proposal 2009462572

TRANSCRIPT

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

CHAPTER 1: INTRODUCTION

1.0 INTRODUCTION OF STUDY

Understanding the nature of savings behavior is critical in

designing policies to promote savings and investment. Given the

differences in the economic environment of the developing and

industrial countries there should be substantial variation in the

household behavior.

The topic that researcher will be discuss in this research paper

is A Study on Determinants of Saving in Malaysia. This research paper

is starts with introduction. For introduction it includes background

of the study, statement of problem, objectives of study, scope of

study, theoretical framework, research hypothesis, limitations of

study, significance of study and definition of terms.

Next chapter is about literature review which discuss of each

dependent and independent variables. Chapter three in this report

consists of methodologies which discuss about the research methods

that used for this study. For the chapter four, it discuss about the

findings that found from the data collected. Last chapter, it discuss

about conclusion and some recommendations from researcher.

1 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

1.1 BACKGROUND OF STUDY

Proper analysis of savers’ behavior requires household or micro

level data on saving patterns and preferences as well as direct

estimates of household savings. Such information will help financial

institutions and policy makers mobilize savings and increase

investments.

Savings play an important role in economic development. Growth

theories have shown that savings is a necessary ingredient to finance

investment which will enhance a country’s productivity. Thus, it would

be important to look at the determinants of people’s saving to fully

understand economic growth.

Saving is the amount of current income which is not spent on

current consumption but reserved for use in the future. In its

simplest form, saving is usually in cash or other bankable deposits.

2 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

In broader terms, a comprehensive definition of saving would be the

value of all assets held, including financial assets, inventories,

livestock, equipment, land and landed assets.

The degree or extent to which these saved assets can be mobilized

for use in the future date differs. For example, bank deposits and

other liquid forms of savings can be readily mobilized in financial

markets in that the savers fund can be easily transformed by the

financial intermediaries to meet the needs of potential borrowers.

On the other hand, savings held in the form of assets, such as

equipments and land may not be as liquid for immediate mobilization.

By contrast, cash may be readily available for use by the savers, but

this is not accessible in the market for lending to other people.

1.1.1 History of Saving Environment in Malaysia

The mobilization of savings is an important prerequisite for

capital formation and hence, national development. Economic

growth can be sustained only if resources are mobilized

efficiently and transformed effectively into productive

activities.

Historically, Malaysia had managed to sustain a high level

of savings. On the whole, the country saved an average of 24% of

3 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

GNP a year over the last three decades, a level amongst the

highest in the world. Because of the availability of adequate

savings for productive long-term investment, Malaysia had

consistently achieved a high rate of growth with relative price

stability.

Growth in the gross domestic product (GDP) at constant

prices had accelerated from an average annual rate of about 5%

(inflation of less than 1% annually) in the 1960s, to 8% in the

1970s (inflation was higher, averaging about6%), but slackened to

5.2% during the 1981-85 period (inflation averaged 4.6% during

this period). This reflected the prolonged global recession in

the early 1980s.

However, the Malaysian economy had since rebounded through

the rest of the 1980s with remarkable resilience in terms of

performance. Real economic growth picked up to average 6.9% per

annum during the 1986-90 period (9.2% a year in 1988-90), with

inflation averaging 2.8% annually.

Throughout the past three decades, Malaysia had basically

relied on the use of realistic 5-year plans to implement its

development strategy, the main aim being to ensure that

4 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

sufficient domestic resources will be forthcoming to meet the

goals of national development.

However, Malaysia is a small and open economy and as such,

fluctuations in its international terms of trade and their impact

on export earnings (and hence, national income) have a

significant influence on the rate and level of its domestic and

national savings.

Consequently, periodic imbalances were reflected in the form

of deficits or surpluses in the current account of the balance of

payments, which were usually "financed" through sufficient

inflows of long term foreign capital so that overall national

external reserves even rose significantly in most of the "lean"

years.

1.2 PROBLEM STATEMENT

The rapid demographic shift in Malaysia is expected to raise both

micro and macro-economic issues. On the microeconomic front, health

care, housing, and other related services for the purpose of improving

the welfare of the elderly need to be addressed. In addition,

5 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

macroeconomic issues related to saving, labor productivity, and

capital flows also need to receive attention.

To derive the saving implications of this economic change, the

determinants of the people’s saving ratio in Malaysia are investigated

using the hypothesis of saving behavior. The saving behavior

hypothesis is tested with the Malaysian data. The investigation deals

with an unresolved issue of the growth rate effect on the saving

ratio.

Malaysia has achieved remarkable growth and development since

independence. During the 1970s, the economy registered a rate of

growth of Gross Domestic Products (GDP) at 7.6 percent per annum

despite the setbacks due to the oil crisis in 1972-1973 and 1979.

Subsequently, growth was somewhat hampered by the recession which

began in late 1979. However, economic growth of the GDP during the

period of 1981 to 1985 managed to sustain at 5.8 percent per annum

(Fourth Malaysia Plan, 1981).

Since the growth in some of these economies is often considered

resource intensive rather than technology intensive (Rosegrant and

Evenson (1992), The World Bank (2007), savings are likely to play a

very important role in promoting real growth. Several empirical

studies found a positive effect of the saving rate on the long term

6 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

growth (Cardenas and Escobar (1998), Motely (1994) and Krieckhaus

(2002) though the growth theory predicted only temporary positive

effect of increased saving rate on the growth rate in the economy due

to corresponding negative effect on capital productivity.

People’s savings, in particular, assist in smoothing out

unexpected variations in income, minimizing the impact of shocks on

consumption. In a country like the Malaysia, where a lot of resident

in rural area are engaged in agriculture and face uncertainty from

weather and natural calamities, it would be helpful to understand how

people deal with fluctuations in incomes. Further, savings serve as a

vehicle of social mobility and of enhancing future income earning

possibilities. Savings indeed have implications in the welfare of

households, macroeconomic, growth and development.

In the Malaysia, however, it has been noted that the savings rate

is becomes fluctuate overtime. On the other hand, there is a

possibility that Malaysian are actually saving more but not through

formal financial instruments. Previous studies on savings look at

differences in the saving behavior of urban and rural households. Some

studies focus on the forms and determinants of rural savings. Due to

the inadequacy of recent and comprehensive data and information

7 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

regarding the behavior of household savers through time, the study

designed to increase savings interest.

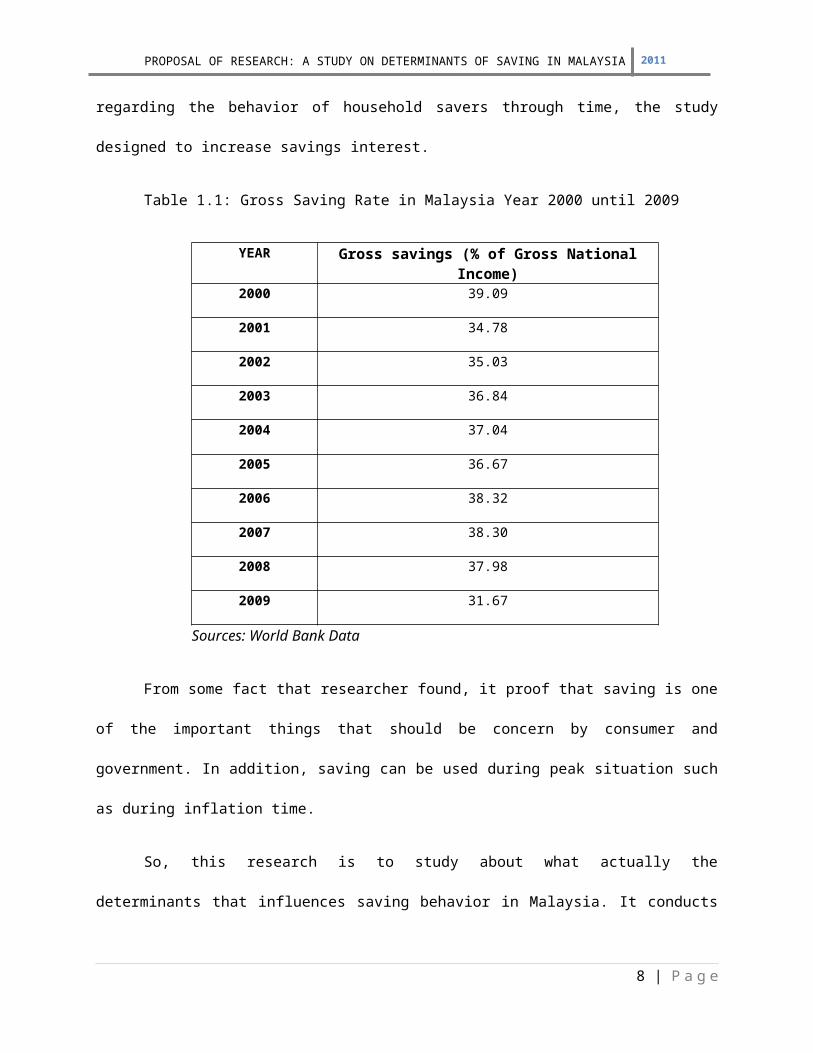

Table 1.1: Gross Saving Rate in Malaysia Year 2000 until 2009

YEAR Gross savings (% of Gross NationalIncome)

2000 39.09

2001 34.78

2002 35.03

2003 36.84

2004 37.04

2005 36.67

2006 38.32

2007 38.30

2008 37.98

2009 31.67

Sources: World Bank Data

From some fact that researcher found, it proof that saving is one

of the important things that should be concern by consumer and

government. In addition, saving can be used during peak situation such

as during inflation time.

So, this research is to study about what actually the

determinants that influences saving behavior in Malaysia. It conducts

8 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

to determine is there relationship between of income, rate of return,

inflation, and consumption on saving in Malaysia.

1.3 OBJECTIVES OF STUDY

The research attempts to achieve several objectives. All of these

objectives must be considered to ensure that the findings are precise

with what researcher is trying to search out.

9 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Below are the objectives that are essential to be achieved for

the purpose of completing the ultimate intention of this research

which is as follow:

i. To give background information about saving.

ii. To study about relationship of income level on saving.

iii. To study about relationship rate of return on saving.

iv. To study about relationship of inflation on saving.

v. To study about relationship of consumption on saving.

10 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

1.4 SCOPE OF STUDY

This research paper will discuss about saving in Malaysia.

Malaysia is one of develop country regarding of their economy. The

Malaysian economy has demonstrated strong resilience in the face of

external uncertainties. Economic growth continues to be broad-based

with all sectors registering higher output.

This study using secondary data as a source to get information

about saving behavior and literature review was founded from internet

materials such as journal and articles that need supported to all

dependent and independent variable to conduct this research.

The research focus is about the income level, rate of return,

inflation, and consumption in Malaysia. The Malaysia data collected is

time series data about 41 years which range from year 1967 until 2007.

Researcher use real Gross Domestic Product (GDP) constant local

currency as income indicator, Deposit Interest Rate as measurement of

rate of return, Consumer Price Index (CPI) for inflation, and Gross

National Expenditure constant local currency for consumption, while

for saving behavior, researcher use Gross Domestic Saving constant

local currency as measurement.

11 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

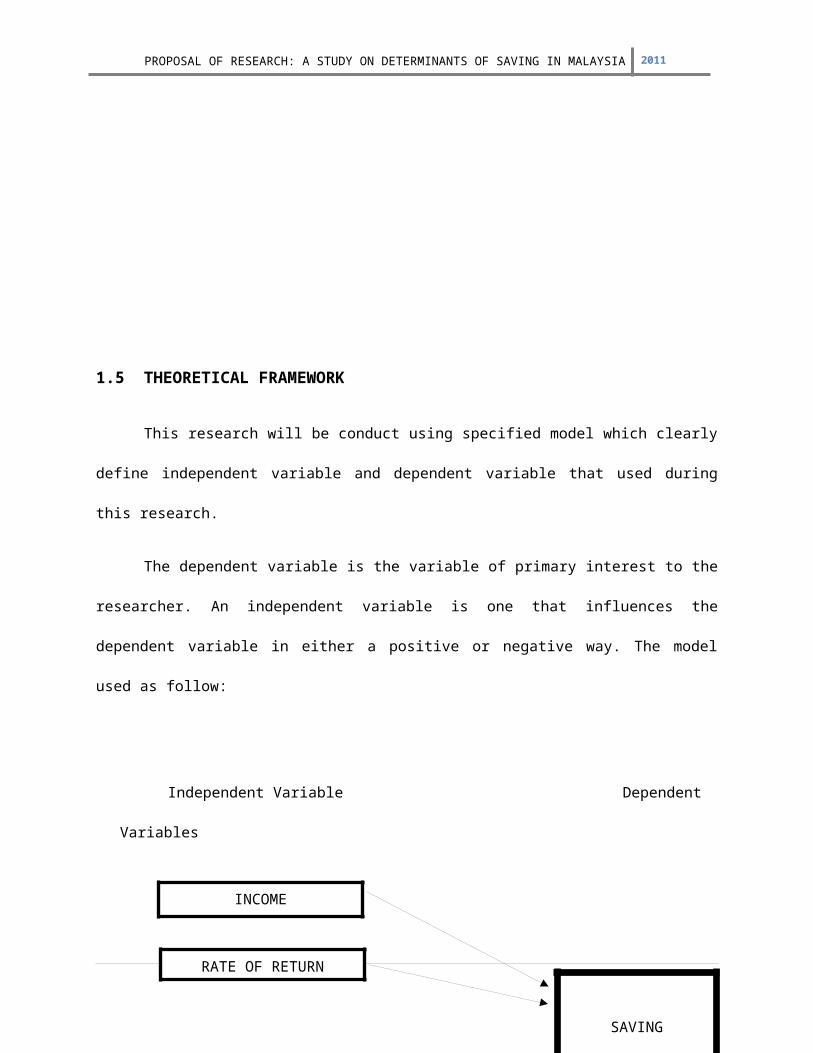

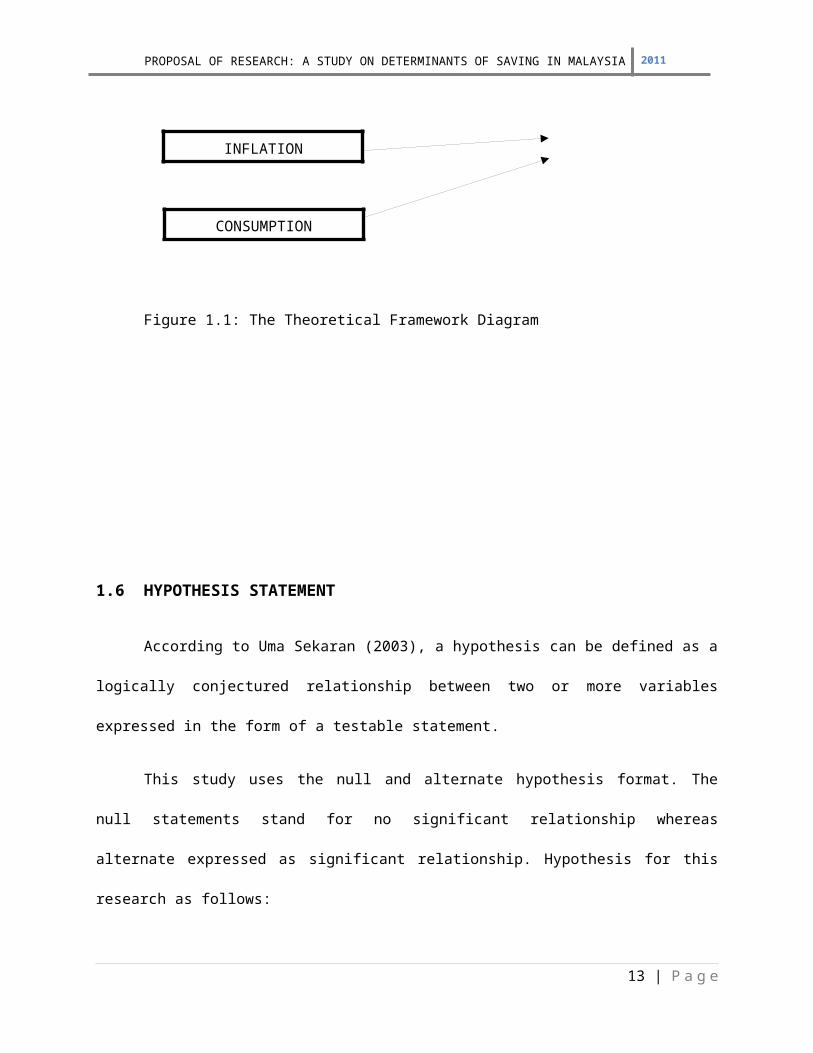

1.5 THEORETICAL FRAMEWORK

This research will be conduct using specified model which clearly

define independent variable and dependent variable that used during

this research.

The dependent variable is the variable of primary interest to the

researcher. An independent variable is one that influences the

dependent variable in either a positive or negative way. The model

used as follow:

Independent Variable Dependent

Variables

12 | P a g e

INCOME

RATE OF RETURN

SAVING

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Figure 1.1: The Theoretical Framework Diagram

1.6 HYPOTHESIS STATEMENT

According to Uma Sekaran (2003), a hypothesis can be defined as a

logically conjectured relationship between two or more variables

expressed in the form of a testable statement.

This study uses the null and alternate hypothesis format. The

null statements stand for no significant relationship whereas

alternate expressed as significant relationship. Hypothesis for this

research as follows:

13 | P a g e

INFLATION

CONSUMPTION

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Hypothesis 1

H0: There is no significant relationship between income and

saving.

H1: There is significant relationship between income and saving.

Hypothesis 2

H0: There is no significant relationship between rate of return

and saving.

H1: There is significant relationship between rate of return and

saving.

Hypothesis 3

H0: There is no significant relationship between inflation and

saving.

H1: There is significant relationship between inflation and

saving.

Hypothesis 4

14 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

H0: There is no significant relationship between consumption and

saving.

H1: There is significant relationship between consumption and

saving.

Hypothesis 5

H0: There is no significant relationship between income, rate of

return, inflation, consumption, and saving.

H1: There is significant relationship between income, rate of

return, inflation, consumption, and saving.

15 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

1.7 LIMITATIONS OF STUDY

This study has some of limitation as follows:

1.7.1 Time Constraint

Time factor is one of the limitations for the researcher to

conduct this study. Since the researcher is in final year and

last semester of study, the schedule is quite tight because have

to attend industrial training. So, the time that researcher have

is only in weekend to conduct this research.

1.7.2 Data Collection

In term of data collection, since this paper is fully use

secondary data as a data collection, the researcher have to find

the most accurate data. However, this data can be obtained in

DataStream System but some of data that researcher need is not

16 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

available and researcher have to find other sources to fulfill

data needed.

1.7.3 Sources of Information

This research information is mainly come from internet

sources. Some articles, journal and web pages are directly

download from internet. So, researcher does not know the

information level of accuracy.

1.8 SIGNIFICANCE OF STUDY

This study gives some benefits to the following parties such as:

1.8.1 Researcher

This report is very important to the researcher itself. The

study is conduct by researcher because to identify the

determinants about the saving in Malaysia. The researcher also

wants to give some information about what factors influences

saving pattern in Malaysia.

17 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

1.8.2 Government

This research would help the government to identify which

factors that influence the level and proportion of national

savings. The information provided by the researcher could help

the government to remain concerned about the economic conditions

regarding the inflation rate and rate of return.

1.8.3 Consumer

This report also gives some information to the consumer. As

we already know, saving is important for future purpose. We did

not know what will happen in next day, so saving is quite

important things that should be concern especially by consumer.

This report will give some information to the consumer about what

factor that actually influences their saving behavior.

1.8.4 Future Researcher

This research also can give information to other researcher

who wants to conduct research regarding this area of interest and

also for other researcher whom want to further this research in

the future. This study can give some information and statistical

regarding saving behavior in Malaysia.

18 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

1.9 DEFINITION OF TERM

Determinant - Factor or element that limits or defines

a decision or condition.

Saving - Portion of disposable income not spent on

consumption of consumer goods.

Gross domestic product - Gross Domestic Product refers to the

market value of all goods and services

produced within a country in a given

period. It is often considered an indicator

of a country's standard of living.

Gross National Expenditure - Gross National Expenditure is total

of all expenditure of all kinds within the

economy, public and private. It is usually

different from Gross Domestic Product (GDP)

because expenditures on imports are

included, but exports (goods produced

within the economy but sold outside of it)

are not.

Deposit Interest Rate - The interest rate paid by financial

institutions to deposit account holders.

19 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Deposit accounts include certificates of

deposit, savings accounts and self-directed

deposit retirement accounts.

CHAPTER 2: LITERATURE REVIEW

2.0 CHAPTER INTRODUCTION

In this chapter, researcher wills discuss some of literature

survey that will support each relationship of each independent

variable for this study. Based on Uma Sekaran (2003), literature

survey is the documentation of a comprehensive review of the published

and unpublished work from secondary sources of data in the areas of

specific interest to the researcher. It includes books, journal,

articles, newspapers, magazine, theses, and government publications.

2.1 PREVIOUS STUDY: SAVING

In pervious study, research paper about saving behavior already

done by many researchers. According to Gavin, Hausmann et al. (1997)

in their research paper Saving Behavior in Latin America: Overview and

Policy Issues, which presents an alternative perspective on the

relationship between saving and growth, saving and inflation

20 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

stabilization, saving and structural reform, and saving and capital

inflows, drawing on the experience of East Asia and Latin America in

the last twenty five years.

In paper named Empirical Analysis of Savings Behavior in European

Countries: New Insights, by Cristina Ruza & Jose M. Montero (2003),

the primary aim of this paper is to carry out an analysis of the

savings behavior by separately analyzing its public and private

components and the private savings components as well. Particularly,

the authors will devote attention to appraise the extent to which the

substitution effect between those magnitudes has held for the last few

decades in the European context.

Other than that, The (Dis)Saving Behavior of the Aged in Japan

paper written by Charles Y. Horioka (2009) also discuss about saving

behavior. In this paper, the researcher survey the previous literature

on the saving behavior of the aged in Japan and then present some

survey data on the saving behavior of the aged in Japan that became

available recently.

In research paper Differences in Household Savings Behavior:

Evidence from Industrial and Developing Countries by Muradoglu G., &

Taskin. F.(1996), The purpose of their study was to learn more about

21 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

the differences in the nature of the household savings behavior in

industrial versus developing countries.

Ferrucci & Miralles (2007), in their working paper series named

Saving Behavior and Global Imbalances the Role of Emerging Market

Economies discus about reduced-form model that relates private saving

to a set of economic fundamentals, while controlling for structural

and institutional differences across countries.

In paper titled Consumption and Saving Behavior: Modeling Recent

Trends illustrates recent trends in household consumption and personal

savings in the UK and the US and discusses some theoretical models

that can be used to interpret them. The trends in these two countries

are interesting for several reasons (Orazio Attanasio, 1997).

Based on Naziruddin & M. Shabri (2003), in paper The Influence of

Religiosity, Income and Consumption on Saving Behavior:The Case of

International Islamic University Malaysia, attempts to measure the

influence of religiosity, income and consumption on saving behavior.

From the empirical results, it is found that the religiosity and other

variables have a significant impact on the students saving behavior.

22 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

2.2 INCOME AND SAVING

Income means the maximum amount an individual can spend during a

period without being any worse off. For the average individual, income

is earned through earning wages by working or making investments into

financial assets. In most countries, the amount of income that an

individual receives is taxed by the government before it is received.

The revenue generated by income taxes is used to finance government

actions and programs as determined by the federal budget.

Theories have shown that income and wealth play a very important

role in determining the level of saving. Other findings in the field

of saving behavior reveal that different sector of population have

different savings motives and behavior and capacities to smooth shocks

and build assets. Savings may depend on education level, age,

macroeconomic environment, demographics, region, and family structure,

labor participation, and access to pension funds system (Attanasio and

Szekely, 2000).

According to Province British Columbia (1994), the relationship

between personal income and savings is one of the key economic

indicators reported in the income and expenditure accounts. Personal

income (the total of labor, transfer and unincorporated business

23 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

income) may be saved, used to purchase goods and services, or

transferred to other individuals, corporations or the government. In

turn, the savings of the personal sector permit investment and

borrowing by businesses and governments. Savings are affected by

factors such as general economic conditions, age, and individual

preferences. However, income is probably the most important

determinant of the savings behavior of individuals. With decreases in

the percentage of personal income retained by consumers (disposable

income) over time, one might wonder whether there has been an effect

on the savings rate of British Columbians.

The life-cycle hypothesis of saving is tested with pooled cross-

age time series data of Korean household survey data from 1977 to

2002. The investigation reveals that real saving rates increase when

the duration of life span and per household real disposable income

rise, whereas they decrease when the growth rate of income and net

worth to GDP ratio rises (Kwack, Sung Yeung, 2003).

Coombs& Freedman (1970) in their economic theory suggested that

income is positively related to savings. Thus, the higher the income

growth rate the higher is the savings rate.

According to Lachlan McGregor (1998), the personal disposable

income is often used for purposes of spending money on goods and

24 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

services that are desired by an individual. However it may also be

used for the purposes of saving as well by not spending a particular

amount of money for consumption. The personal disposable income of a

person could be used for the purposes of investing in saving options

like insurance plans.

The incomes received by households may be categorized into the

part that they spend on consumption goods, the part that they save,

and the part that they are required to pay in taxes. Thus aggregate

income may be represented as a sum of consumption (C), saving (S) and

taxation (T). Bearing in mind that we can represent aggregate income

by GDP, we can summaries the components of income as GDP equal C plus

S plus T (Lachlan McGregor, 1998).

A study by Davis and Schumm (1987), using 1739 low and high

income married couples in both rural and urban states, investigated

savings behavior and satisfaction. Results indicated no relationship

between income and savings among low income families, but it was

related among high income families.

Keynes in economic theory, Income has been considered the most

important factor in the determination of the saving behavior of an

individual. More income means, normally, more saving and vice versa.

25 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Different forms of the functional relationship between saving and

income have been tested. Some studies found a statistically

significant effect of income on saving, and other studies found no

significant effects of income.

Both the Keynesian savings function (1936) and the permanent

income hypothesis indicates a positive effect of income on savings.

Using time series data for forty nine countries, Rossi (1988), for

example, indicated the positive impact of current income levels on

savings rate without differentiating types of income.

According to the permanent income hypothesis by Friedman (1957),

which distinguishes between permanent and transitory components of

income, households will spend mainly the permanent income and

therefore the transitory income will immediately be channeled to

savings with marginal propensity of savings from this income

approaching unity.

Studying a group of developing countries, Gupta (1987) observed

that savings respond positively to transitory income.

Koskela and Viren (1982) studying a group of industrial countries

and defining transitory income as unanticipated changes also concluded

that unanticipated real income had a positive effect on savings.

26 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Based on the survey of consumer finances, Avery and Kennickell

(1991) indicated that in the United States, families with higher real

income and families that received support or large gifts, which is an

alternative definition of transitory income, experienced a higher

level of savings. In addition to permanent and transitory income

components, the rate of growth in income is used as an additional

explanatory variable in empirical savings studies. Increased growth

rates in income are also expected to have a positive effect on

household savings.

Collins (1989), for example, found that income growth would

increase savings especially if it were concentrated in higher saving

households. In this study all three definitions of income, namely,

permanent income, transitory income, and growth rate of income, were

used as explanatory variables.

They do however find a positive relationship between income

growth and saving and this is in line with the findings of Attanasio

(2000).

In other words, the factors other than income generally have a

relatively small effect on consumption and saving of households as a

whole though they might be of importance for individual economic

units. The consideration of income in a functional relationship with

27 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

consumption and saving is therefore the first step to a study of

consumption and savings behaviour of the households. It means, faster

rise in saving than income as income rises (Uma Datta, 1997).

2.3 RATE OF RETURN AND SAVING

In finance, rate of return (ROR), also known as return on

investment (ROI), rate of profit or sometimes just return, is the

ratio of money gained or lost (whether realized or unrealized) on an

investment relative to the amount of money invested. The amount of

money gained or lost may be referred to as interest, profit or loss,

28 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

gain or loss, or net income or loss. The money invested may be

referred to as the asset, capital, principal, or the cost basis of the

investment. ROI is usually expressed as a percentage.

Carmen and Ostry (1995) which generate higher real interest

rates, that means higher return will result in greater savings by

households only if the later decide to defer consumption, in other

words, if the sensitivity of consumption and saving is significant.

According Ostry and M. Reinhart (1996) there is little consensus

in the empirical literature on the interaction between saving and the

real rate of interest in developing countries, Some studies have

concluded that, for a large number of developing countries, there does

not appear to be any systematic relationship between rates of return

and saving behavior which others have suggested that there may be

considerable regional variation in this elasticity.

Saving responds positively to rises in the interest rate only if

the substitution effect is stronger than the income effect. It could

be argued that, for the typical developing economy the net impact of a

change in real interest rate on saving is likely to be positive

( Athukorala,1998 and Sen, 2002).

29 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

The effect of interest rates on savings was inconclusive in the

previous empirical studies. According to consumption decision, an

increase in the rates of return increases savings but real income

effect of higher rates of return can affect savings adversely. In his

survey article, Balassa (1992) argued that the effect of real interest

rates on savings is positive for developing countries.

Examining the household savings behavior in Australia, Ouliaris

(1992) indicated that real interest rates exert a negative influence

on the savings ratio and the fall in real interest rates contributes

to the rise in savings ratio.

According to the Gulnur and Fatma (1996), a cross-section time

series sample from developing countries provides evidence that in the

majority of the cases the response of savings growth to real rates is

not different from zero.

Loayza (2000) find no positive relationship between financial

deepening and saving or between higher real interest rates and saving.

Hussain (2002) in examined the impact of financial liberalization

on resource mobilization and investment in 25 African Countries,

including Ghana and found that the real interest rate does not seem to

be an important factor in the determinant of financial saving and

30 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

total saving but the activities of the informal financial market is an

important determinant of financial savings.

Masson (1998), in an attempt to discover the determinants of

savings across a large number of developed and developing countries

over time finds that the interest rate is a significant explanatory

variable for developed countries in determining savings rates. However

this is not the case in developing countries. They found that growth

in income was associated with higher rates of saving but beyond a

certain point, as income increases savings ratios fall.

Giovannini (1985) in an empirical study found that in most

countries, the response of savings growth to real rates is no

different from zero. He argued that in developing countries,

assumptions about elasticity of substitution may not hold because a

significant proportion of the population may not be able to borrow

even at black market rates.

2.4 INFLATION AND SAVING

In mainstream economics, the word “inflation” refers to a general

rise in prices measured against a standard level of purchasing power.

Previously the term was used to refer to an increase in the money

31 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

supply, which is now referred to as expansionary monetary policy or

monetary inflation. Inflation is measured by comparing two sets of

goods at two points in time, and computing the increase in cost not

reflected by an increase in quality. There are, therefore, many

measures of inflation depending on the specific circumstances. The

Consumer Price Index (CPI) measures the percentage change through time

in the cost of purchasing a constant basket of goods and services

representing the average pattern of purchases made by a particular

population group in a specified time period

Changes in behavior may be related to factors such as economic

growth, unemployment, interest, and inflation rates, all of which can

affect consumer confidence in the economy. This section examines two

of these factors, unemployment and interest rates, as they relate to

the savings of Columbians (British Province British Columbia, 1994).

Studying a group of industrial countries Koskela and Viren (1982)

also observed that savings increase as real rates of interest

increase. The effect of interest rates may also be explained by the

inflation effect: assuming that nominal rates of interest are

constant, a rise in the inflation rate lowers the real cost of

borrowing and hence has a positive effect on consumers’ expenditure

and a negative effect on savings.

32 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

The consumption argument suggests that inflation expectations may

encourage expenditures on durables at the expense of savings. On the

contrary, it is also suggested that inflation decreases the real value

of financial wealth fixed in nominal terms, and households trying to

restore their wealth-income position will increase their savings.

Empirical literature on the effect of inflation on savings provides

evidence that supports both views. Gupta (1987), for example, found

that in a group of Asian countries, both expected and unexpected

components of inflation had a positive effect on savings.

Lahiri’s (1988) results were inconclusive that inflation had

positive effect on savings.

Kauffmann (1990), on the other hand compared the United States

and Germany, and suggested that the lower savings activity of U.S.

households was due to the higher inflation rates in the United States

than in Germany.

Bovenberg and Evans (1990), analyzing personal savings in the

United States, concluded that due to reduced inflation during the

1980s the personal savings rate was reduced.

The most recent study by Zorklu and Barbie (2003), the results of

this study show that because the inflationary pressures in Ghana

33 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

during the reform period resulted in negative real deposit interest

rates and as a result, the savings response was weak.

This confirms earlier work (Aryeetey and Gockel, 1991, Gockel and

Brownbridge, 1998, Gockel and Akoena, 2002). A major lesson from

Ghana's experience high inflationary pressures has a reduced chance of

increasing savings mobilization.

Gulnur and Fatma (1996) in their study said that when savings

rates were estimated for all countries the model used in this study

performed reasonably well, accounting for 35 per cent of the total

variation. In this equation only income growth and inflation rate

variables showed significant coefficients. As income growth increased,

savings rates increased and as inflation increased, savings rates

decreased.

Literature suggests inflation as one such factor contribute to

the saving rate (Deaton, 1977, Chopra, 1988, Haslag, 1997, Heer and

Suessmuth, 2006).

The effect of inflation on savings, however, is ambiguous both in

theory and practice (Heer and Suessmuth, 2006, and Deaton and Paxson,

1993).

34 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Craig and Mark (2006), in their study result stated the

relationship between the savings rate and inflation is positively

correlated. As such, when inflation is high it appears that people

save more, and when the inflation rate is low people save less.

2.5 CONSUMPTION AND SAVING

Consumption means expenditure during a particular period on goods

and services used in satisfaction of needs and wants

35 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

John Maynard Keynes developed a theory of consumption that

focused primarily on the importance of people’s disposable income in

determining their spending. A rise in real income gives people greater

financial resources to spend or save. The rate at which consumers

increase demand as income rises is called the marginal propensity to

consume.

Savings, investment and consumption are closely related. There

will be no investment without savings. Investment, in turn, creates

employment and income for people. Without it and, therefore, without

income, we shall have nothing to save and nothing to spend on consumer

goods and services. What we do not spend is what is saved.

Consumption, therefore, is affected by decisions to spend. If we spend

all our income, there will be no capital accumulation for saving

investment (Funom Makama, 2009).

According to Rose and Kolari (1995), savings is referred to the

postponement of current consumptions. The volume of savings by

individuals’ consumers is a function of number of factors, including

the amount of current and expected income, the stock wealth held by

the individual, the level of interest rate, expectations concerning

the future rate of inflations and other variables.

36 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Regina Chang (1994) noted that, the idea of consumption smoothing

gives a positive correlation between current consumption and saving

because transitory income shocks lead to a higher current income and

increased saving.

As was pointed out by Caroll (1992), this may create a

significant correlation between consumption growth, lagged income and

saving ratio.

Russian households saved much the same in the 1990s, which was

higher than savings in 1976 (Gregory et al. 1999). This finding is

contrary to expectations since there is widespread belief that savings

were actually relatively high in the Soviet era because of shortages

of consumption goods (a form of forced saving) and that saving was

lower with price liberalization.

According to the William and Micheal (2006) in their Economics

book state that both consumption function and saving function have

positive slope. As disposable income rises, consumption and saving

rise. Consumption and saving then are positive functions of disposable

income.

37 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Loayza and Shankar (2000), advocate the use of measures of

savings that correct for consumer durables. In their study stated

that, saving and consumer spending have positive relationship.

W.S.Woytinsky (1948) remarks on the relationship between

consumers’ expenditures, savings and disposable income. He said that

these three indicators have positive relationship.

There are several reasons why one may be interested to study the

saving and consumption behavior of households in developing countries.

Saving is related to growth and economic development. There is a close

link between household consumption and national saving rates over time

(Deaton, 1997).

Athukorala (1998) and Sen (2002) noted that higher interest rate

increases the present price of consumption relative to the future

price (the substitution effect), and thus provides an incentive to

increase saving. However, if the household is a net lender, the

interest rate rise also raises lifetime income, and thus tends to

increase consumption and decrease saving (the income effect).

CHAPTER 3: METHODOLOGY

38 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

3.0 CHAPTER INTRODUCTION

In this chapter, researcher will discuss about the data that

researcher use for this research. Research methodology will discuss

the Research Design, Data Collection Method, and Interpretation that

researcher uses in conducting this study. It is Important for a

researcher to select and determining the appropriate research design

to be choose for providing the framework in conducting the study.

Data can be obtained from primary or secondary resources. To

achieve the objectives of this research which is to identify the

determinants of saving behavior in Malaysia, researcher used secondary

data as data collection methods.

3.1 RESEARCH DESIGN

Research design is a blueprint that provides the detail of

necessary procedure in obtaining the information needed in order to

structure or solve marketing research problem. The researcher used the

secondary data to complete this study.

According to Malhotra (2007), research design is a framework for

conducting the marketing research project. That means research design

39 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

will show the details of the procedures that needed in order for

obtaining the information needed to structure of solving marketing

research problems.

3.2 DATA COLLECTION METHOD

Data collection methods are an integral part of research design

as shown in the shaded portion in the figure. Data can be collected in

a variety of ways, either from primary or secondary resources. To

achieve the objectives of this research which is to identify the

determinants of saving behavior in Malaysia, researcher used secondary

data as data collection methods.

3.2.1 Secondary Data

Data that are collected to be analyzed in this study is by

using the main source that is the secondary data. According to

Malhohotra K. Naresh (2007), secondary data is the data that had

been collected for the purposed other than the problem at the

hand. These data can be lactated quickly and inexpensively,

whereas according to Uma Sekaran (2003), secondary data refer to

40 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

information gathered from sources already existing for examples

journal, articles, government publication, web pages, and book.

The data that researcher collect to conduct this study is

time series data. It uses Malaysia data from year 1967 until

2007, which is 41 years to see the trend whether this dependent

variable has positive or negative relationship between the other

variables. To complete this study, data about income, rate of

return, inflation and consumption are collected from DataStream

database, World Bank data, Malaysia Department of Statistics, and

Malaysia Economy webpage.

There are two types of secondary data which is as follows:

3.2.1.1 Internal Sources

Internal sources consist of sources within the

organization such as annual report of the company and other

report. The sources were obtained from company itself.

3.2.1.2 External Sources

It refers to the sources outside the organization. The

sources that are usually uses for obtaining information are

book, journal, articles, newspaper, magazine, internet,

printed media and pamphlets. Since this research is related

41 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

with Economics and Finance area, the information can be

gathering from Journal of Marketing, Finance and Economy

articles.

3.3 PROCEDURE FOR DATA ANALYSIS

The researcher analyzed the data using the Statistical Package

for the Social Science (SPSS 17.0). This programme can be used to

analyze data collected from surveys, tests, observation or even

secondary data. It can perform a variety of data analysis and

presentation functions including statistical analysis and graphical

presentation of data. Among its features are modules for statistical

data analysis that induce descriptive statistics, analysis of

variance, factor analysis, multivariate analysis, categorical data

analysis and many more. SPSS can also provide a method for examining

the adequacy of the regression model that covers checking assumption

in regression.

In this study, this programme help the researcher to run the

secondary data that already collect. This programme also helps to

facilitate data clearing, and checking for logical inconsistencies. In

addition, by using this program, it can analyze the data collection to

42 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

identify the relationship and correlation between saving with income,

rate of return, inflation and consumption. It also involves in the

process of hypothesis testing.

3.3.1 Descriptive Statistics

Descriptive statistics are used to describe the basic

features of the data in a study. They provide simple summaries

about the sample and the measures. Together with simple graphics

analysis, they form the basis of virtually every quantitative

analysis of data.

3.3.1.1 Measures of Central Tendency

Measures of central tendency provide information about

the most typical or average values of a variable. It

presents the minimum and maximum value, mean, the average,

mode and the median.

Minimum value is the lowest value in the data that

have been collected. In contrast, maximum value is the

highest value in the data that have been collect.

43 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

The mean is defined as the sum of a series of

observations divided by the number of observations in the

series. It is commonly used to describe the central tendency

of variables.

The median is limitation of the mean as an indicator

of central tendency is that its value is greatly affected

when a few observations have very large or very low values.

The median is the middle value in a series of values.

The mode is defined as the most frequent value of a

variable. This indicator might convey more information about

the central tendency of a series when variables have certain

values that are much more frequent than the others.

3.3.1.2 Measures of Dispersion

Measures of dispersion provide information about the

distribution of the values of a variable. They tell us how

widely values are dispersed around their measures of central

tendency. It presents variance, standard deviation, the

skewness and the kurtosis and histograms.

44 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

The variance measures the amount of variation in a

distribution, in some sense, its “width”. It measures the

average of the square of the distance from the mean for each

value.

The standard deviation is a measure of dispersion that

is calculated based on the values of the data. It allows us

to see how widely the data are dispersed around the mean.

Skewness is a measure of whether the peak is centered

in the middle of the distribution. A symmetrical

distribution has a skewness of zero. An asymmetrical

distribution with a long tail to the right (higher values)

has a positive skew. An asymmetrical distribution with a

long tail to the left (lower values) has a negative skew.

Any threshold or rule of thumb is arbitrary, but here

is one, if the skewness is greater than 1.0 (or less than -

1.0), the skewness is substantial and the distribution is

far from symmetrical.

Kurtosis is a measure of the extent to which data are

concentrated in the peak versus the tail. A positive value

indicates that data are concentrated in the peak, while a

45 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

negative value indicates that data are concentrated in the

tail.

Values of skewness and kurtosis have little inherent

meaning, other than large values indicate greater asymmetry.

A rule of thumb is that the absolute value of the ratio of

skewness to its standard error and of kurtosis to its

standard error should be less than 2.

Histograms show the number of observations in each

category. They are very useful because they give a quick

visual of the central tendency, the extent of dispersion,

and also whether any unusually large or small observations

are present.

3.3.2 Reliability Analysis

Zikmund (2000) defined reliability as the degree to which

measures are free from error and therefore yield consistent

results. Sekaran (2003) in other words states that reliability of

a measure established by testing for both consistency and

stability. Cronbach’s alpha is a reliability coefficient that

indicates how well the item in a set is positively correlated to

46 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

one another. As suggested by Sekaran (2003), the reliability less

than 0.60 are generally considered to be poor, those in the range

of 0.70 to be acceptable and those over 0.80 to be good.

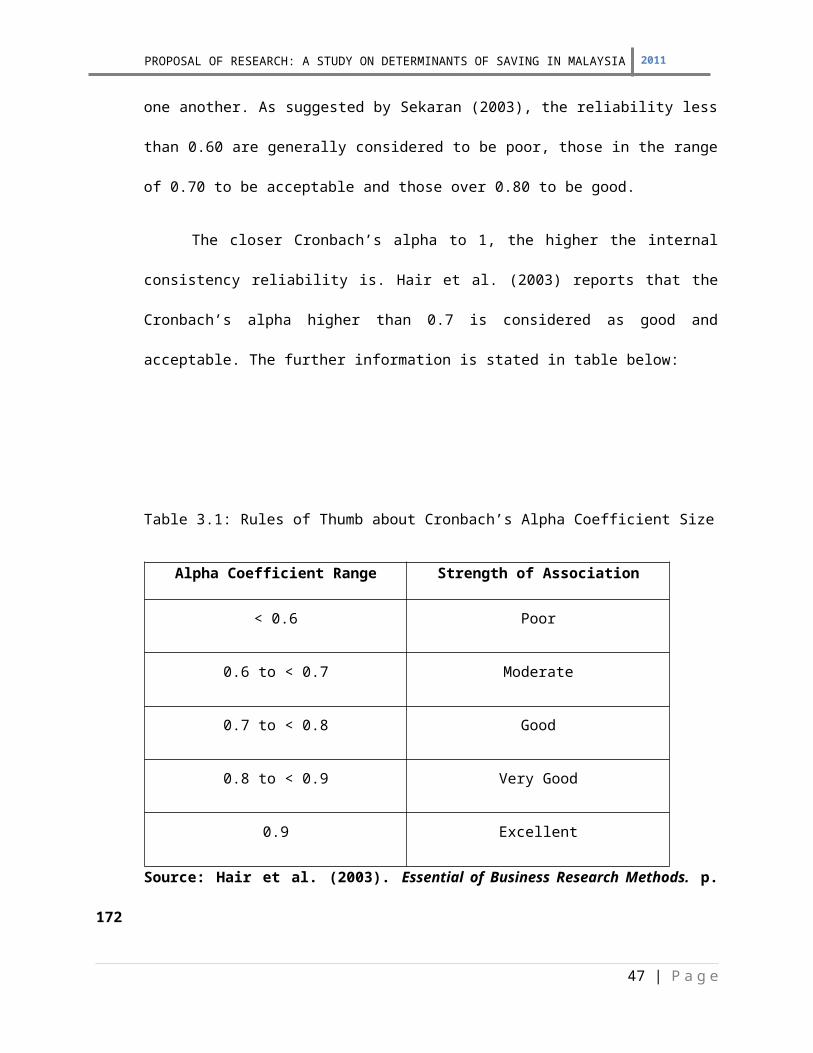

The closer Cronbach’s alpha to 1, the higher the internal

consistency reliability is. Hair et al. (2003) reports that the

Cronbach’s alpha higher than 0.7 is considered as good and

acceptable. The further information is stated in table below:

Table 3.1: Rules of Thumb about Cronbach’s Alpha Coefficient Size

Alpha Coefficient Range Strength of Association

< 0.6 Poor

0.6 to < 0.7 Moderate

0.7 to < 0.8 Good

0.8 to < 0.9 Very Good

0.9 Excellent

Source: Hair et al. (2003). Essential of Business Research Methods. p.

172

47 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

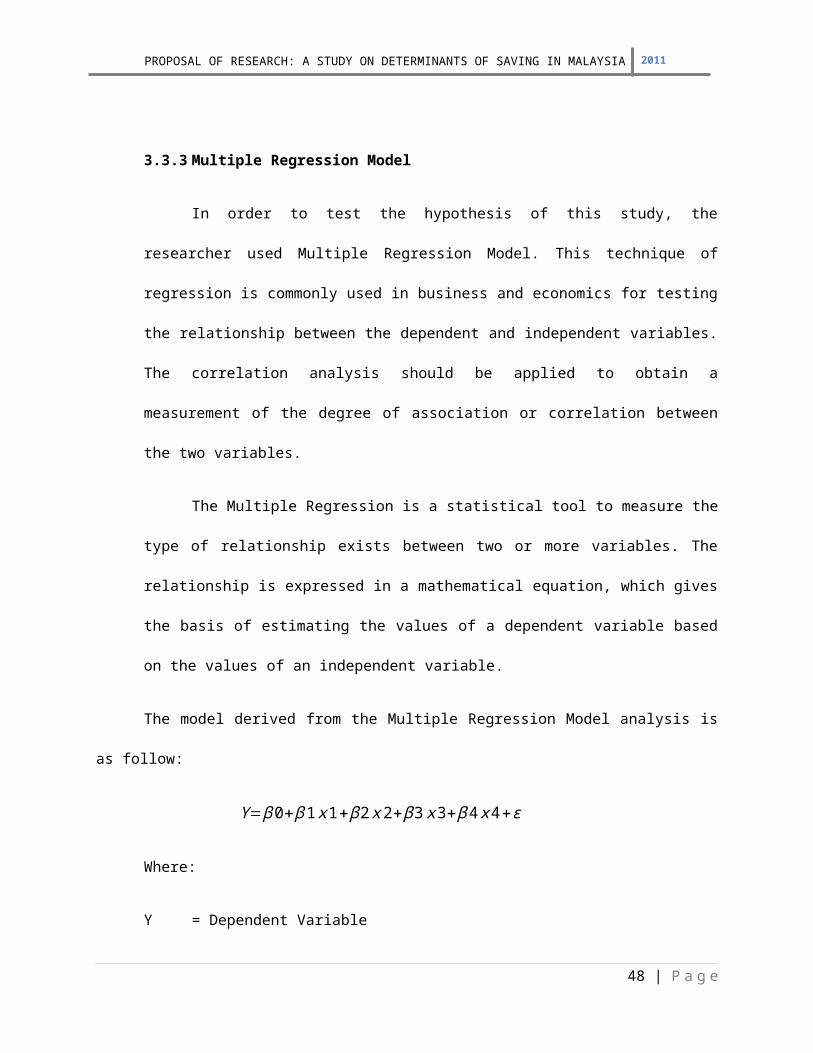

3.3.3 Multiple Regression Model

In order to test the hypothesis of this study, the

researcher used Multiple Regression Model. This technique of

regression is commonly used in business and economics for testing

the relationship between the dependent and independent variables.

The correlation analysis should be applied to obtain a

measurement of the degree of association or correlation between

the two variables.

The Multiple Regression is a statistical tool to measure the

type of relationship exists between two or more variables. The

relationship is expressed in a mathematical equation, which gives

the basis of estimating the values of a dependent variable based

on the values of an independent variable.

The model derived from the Multiple Regression Model analysis is

as follow:

Y=β0+β1x1+β2x2+β3x3+β4x4+ε

Where:

Y = Dependent Variable

48 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

β0 = Constant

β1 = Coefficient describes how changes in income affect the

value of saving.

β2 = Coefficient describes how changes in rate of return affect

the value of saving.

β3 = Coefficient describes how changes in inflation affect the

value of saving.

β4 = Coefficient describes how changes in consumption affect

the value of saving

ε = random error term

3.3.4 Correlation Test

Correlation is a statistical technique that can show whether

and how strongly pairs of variables are related.

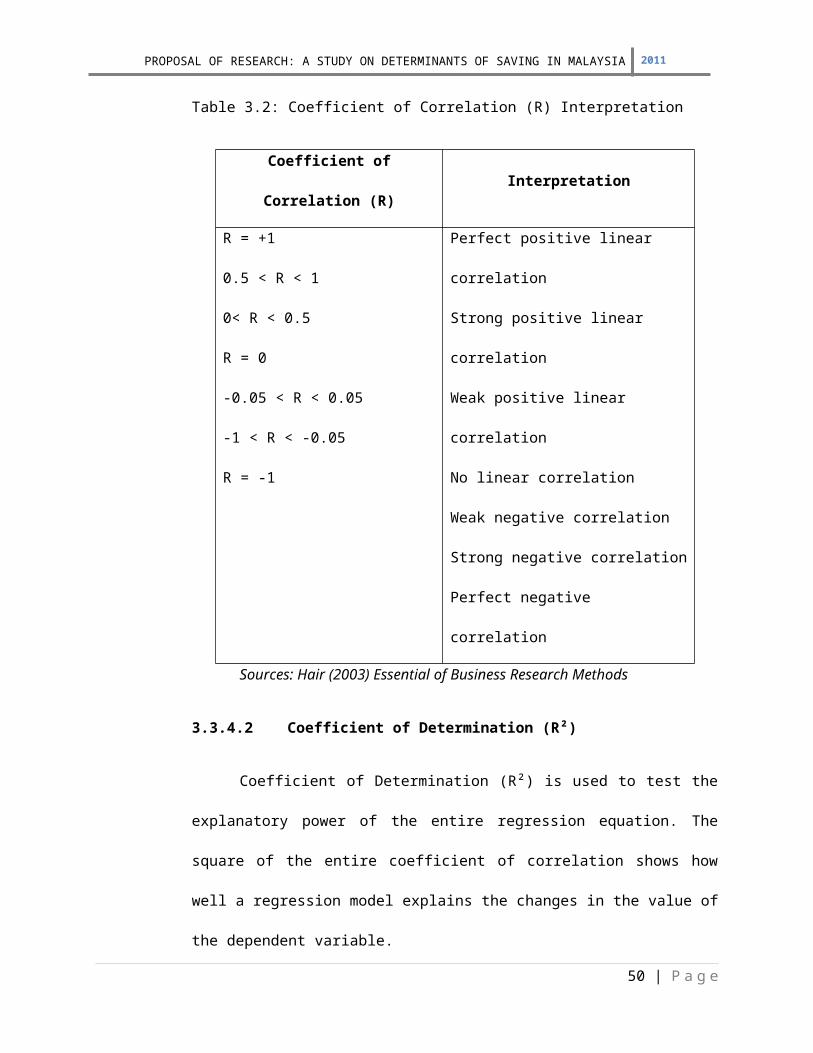

3.3.4.1 Correlation Coefficient (R)

A correlation coefficient (R) shows how much and in

what direction the two variables move together. The

tabulated interpretation mentioned is as follows:

49 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Table 3.2: Coefficient of Correlation (R) Interpretation

Coefficient of

Correlation (R)Interpretation

R = +1

0.5 < R < 1

0< R < 0.5

R = 0

-0.05 < R < 0.05

-1 < R < -0.05

R = -1

Perfect positive linear

correlation

Strong positive linear

correlation

Weak positive linear

correlation

No linear correlation

Weak negative correlation

Strong negative correlation

Perfect negative

correlation

Sources: Hair (2003) Essential of Business Research Methods

3.3.4.2 Coefficient of Determination (R²)

Coefficient of Determination (R²) is used to test the

explanatory power of the entire regression equation. The

square of the entire coefficient of correlation shows how

well a regression model explains the changes in the value of

the dependent variable.

50 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

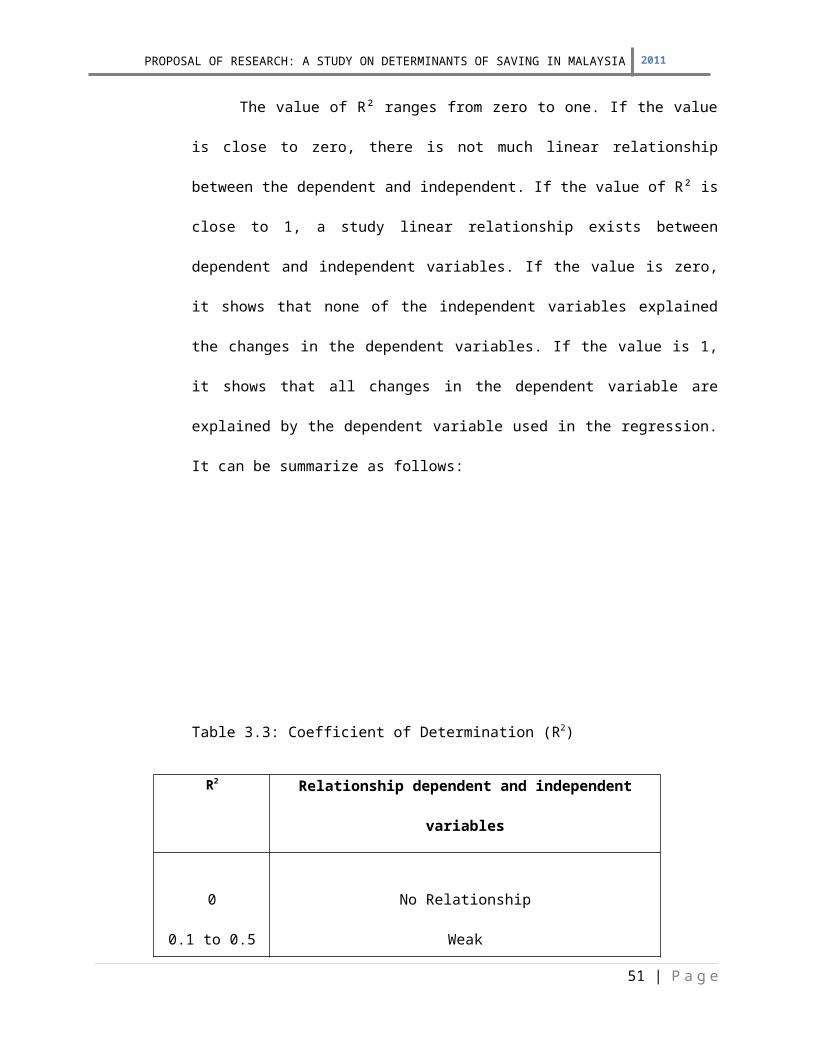

The value of R² ranges from zero to one. If the value

is close to zero, there is not much linear relationship

between the dependent and independent. If the value of R² is

close to 1, a study linear relationship exists between

dependent and independent variables. If the value is zero,

it shows that none of the independent variables explained

the changes in the dependent variables. If the value is 1,

it shows that all changes in the dependent variable are

explained by the dependent variable used in the regression.

It can be summarize as follows:

Table 3.3: Coefficient of Determination (R2)

R2 Relationship dependent and independent

variables

0

0.1 to 0.5

No Relationship

Weak

51 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

0.6 to 0.99

1

Strong

Perfectly explained

Sources: Gujarati (2009),Basic Econometric

3.3.5 Hypothesis Testing

Hypothesis testing means of testing if the if-then statement

generated from the theoretical framework hold true when subjected

to rigorous examination (Sekaran, 2003). It also means procedure

which enable researcher to decide whether to accept or reject

hypothesis.

3.3.5.1 Hypothesis Testing with T-Statistic

T-Statistic or T- calculated will be used to test the

null hypothesis, whether there is significant relationship

between the dependent and independent variables. In order to

test the significant of T-Statistics, the comparison between

the absolute value of the T-Statistics to the tabulated

value of T-critical table with degree of freedom (df) will

be done and normally at 5% level of significant (95% of

confidence interval).

The formula used is as follows:

df = n-k-1

52 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

Where,

df = degree of freedom (from output regression)

n = no of observation

k = no of independent variable

Therefore, the decision rule is:

At 95%, confidence interval;

T-statistics > t-critical value, reject H0 and

accept H1.

T-statistics < t-critical value, reject H1 and

accept H0.

If the numerical value of the statistics is greater

than the critical value of T or less than –t, it is fall in

the rejection region, where the null hypothesis is rejected

and the alternate hypothesis is accepted.

3.3.5.2 Hypothesis with F-Statistic

The study use F-Statistic in order to know how

reliable the overall model. F-Statistics provides an overall

appraisal of the regression equation appeased to evaluating

the significant of each individual component of the entire

53 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

regression model. Besides that, f-statistic is whether a

significant proportion of total variation independent is

explained by the estimated regression equation. If

calculated F-Statistics more than critical value of F, the

regression equation is significant to explain the changes in

dependent variable.

• If calculated F-statistics > 5%, there is a

significant relationship between independent variable

and dependent variable.

• If calculated F-statistics < 5%, the model is not

valid for forecasting.

In the determination of rejection region of F-

Statistics, the one tail used in order to determine the

significant of the combination among the variables. Through

one tail test, it will explain the direction of relationship

between both independent variable and dependent variable. It

is computed as the ratio of two samples variance if the F-

Statistics is bigger than the critical value of F; the

regression equation is significant to explain the change in

dependent variable.

54 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

The formula of F-Statistics defined as follows:

F = [ R² / k ] / [ ( 1 - R² ) / (n - k – 1 ) ]

Whereby;

F = F-statistics

R² = Coefficient of Determination

n = no of observation

k = no of variable

Otherwise, the critical value of F defined as follows:

F = α (k – 1, n – k – 1)

Where,

α = Significant level at 0.05

k = no of variable

n = no of observation

3.4 SUMMARY FOR CHAPTER 4 AND CHAPTER 5

For the next two chapters, researcher will discuss more

details for this study. In chapter 4, researcher will discuss

55 | P a g e

PROPOSAL OF RESEARCH: A STUDY ON DETERMINANTS OF SAVING IN MALAYSIA 2011

about the result from the data collected. In this section,

researcher will clearly explain the result based on the procedure

for data analysis in chapter 3. Researcher will discuss the

relationship between dependent variable and independent variable

based on this study. Furthermore, in chapter 5, researcher will

make conclusion based on the finding in chapter 4. After that

researcher will provides some recommendations based on this

study. Finally, researcher will make overall conclusion for this

study.

56 | P a g e