business planning using life insurance retain, recruit and rewardretain, recruit and reward

TRANSCRIPT

Business Planning Using Life Insurance

Retain, Recruit and Reward

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

2What is Business Insurance?

• The purchase of life insurance by an employer on the life of an employee

• Used to provide an additional benefit in an informally funded non-qualified deferred compensation plan or to protect the business in the event of the death of a key individual.

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

3Types of Business Life Insurance Plans

• Key Person

• Executive Bonus / REBAs

• Deferred Compensation Plan• Salary Deferral• SERPs

• Split Dollar

• Buy-Sell Arrangements

Key Person Insurance

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

5Key Person Insurance

• Insurance Policy taken out on the life of a key employee to protect the business in case of sudden death.

• A key employee is anyone in the business whose loss would affect profits and day-to-day operations.

• Owner, Partner, or irreplaceable executive

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

6Benefits of Key Person Insurance

• Protects the business from financial loss due to the death of key employee

• Business may borrow from the policy cash value*

• Death benefit is received by the company directly free from income taxes**

* Withdrawals and loans from life insurance policies, which are classified as modified endowment contracts, may be subject to tax at the time of withdrawal. A federal tax penalty may also apply if the withdrawal or loan is taken before age 59 ½. Withdrawals and loans also have the effect of reducing the Death Benefit and Cash Surrender Value. Consult your Financial Advisor for more information.

** Although Key-Man Insurance does not require IRS approval the business must ensure they are compliant with IRS Code 101(j) to avoid possible taxation of death benefit for policies placed after 2006.

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

7How Does Key Person Insurance Work?

• Business purchases a life insurance policy on a key employee

• Business is the owner and beneficiary of the policy

• Business pays the entire premium.

Insurance Policy

BusinessEmployee

Employee = Insured Business = Owner / Beneficiary

Business has on-file a

signed 101(j) form by

employee

Non-Qualified Executive Benefit Plans

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

9Non-Qualified Deferred Compensation

• Arrangements between an employee and executive to provide key executives with additional retirement benefits

• Selective and does not need to be offered to all employees

• Used to retain, recruit and reward key employees

10Types of Non-Qualified Deferred Compensation Plans

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Employee Financed

Employer/Employee Financed

Employer Financed

Group Plans

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

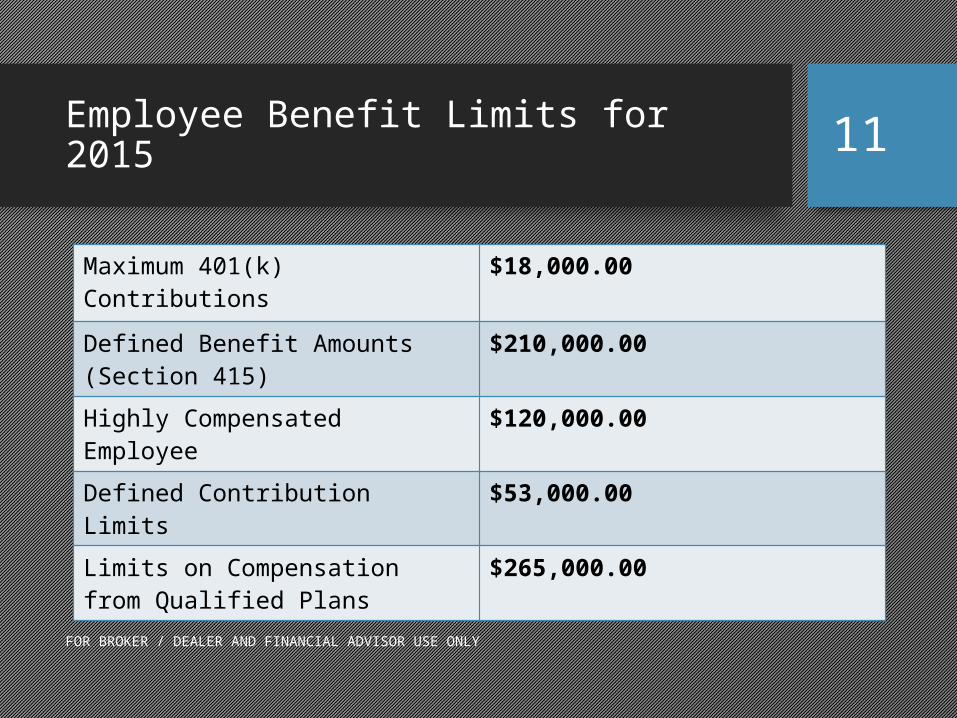

11Employee Benefit Limits for 2015

Maximum 401(k) Contributions $18,000.00

Defined Benefit Amounts (Section 415)

$210,000.00

Highly Compensated Employee $120,000.00

Defined Contribution Limits $53,000.00

Limits on Compensation from Qualified Plans

$265,000.00

12Reverse Discrimination

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

200,000 225,000 250,000 300,000 400,000 500,0000%

10%

20%

30%

40%

50%

60%

70%

Retirement Benefits as % of Final Salary

Retirement Income

13The Power of Deferred Compensation

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

$10K Invested @ 5% $6K Invested @ 5%$0.00

$5,000.00

$10,000.00

$15,000.00

$20,000.00

$25,000.00

$30,000.00

10 yrs 15 yrs 20 yrs

Assumes lump sum deferral amounts of $10,000 growing over 20 years at 5% compared to a lump sum of $6,000 ($1-,000 at 40% after-tax_ also growing at 5% for 20 years.

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

14Salary Deferral Plans

• Executives elect to defer part of their salary

• Often referred to as 401(k) mirror plans

• More flexible than standard Qualified Plans

• Do not have maximum deferral limits

• May exclude rank and file employees

• Executive financed plans

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

15How Salary Deferral Plans Work

• Executive elects to defer a certain amount at the beginning of the year

• The amount is credited to a “phantom” interest bearing account

• Will be distributed for a certain period of time – starting at retirement

16The Power of Salary Deferrals

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Deferred Non-Deferred$0.00

$20,000.00

$40,000.00

$60,000.00

$80,000.00

$100,000.00

$120,000.00

$140,000.00

$160,000.00

$180,000.00

Column1

This example assumes a one-year deferral of $55,000 for 15 years into a phantom account growing at 7.5%. The non-deferred cash assumes the same $55,000 after-tax (40% income tax rate) at 7.5%. Total for deferred is $162,738.25 and non-deferred is $97,642.95

Salary Deferral Withdrawals

17The Salary Deferral Plan – The Concept

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Executive

Employer

Specifics:

• The executive agrees to defer a portion of income• The employer agrees to provide a specific flow of income at a specific future

time.• The employer uses the deferred income to purchase a policy. Policy benefits

are used to fund the agreed to retirement compensation.

Agreement to use deferral to purchase life

insurance policy

Agreement to defer a specified

amount of income

Employer purchases and owns the policy

Life Insurance Company

18The Salary Deferral Plan – The Structure

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Notes:

• The Employer is able to provide significant pre and post retirement benefits on a deferred basis.

• The Employer’s cost is significantly reduced and stabilized with complete recovery possible through direct receipt of tax free death benefit proceeds.

• The executive enjoys substantial retirement and family security benefits.

Executive

Beneficiaries

Employer

Cash Value to fund deferred compensation

Tax Free death benefit to fund

continuing compensation to

heirs

Life Insurance Policy

Pre Retirement Compensation

Post Retirement Compensation

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

19Supplemental Executive Retirement Plan (SERP)

• Employer sponsored non-qualified deferred compensation plan

• Provides retirement benefits to highly compensated executives

• Can be used with qualified plans

• Combats “reverse discrimination”

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

20How Does a SERP Work?

• Corporation and select executives enter into an agreement that pays the executives a certain amount at retirement

• Can be informally funded with life insurance

• Employer is the owner and beneficiary of the policy.

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

21Executive Bonus Plans

• Employer/executive financed plans

• An arrangement between the executive and the corporation

• The corporation pays the premium on a life insurance policy on the executive

• Executive is the owner and beneficiary of the policy.

22Advantages of a Bonus Plan

• Corporation• Simple to install• No minimum or maximum lives• Employer cost may be tax deductible

• Executive• Death benefit protection• Supplemental retirement income• Can access the policy cash value at anytime

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

*Withdrawals and loans from life insurance policies, which are classified as modified endowment contracts, may be subject to tax at the time the withdrawal or loan is made. A federal tax penalty may also apply if the withdrawal or loan is taken before age 59 1/2. Withdrawals and loans also have the effect of reducing the Death Benefit and Cash Surrender Value. Consult your Financial Advisor.

23How Does a Bonus Plan Work?

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

*Withdrawals and loans from life insurance policies, which are classified as modified endowment contracts, may be subject to tax at the time the withdrawal or loan is made. A federal tax penalty may also apply if the withdrawal or loan is taken before age 59 1/2. Withdrawals and loans also have the effect of reducing the Death Benefit and Cash Surrender Value. Consult your Financial Advisor.

Corporation Executive

Insurance Policy

IRS

Bonus Premium Amount

Pays Premium

In retirement, takes withdrawals

Pays tax to IRS on premium

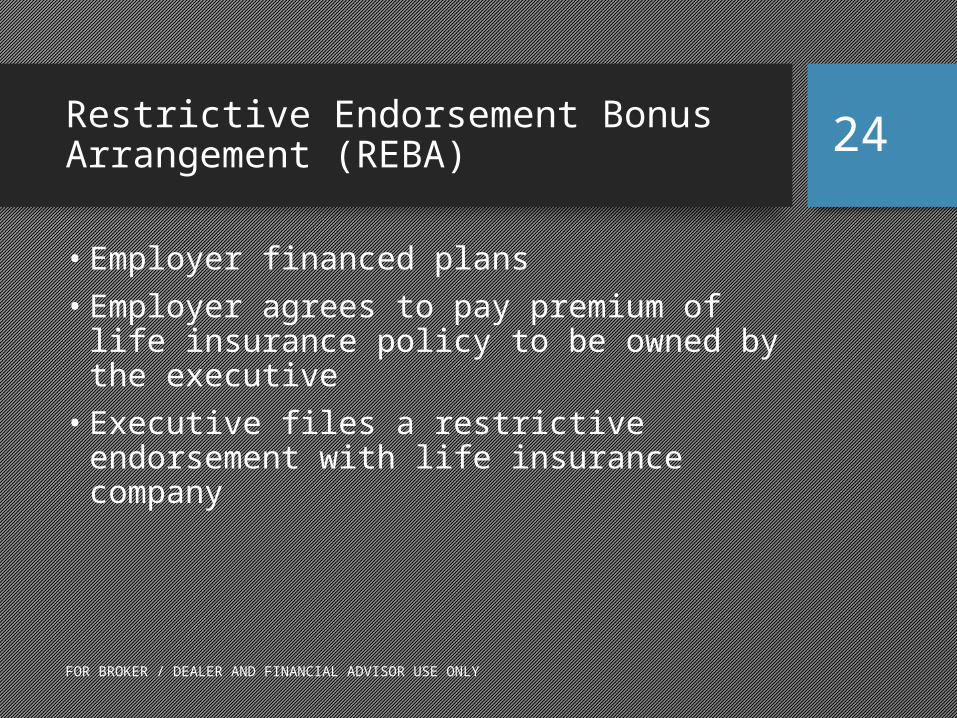

24Restrictive Endorsement Bonus Arrangement (REBA)

• Employer financed plans

• Employer agrees to pay premium of life insurance policy to be owned by the executive

• Executive files a restrictive endorsement with life insurance company

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

25Advantages of a REBA

• Corporation• Distinguished compensation package• Minimal set-up cost• “Golden handcuffs”

• Executive• Portable death benefit• Supplemental retirement income

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

*Withdrawals and loans from life insurance policies, which are classified as modified endowment contracts, may be subject to tax at the time the withdrawal or loan is made. A federal tax penalty may also apply if the withdrawal or loan is taken before age 59 1/2. Withdrawals and loans also have the effect of reducing the Death Benefit and Cash Surrender Value. Consult your Financial Advisor.

26REBA Agreement

• Prevents the executive from• Surrendering the cash value• Taking loans and withdrawals from the policy• Changing ownership• Using the policy as collateral

• Executive Can• Name the beneficiary

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

*Withdrawals and loans from life insurance policies, which are classified as modified endowment contracts, may be subject to tax at the time the withdrawal or loan is made. A federal tax penalty may also apply if the withdrawal or loan is taken before age 59 1/2. Withdrawals and loans also have the effect of reducing the Death Benefit and Cash Surrender Value. Consult your Financial Advisor.

Split Dollar Arrangements

28Advantages Split Dollar Plans

• Corporation• Death benefit protection• Access to cash values• Selective• Simple to implement

• Executive• Death benefit protection• Protects insurability

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

29How Does a Split Dollar Plan Work?

• Corporation and executive enter into an arrangement

• The corporation will pay the bulk of the premium

• The executive pays the economic benefit amount.

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

30Endorsement Method

• Mandatory for plans when the business seeks to recover amount in excess of premium paid, i.e. key person indemnity or deferred compensation.

• Ideal when control of the plan is to be with employer providing benefit, or a Non-Owner employee

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

31Endorsement Method

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Corporate

Execu-tive

Relative Premiums

Policy Premium Split

32Endorsement Method

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Policy Proceeds Split

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$1,800,000

$2,000,000

Executive Death Benefit Excess Corportate Cash ValueCorporate Return of Premium

33Collateral Assignment Method

• In most cases it’s the customary method used to remove proceeds from majority shareholder’s estate

• Debtor-creditor relationship is created

• Places effective control in hands of insured/executive

• Ideal when ultimate objective is to provide continuing post-retirement coverage

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

34Collateral Assignment Method

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Policy Cash Value Split

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

Balance To Executive Employer Return of Premium

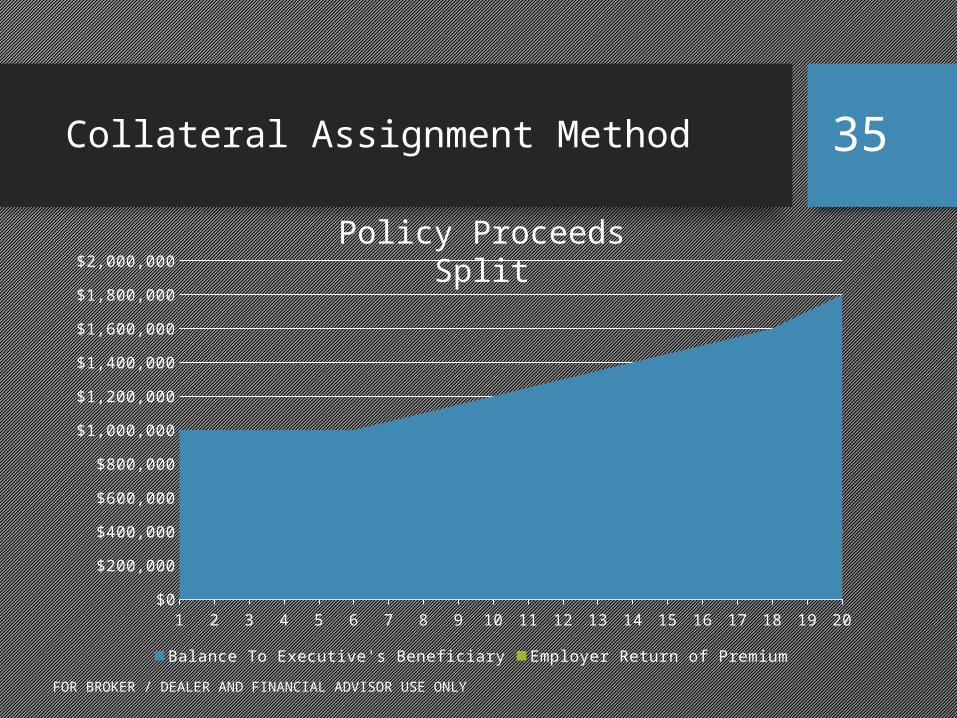

35Collateral Assignment Method

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Policy Proceeds Split

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$1,800,000

$2,000,000

Balance To Executive's Beneficiary Employer Return of Premium

Split Dollar Summary

Buy-Sell Arrangements

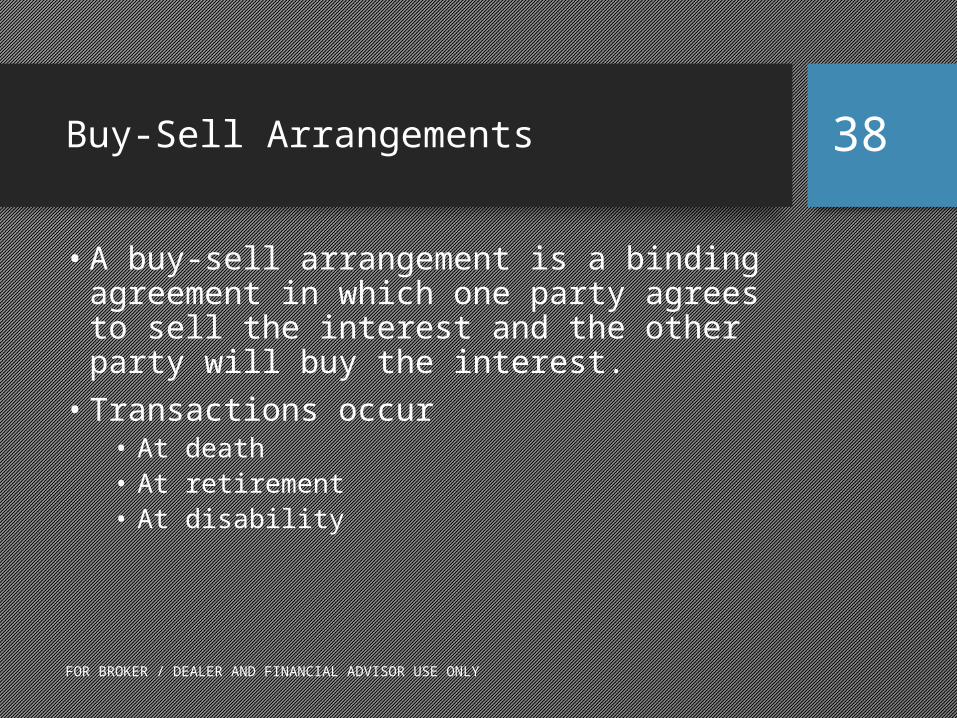

38Buy-Sell Arrangements

• A buy-sell arrangement is a binding agreement in which one party agrees to sell the interest and the other party will buy the interest.

• Transactions occur• At death• At retirement• At disability

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

39Types of Buy-Sell Arrangements

• Stock Redemption or Entity Purchase• Cross Purchase• Wait and See

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

40Stock Redemption or Entity Plan

• The business agrees to buy life insurance on the lives of the owners

• Agreement states that the owners or their estates agree to sell interest in the business and the business agrees to buy it.

• Business is the owner and beneficiary of the life insurance policy.

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

41Stock Redemption or Entity Plan

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Pays Premiums

Agreement Agreement

During Lifetime

The Business owns insurance policies on each owner

Insurance Co.

Owner A Owner B

Business

42Stock Redemption or Entity Plan

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Business

Pays Death Benefit

CashBusinessInterest

Upon A’s Death

Stock Passes

Owner B

A’s Family or Estate

Insurance Co.

43Cross-Purchase Plan

• Owners take life insurance policies out on each other

• Survivor purchases deceased owner’s shares in company

• Life insurance proceeds help to provide the funds

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

44Cross Purchase Plan

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

During Lifetime

Pays Premiums Pays Premiums

Business

Insurance Co.

Owner BOwner A Each Owner Obtains Insurance On the Other

45Advantages of Cross Purchase

• Purchasing shareholder will get step-up in cost basis

• Life insurance proceeds are income tax free

• Avoids possible treatment of redemption as a dividend.

• No AMT or accumulated earnings tax problems

• Can reallocate ownership of the surviving owners by purchasing varying amounts of the deceased owner’s shares.

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

46Cross Purchase Plan

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Stock Passes

CashA’s Family or Estate

Business

Business Interest

Upon A’s Death

Pays Death Benefit

Insurance Co.

Owner B

47Wait and See Agreement

• Owners agree to buy and sell their shares but the price is not determined until death, retirement or disability

• Owners purchase life insurance on each other

• Business has right of first refusal, owner second right, and the business must purchase remaining shares

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

48“Wait and See” funded by owners

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

During Lifetime

Each Owner Obtains Insurance On the Other

Pays Premiums Pays PremiumsBusiness

Agreement

Pays Premiums

Owner BOwner A

Insurance Co.

49“Wait and See” funded by owners

FOR BROKER / DEALER AND FINANCIAL ADVISOR USE ONLY

Upon A’s Death

Stock Passes

Death Benefit

Option toPurchase

2nd

Option toPurchase

MustPurchase

3rd1st $

$

$

Insurance Co.

Owner B

Business

A’s Family or Estate

For More Information

MVP Financial Services, [email protected]

www.mvp4me.com/our-staff

Business Planning Using Life Insurance