currency convertibility

TRANSCRIPT

CHAPTER 1

INTRODUCTION

1.1 Convertibility

Convertibility means the system where anything can be converted

into any other stuff without any question asked about the purpose

1.2 Balance of Payment

Balance of Payment (BoP) is a statistical statement that

summarizes, for a specific period, transactions between residents

of a country and the rest of the world. BoP positions indicate

various signals to businesses. BoP comprises current account,

capital account and financial account.

Signals that the BoP account of a country gives out. For example,

large current account transactions indicate towards openness of

an economy. This was the case with India as reduction in trade

restrictions and duties led to increase in both exports and

imports after 1991. Also large capital account transactions may

indicate well-developed capital markets of an economy.

1 | P a g e

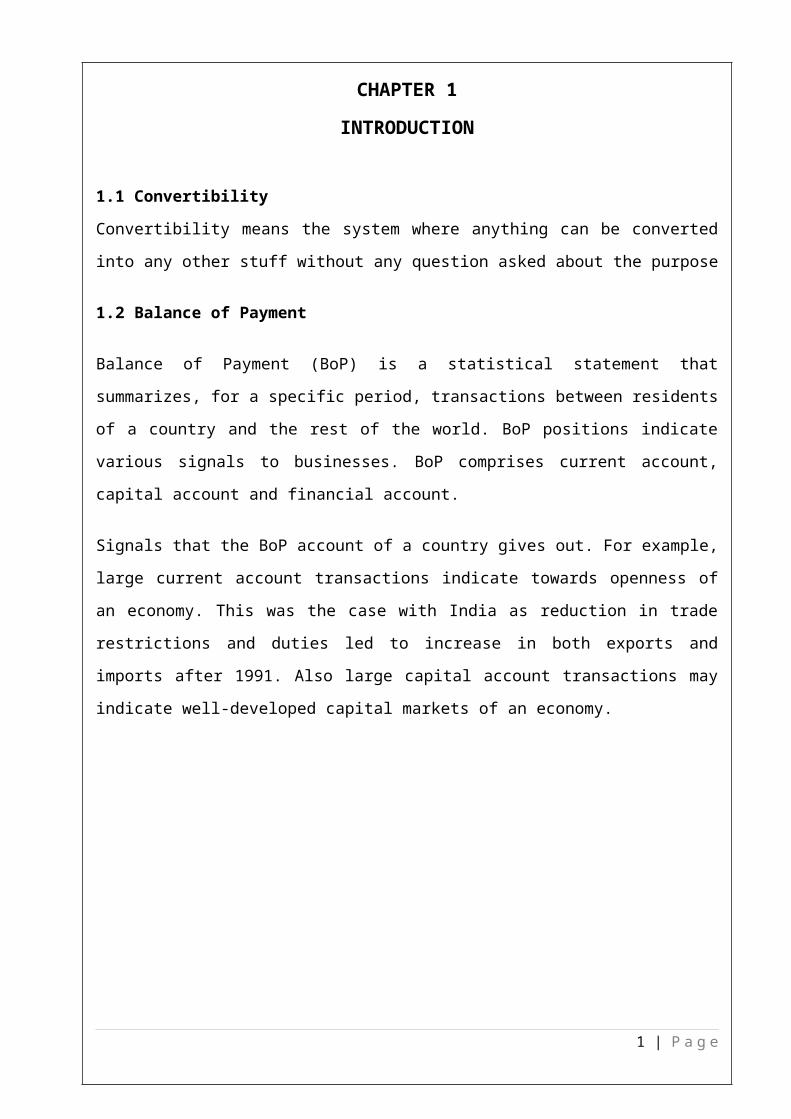

Capital and current account balances for India were quite stable

between 1991 and 2001. After 2001, primarily because of increased

exports of IT services and transfers, current account balance

went into surplus. But due to increasing imports and an

increasing oil bill, it started deteriorating after 2004 and went

into deficit.

Sound fundamentals and a large untapped market coupled with a

deregulated regime allowed foreign investors to invest in India,

thereby increasing capital inflows after 2000. However, the

global meltdown has led to an outflow of capital, which has led

to a sudden fall in the capital account balance after 2007.

Reserves were built up over the years mainly because of capital

inflows. But a deficit in current account and capital outflow led

to a fall in 2008-09.

Healthy BoP positions or surplus in capital and current account

keeps confidence in the economy and among investors. However,

2 | P a g e

healthy BoP positions may be different for different countries.

For example, surplus in current account is often more important

for developed countries than surplus in capital account as most

of them have sufficient capital to fund their investments. On the

other hand, developing countries like India may place more

importance on capital account as reserves and funding for

investment is crucial for them at present.

Large balances often attract foreign investors into an economy,

thus bringing in precious foreign exchange. Often credit ratings

are based on BoP positions, thereby affecting the flows of credit

to businesses. Businesses can make predictions about exchange

rates by studying BoP positions. A healthy BoP position can

signal domestic currency appreciation, hence encouraging

businesses to engage in future contracts accordingly. Also, the

BoP position influences the decisions of policy makers, which are

crucial for any business.

3 | P a g e

CHAPTER 2

INDIA’S BALANCE OF PAYMENT

India presently has a deficit in its current account of BoP,

which has increased substantially after reforms in 1991. In 1991-

92, current account deficit was $1,178 million, which rose to

$17,403 million in 2007-08, and accounted for $36,469 million for

the last three quarters of 2008. After the reforms in 1991,

India’s position of merchandise trade (exports and imports of

goods) kept on deteriorating, but its position on invisibles

(services, current transfers etc) improved during the period.

However, one of the major factors for increasing current account

deficit in the last few years has been a rising oil import bill.

Some countries like Japan and Germany have current account

surpluses, while the USA and UK have deficits.

India has done fairly well on the capital account side. In 2007-

08 it had a capital account surplus of $108,031 million. In the

same year it increased its foreign exchange reserves by $92,164

million, which provided stability to the economy. Foreign

investments have increased manifold since 1991, peaking in 2007-

08 to $44,806 million.

India’s overall current account and capital account deficit is

$20,380 million for April–December 2008, which is expected to

rise to a figure between $25 and 30 billion by the year ending

March 31, 2009. There has been dip in reserves from $309,723

million in March 2008 to $253,000 million in March 2009. Reasons

for this are portfolio flows from foreign institutional investors

and the appreciation of the US dollar. But this may not pose a

4 | P a g e

significant threat to the Indian economy and businesses because

of large pool of reserves that are still providing enough

cushion. However, some businesses like those related to equities

and realty are hit when outflows from these sectors occur. Not

only is there fall in asset prices and erosion of investment

value, but economic activity also gets reduced in these sectors.

However, recent profitability/growth numbers have indicated signs

of a revival. Also political change and expected stability might

bring in foreign exchange and may improve India’s capital account

position and reserves. This may lead to the appreciation of the

Indian rupee and may affect exporters and importers accordingly.

At the same time, reserves infuse stability into the system,

which in turn has positive effects on businesses and investments.

2.1 Capital account convertibility

Refers to convertibility required in the transactions of

capital flows that are classified under the capital account of

the balance of payments. There is no formal definition of capital

account convertibility (CAC). The Tarapore committee set up by

the Reserve Bank of India (RBI) in 1997 to go into the issue of

CAC defined it as the freedom to convert local financial assets

into foreign financial assets and vice versa at market determined

rates of exchange. In simple language what this means is that CAC

allows anyone to freely move from local currency into foreign

currency and back.

5 | P a g e

2.2 Current account convertibility

Refers to currency convertibility required in the case of

transactions relating to exchange of goods and services, money

transfers and all those transactions that are classified in the

current account.

CHAPTER 3

CURRENT ACCOUNT CONVERTIBILITY

6 | P a g e

Current account convertibility refers to freedom in respect of

Payments and transfers for current international transactions. In

other words, if Indians are allowed to buy only foreign goods and

services but restrictions remain on the purchase of assets

abroad, it is only current account convertibility. As of now,

convertibility of the rupee into foreign currencies is almost

wholly free for current account i.e. in case of transactions such

as trade, travel and tourism, education abroad etc.

The government introduced a system of Partial Rupee

Convertibility (PCR) (Current Account Convertibility) on February

29,1992 as part of the Fiscal Budget for 1992-93. PCR is designed

to provide a powerful boost to export as well as to achieve as

efficient import substitution. It is designed to reduce the scope

for bureaucratic controls, which contribute to delays and

inefficiency. Government liberalized the flow of foreign exchange

to include items like amount of foreign currency that can be

procured for purpose like travel abroad, studying abroad,

engaging the service of foreign consultants etc. What it means

that people are allowed to have access to foreign currency for

buying a whole range of consumables products and services. These

relaxations coincided with the liberalization on the industry and

commerce front which is why we have Honda City cars, Mars

chocolate and Bacardi in India.

Components of Current Account Convertibility

Covered in the current account are all transactions (other than

those in financial items) that involve economic values and occur

between resident non-resident entities. Also covered are offsets

to current economic values provided or acquired without a quid

7 | P a g e

pro quo. Specifically, the major classifications are goods and

services, income, and current transfers.

3.1 GOODS

General merchandise covers most movable goods that residents

export to, or import from, non residents and that, with a few

specified exceptions, undergo changes in ownership (actual or

imputed).

3.1.1 Structure and Classification

Goods for processing covers exports (or, in the compiling

economy, imports) of goods crossing the frontier for processing

abroad and subsequent re-import (or, in the compiling economy,

export) of the goods, which are valued on a gross basis before

and after processing. The treatment of this item in the goods

account is an exception to the change of ownership principle.

Repairs on goods covers repair activity on goods provided to or

received from non residents on ships, aircraft, etc. repairs are

valued at the prices (fees paid or received) of the repairs and

not at the gross values of the goods before and after repairs are

made.

Goods procured in ports by carriers covers all goods (such as

fuels, provisions, stores, and supplies) that

resident/nonresident carriers (air, shipping, etc.) procure

abroad or in the compiling economy. The classification does not

8 | P a g e

cover auxiliary services (towing, maintenance, etc.), which are

covered under transportation.

3.1.2 Nonmonetary gold

It covers exports and imports of all gold not held as reserve

assets (monetary gold) by the authorities. Nonmonetary gold is

treated the same as any other commodity and, when feasible, is

subdivided into gold held as a store of value and other

(industrial) gold.

3.2 SERVICES

3.2.1 Transportation

It covers most of the services that are performed by residents

for nonresidents (and vice versa) and that were included in

shipment and other transportation in the fourth edition of the

Manual. However, freight insurance is now included with insurance

services rather than with transportation. Transportation includes

freight and passenger transportation by all modes of

transportation and other distributive and auxiliary services,

including rentals of transportation equipment with crew.

3.2.2 Travel covers goods and services

Health and education—acquired from an economy by non resident

travelers (including excursionists) for business and personal

9 | P a g e

purposes during their visits (of less than one year) in that

economy. Travel excludes international passenger services, which

are included in transportation. Students and medical patients are

treated as travelers, regardless of the length of stay. Certain

others—military and embassy personnel and non resident workers—

are not regarded as travelers. However, expenditures by non

resident workers are included in travel, while those of military

and embassy personnel are included in government services

3.2.3 Communications services

It covers communications transactions between residents and

nonresidents. Such services comprise postal, courier, and

telecommunications services (transmission of sound, images, and

other information by various modes and associated maintenance

provided by/for residents for/by non residents).

3.2.4 Construction services

It covers construction and installation project work that is, on

a temporary basis, performed abroad/in the compiling economy or

in Extra territorial enclaves by resident/non resident

enterprises and associated personnel. Such work does not include

that undertaken by a foreign affiliate of a resident enterprise

or by an unincorporated site office that, if it meets certain

criteria, is equivalent to a foreign affiliate.

3.2.5 Insurance services

10 | P a g e

It covers the provision of insurance to non residents by resident

insurance enterprises and vice versa. This item comprises

services provided for freight insurance (on goods exported and

imported), services provided for other types of direct insurance

(including life and non-life), and services provided for

reinsurance.

3.2.6 Financial services

It covers financial intermediation services and auxiliary

services conducted between residents and nonresidents. Included

are commissions and fees for letters of credit, lines of credit,

financial leasing services, foreign exchange transactions,

consumer and business credit services, brokerage services,

underwriting services, arrangements for various forms of hedging

instruments, etc. Auxiliary services include financial market

operational and regulatory services, security custody services,

etc.

3.2.7 Computer and information services

It covers resident/non resident transactions related to hardware

consultancy, software implementation, information services (data

processing, data base, news agency), and maintenance and repair

of computers and related equipment.

3.2.8 Royalties and license 11 | P a g e

Fees covers receipts (exports) and payments (imports) of

residents and non-residents for (i) the authorized use of

intangible non produced, nonfinancial assets and proprietary

rights—such as trademarks, copyrights, patents, processes,

techniques, designs, manufacturing rights, franchises, etc. and

(ii) the use, through licensing agreements, of produced originals

or prototypes—such as manuscripts, films, etc.

3.2.9 Other business services

It provided by residents to nonresidents and vice versa covers

merchanting and other trade-related services; operational leasing

services; and miscellaneous business, professional, and technical

services.

3.2.10 Personal, cultural, and recreational services

It covers (i) audiovisual and related services and (ii) other

cultural services provided by residents to non-residents and vice

versa.

Included under (i) are services associated with the production of

motion pictures on films or video tape, radio and television

programs, and musical recordings. (Examples of these services are

rentals and fees received by actors, producers, etc. for

productions and for distribution rights sold to the media.)

Included under (ii) are other personal, cultural, and

recreational services—such as those associated with libraries,

museums—and other cultural and sporting activities.

12 | P a g e

3.2.11 Government services

It covers all services (such as expenditures of embassies and

consulates) associated with government sectors or international

and regional

organizations and not classified under other items.

3.3 INCOME

Compensation of employees covers wages, salaries, and other

benefits, in cash or in kind, and includes those of border,

seasonal, and other non-resident workers (e.g., local staff of

embassies).

Investment income covers receipts and payments of income

associated, respectively, with residents’ holdings of external

financial assets and with residents’ liabilities to nonresidents.

Investment income consists of direct investment income, portfolio

investment income, and other investment income. The direct

investment component is divided into income on equity (dividends,

branch profits, and reinvested earnings) and income on debt

(interest); portfolio investment income is divided into income on

equity (dividends) and income on debt (interest); other

investment income covers interest earned on other capital (loans,

etc.) and,in principle, imputed income to households from net

equity in life insurance reserves and in pension funds.

13 | P a g e

CHAPTER 4

BALANCE OF PAYEMENT’S STATISTICS

Balance of Payments statistics (at least estimates of major

items) are regularly compiled, published and are continuously

monitored by companies, banks, and government agencies. Often we

find a news headline like "announcement of provisional US balance

of payment figures sends the dollar tumbling down". Obviously,

the BOP statement contains useful information for financial

decision matters. In the short-run, BOP deficits or surpluses may

have an immediate impact on the exchange rate. Basically, BOP

records all transactions that create demand for and supply of a

currency. When exchange rates are market determined, BOP figures

indicate excess demand or supply for the currency and the

possible impact on the exchange rate. Taken in conjunction with

recent past data, they may confirm or indicate a reversal of

perceived trends. Further, as we will see later, they may signal

a policy shift on the part of the monetary authorities of the

country, unilaterally or in concert with its trading partners.

For instance, a country facing a current account deficit may

raise interest rates to attract short-term capital inflow to

prevent depreciation of its currency. Or it may otherwise tighten14 | P a g e

credit and money supply to make it difficult for domestic banks

and firms to borrow the home currency to make investments abroad.

It may force exporters to realize their export earnings quickly,

and bring the foreign currency home. Movements in a country's

reserves have implications for the stock of money and credit

circulating in the economy. Central bank's purchases of foreign

exchange in the market will add to the money supply and vice

versa unless the central bank "sterilizes" the impact by

compensatory actions such as open market sales or purchases.

Countries suffering from chronic deficits may find their credit

ratings being downgraded because the markets interpret the data

as evidence that the country may have difficulties in servicing

its debt.

4.1 Brief History

During the period 1950-1951 until mid-December 1973, India

followed an exchange rate regime with Rupee linked to the Pound

Sterling, except for the devaluations in 1966 and 1971. When the

Pound Sterling floated on June 23, 1972, the Rupee’s link to the

British units was maintained; paralleling the Pound’s

depreciation and effecting a de facto devaluation.

On September 24, 1975, the Rupee’s ties to the Pound Sterling

were broken. India conducted a managed float exchange regime with

the Rupee’s effective rate placed on a controlled, floating basis

and linked to a “basket of currencies” of India’s major trading

partners.

15 | P a g e

In early 1990s, the above exchange rate regime came under severe

pressures from the increase in trade deficit and net invisible

deficit, which led the Reserve Bank of India (RBI) to undertake

downward adjustment of Rupee in two stages on July 1 and July 3,

1991. This adjustment was followed by the introduction of the

Liberalized Exchange Rate Management System (LERMS) in March 1992

and hence the adoption of, for the first time, a dual (official

as well as market determined) exchange rate in India. However,

such system was characterized by an implicit tax on exports

resulting from the differential in the rates of surrender to

export proceeds.

Subsequently, in March 1993, the LERMS was replaced by the

unified exchange rate system and hence the system of market

determined exchange rate was adopted. However, the RBI did not

relinquish its right to intervene in the market to enable orderly

control.

4.2 Impact on Balance of Payments

The deficits in trade and current accounts of the balance of

payments widened significantly after 1993-94 . The current

account deficit, as a proportion of GDP, rose from 0.5 per cent

in 1993-94 to 1.7 per cent in 1995-96. The gap between domestic

savings and investment required to support the accelerating

growth momentum of the economy widened in the aftermath of

reforms, including trade liberalisation. The increase in the

current account deficit since 1993-94 reflects the availability

of foreign savings, or external resources, to bridge this higher

savings-investment gap. The magnitude of the deficit itself

16 | P a g e

should be no cause for alarm as long as the deficit finances

higher capital formation, and is sustained by capital inflows

without compromising prudent management of India's external debt

position. In fact, capital inflows during the years 1993-94 and

1994-95 have not only financed the current account deficits, but

also led to a foreign currency assets build-up of US $14.4

billion from US $6.4 billion at the end of 1992-93 to US $20.8

billion at the end of 1994-95. Furthermore, the capital inflows

have been preponderantly of the non-debt creating variety with

net foreign borrowings constituting only about 20 per cent of the

total capital inflows during 1993-95. External debt and debt

service indicators have moved in a favourable direction,

reflecting substitution, on a relatively large scale, of non-debt

creating foreign investment for other forms of debt-creating

capital flows, especially since 1993-94.

Foreign investment flows continued to dominate the capital

account inflows, which helped to mitigate the pressure on the

overall balance of payments from the current account in 1995-96.

External assistance and commercial credits remained subdued. Non-

resident deposits were stable. Repayments to the International

Monetary Fund peaked in 1995-96. Residual financing requirements

were met by drawing down foreign currency assets from US$20.8

billion at end-March 1995 to US$15.9 billion by end-February

1996, as part of a policy to manage the balance of payments and

to counter the periodic speculative pressures on the exchange

rate of the rupee during the second half of 1995-96. The

management of the foreign exchange situation in February and

March 1996 brought about a turnaround in exchange market

17 | P a g e

sentiments, and reserves grew by over US $1 billion to reach a

level of US $17.0 billion by end-March 1996. The improvement in

reserves since March, 1996 has also been supported by the stance

of monetary policy announced by the RBI in early February 1996.

The movements in the nominal exchange rate of the rupee were, on

the whole, consistent with maintenance of the competitiveness of

Indian products in international markets.

Developments on the trade account so far during 1996-97 have led

to an easing of the pressure on the current account of the

balance of payments. There are signs of a deceleration in the

growth of foreign trade, particularly of imports. The current

trend seems to indicate that the initial impact of trade

liberalization, which resulted in very high growth rates in

exports and imports during the last three years, is petering out

and trade flows are reverting back to their normal trend

determined by world demand and domestic activity. Export growth

in 1996-97 is likely to be only about 8 to 10 per cent in US

dollar terms compared to 18 to 21 per cent in the last three

years. Similarly, import growth, which averaged about 29 per cent

(on BOP basis) in the last two years, is likely to be only about

6 per cent in the current year. The sharp deceleration in the

growth of imports of items other than petroleum and petroleum

products is only partly explained by the slow-down in industrial

growth. The improvement in the trade deficit brought about by the

slow-down in imports will be largely offset by the anticipated

decline in net invisible receipts. As a result, the current

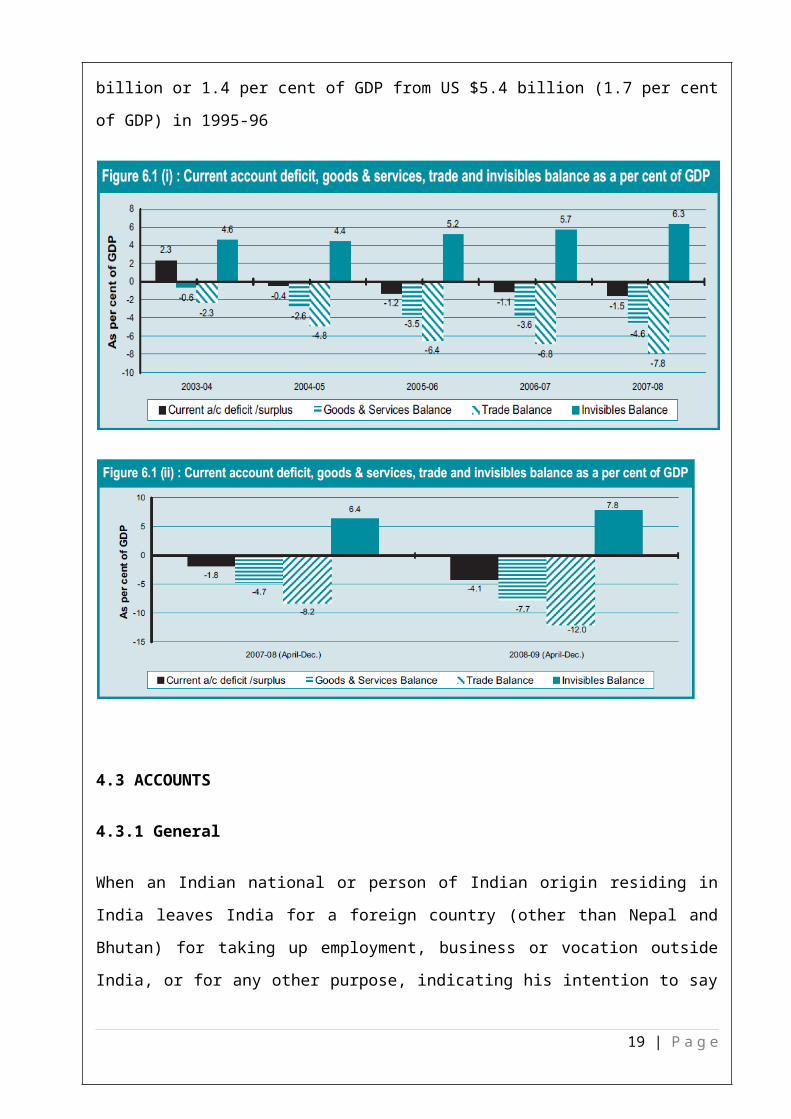

account deficit in 1996-97 is likely to decline to about US $4.9

18 | P a g e

billion or 1.4 per cent of GDP from US $5.4 billion (1.7 per cent

of GDP) in 1995-96

4.3 ACCOUNTS

4.3.1 General

When an Indian national or person of Indian origin residing in

India leaves India for a foreign country (other than Nepal and

Bhutan) for taking up employment, business or vocation outside

India, or for any other purpose, indicating his intention to say

19 | P a g e

outside India permanently or for an indefinite period, he becomes

a person resident outside India. His bank account, if any, in

India is designated as an Ordinary Non-resident Account (NRO

Account). Such accounts can also be opened with funds remitted

from abroad. . As funds in this type of account are non

repatriable, they cannot be remitted abroad to the account

holders or transferred to their NRE Accounts without the Reserve

Bank’s prior permission. Interest earned on these deposits is not

exempt from Indian Income-tax.

4.3.2 Operation of the Account

There are not many restrictions on the operation of this account

and a number of credit and debit transactions can be made after

filling up Form A4.……………………………………….

(a) Proceeds of remittances received in any permitted form

through normal banking channels.

(b) Proceeds of foreign currency notes/traveller cheques tendered

by the account holder during his temporary visit to India.

(c ) Remittance by way of transfer from rupees accounts of non-

resident banks.

(d) Legitimate dues in rupees of the account holder in India.

Certain credits to the accounts such as proceeds of foreign

inward remittances, dividend and interest earned on

shares/securities acquired with the Reserve Bank’s permission

(wherever necessary) and held in India by the account holder,

sale proceeds/maturity proceeds of shares/securities, surrender

20 | P a g e

value of life insurance policies of the account holder and

proceeds of cheques for small amounts upto specified limits can

be made by banks without the Reserve Bank’ permission.

Following debit transactions can also be made after filling Form

A4

(a) All local payments in rupees.

(b) Debits for investment and credits representing sale proceeds

of investments may also be permitted by banks.

Withdrawals from these accounts can be freely made for local

disbursements as well as for investments in Units of UTI,

Government securities and National Plan/Savings Certificates,

without prior approval of the Reserve Bank.

4.3.3 Change of Status from Resident to Non-resident Account vice

versa

All resident accounts of a person with banks in India will

automatically be treated ordinary non-resident accounts on his

becoming non-resident.

Similarly NRO account may be redesignated as resident accounts on

the account of holder becoming resident in India. It may be noted

that residential status of a person will be determined as per the

definition under Foreign Exchange Regulation AEligibility

Any person or entity residing outside India is entitled to

open a NRO account with an authorised dealer or an authorised

bank for transactions conducted in Indian Rupees.

21 | P a g e

Individuals or entities of Bangladeshi or Pakistani

nationality or ownership require approval from the RBI.

4.3.4 Type of Account

The accounts may be maintained in the form of savings or current

or term deposit accounts. The accounts can also be opened jointly

by non-residents with their close relatives resident in India and

operations thereon by the resident account holders can be made

freely. If an account is used only for the personal or business

needs of the resident account holder, it may be opened jointly

even with a person who is not a close relative but this needs

prior permission of the Reserve Bank. Interest earned on balances

in NRO Accounts is not exempt from Indian Income-tax instead

Income-tax (at present @ 20%) is deducted at source i.e. at the

time of payment of interest by the bank. Balance held in NRO

Account can neither be repatriated nor any remittance in foreign

currency is allowed without prior approval of Reserve Bank.

NRO accounts can be opened as current, savings, recurring or

fixed deposit accounts. The RBI determines the rate of interest

on these accounts and issues guidelines for opening, operating

and maintaining them.

4.3.4.a Joint Accounts with Residents/Non-residents

Joint accounts are permitted with resident and non-residents.

4.3.4.b Permissible Credits/Debits –

o Credits -

22 | P a g e

Remittances from outside India through normal banking

channels received in freely convertible foreign

currency.

Any freely convertible foreign currency can be

deposited into the account during the account holder's

visit to India. Foreign currency exceeding USD 5000/-

or its equivalent in the form of cash has to be

supported by a Currency Declaration Form. Rupee funds

must be supported by an Encashment Certificate, if they

are funds brought from outside India.

Current income earned in India, such as rent, dividend,

pension or interest. Even proceeds from sale of assets

including immovable property acquired out of rupee or

foreign currency funds or through inheritance.

o Debits -

All payments towards expenses and investments in India

Payment outside India of current income like rent,

dividend, pension, interest etc. in India of the

account holder.

Repatriation up to USD One million, per calendar year,

for all bonafide purposes with the approval of the

authorised dealer.

4.5 Remittance of Assets

NRIs and PIO may remit upto USD One million per calendar year,

out of balances held in the NRO account which could be acquired

23 | P a g e

from the sale proceeds of assets acquired in India out of rupee

or foreign currency funds or by way of inheritance from a

resident Indian, provided:

4.5.1 Assets acquired in India out of rupee/foreign currency

funds

(i) Immovable property: NRIs and PIO may remit sale proceeds of

immovable property purchased by them when they were resident or

out of Rupee funds as NRI or PIO.

(ii) Other financial assets: There is no lock-in period for

remittance of sale proceeds of other financial assets

4.5.2 Assets acquired by way of inheritance:

Sale proceeds of assets acquired through inheritance can be

remitted. No lock-in period applies here if the authorised dealer

is satisfied that the proceeds are from inherited property.

4.5.3 Remittance of assets out of NRO account by a person

resident outside India other

than NRI/PIO

A foreign national who is not a citizen of Pakistan, Bangladesh,

Nepal or Bhutan and who

has retired as an employee in India,

has inherited assets from a resident Indian, or

24 | P a g e

is a widow residing outside India and has inherited assets

of her deceased husband who was a resident Indian can remit

upto USD one million per calendar year on production of

documentary evidence to support the acquisition by way of

inheritance or legacy of assets to the authorised dealer.

4.5.4 Restrictions

The above facility of repatriation from sale of immovable

property is not extended to citizens of Pakistan, Bangladesh, Sri

Lanka, China, Afghanistan, Iran, Nepal and Bhutan. Remittance of

sale proceeds from other financial assets is not extended to

citizens of Pakistan, Bangladesh, Nepal and Bhutan.

4.5.5 Foreign Nationals of non-Indian origin on a visit to India

Foreign nationals of non-Indian origin are permitted to open a

NRO account (current/savings) on their visit to India with funds

remitted from outside India through normal banking channels or by

foreign exchange brought to India. The balance in the NRO account

is converted by the bank into foreign currency for payment to the

account holder when he leaves India, provided the account was

maintained for less than six months. The account should not be

credited with any local funds during the term, except for

interest accrued on it.

4.5.6 Grant of Loans/ Overdrafts by Authorised Dealers/ Bank to

Account Holders and

Third parties –

25 | P a g e

Loans to NRI account holders and to third parties is granted in

Indian Rupees by authorised dealers (banks) against the security

of fixed deposits provided:

o The loans are utilised only for meeting the borrower's

personal requirements or for business and not for

agricultural/plantation /real estate or relending activities

o RBI regulations pertaining to margin and rate of interest

will apply

o All norms and considerations which apply to loans to trade

and industry will apply to loans and facilities granted to

third parties.

The authorised dealer/bank may allow an overdraft to the account

holder subject to his commercial discretion and compliance with

the interest rate directives.

4.5.7 Change of Resident Status of Account holder -

(a) From Resident to Non-resident

When a resident Indian leaves India for taking up employment or

for carrying on business outside India, his existing account is

designated as a Non-Resident (Ordinary) Account, except in the

case of persons shifting to Bhutan and Nepal. For the latter, the

resident accounts do not change to NRO accounts.

(b) From Non-Resident to Resident

NRO accounts may be re-designated as resident rupee accounts once

the account holder returns to India for taking up employment, or

for carrying on business or for any other purpose indicating his

objective to stay in India for an uncertain period. Where the

26 | P a g e

account holder is only on a temporary visit to India, the account

continues to be treated as non-resident during the visit.

4.5.8 Treatment of Loans/ Overdrafts in the Event of Change in

the Resident Status of the

Borrower -

In case of a resident Indian who had availed of loan or overdraft

facilities while resident in India and who subsequently becomes a

NRI, the authorised dealer may at its discretion allow the loan

facility to continue. In this case, payment of interest and

repayment of loan may be made by inward remittance or out of

bonafide resources in India.

4.5.9 Payment of funds to Non-resident/Resident Nominee

The amount payable to a non-resident nominee from the NRO account

of a deceased account holder is credited to the NRO account of

the nominee.

4.5.10 Facilities to a person going abroad for studies –

Students going abroad for studies are treated as Non-Resident

Indians (NRIs) and are eligible for all the facilities enjoyed by

NRIs. All loans availed of by them as residents in India will

continue to be extended as per FEMA regulations.

4.5.11 International Credit Cards

Authorised dealers are allowed to issue International Credit

Cards to NRIs and PIO, without the permission of the RBI. Such

transactions can be made by inward remittance or out of balances

held in the cardholder's FCNR/NRE/NRO Accounts.

27 | P a g e

4.5.12 Income Tax

The remittances, after payment of tax are allowed to be made by

the authorised dealers on production of a statement by the

remitter and a Certificate from a Chartered Accountant in the

formats prescribed by the Central Board of Direct Taxes, Ministry

of Finance, Government of India.

4.6 NRE ACCOUNT

A Non-Resident External (NRE) account is a bank account that’s

opened by depositing foreign currency at the time of opening a

bank account. This currency can be tendered in the form of

traveler’s checks or notes.

Account Highlights:--

o Savings / Current or Term Deposits accounts in Indian Rupees

can be opened.

o Minimum period of NRE Term deposit is one year and maximum

period is 3 years.

o The balances in these accounts can be repatriated outside

India at any time.

o Transfer to / from other NRE / FCNR Account is possible.

o Accounts in the name of 2 or more NRI's are permitted.

o Nomination facility is available.

o Interest earned on deposit is exempted from Indian Income

Tax.

o Balances in the accounts are free from wealth Tax.

o Gifts to close relatives in India from balances in the

account are exempted from gift tax.

28 | P a g e

o NRE Account can be operated by resident in terms of Power of

Attorney for Local payments.

o Local disbursements from accounts can be made freely.

o Loans / Overdrafts can be availed against the security of

Term Deposits.

o Premature withdrawals are allowed. Interest for such

withdrawals is paid one percent less than the rate payable

for the period of deposit held.

o Standing instructions for local payments are accepted.

o Term Deposits will be allowed to be continued till maturity

at the contracted rate on return to India and re-designated

as resident account.

o The depositor runs the risk of depreciation in Rupee against

foreign currencies.

4.6.1 Schemes available under NRE Account:

o Fixed Deposit (Simple Interest Deposit).

o Recurring Deposit (Monthly Interest Deposit).

o Muthukkuvial Deposit (Reinvestment Plan).

o Pearl Deposit (Reinvestment Plan with Compound Interest

Payment).

4.7 FCNR ACCOUNT

Non-Resident Indians can open accounts under this scheme. The

account should be opened by the non-resident account holder

himself and not by the holder of power of attorney in India.

29 | P a g e

These deposits can be maintained in 5 designated currencies i.e.

U.S. Dollar (USD), Pound Sterling (GBP) and Euro, Australian

Dollar (AUD) & Canadian Dollar (CAD).

These accounts can only be maintained in the form of terms

deposits for maturities of minimum 1 year to maximum 5 years.

These deposits can be opened with funds remitted from abroad in

convertible foreign currency through normal banking channel,

which are of repartiable nature in terms of general or special

permission granted by Reserve Bank of India.

These accounts can be maintained with our branches, which are

authorised for handling foreign exchange business. (List of

branches authorised for handling foreign exchange business linked

at the end).

Funds for opening accounts under PNB Global Foreign Currency

Deposit Scheme or for credit to such accounts should be received

from: -

o Remittance from outside India or

o Traveller Cheques/Currency Notes tendered on visit to

India. International Postal Orders cannot be accepted

for opening or credit to FCNR accounts.

o Transfer of funds from existing NRE/FCNR accounts.

If remittance is received in any currency other than USD, GBP,

Euro, AUD & CAD, it will be converted into one of the designated

currencies of remitter’s choice at the risk & cost of the

depositor.

30 | P a g e

Rupee balances in the existing NRE accounts can also be converted

into one of the designated currencies at the prevailing TT

selling rate of that currency for opening of account or for

credit to such accounts.

4.7.1 Advantages of FCNR (B) Deposits

o Principal alongwith interest freely repatriable in the

currency of your choice.

o No Exchange Risk as the deposit is maintained in

foreign currency.

o Loans/overdrafts in rupees can be availed by NRI

depositors or 3rd parties against the security of these

deposits. However, loans in foreign currency against

FCNR (B) deposits in India can be availed outside India

through our correspondent Banks.

o No Wealth Tax & Income Tax is applicable on these

deposits.

o Gifts made to close resident relatives are free from

Gift Tax.

o Facility for automatic renewal of deposits on maturity

and safe custody of Deposit Receipt is also available.

4.7.2 Payment of Interest

Interest on FCNR (B) deposits is being paid on the basis of 360

days to a year. However, depositor is eligible to earn interest

applicable for a period of one year if the deposit has completed

a period of 365 days.

31 | P a g e

For deposits upto one year, interest at the applicable rate will

be paid without any compounding effect. In respect of deposits

for more than one year, interest can be paid at intervals of 180

days each and thereafter for remaining actual number of days.

However, depositor will have the option to receive the interest

on maturity with compounding effect in case of deposits of over

one year.

CHAPTER 5

CAPITAL ACCOUNT CONVERTIBILITY

Capital Account Convertibility (CAC) means freedom to convert

domestic financial assets into overseas financial assets at

market-determined rates. Simply put, the regime of full

convertibility allows any Indian resident to go to a foreign

exchange dealer or bank and freely convert rupees into dollars,

pounds or Euros to acquire assets abroad. The overseas assets can

be anything; equity, bonds, property or ownership of overseas

firms.

It refers to the abolition of all limitations with respect to the

movement of capital from India to different countries across the

globe. In fact, the authorities officially involved with CAC

(Capital Account Convertibility) for Indian Economy encourage all

companies, commercial entities and individual countrymen for

investments, divestments, and real estate transactions in India

32 | P a g e

as well as abroad. It also allows the people and companies not

only to convert one currency to the other, but also free cross-

border movement of those currencies, without the interventions of

the law of the country concerned.

Capital Account convertibility in its entirety would mean that

any individual, be it Indian or Foreigner will be allowed to

bring in any amount of foreign currency into the country. Full

convertibility also known as Floating rupee means the removal of all

controls on the cross-border movement of capital, out of India to

anywhere else or vice versa. Capital account convertibility or

CAC refers to the freedom to convert local financial assets into

foreign financial assets or vice versa at market-determined rates

of interest. If CAC is introduced along with current account

convertibility it would mean full convertibility.

Complete convertibility would mean no restrictions and no

questions. In general, restrictions on foreign currency movements

are placed by developing countries which have faced foreign

exchange problems in the past is to avoid sudden erosion of their

foreign exchange reserves which are essential to maintain

stability of trade balance and stability in their economy. With

India’s forex reserves increasing steadily, it has slowly and

steadily removed restrictions on movement of capital on many

counts.

The last few steps as and when they happen will allow an Indian

individual to invest in Microsoft or Intel shares that are traded

on NASDAQ or buy a beach resort on Bahamas or sell home or small

industry and invest the proceeds abroad without any restrictions.

5.1 Components of Capital Account: -

33 | P a g e

o Foreign Investment(FDI, FII)

o Banking Capital (NRI Deposits)

o Short term credit

o External Commercial Borrowings(ECB)

5.2 Accounting of total inflow and outflow of Funds is as

follows: -

Increase in foreign ownership of domestic assets – Increase of

domestic ownership of foreign assets = FDI + Portfolio Investment

+ Other investments.

FDI: - At present, there are limits on investment by foreign

financial investors and also caps on FDI ceiling in most sectors,

for example, 74% in banking and communication, 49% in insurance,

0% in retail, etc.

5.3 Need for Capital Account Convertibility: -

o Capital account convertibility is considered to be one of

the major features of a developed economy. It helps attract

foreign investment. It offers foreign investors a lot of

comfort as they can re-convert local currency into foreign

currency anytime they want to and take their money away.

o Capital account convertibility makes it easier for domestic

companies to tap foreign markets. At the moment, India has

current account convertibility. This means one can import

and export goods or receive or make payments for services

34 | P a g e

rendered. However, investments and borrowings are

restricted.

o It also helps in the efficient appropriation or distribution

of international capital in India. Such allocation of

foreign funds in the country helps in equalizing the capital

return rates not only across different borders, but also

escalates the production levels. Moreover, it brings about a

fair allocation of the income level in India as well.

o For countries that face constraints on savings and capital

can utilise such flows to finance their investment, which in

turn stokes economic growth.

o Local residents would be in a position to diversify their

portfolio of assets, which helps them insulate themselves,

better from the consequences of any shocks in the domestic

economy.

o For global investors, capital account convertibility helps

them to seek higher returns by sharing risks.

o It also offers countries better access to global markets,

besides resulting in the emergence of deeper and more liquid

markets.

o Capital account convertibility is also stated to bring with

it greater discipline on the part of governments in terms of

reducing excess borrowings and rendering fiscal discipline.

5.4 Impact of Capital Convertibility

35 | P a g e

As most of us know, resident Indians cannot move their money

abroad freely. That is, one has to operate within the limits

specified by the Reserve Bank of India and obtain permission from

RBI for anything concerning foreign currency.

For example, the annual limit for the amount you are allowed to

carry on a private visit abroad is $10,000: of which only $5,000

can be in cash. For business travel, the yearly limit is $25,000.

Similarly, you can gift or donate up to $5,000 in a year.

The RBI raises the limit if you are going abroad for employment,

or are emigrating to another country, or are going for studies

abroad: the limit in both these cases is $100,000.

You are also allowed to invest into foreign stock markets up to

the extent of $25,000 in a year.

For the average Indian, these 'limits' seem generous and might

not affect him at all. But for heavy spenders and those with

visions of buying a house abroad or a Van Gogh painting, it will

mean a lot.

But with the markets opening up further with the advent of

capital account convertibility, one would be able to look forward

to more and better goods and services.

5.5 Evolution of CAC in India economic and financial scenarios:

36 | P a g e

In early 1990s India was facing foreign reserve crisis, the

foreign reserves were only sufficient to pay off two weeks

import; therefore India was forced to liberalize the economy. In

1994 August, the Indian economy adopted the present form of

Current Account Convertibility, compelled by the International

Monetary Fund (IMF) Article No. VII, the article of agreement.

The primary objective behind the adoption of CAC in India was to

make the movement of capital and the capital market independent

and open. This would exert less pressure on the Indian financial

market. The proposal for the introduction of CAC was present in

the recommendations suggested by the Tarapore Committee appointed

by the Reserve Bank of India.

5.6 Currency Crisis in Emerging Market Economies (EME)

o The East Asian currency crisis began in Thailand in late

June 1997 and afflicted other countries such as Malaysia,

Indonesia, South Korea and the Philippines and lasted up to

the last quarter of 1998. The major macroeconomic causes for

the crisis were identified as: current account imbalances

with concomitant savings-investment imbalance, overvalued

exchange rates, high dependence upon potentially short-term

capital flows. These macroeconomic factors were exacerbated

by microeconomic imprudence such as maturity mismatches,

currency mismatches, moral hazard behaviour of lenders and

borrowers and excessive leveraging.

o The Mexican crisis in 1994–95 was caused by weaknesses in

Mexico's economic position from an overvalued exchange rate,

and current account deficit at 6.5 per cent of Gross

37 | P a g e

Domestic Product (GDP) in 1993, financed largely by short-

term capital inflows.

o Brazil was suffering from both fiscal and balance of

payments weaknesses and was affected in the aftermath of the

East Asian crisis in early 1998 when inflows of private

foreign capital suddenly dried up. After the Russian crisis

in 1998, capital flows to Brazil came to a halt.

o Difficulties in meeting huge requirements for public sector

borrowing in 1993 and early 1994, led to Turkey's currency

crisis in 1994. As a result, output fell by 6 per cent,

inflation rose to three-digit levels, the central bank lost

half of its reserves, and the exchange rate depreciated by

more than 50 per cent. Turkey faced a series of crisis again

beginning 2000 due to a combination of economic and

noneconomic factors.

5.7 Currency Crisis in Emerging Market Economies: -

o Most currency crises arise out of prolonged overvalued

exchange rates, leading to unsustainable current account

deficits. As the pressure on the exchange rate mounts, there

is rising volatility of flows as well as of the exchange

rate itself. An excessive appreciation of the exchange rate

causes exporting industries to become unviable, and imports

to become much more competitive, causing the current account

deficit to worsen.

o Large unsustainable levels of external and domestic debt

directly led to currency crises. Hence, a transparent fiscal

38 | P a g e

consolidation is necessary and desirable, to reduce the risk

of currency crisis.

o Short-term debt flows react quickly and adversely during

currency crises. Receivables are typically postponed, and

payables accelerated, aggravating the balance of payments

position.

o Domestic financial institutions, in particular banks, need

to be strong and resilient. The quality and proactive nature

of market regulation is also critical to the success of

efficient functioning of financial markets during times of

currency crises.

5.8 Challenges to Full Capital Account Convertibility -

o Market risks such as interest rate and foreign exchange

risks become more complex as financial institutions and

corporate gain access to new securities and markets, and

foreign participation changes the dynamics of domestic

markets. For instance, banks will have to quote rates and

take unhedged open positions in new and possibly more

volatile currencies. Similarly, changes in foreign interest

rates will affect banks’ interest sensitive assets and

liabilities.

o Credit risk will include new dimensions with cross-border

transactions. For instance, transfer risk will arise when the

currency of obligation becomes unavailable to borrowers.

Settlement risk (or Herstatt risk) is typical in foreign exchange

operations because several hours can elapse between payments

39 | P a g e

in different currencies due to time zone differences. Cross-

border transactions also introduce domestic market

participants to country risk, the risk associated with the

economic, social, and political environment of the

borrower’s country, including sovereign risk.

o Liquidity risk will include the risk from positions in

foreign currency denominated assets and liabilities.

Potentially large and uneven flows of funds, in different

currencies, will expose the banks to greater fluctuations in

their liquidity position and complicate their asset-

liability management as banks can find it difficult to fund

an increase in assets or accommodate decreases in

liabilities at a reasonable price and in a timely fashion.

o Risk in derivatives transactions becomes more important with

capital account convertibility as such instruments are the

main tool for hedging risks. Risks in derivatives

transactions include both market and credit risks. For

instance, OTC derivatives transactions include counterparty

credit risk. In particular, counterparties that have

liability positions in OTC derivatives may not be able to

meet their obligations, and collateral may not be sufficient

to cover that risk. Collecting and analyzing information on

all these risks will become more challenging with FCAC

because the number of foreign counterparts will increase and

their nature change.

o Operational risk may increase with FCAC. For instance, legal

risk stemming from the difference between domestic and

40 | P a g e

foreign legal rights and obligations and their enforcements

becomes important with fuller capital account

convertibility.

o Adequate prudential regulation and supervision, and

developed capital markets will also be key in addressing the

challenges from FCAC. Prudential regulation and supervision

will need to encompass the existing and new risks associated

with FCAC. In addition, developed capital markets with

adequate liquidity, infrastructure, and market discipline

are necessary to provide market participants with the

relevant risk management instruments.

5.9 Conversion Ratio of 60:40 Till 1992 and LERMS

(Liberalised Exchange Rate Management System)

A market channel in which the exchange rate is determined by

market forces of supply and demand of foreign exchange where

access if free for all transactions (other than those specified

as not free).

An official channel where the exchange rate continues to be

determined by RBI on the base of the value of rupee in relation

to the basket of currencies and fixed, but access to the market

is restricted.

With view to giving effect to the PCR. RBI introduced a system

called the Liberalized Exchange Rate Management System (LERMS)

effective from 1st March 1992.

Till 1st March 1992 all foreign exchange remitted into India was

implicitly handed over to RBI by Authorized Dealers (ADs) and

41 | P a g e

then RBI made a Foreign exchange available for approved purpose.

Under new system, the RBIs retention ratio has been reduced from

100% to 40% of all foreign exchange remittances received with

effect from 1.3.1992. The ADs apply the official exchange rate in

calculating the value of rupees to be paid to the remitter for

this 40% and surrender the exchange to the RBI. The remaining 60%

of the value of the remittance is purchased by AD at a market-

determined exchange rate. AD s, retain this 60% portion for sale

to other AD s, authorized broker or buyer of foreign exchange.

The international financial system is in a state of

introspection, jolted by several financial crises caused by

violent capital movements over the last two decades. On their

part, Indian policy-makers are also in a state of revisionism and

are moving the country to greater capital account openness after

several decades of extensive controls.

The proponents of full capital account convertibility advance

these arguments in its favour:

42 | P a g e

o An arbitrary (i.e. pre-capital mobility) distribution

of capital among different nations is not necessarily

efficient, and all countries, irrespective of whether

they borrow or lend, stand to gain from the

reallocation caused by freer capital mobility. National

income goes up in the country experiencing capital

outflows due to higher interest incomes, while that in

the debtor country increases as the interest paid is

less than the increase in output.

o Capitalists in the labour-abundant economies tend to

lose with a fall in the marginal productivity of

capital, and the opposite happens in labour-scarce

countries, so that developing nations, which are

usually capital-scarce, are doubly blessed under

unhindered mobility of capital — the inflow of capital

raises the national income and produces a healthy,

egalitarian impact on income distribution as well.

o It is argued that if there is only a small correlation

between the returns on investment in different

countries, risk can be reduced by the ownership of

income-earning assets across different countries. Free

mobility of capital, thus, helps reduce the risks that

each country is subjected to.

o Finally, it is argued that when full capital account

convertibility is in place, government profligacy and

distortionary policies are likely to be followed by

currency crises that threaten to make the government

highly unpopular. Therefore, under capital account

convertibility, the salubrious effects of capital

43 | P a g e

mobility are magnified through a change in domestic

policy in the right direction.

CHAPTER 6

TARAPORE COMMITTEE

6.1 TARAPORE COMMITTEE

6.1.1 Establishment

o The first Tarapore committee report on capital account

convertibility (CAC), which came out in May 1997, wanted CAC

to be phased in over three years (1997-2000)

44 | P a g e

o The five-member committee has recommended a three-year time

frame for complete convertibility by 1999-2000. The

highlights of the report including the preconditions to be

achieved for the full float of money are as follows:-

6.1.2 Pre-Conditions Set By Tarapore Committee:

o Gross fiscal deficit to GDP ratio has to come down from a

budgeted 4.5 per cent in 1997-98 to 3.5% in 1999-2000.

o A consolidated sinking fund has to be set up to meet

government's debt repayment needs; to be financed by

increased in RBI's profit transfer to the govt. and

disinvestment proceeds.

o Inflation rate should remain between an average 3-5 per cent

for the 3-year period 1997-2000

o Gross NPAs of the public sector banking system needs to be

brought down from the present 13.7% to 5% by 2000. At the

same time, average effective CRR needs to be brought down

from the current 9.3% to 3%.

o RBI should have a Monitoring Exchange Rate Band of plus

minus 5% around a neutral Real Effective Exchange Rate RBI

should be transparent about the changes in REER.

o External sector policies should be designed to increase

current receipts to GDP ratio and bring down the debt

servicing ratio from 25% to 20%.

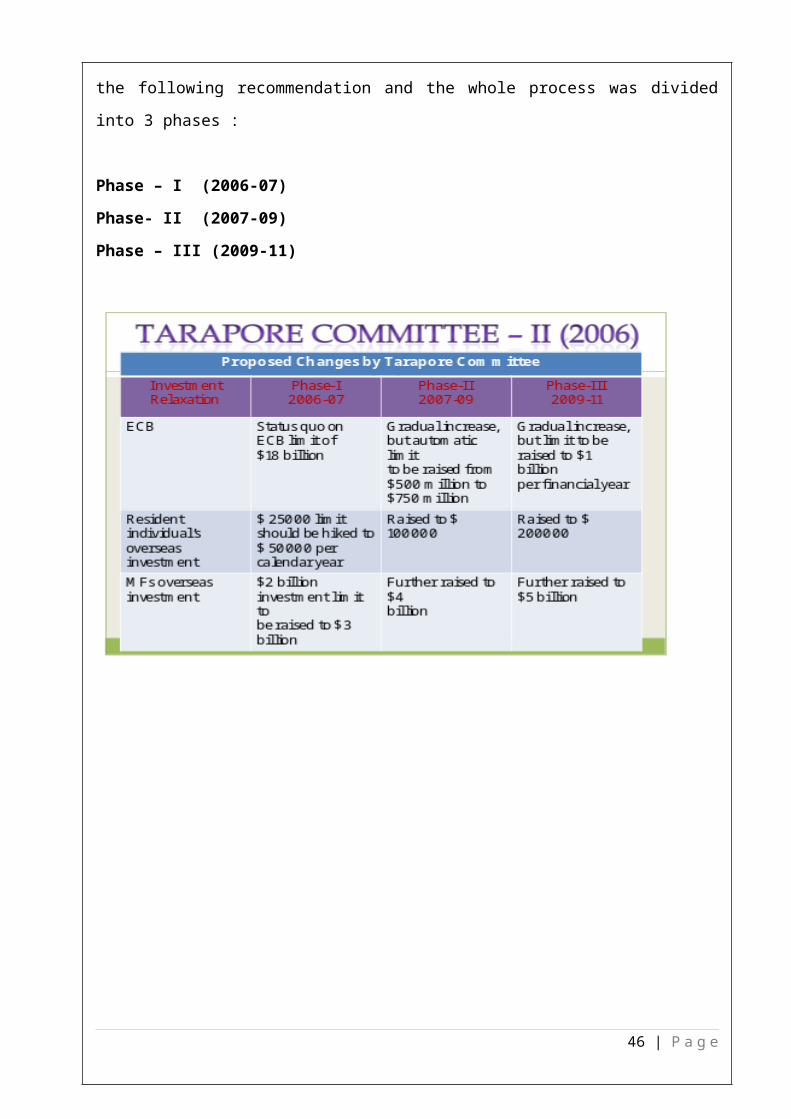

6.2 TARAPORE COMMITTEE -II

In the Year 2006 under Manmohan Singh Government the Tarapore

Committee reappointed to give suggesstion on adoption of Fuller

Capital Account Convertibility (FCAC). The Committee has given

45 | P a g e

the following recommendation and the whole process was divided

into 3 phases :

Phase – I (2006-07)

Phase- II (2007-09)

Phase – III (2009-11)

46 | P a g e

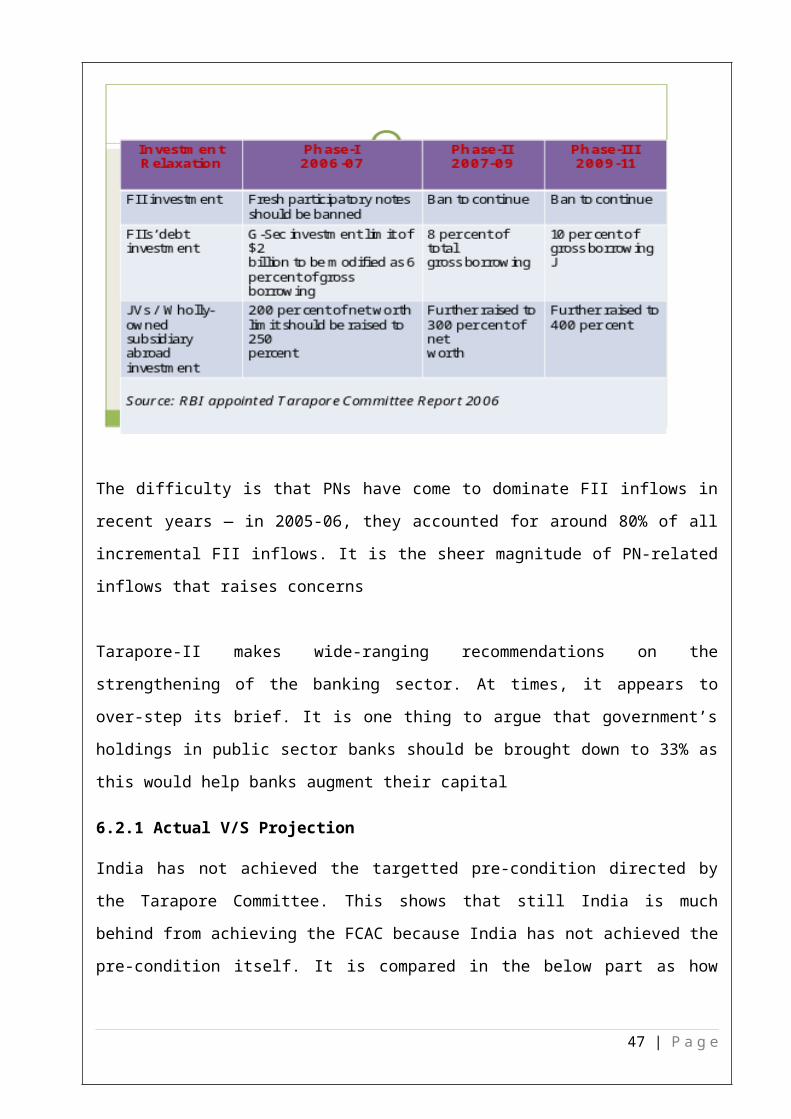

The difficulty is that PNs have come to dominate FII inflows in

recent years — in 2005-06, they accounted for around 80% of all

incremental FII inflows. It is the sheer magnitude of PN-related

inflows that raises concerns

Tarapore-II makes wide-ranging recommendations on the

strengthening of the banking sector. At times, it appears to

over-step its brief. It is one thing to argue that government’s

holdings in public sector banks should be brought down to 33% as

this would help banks augment their capital

6.2.1 Actual V/S Projection

India has not achieved the targetted pre-condition directed by

the Tarapore Committee. This shows that still India is much

behind from achieving the FCAC because India has not achieved the

pre-condition itself. It is compared in the below part as how

47 | P a g e

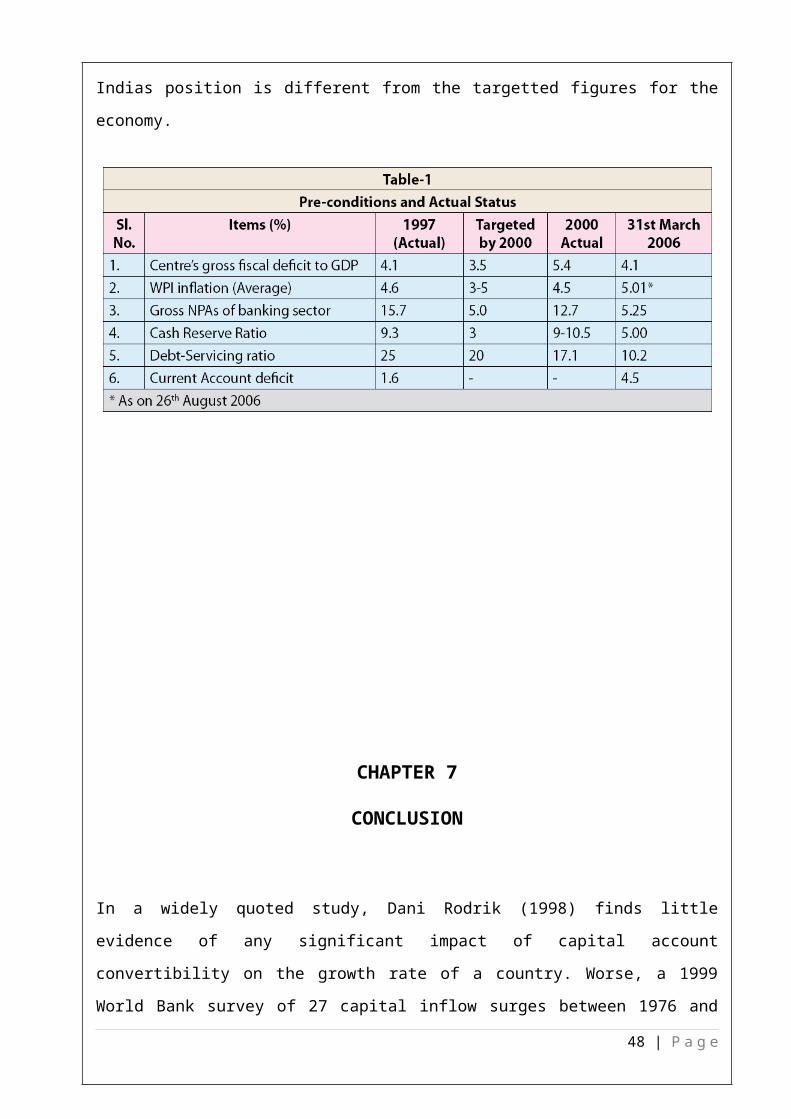

Indias position is different from the targetted figures for the

economy.

CHAPTER 7

CONCLUSION

In a widely quoted study, Dani Rodrik (1998) finds little

evidence of any significant impact of capital account

convertibility on the growth rate of a country. Worse, a 1999

World Bank survey of 27 capital inflow surges between 1976 and

48 | P a g e

1996 in 21 emerging market economies found that in about two-

thirds of the cases, there was a banking crisis, currency crisis

or twin crises in the wake of the surge.

Since the early 1970s, there have been several crises triggered

by speculative capital movements: the Southern Cone financial

crisis in the late 1970s; the Mexican crisis of 1994-95 and the

`Tequila Effect'; the East Asian crisis of 1997; the collapse of

the Brazilian real and its impact on the rest of Latin America;

the Russian crisis of 1998 and the Argentine crisis of 2001.

Contrary to the assumption of the neo-classical model, a large

volume of capital inflows into developing countries has actually

been used for speculative purposes rather than for financing

productive investments.

Capital account convertibility exposes the economy to all sorts

of exogenous impulses generated through financial channels, as

domestic and foreign investors try to shift their funds into or

out of a country. Since financial markets adjust very quickly,

even minor disturbances may exacerbate into major ones.

Under flexible exchange rates, capital inflows lead to an

appreciation of the domestic currency directly. On the other

hand, in a fixed exchange rate regime, increased capital inflows

lead to monetary expansion and price inflation (unless there is

substantial unutilised capacity), which also causes a real

appreciation. In both cases, therefore, capital inflows tend to

cause a real appreciation and the possibility of swollen current

account deficits because of cheaper imports and uncompetitive

exports which, if not controlled in time, will lead to loss of

confidence and capital flight.

49 | P a g e

Because of the massive volume and high mobility of international

capital, it has been observed that the government tries to play

it safe by keeping interest rates high, thus discouraging

domestic private investment. The government also desists from

spending on public investment because, through an expansion in

government spending, it could send signals of impending increases

in fiscal deficits that have the potential of destabilising

capital markets and inducing capital flight.

7.1 Policy implications for India

The experience with liberalisation of inward capital flows in

India has been similar to the economies of Latin America and East

Asia, only the magnitude of these flows has not been large enough

to cause serious macro and micro management problems.

Flexibility in exchange rate: To prevent a nominal appreciation

because of the capital inflows, the RBI has been adding billions

of dollars to its reserves; the foreign exchange reserves with

the RBI are a whopping $69 billion.

However, intervening foreign currency purchases to stabilise the

exchange rate and accumulation of forex reserves have

implications for domestic monetary management, which can be

seriously impaired by divided short-term monetary responses

during a capital surge.

On the other hand, the option of a more flexible exchange rate

would cause an appreciation in the value of the rupee, which may

hurt exports.

50 | P a g e

Hence, the usual macroeconomic trilemma (Obstfield, M and A. M

Taylor 2001) where only two of the three objectives of a fixed

exchange rate — capital mobility and an activist monetary policy

— can be chosen. Since the government has already liberalised

inflows of capital to a large extent, the authorities could

attempt to deal with this problem in one of the following ways:

It could begin relaxing capital controls, allowing individuals to

exchange rupees for dollars. Indeed, some piecemeal measures in

this direction have already been taken. But this, perhaps, is a

risky proposition.

For one thing, the embrace of full convertibility is itself

likely to bring more dollars into the country in the initial

phase and add to the existing upward pressure on the rupee. More

important, given the lack of regulatory capacity, such

convertibility runs the risk of a future financial crisis that

may scuttle the growth process.

Alternatively, the government could tap this opportunity to

liberalise imports. Further liberalisation will stimulate imports

and create the necessary demand for dollars, mopping up the

excess supply of dollars and relieving the government of the

burden of low-yielding foreign exchange reserves.

In as much as the imports are used as inputs for further exports,

the move will kill two birds with one stone — it will relieve the

upward pressure on the rupee, and bring the usual efficiency

gains. In this regard, therefore, import liberalisation seems to

be a distinctly better option.

Banking and capital market regulatory system: The relatively

greater contribution of portfolio capital towards India's capital

51 | P a g e

account, and the fact that these inflows could increase to

significant levels in the future as India's financial markets get

integrated globally, show that an important sphere of concern is

their skilful management to facilitate smooth intermediation.

Banks intermediate a substantial amount of funds in India — over

64 per cent of the total financial assets in the country belong

to banks. However, many Indian banks are undercapitalised, and

their balance sheets characterised by large amounts of non-

performing assets (NPAs).

Unless banking standards are duly brushed up, viable competition

introduced and government interference reduced, it would be

reckless to go in for full capital account convertibility, which

requires flexibility, dynamism and foresight in the country's

banking and financial institutions.

Transparency and discipline in fiscal and financial policies: It

is well known that the last thing that a government wanting to

gain the confidence of investors should do is to be fiscally

imprudent. However, New Delhi does not seem to be paying heed to

this consideration at all.

The ratio of gross fiscal deficit to GDP (including that of

states) increased to 10.4 per cent in 1999-2000 from 6.2 per cent

in 1996-97 and 8.5 per cent in 1998-99, and has hovered around

the 10 per cent figure since then. Such high fiscal deficits can

prove to be unsustainable and frighten away investors. Hence,

there is an immediate need for putting brakes on government

expenditure, and until that has been satisfactorily done, opening

up the capital account fully would carry with it a big risk of

sudden loss of faith of investors and capital flight.

52 | P a g e

BIBLOGRAPHY

Books

o Currency convertibility : Indian and global experiences

by Sumati Varma

o International Trade & Financial Environment by Bhat

M.K.

Magazines

o Business world

News papers

o Economic Times

Websites

o http://timesofindia.indiatimes.com/topic/

CurrencyConvertibility

o www.caclubindia.com

o www.ndtv.com

o www.dnaindia.com

53 | P a g e