restaurant, food & beverage market research

TRANSCRIPT

Richard K. Miller & Associates ————— since 1972 —————

Restaurant, Food & BeverageMarket Research Handbook 2013

RESTAURANT, FOOD & BEVERAGE

MARKET RESEARCH HANDBOOK 2013

14th Edition

RKMA MARKET RESEARCH HANDBOOK SERIES

By: Richard K. Miller and Kelli Washington

Published by:

Richard K. Miller & Associates4132 Atlanta Highway, Suite 110Loganville, GA 30052(888) 928-7562www.rkma.com

Richard K. Miller & Associates————— since 1972 —————

RESTAURANT, FOOD & BEVERAGE

MARKET RESEARCH HANDBOOK 2013

14th Edition

RKMA MARKET RESEARCH HANDBOOK SERIES

Copyright © 2013 by Richard K. Miller & Associates

All rights reserved. Printed in the United States of America.

Use of the electronic edition of this publication is limited to internal use within the purchasing organization.

The electronic edition may be stored on computers, Intranets, servers, and networks by organizationswhich have purchased this publication, and those for which an employee has made such purchase. Copies, including multiple copies, may be printed from the electronic edition for use within the purchasingorganization.

Libraries may store the electronic edition on an archival database or proxy server for access by libraryusers.

Governmental agencies purchasing this publication may share the content within the agency ordepartment. Universities and colleges may share the information within their campus, but not with otheruniversities. Membership associations may use the information within their internal organization, but maynot distribute to their membership.

This publication may not be stored on Internet websites, nor may it be file-shared through the Internet.

This publication may not be resold or distributed without prior written agreement with the publisher.

While every attempt is made to provide accurate information, the author and publisher cannot be heldaccountable for any errors or omissions.

ISBN Number: 1-57783-188-89781577831884

Richard K. Miller & Associates4132 Atlanta Highway, Suite 110Loganville, GA 30052(888) 928-7562www.rkma.com

CONTENTS

PART I: MARKET OVERVIEW. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1 MARKET SUMMARY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 231.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 231.2 Industry Sales. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 231.3 Revenue Distribution. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 251.4 Restaurant Sales Growth. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 251.5 Restaurant Expenditures. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 261.6 Independents and Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 261.7 Chain Restaurant Classification. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 271.8 Restaurant Visits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 281.9 Restaurant Performance Index. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

2 STATE-BY-STATE ANALYSIS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 302.1 Restaurant Sales By State. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 302.2 Restaurant Locations By State.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 312.3 Foodservice Employment By State. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

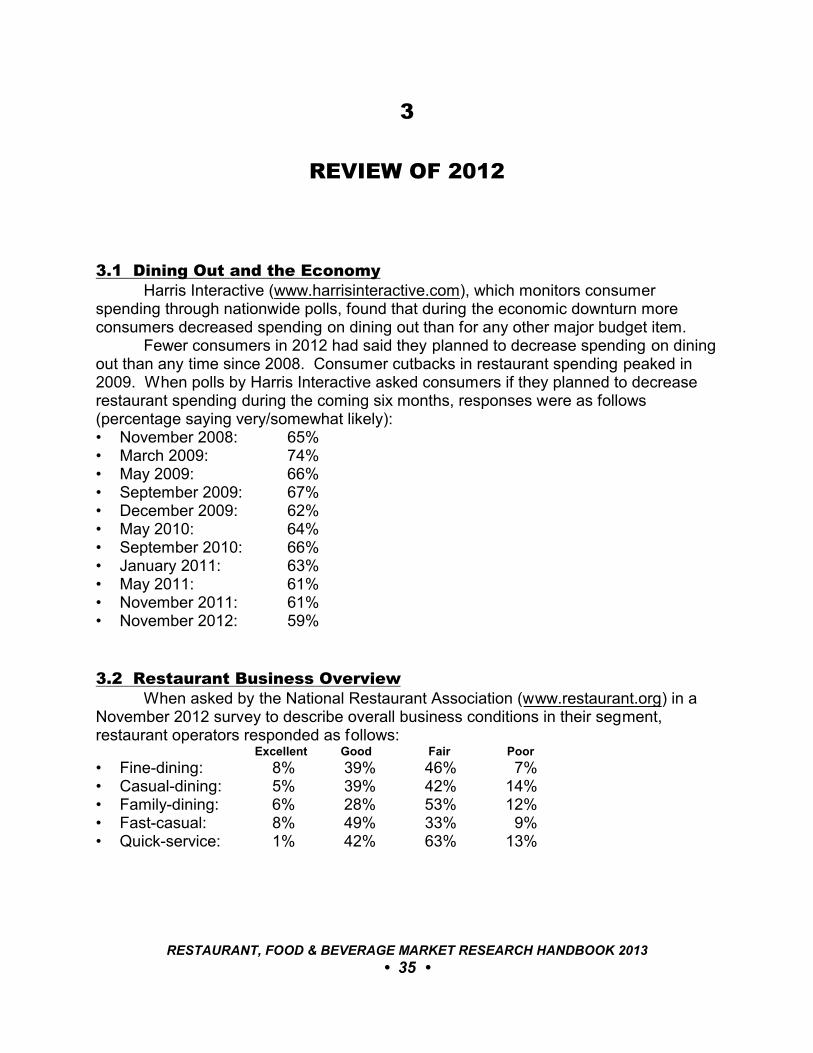

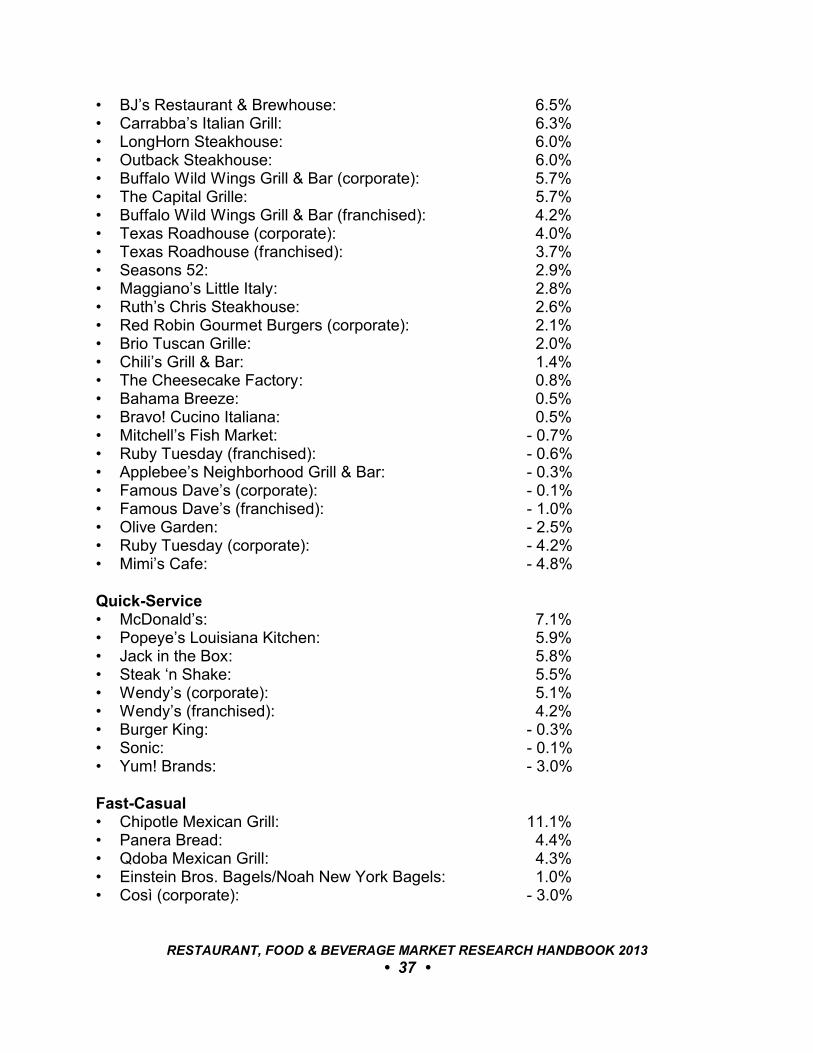

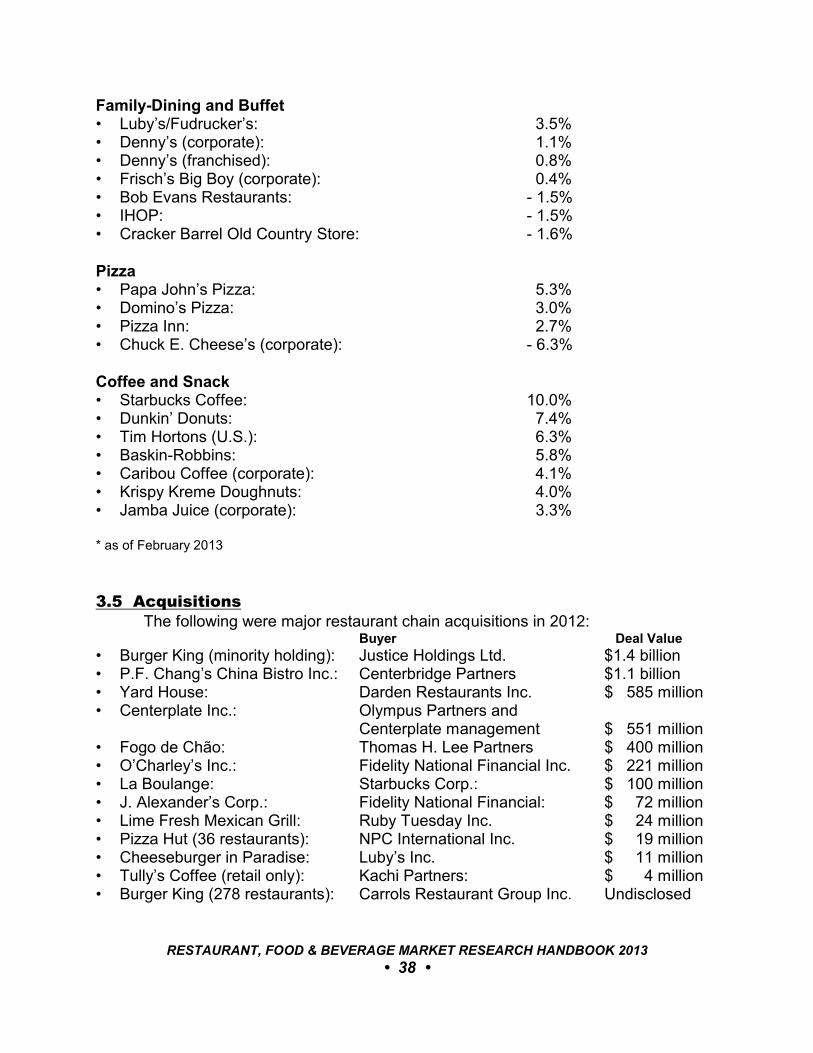

3 REVIEW OF 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353.1 Dining Out and the Economy. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353.2 Restaurant Business Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353.3 Restaurant Counts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 363.4 Same-Store Sales. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 363.5 Acquisitions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

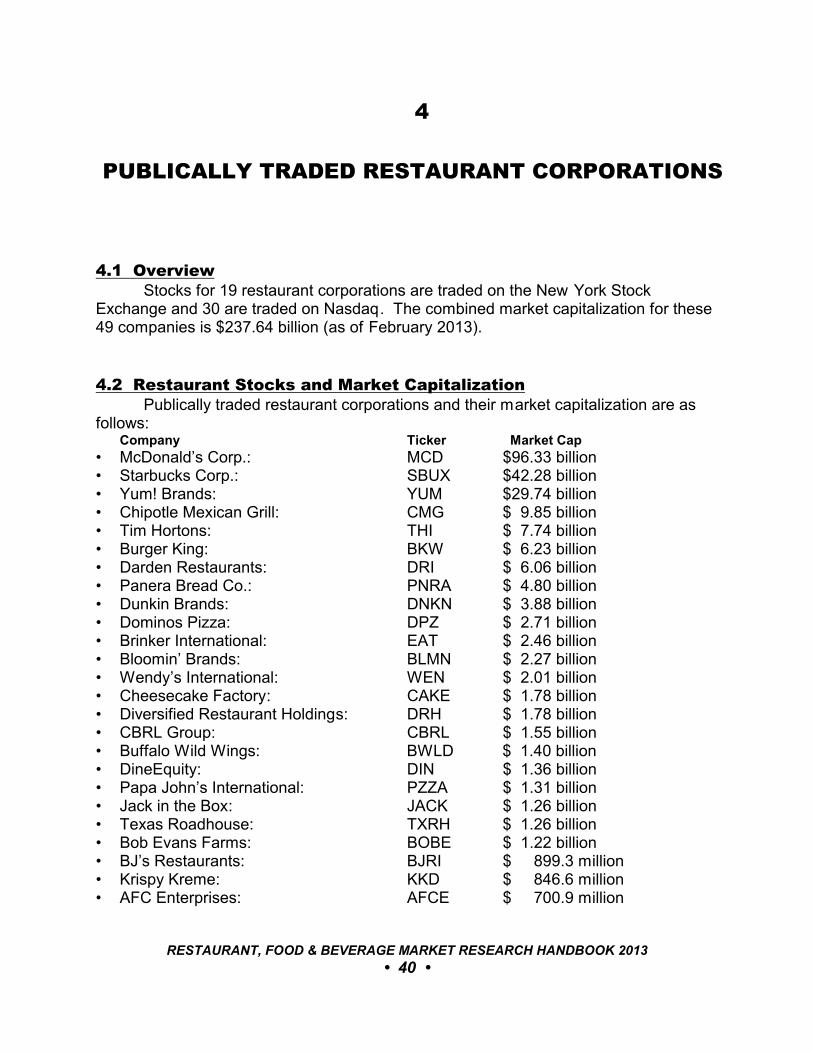

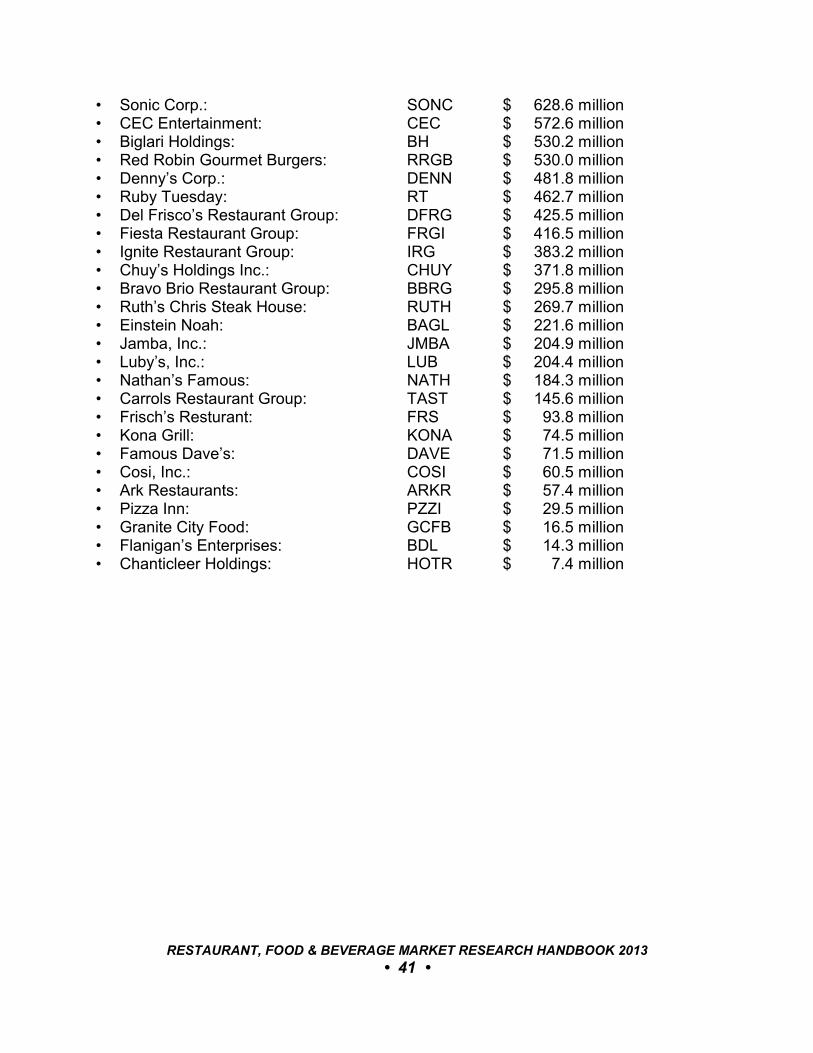

4 PUBLICALLY TRADED RESTAURANT CORPORATIONS.. . . . . . . . . . . . . . . . . 404.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 404.2 Restaurant Stocks and Market Capitalization. . . . . . . . . . . . . . . . . . . . . . . . . 40

PART II: TRENDS FOR 2013. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

5 CULINARY TRENDS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 435.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 435.2 Culinary Themes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 435.3 Top Menu Trends.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 435.4 Top Trends By Category. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

6 FOOD & DINING TRENDS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 476.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 5 •

6.2 Andrew Freeman & Co.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 476.3 Baum + Whiteman. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 496.4 Bon Appétit.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 536.5 Culinary Visions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 556.6 Epicurious. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 586.7 Flavor Forecast. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 596.8 Mintel. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 606.9 Sterling-Rice Group. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 616.10 Supermarket Guru. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 626.11 Technomic. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 646.12 The Food Channel. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 676.13 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

PART III: CITY-BY-CITY ANALYSIS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

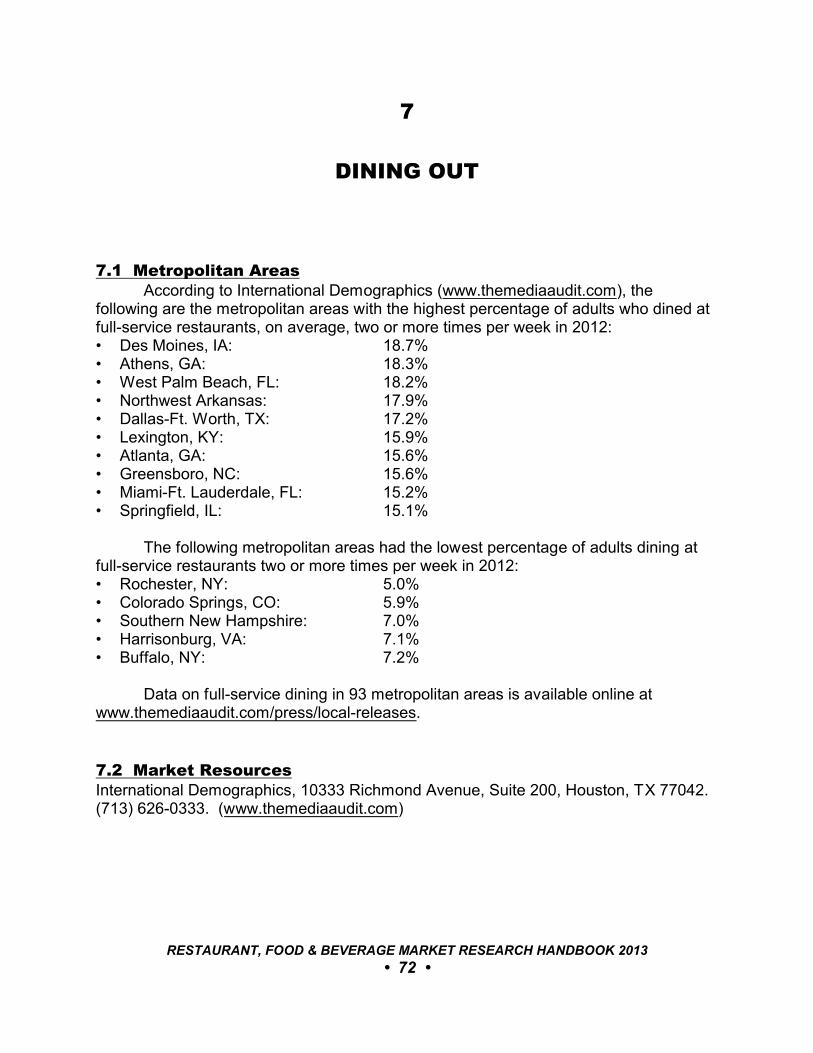

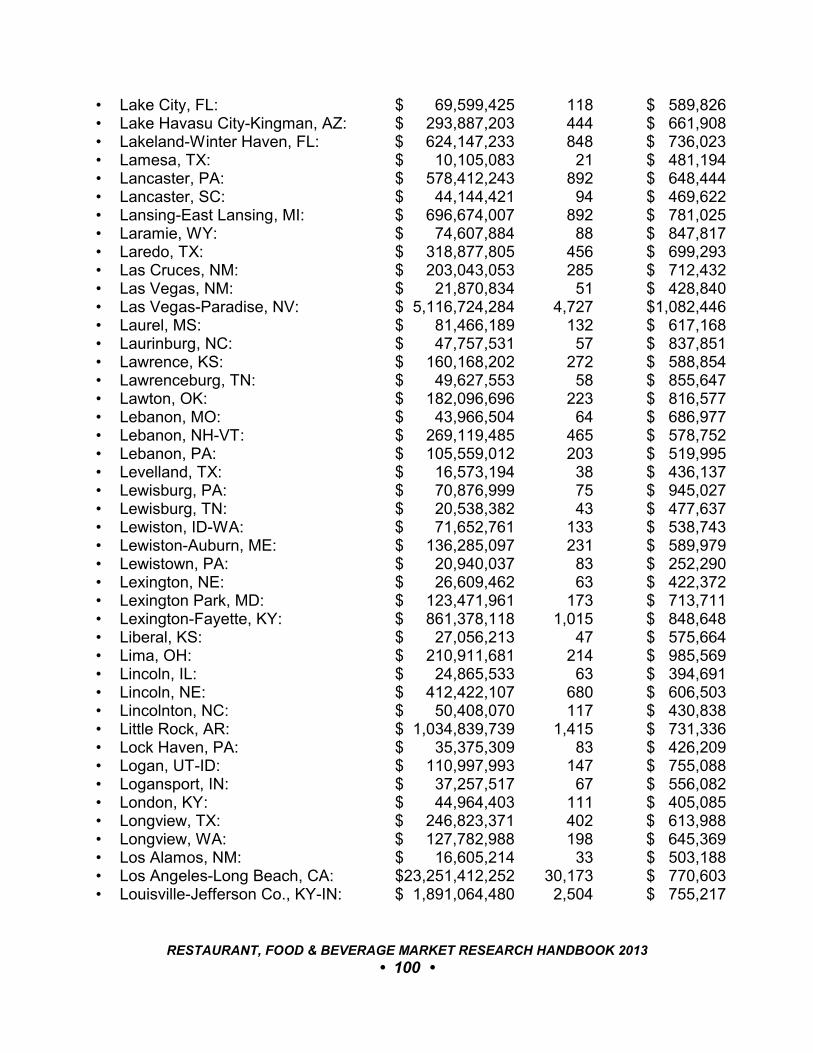

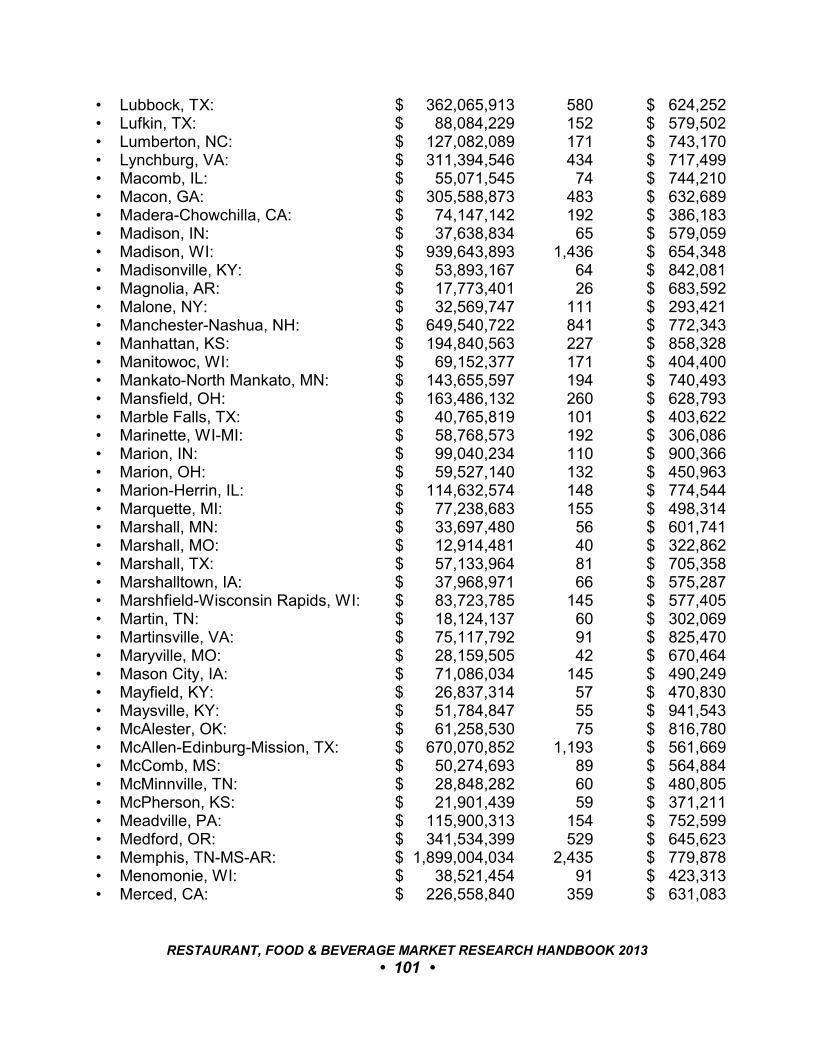

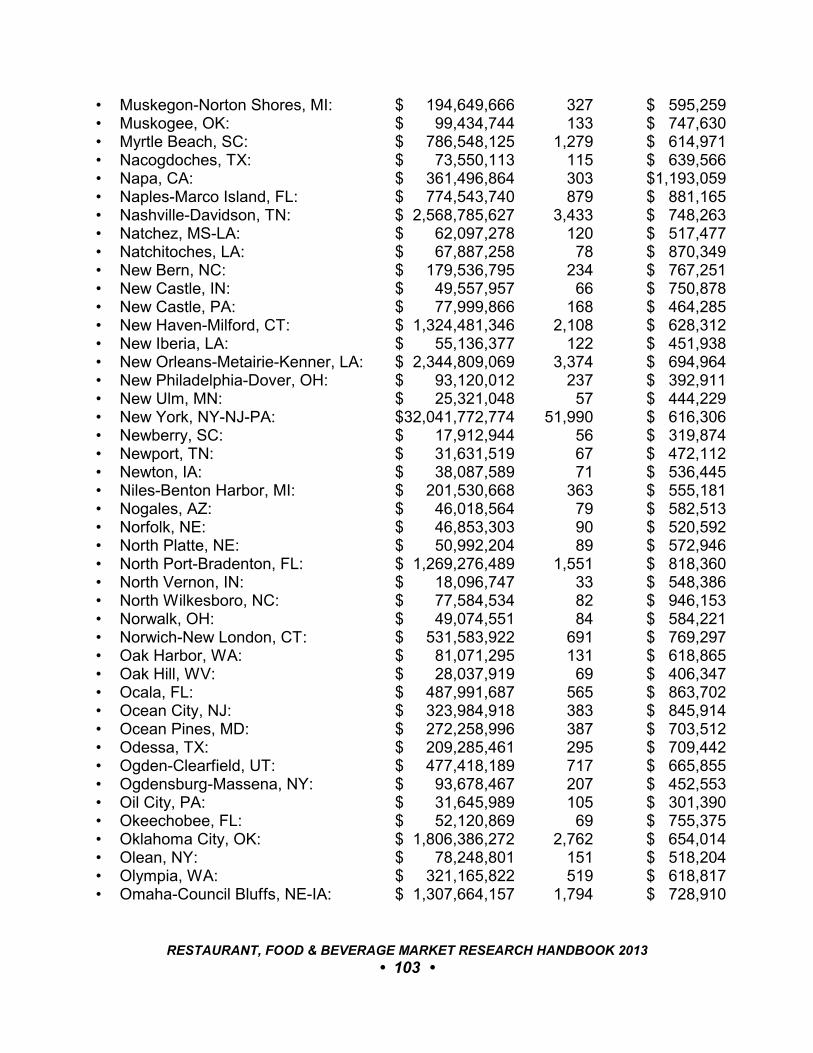

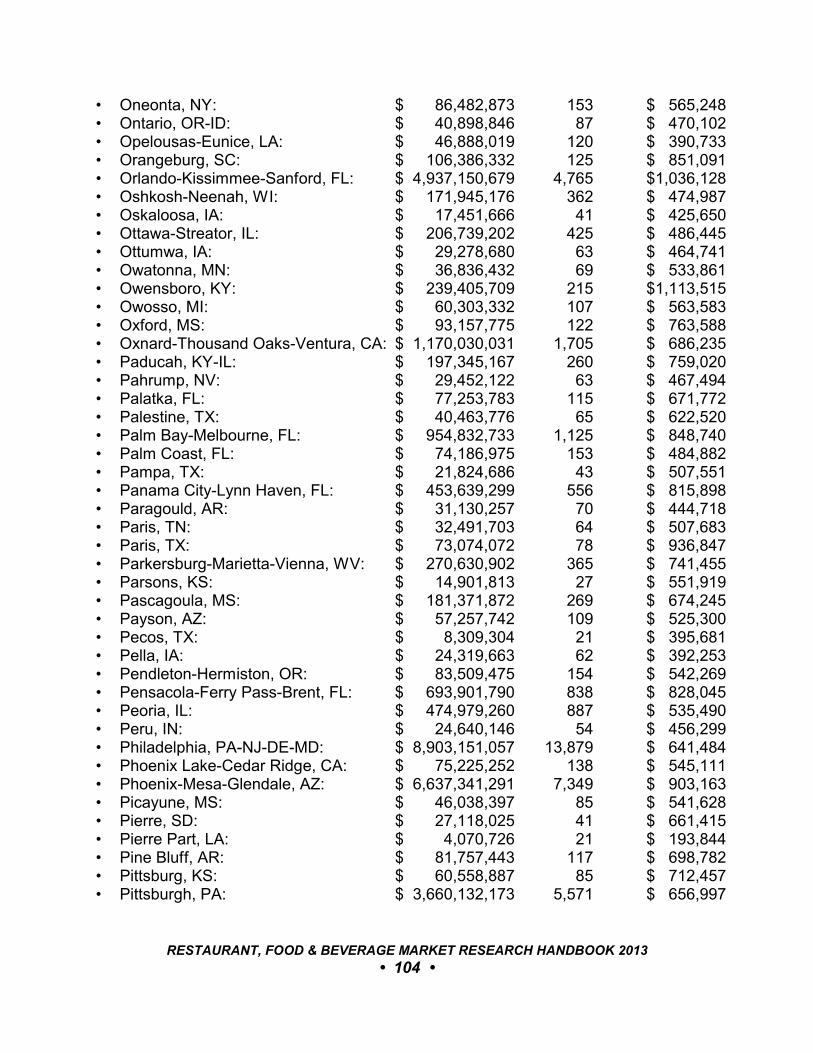

7 DINING OUT. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 727.1 Metropolitan Areas. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 727.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

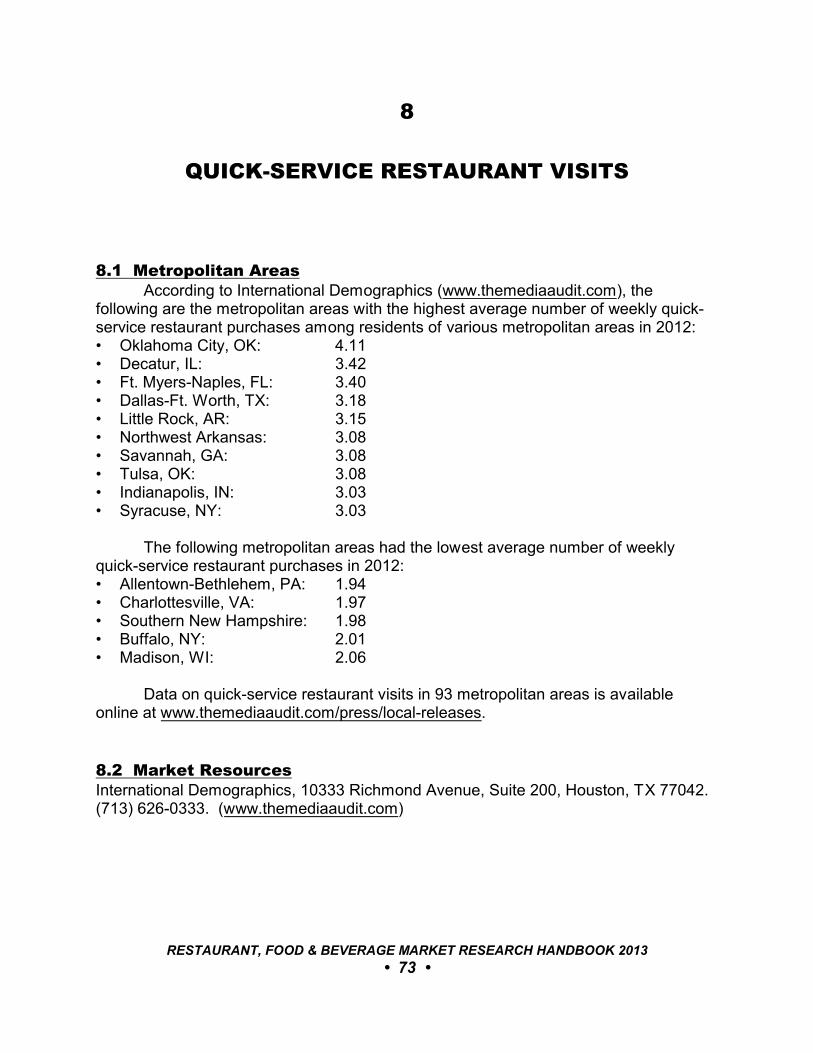

8 QUICK-SERVICE RESTAURANT VISITS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 738.1 Metropolitan Areas. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 738.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

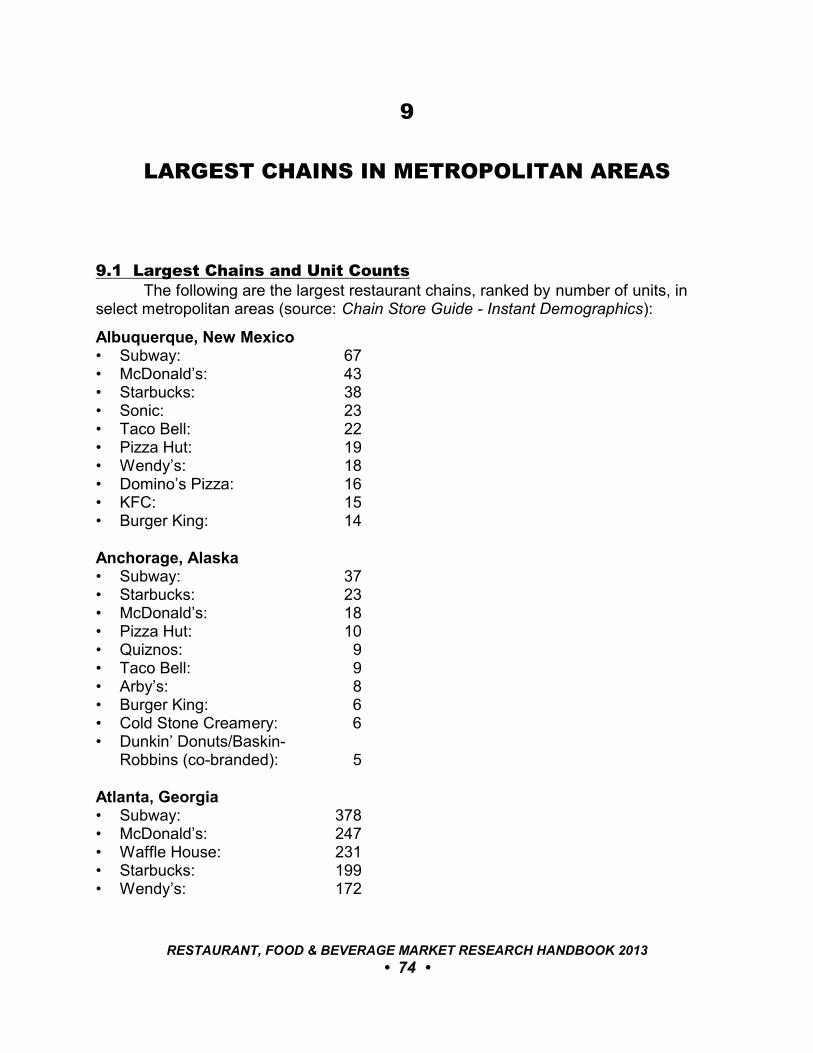

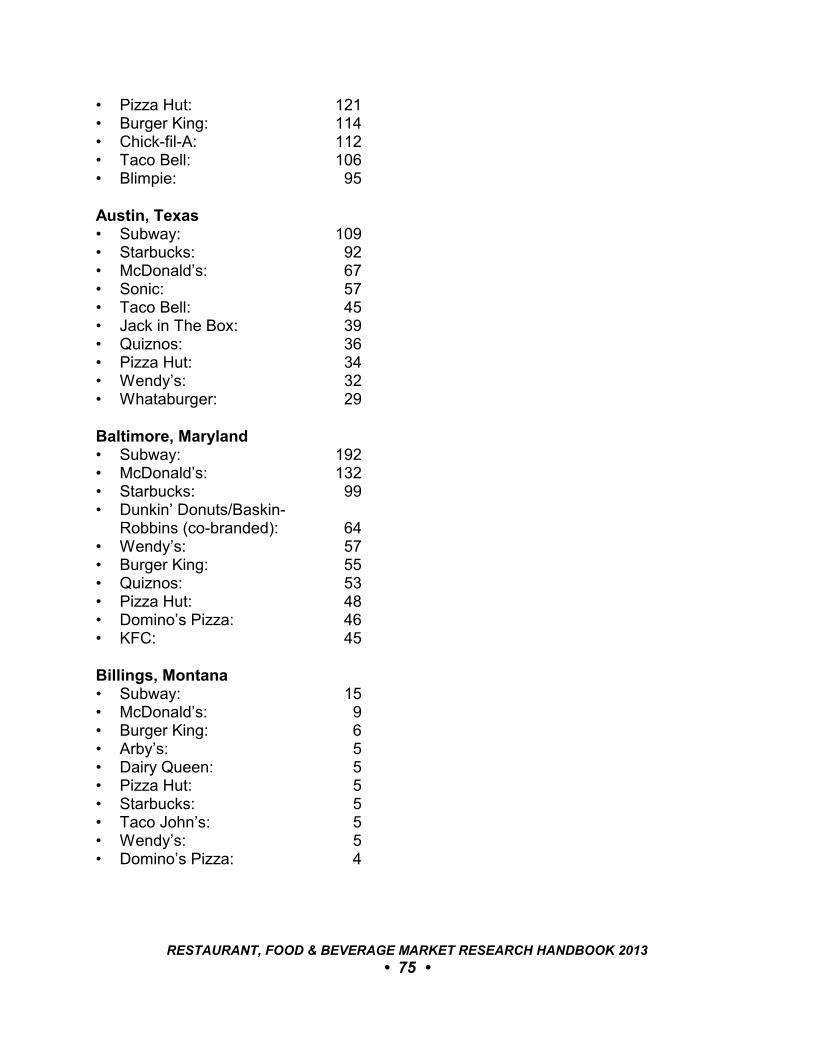

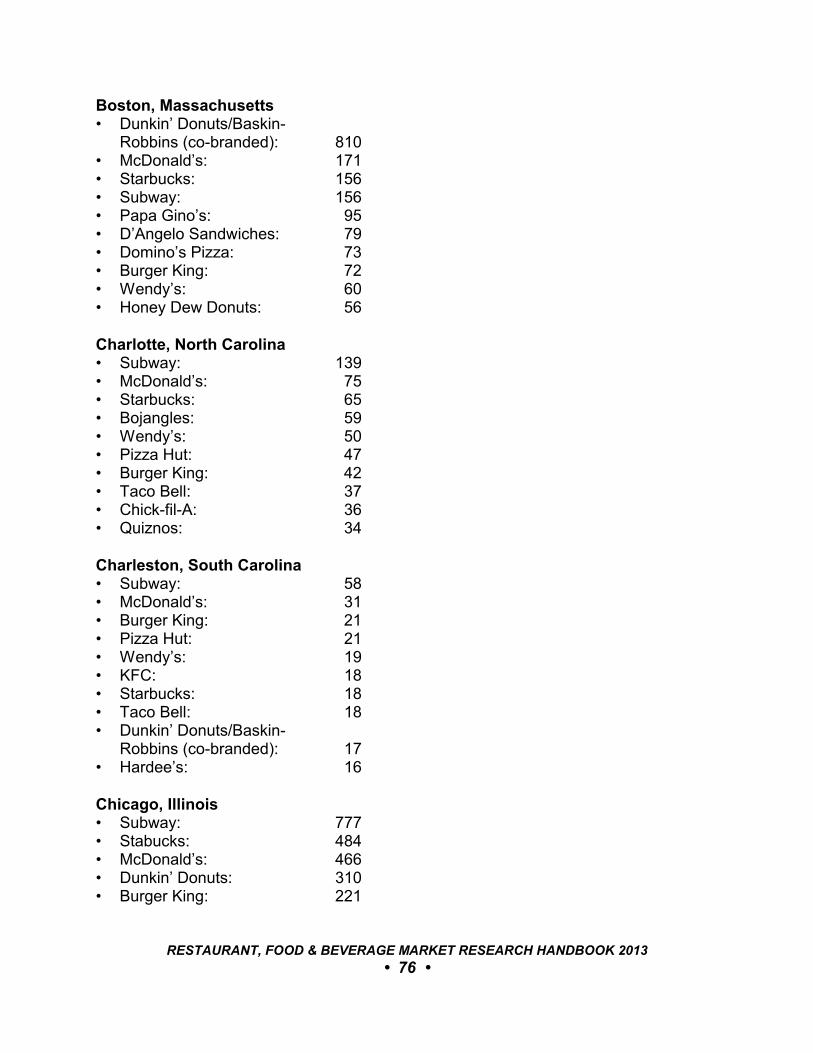

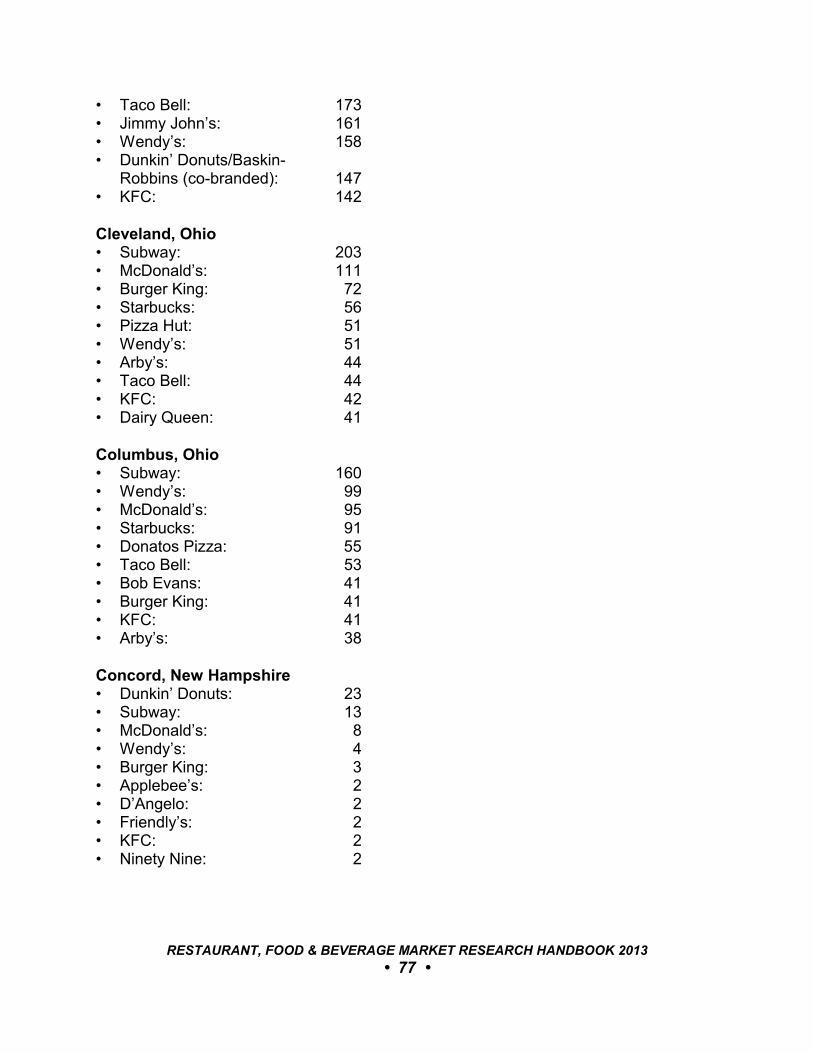

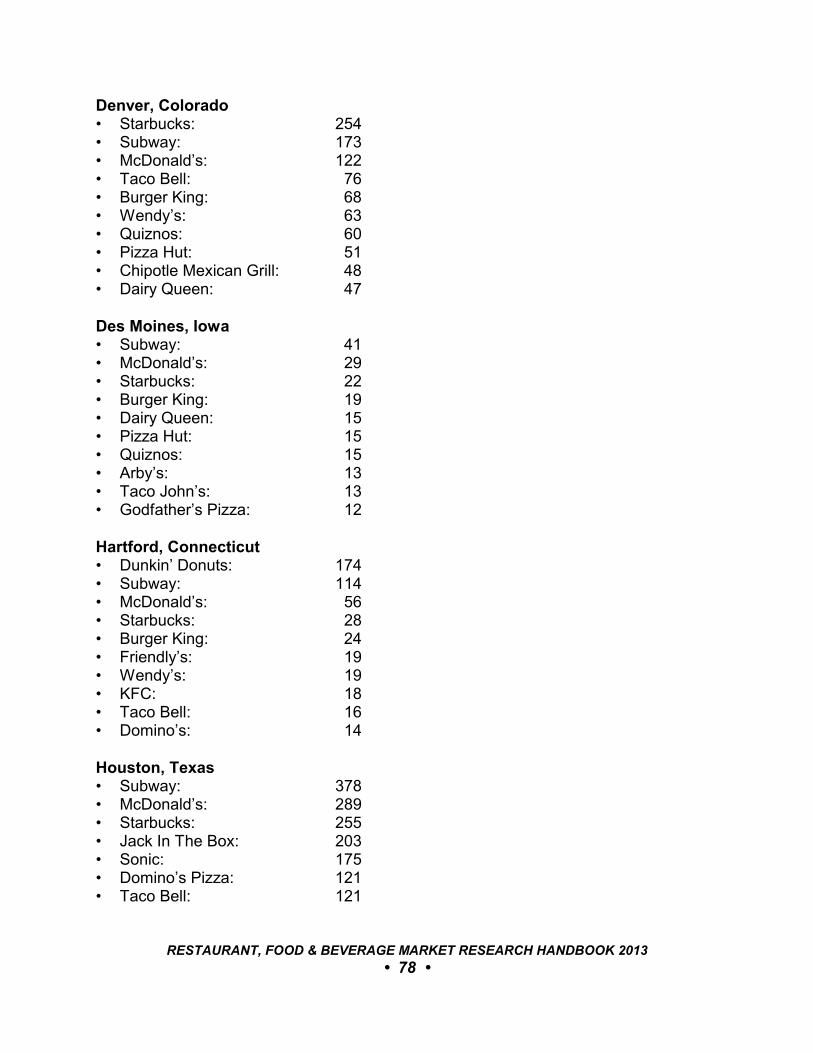

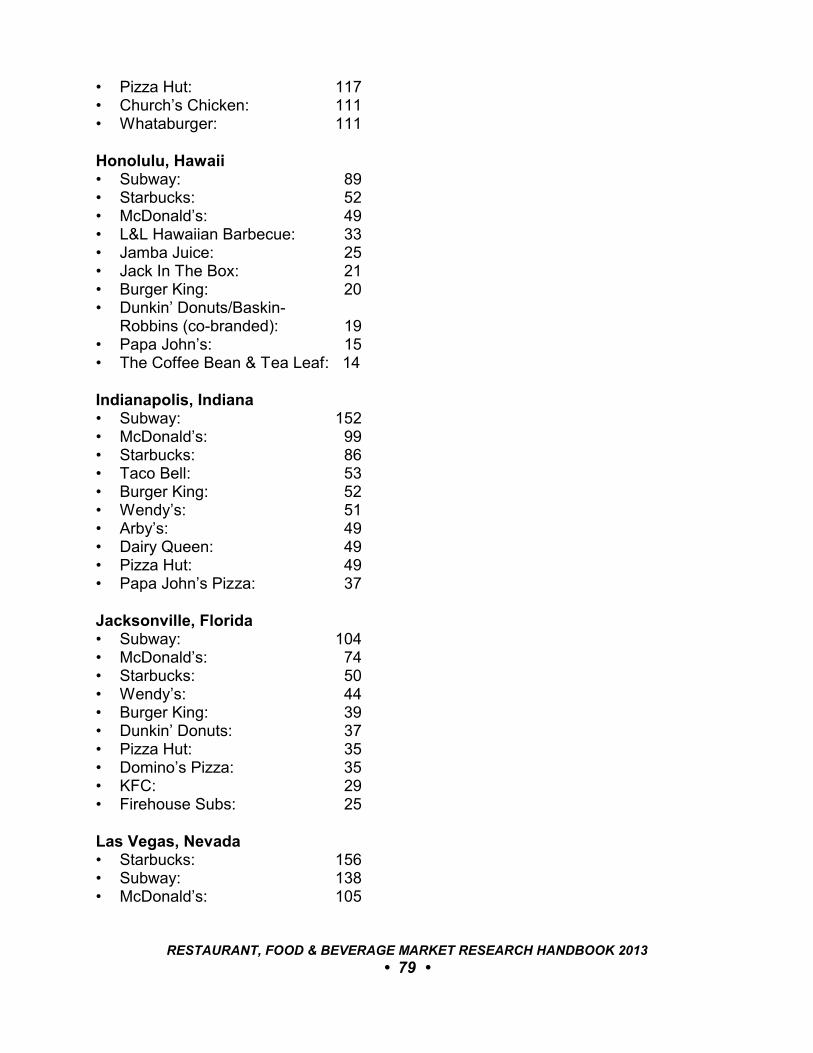

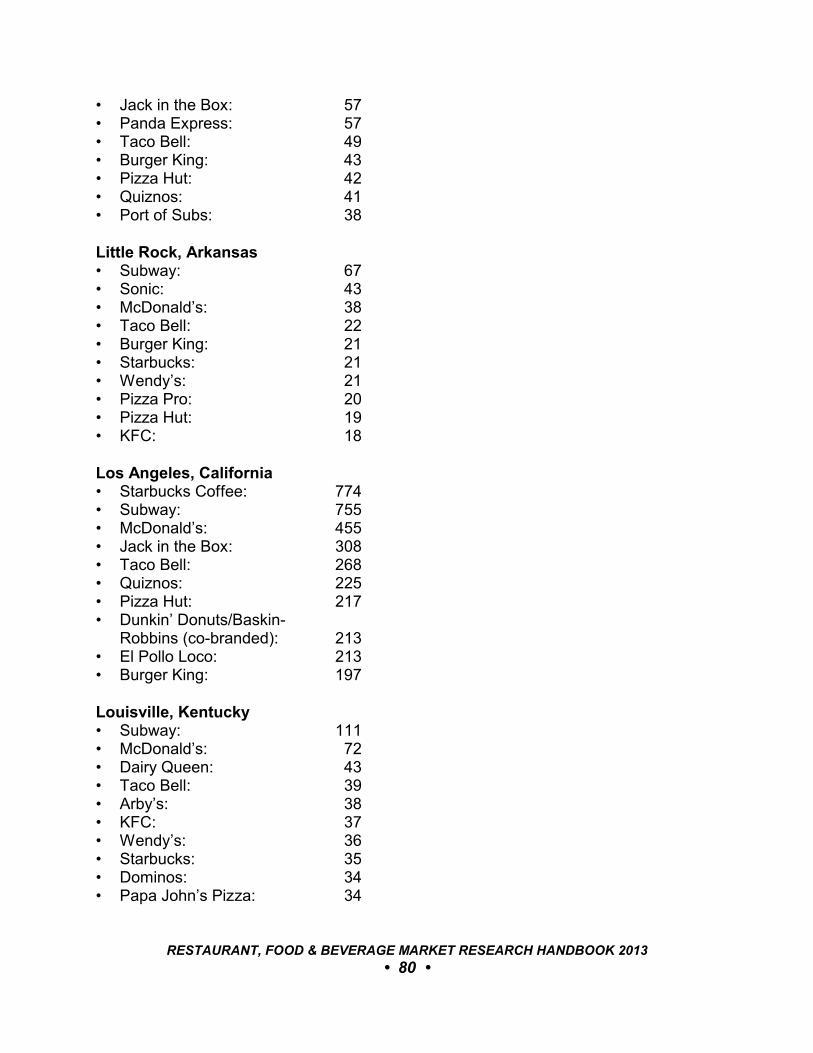

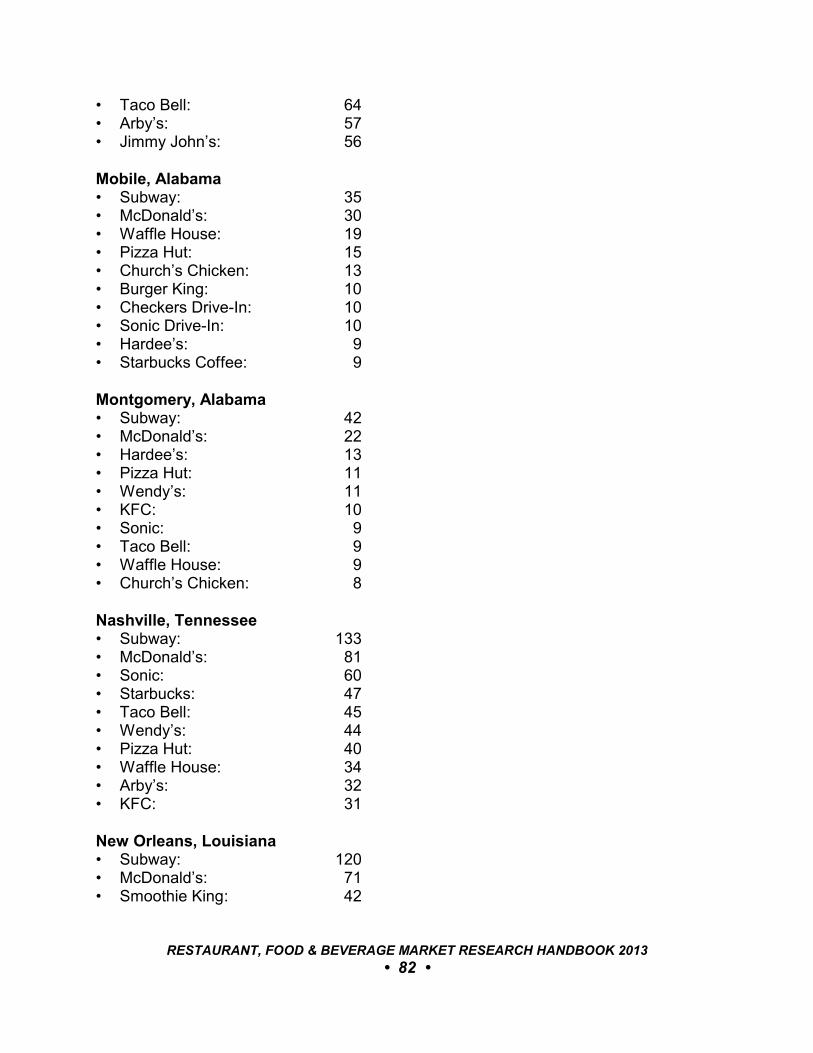

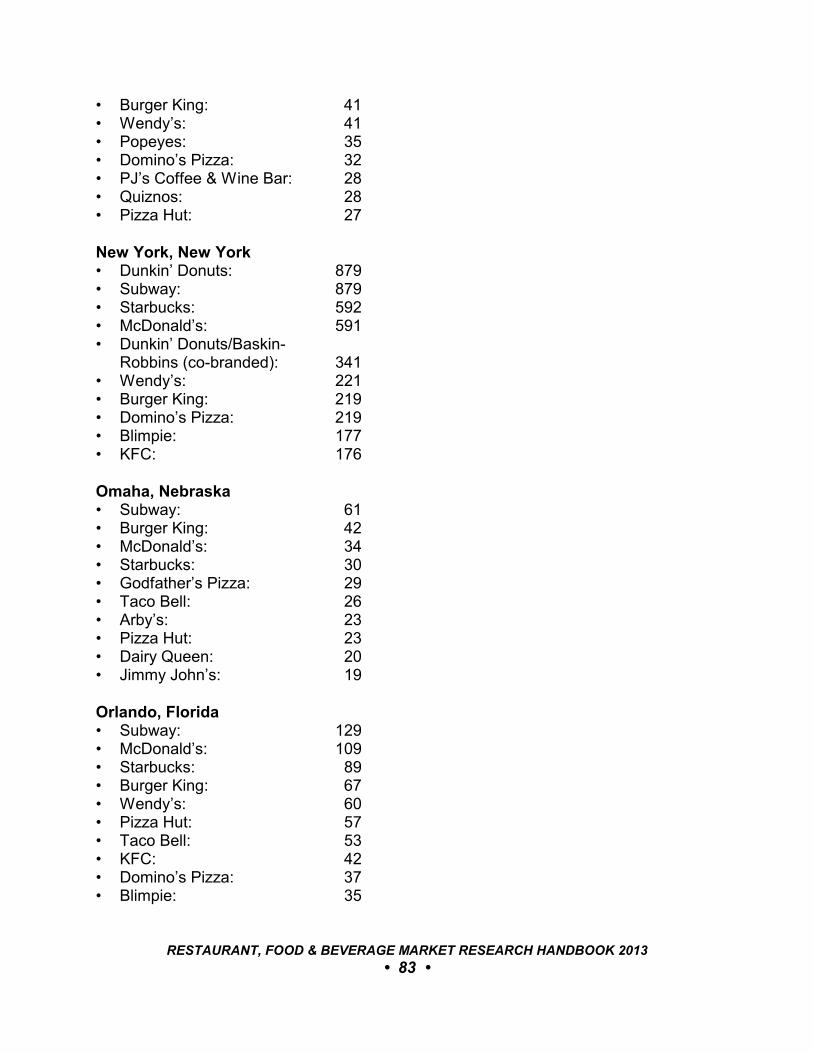

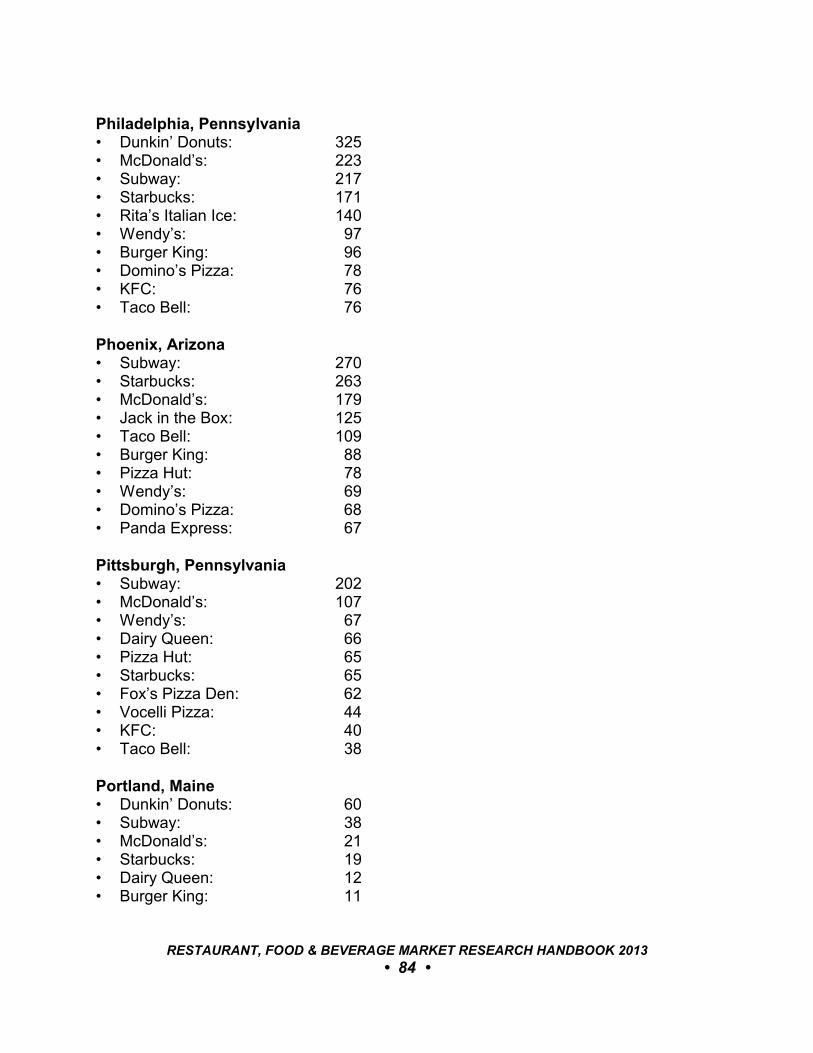

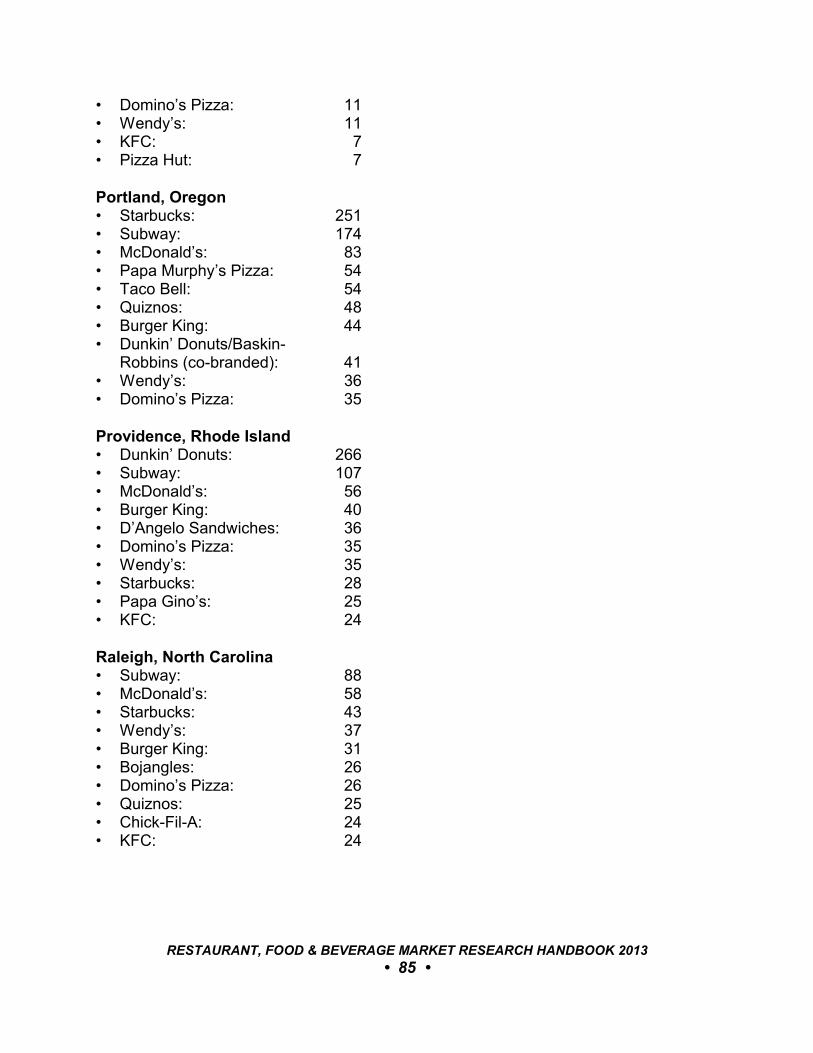

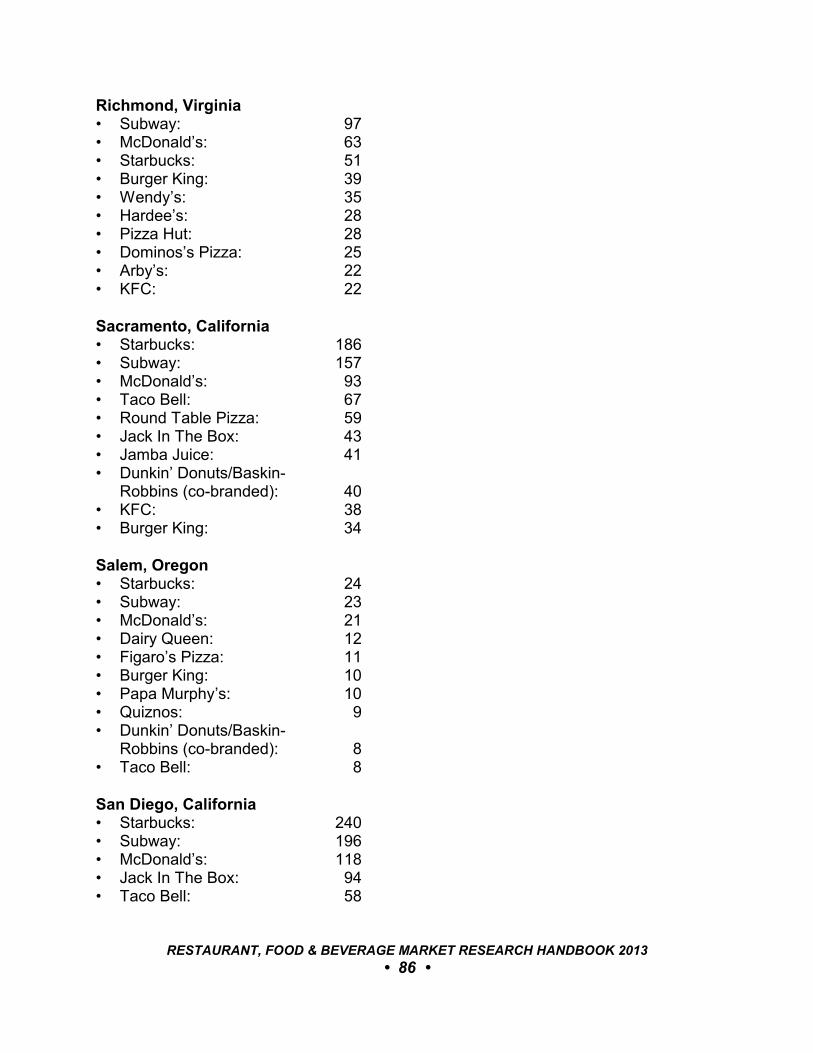

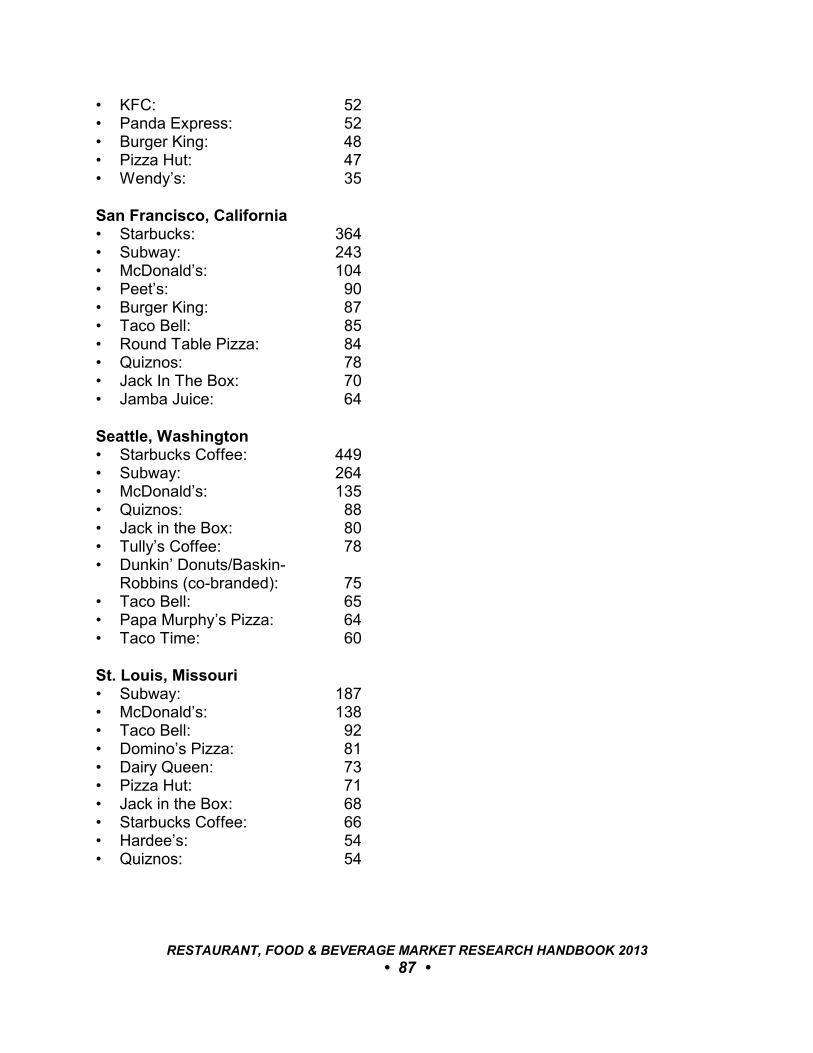

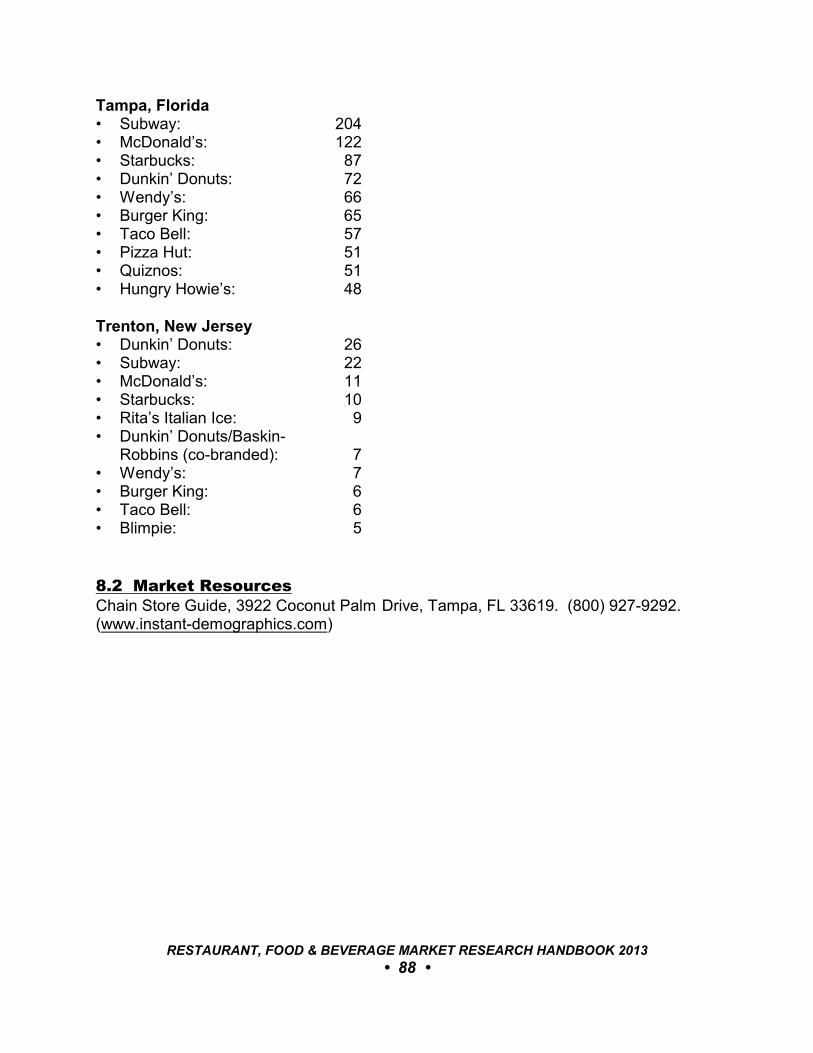

9 LARGEST CHAINS IN METROPOLITAN AREAS. . . . . . . . . . . . . . . . . . . . . . . . . 749.1 Largest Chains and Unit Counts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 748.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

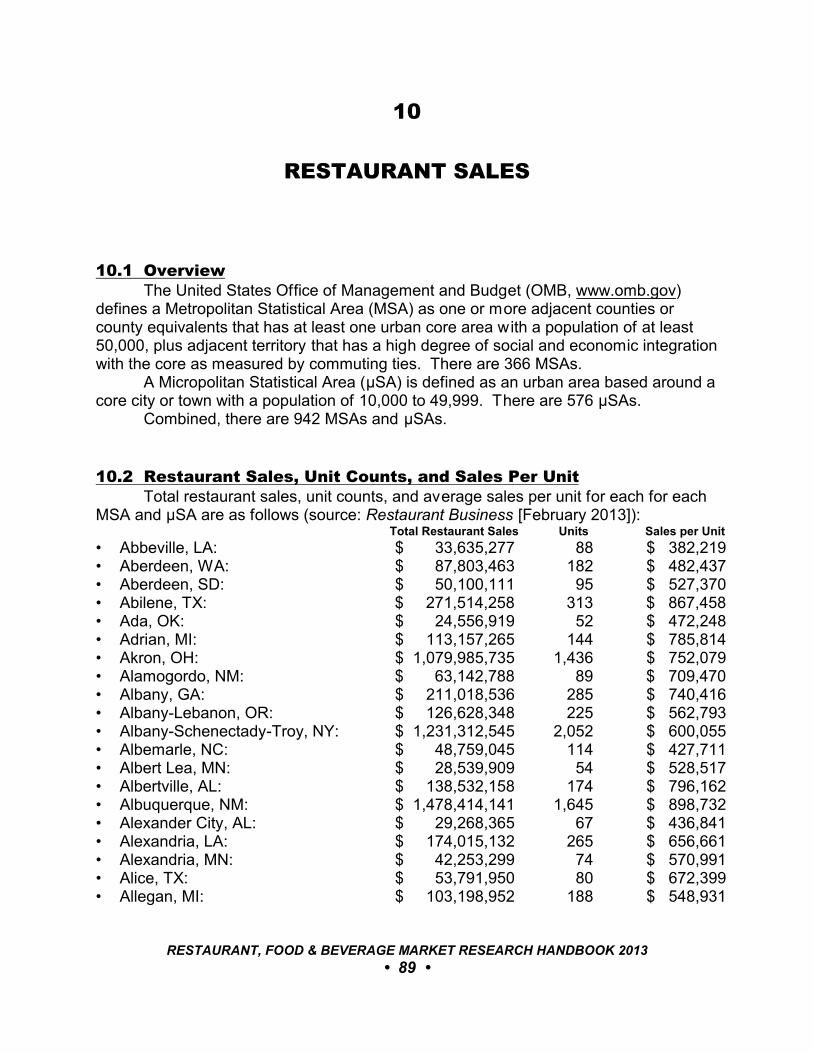

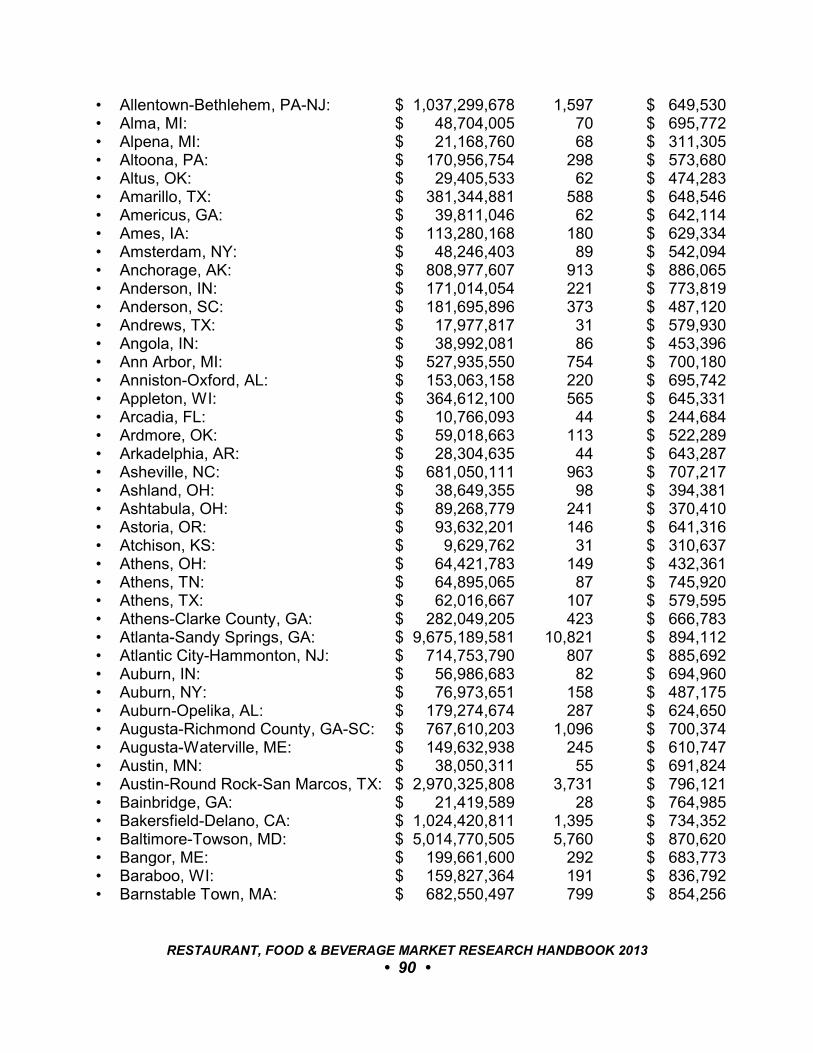

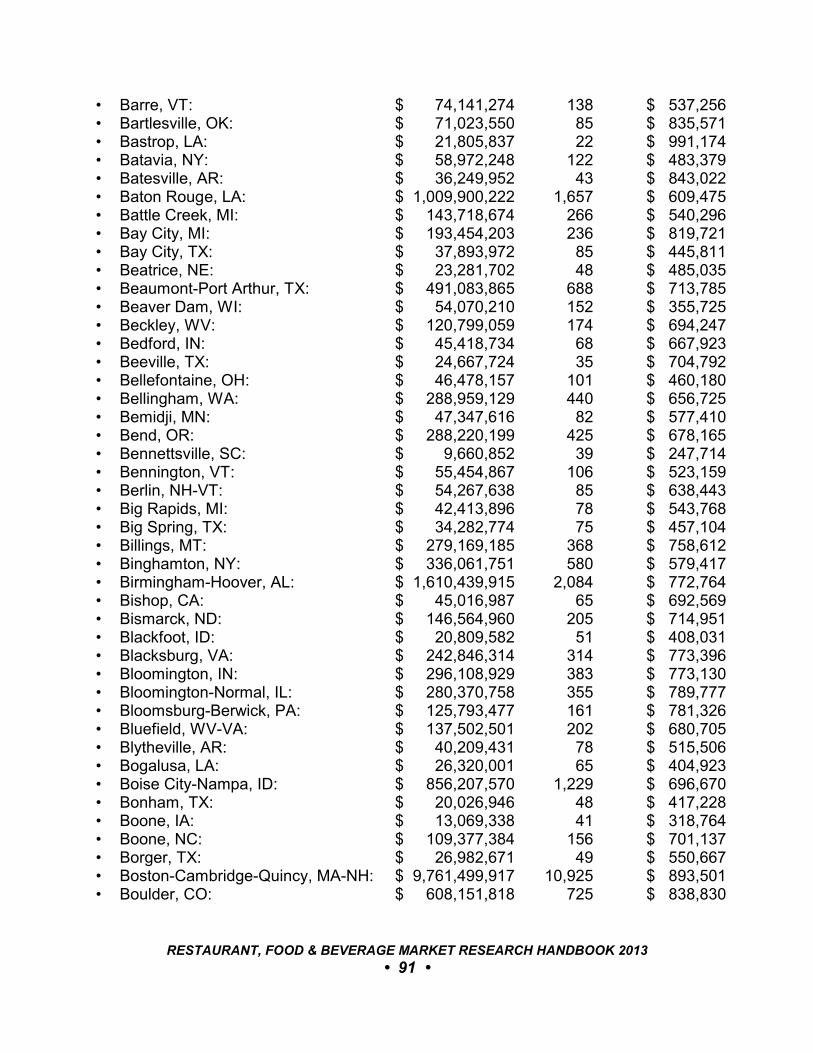

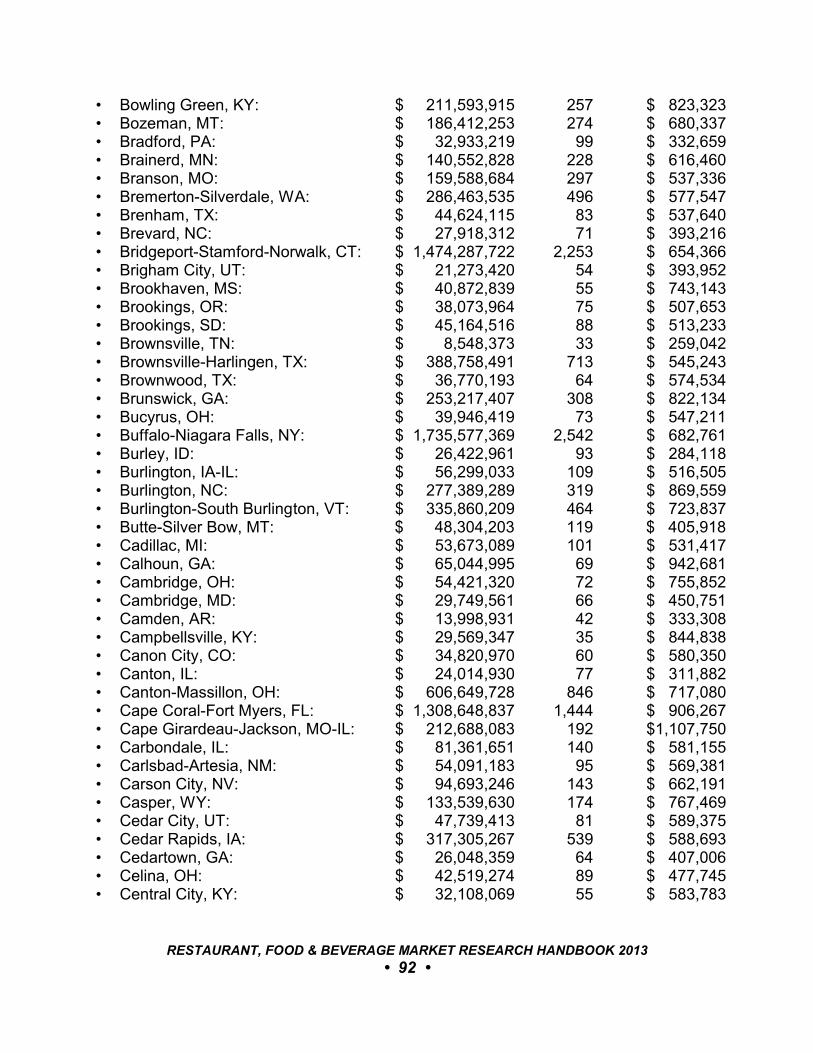

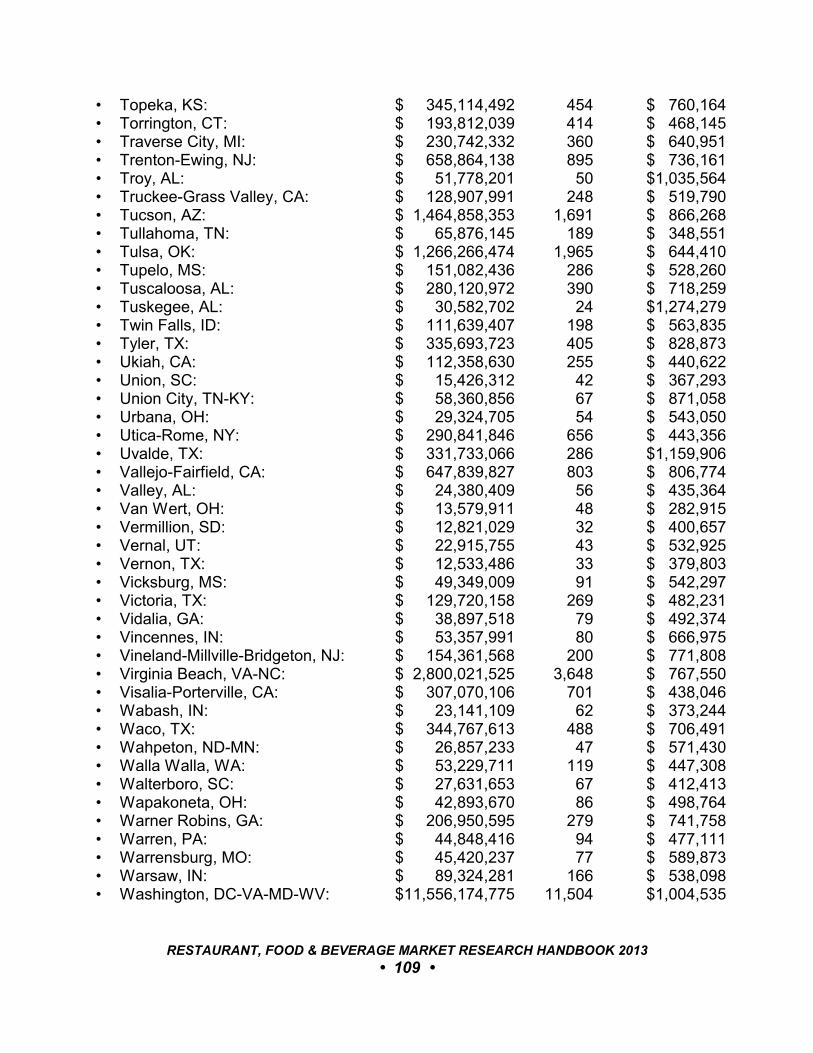

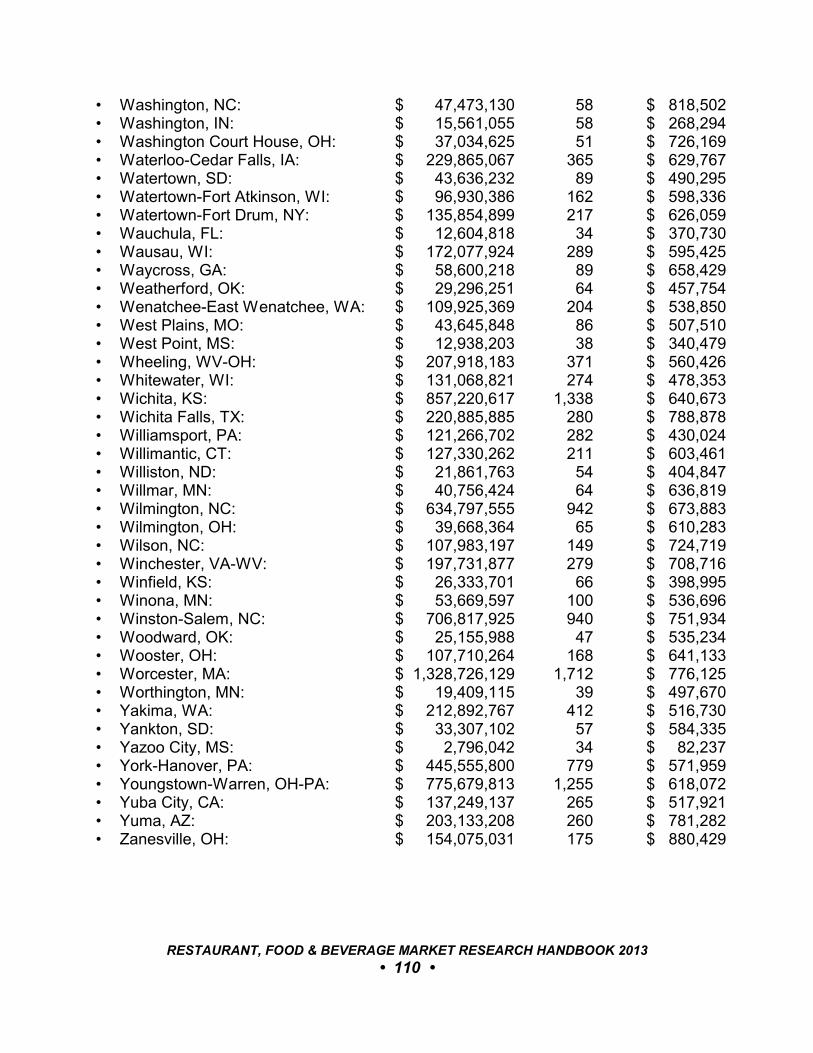

10 RESTAURANT SALES. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8910.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8910.2 Restaurant Sales, Unit Counts, and Sales Per Unit. . . . . . . . . . . . . . . . . . 89

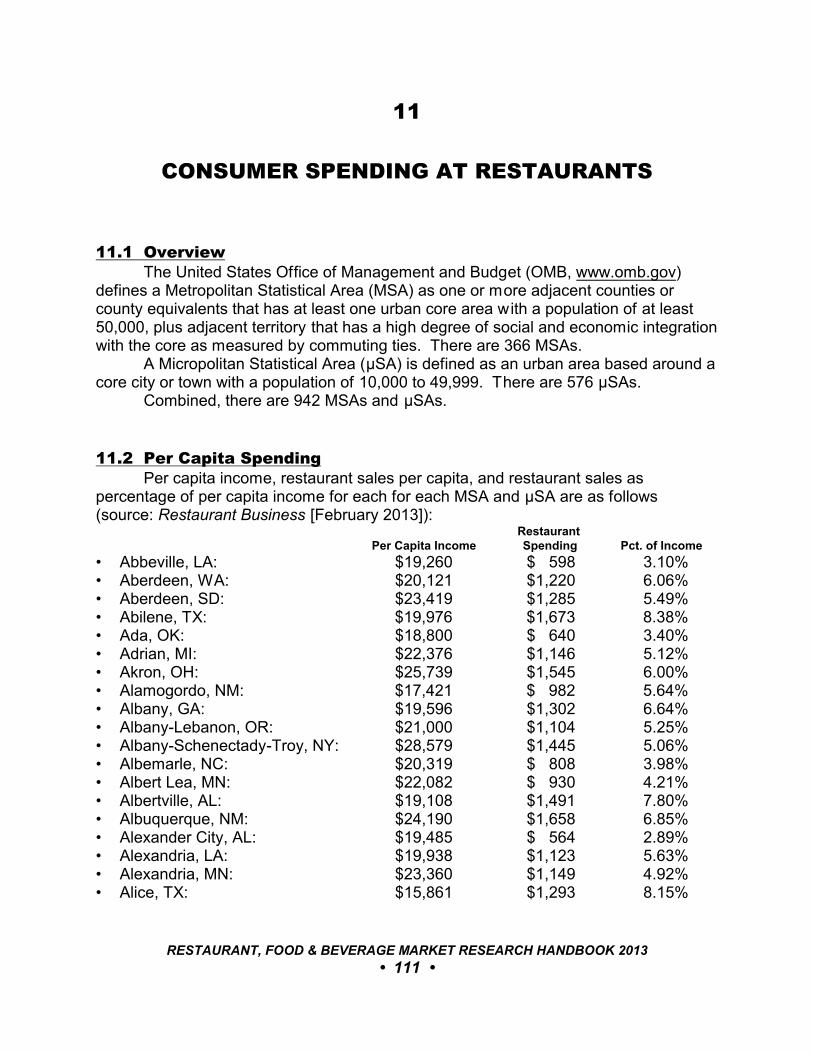

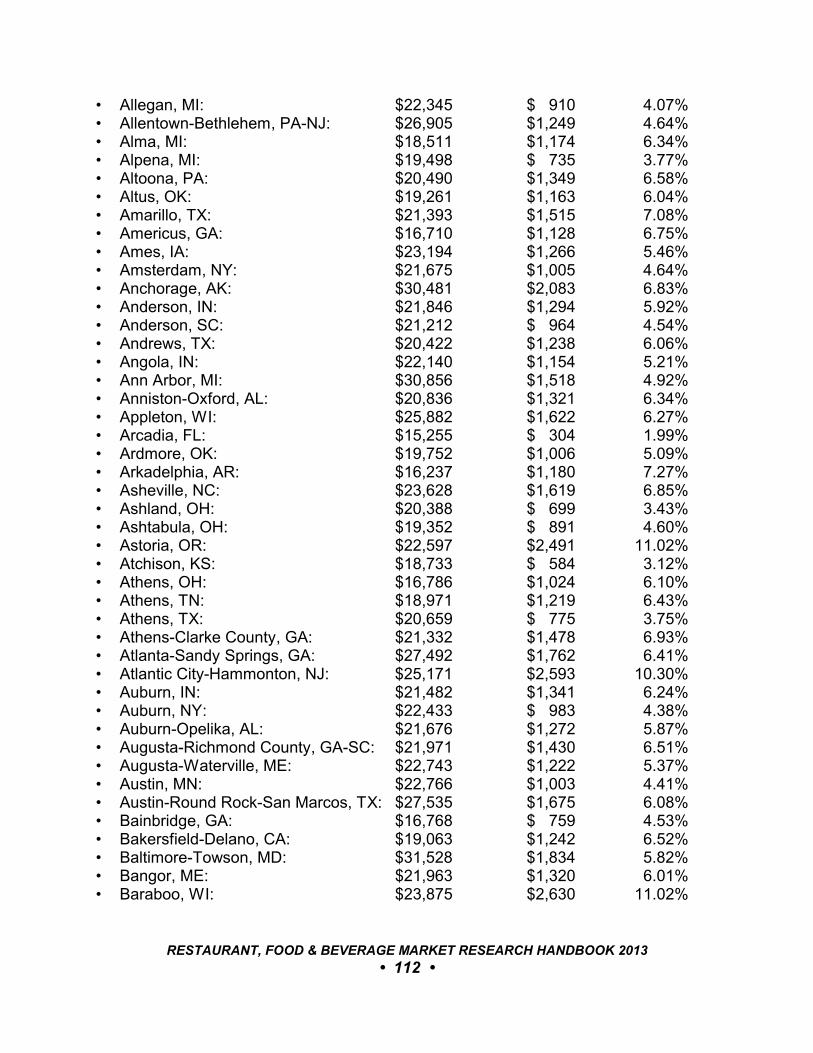

11 CONSUMER SPENDING AT RESTAURANTS. . . . . . . . . . . . . . . . . . . . . . . . . 11111.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11111.2 Per Capita Spending. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

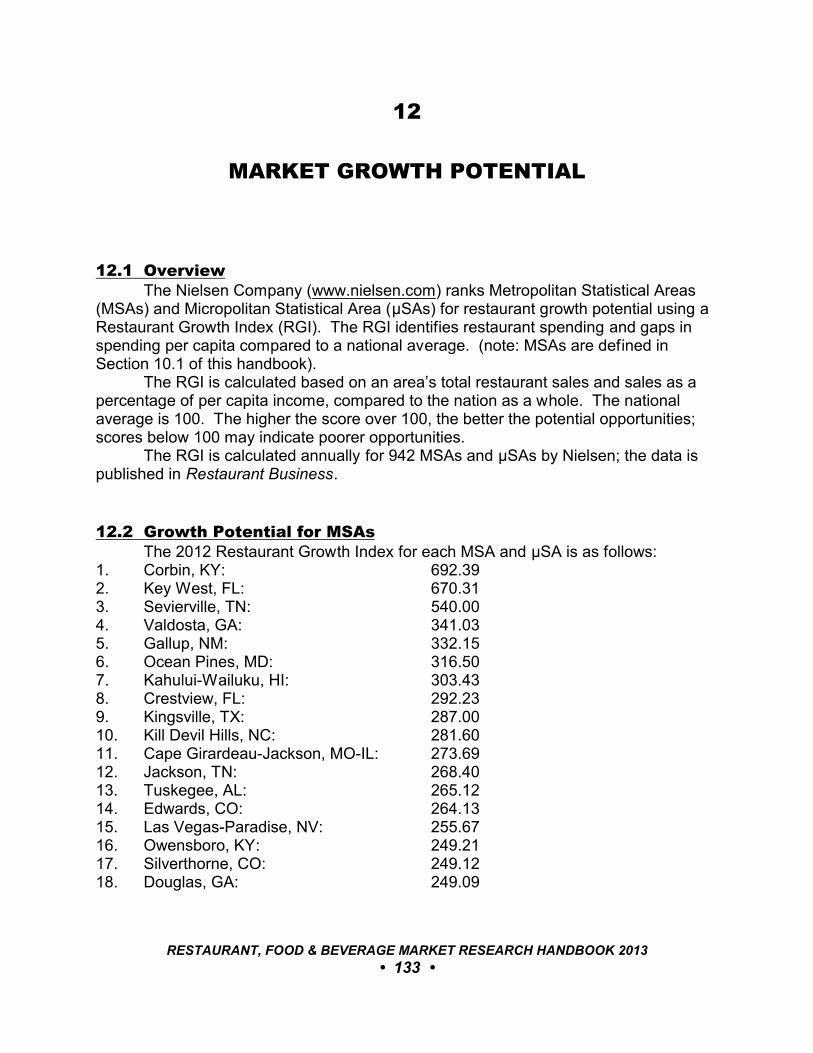

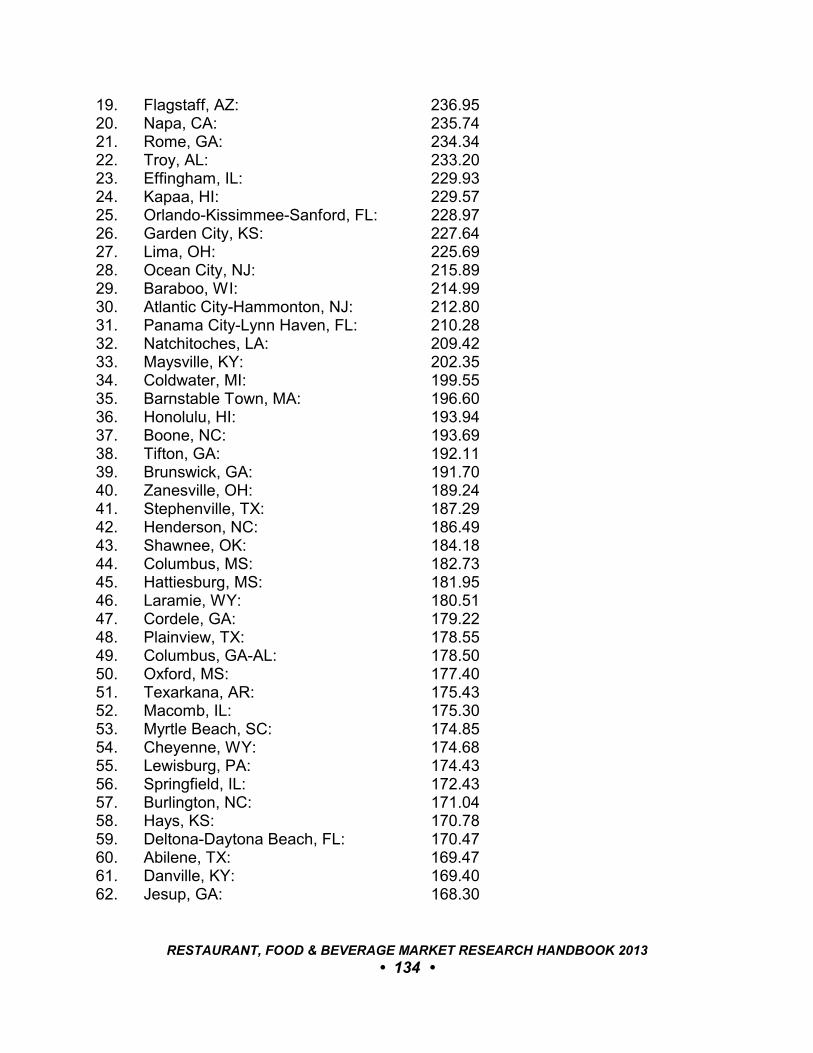

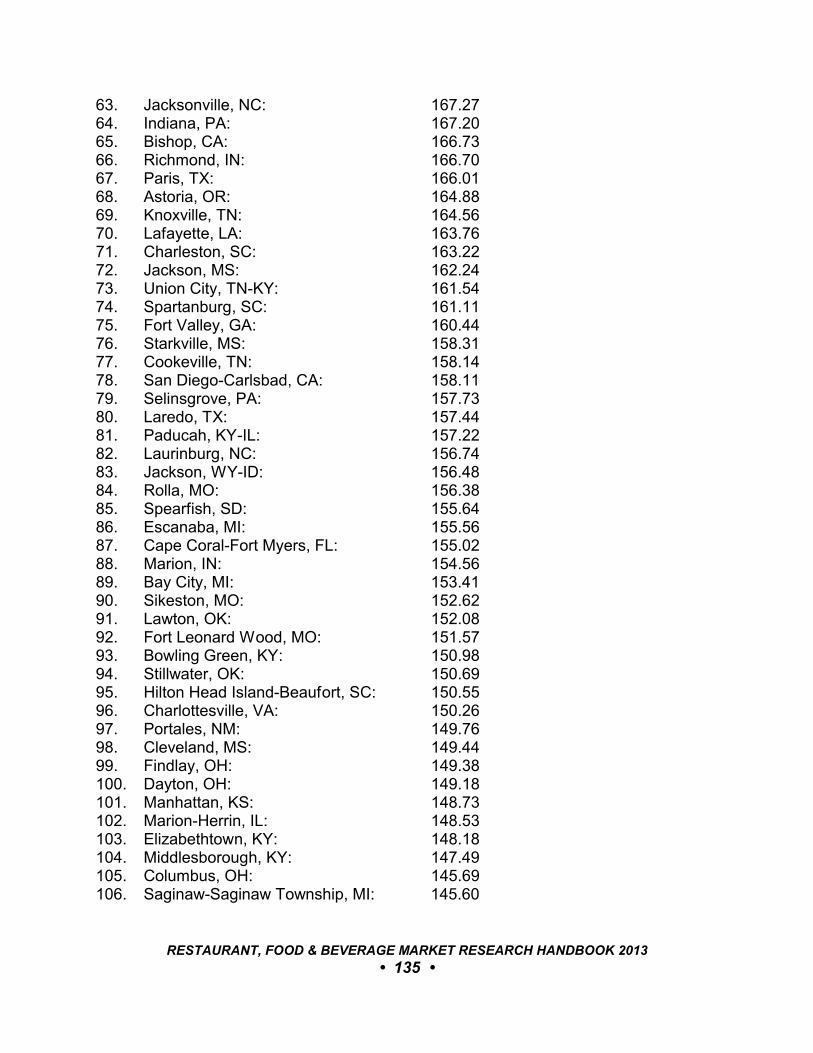

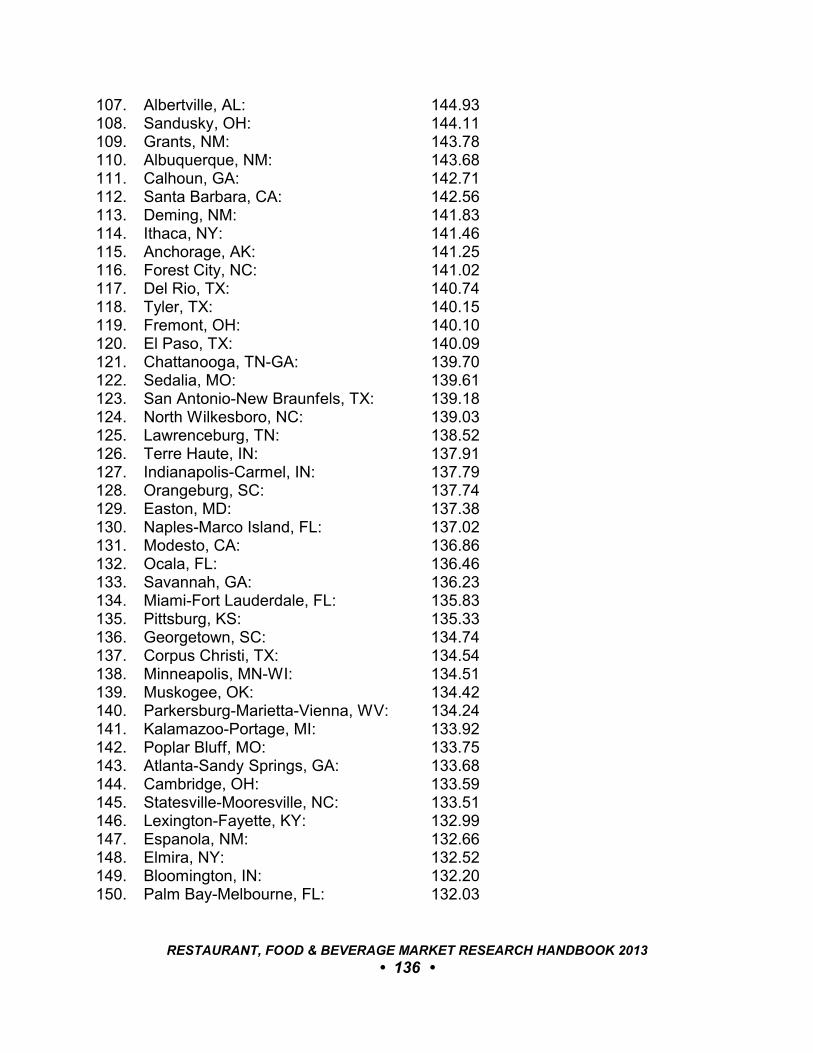

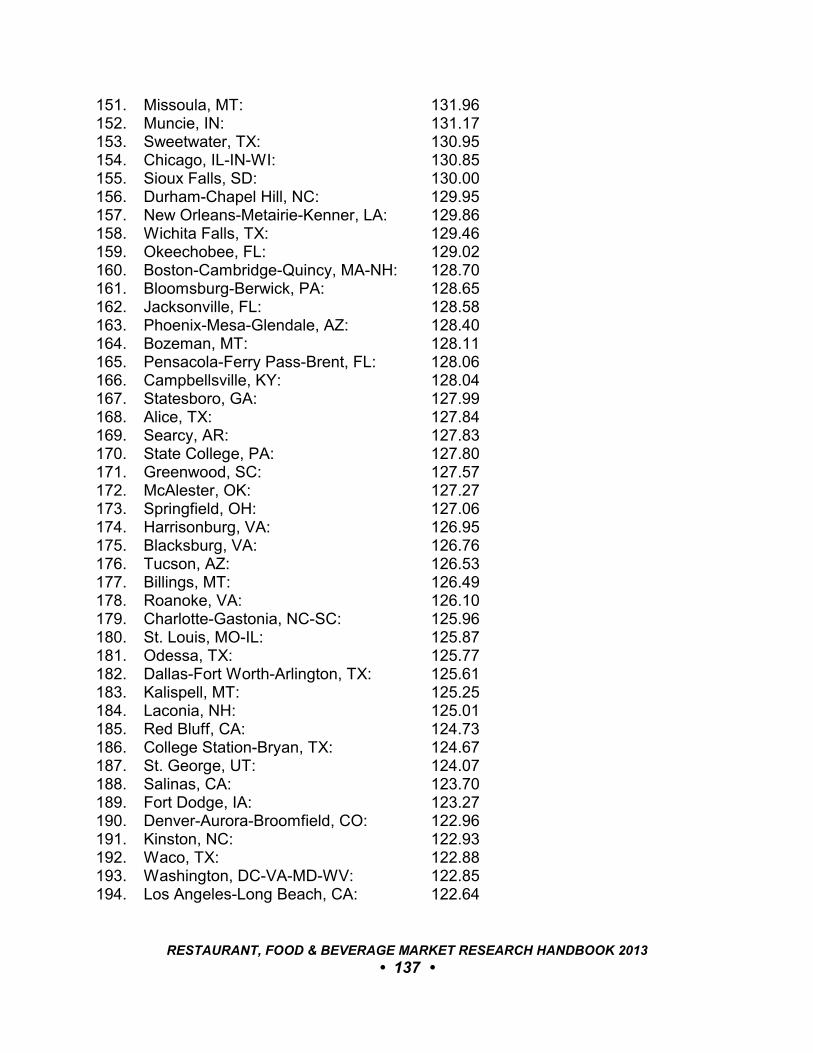

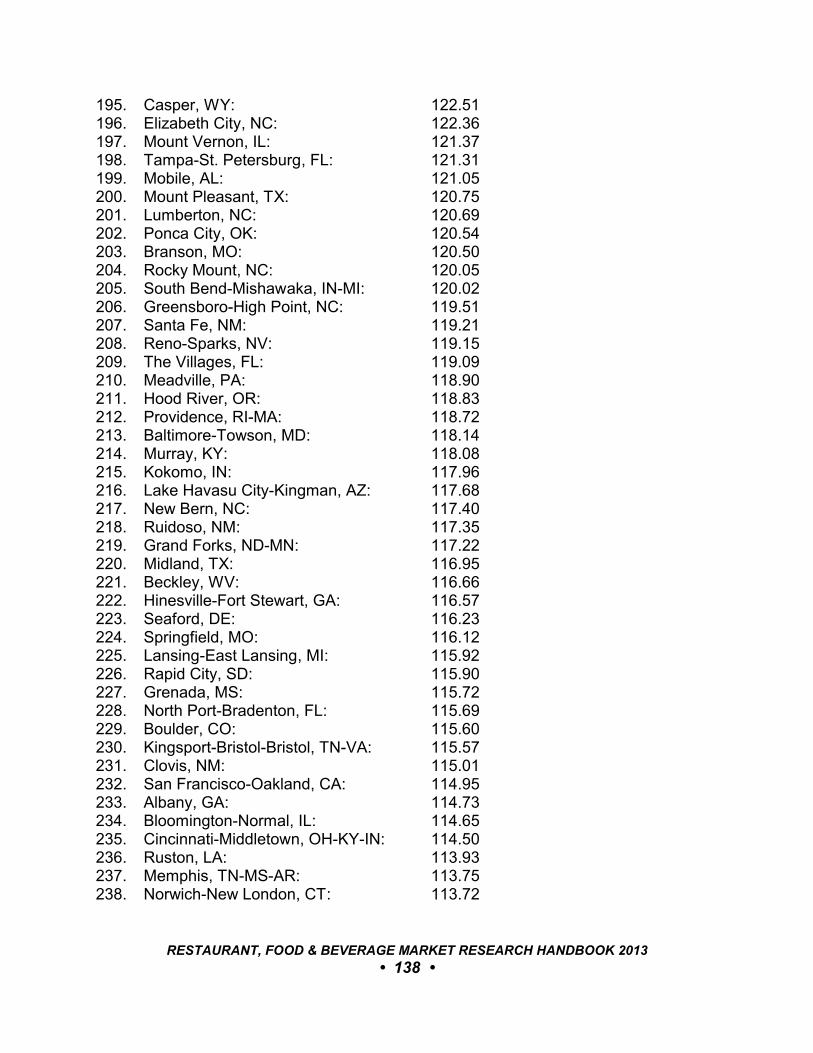

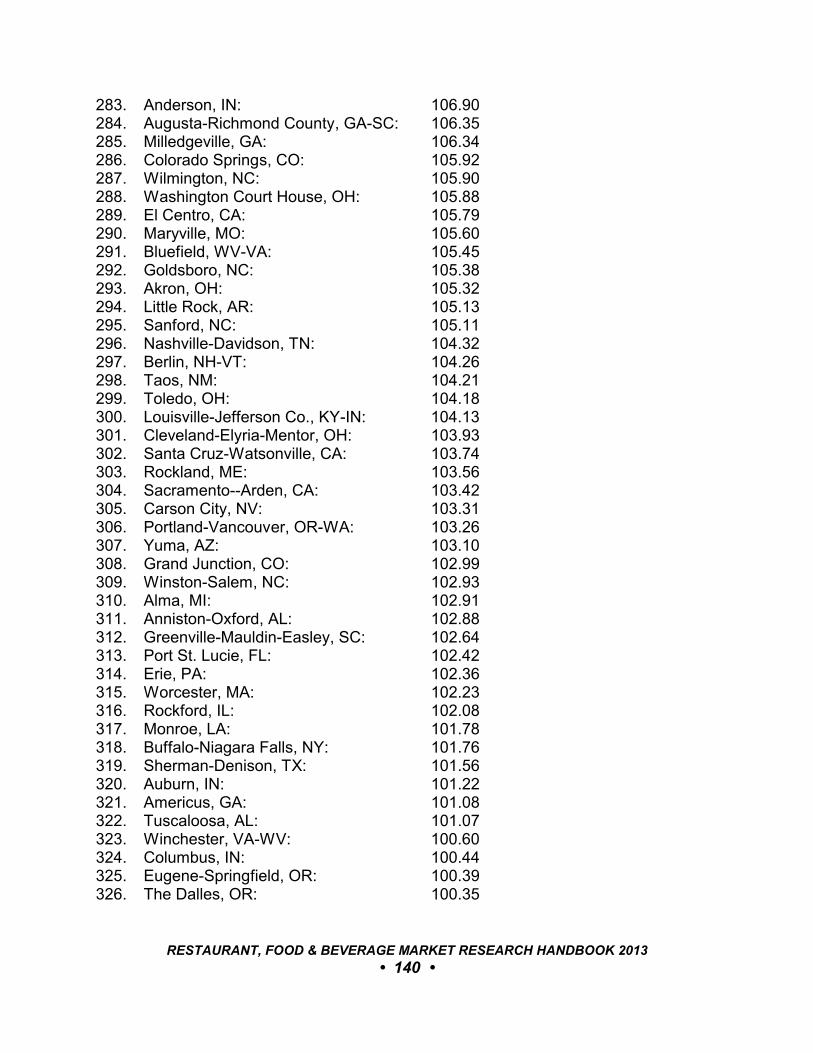

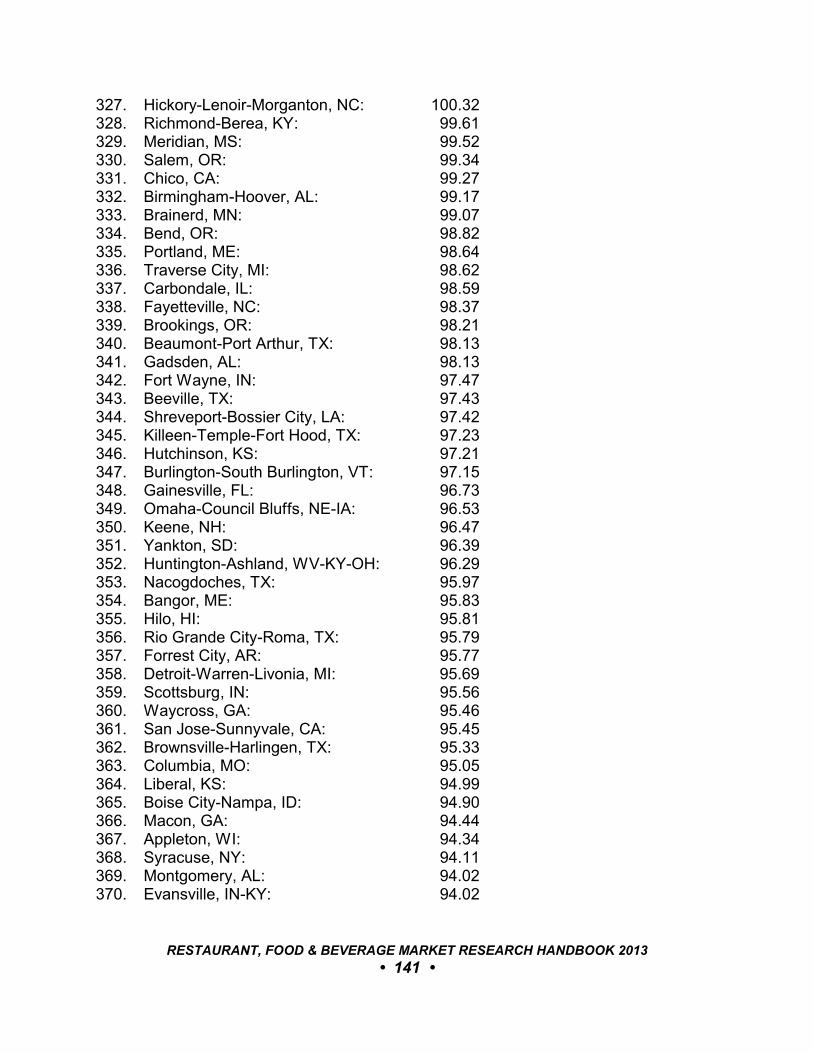

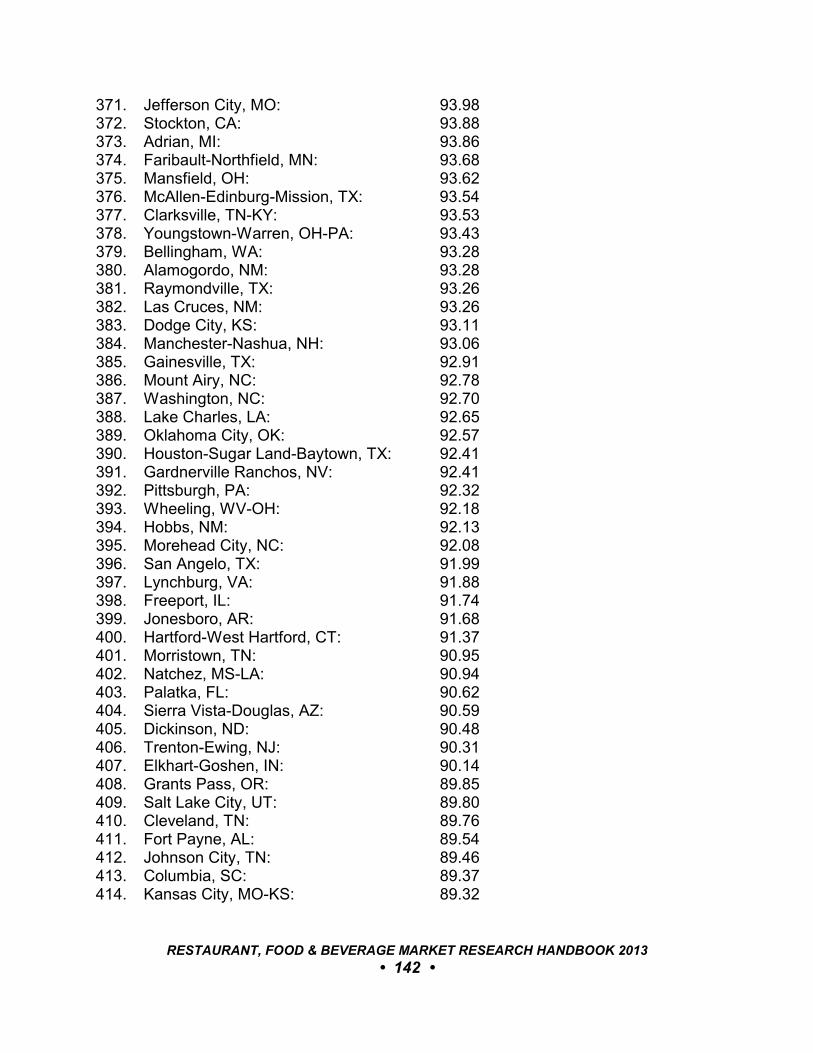

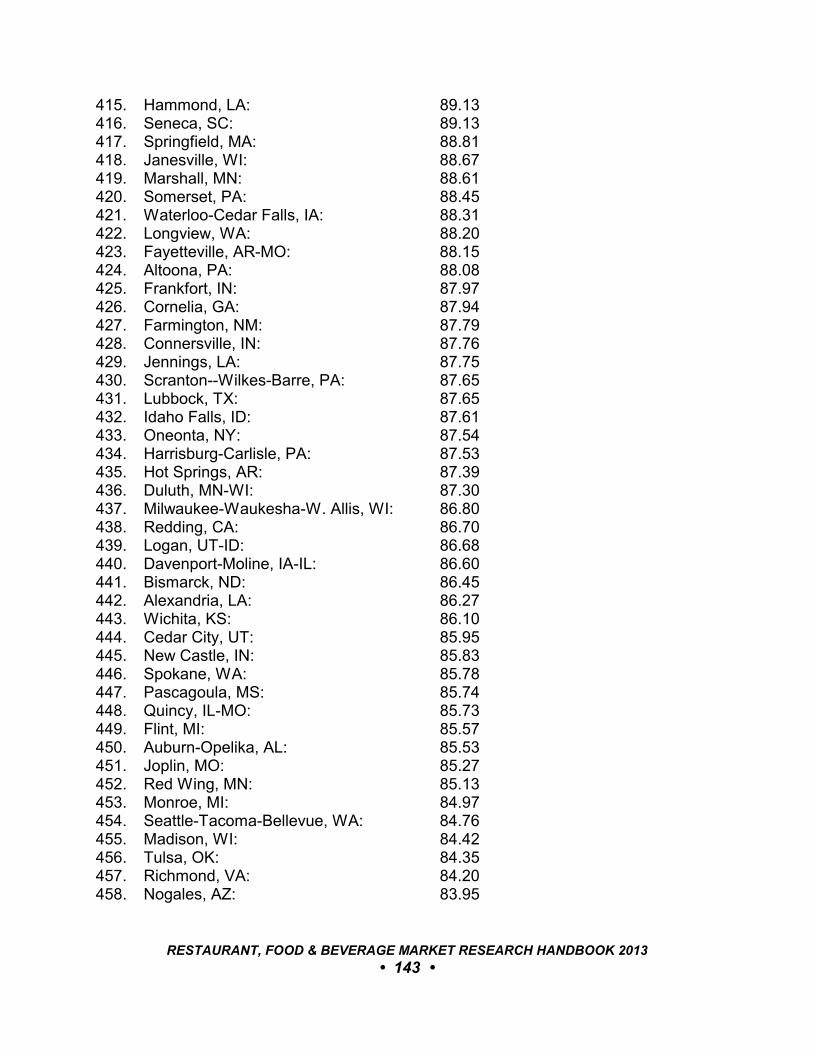

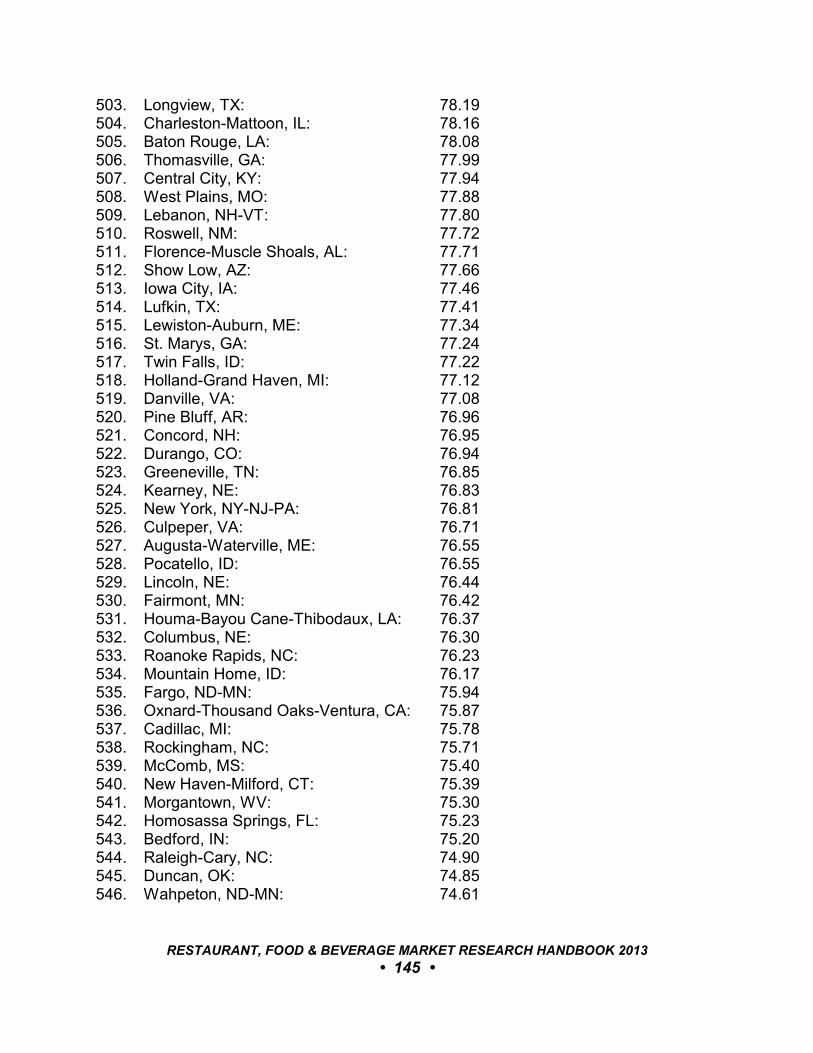

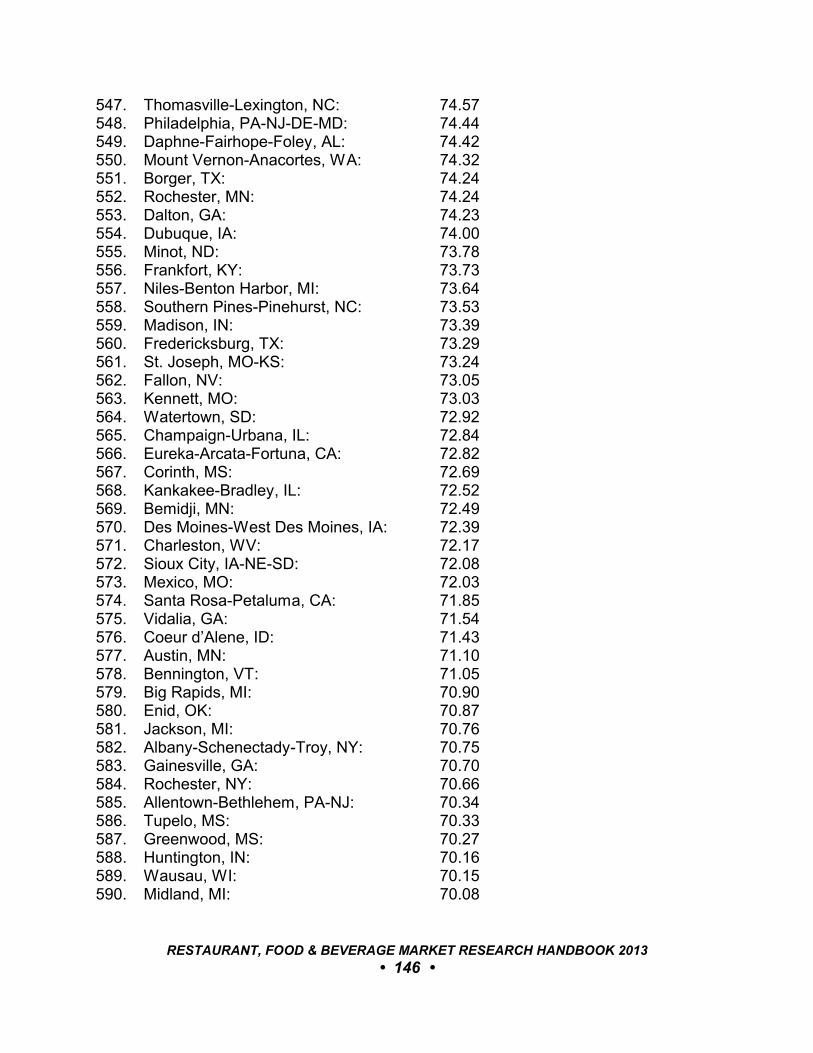

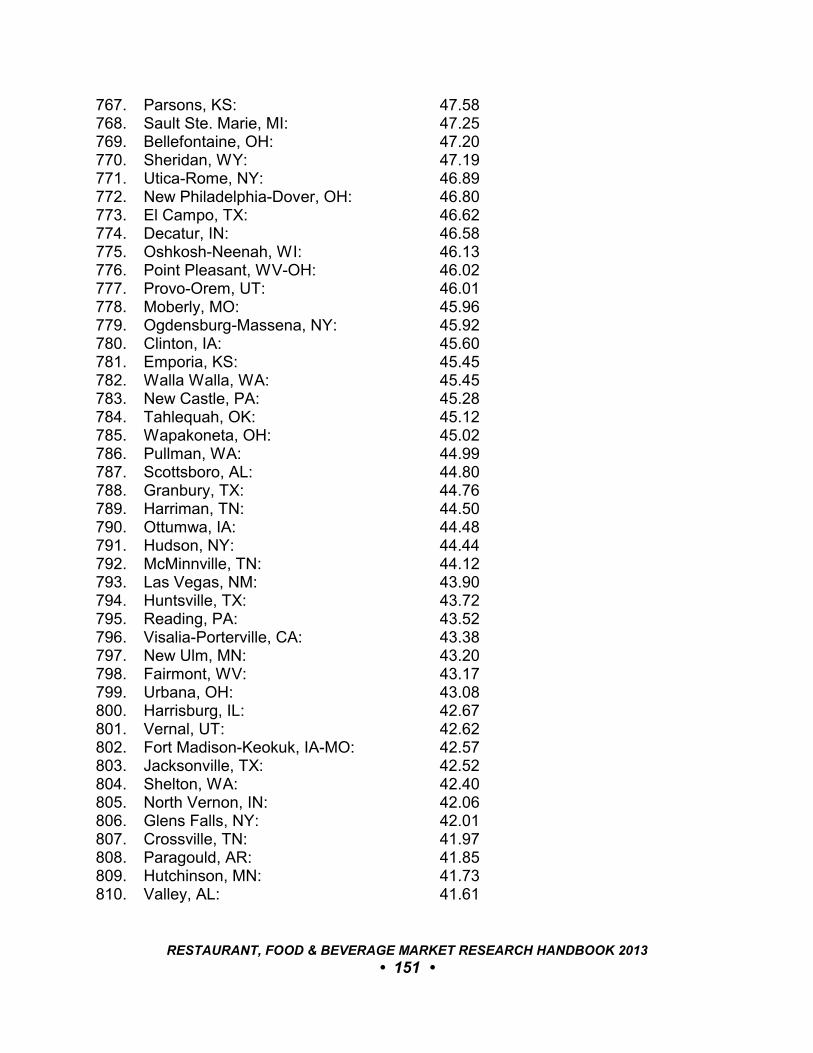

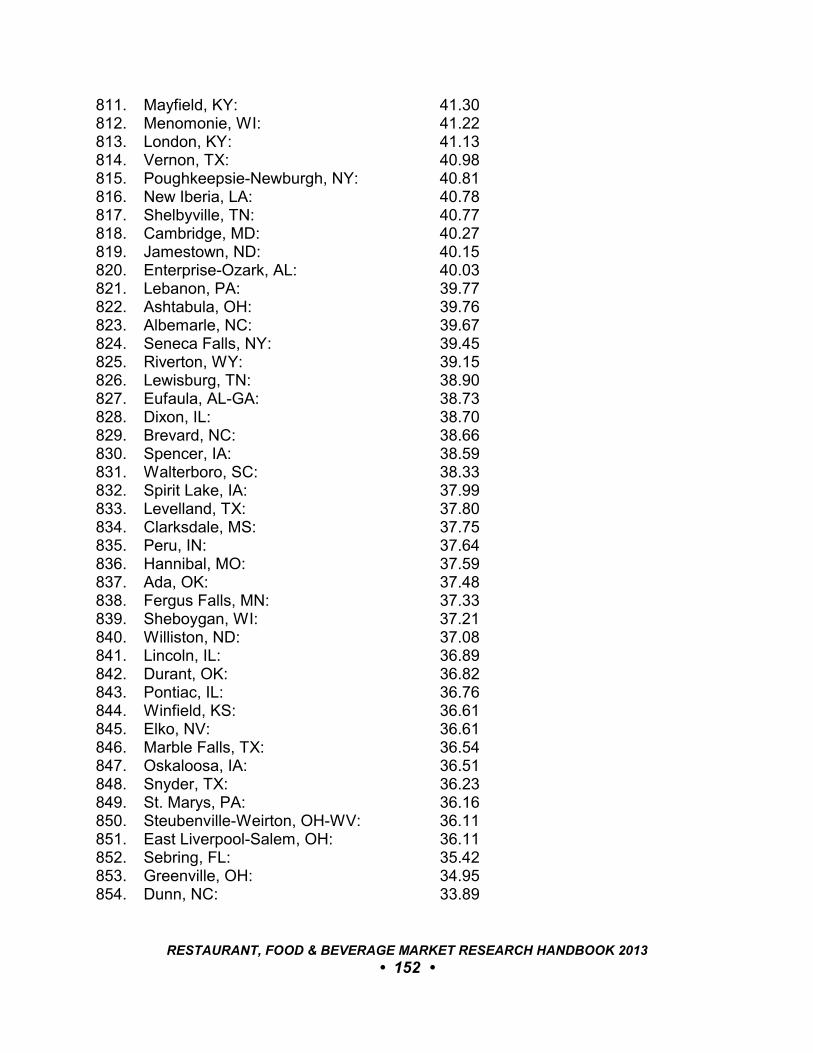

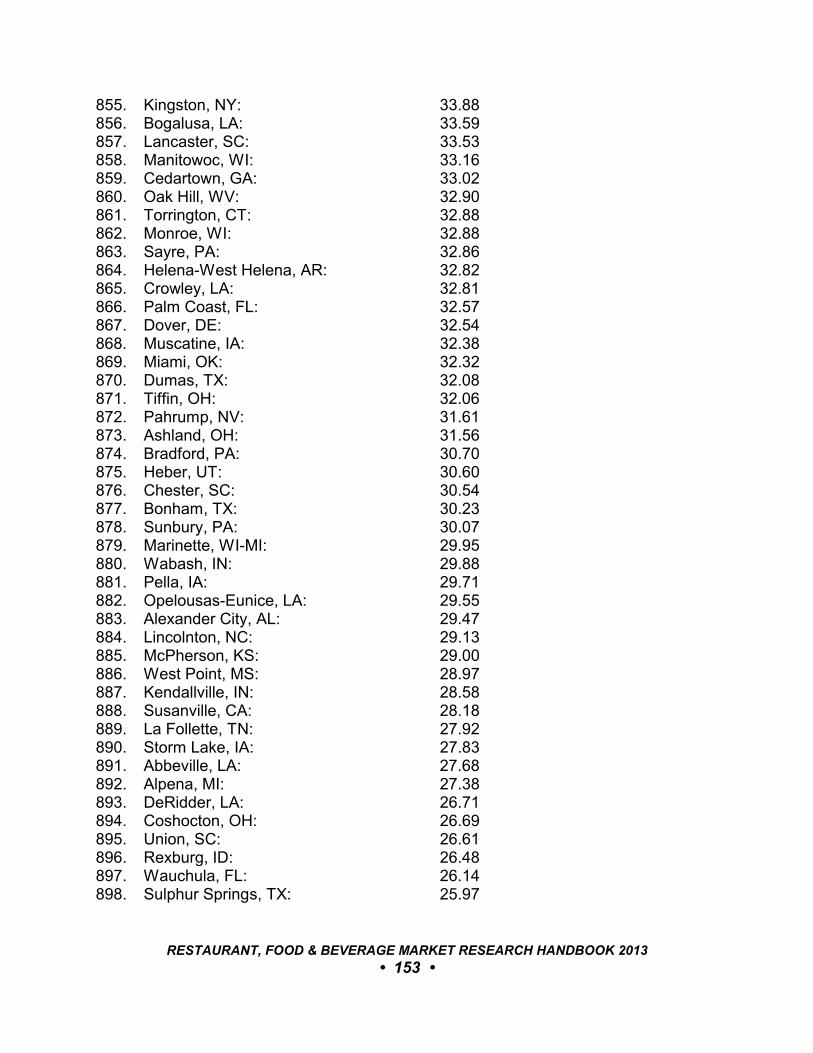

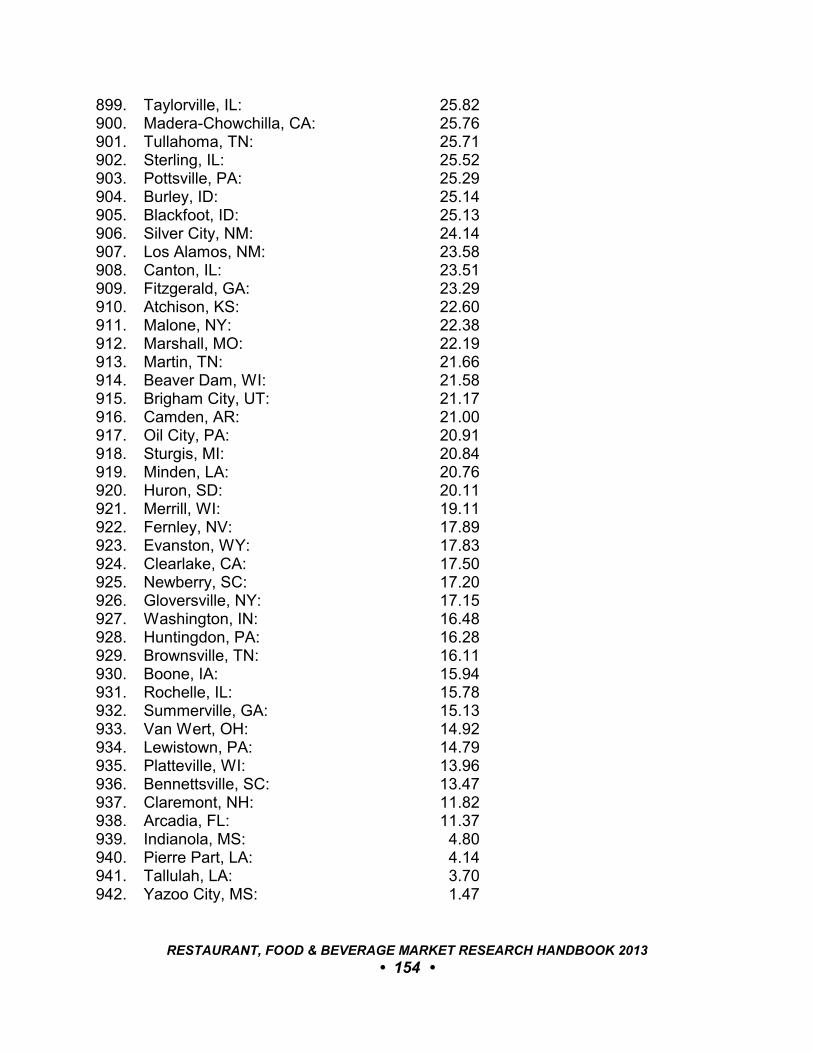

12 MARKET GROWTH POTENTIAL. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13312.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13312.2 Growth Potential for MSAs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13312.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 155

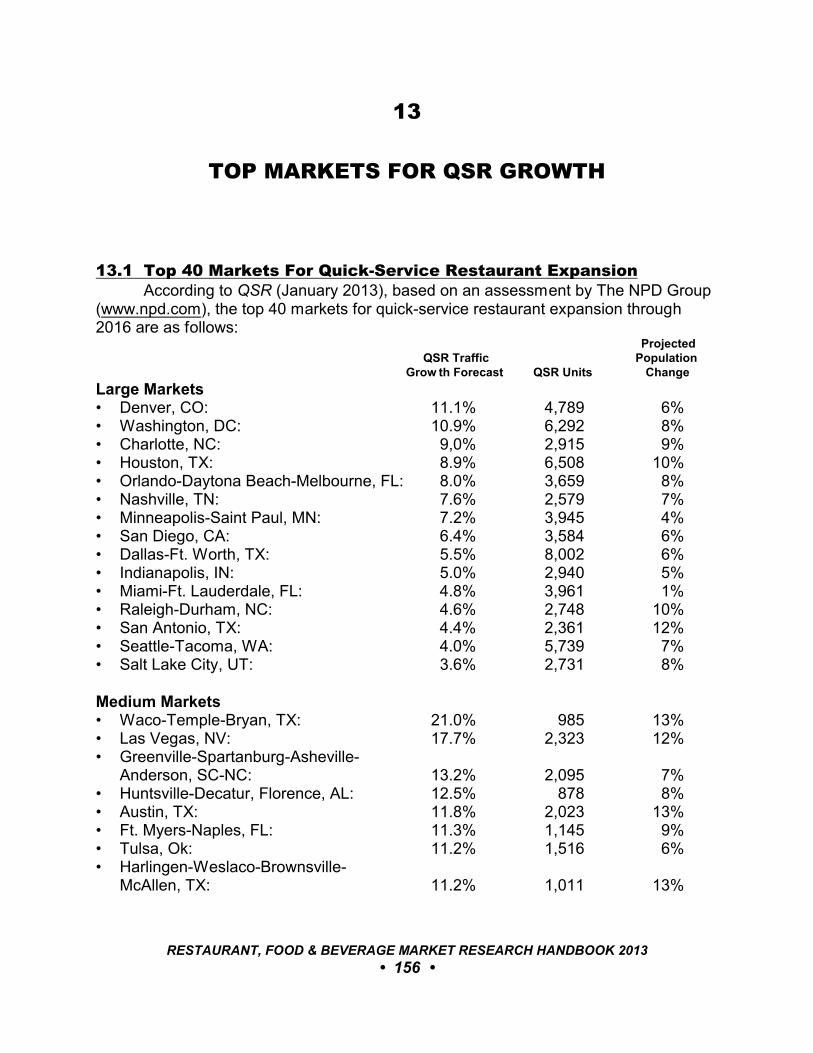

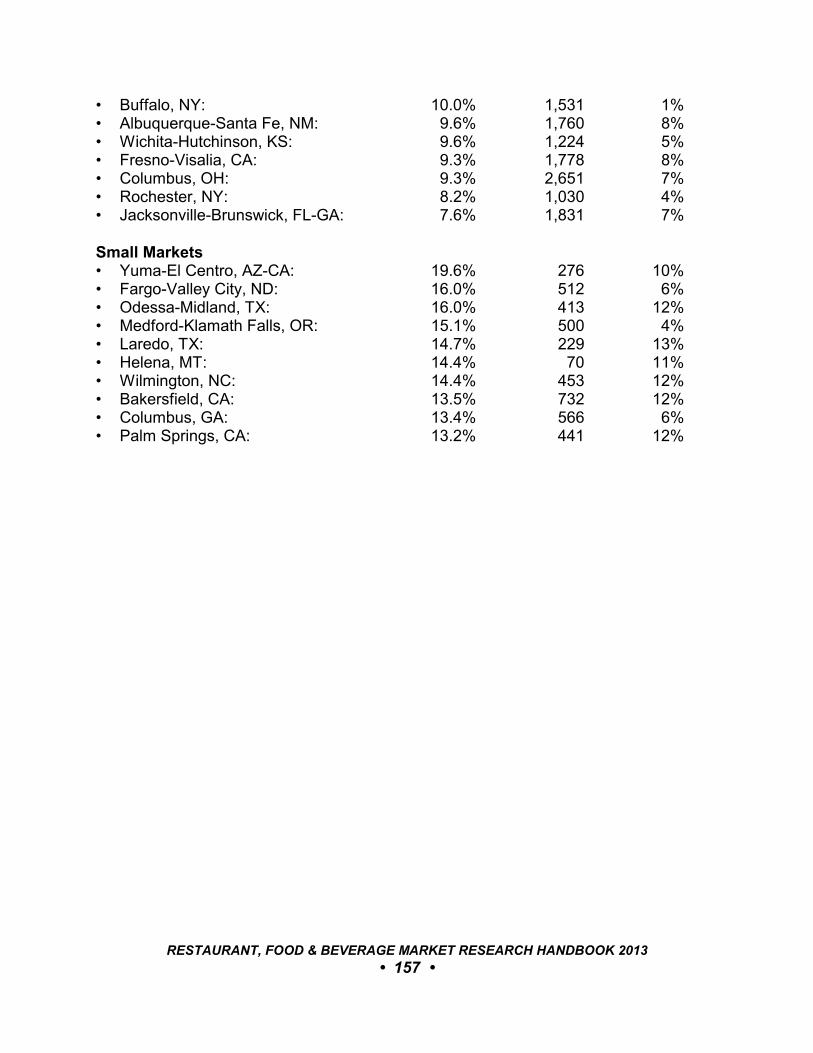

13 TOP MARKETS FOR QSR GROWTH. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15613.1 Top 40 Markets For Quick-Service Restaurant Expansion. . . . . . . . . . . . 156

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 6 •

PART IV: MARKET SEGMENTS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 158

14 CASUAL-DINING RESTAURANTS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15914.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15914.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

15 CATERING & BANQUETS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16115.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16115.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16115.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162

16 COFFEESHOPS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16316.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16316.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

17 CONTRACT-MANAGED FOODSERVICE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16517.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16517.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 166

18 CONVENIENCE STORE FOODSERVICE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16718.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16718.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 167

19 FAMILY-DINING RESTAURANTS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16919.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16919.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169

20 FAST-CASUAL RESTAURANTS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17120.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17120.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17120.3 Comparison of Quick-Service and Fast-Casual.. . . . . . . . . . . . . . . . . . . . 173

21 FINE-DINING. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17521.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17521.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

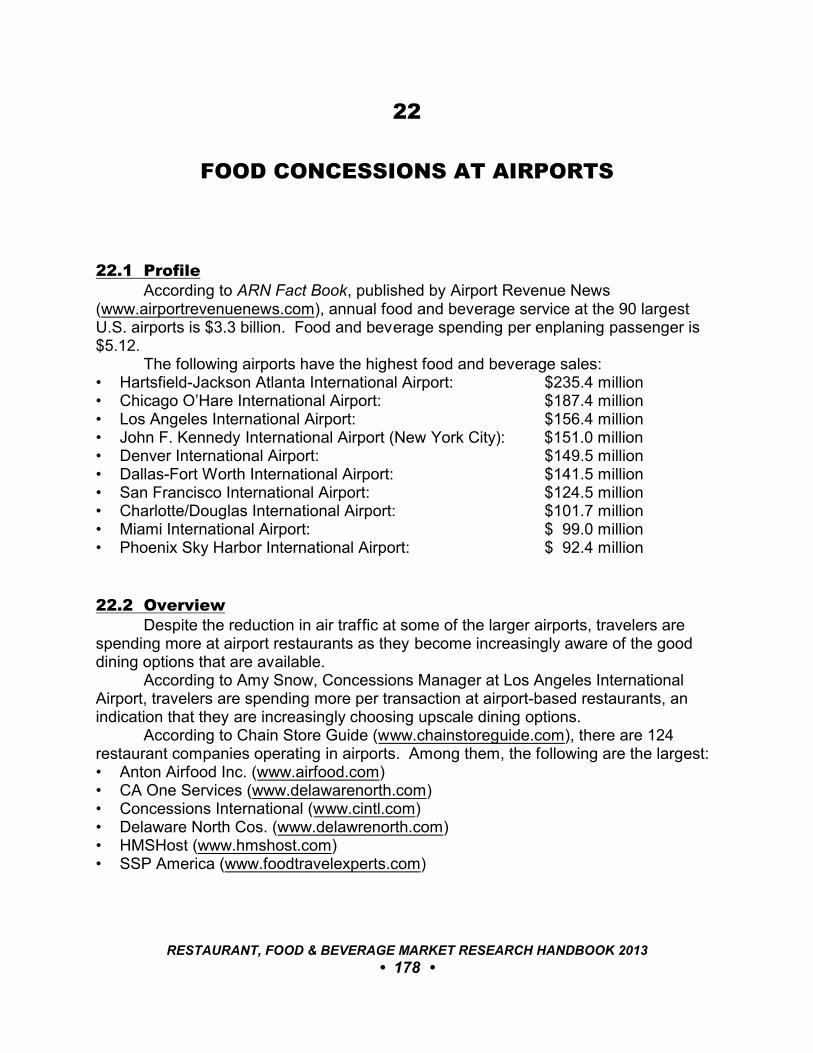

22 FOOD CONCESSIONS AT AIRPORTS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17822.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17822.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17822.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 181

23 FOOD CONCESSIONS AT SPORTS VENUES.. . . . . . . . . . . . . . . . . . . . . . . . 18223.1 Market Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18223.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 7 •

24 FOOD TRUCKS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18424.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18424.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 184

25 MALL-BASED RESTAURANTS & FOOD COURTS. . . . . . . . . . . . . . . . . . . . . 18725.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18725.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18725.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 188

26 PIZZA. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18926.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18926.2 Trends. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 189

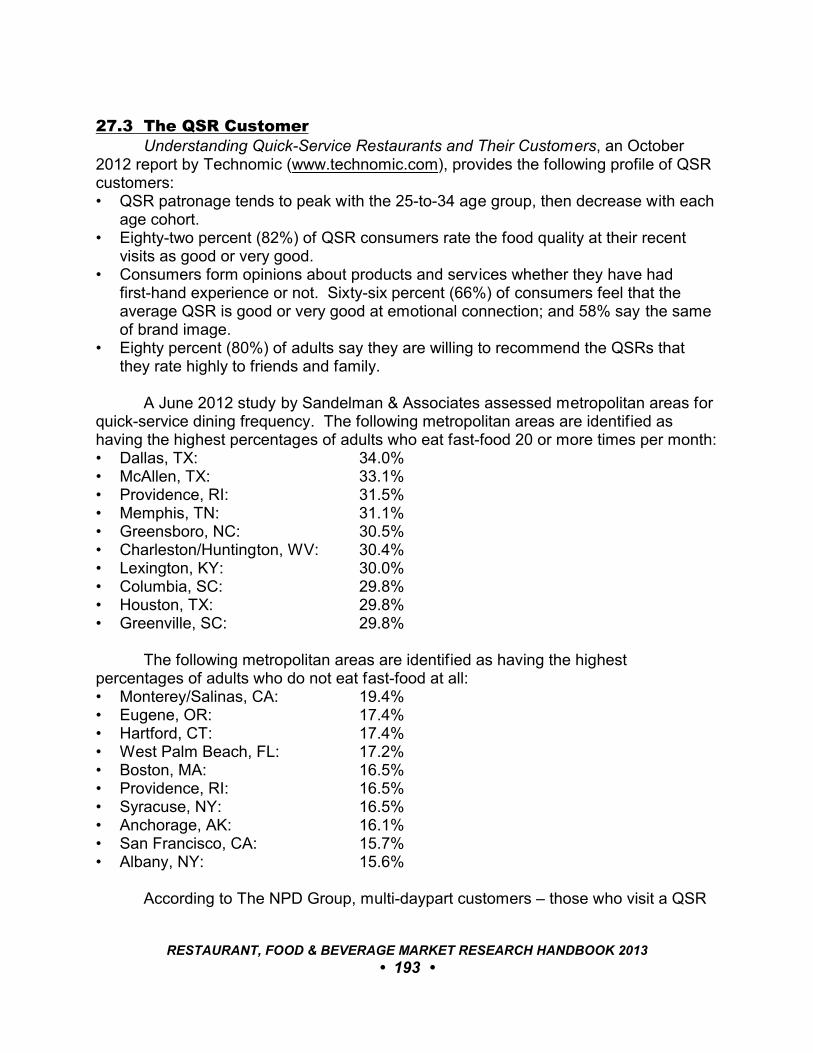

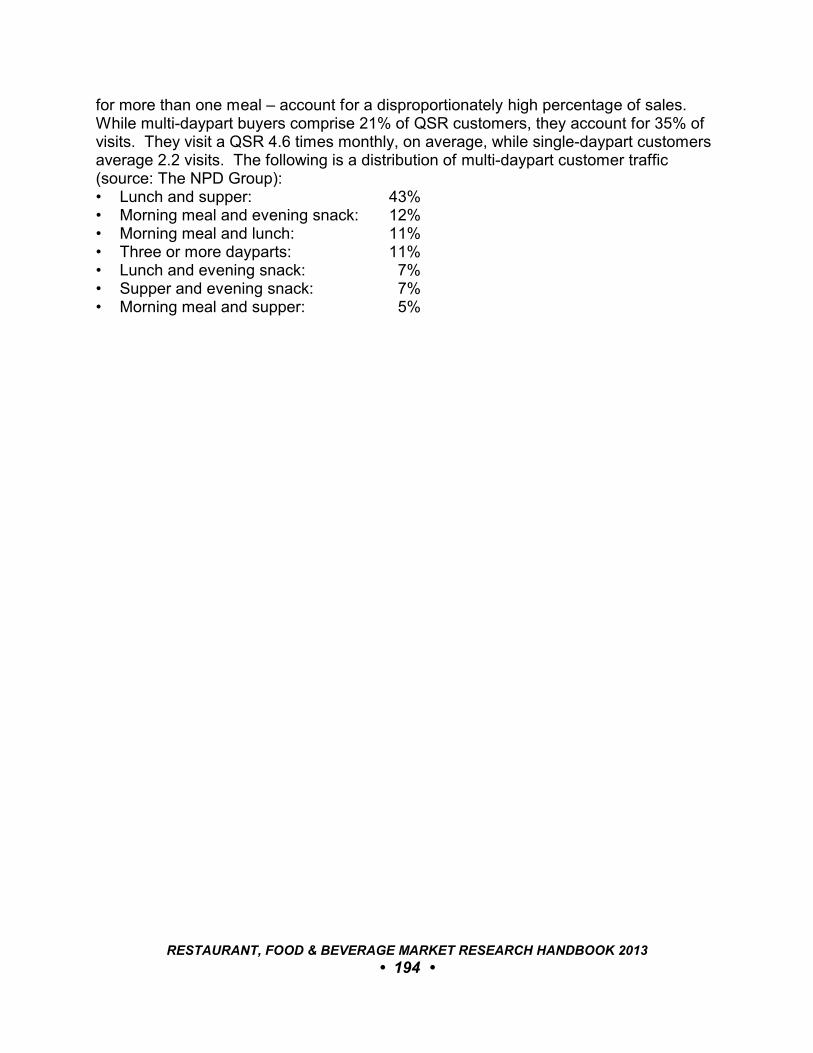

27 QUICK-SERVICE RESTAURANTS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19127.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19127.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19127.3 The QSR Customer. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 193

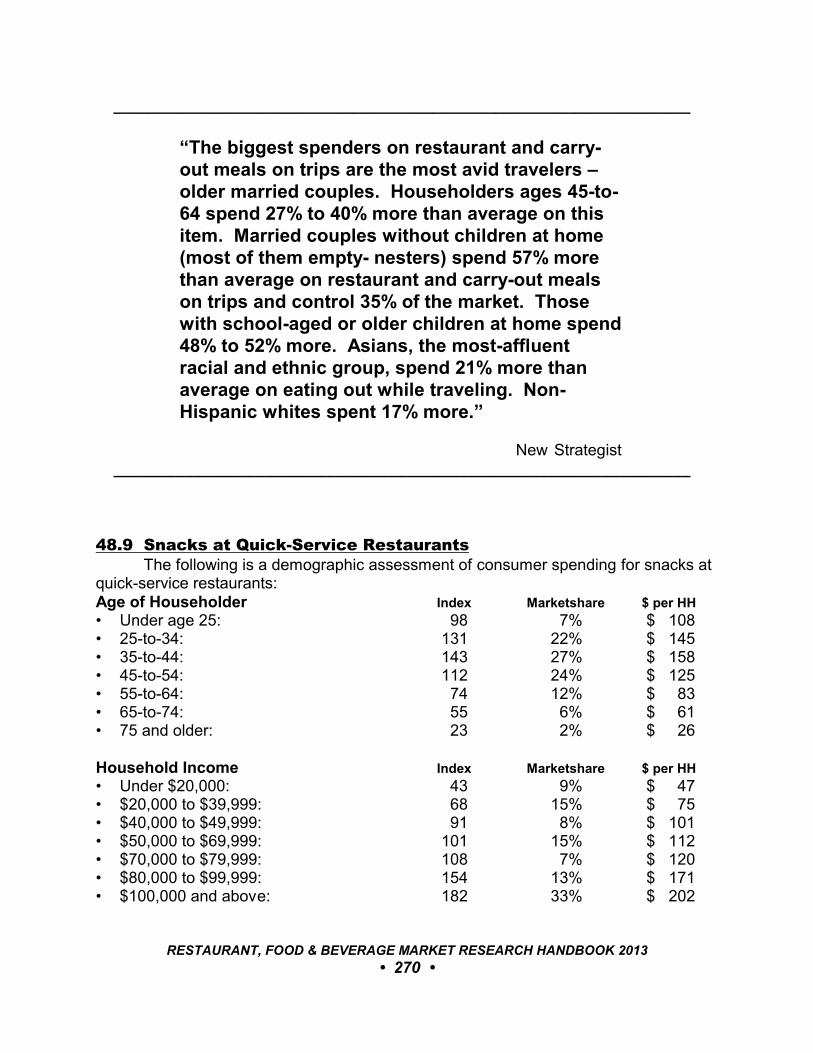

28 SNACKS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19528.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19528.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19528.3 Trends. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 196

29 SUPERMARKET FOODSERVICE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19829.1 Profile. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19829.2 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19829.3 Trends. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 199

PART V: MARKET LEADERS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 201

30 LARGEST BAKERY CAFE CHAINS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20230.1 Largest Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20230.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 202

31 LARGEST BURGER CHAINS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20331.1 Largest Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20331.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 205

32 LARGEST FAMILY-DINING CHAINS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20632.1 Largest Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20632.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 206

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 8 •

33 LARGEST FAST-CASUAL RESTAURANT CHAINS.. . . . . . . . . . . . . . . . . . . . 20733.1 Largest Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20733.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 209

34 LARGEST MEXICAN RESTAURANT CHAINS. . . . . . . . . . . . . . . . . . . . . . . . . 21034.1 Largest Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21034.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 211

35 LARGEST PIZZA CHAINS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21235.1 Largest Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21235.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 214

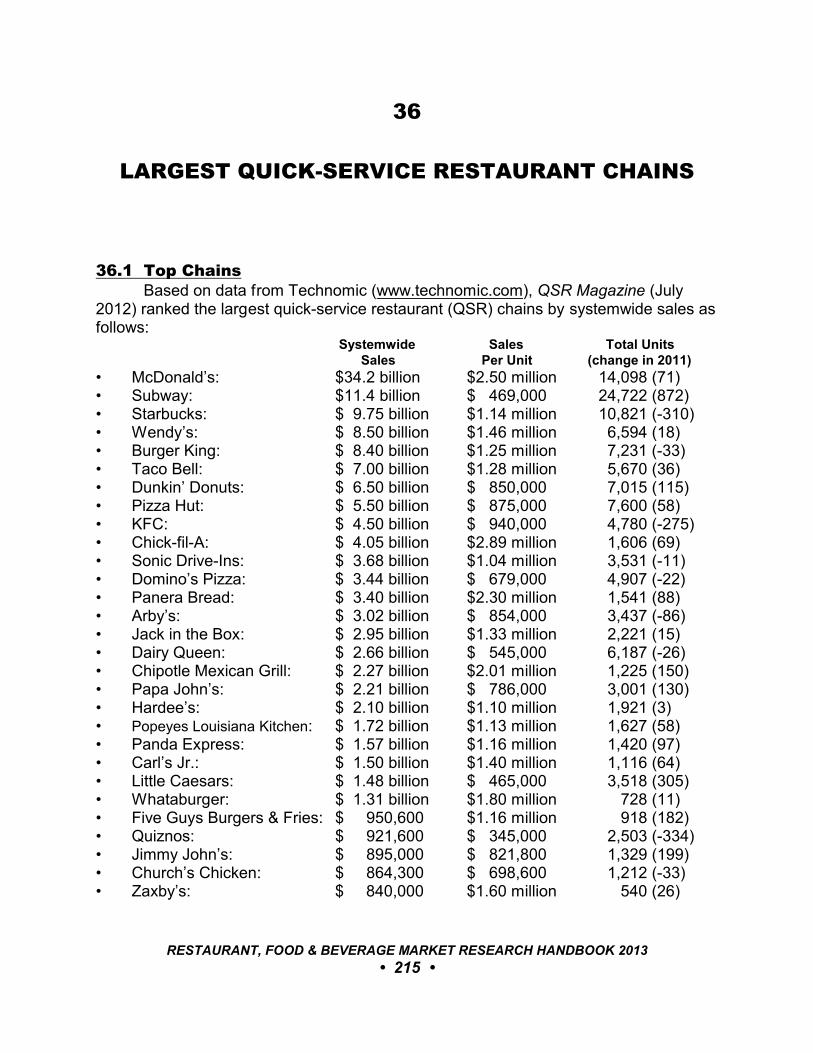

36 LARGEST QUICK-SERVICE RESTAURANT CHAINS. . . . . . . . . . . . . . . . . . . 21536.1 Top Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21536.2 Largest QSR Chains By Category. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 216

37 LARGEST SANDWICH CHAINS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21937.1 Largest Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21937.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 221

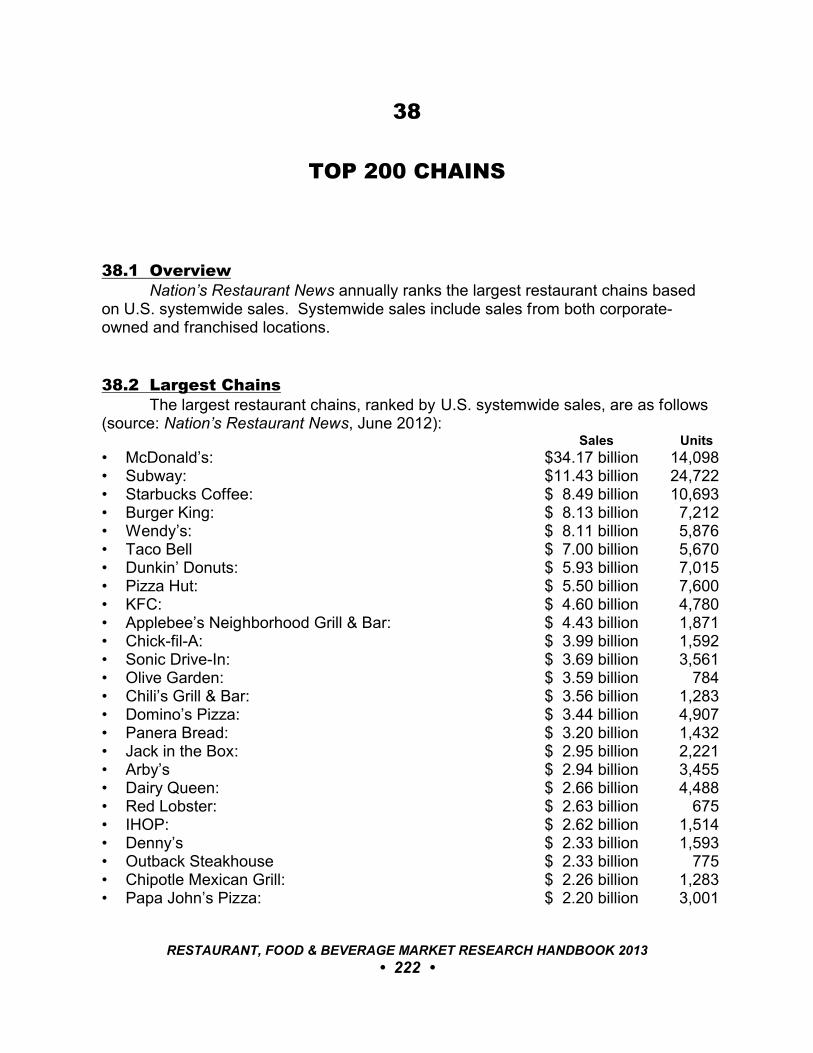

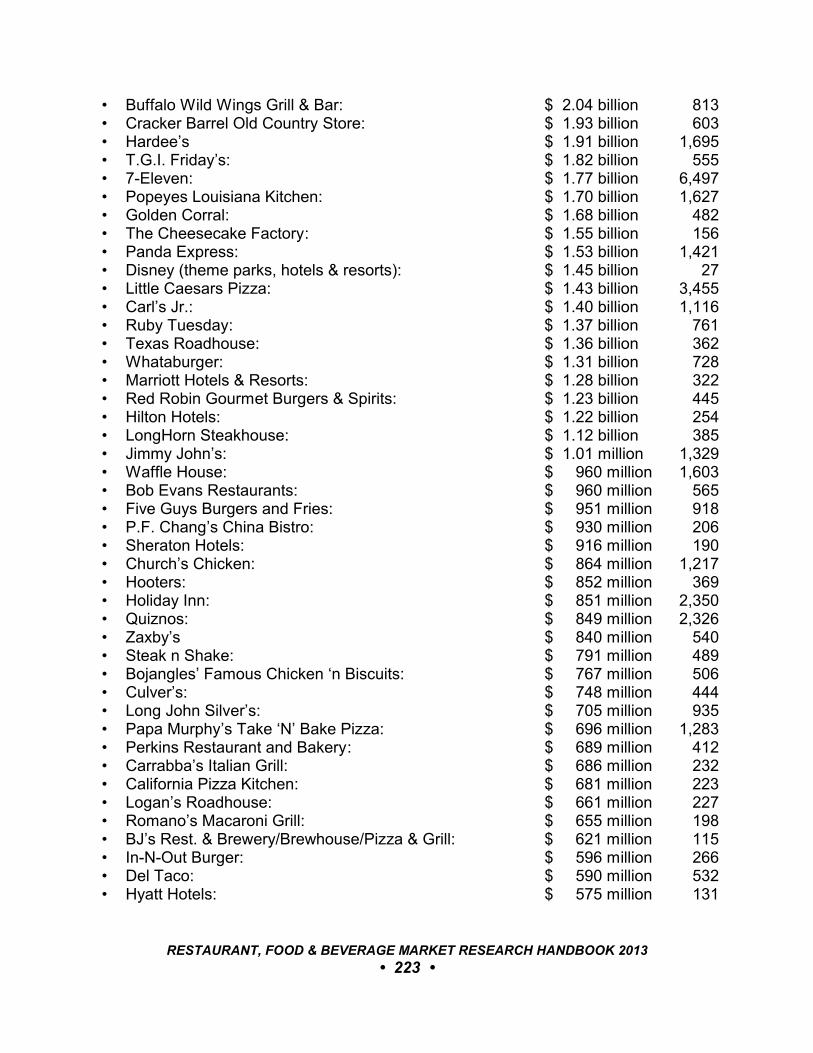

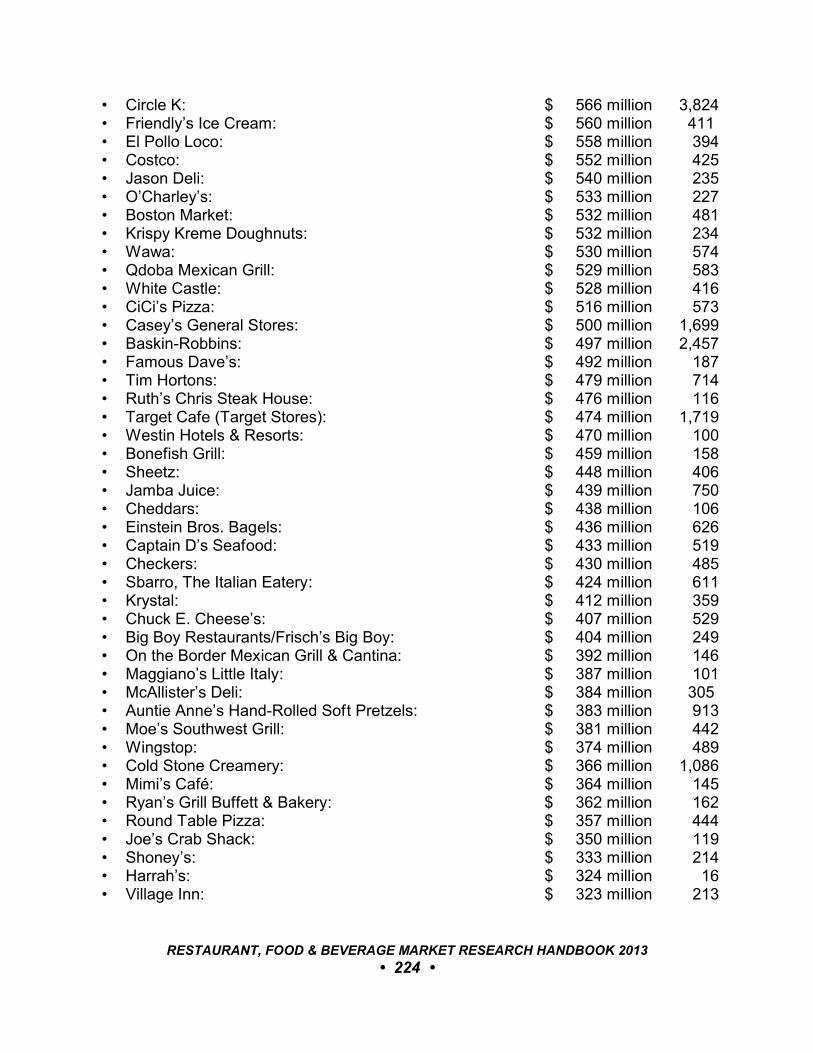

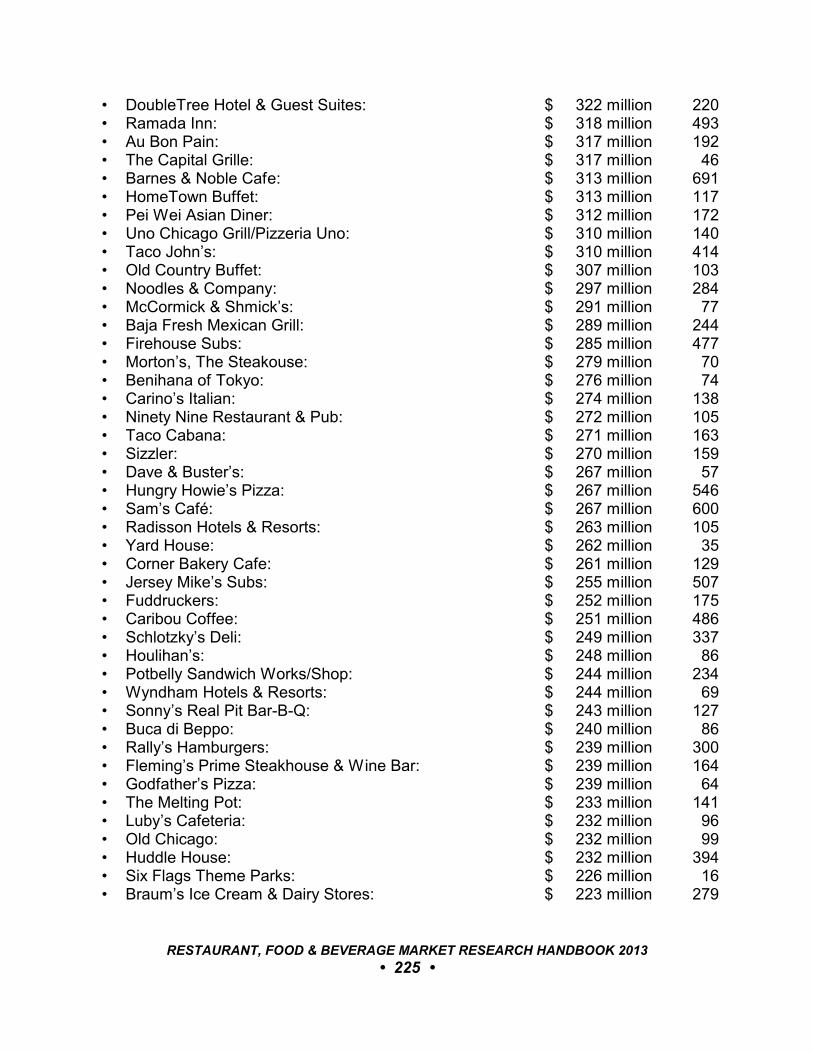

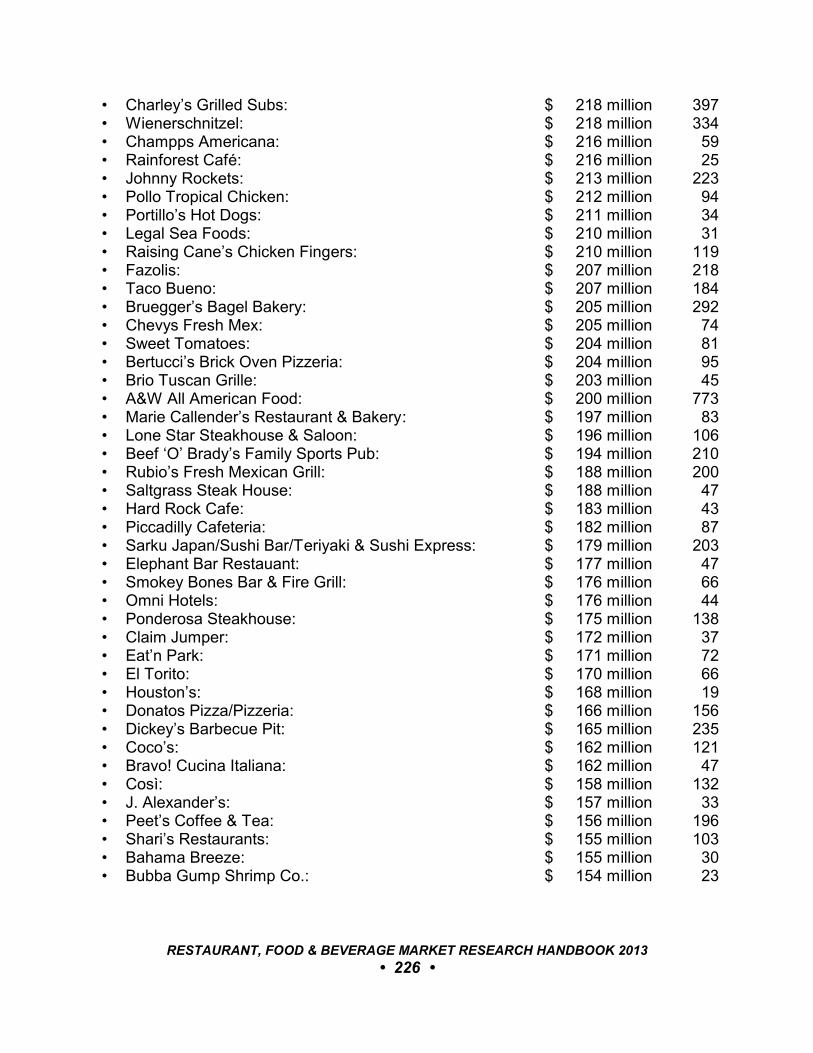

38 TOP 200 CHAINS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22238.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22238.2 Largest Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 222

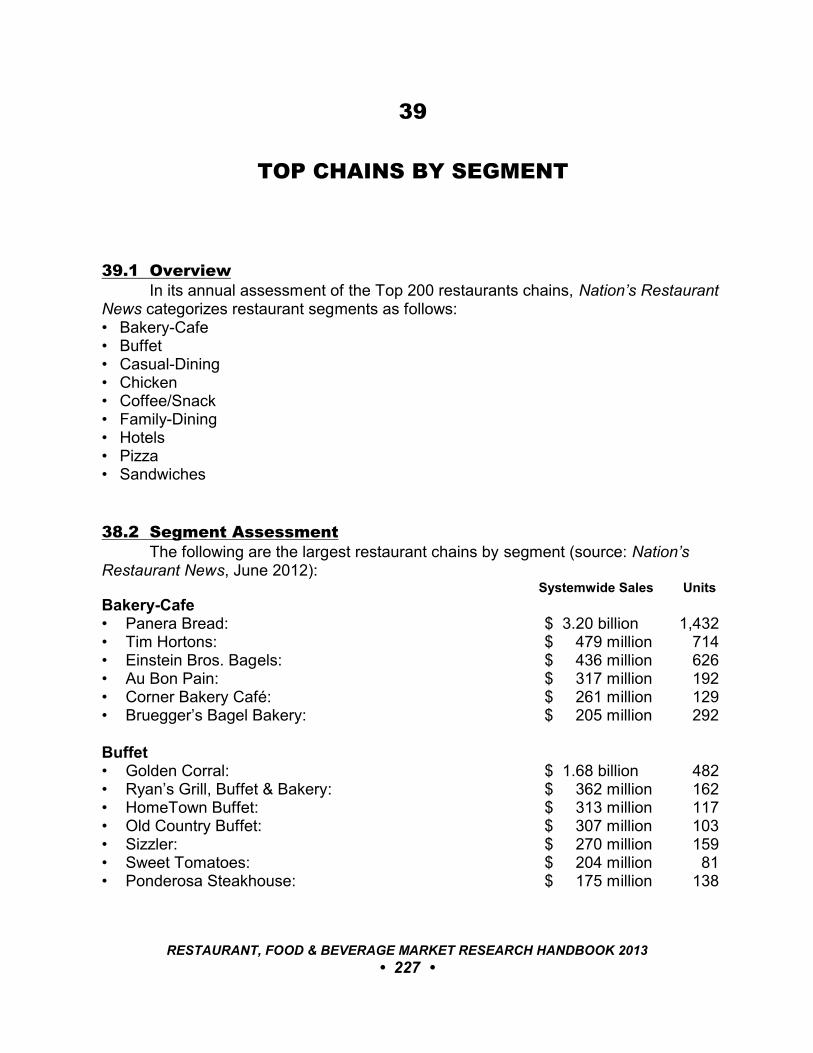

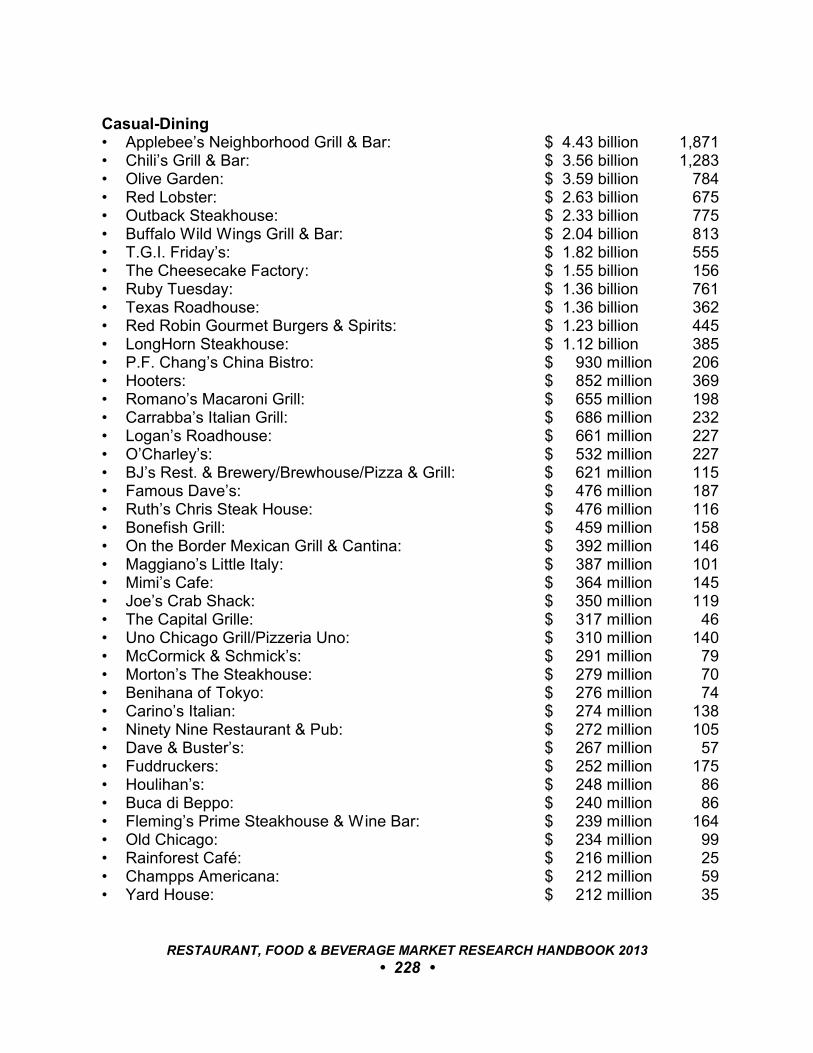

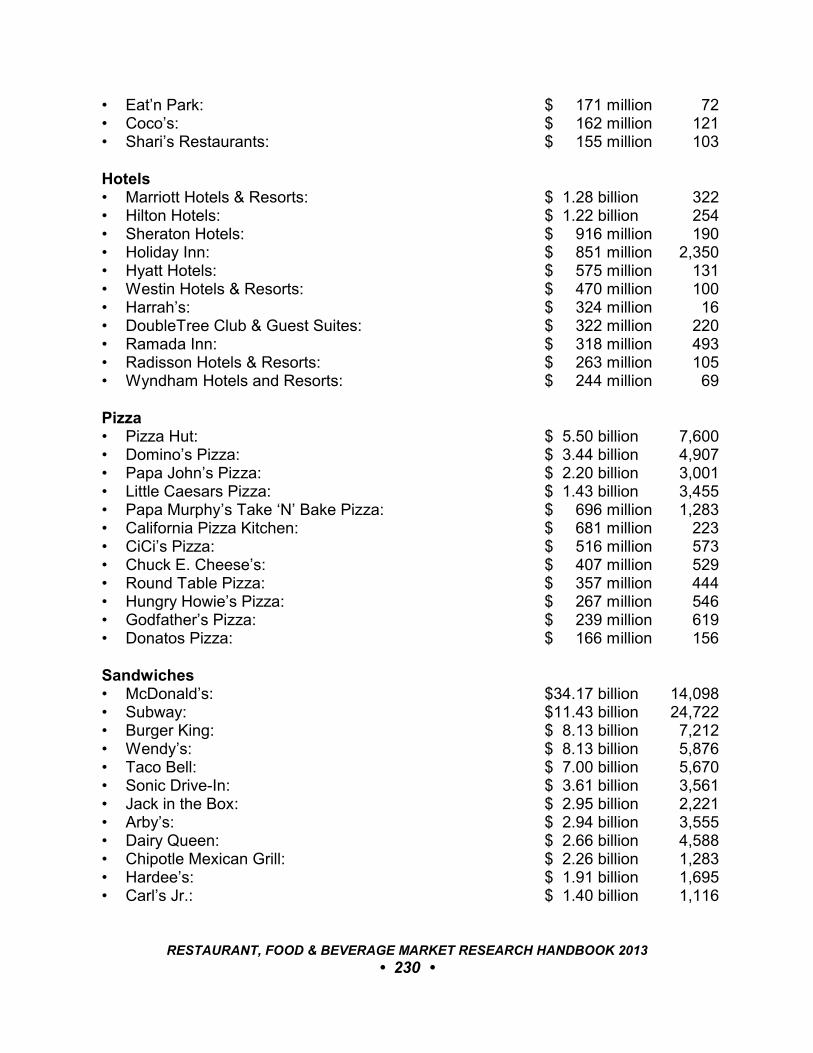

39 TOP CHAINS BY SEGMENT. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22739.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22738.2 Segment Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 227

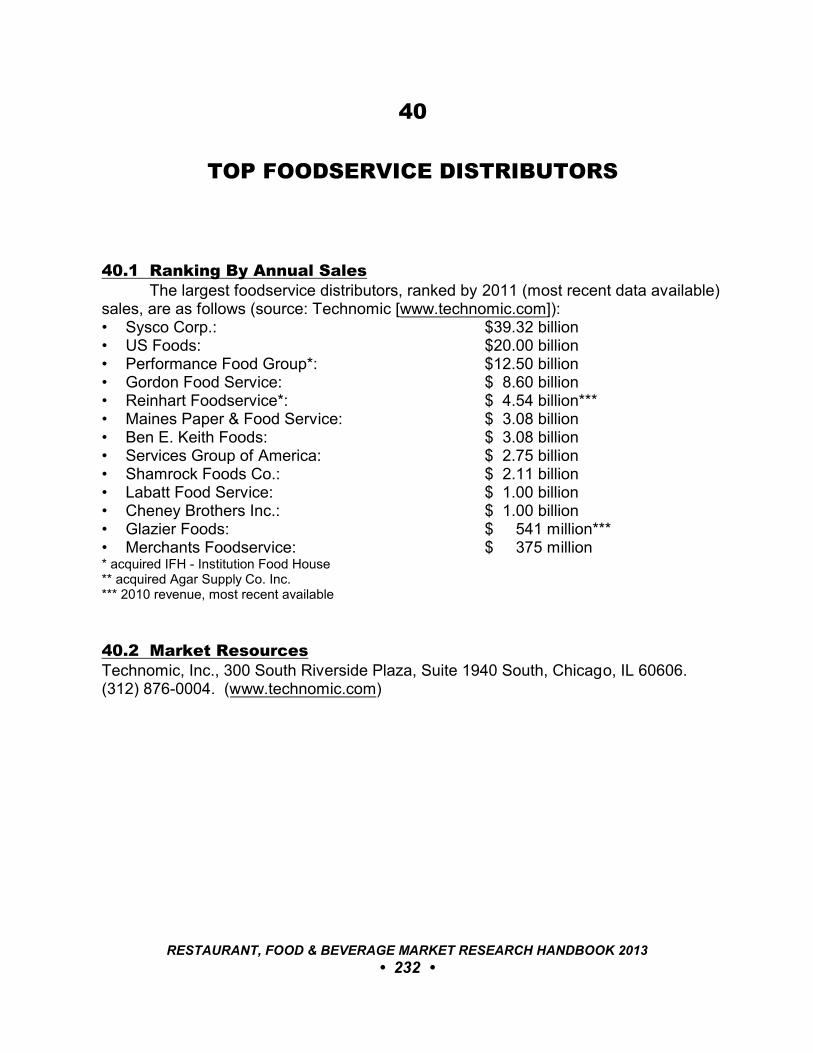

40 TOP FOODSERVICE DISTRIBUTORS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23240.1 Ranking By Annual Sales. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23240.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 232

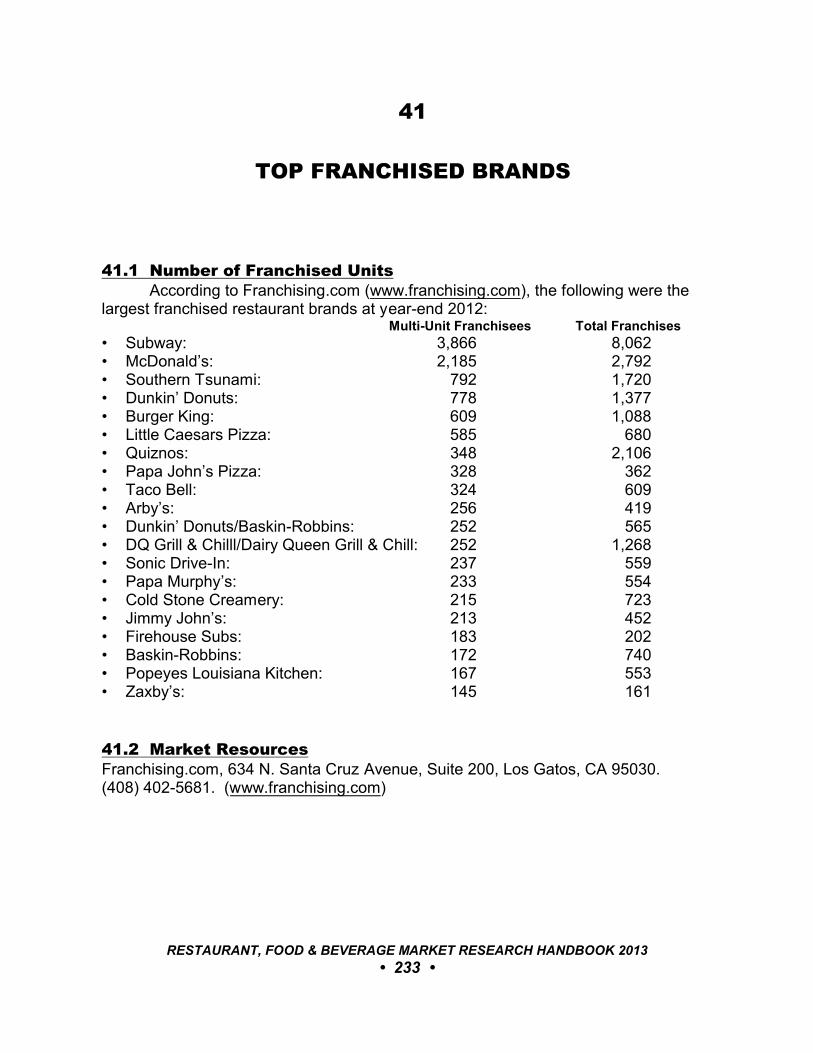

41 TOP FRANCHISED BRANDS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23341.1 Number of Franchised Units. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23341.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 233

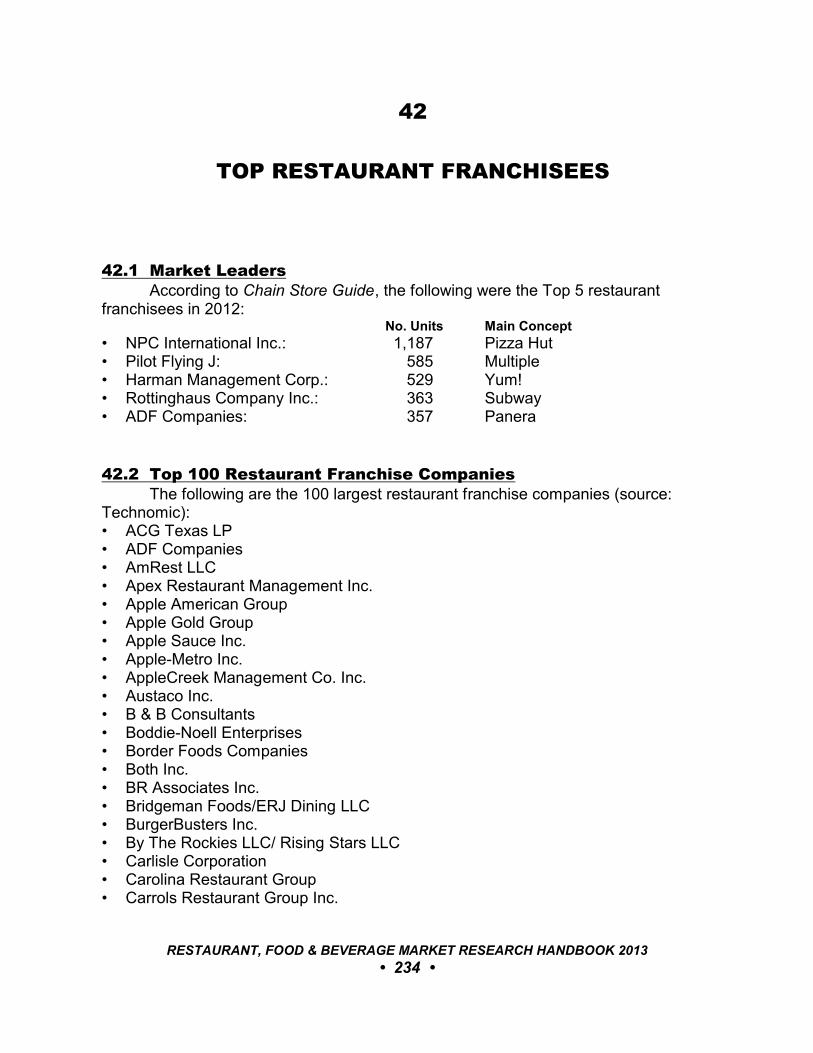

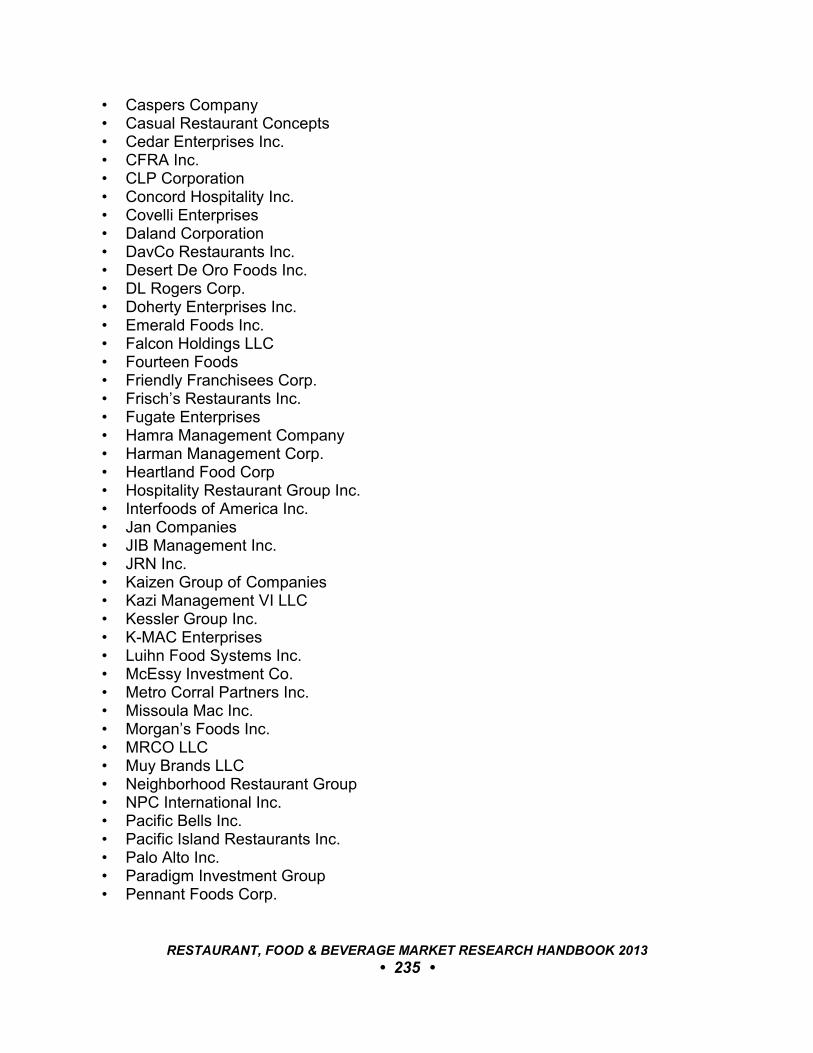

42 TOP RESTAURANT FRANCHISEES. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23442.1 Market Leaders. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23442.2 Top 100 Restaurant Franchise Companies. . . . . . . . . . . . . . . . . . . . . . . . 23442.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 236

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 9 •

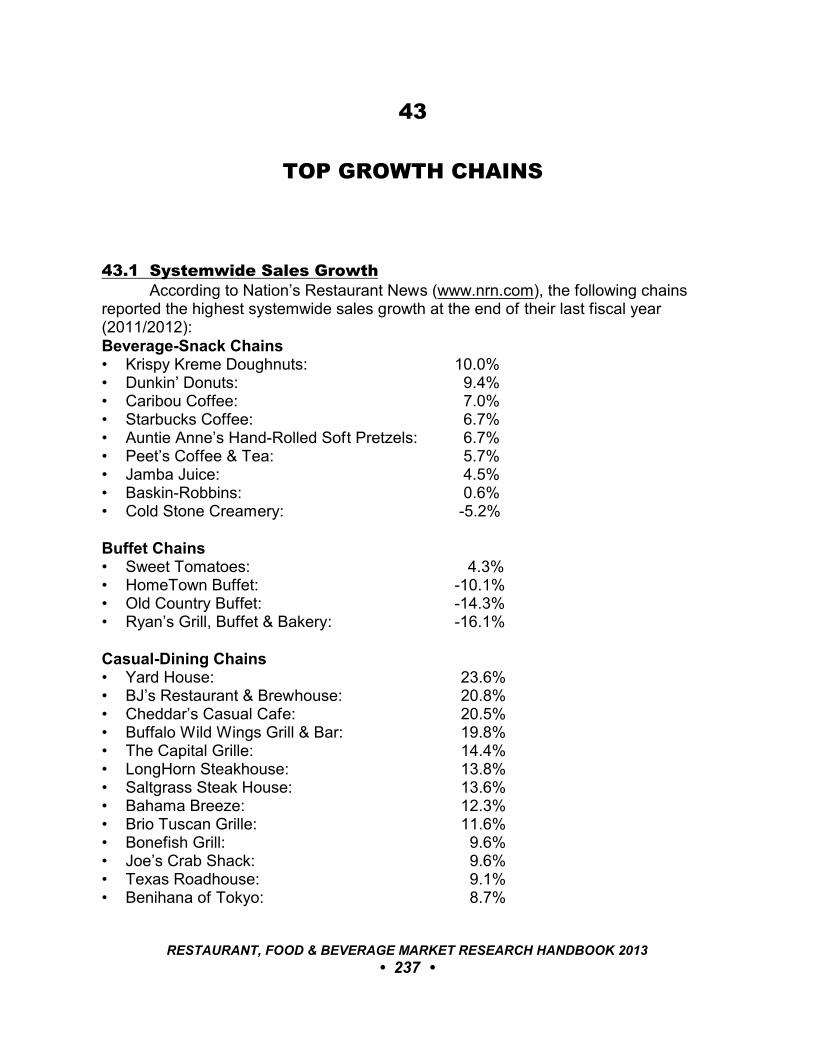

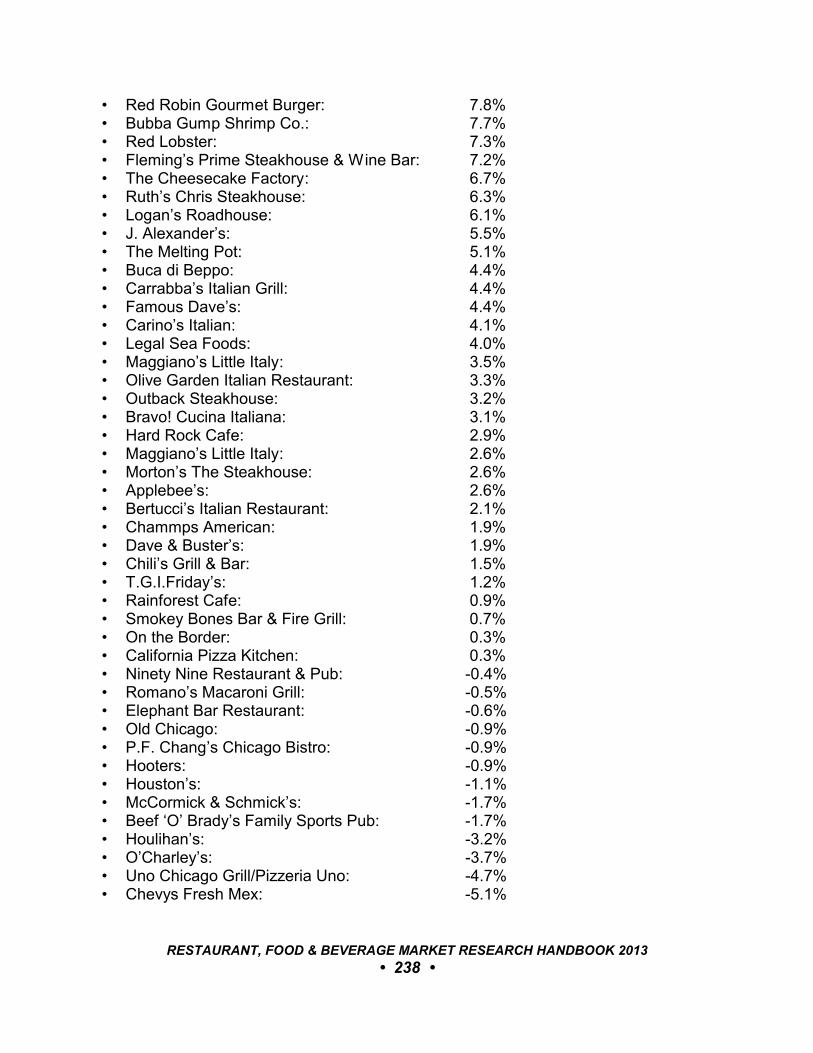

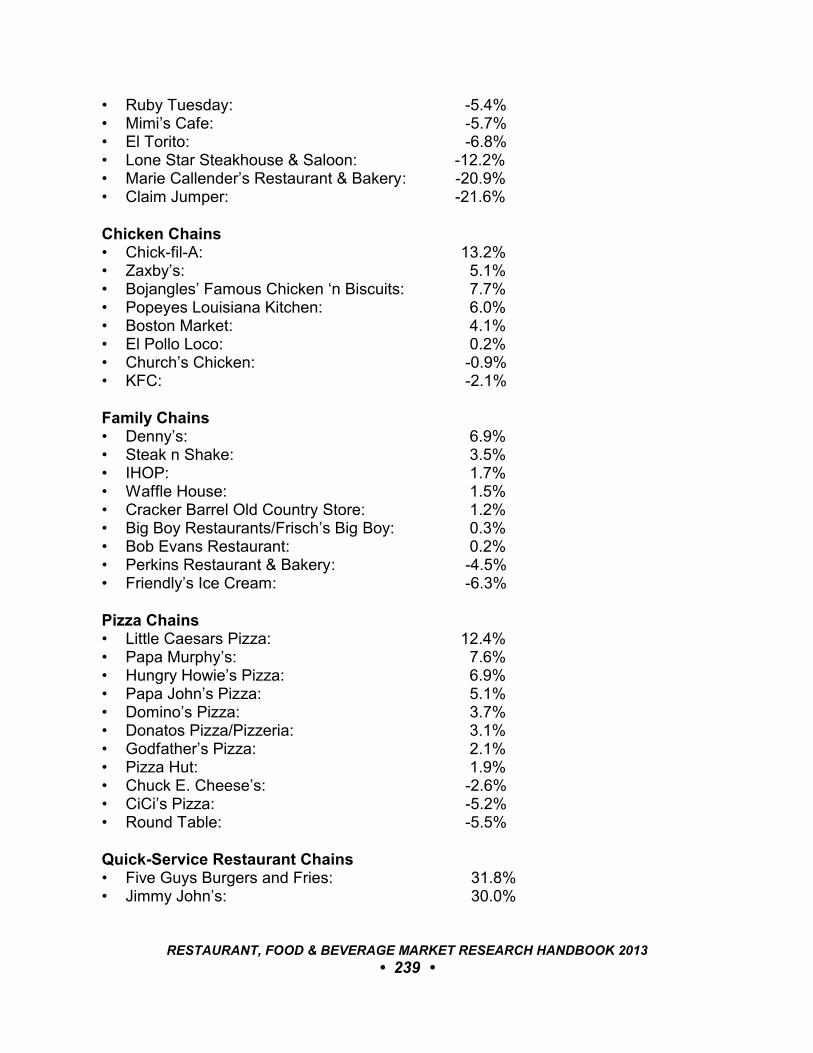

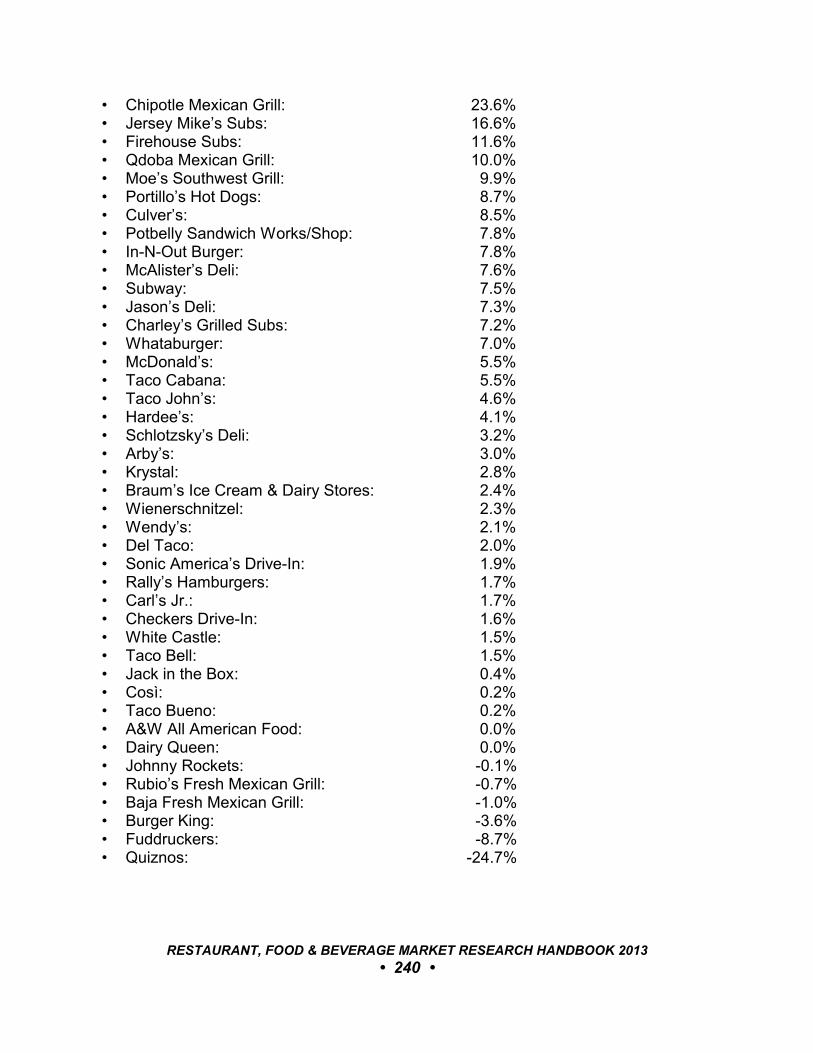

43 TOP GROWTH CHAINS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23743.1 Systemwide Sales Growth.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23743.2 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 241

44 TOP INDEPENDENT RESTAURANTS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24244.1 Rank By Annual Gross Revenue. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 242

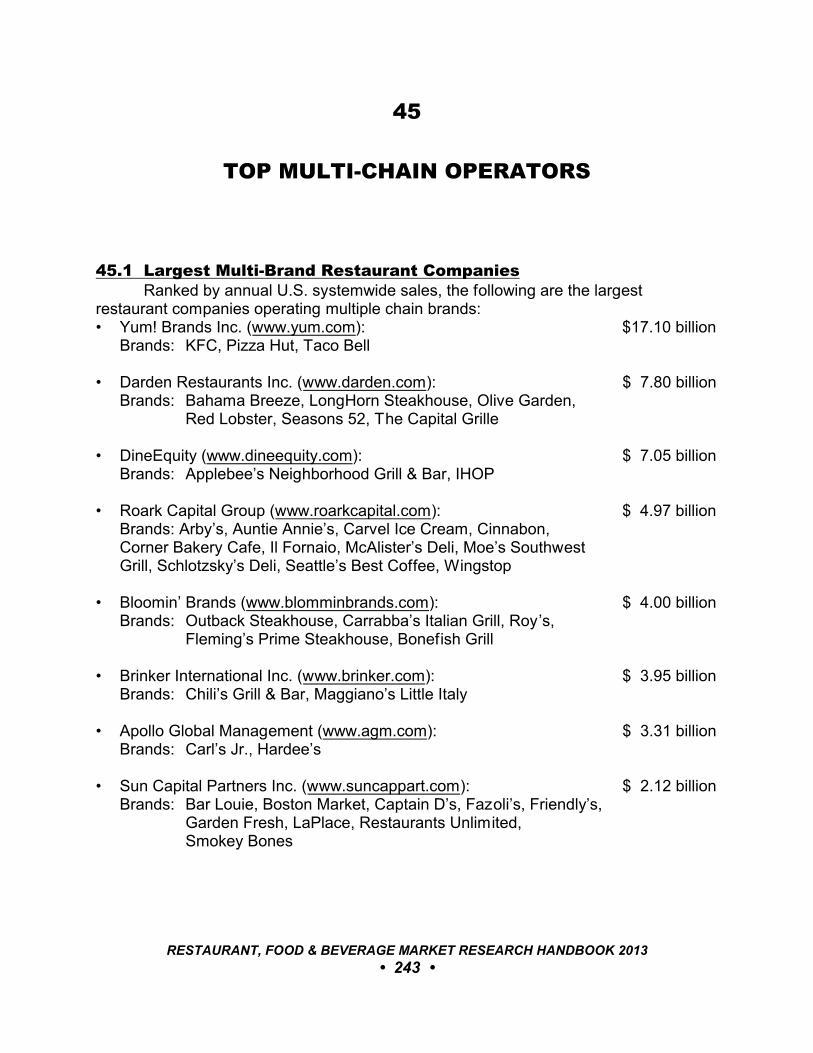

45 TOP MULTI-CHAIN OPERATORS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24345.1 Largest Multi-Brand Restaurant Companies. . . . . . . . . . . . . . . . . . . . . . . 243

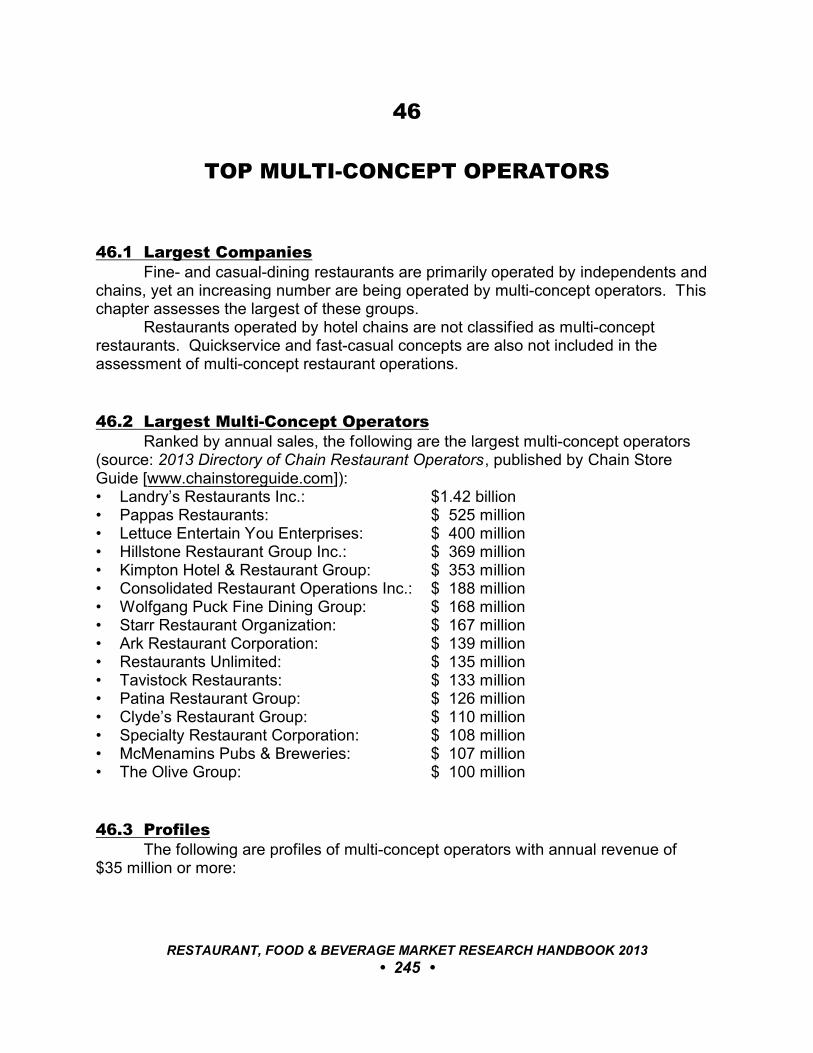

46 TOP MULTI-CONCEPT OPERATORS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24546.1 Largest Companies. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24546.2 Largest Multi-Concept Operators.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24546.3 Profiles.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 245

47 TOP NIGHTCLUBS & BARS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25447.1 Top Clubs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 254

PART VI: THE CUSTOMER. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 257

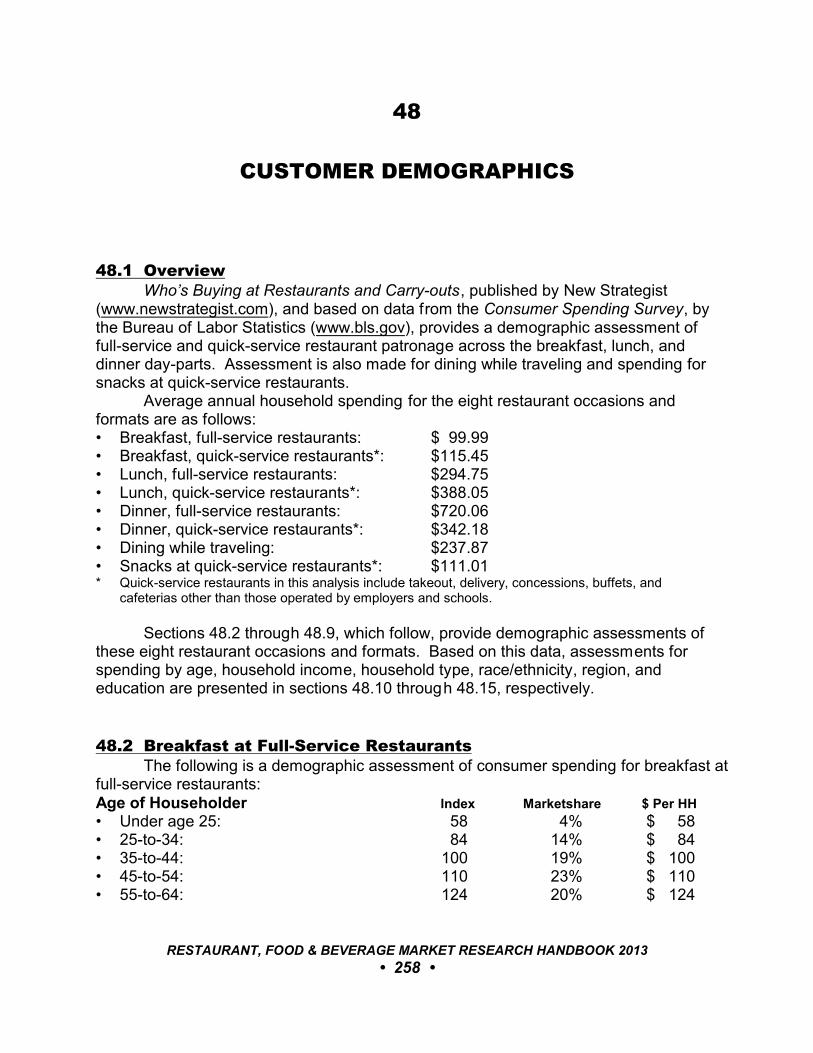

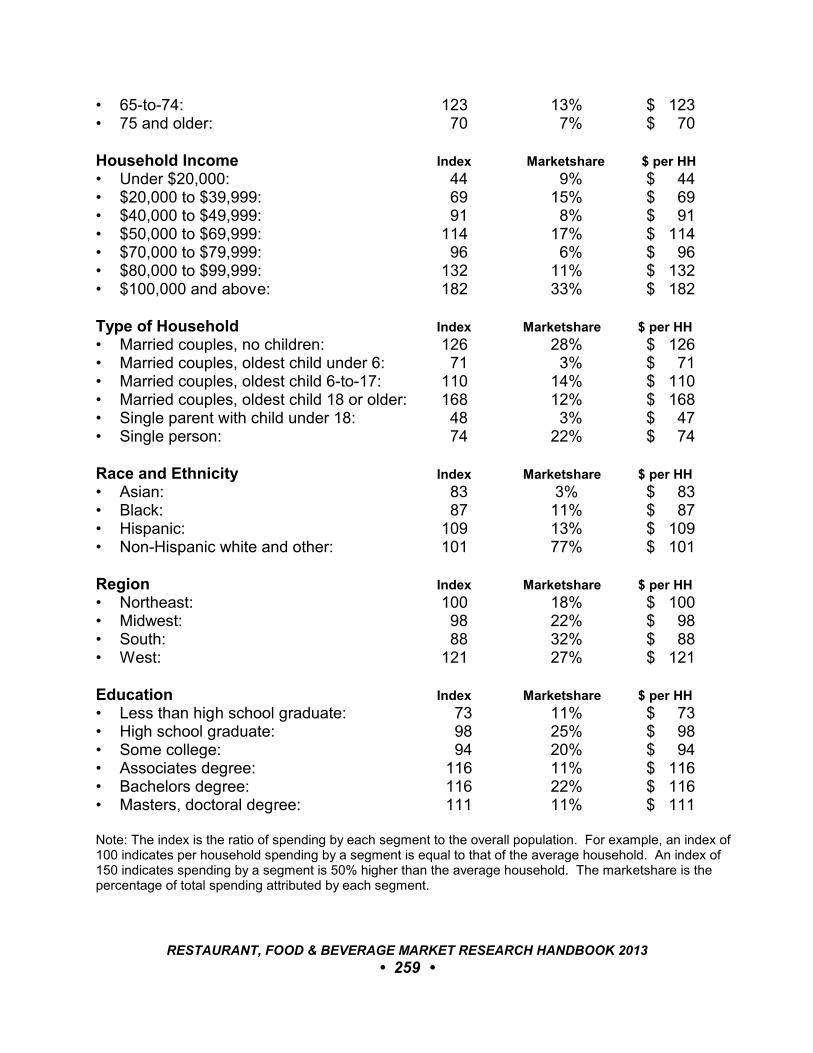

48 CUSTOMER DEMOGRAPHICS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25848.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25848.2 Breakfast at Full-Service Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . 25848.3 Breakfast at Quick-Service Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . 26048.4 Lunch at Full-Service Restaurants.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26248.5 Lunch at Quick-Service Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26348.6 Dinner at Full-Service Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26548.7 Dinner at Quick-Service Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . 26748.8 Dining While Traveling.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26848.9 Snacks at Quick-Service Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . 27048.10 Spending by Age. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27248.11 Spending by Household Income. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27248.12 Spending by Household Type. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27248.13 Spending by Race and Ethnicity. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27248.14 Spending by Region. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27248.15 Spending by Education. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27348.16 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 273

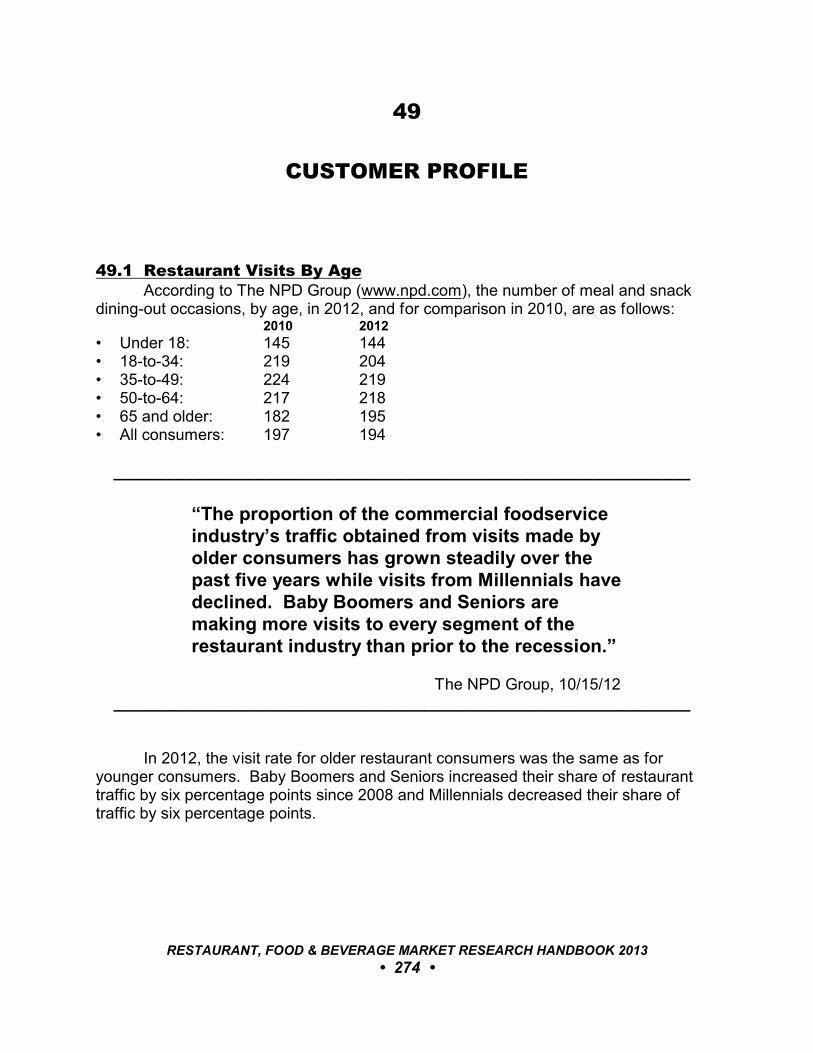

49 CUSTOMER PROFILE.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27449.1 Restaurant Visits By Age. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27449.2 The Full-Service Dining Customer.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27549.3 The Quick-Service Dining Customer. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27549.4 Regular Customers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 276

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 10 •

49.5 Families Dining Out. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27749.6 Value-Focused Customers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27749.7 What Customers Want. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 278

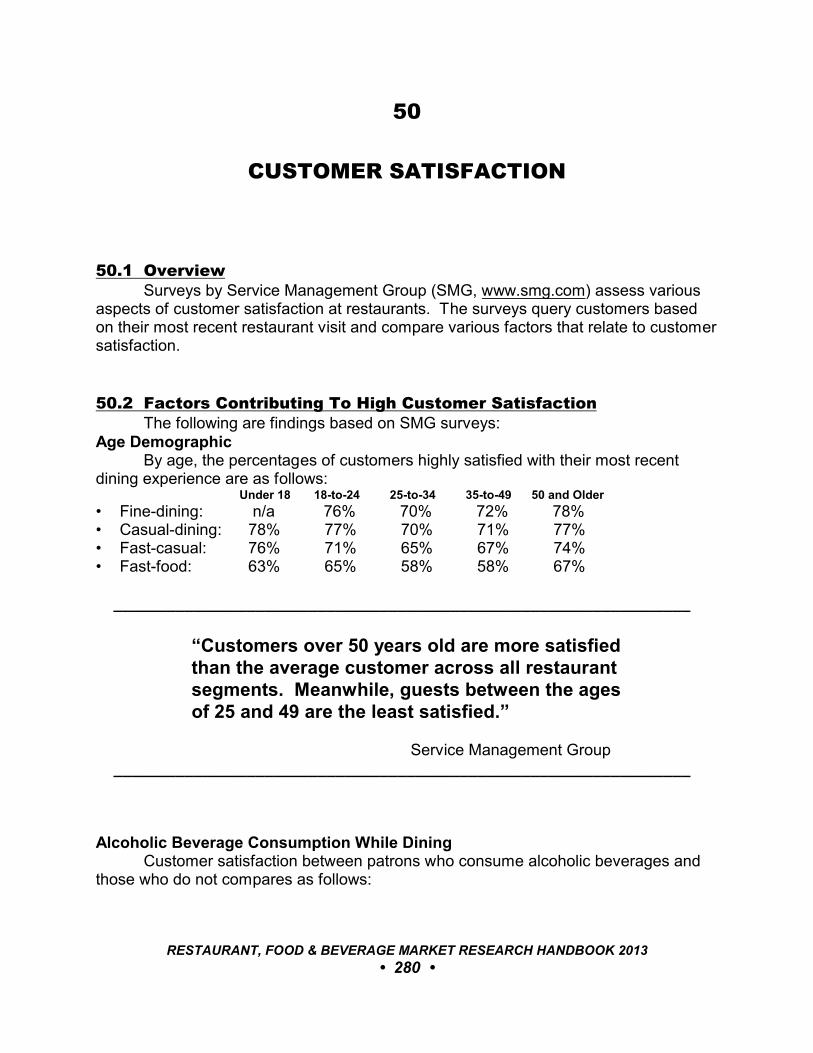

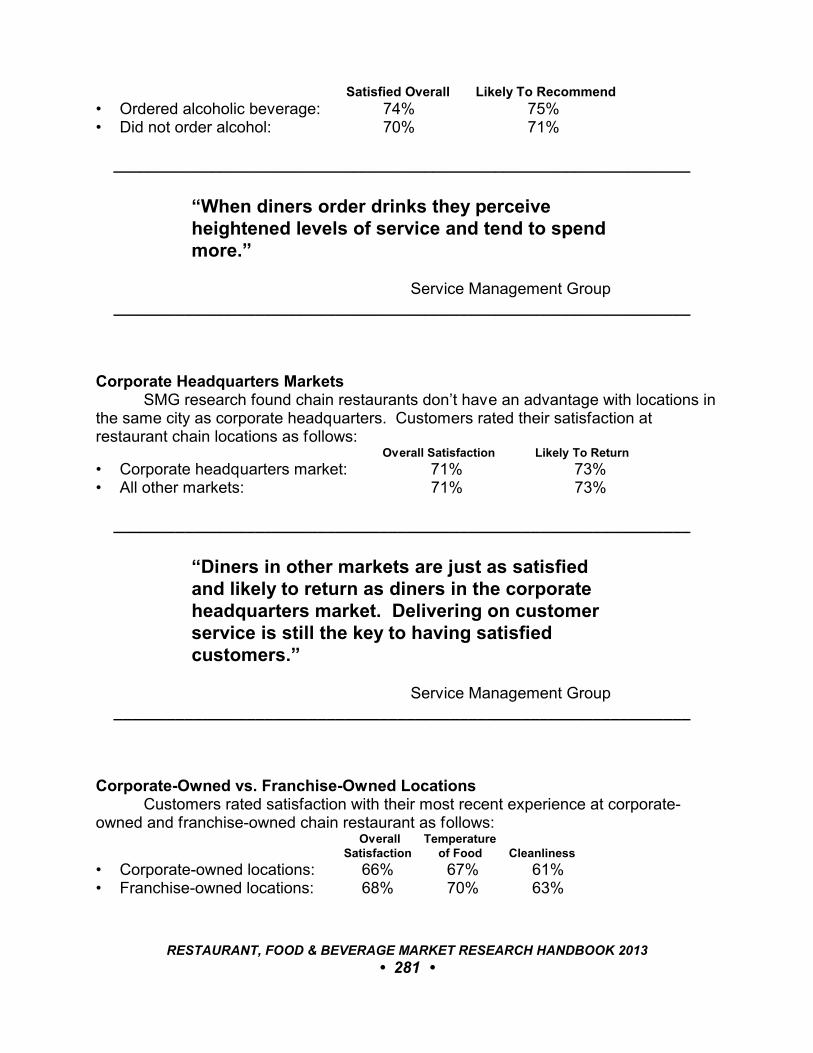

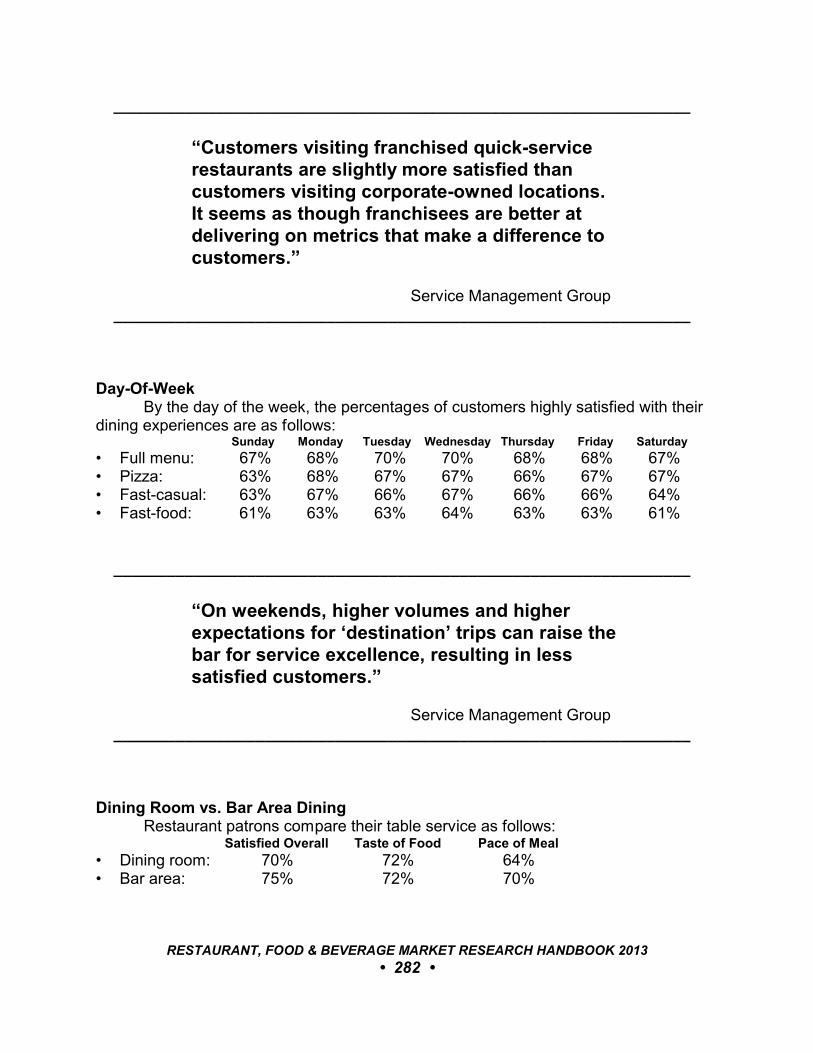

50 CUSTOMER SATISFACTION. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28050.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28050.2 Factors Contributing To High Customer Satisfaction.. . . . . . . . . . . . . . . . 28050.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 291

51 HISPANIC-AMERICAN CUSTOMERS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29251.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29251.2 Market Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29251.3 Hispanic Restaurant Patronage.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29351.4 Hispanic Menu Preferences. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 294

52 MILLENNIAL CUSTOMERS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29652.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29652.2 Restaurant Visits By Millennials.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29652.3 Dining Priorities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29752.4 Restaurant Interactions Online and Mobile. . . . . . . . . . . . . . . . . . . . . . . . 298

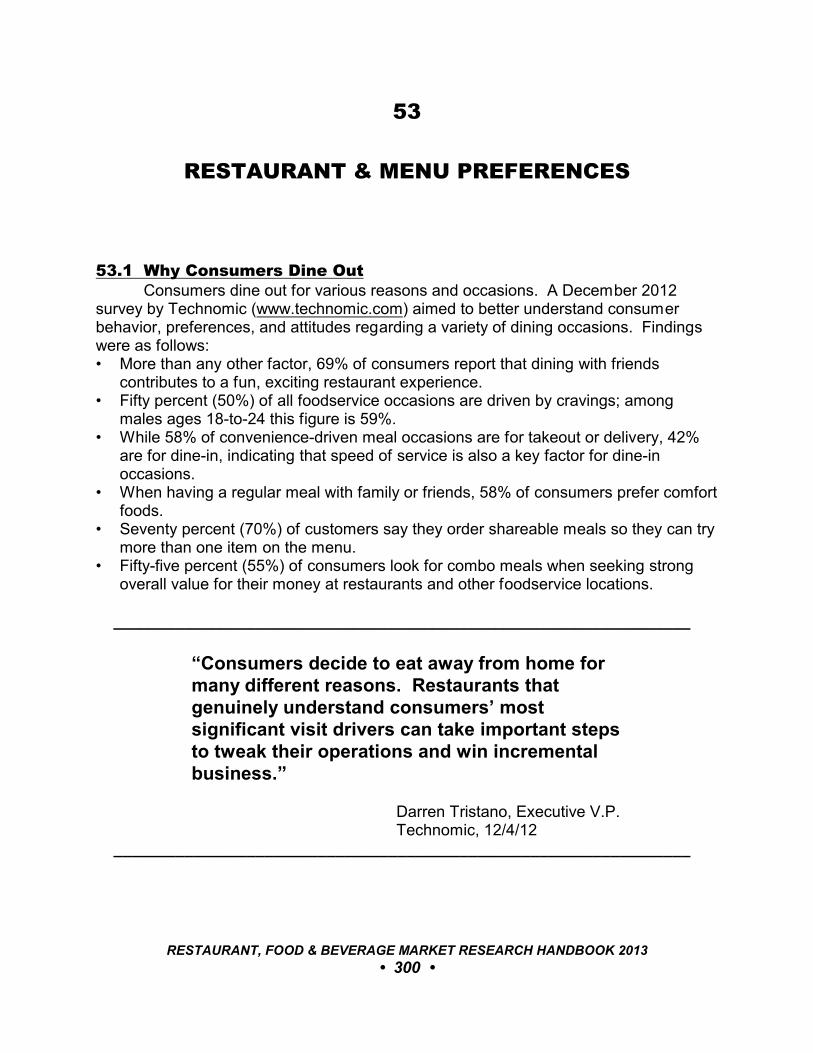

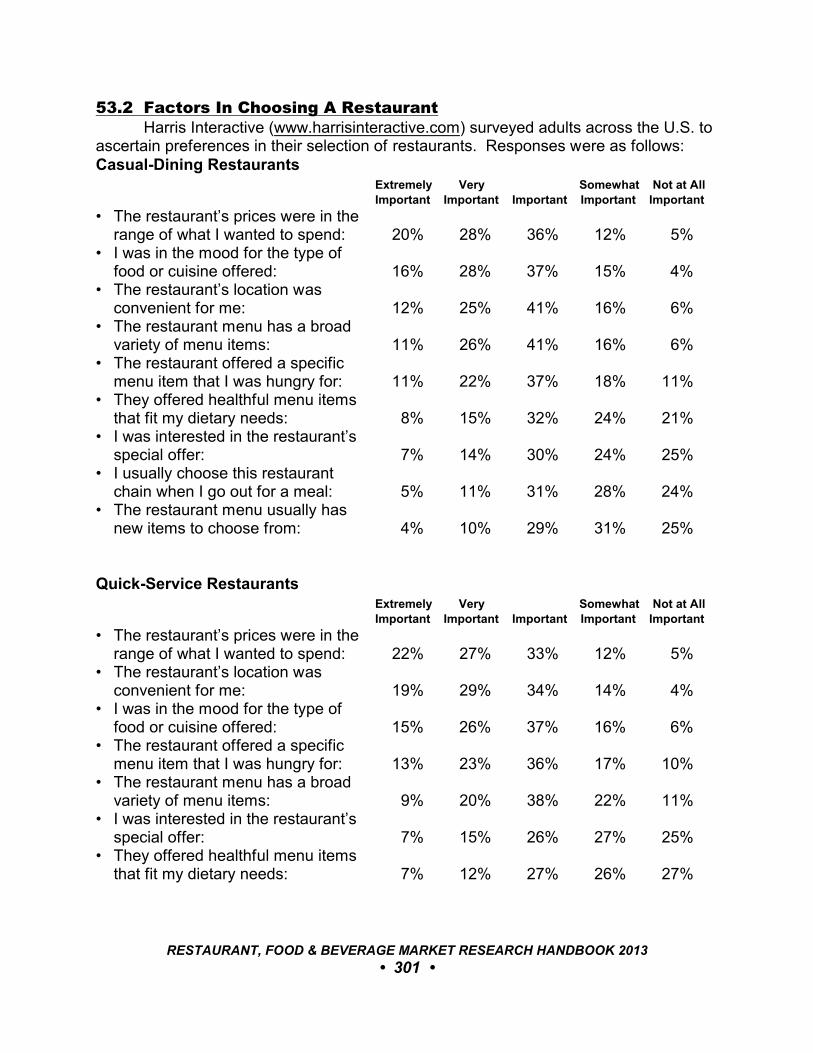

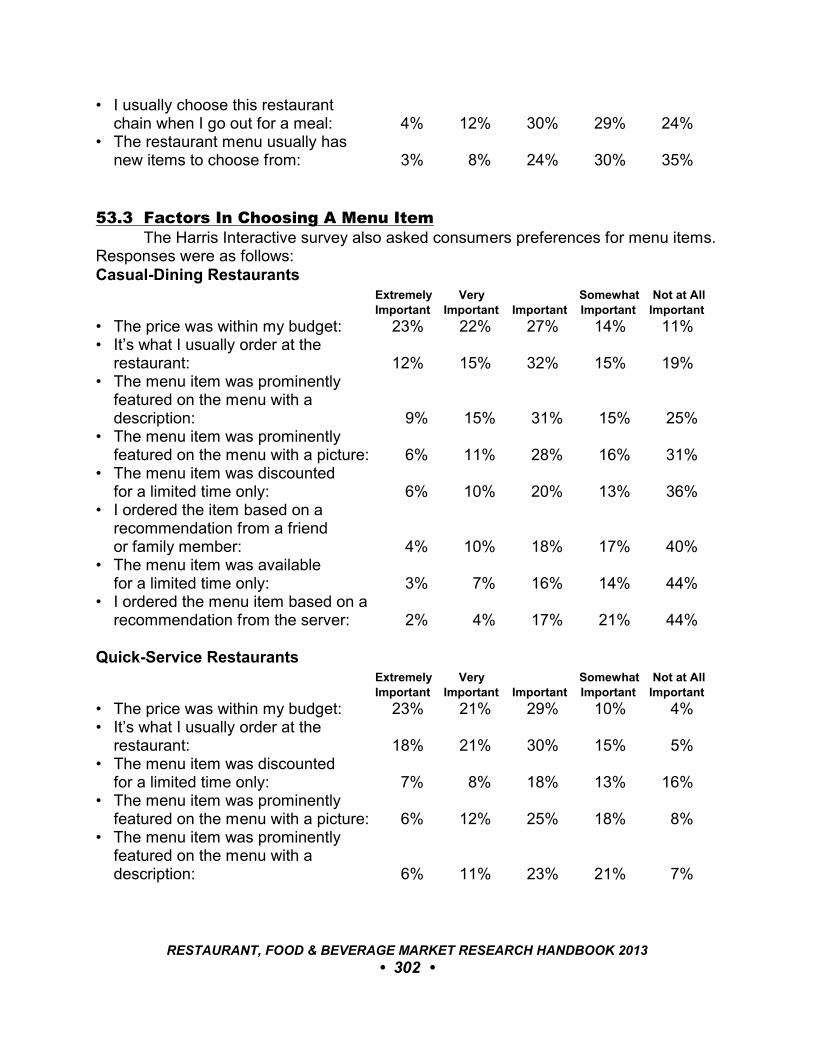

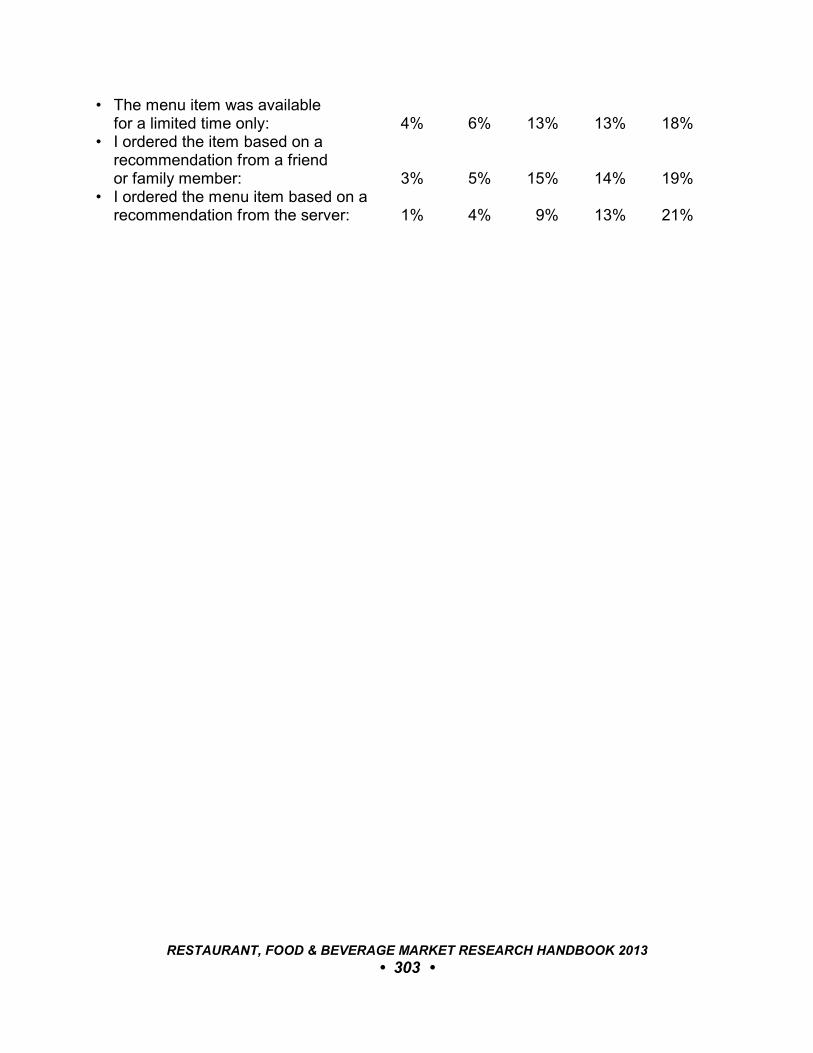

53 RESTAURANT & MENU PREFERENCES. . . . . . . . . . . . . . . . . . . . . . . . . . . . 30053.1 Why Consumers Dine Out.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30053.2 Factors In Choosing A Restaurant.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30153.3 Factors In Choosing A Menu Item. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 302

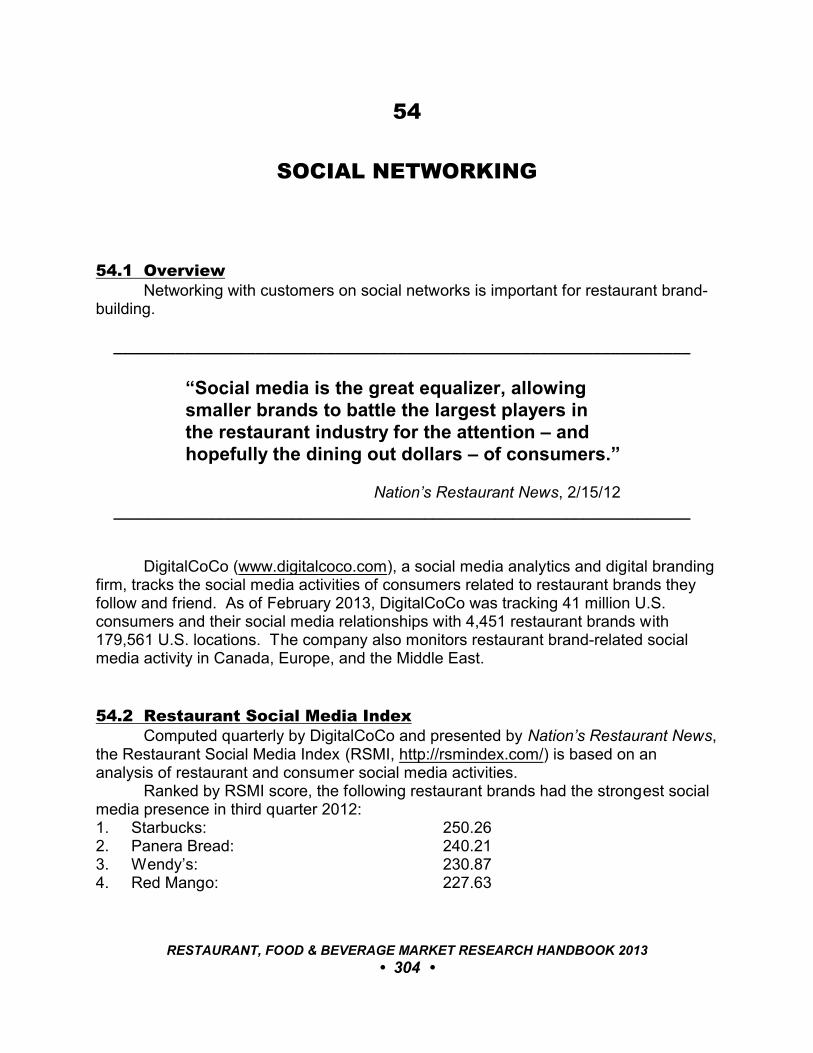

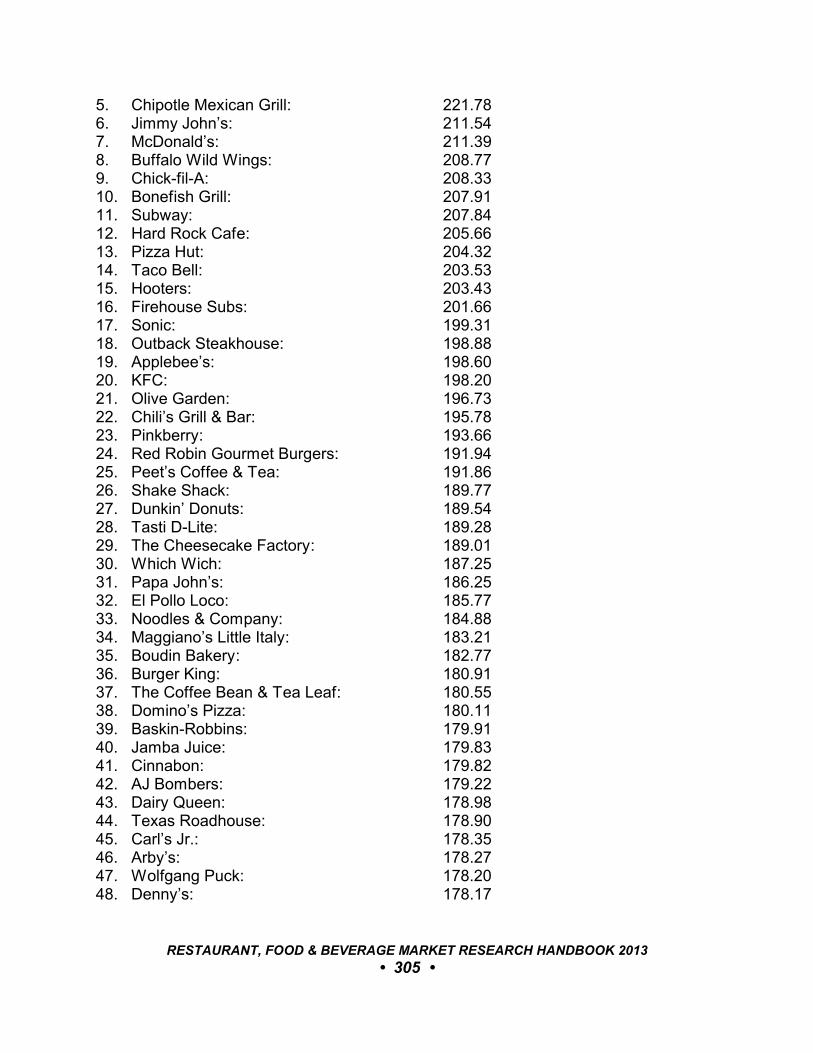

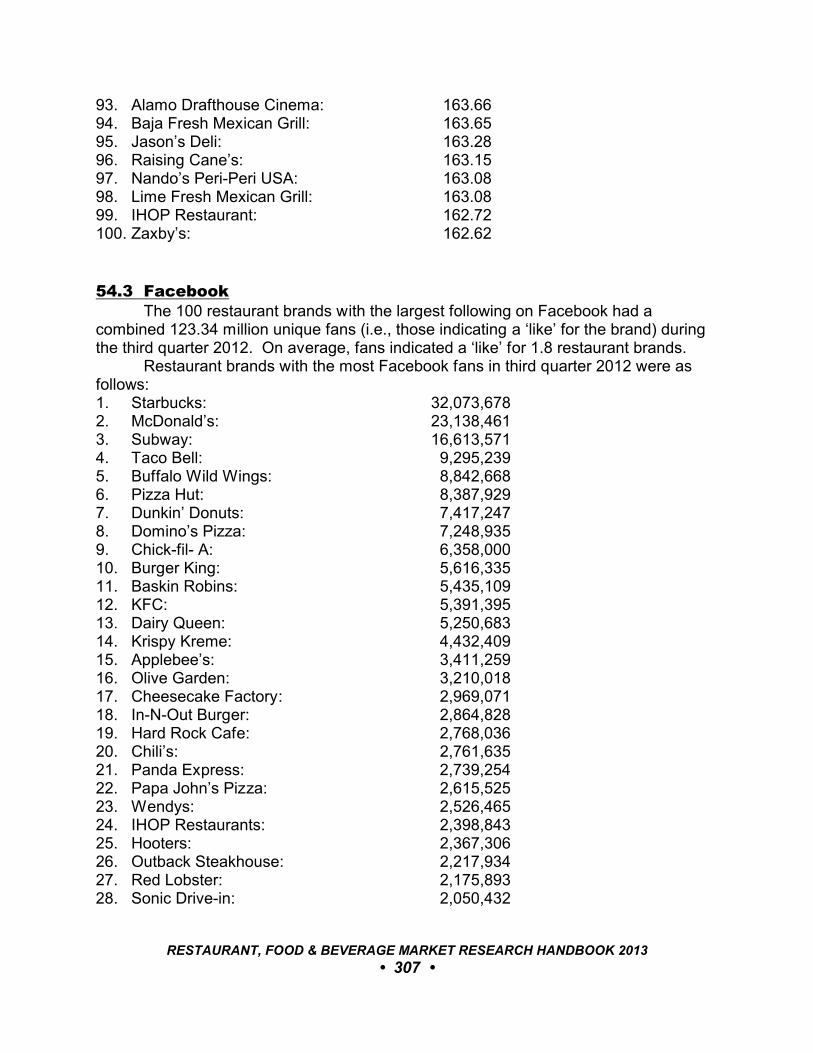

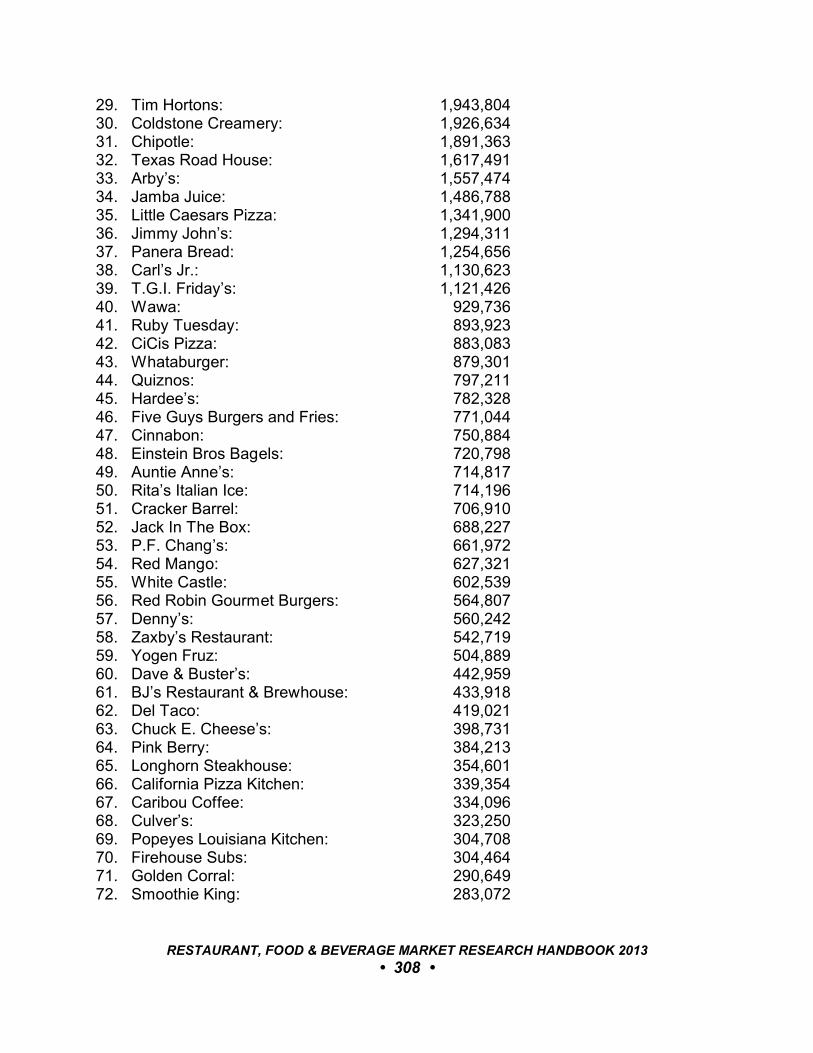

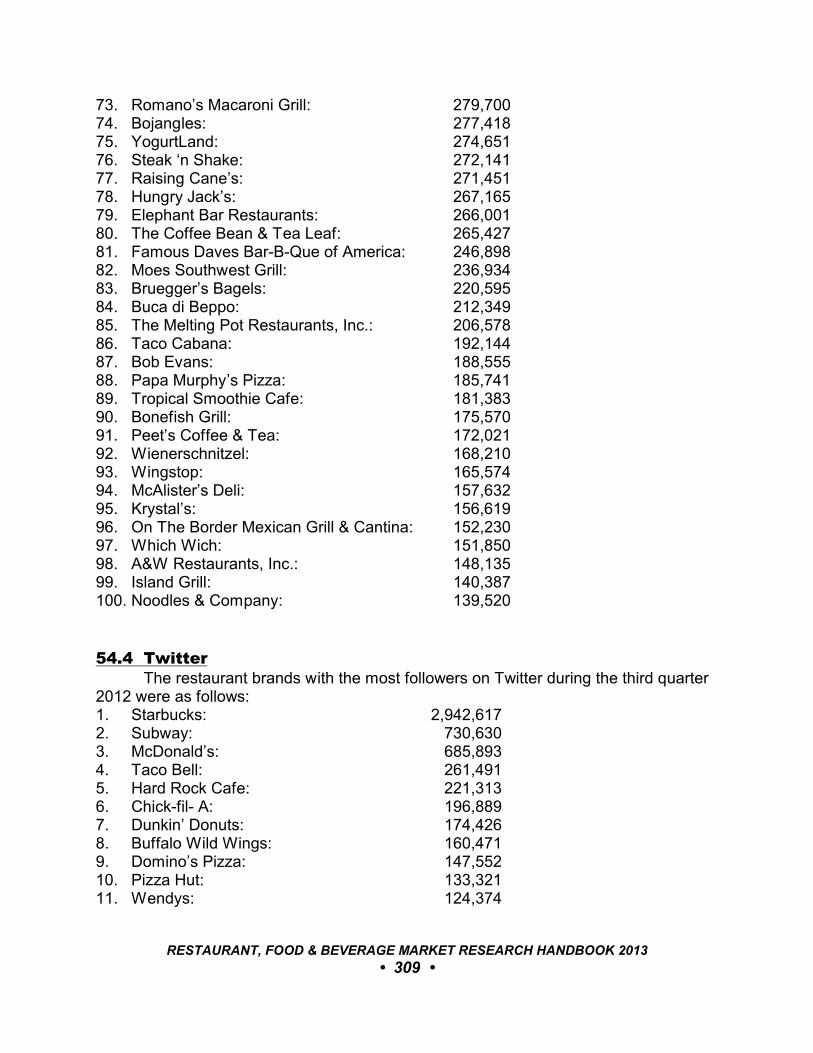

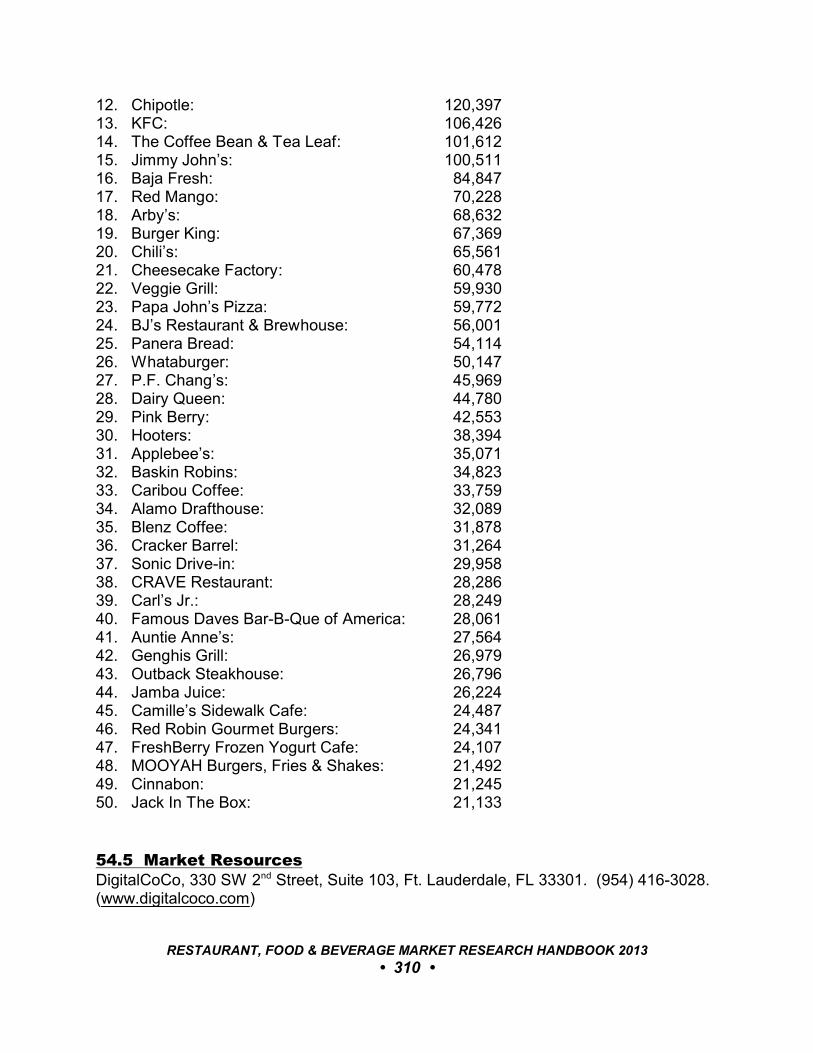

54 SOCIAL NETWORKING. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30454.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30454.2 Restaurant Social Media Index. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30454.3 Facebook.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30754.4 Twitter. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30954.5 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 310

PART VII: DINING TRENDS & ANALYSES. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 311

55 BURGERS & SANDWICHES.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31255.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31255.2 Hamburgers.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31255.3 Hot Dogs & Sausages. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31355.4 Other Sandwiches. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31455.5 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 315

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 11 •

56 CELEBRITY CHEFS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31656.1 Cooking Shows On Television.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31656.2 Top-Earning Chefs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31656.3 Chef Business Ventures. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31756.4 Chef-Inspired Restaurant Concepts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 319

57 CHILDREN’S MEALS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32157.1 The Kids LiveWell Initiative. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32157.2 Healthful Kids’ Menus At QSRs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32157.3 School Meals. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32257.4 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 323

58 CUISINE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32458.1 Regional Cuisine. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32458.2 Ethnic Cuisine. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 327

59 CUSTOMER SERVICE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32859.1 Ranking Customer Priorities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32859.2 Customer Service Strategies. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32859.3 Team Service. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32959.4 Top Restaurants For Service.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 330

60 DAYPARTS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33160.1 Daypart Spending and Traffic. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33160.2 Breakfast. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33260.3 Lunch.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33360.4 Dinner. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 334

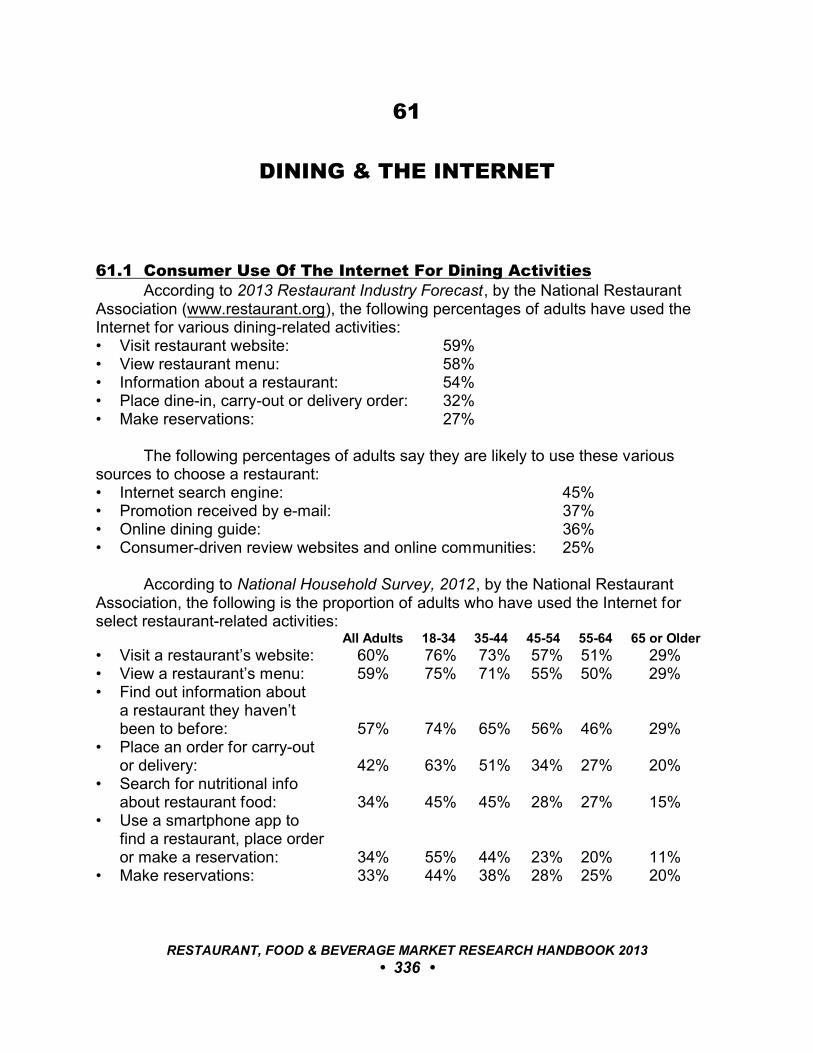

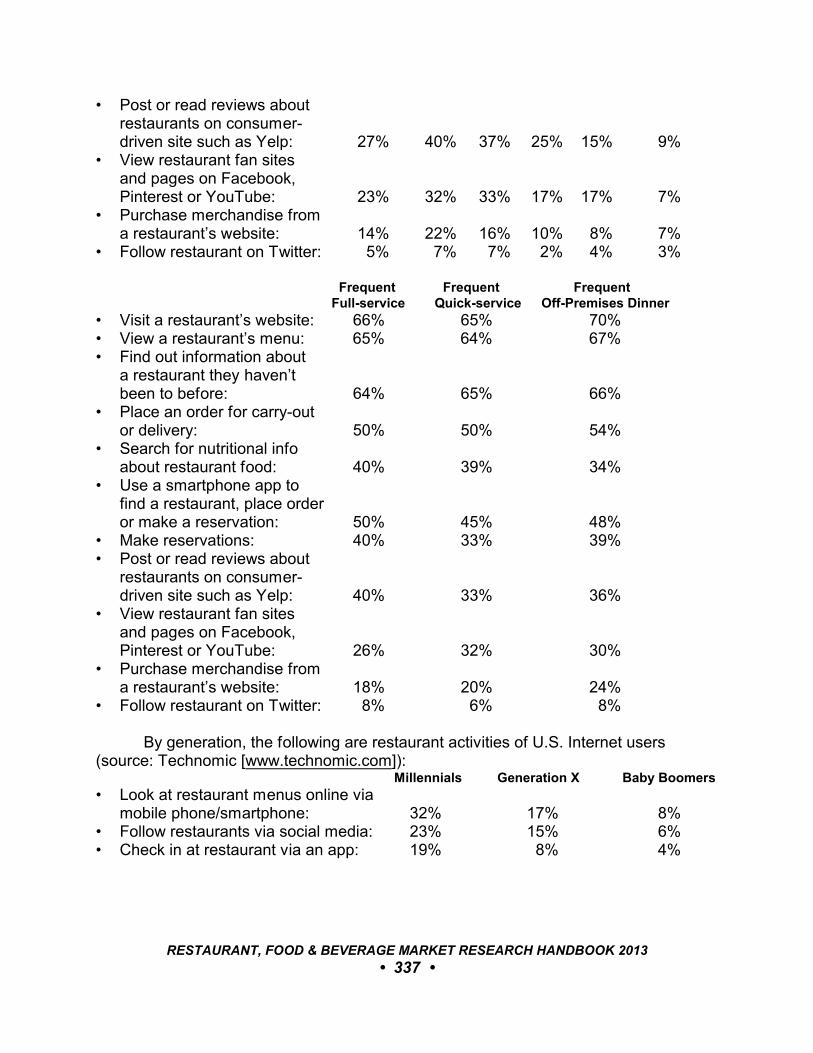

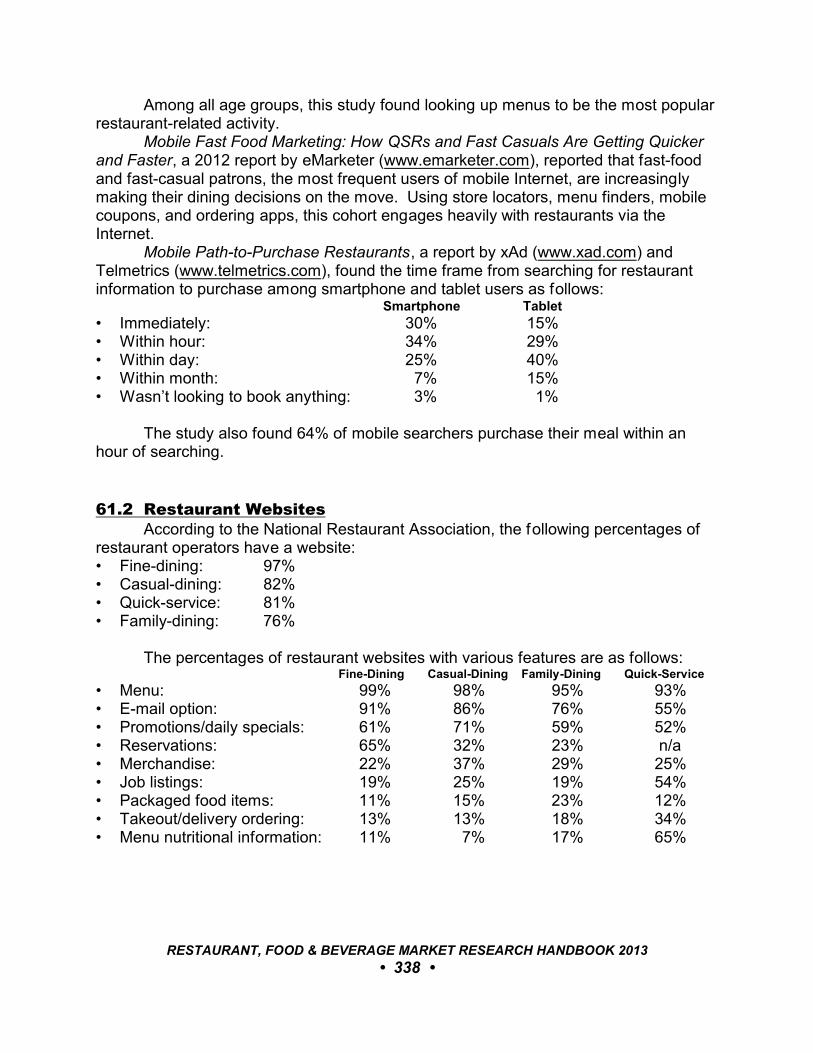

61 DINING & THE INTERNET. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33661.1 Consumer Use Of The Internet For Dining Activities.. . . . . . . . . . . . . . . . 33661.2 Restaurant Websites. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33861.3 Online Reservations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33961.4 Online Reviews. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33961.5 Social Networking. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33961.6 Online Ordering. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34061.7 In-Restaurant Ordering Via Tablet.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 341

62 DINING WHILE TRAVELING. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34262.1 Traveler Dining. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34262.2 Culinary Destinations.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34262.3 Sampling Tours. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34362.4 Culinary Arts Programs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34362.5 Winery Tours. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34462.6 American Whiskey Trail.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 345

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 12 •

63 DINING WITH ENTERTAINMENT. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34763.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34763.2 Live Music and Dining. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34863.3 Theme Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34863.4 Experiential Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34963.5 Mystery Dinner Theaters. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35063.6 Dinner and a Movie. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35063.7 Speakeasies. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35163.8 Novel Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 352

64 DOG-FRIENDLY RESTAURANTS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35464.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35464.2 Dog-friendly Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35464.3 Dog Menus. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 355

65 FOOD & WINE FESTIVALS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35665.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35665.2 Prominent Food Festivals. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35665.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 357

66 HOLIDAY DINING. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35866.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35866.2 Birthdays. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35866.3 Valentine’s Day. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35966.4 Mother’s Day. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35966.5 Father’s Day. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36066.6 Easter. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36066.7 New Year’s Eve. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36066.8 Thanksgiving. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36066.9 St. Patrick’s Day. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36166.10 Oktoberfest. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36166.11 Super Bowl Sunday. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 361

67 LATE-NIGHT HOURS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36367.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36367.2 Late-Night Customer Demographics. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36367.3 Late-Night Operations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 364

68 LICENSING. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36668.1 Market Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36668.2 Case Studies. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36668.3 Market Trends. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36868.4 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 369

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 13 •

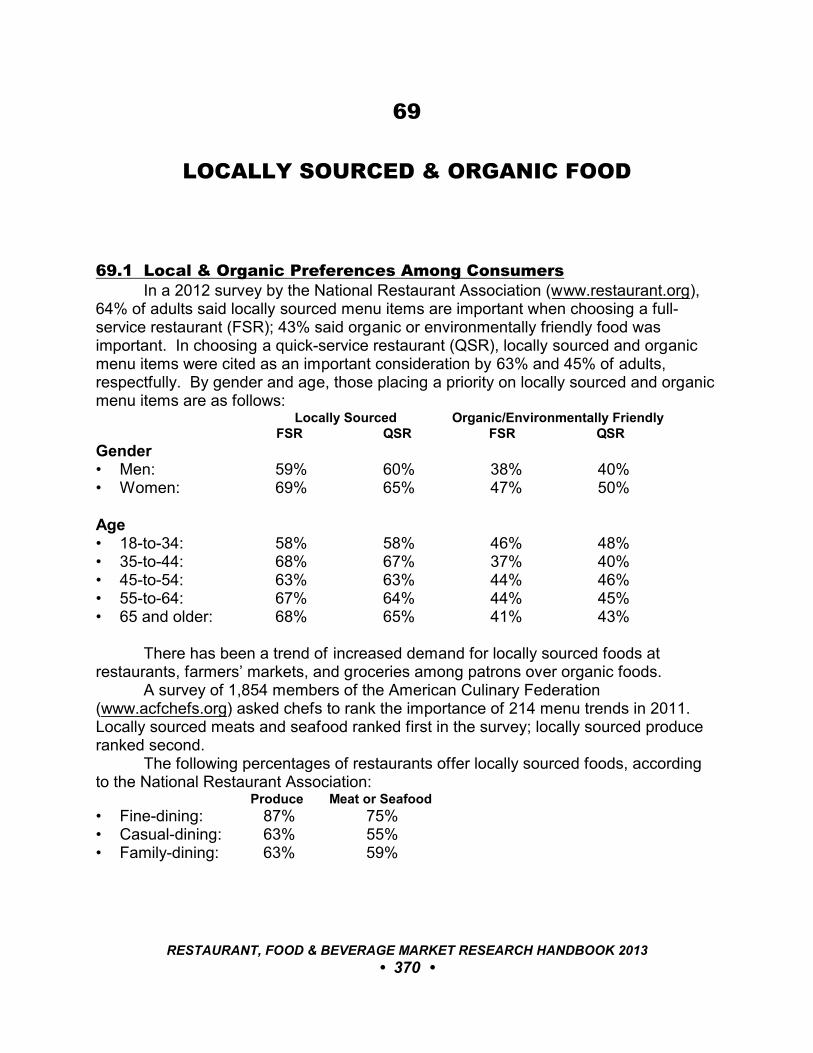

69 LOCALLY SOURCED & ORGANIC FOOD. . . . . . . . . . . . . . . . . . . . . . . . . . . . 37069.1 Local & Organic Preferences Among Consumers. . . . . . . . . . . . . . . . . . . 37069.2 Locavores. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37169.3 Local Sourcing At Limited-Service Restaurants. . . . . . . . . . . . . . . . . . . . 37269.4 Chef- and Restaurant-owned Farms. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37369.5 Organic Menus. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 374

70 LOYALTY PROGRAMS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37570.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37570.2 Restaurant Programs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37570.3 Customer Participation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37570.4 Social Networking With Loyalty Customers. . . . . . . . . . . . . . . . . . . . . . . . 375

71 NON-TRADITIONAL RESTAURANT SITES. . . . . . . . . . . . . . . . . . . . . . . . . . . 37771.1 Pop-Up Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37771.2 Restaurants At Auto Dealerships. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37871.3 Restaurants At Car Washes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37871.4 Restaurants At Museums and Tourist Attractions. . . . . . . . . . . . . . . . . . . 37871.5 Restaurants At Parks and Botanical Gardens. . . . . . . . . . . . . . . . . . . . . . 37971.6 Restaurants At Retail Stores. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 379

72 NUTRITION. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38272.1 Healthful Dining. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38272.2 Portion Control.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38372.3 Menu Labeling. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38372.4 Trans Fat. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38472.5 Reduced Sodium. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 384

73 RESTRICTIVE DIET MENUS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38673.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38673.2 Gluten-Free Menu Items. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38673.3 Kosher Cuisine. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38773.4 Halal Foods. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38873.5 Vegetarian Cuisine. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 388

74 SEAFOOD. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39074.1 Seafood Entrees in Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39074.2 Trends. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39074.3 Sustainable Seafood. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39074.4 Labeling. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 392

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 14 •

75 SNACKING.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39475.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39475.2 Market Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39575.3 Snack Food Trends. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 396

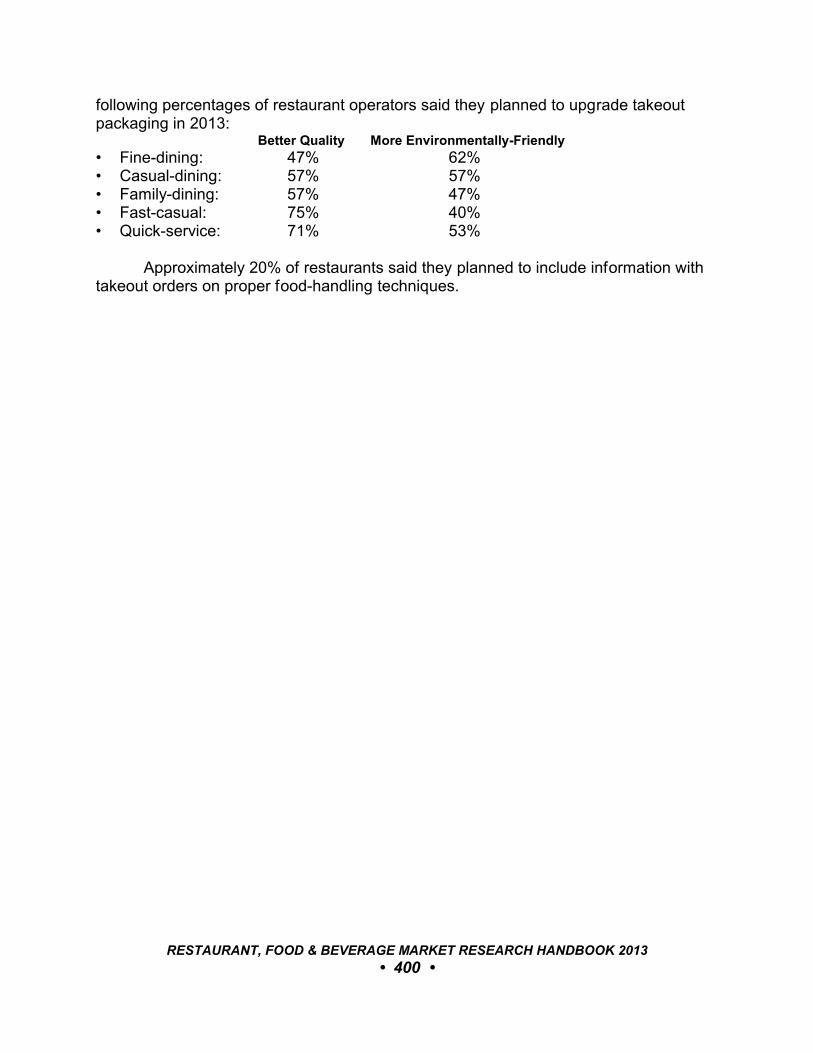

76 TAKEOUT & DELIVERY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39776.1 Market Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39776.2 Takeout and The American Lifestyle. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39776.3 The Takeout and Delivery Customer. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39776.4 Pizza Delivery. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39876.5 Quick-Service Carryout and Delivery.. . . . . . . . . . . . . . . . . . . . . . . . . . . . 39876.6 Takeout At Full-Service Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39976.7 Takeout for Offices and Elsewhere. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39976.8 Takeout Packaging. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 399

77 VALUE-FOCUSED DINING. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40177.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40177.2 Trading Down. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40177.3 Promotions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40377.4 Off-Peak Specials. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 403

PART VIII: BEVERAGE TRENDS & ANALYSES. . . . . . . . . . . . . . . . . . . . . . . . . . . 405

78 BEVERAGE CONSUMPTION & SPENDING. . . . . . . . . . . . . . . . . . . . . . . . . . 40678.1 Beverage Consumption. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40678.2 Beverage Spending. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40678.3 Alcoholic Beverages. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40778.4 Nonalcoholic Beverages. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 411

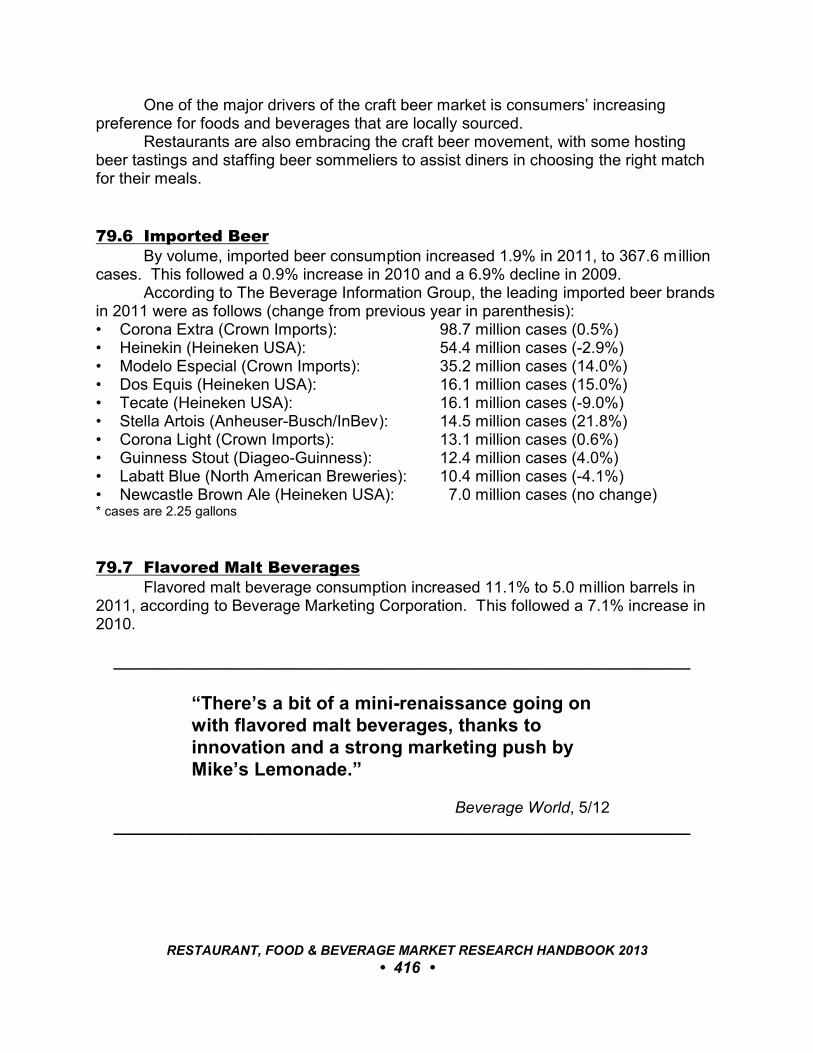

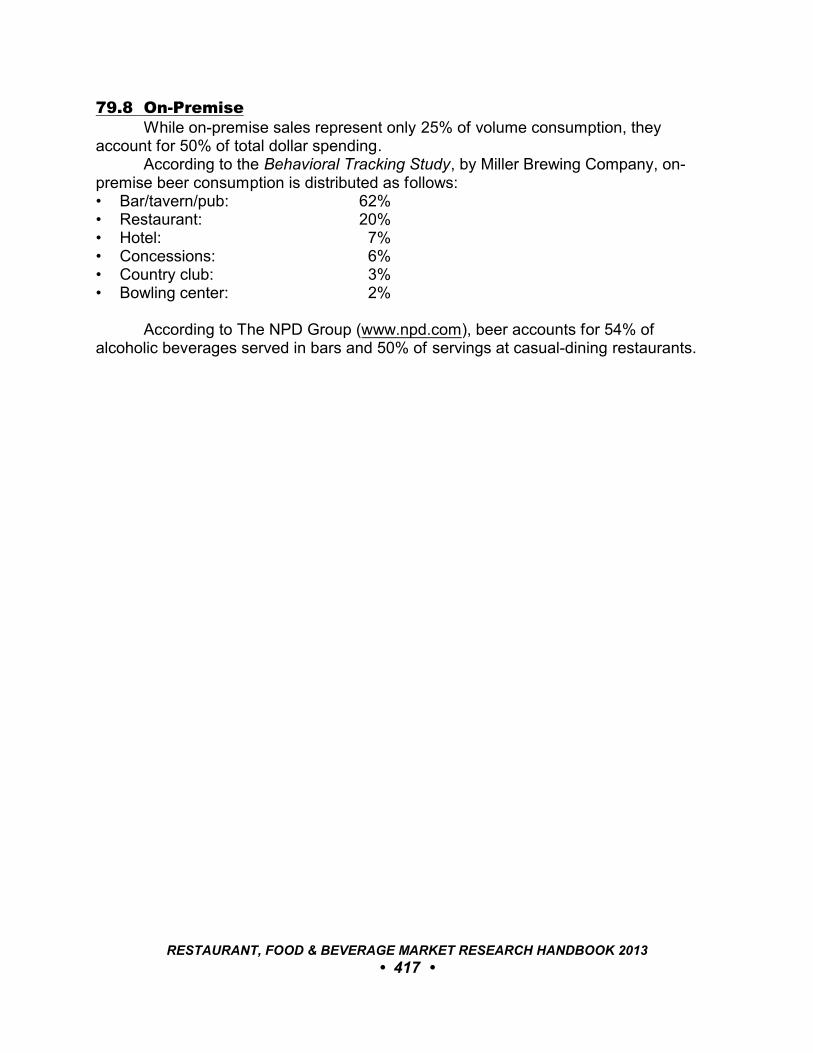

79 BEER. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41279.1 Market Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41279.2 Market Leaders. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41379.3 Top Domestic Beer Brands. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41479.4 Demographics. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41479.5 Craft Beer. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41579.6 Imported Beer. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41679.7 Flavored Malt Beverages.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41679.8 On-Premise. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 417

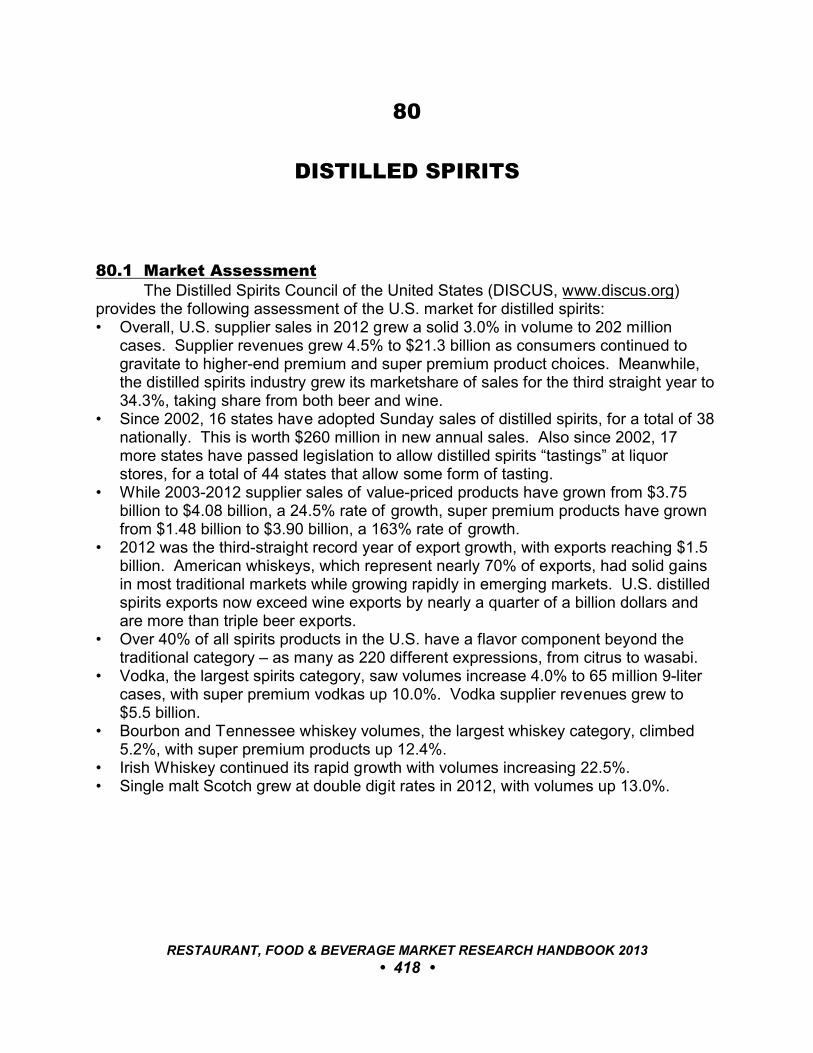

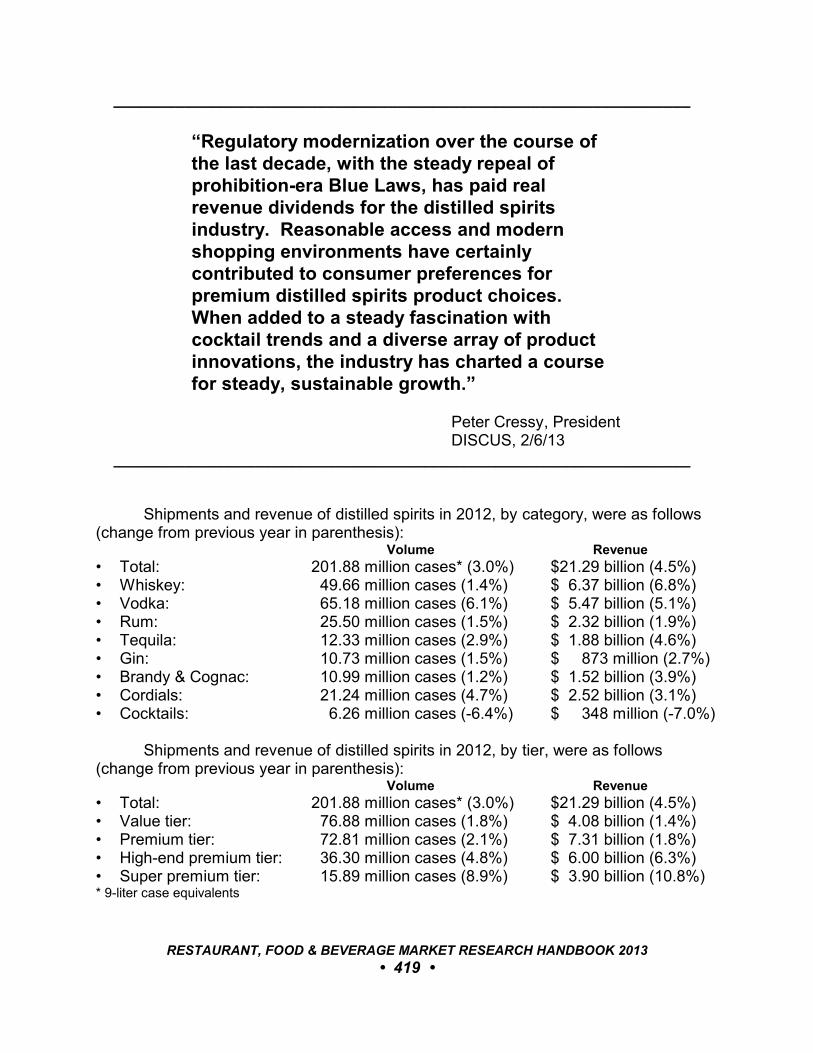

80 DISTILLED SPIRITS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41880.1 Market Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41880.2 Major Brands. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42080.3 Whiskey.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 421

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 15 •

80.4 Vodka. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42380.5 Rum.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42580.6 Tequila.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42780.7 Gin. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42880.8 Brandy and Cognac.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42980.9 Cordials. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 430

81 WINE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43281.1 Market Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43281.2 U.S. Wine Exports. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43381.3 Market Leaders. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43381.4 Wine Consumer Characteristics. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43381.5 Champagne and Sparkling Wine.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43481.6 Oneophiles. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 435

82 REFRESHMENT & FUNCTIONAL BEVERAGES. . . . . . . . . . . . . . . . . . . . . . . 43682.1 Carbonated Soft Drinks. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43682.2 Consumption Demographics. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43882.3 Sports Beverages. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43882.4 Energy Drinks. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43982.5 Juice & Fruit Drinks. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 441

83 COFFEE & TEA. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44483.1 Coffee Consumption. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44483.2 RTD Coffee. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44583.3 Coffeeshops. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44583.4 Tea Consumption. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44583.5 RTD Tea. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44683.6 Tea Stores and Tea Bars. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 447

84 BOTTLED WATER.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44884.1 Consumption and Spending. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44884.2 Consumption Demographics. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44984.3 Market Leaders. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44984.4 Market Drivers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 450

85 MILK.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45185.1 Consumption and Dairy Production. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45185.2 Consumer Spending. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45185.3 Market Drivers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 451

86 BEVERAGE SERVICE IN RESTAURANTS & BARS. . . . . . . . . . . . . . . . . . . . 45386.1 Market Assessment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45386.2 Refreshment and Nonalcoholic Beverage Service in Restaurants. . . . . . 454

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 16 •

86.3 Alcoholic Beverage Service in Full-Service Restaurants. . . . . . . . . . . . . . 45486.4 Alcoholic Beverage Service In Limited-Service Restaurants. . . . . . . . . . . 45786.5 Nonalcoholic Cocktails. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45886.6 Happy Hours. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46086.7 Beverage-Only Restaurant Occasions. . . . . . . . . . . . . . . . . . . . . . . . . . . 461

PART IX: AWARD WINNERS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 462

87 BEST NEW CHEFS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46387.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46387.2 Award Winners 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46387.3 Recent Award Winners. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 463

88 BEST NEW RESTAURANTS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46688.1 Lists For 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 466

89 BENCHMARK AWARDS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46989.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46989.2 Award Winners 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46989.3 Recent Award Winners. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 469

90 BEVERAGE EXCELLENCE AWARDS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47190.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47190.2 Award Winners 2013. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47190.3 Award Winners 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47290.4 Award Winners 2011. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 473

91 CHAIN RESTAURANT CONSUMERS’ CHOICE AWARDS. . . . . . . . . . . . . . . 47491.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47491.2 Award Winners 2013. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47491.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 474

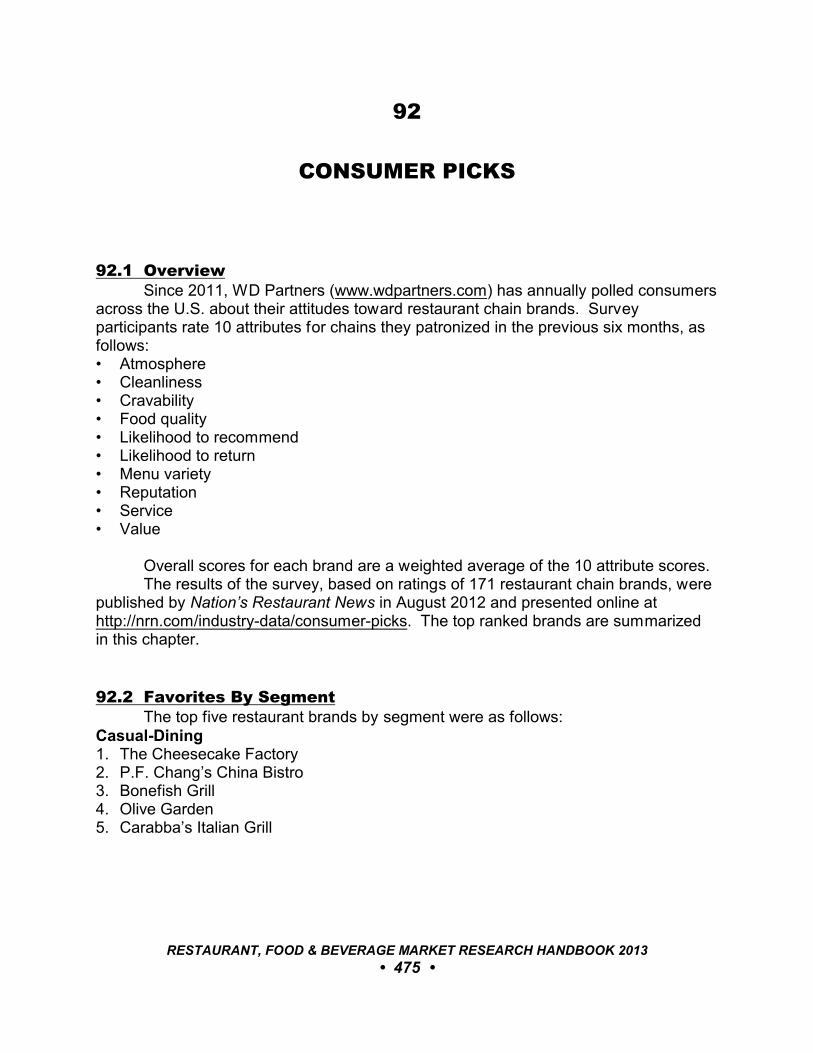

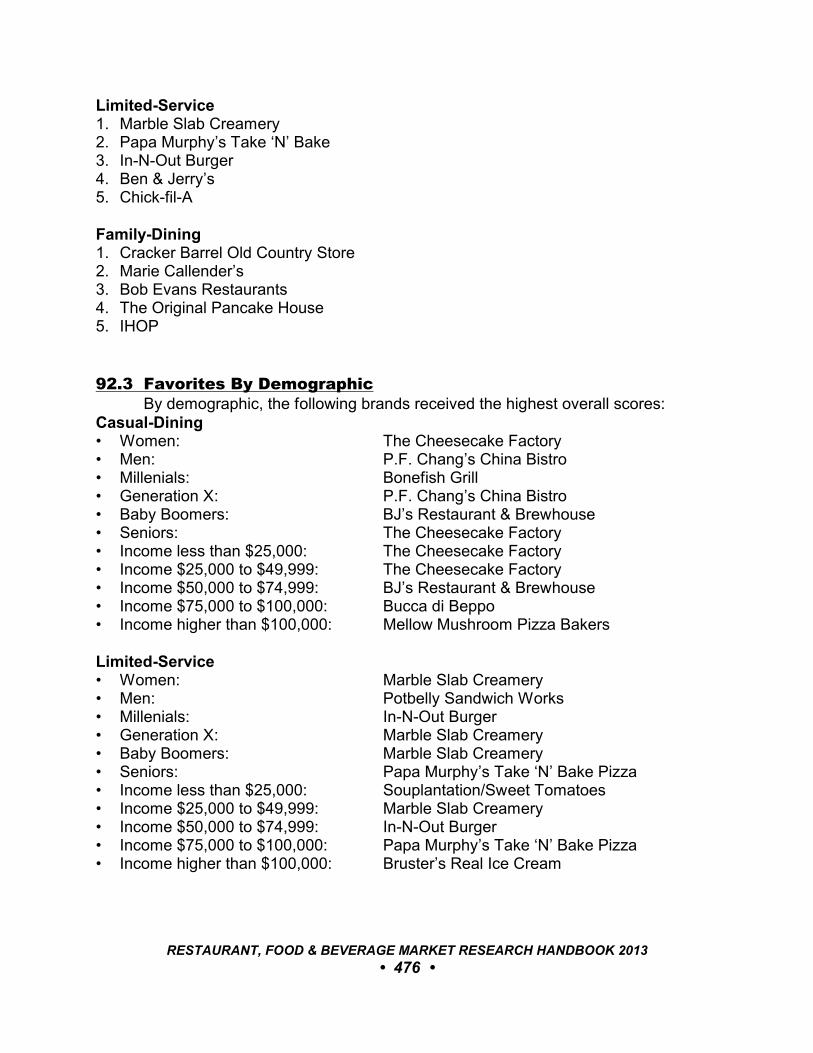

92 CONSUMER PICKS.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47592.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47592.2 Favorites By Segment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47592.3 Favorites By Demographic. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47692.4 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 477

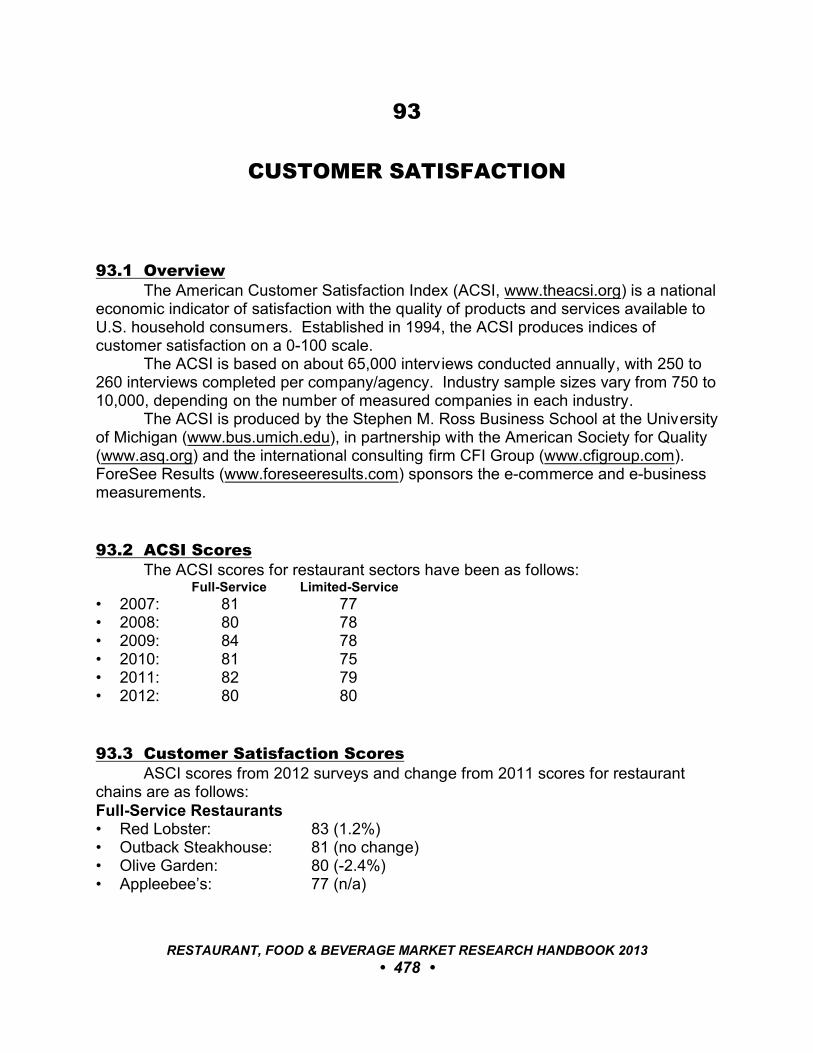

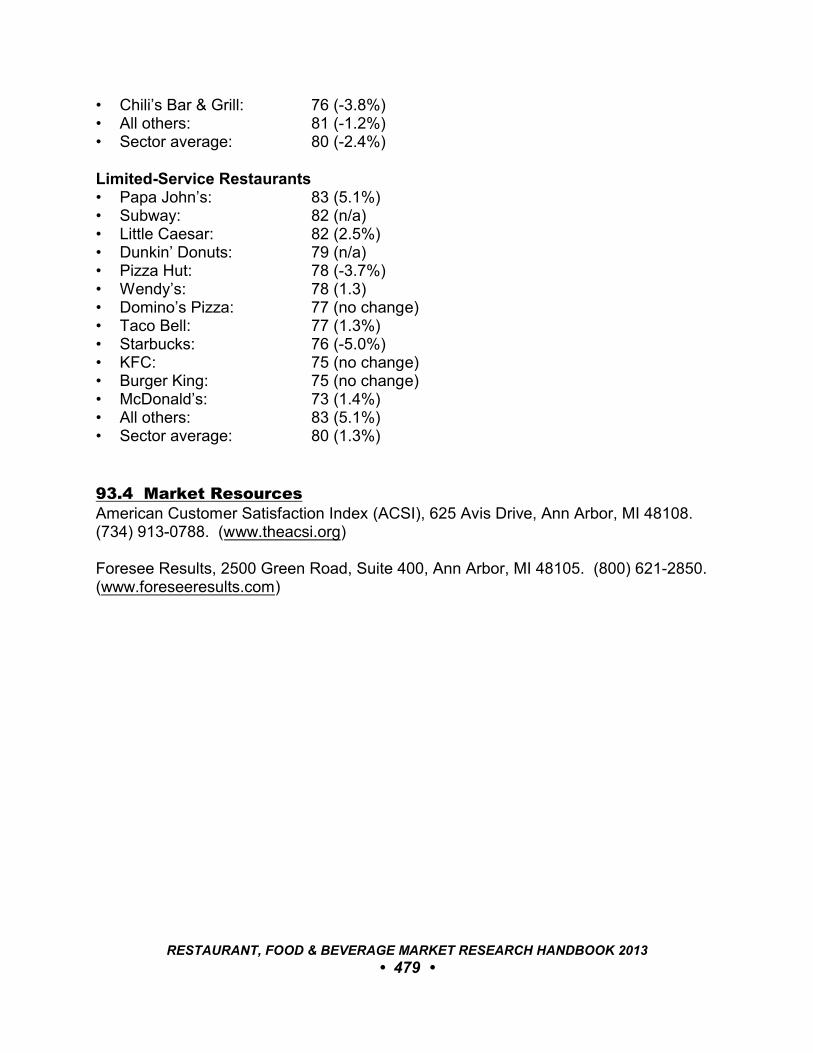

93 CUSTOMER SATISFACTION. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47893.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47893.2 ACSI Scores. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47893.3 Customer Satisfaction Scores. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47893.4 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 479

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 17 •

94 DINERS’ CHOICE AWARDS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48094.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48094.2 Best Restaurant. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48094.3 Best Service. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48394.4 Brunch. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48594.5 Fit For Foodies Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48794.6 Hot Spots. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49094.7 Kid-Friendly Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49294.8 Late-Night Dining. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49394.9 Most Notable Wine Lists. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49694.10 Most Romantic Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49894.11 Most Scenic Views. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50094.12 Outdoor Dining. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50394.13 Top American Cuisine. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 505

95 DISTINGUISHED RESTAURANTS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50895.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50895.2 List Of Distinguished Restaurants 2013. . . . . . . . . . . . . . . . . . . . . . . . . . 508

96 FAVORITE LIMITED-SERVICE RESTAURANTS. . . . . . . . . . . . . . . . . . . . . . . 52196.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52196.2 Top Chains By Segment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52196.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 522

97 FINE-DINING HALL OF FAME. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52397.1 List of Inductees. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 523

98 FIVE- AND FOUR-DIAMOND AWARDS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52698.1 Five-Diamnd Award Winners. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52698.2 Four-Diamnd Award Winners. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 528

99 FUTURE 50. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54499.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54499.2 Fastest Growing Chains 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54499.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 545

100 GREAT STEAK HOUSES. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 546100.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 546100.2 List Of Recognitions 2013.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 546

101 HOT CONCEPTS!. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 547101.1 Award Recipients 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 547101.2 Recent Designations.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 547101.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 549

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 18 •

102 JAMES BEARD FOUNDATION AWARDS. . . . . . . . . . . . . . . . . . . . . . . . . . . 550102.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 550102.2 Award Winners 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 550102.3 Recent Award Winners. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 551102.4 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 552

103 MENU MASTERS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 553103.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 553103.2 Winners By Category. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 553103.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 556

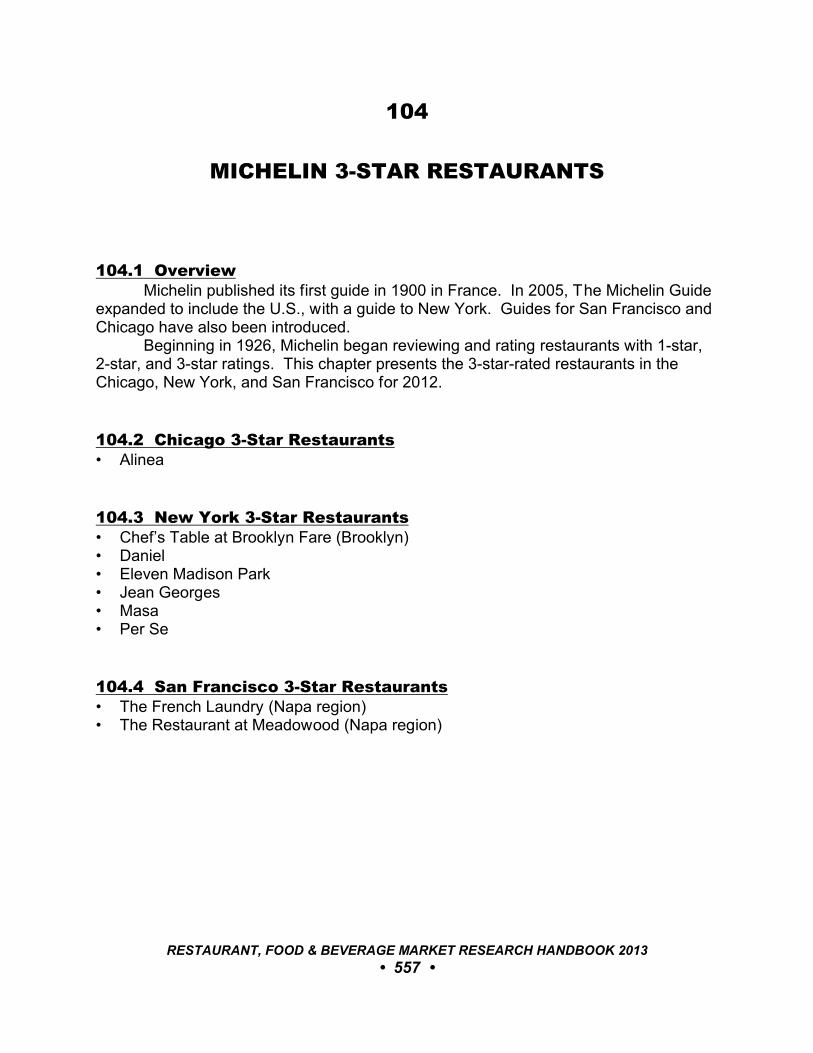

104 MICHELIN 3-STAR RESTAURANTS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 557104.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 557104.2 Chicago 3-Star Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 557104.3 New York 3-Star Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 557104.4 San Francisco 3-Star Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . 557

105 MILLENNIALS’ FAVORITE RESTAURANT CHAINS. . . . . . . . . . . . . . . . . . . 558105.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 558105.2 Favorite Restaurant Chains. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 559105.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 559

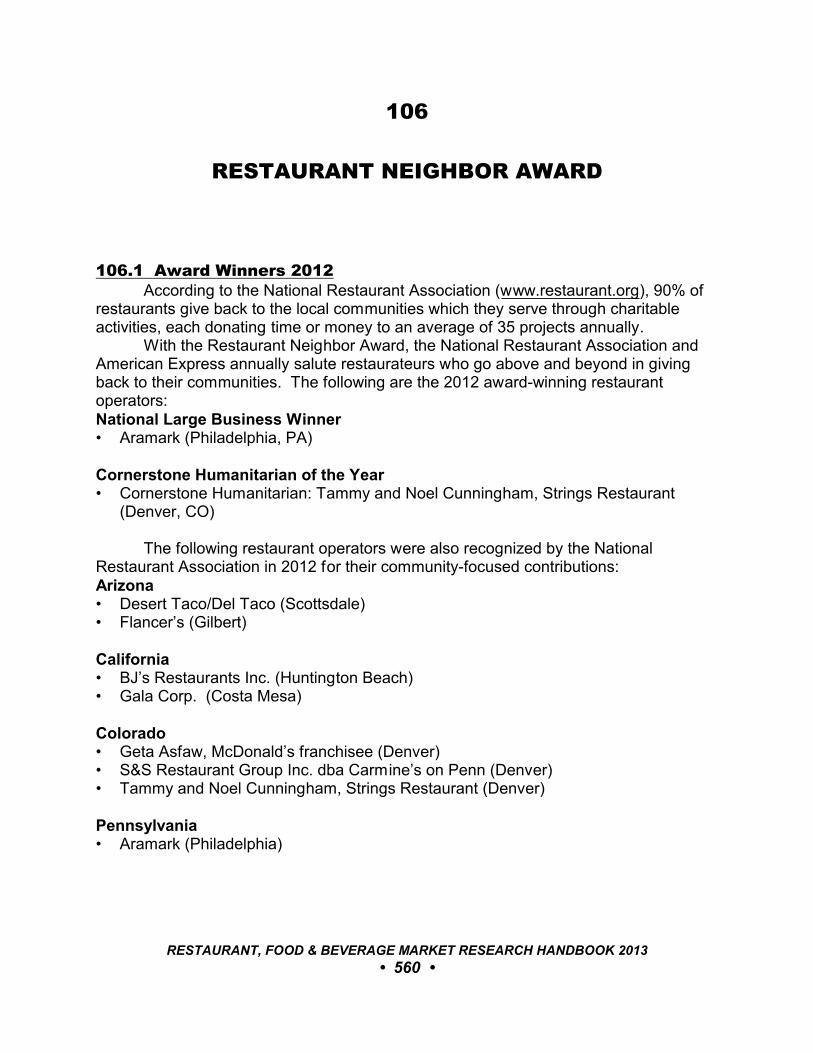

106 RESTAURANT NEIGHBOR AWARD. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 560106.1 Award Winners 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 560

107 SELECTIONS: BON APPÉTIT. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 561107.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 561107.2 Best Restaurant and Snack Shops Sepections. . . . . . . . . . . . . . . . . . 561

108 SELECTIONS: DINERS, DRIVE-INS & DIVES. . . . . . . . . . . . . . . . . . . . . . . . 565108.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 565108.2 List Of Featured Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 565

109 SELECTIONS: FOOD & WINE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 579109.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 579109.2 America’s Best. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 579

110 SELECTIONS: GAYOT. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 589110.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 589110.2 Top 40 List 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 589110.3 Top 10 By Segment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 590

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 19 •

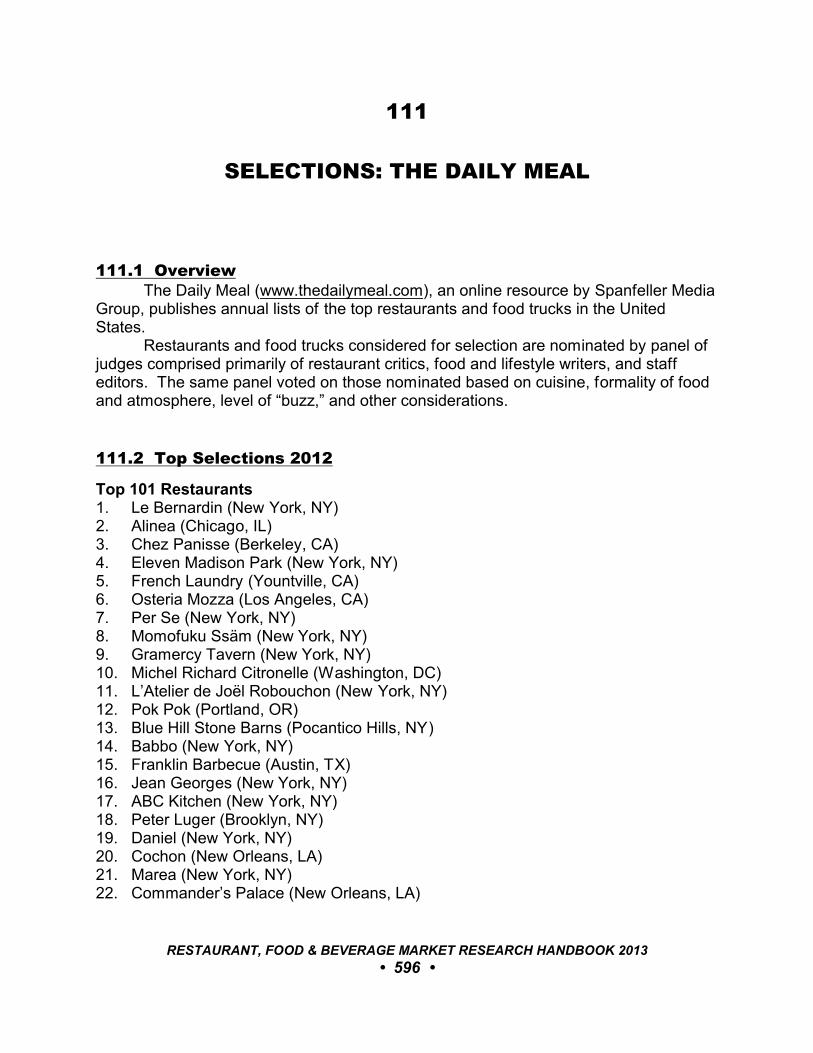

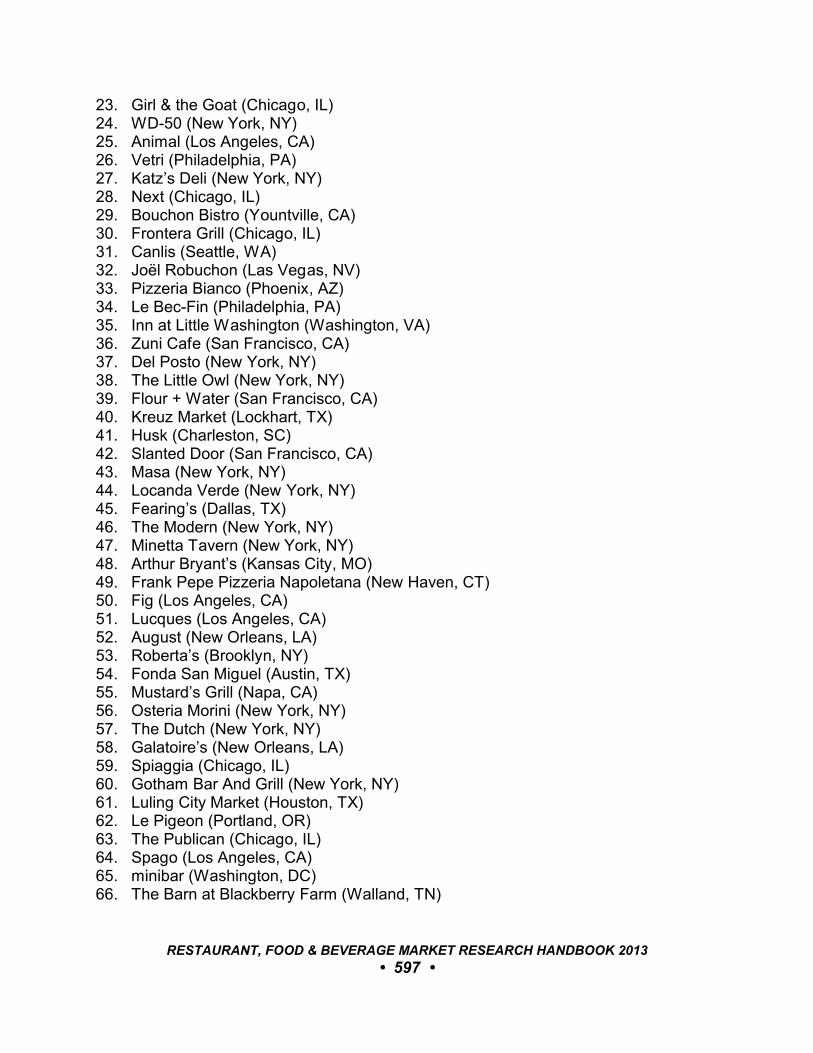

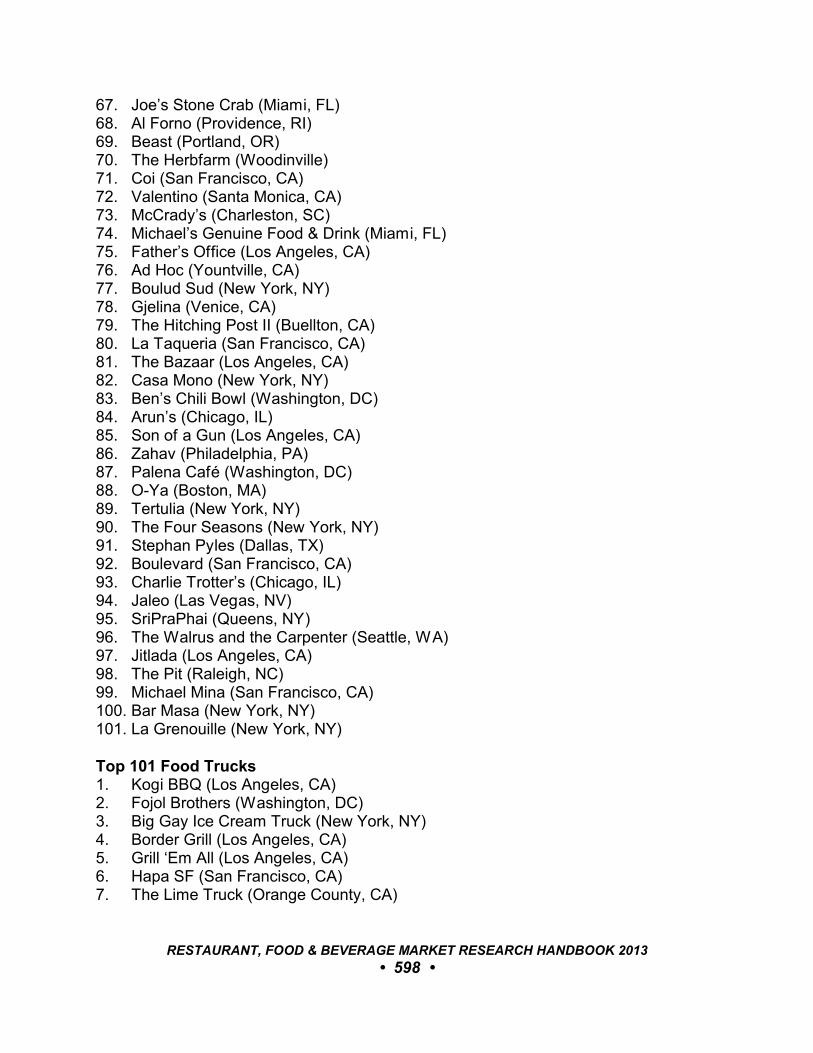

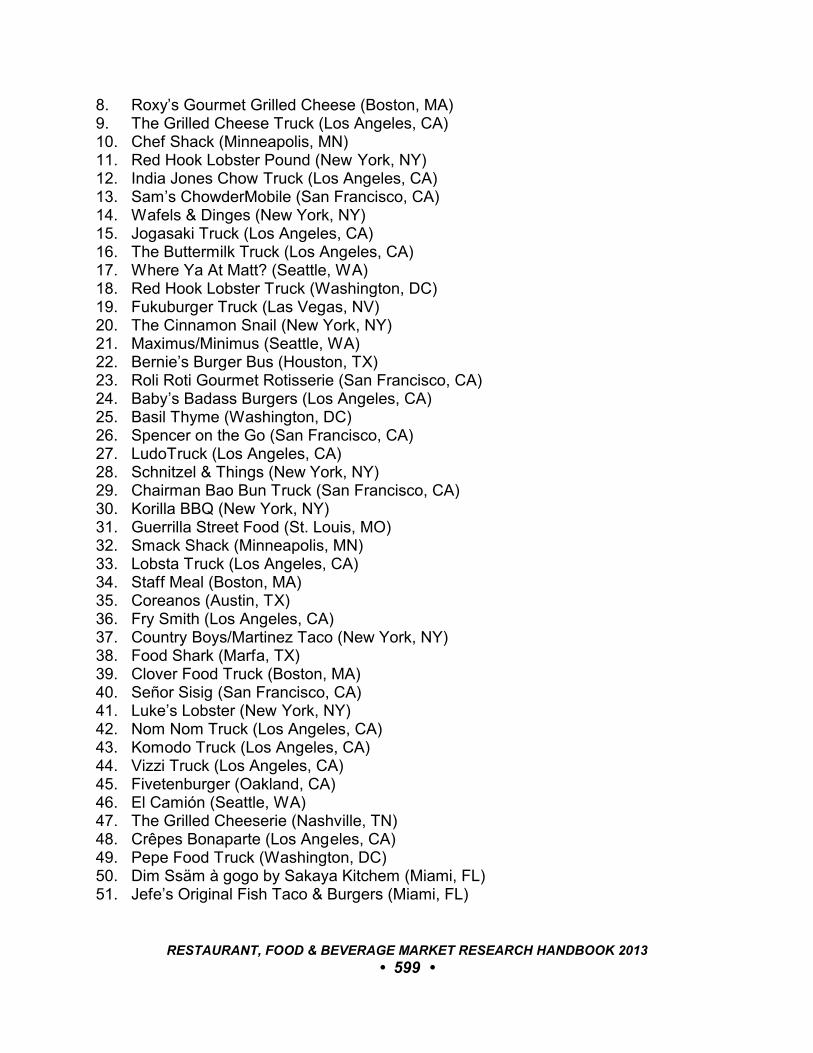

111 SELECTIONS: THE DAILY MEAL. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 596111.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 596111.2 Top Selections 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 596111.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 602

112 SELECTIONS: TRAVEL + LEISURE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 603112.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 603112.2 Restaurant and Beverage Service Selections.. . . . . . . . . . . . . . . . . . . 603

113 SELECTIONS: ZAGAT. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 611113.1 Best Burgers. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 611113.2 Best Business Lunch. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 613113.3 Best Sandwiches. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 614113.4 Best Service. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 615113.5 Business Trip Dining. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 617113.6 Hotel Restaurants. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 625113.7 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 627

114 STAR DIAMOND AWARD.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 628114.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 628114.2 Five Star Diamond Awards 2013. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 628

115 THE NRN 50. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 630115.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 630115.2 Breakout Brands 2013. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 630115.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 632

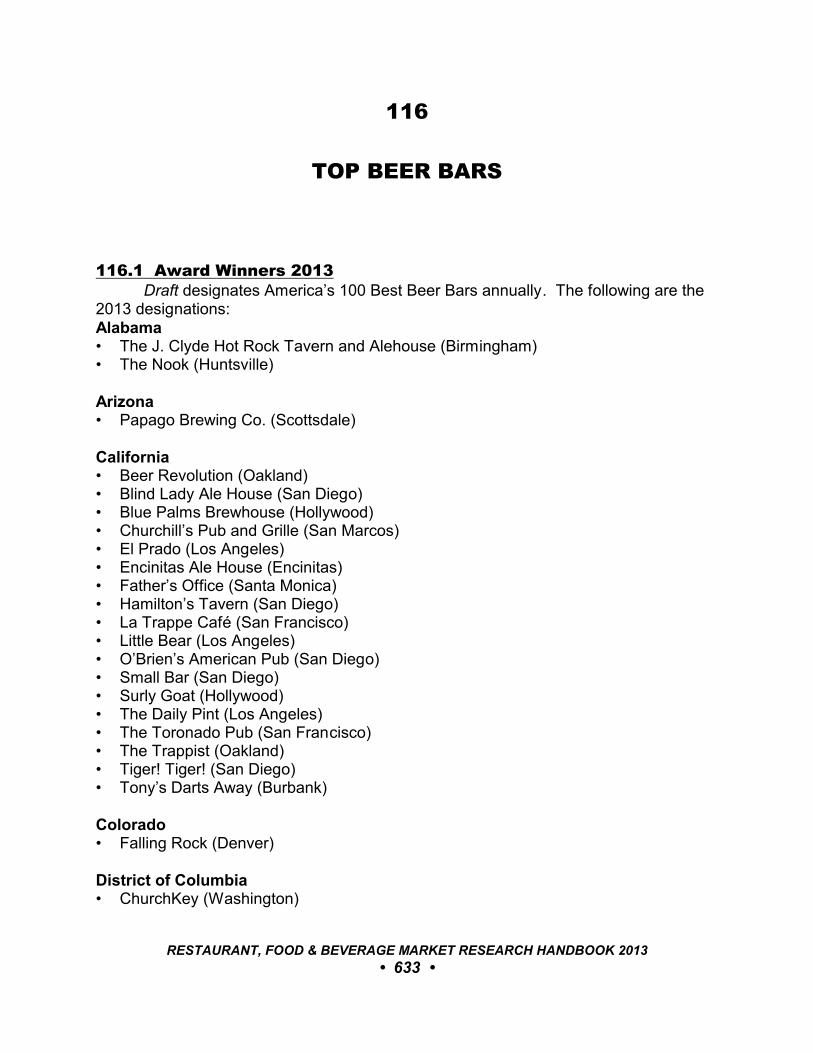

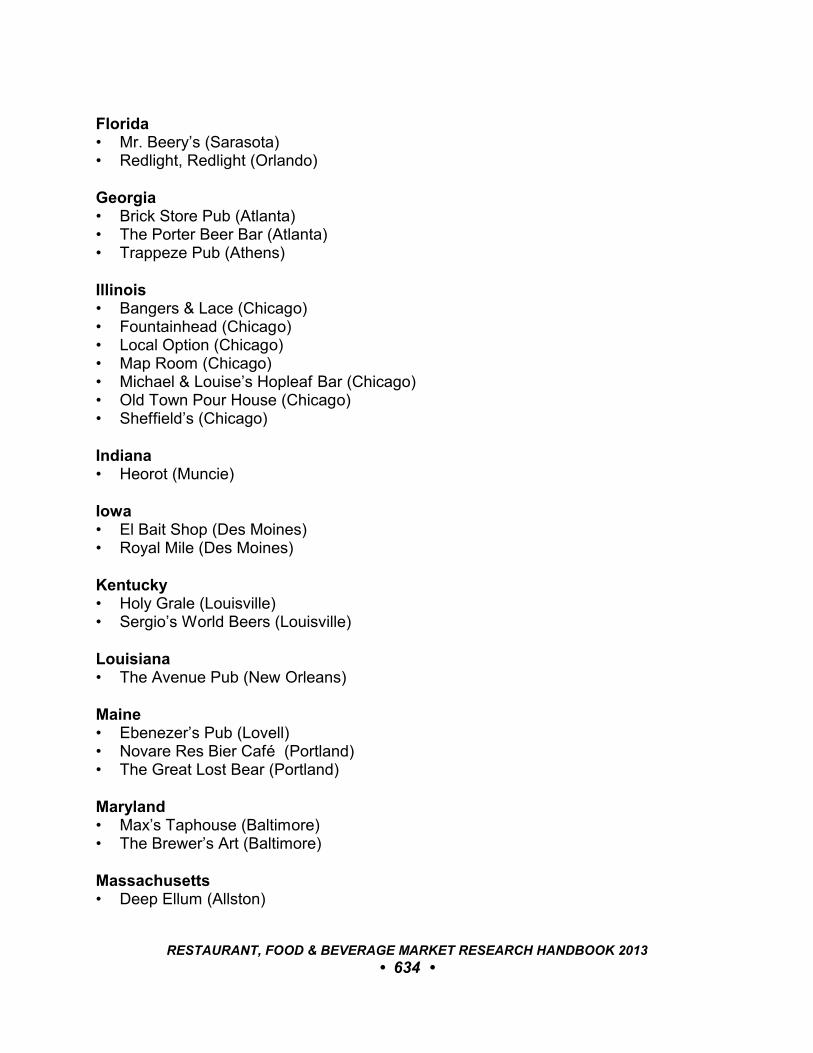

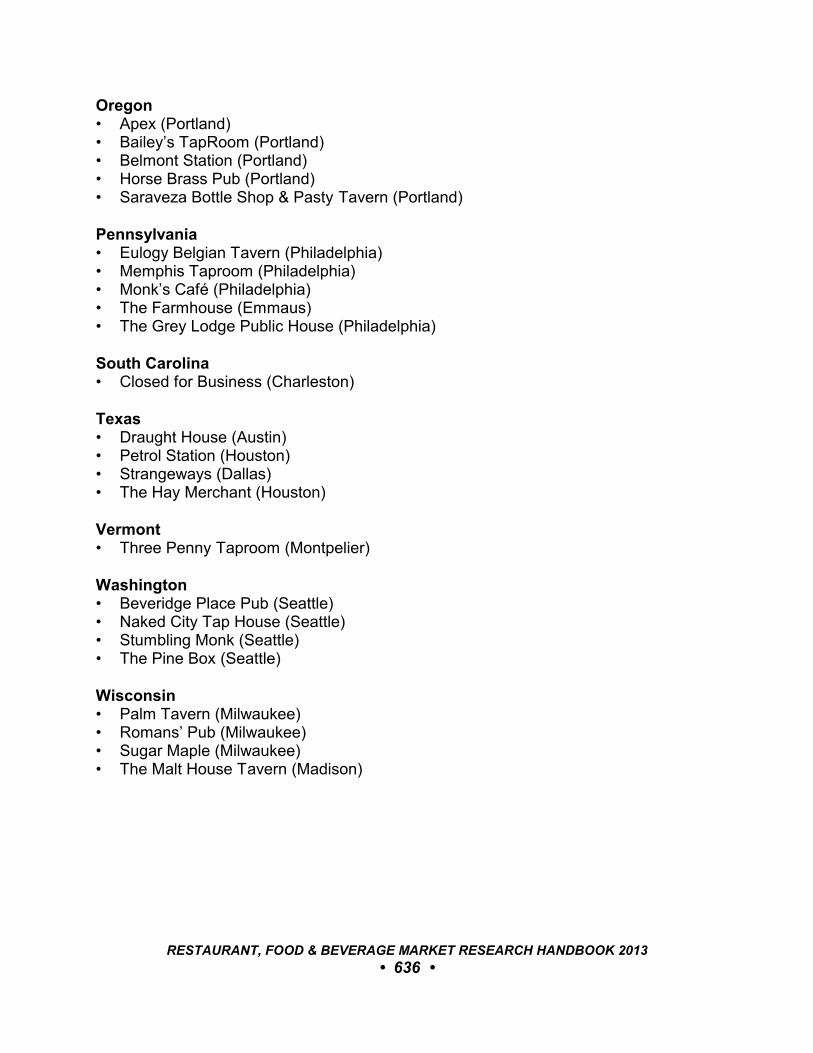

116 TOP BEER BARS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 633116.1 Award Winners 2013. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 633

117 TOP RESTAURANT BRANDS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 637117.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 637117.2 Top Brand Scores 2011. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 637117.3 Market Resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 637

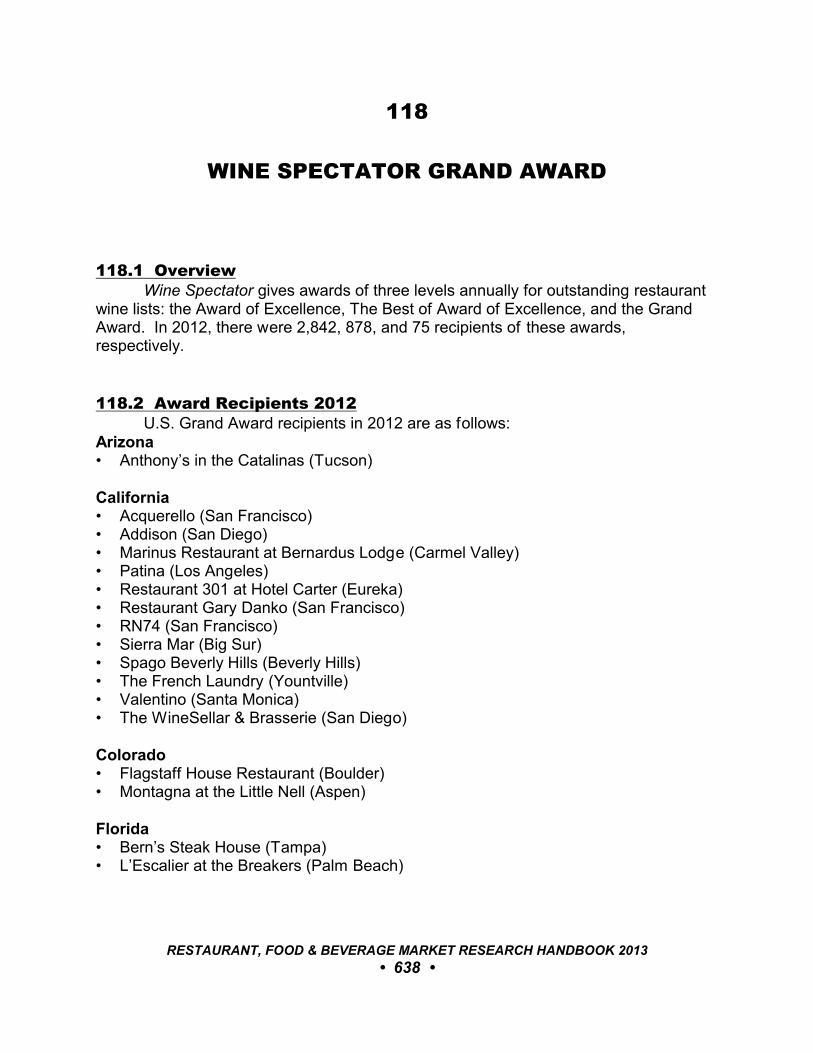

118 WINE SPECTATOR GRAND AWARD. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 638118.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 638118.2 Award Recipients 2012. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 638

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 20 •

PART X: FOOD & BEVERAGE DESIGNATIONS. . . . . . . . . . . . . . . . . . . . . . . . . . . 641

119 NATIONAL FOOD & BEVERAGE HOLIDAYS. . . . . . . . . . . . . . . . . . . . . . . . 642119.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 642119.2 National Food & Beverage Days.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 642119.3 National Food & Beverage Weeks. . . . . . . . . . . . . . . . . . . . . . . . . . . . 653119.4 National Food & Beverage Months. . . . . . . . . . . . . . . . . . . . . . . . . . . . 654

120 STATE FOODS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 658120.1 Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 658120.2 List of Official State Foods. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 658

APPENDIX A - ACADEMIC PROGRAMS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 662

APPENDIX B - ANALYSTS & MARKET CONSULTANTS. . . . . . . . . . . . . . . . . . . . 668

APPENDIX C - ASSOCIATIONS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 671

APPENDIX D - PERIODICALS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 673

APPENDIX E - STATE RESTAURANT ASSOCIATIONS. . . . . . . . . . . . . . . . . . . . . 675

REFERENCES. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 680

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 21 •

PART I: MARKET OVERVIEW

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 22 •

1

MARKET SUMMARY

1.1 OverviewThere are more than 980,000 restaurant and foodservice locations in the United

States. The restaurant share of the food dollar is approximately 48%. The industryemploys 13.1 million people.

1.2 Industry SalesAccording to the National Restaurant Association (www.restaurant.org), total

restaurant industry sales are projected to reach $660.5 billion in 2013, an increase of3.5%, or 0.8% on an inflation-adjusted basis. Sales reached $636.4 billion in 2012. Distribution for 2013 is as follows:COMMERCIAL RESTAURANT SERVICES• Restaurants: $441.9 billion• Retail, vending, recreation, mobile, and other: $ 62.4 billion• Managed services: $ 45.6 billion• Hotel restaurants: $ 33.2 billion• Bars and taverns: $ 19.5 billion• Total: $602.5 billion

NONCOMMERCIAL RESTAURANT SERVICES• Total: $ 55.4 billion

MILITARY RESTAURANT SERVICES• Total: $ 2.5 billion

Sales at full-service restaurants are projected to reach $208.1 billion in 2013, anincrease of 2.9% over 2012 and a real growth rate of 0.2%. Sales at quick-servicerestaurants are projected to reach approximately $188.1 billion in 2013, an increase of4.9% over 2011 and a real growth rate of 1.7%.

The National Restaurant Association projects food and beverage sales forrestaurant and foodservice segments in 2013 as follows (change from 2012 inparenthesis):EATING AND DRINKING PLACES• Full-service restaurants: $208.69 billion (2.9%)• Quick-service restaurants: $188.12 billion (4.9%)

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 23 •

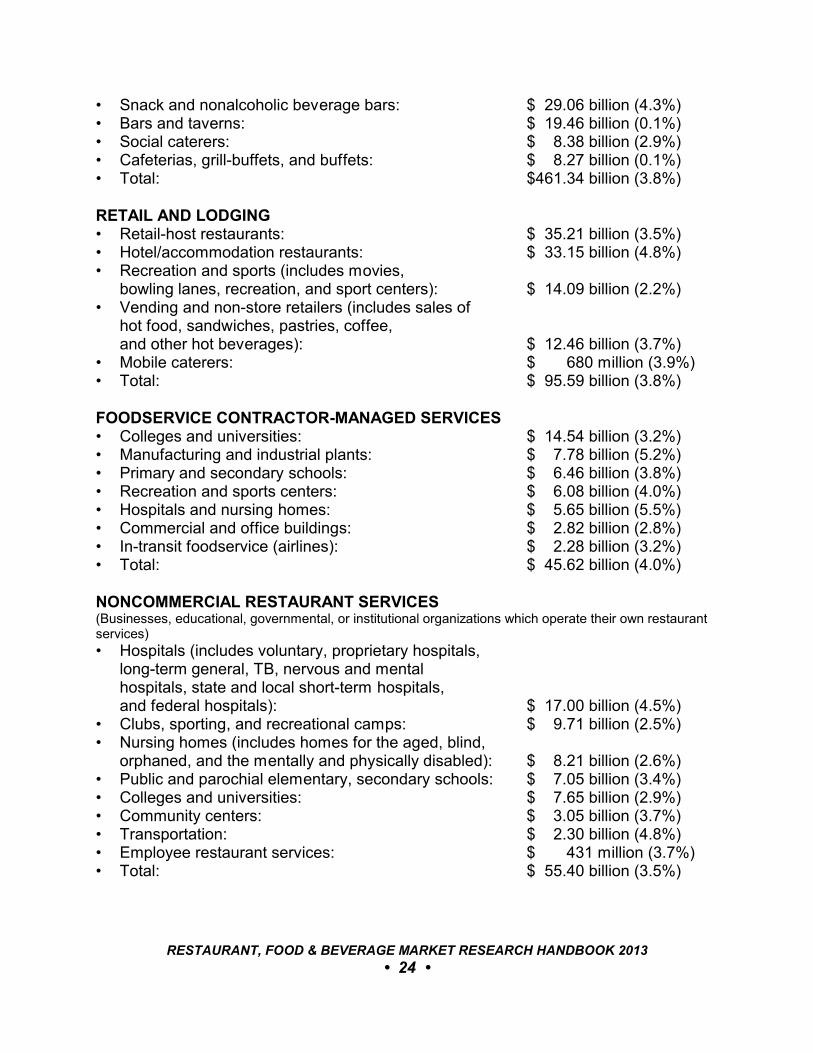

• Snack and nonalcoholic beverage bars: $ 29.06 billion (4.3%)• Bars and taverns: $ 19.46 billion (0.1%)• Social caterers: $ 8.38 billion (2.9%)• Cafeterias, grill-buffets, and buffets: $ 8.27 billion (0.1%)• Total: $461.34 billion (3.8%)

RETAIL AND LODGING• Retail-host restaurants: $ 35.21 billion (3.5%)• Hotel/accommodation restaurants: $ 33.15 billion (4.8%)• Recreation and sports (includes movies,

bowling lanes, recreation, and sport centers): $ 14.09 billion (2.2%)• Vending and non-store retailers (includes sales of

hot food, sandwiches, pastries, coffee, and other hot beverages): $ 12.46 billion (3.7%)

• Mobile caterers: $ 680 million (3.9%)• Total: $ 95.59 billion (3.8%)

FOODSERVICE CONTRACTOR-MANAGED SERVICES• Colleges and universities: $ 14.54 billion (3.2%)• Manufacturing and industrial plants: $ 7.78 billion (5.2%)• Primary and secondary schools: $ 6.46 billion (3.8%)• Recreation and sports centers: $ 6.08 billion (4.0%)• Hospitals and nursing homes: $ 5.65 billion (5.5%)• Commercial and office buildings: $ 2.82 billion (2.8%)• In-transit foodservice (airlines): $ 2.28 billion (3.2%)• Total: $ 45.62 billion (4.0%)

NONCOMMERCIAL RESTAURANT SERVICES(Businesses, educational, governmental, or institutional organizations which operate their own restaurantservices)

• Hospitals (includes voluntary, proprietary hospitals, long-term general, TB, nervous and mental hospitals, state and local short-term hospitals, and federal hospitals): $ 17.00 billion (4.5%)

• Clubs, sporting, and recreational camps: $ 9.71 billion (2.5%)• Nursing homes (includes homes for the aged, blind,

orphaned, and the mentally and physically disabled): $ 8.21 billion (2.6%)• Public and parochial elementary, secondary schools: $ 7.05 billion (3.4%)• Colleges and universities: $ 7.65 billion (2.9%)• Community centers: $ 3.05 billion (3.7%)• Transportation: $ 2.30 billion (4.8%)• Employee restaurant services: $ 431 million (3.7%)• Total: $ 55.40 billion (3.5%)

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 24 •

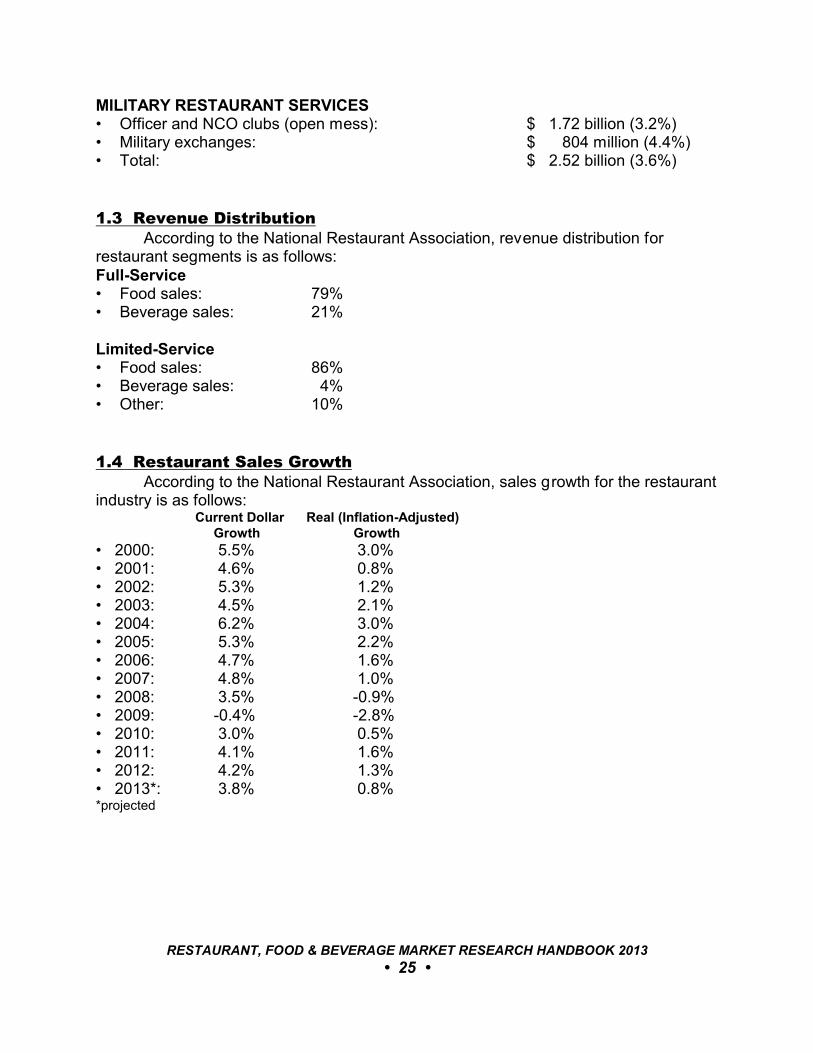

MILITARY RESTAURANT SERVICES• Officer and NCO clubs (open mess): $ 1.72 billion (3.2%)• Military exchanges: $ 804 million (4.4%)• Total: $ 2.52 billion (3.6%)

1.3 Revenue DistributionAccording to the National Restaurant Association, revenue distribution for

restaurant segments is as follows:Full-Service• Food sales: 79%• Beverage sales: 21%

Limited-Service• Food sales: 86%• Beverage sales: 4%• Other: 10%

1.4 Restaurant Sales GrowthAccording to the National Restaurant Association, sales growth for the restaurant

industry is as follows: Current Dollar Real (Inflation-Adjusted) Growth Growth

• 2000: 5.5% 3.0%• 2001: 4.6% 0.8%• 2002: 5.3% 1.2%• 2003: 4.5% 2.1%• 2004: 6.2% 3.0%• 2005: 5.3% 2.2%• 2006: 4.7% 1.6%• 2007: 4.8% 1.0%• 2008: 3.5% -0.9%• 2009: -0.4% -2.8%• 2010: 3.0% 0.5%• 2011: 4.1% 1.6%• 2012: 4.2% 1.3%• 2013*: 3.8% 0.8%*projected

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 25 •

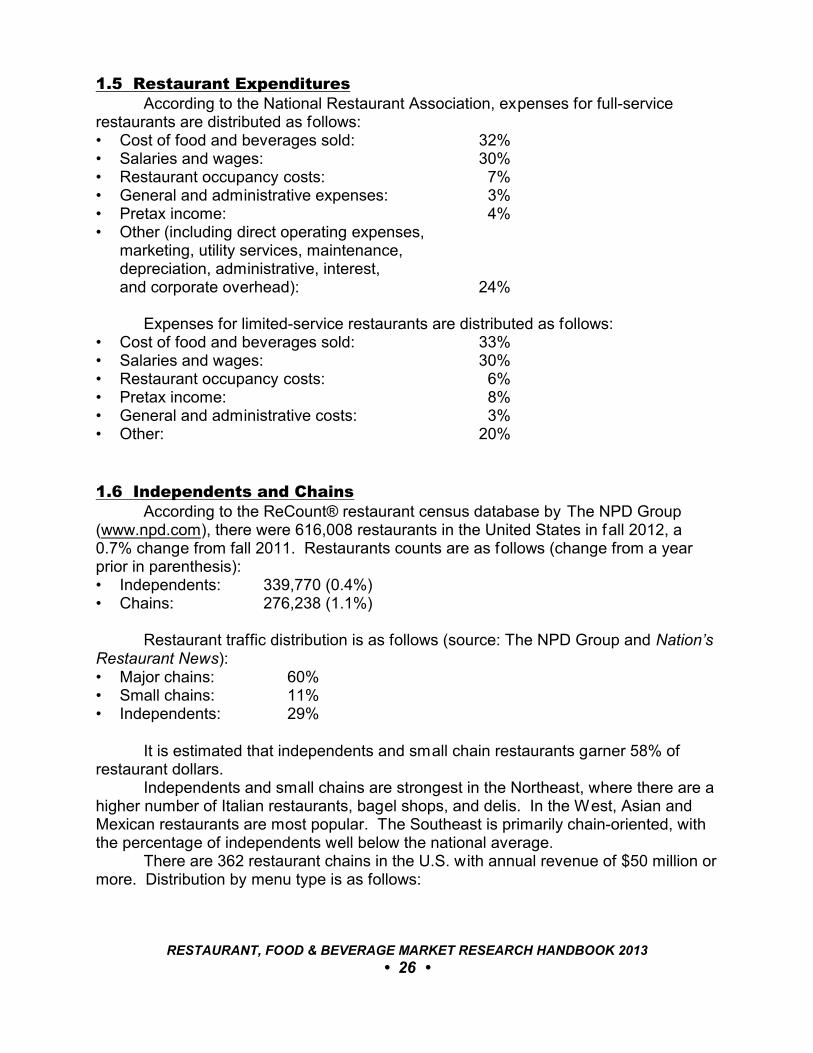

1.5 Restaurant ExpendituresAccording to the National Restaurant Association, expenses for full-service

restaurants are distributed as follows:• Cost of food and beverages sold: 32%• Salaries and wages: 30%• Restaurant occupancy costs: 7%• General and administrative expenses: 3%• Pretax income: 4%• Other (including direct operating expenses,

marketing, utility services, maintenance, depreciation, administrative, interest, and corporate overhead): 24%

Expenses for limited-service restaurants are distributed as follows:• Cost of food and beverages sold: 33%• Salaries and wages: 30%• Restaurant occupancy costs: 6%• Pretax income: 8%• General and administrative costs: 3%• Other: 20%

1.6 Independents and ChainsAccording to the ReCount® restaurant census database by The NPD Group

(www.npd.com), there were 616,008 restaurants in the United States in fall 2012, a0.7% change from fall 2011. Restaurants counts are as follows (change from a yearprior in parenthesis):• Independents: 339,770 (0.4%)• Chains: 276,238 (1.1%)

Restaurant traffic distribution is as follows (source: The NPD Group and Nation’sRestaurant News):• Major chains: 60%• Small chains: 11%• Independents: 29%

It is estimated that independents and small chain restaurants garner 58% ofrestaurant dollars.

Independents and small chains are strongest in the Northeast, where there are ahigher number of Italian restaurants, bagel shops, and delis. In the West, Asian andMexican restaurants are most popular. The Southeast is primarily chain-oriented, withthe percentage of independents well below the national average.

There are 362 restaurant chains in the U.S. with annual revenue of $50 million ormore. Distribution by menu type is as follows:

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 26 •

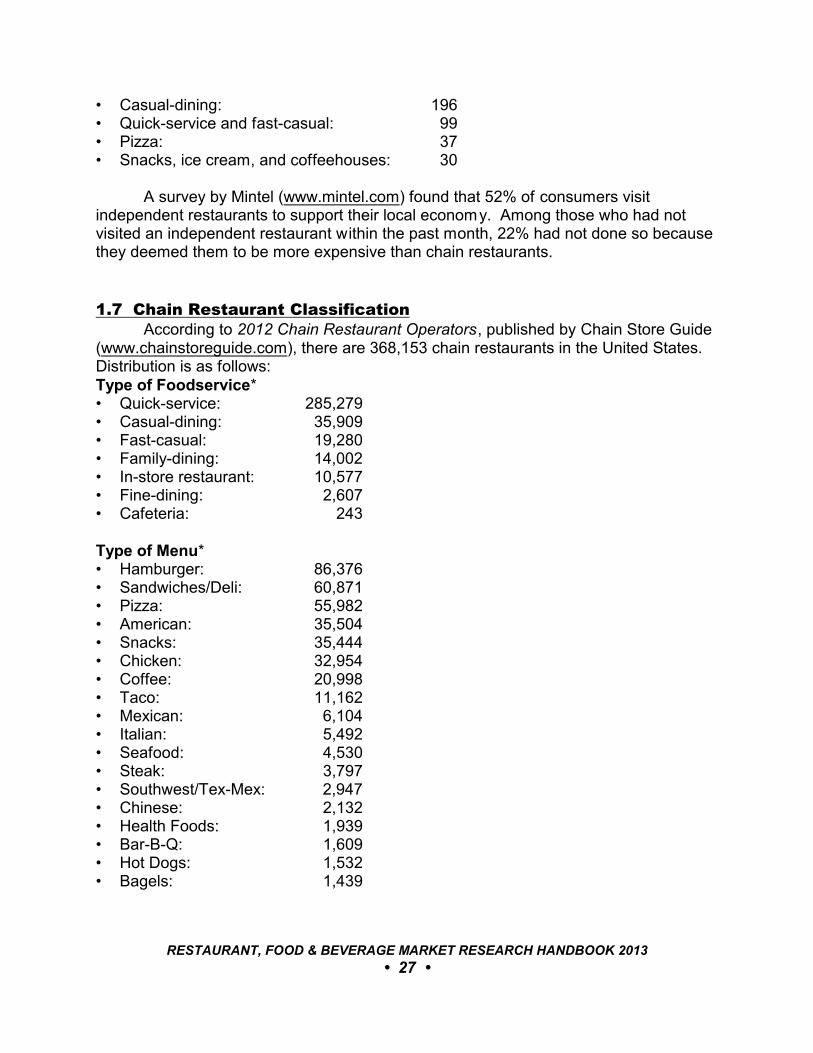

• Casual-dining: 196• Quick-service and fast-casual: 99• Pizza: 37• Snacks, ice cream, and coffeehouses: 30

A survey by Mintel (www.mintel.com) found that 52% of consumers visitindependent restaurants to support their local economy. Among those who had notvisited an independent restaurant within the past month, 22% had not done so becausethey deemed them to be more expensive than chain restaurants.

1.7 Chain Restaurant ClassificationAccording to 2012 Chain Restaurant Operators, published by Chain Store Guide

(www.chainstoreguide.com), there are 368,153 chain restaurants in the United States. Distribution is as follows:Type of Foodservice*• Quick-service: 285,279• Casual-dining: 35,909• Fast-casual: 19,280• Family-dining: 14,002• In-store restaurant: 10,577• Fine-dining: 2,607• Cafeteria: 243

Type of Menu*• Hamburger: 86,376• Sandwiches/Deli: 60,871• Pizza: 55,982• American: 35,504• Snacks: 35,444• Chicken: 32,954• Coffee: 20,998• Taco: 11,162• Mexican: 6,104• Italian: 5,492• Seafood: 4,530• Steak: 3,797• Southwest/Tex-Mex: 2,947• Chinese: 2,132• Health Foods: 1,939• Bar-B-Q: 1,609• Hot Dogs: 1,532• Bagels: 1,439

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 27 •

• Asian: 1,327• Steak/Seafood: 625• Greek/Mediterranean: 605• Japanese: 455• Cajun/Creole: 353• French/Continental: 321• Caribbean: 215• Californian: 170• Southern: 93• Indian: 82• Latin American/Cuban: 60• Spanish: 52• Eastern European: 48• Middle Eastern: 45• Thai: 30• German: 6• Miscellaneous: 843* Some locations offer more than one type of foodservice or menu

Chain Store Guide includes all restaurant groups with two or more locations inthe count of chain restaurants. The NPD Group classifies some small local restaurantgroups as independents. This difference, in part, accounts for the differing counts insections 1.7 and 1.8.

1.8 Restaurant VisitsThe NPD Group (www.npd.com) assesses the total number of annual visits to

restaurants and the average number of visits per capita as follows: Total Visits Visits Per Capita

• 2004 59 million 206• 2010: 60 million 197• 2011: 61 million 196• 2012: 62 million 194• 2014 (projected): 64 million 190

Restaurant traffic has improved slightly since the recession; traffic was up 1% for12-month period ending September 2012, according to NPD’s CREST® foodservicemarket research, although levels remain below those in 2008. Morning meal visits havecompletely recovered to pre-recession levels, up 2% for same 12-month period.

Restaurant visits by age demographic are assessed in Section 49.1 of this handbook.

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 28 •

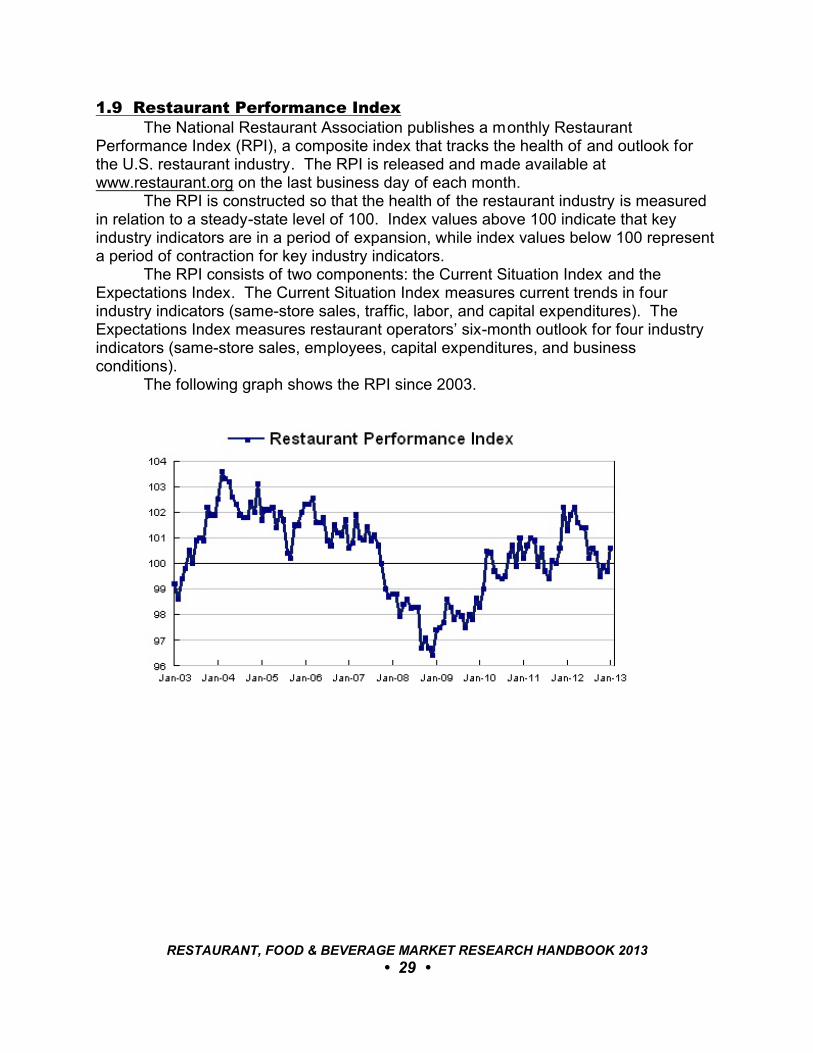

1.9 Restaurant Performance IndexThe National Restaurant Association publishes a monthly Restaurant

Performance Index (RPI), a composite index that tracks the health of and outlook forthe U.S. restaurant industry. The RPI is released and made available atwww.restaurant.org on the last business day of each month.

The RPI is constructed so that the health of the restaurant industry is measuredin relation to a steady-state level of 100. Index values above 100 indicate that keyindustry indicators are in a period of expansion, while index values below 100 representa period of contraction for key industry indicators.

The RPI consists of two components: the Current Situation Index and theExpectations Index. The Current Situation Index measures current trends in fourindustry indicators (same-store sales, traffic, labor, and capital expenditures). TheExpectations Index measures restaurant operators’ six-month outlook for four industryindicators (same-store sales, employees, capital expenditures, and businessconditions).

The following graph shows the RPI since 2003.

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 29 •

2

STATE-BY-STATE ANALYSIS

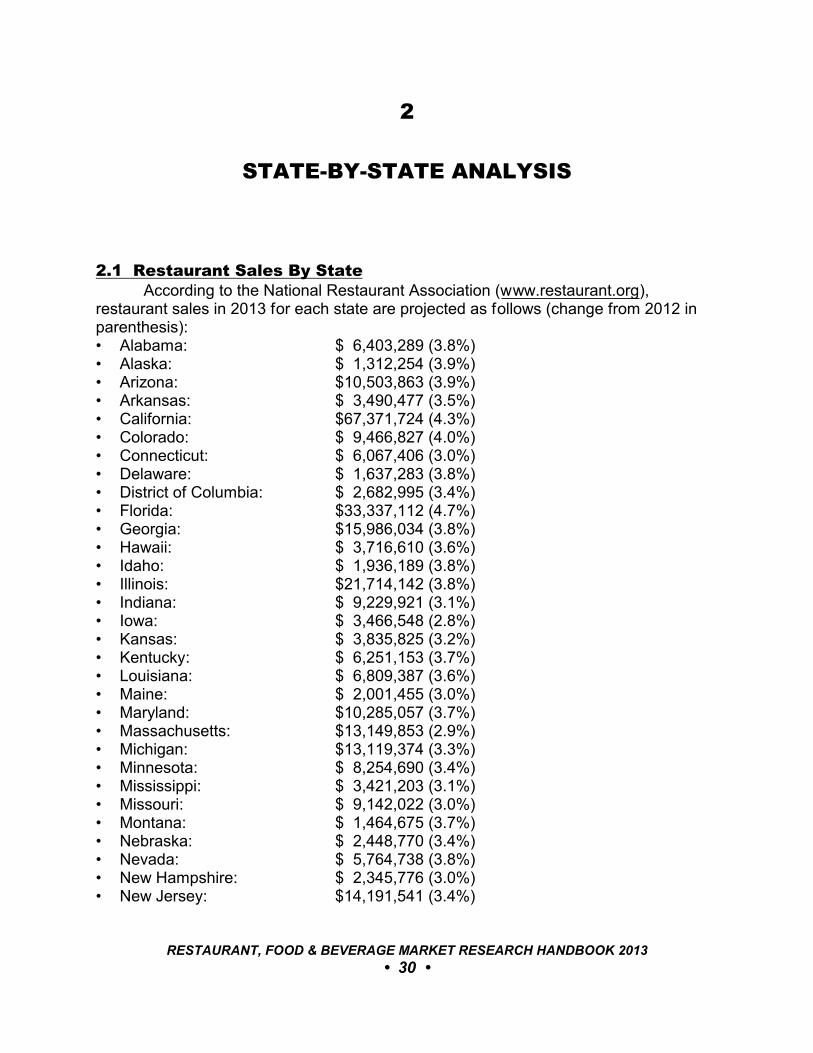

2.1 Restaurant Sales By StateAccording to the National Restaurant Association (www.restaurant.org),

restaurant sales in 2013 for each state are projected as follows (change from 2012 inparenthesis):• Alabama: $ 6,403,289 (3.8%)• Alaska: $ 1,312,254 (3.9%)• Arizona: $10,503,863 (3.9%)• Arkansas: $ 3,490,477 (3.5%)• California: $67,371,724 (4.3%)• Colorado: $ 9,466,827 (4.0%)• Connecticut: $ 6,067,406 (3.0%)• Delaware: $ 1,637,283 (3.8%)• District of Columbia: $ 2,682,995 (3.4%)• Florida: $33,337,112 (4.7%)• Georgia: $15,986,034 (3.8%)• Hawaii: $ 3,716,610 (3.6%)• Idaho: $ 1,936,189 (3.8%)• Illinois: $21,714,142 (3.8%)• Indiana: $ 9,229,921 (3.1%)• Iowa: $ 3,466,548 (2.8%)• Kansas: $ 3,835,825 (3.2%)• Kentucky: $ 6,251,153 (3.7%)• Louisiana: $ 6,809,387 (3.6%)• Maine: $ 2,001,455 (3.0%)• Maryland: $10,285,057 (3.7%)• Massachusetts: $13,149,853 (2.9%)• Michigan: $13,119,374 (3.3%)• Minnesota: $ 8,254,690 (3.4%)• Mississippi: $ 3,421,203 (3.1%)• Missouri: $ 9,142,022 (3.0%)• Montana: $ 1,464,675 (3.7%)• Nebraska: $ 2,448,770 (3.4%)• Nevada: $ 5,764,738 (3.8%)• New Hampshire: $ 2,345,776 (3.0%)• New Jersey: $14,191,541 (3.4%)

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 30 •

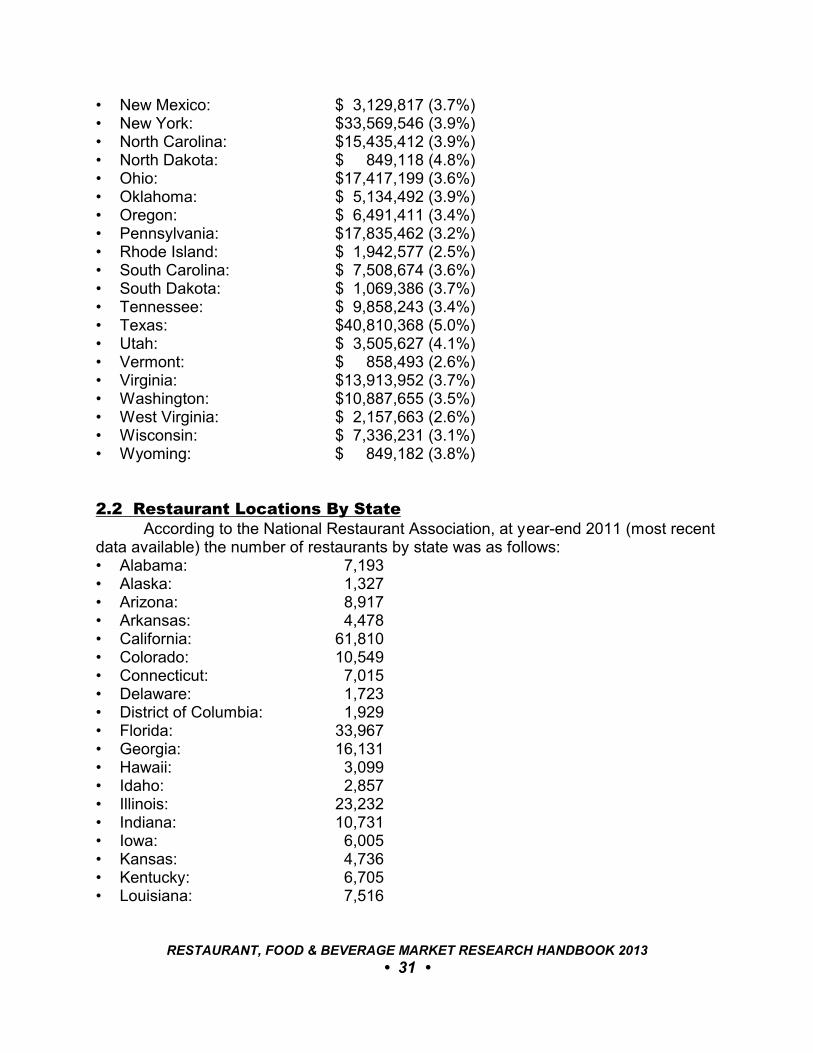

• New Mexico: $ 3,129,817 (3.7%)• New York: $33,569,546 (3.9%)• North Carolina: $15,435,412 (3.9%)• North Dakota: $ 849,118 (4.8%)• Ohio: $17,417,199 (3.6%)• Oklahoma: $ 5,134,492 (3.9%)• Oregon: $ 6,491,411 (3.4%)• Pennsylvania: $17,835,462 (3.2%)• Rhode Island: $ 1,942,577 (2.5%)• South Carolina: $ 7,508,674 (3.6%)• South Dakota: $ 1,069,386 (3.7%)• Tennessee: $ 9,858,243 (3.4%)• Texas: $40,810,368 (5.0%)• Utah: $ 3,505,627 (4.1%)• Vermont: $ 858,493 (2.6%)• Virginia: $13,913,952 (3.7%)• Washington: $10,887,655 (3.5%)• West Virginia: $ 2,157,663 (2.6%)• Wisconsin: $ 7,336,231 (3.1%)• Wyoming: $ 849,182 (3.8%)

2.2 Restaurant Locations By StateAccording to the National Restaurant Association, at year-end 2011 (most recent

data available) the number of restaurants by state was as follows:• Alabama: 7,193• Alaska: 1,327• Arizona: 8,917• Arkansas: 4,478• California: 61,810• Colorado: 10,549• Connecticut: 7,015• Delaware: 1,723• District of Columbia: 1,929• Florida: 33,967• Georgia: 16,131• Hawaii: 3,099• Idaho: 2,857• Illinois: 23,232• Indiana: 10,731• Iowa: 6,005• Kansas: 4,736• Kentucky: 6,705• Louisiana: 7,516

RESTAURANT, FOOD & BEVERAGE MARKET RESEARCH HANDBOOK 2013

• 31 •

• Maine: 2,955• Maryland: 10,234• Massachusetts: 14,179• Michigan: 16,565• Minnesota: 10,028• Mississippi: 4,234• Missouri: 10,462• Montana: 2,561• Nebraska: 3,753• Nevada: 5,316• New Hampshire: 2,853• New Jersey: 17,308• New Mexico: 2,913• New York: 38,596• North Carolina: 16,035• North Dakota: 1,570• Ohio: 21,535• Oklahoma: 5,728• Oregon: 8,569• Pennsylvania: 24,397• Rhode Island: 2,640• South Carolina: 7,643• South Dakota: 1,788• Tennessee: 8,937• Texas: 35,805• Utah: 4,115• Vermont: 1,321• Virginia: 13,646• Washington: 13,557• West Virginia: 3,129• Wisconsin: 12,002• Wyoming: 1,234

2.3 Foodservice Employment By StateAccording to 2013 Restaurant Industry Forecast by the National Restaurant

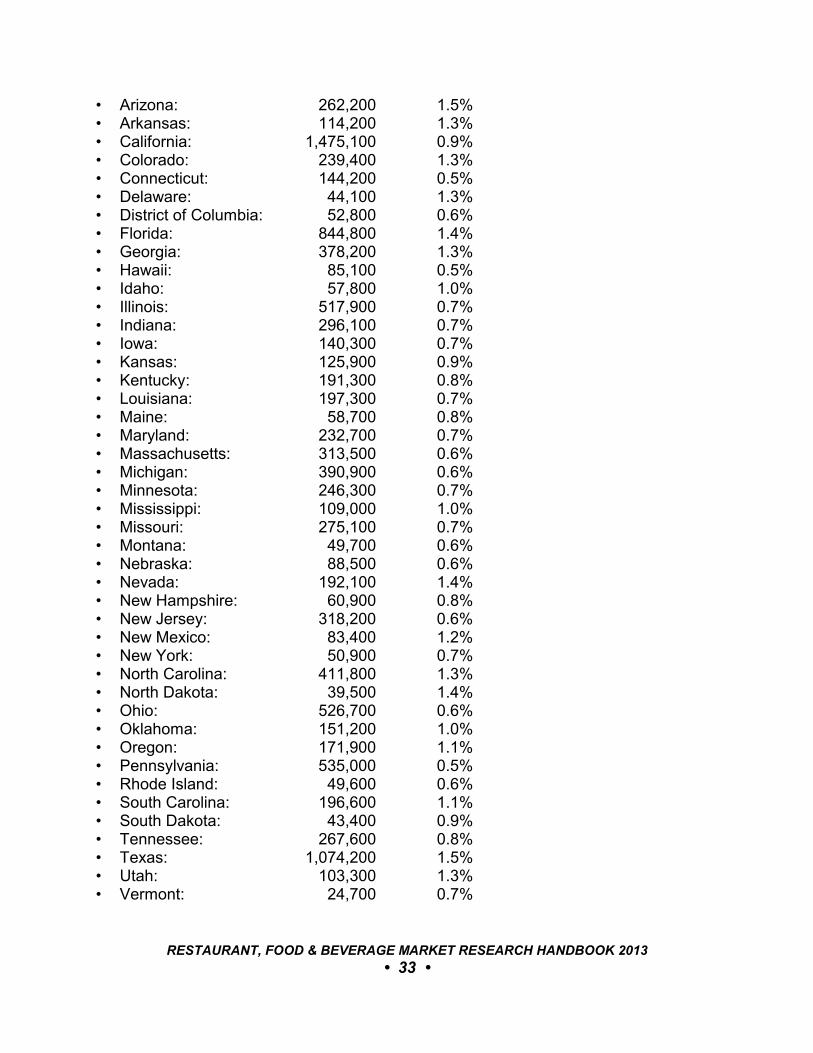

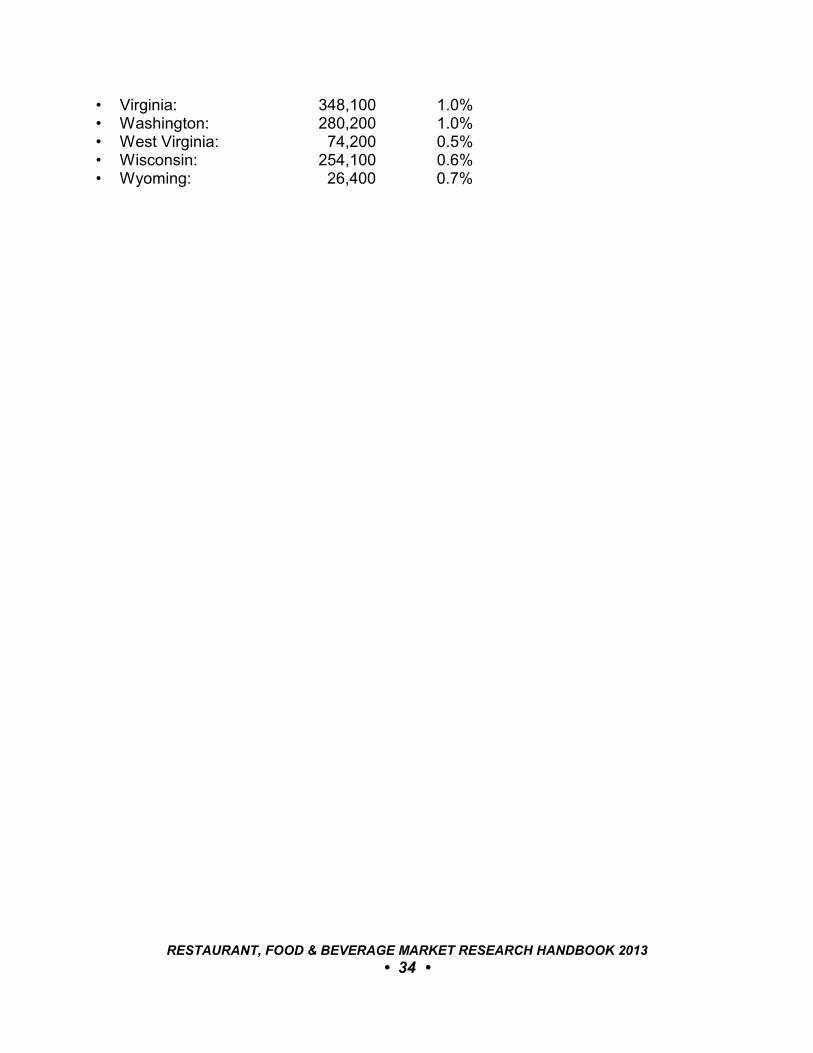

Association, 13.11 million people are employed in the restaurant and foodservicesector, a figure which is projected to increase at an average national rate of 0.9%through 2023.

Current restaurant employment and the projected average annual increasethrough 2023 are as follows: