mobility implication on beverage industry

TRANSCRIPT

TRENDS IN MOBILE TECHNOLOGY AND IT’S IMPACT ON SALES FORCEAUTOMATION STRATEGY FOR A BEVERAGE COMPANY IN VIETNAM

A Research Project

Submitted to the Faculty of the

Manchester Business School

In partial fulfillment of the requirements

For the degree of

Master of Business Administration

By

Sunil Singh,

Student No 7630509

March 2013

ii

© Copyright, Sunil Singh 2013

All rights reserved

iii

I certify that I have read this manuscript and that, in my judgment, it is fully adequate in scope and quality as a research project for the degree of Master of Business Administration

__________________________________ ____________Dr. Shelen Ho March 2013Project Supervisor

iv

ACKNOWLEDGMENTS

Head of IT, ABC Indochina

Director Sales, ABC Vietnam

CEO, Nokia Vietnam,

Director, Visa Money, Visa Singapore

Research Analyst, Nielson Vietnam

My project Supervisor

& my family

v

ABSTRACT

This article addresses the two research questions, what is

the level of sales force automation across ABC bottlers in

Indochina Region and how is it correlated to market size,

market complexity and Sales Performance? What are key trends

in mobility technology and how these trends are expected to

impact sales processes for ABC in Vietnam market? It deals

with the understanding current sales force automation

implementation at a beverage global company and understands

impacts of mobility technology trends on its sales processes

in a key market in Indochina region. It highlights current

research in this area and identifies the research gap for

the further researches. This research paper will provide

information about the mobility trends and its implications

to the beverage company in Vietnam and will show a path for

future research in the area of sales force automation

implementation, which is the gaining significant importance

in executing customer relationship strategy. vi

Keywords: Sales force Automation, customer relationship

management strategy, Beverage industry

vii

TABLE OF CONTENTS

Acknowledgments..........................................iv

Abstract..................................................v

Table of Contents........................................vi

List of Tables..........................................vii

List of Figures........................................viii

[C & t Chapter I: Chapter Title, Use upper and lower case] 1

[C & t Chapter II: Chapter Title, Use upper and lower case]..........................................................2

[C & t Chapter III: Chapter Title, Use upper and lower case]..........................................................3

[C & t Chapter IV: Chapter Title, Use upper and lower case]..........................................................4

[C & t Chapter V: Chapter Title, Use upper and lower case] 5

References................................................6

[Click and type Appendix A: Appendix Title, use upper/lower]..........................................................7

[Click and type Appendix B: Appendix Title, use upper/lower]..........................................................9

viii

LIST OF TABLES

Chapter 3: Research MethodologyTable

3.1

Research Plan

Table

3.2

Research Questionaire A

Table

3.3

Research Questionaire B

Table

3.4

Research Questionaire C

Table

3.5

Research Questionaire D

ix

LIST OF FIGURES

Chapter 1: IntroductionFigure

1.1

Trends on which category has biggest opportunity in future (Source: Euromonitor 2012)

Figure

1.2

How ABC reaches its customers (Source: Company Intranet)

Figure

1.3

Category Share growth across different market type (Source: Euromonitor 2012)

Figure

1.4

Per Capita Consumption of Soft Drink (Source: Euromonitor 2012)

Figure

1.5

ABC’s product availability across total outlet universe in India (Source: Company SharePoint/Neilson Survey, 2011)

Figure

1.6

ABC Primary Value Chain

Chaper-2: Literature ReviewFigure

2.1

Is Mobile the new face of engagement? (Source: ForresterResearch 2012)

Figure

2.2

Is Mobile the new face of engagement? (Source: ForresterResearch 2012)

Figure

2.3

Transforming Sales and Service (Source: Mckinsey Quarterly Report, 2005 No.4)

Figure

2.4

Transforming Sales and Service (Source: Mckinsey Quarterly Report, 2005 No.4)

Figure

2.5

ABC India Distribution Model (Source: Company Intranet)

Figure

2.6

Mapping ABC’s Selling Activities (Adapted based on Moncrief’s classification of sales work)

Figure

2.7

Michael Porter’s Five Industry Forces Analysis

Figure

2.8

CRM Strategy Matrix (Source: Payne & Frow 2005)

Figu 2. Boston Consulting Group (BCG) Growth Share Matrix

x

re 9 (Source: Internet)Figure

2.10

Customized Model – Business Complexity vs. Market Size

Figure

2.11

Adapted from CRM Strategic Framework (Payne and Frow 2005)

Figure

2.12

Adapted from setting agenda for Sales Transformation (David Cravens, 1995)Chapter 4: Research Analysis

Figure

4.1

Which operation has SFA implemented? Source: Response Questionnaire A

Figure

4.2

Primary Focus for SFA Benefits? Source: Response Questionnaire A

Figure

4.3

SFA Solution functional Complexity? Source: Response Questionnaire A

Figure

4.4

SFA Solution scope - % Customers Covered? Source: Response Questionnaire A

Figure

4.5

BCG Matrix 2009 (Source: Response Questionnaire B)

Figure

4.6

BCG Matrix 2012 (Source: Response Questionnaire B)

Figure

4.7

Porter Five Forces for ABC Vietnam (Source: Response Questionnaire C)

Figure

4.8

CRM Strategic Matrix -ABC Vietnam 2012 (Source: ResponseQuestionnaire C)

Figure

4.9

CRM Strategic Matrix – ABC Vietnam 2018 (Source: Response Questionnaire C)

xi

12

[C & T CHAPTER I: CHAPTER TITLE, USE UPPER AND LOWER CASE]

[Click and type Text (Body Text style), Use styles for

more headings]

13

[C & T CHAPTER II: CHAPTER TITLE, USE UPPER AND LOWER CASE]

[Click and type Text (Body Text style), Use styles for

more headings]

14

[C & T CHAPTER III: CHAPTER TITLE, USE UPPER AND LOWER CASE]

[Click and type Text (Body Text style), Use styles for

more headings]

15

[C & T CHAPTER IV: CHAPTER TITLE, USE UPPER AND LOWER CASE]

[Click and type Text (Body Text style), Use styles for

more headings]

16

[C & T CHAPTER V: CHAPTER TITLE, USE UPPER AND LOWER CASE]

[Click and type Text (Body Text style), Use styles for

more headings]

17

REFERENCES

Chapter 1

1. Gebauer, J., & Shaw, M. J. (2004). “Success Factors and

Impacts of Mobile Business Applications: Results from a

Mobile e- Procurement Study.” International Journal of

Electronic Commerce, 8(3), 19-41.

2. Nah, F., Siau, K., & Sheng, H. (2005). “The VALUE of Mobile

Applications: A Utility Company Study” Communications of the

ACM, 48(2), 85-90.

3. “Soft Drinks 2010 Trends and Future Directions” (2011, 01).

Retrieved 07, 2012, from WWW.EUROMONITOR.COM

4. “How ABC reaches its customers”, Retrieved 07, 2012, from

WWW.HCCBPL.IN

18

5. KO Analyst Report. Retrieved 08, 2012, (2010, 12). from

WWW.NYSE.COM

6. Beverage Industry Research. Retrieved 08, 2012, (2010, 12).

from WWW.VALUELINE.COM

7. Company Financial Report. Retrieved 08, 2012, from www.coca-

cola.com

8. “ABC’s product availability across total outlet universe in

India”. Retrieved 08, 2012, from www.nielson.com

9. ABC’s Financial Report 10K SEC Filing. Retrieved 08, 2012,

from www.abc.com

Chapter 2

10. Kotler, P. (1994), “Marketing Management, Analysis, Planning,

Implementation, and Control” Prentice-Hall, Englewood Cliffs,

NJ.

19

11. Baumgartner, T., John, R.H. & Naucler, T. (2005)

“Transforming Sales and Service”, Mckinsey Quarterly, No. 4,

pp. 80-91.

12. Ted Schadler and John C. McCarthy (2012) “Mobile Is The New

Face Of Engagement”, Forrester Research, pp. 3-10

13. Geoffrey Moore (2011), “Systems of Engagement and the Future

of Enterprise IT”, AIIM Whitepaper, pp. 5-15

14. Basole, R.C. and DeMillo, R.A., “Enterprise IT and

Transformation”, Chapter 11 in W.B. Rouse (Ed.) Enterprise

Transformation: Understanding and Enabling Fundamental

Change, John Wiley (2006), New York

15. Mikko Lipasti and Tapio Schrey (2007) “MOBILE SOLUTIONS IN

BUSINESS PROCESSES” Publications in Telecommunications

Software and Multimedia, pp. 74-78

20

16. Newell F. and Seth Godin (2003), “Why CRM Doesn’t Work: How

to win by letting customers Manage the relationship” New

York: Bloomberg Press

17. “BUILDING A MOBILITY STRATEGY - Seven Insights to Promote

Workforce Productivity and Minimize Risk ” Retrieved 08,

2012, from www.executiveboard.com/IT

18. B. Joseph Pine II, James H. Gilmore (1999), “The Experience

Economy: Work Is Theatre & Every Business a Stage” Harvard

Business Press, 2011

19. Kerin, Roger, Hartley, Steven, Rudelius, William. Marketing.

Irwin/McGraw-Hill, 2009

20. William C Moncrief, “Selling activity and sales position

taxonomies for industrial Sales forces”, Journal of Marketing

Research, Volume 23, August 1986, pages 261 - 270.

21. Porter, M.E. (2008) "The Five Competitive Forces That Shape

Strategy", Harvard Business Review, January 2008, pp. 79–93

22. Roberts, M., Liu, R. Hazard, K. (2005) “Strategy,

Technology, and Organizational Alignment: Key Components of

21

CRM Success.” Database Marketing & Customer Strategy

Management, pp. 315-326

23. Payne A. & Frow P. (2005), “A strategic Framework for CRM”

Journal of Marketing, Vol. 69, No. 4, pp. 167-176

24. Payne A. & Frow P. (2006), “Customer Relationship

Management. From Strategy to implementation” Journal of

Marketing, Vol. 22, pp. 135-168

25. BCG Growth Share Matrix, Retrieved on 8th September 2012 from

http://en.wikipedia.org/wiki/Growth-share_matrix

26. Jagdish N Sheth, “The Future of Relationship Marketing”,

Journal of Services Marketing, Volume 16, Number 7, 2002,

pages 590 – 592

27. Bill Donaldson, “Sales Management, Principles, Process and

Practice, 3rd Edition”

28. William C Moncrief, “Selling activity and sales position

taxonomies for industrial salesforces”, Journal of Marketing

Research, Volume 23, August 1986, pages 261 - 270.

22

29. David W Cravens, “The changing role of the salesforce”,

Marketing Management, Volume 4, Number 2, Fall 1995, pages 49

- 57.

Chapter 3

30. Maykut, P., & Morehouse, R. (1994). The qualitative posture:

Indwelling. In Beginning qualitative research: A philosophic

and practical guide (pp.n25–40) London: Falmer Press.

31. Denzin, NK & Lincoln, YS. (1994). "Introduction: Entering the

field of qualitative research." In NK Denzin and YS Lincoln

(Eds.) Handbook of Qualitative Research pp. 1-17 Thousand

Oaks: Sage Publications.

32. David Silverman (1993). “Beginning Research”. Interpreting

Qualitative Data. Methods for Analysing Talk, Text and

Interaction. Londres: Sage Publications.

33. Guba, E. G., & Lincoln, Y. S. (1994). Competing paradigms in

qualitative research. In N. K. Denzin & Y. S. Lincoln (Eds.),

Handbook of qualitative research (pp. 105-117). London: Sage.

23

34. Bryman, A. (2004). Social Research Methods (2 ed.). Oxford:

Oxford University Press.

35. Bryman, A. (2004) ‘Triangulation’, in M. Lewis-Beck, A.

Bryman, and T. F. Liao (eds.) Encyclopedia of Social Science

Research Methods, Thousand Oaks, Sage.

36. Rindfleisch, Aric and Christine Moorman (2001), “The

Acquisition and Utilization of Information in New Product

Alliances: A Strength-of-Ties Perspective,” Journal of

Marketing, 65 (April), 1–18.

37. Jap, Sandy D. (1999), “Pie-Expansion Efforts: Collaboration

Processes in Buyer-Supplier Relationships,” Journal of

Marketing Research, 36 (November), 461-475.

38. Erin Anderson (2004), “Challenges and Advances in Marketing

Strategy Field Research,” in Assessing Marketing Strategy

Performance. Christine Moorman and Donald R. Lehmann, eds.

Cambridge, MA: Marketing Science Institute, 269-292.

39. Ostroff, Cheri, Angelo J. Kinicki, and Mark A. Clark (2002),

“Substantive and Operational Issues of Response Bias Across

24

Levels of Analysis: An Example of Climate-Satisfaction

Relationships,” Journal of Applied Psychology, 87 (2), 355-

368.

40. Podsakoff, Philip M. and Dennis Organ (1986), “Self-Reports

in Organizational Research: Problems and Prospects,” Journal

of Management, 12 (4), 531-544.

41. Van Bruggen, Gerrit, Gary Lilien, and Manish Kacker (2002),

“Informants in Organizational Marketing Research: Why Use

Multiple Informants and How to Aggregate Responses,” Journal

of Marketing Research, 39 (November), 469-478.

42. Adèr, H.J. (2008). Chapter 14: Phases and initial steps in

data analysis. In H.J. Adèr & G.J. Mellenbergh (Eds.) (with

contributions by D.J. Hand), Advising on Research Methods: A

consultant's companion (pp. 333–356). Huizen, the

Netherlands: Johannes van Kessel Publishing.

Chapter 4

43. Porter, M.E. (2008) "The Five Competitive Forces That Shape

Strategy", Harvard Business Review, January 2008, pp. 79–93

25

44. “Soft Drinks in Vietnam Trends and Future Directions” (2013,

01). Retrieved 01, 2013, from www.euromonitor.com

Chapter 5

45. Newell F. and Seth Godin (2003), “Why CRM Doesn’t Work: How

to win by letting customers Manage the relationship” New

York: Bloomberg Press

46. Porter, M.E. (2008) "The Five Competitive Forces That Shape

Strategy", Harvard Business Review, January 2008, pp. 79–93

47. Mikko Lipasti and Tapio Schrey (2007) “MOBILE SOLUTIONS IN

BUSINESS PROCESSES” Publications in Telecommunications

Software and Multimedia, pp. 74-78

48. B. Joseph Pine II, James H. Gilmore (1999), “The Experience

Economy: Work Is Theatre & Every Business a Stage” Harvard

Business Press, 2011

49. Basole, R.C. and DeMillo, R.A., “Enterprise IT and

Transformation”, Chapter 11 in W.B. Rouse (Ed.) Enterprise

Transformation: Understanding and Enabling Fundamental

Change, John Wiley (2006), New York

26

50. Kerin, Roger, Hartley, Steven, Rudelius, William. Marketing.

Irwin/McGraw-Hill, 2009

27

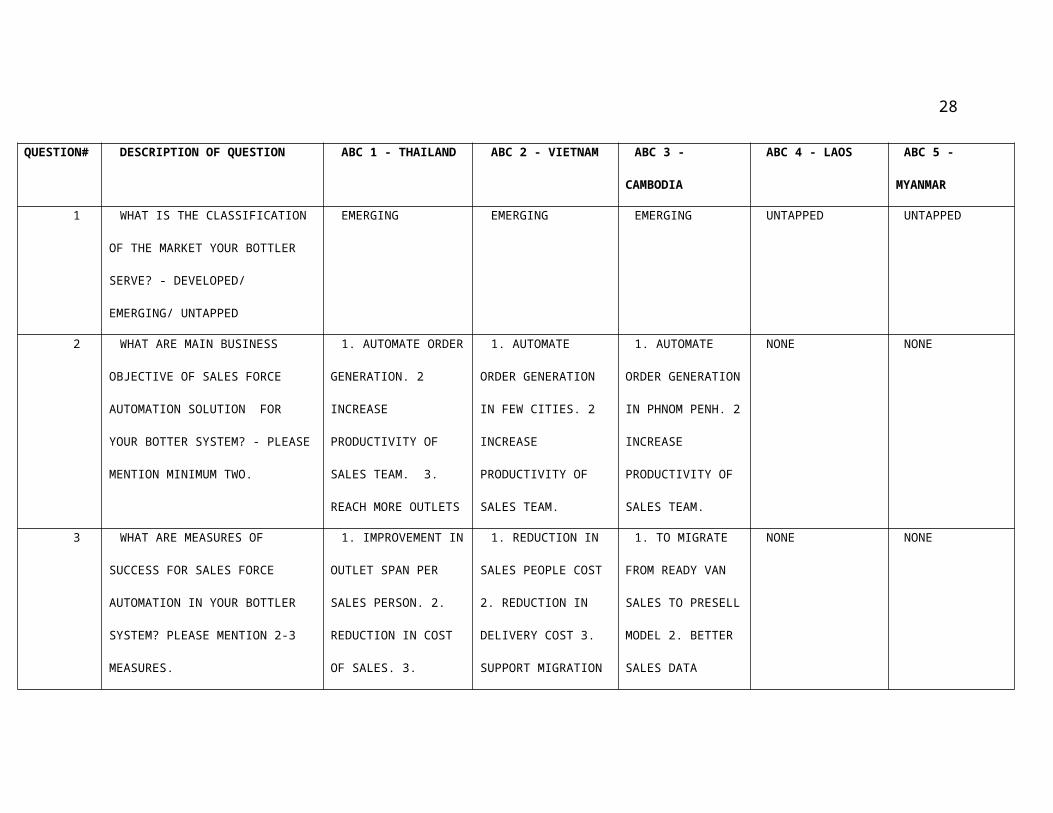

APPENDIX A: SURVEY RESPONSES – QUESTIONAIRE A-D

28

QUESTION# DESCRIPTION OF QUESTION ABC 1 - THAILAND ABC 2 - VIETNAM ABC 3 -

CAMBODIA

ABC 4 - LAOS ABC 5 -

MYANMAR

1 WHAT IS THE CLASSIFICATION

OF THE MARKET YOUR BOTTLER

SERVE? - DEVELOPED/

EMERGING/ UNTAPPED

EMERGING EMERGING EMERGING UNTAPPED UNTAPPED

2 WHAT ARE MAIN BUSINESS

OBJECTIVE OF SALES FORCE

AUTOMATION SOLUTION FOR

YOUR BOTTER SYSTEM? - PLEASE

MENTION MINIMUM TWO.

1. AUTOMATE ORDER

GENERATION. 2

INCREASE

PRODUCTIVITY OF

SALES TEAM. 3.

REACH MORE OUTLETS

1. AUTOMATE

ORDER GENERATION

IN FEW CITIES. 2

INCREASE

PRODUCTIVITY OF

SALES TEAM.

1. AUTOMATE

ORDER GENERATION

IN PHNOM PENH. 2

INCREASE

PRODUCTIVITY OF

SALES TEAM.

NONE NONE

3 WHAT ARE MEASURES OF

SUCCESS FOR SALES FORCE

AUTOMATION IN YOUR BOTTLER

SYSTEM? PLEASE MENTION 2-3

MEASURES.

1. IMPROVEMENT IN

OUTLET SPAN PER

SALES PERSON. 2.

REDUCTION IN COST

OF SALES. 3.

1. REDUCTION IN

SALES PEOPLE COST

2. REDUCTION IN

DELIVERY COST 3.

SUPPORT MIGRATION

1. TO MIGRATE

FROM READY VAN

SALES TO PRESELL

MODEL 2. BETTER

SALES DATA

NONE NONE

29

REDUCTION IN SALES

TEAM TURNOVER

FROM CONVENTION

SALES TO PRESELL

STRATEGY

VISIBILITY

4 MENTION 2-3 PROCESSES THAT

YOU WILL INCLUDE IN THE

SALES FORCE AUTOMATION

SOLUTION OVER 2-3 YEARS?

1. COOLER

TRACKING 2. OUTLET

EXECUTION SURVEY

3.KPI FOR SALES

TEAM

1. PARTIAL CASE

ORDER 2. PROMOTION

BY SALES CHANNEL

3. COOLER SCANNING

(RFID)

1. PARTIAL CASE

ORDER 2.

PROMOTION BY

SALES CHANNEL 3.

COOLER SCANNING

(RFID)

PLAN TO

IMPLEMENT

AUTOMATION OF

ORDER GENERATION

IN 2013

PLAN TO

IMPLEMENT

AUTOMATION OF

ORDER

GENERATION IN

2013

5 HOW MUCH % OF YOUR TOTAL

SALES PEOPLE ARE USING SALES

FORCE AUTOMATION SOLUTION?

50% 10% 3% 0 0

6 HOW MANY PRODUCTION

FACILITIES DO YOU MANAGE

WITHIN YOUR BOTTLER SYSTEM?

14 3 1 0 2

7 HOW MANY DISTRIBUTION

CENTERS DO YOU MANAGE WITHIN

36 6 2 1 13

30

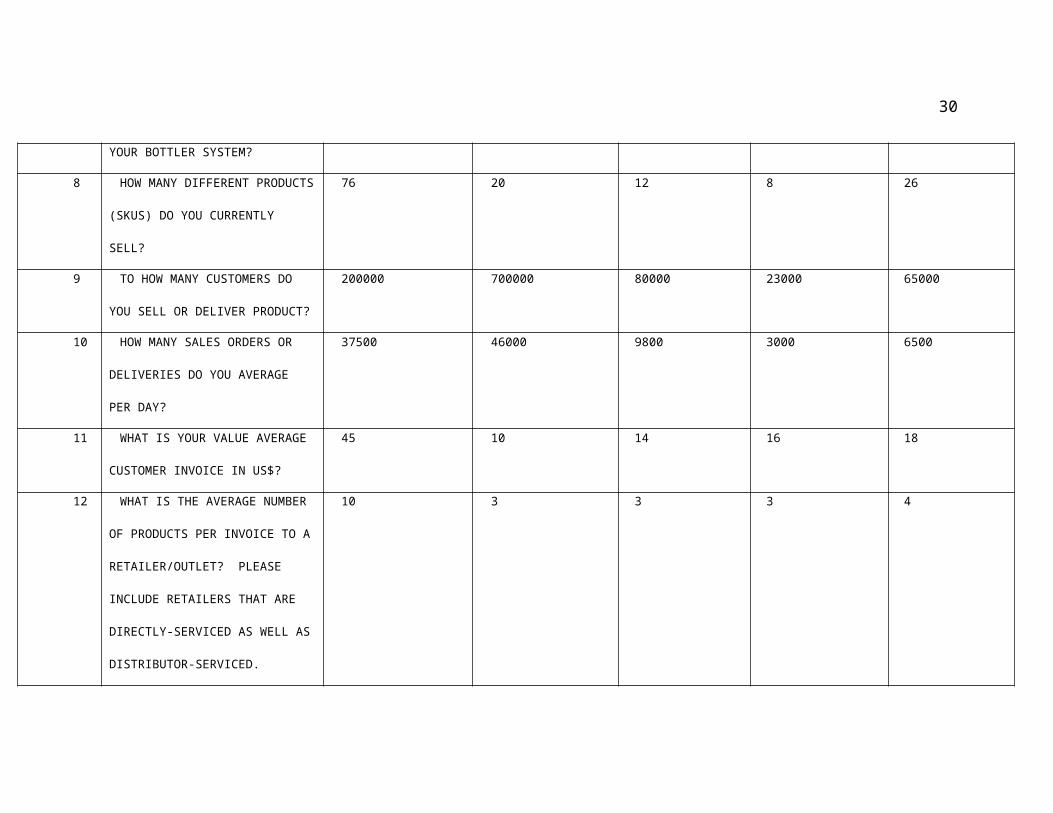

YOUR BOTTLER SYSTEM?

8 HOW MANY DIFFERENT PRODUCTS

(SKUS) DO YOU CURRENTLY

SELL?

76 20 12 8 26

9 TO HOW MANY CUSTOMERS DO

YOU SELL OR DELIVER PRODUCT?

200000 700000 80000 23000 65000

10 HOW MANY SALES ORDERS OR

DELIVERIES DO YOU AVERAGE

PER DAY?

37500 46000 9800 3000 6500

11 WHAT IS YOUR VALUE AVERAGE

CUSTOMER INVOICE IN US$?

45 10 14 16 18

12 WHAT IS THE AVERAGE NUMBER

OF PRODUCTS PER INVOICE TO A

RETAILER/OUTLET? PLEASE

INCLUDE RETAILERS THAT ARE

DIRECTLY-SERVICED AS WELL AS

DISTRIBUTOR-SERVICED.

10 3 3 3 4

31

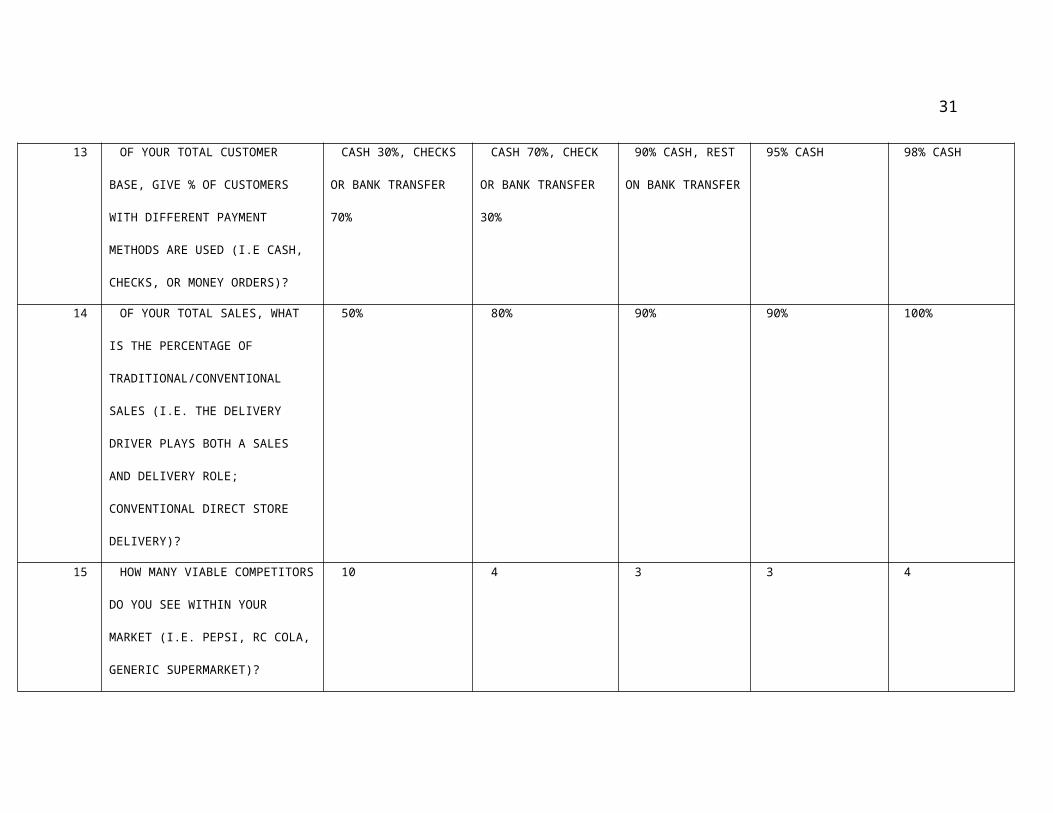

13 OF YOUR TOTAL CUSTOMER

BASE, GIVE % OF CUSTOMERS

WITH DIFFERENT PAYMENT

METHODS ARE USED (I.E CASH,

CHECKS, OR MONEY ORDERS)?

CASH 30%, CHECKS

OR BANK TRANSFER

70%

CASH 70%, CHECK

OR BANK TRANSFER

30%

90% CASH, REST

ON BANK TRANSFER

95% CASH 98% CASH

14 OF YOUR TOTAL SALES, WHAT

IS THE PERCENTAGE OF

TRADITIONAL/CONVENTIONAL

SALES (I.E. THE DELIVERY

DRIVER PLAYS BOTH A SALES

AND DELIVERY ROLE;

CONVENTIONAL DIRECT STORE

DELIVERY)?

50% 80% 90% 90% 100%

15 HOW MANY VIABLE COMPETITORS

DO YOU SEE WITHIN YOUR

MARKET (I.E. PEPSI, RC COLA,

GENERIC SUPERMARKET)?

10 4 3 3 4

32

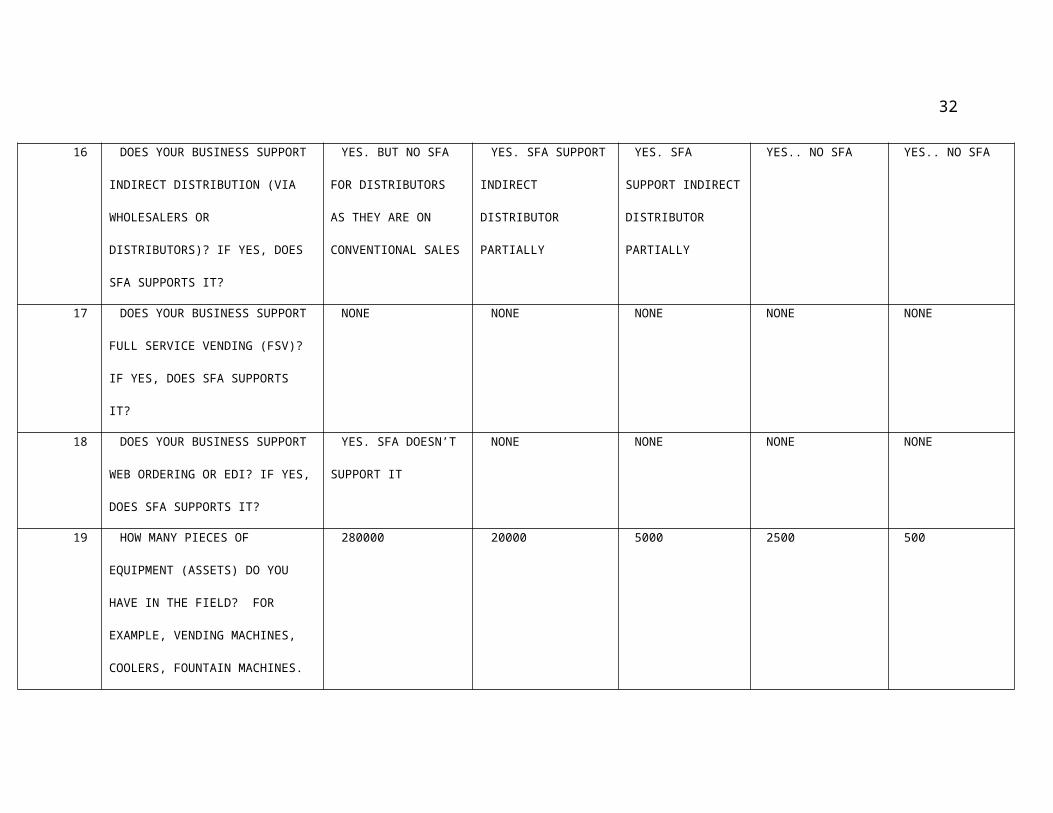

16 DOES YOUR BUSINESS SUPPORT

INDIRECT DISTRIBUTION (VIA

WHOLESALERS OR

DISTRIBUTORS)? IF YES, DOES

SFA SUPPORTS IT?

YES. BUT NO SFA

FOR DISTRIBUTORS

AS THEY ARE ON

CONVENTIONAL SALES

YES. SFA SUPPORT

INDIRECT

DISTRIBUTOR

PARTIALLY

YES. SFA

SUPPORT INDIRECT

DISTRIBUTOR

PARTIALLY

YES.. NO SFA YES.. NO SFA

17 DOES YOUR BUSINESS SUPPORT

FULL SERVICE VENDING (FSV)?

IF YES, DOES SFA SUPPORTS

IT?

NONE NONE NONE NONE NONE

18 DOES YOUR BUSINESS SUPPORT

WEB ORDERING OR EDI? IF YES,

DOES SFA SUPPORTS IT?

YES. SFA DOESN’T

SUPPORT IT

NONE NONE NONE NONE

19 HOW MANY PIECES OF

EQUIPMENT (ASSETS) DO YOU

HAVE IN THE FIELD? FOR

EXAMPLE, VENDING MACHINES,

COOLERS, FOUNTAIN MACHINES.

280000 20000 5000 2500 500

33

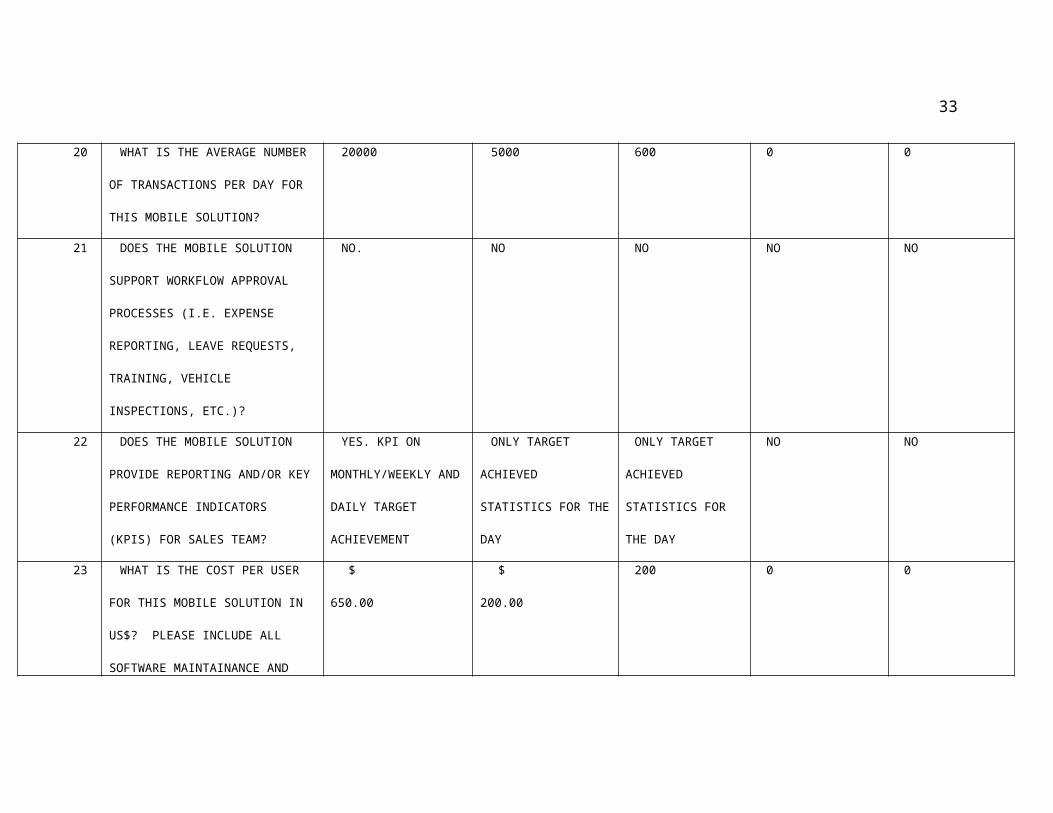

20 WHAT IS THE AVERAGE NUMBER

OF TRANSACTIONS PER DAY FOR

THIS MOBILE SOLUTION?

20000 5000 600 0 0

21 DOES THE MOBILE SOLUTION

SUPPORT WORKFLOW APPROVAL

PROCESSES (I.E. EXPENSE

REPORTING, LEAVE REQUESTS,

TRAINING, VEHICLE

INSPECTIONS, ETC.)?

NO. NO NO NO NO

22 DOES THE MOBILE SOLUTION

PROVIDE REPORTING AND/OR KEY

PERFORMANCE INDICATORS

(KPIS) FOR SALES TEAM?

YES. KPI ON

MONTHLY/WEEKLY AND

DAILY TARGET

ACHIEVEMENT

ONLY TARGET

ACHIEVED

STATISTICS FOR THE

DAY

ONLY TARGET

ACHIEVED

STATISTICS FOR

THE DAY

NO NO

23 WHAT IS THE COST PER USER

FOR THIS MOBILE SOLUTION IN

US$? PLEASE INCLUDE ALL

SOFTWARE MAINTAINANCE AND

$

650.00

$

200.00

200 0 0

34

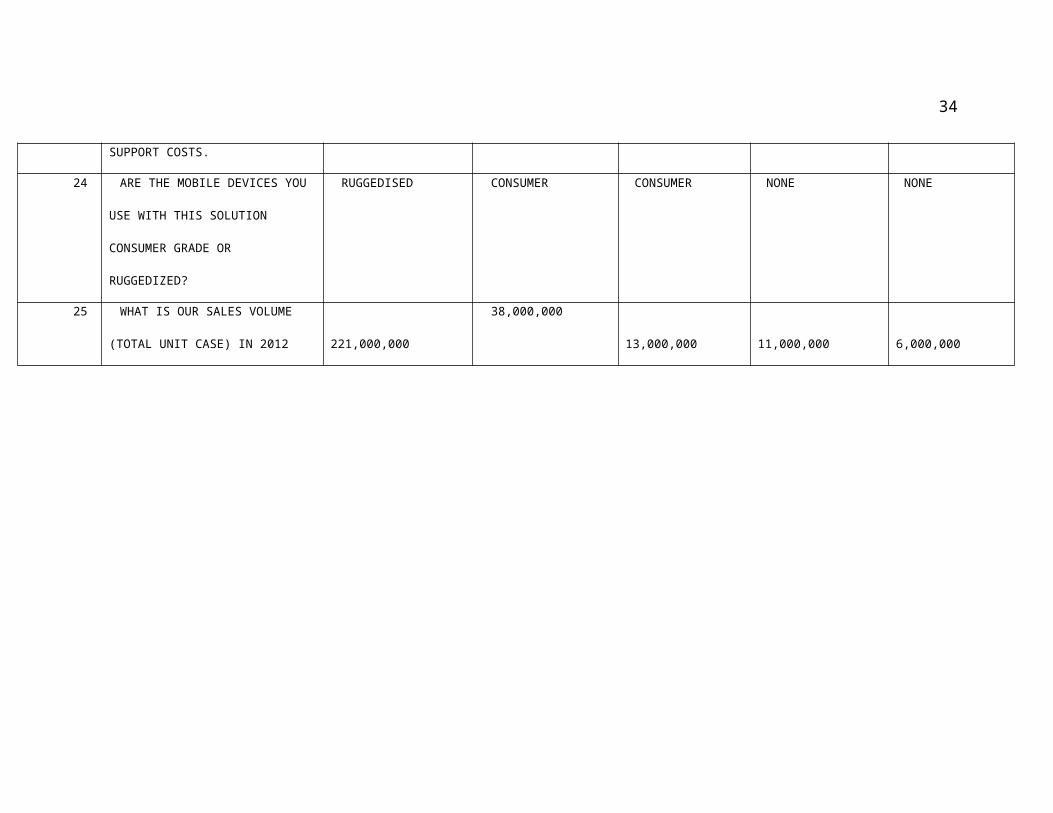

SUPPORT COSTS.

24 ARE THE MOBILE DEVICES YOU

USE WITH THIS SOLUTION

CONSUMER GRADE OR

RUGGEDIZED?

RUGGEDISED CONSUMER CONSUMER NONE NONE

25 WHAT IS OUR SALES VOLUME

(TOTAL UNIT CASE) IN 2012

221,000,000

38,000,000

13,000,000

11,000,000

6,000,000

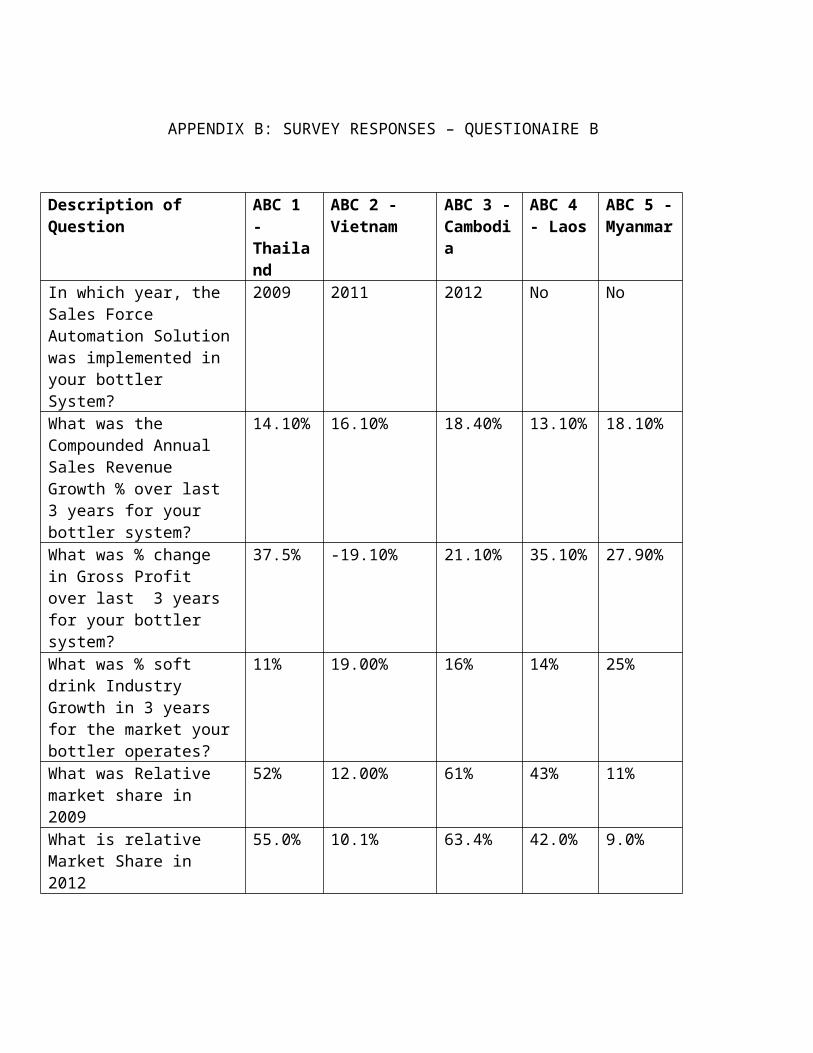

APPENDIX B: SURVEY RESPONSES – QUESTIONAIRE B

Description of Question

ABC 1 - Thailand

ABC 2 - Vietnam

ABC 3 -Cambodia

ABC 4 - Laos

ABC 5 -Myanmar

In which year, the Sales Force Automation Solutionwas implemented in your bottler System?

2009 2011 2012 No No

What was the Compounded Annual Sales Revenue Growth % over last 3 years for your bottler system?

14.10% 16.10% 18.40% 13.10% 18.10%

What was % change in Gross Profit over last 3 years for your bottler system?

37.5% -19.10% 21.10% 35.10% 27.90%

What was % soft drink Industry Growth in 3 years for the market yourbottler operates?

11% 19.00% 16% 14% 25%

What was Relative market share in 2009

52% 12.00% 61% 43% 11%

What is relative Market Share in 2012

55.0% 10.1% 63.4% 42.0% 9.0%

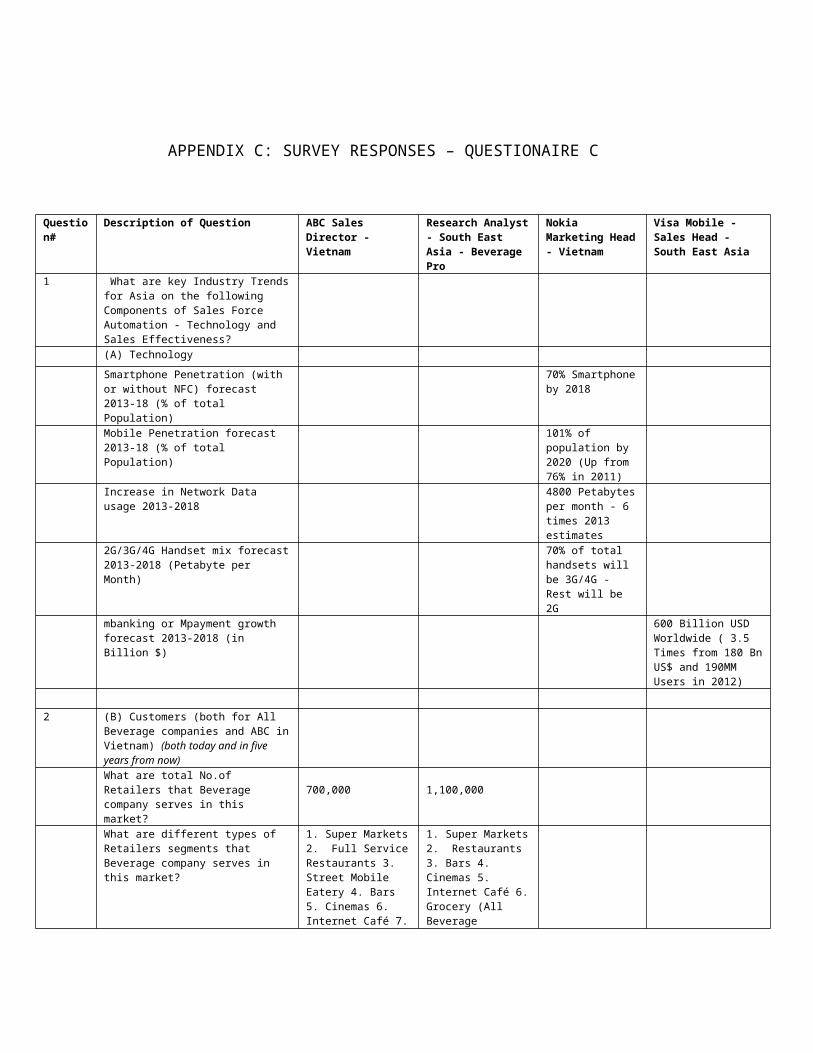

APPENDIX C: SURVEY RESPONSES – QUESTIONAIRE C

Question#

Description of Question ABC Sales Director - Vietnam

Research Analyst- South East Asia - Beverage Pro

Nokia Marketing Head- Vietnam

Visa Mobile - Sales Head - South East Asia

1 What are key Industry Trendsfor Asia on the following Components of Sales Force Automation - Technology and Sales Effectiveness?

(A) Technology Smartphone Penetration (with or without NFC) forecast 2013-18 (% of total Population)

70% Smartphoneby 2018

Mobile Penetration forecast 2013-18 (% of total Population)

101% of population by 2020 (Up from 76% in 2011)

Increase in Network Data usage 2013-2018

4800 Petabytesper month - 6 times 2013 estimates

2G/3G/4G Handset mix forecast2013-2018 (Petabyte per Month)

70% of total handsets will be 3G/4G - Rest will be 2G

mbanking or Mpayment growth forecast 2013-2018 (in Billion $)

600 Billion USD Worldwide ( 3.5 Times from 180 BnUS$ and 190MM Users in 2012)

2 (B) Customers (both for All

Beverage companies and ABC inVietnam) (both today and in five years from now)What are total No.of Retailers that Beverage company serves in this market?

700,000

1,100,000

What are different types of Retailers segments that Beverage company serves in this market?

1. Super Markets2. Full ServiceRestaurants 3. Street Mobile Eatery 4. Bars 5. Cinemas 6. Internet Café 7.

1. Super Markets2. Restaurants 3. Bars 4. Cinemas 5. Internet Café 6.Grocery (All Beverage

Grocery (For ABCand All others)

Companies)

What is the retailer segment mix for ABC has in Vietnam ? - By No. of Customers

By Outlets - 1. Super Markets - 2% 2. Restaurants - 12% 3. Street Mobile Eatery 34% 4. Bars - 9%5. Cinemas - 6%,6. Internet café- 12% 7. Grocery- 25% - (For ABC)

By Outlets - 1. Super Markets - 3% 2. Restaurants - 14% 3. Bars - 8%4. Cinemas - 5%,5. Internet café- 10% 6. Grocery- 60% - (Beverage Industry - Vietnam)

What is the retailer segment mix for ABC has in Vietnam ? - By Sales Volume

By Sales Volume - 1. Super Markets - 5% 2. Restaurants - 16% 3. Street Mobile Eatery 28% 4. Bars - 12% 5. Cinemas -13%, 6. Internetcafé - 17% 7. Grocery -9% (ForABC)

By Sales Volume - 1. Super Markets - 6% 2. Restaurants - 19% 3. Bars - 11% 4. Cinemas -12%, 5. Internetcafé - 12% 6. Grocery -40% (For Beverage Industry - Vietnam)

% of total retailers that ABChas high degree of information in their sales system

1. Super Markets100% 2. Restaurants - 50% 3. Street Mobile Eatery 1%4. Bars - 50% 5.Cinemas - 75% 6.Internet Café 5%7. Grocery 0% -(For ABC)

% of total retailers that ABC(its Sales Team) has "Ability" to exploit that information to give individual service

1. Super Markets50% 2. Restaurants - 50% 3. Street Mobile Eatery 0%4. Bars - 50% 5.Cinemas - 50% 6.Internet Café 0%7. Grocery 0% - (for ABC)

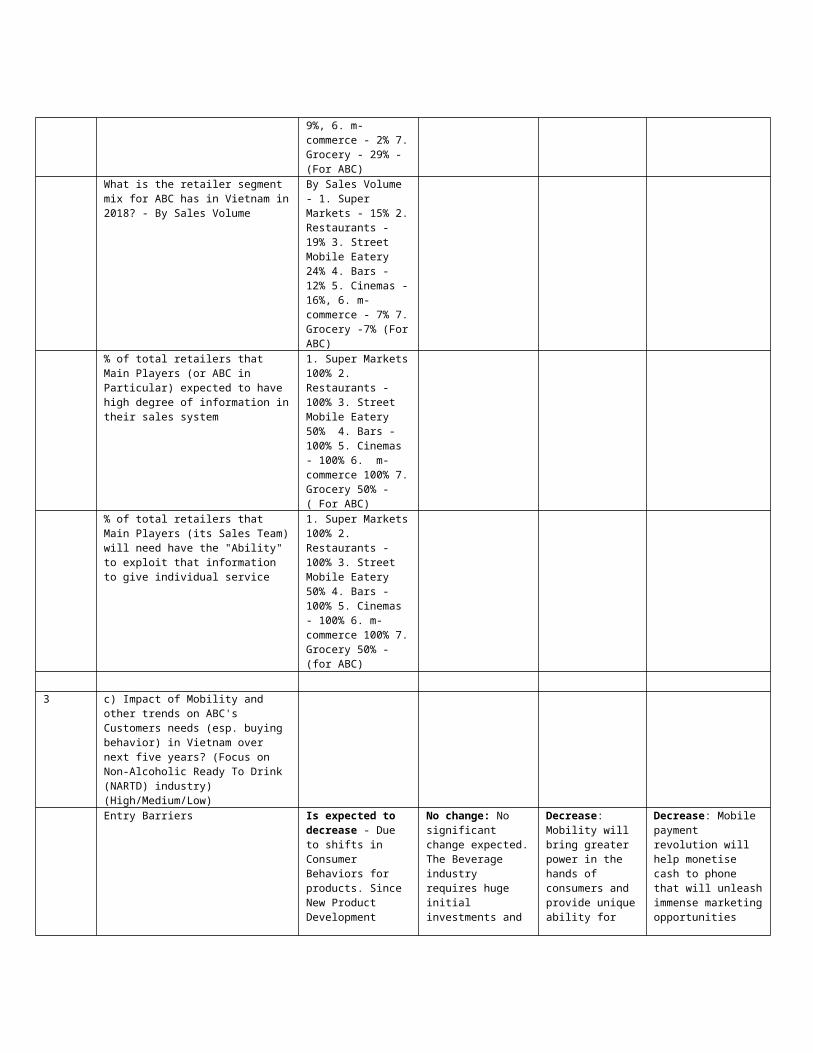

What is the retailer segment mix for ABC has in Vietnam in2018 ? - By No. of Customers

By Outlets - 1. Super Markets - 9% 2. Restaurants - 15% 3. Street Mobile Eatery 30% 4. Bars - 16% 5. Cinemas -

9%, 6. m-commerce - 2% 7.Grocery - 29% - (For ABC)

What is the retailer segment mix for ABC has in Vietnam in2018? - By Sales Volume

By Sales Volume - 1. Super Markets - 15% 2.Restaurants - 19% 3. Street Mobile Eatery 24% 4. Bars - 12% 5. Cinemas -16%, 6. m-commerce - 7% 7.Grocery -7% (ForABC)

% of total retailers that Main Players (or ABC in Particular) expected to have high degree of information intheir sales system

1. Super Markets100% 2. Restaurants - 100% 3. Street Mobile Eatery 50% 4. Bars - 100% 5. Cinemas - 100% 6. m-commerce 100% 7.Grocery 50% -( For ABC)

% of total retailers that Main Players (its Sales Team)will need have the "Ability" to exploit that information to give individual service

1. Super Markets100% 2. Restaurants - 100% 3. Street Mobile Eatery 50% 4. Bars - 100% 5. Cinemas - 100% 6. m-commerce 100% 7.Grocery 50% - (for ABC)

3 c) Impact of Mobility and

other trends on ABC's Customers needs (esp. buying behavior) in Vietnam over next five years? (Focus on Non-Alcoholic Ready To Drink (NARTD) industry) (High/Medium/Low)Entry Barriers Is expected to

decrease - Due to shifts in Consumer Behaviors for products. Since New Product Development

No change: No significant change expected.The Beverage industry requires huge initial investments and

Decrease: Mobility will bring greater power in the hands of consumers and provide uniqueability for

Decrease: Mobile payment revolution will help monetise cash to phone that will unleashimmense marketingopportunities

takes longer forlarge companies like ABC, many small players are expected to surface and mobility will enable these small players quick access to these consumers

chances of success are low that may keep away the new entrant in Vietnam.

marketing to all the way upto individual consumers possible.. This means a new player caneasily reach the consumers directly overcoming theentry barrierscreated by existing market leaderson customer facing supply chain..

that can be exploited both Existing Fast Moving Consumer Goods Companies like ABC as well the innovators.

Buyer Power Increase: There is expected to be greater shiftin favor of buyers across various distribution channels while certain Channelslike Super Markets this shift will much higher; Every channel will have better capabilities andaccess to large number players -Old and new withproducts and pricing information

Increase: In terms of Retailers power,it is surely going increase for certain channels such asModern Trade, Key accounts such as Saigon Corp. Traditional Channel such as grocery customers will loose the power to Super Store Chains.. Internet Channelis expected to grow bigger withas lot off premise transactions will migrate to web - including Mobile

Increase: Consumers and Customers alike will have larger power due to immediate access to information ontheir mobile phones. For consumers - asbeverage decision are impulse driven, they can now find out which is better products whereits available quicker than past.

Increase: Mobile Money will not change the power equation in favorof customers as much in favor of consumers. Consumers due to their increased visibility; will benefit due to access to alternate channels. Similarly new channels or intermediaries would emerge who will "potentially" sell their extraordinary consumer insightsi.e. Facebook/Google

Supplier Power Decrease: Supplier power will decrease inabsolute term; however it will vary for each supplier based on; Diversified Product Portfolio, Brand

Increase: ABC Supplier will have higher power such as Sugar, where continues to increased regulatory control to protect local

Decrease: If the FMCG players in Vietnam doesn’t take action to leverage this mobile revolution they will

Decrease: As the consumers migrateto Mobile money from Cash, the Suppliers will loose some of itscash flow to intermediaries - who will control these platforms.

Strength, differentiated Pricing, Controlover Retailer Channel, Strength of its relationship with its customers. Now if considers RawMaterial suppliers to ABClike - Sugar, Aluminum, Resin,Crowns etc, the power shift is not expected that significantover 3-5 years.

sugar manufacturer. Resin - supplierwill greater power as we foresee supplierconsolidation. For ABC and its competitors there will continue to be increase in power as we foresee M&A of smaller/popular brands by Key market leaders such as Pepsi etc to protect their leadershipacross differentcategories.

loose power tothe one who does. 100% mobile penetration will mean you can now know each consumers.

Mobile money float will remainlocked in these intermediaries who will take itsshare of the margin. This may however be passedonto the consumers ultimately.

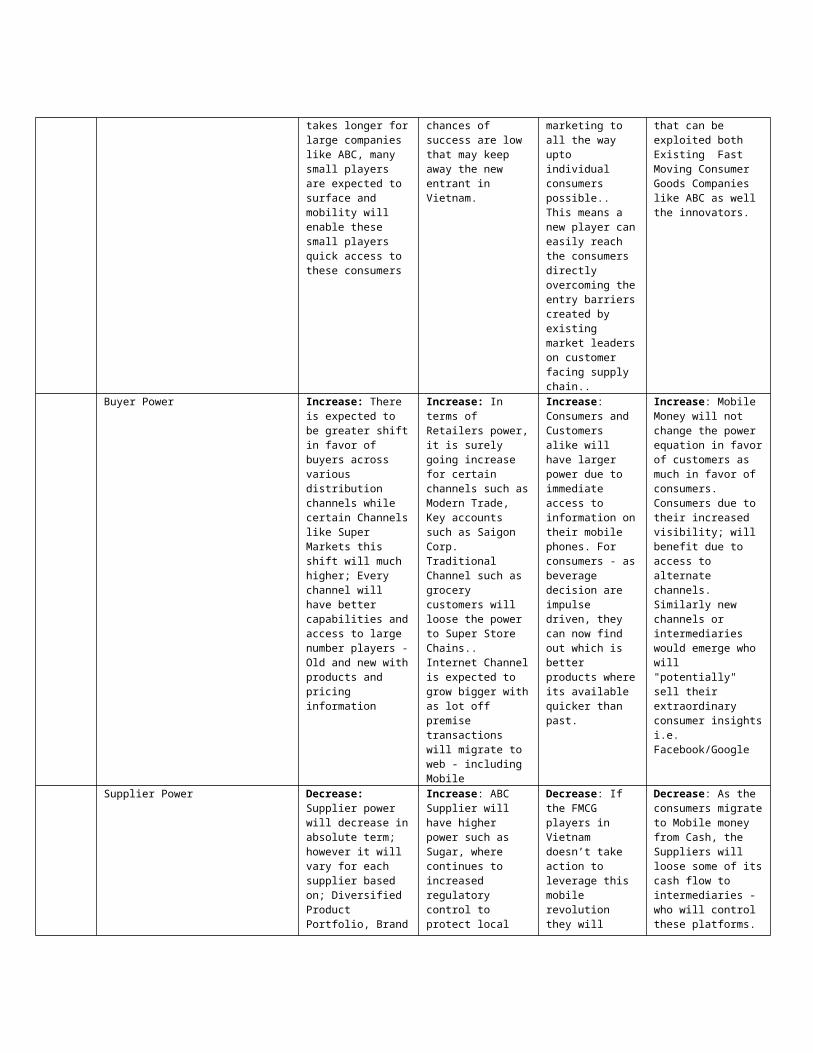

Threats of Substitutes Increase: More players that will offer newerhealthier products

Increase: juice/Energy andTea, Milk based products are expected to posea strong challenge to Carbonates

Increase: Mobility will open new channels of information for consumers and customers alike.

No Change: Mobilepayment per se will not increaseor decrease this threat

Rivalry Increase: In Vietnam, there are already 5 main players andthe competition is growing with every one eyeingshare of 20% growth in the Beverage market.

No Change: No significant change expected.The industry already has highrivalry between THB, Pepsi and other, however each one is ableto maintain leadership in different categories such as Ready to Drink Tea, Energy and Carbonates.

No change: Mobility in itself will not increase or decrease the rivalry between players today.However the rivalry will get extended to new distribution and retail channels opened up by mobility.

No Change: Mobilepayment per se will not increaseor decrease this threat

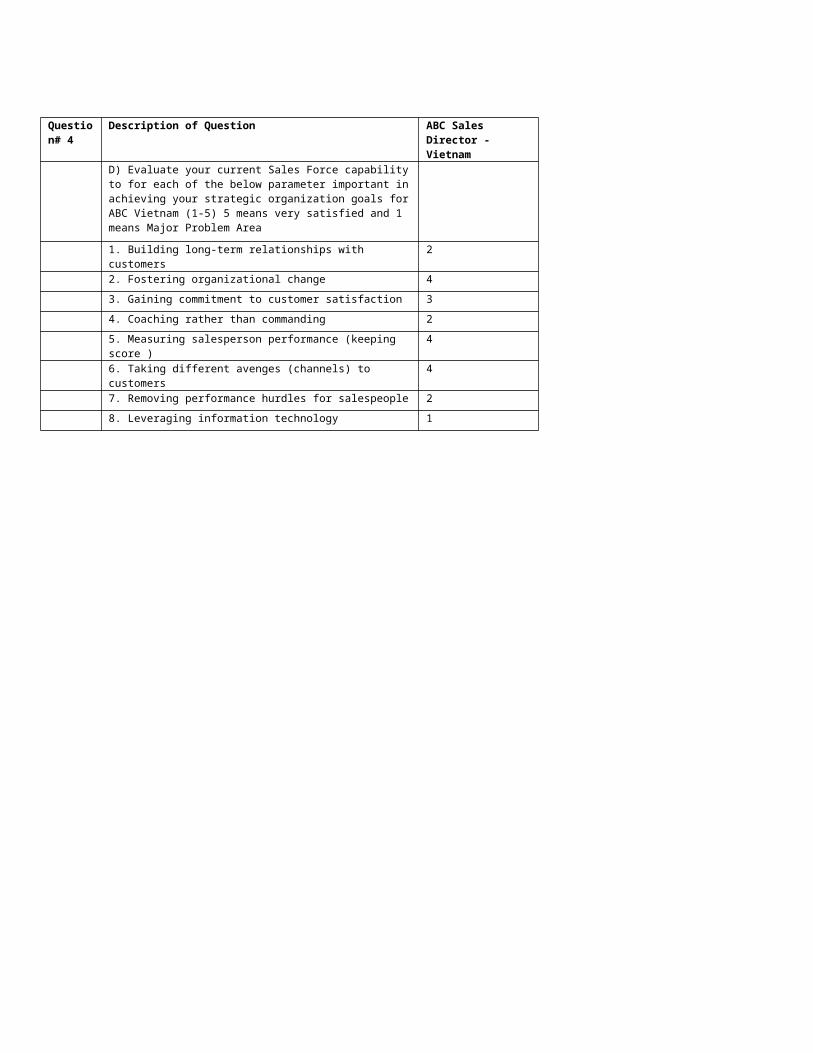

Question# 4

Description of Question ABC Sales Director - Vietnam

D) Evaluate your current Sales Force capabilityto for each of the below parameter important inachieving your strategic organization goals forABC Vietnam (1-5) 5 means very satisfied and 1 means Major Problem Area

1. Building long-term relationships with customers

2

2. Fostering organizational change 43. Gaining commitment to customer satisfaction 34. Coaching rather than commanding 25. Measuring salesperson performance (keeping score )

4

6. Taking different avenges (channels) to customers

4

7. Removing performance hurdles for salespeople 28. Leveraging information technology 1

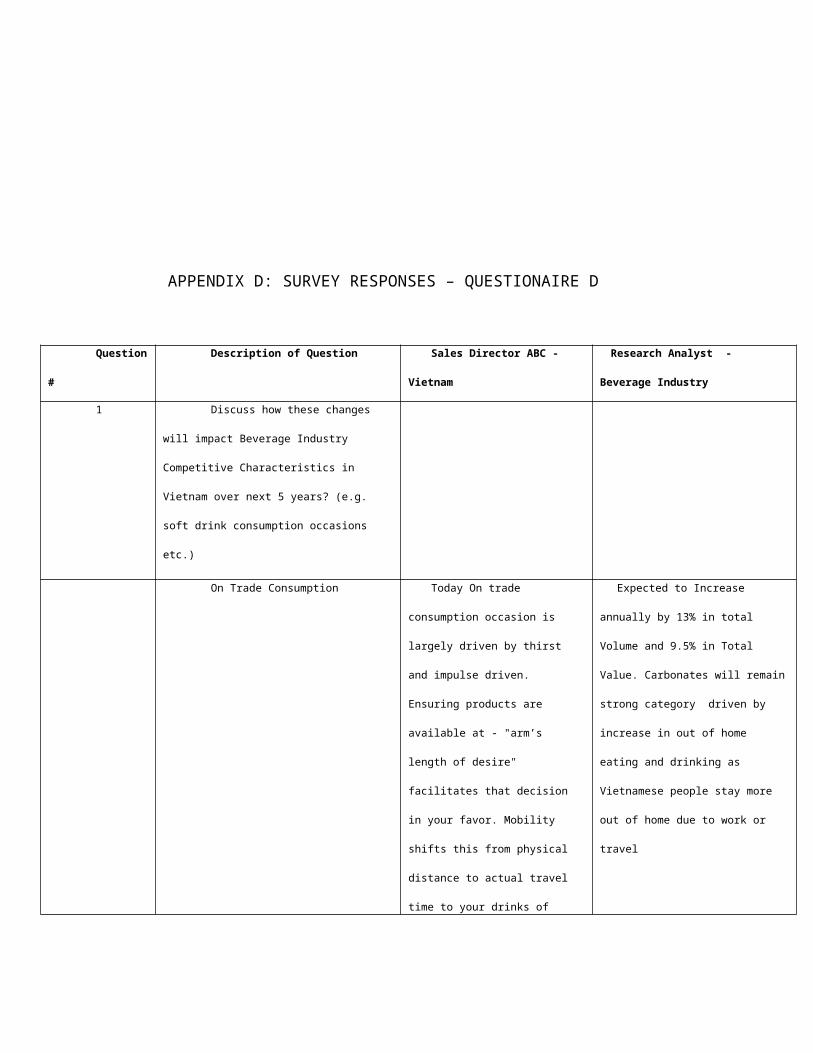

APPENDIX D: SURVEY RESPONSES – QUESTIONAIRE D

Question

#

Description of Question Sales Director ABC -

Vietnam

Research Analyst -

Beverage Industry

1 Discuss how these changes

will impact Beverage Industry

Competitive Characteristics in

Vietnam over next 5 years? (e.g.

soft drink consumption occasions

etc.)

On Trade Consumption Today On trade

consumption occasion is

largely driven by thirst

and impulse driven.

Ensuring products are

available at - "arm’s

length of desire"

facilitates that decision

in your favor. Mobility

shifts this from physical

distance to actual travel

time to your drinks of

Expected to Increase

annually by 13% in total

Volume and 9.5% in Total

Value. Carbonates will remain

strong category driven by

increase in out of home

eating and drinking as

Vietnamese people stay more

out of home due to work or

travel

choice. How effectively ABC

and competitors exploits it

will get the larger share.

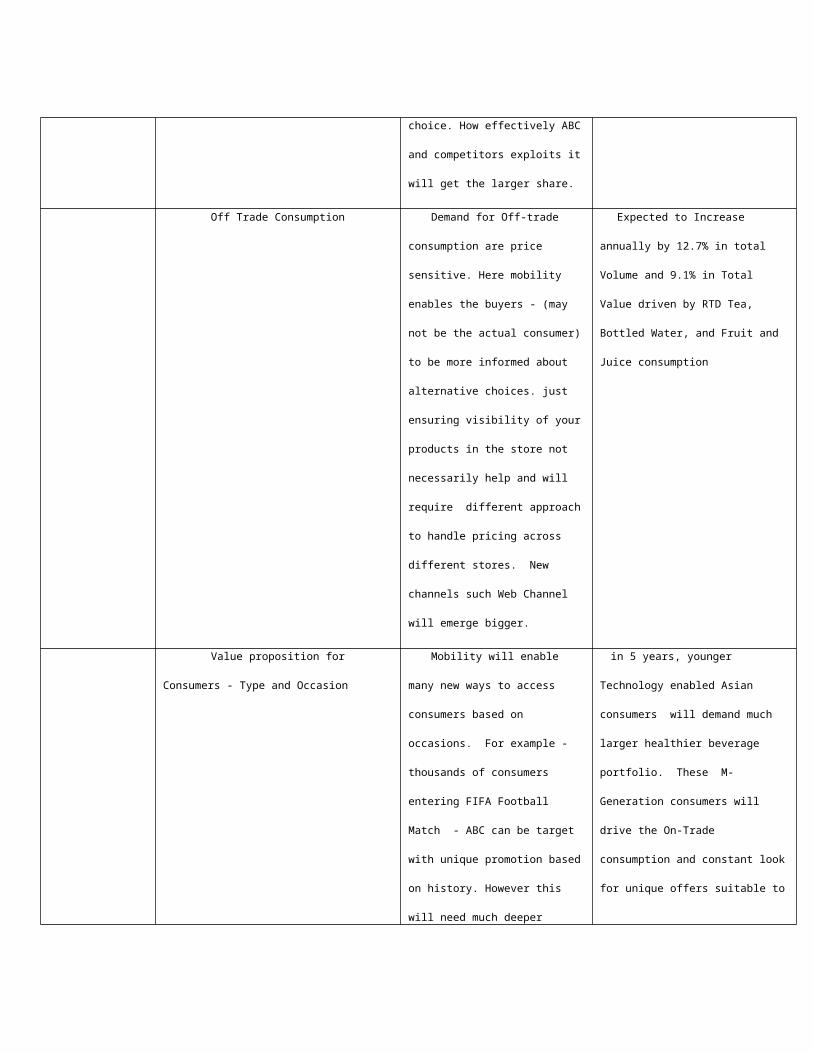

Off Trade Consumption Demand for Off-trade

consumption are price

sensitive. Here mobility

enables the buyers - (may

not be the actual consumer)

to be more informed about

alternative choices. just

ensuring visibility of your

products in the store not

necessarily help and will

require different approach

to handle pricing across

different stores. New

channels such Web Channel

will emerge bigger.

Expected to Increase

annually by 12.7% in total

Volume and 9.1% in Total

Value driven by RTD Tea,

Bottled Water, and Fruit and

Juice consumption

Value proposition for

Consumers - Type and Occasion

Mobility will enable

many new ways to access

consumers based on

occasions. For example -

thousands of consumers

entering FIFA Football

Match - ABC can be target

with unique promotion based

on history. However this

will need much deeper

in 5 years, younger

Technology enabled Asian

consumers will demand much

larger healthier beverage

portfolio. These M-

Generation consumers will

drive the On-Trade

consumption and constant look

for unique offers suitable to

analytics capability which

doesn’t exists.

the consumption occasion.

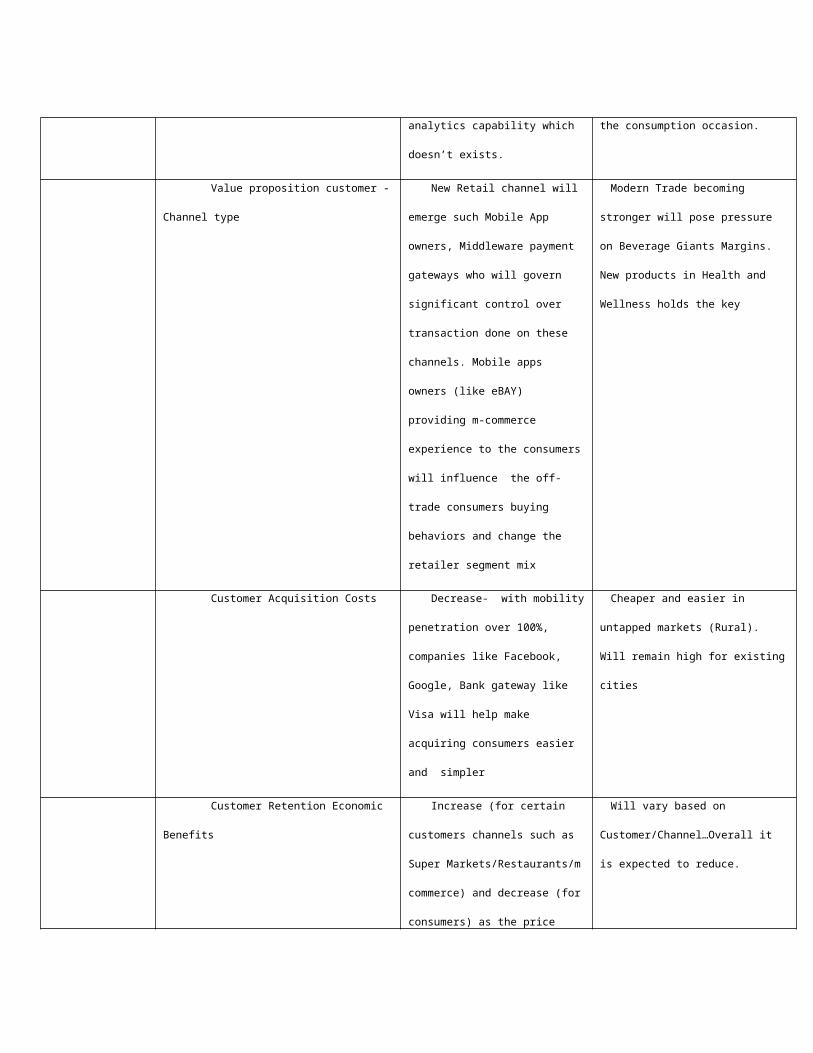

Value proposition customer -

Channel type

New Retail channel will

emerge such Mobile App

owners, Middleware payment

gateways who will govern

significant control over

transaction done on these

channels. Mobile apps

owners (like eBAY)

providing m-commerce

experience to the consumers

will influence the off-

trade consumers buying

behaviors and change the

retailer segment mix

Modern Trade becoming

stronger will pose pressure

on Beverage Giants Margins.

New products in Health and

Wellness holds the key

Customer Acquisition Costs Decrease- with mobility

penetration over 100%,

companies like Facebook,

Google, Bank gateway like

Visa will help make

acquiring consumers easier

and simpler

Cheaper and easier in

untapped markets (Rural).

Will remain high for existing

cities

Customer Retention Economic

Benefits

Increase (for certain

customers channels such as

Super Markets/Restaurants/m

commerce) and decrease (for

consumers) as the price

Will vary based on

Customer/Channel…Overall it

is expected to reduce.

sensitive consumers (off-

trade) shifts quickly,

these benefits will be

insignificant.

2 Discuss how these will

impact customer Strategy for

Beverage companies for that market?

(In terms of)

Customer Choice As Super markets grow in

Vietnam, ABC need to

reengineers its sales

capabilities - Order

generation and

Merchandising to make the

best of the high cost store

space vs. Traditional

Grocery Shops. These

customer will own

information around consumer

buying behavior that need

to leveraged by ABC. Would

need different strategy for

each customer in this

channel require deeper

analytical capabilities.

Private labels will pose a

huge challenge at Super

Market. Beverage companies

continue to add outlets in

Rural Markets while

increasing their portfolio to

grow sales in existing

customers

Customer Characteristics ABC will have full

information about 700000

customers (Retailers) and

Majority of Retailers in

traditional trade will be

more connected and informed

with increase smartphone

penetration; these

customers will be able to

place orders directly. Also

if ABC can know actual

sales of each of their

product form these

retailers every day, it

will help understand

effectiveness of each

promotion much faster.

and will need better value

from sales transaction.

Customer Segmentation Current customer

segments mix will change

significantly with Super

Markets, M-Commerce,

Restaurant/Bars will

constitute 60% of the total

sales by 2020, creating and

executing different

segmentation strategy will

be biggest challenge

significant increase

number of segments

3 Discuss how will these

changes impact Multi Channel

Customer and Sales Integration

Management process for beverage

Companies for that market?

Sales Force Change in Customer

Characteristics and

Sales team need to be

highly computer savvy and

segmentation strategy will

make execution an uphill

task for existing ABC sales

team. For Super Markets,

Mcommerce becoming bigger,

will require different

sales capabilities. In

general, Sales people job

will move away from low

level activities such as

order capturing and more

focus on putting together

the Unique sales

proposition or

merchandising at the store.

Sales force will be

expected to analyse and

consume much more

information around Past

and future trends for each

customer.

needs access to better

analytical abilities to close

sales to bigger customers.

Outlets ABC would need to build

capability to manage

relationship with each of

its 70000 outlets today

thru agile IT systems and

Sales processes. Carbonates

are ABC key strength, ABC

Outlet universe will need

to grow to rural market in

Asia market as same store

sales will be more

competitive and pressure on

keeping market share

would need to add new

outlets in Rural areas to

improve its penetration and

gain market share.

Electronic/Mobile Commerce

(order to cash cycle)

ABC doesn’t accept other

cash or Cheque today from

its customers. Internet

Banking and Mobile Wallet

will require ABC to

integrate its systems with

Intermediaries and Banks

and may impact its cash

flow. It will require to

re-negotiate its credit

terms with customers and

suppliers.

Mobile payment may become

significant portion of

payment method - 30%+

4 Discuss how will beverage

companies in that market will

measure performance of the customer

relationship strategy?

Revenue Growth Net Sales Revenue

Growth, Sales Volume Growth

by Product by Channel,

Profitability Gross Profit by Channel

by Customer by Product

People (Sales) Net Revenue and Gross

profit per Sales person, by

Sales Area

Productivity PJP Compliance, Call

Rate %, Hit Rate %, Range

Selling. Outlet Span

Performance Monitoring

Standards - Qualitative/Quantitative

Sales Force

Effectiveness - SFE

Dashboard which will

monitors Daily Execution at

outlet, Sales Volume Target

Results and KPIs Results for these

Productivity, SFE Dashboard

will be measured daily

basis