preparing financial statements

TRANSCRIPT

INSTITUTE OF DISTANCE LEARNINGK N U S T

EXECUTIVE MBA/MPACEMBA/CEMPA 560

PREPARING FINANCIAL STATEMENTS

THE FINANCIAL ORGANISATION AND DIRECTION OF BUSINESS

INTRODUCTION: Any organized group or business, regardless of its size has certain resources and obligations which are influenced by a number of business transactions undertaken by it for the accomplishment of its objectives. It is not possible for a person or a group of persons to remember the occurrence of these events and their impact on business.

CON’T OF THE FINANCIAL ORGANISATION AND DIRECTION OF BUSINESS

• Therefore these transactions are recorded in certain books known as books of accounts. Not only this, they are also analysed, interpreted and communicated to the interested parties who use the information as basis for their decision. The person responsible for these processes is called ‘accountant’ and the system incorporating these processes is known as ‘accounting’

CON’T OF THE FINANCIAL ORGANISATION AND DIRECTION OF BUSINESS

• Many business decisions were taken without reference to any data. Most firms were closed down because of poor methods of recording data. With the introduction of book-keeping, this problem to some extent has been overcome.

What is book-keeping?It is the art of recording business transactions in terms of money or money’s worth in a regular and systematic manner so that information in regard to them may be readily or quickly obtained. A person who does the work of book-keeping is called a book-keeper; that is he/she keeps the books of accounts.

What is accounting?There are various ways in which accounting may be defined. Some of them are given below:

The American Institute of Accountants defined accounting in 1941 as ‘’the art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events which are, in part at least, of a financial character, and interpreting the results thereof’’.

The American Accounting Association defined accounting as ‘’the process of identifying, measuring and communicating economic information to permit informed judgments and decisions by users of the information’’

•The rather broad definition is appealing because it highlights the fact that accounting exists for a particular purpose. That purpose is to help users of accounting information to make more informed decisions.

• If accounting information is not capable of helping to make better decisions then it is a waste of time and money to produce. Sometimes, the impression is given that the purpose of accounting is simply to prepare financial reports on a regular basis. Whilst it is true that accountants undertake this kind of work, it does not represent an end in itself. The ultimate purpose of the accountants’ work is to influence the decisions of users of the information produced.

BRANCHES OF ACCOUNTING• Accounting as a discipline is constantly developing and expanding. There are several branches of accounting, the major branches of accounting are:

• Financial Accounting• Cost and Management Accounting• Tax Accounting• Auditing• Public Sector Accounting

Financial Accounting

• Financial Accounting focuses on the stewardship function of management by generating reports that explain how financial resources made available by lenders and owners have been applied for the business of the enterprise. Financial Accounting deals mainly with the recording of historical data and the preparation of reports on past events.

Cost and Management Accounting

Cost and Management Accounting focuses on providing information to management to be used for planning, control and decision making purposes. The emphasis is on making estimates about the cost and benefits of future events so as to ensure that the enterprise achieves its objectives.

Tax AccountingTax Accounting is concerned with arranging the tax issues of individuals and organizations. It involves the computation of tax obligations as well as advising on various ways of carrying on business so as to minimize the tax obligation of organizations. Tax Accountants also provide service to government institutions in charge of revenue mobilization for the state. They help in the assessment of taxes.

Auditing

This branch of accounting provides assurance to various users of financial statements that the financial statements are true and fair and that users can reasonably rely on the statements for planning, control and decision making purposes.

Public Sector Accounting

Public Sector Accounting is the branch of accounting that concentrates on public sector organizations such as central government, local government, non-governmental organizations etc. It encompasses financial accounting, cost and management practices in public sector organizations.

USERS OF ACCOUNTING INFORMATION AND THEIR INFORMATION NEEDS

For accounting information to be useful, the accountant must be clear about for whom the information is being prepared and for what purpose the information will be used. There are likely to be various user groups with interest in a particular organization.

MAIN USERS OF FINANCIAL INFORMATION RELATING TO A BUSINESS

o The Loan-Creditor GroupInterested in credit worthiness of the business and long term solvency

o The Employees GroupInterested in profitability, stability and vulnerability of the business since their livelihood is tied to the success of the business

o The GovernmentInterested for tax purposes, safeguarding the interest of both lenders and investors

MAIN USERS OF FINANCIAL INFORMATION RELATING TO A BUSINESS CONT.

o The Analyst Advisory GroupIncludes financial Analysts, journalists, credit-rating agencies &other groups of advisory services.

Interested in general financial performance of business and future prospects for use by media, investors, competitors , etc.

o The Business-Contact GroupIncludes customers, trade creditors and suppliers and competitors etc.

QUALITIES OF GOOD ACCOUNTING INFORMATIONA.Relevance Accounting information must have the ability to influence decisions. Unless this characteristic is present, there really is not any point producing the information. The information may be relevant to the prediction of future events or relevant in helping confirm past events. Relevant implies the following:

TimelinessCompletenessAppropriateness and suitability to user objective

B. Reliability Accounting information is reliable if it

is free from material errors or bias, it is complete and faithfully represents what it purports to represent. Reliability implies reasonable accuracy.

C. Comparability Accounting information should permit

meaningful comparison between one period and another as well as between one company and another. Comparability requires that items which are basically the same should be treated in the same manner for measurement and presentation purposes.

D. UnderstandabilityAccounting reports should be expressed as clearly as possible and should be understood by those for whom the information is aimed. In other words, information must be understandable before it can be useful.

CONSTRAINTS/PROBLEMS ON RELEVANT AND RELIABLE INFORMATION

In theory, financial information should be produced only if the cost of providing that piece of information is less than the benefit, or value, to be derived from its use. Some of the constraints are indicated below.

TimelinessBalance between benefit and cost(cost/benefit analysis)

ACCOUNTING CONCEPTS AND ASSUMPTIONSFundamental accounting concepts are the assumptions that underline the preparation of financial statements. These are usually not stated because their acceptance and use is assumed. If these are not followed, this fact and reasons for not following them must be given.

1 GOING CONCERN CONCEPT: This assumption implies that the business or entity will continue in operational existence for the foreseeable future. This means in particular that the income statement and the statement of financial position assume no intention or necessity to liquidate or curtail significantly the scale of operation. In line with this concept accounts are prepared in short; but regular intervals of equal lengths such as yearly intervals.

•2. THE BUSINESS ENTITY CONCEPT: This concept considers the business enterprise as a separate entity distinguishable from the owners and from all other enterprises. The items recorded in the books of the business are, therefore, restricted to the transactions of the business.

•The only attempt to show how the transactions affect the owner(s) of the business is when they introduce new capital into the business or take drawings out of it. The total drawings figure at the end of the given period will reduce the proprietor’s capital contribution.

ACCOUNTING CONCEPTS AND ASSUMPTIONS CONT.

3. THE HISTORICAL COST CONCEPT: This principle states that assets and other items e.g. expenses incurred are to be shown in the books at the prices they are bought (historic cost).

4 THE MONEY MEASUREMENT CONCEPT: This concept states that accounting statements must be quantified in terms of a monetary unit. This means that transactions are recorded in money terms. It therefore means that expenses, assets, liabilities, revenues, the values of which can be measured in monetary terms with a fair degree of objectivity are recorded in the accounts.

• Note that accounting does not record that the firm has a good or bad management team. It does not show that the poor morale prevalent among the staff is about to lead to a serious strike etc.

• 5. DOUBLE ENTRY PRINCIPLE OR DUAL ASPECT CONCEPT: The principle or concept states that every transaction affects the business in two ways and therefore needs to be recorded in two accounts. That is the receiving account and giving account. The receiving account is debited with the value of benefit received, while the giving account is credited with the same value of benefit given at the same time.

• In other words, the concept states that for every debit entry there is a corresponding credit entry and vice versa. This is the alternate form of the accounting equation:

ASSETS=CAPITAL + LIABILITIES

ACCOUNTING CONCEPTS AND ASSUMPTIONS CONT.6 ACCRUAL OR THE MATCHING CONCEPT: The principle or concept states that in order to measure profit, the revenue for the period must be matched with the cost incurred in order to earn that revenue. This is to say that expenses, the benefits which have been used up in a given accounting year should be reported in the accounts of the period whether or not those expenses have been paid for. Also money paid in respect of expenses the benefits of which have not yet been used, should not be included in the accounts as expenses because the expenses do not relate to the given period.

7 CONSISTENCY PRINCIPLE: It is the requirement that the same interpretation of accounting principle is applied from year to year within the same firm. When a firm has once fixed a method of the accounting treatment of an item, it will enter all similar items that follow in exactly the same way e.g. stock valuation and method of providing for depreciation. This does not mean changes should not be made in methods or procedures, if there is sufficient reason to change from one method to another. However, there should not be habitual and frequent changes.

8. PRUDENCE/CONSERVATISM CONCEPT: ‘Anticipate no profit, provide for all possible losses’. This principle states that accountant will tend to understate rather than overstate profit. Where alternative treatments are available, the treatment that produces the less favourable result should be preferred. Prudence however does not justify the creation of secret or hidden reserves.

INTRODUCTION TO DOUBLE ENTRY

THE ACCOUNTING EQUATIONThe whole of financial accounting is based on a very simple idea. This is called the accounting equation.

RESOURCES IN THE BUSINESS=RESOURCES SUPPLIED BY THE OWNER

This implies that the resources supplied by the owner to set up a firm are all the resources the business has.

In accounting the amount of resources supplied by the owner is called CAPITAL.The actual resources that are then in the business are called ASSETS.Therefore the accounting equation can be related as

CAPITAL=ASSETSUsually, however, people other than the owner e.g. Banks, lenders etc. have supplied some of the assets. Liabilities are the name given to the amount owing to the people for these assets. The equation has now changed to:

ASSETS = CAPITAL + LIABILITIESIt can be seen that the two sides of the equation will have the same total. This is because we are dealing with same thing from two viewpoints. It is

Resources: which are (Assets) = Resources: who supply them (Capital + Liabilities)

It is fact that the totals of each side will always equal one another, and that this will always be true no matter the number of transactions there may be. The actual assets, Capital and liabilities may change, but the total of the assets will always equal the total of the capital + liabilities.

THE BALANCE SHEET AND THE BALANCE SHEET EQUATION

The balance sheet attempts to show the financial position of a business at a point in time. There is currently one professional way of setting out the balance sheet.

Vertical formatThe vertical format is today the most popular form of presentation in Ghana and the International Community.

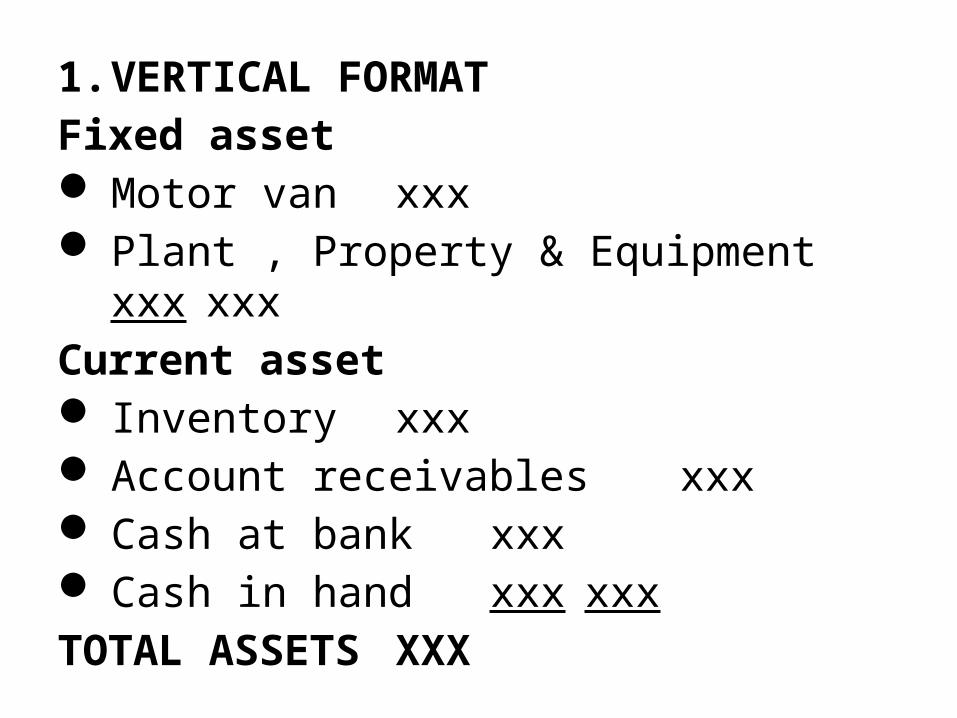

1.VERTICAL FORMATFixed asset Motor van xxx Plant , Property & Equipment

xxx xxxCurrent asset Inventory xxx Account receivables xxx Cash at bank xxx Cash in hand xxx xxxTOTAL ASSETS XXX

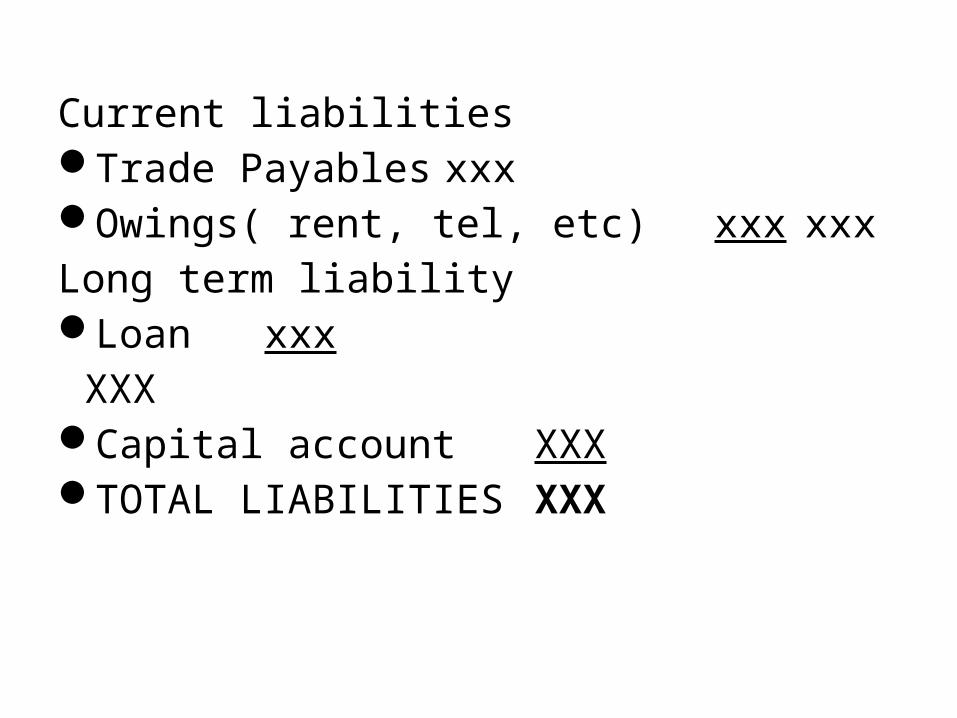

Current liabilitiesTrade Payables xxxOwings( rent, tel, etc) xxx xxxLong term liabilityLoan xxxXXX

Capital account XXXTOTAL LIABILITIES XXX

THE BALANCE SHEET AND THE EFFECTS OF BUSINESS TRANSACTIONS

a. The introduction of capitalOn 1st May, 20x1 Mr. Kwasi started business and deposited ¢10,000 into a bank account opened specially for the business.

Required: draft the balance sheet? b. Purchase of an asset by cheque.On 3rd June, 20x1 Mr. Kwasi buys a building for ¢6,000 paying by cheque. The effect of this transaction is that cash at the bank (Asset) is decreased and new asset (building) appears.

Required: draft the balance sheet?

c. Purchase of an asset and the incurring of liability.

On 6th June, 20x1 Mr. Kwasi buys some goods for ¢5,000 from Mr. Kwame and agrees to pay for them sometime within the next two months.

Required: draft the balance sheet? The effect of this transaction is that a new asset, stock of goods is acquired and a liability for the good is created.

Note: a person to whom money is owed for goods are known as trade payables (creditor) in accounting.

THE BALANCE SHEET AND THE EFFECTS OF BUSINESS TRANSACTIONS CONT.

d. Sale of an asset on creditOn 10th June, 20x1 goods which had cost ¢1,000 were sold to Mr. Cujoe for the same amount; the money is to be paid later.

The effect is reduction in the value of stock of goods and the creation of new asset called Debtors.

Required: draft the balance sheet after the transaction?

Note: a person who owes the firm or the business money is known as trade receivables (debtor) in accounting.

e. sale of asset for immediate payment.

On 20th July, 20x1 goods which had cost ¢500 were sold to Mr. Prosper for the same amount and Mr. Prosper paid for them immediately by cheque.

Required: draft the balance sheet.

f. The payment of liability.On July 25th, 20x1 Mr. Ben pays a cheque of ¢2,000 to Mr. Manso is part payment of the amount owing.

Required: draft the balance sheet

g. Collection of assetMr. Tom who owes Mr. Ben ¢1,000 made a part payment of ¢500 on 29th July 20x1.

Required: draft the balance sheet.

• Quiz.Dr. Commando started a business on 31st December 20x1. Before he actually starts to sell anything, he has bought fixtures ¢200,000 Motor vehicle ¢500,000 and stock of goods ¢350,000. Although he has paid in full for the fixtures and the motor vehicle, he still owes ¢140,000 for some of the goods. Mr. John had lent him ¢300,000. Dr. Commando, after the above he has ¢280,000 in the business bank account and ¢100,000 cash in hand.You are required to calculate his capital and draft his balance sheet.

THE DOUBLE ENTRY SYSTEMWe have seen in our previous studies that every transaction affects two items. For example if a business purchase stock with ¢200,000 and issue cheque, the transaction affects stock of goods ie. Stocks increase by ¢200,000 and cash at bank decrease by ¢200,000. In this case for each transaction bookkeeping entry will have to be made to show an increase in stock and decrease in cash at bank. This is double entry system.

• Double entry system of bookkeeping is good because drawing up balance sheet after every transaction will not give enough information about the business. It does not for instance; tell who the debtors are and how each one of them owes. Let’s recall the double entry rules

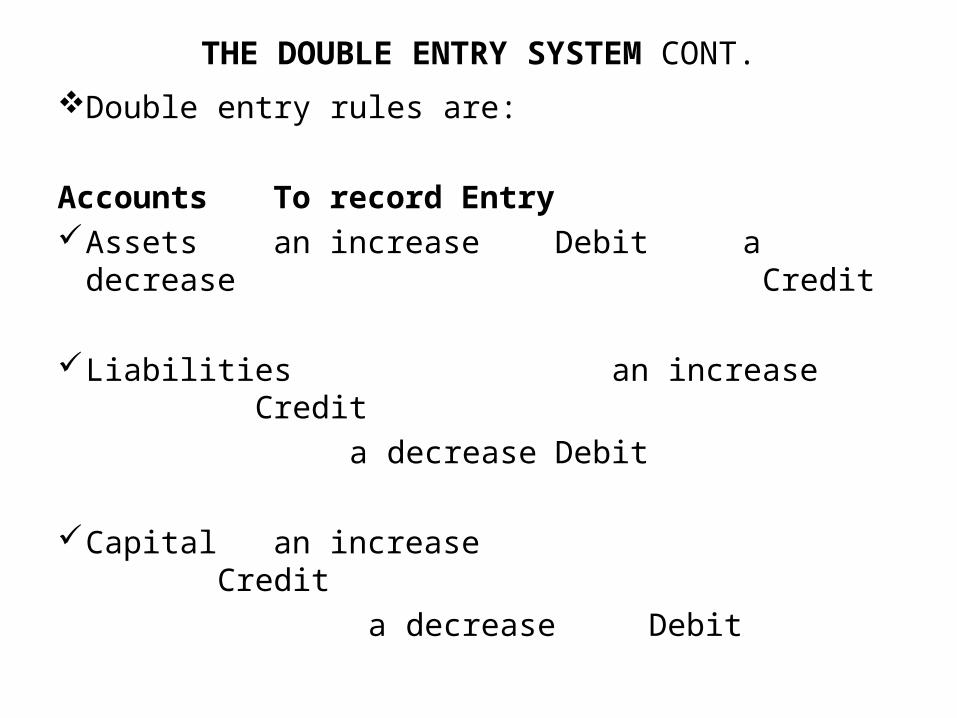

THE DOUBLE ENTRY SYSTEM CONT.Double entry rules are:

Accounts To record Entry Assets an increase Debit a decrease Credit

Liabilities an increase Credit a decrease Debit

Capital an increase Credit a decrease Debit

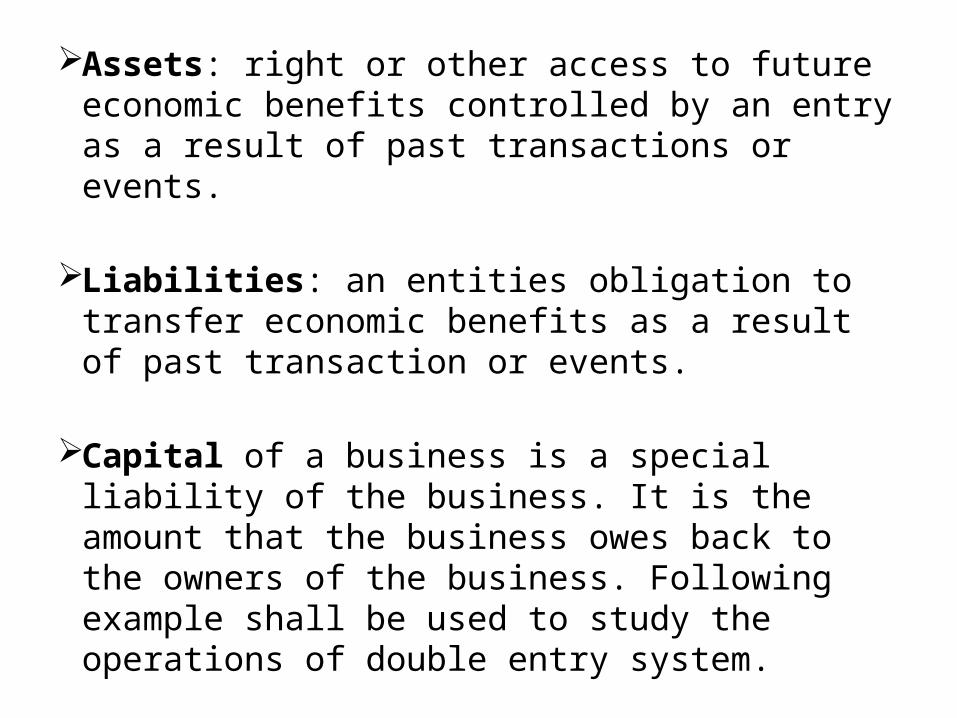

Assets: right or other access to future economic benefits controlled by an entry as a result of past transactions or events.

Liabilities: an entities obligation to transfer economic benefits as a result of past transaction or events.

Capital of a business is a special liability of the business. It is the amount that the business owes back to the owners of the business. Following example shall be used to study the operations of double entry system.

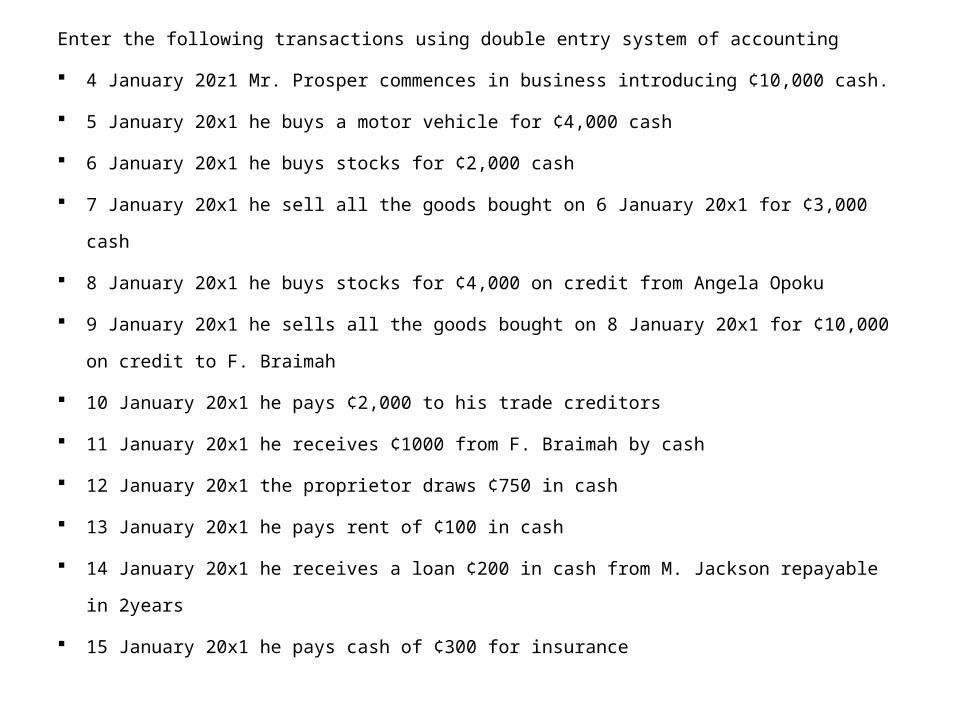

Enter the following transactions using double entry system of accounting

4 January 20z1 Mr. Prosper commences in business introducing ¢10,000 cash.

5 January 20x1 he buys a motor vehicle for ¢4,000 cash

6 January 20x1 he buys stocks for ¢2,000 cash

7 January 20x1 he sell all the goods bought on 6 January 20x1 for ¢3,000

cash

8 January 20x1 he buys stocks for ¢4,000 on credit from Angela Opoku

9 January 20x1 he sells all the goods bought on 8 January 20x1 for ¢10,000

on credit to F. Braimah

10 January 20x1 he pays ¢2,000 to his trade creditors

11 January 20x1 he receives ¢1000 from F. Braimah by cash

12 January 20x1 the proprietor draws ¢750 in cash

13 January 20x1 he pays rent of ¢100 in cash

14 January 20x1 he receives a loan ¢200 in cash from M. Jackson repayable

in 2years

15 January 20x1 he pays cash of ¢300 for insurance

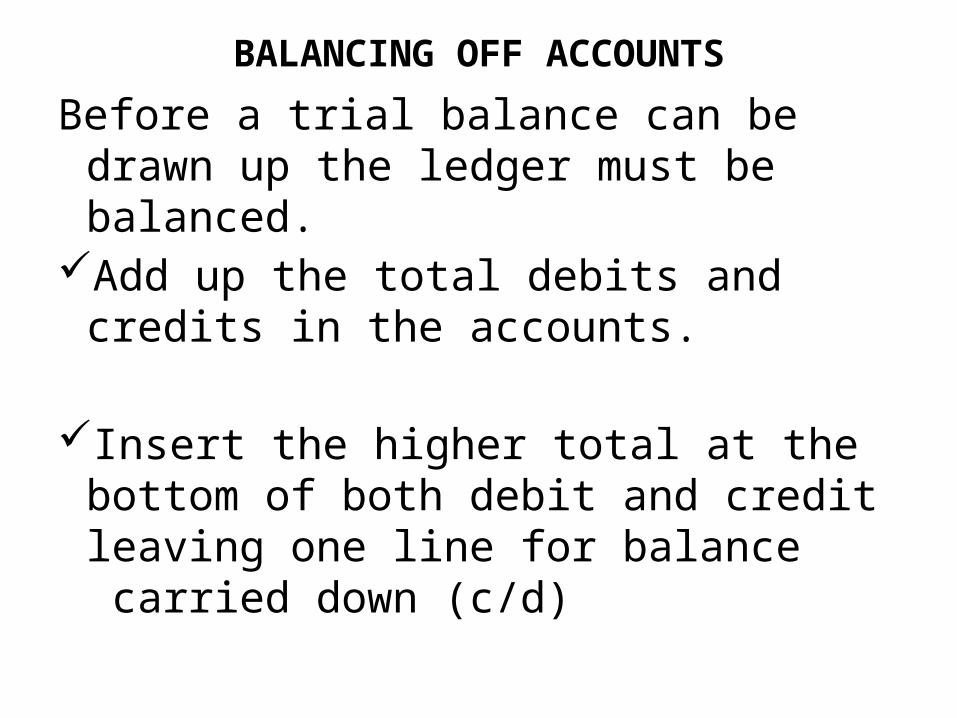

BALANCING OFF ACCOUNTSBefore a trial balance can be drawn up the ledger must be balanced.

Add up the total debits and credits in the accounts.

Insert the higher total at the bottom of both debit and credit leaving one line for balance carried down (c/d)

Insert on the side, which has the lower arithmetical total ,the narrative balance, carried down(c/d)

The same is shown on the other side of the ledger account but underneath the total this is the balance brought down (b/d).

Note: Balance carried down (c/d) is known as closing balance, the balance brought down (b/d) is open balance

THE NATURE AND PURPOSE OF TRIAL BALANCE

• A trial balance is simply a memorandum list of all the ledger account balances. A large number of transactions are recorded in ledger accounts; it means that there is a possibility of errors occurring. Assurance is given by extracting trial balance periodically.

DRAWING UP THE TRIAL BALANCEThis is done by listing each of the ledger account names in the business book showing against each name the balance on that account and whether that balance is a debit balance or a credit balance brought down (b/d). This implies that it is the (b/d) account that determines whether the account is said to have a debit or a credit balance. The debit and the credit totals of the trial balance are equal and opposite credit entry.

DAY BOOKS/BOOKS OF PRIME ENTRY/JOURNALS

These are the books into which financial transactions are first recorded before posted to the ledger. Postings into the books of original entries are usually made from source documents which are often filed in a systematic manner by the entity.

For purposes of convenience, different books have been devised to record different types of business transactions.

The books of original entry are sometimes called the books of prime entry, the day books or the subsidiary journals. The following books constitute the books of original entry:

1.Purchases Day Book/JOURNAL: to record purchases of merchandise on credit

2. Purchases Returns Day Book: to record returns of goods to supplier or grant of allowances by the supplier due to defects or some other reasons. The source document for making entries into the purchases returns day book is either the debit note issued by the business to its credit suppliers or the credit note issued by the supplier to the business.

DAY BOOKS/BOOKS OF PRIME ENTRY/JOURNALS CONT.

3.Sales Day Book/JOURNAL: to record sales of merchandise on credit.

4.Sales Returns Day Book / JOURNAL: to record the return of goods by customers due to defects or other reason. The source document used for recording into the sales returns day book is the credit note issued by the business to the customer or the debit note issued by the a customer to the business.

5.Cash Book CASH/ JOURNAL to record transactions relating to receipts and payments of cash. It serves a dual purpose- as a book of prime entry for all cash transactions as well as the ledger account for the cash and bank account Types of cash books are the one column, the two column and the three column cash books.

Petty Cash Book: This is an extension of the cash book to cover expense items of small values. It is used to record expense items such as taxi fares, postage stamps, stationery expenses; cost of refreshments etc.The imprest system is often used to keep the petty cash book.

Journal Proper:

• In the date column, the date of the transaction is entered. The year is written at the top of the month on the left side and the particular date on the right hand side. The year and the month are not repeated except in the beginning of the new page.

JOURNAL PROPER/GENERAL JOURNAL • This book is used for all other transactions that cannot be captured by any of the books of original entry already discussed.

USES OF JOURNAL PROPER/ GENERAL

1. The recording of Opening and Closing entries

2. Correction of Errors3. Recording purchases and Sales of Fixed Assets on credits

4. Recording the issues (sales) of shares by companies, etc.

5. Writing off bad debts.

Following transactions took place within the month of June 2001

1st June BSEC sold goods worth ¢ 4,000 to SEC

2ND June ¢ 7650 to the Principal’s wife

5th June ¢ 2000 to Cujoe.Require Prepare a sale journal for the above transaction

Example of purchases JournalMr. Cudjoe following purchases in the year 2001.

1st May he purchases Sugar from Madam Mech for ¢3,000

4th June he purchases Gari from Kussi for ¢10,000

7th July he purchases Milk from Miss Degree one for ¢12,000

Required Prepare purchases journal for Mr. Cujoe

CONT.Take note of the following terms and their accounting treatment.

1. Sales Return: goods return by the customer because they might be unsatisfactory Accounting issues:

2. Cash discount allowed: is the discount given to the customer if he pays by a certain date.For example if Mr. Cudjoe is entitled to 10% discount in ¢100,000 worth of sales for prompt payment and he pays early.

Accounting treatment

3. Cash discount received: is a discount received from suppliers if business made payment by certain date. Example if a firm is entitled to 10% discount on ¢100,000 worth of sales for prompt payment and he pays early.

Accounting treatment

4. Purchases return: are goods return to a supplier because they are unsatisfactory. For example if Mr. Prosper purchased ¢200,000 worth of goods and return ¢100,000 worth of goods that are faulty.

Accounting treatment:

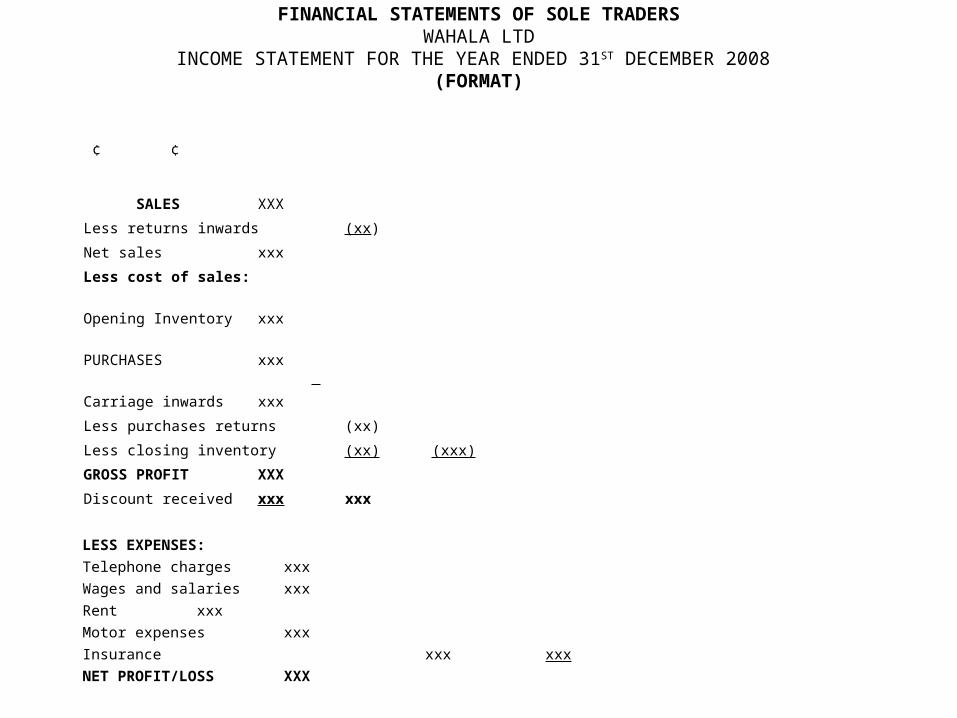

FINANCIAL STATEMENTS OF SOLE TRADERSWAHALA LTD

INCOME STATEMENT FOR THE YEAR ENDED 31ST DECEMBER 2008 (FORMAT)

¢ ¢

SALES XXX Less returns inwards (xx)

Net sales xxxLess cost of sales: Opening Inventory xxx PURCHASES xxx Carriage inwards xxxLess purchases returns (xx)Less closing inventory (xx) (xxx)GROSS PROFIT XXXDiscount received xxx xxx

LESS EXPENSES:Telephone charges xxxWages and salaries xxxRent xxxMotor expenses xxxInsurance xxx xxxNET PROFIT/LOSS XXX

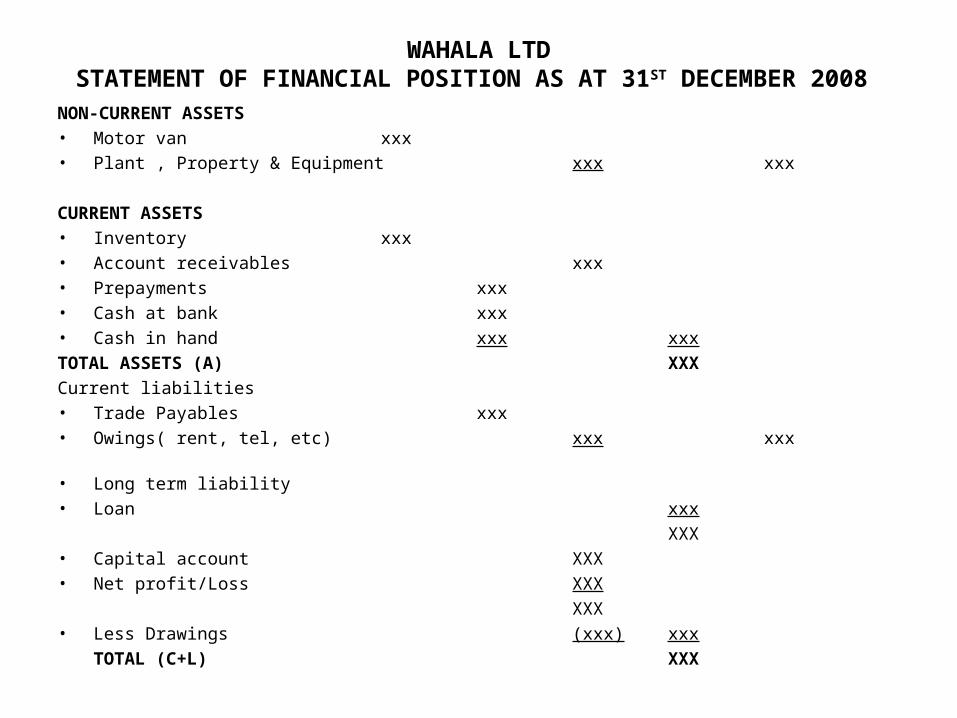

WAHALA LTDSTATEMENT OF FINANCIAL POSITION AS AT 31ST DECEMBER 2008

NON-CURRENT ASSETS• Motor van xxx• Plant , Property & Equipment xxx xxx

CURRENT ASSETS• Inventory xxx• Account receivables xxx• Prepayments xxx• Cash at bank xxx• Cash in hand xxx xxxTOTAL ASSETS (A) XXXCurrent liabilities• Trade Payables xxx• Owings( rent, tel, etc) xxx xxx

• Long term liability• Loan xxx

XXX• Capital account XXX• Net profit/Loss XXX

XXX• Less Drawings (xxx) xxx

TOTAL (C+L) XXX

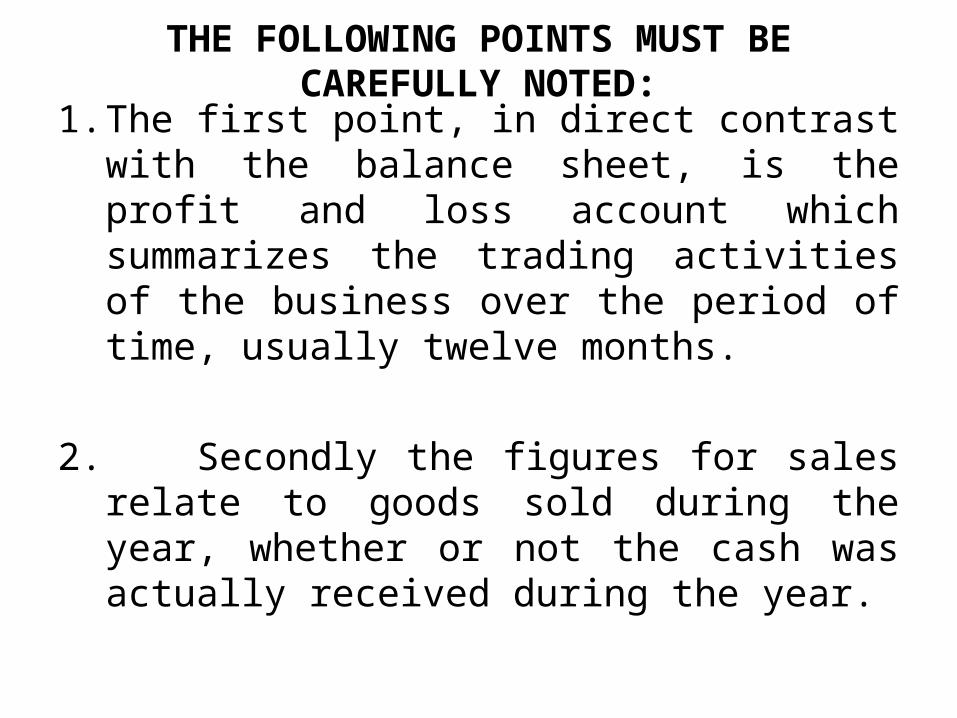

THE FOLLOWING POINTS MUST BE CAREFULLY NOTED:

1.The first point, in direct contrast with the balance sheet, is the profit and loss account which summarizes the trading activities of the business over the period of time, usually twelve months.

2. Secondly the figures for sales relate to goods sold during the year, whether or not the cash was actually received during the year.

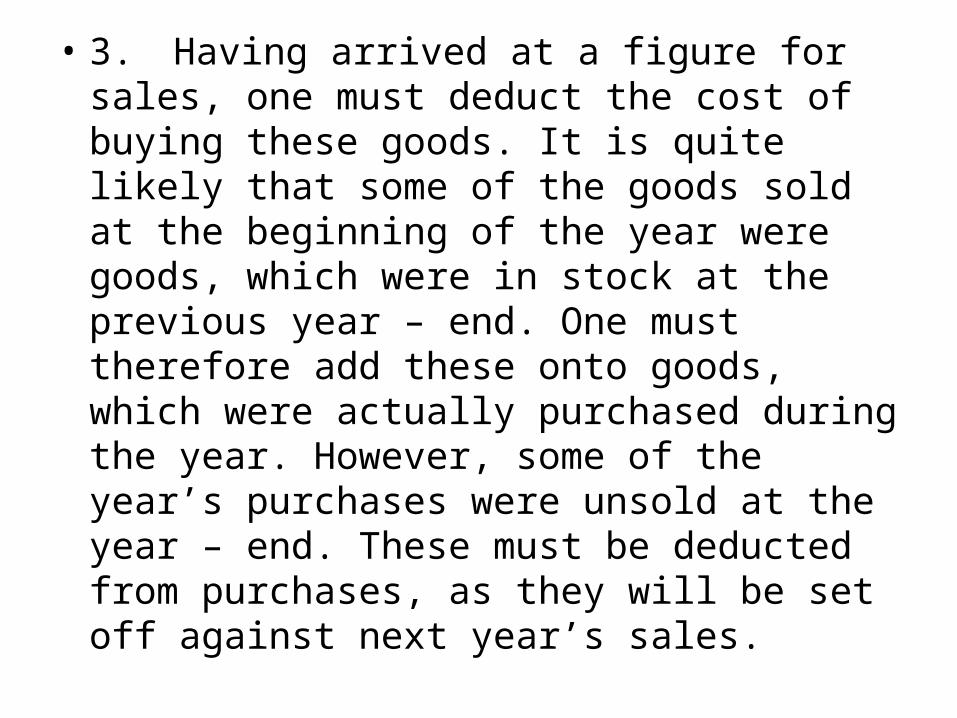

• 3. Having arrived at a figure for sales, one must deduct the cost of buying these goods. It is quite likely that some of the goods sold at the beginning of the year were goods, which were in stock at the previous year – end. One must therefore add these onto goods, which were actually purchased during the year. However, some of the year’s purchases were unsold at the year – end. These must be deducted from purchases, as they will be set off against next year’s sales.

4. Sales less cost of sales gives gross profit.Deducting expenses from the gross profit arrives at net profit. For convenience the profit and loss is divided into two parts. The parts dealing with sales and cost of sales may be referred to as the trading account, the remaining as the profit and loss account.

5. One must be very careful to distinguish between wages and drawings. Wages relate to payment to third parties (employees) and represent a deduction or charge in arriving at the net profit. Amount paid to the proprietor (even if he calls them salary) must be treated as drawings.

It would be wrong to treat drawings as a business expense as the amount drawn is not used to further a sale. They represent an appropriation of profit earned by the business and are eventually deducted from the proprietor’s capital account.

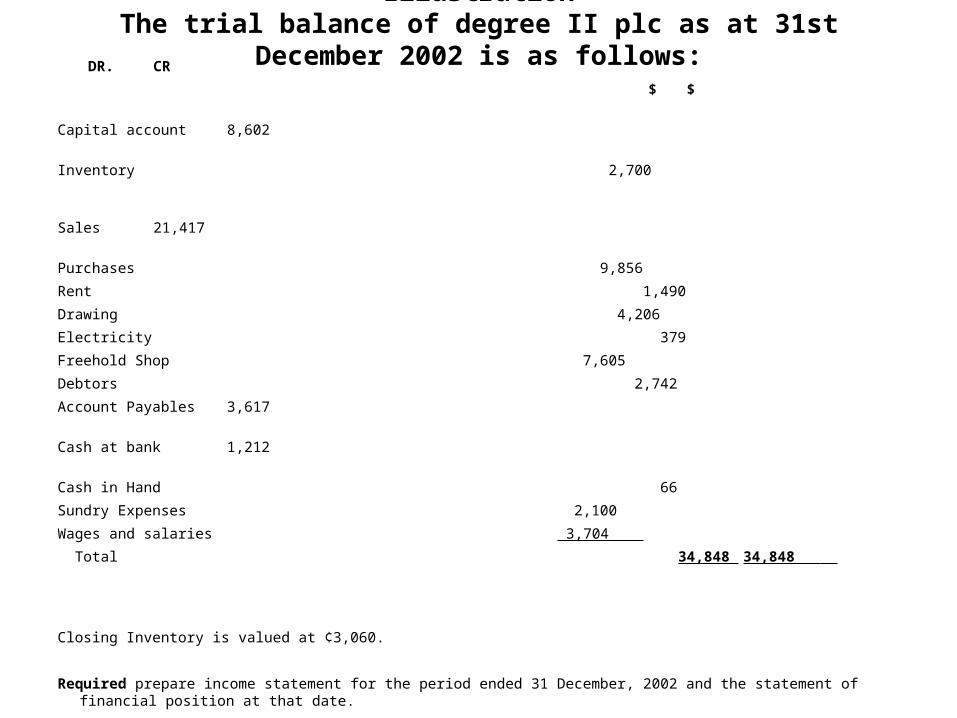

IllustrationThe trial balance of degree II plc as at 31st

December 2002 is as follows: DR. CR $ $

Capital account 8,602

Inventory 2,700

Sales 21,417

Purchases 9,856Rent 1,490Drawing 4,206Electricity 379Freehold Shop 7,605Debtors 2,742Account Payables 3,617

Cash at bank 1,212

Cash in Hand 66 Sundry Expenses 2,100 Wages and salaries 3,704 Total 34,848 34,848

Closing Inventory is valued at ¢3,060.

Required prepare income statement for the period ended 31 December, 2002 and the statement of financial position at that date.