complete act august 00

DESCRIPTION

SAP Actual Costing with Material Ledger presentationTRANSCRIPT

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 1

AActualctual CCostingosting

WWithith

MMaterial aterial LLedgeredger

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 2

IInventory nventory AAccounting ccounting WWithithMMaterial aterial LLedgeredger

Content

Why Why YYOOUU want Multi-Level Actual Costing! want Multi-Level Actual Costing!

Environment of Material LedgerEnvironment of Material Ledger

Traditional Valuation StrategiesTraditional Valuation Strategies

Actual Costing in Three StepsActual Costing in Three Steps

Future Prices; Customizing; GoodiesFuture Prices; Customizing; Goodies

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 3

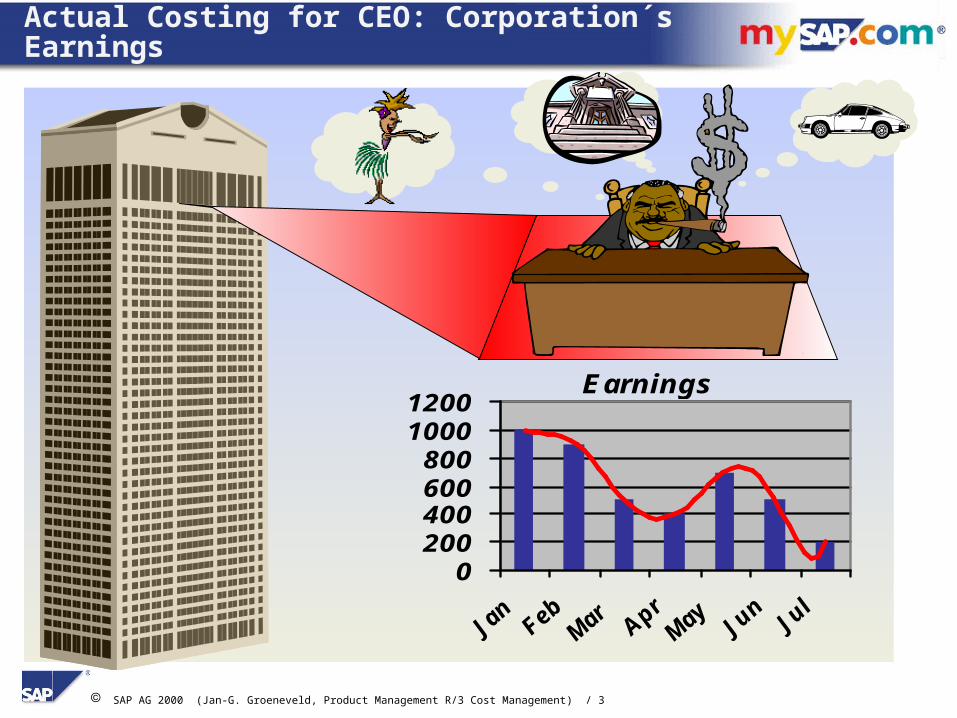

0200400600800

10001200

Earnings

Actual Costing for CEO: Corporation´s Earnings

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 4

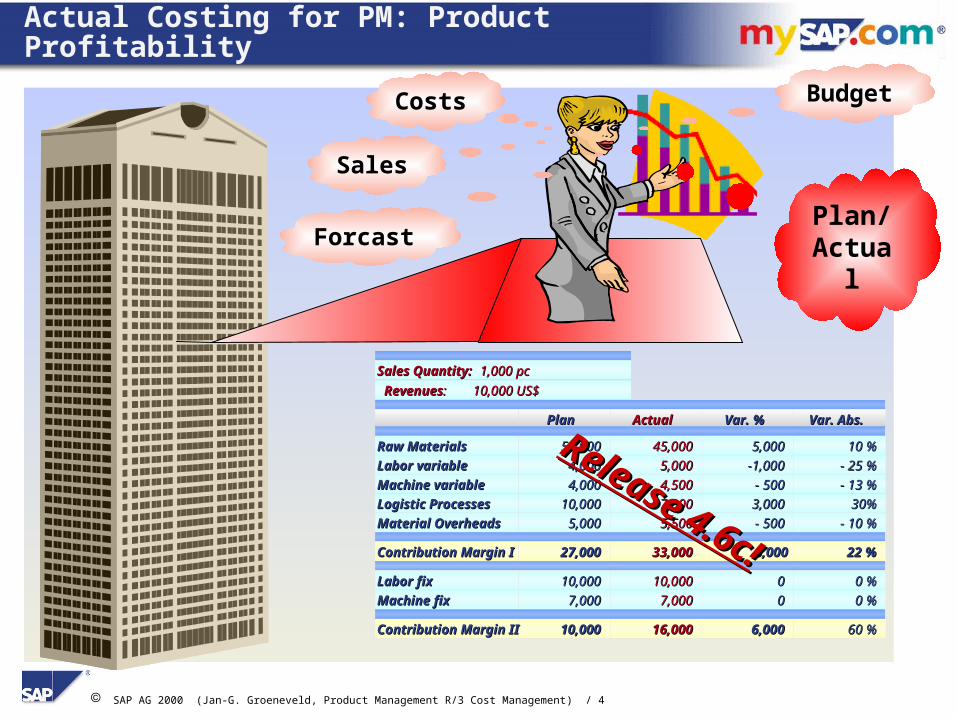

Actual Costing for PM: Product Profitability

PlanPlan ActualActual Var. %Var. % Var. Abs.Var. Abs.

RevenuesRevenues:: 10,000 US$10,000 US$

Sales Quantity:Sales Quantity: 1,000 pc1,000 pc

50,00050,000 45,00045,000 5,0005,000 10 %10 %Raw MaterialsRaw Materials

4,0004,000 5,0005,000 -1,000-1,000 - 25 %- 25 %Labor variableLabor variable

4,0004,000 4,5004,500 - 500- 500 - 13 %- 13 %Machine variableMachine variable

10,00010,000 7,0007,000 3,0003,000 30%30%Logistic ProcessesLogistic Processes

5,0005,000 5,5005,500 - 500- 500 - 10 %- 10 %Material OverheadsMaterial Overheads

6,0006,00027,00027,000 33,00033,000 22 %22 %Contribution Margin IContribution Margin I

10,00010,000 10,00010,000 00 0 %0 %Labor fixLabor fix

7,0007,000 7,0007,000 00 0 %0 %Machine fixMachine fix

10,00010,000 16,00016,000 6,0006,000 60 %60 %Contribution Margin IIContribution Margin II

Release 4.6c!

Release 4.6c!

Plan/Actual

Sales

Costs Budget

Forcast

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 5

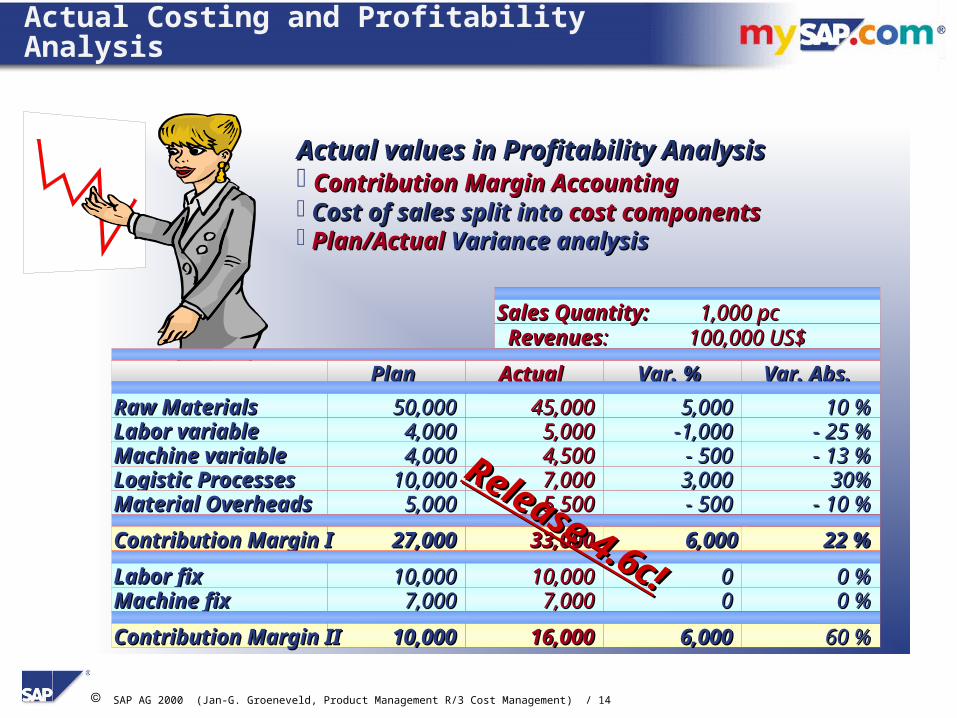

Actual values in Profitability AnalysisActual values in Profitability Analysis Contribution Margin AccountingContribution Margin Accounting Cost of sales Cost of sales split into split into cost componentscost components Plan/ActualPlan/Actual Variance analysis Variance analysis

Contribution Margins with Actual Values

PlanPlan ActualActual Var. %Var. % Var. Abs.Var. Abs.

RevenuesRevenues:: 100,000 US$100,000 US$Sales Quantity:Sales Quantity: 1,000 pc1,000 pc

50,00050,000 45,00045,000 5,0005,000 10 %10 %Raw MaterialsRaw Materials4,0004,000 5,0005,000 -1,000-1,000 - 25 %- 25 %Labor variableLabor variable4,0004,000 4,5004,500 - 500- 500 - 13 %- 13 %Machine variableMachine variable

10,00010,000 7,0007,000 3,0003,000 30%30%Logistic ProcessesLogistic Processes5,0005,000 5,5005,500 - 500- 500 - 10 %- 10 %Material OverheadsMaterial Overheads

6,0006,00027,00027,000 33,00033,000 22 %22 %Contribution Margin IContribution Margin I

10,00010,000 10,00010,000 00 0 %0 %Labor fixLabor fix7,0007,000 7,0007,000 00 0 %0 %Machine fixMachine fix

10,00010,000 16,00016,000 6,0006,000 60 %60 %Contribution Margin IIContribution Margin II

Release 4.6c!

Release 4.6c!

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 6

Actual Costing for InvAcc: Prices and Values

Procurement

BalanceSheet Valuation

Values&

Prices

InventoryCounting

Planning

Stock

Material Plant Std.PriceAct. PriceVar.absVar. %

PC 600 Pentium London 3,500 3,920 420 12 %PC 500 Pentium London 2,500 2,900 400 16 %

PC 330 Pentium Frankfurt 1,500 1,635 135 9 %Monitor 17‘ London 400 432 32 8 %Digital Camera xmsFrankfurt 750 805 55 7,5 %Digital Camera xmsLondon 950 1020 70 7,4 %PC Pentium 200 Frankfurt 800 855 55 7 %

Total ... ... ... ... ...... ... ... ... ... ...

Category Quantity PrelValuePriceDif Price

Trading Inc200 2,000 1,200 16,00Best Price Ltd100 1,000 300 13,00

Prod. Version1500 5,000 500 11,00

Receipts 900 9,000 2,340 12,60Purchase Order 300 3,000 1,500 15,00

Production 500 5,000 500 11,00

Beginning Inventory 100 1,000 160 11,60

Cumulative Inventory1,000 10,000 2,500 12,50Consumption 600 6,000 1,500 12,50Ending Inventory 400 4,000 1,000 12,50

... 100 1,000 340 13,40

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 7

Price Analysis for selected MaterialsPrice Analysis for selected Materials Huge number of monetary and quantity key-figures Multiple sorting and summerization functions Easy-to-customize to fit personal needs Direct drill-down tools to detailed views and documentsEasy error finding

Material Price Analysis

Material Material PlantPlant Std.PriceStd.Price Act. PriceAct. Price Var.absVar.abs Var. %Var. %

PC 600 PentiumPC 600 Pentium LondonLondon 3,5003,500 3,9203,920 420420 12 %12 %PC 500 PentiumPC 500 Pentium LondonLondon 2,5002,500 2,9002,900 400400 16 %16 %

PC 330 PentiumPC 330 Pentium FrankfurtFrankfurt 1,5001,500 1,6351,635 135135 9 %9 %Monitor 17‘Monitor 17‘ LondonLondon 400400 432432 3232 8 %8 %

Digital Camera xmsDigital Camera xms FrankfurtFrankfurt 750750 805805 5555 7,5 %7,5 %Digital Camera xmsDigital Camera xms LondonLondon 950950 10201020 7070 7,4 %7,4 %PC Pentium 200PC Pentium 200 FrankfurtFrankfurt 800800 855855 5555 7 %7 %

TotalTotal ...... ...... ...... ...... ............ ...... ...... ...... ...... ......

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 8

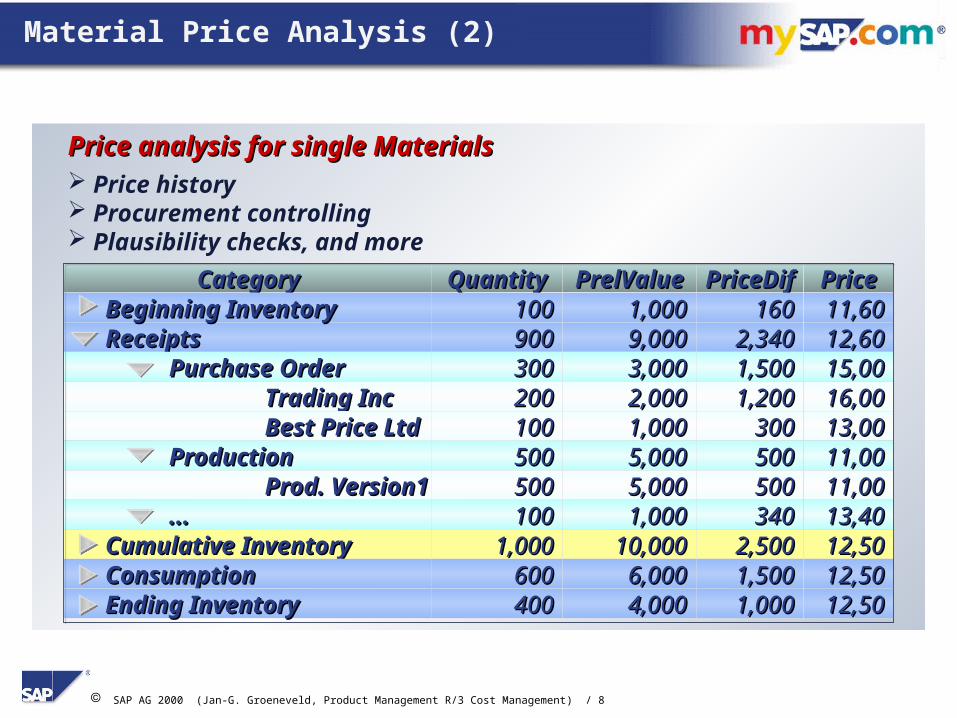

Material Price Analysis (2)

Price analysis for single MaterialsPrice analysis for single Materials Price history Procurement controlling Plausibility checks, and more

CategoryCategory QuantityQuantity PrelValuePrelValue PriceDifPriceDif PricePrice

Trading IncTrading Inc 200200 2,0002,000 1,2001,200 16,0016,00Best Price LtdBest Price Ltd 100100 1,0001,000 300300 13,0013,00

Prod. Version1Prod. Version1 500500 5,0005,000 500500 11,0011,00

ReceiptsReceipts 900900 9,0009,000 2,3402,340 12,6012,60Purchase OrderPurchase Order 300300 3,0003,000 1,5001,500 15,0015,00

ProductionProduction 500500 5,0005,000 500500 11,0011,00

Beginning InventoryBeginning Inventory 100100 1,0001,000 160160 11,6011,60

Cumulative InventoryCumulative Inventory 1,0001,000 10,00010,000 2,5002,500 12,5012,50ConsumptionConsumption 600600 6,0006,000 1,5001,500 12,5012,50Ending InventoryEnding Inventory 400400 4,0004,000 1,0001,000 12,5012,50

...... 100100 1,0001,000 340340 13,4013,40

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 9

IInventory nventory AAccounting ccounting WWithithMMaterial aterial LLedgeredger

Content

Why Why YYOOUU want Multi-Level Actual Costing! want Multi-Level Actual Costing!

Environment of Material LedgerEnvironment of Material Ledger

Traditional Valuation StrategiesTraditional Valuation Strategies

Actual Costing in Three StepsActual Costing in Three Steps

Future Prices; Customizing; GoodiesFuture Prices; Customizing; Goodies

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 10

Product Cost Controlling: Components

BOM RoutingRouting

Material pricesActivity pricesProcess pricesOverhead

Product Cost Planning

Value structure

Quantity Structure:PP Master Data

Standard price

Material Internal OH Process

•Planned costs•Actual costs

Work in processScrap variancesVariancesSettlement

Order

Material $Internal $OH $Process $Total ...

Final costingPeriod-end closing

Preliminary Costing,Simultaneous Costing

Cost Object Controlling

Price diff.Standard price

Material movements

Material settlement:actual price

Value structure

Actual Costing/ Material Ledger

Quantity Structure:Material Movements

Material Ledger

ProcessProcess

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 11

Actual CostingActual CostingMulti-levelMulti-level

Periodic Material PricesPeriodic Material Prices

Parallel CurrenciesParallel CurrenciesValuation with HistoricValuation with Historic

Exchange RatesExchange Rates

Parallel ValuationParallel ValuationTransfer pricesTransfer prices

GroupGroup LegalLegal Profit CenterProfit Center

TransparencyTransparencyof Value Chainof Value Chain

Actual CostingActual CostingMulti-levelMulti-level

Periodic Material PricesPeriodic Material Prices

MaterialMaterialLedgerLedger

Inventory ValuationInventory Valuation

Environment of Material Ledger

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 12

External ProcurementExternal Procurement External ProcurementExternal Procurement

ProductionProduction

ProductionProduction

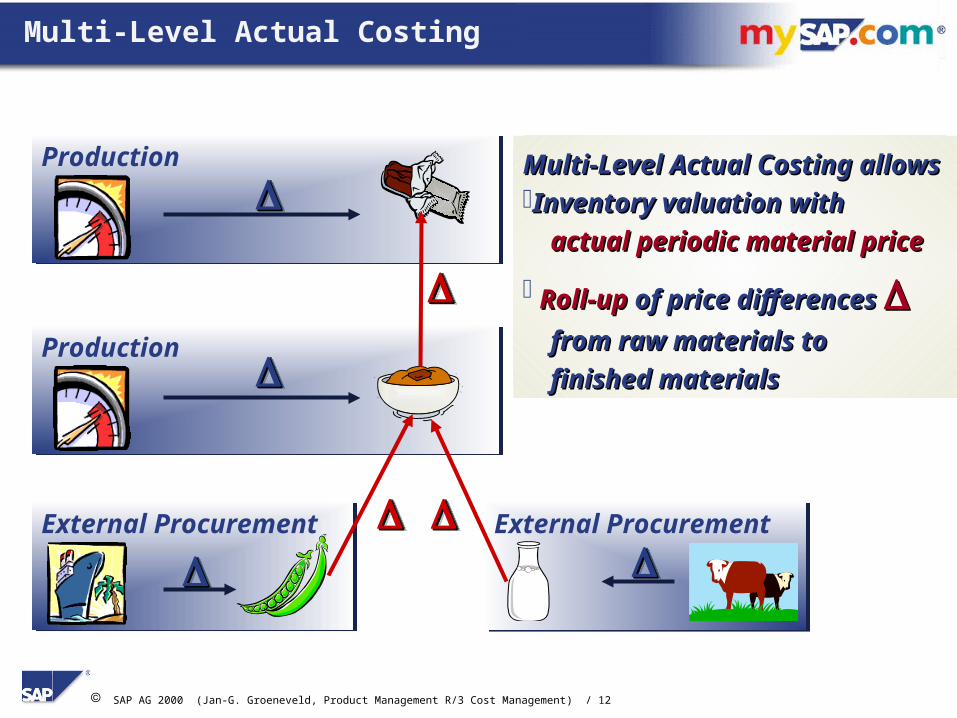

Multi-Level Actual Costing

Multi-Level Actual Costing allows Multi-Level Actual Costing allows Inventory valuation withInventory valuation with

actual periodic material priceactual periodic material price

Roll-upRoll-up of price differences of price differences

from raw materials to from raw materials to

finished materials finished materials

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 13

Integration ofIntegration ofMulti-LevelMulti-Level

Actual CostingActual Costing

Integration of Actual Costing

Profitability Profitability AnalysisAnalysis

Contribution Margins

Release 4.6c!

Release 4.6c!

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 14

Actual values in Profitability AnalysisActual values in Profitability Analysis Contribution Margin AccountingContribution Margin Accounting Cost of sales Cost of sales split into split into cost componentscost components Plan/ActualPlan/Actual Variance analysis Variance analysis

Actual Costing and Profitability Analysis

PlanPlan ActualActual Var. %Var. % Var. Abs.Var. Abs.

RevenuesRevenues:: 100,000 US$100,000 US$Sales Quantity:Sales Quantity: 1,000 pc1,000 pc

50,00050,000 45,00045,000 5,0005,000 10 %10 %Raw MaterialsRaw Materials4,0004,000 5,0005,000 -1,000-1,000 - 25 %- 25 %Labor variableLabor variable4,0004,000 4,5004,500 - 500- 500 - 13 %- 13 %Machine variableMachine variable

10,00010,000 7,0007,000 3,0003,000 30%30%Logistic ProcessesLogistic Processes5,0005,000 5,5005,500 - 500- 500 - 10 %- 10 %Material OverheadsMaterial Overheads

6,0006,00027,00027,000 33,00033,000 22 %22 %Contribution Margin IContribution Margin I

10,00010,000 10,00010,000 00 0 %0 %Labor fixLabor fix7,0007,000 7,0007,000 00 0 %0 %Machine fixMachine fix

10,00010,000 16,00016,000 6,0006,000 60 %60 %Contribution Margin IIContribution Margin II

Release 4.6c!

Release 4.6c!

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 15

Integration ofIntegration ofMulti-LevelMulti-Level

Actual CostingActual Costing

Integration of Actual Costing

Product Cost Product Cost PlanningPlanning

Standard Prices&

Cost ComponentSplit

Profitability Profitability AnalysisAnalysis

Contribution Margins

Release 4.6c!

Release 4.6c!

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 16

Actual Costing and Product Cost Planning

Variance AnalysisVariance AnalysisVariance AnalysisVariance Analysis

Actual Costing with Actual Costing with Cost ComponentsCost Components

Actual Costing with Actual Costing with Cost ComponentsCost Components

BOMRouting

PP Master Data

Mat Proc OHLab

Standard PriceStandard Pricewithwith

Cost Component SplitCost Component Split

Product CostProduct CostPlanningPlanning

Cost Estimate

Material Movements

Mat Proc OHLab

Periodic Unit PricePeriodic Unit Pricewithwith

Cost Component SplitCost Component Split

Multi-LevelMulti-LevelActual CostingActual Costing

Price Determination

Actual Quantity StructureActual Quantity Structure

Same cost componentSame cost component structure as in planning structure as in planning

No Cost EstimatesNo Cost Estimates necessary for Actual necessary for Actual Costing Costing

Optional: Primary costOptional: Primary cost component split component split

Same cost componentSame cost component structure as in planning structure as in planning

No Cost EstimatesNo Cost Estimates necessary for Actual necessary for Actual Costing Costing

Optional: Primary costOptional: Primary cost component split component split

Release 4.6c!

Release 4.6c!

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 17

Integration ofIntegration ofMulti-LevelMulti-Level

Actual CostingActual Costing

Integration of Actual Costing

Product Cost Product Cost PlanningPlanning

Standard Prices&

Cost ComponentSplit

Profitability Profitability AnalysisAnalysis

Contribution Margins

Cost Center Cost Center AccountingAccounting

Actual Prices of Activities and

Business Processes

Release 4.6c!

Release 4.6c!

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 18

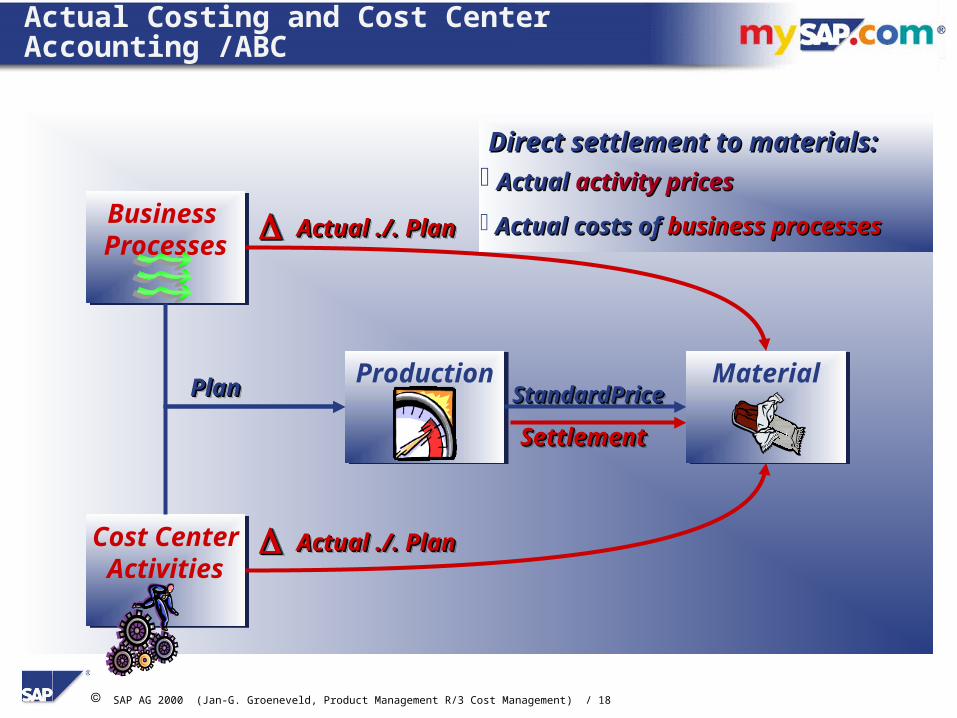

Actual Costing and Cost Center Accounting /ABC

ProductionProduction MaterialMaterial

Cost CenterActivities

Cost CenterActivities

Business ProcessesBusiness Processes

Actual ./. PlanActual ./. PlanActual ./. PlanActual ./. Plan

Actual ./. PlanActual ./. PlanActual ./. PlanActual ./. Plan

PlanPlanPlanPlan StandardPriceStandardPriceStandardPriceStandardPrice

SettlementSettlementSettlementSettlement

Direct settlement to materials:Direct settlement to materials: Actual Actual activity pricesactivity prices

Actual costs of Actual costs of business processesbusiness processes

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 19

IInventory nventory AAccounting ccounting WWithithMMaterial aterial LLedgeredger

Content

Why Why YYOOUU want Multi-Level Actual Costing! want Multi-Level Actual Costing!

Environment of Material LedgerEnvironment of Material Ledger

Traditional Valuation StrategiesTraditional Valuation Strategies

Actual Costing in Three StepsActual Costing in Three Steps

Future Prices; Customizing; GoodiesFuture Prices; Customizing; Goodies

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 20

Material MasterMaterial Master Price ControlPrice Control

Valuation Strategies without Material Ledger

Standard Price(S-Price)

- Constant- Recommended for all material types

Moving average price(V-Price)

- Adjusted with every receipt- If at all, only to be used for raw materials and materials procured externally

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 21

Posting Example: Moving average price 1

StockStock GR/IR AccountGR/IR Account

VendorVendor

Procedure Stock Stock value V price

Begin. inventory: 100 PC at 2.00 100 200.- 2.00

Goods receipt: 100 PC at 3.00 200 500.- 2.50

Invoice receipt: 100 PC at 4.00 200 600.- 3.00

Goods issue: 150 PC at 3.00 50 150.- 3.00

Procedure Stock Stock value V price

Begin. inventory: 100 PC at 2.00 100 200.- 2.00

Goods receipt: 100 PC at 3.00 200 500.- 2.50

Invoice receipt: 100 PC at 4.00 200 600.- 3.00

Goods issue: 150 PC at 3.00 50 150.- 3.00

11

22

33

11 200,-

300,-

100,-

200,-

300,-

100,-

22300,-300,- 22

44

400,-400,-

300,-300,-

44

ConsumptionConsumption

450,-450,-

33

33

450,-450,-

44

If the invoice receipt is for 100 units, the stock

coverageis 200 units:

all differences stock

If the invoice receipt is for 100 units, the stock

coverageis 200 units:

all differences stock

33

Stock Coverage

ok

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 22

With a delayed invoice receiptOf 100 units:

a shortage of 50 units price differences despite MAP

With a delayed invoice receiptOf 100 units:

a shortage of 50 units price differences despite MAP

Posting Example: Moving average price 2

StockStock

Price differencePrice difference

GR/IR accountGR/IR account

VendorVendor

Procedure Stock Stock Value V Price

Begin. inventory: 100 200.- 2.00

Goods receipt: 100 PC at 3.00 200 500.- 2.50

Goods issue: 150 PC at 2.50 50 125.- 2.50

Invoice receipt: 100 PC at 4.00 50 175.- 3.50

Procedure Stock Stock Value V Price

Begin. inventory: 100 200.- 2.00

Goods receipt: 100 PC at 3.00 200 500.- 2.50

Goods issue: 150 PC at 2.50 50 125.- 2.50

Invoice receipt: 100 PC at 4.00 50 175.- 3.50

11

22

33

11 200.-

300.-

50.-

200.-

300.-

50.-

22300.-300.- 22

50.- 50.-

44

44400.-400.-

300.-300.-

44

ConsumptionConsumption

375.-375.-33

33 375.-375.-

44

44

Stock Shortage

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 23

Posting Example: Moving average price 3

Procedure Stock Stock Value V Price

Begin. inventory: 100 200.- 2.00

Goods receipt: 100 PC at 2.20 200 420.- 2.10

Goods receipt: 100 PC at 2.40 300 660.- 2.20

Goods issue: 200 PC at 2.20 100 220.- 2.20

Invoice receipt: 100 PC at 3.00 100 300.- 3.00

Invoice receipt: 100 PC at 3.00 100 360.- 3.60

Procedure Stock Stock Value V Price

Begin. inventory: 100 200.- 2.00

Goods receipt: 100 PC at 2.20 200 420.- 2.10

Goods receipt: 100 PC at 2.40 300 660.- 2.20

Goods issue: 200 PC at 2.20 100 220.- 2.20

Invoice receipt: 100 PC at 3.00 100 300.- 3.00

Invoice receipt: 100 PC at 3.00 100 360.- 3.60

With multiple delayed invoice receipts: Danger of Incorrect Valuation!

With multiple delayed invoice receipts: Danger of Incorrect Valuation!

Eventhough all receipts between 2.- and 3.- were

valuated!

Eventhough all receipts between 2.- and 3.- were

valuated!

Δ 80.- in stockΔ 80.-

in stock

Δ 60.- in stockΔ 60.-

in stock

Stock Coverage

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 24

Characteristics of Price Control V

+ The stock value is adjusted each time goods are received

+ Real-time price fluctations are posted to stock

+ Price difference postings only take place in exceptional cases

- Price fluctuations cannot be adjusted to the finished products of higher levels (S price)

- Only recommended for raw materials or goods procured externally (real-time price for goods receipt known)

- False entries with severe consequences (compounded errors)

- Danger of incorrect valuations with delayed invoice receipt

Moving average price

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 25

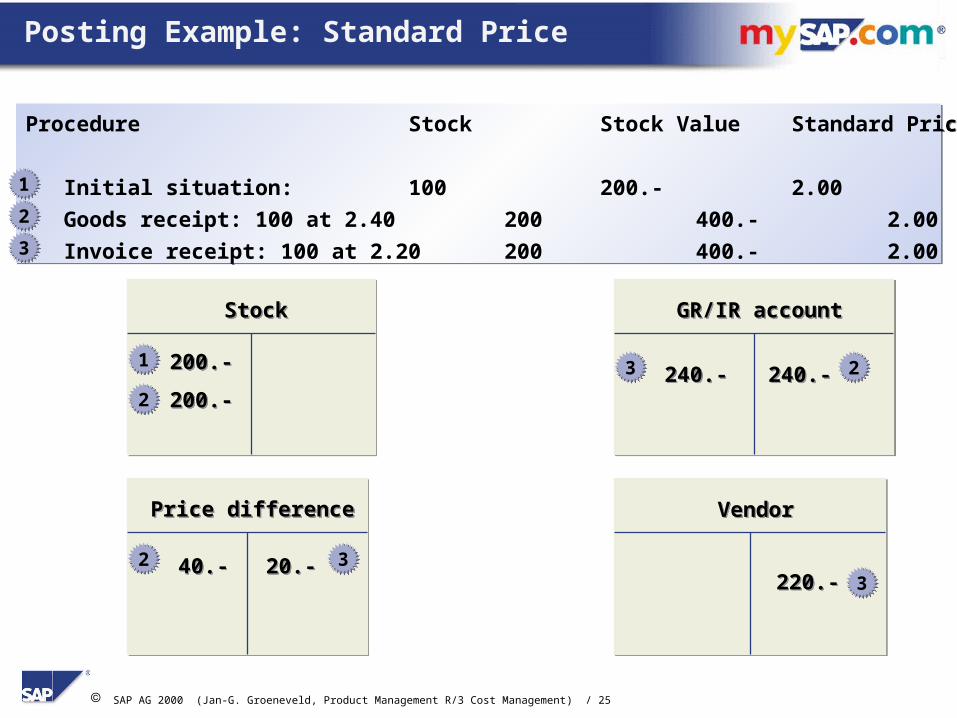

Posting Example: Standard Price

StockStock

Price differencePrice difference

GR/IR accountGR/IR account

VendorVendor

Procedure Stock Stock Value Standard Price

Initial situation: 100 200.- 2.00

Goods receipt: 100 at 2.40 200 400.- 2.00

Invoice receipt: 100 at 2.20200 400.- 2.00

Procedure Stock Stock Value Standard Price

Initial situation: 100 200.- 2.00

Goods receipt: 100 at 2.40 200 400.- 2.00

Invoice receipt: 100 at 2.20200 400.- 2.00

11

22

33

11 200.-

200.-

200.-

200.-22240.-240.- 22

22 40.-40.-

33

333320.-20.-

220.-220.-

240.-240.-

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 26

Characteristics of Price Control S

+ All stock postings take place at the standard price

+ Prices remain constant throughout at least one period

+ Price fluctuations do not debit/credit the cost objects (e.g. orders)

consistant controlling with the standard price as a bench mark

+ Calculation of the standard prices with cost component splits

+ Recommended for all material types

- Price differences cannot be subsequently adjusted to the ending

inventories or the consumed products (sales, production

withdrawals)

Standard Price

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 27

Period-End Closing: Valuation Problems

Valuation PeriodValuation Period

Distribution of Price Differences?

Actual Prices?

Finished Products

Ending Inventory: Raw MaterialsRaw Materials II

Raw Materials I

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 28

Variances of Standard Cost Accounting

External procurement

Ergebnis FI

Order

Order

Cost center Activitytype

Activitytype

V price

S price

S price

Result (FI)Result (FI)Variance categoriesVariance categories Price difference accountPrice difference account==

Cost elementsCost elements

ProductionCost Centers

Result (CO-PA)

Stock accounts

Cost center Activity type

Activity type

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 29

IInventory nventory AAccounting ccounting WWithithMMaterial aterial LLedgeredger

Content

Why Why YYOOUU want Multi-Level Actual Costing! want Multi-Level Actual Costing!

Environment of Material LedgerEnvironment of Material Ledger

Traditional Valuation StrategiesTraditional Valuation Strategies

Actual Costing in Three StepsActual Costing in Three Steps

Future Prices; Customizing; GoodiesFuture Prices; Customizing; Goodies

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 30

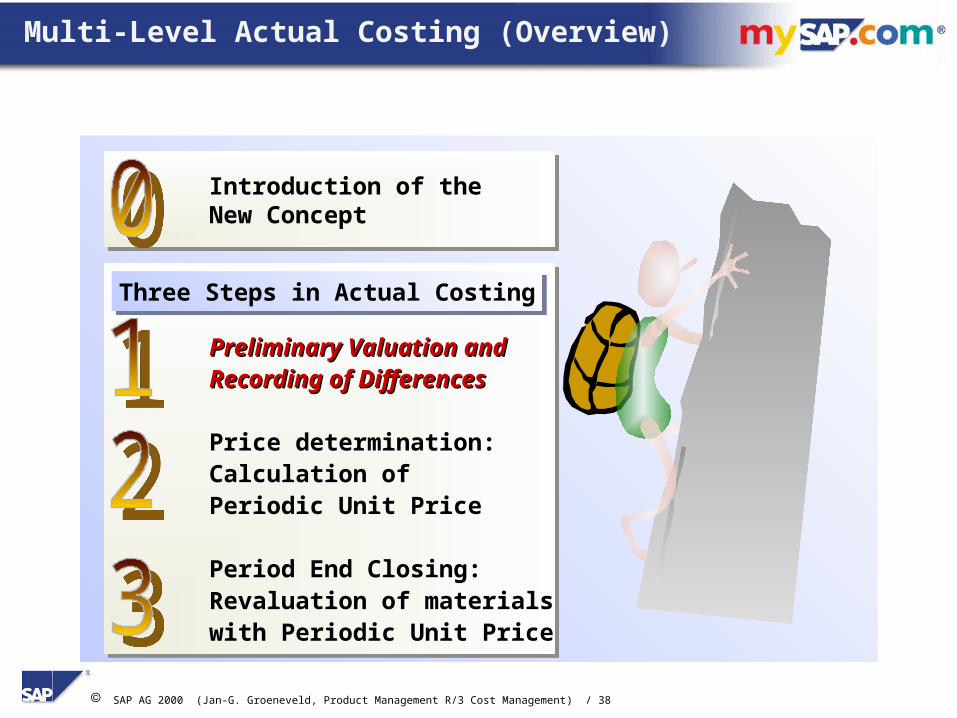

Multi-Level Actual Costing (Overview)

Introduction of theIntroduction of theNew ConceptNew ConceptIntroduction of theIntroduction of theNew ConceptNew Concept

Preliminary Valuation andRecording of Differences

Price determination:Calculation ofPeriodic Unit Price

Period End Closing:Revaluation of materialswith Periodic Unit Price

Preliminary Valuation andRecording of Differences

Price determination:Calculation ofPeriodic Unit Price

Period End Closing:Revaluation of materialswith Periodic Unit Price

Three Steps in Actual CostingThree Steps in Actual Costing

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 31

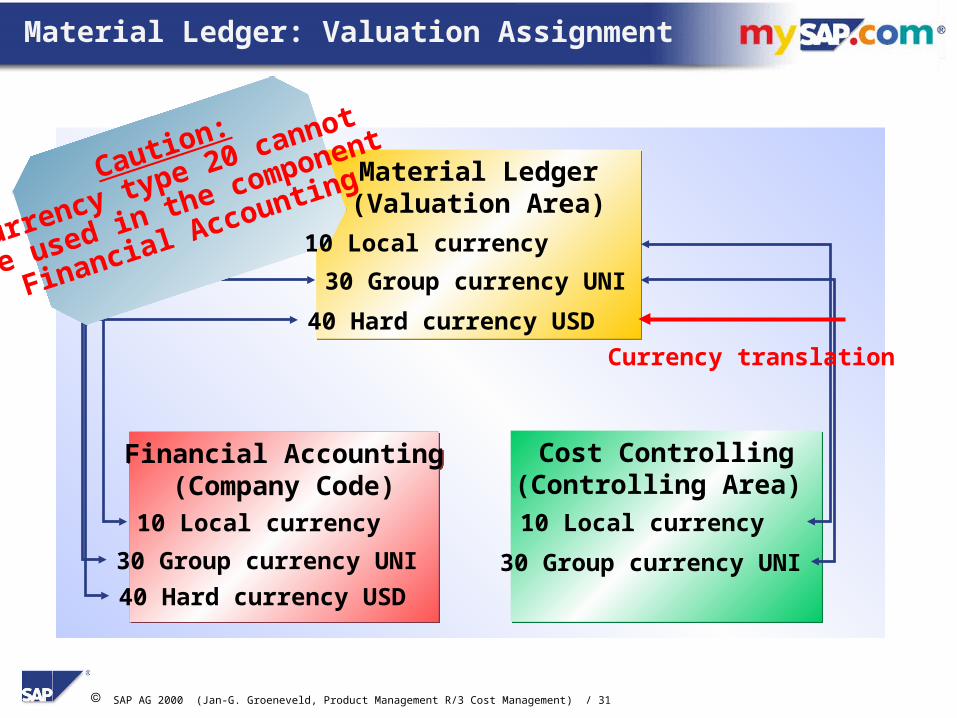

Material Ledger(Valuation Area)Material Ledger(Valuation Area)

40 Hard currency USD

30 Group currency UNI

Cost Controlling(Controlling Area) Cost Controlling

(Controlling Area)

10 Local currency

30 Group currency UNI

Currency translation

Financial Accounting(Company Code)

Financial Accounting(Company Code)

10 Local currency

30 Group currency UNI

40 Hard currency USD

Caution:

Currency type 20 cannot

be used in the component

Financial Accounting

Material Ledger: Valuation Assignment

10 Local currency

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 32

ValuationCompany Code

CurrencyGroup

CurrencyHard

Currency

10

11

12

Legal

Group

Profit-Center

30

31

32

40

Multiple Currencies and Valuations

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 33

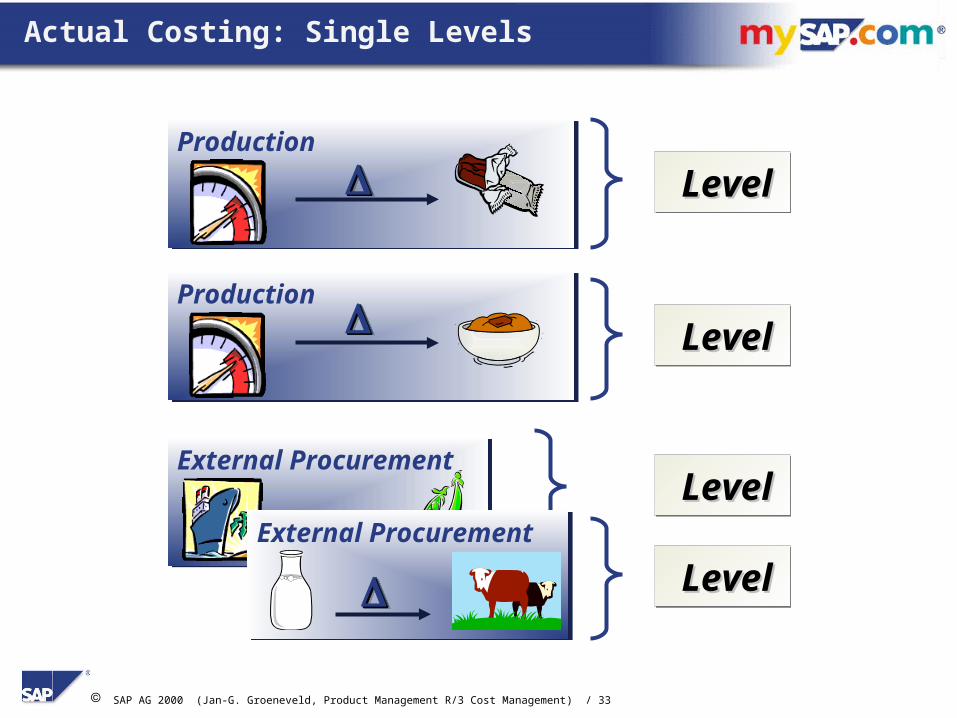

Actual Costing: Single Levels

ProductionProduction

ProductionProduction

LevelLevelLevelLevel

LevelLevelLevelLevel

LevelLevelLevelLevelExternal ProcurementExternal Procurement

External ProcurementExternal Procurement

LevelLevelLevelLevel

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 34

ProductionProduction

ProductionProduction

Actual Costing: Multi-Level

LevelLevelLevelLevel

LevelLevelLevelLevel

LevelLevelLevelLevel

Multi-Multi-LevelLevelMulti-Multi-LevelLevel

External ProcurementExternal Procurement

External ProcurementExternal Procurement

LevelLevelLevelLevel

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 35

External ProcurementExternal Procurement External ProcurementExternal Procurement

ProductionProduction

ProductionProduction

Multi-Level Actual Costing

Material Valuation with Material Valuation with

Multi-Level Actual CostingMulti-Level Actual Costing Preliminary ValuationPreliminary Valuation

During the Period During the Period

Revaluation at Period EndRevaluation at Period End

with Actual Price with Actual Price

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 36

Materials(Receipts)

Materials(Receipts)

Materials(Withdrawals)

Materials(Withdrawals)

Procurement AlternativeProcurement Alternative

Procurement ProcessProcurement Process

Quantity Structure: Elements:

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 37

MaterialsMaterials

ProcurementAlternative

ProcurementAlternative

ProcessProcess

Structured Elements

HierarchicalAssembly

MultipleMethods of

Procurement

Co-Production CyclicalProduction

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 38

Multi-Level Actual Costing (Overview)

Introduction of theNew ConceptIntroduction of theNew Concept

Preliminary Valuation andPreliminary Valuation andRecording of DifferencesRecording of Differences

Price determination:Calculation ofPeriodic Unit Price

Period End Closing:Revaluation of materialswith Periodic Unit Price

Preliminary Valuation andPreliminary Valuation andRecording of DifferencesRecording of Differences

Price determination:Calculation ofPeriodic Unit Price

Period End Closing:Revaluation of materialswith Periodic Unit Price

Three Steps in Actual CostingThree Steps in Actual Costing

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 39

Receipts

Cumulative inventory 1000 250 25.00

Ending inventory 1000 250 25.00

Other receipts/consum

Consumption

Preliminary Preliminary valuationvaluation

Preliminary Preliminary valuationvaluationQuantityQuantityQuantityQuantity

Beginning inventory 1000 250 25.00

PricePricedifferencedifference PricePrice

Differences between Standard Price and actual price

Real time valuation with Standard Price

Average actual price of category (line)

Material Price Analysis: Content

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 40

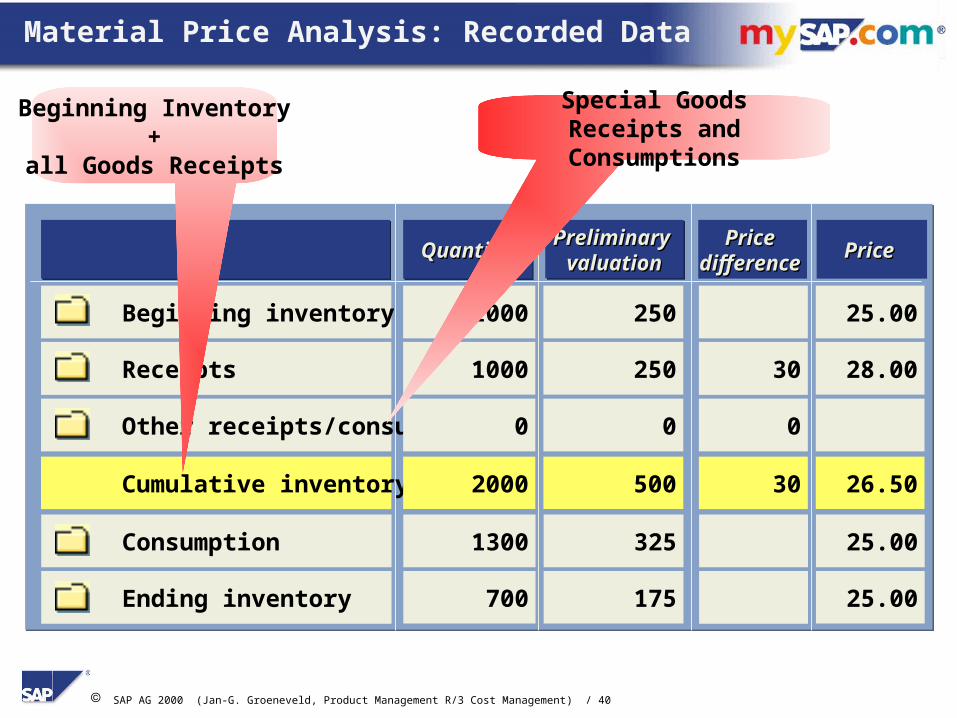

Material Price Analysis: Recorded Data

Receipts 1000 250 30 28.00

Cumulative inventory 2000 500 30 26.50

Ending inventory 700 175 25.00

Other receipts/consum 0 0 0

Consumption 1300 325 25.00

Preliminary Preliminary valuationvaluation

Preliminary Preliminary valuationvaluationQuantityQuantityQuantityQuantity

Beginning inventory 1000 250 25.00

PricePricedifferencedifference PricePrice

Beginning Inventory+

all Goods Receipts

Special Goods Receipts and Consumptions

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 41

Standard Cost Standard Cost EstimateEstimate

Standard Cost Standard Cost EstimateEstimateMaterial MasterMaterial MasterMaterial MasterMaterial Master Material Ledger Material Ledger

Document OverviewDocument OverviewMaterial Ledger Material Ledger

Document OverviewDocument Overview

Document itemsDocument itemsDocument itemsDocument items Source Source documentdocument

Source Source documentdocument

Document Document headerheader

Document Document headerheader

Accounting Accounting documentsdocumentsAccounting Accounting documentsdocuments

FIFIPPPP MMMM

MMMM CO-CO-PCPPCP

COCOCO-CO-PAPACOCO

Receipts 100 10.000 1.000 110

Cumulative inventory 170 17.000 3.400 120

Ending inventory 140 14.000 100

Other receipts/consumption 50 5.000 2.400 148

Consumption 30 3.000 100

Beginning inventory 20 2.000 100

Prel. val.Category Quantity Price diff. Price

Interactive Information

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 42

Price Differences occur with

External procurement (order / invoice value)

In-house production (settlement of orders)

Initial entry of stock balances (external value posted)

Transfer postings (standard price in involved plants)

Subcontracting (subsequent charging)

Debit / credit of material

Price Differences

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 43

Exchange Rate Differences occurExchange Rate Differences occur withwith

Goods Receipts with reference to Purchase Ordersif the exchange rate at the time of Invoice Receiptif the exchange rate at the time of Invoice Receipt

differs from the

exchange rate at the Time of Goods Receipts,Time of Goods Receipts, or from the assumed exchange rateassumed exchange rate

Prerequisite: You activate the treatment of exchange rate differences in Customizing!

Exchange Rate Differences

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 44

The Logistic InvoThe Logistic Invoice Verification ice Verification HAS TO BE HAS TO BE used with used with Material Ledger !!Material Ledger !!

AdvantagesAdvantages Invoice verification across company codes Distributed scenarios Any number of purchase orders / deliveries in a transaction Manual invoice reduction Total-based invoice reduction Supports transfer prices

For more Details, see Note 116272 (Release 4.0), 127366 (Release 4.5), or 144081 (Enjoy SAP)

The Logistic InvoThe Logistic Invoice Verification ice Verification HAS TO BE HAS TO BE used with used with Material Ledger !!Material Ledger !!

AdvantagesAdvantages Invoice verification across company codes Distributed scenarios Any number of purchase orders / deliveries in a transaction Manual invoice reduction Total-based invoice reduction Supports transfer prices

For more Details, see Note 116272 (Release 4.0), 127366 (Release 4.5), or 144081 (Enjoy SAP)

Example: Single-Level Price Differences / Logistics Invoice Verification

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 45

MaterialMaterialLedgerLedger

Inventory ValuationInventory Valuation

Example: Single-Level Price Differences/ Production Orders

Cost ObjectsCost ObjectsCost ObjectsCost Objects

Credit:

Goods Rreceipt:Credit at Standard Price

Work In Process- WIP at actual (total settlement)- WIP at target (periodic settlement)

Credit:

Goods Rreceipt:Credit at Standard Price

Work In Process- WIP at actual (total settlement)- WIP at target (periodic settlement)

Debit:

Material Costs (Standard price)

Activity Prices (optional: Actual Price)

Overhead costs

Process costs (optional: Actual Prices)

Debit:

Material Costs (Standard price)

Activity Prices (optional: Actual Price)

Overhead costs

Process costs (optional: Actual Prices)

Variances:Debit - goods receipt - WIP

Variances:Debit - goods receipt - WIP

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 46

Structured Value Chains: Process Types

1000

...

...

...

...

250

...

...

...

...

30

...

...

...

...

28.00

...

...

...

...

Cumulative inventory 2000 500 30 26.50

Other receipts/cons. 0 0 0

Preliminary Preliminary valuationvaluation

Preliminary Preliminary valuationvaluationQuantityQuantityQuantityQuantity

1000 250 25.00

PricePricedifferencedifference PricePrice

Beginning inventory

Receipts

Production

Purchase order

Stock transfer

Subcontracting

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 47

Controlling Levels of the Material

Process Type Process Type

Purchase orderPurchase order

SubcontractingSubcontracting

Stock transferStock transfer

Reposting/material

Reposting/material

ProductionProduction

Plant/materialPlant/material

Purchasing organization/ vendorPurchasing organization/ vendor

Plant/materialPlant/material

Purchasing organization/ vendorPurchasing organization/ vendor

Plant/materialPlant/material

Issuing plantIssuing plant

Plant/materialPlant/material

Issuing plant/ materialIssuing plant/ material

Plant/materialPlant/material

Production plant/ planning plantProduction plant/ planning plant

BOM / routingBOM / routing

Production versionProduction version

Procurement alternatives

Characteristics of the Controlling LevelsCharacteristics of the Controlling Levels

...

...

...

...

...

Vendor A, Vendor B, ...

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 48

Procurement Alternatives

1000

...

...

...

...

250

...

...

...

...

30

...

...

...

...

28.00

...

...

...

...

Cumulative inventory 2000 500 30 26.50

Preliminary Preliminary valuationvaluation

Preliminary Preliminary valuationvaluationQuantityQuantityQuantityQuantity

1000 250 25.00

PricePricedifferencedifference PricePrice

Beginning inventory

Receipts

Production

Purchase order

Vendor A/ Porg1

Vendor B/ POrg1....IR..

....GR...

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 49

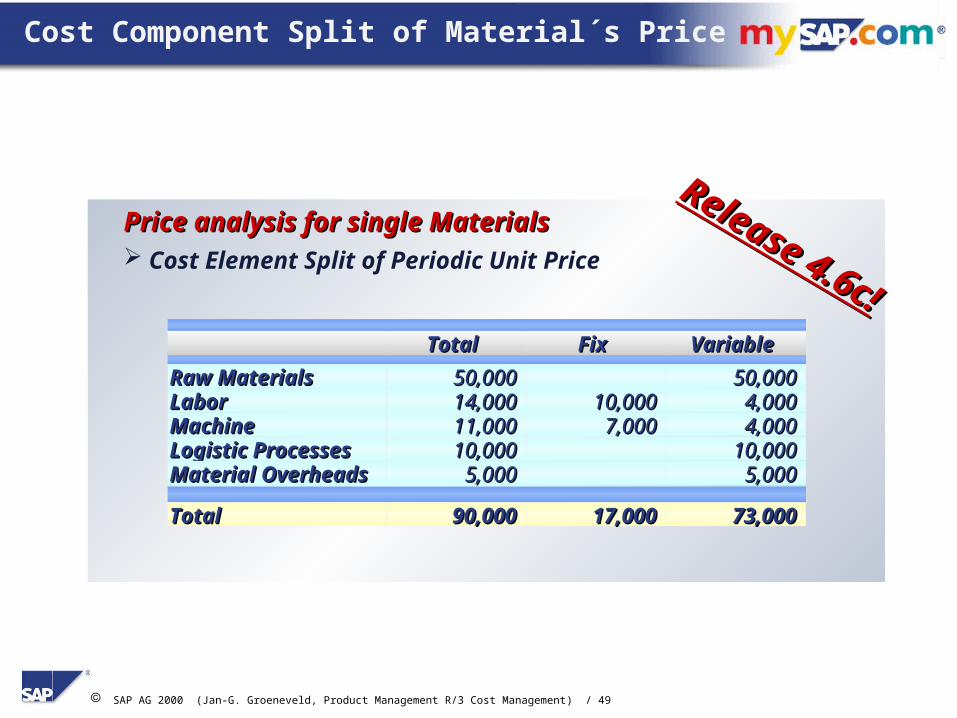

Price analysis for single MaterialsPrice analysis for single Materials Cost Element Split of Periodic Unit Price

Cost Component Split of Material´s Price

50,00050,000 50,00050,000Raw MaterialsRaw Materials14,00014,000 10,00010,000 4,0004,000LaborLabor11,00011,000 7,0007,000 4,0004,000MachineMachine10,00010,000 10,00010,000Logistic ProcessesLogistic Processes

5,0005,000 5,0005,000Material OverheadsMaterial Overheads

90,00090,000 17,00017,000 73,00073,000TotalTotal

TotalTotal FixFix VariableVariable

Release 4.6c!

Release 4.6c!

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 50

Multi-Level Actual Costing (Overview)

Introduction of theNew ConceptIntroduction of theNew Concept

Preliminary Valuation andRecording of Differences

Price determination:Price determination:Calculation ofCalculation ofPeriodic Unit PricePeriodic Unit Price

Period End Closing:Revaluation of materialswith Periodic Unit Price

Preliminary Valuation andRecording of Differences

Price determination:Price determination:Calculation ofCalculation ofPeriodic Unit PricePeriodic Unit Price

Period End Closing:Revaluation of materialswith Periodic Unit Price

Three Steps in Actual CostingThree Steps in Actual Costing

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 51

Cost Controlling: Period End Activities

Cost ObjectControlling

Material Ledger2 3Cost CenterAccounting

Cost Center 1

Cost Center 2

1

External Procurement

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 52

Cost Controlling: Period End Activities Release 4.6

Cost ObjectControlling

Material Ledger2 3Cost CenterAccounting

Cost Center 1

Cost Center 2

1

External Procurement

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 53

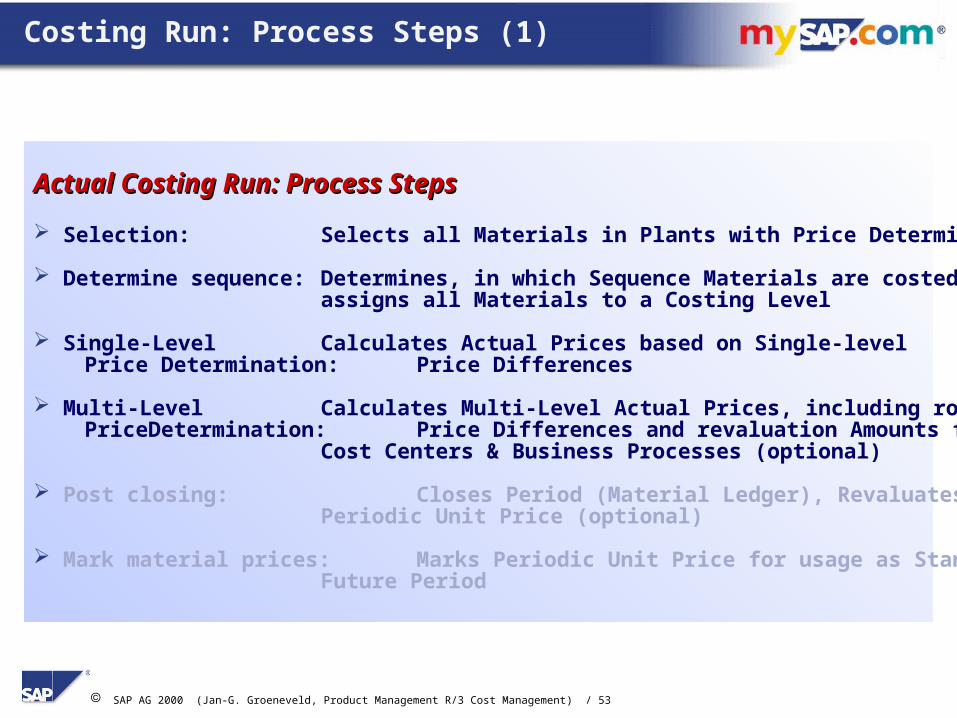

Costing Run: Process Steps (1)

Actual Costing Run: Process StepsActual Costing Run: Process Steps

Selection: Selects all Materials in Plants with Price Determination „3“

Determine sequence: Determines, in which Sequence Materials are costed, andassigns all Materials to a Costing Level

Single-Level Calculates Actual Prices based on Single-level Price Determination: Price Differences

Multi-Level Calculates Multi-Level Actual Prices, including roll-up of PriceDetermination: Price Differences and revaluation Amounts from

Cost Centers & Business Processes (optional)

Post closing: Closes Period (Material Ledger), Revaluates Inventory with Periodic Unit Price (optional)

Mark material prices: Marks Periodic Unit Price for usage as Standard Price in aFuture Period

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 54

Costing Run: Revaluation of Activities andBusiness Processes

ProductionProduction MaterialMaterial

Cost CenterActivities

Cost CenterActivities

Business ProcessesBusiness Processes

Actual ./. PlanActual ./. PlanActual ./. PlanActual ./. Plan

Actual ./. PlanActual ./. PlanActual ./. PlanActual ./. Plan

PlanPlanPlanPlan StandardPriceStandardPriceStandardPriceStandardPrice

SettlementSettlementSettlementSettlement

Direct settlement to materials:Direct settlement to materials: Actual Actual activity pricesactivity prices

Actual costs of Actual costs of business processesbusiness processes

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 55

External ProcurementExternal Procurement External ProcurementExternal Procurement

ProductionProduction

ProductionProduction

Single-Level Price Determination

Single-Level Price DeterminationSingle-Level Price Determination Actual Material Price based onActual Material Price based on

Costs of Procurement Costs of Procurement

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 56

External ProcurementExternal Procurement External ProcurementExternal Procurement

ProductionProduction

ProductionProduction

Multi-Level Price Determination

Multi-Level Price DeterminationMulti-Level Price Determination Roll-up of price differencesRoll-up of price differences

from raw materials to from raw materials to

finished materials finished materials

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 57

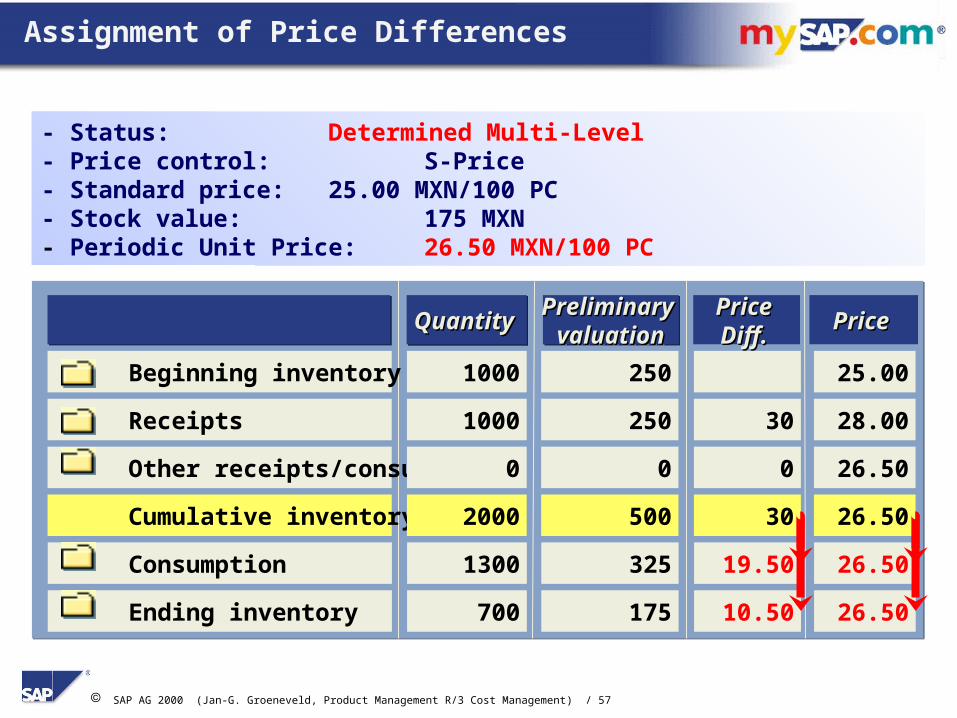

Assignment of Price Differences

- Status: Determined Multi-Level - Price control: S-Price- Standard price: 25.00 MXN/100 PC- Stock value: 175 MXN- Periodic Unit Price: 26.50 MXN/100 PC

Receipts 1000 250 30 28.00

Cumulative inventory 2000 500 30 26.50

Ending inventory 700 175 26.50 10.50

Other receipts/consum 0 0 0 26.50

Consumption 1300 325 19.50 26.50

Preliminary Preliminary valuationvaluation

Preliminary Preliminary valuationvaluationQuantityQuantityQuantityQuantity

Beginning inventory 1000 250 25.00

PricePriceDiDiffff..

PricePrice

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 58

Multi-Level Actual Costing (Overview)

Introduction of theNew ConceptIntroduction of theNew Concept

Preliminary Valuation andRecording of Differences

Price determination:Calculation ofPeriodic Unit Price

Period End Closing:Period End Closing:Revaluation of materialsRevaluation of materialswith Periodic Unit Pricewith Periodic Unit Price

Preliminary Valuation andRecording of Differences

Price determination:Calculation ofPeriodic Unit Price

Period End Closing:Period End Closing:Revaluation of materialsRevaluation of materialswith Periodic Unit Pricewith Periodic Unit Price

Three Steps in Actual CostingThree Steps in Actual Costing

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 59

Costing Run: Process Steps (2)

Actual Costing Run: Process StepsActual Costing Run: Process Steps

Selection: Selects all Materials in Plants with Price Determination „3“

Determine sequence: Determines, in which Sequence Materials are costed, andassigns all Materials to a Costing Level

Single-Level Calculates Actual Prices based on Single-level Price Determination: Price Differences

Multi-Level Calculates Multi-Level Actual Prices, including roll-up of PriceDetermination: Price Differences and revaluation Amounts from

Cost Centers & Business Processes (optional)

Post closing: Closes Period (Material Ledger), Revaluates Inventory with Periodic Unit Price (optional)

Mark material prices: Marks Periodic Unit Price for usage as Standard Price in aFuture Period

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 60

Material consumptionMaterial consumptionVB 325

Material stockMaterial stock325 VBBI 250

ZU 250

GR/IR allocationGR/IR allocationRE 260 260 ZU

VendorVendor280 RE

Price differencePrice difference

ZU 10RE 20

Posting Example: before Closing Entries

GRGR

IRIR

CNSCNS

GRGR

GRGRIRIR IRIR

IRIR

CNSCNS

CNSCNSGRGR

Stock value:175 MXN

Stock value:175 MXN

Standard price: 25 MXN / 100 unitsPeriodic unit price: 26.50 MXN / 100 unitsStandard price: 25 MXN / 100 unitsPeriodic unit price: 26.50 MXN / 100 units

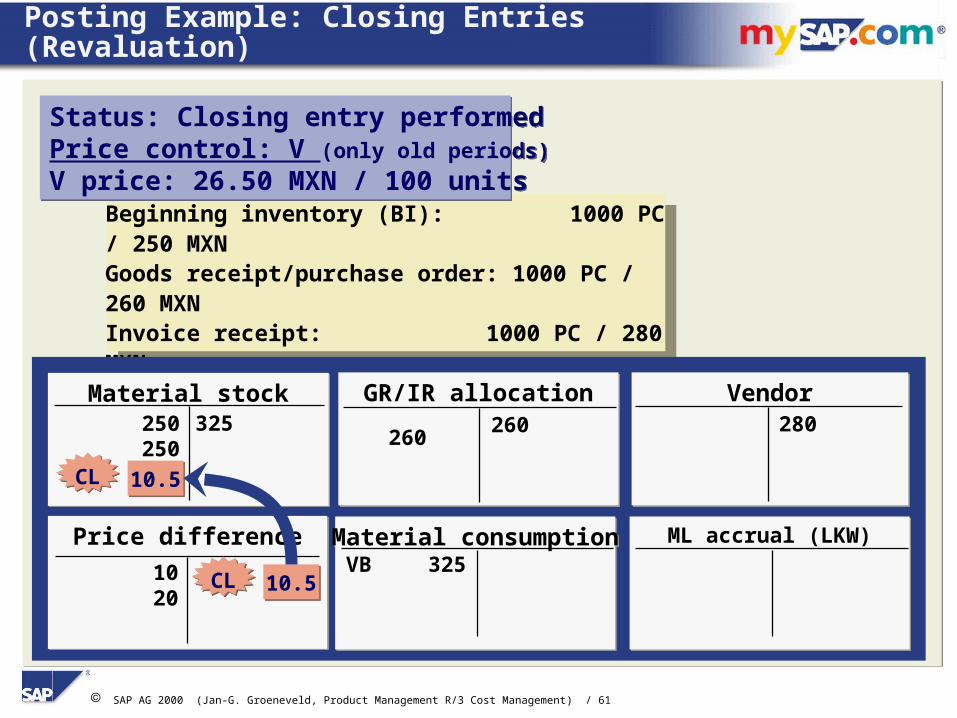

Beginning inventory (BI): 1000 PC / 250 MXNGoods receipt/purchase order: 1000 PC / 260 MXNInvoice receipt: for 1000 PC / 280 MXN Consumption: 1300 PC / 325 MXNEnding inventory: 700 PC

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 61

Beginning inventory (BI): 1000 PC / 250 MXNGoods receipt/purchase order: 1000 PC / 260 MXNInvoice receipt: 1000 PC / 280 MXN Consumption: 1300 PC / 325 MXNEnding inventory: 700 PC

Material consumptionMaterial consumptionVB 325

Material stockMaterial stock325 250

250

GR/IR allocationGR/IR allocation 260 260

VendorVendor280

Price differencePrice difference

10 20

Posting Example: Closing Entries (Revaluation)

Status: Closing entry performedPrice control: V (only old periods)

V price: 26.50 MXN / 100 units

Status: Closing entry performedPrice control: V (only old periods)

V price: 26.50 MXN / 100 units

ML accrual (LKW)ML accrual (LKW)

10.510.5

10.510.5CLCL

CLCL

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 62

Period 1 Period 2

Period 1:Prel.ValuationPeriod 1:Prel.Valuation

Stock Price Dif

Period 1: Act.CostingPeriod 1: Act.Costing

Stock Price Dif

+

Revaluation: Allocation of Price Differences

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 63

Period 1 Period 2

Price ControlDuring Period: Preliminary Valuation Price (S)After Closing Entries: Periodic Unit Price (V)

For Period 1:

Price Control: S

For Period 2:

Price Control S

For Period 1:

Price Control V

For Period 0:

Price Control V

Revaluation: Change of Price Control

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 64

Costing Run: Analysis of the Variances

AC530 1088Level 0 50Level 1 450Level 2 550Level 3 38....

Results overview Material list

Material Plant LevelSL ML CL S price Per. unit price % var.

1850 2560- 3580 1228,83

700 175 0 0

1250 560- 1580 1228.83

0 78- 150 1325,22

Single-level difference

Single-level differenceQuantityQuantity

1000 175 26,5010,50

Multileveldifference Price

Beginning inventory

Receipts

Production

Version1

Version 2....RE..

....WE...

850 560- 923 1123.45

ACT-BCD00 6000 1 750.00 745.00 -0.67ACT-LCD00 6000 1 25.00 26.50 6.00ACT-DCD00 6000 2 1177.50 1228.83 21.40ACT-DCD00 6100 3 1250.00 1188.20 -5.80...

Actual BOMProd. version 01: new machine Output quantity ACT-DCD00: 850 PCInput quantity ACT-LCD00: 888 PCInput quantity ACT-BCD00: 850 PC Inpt int. activity E 530CC00/530AT100 setup hours 12 H Inpt int. activity E 530CC00/530AT200 masch.hour 24 H

Actual BOMProd. version 01: new machine Output quantity ACT-DCD00: 850 PCInput quantity ACT-LCD00: 888 PCInput quantity ACT-BCD00: 850 PC Inpt int. activity E 530CC00/530AT100 setup hours 12 H Inpt int. activity E 530CC00/530AT200 masch.hour 24 H

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 65

IInventory nventory AAccounting ccounting WWithithMMaterial aterial LLedgeredger

Content

Why Why YYOOUU want Multi-Level Actual Costing! want Multi-Level Actual Costing!

Environment of Material LedgerEnvironment of Material Ledger

Traditional Valuation StrategiesTraditional Valuation Strategies

Actual Costing in Three StepsActual Costing in Three Steps

Future Prices; Customizing; GoodiesFuture Prices; Customizing; Goodies

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 66

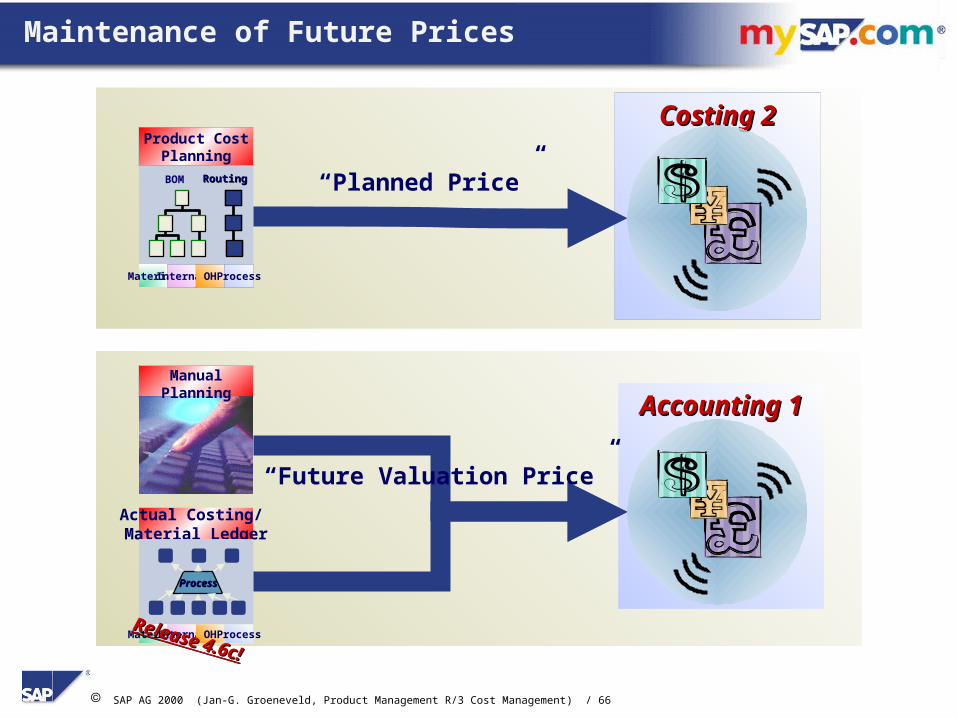

Maintenance of Future Prices

Accounting 1Accounting 1

Actual Costing/ Material Ledger

ProcessProcess

MaterialInternalOHProcessRelease 4.6c!

Release 4.6c!

ManualPlanning

“Future Valuation Price”

BOM RoutingRouting

Product CostPlanning

MaterialInternalOHProcess

“Planned Price”

Costing 2Costing 2

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 67

Release of Future Price

Costing 2Costing 2Accounting 1Accounting 1

CurrentCurrentStandard PriceStandard Price

Costing 2Costing 2Planned PricePlanned Price

Accounting 1Accounting 1Future Valuation PriceFuture Valuation Price Manual ReleaseManual Release

Dynymic ReleaseDynymic Releasewith firstwith first

Material PostingMaterial Posting

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 68

IIMMGG

Customizing: Material Ledger / Actual Costing

Material Ledger Type for each valuation areaMaterial Ledger Type for each valuation area

Activate Actual Costingfor each valuation areaActivate Actual Costingfor each valuation area

Price determination(new materials)Price determination(new materials)

transaction-basedtransaction-based

single/multilevelsingle/multilevel

Activate Material Ledger for each valuation areaActivate Material Ledger for each valuation area

Maintain ML Number RangesMaintain ML Number Ranges

Dynamic Price Changes(optional for each valuation area)Dynamic Price Changes(optional for each valuation area)

Alternative Update Structure(optional for each valuation area)Alternative Update Structure(optional for each valuation area)

Production StartupProduction Startup

Currency and Valuation settingsCurrency and Valuation settings

Optional:Activity Types UpdateOptional:Activity Types Update

nono

yes, only quantitiesyes, only quantities

yes, with actual prices

yes, with actual prices

SAP AG 2000 (Jan-G. Groeneveld, Product Management R/3 Cost Management) / 69

Production Startup

To be starter from the Menu of Material Ledger

Creates Material Ledger Master Records

Converts stock values of Material Ledger to

stock values of Financial Accounting

(second and third currency)

Sets ML indicators in all Material Master records

Sets Material Price Determination Indicator

in Material Masters to „2“ (can be changed to „3“)

Fixes the Currencies used

Sets the Productive Indicator

Production StartupProduction Startup

See Note 108374