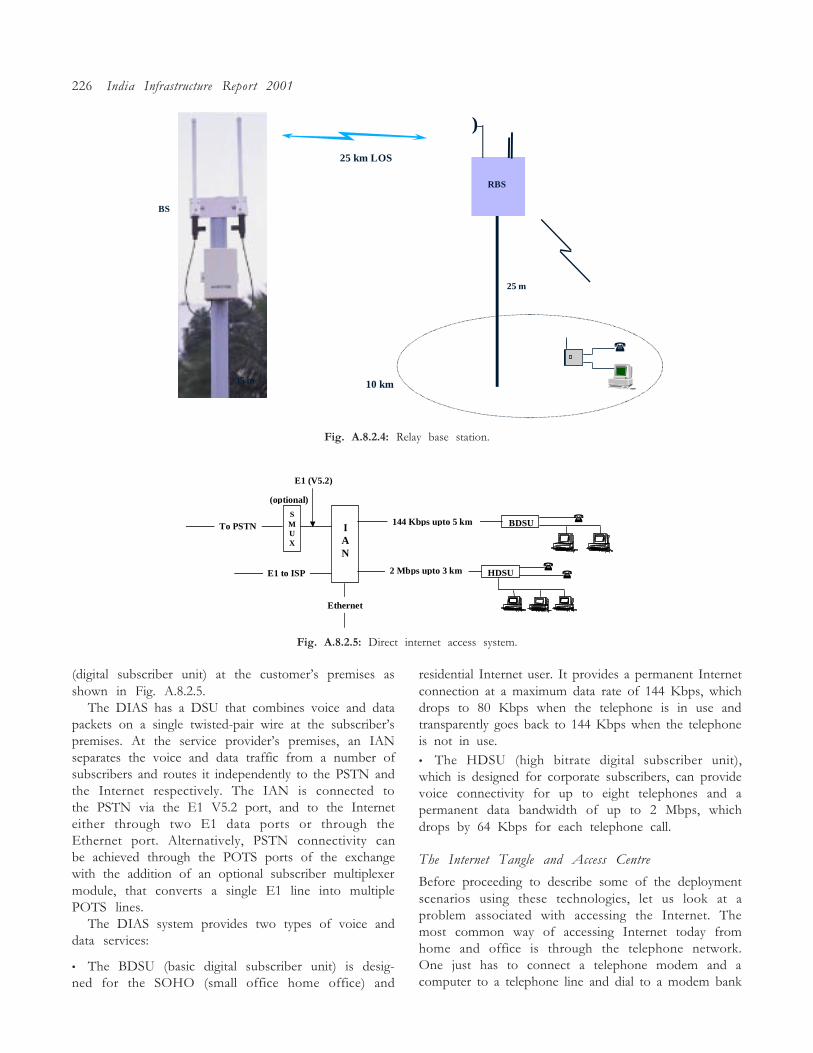

india infrastructure report 2001 - idfc

TRANSCRIPT

INDIA INFRASTRUCTURE REPORT 2001

Editor

Sebastian MorrisProject co-ordinators

Anupam B. Rastogi, IDFCSebastian Morris, IIM (A)

Prem K. Kalra, IIT (K)

INDIA INFRASTRUCTURE REPORT 2001

3iNetworkInfrastructure Development Finance CompanyIndian Institute of Management, Ahmedabad

Indian Institute of Technology, Kanpur

1

1YMCA Library Building, Jai Singh Road, New Delhi 110001

Oxford University Press is a department of the University of Oxford. It furthers theUniversity�s objective of excellence in research, scholarship, and education

by publishing worldwide in

Oxford New YorkAthens Auckland Bangkok Bogota Buenos Aires Calcutta

Cape Town Chennai Dar es Salaam Delhi Florence Hong Kong IstanbulKarachi Kuala Lumpur Madrid Melbourne Mexico City Mumbai

Nairobi Paris Sao Paolo Singapore Taipei Tokyo Toronto Warsaw

with associated companies in

Berlin Ibadan

© Oxford University Press 2000

ISBN 0 19 565.........................

Typeset by Excellent Laser Typesetters, Pitampura, Delhi 110034Printed in India ........................................

and published by Manzar Khan, Oxford University PressYMCA Library Building, Jai Singh Road, New Delhi 110001

When the Infrastructure Development Finance Company (IDFC) was in its formative stages, I felt that much ofits value would depend upon our ability to assimilate relevant knowledge already existing in the area of our interest.Apart from setting up our own policy advisory group to think through problems related to private investmentin infrastructure development, we also felt that we ought to be able to scan the broader environment to help uswith the task at hand.

Harnessing creative talent by developing research programmes in collaboration with the academic community,was one method of achieving this objective. We visited both IIM, Ahmedabad and IIT, Kanpur to see if there wasany interest in the enterprise. To our delight we found considerable enthusiasm for the idea. The result was thefounding of the 3iNetwork�as an open network where new like-minded partners from industry, academia, non-governmental organizations, and even the government can come together to realize its mission in a spirit ofcooperative endeavour.

The 3iNetwork essentially has a dual role: to identify projects within the two academic institutions to furtherthe process of investment in relevant and appropriate infrastructure projects and; to annually document issues ininfrastructure development arising from the evolving political and economic environment in the country. Withregard to the first, we are currently funding nine projects, ranging from virtual reality simulation labs to publicutility pricing for infrastructure services.1

This first attempt by us to document infrastructure issues has resulted in the India Infrastructure Report 2001.This report focuses on the policies required to create an appropriate market structure for infrastructure provisionand the regulatory framework this implies. We envisage that this enterprise will evolve into a periodic documentthat records progress in the country as a whole, and in the various states on matters of both policy evolution andproject development in infrastructure. We intend this to be a standard work of reference with respect to infrastructuredevelopment in India.

IDFC considers itself fortunate to have played the role of a catalyst in this process of bringing together academiaand industry to deliberate upon and solve many of today�s problems. It is our belief that a free, frank, and openexchange of views is necessary to arrive at the most innovative and workable solutions that will find acceptanceamong various stakeholders. We are ultimately concerned with processes that yield optimal solutions for thegovernment, encourage private participation in investment and provision of infrastructure services, provide anenvironment of healthy competition, and, above all offer quality services to citizens. With the right frameworkand willingness to put people first, systems can work to achieve this objective. We need to ask ourselves one simplequestion in this context�is it sustainable, and is this in the interest of the consumer? If the answer is �no� we needto seek alternatives, even if that means eliminating existing structures of governance. Governance is about citizens,for citizens, and has no other purpose. We hope to develop the 3iNetwork into an ever-growing fraternity and,together, make a difference for the people of India.

December 2000 NASSER MUNJEE

1 The range of activity could be viewed on the network�s portal at www.3inetwork.org or at www.idfc.com.

PREFACE

Samir K. Barua Indian Institute of Management, AhmedabadRakesh Basant Indian Institute of Management, AhmedabadAtanu Chakraborty Directorate of Employment and Training, Government of Gujarat, GandhinagarPuneet Chitkara Indian Institute of Technology, KanpurKeshab Das Gujarat Institute of Development Research, AhmedabadSaumyen Guha Indian Institute of Technology, KanpurAmita Gupta Infrastructure Leasing and Financial Services, New DelhiRekha Jain Indian Institute of Management, AhmedabadAshok Jhunjhunwala Indian Institute of Technology, MadrasAbha Singhal Joshi Centre for Human Rights Initiative, New DelhiPrem K. Kalra Indian Institute of Technology, KanpurT. Madhavan Indian Institute of Management, AhmedabadS. Manikutty Indian Institute of Management, AhmedabadB. R. Marwah Indian Institute of Technology, KanpurM. P. Mathur National Institute of Urban Affairs, New DelhiAlice Albin Morris Unnati, Organisation for Development Education, AhmedabadSebastian Morris Indian Institute of Management, AhmedabadAnish Nanavaty Infrastructure Development Finance Company, MumbaiAjay Narayanan Infrastructure Development Finance Company, ChennaiB. P. Pundir Indian Institute of Technology, KanpurG. Raghuram Indian Institute of Management, AhmedabadBhaskar Ramamurthi Indian Institute of Technology, MadrasK.V. Ramani Indian Institute of Management, AhmedabadM. Y. Rao PricewaterhouseCoopers and Development Associates Ltd., BhubaneshwarVivek Raval Unnati, Organisation for Development Education, AhmedabadDheeraj Sanghi Indian Institute of Technology, KanpurSujata Sawant Rail India Technical and Economic Services, Urban Transport Division, New DelhiRajiv Shekhar Indian Institute of Technology, KanpurY. M. Shivamurthy Infrastructure Development Finance Company, MumbaiV. K. Sibal Rail India Technical and Economic Services, Urban Transport Division, New DelhiSidharth Sinha Indian Institute of Management, AhmedabadVinita Sinha Infrastructure Development Finance Company, MumbaiGeetam Tiwari Indian Institute of Technology, DelhiJayanth Varma Securities and Exchange Board of India, Mumbai

CONTRIBUTORS

The 3iNetwork had met several times to discuss the proposition of an infrastructure report and its possible contents,before adopting the theme of industry structure and regulation. Freewheeling discussions among engineers, socialscientists, and practising managers, gave us much insight and many leads to work and write upon. It is now clearto all of us that the topic chosen for the first report could not have been more timely. Nasser Munjee first articulatedthe idea that policy and regulatory contradictions stand in the way of the development of several physicalinfrastructural sectors, especially with respect to private investment. The theme was both broad and unifying. Manymore articles than those carried in the report were written. Not all could be included due to the limitations of spaceand time. Similarly, not all who took active part in the report have written papers. However, their contributionsare as important to the success of the report as that of the writers.

There continue to be uncertainties with regard to the likely and intended industry structure and restructuringin many of the infrastructural areas. This in conjunction with today�s recession, and institutional and organizationalinadequacies, have worked to create a situation wherein a fresh approach to the development of infrastructure isimportant. If this report is able to outline the necessary national effort to create the basic contours of the �secondround of reform� then it would have served its purpose. We are grateful to IDFC, specifically to Nasser Munjeeand Anupam Rastogi who provided us this opportunity.

The need to go beyond stylistic, piecemeal and doctrinaire approaches, to a more thoughtful and pragmatic oneis by now obvious to any one involved in the development of infrastructure in India. For example, neither theextreme positions of �abolish all subsidies�, nor its contrary of the continuance of the status quo, are justified.Therefore, reform today poses a greater challenge than what is generally believed. The challenge is not merelypolitical, but also intellectual�we need to deeply worry about the �incentive compatibility� and the institutionalbasis of any policy. At IIM(A) many of us have long held this view. We were pleasantly surprised to discover similarthinking amongst our colleagues both at IDFC and IIT(K). We worked together closely as part of the 3iNetwork,and in putting together IIR 2001. It became clear to us that the basic problems cut across many of the infrastructuralareas. While vested interests do stand in the way of reform, such interests have usually been a creation of perverseincentives and insensitive policy. The need to direct intellectual capital into infrastructure is an important task aheadfor our country.

The technological dimensions of this task are perhaps as important as the challenge of institutional reform andincentive compatibility. This is especially so in today�s world wherein information technology in its broadest sensehas the potential to redraw the very economic fabric of society through change in the many ways of communication.Similarly, cheap, real time measurement possibilities, advances in data storage and mining create scope for constructedmarkets, light regulation, monitoring and control, direct participation and regulation by people, that are only dimlysensed at this juncture. The telecom sector is being directly turned around by developments in technology, andother sectors will not be able to escape its indirect effects. The aspect of convergence already tends to make obsoletesome of the institutional initiatives at a sectoral level. In this world of uncertainty, and where phenomena mutatefaster than theory, there is a strong need to get back to the basic principles, to �respect� the specificities of the particularsituation and society.

Such a task is seemingly contradictory, but not as useless as a doctrinaire approach would be. Little can be achievedin a democracy like ours without the participation of people in socially important infrastructure such as roads, dams,

ACKNOWLEDGEMENTS

and municipal water. Thus, issues such as land acquisition and people�s right to know, are part of the debate, requiringresolution. Therefore, we also invited persons outside the network but with experience to join the IIR 2001 team.

We see this report as a modest effort to understand infrastructure and its problems, with the recognition thatthere are broader dimensions to the problem. We also hope that at this juncture when the direction to move isnot clear, such an approach is rewarding.

The preliminary papers were presented at the writers� workshop held at IIM(A) in mid-August. We thank allthe special invitees for their comments and lively participation�Sadashiv Rao, Cherian Thomas, Partha Mukhopadhyay,Jayalakshmi Jayaraman, Janak Talsania, Nirmal Mohanty, and Anupam Srivatsava from IDFC, and Subir Gokarnof the National Council of Applied Economic Research (NCAER). I also thank the IIM(A) faculty who participatedin the workshop. To Anupam Rastogi, a special thanks is due for holding together the entire workshop. I am gratefulto the team of rappoteurs consisting of Bharat Verma, Vinisha Thaker, Deepa Keskhani, Trupti Patel, and ChristinaSullivan Sarabhai for painstakingly recording the highlights of the discussions.

A collective effort such as this one is hardly possible without the involvement of several persons. Devika Fernandesof the IDFC was ready to provide much crucial information and data however ill-defined the requests. DeepaKeshkani, Trupti Patel, and Vinisha Thaker took up the �back office� operations at IIM(A). They put together thebibliography, the abbreviations and helped me with the manuscript, besides assisting G. Raghuram and Rekha Jainwith their papers. Ram Mishra looked after the coordination at IIT(K). Urmil Anjaria, my secretary, workedfeverishly to get the various papers in shape. Kavita Iyengar and Shreemoyee Patra at Oxford University Press, Delhinot only did a remarkable job of supervising the entire editorial task within an exceedingly tight schedule but alsoensured that I did not slacken on the deliverables. Christina Sullivan Sarabhai saved me much time by copyeditingmany of the papers.

I would also like to thank Jahar Saha, for encouraging the IIM(A) component of the team in so many ways.My personal indebtedness is also due to Jayanth Varma, G. Raghuram, Sidharth Sinha, Bithin Datta, Rekha Jain,Keshab Das, Anupam Rastogi, Jaya Singhania, Puneet Chitkara, Rakesh Basant, Dheeraj Sanghi, Arun P. Sinha, T. V.Prabhakar, Atanu Chakraborty, Bernard D�Mello, R. Nagaraj, Nasser Munjee, Alice Albin, M. Y. Rao, S. K. Barua,Y. M. Shivamurthy, Anish Nanavaty, Sanjay Dhande, B. R. Marwah, Prem Kalra, K. K. Saxena and Subir Gokarnfor the discussions I had with them on various issues in infrastructure. I gained much from these discussions.

Mahesh Vyas gave the team and me the confidence that came from knowing that the database of the Centre forMonitoring the Indian Economy (CMIE) was always available to us. The report owes much to the informationprovided by the CMIE, and I am indebted to Mahesh Vyas for this.

On behalf of the contributors, I thank all those who have helped us put together this report. However, we aloneare responsible for any errors that remain.

SEBASTIAN MORRIS

viii Acknowledgements

CONTENTS

List of Tables xivList of Boxes xviiList of Figures xviiiList of Abbreviations and Acronyms xix

1 . Overview 1Sebastian Morris

2. Issues in Infrastructure Development Today: The Interlinkages 9Sebastian Morris

Introduction 9The Situation Today 10Macroeconomic Linkages 13The Approach to Reform and Restructuring 15Ill-conceived Reforms 16Leverage Points for Change 17Public Enterprise in Infrastructure 18Pricing and Subsidies 21Regulatory Stances 23The Constraint of Land and Environment 28The Right to Information and Pressures from Below 31

3. Regulation of Tariffs and Interconnection: Case Studies 33Sidharth Sinha

Case 1. Rebalancing of Telecom Tariffs 35Case 2. Interconnection between Fixed and Mobile Networks 42Case 3. Availability-based Tariff (ABT) Order of the CERC 48

4. Regulatory Dilemmas in Infrastructure Financing 53Jayanth Varma

Introduction 53Relaxing Financial Sector Regulations 53Government Support for Infrastructure Financing 58Conclusion 62

5. Structural Issues and Constraints 63

5.1 INTERFACE BETWEEN SECTOR-SPECIFIC REGULATORY BODIES AND

COMPETITION AGENCIES: A CASE OF THE INDIAN TELECOM SECTOR 63Rakesh Basant

The Experience of Other Countries 63

x Con t en t s

Telecom Standards, Intellectual Property Rights (IPRs), and Competition Policy 66The TRAI Ordinance and the Distribution of Responsibilities 66The Allocation of Responsibilities: Some Considerations 67Modifications in the Indian Institutional Structure 70

5.2 POLITICAL AND BUREAUCRATIC HURDLES IN REFORM AND RESTRUCTURING:THE ELECTRICITY SECTOR 71M. Y. Rao

5.3 NEED FOR A BOT LAW: GUJARAT INFRASTRUCTURE DEVELOPMENT ACT 73Atanu Chakraborty

5.4 PROJECT PREPARATION: THE CINDERELLA OF PRIVATE SECTOR PARTICIPATION (PSP) 76Atanu Chakraborty

5.5 HOW MUCH MORE OF THIS INFLICTION?THE CASE OF THE AHMEDABAD�VADOARA EXPRESSWAY 77Amita Gupta and Sebastian Morris

5.6 LAND ACQUISITION: LAW AND PRACTICE 80Y. M. Shivamurthy and Vinita Sinha

Introduction 80Public Purpose 81Acquisition Procedure 82Compensation 83Resettlement and Rehabilitation 84Suggested Amendments to the Legislative Framework 85Conclusion 85

5.7 ENVIRONMENT AND SOCIAL RISKS IN INFRASTRUCTURE DEVELOPMENT 87Ajay Narayanan

Public Pressure and Judicial Intervention 87International Pressures 88Regulatory Framework for the Environment 89The Way Forward 90PAPs as Stakeholders in Project Development 90

5.8 THE RIGHT TO INFORMATION AS A TOOL OF EMPOWERMENT 91Abha Singhal Joshi

6. The Electricity Sector 94

6.1 MISSING INTERCONNECTIONS IN THE POWER SYSTEMS 94Puneet Chitkara, Rajiv Shekhar, and Prem K. Kalra

Introduction 94Bulk Tariffs 95Being Fair to Consumers 96Subsidies 97Resource Mobilization 97Transmission 98Pricing of Transmission Services 100

6.2 POWER SECTOR REFORMS AND REGULATION: THE ROAD AHEAD 104Sebastian Morris

Introduction 104The Current Paradigm 105Overcoming the �Agency Problem� 109Creating the Market 112Values of �X� 118

Cont en t s xi

Market Conduct 119Labour and Modalities 124Conclusion 125

7. Integrated Transport 129

7.1 THE TRANSPORT SECTOR 129G. Raghuram

Estimating Demand 129Transport Myopia 130Segmenting the Market 134Structure of the Transport Sector 136

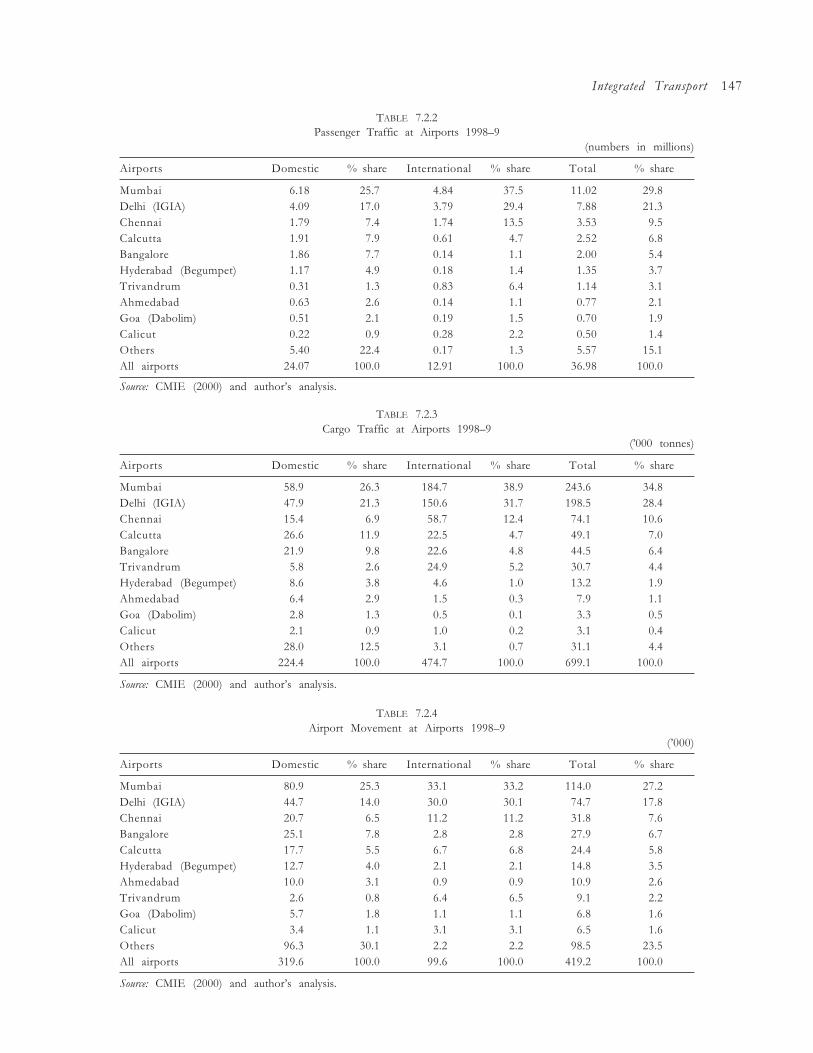

7.2 SECTORAL ISSUES IN TRANSPORTATION 146G. Raghuram

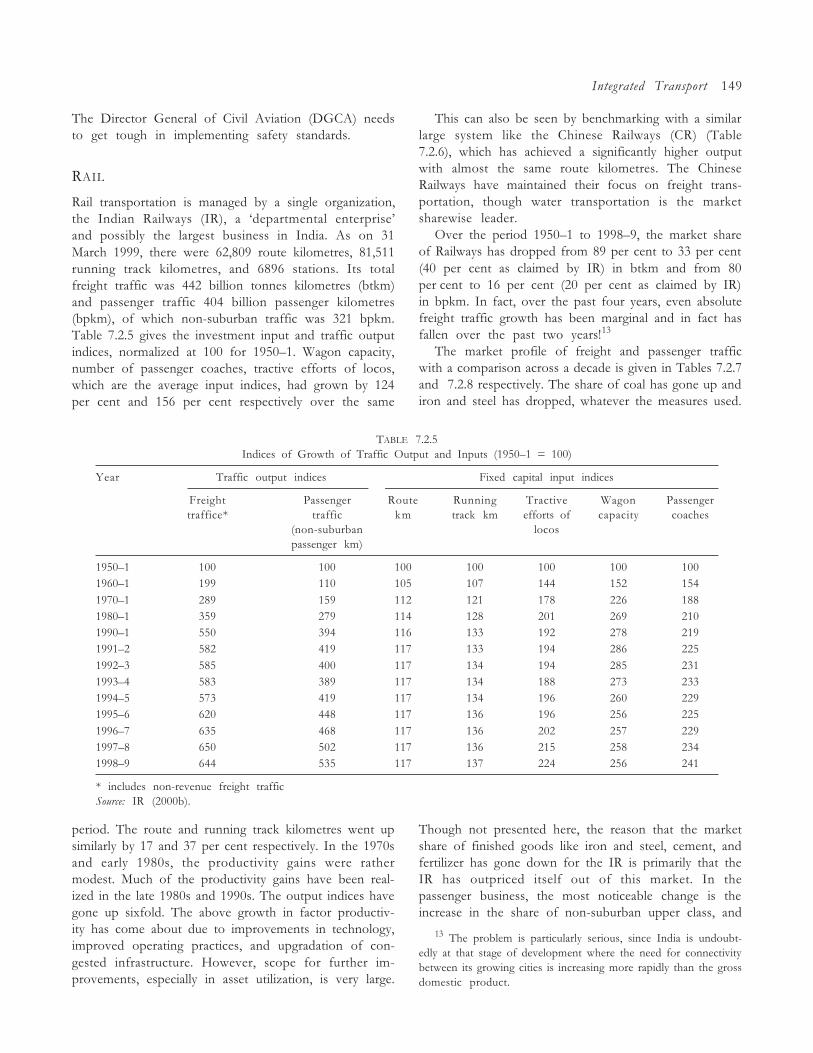

Air 146Rail 149Road Transport 155Maritime Transport 159Pipelines 165Multimodal Transport 166

7.3 PORT AND SHIPMENT MANAGEMENT AT SINGAPORE PORT:THE REVOLUTION IN THE USE OF ELECTRONIC DATA INTERCHANGE 167K. V. Ramani

Management of Container Terminals 168

7.4 AT THE CROSSROADS: PIPELINE INFRASTRUCTURE FOR OIL PRODUCTS 171Samir K. Barua and T. Madhavan

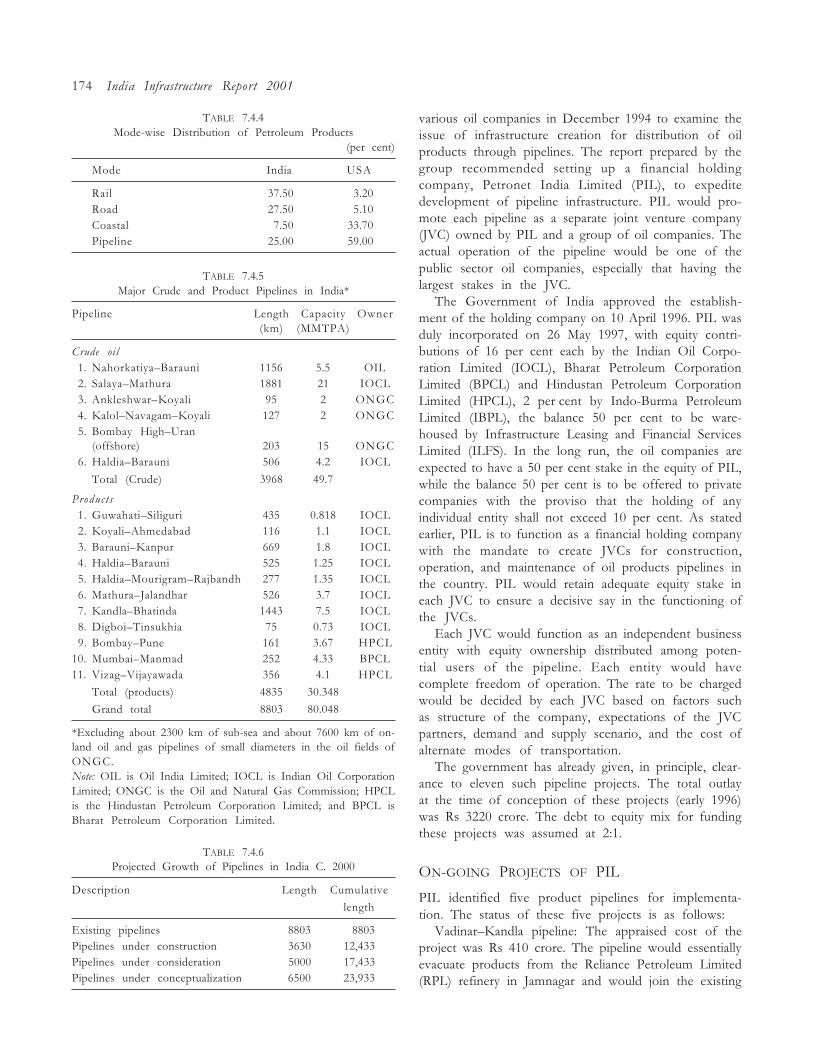

Introduction 171Operation 171Advantage of Pipeline Transportation 171Oil Pipelines in India 171Existing Policy 173On-going Projects of PIL 174Tariff 175Pipeline Projects Remain Unbankable 175Tariff Determination in the US and UK 176The Road Ahead 176Regulatory Framework is Necessary 176

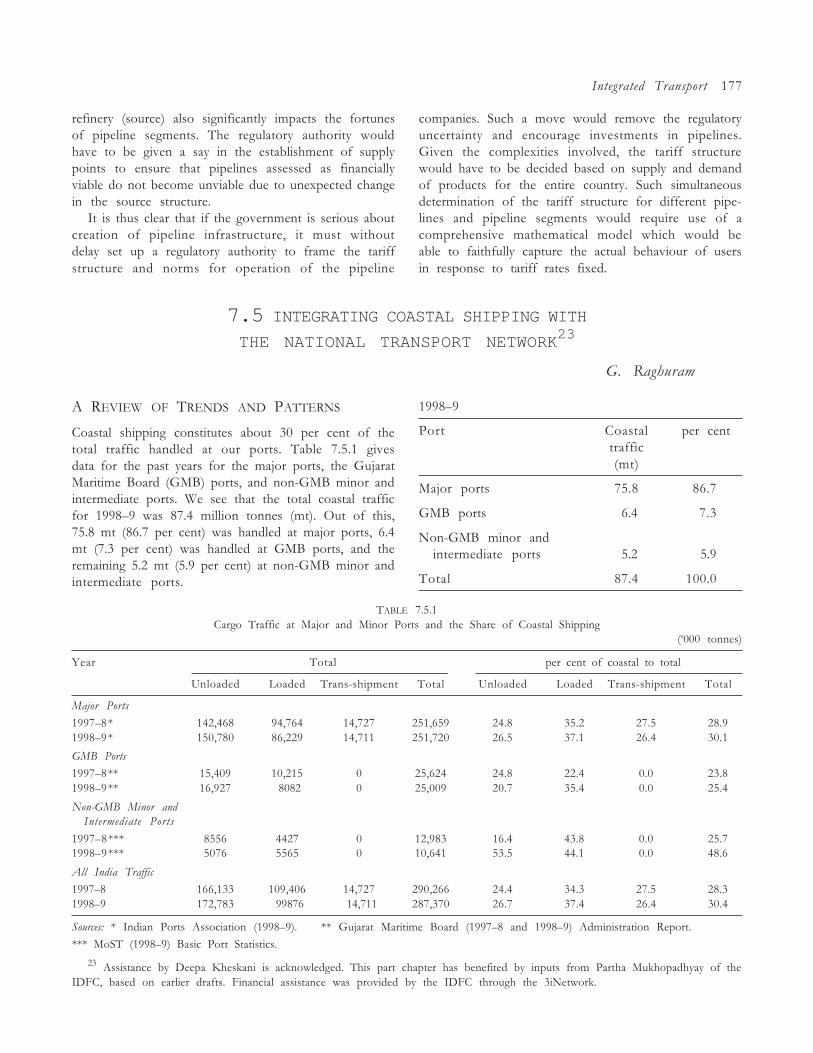

7.5 INTEGRATING COASTAL SHIPPING WITH THE NATIONAL TRANSPORT NETWORK 177G. Raghuram

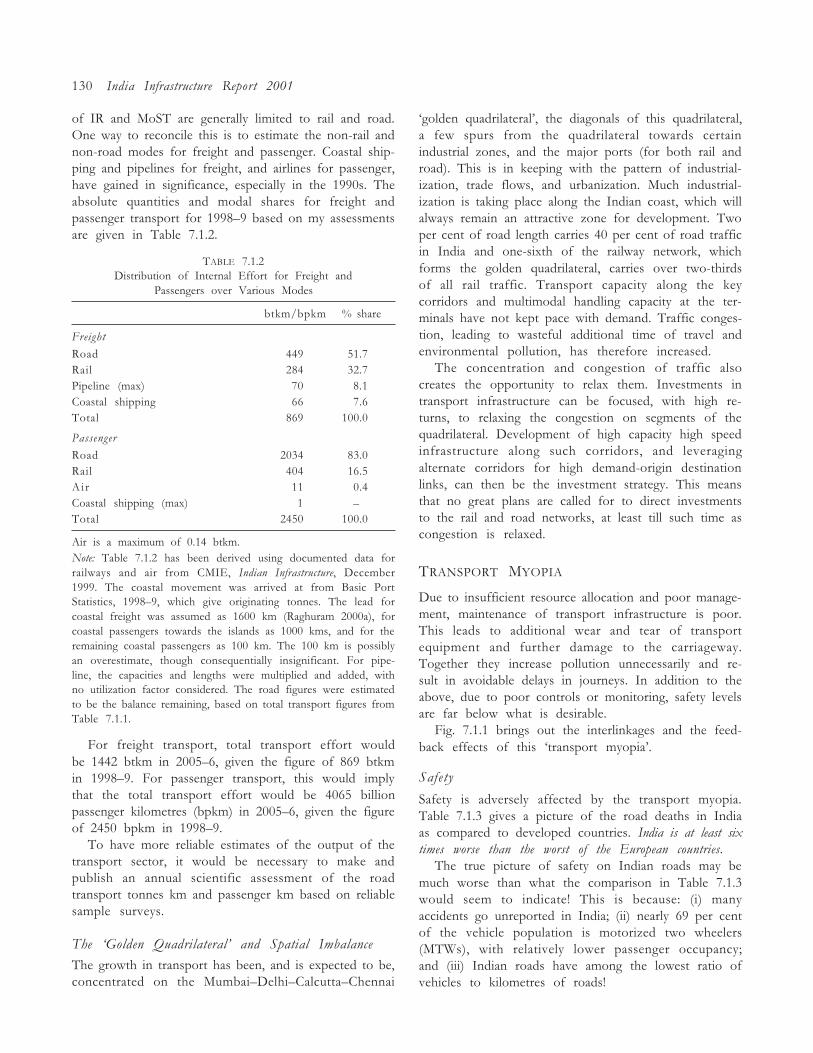

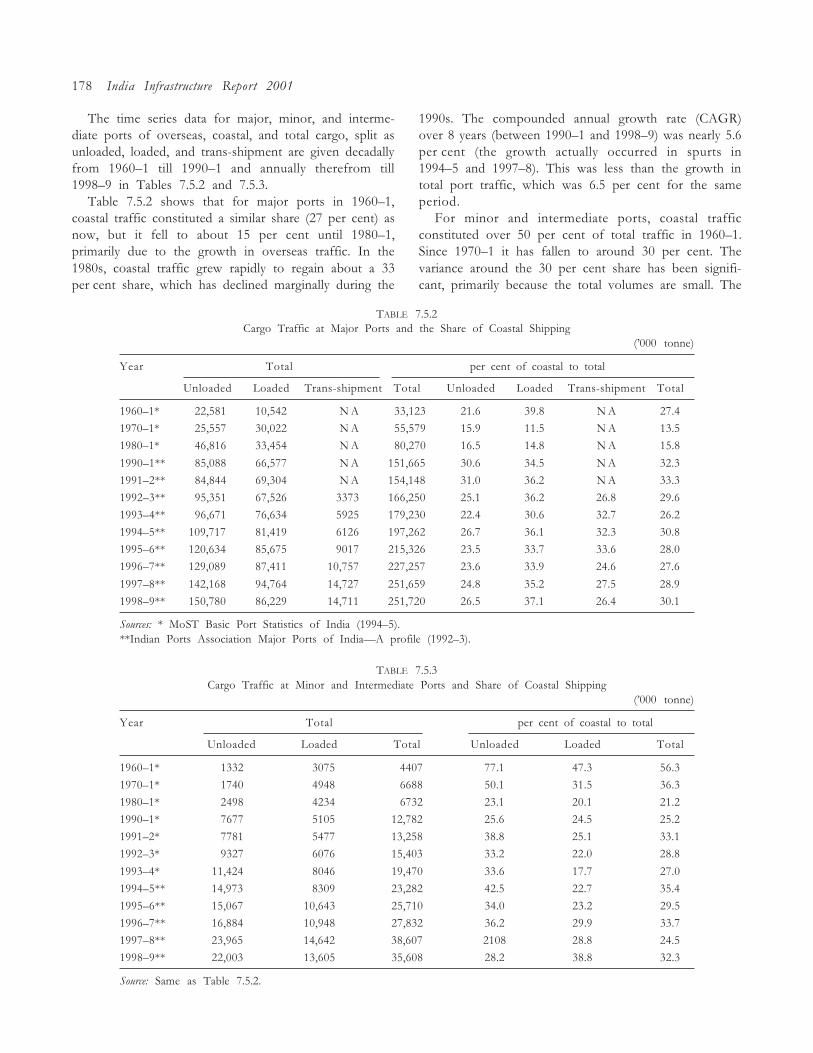

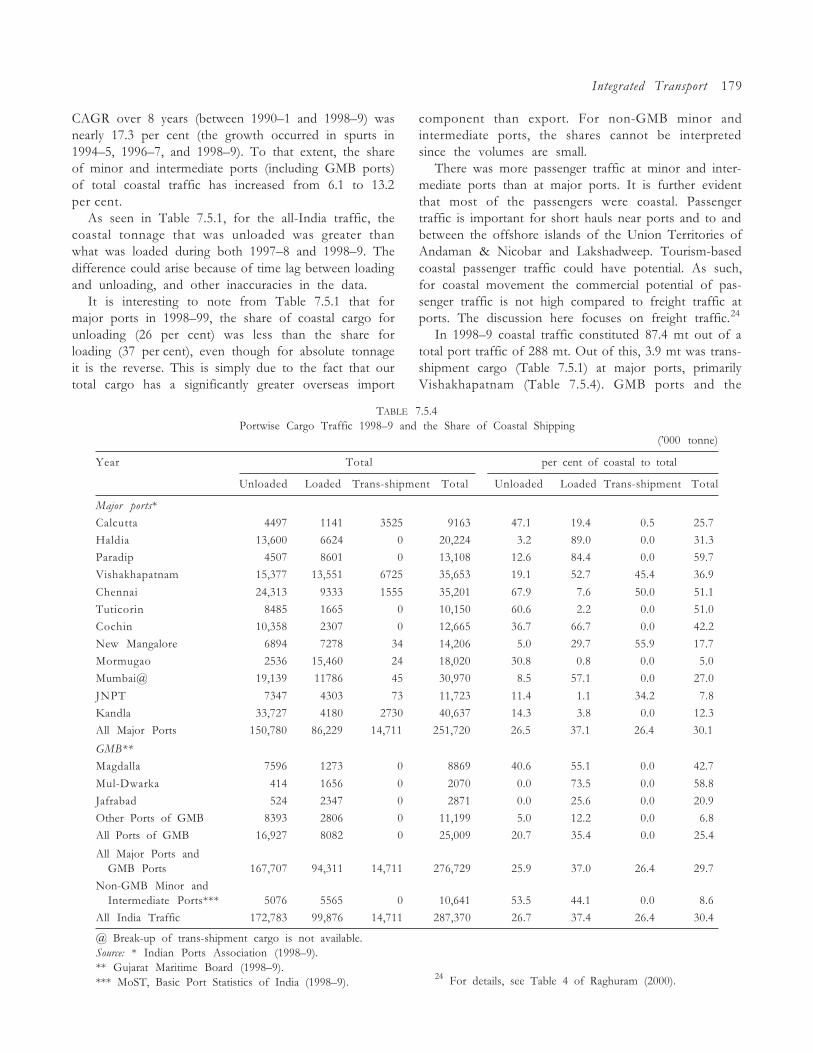

A Review of Trends and Patterns 177Coastal Traffic Profile 180Economics of Coastal Movement 183Traffic Potential 185Utilization of Ships 185Regulatory Issues 186Infrastructure Focus Areas 187

8. The Telecom Sector 189

8.1 A REVIEW OF THE INDIAN TELECOM SECTOR 189Rekha Jain

Introduction 189Basic Services 194

xii Content s

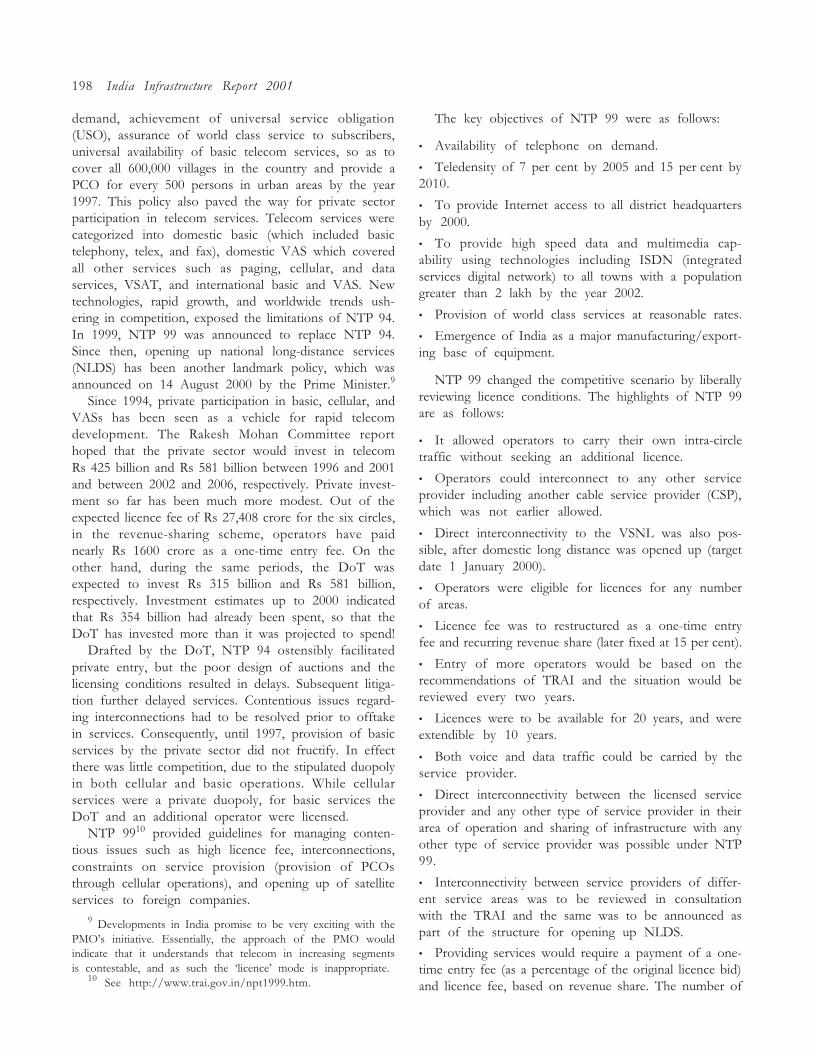

Rural Telecom Services 195International Telecom Services and the VSNL 195National Telecom Policy 1994 and 1999 197Private Participation 199Emergent Issues 201Strengthening the TRAI 202Issues in Licensing 203Bundling 203Unit of Bidding 204Bid Design 204Interconnection Issues 204Universal Service Obligations (USOs) 205Demand Estimates 205Spectrum Management 206Role of Competition 207

8.2 LOOKING BEYOND NTP 99 210Ashok Jhunjhunwala

Introduction 210Where did the Operators go Wrong? 211Some Implications of Revenue Sharing 211NTP 99: Some Specific Issues 214Conclusion 215

8.3 NUMBER PORTABILITY: WHY DO WE NEED IT? 217Dheeraj Sanghi

APPENDICES

8.1.1 Note on IP Telephony and Voice over Internet Protocol (VoIP) 2208.1.2 Data Services before NTP 99 2228.1.3 Scope and Functions of the TRAI 2238.2.1 Efforts of the Telecommunication and Computer Network (TeNet) Group 223

9. The Spatial Context 236

9.1 FINANCES AND FUNCTIONING OF URBAN LOCAL BODIES: A SITUATION REPORT 236M. P. Mathur

Introduction 236ULBs 238Functional Domain of ULBs 239Fiscal Domain of ULBs 240Composition of Own Revenues 241Municipal Expenditure 243Trends in Municipal Finance 244Grants to States for Financing Local Bodies: CFC Recommendations 245Water Supply, Sanitation, and Solid Waste Disposal 246Major Drawbacks in the Existing Tariff Structure 251Privatization in Municipalities 251Innovations in Municipal Accounting Systems 253Conclusion 254

9.2 URBAN AND INTER-URBAN ROAD DESIGNS IN INDIA:ISSUES CONCERNING MIXED TRAFFIC 256Geetam Tiwari

Traffic Patterns and Planning Issues in Indian Cities 256The �Critical Element� in the City Transport Fabric: Vulnerable Road Users 257

Contents xiii

Avoided Costs through Investments in Bicycle/NMV Friendly Infrastructure 257Inter-Urban Transport Issues 259

9.3 VEHICULAR AIR POLLUTION IN INDIA:RECENT CONTROL MEASURES AND RELATED ISSUES 260B. P. Pundir

Vehicular Air Pollution and Emission Regulations 260Emission Control of In-service Vehicles 261Remedial Measures 262Benzene 262Oxygenates 262CNG 262

9.4 IMPLICATIONS OF THE 74TH AMENDMENT ON THE WATER AND

WASTEWATER SECTOR 263Anish Nanavaty

Key Features 264Water Sector Implications 264Extent of Devolution 264

9.5 RURAL DRINKING WATER SUPPLY: ISSUES AND STRATEGIES 269Keshab Das

Introduction 269Statal Role: Chasing Changing Targets 269The Problem of Mobilizing Finance 273Management by Local Community 276Design and Technology 276Concluding Observations 277

9.6 BUS TRANSPORT IN DELHI 277B. R. Marwah, V.K. Sibal, and Sujata Sawant

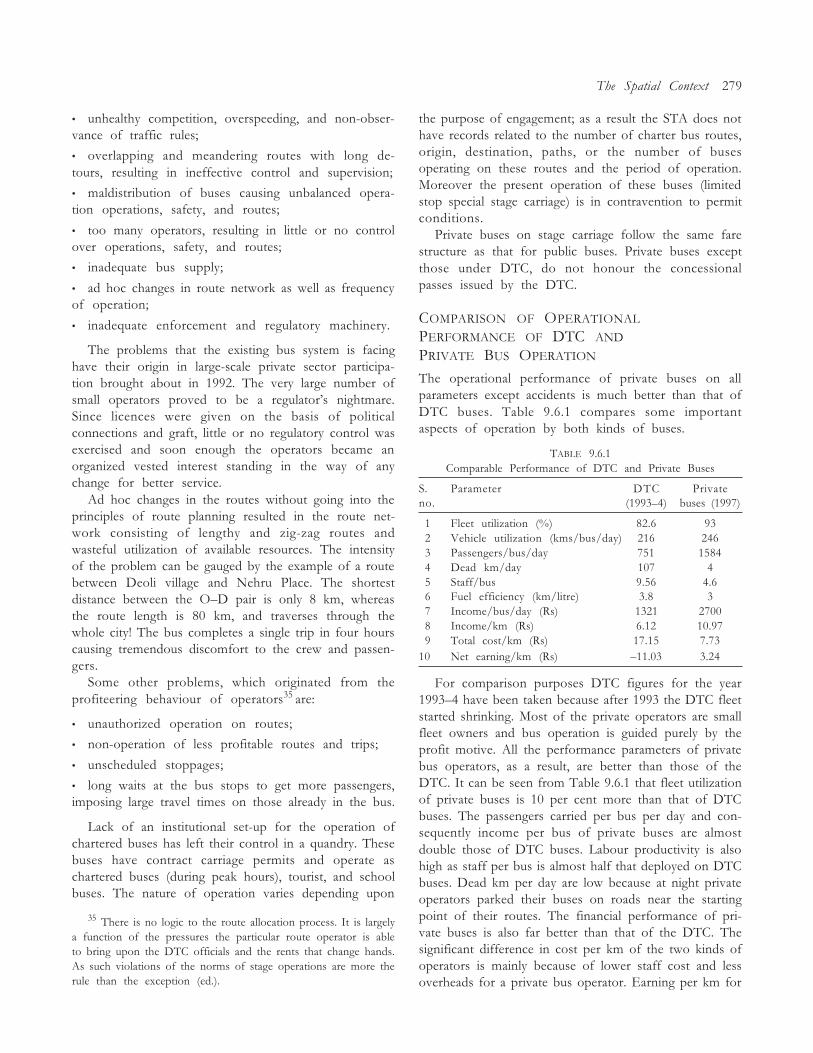

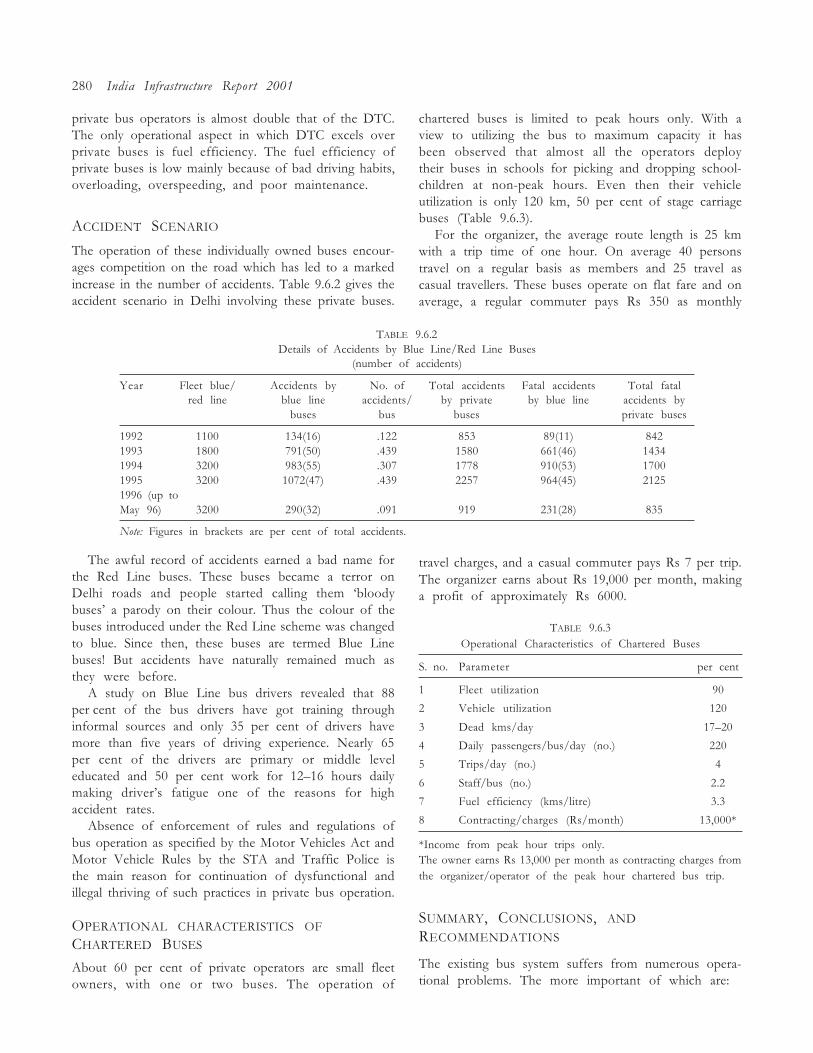

Introduction 277Inadequacy of the Bus Transport System in Delhi 278Growth of the DTC 278Comparison of Operational Performance of DTC and Private Bus Operation 279Accident Scenario 280Operational Characteristics of Chartered Buses 280Summary, Conclusions, and Recommendations 280

9.7 DEALING WITH DROUGHT 281Saumyen Guha

Issues for Implementation 282

Bibl iography 283

TABLES

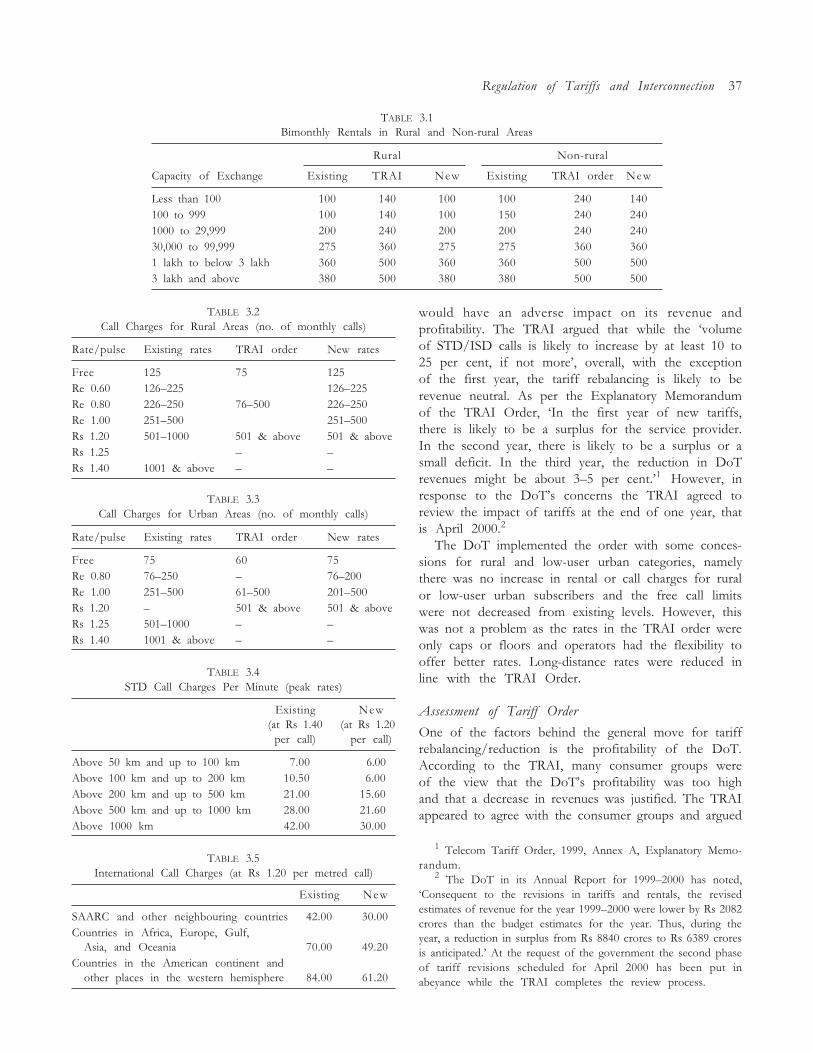

3.1 Bimonthly Rentals in Rural and Non-rural Areas 37

3.2 Call Charges for Rural Areas 37

3.3 Call Charges for Urban Areas 37

3.4 STD Call Charges Per Minute 37

3.5 International Call Charges 37

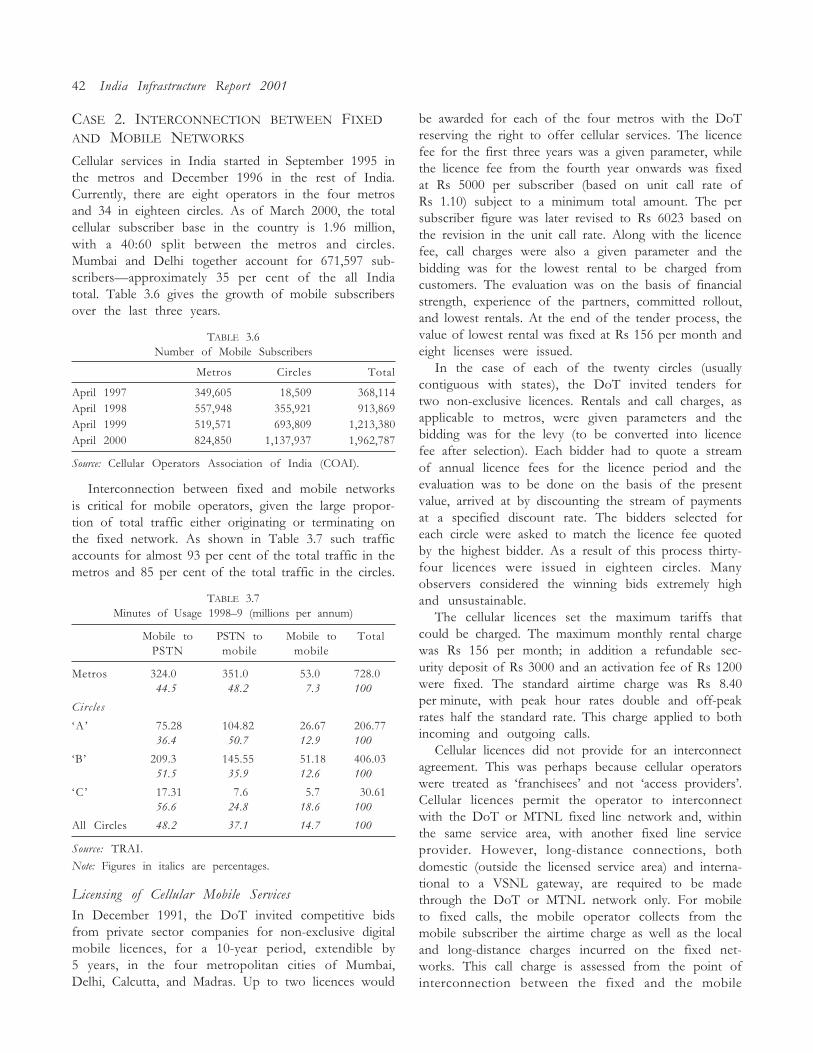

3.6 Number of Mobile Subscribers 42

3.7 Minutes of Usage 1998�9 42

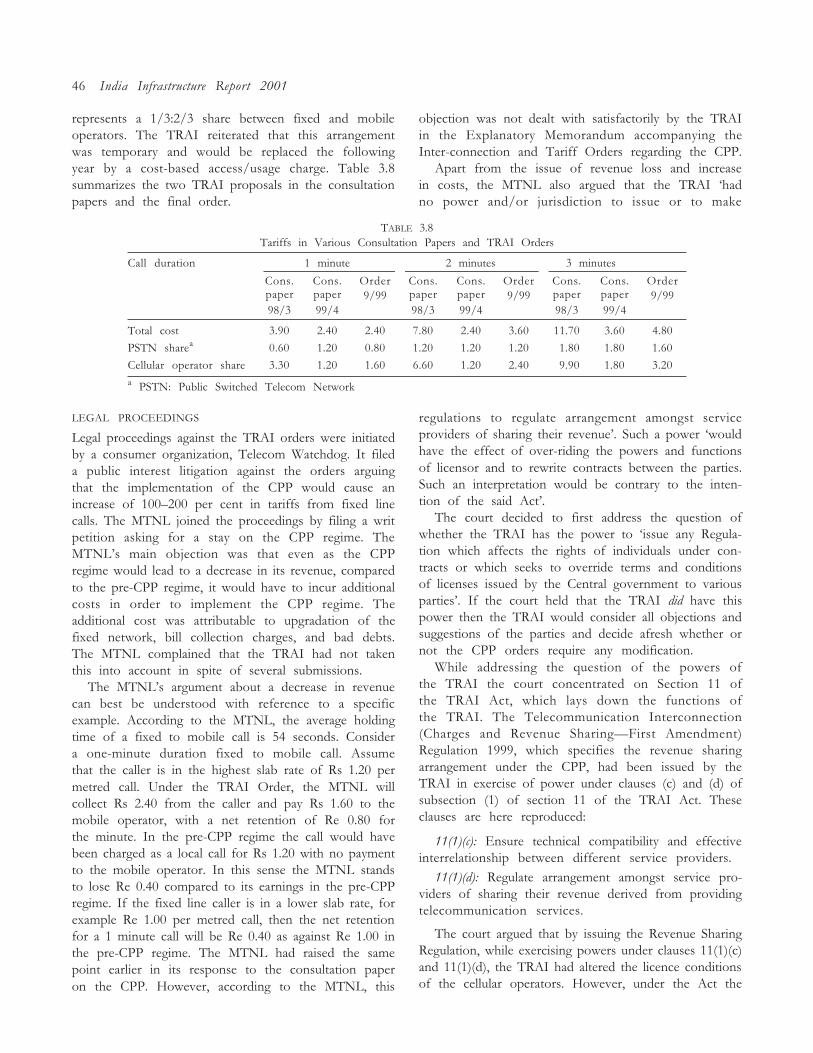

3.8 Tariffs in Various Consultation Papers and TRAI Orders 46

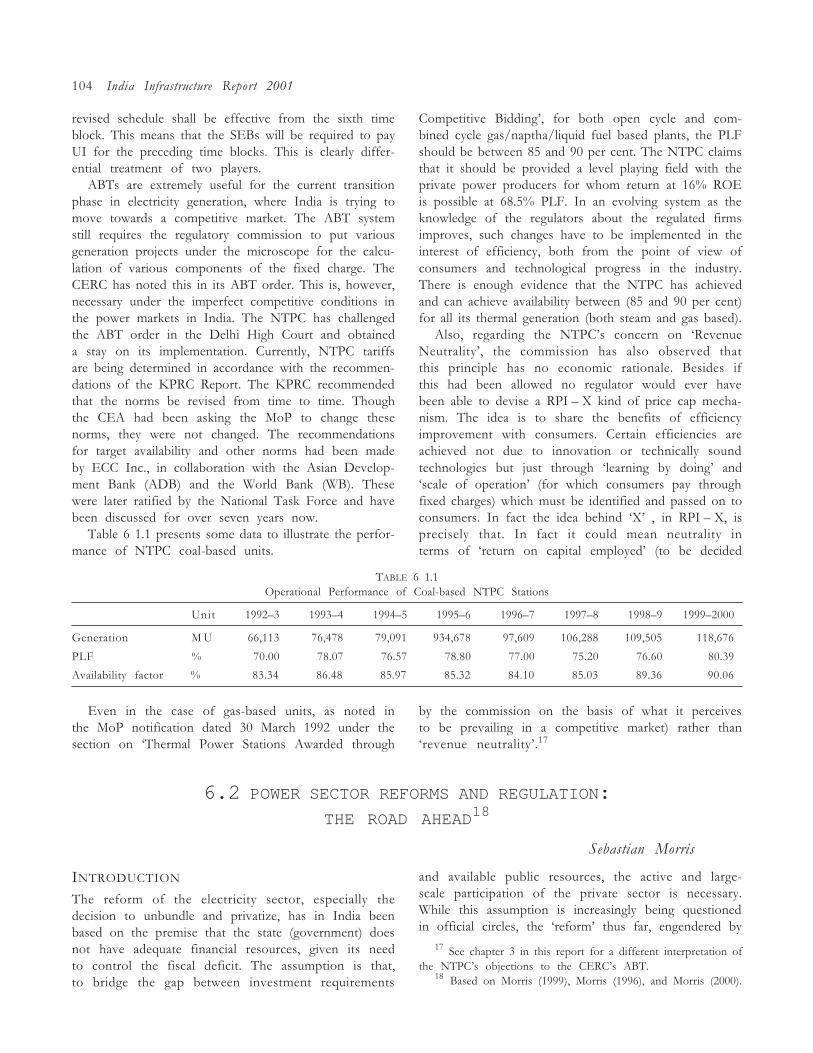

6.1.1 Operational Performance of Coal-based NTPC Stations 104

6.2.1 The Internal Rate of Return of the Difference in the Foreign Exchange FlowsBetween a Nationalist Alternative and an Enron-like Project 107

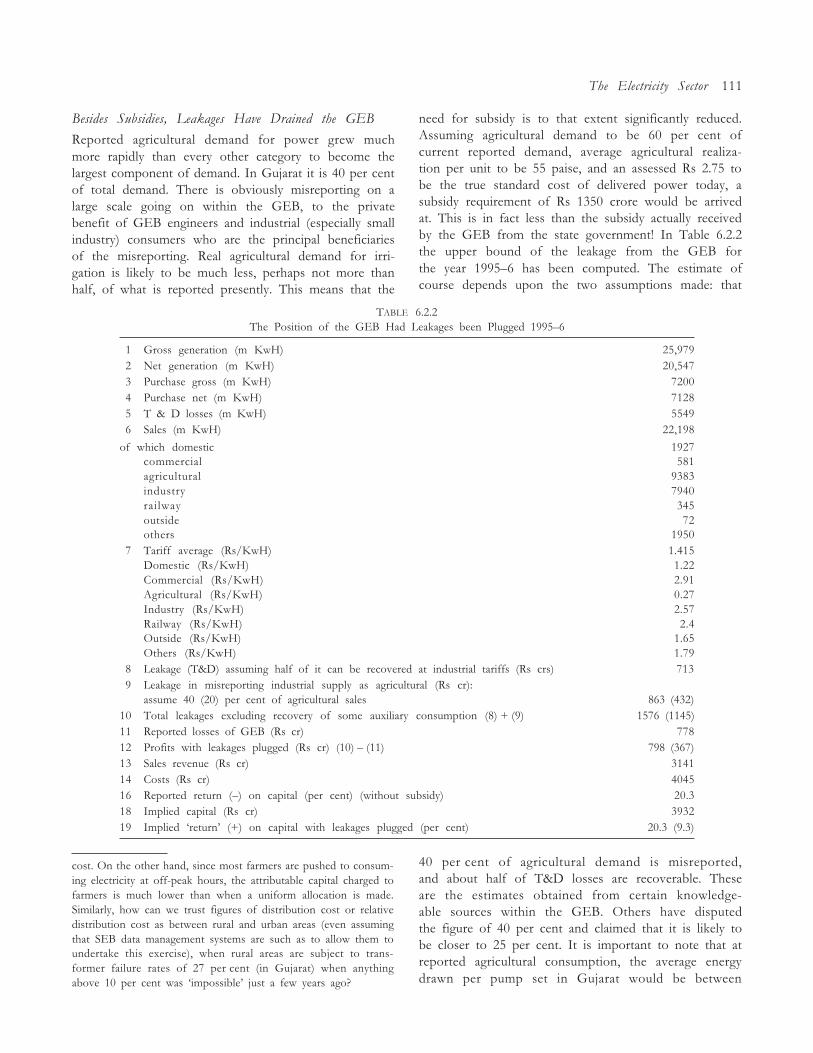

6.2.2 The Position of the GEB Had Leakages been Plugged 1995�6 111

6.2.3 Average Sizes of Various Classes of Consumers of GEB c.1995�6 116

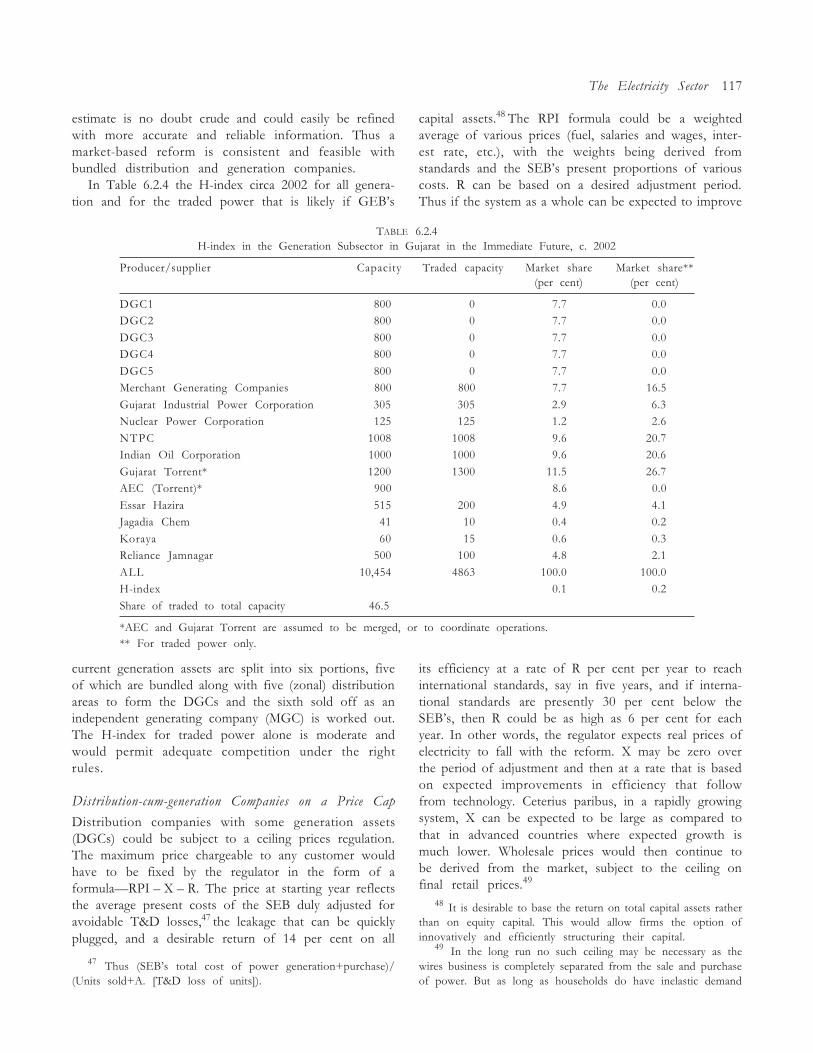

6.2.4 H-index in the Generation Subsector in Gujarat in the Immediate Future c.2002 117

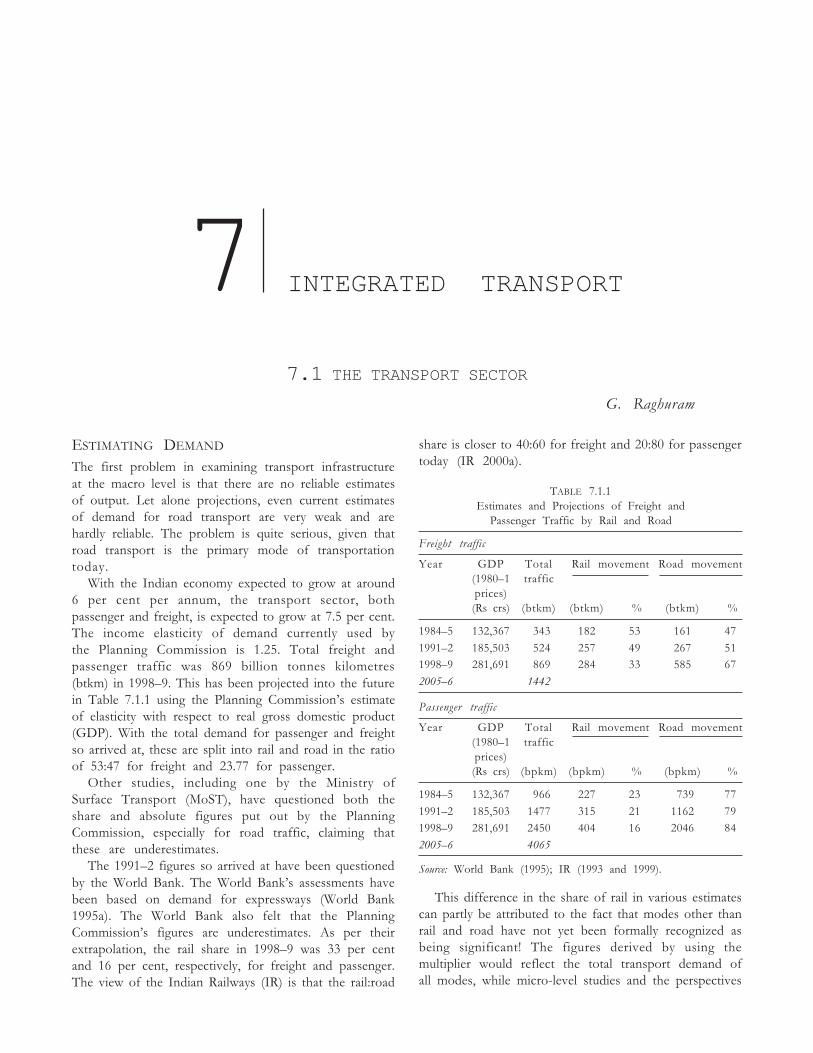

7.1.1 Estimates and Projections of Freight and Passenger Traffic by Rail and Road 129

7.1.2 Distribution of Internal Effort for Freight and Passengers over Various Modes 130

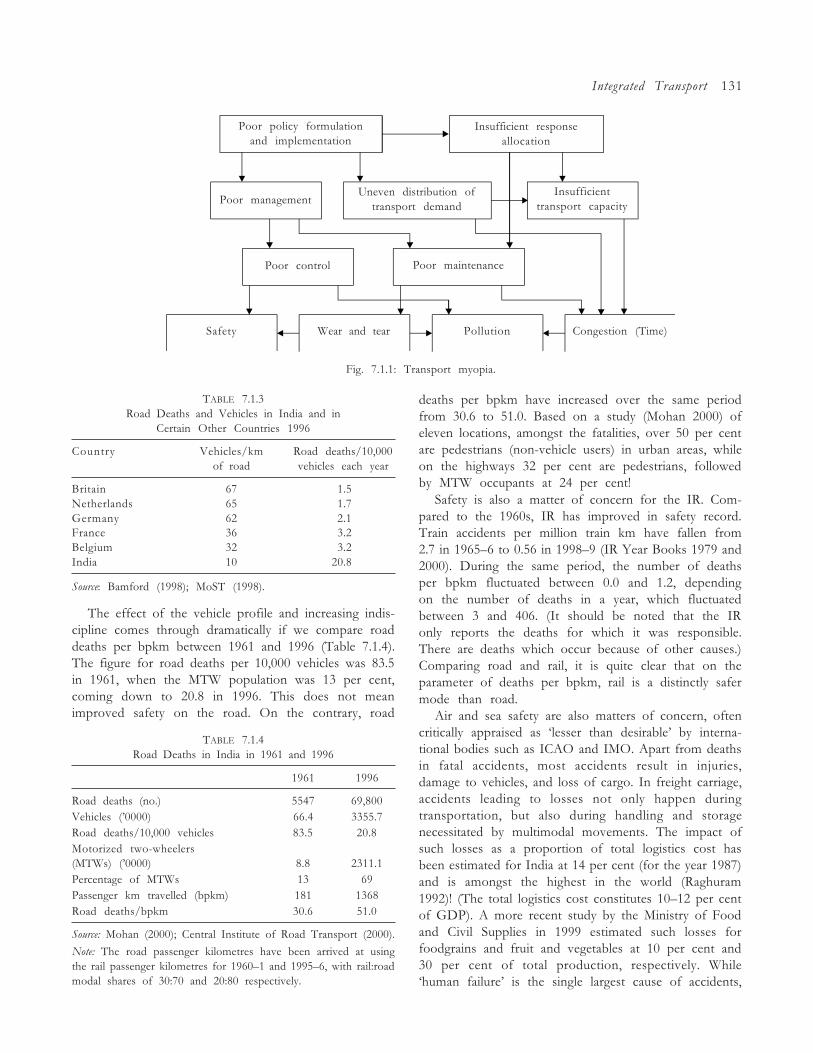

7.1.3 Road Deaths and Vehicles in India and in Certain Other Countries 1996 131

7.1.4 Road Deaths in India in 1961 and 1996 131

7.1.5 Premature Deaths Due to Ambient Air Pollution Exceeding WHO Standard c.1995in Some Indian Cities 133

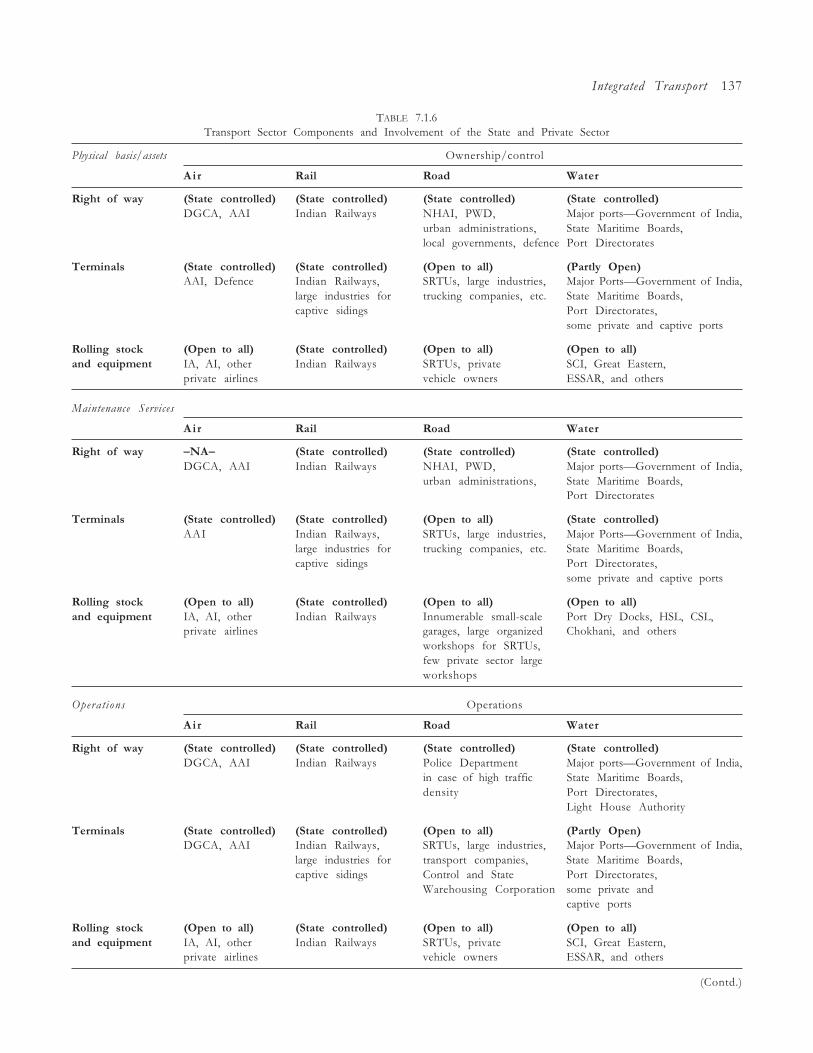

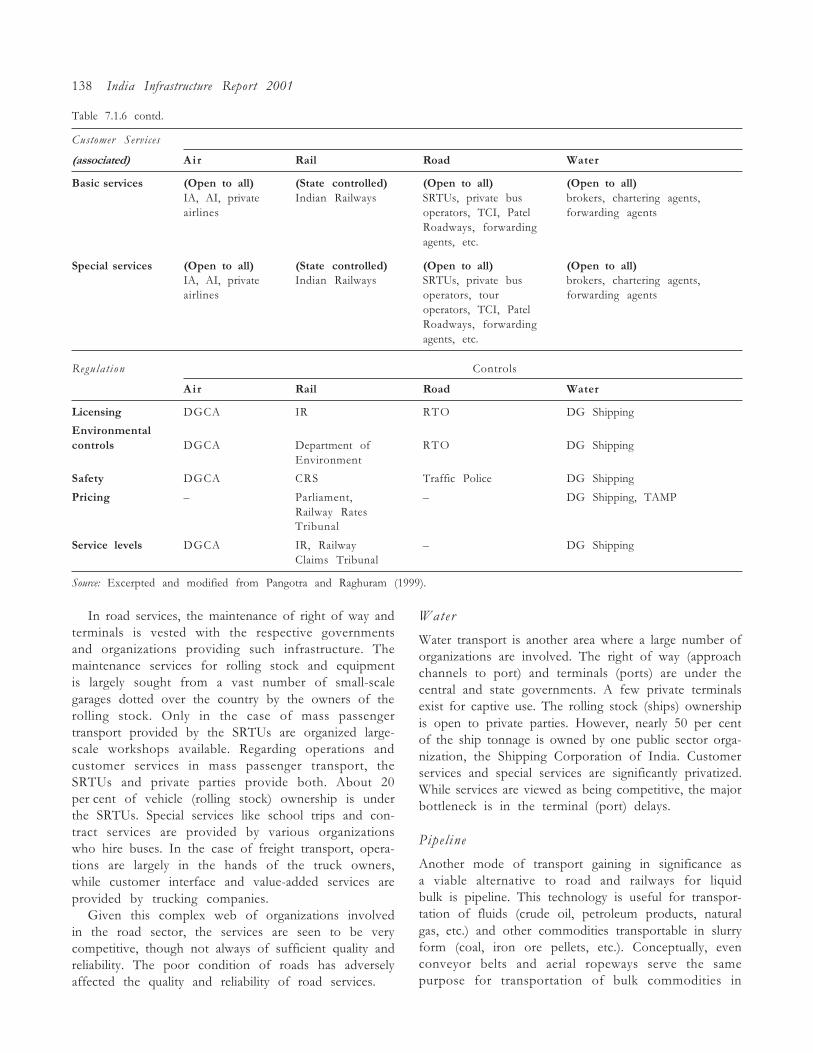

7.1.6 Transport Sector Components and Involvement of the State and Private Sector 137

7.2.1 Traffic at Airports 146

7.2.2 Passenger Traffic at Airports 1998�9 147

7.2.3 Cargo Traffic at Airports 1998�9 147

7.2.4 Airport Movement at Airports 1998�9 147

7.2.5 Indices of Growth of Traffic Output and Inputs 149

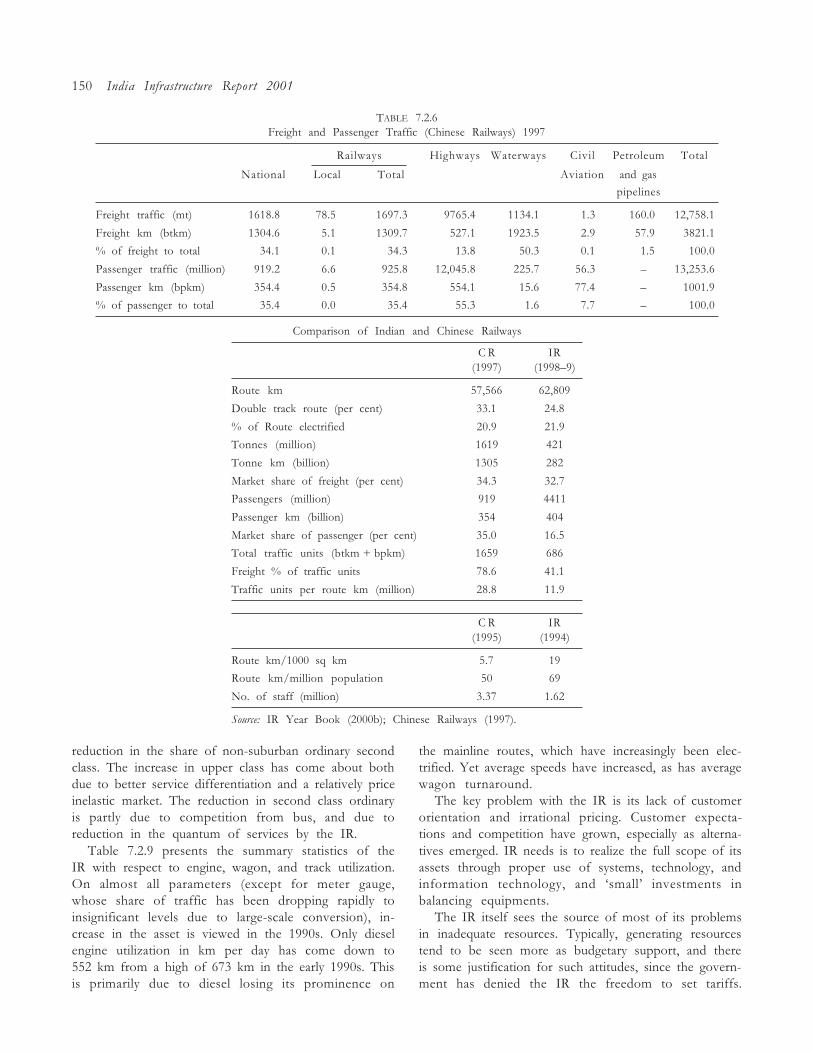

7.2.6 Freight and Passenger Traffic (Chinese Railways) 1997 150

7.2.7 Freight Business of Indian Railways: 1998�9 and 1988�9 151

7.2.8 Passenger Business of IR 152

7.2.9 Utilization of Assets by Railways 153

7.2.10 Road Safety Statistics 1994�5 156

7.2.11 Total Registered Motor Vehicles in India 157

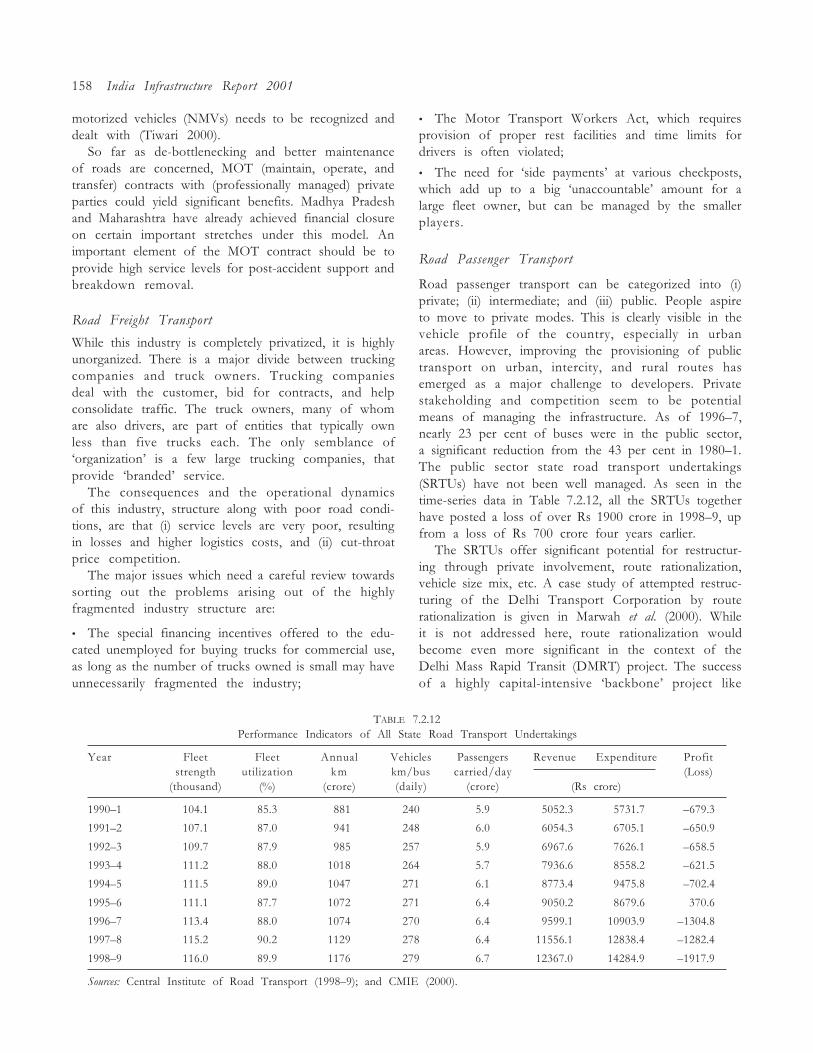

7.2.12 Performance Indicators of All State Road Transport Undertakings 158

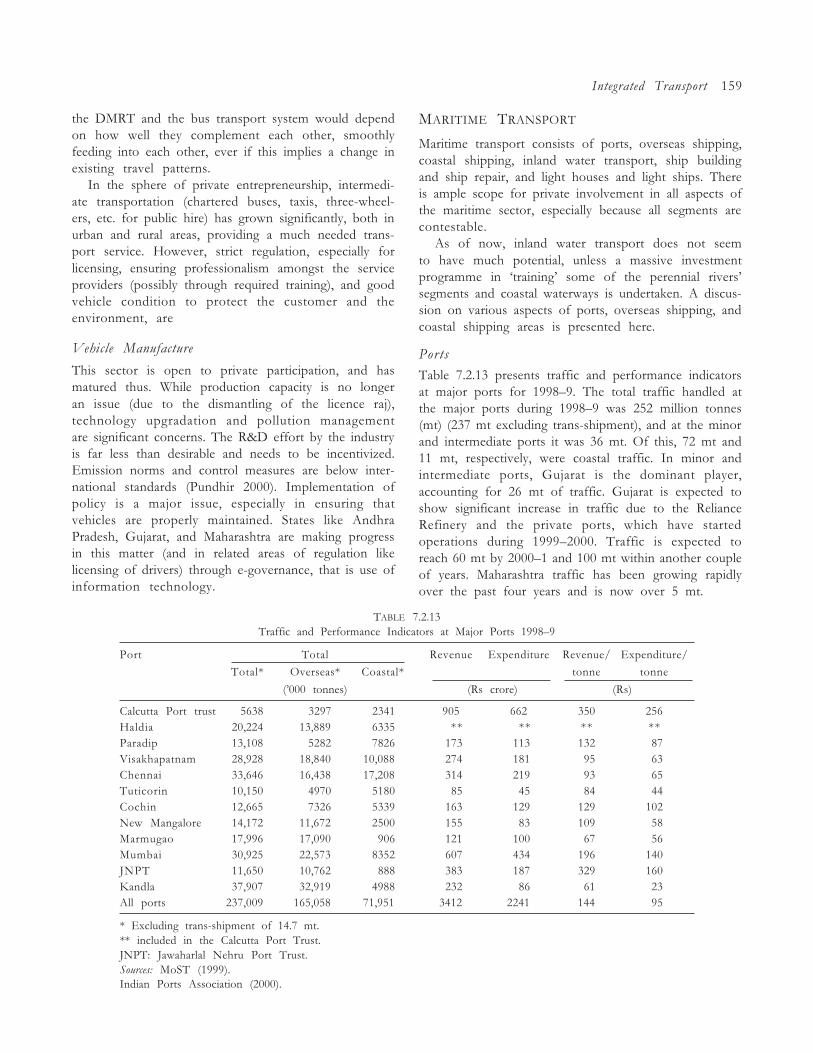

7.2.13 Traffic and Performance Indicators at Major Ports 1998�9 159

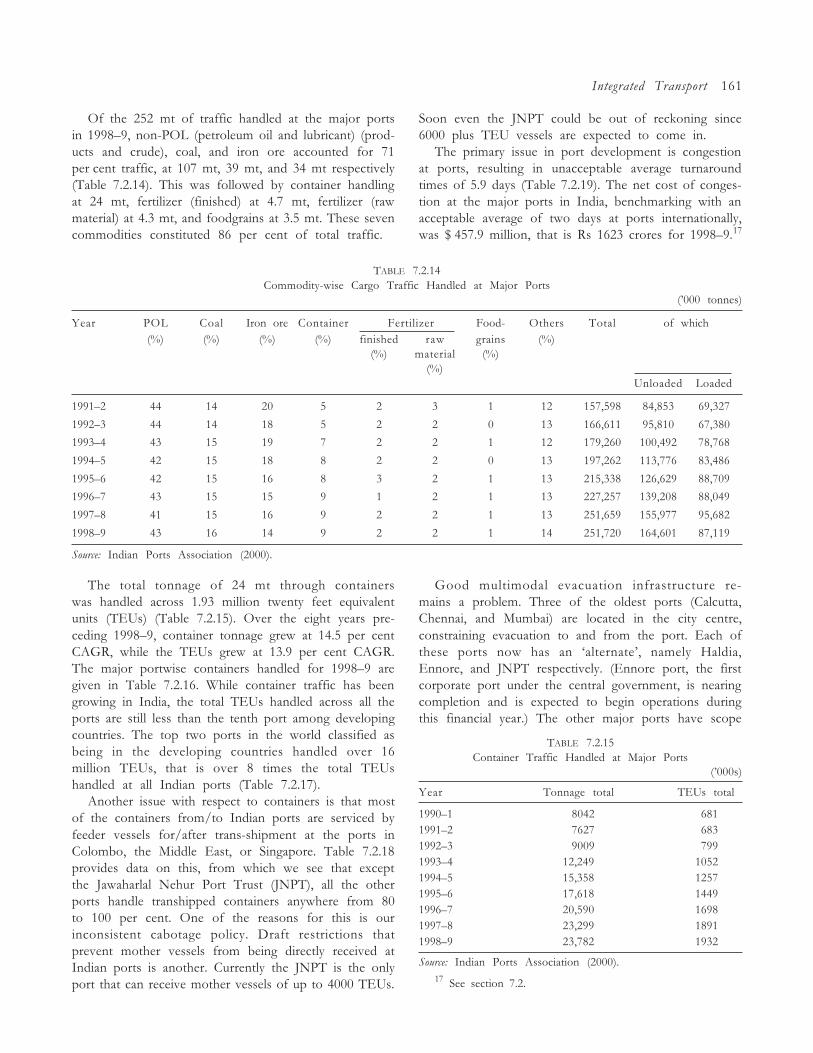

7.2.14 Commodity-wise Cargo Traffic Handled at Major Ports 161

7.2.15 Container Traffic Handled at Major Ports 161

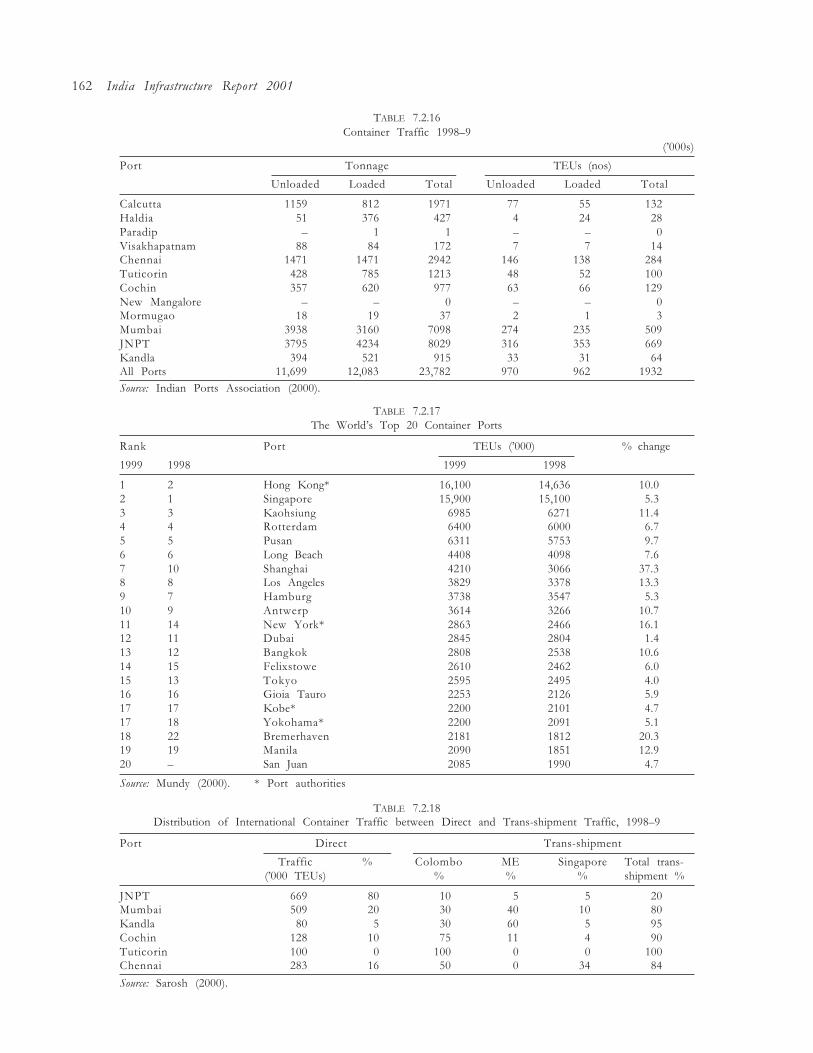

7.2.16 Container Traffic 1998�9 162

7.2.17 The World�s Top 20 Container Ports 162

7.2.18 Distribution of International Container Traffic betweenDirect and Trans-shipment Traffic, 1998�9 162

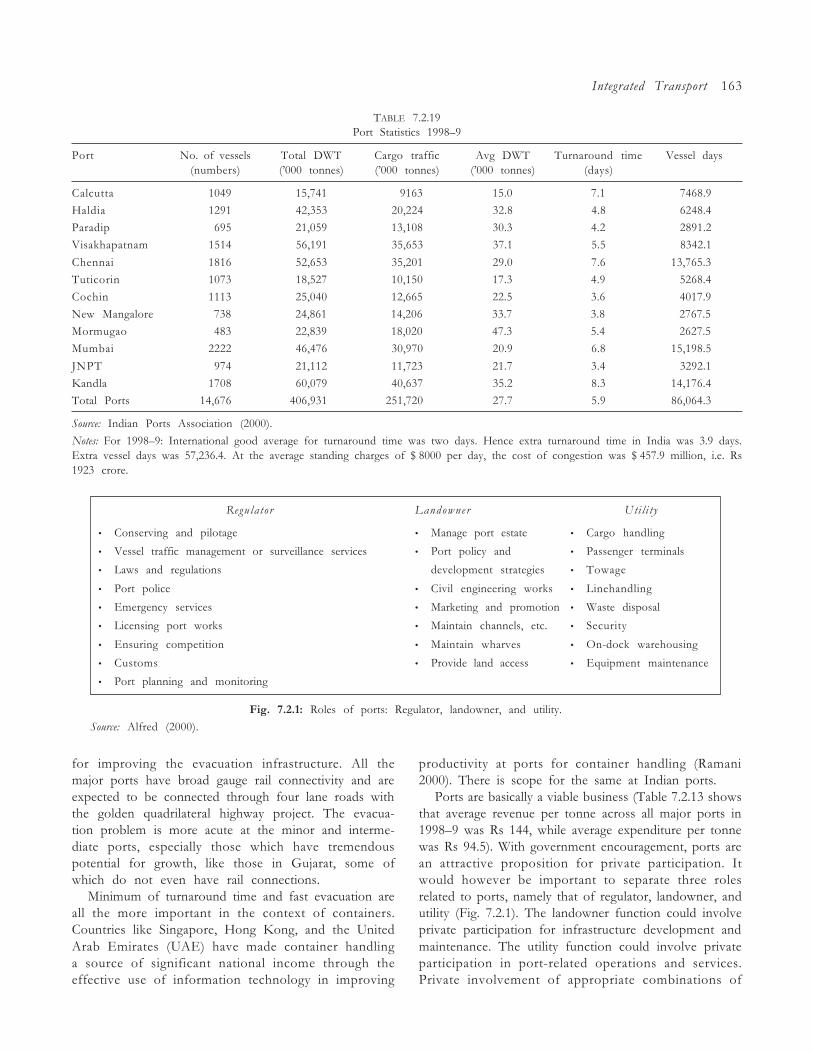

7.2.19 Port Statistics 1998�9 163

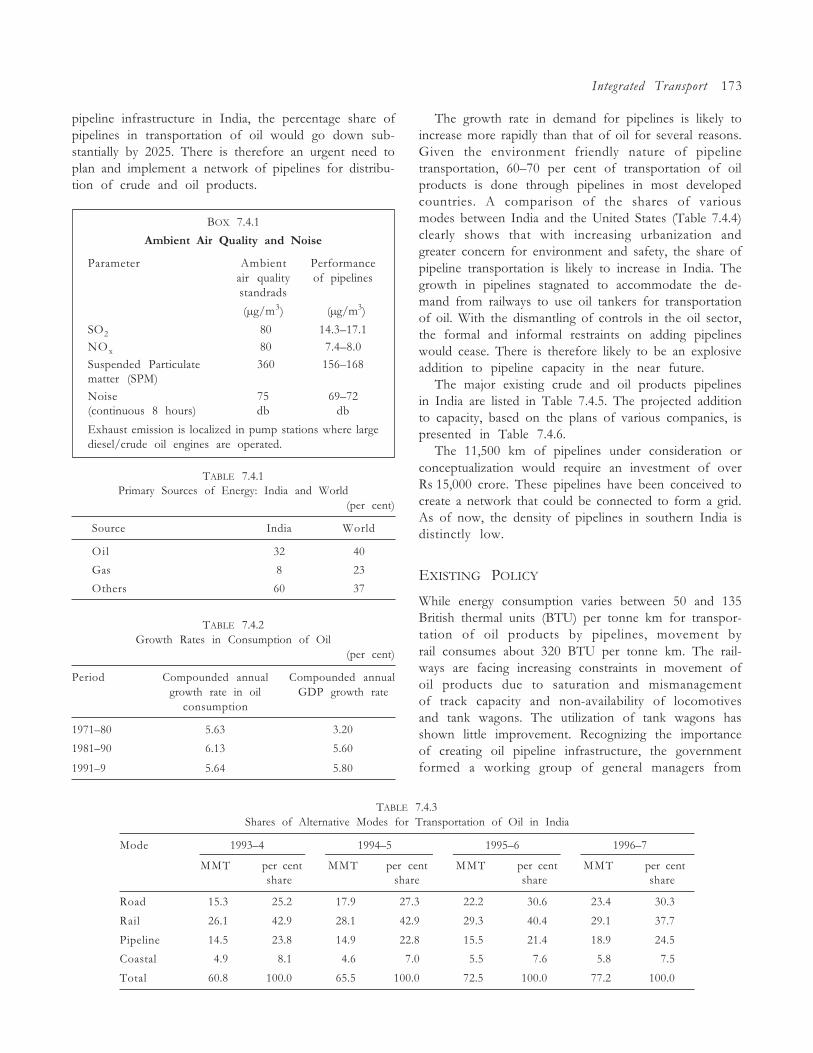

7.4.1 Primary Sources of Energy: India and the World 173

7.4.2 Growth Rates in Consumption of Oil 173

7.4.3 Shares of Alternative Modes of Transportation of Oil in India 173

7.4.4 Mode-wise Distribution of Petroleum Products 174

7.4.5 Major Crude and Product Pipelines in India 174

7.4.6 Projected Growth of Pipelines in India 174

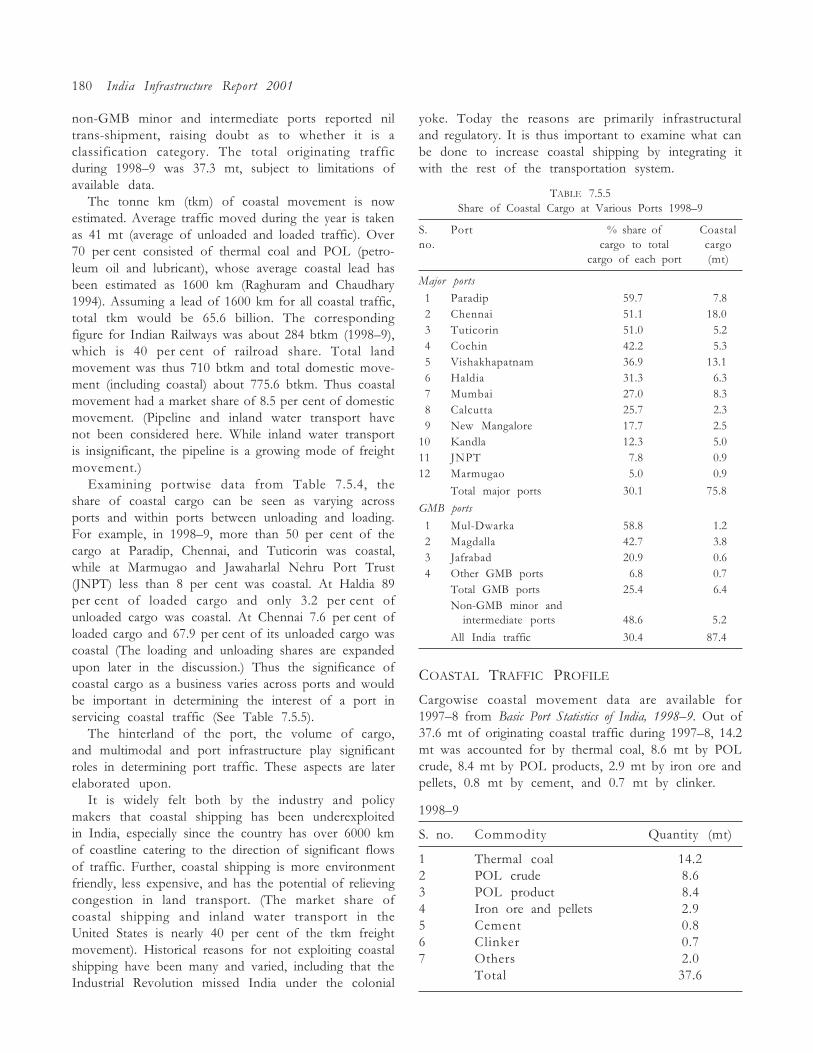

7.5.1 Cargo Traffic at Major and Minor Ports and the Share of Coastal Shipping 177

7.5.2 Cargo Traffic at Major Ports and the Share of Coastal Shipping 178

7.5.3 Cargo Traffic at Minor and Intermediate Ports and the Share of Coastal Shipping 178

7.5.4 Portwise Cargo Traffic 1998�9 and the Share of Coastal Shipping 179

7.5.5 Share of Coastal Cargo at Various Ports 1998�9 180

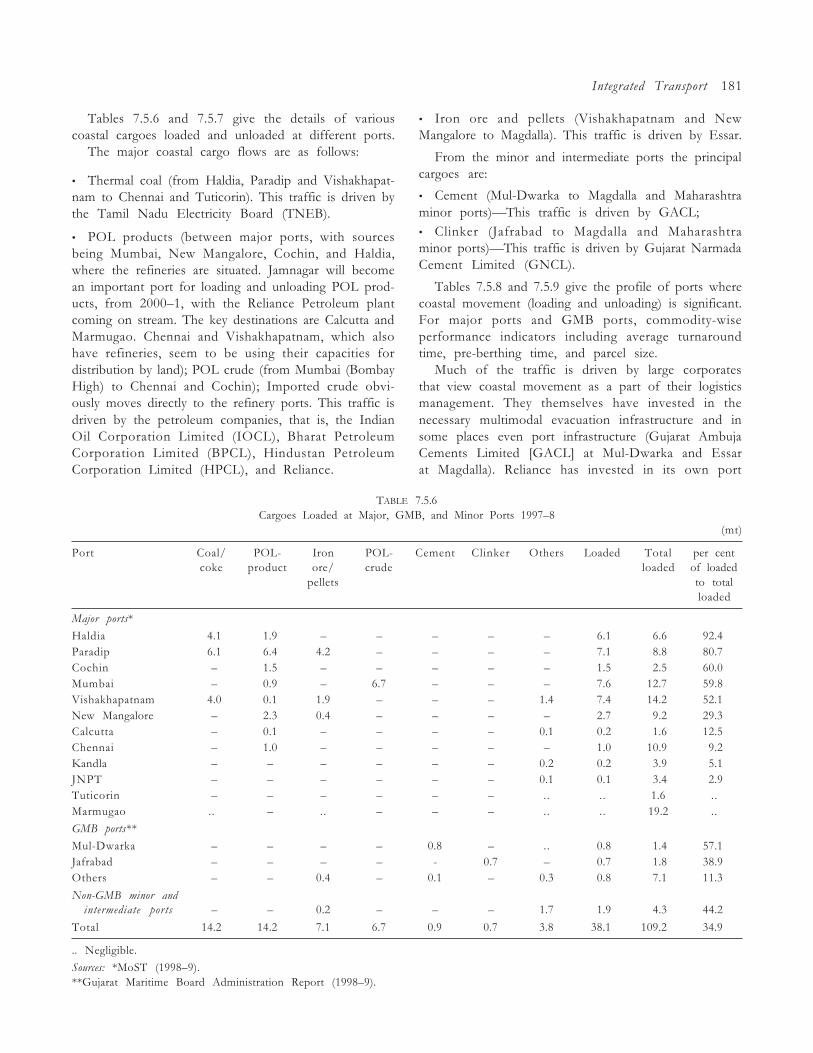

7.5.6 Cargoes Loaded at Major, GMB, and Minor Ports 1997�8 181

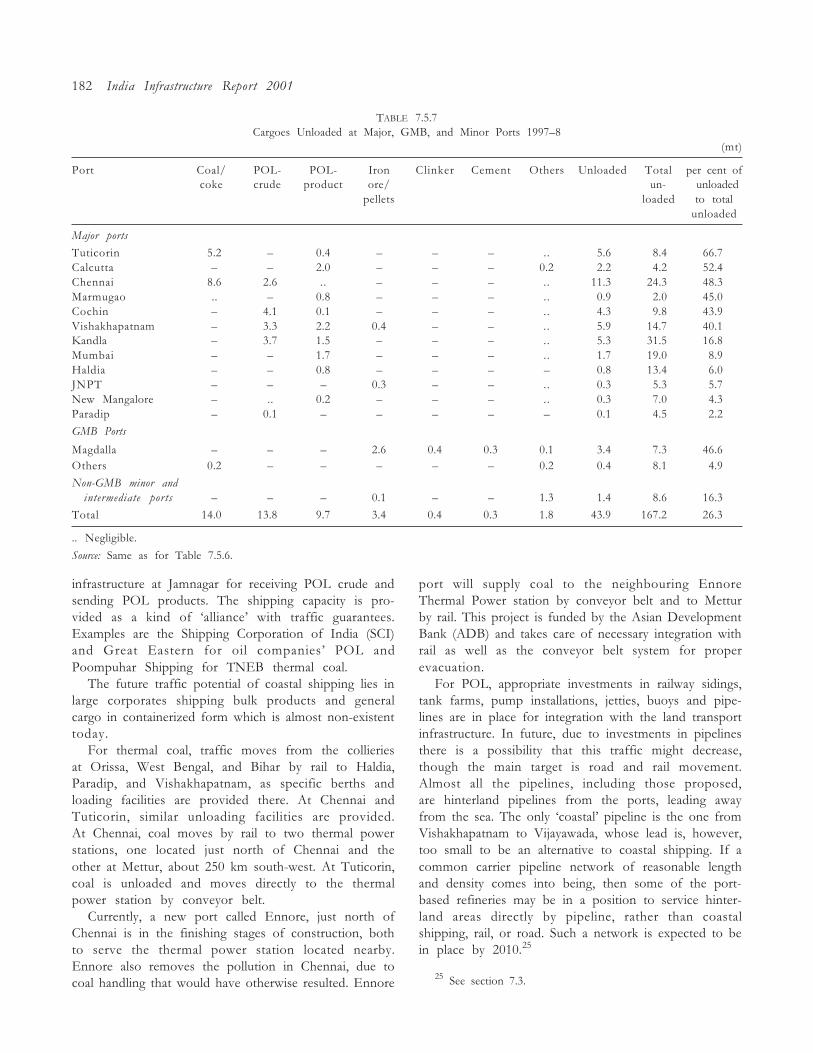

7.5.7 Cargoes Unloaded at Major, GMB, and Minor Ports 1997�8 182

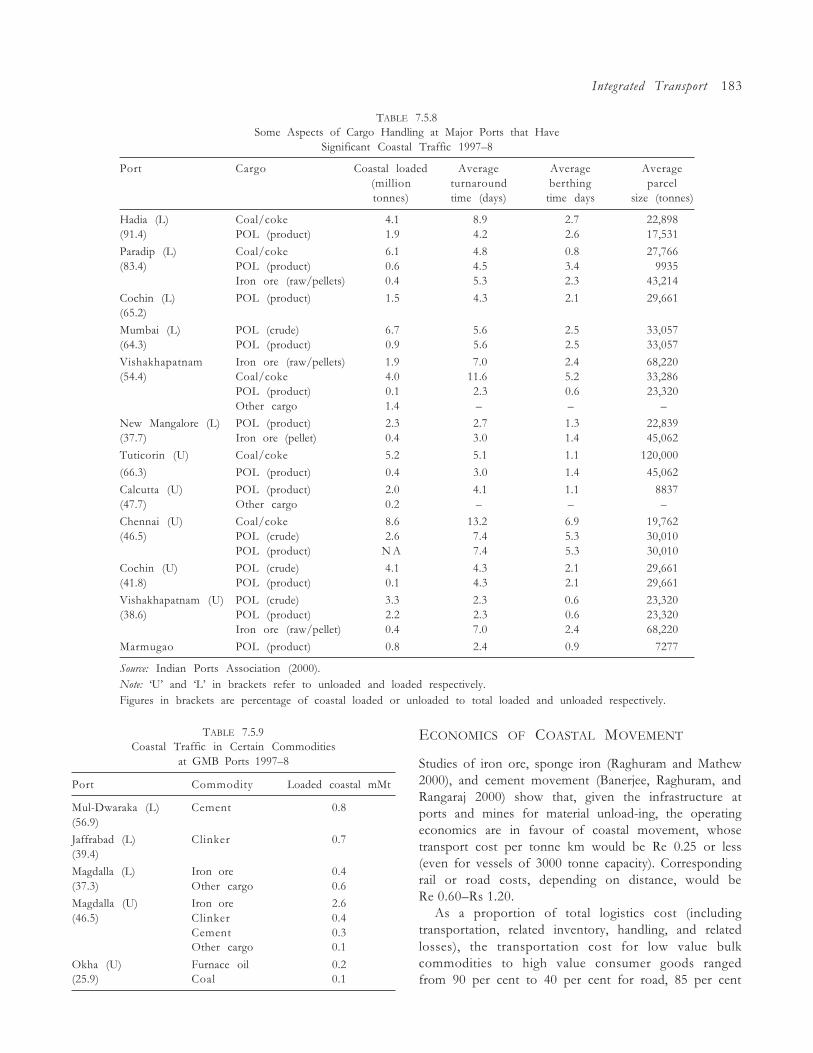

7.5.8 Some Aspects of Cargo Handling at Major Ports thatHave Significant Coastal Traffic 1997�8 183

7.5.9 Coastal Traffic in Certain Commodities at GMB Ports 1997�8 183

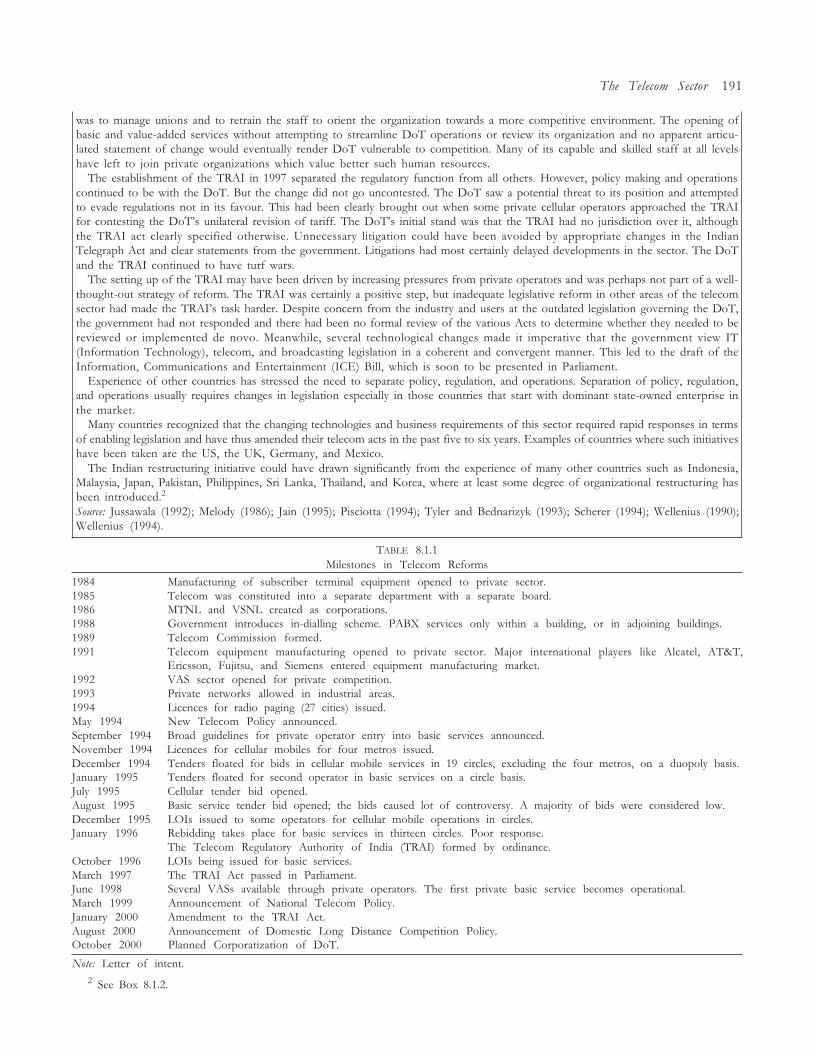

8.1.1 Milestones in Telecom Reforms 191

8.1.2 Share of Telecom Sector in National Plan Outlays 192

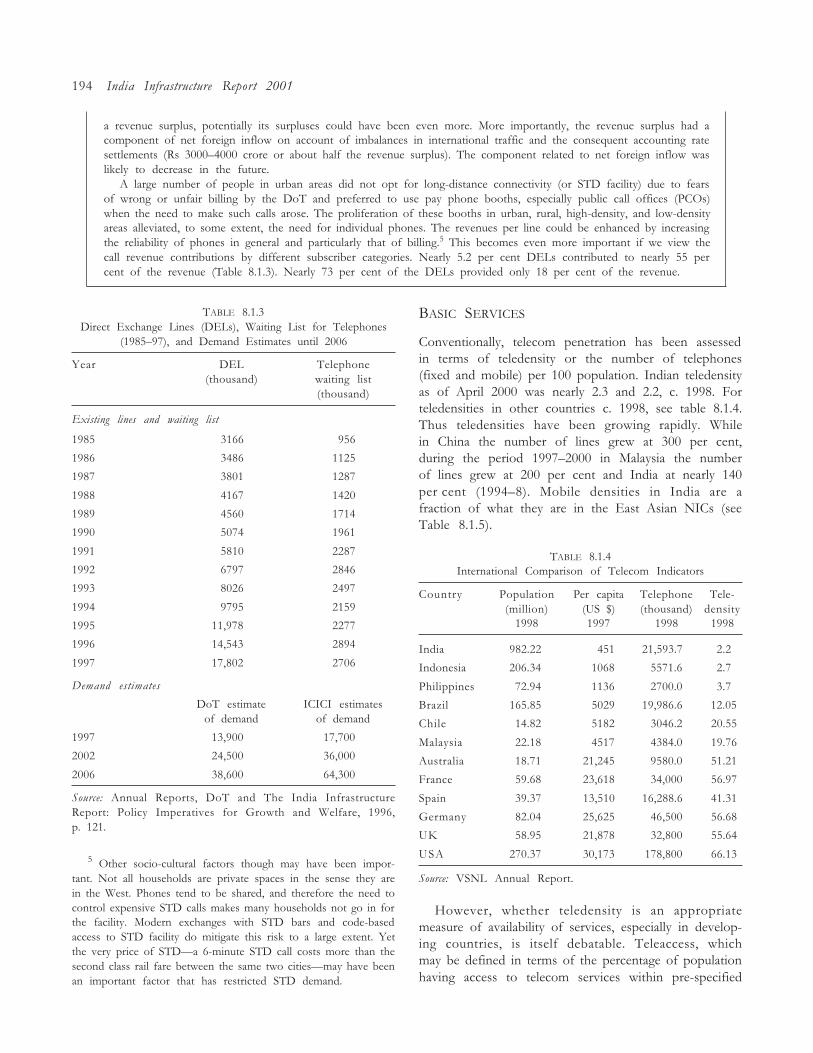

8.1.3 Direct Exchange Lines (DELs), Waiting List for Telephones (1985�97),and Demand Estimates until 2006 194

8.1.4 International Comparison of Telecom Indicators 194

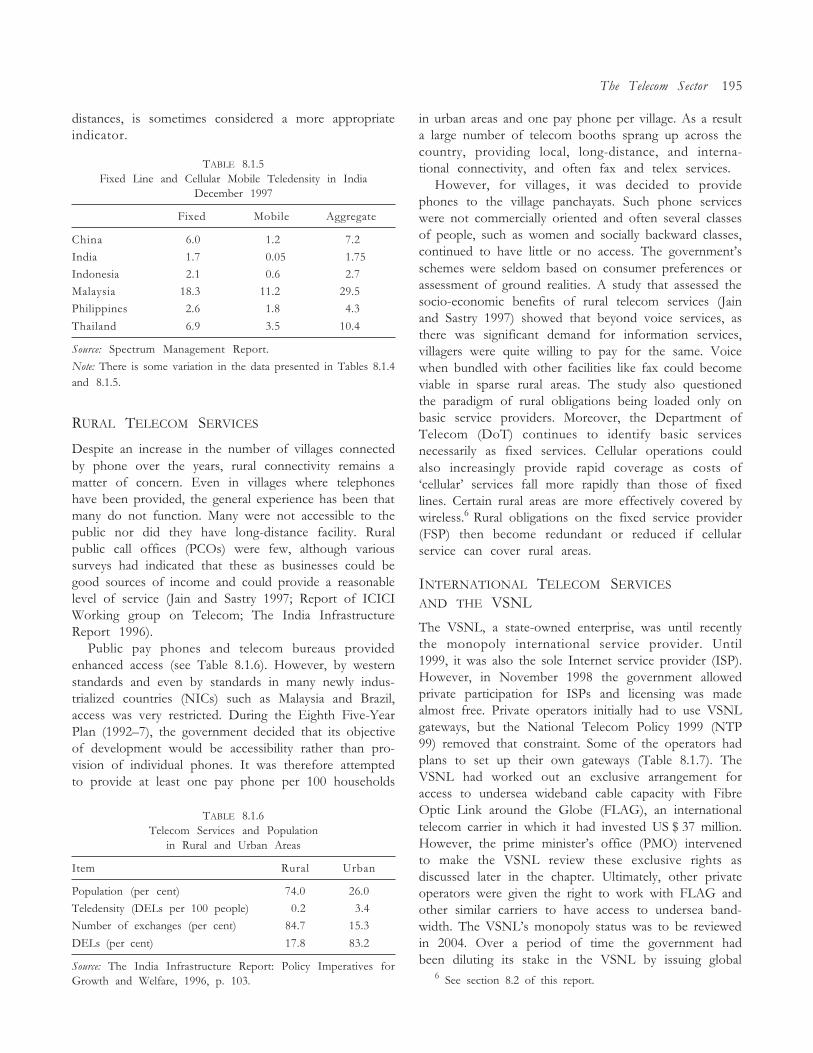

8.1.5 Fixed Line and Cellular Mobile Teledensity in India 195

8.1.6 Telecom Services and Population in Rural and Urban Areas 195

8.1.7 Planned Gateways of Private Operators 196

8.1.8 Distribution of Incoming Telephone Traffic over Originating Countries 196

8.1.9 Distribution of Outgoing Telephone Traffic over Originating Countries 197

8.1.10 List of Basic Service Providers in India and Their Areas of Operation 200

8.1.11 Licence Fee Payable under � Migration Package� 201

8.1.12 Number of Cellular Subscribers c.1999 201

8.1.13 Subscriber Base of Private Basic Service Operators 201

8.1.14 Spectrum Allocation in Some Asian Countries 206

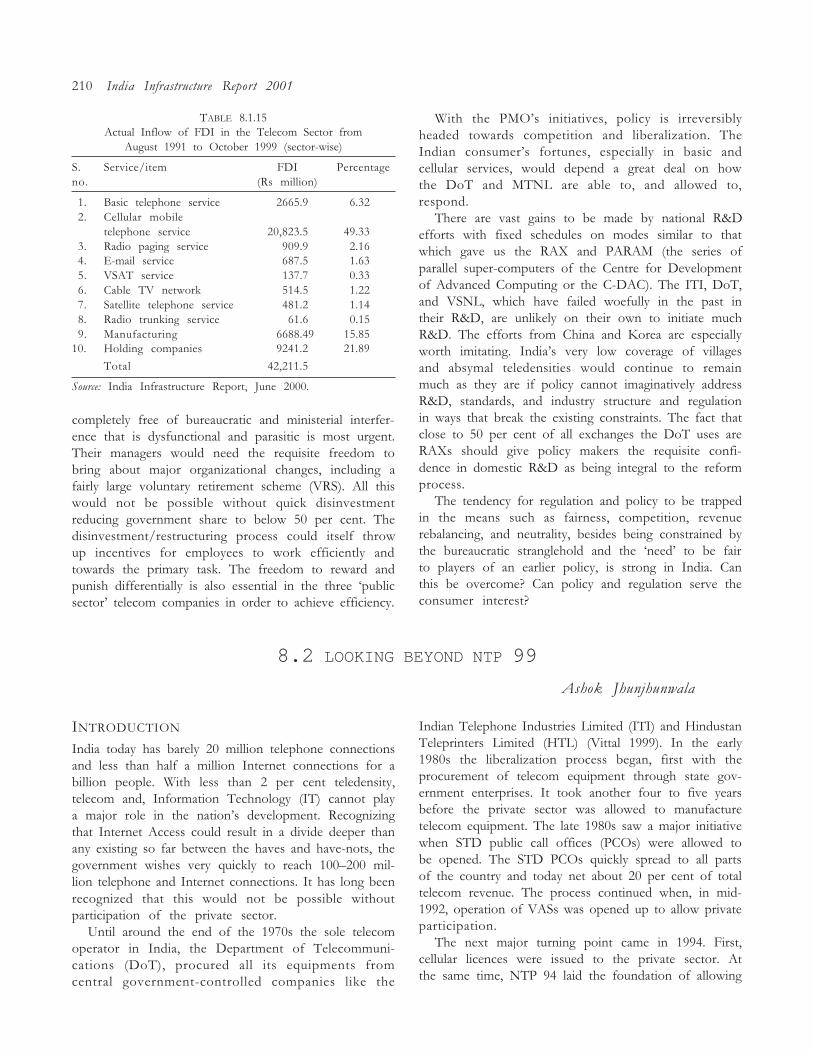

8.1.15 Actual Inflow of FDI in the Telecom Sector fromAugust 1991 to October 1999 210

Tables xv

A.8.1.1 Indicators of Telecom Network in India 230

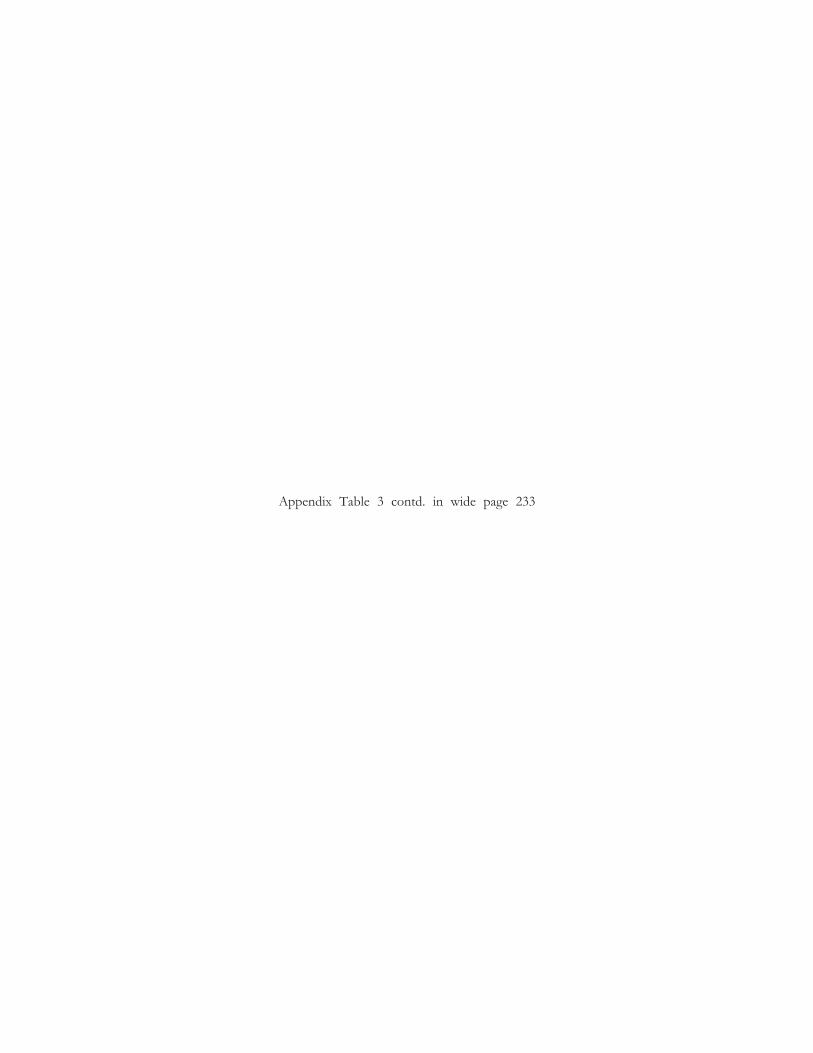

A.8.1.2 Circle-wise Status of DELs and Waiting List 1998�9 232

A.8.1.3 Key Network and Performance Indicators for VSNL 233

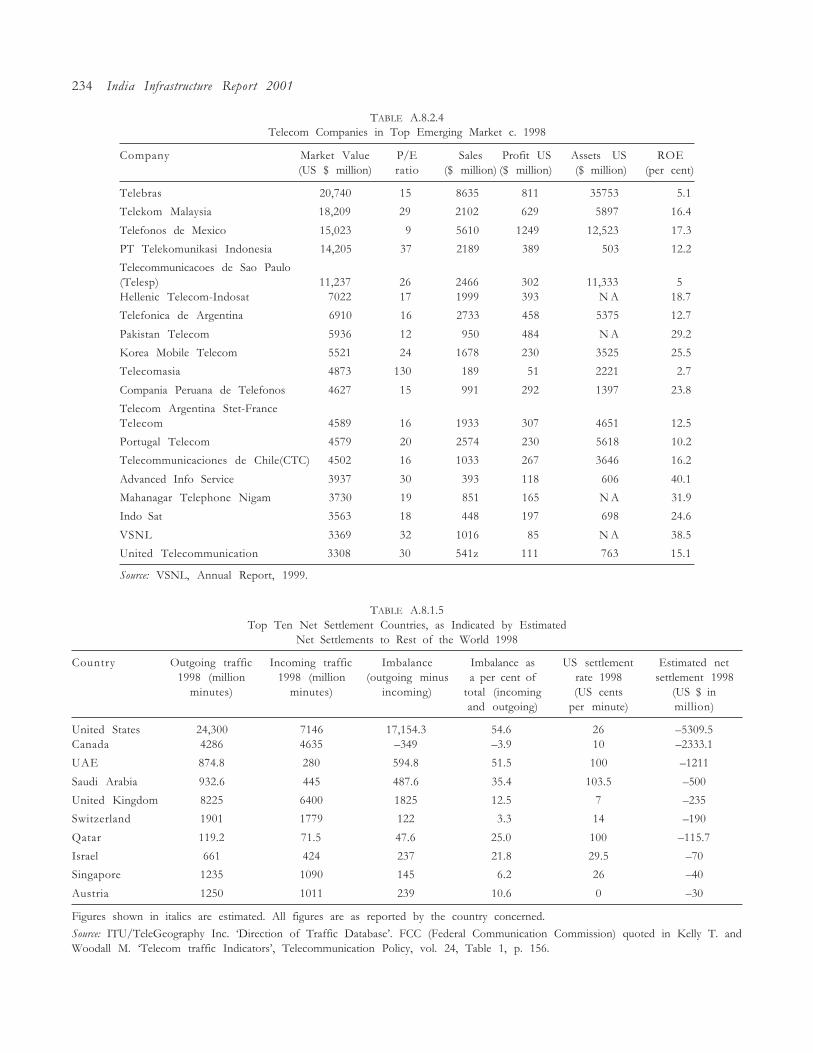

A.8.1.4 Telecom Companies in Top Emerging Market 234

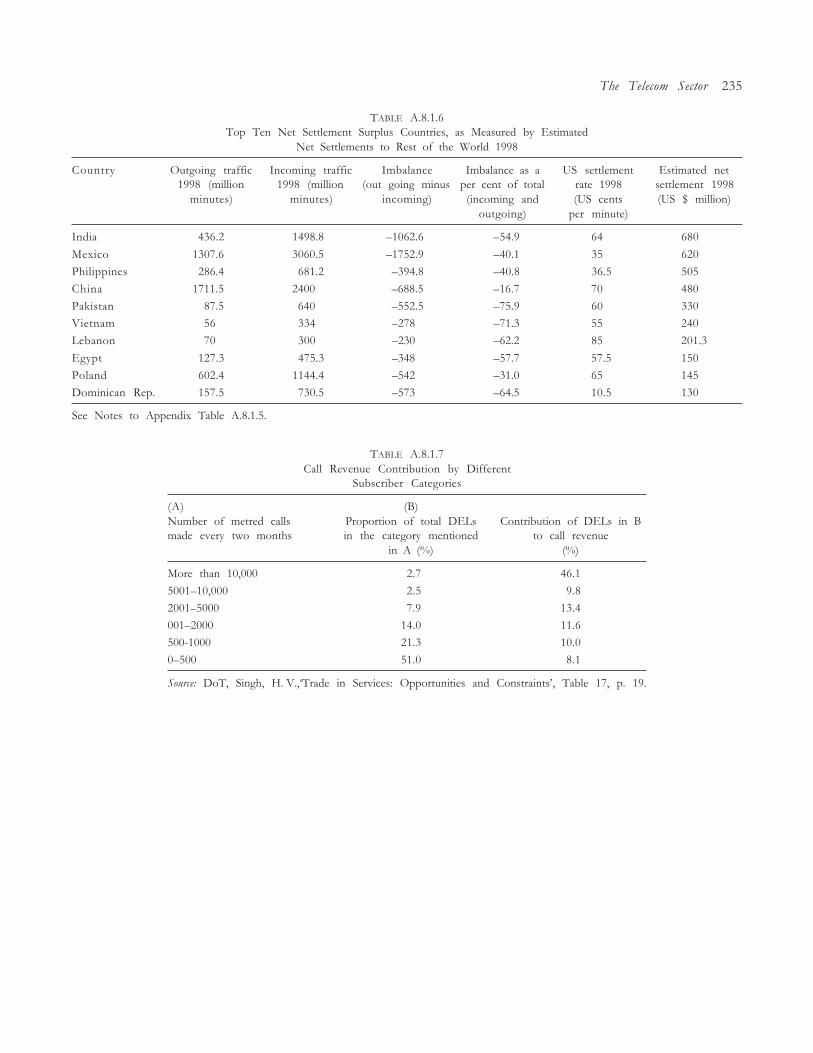

A.8.1.5 Top Ten Net Settlement Countries, as Indicated byEstimated Net Settlements to Rest of the World 1998 234

A.8.1.6 Top Ten Net Settlement Surplus Countries, as Measured byEstimated Net Settlements to Rest of the World 1998 235

A.8.1.7 Call Revenue Contribution by Different Subscriber Categories 235

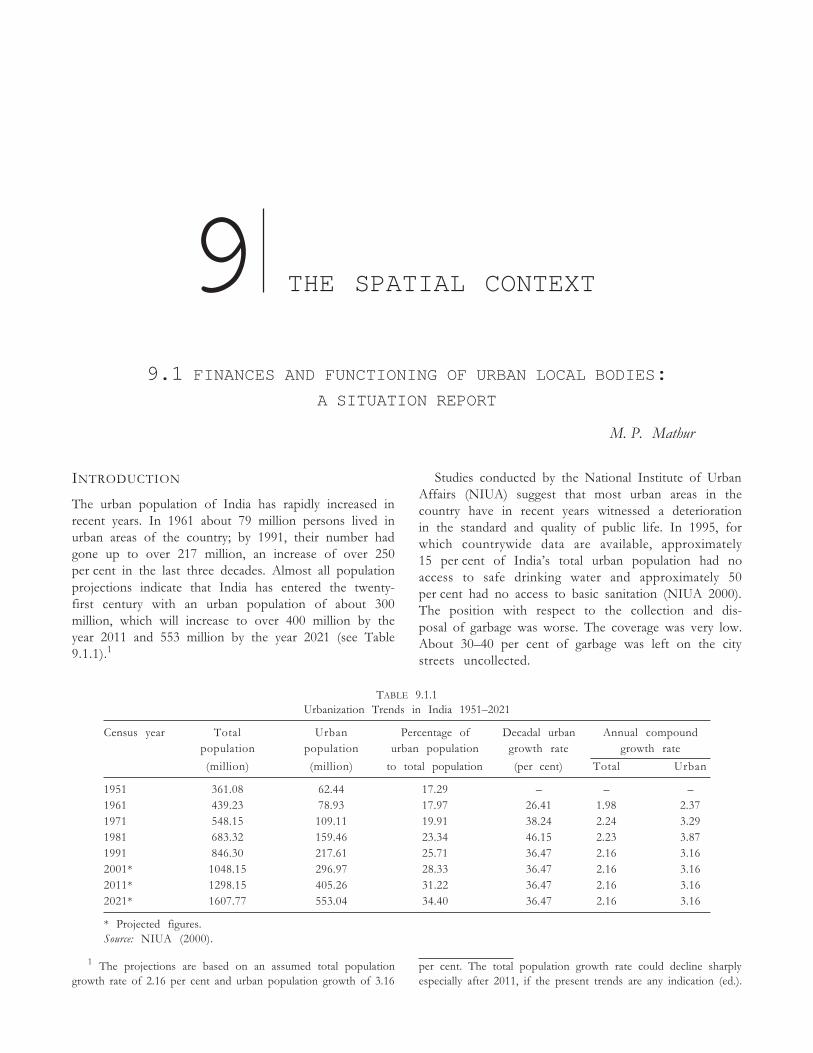

9.1.1 Urbanization Trends in India 1951�2021 236

9.1.2 Revenues of the Centre, States, and Municipalities 1991�2 237

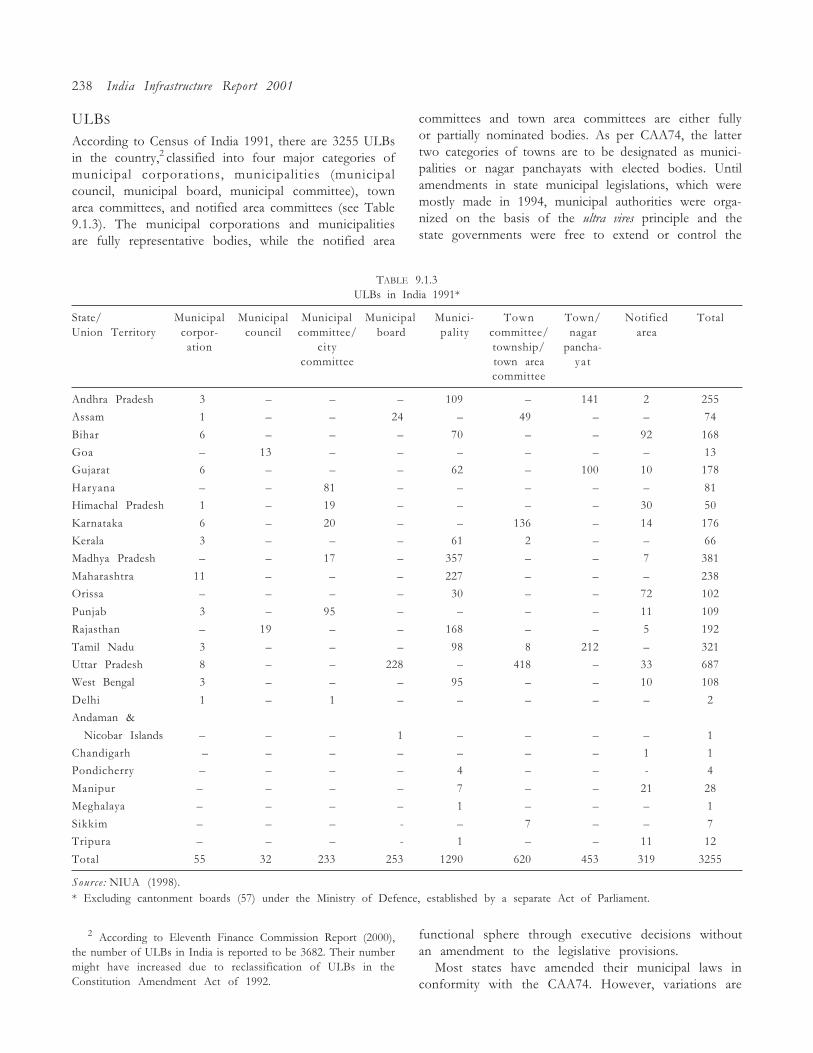

9.1.3 ULBs in India 1991 238

9.1.4 Major Sources of Income for Municipal Bodies in India 240

9.1.5 Source of Municipal Revenues 1997�8 241

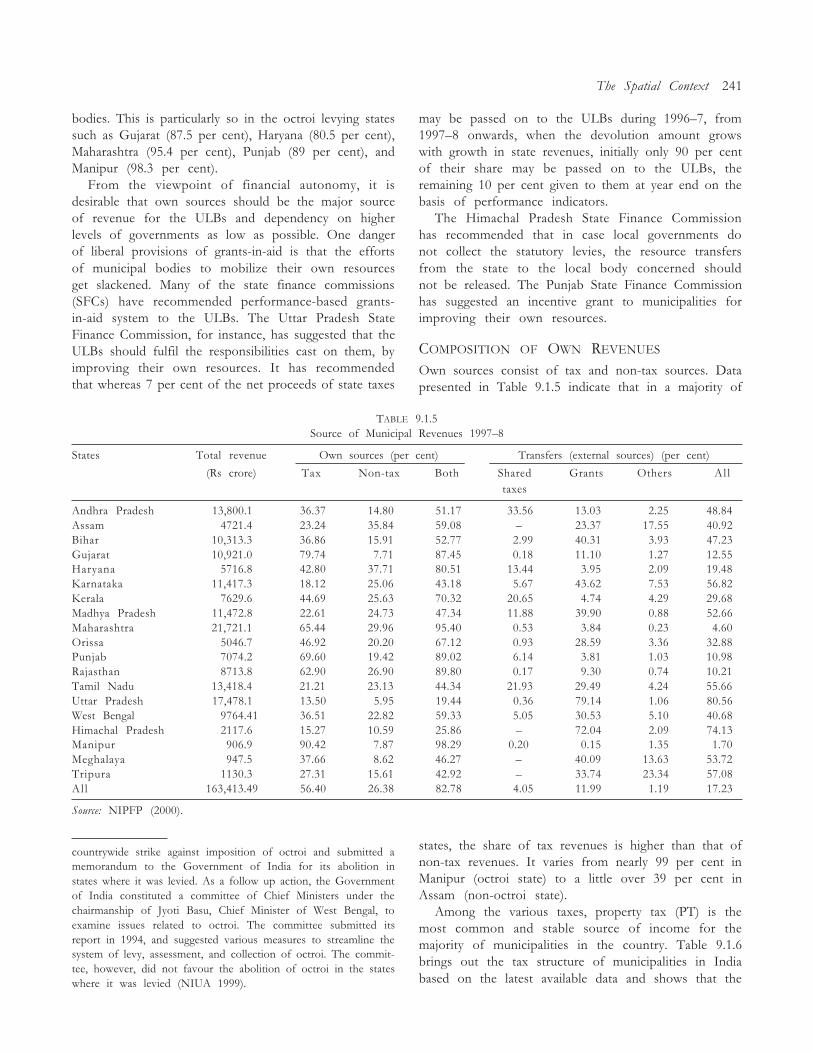

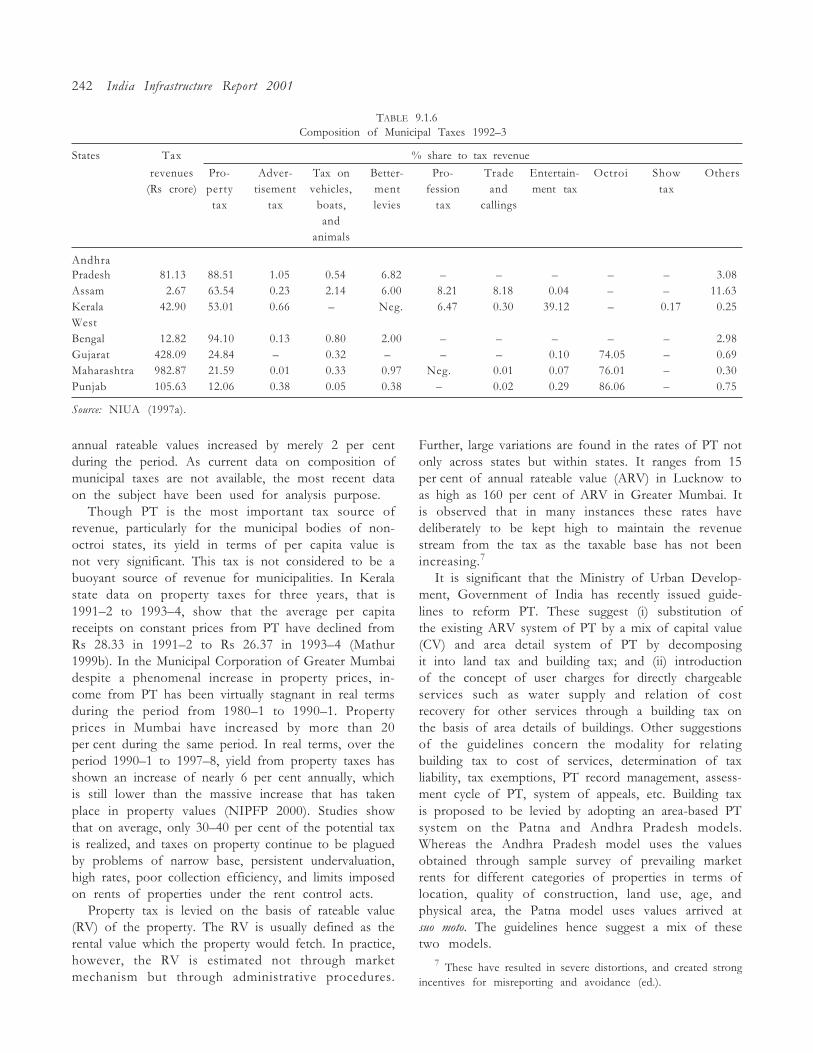

9.1.6 Composition of Municipal Taxes 1992�3 242

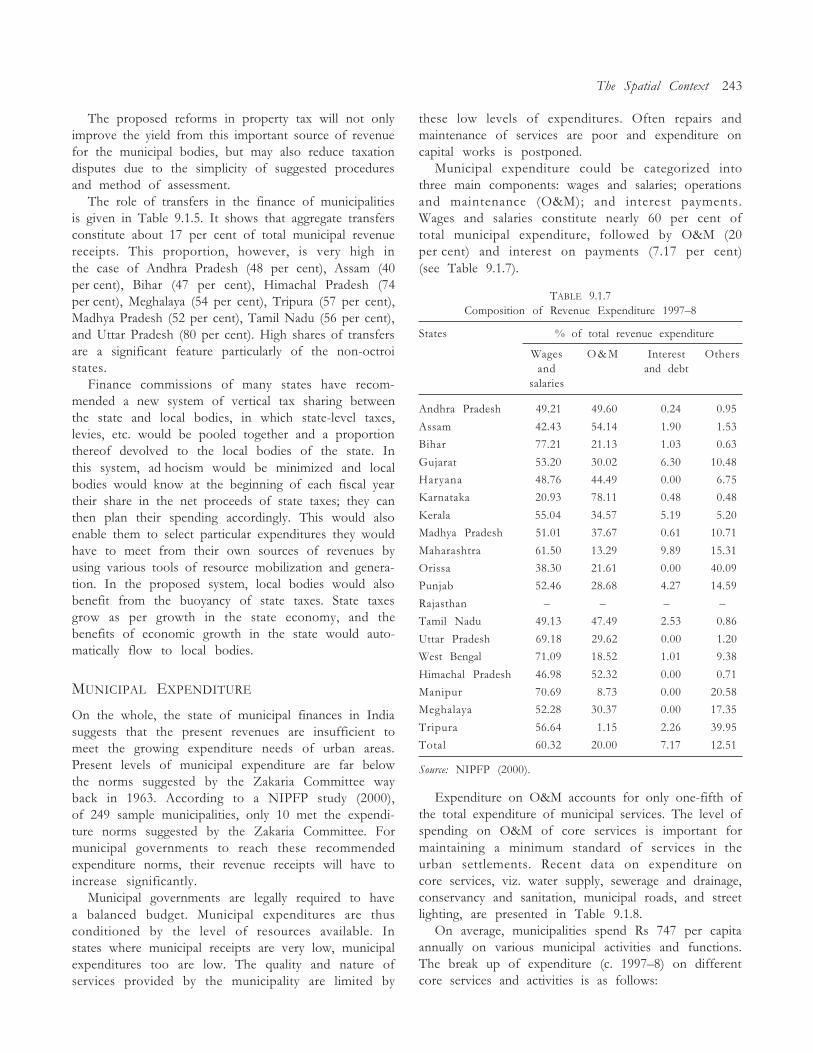

9.1.7 Composition of Revenue Expenditure 1997�8 243

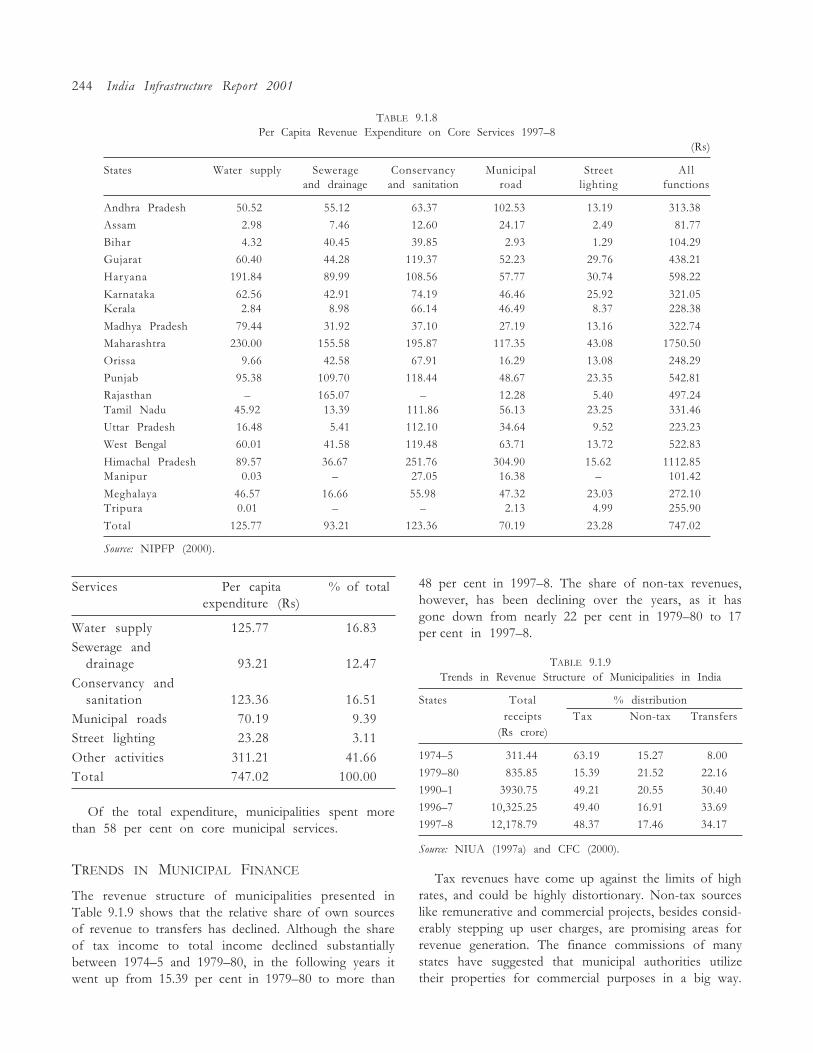

9.1.8 Per Capita Revenue Expenditure on Core Services 1997�8 244

9.1.9 Trends in Revenue Structure of Municipalities in India 244

9.1.10 Trends in Municipal Finances in Selected States 245

9.1.11 Key Indicators for Selected Urban Services 247

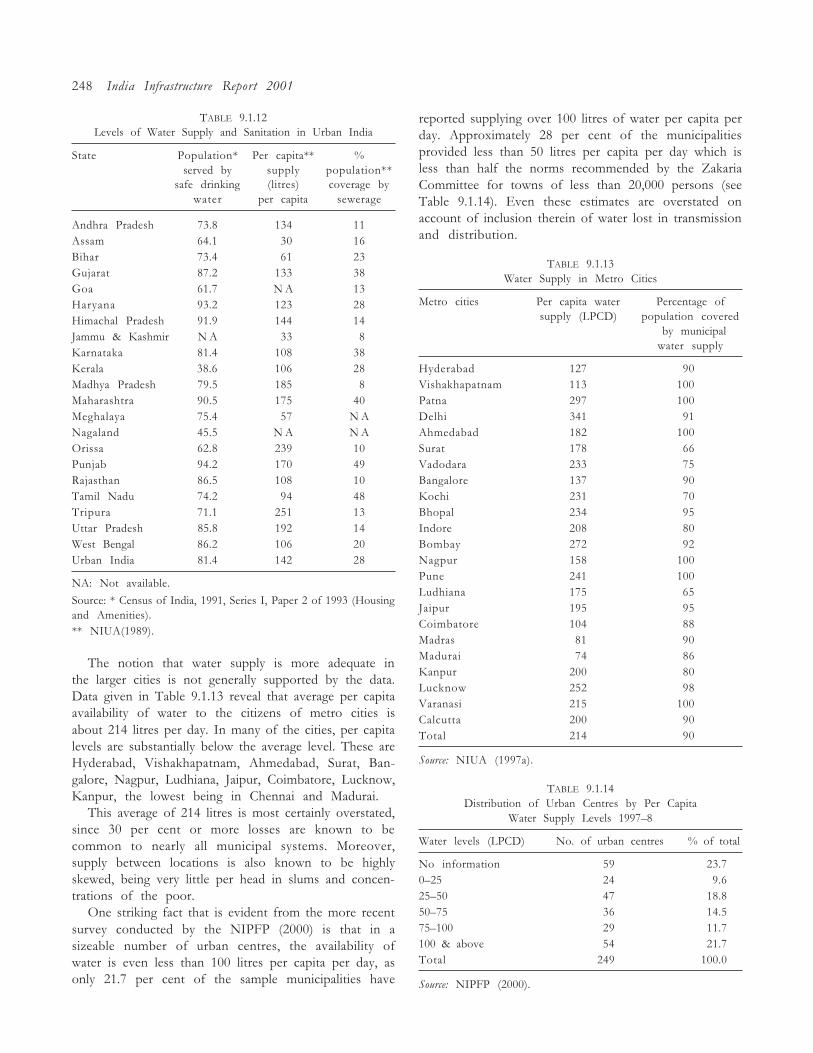

9.1.12 Levels of Water Supply and Sanitation in Urban India 248

9.1.13 Water Supply in Metro Cities 248

9.1.14 Distribution of Urban Centres by Per Capita Water Supply Levels 1997�8 248

9.1.15 Distribution of Urban Centres by Per Capita Expenditure Levels 249

9.1.16 Percentage of Urban Households Classified by Nature of Sanitation Facility 1988�9 249

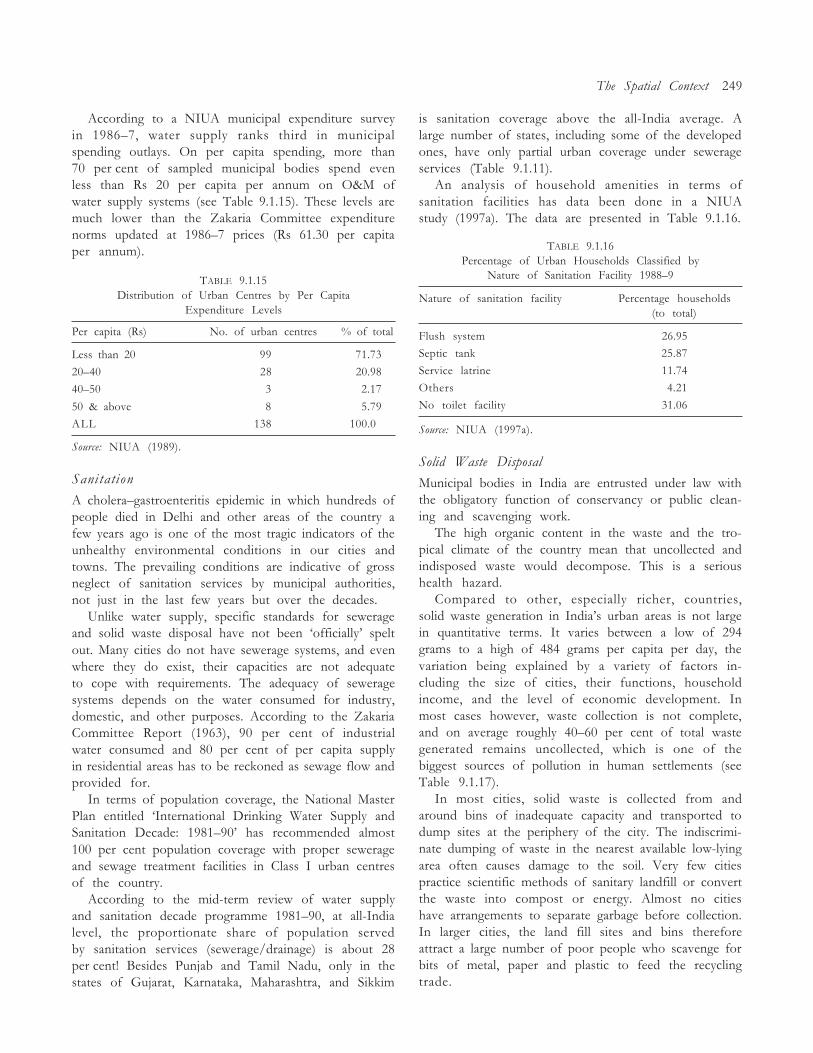

9.1.17 Solid Waste Collection and Generation in Selected Metro Centres of India c.1998 250

9.1.18 Revenue Receipts and Expenditures with regard to Water Supply andSanitation in Selected Cities 1993�4 250

9.1.19 Private Sector Participation in Water Supply and Sanitation Projects 251

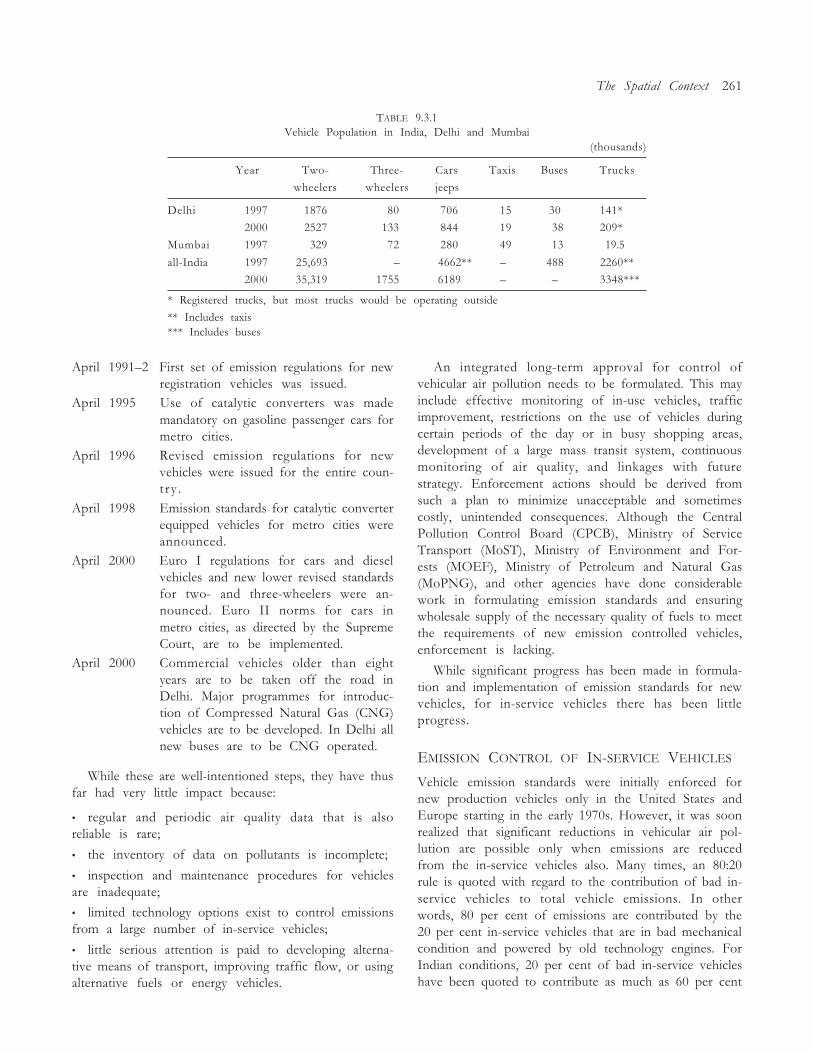

9.3.1 Vehicle Population in India, Delhi and Mumbai 261

9.5.1 Monthly Tariff to Paying Customers for Cross-subsidizing the Poor 1994�5 274

9.5.2 Sources of Drinking Water in Inhabited Villages in India 275

9.6.1 Comparable Performance of DTC and Private Buses 279

9.6.2 Details of Accidents by Blue Line/Red Line Buses 280

9.6.3 Operational Characteristics of Chartered Buses 280

9.7.1 Record of Government Rural Drinking Water Supply Schemes 282

xvi Tables

3.1 Background to Tariff and Interconnection Regulation 34

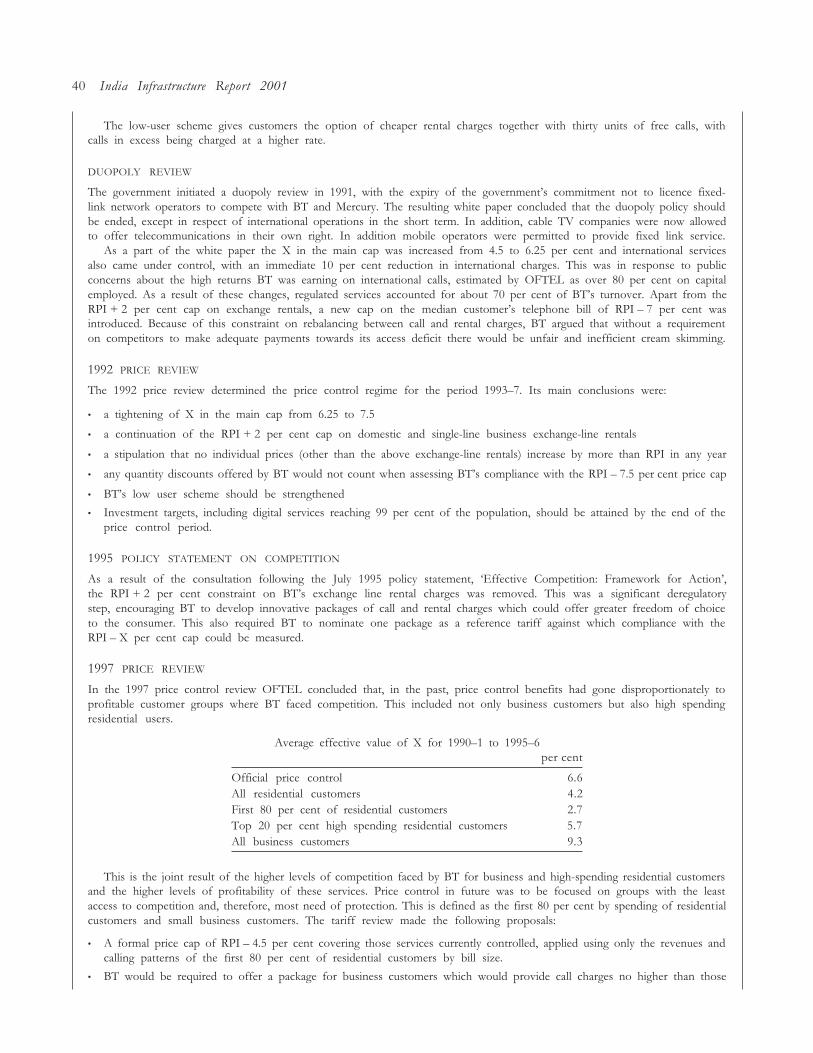

3.2 Rebalancing Tariffs with Price Caps in the UK 39

5.3.1 Key Departments Up In Arms Against the GIDB 75

5.6.1 Land Acquisition Process: The Case of Poshitra Port 86

5.7.1 Hotshot Consultants Copy a Report to Get Project Cleared 88

6.2.1 California Electricity Markets 127

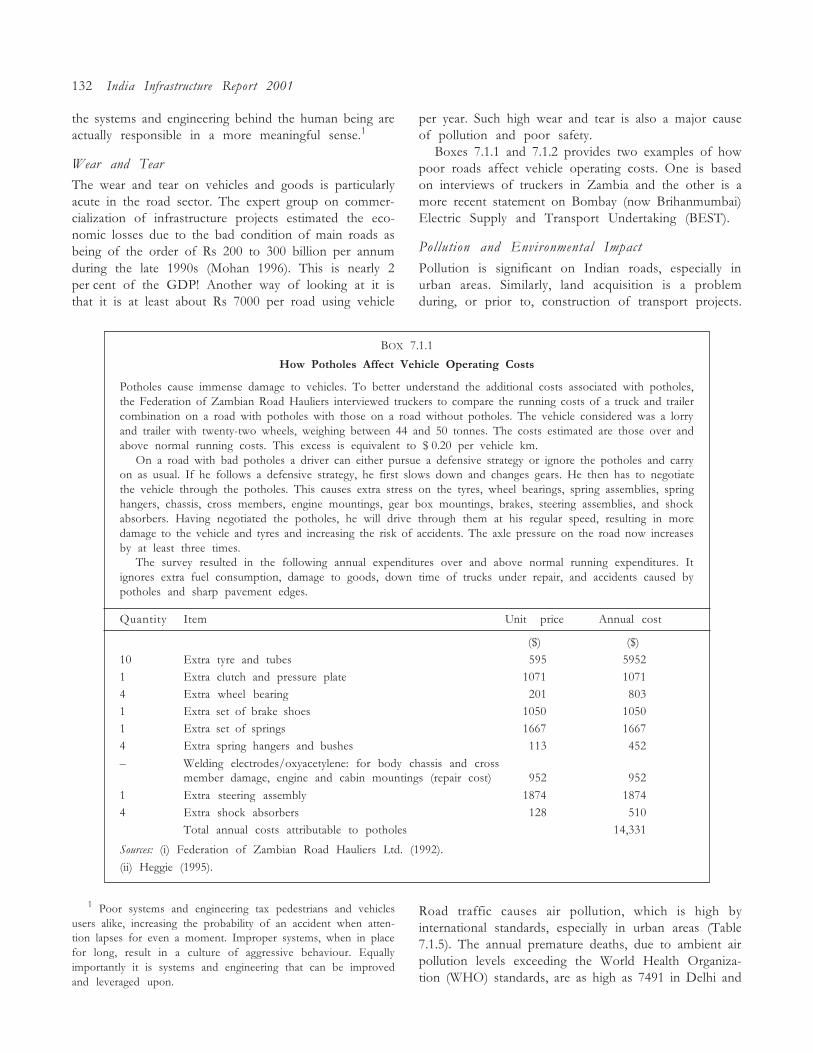

7.1.1 How Potholes Affect Vehicle Operating Costs 132

7.1.2 Deluge, BMC Punch Holes in BEST�s Coffers 133

7.1.3 Constraints which Deplete Rail Transport Capacity butwhich are Removable by Low Investments 141

7.1.4 Low Investment Strategies to De-bottleneck Road Systems 142

7.1.5 Role of Citizens in Monitoring Roads 144

7.1.6 Transport Research and Training 145

7.2.1 A Relook at Passenger Car Equipments in the Indian Context 160

7.4.1 Ambient Air Quality and Noise 173

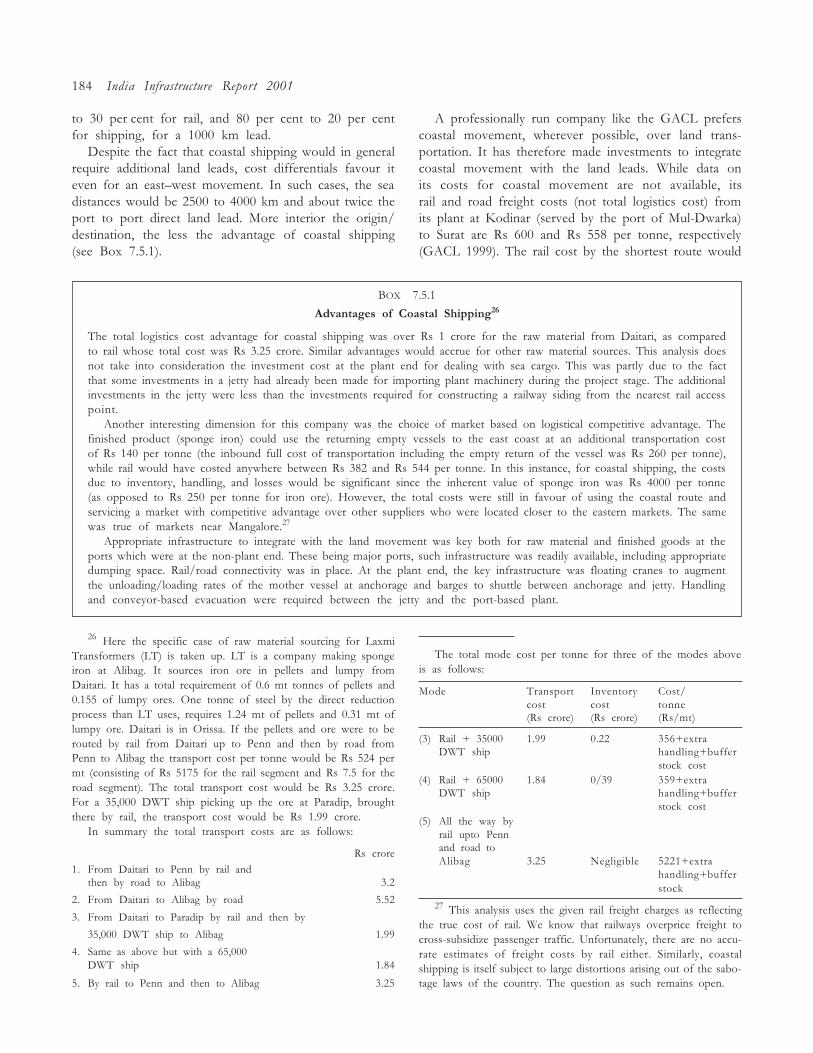

7.5.1 Advantages of Coastal Shipping 184

7.5.2 A Relative Success Story 186

8.1.1 The DOT and the Precursor to Reform 190

8.1.2 A Brief Review of Restructuring in Some Other Countries 192

8.1.3 The Telecom Network and the DoT 193

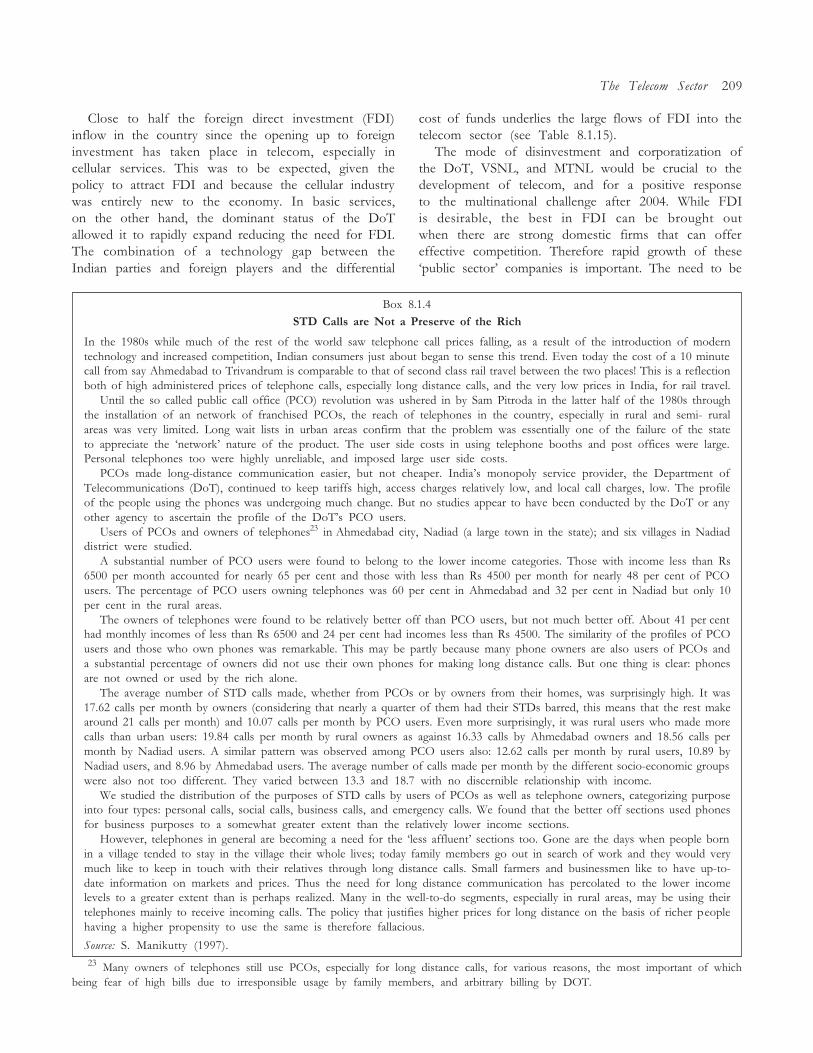

8.1.4 STD calls are Not a Preserve of the Rich 209

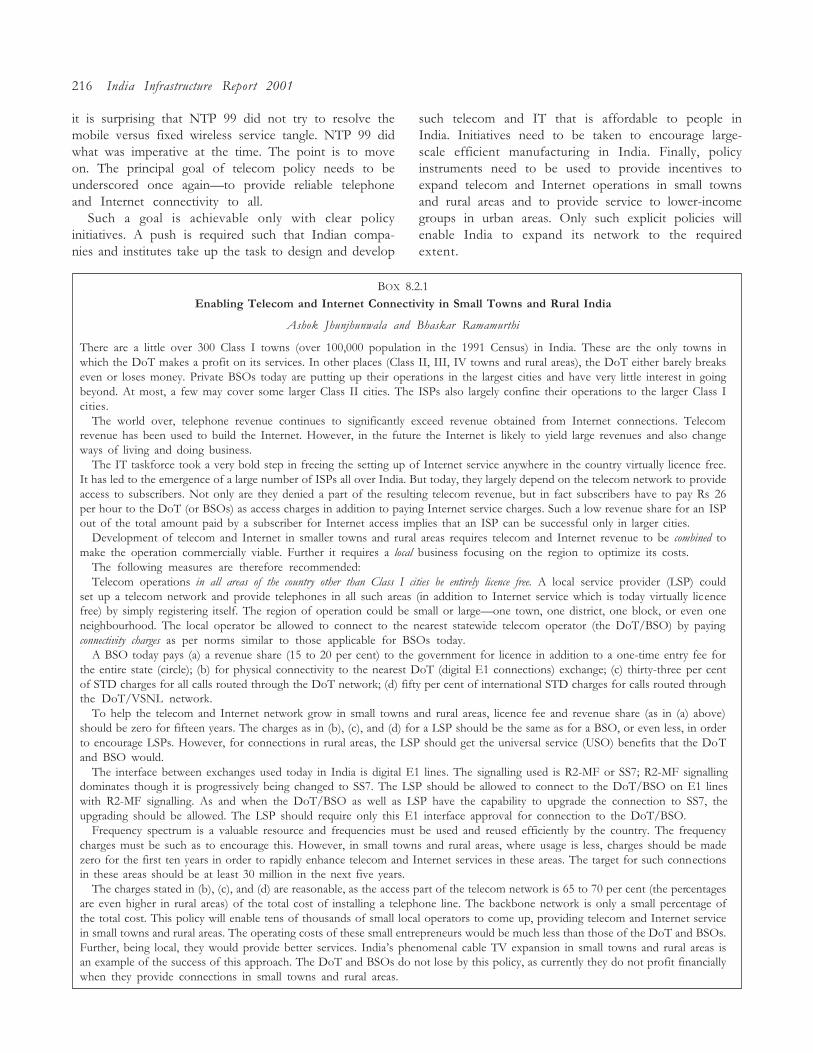

8.2.1 Enabling Telecom and Internet Connectivity inSmall Towns and Rural India 216

9.1.1 Local Governance in Small Towns in Gujarat since the CAA74:First Impressions 255

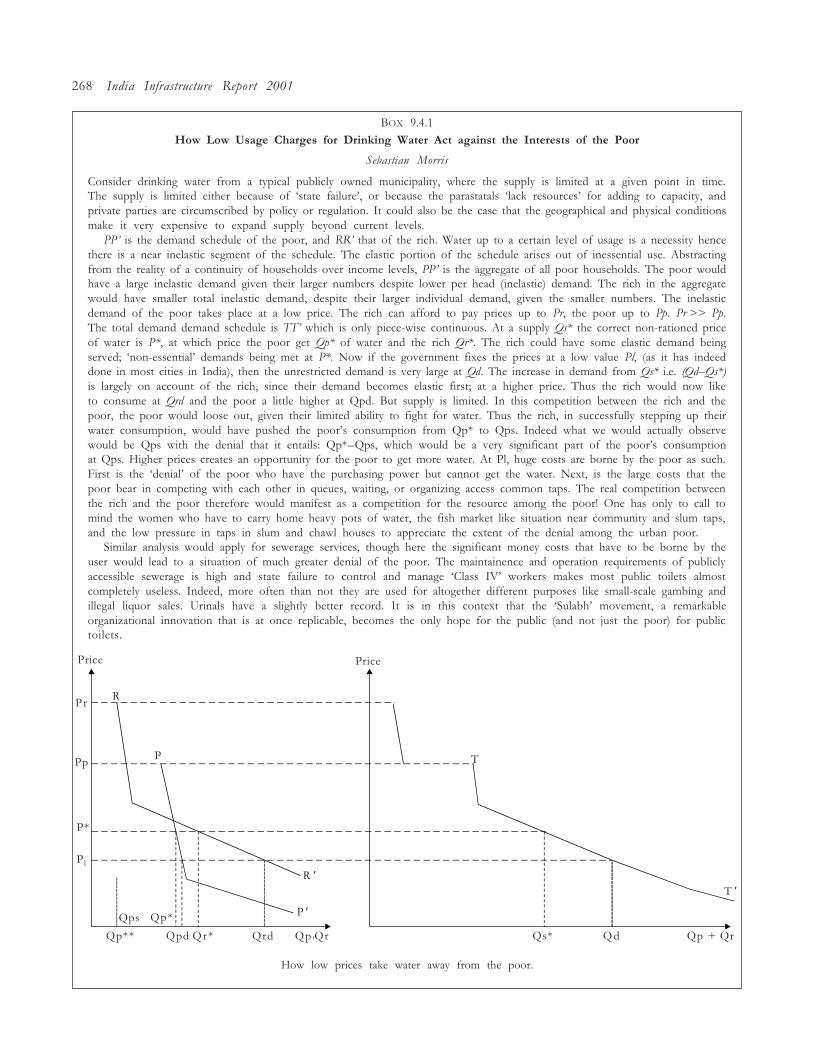

9.4.1 How Low Usage Charges for Drinking Water Actagainst the Interests of the Poor 268

9.5.1 Overexploitation of Groundwater can be Overcome byCorrectly Pricing Electricity and Diesel 270

BOXES

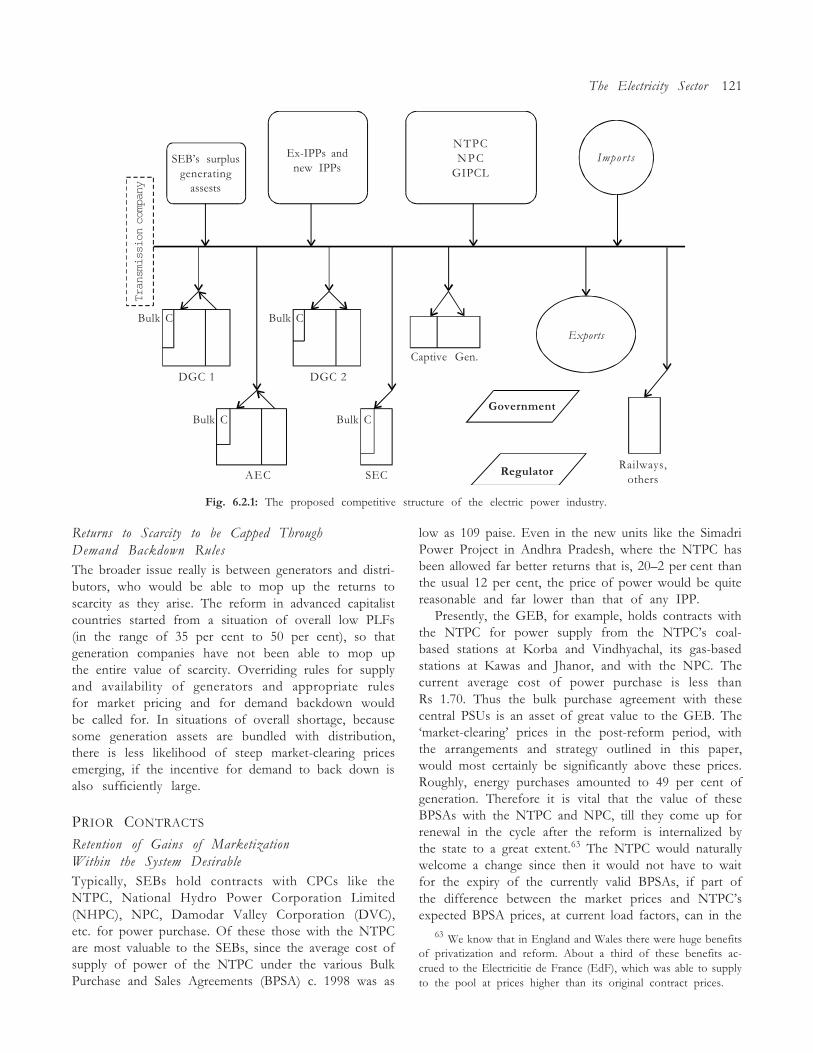

6.2.1 The proposed competitive structure of the electric power industry 111

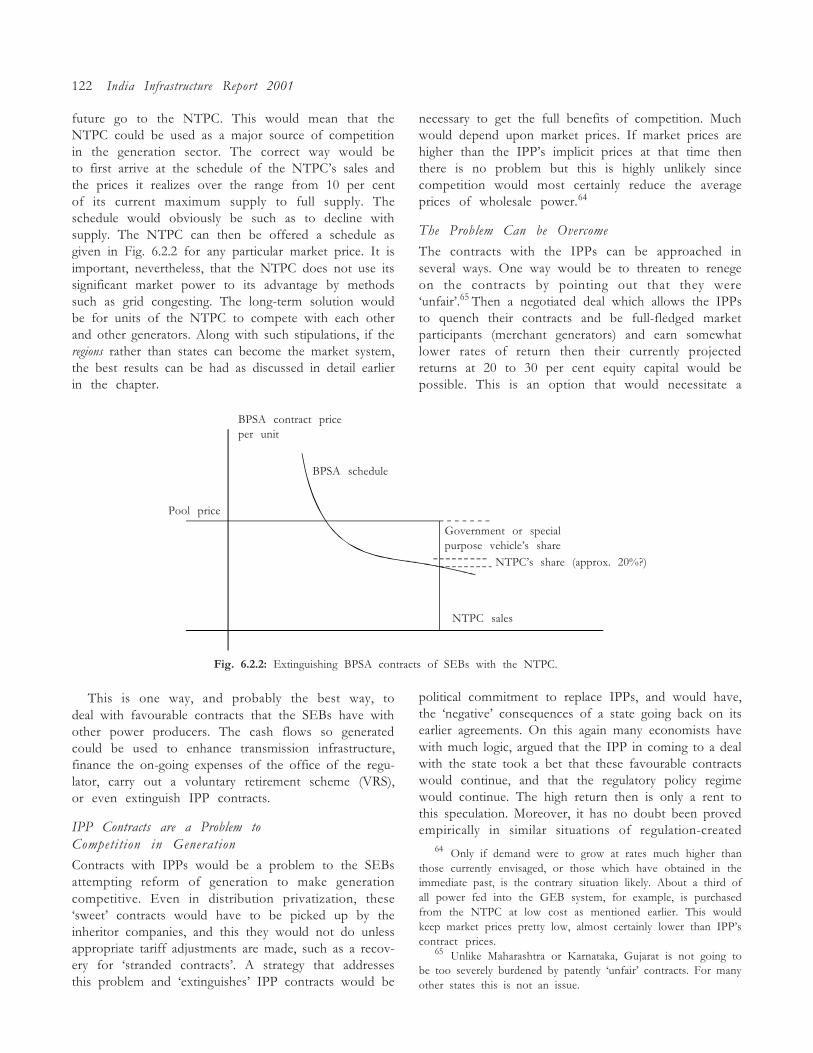

6.2.2 Extingushing BPSA contracts of SEBs with the NTPC 122

7.1.1 Transport myopia 131

7.1.2 Framework to segment users 135

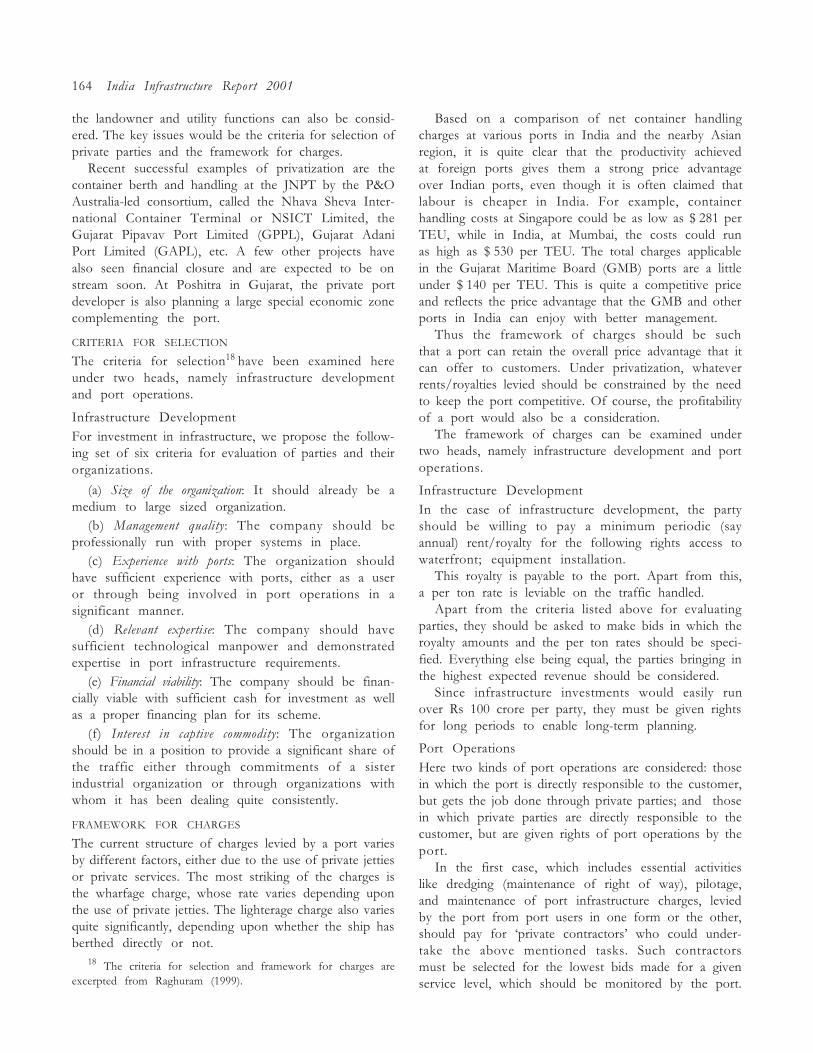

7.2.1 Roles of ports: Regulator, landowner and utility 163

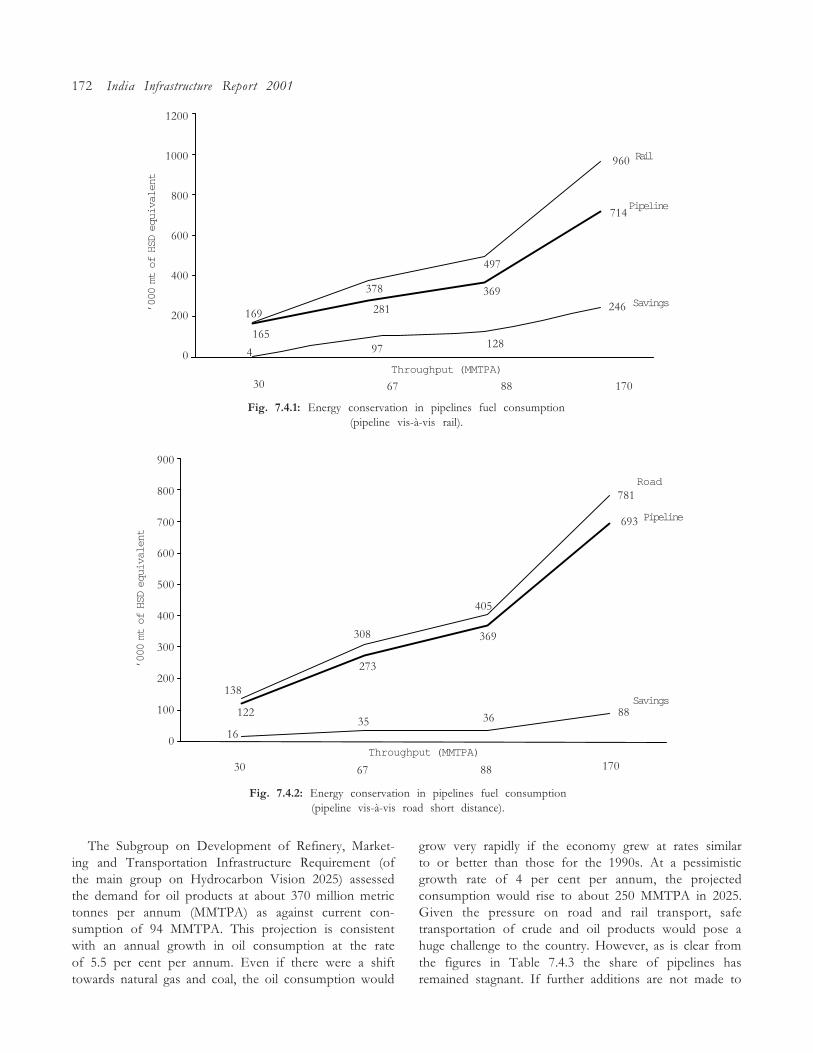

7.3.1 Energy conservation in pipelines fuel consumption(pipeline vis-à-vis rail) 172

7.3.2 Energy conservation in pipelines fuel consumption(pipeline vis-à-vis road short distance) 172

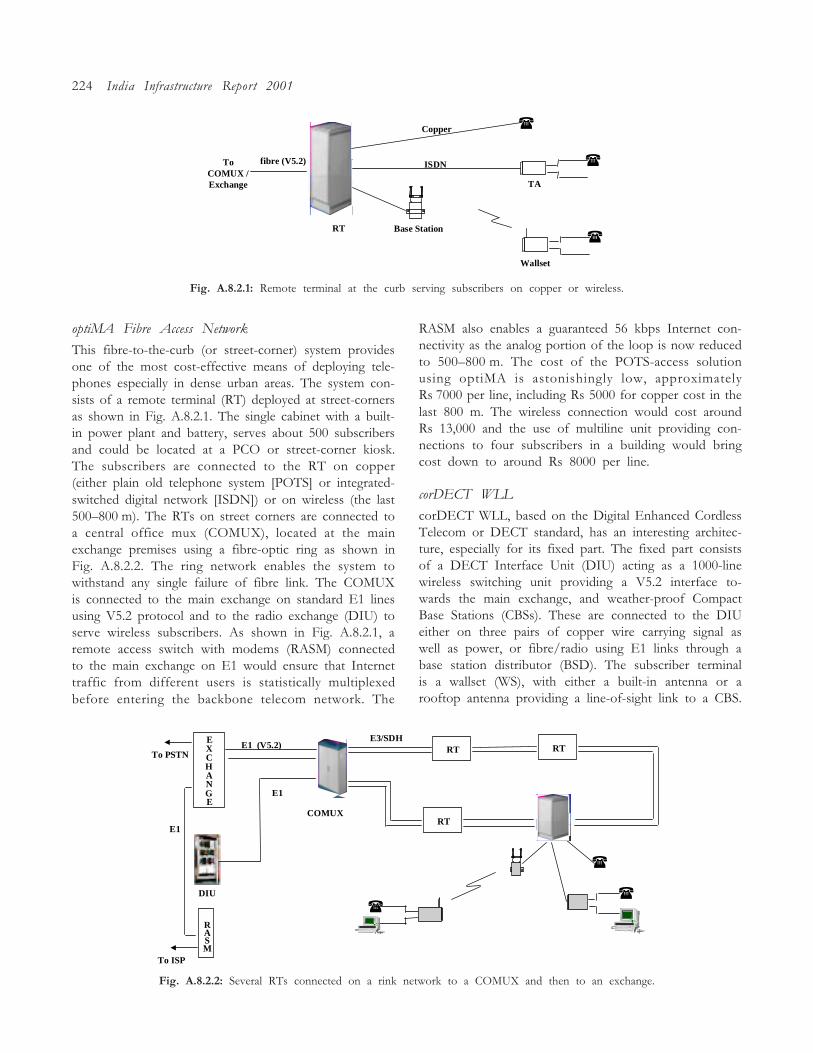

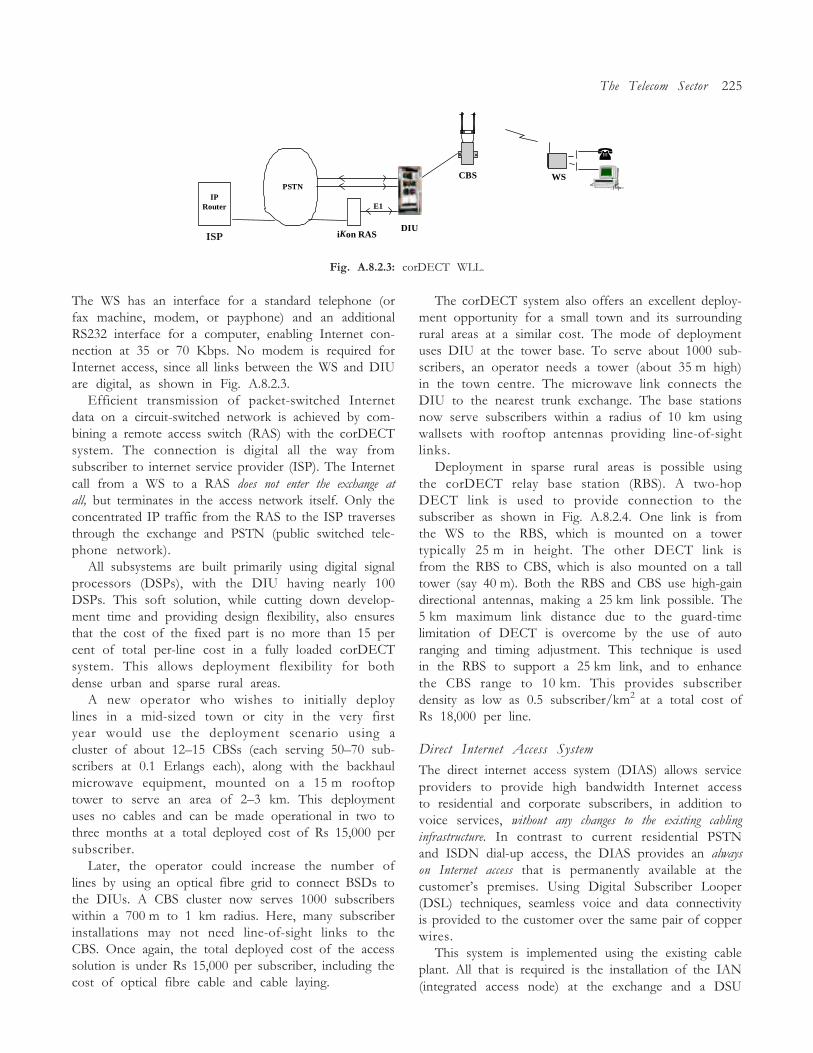

A.8.2.1 Remote terminal at the curb serving subscribers on copper or wireless 224

A.8.2.2 Several RTs connected on a rink network to a COMUX andthen to an exchange 224

A.8.2.3 corDECT WLL 225

A.8.2.4 Relay base station 226

A.8.2.5 Direct internet access system 226

A.8.2.6 Internet usage today 227

A.8.2.7 An AC serving subscribers through a SU 227

A.8.2.8 PDH/SDH Fibre backhaul with drop and insert (D & I) 228

A.8.2.9 AC providing POTS, wireless internet plus simultaneous voice connectivityand DSL connections presiding internet plus voice 228

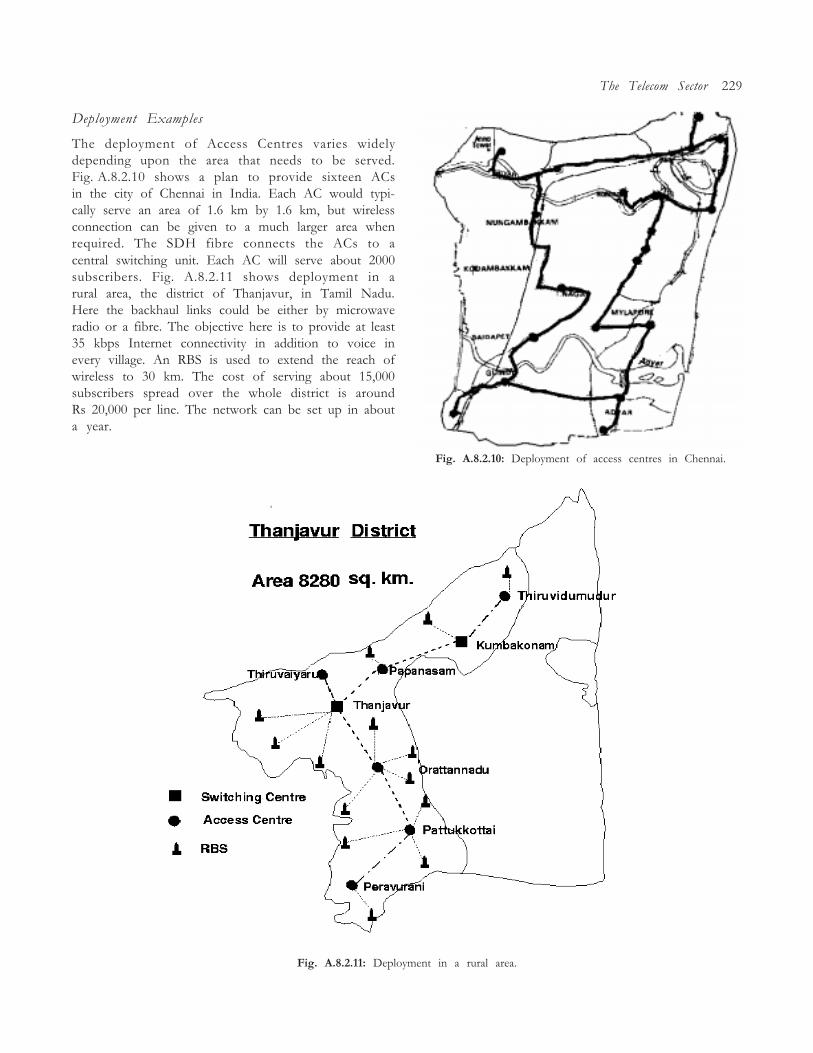

A.8.2.10 Deployment of access centres in Chennai 229

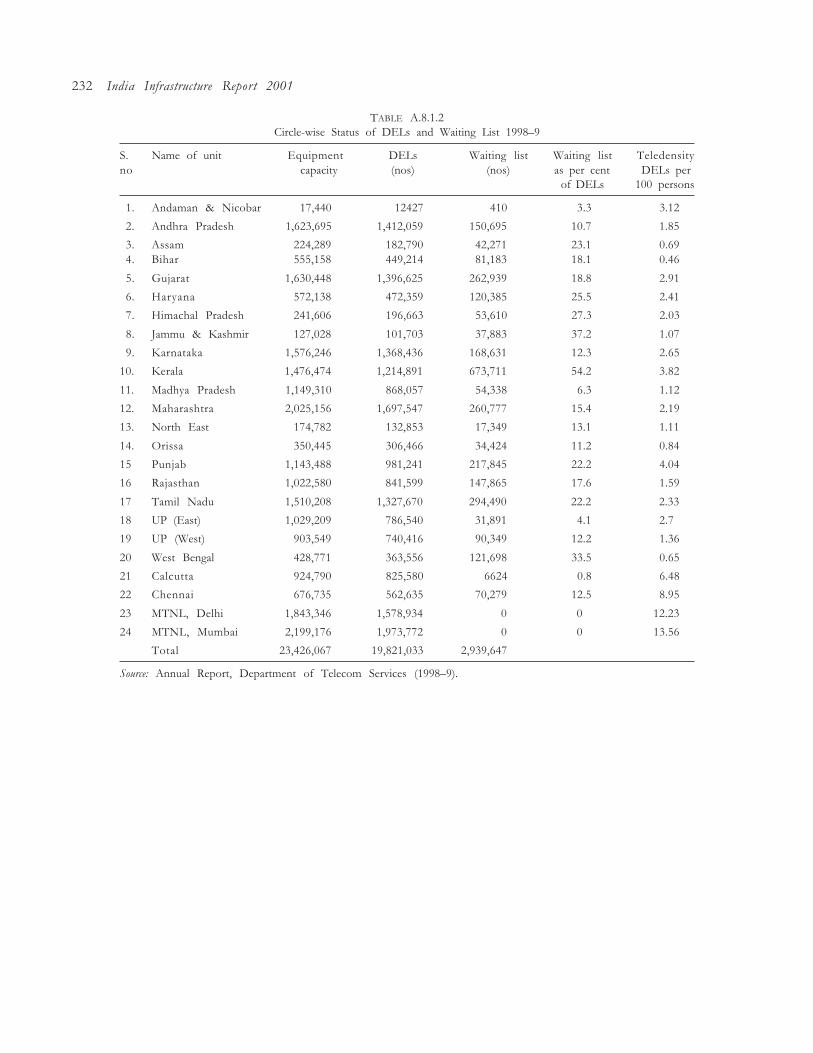

A.8.2.11 Deployment in a rural area 229

9.5.1 Factors causing regression of rural water supply status 272

9.5.2 Improving availability and ensuring sustainability: options 276

FIGURES

AAI Airport Authority of IndiaABT Availability-based TariffACP anti competitive practicesADB Asian Development BankADC Analogue Digital ConverterADSL Asynchronous Digital Subscriber LoopADV animal drawn vehicleAIMTC All India Motor Transport CongressAITD Asian Institute of Transport DevelopmentAPM Administered Pricing MechanismAPSEB Andhra Pradesh State Electricity BoardAPTRANSCO Andhra Pradesh Transmission Company, an inheritor company of the APSEBARV Annual Ratable ValueARWSP Accelerated Rural Water Supply ProgrammeBDSL Basic Rate DSLBDSU Basic Digital Subscriber UnitBFOT build, finance, operate and transferBKPL Barvani�Kanpur PipelineBOLT build, operate, lease, and transferBOO build, operate, and ownBOOT build, own, operate and transferBoP balance of paymentsBoT build, operate and transferBPSA Bulk Purchase and Sales Agreement

(between central power corporations like the NTPC, NHPC, NPC and SEBs)BSD Base Station DistributorBSES Bombay Suburban Electric Supply (Undertaking) LimitedBSO basic service operatorBWSSB Bangalore Water Supply & Sewerage BoardCBD central business districtCBSs Compact Base StationsCCL Continental Construction LimitedC-DOT Centre for Development of TelematicsCEA Central Electricity AuthorityCERC Central Electricity Regulatory CommissionCFC Central Finance CommissionCFSs Container Freight StationsCIDCO City and Industrial Development Corporation

ABBREVIATIONS AND ACRONYMS

CLASS Customs Local Area Signalling ServicesCLEC competitive local exchange carrierC M C Computer Maintenance Corporation Ltd.CMSP Cellular Mobile Service ProviderCNG Compressed Natural GasCOAI Cellular Operators Association of IndiaCOMUS Central Office MuxCONCOR Container Corporation of IndiacorDECT Registered DECT of TeNetCPC Central Power Corporations (NTPC, NHPC, NPC, REC)CPCB Central Pollution Control BoardCPE Customer Premise EquipmentCPHEEO Central Public Health and Environmental Engineering OrganisationCPP Calling Party PaysCRS Commissionerate of Railway SafetyCSP Cable Service ProviderC T U Central Transmission UtilityDEL Direct Exchange LineDFIs Development Financial InstitutionsDGCs Distribution-cum-Generating CompaniesDG-IV General Directorate of Competition of the European UnionDGT Director General, Telecommunications, OFTEL, UKDIAS Direct Internet Access SystemDIU DECT Interface UnitDLD Domestic Long DistanceDMH Dandeli Mini-Hydel ProjectDMRT Delhi Mass Rapid TransitDNPR&R Draft National Policy on Rehabilitation and ResettlementDoT Department of TelecommunicationDPC Dabhol Power Company Ltd.DPA Dubai Ports AuthorityDPCs District Planning CommitteesDPI Department of Programme Implementation (of the Ministry of Planning),

Government of IndiaDSP Digital Signal ProcessorDSU Digital Subscriber UnitDTC Delhi Transport CorporationDTHB direct to home broadcastingDTO Department of Telecom OperationsDTS Department of Telecom ServicesDVC Damodar Valley CorporationECB External Commercial BorrowingECIL Electronics Corporation of India Ltd.EDI Electronic Data InterchangeEHV extra high voltageEIA environment impact analysesEPA Environmental Protection AgencyERC Electricity Regulations Act, 1998ERR economic rate of returnETSI European Telecommunications Standards InstituteEW England & Wales (Pool or electricity System)EZEV Equivalent Zero Emission VehiclesFAC fully allocated costs

xx Abbreviations and Acronyms

FACTS flexible AC transmission systemsFCC Federal Communication CommissionFCVs Fuel Cell VehiclesFDI foreign direct investmentFERC Federal Energy Regulatory CommissionFIRE Financing Institution Reform and ExpansionFLAG fibre optic link around the globeFOI Freedom of Information ActFPI Foundation for Public InterestFSI floor space indexFSP fixed service providersGAIL Gas Authority of India LimitedGAPL Gujarat Adani Port LimitedGATS General Agreement on Trade and ServicesGDCF gross domestic capital formationGDP gross domestic priceGDR Global Depository ReceiptGEB Gujarat Electricity BoardGIDB Gujarat Infrastructure Development BoardGIDC Gujarat Industrial Development CorporationGMB Gujarat Maritime BoardGMSC Global Mobile Service CarrierGNCTD Government of National Capital Territory of DelhiGPPL Gujarat Pipavav Port LimitedGRT gross registered tonnageGSM Group Special MobileGWSSB Gujarat Water Supply and Sewerage BoardHBCP Haldia�Barauni Crude Oil PipelineHDSU high bit rate digital subscriber unitHDT host digital terminalHERC Haryana Electricity Regulatory CommissionHEVs hybrid electric vehiclesHMRPL Haldia�Mourigram�Rajbandh PipelineHUAC high voltage alternating current (transmission)HUDC high voltage direct current (transmission)IAN Integrated Access NodeIBPL Indo-Burma Petroleum LimitedIBRD International Bank for Reconstruction and DevelopmentIC internal combustionICAO International Civil Aviation OrganizationICE Information, Communication and EntertainmentICF Integral Coach FactoryICSEM Institute for Catchment Studies and Environmental ManagementIDC International Data CorporationIDWSSF International Drinking Water Supply and Sanitation DecadeIETP Internet Engineering Task ForceIEGC Indian Electricity Grid CodeIETF Internet Engineering Task ForceIFC International Finance CorporationILEC Incumbent Local Exchange CourierIMO International Monetary OrganizationINF Intelligent Network ForumINSA Indian National Shipowners� Association

Abbreviations and Acronyms xxi

IOCL Indian Oil Corporation LimitedIP Internet ProtocolIPP Independent Power ProjectIPRs Intellectual Property RightsIRR internal rate of returnISDN International Subscriber Dialling NumberISP Internet Service ProviderITI Indian Telephone Industries Ltd.ITS Indian Telecom ServiceITU International Telecommunications UnionITXC Internet Telephony Exchange CarrierJNPT Jawaharlal Nehru Port TrustJRY Jawahar Rozgar YojanaJTM Jabatan Telekom MalaysiaJVC Joint Venture CompanyKBPL Kandla�Bhatinda PipelineKPRC KP Rao Committee (set up to study bulk tariff)KRC Konkan Railway CorporationLAA Land Acquisition Act 1894LEC Local exchange carrierLEV Low Emission VehicleLIBOR London Inter Bank Offer RateLNP Local Number PortabilityLoC Letter of CreditLoI Letter of IntentLPCD Litres per capita per dayLRAC Long run average costsLRDSS Long Range Decision Support SystemLRIC Long Run Incremental CostLRMC Long Run Marginal CostsLSP Local Service ProviderLT Laxmi TransformersMAINS Maritime Information SystemMERC Maharashtra Electricity Regulatory CommissionMGC merchant (independent) generating companyMHV medium and heavy vehicleMIDC Maharashtra Industrial Development CorporationMIGA Multilateral Investment Guarantee agencyMIS Management Information SystemMJPL Mathura�Jalandhar PipelineMMC Monopolies and Mergers Commission of the UKMNP Minimum Needs ProgrammeMOEF Ministry of Environment and ForestsMoP Ministry of PowerMoST Ministry of Surface TransportMOT Maintain, Operate and TransferMoU Memorandum of UnderstandingMPCs Metropolitan Planning CommitteesMRTPC Monopoly and Restrictive Trade Practices CommissionMRTS mass rail transit systemMSEB Maharashtra State Electricity BoardMSO Multiple Service OperatorMSRDC Maharashtra State Roads Development Corporation Limited

xxii Abbreviations and Acronyms

MTBE methyl tertiary butyl etherMTC Mobile Termination ChargeMTNL Maharashtra Transport Nigam LimitedMTW motorized two-wheelersMWS Multi WallsetNABARD National Bank for Rural DevelopmentNBCC National Building Construction Company LimitedNHAI National Highway Authority of IndiaNHPC National Hydro Power Corporation LimitedNIC National Informatics CentreNICs newly industrialized countriesNLC Neyveli Lignite Corporation Ltd.NLDC national long distance carrierNLDO National Long Distance OperatorNLDS National Long Distance ServicesNMHC/NMOG Non-Methane HydrocarbonNORD pool The electricity pool of the Nordic countriesNPC Nuclear Power CorporationNTF National Task ForceNTPC National Thermal Power Corporation Ltd.NZ New Zealand (Pool or electricity system)O C C Oil Co-ordination CommitteeOERC Orissa Electricity Regulatory CommissionOHPC Orissa Hydro Power CorporationoptiMA Registered brand of TeNetOSEB Orissa State Electricity BoardOYW own your wagon (scheme of the Railways)PAFC Phosphoric AcidPAP Project Affected PeoplePCC Public Common CarrierPCS Personal Service CommunicationPCUs Passenger Car Equivalent UnitsPDH Plesiochronous Digital HeirarchyPEMFC Polymeric Electrolyte Membrane Fuel CellsPGCIL Power Grid Corporation of India LimitedPIL Petronet India LimitedPJM Pennsylvania, New Jersey and MarylandPLF plant load factorPOL Petroleum Oil and LubricantPPA Power Purchase AgreementPPP Public�Private PartnershipPRCL Pipavav Rail Corporation LimitedPRIs Panchayati Raj InstitutionsPSEG Public Service Electric and Gas CompanyPSP Private Sector ParticipationPSTN Public Switched Telephone NetworkPTC Power Trading Corporation LimitedPUC Pollution Under ControlQP Quality ProblemRAS Remote Access SwitchRBI Reserve Bank of IndiaRBS Relay Base StationR C Restructuring Commission

Abbreviations and Acronyms xxiii

REC Rural Electrification CorporationRGNDWM Rajiv Gandhi National Drinking Water MissionRLDC Regional Load Despatch CentreR MC Rajkot Municipal CorporationROE return on equityROI return on investmentRo-Ro Roll-on-Roll-OffROW right of wayRPI Retail price indexR T Remote TerminalRTF Regional Task ForceRTO Road Transport OfficeRV Rateable ValueSACFA Standing Advisory Committee on Frequency AllocationSBM Single Buoy MooringSCADA Supervisory Control and Data AcquisitionSCICI Shipping Credit and Industry Corporation of India Ltd.SEBI Securities & Exchange Board of IndiaSEGW Secondary Sector (electricity, gas and water)SEZ Special Economic ZoneSGCP Switching Gateway Control ProtocolSMPL Salaya�Mathura PipelineSOHO Small Office Home OfficeSPM suspended particulate matterSPV Special Purpose VehicleSRMC short run marginal costSRTUs State Road Transport UndertakingsSSA Secondary Switching AreaSTD�PCOs Subscriber Trunk Dialling/Public Call OfficesSTM Syarikat Telekim MalaysiaSTU State Trading Utilitysu subscriber unitSVC Static VAR compensation systemsTAMP Tariff Authority for Major PortsTAS Tattihalla Augmentation SchemeTCI Transport Corporation of India LimitedTCIL Telecommunications Corporation of India Ltd.TeNet Telecommunication and Computer NetworkTEUs twenty feet equivalent unitsTIPHON The Internet Protocol Harmonization over NetworkTNSEB Tamil Nadu State Electricity BoardToU time of useTRAI Telecom Regulatory Authority of IndiaTRANSCO transmission companyTTSC Transport, Trading, Storage and CommunicationUI Unscheduled interchangeULB Urban Local BodyULEV ultra low emission vehicleUnicom United TelecomUPSBC Uttar Pradesh State Bridges Construction Company LimitedUPSEB Uttar Pradesh State Electiricyt BoardUSO Universal Service ObligationVAR Volt Ampere Reactive

xxiv Abbreviations and Acronyms

VoIP Voice over Internet ProtocolVPT Village Panchayat TelephonesVRS Voluntary Retirement SchemeVSAT Very Small Aperture TerminalVSNL Videsh Sanchar Nigam LimitedVTS Vessel Traffic Management or Surveillance ServicesWILL Wireless in Local LoopWNP Wireless Number PortabilityWPC Wireless Planning and Co-ordination WingWS Wall SetZEV Zero Emission Vehicle

Abbreviations and Acronyms xxv

1The overall theme is �regulation and industry struc-

ture�, far more broadly interpreted than is conventional.Indeed, the approach has been to discuss the principalconstraints in the development and commercializationof infrastructure. We also show how the two areinterlinked in a market economy. The principal con-straints, including those of a structural and institutionalnature, which we believe need to be overcome for thefast development of infrastructure are also covered.

Thus the conservative approach to macroeconomicpolicy which may have slowed down growth over thelast three years or so and the land acquisition processeswhich arrest infrastructure development and create dis-sent against development are discussed. Similarly, thelimitations of the principal local bodies (the municipali-ties) that would have to organize much of the urbaninfrastructure are also discussed.

Public enterprise, whether structured as a companyor operating within government departments, findcoverage especially in its potential for commercializa-tion. Government departments and regulatory bodiesprivatizing public enterprise are also discussed.

In this report�in keeping with the overall objectiveof the 3iNetwork, viz. to �lead intellectual capital intoinfrastructure��we attempt to go beyond a discussion ofcurrent constraints to suggest changes in terms of ap-proaches, institutional reorganization, and appropriatepolicy. Thus we do not hesitate to point out the possibleneed for an alternative paradigm with regard to project-affected people. Similarly, we would question the con-sensus around the need to eliminate subsidies. The biggerproblem is the mode of administration of subsidies. Oursuggestions are best seen as attempts to bring to theattention of policy makers, developers, and others, freshavenues for extended consideration.

India Infrastructure Report (IIR) 2001 has several contribu-tors including members of the 3iNetwork, a networkof three institutions: the Infrastructure DevelopmentFinance Company, the Indian Institute of Technology,Kanpur, and the Indian Institute of Management,Ahmedabad.

In little less than six months since the idea of a reportoutlining the developments and constraints in infrastruc-ture was mooted, the members and others outside theseinstitutions wrote on sectors and themes that constitutephysical infrastructure. The coverage no doubt varieswith regard to the sectors. Similarly, not all the impor-tant issues that bear on regulation and industry structurehave been covered. Thus there should have been moredetailed treatment of urban transportation especially theintermodal dimensions. Similarly the constraints im-posed by current practices with regard to land use inurban areas are not covered. The housing sector has beenentirely omitted. Industrial parks had to be omitted forlack of time and because we were anyway not able tocover the important aspects of land use in urban areas.These are important omissions which we hope would betaken up in later issues of the IIR.

Nevertheless, in the chapters here we put forward apicture of infrastructure development in India, review-ing the major developments especially with regard topolicy and regulation. We draw out certain themes thatare interesting and which help in understanding perver-sities such as distortionary prices, systematic exclusionof the poor, very inefficient operations, and largeallocative failures that run through nearly all the sectors.We also outline the nature of both state and marketfailure with regard to infrastructure and of the relation-ship between the two. We also identify, in some sectorsmore than in others, the restructuring tasks ahead.

OVERVIEW

Sebastian Morris

2 India Infrastructure Report 2001

When the idea of such a report was first mooted, itwas felt that problems of infrastructure have an emer-gent character, as reformers and governments learn todo what is right for the economy and the consumer.Thus the mistakes that had been made and need correc-tion (in the view of the contributors) are discussed.The challenge of private sector involvement runs rightthrough the report. This is not because we feel that thestate has no role or only a declining one, but becausewe are convinced that commercialization, which ismore important than ownership, is vital to the realiza-tion of both allocative and operational efficiency ofinfrastructure. And that cannot be realized withouteither a certain degree of privatization or a reorientationof public enterprise away from rules and guidelines totasks. We see as more important the feedback effect ofsome degree of privatization, through the tension forreform that such privatization creates, than the fact ofprivatization per se. Thereby the �state failure� thatlimited public enterprise from delivering can begin to beovercome.

Chapter 2, �Issues in Infrastructure DevelopmentToday: The Interlinkages� (Sebastian Morris), discussescross-sectoral problems, bringing out interrelationshipsand interlinkages. The need for reform is real. It is nolonger a question of merely signalling to the world atlarge that the country is ready to open its doors toprivate and foreign capital. Privatization or commercial-ization of public enterprise and restructuring of manyof the infrastructural areas is an urgent necessity. Thefiscal situation is explosive in power and urban servicesand the opportunities in telecom are too large to bemissed, especially for an economy that has shown somuch potential in software and remote delivery ofservices. Transport services are misdirected by highlydistortionary prices, and pipelines are held back byimproper policy.

The economy would most certainly have enteredinto a phase of infrastructural shortage, given the slowergrowth of infrastructure in the 1990s. This arises becauseof the �limited capacity of the state to invest� and theprivate sector�s unwillingness to do so, since the ex-pected regulatory and policy clarity has not been ob-tained. While the resulting costs of denial are undoubted-ly large, this relative �shortage�, or �infrastructure laterrather than first�, has its own advantages in that theproblem of directing infrastructural investments is hardlythere. The first priority would be to relax the shortages.Appropriability too could improve. But in many areasthe state continues to derive its priorities politically orthrough planning �exercises�. More efficient use of infra-structure is also possible today.

The slowing down of infrastructural investments in

the 1990s has had negative effects on investment demandin general and is most certainly one of the factorsunderlying the slow growth of the economy since1997�8. The economy may have reached a stage wherefrom the demand side a major push in infrastructuralinvestment is necessary. Indeed, the matter may beurgent enough to bring back public investment eventhough it is known to be inefficient.

The problem is not subsidies per se but their modeof administration. Not a single meeting on infrastruc-ture, especially power and water, takes place withoutlamenting the subsidies. Their administration in such amanner as to create moral hazard in the organizationsproviding the service has been an important reason forthe failure of public organizations. Although the vestedinterests against reform are strong, they may not be thegroups that are usually identified as such�workers andsubsidized groups. The vested interests are more likelyto be bureaucrats and politicians who have to give upprivileges they have enjoyed as managers and owners.The emphasis on vested interests as a barrier againstreform may have been overstated. Reforms have notbeen too well conceived, and that more than vestedinterests has limited their scope thus far. The need todayis to create the right market structures to take advantageof competition wherever possible, and institute lightregulation elsewhere. These are tasks that require highlevels of skills and effort.

It is important that public enterprises be allowed tofunction commercially and towards their primary tasks.The pressures against denial of that freedom have in-creased. The possibility of privatization indeed improvesthe prospects for such autonomy, and hence for com-mercialization of public enterprise in infrastructure.�Empty solutions� that merely postpone the day ofreckoning continue to be generated, as when privatizationof State Electricity Boards� (SEBs�) assets by selling thesame to state-level Public Sector Undertakings (PSUs) isproposed, or a sham privatization is proposed to �satisfy�a multilateral agency. The days for such behaviourwould soon be over.

The myth that low prices are in the interest of thepoor needs to be recognized as such and exposed. Lowprices have created the problem of slow expansion orstagnation of the service, and hence have kept a largenumber of the poor as �outsiders�, that is those who aredenied the service since they do not even have access.There is a need to distinguish between subsidization ofaccess and subsidization of use, the former being welfareenhancing. Direct subsidization via stamps or couponsis the need of the hour especially in irrigation, drinkingwater, and electricity. That would allow these servicesto be viably provided by private capital.

O v e r v i e w 3

So deep have been the price distortions that invest-ments have been taking place on the basis of suchdistorted prices. Naturally demand has also been af-fected. As the reform extricates the system out of thesedistortions there would be a phase when the true pricesand demand would be discovered.

The notion that whenever there is a market failurein the neoclassical static sense, an orthodox price regu-lation is called for is quite questionable. When inan area like telecom, growth is expected to be rapidbecause of technological changes and network econo-mies, contestability is high and the orthodox regulatorystance is scarcely appropriate. In telecom, especially,freer entry and more liberal interconnect rules wouldtherefore be justified. Convergence too creates it ownopportunity for one industry to ride on another asInternet today can be expected to ride on cable televisionand high bandwidth cables on existing powerline infra-structure.

The most important structural constraint remainsthe process of land acquisition. The current process andvaluations may not be correct if the specificities ofthe Indian situation and the fact that the land marketitself has been distorted by land use restrictions are takeninto account. On land acquisition and resettlement ofproject-affected people, the law needs to change to createthe space for their inclusion in the project as stakehold-ers. Only this can lower the risk from �displacement�.

Relevant information about public bodies when avail-able with the concerned public can work wonders inmaking such bodies and their officials responsible. Assuch, a genuine right to information Act is necessary forthe reorientation of the state to its people and theirinfrastructural needs.

Chapter 3, �Regulation of Tariffs and Interconnec-tion: Case Studies� (Sidharth Sinha), brings out threecases of tariff rulings by regulators in India, two in thecase of the telecom sector and one in bulk power. Thechapter uncovers the underlying assumptions and con-cerns of the regulator and the regulated, and the limi-tation of these rulings, to make a critical assessment ofthe same. Some of the limitations in the defined powersof the regulator and in the existing structure of theindustry are brought forth.

Independence of the regulator has gained currencybut still remains contested and contingent. The tempta-tion to dilute financial regulation or oversight to allowmore lax standards in lending to infrastructure is naturalbut dangerous. This is discussed in Chapter 4, �Regula-tory Dilemmas in Infrastructure Financing� (JayanthVarma). The author comes to the conclusion that whilecredit enhancements and tax support for funds flowinto infrastructure would be appropriate, dilution of

standards would not be so. The recent experience of theEast Asian countries as well as historical experiencewould show that there is little need for such relaxations,despite the force with which governments and develop-ers may put forward their arguments. Financial markets,especially debt markets are quick to emerge, when theopportunities arise. The problem with infrastructure isusually, and more certainly in India, with the sector assuch�regulatory and policy uncertainties, allocativeinefficiencies arising out of government�s influence ininvestment decisions�than in the need for special finan-cial dispensation for infrastructure. This is not to denythe role of credit enhancement and land grants in the caseof infrastructure with high social returns.

Chapter 5 discusses the principal structural con-straints in infrastructure development in India. As �in-dependent� regulation emerges in many sectors, there isneed to look at the relationship between sector-specificregulators and the competition agencies. There are manyreasons why we should have a competition policy,despite the known limitations of the same in a trans-forming economy. Convergence is an important driverthat in the years to come would question the standardprescription of an �independent� sector-specific regula-tor. Convergence in India could be driven by bothtechnology, as in telecom as voice over Internet Protocol(IP) becomes a distinct possibility, and by the economiesof the �right of way� which tend to be amplified, giventhe many clearances and dealings with governmentbodies that have to be gone through before any networkinvestments can be in place. The first part of Chapter 5,�Interface between Sector-specific Regulatory Bodies andCompetition Agencies� (Rakesh Basant), brings out theconflicts that are likely and flags the loose ends, callingfor a more detailed study of possible options.

In �Political and Bureaucratic Hurdles in Reform andRestructuring� (M. Y. Rao), the history of the birth ofthe Orissa regulator is brought out by one who not onlyhad a ringside view but was actively involved in the earlystages of the reform. The biases and assumptions and thevested interests that had to be overcome in institutionalreform for regulation remain just as relevant today. Weget a feel of the nature of the state and bureaucracy inIndia at the provincial level. Most certainly hardeningbudgets and the crisis-like situation were the drivers forchange. Thus threats more than opportunities are goingto work in the Indian situation.

An important development in the involvement ofthe private sector has been the passage of several build,operate and transfer (BOT) laws by state governments.In �Need for a BOT Law� (Atanu Chakraborty), whohad been involved in the design of the Gujarat Infrastruc-ture Act, brings out the salient features and the processes

4 India Infrastructure Report 2001

involved in bringing forth the legislation. Limitationsapart, such BOT laws bring in the operational efficiencyof the private sector into areas of infrastructure thatare appropriable in part or full. As many state govern-ments gear themselves for reform, the experience ofGujarat would be of interest. Change is not without itshiccups and opponents. In infrastructure, the �power ofthe status quo� is most acute: markets do not naturallyexist. They have to be �created� by design, law, and useof technology. Such unbundling makes the task ofgovernment more challenging. As such the capacity andcapability of the government is vital to the success ofreform and privatization.

�Project Preparation: The Cinderella of Private SectorParticipation (PSP)� (Atanu Chakraborty), as its namesuggests, laments the relative neglect of this ratherpainstaking but important task when the state putsforward projects for the private sector. The task isespecially important if foreign developers are to beinterested in Indian projects. Indian government has todevelop the skills to put forth projects that speakthe same language that developers and foreign institu-tional investors expect. Unfortunately, many govern-ment departments are still to learn what constitutes therelevant details. The creation of specialized bureauscan only be the first step in the diffusion of the relevantskills for project preparation through the state govern-ment system. �How much more of this Infliction? TheCase of the Ahmedabad�Vadodara Expressway� (AmitaGupta and Sebastian Morris) brings out coordinationfailure of government construction in a large project.Few projects have failed on the same scale as thisexpressway. The case is archetypical of what happenswhen a bureaucracy has moved far from the Weberianideal upon which the case for public provisioning rests.Given the current, entirely dysfunctional systems andprocedures within government, the case tells us that themore pertinent question to ask may well have been:�How did such bureaucracies deliver at all?� The answerwe guess may well lie in the work of key persons withinthe system who are willing to creatively interpret theirroles to make things happen. That such persons exist isbeyond doubt. The challenge therefore is to energizethem as change agents within the state system.

In �Land Acquisition: Law and Practice�, Y. M.Shivamurthy and Vinita Sinha bring out the salientfeatures of the Act. The court rulings which have tendedto display much concern for the status of the affectedpersons are also discussed. Land acquisition has beenproblematic but its solution does not lie in the new bill,which seeks to curb certain freedoms of the affectedpersons. Indeed a case is made for a paradigm changein land for infrastructure. No infrastructure, however

socially beneficial, can be built on inadequate compen-sation for those whose land had to be taken away. Thatargument is valid not only from the point of view ofjustice but also because significant reductions in the timefor acquisition and the risks involved cannot come ifevery act of acquisition has to become a tussle, as itcurrently is. On what needs to be done though, thereis some divergence in this report itself. �Land Acquisi-tion: The Case of Poshitra Port� (Alice Albin Morris)documents an ongoing process of land acquisition. Theinadequacies in the practice are brought out, as thepeople experience the process of their lands beingacquired by the government. In this case the governmenthas gone through most of the motions as specified, inthe letter but not in the spirit of the law.

In �Environment and Social Risks in InfrastructureDevelopment� Ajay Narayanan makes a case for the landacquisition law to change in keeping with �case law�. Heargues for larger compensation and also some involve-ment of those affected. The need for the Act to be morein line with the Draft Policy on Project-Affected Peoplesof the Ministry of Rural Development is also discussed.Moreover environmental risks of infrastructural projectsdo not go away with mere adherence to all clearances.Project developers have to do much more, truly reduc-ing if not eliminating the ill effects on the environmentand adequately compensating those affected.

The environmental consciousness of the 1970s andthe 1980s resulted in a formalistic and clearance-basedapproach. As the terms of the clearances were system-atically violated judicial activitism resulted and muchopposition from those affected created risks. The re-sponse of the state which was doing much of theinfrastructural development was more towards bearthese risks and costs and suffer as a consequence, ratherthan to go beyond the law to reduce the risks. Today,with private financial institutions being involved, thatapproach could possibly give way to true risk mitigationas they realize that mere adherence to clearances is noguarantee of freedom from risk. But has this realizationtaken root? Not as yet, if the story �Hotshot ConsultantsCopy a Report to get Project Cleared� (B. S. Nagaraj,Indian Express) is any indication.

What can a harried citizenry, in the face of statefailure and widespread corruption, do? Today lack ofa right to information constrains the average citizenand when he is really desperate, as when his land is beingtaken over for �public� purposes or when a local industrypumps back pollutants into the ground, he has no choicebut to agitate. A thoroughgoing right to information lawcould do much in a democracy, especially in as plurala society as ours. �The Right to Information as a Toolof Empowerment� (Abha Singhal Joshi) argues that the

O v e r v i e w 5

expectations of citizens have been dashed, as the newbill is more an exercise to deny information while havingthe form of a �freedom of information�. It would changenothing and the hoped for instrument for the democratictransformation of society would be one more exampleof �tokenism�. Information with regard to local bodiesand public processes�expenditure statements, plans,allocations etc.�of local bodies and corporations havinga public aspect, when available with the immediatepopulation who are affected by their working, can havedramatic effects on elected and non-elected officials. Thepressures for accountable and responsible working canbe significant, and that, privatization or not, is vital tothe improvement in infrastructure and its orientationtowards the customer.

In Chapter 6, �The Electricity Sector�, the leadpaper �Missing Interconnections in the Power Systems�(Puneet Chitkara, Rajiv Shekhar, and Prem K. Kalra)takes a close look at the present proposals and rulingsof the Central Electricity Regulatory Commission(CERC), bringing out their limitations and suggestingthe direction for change. The contradictions createdby institutions like the Power Trading Corporation,given the need for competitive behaviour among sellersand buyers of wholesale power, are drawn out. Theelectricity grid is in very poor shape with grid frequen-cies for hours on end being either far above or belowthe stipulated 50 cycles. The current attempt is toconvert a problem of indiscipline (that requires for itssolution stiff punitive measures and disconnection) toa commercial schedule of varying rates that give largeincentives for adhering to grid rules, as the proposedavailability-based tariff seeks to do. Would it work?Not at all, argues Chapter 6. The difficulties in thecurrent framework for interstate trade in power and theproblem of �identifying the culprits for grid failures� arealso covered.

In �Power Sector Reforms and Regulation: The RoadAhead� (Sebastian Morris) the roots of the currentproblems including the increasing regulatory and policyrisks are brought out. The need to directly administersubsidies through a stamps-based system is put forth. Noother system would work since anything else wouldcreate a situation of moral hazard for the utility inquestion. More than subsidization it is the vested inter-ests within the SEBs and outside that have stood in theway of reform and restructuring. Leakages are very largeand if they could be plugged most SEBs would becommercially viable entities at tariffs close to currentlevels! That is the principal challenge, and only directsubsidization can succeed in delinking reform from thesubsidy question. A model of reform and regulationthat brings in competition in generation is proposed in

some detail. The aspects of the market creation pro-cesses, the tasks that need to be carried out, the degreeof unbundling, the prospects for competition and themanagement and ownership of transmission, distribu-tion, and generation assets are considered. In any marketmodel the independent power producers� (IPPs�) powerpurchase agreements (PPAs) would become strandedcontracts, imposing great cost on consumers. Variousoptions to extinguish such contracts and boldly gotowards a market model are put forth. Both parts to thechapter on the power sector argue that in not havingbrought out a paper outlining the strategy for regulationand restructuring, the government has imposed muchuncertainty on prospective investors who have thereforekept away. Even if the details of legislation and thepassage of bills would take time, the need for a credibleannouncement of the kind of system and change thegovernment wants is important. If the right to choosethe supplier can be given to bulk buyers, and similarlycaptive units can be allowed to go on the grid, theresistance from the SEBs and their �hedging strategy��to corporatize without any change in the incentivepatterns or in ownership, for example�could be broken.

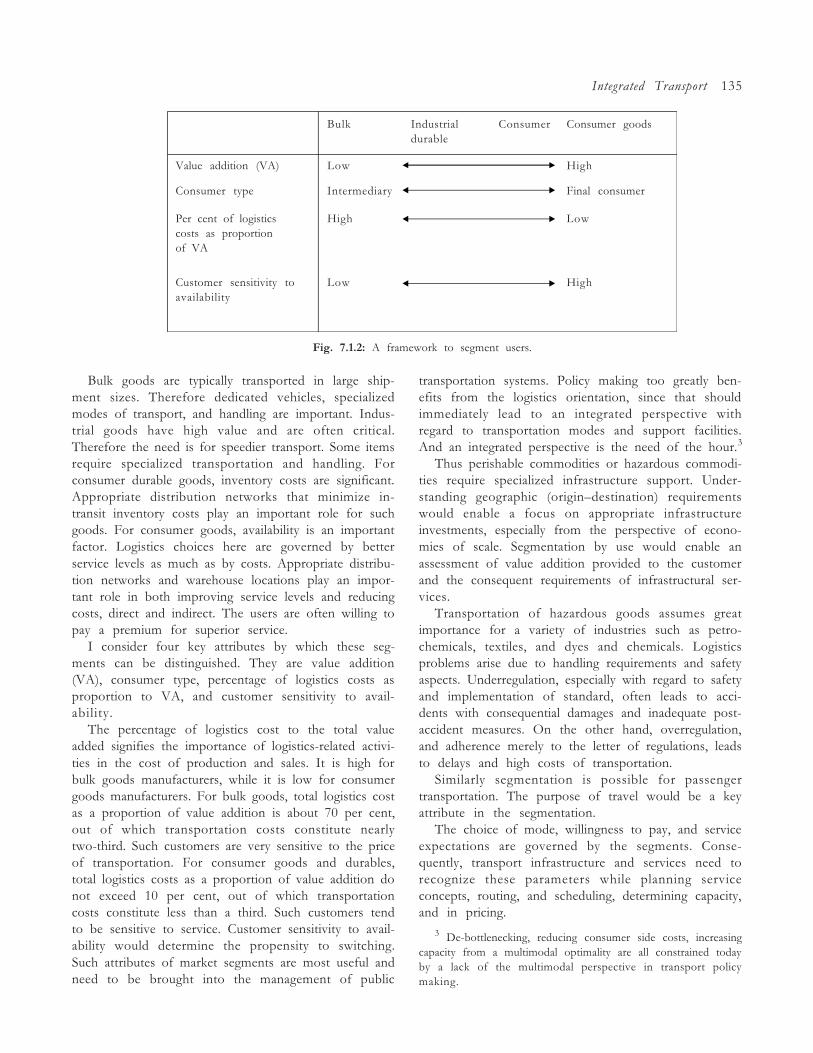

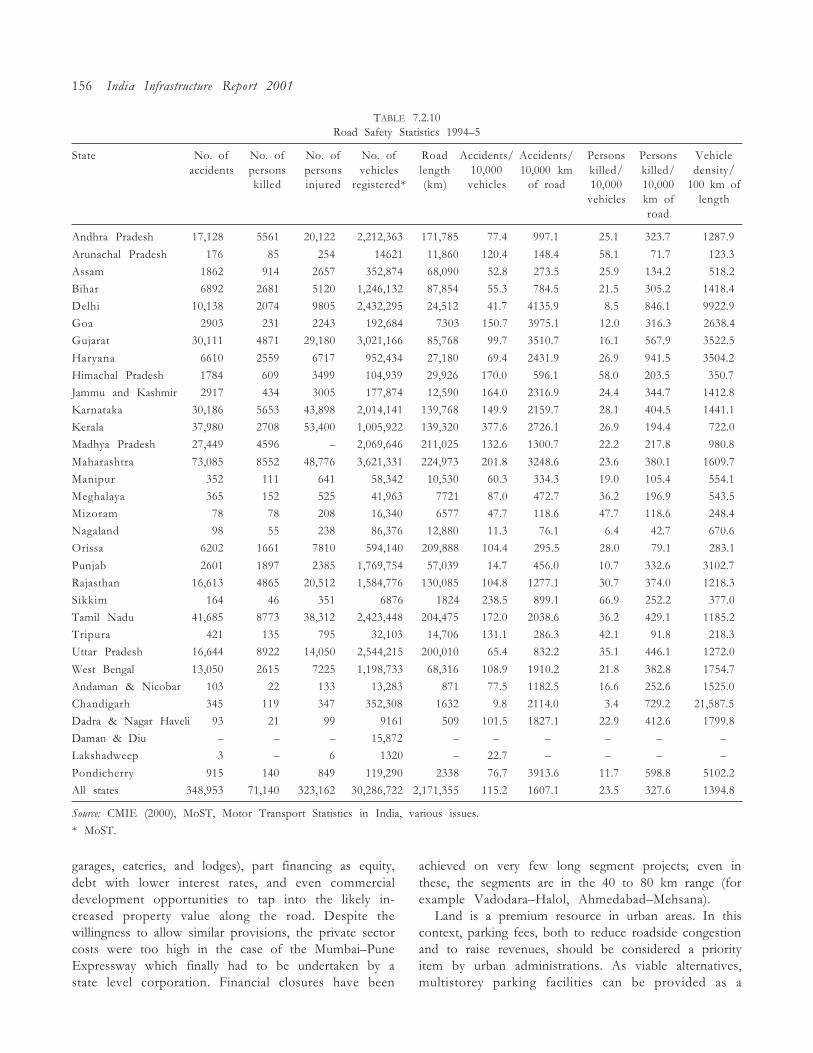

In section 7.1 �The Transport Sector�, G. Raghuramprovides a birds-eye view of the problems with thevarious sectors that constitute transportation. The ne-glect of the intermodal and multimodal aspects and theunderinvestments in the sector resulting in �transportmyopia� are brought out. The effect of absurd prices oninvestment choice and traffic patterns and the hugereturns to relaxation of congestion both in rail and roadthat are possible, especially on the �golden quadrilateral�,are discussed. A schema classifying the various activitiesis presented. The notions of the �network�, �rollingstock�, �terminal�, service, and regulation are appliedacross the sectors to result in a meaningful approach foran integrated treatment of shipping, roads, pipelines,airlines, and railways. Marwah�s paper Box 7.1.4 high-lights the vast returns to debottlenecking roads. Seemingcapacity constraints in roads in many situations are dueto the lack of the attention to bottlenecks on roads thatare prone to arise in the Indian situation�sections ofroads that are damaged, frequent use of certain portionsby animals and slow moving vehicles, and too manyjunctions on highways.

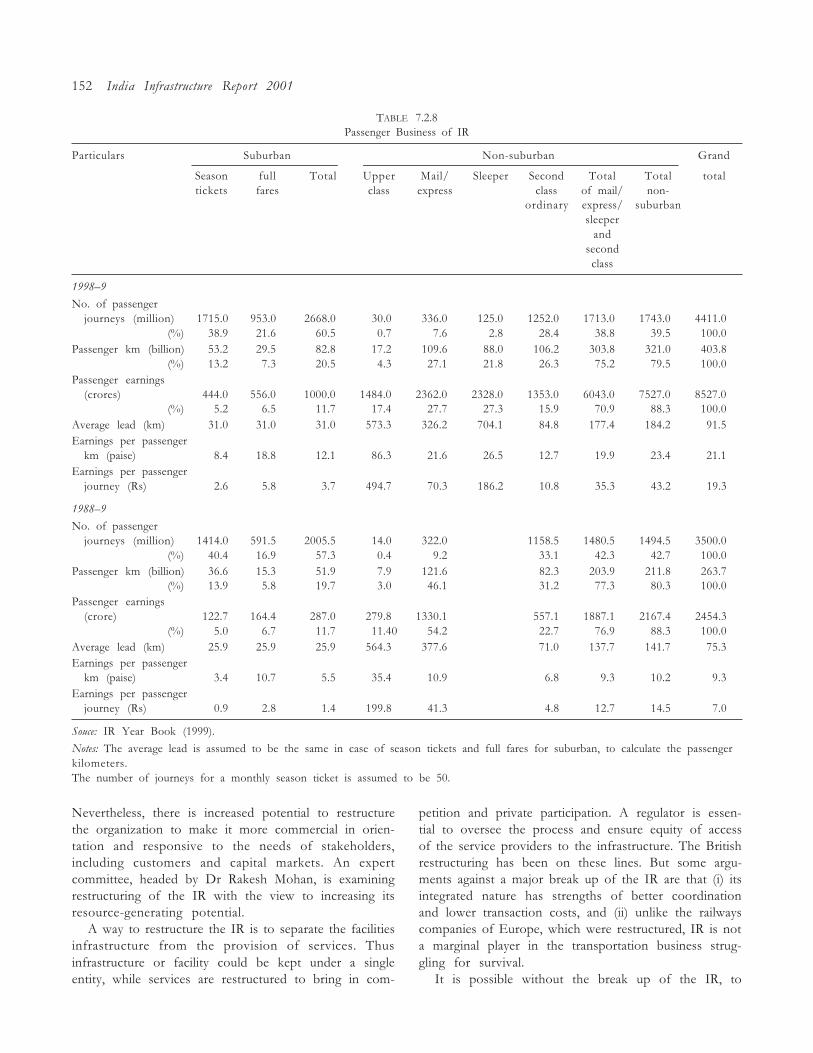

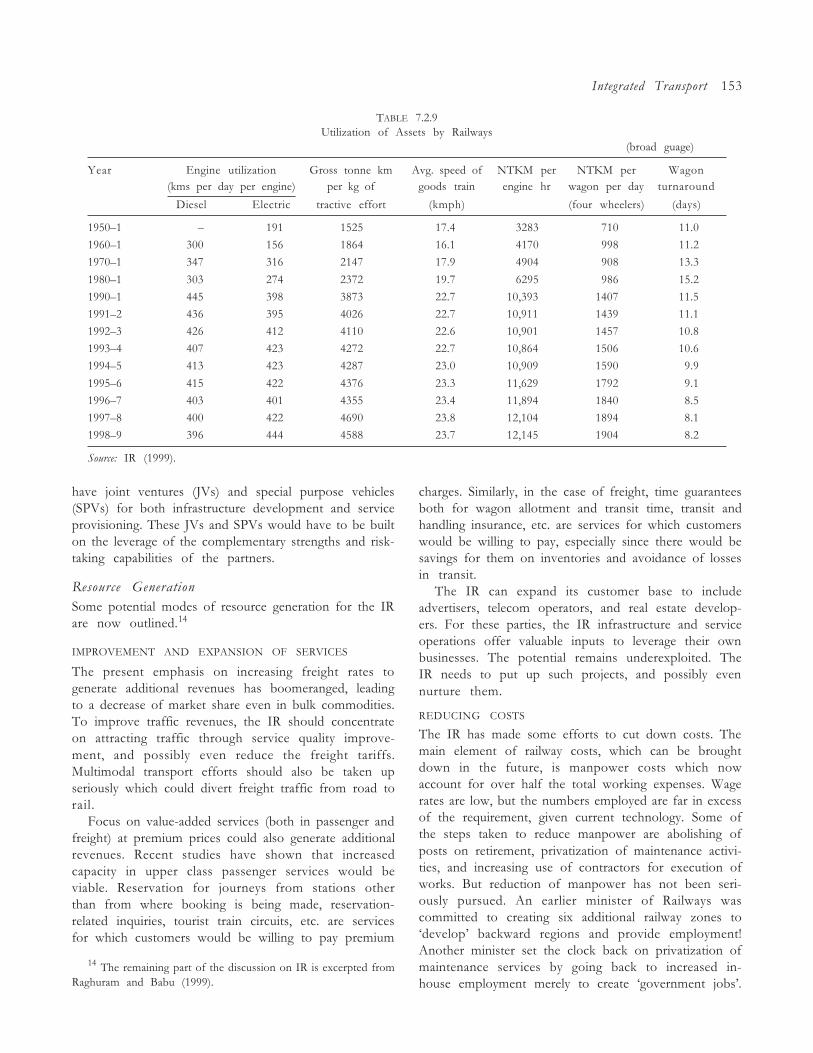

�Sectoral Issues in Transportation� discusses in detaileach of the sectors to the extent possible given thelimitations of publicly available data. Productivity hasbeen improving steadily in the Railways, and the needis really to price their products appropriately and bringabout a customer orientation. The Railways could raisetheir declining share of freight tonne kms by providinglogistic solutions especially to large customers. Railway

6 India Infrastructure Report 2001

privatization, except at the margins for certain kinds ofnon-network related services, is seen by the author asnot immediately feasible. The logistic aspect which issensed only when the provider is willing to see theproblem of transportation from the point of view of thecustomer needs to inform change and improvements inthe sector. In �A Relook at Passenger Car Equivalents(PCEs) in the Indian Context�, Box 7.2.1, Marwahargues that the standard tool of road designers, the PCEwould not work because of the wide variation in vehicletypes, so the need to develop easy to use simulationmodels is very important. If the notion of the PCE hasto be retained, for the Indian highways the standard 1210type truck should be the reference.

�Port and Shipment Management at Singapore Port:The Revolution in the Use of Electronic Data Inter-change (EDI)� (K. V. Ramani) in presenting the develop-ments at Singapore port helps to remind us of thedistance between our best ports and Singapore. TodaySingapore port uses IT and the Web to cut turnaroundtimes from two days to hours!

�At the Crossroads: Creating Pipeline Infrastructurefor Oil Products� (Samir K. Barua and T. Madhavan)reviews the development of oil pipelines in India.Pipelines have been held back due to adverse policy andthe pressure exercised by the Railways to keep forthemselves a large part of the liquid freight movementin India. The present policy of joint ventures and stand-alone companies will not allow pipeline constructionto take off. Financial institutions naturally insist on takeor pay contracts. The policy has not been sufficientlyappreciative of the network nature of pipelines, whereindevelopments in one segment affect on all other seg-ments. The need to quickly move on to a commoncarrier mode for regulation and access to pipeline infra-structure is argued for.

�Integrating Coastal Shipping with the NationalTransport Network� (G. Raghuram) argues that coastalshipping has been constrained by archaic customs andcabotage laws. The potential for coastal shipping,especially in low value bulk items, is at least twiceits current levels. When combined with other modes,that is with appropriate strategies to provide connectiv-ity of urban and industrial places to coastal ports, coastalshipping can emerge as the main mode for carriage ofbulk between the west and east coasts.

The telecom sector in India has perhaps seen themost rapid changes whatever the yardsticks. �Review ofthe Indian Telecom Sector� (Rekha Jain) looks at themajor developments in the institutions, policy, regula-tion, and network and industry since the process ofreform began in the early 1990s. NTP 1999 and theearlier NTP 1994 are discussed. The gradual evolution

of policy from monopoly to licensed oligopoly and nowcompetition is indeed a most positive development. Thepressure on the incumbent as private parties wereallowed in has made the incumbent expand its capacityremarkably. At current tariffs and connection chargesmuch of the demand has been met. The challengetherefore is to bring in new demand. How far has thepolicy succeeded? Not very far, since the high licencefees, the lack of competition in the beginning, thepossible denial of network economies to the players, andindependent regulation itself may have stood in the wayof a rapid fall in prices. While cellular services� have hadsome success, basic services� privatization remains awoeful failure.

�Looking Beyond NTP 99� (Ashok Jhunjhunwala)argues for a paradigm shift into local and small-scalesolutions which alone, in a poor country, can quicklygive us the 100 million subscribers aimed at. For sucha development to take place, use of Indian technologyand breaking out of the bind of interlocking interna-tional credit and technology (and equipment) marketsare necessary. Appropriate policy that allows the appli-cation of such technologies, the unit of licensing to bemore flexibly defined, and smaller players to operate isnecessary. �Enabling Telecom and Internet Connectivityin Small Towns and Rural India� (Ashok Jhunjhunwalaand Bhaskar Ramamurthi) describes ways to achieve asudden jump in Internet and telecom usage. Essentiallythe need is to pursue cost-reducing approaches ratherthan feature-adding research which has a functionality inthe rich countries given high incomes and high telecomdensities. Few transnationals would be interested in cost-reducing research since they would have geared up forthe biggest and most lucrative markets. �Number Port-ability: Why do we need it?� (Dheeraj Sanghi) examinesthe importance of number portability in the working ofthe competitive market for telecom services. The steepfall in 1�800 number prices as the US regulators an-nounced a phased plan for number portability is inter-esting. Despite appearances to the contrary, an earlypursuit of number portability can do much for compe-tition in telecom services. The poor also use STDfacilities at PCOs and the assumption that STD is usedlargely by business and the rich is not quite correct.�STD Calls are Not a Preserve of the Rich� (S. Manikutty)brings this out.

The spatial context of infrastructure could not beas effectively covered in this report as we would haveliked. Industrial parks and rural infrastructure, exceptdrinking water, have not been covered here. Moreimportantly, there are, we know, major distortions inthe market for urban land. Very severe restrictions inland use, cumbersome processes for changes in land

O v e r v i e w 7

use permits, rent control, and punitive taxes on sale ofland create a highly distorted market, wherein the pricesthat rule are no indication of true social costs orscarcities. Investment decisions based on these pricescould carry the distortions further into the economy ashas most certainly happened in the larger cities. Thisproblem still remains to be addressed and it is hopedthat a future issue of the IDR would be able to take upthe topic of urban land and its use. The 74th Amend-ment to the Constitution (CAA74) that sought togive power, autonomy, and fiscal devolution to urbanlocal bodies is an important focus of the chapter on thespatial context of infrastructure. Financing and Func-tioning of Urban Local Bodies: A Situation Report�(M. P. Mathur) examines the present situation statisti-cally. It draws attention to the poor fiscal situation,and lack of autonomy despite the changes since theCAA74. Again, quite like the situation with regard tothe right to information bill, there has been majordivergence between the form and content of the devo-lution. State governments have �hedged� the indepen-dence of urban local bodies, keeping many importantpowers at the state level and making other devolutionscontingent upon the state governments� own assessment.The urban bodies of the largest cities in any case havehad the relevant autonomy and the reasons for theirpoor performance lie elsehere in competitive politics, intheir relationship with state governments, in irrationaltariff policies, in poor organizational processes, espe-cially in the confusion of responsibility between theelected and nonelected officials. The promise held outfor the smaller municipalities by the CAA74 has beenbelied. The urban bodies are under much fiscal stress andthose without access to revenues from octroi and entrytaxes have not even been able to maintain existing levelsof service. The only answer is rationalizing user chargesand better collection of local taxes. The potential thoughis very good, but not generally recognized as such, sincethe paradigm of free water and sewerage is deeplyentrenched. �Local Governance in small towns in Gujaratsince the 74th Amendment: First Impressions� (AliceAlbin Morris and Vivek Raval) brings out the fact thatdespite the CAA74 nothing has really changed in foursmall towns in Gujarat.

�Implications of the 74th Amendment on the Waterand Waste water Sector� (Anish Nanavaty) brings outthe dismal situation with regard to water in mostmunicipalities. The fact that muncipalities do not havethe freedom to chose the organization with whom theycan deal to provide water and sewerage services, is amajor limitation. They have to necessarily deal with theparastatal bodies of the state government. Responsibilityis therefore displaced and poor and indequate coverage