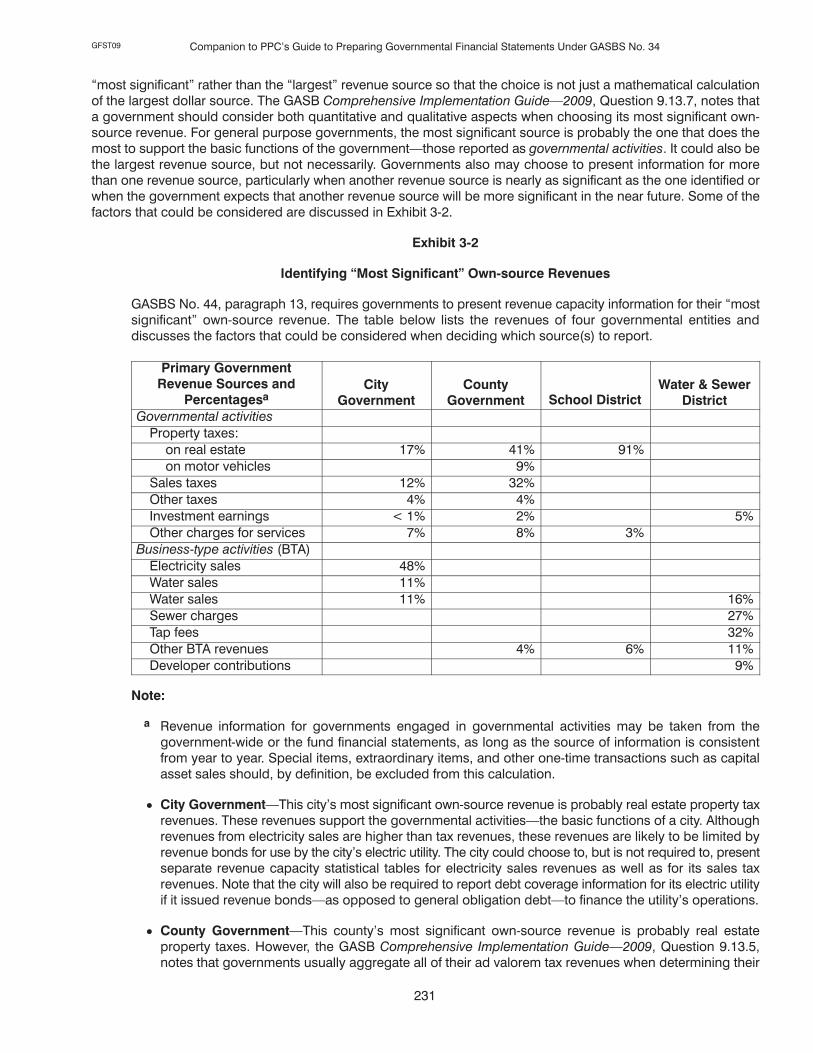

preparing governmental financial statements under gasbs

TRANSCRIPT

GFST09

SELF�STUDY CONTINUING PROFESSIONAL EDUCATION

Companion to PPC's Guide to

PreparingGovernmental

FinancialStatements

Under GASBSNo. 34

Fort Worth, Texas(800) 323�8724trainingcpe.thomson.com

GFST09

ii

Copyright 2009 Thomson Reuters/PPCAll Rights Reserved

This material, or parts thereof, may not be reproduced in another document or manuscript

in any form without the permission of the publisher.

This publication is designed to provide accurate and authoritative information in regard to the subjectmatter covered. It is sold with the understanding that the publisher is not engaged in rendering legal,accounting, or other professional service. If legal advice or other expert assistance is required, theservices of a competent professional person should be sought.From a Declaration of Principles

jointly adopted by a Committee of the American Bar Association and a Committee of Publishers and

Associations.

The following are registered trademarks filed with the United States Patent and Trademark Office:

Checkpoint Tools�PPC's Practice Aids�

PPC's Workpapers�

PPC's Engagement Letter Generator�

PPC's Interactive Disclosure Libraries�

PPC's SMART Practice Aids�

Practitioners Publishing Company is registered with the NationalAssociation of State Boards of Accountancy (NASBA) as a sponsor ofcontinuing professional education on the National Registry of CPESponsors. State boards of accountancy have final authority on theacceptance of individual courses for CPE credit. Complaints regardingregistered sponsors may be addressed to the National Registry of CPESponsors, 150 Fourth Avenue North, Suite 700, Nashville, TN37219�2417. Website: www.nasba.org.

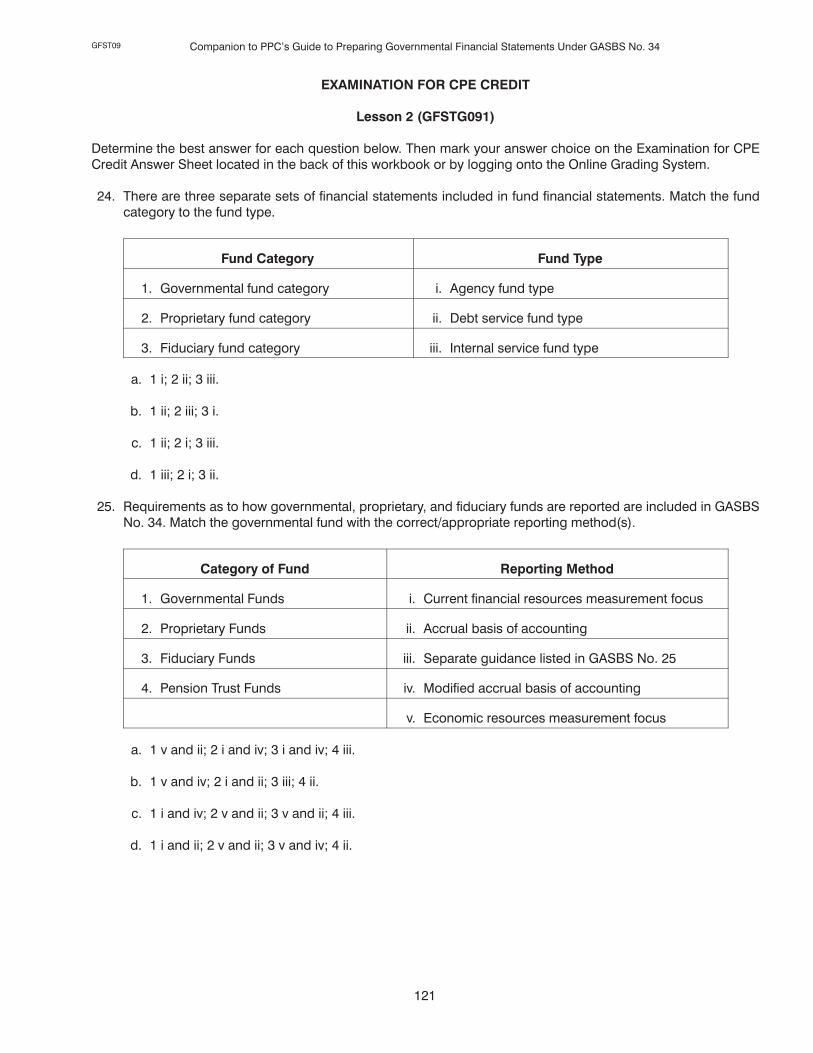

Practitioners Publishing Company is registered with the NationalAssociation of State Boards of Accountancy (NASBA) as a QualityAssurance Service (QAS) sponsor of continuing professionaleducation. State boards of accountancy have final authority onacceptance of individual courses for CPE credit. Complaints regardingQAS program sponsors may be addressed to NASBA, 150 FourthAvenue North, Suite 700, Nashville, TN 37219�2417. Website:www.nasba.org.

Registration Numbers

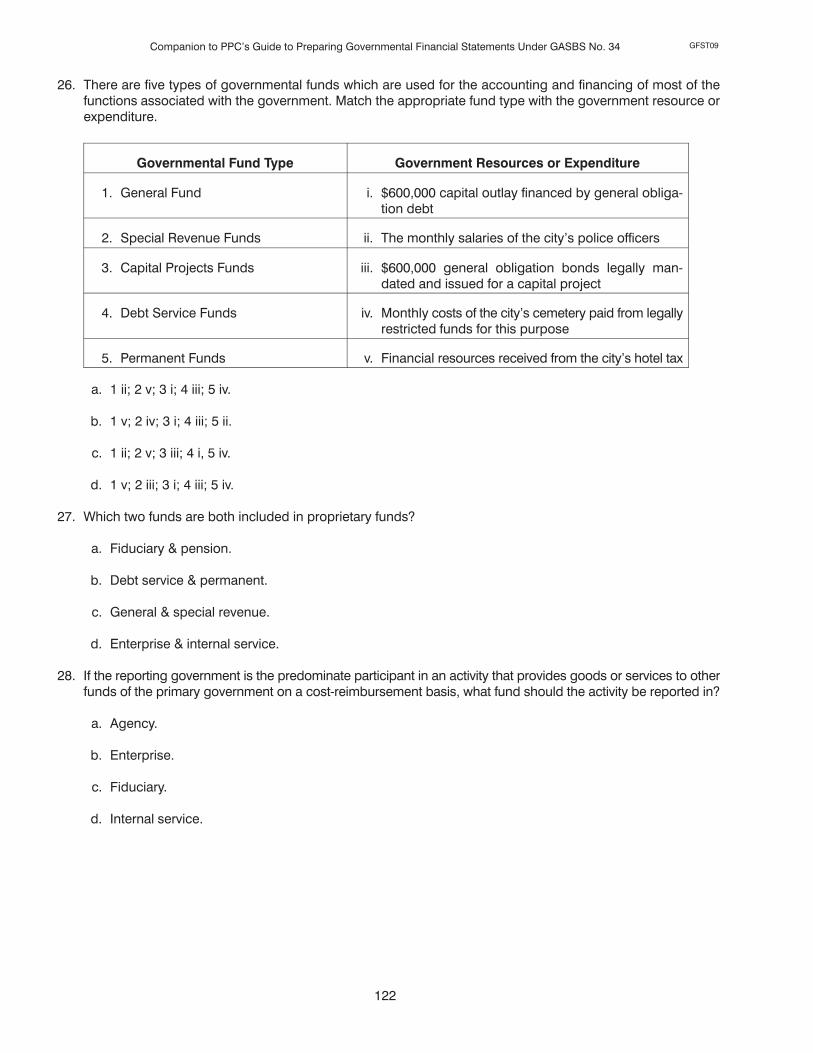

Texas 001615

New York 001076

NASBA Registry 103166

NASBA QAS 006

GFST09

iii

Interactive Self�study CPE

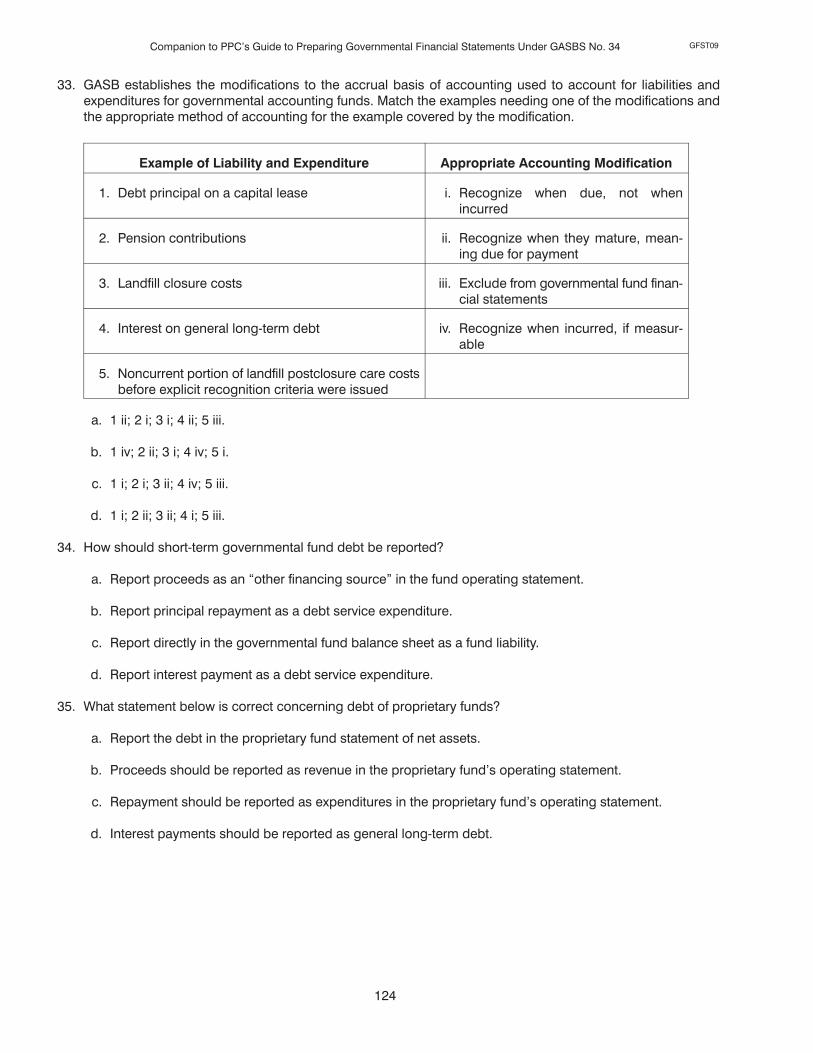

Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

TABLE OF CONTENTS

Page

COURSE 1: Introduction to Governmental Financial Reports and Fund Accounting Overview

Overview 1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Lesson 1: Introduction to Governmental Financial Reports 3. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

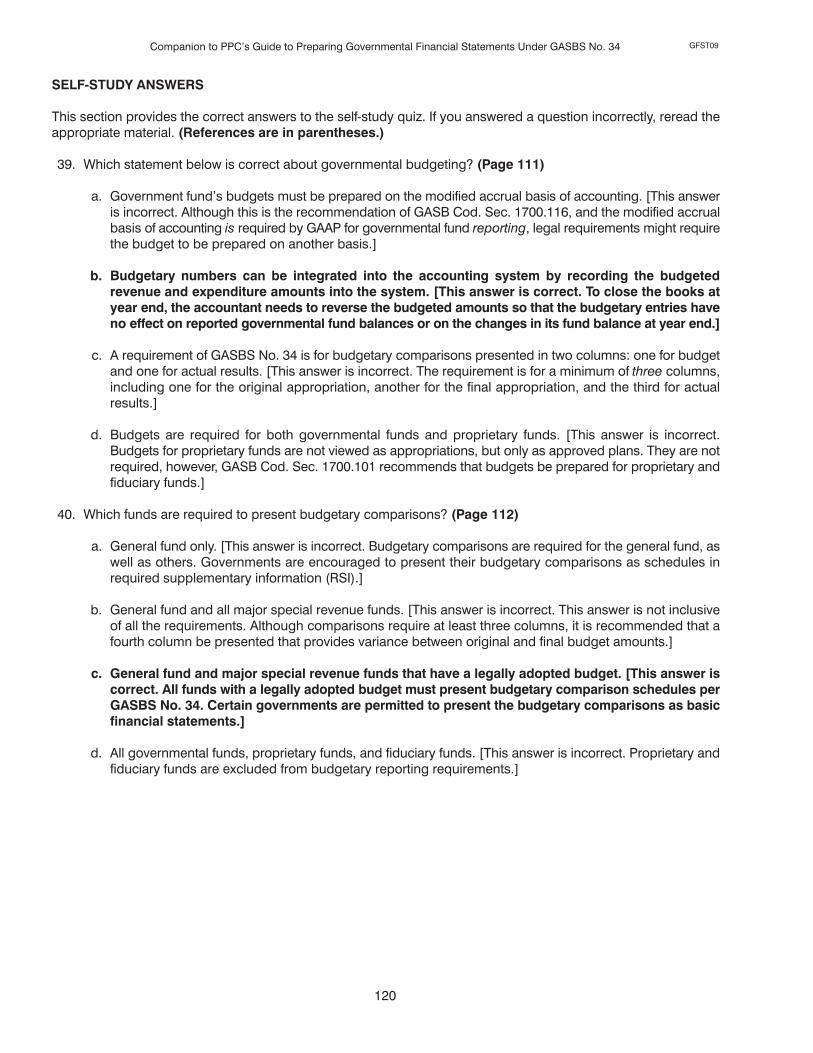

Lesson 2: Fund Accounting Overview 69. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Glossary 127. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Index 131. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

COURSE 2: Budgetary Reporting, Other RSI, MD&A, and CAFR

Overview 133. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Lesson 1: Budgetary Reporting and Other Required Supplementary Information (RSI) 135. . . . . . .

Lesson 2: Management's Discussion and Analysis (MD&A) 161. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Lesson 3: Comprehensive Annual Financial Reports (CAFR) 211. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Glossary 249. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Index 253. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

COURSE 3: Capital Assets

Overview 255. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Lesson 1: The Basics of Capital Assets, Including Valuation, Reporting, and Capitalization 257. . . .

Lesson 2: Capital Assets, Infrastructure, and Impairment 321. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Glossary 387. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Index 391. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

GFST09

iv

To enhance your learning experience, the examination questions are located throughoutthe course reading materials. Please look for the exam questions following each lesson.

EXAMINATION INSTRUCTIONS, ANSWER SHEETS, AND EVALUATIONS

Course 1: Testing Instructions for Examination for CPE Credit 393. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Course 1: Examination for CPE Credit Answer Sheet 395. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Course 1: Self�study Course Evaluation 396. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Course 2: Testing Instructions for Examination for CPE Credit 397. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Course 2: Examination for CPE Credit Answer Sheet 399. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Course 2: Self�study Course Evaluation 400. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Course 3: Testing Instructions for Examination for CPE Credit 401. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Course 3: Examination for CPE Credit Answer Sheet 403. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Course 3: Self�study Course Evaluation 404. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

GFST09

v

INTRODUCTION

Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34 consists of threeinteractive self�study CPE courses. These are companion courses to PPC's Guide to Preparing Governmental

Financial Statements Under GASBS No. 34 designed by our editors to enhance your understanding of the latestissues in the field. To obtain credit, you must complete the learning process by logging on to our Online GradingSystem at OnlineGrading.Thomson.com or by mailing or faxing your completed Examination for CPE CreditAnswer Sheet for print grading by October 31, 2010. Complete instructions are included below and in the TestInstructions preceding the Examination for CPE Credit Answer Sheet.

Taking the Courses

Each course is divided into lessons. Each lesson addresses an aspect of preparing governmental financialstatements under GASBS No. 34. You are asked to read the material and, during the course, to test yourcomprehension of each of the learning objectives by answering self�study quiz questions. After completing eachquiz, you can evaluate your progress by comparing your answers to both the correct and incorrect answers and thereason for each. References are also cited so you can go back to the text where the topic is discussed in detail.Once you are satisfied that you understand the material, answer the examination questions which follow eachlesson. You may either record your answer choices on the printed Examination for CPE Credit Answer Sheet orby logging on to our Online Grading System.

Qualifying Credit HoursQAS or Registry

PPC is registered with the National Association of State Boards of Accountancy as a sponsor of continuingprofessional education on the National Registry of CPE Sponsors (Registry) and as a Quality Assurance Service(QAS) sponsor. Part of the requirements for both Registry and QAS membership include conforming to theStatement on Standards of Continuing Professional Education (CPE) Programs (the standards). The standards weredeveloped jointly by NASBA and the AICPA. As of this date, not all boards of public accountancy have adopted thestandards. Each course is designed to comply with the standards. For states adopting the standards, recognizingQAS hours or Registry hours, credit hours are measured in 50�minute contact hours. Some states, however, require100�minute contact hours for self study. Your state licensing board has final authority on accepting Registry hours,QAS hours, or hours under the standards. Check with the state board of accountancy in the state in which you arelicensed to determine if they participate in the QAS program or have adopted the standards and allow QAS CPEcredit hours. Alternatively, you may visit the NASBA website at www.nasba.org for a listing of states that acceptQAS hours or have adopted the standards. Credit hours for CPE courses vary in length. Credit hours for eachcourse are listed on the �Overview" page before each course.

CPE requirements are established by each state. You should check with your state board of accountancy todetermine the acceptability of this course. We have been informed by the North Carolina State Board of CertifiedPublic Accountant Examiners and the Mississippi State Board of Public Accountancy that they will not allow creditfor courses included in books or periodicals.

Obtaining CPE Credit

Online Grading. Log onto our Online Grading Center at OnlineGrading.Thomson.com to receive instant CPEcredit. Click the purchase link and a list of exams will appear. You may search for the exam using wildcards.Payment for the exam is accepted over a secure site using your credit card. For further instructions regarding theOnline Grading Center, please refer to the Test Instructions preceding the Examination for CPE Credit AnswerSheet. A certificate documenting the CPE credits will be issued for each examination score of 70% or higher.

Print Grading. You can receive CPE credit by mailing or faxing your completed Examination for CPE Credit AnswerSheet to the Tax & Accounting business of Thomson Reuters for grading. Answer sheets are located at the end ofall course materials. Answer sheets may be printed from electronic products. The answer sheet is identified with thecourse acronym. Please ensure you use the correct answer sheet for each course. Payment of $79 (by check orcredit card) must accompany each answer sheet submitted. We cannot process answer sheets that do not includepayment. Please take a few minutes to complete the Course Evaluation so that we can provide you with the bestpossible CPE.

GFST09

vi

You may fax your completed Examination for CPE Credit Answer Sheet to the Tax & Accounting business ofThomson Reuters at (817) 252�4021, along with your credit card information.

If more than one person wants to complete this self�study course, each person should complete a separateExamination for CPE Credit Answer Sheet. Payment of $79 must accompany each answer sheet submitted. Wewould also appreciate a separate Course Evaluation from each person who completes an examination.

Express Grading. An express grading service is available for an additional $24.95 per examination. Courseresults will be faxed to you by 5 p.m. CST of the business day following receipt of your Examination for CPE CreditAnswer Sheet. Expedited grading requests will be accepted by fax only if accompanied with credit cardinformation. Please fax express grading to the Tax & Accounting business of Thomson Reuters at (817) 252�4021.

Retaining CPE Records

For all scores of 70% or higher, you will receive a Certificate of Completion. You should retain it and a copy of thesematerials for at least five years.

PPC In�House Training

A number of in�house training classes are available that provide up to eight hours of CPE credit. Please call ourSales Department at (800) 323�8724 for more information.

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

1

COMPANION TO PPC'S GUIDE TOPREPARING GOVERNMENTAL FINANCIAL STATEMENTS UNDER GASBS NO. 34

COURSE 1

INTRODUCTION TO GOVERNMENTAL FINANCIAL REPORTSAND FUND ACCOUNTING OVERVIEW (GFSTG091)

OVERVIEW

COURSE DESCRIPTION: This interactive self�study course provides an introduction and overview ofgovernmental accounting and fund accounting, including budgetary reporting. Thegeneral requirements of GASBS No. 34 is introduced and discussed. This coursecovers all three categories of funds as well as how to account under each fund forthe sources and uses of financial resources as well as capital assets, long�termliabilities and fund balances, net assets and fund equity.

PUBLICATION/REVISIONDATE:

October 2009

RECOMMENDED FOR: Users of PPC's Guide to Preparing Governmental Financial Statements UnderGASBS No. 34

PREREQUISITE/ADVANCEPREPARATION:

Basic knowledge of governmental accounting and reporting

CPE CREDIT: 8 QAS Hours, 8 Registry Hours

Check with the state board of accountancy in the state in which you are licensed todetermine if they participate in the QAS program and allow QAS CPE credit hours.This course is based on one CPE credit for each 50 minutes of study time inaccordance with standards issued by NASBA. Note that some states require100�minute contact hours for self study. You may also visit the NASBA website atwww.nasba.org for a listing of states that accept QAS hours.

Yellow Book CPE Credit: This course is designed to assist auditors in meeting thecontinuing education requirements included in GAO's Government AuditingStandards.

FIELD OF STUDY: Accounting (Governmental)

EXPIRATION DATE: Postmark by October 31, 2010

KNOWLEDGE LEVEL: Basic

LEARNING OBJECTIVES:

Lesson 1Introduction to Governmental Financial Reports

Completion of this lesson will enable you to:� Define governmental entity and financial reporting entity.� Describe the governmental environment.� Identify the uses and users of governmental financial reports as well as the objectives of governmental financial

reporting.� Describe the GASB project on service efforts and accomplishment reporting and establishing GAAP for state

and local governments.� Identify the requirements of GASBS No. 34.

Lesson 2Fund Accounting Overview

Completion of this lesson will enable you to:� Identify the three categories of funds and the types of funds of each category.

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

2

� Summarize the requirements of measurement focus and basis of accounting for all three types of funds.� Choose the proper accounting and reporting treatment of capital assets, debt and long�term liabilities and

interfund activity.� Define the proper terms for the difference between fund assets and liabilities for each fund category and record

the appropriate accounting entries for each fund category.� Identify the importance of governmental budgets as well as the requirements for reporting of budgetary

comparisons.

TO COMPLETE THIS LEARNING PROCESS:

Send your completed Examination for CPE Credit Answer Sheet, Course Evaluation, and payment to:

Thomson ReutersTax & AccountingR&GGFSTG091 Self�study CPE36786 Treasury CenterChicago, IL 60694�6700

See the test instructions included with the course materials for more information.

ADMINISTRATIVE POLICIES:

For information regarding refunds and complaint resolutions, dial (800) 323�8724 for Customer Service and yourquestions or concerns will be promptly addressed.

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

3

Lesson 1:�INTRODUCTION TO GOVERNMENTALFINANCIAL REPORTS

INTRODUCTION

This lesson discusses the definitions of governmental entity and the financial reporting entity. It describes thegovernment environment as well as the uses, users and objectives of the statements. The general requirementsof the GASB No. 34 reporting model is introduced and discussed to aid the preparer and auditor of governmen�tal financial statements.

LEARNING OBJECTIVES:

Completion of this lesson will enable you to:

� Define governmental entity and financial reporting entity.

� Describe the government environment.

� Identify the uses and users of governmental financial reports as well as the objectives of governmental financialreporting.

� Describe the GASB project on service efforts and accomplishment reporting and establishing GAAP for stateand local governments.

� Identify the requirements of GASBS No. 34.

GENERAL INFORMATION

Scope of the State and Local Governmental Sector

In 2007, the U.S. Bureau of the Census identified more than 89,000 units of local government, in addition to the 50states, classified as follows:

a. Counties 3,033

b. Municipalities 19,492

c. Townships 16,519

d. School districts 13,051

e. Special districts 37,381

89,476

Municipalities, counties and townships include cities, towns, villages, parishes, boroughs, etc. Special districtsinclude port authorities, industrial development and housing agencies, water, park, and planning commissions,etc. In addition, there are thousands of subordinate agencies of these governments, that is, statutory authorities,commissions, corporations, etc., with governmental characteristics that are subject to administrative or fiscalcontrol of independent local governments.

States, counties, cities, towns, etc., provide a broad range of services to citizens, whereas special districts usuallyprovide narrower, specialized services. In addition, governments may operate organizations such as hospitals,colleges, universities, employee benefit plans, or other nonbusiness organizations to provide services.

By any measure, state and local governments play a significant role in the U.S. economy. In 2005�2006, forinstance, state and local governments raised more than $2.7 trillion in revenue, nearly 54% of it in the form of

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

4

property, sales, or income taxes. They spent more than $2.5 trillion, 29% of it for education. In 2006, state and localgovernments employed more than 16.1 million people. Debt at the end of 2006 totaled $860 billion for states and$1.3 trillion for local governments.

The American Recovery and Reinvestment Act of 2009 (Recovery Act) is having a significant impact on spendingby state and local governments. The Recovery Act is providing $250 billion to state and local governmentspri�marily for infrastructure, healthcare, education, and general fiscal stabilization. The federal government has esti�mated that allocation of Recovery Act funds to individual states range from 4.8% to 25.2% of a state's budget. Otherelements of the Recovery Act indirectly benefit state and local governments; for example, bond subsidies and aidto individuals. Recovery Act funding (and spending by state and local governments) can be tracked atwww.recovery.gov.

Besides their economic significance, local governments affect all individuals and organizations in the UnitedStates. They regulate aspects of daily and commercial life through laws, ordinances, regulations, etc. They provideservices such as education, police and fire protection, court systems, transportation, water supply and otherutilities, streets and highways, parks, libraries, etc.

The role of state and local governments, relative to that of the federal government, has expanded in the last fewdecades due, in part, to reduced federal spending at the state and local level along with growth of federallymandated programs imposed upon states and localities. In addition, there has been an increased demand bycitizens for public services. One result has been an increase in the number of special districts created to providespecialized servicesover 43 percent since 1977.

Financing methods have also changed, due, in part, to taxpayer resistance to new taxes and initiatives to limit taxincreases, as well as to governments reaching their debt capacity limits. As a result, traditional financing sourcessuch as property taxes have decreased while sales taxes and user fees have increased.

Scope of This Course

This course is concerned with the measurement, presentation, and disclosure of transactions and balances inaccordance with GAAP in governmental financial statements. Thus, it focuses on the accounting and financialreporting standards for governmental entities as promulgated by the Governmental Accounting Standards Board(GASB). It is not a bookkeeping manual, that is, it is not concerned with preparation of books of original entry.However, it does provide journal entries to illustrate discussion of the accounting for various transactions, particu�larly complex ones or those that affect more than one fund.

GASB Pronouncements Considered. This course includes relevant technical developments as of October 2008.It is current as of:

� GASB Statement No. 56, Codification of Accounting and Financial Reporting Guidance Contained in the

AICPA Statements on Auditing Standards.

� GASB Interpretation No. 6, Recognition and Measurement of Certain Liabilities and Expenditures in

Governmental Fund Financial Statements.

� GASB Technical Bulletin 2006�1 No. 2008�1, Determining the Annual Required Contribution Adjustment for

Postemployment Benefits.

� GASB Concepts Statement No. 5, Service Efforts and Accomplishments Reportingan amendment of

GASB Concepts Statement No. 2.

Nonspecialized Accounting Standards for Business�type Activities. Business�type activities (enterprise funds)have the option to follow FASB pronouncements issued after November 30, 1989, that are developed for businessenterprises. However, this course does not discuss those FASB pronouncements because they are applicable onlyto the very limited number of business�type activities that have elected to apply them.

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

5

Specialized Accounting Standards Not Covered. This course does not cover the specialized accounting stan�dards in the following documents:

a. AICPA Audit and Accounting Guide, Health Care Organizations. Although this course does not discuss theprovisions of the AICPA Health Care Guide in any detail, it will be helpful to preparers of governmentalhealthcare entity financial statements to the extent that GASB requirements apply.

b. FASB Statement No. 71, Accounting for the Effects of Certain Types of Regulation, and related FASBStatements (Nos. 90, 92, and 101).

GASBS No. 34 eliminated the option for governmental not�for�profit organizations to follow the AICPA Not�for�Profitmodel. GASBS No. 35, Basic Financial Statementsand Management's Discussion and Analysisfor Public

Colleges and Universities, requires public colleges and universities to follow the special�purpose governmentprovisions of GASBS No. 34, eliminating the provisions previously in GAAP that allowed public colleges anduniversities to follow the AICPA Audit and Accounting Guide, Audits of Colleges and Universities.

AICPA Not�for�Profit Model. GASBS No. 34 superseded the interim guidance provided by GASBS No. 29, The

Use of Not�for�Profit Accounting and Financial Reporting Principles by Governmental Entities. However, GASBS No.34, paragraph 147, allows governments that reported under the GASBS No. 29 AICPA Not�for�Profit model as ofJune 30, 1999 to report using enterprise fund accounting and reporting even though they may not meet the criteriafor an enterprise fund under GASBS No. 34, paragraph 67. Paragraph 5a. of GASBS No. 29 defined the AICPANot�for�Profit model as being the accounting and financial reporting contained in SOP 78�10 and the AICPA Auditand Accounting Guide, Audits of Voluntary Health and Welfare Organizations. Question 7.103.1 in the GASBComprehensive Implementation Guide2009 clarifies that only those governments reporting under the GASBSNo. 29 AICPA Not�for�Profit model as of June 30, 1999 (the date GASBS No. 34 was issued), qualified for thisexception. Most of these governmental nonprofits do not meet the GASBS No. 34 definition of an enterprise fund.Therefore, the GASB created this limited exception to �grandfather" those governments as business�type activitiesto prevent their having to create governmental fund and modified accrual information for fund�based statements.Now that all the effective dates of GASBS No. 34 have passed, no governmental entity may report using the AICPAnot�for�profit model.

States and Special�purpose Governments. The focus of this course is on governmental accounting principles asthey apply to general purpose governmentscities, other municipalities, and counties. However, the guidance isalso generally applicable to states as well as school districts and many other special�purpose governments.

Performance and Reporting Standards Not Covered. This course covers financial statement preparation stan�dards, that is, GAAP applicable to financial statements of governmental entities. Its guidance is useful to preparersof GAAP financial statements, whether those preparers are accountants in government or in public practice.Performance standards are the standards and procedures that a CPA in public practice must follow when associ�ated with, and reporting on, the financial statements of a client. Performance and reporting standards includestandards for the compilation, review, or audit of financial statements. Discussion of performance and reportingstandards is beyond the scope of this course. Guidance on the performance and reporting for compilation andreview engagements may be found in PPC's Guide to Compilation and Review Engagements and guidance onperformance and reporting for audits of governmental financial statements may be found in PPC's Guide to Audits

of Local Governments. In addition, guidance on performing Single Audits for entities receiving federal awards isprovided in PPC's Guide to Single Audits.

Quality Control Standards Not Covered. Quality control standards relate to the internal system that a CPA firmuses to provide itself with reasonable assurance of conforming to the professional standards (including perfor�mance and reporting standards) in financial statement engagements. Quality control standards apply to compila�tion, review, attestation, and audit engagements. Discussion of quality control standards is beyond the scope of thiscourse. Guidance may be found in PPC's Guide to Quality Control.

Ethics Standards Not Covered. Ethics standards relate to the performance of professional responsibilities by allmembers of the AICPA, whether they are in public practice, government, industry, or education. Those standardsare codified in the AICPA Code of Professional Conduct.

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

6

Acronyms for Authoritative Pronouncements. This course uses the following acronyms to refer to authoritativepronouncements:

a. GASBS No. XGovernmental Accounting Standards Board Statement No. X.

b. GASBC No. XGovernmental Accounting Standards Board Concepts Statement No. X.

c. GASBI No. XGovernmental Accounting Standards Board Interpretation No. X.

d. GASBTB No. XX�XGovernmental Accounting Standards Board Technical Bulletin No. XX�X.

e. GASB Cod. sec. xxxx.xxxGASB Codification section xxxx.xxx (all references are to the June 30, 2009edition).

f. BFCThe Basis for Conclusions section of a referenced GASB standard.

g. GASB Comprehensive Implementation Guide2009this GASB publication contains all previouslyissued GASB Implementation Guides including the April 2009, Guide to Implementation of GASB Statement

53 on Accounting and Financial Reporting for Derivative Instruments and updates them for the effects ofnew GASB pronouncements.

h. SLGThe AICPA Audit and Accounting Guide, State and Local Governments (updated as of March 2009).

i. NCGAS XNational Council on Governmental Accounting Statement No. X.

j. SAS No. XStatement on Auditing Standards No. X.

k. FASBS No. XFASB Statement of Financial Accounting Standards No. X.

l. APBO No. XAccounting Principles Board Opinion No. X.

m. 2005 GAAFRThe GFOA Governmental Accounting, Auditing, and Financial Reporting, issued in 2005(also called The Blue Book).

DEFINING OF A GOVERNMENTAL ENTITY

Definition of a GovernmentTHE BASICS

� Any entity that meets the definition of a government must follow GASB pronouncements(other than the federal government). All others follow FASB pronouncements.

� Nearly all general purpose governments meet the definition of a government simply basedon the fact that they are public corporations or bodies corporate and politic.

� Other organizations may be governments based on one of the four characteristics discussedbelow.

What is a governmental entity? In some cases, the answer is obvious. A state or a city, for instance, obviously is agovernment. In other cases, however, it may not be obvious whether a particular entity should be consideredgovernmental for the purpose of determining whether governmental accounting and reporting standards apply.The determination may be particularly difficult for special districts or entities created under general corporation ornot�for�profit corporation laws and that perform some governmental functions, have some characteristics of gov�ernment, or are controlled by a governmental entity. For example, is a community services center that providesyouth recreation and job training services and is financed through government grants and city contracts a govern�mental entity or a nongovernmental entity? The answer depends on other specific circumstances discussed in thefollowing paragraphs.

The GASB has jurisdiction over accounting and financial reporting standards for state and local governmentalentities, and the Financial Accounting Standards Board (FASB) has jurisdiction over standards for nongovernmen�

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

7

tal organizations. Thus, the determination of whether an entity is a governmental entity or not has importantaccounting consequences.

In March 1996, the GASB and the FASB met jointly to clear the proposed AICPA Audit and Accounting Guide,Health Care Organizations. During that meeting, the GASB and the FASB agreed on a definition of a governmentalorganization that should be used in determining whether an entity should follow GAAP for governments.

Rather than issue a Statement, the two Boards decided to clear AICPA audit and accounting guides containing thedefinition, which rank as level �b" source of GAAP. Previous nonauthoritative guidance in this area consisted of aNovember 1993 GASB staff paper titled �Applicability of GASB Standards" (the GASB Staff Paper). Readers of thiscourse should be aware that determining that an organization is governmental based on the definition does notsupersede guidance in GASBS No. 14, The Financial Reporting Entity, regarding whether to include the organiza�tion in a particular governmental financial reporting entity.

Definition

The following definition of a governmental entity is stated in paragraph 1.01 of The AICPA Audit and AccountingGuide, State and Local Governments (SLG):

Public corporations and bodies corporate and politic are governmental entities. Other entities aregovernmental entities if they have one or more of the following characteristics:

� Popular election of officers or appointment (or approval) of a controlling majority of themembers of the organization's governing body by officials of one or more state or localgovernments;

� The potential for unilateral dissolution by a government with the net assets reverting to agovernment; or

� The power to enact and enforce a tax levy.

Furthermore, entities are presumed to be governmental if they have the ability to issue directly(rather than through a state or municipal authority) debt that pays interest exempt from federaltaxation. However, entities possessing only that ability (to issue tax�exempt debt) and none of theother governmental characteristics may rebut the presumption that they are governmental if theirdetermination is supported by compelling, relevant evidence.

Common Examples

Black's Law Dictionary describes a public corporation as a municipality or a governmental corporation that hasbeen created to administer public affairs or as an instrumentality of the state, founded and owned in the publicinterest. The following entities are common examples of governmental entities.

a. States, territories of the United States, and the District of Columbia.

b. Entities created by or under a state constitution, statute, statutory enabling legislation, or other localordinance, including

(1) Cities.

(2) Counties.

(3) Towns.

(4) Townships.

(5) Villages.

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

8

(6) Parishes.

(7) Boroughs.

(8) School districts.

(9) Special districts.

(10) Public authorities.

c. Entities considered to be a �municipal corporation" because they are declared by statute to be a �publiccorporation" or a �body corporate and politic." Legally separate special�purpose entities may be sodesignated so that they can avoid limitations or requirements placed on the general government, such aslimitations on debt issuance or civil service requirements.

Example of Determination As to Governmental Nature

As an example of the definition in the paragraph above, consider the question posed earlier in this lesson about thegovernmental nature of a community services center that provides youth recreation and job training services andis financed through government grants and city contracts. Presented below are two situations in which the centerwould be considered governmental and one in which it would not. Although these examples are based onIllustration 1 in the GASB Staff Paper, they remain applicable based on the revised definition of a governmentalorganization.

a. The center would be considered to be a governmental organization if it was created by a city ordinancepursuant to state enabling legislation as a �body corporate and politic" and its governing board wasappointed by the city's mayor, and if the center could issue its own tax�exempt debt.

b. The center would be considered to be a governmental organization if it was incorporated as an IRC Section501(c)(3) not�for�profit corporation under the state's not�for�profit corporation laws and if its governingboard consisted entirely of city officials serving ex officio, that is, serving by virtue of their status as cityofficials. The status as governmental would apply even if the center could not issue its own tax�exempt debt.

c. The center would not be considered to be a governmental organization if it was organized by a private civicgroup and incorporated as a Section 501(c)(3) not�for�profit corporation under the state's not�for�profitcorporation laws and if its governing board consisted entirely of private, nongovernmental individuals. Itwould be nongovernmental because it was not created by a governmental organization, no governmentalorganization has control over its operations, and it does not possess any characteristics of government,such as popularly elected officials or the power to tax. The status as nongovernmental would apply evenif a governmental agency issued tax�exempt debt on the center's behalf.

In the first two situations, the center's accounting and financial reporting would be subject to the standards�settingauthority of the GASB. In the third situation, the center would be subject to the standards�setting authority of theFASB. Note that this could result in different accounting and financial reporting by two entities that engage in thesame activities and differ only with respect to their being governmental or nongovernmental organizations.

DETERMINING THE FINANCIAL REPORTING ENTITY

Governments, such as cities, provide services and engage in activities through a variety of organizations that mayhave differing degrees of autonomy from the city's elected officials and differing degrees of financial independenceof the city. Which of these entities should be included in the city's financial statements? The financial reporting entity

refers to the units of government, organizations, and activities included in a particular set of financial statements.

GASBS No. 14, The Financial Reporting Entity, as amended, establishes the criteria for determining what makes upthe financial reporting entity. The financial reporting entity is comprised of a primary government and organizationsfor which the primary government is financially accountable. A primary government is a state government, general

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

9

purpose local government, or special�purpose government that meets certain criteria of GASBS No. 14 denoting itsindependence from other state or local governments. Those criteria include the ability to set its own tax rates andto issue debt.

One should not confuse the definition of a governmental entity with the GASBS No. 14 criteria for a primarygovernment. That is, an entity might meet the definition of a government but not meet the definition of a primarygovernment. Similarly, an entity may not meet the definition of a government but may still be included as acomponent unit of a governmental entity.

Definition of Component Unit

A component unit is a legally separate organization for which the primary government is financially accountable.GASBS No. 14 gives the indicators of financial accountability, such as ability to approve or modify the potentialcomponent unit's budget or service fee rates or being obligated for the unit's debt. A component unit may be agovernmental entity, a nonprofit corporation, or a for�profit corporation. Only its relation to the primary governmentis important in determining whether it is part of a governmental reporting entity. GASBS No. 39, Determining

Whether Certain Organizations Are Component Units, amends GASBS No. 14. It provides guidance on when certainlegally separate tax�exempt organizations for which the primary government is not financially accountable (oftenreferred to as �affiliated organizations") should, nonetheless, be included in a government's financial reportingentity.

Discrete Presentation of Component Units

There are two ways of reporting a component unit in the financial statements of the reporting entity: discretepresentation and blending. These are not options; the method for which the unit qualifies must be followed. Mostcomponent units are discretely presented. Discrete presentation refers to presentation of data for the componentunit in a column to the right of the data columns for the primary government.

Blending of Component Units

Blending means that the component unit is so closely related to the primary government that it is, in effect, the sameas the primary government. In this case, the data for the component unit's funds are combined with the data forcorresponding funds of the primary government.

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

10

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

11

SELF�STUDY QUIZ

Determine the best answer for each question below. Then check your answers against the correct answers in thefollowing section.

1. What guidance did the GASB and the FASB agree upon as the highest authority containing the definition ofgovernmental organization in March of 1996?

a. A new Statement issued at the March 1996 session.

b. The AICPA audit and accounting guides.

c. GASBS No. 14, The Financial Reporting Entity.

2. High Five is a community youth recreation center that also provides job training. High Five is financed throughgovernment grants and city contracts. Under which situation below would High Five be considered anongovernmental organization?

a. High Five is a Section 501(c)(3) organization incorporated under the state's not�for�profit corporation laws.Its board consists entirely of city officials serving ex officio. They do not issue their own tax�exempt debt.

b. High Five is a Section 501(c)(3) not�for�profit corporation, and its board consists entirely of privateindividuals. The organizing group is a private civic group. A governmental agency issues tax�exempt debton High Five's behalf.

c. High Five was created by a city ordinance based on state legislation as a �body corporate and politic," andits board was appointed by the mayor. High Five issues its own tax�exempt debt.

3. Swimming Fish Marina's accountant is trying to determine if they should be included in the city's financialstatements. Which indicator would positively confirm that the Marina is financially accountable to the city?

a. Swimming Fish Marina is a legally separate organization from the city.

b. Swimming Fish Marina is a governmental entity.

c. The city can approve Swimming Fish Marina's budget and service fee rates.

d. Swimming Fish Marina is a nonprofit corporation.

4. Ace Flies North is a nonprofit corporation that is financially accountable to Hay Springs, TX. If the financial datafor Ace Flies North is presented in a column to the right of the data columns for Hay Springs, what method ofreporting is being used?

a. Discrete presentation.

b. Blending.

c. Affiliated.

d. Component unit.

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

12

SELF�STUDY ANSWERS

This section provides the correct answers to the self�study quiz. If you answered a question incorrectly, reread theappropriate material. (References are in parentheses.)

1. What guidance did the GASB and the FASB agree upon as the highest authority containing the definition ofgovernmental organization in March of 1996? (Page 7)

a. A new Statement issued at the March 1996 session. [This answer is incorrect. The FASB and GASBdecided not to issue a new Statement to define governmental organization.]

b. The AICPA audit and accounting guides. [This answer is correct. The GASB and FASB met jointlyand cleared the AICPA audit and accounting guides which contain the definition for governmentalorganization.

c. GASBS No. 14, The Financial Reporting Entity. [This answer is incorrect. GASBS No. 14 contains guidanceabout whether a governmental organization should be included in a particular governmental financialreporting entity.]

2. High Five is a community youth recreation center that also provides job training. High Five is financed throughgovernment grants and city contracts. Under which situation below would High Five be considered anongovernmental organization? (Page 8)

a. High Five is a Section 501(c)(3) organization incorporated under the state's not�for�profit corporation laws.Its board consists entirely of city officials serving ex officio. They do not issue their own tax�exempt debt.[This answer is incorrect. In this situation High Five possesses one or more of the defining characteristicsof being a governmental organization.]

b. High Five is a Section 501(c)(3) not�for�profit corporation, and its board consists entirely of privateindividuals. The organizing group is a private civic group. A governmental agency issues tax�exemptdebt on High Five's behalf. [This answer is correct. In this situation High Five is a nongovernmentalorganization. There are no characteristics present that define a governmental entity. A governmen�tal agency issuing tax�exempt debt on the center's behalf is not enough to define it as governmental.]

c. High Five was created by a city ordinance based on state legislation as a �body corporate and politic," andits board was appointed by the mayor. High Five issues its own tax�exempt debt. [This answer is incorrect.In this situation High Five would be a governmental organization because the center possesses one ormore of the defining characteristics.]

3. Swimming Fish Marina's accountant is trying to determine if they should be included in the city's financialstatements. Which indicator would positively confirm that the Marina is financially accountable to the city?(Page 9)

a. Swimming Fish Marina is a legally separate organization from the city. [This answer is incorrect. Anorganization being legally separate is not enough information to deem it accountable to the city. Thedefining factor would be its relationship to the city, which is not included here.]

b. Swimming Fish Marina is a governmental entity. [This answer is incorrect. A component unit may be agovernmental entity, but still not be financially accountable. We would need to know what the relationshipis between Swimming Fish Marina and the city.]

c. The city can approve Swimming Fish Marina's budget and service fee rates. [This answer is correct.Because the city has the authority of the Marina's budget approval and setting of service fees, theMarina is accountable to the city according to GASBS No. 14, which gives the indictors of financialaccountability. Another indicator would be if the city were responsible for the Marina's debt.]

d. Swimming Fish Marina is a nonprofit corporation. [This answer is incorrect. A component unit may be anonprofit corporation and still not be financially accountable. The relationship between the city and theMarina is what would indicate whether there is financial accountability.]

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

13

4. Ace Flies North is a nonprofit corporation that is financially accountable to Hay Springs, TX. If the financial datafor Ace Flies North is presented in a column to the right of the data columns for Hay Springs, what method ofreporting is being used? (Page 9)

a. Discrete presentation. [This answer is correct. There is not an option for how Ace Flies North andHay Springs, TX report their financial data. The method for which the unit qualifies must be followed.Discrete presentation is how most component units must report.]

b. Blending. [This answer is incorrect. If blending were the method of presentation, Ace Flies North's fundnumbers would be combined with Hay Springs fund numbers. This method is used because Ace FliesNorth, as the component unit, is so closely related to Hay Springs which is the primary government thatit is, in effect, the same as the primary government.]

c. Affiliated. [This answer is incorrect. An affiliated organization is not a method of financial presentation, butrather a term used to describe legally separate tax�exempt organizations for which the primary governmentis not financially accountable.]

d. Component unit. [This answer is incorrect. A component unit is not a method of financial presentation, butrather a term used to describe legally separate organizations for which the primary government isfinancially accountable.]

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

14

UNDERSTANDING THE GOVERNMENT ENVIRONMENT

Some aspects of the governmental sector are similar to the nongovernmental sector. For example, fees may becharged to users of some government services, and the governmental service activity may be operated on acost�recovery basis. In general, the accounting and financial reporting for such �business�type" (proprietary)activities are similar to the accounting for similar activities provided by business enterprises in the private sector.Other aspects of the governmental sector, however, are quite different from the private sector, and the accountingand financial reporting for those aspects are unique. Thus, it is important to understand those unique environmen�tal characteristics.

GASBC No. 1, Objectives of Financial Reporting, paragraph 13, identifies, among others, the following significantgovernment environmental characteristics:

a. Government structure and services

(1) The representative form of government and separation of powers.

(2) The relationship of taxpayers to services received.

b. Control characteristics

(1) The budget as an expression of public policy and as a method of providing control.

(2) The use of fund accounting for control purposes.

c. Other

(1) The political process.

(2) Significant investment in non�revenue�producing capital assets.

The following paragraphs discuss these characteristics and how they affect governmental accounting and financialreporting.

Governmental Structure and Budget

State and local governments operate as representative forms of government in which elected officials and separatebranches of government ultimately are accountable to the electorate. For example, the executive branch preparesa budget that, when approved by the legislative branch, authorizes expenditures and has the force of law. Citizensplay a role in the budget�adoption process, for example, by commenting on a proposed budget at budgethearings. Thus, the adopted budget becomes an expression of public policy of service objectives and priorities.The legally adopted budget also serves as a form of control and a means of demonstrating accountability.

The governmental accounting model recognizes the annual budget's significance by focusing on the flows ofcurrent financial resources in the governmental fund financial statements. This measurement focus is the same asor similar to the measurement focus used in most governments' legally adopted budgets. Using this measurementfocus, certain noncurrent, nonfinancial resources, liabilities, and expenditures are given unique treatment so thatthese assets and liabilities are reported in the same manner as they are in most legally adopted budgets. Inaddition, GAAP requires governments to present budget�to�actual comparisons for their general fund and eachmajor special revenue fund that has a legally adopted annual or biennial budget to demonstrate whether govern�ment officials adhered to the spending authorizations and limitations inherent in the budget.

Fund Accounting. Besides the budget, other legal and contractual provisions govern how governments may raiseand spend resources. For example, a debt agreement may specify the use for which borrowed monies may bespent and may require the accumulation of resources for repaying the debt. Or, legislation authorizing a new tax orfee may restrict the revenues to use for a specific purpose. Or, a grant agreement may stipulate how grant

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

15

resources received from another level of government may be used. Fund accounting is a way governmentstraditionally have controlled the use of resources designated for a specific purpose and have demonstrated thatlegal or contractual provisions governing specific resources have been complied with. Even though computerizedaccounting systems may have diminished the need for fund�based accounting systems, fund�based financialreporting is still a way for governments to demonstrate that resources were used as authorized and that otherfinance�related legal or contractual requirements were adhered to.

Relationship of Taxpayers to Services Received

In a representative democracy, the electorate as a whole authorizes, through actions of elected officials, theimposition of taxes to raise resources needed to provide basic government services. However, individual taxpayersmust abide by that taxing decision and pay taxes whether they want to or not and whether they receive all theauthorized services or not. Because taxes may be based on factors such as income or the value of property owned,the amount of taxes an individual citizen pays usually will not bear a direct relationship to the value of tax�supportedservices that the taxpayer receives. For example, property owners must pay property taxes to finance publiceducation even though they do not have any children in public schools. The fact that individual taxpayers areinvoluntary resource providers increases the need for governmental financial reporting to demonstrate fiscalaccountability to those resource providers.

Absence of Exchange Relationship, Profit Motive, and Competition

There is not an exchange relationship between resources provided to governments and many general governmentservices provided by governments. For example, the fire department generally does not bill a citizen for its servicesin fighting a fire on the citizen's property. Also, governments provide many services that the private sector would notfind cost�effective or profitable to provide, for example, public transportation. The result is that, in some instances,the government is the only provider of a service.

This monopolistic quality and the lack of a profit�motive for providing services can result in difficulty in measuringthe efficiency of many government operations. Unlike the private business sector, the government is not measuredin terms of profit or loss or return on shareowners' investment. Instead, governmental financial reporting mustprovide other methods of evaluating the government's efficiency and effectiveness. Concepts and standards formeasuring governmental service efforts and accomplishments are only now beginning to be developed.

Political Nature of Government

Government is by definition a political process. Elected officials attempt to balance competing claims for limitedresources and conflicting taxpayer desires for more services without tax increases. Elected officials often serve forrelatively short terms and thus have a short�term horizon. There is some incentive for elected officials to satisfycitizens' desires for current services by deferring other services or deferring necessary maintenance of infrastruc�ture (such as streets and bridges) and other non�revenue�producing capital assets. Also, officials may pay forservices with nonrecurring, short�term revenues or by deferring the cash effects of certain types of transactions tomore remote periods. In the past, the focus on measuring and recognizing long�term or deferred commitments orliabilities has been given less emphasis than the focus on current resources and expenditures that correspond tothe time frame of the annual budget. However, management's discussion and analysis (MD&A) and government�wide financial statements, required by GASBS No. 34, address the longer�term focus, that is, interperiod equity.

Business�type Activities of Governments

Some of the unique characteristics of governmental activities, and the related accounting and financial reportingimplications, can be better understood by contrasting those characteristics with characteristics of business�type(proprietary) activities that governments engage in. Business�type activities have counterparts in the private sectorand include activities such as water utilities, sanitation services, golf courses, parking lots and garages, etc. Theseactivities provide the same types of services as are provided by private enterprises. Thus, often there is competitionthat may be absent from governmental activities. If there is competition, the customers have a choice whether touse the government's proprietary service or not (unless the activity is a monopoly of a necessary service, such asa water utility). Both GASBC No. 1 and GASBS No. 34 use the terms governmental activities and business�type

activities. However, those terms are defined only in GASBS No. 34, paragraph 15. Governmental activities �gener�

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

16

ally are financed through taxes, intergovernmental revenues, and other nonexchange revenues." Business�typeactivities �are financed in whole or in part by fees charged to external parties for goods and services." Governmentsare required to report business�type activities separately in their government�wide financial statements.

Exchange Relationship and User Fees. Like private enterprises, government business�type activities charge userfees and thus have an exchange relationship with service recipients. The government�owned activity may chargeuser fees at a level that will recover all costs. However, the activity may be subsidized by the government to keepuser fees at a level considered politically or economically acceptable. In either case, however, fund financialreporting for these activities focuses on measuring all costs of the activity, including, for example, depreciation andcosts related to long�term commitments. It also focuses on reporting net operating income, either to determine thenecessary level of user fees or to determine the extent of subsidization necessary. This measurement focus is thesame as for private�sector enterprises.

Revenue�producing Assets. Business�type activities of governments usually are capital intensive. But becausethe capital assets are revenue�producing (unlike most capital assets associated with governmental activities), theremay be less incentive to defer necessary maintenance. Maintenance will be performed because it is necessary toprovide effective and efficient service that will generate revenue. Because the activity reports depreciation and otherlong�term costs, the related capital assets and long�term liabilities are included in the activity's balance sheet.

Different Status of Budget. Because government business�type activities are fully or partially self�supporting fromuser fees (rather than from taxes), and because they have an exchange relationship with the customers and somerelationship between user fees and services, there is less need for a legally adopted budget like that for governmen�tal activities. Business�type activities use budgets for internal planning and control, but the budgets generally donot have the legal status or political nature of governmental activity budgets. For instance, usually they are notsubject to public comment and are not formally adopted by a legislature or governing body.

Because the budget for proprietary activities generally is not a legal authorization of, or limitation on, spending,there is less need to demonstrate compliance with it. Thus, GAAP financial reporting includes budgetary compari�sons only for certain governmental funds (activities).

Absence of Fund Accounting. For similar reasons, business�type activities generally do not use fund accountingin their financial reporting (although the entire activity may be reported in one separate enterprise fund when theactivity is included in the financial report of the government as a whole). Business�type activities typically maydecide how to spend their revenues and resources to provide the service in the most efficient and effective way.Because the resources usually are not restricted to specified uses, there is no need to segregate the resources andtheir expenditures into funds for financial reporting purposes. (Debt agreements may specify how debt proceedsare to be used and may require the maintenance of certain �funds," but those funds are treated as accounts forfinancial reporting purposes and are not equivalent to fund accounting.)

The differences discussed in the preceding paragraphs are not absolute. For one thing, the organizationaldemarcation between governmental and business�type activities is not always clear. For example, one governmentmay organize its parks as a department of the general government while another government may organize themas a separate business�type activity. As previously mentioned, business�type activities may be subsidized, andtherefore subject to the same political process of obtaining tax�supported subsidies and to resulting heightenedaccountability to the taxpayers. The activities may be a monopoly of necessary service, which affects the relation�ship with the service recipients. Rates, particularly of utilities, may be subject to regulation, which also increasespolitical considerations and affects the relationship with service recipients. The activity may receive governmentgrants that have restrictions on their use and require demonstration of compliance with those restrictions.

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

17

SELF�STUDY QUIZ

Determine the best answer for each question below. Then check your answers against the correct answers in thefollowing section.

5. What is a characteristic of a nongovernmental entity that is similar to a governmental entity?

a. The legally adopted budget serving as a form of control and a means of accountability demonstration.

b. The exchange relationship between the taxes paid and the services received.

c. The profit motive driving the services provided.

d. The accounting and financial reporting for the user fees charged to the user for the services offered.

6. How do governments demonstrate that resources were used as authorized and that other finance�related legalor contractual requirements were adhered to?

a. Budget process.

b. GAAP requirements.

c. Fund�based financial reporting.

d. Resource raising procedures.

7. Sammy Sanitation is a city�governed waste management company that is financed in part through feescharged to external parties for services. What classification of activity is this?

a. Governmental.

b. Business�type.

c. Private enterprise.

d. Private sector.

8. Which statement listed below best describes the difference between business�type and governmentalactivities?

a. Competition is generally present in governmental activities, but absent in business�type activities.

b. The measurement focus of government activities is reporting of net operating income and themeasurement focus is fund accounting for business�type activities.

c. Capital assets of business�type activities are generally revenue�producing and they are not ingovernmental activities.

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

18

SELF�STUDY ANSWERS

This section provides the correct answers to the self�study quiz. If you answered a question incorrectly, reread theappropriate material. (References are in parentheses.)

5. What is a characteristic of a nongovernmental entity that is similar to a governmental entity? (Page 14)

a. The legally adopted budget serving as a form of control and a means of accountability demonstration. [Thisanswer is incorrect. This is a unique environmental characteristic of the governmental sector. The budgetprepared by the executive branch, approved by the legislative branch, and adopted as an expression ofpublic opinion becomes the basis for measurement of meeting legally authorized expenditures.]

b. The exchange relationship between the taxes paid and the services received. [This answer is incorrect. Agovernmental entity may be financed through taxation, which means individual taxpayers are legallybound to pay the taxes regardless of whether or not they receive any of the authorized services.]

c. The profit motive driving the services provided. [This answer is incorrect. Some services which areprovided by governments are not profitable, for example public transportation, and so nongovernmentalentities might not find it cost effective to offer such services.]

d. The accounting and financial reporting for the user fees charged to the user for the services offered.[This answer is correct. This is one aspect that is generally similar between governmental andnongovernmental entities. Business�type activities provided by governments that charge user feeshave similar accounting and financial reporting procedures as these same activities provided bybusiness enterprises in the private sector.]

6. How do governments demonstrate that resources were used as authorized and that other finance�related legalor contractual requirements were adhered to? (Page 15)

a. Budget process. [This answer is incorrect. Budgets can serve as an expression of public policy of serviceobjectives and priorities and once adopted can serve as a form of control and a means of demonstratingaccountability of the resources received but does not indicate whether other finance�related legal orcontractual requirements were adhered to.]

b. GAAP requirements. [This answer is incorrect. GAAP requirements are concerned with financial reportingand do not deal with the legal or contractual requirements of the funding resource.]

c. Fund�based financial reporting. [This answer is correct. Fund�based accounting systems can reportfinancial results in such a way as to demonstrate that legal or contractual requirements werecomplied with and that the use of financial resources were used for the special purpose for whichthey were designated.]

d. Resource raising procedures. [This answer is incorrect. How governments tax the citizenry or apply forgrant or federal subsidies does not demonstrate how the financial resources are used.]

7. Sammy Sanitation is a city�governed waste management company that is financed in part through feescharged to external parties for services. What classification of activity is this? (Page 15)

a. Governmental. [This answer is incorrect. Governmental activities are financed through taxes, intergovern�mental revenues, and other nonexchange revenues. The user fees demonstrate that this is not agovernmental activity.]

b. Business�type. [This answer is correct. The financing for business�type activities come in part orin whole from fees charged to external parties for the goods or services offered. These activitiesprovide the same type of services as are provided by private enterprise.]

c. Private enterprise. [This answer is incorrect. Because the city governs this entity, it is not a privateenterprise.]

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

19

d. Private sector. [This answer is incorrect. Sammy Sanitation is governed by the city and, therefore, is nota part of the private sector.]

8. Which statement listed below best describes the difference between business�type and governmentalactivities? (Page 16)

a. Competition is generally present in governmental activities, but absent in business�type activities. [Thisanswer is incorrect. The exact opposite is true. Many times there are counterparts in the private sector thatcan provide competition for business�type activities offered by a government. Examples of these servicesmight be water utilities or sanitation services.]

b. The measurement focus of government activities is reporting of net operating income and themeasurement focus is fund accounting for business�type activities. [This answer is incorrect. The exactopposite is true. The measurement focus of net operating income for business�type activities is the samefor private�sector enterprises. This analysis helps the government set the user fees or know how muchsubsidization is necessary.]

c. Capital assets of business�type activities are generally revenue�producing and they are not ingovernmental activities. [This answer is correct. User fees (revenue produced by the capital assets)apply to business�type activities. Furthermore, because business�type activities can be capitalintensive and the capital assets are necessary to produce revenue by way of user fees, maintenanceon those assets is not likely to be deferred.]

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

20

THE USES FOR AND THE USERS OF GOVERNMENTAL FINANCIALREPORTS

Users

Who are the users of governmental external financial reports? GASBC No. 1, paragraphs 30�31, identifies thefollowing user groups:

a. Citizens. The government is primarily accountable to the citizenry. This user group includes citizen voters,taxpayers, and service recipients, the media, and advocate groups.

b. Legislative and Oversight Bodies. These bodies represent the citizens and include members of statelegislatures, county commissions, city councils, boards of trustees, school boards, and executive branchofficials who have oversight responsibility for other levels of government or for separately organizedbusiness�type activities.

c. Investors and Creditors. Investors and creditors include individual and institutional investors and creditors,municipal security underwriters, bond rating agencies, bond insurers, and other financial institutions.

Internal government management officials use external financial statements, but they are not identified as a primaryuser because they have access to the information through internal financial reports.

Uses

What use do the users identified in the preceding paragraph make of external governmental financial statements?GASBC No. 1, paragraph 32, lists the following uses:

a. Comparing actual financial results with the legally adopted budget.

b. Assessing financial condition and results of operations.

c. Assessing compliance with finance�related legal and contractual requirements.

d. Assessing efficiency and effectiveness.

The accounting and financial reporting objectives and standards discussed in this course are influenced by theuses made of governmental financial statements.

Comparing Actual and Budgeted Results. All user groups use governmental financial reports to compare actualto budgeted results. Citizens and legislative and oversight bodies make the comparison to assess whetherresources were used as authorized. Other groups assess whether deviations from the budget reflect managementweaknesses, poor budgeting practices, or other circumstances. The budget has less significance for business�typeactivities. Thus, users of financial statements of business�type activities typically are less interested in comparingactual and budgeted results.

Assessing Financial Condition and Results of Operations. Citizens assess whether the reported financialcondition and operating results indicate that the government can continue to provide the current level of serviceswith the current level of resources and the likelihood of tax or service fee increases. Legislative and oversight bodiesuse reported information in planning budgets and programs and to determine the need for tax, fee, or subsidychanges. Investors and creditors use reported information on financial condition to assess the government's abilityto meet its debt service obligations.

Assessing Compliance with Finance�related Legal and Contractual Requirements. Legal and contractualprovisions such as debt covenants, grant restrictions, and statutory taxing or debt limits may control governmentactivities or expenditures. Grantors use governmental fund financial statements to assess whether grant require�ments have been adhered to, and investors and creditors use them to assess compliance with debt covenants.

GFST09 Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

21

Citizens, too, are concerned with the government's compliance with such legal and contractual provisions becauseof the possible consequence of noncompliance, such as loss of grant funds.

Assessing Efficiency and Effectiveness. Citizens and legislative and oversight bodies are particularly concernedwith the economy, efficiency, and effectiveness with which government uses resources provided through taxes orgrants from other levels of government.

GASB OBJECTIVES FOR GOVERNMENTAL FINANCIAL REPORTING

GASBC No. 1 provides the conceptual framework for accounting and financial reporting for state and localgovernments. In GASBC No. 1 (GASB Cod. Appendix B), the GASB articulated the broad external financialreporting objectives that underlie existing, or will influence future, accounting and financial reporting standards.Many, but not all, of the reporting objectives have been achieved in the GASBS No. 34 financial reporting model.Familiarity with the objectives can increase understanding of the nature and purpose of existing standards and thetrend of future standards.

Accountability

GASBC No. 1, paragraph 56, states that �accountability is the cornerstone of all financial reporting in government."That paragraph describes �accountability" as:

Accountability is the cornerstone of all financial reporting in government. . . . The dictionarydefines accountable as �being obliged to explain one's actions, to justify what one does."Accountability requires governments to answer to the citizenryto justify the raising of publicresources and the purposes for which they are used.

Accountability implies stewardship. A government is accountable to citizens for its stewardship of resourcesbecause individual taxpayers provide the resources involuntarily. Many laws and constitutions reflect the conceptof the accountability of government to the people. So should governmental accounting. In paragraph 58, the GASBexpressed the conclusion that governmental financial reporting should demonstrate accountability by providinginformation that will assist in assessing whether a government was �operated within the legal constraints imposedby the citizenry."

Interperiod Equity

GASBC No. 1, paragraph 61, notes that �interperiod equity is a significant part of accountability and is fundamentalto public administration." Although the term �interperiod equity" is not defined in GASBC No.�1 or in other account�ing literature, the Board does discuss the term in the context of balanced budget laws in paragraph 60. It notes thatthe intent of those laws is that �the current generation of citizens should not be able to shift the burden of paying forcurrent�year services to future�year taxpayers." Paragraph 77 introduces other facets of interperiod equity, specifi�cally, whether previously accumulated resources were used up in providing service in the current period or whethercurrent�year revenues were not only sufficient but also increased accumulated resources. As far back as the 1920s,commentators noted that the ease of issuing public debt often led governments to finance unfair portions ofexpenditures through the sales of bonds and thus to unfairly shift the repayment burden to future years. Currently,there is not a perceived problem of capital debt being issued with a term that exceeds the life of the asset itfinances; however, issues involving interperiod equity exist with respect to operating debt, unfunded pensioncontributions, deferred maintenance, claims and judgments, compensated absences, and other postemploymentbenefits.

Many state and local laws and constitutions recognize the need for interperiod equity. For instance, most state andlocal governments have laws requiring balanced budgets and limiting debt to amounts that can be repaid over thelife of the assets that are acquired with the debt. Because of the political nature of government and the resultingshort�term outlook of elected officials, there is a temptation to ignore interperiod equity when providing services tothe current electorate. Thus, as GASBC No. 1, paragraph 59, explains, these laws attempt to �achieve fairness fromone year, one term of office, or one generation to another."

GASBC No. 1, paragraph 61, states that an objective of financial reporting is to provide information to assesswhether current�year revenues are sufficient to pay for current�year services or whether future�year taxpayers willhave to assume the burden for those services.

GFST09Companion to PPC's Guide to Preparing Governmental Financial Statements Under GASBS No. 34

22

The concept of interperiod equity is related to the concept of accountability in that government officials areaccountable for compliance with balanced budget and debt limitation laws that seek to achieve interperiod equity.Thus, financial reporting that demonstrates accountability by providing information that will assist in assessingwhether a government was �operated within the legal constraints imposed by the citizenry" also demonstrates theextent of interperiod equity. The financial reporting objectives of GASBC No. 1 discussed in the following para�graphs reflect the primacy of accountability and interperiod equity.

Financial Reporting Objectives

From this focus on accountability and interperiod equity, the GASB established three basic objectives of financialreporting by state and local governments. GASBC No. 1, paragraphs 77�79, presents the three main financialreporting objectives, each with three subobjectives. The objectives apply to both governmental and business�typeactivities because both types are part of a government and thus are accountable to the public. There may be,however, differences in emphasis in applying the objectives to each type of activity. The objectives are as follows:

a. Assist in Assessing Accountability. Financial reporting should assist in fulfilling government's duty to bepublicly accountable and should enable users to assess that accountability.

(1) Financial reporting should provide information to determine whether current�year revenues weresufficient to pay for current�year services. This objective implies that financial reporting should enablethe assessment of interperiod equity.

(2) Financial reporting should demonstrate whether resources were obtained and used in accordancewith the legally adopted budget and should demonstrate compliance with other finance�related legalor contractual requirements.