malaysia daybreak | 30 october 2013 - i3investor

TRANSCRIPT

REGIONAL DAILY

December 26, 2012

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT.

MALAYSIA

Malaysia Daybreak | 30 October 2013

▌What’s on the Table…

——————————————————————————————————————————————————————————————————————

Oil & Gas - Equipment & Svs - Contract opportunities point North After Perisai's FPSO and Wah Seong's pipe-coating wins in the North Malay Basin, more contracts should be rolled out to support Petronas's and Hess's US$5.2bn development of the basin. A large fabrication contract is up for grabs, with more to come, Upstream reported. The sector remains an Overweight, with the strong contract pipeline arising from Petronas’s capex as catalyst. Our top picks are SapuraKencana among the big caps and Perisai among the small caps.

KLCC Property Holdings - Twins of uncertainty

KLCCP's 9M13 core net profit of RM452m was in line with our estimate at 75% of our full-year forecast. Yoy revenue growth of 13.7% was driven by both its office and retail segments which grew by 17.8% and 14.9%, respectively. Our DDM-based target price is revised downwards from RM7.30 to RM6.90 as we have revised upwards our risk-free rate to be in line with the current average 10-year MGS yields of 3.7-3.8%. We downgrade from an Outperform to Neutral given the risk to KLCCP's earnings and DPU growth in the longer term. We prefer property developers such as Mah Sing, which is our top pick in the sector.

Sunway REIT - Not so sunny outlook

Sunway REIT's 1Q14 net profit of RM55.4m was broadly in line with our estimates, accounting for 24% of our full-year forecasts. Its softer earnings outlook, arising from the closure of Sunway Putra Mall and the lack of new acquisitions, points to a flattish DPU. Thus, we maintain our Neutral call on the stock, with an unchanged DDM-based target price of RM1.45. We believe investor sentiment on M-REITs overall has waned, given the more positive broader market outlook. For exposure to Malaysian property stocks, we suggest a switch to developers, namely Mah Sing, which is our top pick in the property sector.

DiGi.com - Outpacing its rivals

▌News of the Day…

——————————————————————————————————————————————————————————————————————

• CMMT calls off purchase of Tropicana Corp’s two assets

• IOI Corp’s demerger approved by the SC

• SC approves Sunway’s commercial papers up to RM2bn

• Selangor MB "will be busy" with negotiations for takeover of water assets in Nov

• Property developer Titijaya Land Bhd’s IPO by year-end

• Pintaras Jaya Bhd has bagged RM59m piling job

• US S&P/Case-Shiller home price index rose 0.9% in Aug (+0.6% in Jul)

Sources: CIMB. COMPANY REPORTS

Sources: CIMB. COMPANY REPORTS

Key Metrics

FBMKLCI Index

1,550

1,600

1,650

1,700

1,750

1,800

1,850

Oct-12 Dec-12 Feb-13 Apr-13 Jun-13 Aug-13 Oct-13

———————————————————————————

FBMKLCI

1815.65 -2.74pts -0.15%OCT Futures NOV Futures

1817.5 - (-0.14% ) 1820 - (1.00% )———————————————————————————

Gainers Losers Unchanged418 379 303

———————————————————————————

Turnover1809.83m shares / RM1892.342m

3m avg volume traded 1772.81m shares

3m avg value traded RM1897.06m———————————————————————————

Regional IndicesFBMKLCI FSSTI JCI SET HSI

1,816 3,209 4,563 1,456 22,847

————————————————————————————————

Close % chg YTD % chg

FBMKLCI 1,815.65 (0.2) 7.5

FBM100 12,340.62 (0.1) 9.2

FBMSC 15,779.15 0.4 37.4

FBMMES 5,729.33 1.9 36.0

Dow Jones 15,680.35 0.7 19.7

NASDAQ 3,952.34 0.3 30.9

FSSTI 3,208.82 0.0 1.3

FTSE-100 6,774.73 0.7 14.9

Hang Seng 22,846.54 0.2 0.8

JCI 4,562.77 (0.6) 5.7

KOSPI 2,051.76 0.2 2.7

Nikkei 225 14,325.98 (0.5) 37.8

PCOMP 6,543.46 0.1 12.6

SET 1,455.86 0.4 4.6

Shanghai 2,128.86 (0.2) (6.2)

Taiwan 8,420.98 0.2 9.4

Close % chg Vol. (m)

HUBLINE 0.065 0.0 76.9CENSOF HOLDINGS 0.605 5.2 44.2

TALAM TRANSFORM 0.070 (6.7) 41.8

XIDELANG HOLDINGS 0.395 0.0 41.2

R&A TELECOM 0.060 20.0 31.3

EA HOLDINGS 0.155 14.8 30.8

DIGI.COM 5.060 2.6 27.5

DAYA MATERIALS 0.365 5.8 24.2

Close % chg

US$/Euro 1.3748 0.01RM/US$ (Spot) 3.1453 (0.06)

RM/US$ (12-mth NDF) 3.2071 0.30

OPR (% ) 3.00 0.00

BLR (% , CIMB Bank) 6.60 0.00

GOLD ( US$/oz) 1,344 (0.05)

WTI crude oil US spot (US$/barrel) 98.20 (0.49)

CPO spot price (RM/tonne) 2,440 0.83

Economic Statistics

Market Indices

Top Actives

————————————————————————————————————————

Terence WONG CFA T (60) 3 20849689 E [email protected]

Daybreak Malaysia

October 30, 2013

2

Global Economic News…

US producer price index fell 0.1% in Sep (+0.3% in Aug), weaker than consensus estimate of +0.2%. The core rate, which excludes both food and energy, firmed to 0.1% after no change in Aug. The market forecast was for a 0.1% increase. (Bloomberg)

US retail sales slipped 0.1% in Sep (+0.2% in Aug), lower than market estimate for no change. Autos fell 2.2% (+0.7% in Aug). Retail sales excluding autos gained 0.4% (+0.1% in Aug). (Bloomberg)

US S&P/Case-Shiller home price index rose 0.9% in Aug (+0.6% in Jul), ahead of consensus estimate of +0.7%. This is the first monthly pickup since Apr when prices jumped 1.7%. The year-on-year rate is showing special strength, at plus 12.8%. (Bloomberg)

US business inventories rose 0.3% in Aug (+0.4% in Jul), in line with market estimates. (Bloomberg)

US Conference Board's consumer confidence index dropped to 71.2 in Oct (80.2 in Sep), lower than consensus reading of 75.0. (Bloomberg)

Japan's average household spending in Sep rose 3.7% yoy (-1.6% in Aug), outstripping economists' forecasts of 0.5%. Retail trade rose 3.1% yoy in Sep(1.1% in Aug). The average income of working households in Sep also rose 0.9% in real terms. (AFP)

Japan's jobless rate improved to 4.0% in Sep, down by 0.1% pt from the previous month. (AFP)

Japan’s small business confidence improved in Oct to 50.8 from 49.8 the previous month. (Bloomberg)

Australia’s central bank Governor Glenn Stevens said the local currency’s level isn’t supported by costs and productivity in the economy and the nation’s terms of trade are more likely to fall than rise. “It seems quite likely that at some point in the future the Australian dollar will be materially lower than it is today,” Stevens said. (Bloomberg)

The Reserve Bank of India raised its benchmark interest rate for the second straight month to 7.75% from 7.5% to fight accelerating inflation. It cut the marginal standing facility rate from 9% to 8.75%, making short-term funds cheaper for banks. It left the cash reserve ratio unchanged at 4%. (Bloomberg)

South Korea’s current account surplus widened to US$6.57bn in Sep from US$5.68bn in Aug. The goods balance increased from US$5.28bn to US$5.70bn. (Bloomberg)

South Korea's industrial output expanded in Aug by 1.8% mom (-0.3% in Jul), versus a 0.5% gain forecast by the market. (Reuters)

Daybreak Malaysia

October 30, 2013

3

China’s leading index fell to 99.64 in Sep from 99.89 the previous month. (Bloomberg)

Inflation will pick up over the next few quarters before tapering towards the end of 2014. The Monetary Authority of Singapore said domestic food inflation is expected to rise from around 2% in 2013 to close to 3% in 2014. (CNA)

Singapore topped the global ranking on the World Bank’s ease of doing business survey for the upcoming year 2014. Joining it on the list of the top 10 economies with the most business-friendly regulatory environments are

Hong Kong; New Zealand; the United States; Denmark; Malaysia; the republic of Korea; Georgia; Norway; and the United Kingdom. Malaysia ranked 6th (+2 from 8th in 2013), Thailand was ranked 18th (unchanged from 2013), Indonesia ranked 120th (-4 from 116th in 2013), Philippines ranked 108th (+25 from 133th in 2013), China ranked at 96th (+3 from 99th in 2013), India ranked 134th (-3 from 131th in 2013). (World Bank)

Thailand Prime Minister Yingluck Shinawatra said the government stands ready to go ahead with its THB2tr transportation-infrastructure project as a means to prepare for enhanced Thai-Asean links and liberalised trade with both Asean and non-Asean partners. Meanwhile, state subsidies for agricultural products will be adjusted to strengthen the sector before the country joins the full Asean economic integration planned for Jan 1 2016. (The Nation)

Indonesia President Susilo Bambang Yudhoyono says the value of projects realized under the Masterplan for the Acceleration and Expansion of Indonesian Economic Development (MP3EI) has reached RPH737.9tr (US$66.78bn). (Jakarta Post)

Philippines leading economic indicator (LEI) for 4Q13 inched up to 0.181 (0.046 in 3Q), indicating the Philippines was poised to stay on a robust growth path. (Philippines Inquirer)

Malaysian Economic News…

Malaysia has improved its business environment over the past year, by reducing company registration fees and making it easier to obtain construction permits as well as post construction approvals through the establishment of a one-stop shop, said the World Bank Group. Acting Country Director for Malaysia, Constantine Chikosi said Malaysia had also made it easier for firms to receive electricity supply by increasing the efficiency of internal processes and improving its communication and dialogue with contractors.

The World Bank of Doing Business Report 2014, which released yesterday, revealed that Malaysia improved from 25th position in 2007 to sixth position for 2014 (12th in 2013), joining the list of 10 economies in the world with the most business-friendly regulations, along with Singapore, Hong Kong, New Zealand, the US, Denmark, Korea, Georgia, Norway, and the UK.

Chief Secretary to the Government Tan Sri Dr Ali Hamsa said the progress was a testimony to Malaysia's attractiveness as a choice destination for trade and investment to local and foreign investors. (Bernama)

Daybreak Malaysia

October 30, 2013

4

The general insurance industry's gross premiums grew by 5.7% to RM8.33bn for Jan-Jun 2013 from RM7.88bn over the same period of 2012, said General Insurance Association of Malaysia (PIAM). The motor insurance accounted for the largest portion with 44.4%, fire (17.6%) and marine, aviation and transit (10.8%).

Personal accident was at 7.4%; medical and health insurance 6.7%; contractors all risk and engineering 3.3%; liabilities 3.5%; and, workmen's compensation and employer's liability at 1.5%.

Other classes of general insurance contributed 4.8%. (Bernama)

The Finance Ministry is to go on a roadshow to explain the proposed Goods and Services Tax (GST) to the people, particularly those in the rural areas. Deputy Minister Datuk Ahmad Maslan said yesterday the ministry would also make use of the mass media to disseminate information on the GST. "We also have a dedicated website, www.gst.customs.gov.my. We will also use the main television channels for the purpose, and it will be done soon," he said. (Bernama)

The Agriculture and Agro-based Industry Ministry plans to develop 110,170 hectares of idle land in the country for agrofood. Its deputy minister Datuk Tajuddin Abdul Rahman said the ministry was currently identifying owners of idle lands, the soil type and infrastructure requirements. Since 2007, the government had developed 9,213 hectares of land involving 7,517 farmers nationwide and produced 178,141 metric tonnes of yield worth RM78.68m, he said. (Bernama)

The Royal Customs and Excise Department will be ready in terms of manpower, information technology and infrastructure to implement the Goods and Services Tax (GST) in Apr 2015, its director-general, Datuk Seri Khazali Ahmad, said on Tuesday. He said all officers had been trained and given the necessary exposure and training on the GST and its implementation over the last few years.

"We have 17 more months to go, which is a long time for us to explain not only to our officers but also to the people that this new system is not something disadvantageous," he said.

The GST computerisation system to be used by the Customs Department was almost ready. He also said that the department was working on integrating the system with appointed banks and banking agents to assist in the effective implementation of the GST. (Bernama)

Malaysia has received applause from the World Bank Group for the country's efforts in collaborating with the private sector through the Public Private Partnership (PPP) programme. Its International Finance Corporation Singapore and Malaysia Country Manager, Tunde Onitiri described the engagement between the government and the private sector as one of the best globally, especially in respect of infrastructure.

"Malaysia has done a tremendous job on PPP infrastructure such as the Mass Rapid Transit project as well as the Kuala Lumpur-Singapore high speed rail (HSR) link venture. Going forward, the country still has room to grow," he said.

He suggested that apart from infrastructure, other sectors which Malaysia should consider under the PPP, is education and healthcare. (Bernama)

Daybreak Malaysia

October 30, 2013

5

Bursa Malaysia Bhd yesterday announced that it and its subsidiaries will be closed for the Maal Hijrah holiday on next Tuesday, 5 Nov. In a statement, Bursa Malaysia said it and its subsidiaries will resume operations on 6 Nov. (Bernama)

JPB-MRT Resources Sdn Bhd, a joint venture (JV) between JPB Asia Pacific Sdn Bhd and MRT Japan Corporation Company Ltd, will invest RM60m to develop a Research and Development (R&D) centre and high technology green houses in the Northern Corridor Economic Region (NCER) by 2016. The Northern Corridor Implementation Authority (NCIA) Chief Executive Datuk Redza Rafiq said the investment also involves the setting up of 30 units of high technology green houses in Ara Kuda, Tasek Gelugor, in Penang.

He added that for a start, the green houses will produce melons and Japanese pumpkins for the export market.

The JV between the Malaysian and Japanese companies, also includes Nepon Inc, a leading manufacturer for Japanese horticulture growers.

The project will be over four phases and Nepon will supply some of its products for JPB-MRT Resources in setting up the green houses.

The first phase of the project includes the R&D centre and five units of the high technology green houses at an estimated cost of RM17.5m.

The second phase comprises 15 units of the green houses costing RM15m, and under the third phase, 10 more units will be built for the same cost.

The final phase involves the setting up of a collection processing centre in Ara Kuda at a cost of about RM5m and RM7.5m for the training component for master growers. (Bernama)

The Cooperatives Commission of Malaysia (CCM) has target for the cooperative sector to register a higher income of RM32.97bn by year-end from RM31.10bn previously. The chairman of the board of directors of the Cooperative College Malaysia Datuk Yusof Samsuddin said this follows the encouraging performance of 33 cooperatives under the micro, small and medium clusters, which had leapt to the large cluster, with each generating an annual income exceeding RM5m. There were now 10,807 registered cooperatives throughout the country with a membership of 7.03m. (Bernama)

The hike in sugar price is not due to the scrapping of the 34 sen subsidy but because the government inked a three-year raw sugar import deal at a high price, said the DAP National Publicity secretary Tony Pua. He said the government had been buying sugar at 55.7% higher than the market price last month. He said this was because the Domestic Trade, Co-operatives and Consumerism Ministry signed the deal at US$26 (RM78.54) per 100lbs (45.3kg) in Jan last year when the market price for raw sugar then was at US$23.42 (RM73.57).

The international price for sugar had gradually dropped since then, going as low as US$16.70 (RM52.46) per 100lbs last month. The market price for raw sugar now, he said, was US$18.91 (RM59.41) per 100lbs.

Taking that into consideration, the subsidy was not needed and the price of sugar in the market was cheaper than the presently fixed RM2.84/kg, he said. The over 10% difference between the contract price and the market price cost the government a loss of RM64m yearly, he added.

Daybreak Malaysia

October 30, 2013

6

"I had already warned the government at the time that international analysis reports had predicted a fall in sugar prices due to excessive supply but my warning was unheeded and the then International Trade and Industry deputy minister Datuk Mukhriz Mahathir told Parliament that the price was going up," he said.

The government should bear the responsibility for making a bad call and admit its mistake, which had cost the government to pay RM194m a year to import 2.73bn pounds of raw sugar annually, he said. (Malaysian Insider)

The government has been urged to stop setting up new agencies, especially those whose functions overlap with existing government bodies and which hire high-salaried contract staff. DAP's Serdang MP Dr Ong Kian Ming said PM Datuk Seri Najib Razak should walk the talk by cutting expenditure in the Prime Minister's Department and not create more new and expensive agencies.

He was referring to Najib's announcement of a Green Foundation and the Malaysian Global Innovation and Creativity Centre (Magic) during the Budget 2014 speech last Friday.

He said the two new agencies were unnecessary, and pointed out the existence of the Malaysian Green Tech Corporation and the Sustainable Energy Development Authority, he said.

He said agencies such as Agensi Inovasi Malaysia, the Malaysian Productivity Council and others were already doing the job of the newly-announced Magic. (Malaysian Insider)

The crime index has seen a steady drop in the number of reported cases, from 211,645 in 2008 to 153,669 last year. From Jan to Sep this year, the total number of cases reported were 111,020. Home Minister Datuk Seri Dr Ahmad Zahid Hamidi said the index includes violent and property crimes, and drug-related offences.

The number of violent crimes has dropped from 37,817 cases in 2008 to 29,950 last year. This year, 22,357 cases were reported up to Sep.

Property crimes reported last year was 123,719 cases, a drop from 173,828 cases reported in 2008.

Some 857,252 people were arrested for various drug-related offences between 2008 and Sep this year.

Selangor reported the highest number of violent and property crime cases, with 57,752 cases in 2008 and 40,629 cases last year, followed by Kuala Lumpur with 28,438 cases in 2008 and 23,022 cases last year.

Perlis reported the least number of violent and property crime cases with 808 cases in 2008. However, the number has increased to 974 cases last year. (NST)

There is an apparent Western bias in credit rating agencies' assessment of economies and their risk profiles, said CIMB Group Holdings Bhd CEO Dato' Sri Nazir Razak. "If you look at the global financial system today, it was constructed and dominated by the West. If you look at the rating system for example, it is all dominated by S&P and Moody's," he said.

He said the rating agencies "dictate" how countries and banks looked at each other, pointing out that this determined how much capital a bank had to put against a loan it gave to a certain company.

Daybreak Malaysia

October 30, 2013

7

"My question is, why are we only dependent on S&P and Moody's? Are they able to assess our credit worthiness properly? If you look at their history, it is pretty bad because for the longest time they said Spain had a much better credit rating than China - when China was doing all lending while Spain was doing all the borrowing," he said.

"This doesn't make sense and this is a clear example of the Western bias in the system. And until today we still have not evolved an Asian rating agency. I think that Ratings Agency Malaysia (RAM) should evolve to Ratings Agency Asia (RAA)," he quipped.

Despite the present situation, he also noted that there was a "discernible rise" of Asian players and this could be the wider trend over the next few years. (Starbiz)

The government will not do away with the vital revenue-generating excise tax as opposed to the abolishment of Sales and Services Tax (SST) upon the introduction of the recently announced Goods and Services Tax (GST). Minister in the Prime Minister's Department Datuk Seri Idris Jala said Malaysia will not abolish the duty as it is still an important source of revenue. (Malaysian Reserve)

Malaysian and Thai financial institutions are the most vulnerable in the Asia-Pacific region to a deterioration in the household debt segment, as household leverage outpace income growth and undermine household resilience, according to a Standard & Poor's (S&P) report. It said the creditworthiness of the banks' households exposure in the country is less resilient than its peers, as a result of rapidly rising households indebtedness.

In 2012, Malaysia has the highest household debt-to-GDP ratio of 80.5% compared to other Asia-Pacific regions such as Thailand (77.1%), Singapore (76.8%), Korea (75.4%), Taiwan (64.9%), Japan (62.8%) and Hong Kong (58.2%).

Besides that, it said Malaysia and Thailand experienced constrained income levels where the nominal GDP per capita of US$5,677 in Thailand and US$10,393 in Malaysia us low compared to other similarly rated sovereigns. (Malaysian Reserve)

Political News…

Several Umno supreme councillors have hit back at Tun Dr Mahathir Mohamad over his claims that money politics was rampant in the party, saying that it was an insult to the 146,000 delegates who voted in the party polls earlier this month. Going into "damage control", they said their former president's remarks implied that the delegates "were easy to buy with money" and told him to be specific about what he meant instead of making rash statements. Dr Mahathir's comment came on the heels of talk that vote-buying was rampant in the party elections, which had been widened from 2,500 central delegates to 146,000 this time to prevent money politics. (Malaysianinsider)

Backbenchers Club chairman Tan Sri Shahrir Abdul Samad (BN-Johor Baru) has called for an end to sugar monopolies in the country now that the sugar subsidy has been removed. "With the subsidy removed, the sugar industry should be liberalised. Import of the commodity should be allowed for instance from Thailand and allow market forces dictate the price of processed sugar. "Monopolies for sugar supply must be ended. There should also be no cartels fixing the price (of processed sugar)," he said when debating the Supply Bill 2014 in the Dewan Rakyat yesterday. (Malaysianinsider)

Daybreak Malaysia

October 30, 2013

8

Former PM Tun Dr Mahathir Mohamad has said the Malaysian courts are free and it is ridiculous to suggest that he had subverted the judicial system, which had often ruled against his government and party during his tenure. Dr Mahathir cited the courts' latest decision on the use of the word Allah as an example of its independence. He said whereas the High Court decided that use of the word was permitted in Herald, the Court of Appeal disagreed. (Malaysianinsider)

Corporate News…

CapitaMalls Malaysia Trust (CMMT) has called off its proposed acquisition of two properties owned by Tropicana Corp Bhd. In a filing to Bursa Malaysia, the company said that both parties were unable to conclude on the terms of the sale and purchase agreement, and have mutually agreed not to pursue further with the proposed disposal. The two properties owned by Tropicana Corp's unit, Tropicana City Sdn Bhd, are Tropicana City Mall and Tropicana City Office Tower in Selangor. (BT)

Despite scrapping its takeover talks with the Philippines' Bank of Commerce in June, CIMB Group Holdings Bhd is still looking for opportunities in the country. CEO Datuk Seri Nazir Razak said the bank is still committed to having a presence in the Philippines. "It is a key market in Asean and it is integral to what we are doing," he said. (Financial Daily)

IOI Corp Bhd is due to spin off its lucrative property arm IOI Properties Group Bhd and list it on the Main Market of Bursa Malaysia in January next year, with a market capitalisation of more than RM14bn, said IOI Corp executive chairman and plantation tycoon Tan Sri Lee Shin Cheng. The initial public offering (IPO) is slightly off its initial timeframe of end-2013.

"IOI Properties will probably be listed in the first month of next year. The listing preparations are going smoothly as we are now waiting for the final approval from High Court. To date, the Securities Commission and Bursa Malaysia have given (IOI Properties IPO) the green light," Lee added. (Sun)

Sunway Bhd has obtained Securities Commission's approval to issue commercial papers and/or medium term notes of up to RM2bn. It said the proceeds would be used to refinance its existing RM500m CP/MTN programme and to finance the group's working capital, capital expenditure requirement and other general corporate purposes. (StarBiz)

Gadang Holdings Bhd has acquired 80% stake in Indonesia-based power company PT Hidronusa Rawan Energi (HRE) for 10.8bn rupiah (RM3.06m). In a filing with Bursa Malaysia, Gadang said its indirect wholly-owned subsidiary, Asian Utilities Pte Ltd, had entered into a sale and purchase of shares agreement with Angga Panji Kesuma and Aprian Eka Rahadi to acquire 6,000 shares of nominal value 1m rupiah each, representing 80% stake in HRE. (Starbiz)

YTL Group is actively pursuing infrastructure assets in Johor which may include water treatment and power plants, sources said. It is understood that among the assets YTL is eyeing is Ranhill Energy and Resources Bhd’s water treatment plants in the state. Sources said YTL had already started initial discussions to secure large infrastructure projects in Johor. Ranhill has an exclusive licence to supply source-to-tap water to end-customers in Johor. According to reports, the current licence is valid till 2014 and renewable every three years. (Starbiz)

Daybreak Malaysia

October 30, 2013

9

Kuala Lumpur has been listed as one of the favourite prime new-build markets for property and real-estate investors from China, according to a report compiled by Knight Frank. Its global head of residential research Liam Bailey said the Chinese are the most influential buyers in the world's prime new-build sector. "Chinese are the top purchasers of new-build residential properties in Sydney and Hong Kong and are active buyers in both Kuala Lumpur and Bangkok's prime new-build markets," Bailey said yesterday.

Liam said Chinese buyers' global presence is fuelled in part by the strong yuan and a slowing domestic economy, both encouraging them to look further afield in an attempt to diversify investments. He said the next most influential buyers are from Singapore and Russia, followed by the United Kingdom and the United States.

"Given the recent growth in wealth creation in Asia over the last few years, it is, perhaps, no surprise that buyers from this region feature strongly among our list of top global new-build purchasers," he said. (BT)

Kimlun Corp Bhd's unit Kimlun Land Sdn Bhd (KLLSB) has signed a sale and purchase agreement with Bina Plastic Industries Sdn Bhd for the disposal of land in Negri Sembilan for RM46.5m. The company said the disposal of nine parcels of freehold agriculture land, measuring about 17,266ha, is expected to be completed by 1Q14. (BT)

Sarawak Cable Bhd, via its JV unit Sinohydro-Trenergy has secured two contracts worth RM618.6m from Sarawak Energy Bhd (SEB) to lay transmission lines. In a filing with Bursa Malaysia it said the JV has accepted the Letters of Award for the Mapai to Lachau 500kV transmission line project (Package B) for RM352.8m and the Lachau to Tondong 500kV transmission line project (Package C) for RM265.8m. (The Edge)

Selangor Mentri Besar Tan Sri Khalid Ibrahim said the state government "will be busy" with negotiations for the takeover of water assets in November, giving an assurance that the state's water restructuring exercise is on track for completion by the end of the year. Khalid made clear that the Selangor government did not issue a new offer to the concessionaires, with the last offer valued at RM9.65bn. The state is currently ironing out details on "how best to make the offer".

"Langat 2 is also part of the discussion for the water restructuring matter", he said, referring to the long-delayed water treatment plant that will treat some 1.89bn litres of raw water to meet the demand in Selangor, Kuala Lumpur and Putrajaya until 2025. (Financial Daily)

Property developer Titijaya Land Bhd has appointed Alliance Investment Bank Bhd as the principal adviser and underwriter for its initial public offering on Bursa Malaysia's Main Market by the end of the year. This follows the approval granted by the Securities Commission for Titijaya's initial public offering comprising a public issue of 81.7m new shares and an offer for sale of 49.5m existing shares. (BT)

Pintaras Jaya Bhd has bagged a RM59m contract to undertake the piling for a mixed development project in Dengkil, Selangor. It said on Tuesday its unit had received a letter of award from Tristar Acres Sdn. Bhd. to undertake the piling. “The said works are to commence in Nov-2013 with a completion period of 14 months. The contract is valued at RM59m,” it said. (Starbiz)

Daybreak Malaysia

October 30, 2013

10

Only World Group Holdings Bhd (OWG) intends to revitalise the KomtarTower in Penang using 56% of the proceeds from its IPO. In its prospectus exposure, the group said the revitalisation project involved the proposed refurbishment and enhancement of five specified levels within the Komtar Tower to create high-end commercial space for retail, food and beverage, and recreational purposes. The project commenced on Aug 27 and is expected to be completed within 30 months of the leasing date. The group also plans to allocate about 28% of its expansion plans, which include the expansion of its water park, Wet World Water Park in Shah Alam, food and services outlets and growing its franchise programme.

The group plans to issue up to 56.4m new ordinary shares (30.49%) of the group's enlarged issued and paid-up capital, priced at 50 sen each. Of the projected new shares, 5% or 9.2m shares are allocated for the public. Furthermore, four million shares or 2.2% will be allocated for its directors, 18.5m shares or 10% for bumiputra investors and 24.7m shares or 13.3% for selected investors. The OWG group is primarily a provider of leisure and hospitality services incorporating the operation of food services outlets, as well as amusement and recreation outlets comprising water amusement parks and family attractions. (The Edge)

Daybreak Malaysia

October 30, 2013

11

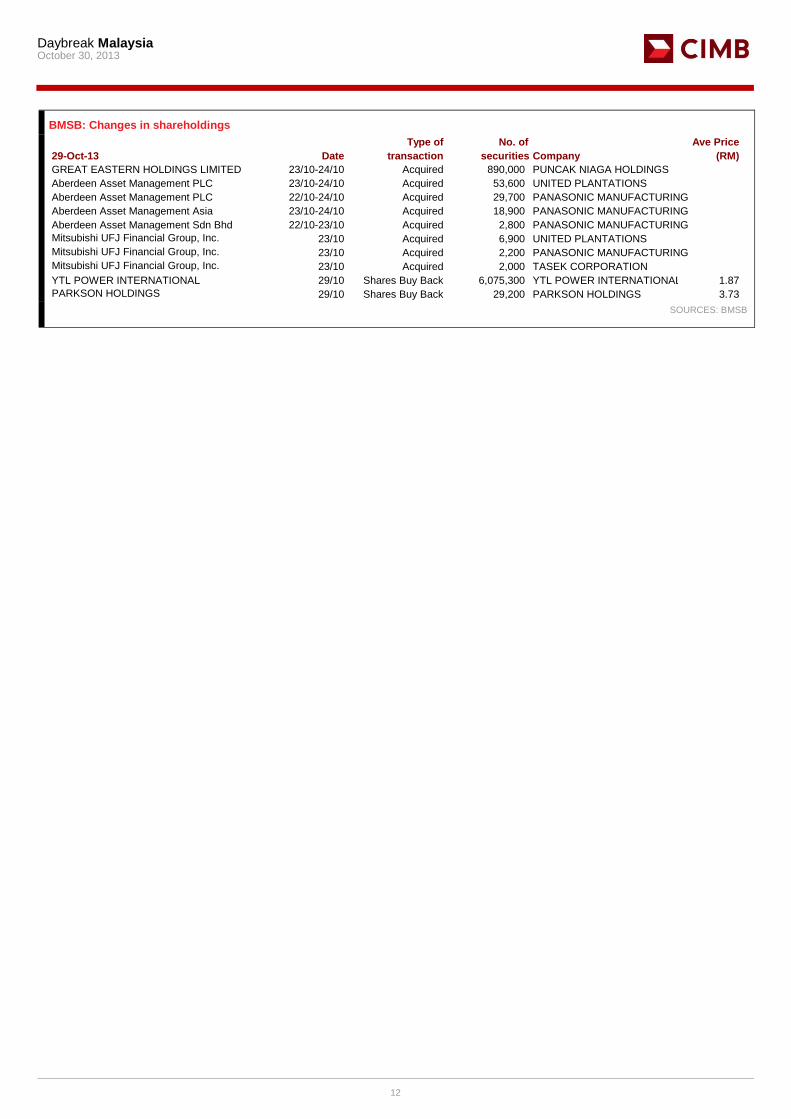

BMSB: Changes in shareholdings

Type of No of Ave Price

29-Oct-13 Date transaction securities Company (RM)

EPF 24/10 Disposed 2,906,100 DIGI.COM

EPF 24/10 Disposed 2,576,900 AMMB HOLDINGS

EPF 24/10 Disposed 1,646,800 TELEKOM MALAYSIA

EPF 24/10 Disposed 1,525,000 PETRONAS CHEMICALS

EPF 23/10 Disposed 1,441,700 AXIATA GROUP

EPF 24/10 Disposed 1,107,400 SIME DARBY

EPF 24/10 Disposed 1,000,000 FELDA GLOBAL VENTURES

EPF 24/10 Disposed 791,500 BURSA MALAYSIA

EPF 24/10 Disposed 650,000 BUMI ARMADA

EPF 24/10 Disposed 638,400 WAH SEONG CORPORATION

EPF 24/10 Disposed 632,400 SAPURAKENCANA PETROLEUM

EPF 24/10 Disposed 503,900 MAXIS

EPF 24/10 Disposed 500,000 CAPITAMALLS MALAYSIA TRUST

EPF 24/10 Disposed 484,400 UEM SUNRISE

EPF 24/10 Disposed 483,000 IOI CORPORATION

EPF 24/10 Disposed 480,300 GAMUDA

EPF 24/10 Disposed 450,200 HONG LEONG BANK

EPF 24/10 Disposed 300,000 LAFARGE MALAYSIA

EPF 24/10 Disposed 131,000 KUALA LUMPUR KEPONG

EPF 24/10 Disposed 120,300 PETRONAS GAS

EPF 24/10 Disposed 107,200 KPJ HEALTHCARE

EPF 24/10 Disposed 100,000 FRASER & NEAVE

EPF 24/10 Disposed 58,300 IGB CORPORATION

EPF 24/10 Disposed 34,000 MMC CORPORATION

EPF 24/10 Disposed 22,800 MBM RESOURCES

EPF 24/10 Disposed 1,800 TAN CHONG MOTOR

Skim Amanah Saham Bumiputera 21/10 Disposed 50,000,000 MALAYAN BANKING

Skim Amanah Saham Bumiputera 23/10-24/10 Disposed 2,270,000 TELEKOM MALAYSIA

Lembaga Tabung Haji 24/10-25/10 Disposed 2,000,000 PROTASCO

Lembaga Tabung Haji 24/10-25/10 Disposed 558,000 GLOMAC

Lembaga Tabung Haji 24/10-25/10 Disposed 515,300 FABER GROUP

Lembaga Tabung Haji 11/10-14/10 Disposed 384,400 BRAHIM'S HOLDINGS

Lembaga Tabung Haji 14/10 & 25/10 Disposed 268,700 MRCB

Lembaga Tabung Angkatan Tentera 21/10 Disposed 100,000 DKSH HOLDINGS

Mitsubishi UFJ Financial Group, Inc. 23/10 Disposed 1,105,300 CIMB GROUP

Mitsubishi UFJ Financial Group, Inc. 23/10 Disposed 10,700 SHANGRI-LA HOTELS

EPF 24/10 Acquired 1,460,500 MALAYAN BANKING

EPF 24/10 Acquired 1,250,500 DIALOG GROUP

EPF 24/10 Acquired 890,300 IJM CORPORATION

EPF 24/10 Acquired 644,300 PUBLIC BANK

EPF 24/10 Acquired 644,200 AIRASIA

EPF 24/10 Acquired 500,000 TOP GLOVE CORPORATION

EPF 24/10 Acquired 300,000 PAVILION REIT

EPF 24/10 Acquired 283,700 POS MALAYSIA

EPF 24/10 Acquired 238,200 IHH HEALTHCARE

EPF 24/10 Acquired 224,000 MALAYSIA AIRPORTS

EPF 24/10 Acquired 205,600 KULIM (MALAYSIA)

EPF 24/10 Acquired 190,300 GENTING PLANTATIONS

EPF 24/10 Acquired 80,000 PERDANA PETROLEUM

EPF 24/10 Acquired 65,000 CAHYA MATA SARAWAK

EPF 24/10 Acquired 21,300 AFFIN HOLDINGS

Skim Amanah Saham Bumiputera 23/10-24/10 Acquired 2,730,000 GAMUDA

Skim Amanah Saham Bumiputera 23/10-25/10 Acquired 2,925,900 MAXIS

Skim Amanah Saham Bumiputera 23/10-25/10 Acquired 1,200,000 CAPITAMALLS MALAYSIA TRUST

Lembaga Tabung Haji 24/10-25/10 Acquired 1,092,100 PARKSON HOLDINGS

Kumpulan Wang Persaraan 24/10 Acquired 506,900 FELDA GLOBAL VENTURES

Kumpulan Wang Persaraan 24/10 Acquired 98,500 KULIM (MALAYSIA)

Kumpulan Wang Persaraan 24/10 Acquired 44,600 GENTING PLANTATIONS

Lembaga Tabung Angkatan Tentera 18/10-23/10 Acquired 487,300 TIEN WAH PRESS HOLDINGS SOURCES: BMSB

Daybreak Malaysia

October 30, 2013

12

BMSB: Changes in shareholdings

Type of No. of Ave Price

29-Oct-13 Date transaction securities Company (RM)

GREAT EASTERN HOLDINGS LIMITED 23/10-24/10 Acquired 890,000 PUNCAK NIAGA HOLDINGS

Aberdeen Asset Management PLC 23/10-24/10 Acquired 53,600 UNITED PLANTATIONS

Aberdeen Asset Management PLC 22/10-24/10 Acquired 29,700 PANASONIC MANUFACTURING

Aberdeen Asset Management Asia 23/10-24/10 Acquired 18,900 PANASONIC MANUFACTURING

Aberdeen Asset Management Sdn Bhd 22/10-23/10 Acquired 2,800 PANASONIC MANUFACTURING

Mitsubishi UFJ Financial Group, Inc. 23/10 Acquired 6,900 UNITED PLANTATIONS

Mitsubishi UFJ Financial Group, Inc. 23/10 Acquired 2,200 PANASONIC MANUFACTURING

Mitsubishi UFJ Financial Group, Inc. 23/10 Acquired 2,000 TASEK CORPORATION

YTL POWER INTERNATIONAL 29/10 Shares Buy Back 6,075,300 YTL POWER INTERNATIONAL 1.87

PARKSON HOLDINGS 29/10 Shares Buy Back 29,200 PARKSON HOLDINGS 3.73 SOURCES: BMSB

Daybreak Malaysia

October 30, 2013

13

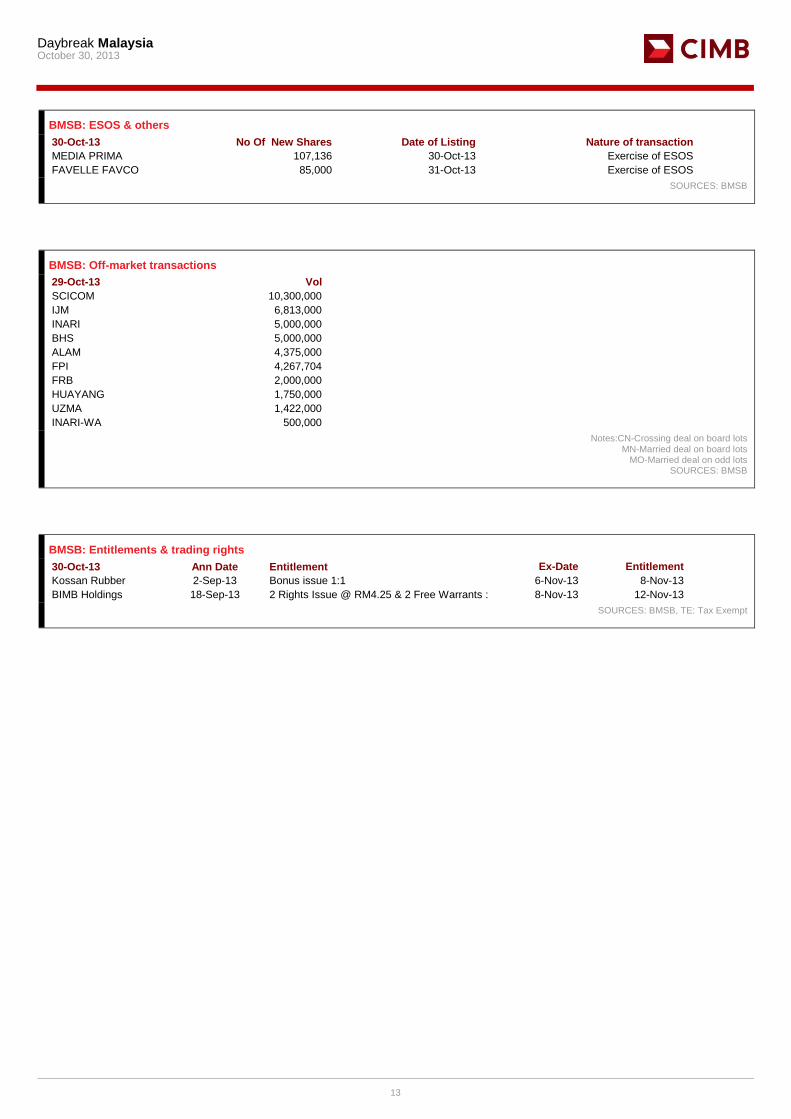

BMSB: ESOS & others

30-Oct-13 No Of New Shares Date of Listing Nature of transaction

MEDIA PRIMA 107,136 30-Oct-13 Exercise of ESOS

FAVELLE FAVCO 85,000 31-Oct-13 Exercise of ESOS SOURCES: BMSB

BMSB: Off-market transactions

29-Oct-13 Vol

SCICOM 10,300,000

IJM 6,813,000

INARI 5,000,000

BHS 5,000,000

ALAM 4,375,000

FPI 4,267,704

FRB 2,000,000

HUAYANG 1,750,000

UZMA 1,422,000

INARI-WA 500,000 Notes:CN-Crossing deal on board lots

MN-Married deal on board lots MO-Married deal on odd lots

SOURCES: BMSB

BMSB: Entitlements & trading rights

30-Oct-13 Ann Date Entitlement Ex-Date Entitlement

Kossan Rubber

Iindustries

2-Sep-13 Bonus issue 1:1 6-Nov-13 8-Nov-13

BIMB Holdings 18-Sep-13 2 Rights Issue @ RM4.25 & 2 Free Warrants :

5

8-Nov-13 12-Nov-13 SOURCES: BMSB, TE: Tax Exempt

Daybreak Malaysia

October 30, 2013

14

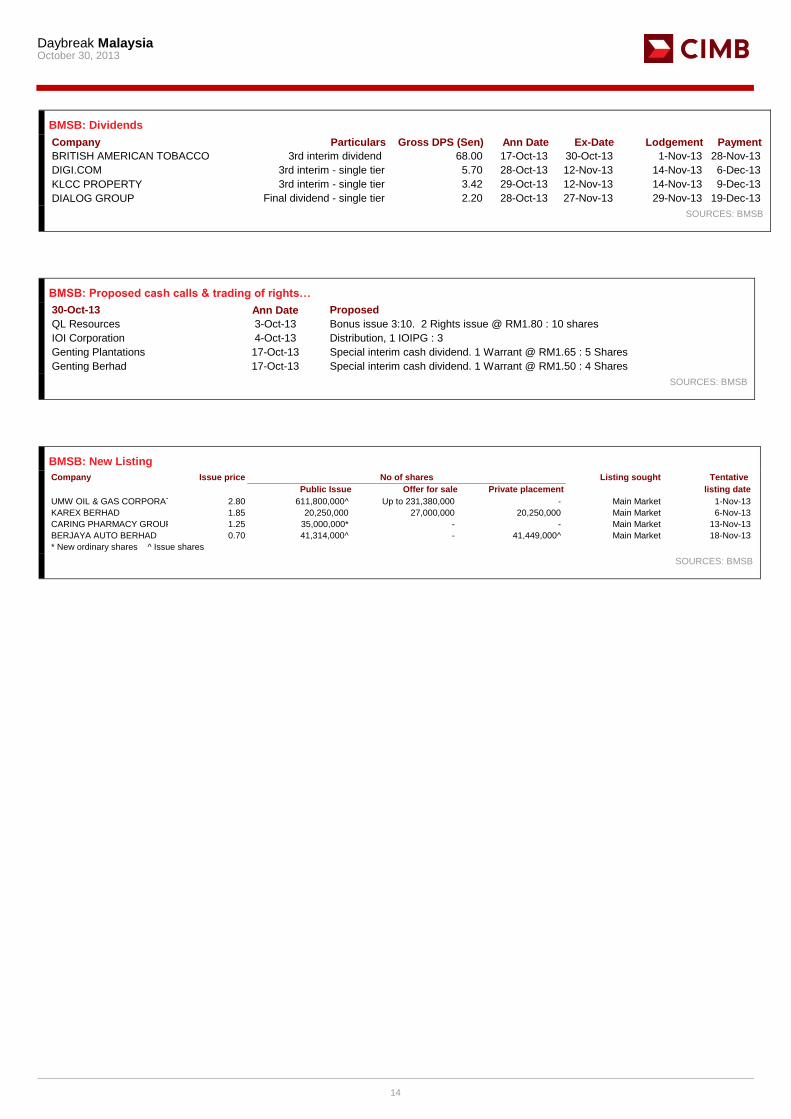

BMSB: Dividends

Company Particulars Gross DPS (Sen) Ann Date Ex-Date Lodgement Payment

BRITISH AMERICAN TOBACCO 3rd interim dividend 68.00 17-Oct-13 30-Oct-13 1-Nov-13 28-Nov-13

DIGI.COM 3rd interim - single tier 5.70 28-Oct-13 12-Nov-13 14-Nov-13 6-Dec-13

KLCC PROPERTY 3rd interim - single tier 3.42 29-Oct-13 12-Nov-13 14-Nov-13 9-Dec-13

DIALOG GROUP Final dividend - single tier 2.20 28-Oct-13 27-Nov-13 29-Nov-13 19-Dec-13 SOURCES: BMSB

BMSB: Proposed cash calls & trading of rights…

30-Oct-13 Ann Date Proposed

QL Resources 3-Oct-13 Bonus issue 3:10. 2 Rights issue @ RM1.80 : 10 shares

IOI Corporation 4-Oct-13 Distribution, 1 IOIPG : 3

Genting Plantations 17-Oct-13 Special interim cash dividend. 1 Warrant @ RM1.65 : 5 Shares

Genting Berhad 17-Oct-13 Special interim cash dividend. 1 Warrant @ RM1.50 : 4 Shares SOURCES: BMSB

BMSB: New Listing

Company Issue price Listing sought Tentative

Public Issue Offer for sale Private placement listing date

UMW OIL & GAS CORPORATION 2.80 611,800,000^ Up to 231,380,000 - Main Market 1-Nov-13

KAREX BERHAD 1.85 20,250,000 27,000,000 20,250,000 Main Market 6-Nov-13

CARING PHARMACY GROUP 1.25 35,000,000* - - Main Market 13-Nov-13

BERJAYA AUTO BERHAD 0.70 41,314,000^ - 41,449,000^ Main Market 18-Nov-13

* New ordinary shares ^ Issue shares

No of shares

SOURCES: BMSB

Daybreak Malaysia

October 30, 2013

15

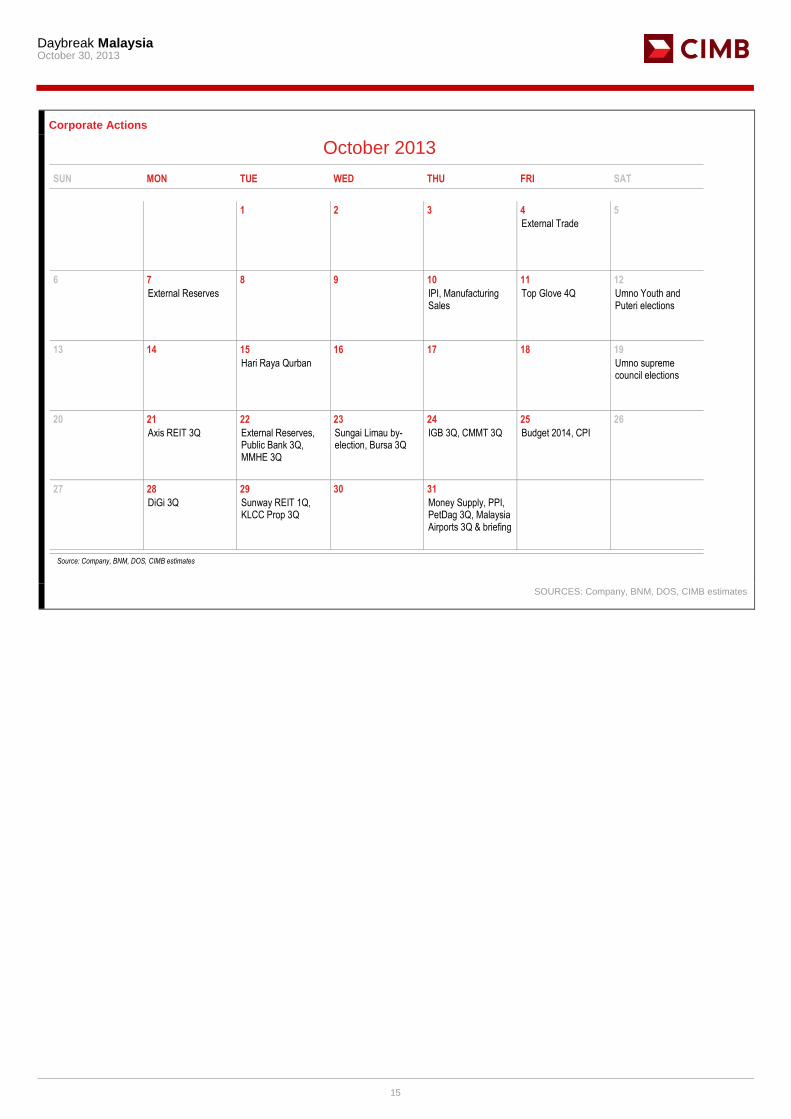

Corporate Actions

October 2013

SUN MON TUE WED THU FRI SAT

1 2 3 4 5

External Trade

6 7 8 9 10 11 12

External Reserves IPI, Manufacturing Sales

Top Glove 4Q Umno Youth and Puteri elections

13 14 15 16 17 18 19

Hari Raya Qurban Umno supreme council elections

20 21 22 23 24 25 26

Axis REIT 3Q External Reserves, Public Bank 3Q, MMHE 3Q

Sungai Limau by-election, Bursa 3Q

IGB 3Q, CMMT 3Q Budget 2014, CPI

27 28 29 30 31

DiGi 3Q Sunway REIT 1Q, KLCC Prop 3Q

Money Supply, PPI, PetDag 3Q, Malaysia Airports 3Q & briefing

Source: Company, BNM, DOS, CIMB estimates

SOURCES: Company, BNM, DOS, CIMB estimates

Daybreak Malaysia

October 30, 2013

16

Corporate Actions

November 2013

SUN MON TUE WED THU FRI SAT

1 2

3 4 5 6 7 8 9

Sungai Limau by-election

Awal Muharram Daibochi 3Q MPC, MISC 3Q, Nestle 3Q, Daibochi briefing

External Trade, Guinness 1Q, F&N briefing

10 11 12 13 14 15 16

IPI, Manufacturing Sales, External Reserves, Mah Sing 3Q, Nestle briefing

Hartalega 2Q, Maxis 3Q

GDP, BOP

17 18 19 20 21 22 23

Media Prima 3Q, Dialog 1Q, Perdana 3Q

CPI, KLK 4Q, Star 3Q, Prestariang 3Q, Bumi Armada 3Q

JTI 3Q, Tomypak 3Q External Reserves, QL 2Q, Kossan 3Q

24 25 26 27 28 29 30

UEM Sunrise 3Q, Wah Seong 3Q

E&O 2Q & briefing, Media Chinese 2Q, Bintulu Port 3Q

Media Chinese briefing, MyEG 1Q

Money Supply, PPI, Cuscapi 3Q, Asia File 2Q

Source: Company, BNM, DOS, CIMB estimates

SOURCES: Company, BNM, DOS, CIMB estimates

Daybreak Malaysia

October 30, 2013

17

DISCLAIMER

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

By accepting this report, the recipient hereof represents and warrants that he is entitled to receive such report in accordance with the restrictions set forth below and agrees to be bound by the limitations contained herein (including the ―Restrictions on Distributions‖ set out below). Any failure to comply with these limitations may constitute a violation of law. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this report may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

Unless otherwise specified, this report is based upon sources which CIMB considers to be reasonable. Such sources will, unless otherwise specified, for market data, be market data and prices available from the main stock exchange or market where the relevant security is listed, or, where appropriate, any other market. Information on the accounts and business of company(ies) will generally be based on published statements of the company(ies), information disseminated by regulatory information services, other publicly available information and information resulting from our research.

Whilst every effort is made to ensure that statements of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable as of the date of the document in which they are contained and must not be construed as a representation that the matters referred to therein will occur. Past performance is not a reliable indicator of future performance. The value of investments may go down as well as up and those investing may, depending on the investments in question, lose more than the initial investment. No report shall constitute an offer or an invitation by or on behalf of CIMB or its affiliates to any person to buy or sell any investments.

CIMB, its affiliates and related companies, their directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, CIMB, its affiliates and its related companies do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory, underwriting or placement services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report.

CIMB or its affiliates may enter into an agreement with the company(ies) covered in this report relating to the production of research reports. CIMB may disclose the contents of this report to the company(ies) covered by it and may have amended the contents of this report following such disclosure.

The analyst responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. No part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations(s) or view(s) in this report. CIMB prohibits the analyst(s) who prepared this research report from receiving any compensation, incentive or bonus based on specific investment banking transactions or for providing a specific recommendation for, or view of, a particular company. Information barriers and other arrangements may be established where necessary to prevent conflicts of interests arising. However, the analyst(s) may receive compensation that is based on his/their coverage of company(ies) in the performance of his/their duties or the performance of his/their recommendations and the research personnel involved in the preparation of this report may also participate in the solicitation of the businesses as described above. In reviewing this research report, an investor should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the duties of confidentiality, available on request.

Reports relating to a specific geographical area are produced by the corresponding CIMB entity as listed in the table below. The term ―CIMB‖ shall denote, where appropriate, the relevant entity distributing or disseminating the report in the particular jurisdiction referenced below, or, in every other case, CIMB Group Holdings Berhad ("CIMBGH") and its affiliates, subsidiaries and related companies.

Country CIMB Entity Regulated by

Australia CIMB Securities (Australia) Limited Australian Securities & Investments Commission

Hong Kong CIMB Securities Limited Securities and Futures Commission Hong Kong

Indonesia PT CIMB Securities Indonesia Financial Services Authority of Indonesia

India CIMB Securities (India) Private Limited Securities and Exchange Board of India (SEBI)

Malaysia CIMB Investment Bank Berhad Securities Commission Malaysia

Singapore CIMB Research Pte. Ltd. Monetary Authority of Singapore

South Korea CIMB Securities Limited, Korea Branch Financial Services Commission and Financial Supervisory Service

Taiwan CIMB Securities Limited, Taiwan Branch Financial Supervisory Commission

Thailand CIMB Securities (Thailand) Co. Ltd. Securities and Exchange Commission Thailand

Information in this report is a summary derived from CIMB individual research reports. As such, readers are directed to the CIMB individual research report or note to review the individual Research Analyst's full analysis of the subject company. Important disclosures relating to the companies that are the subject of research reports published by CIMB and the proprietary positions by CIMB and shareholdings of its Research Analysts’ who prepared the report in the securities of the company(s) are available in the individual research report.

The information contained in this research report is prepared from data believed to be correct and reliable at the time of issue of this report. CIMB may or may not issue regular reports on the subject matter of this report at any frequency and may cease to do so or change the periodicity of reports at any time. CIMB is under no obligation to update this report in the event of a material change to the information contained in this report. This report does not purport to contain all the information that a prospective investor may require. CIMB or any of its affiliates does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information and opinion contained in this report. Neither CIMB nor any of its affiliates nor its related persons shall be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

This report is general in nature and has been prepared for information purposes only. It is intended for circulation amongst CIMB and its affiliates’ clients generally and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. The information and opinions in this report are not and should not be construed or considered as an offer, recommendation or solicitation to buy or sell the subject securities, related investments or other financial instruments thereof.

Investors are advised to make their own independent evaluation of the information contained in this research report, consider their own individual investment objectives, financial situation and particular needs and consult their own professional and financial advisers as to the legal, business, financial, tax and other aspects before participating in any transaction in respect of the securities of company(ies) covered in this research report. The securities of such company(ies) may not be eligible for sale in all jurisdictions or to all categories of investors.

Australia: Despite anything in this report to the contrary, this research is provided in Australia by CIMB Securities (Australia) Limited (―CSAL‖) (ABN 84 002 768 701, AFS Licence number 240 530). CSAL is a Market Participant of ASX Ltd, a Clearing Participant of ASX Clear Pty Ltd, a Settlement Participant of ASX Settlement Pty Ltd, and, a participant of Chi X Australia Pty Ltd. This research is only available in Australia to persons who are ―wholesale clients‖ (within the meaning of the Corporations Act 2001 (Cth)) and is supplied solely for the use of such wholesale clients and shall not be distributed or passed on to any other person. This research has been prepared without taking into account the objectives, financial situation or needs of the individual recipient.

France: Only qualified investors within the meaning of French law shall have access to this report. This report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial instruments and it is not intended as a solicitation for the purchase of any financial instrument.

Hong Kong: This report is issued and distributed in Hong Kong by CIMB Securities Limited (―CHK‖) which is licensed in Hong Kong by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 6 (advising on corporate finance) activities. Any investors wishing to purchase or otherwise deal in the securities covered in this report should contact the Head of Sales at CIMB Securities Limited. The views and opinions in this research report are our own as of the date hereof and are subject to

Daybreak Malaysia

October 30, 2013

18

change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CHK has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CHK. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CHK. Unless permitted to do so by the securities laws of Hong Kong, no person may issue or have in its possession for the purposes of issue, whether in Hong Kong or elsewhere, any advertisement, invitation or document relating to the securities covered in this report, which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong (except if permitted to do so under the securities laws of Hong Kong).

India: This report is issued and distributed in India by CIMB Securities (India) Private Limited (―CIMB India‖) which is registered with SEBI as a stock-broker under the Securities and Exchange Board of India (Stock Brokers and Sub-Brokers) Regulations, 1992 and in accordance with the provisions of Regulation 4 (g) of the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, CIMB India is not required to seek registration with SEBI as an Investment Adviser.

The research analysts, strategists or economists principally responsible for the preparation of this research report are segregated from the other activities of CIMB India and they have received compensation based upon various factors, including quality, accuracy and value of research, firm profitability or revenues, client feedback and competitive factors. Research analysts', strategists' or economists' compensation is not linked to investment banking or capital markets transactions performed or proposed to be performed by CIMB India or its affiliates.

Indonesia: This report is issued and distributed by PT CIMB Securities Indonesia (―CIMBI‖). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBI has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMBI. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBI. Neither this report nor any copy hereof may be distributed in Indonesia or to any Indonesian citizens wherever they are domiciled or to Indonesia residents except in compliance with applicable Indonesian capital market laws and regulations.

Malaysia: This report is issued and distributed by CIMB Investment Bank Berhad (―CIMB‖). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMB has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMB. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

New Zealand: In New Zealand, this report is for distribution only to persons whose principal business is the investment of money or who, in the course of, and for the purposes of their business, habitually invest money pursuant to Section 3(2)(a)(ii) of the Securities Act 1978.

Singapore: This report is issued and distributed by CIMB Research Pte Ltd (―CIMBR‖). Recipients of this report are to contact CIMBR in Singapore in respect of any matters arising from, or in connection with, this report. The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBR has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only. If the recipient of this research report is not an accredited investor, expert investor or institutional investor, CIMBR accepts legal responsibility for the contents of the report without any disclaimer limiting or otherwise curtailing such legal responsibility. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBR.

As of October 29, 2013, CIMBR does not have a proprietary position in the recommended securities in this report.

South Korea: This report is issued and distributed in South Korea by CIMB Securities Limited, Korea Branch ("CIMB Korea") which is licensed as a cash equity broker, and regulated by the Financial Services Commission and Financial Supervisory Service of Korea.

The views and opinions in this research report are our own as of the date hereof and are subject to change, and this report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial investment instruments and it is not intended as a solicitation for the purchase of any financial investment instrument.

This publication is strictly confidential and is for private circulation only, and no part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB Korea.

Sweden: This report contains only marketing information and has not been approved by the Swedish Financial Supervisory Authority. The distribution of this report is not an offer to sell to any person in Sweden or a solicitation to any person in Sweden to buy any instruments described herein and may not be forwarded to the public in Sweden.

Taiwan: This research report is not an offer or marketing of foreign securities in Taiwan. The securities as referred to in this research report have not been and will not be registered with the Financial Supervisory Commission of the Republic of China pursuant to relevant securities laws and regulations and may not be offered or sold within the Republic of China through a public offering or in circumstances which constitutes an offer within the meaning of the Securities and Exchange Law of the Republic of China that requires a registration or approval of the Financial Supervisory Commission of the Republic of China.

Taiwan: This research report is not an offer or marketing of foreign securities in Taiwan. The securities as referred to in this research report have not been and will not be registered with the Financial Supervisory Commission of the Republic of China pursuant to relevant securities laws and regulations and may not be offered or sold within the Republic of China through a public offering or in circumstances which constitutes an offer or a placement within the meaning of the Securities and Exchange Law of the Republic of China that requires a registration or approval of the Financial Supervisory Commission of the Republic of China.

Thailand: This report is issued and distributed by CIMB Securities (Thailand) Company Limited (CIMBS). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBS has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMBS. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBS.

Corporate Governance Report:

The disclosure of the survey result of the Thai Institute of Directors Association (―IOD‖) regarding corporate governance is made pursuant to the policy of the Office of the Securities and Exchange Commission. The survey of the IOD is based on the information of a company listed on the Stock Exchange of Thailand and the Market for Alternative Investment disclosed to the public and able to be accessed by a general public investor. The result, therefore, is from the perspective of a third party. It is not an evaluation of operation and is not based on inside information.

The survey result is as of the date appearing in the Corporate Governance Report of Thai Listed Companies. As a result, the survey result may be changed after that date. CIMBS does not confirm nor certify the accuracy of such survey result.

Score Range 90 – 100 80 – 89 70 – 79 Below 70 or No Survey Result

Description Excellent Very Good Good N/A

United Arab Emirates: The distributor of this report has not been approved or licensed by the UAE Central Bank or any other relevant licensing authorities or governmental agencies in the United Arab Emirates. This report is strictly private and confidential and has not been reviewed by, deposited or registered with UAE Central Bank or any other licensing authority or governmental agencies in the United Arab Emirates. This report is being issued outside the United Arab Emirates to a limited number of institutional investors and must not be provided to any person other than the original recipient and may not be reproduced or used for any other purpose. Further, the information contained in this report is not intended to lead to the

Daybreak Malaysia

October 30, 2013

19

sale of investments under any subscription agreement or the conclusion of any other contract of whatsoever nature within the territory of the United Arab Emirates.

United Kingdom and Europe: In the United Kingdom and European Economic Area, this report is being disseminated by CIMB Securities (UK) Limited (―CIMB UK‖). CIMB UK is authorised and regulated by the Financial Services Authority and its registered office is at 27 Knightsbridge, London, SW1X 7YB. This report is for distribution only to, and is solely directed at, selected persons on the basis that those persons: (a) are persons that are eligible counterparties and professional clients of CIMB UK; (b) have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the ―Order‖); (c) are persons falling within Article 49 (2) (a) to (d) (―high net worth companies, unincorporated associations etc‖) of the Order; (d) are outside the United Kingdom; or (e) are persons to whom an invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000) in connection with any investments to which this report relates may otherwise lawfully be communicated or caused to be communicated (all such persons together being referred to as ―relevant persons‖). This report is directed only at relevant persons and must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this report relates is available only to relevant persons and will be engaged in only with relevant persons.

Only where this report is labelled as non-independent, it does not provide an impartial or objective assessment of the subject matter and does not constitute independent "investment research" under the applicable rules of the Financial Services Authority in the UK. Consequently, any such non-independent report will not have been prepared in accordance with legal requirements designed to promote the independence of investment research and will not subject to any prohibition on dealing ahead of the dissemination of investment research.

United States: This research report is distributed in the United States of America by CIMB Securities (USA) Inc, a U.S.-registered broker-dealer and a related company of CIMB Research Pte Ltd, CIMB Investment Bank Berhad, PT CIMB Securities Indonesia, CIMB Securities (Thailand) Co. Ltd, CIMB Securities Limited, CIMB Securities (Australia) Limited, CIMB Securities (India) Private Limited,and is distributed solely to persons who qualify as "U.S. Institutional Investors" as defined in Rule 15a-6 under the Securities and Exchange Act of 1934. This communication is only for Institutional Investors whose ordinary business activities involve investing in shares, bonds and associated securities and/or derivative securities and who have professional experience in such investments. Any person who is not a U.S. Institutional Investor or Major Institutional Investor must not rely on this communication. The delivery of this research report to any person in the United States of America is not a recommendation to effect any transactions in the securities discussed herein, or an endorsement of any opinion expressed herein. CIMB Securities (USA) Inc, is a FINRA/SIPC member and takes responsibility for the content of this report. For further information or to place an order in any of the above-mentioned securities please contact a registered representative of CIMB Securities (USA) Inc.

Other jurisdictions: In any other jurisdictions, except if otherwise restricted by laws or regulations, this report is only for distribution to professional, institutional or sophisticated investors as defined in the laws and regulations of such jurisdictions.

Recommendation Framework #1 *

Stock Sector OUTPERFORM: The stock's total return is expected to exceed a relevant benchmark's total return by 5% or more over the next 12 months.

OVERWEIGHT: The industry, as defined by the analyst's coverage universe, is expected to outperform the relevant primary market index over the next 12 months.

NEUTRAL: The stock's total return is expected to be within +/-5% of a relevant benchmark's total return.

NEUTRAL: The industry, as defined by the analyst's coverage universe, is expected to perform in line with the relevant primary market index over the next 12 months.

UNDERPERFORM: The stock's total return is expected to be below a relevant benchmark's total return by 5% or more over the next 12 months.

UNDERWEIGHT: The industry, as defined by the analyst's coverage universe, is expected to underperform the relevant primary market index over the next 12 months.

TRADING BUY: The stock's total return is expected to exceed a relevant benchmark's total return by 5% or more over the next 3 months.

TRADING BUY: The industry, as defined by the analyst's coverage universe, is expected to outperform the relevant primary market index over the next 3 months.

TRADING SELL: The stock's total return is expected to be below a relevant benchmark's total return by 5% or more over the next 3 months.

TRADING SELL: The industry, as defined by the analyst's coverage universe, is expected to underperform the relevant primary market index over the next 3 months.

* This framework only applies to stocks listed on the Singapore Stock Exchange, Bursa Malaysia, Stock Exchange of Thailand, Jakarta Stock Exchange, Australian Securities Exchange, Taiwan Stock Exchange

and National Stock Exchange of India/Bombay Stock Exchange. Occasionally, it is permitted for the total expected returns to be temporarily outside the prescribed ranges due to extreme market volatility or other

justifiable company or industry-specific reasons.

CIMB Research Pte Ltd (Co. Reg. No. 198701620M)

Recommendation Framework #2 **

Stock Sector

OUTPERFORM: Expected positive total returns of 10% or more over the next 12 months. OVERWEIGHT: The industry, as defined by the analyst's coverage universe, has a high number

of stocks that are expected to have total returns of +10% or better over the next 12 months.

NEUTRAL: Expected total returns of between -10% and +10% over the next 12 months. NEUTRAL: The industry, as defined by the analyst's coverage universe, has either (i) an equal

number of stocks that are expected to have total returns of +10% (or better) or -10% (or worse), or

(ii) stocks that are predominantly expected to have total returns that will range from +10% to -10%;

both over the next 12 months.

UNDERPERFORM: Expected negative total returns of 10% or more over the next 12 months. UNDERWEIGHT: The industry, as defined by the analyst's coverage universe, has a high number

of stocks that are expected to have total returns of -10% or worse over the next 12 months.

TRADING BUY: Expected positive total returns of 10% or more over the next 3 months. TRADING BUY: The industry, as defined by the analyst's coverage universe, has a high number

of stocks that are expected to have total returns of +10% or better over the next 3 months.

TRADING SELL: Expected negative total returns of 10% or more over the next 3 months. TRADING SELL: The industry, as defined by the analyst's coverage universe, has a high number

of stocks that are expected to have total returns of -10% or worse over the next 3 months.

** This framework only applies to stocks listed on the Korea Exchange, Hong Kong Stock Exchange and China listings on the Singapore Stock Exchange. Occasionally, it is permitted for the total expected returns

to be temporarily outside the prescribed ranges due to extreme market volatility or other justifiable company or industry-specific reasons.

Corporate Governance Report of Thai Listed Companies (CGR). CG Rating by the Thai Institute of Directors Association (IOD) in 2012.

AAV – not available, ADVANC - Excellent, AEONTS – Good, AMATA - Very Good, ANAN – not available, AOT - Excellent, AP - Very Good, BANPU - Excellent , BAY - Excellent , BBL - Excellent, BCH – not available, BCP - Excellent, BEC - Very Good, BGH - not available, BJC – Very Good, BH - Very Good, BIGC - Very Good, BTS - Excellent, CCET - Good, CENTEL – Very Good, CK - Very Good, CPALL - Very Good, CPF - Very Good, CPN - Excellent, DELTA - Very Good, DTAC - Very Good, EGCO – Excellent, ERW – Excellent, GLOBAL - Good, GLOW - Very Good, GRAMMY – Excellent, HANA - Very Good, HEMRAJ - Excellent, HMPRO - Very Good, INTUCH – Very Good, ITD – Very Good, IVL - Very Good, JAS – Very Good, KAMART – not available, KBANK - Excellent, KK – Excellent, KTB - Excellent, LH - Very Good, LPN - Excellent, MAJOR - Good, MAKRO – Very Good, MCOT - Excellent, MINT - Very Good, PS - Excellent, PSL - Excellent, PTT - Excellent, PTTGC - Excellent, PTTEP - Excellent, QH - Excellent, RATCH - Excellent, ROBINS - Excellent, RS – Excellent, SAMART – Excellent, SC – Excellent, SCB - Excellent, SCC - Excellent, SCCC - Very Good, SIRI - Good, SPALI - Very Good, SRICHA – not available, SSI – not available, STA - Good, STEC - Very Good, TCAP - Very Good, THAI - Excellent, THCOM – Very Good, TICON – Very Good, TISCO - Excellent, TMB - Excellent, TOP - Excellent, TRUE - Very Good, TTW – Very Good, TUF - Very Good, VGI – not available, WORK – Good.

Daybreak Malaysia

October 30, 2013

20