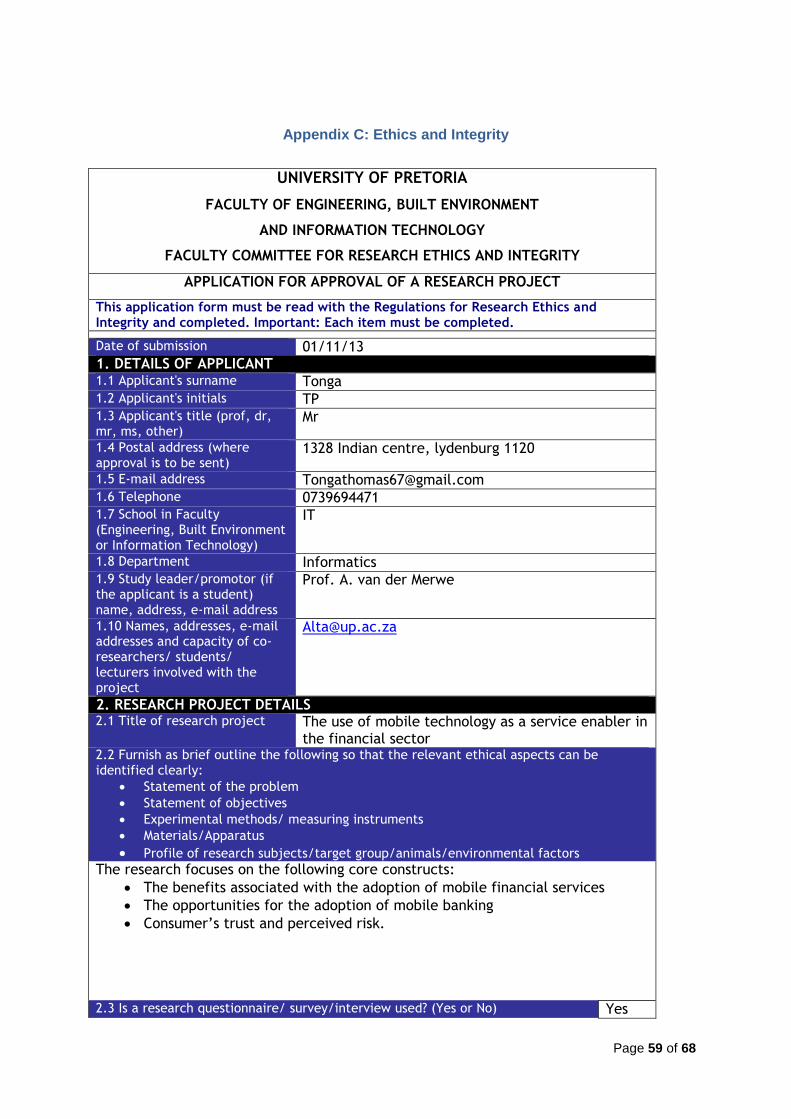

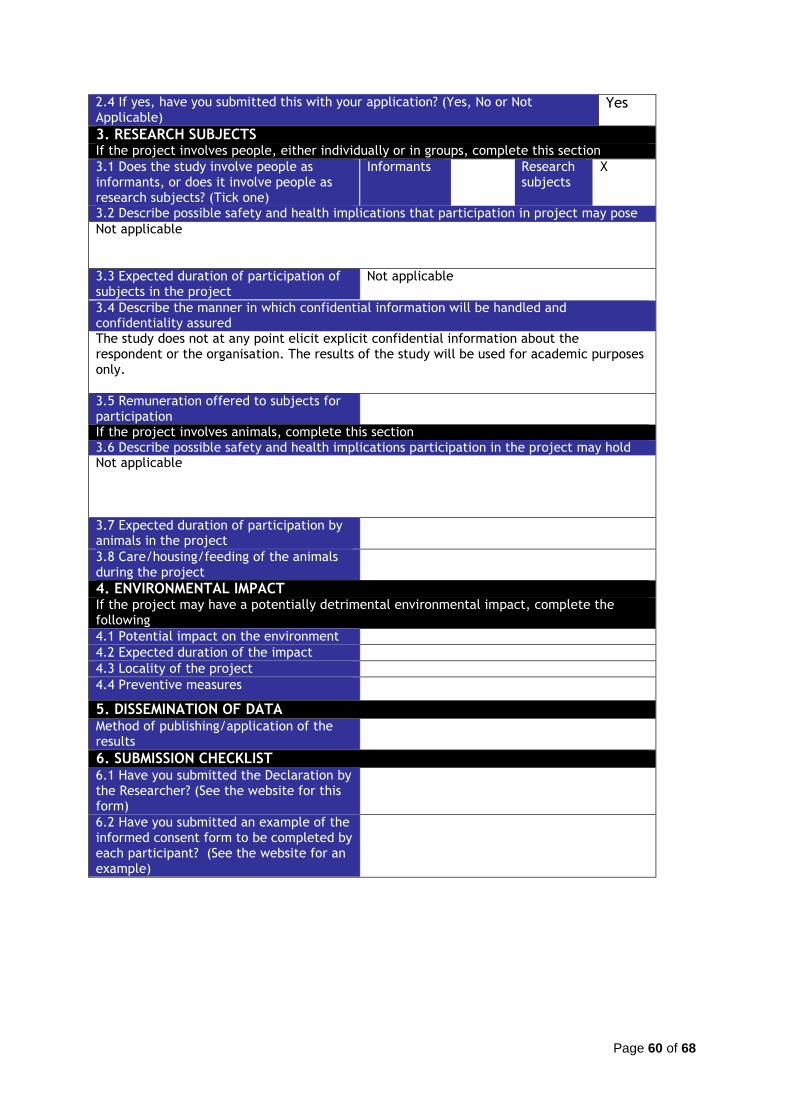

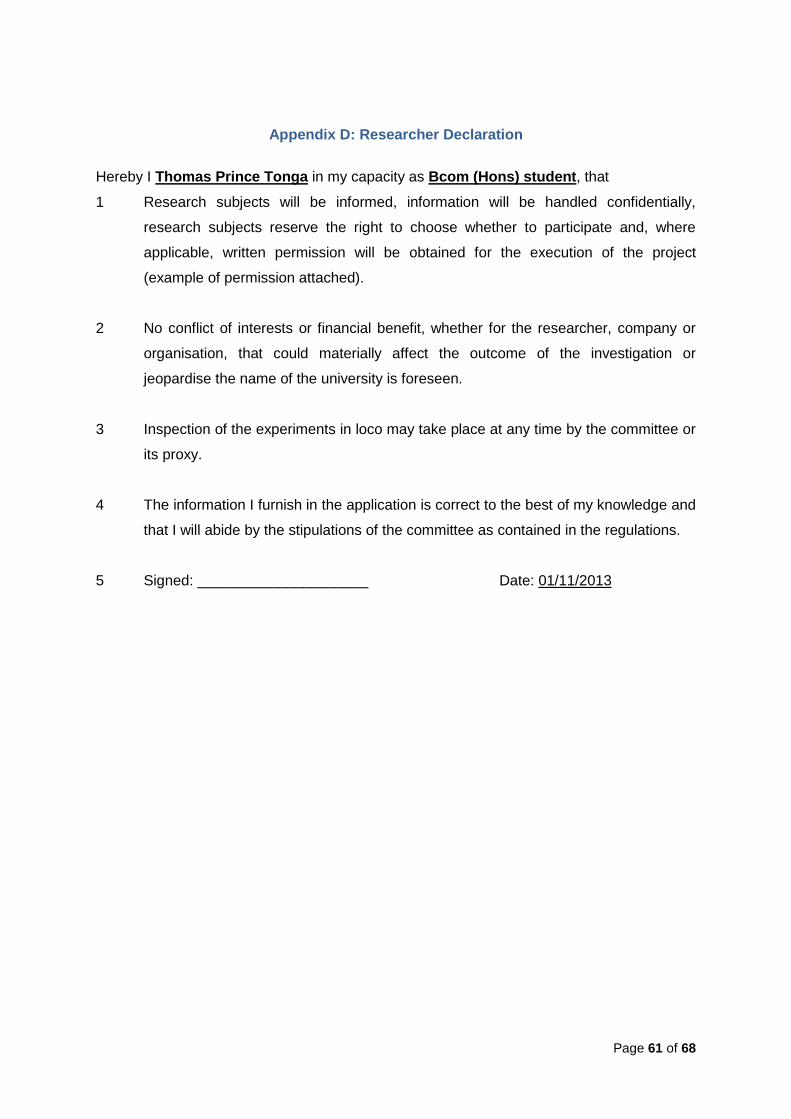

the use of mobile technology as a service enabler in the banking sector

TRANSCRIPT

FACULTY OF ENGINEERING, BUILT ENVIRONMENT AND INFORMATION TECHNOLOGY

FAKULTEIT INGENIEURSWESE, BOU-OMGEWING EN INLIGTINGTEGNOLOGIE

INDIVIDUAL ASSIGNMENT / INDIVIDUELE WERKSOPDRAG

Surname / Van Tonga

Initials / Voorletters T.P.B.

Student Number /Studentenommer

1 0 4 8 7 2 8 1

Module Code / Modulekode

INF : 7 8 0

Assignment number / Opdragnommer

Final Paper (Exam)

Name of Lecturer / Naam van Dosent

Prof A. Van Der Merwe (Supervisor)

Prof C. de Villiers

Date of Submission / Datum ingehandig

01/11/2013

Declaration / Verklaring: I declare that this assignment, submitted by me, is my own work and that I have referenced all the sources that I have used. / Ekverklaardathierdieopdragwatdeur my ingehandig word, my eiewerk is en datekna al die bronnewatekgebruik het, verwys het.

Signature of Student

MARK / PUNT

The use of mobile technology as a service enabler in the banking sector

by

Thomas Tonga

(10487281)

Submitted in partial fulfilment of the requirements for the degree

Bcom (Hons) Informatics

in the

DEPARTMENT OF INFORMATICS

of the

FACULTY OF ECONOMIC MANAGEMENT SCIENCES

UNIVERSITY OF PRETORIA

Supervisor: Prof Alta van der Merwe

01 November 2013

Abstract

This paper explores how organisations, especially those in the banking industry, can

use mobile financial services to better offer services to their consumers.

Furthermore, it explores whether these organisations can gain competitive

advantage using the mobile channel. Initially, a problem statement is discussed to

explore the gaps that currently exist with regards to this study. Then a literature

review regarding these gaps is discussed.

This research is based on an interprevitism paradigm approach. Qualitative and

quantitative data collection techniques were used in this study, this techniques

included; semi-structured interviews, and pre and post-test questionnaires. The

research strategy and methodology are discussed within. An analysis of the data and

findings of the data collected is discussed. A brief summary and conclusion

answering the main question is included at the end of the research paper.

Keywords

Mobile Banking, Mobile Financial Services, Mobile Commerce, Competitive

Advantage

Acknowledgements

Firstly, I would like to give thanks to God almighty for showering me with blessings

that I myself cannot contain, for walking with me throughout the days of my life and

mostly through my studies.

Secondly, I would like to extend my depth of gratitude to my supervisor, Prof Alta

van der Merwe for the support and consultation she provided. She has truly been an

inspiration, providing much appreciated insight and acumen from the initial draft to

the final paper.

I would like to give thanks to my family and friends for their patience, support, and

motivation throughout the research and completion of this paper. And lastly, to

everyone who took part in the development and writing of this paper, including all the

respondents that took time to complete the questionnaires and interview questions,

your support and time is highly appreciated. Without you all, this paper would not be.

THANK YOU!

Table of contents

Chapter 1: Introduction ............................................................................................... 1

1.1. Introduction ...................................................................................................... 1

1.2. Background Information ................................................................................... 1

1.3. Problem Statement .......................................................................................... 2

1.4. Research Objectives and Research Questions ................................................ 3

1.5. Research Scope .............................................................................................. 4

1.6. Chapter Overview ............................................................................................ 4

Chapter 2: Literature Review ...................................................................................... 6

2.1. Introduction ...................................................................................................... 6

2.2. Information Technology in Banking Industry .................................................... 6

2.2.1. Information Technology Adoption .............................................................. 7

2.2.2. Emergence of Mobile Technology ............................................................. 8

2.3. Difference between Mobile Commerce and Mobile Banking ............................ 9

2.4. Mobile Commerce Services ........................................................................... 10

2.4.1. The Use of Mobile Services by Banks ..................................................... 11

2.4.2. Advantages of Adopting Mobile Services ................................................ 12

2.5. Why are people reluctant to using Mobile Banking? ...................................... 15

2.5.1. Security .................................................................................................... 17

2.6. The Future of Mobile Banking ........................................................................ 18

Chapter 3: Research Methodology ........................................................................... 20

3.1. Research Design & Strategy .......................................................................... 20

3.1.1. Introduction .............................................................................................. 20

3.1.2. Research Paradigm ................................................................................. 20

3.1.3. Population and Sampling ......................................................................... 21

3.1.4. Unit of Study ............................................................................................ 22

3.1.5. Sample Size of Participants ..................................................................... 22

3.2. Research Strategy and Data Collection Methods .......................................... 23

3.3. Expected Results ........................................................................................... 24

3.4. Limitation ........................................................................................................ 24

3.5. Ethics ............................................................................................................. 24

3.6. Conclusion ..................................................................................................... 25

Chapter 4: Research Findings .................................................................................. 26

4.1. Introduction .................................................................................................... 26

4.2. Mobile User Statistics..................................................................................... 28

4.2.1. Mobile User Demographics ......................................................................... 28

4.2.2. Type of M-banking Transactions ................................................................. 30

4.2.3. Customer Evaluation of Service Factors ..................................................... 31

4.2.4. Customer Evaluation of Delivery Channel ................................................... 32

4.3. Organisations Statistics .................................................................................. 33

4.3.1. Organisation Demographics ........................................................................ 33

4.3.2. Purpose behind the Introduction of Mobile Banking .................................... 34

4.3.3. Benefits of Mobile Financial Services.......................................................... 35

4.3.4. Competitive Advantage Findings ................................................................ 37

4.3.5. Mobile Trends Findings ............................................................................... 38

4.3.6. Security Findings ........................................................................................ 39

4.4. Conclusions and Recommendations .............................................................. 39

Chapter 5: Conclusion .............................................................................................. 41

5.1. Summary of findings ...................................................................................... 41

5.2. Conclusion ..................................................................................................... 42

5.3. Future research .............................................................................................. 43

Bibliography ............................................................................................................. 44

Appendix A: Sample Questionnaire ......................................................................... 48

Appendix B: Sample Interview Questions ................................................................ 55

Appendix C: Ethics and Integrity .............................................................................. 59

Appendix D: Researcher Declaration ....................................................................... 61

List of Figures

Figure 1: Chapter Overview Model ............................................................................. 5

Figure 2: Number of Mobile Subscribers .................................................................... 9

Figure 3: Mobile User Gender .................................................................................. 29

Figure 4: Mobile Device Usage ................................................................................ 29

Figure 5: Financial Service Delivery Platform ........................................................... 33

Figure 6: Advantages of MFS ................................................................................... 36

Figure 7: Competitive Advantage ............................................................................. 37

List of Tables

Table 1: Mobile Banking Transactions ..................................................................... 31

Page 1 of 68

Chapter 1: Introduction

1.1. Introduction

This paper explores how banks can effectively use mobile financial services (MFS) in

order to offer better services to its consumers and possibly attract potential

customers. The variables explored are uses of MFS, benefits of adoption for banks,

competitive advantage, and consumer preference. The paper defines mobile

commercial services, looks at information technology in the banking sector and

explores why consumers are reluctant to adopt MFS. The paper then looks at how

banks can use MFS to gain competitive advantage.

1.2. Background Information

Mobile devices today allow access to any web page compared to earlier mobile

devices that supported specially formatted web pages. These mobile web browsers

allow users to look up information, communicate with friends, and read news articles

from anywhere and at any time (Kane, et al, 2009). In South Africa, mobile devices

have enjoyed spectacular growth over the past decade. More than 60% of South

Africans, especially students, use mobile phones to access mobile internet

applications (Kreutzer, 2009). This level of usage has proven to be far greater than

the use of computer-based internet. A study conducted by Accenture (2012) shows

that South Africa was ranked as the highest in terms of the most internet usage

through mobile devices compared to other countries, such as France, Germany and

Finland. As the mobile market continues to skyrocket, the use of mobile devices to

access the internet is said to overtake the use of Personal Computers, which causes

a huge opportunity for mobile services.

According to Ondiege (2010), 60% of Africa’s population have no access to banking

services. Nevertheless, because 50% of the adult population have access to mobile

devices, organisations in the financial sector, specifically banks have recognised the

potential of reaching millions of prospective customers by offering access to financial

services through these devices. As banks embark on these opportunities they need

Page 2 of 68

to understand the factors influencing the adoption of these mobile services by users,

and how they can improve these factors in order to meet their business objectives.

By using mobile devices as a mode to conduct business, banks can provide instant

tailor made products and services to their customers based on the customer’s

financial history and buying patterns (Riivari, 2005).

Mobile technology or mobile banking (m-banking) has the potential to change the life

of consumers. It has the power to eliminate the need to physically visit a branch. In

other words, it enables the customer to have access to their financial information

anywhere and anytime and also have access to anytime applications that match their

lifestyles. The study in this paper investigates the various mobile technology trends,

which can be utilised by financial sector organisations in order to make service

delivery to their client feasible. Furthermore, the study will focus on the benefits

associated with the use of mobile technology as a service delivery platform, and how

financial organisations can use m-banking to build competitive advantage.

1.3. Problem Statement

M-banking is a powerful tool that has numerous advantages over traditional banking

solutions, such as, reducing geographical constraints and offering immediacy,

security and efficiency (Ondienge, 2010). The former advantage is the main

advantage for banks and the latter caters for the customers. In order for banks to

fully reap these benefits and to effectively provide m-banking services that

customers seek, they need to understand the entire perspective of m-banking, i.e.

they need to have a conceptual view of mobile technology. Furthermore, they need

to understand how they can use mobile technology to help them offer better service

delivery.

Many studies have been conducted with regards to use of m-banking services, for

example, in their paper Durkin and Howcroft (2003) studied the perception of senior

bankers regarding the use of the internet as a relationship marketing tool. Durkin and

Howcroft’s (2003) study, which was mainly focused on bankers in UK, Sweden and

USA, found that in order for banks to reinforce the bank customer relationship they

Page 3 of 68

need to collect efficient information about customer behaviour patterns. The study in

this paper will focus on bankers in South Africa and will exploit whether the adoption

of mobile technology can help South African banks to effectively use the marketing

tools that these channel provides.

Joseph and Stone (2003) studied the impact of technology on banking sector

service. They looked at the evolution of technology and the customer’s perception on

the impact of this evolution on service delivery. Patricio, Fisk and Cunha (2003)

studied the use of internet banking integrated in a multi-channel offering and found

that customer satisfaction, in a multi-channel context, is dependent not only on the

performance of isolated channels but they tend to use these channels in a

complementary way. The focus of these studies was mainly on the use of self-

service system, which included ATMs, internet banking and telephone banking. The

latter study measured the contribution of each service delivery channel, but focused

on internet as a channel in general. This paper focuses on the evolution of mobile

technology, specifically m-banking and analyse the impact of this evolution on the

banking sector.

1.4. Research Objectives and Research Questions

The core objective of this paper is to investigate how financial institutions can use

mobile services or mobile technology in order to enhance service delivery, i.e. the

paper aims to discover the feasibility of the use of m-banking by banks in order to

offer better service to its clients. In this paper, the opportunities that exist with

regards to use of mobile services are investigated and how these can help the

financial sector to meet their customers forever changing needs. As mobile devices

become omnipresent and many organisations take advantage of these innovations,

a lot of financial institutions are yet to exploit these advantages in order to gain

competitive advantage.

Further, this paper reflects whether consumers prefer mobile technology over the

other available platforms, such as branch, ATM, telephone and internet, and why

financial institutions should adjust to these changes. The various opportunities

Page 4 of 68

available to the banking sector with regards to mobile services will also be

investigated. The following questions are used as guidelines in order to attain the

paper’s objective:

Question 1: How can banks use mobile technology to better enable service

delivery?

Question 2: What are some of the benefits associated with the use of mobile

channel to offer services?

Question 3: Can mobile technology help organisations gain competitive

advantage over its competitors?

Question 4: Do customers prefer mobile services over the other available

platforms?

1.5. Research Scope

This research is conducted in Pretoria, South Africa. The research method, refer to

Chapter 3, is conducted on bank account holders who have a mobile device and on

four of the South African banks, which are based in the surroundings of Pretoria. The

research focuses on the following core constructs:

The benefits associated with the adoption of mobile services

The opportunities for m-banking

Consumer’s trust and perceived risk.

1.6. Chapter Overview

Figure 1 shows the chapter overview of this paper, each chapter entails the

following: Chapter 1 – Introduction, this section gives a brief background of the

problem statement, research objective and research scope. This section is then

followed by Chapter 2 – Literature Review. In this section, I will look at the available

literature regarding the use of MFS in the financial sector and the variables

mentioned above.

Chapter 3 – Research Methodology, discusses the research design and strategy to

be followed. It further discusses paradigm used, the population and sampling

Page 5 of 68

methods used to acquire the data, how the data is analysed and what the

expectations of the results are.

The fourth section, Chapter 4 – Data Analysis and Findings, focuses on the analysis

of the collected data and discusses the findings and results of the research. Finally,

Chapter 5 – Conclusion, I will summarise and conclude the findings of this paper.

The research findings will be discussed and synthesis with the literature.

Chapter 2Literature Review

Chapter 3Research

Methodology

Chapter 4 Research Findings

Chapter 5 Conclusion

Chapter 1Introduction

Interested in research method?

No Yes

Figure 1: Chapter Overview Model

Page 6 of 68

Chapter 2: Literature Review

2.1. Introduction

In this chapter, the existing literature regarding the use of m-banking or mobile

technology in the financial sector is reviewed. The focus of the literature review is

based on how financial institutions, specifically banks can better offer mobile

services through the use of m-banking. The evolution of mobile technology is

reviewed. The literature review then explores mobile commerce, m-banking and the

various mobile services that exist. It further reviews the benefits associated with the

adoption of mobile technology by banks, risks associated with the use of mobile

services and competitive advantage.

2.2. Information Technology in Banking Industry

Information technology (IT) plays an important role across many industries.

According to Padmanabhan (2012) the financial industry, particularly banking

industry, was one of the first to adopt the use of IT in the 1960s in order to influence

economic development across many nations. Banks use technology to take care of

their internal requirements with regards to book keeping and transaction processing.

This enables banks to offer products or services of quality at the utmost speed. The

introduction of m -banking has help banks eliminate the need for customer to set foot

in a bank, i.e. the time and distance barriers associated with accessing banking

services have been alleviated (Padmanabhan, 2012). Firms have adopted IT to

breed changes in managing customer relationships and opens doors to innovation,

which involves adding new services that customers need, expanding existing ones

and improving the service delivery process (Chen & Tsou).

However, technology comes with disadvantages, according to Joseph, Sekhon,

Stone, and Tinson (2005) qouting Durkin and Bennet (1999), states that the

introduction of service delivery technology will change the basic cost dimensions of

business. New technologies will initiate new opportunistic competition which the

Page 7 of 68

current players have never faced before. In order to adjust to this competition and to

be effectively competitive, the entire organisation culture will need to change. This

may force an organisation to follow a direction which contradicts the main business’

strategy, leading to business faillure. Furthermore, Joseph, Sekhon, Stone, and

Tinson (2005) state that when customer decide on what constitutes as good service

quality, they evaluate each aspect of service which is important to them. If an

organisation doesn’t satify their needs and forever changing needs, they simply seek

an organisation which provides these needs. In order for organisation to be effective

when choosing the technology adoption route, they need to keep certain technology

adoption elements in mind.

2.2.1. Information Technology Adoption

Chen and Tsou (2007) suggests the use of Scott Morton's (1995) MIT90 model,

when organisations want to adopt IT. This model consists of four elements:

Information technology infrastructure:

o The IT infrastructure includes the networks that enable an organisation to

effectively share information across departments in an ad hoc fashion.

Effective management of this are a foundation to IT adoption

Strategic alignment:

o The IT and organisation strategies need to be aligned in order to obtain

effective organisation performance

Organizational structure:

o The organisation structure includes the formal lines of communication and

the management hierarchy in an organisation, organisation structure

needs to be re-engineered to improve performance

Individual learning:

o In order for an organisation to gain effective benefits of IT, end-users and

IT personnel in the organisation must acquire new IT related skills and

knowledge.

Chen and Tsou (2007) research illustrates that by adopting these mechanisms

financial firms can sustain and enhance service innovation practices, which leads to

significant effects on competitive advantage and satisfied customers.

Page 8 of 68

2.2.2. Emergence of Mobile Technology

With the emergence of smart phones, technology now offers a multifunctional

wireless infrastructure that is accessible to customers 24/7. Mobile phones, referring

to those that are typically mobile, this includes notebooks and sub notebooks, are

becoming part of our everyday lives. Studies show that they have the potential to

become low-cost delivery channels for financial information, services and

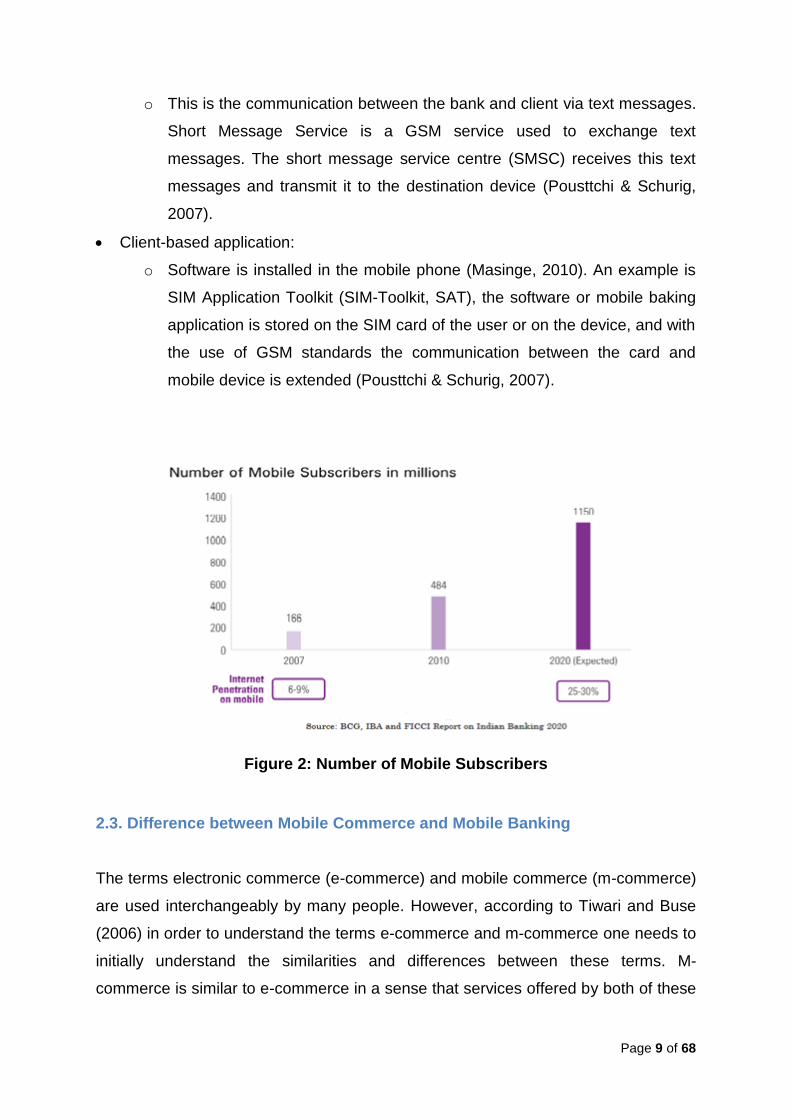

transactions (Duncombe & Boateng, 2009). With nearly 885.99 million mobile

subscribers (Figure 1), the mobile service platform provides an opportunity for banks

to offer banking products and services (KPMG India, 2011). Accenture (2012) in the

their study on the mobile internet, found that South Africa, Brazil and Russia showed

the highest adoption of mobile technology, this is due to the developments in other

emerging markets. Many consumers use mobile devices to access internet

application, this level of usage is far greater than the use of computer-based internet

(Kreutzer, 2009). In his paper, Masinge (2010) quoted ITU (2009) saying that 90% of

South Africans own a mobile device and according to Ondinge (2010) there was a

substantial increase in South Africa’s mobile telephone subscription, from 16860

subscriptions in 2003 to 46436 subscriptions in 2009 with a 18.39% annual growth

rate. According to Deloitte’s (2010) research, about 10% of mobile users conducted

m-banking on their devices. In return, banks have made large investments in m-

banking capabilities. According to KPMG India (2011) the new channel can be built

at low cost, by incorporating internet platforms to mobile devices. For communication

this mobile devices use GSM/GPRS and 3G technologies as typical connections

standards.

In his research Masinge (2010) discovered three technology solutions which m-

banking can be implemented through, which will be discussed below:

Browser-based application:

o This solution is based on micro-websites following the Wireless Application

protocol (WAP). The functions of this solution are similar to those of

electronic banking which uses http (Pousttchi & Schurig, 2007)

Messaging-based application:

Page 9 of 68

o This is the communication between the bank and client via text messages.

Short Message Service is a GSM service used to exchange text

messages. The short message service centre (SMSC) receives this text

messages and transmit it to the destination device (Pousttchi & Schurig,

2007).

Client-based application:

o Software is installed in the mobile phone (Masinge, 2010). An example is

SIM Application Toolkit (SIM-Toolkit, SAT), the software or mobile baking

application is stored on the SIM card of the user or on the device, and with

the use of GSM standards the communication between the card and

mobile device is extended (Pousttchi & Schurig, 2007).

Figure 2: Number of Mobile Subscribers

2.3. Difference between Mobile Commerce and Mobile Banking

The terms electronic commerce (e-commerce) and mobile commerce (m-commerce)

are used interchangeably by many people. However, according to Tiwari and Buse

(2006) in order to understand the terms e-commerce and m-commerce one needs to

initially understand the similarities and differences between these terms. M-

commerce is similar to e-commerce in a sense that services offered by both of these

Page 10 of 68

terms are done electronically over computer-mediated networks. The difference is

that the communication networks used by m-commerce are accessed through

mobile devices and e-commerce is accessed through personal computers, laptops,

etc (Tiwari & Buse, 2006).

M-banking at the other hand refers to the use of mobile telecommunication devices

through which bankers do their bank related transactions (Pikkarainen, Karjaluoto &

Pahnila, 2004). M-banking is also defined as an application of m-commerce which

allows bank clients to access their financial account information or perform bank

related transactions such as balance enquires, money transfer, and purchasing

prepaid airtime from anywhere and at any time (Masinge, 2010). M-banking enables

customer to gain access to information relating to their accounts via the devices

themselves or enables them to transact online (Njenga, 2009). Besides the success

of the applications to get convenience at customer’s fingertips, m-banking also helps

rural household in that they no longer need to travel to post offices or banks to

conduct transactions (KPMG India, 2011).

2.4. Mobile Commerce Services

The market for mobile commerce services also known as mobile financial services

(MFC) is huge and is expanding, the use of mobile devices by users are three times

more than that of Personal Computers (Riivari, 2005). According to Marsh and

McLennan Companies (2012) 20 million users across Europe use their handheld

devices to access their bank account. Out of that 20 million, 3 million users in UK

use their mobile device to manage their money. The research also found that

compared to online banking users, who access their account six times a month, On

average, m-banking user’s accounts are active 16-18 times a month. Many mobile

users are now using their mobile devices to access online services. As the number

of financial transactions carried out through the use of mobile service increase

enormously, we can expect banks to start considering closing this gap (Tiwari, Buse,

& Herstatt, 2006).

Page 11 of 68

Because the focus of this paper is on m-banking, I will not look into the other service

delivery platforms used by banks, such as ATMs, branch, telephone banking and

internet banking. According to Riivari (2005), not only do banks use m-commerce

services channels to render convenient services to customers but they use these

channels to attract new customers and to help them build good brand image. M-

banking also helps to sustain current customers, i.e. it allows banks to build a close

relationship with its clients and also to reduce marketing and fixed or variable costs

(refer to “2.4.2 Advantages of adopting mobile services”). The services offered by m-

banking providers may include transfers between accounts as well as between

peers, view and manage accounts, and receive alerts regarding account activity,

balances and other issues.

2.4.1. The Use of Mobile Services by Banks

The financial sector core business consists of the handling of money but banks have

now taken on a speculative forte (Ricard, Prefontaine, & Sioufi, 2001). In order for a

firm to reap profits, managers in various industries have realised the importance of

providing quality customer service. This strategy is key to improving customer

satisfaction and wining a bigger share of the market. Because of the high increase in

satisfactory service delivery expectations of customers, banks have been forced to

respond with a set of deeper and broader services than they use to in the past

(Joseph, Sekhon, Stone, & Tinson, 2005). As with other industries, banks have also

invested in technology in order to entice new customers, meet the forever changing

needs of their existing customers, to offer better services and to meet the technical

innovation expectations of customers (Stone & Joseph, 2003).

According to a study conducted by Deloitte (2010), banks can realise operational

efficiencies by adopting an integrated channel strategy that includes the various

service delivery channels and m-banking. The cost of a transaction processed via a

mobile phone is ten times lower than transactions processes via an ATM and more

than fifty times lower than via a branch (Deloitte, 2010). Thus banks need to drive

more transactions to mobile phones in order to increase operating efficiencies.

Mobile application can help banks generate high revenues as well. In order to reach

Page 12 of 68

this objective, they need to offer value added and highly innovative MFC while

retaining their technological literate customers (Tiwari, Buse, & Herstatt, 2006).

According to Deliotte (2010), an increase in revenue can be realised by:

Expanding distribution

o M-banking allows banks to expand beyond their current geographic

segment, thus catering to a large pool of consumers.

“Monetizing the value of customer analytics”

o Because m-banking allows banks to have a broader view of their

customers spending patterns. Banks are put in a position whereby they

can develop a new line of business specifically catering for their

consumers’ needs

Real-time access to products and services

o Banks can pin-point a customer’s physical location in order to make

relevant offers to the customer. For example, when a consumer enters a

shopping centre, the banks can be notified and can offer the customer

products or services without them actually acquiring the service.

A research conducted by Future Foundation (2011) found that users of m-banking

are in a very frequent contact with their bank. The study found that this interaction is

far greater than that from any other channel, which creates new opportunities for

banks to build a relationship with customers (Future Foundation, 2011). On the

whole, the mobile channel has proven to be the most effective and efficient way

through which banks can use to communicate with consumers. The study further

found that a third of customers are willing to be contacted by the banks through their

mobile devices if it improves the service they receive.

2.4.2. Advantages of Adopting Mobile Services

Mobile services have a positive impact on customers because they allow customers

to access information and services from anywhere and at any time (Bhatti, 2007).

Customer want to be in control of their account and want ad hoc information, mobile

services thus increase customer satisfaction. According to Future Foundation (2011)

the appeal of m-banking is not one-dimentional, rather consumers benefit from a

Page 13 of 68

number of advantages. Consumers that value their time and ability to regularly

monitor their finances to avoid bank charges, convenience, speed and control are

some of the key factors. “When it comes to service, sometimes it’s what you don’t

get that is most important” (Future Foundation, 2011). Consumers that ulitises m-

banking appreciate not having to go to a branch and the benefit of not having to use

a call centre, some love the idea of checking if they have sufficient funds in their

accounts before purchasing something. Apart from the consumers benefits

discussed above banks can also reap a few benefits as well.

A research conducted by Marsh and McLennan Companies (2012) determined the

following benefits to banks if they embrace m-banking:

Reduced cash handling costs

Large pool of customer, i.e. global reach

Alleviate the need for branches, this helps reduce location costs and cost

associated to employees.

A study also done by Marsh and McLennan Companies (2012) on a medium-sized

Spanish bank that implemented m-banking services showed that the use of m-

banking resulted in a 6% decrease in fraud. A bank can through the use of mobile

technology, inform customers and ask for their confirmation when a transaction is

performed. By combining information services and marketing, banks can improve

customer service by using mobile applications that offer tailor made products based

on the consumer’s financial history, interests and spending patterns (Riivari, 2005).

M-banking assist banks to get to know their clients, banks are therefore able to

provide accessible service (convenience) which attract customer, thus fostering a

long term personalised relationships (Ricard, Prefontaine, & Sioufi, 2001).

2.4.2.1. Competitive Advantage

With the emergence of mobile technology, banks now operate in a highly competitive

market. According to Clemons (1986) referencing Michael Porter states that there

are three generic competitive strategies which form the basis of a business’s

Page 14 of 68

strategy and these generic competitive strategies help to define competitive

advantage:

Differentiation

o Organisations should provide superior value products or services which

are difficult to imitate, difficult to substitute and dominate on premium

prices

Cost leader

o Organisation should provide reasonable value or quality products or

services at low prices

Focus

o Organisations need to study and understand their target market, thus

enabling them to provide better products and services than their

competitors.

Banks that possesses differentiation, cost leadership and focus will be able to

provide services that are unique, faster, and the advantage of charging premium

prices. According to Clemons (1989) this is achieved through differentiation with

innovation, quality or customer service. Furthermore, competitive advantage is

achieved by following a focus strategy. This enables an organisation to target a

specific market, for example, banks target local or high net worth customers. These

customers therefore enjoy the personal touch that big organisations may not be able

to provide. In support of this theory, in their research Stone and Joseph (2003),

found that banks that offer both branch and technology based services are more

competitive than their competitors as consumers prefer to conduct at least a portion

of their bank services via technology-based services.

According to Pearlson and Saunders (2012), Information resources can be used to

influence competitive forces. There are five major competitive forces which can be

used to shape the environment in which a firm operates. These forces include

potential threat of new entrant, bargaining power of suppliers, bargaining power of

buyers, industry competitors and threat of substitute product. For the purpose of this

paper only barging power of buyers and threat of substitute products will be explored

in detail from a banks perspective.

Page 15 of 68

Bargaining power of buyer

Consumers have power to influence the competitive environment in which banks

operate. This power can take the form of easy access to banks or ATMs in order to

purchase the same products and services or the opportunity to get access to

products and services from anywhere and at any time. Banks can use information

resources to build switching costs that make it less desirable for consumers to

purchase from competitors. For example, Apples iTunes software makes it difficult

for customer to use other formats and technologies other than the iPod, this reduces

the power of consumers.

Threat of substitute products

A substitute product is a product from another industry or firm that provides the same

benefits to the buyers as products provided by firms in the same industry (Pearlson

& Saunders, 2012). A product on the marketplace is substitutable depending on the

buyer’s willingness to substitute. Information resources can be used to reduce the

threat of substitution. Thus in order for competitors to be successful, they need to

offer better services to their customers and not just substitute products.

According to Pearlson and Saunders (2012), a resource is only viable when it

enables a bank to become more efficient and effective. It is considered rare when

competitors do not posses it. For example, many banks use ATMs in order to

conduct their operations and customers expect these ATMs in many convenient

locations. However, because these ATMs are offered by most banks, they are no

longer rare and they no longer offer strategic advantage. The aim of this paper is to

explore whether m-banking can be used to offer rare services, reduce threat of

substitute products and reduce power of consumers, thus creating competitive

advantage.

2.5. Why are people reluctant to using Mobile Banking?

Regardless of the time, cost-saving and freedom of location which are benefits of

using online banking, banks still face problems with consumers being reluctant to

use online banking (Pikkarainen, Karjaluoto & Pahnila, 2004). Research conducted

Page 16 of 68

by White and Nteli (2004) shows that there has only been a 6 per cent increase for

the use of the World Wide Web (www) for banking purposes in the UK. Consumers

are sceptic about using online services or online banking because they are uncertain

as to what are best practices with regards to the use of the internet (Durkin &

Howcroft, 2003). In their paper, White and Nteli (2004) says that the level of increase

of the use of internet for banking purposes has stayed stationery while there has

been an increase in the number of internet users. One of many reasons for this is

fear about security.

Despite the reassurance given by banks, customers still have negative perceptions

about using these services. There are various factors which influence the adoption of

mobile services in South Africa. Financial institutions need to understand these

factors in order to increase the rate of adoption (Brown, Zaheeda, Davies & Stroebel,

2003). In their paper, Pikkarainen, Pikkarainen, Karjaluoto and Pahnila (2004)

discovered various reasons why bankers do not use online banking channels. Firstly,

because customers need to have access to the internet in order to use this service,

they face cost challenges. These costs include traditional bank charges, mobile

network charges and mobile device costs. On top of that novice users still need to

learn how to use these services, some people go to say that they have no interest

because a phone is to call and text. Secondly, people also complain about the lack

of social dimension when using online banking. Thirdly, trust has been recognised as

one of the critical factors with influences the success of m-banking. This trust is

categorised into two aspects:

Trust in mobile network providers

Trusting banks.

Masinge (2010) states that consumers have a psychological expectation towards

banks, they expect banks not to act as opportunists when providing their services.

Finally, Pikkarainen, Pikkarainen, Karjaluoto and Pahnila (2004) concurs with White

and Nteli (2004), they say that customers have been afraid of security issues, i.e.

customers are reluctant to adopt MFS because of the security risk associated with

such platforms.

Page 17 of 68

2.5.1. Security

Pikkarainen, Pikkarainen, Karjaluoto, and Pahnila (2004) found that many studies

have already realised the importance of security when it comes to customer

accepting to use online services. Security was found to be the main obstacle to the

adoption of online services in Australia, although people are aware of the risks they

had little understanding of online banking security risks.

KPMG India (2011) found that m-banking services use basic SMS/USSD based data

transfer technologies, which makes it less secure than internet banking. Though the

services offered by banks over the mobile platform are for information dissemination

and small value transactions, Padmanabhan (2012) advises banks to ensure that

they have the best controls and measures in place, i.e. banks need to protect assets

and highly sensitive data they hold about customers from cyber-crimes and

unauthorised access. Features like authentication using OTP and alerts need to be

implemented in order to enhance security (KPMG India, 2011). In their paper,

Pousttchi and Schurig (2007) suggested two security requirements that need to be

considered by banks when introducing m-banking services. Firstly, because m-

banking transmits sensitive data, the data transmission process needs to be

encrypted. Secondly, users need to authorise every transaction or access to the

data, i.e. users need to prove that they are the rightful holder of the account before

any transaction can take place.

In order for customers to trust banks, banks need to educate customers about the

risk of online banking (Padmanabhan, 2012). Literature emphasise that people want

to work or share information with people they trust thus the creation of a strong

relationship between banks and their customers is essential (Brown, Zaheeda,

Davies & Stroebel, 2003). Since traditionally, building trust occurs mostly through

face-to-face contact, the implications of introducing e-banking remain uncertain

whether building long-term relationships will still be possible (Joseph, Sekhon,

Stone, & Tinson, 2005).

Page 18 of 68

2.6. The Future of Mobile Banking

M-banking is being used more and more by banking customers. The banking trend is

increasing simultaneously with the increase in the adoption of smart phones and

tablets, especially amongst the y-generation. A study conducted by the Federal

Reserve (2012) found that nearly 21 percent of mobile device users have used m-

banking in the past 12 months. Eleven percentage non-users reported that they will

use m-banking in the future. In terms of functions performed over m-banking, the

study further found that 90 percent of mobile users use m-banking to check financial

account balances or transaction inquiry. According to the Pew Research Center

(2012) there has been a drastic increase in the number of users that use their mobile

devices to query account balance information, an increase from 18 percent to 29

percent between the years 2011 and 2012. M-banking is seen an additional

customer expectation that compliments other banking channels rather than a service

delivery channel replacement (Federal Reserve, 2012). Banks therefor need to

invest in their channel network in order to make these channels more customer-

centric and user-friendly. By doing so the channel will be more efficient which in turn

contributes to better returns on investment and increased profitability.

Because of the emergence of new mobile technologies, the banking sector is

becoming highly competitive with the traditional channels no longer offering

competitive edge. According to Capgemini (2012), the changes in mobile

technologies have led to the emergence of four technology trends in the retail

banking channels. The trends will be discussed in detail below.

Increased spending on mobility to enhance consumer experience:

o As customers are shifting from PCs to mobile devices, the mobile channel

is now becoming part of the banking channel blend. Banks are said to

spend more than 30 percent on mobile channels in order to improve

customer experience. A focus by banks on mobile innovation will help

them improve customer experience and differentiate them in the highly

competitive environment in which they operate. Banks need to invest more

in digital channels and implement the best solutions which are available on

the market.

Page 19 of 68

Concentration on mobile remote deposit capture (RDC) and mobile marketing to

gain competitive advantage:

o RDC is a technology that allows bankers to remotely scan cheques and

send that image to the bank for deposit, via an encrypted internet

connection (Deloitte, 2010). Banks can use RDC to strengthen the bank-

customer relationship by offering the customers value-added services.

According to Capgemini (2012) the driver for this trend is the rapid

consumer preferences and lifestyle which forces banks to develop ways to

allow customers to transact anytime and anywhere.

o In order to leverage business growth and efficient customer service, they

need to integrate mobile marketing and social media.

Increase on social media and social analytical tools to help make strategic

decisions:

o With an increase in the use of social platforms, customers expect banks to

commune through these platforms as well. They expect customer service

and financial advice through these platforms. Banks need to consider

social media as part of their multi-channel strategy.

o A combination of customer intelligence and social analytics can help banks

gain an insight into customer behaviour and needs.

Focus on multi-channel integration in order to better offer services:

o According to Gartner Inc (2012) one of the problems faced by banks is the

challenge of delivering a seamless experience to customers. Another

challenge is the integration of “backend systems” with “multi-channel front-

end”. In the upcoming years, banks that offer seamless customer

experience for better service delivery through the use of multi-channel will

gain a competitive edge over its competitors.

Page 20 of 68

Chapter 3: Research Methodology

3.1. Research Design & Strategy

3.1.1. Introduction

In order attain the objectives of this study, which is how banks can reap the benefits

associated with the use of MFS to offer better services. The opportunities provided

by m-banking and the risks and challenges faced by banks without and those without

such are studied. In support of this objective, a second objective is studied which aim

to encourage the adoption of MFS as an effective service delivery platform. The

second objective of this paper is to investigate whether customers prefer MFS over

the other available banking service platforms, such as, ATMs, internet banking, and

branch banking. In this chapter, we will look at the research paradigm, the various

research instruments that will be used to conduct the research, the population,

sampling and size of sample and the unit of study. Furthermore, the data collection

techniques are discussed including the challenges and limitations of this paper.

3.1.2. Research Paradigm Researchers have different thinking styles, beliefs and views of their environment,

thus the way they conduct their research studies tend to differ. According to Oates

(2006), a paradigm is a specific way of thinking about problems and practices that

regulate inquiry within a discipline. Therefore, to clarify the researcher’s thinking

style, an exploration of the paradigm chosen for this study will be discussed.

This study makes use of a two methods to explore and advice on how banks can

reap the benefits associated with the use of MFS to offer better services.

Quantitative method is used to provide a representative sample from the population,

so that the results of the sample studied can be generalised back to the population

(Oates, 2006). Because the population of this study is unknown, this method is used

to provide numeric measurements and analysis of the adoption dynamic of mobile

services between banks and customers, thus the study is not generalised back to the

population. Qualitative on the other hand is used, according to Marshall (1996), to

Page 21 of 68

help provide understanding of complex psychological issues. Thus this method will

be used to help understand the issues and benefits relating to the use of m-banking

or MFS by banks.

According to Oates (2006), the philosophical paradigms most mainly used in

Information System research are positivism, interpretivism, and critical research. The

qualitative method is in the same philosophical foundation as the interpretive

paradigm, which is concerned with understanding the social context of Information

Systems (Oates, 2006). The interpretivism paradigm is used in this paper because it

supports the view that there are many truths and multiple subjective realities. This

type of paradigm helps to understand complex ideas and concepts of people in their

natural social settings which is more the focus of this study. Furthermore, the

interpretive paradigm provides an opportunity for the research’s participants to voice

their concerns and practices.

The quantitative method on the other hand is in the same philosophical foundation

as the positivist paradigm. This paradigm forms the foundation of what is called “the

scientific method”, it argues that there is one version of truth or objective reality

(Oates, 2006). But because only the measurement method (quantitative) is adopted

from this paradigm, the paper doesn’t make use of universal laws, mathematical

models and is not based on the empirical testing of hypothesis. Thus the use of

quantitative method in this study is to understand people in their world and to

recognise that multiple interpretations exist.

Qualitative and quantitative data collection techniques were used in this descriptive

study, this techniques included; semi-structured interviews, and pre and post-test

questionnaires. In order to attain different perspectives and to draw attention to the

adoption of MFS by financial institutions, descriptive research methods were used in

this study.

3.1.3. Population and Sampling The population in this study is divided into two parts. Firstly, the population for this

study is consumers with a mobile device and a bank account with any of the four

Page 22 of 68

banks in South Africa. Secondly, according to Marshall (1996) the nature of the

population is defined in such a way that all the members have an equal chance of

selection. Thus the second part of the population follows random sampling, thus the

sample includes the four major banks in South Africa, FNB, Standard Bank, ABSA

and Capitec Bank.

3.1.4. Unit of Study

For the purpose of this study, the unit of analysis is 25 consumers with bank

accounts in South Africa. These consumers also need to own a mobile device. To

better understand the adoption issues of the consumers, the research is not limited

to consumers with a mobile device and a bank account or those with a banks

account but no mobile device. It also includes consumers with bank account and

mobile device or bank account and no mobile device, regardless of their status and

age group. The study however does not include consumers who do not have a bank

account.

The study also focuses on the banks that actually provide these services; the banks

include the four major banks in South Africa, ABSA, FNB, Standard Bank and

Capitec Bank. These banks are limited to only those that are in the Pretoria

surroundings, only each of the main banks will be included in the study.

3.1.5. Sample Size of Participants

According to Marshall (1996), a probability technique is use when an author beliefs

that the sample of respondents chosen are representatives of the overall population.

Because the first part of the study, refer to “3.1.3 Population”, focuses on consumers

with or without mobile device but those consumers with bank accounts with FNB,

Standard Bank, ABSA or Capitec Bank, the sampling method followed in this study is

non-probability. The sampling method is also chosen because the researcher does

not know enough about the population to thoroughly conduct a probability sample.

The second part of this study, refer to “3.1.3 Population”, will use a probability

Page 23 of 68

technique, because the results of the sample study can be generalised back to the

population.

According to Marshall (1996), in order to determine how close one is to the true

population, the margin of error and confidence interval are used. For the purpose of

this study, twenty-six questionnaires were created in order to attain a sample size of

twenty, which is necessary to ensure ninety-five percent level of confidence with a

+/- three percent accuracy range. Interviews will also be conducted with the each of

the four banks in S.A.

3.2. Research Strategy and Data Collection Methods

In this study, a survey interview was used to collect all the data necessary to answer

the main research question. Furthermore, a survey questionnaire was used to

support findings of the main question (refer to instruments in Appendix A and

Appendix B).

The survey interview (Appendix B) was directed at the major bank’s IT managers or

representatives, who have knowledge and insight about the implementation of m-

banking as a service delivery channel in their respective organisations and how

these channels affect or benefit the organisation. The interview seeks to establish

the benefits associated with the use of mobile technology by banks, determine

whether mobile technology can be used to offer better services to consumers and

how banks can effectively use these services to make service delivery more efficient.

An analysis of the risks and challenges of banks with and without such mobile

services will also be conducted.

The survey questionnaire (Appendix A) was mainly directed at the bank’s customers

who make use of the various service delivery platforms offered by the banks. The

respondents may include anyone who has a bank account and a mobile device. The

questionnaire aims to establish whether the respondents/customers prefer MFS over

the other available platforms offered by the banks. It further aims to identify the

issues leading to lack of mobile service adoption.

Page 24 of 68

3.3. Expected Results

Upon conclusion of this research, I expect to come to a solution for the main

research question including its sub-questions. The solution expected is aimed to

advise financial institutions, especially banks how they can better take advantage of

the benefit associated with the use of MFS as a service delivery channel. This is a

solution aimed to help banks to effectively exhaust the benefits provided by MFS, a

solution that will realise competitive advantage and provide knowledge about what

consumers prefer. In support of the main question, I also aim to discover whether

customers really do prefer MFS channel over the other available channels.

3.4. Limitation

The survey will only be conducted on the surroundings of Pretoria. A pre-requisite of

a respondent answering this survey is that one should have a bank account, with any

of the major banks in South Africa, ABSA, FNB, Capitec Bank or Standard Bank,

and/or a mobile device. The questionnaire will be English, thus misunderstanding

and misinterpretation of the questions might occur especially for non-speaking

respondents. This might negatively affect the results.

3.5. Ethics

The author shall adhere to the following general principles of ethics while conducting

the research of this paper:

The author shall obtain informed consent of the respondents before conducting

research on this paper

Respondents have the right not to participate or are not obliged to respond to the

questionnaire distributed or interview conducted by the researcher

The researcher pledges that the data collected shall be handled with out-most

confidentiality and anonymity

The research shall be conducted with close attention and promises not to provide

misinterpretation or misunderstanding of any sort

Page 25 of 68

3.6. Conclusion

Research instrument

Qualitative – interview

Quantitative – user questionnaires

Population and unit of study

consumers with a mobile device

and a bank account

four major banks in South Africa

not consumers with no mobile

device

regardless of status or age group

Pretoria surroundings only

Sample size

Non-probability – with or without cell

phone but with bank account

Probability – banks or financial

institutions

Data collection

Survey based questionnaire distributed

to consumers

Interview with banks that offer mobile

banking services

Page 26 of 68

Chapter 4: Research Findings

4.1. Introduction

In order to explore theories and concepts that are relevant to a research study,

according to Oates (2006), a researcher needs to conduct data analysis, which is the

process of analysing and arranging the collected data. In this section, the aim is to

analysis the collected data in order to answer the questions discussed in Chapter 1.

In order to answer the main question formulated in Chapter 1, “How banks can reap

the benefits associated with the use of mobile technology to offer better services?”,

and its sub-questions, an interview was conducted with the banks representatives.

The first part of the interview questions are designed in such a way as to provide

qualitative data which will be analysed through the use of thematic analysis

(Appendix B). Whilst the second part of the interview questions are constructed in

such a way as to provide quantitative data by utilising a rating for each response to a

question. The rating used had variables ranging from “strongly disagree” to “strongly

agree”. Included in between, in their respective order the other rating were;

“disagree”, “neutral”, “slightly agree”, and “agree”. The interviews with banks focus

on the bank’s perspective about customer behaviour and use of m-banking service

delivery channel. The open-ended interviews were literally transcribed and a cross-

analysis method was used in order to underline different concept and assess

relationship among these concept.

The closed questions questionnaire aims to collect data in order to support the main

questions. This questionnaire aims to find out whether consumers or bankers prefer

MFSs over the other available service delivery channels. Thus the application of

rating scores was incorporated into the design of the questionnaire, in order to obtain

quantitative data. Part of the questionnaire was a section used to collect data about

the usage of MFSs, including the attitude and perception of consumers towards the

use of such services.

Page 27 of 68

The analysis technique applied in this study is thematic analysis and association

cross analysis. This data analysis is manually conducted based on the determined

categorise. This chapter is divided into two parts; the first part, section 4.2 shows

results based on user findings, while section 4.3 will analyse the organisation

statistics gathered by the author. The results that follow in the section below are

presented through the use of tables, figures and graphs.

Page 28 of 68

4.2. Mobile User Statistics

The section below analyses mobile user statistics gathered using a survey

questionnaire, see Appendix A. A few topics regarding the findings are touch upon,

these topics include: user demographics, types of m-banking transactions, customer

evaluation of service factors, and lastly customer evaluation of delivery channel.

4.2.1. Mobile User Demographics

In this section, I focus on a few variables in order to analyse the demographics of the

mobile users evaluated. These variables include the respondent’s gender, mobile

device and bank account status, and whether they use mobile device to transact.

The reason behind the choice of these variables is to determine the gender, and to

screen out respondents that cannot participate in this study.

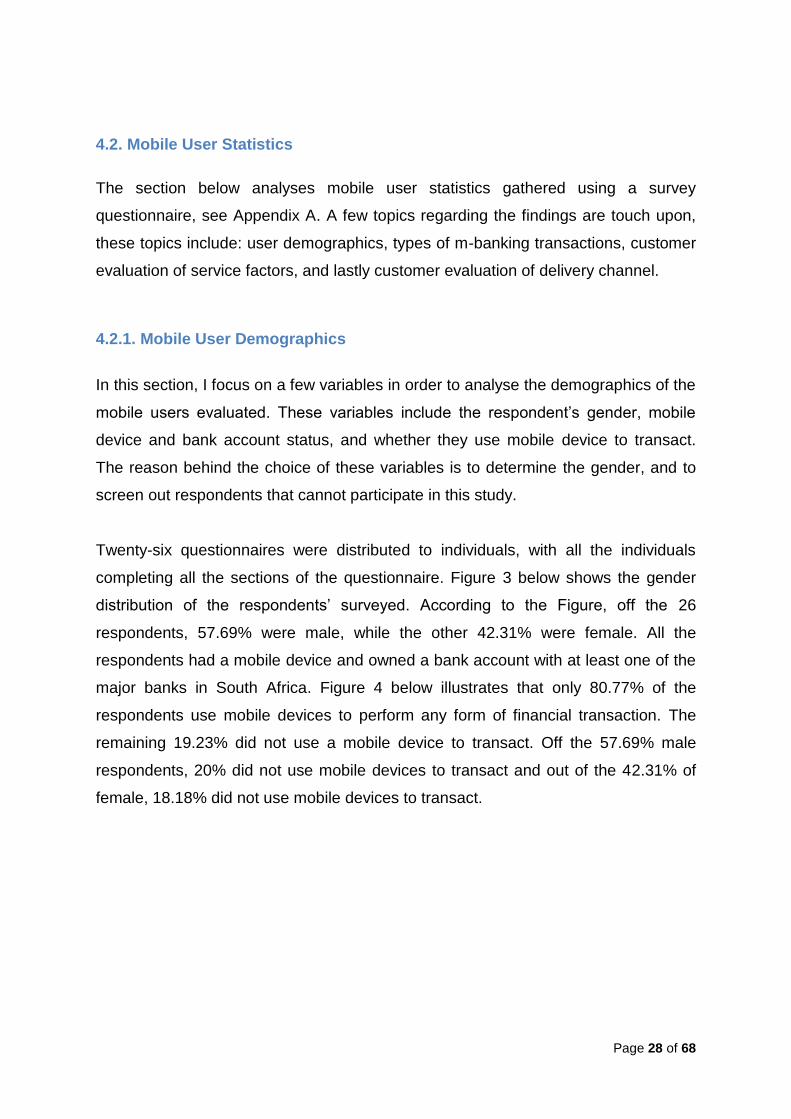

Twenty-six questionnaires were distributed to individuals, with all the individuals

completing all the sections of the questionnaire. Figure 3 below shows the gender

distribution of the respondents’ surveyed. According to the Figure, off the 26

respondents, 57.69% were male, while the other 42.31% were female. All the

respondents had a mobile device and owned a bank account with at least one of the

major banks in South Africa. Figure 4 below illustrates that only 80.77% of the

respondents use mobile devices to perform any form of financial transaction. The

remaining 19.23% did not use a mobile device to transact. Off the 57.69% male

respondents, 20% did not use mobile devices to transact and out of the 42.31% of

female, 18.18% did not use mobile devices to transact.

Page 29 of 68

Figure 3: Mobile User Gender

Figure 4: Mobile Device Usage

Page 30 of 68

From the user demographic analysis and figures above, it is visible that the most

individuals surveyed were males. Furthermore, it is clear that the usage of mobile

device by consumers to conduct financial transactions is higher than those that do

not use the channel. This could be caused by the increase in mobile device users.

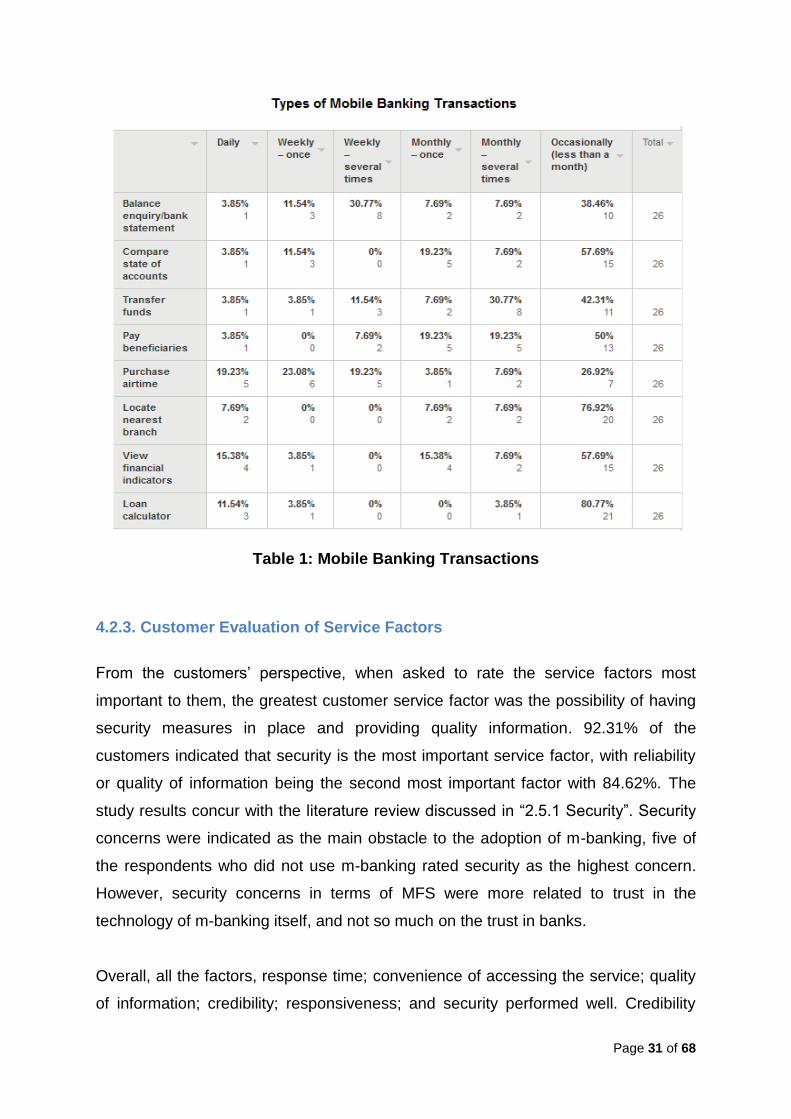

4.2.2. Type of M-banking Transactions

Customers were asked to indicate the types of m-banking transactions that they

conduct via mobile devices and indicate how often they use these type transactions,

the analysis allowed a comparative evaluation of the transactions. The transaction

included: balance enquiry, compare state of accounts, transfer funds, pay

beneficiaries, purchase airtime, locate nearest branch, view financial indicators, and

loan calculator. As shown in Table 1, purchase of airtime is seen as the most

performed transaction, with 19.23% of customers performing such a transaction

daily. From the data analysed, what appeared to be significantly surprising is that

that out of the 19.23% customers, 100% of the people purchasing airtime daily is

female. Due to misinterpretation and misunderstanding 11.5% of respondents who

do not use their mobile device for any form of financial/banking transaction have

completed Question 5 of the “Mobile User Questionnaire”.

A significant 80.77% respondent showed no interest in the use of loan calculators

and 76.92% showed no interest in the use of GPS features to locate nearest bank

branch. This statistics could be due to a number of reasons, such as customers not

having smartphones or customers not being interested in the additional features

offered by banks through the mobile channel. Banks seem to be investing in

additional features such as calculators and so forth that consumers show no interest

in.

Page 31 of 68

Table 1: Mobile Banking Transactions

4.2.3. Customer Evaluation of Service Factors

From the customers’ perspective, when asked to rate the service factors most

important to them, the greatest customer service factor was the possibility of having

security measures in place and providing quality information. 92.31% of the

customers indicated that security is the most important service factor, with reliability

or quality of information being the second most important factor with 84.62%. The

study results concur with the literature review discussed in “2.5.1 Security”. Security

concerns were indicated as the main obstacle to the adoption of m-banking, five of

the respondents who did not use m-banking rated security as the highest concern.

However, security concerns in terms of MFS were more related to trust in the

technology of m-banking itself, and not so much on the trust in banks.

Overall, all the factors, response time; convenience of accessing the service; quality

of information; credibility; responsiveness; and security performed well. Credibility

Page 32 of 68

seems to be related to trust in the technology of m-banking. This is an important

reason for customer preference of m-banking compared with Branch or ATM. The

convenience of accessing banking services through m-banking seems to be of less

importance compared to the other five factors.

M-banking service prices do not seem to be of concern, as 34.62% respondents

rated the pricing level 2, from a scale of 1 being very cheap and 5 being very

expensive. However, the data shows that 4 of the respondents who do not use m-

banking found the service as being somewhat expensive. Three of these

respondents preferred ATMs or internet banking over m-banking. The lack of

adoption of m-banking could be influenced by how customers view the pricing of the

service. If the customers perceive the service to be expensive then they are likely not

to use that specific service.

4.2.4. Customer Evaluation of Delivery Channel

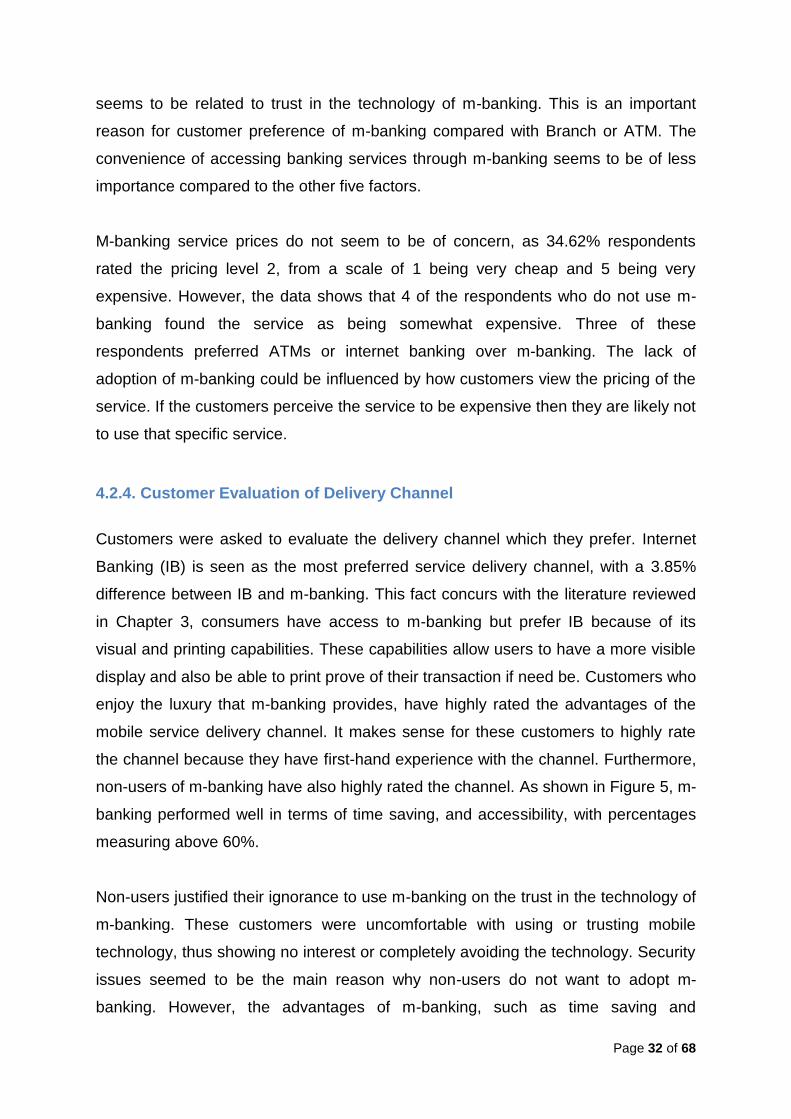

Customers were asked to evaluate the delivery channel which they prefer. Internet

Banking (IB) is seen as the most preferred service delivery channel, with a 3.85%

difference between IB and m-banking. This fact concurs with the literature reviewed

in Chapter 3, consumers have access to m-banking but prefer IB because of its

visual and printing capabilities. These capabilities allow users to have a more visible

display and also be able to print prove of their transaction if need be. Customers who

enjoy the luxury that m-banking provides, have highly rated the advantages of the

mobile service delivery channel. It makes sense for these customers to highly rate

the channel because they have first-hand experience with the channel. Furthermore,

non-users of m-banking have also highly rated the channel. As shown in Figure 5, m-

banking performed well in terms of time saving, and accessibility, with percentages

measuring above 60%.

Non-users justified their ignorance to use m-banking on the trust in the technology of

m-banking. These customers were uncomfortable with using or trusting mobile

technology, thus showing no interest or completely avoiding the technology. Security

issues seemed to be the main reason why non-users do not want to adopt m-

banking. However, the advantages of m-banking, such as time saving and

Page 33 of 68

accessibility seem to encourage current users to continue using the channel, in spite

of the security concerns and the lack of personalisation.

Figure 5: Financial Service Delivery Platform

4.3. Organisations Statistics

In this section, the results obtained from the interview questions, see Appendix B,

are analysed. The variables analysed are: organisation demographics, purpose

behind the introduction of m-banking, benefits of MFS, competitive advantage

findings, mobile trends findings and security findings.

4.3.1. Organisation Demographics

In this section, I will analyse the demographics of the organisations interviewed. The

variables analysed are organisation size and the type of organisation. The purpose

of these analysis is to determine the how big or small the organisations are, and

what type of organisation they are.

There was an estimation of four organisations to be interviewed. In total, three

organisations were interviewed. All of the organisations were large organisations,

Page 34 of 68

with more than 5001 employees. The organisation type for these organisations was

public organisations, all based in the banking/financial services industry.

4.3.2. Purpose behind the Introduction of Mobile Banking

In this section, I discuss the findings of the data analysis of the organisations

purpose behind the introduction of m-banking. Organisations were asked to

emphasise on their purpose for the introduction of m-banking. The study found some

key similarities as to why organisations use mobile channels to add value to their

organisation. What appears common throughout the organisations is that they all

introduce mobile channel to improve customer service, adapt to market demand and

also to position themselves in the forefront of innovation. This indicates that mobile

technology can in essence be used to improve customer service and to gain

competitive advantage. According to the organisations, the mobile platform should

not simply be used to provide information but to offer services which consumers

highly demand. They believe that mobile technology can extend beyond providing

access to account management features. For example, mobile technology can be

used to alert consumers when they have a low balance or insufficient funds to

purchase or pay for something.

The organisations were asked whether the introduction of mobile channel was to

compete with other organisations or not. They argued that the implementation was

not to compete but to improve service delivery. They do this by leveraging off the

latest functionality of the device itself, these functionalities provide them the

opportunity to create value to their customers. They further argue that they do not

simply use the mobile channels to catch-up with the digital age but they are tying it

into their business processes, directly unlocking core business functions and

knowledge. This makes good business sense as IT is merely an enabler of business

processes. The IT strategy thus needs to be aligned with business strategy.

Furthermore, the mobile channel, according to the study, is introduced to give

customers, especially the young, tech-savvy users the convenience of self-service.

Customers are therefore able to manage their finances effectively. According to the

Page 35 of 68

organisations, there has been a huge increase in the younger group opening bank

accounts. This group prefer the mobile channel over the traditional face-to-face,

therefore giving them direct interaction with their finances. Although the

organisations are aware of the implications of no face-to-face relationships between

them and their customers, they seem to have hope in their multi-channel integration

strategy. Consumers use the various channels depending on their individual needs.

If they feel like face-to-face interaction they tend to make use of branch channel, and

for no face-to-face interaction they make use of IB or m-banking.

When the organisations were asked which channel the customers prefer, they

concurred with the literature reviewed in this paper. Customers tend to use those

channels that perform best in satisfying their banking needs. From the organisation’s

perspective, no channel satisfies all the users’ needs, thus that is why banks offer

various banking channels. The channels are used only for the purpose they need to

serve, e.g. branch is used for absolute transactions while m-banking is used for

money transfers and purchase of airtime. From these findings, it seems that

organisations need to focus on integrated multi-channel offering strategies and

management.

4.3.3. Benefits of Mobile Financial Services

Organisations were asked to rate the advantages of MFS. What appears apparent in

Figure 6 is that most organisations benefited from a large pool of customers and

reduced costs. The large pool of consumers has been cause by an increase in the

number of mobile subscribers. With this increase, organisations now leverage the

mobile channel in order to reach out to a large pool of consumers at the lowest

possible cost.

All three organisations benefited from reduced location costs and costs associated to

employees or overhead costs. This has been a result of a decrease in the number of

employees needed to carry daily business tasks or decrease in the cost of serving

customers. Some business processes may no longer be needed due to the

introduction of mobile channel, thus eliminating costs related to these business

Page 36 of 68

processes. From the organisation’s perspective, they benefited from reduced costs

related to call centers and branch banking. Furthermore, mobile channel provided

them the upper hand of getting closer to their customers by using somewhat

analytical tools thus providing better feedback and satisfying customer needs.

Figure 6: Advantages of MFS

What appears significant is that most organisations use mobile channel to improve

customer service, which is the core of this paper. These organisations have realised

that mobile channel helps them to build customer relationship. The mobile channel is

on the rise and the ever-growing base of young people using this channel is

expecting more advanced capabilities. As a result, the tech-savvy consumers expect

high quality customer service at their fingertips. In order for organisations to live up

to this challenges, they need to understand their customers and be able to provide

quality service to this customers via mobile channel. A further significant finding is

that with an increased improvement in customer service, organisations seem to

benefits from a large pool of customers. Satisfied customers and customer who have