m&a und allianzen in life science aktuelle entwicklungen ...€¦ · page 3 m&a und...

TRANSCRIPT

M&A und Allianzen in Life ScienceAktuelle Entwicklungen und Trends Symposium Life Science am Kapitalmarkt

Frankfurt, 3. Juni 2008

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 2

Global biotech industryStrong growth in most areas but…

Visible product progress in EuropeRecord dealsBooming financings

More approved products; progress in Phase II2007 with unprecedented deal valuesVC sets new record of US$7.4 billion

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 3

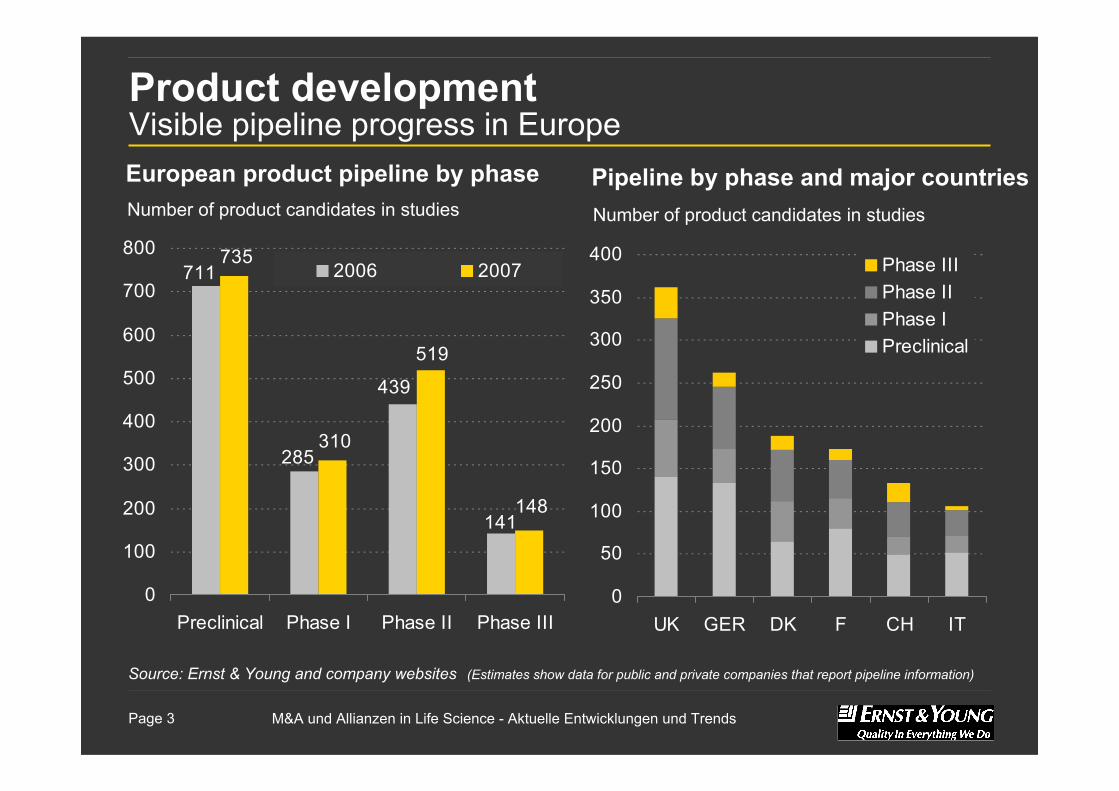

Product developmentVisible pipeline progress in Europe

Source: Ernst & Young and company websites (Estimates show data for public and private companies that report pipeline information)

711

285

439

141

735

310

148

519

0

100

200

300

400

500

600

700

800

Preclinical Phase I Phase II Phase III

2006 2007

European product pipeline by phaseNumber of product candidates in studies

0

50

100

150

200

250

300

350

400

UK GER DK F CH IT

Phase IIIPhase IIPhase IPreclinical

Number of product candidates in studies

Pipeline by phase and major countries

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 4

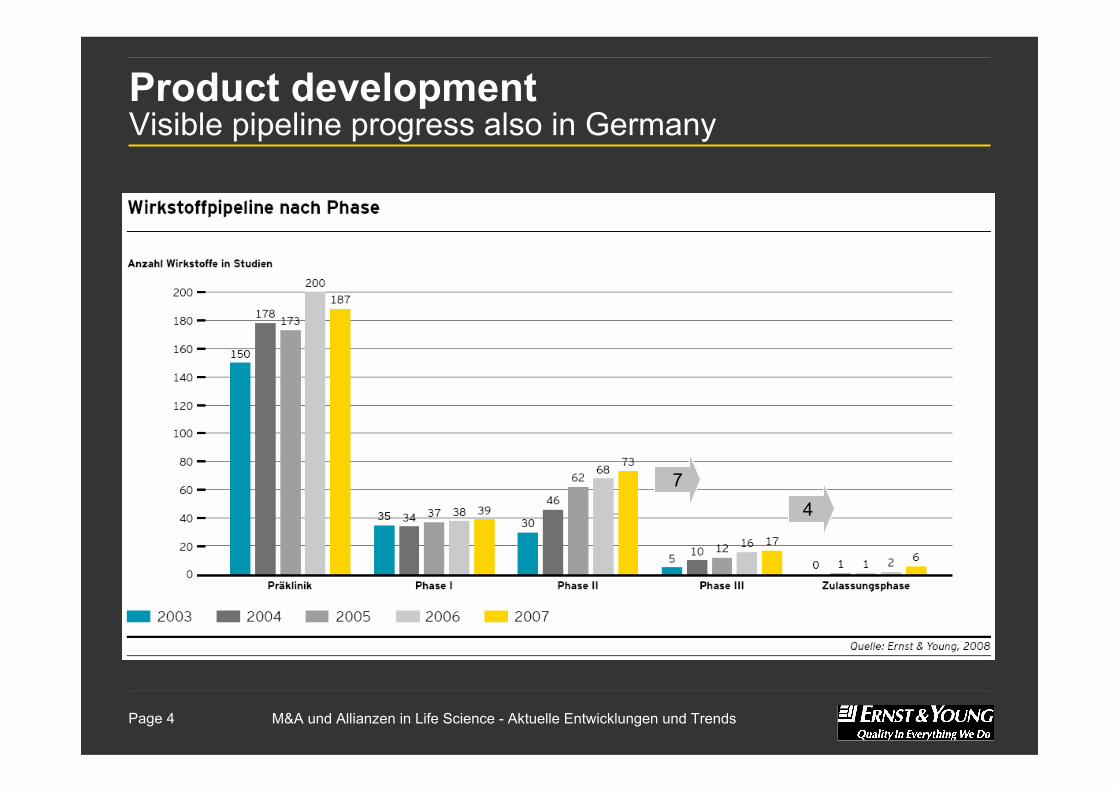

Product developmentVisible pipeline progress also in Germany

74

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 5

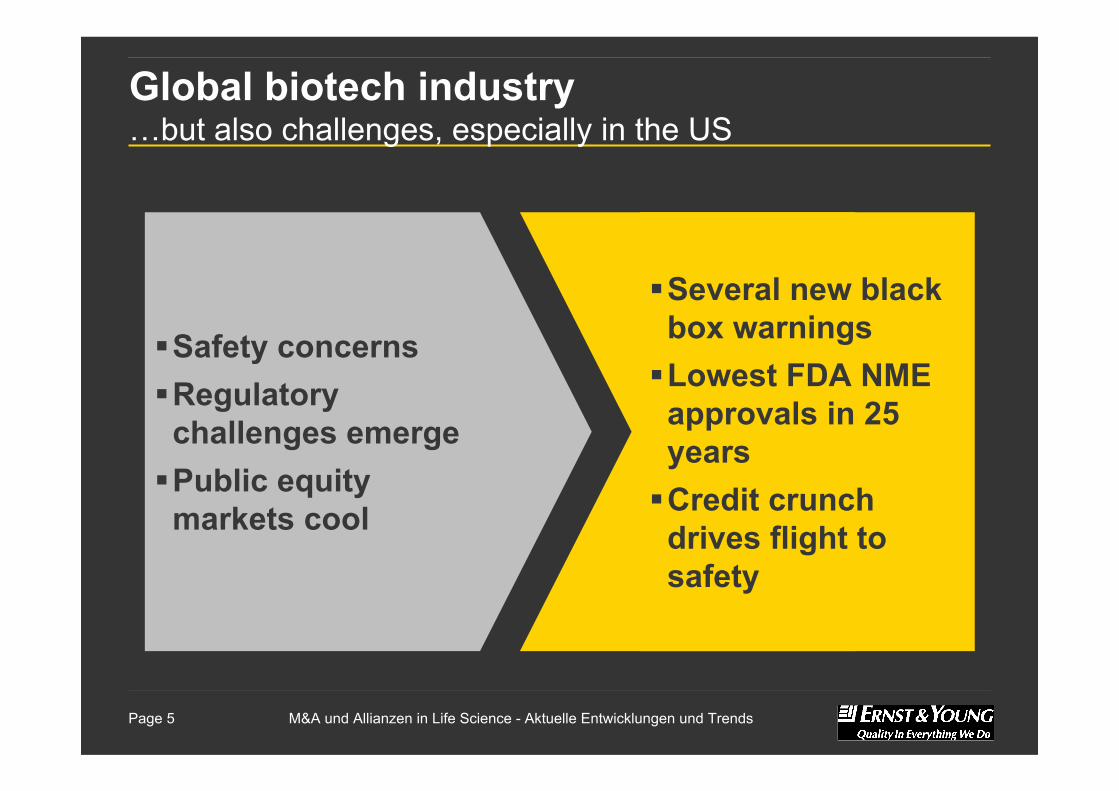

Global biotech industry…but also challenges, especially in the US

Safety concernsRegulatory challenges emergePublic equity markets cool

Several new black box warningsLowest FDA NME approvals in 25 yearsCredit crunch drives flight to safety

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 6

Uncertain public equity marketsCompanies considering IPOs don’t expect the markets improve soon…

24 months39% 24 months

32%

36 months52% 36 months

62%

12 months 6%12 months 9%0%

20%

40%

60%

80%

100%

US Europe

IPO as preferred exit by time planned; share of companies

Source: Ernst & Young company survey. Chart only shows companies that are planning IPOs.

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 7

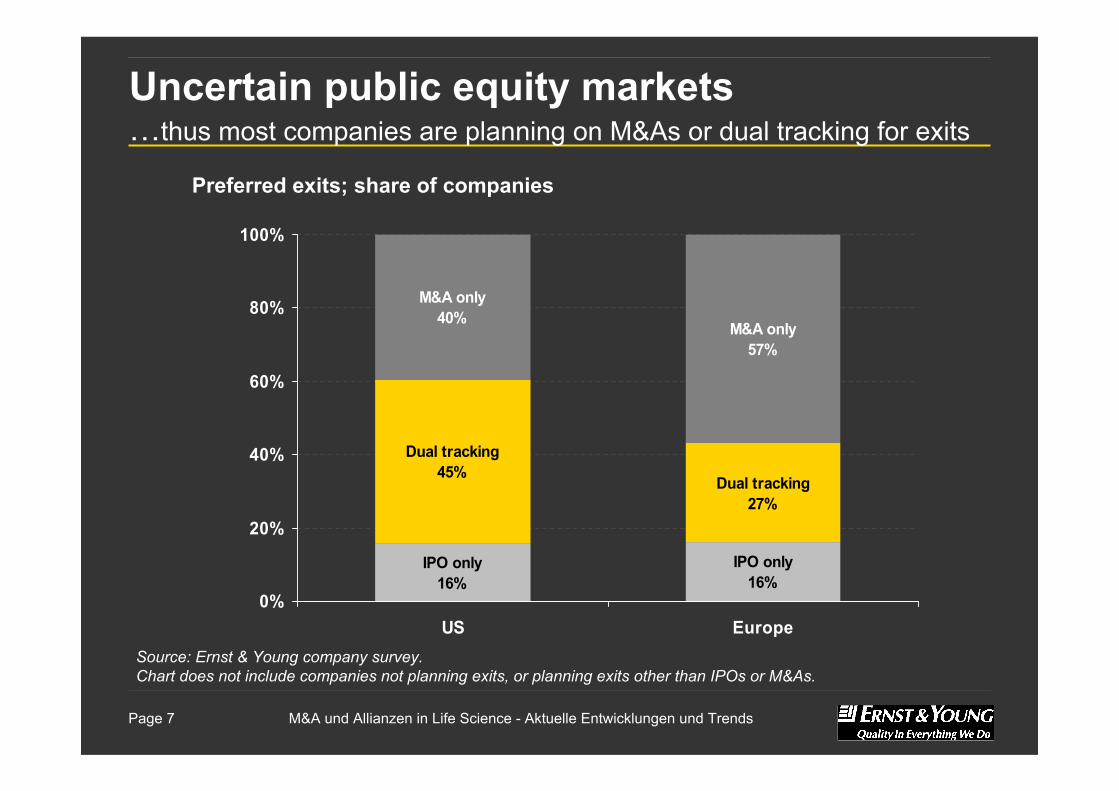

Uncertain public equity markets…thus most companies are planning on M&As or dual tracking for exits

IPO only16%

IPO only16%

Dual tracking45%

Dual tracking27%

M&A only40%

M&A only57%

0%

20%

40%

60%

80%

100%

US Europe

Preferred exits; share of companies

Source: Ernst & Young company survey. Chart does not include companies not planning exits, or planning exits other than IPOs or M&As.

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 8

Long-term outlook:reinvention

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 9

Reinvention

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money- back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal… is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥►

£

R&D

►

?????►

The drug industry is being reinventedby three sweeping trends:

►R&D productivity ►Personalized medicine►Globalization

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 10

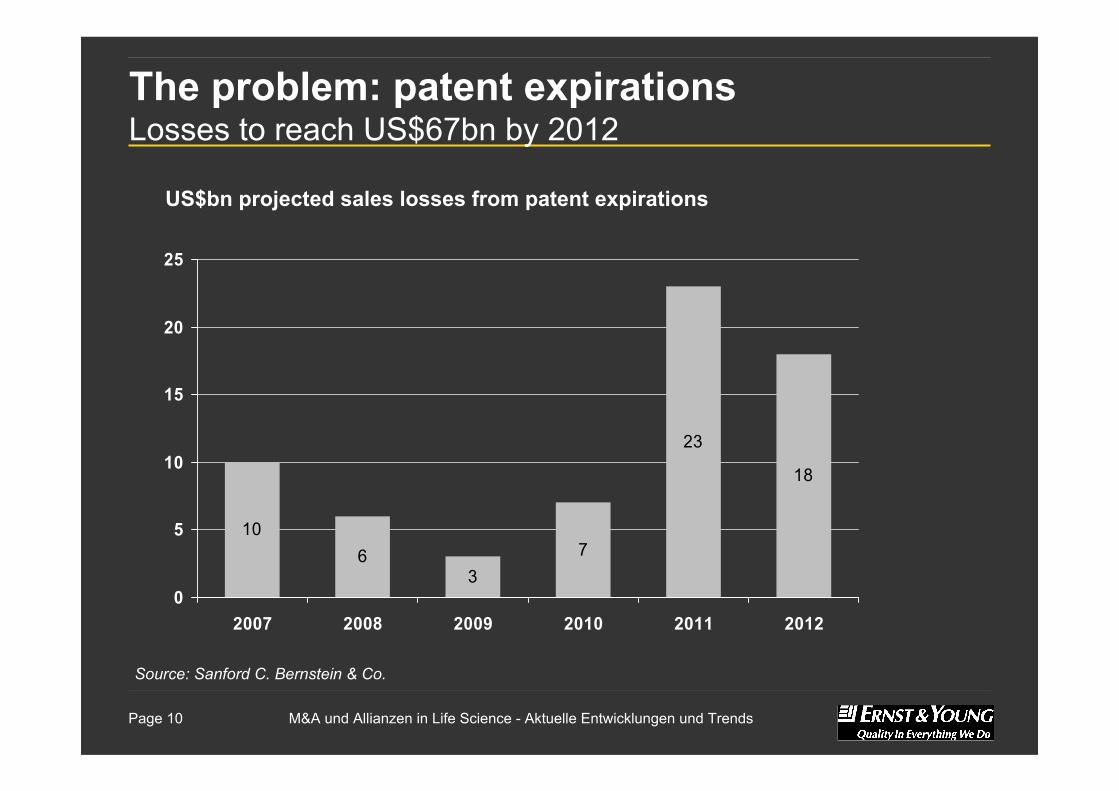

The problem: patent expirationsLosses to reach US$67bn by 2012

106

37

23

18

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012

US$bn projected sales losses from patent expirations

Source: Sanford C. Bernstein & Co.

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 11

Reinventing drug developmentPharma will continue to need biotech to fill their pipelines

Pharma’s patent productivity challenges drive change

Short- term: cost cutting, late- stage acquisitionsLong- term: platform deals, restructuring R&D (smaller teams, networked, more autonomous)

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 12

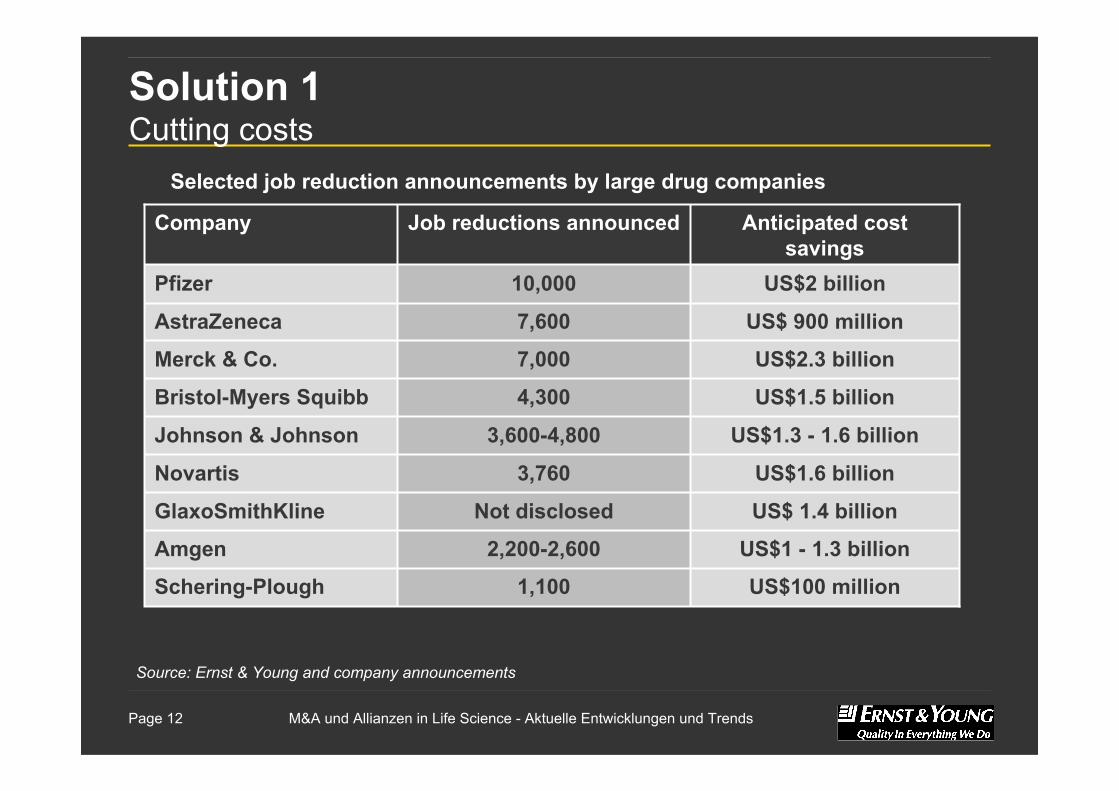

Solution 1Cutting costs

US$ 1.4 billionNot disclosedGlaxoSmithKline

US$1 - 1.3 billion2,200-2,600Amgen

US$100 million1,100Schering-Plough

US$1.6 billion3,760Novartis

US$1.3 - 1.6 billion3,600-4,800 Johnson & Johnson

US$1.5 billion4,300Bristol-Myers Squibb

US$2.3 billion7,000Merck & Co.

US$ 900 million7,600AstraZeneca

US$2 billion10,000Pfizer

Anticipated cost savings

Job reductions announcedCompany

Selected job reduction announcements by large drug companies

Source: Ernst & Young and company announcements

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 13

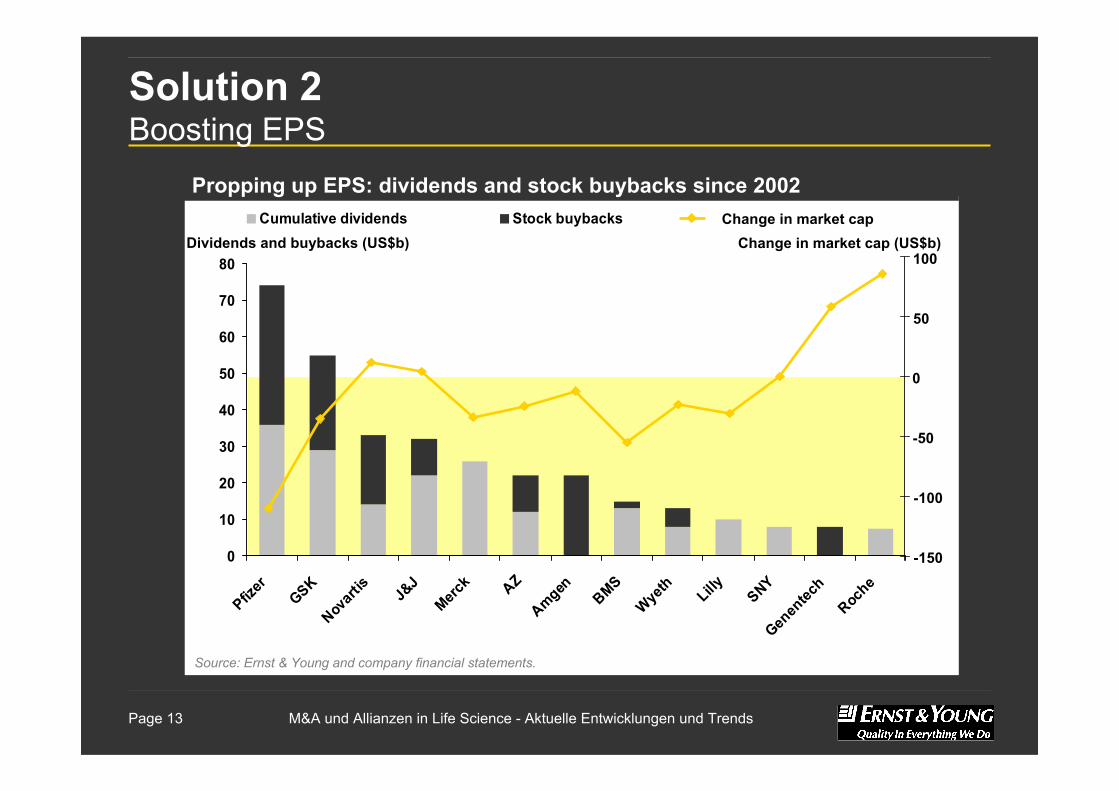

Solution 2 Boosting EPS

0

10

20

30

40

50

60

70

80

Pfizer

GSKNov

artis

J&J

Merck AZ

Amgen

BMS

Wyeth Lilly SNY

Genen

tech

Roche

Cumulative dividends Stock buybacks

Propping up EPS: dividends and stock buybacks since 2002

Source: Ernst & Young and company financial statements.

Dividends and buybacks (US$b)

-150

-100

-50

0

50

100

Change in market capChange in market cap (US$b)

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 14

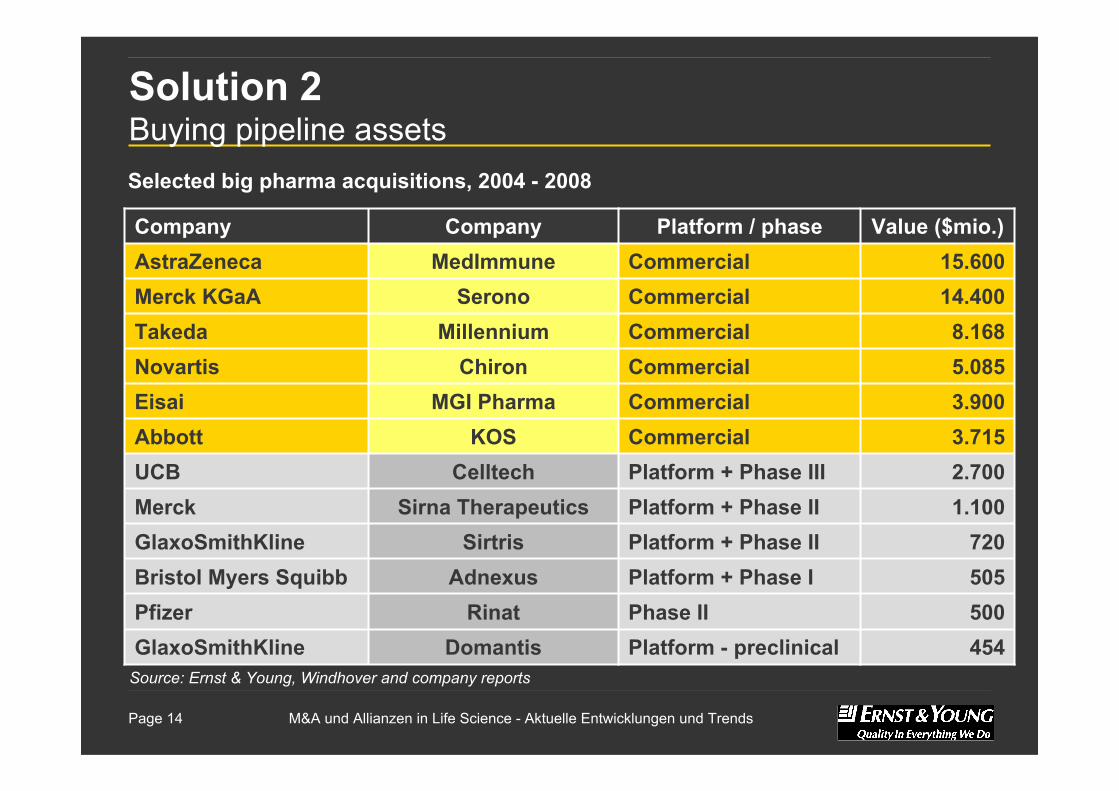

Solution 2 Buying pipeline assets

5.085CommercialChironNovartis

505Platform + Phase IAdnexusBristol Myers Squibb500Phase IIRinatPfizer

720Platform + Phase IISirtrisGlaxoSmithKline

2.700Platform + Phase IIICelltechUCB

Platform - preclinical

Platform + Phase II

CommercialCommercial

CommercialCommercialCommercial

Platform / phase

3.900MGI PharmaEisai

14.400SeronoMerck KGaA8.168MillenniumTakeda

1.100Sirna TherapeuticsMerck

454DomantisGlaxoSmithKline

15.600MedImmuneAstraZeneca

3.715KOSAbbott

Value ($mio.)CompanyCompany

Selected big pharma acquisitions, 2004 - 2008

Source: Ernst & Young, Windhover and company reports

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 15

M&ADevelopments & Trends

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 16

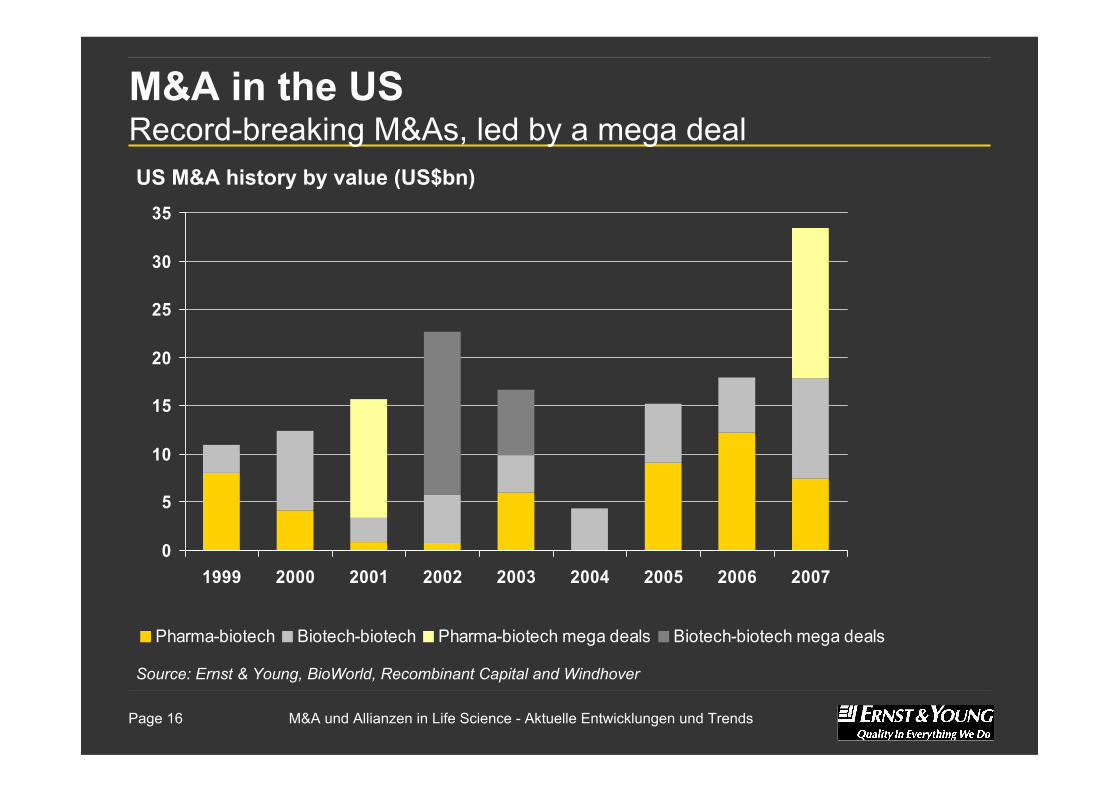

M&A in the USRecord-breaking M&As, led by a mega deal

0

5

10

15

20

25

30

35

1999 2000 2001 2002 2003 2004 2005 2006 2007

Pharma-biotech Biotech-biotech Pharma-biotech mega deals Biotech-biotech mega deals

US M&A history by value (US$bn)

Source: Ernst & Young, BioWorld, Recombinant Capital and Windhover

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 17

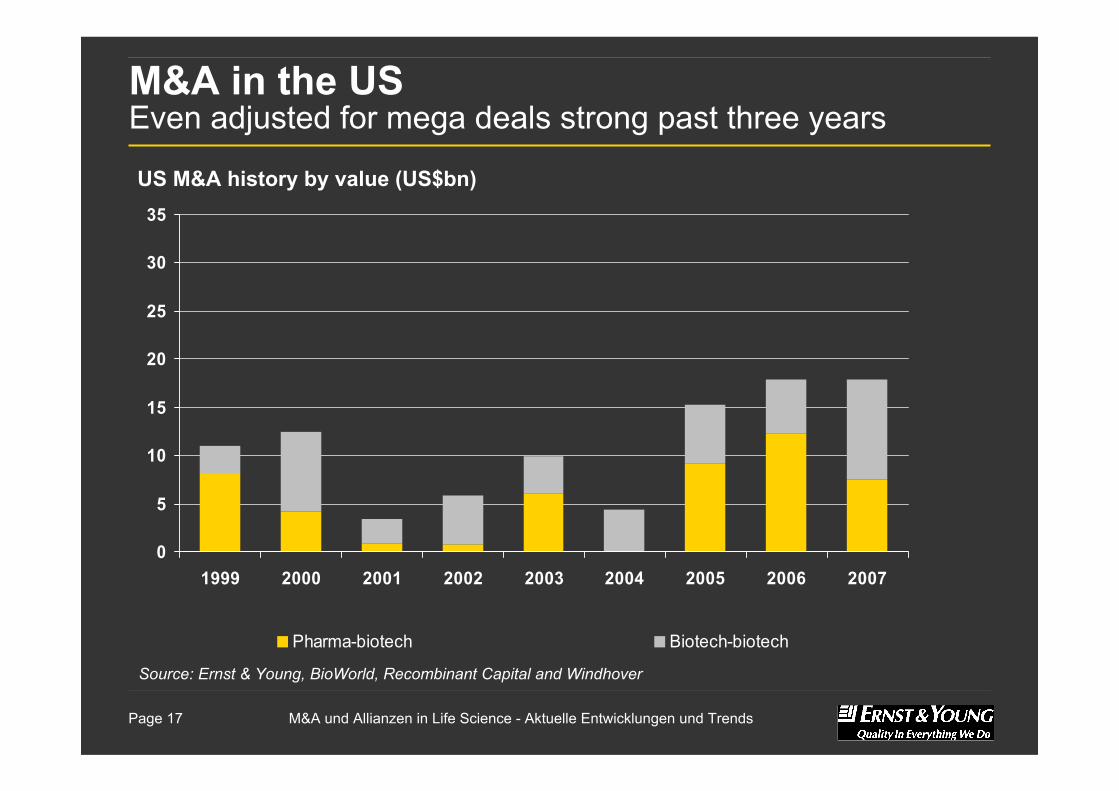

M&A in the US Even adjusted for mega deals strong past three years

0

5

10

15

20

25

30

35

1999 2000 2001 2002 2003 2004 2005 2006 2007

Pharma-biotech Biotech-biotech

US M&A history by value (US$bn)

Source: Ernst & Young, BioWorld, Recombinant Capital and Windhover

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 18

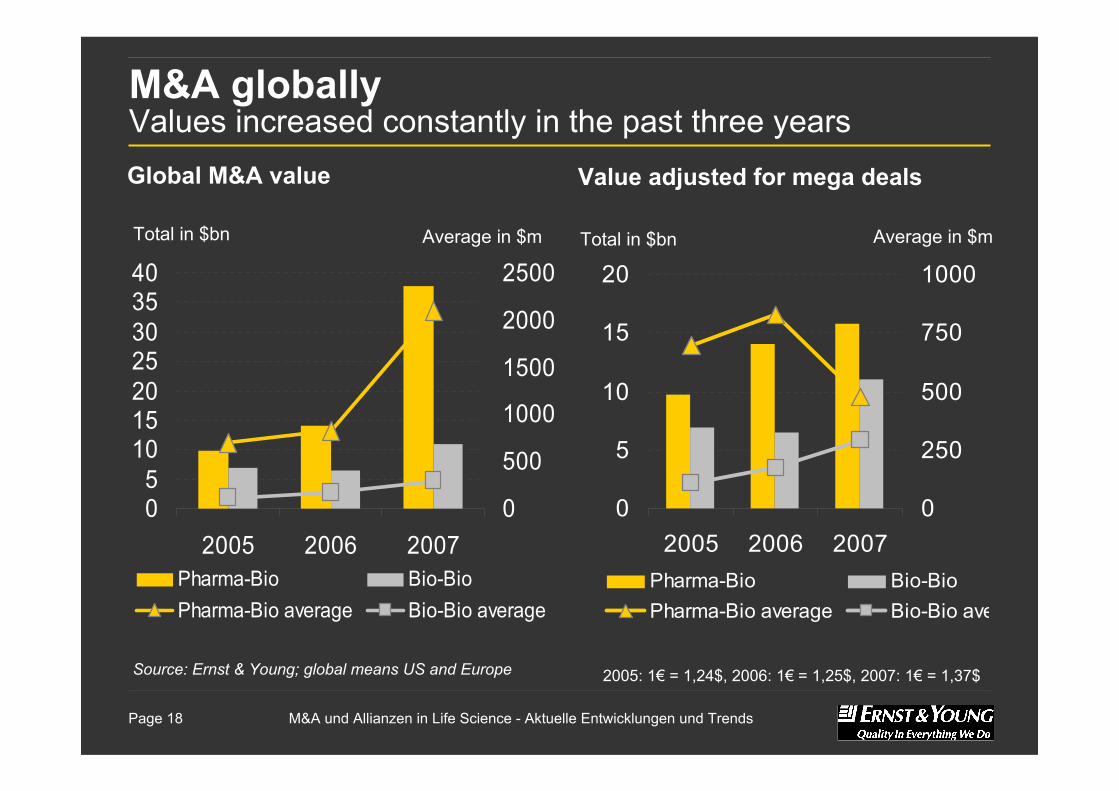

M&A globallyValues increased constantly in the past three years

Source: Ernst & Young; global means US and Europe 2005: 1€ = 1,24$, 2006: 1€ = 1,25$, 2007: 1€ = 1,37$

Total in $bn

Global M&A value

Average in $m

05

10152025303540

2005 2006 20070

500

1000

1500

2000

2500

Pharma-Bio Bio-BioPharma-Bio average Bio-Bio average

0

5

10

15

20

2005 2006 20070

250

500

750

1000

Pharma-Bio Bio-BioPharma-Bio average Bio-Bio ave

Value adjusted for mega deals

Total in $bn Average in $m

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 19

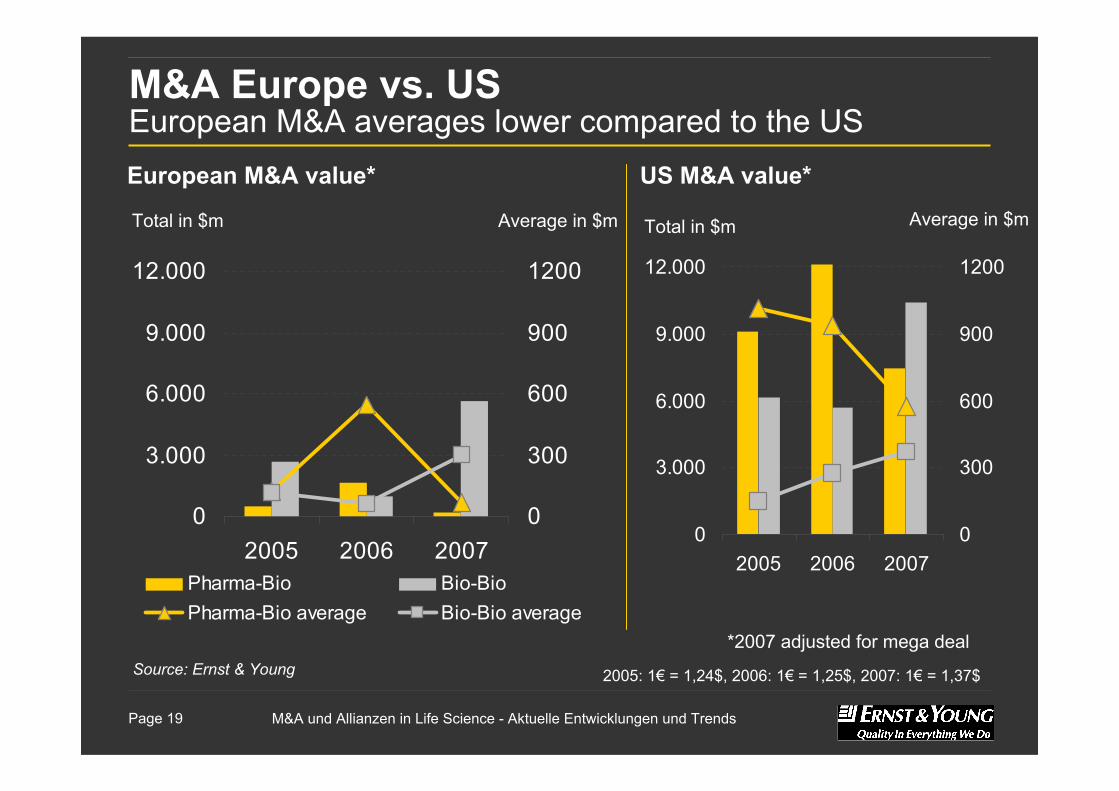

M&A Europe vs. USEuropean M&A averages lower compared to the US

Source: Ernst & Young 2005: 1€ = 1,24$, 2006: 1€ = 1,25$, 2007: 1€ = 1,37$

0

3.000

6.000

9.000

12.000

2005 2006 20070

300

600

900

1200

Total in $m

US M&A value*

Average in $mTotal in $m

European M&A value*

Average in $m

0

3.000

6.000

9.000

12.000

2005 2006 20070

300

600

900

1200

Pharma-Bio Bio-BioPharma-Bio average Bio-Bio average

*2007 adjusted for mega deal

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 20

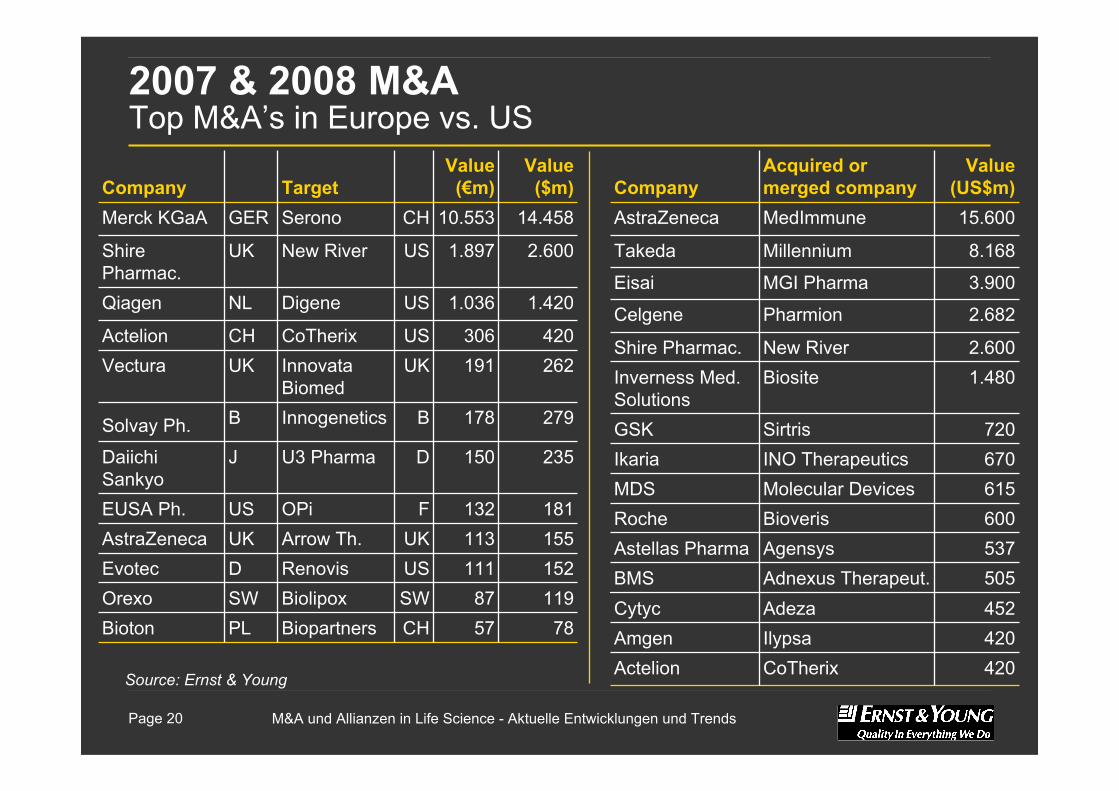

2007 & 2008 M&ATop M&A’s in Europe vs. US

8.168MillenniumTakeda

452AdezaCytyc505Adnexus Therapeut.BMS

420IlypsaAmgen

2.600New RiverShire Pharmac.1.480BiositeInverness Med.

Solutions720SirtrisGSK670INO TherapeuticsIkaria615Molecular DevicesMDS600BioverisRoche537AgensysAstellas Pharma

15.600MedImmuneAstraZeneca

3.900MGI PharmaEisai

2.682PharmionCelgene

420

Value (US$m)

CoTherix

Acquired or merged company

Actelion

Company

279178BInnogeneticsBSolvay Ph.

235150DU3 PharmaJDaiichi Sankyo

155113UKArrow Th.UKAstraZeneca

5787

111

132

191306

1.036

1.897

10.553

Value (€m)

CHSWUS

F

UKUS

US

US

CH

PLSWD

US

UKCH

NL

UK

GER

420CoTherixActelion262Innovata

BiomedVectura

181OPiEUSA Ph.

152RenovisEvotec119BiolipoxOrexo

78BiopartnersBioton

14.458SeronoMerck KGaA

2.600New RiverShire Pharmac.

1.420DigeneQiagen

Value ($m)TargetCompany

Source: Ernst & Young

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 21

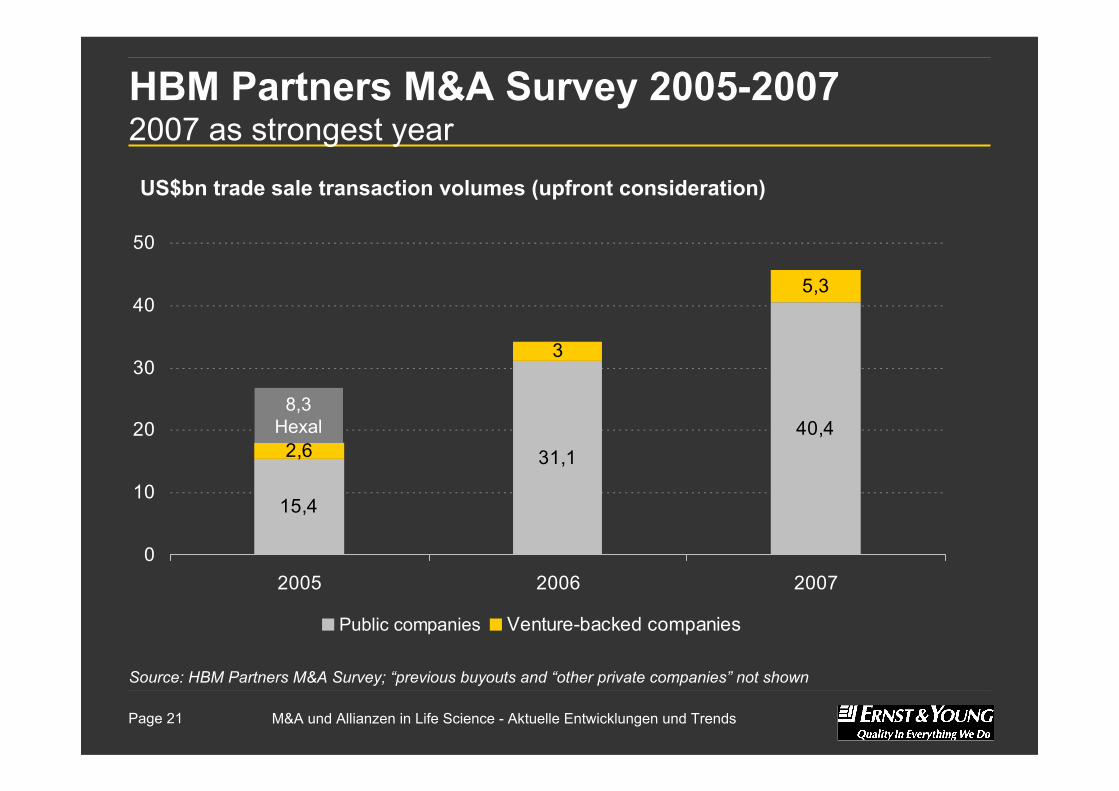

HBM Partners M&A Survey 2005-20072007 as strongest year

US$bn trade sale transaction volumes (upfront consideration)

Source: HBM Partners M&A Survey; “previous buyouts and “other private companies” not shown

15,4

31,140,4

2,6

3

5,3

0

10

20

30

40

50

2005 2006 2007

Public companies Venture-backed companies

8,3Hexal

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 22

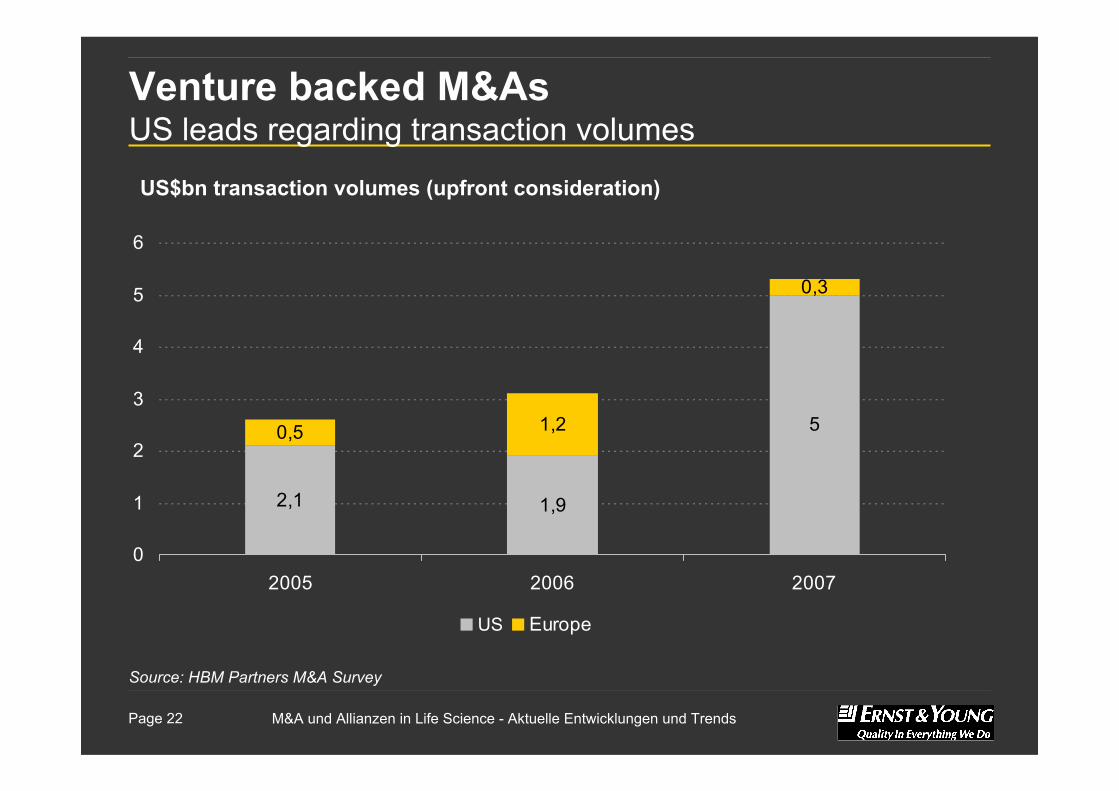

Venture backed M&AsUS leads regarding transaction volumes

US$bn transaction volumes (upfront consideration)

Source: HBM Partners M&A Survey

2,1 1,9

50,5 1,2

0,3

0

1

2

3

4

5

6

2005 2006 2007

US Europe

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 23

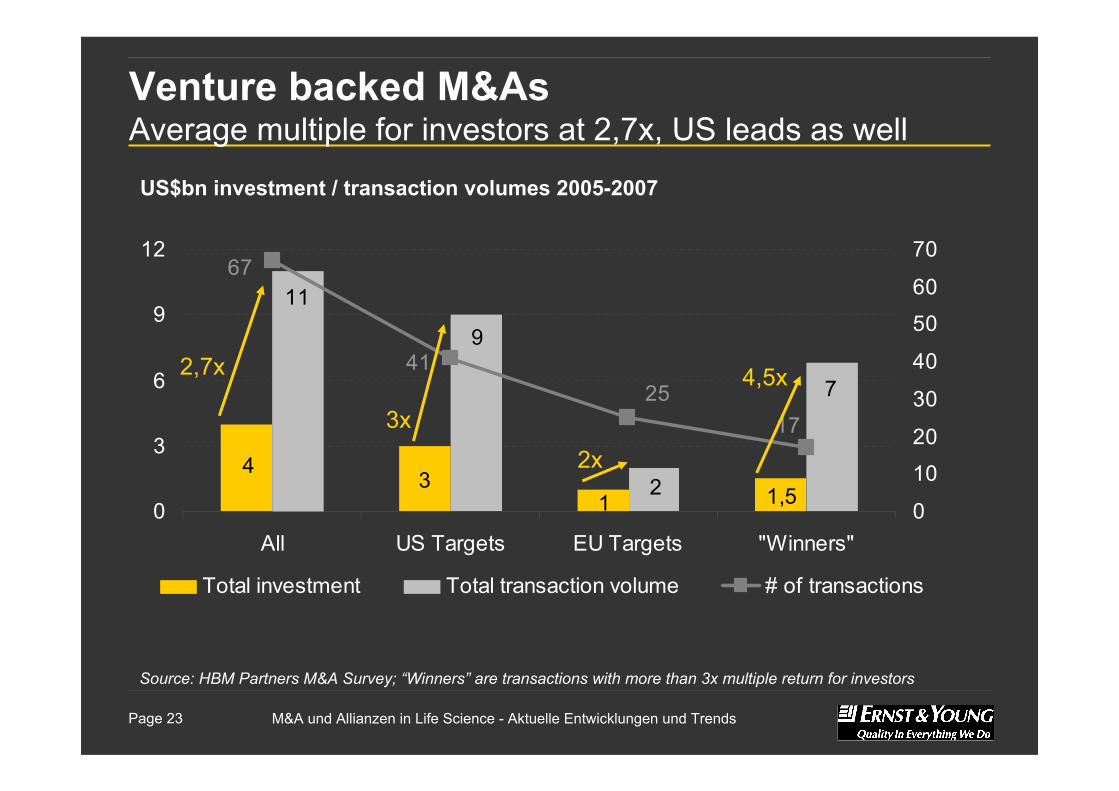

Venture backed M&AsAverage multiple for investors at 2,7x, US leads as well

US$bn investment / transaction volumes 2005-2007

Source: HBM Partners M&A Survey; “Winners” are transactions with more than 3x multiple return for investors

1,513

4

11

9

7

2

2517

41

67

0

3

6

9

12

All US Targets EU Targets "Winners"0

10

20

30

40

50

60

70

Total investment Total transaction volume # of transactions

2,7x

3x

2x

4,5x

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 24

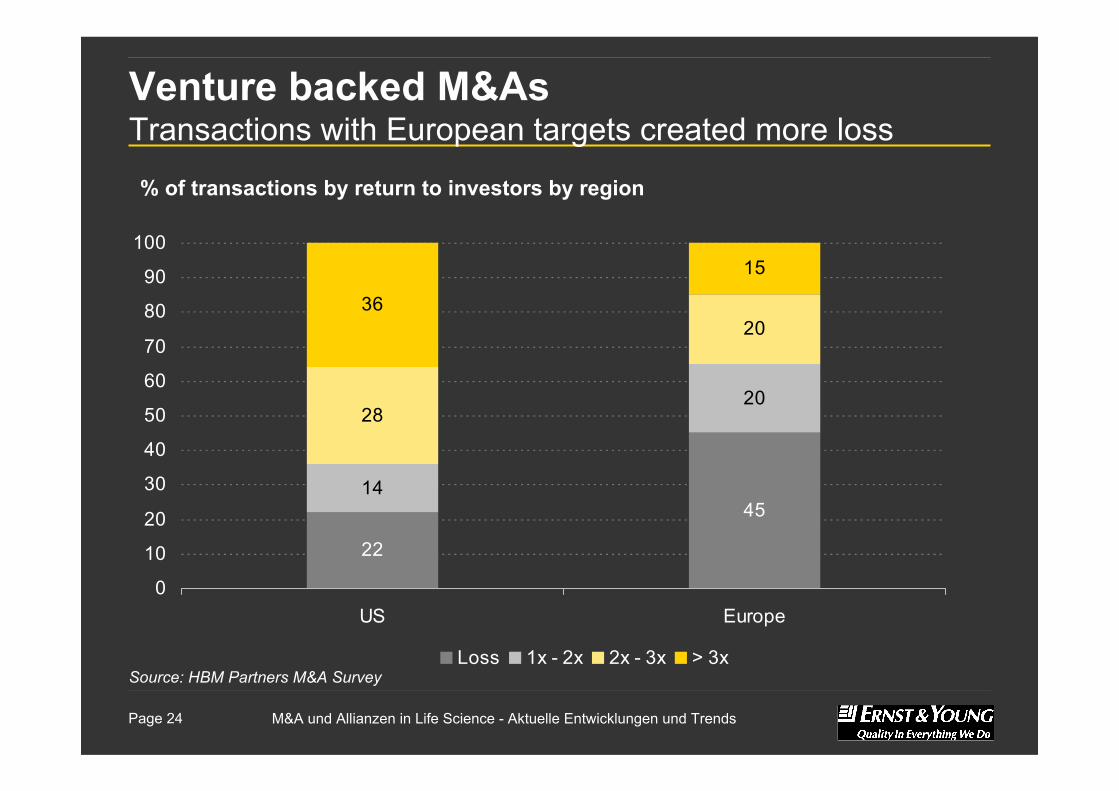

Venture backed M&AsTransactions with European targets created more loss

% of transactions by return to investors by region

Source: HBM Partners M&A Survey

22

4514

2028

2036

15

0

10

20

30

40

50

60

70

80

90

100

US Europe

Loss 1x - 2x 2x - 3x > 3x

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 25

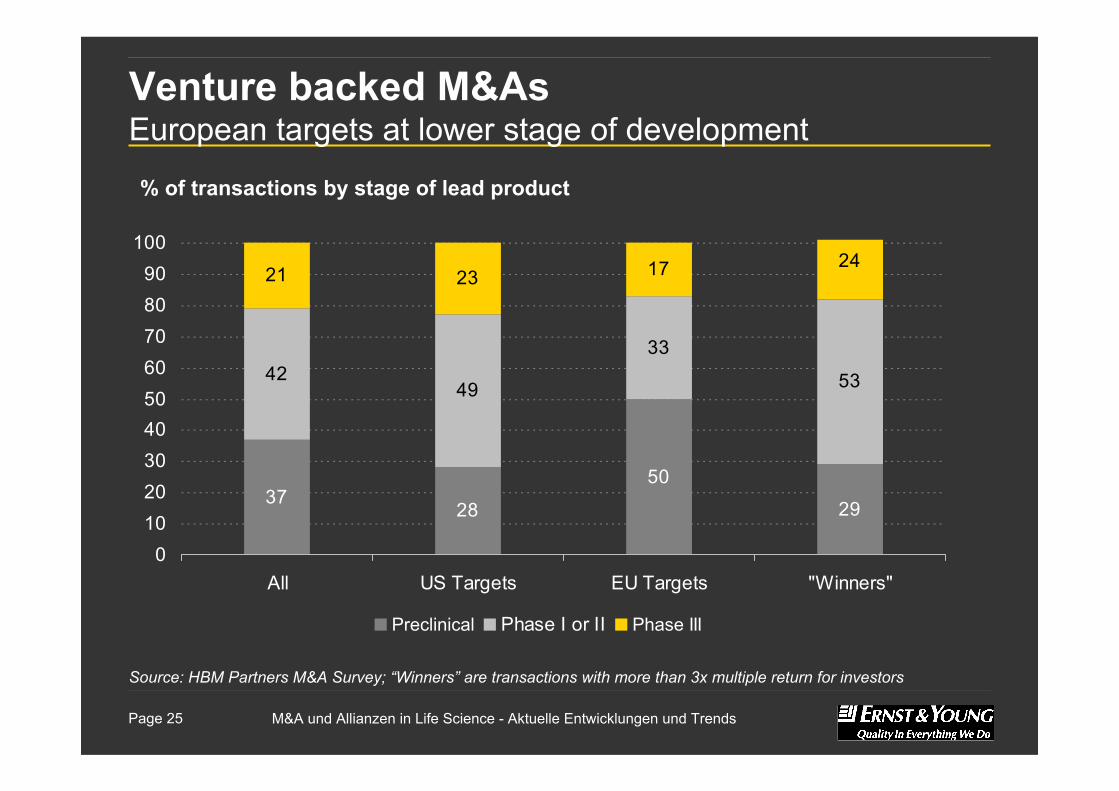

Venture backed M&AsEuropean targets at lower stage of development

% of transactions by stage of lead product

Source: HBM Partners M&A Survey; “Winners” are transactions with more than 3x multiple return for investors

3728

50

29

33

21 23 17 24

534942

0102030405060708090

100

All US Targets EU Targets "Winners"

Preclinical Phase I or II Phase III

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 26

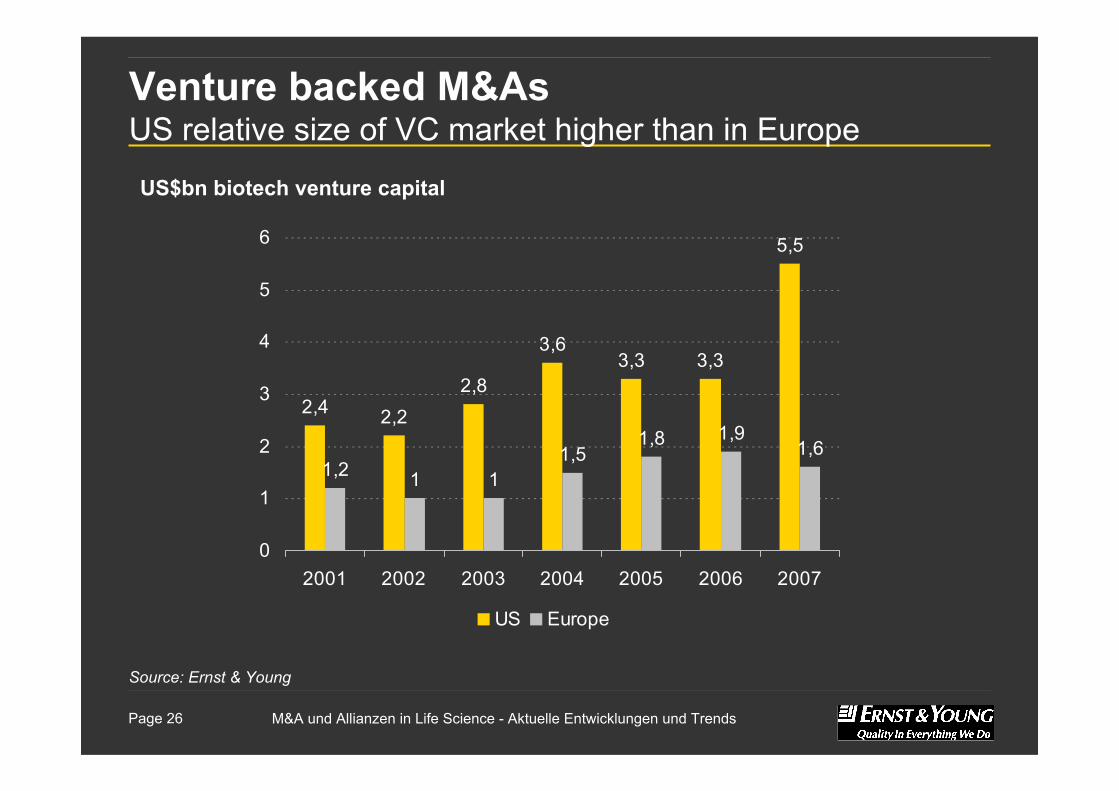

Venture backed M&AsUS relative size of VC market higher than in Europe

US$bn biotech venture capital

Source: Ernst & Young

2,4 2,22,8

3,63,3 3,3

5,5

1

1,8 1,91,61,5

11,2

0

1

2

3

4

5

6

2001 2002 2003 2004 2005 2006 2007

US Europe

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 27

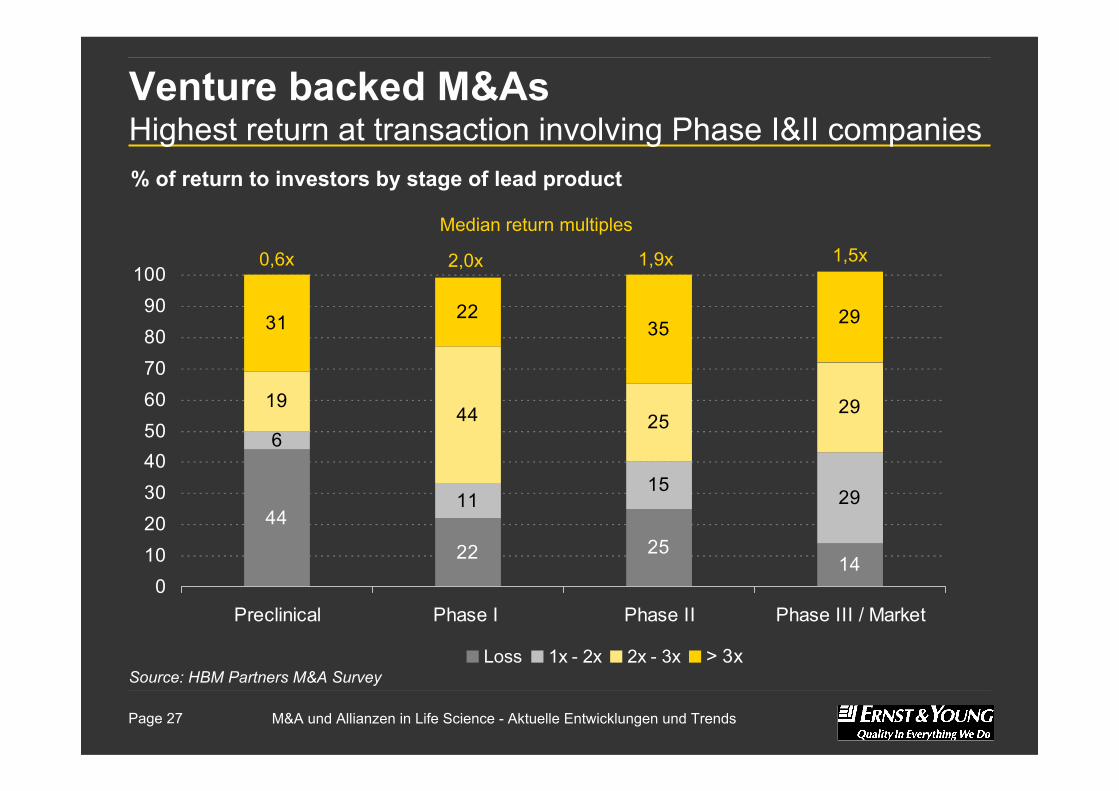

Venture backed M&AsHighest return at transaction involving Phase I&II companies% of return to investors by stage of lead product

Source: HBM Partners M&A Survey

44

22 2514

6

1115

29

1944 25

29

35 292231

0102030405060708090

100

Preclinical Phase I Phase II Phase III / Market

Loss 1x - 2x 2x - 3x > 3x

Median return multiples

0,6x 2,0x 1,9x 1,5x

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 28

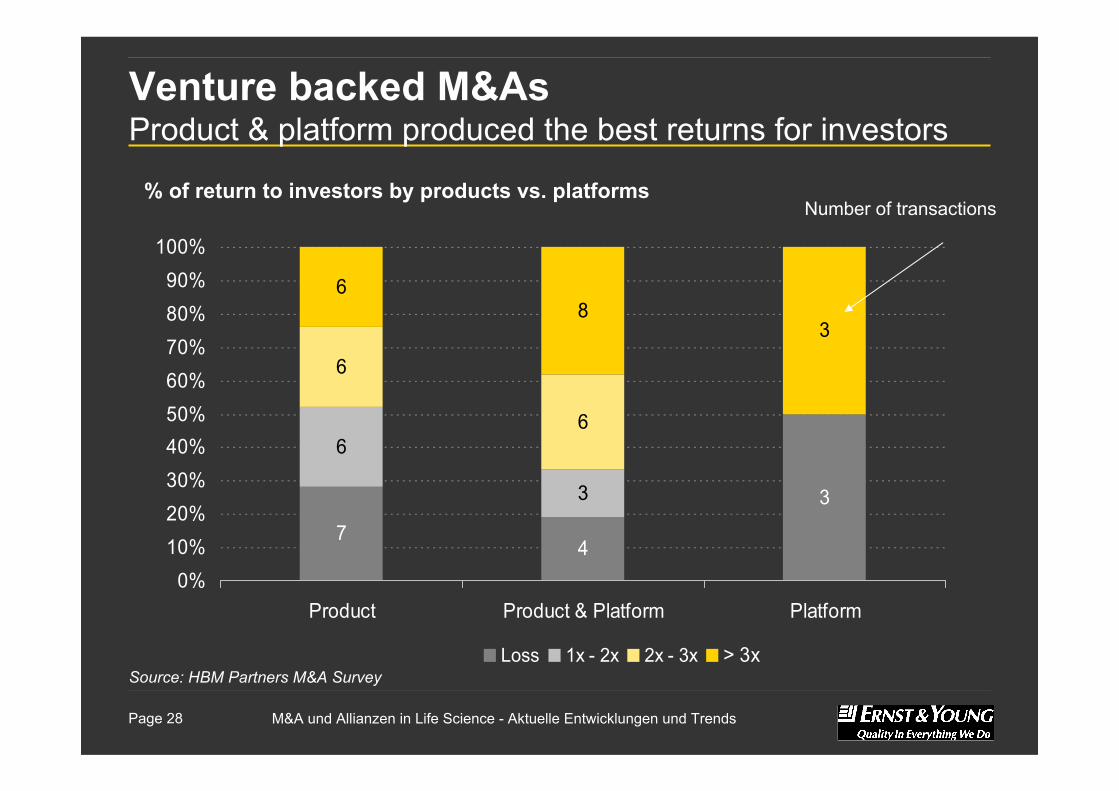

Venture backed M&AsProduct & platform produced the best returns for investors

% of return to investors by products vs. platforms

Source: HBM Partners M&A Survey

74

3

6

3

6

6

38

6

0%10%20%30%40%50%60%70%80%90%

100%

Product Product & Platform Platform

Loss 1x - 2x 2x - 3x > 3x

Number of transactions

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 29

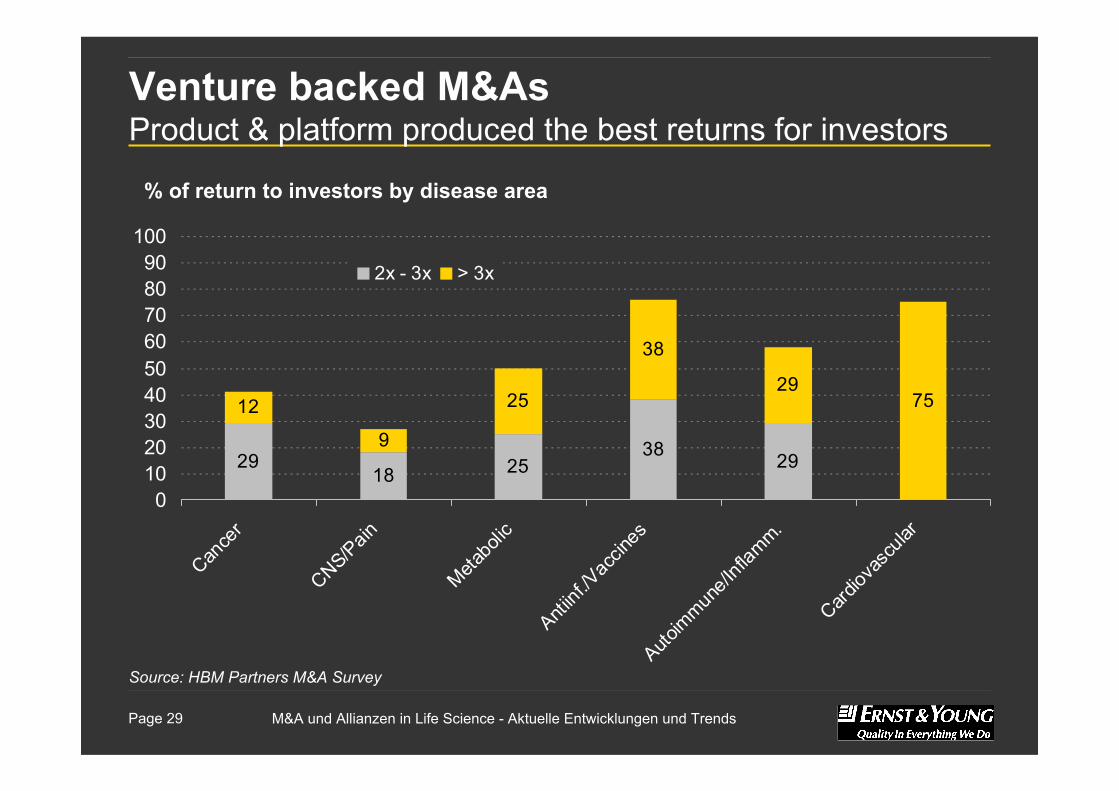

Venture backed M&AsProduct & platform produced the best returns for investors

% of return to investors by disease area

Source: HBM Partners M&A Survey

2918 25

38 29

12

9

38

297525

0102030405060708090

100

Cance

r

CNS/Pain

Metabo

lic

Antiinf

./Vac

cines

Autoim

mune/I

nflam

m.

Cardiov

ascu

lar

2x - 3x > 3x

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 30

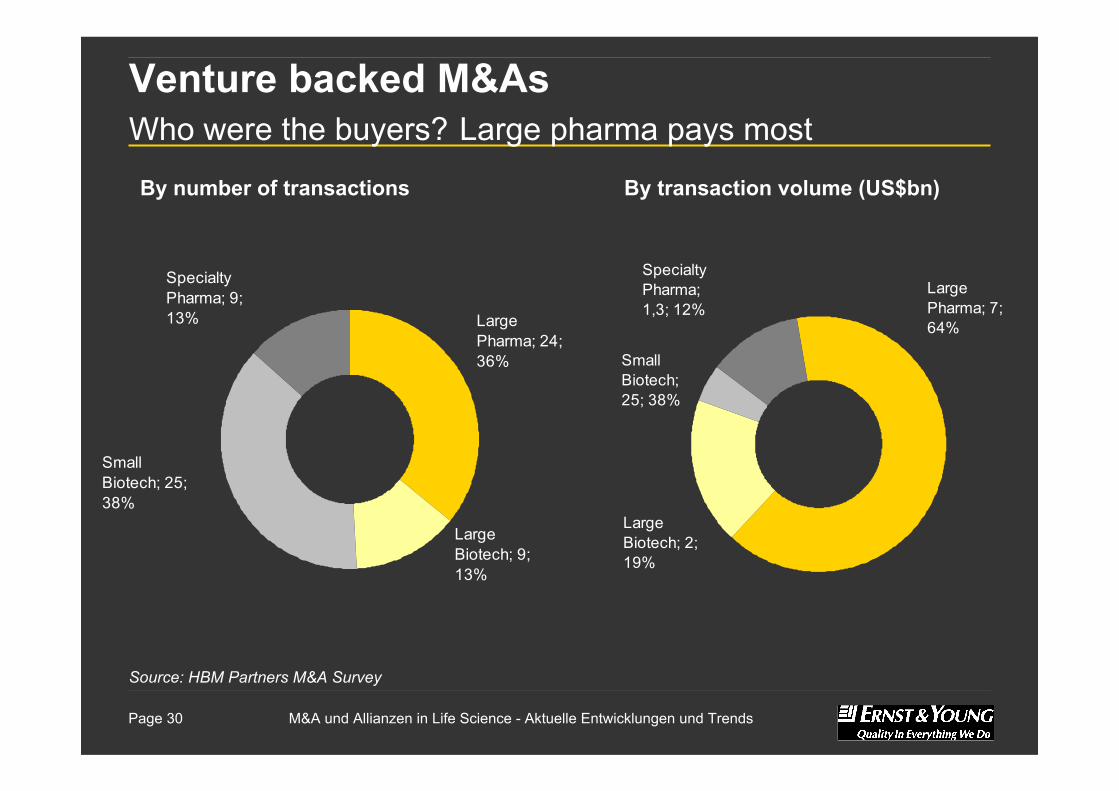

Venture backed M&AsWho were the buyers? Large pharma pays most

By number of transactions

Source: HBM Partners M&A Survey

Large Pharma; 24; 36%

Specialty Pharma; 9; 13%

Large Biotech; 9; 13%

Small Biotech; 25; 38%

By transaction volume (US$bn)

Large Pharma; 7; 64%

Specialty Pharma; 1,3; 12%

Large Biotech; 2; 19%

Small Biotech; 25; 38%

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 31

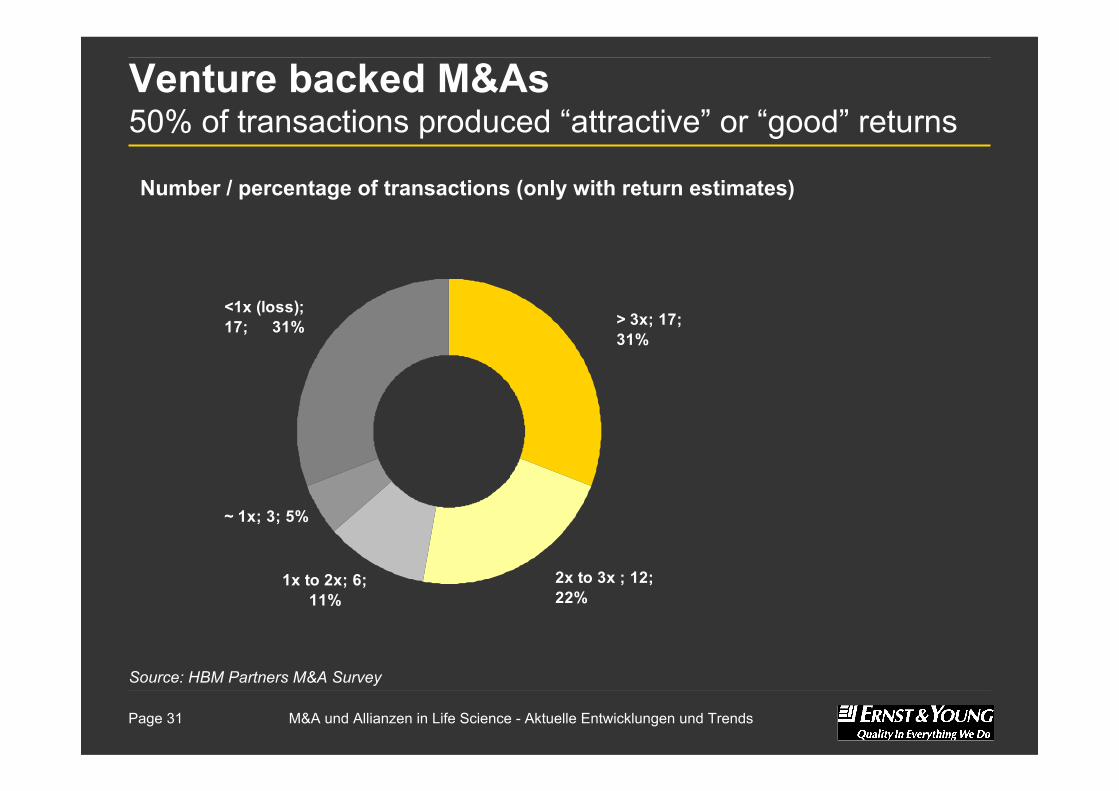

Venture backed M&As50% of transactions produced “attractive” or “good” returns

Number / percentage of transactions (only with return estimates)

Source: HBM Partners M&A Survey

<1x (loss); 17; 31% > 3x; 17;

31%

~ 1x; 3; 5%

2x to 3x ; 12; 22%

1x to 2x; 6; 11%

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 32

AlliancesDevelopments & Trends

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 33

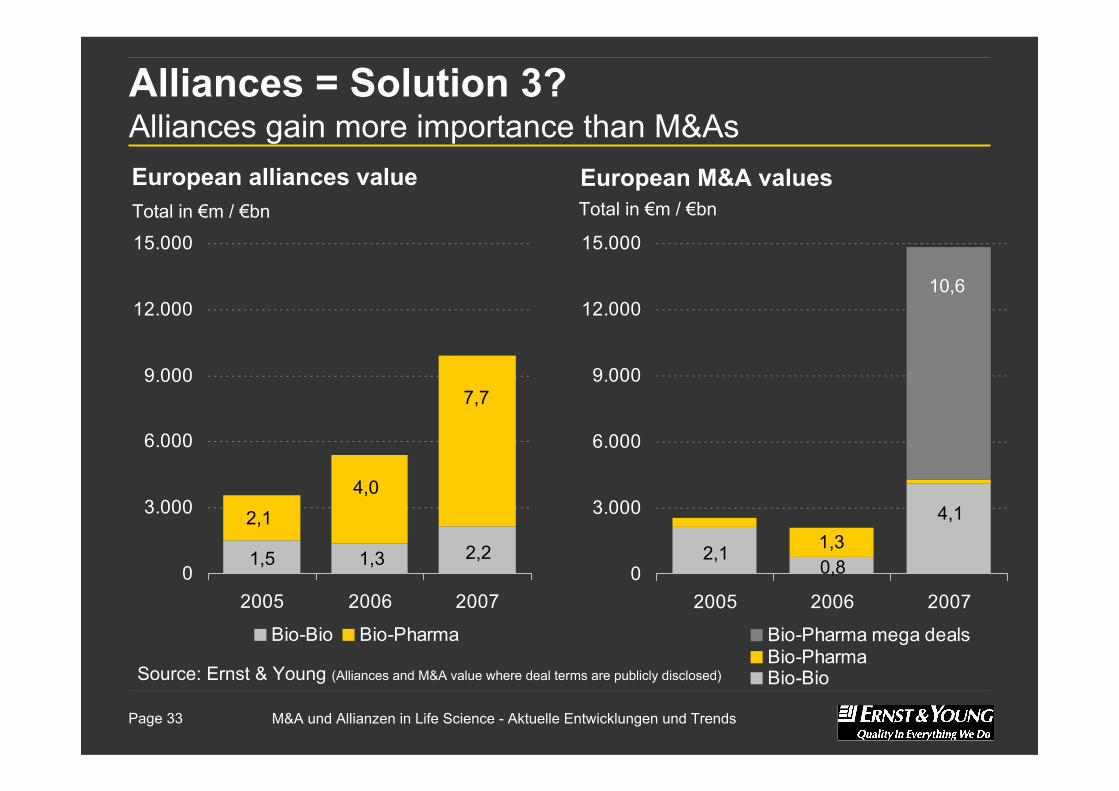

Alliances = Solution 3?Alliances gain more importance than M&As

Source: Ernst & Young (Alliances and M&A value where deal terms are publicly disclosed)

Total in €m / €bn

European alliances value

0

3.000

6.000

9.000

12.000

15.000

2005 2006 2007

Bio-Bio Bio-Pharma

0

3.000

6.000

9.000

12.000

15.000

2005 2006 2007

Bio-Pharma mega dealsBio-PharmaBio-Bio

European M&A valuesTotal in €m / €bn

1,5 1,3 2,2

2,14,0

7,7

2,10,8

4,11,3

10,6

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 34

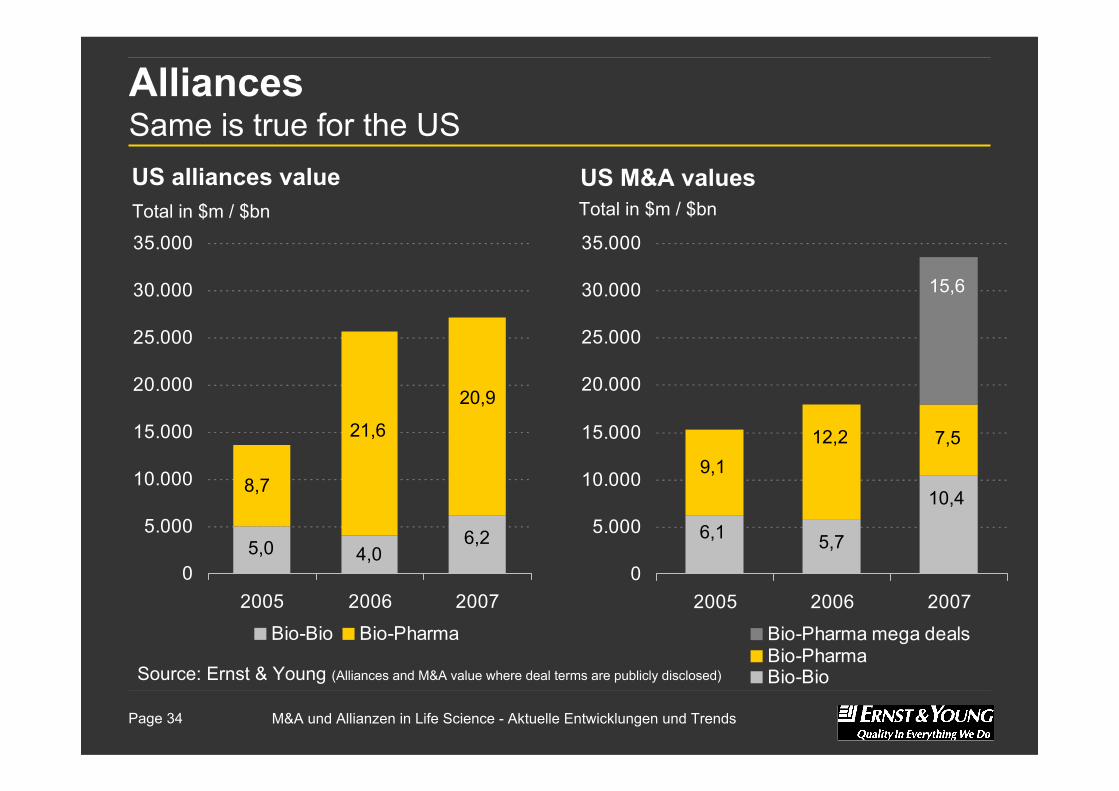

AlliancesSame is true for the US

Source: Ernst & Young (Alliances and M&A value where deal terms are publicly disclosed)

Total in $m / $bn

US alliances value

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

2005 2006 2007

Bio-Bio Bio-Pharma

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

2005 2006 2007

Bio-Pharma mega dealsBio-PharmaBio-Bio

US M&A valuesTotal in $m / $bn

5,0 4,06,2

8,7

21,6

20,9

6,1

10,4

5,7

15,6

9,112,2 7,5

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 35

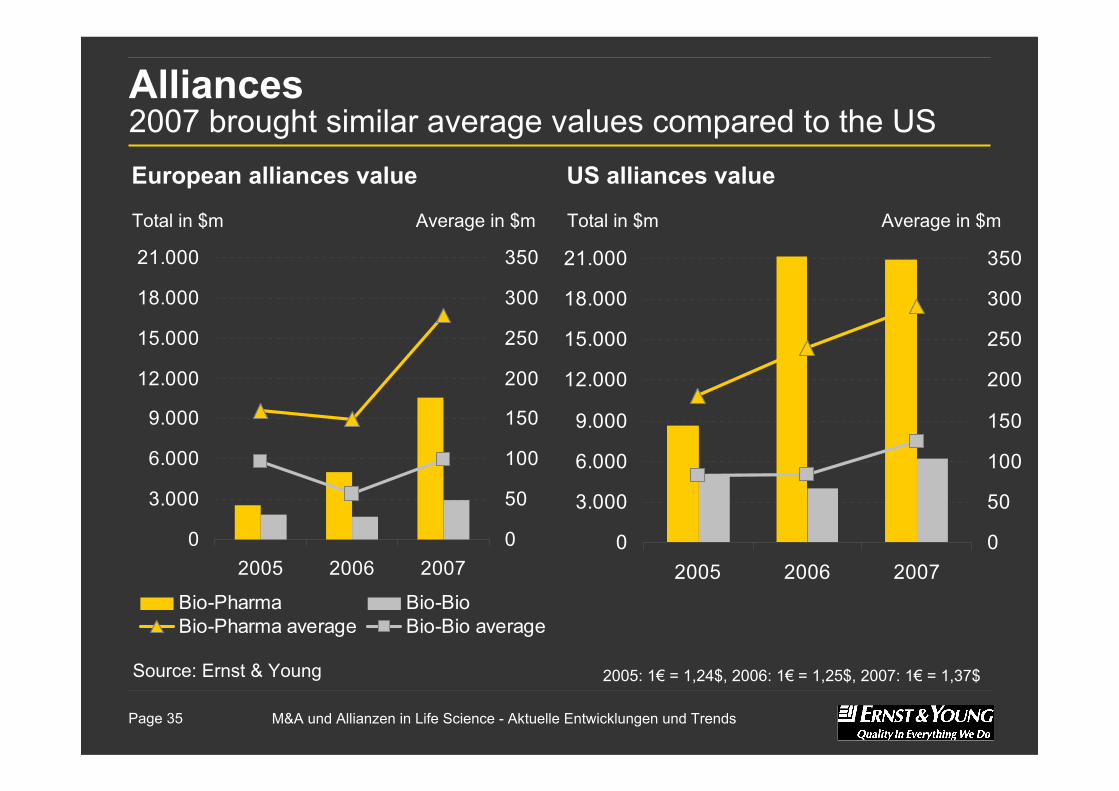

Alliances2007 brought similar average values compared to the US

Source: Ernst & Young 2005: 1€ = 1,24$, 2006: 1€ = 1,25$, 2007: 1€ = 1,37$

0

3.000

6.000

9.000

12.000

15.000

18.000

21.000

2005 2006 20070

50

100

150

200

250

300

350

Total in $m

US alliances value

Average in $mTotal in $m

European alliances value

Average in $m

0

3.000

6.000

9.000

12.000

15.000

18.000

21.000

2005 2006 20070

50

100

150

200

250

300

350

Bio-Pharma Bio-BioBio-Pharma average Bio-Bio average

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 36

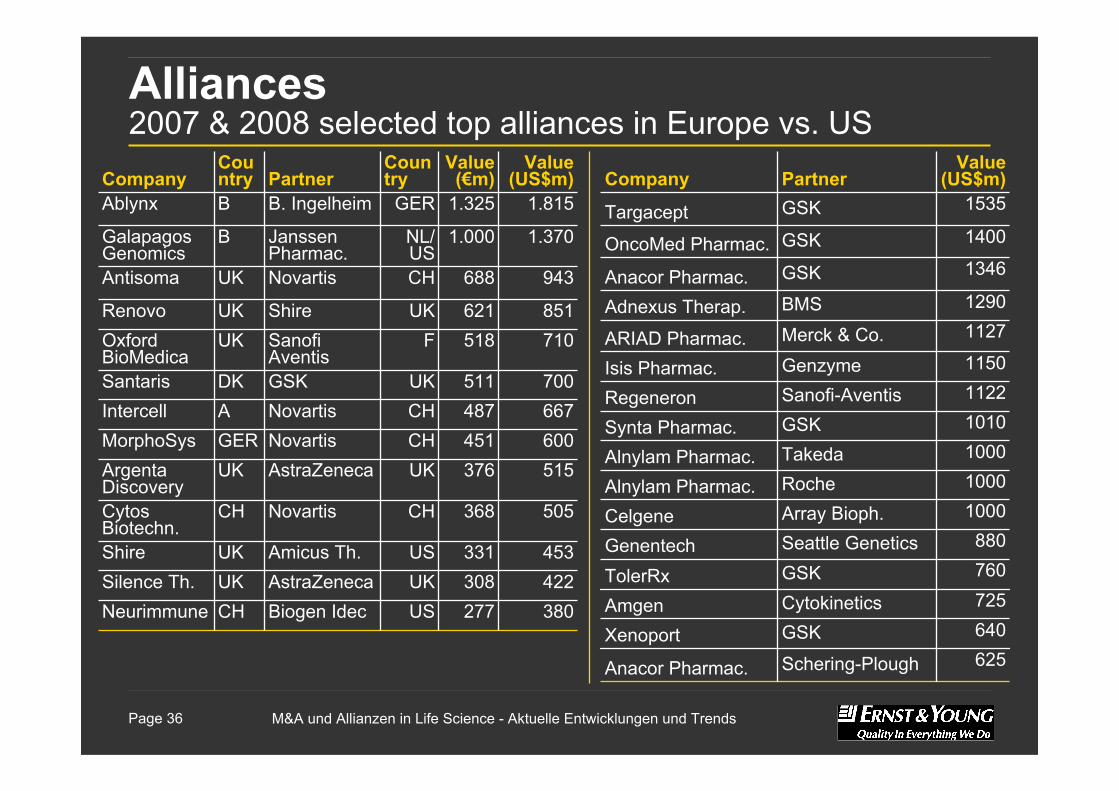

Alliances2007 & 2008 selected top alliances in Europe vs. US

1150GenzymeIsis Pharmac.

1000TakedaAlnylam Pharmac.

625Schering-PloughAnacor Pharmac.

725CytokineticsAmgen

760GSKTolerRx

640GSKXenoport

1290BMSAdnexus Therap.1127Merck & Co.ARIAD Pharmac.

1122Sanofi-AventisRegeneron1010GSKSynta Pharmac.

1000RocheAlnylam Pharmac.1000Array Bioph.Celgene880Seattle GeneticsGenentech

1535GSKTargacept1400GSKOncoMed Pharmac.1346GSKAnacor Pharmac.

Value (US$m)PartnerCompany

453331USAmicus Th.UKShire422308UKAstraZenecaUKSilence Th.

505368CHNovartisCHCytosBiotechn.

667487CHNovartisAIntercell700511UKGSKDKSantaris

277

376451

518621

688

1.000

1.325

Value (€m)

US

UKCH

FUK

CH

NL/US

GER

Country

CH

UKGER

UKUK

UK

B

B

Country

851ShireRenovo710Sanofi

AventisOxford BioMedica

600NovartisMorphoSys515AstraZenecaArgenta

Discovery

380Biogen IdecNeurimmune

1.815B. IngelheimAblynx

1.370Janssen Pharmac.

Galapagos Genomics

943NovartisAntisoma

Value (US$m)PartnerCompany

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 37

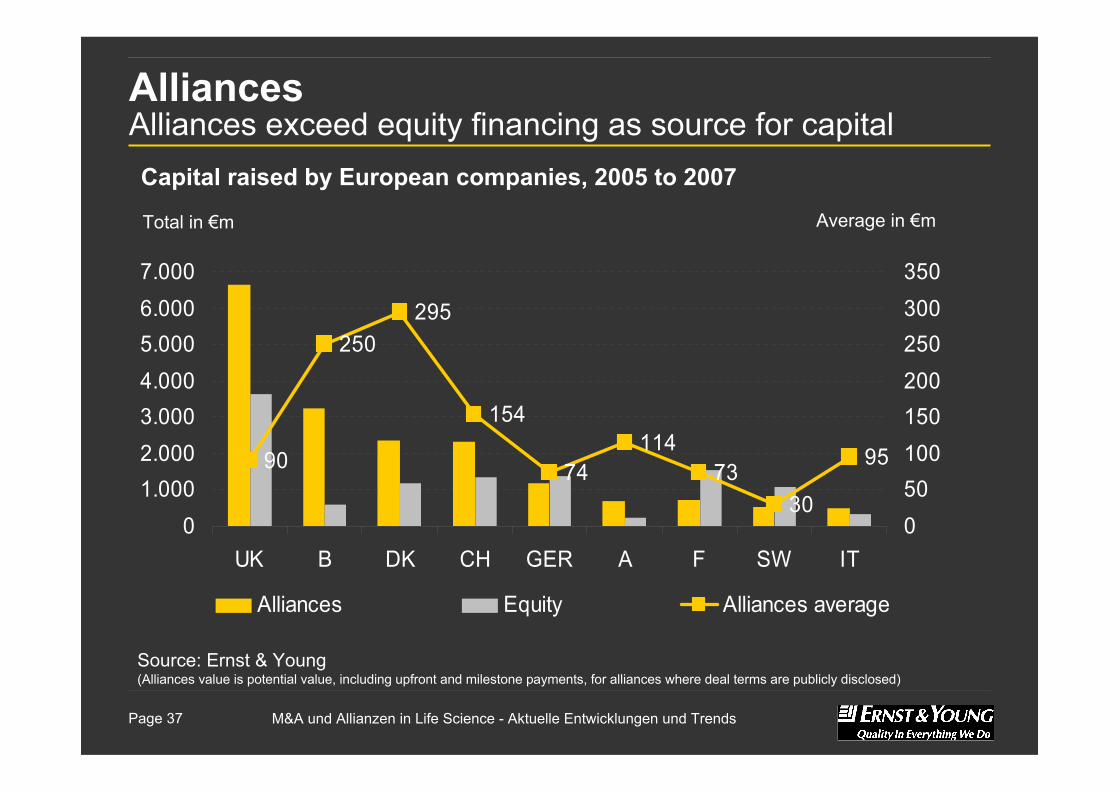

AlliancesAlliances exceed equity financing as source for capital

Source: Ernst & Young(Alliances value is potential value, including upfront and milestone payments, for alliances where deal terms are publicly disclosed)

90

250295

154

74114

7330

95

01.0002.0003.0004.0005.0006.0007.000

UK B DK CH GER A F SW IT050100150200250300350

Alliances Equity Alliances average

Total in €m Average in €m

Capital raised by European companies, 2005 to 2007

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 38

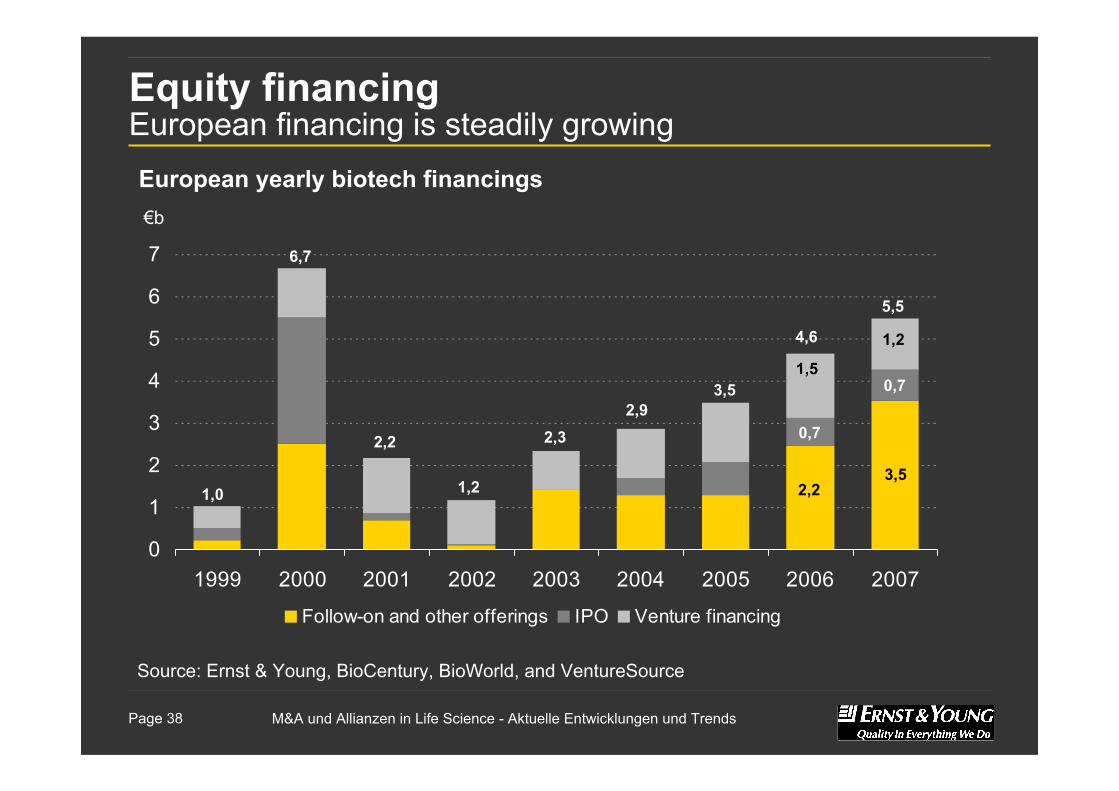

Equity financingEuropean financing is steadily growing

0

1

2

3

4

5

6

7

1999 2000 2001 2002 2003 2004 2005 2006 2007

Follow-on and other offerings IPO Venture financing

European yearly biotech financings€b

Source: Ernst & Young, BioCentury, BioWorld, and VentureSource

3,5

0,7

1,2

2,2

0,7

1,5

5,5

4,6

3,52,9

2,3

1,2

2,2

6,7

1,0

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 39

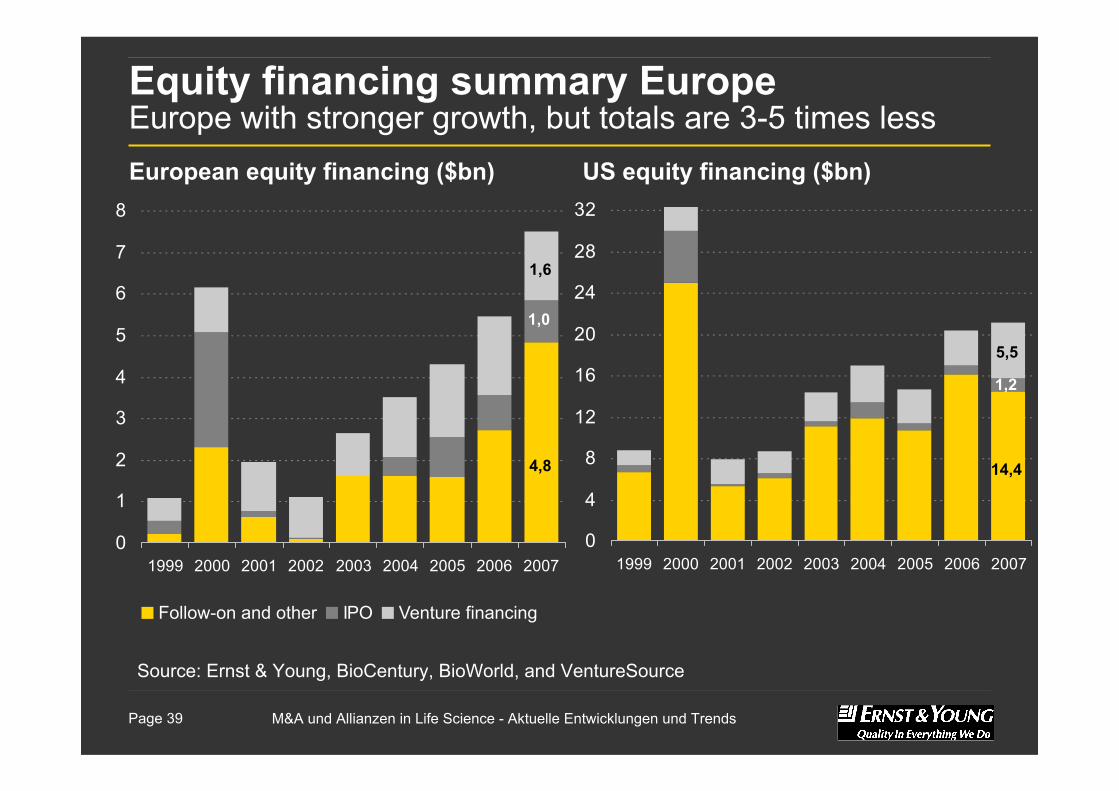

Equity financing summary Europe Europe with stronger growth, but totals are 3-5 times less

Source: Ernst & Young, BioCentury, BioWorld, and VentureSource

0

4

8

12

16

20

24

28

32

1999 2000 2001 2002 2003 2004 2005 2006 2007

14,4

5,5

1,2

0

1

2

3

4

5

6

7

8

1999 2000 2001 2002 2003 2004 2005 2006 2007

Follow-on and other IPO Venture financing

4,8

1,0

1,6

European equity financing ($bn) US equity financing ($bn)

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 40

Outlook

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 41

The business of drug development will fundamentally change

► Approaches to research and development► Business models► The value chain► Deal structures► Balance of power between biotech and big pharma► Partnerships between western companies and companies

in emerging markets

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 42

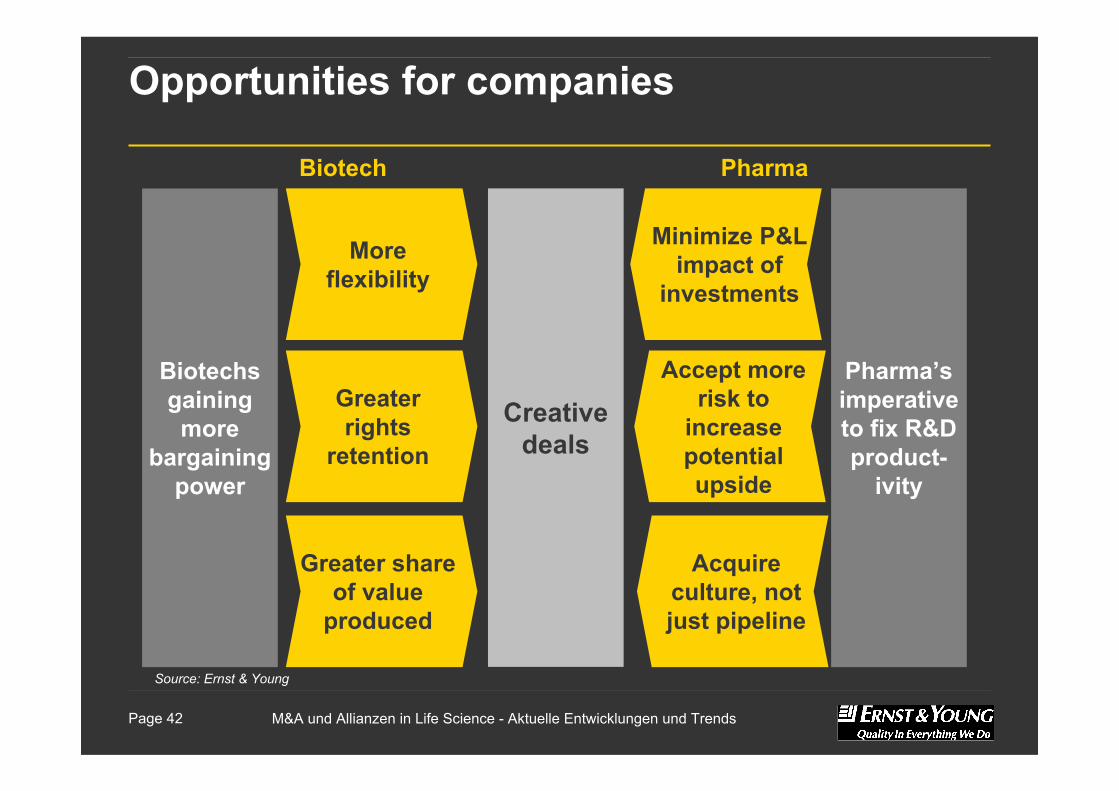

Opportunities for companies

Biotechsgaining more

bargaining power

More flexibility

Greater share of value

produced

Source: Ernst & Young

Pharma’simperative to fix R&D product-

ivity

Greater rights

retention

Minimize P&L impact of

investments

Creative deals

Accept more risk to

increase potential upside

Acquire culture, not just pipeline

Biotech Pharma

M&A und Allianzen in Life Science - Aktuelle Entwicklungen und Trends Page 43

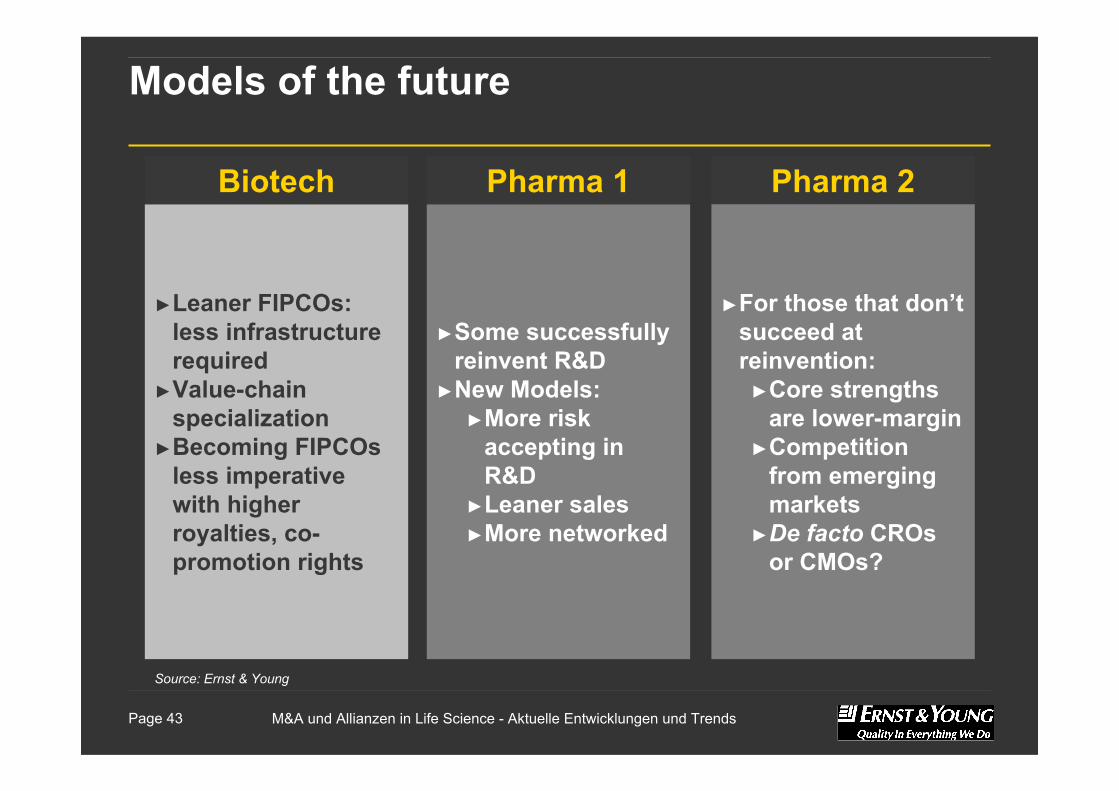

Models of the future

Source: Ernst & Young

►Leaner FIPCOs: less infrastructure required

►Value-chain specialization

►Becoming FIPCOsless imperative with higher royalties, co-promotion rights

Biotech

►Some successfully reinvent R&D

►New Models: ►More risk

accepting in R&D

►Leaner sales►More networked

Pharma 1 Pharma 2

►For those that don’t succeed at reinvention:►Core strengths

are lower-margin►Competition

from emerging markets

►De facto CROsor CMOs?

Thank you