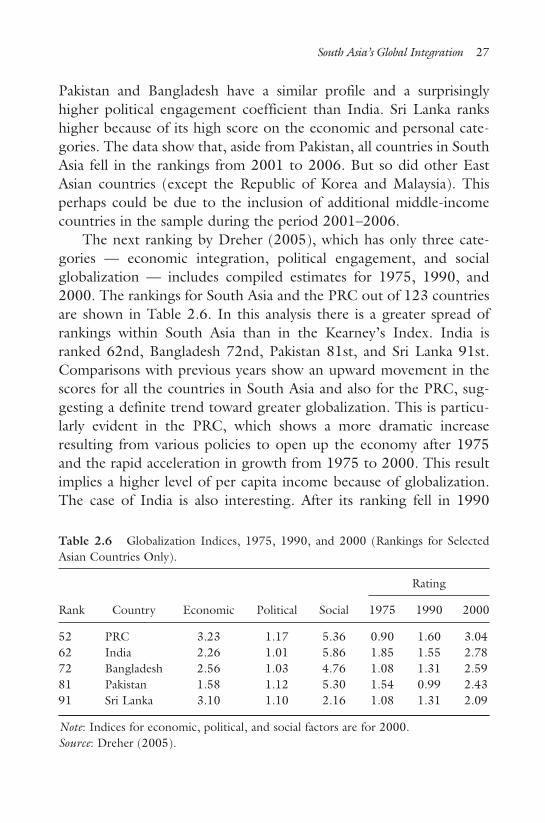

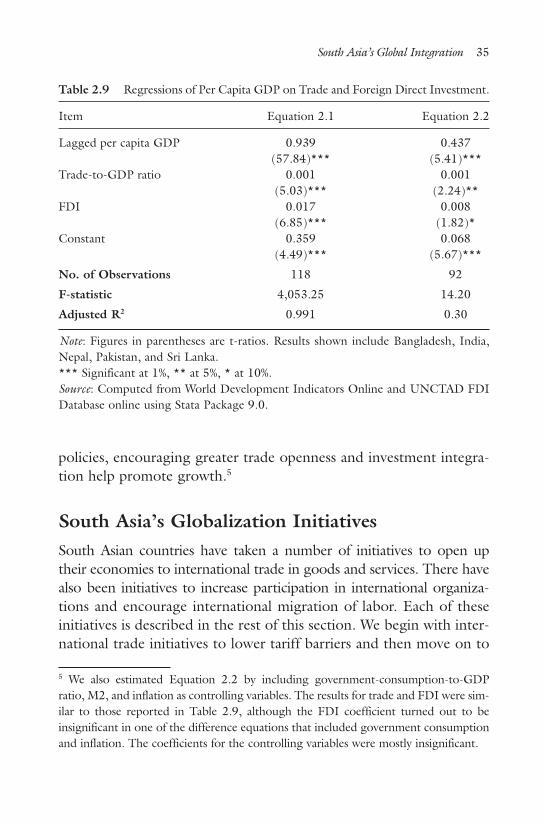

south asia

DESCRIPTION

A Political StudyTRANSCRIPT

RISING TO THE CHALLENGE OF GLOBALIZATION

SOUTH ASIA

This page intentionally left blankThis page intentionally left blankThis page intentionally left blankThis page intentionally left blank

N E W J E R S E Y • L O N D O N • S I N G A P O R E • BE IJ ING • S H A N G H A I • H O N G K O N G • TA I P E I • C H E N N A I

World Scientific

RISING TO THE CHALLENGE OF GLOBALIZATION

SOUTH ASIA

Pradumna B Rana Nanyang Technological University, Singapore

John Malcolm Dowling University of Hawaii, USA

British Library Cataloguing-in-Publication DataA catalogue record for this book is available from the British Library.

For photocopying of material in this volume, please pay a copying fee through the CopyrightClearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, USA. In this case permission tophotocopy is not required from the publisher.

ISBN-13 978-981-281-421-0ISBN-10 981-281-421-3

Typeset by Stallion PressEmail: [email protected]

All rights reserved. This book, or parts thereof, may not be reproduced in any form or by any means,electronic or mechanical, including photocopying, recording or any information storage and retrievalsystem now known or to be invented, without written permission from the Publisher.

Copyright © 2009 by World Scientific Publishing Co. Pte. Ltd.

Published by

World Scientific Publishing Co. Pte. Ltd.

5 Toh Tuck Link, Singapore 596224

USA office: 27 Warren Street, Suite 401-402, Hackensack, NJ 07601

UK office: 57 Shelton Street, Covent Garden, London WC2H 9HE

Printed in Singapore.

SOUTH ASIARising to the Challenge of Globalization

Sandhya - South Asia.pmd 4/9/2009, 11:06 AM1

v

“Rana and Dowling have been keen observers of the South Asian scene forover two decades. This experience and scholarship is amply demonstrated intheir new book. The book has two special features that should make it anecessary reading for all those interested in Asia’s evolving economic geo-graphy. The first is its comparison of the development experience in Chinaand South Asia. The second is the discussion of pan-Asian cooperation andthe prospects of strengthening of economic cooperation between South Asiaand East Asia, an idea whose time is now well within the planning horizon.Their prescription is right on the mark. The book is a welcome addition tothe growing literature on pan-Asian cooperation and will strengthen theimportant cause of regional cooperation in South Asia.”

Rajiv KumarDirector and Chief ExecutiveIndian Council for Research on International Economic Relations

“The basic premise of Rana and Dowling’s remarkable book is that sustain-ing high growth in South Asia is essential for integrating Asia, and forenhancing its role in global affairs. They make many policy suggestions forpursuing inclusive high growth by South Asian countries, so the sub-regioncan be a growth node for the rest of Asia. The book is a welcome additionto growing literature on Asian integration in general, and to managing glob-alization in South Asia in particular.”

Mukul G Asher Professor of Public PolicyLee Kuan Yew School of Public Policy National University of Singapore

“This book provides a thorough assessment about the developments inSouth Asia — a region that has risen significantly on the global stage inrecent decades. As the long time observers of the Asian economies, theauthors are well-positioned for tackling various challenging policy issues fac-ing the region. Policy-makers and students alike should benefit enormouslyfrom the careful analyses and invaluable knowledge that the authors haveoffered in this timely book.”

Wei Ge, Ph.D.Department of EconomicsBucknell University

b670_FM.qxd 12/10/2008 7:38 AM Page v

“There has been a proliferation of books on East Asia’s dynamism and it’sintegration intraregionally as well as with the global economy. In contrast,much less has been written on South Asia which has, until recently, been arelative laggard in economic growth. There are also encouraging signsregarding the gradual integration of India and — to a lesser extent — therest of South Asia with China and the rest of East Asia, leading some to talkabout “Pan-Asian” integration. The revitalization of South Asia has alsogiven impetus for enhanced intra-South Asian economic integration ….There has, however, been little careful and thoughtful analysis of theseimportant trends and ongoings. The book by Rana and Dowling very ablyfills this gap. The authors, both of whom have extensive policy experience inAsia, should be commended for writing a book that offers a thorough anddetailed analysis of the data and provides highly useful and insightful policyrecommendations.”

Ramkishen S. RajanGeorge Mason University, USAand University of Adelaide, Australia

“Rana and Dowling have come up with an interesting analysis of South Asia,a region that has begun to emerge as one of the most dynamic by exploitingopportunities provided by globalization. They also focus on the challenges thatthey face in responding to globalization and regional economic integration.I hope that the book will be widely read.”

Nagesh KumarDirector-GeneralResearch and Information System for Developing Countries

b670_FM.qxd 12/10/2008 7:38 AM Page vi

vii

Contents

Tables ix

Figures xiii

Abbreviations xv

Foreword xvii

Acknowledgments xix

About the Authors xxi

Chapter 1: Introduction and Summary 1

Chapter 2: South Asia’s Global Integration 19

Introduction 19Globalization of South Asia 21Impact of Globalization on South Asia 31South Asia’s Globalization Initiatives 35Future Agenda for Globalization in South Asia 45References 55

Chapter 3: A Comparative Analysis of Economic 57Performance and Policy Reformsin South Asia and the PRC

Introduction 57Comparative Economic Performance 58Raising Living Standards in the PRC and South Asia 75

b670_FM.qxd 12/10/2008 7:38 AM Page vii

Impact of Policy Reforms 98The Unfinished Agenda 110Future Prospects: A Comparison of India and the PRC 116Appendix 3.1: Chronology of Policy Reforms in South Asia 125Appendix 3.2: Governance Indicators 156Appendix 3.3: Unfinished Agenda of Reforms 162

in South Asian CountriesReferences 173

Chapter 4: Economic Integration Between South Asia 175and East Asia: The Second Phaseof Pan-Asian Integration?

Introduction 175Quantitative Measures of Integration 178Economic Complementarities 187Ongoing Policy Efforts 201Conclusions and Policy Recommendations 203Appendix 4.1: Total Trade of South Asia with East Asia: 213

Levels and Growth RatesAppendix 4.2: Pan-Asian Intra-regional and 214

Interregional TradeAppendix 4.3: Revealed Comparative Advantage Indices 216

in South Asia and East Asia, by CountryAppendix 4.4: Annotated List of Free Trade Agreements 224

(FTAs) between South Asia and East AsiaReferences 227

Chapter 5: Economic Integration in South Asia 228

Introduction 228Economic Integration in South Asia 230Lessons from East Asia and Recommendations 238References 242

Author Index 244

Subject Index 246

viii South Asia: Rising to the Challenge of Globalization

b670_FM.qxd 12/10/2008 7:38 AM Page viii

ix

Tables

2.1 Average Per Capita Income Growth for Low- 20and High-Globalization Countries (percentage)

2.2 South Asia’s Total Trade, 1980, 1985, 1990, 221995, 2000, and 2005 ($ million)

2.3 Foreign Direct Investment Inflows, 1980, 1985, 241990, 1995, 2000, and 2005 ($ million)

2.4 Direct Investment and Portfolio Investment in 25India and Pakistan, 1991, 1995, 2000, 2005,and 2007 ($ million)

2.5a Globalization Index Rankings, 2006 262.5b Globalization Index Rankings, 2001 and 2006 262.6 Globalization Indices, 1975, 1990, and 2000 27

(Rankings for Selected Asian Countries Only)2.7 Openness Factor and Indigenous Factor Indicators 28

(1998–2002 Average)2.8 Globalization Rankings 302.9 Regressions of Per Capita GDP on Trade 35

and Foreign Direct Investment2.10 South Asian Free Trade Agreements with Non-Asian 37

Countries2.11 Mean Tariff Rates in East Asia and South Asia, 1985, 39

1990, 1995, 2000, and 2004 (percentage)2.12a World Competitiveness Indicators, 1995 and 2006 41

(rankings)2.12b World Competitiveness Factors, 2000 41

and 2006 (rankings)

b670_FM.qxd 12/10/2008 7:38 AM Page ix

x South Asia: Rising to the Challenge of Globalization

2.13 Workers’ Remittances and Receipts (Balance 44of Payments), 1980, 1985, 1990, 1995, 2000,and 2004 ($ million)

2.14 Effective Rate of Duty on Imports into 46the US, 2005 (percentage)

2.15 Intra-regional Export Shares, 1990 and 2001 48(percentage)

2.16 Interregional and Intra-regional Portfolio 52Investments, 2003 ($ billion)

2.17 Corporate Governance Ratings, 2000 and 2004 533.1 GDP Per Capita, 1980, 1985, 1990, 1995, 2000, 59

and 2006 (constant 2000 $)3.2 Poverty Head-Count Ratio at $1-a-Day, in PPP 61

(percentage of population)3.3 Exports of Goods and Services, 1978, 1991, 2004, 62

and 2005 (percentage of GDP).3.4 Taxes on International Trade, 1990 and 2005 63

(percentage of revenue)3.5 Foreign Direct Investment Inflows and Outflows, 64

1980, 1985, 1990, 1995, 2000, and 2005($ million)

3.6 Cash Surplus/Deficit, 1990, 1995, 2000, 2004, 65and 2005 (percentage of GDP)

3.7 Current Account Balance, 1980, 1985, 1990, 661995, 2000, and 2004 (percentage of GDP)

3.8 Money and Quasi Money (M2), 1978, 1991, 67and 2005 (percentage of GDP)

3.9 Sectoral Share of Employment (percentage 68of total employment)

3.10 Total Reserves minus Gold, 1980, 1985, 1990, 691995, 2000, and 2006 ($ million)

3.11 Total Life Expectancy at Birth, 1980 and 2004 (years) 703.12 Infant Mortality Rate, 1980 and 2004 71

(per 1,000 live births)3.13 Total Adult Literacy Rate, 1990 and 2004 72

(percentage of people 15 and above)

b670_FM.qxd 12/10/2008 7:38 AM Page x

Tables xi

3.14 Share of World GDP (in PPP), 1980, 1990, 2000, 73and 2005 (percentage)

3.15 Gross Capital Formation, 1980, 1985, 1990, 1995, 772000, and 2005 (percentage of GDP)

3.16 Economically Active Population, Age 15 78and above 1980, 1985, 1990, 1995, 2000,and 2005 (percentage)

3.17 Sectoral Output Growth in the PRC (percentage) 813.18 Industrial Output Share, by Form of Ownership, 85

1980, 1984, 1988, 1992, 1996, and 2002(percentage)

3.19 Rigidity of Labor Market Indices, 2005 963.20 Average Growth in GDP and Per Capita GDP 99

(percentage)3.21 Selected Doing Business Indicators, 2005 1013.22 Sectoral Share of Value Added, 1980 and 2005 102

(percentage)3.23 Average Share of Trade in GDP (percentage) 1053.24 Growth in Labor Force and Income and Total 110

Factor Productivity3.25 Composition of Manufactured Output in the PRC, 117

1970, 1980, 1990, and 1997 (percentage of totaloutput of manufactured goods)

3.26 Export Share of Selected Two-Digit Manufacturing 117Industries in the PRC (percentage)

3.27 Export Share of Selected Two-Digit Manufacturing 118Industries in India (percentage)

3.28 Poverty Levels in India and the PRC (percentage 123of people in poverty)

4.1 World Foreign Direct Investment Inflows 183into South Asia and East Asia, 1990, 1995,2000, and 2005 ($ million)

4.2 Top 10 Exports of South Asia to East Asia, 1990 187and 2004

4.3 Top 10 Exports of East Asia to South Asia, 1990 188and 2004

b670_FM.qxd 12/10/2008 7:38 AM Page xi

xii South Asia: Rising to the Challenge of Globalization

4.4 Revealed Comparative Advantage Indices for 190South Asia, 1993 and 2004

4.5 Commodities in Which Various South Asian 191Countries Have Comparative Advantage, 2004

4.6 Revealed Comparative Advantage Indices for 192East Asia, 1993 and 2004

4.7 Commodities in Which Various East Asian 193Countries Have Comparative Advantage, 2004

4.8 Spearman Rank Correlation Coefficients for 195Revealed Comparative Advantage Indices,1993 and 2004

4.9 Trade Complementarity Indices between South Asia 197and East Asia, 1993 and 2004

4.10 Exports of Commercial Services, 1990, 1995, 1982000, and 2005 ($ million)

4.11 Commercial Service Exports for India 199and the PRC by Sector, 1990, 1995, 2000,2003, and 2004 ($ million)

4.12 Revealed Comparative Advantage in Services, 2004 2004.13 Trade Restrictiveness Indices (percentage) 2044.14 Ease of Doing Business Index: Rankings for Asian 206

Countries, 20055.1 Share of South Asian Intra-regional Trade 229

in World Trade, 1980, 1985, 1990, 1995,2000, and 2006 (percentage)

b670_FM.qxd 12/10/2008 7:38 AM Page xii

Figures

2.1 Total Trade and GDP Growth 322.2 Foreign Direct Investment and GDP Growth 332.3 Poverty Head-Count Ratio and Level of Per Capita 34

Income3.1 Per Capita GDP, 1980–2006 (constant 2000 $) 603.2 Share of Value Added in GDP, 1980 (percentage) 793.3 Average Firm Size in India and Comparator 120

Countries, 1990 (value added in $ millionper establishment)

4.1 Total Trade between South Asia and East Asia, 1781990–2006 ($ billion)

4.2 Pan-Asian Intra-regional and Inter-regional Trade, 1802006

4.3 Inter-regional Trade between South Asia 180and East Asia (as a percentage of South Asia’sTotal Trade with the World), 1990–2006

4.4 Inter-regional Trade between South Asia and East Asia 181(as a percentage of East Asia’s Total Trade with theWorld), 1990–2006

4.5 Total Trade Intensity Index between South Asia 182and East Asia, 1990–2006

4.6a Foreign Direct Investment Flows from Selected 184East Asian Countries to India, 2002/03–2006/07($ million)

4.6b Foreign Direct Investment Flows from Selected 184East Asian Countries to Pakistan 1999/00–2005/06($ million)

xiii

b670_FM.qxd 12/10/2008 7:38 AM Page xiii

4.7a Foreign Direct Investment Flows from Selected 185South Asian Countries to ASEAN, 1995–2006($ million)

4.7b Foreign Direct Investment Flows from Selected 185South Asian Countries to the PRC, 1994–2006($ million)

4.8a Infrastructure: Southern Corridor: Shipping 2094.8b Infrastructure: Central Corridor: Air Freight Hubs 2104.8c Infrastructure: Northern Corridor: Asian Highway 2104.8d Infrastructure: Northern Corridor: Trans-Asian 211

Railways5.1 Total World and Intra-regional Exports of East Asia, 239

1980–2006 ($ billion)

xiv South Asia: Rising to the Challenge of Globalization

b670_FM.qxd 12/10/2008 7:38 AM Page xiv

xv

Abbreviations

ASEAN Association of Southeast Asian NationsASEAN + 3 ASEAN plus the People’s Republic of China, Japan,

and the Republic of KoreaBIMSTEC Bay of Bengal Institute for Multi-Sectoral Technical

and Economic CooperationCMI Chiang Mai InitiativeFDI foreign direct investmentFTA free trade agreementGATT General Agreement on Tariffs and TradeGDP gross domestic productICT information and communication technologyILO International Labour OrganizationIMF International Monetary FundIT information technologyMFN most favored nationNAFTA North American Free Trade AgreementNGO nongovernment organizationNPLs nonperforming loansNTBs nontariff barriersOECD Organisation for Economic Co-operation and

DevelopmentPPP purchasing power parityPRC People’s Republic of ChinaPTAs preferential trading arrangementsQRs quantitative restrictionsRCA revealed comparative advantageSAARC South Asian Association for Regional Cooperation

b670_FM.qxd 12/10/2008 7:38 AM Page xv

SAFMs South Asian finance ministersSAFTA South Asia Free Trade AgreementSAGQ South Asian Growth QuadrangleSAPTA SAARC Preferential Trading ArrangementSASEC South Asia Subregional Economic CooperationSEZ special economic zoneSITC Standard International Trade ClassificationSOE state-owned enterpriseTFP total factor productivityTVEs township and village enterprisesUNDP United Nations Development ProgrammeVAT value-added taxWTO World Trade Organization

xvi South Asia: Rising to the Challenge of Globalization

b670_FM.qxd 12/10/2008 7:38 AM Page xvi

xvii

Foreword

After adopting rigid import substitution policies for four decades,beginning in the 1980s and the 1990s the South Asian countries startedto opt for greater economic openness and began the long process ofaligning their economies with those of the rest of the world. This impor-tant book, authored by two acknowledged experts on Asia with manyyears of experience working at the Asian Development Bank (ADB),is devoted to analyzing the recent economic dynamism of South Asiaand the challenges that the region faces in a globalizing world.

The book examines the South Asian experience of globalizationthrough several different lenses. The book compares South Asia’sglobalization efforts with those of East Asia and the rest of the world,giving the reader a broad overview of globalization progress, impact,and potential in South Asia. This comparison demonstrates how,despite recent successes, India and the rest of South Asia are laggingbehind the People’s Republic of China (PRC) in various areas.

The book then presents a penetrating comparative analysis of eco-nomic performance and policy reforms in the PRC and South Asia.The major premise is that policy does matter. Good policies can helplift income growth rates and lower poverty, while poor policies retardgrowth and stall poverty reduction. Both the PRC and South Asiahave been growing rapidly in the past few years, faster than mostother developing countries in Asia and the rest of the developingworld, raising living standards for more than two billion people. Thisis a major accomplishment and to be applauded and it owes much ofits success to policy reforms.

The book moves on to examine the evolving trade relationshipbetween South Asia and East Asia, including the trade relationship

b670_FM.qxd 12/10/2008 7:38 AM Page xvii

xviii South Asia: Rising to the Challenge of Globalization

between the PRC and India. This relationship has important implica-tions for other countries in the region and the global economy.

The final chapter of the book turns to a discussion of mechanismsand modalities for increasing intra-regional trade and fostering regionalcooperation in South Asia. Among these are developing cross-borderinfrastructure, fostering international trade and investment, andincreasing regional financial sector cooperation.

Among the important questions answered in the book are:

• How globalized is South Asia? Has global integration been beneficial?• Economic reforms in South Asia have borne fruit. What does each

country still have to do?• The PRC began the reform process with a lower per capita GDP

than South Asia, but by 2005 its per capita income was more thantwice that of South Asia. Why?

• India has the potential to grow as fast as the PRC over the next twodecades. What policy actions are needed to realize this potential?

• After falling dramatically after 1947, trade integration among theSouth Asian countries is now starting to increase. Can South Asiabe as well integrated in the future as it was before 1947?

• South Asia’s economic relations with East Asia are starting tosurge. Could this eventually lead to an integrated Pan-Asia, similarto what has been achieved in Europe?

This book is timely and helps enhance the understanding of recentSouth Asian economic development and how the surge in SouthAsia’s trade and investment relations with East Asia could pave theway for an integrated Asia. The book will be of value to a wide spec-trum of readers — academics, policy makers, development institu-tions, students of economics, and the general public.

Professor Lim Chong YahAlbert Winsemius Chair Professor of Economics

Director of Economic Growth CentreNanyang Technological University

SingaporeNovember 2008

b670_FM.qxd 12/10/2008 7:38 AM Page xviii

xix

Acknowledgments

If Rip van Winkle had gone to sleep in the 1980s and awakened twoand a half decades later, he would have been surprised by the changesthat have occurred in the South Asian economies and their linkageswith the rest of the world. The changes have been most significant inIndia, but other South Asian countries have also shown economicdynamism. This book seeks to systematically document these changes.

The idea for the book arose when both of the authors wereinvolved in the ADB’s Study on Economic Cooperation between EastAsia and South Asia. We would therefore like to thank the ADB forthis opportunity. In addition, Dr. Rana would also like to thank theNanyang Technological University, where he completed work on thebook, and Neeru, Abhi, and Ayush for their inspiration. Dr. Dowlingwould like to thank the University of Hawaii, where he completedwork on the book, and Maribeth Boritzer for her helpful commentsand suggestions.

Our colleagues and collaborators have also given us much encour-agement throughout the project, especially Professor Lim Chong Yah,and Professor Euston Quah.

Benjamin Endriga provided excellent research assistance. WilheminaPaz provided administrative support. Pauline Chan and Sandhya ofWorld Scientific provided editorial support. We are grateful to them.

b670_FM.qxd 12/10/2008 7:38 AM Page xix

b670_FM.qxd 12/10/2008 7:38 AM Page xx

This page intentionally left blankThis page intentionally left blank

xxi

About the Authors

Pradumna B. RanaDr. Pradumna B. Rana is currently a Senior Fellow at the NanyangTechnological University in Singapore. He was the Senior Director ofthe Asian Development Bank’s (ADB’s) Office of Regional EconomicIntegration which spearheaded the ADB’s support for regional coop-eration and integration in Asia. He joined the ADB in the early 1980sand held senior positions at the research and various operationaldepartments. Earlier he was a Lecturer at the National University ofSingapore and the Tribhuvan University (Nepal), a researcher at theInstitute of Southeast Asian Studies in Singapore, and a consultant tothe World Bank in Washington D.C. He obtained his PhD fromVanderbilt University where he was a Fulbright Scholar and a Mastersin Economics from Michigan State University and Tribhuvan Universitywhere he was a gold medalist. He has published widely in the areas ofAsian economic development and integration, Asian financial crisis,business cycle co-movements, early warning systems of financial crisis,and policy reforms in transition economies. These include half adozen books and numerous articles in international scholarly journalsincluding Review of Economics and Statistics, Journal of InternationalEconomics, Journal of Development Economics, Journal of AsianEconomics, World Development, Developing Economies, and SingaporeEconomic Review. Currently, in addition to this book, he is co-editingbooks on Pan-Asian Integration: Linking East and South Asia (forth-coming Palgrave Macmillan) and National Strategies for RegionalIntegration (forthcoming ADB, Manila).

b670_FM.qxd 12/10/2008 7:38 AM Page xxi

John Malcolm DowlingProfessor Dowling received his Ph. D in Economics from the Universityof Pittsburg and taught at the University of Colorado for 15 yearswhere he became a full professor in 1976. He moved to the AsianDevelopment Bank in the early 1980s where he served as AssistantChief Economist for many years. After retiring from the AsianDevelopment in 1996 he taught at the University of Melbourne inAustralia, Singapore Management University in Singapore and, mostrecently, the University of Hawaii at Manoa. Professor Dowlinghas been the recipient of two Fulbright Fellowships (Iran andThailand) and a Rockefeller Foundation fellowship. He is the authorof numerous articles in professional journals and several books onAsian development topics.

xxii South Asia: Rising to the Challenge of Globalization

b670_FM.qxd 12/10/2008 7:38 AM Page xxii

1

Chapter 1

Introduction and Summary

India and the People’s Republic of China (PRC) were by far therichest countries in the world 2,000 years ago. Even in the early19th century their share of global gross domestic product (GDP) wasnearly 50%. However, by 1950 this share had fallen to a mere 8% asthe industrialized countries in Europe, North America, andAustralasia developed further. This balance persisted until the 1970s(Maddison, 2001). As India, after the mid-1980s and early 1990s,and the PRC, after 1978, began to open up and liberalize, their shareof world income began to rise again. By 1998 it had risen to 16% andby 2005 to 21%. As the PRC and India continue to grow and inte-grate further into the global economy, their economic prospects willdepend more and more on how they manage globalization. The much-quoted 2003 Goldman Sachs study (Wilson and Purushothaman,2003) forecasts that by 2050 three of the four largest economies inthe world will be in Asia and in this order: the PRC, the UnitedStates, India, and Japan. The 2007 Goldman Sachs report (Poddarand Yi, 2007) forecasts that India will overtake the United Statesfaster than expected and be the second largest economy in the worldby 2050 after the PRC. During the 1980s and 1990s, other SouthAsian countries also started to opt for greater openness and began thelong process of realigning their economies with those of the rest ofthe world.1

1 South Asia in this book refers to the seven members of the South Asia Associationfor Regional Cooperation (SAARC), which are Bangladesh, Bhutan, India, Maldives,Nepal, Pakistan, and Sri Lanka. Afghanistan, which became the eighth member of theSAARC in 2007, is not included here.

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 1

The benefits of globalization are many and varied. By opening upto international trade and investment, countries can acquire technol-ogy and some essential inputs that help to raise productivity andincrease economic efficiency. Greater access to a wider market throughglobalization helps to reduce the risk of fluctuations in externaldemand and provides greater scope for exporting a broader range ofexports. Greater openness also helps countries to attract foreign directinvestment (FDI), which brings with it new technology and innova-tion and greater access to industrial country markets. In addition,globalization increases export demand, generates employment, andraises living standards. More open financial markets result in increasedcompetition, lower costs of financial intermediation, better resourceallocation, and deepening of financial markets. More open labor mar-kets bring new flexibility, skills, and expertise. Skilled labor migrationoffers benefits to the economy as returning migrants bring improvedskills and knowledge and a deeper understanding of science, engi-neering, technology, and business, which can make the local economymore productive and open new lines of international communication.But globalization also has associated costs. Maximizing the benefitsand minimizing the potential costs of globalization requires imple-menting appropriate policies at the national, regional and global level.These require good governance, transparency, and a consistent policyenvironment.

An appropriate response to globalization requires a three-pronged approach. First, countries need to integrate with the worldeconomy through the multilateral initiatives for trade and finance.De-linking is not an option, as multilateral initiatives provide frame-works that are fair and equitable for all countries and convey immensebenefits. Domestic policies must be adjusted to take full advantage ofthe benefits of multilateral liberalization. This brings us to the sec-ond point. National policy reforms — in trade and finance, theexchange rate, industrial and financial sectors, and labor policies —have to be developed and implemented within the broad context ofglobalization. These will improve international competitiveness, pro-ductivity, and economic efficiency and resilience. Third, regionalpolicies have to be considered, not only to increase the connectivity

2 South Asia: Rising to the Challenge of Globalization

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 2

of countries to regional groupings but also to bring smaller and per-haps isolated economies under the umbrella of a larger regionalgrouping. The greater economies of production and export diversifi-cation these smaller economies can thus achieve may not be possibleotherwise, even within the broader framework of global integra-tion. Such regional agreements can also be stepping-stones to widerglobalization.

Hence, to respond to globalization, national, regional (interre-gional), and global policies and actions must be implemented. At thenational level, a number of macroeconomic issues, such as exchangerates, monetary stabilization, and fiscal policies, need to be consid-ered. Financial markets must also be developed, and the possible con-tagion effects of actions in other countries, contained. Capital accountliberalization needs to be sequenced properly. Other structuralreforms have to be addressed as well. Regional actions offer anothereffective way to address and manage globalization. These havebecome an important component of the development strategy in EastAsia since the financial crisis of 1997 and 1998.2 The Association ofSoutheast Asian Nations (ASEAN) and ASEAN+3 (ASEAN plus thePRC, Japan, and the Republic of Korea) have become more active,and several new initiatives have been started to stimulate trade andfinancial integration. There has also been a proliferation of bilateraland subregional free trade agreements (FTAs), both within the Asianregion and between Asian economies and other regions. In the areaof monetary and financial cooperation, regional policy dialogues havebegun through various forums comprising ASEAN and ASEAN+3finance ministers and their deputies. A regional resource-poolingscheme, the Chiang Mai Initiative, has been established and effortsare being made to develop multilateral swaps as well as bond marketsdenominated in local currencies. Bridges are also starting to be builtacross the Asian subregions especially between South Asia and EastAsia. East Asia’s momentum of integration with the global economy,including its role in various international forums, is also beingstrengthened.

Introduction and Summary 3

2 See Chapter 5.

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 3

After independence from the British in 1947, both India andPakistan (with what is now Bangladesh) had adopted import-substituting policies and erected high walls of protection on all sec-tors of the economy. This had meant not only high tariffs but alsovarious forms of licensing to control entry into industries. The result-ing “license raj” in both countries had created inefficiencies, pro-moted public sector corruption, and constrained the rate of economicgrowth. The smaller South Asian countries — Bhutan, Maldives, andNepal — had also adopted a similar development strategy. It was basi-cally only in the 1980s and the 1990s — the 1980s in the case ofSri Lanka, the mid 1980s in the case of India and Bangladesh, andthe 1990s in the case of Pakistan and Nepal — that the South Asiancountries started the reform process (Devarajan and Nabi, 2006). Inmany cases reforms have been proceeding in spurts because vestedinterests have applied pressures to slow the reform process.

Since its independence 60 years ago, India has consolidated avibrant and competitive form of democracy, banished famine, morethan halved its absolute poverty rate and dramatically improved liter-acy and health conditions. It has also achieved global competitivenessin information technology (IT), outsourcing, telecommunications,and pharmaceuticals; acquired de facto membership in the club ofnuclear powers; created more billionaires than any other country inAsia and became one of the most dynamic and fastest-growing coun-tries, ranked the world’s fourth-largest in purchasing power parity. Ithas also acquired a new geo-strategic importance.

On the economic side, however, India’s success is relativelyrecent. Some changes occurred slowly and the growth rate of theeconomy rose to 5% a year in the 1980s, much higher than during theearlier decades of independence (when the growth rate was 3% peryear). But the decisive change occurred after the reforms of the early1990s. During the period 1991–2005, the growth rate averaged 6%,compared to 4.9% in 1976–1990. The reforms of the 1980s in SriLanka and in the 1990s in other South Asian countries have alsoborne fruit, and other South Asian countries have also shown eco-nomic dynamism. The Bangladeshi economy grew by an averageof 5% in 1991–2005, compared to 3.9% in 1976–1990, and the

4 South Asia: Rising to the Challenge of Globalization

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 4

Sri Lankan economy, by 4.8% and 4.6%, respectively. The economy ofNepal, which has been ravaged by political problems, grew by an aver-age of 4.3% in 1991–2005. The Pakistani economy has, howeverslowed, from an average of 6.3% in 1976–1990 to 4.3% in 1991–2005.This economic dynamism of the South Asian countries is expected tocontinue in the future, and South Asia’s share of global income isexpected to increase further. For example, the Planning Commissionprojects that the Indian economy will grow by 10% per year in2007–2012. However, as the East Asian crisis has shown, a financialcrisis can be a major setback to an economy, entailing huge economicand social costs but without derailing it. The recovery of the crisis-affected countries in East Asia was swift, but the investment rates havenot recovered yet and the post-crisis growth rates are significantlylower than the pre-crisis ones.

South Asia was spared from the contagion of the 1997 EastAsian financial crisis mainly because it had not deregulated its cap-ital account. However, in the future, as South Asia continues itseconomic reforms and deregulates its capital account and enhancesits integration with the world, a financial crisis cannot be ruled out.Capital account deregulation is necessary in order to attract foreigncapital into local stock and bond markets. Financial sectors inSouth Asia continue to be weak and the system of corporate gov-ernance is less than fully transparent. Like those in East Asia, bankscontinue to bear the brunt of the required financing, and capitalmarkets are less developed. This could create the so-called “doublemismatch” problem, which led to the Asian financial crisis. Theregion can also be buffeted by other types of real and financialshocks. A major lesson for South Asia from the post-crisis experi-ence of East Asia is that globalization can convey large amounts ofbenefits but also presents some challenges, which have to beaddressed effectively.

This book reviews how South Asia is rising to the challenge ofglobalization. How are South Asian countries maximizing the ben-efits of globalization while minimizing its costs? What actions havethey taken at the national, regional (inter-regional), and globallevel? What lessons have the South Asian countries learned from the

Introduction and Summary 5

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 5

East Asian financial crisis and how are they preparing for financialglobalization?

This book comprises five chapters. This chapter contains theintroduction and summary. In Chapter 2, the current status of theregion is compared to that of countries in East Asia and the rest ofthe world, against a variety of globalization indicators. The chaptergives the reader a broad overview of progress, impact, and potentialfor globalization in South Asia. Since globalization has generally beena positive force for greater economic growth throughout the world,the chapter analyzes the globalization experience of South Asia usingthe various indices developed, among others, by Kearney (2006)and the Carnegie Endowment for International Peace (2006) andDreher (2005). South Asia has opened up its economy to foreigninvestment and provided stimulus for growth in international tradesince the 1980s and the 1990s and has become more globalized.There has been a shift in emphasis from an inward-looking importsubstitution strategy to more outward-looking international policieswith a role for the private sector. A variety of indicators of economicgrowth and international trade and finance and others reflect this newlook. Among these are the share of FDI in total investment andincome, the share of trade in GDP, the growth in trade, and the inflowof portfolio capital into the stock market. Although the globalizationscores for South Asia are increasing, they are lower than those for EastAsia and the PRC mainly because of poor health and education, qual-ity of labor force, and institutional strength indicators. By looking athow these indicators are related to economic growth, the chapterdraws a clearer profile of the impact of globalization on economicgrowth and poverty reduction. Globalization initiatives in South Asia,such as lowered barriers to trade, FTAs signed and under negotiation,international migration, and FDI and capital flows, are examined.

The chapter ends with a discussion of an agenda for enhancingglobalization — trade policy, improved competitiveness, policies toencourage inflows of FDI, increased financial integration, and anappropriate international migration policy. Integrating further intothe global economy would benefit South Asia. Initiatives taken sincethe 1980s and 1990s have borne fruit, both in accelerating economic

6 South Asia: Rising to the Challenge of Globalization

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 6

growth and reducing poverty. South Asia must build on this founda-tion to become even more competitive internationally and to acceler-ate economic growth. South Asia can integrate further into the globalcommunity in several ways. Many of these initiatives relate to inter-national trade in goods and services and in the flow of capital, such asreducing trade barriers, improving international competitiveness,attracting FDI, developing new trade agreements, and increasing cap-ital account convertibility. The flow of labor and issues of financialintegration must also be addressed. Recent data on FDI inflows intoIndia are encouraging. According to the United Nations Conferenceon Trade and Development (UNCTAD), India ranked second only tothe PRC as the most preferred destination for global FDI, receiving$17 billion of FDI in 2006, an amount equivalent to the combinedflows for the previous three years.

On the trade front, the chapter recommends further reductions intariffs and nontariff barriers (NTBs). The overall assessment of vari-ous competitiveness indicators for South Asia is positive but there isscope for further improvement, through reforms in business and gov-ernment efficiency by reducing bureaucratic procedures and increas-ing competition. In increasing competitiveness, infrastructureimprovements are critical. Despite recent improvements, includingefforts to involve the private sector, the lack of a modern and efficientinfrastructure foundation continues to inhibit the growth of industryand the private sector in South Asia. The removal of road transporta-tion bottlenecks can be extremely effective in increasing efficiency, byreducing costs and time to market as well as facilitating the movementof temporary labor throughout the country. Cross-border linksshould also be improved as part of the Asian highway network and thetrans-Asian railway system.

Additional measures should be adopted to attract FDI. Amongthese are various institutional and procedural improvements that candemonstrate the attractiveness of South Asia as an FDI destination.First, measures can be taken to harmonize FDI regulations and incen-tives to stop a “race to the bottom,” develop regulations to stop dou-ble taxation, pool experience among South Asian countries todetermine a strategy for attracting FDI into different sectors, and

Introduction and Summary 7

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 7

establish a regional research center devoted to studying the patternand effectiveness of FDI in the region and elsewhere and disseminat-ing the results. Second, a series of procedures can be developed tosimplify entry and exit procedures, set up a fast track for approvals ofFDI investment, allow repatriation of profits, and encourage free flowof FDI within the region. Harmonization of financial regulations isanother key area of need in South Asia. This should be combined withdeepening of the financial infrastructure and financial markets, per-haps using the Asian Bond Market Initiative proposed for East Asiaas a model. Capital account convertibility should not be eschewed;liberalization should, however, be sequenced properly.

Many impediments to increasing migration from South Asia restwith recipient countries in Europe, North America, and Australia.Bilateral negotiations to enhance personal safety and improve work-ing conditions for short-term guest workers should be intensified.Given the increasing importance of remittances in South Asian coun-tries, facilitation of these flows can also be improved. Further integra-tion into the global information and telecommunications labormarket can be encouraged and promoted in a number of ways. Givingsupport to the private sector by upgrading physical infrastructure inservice sectors specializing in IT and communications should be amajor priority as the demand for outsourcing and migration of skilledprofessionals in the IT industry continues to grow. Better coordina-tion between shifting job openings in industrial countries and skilldevelopment in South Asian countries can be developed by encour-aging private sector involvement in IT and communications trainingin South Asia as well as facilitating migration programs that allowskilled and professional workers to migrate for a year or two and thenreturn to use their expertise at home.

Chapter 3 presents a comparative analysis of economic perform-ance and policy reforms in the PRC and South Asia. There are severalreasons for this. First, nearly half of the world’s population has a stakein the ability of both to sustain high rates of growth and raise livingstandards. Second, the PRC and South Asia can benefit from eachother’s experiences. Their unique features make mutual dialogue anddiscussions important. The two are at similar stages of economic

8 South Asia: Rising to the Challenge of Globalization

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 8

development with diverse policy challenges. They both have hugeland masses, diverse climates and geography, similar demands on theenvironment, and, of course, large populations. The major premise ofthis chapter is that policies are important. Good policies can help liftincome growth rates and lower poverty, while poor policies retardgrowth and stall poverty reduction. The chain of events leading frompolicy reforms to growth is not the same for all economies. Specialcircumstances in each economy have to be analyzed as well. History,government, and institutions are also important because they serve asthe background for policy adjustments.

In both India (and its neighbors in South Asia) and the PRCgrowth has been rapid in the past few years, faster than in most otherdeveloping countries in Asia and the rest of the developing world.The fact that living standards have swiftly improved for the more than2 billion people in these countries is a major accomplishment to belauded. While the PRC has grown rapidly for more than threedecades, growth in India and the rest of South Asia has acceleratedonly recently. To provide a better grasp of the details of recent eco-nomic development, the chapter begins with a short review of eco-nomic performance indicators for South Asia and the PRC: thepattern of growth in per capita income; modifications in sector sharesin agriculture, industry, and services; inflation, FDI, and currentaccount balances, along with international reserves; and humanresource indicators such as the incidence of poverty.

This review is followed by a discussion of why living standardshave been rising faster in the PRC than in South Asia. PRC began thereform period with a lower per capita GDP than all the countries inSouth Asia with the exception of Nepal. But by 2005 per capitaincome was more than twice as high in the PRC than in all of SouthAsia with the exception of Sri Lanka. Furthermore, poverty reductionhas been more dramatic and human development indicators haveimproved more rapidly. The differences in initial conditions as well asthe design and sequencing of reforms explain this outcome. Reformsin agriculture and industry took center stage at the start of the reformprocess in the PRC. This facilitated the development of relatively effi-cient commodity markets and the encouragement of quick supply

Introduction and Summary 9

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 9

responses early in the reform process. Macroeconomic reforms (e.g.,fiscal, financial, trade and investment, and exchange rate reforms) andother microeconomic reforms (e.g., industrial policy and public enter-prise, public administration, labor market, and infrastructure reforms)were undertaken later, sometimes in response to distortions and bot-tlenecks that resulted from reforms in the productive sector. SouthAsia, on the other hand, generally put macroeconomic reforms aheadof microeconomic reforms mainly because reforms were undertakenin response to adverse macroeconomic situation and required belt-tightening measures with high social costs.

Although South Asia put macroeconomic reforms ahead ofmicroeconomic ones, more remains to be done at this level. Tariffshave been lowered, yet they are still higher than rates in SoutheastAsia and East Asia. In India, export processing zones are relativelyrecent and small compared with those in the PRC, and they lack effi-cient and cheap connectivity with major ports. Regulations are stillcumbersome and are a disincentive to foreign investors. In othercountries in South Asia, similar reforms are needed in trade, foreigninvestment, and the financial sector, although the details differ fromcountry to country. Additional reforms at the microeconomic level orthe so-called second-generation reforms are needed to make marketswork better. These comprise continued reforms of the agriculture andindustrial sectors; reform of public institutions for improved gover-ence (civil service, bureaucracy, and public administration); reform ofinstitutions that create or maintain human capital (education andhealth); and, improving the environment affecting the private sector(regulatory environment, flexibility in labor markets, legal and physi-cal infrastructure, and clearly-defined property rights). Unlike macro-economic reforms, however, successful implementation of second-generation reforms requires a wider consences in the countries. Thischapter also provides a discussion of the unfinished agenda for SouthAsian countries at a country level and concludes with an analysis offuture growth prospects for the region, which are fairly encouragingprovided reforms remain on track. The unfinished agenda includes,among others, restructuring private enterprises in most countries,improving tax administration in Nepal and Pakistan, implementing

10 South Asia: Rising to the Challenge of Globalization

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 10

various standards and codes and best practices for the financial sector,improving labor market flexibility, and upgrading governance andinfrastructure throughout the region (see Chapter 3, Appendix 3, forfurther details).

A review of the pattern of economic growth and sectoral changesin the PRC and India brings out several aspects that are important inassessing the future prospects for these two giant economies. First isthe overwhelming importance of industrial growth in the PRC.Industry in 2005 accounted for 40% of the country’s GDP, up froma negligible amount only 30 years ago. This growth has not only beenspectacular but has been concentrated for the most part in a fewsectors, primarily Standard International Trade Classification (SITC)categories 5–8 (office machinery, electrical machinery and appliances,telecommunications equipment, and miscellaneous manufacturedgoods).

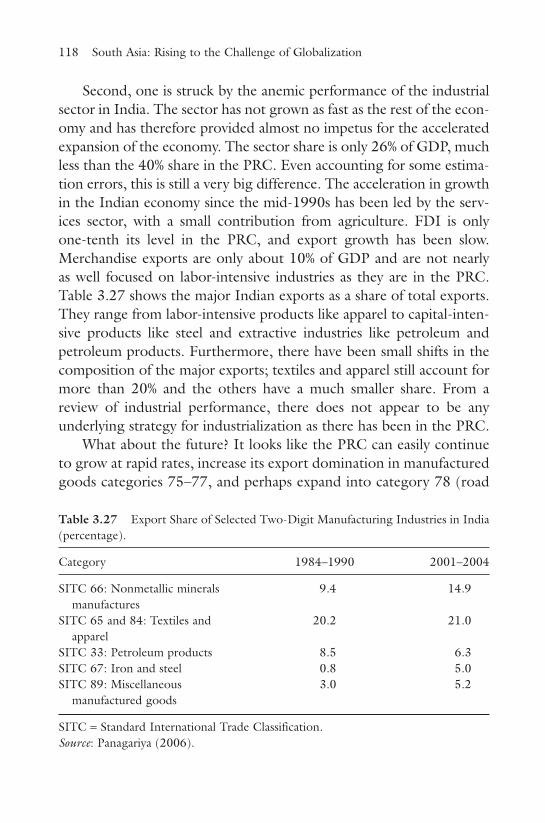

Second, although it is starting to improve, the performance of theindustrial sector in India has been anemic. The sector has not grownas fast as the rest of the economy and has therefore provided littleimpetus for economic expansion. The sector share is only 26% ofGDP, versus 40% in the PRC. Even accounting for some estimationerrors, this is still a very big difference. The acceleration in growth ofthe Indian economy since the mid-1990s has been led by the servicessector, with a small contribution from agriculture. Since the middle ofthis decade, there has also been some turnaround in manufacturingproductivity, mainly because of private sector activities and responsesto reforms. FDI is only one-tenth the level of the PRC’s and exportgrowth has been slow. Merchandise exports are only about 10% ofGDP and are not nearly as well focused on labor-intensive industriesas they are in the PRC.

The PRC can easily continue to grow rapidly and increase itsexport domination in manufactured goods categories 75–77, and per-haps expand into 78 (road vehicles). By 2001–2004 this subsector’sshare of total manufactured output was already 34%, up from a neg-ligible amount in the 1990s. Whether this continued growth in indus-try is in the best interest of the country is another matter, however.A more appropriate strategy would be to put less emphasis on industry

Introduction and Summary 11

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 11

and more on services and the rural development of the backward inte-rior provinces.

Much of the current emphasis in India is to leapfrog over theindustrialization phase of development and focus on a wide variety ofboth high- and low-technology services, primarily in IT and commu-nications. To sustain rapid growth, there has to be an added push todevelop labor-intensive industry as in East Asia and the PRC. Such astrategy would also benefit rural areas as growth would trickle downto the poor. India has the potential to develop a vibrant, efficient, andinternationally competitive industrial sector, but this requires betterinfrastructure as well as labor and industrial policies that are flexibleand allow large-scale industry to operate in labor-intensive industries.

The recent Goldman Sachs report (Poddar and Yi, 2007) arguesthat growth acceleration in India since 2003 represents a structuralincrease rather than simply a cyclical upturn. India could grow by 8%yearly until 2020 (from the 5.7% forecast for 2003), the report adds.But to do this, India needs to address supply-side constraints on busi-ness, infrastructure development (health and education, among oth-ers), and the labor market.

There are encouraging signs that such a takeoff is near in India;however, FDI growth in manufacturing is still slow, labor markets arestill constrained, and business investment in new plant and equipmentis weak. For the outlook for the next decade to change, theGovernment will have to remove all of these bottlenecks. Then it willdefinitely be possible for the industrial sector to exhibit the dynamismthat the IT and related service sectors have been showing in the lastfew years. If this materializes, India could well grow as fast as PRC inthe next two decades, particularly if it is able to raise investment ratesso that they are closer to the rates achieved by the PRC.

Chapter 4 looks at the evolving economic relationship betweenSouth Asia and East Asia. Recently, there has been growing interestin the economic relationships between these two regions. There are,at least, three reasons for this interest. First, two of the most dynamiccountries in the world, namely, the PRC and India, are in theseregions and the evolution of these giant economies, together with grow-ing economic interrelations between the two, could have important

12 South Asia: Rising to the Challenge of Globalization

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 12

implications for other countries in the regions and the global economy.Second, with the surge in regionalism in post-crisis East Asia, a questionthat is frequently being asked is: will growing economic relationsbetween South Asia and East Asia be the second phase and eventuallylead to an integrated Pan-Asia similar to the integration achieved inEurope sometime in the future? Third, during the pre-colonial period,Asia not only dominated the global economy but was one of the mostintegrated regions in the world, will this happen once again? The chap-ter highlights the recent surge and the potential for increased integrationin the future between the two regions. It also recommends a set of poli-cies to further enhance integration between South Asia and East Asia.

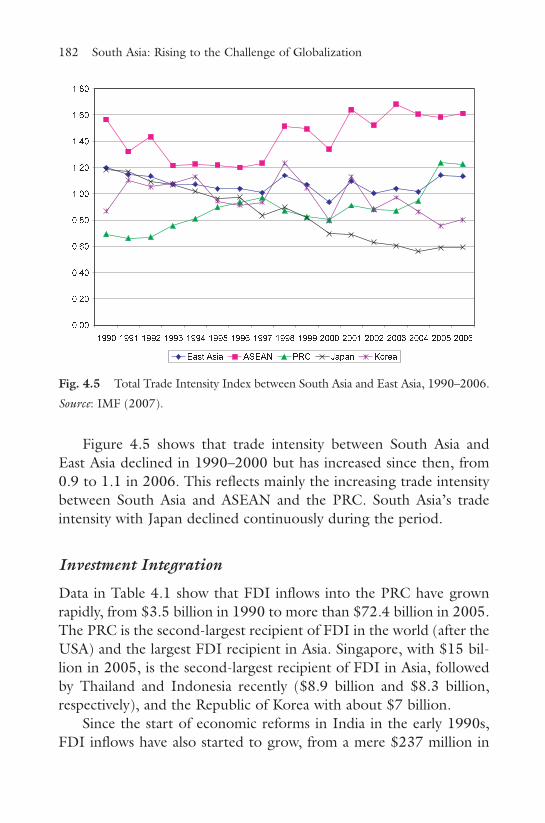

The chapter begins by reviewing trends in economic integra-tion between South Asia and East Asia. South Asia’s merchandisetrade with East Asia has grown significantly in absolute terms. Thistrade is the second-largest component of Pan-Asian trade, suggest-ing that South Asia–East Asia economic relations could be labeledas the “second phase of Pan-Asian integration.” The chapter alsoreviews quantitative measures of economic integration betweenSouth Asia and East Asia, and assesses economic complementaritiesbetween the two regions by looking at the pattern of exports andcomparative advantage. A large part of the increase in SouthAsia–East Asia trade is accounted for by the bilateral trade betweenthe two giant economies of India and the PRC; trade betweenthem has also increased rapidly in recent years. The trends show aswell that East Asia is a more important trading partner for SouthAsia than vice versa.

Trade shares are not sufficient to assess the extent to which coun-tries prefer to trade with each other than with other trading partners.Trade intensity indices are a better way of measuring whether tradebetween two regions is greater relative to their importance in worldtrade. The trade intensity indices between South Asia and East Asiadeclined in the 1990s but have increased since then. This increasereflects mainly the increasing trade intensity between South Asia andASEAN and the PRC. Despite overlaps, exports between the tworegions have some complementarities. South Asia exports mainlyagricultural, primary, and labor-intensive manufactured goods to

Introduction and Summary 13

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 13

East Asia. East Asia’s exports to South Asia, on the other hand, com-prise mainly of capital- and knowledge-intensive products such astelecommunications and sound recording equipment, electricalmachinery, road vehicles, and industrial machines.

Policies in South Asia, particularly in India, have recently soughtto establish trade and investment links with ASEAN and East Asiancountries. India’s engagement with ASEAN began in 1992, and since2005 India has also participated in various East Asia Summits as wellas other meetings with European finance ministers. South Asia andEast Asia have signed a number of FTAs as well.

Which policy actions would increase South Asia–East Asia inte-gration? First, while tariffs and NTBs are already low in many EastAsian countries and while South Asia has made encouraging progressin the same direction, further reductions can be made (especially inNTBs in East Asia, where tariffs are already low). Second, trade liber-alization efforts need to be embedded in a wider program of eco-nomic reforms. South Asian countries and several East Asian countriesneed to make progress in implementing reforms at the microeconomiclevel and the so-called second-generation reforms to enhance trans-parency, good governance, and human captial. Among these reformsare reform of the civil service and of the delivery of public goods, tostrengthen competition, regulations, and property rights and thuscreate an environment conducive to private sector opportunities. Thereform of institutions that create human capital, in health and educa-tion among others, is also required. Third, South and East Asiancountries need to consolidate their FTAs into an Asia-wide FTA. Tomake the proliferation of FTAs between South Asia and East Asiastepping-stones rather than stumbling blocks to multilateralism andto reduce economic inefficiencies due to overlapping rules of originand others, policy makers in the region may wish to adopt the conceptof “open regionalism” and broaden FTAs by creating as large andwide a market as possible. Deepening FTAs by extending their cover-age beyond trade in goods into services, investment, technology, etc.,may reduce the problem of trade diversion. Quantitative estimatessuggest that a broad regional approach will, for the most part, forestalllargely adverse effects on individual Asian countries that may follow

14 South Asia: Rising to the Challenge of Globalization

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 14

when countries and subregions are otherwise left out (Francois, Rana,Wignaraja, forthcoming). The fourth measure that could significantlyaffect trade between South Asia and East Asia is reduction of tradingcosts. This could be brought about by investment in trade-relatedinfrastructure and the streamlining of cross-border procedures (suchas customs procedures and logistic costs) to minimize delays incustoms inspection, cargo handling and transfer, and processing ofdocuments. Finally, trade promotion through skillful economic diplo-macy, regular exchange of business delegations, and civil society partic-ipation could be given much more encouragement. People-to-peoplecontacts can go a long way toward enhancing trade and investmentbetween countries.

Chapter 5 considers the broad topic of regional integrationwithin South Asia and draws lessons from the experience of EastAsia. South Asia was a well-integrated region of the British Empirein the 19th and early 20th century before World War II. In 1947,when Pakistan and India became independent, more than half ofPakistan’s imports came from India and nearly two-thirds of itsexports went to India. Then, after Pakistan was partitioned, tensionsbetween the two countries grew as they bickered over water rights,territory, and currency valuation. These, together with the adoptionof international trade policies that emphasized import substitution,led to a dramatic reduction of trade among South Asian countries.Whatever limited international trade that took place was with indus-trial countries, particularly the United States. Consequently, afterindependence from British rule, trade among the South Asian coun-tries fell from around 20% of total trade to about 4% by the end ofthe 1950s, and to 2% by 1967 (World Bank, 2004). The share ofintra-regional trade in total trade began to increase only after thecountries abandoned import substitution polices in the 1980s andthe 1990s. It now stands at about 4% of total trade.

This chapter explores how the previous strong pattern of tradecan be revitalized. There are several mechanisms and modalitiesfor increasing intra-regional trade and fostering regional coopera-tion, such as developing cross-border infrastructure, fostering inter-national trade and investment (including services), and increasing

Introduction and Summary 15

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 15

cooperation in the financial sector. In infrastructure, under theSouth Asia Subregional Economic Cooperation (SASEC), six prioritysectors have been identified: transport; energy and power; tourism;environment; trade, investment, and private sector cooperation; andinformation and communication technology. Progress is still in theearly stages, although projects are being identified and preliminarywork is being done.

The South Asian Association for Regional Cooperation (SAARC)with its trade initiatives — the SAARC Preferential TradingArrangement (SAPTA) and the South Asia Free Trade Agreement(SAFTA) — is the major institutional entity charged with promotingfree trade in South Asia. SAFTA aims to reduce tariffs among mem-bers to 0%–5% by 2016 and establish a free trade area. However,progress has also been slow. Each country has a list of products thatare not part of the agenda for tariff reduction and these products arehard to eliminate. The hope is that all countries are more committedto free trade than they have been in the past and will be willing tomake mutual concessions to make trade agreements work. Withregard to free trade agreements, two current bilateral agreementsinvolve South Asian countries — those between Sri Lanka and Indiaand between Nepal and India. Although the World Bank (2004)argues that even with free trade the amount of trade within SouthAsia would be relatively small (although certainly bigger than the cur-rent flows), opportunities for more trade within South Asia are con-firmed by a number of studies that consider comparative advantageand geographic proximity. The level of intra-regional trade is expectedto increase in the future but not to the pre-partition level as patternsof comparative advantage have changed. Integration with East Asia(discussed in Chapter 4) will provide additional opportunities forboth South Asia and other regions of Asia to reap the benefits of glob-alization. As Chandra and Kumar (2008) note, South Asia can bene-fit from a twin-track approach: integration within itself and betterintegration with the rest of the world. Integration within South Asiais more likely to succeed if undertaken as part of broader Pan-Asiancooperation. Increased integration in South Asia could also help buildbridges between Central Asia and East Asia.

16 South Asia: Rising to the Challenge of Globalization

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 16

Regarding financial integration, several institutional develop-ments in the past decade were designed to promote greater mone-tary and financial integration in South Asia. Among these is therecent formation of a network of central bank governors and financesecretaries of the SAARC region and a forum of SAARC finance min-isters. These groups discuss and exchange views on macroeconomicissues, and possibilities for harmonizing strategies for the environ-ment and natural disaster relief. A South Asian Development Fund(SADF) has been set up to identify regional projects in industry,energy, agriculture, and services, as well as infrastructure and socialdevelopment projects. The SADF has also financed feasibility studies.For financial and monetary integration within South Asia to progressbeyond these steps, more work must be done to assess whetherenough macroeconomic convergence and political will has beendeveloped before the idea of a common market can be entertained.This work is ongoing.

An important lesson for South Asia from East Asia’s experi-ence is that regionalism can help maximize the benefits of global-ization while minimizing its costs. South Asia should strengthenits efforts to enhance cooperation within the region and with EastAsia. The recent observer status given to the PRC and Japan inSAARC should have a catalytic impact on South Asian integration.Second, expeditious implementation of SAFTA is necessary.Nontariff barriers to trade should be removed. SAFTA should alsobe deepened to cover the service trade and the movement of labor.Third, efforts should be made to strengthen monetary and finan-cial cooperation in South Asia. The region could join ongoingefforts in East Asia (such as the Chiang Mai Initiative and localcurrency bond markets).1 Fourth, in infrastructure cooperation,the SASEC initiative could benefit from interaction with theGreater Mekong Subregion program.

Introduction and Summary 17

1 Recently a $3 billion bilateral swap agreement was signed between India andJapan.

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 17

ReferencesChandra, R and R Kumar (2008). South Asian Integration Prospects and Lessons from

East Asia. Indian Council for International Economic Relations.Devarajan, S and I Nabi (2001). Economic Growth in South Asia, Promising,

Unequalizing, Sustainable? Economic and Political Weekly, August 19.Dreher, A (2005). Does Globalization Affect Growth? Evidence from a New Index

of Globalization. Thurgauer Wirtschaftsinstitut Research Paper Series No. 6.April.

Francois, J, PB Rana and G Wignaraja (eds.) (forthcoming). Pan-Asian Integration:Linking East and South Asia, Chapter 1, Palgrave Macmillan.

Kearney, A. T. Inc. and the Carnegie Endowment for International Peace (2006).The Globalization Index. Foreign Policy (November/December), 74–81.

Maddison, A (2001). The World Economy: A Millennial Perspective. OECD.Poddar, T and E Yi (2007). India’s Rising Growth Potential. Global Economics,

Paper 152. Goldman Sachs.United Nations Conference on Trade and Development (UNCTAD) (2007). World

Investment Report 2007.Wilson, D and R Purushothaman (2003). Dreaming with the BRICS: The Path to

2050. Global Economic Paper No. 99. Goldman Sachs.World Bank (2004). Trade Policies in South Asia: An Overview. Report No. 29929,

Washington, DC.

18 South Asia: Rising to the Challenge of Globalization

b670_Chapter-01.qxd 12/10/2008 7:43 AM Page 18

19

Chapter 2

South Asia’s Global Integration

IntroductionGlobalization is a contentious word that means different things todifferent people. While the general public has grown skeptical of glob-alization, fearing foreign competition and loss of jobs, most econo-mists are optimistic about the longer-term prospects for the worldeconomy and for countries that are joining the global community. Forthem the net effect of globalization is definitely positive. For others,where local producers are threatened by lower-cost imports, the netimpact is negative.

Empirical studies on globalization have measured its impact oneconomic growth and development. Many of these have used inter-national trade flows, direct foreign investment, and other capital flowas measures of globalization. Dollar (1992) and Frankel and Romer(1996) find that trade and openness to trade have both had a positiveand significant impact on economic growth for many countries. Theimpact of capital account liberalization on growth is more debatable.Rodrik (1998) and Alesina, Grilli, and Milesi-Ferretti (1994) do notfind a significant relationship between capital account openness andeconomic growth, and Chandra (2001) finds that there are moredeveloping countries that have suffered than those that have gainedfrom globalization. However, Dollar and Kray (2001) find a positiverelationship between FDI flows and growth.

Several other studies have expanded the definition of globalizationbeyond FDI, openness to trade, and trade flows. These studies (reviewedin the next section of this chapter) look at a much wider range ofindicators to assess the degree of globalization in different economies.

b670_Chapter-02.qxd 11/12/2008 11:02 AM Page 19

The results of these studies generally find that globalization is positivelyrelated to growth in per capita income, using panel data for a variety ofindustrial and developing countries. Dreher (2005) finds that countrieswith high rates of globalization grew faster than countries with lowrates of globalization (see Table 2.1). His regression results imply thatthe PRC’s growth rate was 2.33 percentage points higher in 2000 thanin 1975 as a result of greater integration with the rest of the world. Li,Pang, and Ng (2006) find that openness and local domestic factors likegovernance, human resources, and the quality of the labor force bothcontribute to more rapid economic growth.

Since globalization has generally been a positive force for greatergrowth throughout the world, we can turn to an analysis of the glob-alization experience of South Asia. South Asia has opened up its econ-omy to foreign investment and provided stimulus for the growth ininternational trade essentially sometime in the 1980s and the 1990s.This shift emphasizes the move from an inward-looking import sub-stitution strategy to more outward-looking international policies andthe role of the private sector. A variety of indicators of economicgrowth and international trade and finance reflect this new look.Among these are the share of trade in GDP, the growth in trade, theshare of FDI in total investment and income, and the inflow of port-folio capital into the stock market. By looking at how these indicatorsare related to economic growth we can draw a better profile of theimpact of globalization on economic growth and poverty reduction.

20 South Asia: Rising to the Challenge of Globalization

Table 2.1 Average Per Capita Income Growth for Low- and High-GlobalizationCountries (percentage).

Degree of 1970– 1976– 1981– 1986– 1991– 1996–Globalization 1975 1980 1985 1990 1995 2000

Low globalization 2.62 2.08 0.35 0.68 0.14 1.16(68) (71) (80) (83) (64) (40)

High globalization 2.99 3.02 0.79 2.64 1.24 2.04(38) (38) (36) (36) (59) (82)

Note: Figures in parentheses refer to sample size.Source: Dreher (2005).

b670_Chapter-02.qxd 11/12/2008 11:02 AM Page 20

It is also useful to analyze the changing placement of South Asiaon various indices of globalization. The most popular index is theKearney’s Index (2006), which has four separate categories of global-ization: economic integration, personal contact, technological con-nectivity, and political engagement.3 Each of these dimensions isreflected in a number of different variables. A slightly different seriesof three categories is reported by Dreher (2005). These categories areeconomic integration, social globalization, and political engagement.A paper by Heshmati (2003) uses principal component analysis toderive an index of globalization with the four Kearney variables.Another approach adopted by Li, Pang, and Ng (2006) adds a set ofindigenous factors including health and education, quality of thelabor force, and effectiveness of government and amount of corrup-tion. These indigenous factors enable countries to take advantage ofthe opportunities that globalization offers.

In the next section we review the trends in South Asia’s externaleconomic relations and relative country rankings with respect to var-ious globalization indicators. Simple assessments of the economicimpact of globalization on South Asian economic performance arealso provided. After that we explore possible policy initiatives forincreasing the integration of South Asia into the global economy.

Globalization of South AsiaWe begin this section by reviewing trends in South Asia’s globalizationusing the more traditional measures. From 1980 to 1990, South Asia’sshare of world trade remained at 1%, even though the value of tradegrew strongly from 1985 to 1995 (see Table 2.2). Trade in other

South Asia’s Global Integration 21

3 The economic variable includes trade and FDI. The personal contact variableincludes factors such as international travel and tourism, international telephone traf-fic, and workers’ remittances. The technological connectivity variable includes thenumber of Internet users, Internet hosts, and secure servers. The political engage-ment variable includes membership in international organizations, contributions toUnited Nations peacekeeping missions, international treaties ratified, and govern-ment transfers.

b670_Chapter-02.qxd 11/12/2008 11:02 AM Page 21

22South A

sia: Rising to the C

hallenge of Globalization

Table 2.2 South Asia’s Total Trade, 1980, 1985, 1990, 1995, 2000, and 2005 ($ million).

Country 1980 1985 1990 1995 2000 2005

Bangladesh 3,400.7 3,525.1 5,326.6 9,625.2 14,590.4 22,345.3India 23,263.0 24,594.4 41,804.4 65,024.5 92,961.9 238,590.6Maldives 0.0 93.2 190.0 406.5 465.2 948.2Nepal 0.0 430.0 797.9 1,090.9 1,734.1 2,551.7Pakistan 7,969.1 8,627.0 12,970.4 19,452.3 19,598.4 40,561.4Sri Lanka 3,067.8 3,096.7 4,531.7 8,282.0 12,146.8 16,474.7South Asia 37,700.7 40,366.2 65,621.0 103,881.4 141,496.7 321,471.9

South Asia’s Share of 1.0% 1.0% 1.0% 1.0% 1.1% 1.5%World Trade

Average 5-Year – 1.4% 12.5% 11.7% 7.2% 25.4%Growth Rate

Source: International Monetary Fund, Direction of Trade Statistics CD-ROM, July 2006.

b670_Chapter-02.qxd 11/12/2008 11:02 AM Page 22

parts of the world also increased during this period. However, asreforms began to take hold after 1990 and tariff barriers were low-ered, South Asia’s participation in international trade accelerated evenfaster, and by 2005 its share of world trade had increased by 50%, to1.5%. More importantly, the average rate of growth of world trade peryear also rose rapidly, more than doubling from 2000 to 2005 aftergrowing by nearly 40% from 1995 to 2000. India was responsible forthe bulk of the increase. Its total trade (exports plus imports)increased by 2.5 times from 2000 to 2005. Trade in other economiesalso accelerated after 2000. Pakistan’s total trade more than doubledand that of other countries increased by healthy amounts. From 2000to 2005, South Asia’s total trade grew by an average of more than25% yearly, one of the highest rates in the world.

FDI is another important index of globalization. It reflects theinterest of industrial countries in developing countries and is a keyingredient of technological transfer and innovation. Before reformswere introduced in the 1980s and the 1990s, FDI in South Asia wasonly a trickle and its pace was slow, actually falling between 1980 and1985. South Asia’s share of world FDI flows was less than one-half of1% (see Table 2.3). As reforms began in India and Pakistan, FDI flowsaccelerated somewhat, although they remained small relative to totalworld inflows. From 2000 to 2004, South Asia’s share of world FDIflows increased from 0.22% to 1.04%, still a small amount but morethan a fourfold increase in 6 years. India and Pakistan were the bigrecipients. It is notable that from 2000 to 2005 the total global flowof FDI fell by about 48% as global flows from the US declined.However, inflows into South Asia more than doubled. This pattern ofacceleration in the flow of FDI is a strong sign that South Asia isbecoming further integrated into the global economy.

Portfolio investment and other capital flows are yet another indi-cation of the pace of globalization of capital markets in South Asia.According to data from the Institute of International Finance, equityinvestment in India has increased quite dramatically since liberaliza-tion began in the late 1980s and early 1990s (see Table 2.4). In India,direct investment went from $129 million in 1991 to just over $6 bil-lion in 2006 and was forecast to reach $8 billion in 2007. Portfolio

South Asia’s Global Integration 23

b670_Chapter-02.qxd 11/12/2008 11:02 AM Page 23

24South A

sia: Rising to the C

hallenge of Globalization

Table 2.3 Foreign Direct Investment Inflows, 1980, 1985, 1990, 1995, 2000, and 2005 ($ million).

Country 1980 1985 1990 1995 2000 2005

Bangladesh 8.5 −6.7 3.2 1.9 280.4 692.0Bhutan n.a. n.a. 1.6 0.1 −0.1 9.0India 79.2 106.1 236.7 2,151.0 2,319.0 6,676.0Maldives −0.1 1.2 5.6 7.2 13.0 9.5Nepal 0.3 0.7 5.9 8.0 −0.5 2.4Pakistan 63.6 47.4 250.0 719.0 308.0 2,201.0Sri Lanka 42.9 24.4 43.4 65.0 173.0 272.0South Asia 194.4 173.1 546.4 2,952.2 3,092.8 9,861.9World 55,108.1 57,644.9 207,878.4 341,085.9 1,396,538.6 945,795.0

South Asia’s Share 0.35% 0.30% 0.26% 0.87% 0.22% 1.04%of World FDI

n.a. = not available.Source: UNCTAD FDI database online.

b670_Chapter-02.qxd 11/12/2008 11:02 AM Page 24

flows started more slowly, beginning only in 1993 after some liberal-ization of inflows. There was a big spurt in 1993 and 1994, followedby fluctuations over the next decade including negative flows in 1998(not shown in the table). Since 2000, portfolio inflows have acceler-ated further, but with some fluctuation, reaching over $12 billion in2005 before receding somewhat since then. Since 1991, foreignexchange reserves have also increased in every year except 1995.

In Pakistan, direct equity investment has fluctuated since the late1980s with a slight upward trend, peaking in 1998 at $1.5 billion andthen falling back to around $700 million in the last few years.Portfolio investment has been anemic, and there has been a small out-flow in most years since 2001. International reserves have alsoincreased, but not at the same rate as in India. Much of the accelera-tion in FDI has been the result of policy changes that have made iteasier for foreign investors to develop partnerships with South Asianfirms and also to make portfolio investments in South Asian stock andbond markets.

The Kearney’s Index (2006) has been compiled for the past sev-eral years. Its components are listed in Table 2.5a along with the rank-ings of selected countries (from a total of 62 countries) for 2001 and

South Asia’s Global Integration 25

Table 2.4 Direct Investment and Portfolio Investment in India and Pakistan,1991, 1995, 2000, 2005, and 2007 ($ million).

2007Country 1991 1995 2000 2005 (forecast)

India

Direct investment 129 1,954 3,066 6,093 8,000Portfolio investment 4 2,784 2,590 12,489 6,000Increase in reserves 3,385 −2,936 5,842 15,052 12,000

Pakistan

Direct investment 0 439 471 750 n.a.Portfolio investment 323 1,098 73 −30 n.a.Increase in reserves −112 333 1,254 1,150 n.a.

n.a. = not available.Source: Institute of International Finance website.

b670_Chapter-02.qxd 11/12/2008 11:02 AM Page 25

2006 (Table 2.5b). Except for Sri Lanka, the South Asian economiesranked near the very bottom of the overall ranking in 2006. The PRCalso ranks low on the list. India ranks very low in three categories. Itranks higher in personal contact because of the size of remittances.

26 South Asia: Rising to the Challenge of Globalization

Table 2.5a Globalization Index Rankings, 2006.

Country Economic Personal Technological Political

Bangladesh 61 37 62 49India 59 51 57 60Pakistan 60 34 59 55Sri Lanka 38 27 58 58PRC 28 55 50 47Indonesia 52 59 51 50Korea, Republic of 32 39 19 33Malaysia 3 19 28 48Singapore 1 3 12 29Taiwan 12 33 18 62Thailand 16 49 41 57

Source: Kearney (2006).

Table 2.5b Globalization Index Rankings, 2001 and 2006.

Country 2001 2006

Bangladesh 48* 58India 49* 61Pakistan 56* 56Sri Lanka 32* 46PRC 48* 51Indonesia 38* 60Korea, Republic of 31* 29Malaysia 20* 19Singapore 1 1Taiwan 32* 35Thailand 30* 45

*2002 figures.Source: Kearney (2006).

b670_Chapter-02.qxd 11/12/2008 11:02 AM Page 26