the evaluation of the tanzanian petroleum fiscal regime to projects profitability

TRANSCRIPT

THE EVALUATION OF THE TANZANIAN PETROLEUM FISCAL

REGIME TO PROJECTS PROFITABILITY

Author: Lulu Silas Olan’g

Date: 12 August 2015

A thesis presented in partial fulfilment of the requirements for the degree of MSc.

Petroleum, Energy Economics and Finance at the University of Aberdeen

i

DISCLAIMER ‘I declare that this thesis has been composed by myself, that it has not been accepted in any

previous application for a degree, that the work of which it is a record has been done by

myself, and that all quotations have been distinguished appropriately and the source of

information specifically acknowledged’

Signature:

Name:

Date:

ii

Table of Contents DISCLAIMER ............................................................................................................................................. i

LIST OF FIGURES .................................................................................................................................... iv

LIST OF TABLES ....................................................................................................................................... v

ABSTRACT .............................................................................................................................................. vi

ACKNOWLEDGEMENT .......................................................................................................................... vii

1. INTRODUCTION .............................................................................................................................. 1

1.1 United Republic of Tanzania-Background and profile .......................................................... 1

1.2 History of petroleum industry in Tanzania ............................................................................ 1

1.3 Natural gas sector and its importance to Tanzania............................................................... 2

1.4 Position of Tanzania in the competitive global market of natural gas ................................. 3

1.5 Research Overview ....................................................................................................................... 5

2. LITERATURE REVIEW ...................................................................................................................... 6

2.1 Economic rent and its measurement ........................................................................................... 6

2.2 Petroleum industry performance measurement yardsticks ................................................. 7

2.3 Rent collection Fiscal Devices .............................................................................................. 10

2.4 Current petroleum fiscal system in Tanzania ...................................................................... 19

3 DATA AND METHODOLOGY ......................................................................................................... 23

3.1 Data ....................................................................................................................................... 23

3.1.1 Costs .............................................................................................................................. 23

3.1.2 Production .................................................................................................................... 24

3.1.3 Price .............................................................................................................................. 26

3.1.4 Tax Terms ...................................................................................................................... 27

3.2 Financial Modelling .............................................................................................................. 27

3.3 Sensitivity Analysis ............................................................................................................... 28

3.4 Monte Carlo Simulation ....................................................................................................... 29

4 RESULTS ........................................................................................................................................ 30

4.1 Pre-Tax Results ..................................................................................................................... 30

4.1.1 Sensitivity analysis on pre-tax values .......................................................................... 30

4.1.2 Pre Tax Monte Carlo results ......................................................................................... 32

4.2 Post Tax Results .................................................................................................................... 35

4.2.1 Sensitivity Analysis ....................................................................................................... 36

4.2.2 Monte Carlo Simulations.............................................................................................. 40

4.2.3 Analysis of Alternative regime ..................................................................................... 47

5 CONCLUSION ................................................................................................................................ 52

5.1 Concluding Remarks ............................................................................................................. 52

iii

5.2 Limitation of Research and Recommendation .................................................................... 53

6 BIBLIOGRAPHY .............................................................................................................................. 54

7 APPENDICES .................................................................................................................................. 56

APPENDIX A: Main formulas used in Model Calculations............................................................... 56

APPENDIX B: Conversion factors ..................................................................................................... 57

iv

LIST OF FIGURES Figure 1.1 Regional gas Prices ................................................................................................................ 4

Figure 2.1 Supply Price of Petroleum .................................................................................................... 6

Figure 2.2Progressive Tax .................................................................................................................... 11

Figure 2.3 Progressive Tax .................................................................................................................... 14

Figure 2.4 Production Sharing Agreement .......................................................................................... 18

Figure 2.5 World Petroleum Fiscal Arrangements .............................................................................. 19

Figure 3.1 Production profile field 1(small field) ................................................................................ 24

Figure 3.2 Production Profile field 2 (medium field) ........................................................................... 25

Figure 3.3 Production Profile field 3 (Large field) ............................................................................... 25

Figure 3.4 Influence Diagram ............................................................................................................... 28

Figure 4.1 Contractor Pre-tax NPV field 2 ........................................................................................... 31

Figure 4.2 Contractor Pre Tax NPV field 1 ........................................................................................... 31

Figure 4.3 Contractor Pre-Tax NPV field 3 ........................................................................................... 32

Figure 4.4 Monte Carlo simulation results for pre-tax NPV relative to price-field 1 ......................... 32

Figure 4.5 Monte Carlo simulation results on pre-tax NPV relative to price-field 2 .......................... 33

Figure 4.6 Monte Carlo simulation results on pre-tax NPV relative to price field 3 .......................... 33

Figure 4.7 Monte Carlo simulation results on pre-tax NPV relative to devex-field 1 ........................ 34

Figure 4.8 Monte Carlo simulation results on pre-tax NPV relative to devex-field 2 ........................ 34

Figure 4.9 Monte Carlo simulation results on pre-tax NPV relative to Devex-field 3........................ 34

Figure 4.10 Contractor Post Tax NPV field 1 ....................................................................................... 37

Figure 4.11 Contractor Post tax NPV field 2 ........................................................................................ 37

Figure 4.12 Contractor post Tax NPV field 3 ....................................................................................... 38

Figure 4.13Minimum price indicator ................................................................................................... 38

Figure 4.14 Government take field 1 ................................................................................................... 39

Figure 4.15 Government take field 2 ................................................................................................... 40

Figure 4.16 Government take field 3 ................................................................................................... 40

Figure 4.17 Monte Carlo Simulation results on post tax NPV relative to price-field 1 ...................... 41

Figure 4.18 Monte Carlo simulation results on Post Tax NPV relative to price-field 2...................... 41

Figure 4.19 Monte Carlo simulation results for Post Tax NPV relative to price-field 3 ..................... 42

Figure 4.20 Monte Carlo simulation results for post-tax NPV relative to Devex-field 1 ................... 42

Figure 4.21Monte Carlo simulations results for Post Tax NPV relative to Devex-field 2 .................. 43

Figure 4.22 Monte Carlo simulation results on post tax NPV relative to Devex- field 3 ................... 43

Figure 4.23 Monte Carlo results on government take relative to price-field 1.................................. 44

Figure 4.24 Monte Carlo simulation results on government take relative to price-field 2 ............... 44

Figure 4.25 Monte Carlo simulation results on government take relative to price-field 3 ............... 45

Figure 4.26 Monte Carlo simulation results on government take relative to Devex-field 1 ............. 45

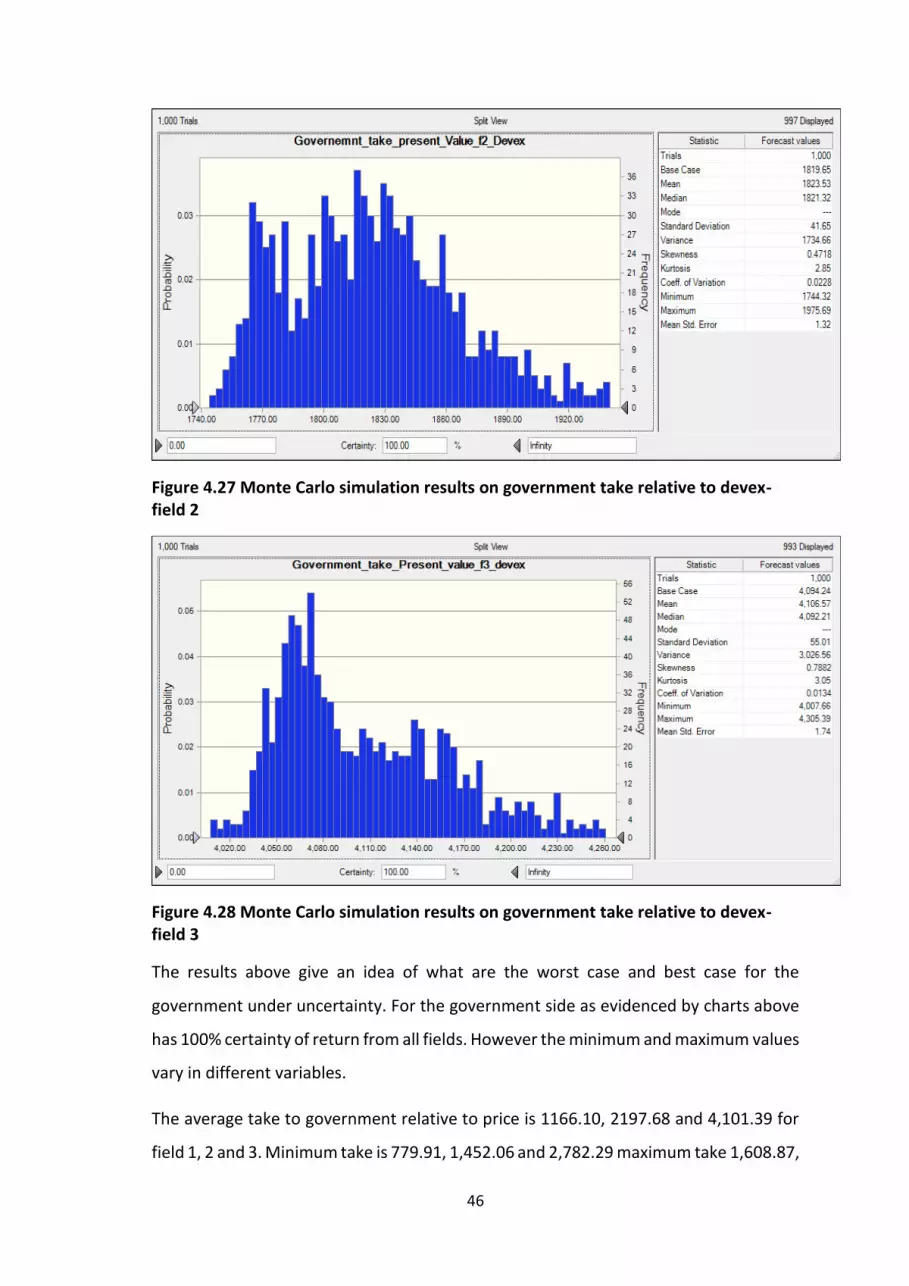

Figure 4.27 Monte Carlo simulation results on government take relative to devex- field 2 ............ 46

Figure 4.28 Monte Carlo simulation results on government take relative to devex-field 3 ............. 46

Figure 4.29 Tax System Comparison-contractor taker for field 1 ....................................................... 48

Figure 4.30 Tax System Comparison-Contractor take for field 2 ........................................................ 49

Figure 4.31 Tax system comparison-contractor take for field 3 ......................................................... 49

Figure 4.32 Tax System Comparison-Government take for field 1 ..................................................... 50

Figure 4.33 Tax System comparison-government take for field 2 ...................................................... 50

Figure 4.34 Tax system comparison-Government take for field 3 ..................................................... 51

v

LIST OF TABLES Table 2.1 Onshore profit gas split ........................................................................................................ 21

Table 2.2 Offshore Profit Split ............................................................................................................. 22

Table 3.1 Field Reserve and related costs ........................................................................................... 23

Table 3.2 Phasing of development expenditure ................................................................................. 24

Table 3.3 Tanzania Well reserve estimates ......................................................................................... 26

Table 3.4 Additional profit tax rates .................................................................................................... 27

Table 4.1 Pre-Tax Results ..................................................................................................................... 30

Table 4.2 Pre Tax Monte Carlo Statistics ............................................................................................. 35

Table 4.3 Post Tax Results .................................................................................................................... 36

Table 4.4 Adjusted PSA terms results .................................................................................................. 48

Table 4.5 Resource rent tax results ..................................................................................................... 48

vi

ABSTRACT Tanzania has been carrying out Petroleum exploration for over 50 years now, of which Gas

has been produced onshore and on shallow waters. The Gas produced has been used for

domestic supply. The recent discoveries of significant reserves in deep waters approximately

50 Tcf has created an opportunity for Tanzania to export. The government contracts

International companies to carry out exploration and development of gas fields. Since Gas is

a depleting resource the issue of efficient taxing system that will generate sustainable return

for the government rises. To cater for this Tanzania has been continuously updating the fiscal

system reaching to the current contractual system.

This dissertation analysed how flexible the current Tanzanian fiscal system is to guaranteeing

project’s profitability, balancing the interest of the government and the investor. The terms

of PSA (2013) ware used to analyse 3 fields of small to large size. From the analysis it was

found that pre-tax fields are profitable. Results after tax shows the system to be favourable

for large fields thus the government can continue using the current system for fields with

reserves above 1 Tcf. An adjusted system where additional profit tax is not charged is highly

recommended for smaller fields.

vii

ACKNOWLEDGEMENT This research paper would have not become complete in its nature without assistance and

guidance from other parties. First and for most I Thank God for granting me knowledge and

good health though out the period of undertaking this research.

Secondly Many Thanks to my Supervisor Dr Marc Gronwald for the assistance and guidance

received throughout the research period. Third I Thank Prof Alexander Kemp for his enormous

assistant throughout the preparation to the completion of this dissertation.

I also extend my utmost appreciation to TPDC officials for their assistance and agreeing to

meet me at such short notice, their inputs have enriched the content of this work.

I want to thank very much my Parents Mr. Silas Olan’g and Mrs. Martha Olan’g for the support

provided to enable me reach this point and finally completion of my project. Thanks to my

immediate siblings for understanding and being there for me through out. Thanks to my

friends and class mate for all the help and support provided whenever needed.

Your support and dedication is highly appreciated, May God bless you all abundantly.

1

1. INTRODUCTION 1.1 United Republic of Tanzania-Background and profile

The United Republic of Tanzania is formed of two Sovereign States. Tanganyika which

became a Sovereign State on 9th December, 1961 and a Republic in 1962 and the

People’s Republic of Zanzibar which was established after the Revolution on 12th

January, 1964 after Zanzibar became independent. In December, 1963 followed the

Union of the two states. Tanzania is in East Africa on the Indian Ocean, to the north are

Uganda and Kenya; to the west; Burundi, Rwanda, and Congo; and to the south;

Mozambique, Zambia, and Malawi. The total area in main land 883.6 and Zanzibar

2.5(“000” sq. km). The population by census of 2012 is 44.9m. (Tanzania National

Bureau of statistics, 2013)

The Tanzanian economy is heavily dependent on Agriculture which grew by 4% in 2014,

the overall economy of the country grew by 7.3% in 2013. Main sectors that contributed

to this growth include information and communication, manufacturing, construction,

mining and quarrying and other services which are supported by public investment in

infrastructure and the energy sector. Electricity production and supply in the country

has increased due to expansion in production capacity from natural gas. According to

the African economic Outlook (2015) Tanzanian economy is projected to grow by 7.5%

in 2017 this follows the expected boost of the natural gas development projects in the

country. Today, gas is used to generate electricity to feed the national grid. Further

expansions are underway including 532 km of 36 inch pipeline, which is being

constructed to transport natural gas from Mtwara and Lindi to Dar Es Salaam. A further

25km of 24 inch subsea line will connect Songo Songo Island to Somanga Fungi.

Investment in Liquefied Natural Gas (LNG) and Compressed Natural Gas (CNG)

processing plants is also being sought. (African Economic Outlook, 2015)

1.2 History of petroleum industry in Tanzania

Intermittently, Tanzania has been exploring Oil and gas since 1950s mainly onshore. The

first natural gas discovery was made in 1974 at the Songo Songo Island in Lindi Region

followed by another discovery at Mnazi Bay (Mtwara Region) in 1982. In respect to this

History of Petroleum Exploration in Tanzania has gone through five main phases to date.

2

The first phase was the year 1952-1964 where four wildcats were drilled along the coast

on Mafia Island, Zanzibar, Pemba and Onshore in the Mandawa Salt Basin. These

Operations were done by BP and Shell but significant hydrocarbons were not

discovered.

The Second phase was the year 1969-1979 where the first Production sharing

agreement was signed between Tanzania Petroleum Development Corporation (TPDC)

and AGIP on the former concessions with BP and Shell. Three onshore and two offshore

wells were drilled, in 1974 significant gas discoveries were made at SongoSongo.

Third phase is the year 1980 to 1991, this period was characterised by increase in Oil

price which stimulated exploration and production activities which led to gas discoveries

in 1982 at Mnazi Bay by AGIP. It is during this period that oil companies’ attention was

drawn to the coast of Tanzania and exploration licences were awarded to companies

including Shell and Texaco.

Then followed a fourth phase, this period was more of a regulatory finalisation period

by the government of Tanzania and TPDC there was least activities going on. These

phase was basically for development of fiscal and technical agreement for Songosongo

development, Mnazi bay field developments and acquisition of exploration licenses

which leads to the current phase.

Following the availability of new data from seismic studies done onshore and offshore

in the year starting 2000. Rights to explore the coast of Tanzania were granted to

several oil and gas companies. These exploration lead to a number of discoveries both

on shore and offshore by 2014 total onshore reserves were estimated to be 8 Tcf and

significant offshore reserves of 45.23 Tcf which totals up to 53.23Tcf.1

1.3 Natural gas sector and its importance to Tanzania

Tanzania’s recent vast discoveries of offshore natural gas strongly signal that it can

become the third-largest gas exporter in Sub-Saharan Africa, following Nigeria and

Mozambique. Based on current discoveries and estimated recoverable reserves in

Tanzania, the IMF report in 2014 projected that the government revenue would be at a

range of $ 3-6 billion annually starting 2020 or later. “Currently Tanzania is a net

1 TPDC 2014-Exploration history

3

importer of petroleum fuels that absorbs on average 55% of the country foreign

exchange earnings.” (Mkenda. A 2014). To alleviate this challenge Ongoing Oil and gas

exploration activities are currently given high priority.

Structural changes that aimed at promoting the growth of private sector led economy,

led to the first Energy policy of Tanzania (1992) to be formulated and revised in 2003.

Markets became more liberal and the government committed to bringing social

economic development. This policy has accelerated the development of energy sector

this includes increased discoveries of gas. In the study (Ebohon. O, 1996) it empirically

proven that energy consumption is complementary to Tanzania and any African country.

With the challenge of power cuts and insufficient supply of electricity in the country

given the huge reserves Tanzania can improve the domestic fuel mix. To do so the

government indicates that a minimum of 10% of gas produced in the country be

supplied in the country at a lower price and also TPDC is to pay royalty in kind (supply

gas). Also Tanzania is to take advantage of the competitive global market of natural gas.

(Ledesma, 2014)

1.4 Position of Tanzania in the competitive global market of natural gas

Natural gas has become an important source of energy in the world and its importance

is expected to continue increasing over time. Following the increase in new sources of

supply and demand in the markets of Asian countries (expected market or Tanzania gas),

where this demand is expected to be met through LNG.

In the natural gas market Tanzania is not alone, is currently competing with other

countries which have different advantages and disadvantages economical and

geographically. Currently Tanzania is competing with its neighbour Mozambique, also

with USA and Australia. Tanzania and Mozambique have almost close advantages in the

market in terms of distance and availability of clean gas2 thus lower processing and

production costs. But unlike Tanzania, Mozambique is having higher reserves. USA and

Australia are considered potential high volume suppliers because of political stability,

close proximity to the market for the case of Australia and low development cost for

USA. On the other hand USA is having a distance disadvantage being further away from

2 Gas which has no significant impurities such as carbon dioxide and sulphur oxide

4

the market and Australia has high development costs. Therefore for Tanzania it is very

crucial to distinguish it’s self in the market to be able to compete effectively in such a

concentrated market. (Ledesma, 2014)

Seeing that Tanzania is currently in a good position of securing market for its gas and

looks to contract private Oil companies mostly foreign companies it’s crucial for the

government to create an enabling environment that attracts investor’s to participate in

the exploration activities. The reason for creating an enabling environment is to reflect

on the industrial challenges of high development costs associated with gas production

and fluctuating prices. Gas pricing is a crucial component in making projects

economically viable.

For companies to secure financing for such high investment projects requires mostly by

entering into long-term contracts with customers. (Kemp, 2015) The decline in prices

and regional price segmentation in gas prices adds uncertainty to the financial outlook

of projects. In 2014 the price of natural gas in different regions dropped as seen in the

chart below while the price of LNG to japan was around $16, US henry Hub $5 and UK

NBP $8 by 2014. It is of importance the price that Tanzania is to use in the market is

competitive and reasonable that is creates enough revenues for the government and

investment incentive to contractor.

Figure 1.1 Regional gas Prices

Source: BP statistical review of world energy (2015)

5

1.5 Research Overview

Development of hydrocarbon sector to Tanzania does not only bring a number of

opportunities but also challenges. The current focus is on the development of the deep

water blocks, which are yet to be declared commercially viable. Commercializing gas is

costly, despite the active exploration activities uncertainty still prevails about gas price,

recoverable reserves and fiscal impact which will affect the design of gas projects.

Main objective of the study is to find out how the current design of the fiscal system

responds to the economic situations looking at prices and costs relative to the

profitability of the upstream petroleum project in a field of either small, medium or

large size. For this purpose 3 fields were chosen with corresponding Operating, and

development costs at given base price that will enable to analyse the risks and rewards

to companies and to the state.

This study mainly will seek:

a) To investigate how effective is the existing fiscal scheme in balancing the

government and investors interests.

b) To estimate the profitability of the selected projects (fields) under the current

hybrid system

c) Assessing project risk under the current regime relative to price and cost

uncertainties

d) Compare current PSA term with alternative fiscal tool on which benefits both

parties.

This paper is divided into 5 main chapters, Chapter one covers the introduction, chapter

2 is the literature Review which discusses the concept of economic rents and their

collection to the state, chapter 3 describes Data, Methodology used which include

financial modelling, chapter 4 discusses the results obtained from financial modelling,

sensitivity analysis and Monte Carlo Simulation, lastly are concluding remarks which

summarises the study discussions and recommendations.

6

2. LITERATURE REVIEW 2.1 Economic rent and its measurement

Tanzania just like other petroleum producing countries expect higher returns to be

generated from project investments. Host government is faced with hard decisions of

what and how will be the share of the revenue to the state since the country uses private

companies for petroleum exploration and production. In theory there are a number of

fiscal tools that can be used. Main tools that can be used for capturing economic rent

are through transfer of rights this is through bidding processes or concessions through

taxes and royalties or profit sharing agreements. (Johnston 2003)

The concept of Economic rent is very vital in the discussion of the design of an efficient

tax system. Economic rent in petroleum industry are returns acquiring to producers in

excess of supply price of the investment, this relates to the alternative investment

opportunities the company may have. In other words it is the revenue if the government

taxes the company can still get sustainable returns from the investment. (Kemp, 2015)

Figure 2.1 Supply Price of Petroleum

Source: (Kemp. A, 2015)

From the Figure above a return OMCP is required to cover production and yields normal

profits, return OMCD+P is required to cover the costs and risks involved In developing

7

new fields. The difference MCT-P is the economic rent, if the government collects any

amount in that area, development activities should be able to continue. (Kemp, 2015)

There are a number of issues that make the decision of determining how a state can

efficiently capture the share of the economic rent generated complex to most producing

countries. Considering the uniqueness of the petroleum industry. The petroleum

industry does not conform to the general definition of perfect competition,

characterised by long lead times and investment costs and especially because

petroleum is a depleting resource. (Kemp, 2015)

The size of economic rents on any projects in the petroleum industry can be determined

by the performance criteria and yardsticks as explained below. At the field development

stage the practical measure of economic rent include the net present value, rate of

return and investors weighted cost of capital. At the exploration stage the measure is

the expected monetary value.

2.2 Petroleum industry performance measurement yardsticks

2.2.1 NPV at various discount rates

Net Present Value (NPV) of an investment is computed to show the value of future

earnings at present day after initial investment costs have been compensated at a

discount rate. NPV can be calculated by the formula shown below:

Where R=revenues, O=operating cost, I=initial investment cost, r=discount rate and

i=period

The NPV decision rule is to undertake an investment whose NPV is positive and abandon

an investment with negative NPV. When comparing projects the best decision is to take

the alternative with the highest NPV, Berk and Dermazo (2007) explain the valuation

principle generally notes that an investment that adds more value is preferred

8

compared to the later not taking into account the investors’ preference to reach to this

conclusion. Thus because of the wealth measurement ability to project investments and

discounting nature it is among the mostly used Discounted cash flow investment

appraisal method.

On the other hand NPV rule is limited in its use, it does not take into account the

flexibility that an investor can have to react to new information. Considering that

flexibility in the petroleum industry is considered of high importance following the high

initial costs of investment which are irreversible. The NPV rule assumes risks to be

unchanging during the project life this is seen in its design where it deals with expected

cash flow at a constant discount rate. (Pindyck&Dixit, 1994)

2.2.2 Internal rate of return

The internal rate of return is the interest rate such that the net present value equals

zero. The calculation of IRR is done after defining the anticipated future cash flows to

be received from the investment. Its formula can be as below:

Where IRR is r in the equation

The IRR rule is based on the decision to take on an investment opportunity if the IRR is

greater than the opportunity cost of capital and turn down a project with IRR less than

the opportunity cost of capital. The IRR method just like the NPV rule are both

discounted cash flow method in that they take into account the time value of money

and shows if the project is profitable.

On the other hand the IRR rule is used when looking at stand-alone projects only if the

project’s negative cash flow precede its positive cash flow. This means that it is not a

proper method for comparing across different projects. Also the IRR rule will give

correct answers but not always that means it is to be used in line with other methods

like the NPV this is because sometimes the IRR could lead to incorrect answers for

example when the NPV is negative but the IRR is higher than the cost of capital. Making

9

a decision basing on IRR alone will in the end reduce the investor’s wealth. (Berk and

Demarzo 2007)

2.2.3 Payback period

Is the time required to recover investment costs, it is sometimes referred to as the

breakeven point. At this point money received equals money spent in Money of the Day

terms which means that it is a non-discounting appraisal method. Payback period

method seems to be insufficient in itself in investment decision since it does not show

the profitability of the investment by not taking into consideration cash flows beyond

the breakeven point. The rule of thumb for payback method is the project with the

shortest period is preferred to project with long period of payback. Whilst it’s

advantageous to use method especially in the oil and gas industry where the price of

the products are highly volatile. This method is best for comparing across projects for

this reason it’s not used in this study. (Mian. M, 2011)

2.2.4 Real profit/investment ratio

This is the ratio of Net present value to investment, this shows how much great returns

can be derived from a unit of investment made. The formula for this method is as seen

below

Where sum of NPV is divided by the sum of present value of investments

In case of limited budget this ratio is useful in ranking which investment gives a higher

return and it sometimes gives a different ranking to that of NPV. Berk and Dermazo

(2007) refer to it as profitability index which is used mostly by firms to rank projects

given constrained resources, however for this method to work there should only be one

constrained to be considered in the calculation and the set of project that maybe

undertaken should exhaust all the available resource.

NPV

PV of I

∑

10

2.2.5 Assessment at exploration stage

At the exploration stage the Expected monetary value (EMV) is considered the most

relevant measure of the project’s return. EMV is the expected Net Present Value from

development less explorations costs.

Denoted:

EMV = P(NPV) - E - P(A)

Where:

EMV = Expected Monetary Value

P = Chance of Discovery

NPV = Net Present Value

E = Initial Exploration Costs

A = Appraisal Costs

As Schuyler and Newendorp (2007) suggest following the uncertainty and risks

associated with the exploration stage risks such as chance of discovery, the EMV is

suited to give the profitability monetary value of the project and the degree of risk and

is the base parameter the decision maker should use to select investments with high

uncertainty.

The decision rule for EMV is to accept the project when EMV is positive, reject a project

when EMV is negative.

2.3 Rent collection Fiscal Devices

The economic rent generated is to be shared between the government and the

operating company(s) which can be complex and requires a design of an appropriate

tool that can be used to ensure the government equally with the company get fair

returns without causing economic distortions. A magnitude of the implied regime

matters in the sense as Bhattacharyya (2011) explains if the policy is very generous the

state will receive a low share which will be questionable by the citizens or it can be very

11

strict and deter investment because of the increased uncertainty to an investor, or

rather cause pre-mature abandonment of fields.

Generally when designing a fiscal regime there are a lot of issues to be considered, it’s

important to keep in mind the objectives of both the government and companies and

should be a function of economic rent. To be termed an efficient tax system a tax system

should be targeted on economic rents be sensitive to varying oil prices, field sizes and

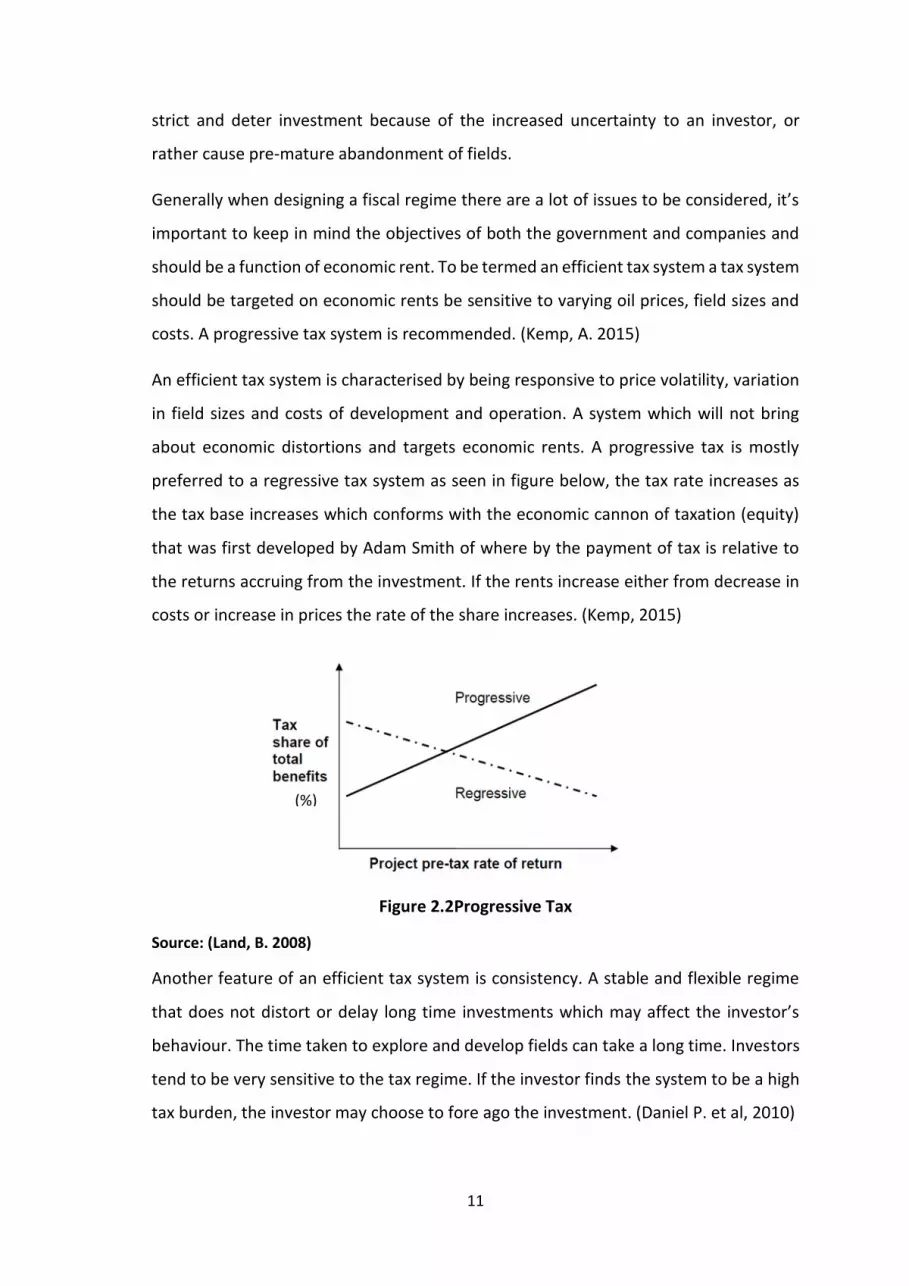

costs. A progressive tax system is recommended. (Kemp, A. 2015)

An efficient tax system is characterised by being responsive to price volatility, variation

in field sizes and costs of development and operation. A system which will not bring

about economic distortions and targets economic rents. A progressive tax is mostly

preferred to a regressive tax system as seen in figure below, the tax rate increases as

the tax base increases which conforms with the economic cannon of taxation (equity)

that was first developed by Adam Smith of where by the payment of tax is relative to

the returns accruing from the investment. If the rents increase either from decrease in

costs or increase in prices the rate of the share increases. (Kemp, 2015)

Figure 2.2Progressive Tax

Source: (Land, B. 2008)

Another feature of an efficient tax system is consistency. A stable and flexible regime

that does not distort or delay long time investments which may affect the investor’s

behaviour. The time taken to explore and develop fields can take a long time. Investors

tend to be very sensitive to the tax regime. If the investor finds the system to be a high

tax burden, the investor may choose to fore ago the investment. (Daniel P. et al, 2010)

(%)

12

A number of instruments can be used to collect rents from petroleum explorations,

most commonly used are taxes (Profit/corporate tax, resource rent tax, brown tax),

Royalties and production sharing Agreements/contracts. Below is the description of the

mostly common used instruments focusing on their characteristics, shortcomings and

their implication to the economy.

2.3.1 Corporate income tax

Income tax is levied on Oil and gas companies like any other company operating in other

economic activities which in some cases with certain provisions the charge levied on

petroleum companies may be higher than other companies. Taxes are levied on

company’s profits which is least likely to hinder field development. An effective tax is a

function of nominal tax rate and pace of write off for exploration costs. Costs are

recovered by order of first the previous unrecovered costs followed by operating,

Exploration and Appraisal then depreciation. The quicker the pace of cost write off the

better as it ensures that the rate of return is not reduced by tax. In some countries the

write off is 100% as production begins, which is less likely to take place in developing

countries such as Tanzania. (Kemp, 1992)

Among the provision that are provided under the income tax regime is project financing

where the interest rate is a deductible cost limited to a certain percentage of total

investment or by imposing a withholding tax on interest sent abroad. This is to avoid

employing a company with high debt and limit abusive transfer pricing between related

companies (Sunley et al 2003). Another provision is permitting Tax credits in countries

such as USA, it’s easier if the tax paid in producing country resembles that of home

country especially if it meets realisations, gross receipts and net income requirements.

Also loss carry forward may be considered in other countries which allows investors to

carry forward losses incurred in a year to the next year at a given level of proportions,

“Loss carry forward is important to be allowed in the petroleum exploration and

development by considering the long lead times and upfront investment” (kemp 2015).

For the above provisions to work most countries ring fence petroleum activities, this

expands the tax base by limiting the consolidation of income and deductions for tax

purposes across projects or contract area. The design of the extent of ring fencing is

13

again entirely based on the country’s fiscal regime, negotiations with IOCs and

preference of early revenues. (Keen, M. and Boadway, R. 2010)

Income tax ensures host government gets a considerable amount of rent as it targets

the profits of the company which makes them more desirable compared to royalty

which will be discussed below. Since the scheme targets the profits it is less likely to

cause disincentives to field developments. (Kemp, 2015)

A challenge with income tax comes with the present value of the depreciation

allowance. Before tax companies are provided with a depreciation allowance on

development costs. The depreciation allowance is calculated by either a rate of around

20% or 5 years on a straight line basis or 20-30% declining balance. As Kemp (2015)

elaborates on the design of depreciation allowance, in some countries depreciation

starts with expenditure while other countries it commences when production has

started. With both the present value of the depreciation allowance is lower than the

initial investment but even lesser if production starts late for countries where allowance

commences with production. (Hannesson 1998)

Another issue with corporate income tax is that it’s not targeted on economic rents. A

generally flat rate not progressively related to profits does not allow for return on equity

may leave the government with lower share or hinder development when oil prices

drop. (Kemp 2015)

2.3.2 Royalties

Royalties are traditionally rewards to landlords for use of natural resources for the right

to use property. Royalties are often not recorded in the fiscal accounts as tax but to an

investor it does not quite make a big difference since the economic impact to projects

is the same. Royalty is levied on gross revenue usually based on well- head values at a

flat rate and widely applied to mineral extraction around the world. According to most

model PSA a commonly used flat rate is 12.5% (Kemp, 2015)

To host governments royalty is more preferable revenues are yield from the very start

of production and it is easy to administer as well compared to other profit based taxes.

It also ensures to the government as a political advantage that foreign companies

14

operate project and are paying something to the state. To a contractor the risks are

shared between the government and companies to some extent (uncertainty of oil

price) while costs are borne by the investor. (Kemp, 1992) Royalties may provide fiscal

stability, predictable tax base and can be less exposed to asymmetric information

challenges (Keen, M. and Boadway, R. 2010)

Royalty has its drawbacks as well. Firstly it is not targeted on economic rents “At best

they constitute imperfect taxes on quasi rents and take no account of sunk costs of

exploration and site development” Keen, M. and Boadway, R. (2010). With a flat rate

commonly 12.5% can cause the government to leave a substantial amount of rent share

with investors when profits increase probably following oil price increase. At the same

time when the revenue after deduction of royalty falls below production cost to the

investor could make marginal fields uneconomic and will cause premature

abandonment of fields. (Kemp, 2015) The figure below elaborates the distorting effects

of royalty.

Figure 2.3 Progressive Tax

(Source; Kemp, 2015)

From above figure initial production is qo with introduction of tax t production reduces

to q1 because it is expensive for companies. With the price p1 the investor is able to

cover its marginal cost there after production q1 it becomes uneconomic to keep

operating.

15

Because most host governments prefer early revenues, to guard against the regressive

nature of the royalty some countries like Denmark and Netherlands in the years around

1973 after the major price increases introduced a sliding scale royalty scheme. Under

the sliding scale scheme the royalty rate increases as production increases. It is basically

a function of field size making more flexible but not sensitive to prices and costs. (Kemp,

1992)

2.3.3 Resource rent tax

Garnaut and Clunies Ross (1975) article is the most referred to in literature as the first

to propose the use of Resource rent tax. Lund, (2009) acknowledges system’s intent to

give a higher return to investors compared to other tax systems such as the income tax.

Resource rent tax (RRT) is the tax on the net cash flow after a specified rate of return

has been obtained from the investment. As Kemp (2015) explains the return on capital

would consist of a basic return equivalent to the rate of interest on risk free long term

borrowing plus a margin enough to cover the risks associated with the investment.

The resource rent tax is designed to target economic rent, the scheme allows the

investor to achieve a specified threshold rate of return before tax is paid. The threshold

is then used to compound the investor’s net cash flow, the cash flow is initially negative

following the exploration and appraisal costs. The cash flow is accumulated by the

threshold rate until the income becomes positive. (Kemp 2015)

A resource rent tax is stable, it varies with changes in oil prices and costs. There is no

early fiscal burden to the investor and risks are shared with the government and provide

an appropriate share of the rent to the government. The resource rent tax allows for

ring fencing, where a firm operating in one project cannot reduce the revenue of the

one project by incorporating the costs of another project otherwise revenues will be

postponed through continuous deductions. Australia resource tax system includes ring

fencing on contract area to enhance the near term revenue from resource rent tax.

(Kemp 2015)

On the other hand the Resource rent tax is faced with a problem of information

asymmetry deciding on the rate of return. The magnitude of the rate of return can either

create an incentive to invest, practice tax avoidance or give low or no return to

16

government.” if the hurdle rate is set too low, the tax may become a major deterrent to

investment, if set too high chances are it will never apply.”(sunley, et al 2003)

RRT is associated with delay of payments to the government. This can be less attractive

to some governments, also because of the high risk sharing between government and

companies. The government does not get upfront payments, due to the wait period

until the company has recovered all its costs and get the desirable rate of return which

is also unknown to the government and probably may not be desirable from the social

point of view. (Hannesson 1998). To increase the government expected revenue

Garnaut, and Ross (1975) suggest a hybrid system of imposing income tax in conjunction

with the RRT.

To cover the possibility of increased profitability in the future and ensure that the

revenue to the government increases as well. But also enable companies to recover

development costs in early years when profits are still low. The government implies a

set of tiers (where the tax rate increases as a certain rate of return has been attained by

the company) that can be imposed when a certain threshold has been met. A challenge

is on deciding the number of tiers to use, (Gaus, Ross 1975) suggest a separate tax to be

levied at more than one threshold interest rate for example a tax rate of 25% may be

levied at a real rate of return of 10 and then when the threshold rate is beyond 10 a tax

rate can increase to 35%.

The problem of gold plating also arises with such a scheme, an investor gets the

incentive to increase his expenditure to get higher returns. This is mostly common with

schemes based on the rate of return (ROR). This problem can however be avoided by

putting the ROR close to the that of the investor but is still a challenge as the IRR Is

unknown to the government. (Kemp, 2015)

2.3.4 Brown Tax

Another type of tax is Brown tax named after E.C Brown, As Kemp (2015) describes it is

a type of tax based on company’s net cash flow with no discounting. All cash flow is

taxed proportionally where the government pays subsidies when the cash flow is

negative and collects taxes when the cash flow is positive. With this scheme the rate can

be set very high but without causing disincentives except when the NPV becomes very

17

small, leaves the IRR post tax unchanged and if NPV was positive pre-tax remains

positive Post Tax.

Brown tax is proportionate in nature and considered completely neutral and effective

at targeting economic rent. But not favoured by government because of the high risk

sharing on costs, price and production. Kemp (2015)

2.3.5 Production Sharing contracts

The concept of production/profit sharing contracts is derived to explain the ownership

of resources. It was firstly used in agriculture where a tenant (rents) does not have the

title of the resources, the title is being retained by the government (land lord). In the

petroleum industry the government contracts a private company to explore and

produce oil and gas. The contractor incurs the investment costs and risks which then

gets compensated out of the production. In this case a contractor is not liable to pay

royalty but in some countries the royalty is paid as the government requires early

revenues. (Johnston, 2003)

In designing a production sharing contract it is very important to consider cost oil/gas

and profit oil/gas. Cost gas is the proportion of total production as specified by the PSC

that the contractor retains to recover investment costs. The cost recovery

conditions/process are similar to depreciation terms used in calculating income tax. A

cost recovery limit is set “a ceiling of 40% - 50% is common” (Kemp 1992) this ensures

there is profit oil as soon as production starts. The remaining gas is the profit gas which

is split between the government and the contractor following specified proportions

indicated in the contract. Because of the limit in some cases not all costs are recovered

and can also delay cost recovery in turn the post-tax rate of return gets affected which

is a great possibility of making projects less commercial. In some countries an uplift is

given to compensate for the delay. Another instance is when the actual cost for recovery

is less than the cost celling the difference goes to the state rather than becoming part

of the profit Oil which creates an incentive for companies to be less cost conscious

(Kemp, 2015)

When splitting profit gas a production sharing scheme can be progressive or at a flat

rate, although originally the scheme had a flat rate which is still is in Indonesia makes

18

the scheme inflexible as it is not responsive to increased production. The profit oil split

can as well be on an incremental basis, with the share to the state increasing as

production increases making it progressive as it responds to the field size as the seen

below where the government’s share of profit Oil increases as production increases.

(Kemp, 2015)

Source: (Kemp 2015)

Profit gas split can also be based on project’s profitability through R-factor or

contractor’s Rate of return. The R-factor can be generally be referred to as the ratio of

cumulative revenues to cumulative investment costs:

Contractor’s revenues after all royalty, tax & Government profit oil share to date

Contractor’s costs to date

The government’s take increases as the R factor/ROR increases. Usually the concept of

resource rent tax is used to determine the state’s share of profit oil/gas where the R-

factor is calculated in a given accounting period and when a certain threshold is reached

as specified in the contract another sharing rate is applied.

The profit sharing scheme is flexible to variation of oil price, field sizes and variation in

investment costs. PSA scheme considered the most efficient tool of collecting rent and

Figure 2.4 Production Sharing Agreement

19

widely used by most petroleum producing countries especially developing countries.

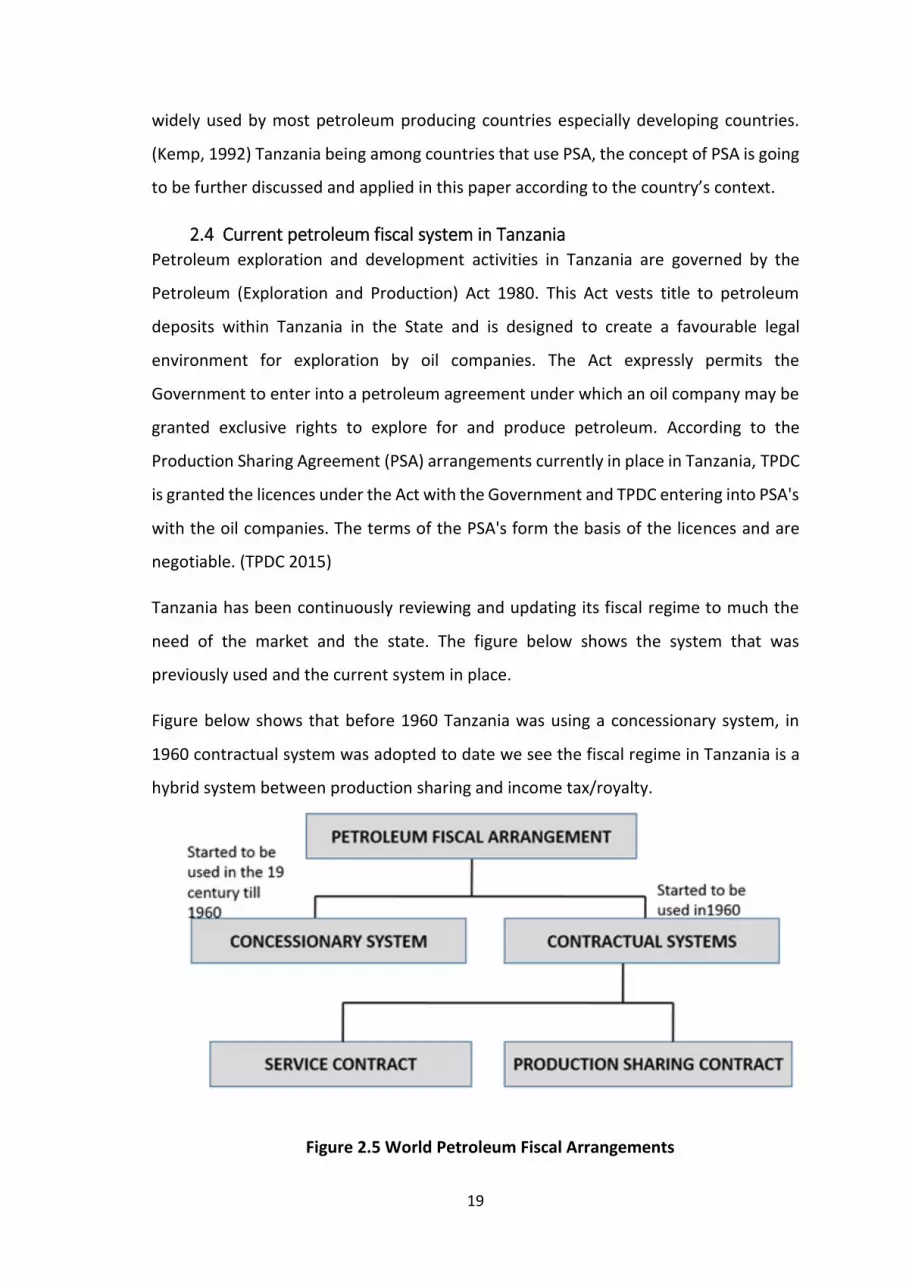

(Kemp, 1992) Tanzania being among countries that use PSA, the concept of PSA is going

to be further discussed and applied in this paper according to the country’s context.

2.4 Current petroleum fiscal system in Tanzania

Petroleum exploration and development activities in Tanzania are governed by the

Petroleum (Exploration and Production) Act 1980. This Act vests title to petroleum

deposits within Tanzania in the State and is designed to create a favourable legal

environment for exploration by oil companies. The Act expressly permits the

Government to enter into a petroleum agreement under which an oil company may be

granted exclusive rights to explore for and produce petroleum. According to the

Production Sharing Agreement (PSA) arrangements currently in place in Tanzania, TPDC

is granted the licences under the Act with the Government and TPDC entering into PSA's

with the oil companies. The terms of the PSA's form the basis of the licences and are

negotiable. (TPDC 2015)

Tanzania has been continuously reviewing and updating its fiscal regime to much the

need of the market and the state. The figure below shows the system that was

previously used and the current system in place.

Figure below shows that before 1960 Tanzania was using a concessionary system, in

1960 contractual system was adopted to date we see the fiscal regime in Tanzania is a

hybrid system between production sharing and income tax/royalty.

Figure 2.5 World Petroleum Fiscal Arrangements

20

Source: TPDC presentation to Mineral and Energy Commission (2015)

2.4.1 Bonuses

According to the 2013 MPSA the Tanzanian government implements two types of

bonuses; Signature bonus of $2.5 million upon signing the Production Sharing

Agreement when an investor wants to operate in the petroleum industry and

Production bonus of $5 million upon commencement of production. For the Tanzanian’s

having bonuses incorporated in the PSA can be beneficial especially the production

bonus Johnston, D (2003) suggests the payments can help in its work plans these may

include training of personnel.

2.4.2 Royalty

Royalty is paid to the government by TPDC on behalf of itself and the Contractor in

respect of petroleum obtained from the Contract Area. By delivering to the Government

12.5% for onshore/shelf areas and 7.5% for offshore of total Crude Oil/Natural Gas

production (prior to Cost Oil and/or Cost Gas recovery). The variations in percentages

depending on the location of either offshore or onshore can be related to the varying

technical difficulties associated with the exploration process. (MPSA 2013)

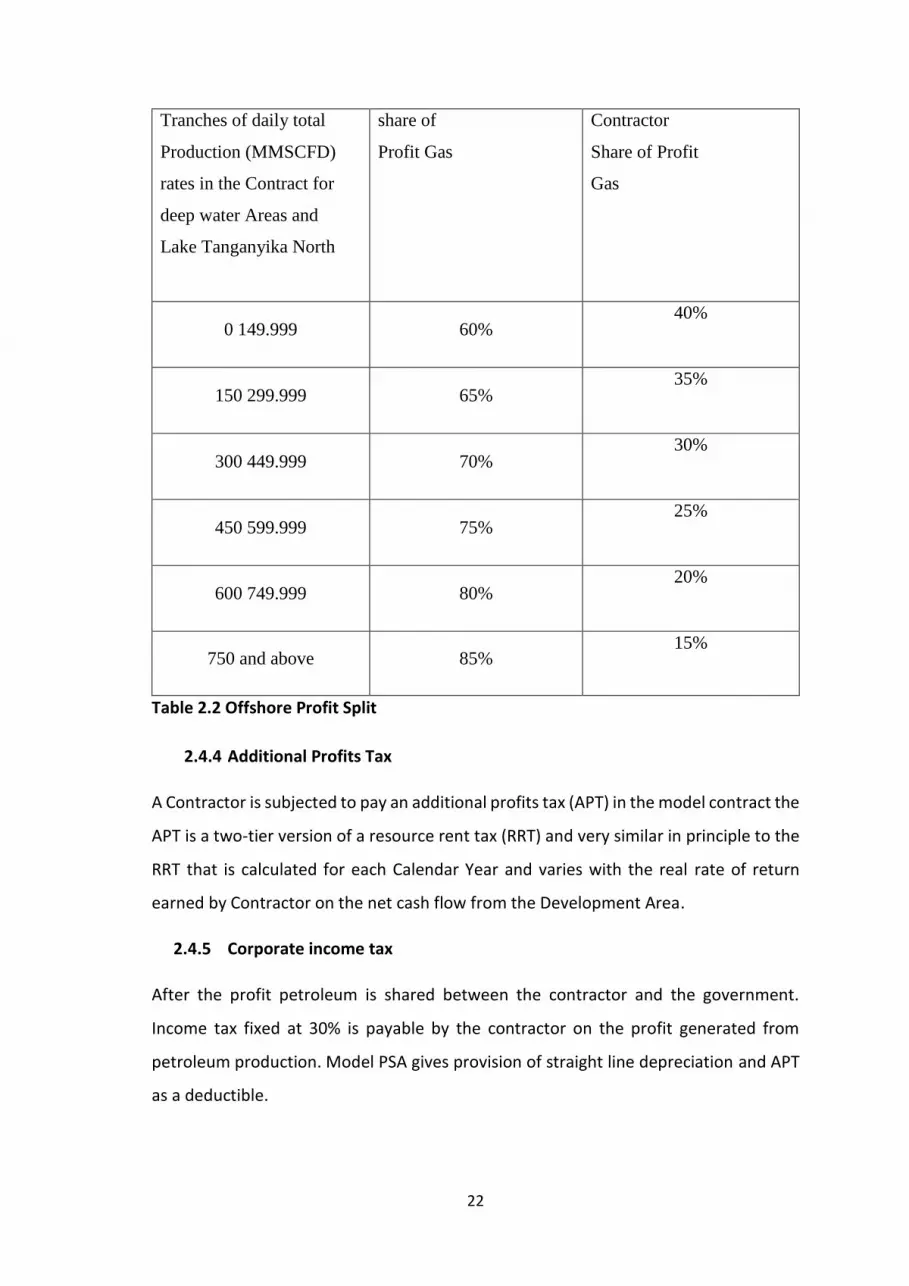

2.4.3 Production Sharing

Produced gas is shared between the government and the contractor. Cost recovery limit

of 50% is set on the revenues net of royalty limited to any calendar year ring fenced to

Exploration Licence or Development Licence. Recoverable costs are recovered from the

date they have been incurred, if there is to the extent in the calendar year the

recoverable costs exceed cost oil unrecovered costs are carried forward to the next

succeeding calendar year(s) until fully recovered.

21

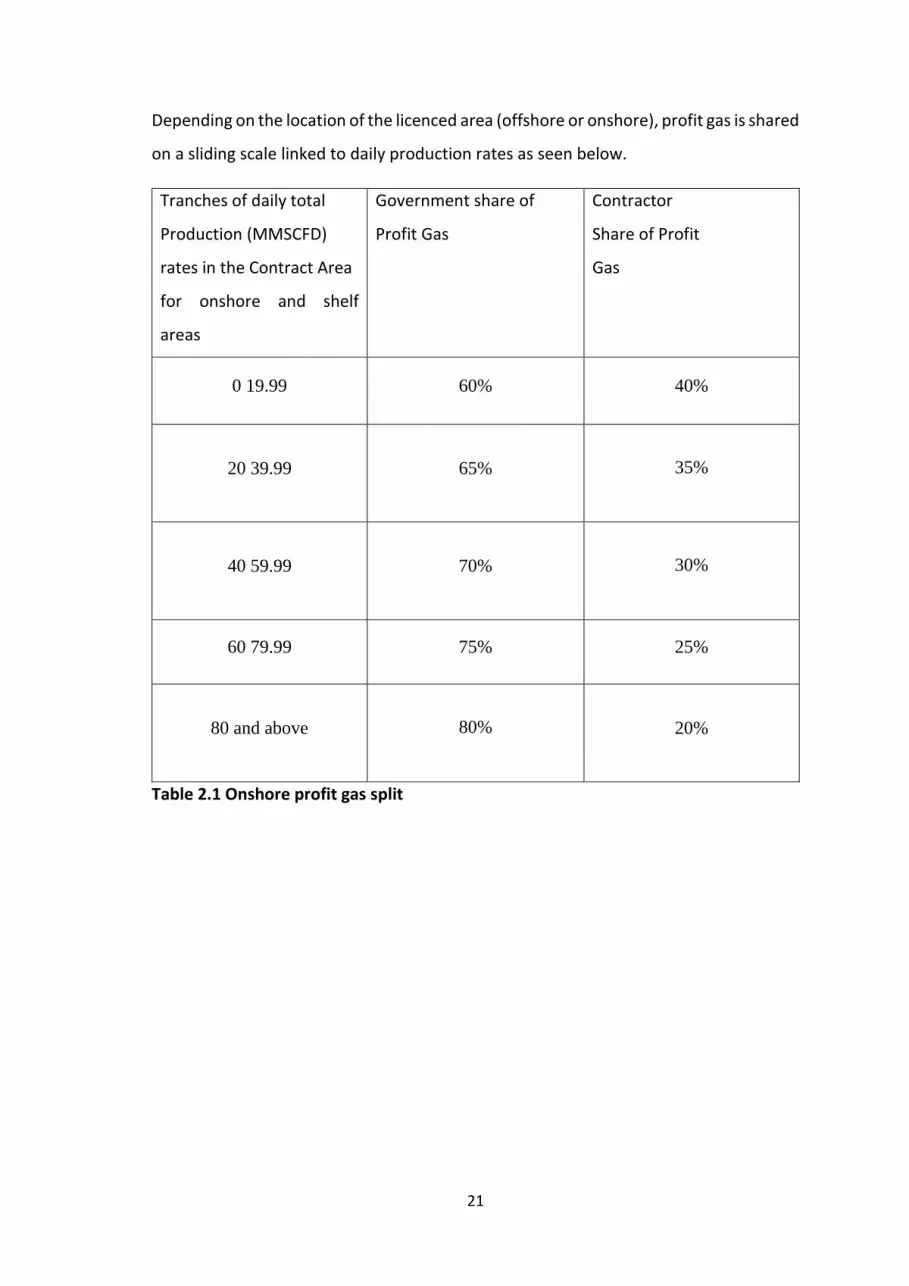

Depending on the location of the licenced area (offshore or onshore), profit gas is shared

on a sliding scale linked to daily production rates as seen below.

Tranches of daily total

Production (MMSCFD)

rates in the Contract Area

for onshore and shelf

areas

Government share of

Profit Gas

Contractor

Share of Profit

Gas

0 19.99 60% 40%

20 39.99 65%

35%

40 59.99 70%

30%

60 79.99 75% 25%

80 and above

80%

20%

Table 2.1 Onshore profit gas split

22

Tranches of daily total

Production (MMSCFD)

rates in the Contract for

deep water Areas and

Lake Tanganyika North

share of

Profit Gas

Contractor

Share of Profit

Gas

0 149.999 60% 40%

150 299.999 65% 35%

300 449.999 70% 30%

450 599.999 75% 25%

600 749.999 80% 20%

750 and above 85% 15%

Table 2.2 Offshore Profit Split

2.4.4 Additional Profits Tax

A Contractor is subjected to pay an additional profits tax (APT) in the model contract the

APT is a two-tier version of a resource rent tax (RRT) and very similar in principle to the

RRT that is calculated for each Calendar Year and varies with the real rate of return

earned by Contractor on the net cash flow from the Development Area.

2.4.5 Corporate income tax

After the profit petroleum is shared between the contractor and the government.

Income tax fixed at 30% is payable by the contractor on the profit generated from

petroleum production. Model PSA gives provision of straight line depreciation and APT

as a deductible.

23

3 DATA AND METHODOLOGY

3.1 Data Sample Gas field data has been used in this research. The choice of fields was based

upon the overall natural gas discoveries in deep waters in Tanzania that has reached

approximately 45.23 Tcf, with wells of varying sizes. To capture the variation small,

medium and large fields were selected to see whether the current fiscal system is

flexible enough in capturing economic rent and how to it affects the profitability of

different fields of varying sizes.

For the above stated purposes fields with recoverable reserves of 500 Bcf, 1000 Bcf and

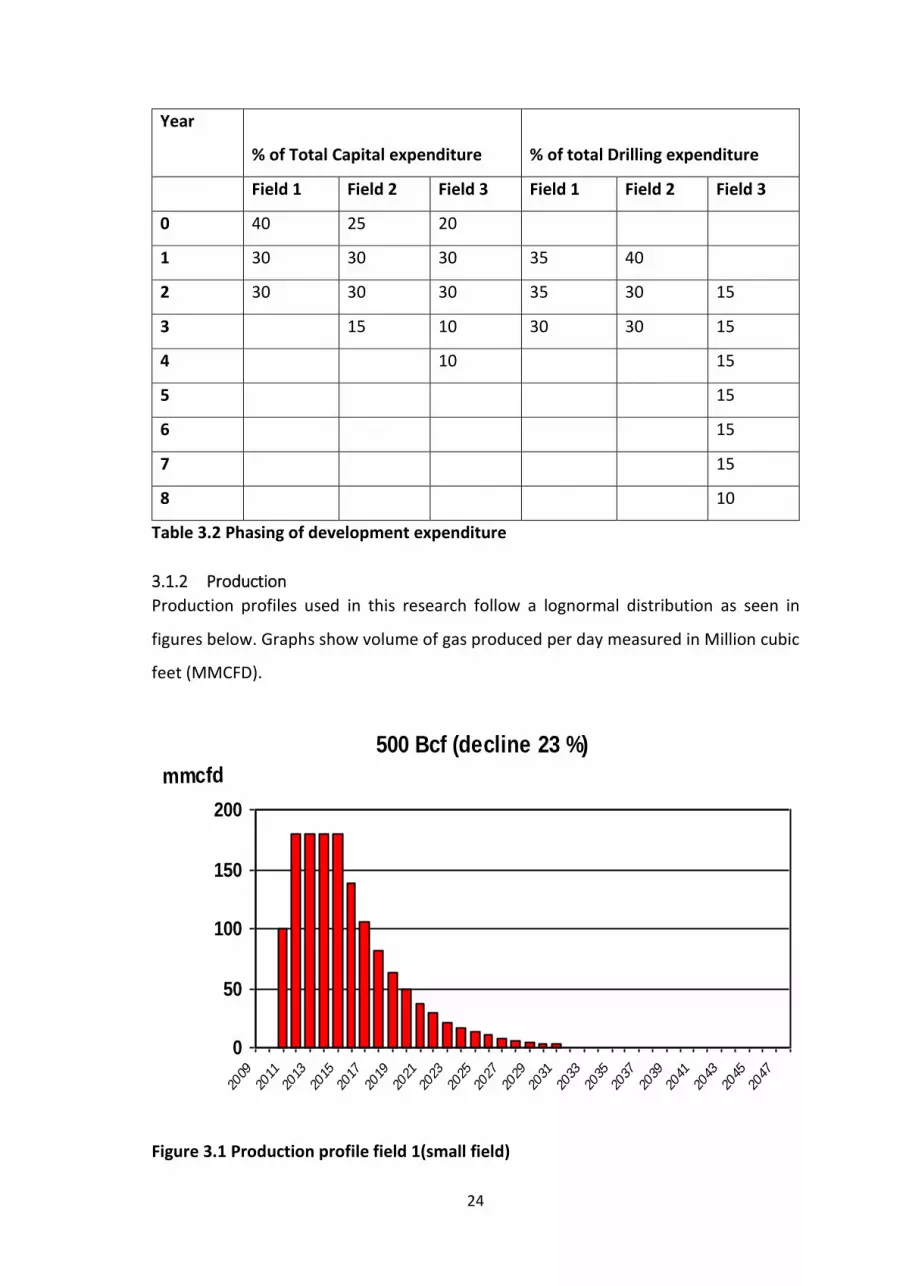

2000 Bcf were chosen. Each field has associated Development costs that were chosen

with the idea of economies of scale related to field size. Field development costs

estimates are not quite certain and in the study by Ledesma, 2013 he estimates the cost

to be $3.5 per MMBTU which are quite low and argues that costs could be lowered over

time in production of gas.

3.1.1 Costs

Compared to the estimate used in this research, costs are to the contrary high in deep

water exploration. For the small field development cost is $15, medium field $12.5 and

$10 per barrels of Oil equivalency (Boe) as adopted from AUPeC report, 2009. This

information and other related costs are summarised in the table below:

Field Size

DATA 1 2 3 Units

Reserves 500 1000 2000 Billion Cubic feet

Development

costs

15 12.5 10 $ Per Barrels of Oil

equivalent

Drilling costs 50 40 35 % of development

cost

Operating costs 6.75 6.0 5.25 % of accumulated

development cost

Table 3.1 Field Reserve and related costs

24

Year

% of Total Capital expenditure

% of total Drilling expenditure

Field 1 Field 2 Field 3 Field 1 Field 2 Field 3

0 40 25 20

1 30 30 30 35 40

2 30 30 30 35 30 15

3 15 10 30 30 15

4 10 15

5 15

6 15

7 15

8 10

Table 3.2 Phasing of development expenditure

3.1.2 Production

Production profiles used in this research follow a lognormal distribution as seen in

figures below. Graphs show volume of gas produced per day measured in Million cubic

feet (MMCFD).

Figure 3.1 Production profile field 1(small field)

500 Bcf (decline 23 %)

0

50

100

150

200

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

2039

2041

2043

2045

2047

mmcfd

25

Figure 3.2 Production Profile field 2 (medium fiel

Figure 3.3 Production Profile field 3 (Large field)

The above production profile were chosen to reflect Tanzania different block reserve

estimates between Chaza-1 and Papa-1 as seen in the 2013 TPDC estimates in the figure

below:

2 Tcf (decline 20 %)

0

100

200

300

400

500

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

2039

2041

2043

2045

2047

mmcfd

26

Well Name Gas Reserve estimate (Tcf)

Pweza-1 1.7

Chewa-1 1.8

Papa-1 2.0

Chaza-1 0.47

Jodari-1 4.1

Mzia-1 and Mzia 2 7.8

Zafarani-1 6.0

Lavani-1 and 2 4.4

Tangawizi-1 6

Table 3.3 Tanzania Well reserve estimates

Source: (extracted from TPDC (2013) online database)

3.1.3 Price

For base year 2015 the Gas price is assumed to be $8.36 per Mmbtu as the possible

price to delivery point3. The price was chosen to reflect the price that is charged before

processing of Liquefied Natural Gas and shipping to Asian Markets. A model including

LNG processing can be model but is beyond the focus of this research which is focused

on the upstream evaluation of the project. The assumption of price comes from the

historical price of gas trades in Tanzania for onshore production which has been $5.36

per Mmbtu to delivery point. To reflect offshore activities and costs the price used in

this research was assumed and slightly increased by the researcher due to lack of

specific data of the prevailing price in Tanzania for Gas to delivery point for offshore

production. (RPS, 2015). For the purpose of this research delivery point is assumed to

be at wellhead for simplicity.

Other information used include inflation rate of 3% following the US dollar used. The

discount rate is assumed to be 10% as the prevailing rate in the industry.

3 The PSA governs upstream activity of a defined delivery point, according to the 2010 Model Addendum for Natural gas the delivery point is specified as the wellhead or other point which may be agreed between TPDC and the contractor.

27

3.1.4 Tax Terms

For the purpose of his research as a base model contract, Production contract of 2013

was used with terms as listed below.

Royalty rate of 7.5%

Corporate income tax is applied at rate of 30% adjusted for depreciation with a

rate of 20% straight line from the start of production.

Cost oil for production sharing is 50% of revenue less royalty

Profit sharing is based on the daily production of gas on a sliding scale as seen in

previous chapter (Table 2.2)

Additional profit tax is payable based on the contractors pre-tax RROR

summarised:

RROR APT rate

≤ 20 0%

20≤R≤30 25%

>30 35%

Table 3.4 Additional profit tax rates

3.2 Financial Modelling

The above data was used for financial analysis using capital budgeting tools that include

NPV, IRR and profit to investment ratio at field development stage. First by calculating

pre-tax and then post tax cash flows for both the government and the contractor to see

how much of profit gas each gets as well as how much tax is being paid. The model gives

detailed statistics and economic indicators under the model production sharing

contract.

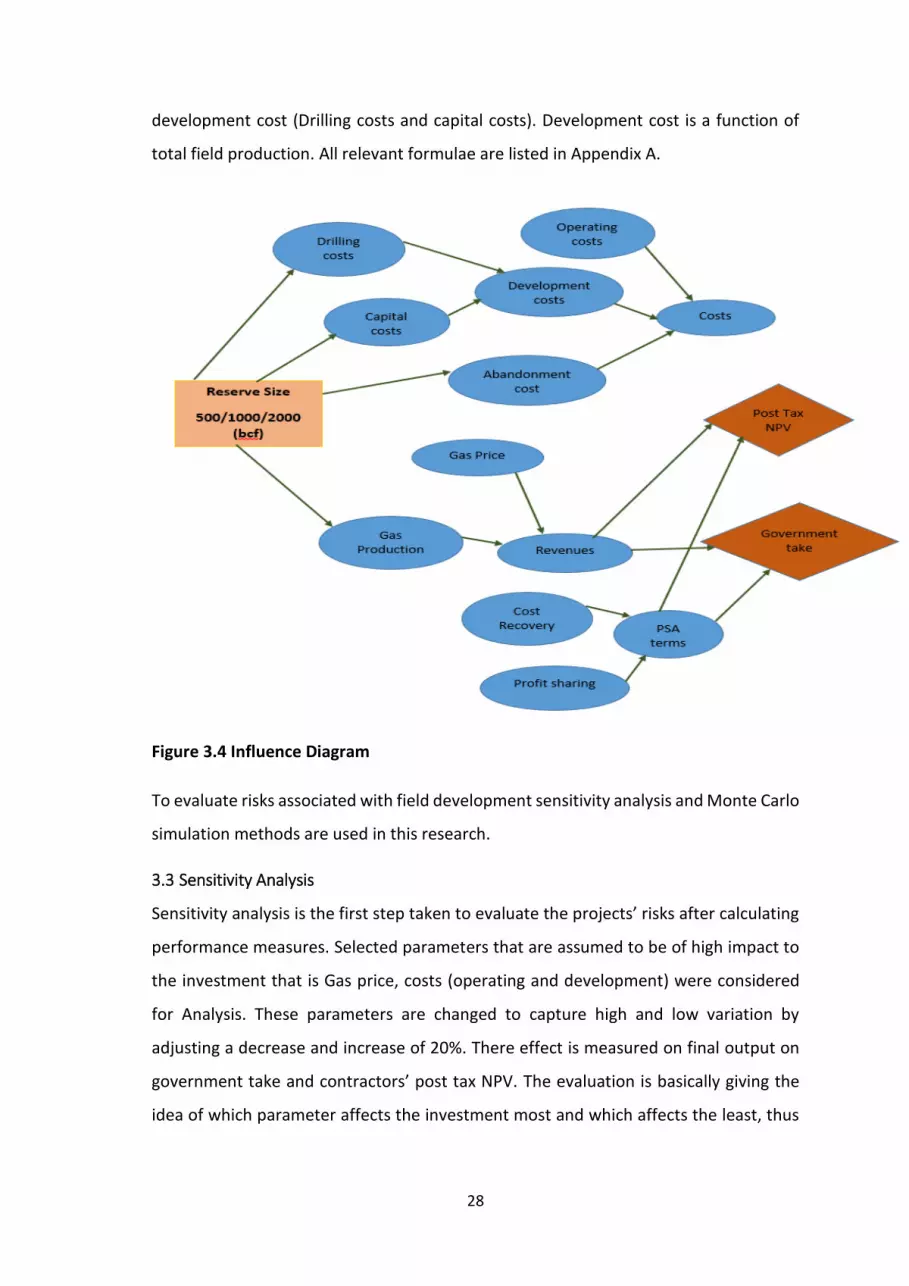

The flow is clearly illustrated by the Influence diagram below, where the main objective

is to get the contractors Net Present value Post tax and government take as indicated

by value nodes. Government take and contractors’ Post tax NPV depend on the

revenues from production and the applied fiscal terms (PSA term) as described above

which is a hybrid including taxes and royalties. Gas price and costs subjected to inflation

are uncertain following market fluctuations. Costs include operating cost and

28

development cost (Drilling costs and capital costs). Development cost is a function of

total field production. All relevant formulae are listed in Appendix A.

Figure 3.4 Influence Diagram

To evaluate risks associated with field development sensitivity analysis and Monte Carlo

simulation methods are used in this research.

3.3 Sensitivity Analysis

Sensitivity analysis is the first step taken to evaluate the projects’ risks after calculating

performance measures. Selected parameters that are assumed to be of high impact to

the investment that is Gas price, costs (operating and development) were considered

for Analysis. These parameters are changed to capture high and low variation by

adjusting a decrease and increase of 20%. There effect is measured on final output on

government take and contractors’ post tax NPV. The evaluation is basically giving the

idea of which parameter affects the investment most and which affects the least, thus

29

an investment decision is likely going to be based on the parameter that affects the

project’s returns most. (Kemp, A. 2015)

3.4 Monte Carlo Simulation

Mont Carlo simulation is run on Gas price and development costs to see the effect on

Government take and contractor’s NPV. Simulations describe the uncertainty in price

and development costs in terms of probabilities. Normal distribution is used assuming

the base case variables are most likely but there is a possibility of approximately 68%

that variables will deviate from the mean especially following the trend in gas price.

When running the simulations it is important to specify a large number of trials to get

approximate accuracy in expected values and outcome. For the purpose of this research

1000 trials have been run. Monte Carlo method is argued to be very useful and since its

early recognition in 1960 most Petroleum companies have used it to make investment

decision as it illustrate the degree of riskiness in projects. (Newendorp and Schuyler

2014)

30

4 RESULTS

4.1 Pre-Tax Results

From spreadsheet modelling preliminary results are obtained and summarised below

are the contractor’s NPV at 10% discount rate, IRR and Real profit/investment ratio.

Table 4.1 below shows the metrics for each field.

Description Field 1 Field 2 Field 3 Unit

Reserves 0.5 1 2 Tcf

Pre Tax NPV 1,086 2,184 4,240 Million $

Pre Tax IRR 28 26 26 Percent

Pre Tax NPV/I 0.92 1.1 1.4

Table 4.1 Pre-Tax Results

At a base price of 8.46 dollars per Mmbtu all fields indicate higher profitability as seen

from values above. The internal rate of return is 28% for small field and 26% for medium

and large fields, these fields showing low IRR could be associated with long production

periods. Field 3 with reserves estimate of 2 Tcf has a high NPV of 4,240 and high return

derived from a unit of investment, a contractors gets a return of 1.4 this is as would be

expected because of the economies of scale where development costs for larger field is

low compared to the medium and small field.

4.1.1 Sensitivity analysis on pre-tax values

To evaluate the risk associated with each field a sensitivity analysis was done and results

are shown in tornado charts below for each respective field. All field remain quite

profitable after a decrease of 20% in Gas price and Production, increase in development

costs and operating costs, Gas price is seen to have a higher impact to contractor’s NPV

followed by production, development costs and least by operating costs as a percentage

of accumulated development cost.

31

400.00 600.00 800.00 1000.00 1200.00 1400.00 1600.00 1800.00

Gas price

Production

Devex

Opex

PRE-TAX NPV

1000.00 1500.00 2000.00 2500.00 3000.00 3500.00

Gas price

Production

Devex

Opex

Pre_Tax NPV

Figure 4.2 Contractor Pre Tax NPV field 2

Figure 4.1 Contractor Pre-tax NPV field 1

32

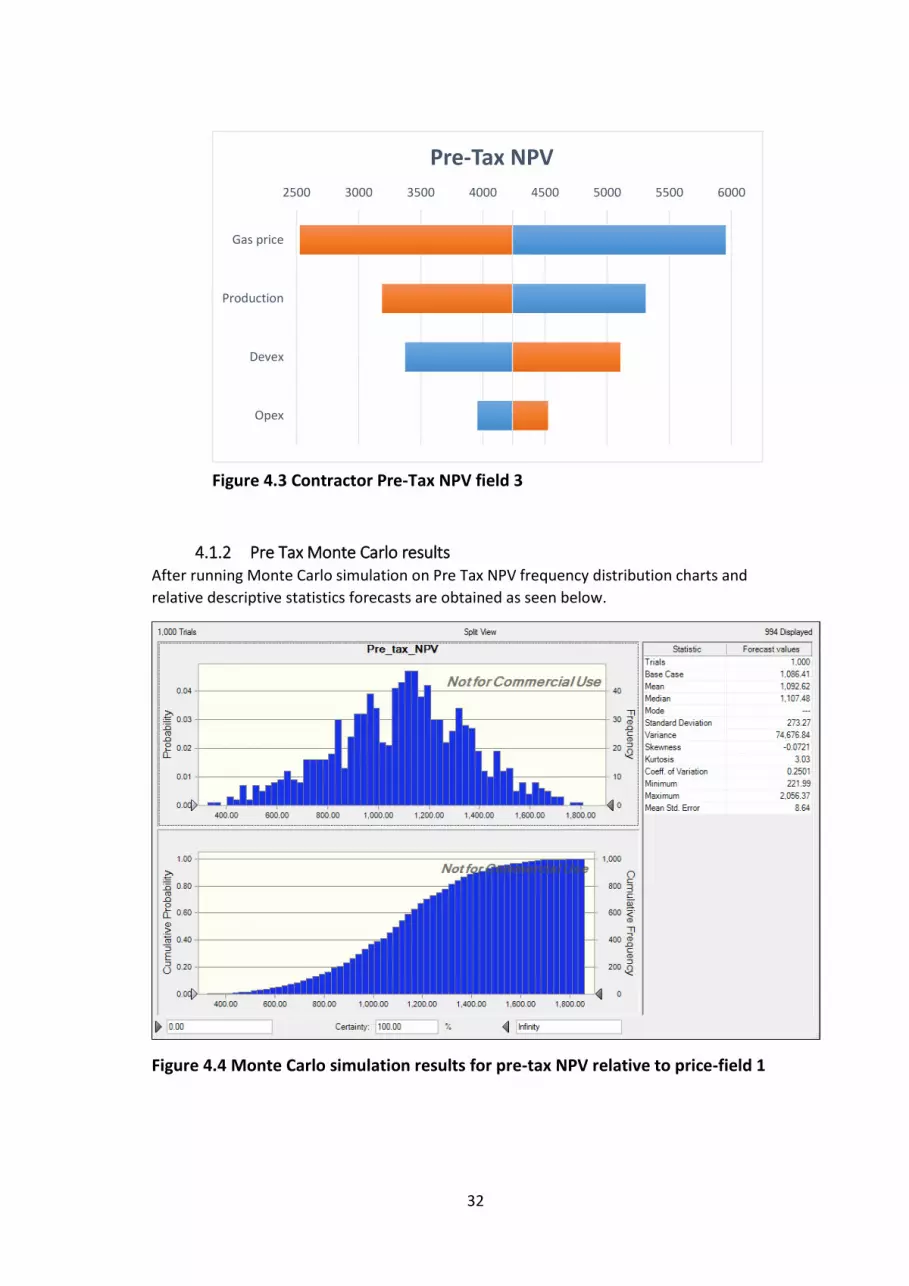

4.1.2 Pre Tax Monte Carlo results After running Monte Carlo simulation on Pre Tax NPV frequency distribution charts and

relative descriptive statistics forecasts are obtained as seen below.

Figure 4.4 Monte Carlo simulation results for pre-tax NPV relative to price-field 1

2500 3000 3500 4000 4500 5000 5500 6000

Gas price

Production

Devex

Opex

Pre-Tax NPV

Figure 4.3 Contractor Pre-Tax NPV field 3

33

Figure 4.5 Monte Carlo simulation results on pre-tax NPV relative to price-field 2

Figure 4.6 Monte Carlo simulation results on pre-tax NPV relative to price field 3

34

Figure 4.7 Monte Carlo simulation results on pre-tax NPV relative to devex-field 1

Figure 4.8 Monte Carlo simulation results on pre-tax NPV relative to devex-field 2

Figure 4.9 Monte Carlo simulation results on pre-tax NPV relative to Devex-field 3

35

From results above the distribution is fairly asymmetrical to the mean Indicating that

the price pulls the contractor NPV negatively and positively almost equally. There is

100% certainty of making profit before taxes for all field sizes. The table below

summarises the average, minimum and maximum profit that can be attained by the

contractor at the given price and development cost. The base case profits (NPV) for

each field fall in between the attained range from simulations as seen below.

Field 1 Field 2 Field 3

Statistics relative to Price

Mean 1,092.62 2,179.06 4,251.55

Minimum 221.99 519.18 1,257.39

Maximum 2,056.37 4,090.44 7,996.59

Statistics relative to Devex

Mean 1,086 2,178 4,231.34

Minimum 555.33 1,389.2 2,967.32

Maximum 1,682.67 3,082.11 5,862.73

Table 4.2 Pre Tax Monte Carlo Statistics

4.2 Post Tax Results

Analysis and discussion of Post Tax result section builds mainly from Pre Tax sensitivity

analysis we have seen Gas Price, production and development cost have a significant

impact to contractor’s return. Therefore after Production sharing as described in

chapter 3 and application of tax terms results on Government’s take and Contractors

NPV are presented. Uncertainty analysis results from Sensitivity analysis and Monte

Carlo simulations are also presented and analysed.

Description Field 1 Field 2 Field 3 Unit

Reserves 0.5 1 2 Tcf

Post Tax NPV 129.49 365.33 789.20 Million $

Post Tax IRR 13 14 14 Percent

Post Tax NPV/I 0.11 0.19 0.27

36

Government

present value

cash flow

956.92 1819.65 3451.35 Million $

Government

cash flow (MOD)

1,793.44 4,054.96 9,661.04 Million $

Contractor cash

flow (MOD)

952.97 2,390.85 5,543.97 Million $

Total

Government

take

65 63 64 Percent

Government

share of

economic rent

88 83 81 Percent

Royalty to the

government

379 799 1,729 Million $

Table 4.3 Post Tax Results

From table 4.3 it can be observed how statistics have changed from pre-tax results

obtained earlier. Post tax NPV obtained is 129.49, 365.33 and 789.20 million dollars for

field 1, field 2 and field 3 respectively. Total government take is (65%) for small field,

63% for medium and 64% for large field. A share of economic rent going to government

is 88% for a small field and 83% and 81% for medium and large field respectively. The

government also gets royalty (gas worth of million dollars) 379, 799 and 1,729 from

small, medium and large field respectively. Practically royalties in Tanzania are paid by

the Tanzania Petroleum Development cooperation, this could be because ideally

royalties are not meant to be incorporated in PSC’s in a place where the investor is a

contractor. It can be observed that after collection of quite a large share of economic

rent by the government all fields remain relatively profitable with positive post tax NPV

and IRR above 10%.

4.2.1 Sensitivity Analysis

Considering the base results it is of interest to measure how the above results would

change at different market situation and geological prospects. Thus below are results

37

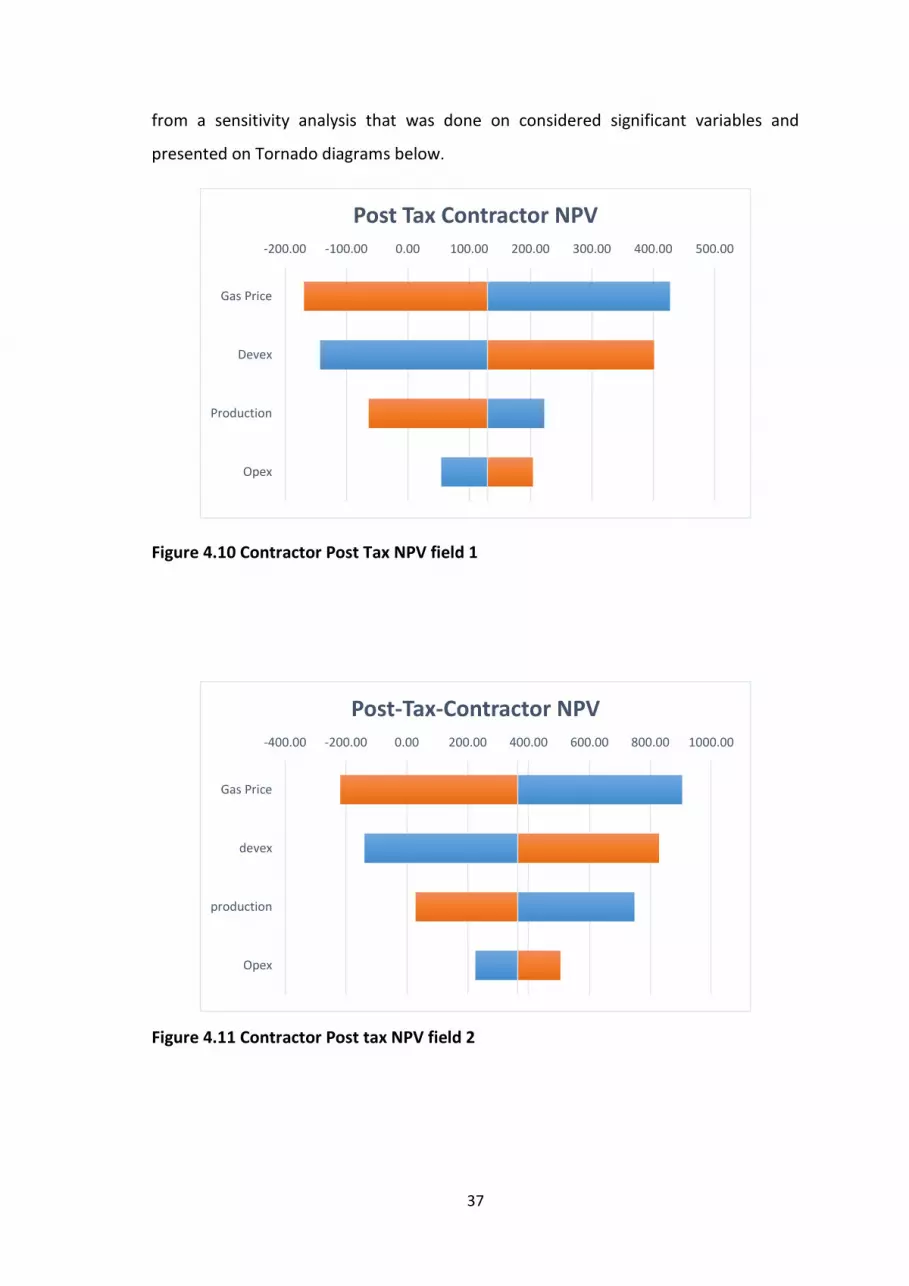

from a sensitivity analysis that was done on considered significant variables and

presented on Tornado diagrams below.

Figure 4.10 Contractor Post Tax NPV field 1

Figure 4.11 Contractor Post tax NPV field 2

-200.00 -100.00 0.00 100.00 200.00 300.00 400.00 500.00

Gas Price

Devex

Production

Opex

Post Tax Contractor NPV

-400.00 -200.00 0.00 200.00 400.00 600.00 800.00 1000.00

Gas Price

devex

production

Opex

Post-Tax-Contractor NPV

38

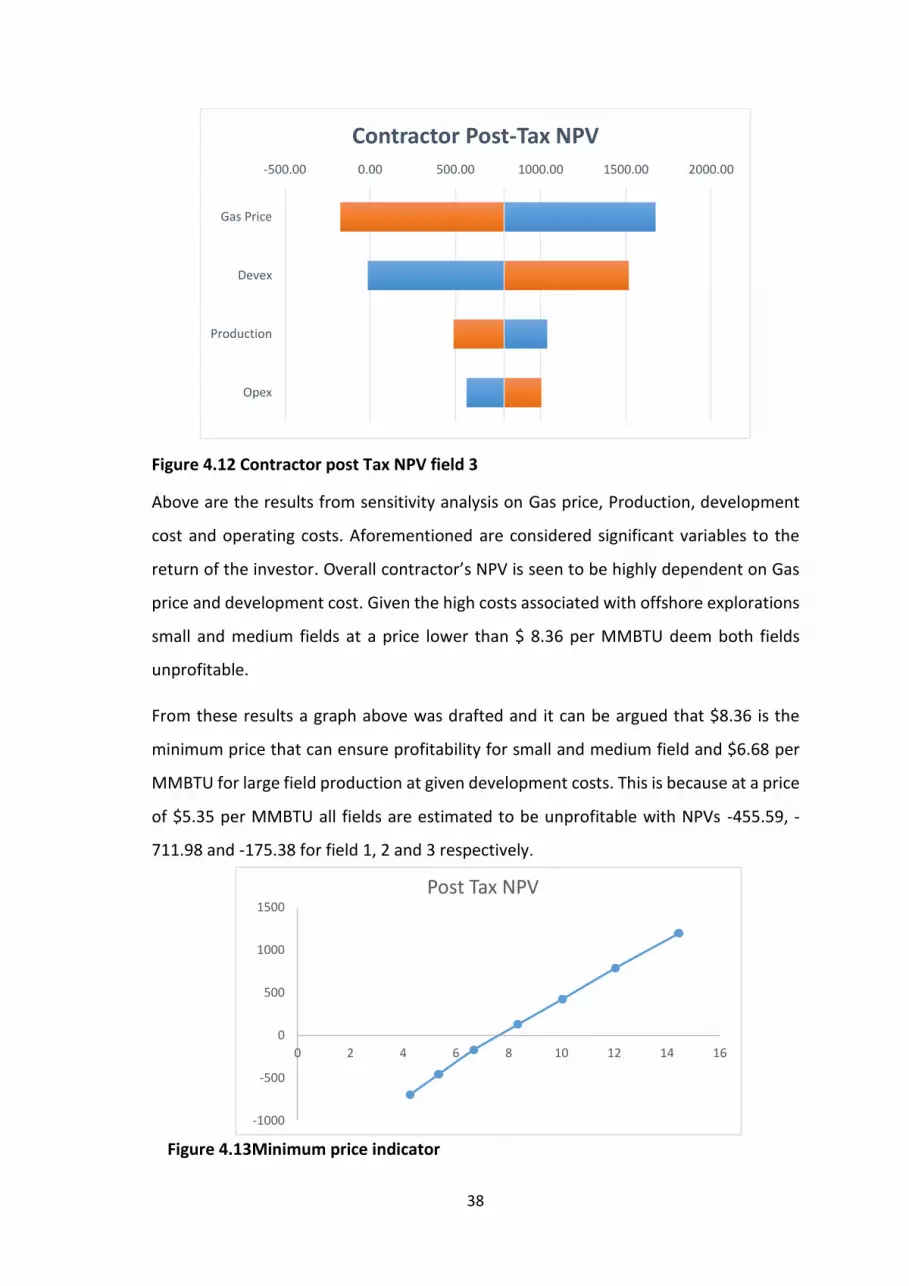

Figure 4.12 Contractor post Tax NPV field 3

Above are the results from sensitivity analysis on Gas price, Production, development

cost and operating costs. Aforementioned are considered significant variables to the

return of the investor. Overall contractor’s NPV is seen to be highly dependent on Gas

price and development cost. Given the high costs associated with offshore explorations

small and medium fields at a price lower than $ 8.36 per MMBTU deem both fields

unprofitable.

From these results a graph above was drafted and it can be argued that $8.36 is the

minimum price that can ensure profitability for small and medium field and $6.68 per

MMBTU for large field production at given development costs. This is because at a price

of $5.35 per MMBTU all fields are estimated to be unprofitable with NPVs -455.59, -

711.98 and -175.38 for field 1, 2 and 3 respectively.

-500.00 0.00 500.00 1000.00 1500.00 2000.00

Gas Price

Devex

Production

Opex

Contractor Post-Tax NPV

-1000

-500

0

500

1000

1500

0 2 4 6 8 10 12 14 16

Post Tax NPV

Figure 4.13Minimum price indicator

39

Lower development costs have seen to result to higher NPV values and 20% increase of

development costs resulting to negative NPVs(-142, -139,-14.31) for field 1,2 and 3

respectively. Since development cost is an unsystematic risk, it is within the investor’s

power and interest to use minimal costs possible.

Government take

Under the current Production sharing system (2013) government take mainly includes

royalty, profit gas share, additional profit tax and corporate income tax. As seen from

figures above total government averages around 80% which indicates that the

government is able to enjoy a good return from all fields as seen in table 4.3.

Sensitivity analysis on government take relative to gas price, production, development

and operating costs was done. Results are as seen on Figures below:

800.00 900.00 1000.00 1100.00 1200.00 1300.00 1400.00 1500.00

Gas Price

production

Devex

opex

Government Present Value Take

Figure 4.14 Government take field 1

40

Figure 4.15 Government take field 2

Figure 4.16 Government take field 3

As results show the government return is highly dependent on the price that the gas

will be traded on and the level of production. A decrease in price and production

decreases the government take and vice versa is true. Development and operating

costs as observed are least significant to government revenues.

4.2.2 Monte Carlo Simulations

A simulation is run on the impact on the contractor’s Post Tax NPV and government

take if price and development costs are considered as random variable. From

sensitivity analysis above development costs and gas price affected the return of the

contractor the most and keeping in mind the high percentage take by the government

1200 1400 1600 1800 2000 2200 2400

Production

Gas Price

Devex

Opex

Government Present Value take

3000.00 3500.00 4000.00 4500.00 5000.00 5500.00

Gas Price

Production

Devex

Opex

Government Present Value

41

it crucial to see the uncertainty that results from each field. Below are figures 4.12,

4.13 and 4.14 of normal distribution charts and statistics results from a Monte Carlo

simulation for the investor. Figures 4.15, 4.16 and 4.17 are for the government.

Figure 4.17 Monte Carlo Simulation results on post tax NPV relative to price-field 1

Figure 4.18 Monte Carlo simulation results on Post Tax NPV relative to price-field 2

42

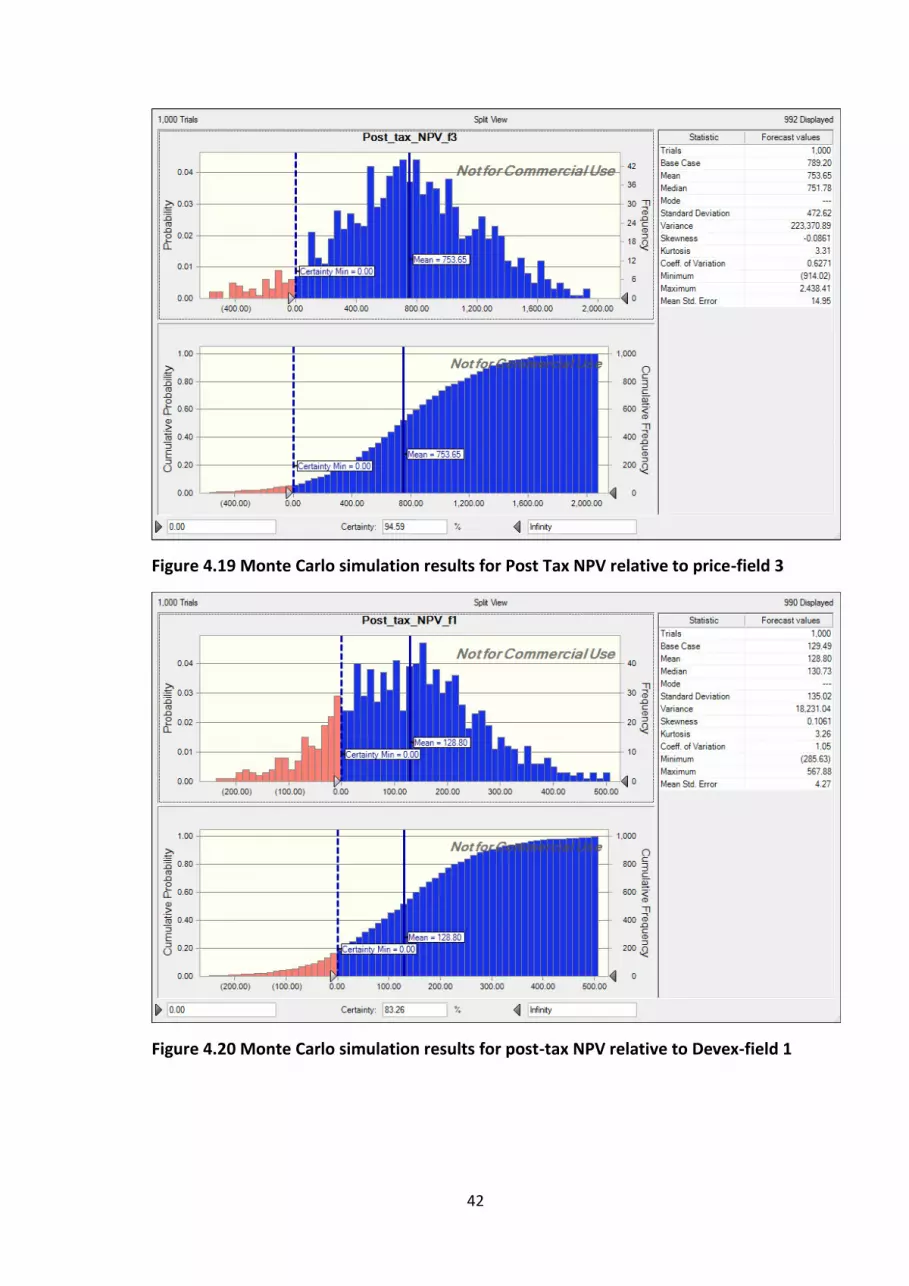

Figure 4.19 Monte Carlo simulation results for Post Tax NPV relative to price-field 3

Figure 4.20 Monte Carlo simulation results for post-tax NPV relative to Devex-field 1

43

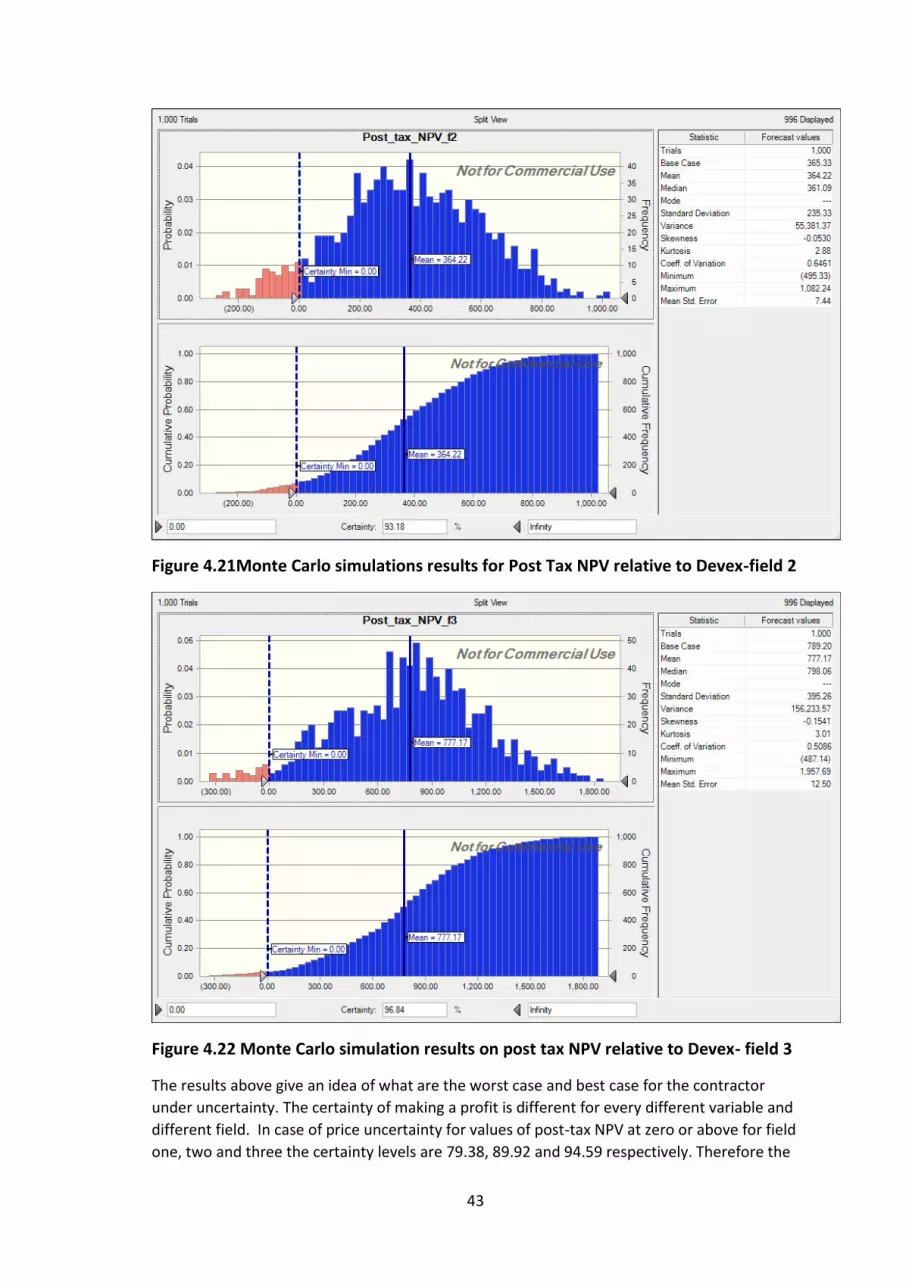

Figure 4.21Monte Carlo simulations results for Post Tax NPV relative to Devex-field 2

Figure 4.22 Monte Carlo simulation results on post tax NPV relative to Devex- field 3

The results above give an idea of what are the worst case and best case for the contractor

under uncertainty. The certainty of making a profit is different for every different variable and

different field. In case of price uncertainty for values of post-tax NPV at zero or above for field

one, two and three the certainty levels are 79.38, 89.92 and 94.59 respectively. Therefore the

44

estimate of the probability of a loss from the simulation for field one is 20.62% field 2 with

10.08% and field three with 5.41%. For development cost again field (3) has a high possibility

of profitability at 96.84 field (2) 93.18 and field (1) 83.26. Field 1 is observed to be the least