a restaurant

TRANSCRIPT

A restaurant case study of leaseaccounting impacts of

proposed changes in leaseaccounting rules

Amrik SinghFritz Knoebel School of Hospitality Management, Daniels College of Business,

University of Denver, Denver, Colorado, USA

Abstract

Purpose – New lease accounting rules are proposed that will fundamentally change the way leasesare accounted for and reported in financial statements. This paper seeks to provide information on theproposed new rules and to illustrate their impact on financial statements and financial ratios using asingle restaurant company.

Design/methodology/approach – The case of a single restaurant company, CEC International, isused to illustrate the potential impact of the new rules. Additional examples are used to illustrate theimpact on financial policies. Financial statements were adjusted and various financial ratios such asinterest coverage, leverage and profitability ratios were computed before and after capitalization.

Findings – The results show that financial statements presented will change dramatically whenlease assets and liabilities are added to the balance-sheet. The expense recognition pattern will changesignificantly and negatively impact performance measures such as interest coverage and capital ratiosbut improve cash flow measures such as EBIT and EBITDA.

Research limitations/implications – Limitations of this study include the assumptions used tocapitalize leases such as interest rate, life of leases, no new leases, and exclusion of contingent rentals.

Practical implications – All restaurant companies and managers must assess the costs andbenefits of complying with the proposed new rules and start analyzing and evaluating their impact onexisting debt agreements, executive compensation plans, and the lease versus buy decision.

Originality/value – This paper serves to inform restaurant managers about the potentialimplications of the new rules, so managers can prepare, plan and formulate strategies to mitigatetheir impact.

Keywords Leasing, Financial ratios, Restaurant industry, Regulation, Accounting

Paper type Case study

IntroductionOn August 17, 2010, the Financial Accounting Standards Board (FASB) and theInternational Accounting Standards Board (IASB) jointly issued an Exposure Draft ofnew lease accounting rules that would fundamentally overhaul and change the wayleases are accounted for and reported in financial statements. The proposed rules willeliminate the existing classification of leases as either finance or operating leases, andinstead require lessees to capitalize all leases and recognize a single model representinga right-to-use the leased asset.

The proposed changes in lease accounting are expected to impact financialstatement presentation and performance measures materially and significantly. The

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/0959-6119.htm

IJCHM23,6

820

Revised 18 February 20118 March 2011

International Journal ofContemporary HospitalityManagementVol. 23 No. 6, 2011pp. 820-839q Emerald Group Publishing Limited0959-6119DOI 10.1108/09596111111153493

balance sheet effects are currently hidden because of the off-balance sheet treatment ofoperating leases under the existing lease accounting standard. The material increase inassets and liabilities and deterioration in certain financial ratios has raised concernsabout the potential financial implications of the rules on firm debt structure andfinancial policies such as debt covenants and executive compensation.

Off-balance sheet operating leases have raised questions and concerns becausecritics have argued that the existing rules allowed companies to understate theirliabilities by structuring leases as operating leases instead of capital leases and indoing so, influenced the outcomes of various profitability and debt financial ratios.Furthermore, in 2005, an estimated 293 firms, comprised mainly of restaurant andretail firms, were forced to restate their financial statements due to various leaseaccounting errors (Scholz, 2008). These restatements were sparked by CKERestaurants, Inc., which discovered the lease accounting errors during its internalreview in 2004. In a 2005 report to Congress, the Securities and Exchange Commission(SEC) was also highly critical of the lease accounting standard and recommended thatthe FASB overhaul the lease standard (Securities and Exchange Commission, 2005).Subsequently the FASB, working together with the IASB, adopted a project tooverhaul the lease accounting rules to address these concerns.

The restaurant industry has been identified in prior research as one of the largestusers of off-balance sheet operating leases (Imhoff et al., 1997). Lease accounting is animportant issue for many restaurant firms. Given their pervasive use, magnitude andgrowing financial lease obligations, the restaurant industry provides an ideal settingfor investigating questions of how the proposed rules will affect financial statementpresentation and what is the likely impact of the rules on financial ratios and financialpolicy decisions.

It is the purpose of this study to investigate the likely impact of the proposed leaseaccounting standard on the balance sheet and income statement presentation byapplying them to a single public restaurant company, CEC Entertainment, Inc., theowner, operator and franchisor of Chuck E. Cheese restaurants. The focus of this paperis on lessee accounting and the potential impacts will then be measured using a set offinancial ratios that are widely used in practice. Finally, the managerial and practicalimplications of the proposed rules on debt agreements, executive compensation and thelease versus buy decision will be presented and discussed.

This study contributes to the existing literature on leasing in the following ways.First, it shows how the presentation of financial statements will be changeddramatically and how the proposed rules will affect various financial statement ratiosthat are widely used in practice to assess credit ratings, debt covenants, and executivecompensation. The case study method was chosen for this purpose because of itsadvantage in highlighting and exploring complex lease accounting issues in far greaterdetail than otherwise possible with a larger set of firms. Additional firm examples andpractical applications are also included to supplement the analysis. Second, this studyserves the purpose of informing and raising awareness among restaurant managers,small business owners, and other hospitality managers about the proposed rules somanagers can formulate strategies to mitigate the likely impact on corporate policies.Finally, this study serves the need of financial statement users, academics, andregulators who will find it informative and relevant.

Changes in leaseaccounting rules

821

Current and proposed leasingCurrent standardOperating leases provide a number of advantages over capital leases including 100percent financing of assets, preservation of capital, tax benefits, and protection againstobsolescence, cheaper financing, and flexibility of lease terms. For example, companieswith limited debt capacity or liquidity constraints can finance the acquisition of assetswith low payments and longer lease terms compared with traditional costs offinancing. Under the existing lease accounting rule (Financial Accounting StandardsBoard, 1976, p. 8), leases are capitalized if any one of the following criteria is met:

. the lease transfers ownership of the asset to the lessee;

. the lease contains a bargain purchase option;

. the lease term is equal to 75 percent or more of the estimated economic life of theleased asset; and

. the present value of the minimum lease payments equals or exceeds 90 percent ofthe fair value of the leased asset.

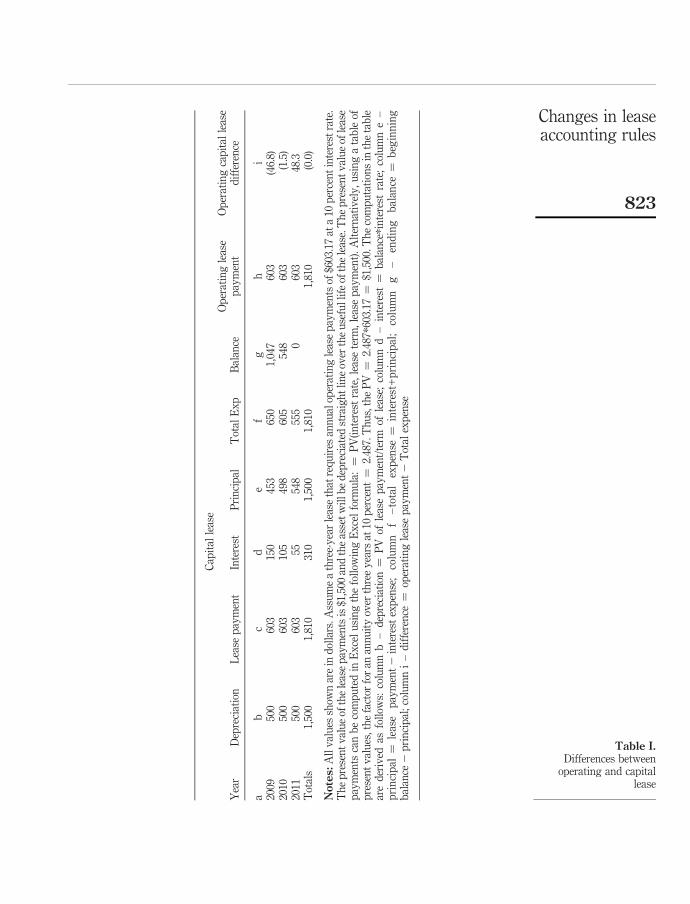

If none of the above criteria is met, then a lease is classified as an operating lease. In anoperating lease, the rental payments are treated as regular expenses when incurred,flowing through the income statement without recognizing an asset or liability on thebalance sheet. On the other hand, a capital lease is treated like the acquisition of anasset in a financing transaction, giving rise to the recognition of an asset and a liabilityon the balance sheet, while the expenses are charged to both interest and depreciation.The impact of a capital lease on the balance sheet is thus an increase in asset, whichwill produce a lower return on asset ratio while the increase in liability results in ahigher debt-to-equity ratio. Although the total expenses for both types of leases will beidentical over the lease term, the total depreciation and interest expense in a capitallease will, however, exceed the operating lease payments in earlier years resulting inlower reported net income. This timing difference is illustrated in Table I, which showsthe total expenses in a capital lease (column f) to be greater than the operating leaseexpense of $603 (column c) by $47 in the first year but by the third year, the outcome isreversed. The total expenses in both leases will remain the same at the end of the leaseterm ($1,810) (columns f and h).

Proposed leasing rulesOn August 17, 2010, the Financial Accounting Standards Board (2010) jointly with theIASB issued an Exposure Draft of the proposed new rules on lease accounting. Theproposed guidance would eliminate the classification of leases as either finance oroperating leases. Instead the Boards proposed a single lease accounting model in whichall lessees would recognize a “right-of-use” asset representing a right to use the leasedasset and a corresponding liability representing an obligation to make rental payments(Financial Accounting Standards Board, 2010, p. 16). The Boards concluded that theright-of-use of an asset and the obligations to make rental payments in a lease met thedefinition of an asset and a liability in their respective conceptual accountingframeworks. At the inception of the lease, a lessee would be required to measure theright-of-use asset and lease finance liability at the discounted present value of theexpected lease payments over the lease term using the lessee’s incremental borrowing

IJCHM23,6

822

Cap

ital

leas

e

Yea

rD

epre

ciat

ion

Lea

sep

aym

ent

Inte

rest

Pri

nci

pal

Tot

alE

xp

Bal

ance

Op

erat

ing

leas

ep

aym

ent

Op

erat

ing

cap

ital

leas

ed

iffe

ren

ce

ab

cd

ef

gh

i20

0950

060

315

045

365

01,

047

603

(46.

8)20

1050

060

310

549

860

554

860

3(1

.5)

2011

500

603

5554

855

50

603

48.3

Tot

als

1,50

01,

810

310

1,50

01,

810

1,81

0(0

.0)

Notes:

All

val

ues

show

nar

ein

dol

lars

.Ass

um

ea

thre

e-y

ear

leas

eth

atre

qu

ires

ann

ual

oper

atin

gle

ase

pay

men

tsof

$603

.17

ata

10p

erce

nt

inte

rest

rate

.T

he

pre

sen

tv

alu

eof

the

leas

ep

aym

ents

is$1

,500

and

the

asse

tw

illb

ed

epre

ciat

edst

raig

ht

lin

eov

erth

eu

sefu

llif

eof

the

leas

e.T

he

pre

sen

tv

alu

eof

leas

ep

aym

ents

can

be

com

pu

ted

inE

xce

lu

sin

gth

efo

llow

ing

Ex

cel

form

ula

:¼

PV

(in

tere

stra

te,

leas

ete

rm,

leas

ep

aym

ent)

.A

lter

nat

ivel

y,

usi

ng

ata

ble

ofp

rese

nt

val

ues

,th

efa

ctor

for

anan

nu

ity

over

thre

ey

ears

at10

per

cen

t¼

2.48

7.T

hu

s,th

eP

V¼

2.48

7 *60

3.17

¼$1

,500

.Th

eco

mp

uta

tion

sin

the

tab

lear

ed

eriv

edas

foll

ows:

colu

mn

b–

dep

reci

atio

n¼

PV

ofle

ase

pay

men

t/te

rmof

leas

e;co

lum

nd

–in

tere

st¼

bal

ance

*in

tere

stra

te;

colu

mn

e–

pri

nci

pal

¼le

ase

pay

men

t2

inte

rest

exp

ense

;co

lum

nf

–to

tal

exp

ense

¼in

tere

st+

pri

nci

pal

;co

lum

ng

–en

din

gb

alan

ce¼

beg

inn

ing

bal

ance

2p

rin

cip

al;

colu

mn

i–

dif

fere

nce

¼op

erat

ing

leas

ep

aym

ent2

Tot

alex

pen

se

Table I.Differences between

operating and capitallease

Changes in leaseaccounting rules

823

rate (Financial Accounting Standards Board, 2010, p. 17). The lease term is the longestpossible lease term that is more likely than not to occur and this determination wouldbe based on an assessment of all contractual, non-contractual and business factorsincluding the likelihood of renewals, terminations and purchase options. The expectedlease payments would include not only the fixed rental payments under the lease butalso any contingent rental payments and residual value guarantees. The right-of-useasset would also be measured at the amount of the liability to make lease paymentsplus any prepaid rent and recoverable initial direct costs incurred by the lessee.Subsequently, the asset will be amortized on a systematic basis over the shorter term ofthe lease or the economic life of the leased asset. On the other hand, the lease paymentwould be allocated between a reduction in the principal amount of outstanding leaseliability and interest expense. Instead of recognizing rent expense under the existingstandard, the lessee will recognize an amortization expense and interest expense on theincome statement. Furthermore, at each reporting period, lessees will be required toreassess the liability amounts and make revisions for changes in payments if facts andcircumstances related to the lease term or future contingent rentals change. Changesrelated to current or prior periods would be recognized immediately in the incomestatement (Financial Accounting Standards Board, 2010, pp. 18-19).

The disclosure requirements would increase significantly under the proposed newrules. On the balance sheet, lessees will be required to present the right-of-use assetseparately from other property, plant and equipment while the liability is presentedseparately from other financial liabilities. On the income statement, amortization andinterest expense will also be presented separately. Unlike the existing rules where leasepayments are included in operating activities in the statement of cash flows, theproposed rules will require that such lease payments be classified as financingactivities and presented separately from other repayments (Financial AccountingStandards Board, 2010, p. 20). Since the new rules will be applied retroactively,companies with all outstanding leases will apply a simplified retrospective approachon the date of initial application. Lessees would determine the liability as the presentvalue of the outstanding lease payments discounted using the lessee’s incrementalborrowing rate and measure the right-of-use asset on the same basis as the liability.

Literature reviewMuch of the research to-date on leasing has focused on the effects of capitalizingoperating leases on financial statements and the impact of Statement of FinancialAccounting Standard 13 (SFAS 13) on equity risk, capital structure and stock prices.

Effect on financial statementsPrior research from the 1990s showed capitalization of operating leases to have asignificant effect on risk and return measures. Using a small sample of 14 firms, Imhoffet al. (1991) found an average (median) decrease of 34 percent (10 percent) in return onassets and an average (median) increase of 191 percent (47 percent) in debt-to-equityratios for high lease (low lease) firms. On the international front, Beattie et al. (1998)drew similar conclusions among a sample of 232 UK firms. Using the constructivelease capitalization methodology proposed by Imhoff et al. (1991), Beattie et al. (1998)found that operating leases represented an average of 39 per cent of total debt and 6 percent of total assets. Six of nine ratios (profit margin, return on assets (ROA), asset

IJCHM23,6

824

turnover, and three measures of leverage were significantly affected by capitalizingoperating leases. Significant inter-industry variations indicated a greater impact on theservices sector (retail, hotel, media etc.) relative to other sectors. Similar findings of asignificant effect of capitalizing leases on the balance sheet and income statement havebeen observed among New Zealand firms (Bennett and Bradbury, 2003) German firms(Fulbier et al., 2006) and the UK retail sector (Goodacre, 2003).

Effect on equity riskPrior studies have also documented that capital leases behave similarly to debt in theireffect on equity risk (Bowman, 1980). Imhoff et al. (1993) extended this line of researchto show that the present value of operating leases is also positively associated withequity risk. Similar results have been reported by Ely (1995) indicating that debt andoperating leases were positively correlated with equity risk. Imhoff et al. (1993) alsofound no evidence that companies adjust financial statement data to reflect operatingleases in determining executive compensation. More recently, Ge et al. (2008) revisitedearlier studies and re-examined the association between stock prices and operatingleases. Their findings show that operating lease adjustments to accounting ratios werenot positively related to stock returns indicating that investors were not using thediscounted present value method in capitalizing operating leases in their assessment ofrisk and performance. The researchers explained that investors either paid limitedattention to footnote disclosures or were aware of the operating lease effects but choseto ignore them because of the high information processing costs. They concluded thatexisting lease disclosures were inadequate and costly for investors providing furthersupport for the recognition of operating leases as assets and liabilities on the balancesheet.

Effect on capital structureResearch studies have also shown no effect on the market’s assessment of a firm’sequity risk after the adoption of SFAS 13 (Finnerty et al., 1980; Abdel-khalik, 1981). Onthe other hand, Imhoff and Thomas (1988) documented a significant change in thecapital structure of firms after the adoption of SFAS 13. A sharp decline in capitalleases and substantial increases in operating leases was observed. Most firmsemployed capital structure changes to mitigate the impact of SFAS 13 by renegotiatinglease contract terms to avoid the capital lease criteria and increasing non-leasefinancing as evidenced by an increase in equity and reduction in leverage. With theimpending changes to lease accounting, firms again have incentives to mitigate anyadverse impact on capital structure.

Effect of debt covenant violationsChanges in accounting regulations also have the potential to induce technicalviolations in debt agreements. Fogelson (1978) argues that firms should anticipatethese changes and limit the impact of costly contractual amendments prior to theimplementation of accounting regulations. The empirical evidence substantiates thattechnical violation of debt covenants is costly when lenders exercise control of firmactivities and impose additional refinancing costs (Beneish and Press, 1993). El-Gazzar(1993) provides evidence that stock prices declined significantly in those cases wherecapitalization of operating leases would have increased the probability of technical

Changes in leaseaccounting rules

825

default. Beneish and Press (1995) also show that announcements of technical defaultare associated with significant stock price declines that negatively impact shareholderwealth. In a more recent study, Chava and Roberts (2008) show that debt covenantviolations will lead to sharp declines in capital investments when lenders intervene inmanagement.

Hospitality leasing researchWithin the hospitality industry, the research on leasing has been limited to just a fewstudies. Only one study by Marler (1993) provided some evidence that restaurantcompanies preferred operating leases over capital leases with operating leaseobligations exceeding capital lease obligations by a ratio of nine to one. Despite somemixed evidence, her results suggested that only liquidity and solvency ratios weremost affected by lease capitalization. In another study, Upneja and Dalbor (1999)examined a sample of 95 restaurant firms to determine the association between debtfinancing and marginal tax rates. Despite facing some data limitations in their proxyfor operating leases, they found that marginal tax rates were significantly andnegatively related to operating leases. This implied that restaurant firms with lowermarginal tax rates were more likely to use operating leases instead of purchasingassets while firms with high marginal tax rates were more likely to employ capitalleases. The researchers also noted that firms with higher tax rates and in goodfinancial position were more likely to rely on debt financing to purchase assets.

Lease capitalization methodology for CEC EntertainmentThis case study investigates the likely impacts of the proposed new lease accountingstandard on the financial statement presentation and financial ratios of CECEntertainment, Inc., and the implications for various corporate financial policies. CECEntertainment was selected for this case study because of previous financialrestatements stemming from lease accounting errors. Financial statement data for thecompany was obtained from the annual 10-K financial report filed with the SEC (CECEntertainment, 2010) and retrieved from the SEC’s Edgar database. This data was thenused to capitalize operating leases and compute various financial ratios to assess theirlikely impact on financial statements.

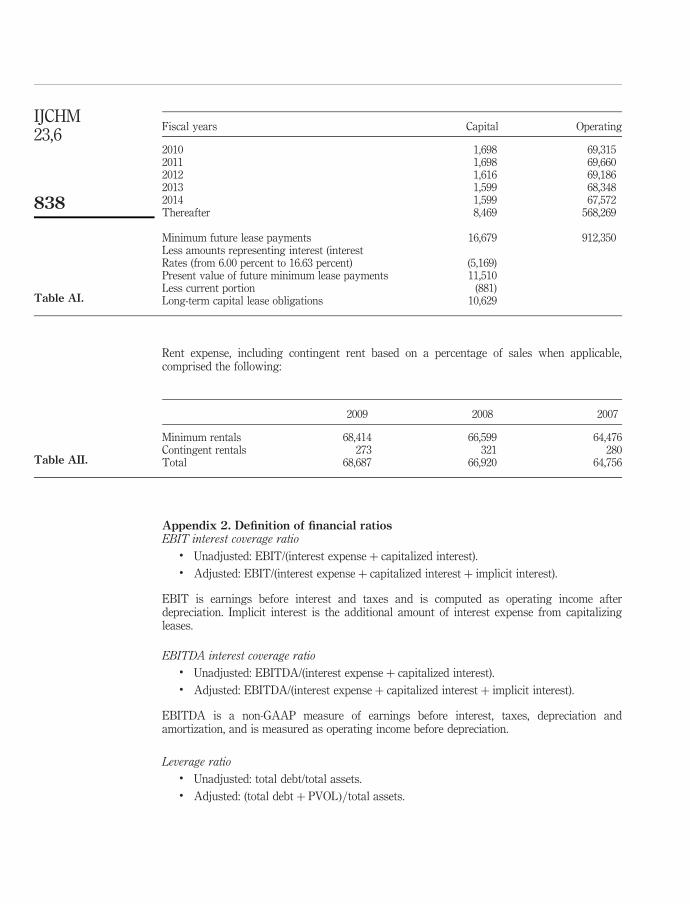

CEC Entertainment is a restaurant company that owns and operates 497 ChuckE. Cheese restaurants excluding 48 franchised restaurants in the US andinternationally. Of these 497 restaurants, 438 restaurants occupy leased premiseswhile 59 restaurants operate on owned sites. On the balance sheet for fiscal year 2009,CEC Entertainment recorded capital lease assets of $16.020m and $15.862m for 2009and 2008, respectively. These capital lease assets were primarily buildings for some ofits store locations. Including accumulated depreciation, the net book value of thesecapital lease assets amounted to $9.120m and $9.962m, respectively, for 2009 and 2008.On the other hand, its obligations under capital leases were estimated at $11.510m and$12.208m for the same period. Other relevant information on operating lease paymentsis presented in Appendix 1.

Capitalizing operating leasesOperating leases for CEC Entertainment are capitalized using the discounted presentvalue approach as recommended in the proposed standard. The lease capitalization

IJCHM23,6

826

methodology (Tables II-V) has been used in prior studies (Imhoff et al., 1991, 1997;Beattie et al., 1998) to capitalize operating leases[1]. A set of simplifying assumptionswas made in the computation of the present value of operating lease payments sincevariations in lease terms, timing of payments, incremental borrowing rates, andrenewal options, etc., are observed in practice from lease to lease. These assumptionsinclude the following:

. lease payments occur annually at the end of the year and no new leases wereentered into by the company from the beginning of fiscal year 2010;

. lease payments exclude contingent rentals, executory costs, sublease income,residual value guarantees or renewal options due to their added complexity andlack of additional financial statement disclosures;

. the present value of the lease liability is equal to the lease asset at the inception ofthe lease and zero at the end of the lease;

. assets are depreciated using the straight-line method of depreciation, while thelease payments are amortized using the effective interest method; and

. all the computations are performed using a 35 percent marginal tax rate.

The first step in the capitalization process was to estimate the discounted present valueof operating leases (PVOL). The PVOL is the amount that will appear as a liability andas an asset on the balance sheet assuming capitalization of all operating leases. CECEntertainment disclosed that its interest rate on capital leases ranged from 6 percent to17 percent. To compute an effective interest rate for CEC Entertainment the followingcomputations were made using the capital lease disclosures in Appendix 1:

Capital lease payment for 2010 ($1,698)Less: current principal portion ($881)Equals: interest portion ($817)Divided by PV value of leases (11,510)Equals: effective interest rate (7.1 percent).

The estimated incremental borrowing rate for CEC Entertainment is thus estimated tobe 7.1 percent, rounded to 7 percent. The estimation of the average annual leasepayments beyond year five is shown in Table II.

To estimate the annual lease amount beyond 2015, the “thereafter” payment of$568,269 is first divided by $67,572 (Year 5 or 2014 payment) to yield an initial estimateof 8.4 years, which is then rounded up to nine years. The assumption is that beyond2014, the annual lease payments would continue at an approximate amount of $63,141($568,269/9) for nine years for a total term of 14 years (including the first five years).Based on this estimate, the annual lease payments were then discounted at 7 percentover 14 years to yield a discounted present value (PVOL) of $575,728 as shown inTable III. The present value of lease payment amount of $575,728 is then added toexisting assets and to the long-term debt liability on the balance sheet. These amountsare only equal at the inception of the lease but will be unequal over the lease life. Theasset amount is further reduced by depreciation while the liability amount is reducedby the lease payment schedule using the effective interest method. The annualstraight-line depreciation is estimated by dividing the PVOL amount of $575,728 by 14years to yield a constant rate of $41,123 from 2010 onwards. The interest expense is

Changes in leaseaccounting rules

827

estimated as $40,301 ($575; 728*7 percent) with $28,113 ($68; 414-$40; 301) allocatedtowards principal reduction.

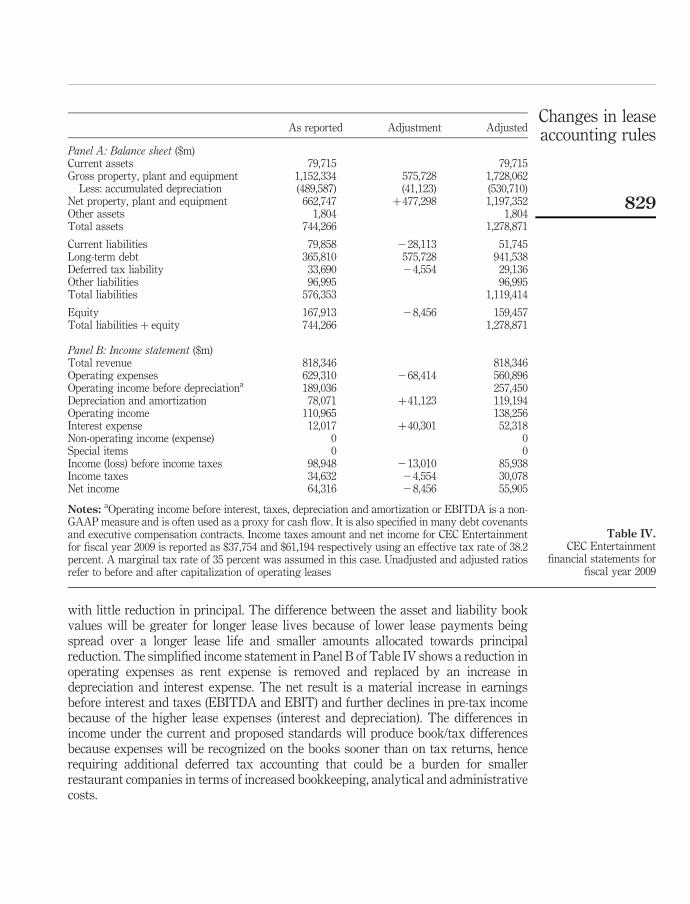

ResultsImpact on financial statementsThe results of the capitalization process are shown in Panels A and B of Table IV,which present the balance sheet and income statement effects before and aftercapitalization for fiscal 2009 for CEC Entertainment. In particular, the additionalamount of off-balance operating lease liability represents 50 times its capital leasesobligations and accounts for more than half or 61 percent ($575,728/$941,538) of CECEntertainment’s total long-term debt (including operating leases). This is a materialand significant amount of off-balance sheet debt. Similar results are expected for manyrestaurant firms with significant amounts of off-balance sheet operating leases basedon an analysis of other restaurant companies.

Over the life of the leases, the liability amounts will exceed the asset amountsbecause the early payments on the leases will comprise of largely interest payments

Year Present values ($)

1 64,7802 60,8443 56,4764 52,1425 48,178Thereafter 293,307Total 575,728

Notes: Number of years embedded is estimated as $568,269/$67,572 ¼ 8.41, rounded to 9 years.Total useful life 14. Estimated lease payments after 2014 $63,141. Lease payments are discountedat 7 percent

Table III.Estimating present valueof lease payments:estimating present values

Year Lease payments ($)

2010 69,3152011 69,6602012 69,1862013 68,3482014 67,572Thereafter 568,269

Number of years embedded in “thereafter” estimate 9Estimated total useful life of leases 14Estimated lease payments after 2014 ($) 63,141Discount rate (percent) 7

Notes: Number of years embedded is estimated as $568,269/$67,572 ¼ 8.41, rounded to 9 years.Total useful life 14. Estimated lease payments after 2014 $63,141. Lease payments are discountedat 7 percent

Table II.Estimating present valueof lease payments:estimating paymentsbeyond 2014

IJCHM23,6

828

with little reduction in principal. The difference between the asset and liability bookvalues will be greater for longer lease lives because of lower lease payments beingspread over a longer lease life and smaller amounts allocated towards principalreduction. The simplified income statement in Panel B of Table IV shows a reduction inoperating expenses as rent expense is removed and replaced by an increase indepreciation and interest expense. The net result is a material increase in earningsbefore interest and taxes (EBITDA and EBIT) and further declines in pre-tax incomebecause of the higher lease expenses (interest and depreciation). The differences inincome under the current and proposed standards will produce book/tax differencesbecause expenses will be recognized on the books sooner than on tax returns, hencerequiring additional deferred tax accounting that could be a burden for smallerrestaurant companies in terms of increased bookkeeping, analytical and administrativecosts.

As reported Adjustment Adjusted

Panel A: Balance sheet ($m)Current assets 79,715 79,715Gross property, plant and equipment 1,152,334 575,728 1,728,062

Less: accumulated depreciation (489,587) (41,123) (530,710)Net property, plant and equipment 662,747 þ477,298 1,197,352Other assets 1,804 1,804Total assets 744,266 1,278,871

Current liabilities 79,858 228,113 51,745Long-term debt 365,810 575,728 941,538Deferred tax liability 33,690 24,554 29,136Other liabilities 96,995 96,995Total liabilities 576,353 1,119,414

Equity 167,913 28,456 159,457Total liabilities þ equity 744,266 1,278,871

Panel B: Income statement ($m)Total revenue 818,346 818,346Operating expenses 629,310 268,414 560,896Operating income before depreciationa 189,036 257,450Depreciation and amortization 78,071 þ41,123 119,194Operating income 110,965 138,256Interest expense 12,017 þ40,301 52,318Non-operating income (expense) 0 0Special items 0 0Income (loss) before income taxes 98,948 213,010 85,938Income taxes 34,632 24,554 30,078Net income 64,316 28,456 55,905

Notes: aOperating income before interest, taxes, depreciation and amortization or EBITDA is a non-GAAP measure and is often used as a proxy for cash flow. It is also specified in many debt covenantsand executive compensation contracts. Income taxes amount and net income for CEC Entertainmentfor fiscal year 2009 is reported as $37,754 and $61,194 respectively using an effective tax rate of 38.2percent. A marginal tax rate of 35 percent was assumed in this case. Unadjusted and adjusted ratiosrefer to before and after capitalization of operating leases

Table IV.CEC Entertainment

financial statements forfiscal year 2009

Changes in leaseaccounting rules

829

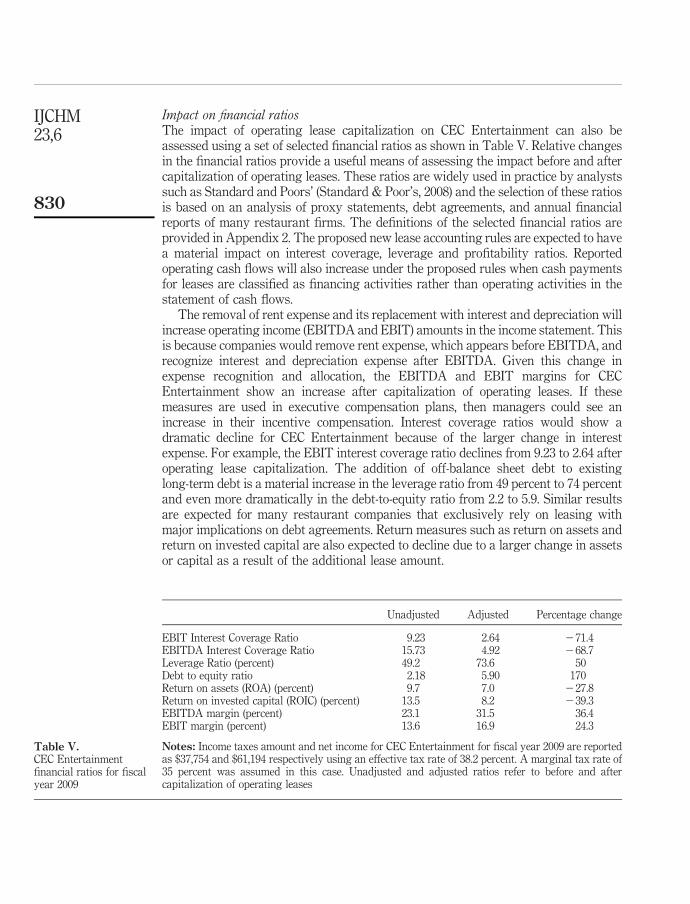

Impact on financial ratiosThe impact of operating lease capitalization on CEC Entertainment can also beassessed using a set of selected financial ratios as shown in Table V. Relative changesin the financial ratios provide a useful means of assessing the impact before and aftercapitalization of operating leases. These ratios are widely used in practice by analystssuch as Standard and Poors’ (Standard & Poor’s, 2008) and the selection of these ratiosis based on an analysis of proxy statements, debt agreements, and annual financialreports of many restaurant firms. The definitions of the selected financial ratios areprovided in Appendix 2. The proposed new lease accounting rules are expected to havea material impact on interest coverage, leverage and profitability ratios. Reportedoperating cash flows will also increase under the proposed rules when cash paymentsfor leases are classified as financing activities rather than operating activities in thestatement of cash flows.

The removal of rent expense and its replacement with interest and depreciation willincrease operating income (EBITDA and EBIT) amounts in the income statement. Thisis because companies would remove rent expense, which appears before EBITDA, andrecognize interest and depreciation expense after EBITDA. Given this change inexpense recognition and allocation, the EBITDA and EBIT margins for CECEntertainment show an increase after capitalization of operating leases. If thesemeasures are used in executive compensation plans, then managers could see anincrease in their incentive compensation. Interest coverage ratios would show adramatic decline for CEC Entertainment because of the larger change in interestexpense. For example, the EBIT interest coverage ratio declines from 9.23 to 2.64 afteroperating lease capitalization. The addition of off-balance sheet debt to existinglong-term debt is a material increase in the leverage ratio from 49 percent to 74 percentand even more dramatically in the debt-to-equity ratio from 2.2 to 5.9. Similar resultsare expected for many restaurant companies that exclusively rely on leasing withmajor implications on debt agreements. Return measures such as return on assets andreturn on invested capital are also expected to decline due to a larger change in assetsor capital as a result of the additional lease amount.

Unadjusted Adjusted Percentage change

EBIT Interest Coverage Ratio 9.23 2.64 271.4EBITDA Interest Coverage Ratio 15.73 4.92 268.7Leverage Ratio (percent) 49.2 73.6 50Debt to equity ratio 2.18 5.90 170Return on assets (ROA) (percent) 9.7 7.0 227.8Return on invested capital (ROIC) (percent) 13.5 8.2 239.3EBITDA margin (percent) 23.1 31.5 36.4EBIT margin (percent) 13.6 16.9 24.3

Notes: Income taxes amount and net income for CEC Entertainment for fiscal year 2009 are reportedas $37,754 and $61,194 respectively using an effective tax rate of 38.2 percent. A marginal tax rate of35 percent was assumed in this case. Unadjusted and adjusted ratios refer to before and aftercapitalization of operating leases

Table V.CEC Entertainmentfinancial ratios for fiscalyear 2009

IJCHM23,6

830

Implications for the restaurant industryIn addition to the likely impact on the financial statement presentation and financialratios, the proposed new rules are also expected to affect corporate financial policiessuch as executive compensation, debt agreements and the lease versus buy decision.

Executive compensationChanges in lease accounting rules will affect management compensation policies ifmanagement performance and compensation is based on profitability ratios such asEBITDA, EBIT or pre-tax income. Under the proposed rules managementcompensation will likely increase if compensation is based on EBITDA margins.Red Robin Gourmet Burgers for example, uses EBITDA as a performance objective inits cash bonus incentive program for its top executives. The firm does not adjust itsEBITDA for the impact of operating leases in determining its incentive compensation.This observation is also consistent with prior research that shows a lack of evidencethat firms adjust reported income amounts to reflect operating leases whendetermining executive compensation (Imhoff et al., 1993). The following exampleillustrates how changes in the proposed rules will have an impact on executivecompensation for Red Robin Gourmet Burgers Inc.:

Example: Red Robin Gourmet Burgers set an EBITDA-based bonus target range of 90percent to 135 percent for its top executive in its 2009 cash bonus incentive program. Thetarget level EBITDA for fiscal year 2009 was set at approximately $104.5m with a minimumtarget of $99m or 95 percent below target ($104:5m*95 percent ¼ $99m) and a maximum of$110m or 105 percent above target. The estimated EBITDA for 2009 was estimated atapproximately $89m which fell below the minimum level of $99m. As a result, Red Robin didnot pay out any cash bonuses to its executives for fiscal year 2009. If the company’s operatingleases were capitalized under the proposed rules, the removal of base rent expense of $41mwould increase the estimated EBITDA to $130m ($89m þ $41m) which would fall 124 percent($130=$104:5 £ 100) above the target. The incentive bonus compensation that would be paidout to its top executive, set at a minimum target level of 90 percent based on a base salary of$725,000, would thus be an additional $625,000 ($725; 000*90 percent). At 124 percent abovetarget, the bonus compensation would amount to $899,000 up to a maximum of $978,750($725; 000*135 percent) (Red Robin Gourmet Burgers, Inc., 2010a, b).

Ruth & Chris Steakhouse and California Pizza Kitchen are among other restaurantcompanies that use EBITDA for their executive compensation plans. On the otherhand, CKE Restaurants and BJ’s Restaurants incorporate pre-tax income into theirrespective executive compensation plans. All of these compensation plans will beaffected by the capitalization of operating leases. Consequently, restaurant companiesshould re-examine their compensation plans in light of the proposed changes. As analternative managerial performance benchmark, managers should include rentexpense in their computation of EBITDA so the performance measure representsEBITDAR (earnings before interest, taxes, depreciation, amortization and rent). Thisnon-GAAP metric is commonly used in practice by many financial analysts as anindicator of a firm’s financial performance.

Debt agreementsThe proposed changes could also have a significant effect on leverage ratios that areused to evaluate a company’s financial performance and compliance with loancovenants or other agreements that reference those items. For example, debt ratios

Changes in leaseaccounting rules

831

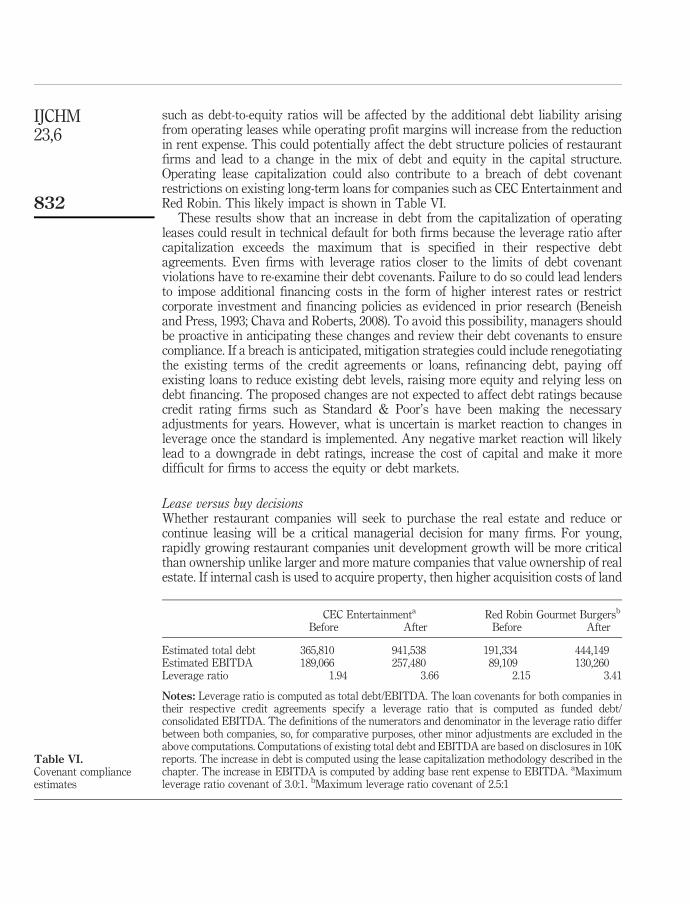

such as debt-to-equity ratios will be affected by the additional debt liability arisingfrom operating leases while operating profit margins will increase from the reductionin rent expense. This could potentially affect the debt structure policies of restaurantfirms and lead to a change in the mix of debt and equity in the capital structure.Operating lease capitalization could also contribute to a breach of debt covenantrestrictions on existing long-term loans for companies such as CEC Entertainment andRed Robin. This likely impact is shown in Table VI.

These results show that an increase in debt from the capitalization of operatingleases could result in technical default for both firms because the leverage ratio aftercapitalization exceeds the maximum that is specified in their respective debtagreements. Even firms with leverage ratios closer to the limits of debt covenantviolations have to re-examine their debt covenants. Failure to do so could lead lendersto impose additional financing costs in the form of higher interest rates or restrictcorporate investment and financing policies as evidenced in prior research (Beneishand Press, 1993; Chava and Roberts, 2008). To avoid this possibility, managers shouldbe proactive in anticipating these changes and review their debt covenants to ensurecompliance. If a breach is anticipated, mitigation strategies could include renegotiatingthe existing terms of the credit agreements or loans, refinancing debt, paying offexisting loans to reduce existing debt levels, raising more equity and relying less ondebt financing. The proposed changes are not expected to affect debt ratings becausecredit rating firms such as Standard & Poor’s have been making the necessaryadjustments for years. However, what is uncertain is market reaction to changes inleverage once the standard is implemented. Any negative market reaction will likelylead to a downgrade in debt ratings, increase the cost of capital and make it moredifficult for firms to access the equity or debt markets.

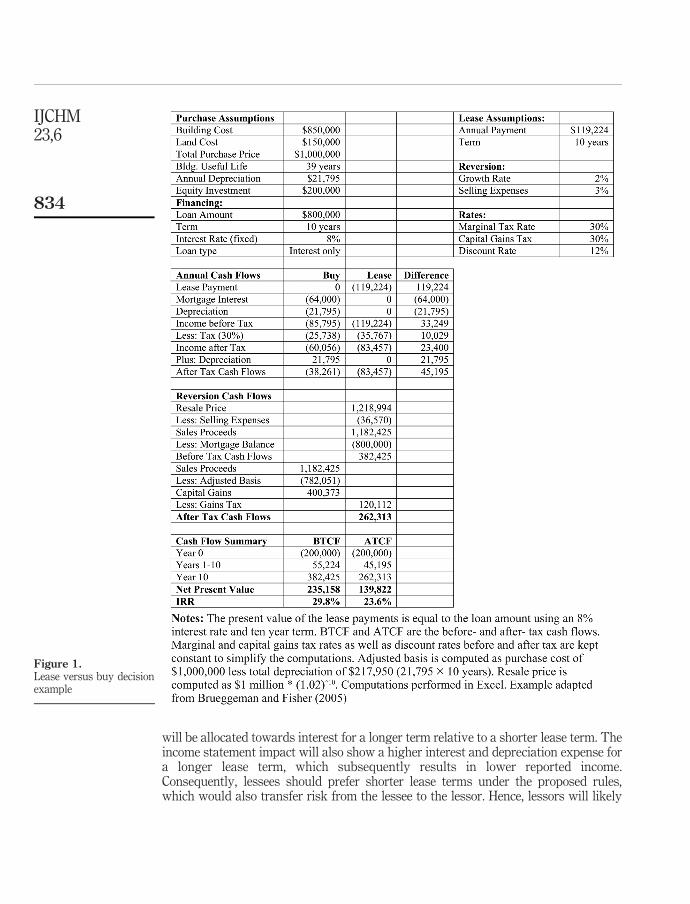

Lease versus buy decisionsWhether restaurant companies will seek to purchase the real estate and reduce orcontinue leasing will be a critical managerial decision for many firms. For young,rapidly growing restaurant companies unit development growth will be more criticalthan ownership unlike larger and more mature companies that value ownership of realestate. If internal cash is used to acquire property, then higher acquisition costs of land

CEC Entertainmenta Red Robin Gourmet Burgersb

Before After Before After

Estimated total debt 365,810 941,538 191,334 444,149Estimated EBITDA 189,066 257,480 89,109 130,260Leverage ratio 1.94 3.66 2.15 3.41

Notes: Leverage ratio is computed as total debt/EBITDA. The loan covenants for both companies intheir respective credit agreements specify a leverage ratio that is computed as funded debt/consolidated EBITDA. The definitions of the numerators and denominator in the leverage ratio differbetween both companies, so, for comparative purposes, other minor adjustments are excluded in theabove computations. Computations of existing total debt and EBITDA are based on disclosures in 10Kreports. The increase in debt is computed using the lease capitalization methodology described in thechapter. The increase in EBITDA is computed by adding base rent expense to EBITDA. aMaximumleverage ratio covenant of 3.0:1. bMaximum leverage ratio covenant of 2.5:1

Table VI.Covenant complianceestimates

IJCHM23,6

832

and buildings could slow or limit future growth and expansion by tying up valuableinternal cash resources. Purchase and ownership of the real estate (both land andbuilding) will certainly increase assets and debt liabilities on the balance sheet. Asidefrom the benefits of higher future property values, duration matching of assets,liabilities, and cash flows, and a longer depreciation tax shield, an increase in propertyownership could also imply greater exposure to economic downturns that could lead toimpairment of assets and reduce property values. A high fixed cost base for manyrestaurant companies could also impact the degree of operating leverage andcontribute to future volatility in earnings. Restaurant managers should carefully weighall of the costs and benefits associated with the lease versus buy decision betweenleasing all of their sites (both land and building), owning some combination (leaseland/own building) or purchasing both the land and buildings. A practical applicationof the lease versus buy decision is shown in Figure 1. In this case the decision whetherto lease or buy should be made on an after-tax basis based on the differences in cashflows between the two alternatives. As shown in the example, the annual after-tax cashflow savings from owning the property is $45,195 relative to leasing it. At the end often years, an additional $262,313 in cash flows will be generated from the sale of theproperty if it is owned. Based on the equity investment of $200,000 and the annualafter-tax incremental cash flows of $45,195 plus the $262,313 in year 10, the after-taxnet present value (NPV) is a positive $139,822 representing an internal rate of return(IRR) of 23.6 percent. This result implies that a firm should lease the property if it isable to earn a return greater than 23.6 percent given the opportunity cost and riskassociated with the investment otherwise it should own the property.

Other likely impactsA likely impact of the new rules could be a decision by some restaurant firms to reducethe number of company-owned and operated restaurants on leased sites. This could beachieved by shifting the risk and cost to franchisees through asset dispositions.Similarly, companies that own and operate restaurants and facing the prospects ofadditional increases in leverage could identify restaurant sites within their portfoliothat no longer meet their needs and sell them off to existing or new franchisees. Indoing so, these companies will not only reduce leverage levels but also free up capitalto fund future growth and expansion.

Given the high failure rate of restaurants and the recurring frequency with whichrestaurant companies increasingly report lease termination costs for poorly performingrestaurants, modification of existing lease terms is a very likely outcome under theproposed rules. This is consistent with the actions of firms in response to the adoptionof SFAS 13 (Imhoff and Thomas, 1988). Managers will probably resort to restructuringexisting leases or enter into new leases with shorter terms of five or ten years with norenewal options, employ termination clauses and residual value guarantees (Goodacre,2003). The advantage of a shorter lease term over a longer lease term can be illustratedwith an example in Table VII that compares the first five years of a 20-year capitallease versus a five-year capital lease. The data in Table VII shows the present value ofthe operating lease to be higher for a 20-year lease compared to a five-year lease. Thisalso means higher asset and debt liability amounts recorded on the balance sheet thelonger the lease term and a lesser amount for a shorter lease term. Depreciation is alsolower for a 20-year lease because of the longer lease term. More of the lease payment

Changes in leaseaccounting rules

833

will be allocated towards interest for a longer term relative to a shorter lease term. Theincome statement impact will also show a higher interest and depreciation expense fora longer lease term, which subsequently results in lower reported income.Consequently, lessees should prefer shorter lease terms under the proposed rules,which would also transfer risk from the lessee to the lessor. Hence, lessors will likely

Figure 1.Lease versus buy decisionexample

IJCHM23,6

834

bear a greater risk from early lease terminations by lessees or failure to exercise leaserenewal options due to poor financial performance of restaurants (Goodacre, 2003). Asa result, lessors can be expected to demand longer lease terms, demand higher rentalcompensation or make greater use of termination penalties to compensate for theadditional risk incurred.

Summary and conclusionsThis case study presented a discussion of the proposed changes in lease accountingchanges and highlighted their potential impacts on restaurant firms. More specifically,the case of CEC Entertainment was used to illustrate the likely impacts on financialstatement presentation and various financial performance measures. The results ofthis study provide some evidence to suggest that interest coverage and capital ratioswill decline, debt-related ratios will increase dramatically, and performance measuressuch as EBITDA and EBIT are expected to change without changing the underlyingcash flows. These performance measures will also affect executive compensation plansbecause of their use by some companies in determining such compensation. Inaddition, this study showed how the proposed changes will likely affect debt covenantratios and potentially lead companies to reconsider the lease versus buy decision. Theextent to which a restaurant company is affected by changes in the rules will certainlyvary depending on the magnitude of leasing activity for each firm as well as theexisting structure and portfolio of leases within each firm.

A major challenge facing many restaurant firms will be the requirement to reassesslease terms, contingent rentals, and residual value guarantees at each reporting date.Requiring reassessment of each individual lease in each reporting period will increasethe time and cost of compliance because of the challenges faced in applying judgmentand making estimates. Given the increase in financial reporting and data requirements,companies will also have to evaluate their existing accounting and informationsystems, processes and controls to determine whether additional investments arerequired to comply with the proposed rules.

It will be critical important for restaurant companies and managers to immediatelyassess and evaluate the likely impacts of the proposed changes on their financialstatements and ratios and to formulate financial policies and strategies to mitigate anyadverse impacts. In the interim, companies entering into new leases should also beaware of the new rules and consider their practical implications on future leasingactivities. If a negative impact is anticipated, then managers could employ a number of

Lease termTwenty years Five years

Annual payments ($) 1,000 1,000Interest rate (percent) 10 10PVOL ($) 8,514 8,514Annual depreciation ($) 426 758Total depreciation ($, five years) 2,128 3,791Total interest ($, five years) 4,093 1,209Total principal ($, five years) 907 3,791Depreciation þ interest 6,221 5,000

Table VII.Comparative analysis of

20-year lease versusfive-year lease

Changes in leaseaccounting rules

835

strategies to modify existing lease terms and structures, including among others, theuse of shorter rental terms and avoiding renewal options. Companies that planproactively ahead of final adoption will also minimize future administrative,operational, and financial costs of compliance. Despite its potential drawbacks formany restaurant companies, the new lease accounting standard is expected to provideinvestors and financial statement users with more precise information to assess andvalue the debt obligations of firms. Incrementally new lease financial data anddisclosures will also enable external users of financial statements to more accuratelyassess the financial risks undertaken by firms.

When the standard is finally implemented in the next two or three years, futureresearch should investigate the actual ex post impact of the standard on financialstatements, firm behavior, capital structure, risk and return measures, and stock prices.Finally, this case study is limited by the assumptions employed in capitalizing leasesand the exclusion of many features of operating leases such as residual valueguarantees, renewal terms and contingent rentals in assessing the likely impacts.

Note

1. See studies by Imhoff et al. (1991, 1997) for details and discussion of the lease capitalizationmethodology.

References

Abdel-khalik, A. (1981), “The economic effects of leases of FASB Statement No. 13, Accountingfor Leases”, Financial Accounting Standards Board, Norwalk, CT.

Beattie, V., Edwards, K. and Goodacre, A. (1998), “The impact of constructive operating leasecapitalisation on key accounting ratios”, Accounting and Business Research, Vol. 28 No. 4,pp. 233-54.

Beneish, M. and Press, E. (1993), “Costs of technical violation of accounting-based debtcovenants”, The Accounting Review, Vol. 68 No. 2, pp. 233-57.

Beneish, M. and Press, E. (1995), “The resolution of technical default”, The Accounting Review,Vol. 70 No. 2, pp. 337-53.

Bennett, B. and Bradbury, M. (2003), “Capitalizing non-cancelable operating leases”, Journal ofInternational Financial Management and Accounting, Vol. 14 No. 2, pp. 101-14.

Bowman, R. (1980), “The debt equivalence of leases: an empirical investigation”, The AccountingReview, Vol. 55 No. 2, pp. 237-53.

CEC Entertainment (2010), “Form 10-K – 2009 Annual Report”, Securities and ExchangeCommission, Washington, DC.

Chava, S. and Roberts, M. (2008), “How does financing impact investment? The role of debtcovenants”, Journal of Finance, Vol. 63 No. 5, pp. 2085-121.

El-Gazzar, S. (1993), “Stock market effects of closeness of debt covenant restrictions resultingfrom capitalization of leases”, The Accounting Review, Vol. 68 No. 2, pp. 258-72.

Ely, K. (1995), “Operating lease accounting and the market’s assessment of equity risk”, Journalof Accounting Research, Vol. 33 No. 2, pp. 397-415.

Financial Accounting Standards Board (1976), Statement of Financial Accounting StandardsNo. 13: Accounting for Leases, Financial Accounting Standards Board, Norwalk, CT.

Financial Accounting Standards Board (2010), Exposure Draft: Leases, Financial AccountingStandards Board, Norwalk, CT.

IJCHM23,6

836

Finnerty, J., Fitzsimmons, R. and Oliver, T. (1980), “Lease capitalization and systematic risk”,The Accounting Review, Vol. 55 No. 4, pp. 631-9.

Fogelson, J. (1978), “The impact of changes in accounting principles on restrictive covenants incredit agreements and indentures”, The Business Lawyer, Vol. 33, pp. 769-87.

Fulbier, R., Silva, J. and Pferdehirt, M. (2006), “Impact of lease capitalization on financial ratios oflisted German companies”, working paper, WHU – Otto Beisheim School of Management,Vallendar.

Ge, W., Imhoff, G. and Lee, L. (2008), “Investment decisions and off-balance-sheet leases: dowe really need further rule change?”, working paper, University of Washington, Seattle,WA.

Goodacre, A. (2003), “Operating lease finance in the UK retail sector”, International Review ofRetail, Distribution and Consumer Research, Vol. 13 No. 1, pp. 99-125.

Imhoff, E. and Thomas, J. (1988), “Economic consequences of accounting standards: the leasedisclosure rule change”, Journal of Accounting and Economics, Vol. 10 No. 4, pp. 277-310.

Imhoff, E.A., Lipe, R.C. and Wright, D. (1991), “Operating leases: impact of constructivecapitalization”, Accounting Horizons, Vol. 5 No. 1, pp. 51-63.

Imhoff, E.A., Lipe, R.C. and Wright, D. (1993), “The effects of recognition versus disclosure onshareholder risk and executive compensation”, Journal of Accounting, Auditing, andFinance, Vol. 8 No. 4, pp. 335-68.

Imhoff, E.A., Lipe, R.C. and Wright, D. (1997), “Operating leases: income effects of constructivecapitalization”, Accounting Horizons, Vol. 11 No. 2, pp. 12-32.

Marler, J.H. (1993), “Off-balance-sheet lease financing in the restaurant industry”, Journal ofHospitality Financial Management, Vol. 3 No. 1, pp. 15-28.

Red Robin Gourmet Burgers, Inc. (2010a), “Form 10-K – 2009 Annual Report”, Securities andExchange Commission, Washington, DC.

Red Robin Gourmet Burgers, Inc. (2010b), “Form DEF 14A Proxy Statement”, Securities andExchange Commission, Washington, DC.

Scholz, S. (2008), “The changing nature and consequences of public company financialrestatements: 1997-2006”, US Department of the Treasury, Washington, DC.

Securities and Exchange Commission (2005), “Report and recommendations pursuant to Section401(c) of the Sarbanes-Oxley Act of 2002 on arrangement with off-balance-sheetimplications, special purpose entities, and transparency of filings by issuers”, Securitiesand Exchange Commission, Washington, DC.

Standard & Poor’s (2008), “Corporate ratings criteria”, Standard & Poor’s, New York, NY.

Upneja, A. and Dalbor, M. (1999), “An examination of leasing policy, tax rates, and financialstability in the restaurant industry”, Journal of Hospitality & Tourism Research, Vol. 23No. 1, pp. 85-99.

Appendix 1. CEC Entertainment operating lease payments from lease footnotedisclosures, FY 2009 Annual 10-K Report8. Commitments and Contingencies:Leases. We lease certain store locations and related property and equipment under operating andcapital leases. All leases require us to pay property taxes, insurance and maintenance of theleased assets. The leases generally have initial terms of ten to 20 years with various renewaloptions.

Future minimum lease payments under our capital and operating leases as of January 3, 2010are as follows (in thousands):

Changes in leaseaccounting rules

837

Rent expense, including contingent rent based on a percentage of sales when applicable,comprised the following:

Appendix 2. Definition of financial ratiosEBIT interest coverage ratio

. Unadjusted: EBIT/(interest expense þ capitalized interest).

. Adjusted: EBIT/(interest expense þ capitalized interest þ implicit interest).

EBIT is earnings before interest and taxes and is computed as operating income afterdepreciation. Implicit interest is the additional amount of interest expense from capitalizingleases.

EBITDA interest coverage ratio. Unadjusted: EBITDA/(interest expense þ capitalized interest).. Adjusted: EBITDA/(interest expense þ capitalized interest þ implicit interest).

EBITDA is a non-GAAP measure of earnings before interest, taxes, depreciation andamortization, and is measured as operating income before depreciation.

Leverage ratio. Unadjusted: total debt/total assets.. Adjusted: (total debt þ PVOLÞ=total assets.

2009 2008 2007

Minimum rentals 68,414 66,599 64,476Contingent rentals 273 321 280Total 68,687 66,920 64,756Table AII.

Fiscal years Capital Operating

2010 1,698 69,3152011 1,698 69,6602012 1,616 69,1862013 1,599 68,3482014 1,599 67,572Thereafter 8,469 568,269

Minimum future lease payments 16,679 912,350Less amounts representing interest (interestRates (from 6.00 percent to 16.63 percent) (5,169)Present value of future minimum lease payments 11,510Less current portion (881)Long-term capital lease obligations 10,629Table AI.

IJCHM23,6

838

Debt to equity ratio. Unadjusted: total debt/stockholder’s equity.. Adjusted: (Total debt þ PVOLÞ=stockholder’s equity.

Return on assets. Unadjusted: EBIT after tax/total assets.. Adjusted: EBIT after tax/(total assets þ PVOL).

Return on invested capital (ROIC) ratio. Unadjusted: EBIT after tax/total capital.. Adjusted: EBIT after tax/(total capital þ PVOLÞ.

Total capital is the sum of total debt, minority interest and stockholder’s equity.

EBITDA margin ratio. Unadjusted: EBITDA/sales.. Adjusted: EBITDA/sales.

EBIT margin ratio. Unadjusted: EBIT/sales.. Adjusted: EBIT/sales.

Corresponding authorAmrik Singh can be contacted at: [email protected]

Changes in leaseaccounting rules

839

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints