payment systems and cash management implications

TRANSCRIPT

Payment systems and cash management implications

Nicola Coyne Head of Immediate Payments,Barclays Corporate Banking

2 | Payment systems and cash management implications | 25 February 2020

• Cash & digital payments in the new economy

• Real-time payments

• Request to Pay

• The changing regulatory landscape

Agenda

3 | Payment systems and cash management implications | 25 February 2020

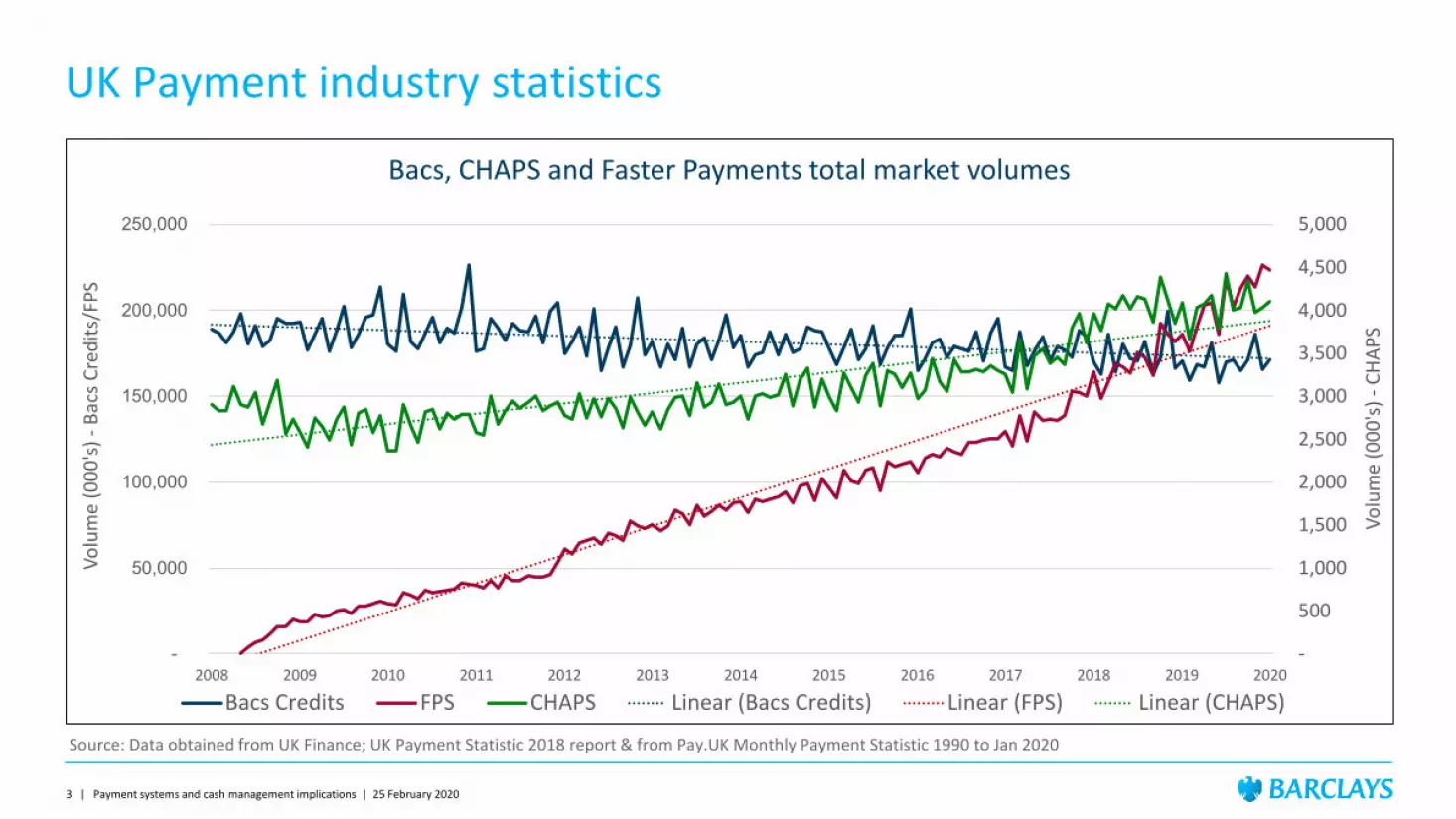

UK Payment industry statistics

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

-

50,000

100,000

150,000

200,000

250,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Volu

me

(000

's) -

CHAP

S

Volu

me

(000

's) -

Bacs

Cre

dits

/FPS

Bacs, CHAPS and Faster Payments total market volumes

Bacs Credits FPS CHAPS Linear (Bacs Credits) Linear (FPS) Linear (CHAPS)

Source: Data obtained from UK Finance; UK Payment Statistic 2018 report & from Pay.UK Monthly Payment Statistic 1990 to Jan 2020

4 | Payment systems and cash management implications | 25 February 2020

UK Payment industry statistics

Data obtained from UK Finance; UK Payment Statistic 2018 report & from Pay.UK Monthly Payment Statistic 1990 to Jan 2020

£-

£1,000,000

£2,000,000

£3,000,000

£4,000,000

£5,000,000

£6,000,000

£7,000,000

£8,000,000

£9,000,000

£-

£50,000

£100,000

£150,000

£200,000

£250,000

£300,000

£350,000

£400,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Valu

e in

£m

-CH

APS

Valu

e in

£m

-Ba

cs C

redi

ts/F

PS

Bacs, CHAPS and Faster Payments total market values

Bacs Credits FPS CHAPS Linear (Bacs Credits) Linear (FPS) Linear (CHAPS)

5 | Payment systems and cash management implications | 25 February 2020

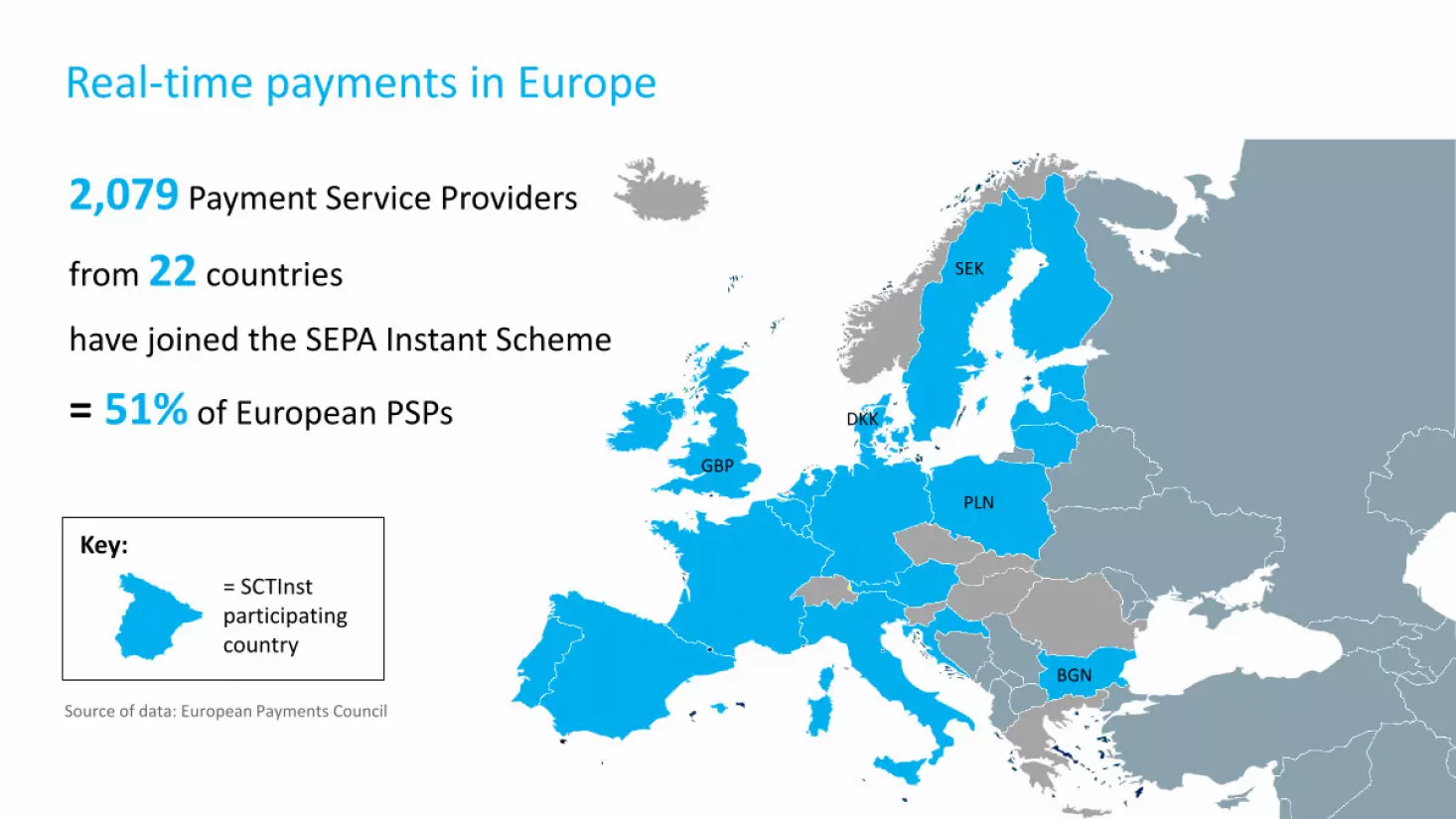

Real-time payments in Europe

SEK

PLN

GBP

BGN

DKK

2,079 Payment Service Providers

from 22 countries

have joined the SEPA Instant Scheme

= 51% of European PSPs

= SCTInst participating country

Key:

Source of data: European Payments Council

6 | Payment systems and cash management implications | 25 February 2020

SEPA vs FPS initial take-up

0.08%0.64%

1.02%

2.83%

4.39%

5.53%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Q12018

Q22018

Q32019

Q42018

Q12019

Q22019

Q32020

Q42019

SCT INST volumes as a % of total CT* volumes

0.00%

0.01%0.01%

0.01%0.02%

0.02%

0.00%0.00%0.00%0.01%0.01%0.01%0.01%0.01%0.02%0.02%0.02%

Q32008

Q42008

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

FPS volumes as a % of total CT** volumes

Source: European Payments Council. *total CT volumes are SCT+SCT Inst

Source: UK Finance; UK Payment Statistic 2018 report and Pay.UK Monthly Payment Statistic 1990 to Jan 2020** total CT volumes are BACS + FPS

7 | Payment systems and cash management implications | 25 February 2020

What is Request to Pay?

Payer = Authorising PartyPayee = Initiating Party

BeneficiaryPSP

PayerPSP

2. Request for payment

7. Payment sent

5. Approve response

1. 8. 4. 3. 6.

R2P system

Request payment

Funds received

Request authorisation

Approve to pay

8 | Payment systems and cash management implications | 25 February 2020

How might Request to Pay be used by your business?

Fully electronic invoicing – Efficient reconciliation of credits -reduced processing fees for Corporates

Invoicing

9 | Payment systems and cash management implications | 25 February 2020

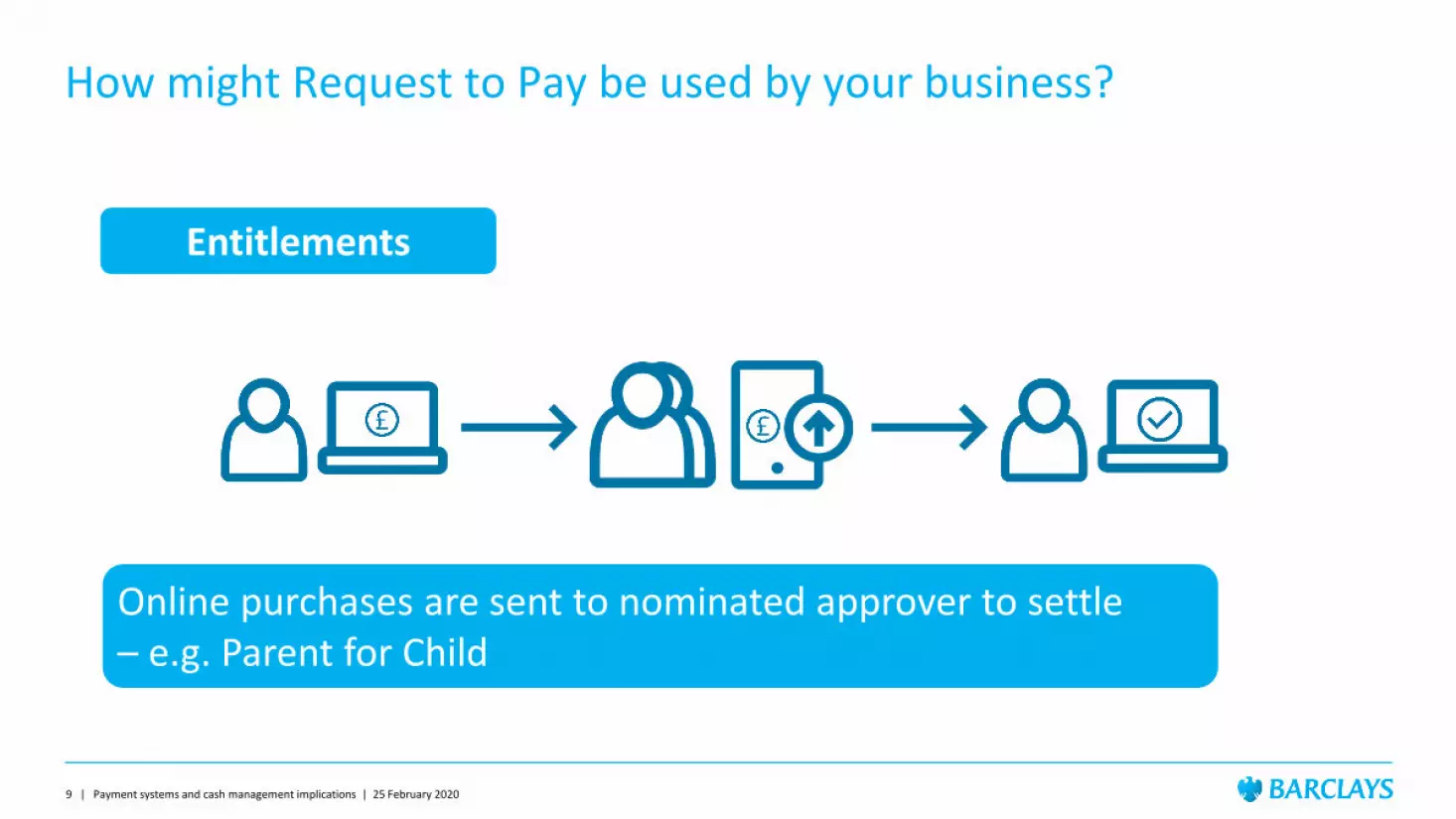

How might Request to Pay be used by your business?

Online purchases are sent to nominated approver to settle – e.g. Parent for Child

Entitlements

10 | Payment systems and cash management implications | 25 February 2020

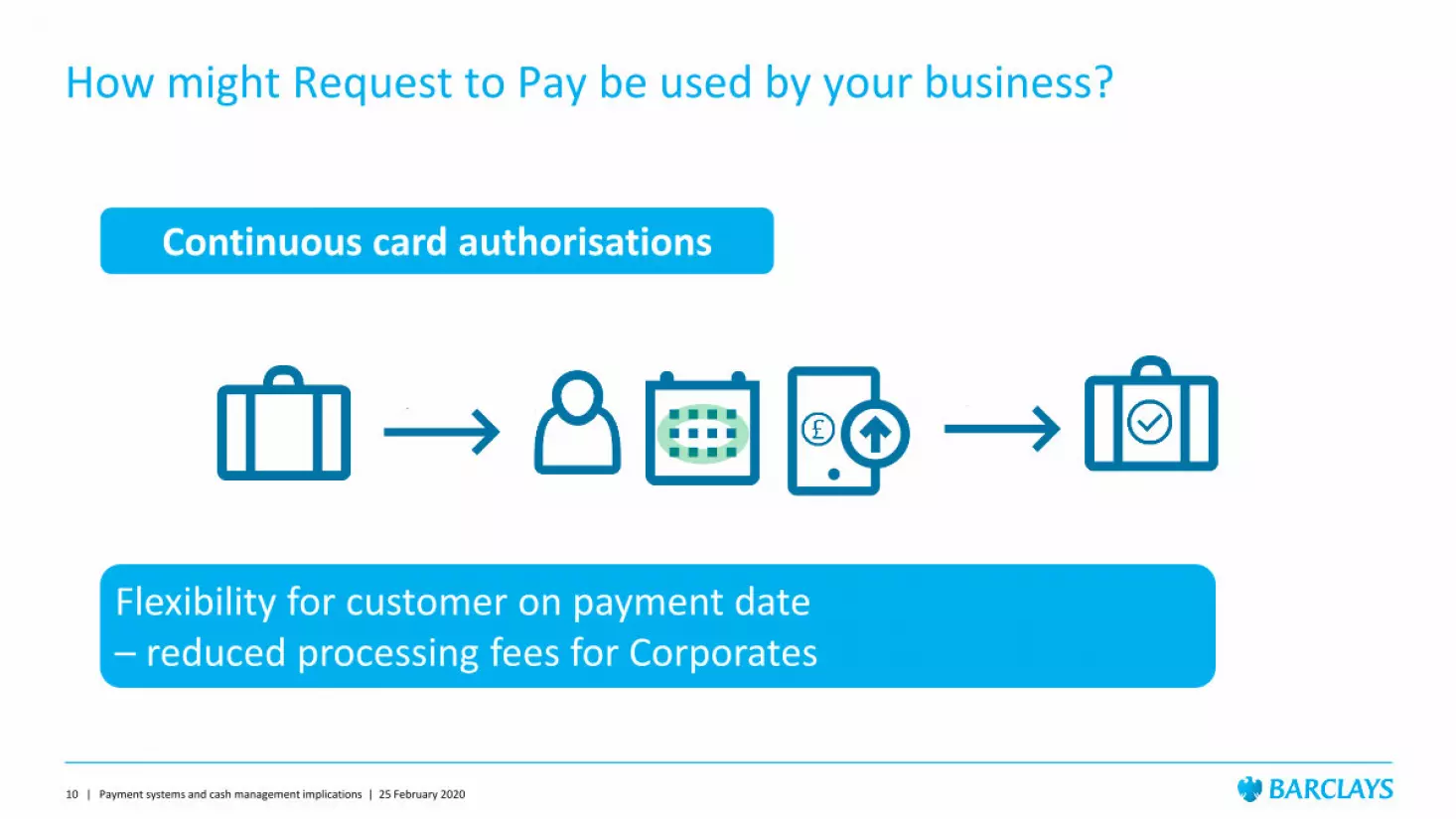

How might Request to Pay be used by your business?

Flexibility for customer on payment date – reduced processing fees for Corporates

Continuous card authorisations

11 | Payment systems and cash management implications | 25 February 2020

Plethora of Regulation

e.g. PSD2, FTR, CoP, Basel III, ISO20022 and Brexit

• How do these Regulations impact cash management?

• Brexit – Does it change anything?

– Euro wires

– SEPA

The changing regulatory landscape

12 | Payment systems and cash management implications | 25 February 2020

“No-deal” BrexitPost December 31st, if no deal is agreed then the UK will be deemed to have left the EU and the EEA. If that is the case then the possible charging options for a payment from the UK to Europe will be OUR/BEN/SHA (for PSD2 purposes, the UK will then be a ‘one-leg out’ country). SEPA may provide a cost-effective alternative.

Wire Transfers from the UK to the EU

OUR = remitter pays all charges BEN = beneficiary pays all charges SHA = remitter pays remitter bank charges & beneficiary pays their bank charges, ODC = Overseas delivery charge

EU hubPrincipal amount

Charge Amount

OUR €10,000

SHA €10,000

BEN €10,000

Sending feeCharge Amount Deduction

OUR £XX + ODC N/A

SHA £XX N/A

BEN A. Paid by bene

Intermediary feeCharge Amount Deduction

OUR Paid by UK bank

SHA B. Paid by bene

BEN B. Paid by bene

Fee

Charge Amount Deduction

OUR Paid by UK bank

SHA C. Paid by bene BEN C. Paid by bene

Beneficiary receives

Charge Amount

OUR €10,000

SHA €10,000 minus charges(B+C)BEN €10,000 minus charges(A+B+C)

SenderSending fee:

£XXFee:€XX+ Beneficiary

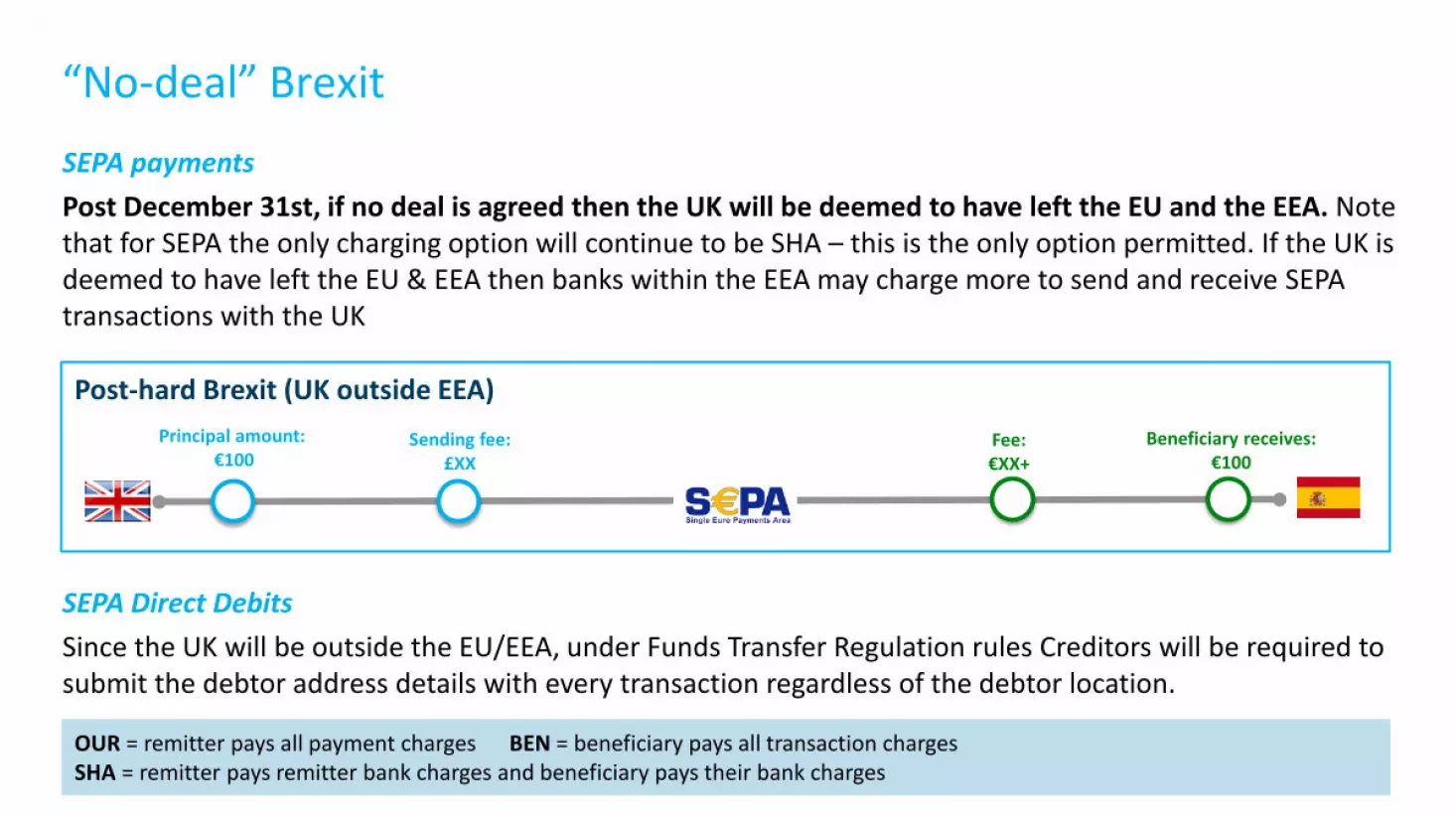

Post-hard Brexit (UK outside EEA)

13 | Payment systems and cash management implications | 25 February 2020

SEPA paymentsPost December 31st, if no deal is agreed then the UK will be deemed to have left the EU and the EEA. Note that for SEPA the only charging option will continue to be SHA – this is the only option permitted. If the UK is deemed to have left the EU & EEA then banks within the EEA may charge more to send and receive SEPA transactions with the UK

SEPA Direct DebitsSince the UK will be outside the EU/EEA, under Funds Transfer Regulation rules Creditors will be required to submit the debtor address details with every transaction regardless of the debtor location.

“No-deal” Brexit

OUR = remitter pays all payment charges BEN = beneficiary pays all transaction charges SHA = remitter pays remitter bank charges and beneficiary pays their bank charges

Post-hard Brexit (UK outside EEA)Principal amount:

€100Sending fee:

£XXBeneficiary receives:

€100Fee:€XX+

14 | Payment systems and cash management implications | 25 February 2020

Questions?

15 | Payment systems and cash management implications | 25 February 2020

Barclays offers corporate banking products and services to its clients through Barclays Bank PLC. This presentation has been prepared by Barclays Bank PLC ("Barclays"). This presentation is for discussion purposes only, and shall not constitute any offer to sell or the solicitation of any offer to buy any security, provide any underwriting commitment, or make any offer of financing on the part of Barclays, nor is it intended to give rise to any legal relationship between Barclays and you or any other person, nor is it a recommendation to buy any securities or enter into any transaction or financing. Customers must consult their own regulatory, legal, tax, accounting and other advisers prior to making a determination as to whether to purchase any product, enter into any transaction of financing or invest in any securities to which this presentation relates. Any pricing in this presentation is indicative. Although the statements of fact in this presentation have been obtained from and are based upon sources that Barclays believes to be reliable, Barclays does not guarantee their accuracy or completeness. All opinions and estimates included in this presentation constitute the Barclays’ judgment as of the date of this presentation and are subject to change without notice. Any modelling or back testing data contained in this presentation is not intended to be a statement as to future performance. Past performance is no guarantee of future returns. No representation is made by Barclays as to the reasonableness of the assumptions made within or the accuracy or completeness of any models contained herein.

Neither Barclays, nor any officer or employee thereof, accepts any liability whatsoever for any direct or consequential losses arising from any use of this presentation or the information contained herein, or out of the use of or reliance on any information or data set out herein.

Barclays and its respective officers, directors, partners and employees, including persons involved in the preparation or issuance of this presentation, may from time to time act as manager, co-manager or underwriter of a public offering or otherwise deal in, hold or act as market-makers or advisers, brokers or commercial and/or investment bankers in relation to any securities or related derivatives which are identical or similar to any securities or derivatives referred to in this presentation.

Copyright in this presentation is owned by Barclays (© Barclays Bank PLC, 2020). No part of this presentation may be reproduced in any manner without the prior written permission of Barclays.

Barclays Bank PLC is a member of the London Stock Exchange.

Barclays Bank PLC is registered in England (Company No. 1026167) with its registered office at 1 Churchill Place, London E14 5HP. Barclays Bank PLC is authorised by the Prudential Regulation Authority, and regulated by the Financial Conduct Authority (Financial Services Register No. 122702) and the Prudential Regulation Authority. Barclays is a trading name and trade mark of Barclays PLC and its subsidiaries.

Disclaimer