subsidies’ unintended inequities: how dynamic finance addresses “just rewards” dilemma

TRANSCRIPT

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

1

Subsidies’ unintended inequities: How dynamic finance addresses “just rewards” dilemma

Ricardo G Barcelona – King’s College, London, [email protected]

Bernardo M Villegas – University of Asia and the Pacific, Philippines

Energy subsidies uncannily work against policy’s avowed intentions of wide scale renewable energy deployment. Perversely, technology-‐specific subsidies encourage investments in “expensive” technologies where consumers de facto underwrite the costs differences. Consequently, investing firms retain excess returns while assuming limited financial risks. Consumers respond by coaxing the regulator a posteriori to cut subsidies to rebalance “just rewards” commensurate to firms’ risk-‐taking. This paper suggests that a dynamic approach to corporate finance better addresses “just rewards” dilemma. This is feasible when optimisation is undertaken as a portfolio decision under flexibility conditions. Hence, by leaving firms to respond strategically according to their resource endowment and aspirations, a more equitable route becomes available. The competitive market allocates through a pricing mechanism benefits, risks and burdens among firms and consumers.

Key words: Energy subsidies, carbon tax, floor power price

1. Introduction Corporate finance is premised on rational human behaviour that ignores explicit considerations of ethical and moral values. Under this positivist construct, the economic dimension follows utilitarian notion where returns (or future cash flows) are traded against risks (or deviations from expected outcome)1 . In turn, regulation apportions economic externalities to stakeholders through the state’s coercive power to tax2. Within this context, “just rewards” follow that risk-‐taking is compensated with commensurate returns. The translation to practice is proving problematic. Within the narrow remit of capital budgeting, marginal theory of value produces unintended inequities. This happens when firms appropriate returns that are divorced from the financial risks that they assume. To illustrate this phenomenon, we examine the case of subsidies to renewable energy and the role that financial analysis may have played in perpetuating inequitable outcomes.

1 John R Hicks (1946). Value and capital. (2nd edition). London: Oxford University Press. 2 George J Stigler (1971). “The theory of economic regulation”. The Bell Journal of Economics and Management Science, 2(1), 3-‐21.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

2

Subsidies3 are seen as sine qua non to wide scale renewable energy deployment. Recognised for their social benefits in reducing pollution, renewable energy’s higher private costs (i.e. capital spend) when compared to fossil fuel technologies are often compensated through subsidies. While “social compensation” represents an accepted wisdom in energy investment and policy circles4, policy outcomes often fall short of objectives5. Increasingly, renewable energy returns are dependent to varying extent on subsidies. In effect, firms assume less financial risks, with subsidies that consumers de facto underwrite underpinning their “secure cash flows”. This phenomenon raises a fundamental question: Why energy subsidies often fail to achieve policy objectives, while perpetuating inequitable resource allocation? Corporate finance inadvertently participates in subsidies’ unintended inequities through the practices followed in capital budgeting. This occurs at two levels: One, in setting subsidies as static “social compensation” consistent with the grid price parity premise; and two, in incorrectly evaluating energy investments optimised as discrete investments. Subsidies are set following grid price parity logic. This takes the differences in life cycle costs of energy (LCOEs)6, calculated under static price assumptions, between fossil fuel and renewable energy technologies. Inadvertently, subsidies over-‐compensate renewable energy when actual output prices are above their LCOEs (or vice versa). Capital budgeting, employing net present values (NPVs), follows a pecking order when ranking competing opportunities from highest to lowest positive values. The logic suggests that capital is committed first to the highest NPV project, with investments continuing to be made until the final marginal sum is committed7. Two assumptions underpin this pecking order. One, the investment performs according to plan; and two, greater returns certainty equate to lower risks, hence increasing value when cash flows are discounted at lower rates. For renewable energy, subsidies are said to reduce the investing firms’ financial risks. Under a static and unchanging world, NPVs may correctly rank the opportunities according to their financial merits, given that certainty in outcomes effectively reduces risks. However, under dynamic markets, the pecking order falls apart no sooner than 3 Broadly applied to incentives and subsidies to renewable energy aimed at encouraging adoption. The forms used in energy markets are outlined in Enzensberger, N., Wietschel, M. and Rentz, O. (2002). “Policy instruments fostering wind energy projects – A multi-‐perspective evaluation approach”. Energy Policy, 30(9), 793-‐801. 4 Stern, N. (2006). The economics of climate change: The Stern review. Cambridge, United Kingdom: Cambridge University Press. 5 Toke, D., Breukers, S., and Wolsink, M. (2008). “Wind power deployment outcomes: How can we account for the differences?” Renewable and Sustainable Energy Reviews, 12(4), 1129-‐1147. 6 A detailed calculation methodology is provided in Roth, I.F. and Ambs, L.L. (2004). “Incorporating externalities into a full cost approach to electric power generation life cycle costing”. Energy, 29, 2125-‐2144. 7 John R. Graham and Campbell R. Harvey (2001): “The theory and practice of corporate finance: Evidence from the field”. Journal of Financial Economics, 60 (2/3), 187-‐243.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

3

the first encounter with volatilities. In the process, firms would either prefer investments with low volatilities, or require greater guarantees of secure returns before committing their capital. The latter is achieved by higher subsidies, or transferring risks to consumers through take-‐or-‐pay contracts. Applied to energy investments, proven fossil fuel technologies are preferred for their predictable cash returns. While this comes at the expense of renewable energy, the consequences to technology choices run counter to the “social compensation” notion. Subsidies deter technology innovation, while reversing the benefits from “learning curve” effects8 where lower costs follow wider deployment. When cost reductions fail to materialise, “social compensation” will have to rise to make up for the higher costs differences. In an imperfect market economy, “what moves us, reasonably enough, is not the realisation that the world falls short of being completely just – which few of us expect – but that there are clearly remediable injustices around us which we want to eliminate”9. Energy subsidies, and its implications for capital allocation, appear to be a place to start. Technology-‐specific subsidies are predicated on endowing a government with a foresight (that it does not possess) to identify a priori technological champions that deserve support. This abdicates a firm’s risk-‐taking to the government and hence, questions the investing firm’s rights to retain any excess returns from subsidies. In this paper, we posit that grid price parity principles render indeterminate a “correct” setting of subsidies when energy prices are volatile. This leads to uncertainty of benefits resulting in low deployment rates while increasing rent-‐extraction opportunities. Capital budgeting suffers from a similar malaise. When proven technologies are preferred, technological innovations such as advances in renewable energy will experience greater difficulties in being adopted. A dynamic approach to finance better addresses the “just rewards” dilemma. When optimisation is undertaken as a portfolio decision under flexible conditions, renewable energy’s hedge value against rising fuel prices can be explicitly evaluated. This is combined with carbon taxation as pricing signal to adopt non-‐polluting technologies. Consequently, firms retain their right to decide on their technology choices informed by their resources endowment, portfolio aspirations and capabilities. In the process, renewable energy technologies are adopted or discarded based on their economic and technological virtues, when the costs of pollution are fully internalised. Operating under competitive markets, with a dynamic approach to finance correctly informing the firm’s technology decisions and policy, a more equitable route to resource allocation becomes feasible.

8 Cliff Chen, Ryan Wiser and Mark Bollinger (2007). Weighing costs and benefits of state renewable portfolio standards: A comparative analysis of state-‐level policy impact projections. Berkeley, California: Ernest Orlando Lawrence Berkeley National Laboratory, Berkeley, LBNL-‐62580. 9 Sen, A.K. (2009). The idea of justice. Cambridge, Massachusetts: Harvard University Press.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

4

2. Resource allocation and subsidies How societies allocate scarce resources often start with some notion of distributive justice. In one form or another, scarce resources may be allocated according to an accepted concept of equity, equality and need as values within a community. The importance of one value over another may vary in its emphasis over time10 while contending with the competing needs or claims by individuals11. There appears to be at least two schools of thoughts that dominate the debate in distributive justice literature. One is represented by a utilitarian notion popular in economic theory, and the other is a philosophical strand on what constitutes a just society. While generally agreeing on the values of equity, equality and needs as the foundation for a just society, they differ on what it is that they are aiming to allocate that satisfies their notions of fairness. The debate on “just rewards” is skewed by a utilitarian bias for quantification towards allocating outputs based on some notions of fairness12. In this context, traditional finance discipline considers economics as a strict allocation problem, where the behaviour of economic actors is assumed to be selfish and rational”13. Altruistic motives are inconsequential to the profit optimisation function. Hence, output is allocated devoid of moral or ethical values according to their marginal utility irrespective of their social consequences. The “view that a person is actuated only by self-‐interest is persistent in economic models. This view is not very realistic”14. This observation led Sen to propose an egalitarian view of justice based on capability15. This takes into account the ability to function in various ways – to be mobile, to understand the world around them, and to have a social life – is predicated on access to resources. Optimisation of benefits and the just allocation of resources are predicated on individual responsibility16 where a just society is characterised by an “equality of access to advantage”17. The debates on energy policies, where subsidies and social choice loom large, follow a similar divide as to what subsidies are attempting to equalise. Specifically:

10 Deutsch, M. (1975). “Equity, equality and need: What determines which value will be used as the basis of distributive justice?”. Journal of Social Issues, 31(3), 137-‐149. 11 Roemer, J.E. (1998). Theories of distributive justice. Massachusetts: Harvard University Press. 12 Rawls, J. (1999). A theory of justice, revised edition. Cambridge, Massachusetts: Harvard University Press. 13 Aloy Soppe (2004). “Sustainable corporate finance”. Journal of Business Ethics, 3(1/2), 213-‐224. 14 Sen, A.K. (1977). “Rational fools: A critique of the behavioural foundations of economic theory”. Philosophy and Public Affairs, 6(4), 317-‐344. 15 Sen, A.K. (1979). “Equality of what?”. The Tanner Lecture on Human Values. Stanford University: May 22, 1979. 16 Dworkin, R. (1981). “What is equality? Part 1: Equality of welfare, Part 2: Equality of Resources” Philosophy and Public Affairs, 10, 185-‐246 and 283-‐245. 17 Cohen, G.A. (1997). “Where the action is: On the site of distributive justice”. Philosophy and Public Affairs, 26(1), 3-‐30.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

5

1. Level technology playing field is achieved by equalising costs through grid price parity that favours specific subsidies to “technology champions”;

2. Evolutionary technology adaptation equalises access by maximising viable technologies through a pricing mechanism such as carbon taxation.

Within a market economy, subsidies result in differentiated pricing that flatters the returns of preferred technologies. In contrast, carbon taxation maintains unified pricing. The influence on financial allocation of benefits and risks are not inconsequential. While subsidies’ tiered pricing in theory directs capital to preferred technologies, they seldom achieve the outcomes 18 that financial theories would predict. Carbon taxation is a political hot potato that politics prefer to treat with benign neglect. However, its simplicity and progressive nature has its appeal. Generally, higher income groups tend to consume more carbon intensive products.

2.1 The paradox of energy subsidies: How unintended inequities happen Subsidies set out to level the technology playing field by equalising the costs differences between fossil fuel and renewable energy. Through the grid price parity logic, this works by “guaranteeing” minimum returns to investing firms in preferred technologies (i.e. wind, solar or other renewable energy sources)19. Implicitly, policy assumes that when costs are equalised, investments would be committed to renewable energy following capital budgeting’s pecking order. When input costs (i.e. fuel) and power prices are fixed, the equalisation function is a straightforward arithmetical application of a difference equation. However, dynamic energy markets produce volatile prices that render the calculation indeterminate when infinite number of results occurs. As benefits become uncertain20, the unintended effects tend to distort the notion of “just rewards”. Specifically:

1. Subsidies spiral: Boom-‐bust investment cycles exaggerate the equipment supply imbalances21 that reverse the declining costs attributed to “learning curve effects”. As equipment prices escalate, higher subsidies are required. When acceded, higher subsidies could fuel another equipment price spiral, farther worsening the costs differences.

2. Capital inefficiency: As subsidies spiral, policy-‐supported renewable energy offers increasingly attractive returns secured by subsidies. This result in firms to

18 IPCC. (2011). Summary for policy makers. In IPCC Special Report on Renewable Energy Sources and Climate Change Mitigation. Cambridge, United Kingdom: Cambridge University Press. 19 Brown, M. (2001). “Market failures and barriers as a basis for clean energy policies”. Energy Policy, 29(14), 1197-‐1207. 20 Jaffe, A.B. and Stavins, R.N. (1994). “The energy paradox and the diffusion of conservation technology”. Resource and Energy Economics, 16, 91-‐122. 21 Chen, C., Wiser, R. and Bollinger, M. (2007). Energy status report. Sacramento, California: California Energy Commission.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

6

appropriates excess returns from “expensive technologies” while assuming limited financial risks.

3. Innovation deterrent: Rising equipment prices when supplies tighten deter

innovation to reduce costs. Higher deployment could produce excess returns for equipment manufacturers, as they occurred from 2001 -‐ 200922.

Consumers respond by coaxing regulator to cut subsidies as a way of reigning in the investing firm’s excess returns, as they did in Spain and Germany23. The affected investing firm considers such change, often resulting from changing government priorities, as heightened regulatory risks. In the process, capital flight occurs or investments come to a stand still, with equipment manufacturers experiencing demand-‐induced price collapse. In reality, a firm’s heavy reliance on subsidies effectively abdicates the exercise of their technology choice to a government (erroneously) bestowed with foresight on future technological evolution. Clearly, this is far from a realistic view. What actually occurs is restraining the tendency to accumulate with repeated adaptation of regulations. Without these restraints, the allocation problem would be resolved by ever-‐rising demand for subsidies. As subsidies dominate returns, the provision of a public good (i.e. pollution reducing technology) is overwhelmed by the opportunity to extract more economic rent.

2.2 Carbon pricing as a resource allocation signal Carbon taxation implies a subtle shift in the regulator’s function. From being the promoter of “technology champions”, carbon taxes are aimed at penalising known polluting technologies. When retaining a unified price for energy output, the choice of technology solutions is largely left with investing firms. This follows Sen’s “equality of access to capability” argument24. In this context, carbon taxation serves two purposes: a) as a penalty for pollution25, and b) as an inducement to substitute “dirty” with “clean” technology26. In their more recent forms, the appropriate level of carbon taxes is relaxed to fall below Pigou’s prescribed equality to the cost of marginal environmental damage27. This holds some promise for reframing carbon taxation as an explicit pricing signal that takes into

22 Mark Bollinger and Ryan Wiser (2011). Understanding trends in wind turbine prices over past decade. Berkeley, California: Ernest Orlando Lawrence Berkeley National Laboratory. 23 Global Sustainability Institute. (2011). “Fiscal deficit forces Spain to slash renewable energy subsidies”. Subsidies Watch, 40, September 2011. 24 Sen (2009) supra 9. 25 Goodstein, E. (2003). “The death of Pigouvian tax? Policy implications from the double dividend debate”. Land Economics, 79(3), 402-‐414. 26 Baumol, W.J. and Oates, W.E. (1975). The theory of environmental policy. New Jersey: Prentice Hall. 27 Fullerton, D. (1997). “Environmental levies and distortionary taxation: A comment”. The American Economic Review, 87(1), 245-‐251.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

7

account the influence on adoption of market structures, technological evolution and carbon emissions. Renewable energy adoption is a form of technological innovation that can be evaluated within the context of technological systems28. This involves applying a portfolio perspective, where renewable energy is added to extant fossil-‐fuel-‐dominated supplies. The innovation and technology diffusion processes could occur through individual and collective actions29 of firms, with the government playing an enabling but dynamic role through taxation30. The resource-‐recombination perspective provides a framework for examining the question of how the returns from innovation are appropriated by firms. Demand effects are transmitted through energy prices, while supply factors arises from technological evolution and experience 31 . Within this construct, slow market adjustments occur when market and support regimes are stable32. In contrast, rapid adaptation happens when disruptions render a market unpredictable33. In this context, flexibility is required in the production system in order to re-‐allocate the resources smoothly and without cost escalation34. The strategic tension arises when a firm’s early commitment sets in motion network benefits such as learning curve effects 35 . The exercising firm cannot exclusively appropriate these collective benefits. Hence, as capacity costs decline when learning curve effects operate, early adopters bear the costs of innovation while late adopters reap the benefits from expanded diffusion. Strategically, these uncertainties demand of firms the managerial capabilities to correctly exercise their strategic options. Incorporating these dynamics in evaluating the financial returns, uncorrelated costs of fossil fuel and renewable energy technologies when combined results in diversification benefits. That is, as energy costs and prices interact, zero-‐fuel-‐costs renewable energy provides a hedge against rising fuel costs. 28 Jacobson, S. and Bergek, A. (2004). “Transforming the energy sector: The evolution of technological systems in renewable energy technology”. Industrial and Corporate Change, 13(5), 815-‐849. 29 Gallagher, K.S., Grübler, A., Kuhl, L., Nemet, G. and Wilson, C. (2012). “The energy technology innovation system”. Annual Review of Environment and Resources, 37, 137-‐162. 30 Lewis, J.I. and Wiser, R.H. (2007). “Fostering a renewable energy technology industry: An international comparison of wind industry policy support mechanisms”. Energy Policy, 35(3), 1844-‐1857. 31 Verdolini, E. and Galeotti, M. (2011). “At home and abroad: An empirical analysis of innovation and diffusion in energy technologies”. Journal of Environmental Economics and Management, 61(2), 119-‐134. 32 Luiten, E., Lente, H.V. and Blok, K. (2006). “Slow technologies and government intervention: Energy efficiency in industrial process technologies”. Technovation, 26, 1029-‐1044. 33 Jaffe, A.B., Newell, R.G. and Stavins, R.N. (2005). “A tale of two market failures: Technology and environmental policy”. Ecological Economics, 54(2-‐3), 164-‐174. 34 Eliasson, G. and Taymaz, E. (2002). “Institutions, entrepreneurship, economic flexibility and growth – Experiments on an evolutionary micro-‐to-‐macro model”. In Canner, U. (ed). Economic evolution, learning and complexity. Berlin-‐Heidelberg: Springer-‐Verlag. 35 Watanabe, C., Nagamatsu, A. and Griffy-‐Brown, C. (2003). “Behavior of technology in reducing prices of innovative goods – An analysis of the governing factors of variance of PV module prices”. Technovation, 23, 423-‐436.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

8

Carbon taxes increase power prices that raise renewable energy’s returns, while reducing fossil fuel technologies’ earnings. When examined under a technology system, the setting of carbon taxes is dependent as to how (a) firms interact and deal with uncertainties, (b) networks benefits induce or hinder adoption decisions, and (c) institutions act to influence connectivity through a market, or incentive structures and demand through policy actions. This dynamic approach contrasts with the social notion of subsidies. While subsidies pre-‐judge (often incorrectly) a technology champion, influenced by a utilitarian bias to equalise returns or costs, carbon taxes establish a power price level to allow equal market access to viable and competing renewable energy. When decisions on technology choice are left with firms, the consequences of their decisions (gains or losses) could justifiably accrue to the investing firms. Hence, carbon taxation conforms to the “just rewards” notion that the application of subsidies distorts.

3. Findings We use energy market data36 to empirically test through simulations how grid price parity fulfils the costs equality and returns predictability criteria. The standardised data facilitates cross-‐technology comparisons, particularly when applied to calculating the life cycle costs of energy (LCOEs). Portfolio returns are estimated from the technology mix, using data from LCOEs as costs inputs, applying residual returns (or economic value added) calculations37. These results are then contrasted with the outcomes using carbon taxation, through its influence on pricing, in addressing the appropriation of returns of mixed energy technologies portfolios. Whenever appropriate, we compare the outcomes of subsidies under a coal or gas system. As power markets liberalised, combined cycle gas turbines (CCGTs) progressively replaced coal as the technology that sets the market price. For this reason, gas is used as the reference technology for estimating cost differences with renewable energy following the grid price parity logic.

3.1 Flawed logic of grid price parity leads to green paradox The required subsidies rise with the costs of renewable energy, where “expensive” solar is subsidised to a greater extent than “cheaper” wind power. Hydro and geothermal, while considered as renewable energy, usually do not benefit from subsidies, given that they are considered as part of the mainstream supplies.

36 EIA – Energy Information Administration (2011). The electricity market module of the National Energy Modelling System: Model documentation report. July 2011. Washington, D.C.: US Energy Information Administration. 37 Residual returns are returns over and above the firm’s costs of capital. Detailed residual income formula are shown in McCormack, J.L. and Vytheeswaran, J. (1998): “How to use EVA in the oil and gas industry”. Journal of Applied Corporate Finance, 11 (3), 2422–2437.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

9

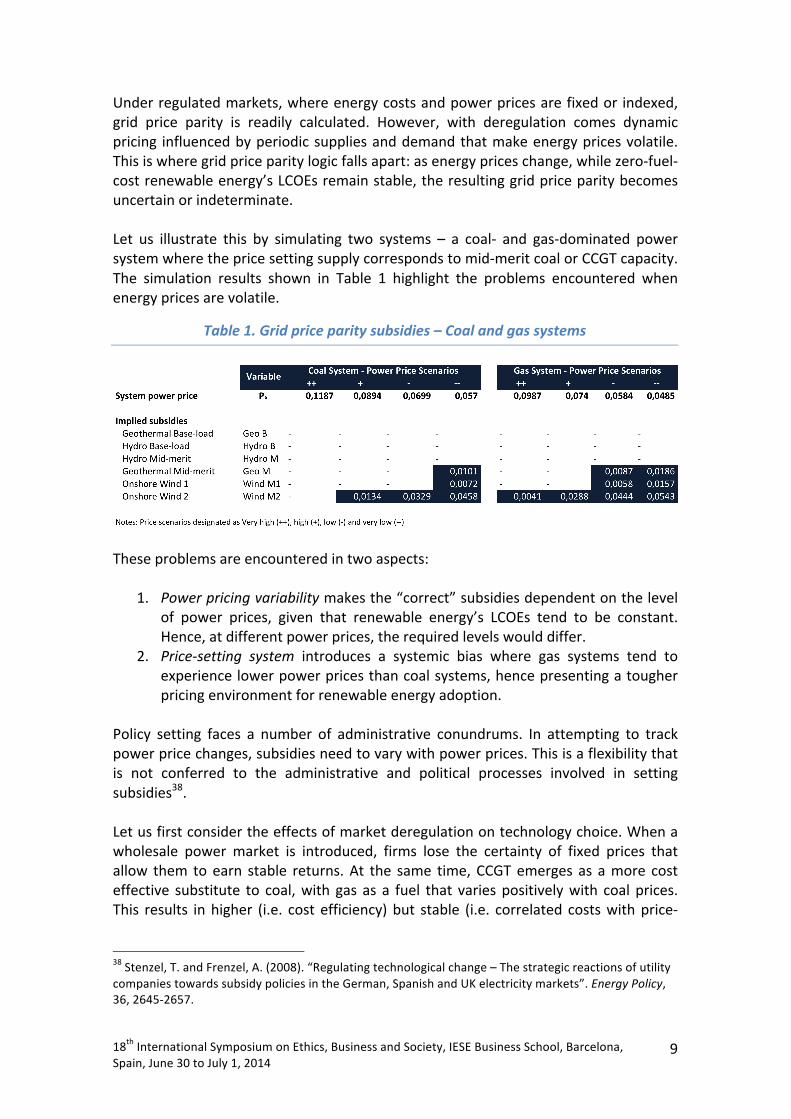

Under regulated markets, where energy costs and power prices are fixed or indexed, grid price parity is readily calculated. However, with deregulation comes dynamic pricing influenced by periodic supplies and demand that make energy prices volatile. This is where grid price parity logic falls apart: as energy prices change, while zero-‐fuel-‐cost renewable energy’s LCOEs remain stable, the resulting grid price parity becomes uncertain or indeterminate. Let us illustrate this by simulating two systems – a coal-‐ and gas-‐dominated power system where the price setting supply corresponds to mid-‐merit coal or CCGT capacity. The simulation results shown in Table 1 highlight the problems encountered when energy prices are volatile.

Table 1. Grid price parity subsidies – Coal and gas systems

These problems are encountered in two aspects:

1. Power pricing variability makes the “correct” subsidies dependent on the level of power prices, given that renewable energy’s LCOEs tend to be constant. Hence, at different power prices, the required levels would differ.

2. Price-‐setting system introduces a systemic bias where gas systems tend to experience lower power prices than coal systems, hence presenting a tougher pricing environment for renewable energy adoption.

Policy setting faces a number of administrative conundrums. In attempting to track power price changes, subsidies need to vary with power prices. This is a flexibility that is not conferred to the administrative and political processes involved in setting subsidies38. Let us first consider the effects of market deregulation on technology choice. When a wholesale power market is introduced, firms lose the certainty of fixed prices that allow them to earn stable returns. At the same time, CCGT emerges as a more cost effective substitute to coal, with gas as a fuel that varies positively with coal prices. This results in higher (i.e. cost efficiency) but stable (i.e. correlated costs with price-‐

38 Stenzel, T. and Frenzel, A. (2008). “Regulating technological change – The strategic reactions of utility companies towards subsidy policies in the German, Spanish and UK electricity markets”. Energy Policy, 36, 2645-‐2657.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

10

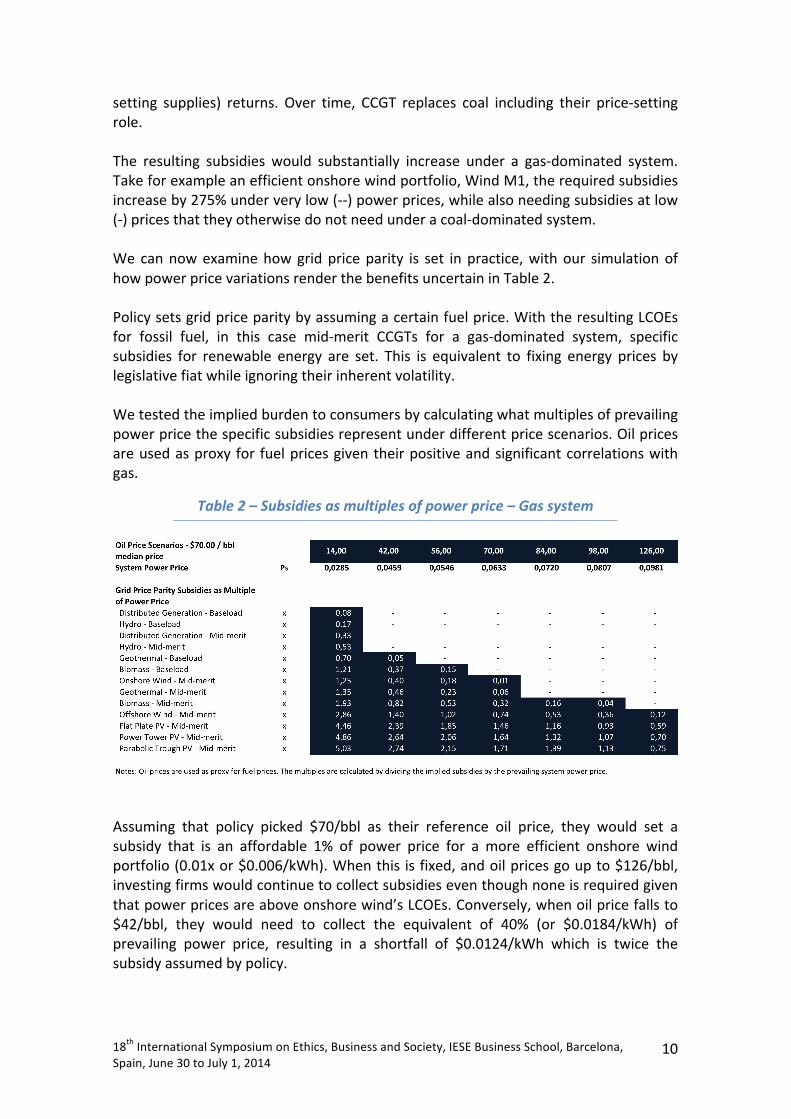

setting supplies) returns. Over time, CCGT replaces coal including their price-‐setting role. The resulting subsidies would substantially increase under a gas-‐dominated system. Take for example an efficient onshore wind portfolio, Wind M1, the required subsidies increase by 275% under very low (-‐-‐) power prices, while also needing subsidies at low (-‐) prices that they otherwise do not need under a coal-‐dominated system. We can now examine how grid price parity is set in practice, with our simulation of how power price variations render the benefits uncertain in Table 2. Policy sets grid price parity by assuming a certain fuel price. With the resulting LCOEs for fossil fuel, in this case mid-‐merit CCGTs for a gas-‐dominated system, specific subsidies for renewable energy are set. This is equivalent to fixing energy prices by legislative fiat while ignoring their inherent volatility. We tested the implied burden to consumers by calculating what multiples of prevailing power price the specific subsidies represent under different price scenarios. Oil prices are used as proxy for fuel prices given their positive and significant correlations with gas.

Table 2 – Subsidies as multiples of power price – Gas system

Assuming that policy picked $70/bbl as their reference oil price, they would set a subsidy that is an affordable 1% of power price for a more efficient onshore wind portfolio (0.01x or $0.006/kWh). When this is fixed, and oil prices go up to $126/bbl, investing firms would continue to collect subsidies even though none is required given that power prices are above onshore wind’s LCOEs. Conversely, when oil price falls to $42/bbl, they would need to collect the equivalent of 40% (or $0.0184/kWh) of prevailing power price, resulting in a shortfall of $0.0124/kWh which is twice the subsidy assumed by policy.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

11

Repeating the calculations for other renewable energy technologies, the same conclusions are reached. Solar power remains exorbitant at all oil price levels in spite of the sharp falls in panel costs experienced since 2008. Applying specific subsidies to technology champions result in a two-‐tier power price market. One price is applied to fossil fuel supplies (often lower) while another is paid to renewable energy (often higher). In the absence of consumer choice, the higher power prices used to fund the payment of subsidies are imposed on consumers. In effect, consumers de facto underwrite any excess returns that investing firms appropriate. The inadvertent generosity of subsidies poses questions about an imbalance of risks and returns for renewable energy. By assuming minimal risk, guaranteed high returns are captured by firms. This places policy under some strain: When power prices are low, renewable energy’s prices will appear exorbitant in comparison, given that they will significantly exceed the prevailing market prices for power. Conversely, when power prices are high, returns from renewable energy increase substantially. Under this scenario, the regulators are under pressure to claw-‐back “excessive” returns to satisfy a policy imperative for “fairness”.

3.3 Energy markets are different … and why they matter Subsidies and carbon taxation are often set independently of market structures, while ignoring the influence of competitor’s actions on an investing firm’s decisions. Naively, renewable energy markets are judged as attractive when their subsidies or carbon tax are higher (or vice versa). However, this approach fails to explain a paradox, where markets with higher subsidies or carbon taxes do not always achieve higher investments. Part of the answer lies in how firms discriminate their investment thresholds, which coincide with a value at which a firm is prepared to commit capital. Following Sen’s “equality of access to capability” argument, policy support is reframed to create the conditions under which a maximum number of renewable energy technologies become viable with a minimum of subsidies. To address this question, let us examine how investing firms respond to opportunities relative to their market position using option-‐game-‐theoretic logic39. Under dynamic markets, when firms invest, their actions often elicit responses from competitors that are often non-‐cooperative. These competing actions lead firms to pre-‐empt, to follow or to differentiate their strategies on technology selection according to their portfolio aspiration.

39 A detailed explanation of the methodology is found in Chevalier-‐Roignant, B. and Trigeorgis, L. (2011). Competitive strategy: Options and games. Cambridge, Massachusetts: Massachusetts Institute of Technology Press.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

12

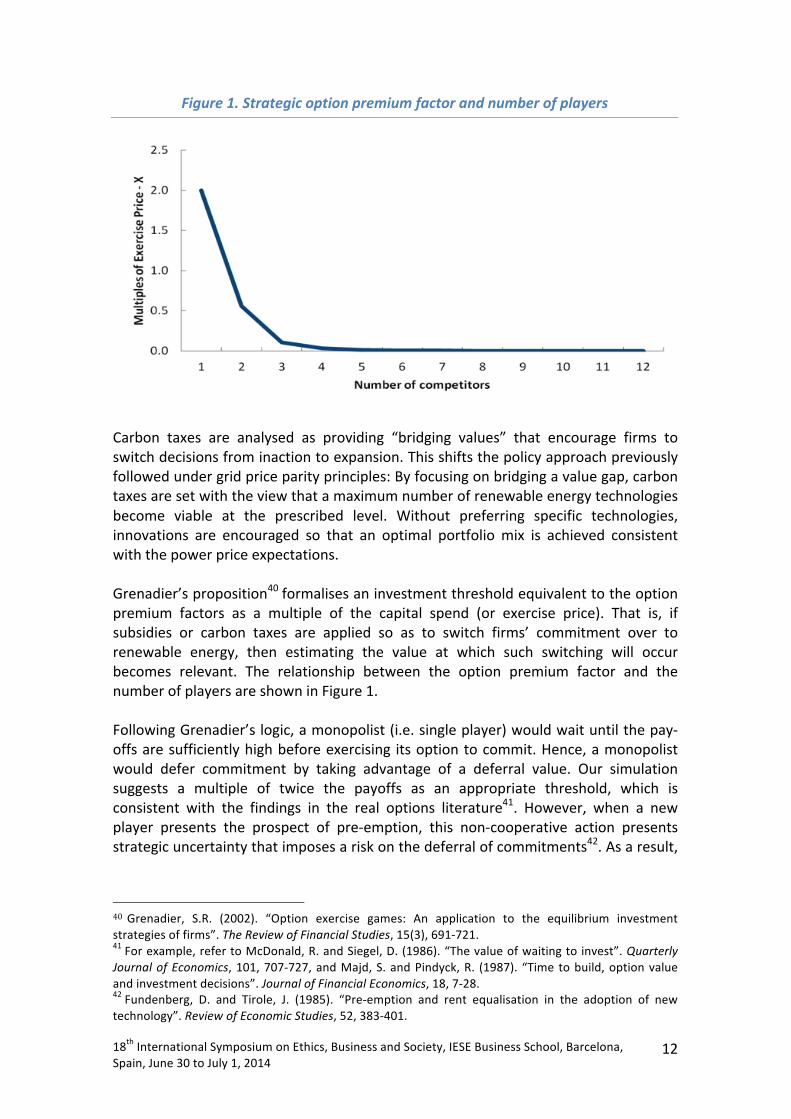

Figure 1. Strategic option premium factor and number of players

Carbon taxes are analysed as providing “bridging values” that encourage firms to switch decisions from inaction to expansion. This shifts the policy approach previously followed under grid price parity principles: By focusing on bridging a value gap, carbon taxes are set with the view that a maximum number of renewable energy technologies become viable at the prescribed level. Without preferring specific technologies, innovations are encouraged so that an optimal portfolio mix is achieved consistent with the power price expectations. Grenadier’s proposition40 formalises an investment threshold equivalent to the option premium factors as a multiple of the capital spend (or exercise price). That is, if subsidies or carbon taxes are applied so as to switch firms’ commitment over to renewable energy, then estimating the value at which such switching will occur becomes relevant. The relationship between the option premium factor and the number of players are shown in Figure 1. Following Grenadier’s logic, a monopolist (i.e. single player) would wait until the pay-‐offs are sufficiently high before exercising its option to commit. Hence, a monopolist would defer commitment by taking advantage of a deferral value. Our simulation suggests a multiple of twice the payoffs as an appropriate threshold, which is consistent with the findings in the real options literature41. However, when a new player presents the prospect of pre-‐emption, this non-‐cooperative action presents strategic uncertainty that imposes a risk on the deferral of commitments42. As a result,

40 Grenadier, S.R. (2002). “Option exercise games: An application to the equilibrium investment strategies of firms”. The Review of Financial Studies, 15(3), 691-‐721. 41 For example, refer to McDonald, R. and Siegel, D. (1986). “The value of waiting to invest”. Quarterly Journal of Economics, 101, 707-‐727, and Majd, S. and Pindyck, R. (1987). “Time to build, option value and investment decisions”. Journal of Financial Economics, 18, 7-‐28. 42 Fundenberg, D. and Tirole, J. (1985). “Pre-‐emption and rent equalisation in the adoption of new technology”. Review of Economic Studies, 52, 383-‐401.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

13

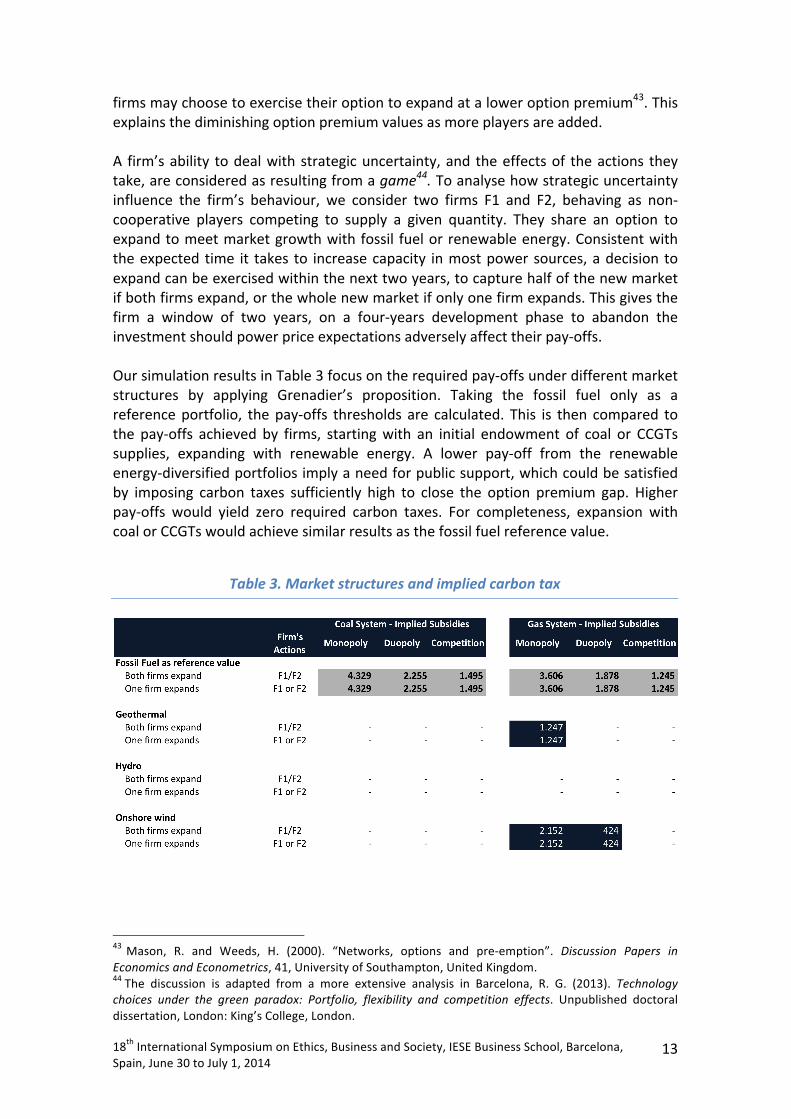

firms may choose to exercise their option to expand at a lower option premium43. This explains the diminishing option premium values as more players are added. A firm’s ability to deal with strategic uncertainty, and the effects of the actions they take, are considered as resulting from a game44. To analyse how strategic uncertainty influence the firm’s behaviour, we consider two firms F1 and F2, behaving as non-‐cooperative players competing to supply a given quantity. They share an option to expand to meet market growth with fossil fuel or renewable energy. Consistent with the expected time it takes to increase capacity in most power sources, a decision to expand can be exercised within the next two years, to capture half of the new market if both firms expand, or the whole new market if only one firm expands. This gives the firm a window of two years, on a four-‐years development phase to abandon the investment should power price expectations adversely affect their pay-‐offs. Our simulation results in Table 3 focus on the required pay-‐offs under different market structures by applying Grenadier’s proposition. Taking the fossil fuel only as a reference portfolio, the pay-‐offs thresholds are calculated. This is then compared to the pay-‐offs achieved by firms, starting with an initial endowment of coal or CCGTs supplies, expanding with renewable energy. A lower pay-‐off from the renewable energy-‐diversified portfolios imply a need for public support, which could be satisfied by imposing carbon taxes sufficiently high to close the option premium gap. Higher pay-‐offs would yield zero required carbon taxes. For completeness, expansion with coal or CCGTs would achieve similar results as the fossil fuel reference value.

Table 3. Market structures and implied carbon tax

43 Mason, R. and Weeds, H. (2000). “Networks, options and pre-‐emption”. Discussion Papers in Economics and Econometrics, 41, University of Southampton, United Kingdom. 44 The discussion is adapted from a more extensive analysis in Barcelona, R. G. (2013). Technology choices under the green paradox: Portfolio, flexibility and competition effects. Unpublished doctoral dissertation, London: King’s College, London.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

14

Competition facilitates the reduction of carbon taxes. That is, when a monopolist faces no threat of pre-‐emption, they would rather wait until the option value is twice the competitive market’s level, often induced by rising prices as supplies tighten. Under a gas system, a monopolist firm F1 or F2 would require a value increase from carbon taxes of $1,247 mln to exercise its option to commit to geothermal power. For onshore wind, the carbon tax threshold is higher, a value increase of $2,152 mln for a monopolist, while falling to $424 mln under a duopoly. That is, the threat of pre-‐emption encourages earlier exercise of the investment by partially foregoing a monopoly rent. A similar coal-‐gas divide is observed as we highlighted in our grid price parity simulation, with specific policy implications:

1. Market structures: Subsidies under grid price parity to a monopolist compound the monopoly rent, while remaining ineffective if set below the option premium gap.

2. Policy focus: Under monopolistic structures, increasing competition rather than

handing out more subsidies could prove more effective in encouraging investments.

Carbon taxes benefit from retaining a unified pricing for power that simplifies capital allocation within a functioning market economy. Carbon taxes offer the prospect of differentiating according to the emission levels of fossil fuel technologies, implying a better allocation of penalties that is technically verifiable. As a result, by correctly internalising pollution costs, technological innovations are encouraged in a) reducing fossil fuel emissions; or b) enhancing capital cost efficiency of renewable energy to accelerate substitution of fossil fuel technologies. When renewable energy’s portfolio hedge value is considered, the economic and political concerns in introducing carbon taxes are less daunting. With sufficient competitive pressures, the appropriate carbon taxes to effect renewable energy deployment are sufficiently low where they are only needed when power prices fall below their historic trend. Mechanisms to address the effects of carbon taxes on low-‐income consumers and competitiveness of adopting vs non-‐adopting markets are discussed in a previously published paper45. In summary, precedents in Australia and British Columbia, Canada have experimented by re-‐allocating carbon tax proceeds to fund price discounts to poor consumers affected by power price increases. Scandinavia is a successful example of how heavy carbon taxes result in high levels of renewable energy adoption and technological innovations. Adopting countries may consider using the trade tariffs as mechanism for clawing back free riders’ “costs advantage” from non-‐application of carbon taxes. 45 Refer to Barcelona, R.G. (2012). “Failed with subsidies? – Try CO2 tax!”. Renewable Energy Law and Policy Review, 2, 121-‐130.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

15

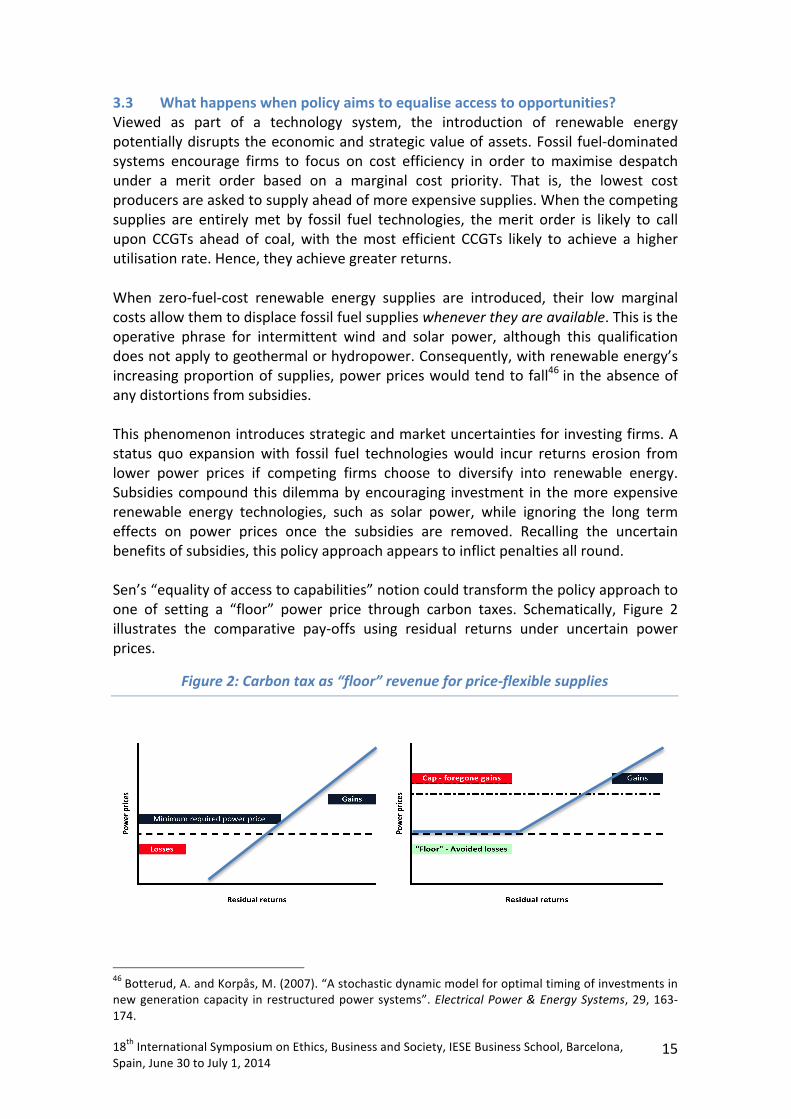

3.3 What happens when policy aims to equalise access to opportunities? Viewed as part of a technology system, the introduction of renewable energy potentially disrupts the economic and strategic value of assets. Fossil fuel-‐dominated systems encourage firms to focus on cost efficiency in order to maximise despatch under a merit order based on a marginal cost priority. That is, the lowest cost producers are asked to supply ahead of more expensive supplies. When the competing supplies are entirely met by fossil fuel technologies, the merit order is likely to call upon CCGTs ahead of coal, with the most efficient CCGTs likely to achieve a higher utilisation rate. Hence, they achieve greater returns. When zero-‐fuel-‐cost renewable energy supplies are introduced, their low marginal costs allow them to displace fossil fuel supplies whenever they are available. This is the operative phrase for intermittent wind and solar power, although this qualification does not apply to geothermal or hydropower. Consequently, with renewable energy’s increasing proportion of supplies, power prices would tend to fall46 in the absence of any distortions from subsidies. This phenomenon introduces strategic and market uncertainties for investing firms. A status quo expansion with fossil fuel technologies would incur returns erosion from lower power prices if competing firms choose to diversify into renewable energy. Subsidies compound this dilemma by encouraging investment in the more expensive renewable energy technologies, such as solar power, while ignoring the long term effects on power prices once the subsidies are removed. Recalling the uncertain benefits of subsidies, this policy approach appears to inflict penalties all round. Sen’s “equality of access to capabilities” notion could transform the policy approach to one of setting a “floor” power price through carbon taxes. Schematically, Figure 2 illustrates the comparative pay-‐offs using residual returns under uncertain power prices.

Figure 2: Carbon tax as “floor” revenue for price-‐flexible supplies

46 Botterud, A. and Korpås, M. (2007). “A stochastic dynamic model for optimal timing of investments in new generation capacity in restructured power systems”. Electrical Power & Energy Systems, 29, 163-‐174.

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

16

In the absence of “floor” price and volume flexibility, power supplies would earn the revenues derived from the prevailing prices and volume. Hence, losses would be incurred when power prices fall below a given threshold (i.e. minimum required power price for positive returns). To cushion against such losses, the manager could choose not to supply, hence incurring zero returns by not supplying for a given period. Alternatively, a “floor” price would eliminate the possibility of a loss when set above a threshold that complies with a positive returns condition. In effect, when power prices are below the “floor” price, the supplied power earns the fixed “floor” price. The “floor” price is provided by the carbon tax when there is managerial flexibility to vary the power prices, which a functioning energy market would provide. This price flexibility satisfies the notion that when firms are given equal access to an energy market’s opportunities, they would likely optimise their choice of technologies. More likely, rent-‐extraction is constrained by competitors’ actions when subsidies do not flatter, hence distort, the returns from preferred technologies. Under a floor pricing system, a minimum price is set through carbon tax for renewable energy, while no cap is applied to power prices. This is the prevailing system in Spain, where above a certain power price threshold, renewable energy “loses” its feed-‐in tariffs and receives the prevailing market price for power. In effect, renewable energy is provided with floor revenues, while reaping unconstrained benefits from higher prices. As illustrated in Table 4, when power price floors are established, thereby eliminating “losses” below the high power price (+) threshold, onshore wind pay-‐offs substantially increase to achieve expected returns on a par with geothermal and hydro. In contrast, geothermal and hydro do not benefit as much as onshore wind does from power price floors as both technologies are already viable without the need for any subsidies or carbon tax, except, for geothermal, when expected power prices fall below a low price scenario (-‐) under a gas system.

Table 4. Floor pricing – Coal and gas systems

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

17

The ability to estimate the strategic pay-‐offs (SPOe) provide a common framework for policy and the investing firms to reconcile their strategic objectives. While our simulation appears to suggest investing firms to disproportionately appropriate returns, policy could vary carbon taxes so as to influence the pace of deployment and retention of returns. By reducing the carbon taxes, policy may signal to influence in the way supplies mix are rebalanced through power pricing. In the process, policy’s role is transformed into an active economic agent that facilitates renewable energy deployment, while leaving investing firms to take risks and justifiably appropriate returns that are consistent with their risk-‐taking. By using power pricing as a preferred policy mechanism, distortions from subsidies are minimised that potentially avoid favouring the more expensive renewable energy technologies such as solar power.

4. Conclusions When the question “who pays, who benefits” is posed, the “common wisdom” on energy subsidies that comes to be accepted in investment and policy circles needs a rethink. Far from satisfying policy criteria for fairness, subsidies often fail to meet substantive aspects of equity, equality or needs. The exceptions pertain to enabling persons in extreme poverty to meaningfully participate in socio-‐economic pursuits. To a large extent, the limited remit of capital budgeting is contributory to subsidies’ unintended inequities. When uncertainties and competitors’ actions are explicitly considered, and the effects of strategic moves are evaluated as portfolio decisions under flexible conditions, the notion of “just rewards” are reconciled with the firms’ risk-‐taking that justifies commensurate returns. Grid price parity principles, when applied as the bases for setting “correct” subsidies, are alluring for their conceptual simplicity. They work best when energy prices are fixed, either contractually or by legislative fiat. Our simulation shows that when subsidies are fixed under assumed fuel costs, the “correct” levels under-‐ or over-‐shoot the required levels when energy prices are volatile. Consequently, subsidies contribute disproportionately to returns of investing firms while reducing the same firms’ financial risks. This phenomenon is problematic for equitable resource allocation. Differentiated subsidies give more to “expensive” solar than “cheaper” wind power to equalise their costs (or returns) with fossil fuel technologies. Potentially, investing firms may be tempted to maximise the recovery of subsidies as “secure” returns that inadvertently encourage rent-‐extraction. Consumers are unlikely to stand for this apparent misallocation of benefits and risks, raising the prospect of a consumer backlash that could ultimately lead to cuts in subsidies in order to rebalance “just rewards”. When firms over-‐rely on subsidies, they abdicate their risk-‐taking role that justifies their appropriation of returns. This poses an irreconcilable dilemma for firms and policy: If firms take minimal financial risks, because subsidies are supposed to have secured their returns, then the firms’ rights to appropriate returns above a notional

18th International Symposium on Ethics, Business and Society, IESE Business School, Barcelona, Spain, June 30 to July 1, 2014

18

risk free rate are hardly defensible. Perhaps, for these reasons, subsidies often fail to meet policy objectives given the inherent disequilibrium that jeopardises their sustainability. Carbon taxation maximises access to a range of viable energy technologies by asserting their influence on energy pricing. The level of carbon taxes gives the appropriate pricing signals, firms may respond by changing the mix in order to optimise their portfolios. In effect, technology choices are not predetermined when portfolio hedge, the firm’s position within a given market (i.e. monopolist or price-‐taker), and their uncertainties are taken into account. Thus, by focusing on influencing energy pricing, carbon taxation offers the prospect of differentiating penalties for pollution to verifiable emissions from fossil fuel technologies. As a result, when pollution costs are fully internalised, innovations could occur in reducing carbon emissions or renewable energy’s capital costs. The risk-‐taking exercised by investing firms through their explicit choice of technologies avoids the irreconcilable dilemmas previously observed as occurring for subsidies. Indirectly, consumption of carbon-‐emissions-‐intensive goods often rises with increasing income. With carbon taxes applied on the consumption of such goods, the resulting burden is more likely placed on those with higher income. Carbon taxation could be modified as a “floor” power price while retaining managerial flexibility on volume despatch and pricing of supplies. When set above a minimum power price threshold, losses for renewable energy could be avoided arising from lower prices. Our simulation highlights these observations: When “floor” power prices are at an appropriate level, renewable-‐energy-‐diversified portfolios achieve higher returns than fossil-‐fuel-‐only portfolios. The differences imply foregone values incurred by non-‐diversifying firms. Potentially, as these value differences widen, fossil-‐fuel-‐only portfolios may take this cue to diversify into renewable energy. When policy uses pricing signals to influence renewable energy adoption, while consciously working within the context of the firms’ investment decision criteria, resource allocation could follow a more equitable route feasible under a functioning market economy. Consequently, carbon taxation may be periodically varied to adapt to changing market circumstances that impact firms’ values and the pace of technological evolution. Within the context of energy’s oligopolistic markets, regulatory actions could achieve greater influence by dismantling the barriers to competition. For renewable energy deployment, competitive markets require less regulatory support when firms are left to strategically respond according to their resource endowment and aspirations.