boletim do banco central do brasil – annual report 2011 · 2013-05-27 · 2 boletim do banco...

TRANSCRIPT

ISSN 1517-7270CGC 00.038.166/0001-05

Boletim do Banco Central do Brasil Brasília v. 47 Annual 2011 P. 1-222 Report

2 Boletim do Banco Central do Brasil – Annual Report 2011

Boletim do Banco Central do BrasilPublished annually by the Banco Central do Brasil/Department of Economics (Depec). The contents and their correspondent statistical tables are under the charge of the following component parts:

The Brazilian Economy – Consultative Group on Domestic Economic Activity (Coace) (E-mail: [email protected]); Money and Credit – Monetary and Banking Division (Dimob) (E-mail: [email protected]); Capital and Financial Markets – Monetary and Banking Division (Dimob) (E-mail: [email protected]);Public Finance – Public Finance Division (Difin) (E-mail: [email protected]);Economic-Financial Relations with the International Community – Balance of Payments Division (Dibap) (E-mail: [email protected]);The International Economy – Consultative Group on Economic Research and Analysis (Copec)(E-mail: [email protected]);International Financial Organizations – Departament of Foreign Debt and External Relations (Derin)(E-mail: [email protected]);

Information on the Boletim:

Phone (55.61) 3414-1009Fax (55.61) 3414-2036

Subscription request: complete and print the form that can be found at the site www.bcb.gov.br, and send it with a cheque for the appropriate amount payable to Banco Central do Brasil, at the following prices: R$375,00 (domestic) and US$231,00 (abroad) to the General Control of Publications. Subscription to the Boletim includes twelve monthly issues, the Annual Report and four issues of the Inflation Report.

Reproduction permitted only if source is stated: Boletim do Banco Central do Brasil, Volume 47, Annual Report 2011

General Control of Publications

Banco Central do BrasilSecre/Surel/CogivSBS – Quadra 3 – Bloco B – Edifício-Sede – 1º andarCaixa Postal 8.67070074-900 Brasília – DF – BrazilPhones: (55.61) 3414-3710 and 3414-3565Fax: (55.61) 3414-3626E-mail: [email protected]

Single copy: US$21.16

Statistical Conventions: ... data not available. - nil or non-existence of the event considered.0 ou 0.0 less than half the final digit shown. * preliminary figures.

A hiphen (-) between years (1970-75) indicates the years covered, including the beginning and ending years.A bar (/) between years (1970/75) indicates the average of the years covered, including the beginning and ending years, or even crop or agreement year, when mentioned in the text.

Minor discrepancies between constituent figures and totals as well as percentage changes are due to rounding.

There are no references to sources in tables and graphs originated in the Banco Central do Brasil.

Address

Banco Central do BrasilSecre/Surel/DiateSBS – Quadra 3 – Bloco B – Edifício-Sede – 2º subsolo70074-900 Brasília - DFIDDD: (55) 0800 9792345Fax: (55.61) 3414-2553Internet: <http//www.bcb.gov.br>

Summary 3

Summary

Introduction ....................................................................................................11I- The Brazilian Economy ................................................................................ 13 Activity level ................................................................................................... 13 Gross Domestic Product ................................................................................. 13 Central Bank Index of Economic Activity ...................................................... 17 Investments ..................................................................................................... 18 Industrial output indicators ............................................................................. 20 Services ........................................................................................................... 23 Commerce Indicators ...................................................................................... 24 Agricultural output indicators ......................................................................... 26 Livestock ......................................................................................................... 28 Agricultural policy .......................................................................................... 28 Productivity ..................................................................................................... 29 Energy ........................................................................................................... 29 Employment indicators ................................................................................... 30 Wage and earnings indicators ......................................................................... 32 Price indicators ............................................................................................... 33 General price indices ...................................................................................... 33 Consumer price indices ................................................................................... 34 Regulated prices .............................................................................................. 36 Cores ........................................................................................................... 37

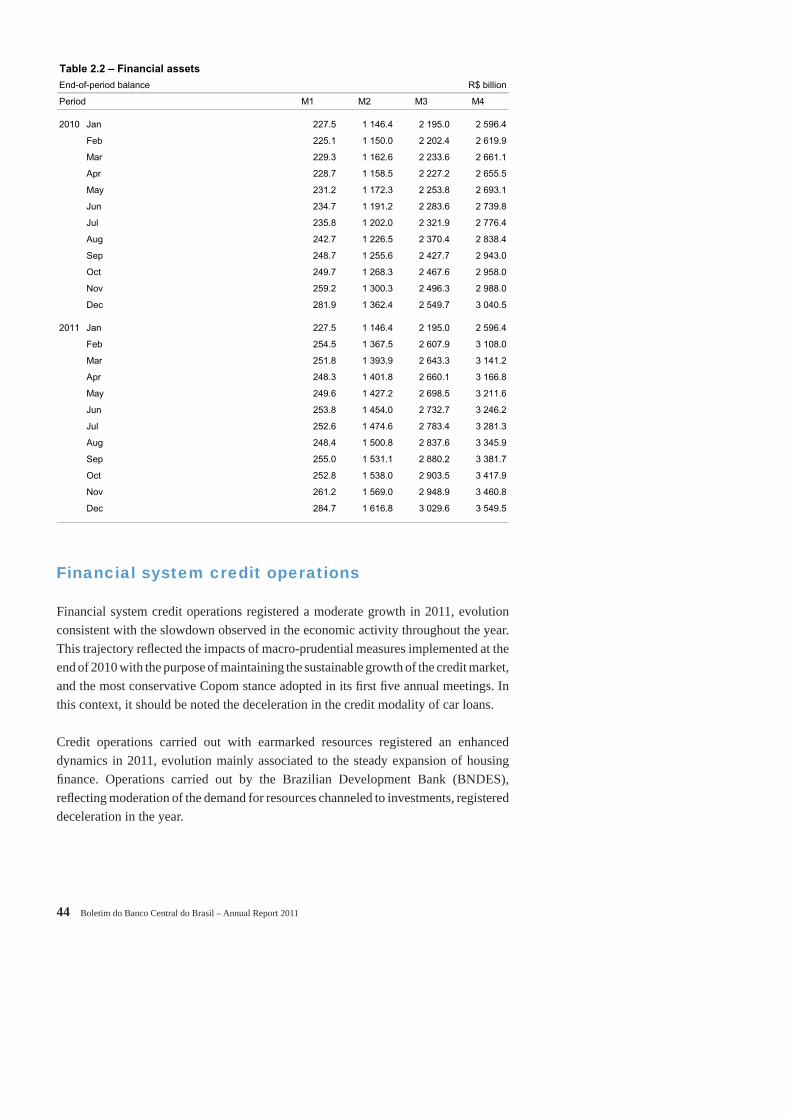

II- Money and Credit ......................................................................................... 39 Monetary policy .............................................................................................. 39 Monetary aggregates ....................................................................................... 39 Financial system credit operations .................................................................. 44 National Financial System .............................................................................. 50

4 Boletim do Banco Central do Brasil – Annual Report 2011

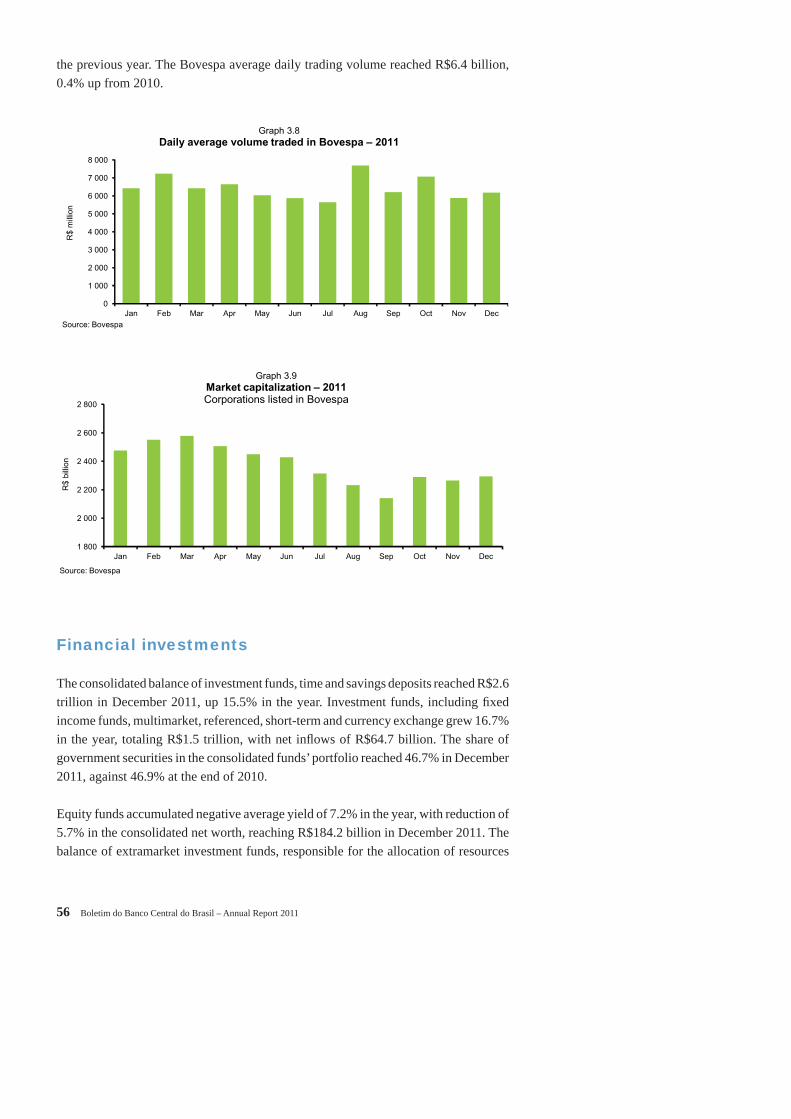

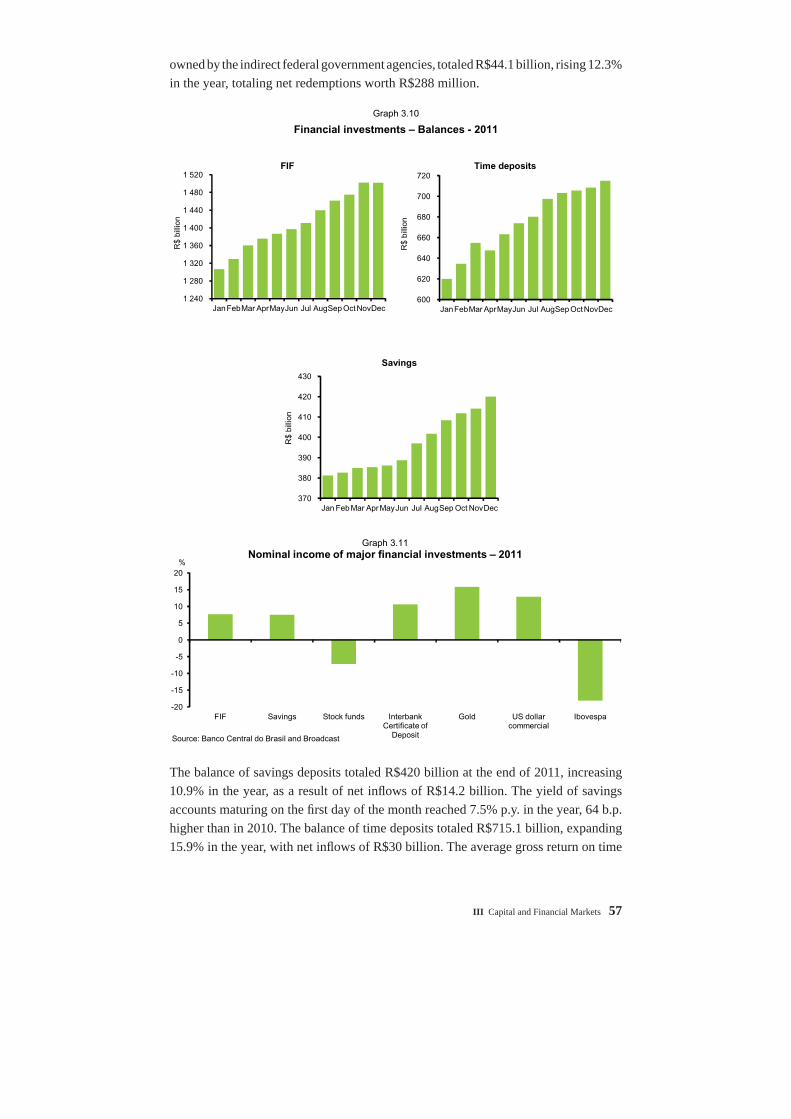

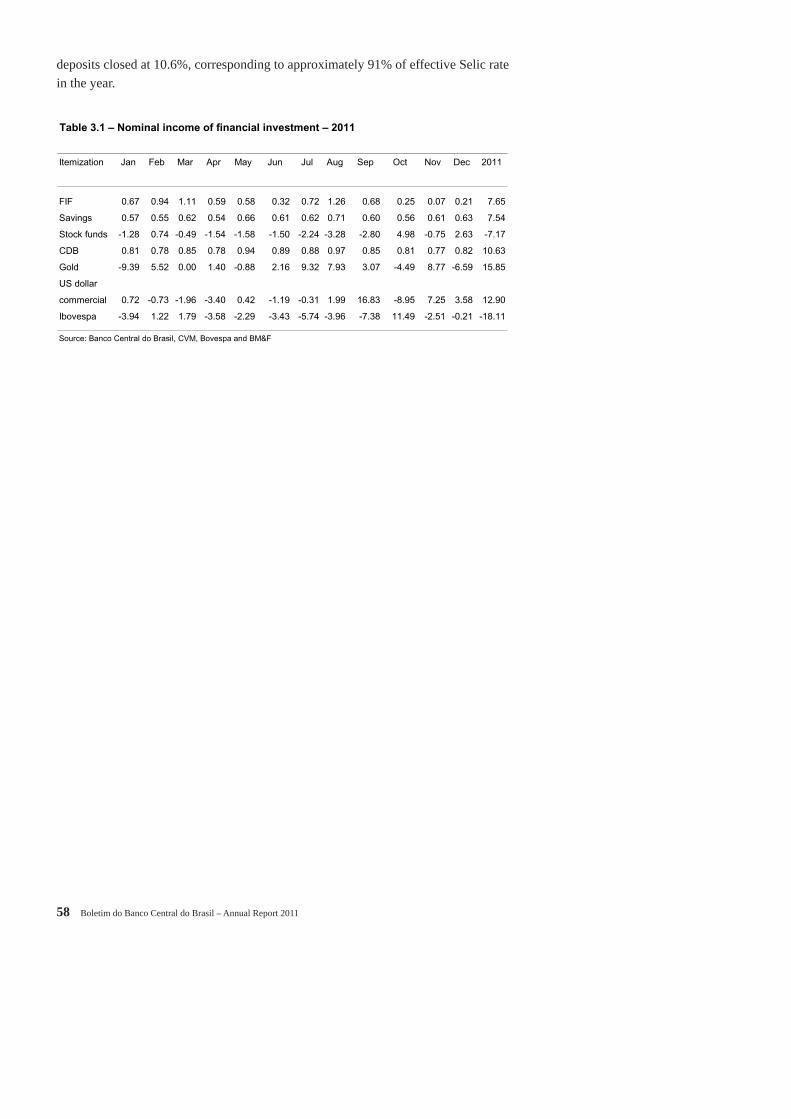

III- Capital and Financial Markets .................................................................... 53 Real interest rates and market expectations .................................................... 53 Capital markets ............................................................................................... 54 Financial investments ..................................................................................... 56

IV- Public Finance ............................................................................................... 59 Tax, fiscal and budget policies ........................................................................ 59 Other economic policy measures .................................................................... 60 Public Sector Borrowing Requirements ......................................................... 61 Federal securities debt .................................................................................... 65 Public Sector Net Debt ................................................................................... 69 Collection of federal taxes and contributions ................................................. 73 Social Security ................................................................................................ 74 State and municipal finances .......................................................................... 75

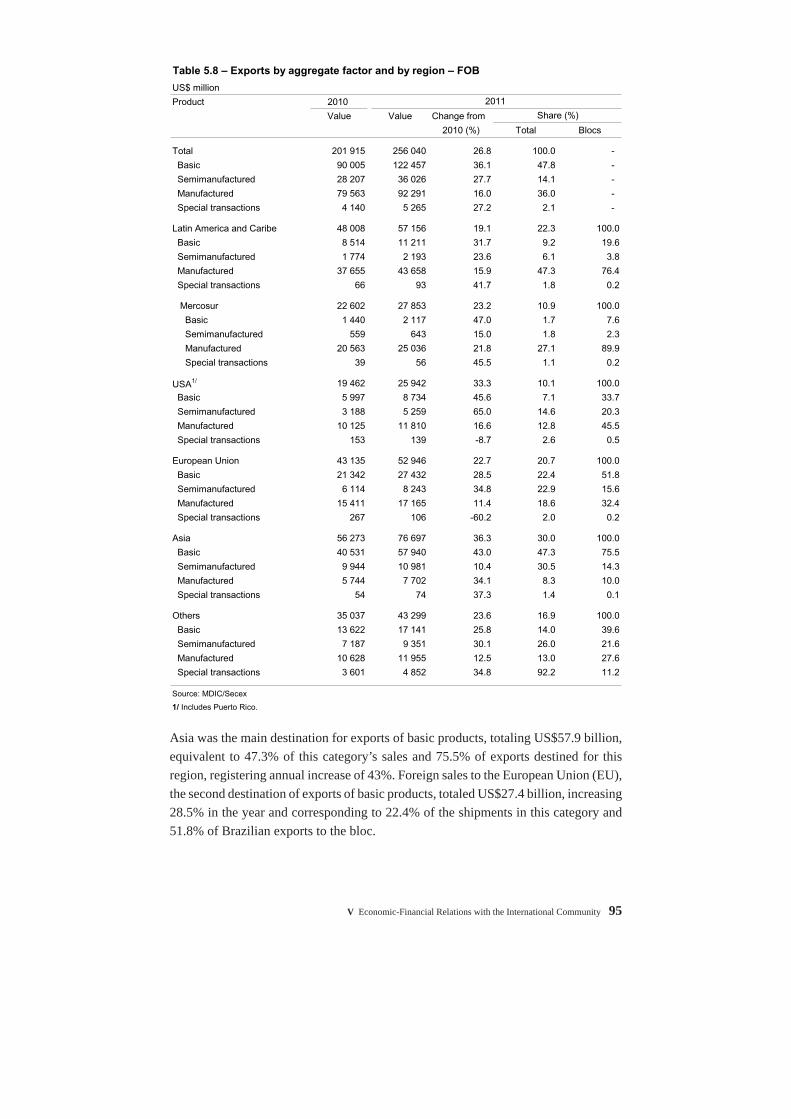

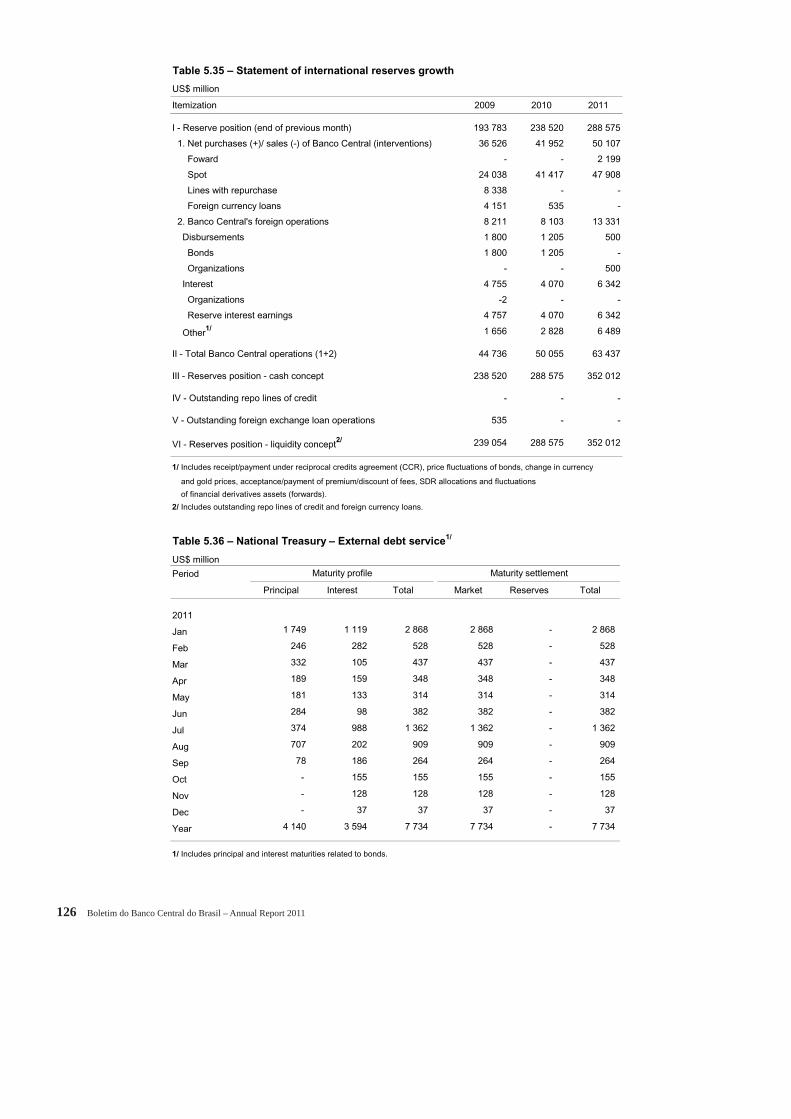

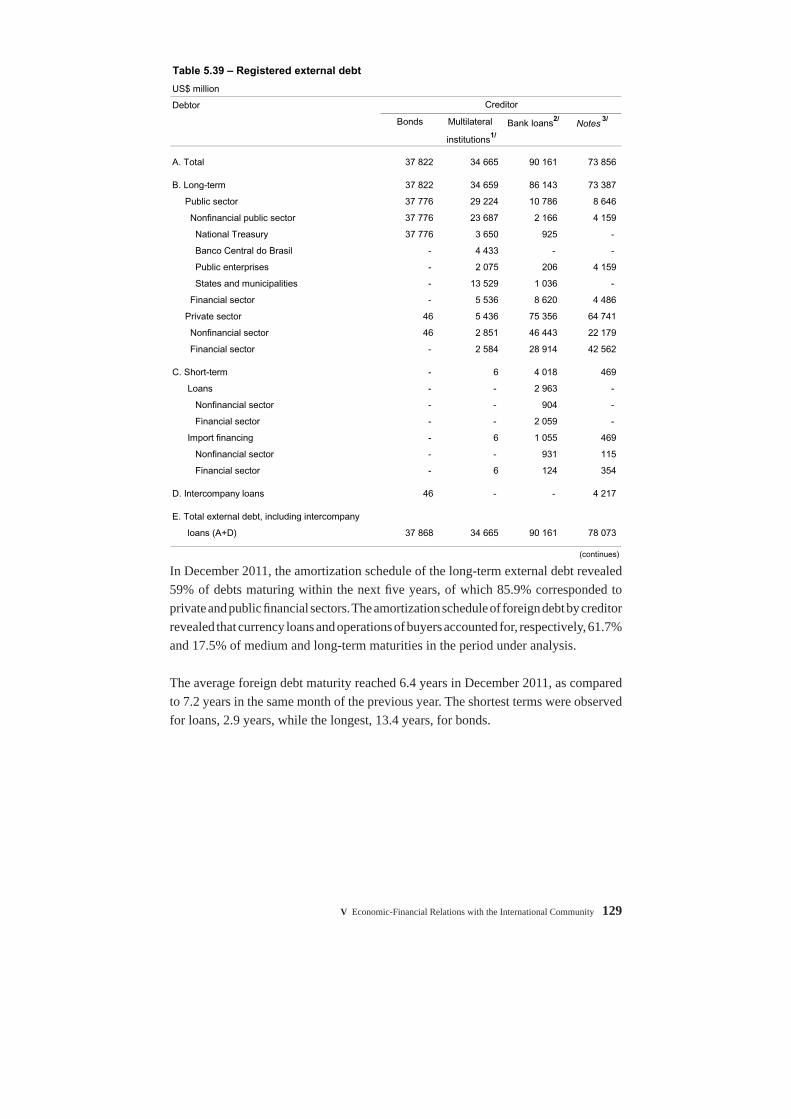

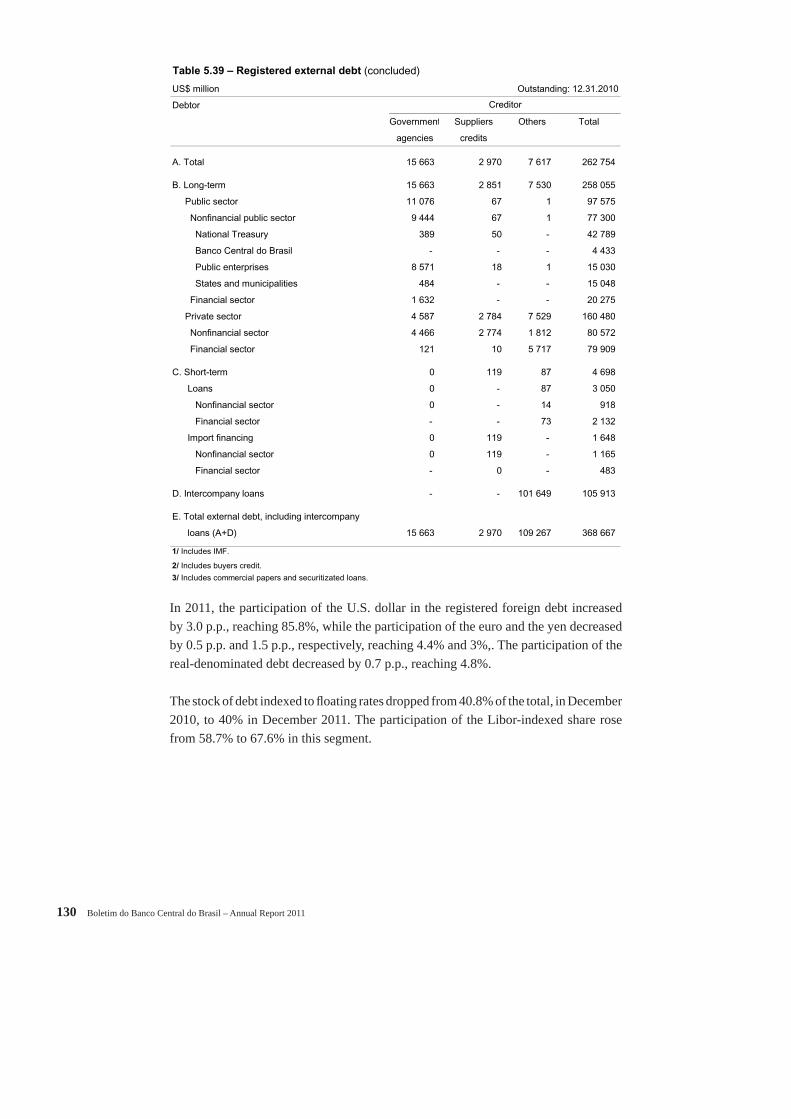

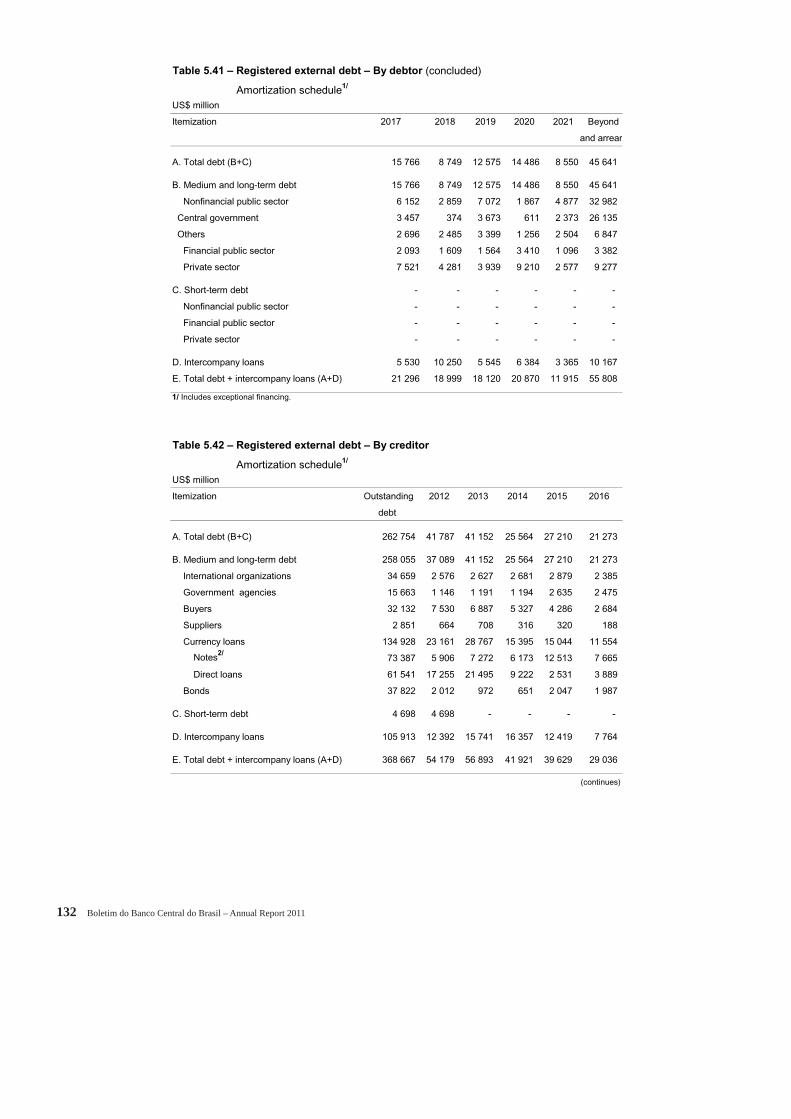

V- Economic-Financial Relations with the International Community ......... 77 Foreign Trade Policy ....................................................................................... 77 Exchange policy .............................................................................................. 82 Exchange movement ....................................................................................... 85 Balance of payments ....................................................................................... 86 Trade balance .................................................................................................. 88 Trade exchange ............................................................................................. 108 Services ......................................................................................................... 109 Income ..........................................................................................................113 Current unilateral transfers ............................................................................115 Financial account ..........................................................................................116 International reserves ................................................................................... 125 National Treasury external debt service ........................................................ 125 Foreign debt .................................................................................................. 127 Foreign sustainability indicators .................................................................. 134 External funding operations .......................................................................... 136 Brazilian foreign debt bonds ......................................................................... 137 International Investment Position (IIP) ......................................................... 138 IMF financing and relationship with Brazil ................................................. 139

VI- The International Economy ....................................................................... 141 Economic activity ......................................................................................... 141 Monetary policy and inflation ....................................................................... 146 International financial market ....................................................................... 151 Commodities ................................................................................................. 155

Summary 5

VII- International Financial Organizations ...................................................... 157 International Monetary Fund ........................................................................ 157 G-20 ......................................................................................................... 159 Bank for International Settlements (BIS) ..................................................... 161 Center for Latin American Monetary Studies (Cemla) ................................. 163

VIII- Main Economic Policy Measures ............................................................... 165 Constitutional Amendment ........................................................................... 165 Supplementary Law ...................................................................................... 165 Laws ......................................................................................................... 165 Provisional Measures .................................................................................... 168 Legislative Decrees ....................................................................................... 170 Decrees 170 National Monetary Council Resolutions ....................................................... 176 Foreign Trade Council Resolutions .............................................................. 185 Central Bank of Brazil Circulars .................................................................. 195 Circulars of the Foreign Trade Secretariat .................................................... 199 Federal Revenue Secretariat of Brazil Directives ......................................... 200 Foreign Trade Secretariat Directives ............................................................ 201 National Treasury Secretariat Directives ...................................................... 201 Normative Instructions of the Federal Revenue Secretariat of Brazil .......... 204 Interpretative Declaratory Acts of the Federal Revenue Secretariat ............. 205 Central Bank of Brazil Communiqués .......................................................... 205 Circular Letters of the Central Bank of Brazil .............................................. 205

Appendix ...................................................................................................... 207

6 Boletim do Banco Central do Brasil – Annual Report 2011

Statistical Tables

Chapter I 1.1 GDP at market price ......................................................................... 14 1.2 GDP real change rates – Under the prism of production ................ 15 1.3 GDP real change rates – Under the prism of expenditure ................ 15 1.4 GDP – Quarterly growth/previous quarter – Seasonally adjusted ... 16 1.5 Gross Domestic Product – At current value ..................................... 17 1.6 Gross capital formation (GCF) .......................................................... 18 1.7 Selected capital goods production .................................................... 19 1.8 BNDES disbursement ....................................................................... 20 1.9 Industrial production ......................................................................... 21 1.10 Industrial capacity utilization .......................................................... 22 1.11 Agricultural production – Major crops ............................................. 26 1.12 Agricultural production, harvested area and average earnings – Major crops ..................................................................... 27 1.13 Apparent consumption of oil derivatives and fuel alcohol ............. 30 1.14 Electric energy consumption ............................................................ 30 1.15 Formal employment – New jobs openings ........................................ 31 1.16 Average earnings of occupied people – 2011 ................................... 32 1.17 IPCA items share in 2011 ................................................................. 38 1.18 IPCA items share in 2011 ................................................................. 39 1.19 Major items included in the IPCA during 2011 ............................... 36 1.20 Regulated prices in 2011 – Selected items ....................................... 37 1.21 Consumer prices and core inflation in 2011 ..................................... 38

Chapter II 2.1 Collection rate on mandatory reserves ............................................. 42 2.2 Financial assets ................................................................................. 44 2.3 Credit operations ............................................................................... 45 2.4 Nonearmarked credit operations ....................................................... 46 2.5 Earmarked credit operations .............................................................. 49 2.6 BNDES disbursements ..................................................................... 50 Chapter III 3.1 Nominal income of financial investment – 2011 .............................. 58

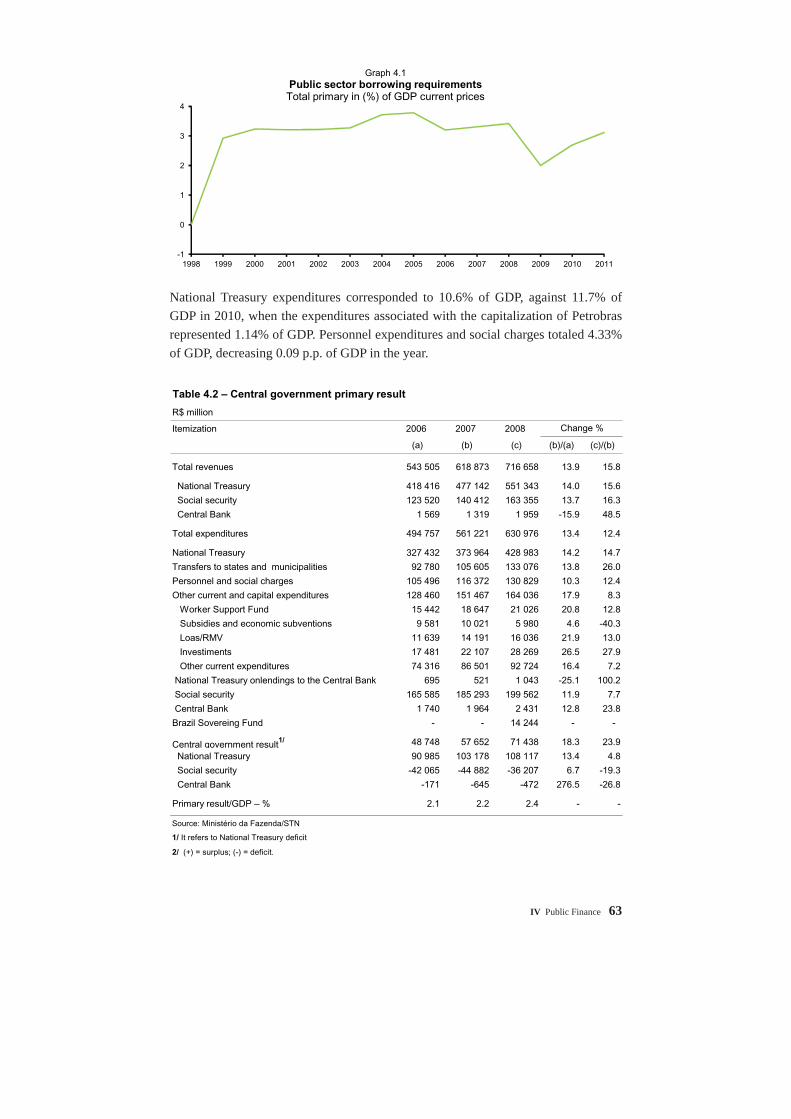

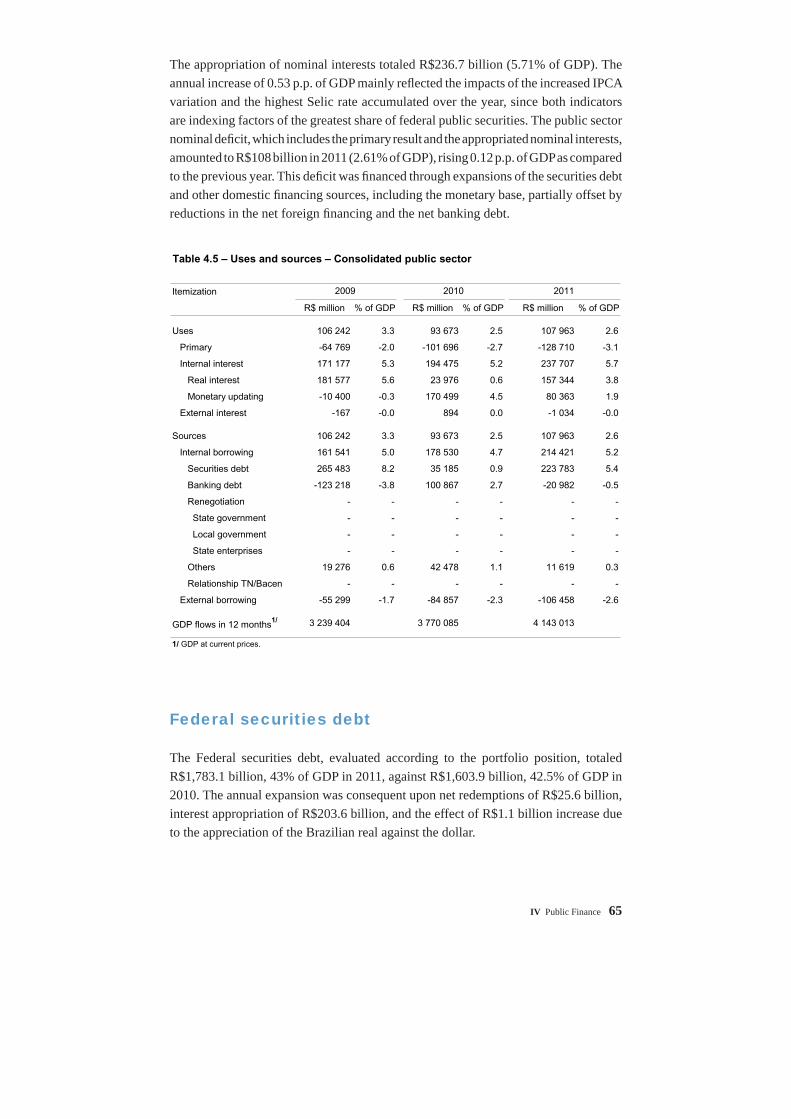

Chapter IV 4.1 Public sector borrowing requirements .............................................. 62 4.2 Central government primary result .................................................. 63 4.3 Gross revenue of National Treasure ................................................. 64 4.4 National Treasure expenditures ........................................................ 64 4.5 Uses and sources – Consolidated public sector ................................ 65 4.6 Federal securities – Portfolio position .............................................. 66 4.7 Federal public securities ................................................................... 67

Summary 7

4.8 Public sector net debt growth ...................................................... 69/70 4.9 Public Sector Net Debt ..................................................................... 71 4.10 Gross and net government debt ........................................................ 72 4.11 Gross federal revenues ..................................................................... 73 4.12 Income Tax and Industrialized Products Tax ................................... 74 4.13 Social Security.................................................................................. 74 4.14 Payment of the Tax on the Circulation of Merchandise and Services (ICMS) ............................................................................... 75 4.15 Federal government onlendings to states and municipalities ............ 76

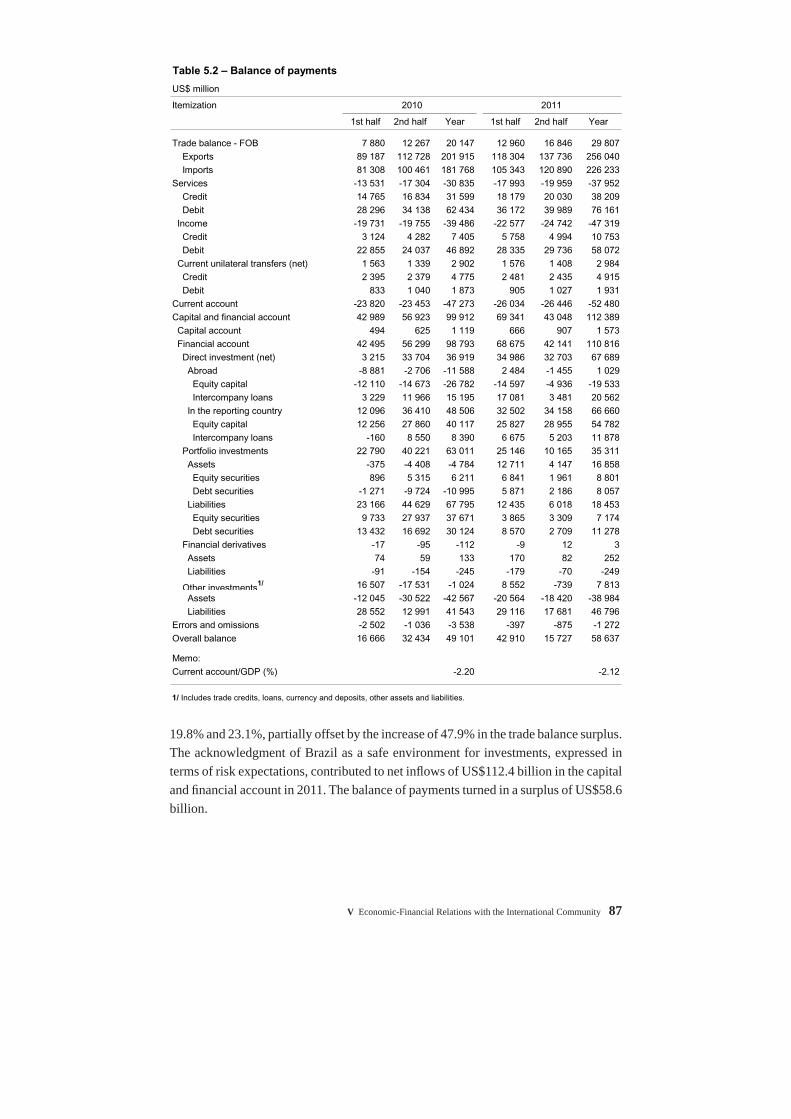

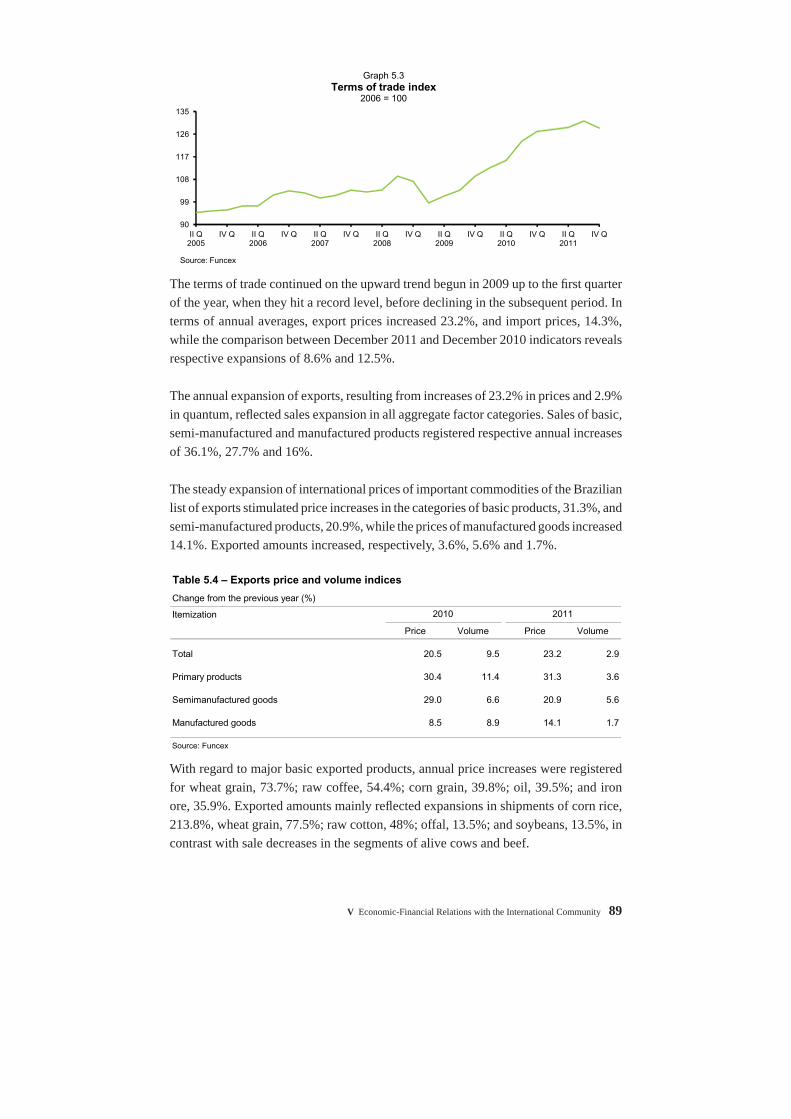

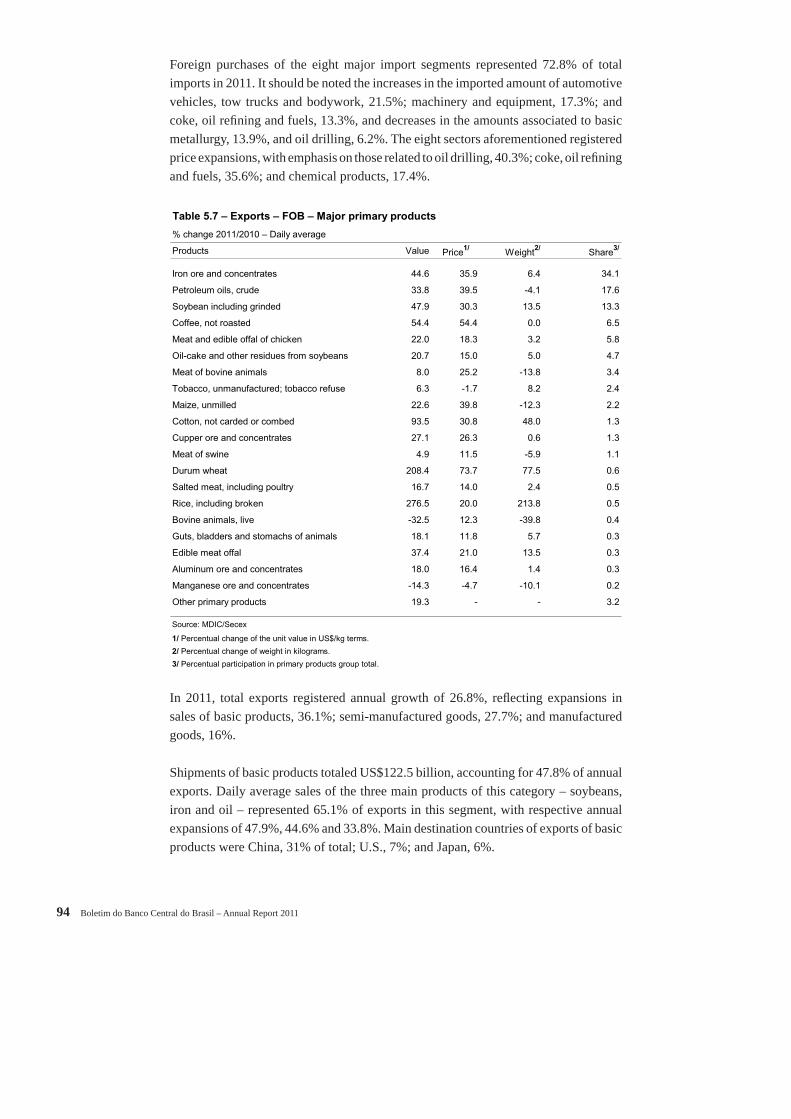

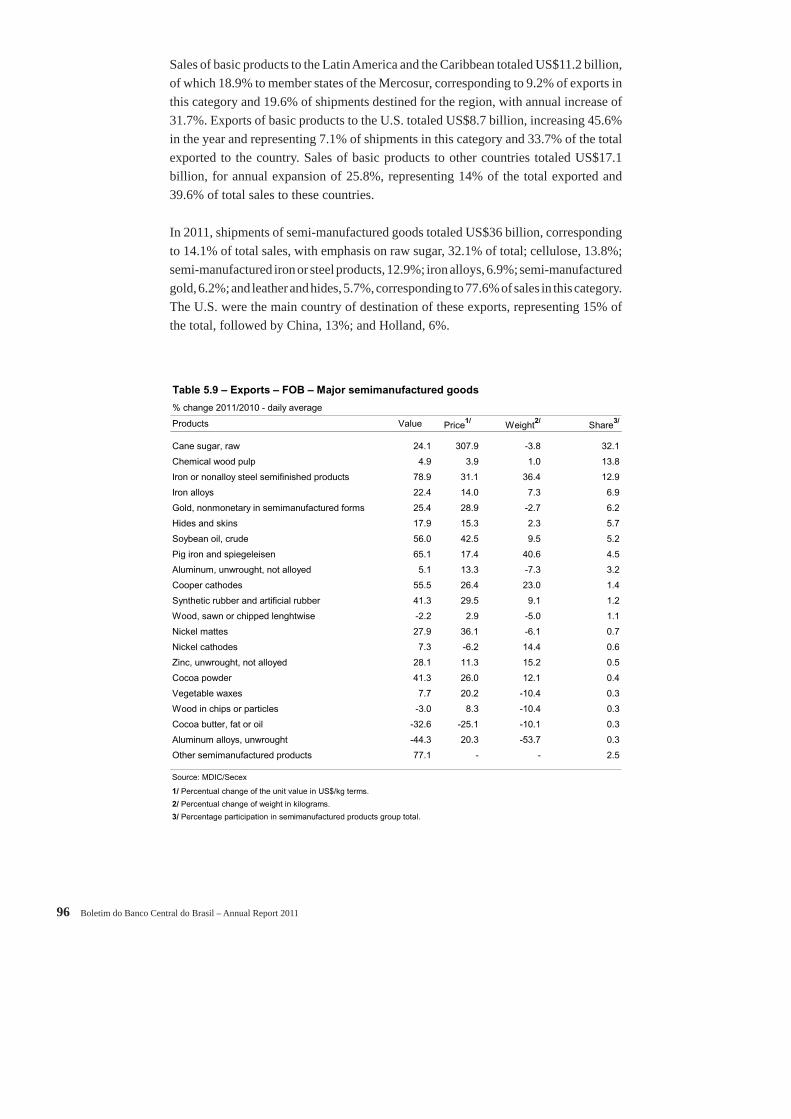

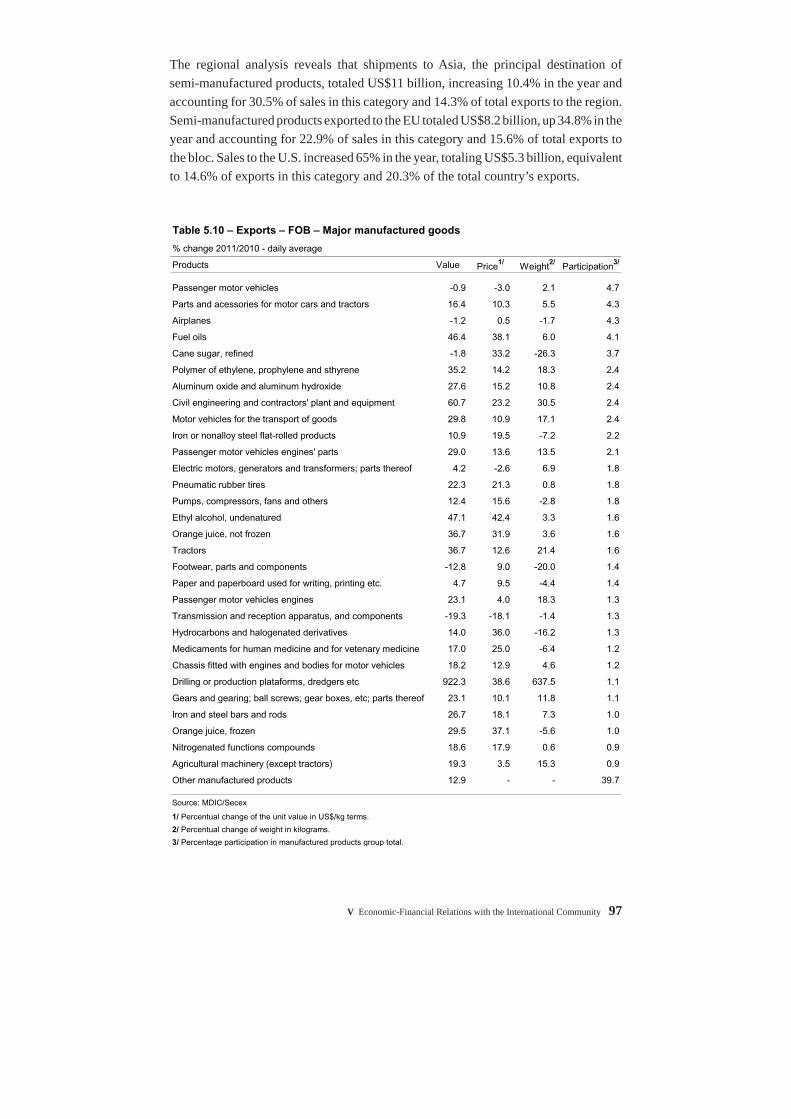

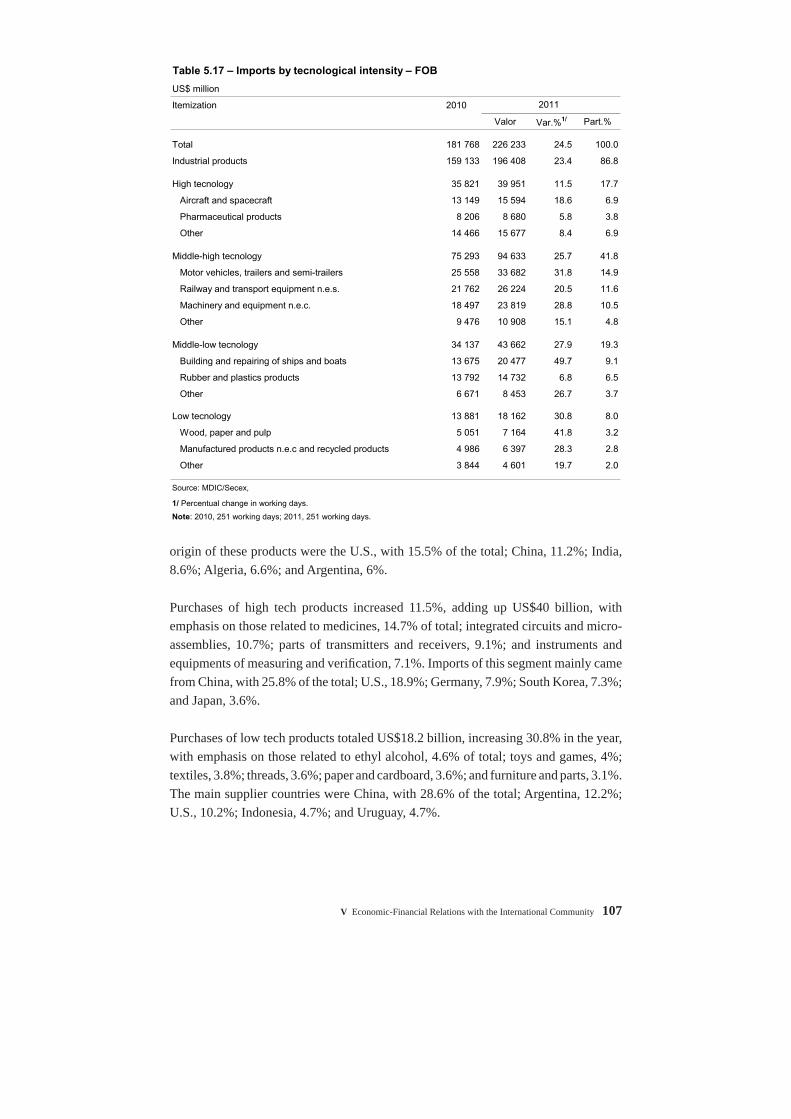

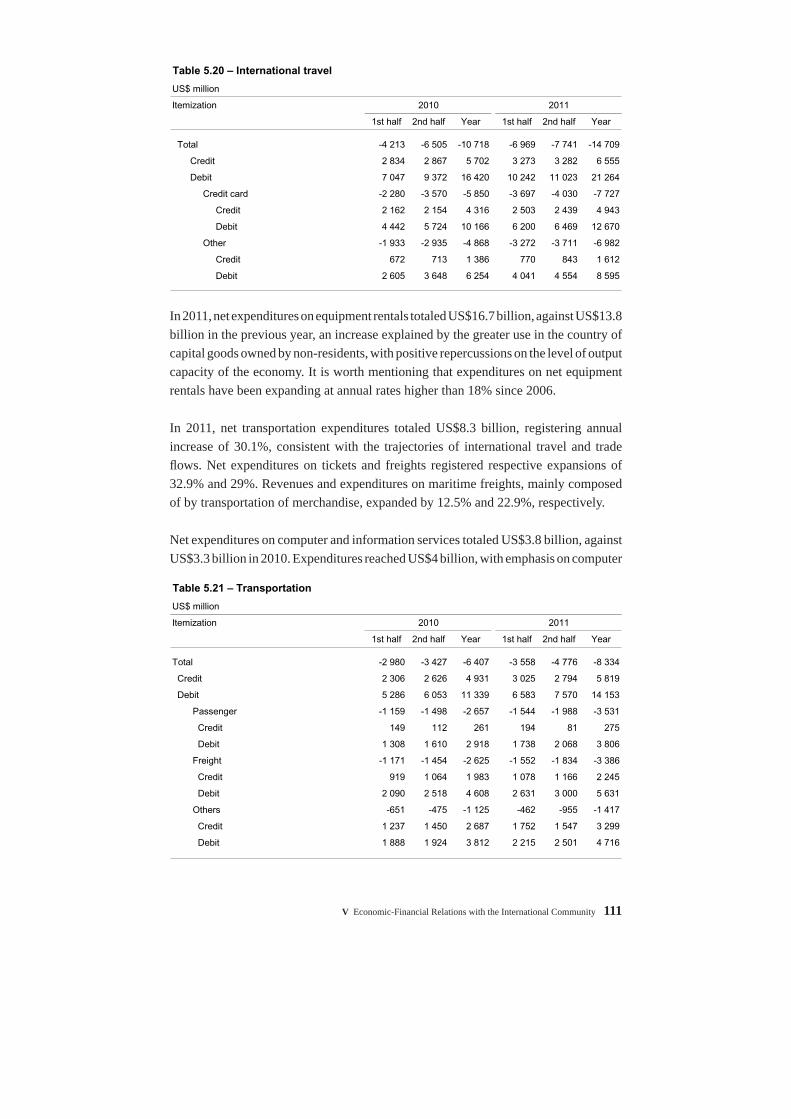

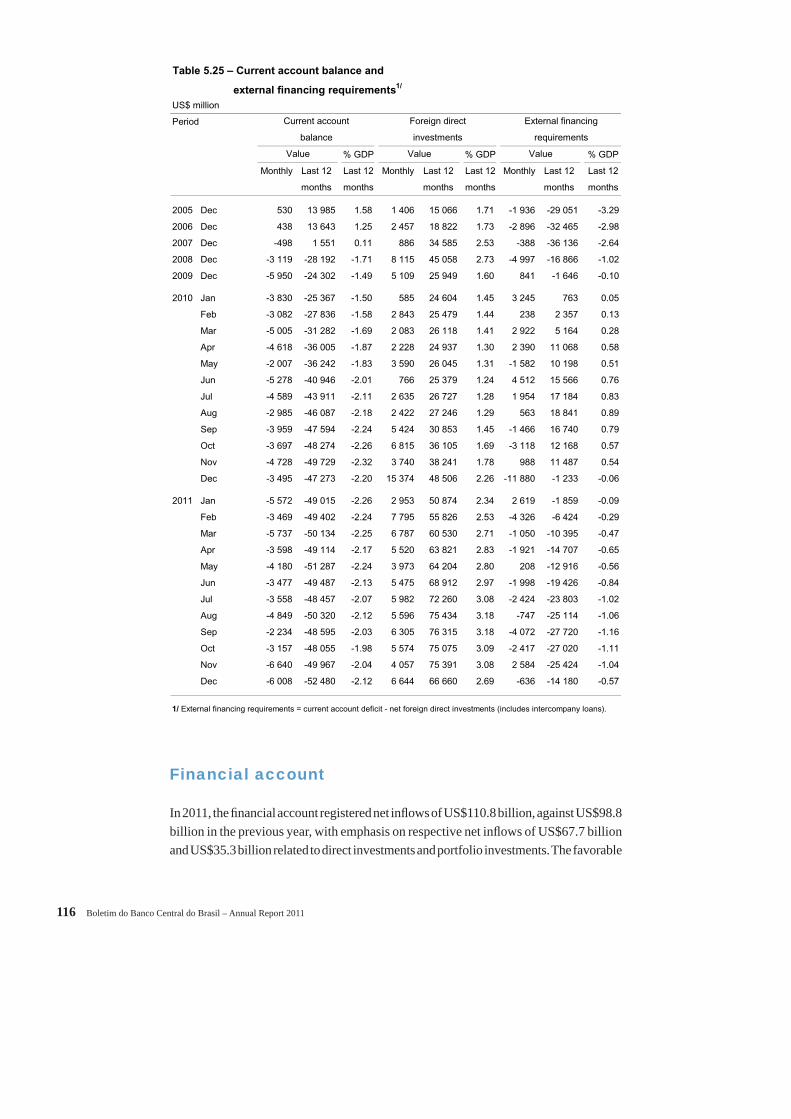

Chapter V 5.1 Foreign exchange operations ............................................................ 85 5.2 Balance of payments ........................................................................ 87 5.3 Trade balance – FOB ........................................................................ 88 5.4 Exports price and volume indices .................................................... 89 5.5 Imports price and volume indices .................................................... 91 5.6 Exports by aggregate factor – FOB .................................................. 93 5.7 Exports – FOB – Major primary products ....................................... 94 5.8 Exports by aggregate factor and by region – FOB ........................... 95 5.9 Exports – FOB – Major semimanufactured goods ........................... 96 5.10 Exports – FOB – Major manufactured goods .................................. 97 5.11 Exports by main products and countries – FOB .............................. 99 5.12 Exports by tecnological intensity – FOB ....................................... 100 5.13 Imports – FOB ................................................................................ 101 5.14 Imports – FOB – Major products ................................................... 103 5.15 Imports by category of use and by region – FOB .......................... 104 5.16 Imports by main products and trade partners – FOB ..................... 106 5.17 Imports by tecnological intensity – FOB ....................................... 107 5.18 Brazilian trade by region – FOB .................................................... 109 5.19 Services ........................................................................................... 110 5.20 International travel .......................................................................... 111 5.21 Transportation ................................................................................. 111 5.22 Business, technical and professional services ................................. 112 5.23 Income ............................................................................................. 114 5.24 Current transfers .............................................................................. 115 5.25 Current account balance and external financing requirements ........ 116 5.26 Private sector medium and long-term rollover rates ....................... 117 5.27 Foreign direct investments .............................................................. 118 5.28 Foreign direct investments inflows – Equity capital – Distribution by immediate investing country ................................. 120 5.29 Foreign direct investments inflows – Equity capital – Distribution by economic activity sector ....................................... 121 5.30 Portfolio investments – Liabilities ................................................. 122 5.31 Other foreign investments .............................................................. 123 5.32 Brazilian direct investments abroad ............................................... 123

8 Boletim do Banco Central do Brasil – Annual Report 2011

5.33 Brazilian portfolio investments abroad .......................................... 124 5.34 Other brazilian investments abroad ................................................ 124 5.35 Statement of international reserves growth .................................... 126 5.36 National Treasury – External debt service ..................................... 126 5.37 National Treasury – External debt sovereign bonds buyback operations ....................................................................................... 127 5.38 Gross foreign indebtedness ............................................................ 128 5.39 Registered external debt .......................................................... 129/130 5.40 Public registered external debt – Breakdowm of principal by debtor and by guarantor................................................................... 131 5.41 Registered external debt – By debtor ...................................... 131/132 5.42 Registered external debt – By creditor .................................... 132/133 5.43 Average maturity term – Registered external debt ......................... 133 5.44 Indebtedness indicators .................................................................. 135 5.45 Issues of the Republic .................................................................... 136 5.46 International investment position ............................................ 138/139 5.47 Brazilian financial position in the IMF .......................................... 140

Chapter VI 6.1 Major countries .............................................................................. 144

Graphs

Chapter I 1.1 Gross Fixed Capital Formation ........................................................ 19 1.2 Industrial production ....................................................................... 20 1.3 Industrial production – Seasonally adjusted data ............................. 21 1.4 Industrial production – By category of use ...................................... 22 1.5 Industrial capacity utilization ........................................................... 23 1.6 Broad sales volume Index in the Trade Sector ................................. 24 1.7 Consumer Confidence Index ............................................................ 25 1.8 Animal production............................................................................ 28 1.9 Average unemployment rate ............................................................. 31 1.10 Level of formal employment ............................................................ 32 1.11 Real average earnings ....................................................................... 32 1.12 Consumer price indices .................................................................... 34 Chapter II 2.1 Money supply (M1) – Income velocity ............................................. 40 2.2 Currency outside banks – Seasonally adjusted at December 2011 prices .................................................................. 40 2.3 Demand deposits – Seasonally adjusted at December 2011 prices... 40 2.4 Monetary base and money supply (M1) – Average daily balances .. 41

Summary 9

2.5 Financial assets – As percentage of GDP ......................................... 43 2.6 Credit by borrower’s economic activity – Financial system ............ 45 2.7 Interest rates of credit operations with nonearmarked resources ..... 47 2.8 Interest rates of credit operations – Individuals .............................. 47 2.9 Interest rates of credit operations – Corporations ........................... 47 2.10 Spread of credit operations with nonearmarked resources ............... 48 2.11 Default rate of credit operations with nonearmarked resources ....... 48

Chapter III 3.1 Over/Selic rate .................................................................................. 53 3.2 Over/Selic rate x dollar x 360-day swap .......................................... 53 3.3 Yield curve – ID x fixed rate swap ................................................... 54 3.4 Over/Selic cumulative 12-month rate .............................................. 54 3.5 Primary issues .................................................................................. 55 3.6 Ibovespa ........................................................................................... 55 3.7 Ibovespa x Dow Jones x Nasdaq – 2011 .......................................... 55 3.8 Daily average volume traded in Bovespa – 2011 ............................. 56 3.9 Market capitalization – 2011 – Corporation listed in Bovespa ........ 56 3.10 Financial investments – Balances .................................................... 57 3.11 Nominal income of major financial investments – 2011 ................. 57

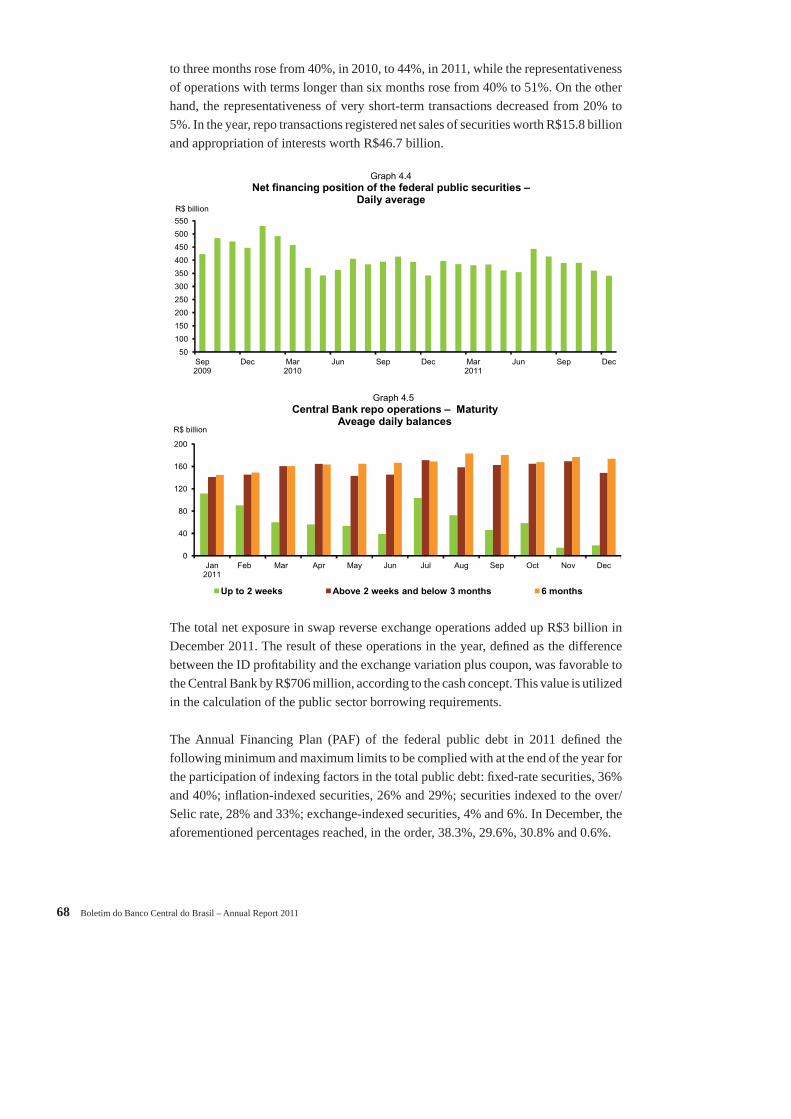

Chapter IV 4.1 Public sector borrowing requirements ............................................... 63 4.2 Federal public securities ................................................................... 67 4.3 Federal securitized debt structure ...................................................... 67 4.4 Net financing position of the federal public securities ...................... 68 4.5 Central Bank repo operations ............................................................ 68 4.6 Social security ................................................................................... 75

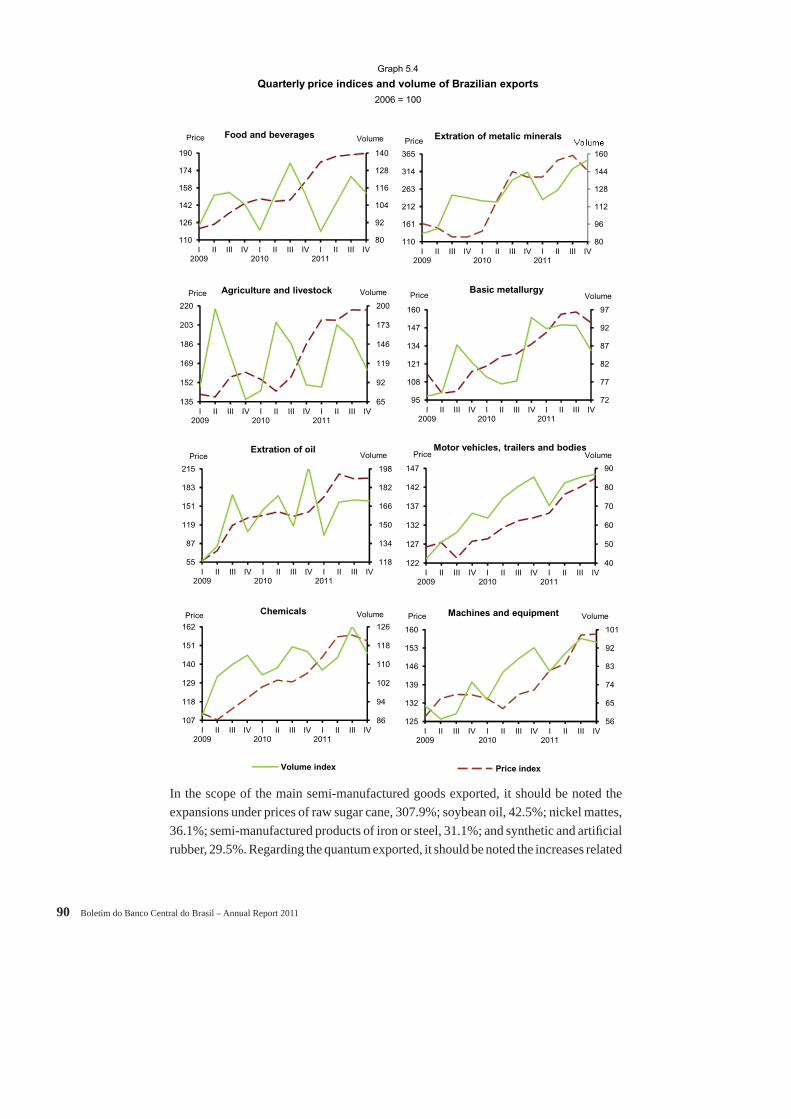

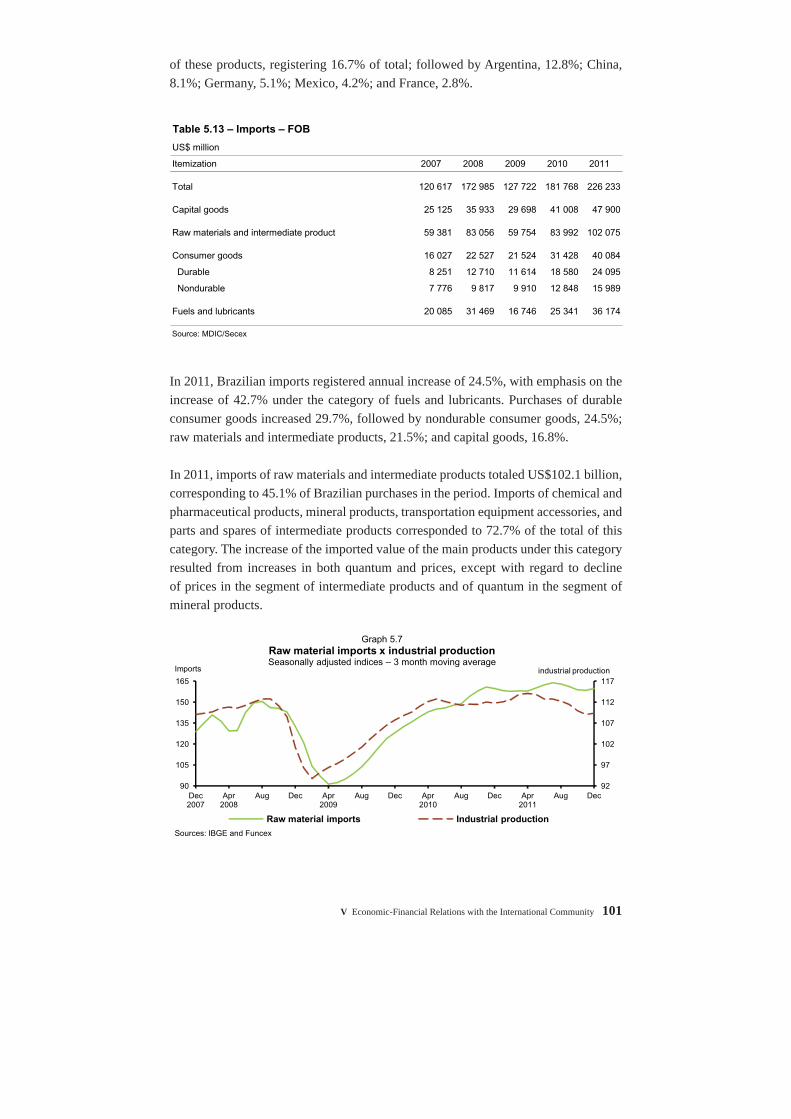

Chapter V 5.1 Current accounts balance and external financing requirements ....... 88 5.2 Exports and imports – FOB .............................................................. 88 5.3 Terms of trade index ......................................................................... 89 5.4 Quarterly price indices and volume of Brazilian exports ................. 90 5.5 Quarterly price indices and volume of Brazilian imports ................ 92 5.6 Exports by aggregate factor – FOB .................................................. 93 5.7 Raw material imports x industrial production ................................ 101 5.8 Brazilian imports by end use category – FOB (% growth) ............ 102 5.9 Brazilian imports by end use category – FOB (% change) ............ 105 5.10 International reserves ..................................................................... 125 5.11 Average term of registered external debt ....................................... 134 5.12 Registered external debt composition ............................................ 134 5.13 Sustainability indicators ................................................................. 136 5.14 Prices of Brazilian securities abroad .............................................. 137

10 Boletim do Banco Central do Brasil – Annual Report 2011

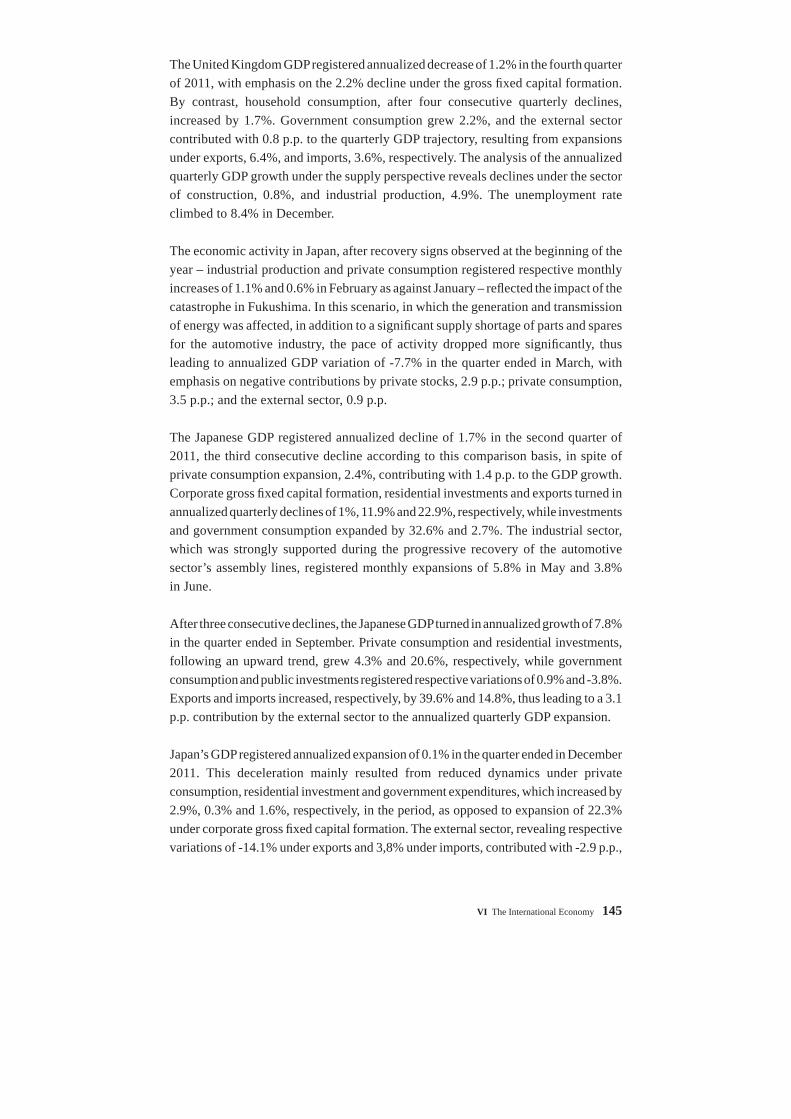

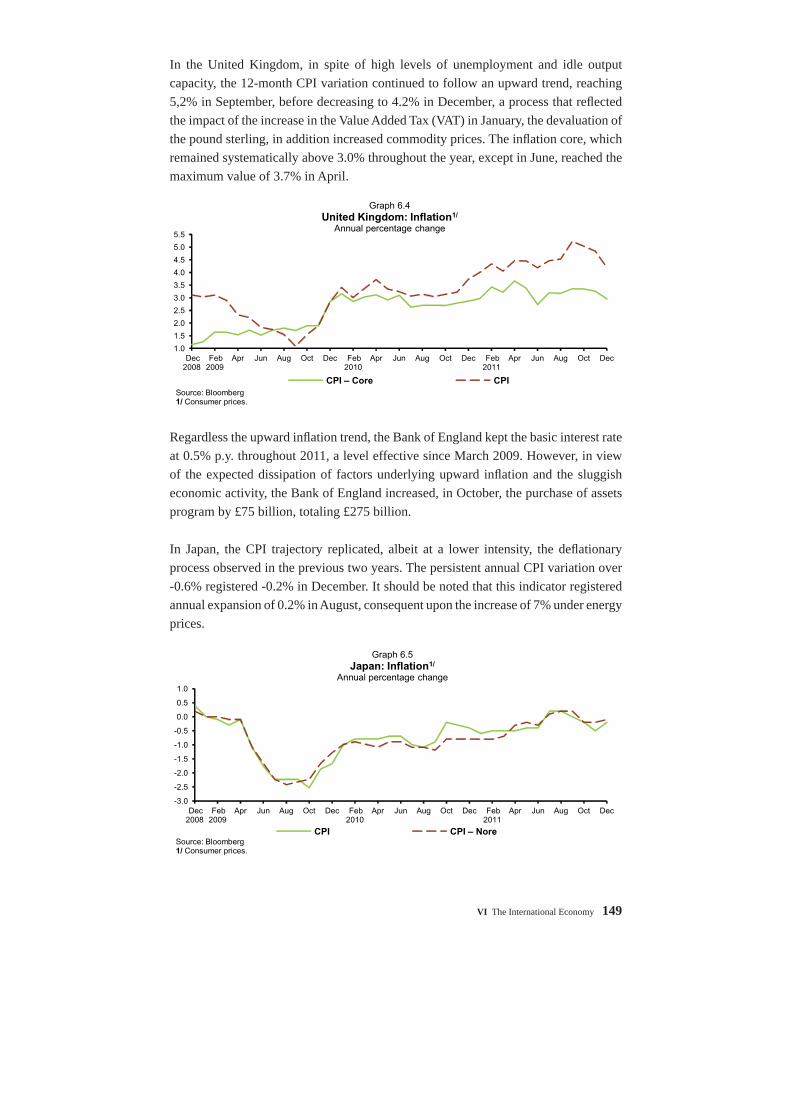

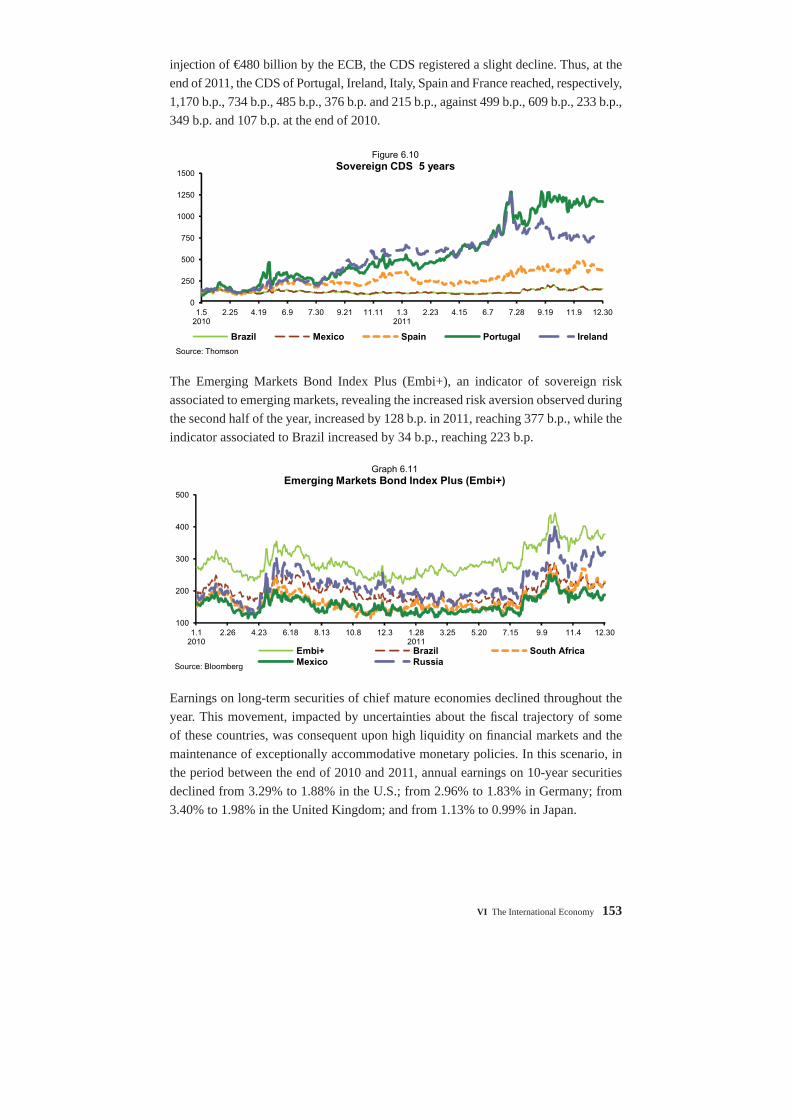

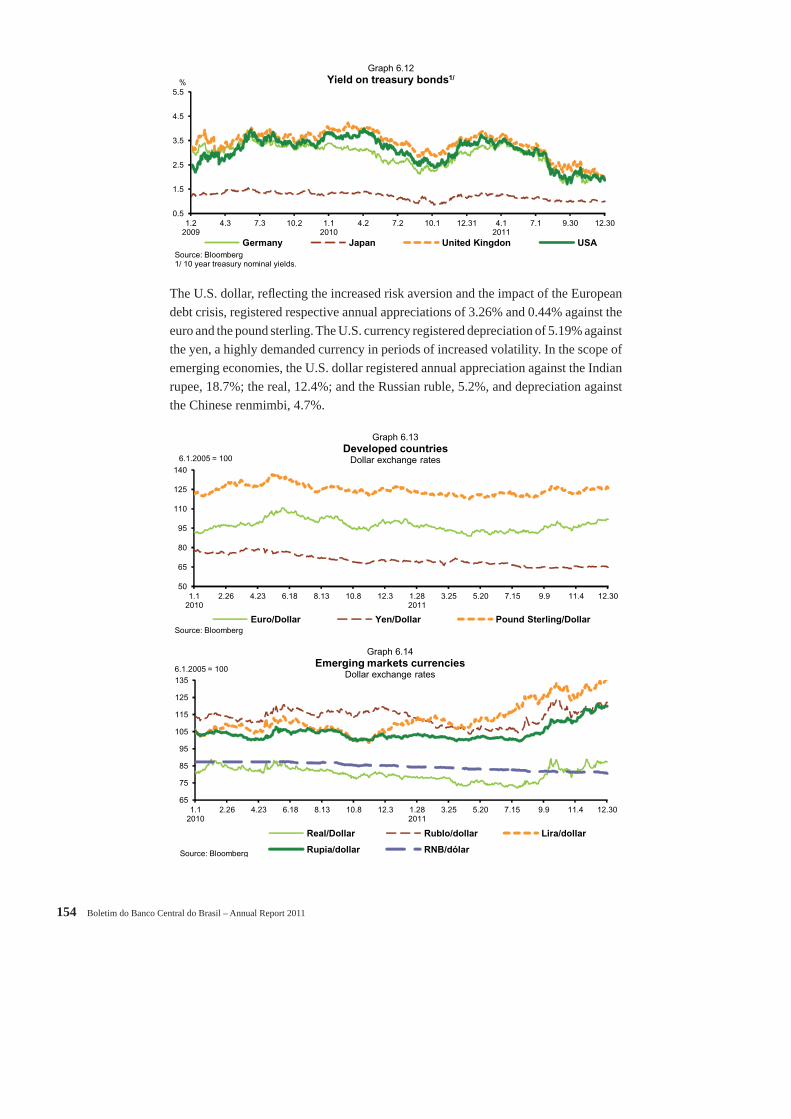

Chapter VI 6.1 Official interest rates ...................................................................... 147 6.2 USA: Inflation ................................................................................ 147 6.3 Euro area: Inflation ......................................................................... 148 6.4 United Kingdom: Inflation ............................................................. 149 6.5 Japan: Inflation ............................................................................... 149 6.6 China: Inflation ............................................................................... 150 6.7 Stock exchanges – USA, United Kingdon, Japan and German ..... 151 6.8 VIX ................................................................................................. 152 6.9 Stock exchanges – Emerging markets ............................................ 152 6.10 Sovereign CDS 5 years .................................................................. 153 6.11 Emerging Markets Bond Index (Embi+) ........................................ 153 6.12 Yield on treasury bonds .................................................................. 154 6.13 Developed countries – Dollar exchange rates ................................ 154 6.14 Emerging markets currencies ......................................................... 154 6.15 IC-Br index ..................................................................................... 155 6.16 Brent oil – Spot market .................................................................. 156

Introduction 11

Introduction

The global economic activity, following a strong recovery observed at the beginning of 2011, started to refl ect the upward trajectory of commodity prices begun in the previous year; the worsening of the fi scal crisis in some European countries; geopolitical confl icts in the North Africa and Middle East; and economic impacts of the strong earthquake that hit Japan. In this scenario, economic activity decelerated signifi cantly in leading mature economies, except in the Eurozone. Infl ation, basically refl ecting the supply shock of commodities observed since the second half of 2010, continued to follow an upward trend in major developed and emerging economies, where the tightening cycles of monetary and fi scal policies were intensifi ed.

In the second quarter of the year, businessmen and consumers’ expectations were negatively affected by the worsening of the fi scal crisis in Europe, of some fi scal-related issues in the U.S., coupled with the perspective of moderate activity growth in these economies and its likely effects over leading mature and emerging economies. In this context, in which important European economies slowed down and the Japanese economy registered another decline, the increase of risk perception led to high volatility on fi nancial markets.

The reduction of growth forecasts in leading economies intensifi ed in the second half of 2011. In this context, in spite of renewed consumption support to activity growth in the U.S., activity expansion in Japan due to measures aimed at reconstruction and post-catastrophe recovery of production lines, coupled with a slight growth deceleration in China, the Eurozone economy registered a signifi cant slowdown. In this framework, coupled with the environment of high volatility on fi nancial markets, the world economy continued to follow a disinfl ationary trajectory.

In line with the evolution of the international scenario, the Brazilian economy did not succeed to repeat the vigorous growth rate registered in the previous year. The moderation of economic activity in 2011 was also consistent with policy measures implemented since the end of 2010 aimed to adjust domestic liquidity conditions and the mismatch between aggregate supply and demand. In this context, the Gross Domestic Product (GDP) registered annual expansion of 2.7% in 2011.

12 Boletim do Banco Central do Brasil – Annual Report 2011

It should be noted that, in a context of global economic deceleration, the expansion of the Brazilian economy continued to be fueled by domestic demand, with emphasis on the dynamics of consumption, which registered the eighth consecutive annual growth, mainly refl ecting the impact on household income of favorable labor market conditions and the maintenance of government social programs.

In this scenario, according to a pre-established schedule, the Central Bank Monetary Policy Committee (Copom) carried out eight ordinary meetings in the year. In the fi rst fi ve meetings, by evaluating that the risks for the consolidation of a positive infl ation scenario were associated, in the external scope, to the increased commodity prices and, in the internal scope, to the mismatch between the growth rates of domestic absorption and supply expansion capacity, Copom implemented fi ve consecutive risings in the basic interest rate, totalizing 175 b.p., which was fi xed at 12.50% p.y. in July.

In the meetings carried out in August, October and November, Copom evaluated that the impact of supply shocks observed in the fi rst half of the year on infl ation as well as the risks associated with the persistent mismatch between the growth rates of supply and demand started to diminish. In this scenario, in which the level of utilization of installed capacity started to decline and the international scenario further deteriorated, Copom, by assessing that the prospective infl ation scenario was favorable, carried out three consecutive cuts in the Selic rate, totalizing 150 b.p., which was fi xed at 11,0% p.y. in the November meeting.

With regard to the external sector, the perception about the solidness of Brazilian external accounts offset the impact of international fi nancial markets volatility. This sentiment, in a scenario of sustained consistence of macroeconomic policy based on infl ation targets, fi scal responsibility and fl oating exchange system, refl ected in the signifi cant improvement of Brazilian sovereign credit ratings by the agencies Fitch, in April, Moody’s, in June, and Standard and Poor’s, in November.

In this context, the Brazilian external position was positive in 2011 according to several aspects: the defi cit in current transactions, measured as a GDP ratio, was reduced in comparison with the previous year; the trade in goods and services increased; the net external liabilities, expressed by the International Investment Position (IIP), decreased in absolute terms; and the coverage of the stock of international reserves over the debt’s principal with 12-month maturity improved signifi cantly.

Worries about the evolution of the sovereign debt of important European countries did not affect the volume of funds obtained by the Brazilian private sector. According to previous estimates published by the United Nations Conference on Trade and Development (Unctad) through the Global Investment Trends Monitor, Brazil was the fi fth greatest recipient of net fl ows, behind the U.S, U.K., China and Hong Kong.

I The Brazilian Economy 13

IThe Brazilian Economy

Activity level

Following the strong expansion in 2010, the Brazilian economy registered a moderate growth pace in 2011. This evolution was consistent with the policy measures implemented since the end of 2010 and the deteriorating international economic scenario, especially as of the second half of the year. In this context, the GDP registered annual expansion of 2.7% in 2011, compared to 7.5% in 2010.

It should be noted that, in the context of reduced foreign demand, economic expansion was supported by domestic demand, with emphasis on the dynamics of household consumption, which, mainly refl ecting the favorable labor market and the maintenance of governmental programs aimed at income distribution, registered the eighth consecutive annual growth.

Gross Domestic Product

According to the Quarterly National Accounts of the Brazilian Institute of Geography and Statistics (IBGE), the GDP grew 2.7% in 2011. In current values, the GDP at market prices totaled R$4,143 billion in the year.

The analysis under the perspective of demand reveals that the annual GDP expansion resulted from contributions of 3.4 p.p. of the domestic component and -0.7 p.p. of the external sector. Investments, refl ecting the favorable evolution of the civil construction sector and the absorption of capital goods, expanded 4.7%, while household consumption and government consumption grew by 4.1% and 1.9%, respectively. The negative contribution of the external sector refl ected expansions of 9.7% under imports and 4.5% under exports.

In the scope of supply, agriculture expanded 3.9%, services, 2.7%, and industry, 1.6%. The performance of the agricultural sector refl ected annual expansion of 7% in the grain harvest and respective variations of -2.8%, 6.6% and 9.4% in the slaughters of cattle,

I

14 Boletim do Banco Central do Brasil – Annual Report 2011

poultry and swine. The expansion of the sector of services was basically fueled by the segments of information services, 4.9%; fi nancial intermediation, insurance, pension and related services, 3.9%; commerce, 2.4%; and transportation, storage and postal services, 2.8%. The performance of the last two segments refl ected the trajectory of the agricultural and industrial sectors. The industrial performance was specially supported by the segments of production and distribution of electricity, gas and water, 3.8%; civil

Table 1.1 – GDP at market price

Year At 2011 Real Implicit At current Population Per capita GDP

prices change deflator prices1/ (million) At 2011 Real At current

(R$ (%) (%) (US$ prices change prices1/

million) million) (R$) (%) (US$)

1980 1 882 456 9.2 92.1 237 772 118 563 15 877 7.0 2 005

1981 1 802 452 -4.3 100.5 258 553 121 213 14 870 -6.3 2 133

1982 1 817 412 0.8 101.0 271 252 123 885 14 670 -1.3 2 190

1983 1 764 162 -2.9 131.5 189 459 126 573 13 938 -5.0 1 497

1984 1 859 427 5.4 201.7 189 744 129 273 14 384 3.2 1 468

1985 2 005 373 7.8 248.5 211 092 131 978 15 195 5.6 1 599

1986 2 155 576 7.5 149.2 257 812 134 653 16 008 5.4 1 915

1987 2 231 668 3.5 206.2 282 357 137 268 16 258 1.6 2 057

1988 2 230 329 -0.1 628.0 305 707 139 819 15 952 -1.9 2 186

1989 2 300 807 3.2 1 304.4 415 916 142 307 16 168 1.4 2 923

1990 2 200 722 -4.3 2 737.0 469 318 146 593 15 013 -7.1 3 202

1991 2 223 389 1.0 416.7 405 679 149 094 14 913 -0.7 2 721

1992 2 211 303 -0.5 969.0 387 295 151 547 14 592 -2.2 2 556

1993 2 320 205 4.9 1 996.1 429 685 153 986 15 068 3.3 2 790

1994 2 456 003 5.9 2 240.2 543 087 156 431 15 700 4.2 3 472

1995 2 559 740 4.2 93.9 770 350 158 875 16 112 2.6 4 849

1996 2 614 787 2.2 17.1 840 268 161 323 16 208 0.6 5 209

1997 2 703 044 3.4 7.6 871 274 163 780 16 504 1.8 5 320

1998 2 703 999 0.0 4.2 843 985 166 252 16 264 -1.5 5 077

1999 2 710 870 0.3 8.5 586 777 168 754 16 064 -1.2 3 477

2000 2 827 605 4.3 6.2 644 984 171 280 16 509 2.8 3 766

2001 2 864 735 1.3 9.0 553 771 173 808 16 482 -0.2 3 186

2002 2 940 882 2.7 10.6 504 359 176 304 16 681 1.2 2 861

2003 2 974 603 1.1 13.7 553 603 178 741 16 642 -0.2 3 097

2004 3 144 521 5.7 8.0 663 783 181 106 17 363 4.3 3 665

2005 3 243 877 3.2 7.2 882 439 183 383 17 689 1.9 4 812

2006 3 372 239 4.0 6.1 1 088 767 185 564 18 173 2.7 5 867

2007 3 577 656 6.1 5.9 1 366 544 187 642 19 066 4.9 7 283

2008 3 762 678 5.2 8.3 1 650 897 189 613 19 844 4.1 8 707

2009 3 750 271 -0.3 7.2 1 625 636 191 481 19 586 -1.3 8 490

2010 4 032 805 7.5 8.2 2 143 921 193 253 20 868 6.5 11 094

2011 4 143 013 2.7 7.0 2 475 066 194 947 21 252 1.8 12 696

Source: IBGE

1/ Estimates obtained by the Banco Central do Brasil dividing the GDP at current prices by the annual average buying

rate of exchange.

I The Brazilian Economy 15

construction, 3.6%; and mining activities, 3.2%, as against the sluggish performance of the manufacturing industry, which grew 0.1% in the year.

The analysis of seasonally adjusted data reveals that the GDP grew moderately during the fi rst two quarters of 2011, as compared to the respective quarters of the previous year, then slowed down slightly in the third quarter of the year, when the economic activity was impacted by the deterioration of the international scenario, and resumed the growth trajectory in the fi nal quarter of the year.

The GDP grew 0.6% in the fi rst quarter of the year, in comparison with the fourth quarter of 2010. The analysis under the prism of supply reveals that the quarterly

Table 1.2 – GDP real change rates – Under the prism of production

Percentage

Itemization 2009 2010 2011

GDP -0.3 7.5 2.7

Crop and livestock sector -3.1 6.3 3.9

Industrial sector -5.6 10.4 1.6

Mineral extraction -3.2 13.6 3.2

Manufacturing -8.7 10.1 0.1

Building -0.7 11.6 3.6

Production and distribution of electricity, gas and water supply 0.9 8.1 3.8

Service sector 2.1 5.5 2.7

Commerce -1.0 10.9 3.4

Transportation, storage and postal services -3.6 9.2 2.8

Information services 0.8 3.7 4.9

Financial intermediation, insurance, complementary pension system

and related services 7.8 10.0 3.9

Other services 3.2 3.7 2.3

Real estate activities and rent 2.6 1.7 1.4

Public administration, health and education 3.0 2.3 2.3

Source: IBGE

Table 1.3 – GDP real change rates – Under the prism of expenditure

Percentage

Itemization 2009 2010 2011

GDP -0.3 7.5 2.7

Family consumption 4.4 6.9 4.1

Government consumption 3.1 4.2 1.9

Gross Fixed Capital Formation -6.7 21.3 4.7

Exports of goods and services -9.1 11.5 4.5

Imports of goods and services -7.6 35.8 9.7

Source: IBGE

16 Boletim do Banco Central do Brasil – Annual Report 2011

GDP performance resulted from respective increases of 4.4%, 1.7% and 0.4% under the primary sector, industry and services. It should be noted that the agricultural sector had been negatively impacted in the second half of 2010, while the sector of services had been following an upward trajectory since the beginning of 2009.

Under the perspective of demand, expansions under Gross Fixed Capital Formation (GFCF) and household consumption closed at 1.2% and 0.5% in the fi rst quarter of the year, respectively, while the government consumption decreased 0.1%. Additionally, exports and imports declined 2.6% and 1.3%, in the same order.

GDP increased 0.5% in the second quarter of 2011 as compared with the previous quarter. The analysis under the output perspective reveals respective quarterly variations of -1.1%, -0.3% and 0.6% in the segments of agriculture, industry and service. It is worth noting the dynamics of the sector of services, which registered the tenth consecutive quarterly expansion, while the industrial production slowed down in the period.

Under the perspective of demand, in which the domestic component supported GDP expansion, it should be noted the 2.0% expansion under government consumption, followed by respective quarterly expansions of 1.1% and 0.5% under GFCF and household consumption. The external sector gave a negative contribution to the GDP evolution in the quarter, as imports increased 5.4% and exports, 2.5%.

In the third quarter of 2011, GDP decreased 0.1% in comparison with the previous year. The analysis under the perspective of production reveals quarterly increase of 2.5% in the agricultural sector, in contrast with declines in the sector of services, 0.2%, and

Table 1.4 – GDP – Quarterly growth/previous quarter – Seasonally adjusted

Percentage

Itemization

I II III IV

GDP at market price 0.6 0.5 -0.1 0.3

Under the prism of product

Crop and livestock sector 4.4 -1.1 2.5 0.9

Industrial sector 1.7 -0.3 -1.1 -0.5

Service sector 0.4 0.6 -0.2 0.6

Under the prism of expenditure

Family consumption 0.5 0.5 -0.1 1.1

Government consumption -0.1 2.0 -0.8 0.4

Gross Fixed Capital Formation 1.2 1.1 -0.4 0.2

Exports of goods and services -2.6 2.5 1.9 1.9

Imports of goods and services -1.3 5.4 -0.5 2.6

Source: IBGE

2011

I The Brazilian Economy 17

industry, 1.1%, the worst quarterly industrial result since the start of the international crisis in 2008/2009.

With regard to domestic components of demand, household consumption declined by 0.1%; GFCF by 0.4%; and government consumption by 0.8%. In the scope of the external sector, exports grew 1.9% and imports decreased 0.5%.

GDP expanded 0.3% in the last quarter of the year, in comparison with the immediately previous quarter. The analysis under the perspective of production reveals respective quarterly expansion under agriculture and services, 0.9% and 0.6%, in contrast with the 0.5% decline under industry, the third negative sector’s result in the sequence in this comparison basis.

Insofar as demand is concerned, the domestic component registered expansion under household consumption, 1.1%, government consumption, 0.4%; and GFCF, 0.2%. Meanwhile, in the scope of the external sector, exports and imports increased by 1.9% and, 2.6%, respectively.

Central Bank Index of Economic Activity

The Central Bank Index of Economic Activity – Brazil (IBC-Br) increased 2.7% in 2011, as against expansion of 7.6% observed in the previous year. The seasonally adjusted analysis reveals that the indicator grew 1.4% in the quarter ended in March, as compared

Table 1.5 – Gross Domestic Product – At current value

In R$ million

Itemization 2008 2009 2010 2011

Gross Domestic Product at market prices 3 032 203 3 239 404 3 770 085 4 143 013

Under the prism of product

Crop and livestock sector 152 612 157 232 171 177 192 653

Industrial sector 719 987 749 699 905 852 972 156

Service sector 1 707 850 1 887 448 2 150 151 2 366 062

Under the prism of expenditure

Final consumption expenditure 2 398 945 2 666 752 3 045 956 3 356 136

Family consumption 1 786 840 1 979 751 2 248 624 2 499 489

Government consumption 612 105 687 001 797 332 856 647

Gross Capital Formation 627 497 577 846 763 012 817 261

Gross Fixed Capital Formation 579 531 585 317 733 712 798 720

Changes in inventories 47 966 -7 471 29 300 18 540

Exports of goods and services 414 295 355 653 409 868 492 570

Imports of goods and services (-) 408 534 360 847 448 752 522 953

Source: IBGE

18 Boletim do Banco Central do Brasil – Annual Report 2011

with the quarter ended in December 2010, followed by declines of 0.2% and 0.3% in the next two quarters and expansion of 0.1% in the last quarter of the year.

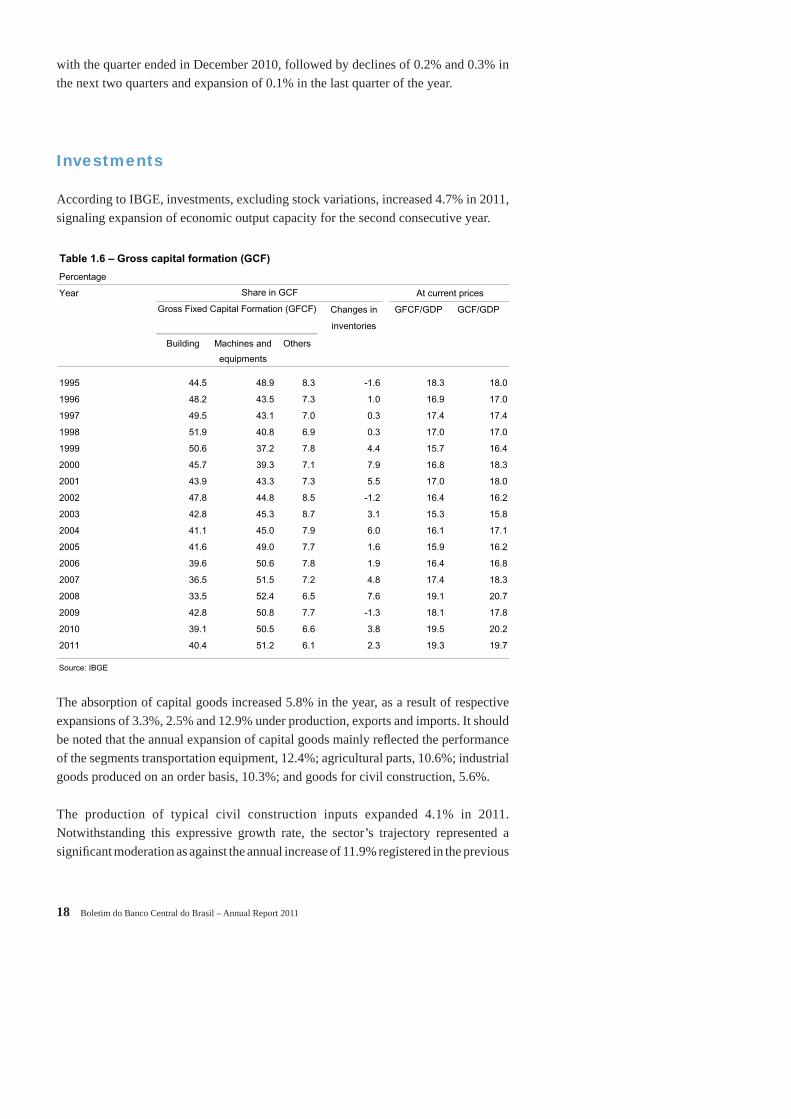

Investments

According to IBGE, investments, excluding stock variations, increased 4.7% in 2011, signaling expansion of economic output capacity for the second consecutive year.

The absorption of capital goods increased 5.8% in the year, as a result of respective expansions of 3.3%, 2.5% and 12.9% under production, exports and imports. It should be noted that the annual expansion of capital goods mainly refl ected the performance of the segments transportation equipment, 12.4%; agricultural parts, 10.6%; industrial goods produced on an order basis, 10.3%; and goods for civil construction, 5.6%.

The production of typical civil construction inputs expanded 4.1% in 2011. Notwithstanding this expressive growth rate, the sector’s trajectory represented a signifi cant moderation as against the annual increase of 11.9% registered in the previous

Table 1.6 – Gross capital formation (GCF)

Percentage

Year At current prices

Changes in GFCF/GDP GCF/GDP

inventories

Building Machines and Others

equipments

1995 44.5 48.9 8.3 -1.6 18.3 18.0

1996 48.2 43.5 7.3 1.0 16.9 17.0

1997 49.5 43.1 7.0 0.3 17.4 17.4

1998 51.9 40.8 6.9 0.3 17.0 17.0

1999 50.6 37.2 7.8 4.4 15.7 16.4

2000 45.7 39.3 7.1 7.9 16.8 18.3

2001 43.9 43.3 7.3 5.5 17.0 18.0

2002 47.8 44.8 8.5 -1.2 16.4 16.2

2003 42.8 45.3 8.7 3.1 15.3 15.8

2004 41.1 45.0 7.9 6.0 16.1 17.1

2005 41.6 49.0 7.7 1.6 15.9 16.2

2006 39.6 50.6 7.8 1.9 16.4 16.8

2007 36.5 51.5 7.2 4.8 17.4 18.3

2008 33.5 52.4 6.5 7.6 19.1 20.7

2009 42.8 50.8 7.7 -1.3 18.1 17.8

2010 39.1 50.5 6.6 3.8 19.5 20.2

2011 40.4 51.2 6.1 2.3 19.3 19.7

Source: IBGE

Share in GCF

Gross Fixed Capital Formation (GFCF)

I The Brazilian Economy 19

year, consistent with the maintenance, albeit at a less intense pace, of growth trend in the labor market and housing fi nance.

Disbursements of the BNDES system – Brazilian Development Bank, the Special Agency for Industrial Financing (Finame) and BNDES Participações S.A. (BNDESpar) – totaled R$138.9 billion in 2011, decreasing 17.5% in comparison with the previous year, when expansion had closed at 23.5%. The analysis by sectors reveals that resources channeled to the mining industry, in spite of 136.5% expansion in the year, corresponded to 2.6% of the total. Disbursements for the manufacturing industry, accounting for 29% of the total, decreased 47.9%, while disbursements channeled to the segments of commerce and services, and agriculture, represented 61.4% and 7% of the total, in the order, for respective annual variations of 7.2% and -3.6%. Excluding the disbursement of R$24.8 billion related to Petrobras capitalization, which took place in September 2010, total disbursements and disbursements channeled to the manufacturing industry decreased by 3.3% and 23.3% in the year, respectively.

Table 1.7 – Selected capital goods production

Itemization

2009 2010 2011

Capital goods -17.4 20.9 3.3

Industrial -28.1 22.1 4.0

Serial -31.6 27.3 2.8

Non-serial -6.6 -0.5 10.3

Agricultural -28.5 31.7 -4.4

Agricultural parts -38.4 13.9 10.6

Building -48.5 95.8 5.6

Electric energy -32.5 -3.8 -11.1

Transportation -8.8 26.0 12.4

Mixed -14.7 13.4 -4.4

Source: IBGE

Percentage change

-10

-5

0

5

10

15

20

25

14

15

16

17

18

19

20

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

% o

f GD

P

Graph 1.1Gross Fixed Capital Formation

GDP share Real change

Source: IBGE

Rea

l cha

nge

20 Boletim do Banco Central do Brasil – Annual Report 2011

The Long Term Interest Rate (TJLP), used as indexing factor for loans granted by the BNDES system, remained stable at 6% p.y. throughout 2011.

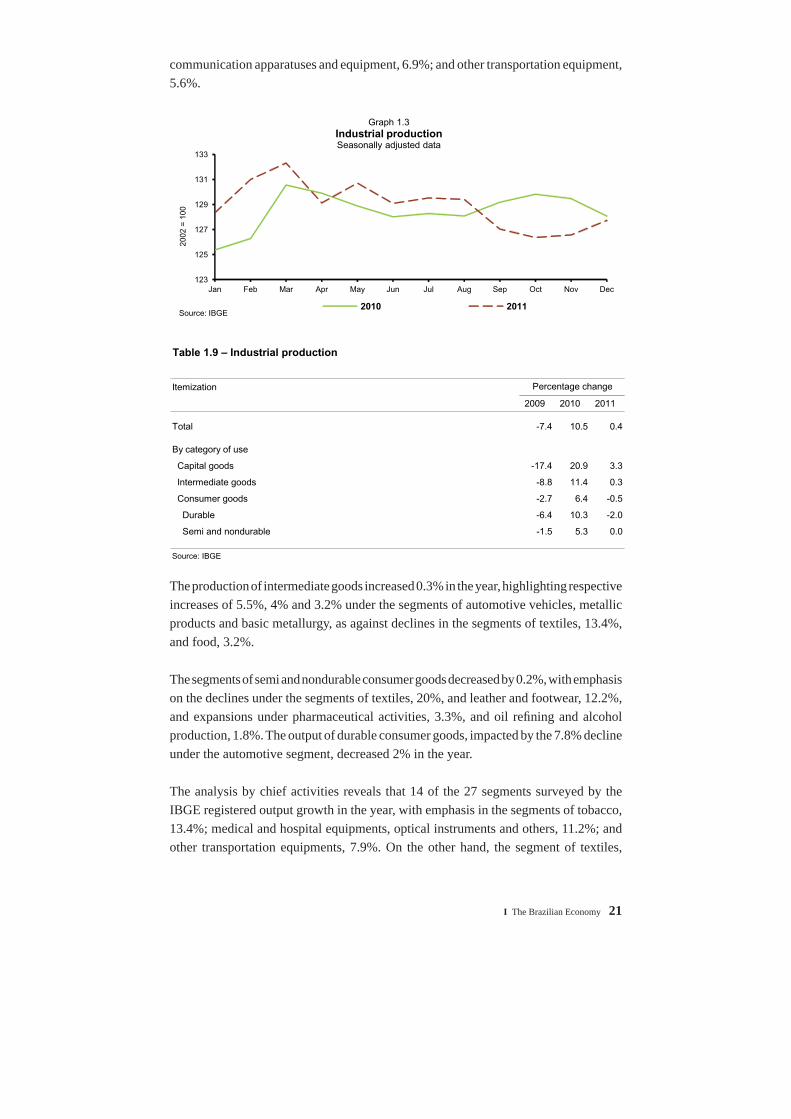

Industrial output indicators

According to the IBGE Monthly Industrial Survey – Physical Production (PIM-PF), physical industrial output registered annual growth of 0.4% in 2011, following expansion of 10.5% in 2010 and decline of 7.4% in 2009. The industrial performance resulted from expansions under the mining and manufacturing segments, 2.1% and 0.2%, respectively. It should be noted that the industrial sector, after expanding 1.1% in the fi rst quarter of the year, as compared to the previous quarter, declined by 0.7%, 0.8% and 1.4% in the following quarters of the year.

The annual industrial output trajectory by category of use reveals an enhanced performance of the sector of capital goods, which grew 3.3% in 2011, with emphasis on the performance of the segment of automotive vehicles, 15.4%; electronic material,

-10

-5

0

5

10

15

20

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Graph 1.2Industrial production

Total Mineral extraction Manufacturing

Source: IBGE

Per

cent

age

chan

ge

Table 1.8 – BNDES disbursement1/

In R$ million

Itemization 2009 2010 2011

Total 136 356 168 423 138 873

By sector

Manufacturing industry 60 302 77 255 40 270

Commerce and service 65 979 79 528 85 265

Crop and livestock 6 856 10 126 9 759

Extraction industry 3 219 1 514 3 579

Source: BNDES

1/ Includes BNDES, Finame and BNDESpar.

I The Brazilian Economy 21

communication apparatuses and equipment, 6.9%; and other transportation equipment, 5.6%.

The production of intermediate goods increased 0.3% in the year, highlighting respective increases of 5.5%, 4% and 3.2% under the segments of automotive vehicles, metallic products and basic metallurgy, as against declines in the segments of textiles, 13.4%, and food, 3.2%.

The segments of semi and nondurable consumer goods decreased by 0.2%, with emphasis on the declines under the segments of textiles, 20%, and leather and footwear, 12.2%, and expansions under pharmaceutical activities, 3.3%, and oil refi ning and alcohol production, 1.8%. The output of durable consumer goods, impacted by the 7.8% decline under the automotive segment, decreased 2% in the year.

The analysis by chief activities reveals that 14 of the 27 segments surveyed by the IBGE registered output growth in the year, with emphasis in the segments of tobacco, 13.4%; medical and hospital equipments, optical instruments and others, 11.2%; and other transportation equipments, 7.9%. On the other hand, the segment of textiles,

123

125

127

129

131

133

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2002

= 1

00

Graph 1.3Industrial productionSeasonally adjusted data

2010 2011Source: IBGE

Table 1.9 – Industrial production

Itemization

2009 2010 2011

Total -7.4 10.5 0.4

By category of use

Capital goods -17.4 20.9 3.3

Intermediate goods -8.8 11.4 0.3

Consumer goods -2.7 6.4 -0.5

Durable -6.4 10.3 -2.0

Semi and nondurable -1.5 5.3 0.0

Source: IBGE

Percentage change

22 Boletim do Banco Central do Brasil – Annual Report 2011

leather and footwear, and offi ce machines and computer equipment registered respective annual declines of 14.8%, 10.4% and 4.9%. Output of the foodstuff sector, the most important general industry segment, decreased 0.2% in 2011.

Industrial output expanded in nine of the thirteen federation units surveyed by the IBGE, with emphasis on Paraná, 7%; Espírito Santo, 6.8%; and Goiás, 6.7%. On the other hand, declines were observed in Ceará, 11.7%; Santa Catarina, 4.8%; and Bahia, 4.4%. The industrial output in the state of São Paulo, which holds the greatest share in national industry, grew 0.6% in 2011.

The level of utilization of installed capacity (Nuci) of the industrial segment followed a downward trajectory in 2011, reaching 83.4% in December, as compared to 84.9% in the same period of 2010. In terms of annual average, the Nuci decreased 0.8 p.p. in 2011, reaching 84%. Personnel employed in the industrial sector increased 1% in 2011.

The seasonally adjusted Industry Confi dence Index (ICI), of the Getulio Vargas Foundation (FGV), reached 101.8 points at the end of 2011, a level 12.7 points down from December 2010. The component that evaluates the current situation reached 102.4 points and that related to expectations, 101.1 points, declining by 13.8% and 11.7%, respectively, as compared to December 2010.

100

120

140

160

180

200

Jan2010

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan2011

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2002

=100

Graph 1.4Industrial production – By category of use

Seasonally adjusted data

Capital goods Intermediate goods

Durable goods Semi and nondurable goodsSource: IBGE

Table 1.10 – Industrial capacity utilization1/

Percentage

Itemization 2009 2010 2011

Manufacturing industry 80.2 84.8 84.0

Consumer goods 82.5 85.4 83.2

Capital goods 75.5 83.4 84.4

Building material 85.3 90.1 89.1

Intermediate goods 80.8 85.8 85.5

Source: FGV

1/ Average in the year.

I The Brazilian Economy 23

It is worth mentioning that the modest industrial performance observed in 2011 refl ected the increase of foreign competitiveness, associated, on the one hand, with the appreciation of domestic currency, and, on the other, with increased labor cost. Thus, it should be noted that the quantum of imports of intermediate goods and consumer durable goods grew 6.5% and 27.1%, respectively, in 2011, while the average real wage in the industrial segment increased 4.3%, refl ecting the enhanced labor market dynamics. In this framework, the federal government, with the aim of stimulating manufacturing activities, implemented, in August, a set of measures called Greater Brazil Plan, attempting to increase investments and technological efforts1.

Services

The growth registered in the sector of services, although less accentuated than in 2010, fueled economic expansion in 2011. The FGV Service Confi dence Index (ICS), which refl ects the sector’s businessmen confi dence, registered an average level of 131.2 points in 2011, above the indifference line of 100 points, signaling positive businessmen expectations. All the same, the indicator declined 1% in the year, after expanding 16.2% in 2010. This trajectory resulted from declines of 1.2% under the component related to the Current Situation Index (ISA) and 0.9% under the Expectations Index (EI).

The Purchase Manager Index (PMI-Services), related to the business activities component, reached an average of 53 points in 2011, compared to 52.6 points in 2010, suggesting the maintenance of the sector’s dynamics.

80

81

82

83

84

85

86

Jan2010

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan2011

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

%

Graph 1.5Industrial capacity utilization

CNI FGVSources: CNI and FGV

1/ For more details about the Greater Brazil Plan, see Chapter IV of this report.

24 Boletim do Banco Central do Brasil – Annual Report 2011

Commerce Indicators

In 2011, retail activity indicators, refl ecting the continuity of a favorable scenario in the credit and labor markets, kept on the upward trend observed over the last years, although at a more moderate pace. Thus, according to the IBGE Monthly Trade Survey (PMC), the Sales Volume Index increased 6.6% in 2011, as compared to expansions of 12.2% in 2010, 6.8% in 2009 and 9.9% in 2008. In the restricted concept, which excludes the segments of automotive vehicles and building materials, expansion came to 6.7%, 10.9%, 5.9% and 9.1% in the years aforementioned, respectively. It should be highlighted sales expansions in the following segments during the year: computer and communication equipment and materials, 19.6%; furniture and appliances; 16.6%, pharmaceutical, medical, orthopedic, perfumery and cosmetic products; 9.7%, and construction materials, 9.1%.

The regional analysis reveals that expanded retail sales registered annual increase of 7.8% in the South region, followed by increases of 7.2% in the Southeast; 6.5% in the Central-West; 6.4% in the Northeast; and 6.1% in the North. Among the federation units, sales expanded in Tocantins, 22.2%; Espírito Santo, 15%; Paraíba, 10%; Maranhão, 9.6%; Roraima, 9.5%; and in Mato Grosso, 9.2%;, and declined in Amapá, 4.6%.

Nominal sales revenues increased 9.4% in 2011, as a result of expansion of 6.6% in the sales volume and 2.6% in prices. Apart from respective increases of 3.4% and 4.6% in the segments of stationery, computer and communication equipment, and vehicles, motorcycles, parts and spares, nominal revenue growth rates exceeded the annual infl ation rate of 6.5% as measured by the IBGE Extended National Consumer Price Index (IPCA) in the period in all surveyed segments. It is noteworthy annual expansion of nominal revenues in the segments of pharmaceutical, medical, orthopedic, perfumery and cosmetic products, 14.1%; furniture and appliances, 13.1%; building materials, 12.9%; textiles, apparel and footwear, 11.8%,; and in hypermarkets, supermarkets, food products, beverages and tobacco, 11.4%

170

180

190

200

210

Jan 2010

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan 2011

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2003

= 1

00

Graph 1.6Broad Sales volume Index in the Trade Sector

Seasonally adjusted data

Source: IBGE

I The Brazilian Economy 25

Sales of the automotive sector, refl ecting the macro-prudential measures implemented in December 2010, slowed down as against the previous years. In this context, sales of cars and light commercial vehicles registered annual increase of 2.9% in 2011, according to the National Federation of Automotive Vehicle Distribution (Fenabrave), the lowest rate since 2004. Similarly, sales of national cars in the domestic market, released by the National Association of Automotive Vehicle Manufacturers (Anfavea) decreased 2.8% in 2011. It should be noted the increased participation of imported vehicles on domestic market sales, from 21.7% in December 2010, to 27% in December 2011.

According to the Brazilian Association of Supermarkets (Abras), real supermarket sales, which accounts for approximately 32% of the Monthly Retail Trade Survey (PMC), kept on the upward trend begun in 2007, expanding 3.7% in 2011, although at a more moderate pace than in the previous three years. The slowdown refl ected the increase in food prices, associated with the shock of agricultural commodities observed in the second half of 2010.

In 2011, commerce default indicators increased as compared with 2010. The average default rate in the São Paulo Metropolitan Region (RMSP), measured by the São Paulo Trade Association (ACSP) closed at 5.7% in 2011, as against 5.2% in the previous year, according to net consultations with the SPC in relation to total consultations.

The National Confi dence Index (INC), elaborated by the Ipsos Public Affairs for the ACSP, registered annual growth of 2.5% in 2011, compared to 15.6% in the previous year. Regionally, it is noteworthy the increase in consumer confi dence in the South, 10.3%, Southeast, 3.3%, and in the North/Central-West region, 0.6%, as opposed to decrease in the Northeast Region, 3.3%.

The FGV Consumer Confi dence Index grew 0.6% in the year, as a result of increase of 4.8% in the Current Situation Index (ISA) and decrease of 2.1% in the Expectations Index (IE).

80

95

110

125

140

155

Jan 2010

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan 2011

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Graph 1.7Consumer Confidence Index

ICC Consumer expectations Current economic situation

Source: FGV

Sep 2005=100

26 Boletim do Banco Central do Brasil – Annual Report 2011

Agricultural output indicators

According to the IBGE Systematic Survey of Agricultural Production (LSPA), the harvest of cereals, leguminous and oilseeds registered annual increase of 7% in 2011, reaching the record of 159.9 million tons of grains. This trajectory, refl ecting expansions of 4.6% in the harvested area and 2.3% in the average yield, was partially favored by respective annual increases of 18.9% and 9.4% under the harvests of rice and soybeans. In the regional scope, it should be highlighted the respective participations of 19.7%, 19.5% and 18.5% of the states of Paraná, Mato Grosso and Rio Grande do Sul in the country’s overall production of grains.

The production of soybeans totaled 74.9 million tons in 2011, for annual expansion of 9.4%, resulting from increases of 3.3% in the harvested area and 5.9% in the average productivity, refl ecting historical productivity records registered in major producing areas, Mato Grosso, Paraná and Rio Grande do Sul. Soybeans exports grew 13.5% in the year, as compared to expansion of 1.8% observed in 2010.

The rice harvest totaled 13.4 million tons, for annual increase of 18.9%, resulting from expansion 17.2% under the average productivity and 1.4% in the harvested area. This trajectory mainly refl ected the favorable weather conditions in the Rio Grande do Sul, the major producing state.

Table 1.11 – Agricultural production – Major crops

Millions of tons

Products 2010 2011

Grain production 149.6 160.1

Cotton seed 1.8 3.1

Rice (in husk) 11.3 13.4

Beans 3.2 3.5

Corn 56.1 56.3

Soybeans 68.5 74.9

Wheat 6.0 5.7

Others 2.7 3.2

Change in grain production (%) 11.6 7.0

Other crops

Bananas 7.0 6.7

White potatoes 3.6 3.9

Cocoa (beans) 0.2 0.2

Coffee (manufactured) 2.9 2.7

Sugarcane 719.2 715.1

Tobacco (in leaf) 0.8 1.0

Oranges 19.1 19.8

Cassava 24.4 25.3

Tomatoes 3.7 4.1

Source: IBGE

I The Brazilian Economy 27

The corn harvest reached 56.3 million tons, for annual increase of 0.4%, in a scenario of respective variations of 3.4% and -2.9% under the harvested area and average productivity. This performance resulted from expansion of 3.2% in the fi rst harvest, favored by positive weather conditions, and decrease of 3.7% in the second harvest, impacted by adverse weather conditions in the state of Paraná.

The production of beans totaled 3.5 million tons, for an increase of 9.3% in the year, with emphasis on the performance of the fi rst harvest. The annual growth resulted from increases of 6.4% in the harvested area and 2.8% in the average productivity.

The production of cotton seed reached 3.1 million tons in 2011. The annual growth of 72.7% mainly refl ected the increase of 70.2% in the harvested area.

The wheat crop decreased 5.6% in the year, totaling 5.7 million tons. Average productivity declined by 3.9%, impacted by frosts and dry weather conditions observed in the South region, while the harvested area decreased by 1.9%.

The sugar cane harvest totaled 715.1 million tons. The annual decrease of 0.6% refl ected respective variations of -5.3% and 5% under the average productivity and the harvested area.

The production of coffee, due to the biannual productivity cycle, declined to 2.7 million tons, an annual decrease of 7.5%, consequent upon decreases of 2.3% in the harvested area and 5.3% in the average productivity.

Table 1.12 – Agricultural production, harvested area and average earnings – Major crops

Percentage change

Products

2010 2011 2010 2011 2010 2011

Grain production 11.6 7.0 -1.5 4.6 13.4 2.3

Cotton (seed) 0.0 72.7 1.9 70.2 -1.8 1.4

Rice (in husk) -10.3 18.9 -6.2 1.4 -4.4 17.2

Beans -9.1 9.3 -16.6 6.4 9.0 2.8

Corn 9.4 0.4 -7.1 3.4 17.8 -2.9

Soybeans 20.3 9.4 7.1 3.3 12.4 5.9

Wheat 21.6 -5.6 -10.5 -1.9 35.9 -3.9

Source: IBGE

Area Average earningsProduction

28 Boletim do Banco Central do Brasil – Annual Report 2011

Livestock

According to the IBGE Quarterly Survey of Animal Slaughters, the production of poultry, cattle and swine totaled, in the order, 11.4 million, 6.8 million and 3.4 million tons in 2011, for respective annual variations of 6.6%, -2.8% and 9.4%. Exports turned in respective annual variations of 3.2%, -13.8% and -5.9%.

Agricultural policy

The 2011/2012 agricultural and livestock plan, published in the month of June by the Ministry of Agriculture, Livestock and Supply (Mapa), made available R$122.2 billion, 7.2% up as compared to the previous plan, of which R$107.2 billion targeted to the commercial agriculture and R$15 billion to the family agriculture.

In the context of commercial agriculture, R$80.2 billion were channeled to working capital and marketing operations, representing annual increase of 6.1%, of which R$64.1 billion granted at controlled interest rates (6.75% p.y.) and R$16.1 billion at market interest rates. Resources channeled to investments totaled R$20.5 billion, up 13.9% in the year, of which R$10.5 billion granted by the BNDES and Banco do Brasil.

The Program for Sustainable Agribusiness Production (Produsa) and the Program for Commercial Planting and Recover of Forests (Propfl ora) were incorporated to the Program for Reducing Greenhouse Gas Emissions in Agriculture (Programa ABC). The resources for the Program for Modernization of Agriculture and Conservation of Natural Resources (Moderagro) reached R$3.15 billion and R$850 million, respectively.

0.6 4.7

-2.8

11.2

5.1

9.4

-2.7

7.66.6

-8

-4

0

4

8

12

16

2009 2010 2011

Graph 1.8Animal production

Cattle Swine Poultry

Per

cent

age

chan

ge

Source: IBGE

I The Brazilian Economy 29

Productivity

Industrial labor productivity, defi ned as the ratio between the index of physical production and the number of hours paid to personnel employed in the manufacturing sector, both released by the IBGE, registered stability in 2011, as compared with expansion of 6.1% in 2010 and decline of 2.2% in 2009. Productivity remained stable in the manufacturing industry, and expanded 1.3% in the mining industry. Among the sectors surveyed, the most signifi cant gains occurred in the activities of tobacco, 20.2%; paper and graphics, 10%; and timber, 10.1%, as opposed to losses observed in the sectors of textiles, 13.5%; machines and apparatuses, exclusively electrical, electronic, precision and communications equipment, 6.1%; and leather and footwear, 4.7%.

Industrial labor productivity decreased in six of the ten federation units surveyed by the IBGE, with emphasis on declines observed in Ceará, 9.4%; Bahia, 5.9%; and Pernambuco, 5.6%, as opposed to expansion in Espírito Santo, 6.4%; Paraná, 6.2%; and São Paulo, 2.1%.

In the agricultural sector, average productivity, estimated by the ratio between the production of grains and the harvested area, increased 2.3% in the year. This trajectory was consistent with respective annual growth rates of 5.6% and 29.8% under national production and imports of agricultural fertilizers. According to the Anfavea, sales of agricultural machinery on the domestic market decreased 5.1% in the year, as a result of respective declines of 27.7% and 6.8% in sales of motorized cultivators and wheeled tractors and increase of 18% in sales of harvesters.

Energy

Oil production, including liquefi ed natural gas (LNG), increased 2.6% in the year, compared to 5.3% in 2010, according to the National Petroleum Agency (ANP). The average production reached 2.193 million barrels/day (mbd), compared to 2,137 mbd in the previous year, registering a record level in December, 2,301 mbd, and the lowest level in August, 2,140 mbd. The production of natural gas increased 4.9% in 2011, reaching an average of 0,415 mbd.

Total oil processed in refi neries increased 4.3% in 2011, reaching 1,831 mbd. Imports of oil increased 2% in the year, totaling 0.355 mbd, while exports decreased 4.2%, remaining at 0,605 mbd.

In 2011, consumption of oil derivatives in the domestic market grew 6.9%, with emphasis on automotive gasoline, 18.8%; aviation kerosene, 10.8%; diesel oil, 5.2%: and aviation gasoline, 0.7%, as against declines in the consumption of fuel oil, 25.1%,

30 Boletim do Banco Central do Brasil – Annual Report 2011

and lighting kerosene, 7.1%. Alcohol consumption decreased 13.6% in the year, as a result of decline under sales of hydrated alcohol, 28.7%, and expansion under sales of anhydrous alcohol, 18.5%.

In 2011, the national consumption of electricity rose 3.3%, according to the Energy Research Company (EPE), a federal public company under the Ministry of Mines and Energy (MME). Expansions were observed in the commercial, 6.3%; residential, 4.5%; and other segments, 2.7%, including public lighting, services and public sector, and the rural sector; and industrial, 2.2%.

Electricity consumption registered annual growth in all of the fi ve geographic regions of the country, with expansions of 8.6% in the Central-West region, 5.7% in the North region, 3.8% in the South region, 2.7% in the Southeast region and 0.9% in the Northeast region.

Employment indicators

In 2011, the labor market maintained a favorable trajectory. The annual average unemployment rate, published by the IBGE Monthly Employment Survey (PME),

Table 1.13 – Apparent consumption of oil derivatives and fuel alcohol

Daily average (1,000 b/d)

Itemization 2009 2010 2011

Petroleum 1 481 1 651 1 764

Fuel oil 86 84 63

Gasoline 328 392 466

Diesel oil 763 848 892

Liquid gas 209 216 222

Other derivatives 95 109 121

Fuel alcohol 393 381 329

Anhydrous 109 122 144

Hydrated 284 259 185

Source: ANP

Table 1.14 – Electric energy consumption1/

GWh

Itemization 2009 2010 2011

Total 388 676 416 456 430 188

By sectors

Commercial 65 325 69 141 73 502

Residential 100 751 107 235 112 089

Industrial 166 163 180 779 184 685

Other 56 440 59 299 60 912

Source: EPE

1/ Self-producers not included.

I The Brazilian Economy 31

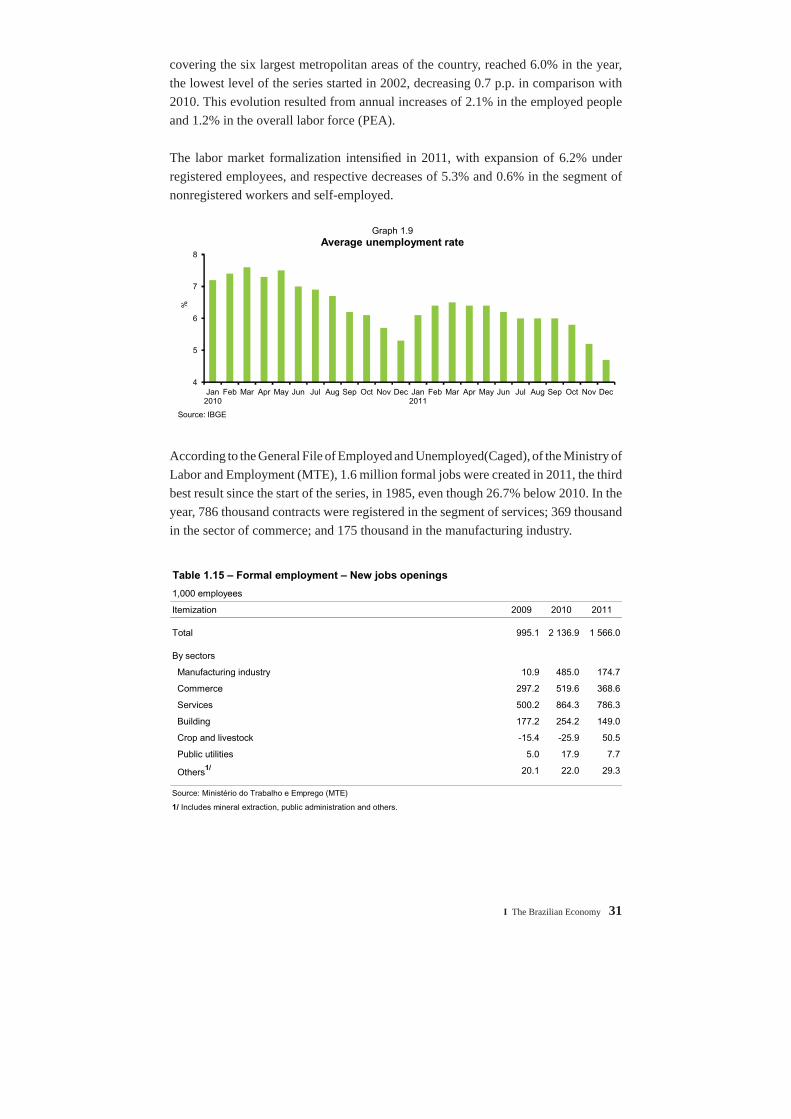

covering the six largest metropolitan areas of the country, reached 6.0% in the year, the lowest level of the series started in 2002, decreasing 0.7 p.p. in comparison with 2010. This evolution resulted from annual increases of 2.1% in the employed people and 1.2% in the overall labor force (PEA).

The labor market formalization intensifi ed in 2011, with expansion of 6.2% under registered employees, and respective decreases of 5.3% and 0.6% in the segment of nonregistered workers and self-employed.

According to the General File of Employed and Unemployed(Caged), of the Ministry of Labor and Employment (MTE), 1.6 million formal jobs were created in 2011, the third best result since the start of the series, in 1985, even though 26.7% below 2010. In the year, 786 thousand contracts were registered in the segment of services; 369 thousand in the sector of commerce; and 175 thousand in the manufacturing industry.

4

5

6

7

8

Jan2010

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan2011

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Graph 1.9Average unemployment rate

%

Source: IBGE

Table 1.15 – Formal employment – New jobs openings

1,000 employees

Itemization 2009 2010 2011

Total 995.1 2 136.9 1 566.0

By sectors

Manufacturing industry 10.9 485.0 174.7

Commerce 297.2 519.6 368.6

Services 500.2 864.3 786.3

Building 177.2 254.2 149.0

Crop and livestock -15.4 -25.9 50.5

Public utilities 5.0 17.9 7.7

Others1/ 20.1 22.0 29.3

Source: Ministério do Trabalho e Emprego (MTE)

1/ Includes mineral extraction, public administration and others.

32 Boletim do Banco Central do Brasil – Annual Report 2011

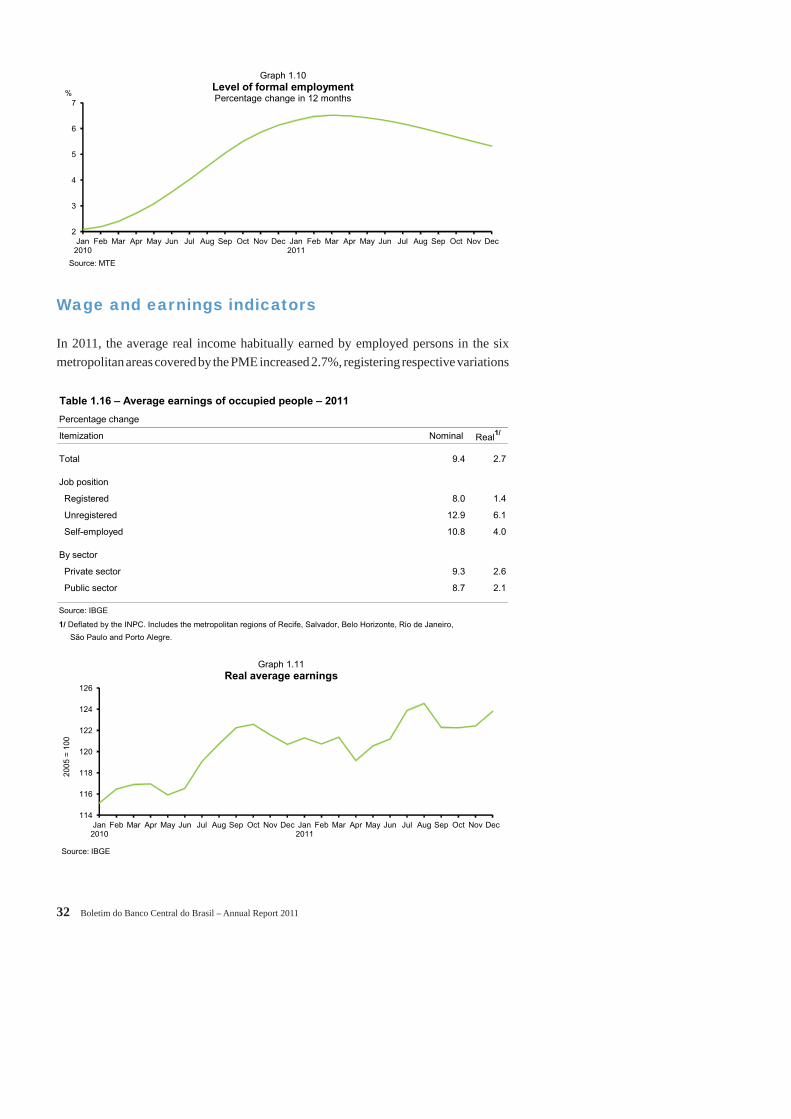

Wage and earnings indicators

In 2011, the average real income habitually earned by employed persons in the six metropolitan areas covered by the PME increased 2.7%, registering respective variations

2

3

4

5

6

7

Jan2010

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan2011

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

%

Graph 1.10Level of formal employmentPercentage change in 12 months

Source: MTE

Table 1.16 – Average earnings of occupied people – 2011

Percentage change

Itemization Nominal Real1/

Total 9.4 2.7

Job position

Registered 8.0 1.4

Unregistered 12.9 6.1

Self-employed 10.8 4.0

By sector

Private sector 9.3 2.6

Public sector 8.7 2.1

Source: IBGE

1/ Deflated by the INPC. Includes the metropolitan regions of Recife, Salvador, Belo Horizonte, Rio de Janeiro,

São Paulo and Porto Alegre.

114

116

118

120

122

124

126

Jan 2010

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan 2011

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2005

= 1

00

Graph 1.11Real average earnings

Source: IBGE

I The Brazilian Economy 33

of 1.4% and 6.1% in the segments of registered and nonregistered workers in the private sector. Among the activity sectors, the most signifi cant gains were registered in the manufacturing industry, 5.1%; construction, 5%; and commerce, 1.7%, as against the decline of 1.8% in the sector of services. Real overall wages, the product of the average real income habitually earned by the number of employed persons, grew 4.8% in the year.

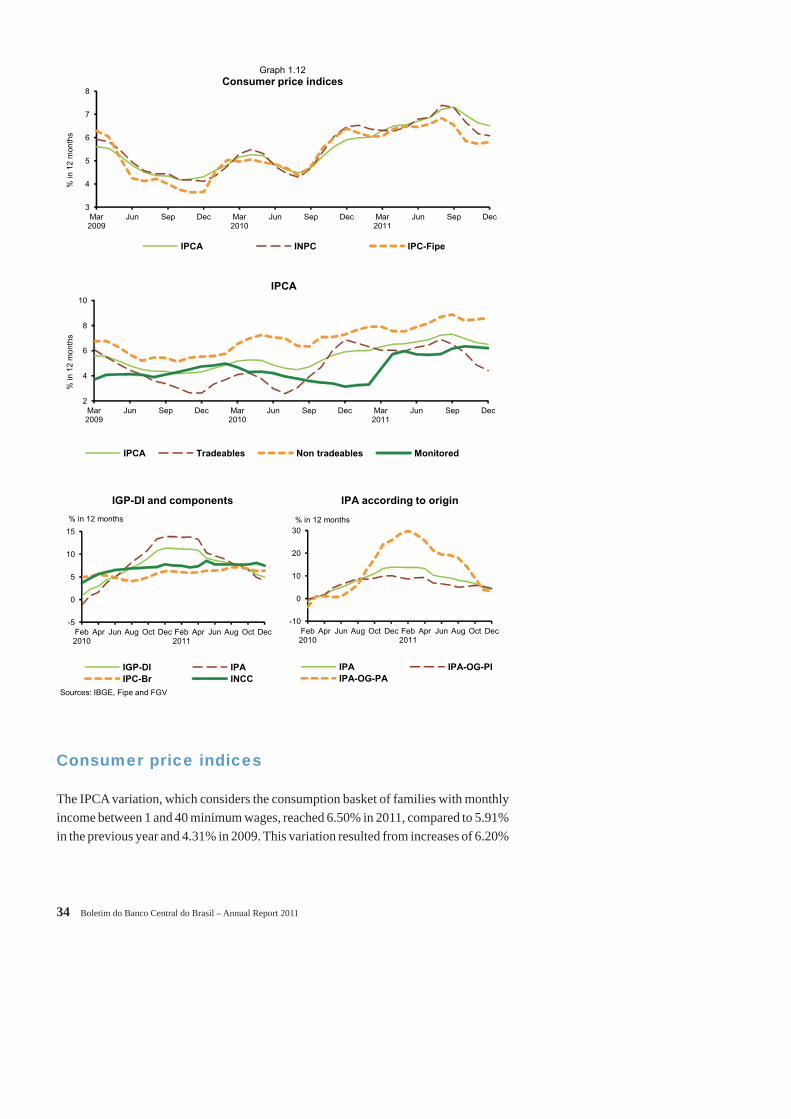

Price indicators

The upward trend of consumer price indices in 2011 mainly refl ected the performance of regulated prices, with emphasis on price increases in the segments of gasoline, urban buses, airline tickets and water and sewage fees. Market prices, revealing deceleration in the segments of food and domestic goods, registered less signifi cant increase in 2011. The IPCA variation calculated by the IBGE closed at 6.50%, remaining within the interval stipulated by the National Monetary Council (CMN) in the framework of the infl ation targeting system.

General price indices

The General Price Index (IGP-DI), published by the FGV, which aggregates the Extended Producer Price Index (PPI), the Consumer Price Index (CPI) and the National Cost of Construction Index (INCC), with respective weights of 60%, 30% and 10%, registered variation of 5.00% in 2011, as compared to 11.30% in the previous year.

The IPA increased 4.12% in the year, as compared to 13.85% in 2010, resulting from respective annual variations of 4.46% and 3.15% in the prices of industrial and agricultural products, which had increased 10.13% and 25.61%, respectively, in 2010. The IPC increased 6.36% and the INCC, 7.49%, compared to 6.24% and 7.77%, respectively, in 2010.

34 Boletim do Banco Central do Brasil – Annual Report 2011

Consumer price indices

The IPCA variation, which considers the consumption basket of families with monthly income between 1 and 40 minimum wages, reached 6.50% in 2011, compared to 5.91% in the previous year and 4.31% in 2009. This variation resulted from increases of 6.20%

3

4

5

6

7

8

Mar 2009

Jun Sep Dec Mar 2010

Jun Sep Dec Mar 2011

Jun Sep Dec

% in

12

mon

ths

Graph 1.12Consumer price indices

IPCA INPC IPC-Fipe

-5

0

5

10

15

Feb2010

Apr Jun Aug Oct Dec Feb2011

Apr Jun Aug Oct Dec

IGP-DI and components

IGP-DI IPA

IPC-Br INCC

% in 12 months

Sources: IBGE, Fipe and FGV

-10

0

10

20

30

Feb2010

Apr Jun Aug Oct Dec Feb2011

Apr Jun Aug Oct Dec

IPA according to origin

IPA IPA-OG-PI

IPA-OG-PA

% in 12 months

2

4

6

8

10

Mar 2009

Jun Sep Dec Mar 2010

Jun Sep Dec Mar 2011

Jun Sep Dec

% in

12

mon

ths

IPCA

IPCA Tradeables Non tradeables Monitored

I The Brazilian Economy 35

Table 1.17 – IPCA items share in 2011

Percentage change

Groups IPCA

Weight1/ Accumulated Accumulated Accumulated Index

change in change in share share2/

2010 2011 in 2011

IPCA 100.00 5.91 6.50 6.50 100.00

Meals away from home 8.23 9.82 10.47 0.86 13.25

Domestic services 3.61 11.81 11.38 0.41 6.32

Educational institutions 5.07 6.64 8.09 0.41 6.30

Rent 2.88 7.43 11.00 0.32 4.86

Recreation 3.43 5.31 5.89 0.20 3.11

Milk and dairy products 2.03 11.42 8.06 0.16 2.52

Meats 2.48 29.66 3.62 0.09 1.38

Sugar (refined and crystal) 0.59 23.38 1.06 0.01 0.10

Beans 0.33 51.55 -5.57 -0.02 ...

Used automobiles 1.10 -2.01 -3.71 -0.04 ...

TV sets and the like 0.47 -12.25 -11.26 -0.05 ...

Non-processed food 1.68 0.32 -3.75 -0.06 ...

Automobiles 2.23 -1.04 -2.87 -0.06 ...

Source: IBGE1/ Average weight in 2011.2/ It is obtained by dividing the accumulated share in the year by the accumulated change in the year.

Table 1.18 – IPCA items share in 2011

Percentage change

Groups IPCA

Weight1/ Accumulated Accumulated Accumulated Index

change in change in share share2/

2010 2011 in 2011

IPCA 100.00 5.91 6.50 6.50 100.00