0

500

1,000

1,500

2,000

2012 2013 2014 2015 2016

Amou

ntKS

hs. M

illio

ns

Year

Increase in Net Assets

5.16 6.73 8.61 9.83 11.34

0

5

10

15

2012 2013 2014 2015 2016

Fund

Val

ue(K

Shs.

Billi

ons)

Year

Fund Growth

6,117 6,087

6,394

6,792

7,180

6,0006,2006,4006,6006,8007,0007,200

2012 2013 2014 2015 2016

Tota

l Num

ber

Year

Membership Growth

The increase in net assets was Kshs 1.5 billion during the year (2015: 1.22 Billion). This increase is the net movement of

the returns from investments, contributions received during the year as well payments of the retirement benefits to exiting

members.

The net asset available for members continues to grow steadily over the years. At the end of the current financial year, the Net assets available for members stood at Kshs 11.34 Billion (2015: 9.83 Billion). The Trustees rolled out various strategic initiatives aimed at expanding the assets under management.

The Fund membership grew to 7,180 from 6,792 recorded in the previous year which was a 6% growth. This was mainly

attributed to the higher number of new entrants compared to exiting members during the year.

Over the years the Fund has been able to maintain administrative expenses to the Fund Value below the recommended

limit of 1% which is an affirmation of the sound financial management systems and controls established by the board.

KEY HIGHLIGHTS

26.8%

12.9%13.5%

7.5% 7.0%

0%

5%

10%

15%

20%

25%

30%

2012 2013 2014 2015 2016

% R

etur

n on

Inve

stm

ents

Year

Return on Investments

1,705.1 1,567.5

1,881.1

1,225.5

1,503.6

0

500

1,000

1,500

2,000

2012 2013 2014 2015 2016

Amou

ntKS

hs. M

illio

ns

Year

Increase in Net Assets

5.16 6.73 8.61 9.83 11.34

0

5

10

15

2012 2013 2014 2015 2016

Fund

Val

ue(K

Shs.

Billi

ons)

Year

Fund Growth

6,117 6,087

6,394

6,792

7,180

6,0006,2006,4006,6006,8007,0007,200

2012 2013 2014 2015 2016

Tota

l Num

ber

Year

Membership Growth

8

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

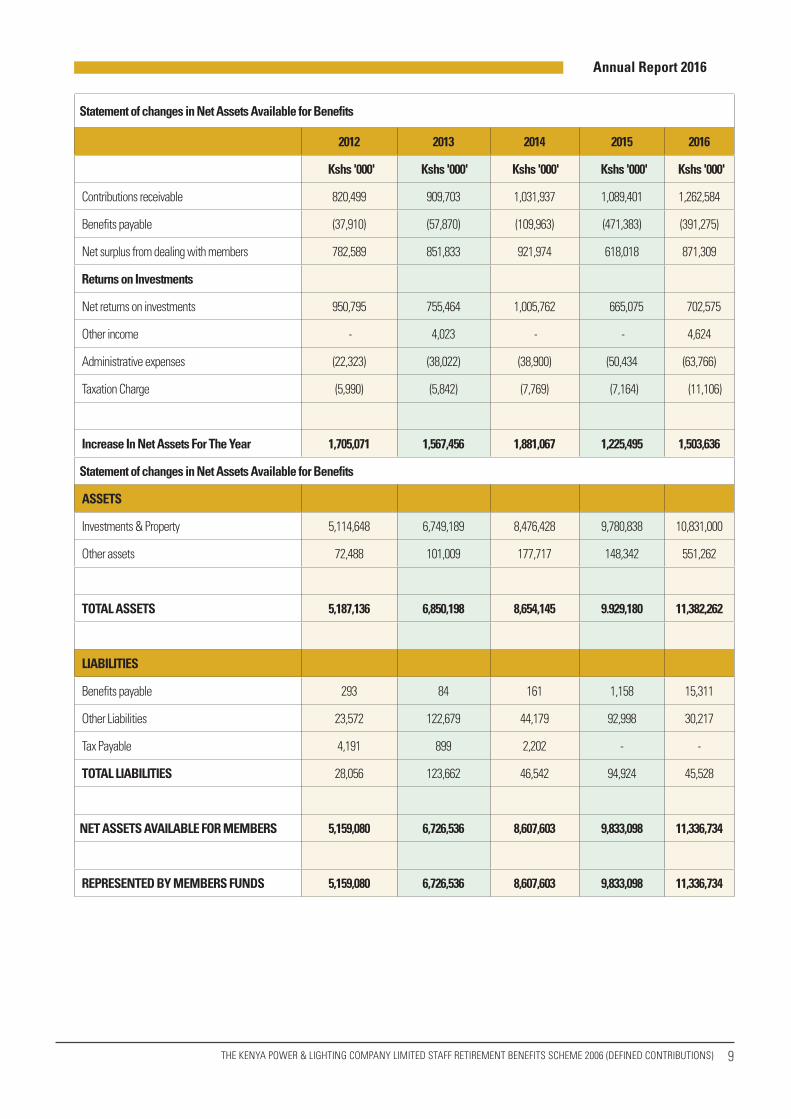

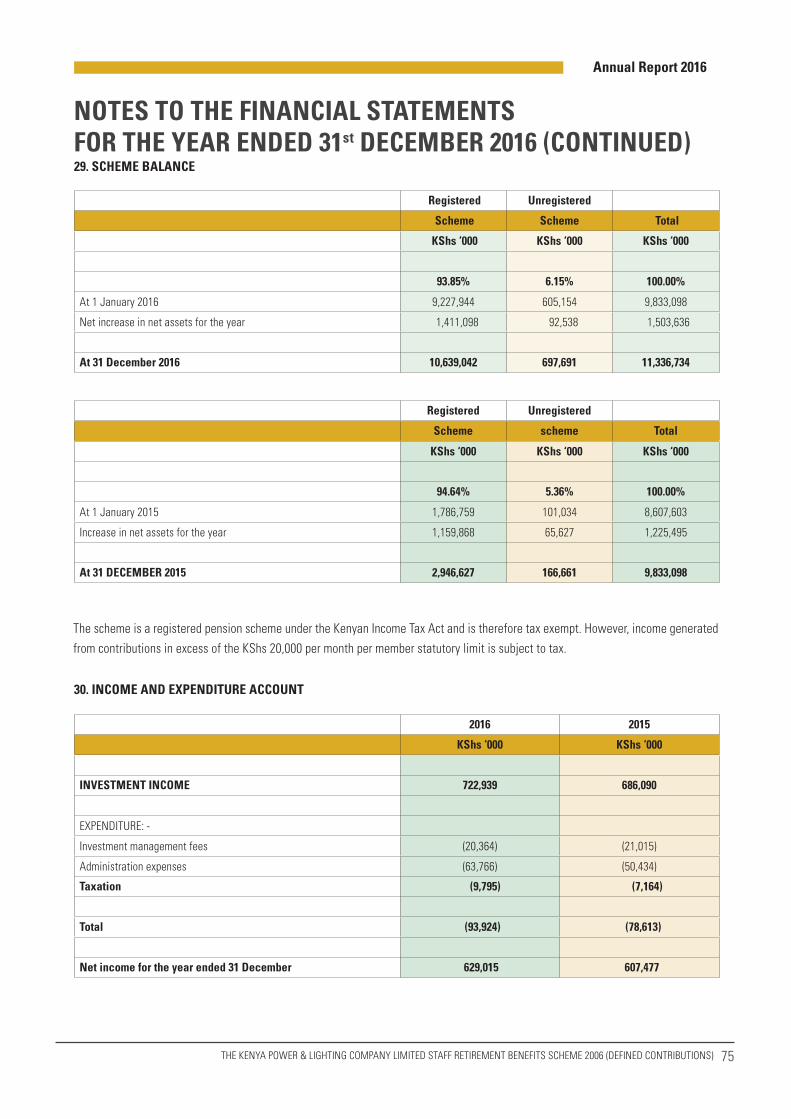

Statement of changes in Net Assets Available for Benefits

2012 2013 2014 2015 2016

Kshs '000' Kshs '000' Kshs '000' Kshs '000' Kshs '000'

Contributions receivable 820,499 909,703 1,031,937 1,089,401 1,262,584

Benefits payable (37,910) (57,870) (109,963) (471,383) (391,275)

Net surplus from dealing with members 782,589 851,833 921,974 618,018 871,309

Returns on Investments

Net returns on investments 950,795 755,464 1,005,762 665,075 702,575

Other income - 4,023 - - 4,624

Administrative expenses (22,323) (38,022) (38,900) (50,434 (63,766)

Taxation Charge (5,990) (5,842) (7,769) (7,164) (11,106)

Increase In Net Assets For The Year 1,705,071 1,567,456 1,881,067 1,225,495 1,503,636

Statement of changes in Net Assets Available for Benefits

ASSETS

Investments & Property 5,114,648 6,749,189 8,476,428 9,780,838 10,831,000

Other assets 72,488 101,009 177,717 148,342 551,262

TOTAL ASSETS 5,187,136 6,850,198 8,654,145 9.929,180 11,382,262

LIABILITIES

Benefits payable 293 84 161 1,158 15,311

Other Liabilities 23,572 122,679 44,179 92,998 30,217

Tax Payable 4,191 899 2,202 - -

TOTAL LIABILITIES 28,056 123,662 46,542 94,924 45,528

NET ASSETS AVAILABLE FOR MEMBERS 5,159,080 6,726,536 8,607,603 9,833,098 11,336,734

REPRESENTED BY MEMBERS FUNDS 5,159,080 6,726,536 8,607,603 9,833,098 11,336,734

9

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

I would like to express my gratitude on behalf of the

Board to the Sponsor and all our stakeholders who have

continued to work tirelessly to support the Fund as it navigates

through the challenging economic and investment

environment.Dear members, it is my pleasure to welcome you all to the

11th Annual General Meeting of our Fund, Kenya Power Pension Fund and to present to you the Annual Report and

Accounts of the Fund for the financial year ended 31st December, 2016. I am indeed honored as this is my first year of serving as the Chairman of the Fund.

ECONOMIC HIGHLIGHTSGlobal economyThe Global economy grew by 2.9% in 2016 which was a decline from the growth levels of 3.1% registered in 2015. The decline was attributed to a constrained international trade as well as the effects of uncertainties occasioned by the world phenomenon key among these being the exit of the United Kingdom from the European Union as well as elections in the United States.

CHAIRMAN’S REPORT

10

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

Domestic economyThe Kenyan economy grew by 5.8% in 2016 compared to 5.7% in 2015. This growth was mainly driven by growth in the tourism, information & communication, real estate as well as transport and storage sectors. The growth was constrained by decline recorded in the agriculture, manufacturing and financial services sectors.

Investment environmentInflation was contained within the Central Bank of Kenya (CBK) target band (2.5% -7%) to average at 6.3% compared to an average of 6.1% during the same period in 2015. The slight increase in inflation was primarily due to increases in prices of food and beverages during the period under review. This rise was however countered by significant decreases in prices of utilities and transport.

On the foreign exchange front the local currency registered some stability against major currencies during the year supported by monetary policy measures taken by CBK, resilient diaspora remittances and healthy forex reserves. The Shilling weakened by 0.2% and 12.8% against the US Dollar and the South African Rand while gaining by 3.0% and 16.1% against the Euro and Sterling Pound respectively. It also gained 6.9%, 0.8% and 9.3% against Uganda shilling, the Tanzanian shilling and Rwandan franc respectively.

The Nairobi Securities Exchange (NSE) 20 share index and the NSE All Share Index declined by 21.1% and 8.5% respectively in 2016. This downturn was precipitated by a host of global and local factors. One of the local factor was the amendment of the Banking Act in September 2016 which introduced caps on the lending rates to be charged by the commercial banks as well as interest to be paid for customers’ deposits. The investors’ sentiments and the perceived negative impact of the caps on the performance of the banking sector resulted to decline in the share prices of the banks listed in the Nairobi Securities Exchange.

The 2016 period registered a decline in interest rates as compared to 2015 with the indicative rates for the short term securities declining. The 91 day rate averaged 8.6% compared to 11.0% for 2015. The 182 day and the 364 Treasury Bills averaged 10.9% and 11.7% compared to 12.2% and 12.9% respectively in 2015. Stability of interest rates continued to be the focus of the CBK as it aims to spur the economic growth.

Rising value of land as well as dynamics in the entire property value chain continued to pose the biggest challenge to successes in the property market for developers, occupiers/owners and investors. The investment space for properties continued to record volatility in the various aspects which affected the supply and demand of the various property products. It is expected that such volatility will continue in the coming periods with demand and supply expected to experience shifts.

PENSION INDUSTRY AND REGULATORY ENVIRONMENTThe industry regulator Retirement Benefits Authority, (RBA) whose mandate is to develop the Retirement Benefits Industry and to provide policy advice to the government on matters relating to the retirement benefits sector has played a major role in creating national awareness of the sector. RBA engages in pertinent research that informs priority areas of development and policy directions. Through the regulator, various innovative products including occupational, individual and umbrella Schemes have been developed to help cater for members during their retirement. The Pension industry has continued to grow over the years with the total pension industry asset value as at the end of 2016 being over Kshs 1.0 trillion.

The Trustee Development Program Kenya (TDPK) training has played an important role in ensuring that there is prudent management of Funds and thereby maintain confidence in the management of the pension funds. All Trustees of pension schemes in Kenya were required to undergo the training by 31st December 2016. The Fund complied fully with this regulatory requirement.

During the year, legislative and regulatory changes were contained in the 2016/2017 budget. Among the changes introduced which were effective 9th June 2016 included the following;

a) In order to protect Trustees against victimization or discrimination while performing their duties, an amendment was made that a Trustee shall not be victimized, removed from office of trustee or discriminated against for having performed the function of office in accordance with the Trust Deed and Rules of a scheme or any law without due process of the law.

11

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

b) Contributions by or on behalf of a member together with interest and other accrued income thereon shall vest on a member immediately. Previously the member was only entitled to the Employer’s contributions after one year of service.

c) Regulation 14 of the RBA Regulations was amended to provide for the schedule of rates of contributions to allow for additional voluntary contributions by a member in respect of funding of a medical fund to be accessed at retirement.

d) Regulation 19 was also amended to ensure that the scheme rules provide for a member who may wish to transfer a portion of the member’s benefits to medical-cover provider where the member has been unable to build a post-retirement medical fund from additional contributions. This is aimed at allowing members to save for their medical expenses during their working life.

e) In a bid to provide pension funds with more investment options, the investment guidelines were amended to include Real Estate Investment Trust (REITS), exchange traded derivatives and the separation of listed and un-listed corporate bonds and commercial paper. Retirement Schemes can now invest in all exchange traded derivatives contracts and all listed REITS incorporated in Kenya as long as they are registered with Capital Markets Authority (CMA).

f) On winding up of schemes, Regulation 8A provides that the liquidator shall be required, in the preparation of the preliminary accounts, to provide for the distribution of surpluses identified which shall be on a 50-50 basis between the members and the sponsor. The surpluses will not have to be distributed based on the invested income, unvested benefits and the proportion of the contribution made by the employer and employee as was previously required.

The Fund continue to enhance its compliance and monitoring mechanisms to ensure that all the changes are adhered and also take advantage of the improvement in the operating environment created by such development. The Fund has put in place an elaborate compliance tool that track the compliance levels against the legislative and regulatory requirements.

FUND’S FINANCIAL PERFORMANCEThe Fund achieved an annual gross return of 7% in 2016 (7.5% in 2015). This performance was registered against a backdrop of challenging investment environment during the year which weighed down the performance of the various assets classes. The total asset market value of the Fund as at the end of the year stood at KShs. 11.33 billion up from KShs. 9.83 billion at the end of 2015. The increase is attributed to both the pension contributions as well as investment income earned during the period.

The Board of Trustees endeavor to prudently invest available funds in an optimized portfolio that yields favorable returns. The overall investment policy is geared towards the achievement of superior investment returns while mitigating against volatility of the returns. The long-term investment objective is to achieve a long term return on investments in excess of inflation through diversified asset allocation as well as continuous performance monitoring.

CORPORATE GOVERNANCE AND AWARDSThe Board of Trustees is committed to ensuring that systems, procedures and practices within the Fund reflect a high standard of corporate governance. An effective corporate governance system is critical in fostering a culture that values ethical behavior, integrity and respect to protect members and other stakeholders’ interests at all times

The Fund participated for the fifth time in the Financial Reporting (FiRe) awards in year 2016, in which, the Fund emerged the 1st runners up in the Not for Profit category and 2nd runners up in the IFRS category. The FiRe Award is an initiative of the Institute of Certified Public Accountants of Kenya (ICPAK) the Capital Markets Authority (CMA) and the Nairobi Securities Exchange (NSE) and aims at enhancing accountability, transparency and integrity in compliance with the international Financial Reporting Standards (IFRS). The awards are in recognition of excellence in financial reporting, fostering sound corporate governance practices and enhancing corporate social responsibility and environmental reporting in East Africa.

BOARD COMPOSITION I would like to report to you that during the period under review, the composition of the Board changed. Three members of the board retired during the period and similar number were

12

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

appointed or elected to the board in accordance with the Fund’s policy. The changes is as shown on page 4 of this report. The composition remains compliant with the requirement of the Retirement Benefits Act.

DECLARED INTEREST The Trustees declared an annual interest rate of 6.3% in 2016 (6.8% in 2015). The Fund maintained the quarterly interest declaration policy during the year 2016 which ensures that the Fund maintains a zero reserve and therefore members exiting the Fund during the year obtain a prorated rate of return at the point of exit. OUTLOOKThe global as well the domestic economies are projected to improve in 2017 with stability in the commodity prices expected. However, the local economy would likely be affected by the political development as this will be an election year. The Trustee will continue monitoring the development in the macro environment and align its investment strategies to take advantage of investment opportunities as well mitigating against the investments risks.

The Trustees will continue with its implementation of the 2016-2020 strategic plan that aims at making the Fund the

best-in-class occupational scheme in the whole of Africa. This is an ambitious plan aimed at ensuring the Fund maximizes investment performance as well as enhancing member offerings. The future of the Fund will ever be exciting.

APPRECIATIONI would like to express my gratitude on behalf of the Board to the Sponsor and all our stakeholders who have continued to work tirelessly to support the Fund as it navigates through the challenging economic and investment environment. I also wish to thank my fellow Board members for their selfless contribution to the Fund over the past year and for supporting me as the Chairman. The Secretary to the Board and his team have also worked tirelessly to ensure prudent management of the day to day operations of the Fund. I would not forget the members for your continued support, encouragement and feedback.

Ernest Nadome ChairmanKPLC Staff Retirement Benefits Scheme 2006

13

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

Wanachama wapendwa, ni furaha yangu kuwakaribisheni nyote kwa Mkutano Mkuu wa kila Mwaka wa Hazina yetu,yaani Hazina ya Malipo

ya Uzeeni ya Wafanyikazi wa Shirika la Kawi la Kenya (Kenya Power Pension Fund). Hiki ni kikao cha mara ya kumi na moja ambapo nawawasilishieni ripoti ya mwaka na taarifa ya kifedha ya hazina yetu kwa kipindi cha mwaka uliokamilika tarehe 31, mwezi wa Disemba, mwaka wa 2016. Hakika, ni kwa heshima kubwa ikiwa huu ndio mwaka wangu wa kwanza nikitumika kama mwenyekiti wa hazina hii.

VIDOKEZO MUHIMU VYA KIUCHUMIUchumi wa KimataifaUchumi wa kimataifa ulikua kwa kiwango cha asilimia mbili nukta tisa (2.9%) katika mwaka wa 2016, hii ikisawiri kupungua kutoka kwa viwango vya ukuaji vya asilimia tatu nukta moja (3.1%) vilivyofikiwa katika mwaka wa 2015. Kuzorota huku kunaelezewa kuwa kulitokana na hali tete katika biashara za kimataifa pamoja na athari za kutokuwepo kwa udhabiti kutokana na matukio ya kiulimwengu, la msingi likiwa ni pamoja

RIPOTI YA MWENYEKITI

Ningependa kuwarudishia shukrani jazila kwa niaba ya Bodi na Mdhamini na washikadau wote ambao

wanaendelea kufanya kazi bila kuchoka ili kuboresha hazina hii wakati inapojaribu kupinda na kupenyeza kwenye hali ngumu

ya kiuchumi na kiuwekezaji.

14

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

na kujiondoa kwa Umoja wa Milki za Uingereza (United Kingdom) kwenye Muungano wa Mataifa ya Uropa (European Union) na kura za urais nchini Marekani.

Uchumi wa KitaifaUchumi wa Kenya ulikua kwa kiwango cha asilimia tano nukta nane (5.8%) katika mwaka wa 2016 ikilinganishwa na asilimia tano nukta saba (5.7%) mwaka wa 2015. Ukuaji huu ulitokana zaidi na kuimarika kwa sekta za utalii, habari na mawasiliano, mali isiyohamishika pamoja na ile sekta ya usafiri na uhifadhi. Kuzorota kwa sekta za kilimo, uzalishaji wa kiviwanda na ile ya huduma za kifedha kulitatiza ukuaji zaidi wa kiuchumi katika kipindi kinachorejelewa.

Mazingira ya KiuwekezajiMfumuko wa bei ulidhibitiwa ndani ya kiwango kilicholengwa na Benki Kuu ya Kenya cha kati ya asilimia mbili nukta tano (2.5%) na asilimia saba (7%) kwa kiwango wastani cha asilimia sita nukta tatu (6.3%) ikilinganishwa na kile cha asilimia sita nukta moja (6.1%) kwa kipindi sawa na hicho mwaka wa 2015. Kuongezeka kidogo kwa kiwango cha mfumuko huo wa bei kimsingi ulitokana na kuongezeka kwa bei ya vyakula na vinywaji katika kipindi kinachotathminiwa. Hata hivyo, kuongezeka huku kulidhibitiwa na kuanguka kwa kiwango kikubwa katika bei za huduma tumizi na usafiri.

Kwenye ubadilishanaji wa fedha za kigeni, Shilingi ya kitaifa ilionyesha kuimarika kwa kiwango kidogo dhidi ya fedha za kigeni katika mwaka uliopita ikiongozwa na sera mwafaka za kifedha zilizowekwa na Benki Kuu ya Kenya, pamoja na hali dhabiti ya fedha zinazotumwa na wakenya waliopo kwenye nchi za nje na hali bora ya hifadhi ya fedha za kigeni. Shilingi ya Kenya ilidhoofika kwa asilimia sufuri nukta mbili (0.2%) na asilimia kumi na mbili nukta nane (12.8%) dhidi ya Dola ya Marekani na Randi ya Afrika Kusini mtawalio, huku ikiimarika kwa asilimia tatu nukta sufuri (3.0%) na asilimia kumi na sita nukta moja (16.1%) dhidi ya Yuro na Pauni ya Uingereza mtawalio. Aidha, iliimarika kwa asilimia sita nukta tisa (6.9%), asilimia sufuri nukta nane (0.8%) na asilimia tisa nukta tatu (9.3%) dhidi ya Shilingi ya Uganda, ile ya Tanzania na Franki ya Rwanda mtawalio.

Kiwango cha Hisa Mahsusi katika Soko la Nairobi (NSE 20 share index) na kile cha Hisa Jumla cha Soko la Hisa la Nairobi (NSE All Share Index- NASI) kilizoroteka ama kuanguka kwa asilimia ishirini na moja nukta moja (21.1) na asilimia nane nukta tano (8.5%) mtawalio katika mwaka wa 2016. Hali hii ya kuanguka

ilitokana na mseto wa sababu za kimataifa na zile za humu nchini. Sababu mojawapo ya humu nchini ni marekebisho kwa sheria za benki katika mwezi wa Septemba mwaka wa 2016 ambayo yalileta udhibiti wa viwango vya mikopo vinavyotozwa na benki za kibiashara sawa na riba inayolipwa kutokana na amana ya wateja wa benki (customer bank deposits). Hisia na mitazamo ya wawekezaji na fikra za athari hasi (negative impact) inayotokana na kurekebeshwa huko kwa sheria ya udhibiti wa viwango vya malipo yanayotozwa kwa mikopo na riba zinazolipwa kwa amana ya wateja ilionekana kuathiri utendaji wa sekta ya benki na kusababisha kuanguka kwa bei za hisa za benki zilizoratibiwa kwenye Soko Kuu la Hisa la Nairobi (NSE).

Kipindi cha mwaka wa 2016 kilionyesha kuanguka kwa viwango vya riba ikilinganishwa na mwaka wa 2015 huku viwango-viashiria vya muhula mfupi vya hisa vikizoroteka. Kiwango cha siku ya tisini na moja (91 day rate) kilikuwa katika kiwango wastani cha asilimia nane nukta sita (8.6%) ikilinganishwa na asilimia kumi na moja (11.0%) katika mwaka wa 2015. Bili za Hazina (Treasury Bills) za siku ya 182 na 364 zilikuwa kwa kiwango wastani cha asilimia kumi nukta tisa (10.9%) na asilimia kumi na moja nukta saba (11.7%) mtawalio ikilinganishwa na asilimia kumi na mbili nukta mbili (12.2%) na asilimia kumi na mbili nukta tisa (12.9%) mtawalio kwenye kipindi cha mwaka wa 2015. Lengo la kudhibiti viwango vya riba ili kufanikisha ukuaji wa kiuchumi, kwa Benki Kuu ya Kenya, lilisalia kuwa la kimsingi.

Kuendelea kuongezeka kwa thamani ya ardhi sawa na mienendo ya mfumo mzima wa mali kiuwekezaji iliendelea kutoa changamoto kubwa kwa ufanisi wa soko la mali kwa watengenezaji/wajenzi, waingiaji au wamiliki pamoja na wawekezaji. Mwanya wa kiuwekezaji kwa mali uliendelea kuashiria hali tete katika masuala yote yaliyoathiri mfumo mzima wa uzalishaji na ununuzi wa bidhaa tofauti tofauti za mali. Inatarajiwa kuwa hali tete kama hiyo itaendelea kwa kipindi kijacho huku uzalishaji na ununuzi ukitarajiwa kuyumbayumba.

SEKTA YA PENSHENI/MALIPO UZEENI NA MAZINGIRA YA UDHIBITIMdhibiti wa sekta ya malipo ya uzeeni, Mamlaka Simamizi ya Faida za Malipo ya Uzeeni {Retirement Benefits Authority, (RBA)} ambayo wajibu wake mkubwa ni kukuza sekta ya malipo ya uzeeni na kupeana ushauri wa kisera kwa serikali kuhusiana na maswala ya sekta ya malipo ya uzeeni, imechukuwa nafasi

15

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

kubwa mno katika kuhamasisha taifa juu ya sekta hii. RBA inafanya utafiti wa kina unaotoa mwelekeo kuhusu maeneo mwafaka ya kimaendeleo na mwelekeo wa kisera. Kupitia kwa mdhibiti, bidhaa mbalimbali bunifu zimetengenezwa ili kuwezesha kuwasaidia wanachama uzeeni wakati wa kustaafu kwao ukiwemo ule wa kitaaluma/kikazi, kibinafsi na ule wa miradi jumla (umbrella schemes). Sekta ya malipo ya uzeeni ama pensheni imeendelea kuimarika na kukua kwa miaka iliyopita huku jumla ya kiwango chake kufikia mwisho wa mwaka 2016 kikiwa Shilingi za Kenya trilioni moja ( Kshs. 1 trillion).

Mafunzo ya Mpango wa Kukuza Wadhamini, Kenya (Trustee Development Program Kenya-TDPK) yametekeleza wajibu muhimu sana kwa kuhakikisha kuwa kunakuwepo usimamizi mwafaka wa Hazina na hivyo kuendelea kukuza hali ya uaminifu katika usimamizi wa mfuko wa malipo ya uzeeni. Wadhamini wote wa miradi yote ya pensheni nchini Kenya walitakiwa kuwa wameshiriki mafundisho kufikia tarehe 31, mwezi Disemba 2016. Hazina hii ilitimiza takwa hili la mamalaka-dhibiti kikamilifu.

Katika mwaka, mabadiliko ya kisheria na kiusimamizi yalidhibitiwa kwenye bajeti ya 2016/2017. Miongoni mwa mabadiliko yaliyoletwa ambayo yalianza kutekelezwa tarehe 9/6/2016 ni;

(a) Ili kulinda wadhamini dhidi ya uonevu na ubaguzi katika kutekeleza majukumu yao, badiliko la kisheria kuwa mdhamini hataonewa, mdhamini hatangólewa au kutolewa ofisini ama kutendewa ubaguzi dhidi yake kutokana na kutekeleza majukumu yake kama ilivyo dhima ya ofisi yake kwa minajili ya Hati ya Dhamana na Kanuni (Trust Deed and Rules) ya mpango wowote au sheria yoyote bila ya kufuata utaratibu wa sheria.

(b) Matoleo na ama kwa niaba ya mwanachama pamoja na riba yake na faida nyingine yoyote inayotokana nayo itakuwa mikononi mwa mwanachama mara moja. Hapo awali, mwanachama alikuwa tu na haki ya kupokea matoleo ya mwajiri baada ya mwaka mmoja wa kuhudumu.

(c) Sheria ya udhibiti ya 14 ya Sheria za Mamalaka Simamizi ya Malipo ya Uzeeni (RBA Regulations) ilibadilishwa ili kutoa nafasi kwa mpango wa viwango vya matoleo ili kuwezesha kuzidisha matoleo na mwanachama kwa kujitolea, zaidi na kiwango rasmi kwa minajili ya kutolea mfuko wa matibabu/afya utakaopokelewa wakati wa

kustaafu. (d) Sheria ya udhibiti ya 19 pia ilirekebishwa ili kuhakikisha

kuwa sheria za Hazina zinatoa nafasi kwa mwanachama ambaye angependelea kuhamisha sehemu ya akiba zake kuelekezwa kwenye shirika linalompa bima ya matibabu/afya ambako ameshindwa kuweka mpango wa bima ya afya baada ya kustaafu kwa matoleo zaidi. Hili linalenga kuwawezesha wanachama kuweka fedha kwa gharama za kiafya/kimatibabu kwa wakati wanaofanya kazi.

(e) Kwa minajili ya kutoa hazina ya uzeeni ambayo ina nafasi nyingi za uwekezaji, muongozo wa uwekezaji ulibadilishwa ili kujumlisha REITS, vitokanavyo na kufanyiwa ubadilishanaji wa kimauzo (exchange related derivatives) na kutofautisha kwa dhamana za kiushirika zilizoratibiwa na zile zisizoratibiwa (listed and unlisted bonds) na waraka wa kibiashara (commercial paper). Hazina za uzeeni sasa zinaweza kuwekeza katika kandarasi za mauzo ya kiubadilishanaji na REITS zote zilizoratibiwa na kufungamanishwa nchini Kenya mradi tu ziwe zimesajiliwa na Mamlaka ya Soko la Mtaji Kenya (Capital Markets Authority, CMA).

(f) Kwa kuvunjwa kwa hazina, sheria ya udhibiti 8A, inaeleza kuwa mwenye kubadilisha mtaji (liquidator) atahitajika, kwa kuandaa akaunti za awali, ili kuwezesha ugawanaji wa faida ya ziada iliyopatikana ambayo itatekelezwa kwa misingi ya asilimia hamsini kwa hamsini yaani nusu bin nusu kati ya wanachama na mdhamini. Faida hiyo ya ziada haitakuwa lazima igawanywe kulingana na kiwango cha fedha kilichowekezwa, faida zisizowekezwa na kiwango cha matoleo kilichofanywa na mwajiri na mwajiriwa kama ilivyotakiwa kisheria hapo awali.

Hazina inaendelea kuboresha hali yake ya kuafikiana na kufwatilia kwa karibu utendaji ili kuhakikisha kuwa mabadiliko yote yanalingana na kuendana pamoja na kunufaika na kuimarika kwa mazingira ya utendaji kazi unaoletwa na maendeleo hayo. Hazina imeweka kifaa madhubuti cha kuafikia matakwa kinachofwatilia unyo unyo kutathmini viwango vya uafikiaji dhidi ya matakwa ya kisheria na kiudhibiti. MATOKEO/UTENDAJI WA KIFEDHA WA HAZINAHazina ilipata faida jumla kimwaka ya asilimia saba (7%) mwaka wa 2016 (7.5% katika mwaka 2015). Kiwango hiki cha faida kilisajiliwa dhidi ya changamoto kuu katika mazingira ya kiuwekezaji katika mwaka uliopita ambazo zilizorotesha matokeo katika vitengo tofauti vya mali. Thamani jumla ya

16

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

hazina kufikia mwisho wa kipindi cha mwaka 2016 ilisimamia kwenye shilingi za Kenya bilioni kumi na moja nukta tatu tatu (Kshs 11.33 bilion) hii ikiwa imeimarika kutoka kwa shilingi za Kenya bilioni tisa nukta nane tatu (Kshs 9.83 bilion) mwaka wa 2015. Ongezeko hili linakisiwa kuwa lilitokana na matoleo pamoja na faida ya kiuwekezaji iliyopatikana katika kipindi hicho husika.

Bodi ya Wadhamini inajizatiti kuwekeza fedha zilizopo kimakinifu kwa mpango mwafaka wenye upeo wa juu zaidi wa mazao au faida yenye kuridhisha. Sera nzima ya uwekezaji kijumla inalenga kufanikisha upatikanaji wa faida kubwa zaidi iwezekanavyo huku ikijilinda dhidi ya hali-tete ya faida hizo. Lengo kuu la kipindi kirefu la kiuwekezaji ni kufikia faida za mda mrefu kwenye maekezo kwa kuzidi mfumuko kupitia upanuzi wa maeneo mbalimbali ya kuwekeza mali pamoja na kufuatilia kwa karibu utendaji wa maekezo hayo. USIMAMIZI WA KIUSHIRIKA NA TUZOBodi ya Wadhamini inashikilia nia yake ya kuhakikisha kuwa mifumo, taratibu na matendo mazoea kwenye Hazina yanasawiri kiwango cha juu zaidi cha usimamizi wa kimashirika. Mfumo mzuri wa usimamizi kiushirika ni muhimu sana katika kukuza utamaduni unaothamini tabia ama hulka njema, uadilifu na heshima ili kutunza na kulinda maslahi wanachama na washikadau wengineo wakati wowote.

Hazina ilishiriki kwa mara ya tano katika Tuzo za Utoaji Ripoti za Kifedha (Financial Reporting- FiRe) mwaka 2016 na kuibuka wa pili katika kitengo cha Isiyo kwa Faida (Not for Profit Category) na wa tatu katika kitengo cha IFRS. Tuzo za FiRe ni juhudi ya Taasisi ya Wahasibu wa Umma Walioidhinishwa wa Kenya (Institute of Certified Public Accountants of Kenya-ICPAK), Mamlaka ya Masoko ya Mtaji (Capital Markets Authority-CMA) na Soko la Nairobi la Ubadilishanaji Hisa (Nairobi Securities Exchange-NSE) na hulenga katika kukuza uwajibikaji, uwazi na uadilifu kuoana na viwango vya kimataifa vya kutoa ripoti za kifedha (International Financial Reporting Standards-IFRS). Tuzo hizi zinatokana na kutambua ubora wa kutoa ripoti za kifedha, kukuza hulka njema za usimamizi wa mashirika na kuinua uwajibikaji wa ushirika kijamii wa mashirika na utoaji ripoti kimazingira Afrika Mashariki.

MUUNDO WA BODINingependa kuwataarifu kuwa kwa kipindi kinachorejelewa, uwanachama wa Bodi ya Hazina ulibadilika kwenye mwaka 2016. Wanakamati watatu wa bodi walistaafu wakati wa muhula huo na jumla ya nambari hiyo hiyoya wengine

wakateuliwa kwa kulingana na kanuni za sera ya Hazina. Mabadiliko haya ni kama mnavyoona kwenye ukurasa wa 4 wa ripoti hii. Muundo wa bodi kama ilivyo ni kwa kulingana na kanuni na sheria za malipo ya uzeeni (Retirement Benefits Act).

MATANGAZO YA RIBAWadhamini walitangaza kiwango cha riba cha mwaka cha asilimia sita nukta tatu (6.3%) kwenye kipindi cha mwaka wa 2016 (6.8% mwaka wa 2015). Hazina ilidumisha sera ya kutangaza riba ya robo mwaka kwenye kipindi cha mwaka wa 2016 ambayo inahakikisha kuwa hazina inadumisha kiwango sufuri cha salio ya wanachama wanaondoka kwenye Hazina katika mwaka na hivyo kufikia kiwango kilichoidhinishwa cha faida wakati wa kuondoka.

MTAZAMOUchumi wa kimataifa na ule wa kitaifa unatazamiwa kuimarika kwenye mwaka wa 2017 kutokana na udhabiti unaotarajiwa kwenye bei za bidhaa. Hata hivyo, uchumi wa humu nchini bila shaka una uwezekano wa kuathiriwa na matukio ya kisiasa kwani ni mwaka wa uchaguzi. Wadhamini wataendelea kufwatilia na kuchunguza maendeleo kwenye mazingira mapana kiuchumi na kuambatanisha uwekezaji wake ili kunufaika na nafasi ibuka za kiuwekezaji pamoja na kujilinda dhidi ya hatari za kiuwekezaji zitakazoibuka.

SHUKRANINingependa kuwarudishia shukrani jazila kwa niaba ya Bodi na Mdhamini na washikadau wote ambao wanaendelea kufanya kazi bila kuchoka ili kuboresha hazina hii wakati inapojaribu kupinda na kupenyeza kwenye hali ngumu ya kiuchumi na kiuwekezaji. Ningependa pia kuwashukuru wanabodi wenzangu kwa kujitolea kwao kwa hazina hii kwa kipindi cha mwaka mzima uliopita na kuendelea kuniunga mkono mimi kama mwenyekiti. Katibu wa bodi na kikundi chake pia wamefanya kazi bila kuchoka kuhakikisha kuwa kuna usimamizi bora na makinifu wa shughuli za kila siku za Hazina hii. Siwezi kuwasahau wanachama kwa kuendelea kutuunga mkono, kutuhimiza na kutupa maoni.

Ernest NadomeMwenyekitiMradi wa Hazina ya Malipo ya Uzeeni wa Wafanyikazi wa Kampuni ya Kawi, Kenya 2006.

17

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

I would like to thank the Board of Trustees for their unwavering

support and guidance as well as the stakeholders for their

contributions in service delivery to the Fund.

DEAR MEMBER,

The Kenya Power Pension Fund registered positive growth in the past year despite the challenging investment environment, as evidenced by a depressed stock market,

volatility in the Kenya Shilling and the interest rates. The positive performance was achieved through implementation of the investment strategies as per the Fund’s strategic plan. Attention was placed on the monitoring and evaluation of this implementation strategy where necessary alignments were made to respond to the prevailing environment at any given time with keen focus on achieving long term investment objectives.

FUND INVESTMENTSThe Board of Trustees of the Fund have the responsibility of establishing and maintaining policies and objectives for all

SECRETARY’S REPORT

18

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

aspects of the Fund’s operations. Central to this is the Board’s responsibility for the prudent investment of the Fund’s assets.

The Fund continues to diversify its investment into alternative assets classes which included the property and private equity investments. These assets classes expanded the investment horizon as well as created opportunity for diversifications owing to their un-correlation with the capital markets investments. All these investments are undertaken while ensuring compliance with the RBA regulations on investments and the Fund’s Investments Policy Statement.

In 2016, the Fund initiated the due diligence process for the second Private Equity Fund as it seeks to maximize the opportunities created by this asset class. This process was projected to be completed and final documents executed in the first quarter of 2017 with investments activities expected to commence immediately thereafter. The shift towards the private equity space will continue in the coming periods as the Fund seeks to align its portfolio to be in line with the strategic plan.

The Fund continued with the execution of its elaborate plan on properties development which has over the years not only provided superior returns but also contributed immensely to the national development of the housing sub sector. The Fund made substantial progress in the construction of the Bogani Park units located in the leafy suburb of Karen, approximately 20 Kilometers from Nairobi Central Business District. The development comprises forty-five (45) four and five-bedroom town houses each on a half an acre plot. The disposal drive commenced in earnest during the period and it is envisaged that the units will be fully sold within the set timelines.

Besides the above activities in the alternative asset space, the Fund continued to refine the monitoring and evaluation of the performance in other assets classes. The underlying objective being to maximize the returns while mitigating against the risks associated with such investments. In addition constant engagement with all the stakeholders within the investment space was maintained throughout the period. This engagement provided the necessary alignment of the strategies and objectives.

Define Benefit Secretariat is responsible for close monitoring and reporting on implementation of the investment strategy. This continued analysis is to ensure that the Fund remains focused on the short term and long-term performance and sustainability.

STRATEGIC PLANNINGThe Kenya Power Pension Fund (KPPF) adopted a new strategic plan for the period 2016 to 2020. KPPF’s purpose which informs everything it does is to deliver value and quality of life in retirement to its members. KPPF’s vision is to be the best-in-class occupational scheme in the whole of Africa. Best-in-class means to be both (i) an outperformer – achieving superior returns relative to peers within acceptable risk parameters and (ii) a pioneer – using innovative and trend-setting strategies in order to benefit its members. KPPF will benchmark itself against not only the best pension funds in Kenya, but also the leading pension funds in Africa.

FUND ADMINISTRATIONThe Defined Contribution Fund has outsourced administrative functions to the Secretariat of the Defined Benefits Fund. The following functions have been outsourced:

• Scheme Administration• Finance & Investments• Property Management & Development• Risk Management• Customer Service• Procurement

There is in place an elaborate contractual agreement governing the engagement with the DB secretariat that ensure among other things the services being provided are to the satisfactory levels.

MEMBER ENGAGEMENTThe Fund is committed to providing high quality service to its members. The Fund endeavors to continuously engage its membership through effective communication and information sharing initiatives. To this end, it has created various communication channels and continuously updates members on the development within the Fund.

Each year, the Fund organizes and conducts education programs targeting both the in service and retired members. The objective for these education programs is to inform and update members on the status and performance of the Fund as well as prepare them for retirement. In addition, on a quarterly basis a newsletter updating members on the fund activities is prepared and circulated.

During the year, the Fund conducted a member satisfaction survey which is part of the bi-annual exercise aimed at determining the satisfaction levels. The overall members’

19

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

satisfaction index stood at 84.2% which was an improvement from 2014’s satisfaction index that was 83.7%. This improvement is an affirmation of the effectiveness of the customer service strategy being implemented by the Fund. The Fund has incorporated the implementation of the recommendations and feedback from the survey in the annual activity plan for the coming periods.

Innovation and ICT remains the pillars for successes of the current generation entities. The Fund has taken a lead from this front by integrating the duo in its processes and activities. The interactive system created a platform for real time engagement with members. In addition the internal processes are supported by an elaborate ICT systems to ensure effectiveness and efficiency within the Fund. Finally the continuous improvement principle dictates that the Fund refine its processes and take opportunity of new development.

PROCUREMENT The new public procurement law (Public Procurement and Asset Disposal Act 2015) took effect from 7th January 2016. Among the changes introduced was inclusion of the pension funds for public entities in the list of entities required to comply with the new law. To facilitate compliance, the DB secretariat which provides the administration services to the Fund, established a procurement department to handle all matters relating to procurement.

RISK MANAGEMENTThe Fund recognizes that risk management is fundamental to achieving corporate goals. Therefore it has put in place processes for identifying, assessing, monitoring and managing risks to ensure that the Fund’s objectives are achieved and risk mitigated. The framework is reviewed continuously to align it

to the realities of the operating environment. The risk register is reviewed every quarter where the effectiveness of the risk mitigating measures is reviewed.

OUTLOOK In 2017, the Fund will seek to achieve optimal returns, adjusted for risk through the implementation of the new asset allocation targets that better reflect the Fund’s moderately aggressive strategy. The Fund would also enhance its performance management framework through a more regular engagement with its fund managers which has been identified as an area of improvement.

Given the overarching purpose to deliver value to members in retirement, the Fund will continue to enhance and innovate around its offering to members. Members are becoming increasingly sophisticated and have higher expectations, the Fund therefore needs to adapt its products and services to be in pace with this development. It will also leverage mobile and digital technology to create deeper relationships with its membership.

APPRECIATION

I would like to thank the Board of Trustees for their unwavering support and guidance as well as the stakeholders for their contribution in service delivery to the Fund.

H.K. KyandaSecretary

20

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

Kwa Mwanachama

Hazina ya Malipo ya Uzeeni ya Wafanyikazi wa Shirika la Kawi, Kenya ilifikia ukuaji yakinifu kwa kipindi cha mwaka uliopita licha ya hali ngumu ya mazingira

ya kiuwekezaji, kama inavyoshudiwa kwa soko la hisa linalopungua, hali tete ya thamani ya shilingi ya Kenya na viwango vya riba. Matokeo hayo yakinifu yalipatikana kupitia utekelezwaji wa mbinu mahsusi ya kiuwekezaji kama ilivyo kwenye kielelezo cha mikakati ya uwekezaji cha Hazina. Mkazo ulitiliwa zaidi kwenye kufuatilia kwa karibu na kutathminiwa kwa utekelezwaji huo ambapo kulifanywa uambatanishaji muhimu ili kuafikiana na mazingira ya wakati husika kwa kipindi chochote kile huku makini ikitiliwa zaidi kwenye malengo ya kipindi kirefu ya faida za kiuwekezaji.

UWEKEZAJI WA HAZINABodi ya Wadhamini ya Hazina ina jukumu la kuweka na kudumisha sera na malengo kwa maswala yote yanayohusu

RIPOTI YA KATIBU

Ningependa kuishukuru Bodi ya Wadhamini kwa

kuendelea kupeana msaada wao usiotikisika na mwelekeo,

pamoja na washikadau wengine wote kwa mchango wao katika

kutoa huduma kwa Hazina.

21

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

shughuli za Hazina. Kitovu chake ni jukumu la Bodi la kufanya uwekezaji wa busara wa mali ya Hazina.

Hazina inaendelea kupanua uwanda wake wa kiuwekezaji kwa kuzingatia vitengo mbadala vya uwekezaji-mali ambao ulihusisha mali na uwekezaji binafsi wa kifedha. Hivi vitengo mbalimbali vya mali vilipanua upeo wa uwekezaji huku vikitoa nafasi mseto za kiuwekezaji kwa kutohusiana na uwekezaji kwenye soko la mtaji. Juhudi hizi zote za kiuwekezaji huchukuliwa kuambatana na kuafikiana na kanuni za Mamlaka Simamizi ya Hazina ya Malipo ya Uzeeni kudhibiti uwekezaji na pia kwa taratibu zilizoko kwenye uratibu wa sera za uwekezaji za Hazina (Fund’s Investment Policy Statement).

Kwenye mwaka wa 2016, Hazina ilianzisha mchakato mzima kwa bidii tekelezi wa Mfuko Binafsi wa Kifedha (Private Equity Fund) katika kutafuta kunufaika kikamilifu na nafasi zinazotokea kwenye kitengo cha mali. Mchakato huu ulikisiwa kukamilika na nyaraka za mwisho kutekelezwa kwa muhula robo wa mwisho wa mwaka wa 2017 huku juhudi za kiuwekezaji zikitarajiwa kungóa nanga moja kwa moja baada ya utekelezwaji huo. Mabadiliko ya kuegemea kitengo cha mauzo binafsi ya kifedha utaendelea kwa vipindi vijavyo kwani Hazina inatazamia kuendelea kuambatanisha sehemu yake sawa na mpango wake mahsusi kimikakati.

Hazina iliendelea kutekeleza mpango wake pana kwa kukuza mali ambao kwa miaka mingi iliyopita umetoa matokeo bora zaidi pamoja na kuchangia pakubwa maendeleo ya kitaifa ya sekta ndogo ya nyumba na makaazi. Hazina ilifikia ukuaji muhimu katika ujenzi wa majumba wa Bogani Park ambayo yapo kwenye sehemu ya kifahari ya kimakaazi ya Karen, takriban kilomita ishirini (20Km) kutoka katikati mwa jiji la Nairobi. Ujenzi huu unajumlisha majumba arubaini na tano (45) yenye vyumba vinne au vitano vya kulala kila mojawapo ya majumba hayo ikikalia eneo la nusu eka (half acre plot). Shughuli ya kuondoa majumba hayo kwa kuuza ilianza kwa kasi mno kwenye kipindi husika na inatazamiwa kuwa vyumba vyote vitakuwa vimeuzwa kufikia mwisho wa kipindi maalum kilichowekwa.

Kando na shughuli zilizorejelewa tayari kwenye nafasi mbadala ya mali, Hazina iliendelea kupiga msasa ufuatilizi na utathmini wa utendaji kwenye vitengo vinginevyo vya kiuwekezaji. Lengo la kimsingi katika juhudi hizi zote likiwa kuendeleza na kukuza faida huku ikijilinda dhidi ya hatari zinazohusiana na uwekezaji wa sampuli hiyo. Kwa kuongezea, ushirikishi endelevu wa

washikadau wote kwenye nafasi ya uwekezaji ulidumishwa mkwa kipindi kizima. Ushirikishi huu ulitoa muambatanisho muhimu wa mikakati na malengo.

Sekretarieti ya Faida Mahsusi (Defined Benefits Secretariat) ina jukumu la ufuatilizi wa karibu na kuripoti kuhusu utekelezwaji wa mikakati ya uwekezaji. Tathmini hii endelevu ni muhimu kuhakikisha kuwa Hazina inasalia makinifu kwenye malengo yake ya muhula mfupi na utendaji wake kwa muhula mrefu na uendelevu wake.

MIKAKATI NA MIPANGOHazina ya Pensheni ya Kampuni ya Kawi (Kenya Power Pension Fund-KPPF) ilipitisha mpango mpya wa kimikakati kwa kipindi 2016 hadi 2020. Lengo la KPPF linaloarifu shughuli zote za hazina ni kuleta faida na thamani kubwa kwa maisha ya uzeeni ya wanachama wake. Ruwaza ya KPPF ni kuwa bora-kwenye-kitengo (best-in-class) kwenye hazina za kikazi kote barani Afrika. Bora-kwenye-kitengo inamaanisha; Kwanza, kuwa mtendaji wa kuzidi viwango vya kawaida kwa kufikia mazao ama faida ya juu zaidi miongoni mwa mashirika-wenza kwa kuzingatia vigezo vya hatari kubalifu na, Pili, kuwa mwanzilishi au mvumbuzi muasisi kwa kutumia mikakati bunifu na yakupigiwa mfano ili kufaidi wanachama wake. KPPF inaweka mikakati kwa kujilinganisha sio tu na hazina za malipo ya uzeeni nchini Kenya bali pia dhidi ya hazina za pensheni zinazofanya vyema zaidi barani Afrika.

USIMAMIZI WA MFUKO WA HAZINAHazina ya Mfuko wa Michango Mahsusi imeweza kuratibu kwa Sekretariati ya Mfuko wa Faida Mahsusi huduma ya usimamizi ya kutoka nje. Huduma zifwatazo zimeratibiwa kutoka nje; • Usimamizi Mradi• Fedha na Maekezo• Usimamizi Mali na Uendelezaji• Usimamizi wa Hatari ibuka• Huduma kwa Wateja• Manunuzi

Pana mpango maalum wa makubaliano kikandarasi unaosimamia ushirikiano na Sekretariati ya DB kuhakikisjha miongoni mwa mambo mengineyo kuwa huduma zinazotolewa ni za kiwango bora zaidi na zenye kuridhisha.

USIMAMIZI WA WANACHAMAHazina imejitolea kikamilifu katika kupeana huduma ya kiwango bora zaidi kwa wanachama wake. Hazina inajizatiti

22

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

kuendelea kushirikisha wanachama wake kupitia njia pana za kimawasiliano na mbinu za kubadilishana taarifa. Kwa kufikia hili, hazina imetengeneza njia mbalimbali za mawasiliano na kutoa taarifa za moja kwa moja kuwajuza wanachama juu ya maendeleo katika Hazina.

Kila mwaka, Hazina huandaa na kutekeleza mpango wa mafundisho unaolenga wanachama wanaondelea kazini na wale waliostaafu. Lengo la mpango huu wa mafunzo ni kuwataarifu na kuwajuza wanachama juu ya hali kamili na utendaji wa Hazina pamoja na kuwaandaa kwa kustaafu kwao. Kwa kuongezea, kwa muhula wa robo mwaka, jarida la kuwajuza na kuwaarifu wanachama huandaliwa na kuchapishwa na kusambazwa.

Katika mwaka, Hazina ilifanya utafiti kuhusu kuridhika kwa wanachama wake kama sehemu ya shughuli za kila mwaka zinazolenga kutathmini viwango vya kuridhishwa na huduma zinazotolewa. Kiwango cha jumla cha kuridhika kwa wanachama kilikuwa asilimia themanini na nne nukta mbili (84.2%) ambacho kilisawiri kuimarika kutoka kwa kiwango cha uridhisho cha mwaka 2014 cha asilimia themanini na tatu nukta saba (83.7%). Kuimarika huku kulikuwa idhibati tosha ya ubora wa mikakati ya huduma kwa wateja inayotekelezwa na Hazina. Hazina imeshirikisha utekelezwaji wa mapendekezo na maoni kutoka kwa utafiti kwenye mpango wa juhudi za kila mwaka kwa vipindi vijavyo.

TEKNOLOJIA HABARI NA MAWASILIANO (TEKNOHAMA)Ubunifu na teknolojia vinasalia kuwa vyamba-jengo vikuu vya ufanisi wa juhudi-jumla kwa kizazi cha sasa. Hazina imechukuwa uongozi katika ulingo huu kwa kujumlisha viwili hivi (ubunifu na teknolojia) katika michakato na juhudi zake zote. Mfumo kimtagusano ulitengeneza ukumbi wa kuingiliana moja kwa moja na wanachama. Kwa kuongezea, michakato ya ndani ya hazina inasaidiwa na mfumo dhabiti wa TEKNOHAMA kuhakikisha kuwepo ufanisi na utenda-kazi bora kwenye Hazina. Mwisho, msingi endelevu wa uimarishaji unahitaji Hazina kuboresha michakato yake na kuchukuwa nafasi ya maendeleo mapya inayopatikana.

MANUNUZI (PROCUREMENT)Sheria mpya ya umma ya manunuzi (Public Procurement and Asset Disposal Act 2015) ilianza kutekelezwa tarehe 7/1/2016. Miongoni mwa mabadiliko iliyoleta ni pamoja na kushirikisha hazina za malipo ya pensheni kwa asasi za umma

kwa ratiba ya asasi zinazohitajika kuafikiana na sheria hiyo mpya. Ili kufanikisha uwiano na uafikiano huu, Sekretariati ya DB ambayo hupeana huduma za kiusimamizi kwa Hazina, ilianzisha idara ya manunuzi itakayohusika na maswala yote ya manunuzi.

USIMAMIZI WA HATARI (RISK MANAGEMENT)Hazina inatambua kuwa usimamizi wa hatari ni jambo la kimsingi katika kufikia malengo ya kiushirika. Kwa hivyo, Hazina imeweka tayari michakato ya kutambua, kutathmini, kufuatilia na kusimamia hatari ili kuhakikisha kuwa Hazina inafikia malengo yake na kuwa hatari zinazuiwa ama kudhibitiwa. Mfumo tekelezi hutathminiwa upya kila mara ili kuuambatanisha na uhalisia wa mazingira ya kazi. Sajili ya hatari hupitiwa kila muhula wa robo mwaka ambapo uwezo wake kiufanisi katika mikakati ya kudhibiti hatari hutathminiwa upya na pia sajili hiyo kuratibiwa kuafiki hali ilivyo wakati huo huo.

MTAZAMOKwenye mwaka wa 2017, Hazina itatafuta kufikia kiwango cha juu zaidi cha faida iliyokarabatiwa dhidi ya hatari kupitia utekelezwaji wa malengo mapya ya kuekeza mali ambayo yanasawiri mkakati makinifu wa Hazina. Hazina itaboresha pia mfumo wake wa utendaji kiusimamizi kupitia njia ya kila mara ya ushirikiano pamoja na mameneja au wasimamizi wa Hazina ambao umetambuliwa kama sehemu mojawapo inayohitaji kuimarishwa.

Kutokana na jukumu kuu la kuleta thamani kwa wanachama uzeeni mwao baada ya kustaafu, Hazina itaendelea kuboresha na kubuni zaidi kwenye matoleo yake kwa wanachama. Wanachama wanazidi kusasaika na wana matarajio ya juu zaidi. Hazina kwa hivyo inahitaji kukabiliana na bidhaa na huduma zake ili ziendane na mabadiliko haya. Aidha Hazina itatafuta mwafaka na teknolojia za simu pamoja na zile za kidigitali ili kuunda mahusiano bora na wanachama.

SHUKRANINingependa kuishukuru Bodi ya Wadhamini kwa kuendelea kupeana msaada wao usiotikisika na mwelekeo, pamoja na washikadau wengine wote kwa mchango wao katika kutoa huduma kwa Hazina.

H.K. KyandaKatibu

23

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

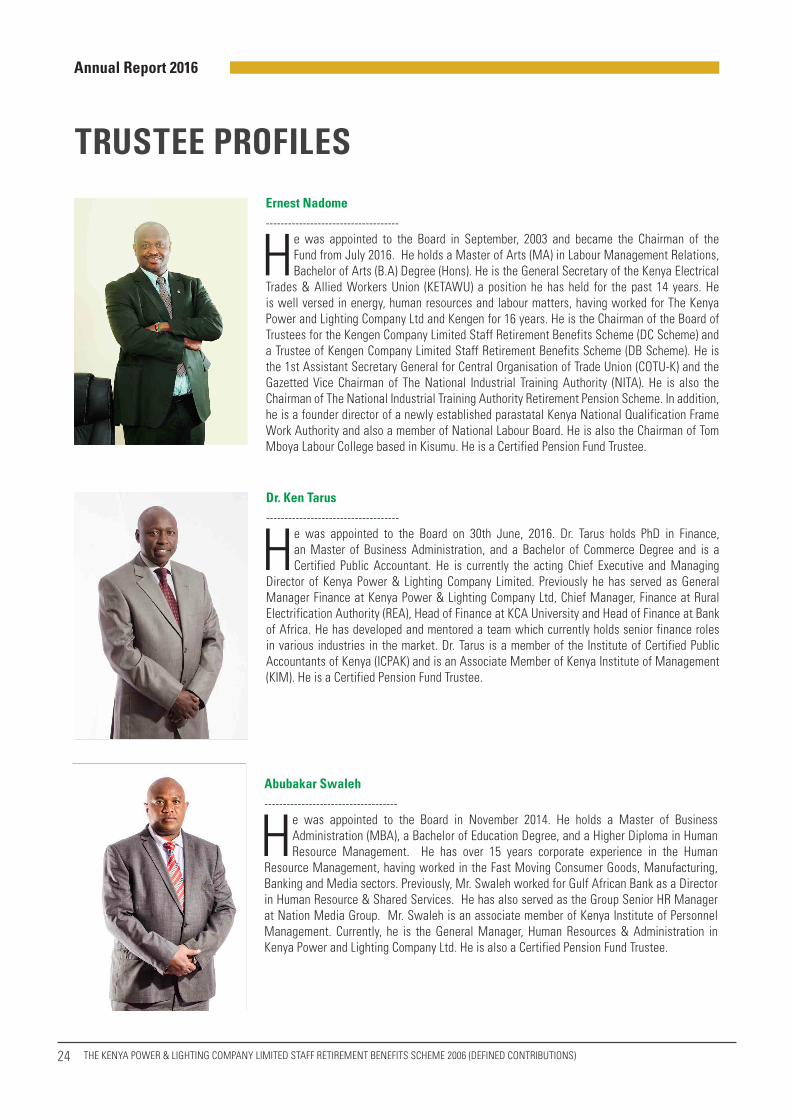

TRUSTEE PROFILESErnest Nadome------------------------------------

He was appointed to the Board in September, 2003 and became the Chairman of the Fund from July 2016. He holds a Master of Arts (MA) in Labour Management Relations, Bachelor of Arts (B.A) Degree (Hons). He is the General Secretary of the Kenya Electrical

Trades & Allied Workers Union (KETAWU) a position he has held for the past 14 years. He is well versed in energy, human resources and labour matters, having worked for The Kenya Power and Lighting Company Ltd and Kengen for 16 years. He is the Chairman of the Board of Trustees for the Kengen Company Limited Staff Retirement Benefits Scheme (DC Scheme) and a Trustee of Kengen Company Limited Staff Retirement Benefits Scheme (DB Scheme). He is the 1st Assistant Secretary General for Central Organisation of Trade Union (COTU-K) and the Gazetted Vice Chairman of The National Industrial Training Authority (NITA). He is also the Chairman of The National Industrial Training Authority Retirement Pension Scheme. In addition, he is a founder director of a newly established parastatal Kenya National Qualification Frame Work Authority and also a member of National Labour Board. He is also the Chairman of Tom Mboya Labour College based in Kisumu. He is a Certified Pension Fund Trustee.

Abubakar Swaleh------------------------------------

He was appointed to the Board in November 2014. He holds a Master of Business Administration (MBA), a Bachelor of Education Degree, and a Higher Diploma in Human Resource Management. He has over 15 years corporate experience in the Human

Resource Management, having worked in the Fast Moving Consumer Goods, Manufacturing, Banking and Media sectors. Previously, Mr. Swaleh worked for Gulf African Bank as a Director in Human Resource & Shared Services. He has also served as the Group Senior HR Manager at Nation Media Group. Mr. Swaleh is an associate member of Kenya Institute of Personnel Management. Currently, he is the General Manager, Human Resources & Administration in Kenya Power and Lighting Company Ltd. He is also a Certified Pension Fund Trustee.

Dr. Ken Tarus ------------------------------------

He was appointed to the Board on 30th June, 2016. Dr. Tarus holds PhD in Finance, an Master of Business Administration, and a Bachelor of Commerce Degree and is a Certified Public Accountant. He is currently the acting Chief Executive and Managing

Director of Kenya Power & Lighting Company Limited. Previously he has served as General Manager Finance at Kenya Power & Lighting Company Ltd, Chief Manager, Finance at Rural Electrification Authority (REA), Head of Finance at KCA University and Head of Finance at Bank of Africa. He has developed and mentored a team which currently holds senior finance roles in various industries in the market. Dr. Tarus is a member of the Institute of Certified Public Accountants of Kenya (ICPAK) and is an Associate Member of Kenya Institute of Management (KIM). He is a Certified Pension Fund Trustee.

24

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

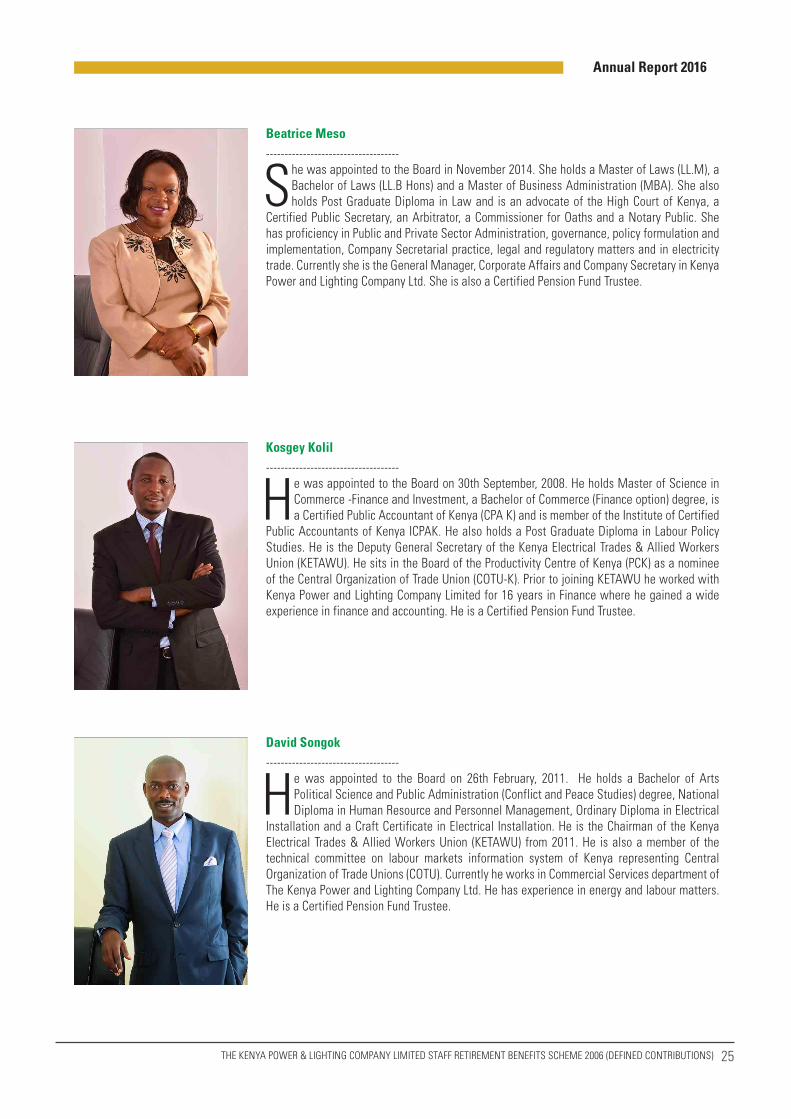

Beatrice Meso------------------------------------

She was appointed to the Board in November 2014. She holds a Master of Laws (LL.M), a Bachelor of Laws (LL.B Hons) and a Master of Business Administration (MBA). She also holds Post Graduate Diploma in Law and is an advocate of the High Court of Kenya, a

Certified Public Secretary, an Arbitrator, a Commissioner for Oaths and a Notary Public. She has proficiency in Public and Private Sector Administration, governance, policy formulation and implementation, Company Secretarial practice, legal and regulatory matters and in electricity trade. Currently she is the General Manager, Corporate Affairs and Company Secretary in Kenya Power and Lighting Company Ltd. She is also a Certified Pension Fund Trustee.

Kosgey Kolil------------------------------------

He was appointed to the Board on 30th September, 2008. He holds Master of Science in Commerce -Finance and Investment, a Bachelor of Commerce (Finance option) degree, is a Certified Public Accountant of Kenya (CPA K) and is member of the Institute of Certified

Public Accountants of Kenya ICPAK. He also holds a Post Graduate Diploma in Labour Policy Studies. He is the Deputy General Secretary of the Kenya Electrical Trades & Allied Workers Union (KETAWU). He sits in the Board of the Productivity Centre of Kenya (PCK) as a nominee of the Central Organization of Trade Union (COTU-K). Prior to joining KETAWU he worked with Kenya Power and Lighting Company Limited for 16 years in Finance where he gained a wide experience in finance and accounting. He is a Certified Pension Fund Trustee.

David Songok------------------------------------

He was appointed to the Board on 26th February, 2011. He holds a Bachelor of Arts Political Science and Public Administration (Conflict and Peace Studies) degree, National Diploma in Human Resource and Personnel Management, Ordinary Diploma in Electrical

Installation and a Craft Certificate in Electrical Installation. He is the Chairman of the Kenya Electrical Trades & Allied Workers Union (KETAWU) from 2011. He is also a member of the technical committee on labour markets information system of Kenya representing Central Organization of Trade Unions (COTU). Currently he works in Commercial Services department of The Kenya Power and Lighting Company Ltd. He has experience in energy and labour matters. He is a Certified Pension Fund Trustee.

25

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

Johnstone Sakwa ------------------------------------

He was appointed to the Board in July 2016. He holds a Business Administration Degree, (Marketing), a Higher Diploma in Electrical Engineering and is also a Registered Graduate Technician Engineer. Currently, he works as a Prepaid Metering Section in charge within

the Revenue Protection Unit of Customer Service in Kenya Power. He is also a member of the National Cohesion and Values Committee within Kenya Power and Lighting. He is a Certified Pension Fund Trustee.

Zilpa Ayara ------------------------------------

She was appointed to the Board in July 2016. She has 30 years’ work experience in various departments in Kenya Power & Company Limited. Currently working at the Kenya Power National Contact Center as a Quality control officer, a founder Committee member of

Kenya Power Fariji Fund and Committee member Safety Health and Environment (SHE) Central Office. A holder of Bachelor of Commerce Degree – Marketing Option, Diploma in Business Management, Call Center Quality Assurance Certificate and Credit/Debt Control Management Certificate. A member of Kenya Institute of Management (KIM). Currently, the chairman of PTA(Parents Teachers Association, member Board Of Management ) Huruma Girls High School, Board Member Of Upper Hill School and Chairperson of AIC- Jericho Church Members Welfare. She is a Certified Pension Fund Trustee.

Henry Kyanda – Secretary------------------------------------

He was appointed Secretary to the Board in 2006. He holds a Master of Business Administration (MBA) Degree (Strategic Management) and Bachelor’s degree in International Business Administration (Finance). He has wide experience in the Pensions

industry having previously worked as the Principal Pensions Officer at The Kenya Power and Lighting Company Ltd. Prior to joining Kenya Power he worked in the investment management industry. He has wide experience in pensions, banking and investments spanning over 15 years. He is also a Certified Pension Fund Trustee.

26

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

STATEMENT ON CORPORATE GOVERNANCE Board of Trustees

The Board of Trustees is committed to upholding the highest governance, legal, and ethical standards in all activities and has therefore adopted best practice

guidelines aimed at strengthening the operating climate and providing necessary guidelines whenever situations warrants. The board sets the strategic direction of the Fund, puts in place policies as well as providing the necessary oversight in the management of the Fund in pursuance of the achieving the Fund’s key objectives.

Board ManualThe Board maintains a Board Manual which is a reference guide on all governance matters and conduct of the Fund’s affairs. It establishes the corporate governance framework, policies and practices to ensure that at all time the Fund’s operations meets the expectation of the stakeholders. It expounds and explains the collective and individual powers, duties, obligations, and responsibilities of the Trustees. The manual is reviewed annually to incorporate any necessary changes that ensures consistency with the Board’s objectives, current law and best practice. Board ResponsibilitiesThe Board Manual sets out the Trustee’s roles and responsibilities which are summarized below:

• Formulation and approval of the Fund’s vision, mission and core values and formulation & approval of the Fund’s strategy, business plan and principles of investments.

• Approval of annual budget and the final financial statements and interest on members’ balances.

• Review and evaluation of Investment Managers Performance and approval of risk management strategy.

• Settlement of major litigation/claims• Appointment of all service providers • Approval of banking/authority levels, policies, procedures

and manuals

• Periodic formulation and review of ICT policies, procedures, strategies and work plans.

Board Chairman The Chairman of the Board is elected by the Board of Trustees in accordance with provisions of the Fund’s Trust Deed and Rules. The roles and responsibilities of the Chairman are distinct and separate from those of the Administrator of the Fund which creates the necessary independence in the discharge of respective responsibilities.

The Chairman is responsible for the overall Board leadership and its effectiveness. He sets the agenda for Board meetings, chairs all meetings and the Fund’s Annual General Meeting (AGM). He also ensures adequate induction of new Trustees to orient them with Board’s role, key tasks, processes, policies, and awareness of conflict of interest, as well as trainings for all Trustees to keep them abreast with good corporate governance practices and developments in the industry. He ensures key tasks of the Board are achieved satisfactorily and maintains an independent working relationship with the Administrator of the Fund. Board Structure and CompositionThe Board’s size and composition is guided by the Retirement Benefits (Occupation Retirement Benefits Schemes) Regulations 2000 issued by RBA, which states that a defined contributions scheme shall not have less than four (4) and not more than nine (9) Trustees and that the number of Trustees elected by the members shall be at least 50% of the Board composition. In compliance with this requirement, and in accordance with the Trust Deed and Rules, the Board is composed of eight Trustees, three of whom are Sponsor-appointed and five (5) are member-elected as detailed below;

27

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

Member elected Trustees serves a 3-year renewable term, while sponsor-appointed Trustees can be re-appointed or maybe removed at any time by the Sponsor. However, this practice will be reviewed to align it with the recent changes in the regulatory framework which has limited the term of a Trustee to maximum of two terms of three years each.

The Board strive to ensure that all time the skills mix of the board is appropriate and updated to steer the Fund within the environment that is ever changing. Key among the existing skill pool include expertise in governance, human resources, legal, and finance and risk management.

The entire board is independent of the Administrator. This arrangement ensures that that Board’s activities, discussions and decisions benefit from predominantly outside views and experiences.

Board Induction programs & TrainingEach Trustee on appointment is provided with sufficient information to enable him/her perform his/her roles. Induction of newly-appointed Trustees is organized by the Secretary to the Board. The Board ensures that all Trustees keep abreast of both practical and theoretical developments, and that their expertise is constantly relevant. Trustee development comprises of induction and enhancement of skills derived from regular evaluations.

Every year the Secretary in liaison with the Board carries out a Trustees training needs analysis and prepares a training calendar which is implemented during the year.

In addition, according to the Capacity Building of Trustees of Retirement Benefits Schemes Prudential Guideline Number RBA 001,2013 all Trustees of Retirement Benefits Schemes and Directors of Corporate Trustees of any retirement benefits scheme in Kenya are required to undergo training in order to be certified and approved by the Retirement Benefits Authority. All the Trustees have undertaken this training and are certified as Trustees. Board Remuneration and compensation The Board’s compensation is determined and approved by the Sponsor. The levels are reviewed periodically to ensure that they are reasonable taking into consideration the affordability of the Fund. The details of the compensation for 2016 is as shown on note 25 of the notes to the financial statements.

Board evaluation The Board undertakes self-evaluation on its performance internally every year while the external facilitated reviews is done every two years. The aim of this exercise is to gauge the performance levels of the Board as well provisions of feedback on areas of improvement which goes a long way in ensuring a sustainable governance structure is always maintained. Board MeetingsThe Board and its Committees meet regularly in accordance with the annual board work plan and at least quarterly in a year. The work plan also sets out the key agenda to be discussed in every meeting.

The Fund uses one of the latest technology solutions in the

Dr. Ken Tarus Sponsor appointed

Beatrice Meso Sponsor appointed

Abubakar Swaleh Sponsor appointed

Ernest Nadome Member elected – representing Workers Union members

Koskey Kolil Member elected – representing Workers Union members

David Songok Member elected – representing Workers Union members

Johnstone Sakwa Member elected

Zilpa Ayara Member elected

28

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

market, a system known as e-Board, to assist in management of Board functions using ICT. All Board and Committee meetings are now managed seamlessly via the e-Board system. Via this system, Trustees can access and review necessary information on the items to be discussed prior to any meeting of the Board. This has been valuable in enabling Trustees prepare adequately and hold meetings easily and efficiently, saving on time and eliminating the manual paper-based way of reviewing and approving documents. Board CommitteesThe Board has established committees to assist it in discharging its responsibilities and obligations. It delegates specific functions to selected Committees with defined formal terms of reference, without abdicating its ultimate responsibility. Currently the Board has four standing committees as indicated below;

a) Risk and Auditb) Strategy, Finance & Investment c) Project Implementation d) Governance, Human Resources & Compensation

The membership and chairmanship of these committees is regularly reviewed by the Board to ensure their effective operations. In constituting the committees individual area of expertise and qualifications form the basis for appointment to the specific committee.

The Chairmen of the committees appraises the full Board of their activities on a quarterly basis through oral and/or written reports.

The details of the committees are as follows;

a) Risk & Audit Committee

The Risk & Audit Committee is chaired by Beatrice Meso with Kosgey Kolil & Zilpa Ayara as members. The responsibilities of the Committee includes but is not limited to:

• To review and recommend to the Board appropriate risk management policies and procedures

• To monitor the implementation of risk management strategies

• To reviewing the effectiveness and reliability of management information systems, risk and internal controls systems and the efficiency and effectiveness of both external and internal audit

• Liaison with internal and external auditors in their undertakings of respective assignments

• Advise the Board on any issues pertaining to the appointment, remuneration and dismissal of auditors

• Consider and make recommendation to the Board on IT governance including ICT policies planning.

b) Strategy, Finance & Investment Committee

The Strategy Finance & Investment Committee is chaired by Dr. Ken Tarus with Beatrice Meso and Johnstone Sakwa as members. The responsibilities of the Committee includes but is not limited to:

• To advise on the development and implementation of the strategic plan

• Consider and make recommendations to the board concerning new strategic initiatives, alliances and potential partnerships

• To monitor portfolio performance and implementation of investment strategies

• Advise the Board on appointment of investment managers, custodians and bankers to monitor and evaluate performance of these service providers

• To review and make recommendations to the Board on proposed new investments, capital developments

• To review and make recommendations on the annual budgets for the Fund including monitoring the performance

c) Governance, HR & Compensation Committee

The Governance, HR & Compensation Committee is chaired by Abubakar Swaleh with Zilpa Ayara, David Songok and Johnstone Sakwa as members. The responsibilities of this Committee includes but is not limited to:

29

Annual Report 2016

THE KENYA POWER & LIGHTING COMPANY LIMITED STAFF RETIREMENT BENEFITS SCHEME 2006 (DEFINED CONTRIBUTIONS)

• Oversee the governance, compliance and communication function of the Fund.

• Responsible for staff and operational policies in order to align the Fund’s operations with best practice.

• Orientation and induction of new Trustees including training and development of Board of Trustees

• Review and advise the Board on the annual procurement plans and also advise management on the procurement matters

d) Project Implementation Committee (PIC)

The Project Implementation committee is chaired by David Songok with Kosgey Kolil, Abubakar Swaleh as members. The responsibilities of this Committee includes but is not limited to:

• To oversee the implementation of the Project in accordance with the directives and approvals from the Board.

• To monitor the progress of implementation for the project.

• To ensure that appropriate mechanisms are put in place to ensure close cooperation amongst the consultants involved in the implementation of the Project.

• To give necessary advice, guidance and support to the Project Manager and the other consultants on all project related matters to ensure that the project is well implemented.

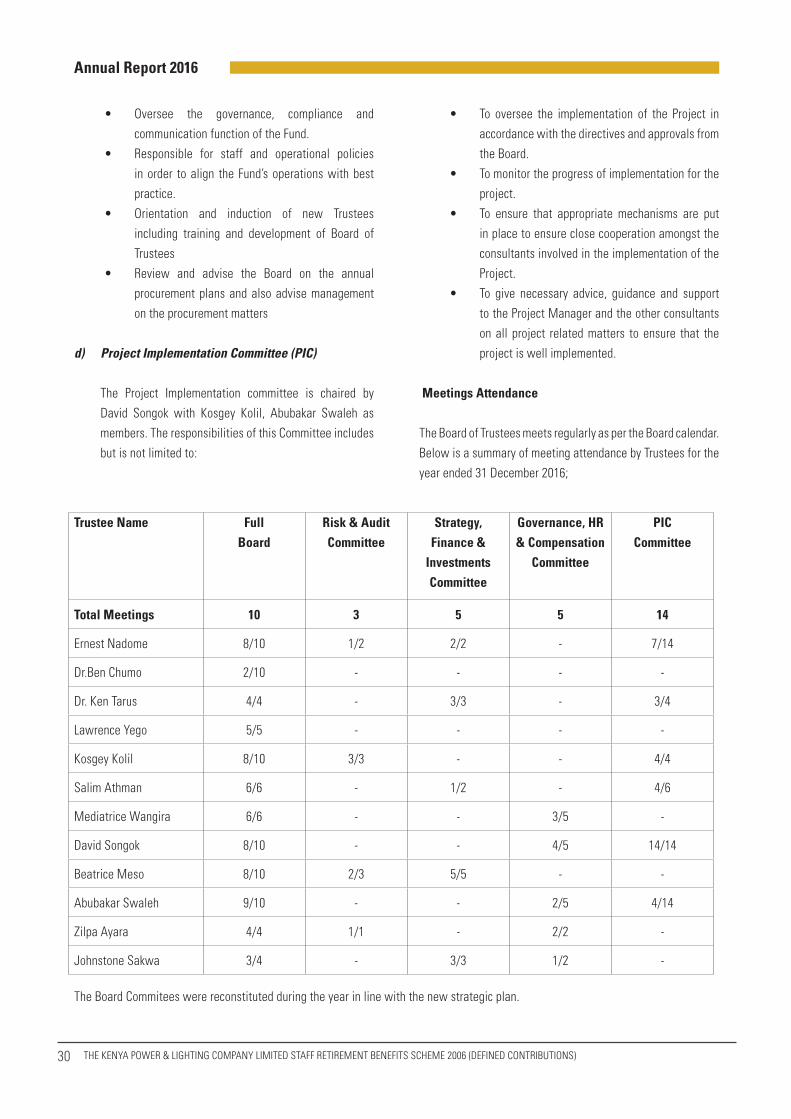

Meetings Attendance

The Board of Trustees meets regularly as per the Board calendar. Below is a summary of meeting attendance by Trustees for the year ended 31 December 2016;