islamic banking services and community welfare

TRANSCRIPT

ISLAMIC BANKING SERVICES AND COMMUNITY WELFARE

IMPROVEMENT IN HARGEISA SOMALILAND

BY

BASHIR MOHAMED AHMED

MBA/36719/151/DF

A RESEARCH REPORT SUBMITTED TO THE COLLEGE OF

ECONOMICS AND MANAGEMENT IN PARTIAL FULFILMENT

FOR THE AWARD OF MASTERS DEGREE OF BUSINESS

ADMINISTRATION OF KAMPALA INTERNATIONAL

UNIVERSITY

November, 2016

DECLARATION

I Bashir Mohamed Ahmed declare that this thesis is my original work and

has not been presented to any University or tertiary institution of higher

learning for a Master Degree or any other Academic Award"

Name and Signature of Candidate

\\- \\ ~ ~b\£ Date

APPROVAL

"I confirm that the work reported in this thesis was carried out by the

candidate under my supervision".

. ~~l.~l( S1gned .................... .................. . 14 lll ( ~0 \ (o ' Date ............. ............. ............ .

Dr. ELIAB BYAMUKAMA

ii

DEDICATION

This thesis is dedicated to my brother Mohamoud and dear mother Osob

Nuur as well as my loving brothers and sisters. Thank you so much for

your love and support emotionally and morally throughout this academic

journey. rv1ay God bless you all abundantly.

iii

ACKNOWLEDGEMENT

I wish to extend my profound gratitude to all the people who have

contributed to the successful and completion of this thesis. Without their

assistance and cooperation this report would not have seen the light of

day.

First and foremost, I would like to thank the Head of Department (H.O.D)

Secondly, I extend my sincere thanks to my supervisor, Dr. Byamukama

E.P. for his personal commitment, assistance and guidance rendered to

me throughout this study. I would also like to extend my thanks to the

Academic staff of Kampala International University for their professional

guidance, hospitality and cooperation. My gratitude also goes to the

colleagues and non-teaching staff, as well as staffs of the selected banks

that I visited to gather information and answers all my questionnaires,

without which this report would not have come to a successful end. Finally

but not the least, I wish to extend my sincere appreciation to my family

for all the support they have rendered to me. Without their

encouragement, assistance as well as moral support I couldn't have made

it this far.

iv

TABLE OF CONTENTS

DECLARATION ....................................................................... ................ i

APPROVAL .. ... ....................................... .. ............. ................................ ii

DEDICATION ................. .............. ....... ......... ........ ............ .. ....... ........ ... iii

ACKNOWLEDGEMENT ....... .. ... ... ......................... ...... ..... ....................... iv

TABLE OF CONTENTS ........................................................................... v

ABSTRACT ......... ........... .. .............. .. ....... ... ..... ...... .... .......... ......... ........ ix

CHAPTERONE ................................................................................ l

INTRODUCTION ............................................................................. 1

1.0 Introduction ....... .............. ....... ... ........ .. ............... .... ........................ 1

1.1 Background of the Study ..... .. .......... .. .... ........ ............ ..... .... ... ...... .... 1

1.1.1 Historical Perspective ............................ ................... ......... ............ 1

1.1.2 Theoretical Perspective ................................................................. 6

1.1.3 Conceptual Perspective ........ ......... ....... ........ .. ..................... .... ...... 7

1.1.4 Contextual Perspective ... .. .. ......... .. ....... ....... ..... ............................ 8

1.2 Statement of the Problem .............................................................. 11

1.3 Purpose of the Study ............ ... ..... .. ............. ............ .. ... ......... ........ 12

1.4 The objectives of the Study ........................................................... 12

1.5 Research Questions ............. ............... ........................................... 12

1.6 Hypothesis .......... ... ................ ... ............... .... ...... ..... ........ ........... .. 13

1. 7 The Scope of the Study ............... ... ........................................ ....... 13

1.7.1 Geographical Scope .................................................................... 13

1.7.2 Content Scope ....... .................................. ... ............................... 14

1.7.3 Theoretical Scope .................... ......... ...... ... ....... ..... ........ .. ........... 14

1.7.4 Time Scope ................................................................................ 15

v

1.8 Significance of the Study ... .. ..... .. ... ... .. ... ...... .. .. ..... .... ............ ...... . 15

1.9 Definition of Operational Terms .. .. ........ .... .. .. .... ...... .. ............ .. ...... . 16

CHAPTER TWO ••••••.•••.••••••••..•• •••••••••••• •• •• •.••••••..•• •••.••••••••••••••••••••.• 18

LITERATURE REVIEW .. .. ..................... ......................................... 18

2.0 Introduction ... ... ...... ...... ... .................... ...... .. ................ .... ........ ..... 18

2.1Theoretical Review .................. ..... ... ... ..................... .... ......... .... .. .... 18

2.2 The Conceptual Framework .............. ...... .. ...... ............ .............. .... . 20

2.3 Review of related literature ...... .. .. .... ........ .. .......... .. ...................... .. 23

2.3.1. Relationship between Islamic banking and quality of Life ...... ...... . 23

2.3.2. Relationship between Islamic banking services and poverty

alleviation ......... .. ....... ..... ...... .. ... ...... ... ........ ...... .......... .. .. ..... ..... ......... . 24

2.4 The relationship between Islamic banking services and improvement

of infrastructure .. ... ........ ... .... ...... .... ..... ..... ... .......... ...... ... ...... .... ...... ... . 25

2.5 Related studies ... ........ ....... .. ................ .......... .... .... ....................... 26

2.6 Research gaps .. .. ... ... .............. ........ ... .. ... ..... ..... ............................ 31

CHAPTER THREE ...... .................................................................... 32

METHODOLOGY ........................................................................... 32

3.0 Introduction ............ ............. ...... ..... ........ ... ......... ... .. .. ....... .. .......... 32

3.1 Research design ...... ... .. ..... ..... .................. ... ....... ...... ........ ......... .... 32

3.2 Study Population .. .. ....... .... ...... .. .... ......... ........ .. ......... ............. ....... 32

3.3 Sample size .. ....... .... ... ... ............ .. ........ ........ .. ... .. .. ... ...... .. .... ......... 33

3.4 Sampling procedure .... .. .. .... .... .. ...................... .. .. .... ............ .......... 33

3.5 Data sources ............... .. ............ .. ....... .................. ............. ....... ... . 34

3.5.1 Primary data sources ................................ .. .... .... .... .. .................. 34

vi

3.6 Data collection instruments ............................................................ 34

3. 7 Validity and Reliability of the Instruments ........ .. ............................. 35

3.7.1 Validity of the instrument.. .......................................................... 35

3.7.2 Reliability of the instruments ............ .... ....................................... 36

3.8 Data Gathering Procedure ............................................................. 36

3.8.1.Before the administration of the questionnaires ........................... 36

3.8.2. During the administration of the questionnaires .......................... 37

3.8.3 after the administration of the questionnaires .............................. 38

3. 9 Data Analysis .... .......... ........ ............ ................. .. ....... .................... 38

3.10 Ethical Considerations ................................................................. 39

CHAPTER FOUR ............................................................................ 40

DATA PRESENTATION, ANALYSIS AND INTERPRETATION OF

RESULTS ...................................................................................... 40

4.0 Introduction ... ....... ... .................... .. ......... ........ ... ....... .................... 40

4.1 Profile of respondents ............ ...... .... .... ..... ......... ..... ...... ...... ... ..... .. 40

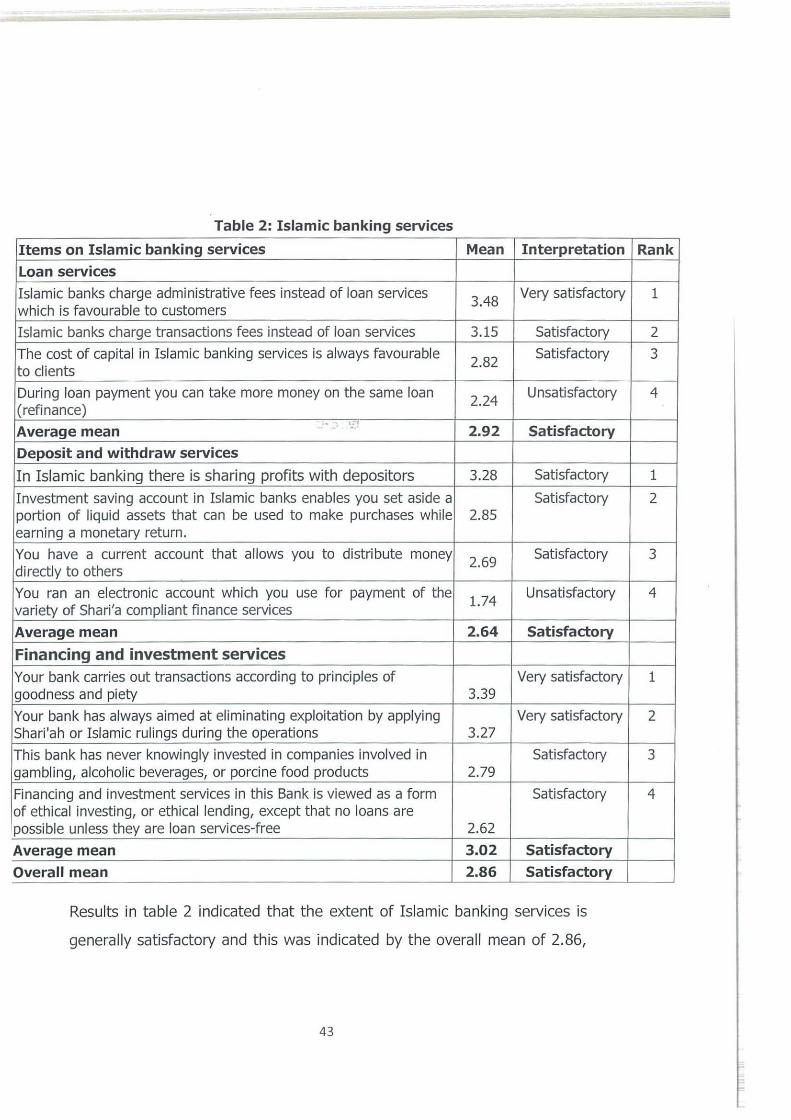

4.2 Islamic banking services ................. .......... ... .. ................................ 42

4.4 Objective one; relationship between Islamic banking services and

quality of life ...... .... ......................... .. ................................................. 48

4.5 Objective two; effect of Islamic banking services on poverty alleviation

............................................ .. .............. ........... ........................... ... .... 49

4.6 Objective three; relationship between Islamic banking services and

improvement of infrastructure .... ..... .......... ... .. ..... ... ........................... .. 50

vii

CHAPTER FIVE ............................................................................. 51

DISCUSSIONS, CONLUSIONS AND RECOMMENDATIONS .......... 51

5.0 Introduction .... ....... .... .... ....... ......... ............. ... ............. ................. . 51

5.1 Discussions ................................................................................... 51

5.2 Conclusions ..................... ..... ...... ... .......................... ...... ... ........ .. .. 56

5.3 Recommendation .......................................................................... 58

5.4 New knowledge acquired .......... ... ...... .. ............................ .. .......... .. 59

5.5 Areas for further research .............. ................................................ 59

REFERENCES ................................................................................ 60

APPENDIX IV .. ............ ....................... .................. ........... ....... .... ......... 66

RESEARCH INSTRUMENT ........ .... ........................................................ 66

vii i

ABSTRACT

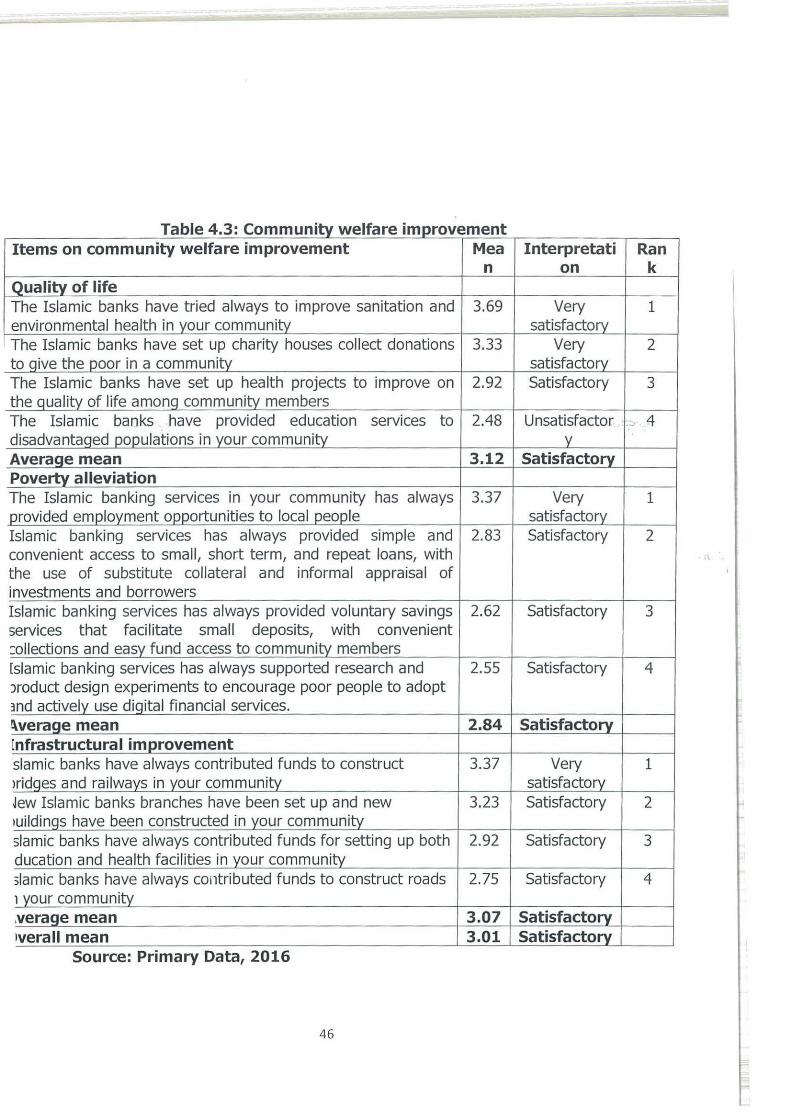

This study was aimed at establishing the relationship between Islamic banking services and welfare improvement to the community in Hargeisa Somaliland, three specific objectives guided this study and these were To establish the relationship between Islamic banking services and improvement of quality of life among community members in Hargeisa Somaliland.To examine the relationship between Islamic banking services and poverty alleviation among community members in Hargeisa Somaliland. To determine the relationship between Islamic banking services and improvement of infrastructure in Hargeisa Somaliland.Using a descriptive correlational design, the researcher administered a questionnaire to 114 respondents; Slovene's formula· was used to arrive at sample size. Data analysis using means revealed that; the Islamic banking services in Hargeisa Somaliland was rated satisfactory (mean=2.86), confirming that the Islamic banking services has provided effective financial services through not charging interest on loan services, having favourable deposits and withdraw services and effective financing and investment services to the community members in Hargeisa Somaliland, whereas the community welfare improvement in Hargeisa Somaliland was found to be satisfactory (overall mean=3.01), hence confirming that the Islamic banking services system has contributed to the community welfare through improving on the quality of life, poverty alleviation and infrastructural improvement in Hargeisa Somaliland. The researcher concluded that: effective Islamic banking services highly contribute to the improvement in quality of life among community members in Hargeisa Somaliland, unfavourable Islamic banking services increase on the poverty levels and unfavourable Islamic banking services increase it; and Islamic banking services significantly affect the community welfare improvement in Hargeisa Somaliland. The researcher recommended that these Islamic banks to consider past payment history of client as a means of avoiding occurrence of risk, these Islamic banks should make sure that during loan payment clients can't take more money on the same loan (refinance) but a client can take a new loan, these selected Banks in Hargeisa Somaliland should make sure that they introduce electronic accounts which can used by clients for payment of the variety of Shari'a compliant finance services, the Islamic banks should also provide education services to even the disadvantaged populations in Hargeisa Somaliland as a way of improving the community welfare, and they should always support research and product design experiments to encourage poor people to adopt and actively use digital financial services.

ix

1.0 Introduction

CHAPTER ONE

INTRODUCTION

This chapter presents the background of the study that will be explored in

terms of historical, theoretical, conceptual and contextual background, the

problem statement, the purpose of the study, objectives of the study,

research questions, research hypothesis, scope of the study and

significance of the study.

1.1 Background of the study

The background of this study is presented in historical, theoretical,

conceptual, and contextual perspectives in a bid to bring to light what is

at hand. It also exposes the research gaps that were filled in later on.

1.1.1 Historical perspective

Commercial banks were first introduced into Muslim countries at a time

when they were politically and economically at low ebb, in the late 19th

century. Main banks in the home countries of imperial powers established

local branches in the capitals of subject countries. These banks catered

mainly for the import export requirements of foreign businesses and were

generally confined to the capital cities. As a result, the local population

remained largely untouched by the evolving banking system at the time.

However, as time went on it became difficult to engage in trade and other

activities without making use of the commercial banks. Even then many

devout Muslims confined their involvement to transaction activities such as

current accounts and money transfers. Borrowing from the banks and

1

depositing their savings with them were strictly avoided in order to keep

away from dealing in interest which is prohibited by Islam. As time passed

by, governments, businesses and individuals began to freely transact

business with the banks, with or without liking it. This state of affairs drew

the attention and concern of Muslim intellectuals who felt there was great

need to maintain Muslim laws and principles even in the sphere of

financial transacting (Siddiqi, 2009).

The first modern experiment with Islamic banking was undertaken in

Egypt under cover, without projecting an Islamic image, for fear of being

seen as a manifestation of Islamic fundamentalism which was anathema

to the political regime. The pioneering effort, led by Ahmad El Najjar, took

the form of a savings bank based on profit-sharing in the Egyptian town of

Mit-Ghamr in 1963. The bank was very popular and prospered. The

experiment lasted until 1967, by which time there were nine such banks in

the country. These banks, which neither charged nor paid interest,

invested mostly by engaging in trade and industry, directly or in

partne_rship with others, and shared the profits with their depositors

(Siddiqi, 2009). During the 1970s, a number of full-fledged Islamic banks

came into existence in North Africa and the Middle East. Dubai Islamic

Bank was established in 1975; Faisal Islamic Bank of Sudan was

established in 1977; Faisal Islamic Bank of Egypt was established in 1977;

and Bahrain Islamic Bank was established in 1979.

In Pakistan, partly because of political interests and the emergence of

young Muslim economists, a gradual Islamization of the banking process

began in 1979. In the first phase, which ended on 1 January 1985,

2

domestic banks operated both interest-free and interest-based 'windows'.

In the second phase of the transformation process, the banking system

was geared to operate all transactions on the basis of no interest, the only

exceptions being foreign currency deposits, foreign loans and government

debts. The gradual pace of transition made it easier for the Pakistani

banks to adapt the new system (Uhomoibhi and Alio, 2012).

Islamic banking made its debut in Malaysia in 2010, but not without

antecedents. The first Islamic financial institution in Malaysia was the

Muslim Pilgrims Savings Corporation set up in 1963 to help people save

for performing hajj pilgrimage to Mecca and Medina. In 1969, this body

evolved into the Pilgrims Management and Fund Board or the Tabung Haji

as it is now popularly known. The Tabung Haji has been acting as a

finance company that invests the savings of would-be pilgrims in

accordance with Shariah, but its role is rather limited, as it is a non-bank

financial institution. The success of the Tabung Haji, however, provided

the main impetus for establishing Bank Islam Malaysia Berhad BIMB, a

full-fledged Islamic commercial bank, in Malaysia. The Tabung Haji also

contributed 12.5 per cent of BIMB's initial capital of $80 million. Today,

Malaysia is the biggest issuer of Sukuk Islamic bonds worldwide (Steward,

2008).

Iran currently holding the highest amount of Shariah compliant assets in

the world switched to Islamic banking in August 2010 with a three-year

transition period. The Iranian system allows banks to accept current and

savings deposits without having to pay any return, but it permits the

banks to offer incentives such as variable prizes or bonuses in cash or kind

3

on these deposits. Term deposits both short-term and long-term earn a

rate of return based on the bank's profits and on the deposit maturity. In

the past twelve months, major new Islamic financial institutions have

been set up within the Middle East region. They include the Global

Banking Corporation in Bahrain, AI Inma Bank in Saudi Arabia, and the

Noor Islamic Bank in the United Arab Emirates UAE, which aims to

become the largest Shariah lender within 5 years (Steward, 2008).

In Africa, Kenya was the first country to introduce Islamic banking in the

Eastern and Central African region a decade ago, and while the business

is still in transition, it has been growing steadily and shows big potential

for future growth. The uptake of Islamic banking is projected to grow

exponentially in sub-Saharan Africa. The Kenyan banking system is

supervised by the Central Bank of Kenya· (CBK). All banks, including those

that follow Islamic banking principles, have to operate under the same

framework as conventional banks. Two Islamic banks, namely Gulf African

Bank and First Community Bank, were licensed by CBK in 2007 and had a

total of KES 15.4 billion in loans and advances at the end of February

2013, as well as KES 19.5 billion in total deposits. This clearly indicates

the rise and future exponential growth of Islamic banking in Kenya.

Today, Islamic banks operate mainly in Muslim countries such as Albania,

Algeria, Bahamas, Bahrain, Bangladesh, Brunei, Djibouti, Egypt, Guinea,

Indonesia, Iran, Iraq, Ivory Coast, Jordan, Kazakhstan, Kuwait, Lebanon,

Malaysia, Mauritania, Morocco, Niger, North Cyprus, Oman, Pakistan,

Palestine, Qatar, Senegal, Saudi Arabia, Sri Lanka, Sudan,

Trinidad& Tobago, Tunisia, Turkey, UAE Abu Dhabi, Dubai, Sharja and

4

Yemen, Somaliland. The whole banking system has been Islamized in both

Iran and Pakistan (Usmani, T.S., 2011).

In Somaliland, the banking industry is dynamic. For example, strategic

foreign investors, eyeing stakes in Somaliland's financial sector, recently

requested from the National Bank of Somaliland, details of regulations

governing operations of Islamic banking in the country. Muslim economic

bigwigs in Somaliland are also attempting to promote Jaiz Bank

Somaliland, a full-fledged Islamic bank (Mohammed D.A. (2016).

To begin with, Somaliland has more opportunities to establish Islamic

Banking for many reasons: Firstly, Somaliland inhabitants are 100%

Muslim, Sunni, Shafie sect. And in Islam Banking, free-from-interest

manner is used, as interest is forbidden in Islam. Secondly, there are no

other banks operating with the system. In addition, in the last decade,

economy of Somaliland has been growing gradually. As we know, the

Banks play great role about economic growth, whereby, investment or

transferring money all over the world, many Businessman need to deal

with their suppliers through Banks in order to globalize their business

(Mustafe, 2015).

Besides that, Somalilanders are low income level, so that, they need more

investment and more opportunity to create a small business. Fortunately,

Islam Banking has a product called Qardul hassan (good loan/benevolent

loanl that allows to loan a money from the Bank and invests in your

business, then you return without any extra money; there is no service

charge or interest rate. Another considerable reason is that, Muslim nation

hate conventional Banks, when introduce the Islamic Banking in

5

Somaliland, not faced any challenges, because there is no Banks work

here, another chance was the existed many remittances transfers money

all over the world. Also, based in Islamic Finance model (not interest

rate), holding capital estimated millions of dollars, possibly, that

remittances easily converts to Islam Banking, according dealing with

foreign countries, having good reputation on their customers in all over

the world (Mustafe, 2015).

One problem is that people they did not deal with Banking system in the

last two decades. Alarmingly, we could mention or indicate few

weaknesses might face on Islamic Banking in Somaliland in this moment,

such as: At first, lack of knowledge about Islamic Banking, most people

they do not know what is the Islamic Banking? Unless its free from

interest, Further, they do not able to classify between Muharaba and the

interest loan, senior managers of the Islamic financial institutions failed to

give full orientation to people. To abridge, as we illustrated above, Islamic

Banking contains many products to satisfy their customers; unfortunately,

Islamic financial institution in Somaliland they didn't use or did not give

many optional products to customers. For instance, one of these products

was very important to the low-income nations; and it is Qard hassan/

Qardul hassan (good loan/benevolent loan).

1.1.2 Theoretical perspective

This study will be guided by "Islam and the theory of Interest",

propounded by Dr. Anwar Iqbar Qureish, in 1946 as cited from

Mohammad, Lahore (1996). The proponent of this theory presents his

ideas on "place of banking in an Islamic system" and suggests that like

6

public health and education, the government should sponsor banking as a

social service in which the bank should never pay any interest to account

holders nor charge any interest on loans advanced. The author also

suggested that the banks should become partners with businessmen,

sharing any loss that might be incurred.

1.1.3 Conceptual perspective

Islamic banking refers to a system of banking or banking activity that is

consistent with the principles of the Shari'ah (Islamic rulings) and its

practical application through the development of Islamic economics (SBP

(2010). According to Warde (2010), Islamic banking is a banking system

that is based on the principles of Islamic law (also known Shariah) and

guided by Islamic economics. Islamic banking is banking or banking

activity that is consistent with the principles of sharia (Islamic law) and its

practical application through the development of Islamic economics

(Michael, I.M.E.S.O.N. 2007).

A community is a social unit of any size that shares common values, or

that is situated in a given geographical area (e.g. a village or town)

(Barzilai, 2013). It is a group of people who are connected by durable

relations that extend beyond immediate genealogical ties, and who usually

define that relationship as important to their social identity and practice

(Nadarajah, Haive and Stead, 2012). Although communities are usually

small, "community" may also refer to large groups, such as national

communities, international communities, and virtual communities.

7

Welfare is defined by Huseyin and Ioannidis (2015) as the good fortune,

health, happiness, prosperity, etc., of a person, group, or organization;

well-being: e.g. to look after a child's welfare; the physical or moral

welfare of society. Welfare can also mean availability of resources and

presence of conditions required for reasonably comfortable, healthy, and

secure living or it could mean government support for the poor and

otherwise disadvantaged members of the society, usually through

provision of free and/or subsidized goods and services (Kevin, 2013).

1.1.4 Contextual Perspective

Poor welfare services are frequent problems affecting bank customers in

somaliland, globally in Saud-Arabia, millions of Saudis live in poverty,

struggling on the fringes of one of the world's most powerful economies,

where job-growth and welfare programs have failed to keep pace with a

booming population that has soared from 6 million in to 28 million today

(Dar, Presley 2010). Under King Abdullah, the government has spent

billions to help the growing numbers of poor people, estimated to be as

much as a quarter of the native Saudi population. But critics complain that

those programs are inadequate, and that some royals seem more

concerned with their wealth and the country's image than with helping the

needy (Fahmy, 2011). Last year, for example, three young Saudi video

bloggers were arrested and jailed for two weeks after they produced an

online video about poverty in Saudi Arabia. Much of the welfare spending

comes from the Islamic system of zakat, a religious requirement that

individuals and corporations donate to charity 2.5 percent of their wealth

the money is paid to the government and distributed to the needy. Living

in Saudi Arabia is like living in a charitable foundation, it is part and parcel

8

of the way they are made up, and Prince Sultan said, "if you are not

charitable, you are not a Muslim." Despite those efforts, poverty and

anger over corruption continue to grow, whereby vast sums of money end

up in the pockets of the royal family through a web of nepotism,

corruption and cozy government contracts (SBP 2010).

In Africa specifically South Africa, the community social welfare services

are delivered as a concurrent function by provincial governments, the

ability of provinces to redirect welfare funds to other services and

priorities means that developmental welfare services continue to be

underfunded (Haran, Sudin 2014). Lack of capacity in provincial

governments to plan, implement, monitor and evaluate service delivery

outcomes also hampered service delivery. Power struggles between

government officials and non-profit organisation (NPO) partners also held

back the potential benefits that might have been realised by the

partnership model. In addition, services delivered by NPOs reached a

limited number of people and were not extended to rural and

underserviced areas. Many NPOs are concentrated in urban areas. Lack of

institutional capacity, including loss of staff by NPOs to government,

inadequate numbers of social workers, community development workers,

child and youth care workers and paraprofessionals has been a serious

impediment (Haron, Shanmugan, 2009).

Overview of Islamic Banking Service in Somali land

Having survived a civil war and living in international isolation, Somaliland,

a de facto independent state in the territory of Somaliland, is gradually

developing its financial sector. The banking services are interest-free in

this entirely Muslim republic. But does it mean they are Shari'ah-

9

compliant. In 1991, the unified country of Somaliland de facto ceased to

exist. The civil war, which had broken out three years earlier, had led to

the breakup of the state into three separate areas: Somaliland and

Puntland. At the time one could hardly call the former British colony and

then province of Somaliland as a country. It was virtually a bare territory

with its infrastructure completely destroyed by the war. The world

community did not rush to recognize the new state and hardly anyone

would have predicted that the country would survive. But 25 years on,

Somaliland continues to exist as a state despite international political

isolation and weak central government.

The main source of welfare for Somaliland's citizens is not international

aid, but money sent by their relatives from abroad. Because of the

underdevelopment of the financial sector, money transfer operators have

practically taken on the role of banks. The situation within the country's

banking sector presents a paradox. Officially, there are three banks in

Somaliland; Bank of Somaliland, Dahabshil international Bank and Salama

Bank. The paradox is that the first bank, which is nominally a central

bank, plays the role of a commercial financial institution, while the latter is

more of a state treasury than a fully-fledged commercial bank. The main

task of the Bank of Somaliland is to support the national currency and

fight inflation. In order to do so, the bank carries out currency

interventions, buying considerable sums in local currency (shillings) for US

dollars.

10

1.2 Statement of the Problem

Despite the many financial institutions in Somaliland springing up, there is

concern of the low representation of Islamic Banks in the country which

has hampered community welfare improvement (Central Bank report

2014). There are low levels of community welfare improvement in

Hargeisa Somaliland (Mohammed 2016). Most of the community members

are characterized by having minimum level of income for food and

clothing, adequate housing, education and poor health care, (Mustafe,

2015). All these are indicators of low levels of community welfare

improvement.

The worsening condition of welfare improvement in the country will affect

the standard of living of the community which will affect the mortality rate

of the people in the country (Haren, 2014). The low levels of community

welfare improvement in Hargeisa Somaliland may be caused by factors

such as lack of government support, the level of the political system in the

country as politically unstable atmosphere, limited number of banks to

practice according to Islamic banking principles, the unemployment rate

among others, (Siddiqi, 2009). This study is intended to establish the

relationship between Islamic banking and welfare improvement in the

community in Hargeisa Somaliland. The researcher chose Islamic banking

because with its principles of encouraging the community to borrow

money with no interest will enable the community to borrow loans and put

it in various investments so as to have welfare improvement. There has

never been a study conducted about Islamic banking and welfare

improvement in Hargeisa Somaliland, therefore, this study is intended to

close the contextual gap that was existing previously.

11

1.3 Purpose of the study

The purpose of this study was to establish the relationship between

Islamic banking services and community welfare improvement in Hargeisa

Somaliland.

1.4 The objectives of the study

i) To establish the relationship between Islamic banking services and

improvement of quality of life among community members in

Hargeisa Somaliland.

ii) To examine the relationship between Islamic banking services and

poverty alleviation among community members in Hargeisa

Somaliland.

iii) To determine the relationship between Islamic banking services

and improvement of infrastructure in Hargeisa Somaliland.

1.5 Research Questions

i) What is the relationship between Islamic banking services on

improvement of quality of life among community members in

Hargeisa Somaliland?

ii) What is the relationship between Islamic banking services and

poverty alleviation among community members in Hargeisa

Somaliland?

iii) What is the relationship between Islamic banking services and

improvement of infrastructure in Hargeisa Somaliland?

12

1.6 Hypothesis

Ho There is no significant relationship between Islamic banking services

and community welfare improvement in Hargeisa Somaliland.

1.7 The Scope of the study

1.7 .1 Geographical scope

The study was carried out among the selected Islamic Banking institutions

in Hargeisa Somaliland, whereby it concentrated on loan services, deposits

and withdrawals services, financing and investment service's customers,

employees, managers and other experts who are knowledgeable about

banking services. Hargeisa is the most populous city in the state of

Somaliland, a self-declared state that is internationally recognized as an

autonomous region of Somalia, situated in the Woqooyi Galbeed region in

Northwestern Somalia. Dahabshiil is the 'rags to riches' story of an African

entrepreneur specifically whose business was interrupted after the Somali

civil war. With limited resources and a strong network of contacts they set

about rebuilding the company, which two decades later is now the largest

international money transfer businesses in the Horn of Africa including the

Islamic banking system in Hargeisa Somaliland. Premier Bank Limited is

found in Hargeisa and it transacts its business using major international

currencies, is a fully fledged Islamic Bank providing several financial

services. It has partnered with MasterCard and SWIFT to deliver global

online financial services including Automated Teller Machines. Dar- Salaam

bank is a fully sharia compliant institution, DSB was instituted as a fully

fledged bank under Somaliland bank Act 55/2012. The address of the

bank is Salaam building, Khairie road (Opposite aero plane Monument

13

Park), this Bank offers retail, corporate micro finance and other related

services to spearhead the economic development of Somaliland and entire

region (Mohammed, 2016).

1.7 .2 Content scope

The study intended to examine the role of Islamic banking services on

community welfare improvement in Hargeisa Somaliland, and to correlate

if there is a significant relationship. This study examined Islamic banking

services in terms of loan services, deposit and withdraw services and

Financing and investment services. The study also examined community

welfare improvement in terms of quality of life, poverty alleviation and

improvement in infrastructure.

1.7.3 Theoretical scope

The study was anchored on Islam and Interest theory which indicated that

the government should sponsor banking as a social service in which the

bank should never pay any loan services to account holders nor charge

any loan services on loans advanced (Jankowicz, 2010) . The theory still

shows that the banks should become partners with businessmen, sharing

any loss that might be incurred (Shahin, 2009), Banking institutions act as

financial intermediaries between savers and investors, Banks are of

significant help in assisting the process of capital formation and

development. With the progress of trade and industry and increased

financing requirements of productive enterprises, direct finance proved an

inadequate mechanism for such transference and banks emerged on the

scene to undertake financial intermediation between savers and investors.

The attitude of Islam to all known innovations is that nothing should stand

14

in the way of their adoption if they are useful for human society and do

not conflict with the fundamental teachings of the Qur'an and the Sunnah

(Khan, 2010).

1.7.4 Time scope

The study covered the data on Islamic banking from 2010 to date, this

being the period in which poor community welfare was reported most in

Hargeisa Somaliland. Still this period was considered appropriate as it

gave enough duration to study the cause of low community welfare

improvement in Hargeisa Somaliland.

1.8 Significance of the Study

The study would be useful in the following ways:

It is expected that the findings of this study will be useful to Hargeisa

Somaliland on how to engage in Islamic banking services for better

community welfare improvement.

The findings of this study will be useful to managers of Islamic banks on

how to emphasize on Islamic banking services for welfare improvement of

communities.

The study findings will also benefit the other members of Hargeisa

Somaliland such as employees and other support staff on how to attain

welfare improvement.

15

- - . ---__;____~ ___ _:__-~----•

The researcher expects that this study will yield data and information that

will be useful for understanding the effects of Islamic banking services on

community welfare improvement.

The future researchers will utilize the findings of this study to embark on

Islamic banking services and community welfare improvement in Hargeisa

Somaliland.

1.9 Definition of operational terms

A community is a social unit of any size that shares common values, or

that is situated in a given geographical area (e.g. a village or town)

(Barzilai, 2013). It is a group of people who are connected by durable

relations that extend beyond immediate genealogical ties, and who usually

define that relationship as important to their social identity and practice

(Nadarajah, Haive and Stead, 2012) . Although communities are usually

small, "community" may also refer to large groups, such as national

communities, international communities, and virtual communities.

Welfare is defined by Huseyin and Ioannidis (2015) as the good fortune,

health, happiness, prosperity, etc., of a person, group, or organization;

well-being: e.g. to look after a child's welfare; the physical or moral

welfare of society. Welfare can also mean availability of resources and

presence of conditions required for reasonably comfortable, healthy, and

secure living or it could mean government support for the poor and

otherwise disadvantaged members of the society, usually through

provision of free and/or subsidized goods and services (Kevin, 2013).

16

The operational definition of community improvement welfare in this study

will mean that a social unit of any size that shares common values or that

is situated in a given geographical area benefits from government support

intended to improve their healthcare, quality of life or Physical and

psychological health.

Infrastructure refers to roads, bridges, railways, water-ways, airways,

and other forms of transportation and communications as well as water

supplies, electricity and telephone. It also includes financial institutions

and such public services as health and education. More generally it

includes all institutional prerequisites of efficient working of competitive

markets and expansion in production.

17

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

This chapter shows theoretical review, the conceptual framework, and

additional literature review.

2.1 Theoretical Review . . l •

This study based on the theory of Islamic banking of Iqbar (1946)

expanded by Mohammad (2014). The theory of Islamic banking is based

essentially on the premise that interest, which is strictly forbidden in

Islam, is neither a necessary nor a desirable basis for the conduct of

banking operations, and that Islamic teachings provide a better

foundation for organizing the working of banks. Muslim economists have

pointed out that it is a historical accident that interest has become the

kingpin of modern banking.

In the period of colonial domination of Muslim countries by Western

powers, the interest based system became solidly entrenched. It is this

string of historical circumstances, Muslim scholars argue, which has led to

the present-day dominance of interest in financial transactions all over the

globe. Had the societies developed in a different fashion and paid greater

heed to the injunctions of religion, the development of the financial

system would have surely taken a different course, and we could have

had in actual operation an alternative system free of interest but fully

meeting the needs of modern society.

18

Muslim scholars recognize the important role banks play in the economy

of a country in modern times (Uhomoibhi and Alia, 2012; Ghafoor, 2014).

Banking institutions act as financial intermediaries between savers and

investors. They can be of significant help in assisting the process of capital

formation and development. There was no prototype of modern banks in

the early history of Islam. Even in Western countries, banking in the form

in which it exists today is of comparatively recent origin. Before the

advent of modern banking, direct finance, where the owner of capital

deals directly with the user of capital, was the customary mode of

transference of funds from savers to investors. Since banks perform a

useful service of financial intermediation, they are wholly acceptable in a

Muslim society. What is not acceptable, however, from the shari'ah point

of view, is the use of interest rate mechanism in the process of financial

intermediation (Uhomoibhi and Alia, 2012).

For long Muslims the world over were beset with a dilemma. Islam

prohibits the giving and taking of interest while it looked almost

impossible to steer clear of interest in the modern world where interest

played a key role in most of the financial transactions. The contemporary

Islamic resurgence has begun to provide an answer to this dilemma.

Theoretical work by Muslim scholars has sought to demonstrate that it is

possible to run an economy without interest even in modern times.

Replacement of interest based banking by interest-free banking has

received the greatest attention in this endeavor (Khan and Bhatti, 2011).

The basic postulate that has guided all theoretical work on Islamic

banking is that while interest is forbidden in Islam, trade and profit is

19

... ..-..-~"- .. ~ -:"""~~'" - . -- --------------

permissible. Conventional banking uses the interest rate mechanism to

perform its task of financial intermediation. Muslim scholars have

developed a radically different model of banking which does not make use

of interest. It relies instead on profit/loss sharing for purposes of financial

intermediation (Hijazi, T.S., Hanif, M., (2010)).

The implication of this theory is that Islamic banking is that, Islamic can

provide the people of Somaliland with funds at no interest which will -:- i.' ·r· enable the borrow and invest and investment will improve the earning

ability and hence get funds for consumption and this is a way to improve

the welfare of the community through enabling borrowing by the

community which enhances investment and hence improves the welfare of

the community through improved standard of living.

The government therefore, should look for ways of emphasizing Islamic

banking so as enable the community borrow loans with no interests to

enhance the investment levels and improve the welfare of the community.

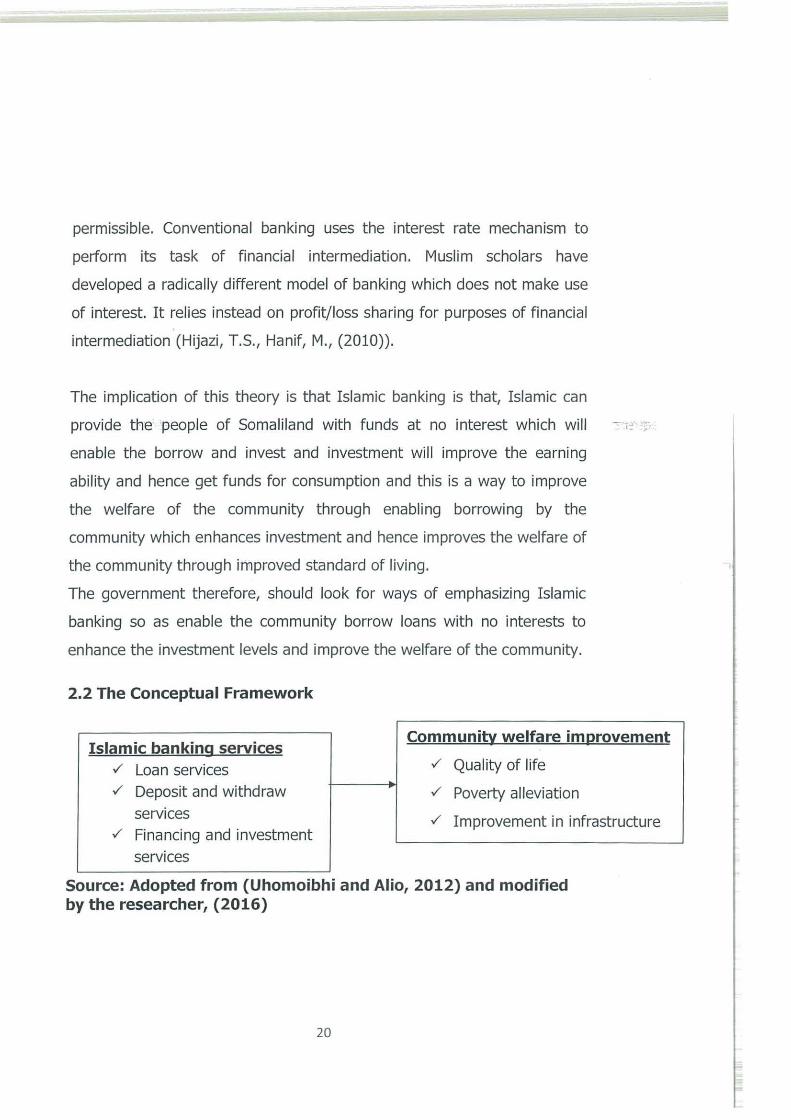

2.2 The Conceptual Framework

Islamic banking services Community welfare improvement

../ Loan services ../ Quality of life

../ Deposit and withdraw ../ Poverty alleviation services ../ Improvement in infrastructure

../ Financing and investment services

Source: Adopted from (Uhomoibhi and Alio, 2012) and modified by the researcher, (2016)

20

The conceptual framework indicates the independent and dependent

variables in the topic under investigation and their relationship on one

another. The independent variable is Islamic banking while the dependent

variable is community welfare improvement. Islamic banking affects

community welfare improvement in terms loan services, deposit and

withdraw services and financing and investment. The study also examined

community welfare improvement in relation to quality of life, poverty

alleviation and improvement in infrastructure. The functions of Islamic

banks are: to collect deposits from the people on profit-and-loss sharing

basis; to provide all necessary banking services to its customers; to

finance those projects which generates employment; to allocate financial

resources (financing) in a way that it ensures equitable distribution of

income; to act as a development institution; to promote entrepreneurship

by providing finance on profit and loss basis; to transform saving into

investment in such a way that it benefits to the majority; to provide

expertise and technical advice to the finance-taker in order to improve the

process of production and profitability; to disperse financing and

discourage its concentration (Ghafoor, 2014).

An Islamic bank is a deposit-taking banking institution whose scope of

activities includes all currently known banking activities, excluding

borrowing and lending on the basis of interest (Iqbal, 2011). On the

liabilities side, it mobilizes funds on the basis of a mudarabah or wakalah

(agent) contract. It can also accept demand deposits which are treated as

interest-free loans from the clients to the bank. On the assets side, it

advances funds on a profit-and-loss sharing or a debt-creating basis, in

21

accordance with the principles of the Sharlah. It plays the role of an

investment manager for the owners of time deposits, usually called

investment deposits. In addition, equity holding as well as commodity and

asset trading constitute an integral part of Islamic banking operations. An

Islamic bank shares its net earnings with its depositors in a way that

depends on the size and date-to-maturity of each deposit. Depositors

must be informed beforehand of the formula used for sharing the net

earnings with-fhe bank (Khan and Bhatti, 2011).

Even though both types of institutions (Islamic banking and Conventional

banking) are providing financing to productive channels for reward. The

difference lies in financing agreement. Conventional banks are offering

loan for a fixed reward whil~ IFis cannot do that because they cannot

charge interest. IFis can charge profit on investments but not interest on

loans. In conventional banking three types of loans are issued to clients

including short term loans, overdrafts and long-term loans. Islamic banks

cannot issue loans except interest free loans (Qarz e Hasna) for any

requirement however they can do business by providing the required

asset to client (Hanif, 2010).

The most essential feature of Islamic banking is that it is interest-free.

Islamic banks neither charge nor pay interest. Islam prohibits Muslims

from taking or giving interest riba regardless of the purpose for which

such loans are made and regardless of the rates at which interest is

charged (Uhomoibhi and Alia, 2012). The prohibition of riba is mentioned

in four different revelations in the Qur'an. The first revelation emphasizes

22

-:-.-·: r:;

that interest deprives wealth of God's blessings. The second revelation

condemns it, placing interest in juxtaposition with wrongful appropriation

of property belonging to others. The third revelation enjoins Muslims to

stay clear of interest for the sake of their own welfare. The fourth

revelation establishes a clear distinction between interest and trade,

urging Muslims to take only the principal sum and to forgo even this sum

if the borrower is unable to repay.

r·. - . 2.3 Review of related literature

This section reviewed literature regarding the Islamic banking and the

relationship with community welfare improvement basing on study

objectives.

2.3.1. Relationship between Islamic banking and quality of Life

There is a growing interest among Muslim economist about the potential

of microfinance scheme in alleviating poverty (Iqbal & Molyneux, 2005).

Indeed microfinance is widely acclaimed as a new innovative approach to

alleviate poverty (Robinson, 2001). Microfinance institutions receive

money by way of deposits and interests which is lent or used to finance

business in form of loans or facilities to micro-small enterprises and low

income households, deposit taking and also non-deposit taking

(Microfinance institutions Act, 2006). Microfinance industry in Kenya has

grown over the past two decades in response to lack of access to formal

financial services for most of Kenya's poor people .The World Bank has

recognized microfinance programme as an approach to address income

inequalities and poverty (Microcredit Summit, 2004).

23

Panich (2007) noted that welfare is thus mainly connected to individuals

perception and utility of the use of income. This also makes it very difficult

to measure welfare at the macro level as individuals" evaluation of the

utility gained from income will differ, but often the consumers" choice as

reflected by the market has been used as a proxy and this explains why

GDP per capita is seen as a good indicator. The approach of using

individual utility can also be part of the explanation of why it so far has

not been possible to establish a single and clear type of societal welfare

function. Individual welfare involves how utility can be maximized by

choices made by the individual (Walker, 2005).

2.3.2. Relationship between Islamic banking services and

poverty alleviation

Estes (2004) indicated that Islamic banks provide small loans to people

who need capital to start a small business and become self-employed to

help them build a sustainable future and Welfare refers to a set of

specialized programs and services designed to meet the income security,

social services and related needs of persons who are unable to provide for

their own basic needs. The assumption mostly made of all islamic banks

loans is that the intervention will change household welfare with regards

to access to more income in a way that lead to achievement of higher

household consumption of goods and services and overall socio-economic

well-being. In order to assess improvement of household welfare as a

result of Islamic banks loan acquisition, there are various variables such

as; household income, Women empowerment (Gender), improved

24

--;; t.~J:-

_.r '"• _:;..• ~-.::-.. .:;.,..Z~'••~'";:'",-- " - •

--~~~--

education, healthcare, Poverty reduction, number of Small business and

consumption according to the Human Development Report (2005).

Sinclair (2001) noted that with Islamic banks, poor people are given an

opportunity to change their lives with capital. One of the major reasons

for social and economic inequality is financial exclusion. Poor and

disadvantaged people have no access to capital and financial services,

especially affordable credit (Whyley and Brooker, 2004). Islamic banking

is concerned with much more than refraining interest; it is a system that

aims at making positive contribution to the fulfillment of the socio

economic objectives. Islamic banks may emulate the existing model of

Islamic banks practices, the activities must be carried out in ways which

do not conflict with the principles of Islam. Islamic banking has the same

purpose as conventional banking except that it operates in accordance

Islamic rules on transaction (Kempson & Whyley, 2000).

2.4 The relationship between Islamic banking services and

improvement of infrastructure

Malik (2007) noted that concentrating investment in infrastructure by

Islamic banks is extremely important for the attainment of the main

development targets, namely industrialization, urbanization, and trade

promotion to get over the shortage of development capital in countries.

To decide the priorities of investment in infrastructure sectors is also

important. Good infrastructure helps to raise productivity and lower costs

in the directly productive activities of the economy. Shahin (2009)

asserted that insufficient capital for infrastructure development could be

supplemented with foreign capital such as foreign aid, loan, and foreign

25

direct investment, hence confirming that Islamic banking services are

important in this case (Meezan Bank, 2011).

Steward, M. (2008) noted that it is obviously important that Islamic

banking services include aid go not only to the poorest countries but also

to the poorest people within recipient countries. And the greater part of

the aid budget that is devoted to rural development and the social

infrastructure, rather than to industrial development, fundamental

research, railways, urban hossing, etc., the greater proportion of Islamic

banking services such as aid which goes directly to the poor. Kocher

Lakota and Yi (2006) presented evidence supporting endogenous growth

models using time series data for the Saudi Arabia, together with various

policy variables including the infrastructure to show that there is no policy

variable that permanently raises the economic growth rate other than aid

from Islamic banking (Amato, 2012).

Bellalah (2009) emphasized that balanced investment to all industry is

efficient for infrastructural development in developing countries. Bokhari

(2007) insisted that balanced investment policy is impossible because

developing countries are always suffering from the shortage of capital.

Therefore, it is important to decide the priorities of investment in

industries and sectors, and to concentrate investment on infrastructural

development in the early stage of development (EIIouz, 2009).

2.5 Related studies

Siddiqi (2010) found out that Islamic banks do not charge interest rates

and consumer loans are unattractive since there is no profit to be derived

in the form of interests on the loans. Hence, Islamic banks deliberately

26

avoid consumer lending. Islamic researchers e.g. have tried to excuse the

Islamic banks. While recognizing the need for such interest-free loans I benevolent loans qard hasan, especially for meeting basic needs, they

seem to think it is the duty of the community and the State through its

treasury baitul mal to cater for these basic needs. Downplaying the role of

Islamic banks in providing consumer loans, they suggest that Islamic

banks give limited overdraft facilities without interest instead. They also

7~ ':r::. consider a portion of bank loanable funds being set aside for consumer

loans, provided repayment will be guaranteed by the State. This, they

reckon, will minimize the risks involved in consumer lending (Nasib, 2012).

Rahman (2012) carried out a study to establish attitudes of Muslims

towards~ Islamic Banking and Finance in the North West of England. The , ., presence and ever growing considerable segment of Muslim population in

the UK and their social, cultural and religious identity require a faith based

banking system which is compatible with their beliefs and values. The

demographics of the Muslim population and the ideological differences

supported the argument that the Islamic banks can produce significant

socio-economic impact. The social aspect of banking institutions is a new

development in the discipline.

Adi (2010) noted that businesses do not function in isolation from the

society around them. In fact, their ability to compete depends heavily on

the circumstances of the locations where they operate. Improving

education, for example, is generally seen as a social issue, but the

educational level of the local workforce substantially affects a company's

27

potential competitiveness. Well-established Islamic publishing companies

like Iqra International/s Books for Schools in USA and donation of books

for building community libraries by the Islamic Foundation in UK are such

examples. The more social improvement relates to a compants business/

more it leads to economic benefits as well. In establishing a Networking

Academy, for example, Islamic Bank Ltd has focused not on the

educational system overall, but on the training needed to produce young

competent persons a particular·-kind of education that made the most

difference to competitive context of Islamic Bank Bangladesh Ltd.

Furthermore, it has established Islamic Bank Foundation which established

a number of schools of International standard in the different places in

Bangladesh. The Ibn Sinha Group of the Islamic Bank Ltd established

specialized as well as general hospitals which are providing healthcare

service to the poor with nominal fees. In 2014, bank has initiated rural

poverty elevation programme under its Rural Development Scheme (RDS).

To handle this scheme, Islamic Bank Ltd has introduced Islamic

microfinance programme through its rural branches to bring all the

villages of the needful countries under the coverage of this scheme (IBBL;

Annual Report, 2014).

Ariff (2012) found out that Islamic banks lend money without interest but

cover the expenses by levying a service charge not exceeding the

proportionate cost of the operation, excluding the cost of funds and

provisions for bad and doubtful debts. Prospective borrowers are always

required to pay this charge on each application, regardless of the amount

28

required, the term of the loan or whether the application is granted or

rejected (Meezan Bank, 2011).

Some scholars have put forward economic reasons to explain why interest

is banned in Islam. It has been argued, for instance, that interest, being a

pre-determined cost of production, tends to prevent full employment

(Khan, 2011); and Ahmad (2013). In the same vein, it has been

contended that international monetary crises are largely due to the ~r~ ~ ~

institution of interest (Khan, 2013) and that trade cycles are in no small

measure attributable to the phenomenon of interest. Others have argued

that interest is not very effective as a monetary policy instrument even in

capitalist economies and have questioned the efficacy of the rate of

interest as a <;Jeterminant of saving and investment (Ariff, 2012).

Hassan, M.K. (2010) noted that the applicants to whom a loan is granted

may be required to pay an additional prescribed fee for all the entries

made in the bank's registers. This total charge is usually less than the

interest charged by conventional banks a bonus for borrowers, and may

be subject to a maximum set by the banking authorities as is the practice

in Pakistan. The usual benchmark for the service charge is the actual

expenditure which the bank incurs in scrutinizing the application and

making its decision, and in maintaining the account until the loan is

repaid . The bank sets aside a part of its funds to grant no-cost loans to

needy persons such as small farmers, entrepreneurs, producers, etc. and

to needy consumers. In Pakistan, these are qa1 d-e-hasana loans given on

compassionate grounds free of any interest or service charge and

repayable if and when the borrower is able to pay. Overdrafts: here

29

Islamic banks usually provide overdrafts, subject to a certain maximum,

free of charge (Nooraslinda, 2013).

Duan (2012) found out that Islamic banks act as a mudarib which

manages their funds to generate profits. Since they are not entitled to

interest income from the productive utilization of their deposits, the profits

generated are then shared with them. Profit-sharing ratios and the modes

of payment vary from place to place, from bank to bank and from time to .

time, depending on supply and demand conditions. Profits are

provisionally declared on a monthly basis in Malaysia, on a quarterly basis

in Egypt, on a half-yearly basis in Bangladesh and Pakistan, and on an

annual basis in Sudan (Weber, 2012).

Alio (2012) found out that deposits in Islamic banks are collected from

savers under both type of institutions for reward irrespective a bank is

operating under conventional system or Islamic system. The difference

lies in agreement of reward. Under conventional system reward is fixed

and predetermined while under Islamic deposits are accepted through

Musharaka and Mudaraba where reward is variable. Under conventional

banking return is higher on long-term deposits and lower for short-term

deposits. Same is the practice in Islamic banking to share profit with

depositors. Higher weight for profit sharing is assigned to long-term

deposits being available to bank for investing in longer term projects

yielding superior returns and lower weight for short-term deposits which

cannot be invested in long term projects (Hijazi, 2010).

Ali (2013) observed that deposits in Islamic banks are treated as shares

and accordingly their nominal values are not guaranteed. In the same

30

vein, both shareholders and depositors are residual claimants to Islamic

banks' profits (AAOIFI, 2009). The current or demand deposit account, as

in the case of conventional banks, gives no return to the depositors. It is

essentially a safe-keeping alwadiah or wadiah arrangement between the

depositors and the bank, which allows the depositors to withdraw their

money at any time and permits the bank to use the depositors' money. As

in the case of conventional banks, cheque books are issued to the current

account deposit holders (Warde, 2010). .:'"''' ~r

2.6 Research gaps

The researcher identified the following gaps in the previous researcher's

literature which needs attention. The findings in the previous study,

conducted by Moh~tmed Omar (2011), about Islamic banking and success

of elected banks in Mogadishu Somalia, indicate that in reviewing

literature, the study looked at only Islamic banks aspects without looking

at the aspects of the success of the banks, therefore, there is a content

gap identified in the previous researcher's literature. In the previous

study, conducted by Mohamed Omar (2011), about Islamic banking and

success of elected banks in Mogadishu Somalia, the researcher failed to

come up with a good theory that could guide the study, therefore, a

theoretical gap has been identified in the previous researcher's work

which also needs serious attention. There has never been a study about

Islamic banking and community welfare improvement in Hargeisa

Somaliland. There is also contextual gap which the current researcher

needs to put more attention. This study therefore, is intended to bridge

the theoretical, content and contextual gaps in the previous researcher's

literature.

31

CHAPTER THREE

METHODOLOGY

3.0 Introduction

This chapter provides the overview of research methodology adopted,

design, target population, sample size, sampling techniques, data sources,

research instruments, validity and reliability of the instrument, data

gathering procedure, data analysis, etliical -considerations, and limitations

of the study.

3.1 Research design

Research design provides an overall guidance for the collection

and analysis of data of a study (Churchill1979).

The study used quantitative approach. The study used descriptive co

relational design; this design enabled the researcher to determine the

degree of the relationship between Islamic banking and community

welfare improvement in Hargeisa Somaliland. It dealt with the relationship

between variables, testing of hypothesis and development of

generalizations and use of theories that have universal validity. It also

involved events that had already taken place and were related to present

conditions (Kothari, 2009).

3.2 Study Population

The target population of this study comprised of 160 respondents who

consisted of community from selected villages in Hargeisa Somaliland.

These respondents comprised of members of the customer of Dahabshil

32

Bank in Gan Libah village with a total of 77 members, 66 of the customer

members of Salama Bank in Ibrahim Kodbur village and 17 customer

members of Preimer bank from Mohamoud Haybe village.

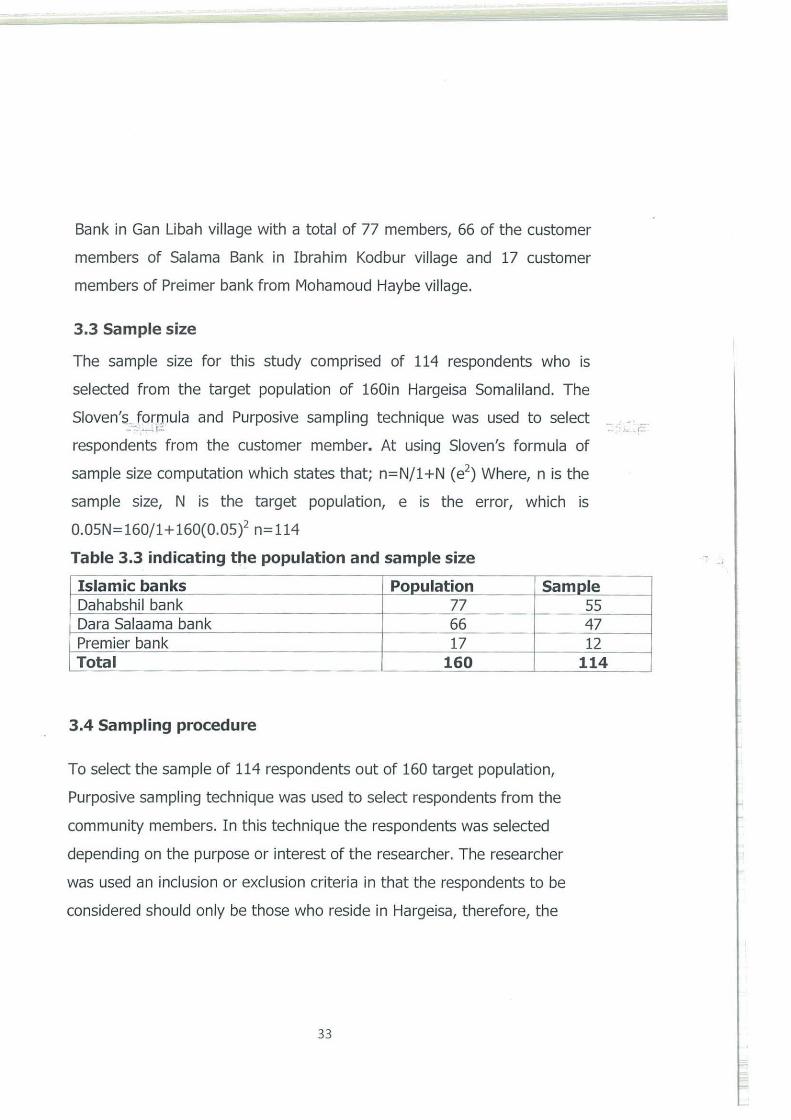

3.3 Sample size

The sample size for this study comprised of 114 respondents who is

selected from the target population of 160in Hargeisa Somaliland. The

Sloven's formula and Purposive sampling technique was used to select - ,. respondents from the customer member. At using Sloven's formula of

sample size computation which states that; n=N/1 +N ( e2) Where, n is the

sample size, N is the target population, e is the error, which is

0.05N=160/1+160(0.05)2 n=114

Table 3.3 indicating the population and sample size

Islamic banks Population Sample Dahabshil bank 77 Dara Salaama bank 66 Premier bank 17 Total 160

3.4 Sampling procedure

To select the sample of 114 respondents out of 160 target population,

Purposive sampling technique was used to select respondents from the

community members. In this technique the respondents was selected

depending on the purpose or interest of the researcher. The researcher

was used an inclusion or exclusion criteria in that the respondents to be

considered should only be those who reside in Hargeisa, therefore, the

33

55 47 12

114

J -

.Jr.. .. r:.

inclusion criteria here was residence and customers of these selected

banks.

3.5 Data sources

The research used primary.

3.5.1 Primary data sources

The researcher obtained primary data by use of questionnaires.

3.6 Data collection instruments

The data collection instrument in this study was basically questionnaires.

Questionnaires by definition mean a set of printed questions addressed by

the researcher to the respondent for him or her to answer and after

answering return the questionnaires to the researcher. The questionnaires

were administered personally by the researcher to the respondents and

collected after time interval. The questionnaires comprised of both open

ended and closed ended questions that required the respondents to

answer all the questions to the best of their knowledge. The

questionnaires were used because they are cheap, quicker, they cover

many respondents, and they are free from interview bias and give

accurate information since respondents take their time to answer the

questions. However, they have a disadvantage of non-despondence.

34

3.7 Validity and Reliability of the Instruments

3.7.1 Validity of the instrument

Validity is the degree to which results obtained from the analysis of the

data actually represents the phenomenon under study. This study look at

three kinds of validity: face validity, content validity and construct validity.

Face validity was ensured by giving the questionnaires to two experts to

check whether the questions are relevant to the contents. Content validity

was ensured by subjecting the researcher devised questionnaires on

Islamic banking and community welfare improvement in Hargeisa

Somaliland that consisted of all the elements of the concept of Islamic

banking and community welfare improvement. To determine the content

validity, content validity index was determined first where the instrument

was redesigned with questions about the content such as very relevant,

relevant, somewhat relevant and not relevant. The instrument was given

to two experts to tick against these questions and give their answers

according to their perception on the relevance of the content. Then the

content validity index (CVI), was calculated as follows;

CVI= Number of questions very relevant, relevant and somewhat

relevant/total number of questions. The CVI should be 0. 7 and above for

the instrument to be proved as having the real content validity.

No of questions declared valid CVI = Total no of Questions in the Questionnaire

24 CVI = 29 CVI= D....82

35

. :

A CVI of 0.82 was used to declare that the research instrument was valid

since it was above 0.7 which is the minimum CVI index required to declare

a research instrument valid (Amin, 2005)

3.7.2 Reliability of the instruments

Reliability is a measure of the degree to which research instruments yield

consistent results or data after repeated trials. The test-retest technique

was used to assess the reliability (accuracy) of the instruments. The

researcher devised the instruments to twelve qualified respondents, five

from the customers of Dahabshil bank from community members of

Ganalibah village and four Dara Salaam in Ibrahim Kodbur village

community members and two from Mohamoud Habye village in Hargeisa

Somaliland. These respondents were not included in the actual study. In

this test- retest technique, the questionnaires were administered twice to

the same subjects after the appropriate groups of the subject are

selected, then the initial conditions were kept constant, the scores were

then correlated from both testing periods to get the coefficient of

reliability or stability. The tests and the trait measured if they were stable,

indicated consistent and essentially the same results in both times (Treece

and Treece, 1973).

3.8 Data Gathering Procedure

3.8.1. Before the administration of the questionnaires

• An introduction letter was obtained from the college on higher

degrees and Research for the researcher to solicit approval to

36

conduct the study from respective Community leaders in Hargeisa

Somaliland.

• When approved, the researcher visited the different villages in

Hargeisa and then Purposive sampling technique was used to select

the respondents from the customers of the banks from the

community members to arrive at the minimum sample size.

• The respondents were explained about the study and were

requested to sign the Informed Consent Form.

• Reproduced more than enough questionnaires for distribution.

• Select research assistants assisted in the data collection; brief and

orient them in order to' be consistent in administering the

questiohnaires.

3.8.2. During the administration of the questionnaires

• The respondents were requested to answer completely and not to

leave any part of the questionnaires unanswered.

• The researcher and assistants emphasized retrieval of the

questionnaires within five days from the date of distribution.

• On retrieval, all returned questionnaires were checked if all

questions are answered.

37

3.8.3 after the administration of the questionnaires

The data gathered was edited, encoded into the computer and

statistically treated using the Statistical Package for Social Sciences

(SPSS).

3.9 Data Analysis

The study used simple tables and frequency counts (frequencies and

percentages) to analyze the profile of respondents. Similarly, mean was

used to analyze the extent Islamic banking and community welfare

improvement in Hargeisa Somaliland, Correlation analysis using Pearson's

coefficient values was used to analyze the relationships between the

independent and dependent variables.

The following mean range was used to arrive at the mean of the individual

indicators and interpretation:

The frequency and percentage distribution was used to determine the

demographic characteristics of the respondents.

The mean was applied for the extent of Islamic banking service and the

level of community welfare improvement. An item analysis illustrated the

strengths and weaknesses based on the indicators in terms of mean and

rank. From these strengths and weaknesses, the recommendations will be

derived.

The following mean ranges were used to arrive at the mean of the

individual indicators and interpretation as cited from Amin, (2012):

38

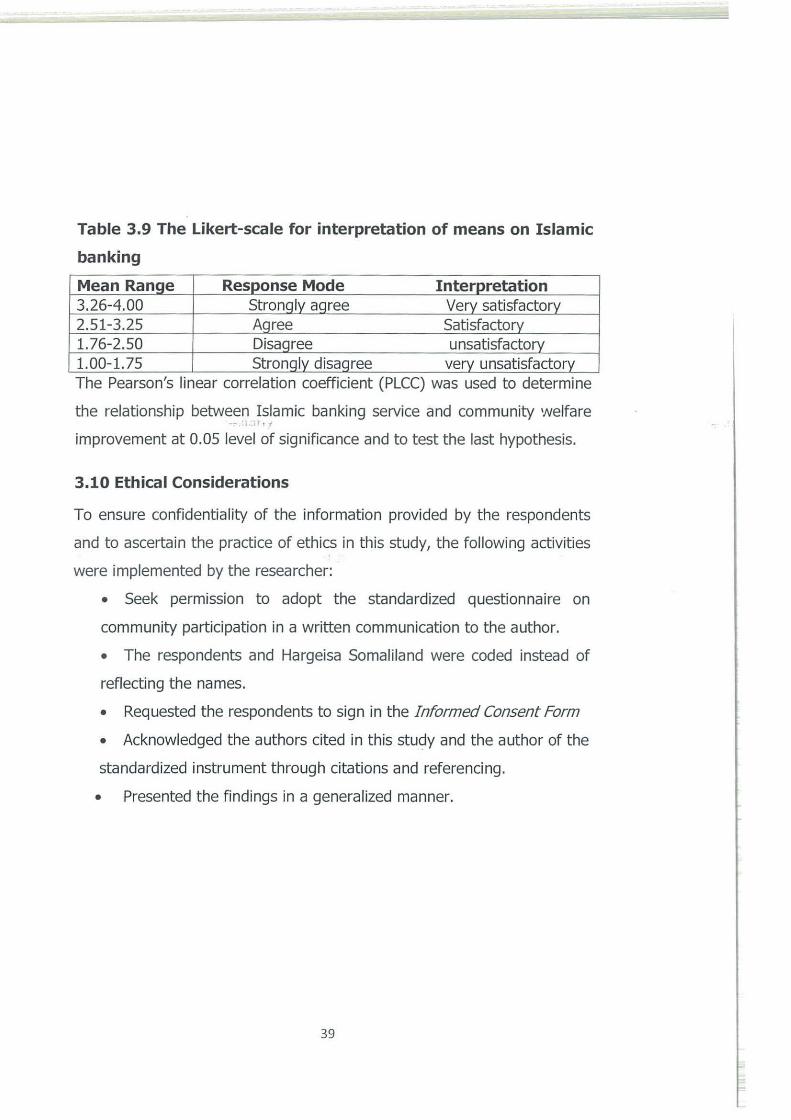

Table 3.9 The Likert-scale for interpretation of means on Islamic

banking

Mean Range Response Mode Interpretation 3.26-4.00 Strongly agree Very satisfactory 2.51-3.25 Agree Satisfactory_ 1.76-2.50 Disagree unsatisfactory 1.00-1.75 Strongly. disagree very unsatisfactory The Pearson's linear correlation coefficient (PLCC) was used to determine

the relationship between Islamic banking service and community welfare - I

improvement at 0.05 level of significance and to test the last hypothesis.

3.10 Ethical Considerations

To ensure confidentiality of the information provided by the respondents

and to ascertain the practice of ethics in this study, the following activities

were implemented by the researcher:

• Seek permission to adopt the standardized questionnaire on

community participation in a written communication to the author.

• The respondents and Hargeisa Somaliland were coded instead of

reflecting the names.

• Requested the respondents to sign in the Informed Consent Form

• Acknowledged the authors cited in this study and the author of the

standardized instrument through citations and referencing.

• Presented the findings in a generalized manner.

39

CHAPTER FOUR

DATA PRESENTATION, ANALYSIS AND INTERPRETATION OF

RESULTS

4.0 Introduction

This chapter presents the demographic characteristics of respondents,

Islamic banking services, community welfare improvement, relationship

between Islamic banking services and quality of life, relationship between

Islamic banking services and poverty alleviation and the relationship

between Islamic banking services and improvement in infrastructure in

Hargeisa Somaliland.

4.1 Profile of respondents

Respondents were asked to present information regarding their age,

gender, highest level of education and work experience, results are

presented in tablel below;

40

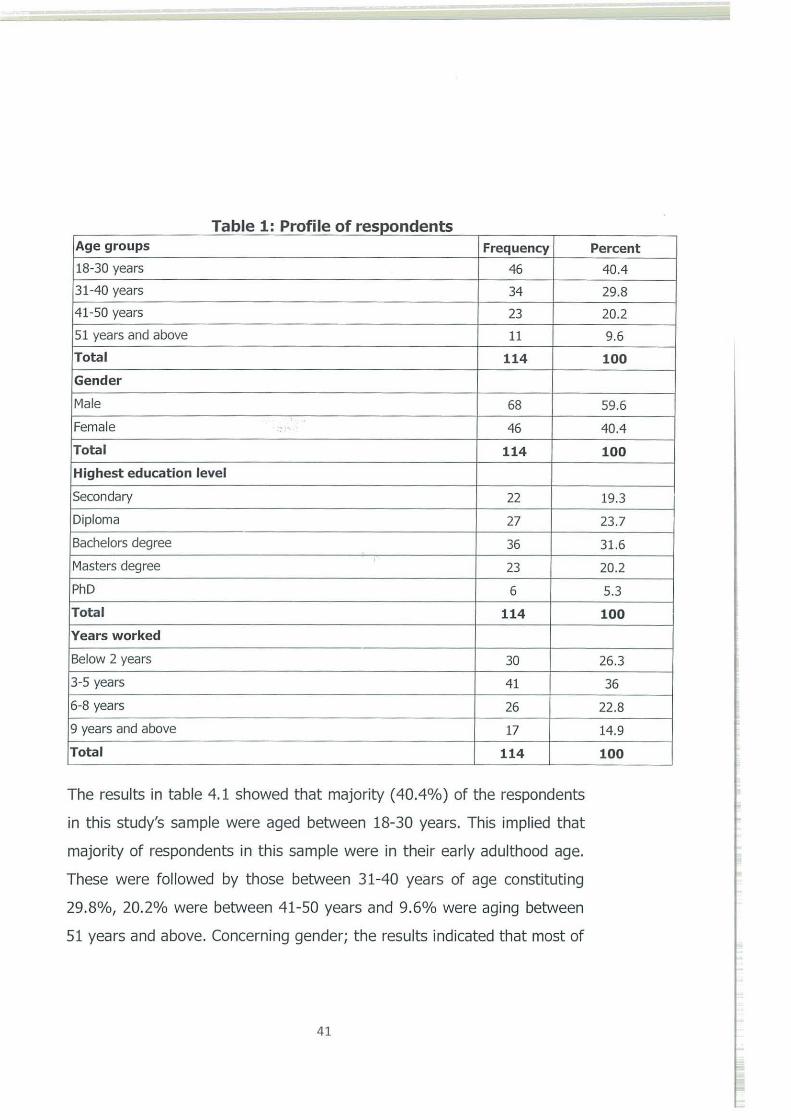

T bl 1 P fil f d ts a e . ro 1 eo respon en . Age groups Frequency

18-30 years 46

31-40 years 34

41-50 years 23

51 years and above 11

Total 114

Gender

Male 68

Female = 46

Total 114

Highest education level

Secondary 22

Diploma 27

Bachelors degree 36

Masters degree .

23

PhD 6

Total 114

Years worked

Below 2 years 30

3-5 years 41

6-8 years 26

9 years and above 17

Total 114

The results in table 4.1 showed that majority ( 40.4%) of the respondents