spire presentation 4th sea automotive summit 2015 indonesia (08 apr2015)

TRANSCRIPT

1

Indonesia Automotive Insight:The New Era of LCGC/LEC

Prepared for : 4th South East Asia Auto Summit, Indonesia 2015

8th & 9th April 2015, Jakarta

2

Topic

1 A Year Before …

2 Indonesia Macro Economic Outlook 2015

3 Low Cost Green Car/Low Emission Car –A Toddler or Sumatran Tiger?

4 Low Cost Green Car/Low Emission Car –Market Opportunity & Challenge

3

A Year Before…

4

A Year Before…Indonesia Automobile Sales in 2014

541 602

781 880 879 895

975

223

292

335

350 329 334 325

765

894

1,116

1,230 1,208 1,229 1,300

2010 2011 2012 2013 2014 2015 2015

Domestic Sales of AutomobileBy Category 2010 - 2015

Passanger Vehicle (PV) Commercial Vehicle (CV) TOTAL SALES VOLUME

11.2%

30.9%

29.7%

14.8%

4.3%

12.7%

0.06%

6.1%16.9%

24.8%

10.2%1,8%

GAIKINDO Prediction

SPIRE Prediction

Source: GAIKINDO, Spire Data & AnalysisESTIMATED SALES GROWTH

Passenger Vehicle (PV)

5

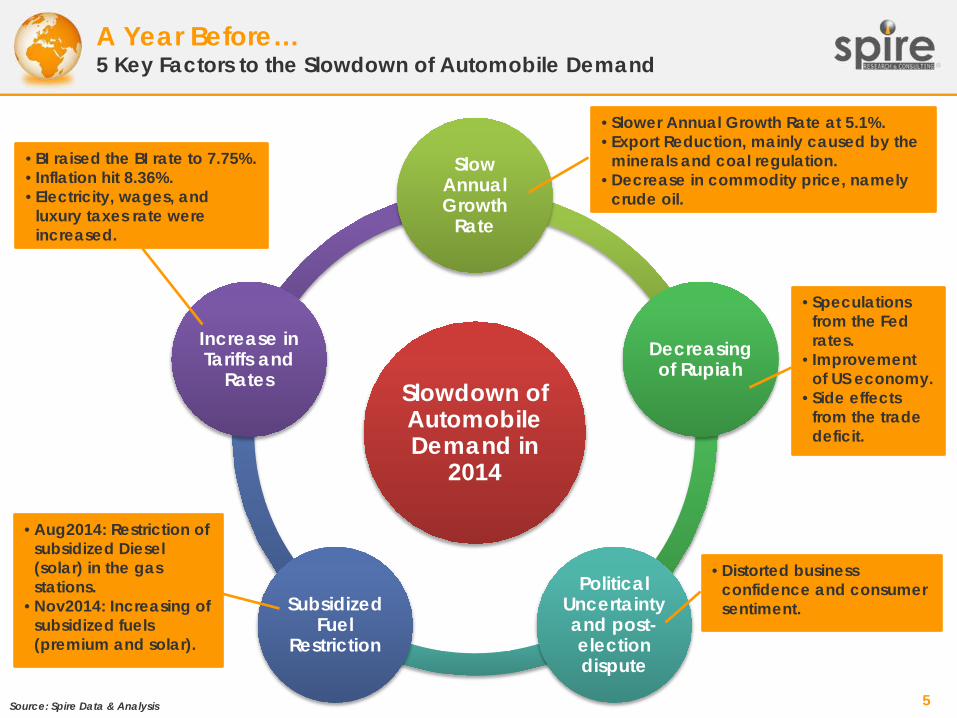

A Year Before…5 Key Factors to the Slowdown of Automobile Demand

Slowdown of Automobile Demand in

2014

Slow Annual Growth

Rate

Decreasing of Rupiah

Political Uncertainty and post-election dispute

Subsidized Fuel

Restriction

Increase in Tariffs and

Rates

• Speculations from the Fed rates.

• Improvement of US economy.

• Side effects from the trade deficit.

• Distorted business confidence and consumer sentiment.

• Slower Annual Growth Rate at 5.1%.• Export Reduction, mainly caused by the

minerals and coal regulation.• Decrease in commodity price, namely

crude oil.

• Aug2014: Restriction of subsidized Diesel (solar) in the gas stations.

• Nov2014: Increasing of subsidized fuels (premium and solar).

• BI raised the BI rate to 7.75%.• Inflation hit 8.36%.• Electricity, wages, and

luxury taxes rate were increased.

Source: Spire Data & Analysis

6

Indonesia Macro Economic Outlook 2015

7

INDONESIA MACRO

ECONOMIC OUTLOOK IN

2015

5.5% growth rate (est.) this year with 5-7% y-o-y growth over the next 5 yearsMainly driven by growth of domestic consumption and productivity rather than export and manufacturing

60 mn productive-age population15 mn household have > USD10k annual disposable income, with 3-4% growth per annum

IDR 290T for infrastructure developmentFocusing on logistics, transportation, energy & electricity, public services, and other industry-supporting infrastructure

Investment target is IDR 520T, facilitated by single window investment serviceTargeting >100 investment by 2020, 35% for outer Java

Source: BPS, Central Bank of Indonesia, Spire Data & Analysis

8

A New Beginning of Indonesia Auto 2015

9

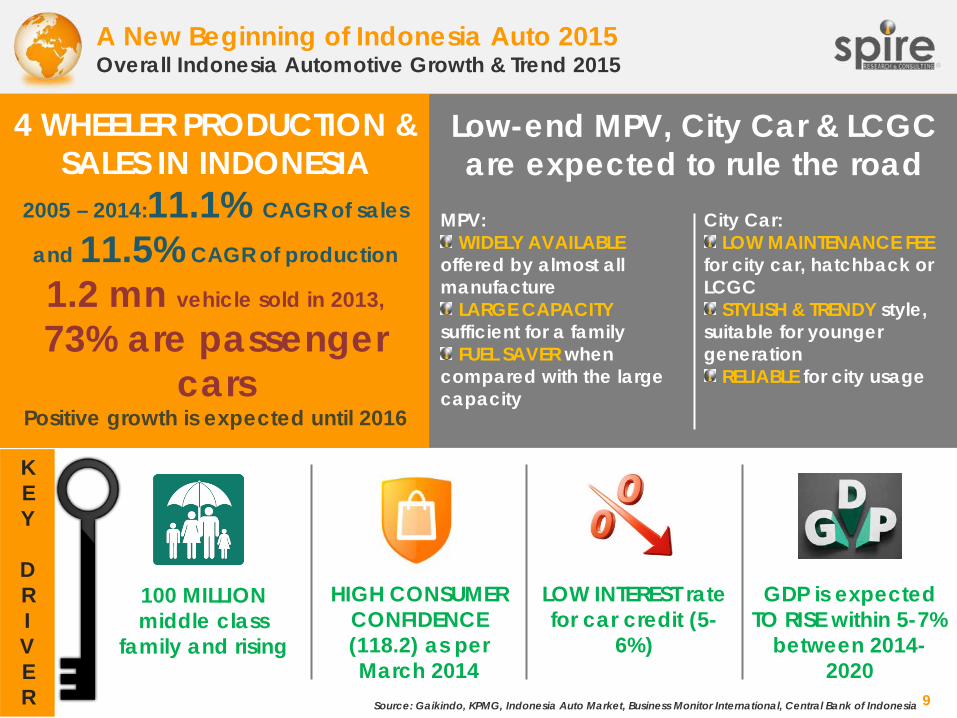

4 WHEELER PRODUCTION & SALES IN INDONESIA

2005 – 2014:11.1% CAGR of sales

and 11.5% CAGR of production

1.2 mn vehicle sold in 2013,

73% are passenger cars

Positive growth is expected until 2016

KEY

DRIVER

A New Beginning of Indonesia Auto 2015 Overall Indonesia Automotive Growth & Trend 2015

100 MILLION middle class

family and rising

HIGH CONSUMER CONFIDENCE (118.2) as per March 2014

LOW INTEREST rate for car credit (5-

6%)

GDP is expected TO RISE within 5-7%

between 2014-2020

Source: Gaikindo, KPMG, Indonesia Auto Market, Business Monitor International, Central Bank of Indonesia

Low-end MPV, City Car & LCGC are expected to rule the road

MPV:WIDELY AVAILABLE

offered by almost all manufacture

LARGE CAPACITY sufficient for a family

FUEL SAVER when compared with the large capacity

City Car:LOW MAINTENANCE FEE

for city car, hatchback or LCGC

STYLISH & TRENDY style, suitable for younger generation

RELIABLE for city usage

10

18 Months of Low Cost Green Car/Low Emission Car – A Toddler or

Sumatran Tiger?

11

A New Beginning of Indonesia Auto 2015 Market Entry & Growth Strategy

COMPETITOR ANALYSIS

BUSINESS PARTNER

SELECTION

CORPORATE SOCIAL

RESPONSIBILITY CONSULTING

CHANNEL HEALTH

MANAGEMENT

KNOWLEDGE PROCESS

OUTSOURCING

GEO-MARKETING

DECISION ANALYTICS

CUSTOMER VALUE

CO-CREATION CONSULTING

MARKET ENVIRONMENT

RESEARCHMARKET

SIZING AND FEASIBILITY

VALUE CHAIN ANALYSIS

PRICE RESEARCH

SUPPLY CHAIN MANAGEMENT CONSULTING

CUSTOMER DECISION

DYNAMICS ANALYSIS

COUNTRY RESEARCH

CONSUMER RESEARCH

CROSS-BORDER

CONSULTING

THOUGHT LEADERSHIP

CONSULTING

ANTI-COUNTERFEIT CONSULTING

HOLISTIC MARKET ENVIRONMENT RESEARCH

12

Toyota Agya (39%)

A New Beginning of Indonesia Auto 2015 The LCGC Program in Indonesia – Domestic Sales and Brand Domination

Source: Gaikindo, Spire Data & Analysis

Daihatsu Ayla(26%) Honda Brio

Satya(13%)

Datsun Go Family(12%)

LCGC Market 2014

by Brand Suzuki Wagon R

(10%)

51

172

2013 2014

LCGC Domestic Sales2013 - 2014

5 players are playing in this market: Toyota, Daihatsu, Honda, Suzuki & Nissan-

Datsun.

13

51

172 181 200

2013 2014 2015F 2015F

LCGC Domestic Sales2013 - 2015

A New Beginning of Indonesia Auto 2015 The LCGC Program in Indonesia – Prediction on Domestic Sales

Sales are tripled in 2014. How is the situation for 2015?

In 18 months since the launch, domestic sales of LCGC has reached 223,000 units.LCGC are popular in Indonesia since these cars are fuel efficient and relatively cheap—starting from less than IDR 100 mn price tag.The LCGC segment will gain huge opportunity in 2015. Spire predicts the sales to hit 200,000.

Source: Gaikindo, Spire Data & Analysis

GAIKINDO Predicts 5% Sales Increase

Spire Predicts 16% Sales Increase

14

A New Beginning of Indonesia Auto 2015 The LCGC Program in Indonesia – Our Previous Prediction…

Presented by Spire on2nd Annual SEA Automotive Summit 2013, 26

June 2013

15

Low Cost Green Car/Low Emission Car – Market Opportunity &

Challenge

16

A New Beginning of Indonesia Auto 2015 The LCGC Program in Indonesia – Market Opportunity & Challenge

Source: Gaikindo, BPS, Central Bank of Indonesia, Spire Data & Analysis

Indonesian people are price-sensitive. LCGC has

80 – 120 mn price tag, affordable to middle

class.

Current government applied fixed subsidy for fuel, making fuel-saving the best choice for car

owners.

LCGC are luxury tax-free, enabling the

manufacturer to have lower production cost.

Manufacturers need to make a low cost product without

sacrificing the quality. Lower price can easily be equated with low

quality.

Lower price may resulted in less profit

for the manufacturers.

With 5 players currently on the market, the

players need to compete each-other.

Brands need to be aware of cannibalism. e.g. for Toyota, Agya

may eat Avanza’smarket share.

Low cost products may lend appearance of

low brand image.

17

Tel: (62) 5794 5800 Fax: (62) 5794 5808

Wisma 46, Kota BNI 25th Floor, Unit #07-09

Jakarta [email protected]

www.spireresearch.com