influencing characteristics of crypto-currency adoption

TRANSCRIPT

INFLUENCING CHARACTERISTICS OF CRYPTO-CURRENCY ADOPTION

THESIS

Submitted in Partial Fulfillment of

the Requirements for

the Degree of

MASTER OF SCIENCE (Management of Technology)

at the

NEW YORK UNIVERSITY

POLYTECHNIC SCHOOL OF ENGINEERING

by!

Esia Yosupov!

May 2015

iii

ABSTRACT

INFLUENCING CHARACTERISTICS OF CRYPTO-CURRENCY ADOPTION

by

Esia Yosupov

Advisor: Prof. Nasir Memon, Ph.D.

Co-Advisor: Prof. Joseph Stanley Nadan, Ph.D.

Submitted in Partial Fulfillment of the Requirements for

the Degree of Master of Science (Management of Technology)

May 2015

!

Crypto-currencies (or digital currencies) have gained popularity in the recent few years,

considering its young existence of six years. Crypto-currencies are simply enabling means to

transact in the virtual space globally without the need of intermediaries and third parties. It is

built on the “Blockchain” technology, which provides an innovative means of transfer. This

paper investigates crypto-currencies, its underlying technology, and the motivation of its

development and adoption. It further takes the next step in evaluating consumer’s mindsets

around crypto-currencies utilizing the patented IdeaMap® and RDE methods to identify the

most influencing characteristics of crypto-currencies. Three distinct segments were

identified, where each segment is concerned with discrete elements involving cost, privacy,

and accessibility. It concludes that the creation of new services and applications will drive

widespread adoption of digital currencies.

iv

Table of Contents

1. Introduction ...................................................................................................................... 1

1.1 Background ...................................................................................................................... 2

1.2 Problem Statement ........................................................................................................... 3

1.3 Research Questions .......................................................................................................... 4

1.4 Proposed Hypothesis ........................................................................................................ 4

2. Literature Review ............................................................................................................ 5

2.1 Crypto-currencies ............................................................................................................. 5

2.1.1 Technical ................................................................................................................... 5

2.1.2 Acceptance and development ..................................................................................... 6

2.1.3 Regulations ................................................................................................................ 7

2.2 Market Research .............................................................................................................. 7

2.3 Mind Genomics .............................................................................................................. 11

3. Research Methodology .................................................................................................. 15

3.1 Experimental Design by Mind Genomics ...................................................................... 15

4. Understanding crypto-currencies ................................................................................. 22

4.1 What is a crypto-currency? ............................................................................................ 22

4.1.1 Types of crypto-currencies ...................................................................................... 22

4.1.2 The Current state of crypto-currencies ................................................................... 23

4.2 Technological Innovation: Blockchain .......................................................................... 25

4.2.1 The Distributed Ledger ............................................................................................ 25

4.2.2 Bitcoin Blockchain Mechanism ............................................................................... 27

4.2.3 Transactions on the Blockchain .............................................................................. 30

4.3 Advantages ..................................................................................................................... 34

4.3.1 Payment strategy ..................................................................................................... 34

4.3.2 Lower or Zero Costs ................................................................................................ 34

4.3.3 New Classes of Payment .......................................................................................... 35

4.3.4 Processing Times ..................................................................................................... 36

4.3.5 Cross Border ............................................................................................................ 36

v

4.3.6 Security .................................................................................................................... 36

4.3.7 Privacy ..................................................................................................................... 36

4.3.8 Transparency ........................................................................................................... 37

4.3.9 Accessibility ............................................................................................................. 37

4.4 Challenges ...................................................................................................................... 39

4.4.1 Regulations .............................................................................................................. 39

4.4.2 Crime risks ............................................................................................................... 42

4.4.3 Risk to Users ............................................................................................................ 43

4.5 The Blockchain: Beyond Payment System .................................................................... 44

4.5.1 Smart contracts ........................................................................................................ 46

4.5.2 Property Title ........................................................................................................... 47

5. Experimental Results ..................................................................................................... 49

5.1 Total Sample Preferred Element Order (TSPEO) .......................................................... 49

5.2 Profile Preferred Element Order (PPEO) ....................................................................... 52

5.3 Segments Preferred Element Order (SPEO) .................................................................. 55

5.4 Discussion ...................................................................................................................... 60

5.5 Contribution ................................................................................................................... 61

5.6 Result implications: Market opportunities ..................................................................... 63

6. Final Remarks ................................................................................................................ 66

6.1 Conclusion ..................................................................................................................... 66

6.2 Limitations ..................................................................................................................... 68

6.3 Further Research ............................................................................................................ 68

7. Bibliography ................................................................................................................... 69

8. Appendices ...................................................................................................................... 74

vi

Table of Figures

FIGURE 1 – BASIC APPROACH TO THE MIND GENOME .............................................................. 12

FIGURE 2 – HIGH-LEVEL STEPS OF THE EXPERIMENTAL DESIGN PROCESS ............................... 15

FIGURE 3 – THE “WELCOME” SCREEN OF THE TEST STIMULI .................................................... 18

FIGURE 4 – THREE ELEMENTS VIGNETTE, AND THE RATING SCALE ........................................ 20

FIGURE 5 –KEY METRICS BITCOIN ADOPTION OF 2015 COMPARED WITH YEAR 2014 .............. 24

FIGURE 6 – WORLD MAP OF THE DECENTRALIZED BITCOIN NETWORK ................................... 26

FIGURE 7 – A GENERAL WORKFLOW OF THE BITCOIN BLOCKCHAIN PROCESS ........................ 29

FIGURE 8 – A STEP-BY-STEP OF THE BITCOIN TRANSACTION PROCESS ................................... 33

FIGURE 9 - A COMPARISON BETWEEN TRADITIONAL PAYMENT TRANSACTION AND BITCOIN . 35

FIGURE 10 – CRYPTO-CURRENCIES ATM WORLD MAP ........................................................... 38

FIGURE 11 – NUMBER OF BITCOIN ATMS BY CONTINENTS ..................................................... 38

FIGURE 12 – MOST COMMON CRYPTO-CURRENCY MALWARE BY FAMILY .............................. 42

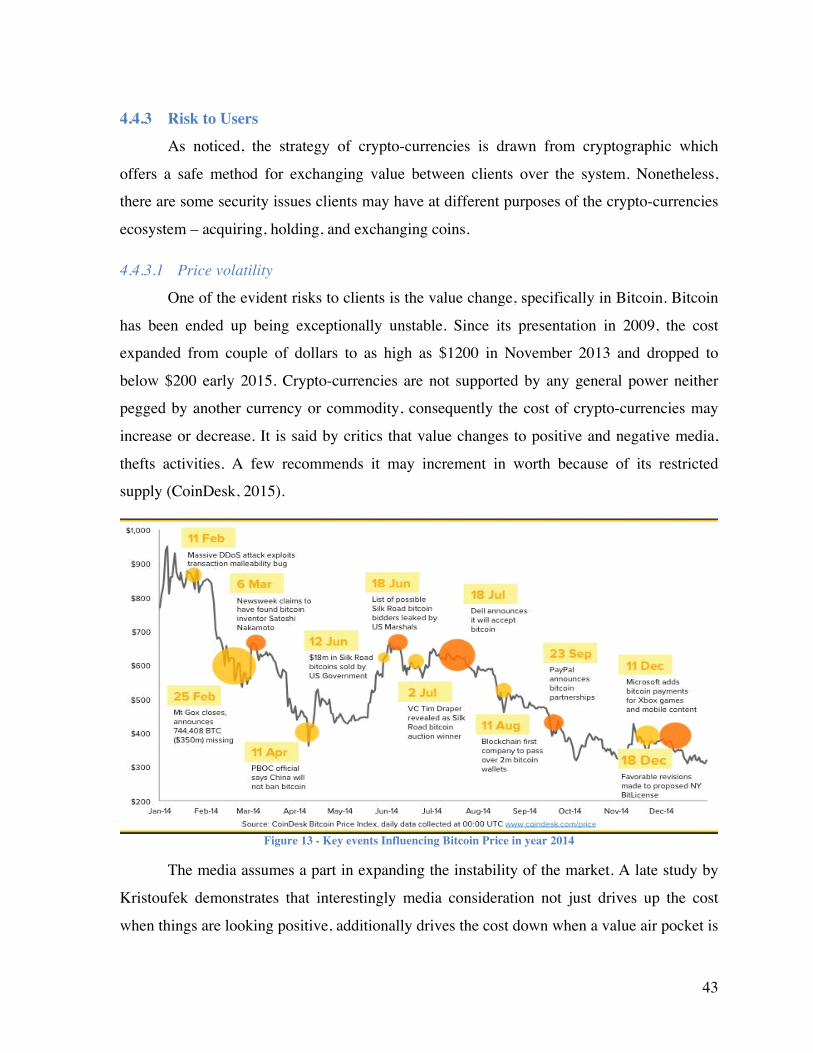

FIGURE 13 – KEY EVENTS INFLUENCING BITCOIN PRICE IN YEAR 2014 ................................... 43

FIGURE 14 – BITCOIN VS. EARLY INTERNET VC INVESTMENTS ($ MILLIONS) .......................... 45

FIGURE 15 – THE ECOSYSTEM OF CRYPTO-CURRENCIES .......................................................... 48

vii

List of Tables

TABLE 1 - TWENTY CHARACTERISTICS OF A DIGITAL CURRENCY ............................................ 17

TABLE 2 – THE LEADING FIVE CRYPTO-CURRENCIES .............................................................. 23

TABLE 3 – TSPEO: TOTAL SAMPLE PREFERRED ELEMENTS ORDER ....................................... 51

TABLE 4 – TSPEO: TOTAL SAMPLE PREFERRED ELEMENT ORDER: FIVE TOP AND THE BOTTOM

ELEMENTS. .............................................................................................................. 52

TABLE 5 – S2PEO: SEGMENT TWO PREFERRED ELEMENT ORDER ........................................... 56

TABLE 6 – S1PEO: SEGMENT ONE PREFERRED ELEMENT ORDER ............................................ 57

TABLE 7 – S2FEO: SEGMENT TWO PREFERRED ELEMENT ORDER ............................................ 58

TABLE 8 – S3PEO: SEGMENT THREE PREFERRED ELEMENT ORDER ........................................ 59

TABLE 9 – PREFERRED MESSAGING FOR CUSTOMERS .............................................................. 62!!

List of Appendices

APPENDIX A – PARTICIPATES PROFILE QUESTIONS ................................................................. 74

APPENDIX B – STUDY PARTICIPANT’S PROFILE INFORMATION S. .............................................. 75

APPENDIX C – EXPERIMENTAL STUDY ON DIGITAL CURRENCIES – DATA RESULTS ................ 77 !

1

1. Introduction

According to David Andolfatto, vice president and head of research at the Federal

Reserve Bank of St. Louis, “Bitcoin has provided the breakthrough innovation” (Andolfatto,

2014). The same viewpoint shared by Marc Andreessen co-founder of Netscape, co-author of

Mosaic and Bitcoin investor, as; “Bitcoin gives us, for the first time, a way for one Internet

user to transfer a unique piece of digital property to another Internet user, such that the

transfer is guaranteed to be safe and secure, everyone knows that the transfer has taken

place, and nobody can challenge the legitimacy of the transfer. The consequences of this

breakthrough are hard to overstate” (Andreesen, 2014). The motivation behind the

statements of David and Marc is the introduction of “a peer to peer electronic cash system …

based on cryptographic proof instead of trust.” (Satoshi, 2008).

The fundamental innovation in crypto-currencies is the subordinate technology (the

ledger) that empowers trust-less transactions without the need of an intermediary. For each

exchange system to exist there must be trust between two sides. Today, we can make online

transactions in light of the fact that we trust banks and organizations like PayPal.

Nonetheless, fraud issues and compromise of personal information on the web has been

initiated to reexamine existing models (Ali, Barrdear, Clews, & Southgate, 2014).

Exiting models are referred to the payment systems used in modern economies today,

which has not significantly changed from the early monetary system of the 16th century. The

development of technology, allowed ledgers to operate more efficiently (such as converting

paper notes to digital notes), however the structural, centralized payment system has

continued as and still holds the fundamentals from those roots (Ali, Barrdear, Clews, &

Southgate, 2014). While a great part of the emphasis on virtual currencies has been

coordinated at their ability to substitute or supplement fiat currencies, there is a developing

view that the real innovation is the decentralized ledger of transactions called the

“Blockchain”. Proponents of Blockchain technology believe that this system could have far-

reaching impacts on the wider industries and applications (Long, Lee, Steiner, Wood, &

Handler, 2015).

The protocol of Blockchain describes how to keep a public ledger of transactions

considering a protected and secure approach to exchange distinct bit of digital property

2

starting with one client then onto the next: everybody realizes that the exchange has occurred

and no one can challenge its legitimacy. The protocol is a major disruptive creation and can

possibly supplant any central handling power with a decentralized distributed

cryptographically secure equivalent, enhancing proficiency and versatility (Swan, 2015).

1.1 Background The idea of crypto-currencies or virtual currencies has been an alluring idea dating as

far back as the late 20th century. Groups were keen on accomplishing privacy and libertarian

goals by utilizing cryptography (Grinberg, 2011). David Chaum, in the 1980s, had acquired

various digital currency licenses identified with guaranteeing anonymity and privacy utilizing

cryptography, presented the first “untraceable payments” protocol in 1983. As he stated in

the paper “A new kind of cryptography, blind signatures … it allows realization of

untraceable payments systems which offer improved auditability and control compared to

current systems, while at the same time offering increased personal privacy” (Chaum, 1998).

All through the 1990s, numerous variations of the Chaum’s unique plan were

acquainted. For example, Digital Cash (DigiCash) attempted to bring electronic money

protocol into practice. In any case, DigiCash, that went bankrupt in 1998, as an after effect of

poor administration and unsuccessful deals. Essentially, clients ended up having no second

thoughts about entering credit card information online (Grigg, 1999).

In 1998, another protocol was proposed, a digital, circulated, unknown currency

called “b-money” that would permit “untraceable pseudonymous entities to cooperate with

each other more efficiently, by providing them with a medium of exchange and a method of

enforcing contracts…” (Wei, 1999). But practically speaking the protocol was impractical

and could not be executed (Grinberg, 2011).

Every new plan expected to remove the bank as an essential body in controlling

online purchases for cost, and privacy advantages. However, a few plans did not work, others

have fallen under design faults primarily because of lack of trust1 in transactions. Other

different reasons incorporated a mix of administrative inadequacy and questionable

lawfulness ( Hughes, Middlebrook, & Broox, 2007). Indeed, even today, there are virtual

1 Referred to the double spending problem in conducting online transactions. Banks or third parties play a role is verifying that the money is not spend previously.

3

currencies accessible on the Internet, for example, Pecuin, e-gold, Linden dollars and even

Facebook credits, however none of those virtual currencies are successful or gained mass

adoption (Grinberg, 2011).

As one can see Bitcoin is not the first private money, not the first digital currency,

and not the first currency in view of cryptography, but rather it has been the first to depend

on distributed, decentralized system to solve the double spending problem while at the same

time utilizing the lessons adapted by the past experiments. It was proposed by Nakamoto in

2008 and released as open source code the accompanying year (Satoshi, 2008).

1.2 Problem Statement Crypto-currencies have gained a lot of attention in the recent years. It introduces a

technology that is new and considerably disruptive, but there is a relatively limited research

done in the topic. The future of crypto-currencies is unclear nevertheless it is a fast changing,

still developing, environment. As we write this paper, there are still new developments and

changes affecting positively the crypto-currencies ecosystem.

Crypto-currencies has been existent for six years, however there is a growing public

concerns with what this technology entails, and how it can be used, and what are the

motivation for adopting and developing it.

4

1.3 Research Questions The discussion above leads towards the question of our research in this paper:

What are the features of crypto-currencies influencing its adoption?

In order to answer the key research question we defined sub research questions:

• Sub Research Question 1: What are crypto-currencies and its underline technology?

• Sub Research Question 2: What are the benefits and the risks associated with the

development and adoption of crypto-currencies?

1.4 Proposed Hypothesis Proposed hypothesis to examine are:

Hypothesis 1: Adoption of crypto-currencies involves the benefits of cost, privacy and

security.

Hypothesis 2: Lack of consumer protection is a barrier to mass adoption of crypto-currencies.

5

2. Literature Review

2.1 Crypto-currencies Given the fact that crypto-currencies has been in existence for about six years, there is

little scholastic research available on the subject. It is only in the recent years, the subject

attracted scholars and researchers to investigate this phenomenon. Because of its premature

age, there is limited data available to analyze crypto-currencies. Most exchanges platforms of

crypto-currencies and fiat money has been established just in year 2010. Scholastic sources

resulted for the most part in articles identified with technology, regulation, and social

implications of early use of Bitcoin and other related crypto-currencies.

The most relevant articles were chosen in view of the relevance of the material

identified with the exploration inquiries of this postulation. Literature on the subject of

crypto-currencies can be grouped under three subjects. The primary subject spins around the

technicality of crypto-currencies, which basically concentrates on portraying its innovative

viewpoints. The second subject incorporates economic literature of crypto-currencies focuses

on financial incentives and its role of money. Finally, the third subject incorporates

regulations and laws in development and acknowledgement of crypto-currencies.

2.1.1 Technical Dominant part of exploration in crypto-currencies spins around its technical details.

Numerous research papers mean to study the workings behind crypto-currencies. The basics

of crypto-currencies are the fundamentals of cryptography. (Babaioff, Oren , Zohar , &

Shahar, 2011) found that there is a fundamental issue with the miming process rewards in the

Bitcoin Protocol. They suggest an improved design for the Bitcoin protocol to eliminate the

problem. Researchers have additionally examined the security and privacy of crypto-

currencies exchanges. (Moore & Nicolas, 2013) research resulted with a high risk of

breaking security of crypto-currency exchange platforms. Another issue concerning its

technicality is in the pre-mining procedure where first miners may gain high rewards when a

new crypto-currency is released to the public.

6

(Ali, Barrdear, Clews, & Southgate, 2014) suggests that key innovation of digital

currencies is the Blockchain technology, which permits electronic payments to operate within

a completely de-centralized system, with no intermediaries such as banks.

2.1.2 Acceptance and development The acknowledgement of crypto-currencies was investigated by (Luther , 2013)

assumed that the low acknowledgement of crypto-currencies is due to the absence of a

massive economic dependability and government support. In his report, Luther looks for

explanations why crypto-currencies such as Bitcoin hasn’t acquired an intensive adoption,

reasoning in low network effects and high switching costs from conventional financial

systems to crypto-currency. He actually conveys that crypto-currencies, like Bitcoin, will not

probably to achieve wide acceptance without the “significant income connected

precariousness or government help” (Luther , 2013).

Interestingly, one can likewise hope to measure up the acknowledgement of digital

currency to prior comparable systems, and observe that it has really been extremely

successful. (Barber, Boyen, Shi, & Uz, 2012) argued this point of view and compared Bitcoin

with other e-money schemes. They discover numerous ways in which Bitcoin is by far

superior to past systems. The most significant factor is to incentivize users to join in the

Bitcoin network. Also, they argue that the design of Bitcoin is not impeccable and has

weaknesses and flaws. It concludes that if executed effectively, “the core design could

support a robust decentralized currency” (Barber, Boyen, Shi, & Uz, 2012).

Similarly (Maurer, Nelms, & Swartz, 2013) take a glance at the favorable

circumstances of Bitcoin from social semiotics angle, characterizing Bitcoin as “practical

materialism” and suggests that its anonymity, low exchange costs and decentralized design

replays raises debates.

Other papers surrounding the acceptance and development investigate whether digital

currencies can fulfill the properties of fiat money, and to what degree it can disrupt or

compliment current financial establishments (Lo & Wang, 2014). (Lazcano, 2013) came up

with yet another exciting viewpoint of economic growth and explains what sort of contour

banking market has considered numerous economic inventions that whatsoever keeps of the

economic world has later grasped. It's probable to label Bitcoin to be a product of contour

banking because it’s a program that operates beyond official economic system. Such style,

7

Bitcoin might probably portray such an innovation that legal financial system will welcome

in some form in future.

2.1.3 Regulations Because of criminal interest and money laundering linked with Bitcoin, it had pulled

in lot of negative media. Subsequently, administrative and legitimate bodies noting to

investigate the risks digital currencies may impose. A few nations have cautioned against the

utilization of crypto-currencies. Others have taken substantial administrative measures to

discourage end users.

Governments attempt to address consumers’ protection in using crypto-currencies.

They likewise revise current laws and regulations that may officially cover digital currencies

and caution against posing limiting laws on digital currencies that could restrict the new

technology before it has an opportunity to develop. What’s more, they give a few suggestions

about how to treat digital currencies going forward (Brito & Castillo, 2013).

(Lee , Long, McRae, & Handler, 2015) discusses Bitcoin noticing its growing value

and proposing a few factors behind its success. Furthermore Bitcoin is compared with other

e-trade currencies and gold-sponsored currencies. It recommends its decentralization and

ambiguity is in maturity of its development. One illustration of financial instability citing end

users to utilize a system without an official endorsement is the instance of Swiss Dinar in

Iraq (Grinberg, 2011). For this situation, seemingly noteworthy financial insecurity was the

cause behind consumers to utilize money that was formally surrendered and did not have any

natural value. Then again, it is significant to recollect that on account of Swiss Dinar, it was

the earlier system that individuals were willing to utilize, making such move to Bitcoin

unusual in the event of fiscal instability.

2.2 Market Research Marketing research is outlined as the systematic gathering and analysis of marketing-

related data to produce information that can be used in making decisions (Kotler & Keller,

2011). Research needs adhering to a scientific series of measures, which will generate

reliable and valid knowledge. Through analysis and model, the information is altered into

appropriate knowledge for the purpose of decision-making functions.

8

Considering crypto-currencies as not simply a traditional product, it is a product that

thought to be high tech. considering the Technology Adoption Life Cycle that classifies the

market and their reaction to an advanced product. Customers have an inclination to drop on

an axis of raising tenderness to risk. At first outlined by (Rogers, 2003), consumers belong to

one among five easy classifications: innovators, early adopters, early majority, late majority

or laggards. Geoffrey Moore, in his book Crossing the Chasm, proposes an alternate of the

initial Technology Adoption Lifecycle. He shows that for discontinuous or disruptive

inventions, there is a chasm or gap between the primary two groups: innovators and early

adopters to the early and the late majority. It is within the chasm that services and application

fail. As suggested by Moore, the technology adoption life cycle itself is nonlinear with

periods of slow growth followed by speedy growth (Moore G. A., Crossing the Chasm,

2006). Complicated systems should be studied holistically with specific attention to the

affiliation and adaptation between system parts (Moore G. A., Inside the Tornado, 2005).

How market research is completed nowadays on high tech?

Businesses have historically committed to massive analysis and development

departments to drive innovation and provide sustainable growth. That product, however, is

eroding thanks to variety of factors. What is rising is basically a lot of open product,

wherever corporations perceive that not whole all wonderful many concepts ought to are

available the firm on and not whole all wonderful many concepts developed among the

organization may well be properly sold-out internally (Chesbrough & Crowther, 2006).

The first decades of selling analysis dedicated to sorts of sampling, collecting data

and systematic techniques. Researchers additionally dedicated to approaches to live strategies

like for example concepts, perceptions, tastes, attitudes, personalities and lifestyles.

The time of the Seventies and Nineteen Eighties is sometimes called the golden era of market

research. Throughout this point research strategies turned a lot of scientific. Computing

power created getting and examining data quicker, easier, cheaper, and more accurate.

Businesses spent substantial resources into research to understand the market, the client, and

the deciding process. Analysis study results became the support or explanation for selecting

specific tactic methods and strategies (SagePub).

9

Through the late Nineteen Nineties and early 2000s a cultural shift in research started

at first to occur. Decision makers required considerably quite support for promoting

decisions. They wished promoting researchers to supply concepts in to what the data meant.

Just explaining potential areas, traits of customers, and the selection method was no

additional adequate. Decision makers required concepts in to why specific potentialities were

created by customers and the way the results of a research study will offer an improved data

of the best strategies and ways.

Now a days, starting to enter still another, newer phase of selling analysis the

informatory phase. Simply providing concepts could no additional be enough. Managers

need promoting researchers to be space of the choice, to supply feedback and approach into

promoting selections (SagePub).

Literature within the market research in crypto-currencies was reviewed. As was

observed, research was conducted applying normal surveys to grasp what individuals believe

crypto-currencies are. Numerous surveys directed by Central banks, consulting firms,

government and reputed specializing crypto-currencies news sites such as coindesk.com and

bitcointalk.com expected to uncover what the extensive population think about crypto-

currencies and its difficulties to adoption.

Juniper Research was the first effort to conduct market research by reviewing the

future of crypto-currencies, searching for market trends and competitive landscape. Juniper

Research was the primary business to analyze and to measure the activities and potentialities

within the fast-moving crypto-currency area (Juniper Research, 2015). It concluded positive

concepts for the following five years.

Banks have accomplished amount of surveys. The Canada’s Central bank has written

an operating paper that has discovered little proof that arbitrage prospects in crypto-currency

areas exist (Gandal & Halaburda, 2014). The Commonwealth of Massachusetts Section of

Banks conducted a consumer survey that assesses the buyer Attitudes on Bitcoin and

different electronic currencies (Commonwealth of Massachusetts Division of Banks, 2014).

Consulting corporations such as Accenture reviewed consumer selection can form the

continued way forward for funds, surveying North America payment clients (Accenture,

2014). PwC, client intelligence in press and entertainment, has explored Bitcoin risks, and

benefits in the media (PwC, 2014). Coin Center, a non-profit analysis and support category

10

has released data from a five-month survey uncovering how well the American people know

and understand Bitcoins (Coin Center, 2015). Lastly, the most recent survey concluded that

8% of business would accept Bitcoin in next twelve months (Perez, 2015).

To get a more in-depth understanding of the creation of crypto-currencies, this paper

examines the technology of crypto-currencies from the innovative product perspective. We

are attempting to help partners to comprehend adoption of crypto-currencies from product

point of view. We intend to analyze the particular attributes of crypto-currencies impacting

wide adoption. To the author’s knowledge, this approach hasn’t been taken before.

11

2.3 Mind Genomics Mind genomics is a market research methodology designed to systematically map end

users’ observations and inclinations. The approach is to identify a little subset of grouping

messages that takes into consideration by a significant and frugal category of new populace

into example based segments to accomplish better focusing on (Moskowitz H. , Gofman,

Beckley, & Ashman, 2006).

Basically, it is an inductive approach plans to better see how individuals respond to

diverse ideas. As individuals are inalienably quite different from one another, they sort out

and react to ordinary encounters, in an unexpected way. Mind genomics is frequently

depicted as “the experimental exploration of the everyday” on the grounds that it recognizes

what sort of messages interests consumers. Those messages then used to identify recently

gathered segments of mindsets. The “mindset” just speaks to set of thoughts, which portrays

the way individuals consider a specific service or product. “Genome” is utilized as a

metaphor; the Mind Genome is expressed as a set of thoughts that “move together”

(Moskowitz H. , Gofman, Beckley, & Ashman, 2006).

The exploration of Mind Genomics joins the science of genomics and the technology

of informatics. Its premise is determined in a formal and organized way utilizing four

standards: Stimulus–response (from experimental brain science), Conjoint investigation

(from customer examination and insights), Internet-based testing (from marketing

exploration), and various tests to identify examples of mind-sets (designed after genomics).

Practically speaking, the system for Mind Genomic can be utilized to build new,

innovation thoughts in business applications. Mind Genomics provides with actionable

results. In the book of “Selling Blue elephants”, the writers express a test of making new

services and items that regularly consumers cannot verbalize precisely what they need, aspire

to, or like. Hence, identifying and experimentally investigating the components that could

drive consumer’s enthusiasm utilizing systematically designed models and join highlights

into the best possible mixes. This methodology is known as the Rule Developing

Experimentation (RDE). The experimental configuration of Mind Genomics based, on RDE,

involved seven stages (Moskowitz & Gofman, 2007):

12

Step 1: Raw material, characterize the problem: thoroughly considering the problem

and identifying gatherings of highlights

Step 2: Design the experiment utilizing these elements

Step 3: Gather customer responses to the models

Step 4: Analyze individual results

Step 5: Optimization

Step 6: Uncover attitudinal segments

Step 7: Generate principles to make new items

The outcome is significant standards (bearings) for managed upper hand and having the

capacity to know the variable based on the math of consumers’ minds before they can even

comprehensible the need. The general fundamental approach to the Mind Genome is shown

in Figure 1 (Moskowitz H. , 2014)

Figure 1 - Basic approach to the Mind Genome

Groundwork)of)Mind)Genomics)

The premise of Mind Genomics is conjoint analysis, which is a key tool to

comprehend and organize characters in marketing. The science of Mind Genomics was

presented in 2005, however the thought of Mind Genomics began in a paper by (Moskowitz

H. , Gofman, Itty, Katz, Manchaiah, & Ma, 2001) fifteen years prior. Since then, it has been

13

broadly surveyed, with case histories, in a book expounded on ten years back (Moskowitz,

Porretta & Silcher, 2005). Its originator, Dr. Howard R. Moskowitz, is a surely understood

experimental clinician in the field of psychophysics and a designer of world-class market

research technology. Among many others, he had received the Sigma Xi’s 2010 Walston

Chubb Award for Innovation. His work generally distributed in the exploratory press (20

books and more than 300 logical articles), he is referred to worldwide as the main

mastermind and inventor of cutting edge research technology in the region of new product

and idea development (Walston Chubb Award, 2010).

The scholarly legacy of Mind Genomics gets from the spearheading work of analysts,

managing the outline of experiments (Moskowitz & Gofman, 2007), and from the use of this

work called conjoint analysis. Conjoint analysis, is the quantitative structure, can be

diminished to a straightforward engaging articulation, to be specific the utilization of

experimental configuration to comprehend responses to thoughts by measuring responses to

mixtures of thoughts. Conjoint analysis utilizes experimental configuration, combining little

parts, creating blends, gaining subjective responses to those mixes, and afterward finding

what segments drive the responses (Moskowitz & Gofman, 2007).

Based on conjoint analysis, the study of Mind Genomics intends to make a collection

of information about how individuals react to the parts of an unpredictable boost. Then, it

creates databases that include product portrayals or situational “vignettes”. At surface level,

the science evaluates what is essential. At a more profound level, the science makes a

collection of learning that uncovers how individuals consider diverse themes, functioning

from responses to complex vignettes descending to all the more fine-grained granularity

concerning how particular segments contribute.

Mind Genomics contrasts from other exploration systems. Standard surveys exhibit

the elements to the respondents autonomously, in a straight, incoherent style, one element at

once, and trains respondent to rate that one element. Then again, Mind Genomics

experimental design gives significantly more capable results by examining how gatherings of

viewpoints “move together”. It consolidates distinctive elements into what called “vignettes”

(which are straightforward explanations of thoughts), requesting that respondents respond to

a mix of vignettes. It creates ideas that can be than tried utilizing computer software

14

presentation of boosts and programmed investigation making it possible to reveal mind-set

segments quickly and effectively (Moskowitz H. , 2012).

The work of Mind Genomics is widely utilized as a part of diverse commercial

enterprises, for example, sustenance and technology and helps organizations worldwide to

optimize products, informing and illustrations plan. Its real customers (recorded on its site)

are Samsung, Coca-Cola. One demonstrated example of overcoming adversity utilizing this

methodology can be seen by the account of Hewlett-Packard (HP) that utilized the RDE

technique to test and optimize new ideas among focused on consumers. RDE studies yield

the advantage of extra buyer bits of knowledge and division opportunities (Moskowitz &

Gofman, 2007).

15

3. Research Methodology

3.1 Experimental Design by Mind Genomics The Experimental design by Mind Genomics was found to be a successful technique

in identifying functional use of information and bits of knowledge to make better products,

applications and services. The technics utilized in this analysis is to use the study of Mind

Genomics. Our aim is to assess the strongest perspectives (i.e., traits or qualities) that will

influence consumers (diverse partners) to utilize a digital currency. Figure 2 shows the

experimental design process.

Figure 2 - High-level steps of the Experimental Design Process

Experimental)Design)Steps)

The experimental investigation of the everyday is applied to the technology of digital

currencies. The destinations are to find the strongest characteristics of a digital currency, and

additionally the weakest traits of a digital currency and to identify 2 to 3 segments that are

like-minded.

)

)

16

Step)1)–)Design)Silos)and)Elements)))

The principal venture of Mind Genomics study starts with raw material. Silos are the

classifications of the product or its experience. Elements are statements that portray the silos.

The stimuli falls into four silos, every silo contains five elements. The silo portrays a general

thought though the elements are the particular instantiations of the general thought. Elements

were not picked randomly but instead created by a structured technique, first identifying

classes and then elements at which accredited to the classifications picked. The four silos

identified with the digital currency experience were distinguished as the following: 1)

Features of Digital Currency 2) Ease of Use 3) Cost 4) Security and Privacy. The elements

are communicated in straightforward definitive articulations mode. The revelatory

articulations are composed in non-specialized terms so any customer can comprehend it.

Table 1 shows each of the four silos and its five elements.

Design)size)considerations)

Preferably, the experiment is developed by 6X6 configuration; six silos with six

relating elements. Totaling in 36 elements, prompting 48 vignettes (or ideas). The length of

time of finishing the experiment of 6X6 configuration is more or less 15 - 20 minutes. The

ideal design for our purpose is a 4X5 configuration. Totaling in 20 elements, prompting 30

vignettes, lessens the length of time around 8 to 10 minutes. It is recommended that lower

term have higher likelihood of respondents to finish the experiment.

The primary step is thought to be the most difficult part on the grounds that it obliges

domain expertise. It is suggested that IdeaMap® designed to end up more progressed through

repeated experimentation (Moskowitz & Gofman, 2007). We had the capacity qualify our

element development by giving a profound investigation of crypto-currencies, and consulting

with specialists in the area of cryptographic. Also, the advantages of crypto-currencies that

we identified were converted to element.

17

Table 1 - Twenty characteristics of a Digital Currency

Silo A: Features of Digital Currency A1 It is a decentralized network…not controlled by an individual or a company A2 Your account balance can be printed on a paper A3 Once payment is made you can’t “undo” it … it is not reversible or disputable A4 It can be used globally A5 Instantly transfer money or make a payment worldwide Silo B: Ease of Use B1 Easy to use … via an application on a smart-device or a computer B2 A human “teller” may convert your digital money to (from) cash B3 Most local ATMs worldwide accept this digital currency B4 More than 30% businesses worldwide now accept this digital money B5 Use this digital currency to make micro payments...as small as a penny Silo C: Cost C1 It is 50% cheaper for business owners to process this digital currency than a credit card C2 There is a negligible fee to convert this currency to any other digital currency or cash C3 Creating a digital “wallet” is as easy as downloading an app…no need for a special device or knowledge C4 People without a bank account may use this digital currency C5 The number of coins produced are limited ... the value may increase in the future Silo D: Security and Privacy D1 No identity theft…it doesn’t expose your personal information D2 This digital currency has a very strong mathematical algorithm…it has never been broken D3 This digital currency is insured … just like a credit card D4 Unlike cash…this digital currency is resistant to counterfeiting D5 Proof of a transaction is verified without involving a third party

Step)2)–)Design)a)Rating)Question)

The rating question that was formed is: Rating Question: “How would you value this

digital currency?” The rating was picked on a scale purpose of 1 to 9, where 1 is being the

slightest worth and 9 is being justified regardless of a considerable measure. The rating

question will be rehashed all through the whole experiment. We performed pretests before to

guarantee that it suits the distinctive elements that may show up on the screen. It is critical to

note that, generally, specialists utilization rating question on a level of likeability. Mind

Genomics on the other hand, utilizes the value that offers a higher significance instead of just

whether something is preferred or not.

)

18

Step)3)–)Prepare)a)“welcome”)page))

The welcome page is the first screen the respondents visit. It presents the point and

the reason for the study. It tells the respondent what the rating questions is, and highlights the

way that vignettes are unique in relation to one another despite the fact that they may show

up the same. Finally, it informs on the estimated length of time regarding the stimuli test, and

headings to start the study. Figure 3 demonstrates the welcome page that every respondent

will see on the screen once the study starts.

Figure 3 - The “welcome” screen of the Test Stimuli

Step)4)–)Prepare)Profile)questions))

Step 4 includes profile questions that were agreed to serve the speculation and

understanding our subjects better and know their experience. Appendix 1 shows the seven

questions that were included in the study.

Step)5)–)Invitation)Email))

We recognized two target groups for our experiment and designed a focused

invitation for every gathering. The primary gathering is the essential clients of the well-

19

known site Bitgazetteer.com serving in the area of crypto-currencies. The site offers clients

complete worldwide postings of businesses and services that acknowledge crypto-currencies,

accessible crypto-currencies ATMs, and postings distributed by clients. The gathering of

clients is effectively communicating with crypto-currencies, it is possible that they are

entrepreneurs involved with digital currencies or clients who are intrigued spending their

digital currency money. The second gathering that was distinguished is the dynamic

individuals in the crypto-currencies field, for example, new start-ups. Both invitations were

composed in a manner that welcomes cooperation and recommends the results may be to

their greatest advantage.

Running)the)Experiment)

The information from steps 1 through 5 was submitted to IdeaMap® suite2. The

online study was displayed to the members in the accompanying request: welcome screen, 30

screens of permutated element mixes with one rating question asked, 7 profile questions, and

a thank you screen. Every screen is alluded to an idea, shows a mix of elements, or vignettes,

which are made by experimental configuration. Vignettes are involved 2–4 elements; every

silo contributes a most extreme of one element to a vignette. The 20 elements are measurably

autonomous of one another. Figure 4 demonstrates an illustration of a 3-element Vignette,

and the rating question scale beneath. The vignette joins three elements, every focused, one

over the other, with no endeavor to join the elements in fitting syntactic structure. Thusly,

respondents have no problem perusing the four elements, and relegating a rating.

In practice, this configuration is simple for the respondent in light of the fact that the

thoughts are separated and focused. The respondent doesn’t need to chase through a thickly

worded section so as to locate the essential information. This approach of focusing the

element and disposing of connectives is a standard approach in conjoint investigation.

2 www.ideamap.net

20

Figure 4 - Three Elements Vignette, and the Rating Scale

After the respondent chooses the rating, the vignette and the rating scale change to be

trailed by the following vignette. The software project controls the whole process. The

respondent need not click additional keys to present the rating, making the process easier. At

long last, the system “permutes” the experimental configuration, so that every respondent

winds up assessing an extraordinary arrangement of mixes. The fundamental experimental

outline stays in place, however the change guarantees that the genuine blends vary starting

with one respondent then onto the next.

Explaining)the)rating)process)

Each member’s ratings are changed over into a parallel response. Ratings of 1–6 are

changed over to the value “0,” and ratings 7–9 are changed over to the worth “100.” Ratings

of 0 alluded to “idea rejecters”, ratings of 100 allude to “idea acceptors”. Aggregate of 30

ideas are exhibited to every member, if a rating given to one idea is 7-9 it is considered

acceptor, if 1-6 rating is given for another idea it is viewed as a “rejecter”. That is,

acceptance/rejecter is unexpected in response to an individual idea, not to the whole item.

21

The information for every member are liable to relapse displaying, which is

impeccably legitimate for these sorts of results as every member assessed 37 ideas set up

particularly to be analyzed by relapse demonstrating. The experimental outline guarantees

that each of the 20 elements are factually autonomous of every other. The model is a basic

and straightforward in an added substance mathematical statement structure:

Where is the additive constant (the expected value of the rating when elements 1 to 20 are

all 0), and , and are elements 1, 2 and 20, respectively. Each participant generates

his own additive model for the study in which he or she participated.

Rating = k0 + k1 +...+ k20

k0

k1 k2 k20

22

4. Understanding crypto-currencies

4.1 What is a crypto-currency? A large segment of the crypto-currencies today relay on a decentralized digital

currency system, utilizes at a distributed information structure known as the Blockchain, a

log containing all transactions records (Bitcoin.org).

The structure of any current crypto-currency is drawn on a 3-layer technology stack:

Blockchain, Protocol, and Currency. The first layer is the hidden technology, the Blockchain.

It is the decentralized ledger recording transactions. It is a substantial database that is

imparted among all system hubs, overhauled by miners, checked by everybody and is not

controlled by anyone (Bitcoin.org).

The Blockchain technology gives an electronic public exchange record of honesty

without central power. The exchange record is a ledger of all transactions that have occurred

inside a set protocol, recorded in a refined, conveyed information structure. The information

structure is decentralized and imparted by all hubs, i.e. computers, inside the partaking

system or network of systems.

The center level of the stack is the Protocol. It is the product or the system that

handles the exchange of money over the Blockchain. At long last, on the highest point of the

stack is the Currency itself. Bitcoin was the initially made crypto-currency, which provides

all the three layers on the stack. Many new types of crypto-currencies were created, by

altering the convention (or the first code) of Bitcoin.

4.1.1 Types of crypto-currencies It is proposed that there are more than 555 sorts of crypto-currencies till date3. Every

currency is ordinarily a currency and a protocol using the Bitcoin Blockchain. The most well

known crypto-currencies concurring their market top are Bitcoin, Ripple, Dash, and

BitShares. Some may have its own Blockchain, for example, Litecoin and Ripple. It has a

different Blockchain significance it had its own decartelized ledger.

3 See http://coinmarketcap.com last visited May 4th, 2015

23

The distinctive sorts of crypto-currencies can further investigated by its protocol.

Table 2 blueprints differences in the convention of the main five crypto-currencies till date4.

All utilize the methodology of mining to secure the system and give a strategy to the issuance

of new currency. Most currencies typically have a maximum supply. There are substantial

contrasts in the more specialized side of the currency. One large difference is in the hashing

algorithm that is utilized. For example, Bitcoin utilizes SHA-256 yet a few currencies have

selected a Scrypt algorithm. Table 2 – The Leading Five Crypto-currencies

Coin Name Block Created (Year)

Algorithm Max Supply (million)

Block Time (min)

Block Reward (coins)

Bitcoin 2009 SHA-256 21 10.00 25

Litecoin 2011 scrypt 82 2.50 50

Ripple 2013 RPCA 99 0.05 N/A

Dash 2014 X11 22 2.50 2.84

BitShares 2014 SHA-512 2 5 2

4.1.2 The Current state of crypto-currencies To comprehend the present state of crypto-currencies, we decide to depict Bitcoin, as

by a wide margin it is the most prevalent crypto-currency. What truly makes crypto-

currencies, for example, Bitcoin so well known? We should take a look at the present metrics

adoption. The Crypto ecosystem is bargained of distinctive performers: infrastructure,

wallets, exchanges, payment services, mining, and financial services.

In the pre-winter of 2013, the first Bitcoin ATM was built and speculator support for

the virtual currency was enthusiastic to the point that for a brief period in late November,

Bitcoin exchanged at costs higher than gold. Notwithstanding concerns over cybersecurity,

Bitcoin is progressively acknowledged by online and brick and mortar retailers. In January

2014, Overstock.com turned into one of the first substantial US online retailers to

acknowledge Bitcoin, and in September 2014, it turned into the first to acknowledge Bitcoin

payments in all remote countries. By the late spring of 2014, Microsoft, Dish Network,

4 Source: http://www.coinwarz.com/cryptocurrency/coins, http://coinmarketcap.com/currencies/views/all, last accessed May 8th, 2015

24

Expedia and Dell all began accepting Bitcoin. An expected 63,000 retailers overall

acknowledged Bitcoin by the mid-year of 2014, and that number was anticipated to achieve

100,000 by the end of 2014 (CoinDesk, 2015).

Notwithstanding stores that directly acknowledge payment in Bitcoins, the virtual

currency can be utilized at different retailers, for example, Amazon, CVS, Target, Zappos,

Home Depot and Entire Foods, by acquiring gift cards through eGifter or Gyft. Further,

Xapo, which offers online Bitcoin wallets and underground Bitcoin vaults, recently

discharged the world’s first plastic upheld by Bitcoins. The rate of development in the

quantity of Bitcoin-accepting dealers kept on tapering off this quarter. Exchanges around the

lull of dealer adoption propose the crucial problem is not an absence of vendor enthusiasm

for Bitcoin, instead a deficiency of purchaser adoption.

Figure 5 highlights key metrics in Bitcoin adoption of the first quarter of 2015

compared to the year of 2014 (CoinDesk, 2015). There were about 1 million brand new

Bitcoin storage wallets created in Q1 of 2015, constitute with 14% growth quarter-over-

quarter. The aggregate amount of Blockchain storage wallets approved about three zillion

within February. The rate connected with wallets growth is virtually standard all around the

last calendar year, driving a number of become involved concerning the believability of the

figures and also troubles in what amount of storage wallets tend to be correctly utilized for

bona fide transactions. Income Work area will be forecasting 12 zillion complete Bitcoin

storage wallets through the finale connected with 2015.

Figure 5 –Key Metrics Bitcoin Adoption of 2015 compared with year 2014

25

4.2 Technological Innovation: Blockchain

4.2.1 The Distributed Ledger A vital issue for just about any electronic payment program is ways to assure that

how the money cannot be double spent. In physical world, the materialistic exchange activity

maintains the payer from spending the same money more than once.

A payment program that depends upon electronic records will need to have a

technique for counteracting double spending on the triggers that it’s easy to manage

electronic records. The strategy employed by current banking system, which developed as a

modern computerized record keeping system from earlier paper-based, is for special

consortium (ordinarily banks) to steadfastly maintaining the master ledgers to keep up every

customer’s transaction record electronically. Thusly, they maintain records noted in the

ledger of 1 central entity (commonly the central bank). Whoever is maintaining these ledgers

have the ability to stop any transaction if they think if is not legitimate. For customers in

order to use this system, they must trust that these consolidated electronic ledgers are safe,

reliable and maintained well.

The difficult task will be how to give and take money online without a trusted third

party, for instance, PayPal, making certain that exactly the same money being spent more

than once. A choice of strategy would be to actualize a totally decentralized payment

program, where copies of the ledger are imparted between all clients, and a technique is

established where customers recognize to amend to the ledger. Since everyone can check

always any planned change contrary to the ledger, this process evacuates the necessity for a

central agency and subsequently for clients to possess rely upon the uprightness of any single

entity.

Any electronic payment program will need to have a dependable process for saving

transactions that clients may possibly concur is precise. For a decentralized program like

Bitcoin that makes two difficulties. The key is contriving a secure and trustworthy process

for replacing a community ledger as there are heap copies spread all over the world. The

second is, without a central agency to maintain or co-ordinate resources, making the

important motivations for clients to contribute resources to confirming transactions. The key

ideas were initially delineated by (Satoshi, 2008).

26

Before the innovation of the Blockchain, it essentially was impractical to organize

singular exercises over the Internet without a centralized body guaranteeing that nobody has

tinkered with the information. A gathering of inconsequential people couldn’t affirm that an

occasion had happened without depending on a central agency to check that this specific

transaction was not deceitful or invalid. Indeed, numerous computer researchers did not

accept that distributed gathering of individuals could achieve accord without a typical

clearinghouse.

Satoshi’s answer was what has ended up known as the Blockchain: a ledger of all

transactions possessed and observed by everybody yet when it is all said and done controlled

by none. It is similar to a titan intuitive spreadsheet everybody has admittance to and

upgrades to affirm every digital credit is distinct. Blockchain technology makes it so that

something that beforehand obliged a centralized power can now be overseen through group.

A Blockchain is just an ordered database of transactions recorded by a system of computers

(Bitcoin Foundation WIKI). Figure 6 shows how robust is the supporting decentralized

network. There are 6441 full bitcoins global nodes running all over the world5.

Figure 6 – World Map of the Decentralized Bitcoin Network

5 Source: getaddr.bitnodes.io. As of April 2015. Last accessed May 9th, 2015

27

4.2.2 Bitcoin Blockchain Mechanism

To accomplish a protected and usable system, “Blockchain” depends on

cryptography. The Blockchain is basically a publicly visible ledger that records all

transactions on the system, with every client on the system holding a duplicate of the ledger.

At the point when another transaction is started by a user, it is assembled with different

transactions and these groupings—or ‘‘blocks’’ are intermittently added to the ledger. The

blocks are distributed to every client of the system, and the veracity of the block is affirmed

by the distributed figuring force of the clients joined. When an transaction is endorsed and

sent, it is irreversible on the grounds that just the approval of the sending party is expected to

start the decentralized methodology.

At its most essential, the Bitcoin programming makes an algorithm, or numerical

riddle, that is extremely hard to tackle. The riddle can be handled either by individual clients

acting alone or by “pools” of clients that gather as one to impart figuring force and to

reduction the danger of fizzled attempts. (Bitcoinmining.com). Those endeavoring to

illuminate the riddle by running the Bitcoin program on their computers, committed servers,

or specific equipment are known as Bitcoin “miners”. The Bitcoin programming uses the

Internet to connect every mining machine (computer) together in one huge distributed

system, implying that each machine is joined with the system without the utilization of any

central nexus, for example, and a server (Bitcoin.org).

In its most basic terms, the Bitcoin system utilizes the mining process to bring new

Bitcoins into flow, as well as to confirm each and every Bitcoin transaction that has ever

happened. Bitcoin consequently works freely of any controlling central power, on the

grounds that no outside operators or altruistic manager is expected to screen, track, and

guarantee the substantial use of Bitcoins. This blend of the Bitcoin creation system with the

Bitcoin confirmation component is typified in what is known as “blocks.” (Bitcoin

Foundation WIKI).

Each new transaction of X Bitcoins from Party A to Party B that has yet to be

checked is packaged together with different as-of yet unsubstantiated transactions and put

away into a document called a block. Every block that has ever been acknowledged by the

Bitcoin system frames a piece of a long, constant record known as the Blockchain; every

endorsed block shapes a connection in a chain that follows back sequentially to the first

28

“Genesis block” made by Nakamoto in January 2009. Because these blocks contain the

records of all confirmed, effective Bitcoin transactions, Bitcoins Blockchain adequately

unctions as a huge, endless public ledger that subtle elements both the time and the

gatherings of each effective Bitcoin transaction. All in all, this record does not contain or

require any information as to the genuine identities of Party A or Party B, who take cover

behind cryptographic locations that role as aka for the transaction and storage of Bitcoins.

Since it is impractical to focus the proprietor of a Bitcoin pseudonym/account without

extra information, Bitcoin is hence regularly alluded to as a “pseudo-anonymous” crypto-

currency. To develop the prior allegory, when miners are given new “veins” to mine each

round, every miner or pool is given an exclusive “block” that can possibly be the following

block added to the Blockchain. Every potential block that is passed out contains not just a

heap of Bitcoins transactions holding up to be checked, additionally an obscure number

produced from a cryptographic hash function, which is that block’s exclusive “hash.” The

hash number yield by the function can’t be returned or predicted. Every block likewise has a

second number value called the “nonce,” which is the piece of the block that is modified by

the mining process (Bitcoin foundation WIKI).

With the goal miners should check their allotted blocks and get their Bitcoin rewards,

they need to succeed in getting the nonce value beneath the hash value, in this way

understanding the “riddle” and creating proof-of-work, as such, mining happens as miners in

a pool take advantage whatever computer processing power as could reasonably be expected

to take “swings” at the nonce as fast as would be prudent in an incensed race to “strike gold”

by being the first mining group to get their block’s nonce value below their block’s hash

value (Ali, Barrdear, Clews, & Southgate, 2014). The first block to have its nonce reduced

below its hash value announce itself to rest of the system, which then uses the Bitcoin

program to affirm the success. Figure 7 illustrating general workflow of how the bitcoin

Blockchain works6.

When this happens, the confirmed block is added to the block chain, its effective

miners are remunerated with Bitcoins, others who had been chipping away at their own

blocks gets nothing, and another round starts as fresh blocks are issued, another block must

6 Provided by Marc at http://egmr.net/2014/12/marcos-musing-bitcoin/

29

be checked and added to the chain if all the transactions it contains are not officially recorded

in the past block.

Figure 7 – A General Workflow of the Bitcoin Blockchain Process

In the event that Party A makes a purchase from Party B utilizing X Bitcoins, Party A

could hypothetically instantly go furthermore launch an arrangement with Party C by

spending the same X Bitcoins. In any case, Party B and Party C can basically wait for the

confirmation procedure to complete before giving Party A the purchased products or

services. Once the transaction with Party B clears and is memorialized in the Blockchain

“ledger,” the block chain will dismiss any transaction with Party C using the same X

Bitcoins. Because the transaction with Party C does not clear, Party C does not give out his

merchandise or services, along these lines guaranteeing that Party A can’t spend the same

Bitcoin more than once. In principle, Party C could give Party A’s buy without waiting for

the verification process. Then again, Party C ordinarily won’t do as such, in light of the fact

that he realizes that there is a uncertainty that his exchange including X Bitcoins from Party

A will be terminates by the block chain if Party A has effectively gone through the Bitcoins

30

with Party B, implying that the system won’t perceive the payment of X Bitcoins from Party

A to Party C. Regardless of the possibility that Party C decides to acknowledge the exchange

without waiting for confirmation and gets defrauded therefore, the Bitcoin system is

unaffected—it still just considered the X Bitcoins being utilized as a part of a solitary

exchange (Party A to Party B) and as continually fitting in with one owner at once. Party C

basically misses out by having doled out something for nothing.

4.2.3 Transactions on the Blockchain The whole transaction procedure on Blockchain is hence depends on a system that

addresses and get over the double spending problem.

1 - Agreeing the transaction

A is a Bitcoin miner who has beforehand worked and verified set of transactions and

got 25 new Bitcoins as a prize. B is a furniture seller who sells furniture on line and

acknowledges Bitcoin. A would like to give 2 Bitcoins to B for some furniture and is ready to

pay 0.01 Bitcoins as an exchange fee7.

2 - Creating the transaction message

A makes a communication with three crucial factors: mentioning the previous

transaction by which A received the Bitcoins, the destination bitcoin addresses and the

amounts to pay. The communication may also have few other factors, such as, conditions if

any, digital signatures and any other elements that A may want to place on the payment.

The amount of Bitcoins on any address is gotten from the previous transactions,

which are publicly available on the Blockchain for examination. In the current example, there

is a record of 25 Bitcoins from A’s earlier mining activity which will become as an input for

new transaction8.

7 Bitcoin customers are under no conventional prerequisite to pay for exchange fees and if they decide to have the exchange fees then its up to their discretion. Whatever the case, Bitcoin miners have the ability to pick which transactions they exercise, thus more fee provided to them gives a far more notable encouraging power to accept A’s transaction. 8 Bitcoin transactions might have a number of inputs or outputs.

31

Inputs:

• 25 Bitcoins from A.

Output:

• 2 Bitcoins to B.

• 22.99 Bitcoins to A.

• 0.01 Bitcoins as an exchange fee to whatsoever miner effectively checks the transaction.

It is also feasible for A to put few restrictions on the payment, so as that B cannot move

forward and spend earnings until they are met9.

3 - Signing the transaction message

When the communication has been developed, A electronically signs it demonstrating

that A regulates the payer address. To produce a digital signature10, A encodes the data and

signs with corresponding private key. Then, the digital signature can be decoded with the

same public key, which A broadcasts to the system where the transaction could be verified.

4 - Broadcasting the transaction message

A broadcasts the signed communication to the system for verification. Bitcoin miners

are orchestrated in a P2P network11, an informal network of connections without any central

co-ordination. Though the bitcoin miners are not under any obligation to accomplish as a

result, the Bitcoin protocol pushes all communications to be delivered across the network,

offering the communication to all peers on the network. That shows that A’s transaction

could maybe not be transmitted to the entire system at once but rather randomly goes to an

arbitrary section of A’s peers first.

9 In normal situations, most payments do not force any restrictions but nonetheless more perplexing transactions may possibly collaborate numerous restrictions to be satisfied before any payments are released. This capacity enables the system to be extended to assistance more complex transactions. 10 Like regular signatures, electronic signatures provide evidence that a transaction is created by the individual who wishes to make a payment. The digital signature is a manifestation of public-key cryptography. The purpose of the public-key is to decode communications by having a “private” key. 11 The P2P network techniques are generally implied to effectively and acceptably share data between users.

32

5 - Transaction verification

Miners collect A’s new record and join it with the others in to new candidate blocks.

Chances are they contend to confirm them in ways that other miners may acknowledge.

Evidence of block transaction verification has two elements: validation and achieving

consensus.

Looking for a block of transactions, including appropriate digital signatures, will take

only a short time. Making consensus is purposely more difficult and involves every miner to

produce the ability of handling resources named as proof-of-work. Comparatively, proof-of-

work needs to be hard to accomplish, nonetheless an easy task to verify. That enables the

incentives of the system to be altered for transaction affirmation by making this simple to

recognize an inaccurate transaction.

The proof-of-work technique employed by Bitcoin Blockchain means that the time

taken for a miner to successfully verify a block of transactions is arbitrary. Anyway, as new

miners join the system, or existing miners invest to increase the computing power of the

machines, the time taken for a fruitful verification may possibly fall. In order to give time for

news of every successful verification to reach the entire system, the complication of the

proof-of-work is adjusted regularly and might be balanced, which means that the average

time between blocks maintains ten minutes constant for Bitcoin, hinting that payments are

not spontaneous.

6 - Success

C is a bitcoin miner and fruitful at verifying a block with A’s transaction inside it,

therefore C will receive reward of new Bitcoins, and also the transaction fees from A’s

transaction. C broadcasts the successful verification result and the remaining miners add the

block to the end of their copies of the block chain and get back to stage 5. Lastly, B receives

2 Bitcoins as a payment, and delivers the furniture to A12 (Satoshi, 2008).

12 Bitcoin Blockchain transactions which (i) offers miners new Bitcoins as a value and (ii) provides the miner any transaction costs made available from transactions within the block. The specific situation of new Bitcoins to every Bitcoin Blockchain deal is halved every 210,000 blocks, on an average of every four years at the rate of ten minutes per block. The existing allocation is 25 Bitcoins every block, which will have 12.5 Bitcoins every block in 2017.

33

Figure 8 illustrates a step-by-step simple example how a bitcoin transaction works13.

Figure 8 - A Step-by-Step of the Bitcoin Transaction Process

13 Provided by Joshua J. Romero, Brandon Palacio & Karlssonwilker Inc: https://bitcoinbazaar.wordpress.com/2013/05/12/how-bitcoin-works-by-joshua-j-romero-brandon-palacio-karlssonwilker-inc/

34

4.3 Advantages The motivation for the development and the adoption of digital currencies has been

partitioned into two areas. Primarily is to research the advantages of digital currencies as

exchange of money. Secondly, is to examine the potential advantages of the underline

technology of digital currencies: the Blockchain.

4.3.1 Payment strategy Potential advantage offered by digital currencies is a modernized way for payment to

existing methods (i.e. credit cards). . It facilitates cheaper and faster payments. Because of its

desterilized design, it can give a more efficient infrastructure for the exchange of money by

avoiding traditional mediators, to guarantee the procedure and confirm that transactions are

genuine.

4.3.2 Lower or Zero Costs

The cost advantage utilizing digital currencies is noticeable as a part of processing

payment transactions (the fees fluctuates relying upon which exchange is being utilized), and

exchanging money. A seller who accepts any type of digital currency enjoys lower

transaction costs when comparing with and traditional bank, normally on a level of 2-4

percent for every transaction. Some well-known exchanges, for example, Bitpay offers 0%

transaction fees, Coinbase offers to change over Bitcoins to USD for a 1% transaction feee in

addition to $0.15 ACH exchange charge. Expenses rely on upon volume, yet general charges

are lower in comparison to banks (TheBlogChain, 2015).

Another focal point is remitting money abroad. The quantities of transfers really

uncover its potential. Presently, remitting money abroad charges include 8% to 12% of the

total payment (utilizing customary wire services, for example, Western Union or

MoneyGram) and settlements can take a few days to complete (Zhen, 2013). Wire transfers

in the United States can run as much as $30 every exchange locally and $50 globally. As

indicated by a report by Goldman Sachs, the total remittance utilizing Bitcoins as a part of

2013 measured at $4 billion. The normal cost of remittance charged by Bitcoin wallet

application sources is of only 1.0 percent (Goldman Sachs, 2014).

35

4.3.3 New Classes of Payment

The use of digital currencies enables opportunities of new classes of payment that are

not economical with existing payments systems, for example, micropayment. Micropayment

is a small financial transaction, and there is no capacity to utilize a charge card online for

amounts less than $1. As of today it is not practical for businesses to monetize very low cost

goods and services and accept micropayments. Crypto-currencies tackle this sort of issue.

Case in point, the scheme of Bitcoin can be divided down by 8 decimal places (0.00000001)

and Ripple is divisible into 6 decimal places 0.000001. Also, other new innovative ideas

were proposed to enable micro transactions for tipping in eateries14 amd smaller scale

payrolls paying workers by the hour\day\week 15. Figure 9 describes the comparison between

traditional payment transaction and bitcoin in a greater detail.

Figure 9 - A Comparison between Traditional Payment Transaction and Bitcoin

14 See https://www.changetip.com 15 See https://www.bitwage.co

36

4.3.4 Processing Times

Current bank payment systems such as credit cards can take a few hours, if not days,

to move money between ledgers. Traditional payment services might just be accessible at

business hours, though transactions in digital currencies are open for business 24/7.

Transactions are instant and accessible throughout the day. This advantage is truly fulfilled

by using the Internet, which can be used on any device that has a connection to the network.

Transactions can be made using a smart device such a phone or tablet by simply installing an

application.

4.3.5 Cross Border Another opportunity, specifically for smaller organizations, is to reach worldwide

markets that are often foimposed upon to large costs and delays. Globalization has empowers