is islamic banking for india? what are the key factors affecting the sector

TRANSCRIPT

Is Islamic Banking for India? What are the key factors affecting the sector

1

Is Islamic Banking for India? What are the key factors affecting the sector

2

TABLE OF CONTENTS Page

Chapter 1: Introduction

1.1. Introduction: Why Islamic Banking? 4

1.1.1 Prohibition of Riba 5

1.1.2 Prohibition of Gharar 7

1.2. Golden rules of Business in Islam 7

1.3. Financial instruments of Islamic banking

8

Chapter 2: Literature Review

2.1 Competitive advantage of Islamic Banking

2.2 Competition in banking industry 23

2.3 Competition in Islamic banking perspective 26

2.4 Customers’ acceptance on Islamic banking 33

Chapter 3: Methodology 3.1 Research Question 37

3.2 Research methodology 37

Islamic Banking and Finance: Is it complementing or competing the

conventional banks MBA

Dahang Bunchuan 8

3.2.1 Questionnaires for banks’ managers 3.2.2 Questionnaires for bank’s

customers (IBB’s customers)

Chapter 4: Background of Brunei Banking Industry

4.1. Banking industry in Brunei Darussalam 40

4.2 Industry size 41

4.3 Regulatory body 44

4.2. Brief History of the Islamic bank of Brunei Bhd 45

4.3. Performance analysis 46

Chapter 5: Research Findings

Is Islamic Banking for India? What are the key factors affecting the sector

3

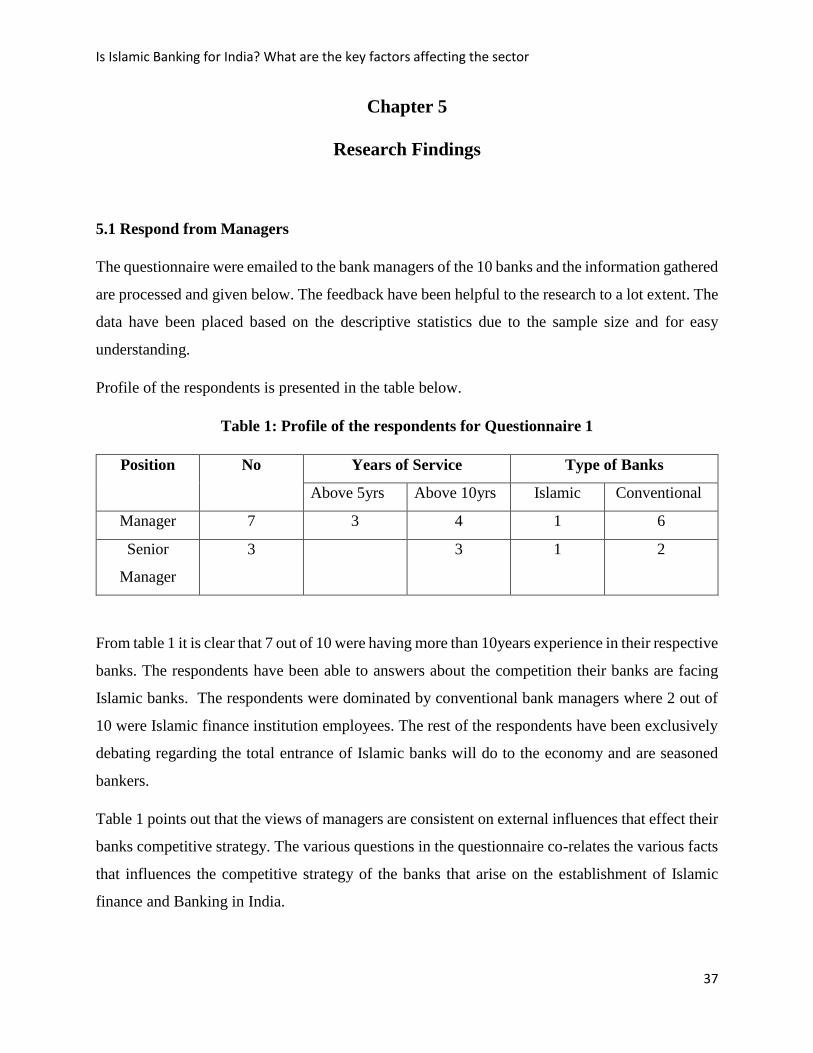

5.1 Respond from managers 51

5.2 Respond from customers 55

Chapter 6: Conclusion 61

Chapter 7: Recommendation 64

Appendix 66

I. Questionnaires for banks’ managers

II. Questionnaires for bank’s customers

Reference

Is Islamic Banking for India? What are the key factors affecting the sector

4

Chapter 1

Introduction

Why Islamic banking?

Islamic banking has been followed by Muslim nations over the centuries and the first ever Islamic

bank was established in Egypt in 1963 as an experiment to cater the demands of Muslims in

accordance to their religious demands (Al-Omar & Abdel-Haq, 1996). This lead to the

establishment of interest free banks globally as many governments found this idea very beneficial

for their development. Islamic banks began in places where there was Muslim community. The

first private Islamic bank was the Dubai Islamic bank established in 1975 and has become the

largest Islamic bank by 1987. This idea has been widely adopted and the basic of banking in these

nations. The idea was adopted by many nations and countries from South East Asia like Malaysia

has been playing a vital role in the development of modern Islamic banking. It is found that where

there is a Muslim community an Islamic financial institution will be set up to carter to their needs.

The Islamic banking system is an entirely different perspective from normal banking, these banks

were favored by the Islamic community as it proved to be an alternative to their banking needs.

Islamic banking is 2 decades old and their rapid success and demand pose a great threat to

conventional banks. When competition became fierce the conventional bankers has been noticing

the development of these banks and how they get away with their customers and deposits. Ever

since their market entry they are considered as a niche market player who cater to the needs of the

Muslims. But when looking into the real statistics it can be found that they do not cater only for

Muslims but for the Non-Muslims as well. The investors who came across the system has realized

the full potentials and been using it and these investors is not always Muslims. This is the case of

India where the Non-Muslim population is higher.

The purpose of Islamic banks and conventional banks are the same that is to act an intermediary

between the depositor and borrowers. But in case of Islamic banks the relation is beyond investors

and depositors, the bank acted as partners and entrusted to invest and to share profits when

generated (Kahf, 2002). This concept of profit and loss sharing is an entirely different concept

from that of conventional banks. In a conventional bank the relationship between the depositor and

borrowers to the bank are interest based, depositors will be paid interest for their deposits whereas

Is Islamic Banking for India? What are the key factors affecting the sector

5

borrowers has to pay interest for the sum borrowed. Traditional banks began to decline on the

wake of ill-effect of interests. The decline in trade has forced the banks to shift focus to promissory

notes, profit sharing and other similar instruments which increase the trade, development and

productivity in the society (Choudhury M.A., 2000). Nowadays these activities have become quite

popular with banks of the two systems, it has solved many issues regarding credit risks and

liquidity. Islamic banks are established based on religious obligation (Fardhu Kifayah) to the

leader of the Muslim society. It is the duty of the head of the state to provide all amenities to the

people so they can lead a social and religious life adhering to the teachings of the Quran.

When Islamic banking was established many considered to be a marketing gimmick to attract

customers to their institutions. El-Gamal (2000) had shown his dissatisfaction regarding the

misconception of Islamic banking as it fail to understand the real meaning of Islamic banking and

was absurd. The total concept of Islamic banking is entirely different and when compare with

conventional banks the process involved in the Islamic financial instruments is entirely different

from the conventional instruments and only an Islamic banking person can understand the

difference and they are enjoying this particular feeling all over the world.

The major difference of Islamic banks is the presence of Shari’ah board which determines the

many factors of the Islamic bank and differentiate it from the conventional banks. In the case of

conventional banks for a new product innovation will need only approval from the board of

directors but in the case of Islamic banks it is entirely different and product innovation need

approval from Shari’ah law as all financial products should follow Quran and Hadith and the board

of directors to approve a product without the approval of the board. The board itself has no power

in deciding or approving financing application from the banks customers. In case of conventional

bank the board decides on the loan request but in case of Islamic banks this view helps to prevent

these banks pursing its product innovation based on profit maximization goal alone but a more

balance goal taking into consideration of social and religious aspect of it.

1.1.1 Prohibition of Riba

Islamic bank works on this basis of Shari’ah principles and according to these principles collection

of interest is prohibited. The prohibition of Riba (usury) is one of the crucial factors for the

existence of Islamic bank. The interest that are earned from deposits or by lending out loans is not

permitted under Shari’ah law. Any transaction that has the element of Riba is against Islamic law.

Is Islamic Banking for India? What are the key factors affecting the sector

6

The concept of earning interest from transactions is haram as it clearly said earning money from

money is not acceptable under Islamic law (Ahmad, M., 2004). When money is used to earn extra

income without any hard word is completing against as it is stated that it is equivalent to waging

war against God and his Prophet (Ariff, M., 1988). The usury does not care or concern about the

poor as it is a mode of exploitation of the poor debtor by the rich creditor (Gamal, 2000). Khan

(1986) increases his support furthermore on the view why Riba is not allowed due to its negative

justice nature, whereas Islam promotes socio economic justice, religious peace and harmony.

Quran asks the followers to be follow an equal relationship with all fellow citizens irrespective of

their social standings. It is clearly discussed why Riba is not allowed in Islam as it does not treat

everyone equally and increase the difference between the rich and the poor. If Riba is totally

prohibited globally the difference between the rich and poverty nations will be erased, nowadays

poor nations lives under the mercy of rich nations.

Conventional banks earns money through charging interests for the products and that is where

Islamic bank differ from these banks. Money is an instrument used as a medium of exchange for

products. Money should never be used to earn more money and this how modern banks provides

fixed returns for fixed deposits or charging higher rate of interests to earn more money. The

prohibition of return of money is because as they are added as capital in the economic sense of it.

This is where Islamic bank comes into play where the depositors are ensured the money they

supplied are treated as investment and return/profit are shared among the investors as they are

generated by the bank (Tannenbaum, 1998). Based on this principle there is no fixed return on

investment made by depositors in the Islamic banks, when profits are generated it is shared with

the investor so no fixed return contracts are provided in their investments, but an estimate is

provided.

Usury is considered as unethical by many religions even from the ancient past and it is not a term

of the modern world. it is criticized to create more harm than good to the society. No viable

alternatives have been found until the establishment of Islamic banking. This proved to be a

solution for not only Muslims but also to people who are looking forward to invest in ethical

investment as it is an act of social justice to the society.

Is Islamic Banking for India? What are the key factors affecting the sector

7

1.1.2 Prohibition of Gharar

Gharar is the term used to represent uncertainty or risk in the Islamic banking. The Shari’ah law

clearly states that any transactions that taking place under Islamic banking should contain any

Gharar. The law states that parties involved in any contract should have any ambiguous doubts as

all facts of the contracts should be clear to both the parties, in the financial case they should be

given detailed information regarding their investments. This cut through clarity of deals acts as an

equally good for both the parties and ensures socio-economic justice. This is based on the logic

that business depends on the economy and fluctuations in the economy will affect the returns and

no proper profit generation cannot be guaranteed. Even with so much technological advancements

there has been deviations in the final financial data with the forecasted reports. So the investors

and bank should be willing to share the risk as market situation varies all the time and customers

should be informed profit will be gained at the first instance of investment. Such a prohibition will

act as a defense system against the unfortunate events in contracts.

1.2 Golden Rules of Business in Islam

In Islam it is prohibited to do any business which consist of uncertainties and gambling, as it is

treated misuse of wealth entrusted by god upon us. So any business ideas developed should satisfy

the strict rules and policies of Quran, if in doubt it should be communicated with religious scholars.

This limitation prohibits Islamic banking practitioners from doing prohibited activities and

reminds them to follow the teachings of Quran. Business like entertainment industry, gambling

industry, alcohol and pork is considered haram and should not be used in any transactions. They

are strictly prohibited at all times to the Muslim community. The Islamic financial system has four

basic principles (Hawary, 2004).

1. Risk sharing: It is one of the mostly discussed basic principles of Islamic banking, as risk

sharing brings forward many new investors to bank with them. When the bank and the

investors enters into a contract the investor cannot be guaranteed fixed income, only an

estimate can be provided. Income is provided when profits are generated from them.

2. Materiality: When transactions take place it should be linked or related to a real economic

transaction so there is a materiality which is essential as per Shari’ah rules of business

transactions.

Is Islamic Banking for India? What are the key factors affecting the sector

8

3. No Exploitation: Social justice is the key ideology of Islamic banking, any exploitation of

transactions is not permissible under Islamic banking. Such practices are not encouraged

by Islamic bank practitioners.

4. Haram: anything that is deemed to be haram according to Quran should not be supported

by Islamic banks. Financing of sinful activities are considered haram especially

transactions on alcohol and pork, entertainment and gambling.

The basic principles of Islamic banking differs across the four Islamic schools and the final

interpretation of rules of Shari’ah will possess minor differences on the various concept of Islamic

banking system depending on the Islamic school they follow.

1.3 Financial instruments of Islamic banking

The understanding of Islamic financial instruments is necessary so as to understand how the system

differ from the conventional banking system. These products are advanced interest free versions

of conventional bank products which are suitable for investors all around the world.

1. Ijarah: The Arabic term Ijarah is used to describe the lease or lease agreement. The bank

will buy the productive asset and is leased to the needed person so as to generate income.

The main reason for the bank to own the equipment is basically the customer will be short

of funds but has the ability to rent it out to carry out his need. Both party of the contract

should have better understanding about the asset to be leased their overall value before the

contract is agreed upon. Contract terminates on the agreed duration of lease and the user

can own the asset at a nominal price. Most commonly used lease product is Al-Ijara

wa’lqitna, which is lease purchase agreement widely used for leasing cars or trucks. This

product is an alternative to the hire purchase loan in the conventional banking system.

2. Istisna: the Arabic term is used to describe the deferred payment or delivery. In this product

both the parties agrees to pay on various progressions of the contract or at the delivery of

Is Islamic Banking for India? What are the key factors affecting the sector

9

final product. This contract is widely used to finance industrial and housing projects. The

payment method will be agreed upon both the parties before the final contract is drawn.

3. Mudarabah: The term is used to define trustee finance contract. In such a contract the bank

will become the capital provider or investor for the entrepreneurs business. It is the duty of

the entrepreneur to invest his business skill and knowledge to earn income. Profits are

shared on an agreed fixed ratio between both the parties. Failure of the business will lead

the bank to lose the money invested and the entrepreneur to lose his valuable time and

effort he invested. The risk shared depends on the ratio of profit agreed.

4. Murabahah: The basic concept of this contract both the parties involved in the deal is aware

the actual cost of the product, both the parties discuss and agrees to give a marginal price

on the product as installments which does not exceed over the agreed total cost. This

contract is similar to cost plus sale concept.

5. Musyarakah: the product that changed the entire conventional banking concept was the

equity participation. The concept is similar to joint venture agreement where both parties

that is the investor and the owner of project has equity shares in it. The level of management

and power is decided based on the amount of share each party hold. In case of failure of

the project the loss is shared based on the amount of equity shares owned. This particular

product has brought many new potential businessmen and investors in to the economy.

Is Islamic Banking for India? What are the key factors affecting the sector

10

Chapter 2: Literature Review

2.1 Competitive advantage of Islamic Banking

Islamic Banking emerged during the economic recession and has outperform the conventional

banking system and seasoned banks. Islamic banking is a traditional banking concept which

follows the rules of the Quran and operates under Sharia law. The Islamic banking is a new

financial system taking advantage of the advanced conventional banking system. Islamic banking

system falls under a certain position based on their market they are associated and compete with.

These new banking system are referred to BCG (Boston Council Group).

The Islamic Banking concept has put forward a lump sum amount to the global economy. The

Sharia law prohibits Muslims from giving interest or lending money for interest as it is considered

as sin (haram). The IDB (Islamic Development Bank) in Jeddah operation is not limited in the

Saudi Arabia market alone, it has large presence in many developing nations especially South East

Asia and the European countries. Their rich oil resources makes immense income as they are

originated in the country. The capability and size of IDB makes it a global competitor and has been

aggressively promoting its financial products globally especially South East Asia due to the large

Muslim population in these areas. The bank falls under cash cow classification

The global competitiveness can be proved more as these banks set up offices in Britain taking their

fight to major international banks. It clearly shows the banks capability to compete with established

banks in mature market. The competency in UK market is intense due to the presence of large

number of banking and non-banking institutions in the UK and the society which is a lot familiar

with conventional banking system than Islamic Banking. The bank falls under dog classification.

The banks share is low when compared with conventional banks, the cash flow has to be abundant

along these periods as it marks the long-term success of these banks and can also raise liquidity

problems which my raise to closure of these institutions.

The growth of Islamic Banking in lower Muslim community area is very low. Islamic Banking has

shown growth in USA where Muslims are a minority, but nowadays it is failing to capture market

share due to the many terrorism activities as well as further tightened by the regulatory requirement

in US that makes Islamic banking/finance has no spot for growth or to compete fairly in the market.

Is Islamic Banking for India? What are the key factors affecting the sector

11

Banks or financial institutions which are situated around Muslim minority like US are categorized

as Question mark also known as problem child.

The Islamic Bank in middle-eastern nations are showing exceptional growth due to the excess cash

flow generated by selling of the natural resources like oil and gas. The Islamic Bank of Brunei can

be considered as the star as it is rich in the resources and have been proving to be growing rapidly.

On every Venue the Head of the State, His Majesty the Sultan of Brunei promotes Islamic Banking

as it fits his aspiration to change Brunei into Global financial hub for Islamic Banking and Finance.

The Bank of Brunei enjoys high market share and has created a household name in the banking

industry, But due to the size of the economy, rapidly matured market and lending activities getting

saturated (Dahang Bunchuan, 2006). The acceptance of deposits and domestic growth venue is

very limited.

Banking is a highly complicated and competitive market. Special legislation has been made for

Islamic Banks to strive among other banking institutions. These protective legislations helps them

to compete fairly in the countries they are established like Pakistan, Sudan, the middle-east and

even small nation like Brunei. Islamic Banking has acquired its own unique competitive advantage,

Porter advocates that for an organization to achieve competitive advantage it has to align its

strategies that suits to the market that they are entering (Dobson et al, 2004). Since Islamic Banking

uses conventional banking system as its platform, the Islamic bank should stand out with its own

set of uniqueness in order to compete with seasoned banks. The Islamic Bank differentiate itself

from other bank with its own financial instruments, product differentiation in order to attract

investors, depositors and individuals to bank with them.

Porter (1997) mentioned that conventional banks has lost the competitiveness as they were lack of

product differentiation and specific strategies on their pursuit to grow and earn profits. Porter

(1997) argued that strategies like merger are not a strategy for attaining competitive advantage but

a value destroying effort as the new entity will be clouded with more unclear strategy in the long

run. Islamic bank is just like a newborn to many developed and developing nations, it is making

its first step in India as the government finds Islamic Banking as a major source to the national

Infrastructure development. The Government of India plans to borrow £147billion from Islamic

Banks to tally the deficit to complete the project Vision 2020. Islamic Bank being new to the

banking system has to develop its own set of skills so as to differentiate it from banks like

Is Islamic Banking for India? What are the key factors affecting the sector

12

conventional banks in India and other South East Asian nations. The ability of Islamic bank to

develop market oriented products which are different from the conventional ones will be their

competitive edge.

The main basic advantage for Islamic Banks is that the Muslim community is very close, they

always get together once in a week for their Friday prayers and gather together for other communal

functions. These periods are of key importance and crucial for disseminating information regarding

Islamic Banking products. This type of Joint community is mostly seen in middle-east and Asian

nations and are rise in the west. The community play a main role in the success rate of these banks

as their marketing effort will be realized based on the presence of the community. Lack of close

knit community in many nations led Islamic banks resorts aggressive marketing strategy:

advertisements on large screens in town centre and shopping malls and meeting potential

individuals in person. Islamic bank began introduction and spreading information through word of

mouth, the traditional method of marketing. With advancement of technology, the marketing

strategy has evolved and is more apparent and visible to competitors.

The growth of the market and the financial industry is slow indicating the market has reached the

maturity stage and needs new ideas and products to rejuvenate it. Islamic banks has been preferred

as the first choice of Muslims and other ethical investors. Islamic banks offers excellent global

opportunity for growth and profitability for worldwide Muslims and other investors who wishes

to bank with them. The opportunities can be spread up to four key market segments like global

consumer banking, commercial banking, global corporate banking and global investment banking

(Matthews et al, 2004). A study was made in UK to understand the potential market for Islamic

Banking products and services on the mortgage segment. The research helped to identify the

differences between the conventional mortgages to the Islamic concept of mortgage which used

Murabaha and Ijara concepts. The major difference among the two were the conventional was

based on debt with interest whereas the Islamic mortgage concept used equity base. In such an

instance the customer share the equity or ownership as well as the risk. There is no interest involved

in any financial transactions compared to the conventional mortgages, thereby prohibits the

element of unethical transactions.

The survival of Islamic banks depends upon the regulations and legislations of the country they

are operating. The regulations for entry of foreign banks or new banks favor Islamic Banking with

Is Islamic Banking for India? What are the key factors affecting the sector

13

a competitive edge. A large number of Islamic banks are established in developing countries and

the major concern was the threat they possess from strong and stable foreign banks, which is

considered unfair due to their size and presence globally. The Islamic Banks are mainly local banks

has to be protected with legislation for their initial survival. Mishkin (2005) argues that entry of

foreign banks favor the nation by providing more financial stability and create a more efficient

banking system in the nation. His argument is further supported by defending that the presence of

foreign banks in the developing economies will act as an insulator to any domestic shocks. This

argument has validity as banks are pressured on the global competition regardless of what system

they follow. The banking market is not limited to the domestic market but to a much wider global

market and is more on the forefront than ever.

2.2 Competition in Banking Industry

Banks solely operates on investments and deposits and earn profit through loans. Competition in

the banking sector from the day they have been started operating. The economy or household of

any nation cannot be separated from their respective banks. These factors are closely tied up with

deposits, loan and other types of financial services (Shaffer, 2003). The factor of demand and

supply of financial products for business, economy and household were largely depend on the

pricing of these services by the bank, they were normally determined by the level of competition

in the business. The level of competition will again also depend on the scope of operating market

i.e. the domestic market or global market.

The popular saying “the more the merrier” is not true in the case of banking industry. Shaffer

(2003) argues that the large number of banks existing in a market create more adverse borrower

selection situations and moral hazard. The argument proves to be true in situations where many

bank chase after a few potential customers and are most likely that a single business may have

several borrowings from different banks which in a later stage create more loan loss for banks

involved. Normally in a concentrated market banks prove to be aggressive in promoting their

financial products to new customers or in other aspect providing loans to reach their budgeted

target. The information collected by banks proved to be asymmetric, customers in such case takes

advantage of the situations by gaining more loans on hope that the investment can repay the loan.

The main tools in a banks competition are the pricing of its loan and deposits. The fewer banks

that operate in a market they are more likely to charge higher interest rates which means there will

Is Islamic Banking for India? What are the key factors affecting the sector

14

be less activity in lending and banks practice more on credit rationing as competition heighten

(Zarutskie, R.2006). In her findings, she mentions that the effect of banks competition was more

visible for private firms than the big firms. Smaller firms get less funding from banks due to the

asymmetry in their information provided compared to the older and bidder firm. The study does

not indicate the increase in bank competition increases the funding but it is more depended on the

asymmetric information of the borrower.

In high level of market concentration in smaller economies the loan rates are higher than the

deposit rates when compared to a lesser concentration market. The main reason for this difference

was the fact that local business and households are dependent on the basic banking or financial

services that were normally located within the vicinity if their home or business (Hannan & Prager,

2004). This is one of the major reasons why banks open up branches in countryside and rural areas

which are of strategic importance to get near to potential customers. Even with the emergence of

advance technology, branching out is a proven successful strategy that will increase the reach and

market share which will enhance the banks overall performance. Localization is a strategy

followed by major banking giant HSBC for quiet sometime and has proved to be a great success.

It is a strategy that other banks should have a look. Based on this study it is found out that the

interest rates seems to be same even in rural areas where the banks had branches. This aspect of

pricing reminds us of the perfect competition scenario where the customers know the price offered

by every vendors of the same product. Branching out has been a traditional competitive strategy

for banks as they proved their competitive edge by showing their reach and geographic location

has been of prime importance when considering this strategy in capturing maximum market share

in the minimal effort. Banks those established their branches normally compete aggressively to

secure deposits whereas multi market banks source out their fund elsewhere which is less cheaper

and volatile in nature. In term of pricing strategy the multimarket bank has uniform prices and are

lesser compared to the local banks which have to tailor their price on loan or deposits to meet the

local demand and supply.

The study of effect of single currency EUR has different competition strategy. Bandt and Davis

(2000) points out in situation like this the cross border competition increases due to the downward

pressure of profitability. The competition has become intense for loans, investments and other

services provided by banks. There was a sizeable change of target revenue for the non-interest

Is Islamic Banking for India? What are the key factors affecting the sector

15

income. Llewellyn’s (1996) argues there is a large decline on traditional banking, seasoned big

banks has been shifting focus to the off balance sheet activities. Competition in domestic market

are monopoly of local banks as they are capable to adapt according to their local environment.

Whereas bigger banks will directly compete with other bigger banks for the different product

portfolio such as huge investment funding where the smaller banks are not capable of providing

it.

The intensity or level of competition depends on the market size and structure and the level of

concentration as we have discussed higher the concentration it benefits the customer with lower

interest rates whereas lower the concentration the interest will be high and funding is low. A study

by Casu and Girrardone (https://www.essex.ac.uk/AFM/finance-discussion-papers/DP05-02.pdf)

points out that in a concentrated market the level of competition will diminish as the banks move

towards monopolistic status and it also shows that an efficient bank will not compete directly and

in an aggressive manner in the market. Based on these findings it is proved most of the efficient

banks increase their market share and competitive edge through merger and acquisition. This

approach is consistent with the theories: economic of scale and economic of scope where these big

bank can harness their capability due to their management capability and technological

advancements. Modern day banks improve their market share and efficiency by pursuing measures

such a cost cutting and improving the process so they can serve the customers in a more efficient

manner. This finding justifies the previous findings on bank competition. Deregulation of banks

has stirred up the competition even further across borders and foreign markets. This has adversely

affected the Islamic Banking sector as the way they compete is through a secure regulation and

legislation and deregulation of banks effects their business as by learning the way conventional

banks does in the wake of globalization. Islamic banks being a new addition to the banking industry

has taken advantage of the existing ready banking infrastructure that was established by the

conventional banks and modified them so they are permissible according to the Shari’ah context.

Dow Jones Islamic Index system is the most apparent system used by Islamic finance. It was

originally the conventional banking and financial venue for investment which was resurrected in

a way to suit the Islamic Banking concept.

The main growth of the banking industry is at Asia Pacific as countries along this region are

developing and are open for foreign investment. Islamic Banking being new to the banking sector

Is Islamic Banking for India? What are the key factors affecting the sector

16

and the market is not exploited to the potential Islamic banks has a fair chance of competition and

grabbing market share. In a report by Deloitte (2005), they have identified the hot spots of cross

border investments in the Asia Pacific. Asian nations such as China, India and Thailand are having

a steep growth in their economy and consumer’s affluence is increasing, demanding for better

financial products and services are on the demand to meet the ever changing market environment.

An extra benefit to Islamic banks are that the three said countries have a large Muslim population

that may become their focused customers by entering the market. Studies have proved that Islamic

banks in India will bring forward the wealth of Muslim community into the economy and will

accelerate the development of nation in a faster rate. Thailand has responded to the situation by

developing an Islamic bank with equity partnership by the Islamic Bank of Brunei

(http://www.muslimnews.co.uk/news). India has developed Islamic Banks along the period and

these banks does not operate under the banking regulation of India, they act as Non-Banking

Finance companies (Khan, 2001). The Indian government is creating a legislation to include

Islamic Banks into the banking regulation as they have identified the potential of these banks and

Muslim investment. The demand from international customers and regulators will pressure India

to modify the existing regulation. China becoming a superpower has not yet used the Islamic

banking sector. China has a considerable number of Muslim population and they are located in the

impoverished inner region. With the larger Muslim community, Islamic banks will have the

advantage community wise and gradually developing the standards of life.

2.3 Competition in Islamic Banking perspective.

Tilva and Tuli (www.globalwebpost.com) shows the growth impact of Islamic Banking on

conventional banking sector and how dramatically competitive environment has changed. The

sophisticated financial instruments developed by Islamic banks were the main drivers of

aggressive and stiff competition in the banking industry. This factor created a large sum of funds

being transferred from conventional banking system to Islamic banking system. The major blow

to the conventional banking sector was the introduction of Shari’ah compliant investment

instruments being made readily available in the international market. Alternate venues are

provided to the Muslim and Non-Muslim investors looking forward to ethical investment by the

FTSE Global Islamic Index (London Stock Exchange) and the Dow Jones Islamic Market Index

(NYSE). Brown, K., further supported that Islamic banks are viable options to attract funds even

Is Islamic Banking for India? What are the key factors affecting the sector

17

though they are not profitable as conventional banks. With extensive support from the government

like in Pakistan, Iran and Sudan conventional banks finds it hard to enter the market where as in

Malaysia the banking regulation allows to operate Islamic windows. This has led many seasoned

conventional banks to establish their Islamic subsidiary, prominent banks such as HSBC started

HSBC Amanah Finance and Citi Bank with its Islamic Banking branch in the middle-east. Many

other banks has been following the suit to attract investments in the region.

According to Kahf, M. (2002), the strategic alliance formed between the Muslim scholars and

bankers to create complex financial instruments in a more sophisticated way of engineering new

financing modes which has been the successful factors in the Islamic Banking industry. These

factors led Islamic Banking from a domestic Bank into a much more globally operating banks. The

relationship between the religious scholars and practitioners has created a new dimension in the

educational world, while considering globally we can see many experts are Non-Muslims as well.

The interest in Islamic banking is not only seen by Muslim experts but Non- Muslim experts as

well and they are able to foresee a large opportunity ahead in the world of banking industry.

Various said factors and evidences has created a huge impact on the banking industry especially

to the conventional banking system. They are acknowledged as a large threat by politicians,

practitioners as well as academicians. Richard Duncan, head of Islamic finance at ANZ

International Merchant Banking Predicts that “Islamic finance will become a very big, established

player in project finance over the next five years,” (Shepherd Jr, 1999). This has been a strong

message from the practitioner of Islamic Banking and Finance and there were many evidences on

this statement that make it a great concern to the conventional banks. The Islamic Banking has

been transferred very dramatically over the decades. Banks based on US such as Citi Bank already

been pursuing Islamic banking system especially in the investment banking system where they

have a better advantage compared to the middle-east.

Based on analysis made by Iley and Megalli (2002), UBS initiative in attracting Muslim customers

proved the interest by Western Bankers in tapping the multibillion opportunity of investment has

increased in recent the last two decades. UBS being one of the largest bank in the world used its

Noriba bank as a platform to reach its global Muslim customers supported by their well-equipped

and experience workforce which are legendary. With robust technology capability and the vast

Is Islamic Banking for India? What are the key factors affecting the sector

18

knowledge that they have make at a greater advantage in competing with Islamic banking all over

the world.

Martin. J, (1997) clarifies this concern basically due to the acceptance of Islamic financial

instruments and the existence of demands from even multinational companies like General Motors,

IBM and Xerox. The concern was raised as the particular sector grown was to be estimated be

around 10 to 15% (Burghardt and FuB, 2004, El-Hawary et al, 2004 and Zaher and Hassan,

2001:166). This phenomenon is not only limited to middle-eastern or Asian nations but to the

western nations as well. Conventional banks stepping into dual system of operation creates a stiffer

competition for the Islamic banks as they operate based on the Shari’ah context. They does not

have the benefit of economy of scale and economy of scope as what their adversaries are.

Llewellyn, D.T (1996) clarifies that the banking in generally faces a decline in their comparative

advantage due to the competition it faces in the industry. The exclusive rights and monopolistic

status they enjoyed are gradually diminishing as the change in regulatory requirement and

government policy. Technology pays a major role in the way bank operates and the changes do

directly benefit the customers. This concept generally affects the way conventional bank operates

and Islamic bank as well even they operate on a different system any changes in the basic banking

of conventional principles will also affect the Islamic Banking sector.

The gradual decline of traditional banking system has made them to research further on way to

gain momentum in the banking business. Islamic bank has been a great breakthrough for the

conventional banking system as it made them to further research in great depth to the system. The

rise in rise and gas prices forced the banks in western countries to look more aggressive in

attracting the excess funds that these oil producing nations which are predominantly Islamic

nations. Islamic bank has been exceptionally growing globally. It has shown a £297 billion in

assets in 2006 and is still growing in the rate of 10% - 15% (www.investoffshore.com). This is a

huge improvement compared to the Islamic bank in 1970s when it was first recognized in the

banking world. The given figure is not significant when comparing to the global Muslim

population contribution from around 1.5 billion Muslims, the potential of the market cannot be

ignored. The majority of the Muslim communication lives in oil rich countries, the value of oil gas

increases the excess cash flows the prices are sky rocketing. It is not a coincidence that the extra

Is Islamic Banking for India? What are the key factors affecting the sector

19

income generated are in these Muslim nations and these funds has to be deployed in a manner

permissible under Shari’ah law.

The introduction of Islamic banking and finance in the banking sector has created has a new

competition globally. Islamic banking is no more belong to the domain of Muslim community but

more on an international perspective as investors and project owners are looking for alternatives

to the current conventional financial system. Governments are over concerned and protected about

their domestic market, these needs to be revisited on to explain the benefits of having an open

market and allowing foreign banks to establish and compete in domestic and international market.

There is no doubt financial globalization has its risk but the overall benefit outweigh the risks.

Schmukler S.L., (2004) defend the idea that globalization does have its benefit especially on the

capital flows. The existence of capital flows proves to be a huge benefit for the country financial

system. The borrowers can choose from better options in getting funds for their project and not too

dependent on domestic funds which proves to be expensive. The argument for globalization does

not limit to cheap funds, it also increases the transparency, improve corporate governance, increase

technical capabilities and improve business environment, which involve other institutions.

Mishkin (2005) supported these arguments especially in transparency and corporate governance

supported by strong legal system may reduce moral hazard problems. When financial institutions

foresee that they are less likely to experience moral hazard problem which always rise I financial

matters. It will motivate them to lend more which in return will create a better economic condition

as new investments can be pursued. Banking industry is no different from other industry, here

changes are inevitable in case of any business and there are rapid change in demands of complex

customers. Khan, M.F. (1999) believes that there are many factors that drive these speed some are:

1. Strategies for minimal and cost reduction.

2. Changing client needs for financing and investment.

3. The emergence of new potential market with different market structure.

4. Advancement of technology aided products and services.

5. Changes in regulation and modernization.

The above factors affects not only the conventional banking system but also the Islamic banking

system as well. Irrespective of the banking systems they compete with each other more new and

existing players will be joining the market making competition much fiercer. Furthermore new

Is Islamic Banking for India? What are the key factors affecting the sector

20

regulations has greater impact on Islamic bank on comparison with conventional banks.

Regulatory changes such as the relaxing of the Glass-Steagall Act (1933) before October 20, 1999

banks activities in US were very restrictive and banks were highly regulated when developing

products and service and they were also prohibited from engaging in securities market which also

include other investment activities like sale of mutual funds. When these regulations were relaxed

the conventional banks can operate on these sectors and wholly started subsidiaries to deal with

investment banking which is the main business of Islamic banking. US based banks have

subsidiaries outside US which are Islamic Banking subsidiaries, they compete with existing

Islamic Banks for their customers. The competition seems to be one sided as the conventional bank

can operate in both sides whereas Islamic banking cannot operate in the conventional manner. This

one-sided competition justifies the countries initiative to protective legislation from threat of new

entrants.

Taylor (2003) points out that the main weakness of conventional commercial banks is the

restriction implied to own properties in the US. As Islamic banks deal with equity ownership and

the said restriction will doubt Islamic banks from establishing in that country. This restriction will

effect Islamic banks financial instruments like Murabaha (cost-plus financing) and Bai Bithaman

Ajil (deferred payment financing). The regulation does not prohibit the Ijarah (lease financing)

agreement because leasing is the common feature of commercial banks in US. The regulations has

prohibited from any Islamic banks starting in US. In order to serve the needs of the Muslim

community, LARIBA finance house has been established since 1987 in the city of Pasadena,

California. They have expanded their operations all over US and be lending small and medium

ventures through Ijarah (leasing) and Musyarakah (joint venture) model

(http://www.lariba.com/company/index.htm). HSBC has launched their Islamic banking

subsidiary HSBC Amanah to provide interest free services and products to the Muslim community

in the US. The competition is not only limited to conventional banks and Islamic bank in the

Islamic countries but on the western turf. As the openness of the new regulations will create more

pressure for the existing conventional banks in the western nations especially US.

The western countries are researching ways to incorporate Islamic Banking to their banking

framework. Muslim countries such as Pakistan, UAE, and Malaysia are trying to create a more

stable and stronger Islamic banking framework that can compete with the likes of international

Is Islamic Banking for India? What are the key factors affecting the sector

21

financing and investment arena. Malaysia aspires to be the global Islamic banking hub by utilizing

by taking advantage of Labuan Offshore Financial Centre (LOFSA) which is confirmed by the

Governor of central bank of Malaysia Dr. Zeta Akhtar Aziz at the ASLI’s World Islamic Economic

Forum in Kuala Lumpur in October 2005. She says that Islamic bank proves more attractive not

only to the Muslim community but to Non-Muslims as well, this reflects the competitiveness of

Islamic banking over conventional banking. Malaysia has liberalized its regulation for foreign

Islamic banks to establish in Malaysia. Since then there are three established Islamic foreign banks

which has been granted license to operate. This step supports the argument made by Mishkin

earlier that the entry of foreign banks contribute to the financial stability of the country due to their

prudent, risk management capability and technological advancements which will help to cushion

against any domestic shock in the future.

The regulatory measures differ from country to country. It is predicted that the Islamic bank will

attract 40% to 50% of the total saving of the Muslim population to the economy that they are

operating. The ethical investors will become more interested in conventional banks which has

respectively established Shari’ah compatible banks in those countries, they have identified as

potential markets (Hawary et al, 2004). The above results satisfies Khan’s argument that

conventional banking subsidiaries are tapping into the Islamic banking market. This concern has

its oen merit and has been proven over the last two decades. One such example is HSBC Amanah

who not only established themselves in Middle-east but in Asia, Europe and America, they have

increased their presence to the current 20 OIC countries which also competes with local Islamic

banks. Another example of western bank tapping into Islamic bank market is the Citi bank and is

termed as the largest Islamic investment bank in the world.

The above research proves that Islamic banking is not only meant to Islamic communities but for

the Non-Muslims as well. It has more global appeal for investors and borrowers, the Islamic

Banking potential is quiet high and they have to reposition themselves in the domestic and

international market to be a competitor in the current and future banking industry.

2.4 Customer acceptance on Islamic banking

Customer acceptance has been a prime factor in the case of Islamic banking, there is always a

cloud of doubt that Islamic banking is just for the Muslim community but it is not true any

personnel who want to invest in ethical investment can bank with Islamic bank. The Islamic banks

Is Islamic Banking for India? What are the key factors affecting the sector

22

provide ethical investments as we have discussed earlier because they work in the Shari’ah contest

which prohibit them from collecting any Riba (interest). It is no doubt the majority of bank’s

customer is from the Muslim community but all countries it operate is not highly populated Muslim

countries. The above statement proves that Islamic banks also deal with non- Muslim customers

as they are potential customers for Islamic bank as well. The competition for new customers in the

market are one sided as conventional banks coming up with their Islamic bank subsidiaries to gain

a share of the market domestically and internationally. This situation was acknowledged by Haron

et al (1994) on their research in Islamic banks in Asia. The study has determined three of the

following factors.

Banking Preference of Muslim and Non-Muslim.

Factors that influence their selection and the diversity.

Perception of the benefits of service offered.

The study concludes that there was no noticeable difference on their selection criteria and

preferences. Therefore there is a notion that Islamic bank products are niche and cannot be hugely

depended to attract new customers as many people intention and motivation to bank highly varies.

Time is the key factor of any modern banking, banks are coming with latest technology for time

cuts to provide excellent services. Nowadays customers focus on this principle as time is a key

factors and customers depend on banks which can provide fast feedback to their requests and

transactions.

Consumer inclination towards Islamic bank products depend on their availability and feasibility

and how fast the delivery channels are. The level of involvement is quiet low for the financial

products as customers are aware of the basic features of the product and services. This behavior is

known as repeat-passive where their pattern of purchase is always repeated and describes

customers are loyalty behavior (Beckett et al, 2000). The main reason for this situation is the

relation of the bank to the customers and also the influence of the community and family members.

Becket et al (2000) further strengthen the concept by putting forward that customers’ loyalty to

the bank was due the switching costs involved in the process. Differentiation were one of the other

key factors that customers do not change their banks very often. The Islamic banking customers

are normally motivated by convenience the bank provides and the inertia to forge new relationship

with unknown new bankers. Crowe et al (2006) found out that new products like credit card, debit

Is Islamic Banking for India? What are the key factors affecting the sector

23

card and other services helps to determine their choice as they are major products in today’s life.

Credit card, debit card and mobile banking is on the top priority of modern customers as time is of

great importance. In countries like UK the payment through credit cards or debit card is a norm

and widely used and it has proved to be a potential part of banking service globally.

The competition in any industry is high as every company compete globally, for a customer to

highly successful in the market and to stay ahead in competition they have to adapt and promote

products that satisfies their customer needs and it does not go out of their banking principles

(Kotler, 1988 and Mclver & Naylor, 1986). The study conducted by Zainuddin et al provides the

difference in perception between users of Muslim community, Non-Muslim and non-users over

the Asia Pacific. The data obtained from the research was of key importance to the Islamic banks

as they were able to understand the needs of the customer and to decide their products and market

them in a manner to attract potential new customers and to retain their existing customers. It was

also noted that those who were married tend to have more saving habits and had more information

of Islamic bank products than those who were single as their spending habit was high and less

income. There is a notion that previous studies made by different authors was supported by the

influence of the community, family members and friends. In research conducted in South East

nations the research is mostly influenced by family members and closed social group as the bond

is high and this are the key factors which helps in the marketing of Islamic banks.

The educational level plays a major role for customer banking with Islamic banks. A study made

by Metawa and Almossavi (1998) on two UAE based Islamic banks they found out that the

customer base of Islamic banks are educated personals. 40% of the customers had a diploma and

a 50% of its customers hold a bachelor degree. This indicates the statement regarding Islamic

banking customers as most of them are mostly educated and holds a stable income. Education

proved to help the banks customers to understand the value and benefits of banking with these

banks. They were able to understand the total Islamic banking concept than the less educated

population. Being a Muslim nation the awareness of Islamic banking is not high in UAE and many

other Asian nations such as Pakistan and Muslim populated countries like India and China. It is

said that above 30% of the population is not aware of the Islamic Banking concept and more than

two third does not use its facilities. This proves that the community and region alone does not

promote these banks as they have to come up with strong marketing ideas to attract potential

Is Islamic Banking for India? What are the key factors affecting the sector

24

customers. Islamic banking has to come up awareness program to promote and market them to

their full potential. The conventional banks are highly aggressive and well-motivated in promoting

their products and services, if Islamic banks fails to market their products with the same

aggressiveness they will lose the competition. The conventional banks needs their customers to be

well informed in order not to lose their business.

Is Islamic Banking for India? What are the key factors affecting the sector

25

Chapter 3

Methodology of Research

3.1 Research Questions

The research question was based on understanding their conventional banks of the Indian banking

system and to determine how they differ from banks in the foreign markets. The questionnaire was

also focused to determine the level of competition an Islamic bank is going to face when they start

their operations in the Indian banking industry. When Islamic banks were introduced at first it was

considered as a complimentary system to support the conventional banks, but their differentiation

has made a huge impact on how consumers expect these banks to operate and how their product

ensured security and returns. Indian banking industry is complex and is one of the major banking

industry which regulates the entry of foreign banks into the banking scene other than through

merger or acquisition. The questionnaire also focus on customers view about these banks as

religious funding houses or is it considered to be a major investment opportunity. Various

evidences are proving that Islamic banks are being highly aggressive in competition to get its share

of Muslim customers in Muslim populated nations and in the European and western countries. The

literature review looks into the arguments raised by scholars and practitioners alike.

3.2 Case Study

Many debates and case studies were considered in this research to derive the current status of

Islamic banking in India and the government decision to set up new legislation so as to include the

Islamic banks in to the Indian banking scene. Arguments raised by conventional banks and other

religious institutions and economists alike on the Islamic banking concept in India. The plans

government wishes to be carried out if they are able to incorporate Islamic banks into the economy

and gather the potential funds into the market to accelerate the companies development. Reviews

on Islamic finance houses that currently operate as non- banking institutions.

3.3 Interviews

A closed social group of Indian students were asked about their views on Islamic banking concept

and how they consider this bank differ from the Indian banks and their potential in a market like

Is Islamic Banking for India? What are the key factors affecting the sector

26

India and the likeness to bank with such banks if they start operating in India. A group of

businessmen and investment bankers were ask how likely they will invest with Islamic banks and

will they share the risk and bank with Islamic banks. The demand for these banks in the current

Indian market. Another group of salaried persons were asked the above same questions to

understand the success rate of Islamic bank in a nation like India which holds the second largest

Muslim population globally. The interview has proven to be a valuable addition.

3.4 Research methodology

In order to ascertain the level of competence and customer preference that Islamic bank has in

India an Islamic finance house Cheeraman Financial Services is considered, this is the only current

fully fledged Islamic finance house operating in India. Questionnaire were designed for the

following.

1. Managers of Banks and finance houses.

2. Customers of the finance house and other banks.

3. Case studies

4. Online Interview of social groups

In many research carried out in the past there were not much data regarding an operational Islamic

financial house and views of practitioners of conventional banking was considered, it just floated

around the religion and politicians. Over the years Islamic bank has shifted focus and has being

noticed by potential investors and international Islamic banks as they have recognized the great

benefit and unexplored potential of the market. The practitioners were considered especially the

managers when the questionnaire is designed as they are the first person to opinion regarding the

financial instruments. Market them at a wake of a competition or decline in the performance of the

bank.

3.4.1 The Bankers

The questionnaire to the bankers was of key importance as they were able to explain the

competition in the financial industry and threats that can be raised Islamic banks to the current

banking system and how they plan to differentiate and compete with Islamic banks. The

questionnaire helps to determine how bankers cover various aspects of influences that trigger for

stiff competition in the banking industry in India. The influences were considered on Porters

Is Islamic Banking for India? What are the key factors affecting the sector

27

strategic competitive analysis method for determining the level of competition in the particular

industry. The level of competition is based on considering the factors like customers, providers,

barriers to entry, externals and repositioning of their organization. These are the main five forces

of competitive strategy that porter advocate and are broadly used by many industries to formulate

their competitive strategy.

3.4.2 The Banks Customers (CFSL)

A second questionnaire is also created for the customers of financial house in order to understand

the level of acceptance of these institutions and preference of Islamic banking against the

conventional banks. The questionnaire helps to point out the current inclination and customer

knowledge of Islamic banking concept in the Indian market. The questionnaire was translated to

Malayalam language to increase the sample pool and to gain a more clarified result. The other

reason for preferring Malayalam is their traditional language and first language to many South-

Indians over English.

3.4.3 Case Studies

Various case studies regarding the current debate on the whole Islamic banking concept is taken

into consideration, in order to determine the direction of progression and the solution derived by

the government. Views from non- Muslims and other practitioners on Islamic banking and benefit

and threat to the market. How the bank can be considered to operate within the existing banking

system and who all can bank with these banks, considering the success of Islamic banks in

European and Western nations and how any nations incorporating Islamic bank into their banking

industry.

3.4.4 Interviews

Interviews have been a key to understand the views of different sample social groups. Groups of

students, investors and salaried people were interviewed to understand what they expect from these

banks and how they consider these banks to change the Indian Banking industry within a short

period of time. How these banks can support their projects over time.

Is Islamic Banking for India? What are the key factors affecting the sector

28

3.4.5 Sample Size

The sample size for the bank managers are very limited based on the availability and of key banks,

total of 10 managers were considered from different financial houses and 25 customers were

considered for the questionnaire from various background to suit the result and group of three

different sector of people was considered for online interviews to ascertain the expectations of the

potential customers and the success or failure of these banks. How they react to the aggressive

marketing strategy of the conventional banks and how often they bank with these banks. There are

more than 10 banks and financial houses in India who are the key players. Questions have been

carried out to the managers and some customers in the conventional banks. The main players are

listed below:

1. HDFC

2. Industrial Development Bank of India

3. State Bank of India

4. State Bank of Travancore

5. South Indian Bank

6. Federal bank

7. ICICI

8. Axis bank

9. Muthoot Fin Corp

10. Cheraman Financial Service Limited(CFSL)

These financial institutions has been major market players and have been preferred by many

business and industries nationally. Their view on the competitive edge and current competition on

the market, how Islamic bank can possess threat to them is discussed to better understand the

Indian banking scene.

3.4.6 Limitation

The basic limitation was the quantity of sample size and the research is based on an international

land, the research data has not been up to the exact expectations. In a country like Indian there are

more than 20 languages and understanding every person’s view was a bit difficult so samples have

been selected from people whose language was understandable. Financial data relevant for the

Is Islamic Banking for India? What are the key factors affecting the sector

29

research has been downloaded from the CFSL institution website and current financial year data

has not yet been audited. The financial institution has started the operation recently and is India’s

first Islamic finance institute. The success or failure of this institution marks the starting of Islamic

banking in India. Furthermore the Islamic finance institute broad view of management cannot be

taken too strong as they just have been established over a year. The Limitations are high.

Is Islamic Banking for India? What are the key factors affecting the sector

30

Chapter 4

Background of Indian Banking Industry

4.1 Banking Industry in India

Indian bank has been the back bone of Indian economy even it faces slow growth and plague of

bad loans, Indian banking industry was the only industry which stood unaffected during recession

and has been going strong ever still. It has come across many difficulties over the period of foreign

rule, partition of India and now it stand high too face banks of the modern world. The historic

bankers of India were the money lenders who lends money at a higher interest rate based on

securities, they slowly diminished with the introduction of co-operative banks and commercial

banks. In the Indian banking industry the co-operative banks and commercial banks stands side by

side to support the development of the Indian economy and helps the agricultural and rural

development to accelerate the growth of infrastructure and the standard of living of the people.

Basically the earlier profession of Indians are farming and government are providing various

benefits to the farmers to uplift the farming industry.

The co-operative banks are governed by the respective co-operative acts of state government.

Since banks became regulated by the RBI after 1st March 1966, the co-operative bank were also

regulated by the RBI after amendment to the Banking Regulation Act 1949. The Reserve Bank is

responsible for licensing new financial institutions and making amendments in the banking sector

of India. RBI controls the rate of interest, credit limit of banks and lending limits to industries.

Banking originated in India in the 18th century when the General Bank of India came into existence

in 1786, followed by the Bank of Hindustan. Both these banks are not functioning, after this Indian

government established three presidency banks which was later amalgamated into Imperial Bank

of India which is the current State Bank of India.

The current industry is crowded by a lot of banks most of them are private commercial banks

which have been owned by international banks. The current private banks are earlier public banks

which were not performing to the potential as these banks has been revived through privatization.

The competition in the Indian banking industry is higher than ever as many private commercial

banks entered the market and the threat of entry from Islamic banks and foreign banks is high. The

Is Islamic Banking for India? What are the key factors affecting the sector

31

Indian banking market is often said as not exploited to the best potential and banks have been

developing products to attract the customers to the banking scene to derive more money into the

market. India is globally known for the hold of black money it possess in various international

banks. Government has been coming up with new legislations to bring these money into the Indian

market.

The current projects of the Indian government wishes to make India a superpower by 2020 and the

project is named “VISION 2020”. The government expect to complete the project with the help of

the banking industry and to accelerate it further the government is allowing foreign investment

which is a great threat for Indian banks as new bankers will be coming into the scene. The banking

industry needs to evolve further to meet the expectations of the public even they provide service

any foreign banks can provide, the main difference between international banks and Indian banks

is basically the interest rate. Indian bank charges higher interest rate than the foreign banks and

Asians especially Indians are well known for their saving habit. The cash flow of India banks are

high the only remark is bad loans which is due to the bias information in the economy and illegal

money lenders who launder unaccounted money into the economy causing inflammation in the

economy. When these factors have been sorted out India can reach its dream. The government has

ordered to make all financial transactions through banks to industries, so that they can keep track

of funds in the economy and nowadays to increase banking whole over the nation. The government

is starting national accounts for all its citizens and providing their pension and other benefits to

this account and citizens will start banking. It will also help to keep out the illegal money into the

economy thereby accelerating the growth of the nation and accelerating the growth of banking in

the nation.

The Islamic banking is welcomed by the RBI and has given special legislation to work as NBFI

(Non-Banking Financial Institutions) in India, The government is researching how to incorporate

Islamic bank into the current regulations. Changes to be made so that both the industry and the

government will be benefited with Islamic banking as the government plans to level their £147

billion deficit by tapping into the Muslim community resource. Basically these banks are reported

have improving the living standard of its customers where they operate and India needs such a

support so that can give the best to its people. Many Islamic banks has already expressed their

interests join the Indian banking scene to help the government to make the project success.

Is Islamic Banking for India? What are the key factors affecting the sector

32

4.2 Industry size

The industry size of the Indian banking system can be pared with the well developed economies

as the growth of Indian banking industry has been qualitative then competitive. The threat of new

entry is really low until the government or the regulatory body soften the rules for their entry. The

Banking industries is mostly privatized except for the gramin banks, co-operative banks, and

PBS’s which act as the main government public bank after Reserve bank of India. Indian

dependency on its commercial bank is really high to accelerate the GDP. Foreign banks can only

enter the market through mergers and acquisition.

In 2012 the Indian parliament passes the banking laws amendment act which made the RBI the

final word on issuing new lines as this gives a greater scope for many banks. The landscape of the

banking industry has been entirely changed by the new bill. The style and mode of operation of

banks are entirely changing it is said that in the next 5 to 10 years, the industry is to develop 2

million new jobs driven by the efforts of the government and RBI. Two new banks have been

allowed by the RBI and is creating new ways to spot bad loans and to deal with rogue borrowers.

The market size of Indian banking is valued at £1.1 trillion in February 2013 and is expected to

reach £25.8 trillion in February 2015. The compound annual growth rate of banks from February

2006-2013 was is 21.2%. The total deposits were amounted to £1 trillion on February 2013. As it

can be clearly understood that the development of Indian economy is quiet high and it has still to

be explored. India’s domestic banks Like Jammu & Kashmir bank is trying to establish its branches

in London and Dubai to enhance the relationship of the bank with current customers, who have

business interest in West Asia and Europe. It is said that Indian banking industry has the potential

to be the fifth largest banking sector globally by 2020 and to be the third largest by 2025.

Nowadays banks in India are turning their attention to technological advancements and servicing

clients as it the wake of new competitors.

Currently Indian domestic banks are tapping into the foreign market as they have been

technologically advanced and to develop their interests into the foreign market. The banking sector

finds the regulatory bodies have reduced the strict regulations and been coming up with product

innovation in order not be shattered when competition from big banks threaten the market.

Is Islamic Banking for India? What are the key factors affecting the sector

33

4.3 Regulatory Body

The main regulatory body of Indian banking is the Reserve Bank of India which is the central

banking institutions. It controls the monetary policy of the Indian currency. The reserve bank was

nationalized in the year 1949 after India gained independence on 15th August 1947. The RBI plays

an important role in the major economic development of the nation and has been supporting the

government on financial matters. The RBI regulates the entire Indian banking industry and is a

member of the Asian clearing union. The general administration and supervision of the reserve

banks is entrusted to 20 member Central board of directors. The 20 member board of directors

consist of a Governor, 4 Deputy Governors, a finance ministry representative, 10 government

nominated directors to represent the various important elements of the Indian economy and 4

directors to represent the local board headquartered at Indian metros.

Under section 22 of the Reserve Bank of India Act 1934, the bank has the sole right to issue bank

notes of all denominations. It is the issue of currency in India, it has an issue house whose liabilities

and assets are kept separate from the banking house. The bank regulates and supervised the finance

sector. It designs the financial system of the nation in order to maintain public confidence in the

system, promote and protect depositor’s interests and providing cost effective banking to the

general public of India. The Banking Ombudsman scheme has been formulated by the RBI

(Reserve Bank of India) for an effective addressing of customer complaints. The RBI controls the

GDP, monetary supply and the design of the currencies. The co-operative banks of India are not

entitled to set up branches according to their discretion as the RBI governs them. Section 35 of the

Indian Banking Act entitles RBI to conduct inspection of banks on its own consent or by the

direction of the central government. This will ensure customers will get the best of their banks and

any fraudulent activities will not be promoted by bank as if found guilty they will lose their banking

license.

The RBI of India has announced new measures in the Bi-monthly monetary policies on June 3,

2014 in which the foreign exchange limit has been raised to £75000 from the previous £45000

limit. RBI has also soften the rules for credit to exporters as exporters are entitled to receive long

term advance credit from banks for a maximum period of 10 years to service their contracts.

Exporters who wish to receive finance from the banks should have a satisfactory record for three