chapter 2 value proposition - library binus

TRANSCRIPT

CHAPTER 2

VALUE PROPOSITION

2.1 Market and Industry Analysis

2.1.1 Market Analysis

Dress It is a marketplace that brings together fashion designers (sellers) with a fashion enthusiasts

(buyer). This idea began when such assumption came out. There are high needs from buyers to use

products that matches with themselves. People have limited information and the source to get right

information. Fashion Industry is growing fast after applying E-commerce. By looking further at

the growth of the fashion industry in Indonesia, it is not only a matter of buyers and sellers, but for

all.

Over the past decade, the global supply chain in the textile and apparel sector has undergone

significant changes. Three key drivers have brought about these changes: the phase-out of the

Multi-Fiber Arrangement (MFA) in January 2005; consumer demand for new fashions and shorter

seasons; and increasing demand—from consumers, multinational brands, and retailers—for

products produced under the right conditions. Until 2005, apparel manufacturers around the world

enjoyed a measure of protection from cost- competitive Asian giants such as China and India

thanks to the quotas afforded by the MFA. Since the withdrawal of the MFA began, it has become

clear that many countries’ apparel sectors were, to varying degrees, dependent on the quota

protections for their survival. The MFA phase-out raised the specter of competition from China

and India driving some countries out of the apparel business.

21

In fact, Chinese ready-made apparel imports increased by over 40 percent when the MFA phase-

out began, making up 28 percent of total U.S. apparel imports (U.S. Census Bureau). The U.S.

Government subsequently capped Chinese exports to the U.S. market through 2008. As protected

access to the U.S. market is poised to expire, the challenge of fierce competition from China looms.

As a result of the end of the MFA, brands have radically condensed their global supply chains.

Moreover, over the last decade, the global apparel supply chain has seen changes in consumer

demand that have affected the terms of competition. These include shorter fashion seasons,

increasing the importance of speed-to-market as a competitiveness factor. Cost remains an

important consideration, but many brands and retailers (with the exception of discounters that

emphasize price) weigh cost along with a number of other elements, such as quality, innovation,

and speed-to-market in their sourcing decisions.

Indonesia has weathered substantial global volatility thanks to sound macroeconomic

fundamentals and strong policy coordination, according to the World Bank’s December 2018

Indonesia Economic Quarterly.

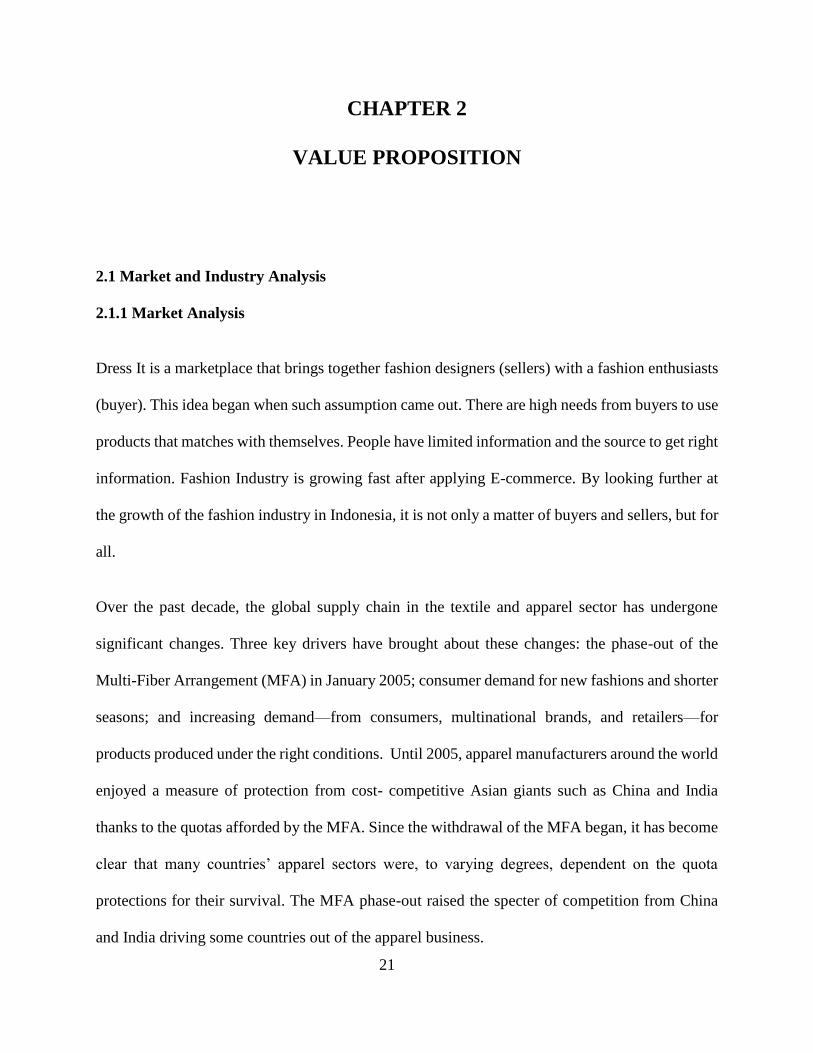

From World Bank, Indonesia ranking among the world by seeing the competitiveness and

efficiency indicators, getting better year by year.

Figure 2.1: Indonesia Competitiveness and Efficiency Indicators

Source: World Bank (2019)

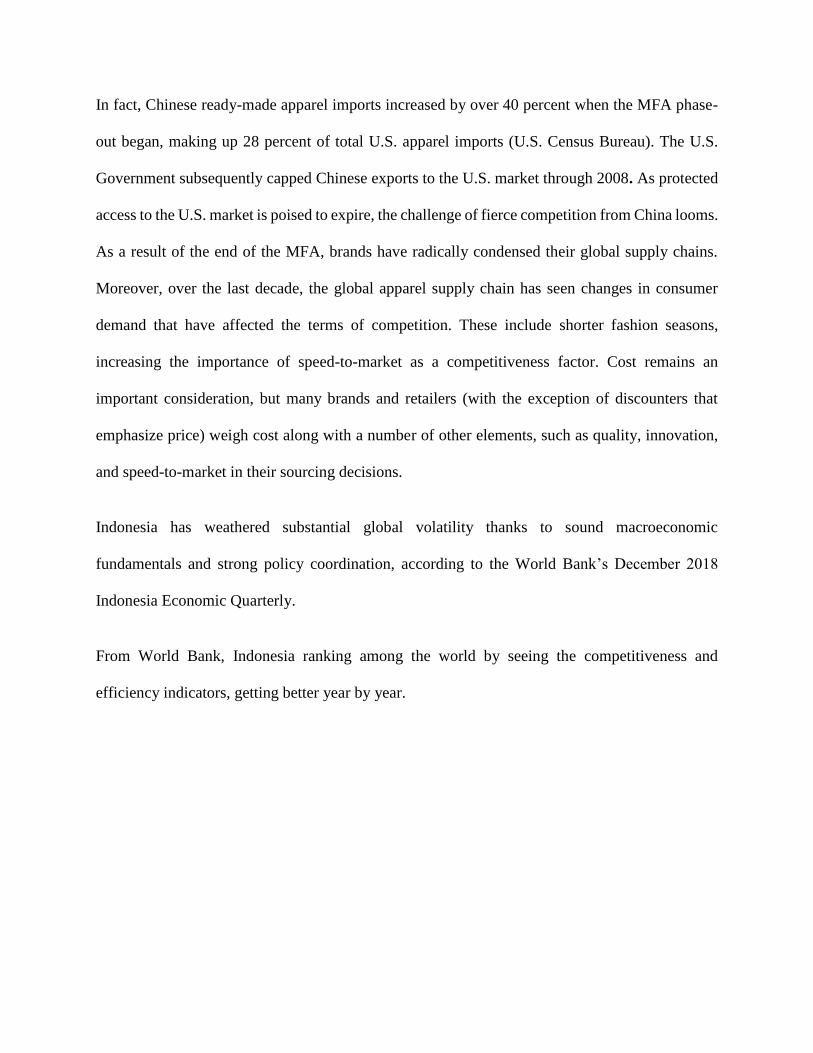

December 2018 Indonesia’s GDP growth during the third quarter remained broadly steady at 5.2%,

driven by domestic demand. Stronger domestic demand, due to increased social spending and a

strong labor market, is expected to more than offset the drag from the external sector.

Figure 2.2: Indonesia GDP growth (annual %)

Source: World Bank (2019)

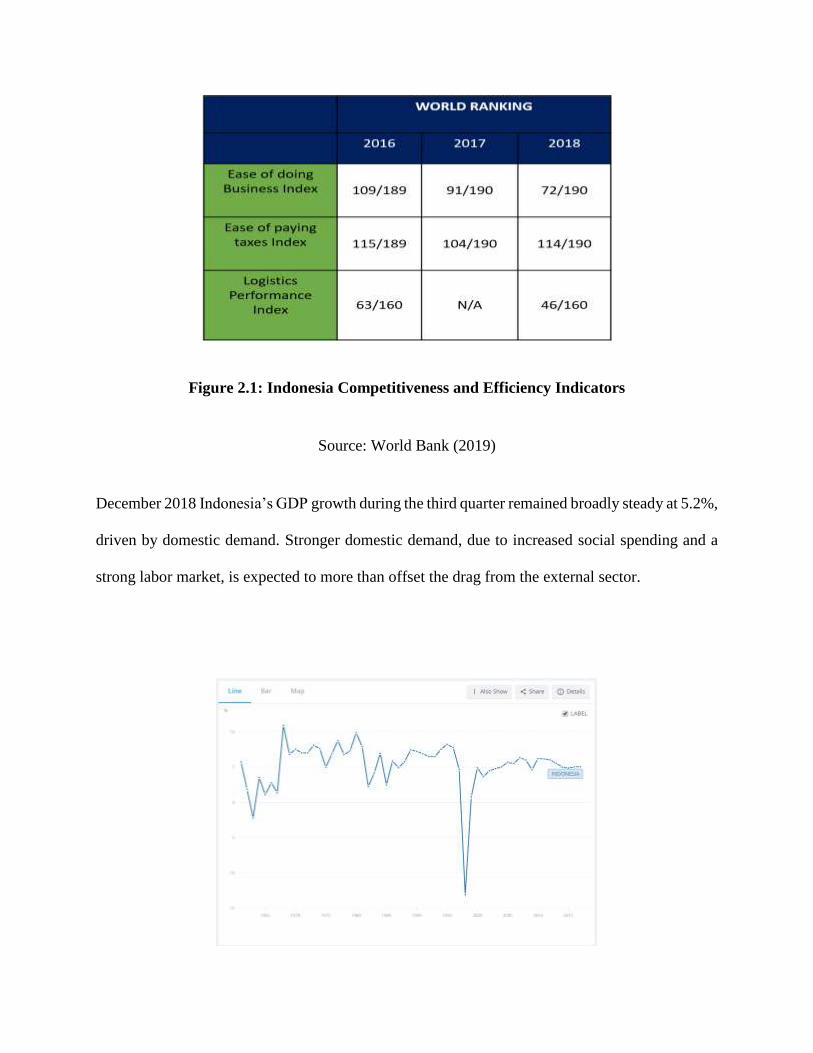

Figure 2.3: Indonesia GNI per capita, Atlas method (current US$)

Source: World Bank (2019)

Figure 2.4: Indonesia Poverty headcount ratio

Source: World Bank (2019)

The landscape of players and channels that operate in the global apparel market are showing the

following trends:

Medium to large retailers are increasing the size of their core orders.

Buyers are sourcing styles that are less complicated than a year ago, though complexity

requirements remain generally high. Garments have been decreased in complexity in order to

reduce the need to outsource panels to China and to keep production in one country.

Distribution channels are getting shorter, but the role of buying agents remains strong

As more large retailers in developed markets are opting to source directly, bypassing importers,

and other layers of intermediaries are being eliminated. Global production has become

commonplace for larger retailers, as increased competitive pressure drives them to reduce costs,

many see the trend extending to smaller retailers as well. One should note, however, that from the

perspective of developing-country producers, direct sourcing rarely eliminates the role of the

buying agent or exporter. There is nearly always a third party responsible for overseeing

production. Even very large retailers prefer to work with an intermediary in the region of origin,

though in some cases the largest retailers may have their own offices in-country.

Retail companies are permanently buying “brand licenses”

It is to merchandize garments from recognized brands, such as Jones New York, Kenneth Cole,

Cole Haan, Timberland, and others. One of the largest such companies, buying from Asian and

Latin American factories for the U.S. market, is the G-III group, which recently acquired Andrew

Marc for $42 million. G-III carries out the entire buying cycle—from product design and pattern

making to direct sourcing from factories—to reduce costs.

A trend toward multi-channel businesses is growing

It is because nearly all discounters, department stores, and specialty stores—as well as more and

more independent retailers—have retail websites; some have mail-order catalogues as well.

Meanwhile, catalogue and internet retailers are opening “brick and mortar” locations as well as

operating wholesale divisions, and wholesale importers are launching websites and/or opening

retail locations to offset a decrease in sales to large retailers.

The market is becoming increasingly polarized

Low-end and luxury market segments are growing, while middle markets are stagnating or

shrinking. At the low end, cheap imports are driving down average retail prices, leading to

consumer expectations of better quality at a lower price. In the United States, with the exceptional

growth of discount stores, apparel products are becoming increasingly disposable. Improved

quality and delivery combined with lower costs through cheaper labor and more efficient

production remain the key competitive requirements for producers worldwide.

Smooth interaction and excellent communication is increasingly important during the

product design process.

As illustrated in the chart below (Figure 2), designing and producing initial apparel samples has

become a very complex process. At the same time, it is a critical link in the global apparel value

chain. Apparel production companies that can respond quickly with exactly matched samples,

including short response times for production and later alterations, can develop a competitive edge

against other suppliers.

2.1.2 Industry Analysis

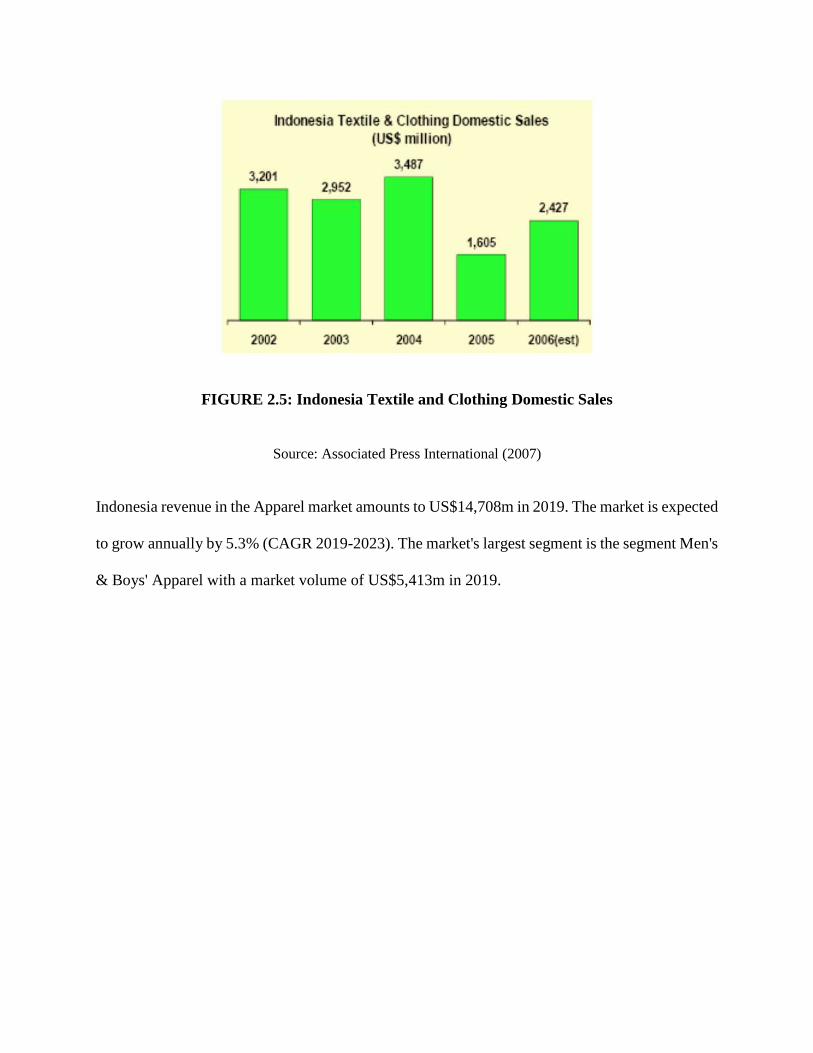

Indonesia is the fourth most populous country in the world, with 260 million people. While security

concerns and natural disasters have harmed tourism and the domestic economy in some years, the

average yearly domestic sales of apparel have been $2.7 billion. This is almost equivalent to

Indonesia’s apparel sales to the U.S. market and should not be overlooked. The chart below shows

values for Indonesia’s textile and clothing domestic sales from 2002 to 2006:

FIGURE 2.5: Indonesia Textile and Clothing Domestic Sales

Source: Associated Press International (2007)

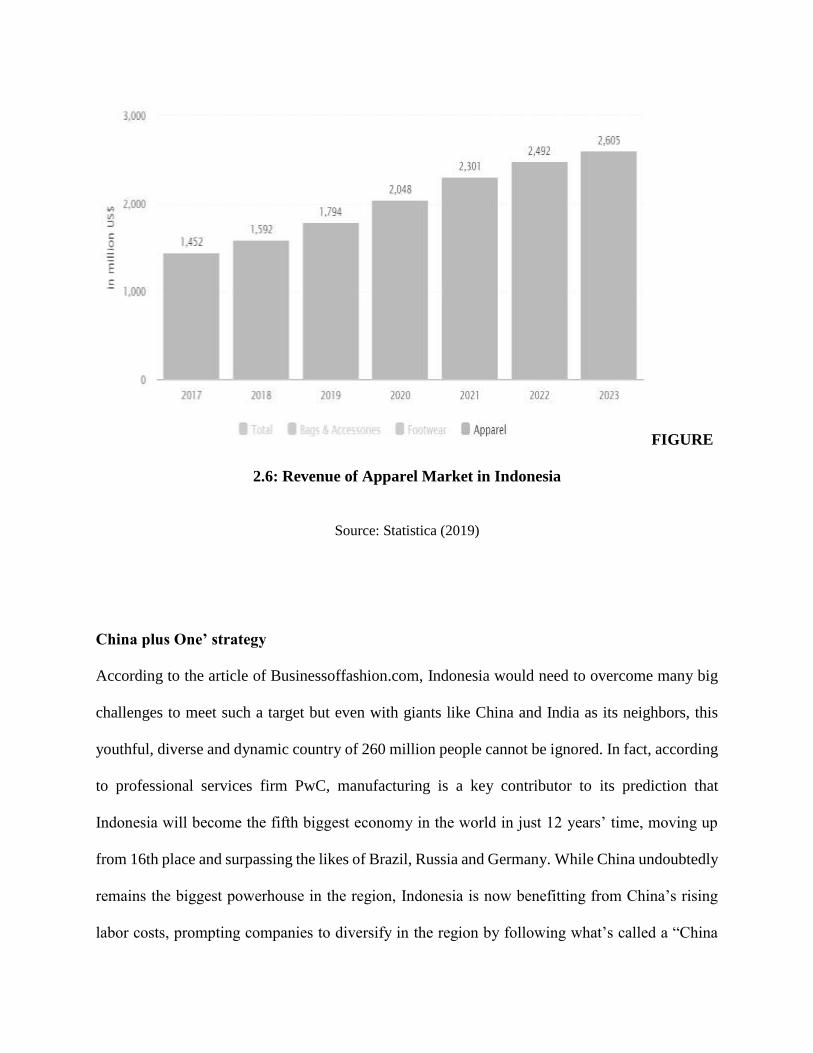

Indonesia revenue in the Apparel market amounts to US$14,708m in 2019. The market is expected

to grow annually by 5.3% (CAGR 2019-2023). The market's largest segment is the segment Men's

& Boys' Apparel with a market volume of US$5,413m in 2019.

FIGURE

2.6: Revenue of Apparel Market in Indonesia

Source: Statistica (2019)

China plus One’ strategy

According to the article of Businessoffashion.com, Indonesia would need to overcome many big

challenges to meet such a target but even with giants like China and India as its neighbors, this

youthful, diverse and dynamic country of 260 million people cannot be ignored. In fact, according

to professional services firm PwC, manufacturing is a key contributor to its prediction that

Indonesia will become the fifth biggest economy in the world in just 12 years’ time, moving up

from 16th place and surpassing the likes of Brazil, Russia and Germany. While China undoubtedly

remains the biggest powerhouse in the region, Indonesia is now benefitting from China’s rising

labor costs, prompting companies to diversify in the region by following what’s called a “China

plus One” strategy. Like China, Indonesia has the advantage of a domestic supply of raw materials,

an expansive labor force and a big domestic economy that is transitioning steadily from low

income to middle income economy. Unlike China, however, it is integrated into the Association

of Southeast Asian Nations (ASEAN).

Besides, manufacturing companies in Indonesia are getting increasingly sophisticated with vertical

operations of spinning, weaving, printing and garment plants — making them a one-stop

destination for international clients. One such example is a gargantuan Java-based company called

Sritex, which produced 8 million pieces of apparel a year and boasts of bigwigs like Uniqlo, Guess

and H&M as long-time clients.

Fast fashion, diffusion and sportswear

According to H&M’s global head of production, Helena Helmersson, the Swedish firm is

optimistic about expanding further in Indonesia and establishing a long-term presence there. “The

advantage of manufacturing in Indonesia is the great mix of fashion, price and sustainability,” she

said on the businessoffashion.com article

Today the biggest international buyers in Indonesia are fast fashion giants or those operating

diffusion labels of designer brands. It is high-volume sportswear production that allows major

multinational sportswear brands — Adidas, Mizune, Asics, New Balance, Nike, Pentland and

Puma — to not only keep up with global demand, but also expand into new countries. Because of

its investments in technology, innovation and training, Indonesia is being increasingly perceived

not as the cut-and-sew factories of Vietnam and Bangladesh, but as a more advanced sourcing

opportunity. And where it cannot compete on price, it can on scale.

An archipelago of specialists

From the article that authors found on techinasia.com, they state of 9 giant E-Commerce players

in Indonesia. All of the E-Commerce players are focusing on fashion, the demand of textile,

apparel and footwear production is scattered across many of Indonesia’s 17,000 islands but the

sector hubs are mostly based on the islands of Java — where the country’s commercial and fashion

capital Jakarta is located — as well as Sumatra, Sulawesi and Bali. A report published by

Indonesia’s Directorate General of National Export Development, cites Sukabumi, a city in West

Java, as the most attractive destination for garment manufacturing investors. But the city of

Bandung is seen as the most developed for garment manufacturing, producing as much as 40

percent of the annual output value of garments in the country. Even Jakarta trails behind Bandung.

Since Indonesia has an abundant supply of raw materials and animal derivatives of cow, sheep,

alligator, snakes and others, the footwear (sports and non-sports) industry is flourishing. The

Ministry of Trade confirms that Indonesia was one of the world’s top ten footwear producers in

the world. Investor confidence is emboldened by the fact that global brands like Nike identify the

country as one of their biggest production hubs. Adis Dimension Footwear, the local Indonesian

unit of American multinational footwear and sportswear giant owns a factory in Tangerang, Java,

with a production capacity of 20 million pairs per year. In 2015, it announced it was setting up a

new $60 million factory in West Java with a production capacity of 10 million pairs of shoes per

year. About half of raw materials are domestically-sourced — a big advantage in terms of both

cost and operations. Following the rapid development of technology, based on techinasia.com

article many fashion brands retailers sell their goods through E-Commerce channels, in this thesis

also examine the advantages of each of these E-Commerce, including:

Zalora

Zalora is probably one of the most famous e-commerce fashion sites in Asia. This site offers a

variety of products for men and women and has one of the largest collections of famous brands in

Indonesia. Zalora also has several local designers and producers that enable them to meet the needs

of various kinds of consumers and still offer competitive prices compared to several retail outlets

in Indonesia.

VIP Plaza

One thing that distinguishes VIP Plaza from most online stores in Indonesia is that this site

prioritizes the flash sales been offered. VIP Plaza gives discounts of up to 80 percent for one item

each day for a certain duration.

BerryBenka

The site, which initially only provided fashion products for women, now also provides a choice of

fashion products for men. Unlike the sites mentioned earlier, BerryBenka prefers to partner with

local and independent producers rather than more well-known brands, so this site has a unique

catalog compared to some of their competitors.

Maskoolin

Targeting consumers more specifically, Maskoolin provides a variety of men's fashion needs such

as shirts, shirts, shoes, snapbacks, watches, and other products. With the tagline "Men Shopping

Assistant", Maskoolin presents a complete catalog of various famous brands such as Rip Curl,

Herschel, Nike, and many others.

HijUp

E-commerce, which was founded in 2011, claims to be the "biggest Islamic fashion online mall".

HijUp sells a variety of Muslim fashion products such as Muslim clothing, hijab, scarves, bags,

shoes, and other Muslim accessories. Interestingly, besides fashion, HijUp also sells products such

as books, Al-Qur'an, magazines and DVDs with Islamic nuances. In addition to selling products,

the HijUp team also offers many hijab usage tutorials and has creative content such as Lookbook

and Fashion Show. The content is certainly very useful for those who are interested in fashion.

Etclo

Etclo is a premium fashion e-commerce site similar to some of the shops mentioned earlier. But

the thing that distinguishes Etclo is that this site displays designs that are based more on the Asian

market, rather than imitating trends and designs that are popular in European or US markets. The

Etclo site also provides Lookbook and Etclorama features that provide a variety of fashion

inspirations for visitors.

PinkEmma

PinkEmma exclusively focuses on women's fashion. However, different from the sites mentioned

earlier, PinkEmma does not focus on just one demographic but has products that appeal to all

women ranging from teenagers, mothers, to executives. Their collections consist of famous brands

to new brands that are rarely heard. Customer could say e-commerce has a lot of products.

BrandClozet

Similar to VIP Plaza, BrandClozet is a fashion e-commerce site that focuses on flash sale. Every

day, this site displays sale offers from various local and international fashion brands. Every sale

offer on this site has a minimum duration of seven days.

Bimbi

Bimbi is arguably the most different e-commerce site on this list. This site focuses on selling

branded fashion products for children. More than 50 international brands such as Armani Junior,

Hugo Boss, Little Marc Jacobs, or Kenzo are provided by this site.

Hijabenka

The Muslim fashion e-commerce site, which was launched in early June last year, is part of

BerryBenka. Hijabenka focuses on selling Muslim fashion products such as hijab, Muslim

clothing, mukena, bags, and other accessories. Besides selling Muslim fashion for women,

Hijabenka also sells Muslim fashion for men like koko clothes. Broadly speaking, this site is not

so much different from the Berrybenka site. Hijabenka provides a variety of transaction methods,

namely credit cards, bank transfers, and cash on delivery (COD).

8wood

8wood is an e-commerce site that focuses on providing women's fashion products. Although it

does not offer products from big brands, this startup founded by celebrity Alice Norin has a stylish

team that is responsible for choosing and matching the right products to attract visitors' attention.

Saqina

Saqina was originally an offline Muslim fashion store founded in 2007 in Mojokerto, Central Java.

In 2008, Saqina began to explore online e-commerce businesses that not only sell products

belonging to fashion brands in Indonesia, but also produce their own fashion labels. Even though

the site began in 2008, Saqina was really serious about her online business in 2013 and closed all

of her offline stores. Muslim fashion collections available in Saqina are mostly self-produced from

hijab, sarongs, koko clothes, robes, mukena, and other Muslim accessories. In addition to buying

unit products, customers can also buy products at wholesale with certain discounts.

Muslimarket

Muslimarket is the most recent player on this list. Just like Saqina, besides selling a variety of

Muslim fashion products for men and women, this site also sells various kinds of worship

equipment and Islamic products. Interestingly, Muslimarket applies the concept of "shopping

while shopping" for buyers. Later, the money that is needed will be channeled to Islamic

foundations to be used to help empower Muslim producers.

Cloth.Inc

Cloth Inc. is one of the few sites on this list that focuses on female consumers. Different from

previous sites, Cloth Inc. takes care of all the product production processes on its site, to become

a homemade clothing line. Starting from the process of product design, material selection, to the

end of production all of which are done in their production house. In addition to providing search

filters by product type, Cloth Inc. also provides product filters according to the season.

WokuWoku

Founded by celebrity couple Irwansyah and Zaskia Sungkar, WokuWoku specializes in selling

fashion products belonging to celebrities in Indonesia. Fashion labels belonging to celebrities such

as Vidi Aldiano, Barli Asmara, or Tantri "Kotak’ can be found on this site.

Below Cepek

BelowCepek is a site that focuses on selling women's clothing. As the name implies, the products

offered on this site are sold for under Rp100, 000. All their products are locally made and have

their own labels, unlike other online shops that sell many brands on the market. Even though their

collections are still a little at first, there are many menus to help customer find the variety of

products the customer are looking for.

2.1.2.1 Porter’s Five Forces

The five forces identified by Porter are divided into:

Porter's Five Forces Framework is a tool for analyzing competition of a business. It draws

from industrial organization (IO) economics to derive five forces that determine the competitive

intensity and, therefore, the attractiveness (or lack of it) of an industry in terms of its profitability.

An "unattractive" industry is one in which the effect of these five forces reduces overall

profitability. The most unattractive industry would be one approaching "pure competition", in

which available profits for all firms are driven to normal profit levels. The five-forces perspective

is associated with its originator, Michael E. Porter of Harvard University. This framework was

first published in Harvard Business Review in 1979.

Porter refers to these forces as the microenvironment, to contrast it with the more general

term microenvironment. They consist of those forces close to a company that affect its ability to

serve its customers and make a profit. A change in any of the forces normally requires a business

unit to re-assess the marketplace given the overall change in industry information. The overall

industry attractiveness does not imply that every firm in the industry will return the same

profitability. Firms are able to apply their core competencies, business model or network to achieve

a profit above the industry average. A clear example of this is the airline industry. As an industry,

profitability is low because the industry's underlying structure of high fixed costs and low variable

costs afford enormous latitude in the price of airline travel. Airlines tend to compete on cost, and

that drives down the profitability of individual carriers as well as the industry itself because it

simplifies the decision by a customer to buy or not buy a ticket. A few carriers Richard

Branson's Virgin Atlantic is one--have tried, with limited success, to use sources of differentiation

in order to increase profitability.

Porter's five forces include three forces from 'horizontal' competition--the threat of substitute

products or services, the threat of established rivals, and the threat of new entrants--and two others

from 'vertical' competition - the bargaining power of suppliers and the bargaining power of

customers.

Porter developed his five forces framework in reaction to the then-popular SWOT analysis, which

he found both lacking in rigor and ad hoc. Porter's five-forces framework is based on the structure–

conduct–performance paradigm in industrial organizational economics. It has been applied to try

to address a diverse range of problems, from helping businesses become more profitable to helping

governments stabilize industries. Other Porter strategy tools include the value chain and generic

competitive strategies.

Threat of new entrants

Profitable industries that yield high returns will attract new firms. New entrants eventually will

decrease profitability for other firms in the industry. Unless the entry of new firms can be made

more difficult by incumbents, abnormal profitability will fall towards zero (perfect competition),

which is the minimum level of profitability required to keep an industry in business.

Threat of substitutes

A substitute product uses a different technology to try to solve the same economic need. Examples

of substitutes are meat, poultry, and fish; landlines and cellular telephones; airlines, automobiles,

trains, and ships; beer and wine; and so on. For example, tap water is a substitute for Coke, but

Pepsi is a product that uses the same technology (albeit different ingredients) to compete head-to-

head with Coke, so it is not a substitute. Increased marketing for drinking tap water might "shrink

the pie" for both Coke and Pepsi, whereas increased Pepsi advertising would likely "grow the pie"

(increase consumption of all soft drinks), while giving Pepsi a larger market share at Coke's

expense.

Bargaining power of customers

The bargaining power of customers is also described as the market of outputs: the ability of

customers to put the firm under pressure, which also affects the customer's sensitivity to price

changes. Firms can take measures to reduce buyer power, such as implementing a loyalty program.

Buyers' power is high if buyers have many alternatives. It is low if they have few choices.

Bargaining power of suppliers

The bargaining power of suppliers is also described as the market of inputs. Suppliers of raw

materials, components, labor, and services (such as expertise) to the firm can be a source of power

over the firm when there are few substitutes. If you are making biscuits and there is only one

person who sells flour, you have no alternative but to buy it from them. Suppliers may refuse to

work with the firm or charge excessively high prices for unique resources.

Competitive rivalry

For most industries the intensity of competitive rivalry is the major determinant of the

competitiveness of the industry. Having an understanding of industry rivals is vital to successfully

market a product. Positioning pertains to how the public perceives a product and distinguishes it

from competitors. A business must be aware of its competitors' marketing strategies and pricing

and also be reactive to any changes made.

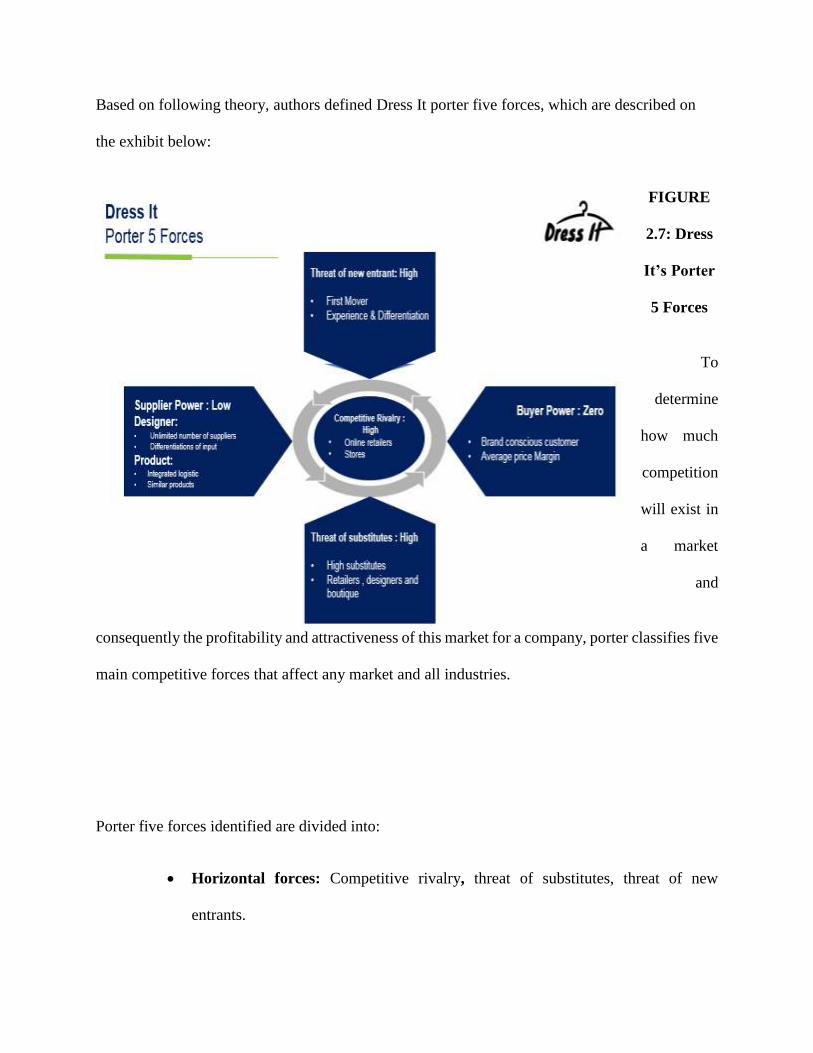

Based on following theory, authors defined Dress It porter five forces, which are described on

the exhibit below:

FIGURE

2.7: Dress

It’s Porter

5 Forces

To

determine

how much

competition

will exist in

a market

and

consequently the profitability and attractiveness of this market for a company, porter classifies five

main competitive forces that affect any market and all industries.

Porter five forces identified are divided into:

Horizontal forces: Competitive rivalry, threat of substitutes, threat of new

entrants.

Vertical forces: Bargaining power of customers and bargaining power of buyers.

1. Competitive Rivalry, is one of important force by potter, a measure of the extent of

competition among the existing companies in the market. More companies competing each

other’s the competitive pressure will drive the price, profit and strategy.

Some reason causing the competitive rivalry may high such as similar sized, strategies,

product or features companies operate in one market or can be the growth in the industry

is low.

Dress It competitive rivalry categorized as high because for fashion already have many

stores and online retailers operate in the market as showing in the Dress It five forces.

2. Threat of new Entrants, one of the forces to shape the competitive structure, refers to the

threat new competitors pose to existing in an industry. A profitable industry will attract

more competitors looking to achieve profits.

Potential new entrants into the market place also can be one of the competitive threat to a

company’s business, not only from existing players in the market. Barriers to entry in the

market change the dynamic of the industry.

When a potential market has low barriers to exit but high barriers to entry is the most

attractive scenario for a new company, to determine the level of difficulty faced by a

company when trying to enter the market is by the economic situation. A high threat of

new entrance can make an industry more competitive and decrease profit potential for

existing competitors.

There are some situation when barriers to entry are may stem such as:

High switching costs for customers

Access to specialized technology or infrastructure

Need high initial investment

Obstacle by government regulation, economic of scale, patents and proprietary

knowledge

Difficulty in accessing distribution channels and raw material.

A low threat of entry makes an industry less competitive and increases potential profit for

the existing company in the market. New entrants are deterred by barriers to entry. In

Indonesia e-commerce spend fashion and beauty become the number one by the category

its showing how big is the economic scale of fashion and beauty industry.

Dress It’s threat of new entrants categorized is high as the first mover in Indonesia fashion

industry which access by using website technology. It’s also become one of Dress It’s

advantages as first mover, on the other hand it has personal stylist experienced as the

differentiation for better service quality. Dress It profitability does not require economies

of scale, customer switching costs are low, proprietary materials and the location also no

issue.

3 Threat of Substitutes, According to Porter’s 5 forces the definition threat of substitutes is

the availability of a product that the customer can purchase instead of the industry’s

product. A product from another industry that offers similar benefit to the customer as the

product produced by the company within the industry called as a substitute product.

Several factors determine whether or not there is threat of substitutes a product in an

industry such as switching costs, brand loyalty, relative price, function, attributes, or the

performance of a product. Dress It’s threat of substitutes categorized as high because have

some risk there are:

Substitutes product and service is high, customer can find cheaper product

in other fashion industry such as stores, retailers, designers, boutique or

traditional fashion market.

Customer switching costs are low and using website easily to get

Substitute’s product quality and performance is equal in fashion industry

because using the well-known brand from current market.

4 Bargaining Power of Buyers, the idea is the bargaining power of buyers in an industry

affects the competitive environment for the seller and influences the seller’s ability to achieve

profitability.

Refers to the pressure customers can exert on businesses to get them to provide higher quality

products, better customer service, and lower prices.

Several factors determine buyer bargaining power defined by Porter’s Five Forces such as:

There are few buyers and many sellers and buyers are more concentrated than sellers

The cost of switching from one seller’s product to another seller’s product are low

Buyers can easily backward integrate or begin to produce the seller’s product

themselves

Dress It’s bargaining power of buyers categorized as zero because have high and low inside.

Buyer is well conscious regarding the brand of product but have high differentiated because

the service experienced through consults with designers and average margin price for both,

product and service.

5 Bargaining Power of Suppliers, the idea is the bargaining power of suppliers in an industry

affects the competitive environment for the buyer and influences the buyer’s ability to achieve

profitability.

Refers to the pressure suppliers can exert on businesses by raising prices, lowering quality,

or reducing availability of their products.

Several factors determine suppliers bargaining power defined by Porter’s Five Forces such

as:

There are few suppliers and many buyers and suppliers are more concentrated than

buyers

The cost of switching from one suppliers product to another suppliers product are high

The supplier’s product is highly differentiated

The buyer does not represent a large portion of the supplier’s sales

Substitute products are unavailable in the marketplace

Dress It’s bargaining power of suppliers categorized as low from designer or even product

itself. Buyer is well conscious regarding the brand of product, unlimited numbers of the

suppliers.

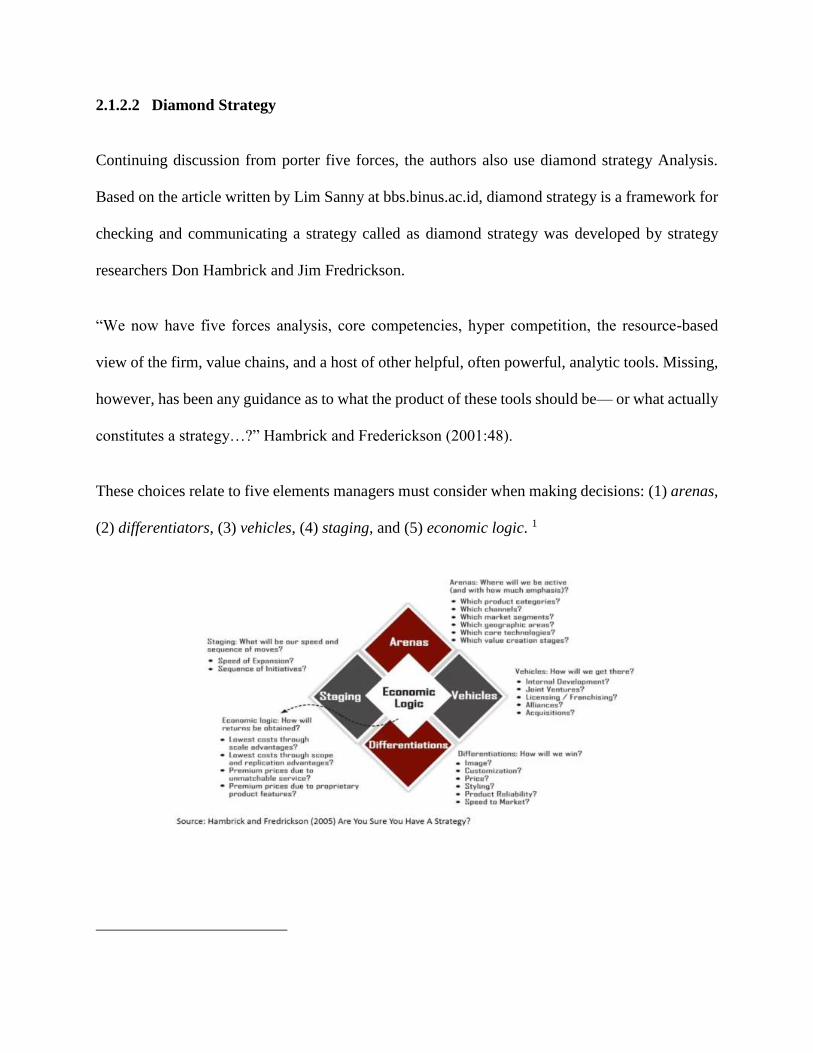

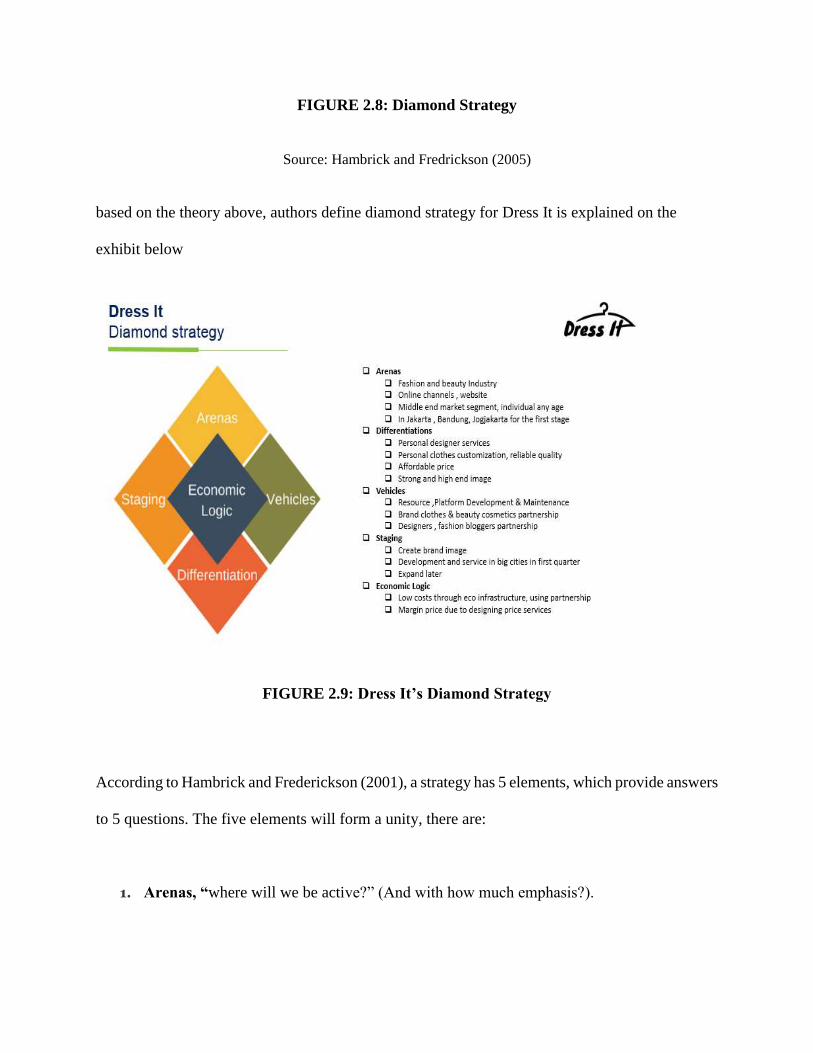

2.1.2.2 Diamond Strategy

Continuing discussion from porter five forces, the authors also use diamond strategy Analysis.

Based on the article written by Lim Sanny at bbs.binus.ac.id, diamond strategy is a framework for

checking and communicating a strategy called as diamond strategy was developed by strategy

researchers Don Hambrick and Jim Fredrickson.

“We now have five forces analysis, core competencies, hyper competition, the resource-based

view of the firm, value chains, and a host of other helpful, often powerful, analytic tools. Missing,

however, has been any guidance as to what the product of these tools should be— or what actually

constitutes a strategy…?” Hambrick and Frederickson (2001:48).

These choices relate to five elements managers must consider when making decisions: (1) arenas,

(2) differentiators, (3) vehicles, (4) staging, and (5) economic logic. 1

FIGURE 2.8: Diamond Strategy

Source: Hambrick and Fredrickson (2005)

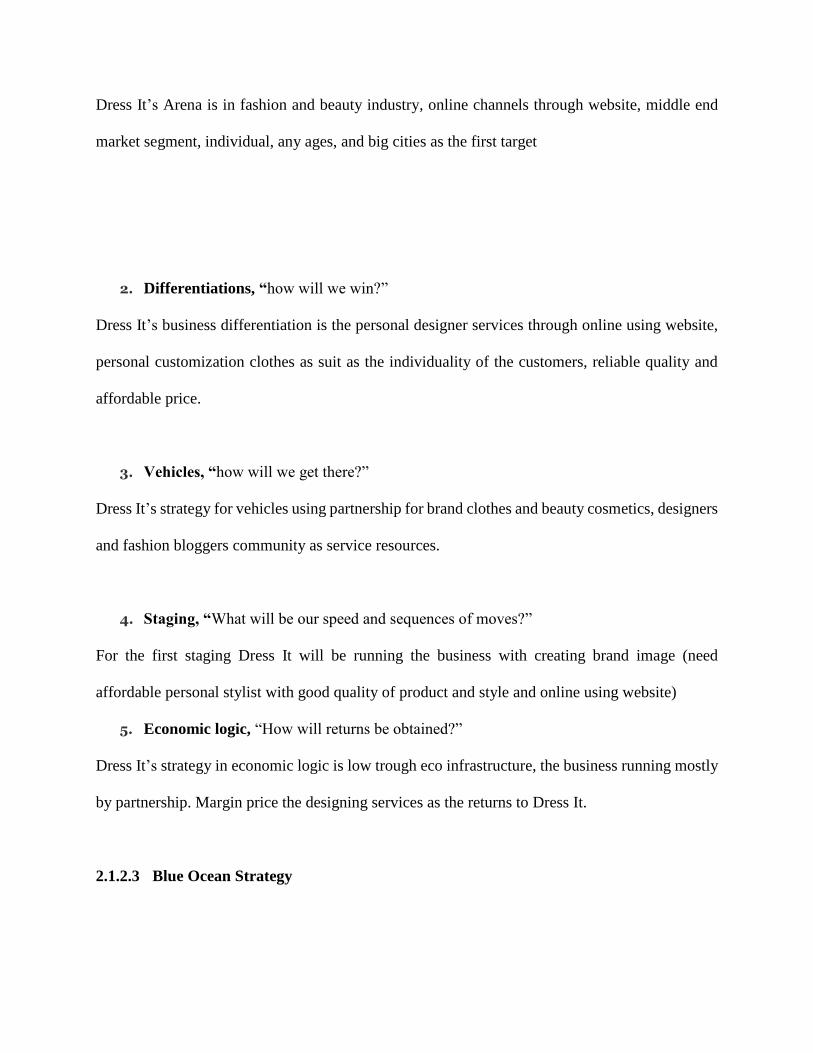

based on the theory above, authors define diamond strategy for Dress It is explained on the

exhibit below

FIGURE 2.9: Dress It’s Diamond Strategy

According to Hambrick and Frederickson (2001), a strategy has 5 elements, which provide answers

to 5 questions. The five elements will form a unity, there are:

1. Arenas, “where will we be active?” (And with how much emphasis?).

Dress It’s Arena is in fashion and beauty industry, online channels through website, middle end

market segment, individual, any ages, and big cities as the first target

2. Differentiations, “how will we win?”

Dress It’s business differentiation is the personal designer services through online using website,

personal customization clothes as suit as the individuality of the customers, reliable quality and

affordable price.

3. Vehicles, “how will we get there?”

Dress It’s strategy for vehicles using partnership for brand clothes and beauty cosmetics, designers

and fashion bloggers community as service resources.

4. Staging, “What will be our speed and sequences of moves?”

For the first staging Dress It will be running the business with creating brand image (need

affordable personal stylist with good quality of product and style and online using website)

5. Economic logic, “How will returns be obtained?”

Dress It’s strategy in economic logic is low trough eco infrastructure, the business running mostly

by partnership. Margin price the designing services as the returns to Dress It.

2.1.2.3 Blue Ocean Strategy

Based on the article that authors found at blueoceanstrategy.com, there’s an explanation about blue

ocean. A blue ocean is an analogy to describe the wider, deeper potential to be found in unexplored

market space. Creating a new demand, creating and capturing uncontested market space thereby

making the competition irrelevant.

The simultaneous pursuit of differentiation and low cost to open up a new market space called as

blue ocean strategy. There are many opportunity for growth that is both profitable and rapid,

demand is created rather than fought over in blue oceans.

Chan Kim and Renée Mauborgne have created a comprehensive set of analytic tools and

frameworks to create blue oceans of new market space, one of used for Dress It business strategy

is the ERRC Grid

A simple matrix that drives companies to focus simultaneously on eliminating and reducing, as

well as raising and creating while unlocking a new blue oceans called as The Eliminate – Reduce

– Raise – Create (ERRC Grid)

The grid gives companies four immediate benefits there are:

Pushes company to simultaneously pursue differentiation and low cost to break the

value-cost trade off

Easily to be understood by managers at any level, creating a high degree of

engagement in its application

Immediately flags companies that are focused only on raising and creating to

maintain the costs structure

Drives companies to thoroughly scrutinize every factor the industry competes on,

help to discover the range of implicit assumptions the company unconsciously

make in competing

FIGURE 2.10: ERRC GRID

Source: Blue Ocean Strategy

Based on the article above, and sees the opportunity of Dress It, authors define dressit blue ocean

strategy which are follow on the exhibit below:

FIGURE 2.11: Dress It’s Blue Ocean Strategy

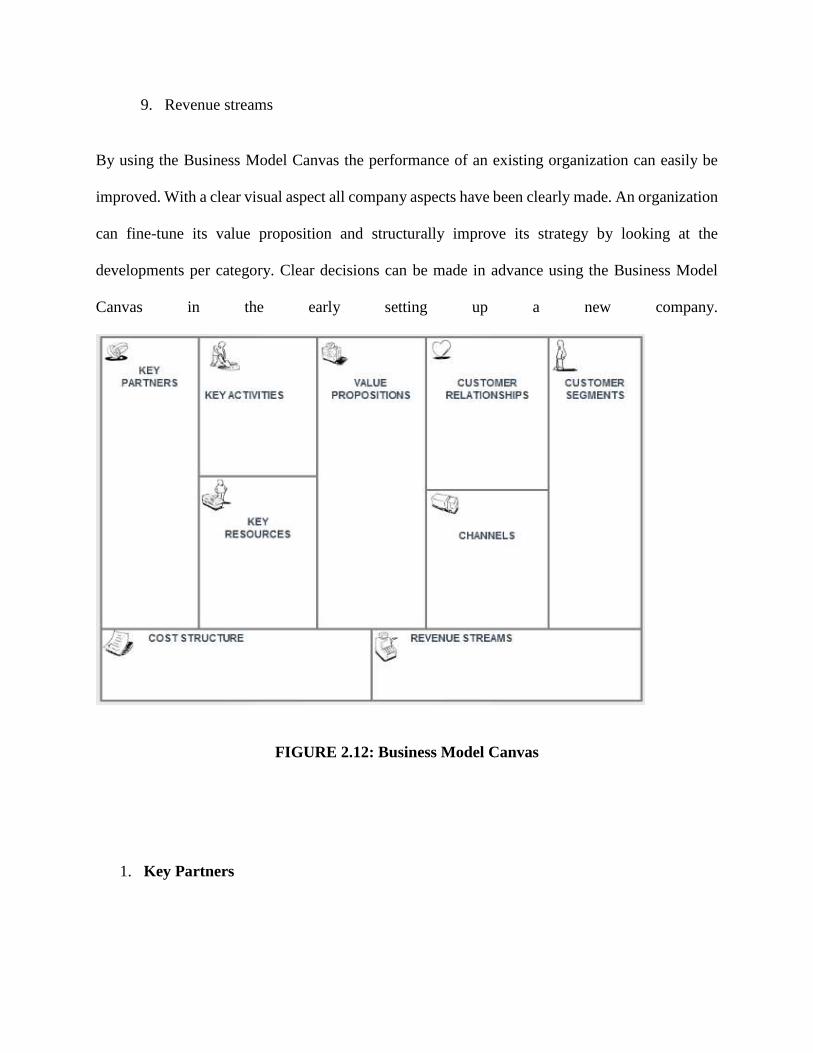

2.2 Concept of Business Model Canvas

A strategic management and lean startup template for developing new or documenting existing

business models, a graphic represented of a number of variables that show the values of an

organization it’s called as the Business Model Canvas or BMC model.

The Business Model Canvas can be deployed as a strategy tool for the development of a new

organization. Furthermore, it also analyses the (business) situation of an existing business.

In 2008 initially proposed by Alexander Osterwalde the Business Model Canvas was developed.

And management Information Systems professor Yves Pigneur in a practical way in 2010.

Alexander Osterwalde and Yves Pigneur defined nine categories for the Business Model Canvas

which refer to as the building blocks of an organization.

The building block are:

1. Key partners

2. Key activities

3. Key resources

4. Value propositions

5. Customer relationships

6. Channels

7. Customer segments

8. Cost structure

9. Revenue streams

By using the Business Model Canvas the performance of an existing organization can easily be

improved. With a clear visual aspect all company aspects have been clearly made. An organization

can fine-tune its value proposition and structurally improve its strategy by looking at the

developments per category. Clear decisions can be made in advance using the Business Model

Canvas in the early setting up a new company.

FIGURE 2.12: Business Model Canvas

1. Key Partners

For both start-up organizations and existing organizations it may be important to create alliances

with partners. For instance when fighting the competition and combining knowledge and

specialization. Essential information will be acquired by knowing in advance which partners may

constitute a valuable relationship.

2. Key Activities

By having a good knowledge of the core activities of a company, a good understanding of the

value proposition of the organization will be obtained. It is not just about production, but also

about a problem-solving approach, networking and the quality of the product and/or service. When

the organization knows what the added value for the customer is, a better relationship may develop

with existing customers, which may be helpful in the canvassing of new customers therefore, and

which makes it easier to keep the competition at bay.

3. Key Resource

Resources are means that a company needs to perform. They can be categorized as physical,

intellectual, financial or human resources. Physical resources may include assets such as business

equipment. Intellectual resources include among other things knowledge, brands and patents. The

financial resources are related to funds flow and sources of income and human resources comprises

the staffing aspect.

4. Value Propositions

The value proposition is about the core of a company’s right to exist, it meets the customer’s

need. How does an organization distinguish itself from the competition? This distinction focuses

on quantity such as price, service, speed and delivery conditions on the one hand, and on the other

hand it also focuses on quality including design, brand status and customer experience and

satisfaction.

5. Customer Relationships

It is essential to interact with customers. The broader the customer base the more important it is to

divide your customers into different target groups. Each customer group has specific needs. By

anticipating the customer needs, the organization invests in different customers. A good service

will ensure good and stable customer relationships that will be ensured in the future.

6. Channels

An organization deals with communications, distribution and sales channels. It is not just about

customer contact and the way in which an organization communicates with their customers. The

purchase location and the delivery of the product and/or services provided are decisive elements

in this. Channels to customers have five different stages: awareness of the product, purchase,

delivery, evaluation & satisfaction and after sales. In order to make good use of the channels and

to reach as many customers as possible, it is advisable to combine off-line (shops) and online (web

shops) channels.

7. Customer Segments

As organizations often provide services to more than one customer group, it is sensible to divide

them into customer segments. By identifying the specific needs and requirements of each group

and which value they attach to this, products and services can be better geared towards these needs

and requirements. This will lead to greater customer satisfaction, which in turn will contribute to

a good value proposition.

8. Cost Structure

By gaining an insight into cost structure, an organization will know what the minimum turnover

must be to make a profit. The cost structure considers economies of scale, constant and variable

costs and profit advantages. When it is obvious that more investments must be made than the

organization is generating in revenue, the costs will have to be adjusted. Often an organization will

opt for deleting a number of key resources.

9. Revenue Streams

In addition to the cost structure, the revenue streams will provide a clear insight into the revenue

model of an organization. For example, how many customers does an organization need on an

annual basis to generate a profit? How much revenue does it need to break even? The revenue

streams are cost drivers. In addition to the revenue from the sale of goods, subscription fees, lease

income, licensing, sponsoring and advertising may also be an option.

2.3 Research Methodology

The method used in the preparation of this thesis, is by using the questionnaire method, Dress It

target data collection from 300 peoples, of whom are office workers, entrepreneurs, socialites,

and fashion bloggers. Dress It wants to get insight into their habits in buying and choosing

clothes.