ferc audits - bracewell.com · o rtos and isos o independent power producers o marketers ‒...

TRANSCRIPT

FERC AUDITS

Power Regulatory Webinar Series October 26, 2016

2

AGENDA

• Authorities

• Organizational Overview

• Division of Audits and Accounting

• FERC’s Expectations

• The Audit Process

• Trends in FERC Audits

• Notable Audits

3

AUDIT AUTHORITY

• Audits may be conducted pursuant to Section 301 of the Federal Power Act and Section 8 of the Natural Gas Act

• Section 301(b) of the FPA allows the audit team to: ‒ Access copies of any accounts, records, or memoranda that pertain to the

audit; requires licensees and public utilities to furnish, within reasonable time frames, any information that the Commission may require; and

‒ Requires licensees and public utilities to grant agents of the Commission free access to their property, accounts, records and memoranda

• See Revised Policy Statement on Enforcement, 123 FERC ¶ 61,156 (2008). ‒ Details the steps of an audit, discovery techniques, methodology used during

an audit, and the investigation process

4

ORGANIZATION

• Office of Enforcement ‒ Division of Investigations

‒ Divisions of Audits and Accounting

‒ Division of Energy Market Oversight

‒ Division of Analytics and Surveillance

• Division of Audits ‒ Oversees the Commission’s audit program

‒ Oversight of jurisdictional entities

5

THE AUDIT PROCESS - OVERVIEW

6

THE AUDIT PROCESS – SELECTION AND COMMENCEMENT

• FERC identifies the companies to be audited ‒ Identification of the most relevant risks facing the industry

‒ Cyclical audits

‒ Inherent risks

‒ Compliance programs

‒ Focus on problem topics

• Types of entities audited: ‒ Public utility holding companies

‒ Public utilities, including o Independent transmission companies

o RTOs and ISOs

o Independent power producers

o Marketers

‒ Reliability Organizations

7

THE AUDIT PROCESS

• FERC issues an audit commencement letter ‒ Description of the purpose and scope of the audit

‒ Identification of FERC’s audit team

‒ Publicly available

• Audit Starting Dates ‒ Most audits commence in the fall (Oct. – Nov.), the beginning of the fiscal year

‒ Audits may commence at later points in the fiscal year

8

RECEIPT OF THE COMMENCEMENT LETTER

• Preparation

• Internal response

• Organization and oversight

• Role of attorneys

9

THE AUDIT PROCESS – COLLECTING DATA

• Staff collects data ‒ Non-public communications ‒ Data requests seeking financial and operational information,

procedures, manuals, org charts, reports, emails, and studies ‒ Data responses provided either electronically or hardcopy ‒ Site visits to review on-site materials and conduct interview ‒ Site visit will commence with an opening conference and concludes

with a wrap-up conference discussing potential findings or areas of concern

‒ Additional interviews may be performed by phone

10

THE AUDIT PROCESS – COLLECTING DATA

• What should the company expect? ‒ Data request volume

‒ Data response accuracy

‒ Scope expansion

• How to manage site visits?

• How to respond to potential findings?

11

THE AUDIT PROCESS

• Staff compiles and analyzes data

• Staff conducts exit interview ‒ Staff presents preliminary findings and recommendations

‒ Staff will have received OE leadership approval of the preliminary findings

‒ Staff may have coordinated with other FERC offices: Office of General Counsel or Office of Energy Market Regulation

‒ Staff will inform the company of the coordination

12

THE AUDIT PROCESS

• Staff provides the company a draft audit report ‒ If the report contains significant, unique, or contested findings, Staff will distribute

the draft report to other offices and/or the Commission itself, prior to delivery to the company

‒ Company has 15 days to work with Staff for clarifications, submit additional information, correct errors

‒ Company may present recommendations ‒ Company submits a written response to the draft report, stating whether it agrees

with the findings and describing any corrective actions taken ‒ Staff may incorporate or address comments in a revised report

13

THE AUDIT PROCESS

• The draft report and the company’s response is distributed to other officesand the Commission‒ Company response will become public when final report issued

• For disputed matters, the Commission may require further analysis orinformation

• Commission issues a final report‒ Undisputed matters – final agency action

‒ Disputed matters – not final agency action

14

THE AUDIT PROCESS – CONTESTING DISPUTED MATTERS

• Company will have 30 days to respond to the final report to elect either

‒ Shortened procedures (briefs); or ‒ Trial-type proceeding

• For shortened procedures, Staff and the company will file an initial brief, followed by reply briefs

• Trial-type hearing may be elected if material issues of fact in dispute • Procedures found in 18 C.F.R. Part 41

15

THE AUDIT PROCESS – IMPLEMENTATION AND REVIEW

• Final audit reports often require companies to file plans for implementing the

audit recommendations • Corrective actions may be taken by the company during the audit process • Division of Audits and Accounting tracks implementation until all

recommendations completed • Audit closed once all recommendations implemented

16

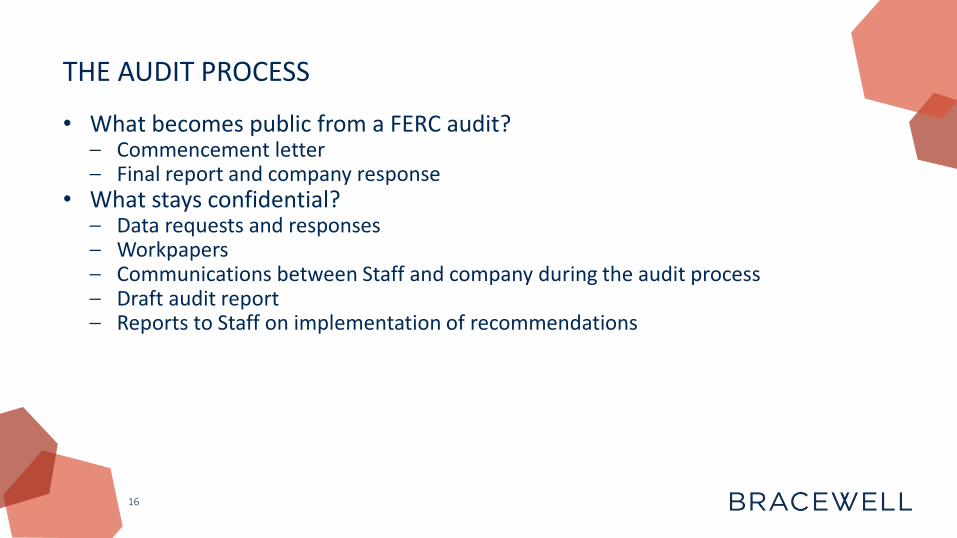

THE AUDIT PROCESS

• What becomes public from a FERC audit? ‒ Commencement letter ‒ Final report and company response

• What stays confidential? ‒ Data requests and responses ‒ Workpapers ‒ Communications between Staff and company during the audit process ‒ Draft audit report ‒ Reports to Staff on implementation of recommendations

17

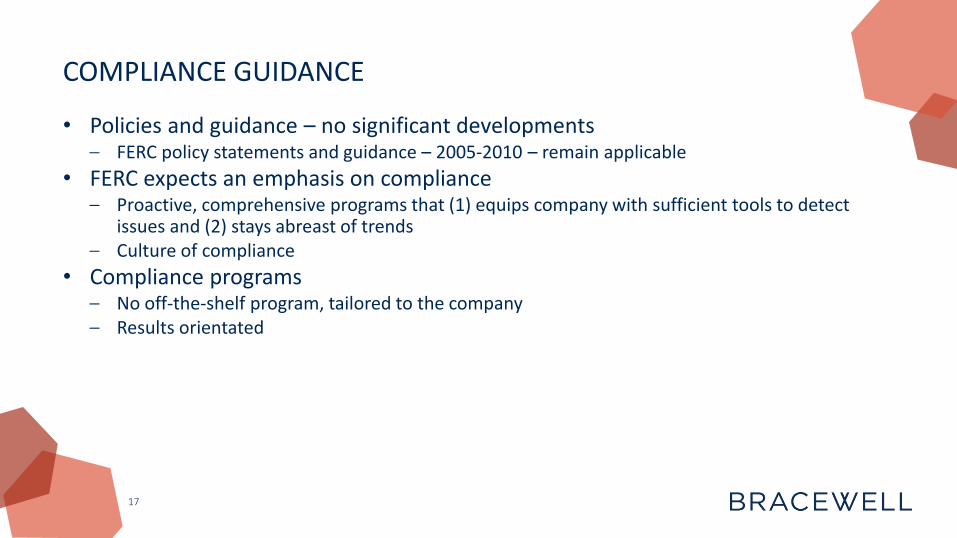

COMPLIANCE GUIDANCE

• Policies and guidance – no significant developments ‒ FERC policy statements and guidance – 2005-2010 – remain applicable

• FERC expects an emphasis on compliance ‒ Proactive, comprehensive programs that (1) equips company with sufficient tools to detect

issues and (2) stays abreast of trends ‒ Culture of compliance

• Compliance programs ‒ No off-the-shelf program, tailored to the company ‒ Results orientated

18

COMPLIANCE GUIDANCE

• Senior management active involvement • Adequate staffing and dedication to compliance • Compliance officer who operates independently and has access to senior

management • Training • Reporting mechanisms • Polices and procedures • Recordkeeping • Auditing and monitoring

19

TYPES OF AUDITS

• Financial Audits (FA Dockets) ‒ Accounting, books and records, formula rates, financial reporting compliance

• Operational Audits (PA Dockets) ‒ FERC orders (Section 203 or 204 authorizations, merger authorizations,

transmission rate incentives), market-based rate and EQR reporting, demand response, capacity markets, open access tariffs and market rules

20

HOLDING COMPANY AUDITS

• Topics ‒ Cross subsidization restrictions on affiliate transactions ‒ Accounting, recordkeeping, and reporting under Part 366 (PUHCA) ‒ USofA for centralized service companies ‒ Preservation of records ‒ Form No. 60 (Report of Centralized Service Companies) ‒ Part 101 accounting requirements for transactions with associated companies ‒ Form No. 1 ‒ Merger and acquisition conditions

21

HOLDING COMPANY AUDITS

• Recent holding company audits: ‒ National Grid – initiated Nov. 2015 ‒ Approximately 9 holding company audits initiated in 2010-2012

• Common findings ‒ Form No. 60 reporting errors ‒ Form No. 1 reporting errors ‒ Misclassifications certain expenses to the wrong accounts ‒ Properly accounting and supporting allocation of employee time

22

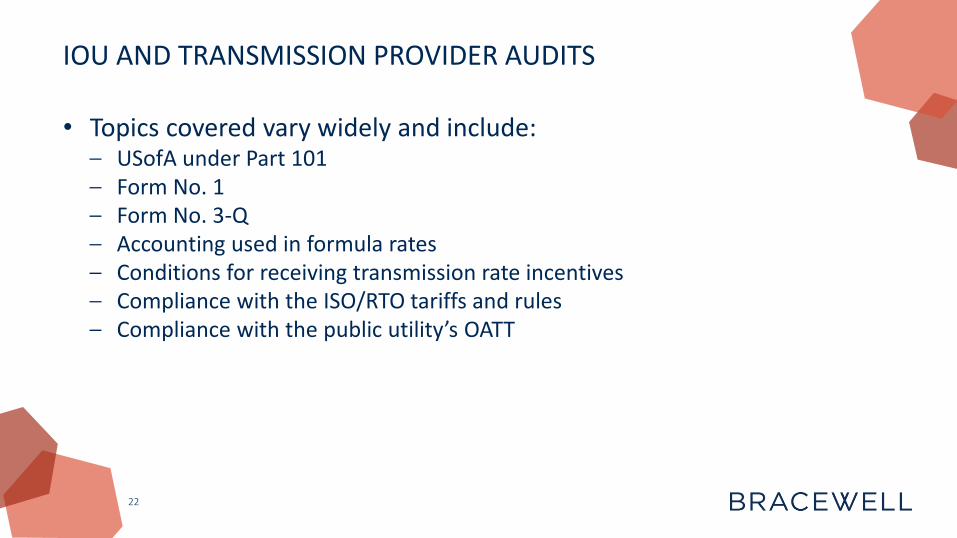

IOU AND TRANSMISSION PROVIDER AUDITS

• Topics covered vary widely and include: ‒ USofA under Part 101 ‒ Form No. 1 ‒ Form No. 3-Q ‒ Accounting used in formula rates ‒ Conditions for receiving transmission rate incentives ‒ Compliance with the ISO/RTO tariffs and rules ‒ Compliance with the public utility’s OATT

23

IOU AND TRANSMISSION PROVIDER FINANCIAL AUDITS

• Frequency ‒ 2016 – 2 audits ‒ 2015 – 8 audits ‒ 2014 – 0 audits ‒ 2013 – 4 audits

• Common findings ‒ Incorrectly excluding or including certain expenses in the formula rate calculation, resulting in

over- or under-billing customers ‒ Failure to report all cost allocation methods in Form No. 60 ‒ Improper accounting of certain affiliate payroll costs ‒ Form Nos. 1 and 3-Q reporting errors

24

MARKETING AUDITS

• Frequency ‒ 2016 – 1 audit ‒ 2015 – 2 audits ‒ 2014 – 5 audits ‒ 2013 – 6 audits

• Topics covered included:

‒ Compliance with the seller’s MBR tariff ‒ Compliance with EQR reporting obligations ‒ Compliance with participation requirements in capacity markets or demand response

programs

25

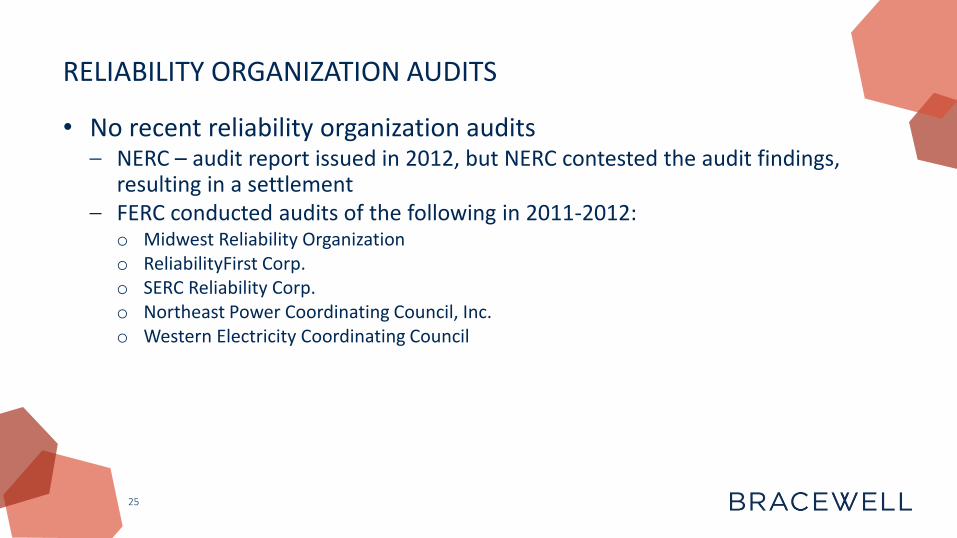

RELIABILITY ORGANIZATION AUDITS

• No recent reliability organization audits ‒ NERC – audit report issued in 2012, but NERC contested the audit findings,

resulting in a settlement ‒ FERC conducted audits of the following in 2011-2012:

o Midwest Reliability Organization o ReliabilityFirst Corp. o SERC Reliability Corp. o Northeast Power Coordinating Council, Inc. o Western Electricity Coordinating Council

26

RTO AND ISO AUDITS

• ISO-NE and MISO: FERC initiated audits in November 2015 ‒ Topics:

o Compliance with the ISO/RTO’s obligations under its tariff o Compliance with Order No. 1000 – transmission planning o Part 101 accounting o Part 141 financial reporting obligations o Recordkeeping

• SPP: FERC conducted an audit 2015-2016 ‒ Topics:

o Compliance with the SPP OATT (particularly implementation of the Integrated Marketplace) o Compliance with Order No. 710 – wholesale competition in regions with organized electric markets o Part 101 accounting o Part 141 financial reporting and Form No. 1

• ISO-NE and MISO were last audited in 2008-2009 • CAISO (2011); PJM (2004)

27

SINGLE ISSUE AUDITS

• FERC may focus audit resources on topics of interest ‒ Compliance with orders authorizing the issuance of short-term debt or the

disposition and acquisition of jurisdictional facilities ‒ Compliance with nuclear plant decommissioning trust fund accounting

requirements ‒ Compliance with FERC-imposed merger conditions or accounting of cost

related to an attempted merger ‒ Compliance with incentive rate authorizations

28

AUDIT DURATION

• Audit durations vary widely ‒ Holding company audits: 13-22 months ‒ Public utility financial audits: 16-32 months; average is 2 years ‒ Nuclear decommissioning trust fund accounting: 7-32 months ‒ MBR audits: average is roughly 2 years

• Shortest: 7 months (nuke plant decommissioning trust fund) • Longest: 32 months (nuke plant decommissioning trust funds)

29

AUDIT FREQUENCY AND REGIONS

• Companies are typically not audited in back-to-back years ‒ PacifiCorp – settled an investigation in 2012 regarding violation of its OATT ‒ PacifiCorp – audit initiated March 2016 for formula rate accounting and compliance with its OATT and

business practices ‒ Ameren Corp – PUHCA audit report issued in 2010 ‒ Ameren Illinois – accounting and financial reporting audit report issued in 2015 ‒ Duke Energy Corp. – PUHCA audit completed in 2010 ‒ Duke Energy Corp. – Compliance with merger conditions audit completed in 2016.

• Regions

‒ Each year, audits span nearly every geographic region ‒ Audits include companies within and outside RTOs/ISOs

30

TRENDS IN FERC AUDITS: FERC ENFORCEMENT REPORTS

• 2011

‒ 56 financial and operational audits completed ‒ 300 recommendations ‒ $290,000 in refunds and recoveries

• 2012 ‒ 44 financial and operational audits completed ‒ 399 recommendations ‒ $5.84 million in refunds and recoveries

• 2013 ‒ 29 financial and operational audits completed ‒ 360 recommendations ‒ $15.4 million in refunds

31

TRENDS IN FERC AUDITS: FERC ENFORCEMENT REPORTS

• 2014 ‒ 19 financial and operational audits of public utilities and gas pipelines completed

‒ 162 recommendations for corrective action

‒ $11.7 million in refunds and recoveries

• 2015 ‒ 22 financial and operational audits of public utilities and gas pipelines completed

‒ 360 recommendations for corrective action

‒ $16.8 million refunded to ratepayers, and $9.5 million prevented from inclusion in formula rates

‒ Oil pipeline 1audits included

32

TRENDS IN FERC AUDITS: 2014-2015

• Formula Rate Issues o Still an area of focus by DAA

» Inclusion of merger-related costs in rates without FERC approval

» Proper accounting for tax prepayments

» Improperly including Asset Retirement Obligation (ARO) amounts in formula rates without FERC approval

» Using state-approved, instead of FERC-approved depreciation rates

» Including merger goodwill in the equity component of the capital structure, which FERC has long excluded from rates

• EQR reporting and MBR tariff compliance

• Failure to submit and account for nuclear decommissioning trust funds

33

RECENT AUDITS REPORTS

• Dynegy Audit Report (Oct. 14, 2016) – Market-base rate compliance, uplift payments, EQR reporting

• Westar and Kansas Gas & Electric (Sept. 29, 2016) – Part 101 accounting compliance, formula rate compliance, financial reporting

34

QUESTIONS?

Bob Pease represents and advises energy and commodity clients in enforcement and regulatory matters before the Federal Energy Regulatory Commission (FERC) and Commodity Futures Trading Commission (CFTC). His experience includes power markets; natural gas trading; natural gas pipelines; exchange trading and FERC audits. He has conducted compliance training on manipulation, disruptive trading practices, high frequency and algorithmic trading and energy trading and marketing.

Bob Pease

Senior Counsel T: +1.202.828.5824

E: [email protected] W: bracewell.com/pease

Ty Johnson

Ty Johnson is a member of Bracewell LLP’s energy regulatory practice, and he counsels domestic and foreign energy-industry clients on regulatory matters before the Federal Energy Regulatory Commission and the Department of Energy. Mr. Johnson advises clients participating in the electric energy markets and clients with renewable power projects. Mr. Johnson also has experience with regulatory proceedings involving the Bonneville Power Administration. He has counseled clients involved in regulatory litigation before FERC and in related appellate litigation.

Attorney

T: +1.206.204.6211

W: bracewell.com/tjohnson

Bob Pease

Associate

35

WE KNOW ENERGY®

T E X A S | N E W Y O R K | W A S H I N G T O N , D C | C O N N E C T I C U T | S E A T T L E | D U B A I | L O N D O N b r a c e w e l l . c o m

This presentation is provided for informational purposes only and should not be considered specific legal advice on any subject matter. You should contact your attorney to obtain advice with respect to any particular issue or problem. The content of this presentation contains general information and may not reflect current legal developments, verdicts or settlements. Use of and access to this presentation does not create an attorney-client relationship between you and Bracewell.