astro malaysia holdings - i3investor

TRANSCRIPT

PP13693/03/2013(032114)

The return of the Pay-TV giant!

Astro Malaysia Holdings Bhd (AMH) is on track to raise some RM4.6bn from its listing

after it acquired the Malaysian businesses of Astro All Asia Networks Limited (AAAN)

(which was privatized back in 2010) as part of its reorganization process in March 2011

and April 2011. We initiate coverage on AMH with a HOLD recommendation. Our target

price of RM3.09 is based on DCF valuation (WACC: 7.4%, β: 1.5, terminal growth: 1%).

SE Asia’s leading integrated consumer media entertainment group � Astro Malaysia Holdings Bhd (AMH) is one of Southeast Asia’s leading integrated

consumer media entertainment group, engaging primarily in the creation,

aggregation and distribution of content over multiple delivery platforms including

TV, radio, publications and digital media within Malaysia.

� AMH was incorporated in February 2011 and acquired the Malaysian businesses of

Astro All Asia Networks Limited (AAAN) as part of the Group’s reorganization in

March 2011 and April 2011. AMH is housing the Malaysian businesses of AAAN.

Investment merits � Higher pay-TV penetration rates to drive the subscriber base. Although Malaysia

has a higher pay-TV penetration rate of 50% compared to its regional peers such as

Vietnam (19%) and Thailand (14%), it is still lagging behind some of the higher

income countries such as South Korea (122%) and Singapore (70%). We believe the

penetration rate in Malaysia will continue to grow given the increasing household

income level as well as rising proportion of households in the higher income bands.

� Value-added service and innovative initiatives to sustain residential ARPU growth.

AMH’s residential average revenue per user (ARPU) has remained flattish for two

consecutive years since FY08. However, thanks to the introduction of value added

services and innovative initiatives since Dec 2009, its residential ARPU has since

consistently increased and in 1HFY13 recorded an all-time high ARPU of RM92. We

believe that HD and PVR are strong drivers for ARPU growth as global data has

shown that the launch of these value-added services by regional pay-TV players

appears to have a positive impact on its ARPU. � Leading position creates significant barriers to entry. We view that given AMH’s

leading position as: (i) the exclusive Direct-to-Home (DTH) licence holder in

Malaysia with nationwide reach of 6.7m households, (ii) a rich content distributor

with exclusive rights for some of the third party internationally sourced channels in

Malaysia, and (iii) a Group with deep pockets for high capex requirements; have

created significant barriers for competitors to enter into the market.

Key risks � Extensive regulation

� Potential of losing the DTH licence

� Satellites failure

� Failure and disruption on broadcast facilities

� Escalation of content cost

� Foreign currency risk

Valuation � Initiate coverage on AMH with a HOLD recommendation as our target price of

RM3.09 has only 3% upside from the indicative IPO price of RM3.00 which could be

revised lower depending on the book-building exercise.

� Given the strong cash generation profile of AMH and potentially high cash flow (due

to stable earnings streams, visibility of capex and AMH’s target dividend payout

ratio of not less than 75% of its consolidated profit starting from FY14), we value

AMH using DCF method based on an explicit forecast period of 10 years.

Initiating Coverage 25 September 2012

Astro Malaysia Holdings MEDIA

Hold Bloomberg Ticker: ASTRO MK

12-month upside potential

IPO price (RM) 3.00

Listing sought Main market

Closing date of application 1 Oct 12

Listing date 19 Oct 12

Market cap @ IPO Price (RMm) 15,592

Issued shares (m) 5,197

12-month upside potential

Target price 3.09

IPO price 3.00

Capital upside (%) 3.0

Net dividends (%) 3.4

Total return (%) 6.4

Major shareholders (Post-IPO) %

Astro Networks (Malaysia) 70.8

Analyst

Team Coverage

+603 2089 2980

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 2

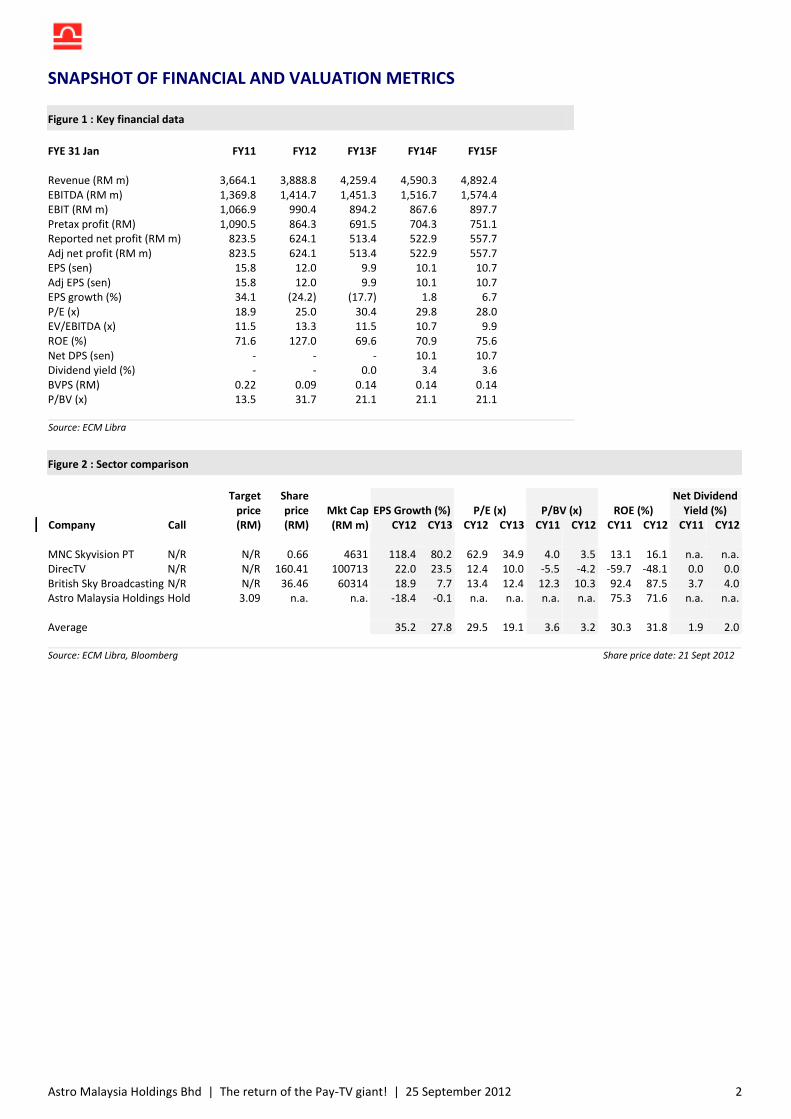

SNAPSHOT OF FINANCIAL AND VALUATION METRICS

Figure 1 : Key financial data

FYE 31 Jan FY11 FY12 FY13F FY14F FY15F

Revenue (RM m) 3,664.1 3,888.8 4,259.4 4,590.3 4,892.4

EBITDA (RM m) 1,369.8 1,414.7 1,451.3 1,516.7 1,574.4

EBIT (RM m) 1,066.9 990.4 894.2 867.6 897.7

Pretax profit (RM) 1,090.5 864.3 691.5 704.3 751.1

Reported net profit (RM m) 823.5 624.1 513.4 522.9 557.7

Adj net profit (RM m) 823.5 624.1 513.4 522.9 557.7

EPS (sen) 15.8 12.0 9.9 10.1 10.7

Adj EPS (sen) 15.8 12.0 9.9 10.1 10.7

EPS growth (%) 34.1 (24.2) (17.7) 1.8 6.7

P/E (x) 18.9 25.0 30.4 29.8 28.0

EV/EBITDA (x) 11.5 13.3 11.5 10.7 9.9

ROE (%) 71.6 127.0 69.6 70.9 75.6

Net DPS (sen) - - - 10.1 10.7

Dividend yield (%) - - 0.0 3.4 3.6

BVPS (RM) 0.22 0.09 0.14 0.14 0.14

P/BV (x) 13.5 31.7 21.1 21.1 21.1

Source: ECM Libra

Figure 2 : Sector comparison

EPS Growth (%) P/E (x) P/BV (x) ROE (%)

Net Dividend

Yield (%)

Company Call

Target

price

(RM)

Share

price

(RM)

Mkt Cap

(RM m) CY12 CY13 CY12 CY13 CY11 CY12 CY11 CY12 CY11 CY12

MNC Skyvision PT N/R N/R 0.66 4631 118.4 80.2 62.9 34.9 4.0 3.5 13.1 16.1 n.a. n.a.

DirecTV N/R N/R 160.41 100713 22.0 23.5 12.4 10.0 -5.5 -4.2 -59.7 -48.1 0.0 0.0

British Sky Broadcasting N/R N/R 36.46 60314 18.9 7.7 13.4 12.4 12.3 10.3 92.4 87.5 3.7 4.0

Astro Malaysia Holdings Hold 3.09 n.a. n.a. -18.4 -0.1 n.a. n.a. n.a. n.a. 75.3 71.6 n.a. n.a.

Average 35.2 27.8 29.5 19.1 3.6 3.2 30.3 31.8 1.9 2.0

Source: ECM Libra, Bloomberg Share price date: 21 Sept 2012

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 3

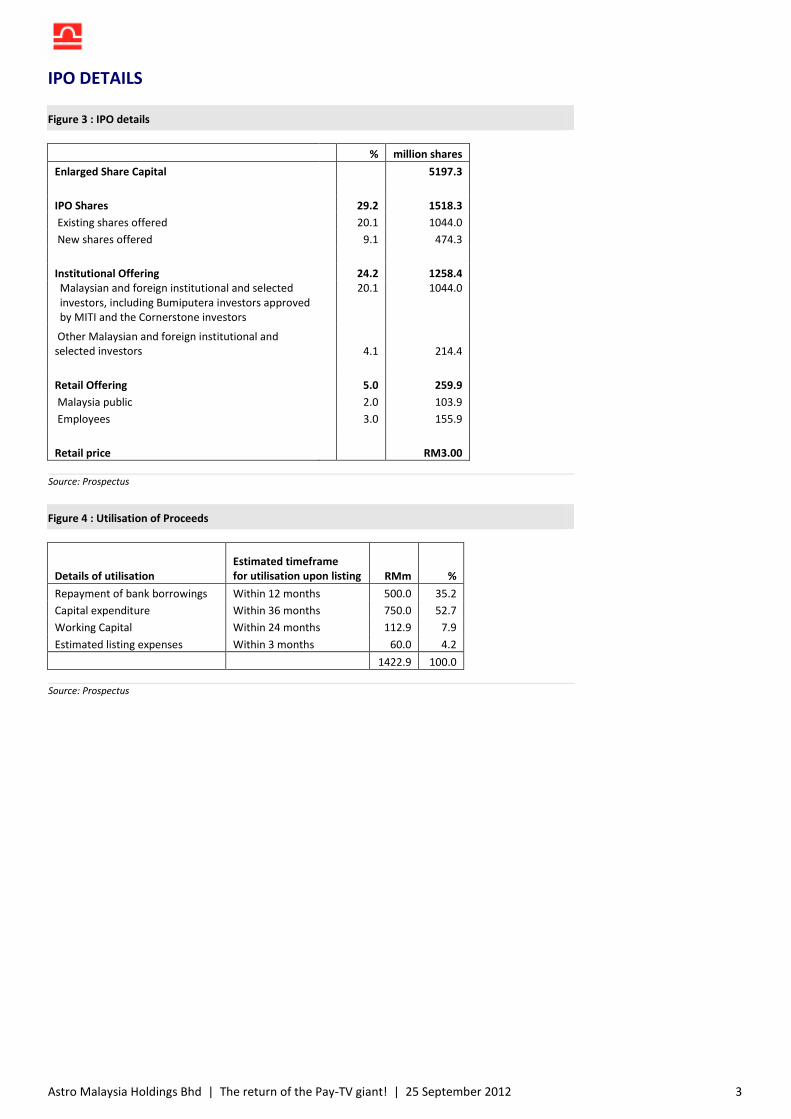

IPO DETAILS

Figure 3 : IPO details

% million shares

Enlarged Share Capital 5197.3

IPO Shares 29.2 1518.3

Existing shares offered 20.1 1044.0

New shares offered 9.1 474.3

Institutional Offering 24.2 1258.4

Malaysian and foreign institutional and selected

investors, including Bumiputera investors approved

by MITI and the Cornerstone investors

20.1 1044.0

Other Malaysian and foreign institutional and

selected investors 4.1 214.4

Retail Offering 5.0 259.9

Malaysia public 2.0 103.9

Employees 3.0 155.9

Retail price RM3.00

Source: Prospectus

Figure 4 : Utilisation of Proceeds

Details of utilisation

Estimated timeframe

for utilisation upon listing RMm %

Repayment of bank borrowings Within 12 months 500.0 35.2

Capital expenditure Within 36 months 750.0 52.7

Working Capital Within 24 months 112.9 7.9

Estimated listing expenses Within 3 months 60.0 4.2

1422.9 100.0

Source: Prospectus

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 4

COMPANY OVERVIEW

Background and history

Astro Malaysia Holdings Bhd (AMH) is one of Southeast Asia’s leading integrated consumer

media entertainment groups, engaging primarily in the creation, aggregation and distribution of

content over multiple delivery platforms including TV, radio, publications and digital media

within Malaysia. AMH’s leading position is reflected by its 156 TV channels (as at 30 Jun 2012), of

which 68 are Astro-created and branded channels. It distributes content to its customers via

broadcast and on-demand programmes through its Direct-to-Home (DTH) satellite TV, Internet

Protocol TV (IPTV) and Over-The-Top (OTT) platforms, making its TV offerings increasingly

platform-agnostic in reaching its customers.

AMH was incorporated in Feb 2011 and acquired the Malaysian businesses of Astro All Asia

Networks Limited (AAAN) as part of the Group’s reorganization process in March 2011 and April

2011. AMH is currently housing the Malaysian businesses of AAAN. To recap, AAAN was

previously listed in October 2003 on the then Main Board of Bursa Malaysia. In 2010, Astro

Holdings Sdn Bhd (AHSB) undertook a conditional take-over offer at RM4.30 to acquire all the

voting shares in AAAN. Subsequently, AAAN was delisted from Bursa Malaysia in June 2010.

Figure 5 : Reorganisation structure

Source: Prospectus

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 5

Figure 6 : Milestones of AMH

Year Milestone

1996 Launch MEASAT-1, Measat Broadcast Metwork Systems SB (MBNS), commenced digital DTH satellite pay- TV services

with 22 TV and five radio stations.

Astro introduced format radio programming, the first broadcaster to introduce this into the Malaysia market.

1997 MBNS was granted a renewable 25- year broadcasting licence for the provision of broadcasting services in Malaysia, with

exclusivity on DTH satellite TV services until 2017 and non- exclusivity until 2022.

2003 Surpassed 1 million residential pay-TV subscribers.

2007 Surpassed 2 million residential pay-TV subscribers.

Introduced Astro On Demand, Malaysia's first TV Near Video-On-Demand (NVOD) service.

2009 Launched Astro B.yond initiative which comprises of hybrid DTH and broadband-enabled set-top boxes and distribution

platform to provide HD services.

Launched Astro.B.yond with the first HD transmission in Malaysia.

Won the "CASBAA Chairman's Award" for Astro outstanding contribution to the pay-TV industry in the region.

2010 Brought the first 3D broadcast in Malaysia and Southeast Asia for the 2010 FIFA World Cup.

Launched Astro B.yond Personal Video Recorder (PVR).

Launched innovative Astro Tutor TV UPSR examination revision channel.

Awarded the gold award in the Media and Entertainment category at the Putra Brands Awards 2010, Malaysia's premier

consumer brand awards.

2011 Introduced IPTV services through Astro B.yond IPTV, in collaboration with TIME, to deliver IPTV through TIME's fibre optic

broadband network.

Launched Astro First, first movie pay-per-view with near cinema window offerings in Malaysia, made available through

Astro set-top boxes.

Launched Super Packs which comprises the best of Astro content, including HD and PVR services, to enhance Astro value

proposition for their customers.

Surpassed 3 million residential pay-TV subscribers.

Awarded the gold award in the Media and Entertainment category at the Putra Brands Awards.

2012 Awarded the Brand of the Year and the gold awards in the Media and Entertainment category at the Putra Brand Awards.

Launched Astro On-The-Go, Astro Over-the Top (OTT) entertainment service for smartphones, tablets, PCs and

broadband-based VOD.

Launched NJOI, Malaysia's first non- subscription based DTH satellite TV with 18 TV and 20 radio channels.

Source: Prospectus

Group structure

Figure 7 : Group corporate structure

Source: Astro Prospectus

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 6

Business segment

AMH primarily operates in four business segments:

� TV business

� Radio business

� Publications business

� Digital services business

Figure 8 : Revenue breakdown

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY2010 FY2011 FY2012

RMm

TV Radio Others

Source: Prospectus

TV business

AMH is the largest pay-TV operator in Malaysia with over 3.1 million residential subscribers,

which commands c.99% market share of residential pay-TV market and 50% penetration rate of

Malaysian TV households in Malaysia. It is actively involved in content creation, aggregation and

distribution capabilities in ten major languages and dialects to cater to the interests of Malaysia’s

three main ethnic groups. As a content creator, AMH has already produced a total c.40,000 hours

of TV content as of 22 Jun 2012 with 8,000 hours TV content produced in FY12 alone. Meanwhile,

on content distribution, it has already broadcast a total of 156 TV channels for both Standard

Definition (SD) and High Definition (HD), of which 68 are Astro-created and branded channels via

broadcast and on-demand programmes through its DTH satellite TV, IPTV and OTT platforms.

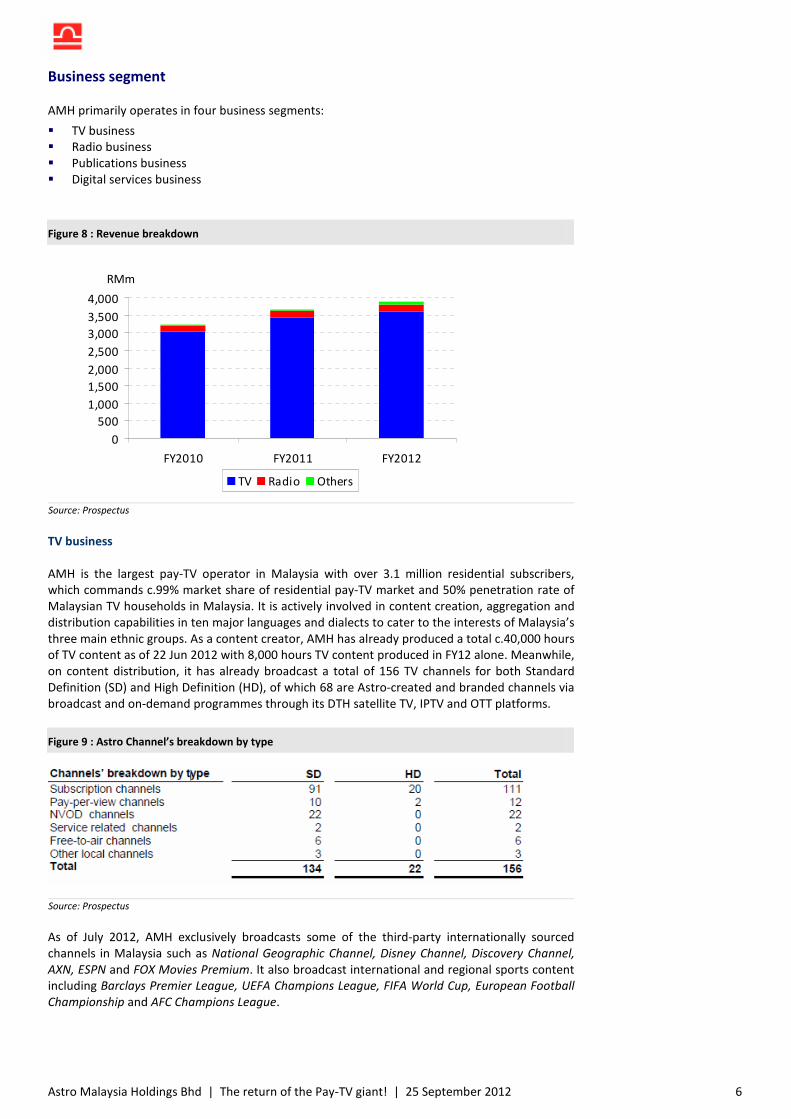

Figure 9 : Astro Channel’s breakdown by type

Source: Prospectus

As of July 2012, AMH exclusively broadcasts some of the third-party internationally sourced

channels in Malaysia such as National Geographic Channel, Disney Channel, Discovery Channel,

AXN, ESPN and FOX Movies Premium. It also broadcast international and regional sports content

including Barclays Premier League, UEFA Champions League, FIFA World Cup, European Football

Championship and AFC Champions League.

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 7

Radio business

Astro Radio broadcasts radio content through 9 of its FM stations (also available on its DTH

satellite TV, IPTV, mobile and Internet platforms) while the other 11 additional direct-to-user

radio stations are broadcast only on its DTH satellite TV, IPTV, mobile and Internet platforms. It

has the highest rated radio stations in the Malay, Chinese, Indian and English languages in terms

of listenership in April 2012. As at April 2012, AMH’s radio stations collectively reached c.13

million weekly radio listeners, translating into 52% of Malaysia’s total listenership and

commanding 53% of radio adex share.

Figure 10 : Share of listenership by operator

49% 51% 54% 52% 50% 52%

21% 20% 21%

15% 14%13% 12%

6% 6% 7% 9% 11%13%7% 6% 5% 5% 6% 0%

24%25%22%

10%14%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 1Q2012

Astro Radio Radio Televisyen Malaysia Media Prima The Star Others

Source: Prospectus

Publications business

Astro Publications published seven print magazines with total 7.7 million circulations in 2010,

including its TV viewing guide, AstroView, which is the most widely circulated magazine in

Malaysia with a circulation of c.6 million in 2010. There are 4 different editions of AstroView in

circulation with 3 editions in different languages and a Traveller edition for commercial

establishments. Notably, its other commercial publications with a combined circulation of 1.7

million in 2010 include FourFourTwo, Style and FHM (in English), InTrend (in Malay) and men’s

uno and iFeel (in Chinese).

Figure 11 : AMH’s TV viewing guide (AstroView) Figure 12 : One of AMH’s commercial publications (FHM)

Source: Online source Source: Online source

Digital services business

Astro Digital develops and manages online and mobile portals to provide sports, entertainment

and other key content to online audiences. These digital services allow Astro Digital to expand its

reach and engage with its customers and viewers by providing digital content such as the latest

news and sporting results, behind-the-scene and special features, programme highlights and

social integration. In addition, its digital media platforms provide another medium for

advertisements, forming part of its integrated media advertisement offering.

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 8

INVESTMENT MERITS

The subscription revenue is the key driver for revenue growth, and we view that its growth

momentum going forward will be underpinned by growth in subscriber base coupled with

consistent growth in residential ARPU.

Figure 13 : Breakdown of AMH’s TV revenue

0

1,000

2,000

3,000

4,000

5,000

FY2010 FY2011 FY2012 FY2013E FY2014E FY2015E

RM

'00

0

Subscription Airtime sales Others

Source: Astro, ECM Libra’s estimates

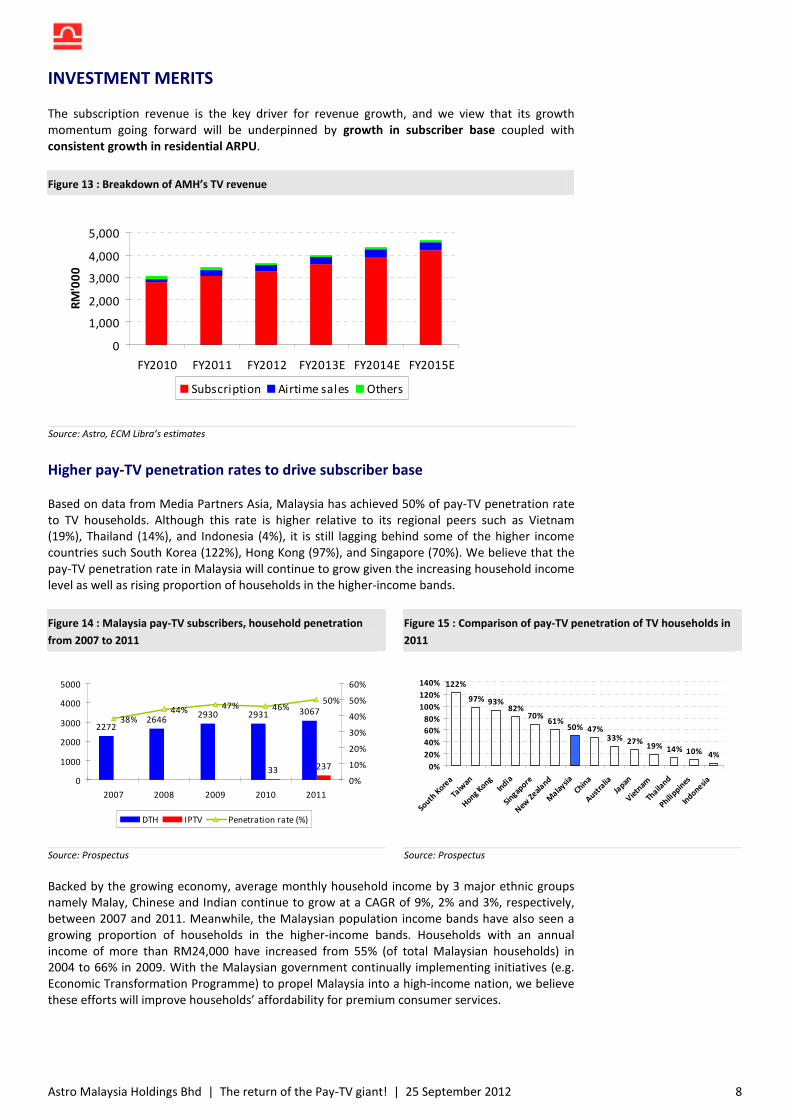

Higher pay-TV penetration rates to drive subscriber base

Based on data from Media Partners Asia, Malaysia has achieved 50% of pay-TV penetration rate

to TV households. Although this rate is higher relative to its regional peers such as Vietnam

(19%), Thailand (14%), and Indonesia (4%), it is still lagging behind some of the higher income

countries such South Korea (122%), Hong Kong (97%), and Singapore (70%). We believe that the

pay-TV penetration rate in Malaysia will continue to grow given the increasing household income

level as well as rising proportion of households in the higher-income bands.

Figure 14 : Malaysia pay-TV subscribers, household penetration

from 2007 to 2011

Figure 15 : Comparison of pay-TV penetration of TV households in

2011

22722646

2930 2931 3067

33 237

38%44%

47% 46%50%

0

1000

2000

3000

4000

5000

2007 2008 2009 2010 2011

0%

10%

20%

30%

40%

50%

60%

DTH IPTV Penetration rate (%)

122%

97% 93%82%

70%61%

50% 47%33% 27%

19% 14% 10% 4%

0%

20%

40%

60%

80%

100%

120%

140%

South

Kore

a

Taiw

an

Hong Kong

India

Singap

ore

New

Zeal

and

Mala

ysia

China

Austra

lia

Japan

Vietn

am

Thaila

nd

Philippin

es

Indonesia

Source: Prospectus Source: Prospectus

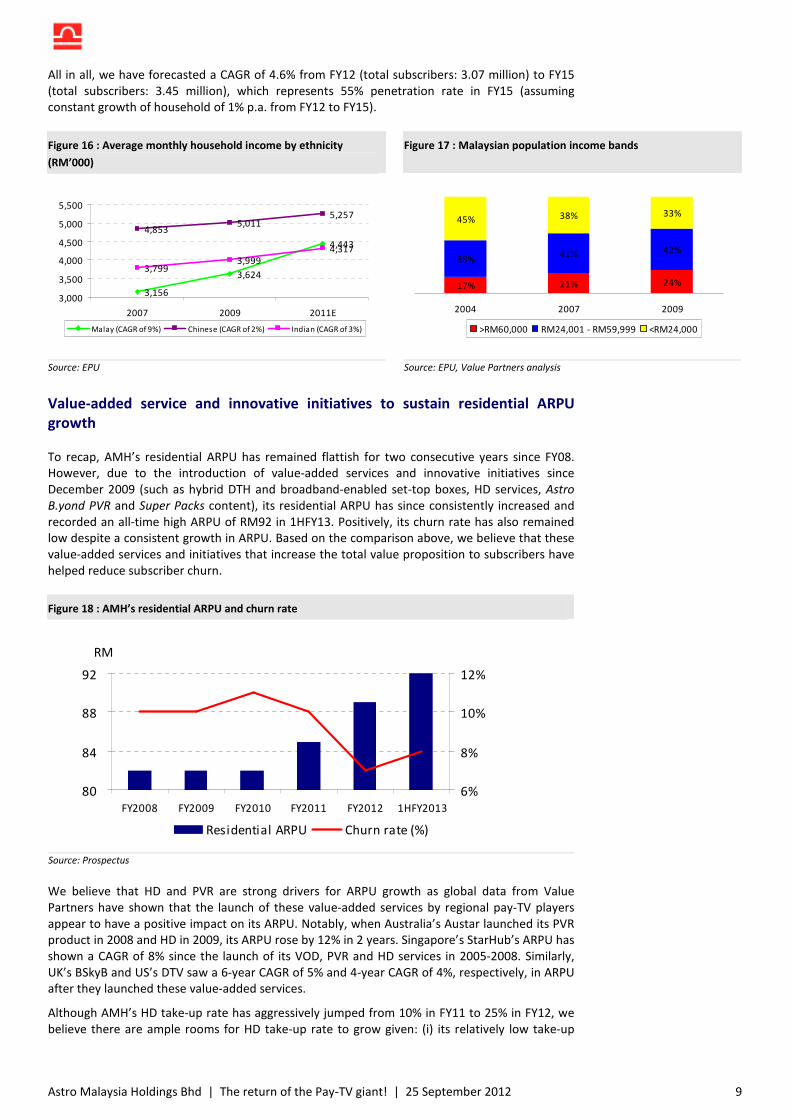

Backed by the growing economy, average monthly household income by 3 major ethnic groups

namely Malay, Chinese and Indian continue to grow at a CAGR of 9%, 2% and 3%, respectively,

between 2007 and 2011. Meanwhile, the Malaysian population income bands have also seen a

growing proportion of households in the higher-income bands. Households with an annual

income of more than RM24,000 have increased from 55% (of total Malaysian households) in

2004 to 66% in 2009. With the Malaysian government continually implementing initiatives (e.g.

Economic Transformation Programme) to propel Malaysia into a high-income nation, we believe

these efforts will improve households’ affordability for premium consumer services.

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 9

All in all, we have forecasted a CAGR of 4.6% from FY12 (total subscribers: 3.07 million) to FY15

(total subscribers: 3.45 million), which represents 55% penetration rate in FY15 (assuming

constant growth of household of 1% p.a. from FY12 to FY15).

Figure 16 : Average monthly household income by ethnicity

(RM’000)

Figure 17 : Malaysian population income bands

3,156

3,624

4,443

4,8535,011

5,257

3,7993,999

4,317

3,000

3,500

4,000

4,500

5,000

5,500

2007 2009 2011E

Malay (CAGR of 9%) Chinese (CAGR of 2%) Indian (CAGR of 3%)

17% 21% 24%

38%41% 42%

45% 38% 33%

2004 2007 2009

>RM60,000 RM24,001 - RM59,999 <RM24,000

Source: EPU Source: EPU, Value Partners analysis

Value-added service and innovative initiatives to sustain residential ARPU

growth

To recap, AMH’s residential ARPU has remained flattish for two consecutive years since FY08.

However, due to the introduction of value-added services and innovative initiatives since

December 2009 (such as hybrid DTH and broadband-enabled set-top boxes, HD services, Astro

B.yond PVR and Super Packs content), its residential ARPU has since consistently increased and

recorded an all-time high ARPU of RM92 in 1HFY13. Positively, its churn rate has also remained

low despite a consistent growth in ARPU. Based on the comparison above, we believe that these

value-added services and initiatives that increase the total value proposition to subscribers have

helped reduce subscriber churn.

Figure 18 : AMH’s residential ARPU and churn rate

80

84

88

92

FY2008 FY2009 FY2010 FY2011 FY2012 1HFY2013

RM

6%

8%

10%

12%

Residential ARPU Churn rate (%)

Source: Prospectus

We believe that HD and PVR are strong drivers for ARPU growth as global data from Value

Partners have shown that the launch of these value-added services by regional pay-TV players

appear to have a positive impact on its ARPU. Notably, when Australia’s Austar launched its PVR

product in 2008 and HD in 2009, its ARPU rose by 12% in 2 years. Singapore’s StarHub’s ARPU has

shown a CAGR of 8% since the launch of its VOD, PVR and HD services in 2005-2008. Similarly,

UK’s BSkyB and US’s DTV saw a 6-year CAGR of 5% and 4-year CAGR of 4%, respectively, in ARPU

after they launched these value-added services.

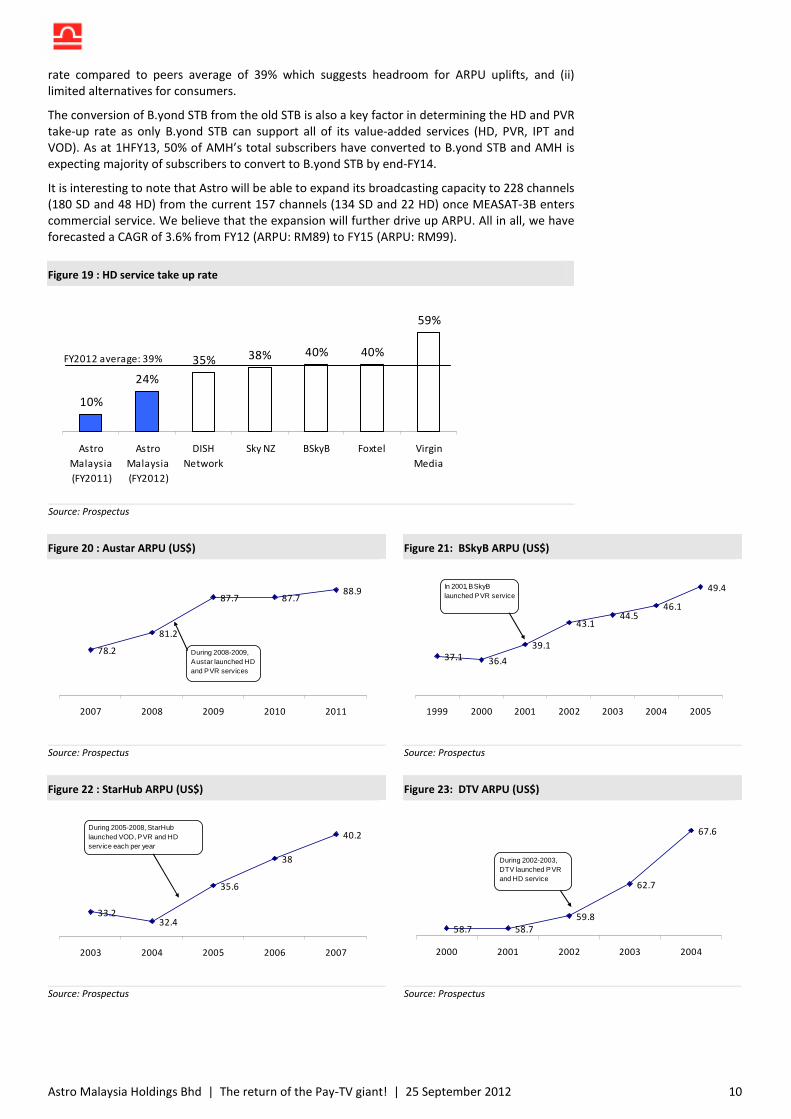

Although AMH’s HD take-up rate has aggressively jumped from 10% in FY11 to 25% in FY12, we

believe there are ample rooms for HD take-up rate to grow given: (i) its relatively low take-up

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 10

rate compared to peers average of 39% which suggests headroom for ARPU uplifts, and (ii)

limited alternatives for consumers.

The conversion of B.yond STB from the old STB is also a key factor in determining the HD and PVR

take-up rate as only B.yond STB can support all of its value-added services (HD, PVR, IPT and

VOD). As at 1HFY13, 50% of AMH’s total subscribers have converted to B.yond STB and AMH is

expecting majority of subscribers to convert to B.yond STB by end-FY14.

It is interesting to note that Astro will be able to expand its broadcasting capacity to 228 channels

(180 SD and 48 HD) from the current 157 channels (134 SD and 22 HD) once MEASAT-3B enters

commercial service. We believe that the expansion will further drive up ARPU. All in all, we have

forecasted a CAGR of 3.6% from FY12 (ARPU: RM89) to FY15 (ARPU: RM99).

Figure 19 : HD service take up rate

10%

24%

35% 38% 40% 40%

59%

Astro

Malaysia

(FY2011)

Astro

Malaysia

(FY2012)

DISH

Network

Sky NZ BSkyB Foxtel Virgin

Media

FY2012 average: 39%

Source: Prospectus

Figure 20 : Austar ARPU (US$) Figure 21: BSkyB ARPU (US$)

78.2

81.2

87.7 87.788.9

2007 2008 2009 2010 2011

During 2008-2009, Austar launched HD and PVR services

37.1 36.4

39.1

43.144.5

46.1

49.4

1999 2000 2001 2002 2003 2004 2005

In 2001, BSkyB launched PVR service

Source: Prospectus Source: Prospectus

Figure 22 : StarHub ARPU (US$) Figure 23: DTV ARPU (US$)

33.232.4

35.6

38

40.2

2003 2004 2005 2006 2007

During 2005-2008, StarHub launched VOD, PVR and HD service each per year

58.7 58.7

59.8

62.7

67.6

2000 2001 2002 2003 2004

During 2002-2003, DTV launched PVR and HD service

Source: Prospectus Source: Prospectus

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 11

Leading position creates significant barriers to entry

In our view, AMH’s leading position as (i) an exclusive DTH licence holder in Malaysia with

nationwide reach of 6.7 million households, (ii) a rich content distributor that owns the exclusive

rights for some of the third party internationally sourced channels in Malaysia, and (iii) a Group

with deep pockets for high capex requirements; have created significant barriers for competitors

to enter into the market.

To recap, with an exclusive DTH licence (until 2017), AMH is the largest pay-TV operator in

Malaysia which commands c.99% market share of residential pay-TV market and 50%

penetration rate of Malaysian TV households in Malaysia. While we believe that the current

head-to-head battle is only limited to alternative IPTV offerings, we view that the impact from

IPTV players such as Hypp TV is non-detrimental due to TM’s limited reach of households (target

of 1.3 million by end-2013), compared to AMH’s 6.7 million households via its DTH services.

Positively, to strengthen its foothold in the market, it has also collaborated with Maxis to

exclusively develop and co-market unique consumer offerings combining its Astro B.yond IPTV

and Astro On The Go services with Maxis’ fibre, mobile, wireless internet and ADSL services.

AMH has proven its leadership as an unrivalled content powerhouse in Malaysia by obtaining

some exclusive rights for popular content and produce a broad suite of local vernacular content

that is tailored to meet the diverse multi-lingual needs of different ethnic groups. As of July 2012,

AMH exclusively broadcasts some of the third party internationally sourced channels in Malaysia

such as National Geographic Channel, Disney Channel, Discovery Channel, AXN, ESPN and FOX

Movies Premium. It also broadcasts international and regional sports content including Barclays

Premier League, UEFA Champions League, FIFA World Cup, European Football Championship and

AFC Champions League. Coupled with its well-bundled packages such as Super Packs which act as

a ‘buffet’-style content to appeal to different customer segments, we believe that its pioneer

leadership as a content creator, aggregator and distributor will continue to thwart new entrants.

Recall that the privatized Astro All Asia Networks (AAAN) which began its services in 1996 with 22

channels took a decade to break even despite being a pioneer in the DTH Pay-TV business. We

believe that a new DTH TV-operator is likely to take a longer gestation period due to rising capex

as well as expensive satellite transponder capacity.

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 12

INDUSTRY OUTLOOK

Pay-TV sector

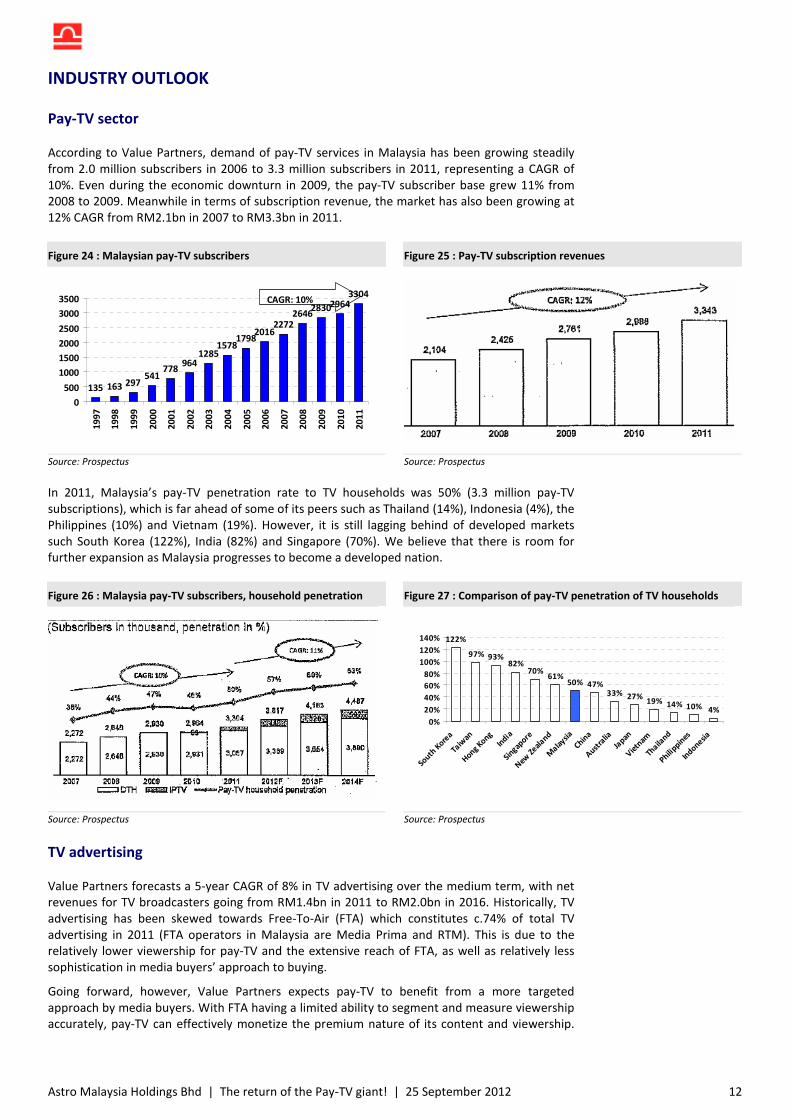

According to Value Partners, demand of pay-TV services in Malaysia has been growing steadily

from 2.0 million subscribers in 2006 to 3.3 million subscribers in 2011, representing a CAGR of

10%. Even during the economic downturn in 2009, the pay-TV subscriber base grew 11% from

2008 to 2009. Meanwhile in terms of subscription revenue, the market has also been growing at

12% CAGR from RM2.1bn in 2007 to RM3.3bn in 2011.

Figure 24 : Malaysian pay-TV subscribers Figure 25 : Pay-TV subscription revenues

135 163 297541

778964

12851578

17982016

22722646

283029643304

0

500

1000

1500

2000

2500

3000

3500

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

CAGR: 10%

Source: Prospectus Source: Prospectus

In 2011, Malaysia’s pay-TV penetration rate to TV households was 50% (3.3 million pay-TV

subscriptions), which is far ahead of some of its peers such as Thailand (14%), Indonesia (4%), the

Philippines (10%) and Vietnam (19%). However, it is still lagging behind of developed markets

such South Korea (122%), India (82%) and Singapore (70%). We believe that there is room for

further expansion as Malaysia progresses to become a developed nation.

Figure 26 : Malaysia pay-TV subscribers, household penetration Figure 27 : Comparison of pay-TV penetration of TV households

122%

97% 93%82%

70%61%

50% 47%33% 27%

19% 14% 10% 4%

0%

20%

40%

60%

80%

100%

120%

140%

South

Kore

a

Taiw

an

Hong Kong

India

Singap

ore

New

Zeal

and

Mala

ysia

China

Austra

lia

Japan

Vietn

am

Thaila

nd

Philippin

es

Indonesia

Source: Prospectus Source: Prospectus

TV advertising

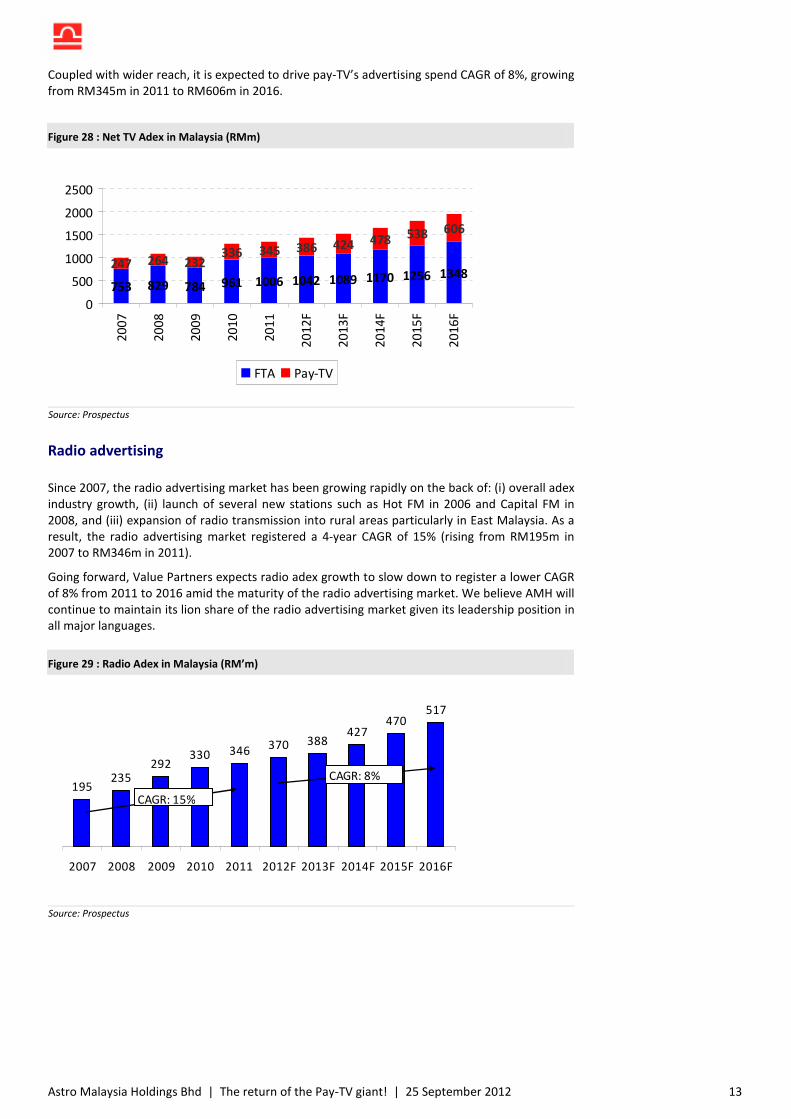

Value Partners forecasts a 5-year CAGR of 8% in TV advertising over the medium term, with net

revenues for TV broadcasters going from RM1.4bn in 2011 to RM2.0bn in 2016. Historically, TV

advertising has been skewed towards Free-To-Air (FTA) which constitutes c.74% of total TV

advertising in 2011 (FTA operators in Malaysia are Media Prima and RTM). This is due to the

relatively lower viewership for pay-TV and the extensive reach of FTA, as well as relatively less

sophistication in media buyers’ approach to buying.

Going forward, however, Value Partners expects pay-TV to benefit from a more targeted

approach by media buyers. With FTA having a limited ability to segment and measure viewership

accurately, pay-TV can effectively monetize the premium nature of its content and viewership.

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 13

Coupled with wider reach, it is expected to drive pay-TV’s advertising spend CAGR of 8%, growing

from RM345m in 2011 to RM606m in 2016.

Figure 28 : Net TV Adex in Malaysia (RMm)

753 829 784 961 1006 1042 1089 1170 1256 1348247 264 232

336 345 386 424 478 538 606

0

500

1000

1500

2000

2500

20

07

20

08

20

09

20

10

20

11

20

12

F

20

13

F

20

14

F

20

15

F

20

16

F

FTA Pay-TV

Source: Prospectus

Radio advertising

Since 2007, the radio advertising market has been growing rapidly on the back of: (i) overall adex

industry growth, (ii) launch of several new stations such as Hot FM in 2006 and Capital FM in

2008, and (iii) expansion of radio transmission into rural areas particularly in East Malaysia. As a

result, the radio advertising market registered a 4-year CAGR of 15% (rising from RM195m in

2007 to RM346m in 2011).

Going forward, Value Partners expects radio adex growth to slow down to register a lower CAGR

of 8% from 2011 to 2016 amid the maturity of the radio advertising market. We believe AMH will

continue to maintain its lion share of the radio advertising market given its leadership position in

all major languages.

Figure 29 : Radio Adex in Malaysia (RM’m)

195235

292330 346

370 388427

470517

2007 2008 2009 2010 2011 2012F 2013F 2014F 2015F 2016F

CAGR: 15%

CAGR: 8%

Source: Prospectus

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 14

RISKS

� Extensive regulation. The Communication and Multimedia Act (CMA) allows licensees to set

rates provided that the rates comply with Section 198 of the CMA but there are provisions in

the CMA which prescribe the circumstances in which the Ministry of Information,

Communication and Culture of Malaysia (Ministry), on the recommendation of the

Malaysian Communications and Multimedia Commission (MCMC), may intervene to the set

rates.

AMH currently possesses licences issued under the Communication and Multimedia Act

(CMA) to provide, among others, multi-channel subscription TV and radio broadcasting

services. According to the CMA, the Ministry may take action to modify, vary or revoke the

special conditions on existing individual licences issued under the CMA. The CMA also allows

the Ministry, to suspend or cancel a licence granted under certain circumstances.

� Potentially losing the DTH licence. AMH’s exclusive rights for DTH broadcasting in Malaysia

under its licence expire on 28 Feb 2017, while its non-exclusive rights expire on 28 Feb 2022.

The CMA provides that the Ministry may take action to modify, vary or revoke the special

conditions on existing individual licences issued under the CMA. The CMA also allows the

Ministry, on the recommendation of the MCMC to suspend or cancel a licence granted under

the CMA in certain circumstances.

� Satellites failure. AMH is currently dependent on MEASAT-3 and MEASAT-3A (with life

expectancies of up to 2021 and 2024, respectively) to provide DTH satellite broadcasting

services in Malaysia and Brunei. Although MEASAT-3 and MEASAT-3A provide back-up and

recovery functions for each other, in the event of failure of either satellite or should the

service levels of either one of the satellites degrade or become unavailable, AMH may not be

able to provide full service to its customers.

AMH has leased 18 Ku-band transponders on MEASAT-3B (which is expected to be launched

in 2014) from MEASAT International (South Asia) Ltd (MISA) in order to expand the number

of its TV channels. Should there be any failure or delay in the launch or commencement of

the commercial operations of MEASAT-3B, or should MISA fails to provide the MEASAT-3B

Ku-band capacity to AMH, its TV channel expansion plans may be delayed or disrupted.

� Failure and disruption on broadcast facilities. AMH has two broadcast facilities—the All Asia

Broadcast Centre in Bukit Jalil and Cyberjaya Broadcast Centre in Cyberjaya. The broadcast

facilities are vulnerable to damage or cessation of operations due to fire, floods, severe

storms, power loss, acts of terrorism and other potential catastrophic events. It may also

experience failures or shutdowns relating to the individual components of the broadcast

facilities or catastrophic failure of all of AMH’s broadcast facilities. In addition, no alternative

third-party Ku-band uplink facilities are currently available for lease in Malaysia.

� Escalation of content cost. AMH ability to retain existing subscribers and attract new

subscribers depends on their ability to deliver content that is popular with TV audiences and

entices consumers to subscribe to their services. The increase in the cost of sourcing and

procuring external content, especially relating to sports and premium content may result in

AMH’s inability to obtain attractive TV content from third parties at reasonable rates.

Content cost is approximately 50% of AMH’s cost of sales and this may escalate due to

intense competition for external content especially those relating to sports and premium

cost.

� Foreign currency risk. AMH incurred and expects to continue to incur, significant expenses

that are denominated mainly in USD such as purchases of set-top boxes, international

content costs and transponder lease payments. Hence movement of USD against the RM

may have a significant effect on AMH’s financial condition. A depreciation of the RM against

the USD could increase the costs of equipment and content cost that is necessary for the

operation of AMH’s business.

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 15

VALUATION & RECOMMENDATION

We initiate coverage on AMH with a HOLD recommendation as our target price of RM3.09 has

only 3% upside from the indicative IPO price of RM3.00 which could be revised lower depending

on the book-building exercise. Given the strong cash generation profile of AMH and potentially

high cash flow (due to stable earnings streams, visibility of capex and AMH’s target dividend

payout ratio of not less than 75% of its consolidated profit starting from FY14), we value AMH

using the DCF method based on explicit forecast for a period of 10 years. Our DCF-derived target

price of RM3.09 is based on the Weighted Average Cost of Capital (WACC) of 7.4%. Key

assumptions include market risk premium of 10.6%, risk free rate of 3.42% (yield for 10-year

Malaysian Government Securities), Beta of 1.5 (which is higher than FTA-TV player Media Prima’s

of 1.1), and terminal growth rate of 1%.

We forecast FY13, FY14, and FY15 adjusted net profit growth of -18%, 2%, and 7% respectively,

assuming higher operating expenses particularly in marketing and installation expenses,

particularly in FY13-FY14 to account for the migration of majority subscriber base to B.yond STB

before its profit normalises. We also incorporated higher content cost in FY13 and FY15 for major

sport events such as the Euro Cup /Olympics and FIFA respectively. At the top line, we believe

that our revenue growth assumption range of 6.6%-9.5% p.a. will be supported by healthy

subscribers and ARPU growth.

We have also assumed a dividend payout of 100% from FY14 onwards as our projected free cash

flow of c.RM940m-1,361m in FY13-FY15 (after incorporating the additional capex for B.yond STB)

allows AMH to adopt a 100% dividend payout (RM523m-558m in FY14-FY15) and also a potential

capital management.

At our target price of RM3.09, AMH would be trading on a CY13 PER of 30.6x compared to global

peers average of 19.1x (Figure 2), given its dominant position (99% market share) in Malaysia. It

is also supported by our forecast net dividend yield of 3.3% p.a., which is comparable to

Malaysian 12-month fixed deposit rates.

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 16

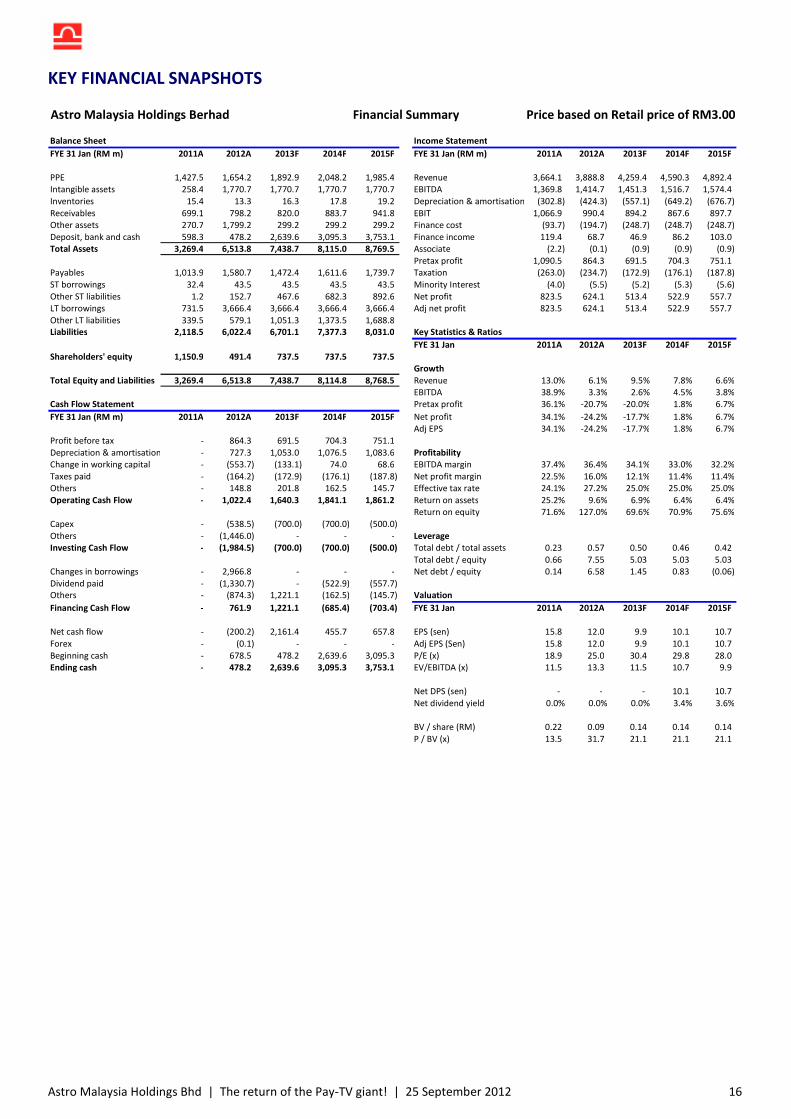

KEY FINANCIAL SNAPSHOTS

Astro Malaysia Holdings Berhad Financial Summary Price based on Retail price of RM3.00

Balance Sheet Income Statement

FYE 31 Jan (RM m) 2011A 2012A 2013F 2014F 2015F FYE 31 Jan (RM m) 2011A 2012A 2013F 2014F 2015F

PPE 1,427.5 1,654.2 1,892.9 2,048.2 1,985.4 Revenue 3,664.1 3,888.8 4,259.4 4,590.3 4,892.4

Intangible assets 258.4 1,770.7 1,770.7 1,770.7 1,770.7 EBITDA 1,369.8 1,414.7 1,451.3 1,516.7 1,574.4

Inventories 15.4 13.3 16.3 17.8 19.2 Depreciation & amortisation (302.8) (424.3) (557.1) (649.2) (676.7)

Receivables 699.1 798.2 820.0 883.7 941.8 EBIT 1,066.9 990.4 894.2 867.6 897.7

Other assets 270.7 1,799.2 299.2 299.2 299.2 Finance cost (93.7) (194.7) (248.7) (248.7) (248.7)

Deposit, bank and cash 598.3 478.2 2,639.6 3,095.3 3,753.1 Finance income 119.4 68.7 46.9 86.2 103.0

Total Assets 3,269.4 6,513.8 7,438.7 8,115.0 8,769.5 Associate (2.2) (0.1) (0.9) (0.9) (0.9)

Pretax profit 1,090.5 864.3 691.5 704.3 751.1

Payables 1,013.9 1,580.7 1,472.4 1,611.6 1,739.7 Taxation (263.0) (234.7) (172.9) (176.1) (187.8)

ST borrowings 32.4 43.5 43.5 43.5 43.5 Minority Interest (4.0) (5.5) (5.2) (5.3) (5.6)

Other ST liabilities 1.2 152.7 467.6 682.3 892.6 Net profit 823.5 624.1 513.4 522.9 557.7

LT borrowings 731.5 3,666.4 3,666.4 3,666.4 3,666.4 Adj net profit 823.5 624.1 513.4 522.9 557.7

Other LT liabilities 339.5 579.1 1,051.3 1,373.5 1,688.8

Liabilities 2,118.5 6,022.4 6,701.1 7,377.3 8,031.0 Key Statistics & Ratios

FYE 31 Jan 2011A 2012A 2013F 2014F 2015F

Shareholders' equity 1,150.9 491.4 737.5 737.5 737.5

Growth

Total Equity and Liabilities 3,269.4 6,513.8 7,438.7 8,114.8 8,768.5 Revenue 13.0% 6.1% 9.5% 7.8% 6.6%

EBITDA 38.9% 3.3% 2.6% 4.5% 3.8%

Cash Flow Statement Pretax profit 36.1% -20.7% -20.0% 1.8% 6.7%

FYE 31 Jan (RM m) 2011A 2012A 2013F 2014F 2015F Net profit 34.1% -24.2% -17.7% 1.8% 6.7%

Adj EPS 34.1% -24.2% -17.7% 1.8% 6.7%

Profit before tax - 864.3 691.5 704.3 751.1

Depreciation & amortisation - 727.3 1,053.0 1,076.5 1,083.6 Profitability

Change in working capital - (553.7) (133.1) 74.0 68.6 EBITDA margin 37.4% 36.4% 34.1% 33.0% 32.2%

Taxes paid - (164.2) (172.9) (176.1) (187.8) Net profit margin 22.5% 16.0% 12.1% 11.4% 11.4%

Others - 148.8 201.8 162.5 145.7 Effective tax rate 24.1% 27.2% 25.0% 25.0% 25.0%

Operating Cash Flow - 1,022.4 1,640.3 1,841.1 1,861.2 Return on assets 25.2% 9.6% 6.9% 6.4% 6.4%

Return on equity 71.6% 127.0% 69.6% 70.9% 75.6%

Capex - (538.5) (700.0) (700.0) (500.0)

Others - (1,446.0) - - - Leverage

Investing Cash Flow - (1,984.5) (700.0) (700.0) (500.0) Total debt / total assets 0.23 0.57 0.50 0.46 0.42

Total debt / equity 0.66 7.55 5.03 5.03 5.03

Changes in borrowings - 2,966.8 - - - Net debt / equity 0.14 6.58 1.45 0.83 (0.06)

Dividend paid - (1,330.7) - (522.9) (557.7)

Others - (874.3) 1,221.1 (162.5) (145.7) Valuation

Financing Cash Flow - 761.9 1,221.1 (685.4) (703.4) FYE 31 Jan 2011A 2012A 2013F 2014F 2015F

Net cash flow - (200.2) 2,161.4 455.7 657.8 EPS (sen) 15.8 12.0 9.9 10.1 10.7

Forex - (0.1) - - - Adj EPS (Sen) 15.8 12.0 9.9 10.1 10.7

Beginning cash - 678.5 478.2 2,639.6 3,095.3 P/E (x) 18.9 25.0 30.4 29.8 28.0

Ending cash - 478.2 2,639.6 3,095.3 3,753.1 EV/EBITDA (x) 11.5 13.3 11.5 10.7 9.9

Net DPS (sen) - - - 10.1 10.7

Net dividend yield 0.0% 0.0% 0.0% 3.4% 3.6%

BV / share (RM) 0.22 0.09 0.14 0.14 0.14

P / BV (x) 13.5 31.7 21.1 21.1 21.1

Astro Malaysia Holdings Bhd | The return of the Pay-TV giant! | 25 September 2012 17

DISCLOSURE & DISCLAIMER

Stock rating definitions

Strong buy - High conviction buy with expected 12-month total return (including dividends) of 30% or more

Buy - Expected 12-month total return of 10% or more

Hold - Expected 12-month total return between -10% and 10%

Sell - Expected 12-month total return of -10% or less

Trading buy - Expected 6-month total return of 10% or more arising from positive newsflow. However, upside may not be

sustainable.

Sector rating definitions

Overweight - Industry expected to outperform the market over the next 12 months

Neutral - Industry expected to perform in-line with the market over the next 12 months

Underweight - Industry expected to underperform the market over the next 12 months

Disclaimer

This report is for information purposes only and general in nature. The information contained in this report is based on data and

obtained from sources believed to be reliable. However, the data and/or sources have not been independently verified and as

such, no representation, express or implied, is made with respect to the accuracy, completeness or reliability of the information

or opinions in this report. Accordingly, neither we nor any of our related companies and associates nor persons related to us

accept any liability whatsoever for any direct, indirect or consequential losses (including loss of profits) or damages that may

arise from the use of or reliance on the information or opinions in this publication. Any information, opinions or

recommendations contained herein are subject to change at any time without prior notice.

It is not possible to have regard to the specific investment objectives, the financial situation and the particular needs of each

person who may receive or read this report. As such, investors should seek financial, legal and other advice regarding the

appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

Under no circumstances should this report be considered as an offer to sell or a solicitation of an offer to buy any securities

referred to herein. This company and its related companies, their associates, directors, connected parties and/or employees

may, from time to time, own, have positions or be materially interested in any securities mentioned herein or any securities

related thereto, and may further deal with such securities and provide advisory, investment or other services for any company

or entity mentioned in this report. In reviewing this report, investors should be aware that any or all of the foregoing, among

other things, may give rise to real or potential conflict of interests.

Published & printed by:

ECM Libra Capital Sdn Bhd (579116-A)

2nd Floor, West Wing, Bangunan ECM Libra

No. 8 Jalan Damansara Endah

Damansara Heights

50490 Kuala Lumpur

Tel: (603) 2089 1888

Fax: (603) 2096 1868