pesa industry review; exploration

TRANSCRIPT

APPEA Journal 2014—1Third proof—Johns 27 february 2014

D.R. Johns and P.G. Desplandsantos 60 flinders streetadelaide, sa [email protected]

absTraCT

Exploration activity in Australia in 2013 occurred across a broad spectrum of conventional and unconventional plays.

Competition for acreage was buoyant with large tracts of key onshore basins either licensed or under application. Offshore, there were new awards on the western Australian margin and in the Bight Basin off SA.

Offshore 3D seismic acquisition was reduced from anoma-lously high levels in 2012. Onshore 2D seismic acquisition was at historic highs and onshore 3D was the most ever recorded.

Overall drilling levels were maintained despite a decline offshore. Of 13 offshore wells drilled, six were discoveries. Sixty-nine exploration wells (excluding CSG wells) were drilled onshore. Fifty addressed conventional, and 19 were unconventional shale or basin-centered gas targets. Sixty of the 69 wells were drilled in the Cooper/Eromanga Basin where conventional oil and gas exploration yielded 11 oil and six gas discoveries.

Drilling and fraccing campaigns in the Nappamerri Trough unconventional gas plays provided early encourag-ing results.

213 exploration and appraisal CSG wells were drilled in the CSG basins of Queensland and NSW. In Queensland a record total of 1,317 CSG wells were drilled in fiscal year 2012/2013.

Shale gas exploration activity was increasingly focused on the Palaeozoic and Proterozoic Basins of Western, Central and Northern Australia with major oil and gas companies involved in joint ventures preparing for drilling in 2014. The results of these programmes will have an important bearing on the future direction of exploration in these plays.

KeyWords

Australia, exploration, petroleum, hydrocarbons, wells, seis-mic, permits, history, oil and gas, conventional, unconventional, discoveries, McArthur, South Nicholson, Georgina, Browse, Amadeus, Canning, Carnarvon, Bight, Ceduna, Cooper/Ero-manga, Nappamerri Trough, coal seam gas, basin-centered gas, Northern Territory, Western Australia, South Australia, Queensland, New South Wales, Victoria, Tasmania.

inTroduCTion

This paper is a review of petroleum exploration activity in Australia in calendar year 2013. Exploration health is often in-dicated by activity levels in the various stages of the exploration

cycle; that is, acreage procurement, seismic acquisition, explo-ration drilling and new field discoveries. This paper reviews 2013 exploration activity levels in Australia and, where possible, provides a more detailed analysis by state, basin and resource type. The data are presented in the form of tables, charts and maps.

Exploration activity is influenced by many factors but per-ceived prospectivity, commercial and economic considerations, competition for acreage, new ideas, and technological devel-opments are some of the key drivers. In this paper some sug-gestions are made concerning medium to long term trends in activity evident in the data. This paper, however, is not intended to be a detailed or thorough analysis of exploration trends, and readers are encouraged to draw their own conclusions from the data provided.

In Australia, as well as the traditional conventional resource plays, unconventional resources such as CSG, shale gas and basin-centered gas plays are all being pursued as explorers seek to discover new hydrocarbon resources. Exploration of these di-verse plays is affected by local and overseas drivers. In particu-lar, the successful exploitation of unconventional plays in the US has generated a great deal of interest in frontier Australian shale plays in the Permian Cooper Basin and in the Proterozoic and Palaeozoic shale plays of the Canning, McArthur, South Nicholson and Georgina basins, and has led to the participation of major oil and gas companies in the shale plays.

In Eastern and Central Australia, the forecast increase in demand for gas from LNG plants being constructed in Queensland, and the scenario of a higher gas prices in the east coast domestic gas market—that will reflect competition with the higher priced international gas markets (Wood and Carter, 2013)—is a new element impacting gas exploration. Whether this was a factor or not, the attraction of onshore gas plays, and in particular unconventional plays, to major oil and gas com-panies was confirmed when Chevron reached an agreement with Beach Energy to farm-in to the basin-centered gas and shale plays of the Nappamerri Trough (Beach Energy, 2013a).

Ultimately the goal of petroleum exploration is to find com-mercial oil and gas resources. Discoveries made during the year are described here as far as public domain data will allow. These descriptions are not detailed. Nevertheless, it is hoped there is sufficient detail in the descriptions and in the data and analyses provided in this paper to enable the reader to obtain a reasonable and balanced perspective of exploration activity and results in Australia in 2013.

aCreaGe aCTiViTy suMMary

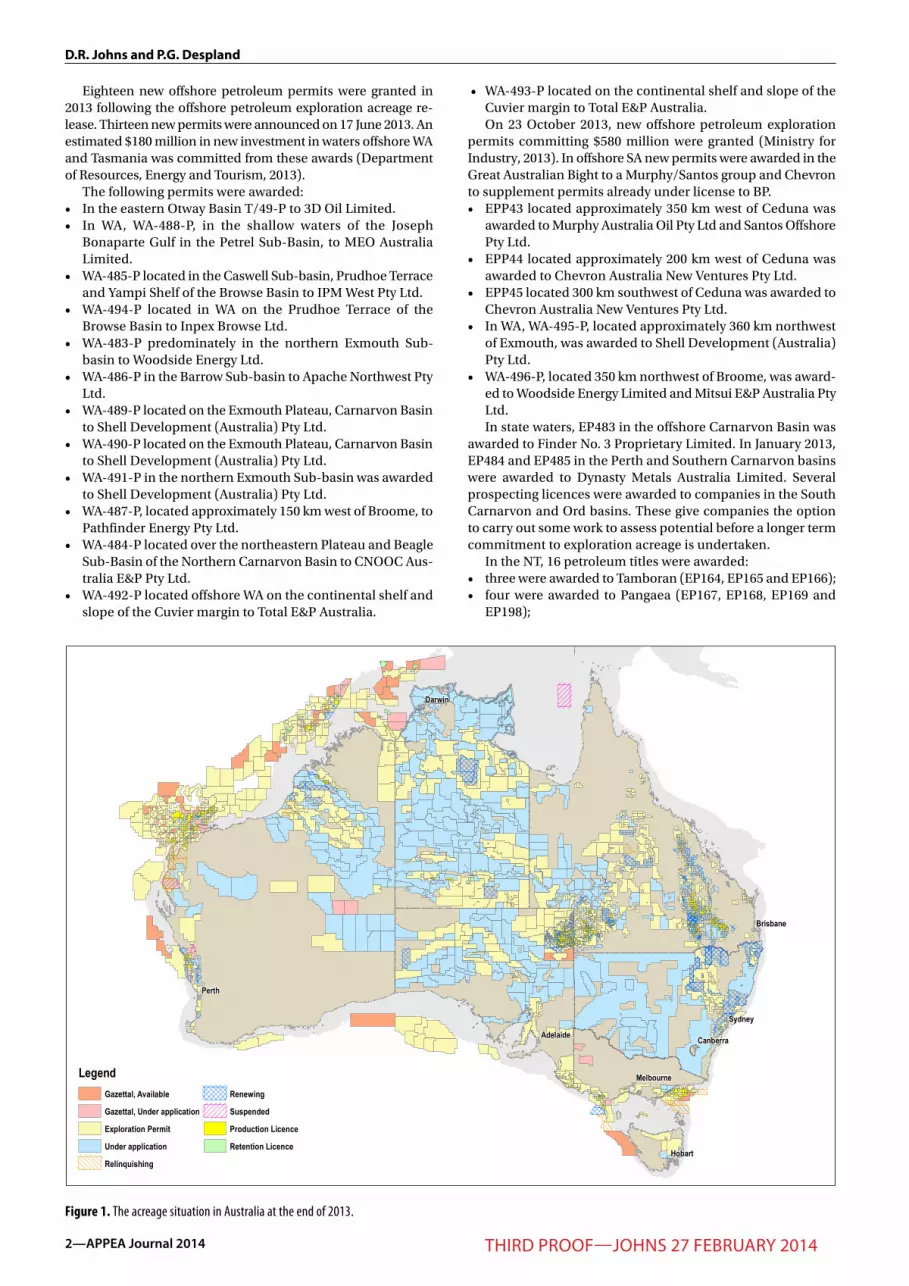

The exploration license map of Australia demonstrates that vast areas are covered either with active permits or with permits under application (Fig. 1). In the onshore, interest in unconventional resource plays is driving the licensing. In the offshore, despite declining drilling activity levels, interest in acreage has been maintained at high levels as indicated by new awards (Fig. 2).

2013 PESA industry review: exploration Lead authorRhodriJohns

2—APPEA Journal 2014 Third proof—Johns 27 february 2014

D.R. Johns and P.G. Despland

Eighteen new offshore petroleum permits were granted in 2013 following the offshore petroleum exploration acreage re-lease. Thirteen new permits were announced on 17 June 2013. An estimated $180 million in new investment in waters offshore WA and Tasmania was committed from these awards (Department of Resources, Energy and Tourism, 2013).

The following permits were awarded:• In the eastern Otway Basin T/49-P to 3D Oil Limited. • In WA, WA-488-P, in the shallow waters of the Joseph

Bonaparte Gulf in the Petrel Sub-Basin, to MEO Australia Limited.

• WA-485-P located in the Caswell Sub-basin, Prudhoe Terrace and Yampi Shelf of the Browse Basin to IPM West Pty Ltd.

• WA-494-P located in WA on the Prudhoe Terrace of the Browse Basin to Inpex Browse Ltd.

• WA-483-P predominately in the northern Exmouth Sub-basin to Woodside Energy Ltd.

• WA-486-P in the Barrow Sub-basin to Apache Northwest Pty Ltd.

• WA-489-P located on the Exmouth Plateau, Carnarvon Basin to Shell Development (Australia) Pty Ltd.

• WA-490-P located on the Exmouth Plateau, Carnarvon Basin to Shell Development (Australia) Pty Ltd.

• WA-491-P in the northern Exmouth Sub-basin was awarded to Shell Development (Australia) Pty Ltd.

• WA-487-P, located approximately 150 km west of Broome, to Pathfinder Energy Pty Ltd.

• WA-484-P located over the northeastern Plateau and Beagle Sub-Basin of the Northern Carnarvon Basin to CNOOC Aus-tralia E&P Pty Ltd.

• WA-492-P located offshore WA on the continental shelf and slope of the Cuvier margin to Total E&P Australia.

• WA-493-P located on the continental shelf and slope of the Cuvier margin to Total E&P Australia.On 23 October 2013, new offshore petroleum exploration

permits committing $580 million were granted (Ministry for Industry, 2013). In offshore SA new permits were awarded in the Great Australian Bight to a Murphy/Santos group and Chevron to supplement permits already under license to BP.• EPP43 located approximately 350 km west of Ceduna was

awarded to Murphy Australia Oil Pty Ltd and Santos Offshore Pty Ltd.

• EPP44 located approximately 200 km west of Ceduna was awarded to Chevron Australia New Ventures Pty Ltd.

• EPP45 located 300 km southwest of Ceduna was awarded to Chevron Australia New Ventures Pty Ltd.

• In WA, WA-495-P, located approximately 360 km northwest of Exmouth, was awarded to Shell Development (Australia) Pty Ltd.

• WA-496-P, located 350 km northwest of Broome, was award-ed to Woodside Energy Limited and Mitsui E&P Australia Pty Ltd. In state waters, EP483 in the offshore Carnarvon Basin was

awarded to Finder No. 3 Proprietary Limited. In January 2013, EP484 and EP485 in the Perth and Southern Carnarvon basins were awarded to Dynasty Metals Australia Limited. Several prospecting licences were awarded to companies in the South Carnarvon and Ord basins. These give companies the option to carry out some work to assess potential before a longer term commitment to exploration acreage is undertaken.

In the NT, 16 petroleum titles were awarded:• three were awarded to Tamboran (EP164, EP165 and EP166);• four were awarded to Pangaea (EP167, EP168, EP169 and

EP198);

")

")

")

")

")

")

")

")

Perth

Sydney

Hobart

Darwin

Canberra

Brisbane

Adelaide

MelbourneLegendGazettal, Available

Gazettal, Under application

Exploration Permit

Under application

Relinquishing

Renewing

Suspended

Production Licence

Retention Licence

Figure 1. The acreage situation in Australia at the end of 2013.

APPEA Journal 2014—3Third proof—Johns 27 february 2014

2013 pesa industry review: exploration

• two each were awarded to Armour (EP191 and EP192) and Tom Oates (EP300 and EP301); and,

• the remainder single licences were awarded to Territory Oil and Gas (NTC/P10), Conarco Minerals (EP144), Minerals Australia/Jacaranda Minerals (EP153), Imperial Oil and Gas (EP184), and Paltar Petroleum (EP232).Blue Energy farmed in to Australian Oil and Gas Limited’s

acreage position in the Wiso Basin (Blue Energy, 2013a).In Victoria two petroleum permits PEP150 (Origin/Mawson

Petroleum) and PEP171 (Beach Energy /Somerton Energy) were awarded during the year.

In SA in 2012, one block in the Cooper Basin (CO2012-A) and one block in the Otway Basin (OT2012-A) were released. In May Bridgeport Energy was named as the winning bidder for acreage release block CO2012-A and NP Oil and Gas Holdings Ltd (a sub-sidiary of UK-based Northern Petroleum) was announced as the successful bidder for the exploration licence in the Otway Basin.

In Queensland acreage was released under competitive tender and competitive cash bidding processes initiated by the Queensland Government. The full results are still to be an-nounced but a total of 24 authority to prospects (ATPs) were awarded across the state during the year.

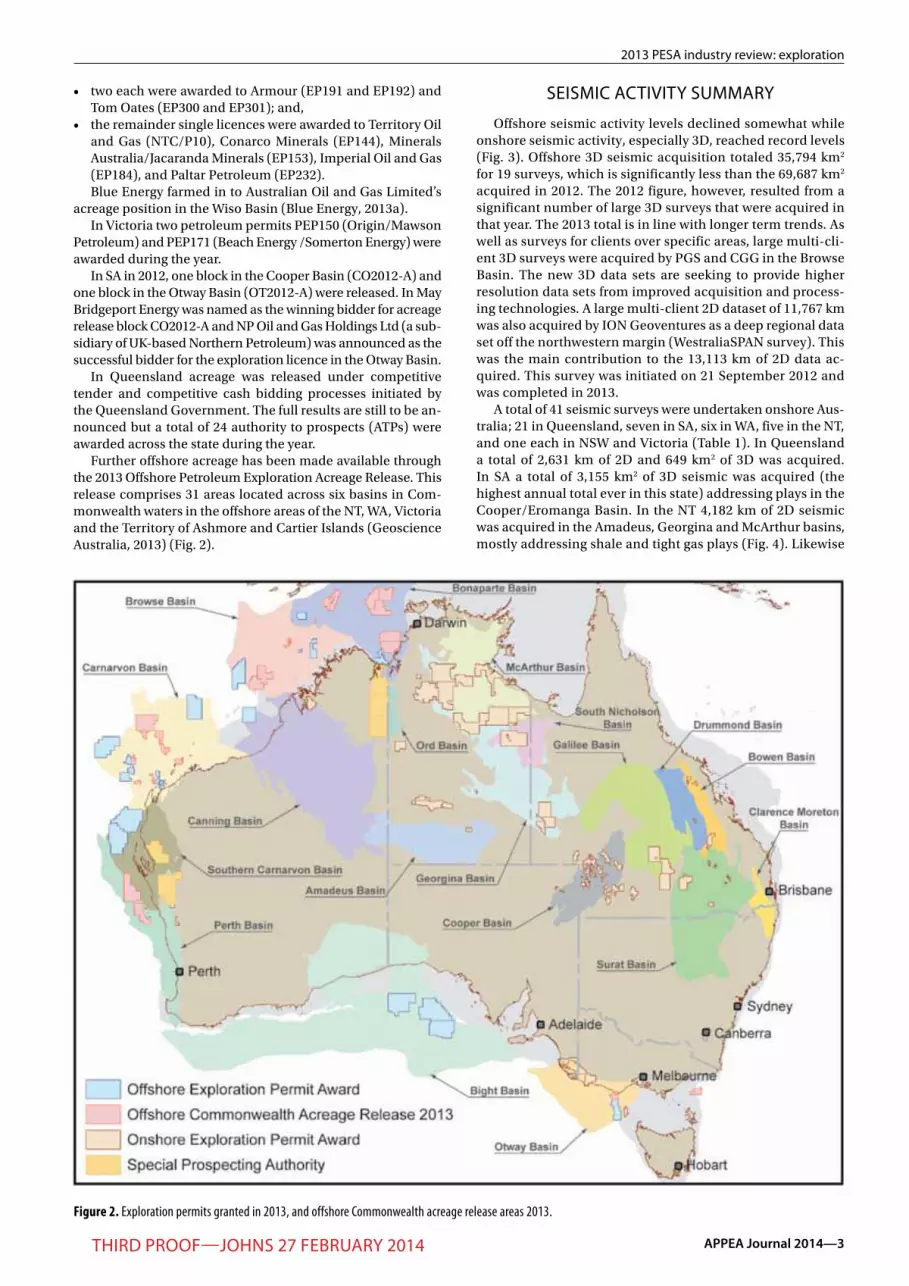

Further offshore acreage has been made available through the 2013 Offshore Petroleum Exploration Acreage Release. This release comprises 31 areas located across six basins in Com-monwealth waters in the offshore areas of the NT, WA, Victoria and the Territory of Ashmore and Cartier Islands (Geoscience Australia, 2013) (Fig. 2).

seisMiC aCTiViTy suMMary

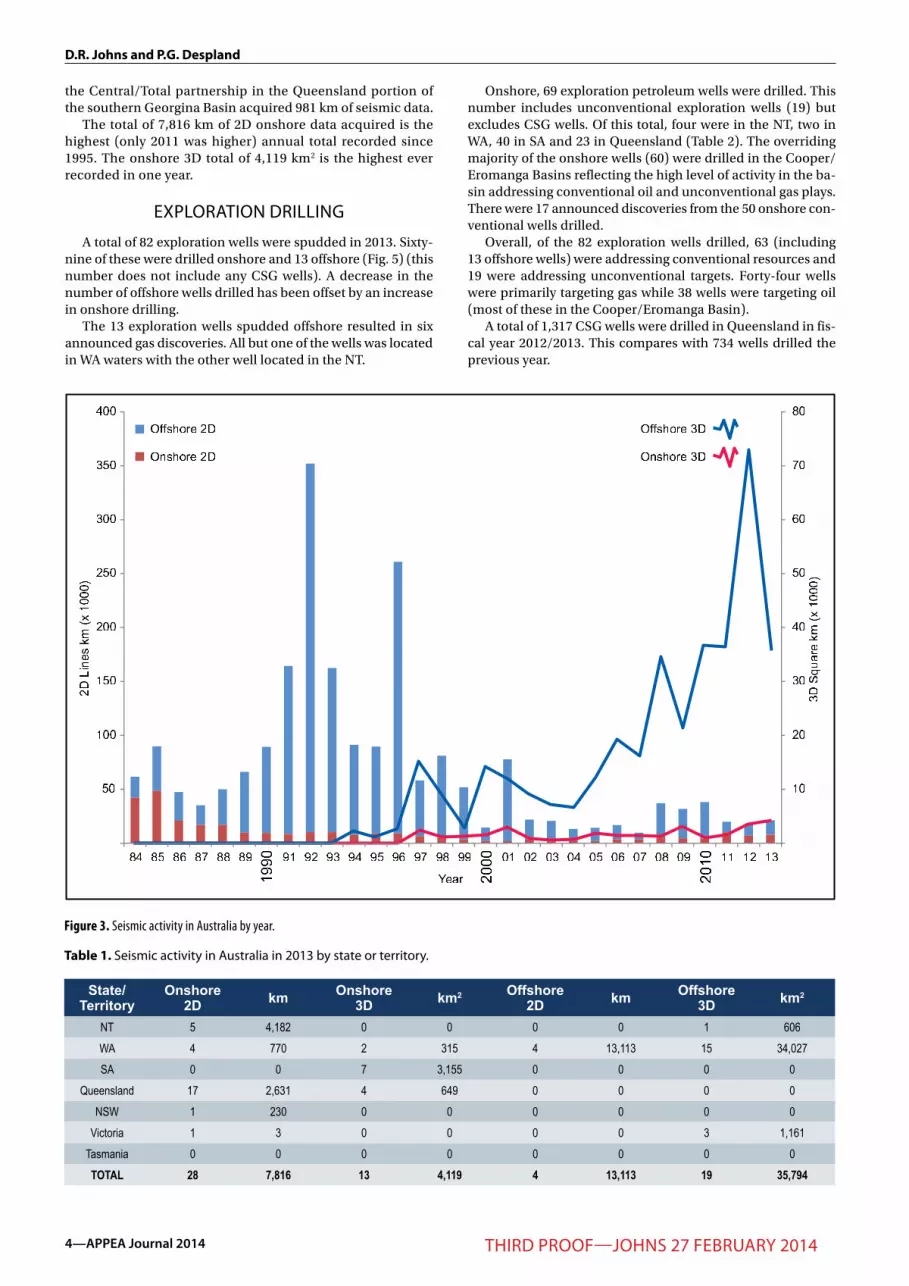

Offshore seismic activity levels declined somewhat while onshore seismic activity, especially 3D, reached record levels (Fig. 3). Offshore 3D seismic acquisition totaled 35,794 km2 for 19 surveys, which is significantly less than the 69,687 km2 acquired in 2012. The 2012 figure, however, resulted from a significant number of large 3D surveys that were acquired in that year. The 2013 total is in line with longer term trends. As well as surveys for clients over specific areas, large multi-cli-ent 3D surveys were acquired by PGS and CGG in the Browse Basin. The new 3D data sets are seeking to provide higher resolution data sets from improved acquisition and process-ing technologies. A large multi-client 2D dataset of 11,767 km was also acquired by ION Geoventures as a deep regional data set off the northwestern margin (WestraliaSPAN survey). This was the main contribution to the 13,113 km of 2D data ac-quired. This survey was initiated on 21 September 2012 and was completed in 2013.

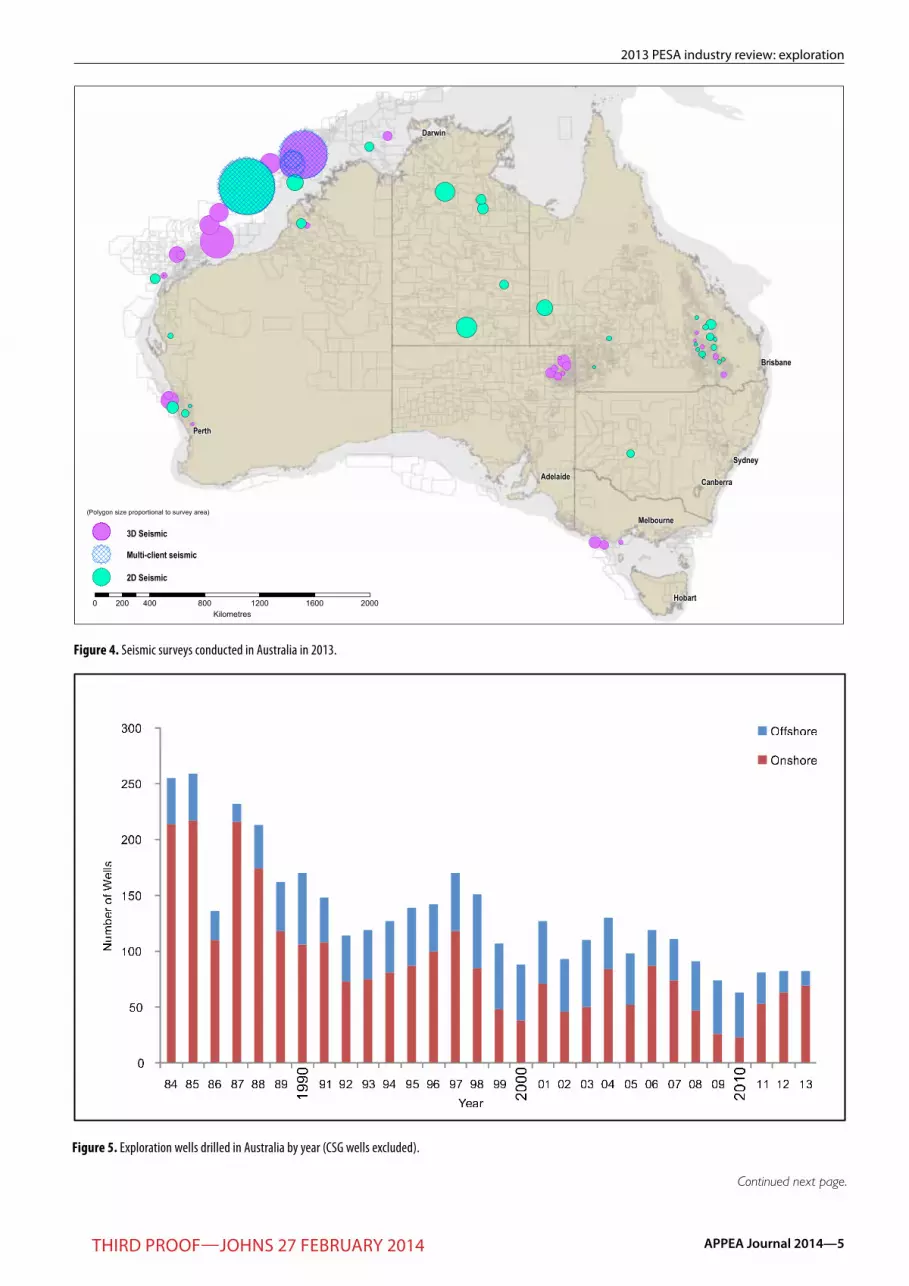

A total of 41 seismic surveys were undertaken onshore Aus-tralia; 21 in Queensland, seven in SA, six in WA, five in the NT, and one each in NSW and Victoria (Table 1). In Queensland a total of 2,631 km of 2D and 649 km2 of 3D was acquired. In SA a total of 3,155 km2 of 3D seismic was acquired (the highest annual total ever in this state) addressing plays in the Cooper/Eromanga Basin. In the NT 4,182 km of 2D seismic was acquired in the Amadeus, Georgina and McArthur basins, mostly addressing shale and tight gas plays (Fig. 4). Likewise

Figure 2. Exploration permits granted in 2013, and offshore Commonwealth acreage release areas 2013.

4—APPEA Journal 2014 Third proof—Johns 27 february 2014

D.R. Johns and P.G. Despland

the Central/Total partnership in the Queensland portion of the southern Georgina Basin acquired 981 km of seismic data.

The total of 7,816 km of 2D onshore data acquired is the highest (only 2011 was higher) annual total recorded since 1995. The onshore 3D total of 4,119 km2 is the highest ever recorded in one year.

eXpLoraTion driLLinG

A total of 82 exploration wells were spudded in 2013. Sixty-nine of these were drilled onshore and 13 offshore (Fig. 5) (this number does not include any CSG wells). A decrease in the number of offshore wells drilled has been offset by an increase in onshore drilling.

The 13 exploration wells spudded offshore resulted in six announced gas discoveries. All but one of the wells was located in WA waters with the other well located in the NT.

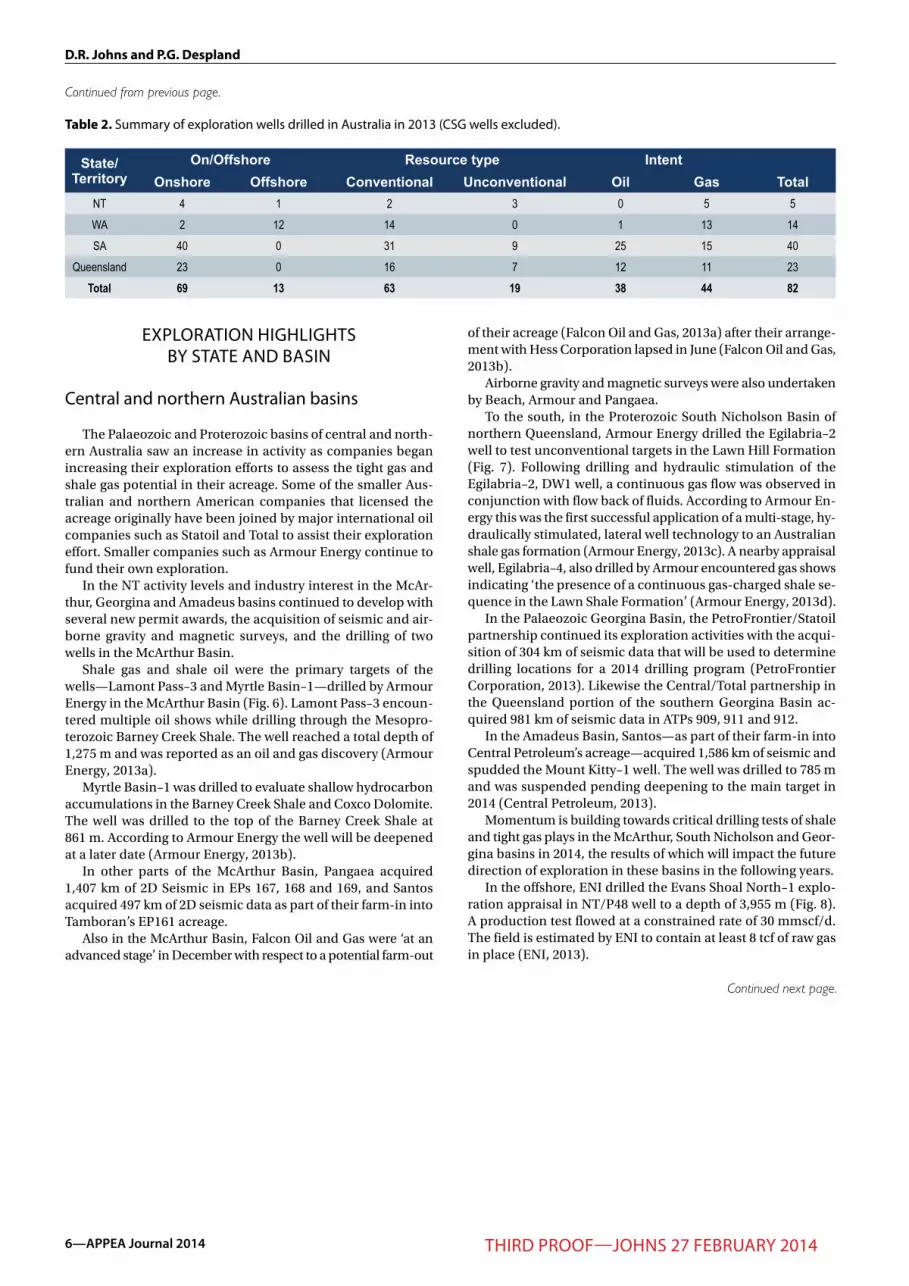

Onshore, 69 exploration petroleum wells were drilled. This number includes unconventional exploration wells (19) but excludes CSG wells. Of this total, four were in the NT, two in WA, 40 in SA and 23 in Queensland (Table 2). The overriding majority of the onshore wells (60) were drilled in the Cooper/Eromanga Basins reflecting the high level of activity in the ba-sin addressing conventional oil and unconventional gas plays. There were 17 announced discoveries from the 50 onshore con-ventional wells drilled.

Overall, of the 82 exploration wells drilled, 63 (including 13 offshore wells) were addressing conventional resources and 19 were addressing unconventional targets. Forty-four wells were primarily targeting gas while 38 wells were targeting oil (most of these in the Cooper/Eromanga Basin).

A total of 1,317 CSG wells were drilled in Queensland in fis-cal year 2012/2013. This compares with 734 wells drilled the previous year.

Figure 3. Seismic activity in Australia by year.

State/ Territory

Onshore 2D km Onshore

3D km2 Offshore 2D km Offshore

3D km2

NT 5 4,182 0 0 0 0 1 606WA 4 770 2 315 4 13,113 15 34,027SA 0 0 7 3,155 0 0 0 0

Queensland 17 2,631 4 649 0 0 0 0NSW 1 230 0 0 0 0 0 0

Victoria 1 3 0 0 0 0 3 1,161Tasmania 0 0 0 0 0 0 0 0TOTAL 28 7,816 13 4,119 4 13,113 19 35,794

Table 1. seismic activity in australia in 2013 by state or territory.

APPEA Journal 2014—5Third proof—Johns 27 february 2014

2013 pesa industry review: exploration

")

")

")

")

")

")

")

")

Perth

Sydney

Hobart

Darwin

Canberra

Brisbane

Adelaide

Melbourne

0 400 800 1200 1600 2000200Kilometres

3D Seismic

Multi-client seismic

(Polygon size proportional to survey area)

2D Seismic

Figure 4. Seismic surveys conducted in Australia in 2013.

Figure 5. Exploration wells drilled in Australia by year (CSG wells excluded).

Continued next page.

6—APPEA Journal 2014 Third proof—Johns 27 february 2014

D.R. Johns and P.G. Despland

eXpLoraTion hiGhLiGhTs by sTaTe and basin

Central and northern australian basins

The Palaeozoic and Proterozoic basins of central and north-ern Australia saw an increase in activity as companies began increasing their exploration efforts to assess the tight gas and shale gas potential in their acreage. Some of the smaller Aus-tralian and northern American companies that licensed the acreage originally have been joined by major international oil companies such as Statoil and Total to assist their exploration effort. Smaller companies such as Armour Energy continue to fund their own exploration.

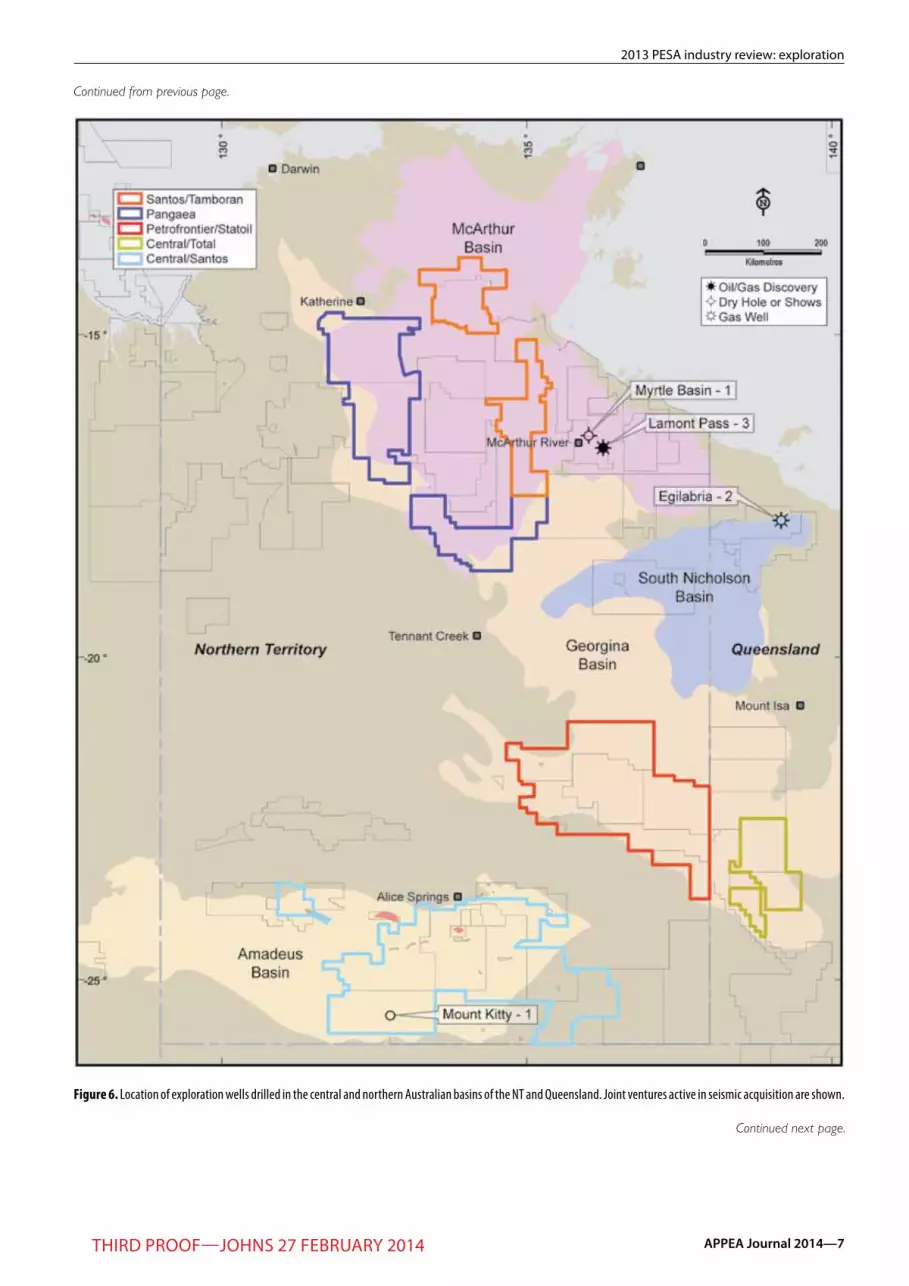

In the NT activity levels and industry interest in the McAr-thur, Georgina and Amadeus basins continued to develop with several new permit awards, the acquisition of seismic and air-borne gravity and magnetic surveys, and the drilling of two wells in the McArthur Basin.

Shale gas and shale oil were the primary targets of the wells—Lamont Pass–3 and Myrtle Basin–1—drilled by Armour Energy in the McArthur Basin (Fig. 6). Lamont Pass–3 encoun-tered multiple oil shows while drilling through the Mesopro-terozoic Barney Creek Shale. The well reached a total depth of 1,275 m and was reported as an oil and gas discovery (Armour Energy, 2013a).

Myrtle Basin–1 was drilled to evaluate shallow hydrocarbon accumulations in the Barney Creek Shale and Coxco Dolomite. The well was drilled to the top of the Barney Creek Shale at 861 m. According to Armour Energy the well will be deepened at a later date (Armour Energy, 2013b).

In other parts of the McArthur Basin, Pangaea acquired 1,407 km of 2D Seismic in EPs 167, 168 and 169, and Santos acquired 497 km of 2D seismic data as part of their farm-in into Tamboran’s EP161 acreage.

Also in the McArthur Basin, Falcon Oil and Gas were ‘at an advanced stage’ in December with respect to a potential farm-out

of their acreage (Falcon Oil and Gas, 2013a) after their arrange-ment with Hess Corporation lapsed in June (Falcon Oil and Gas, 2013b).

Airborne gravity and magnetic surveys were also undertaken by Beach, Armour and Pangaea.

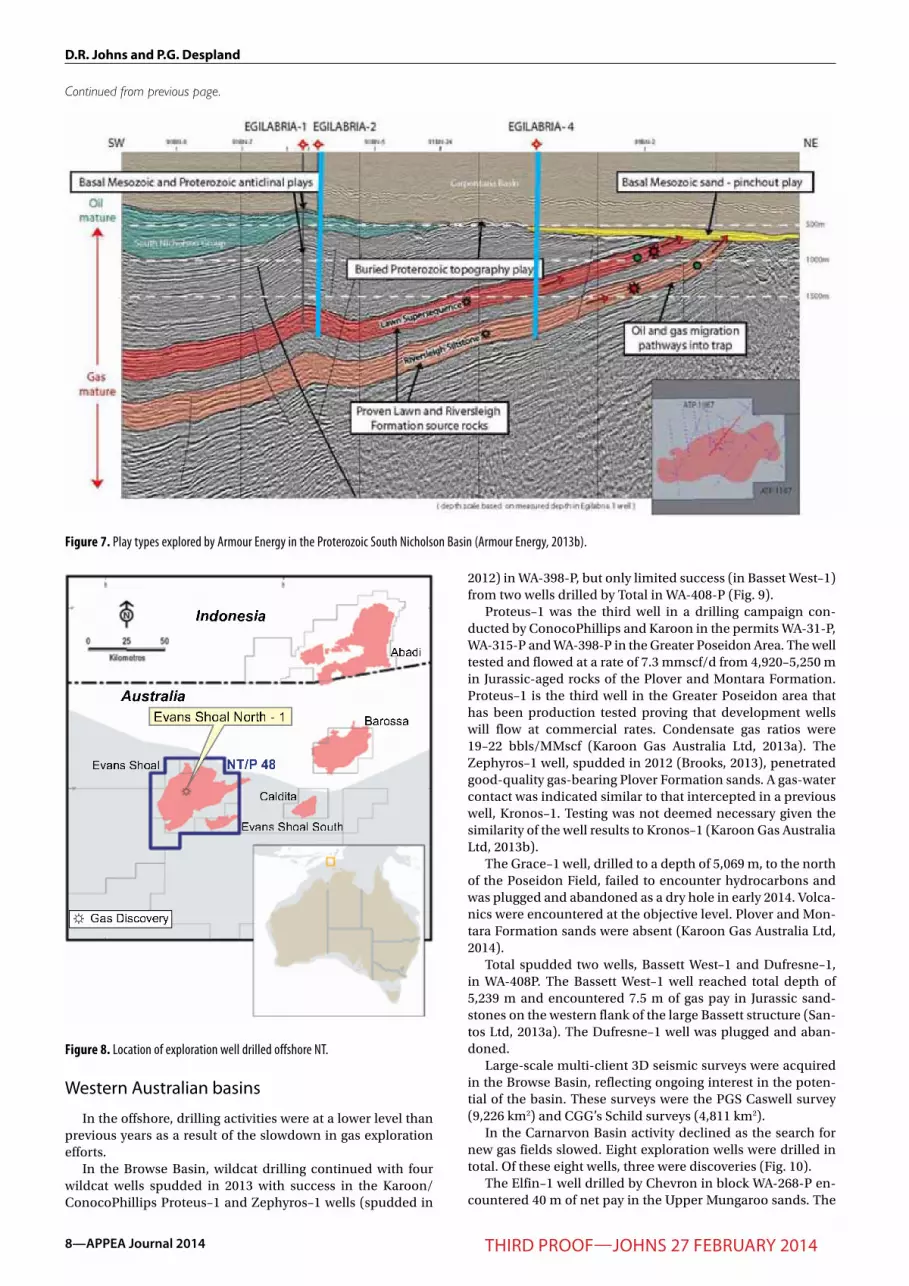

To the south, in the Proterozoic South Nicholson Basin of northern Queensland, Armour Energy drilled the Egilabria–2 well to test unconventional targets in the Lawn Hill Formation (Fig. 7). Following drilling and hydraulic stimulation of the Egilabria–2, DW1 well, a continuous gas flow was observed in conjunction with flow back of fluids. According to Armour En-ergy this was the first successful application of a multi-stage, hy-draulically stimulated, lateral well technology to an Australian shale gas formation (Armour Energy, 2013c). A nearby appraisal well, Egilabria–4, also drilled by Armour encountered gas shows indicating ‘the presence of a continuous gas-charged shale se-quence in the Lawn Shale Formation’ (Armour Energy, 2013d).

In the Palaeozoic Georgina Basin, the PetroFrontier/Statoil partnership continued its exploration activities with the acqui-sition of 304 km of seismic data that will be used to determine drilling locations for a 2014 drilling program (PetroFrontier Corporation, 2013). Likewise the Central/Total partnership in the Queensland portion of the southern Georgina Basin ac-quired 981 km of seismic data in ATPs 909, 911 and 912.

In the Amadeus Basin, Santos—as part of their farm-in into Central Petroleum’s acreage—acquired 1,586 km of seismic and spudded the Mount Kitty–1 well. The well was drilled to 785 m and was suspended pending deepening to the main target in 2014 (Central Petroleum, 2013).

Momentum is building towards critical drilling tests of shale and tight gas plays in the McArthur, South Nicholson and Geor-gina basins in 2014, the results of which will impact the future direction of exploration in these basins in the following years.

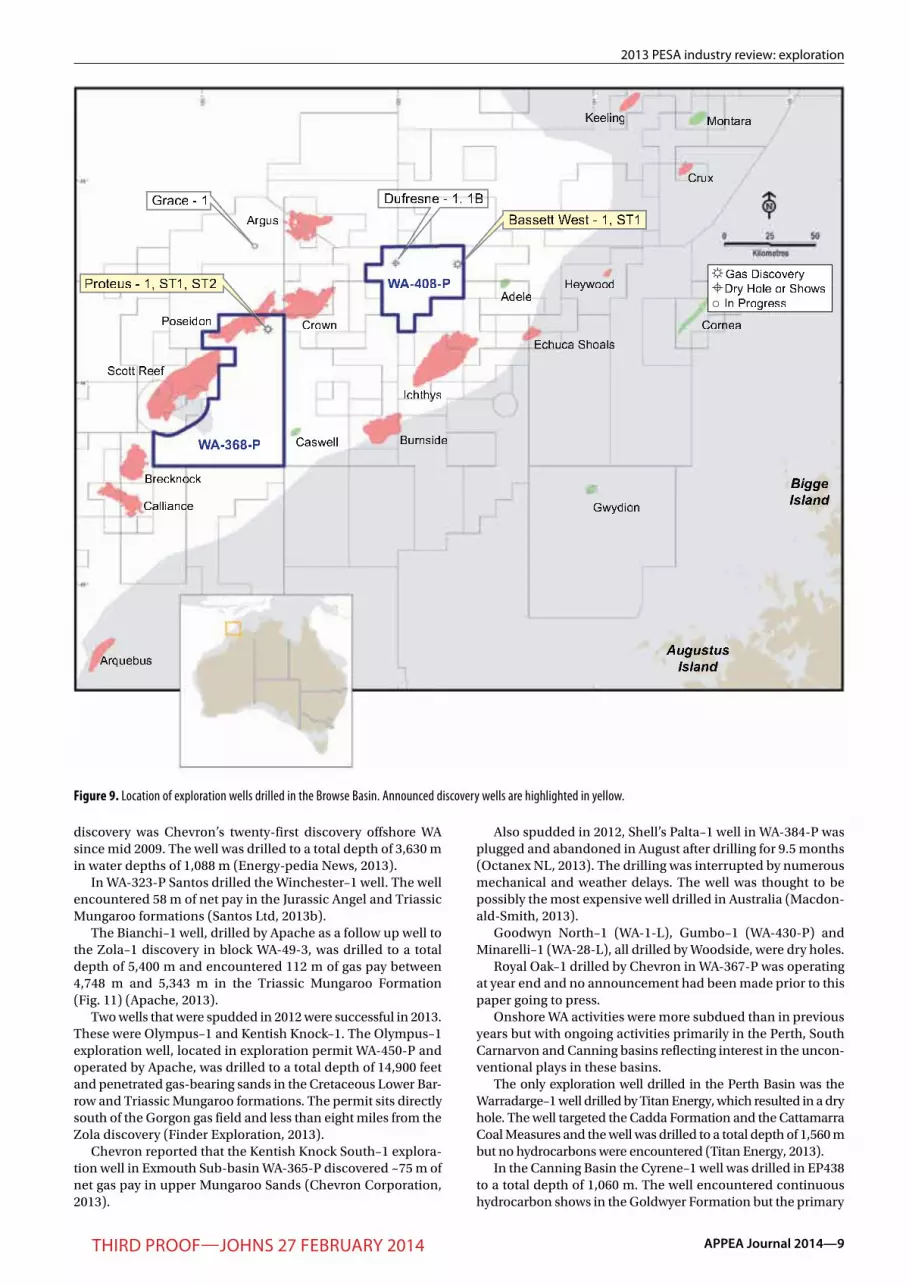

In the offshore, ENI drilled the Evans Shoal North–1 explo-ration appraisal in NT/P48 well to a depth of 3,955 m (Fig. 8). A production test flowed at a constrained rate of 30 mmscf/d. The field is estimated by ENI to contain at least 8 tcf of raw gas in place (ENI, 2013).

State/Territory

On/Offshore Resource type IntentOnshore Offshore Conventional Unconventional Oil Gas Total

NT 4 1 2 3 0 5 5WA 2 12 14 0 1 13 14SA 40 0 31 9 25 15 40

Queensland 23 0 16 7 12 11 23Total 69 13 63 19 38 44 82

Table 2. summary of exploration wells drilled in australia in 2013 (CsG wells excluded).

Continued from previous page.

Continued next page.

APPEA Journal 2014—7Third proof—Johns 27 february 2014

2013 pesa industry review: exploration

Continued from previous page.

Figure 6. Location of exploration wells drilled in the central and northern Australian basins of the NT and Queensland. Joint ventures active in seismic acquisition are shown.

Continued next page.

8—APPEA Journal 2014 Third proof—Johns 27 february 2014

D.R. Johns and P.G. Despland

Western australian basins

In the offshore, drilling activities were at a lower level than previous years as a result of the slowdown in gas exploration efforts.

In the Browse Basin, wildcat drilling continued with four wildcat wells spudded in 2013 with success in the Karoon/ConocoPhillips Proteus–1 and Zephyros–1 wells (spudded in

2012) in WA-398-P, but only limited success (in Basset West–1) from two wells drilled by Total in WA-408-P (Fig. 9).

Proteus–1 was the third well in a drilling campaign con-ducted by ConocoPhillips and Karoon in the permits WA-31-P, WA-315-P and WA-398-P in the Greater Poseidon Area. The well tested and flowed at a rate of 7.3 mmscf/d from 4,920–5,250 m in Jurassic-aged rocks of the Plover and Montara Formation. Proteus–1 is the third well in the Greater Poseidon area that has been production tested proving that development wells will flow at commercial rates. Condensate gas ratios were 19–22 bbls/MMscf (Karoon Gas Australia Ltd, 2013a). The Zephyros–1 well, spudded in 2012 (Brooks, 2013), penetrated good-quality gas-bearing Plover Formation sands. A gas-water contact was indicated similar to that intercepted in a previous well, Kronos–1. Testing was not deemed necessary given the similarity of the well results to Kronos–1 (Karoon Gas Australia Ltd, 2013b).

The Grace–1 well, drilled to a depth of 5,069 m, to the north of the Poseidon Field, failed to encounter hydrocarbons and was plugged and abandoned as a dry hole in early 2014. Volca-nics were encountered at the objective level. Plover and Mon-tara Formation sands were absent (Karoon Gas Australia Ltd, 2014).

Total spudded two wells, Bassett West–1 and Dufresne–1, in WA-408P. The Bassett West–1 well reached total depth of 5,239 m and encountered 7.5 m of gas pay in Jurassic sand-stones on the western flank of the large Bassett structure (San-tos Ltd, 2013a). The Dufresne–1 well was plugged and aban-doned.

Large-scale multi-client 3D seismic surveys were acquired in the Browse Basin, reflecting ongoing interest in the poten-tial of the basin. These surveys were the PGS Caswell survey (9,226 km2) and CGG’s Schild surveys (4,811 km2).

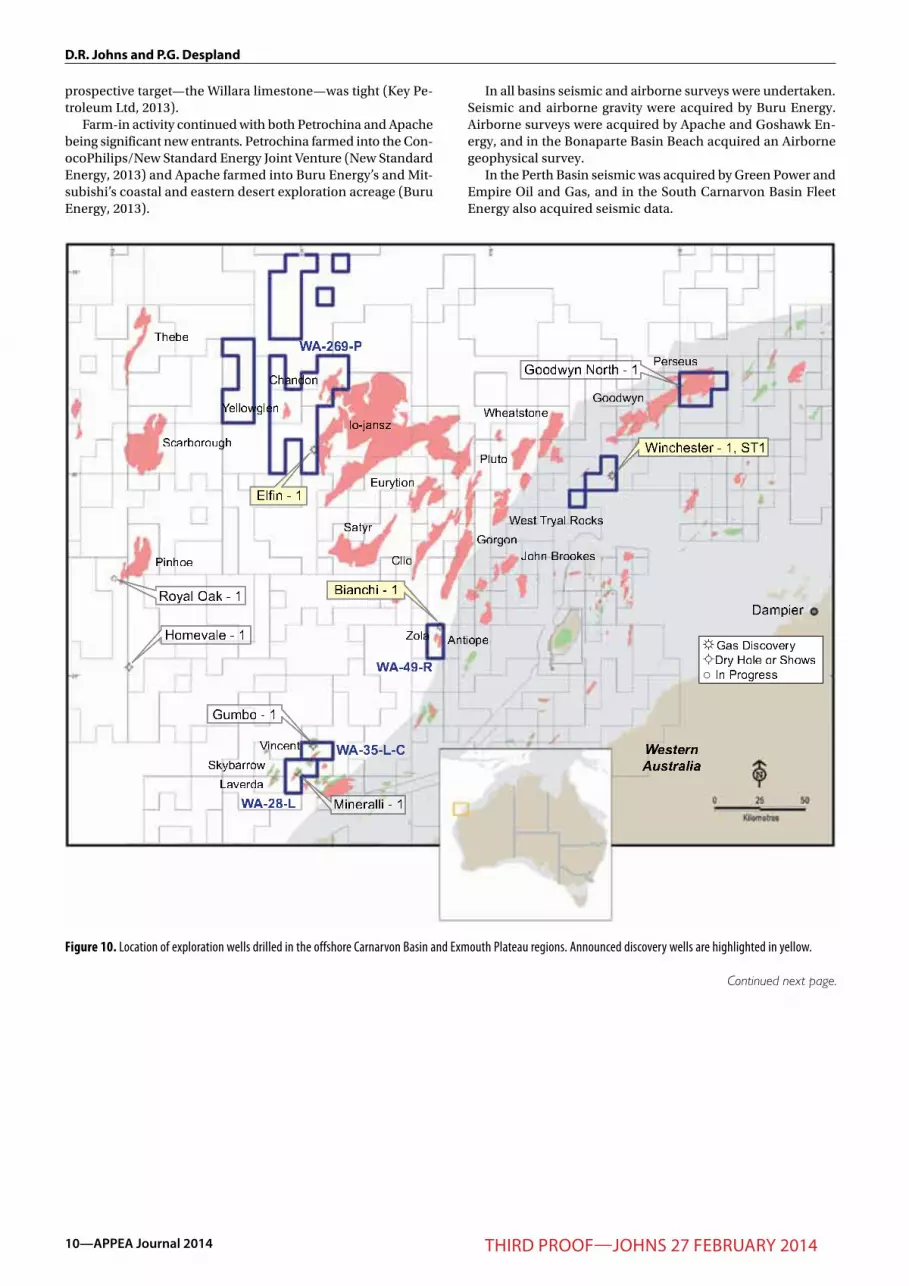

In the Carnarvon Basin activity declined as the search for new gas fields slowed. Eight exploration wells were drilled in total. Of these eight wells, three were discoveries (Fig. 10).

The Elfin–1 well drilled by Chevron in block WA-268-P en-countered 40 m of net pay in the Upper Mungaroo sands. The

Figure 7. Play types explored by Armour Energy in the Proterozoic South Nicholson Basin (Armour Energy, 2013b).

Figure 8. Location of exploration well drilled offshore NT.

Continued from previous page.

APPEA Journal 2014—9Third proof—Johns 27 february 2014

2013 pesa industry review: exploration

discovery was Chevron’s twenty-first discovery offshore WA since mid 2009. The well was drilled to a total depth of 3,630 m in water depths of 1,088 m (Energy-pedia News, 2013).

In WA-323-P Santos drilled the Winchester–1 well. The well encountered 58 m of net pay in the Jurassic Angel and Triassic Mungaroo formations (Santos Ltd, 2013b).

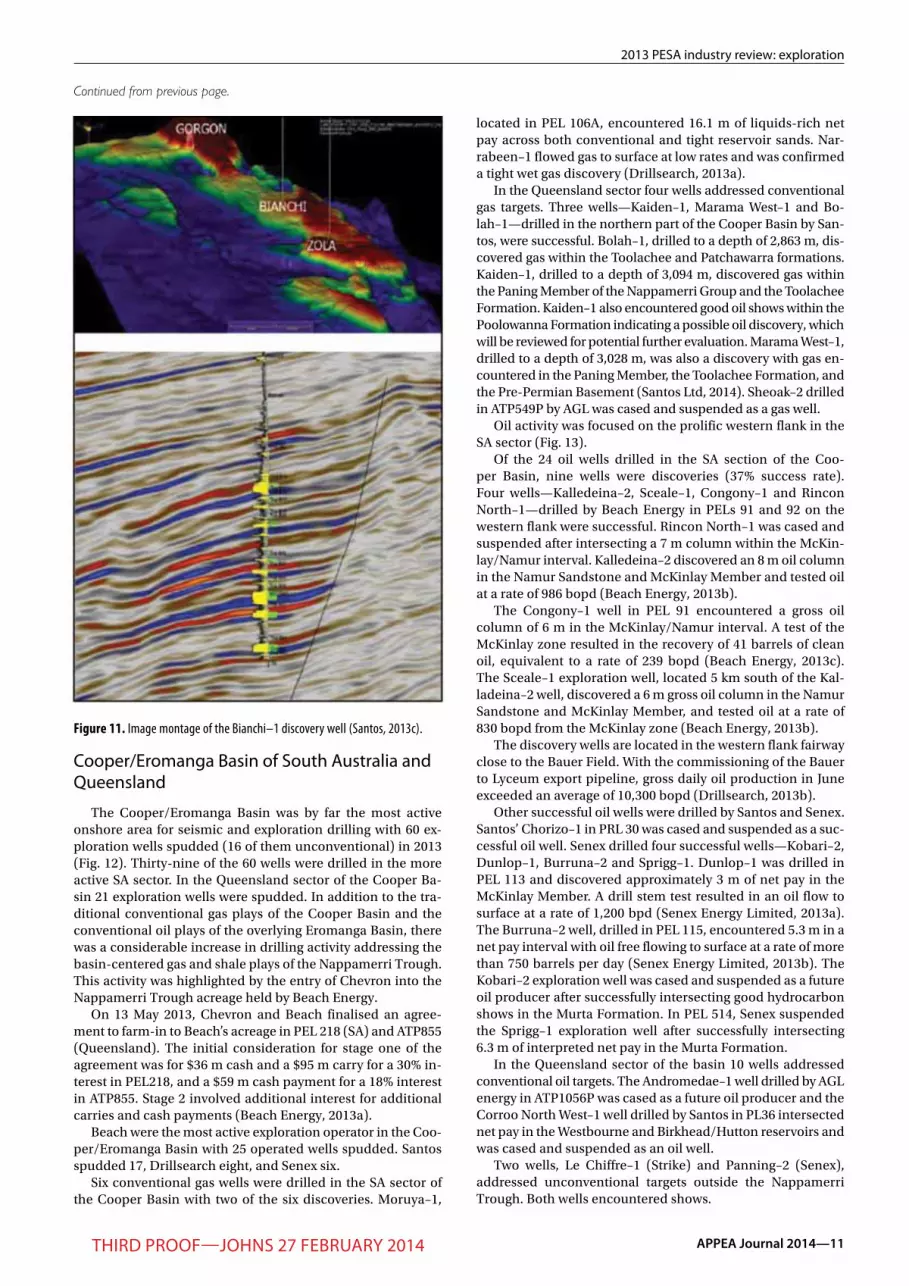

The Bianchi–1 well, drilled by Apache as a follow up well to the Zola–1 discovery in block WA-49-3, was drilled to a total depth of 5,400 m and encountered 112 m of gas pay between 4,748 m and 5,343 m in the Triassic Mungaroo Formation (Fig. 11) (Apache, 2013).

Two wells that were spudded in 2012 were successful in 2013. These were Olympus–1 and Kentish Knock–1. The Olympus–1 exploration well, located in exploration permit WA-450-P and operated by Apache, was drilled to a total depth of 14,900 feet and penetrated gas-bearing sands in the Cretaceous Lower Bar-row and Triassic Mungaroo formations. The permit sits directly south of the Gorgon gas field and less than eight miles from the Zola discovery (Finder Exploration, 2013).

Chevron reported that the Kentish Knock South–1 explora-tion well in Exmouth Sub-basin WA-365-P discovered ~75 m of net gas pay in upper Mungaroo Sands (Chevron Corporation, 2013).

Also spudded in 2012, Shell’s Palta–1 well in WA-384-P was plugged and abandoned in August after drilling for 9.5 months (Octanex NL, 2013). The drilling was interrupted by numerous mechanical and weather delays. The well was thought to be possibly the most expensive well drilled in Australia (Macdon-ald-Smith, 2013).

Goodwyn North–1 (WA-1-L), Gumbo–1 (WA-430-P) and Minarelli–1 (WA-28-L), all drilled by Woodside, were dry holes.

Royal Oak–1 drilled by Chevron in WA-367-P was operating at year end and no announcement had been made prior to this paper going to press.

Onshore WA activities were more subdued than in previous years but with ongoing activities primarily in the Perth, South Carnarvon and Canning basins reflecting interest in the uncon-ventional plays in these basins.

The only exploration well drilled in the Perth Basin was the Warradarge–1 well drilled by Titan Energy, which resulted in a dry hole. The well targeted the Cadda Formation and the Cattamarra Coal Measures and the well was drilled to a total depth of 1,560 m but no hydrocarbons were encountered (Titan Energy, 2013).

In the Canning Basin the Cyrene–1 well was drilled in EP438 to a total depth of 1,060 m. The well encountered continuous hydrocarbon shows in the Goldwyer Formation but the primary

Figure 9. Location of exploration wells drilled in the Browse Basin. Announced discovery wells are highlighted in yellow.

10—APPEA Journal 2014 Third proof—Johns 27 february 2014

D.R. Johns and P.G. Despland

prospective target—the Willara limestone—was tight (Key Pe-troleum Ltd, 2013).

Farm-in activity continued with both Petrochina and Apache being significant new entrants. Petrochina farmed into the Con-ocoPhilips/New Standard Energy Joint Venture (New Standard Energy, 2013) and Apache farmed into Buru Energy’s and Mit-subishi’s coastal and eastern desert exploration acreage (Buru Energy, 2013).

In all basins seismic and airborne surveys were undertaken. Seismic and airborne gravity were acquired by Buru Energy. Airborne surveys were acquired by Apache and Goshawk En-ergy, and in the Bonaparte Basin Beach acquired an Airborne geophysical survey.

In the Perth Basin seismic was acquired by Green Power and Empire Oil and Gas, and in the South Carnarvon Basin Fleet Energy also acquired seismic data.

Figure 10. Location of exploration wells drilled in the offshore Carnarvon Basin and Exmouth Plateau regions. Announced discovery wells are highlighted in yellow.

Continued next page.

APPEA Journal 2014—11Third proof—Johns 27 february 2014

2013 pesa industry review: exploration

Cooper/eromanga basin of south australia and Queensland

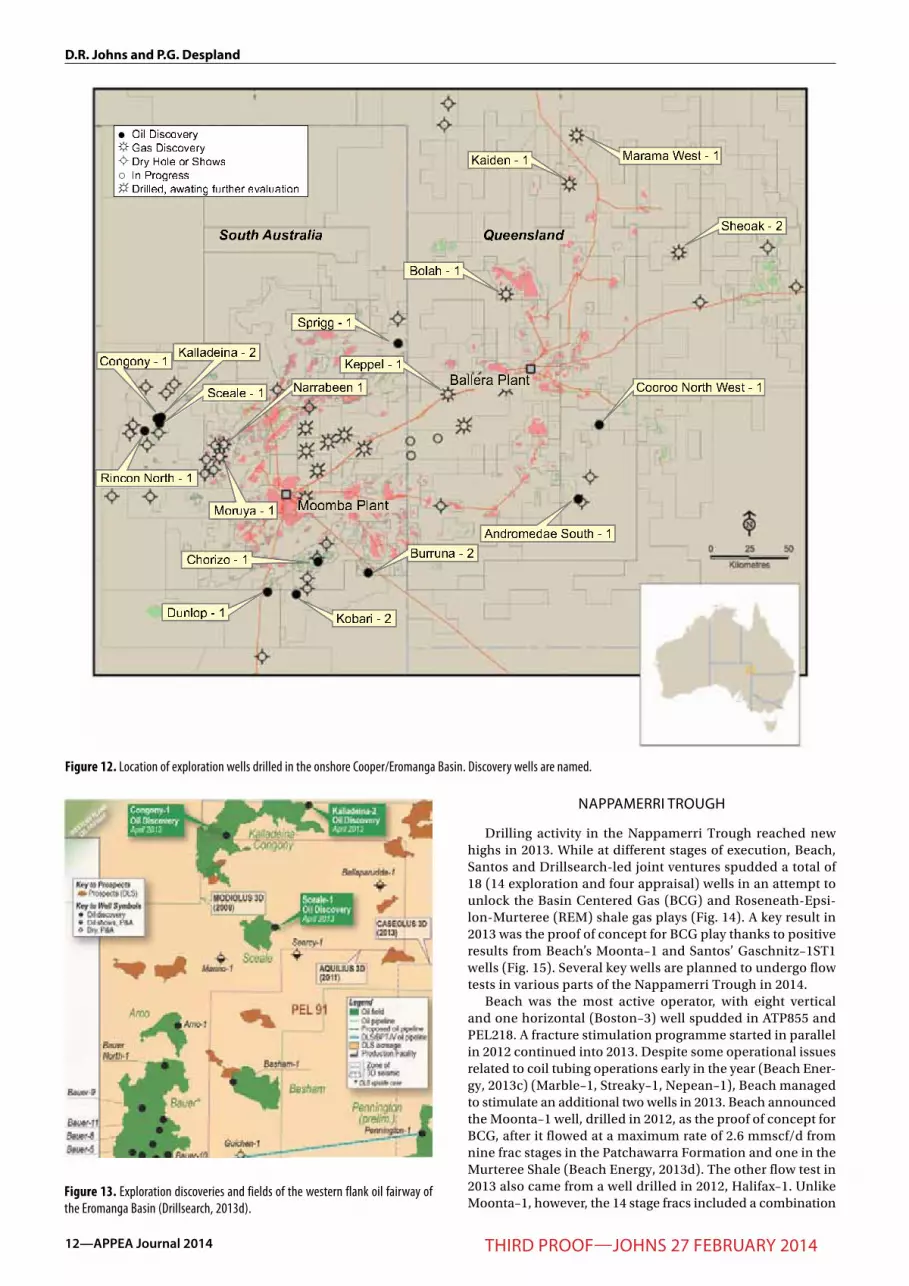

The Cooper/Eromanga Basin was by far the most active onshore area for seismic and exploration drilling with 60 ex-ploration wells spudded (16 of them unconventional) in 2013 (Fig. 12). Thirty-nine of the 60 wells were drilled in the more active SA sector. In the Queensland sector of the Cooper Ba-sin 21 exploration wells were spudded. In addition to the tra-ditional conventional gas plays of the Cooper Basin and the conventional oil plays of the overlying Eromanga Basin, there was a considerable increase in drilling activity addressing the basin-centered gas and shale plays of the Nappamerri Trough. This activity was highlighted by the entry of Chevron into the Nappamerri Trough acreage held by Beach Energy.

On 13 May 2013, Chevron and Beach finalised an agree-ment to farm-in to Beach’s acreage in PEL 218 (SA) and ATP855 (Queensland). The initial consideration for stage one of the agreement was for $36 m cash and a $95 m carry for a 30% in-terest in PEL218, and a $59 m cash payment for a 18% interest in ATP855. Stage 2 involved additional interest for additional carries and cash payments (Beach Energy, 2013a).

Beach were the most active exploration operator in the Coo-per/Eromanga Basin with 25 operated wells spudded. Santos spudded 17, Drillsearch eight, and Senex six.

Six conventional gas wells were drilled in the SA sector of the Cooper Basin with two of the six discoveries. Moruya–1,

located in PEL 106A, encountered 16.1 m of liquids-rich net pay across both conventional and tight reservoir sands. Nar-rabeen–1 flowed gas to surface at low rates and was confirmed a tight wet gas discovery (Drillsearch, 2013a).

In the Queensland sector four wells addressed conventional gas targets. Three wells—Kaiden–1, Marama West–1 and Bo-lah–1—drilled in the northern part of the Cooper Basin by San-tos, were successful. Bolah–1, drilled to a depth of 2,863 m, dis-covered gas within the Toolachee and Patchawarra formations. Kaiden–1, drilled to a depth of 3,094 m, discovered gas within the Paning Member of the Nappamerri Group and the Toolachee Formation. Kaiden–1 also encountered good oil shows within the Poolowanna Formation indicating a possible oil discovery, which will be reviewed for potential further evaluation. Marama West–1, drilled to a depth of 3,028 m, was also a discovery with gas en-countered in the Paning Member, the Toolachee Formation, and the Pre-Permian Basement (Santos Ltd, 2014). Sheoak–2 drilled in ATP549P by AGL was cased and suspended as a gas well.

Oil activity was focused on the prolific western flank in the SA sector (Fig. 13).

Of the 24 oil wells drilled in the SA section of the Coo-per Basin, nine wells were discoveries (37% success rate). Four wells—Kalledeina–2, Sceale–1, Congony–1 and Rincon North–1—drilled by Beach Energy in PELs 91 and 92 on the western flank were successful. Rincon North–1 was cased and suspended after intersecting a 7 m column within the McKin-lay/Namur interval. Kalledeina–2 discovered an 8 m oil column in the Namur Sandstone and McKinlay Member and tested oil at a rate of 986 bopd (Beach Energy, 2013b).

The Congony–1 well in PEL 91 encountered a gross oil column of 6 m in the McKinlay/Namur interval. A test of the McKinlay zone resulted in the recovery of 41 barrels of clean oil, equivalent to a rate of 239 bopd (Beach Energy, 2013c). The Sceale–1 exploration well, located 5 km south of the Kal-ladeina–2 well, discovered a 6 m gross oil column in the Namur Sandstone and McKinlay Member, and tested oil at a rate of 830 bopd from the McKinlay zone (Beach Energy, 2013b).

The discovery wells are located in the western flank fairway close to the Bauer Field. With the commissioning of the Bauer to Lyceum export pipeline, gross daily oil production in June exceeded an average of 10,300 bopd (Drillsearch, 2013b).

Other successful oil wells were drilled by Santos and Senex. Santos’ Chorizo–1 in PRL 30 was cased and suspended as a suc-cessful oil well. Senex drilled four successful wells—Kobari–2, Dunlop–1, Burruna–2 and Sprigg–1. Dunlop–1 was drilled in PEL 113 and discovered approximately 3 m of net pay in the McKinlay Member. A drill stem test resulted in an oil flow to surface at a rate of 1,200 bpd (Senex Energy Limited, 2013a). The Burruna–2 well, drilled in PEL 115, encountered 5.3 m in a net pay interval with oil free flowing to surface at a rate of more than 750 barrels per day (Senex Energy Limited, 2013b). The Kobari–2 exploration well was cased and suspended as a future oil producer after successfully intersecting good hydrocarbon shows in the Murta Formation. In PEL 514, Senex suspended the Sprigg–1 exploration well after successfully intersecting 6.3 m of interpreted net pay in the Murta Formation.

In the Queensland sector of the basin 10 wells addressed conventional oil targets. The Andromedae–1 well drilled by AGL energy in ATP1056P was cased as a future oil producer and the Corroo North West–1 well drilled by Santos in PL36 intersected net pay in the Westbourne and Birkhead/Hutton reservoirs and was cased and suspended as an oil well.

Two wells, Le Chiffre–1 (Strike) and Panning–2 (Senex), addressed unconventional targets outside the Nappamerri Trough. Both wells encountered shows.

Continued from previous page.

Figure 11. Image montage of the Bianchi–1 discovery well (Santos, 2013c).

12—APPEA Journal 2014 Third proof—Johns 27 february 2014

D.R. Johns and P.G. Despland

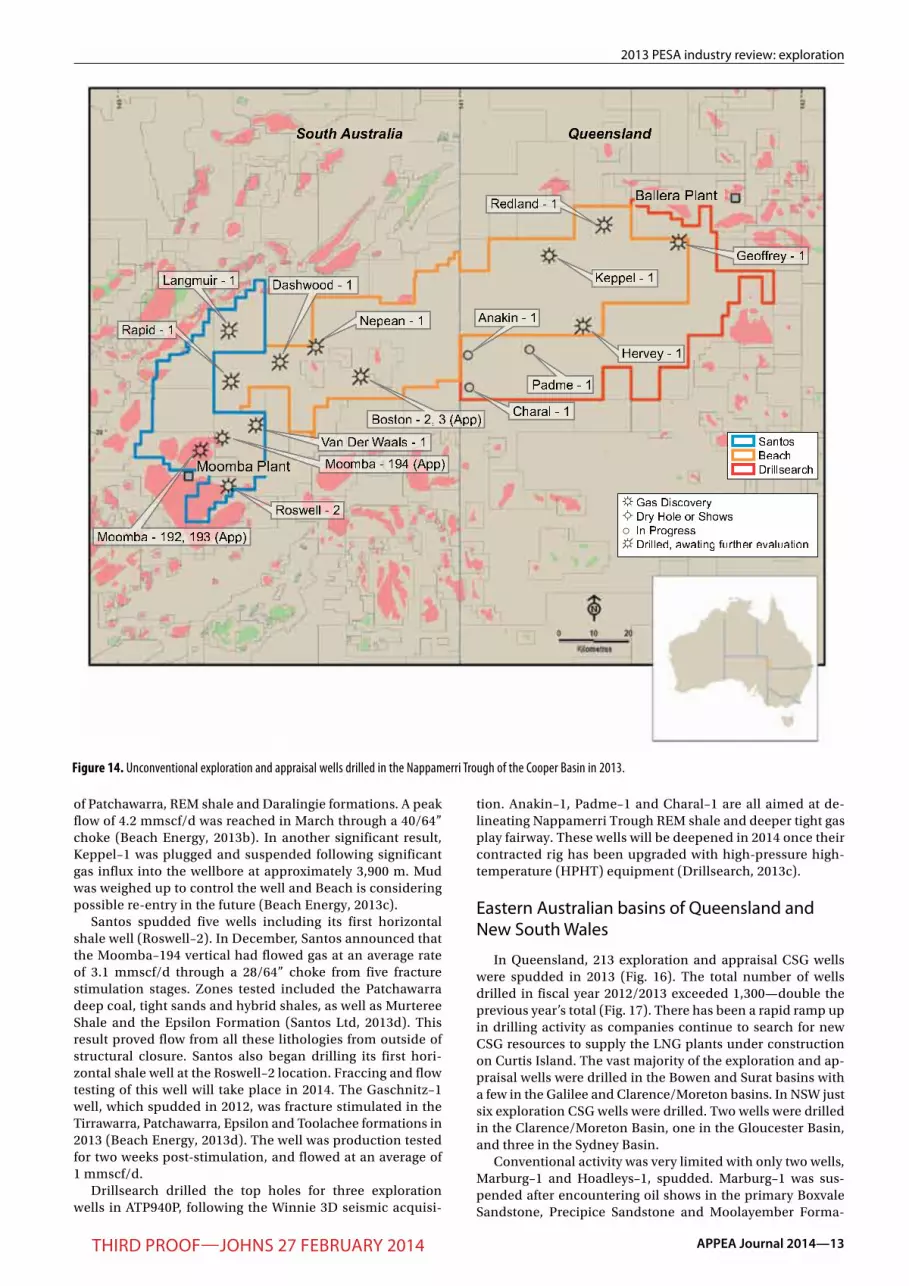

nappaMerri TrouGh

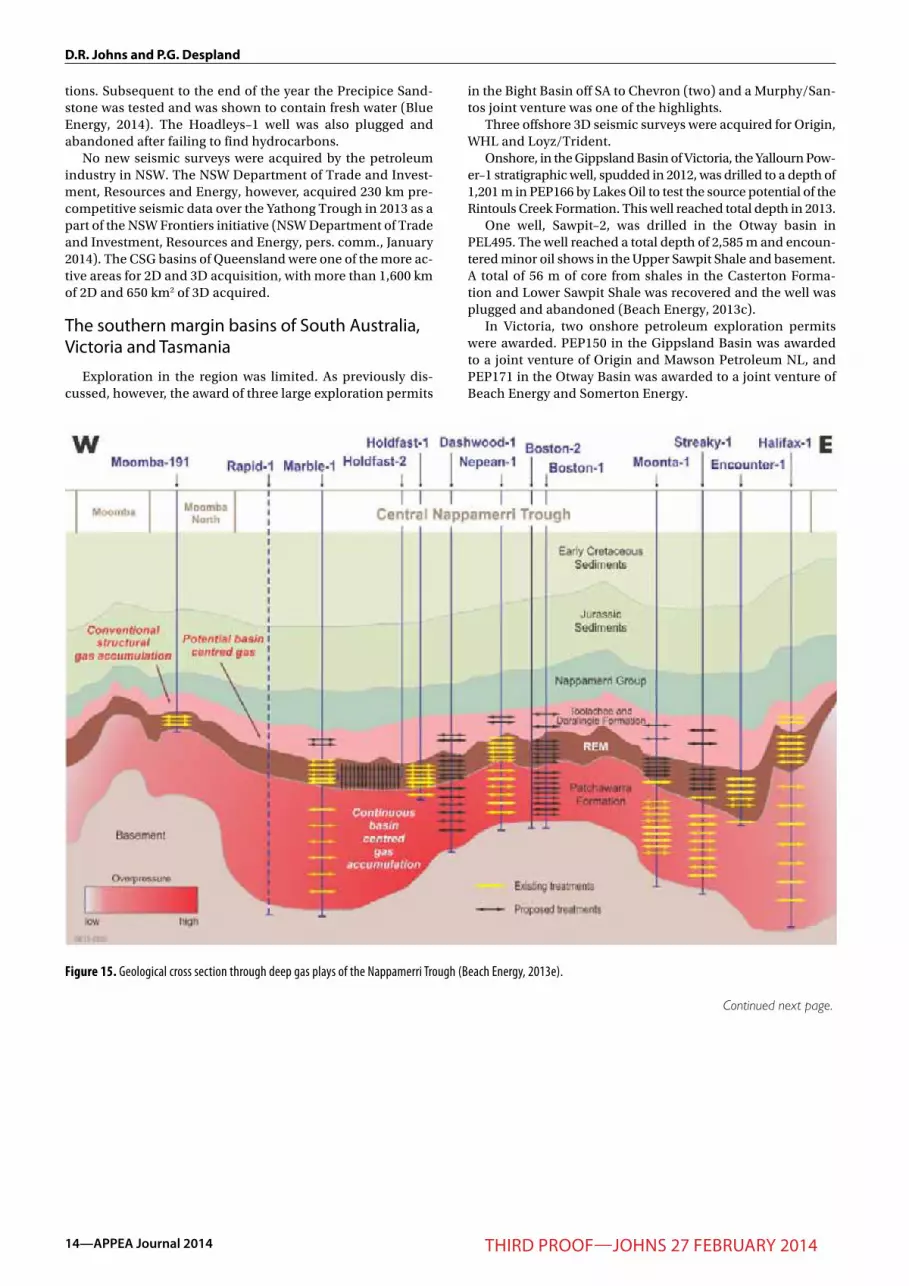

Drilling activity in the Nappamerri Trough reached new highs in 2013. While at different stages of execution, Beach, Santos and Drillsearch-led joint ventures spudded a total of 18 (14 exploration and four appraisal) wells in an attempt to unlock the Basin Centered Gas (BCG) and Roseneath-Epsi-lon-Murteree (REM) shale gas plays (Fig. 14). A key result in 2013 was the proof of concept for BCG play thanks to positive results from Beach’s Moonta–1 and Santos’ Gaschnitz–1ST1 wells (Fig. 15). Several key wells are planned to undergo flow tests in various parts of the Nappamerri Trough in 2014.

Beach was the most active operator, with eight vertical and one horizontal (Boston–3) well spudded in ATP855 and PEL218. A fracture stimulation programme started in parallel in 2012 continued into 2013. Despite some operational issues related to coil tubing operations early in the year (Beach Ener-gy, 2013c) (Marble–1, Streaky–1, Nepean–1), Beach managed to stimulate an additional two wells in 2013. Beach announced the Moonta–1 well, drilled in 2012, as the proof of concept for BCG, after it flowed at a maximum rate of 2.6 mmscf/d from nine frac stages in the Patchawarra Formation and one in the Murteree Shale (Beach Energy, 2013d). The other flow test in 2013 also came from a well drilled in 2012, Halifax–1. Unlike Moonta–1, however, the 14 stage fracs included a combination

Figure 13. Exploration discoveries and fields of the western flank oil fairway of the Eromanga Basin (Drillsearch, 2013d).

Figure 12. Location of exploration wells drilled in the onshore Cooper/Eromanga Basin. Discovery wells are named.

APPEA Journal 2014—13Third proof—Johns 27 february 2014

2013 pesa industry review: exploration

of Patchawarra, REM shale and Daralingie formations. A peak flow of 4.2 mmscf/d was reached in March through a 40/64” choke (Beach Energy, 2013b). In another significant result, Keppel–1 was plugged and suspended following significant gas influx into the wellbore at approximately 3,900 m. Mud was weighed up to control the well and Beach is considering possible re-entry in the future (Beach Energy, 2013c).

Santos spudded five wells including its first horizontal shale well (Roswell–2). In December, Santos announced that the Moomba–194 vertical had flowed gas at an average rate of 3.1 mmscf/d through a 28/64” choke from five fracture stimulation stages. Zones tested included the Patchawarra deep coal, tight sands and hybrid shales, as well as Murteree Shale and the Epsilon Formation (Santos Ltd, 2013d). This result proved flow from all these lithologies from outside of structural closure. Santos also began drilling its first hori-zontal shale well at the Roswell–2 location. Fraccing and flow testing of this well will take place in 2014. The Gaschnitz–1 well, which spudded in 2012, was fracture stimulated in the Tirrawarra, Patchawarra, Epsilon and Toolachee formations in 2013 (Beach Energy, 2013d). The well was production tested for two weeks post-stimulation, and flowed at an average of 1 mmscf/d.

Drillsearch drilled the top holes for three exploration wells in ATP940P, following the Winnie 3D seismic acquisi-

tion. Anakin–1, Padme–1 and Charal–1 are all aimed at de-lineating Nappamerri Trough REM shale and deeper tight gas play fairway. These wells will be deepened in 2014 once their contracted rig has been upgraded with high-pressure high-temperature (HPHT) equipment (Drillsearch, 2013c).

eastern australian basins of Queensland and new south Wales

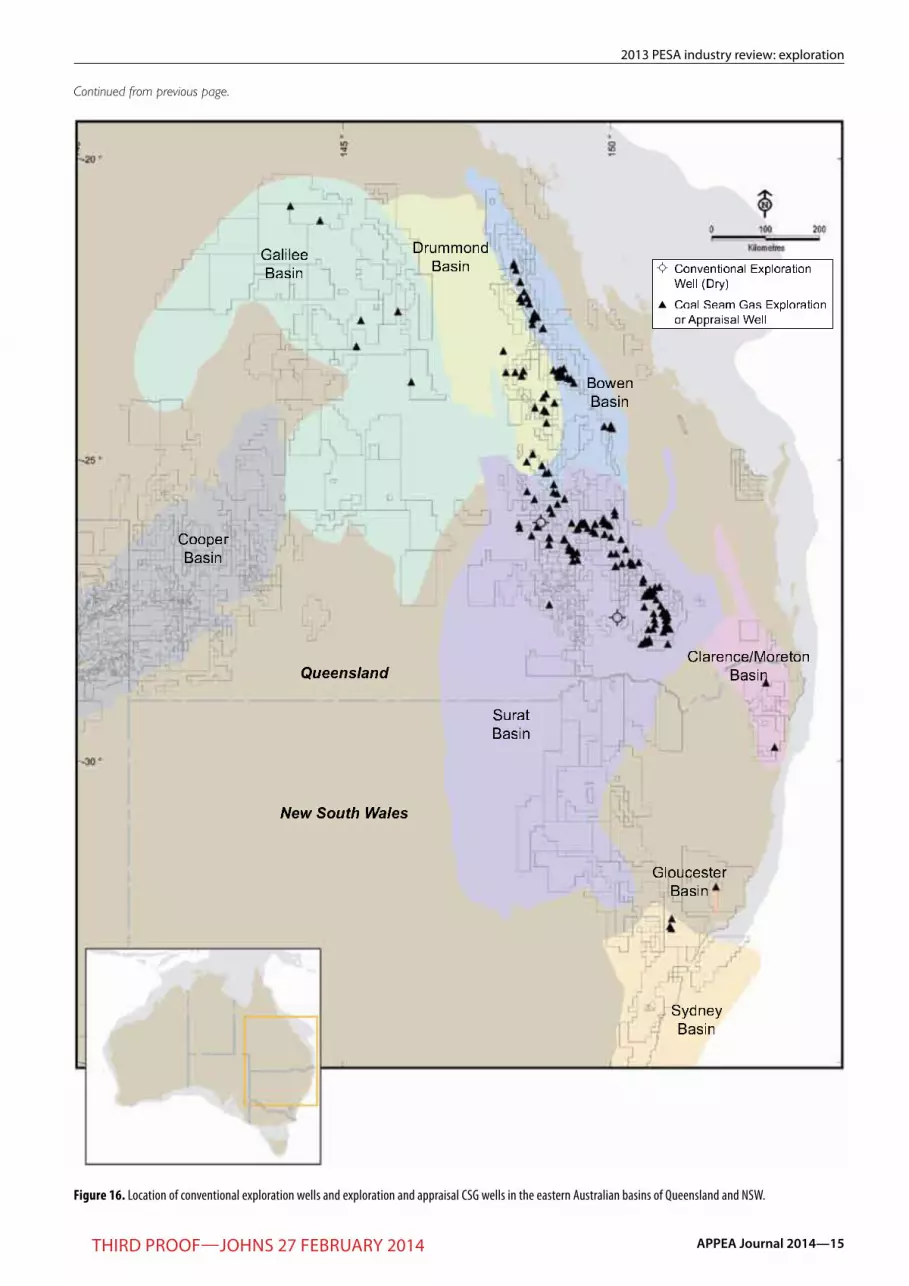

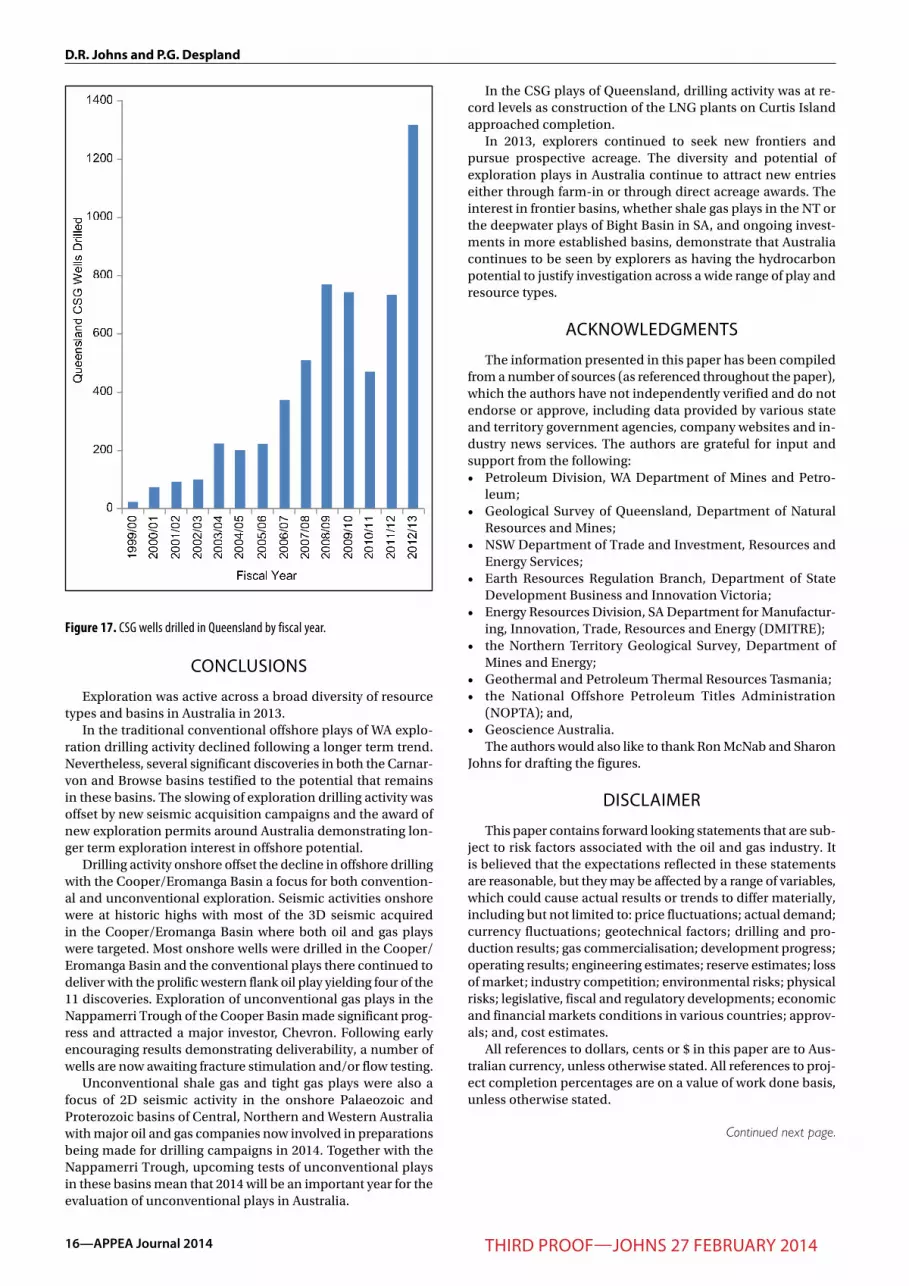

In Queensland, 213 exploration and appraisal CSG wells were spudded in 2013 (Fig. 16). The total number of wells drilled in fiscal year 2012/2013 exceeded 1,300—double the previous year’s total (Fig. 17). There has been a rapid ramp up in drilling activity as companies continue to search for new CSG resources to supply the LNG plants under construction on Curtis Island. The vast majority of the exploration and ap-praisal wells were drilled in the Bowen and Surat basins with a few in the Galilee and Clarence/Moreton basins. In NSW just six exploration CSG wells were drilled. Two wells were drilled in the Clarence/Moreton Basin, one in the Gloucester Basin, and three in the Sydney Basin.

Conventional activity was very limited with only two wells, Marburg–1 and Hoadleys–1, spudded. Marburg–1 was sus-pended after encountering oil shows in the primary Boxvale Sandstone, Precipice Sandstone and Moolayember Forma-

Figure 14. Unconventional exploration and appraisal wells drilled in the Nappamerri Trough of the Cooper Basin in 2013.

14—APPEA Journal 2014 Third proof—Johns 27 february 2014

D.R. Johns and P.G. Despland

tions. Subsequent to the end of the year the Precipice Sand-stone was tested and was shown to contain fresh water (Blue Energy, 2014). The Hoadleys–1 well was also plugged and abandoned after failing to find hydrocarbons.

No new seismic surveys were acquired by the petroleum industry in NSW. The NSW Department of Trade and Invest-ment, Resources and Energy, however, acquired 230 km pre-competitive seismic data over the Yathong Trough in 2013 as a part of the NSW Frontiers initiative (NSW Department of Trade and Investment, Resources and Energy, pers. comm., January 2014). The CSG basins of Queensland were one of the more ac-tive areas for 2D and 3D acquisition, with more than 1,600 km of 2D and 650 km2 of 3D acquired.

The southern margin basins of south australia, Victoria and Tasmania

Exploration in the region was limited. As previously dis-cussed, however, the award of three large exploration permits

in the Bight Basin off SA to Chevron (two) and a Murphy/San-tos joint venture was one of the highlights.

Three offshore 3D seismic surveys were acquired for Origin, WHL and Loyz/Trident.

Onshore, in the Gippsland Basin of Victoria, the Yallourn Pow-er–1 stratigraphic well, spudded in 2012, was drilled to a depth of 1,201 m in PEP166 by Lakes Oil to test the source potential of the Rintouls Creek Formation. This well reached total depth in 2013.

One well, Sawpit–2, was drilled in the Otway basin in PEL495. The well reached a total depth of 2,585 m and encoun-tered minor oil shows in the Upper Sawpit Shale and basement. A total of 56 m of core from shales in the Casterton Forma-tion and Lower Sawpit Shale was recovered and the well was plugged and abandoned (Beach Energy, 2013c).

In Victoria, two onshore petroleum exploration permits were awarded. PEP150 in the Gippsland Basin was awarded to a joint venture of Origin and Mawson Petroleum NL, and PEP171 in the Otway Basin was awarded to a joint venture of Beach Energy and Somerton Energy.

Figure 15. Geological cross section through deep gas plays of the Nappamerri Trough (Beach Energy, 2013e).

Continued next page.

APPEA Journal 2014—15Third proof—Johns 27 february 2014

2013 pesa industry review: exploration

Continued from previous page.

Figure 16. Location of conventional exploration wells and exploration and appraisal CSG wells in the eastern Australian basins of Queensland and NSW.

16—APPEA Journal 2014 Third proof—Johns 27 february 2014

D.R. Johns and P.G. Despland

ConCLusions

Exploration was active across a broad diversity of resource types and basins in Australia in 2013.

In the traditional conventional offshore plays of WA explo-ration drilling activity declined following a longer term trend. Nevertheless, several significant discoveries in both the Carnar-von and Browse basins testified to the potential that remains in these basins. The slowing of exploration drilling activity was offset by new seismic acquisition campaigns and the award of new exploration permits around Australia demonstrating lon-ger term exploration interest in offshore potential.

Drilling activity onshore offset the decline in offshore drilling with the Cooper/Eromanga Basin a focus for both convention-al and unconventional exploration. Seismic activities onshore were at historic highs with most of the 3D seismic acquired in the Cooper/Eromanga Basin where both oil and gas plays were targeted. Most onshore wells were drilled in the Cooper/Eromanga Basin and the conventional plays there continued to deliver with the prolific western flank oil play yielding four of the 11 discoveries. Exploration of unconventional gas plays in the Nappamerri Trough of the Cooper Basin made significant prog-ress and attracted a major investor, Chevron. Following early encouraging results demonstrating deliverability, a number of wells are now awaiting fracture stimulation and/or flow testing.

Unconventional shale gas and tight gas plays were also a focus of 2D seismic activity in the onshore Palaeozoic and Proterozoic basins of Central, Northern and Western Australia with major oil and gas companies now involved in preparations being made for drilling campaigns in 2014. Together with the Nappamerri Trough, upcoming tests of unconventional plays in these basins mean that 2014 will be an important year for the evaluation of unconventional plays in Australia.

In the CSG plays of Queensland, drilling activity was at re-cord levels as construction of the LNG plants on Curtis Island approached completion.

In 2013, explorers continued to seek new frontiers and pursue prospective acreage. The diversity and potential of exploration plays in Australia continue to attract new entries either through farm-in or through direct acreage awards. The interest in frontier basins, whether shale gas plays in the NT or the deepwater plays of Bight Basin in SA, and ongoing invest-ments in more established basins, demonstrate that Australia continues to be seen by explorers as having the hydrocarbon potential to justify investigation across a wide range of play and resource types.

aCKnoWLedGMenTs

The information presented in this paper has been compiled from a number of sources (as referenced throughout the paper), which the authors have not independently verified and do not endorse or approve, including data provided by various state and territory government agencies, company websites and in-dustry news services. The authors are grateful for input and support from the following:• Petroleum Division, WA Department of Mines and Petro-

leum;• Geological Survey of Queensland, Department of Natural

Resources and Mines;• NSW Department of Trade and Investment, Resources and

Energy Services;• Earth Resources Regulation Branch, Department of State

Development Business and Innovation Victoria;• Energy Resources Division, SA Department for Manufactur-

ing, Innovation, Trade, Resources and Energy (DMITRE);• the Northern Territory Geological Survey, Department of

Mines and Energy; • Geothermal and Petroleum Thermal Resources Tasmania;• the National Offshore Petroleum Titles Administration

(NOPTA); and,• Geoscience Australia.

The authors would also like to thank Ron McNab and Sharon Johns for drafting the figures.

disCLaiMer

This paper contains forward looking statements that are sub-ject to risk factors associated with the oil and gas industry. It is believed that the expectations reflected in these statements are reasonable, but they may be affected by a range of variables, which could cause actual results or trends to differ materially, including but not limited to: price fluctuations; actual demand; currency fluctuations; geotechnical factors; drilling and pro-duction results; gas commercialisation; development progress; operating results; engineering estimates; reserve estimates; loss of market; industry competition; environmental risks; physical risks; legislative, fiscal and regulatory developments; economic and financial markets conditions in various countries; approv-als; and, cost estimates.

All references to dollars, cents or $ in this paper are to Aus-tralian currency, unless otherwise stated. All references to proj-ect completion percentages are on a value of work done basis, unless otherwise stated.

Continued next page.

Figure 17. CSG wells drilled in Queensland by fiscal year.

APPEA Journal 2014—17Third proof—Johns 27 february 2014

2013 pesa industry review: exploration

appendiX

Continued from previous page.

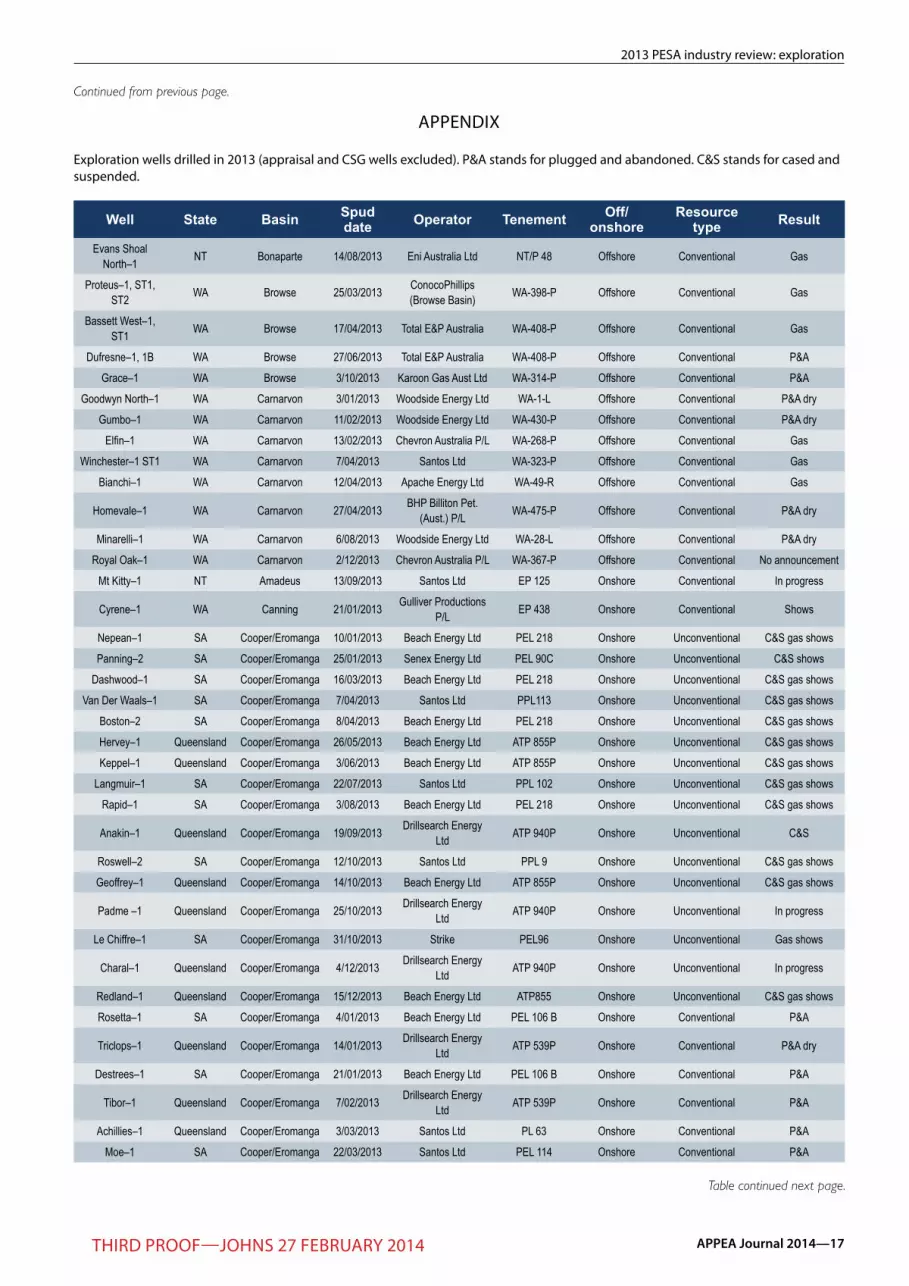

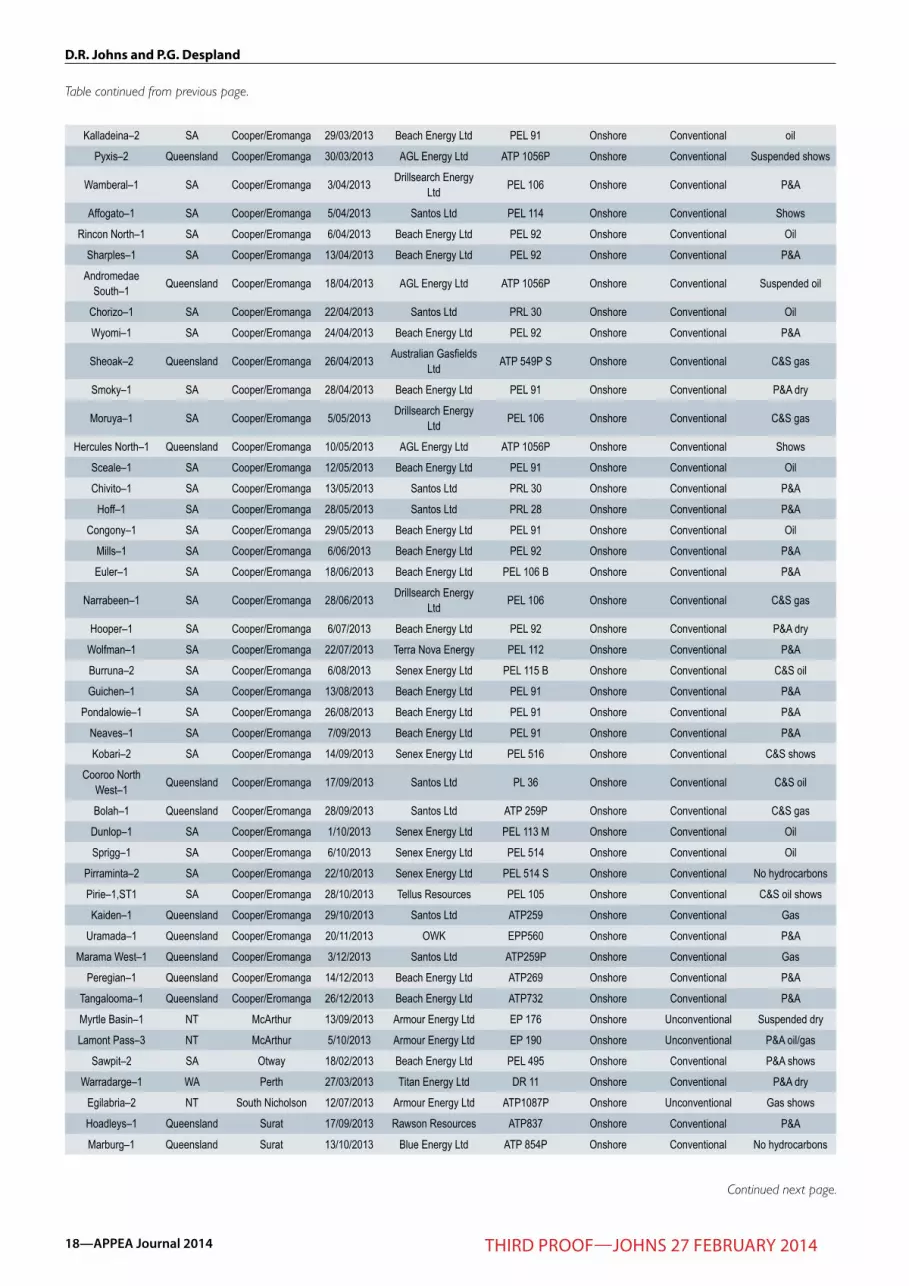

exploration wells drilled in 2013 (appraisal and CsG wells excluded). p&a stands for plugged and abandoned. C&s stands for cased and suspended.

Table continued next page.

Well State Basin Spud date Operator Tenement Off/

onshoreResource

type Result

Evans Shoal North–1 NT Bonaparte 14/08/2013 Eni Australia Ltd NT/P 48 Offshore Conventional Gas

Proteus–1, ST1, ST2 WA Browse 25/03/2013 ConocoPhillips

(Browse Basin) WA-398-P Offshore Conventional Gas

Bassett West–1, ST1 WA Browse 17/04/2013 Total E&P Australia WA-408-P Offshore Conventional Gas

Dufresne–1, 1B WA Browse 27/06/2013 Total E&P Australia WA-408-P Offshore Conventional P&A

Grace–1 WA Browse 3/10/2013 Karoon Gas Aust Ltd WA-314-P Offshore Conventional P&A

Goodwyn North–1 WA Carnarvon 3/01/2013 Woodside Energy Ltd WA-1-L Offshore Conventional P&A dry

Gumbo–1 WA Carnarvon 11/02/2013 Woodside Energy Ltd WA-430-P Offshore Conventional P&A dry

Elfin–1 WA Carnarvon 13/02/2013 Chevron Australia P/L WA-268-P Offshore Conventional Gas

Winchester–1 ST1 WA Carnarvon 7/04/2013 Santos Ltd WA-323-P Offshore Conventional Gas

Bianchi–1 WA Carnarvon 12/04/2013 Apache Energy Ltd WA-49-R Offshore Conventional Gas

Homevale–1 WA Carnarvon 27/04/2013 BHP Billiton Pet. (Aust.) P/L WA-475-P Offshore Conventional P&A dry

Minarelli–1 WA Carnarvon 6/08/2013 Woodside Energy Ltd WA-28-L Offshore Conventional P&A dry

Royal Oak–1 WA Carnarvon 2/12/2013 Chevron Australia P/L WA-367-P Offshore Conventional No announcement

Mt Kitty–1 NT Amadeus 13/09/2013 Santos Ltd EP 125 Onshore Conventional In progress

Cyrene–1 WA Canning 21/01/2013 Gulliver Productions P/L EP 438 Onshore Conventional Shows

Nepean–1 SA Cooper/Eromanga 10/01/2013 Beach Energy Ltd PEL 218 Onshore Unconventional C&S gas shows

Panning–2 SA Cooper/Eromanga 25/01/2013 Senex Energy Ltd PEL 90C Onshore Unconventional C&S shows

Dashwood–1 SA Cooper/Eromanga 16/03/2013 Beach Energy Ltd PEL 218 Onshore Unconventional C&S gas shows

Van Der Waals–1 SA Cooper/Eromanga 7/04/2013 Santos Ltd PPL113 Onshore Unconventional C&S gas shows

Boston–2 SA Cooper/Eromanga 8/04/2013 Beach Energy Ltd PEL 218 Onshore Unconventional C&S gas shows

Hervey–1 Queensland Cooper/Eromanga 26/05/2013 Beach Energy Ltd ATP 855P Onshore Unconventional C&S gas shows

Keppel–1 Queensland Cooper/Eromanga 3/06/2013 Beach Energy Ltd ATP 855P Onshore Unconventional C&S gas shows

Langmuir–1 SA Cooper/Eromanga 22/07/2013 Santos Ltd PPL 102 Onshore Unconventional C&S gas shows

Rapid–1 SA Cooper/Eromanga 3/08/2013 Beach Energy Ltd PEL 218 Onshore Unconventional C&S gas shows

Anakin–1 Queensland Cooper/Eromanga 19/09/2013 Drillsearch Energy Ltd ATP 940P Onshore Unconventional C&S

Roswell–2 SA Cooper/Eromanga 12/10/2013 Santos Ltd PPL 9 Onshore Unconventional C&S gas shows

Geoffrey–1 Queensland Cooper/Eromanga 14/10/2013 Beach Energy Ltd ATP 855P Onshore Unconventional C&S gas shows

Padme –1 Queensland Cooper/Eromanga 25/10/2013 Drillsearch Energy Ltd ATP 940P Onshore Unconventional In progress

Le Chiffre–1 SA Cooper/Eromanga 31/10/2013 Strike PEL96 Onshore Unconventional Gas shows

Charal–1 Queensland Cooper/Eromanga 4/12/2013 Drillsearch Energy Ltd ATP 940P Onshore Unconventional In progress

Redland–1 Queensland Cooper/Eromanga 15/12/2013 Beach Energy Ltd ATP855 Onshore Unconventional C&S gas shows

Rosetta–1 SA Cooper/Eromanga 4/01/2013 Beach Energy Ltd PEL 106 B Onshore Conventional P&A

Triclops–1 Queensland Cooper/Eromanga 14/01/2013 Drillsearch Energy Ltd ATP 539P Onshore Conventional P&A dry

Destrees–1 SA Cooper/Eromanga 21/01/2013 Beach Energy Ltd PEL 106 B Onshore Conventional P&A

Tibor–1 Queensland Cooper/Eromanga 7/02/2013 Drillsearch Energy Ltd ATP 539P Onshore Conventional P&A

Achillies–1 Queensland Cooper/Eromanga 3/03/2013 Santos Ltd PL 63 Onshore Conventional P&A

Moe–1 SA Cooper/Eromanga 22/03/2013 Santos Ltd PEL 114 Onshore Conventional P&A

18—APPEA Journal 2014 Third proof—Johns 27 february 2014

D.R. Johns and P.G. Despland

Kalladeina–2 SA Cooper/Eromanga 29/03/2013 Beach Energy Ltd PEL 91 Onshore Conventional oil

Pyxis–2 Queensland Cooper/Eromanga 30/03/2013 AGL Energy Ltd ATP 1056P Onshore Conventional Suspended shows

Wamberal–1 SA Cooper/Eromanga 3/04/2013 Drillsearch Energy Ltd PEL 106 Onshore Conventional P&A

Affogato–1 SA Cooper/Eromanga 5/04/2013 Santos Ltd PEL 114 Onshore Conventional Shows

Rincon North–1 SA Cooper/Eromanga 6/04/2013 Beach Energy Ltd PEL 92 Onshore Conventional Oil

Sharples–1 SA Cooper/Eromanga 13/04/2013 Beach Energy Ltd PEL 92 Onshore Conventional P&A

Andromedae South–1 Queensland Cooper/Eromanga 18/04/2013 AGL Energy Ltd ATP 1056P Onshore Conventional Suspended oil

Chorizo–1 SA Cooper/Eromanga 22/04/2013 Santos Ltd PRL 30 Onshore Conventional Oil

Wyomi–1 SA Cooper/Eromanga 24/04/2013 Beach Energy Ltd PEL 92 Onshore Conventional P&A

Sheoak–2 Queensland Cooper/Eromanga 26/04/2013 Australian Gasfields Ltd ATP 549P S Onshore Conventional C&S gas

Smoky–1 SA Cooper/Eromanga 28/04/2013 Beach Energy Ltd PEL 91 Onshore Conventional P&A dry

Moruya–1 SA Cooper/Eromanga 5/05/2013 Drillsearch Energy Ltd PEL 106 Onshore Conventional C&S gas

Hercules North–1 Queensland Cooper/Eromanga 10/05/2013 AGL Energy Ltd ATP 1056P Onshore Conventional Shows

Sceale–1 SA Cooper/Eromanga 12/05/2013 Beach Energy Ltd PEL 91 Onshore Conventional Oil

Chivito–1 SA Cooper/Eromanga 13/05/2013 Santos Ltd PRL 30 Onshore Conventional P&A

Hoff–1 SA Cooper/Eromanga 28/05/2013 Santos Ltd PRL 28 Onshore Conventional P&A

Congony–1 SA Cooper/Eromanga 29/05/2013 Beach Energy Ltd PEL 91 Onshore Conventional Oil

Mills–1 SA Cooper/Eromanga 6/06/2013 Beach Energy Ltd PEL 92 Onshore Conventional P&A

Euler–1 SA Cooper/Eromanga 18/06/2013 Beach Energy Ltd PEL 106 B Onshore Conventional P&A

Narrabeen–1 SA Cooper/Eromanga 28/06/2013 Drillsearch Energy Ltd PEL 106 Onshore Conventional C&S gas

Hooper–1 SA Cooper/Eromanga 6/07/2013 Beach Energy Ltd PEL 92 Onshore Conventional P&A dry

Wolfman–1 SA Cooper/Eromanga 22/07/2013 Terra Nova Energy PEL 112 Onshore Conventional P&A

Burruna–2 SA Cooper/Eromanga 6/08/2013 Senex Energy Ltd PEL 115 B Onshore Conventional C&S oil

Guichen–1 SA Cooper/Eromanga 13/08/2013 Beach Energy Ltd PEL 91 Onshore Conventional P&A

Pondalowie–1 SA Cooper/Eromanga 26/08/2013 Beach Energy Ltd PEL 91 Onshore Conventional P&A

Neaves–1 SA Cooper/Eromanga 7/09/2013 Beach Energy Ltd PEL 91 Onshore Conventional P&A

Kobari–2 SA Cooper/Eromanga 14/09/2013 Senex Energy Ltd PEL 516 Onshore Conventional C&S shows

Cooroo North West–1 Queensland Cooper/Eromanga 17/09/2013 Santos Ltd PL 36 Onshore Conventional C&S oil

Bolah–1 Queensland Cooper/Eromanga 28/09/2013 Santos Ltd ATP 259P Onshore Conventional C&S gas

Dunlop–1 SA Cooper/Eromanga 1/10/2013 Senex Energy Ltd PEL 113 M Onshore Conventional Oil

Sprigg–1 SA Cooper/Eromanga 6/10/2013 Senex Energy Ltd PEL 514 Onshore Conventional Oil

Pirraminta–2 SA Cooper/Eromanga 22/10/2013 Senex Energy Ltd PEL 514 S Onshore Conventional No hydrocarbons

Pirie–1,ST1 SA Cooper/Eromanga 28/10/2013 Tellus Resources PEL 105 Onshore Conventional C&S oil shows

Kaiden–1 Queensland Cooper/Eromanga 29/10/2013 Santos Ltd ATP259 Onshore Conventional Gas

Uramada–1 Queensland Cooper/Eromanga 20/11/2013 OWK EPP560 Onshore Conventional P&A

Marama West–1 Queensland Cooper/Eromanga 3/12/2013 Santos Ltd ATP259P Onshore Conventional Gas

Peregian–1 Queensland Cooper/Eromanga 14/12/2013 Beach Energy Ltd ATP269 Onshore Conventional P&A

Tangalooma–1 Queensland Cooper/Eromanga 26/12/2013 Beach Energy Ltd ATP732 Onshore Conventional P&A

Myrtle Basin–1 NT McArthur 13/09/2013 Armour Energy Ltd EP 176 Onshore Unconventional Suspended dry

Lamont Pass–3 NT McArthur 5/10/2013 Armour Energy Ltd EP 190 Onshore Unconventional P&A oil/gas

Sawpit–2 SA Otway 18/02/2013 Beach Energy Ltd PEL 495 Onshore Conventional P&A shows

Warradarge–1 WA Perth 27/03/2013 Titan Energy Ltd DR 11 Onshore Conventional P&A dry

Egilabria–2 NT South Nicholson 12/07/2013 Armour Energy Ltd ATP1087P Onshore Unconventional Gas shows

Hoadleys–1 Queensland Surat 17/09/2013 Rawson Resources ATP837 Onshore Conventional P&A

Marburg–1 Queensland Surat 13/10/2013 Blue Energy Ltd ATP 854P Onshore Conventional No hydrocarbons

Table continued from previous page.

Continued next page.

APPEA Journal 2014—19Third proof—Johns 27 february 2014

2013 pesa industry review: exploration

DRILLSEARCH, 2013a—Moruya-1 wet gas well delivers encour-aging test results. ASX release. Sydney: Drillsearch.

DRILLSEARCH, 2013b—Western Flank Oil Fairway produc-tion exceeds 10,000 barrels of oil per day. ASX release. Sydney: Drillsearch.

DRILLSEARCH, 2013c—Drillsearch Annual Report. Published 18 October 2013. Sydney: Drillsearch.

DRILLSEARCH, 2013d—Asian road show presentation. ASX release. Sydney: Drillsearch.

ENERGY-PEDIA NEWS, 2013—Australia: Chevron announces natural gas discovery offshore Australia. Published 23 April 2013. Energy-Pedia News.

ENI, 2013—ENI successfully drills Evans Shoal North-1 well in Timor Sea. Published 24 October 2013. Rigzone.

FALCON OIL AND GAS LTD, 2013a—Australia Beetaloo Basin agreement to reduce overriding royalty to 1%. Press release, 17 December 2013. Dublin: Falcon Oil and Gas.

FALCON OIL AND GAS, 2013b—Falcon retains interest in Beet-aloo permits, Northern Australia. Hess request to defer drilling decision rejected by Falcon Board. Press release, 1 July 2013.Dublin: Falcon Oil and Gas.

FINDER EXPLORATION, 2013—Olympus-1 discovery and rig release. Media release, 11 April 2013. Perth: Finder Exploration.

GEOSCIENCE AUSTRALIA, 2013—Australia 2013 Offshore Petroleum Exploration Acreage Release. Canberra: Australian Government Department of Industry.

KAROON GAS AUSTRALIA LTD, 2013a—Proteus-1 ST2 suc-cessfully flows condensate bearing gas. ASX release. Sydney: Karoon Gas Australia.

KAROON GAS AUSTRALIA LTD, 2013b—Zephyros-1 explora-tion well in WA-398P. Progress report No 9. ASX release. Sydney: Karoon Gas Australia.

KAROON GAS AUSTRALIA LTD, 2014—Grace exploration well in WA-314P. Progress report no 9. ASX release. Sydney: Karoon Gas Australia.

KEY PETROLEUM LTD, 2013—Quarterly report for the period ending 31 March 2013. ASX release. Sydney: Key Petroleum.

MACDONALD-SMITH, A., 2013—Shell’s costly Palta-1 explo-ration well disappoints. Australian Financial Review. Sydney: Fairfax Media Publications.

MINISTRY FOR INDUSTRY, 2013—$580 million new invest-ment in offshore exploration. Media release 23 October 2013. Canberra: Ministry for Industry, Australian Government.

NEW STANDARD ENERGY, 2013—Petrochina settles Canning Basin interest. ASX release. Sydney: New Standard Energy.

OCTANEX N.L., 2013—Outcome of Palta-1 exploration well. WA-384P Southern Exmouth Sub-basin. ASX release. Sydney: Octanex.

referenCes

APACHE, 2013—Apache confirms gas discovery at Bianchi-1 offshore Western Australia. News release, 16 July 2013. Houston: Apache Corporation.

ARMOUR ENERGY, 2013a—2013 NT and QLD campaigns conclude with NT discovery. ASX release. Sydney: Armour Energy.

ARMOUR ENERGY, 2013b—Operational update – Northern Ter-ritory drilling campaign. ASX release. Sydney: Armour Energy.

ARMOUR ENERGY, 2013c—Egilabria-2 – First continuous post-stimulation gas flows. ASX release. Sydney: Armour Energy.

ARMOUR ENERGY, 2013d—Egilabria-4 reaches total depth with multiple gas shows. ASX release. Sydney: Armour Energy.

BEACH ENERGY, 2013a—Completion of initial farm-in by Chevron. ASX release. Sydney: Beach Energy.

BEACH ENERGY, 2013b—Monthly drilling reports. ASX release. Sydney: Beach Energy.

BEACH ENERGY, 2013c—Quarterly reports. ASX release. Syd-ney: Beach Energy.

BEACH ENERGY, 2013d—Cooper Basin SACB JV unconven-tional and NTNG exploration update. ASX release. Sydney: Beach Energy.

BEACH ENERGY, 2013e—Moonta-1 delivers highest gas flow rate to date from Beach’s unconventional program. ASX release. Sydney: Beach Energy.

BEACH ENERGY, 2013f—Investor briefings presentation. ASX release. Sydney: Beach Energy.

BLUE ENERGY, 2013—Blue Energy expands with farm-in to vast Northern Territory acreage position. ASX release. Sydney: Blue Energy.

BLUE ENERGY, 2014—Marburg 1 exploration well update. ASX release. Sydney: Blue Energy.

BROOKS, D., 2013—2012 PESA industry review—exploration. APPEA Journal (53), 141–64.

BURU ENERGY, 2013—Apache farms-in to Buru and Mitsubi-shi’s coastal and desert acreage in the Canning Basin. ASX release. Sydney: Buru Energy.

CENTRAL PETROLEUM, 2013—Operations report for the quar-ter ending 30 September 2013. ASX release. Sydney: Central Petroleum.

CHEVRON CORPORATION, 2013—Chevron announces further natural gas discovery offshore Australia (Feb. 7, 2013). Press release. San Ramon: Chevron Corporation.

DEPARTMENT OF RESOURCES, ENERGY AND TOURISM, 2013—New $180m investment in offshore exploration. Media release, 17 June 2013. Canberra: Australian Government.

Continued from previous page.

20—APPEA Journal 2014 Third proof—Johns 27 february 2014

D.R. Johns and P.G. Despland

PETROFRONTIER CORPORATION, 2013—PetroFrontier Corp. completes seismic program on Southern Georgina Basin per-mits, Australia and updates corporate activities. Press release, 6 September 2013. Calgary: PetroFrontier Corporation.

SANTOS LTD, 2013a—Gas discovery in the Browse Basin. ASX release. Sydney: Santos Ltd.

SANTOS LTD, 2013b—Quarterly activities reports. ASX release. Sydney: Santos Ltd.

SANTOS LTD, 2013c—Santos 2013 investor seminar. Published 4 December 2013. Adelaide: Santos Ltd.

SANTOS LTD, 2013d—Further shale gas success at Moom-ba-194 in the Cooper Basin. ASX release. Sydney: Santos Ltd.

SANTOS LTD, 2014—Fourth quarter activities report for period ending 31 December 2013. ASX release. Sydney: Santos Ltd.

SENEX ENERGY LIMITED, 2013a—Oil discovery at Dunlop-1 flows 1200 barrels per day. ASX release. Sydney: Senex Energy Ltd.

SENEX ENERGY LIMITED, 2013b—Oil discovery at Burruna-2. ASX release. Sydney: Senex Energy Ltd.

TITAN ENERGY, 2013—Titan Energy Ltd March 2013 quarterly activities report. ASX release. Sydney: Titan Energy.

WOOD, T. AND CARTER, L., 2013—Getting gas right: Australia’s energy challenge. Grattan Institute report no. 2013-6, June 2013. Melbourne: Grattan Institute.

Rhodri Johns is Manager of opportuni-ty Capture at santos. he is a geologist, a graduate of Manchester university, and has a phd from Cambridge university. he started his career with shell in the netherlands, and worked for sun oil in London for several years before mov-ing to adelaide to work for santos. as Manager of opportunity Capture, rhodri

leads a group of exploration geoscientists who are responsible for basin and play analysis and identifying new opportunities.

Patrick Despland obtained a Msc in ge-ology from the université de Lausanne, switzerland, in 2004. upon completion of his academic studies, and a short stint with the research Centre on al-pine environments as a field geologist, patrick migrated to australia where he joined iluka resources in the mineral sands industry. in 2006, patrick moved

across to santos in adelaide where he presently works as a senior Geologist in the opportunity Capture team. his role involves regional-scale technical studies and the review of new ventures opportunities across the asia-pacific region.

THE AUTHORS