apple pay industry analysis

TRANSCRIPT

Near Field Communication, more widely known as NFC, is a short-‐range

communication technology1 facilitating the electronic transfer of data from two

NFC enabled devices. The “bidirectional nature of communication”2 makes NFC

an ideal technology to provide ubiquitous wireless networking capability and

instantaneous data transfer.

The technology was first integrated into a mobile device in 2007 when Nokia

released the 6131 NFC device, capable of transferring basic data such as images

and contacts3 within a 4cm range. Since inception, blue-‐chip companies have

developed a range of applications including those in the healthcare, security and

data collection fields, encouraged by ABI Research, predicting that over 1.95

billion NFC-‐enabled devices will be shipped by 20174.

NFC has the capability in particular to transform the landscape for mobile

payment and commerce, an industry in the US worth over $35bn5 annually,

transacting $4.9 trillion payments6 on cards every year. Apple’s CEO Tim Cook

announced the introduction of their new NFC based technology Apple Pay on 9th

September 2014 providing a challenge to existing mobile payments providers

with an easy, secure and private way to pay7. There is over $14bn of card fraud

each year in the US alone8.

1 (Kerem OK, 2010) 2 (NFC Forum) 3 (Nokia, 2007) 4 (ABI Research, 2013) 5 (Forbes, 2013) 6 (Shieber, 2014) 7 (Apple Inc., 2014) 8 (Business Insider, 2014)

In this report I will explore Apple’s future mobile payment plans and analyze

their commercial viability, competitive stance and relative impact upon society.

Figure 1 – Apple’s proof of concept tests utilizing AuthenTec Biometrics along side

integrated NFC technologies9

9 (iDownload Blog, 2014)

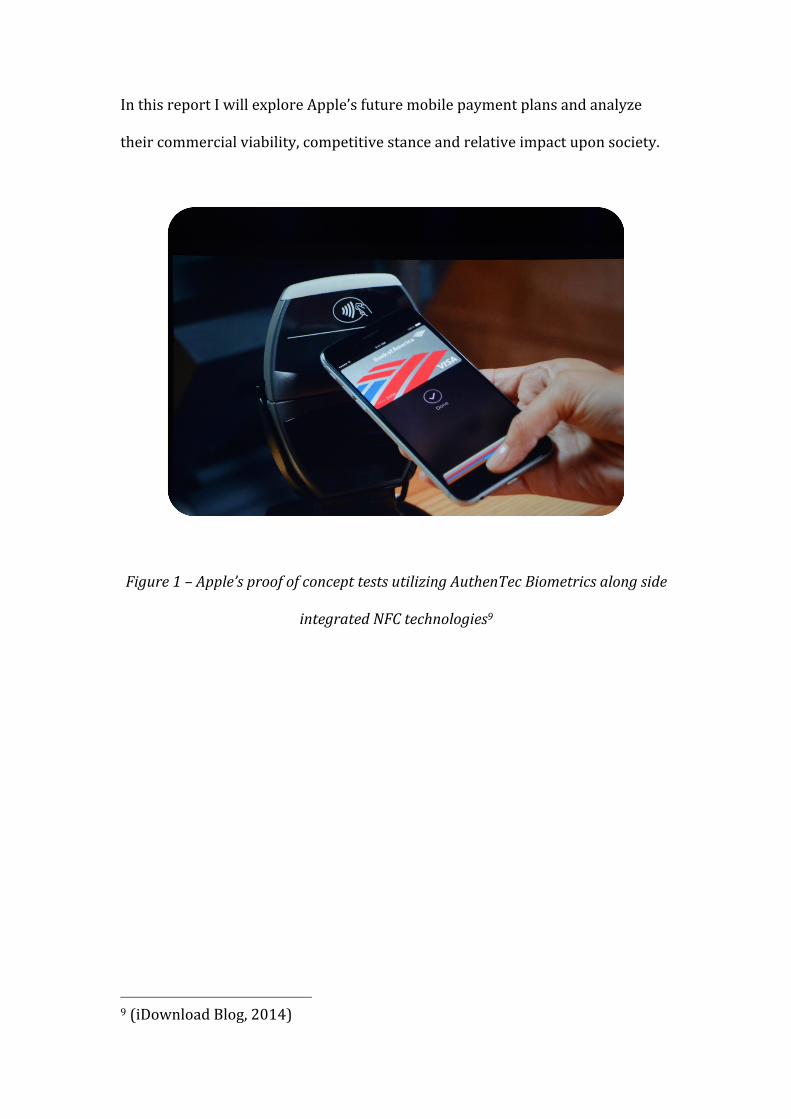

Impact upon Society Apple is claiming it’s new Pay technology will be the safest “mass consumer

payment method10” combining an advanced biometrics identifier, a patented11

tokenization technology to randomize credit card numbers at POS and a new

“secure element” chip embedded inside the new iPhone 6 to encrypt user data.12

Security is the largest area of concern for consumers as shown in Figure 2.

Figure 2 – The most important factor consumer’s care about with respect to mobile

payments

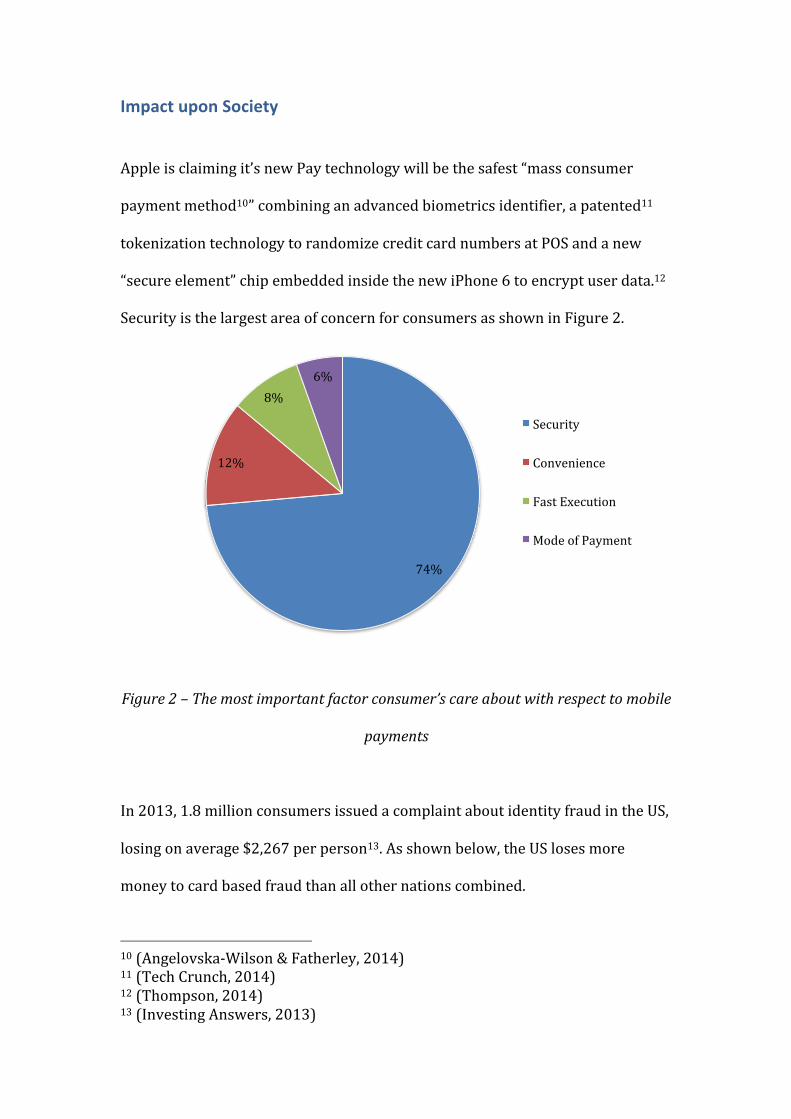

In 2013, 1.8 million consumers issued a complaint about identity fraud in the US,

losing on average $2,267 per person13. As shown below, the US loses more

money to card based fraud than all other nations combined.

10 (Angelovska-‐Wilson & Fatherley, 2014) 11 (Tech Crunch, 2014) 12 (Thompson, 2014) 13 (Investing Answers, 2013)

74%

12%

8% 6%

Security

Convenience

Fast Execution

Mode of Payment

Figure 3 – Global Cost of Payment Fraud14

Consumers will also benefit from a much simpler and faster service at the point

of sale, removing the need to carry multiple cards, cash and coins and thereby

preventing loss and theft. In the UK, the average citizen holds £85 of cash leading

to a loss of £765m over the last five years15.

If an iPhone has been stolen, consumers will have the ability to locate and

remove card data held on the device via Apple’s “Find my iPhone” service which

could one day replace the need for banks to staff 24-‐hour hotlines and support

centers.

14 (Business Insider, 2014) 15 (Guardian, 2010)

3.2 3.6 4.8 5.5

7.1

3.7 4

5.4 6.2

6.8

0

2

4

6

8

10

12

14

16

2009 2010 2011 2012 2013

Fraud Losses in $BN

United States Rest of the World

Smartphone theft is a pressing issue as over 742,00016 mobiles have been stolen

in the past two years. 3% of these crimes instigated minor injuries to the victim.

Apple Pay increases the value of mobile devices with the capacity to access bank

accounts and card information.

Customers will also be able to monitor and reap the rewards from discount

codes, tickets and vouchers through a rereleased Passbook application, helping

to reduce the number of unspent gift cards, which totaled $41 billion from 2005-‐

201117.

However, Apple came under scrutiny from consumers over photos leaked from

the iCloud accounts of various celebrities as well as the discovery by the German

Chaos Computer Club that the fingerprints reader can be fooled using a shiny

surface and glue18, leaving consumers at risk of innovation abuse.

In addition to this, consumers may become victims of Apple’s rapid innovative

success, as retailers start to reject traditional payment methods as they become

more obsolete and outdated.

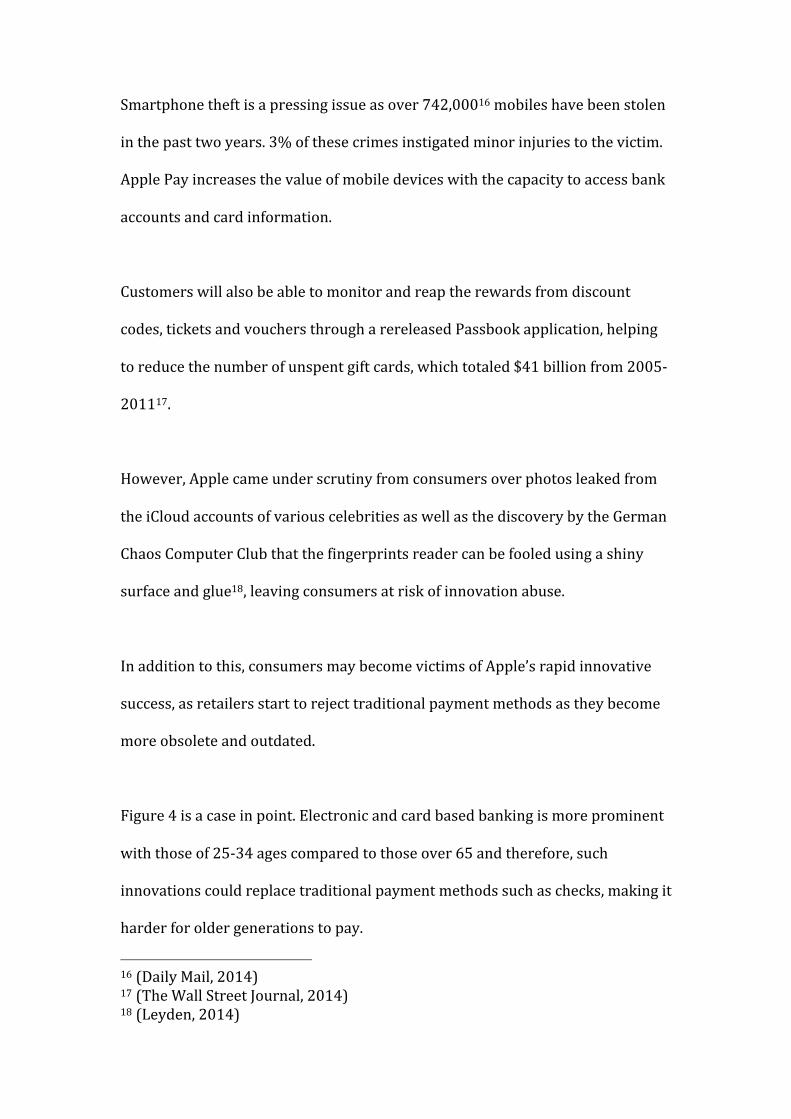

Figure 4 is a case in point. Electronic and card based banking is more prominent

with those of 25-‐34 ages compared to those over 65 and therefore, such

innovations could replace traditional payment methods such as checks, making it

harder for older generations to pay.

16 (Daily Mail, 2014) 17 (The Wall Street Journal, 2014) 18 (Leyden, 2014)

Figure 4 – Average number of Payments per Age Group19

Apple is however facing regulatory issues from the Consumer Financial

Protection Bureau20 as they may not have the correct license to “provide

services” on behalf of “card providers” according to Adam Levitin, a professor of

Law at Harvard University21. Apple needs to be conscious of a highly regulated

industry both in the US and elsewhere (e.g UK’s FCA body), which could impact

their international expansion plans and adoption of the technology.

19 (The Financial Brand, 2014) 20 (Market Watch, 2014) 21 (Georgetown Law, 2014)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

18-‐24 25-‐34 35-‐44 45-‐54 55-‐64

Cash Check Electronic / Card

65+

Market Attractiveness

Since its launch, Apple has sold 20 million iPhone 6 and 6 Plus devices in the

global market place, aiming to sell over 80 million before the end of the

quarter22, increasing the size of the accessible market for Apple Pay services.

For many years, the financial sector has been under pressure as rapid

developments in technology have confronted traditional banking methodologies

an industry restricted by regulation and controls. The world’s largest banking

corporations are therefore being forced to rework their strategies to respond to

digital-‐driven change and provide consumers with a modern banking service.23

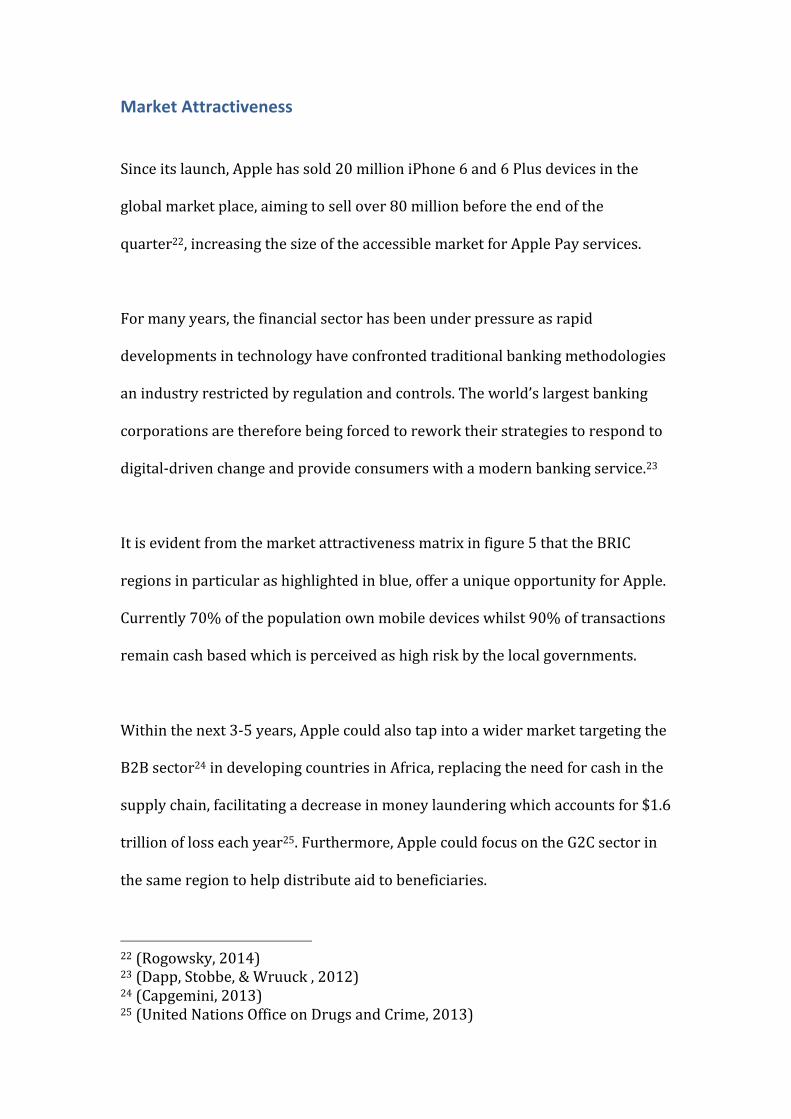

It is evident from the market attractiveness matrix in figure 5 that the BRIC

regions in particular as highlighted in blue, offer a unique opportunity for Apple.

Currently 70% of the population own mobile devices whilst 90% of transactions

remain cash based which is perceived as high risk by the local governments.

Within the next 3-‐5 years, Apple could also tap into a wider market targeting the

B2B sector24 in developing countries in Africa, replacing the need for cash in the

supply chain, facilitating a decrease in money laundering which accounts for $1.6

trillion of loss each year25. Furthermore, Apple could focus on the G2C sector in

the same region to help distribute aid to beneficiaries.

22 (Rogowsky, 2014) 23 (Dapp, Stobbe, & Wruuck , 2012) 24 (Capgemini, 2013) 25 (United Nations Office on Drugs and Crime, 2013)

Figure 5 – Global Market Attractiveness Matrix of m-‐payments 26

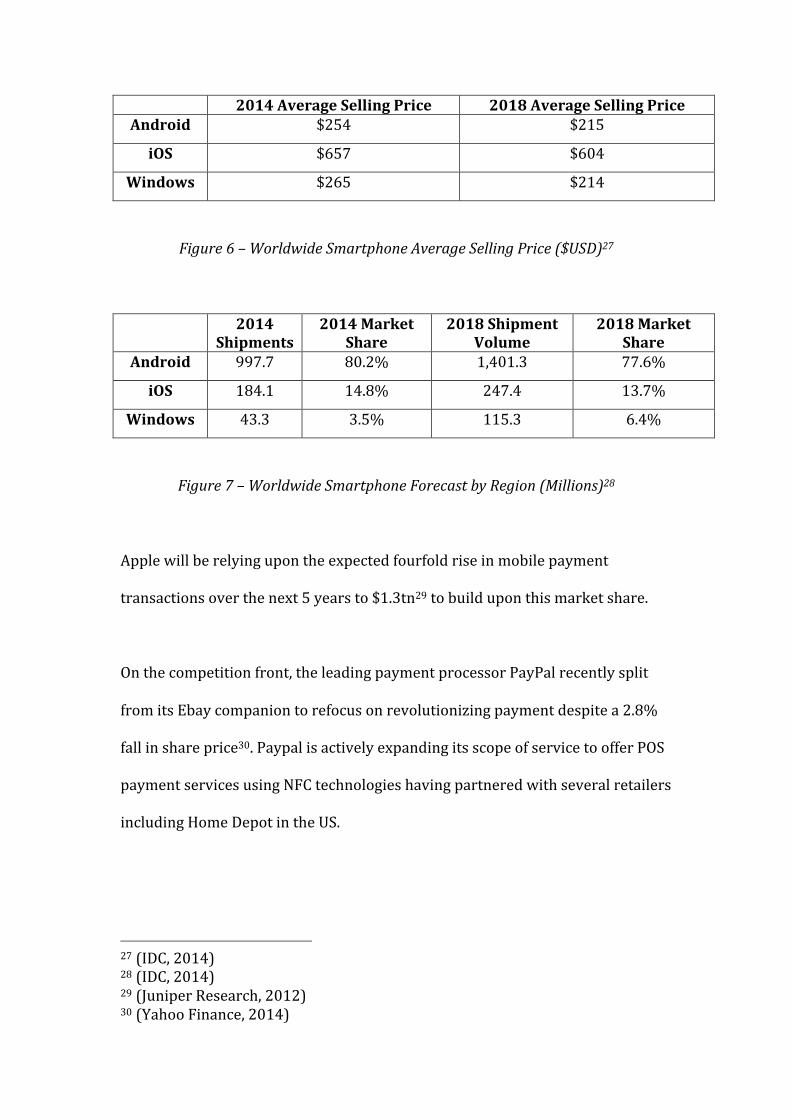

However, Apple has limited the size of its addressable market by pricing its

products above competition. Figure 6 shows that the average price difference in

2018 of an android versus an iOS device will be $400, which makes Apple’s

platform potentially unappealing in developing markets. This is reflected in the

significant difference in the current market share in Figure 7 between the

respective platforms, Android 80.2%, vs Apple 14.8% which will prove to be a

further challenge for growth.

26 (Arthur D Little, 2013)

2014 Average Selling Price 2018 Average Selling Price Android $254 $215

iOS $657 $604

Windows $265 $214

Figure 6 – Worldwide Smartphone Average Selling Price ($USD)27

2014 Shipments

2014 Market Share

2018 Shipment Volume

2018 Market Share

Android 997.7 80.2% 1,401.3 77.6%

iOS 184.1 14.8% 247.4 13.7%

Windows 43.3 3.5% 115.3 6.4%

Figure 7 – Worldwide Smartphone Forecast by Region (Millions)28

Apple will be relying upon the expected fourfold rise in mobile payment

transactions over the next 5 years to $1.3tn29 to build upon this market share.

On the competition front, the leading payment processor PayPal recently split

from its Ebay companion to refocus on revolutionizing payment despite a 2.8%

fall in share price30. Paypal is actively expanding its scope of service to offer POS

payment services using NFC technologies having partnered with several retailers

including Home Depot in the US.

27 (IDC, 2014) 28 (IDC, 2014) 29 (Juniper Research, 2012) 30 (Yahoo Finance, 2014)

Smartphone competitor Samsung also introduced TecTile, an alternative open

sourced attachable device retailing at a low price point of at £8.71, a compelling

offering for consumers in developing regions31.

Mobile phone operators may also be viable competitors as they have access to an

increasing mass of devices with NFC enabled technologies. In 2012, Vodafone

announced an agreement with Visa to utilize Sim cards to store card details.

E-‐commerce retailers such as Amazon are also entering the market acquiring

GoPago, a provider of mobile payment apps and POS retail software. Similarly

IBM announced their own two-‐factor security system for mobile transactions by

incorporating smartphones into a private cloud network and submitting 270

patents in wireless innovations32 which could limit Apple’s expansion plans.

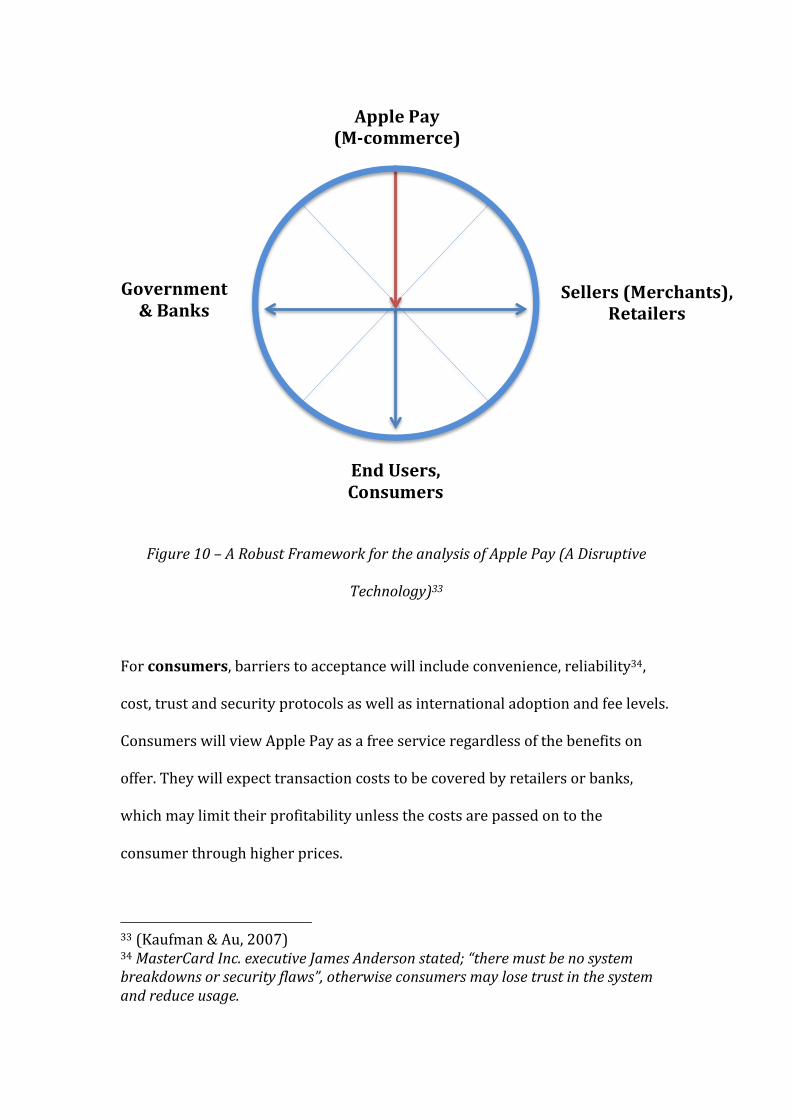

Barriers to Acceptance Commercialization will depend on a number of stakeholders; customer

acceptance, retailer and merchant conversion as well as the continued support

from local governments and banks.

31 (Samsung News, 2012) 32 (IBM Labs, 2013)

Figure 10 – A Robust Framework for the analysis of Apple Pay (A Disruptive

Technology)33

For consumers, barriers to acceptance will include convenience, reliability34,

cost, trust and security protocols as well as international adoption and fee levels.

Consumers will view Apple Pay as a free service regardless of the benefits on

offer. They will expect transaction costs to be covered by retailers or banks,

which may limit their profitability unless the costs are passed on to the

consumer through higher prices.

33 (Kaufman & Au, 2007) 34 MasterCard Inc. executive James Anderson stated; “there must be no system breakdowns or security flaws”, otherwise consumers may lose trust in the system and reduce usage.

Apple Pay (M-‐commerce)

End Users, Consumers

Sellers (Merchants), Retailers

Government & Banks

Apple can overcome any barriers to acceptance by offering additional services

and functionality such as the digital storage of keys, tickets and a means of

storing identification records35. Gamification and rewards may also convince

consumers to use this platform over competitor offerings.

Retailers will also need to be convinced that Apple Pay will speed up payment

times, improve their security protocol and eliminate the audit of cash based

transactions. As in the case of Amazon’s successful development of the 1-‐click

buy process, retailers may find the added simplicity of such a payment system

very attractive. Merchants will be able to benefit from real time reporting of cash

flows and accompanying purchase data analysis.

Retailers will assume that Apple’s technologies will seamlessly work. Poor Wi-‐Fi,

unreliable fingerprint readers and substandard staff training will ultimately

frustrate customers and result in poor customer service ratings. Integration with

existing retailer systems may prove complex and time consuming.

Implementation costs are also likely to be high, the average NFC reader and

software bundle costing each $49936.

Apple has also faced some criticsm from the Merchant Customer Exchange Group

(MCX)37, a large consortium of retailers including Walmart, Target, Best Buy and

Wendy’s who plan to use their own NFC enabled white label solutions 38.

35 (NFC Forum, 2007) 36 (Wall Street Journal , 2014) 37 (Hamblen, 2012) 38 (Woods, 2014)

Apple also face challenges from retailers themselves such as Starbucks who was

one of the first retailers in the world to allow payments on mobile operating

platforms. Apple may be reluctant to integrate and open up their proprietary

technology to 3rd party developers.

Banking institutions are both stakeholders and competitors as they will have

their own mobile payment initiatives such as in the case of Barclays and their

voice biometrics for customer authentication to be released in 201539.

On a positive front for Apple, credit rating agency, Fitch reported, “thus far, 11

banks, representing 83% of the credit card purchase volume in the US are

expected to agree to support Apple Pay.”40

Feasibility of Concept

Apple’s go to market strategy differs from the current practice where the

merchant is charged by the Bank provider for a fee per transaction. For Apple

Pay, banks will be charged instead a fee of 0.15% for each transaction and the

retailers will bear no cost except at time of implementation. Despite the

additional fees, Banks will be motivated by the potential reduction in cash based

transactions and the removal of minimum spend limits currently in operation.

39 (ComputerWeekly.com, 2014) 40 (Reuters, 2014)

Apple is also likely to be very profitable. With over $12 billion41 of transactions

in the US each and every day, Apple’s 6% coverage of iPhone 6 devices will

generate $1.4 million of daily revenue for the company. Juniper research claims

that by 2017 over 54% of all future payments could be driven by NFC based

technology42 as the services grow across the world.

Apple is also expecting to benefit from an upcoming change in regulation

whereby from October 2015, “any merchants that do not support Europay,

Mastercard and Visa credit cards with integrated circuits that enable point of

sale authentication and help prevent fraud will be liable for fraudulent use of

counterfeit, lost and stolen cards.43” This will be a significant legislative

development in the US where only 14% of merchants support modern credit

card chip and pin services. This in effect means that the burden of responsibility

transfers from the bank to the retailer who will now be held accountable for any

fraud if they are not adopting these new, more security conscious pin and chip

services44. This will in turn reduce the net cost incurred by the bank who were

previously covering the incidence of fraud.

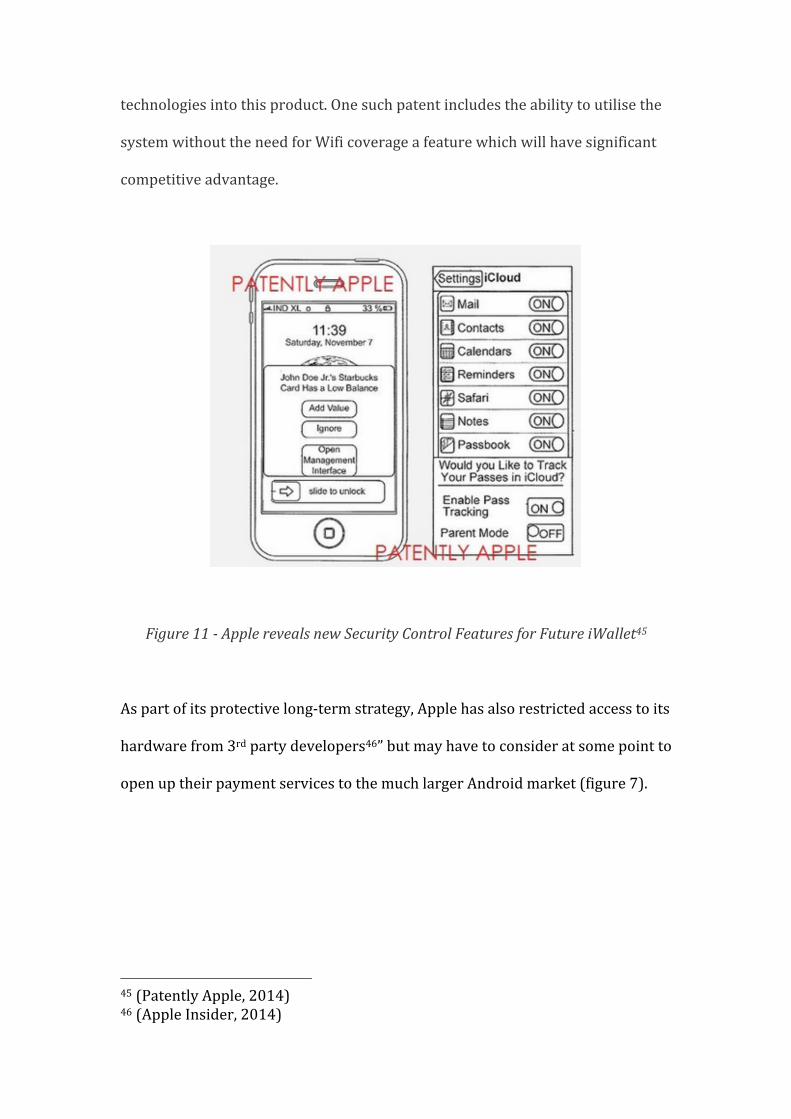

On June 11, 2013, the US Patent and Trademark Office officially published a

series of 37 newly granted patents for Apple Inc in relation to these new

payment services. These patents prove that Apple has the necessary

technological know how in place to be able to integrate NFC and AuthenTec’s ID

41 (CNBC, 2014) 42 (Juniper Research, 2012) 43 (Total System Services, 2014) 44 (Financial Times, 2014)

technologies into this product. One such patent includes the ability to utilise the

system without the need for Wifi coverage a feature which will have significant

competitive advantage.

Figure 11 -‐ Apple reveals new Security Control Features for Future iWallet45

As part of its protective long-‐term strategy, Apple has also restricted access to its

hardware from 3rd party developers46” but may have to consider at some point to

open up their payment services to the much larger Android market (figure 7).

45 (Patently Apple, 2014) 46 (Apple Insider, 2014)

Experience and Strategy Apple has notoriously entered markets late but when it gets there has always

delivered exceptional customer value and simplicity.

To strengthen their knowledge of the financial services market, Apple has

acquired expertise in the market place, hiring, amongst others, the director of

mobile at Visa Europe, Mary Harris who also happened to take charge of

Telefonica’s NFC division.47

Strategic partnerships with leading players in the financial services market such

as Visa, Mastercard and American Express will strengthen the proposition. Apple

have already convinced over 220,000 US stores across 35 major highstreet retail

brands48 that Apple pay is the chosen route for a secure mobile payment service.

Square, a financial merchant services aggregator, also announced a strategic

partnership with Apple as broadcasted by their CEO Jack Dorsey49.

Conclusion

Apple will effectively leverage the power of its brand and successful track record

to seamlessly integrate its payment product into its array of software products.

47 (Kennedy, 2014) 48 (Computer World, 2014) 49 (Mashable, 2014)

In my opinion, for Apple Pay to fulfill its potential, it is of great importance that

each member of the value chain engages with the new intuitive payment

mechanism to heighten its public perception. Worldwide acceptance depends on

Apple’s ability to secure long-‐term partnership support from payment networks,

merchants and consumers.

Competition in the m-‐payments industry is fierce and Apple will therefore have

to strategically position its commission model appropriately to withstand entry

into the market.

Apple Pay sits within a complex ecosystem of stakeholders and influencers

whom will be banking on Apple’s highly regarded executional ability to shake up

an outdated industry.

Bibliography 99Bitcoins. (2014). Bitcoin Worldwide adoption and legal status. Sydney: 99Bits. ABI Research. (2013, March 21). Is NFC Finally Becoming Mobile's Next Big Thing? Wall Street Journal , p. 10. Addyman, C. (2014, April 17). How NFC Technology could be used in the future. Retrieved September 28, 2014, from Geek Time: http://www.geektime.com/2014/04/17/how-‐nfc-‐technology-‐could-‐be-‐used-‐in-‐the-‐future/ Angelovska-‐Wilson, A., & Fatherley, C. J. (2014). Mobile Payments – The Future is NOW. London: Reed Smith. Apple Inc. (2014, September 9). Apple Announces Apple Pay. Retrieved September 28, 2014, from Apple Press Info: https://www.apple.com/uk/pr/library/2014/09/09Apple-‐Announces-‐Apple-‐Pay.html Apple Insider. (2014, September 16). Apple to limit iPhone 6 NFC to Apple Pay, restrict developer access. Retrieved September 28, 2014, from Apple Insider: http://appleinsider.com/articles/14/09/16/apple-‐to-‐limit-‐iphone-‐6-‐nfc-‐to-‐apple-‐pay-‐restricts-‐developer-‐access Arthur D Little. (2013). M-‐Payments in M-‐Bric. Berlin: Arthur D Little. Bower, J. L., & Christensen, C. M. (1995). Disruptive Technologies: Catching the Wave. Harvard, Business Review. Boston: Harvard Business Review. Brown, B. (2011, November 28). Father of RFID, Charles Walton, passes at 89. Retrieved September 28, 2014, from Network World: http://www.networkworld.com/article/2183529/wireless/father-‐of-‐rfid-‐-‐charles-‐walton-‐-‐passes-‐at-‐89.html Brown, B. (2011, November 28). Father of RFID, Charles Walton, passes at 89. Retrieved September 27, 2014, from Network World: http://www.networkworld.com/article/2183529/wireless/father-‐of-‐rfid-‐-‐charles-‐walton-‐-‐passes-‐at-‐89.html Business Insider. (2014, September 4). Here's What The Global Smartphone Market Looks Like Ahead Of The iPhone 6 Launch. Retrieved October 4, 2014, from Business Insider: http://www.businessinsider.com/the-‐state-‐of-‐the-‐smartphone-‐industry-‐2014-‐9 Business Insider. (2014, Mar 5). The US Sees More Money Lost To Credit Card Fraud Than The Rest Of The World Combined. Retrieved Sept 23, 2014, from Businss Insiders: http://www.businessinsider.com/the-‐us-‐accounts-‐for-‐over-‐half-‐of-‐global-‐payment-‐card-‐fraud-‐sai-‐2014-‐3 Capgemini. (2013). World Payments Report 2013. Capgemini. New York: Capgemini.

CNBC. (2014, September 15). Apple wages war on the wallet. Retrieved October 15, 2014, from CNBC: http://www.cnbc.com/id/102000065 Computer World. (2014, October 17). Apple Pay hits U.S. stores Monday -‐-‐ assuming buyers can find anywhere to use it. Retrieved October 18, 2014, from Computer World: http://www.computerworld.com/article/2834651/apple-‐pay-‐hits-‐u-‐s-‐stores-‐monday-‐assuming-‐buyers-‐can-‐find-‐anywhere-‐to-‐use-‐it.html ComputerWeekly.com. (2014, September 5). Barclays bank launches biometric authentication. Retrieved Septmeber 28, 2014, from ComputerWeekly.com: http://www.computerweekly.com/news/2240228235/Barclays-‐bank-‐launches-‐biometric-‐authentication ComputerWeekly.com. (2014, October 17). MasterCard develops biometric authentication card. Retrieved October 18, 2014, from ComputerWeekly.com: http://www.computerweekly.com/news/2240232881/MasterCard-‐supports-‐Zwipe-‐biometric-‐authentication-‐card Daily Mail. (2014, September 8). Call for alarm: 2,000 mobiles stolen every day (and iPhone is top target). Daily Mail , 32. Dapp, T. F., Stobbe, A., & Wruuck , P. (2012). The Future of Mobile Payments. Deutsche Bank, DB Research. Frankfurt: Deutsche Bank. e-‐Society. (2013). Proceedings of the International Conference -‐ E-‐society 2013. Proceedings of the International Conference -‐ E-‐society 2013 (p. 534). Lisbon: IADIS. Finn, C., & Lusignan, C. (2014). Global Non-‐Cash Payments Forecast to Grow by Nearly Ten Percent Reveals World Payments Report 2014. Capgemini. New York: Capgemini. Forbes. (2013, November 27). Here Comes The Mobile Payments Bubble -‐-‐ Why Aren't We Scared Yet? Retrieved October 10, 2014, from Forbes: http://www.forbes.com/sites/groupthink/2013/11/27/here-‐comes-‐the-‐mobile-‐payments-‐bubble-‐why-‐arent-‐we-‐scared-‐yet/ France-‐Presse, A. (2014, September 15). Apple a Decade Behind Japan Mobile Payment Curve. Retrieved September 28, 2014, from NDTV Gadgets: http://gadgets.ndtv.com/mobiles/news/apple-‐a-‐decade-‐behind-‐japan-‐mobile-‐payment-‐curve-‐591866 France-‐Presse, A. (2014, September 15). Apple a Decade Behind Japan Mobile Payment Curve. Retrieved October 1, 2014, from NDTV Gadgets: http://gadgets.ndtv.com/mobiles/news/apple-‐a-‐decade-‐behind-‐japan-‐mobile-‐payment-‐curve-‐591866 Gartner. (2013). Gartner Says Worldwide Mobile Payment Transaction Value to Surpass $235 Billion in 2013. Gartner. Los Angeles: Gartner.

Gates, B. (2014, October 2). Bill Gates on "The future of Payments". (Bloomberg, Interviewer) Bloomberg. Georgetown Law. (2014, Sept 20). Adam J. Levitin. Retrieved Oct 2, 2014, from Harvard University: http://www.law.georgetown.edu/faculty/levitin-‐adam-‐j.cfm Guardian. (2010, Aug 18). Lost wallets: only one in five returned, research says. The Guardian , 29. Hamblen, M. (2012, August 15). Walmart, Target others team to offer mobile payments network. Retrieved September 27, 2014, from Computer World: http://www.computerworld.com/article/2505837/data-‐center/walmart-‐-‐target-‐others-‐team-‐to-‐offer-‐mobile-‐payments-‐network.html IBM Labs. (2013, Oct 13). Two-‐factor security for mobile transactions. Retrieved Oct 10, 2014, from IBM Innovations: http://www.zurich.ibm.com/news/13/two_factor_security.html IDC. (2014). Smartphone Momentum Still Evident with Shipments Expected to Reach 1.2 Billion in 2014 and Growing 23.1% Over 2013. IDC. New York: IDC. iDownload Blog. (2014, Sept 10). Discover confirms joining Apple Pay ‘in the future’. Retrieved Oct 10, 2014, from iDownload Blog: http://www.idownloadblog.com/2014/09/10/discover-‐to-‐join-‐apple-‐pay/ Investing Answers. (2013, Sept 21). 17 Shocking Facts About Identity Theft And Fraud In America. Retrieved Sept 28, 2014, from Investing Answers: http://www.investinganswers.com/personal-‐finance/credit/17-‐shocking-‐facts-‐about-‐identity-‐theft-‐and-‐fraud-‐america-‐4677 Juniper Research. (2012). The Mobile Payments Strategies Briefing 2012-‐2017. Berlin: Juniper Research. Kaufman, R. J., & Au, Y. A. (2007). The economics of mobile payments: Understanding stakeholder issues for an emerging financial technology application. Electronic Commerce Research and Applications 7 , 7, 141-‐164. Kennedy, L. (2014, September 29). Top Visa NFC expert poached by Apple. Retrieved October 2, 2014, from Payment Eye: http://www.paymenteye.com/2014/09/29/top-‐visa-‐nfc-‐expert-‐poached-‐by-‐apple/ Kerem OK, V. C. (2010). Current Benefits and Future Directions of NFC Services. ISIK University, Department of Information Technologies, . Istanbul: 2010 International Conference on Education and Management Technology. Kim, C. (2010). An empirical examination of factors influencing the intention to use mobile payment. Computers in Human Behavior , 26 (3), 310-‐322. Leyden, J. (2014, September 23). Apple's new iPhone 6 vulnerable to last year's TouchID fingerprint hack. Retrieved October 2, 2014, from The Register:

http://www.theregister.co.uk/2014/09/23/iphone_6_still_vulnerable_to_touchid_fingerprint_hack/ Market Watch. (2014, September 11). Law professor thinks Apple turned self into a regulated financial institution. Retrieved October 2, 2014, from Market Watch: http://blogs.marketwatch.com/thetell/2014/09/11/this-‐law-‐professor-‐thinks-‐apple-‐just-‐turned-‐itself-‐into-‐a-‐regulated-‐financial-‐institution/ Mashable. (2014, September 9). Penny for Your Thoughts: Mobile Payment Services Adjust to Apple Pay. Retrieved October 3, 2014, from Mashable: http://mashable.com/2014/09/09/apple-‐pay-‐competitors/ Millennial Distruption Network. (2014). Banking is at the highest risk of disruption. San Francisco: Millennial Distruption Network. Morozov, E. (2012, April 2). My piece on the history of facial recognition technologies. Retrieved September 27, 2014, from Blog: http://evgenymorozov.tumblr.com/post/20347146711/my-‐piece-‐on-‐the-‐history-‐of-‐facial-‐recognition NearfieldCommunication.org. (2014, Jan 10). Technology Standards. Retrieved September 28, 2014, from Nearfiled Communication: http://www.nearfieldcommunication.org/technology.html NewsDay. (2014, Oct 17). Apple Pay looks to cash in on consumer concerns. Retrieved Oct 18, 2014, from Newsday: http://www.newsday.com/business/apple-‐pay-‐looks-‐to-‐cash-‐in-‐on-‐consumer-‐concerns-‐1.9516494 NFC Forum. (2007). The Keys to Truly Interoperable Communications. NFC Forum. California: NFC Forum. Nokia. (2007, Jan 7). Nokia 6131 NFC. (P. Arena, Producer) Retrieved October 2, 2014, from phonearena.com: http://www.phonearena.com/phones/Nokia-‐6131-‐NFC_id1884 Patently Apple. (2014, August 14). Apple Pay, iWallet, NFC Related. Retrieved September 26, 2014, from Patently Apple: http://www.patentlyapple.com/patently-‐apple/tech-‐nfc/ Payments Industry Intelligence . (2014, August 26). MasterCard and Visa targeted in Target lawsuit. Retrieved September 28, 2014, from Payments Cards and Mobile: http://www.paymentscardsandmobile.com/mastercard-‐visa-‐targeted-‐target-‐lawsuit/ Reuters. (2014, September 11). Fitch: iPhone Takes a Bite of the Mobile Card Payment Apple. Retrieved September 28, 2014, from Reuters: http://www.reuters.com/article/2014/09/11/fitch-‐iphone-‐takes-‐a-‐bite-‐of-‐the-‐mobile-‐idUSFit75257920140911

Rogowsky, M. (2014, October 5). Is Apple Nearing 20 Million iPhone 6 Sales Already? Signs Point To Yes. Retrieved October 8, 2014, from Forbes: http://www.forbes.com/sites/markrogowsky/2014/10/05/iphone-‐6-‐launch-‐continues-‐hot-‐streak/ Samsung News. (2012, Oct 24). SAMSUNG Mobile Expands NFC Capabilities with TecTile™ Version 3.0. Retrieved Sept 28, 2014, from Samsung News: http://www.samsung.com/us/news/20301 Shieber, J. (2014, April 15). Seeking Growth, The Payments Industry Embraces New Technologies. Retrieved September 28, 2014, from TechCrunch: http://techcrunch.com/2014/04/15/seeking-‐growth-‐the-‐payments-‐industry-‐embraces-‐new-‐technologies/ Slater-‐Robins, M. (2014, September 23). Apple could change the way we shop. Retrieved September 28, 2014, from Tech Radar: http://www.techradar.com/news/world-‐of-‐tech/why-‐apple-‐pay-‐is-‐a-‐really-‐really-‐big-‐deal-‐for-‐well-‐everyone-‐1266384/2 Tech Crunch. (2014, October 13). Apple Patent On The NFC Mechanics Of Apple Pay Details Its Inner Workings. Retrieved October 15, 2014, from Tech Crunch: http://techcrunch.com/2014/10/09/apple-‐patent-‐on-‐the-‐nfc-‐mechanics-‐of-‐apple-‐pay-‐details-‐its-‐inner-‐workings/ The Financial Brand. (2014, May 6). 6 Reasons Why Cash is Still The King of Payments. Retrieved Oct 2, 2014, from The Financial Brand: http://thefinancialbrand.com/39408/consumer-‐cash-‐usage-‐banking-‐payment-‐research/ The Wall Street Journal. (2014, Dec 24). Number of the Week: Billions in Gift Cards Go Unspent. Retrieved Oct 19, 2014, from Wall Street Journal: http://blogs.wsj.com/economics/2011/12/24/number-‐of-‐the-‐week-‐billions-‐in-‐gift-‐cards-‐go-‐unspent/ Thompson, C. (2014, September 11). How hackers could still get around Apple Pay security. Retrieved September 28, 2014, from CNBC: http://www.cnbc.com/id/101992749#. Total System Services. (2014). U.S. EMV Adoption. New York: Total System Services. Twitter. (2014, September 9). Jack Dorsey. Retrieved October 2, 2014, from Twitter: Twitter.com UniBul Credit Card Blog. (2013, Oct 10). Developing Markets Drive Global Non-‐Cash Payments Growth . Retrieved Oct 1, 2014, from UniBul: http://blog.unibulmerchantservices.com/developing-‐markets-‐drive-‐global-‐non-‐cash-‐payments-‐growth/

United Nations Office on Drugs and Crime. (2013). Illicit money: how much is out there? New York: United Nations Office on Drugs and Crime. Wall Street Journal . (2014, Sept 10). Will Stores Warm Up to Apple Pay? Retrieved Oct 2, 2014, from The Wall Street Journal: http://online.wsj.com/articles/will-‐stores-‐warm-‐up-‐to-‐apple-‐pay-‐1410392952 Walton, C. A. (1983). Patent No. US 4384288 A. USA. Woods, D. (2014, October 8). Where Does Apple Pay Fall Short? Retrieved October 10, 2014, from Forbes Online: http://www.forbes.com/sites/danwoods/2014/10/08/where-‐does-‐apple-‐pay-‐fall-‐short/ Yahoo Finance. (2014, Oct 19). Ebay Share Price. Retrieved Oct 19, 2014, from Yahoo Finance.