effect of internet banking service quality on customer satisfaction: evidence from ghanaian banking...

TRANSCRIPT

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 1

Abstract—The paper examines the influence of Internet Banking Service Quality (IBSQ) on

Customer Satisfaction (CS) in the Ghanaian banking industry. The study was a cross-sectional

survey that employed the use self-administered questionnaire to collect data from a sample of

200 respondents through personal contact. Through Structural Equation Modelling approach,

the findings indicatethat,of the five IBSQ dimensions, web designfactors

havesignificantlypositive influence on CS, explaining about 79.6% of CS with IBSQ. In spite of

the limitations of the study, the findings offer important theoretical and managerial implications.

The paper contributes to the literature in area of e-Service quality and customer satisfaction in

electronic banking.

Index Terms—banking industry, Customer satisfaction, Ghana, e-service quality, internet

banking, internet banking quality, service quality.

I. INTRODUCTION

Information and communications technologies (ICTs) have become an important tool that has

revolutionalised many areas of life including business and commerce. Information systems are now

used in business to bring in new products, service market opportunities and developing more

information system that is business oriented and supports management processes such as planning,

controlling and co-ordination [1]. One of the areas that ICTs have impacted over the last decade is the

banking industry. Most banks in developed and developing parts of the world are now offering internet

banking services with various levels of sophistication as a competitive strategy [2], [3]. Banking is one

of the services that are information intensive and an ideal centre for successful development of e-

commerce because it provides the opportunity to use the internet and e-commerce to facilitate quick

business transactions that results in customer satisfaction [4].

Banking started in Ghana in 1894 by the establishment of the Bank of British West Africa until

1957 [5]. According to the Ghana Banking Survey (GBS) currently there are 25 banks licensed to

operate in Ghana [6], two of which are the banks under study. In Ghana, the deployment of ICTs in the

banking industry has grown from one level of complexity to another since the government of Ghana

established an ICT framework to facilitate the development of ICT in all sectors of the economy

(ICT4AD, 2003). Aside the ICT4AD project, the government in collaboration with the private sector

has initiated the e-zwich electronic payment platform in 2008 to facilitate business, competition and

better delivery of services in the economy [6]. Currently, some banks like United Bank for Africa,

Merchant Bank Ghana, ECOBANK Ghana, Barclays Bank Ghana, among others have adopted internet

banking platform and a wide range of electronic products and transactions, some of which allow

customers to receive their monthly bank statements via e-mail, online checking of accounts balance,

online transfer of funds, the use of electronic cash systems, and for communicating to customers on

regarding bank statements, other banks use internet banking services to allow business customers to

make inter-bank financial transactions and information sharing [7]-[9].

Competition in the Ghanaian banking industry is becoming keener as the more and more banking

players enter the market. In response, many financial institutions are directing their strategies towards

increasing customer satisfaction and loyalty through improved service quality [7]-[9]. Therefore,it

becomes important for managementof the banks to ensure that they deliver service quality that drives

Effect of Internet Banking Service Quality on Customer Satisfaction: Evidence from

Ghanaian Banking Industry

Simon Gyasi Nimako, Nana Kwame Gyamfi, AbdilMumuni Moro Wandaogou.

Department of Management Studies Education,

University of Education, Winneba, Kumasi – Ghana, West Africa

E-mail: [email protected]

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 2

customer satisfaction and loyalty [10]-[13]. Firms that provide superior service quality as measured by

customer satisfaction also experience higher economic returns than competitors that are not so service-

oriented [12]-[14].

Existing literature has focused on e-banking in Asian countries including Malaysia [15], Thailand

[16] and India [17]. Few research that have contributed knowledge on Sub-Saharan Africa include a

study on regulating Internet banking in Nigeria [18], on the determinants of Internet and cell-phone

banking adoption in South Africa [19], an initial exploration in Ghana [8], [9]. Sub-Saharan Africa is

a region in dire need of development and probably one with the greatest need of research attention in

e-banking. In view of the many benefits that could accrue to Ghana from successful implementation of

electronic business solutions, a study that focuses on such an under-researched part of the world would

be very useful to practitioners and scholars. Very little is known regarding the relationship between

internet banking service quality and customer satisfaction in the banking industry in Ghana. Therefore,

more empirical studies in this area are needed to inform policy direction and further theoretical

discourse regarding internet banking effects in developing country Sub-Sahara Africa context. In view

of this, the main purpose of this paper is to examine the influence of internet banking service quality

(IBSQ) on customer satisfaction (CS) in the Ghanaian banking industry (GBI).

II. LITERATURE REVIEW AND HYPOTHESES

A. Service Quality

Service quality (SQ) has received a great deal of attention in the marketing literature from both

scholars and practitioners in business. Many studies have established that SQ is a crucial driver of

satisfaction [11]-[13], profitability [10], and a key competitive advantage for modern business firms

[11], [12], [20]. Indeed, SQ is not just a corporate offering, but a competitive weapon which is

necessary for corporate profitability and survival [14]. SQ has been defined as the difference between

customer expectations for service performance prior to service encounter and their perception of the

service received [21]. Reference[22] defined SQ as the subjective comparison that customers make

between the quality of service that they wish to receive and what they actually get.

Regarding the dimensions and aspects of SQ of firms, some past studies such as [11], [23] have

established different conceptualizations of the SQconstruct. This has resulted in different instruments

for measuring SQ. Reference[11] maintains that SQ has both process and outcome dimensions that are

critical to service context, which have been verified in some previous studies [23], [24]. Reference [23]

develop the dimensions of SQ in their GAP and Extended GAP analyses based on which they

developed the popular SERVQUAL model. The SERVQUAL model has been modified in many

previous studies to suit a particular context. This has been noted by [23, p. 31] that the SERVQUAL

instrument could be “adapted or supplemented to fit the characteristics or specific research needs of a

particular organisation”. However, due to the differences between traditional service and electronic

service, obviously SERVQUAL scale is not suitable for measuring SQ in electronic or internet

environment due to the absence of staff, absence of traditional tangible elements, and self-service of

customers [25]. It has been argued in many past studies that new scales need to be developed for e-

service quality [25], [26].

B. E-service Quality

E-service has been an interesting and important area to scholars and practitioners alike. E-service

has been defined as a web-based service or an interactive service that is delivered on the internet [3].

Reference[27]conceptualises e-service as deeds, efforts, or performances whose delivery is mediated

by information technology. Generally, it can be defined as an interactive content-centered and internet-

based customer service that is driven by customers and integrated with the support of technologies and

systems offered by service providers, which aim at strengthening the customer-provider relationship.

Given the technology quality dimensions of e-service quality that are different from the traditional

service context, e-service quality has been regarded as having the potential to not only deliver strategic

benefits but also to enhance operational efficiency and profitability [3].

A review of existing literature indicates that many past studies have found different dimensions for

e-service quality that are useful for different research contexts [25], [26]. Reference[28] found the

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 3

following e-service quality aspects: site design, reliability, delivery, ease of use, enjoyment and control

in the context of E-service. It has been found by [29] that ease of use, aesthetic design, processing

speed, and security in online retailing are essential e-service qualities. Kim et al. [30] identified nine e-

service quality items, being: efficiency, fulfillment, system availability, privacy, responsiveness,

compensation, contact, information and graphic style in online retailing.

Recent studies show a combination of traditional SERVQUAL and the web-interface quality

dimensions. Reference[25] proposed eight dimensions of e-service quality, which are: website design,

reliability, responsiveness, security, fulfillment, personalization, information and empathy. Past studies

on determinants of e-service quality adoption also indicate that e-service experience has impacted on

customers’ perceptions and evaluation of e-service quality [31]. Reference [32] opine that the

perceived web site quality and customer satisfaction is relevant to customers’ loyalty to the web site. In

view of the above, e-service quality dimensions would be explored in the internet or e-banking context.

C. Internet Banking Service Quality

Internet banking could be conceptualized within the context of electronic banking. Though it has been

variously defined, according to [33], electronic banking is the delivery of banks’ information and

services by banks to customers via different delivery platforms that can be used with different terminal

devices such as personal computer and mobile phone with browser or desktop software, telephone or

digital television. Reference [34, p. 2]maintain that internet banking is situation where “customers can

access their bank account via the internet using a PC or mobile phone and web-browser.” Internet

banking has received considerable interest from scholars and practitioners as a result of the value and

usefulness customers derive from internet banking, as well as the practical value of implications it

offers marketers. A bank could enhance its reputation, customer retention, get new customers and

increase financial performance by delivering superior quality internet banking services to its valued

customers [35] - [37].

Reference [38] in an explorative study in Irish online banking context found ten dimensions of

online retail banking, which are: web usability, security, information quality, access, trust, reliability,

flexibility, responsiveness, self-recovery, and personalization/customization. In the empirical work of

Ho and Lin [26] in an emerging economy of Taiwan Internet banking sector, they developed and

validated a five dimension internet banking service quality with 17-item measurement scale for

measuring the service quality in internet banking. The five emerged dimensions were based on e-

service quality model of [32], namely: web design, customer service, assurance, preferential treatment

and information provision.

First is Web design: This dimension covers the design of the web site and includes items like web

content layout, content updating, navigability, and user-friendliness. These are consistent with findings

of previous studies [39], [37], [40].

Second is Customer Service: Customer service has been recognized as an important element for

enhancing service quality in online shopping and banking [3]. Elements in customer service dimension

have been noted in many previous studies [41], [42]. This dimension has to do with service reliability,

customer sensitivity, personalized service, and fast response to complaints that have been described as

responsiveness to customer needs and complaints [23].

Third is Assurance: Many previous studies have demonstrated that assurance is one of the critical

elements of online banking service quality [29], [42]. The assurance dimension describes impressions

by the service providers that convey a sense of security and credibility [23]. Security and privacy are

related items that affect the confidence to adopt online banking services [43].

Fourth is Preferential treatment: This is related to the added value of using internet banking

services. Where customers perceive that the incentive of online banking is attractive then they would

be more willing to use internet banking.

Fifth is Information provision: Information provision has become one of the key elements of

online service quality as customer would need the right information that enables them complete online

banking transactions successfully [25].

In this study, internet banking service quality is, thus, conceptualized as a construct with five

dimensions that were identified in the empirical work of [25].

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 4

D. Customer Satisfaction

Customer satisfaction (CS) has become a major area of marketing that has received considerable

publications from practitioners and scholars in the last two decades. CS has been recognized as an

important element that drives customer retention, loyalty and post-purchase behavior of customers[10],

[20], [44]. Many studies confirm that the measurement of CS regarding the service quality of firms is a

necessary means by which organizations delve into the minds of its customers for useful feedback that

could form the basis for effective marketing strategy [14]. Since firms exist to satisfy customers by

meeting their requirements, it is crucial for banks that offer internet banking services to periodically

and consistently measure the satisfaction of their customers. As the IBSQ delivery may influence CS it

becomes important to study and understand which IBSQ dimensions are having significant influence

on CS so as to inform management strategy.

Customer satisfaction has been defined in different context by different authors. According to

reference [20, p.144] “Satisfaction is a person’s feeling of pleasure or disappointment resulting from

comparing a product’s performance (outcome) in relation to his or her expectation.” While some

authors perceive satisfaction as a cumulative, others view it as transactional. On the one hand from a

transactional-specific perspective, CS is based on a one time, specific post-purchase evaluative

judgement of a service encounter [45]. On the other hand, in the cumulative CS perspective, CS is

conceptualised as an overall customer evaluation of a product or service based on purchase and

consumption experiences over a time period[46]. It is argued that since cumulative satisfaction is based

on a series of purchase and consumption experiences, it is more useful and reliable as a diagnostic and

predictive tool than the transaction perspective that is based on a one-time purchase and consumption

experience. Therefore, in this study, customer satisfaction is measured from the last twelve months of

using internet banking facilities of the two banks, so CS is conceptualised as cumulative and adopts the

definition of satisfaction given by [47] as operational definition in this paper: CS is “The process of

customer overall subjective evaluation of the product/service quality against his/her expectation or

desires over a time period.”

E. Influence of IBSQ on Customer Satisfaction

The fact that service quality of a firm has a positive influence on satisfaction of customers is well

documented in the literature [11]-[14], [47]. Internet banking quality has also been found to be a driver

of customer satisfaction in different service contexts [48], [49]. Improvement in the internet service

quality could be made if customers’ satisfaction and perception of it and how IBSQ affects CS can be

measured in the first place. Effective measurement the impact of IBSQ on customer satisfaction could

be very useful in the allocation of resources based on critical factors and in the segmentation of

customers in meeting their needs and wants [11]-[14]. However, it is a documented fact in the

literature that different service context could induce unique and critical electronic service quality

variables useful to the service context. As a result, current research keeps exploring the impact of

IBSQ in different countries and industries. Therefore, this paper examines IBSQ and how it is related

to customer satisfaction in a Sub-Sahara Africa country context for theoretical and managerial

implications.

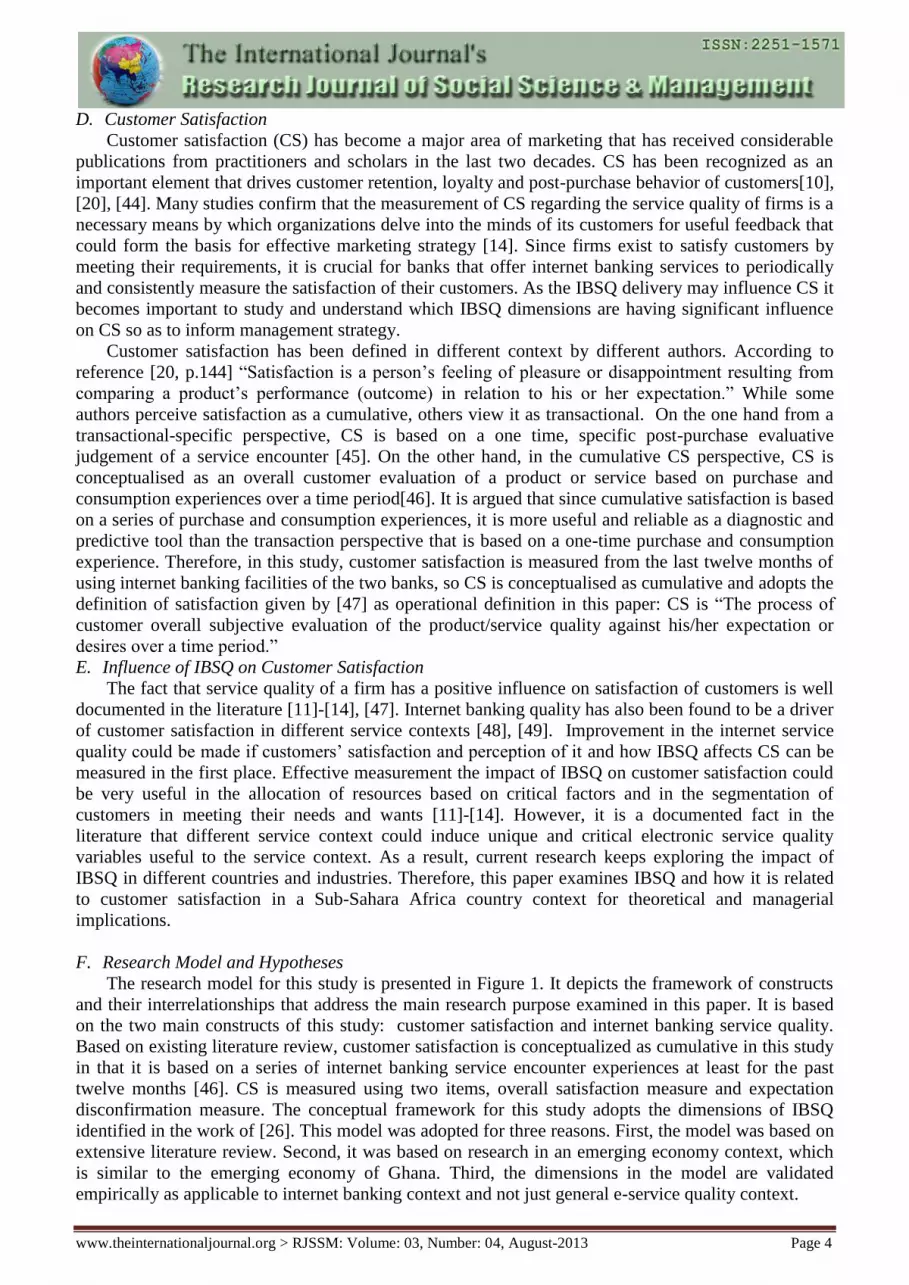

F. Research Model and Hypotheses

The research model for this study is presented in Figure 1. It depicts the framework of constructs

and their interrelationships that address the main research purpose examined in this paper. It is based

on the two main constructs of this study: customer satisfaction and internet banking service quality.

Based on existing literature review, customer satisfaction is conceptualized as cumulative in this study

in that it is based on a series of internet banking service encounter experiences at least for the past

twelve months [46]. CS is measured using two items, overall satisfaction measure and expectation

disconfirmation measure. The conceptual framework for this study adopts the dimensions of IBSQ

identified in the work of [26]. This model was adopted for three reasons. First, the model was based on

extensive literature review. Second, it was based on research in an emerging economy context, which

is similar to the emerging economy of Ghana. Third, the dimensions in the model are validated

empirically as applicable to internet banking context and not just general e-service quality context.

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 5

The study, therefore, sought to examine the extent to which these IBSQ items influence CS in the

context of banking industry in a developing country, Ghana. These IBSQ dimensions are Web design,

Customer service, Assurance, Preferential treatment and Information provision [26]. Therefore, based

on the literature reviewed, we propose that IBSQ dimensions will have significantly positive influence

on customer satisfaction, and specifically hypothesize that:

H1: Web design will have positive influence on customer satisfaction.

H2: Customer service will have significantly positive effect on customer satisfaction

H3: Assurance will have significantly positive effect on customer satisfaction

H4: Preferential treatment will have significantly positive effect on customer satisfaction

H5: Information provision will have significantly positive effect on customer satisfaction

Fig. 1 Research Model. It depicts the hypothesized relationships between IBSQ and satisfaction that

will be tested.

III. METHODOLOGY

A. Population and dataset

The target population consists of internet banking customers of Ghana Commercial Bank Ltd.

(GCB) and Merchant Bank Ghana Limited (MBG) who have used internet banking services for at least

the past twelve months.Originally, the main two banks were chosen for a comparative study as a result

of their unique differences in operational focus with similar internet banking platform.. While GCB is

mainly into tradition banking products (e.g. savings/current account) with little investment banking

service, MBG is typically into investment banking products (e.g. Funds/Portfolio Management, Money

Market Operations, Investor Search & Joint Venture Arrangement) as well as other specialist services

(e.g. Registrar Services, and Corporate Finance & Advisory Services). As a result of the richness of the

dataset, the present paper utilizes the same dataset to study how consumer evaluation of IBSQ affects

their satisfaction using structural equation modelling approach for both managerial and theoretical

implications.

B. Sampling

The dataset involved 200 conveniently sampled respondents, 100 from each sub-group. In selecting

the 200 respondents, a purposive sampling method was used to consciously select customers who meet

the criteria of having used internet banking services for the past twelve months.

C. Data Collection Instrument

A self-administered structured questionnaires was developed based on the literature reviewed to gain

insight into customers’ satisfaction with internet banking service quality in GCB and MBG. The self-

administered questionnaire contained three sections. Section one contained bio data of respondents –

gender, age, education, income and marital status. Section two focused on CS and section three

contained mainly five dimensions with 17 items for internet banking service quality dimensions

developed by Ho and Lin (2010). Overall satisfaction with the internet banking service quality was

measured by asking respondents to rate their satisfaction with IBSQ using a five-point satisfaction

scale and five-point a disconfirmation scale: Much worse than expected (1), worse than expected

Web design

Customer service

Assurance

Preferential treatment

Satisf-

action

Information provision

H1

H2

H3

H5

H4

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 6

(2),equal to expectation (3), better than expected (4) and much better than expected (5). In all, (17)

items asked about satisfaction with five dimensions of internet banking service quality adapted from

[26], two items related to overall CS with internet banking service quality, and five (5) items related to

the respondents characteristics. To assess the initial measurement scale reliability, all items in the

model are derived from the literature for strong construct validity, and from Table 1, the Cronbach

alpha reliability indicate values greater than the recommended 0.70 [50], implying acceptable level of

reliability for each construct, except Assurance, which was 0.661 that is close to 0.70. Therefore, the

items in the measurement scale are considered to possess high-internal consistency and reliability.

IV. DATA ANALYSIS

A. Data Analysis Methods

Data were analysed using SPSS 16.0 for windows. Data was analysed using SPSS version 16.0 and

Amos version 18.0 to perform Confirmatory Factor Analysis (CFA) and Structural Equation

Modelling (SEM) to test the hypothesized relationships among the constructs in proposed model

(Figure 1). SEM approach involves several methods such as covariance structure analysis, latent

variable analysis, confirmatory factor analysis, path analysis and linear structural relations analysis,

and can estimate the interdependent, multiple regression equation simultaneously among different

constructs [51]. In SEM, first the reliability and validity of the constructs are assessed, followed by

assessment of model fitness and then the path co-efficients of the hypothesized relationships.

B. Respondents’ Characteristics

The study involved respondents with varied background characteristics.In terms of gender, 51.8% of

the respondents were males and 48.2% were females. 12.9% of the respondents were below 25 years

and 38.1% were between 25 and 35 years, and 30.2% between 36 and 45 years respectively, while

16.5% and 2.2% were between 46 and 55 years and 56 years and above respectively. This implies that

majority of them were in the economically active population (25 – 45 years). All respondents were

educated with majority of them, 79.1% having tertiary education, while 7.9% had Senior High School

(SHS) and 12.9% had post-SHS education. In terms of monthly income, few of them, 2.9% earned

below GH¢100, 33.1% earned between GH¢101 to ¢500, while 27.3% and 18.7% earned between

GH¢501 to GH¢1000 and GH¢1001 – 1500 respectively. 18% of them earned above GH¢1500. 64.7%

of the respondents were married, 31.7% were single and 3.6% had other marital status. Finally, 55% of

the respondents belonged to GCB while the rest 44.6 belonged to MBG.

C. Reliability

Reliability refers to the extent to which a measuring instrument yields consistent results under

similar conditions [51]. It is judged by strong theoretical basis for all construct indicators, high factor

loadings greater than or equal to 0.5 and high composite reliability (CR) value greater than or equal to

0.7 [51]. As mentioned earlier, all items in the model are derived from the literature, construct item

reliability values are shown by the factor loadings (FL) presented in Table 2. Two items, one each of

Customer Service and Assurance dimensions had FL lower than 0.5, so they were removed. The rest of

the items as indicated in Table 2have high factor loading above 0.05, implying that the individual

items explain well the variances of the construct they represent. After the refinement of scale,from

Table 2, the Cronbach alphas indicate values greater than 0.70 for each construct, implying acceptable

level of reliability for each construct.

D. Construct Validity

Construct validity are assessed through convergent validity and discriminant validity [51].

Convergent validity could be assessed through item reliability, composite reliability, and the average

variance extracted (AVE) [52]. As already demonstrated for item reliability in Table 2, the factor

loadings of items to their respective constructs are strong providing evidence to support the convergent

validity of the items measured [51], [52]. The composite reliability, which is a measure of internal

consistency comparable to coefficient alpha [52], is above 0.70, implying acceptable level of reliability

for each of constructs. Finally, convergent validity is judged to be adequate when AVE equals or

exceeds 0.50. As shown in Table 3, all the AVE values in the diagonal are greater than 0.5 and the

composite reliability (CR) are all above the recommended 0.70. Therefore, taken together, the

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 7

evidence from the high composite reliability values, high factor loadings, combined with high AVE

estimates provide strong evidence in support of convergent validity.

E. Discriminant Validity

Discriminant validity refers to the extent to which the measure of a construct does not correlate with

measures of other constructs, and thus measures the extent to which constructs are different. At the

construct level, discriminant validity is considered adequate when the variance shared between a

construct and any other constructs in the model (covariance) is less than the variance which that

construct shares with its measures (AVE) [51]. As indicated in Table 3, the AVE estimates in the

diagonal are greater than the covariance below the diagonal (inter-construct correlations), therefore,

discriminant validity appears satisfactory at the construct level in the case of all constructs. This

indicates that each construct shared more variance with its items than it does with other constructs.

Since the results show good discriminant validity for the constructs, the constructs in the proposed

research model are deemed to be adequate.

F. Model Goodness-of-fit

In using SEM, the structural model is expected to show a good model fit index before proceeding to

examine the psychometric properties of the model. The usual method is the use of the chi-square

method or the ratio of the chi-square to its degree of freedom, with a value less than 3 indicating

acceptable fit [51], [53]. However, due to the fact that the chi-square of the default model could be

affected by large sample size greater than 250, many researchers recommend a combination of several

fitness indices for judging fitness of a structural model [51]. Several benchmarks for good-fit indices

have been suggested by many scholars [51], [53] as shown in Table 4. Reference [51] advise that to

provide strong evidence of good model fit, a combination of at least one absolute goodness-of-fit

measure, one absolute badness-of-fit index, one incremental fit measure and one comparative fit index

should be used.

In this study, as shown in Table 4, all the fit-indices are either very close to or better than their

corresponding recommended values. Though the Chi-square to the degree of freedom (CMIN) shows a

significant value (p = 0.000), the rest of the fit indices appear satisfactory: GFI= 0.886, AGF = 0.842,

RMSR = 0.045, RMSEA = 0.076, NFI = 0.931, CFI = 0.952, PGF = 0.637. Therefore, there is good fit

for the model. Thus, we proceed to examine the regression co-efficients for the estimated structural

model.

TABLE 1

INITIAL CRONBACH ALPHA RELIABILITY STATISTICS

Code Item Alpha

Web design

WD1 Easy completion of online transactions.

0.880 WD2 Easy logging on online portal.

WD3 Easy understanding which button to be clicked for the next step.

WD4 Helping customer to complete a transaction quickly.

Customer service

CUS1 Sufficient and real time financial information provided by the internet

banking portal site.

0.870 CUS2 Validity of the hyperlinks on the bank's portal.

CUS3 Quickness of the Web page on bank's portal site loading.

CUS4 Banking portal to perform service correctly at the first time.

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 8

CUS5 Prompt reception of responses to customer request.

CUS6 Internet banking system’s ability to guide customer to resolve problems

Assurance

AS1 Reliability and credibility of transactions on the banking portal.

0.661 AS2 Protection/security of customer transaction data...

AS3 Feeling of relief of customer to transact on internet banking

Preferential treatment

PT1 Offering preferentially lower fees/ rates and charges 0.860

PT2 Reasonability of the transaction fee for this banking portal site.

Information provision

IP1 Complete and sufficiency of the information… 0.819

IP2 Accuracy of the online transaction process of the bank.

Table 1 shows the measurement constructs, their indicators and their respective Cronbachapha

reliability values.

TABLE 2

FACTOR LOADINGS, RELIABILITY AND DESCRIPTIVES

Items FL α CR MEAN SD

CS 0.981 0.991

Item 1 0.992 3.09 1.253

Item 2 0.973 3.37 1.261

WD

Item 1 0.822 0.880 0.897 3.31 0.74

Item 2 0.780 3.20 0.76

Item 3 0.800 3.27 0.77

Item 4 0.809 3.15 0.75

CUS 0.852 0.859

Item 1 0.801 3.26 0.78

Item 2 0.648 3.18 0.62

Item 3 0.620 2.36 0.62

Item 4 0.819 0.898 3.14 0.79

Item 5 0.819 2.22 1.09

AS 0.792 0.900

Item 1 0.761 3.41 0.86

Item 2 0.863 3.34 0.79

PT

Item 1 0.934 0.860 0.942 2.62 0.90

Item 2 0.844 2.12 1.22

IP 0.819 0.915

Item 1 0.850 3.5 0.74

Item 2 0.825 3.89 0.86

Note: FL –Factor Loading; α–Cronbach alpha;CR – Composite reliability; SD –Standard deviation;

X – Means;

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 9

TABLE 3

AVE AND INTERCONSTRUCT CORRELATIONS

Const. CS WD CUS AS PT IP

CS 0.731

WD 0.365 0.601

CUS 0.451 0.412 0.814

AS 0.320 0.281 0.385 0.603

PT 0.527 0.417 0.826 0.394 0.883

IP 0.291 0.365 0.249 0.270 0.279 0.631

Note: The covariance are below the diagonal, AVE estimates are in diagonal;

TABLE 4

MODEL GOODNESS-OF-FIT

Goodness-of-fit Indices, Bench-mark value

Absolute goodness of fit

Chi-square (CMIN) P >0.05 0.000

Chi-square/degree of freedom ≤ 3 2.240

Goodness-of-fit Index (GFI) ≥ 0.90 0.886

Adjusted Goodness-of-fit (AGF) ≥ 0.80 0.842

Absolute badness of fit

Root Mean Square Residual (RMSR) ≤ 0.1 0.045

Root mean Square Error of Approximation (RMSEA) ≤ 0.08 0.076

Incremental fit measure

Normed Fit Index (NFI) ≥0.90 0.931

Comparative Fit Index (CFI) ≥ 0.90 0.952

Parsimony fit measure

Parsimony Goodness-of-Fit (PGF) ≥ 0.50 0.637

G. Assessing Hypothesized Relationships

Table 5 and Figure 2 provide a summary of the results for testing the hypotheses and analysing the

path co-efficients respectively.They show that all the hypotheses were not supported by the data,

except one. Specifically, it indicates that Web design (WD) factors significantly influence CS (β =

0.796, p < 0.05), supporting hypothesis H1. Satisfaction is not influenced by the following dimensions,

given a 0.05 significant value: Customer service (β = -0.558, p = 0.395), Assurance dimension (β =

0.265, p = 0.179), Preferential treatment (β = 0.490, p = 0.208), and Information provision (β = 0.004,

p = 0.971). Thus,no support was found for hypotheses H2, H3 and H4 and H5 respectively.

Moreover, the results indicate that Web design factors influence CS by 79.6% in GBI context. The

square multiple correlation (R-square) also indicates that, generally, the proposed model helps predict

CS by 74.1% (R2 = 0.741). Thus, 74.1% of the variances in CS could be explained by the proposed

model in the research context.

TABLE 5

RESULTS FOR HYPOTHESIS TESTING

Hypothesized Path

Std.β S.E. C.R. p-value

Rk

H1 CS <---WD .796 .337 2.875 .004* S

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 10

H2 CS<--- CUS -.558 .590 -.850 .395 NS

H3 CS<--- AS .265 .239 1.344 .179 NS

H4 CS<--- PT .490 .249 1.259 .208 NS

H5 CS<--- IP .004 .123 .036 .971 NS

Notes: *Significant at 0.05, Std.β = Standardised regression co-efficient; S.E. = Standard error, P-

value = significance of co-efficients are Maximum Likelihood Estimates, C.R.- Critical Ratio, RK –

Remarks, S-supported, NS – Not Supported.

Fig. 2 Estimated research model. It depicts the regression co-efficients indicating the impact of internet

banking service quality dimensions on customer satisfaction (CS).*significant at 0.05.

V. DISCUSSION AND IMPLICATIONS

A. Theoretical Implications

The main aim of this paper was to determine the IBSQ factors that significantly drive CS in the

Ghanaian banking industry. This paper, therefore, has validated a theoretical model predicting CS in e-

banking context. The proposed model found one significant determinant of CS, which is Web design,

having four factors such as easy completion of online transactions, easy logging on online portal, easy

understanding which button to be clicked for the next step and helping customer to complete a

transaction quickly.These are therefore, the four items that are critical drivers of CS of IBSQ in the

GBI.

Theoretically, the paper adds to the general marketing and e-banking literature that CS could be

influenced by aspects of IBSQ[32], [37], [48]. The study did not find support for four aspects of IBSQ,

which are: Customer service, Assurance, Preferential treatment and Information provision.

The paper provides empirical evidence that not all IBSQ factors may significantly drive CS in every

service context. The extent to which IBSQ factor will induce CS may depend a number of factors

ranging from technology readiness [54], individual user adoption level, level of ICT technical know-

how, to the level of development of national e-banking platforms to enhance industry-wide delivery of

quality electronic banking services and products, among others.

Thefinding that CS is significantly influenced by web design factors of IBSQ in the Ghanaian

banking industry, should be understood in the context of adoption and innovation stage of internet

banking in Ghana. In the Ghanaian banking industry, internet banking is still at the infant stage in

Ghana, and its adoption is still relatively low. Therefore, most customers seem to be much more

concerned about the basics in using e-banking – web design factors. Web design factors becomes the

first issue of concern for most online users. This is because the value of the rest of the functions of

internet banking services dependents, to a large extent, on the functionability of the web page, its links

and the speed and user friendliness of the internet banking portal.

While the findings of this paper challenge those of previous studies that have found support for

Customer service, Assurance, Preferential treatment and Information provision[25], [26], [32], it does

not imply that those other IBSQ factors are not useful in the Ghanaian banking industry, rather they

Web design

Customer service

Assurance

Preferential treatment

CS

Information provision

-0.558

0.796*

0.004

0.265

0.490

R2= 0.741*

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 11

imply that those factors should still be given attention as they operate together with web design factors

in an integrative way. However, banking management should give much attention to wed design

factors in order to achieve higher levels of customer satisfaction with IBSQ, while the other factors are

to be provided, at least at the minimum level.

B. Managerial Implications

This paper offers several implications and recommendations to management of electronic banks in

general, and internet banks in particular. First, it was found that Web design has the strongest influence

on CS. This implies thatmanagement should give more attention to web design factors and devote

resources to providing excellent web design features that delivers high level of efficiency and

functionability of internet banking portal that meet and exceed customers’ expectations.

In order to ensure that web design of the internet banking is effective and efficient for customer

satisfaction, it is recommended that:

1. Internet banking portal should provide easy completion of online transactions. For easy

completion of online transactions, management should ensure that there are simple instructions

to guide users on how to use various banking services and online activities [55]. In addition to

this, the site should have frequently asked questions [FAQs] function to help users with common

questions such as online bank transfers, charges for online services, protecting passwords,

privacy, security issues about online bank transaction, use of search facility, and other relevant

information [56].

2. Internet banking portal site should provide easy logging on online portal. The internet banking

portal should have effective log on system that is valid and easy for users to enter their user

names and passwords. The log on features should be convenient to users and should not be

difficult for users to be verified using their user identifications and credentials before being able

to do their online banking transaction [57].

3. Internet banking web stie should provide easy understanding to customers of which button to be

clicked for the next step. The management should ensure that web site designers ensure that the

links provided customers on the site are valid, and ensure user-friendly background

characteristics such as colour, legibility, readability, and easy to identify and control buttons

[55], [56]. This is because ease of navigation enhances user efficiency and re-use behaviour [56].

4. Internet banking site should be able to help customer to complete a transaction quickly. Online

transactions should provide competitive advantage by enabling consumers to complete

transactions quickly and faster than offline transactions [2], [4], [25], [26], [38], [55]. This means

that management should ensure that internet banking portals are enhanced with greater

bandwidth for greater speed for browsing, and quick opening of web pages for online

transactions. Thus, it should nottake too much time for web pages to open for users to do their

online banking transaction [57].

VI. CONCLUSION AND LIMITATIONS

In conclusion, the purpose of the study was to empirically examine the influence of IBSQ factors

on CS in Ghanaian banking industry. The paper concludes that within Ghanaian banking industry, web

design factors significantly influences CS and that the rest of the IBSQ identified in the literature may

not significantly linked to CS in the research context, given the relatively infant stage of internet

banking development in Ghana and the low level of its adoption.

The findings of this paper should be interpreted within its limitations. First, the study included

respondents from only two well established internet banking firms in Ghana. As the banking industry

in Ghana matures, it might be that other IBSQ factors might become critical in determining CS.

Therefore, future research should widen the scope of the study in terms of the sample size and its

composition and the factors of IBSQ to include. This should provide deeper empirical insight on IBSQ

and CS linkage and compare the results with those found in this paper and previous studies to enhance

the theoretical discourse on IBSQ in banking industry in developing counties.

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 12

REFERENCES

[1] Z. Liao and M.T. Cheung, “Measuring consumer satisfaction in internet banking: a core

framework”, Association for Computing Machinery.Communications of the ACM, Vol. 51 No. 4,

pp. 47-51, 2008.

[2] C. Garau, “Online banking in transition economies: The implementation and development of

online banking systems in Romania”, International Journal of Bank Marketing, 20 (6), 285-296,

2002.

[3] V.A. Zeithaml, A. Parasuraman, and A. Malhotra, “A conceptual framework for understanding e-

service quality: implications for future research and managerial practice”, Working Paper 00-115,

Marketing Science Institute, Cambridge, MA, 2001.

[4] Z. Liao and M.T. Cheung, “Internet-based E-Banking and Consumer Attitudes: An Empirical

Study”. Information and Management, Vol. 39, pp. 283–295, 2002.

[5] History of Banking in Ghana, downloaded at http://www.ehow.com/facts_5510268_history-

banking-ghana.html retrieved on April 20, 2010

[6] Ghana Banking Survey, 2012. Downloaded at www.pwc.com/gh/en/pdf/ghana-banking-survey-

2012.pdf

[7] J. Abor, “Technological innovations and banking in Ghana: An evaluation of customers’

perceptions”, American Academy of Financial Management, 1, 1-16, 2004. [Online] Available:

http://www.financialcertified.com/armstrong.html on June 6, 2011.

[8] R. Boateng, “Developing E-banking Capabilities in a Ghanaian Bank: Preliminary Lessons”,

Journal of Internet Banking and Commerce, August 2006, vol. 11, no.2, 2006.

(http://www.arraydev.com/commerce/jibc/)

[9] A. Woldie, R. Hinson, H. Iddrisu, and R. Boateng, “Internet banking: an initial look at Ghanaian

bank consumer perceptions”, Banks and Bank Systems, Volume 3, Issue 3, 35-46, 2008.

[10] J.L. Heskett, E. Sasser and L. Schlesinger, The Service Profit Chain, Free Press, New York, 1997.

[11] C. Grönroos, “Service model and its marketing implications”. Eur. J. Market., 18(4): 36-44,1984.

[12] C. Lovelock and J. Wirtz (2007) Services Marketing: People, Technology, Strategy (6th ATDF

JOURNAL Volume 7, Issue 3/4 2010 Ed.), Pearson Prentice Hall, New Jersey

[13] V. Zeithaml, “Service Quality, Profitability and Economic worth of customers: what we know and

what we need to learn”. Academy of Marketing Journal,Winter, 2000.

[14] V.A. Zeithaml, L.L. Berry, & A. Parasuraman, “The behavioral consequences of service quality”,

Journal of Marketing, Vol. 60 No. 2, pp. 31-46, 1996.

[15] C.L. Goi “E-banking in Malaysia: Opportunities and Challenges”, Journal of Internet Banking and

Commerce, Vol. 10 No. 3, Dec 2005.

[16] R. K. Srivastava (India), Customer’s perception on usage of internet banking. Innovative

Marketing, Vol. 3, Issue 4, 2007.

[17] S. Rotchanakitumnual, and M. Speece, “Barriers to Internet Banking Adoption: AQualitative

Study among Corporate Customers in Thailand”. International Journal of Bank, Marketing. 21 (6),

312-23. 2003.

[18] S.C. Chimeke and A.E Ewiekpafe and F.O. Chete“The Adoption of Internet Banking in Nigeria:

An empirical investigation”, Journal of Internet Banking and Commerce, Vol.11, No., 2006.

[19] I. Brown, and A. Molla, “Determinants of Internet and cell phone banking adoption in South

Africa. Journal of Internet Banking and Commerce, 10 (1), 2005.

[20] P. Kotler and K. Keller, “Marketing Management”, 12th Ed., Pearson Education Inc, New Jersey,

2006.

[21] P. Asubonteng, K.J. McCleary, and J. E. Swan, “SERVQUAL revisited: a critical review of

SERVICE QUALITY”, Journal of Services Marketing, 10 (6), pp. 62-81, 1996.

[22] D. Gefen, “Reflections on the Dimensions of Trust and Trustworthiness among Online

Consumers,” The Data Base for Advances in Information Systems, 333, 38-53, 2002.

[23] A. Parasuraman, V.A. Zeithaml, and L.L. Berry, “SERVQUAL: a multiple-item scale for

measuring consumer perceptions of services quality”, Journal of Retailing, Vol. 64 No. 1, pp. 12-

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 13

40, 1988.

[24] K. Gi-Du, and J. James, “Service Quality Dimensions: An Examination of Grönroos’ Service

Quality Model”, Managing Service Quality 14(4), pp. 266–277, 2004.

[25] H. Li and R. Suomi, “A Proposed Scale for Measuring E-service Quality,”International Journal of

u- and e-Service, Science and Technology Vol. 2, No. 1, pp. 2-9, 2009.

[26] C. B. Ho and W. Lin, “Measuring the service quality of internet banking: scale development and

validation, European Business Review, Vol. 22 No. 1, 2010, pp. 5-24, 2010, DOI

10.1108/09555341011008981.

[27] J. Rowley, “An analysis of the e-service literature: Towards a research agenda”. Internet Research,

Vol. 16 No. 3, pp. 339-359, 2006.

[28] P.A. Dabholkar, “Consumer evaluations of new technology-based self-service options: an

investigation of alternative models of service quality”, International Journal of Research in

Marketing , Vol. 13, pp. 29-51, 1996.

[29] B. Yoo, and N. Donthu, “Developing a scale to measure the perceived quality of an internet

shopping site (SITEQUAL)”, Quarterly Journal of Electronic Commerce, Vol. 2 No. 1, pp. 31-46,

2001.

[30] M. Kim, J.H Kim, and S.J. Lennon, “Online Service Attributes Available on Apparel Retail Web

sites: An E-S-QUAL approach”, Managing Service Quality, Vol. 16 No. 1, pp. 51-77, 2006.

[31] Z. Yang, and M. Jun, “Consumer Perception of E-Service Quality: From Internet Purchaser and

Non-Purchaser Perspectives”, Journal of Business Strategies, Vol. 19 No. 1, pp. 19-41. 2002.

[32] E. Cristobal, n. C. Flavia and u, M. Guinali, “Perceived e-service quality: measurement validity

and effects on consumer satisfaction and web site loyalty”, Managing Service Quality, Vol. 17 No.

3, pp. 317-40, 2007.

[33] E. Daniel, “provision of electronic banking in the U.K. and Ireland,” International Journal of Bank

Marketing, Vol. 17, pp.211-232, 1999.

[34] L. Arunachalam, and M. Sivasubramanian, ‘The future of Internet Banking in India’, Academic

Open Internet Journal, Vol. 20, 2007. Available online at: www.acadjournal.com

[35] M. Jun and S. Cai, “The key determinants of internet banking service quality: a content analysis”,

The International Journal of Banking Marketing, Vol. 19 No. 7, pp. 276-91, 2001.

[36] M. Joseph, C. McClure, & B. Joseph, “Service quality in the banking sector: the impact of

technology on service delivery”. International Journal of Bank Marketing, 17 (4), 182-191, 1999.

[37] Z. Yang, and X. Fang, “Online service quality dimensions and their relationships with

satisfaction”, International Journal of Service Industry Management, Vol. 15 No. 3, pp. 302-26,

2004.

[38] M. Loonam and D. O’Loughlin, “Exploring e-service quality: a study of Irish online banking”.

Marketing Intelligence & Planning Vol. 26 No. 7, pp. 759-780, 2008, DOI

10.1108/02634500810916708.

[39] A.M. Aladwania, and P.C. Palvia, “Developing and validating an instrument for measuring user-

perceived web quality”, Information & Management, Vol. 39 No. 6, pp. 467-76, 2002.

[40] Z. Yang, M. Jun, and R.T. Peterson, “Measuring customer perceived online service quality: scale

development and managerial implications”, International Journal of Operations & Production

Management, Vol. 24 No. 11, pp. 1149-74, 2004.

[41] C.N. Madu, and A.A. Madu, “Dimensions of equality”, International Journal of Quality &

Reliability Management, Vol. 19 No. 3, pp. 246-59, 2002.

[42] M. Wolfinbarger, and M.C. Gilly, “eTailQ: dimensionalizing, measuring and predicting e-tail

quality”, Journal of Retailing, Vol. 79 No. 3, pp. 183-98, 2003.

[43] M. Wolfinbarger and M.C. Gilly, “ComQ: dimensionalizing, measuring and predicting quality of

the e-tailing experience”, MSI Working Paper Series No. 02-100, Marketing Science Institute,

Cambridge, MA, pp. 1-51, 2002.

[44] R.T. Rust and R.L. Oliver, “Service quality: Insights and Managerial Implications from the

Frontier”, in Rust, R. and Oliver, R. (Eds), Service quality: New Directions in Theory and

Practice, Sage Publications, Thousand Oaks, CA, pp. 1-20, 1994.

www.theinternationaljournal.org > RJSSM: Volume: 03, Number: 04, August-2013 Page 14

[45] R.L. Oliver, “Cognitive, Affective, and Attribute Bases of the Satisfaction Response”, Journal of

Consumer Research, 20, pp. 418-30, 1993a.

[46] E.W. Anderson, C. Fornell, and D.R. Lehmann, “Customer satisfaction, market share and

profitability”, Journal of Marketing, Vol. 58 No. 3, pp. 53-66, 1994.

[47] G. S. Nimako, K. F. Azumah, F. Donkor, and V. Adu-Brobbey, “Overall Customer Satisfaction in

Ghana’s Mobile Telecommunication Networks: Implications for Management and Policy”. African

Technology Development Forum, Vol. 7, 3/4, pp. 35-49. 2010.

[48] A. Musiime and M. Ramadhan, “Internet banking, consumer adoption and customer satisfaction”,

African Journal of Marketing Management, Vol. 3(10), pp. 261-269, October 2011 Available

online at http://www.academicjournals.org/AJMM ISSN 2141-2421 '2011 Academic Journals

[49] M. Rod, N.J. Ashill, J. Shao and J. Carruthers, “An examination of the relationship between

service quality dimensions, overall internet banking service quality and customer satisfaction - A

New Zeland study”, Marketing Intelligence & Planning. – Vol. 27. No. 1, 2009.

[50] D. Straub, M. Boudreau, and D. Gefen, “Validation guidelines for IS positivist research”,

Communications of the Association for Information Systems, 13:380-427, 2004.

[51] J.F. Jr. Hair, W.C. Black, B.J. Babin, R.E. Anderson and R.L. Tatham, “Multivariate Data

Analysis”. 6th Edn., Upper Saddle, NJ: Pearson Prentice Hall, 2006.

[52] C. Fornell, and D.F. Larcker, “Evaluating structural equation models with unobservable variables

and measurement error”. J. Market. Res., 48(1): 39-50, 1981.

[53] Y.K.C. Patrick, “Re-Examination a Model for Evaluating Information Centre Success Using a

Structural Equation Modelling Approach.” Decision science, 28(2): 309-334, 1997.

[54] H.R. Yen, “An attribute-based model of quality satisfaction for internet self-service technology”,

The Service Industries Journal, 25(5), 641-659,2005.

[55] R. Van der Merwe, and J. Bekker, “A Framework and Methodology for evaluating e-commerce

Web sites. Internet Research: Electronic Networking Applications and Policy, 13[1], 74-93, 2003.

[56] S. Pather, and S. Usabuwera, “Implications of e-Service Quality Dimensions for the Information

Systems Function.” In `43rd Hawaii International Conference on System Sciences (HICSS), IEEE,

2010.

[57] K. C. Laudon and C.G. Traver, “E-commerce: Business, Technology, Society”. 2nd rev. ed.

Pearson Addison Wesley, USA, 2003.