the role of relationship marketing as a tool for growth in ghanaian banking sector

TRANSCRIPT

THESIS PRESENTATION

EMMANUEL TETTEY

THE ROLE OF RELATIONSHIP MARKETING AS A TOOL FOR GROWTH IN THE GHANAIAN

BANKING SECTOR

Introduction• RM - establish, maintain, and enhance long term relationships with customers

• Building customer loyalty

• Satisfying the needs of customers at a profitable level

• Mixture of marketing, quality and customer service

• To retain customers for long term benefits

• Customers may switch loyalties if they perceive better benefits from a competitor.

• Shifting from transactional marketing to relationship marketing

Objective of Study• To determine the effectiveness of HFC Bank Ghana's marketing in gaining competitive advantage over its competitors.

• To know how complaints f customers are being treated by HFC bank Ghana.

• Determine the effectiveness of HFC Bank Ghana's marketing in gaining competitive advantage over its competitors.

• To know how complaints f customers are being treated by HFC bank Ghana.

Case Company• HFC formed on 07/05/1990 as a mortgage financing institution

• Issued with a Universal Banking License by Bank of Ghana on 17/11/2003 as a banking institution.

• Leading mortgage provider with over 30% share in the mortgage industry

• 26 fully networked branches as well 30 Automated Teller Machine (ATM) that operates in 8 regions.

• Vision: “To become a leading Universal Banking Institution in the West Africa sub-region, providing world – class financial service”

• Mission: “To create wealth and better life for our customers”

• Core Values: “Integrity, Professionalism, Efficiency, Honesty, Trust, Customer Focus, Team Work”

Methodology• General population was mainly the corporate customers

• quantitative form of research Well structured questionnaire

• Sample size of 100 customers

• primary and secondary data sources was used

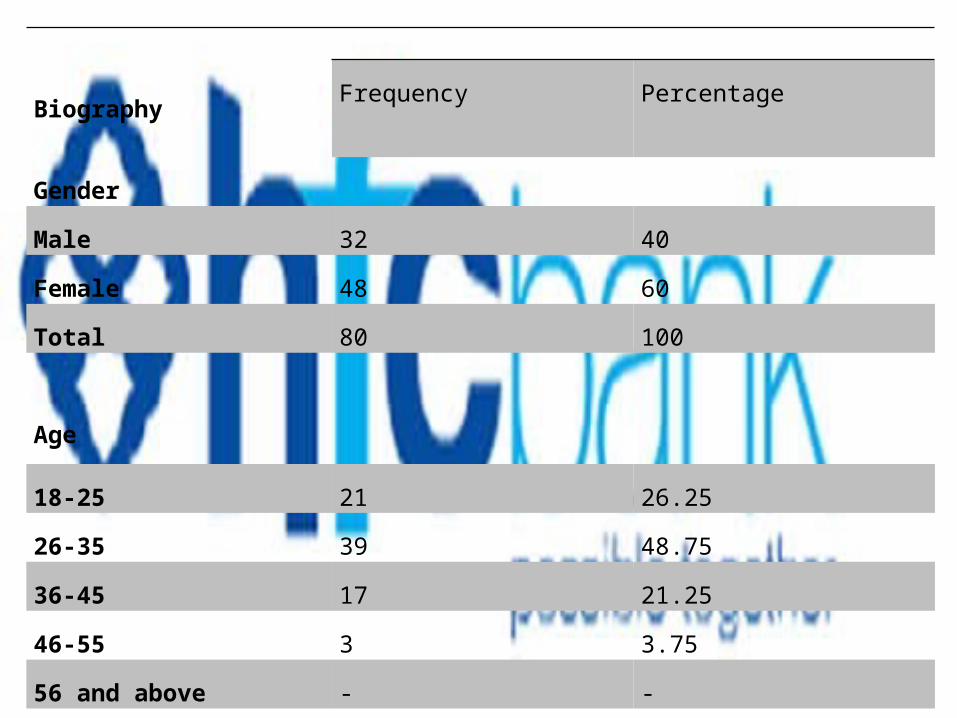

Biography Frequency Percentage

Gender

Male 32 40

Female 48 60

Total 80 100

Age

18-25 21 26.25

26-35 39 48.75

36-45 17 21.25

46-55 3 3.75

56 and above - -

Total 80 100

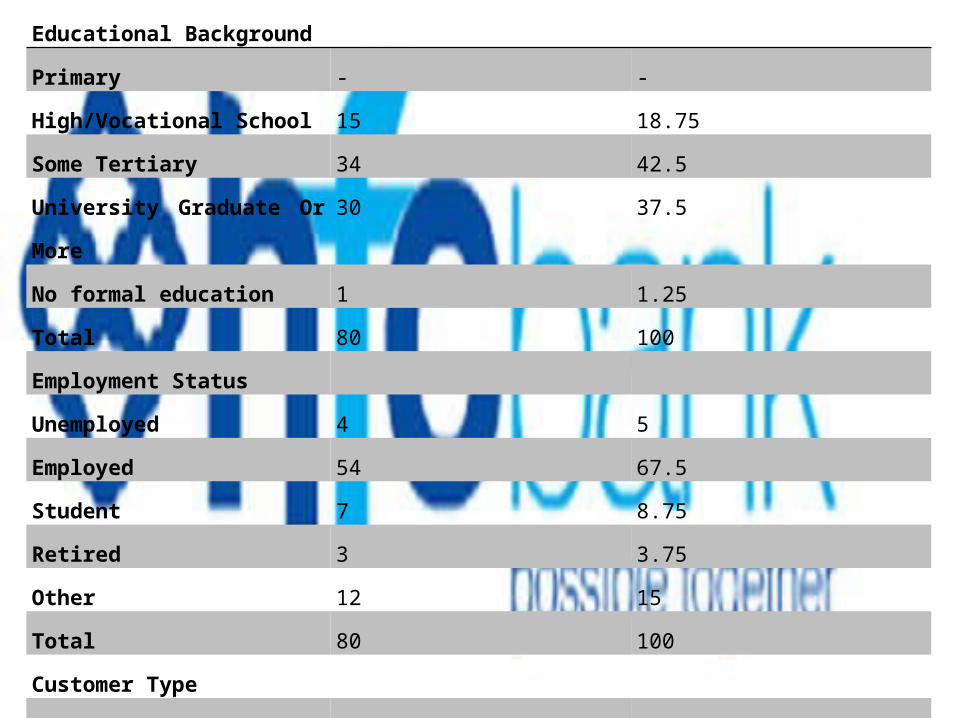

Educational Background

Primary - -

High/Vocational School 15 18.75

Some Tertiary 34 42.5

University Graduate Or

More

30 37.5

No formal education 1 1.25

Total 80 100

Employment Status

Unemployed 4 5

Employed 54 67.5

Student 7 8.75

Retired 3 3.75

Other 12 15

Total 80 100

Customer Type

Corporate 44 55

Individual 30 37.5

Sole proprietorship 6 7.5

Joint Account - -

Total 80 100

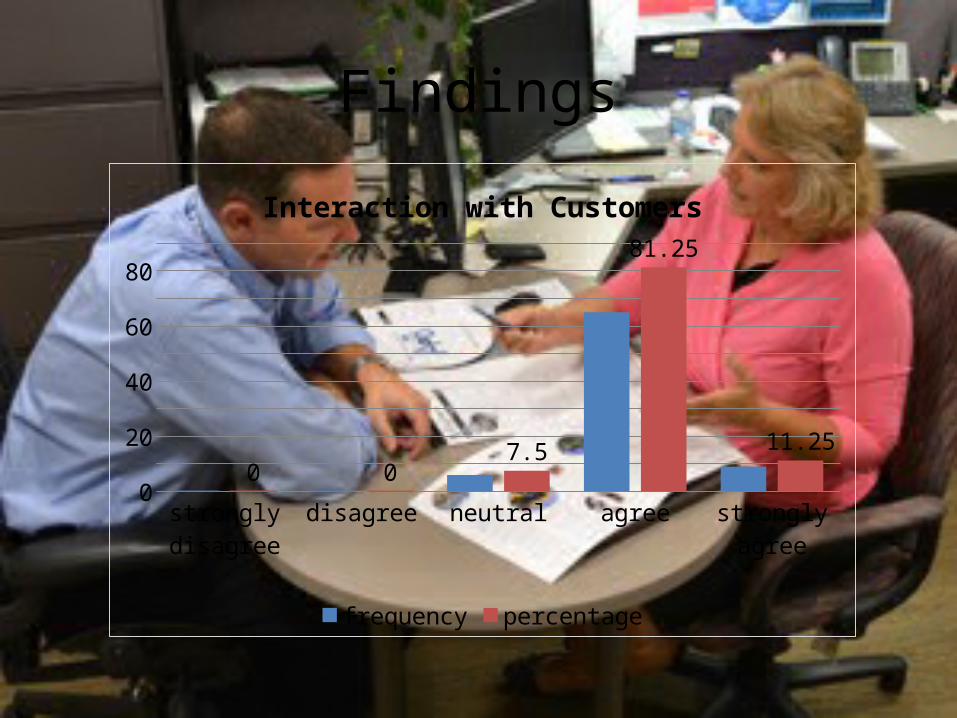

Findings

strongly disagree

disagree neutral agree strongly agree

0

20

40

60

80

0 07.5

81.25

11.25

Interaction with Customers

frequency percentage

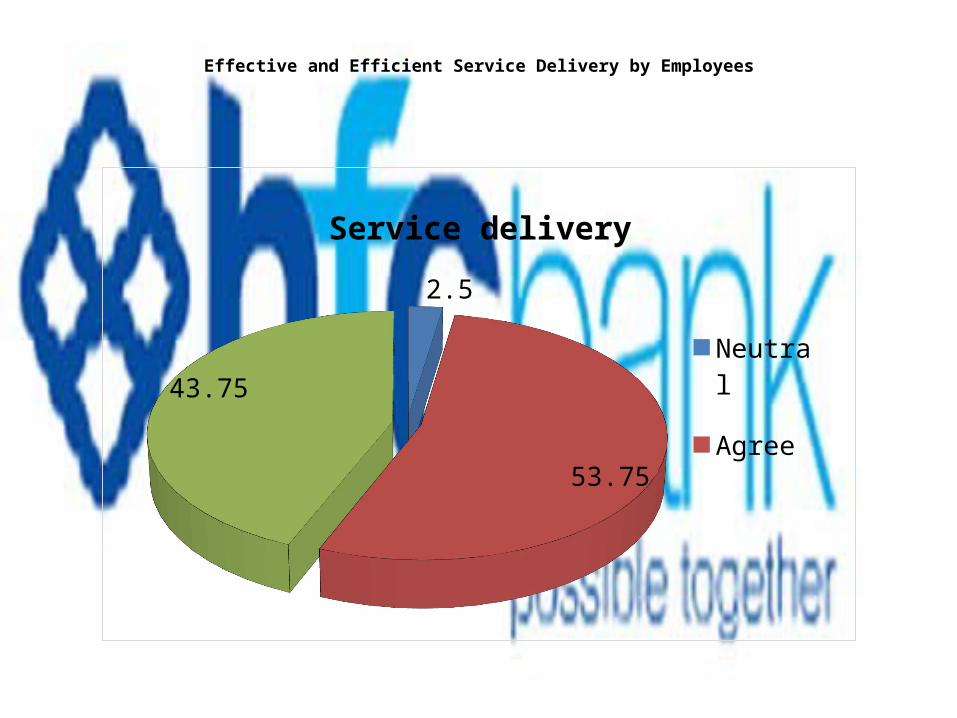

Effective and Efficient Service Delivery by Employees

2.5

53.75

43.75

Service delivery

Neutral

Agree

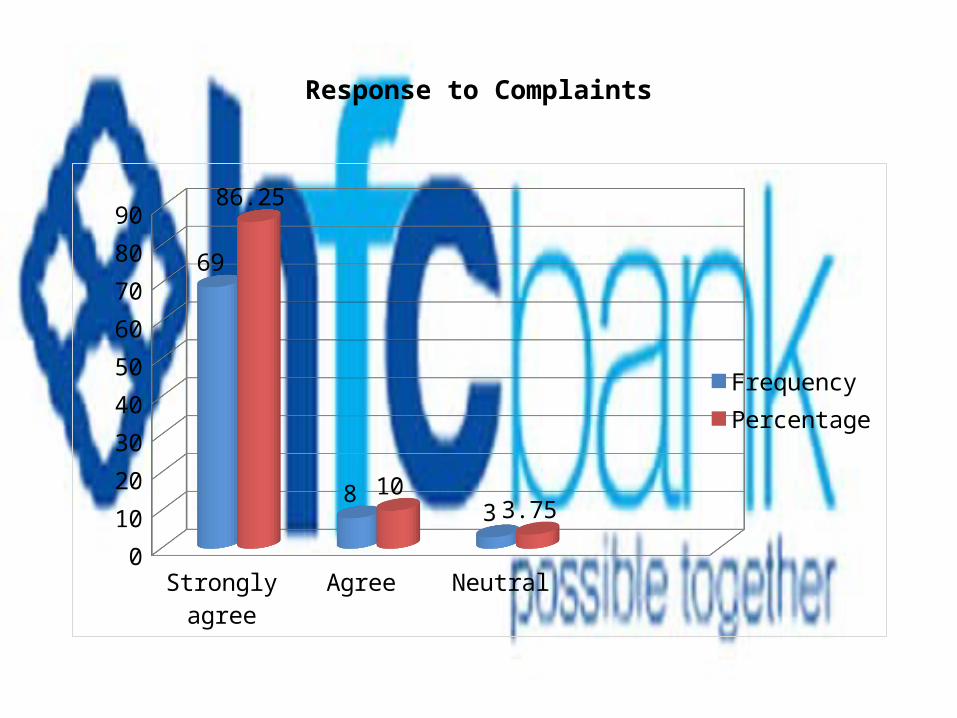

Response to Complaints

Strongly agree

Agree Neutral0102030405060708090

69

8 3

86.25

103.75

FrequencyPercentage

High security on Account

Strongly disagree

disagree

neutral

agree

Strongly agree

010203040

frequency

frequency

Customer level of Satisfaction

NeutralAgree

strongly agree

01020304050607080

418

58

5

22.5

72.5

frequencypercentage

Essential Factor considered in choosing this bank

010203040

12

29

1420

515

36.25

17.525

6.25

FrequencyPercentage

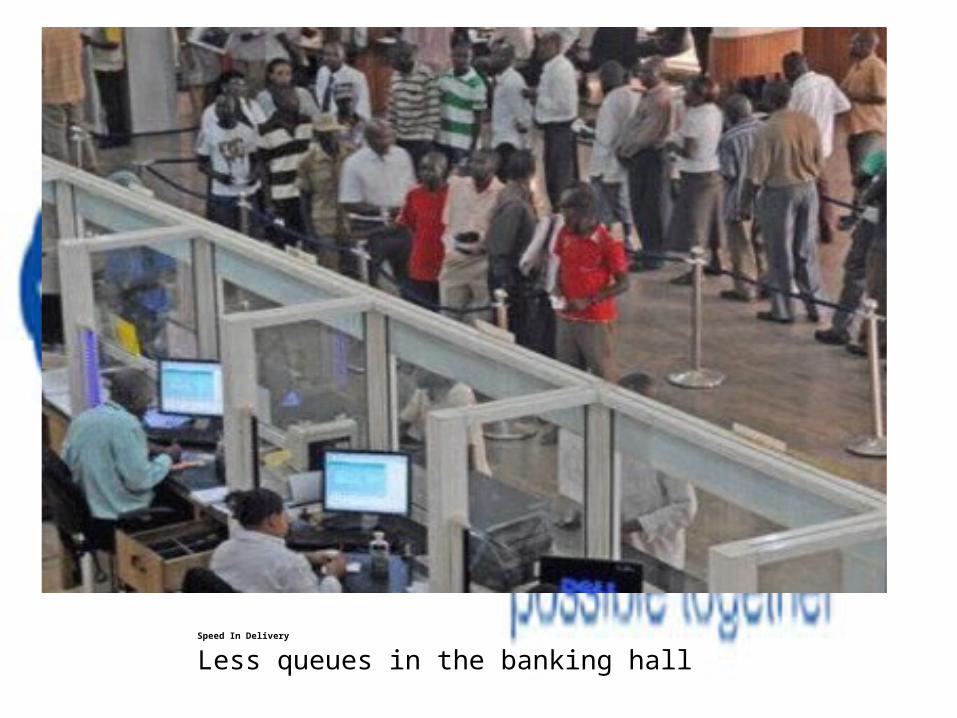

Speed In Delivery

Less queues in the banking hall

Problems Encountered by customers

delay in foreign

transaction51%

Breakdown of ATM30%

Bureaucracy in loan

processing18%

Problems Encountered

Summary• Loyal customers transacting business with them

• Reliable Bank

• Employees are friendly and deliver effective service

• Customers treated as number one asset of the bank

• The bank shows great commitment• • Majority of customers are staisfies with the bank offerings.

• Positive WOM.

Recommendation• Setting up a central complaints unit

• Outwit its competitors by managing customers effectively

• Improved IT

• Embark on more retention strategies

• Provide excellent services to its valued customers

• Train the best people with the best professional attitudes

THE ENDTHANK YOU KIITOS謝謝!Merci!cảm ơn bạnMed-ah-ceeAkpe Nami.