outbound foreign direct investment in china’s finance sector: implications for domestic banking...

TRANSCRIPT

OUTBOUND FOREIGN DIRECT INVESTMENT IN CHINA’S FINANCE SECTOR:

IMPLICATIONS FOR DOMESTIC BANKING REFORM

by

Brandy Au

______________________________________________________________

A Thesis Presented to the FACULTY OF THE USC GRADUATE SCHOOL

UNIVERSITY OF SOUTHERN CALIFORNIA In Partial Fulfillment of the

Requirements for the Degree MASTER OF ARTS

(POLITICS AND INTERNATIONAL RELATIONS)

August 2011

Copyright 2011 Brandy Au

All rights reserved

INFORMATION TO ALL USERSThe quality of this reproduction is dependent on the quality of the copy submitted.

In the unlikely event that the author did not send a complete manuscriptand there are missing pages, these will be noted. Also, if material had to be removed,

a note will indicate the deletion.

All rights reserved. This edition of the work is protected againstunauthorized copying under Title 17, United States Code.

ProQuest LLC.789 East Eisenhower Parkway

P.O. Box 1346Ann Arbor, MI 48106 - 1346

UMI 1500843

Copyright 2011 by ProQuest LLC.

UMI Number: 1500843

ii

Table of Contents

List of Tables iv

List of Figures v

Abbreviations vi

Abstract viii

Chapter 1: The Banking System in China, Reforms, and Outbound Foreign Direct Investment 1

Chapter 2: Theories of OFDI and Application to China’s Finance Sector 6 2.1 An Overview of the Eclectic (OLI) Paradigm 6 2.2 Finance Sector-Specific Explanations of OFDI 7

Chapter 3: China’s Banks: Structure, Evolution, and Role 11

3.1 China’s Banking System in Comparison to Other Countries 11 3.2 Development of the People’s Bank of China and the State-Owned Commercial Banks 13 3.3 The Role of Household Deposits in the Banking System 16 3.4 Reforms in the Banking System 17

Chapter 4: An Assessment of China’s Banks 22

4.1 Fragility 22 4.2 Iron-Fisted State Control 25 4.3 China’s “Too Big to Fail” Banks 26 4.4 Economic Growth and Overdependence on the Banking System 27

Chapter 5: The Role of the Banking System in Outbound Foreign Direct

Investment 29 5.1 Lending Guidelines for State-owned Commercial Banks and Corporate Clients 29 5.2 Significant Developments in OFDI by China’s Banks 31 5.3 ICBC’s Lower-Profile Foreign Bank Investments 36

Chapter 6: The Link between Finance and Non-Finance Sector OFDI and

Implications for Banking Reforms 41 6.1 Finance Sector OFDI Strategies and National Economic Development Goals 41

6.1.1 The Internalization Factor in Practice 41 6.1.2 Beyond Wholly Owned Subsidiaries 42

iii

Chapter 7: Has OFDI Made China’s State-Owned Commercial Banks More Competitive? 46

Chapter 8: Implications and Going Forward 49

8.1 The Potential for Foreign Direct Investment in the Finance Sector 49 Bibliography 53 Appendices 60

Appendix A: Household Deposits, Total and as a Percentage of Total Bank Funds 60

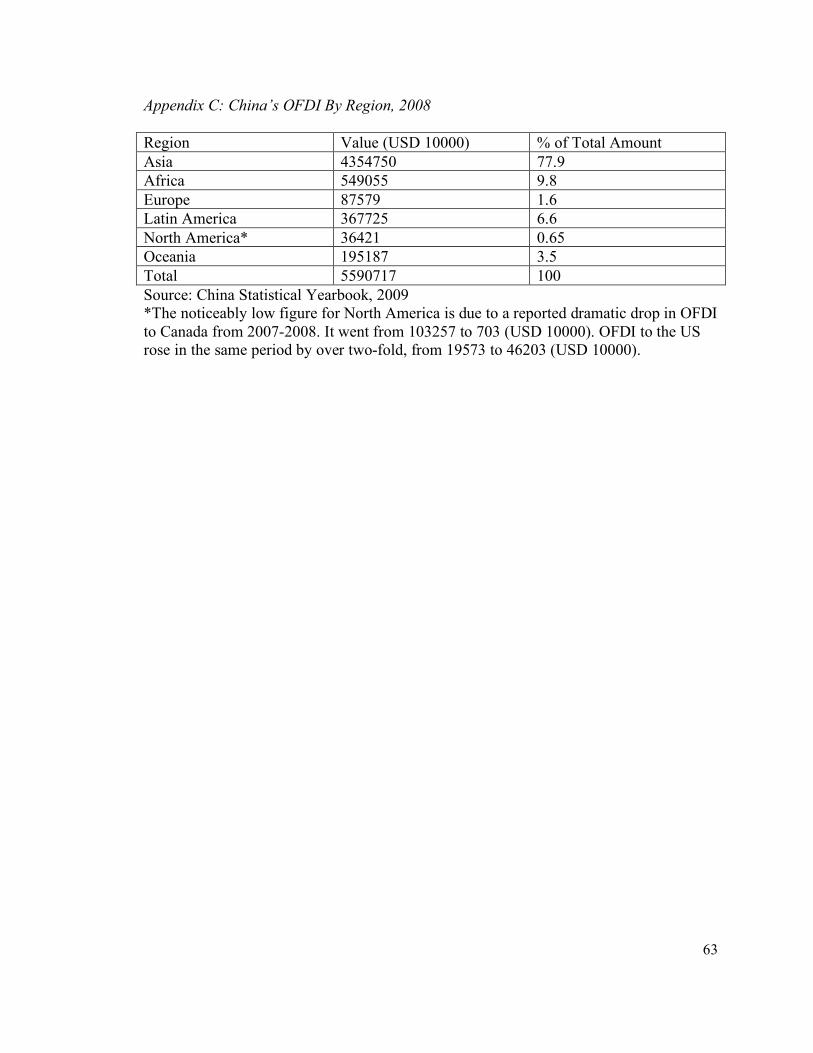

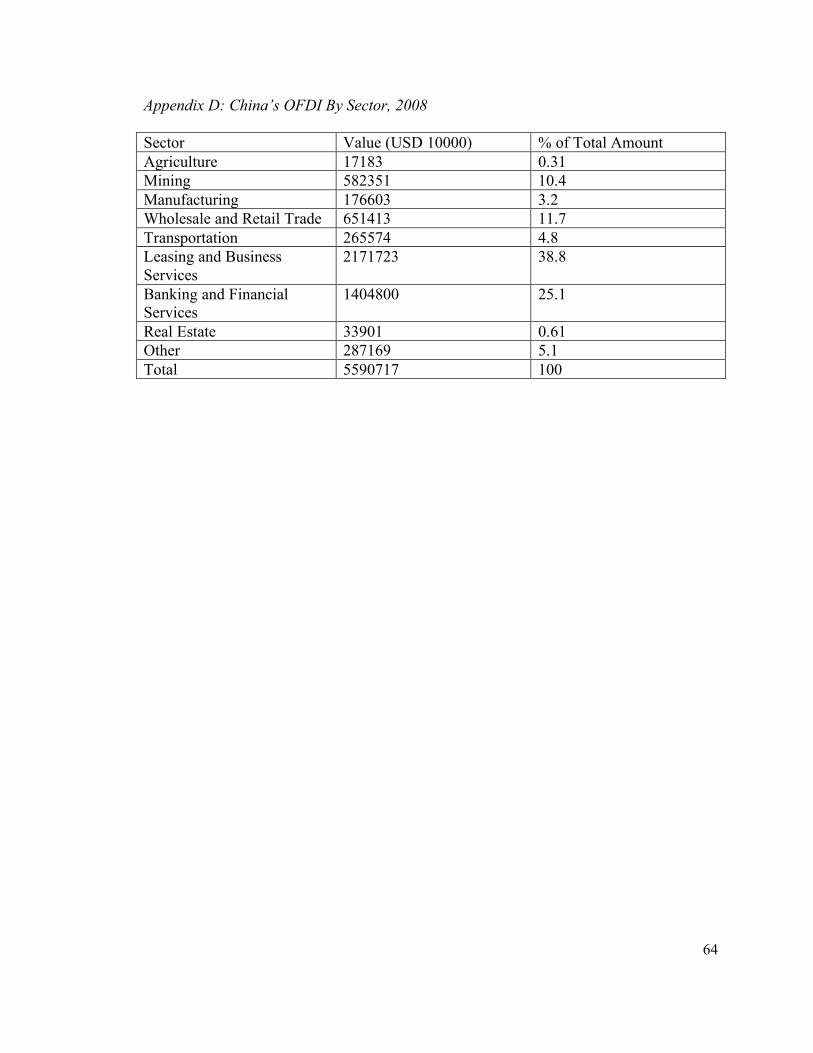

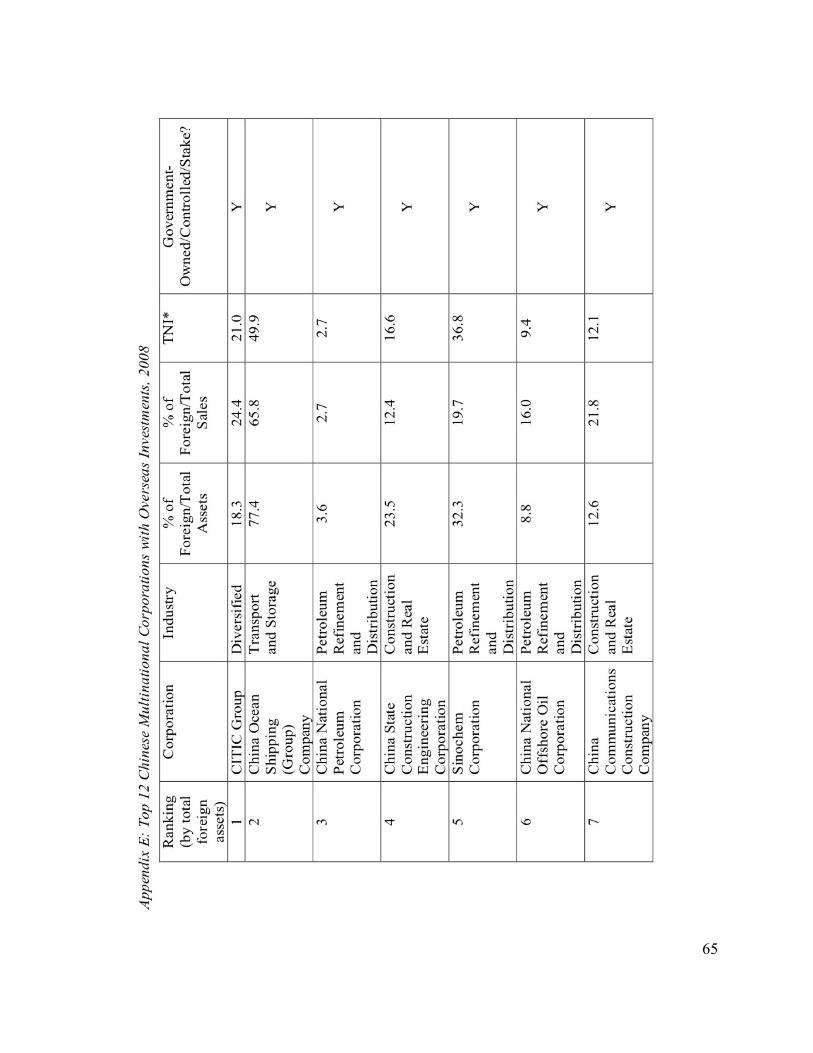

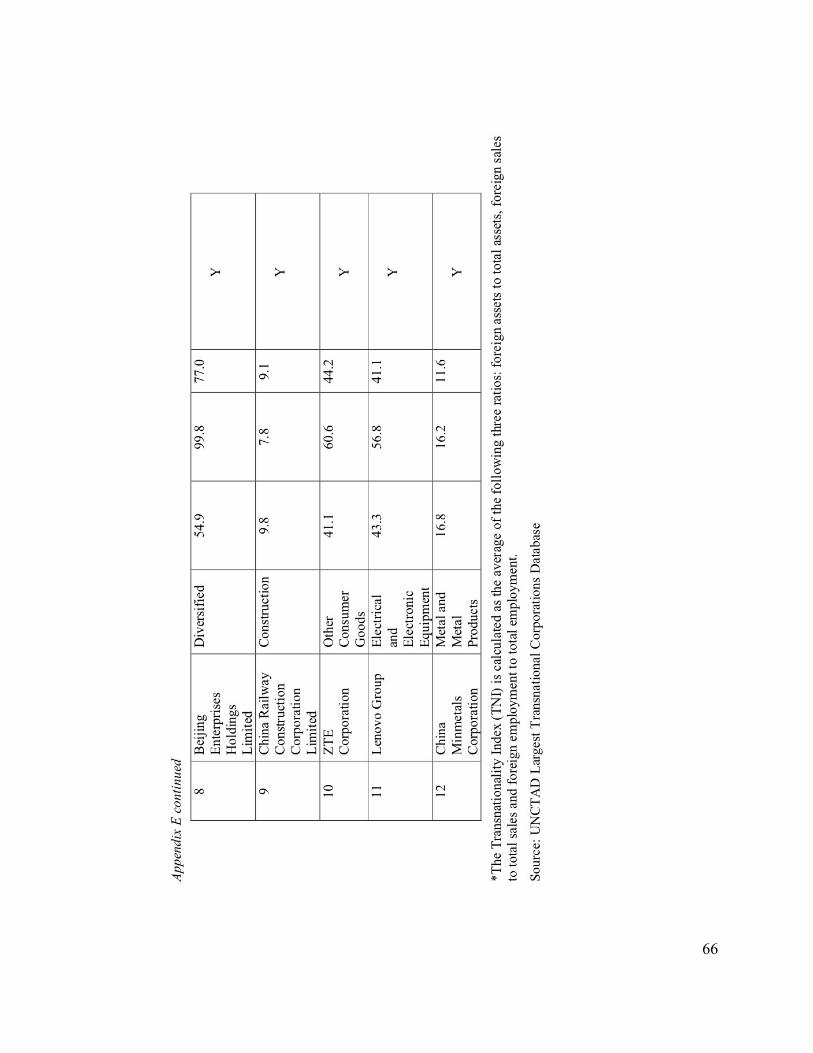

Appendix B: Foreign Exchange Reserves, China 62 Appendix C: China’s OFDI By Region, 2008 63 Appendix D: China’s OFDI By Sector, 2008 64 Appendix E: Top 12 Chinese Multinational Corporations with

Overseas Investments, 2008 65

iv

List of Tables

Table 1: OFDI in China’s Finance Sector and Applicability of the Eclectic Paradigm 7

Table 2: Factors Influencing Finance Sector FDI 10

Table 3: Profile of China’s State-Owned Commercial Banks, 2010 16

Table 4: Chinese Financial Institutions and OFDI in the Finance Sector,

Major Deals 38

v

List of Figures

Figure 1: Household Deposits as a Percentage of Total Bank Funds 17

Figure 2: Corporate Loans Made by ICBC, CCB, and ABC 28

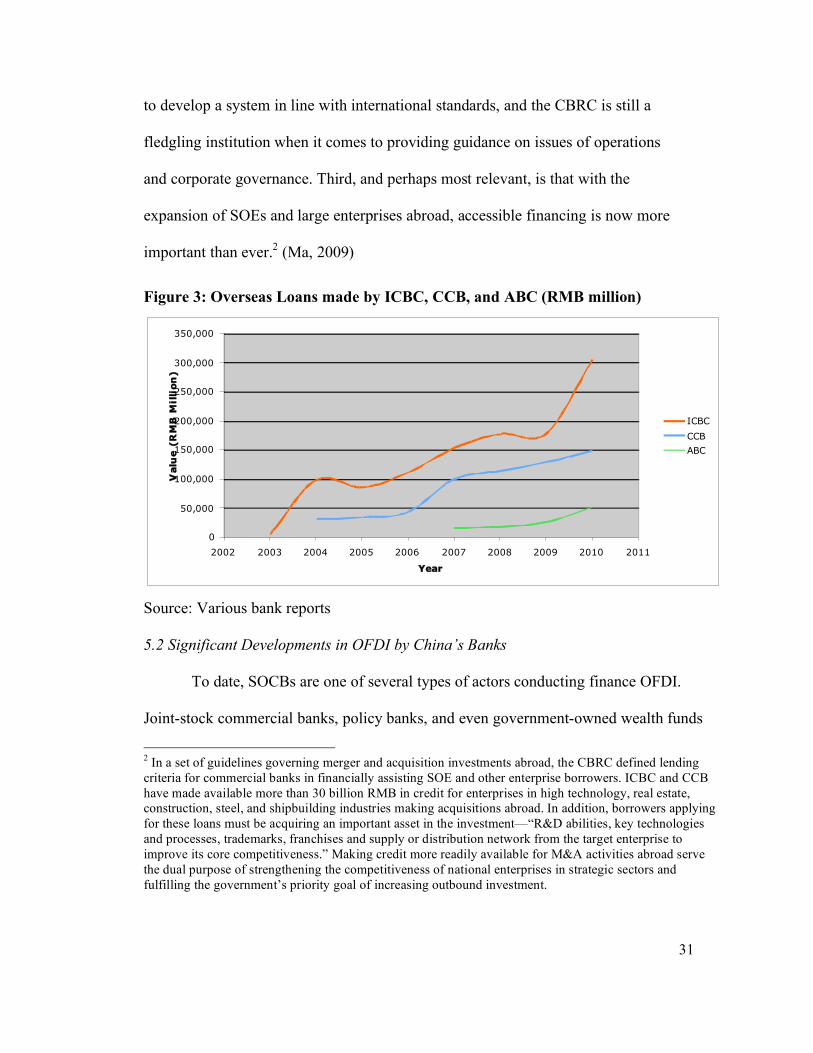

Figure 3: Overseas Loans made by ICBC, CCB, and ABC 31

Figure 4: ICBC and BEA-USA Profiles 36

Figure 5: China’s Outbound Foreign Direct Investment, 1976-2006 40

Figure 6: China’s OFDI By Region, Percentage of Total Amount, 2005-2010 40

vi

Abbreviations

ABC Agricultural Bank of China

AMC Asset Management Company

ASEAN Association of Southeast Asian Nations

BBL Bangkok Bank Public Company Limited

BCBS Basel Committee on Banking Supervision

BEA-USA Bank of East Asia, USA

BOC Bank of China

CAR Capital Adequacy Ratio

CBRC China Banking Regulatory Commission

CCB China Construction Bank

CDB China Development Bank

CFIUS Committee on Foreign Investment in the US

CIC China Investment Corporation

FTA Free Trade Agreement

ICBC Industrial and Commercial Bank of China

IPO Initial Public Offering

MOF Ministry of Finance

NPL Non-Performing Loan

OFDI Outbound Foreign Direct Investment

PBOC People’s Bank of China

vii

ROA Return on Assets

SAFE State Administration of Foreign Exchange

SASAC State-owned Assets Supervision and Administration Commission

SOCB State-Owned Commercial Bank

SOE State-Owned Enterprise

SPC State Planning Commission

UCBH United Commercial Bank Holdings

viii

Abstract

Economic liberalization has occurred at a rapid pace in China since the start of

economic reforms in 1978. One sector that has lagged behind when it comes to

liberalization, however, is that of the banking and finance sector. The lack of

liberalization, and more generally, structural reform in China’s banking system is due to

its irreplaceable role as financier of the national economy. With no alternative forms of

financing, state-led economic development in China has consistently been dependent on

bank lending. In particular, large state-owned enterprises (SOEs) are the entities that have

benefited most from government-mandated preferential lending policies.

This critical role of financial support has extended beyond the domestic realm in

recent years to include assisting enterprises in their outbound foreign direct investment

(OFDI). As China’s general OFDI increases, so has finance sector-specific OFDI.

Finance sector-specific OFDI theoretically can assist in the reform process for China’s

state-owned banks, but this does not seem to be a primary motivation for banks to invest

abroad. Rather, finance sector OFDI indicates an extension of banks supporting state-

owned and large enterprises abroad. This project makes the argument that this added

imperative role will provide even less of an incentive for policymakers to mandate

desperately needed reforms, to the detriment of the banking system.

1

Chapter 1: The Banking System in China, Reforms, and Outbound Foreign Direct Investment

China’s economy has experienced phenomenal change in the short time span of

thirty-three years, marked by the official start of reforms in 1978. Moving from an

isolated command economy with poor performance to a market-based, export-oriented,

and globally integrated one that has achieved remarkable levels of growth is no small feat

on the part of policymakers and enterprising firms. Many sectors of China’s economy

have liberalized, allowing for impressive sums of inward foreign direct investment and

the ability of Chinese firms to undertake profit-seeking activities and investments with

comparatively fewer restraints.

There is one sector that has lagged in the liberalization process, and that is the

financial and banking system. For the most part, the government has relinquished very

little control over China’s banking institutions, keeping them shielded from foreign

investment and competition. Unlike other sectors where China has allowed, even invited,

foreign direct investment, in the financial system banks are still majority state-owned and

operate based on government-mandated criteria. The casualty resulting from this setup is

that China’s banks have become stagnant performers, plagued by operational

inefficiencies, non-performing loans and bad assets; exposed to precarious risk situations;

and subject to political interests without the independence to operate in a profit-seeking

manner. This has severely eroded the competitive abilities of banks and compromised the

2

health of the domestic financial system. Without state support, China’s banks would be

wholly incapable of competing with their foreign counterparts.

The puzzle under discussion is why, despite desperately being in need of reforms,

China’s banking system has yet to take the necessary steps to address the issues

highlighted above. Central and local government officials have been reluctant and

resisted enacting policies that would assist in the reform process. The reason for this is

that banks in China play an indispensable role—that of financing economic activity of the

equally important state-owned enterprises (SOEs). “In China, the banks are the financial

system,” serving as the only source of credit to borrowers. (Walter and Howie, 2011, p.

25) In other words, the banks are responsible for ensuring a steady stream of capital and

monetary loans to the engines fueling China’s economic growth. The logic is

straightforward. Without the banks, there is no capital. Without capital, SOEs cannot

operate. If SOEs become non-operational, economic growth would decline and political

and social stability would be disrupted. In a literal sense China’s banks are the foundation

of the economy, but in a more philosophical sense they are the foundation of the Chinese

leadership’s legitimacy vis-à-vis economic development. The irreplaceable role of the

banking system is no exception when it comes to supporting the activities of SOEs and

other enterprises’ investment activities overseas, which is the focus of this thesis.

Because of this added function, reforms in the banking system will, even more so, be

further delayed.

This thesis will examine the role of the banks in supporting outbound foreign

direct investment (OFDI) activities in non-finance sectors, and argue that such a function

3

is one of many that make China’s banks indispensable in the national economy. In recent

years, increasing total OFDI has become an explicitly stated goal as part of a

comprehensive national economic development strategy.1The government is encouraging

firms to invest abroad and taking its own steps to fulfill this mandate, such as directing

investment abroad via the state-owned sovereign wealth fund China Investment

Corporation (CIC). Like many other sectors of the economy, the banking sector has also

gone global by engaging in OFDI, but it is not for reasons of supporting the reform

process or building competitiveness. Although bank reforms are an important part of the

government agenda, improving the performance of banks is a secondary consideration

when discussing finance sector OFDI. Ultimately, OFDI is undertaken by banks to

support and facilitate the overseas activity of non-finance firms. Because of this

particular role that only became crucial with China’s goal of increasing overall outbound

foreign direct investment, it provides even less of an incentive for policymakers to

implement the necessary reforms in order to improve the status of the banking system.

Needless to say, no reforms would take place that would jeopardize the banks’ role of

financing SOEs.

This argument has several implications. On a theoretical level, China’s OFDI

activity in the banking and financial services sector does not adhere neatly to traditional

theories of foreign direct investment, including the eclectic paradigm postulating that

firms invest abroad in order to exploit various ownership, location, and internalization

factors. (Dunning, 2002, p. 103-104) Banks, thought of as firms, do not possess

1 Specifically, this is articulated in the National People’s Congress 10th and 12th Five Year Plans, which will be discussed later.

4

competitive advantages that they can exploit abroad, especially when it comes to those

that are ownership-specific. China’s banks theoretically could go abroad with the

intention to seek factors of production that would make them more competitive, such as

managerial capital with the ability to train staff and strengthen business practices in

services that are offered. Foreign management can also assist in developing a system to

determine and address financial risk, meeting international banking standards and

regulations, and assessing creditworthiness of borrowers to make functional loans with a

probability of return. Interestingly enough, these are not primary reasons for investing

abroad. The unique role of state-owned banks requires a case-specific approach to

explain their behavior.

In terms of policy implications, the very specific role that banks—especially state-

owned commercial banks (SOCBs)—play in the national economy means that reforms

have been and will continue to be delayed. Policymakers have been selective about what

aspects to reform, and political leaders will implement reforms insofar as they do not

compromise the relationship between banks and SOEs. Selective and incomplete reform

has occurred, and patterns of OFDI in the finance sector will continue to be driven by

national economic development goals.

This thesis primarily analyzes China’s SOCBs, although China’s financial system

is more pluralistic, including non-SOCB firms such as joint stock commercial banks,

regional- and city-level banks, and credit cooperatives. The SOCBs are the primary focus

because they hold the bulk of national deposits—over 70 percent—and moreover,

provide the majority of lending to China’s SOEs. (Walter & Howie, 2011, p. 27) These

5

banks have been designated as the primary vehicles by which SOEs are financed and

hence, they are a critical apparatus that deserves further analysis.

The thesis will first provide a theoretical overview of finance sector FDI as it

relates to China’s case. The next section covers important trends in China’s general OFDI

profile as they relate to national economic development goals, and how this policy

priority impacts reforms in the banking system. Following this is a discussion about the

banking system’s development, problems, reform efforts, and how such efforts have fared

to date. The next section proposes some motivations for finance sector OFDI and

implications for the domestic reform process, tying the two distinct phenomena together.

Although it is generally too early to assess what the impact has been, meaningful

observations can still be made about the intentions of these transactions. A final section

concludes and discusses prospects for China’s banks and finance sector OFDI.

6

Chapter 2: Theories of OFDI and Application to China’s Finance Sector

The purpose of this section is to provide theoretical motivations for why banks

invest abroad, and assess the applicability of such explanations to China’s case.1

(Buckley, Clegg, Cross, Liu, Voss, & Zheng, 2007; Child & Rodrigues, 2005; Deng,

2007; Wang, 2002) Firms in the finance sector—not just in China, but across countries—

tend to have a unique set of motivations when it comes to OFDI that are not captured by

more general theories. Hence, a myriad of theoretical explanations must be considered

when examining the behavior of Chinese banks abroad. After the discussion, it will be

clear that Chinese finance sector OFDI requires a combination of different approaches in

order to accurately capture its motivations for going abroad.

2.1 An Overview of the Eclectic (OLI) Paradigm

Perhaps the most well-known theory of foreign direct investment and

international production is the eclectic paradigm, developed by the late economist John

Dunning and used to explain patterns of firm investment in foreign localities. The theory

contains three classes of factors in which firms possess an advantage and, in turn, exploit

abroad—ownership, location, and internalization. (Buckley et al, 2008, p. 718; Child &

Rodrigues, 2005, p. 383) These factors have provided useful theoretical explanations for

the investment by foreign firms abroad, especially for developed economies, but this

mainstream approach only partially describes the behavior of Chinese banks. Like many

1 The literature on “late industrializer” economies emerged after approaches such as John Dunning’s eclectic paradigm, developed out of advanced economies’ industrialization experiences, failed to account for countries such as South Korea and more recently, China.

7

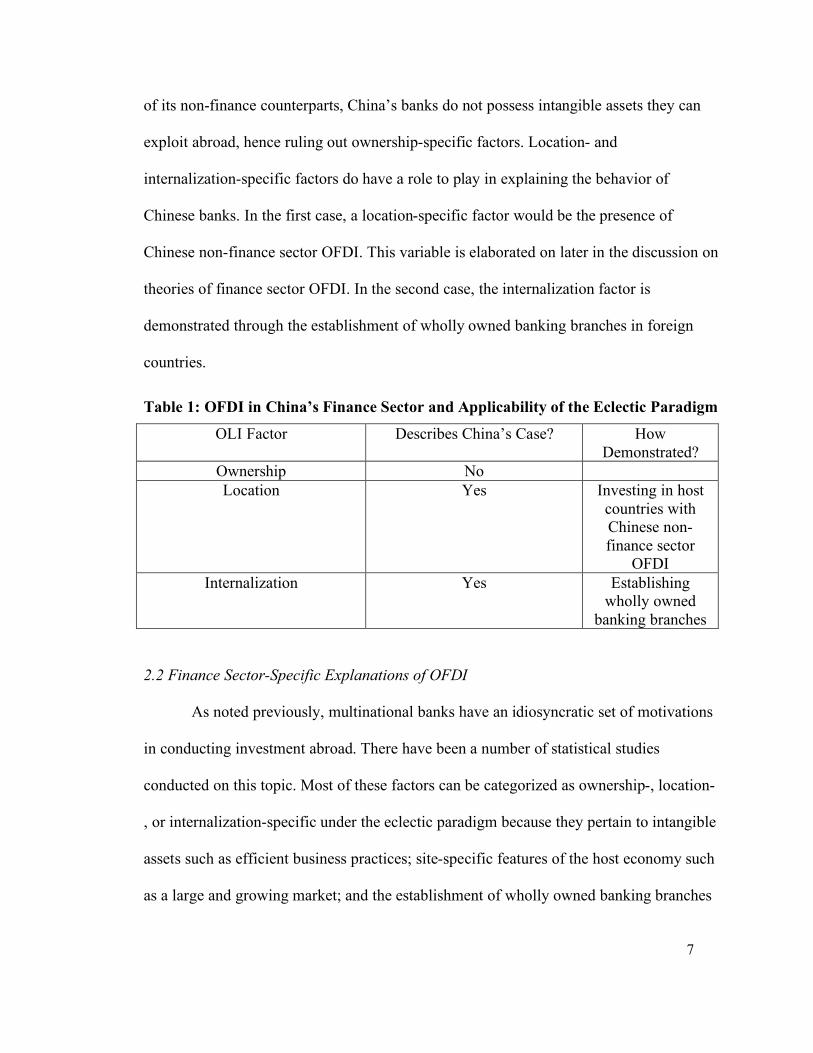

of its non-finance counterparts, China’s banks do not possess intangible assets they can

exploit abroad, hence ruling out ownership-specific factors. Location- and

internalization-specific factors do have a role to play in explaining the behavior of

Chinese banks. In the first case, a location-specific factor would be the presence of

Chinese non-finance sector OFDI. This variable is elaborated on later in the discussion on

theories of finance sector OFDI. In the second case, the internalization factor is

demonstrated through the establishment of wholly owned banking branches in foreign

countries.

Table 1: OFDI in China’s Finance Sector and Applicability of the Eclectic Paradigm

OLI Factor Describes China’s Case? How Demonstrated?

Ownership No Location Yes Investing in host

countries with Chinese non-finance sector

OFDI Internalization Yes Establishing

wholly owned banking branches

2.2 Finance Sector-Specific Explanations of OFDI

As noted previously, multinational banks have an idiosyncratic set of motivations

in conducting investment abroad. There have been a number of statistical studies

conducted on this topic. Most of these factors can be categorized as ownership-, location-

, or internalization-specific under the eclectic paradigm because they pertain to intangible

assets such as efficient business practices; site-specific features of the host economy such

as a large and growing market; and the establishment of wholly owned banking branches

8

in a host economy. The last two of these three factors are demonstrated in the behavior of

Chinese banks.

In a paper researching the determinants of foreign direct investment activity by

banks, Moshirian proposes and tests a number of factors believed to be significant in the

decision of financial institutions based in Germany, Britain, and the US to invest abroad.

(Moshirian, 2001) Another paper by Buch looks at motivations for German banks to

invest abroad. (Buch, 2000) As in Moshirian’s findings, German FDI from non-finance

sectors is a significant determinant of FDI from the finance sector. Preceding studies by

Goldberg and Johnson and Sagari look at how different macroeconomic variables affect

foreign direct investment decisions by US banks. (Goldberg & Johnson, 1990; Sagari,

1992) Lastly, Yamori assesses the impact of factors already delimited in the studies

mentioned as motivations for Japanese banks to invest in subsidiaries abroad. (Yamori,

1998)

Many factors defined in these studies are not directly applicable to China’s case

because they are relevant factors for more developed banking systems that can be

exploited. China’s banks are still very much developing standardized commercial and

personal banking services and cannot be considered mature financial institutions in this

sense. Sagari considers the relationship enjoyed between a bank and its foreign clientele

as an “intangible asset” in accordance with the ownership-specific factor of the eclectic

paradigm, a characteristic that Chinese banks do not possess. (Sagari, 1992, p. 7)

Expansion of banking institutions into a foreign market requires sufficient demand by the

host country, supported by recognition of the bank’s name and the ability to offer

9

competitive services. In fact, it is many of the ownership-specific factors held by

developed financial institutions that China would gain by going abroad—the ability to

undertake complex financial transactions and being staffed by experienced management

and bankers, as examples. (Sagari, 1992, p. 8)

Non-finance sector OFDI and possibly bilateral trade can serve as explanatory

factors for China’s case. Moshirian finds a positive and statistically significant correlation

between FDI activity in the banking sector and FDI activity in non-finance sectors going

to the same country for all three cases under study. (Moshirian, 2001, p. 322) The results

can be interpreted to mean that banks will go abroad to the same host economy in order

to service non-finance sector firms from the home country. A qualitative assessment of

China’s OFDI activity in the banking sector demonstrates this tendency, as the discussion

about ICBC’s investments in Standard Bank in South Africa and small banks in

Southeast Asia later will corroborate. In terms of investing in host economies with which

China has significant bilateral trade, this factor cannot be ruled out, though a more

rigorous methodology for testing it would have to be conducted in order to make

definitive statements about the nature of the link. As China’s trade and OFDI activity are

simultaneously increasing, it is important not to automatically correlate these two

economic patterns simply because they are both increasing in a given host economy.

10

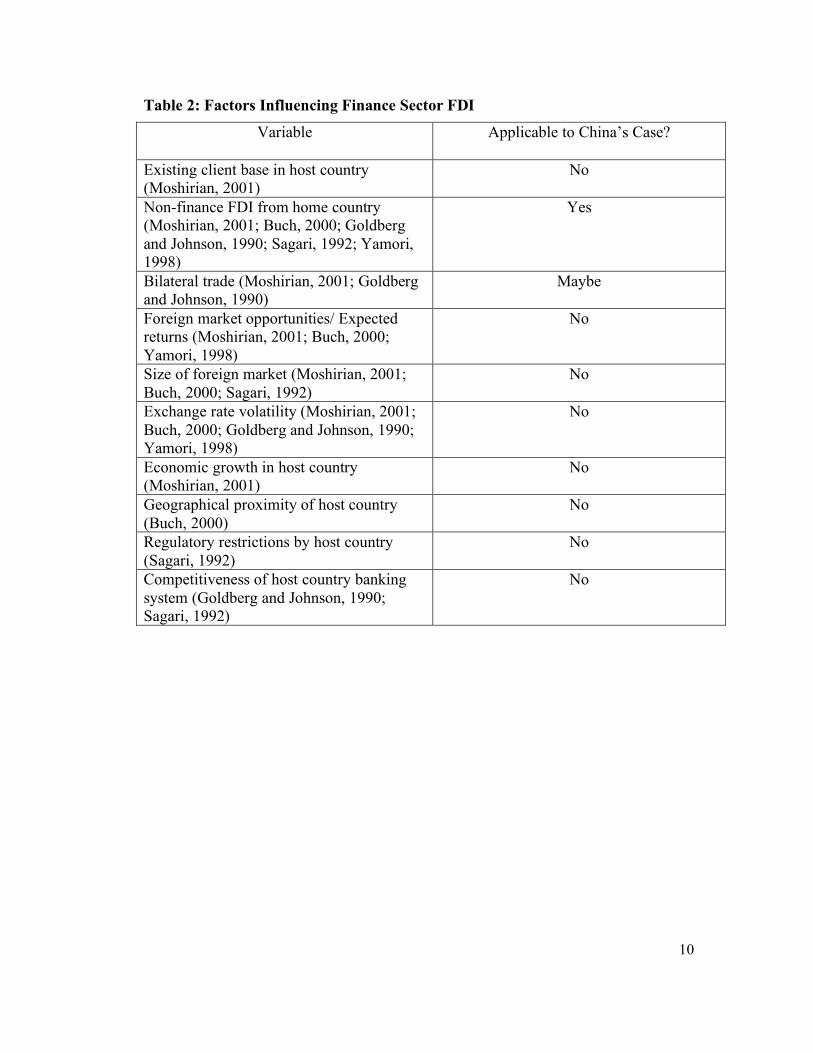

Table 2: Factors Influencing Finance Sector FDI

Variable Applicable to China’s Case?

Existing client base in host country (Moshirian, 2001)

No

Non-finance FDI from home country (Moshirian, 2001; Buch, 2000; Goldberg and Johnson, 1990; Sagari, 1992; Yamori, 1998)

Yes

Bilateral trade (Moshirian, 2001; Goldberg and Johnson, 1990)

Maybe

Foreign market opportunities/ Expected returns (Moshirian, 2001; Buch, 2000; Yamori, 1998)

No

Size of foreign market (Moshirian, 2001; Buch, 2000; Sagari, 1992)

No

Exchange rate volatility (Moshirian, 2001; Buch, 2000; Goldberg and Johnson, 1990; Yamori, 1998)

No

Economic growth in host country (Moshirian, 2001)

No

Geographical proximity of host country (Buch, 2000)

No

Regulatory restrictions by host country (Sagari, 1992)

No

Competitiveness of host country banking system (Goldberg and Johnson, 1990; Sagari, 1992)

No

11

Chapter 3: China’s Banks: Structure, Evolution, and Role 3.1 China’s Banking System in Comparison to Other Countries

In a state-controlled finance sector like China’s, banks constitute the majority of

financing in the economy and do not operate under market forces. For example, interest

rates are set by the government as opposed to being determined by independent bank

policies. Instruments such as ceilings are utilized to artificially achieve a specific rate in

order to meet state preferences and goals. (Lukauskas, 2002) As a result, state control

results in distortion. China’s financial repression policies are not a novel phenomenon

when examining the experiences of other East Asian countries. One view is the “late

industrializer” perspective. As Lukauskas argues, in these types of economies

“governments have…little choice but to opt for a bank-based financial system under tight

state control. Restriction is necessary because existing markets cannot adequately support

a process of industrialization…without government intervention.” (Lukauskas, 2002, p.

384) During their respective periods of industrialization, Japan and Korea practiced

financial repression as well, shielding their banking sectors from competition. Many of

the same policies enacted are observed in China’s current banking system. Some of the

parallel features include low deposit yields for savers, the suppression of bond markets,

and the prevalence of “policy loans” for priority borrowers. (Lukauskas, 2002, p. 390-

391, 394) Similarly, the Chinese banks’ feature of holding an overwhelming share of

deposits was seen in Korea during the 1970s and 1980s, with “government-owned or

controlled financial institutions [holding] 90 percent of total banking system deposits.”

(Lukauskas, 2002, p. 391) Credit was allocated to certain sectors of the economy—

12

namely export-oriented and ones dominated by large industrial conglomerates—per state

mandate. Small and private borrowers experienced limited availability in credit access.

The functions of the commercial banking system in Korea are similar to China’s

as well. During strict control, the “commercial banks were little more than government

agencies delegated the task of mobilizing savings and allocating them according to

directives and guidelines issued by the government.” (Park & Kim, 1994, p. 215) In

China’s current financial system, banks are also saddled with the task of taking household

deposits and allocating credit to sectors the government considers a priority for economic

development. Outside of this, banks have little policy discretion and functional

autonomy. Similarities aside, Lukauskas discusses a different set of reasons from China’s

that motivated Japan to repress its finance sector. From a “public interest perspective,”

banks were shielded from competition in order to build up their competitiveness. Policies

such as restricted entry into the banking sector, fixed ceiling rates, and the suppressed

development of bond markets were supposed to create a “small number of efficient,

highly profitable banks.” (Lukauskas, 2002, p. 391) In turn, banks gained expertise, better

operational capabilities, and developed systems to monitor performance. (Lukauskas,

2002, p. 391-392) Seen from this perspective, the goal of restrictive policies was for the

benefit of the banks themselves. Comparatively speaking, Japan also practiced a level of

financial repression less severe than Korea, the latter of whose objectives more closely

resemble China’s.

Some comparisons between China and Korea can be made regarding the

implications of financial repression. State involvement in the banking sector in Korea

13

eventually resulted in a moral hazard problem. As the government became more

entrenched in the banking system, it bore an increasing amount of the risk associated with

non-performing loans, inefficiency, and instability. (Lukauskas, 2002, p. 406) Extrication

became difficult and the government had no choice but to bail out banks that got into

trouble. As will later be discussed, China faces a similar problem in having to save its

banks during periods of irreparable insolvency. China’s central bank (the PBOC) acts as a

lender of last resort and an injector of capital, roles which all too often are utilized by the

banks.

3.2 Development of the People’s Bank of China and the State-Owned Commercial Banks

The development of China’s modern banking system unfolded as quickly as the

rest of the economy during the reform period. In order for economic development to

progress, China needed an efficient and functional financial system that could facilitate

transactions and provide capital. On the state-led economic reform agenda, it was decided

that the banking system would undertake restructuring of its own and be responsible for

providing credit to China’s state-owned enterprises, entities that in turn the state upheld

as integral to economic development. Because the government no longer directly

financed SOEs, banks became the primary vehicle by which it was able to exercise

decisionmaking authority over the allocation of financing. As a result, in China’s modern

banking sector four large banks dominate lending to SOEs, other enterprises, and

individuals. From 1983 to 1994, bank lending as a source of capital for SOEs grew from

14.3 percent to 25.7 percent, an increase of approximately eleven percentage points.

During the same time period, direct government financing fell from 40.6 percent to 5.0

14

percent. (Cull & Xu, 2002, p. 535) In fact, the decreasing share of government financing

is what Shih attributes to the banking system’s current non-performing loan problem.1

(Shih, 2008, p. 107, 120) After the first bailout of banks over-saddled by NPLs, the

government pledged that this rescue effort would be the first and last of its kind. (Shih,

2008, p. 120) As will be noted below, this was not the case. As Walter and Howie

describe, “…the Party treats its banks as basic utilities that provide unlimited capital to

the cherished state-owned enterprises. With all aspects of banking under Party control,

risk is thought to be manageable.” (Walter & Howie, 2011, p. 25; Jefferson & Rawski,

1994, p. 51)

China’s central bank, the People’s Bank of China, became a separate entity from

the Ministry of Finance in 1978. Prior to this critical year that marked the pre- and post-

economic reform periods, China only had one bank—the People’s Bank of China—kept

as a nominal institution without any semblance of policymaking power. (Okazaki, 2007,

p. 6) In 1984, the PBOC officially ended its commercial banking functions and became

China’s central bank. It became responsible for overseeing and setting national monetary

policy, as central banks in most other countries do. However, it had another key

responsibility unique to a state-planned economy, and this was managing the funding of

1 During the early 1980s household deposits in banks began to increase exponentially, which “did not escape the notice of central leaders, who began to see banks as a source of funding.” They became “second treasuries” for SOEs and development projects. During the early 1980s household deposits in banks began to increase exponentially, which “did not escape the notice of central leaders, who began to see banks as a source of funding.” They became “second treasuries” for SOEs and development projects. Lax repayment guidelines as a tradeoff for growth-inducing investment meant that many loans went un-repaid. Defaulting was also exacerbated by the requirement that “a company was first and foremost obligated to hand in the mandated amount of taxes to the central government and to pay workers’ wages before repaying banks.” (Shih, 2008, p. 109)

15

SOEs and their economic projects. (Okazaki, 2007, p. 9) To assist in this endeavor, four

large banks were restructured or reestablished to serve different sectors of the economy—

the Agricultural Bank of China (ABC), Industrial and Commercial Bank (ICBC), China

Construction Bank (CCB), and the Bank of China (BOC).2 (Cull & Xu, 2002, p. 537;

Wu, 2005, p. 220; Naughton, 2006, p. 455) Since this initial restructuring, the roles of the

PBOC and SOCBs have become increasingly defined. In the case of the SOCBs, their

roles have become more general and functions have overlapped. As the PBOC

transitioned into its roles of serving as China’s central bank and monetary policy

authority, the SOCBs gradually took over the commercial functions of lending and

accepting deposits, as well as offering an array of other financial services, functions for

which the PBOC used to be responsible. Combined, they have consistently constituted

the majority of commercial banking activity. Even with the proliferation of other types of

financial institutions, SOCBs were still responsible for four-fifths of all outstanding loans

and 61 percent of total financial assets between 1995 and 1996. (Lardy, 1998, p. 80)

2 The division of labor for the banks was as follows: the ABC would lend credit to rural areas and agricultural economic activity, the ICBC would be responsible for overseeing national savings and loans, the CCB would specialize in financing investment in fixed assets, and the BOC, a spin-off of the PBOC, would be responsible for foreign exchange activity.

16

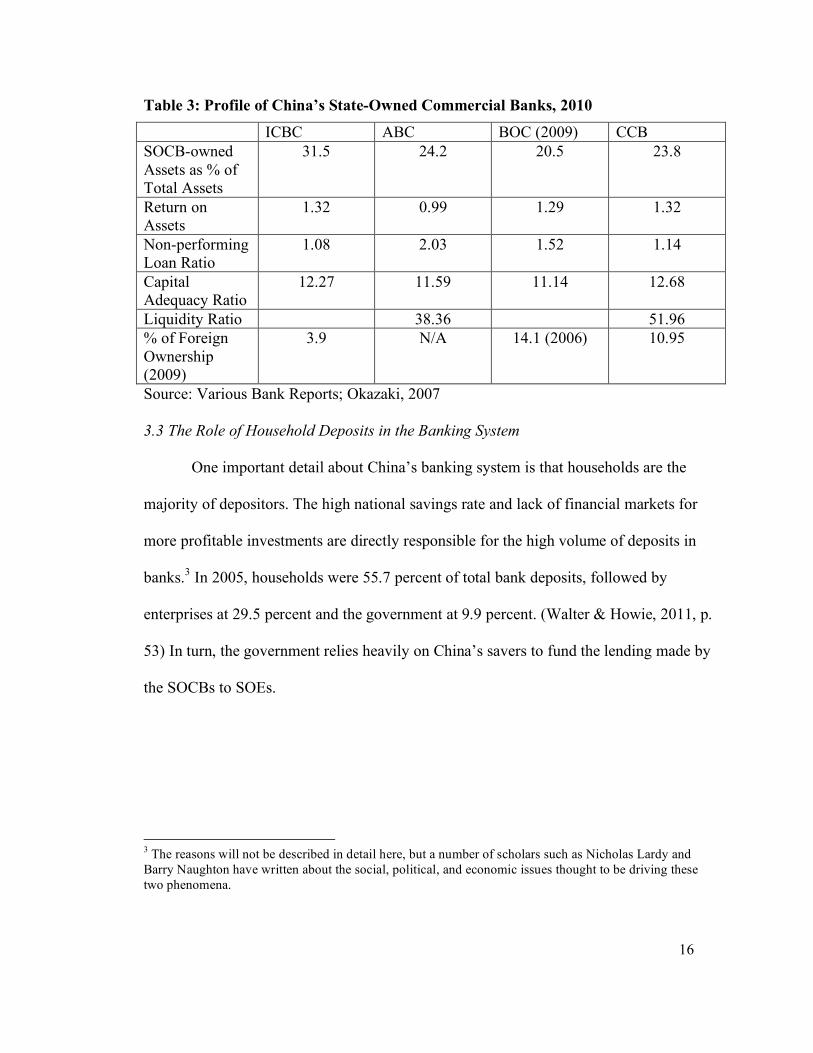

Table 3: Profile of China’s State-Owned Commercial Banks, 2010

ICBC ABC BOC (2009) CCB SOCB-owned Assets as % of Total Assets

31.5 24.2 20.5 23.8

Return on Assets

1.32 0.99 1.29 1.32

Non-performing Loan Ratio

1.08 2.03 1.52 1.14

Capital Adequacy Ratio

12.27 11.59 11.14 12.68

Liquidity Ratio 38.36 51.96 % of Foreign Ownership (2009)

3.9 N/A 14.1 (2006) 10.95

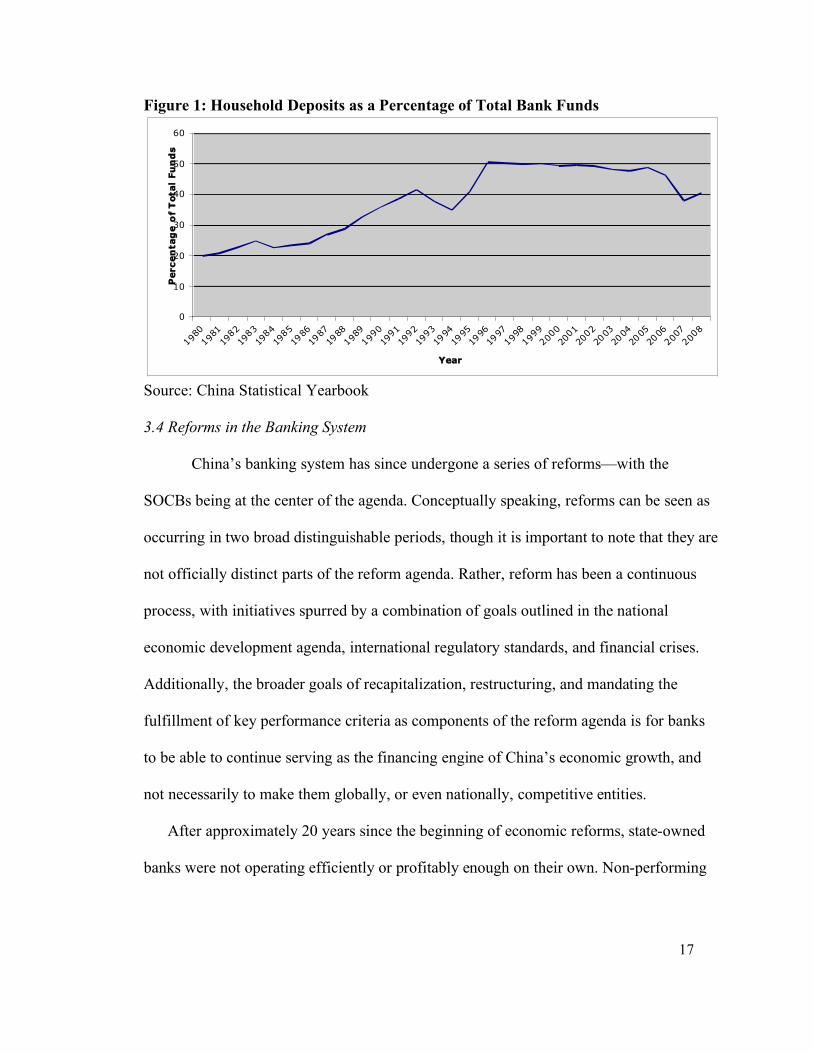

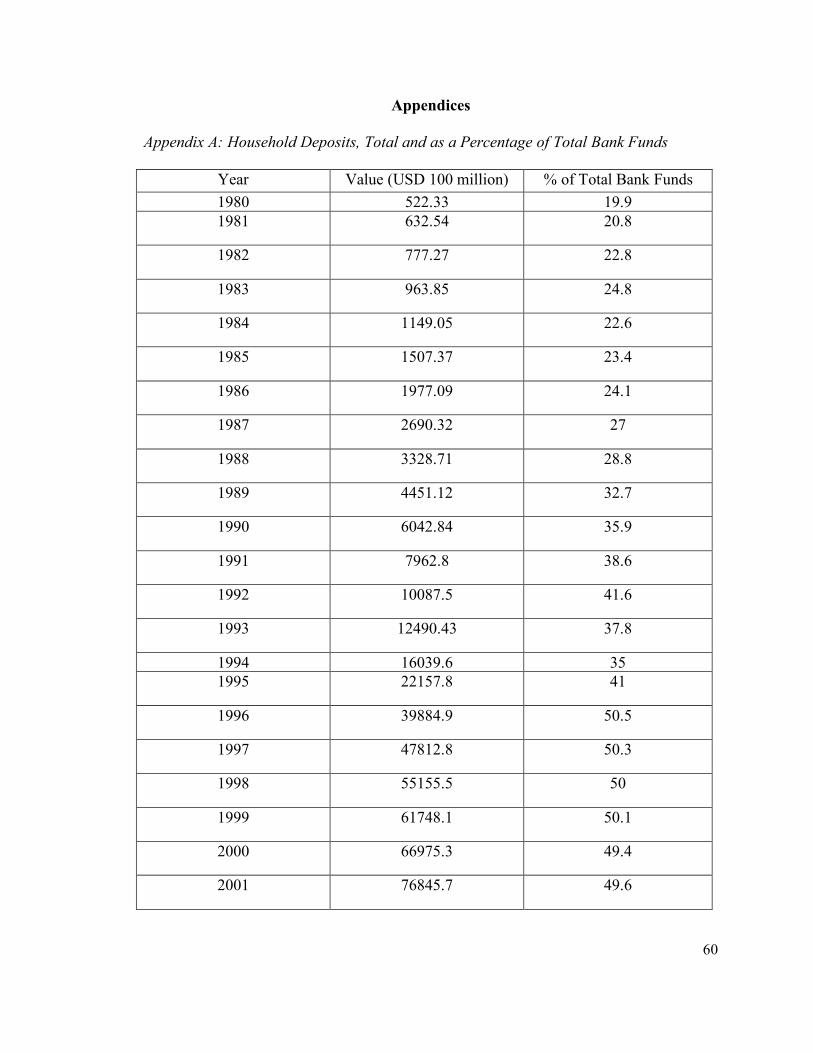

Source: Various Bank Reports; Okazaki, 2007 3.3 The Role of Household Deposits in the Banking System

One important detail about China’s banking system is that households are the

majority of depositors. The high national savings rate and lack of financial markets for

more profitable investments are directly responsible for the high volume of deposits in

banks.3 In 2005, households were 55.7 percent of total bank deposits, followed by

enterprises at 29.5 percent and the government at 9.9 percent. (Walter & Howie, 2011, p.

53) In turn, the government relies heavily on China’s savers to fund the lending made by

the SOCBs to SOEs.

3 The reasons will not be described in detail here, but a number of scholars such as Nicholas Lardy and Barry Naughton have written about the social, political, and economic issues thought to be driving these two phenomena.

17

Figure 1: Household Deposits as a Percentage of Total Bank Funds

0

10

20

30

40

50

60

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Year

Percen

tag

e o

f T

otal

Fu

nd

s

Source: China Statistical Yearbook 3.4 Reforms in the Banking System

China’s banking system has since undergone a series of reforms—with the

SOCBs being at the center of the agenda. Conceptually speaking, reforms can be seen as

occurring in two broad distinguishable periods, though it is important to note that they are

not officially distinct parts of the reform agenda. Rather, reform has been a continuous

process, with initiatives spurred by a combination of goals outlined in the national

economic development agenda, international regulatory standards, and financial crises.

Additionally, the broader goals of recapitalization, restructuring, and mandating the

fulfillment of key performance criteria as components of the reform agenda is for banks

to be able to continue serving as the financing engine of China’s economic growth, and

not necessarily to make them globally, or even nationally, competitive entities.

After approximately 20 years since the beginning of economic reforms, state-owned

banks were not operating efficiently or profitably enough on their own. Non-performing

18

loans were pervasive on bank balance sheets after a few decades of sub-par lending

practices. SOEs that borrowed from the banks were operating at a loss or not making

enough profit to cover their debt. (Lardy, 2003, p. 70) Declining bank profitability in the

mid-1990s meant that the state-owned banks required more capital than was already on

their balance sheets in order to keep operating and stay solvent. The government’s

strategy was to inject fresh capital into the banks’ portfolios. They were termed

differently—“value preservation subsidies”; “deposit index subsidies”—but ultimately

the injection of capital caused a boost in reported bank profits. (Lardy, 1998, p. 105)

China Construction Bank reported almost a doubling of pre-tax profits, while the

Agricultural Bank of China reported a tripling of profits in 1995. (Lardy, 1998, p. 105)

Lardy estimates that the value of capital injections totaled 16.2 billion RMB in 1995.

(Lardy, 1998, p. 263)

The Asian Financial Crisis in 1997 was also a dramatic wake-up call for

policymakers to restructure the increasingly unsustainable lending system. They viewed

China’s banks as a serious liability with the potential to devastate the economy if left

unreformed. As a result, China undertook a deeper series of reforms beyond capitalizing

the banks. The first important step was to bring banks in line with international standards.

It committed to regulatory and supervisory standards set forth by the Basel Committee on

Banking Supervision (BCBS) at the time. Notable among the list of “core principles”

were items that:

• Established stringent criteria on ownership and acquisition activity by banks;

• Set minimum capital-adequacy ratios;

19

• Supervised policies and practices surrounding the evaluation of credit risk in

loans;

• Required transparent accounting policies and practices captured on accessible

records. (Basle Committee on Banking Supervision, 1997)

Committing to adhere to a set of international standards signaled China’s seriousness

about reforming its banking system. In addition, the “aggregate lending quotas” set under

the official credit plan was abolished, replaced by increased, albeit restricted,

independence of the banks to make decisions on financing allocation. (Okazaki, 2007, p.

19) All SOCBs were required to attach a risk assessment to each loan given out, in order

to increase the transparency of credit risks that banks faced. With every outstanding loan,

banks also had to set aside a certain percentage of capital reserves depending on the

borrower’s repayment risk, which was in addition to a specified amount of reserves

already set aside for the total number of general loans. (Okazaki, 2007, p. 22-23)

Undoubtedly these were measures undertaken with the general principles set forth by the

BCBS as guidance.

As part of the recapitalization effort and the desire to attract foreign capital, in an

unofficial second wave of reform during the early 2000s SOCBs were effectively

converted into jointly owned banks by changing their ownership structure. This strategy

entailed recapitalizing the SOCBs so that they would be prepared for an initial public

offering on stock exchanges and be more attractive to foreign investors—both moves

serving to secure important sources of much-needed capital. With the SOCBs going

public, the state no longer maintained 100 percent ownership. High-ranking bank

20

officials hoped that with foreign—or at least diversified—ownership, political interests

plaguing banks would be alleviated.4 (Voss, 2009, p. 140; Naughton, 2006, p. 463;

Okazaki, 2007, p. 21, 27, 30)

With the global financial crisis of 2008, China further realized the deep structural

problems that, if not rectified, would threaten to destabilize its banks and the largest

stakeholder in the financial system—the government itself. A number of measures were

enacted to counter the slowdown in economic growth, including closer monitoring of

overseas bank assets and system-wide credit risk, tightening supervision of the largest

banks, i.e. the SOCBs, and adjusting capital-adequacy ratios to account for global

financial developments. (China Banking Regulatory Commission, 2009) In addition, to

insulate the effects of badly hit foreign financial institutions operating in China, the China

Banking Regulatory Commission (CBRC) mandated several measures to minimize risk

contagion and maintain performance quality, including keeping the CAR at high levels,

maintaining a low NPL ratio, and stabilizing the liquidity ratio.5 The CBRC has

4 To prepare for this, an “investment” company called the Central Huijin Investment Company was established in 2003, backed by the government agency State Administration of Foreign Exchange (SAFE). SAFE was established in 1979 under the Bank of China and is responsible for administering the usage and flow of foreign exchange and recommending foreign exchange policies to the PBOC. Huijin effectively provided capital for the state-owned commercial banks, largely using massive amounts of foreign exchange reserves from the central government. In addition, the central government established asset management companies (AMCs) to temporarily wipe out NPLs from the SOCBs’ liability sheets. For each of the SOCBs there was an AMC created to manage NPLs on their balance sheets: Huarong, Great Wall, Orient, and Cinda. All four AMCs were created in 1999. The specific functions of the AMCs were to “purchase nonperforming loans at face value from the banks in exchange for equity positions in the borrowing firms.” (Lardy, 2003, p. 72) 5 Foreign financial institutions have had consistently higher CARs than Chinese counterparts; the figure stood at 21.22 percent. The NPL ratio was 0.85 percent, compared to 1.58 percent for Chinese financial institutions. The liquidity ratio for foreign financial institutions was 58.83 percent, while for Chinese financial institutions the figure was 46.4 percent. These figures are from 2009. (China Banking Regulatory Commission, 2009)

21

encouraged banks to follow the standards laid out in updated Basel III guidelines, and

annual reports released by SOCBs include discussions on how they are attempting to

achieve these standards.

22

Chapter 4: An Assessment of China’s Banks

Despite reform efforts, China’s banking system still suffers from persistent

performance-related problems. Key issues that need to be addressed include the fragile

and precarious risk situation of the banks, inefficient operations due to monopolized state

control that has severely hindered competitiveness, the continued existence of non-

performing loans and “bad” assets, and the incredibly troubling moral hazard present

between the government and state-owned banks. The longstanding need to support SOEs

domestically, and now internationally as well, increases the gravity of the banking

system’s role in the national economy, and suggests that fundamental reform becomes an

even more remote possibility.

4.1 Fragility

Bank reforms have produced mixed results. In some issue areas, SOCBs have

experienced improved governance and adherence to international standards. The

establishment of a government agency wholly dedicated to bank regulatory supervision

and oversight, the CBRC, is one attempt to follow the international framework.1 The

government anticipates CBRC to become a fully functioning regulatory and supervisory

agency for the banking sector, akin to its counterparts in developed countries that perform

the same duties.

1 This observation is made due to the idea that an autonomous monitoring agency to keep banks in line with national regulatory performance standards is one impermissible feature of developed banking systems.

23

Under CBRC mandate, capital-adequacy ratios have generally met the Basel

standard of eight percent by most financial institutions.2 (Okazaki, 2007, p. 46-47)

However, risk-alleviating provisions are still inadequate.3 (China Banking Regulatory

Commission, 2009; “China’s Banking Industry,” 2005) The most pertinent problems are

structural in nature and will not be alleviated simply by adhering to international

standards. For one, many of the SOEs receiving loans from banks are unprofitable.

Returns on investment projects and industrial output have been disappointingly low.

From the early 1980s to the mid-1990s, SOE profitability decreased from 25 percent to

12-13 percent.4 (Cull & Xu, 2002, p. 536-537) During the 1980s and 1990s, it is

estimated that returns from loans made to SOEs fell from 1.4 percent to 0.3 percent.

(Lardy, 1998, p. 100)

The low profitability of SOEs directly impacts the profitability of its lenders.

Accumulating triangular debt, in which SOEs owe each other, must first be repaid before

debt to the bank is paid back.5 (Shih, 2008, p. 145) This is an important reason why low

2 CARs for the SOCBs were reported as the following at the end of 2006: ICBC’s was 14.05 percent, BOC’s was 13.59 percent, CCB’s was 12.11 percent, and BoComm’s was 10.83 percent. The figure for ABC was not available. 3 Although China has met the minimum eight percent CAR set by the Basel standard, the ratio is merely a guideline. In 2009 China’s banking system-wide CAR stood at 11.4 percent. Developing banking systems typically have higher CARs. Indonesia, for example, has a CAR of 19.9 percent, and Thailand’s is at 12.7 percent. Developed banking systems in East Asia also have CARs beyond the minimum requirement—Singapore’s is at 14.8 percent, Hong Kong is at 15.4 percent, and Taiwan is at 10.7 percent. Banking systems in emerging markets need higher CARs to address macroeconomic shocks that tend to have a more volatile effect on the economy. 4 The authors measure profit as the ratio of pre-tax profits to the total value of output. 5 Having to pay back debt to other SOEs before paying the bank back was mandated at the central level in the 1990s by former Premier Zhu Rongji.

24

profitability of SOEs directly and adversely impacts the ability to pay back bank loans. In

China’s case, the profitability rate is not nearly sufficient to cushion volatility and the

risks associated with an emerging economy.6 (Lardy, 2003, p 70; “China’s Banking

Industry,” 2005) Research by The Economist estimates that for every one dollar of

output, five dollars of new capital must be injected into the system. (“China’s Banking

Industry,” 2005) For China’s banks to sustain their current level of lending and not

receive any external capital, i.e. from the central government, the return on assets would

have to be at least 2.1 percent, approximately five times higher than current levels.

(“China’s Banking Industry,” 2005) That is aside from any macroeconomic shocks that

may occur.

However, making unprofitable loans seems to be a structural trend that will

continue due to central government priorities. As Lardy mentions, state-mandated lending

to SOEs, profitable or otherwise, is classified as a “closed-end loan.” “In principle, these

loans are to be limited to financing potential profitable activities of heavily indebted

money-losing firms. For example, unprofitable firms with signed contracts to produce

goods for the export market are eligible for closed-end loans if the exports are expected

to be profitable.” (Lardy, 2003, p. 89) It is clear from this definition where NPLs first

arise and why they have become such a headache for the SOCBs—lax standards of

evaluation on who may receive a loan, and the fact that SOEs receive preferential

treatment for access to capital regardless of their profitability and performance, if they are 6 In 1985, the profitability of state-owned banks was 1.4 percent. In 1997, the figure had fallen to 0.2 percent. In the mid-1990s, the largest SOCB, ICBC, had a profitability rate of 0.42 percent, measured by return on assets (ROA). At the end of 2004, overall bank profitability was at 0.4 percent, a small improvement.

25

deemed to be important to the central or local government’s economic development

agenda.

4.2 Iron-Fisted State Control

Although the “big four” banks have successfully listed on public stock exchanges,

a closer look reveals that a majority of bank shares are not traded. The figures tell the

story—29.3 percent of ICBC’s shares are tradable, 34.0 percent of CCB’s, 24.5 percent

of BOC’s, and 41.8 percent of BoComm’s. (Walter & Howie, 2011, p. 39) The listing of

SOCBs on stock exchanges is considered more of a signal to foreign investors that such

banks are healthy, sufficient to become a publicly listed company, rather than to actually

diversify ownership, as any profile of the SOCBs reflecting dominant state ownership

would indicate. Walter and Howie argue, “The Big 4 banks [SOCBs] form the very core

of the Party’s political power…[though] China’s banks have taken on an international

guise by public listings, advertising campaigns and consumer lending…such change is

superficial…in China there is…the drive to create a fortress, but it is one that seeks to

insulate the banks from all external and internal sources of change in the belief that risk

should remain under the Party’s control.” (Walter & Howie, 2011, p. 79-80) The

overwhelmingly high-priced IPOs in three of the SOCBs on the Hong Kong and

Shanghai Stock Exchanges are a case in point. The reason for this was due to the role of

bids by government-backed or affiliated organizations. (Naughton, 2006, p. 469) They

included AMCs, “national champion” SOEs, and financial or insurance subsidiaries, all

tied in one form or another to central government agencies. (Walter & Howie, 2011, p.

178-181) The presence of their offerings made IPO shares extremely competitive, hence

26

bidding up the price and edging out small, and largely private, investors. By keeping

ownership in the hands of investors with strong ties to the government, state control

would not be obviated. This would allow the government to hold onto the ability to

mandate banks to carry out its preferred lending policies.

4.3 China’s “Too Big to Fail” Banks

On balance sheets China’s banks look impressive. In terms of asset size, the big

four SOCBs rank in the top 30 globally.7 (Okazaki, 2007, p. 44) A closer look indicates

that the quality of assets is suboptimal. All four banks have consistently been plagued

with a high level of non-performing loans (NPLs), especially when compared to global

counterparts. NPLs are part of every bank’s balance sheet, but in China the problem is

especially pronounced. (Naughton, 2006, p. 461) Bad debt such as NPLs is classified on

balance sheets as assets, which paints a deceiving picture of the banks’ assets to liabilities

ratio and the overall health condition of the bank. The total amount of NPLs is so

significant that it dwarfs the reserves usually used to cover a write-off of debt. Lardy

states, “The nonperforming loans that several of China’s four largest banks ultimately

will have to write off almost certainly exceed the combined value of their reserves and

their own capital. On a realistic accounting, these banks’ capital adequacy is negative,

and they are insolvent.” (Lardy, 1998, p. 95; Italics my emphasis) In the past 10 years,

NPLs have decreased, which may indicate better repayment levels by SOEs.

7 At the end of 2006, ICBC ranked 21st globally with total assets of 961.6 (US$ billion), 26th with 684.4, BOC 27th with 682.0, and CCB 28th with 697.7.

27

The problem of moral hazard is demonstrated in the broad waves of capital

injection and recapitalization that occur every few years since the 1990s. In the mid-

1990s the reported boost in profits was due to capital provided to the large banks by the

MOF. (Lardy, 1998, p. 105) During the 2000s, recapitalization occurred with the

introduction of the government investment agencies. These examples demonstrate that

government-backed recapitalization schemes will serve to undermine banks’ incentive to

adopt fundamental reforms, if it is known that they are guaranteed. (Lardy, 1998, p. 144)

If the SOCBs require another capital injection or restructuring, there is little doubt that

the central government will once again come to their rescue. The banks are simply too

important to allow them to fail. At the same time, the issue of moral hazard points to,

more than anything, the need for reforms to take place that would alleviate this problem.

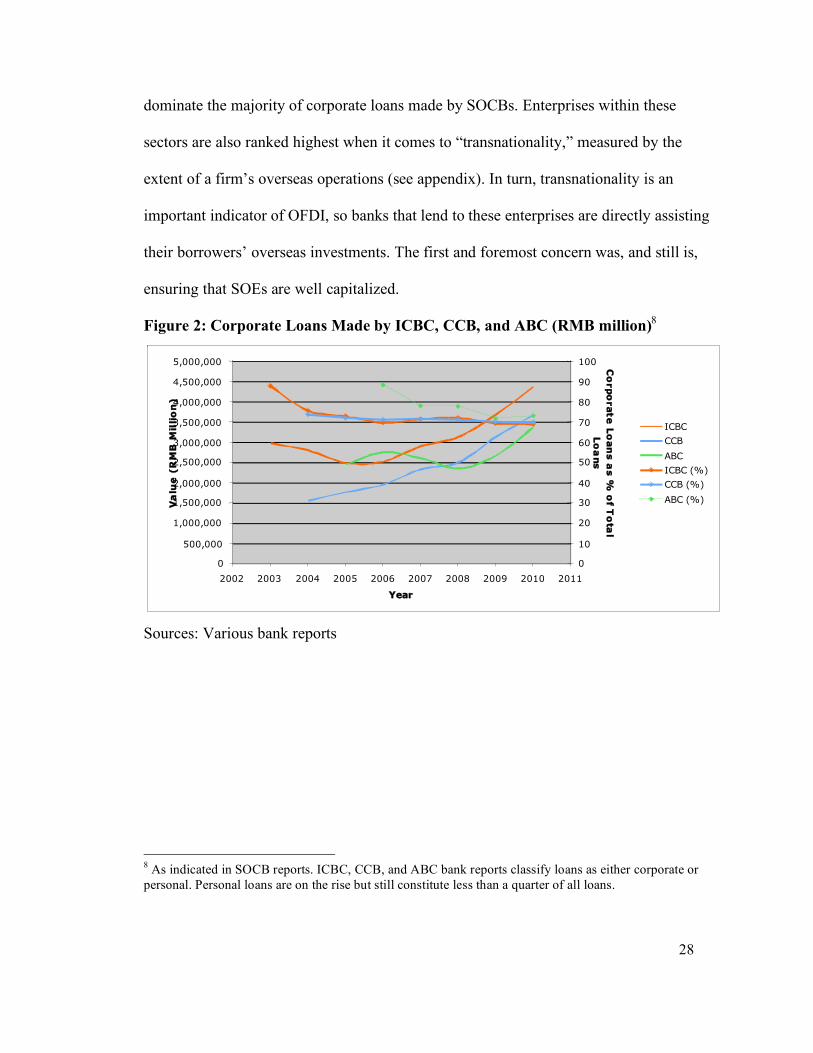

4.4 Economic Growth and Overdependence on the Banking System

Given all these problems, why have reforms not been more stringently

undertaken? Simply put, there is no alternative form of financing for China’s SOEs. Bank

support takes the form of credit provision for and underwriting losses of the SOEs within

these sectors. (Lardy, 1998, p. 83) Returns from loans are not a priority concern. Before

its abolishment, banks were guided by annual “aggregate lending quotas” set by the State

Planning Commission (SPC) in granting loans to SOEs, with little regard to profitability

and risk. (Okazaki, 2007, p. 11) Furthermore, a large part of total lending is made up of

what is officially called “policy loans,” essentially credit extended to government-

designated “priority sectors” of the economy. Such sectors include manufacturing,

wholesale and retail operations, transportation, real estate, and energy firms, which

28

dominate the majority of corporate loans made by SOCBs. Enterprises within these

sectors are also ranked highest when it comes to “transnationality,” measured by the

extent of a firm’s overseas operations (see appendix). In turn, transnationality is an

important indicator of OFDI, so banks that lend to these enterprises are directly assisting

their borrowers’ overseas investments. The first and foremost concern was, and still is,

ensuring that SOEs are well capitalized.

Figure 2: Corporate Loans Made by ICBC, CCB, and ABC (RMB million)8

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Year

Va

lue

(R

MB

Mil

lio

n)

0

10

20

30

40

50

60

70

80

90

100 Co

rpo

rate L

oan

s a

s %

of T

ota

l

Lo

ans

ICBC

CCB

ABC

ICBC (%)

CCB (%)

ABC (%)

Sources: Various bank reports

8 As indicated in SOCB reports. ICBC, CCB, and ABC bank reports classify loans as either corporate or personal. Personal loans are on the rise but still constitute less than a quarter of all loans.

29

Chapter 5: The Role of the Banking System in Outbound Foreign Direct Investment

The discussion so far has focused on the banking system’s domestic role in

lending to SOEs. One aspect given less attention in the general scholarship is how banks

are supporting national enterprises abroad. Commercial banks have been issued a number

of lending guidelines to support the overseas investment activities of enterprises, which

will be briefly discussed in the following section. Just as importantly, banks have lent

direct support abroad. OFDI by the non-finance sector really took off beginning in 2004,

and finance-sector OFDI followed soon thereafter, experiencing a substantial increase

beginning in 2007. Just as SOEs have needed capital to conduct domestic economic and

production activities, they also require financing for investment endeavors abroad. This

section reviews notable investments made abroad by Chinese banks, which serves as an

important context in which to situate the discussion on how banks are supporting the

OFDI endeavors of their non-finance counterparts.

5.1 Lending Guidelines for State-owned Commercial Banks and Corporate Clients

As noted previously, state-owned banks are expected to prioritize enterprise

borrowing according to government-mandated criteria. Though the restrictions and

lending quotas have eased, for the most part corporate loans still dominate the majority of

lending that occurs in SOCBs. In line with reform efforts, the guidelines for these priority

loans have evolved over time to include risk provisioning and include attempts at

following international banking standards. For example, beginning in 1994 banks were

limited to lending 15 percent of their total capital to any one single borrower to minimize

30

loan concentration. (Lardy, 1998, p. 96) During the late 1990s the central government

eased the mandating of lending based on non-commercial criteria, at least officially. A

PBOC official noted in an interview that factors such as asset-liability ratios, reserve

funds, deposit-loan ratios, and the time frame of the loan now had to be taken into

consideration by commercial banks in order for a loan to be approved. (“People’s Bank

Official Explains Decision to Abolish Loan Quotas,” 1998) At the same time they were

expected to give

priority to supporting state-owned large- and medium-sized enterprises [as well as] give proper consideration to medium-sized and small enterprises and money-losing enterprises that can guarantee the capital repayment and interest payment, have a ready market for their products, and have competitive ability and development potential; should vigorously support the re-employment of laid-off workers; and should…cultivate and develop new economic growth areas. (“People’s Bank Official Explains Decision to Abolish Loan Quotas,” 1998)

Although this has been the official mandate, a number of factors prevent

its realization. First, there has been lax oversight over local governments. Bank

branches operate under the jurisdiction of the local government, made up of

policymakers who have an incentive to lend to favored enterprises and/or projects

in which they have a personal or business-related interest. Although the decree

may come from the central bank, local bank branches and government officials

have shown little interest in implementing it.1 Second, banks are still weak when

it comes to having a system of risk assessment and evaluating creditworthiness

based on commercial criteria. Internally, banks do not have the expertise required

1 For a detailed account of local politics surrounding the financial system in China see Victor Shih, Factions and Finance in China: Elite Conflict and Inflation, 2008, Cambridge University Press.

31

to develop a system in line with international standards, and the CBRC is still a

fledgling institution when it comes to providing guidance on issues of operations

and corporate governance. Third, and perhaps most relevant, is that with the

expansion of SOEs and large enterprises abroad, accessible financing is now more

important than ever.2 (Ma, 2009)

Figure 3: Overseas Loans made by ICBC, CCB, and ABC (RMB million)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Year

Valu

e (

RM

B M

illi

on

)

ICBC

CCB

ABC

Source: Various bank reports 5.2 Significant Developments in OFDI by China’s Banks

To date, SOCBs are one of several types of actors conducting finance OFDI.

Joint-stock commercial banks, policy banks, and even government-owned wealth funds

2 In a set of guidelines governing merger and acquisition investments abroad, the CBRC defined lending criteria for commercial banks in financially assisting SOE and other enterprise borrowers. ICBC and CCB have made available more than 30 billion RMB in credit for enterprises in high technology, real estate, construction, steel, and shipbuilding industries making acquisitions abroad. In addition, borrowers applying for these loans must be acquiring an important asset in the investment—“R&D abilities, key technologies and processes, trademarks, franchises and supply or distribution network from the target enterprise to improve its core competitiveness.” Making credit more readily available for M&A activities abroad serve the dual purpose of strengthening the competitiveness of national enterprises in strategic sectors and fulfilling the government’s priority goal of increasing outbound investment.

32

have participated in overseas investments.3 To provide a chronological narrative of how

finance sector OFDI has evolved, the discussion below is not limited to activity by

SOCBs. Many of these financial actors invest abroad with intentions similar to those of

SOCBs. It is still important to keep in mind, ultimately, that SOCBs are expected to

increase their OFDI due to the integral role they already play domestically in providing

SOEs with financial support.

One example of a finance sector firm making an investment overseas for the

purpose of supporting Chinese enterprises is that of China Minsheng Bank. In September

2007 China Minsheng Bank, a privately owned medium-sized commercial bank, bought

4.9 percent of San Francisco-based United Commercial Bank (UCBH) valued at $96.1

million dollars. As part of a two-part investment strategy, Minsheng would increase its

total holdings to 9.9 percent in a year, with the ultimate option of increasing the figure to

twenty percent two years after the initial purchase. (Oliver, 2007) The ultimate value of

the deal was estimated to be $129 million dollars. (Braithwaite & Anderlini , 2009) This

was China’s first investment deal in an American bank, and it happened to be one that

served primarily a Chinese-American population. Unfortunately for Minsheng, UCBH

failed in 2009 due to a number of stress factors adversely impacting its profitability—a

significant one being the number of construction and mortgage loans it had on its books

when the Global Financial Crisis hit—and Minsheng, at the time its largest shareholder,

had to write off the investment. (“All the World’s a Stage, 2010) The extent of UCBH’s

3 As of 2009 SOCBs have a combined 86 branches overseas, covering commercial and investment banking and insurance services.

33

financial deterioration became apparent when in 2009 top executives at UCBH resigned

because they had been deemed responsible for unlawfully modifying loan terms and

withholding information from external auditors in order to cover up the amount of

troubled loans. (Calvey, 2009) Minsheng applied to acquire UCBH, but was subsequently

denied by US federal regulators. (Braithwaite & Anderlini, 2009) With the failed UCBH

deal, China’s eighth-largest commercial bank had paid a high cost for an opportunity to

expand into the US and support rapidly increasing OFDI in this particular market.

In October 2007 ICBC bought a 20 percent share of Standard Bank in South

Africa for $5.6 billion dollars. (“Trojan Dragons,” 2007) The deal was noteworthy in the

sense that it was one the biggest foreign direct investment transactions not only in

Africa’s banking sector, but in the continent’s entire economy.4 It was called a

“watershed,” with Standard Bank chief executive Jacko Maree stating, “It is the biggest

foreign investment by any Chinese company ever and it is the largest foreign direct

investment into South Africa since the end of apartheid. Its significance goes way beyond

the actual deal between the banks.” (Timewell, 2007) In recent years Africa has become

an economically important place for China, so there was no doubt that this consideration

was central in the decision to invest in Standard Bank. Standard Bank is a comparatively

smaller bank with ICBC in terms of market capitalization and net profit, but it has

extensive reach continentally and even globally, with branch operations in 18 African

countries and 20 countries outside of Africa. (Timewell, 2007; Kandell, 2010) With

4 This particular deal is considered exceptional because of the unique strategic nature of the purchase, and hence I spend more time discussing it in this section and elaborating on it in the subsequent section.

34

approval of the deal by regulators, it stood as one of the biggest banking partnerships in

Africa, comparable to the one between Britain-based Standard Chartered and Absa Group

(the Johannesburg-based arm of Barclays) in terms of extent of operations. (Timewell,

2007; Kandell, 2010) In the partnership, Standard Bank received financing from ICBC

for loans it made to borrowers working on infrastructure development projects. ICBC,

along with the Bank of China, China CITIC Bank Corporation, China Development

Bank, and ICBC (Macau), funded a one billion dollar loan for Standard Bank to maintain

liquidity and boost its balance sheet. (Timewell, 2007; Kandell, 2010) Standard Bank

also received capital from ICBC to refinance a copper mine in Zambia to the amount of

$400 million dollars and finance trade of the cocoa crop in Ghana, both projects that

likely would not have been possible without the financial backing of ICBC. (Timewell,

2007; Kandell, 2010) Both banks have partnered to provide loans for Chinese companies

in Africa working on petroleum-related and electric equipment manufacturing projects.

(Enrich, Dean, & Stevens, 2011) ICBC, since it now had a partnership with a well-

connected local entity, became more competitive in assisting Chinese enterprises win

bids for government-backed infrastructure and development projects. One example

involved a coal energy plant-building project in Botswana. It received several foreign

bids, including those from France, India, and Malaysia, but the $970 million dollar

contract was eventually granted to one of ICBC’s clients, China’s state-owned China

National Electric Equipment Corporation. (Enrich et al, 2011) Standard Bank has

operations in Botswana and had known about the project plans, due to consistent energy

35

shortages, for years. There are more plans to cooperate on financing infrastructure

projects, and there is little doubt that they will involve Chinese enterprises.

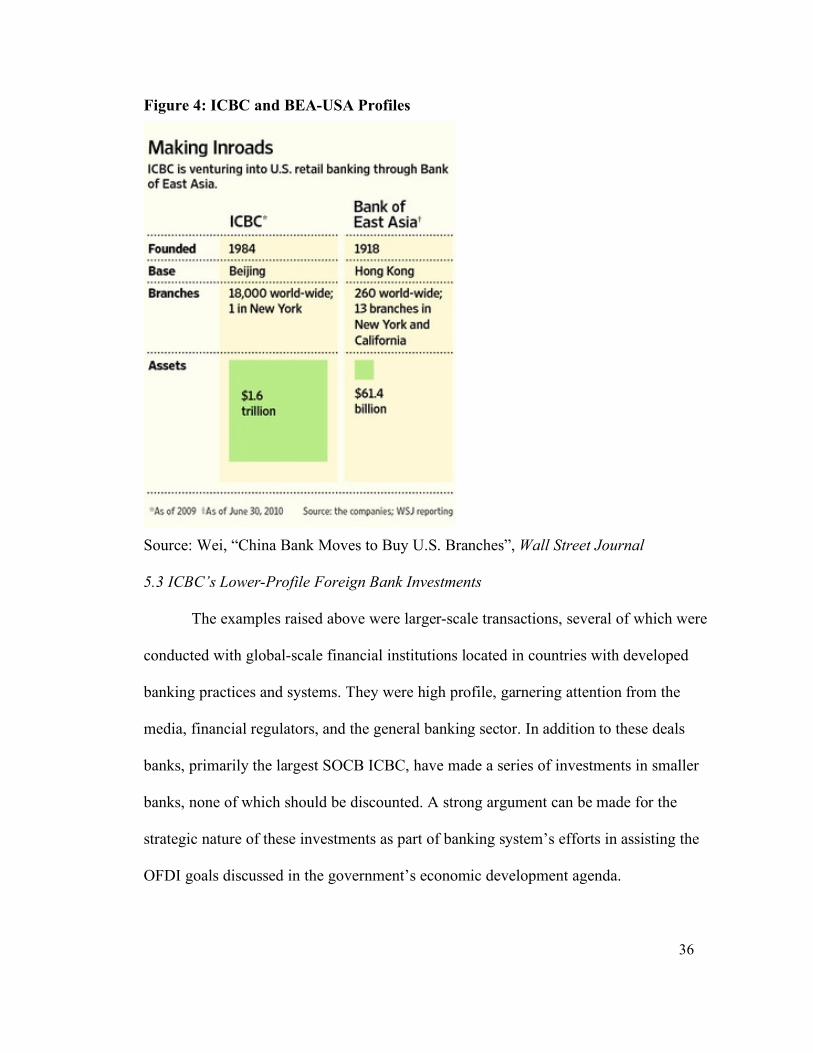

The most recent proposed purchase is that of ICBC and the Bank of East Asia,

USA (BEA-USA) in January 2011. BEA was founded in Hong Kong and is currently its

third largest commercial bank, with operations overseas in Canada, the United States, and

Britain. Under the proposed purchase, ICBC would buy eighty percent of BEA-USA’s

common stock shares for 140 million US dollars. (Reiss, Patrikis, Zou, Wall, &

Cuccinello, 2011; “Chinese Bank Acquisitions in the United States,” 2011) This is the

first purchase that, if approved by the Board of Governors of the Fed, the Committee on

Foreign Investment in the US (CFIUS), the China Regulatory Banking Commission

(CRBC), and the Hong Kong Monetary Authority, would make a Chinese SOCB a

controlling shareholder in a foreign bank, and quite non-coincidentally, an American-

based one. (Reiss et al, 2011; “Chinese Bank Acquisitions in the United States,” 2011)

The ICBC—BEA-USA deal is the latest in a flurry of overseas investments Chinese

financial institutions have been making in recent years in an effort to internationalize the

banking system, and the process does not show signs of slowing down.

36

Figure 4: ICBC and BEA-USA Profiles

Source: Wei, “China Bank Moves to Buy U.S. Branches”, Wall Street Journal 5.3 ICBC’s Lower-Profile Foreign Bank Investments

The examples raised above were larger-scale transactions, several of which were

conducted with global-scale financial institutions located in countries with developed

banking practices and systems. They were high profile, garnering attention from the

media, financial regulators, and the general banking sector. In addition to these deals

banks, primarily the largest SOCB ICBC, have made a series of investments in smaller

banks, none of which should be discounted. A strong argument can be made for the

strategic nature of these investments as part of banking system’s efforts in assisting the

OFDI goals discussed in the government’s economic development agenda.

37

ICBC has taken the lead on OFDI in the banking sector. In December 2006, it

bought 90 percent of Bank Halim Indonesia for $8.9 million dollars, a bank far smaller in

asset size than ICBC. (Timewell, 2007) It was the first overseas investment by one of

China’s state-owned commercial banks. An official ICBC press release noted, “It is the

first time that ICBC has taken over a foreign bank…and [the investment] should give the

bank experience to expand into international financial markets.” (“ICBC Says it Will Buy

Indonesian Bank,” 2007) In August 2007 ICBC bought 80 percent of Seng Heng Bank,

based in Macau, for $584 million dollars, and in June 2009 ICBC bought 70 percent of

Bank of East Asia Canada for $72 million dollars. (Luo, 2009; Timewell, 2007) ICBC

had the option of raising the stake to 80 percent a year after the transaction. (Alexander,

2009) Finally, in September 2009 ICBC came to an agreement with Thailand’s Bangkok

Bank Public Company Limited (BBL) to buy the entire 19.26 percent share of ACL Bank

Public Company Limited owned by BBL, valued at $106 million dollars. (“Industrial and

Commercial Bank of China to Buy Thailand’s ACL Bank ,” 2009) As of April 2010

ICBC completed its acquisition of ACL, Thailand’s smallest bank, purchasing a 97.24

percent share for $551 million dollars. (Jittapong, 2010)

Compared to ICBC’s investments in Standard Bank and Bank of East Asia USA,

these were lower-profile transactions due to the small size of the banks acquired, even as

they resulted in a majority holding. The ICBC-Bank Halim Indonesia deal was conducted

shortly after the former successfully listed on the Hong Kong and Shanghai stock

exchanges, arguably a concurrent strategic move made in an effort to raise ICBC’s profile

in the international banking system. This deal, and the acquisition of Thailand’s ACL

38

Bank, were approved easily and conducted with relatively little obstruction by regulators.

As to the aforementioned ICBC-BEA Canada deal, it later became apparent that it was a

precursory move, serving as a stepping-stone for ICBC to propose a majority share

purchase of BEA Canada’s American counterpart. (Wei, 2011) As ICBC Chairman Jiang

Jianqing stated, the investment in BEA Canada would “enable ICBC to establish its

banking business and customer base in Canada…provid[ing] a strong platform to further

expand…businesses across North America.” (Alexander, 2009)

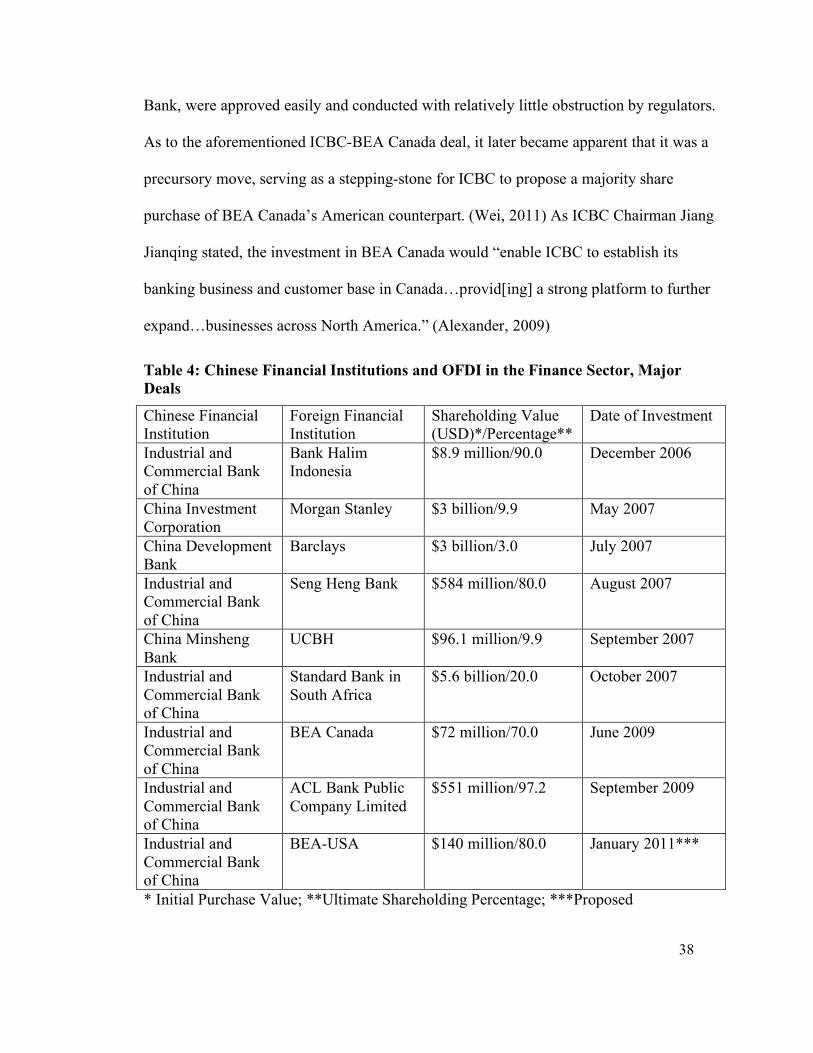

Table 4: Chinese Financial Institutions and OFDI in the Finance Sector, Major Deals

Chinese Financial Institution

Foreign Financial Institution

Shareholding Value (USD)*/Percentage**

Date of Investment

Industrial and Commercial Bank of China

Bank Halim Indonesia

$8.9 million/90.0 December 2006

China Investment Corporation

Morgan Stanley $3 billion/9.9 May 2007

China Development Bank

Barclays $3 billion/3.0 July 2007

Industrial and Commercial Bank of China

Seng Heng Bank $584 million/80.0 August 2007

China Minsheng Bank

UCBH $96.1 million/9.9 September 2007

Industrial and Commercial Bank of China

Standard Bank in South Africa

$5.6 billion/20.0 October 2007

Industrial and Commercial Bank of China

BEA Canada $72 million/70.0 June 2009

Industrial and Commercial Bank of China

ACL Bank Public Company Limited

$551 million/97.2 September 2009

Industrial and Commercial Bank of China

BEA-USA $140 million/80.0 January 2011***

* Initial Purchase Value; **Ultimate Shareholding Percentage; ***Proposed

39

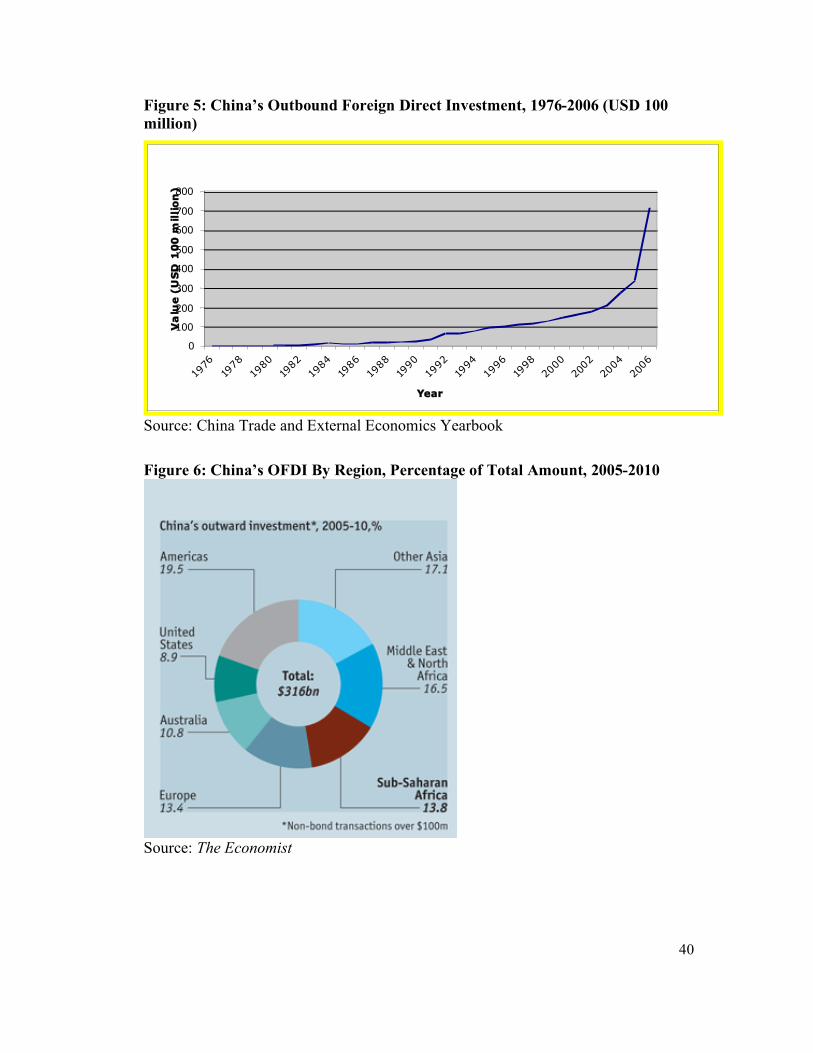

Like non-finance sector OFDI, the finance sector is going global. In light of the

central government’s focus on “rebalancing” the economy, OFDI will be important

means to achieve this goal.5 (“Fourth Plenary Session, 11th National People’s Congress,”

2011; Harris, 2011) In places like South Africa, Australia, and Canada, China is buying

rights to primary commodities and natural resources such as metals, coal, and timber. In

Latin American countries, China is investing in agricultural goods and minerals. In the

Middle East and Central Asia, China is investing in oil and natural gas. (Gao, 2009, p.

237-240; Wang, 2002, p. 196, 201; Brown, 2008, p. 148) Europe and the US have

received OFDI from China as well, in high-technology industries such as

telecommunications, renewable energy, biotechnology, and pharmaceuticals. (Child &

Rodrigues, 2005, p. 391; Rosen & Hannemann, “An American Open Door?”, p. 30) With

OFDI on an upward swing and becoming increasingly prominent in China’s national

economic development plans, one will expect finance sector OFDI to increase as well to

support this priority. The role of commercial banks as financiers becomes more important

than ever.

5 Cumulative OFDI in 2010 reached $220 billion dollars. In the Twelfth Five-Year Plan (2011-2015), reorienting the balance of payments became an additional motivation to invest abroad. The plan stated the need to continue “opening-up” to the global economy—not only by reorienting imports and exports in a more balanced manner within its trade profile, but also by sustaining the “going global” policy in increasing outbound investment to reach a level comparable with inward investment.

40

Figure 5: China’s Outbound Foreign Direct Investment, 1976-2006 (USD 100 million)

0

100

200

300

400

500

600

700

800

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Year

Va

lue

(U

SD

10

0 m

i lli

on

)

Source: China Trade and External Economics Yearbook Figure 6: China’s OFDI By Region, Percentage of Total Amount, 2005-2010

Source: The Economist

41

Chapter 6: The Link between Finance and Non-Finance Sector OFDI and Implications for Banking Reforms

Given the discussion of problems in the banking system, reluctance on behalf of

the government to enact reforms begs explanation. The answers can largely be found in

the underlying motivating factors driving the finance sector transactions described earlier

in the thesis. While some reasons are related to strengthening China’s banks and assisting

in the reform process—such as asset-seeking—they are indirect and marginal. At its very

core, the phenomenon of China’s finance sector ODFI can be traced back to the need to

support SOEs abroad. Finance sector OFDI that has occurred furthers the ultimate

objective of keeping the banking system as a linchpin of SOE financing. This priority

outweighs the preferences of policymakers to engage in reforms that would jeopardize

the relationship between lender and borrower.

6.1 Finance Sector OFDI Strategies and National Economic Development Goals 6.1.1 The Internalization Factor in Practice

The main reason Chinese banks are conducting investment abroad is

straightforward—they are following non-finance sector OFDI. All five SOCBs have

operations outside China, while joint-stock commercial banks have made similar

ventures. (China Banking Regulatory Commission, 2009) As of 2011, ICBC has

established branches in Malaysia, Abu Dhabi, Vietnam, Kazakhstan, across Europe, and

the US. BOC has branches in Australia, Brazil, South Africa, Vietnam, across Europe,

and the US. These are wholly owned subsidiaries not involving local firms. Many are

located in countries where there is already a substantial volume of investment or business

activity conducted by Chinese nationals, giving the host country an incentive to approve

42

the establishment of bank branches that will be responsible for financing Chinese

investment projects, especially in OFDI-heavy sectors such as manufacturing. The

establishment of branches overseas can be considered an act of internalization under the

eclectic paradigm. Chinese banks have decided to absorb the costs associated with:

partnering with a local firm, potential taxes or fees levied on foreign corporations doing

business in the host country, and overcoming foreignness and unfamiliarity with business

rules governing the host country, because directly serving clients in the host market is

expected to outweigh the transaction costs described. There is no impetus to build brand

recognition in this case because a majority of the clients served are already familiar with

the bank brand and services, and are more interested in having a convenient way to

repatriate profits back to China.

6.1.2 Beyond Wholly Owned Subsidiaries

Internalization via the establishment of wholly owned banking branches is one

way Chinese banks are supporting economic activity overseas. Overseas branches are

able to take deposits and provide an array of retail banking services to their clientele, but

they have yet to operate in conjunction with local banks to broaden their client base and

expand into commercial banking functions. Establishing wholly owned subsidiaries can

also be a difficult endeavor given strict rules governing the operations of foreign banks in