“complete guide to tax cuts and jobs act”

TRANSCRIPT

ldquoComplete Guide toTax Cuts and Jobs Actrdquo

Tax Educatorsrsquo Network Inc

Prof John J Connors JD CPA LLM

Tax Educatorsrsquo Network (TEN) Inc

12403 North Hawks Glen Court

Mequon WI 53097-2140

TaxesProfmsncom

Prof John J Connors JD CPA LLM

As an accounting graduate of La Salle University in Philadelphia ProfConnors went on for his law degree at the University of Notre Damegraduating in 1980 After serving as an instructor in the School of BusinessAdministration he obtained his Masters of Law in Taxation at the Universityof Miami Law School in Coral Gables Florida He then served on the graduatetax faculty at the University of Wisconsinrsquos School of Business in MilwaukeeWI

His professional background includes experience in income and estate taxplanning as well as individual partnership and corporate tax returnpreparation and research as a senior tax consultant for Price Waterhouse inthe Philadelphia and South Bend offices Prof Connors also worked onexpatriate and corporate tax matters as an international tax consultant for theChrysler Corporation in London England

Prof Connors currently conducts a national consulting practice designedespecially for tax professionals based out of Milwaukee WI He also publishesa tax newsletter devoted exclusively to practitioners entitled the Monthly TaxUpdate He has been the outside editor for CCHrsquos Federal Tax Course andhas spoken at numerous tax institutes workshops and conferences aroundthe country And his ldquoComplete Guide to Depreciation Amortization ampTransfers of Property - Issues Strategies amp Answersrdquo is sold to taxpractitioners throughout the US along with a brand new publication entitledldquoLLCs Taxed as Partnershipsrdquo

As a nationally known speaker on a variety of tax topics Prof Connors hasconsistently earned average overall ratings in excess of 47 (ie on a 50scale) for his knowledge and presentation skills as well as the quality of hismaterials He was chosen as a Distinguished Discussion Leader for the NewYork Society of CPAs Foundation for Accounting Education And in 2013 hereceived the AICPA prestigious Sidney Kess Award for ldquoExcellence inContinuing Educationrdquo

copy Tax Educatorrsquos Network (TEN) Inc - 2018

ldquoComplete Guide toTax Cuts and Jobs Actrdquo

Table of Contents

Introduction 1LTax Policy Center Estimate of TCJA Effect 2LJCT ldquoBlue Bookrdquo on TCJA Might Not Be Available Until Yearend 2LCBO Report Provides Optimistic Outlook Due to TCJA (The Budget and Economic Outlook

2018-2028) 2LTIGTA Audit Evaluates IRS Handling of New Tax Cuts and Jobs Act (Audit Report No 2018-44-

027) 2LCBO States Recent Tax Cuts Will Cause Budget Deficit to Sharply Increase (Budget and

Economic Outlook 2018 to 2028) 3LConsolidated Appropriations Act Contains Technical Corrections to TCJA (PL 115-141) 3LIRS Outlines Initial Plan for Guidance on Implementing New Tax Act Provisions (Department

of the Treasury 2017-2018 Priority Guidance Plan (Feb 7 2018)) 4LIRS Releases Second Quarter Update to 2017-2018 Priority Guidance Plan 5LIRS Dedicates Special Website to Updates on New Tax Cuts and Jobs Act (e-News for Tax

Professionals 2018-6) 5LVarious State Approaches to Conformity with TCJA 5

Business Tax Provisions 621 Flat C Corporation Tax Rate 6LAlternatives for Handling C Corp Profits 7LImpact of Blended Rates for Fiscal Year C Corporations 8LPossible Windfall in Corporate Tax Revenues for States 921 Rate Also Available for PSCs 1021 C Corp Rate v 37 for S Corp Owners and Partners 10LC Corp Electing S Status Allowed Built-In Loss for Bonuses Pegged Against Cash Basis

Receivables (PLR 200925005) 11100 Bonus Depreciation 12LTechnical Correction Needed for ldquoQualified Improvement Propertyrdquo 14Increased Sec 179 Immediate Expensing Election 15LIRS Fact Sheet Highlights New Rules amp Limits for Depreciation and Expensing under TCJA (FS-

2018-9) 18LCRS Report Analyzes Impact of Sec 179 and Bonus Depreciation on Asset Acquisitions (CRS

Report RL31852) 2025-Year Classlife for Real Estate Rejected 21Recovery Period for Other Types of Real Property 21Luxury Car Caps Dramatically Increased 23LIRS Releases 2018 Vehicle Depreciation Limits (Rev Proc 2018-25) 24LDepreciation Limits Increased for Purposes of Computing FAVR Plan Allowance (Notice 2018-

42) 24MACRS 5-Year Recovery Period and 200 DB for Certain Farm Property 24Listed Property Substantiation Rules Dropped for Computers amp Peripheral Equipment 26Corporate Alternative Minimum Tax Repealed 26Like-Kind Exchanges Now Only Available for Real Estate 26

-i-copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

Carried Interest Holding Period Extended to 3 Years 28LNew Carried Interest Rule Not Avoided by Having S Corporation Hold Interest (Notice 2018-18)

29Restricted Stock Now Ineligible for Sec 83(b) Elections 29Transportation amp On-Premise Gym Fringe Benefits Curtailed 29LIRS Releases Updated Version of Publication 15-B 30Entertainment and Meal Expenses Curtailed 30LTax Deduction Status for Various Types of Business Meals Under the New Tax Act 32Employer-Provided Housing 36Treatment of Certain Self-Created Property 36Non-Owner Capital Contributions 37Rollover of Publicly Traded Securities Gain 37Tax Incentives for Investment in Qualified Opportunity Zones 38LldquoOpportunity Zonesrdquo Might Provide Significant Tax Savings Under TCJA 39L Treasury amp IRS Announce Designated TCJA Opportunity Zones (Treasury Press Release

Treasury IRS Announce First Round Of Opportunity Zones Designations for 18 States) 39

Transfers of Patents 40Nonqualified Deferred Compensation 40Employee Achievement Awards 40Length of Service Award Programs for Public Safety Volunteers 41

Accounting Method Changes 41Taxable Year of Inclusion 41

Other Small Business Accounting Method Reforms 42Cash Method of Accounting 42Cash Method and Farms 43Businesses with Inventories 43Uniform Capitalization Rules 44Accounting for Long-Term Contracts 44

Capitalization Rules 45Costs of Replanting Citrus Plants Lost Due to Casualty 45

Deductions amp Exclusions 45Limits on Interest Expense Deduction 45LElecting Real Property Trades and Businesses Not Subject to Limitation on Deduction of

Business Interest 47LIRS Offers Guidance on New Business Interest Expense Limitations (IR 2018-82) 48Ordinary REIT Dividends Reduced by Sec 199A Deduction 52Modification of Net Operating Loss Deduction 52LTechnical Correction Needed for Effective Date of NOL Change 53Dividend Received Deduction 53Sec 199 QPAD Deduction 54Deduction of FDIC Premiums 54Research and Development Costs 54Limitation on Excessive Employee Compensation 55Litigation Costs Advanced by Attorneys in Contingency Cases 56LIRS Issues Transitional Guidance on Nondeductible Fines and Penalties (Notice 2018-23)

-ii-copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

57No Deduction for Amounts Paid For Sexual Harassment Subject to Non-Disclosure Agreement

57Local Lobbying Expenses 57New Deferral Election for Qualified Equity Grants 57

Business Tax Credits 59Certain Unused Business Credits 59New Credit for Employer-Paid Family and Medical Leave 59LGuidance Provided on New Employer-paid Family and Medical Leave Credit (FAQs) 60Employer Tip Credit 61Employer-Provided Child Care Credit 61Rehabilitation Credit 61Work Opportunity Tax Credit 62New Market Tax Credit 62Disabled Access Credit 62Residential Energy Efficient Property Credit 62Orphan Drug Credit Modified 63

Partnership Tax Provisions 63Technical Terminations of Partnerships 63ldquoLook-Through Rulerdquo Applied to Gain on Sale of Partnership Interest 63Partnership ldquoSubstantial Built-In Lossrdquo Modified 64Charitable Contributions amp Foreign Taxes in Partnerrsquos Share Of Loss 65

S Corporation Tax Provisions 66Revocations of S Corp Elections 66LTechnical Correction Needed Re Revocation of S Corp Election 67LTax Professionals Asking for 6-Month Extension to Make 2018 S Corp Elections 67Qualifying Beneficiaries of an ESBT 68

New 20 Deduction for K-1 and Proprietorship Profits and Net Rental Income 68Various Approaches Congress Took w Sec 199A DeductionSpecial Tax Rate 69LJCT Estimates Distributional Effect of Sec 199A Deduction 69Highlights of New Sec 199A 20 Deduction of ldquoQualified Business Incomerdquo 69Final Sec 199A 20 Deduction Includes Net Rental Income As Well 71IRS Guidance Desperately Needed 72Sec 199A Deduction Cannot Exceed Taxable Income Without Net Capital Gain 72Taxpayers Receiving QBI From Fiscal Year Businesses 73Passive v Nonpassive K-1 Investors amp Rental Property Owners 73Sec 199A Deduction Not Allowed Against Gross or Adjusted Gross Income 75Sec 199A Deduction Not Allowed in Computing Self-Employment Tax 75Definition of Qualified Business Income 75Qualified Business Income Does Not Include Wages Paid to S Corp OwnerEmployee or

Guaranteed Payments Made to Partners 76Location of Qualified Business for Purposes of Sec 199A Deduction 76ldquoSpecified Service Businessrdquo Defined 76LSplitting Off of S Corporationrsquos Separate Businesses Qualified as Divisive Re-Org (PLR

201402002) 79LOnce Again Divisive D Re-Org Solves Problem of Family Disharmony (PLR 201411012)

-iii-copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

7920 Deduction for K-1 Income and Net Profit from Proprietorships 81LCritical Steps to Implementing Sec 199A Deduction 81Critical 1st Step - Determine Projected Taxable Income for 2018 83Calculating Sec 199A 20 Deduction Where Taxable Income Thresholds Not Exceeded 83Critical 2nd Step - Determine Limited 20 Deduction If Projected Taxable Income Falls Within

Phaseout Range ($157500 to $207500 for Unmarried Taxpayers and $315000 to$415000 for MFJ) 85

Taxpayer Planning Steps to Keeping Taxable Income Before Sec 199A DeductionBelowThresholds 86

50 or 20 Wage Limitations 8625 Investment in Capital Limitation 89Dispositions of Sec 1231 Assets and 25 Capital Formula 91Do Sec 754 or Sec 338(h)(10) Elections Create ldquoUnadjusted Basisrdquo for Purposes of the 25

Capital Formula Limitation 91Impact of Purchase Price Allocations under Code Sec 1060 92Critical 3rd Step - Determine ldquoSpecified Service Businessrdquo Status If Taxable Income Exceeds End

of Taxable Income Phaseout Range of $207500 or $415000 94Critical 4th Step - Determine If 20 Sec 199A Deduction Exceeds 20 of Overall Taxable

Income Before Deduction Less Any Net Capital Gain (Defined as Excess If Any of LTCGover STCL) 97

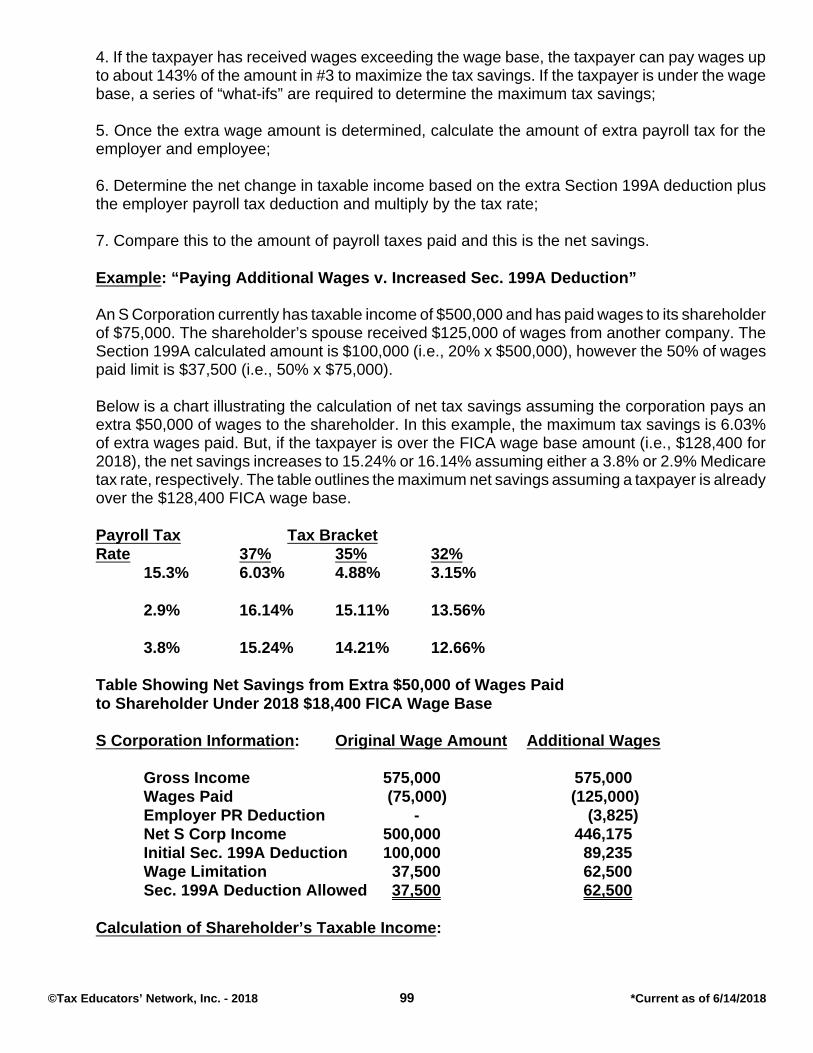

LDoes Tax Benefit of Sec 199A Deduction Offset Additional Payroll Taxes Due If Wages AreIncreased for Purposes of 5025 ldquoWage Limitationsrdquo 98

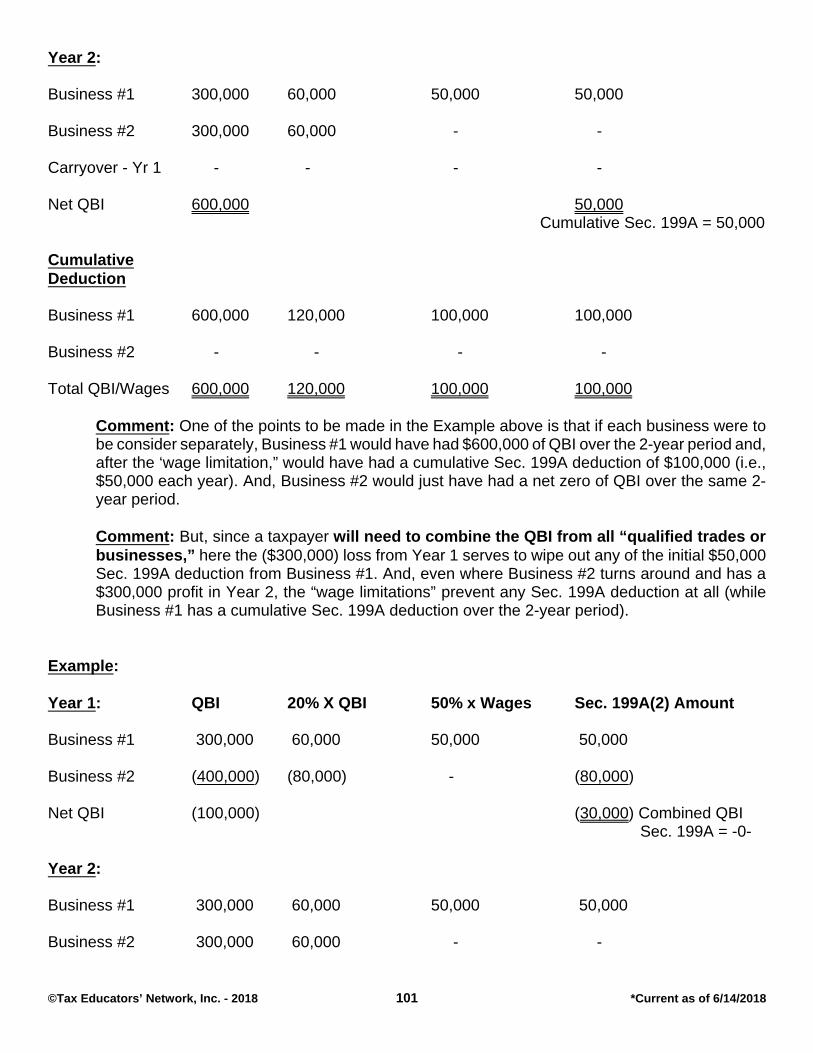

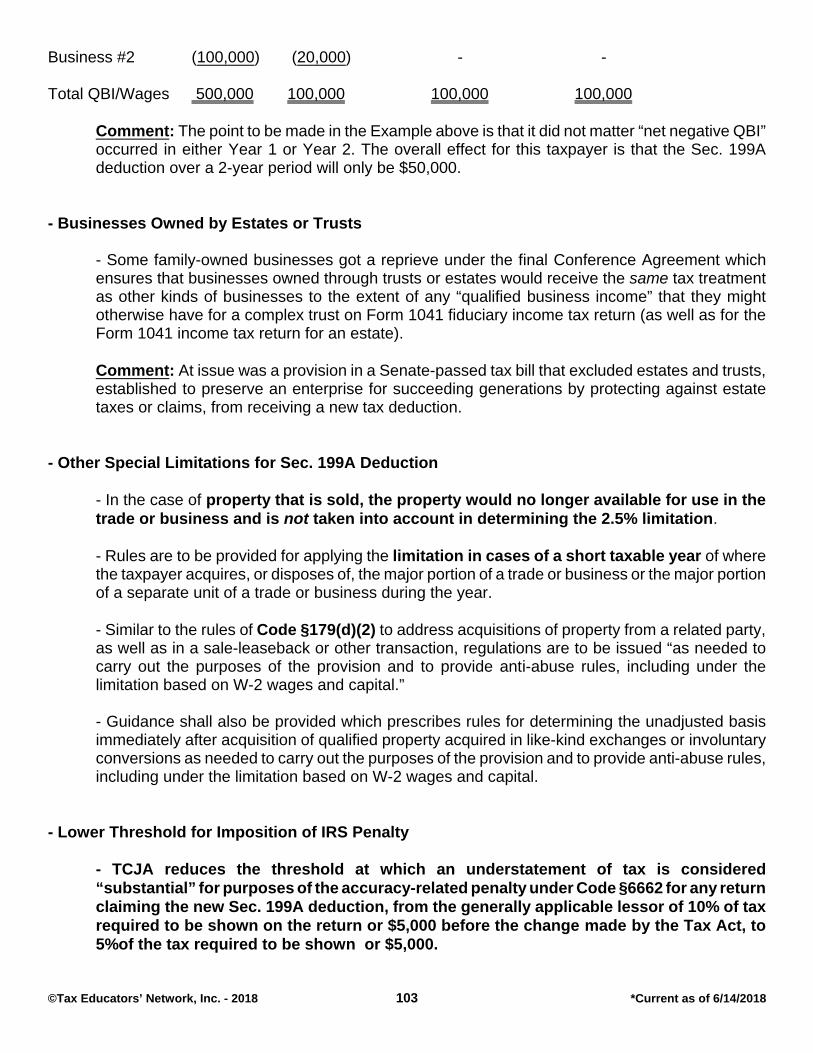

Calculating QBI with Multiple Businesses 100Calculation of Sec 199A Deduction with Negative QBI 100Businesses Owned by Estates or Trusts 103Other Special Limitations for Sec 199A Deduction 103Lower Threshold for Imposition of IRS Penalty 103Specified Agricultural or Horticultural Cooperatives 104LRecent Budget Bill Includes Fix to Code Sec 199As Treatment of Sales to Cooperatives

104LTax Professionals Asking for 6-Month Extension to Make 2018 S Corp Elections 105

Individual Tax Calculations 105Tax Rates and Brackets 105LIRS to Issue New Form 1040-SR for 2019 108LIRS Issues 2018 Version of Employers Tax Guide (IRS Pub 15 Circular E) 108LIRS Issues Guidance on Withholding Rules (Notice 2018-14) 109LIRS Releases Updated 2018 Withholding Tables (IR 2018-5) 110LIRS Releases Updated Withholding Calculator and New Form W-4 (IR 2018-36) 110Capital Gains amp Dividends Preferential Rates Retained 111Standard Deductions Dramatically Increased 112Personal and Dependency Exemptions 114Phase-Out of Personal and Dependency Exemptions 115Kiddie Tax 115Alternative Minimum Tax 117AMT Exemption Amounts Increased 117AMT Exemption for Child Subject to Kiddie Tax 118AMT Exemption Phaseout Increased 118LTechnical Correction Needed for AMT Exemption Amount and Phaseout for Trusts and Estates

-iv-copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

118AMT Tax Rates - 26 v 28 118Treatment of AMT Carryforwards 119

Individual Deductions 119Miscellaneous Itemized Deductions 119Phase-Out of Itemized Deductions 121Mortgage Interest Deduction 121LIRS Clarifies Interest on Home Equity Loans Often Still Deductible (IR 2018-32) 124State and Local Tax Deduction 128LImpact of $10000 SALT Deduction on Form 8960 Calculation of NII 129LNonresident State Income Tax on Law Partners K-1 Income Not Deductible on Schedule E

(Cutler TC Memo 2015-73 (492015)) 129LRecent Developments Regarding Various State Workarounds Challenges to SALT Deduction

Limitation 130LIRS to Propose Regulations on State and Local Tax Deduction (Notice 2018-54) 131Medical Expenses 131Medical Savings Accounts 132Charitable Contribution of Cash Now Allowed Up to 60 of AGI 132LTechnical Correction Needed for Cash Contributions Subject to New 60 AGI Limitation

133Personal Casualty Loss Deduction 134LIRS Offers New Safe Harbors for Calculating Personal Casualty Losses (Rev Proc 2018-08)

134Gambling Losses 134Alimony Deduction Eliminated After 2018 135Moving Expense Deductions 135Net Operating Losses 136Changes to ABLE Accounts 137Deduction for Living Expenses of Members of Congress Eliminated 138Deduction For Amounts Paid For College Athletic Seating Rights 139

Individual Credits and Exclusions 139Increased Child Tax Credit 139Dependent Care Assistance and Child Care Expenses 141Adoption Credit 141LAdoption Credit and Exclusion Amounts Set for 2018 (Rev Proc 2018-18) 141Credit for Plug-In Electric Vehicles 142Credit For The Elderly amp Permanent Disabled 142Moving Expenses and Reimbursements 142Qualified Bicycle Commuting Reimbursements 143Repeal of Exclusion for Advance Refunding Bonds 143Exlusion of Gain from Sale of Principal Residence Left Unchanged 144

Educational Tax Breaks for Individuals 144Education Tax Incentives 145Educational Savings Account 145Section 529 Plan Distributions 145Qualified Tuition Program (QTP) Distributions for Apprenticeships 145Treatment of Discharged Student Loan Indebtedness 146

-v-copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

Educatorrsquos Deduction 146Qualified School Construction Bonds 146Student Loan Interest 146Tuition and Fees Deduction 147Exclusion for Savings Bond Interest 147Tuition Waivers 147Employer-Provided Education Assistance 147

Individual Health Insurance Mandate 147Individual Health Insurance Penalty Eliminated 148

Retirement Plans 148Qualified Retirement Plans 148L2018 Retirement Plan Limits Not Affected by New Tax Act (IR 2018-19) 148Roth IRA Recharacterization Rule Repealed 148LIRS Clarifies Effective Date of New Roth Conversion Recharacterization Prohibition 150Reduction in Minimum Age for Allowable In-Service Distributions 150Modified Rules on Hardship Distributions 150Extended Rollover Period for the Rollover of Plan Loan Offset Amounts in Certain Cases

150

Estate and Generation-Skipping Transfer Taxes 151Doubling of Unified Credit Equivalent 151

Income Tax Rates for Trusts and Estates 152

Tax-Exempt Entities 152Unrelated Business Taxable Income 152Streamlined Excise Tax on Private Foundation Income 153Excise Tax on Private Colleges and Universities 153Excise Tax on Excess Tax-Exempt Organization Executive Compensation 154Johnson Amendment Restricted 154New Reporting for Donor Advised Funds 155

IRS Practice and Procedural Changes 155Time To Contest IRS Levy Extended 155LTaxpayers Now Given More Time to Contest Erroneous IRS Levies 155Due Diligence Requirements for Claiming Head of Household 155

Foreign Tax Provisions 156Deduction for Foreign-Source Portion of Dividends 156Taxation of Foreign Profits 156Taxation of Payments Made to Foreign Businesses Operation in US 157Repatriation of Foreign Earnings 157LIRS Issues Guidance on New Deemed Repatriation Tax (Notice 2018-7) 157LIRS Provides Additional FAQ Guidance on Deemed Repatriation Tax 157LIRS Issues Additional Guidance on New Deemed Repatriation Tax (Notice 2018-13) 158LIRS Outlines Regs to Be Issued on ldquoDeemed Repatriation Transition Taxrdquo (IR 2018-79)

158

-vi-copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

Possibility of 100+ Marginal Rate within Certain Phaseout Ranges 159

Case Study 1 - MFJ w $350000 Rental K-1 amp Schedule C Income 160

Impact of House Ways amp MeansTax Reform Proposals 11-2-17Using Client 2016 Tax Return 160

Impact of Senate Finance CommitteeTax Reform Proposals 12-1-17Using Client 2016 Tax Return 161

Impact of Revised Senate VersionTax Reform Proposals 12-2-17Using Client 2016 Tax Return 162

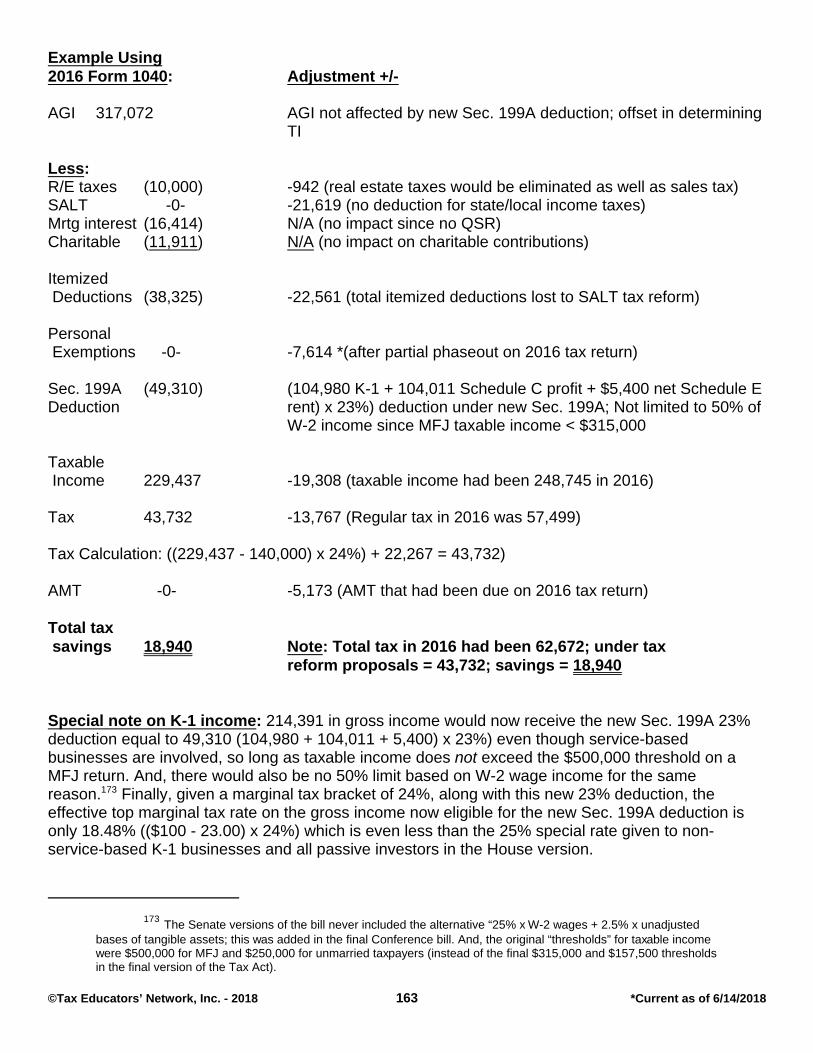

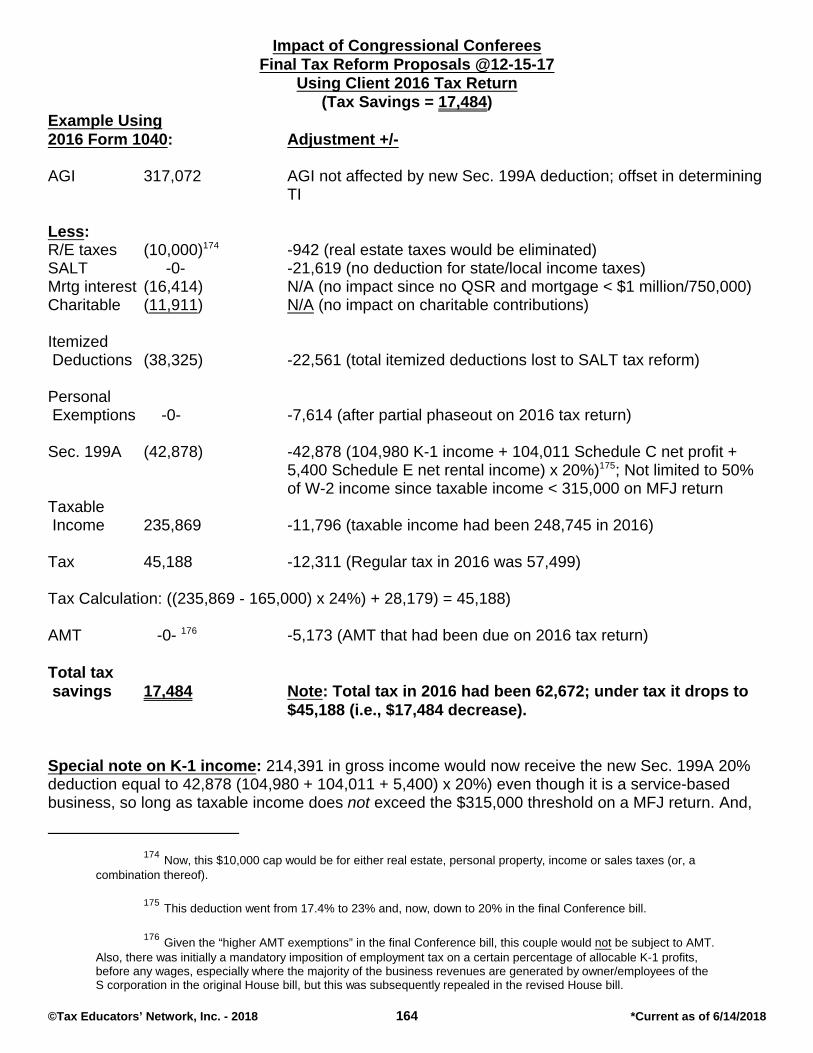

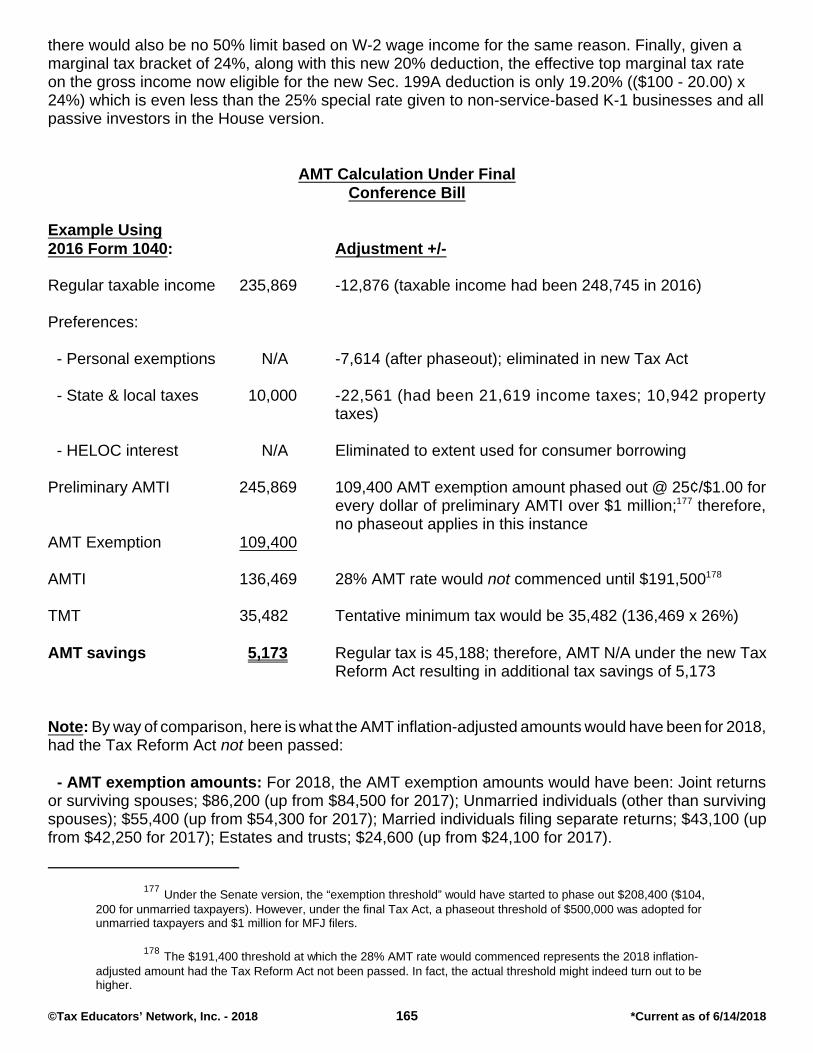

Impact of Congressional ConfereesFinal Tax Reform Proposals 12-15-17Using Client 2016 Tax Return 164

AMT Calculation Under FinalConference Bill 165

Case Study 2 - MFJ w $70000 W-2 Income and Three Dependents(Tax savings = 1640) 166

Case Study 3 - MFJ w $310000 W-2 Income and Three Dependents(Tax savings = 10842) 167

Case Study 4 - MFJ w $700000 W-2 Income and $500000 DividendsLTCGs(Tax savings = 30865) 168

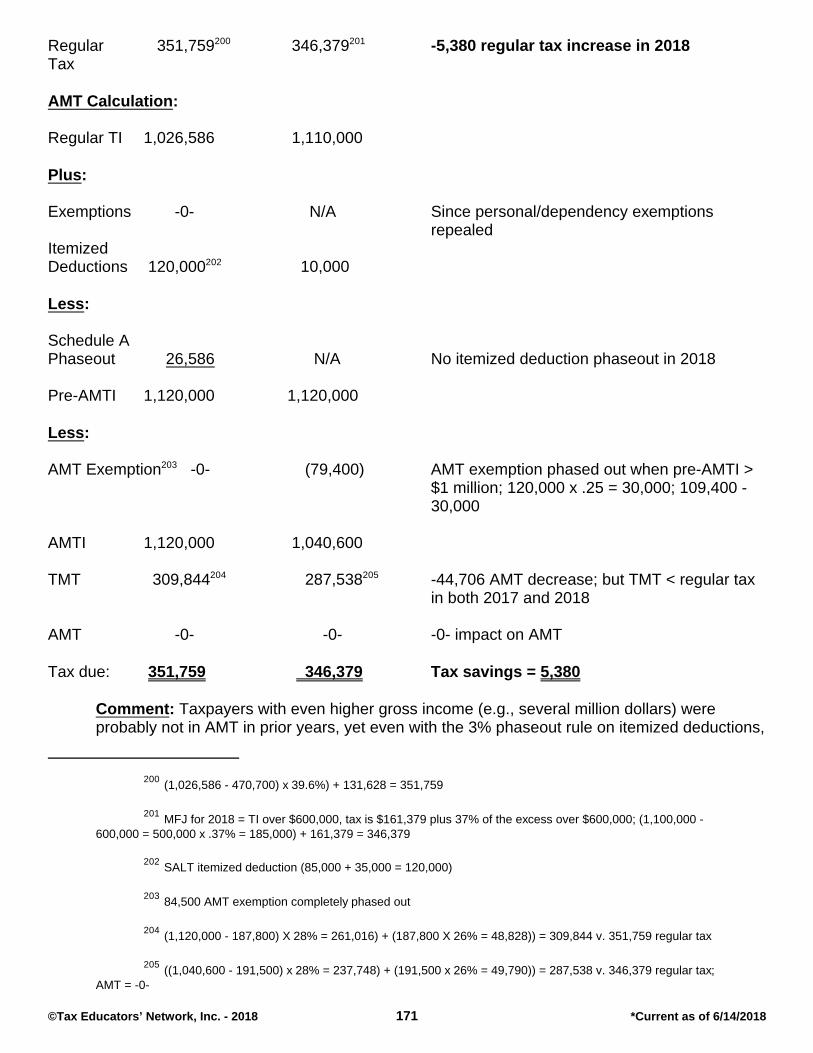

Case Study 5 - MFJ w $1200000 W-2 Income and No DividendsLTCG(Tax savings = 5380) 170

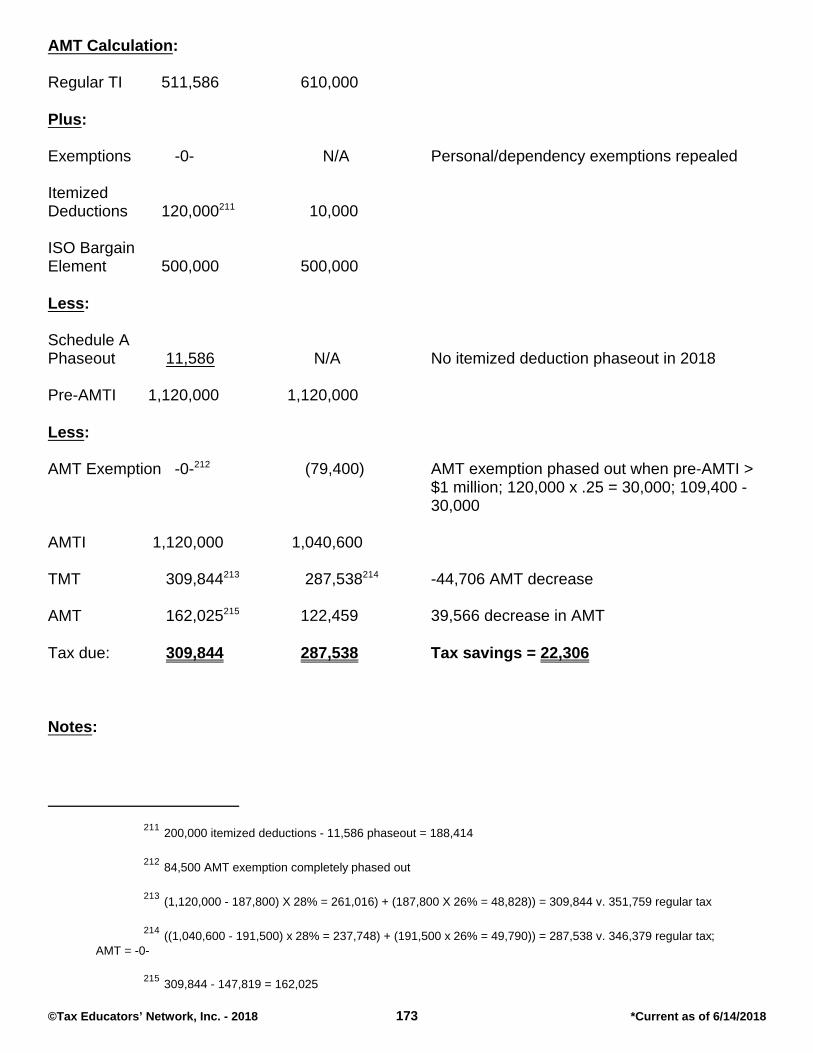

Case Study 6 - MFJ w $700000 W-2 Income and $500000 AMT Adjustment(Tax savings = 22306) 172

-vii-copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

Summary of Tax Reform Proposals

Introduction In most cases the changes listed below would be effective for tax years beginning after2017 However a few of them will potentially impact 2017 tax returns for certain clients The TCJA makessignificant revisions to almost every area including changes affecting individuals real estate pensionand employee benefits insurance companies tax-exempt bonds exempt organizations and foreignincome and foreign persons And these changes would radically alter the taxation of all businesses Asa result clients should begin to evaluate how these changes will affect both their business and individualtax situations The choice-of-entity question will especially be a key component of their future taxplanning1

One of the major distinctions between the House and Senate bills was that the latter version providesfor a ldquosunsetrdquo of the most of the individual provisions after 2025 Of course Congress could certainly actin the interim to extend these provisions (or maybe drastically change the tax law yet again) On theother hand most of the business changes are permanent in nature

Because the new Tax Act was rushed through Congress without the needed debate or hearings thereare numerous provisions where we need significant clarification or maybe even some technicalcorrections But as to a technical corrections bill this new law would need the usual 60 votes in theSenate to pass If so it might be even harder to get needed changes made to the Tax Cuts and JobsAct2 As a result it is much more likely that the Treasury and the IRS will have to come out with thenecessary regulations and rulings to give us the guidance vital to the implementation of these newprovisions

Comment There were several tax provisions that expired at the end of 2016 as follows (1) PMIas additional mortgage interest (2) 10 residential energy credit (3) $20004000 tuition and feesdeduction and (4) $2 million COD exception for forgiven mortgage indebtedness on a principalresidence At this point it seems unlikely that these tax breaks will be resurrected in time for theupcoming tax return busy season

Comment Although the Congress was locked into the requirement that the new tax law not costmore than a projected $15 trillion over the next 10 years the Joint Committee on Taxation (JCT)on Dec 22 published a document titled Macroeconomic Analysis of the ConferenceAgreement for HR 1 the Tax Cuts and Jobs Act (JCX-69-17) which projected that there willonly be a net revenue loss of $107 trillion during that time frame On the other hand theCongressional Budget Office (CBO) and the Joint Committee on Taxation have determined thatprovisions in the new Tax Act would increase deficits over the 2018-2027 period by $15 trillion(not including any macroeconomic effects) in a recent letter to Sen Ron Wyden (D-OR) rankingmember of the Senate Finance Committee estimated additional debt service would increase thedeficit by $18 trillion over the 10-year period As a result of those higher deficits debt held by thepublic would increase from the 912 of gross domestic product in CBOs June 2017 baseline to

1 The final Conference bill is 1097 pages long and contains all of the details with regard to the provisions

summarized below and can be found at httpdocshousegovbillsthisweek20171218CRPT-115HRPT-466pdfThe language was finalized late Thursday night (1214) and GOP leaders had to make 100 sure they had the votesbecause after noon Friday (1215) there could no longer be any changes Furthermore the Joint Committee onTaxation estimates the bill will lower federal revenue by $1456 trillion over 10 years mdash a key finding as the bill couldnot add more than $15 trillion in debt and qualify for special Senate reconciliation rules

2 Another source of information on the Tax Cuts and Jobs Act is JOINT EXPLANATORY STATEMENT OF

THE COMMITTEE OF CONFERENCE

1copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

975

LTax Policy Center Estimate of TCJA Effect The Tax Policy Center issue a report which concluded that

- 80 of taxpayers will receive a tax cut- 15 will see no change- 5 will see a tax increase- ldquoMiddle-class taxpayersrdquo will see an average tax savings of $930- Top 1 will supposedly save an average of $51140

LJCT ldquoBlue Bookrdquo on TCJA Might Not Be Available Until Yearend Tax professionals are eagerly awaiting a legislative publication explaining the new tax law Namely theso-called ldquoblue bookrdquo is published by the Joint Committee on Taxation a nonpartisan staff ofcongressional aides who work with Senate and House tax writers It comes out every two years and alsogenerally when key tax legislation is enacted Tax practitioners were hoping to see the blue book onTCJA law by summer but it now looks as if this publication will not be released until close to year-end (TCJA Blue Book)

LCBO Report Provides Optimistic Outlook Due to TCJA (The Budget and Economic Outlook2018-2028) The Tax Cuts and Jobs Act (TCJA) changes the incentives of businesses and individuals with a net result that thosechanges are expected to encourage saving investment and work according to a recent blog post on theCongressional Budget Offices (CBO) website CBO projects that the acts effects on the US economy over the2018-2028 period will include higher levels of investment employment and gross domestic product (GDP) it saidThe TCJA is projected to initially boost real GDP in relation to real potential GDP (ie the economys maximumsustainable level of production) This is due to the fact that the TCJA increases overall demand for goods andservices by raising households and businesses after-tax income In developing its baseline budget projections CBOincorporated the effects of the tax act taking into account economic feedback especially the ways in which the actis likely to affect the economy and in turn affect the budget The JCTA raised CBOs estimated cumulative primarydeficit (which excludes costs of debt servicing) by $13 trillion and increased projected debt service costs by some$600 billion The total projected deficit over the 2018-2028 period totals about $19 trillion Before taking economicfeedback into account CBO estimated that the tax act would increase the primary deficit by $18 trillion anddebt-service costs by roughly $450 billion the blog said The feedback is estimated to lower the cumulative primarydeficit by about $550 billion mostly because the act is projected to increase taxable income and thus push taxrevenues up it added The growth in debt service costs is attributed to higher interest rates The blog also addressedthe uncertainty surrounding CBO estimates stating CBOs estimates of the economic and budgetary effects of the2017 tax act are subject to a good deal of uncertainty But the agency was uncertain about various issues Forexample the way the act will be implemented by the Treasury how households and businesses will rearrange theirfinances in the face of the act and how households businesses and foreign investors will respond to changes inincentives to work save and invest in the United States That uncertainty implies that the actual outcomes may differsubstantially from the projected ones (Misc TCJA)

LTIGTA Audit Evaluates IRS Handling of New Tax Cuts and Jobs Act (Audit Report No2018-44-027)The Treasury Inspector General for Tax Administration (TIGTA) released an audit which evaluated theServicersquos efforts in implementing the Tax Cuts and Jobs Act (TCJA) of 2017 The law contains 119provisions that are administered by the agency and affect both domestic and international taxes TheIRSs Legislative Affairs function monitored the pending legislation to identify provisions that affectedthe agency and kept the various IRS operating divisions abreast of developments This allowed theoperating divisions to assess how to handle the implementation Once enacted the IRS immediatelybegan the task of implementing these provisions The agency also created a sophisticated oversightstructure to coordinate all the required implementation activities Working with the Treasury Department

2copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

the IRS estimated that implementation of the TCJA would cost approximately $397 million which includesthe hiring of an estimated 1734 full-time equivalent positions to implement tax reform over the next twocalendar years The IRS took adequate steps to create the required withholding tables The IRS inconjunction with the Department of the Treasury designed the Tax Year 2018 withholding tables to workwith an employees existing Form W-4 Employees Withholding Allowance Certificate to minimizepotential burden on employees and employers The audit also praised the manner in which the IRSupdated its online Withholding Calculator (Misc TCJA)

LCBO States Recent Tax Cuts Will Cause Budget Deficit to Sharply Increase (Budget andEconomic Outlook 2018 to 2028) An economic report by the Congressional Budget Office (CBO) The Budget and Economic Outlook2018 to 2028 indicates that the US budget deficit ldquowill increase markedlyrdquo over the next few yearsmainly because of deep tax cuts approved in the Tax Cuts and Jobs Act Despitestronger-than-predicted economic growth ahead the CBO said the deficit will grow to $804 billion in fiscalyear 2018 which ends on Sept 30 up from $665 billion in fiscal year 2017 The deficit that CBO nowestimates for 2018 is $242 billion larger than the one that it previously projected for that year in June2017 Accounting for most of that difference is a $194 billion reduction in projected revenues mainlybecause the TCJA is expected to reduce collections of individual and corporate income taxes In the nextfew years deficits will grow substantially before stabilizing in 2023 resulting in a projected cumulativedeficit of $117 trillion for 2018-2027 the CBO said

CBOs current economic projections differ from those that the agency made in June 2017 in a numberof ways The most significant is that potential and actual real gross domestic product (GDP) are projectedto grow more quickly over the next few years CBO forecasts 33 growth in 2018 in GDP and 24GDP growth in 2019 By way of comparison last year grew by 26

CBO expects corporations income tax payments net of refunds to decline by $54 billion in 2018 to$243 billion The projected decline in corporate income tax receipts mainly results from changes madeby the TCJA The largest part of the projected revenue decline stems from the corporate tax ratereduction itself from 35 to 21 In addition the prospective reduction in the corporate tax rate inJanuary 2018 provided an opportunity for some firms to accelerate expenses such as employeescompensation into the 2017 tax year in order to claim deductions at the 35 rate in effect for that yearthus lowering their tax liabilities in fiscal year 2018

Furthermore the TCJA allows businesses to fully expense (ie under either Sec 179 or bonusdepreciation) equipment they purchased and put into service beginning in the fourth quarter of calendaryear 2017 The ability to deduct the full value of such investments will also lower taxable income in fiscalyear 2018 The lower taxes resulting from those provisions are partly offset by new revenues stemmingfrom a one-time tax on previously untaxed foreign profits expected to be paid from 2018 through 2026 (Misc TCJA)

LConsolidated Appropriations Act Contains Technical Corrections to TCJA (PL 115-141) The Consolidated Appropriations Act 2018 was signed into law on 32318 The provisions of theAct include a $13 trillion spending bill that funds the federal government through 93018 and avoids afederal government shutdown The Act also contains provisions for several technical corrections Themost significant are (1) a fix to the so-called grain glitch to change a provision in the Tax Cuts andJobs Act that gave preference to farmer-owned cooperatives over other types of entities (2) provisionsto correct and clarify the partnership audit rules enacted under the Bipartisan Budget Act of 2015 and(3) provisions to increase the low-income state housing credit ceiling for calendar years 2018-2021 andthe creation of a new category of low-income housing project credit qualification (Misc Consolidated

3copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

Appropriations Act)

LIRS Outlines Initial Plan for Guidance on Implementing New Tax Act Provisions (Department ofthe Treasury 2017-2018 Priority Guidance Plan (Feb 7 2018)) The IRS has issued its second quarter update to the 2017-2018 Priority Guidance Plan describingthe guidance that the IRS intends to issue during by June 30 2018 as part of its initial implementationof the recently enacted Tax Cuts and Jobs Act (TCJA)

Comment One provision of particular interest to taxpayers and practitioners is the new Codesect199A 20 deduction with regard to ldquoqualified business incomerdquo The IRS has stated that it willissue computational definitional and anti-avoidance guidance on this new provision

The Guidance Plan lists the following 18 action items relating to the TCJA

- Guidance on certain issues related to the new business credit under Code sect45S with respect to wagespaid to qualifying employees during family and medical leave

- Guidance under Code sect101 Code sect1016 and new Code sect6050Y regarding ldquoreportable policy salesrdquoof life insurance contracts

- Guidance under Code sect162(m) regarding the application of the effective date provisions to theelimination of the exceptions for commissions and performance-based compensation from the definitionof compensation subject to the $1 million deduction limit for covered employees of publicly-tradedcorporations

- Guidance under Code sect162(f) (on the deductibility of certain fines and penalties) and new Codesect6050X (requiring government agencies or similar entities to report certain settlement payments to IRSand the taxpayer)

- ldquoComputational definitional and other guidancerdquo under new Code sect163(j) (which limits the deductionfor interest paid to 30 of adjusted taxable income for businesses with more than $25 million in grossreceipts)

- Guidance on new Code sect168(k) (100 bonus depreciation)

- ldquoComputational definitional and anti-avoidance guidancerdquo under new Code sect199A (the 20 qualifiedbusiness income deduction)

- Guidance adopting new small business accounting method changes under Code sect263A Code sect448Code sect460 and Code sect471

- ldquoDefinitional and other guidancerdquo under new Code sect451(b) (under which income inclusion for taxpurposes cannot be later than for certain financial reporting purposes) and Code sect451(c) (allowingdeferral of advance payments in certain circumstances)

- Guidance on computation of unrelated business taxable income (UBTI) for separate trades orbusinesses under new Code sect512(a)(6)

- Guidance implementing changes to Code sect529 (qualified tuition programs)

4copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

- Guidance implementing new Code sect965 (deemed repatriation rules) and other international sectionsof the TCJA (IRS notes that such guidance Notice 2018-7 was released on Dec 29 2017)

- Guidance implementing changes to Code sect1361 regarding electing small business trusts

- Guidance regarding Opportunity Zones under Code sect1400Z-1 and Code sect1400Z-2

- Guidance under new Code sect1446(f) for dispositions of certain partnership interests (IRS noted thatsuch guidance Notice 2018-8 was released on Dec 29 2017)

- Guidance on computation of estate and gift taxes to reflect changes in the basic exclusion amount

- Guidance regarding withholding under Code sect3402 and Code sect3405 and optional flat rate withholding

- Guidance on certain issues relating to the excise tax on excess remuneration paid by applicabletax-exempt organizations under Code sect4960

LIRS Releases Second Quarter Update to 2017-2018 Priority Guidance Plan The IRS has released the second quarter update to its 2017-2018 priority guidance plan The plancontains guidance projects the IRS hopes to complete during the period 7117 through 63018 Amongthe 29 new projects added to the plan 18 of them have been designated as near term priorities as aresult of the Tax Cuts and Jobs Act (TCJA) These include (1) computational definitional and anti-avoidance guidance on the new Section 199A deduction for qualified business income (2) rules relatingto the new Section 45S employer credit for paid family and medical leave (3) computational definitionaland other guidance on the business interest limitation under Code sect163(j) and (4) guidance on adoptingnew small business accounting method changes (Misc TCJA)

Comment The IRS may update this list during the year as it considers comments from taxpayersand tax practitioners

LIRS Dedicates Special Website to Updates on New Tax Cuts and Jobs Act (e-News for TaxProfessionals 2018-6) The IRS recently announced that it has created a special page on its website titled Resources for TaxLaw Changes According to the Service the page is designed to assist the tax community in trackinginformation related to the Tax Cuts and Jobs Act (TCJA) The frequently updated page will include aone-stop listing of new legal guidance news releases Frequently Asked Questions and otherinformation related to TCJA the IRS stated Therefore the Service recommended that tax professionalsregularly check the page for the latest updates (Misc TCJA)

LVarious State Approaches to Conformity with TCJA For companies operating in numerous states issues arise especially where the individual states choosenot to conform to the provisions contained in TCJA In other words the state income tax implications ofthe new Tax Act vary widely depending on statesrsquo automatic or fixed conformity to the Internal RevenueCode as well as the statesrsquo ldquoappetiterdquo for amending their own tax laws in the face of TCJA Generallyspeaking the Tax Act will have the effect of increasing most businessesrsquo effective state income tax ratesdue to the broadened federal income tax base without a corresponding reduction in the state income taxrate (Misc State Tax Conformity)

5copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

Business Tax Provisions

- 21 Flat C Corporation Tax Rate3

- Corporate tax rate would generally be taxed at a flat 21 rate for tax years beginning in2018 Therefore the current graduated rates4 of 15 (for taxable income of $0-$50000) 25 (fortaxable income of $50001-$75000) 34 (for taxable income of $75001-$10000000) and 35(for taxable income over $10000000) will be eliminated5

Comment There is the obvious ldquochoice-of-entityrdquo question now that C corps (includingPSCs) receive a flat 21 tax rate on all taxable income Some have argued that this isespecially true where a K-1 entity will not be entitled to the new Code sect199A 20 deductionfor ldquoqualified business incomerdquo But as discussed below if a C corp pays out its profits aswages this ordinary income would face a marginal tax rate of up to 37 on an employeeownerrsquospersonal tax return (let alone a minimum of 29 in employment taxes for a closely-held C corp)This would basically be the same result had an S corp paid out wages or for any SE income toa partnerLLC member Dividends on the other hand are nondeductible to the C corp but onlyface a 20 top rate with no employment taxes Yet when you factor in the 21 rate that the Ccorp has already paid on such profits the effective ldquodouble taxationrdquo rate approximates 37 aswell6

Comment For smaller regular C corps which held back up to $50000 of profits under current lawthis taxable income would have only faced a 15 marginal tax rate And if invested in a dividend-paying mutual fund for instance the C corp would have also received a Code sect243 dividendreceived deduction of 70 (resulting in an effective tax rate on such dividends of only 45)Under the new Tax Act these dividends would now be subject to a 105 effective tax rate(ie after a 50 DRD and the new 21 C corp tax rate)

Comment When preparing 2017 C corporation tax returns special attention should be paidto taking the maximum amount of deductions especially with Sec 179 and bonusdepreciation Using an extreme example for a smaller C corporation having taxable incomebetween $100000 and $335000 it would face a marginal tax rate of 39 Even a PSC wouldface a flat tax rate of 35 on any taxable income So deductions in 2017 have the benefit of thesehigher marginal tax rates while those delayed until 2018 (and later years) receive only a 21 taxbenefit

3 By increasing corporate rate to 21 instead of 20 the effective date will now remain for ldquotax years

beginning after 2017rdquo instead of being delayed for until 2019 Code Sec 11(b) as amended by Act Sec 13001

4 These graduated rates produced an effective corporate tax rate of 2225 on the first $100000 of Ccorporation taxable income But from $100000 to $335000 of C corporation taxable income under the ldquooldrdquo lawthere was an effective 39 tax rate Thus with a flat 21 flat tax rate on all C corp taxable income this is effectivelyan 18 decrease (and with TI gt $335000 a drop from 35 to only 21)

5 Given that the top C corp rate would be a flat 21 there should be a corresponding reduction of the Codesect1374 S corp built-in gains rate of 35 and the Code sect1375 35 penalty on ldquoexcess passive investment incomerdquo Onthe other hand both the Code sect531 accumulated earnings tax penalty and the Code sect541 personal holding companypenalty would remain at just 20 given this remains the top rate on dividend income

6 And this 37 combined rate is before any possible imposition of the Code sect1411 38 Medicare surtax

6copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

Comment A number of commentators7 are insisting that there will be a proration of taxrates for fiscal year C corporations based upon the days before January 1 2018 and thedays after that date [Sec 15(a)(2)] Therefore if you have a September 30 2018 year-end youwill calculate the taxable income from October 1 2017 to December 31 2017 at the old rates andafter that date at the new rates This will be based upon the number of days in each period

Comment As a consequence of having a 2017-2018 blended tax rate all fiscal year corporationswill be in a higher tax bracket in 2017-2018 then they will be in future years when they will betaxed at 21 As a result deductions in their 2017-2018 tax years will yield a greater tax benefitthan in later years while income will be taxed at a higher rate in their 2017-2018 tax years thenit will be in later years So fiscal year corporations can obviously benefit from taking steps thatmove deductions away from future years into the current year while moving income from thecurrent fiscal year to future years

LAlternatives for Handling C Corp Profits

Example ldquoPaying Out Nondeductible DividendrdquoOn $100 of C corporation profits $21 would be paid in federal income taxes Then of the $79remaining to pay a nondeductible dividend 208 or about $16 would be subject to tax at theshareholder level As a result this $100 of corporate profit would face a combined effective taxrate of 37 which is also the top marginal tax rate on ordinary income for individuals starting in2018

Example ldquoCorporate Profits Paid Out as Deductible WagesrdquoIf this $100 of C corporation profits had been paid out as wages there would have been acorresponding deduction to the corporation with the owneremployee picking up this ordinarywage income at marginal rates of up to 37 In addition even if the FICA cap (ie $128400in 2018) is exceeded there would still be the 29 in employments taxes to be considered (145for the employer and employee each) Finally the 9 Medicare surtax would also have to beconsidered if the taxpayerrsquos AGI exceeded the $200000250000 thresholds (depending on filingstatus)

Choice of Entity As far as the ldquochoice-of-entityrdquo question had this $100 of profit instead flowedthrough on an ownerrsquos K-1 from an S corporation or a partnership it could have possibly receiveda 20 deduction (given that the partnerS corp shareholders taxable income did not exceed$315000 on a MFJ return ($1575000 for an unmarried taxpayer) And even if it did exceed theseaforementioned ldquothreshold amountsrdquo then as long as this was not a ldquoserviced-based businessrdquothe 20 deduction would be allowed as long as it did not exceed 50 of any wages paid by thecompany (or an alternative formula for capital intensive businesses) The bottom line is given that

7 Some of the larger accounting firms such as EY KPMG and Deloitte are advising that fiscal year corporatefilers should prorate the tax rate for fiscal years which include days prior to and after 12312017 However thelanguage in the Conference Agreement does not seem to support this position It clearly states that the new flat 21C corporate rate is for ldquotax years beginning after 2017rdquo Nevertheless it seems the actual Conference Report underSubtitle C (page 115) - Business-related Provisions - is silent with regard to fiscal year corporations (ie it doesnot incorporate the language tax years beginning after 2017) So in the absence of this guidance some experts(apparently) are instead looking to Code sect15(c) Effective Date of Change for the rules applicable to corporate taxyears which include days before and after the laws effective date

8 This of course ignores the possible imposition of the Code sect1411 38 Medicare surtax

7copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

the 20 deduction was allowed this would leave $80 (of the original $100 of profit) which couldbe taxed at a marginal rate of up to 37 resulting in a effective tax rate of 2969

- Another option would be to just accumulate this $100 of profit as additional working capital whichcould be invested in a mutual fund for instance yielding a dividend each month First of all theC corporation would have $79 (of the original $100 of profit) to invest And Code sect243 wouldpermit 5010 of this dividend to be excluded from the C corporationrsquos taxable income whenreceived

Example ldquoRetaining C Corp Profits as Invested Working CapitalrdquoIf a C corp had a $100 of profit should it be paid out as additional wages which would face a topmarginal tax rate of 37 along with at least 29 of employment taxes Or should the C corpinstead accumulate this working capital and invest it in a mutual fund paying 7 The C corpshareholder would only have at best about $60 to invest after federal income and employmenttaxes on wages and would then face up to a 20 tax rate on any dividends or LTCGs leaving$80 after-tax per $100 On the other hand the C corporation would have $79 to invest after-taxand would only pay an effective tax rate of 105 of each $100 of return on investment (($100 x50 DRD) x 21) Of course the C corporation would have to watch out for both the AET taxpenalty under Code sect53l (where up to $150000 or $250000 of accumulated earnings could beretained without question) as well as the Code sect541 personal holding company penalty

Example ldquoC Corp Profits Used to Make Retirement Plan Pay-InrdquoA final option might be for the C corporation to contribute the $100 profit into a qualified retirementplan There would be no income taxes due on this amount although employment taxes of at least29 would be owed

LImpact of Blended Rates for Fiscal Year C Corporations

- Due to the fact that the Tax Cuts and Jobs Act reduced the corporate income tax rate from amaximum of 35 to a flat 21 and that changes interaction with Code sect15(a) which coverschanges in rates during a tax year fiscal year corporations will have a blended 2017-2018 taxrate More importantly the one-year existence of that blended rate has planning implications

- With regard to this ldquoblended tax raterdquo before enactment of TCJA corporations were taxed underCode sect11(b) at graduated rates that ranged from 15 to 35 The new flat 21 tax rate providesthat the lowered corporate income tax rate is effective for tax years that begin after Dec 31 2017However for fiscal years that ldquostraddlerdquo the 123117 date the blended procedure outlined belowmust be followed

- Code sect15(a) provides that when tax rates change during a taxpayers tax year (ie a ldquostraddleyearrdquo) the taxpayers tax for the straddle year is computed using a blended tax rate In otherwords the taxpayer is required to

9 Of course separately-stated dividends LTCGs or Sec 1231 gains would receive an even lower rateversus a C corporation which would face a flat 21 tax rate regardless of the source of income

10 The dividend received deduction had been 70 but will be reduced to just 50 under the Tax Actstarting in 2018

8copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

(1) Calculate two tentative taxes for the straddle year by applying each tax rate to thetaxpayers income for the year

(2) Multiply each tentative tax by the proportion of the straddle year to which each tax rateapplies and

(3) Adds the results of the two calculations

Example A C corporationrsquos tax year ends September 30 2018 and its taxable income is $10million To compute its tax the corporation first determines the tax on the taxable income of $10million based on the pre-2018 rates That tax $35 million is multiplied by the ratio of 92 days inJays 2017-2018 tax year (ie the number of days in the 2017 calendar year) over 365 to arriveat approximately $875000 Next the tax on the taxable income of $10 million based on the 2018rates is determined The tax of $21 million is multiplied by the ratio of 273 days in the companyrsquos2017-2018 tax year (ie the number of days in the 2018 calendar year) over 365 to arrive atapproximately $1575000 The corporation then adds $875000 and $1575000 to determine totaltax due of $2450000 Dividing the total tax of $2450000 by taxable income of $10 million yieldsa blended statutory rate of 245 for a fiscal year ending on Sept 30 2018

Comment The blended statutory rate drops by 117 per month ((35-21)12)) For examplea corporation with an October year end will have a blended rate roughly 117 lower than thecompany mentioned in the example above

Planning Point Because of this 2017-2018 blended tax rate all fiscal year corporations will bein a higher tax bracket in 2017-2018 then they will be in future years when they will be taxed at21 Therefore deductions in their 2017-2018 tax years will have greater value than in lateryears and income will be taxed at a higher rate in their 2017-2018 tax years then it will be in lateryears As a result fiscal year corporations would obviously benefit by taking steps that accelerateddeductions into the months in 2017 while deferring income from 2017 to future years

LPossible Windfall in Corporate Tax Revenues for States States may receive a major boost in their corporate tax revenues as a result of the Tax Cuts and JobsAct according to a new report The report prepared by EYrsquos Quantitative Economics and Statisticsunit on behalf of the Council On State Taxationrsquos State Tax Research Institute estimates thenationwide overall increase in state corporate income tax bases is 12 percent over the next 10 yearsalthough it predicts significant variations between the states by year The report estimates the averageexpansion in the state corporate tax base to be 8 percent from 2018 through 2022 increasing to 135percent for 2022 through 2027 The growing increase in later years is due mainly to the impact ofresearch and experimentation expense amortization starting in 2022 and the change in the interestlimitation that same year

Another important factor behind the projected increase in corporate tax revenue is because statesusually conform to federal provisions that broaden the corporate tax base but not to provisions thatreduce corporate tax rates The magnitude of increased corporate tax collections for each state willdepend on how it chooses to conform to the changes in the federal tax code from the new law thecomposition of its economy and the way in which specific provisions within the Tax Cuts and Jobs Actare implemented at the federal level

The states that are expected to get the greatest estimated percentage change in state corporate taxbase from the new tax law are mainly those that tax certain types of foreign income The impact will also

9copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

vary by industry based on the tax and financial profiles of companies in each industry sector The studyestimates the change in the state corporate tax base expansion by sector manufacturing (12 percent)capital intensive services (17 percent) labor intensive services (9 percent) finance and holdingcompanies (8 percent) and other industries (13 percent) (Misc TCJA)

- 21 Rate Also Available for PSCs

- Although the House version would have imposed a separate 25 flat tax rate on PSCs the finalConference version of the Tax Act declined to do so

- As a result personal service corporations would also be subject to a flat 21 corporatetax rate (ie the same as any other C corporation) rather than the current 35 rateeffective for tax years beginning after 2017 A personal service corporation is a corporation theprincipal activity of which is the performance of personal services in the fields of health lawengineering architecture accounting actuarial science performing arts or consulting and suchservices are ldquosubstantially performedrdquo by the employee-owners

Comment Cf Code sect448 for the definition of a PSC But since the same 21 rate appliesto all C corporations the specific classification of a company as a PSC is no longerimportant to ascertain On the other hand for purposes of the new 20 deduction on K-1profits covered below the definition of a service-based business appears to be muchbroader than this ldquooldrdquo definition of PSCs

- 21 C Corp Rate v 37 for S Corp Owners and Partners

- Should a PSC decide to convert to S corporation status it would still face the possible impositionof the Code sect1374 built-in gains tax for the first 5 years after the effective date of the S electionBut as mentioned above the BIG rate should be dropping to just 21 since it will be the highest(and only) C corporation tax rate for tax years beginning after 2017

- On the other hand if a S corp business is ldquoservice-basedrdquo with its owneremployees havingtaxable incomes significantly above the respective phaseout points for the Sec 199A ldquothresholdamountsrdquo (ie gt $207500 and $415000) they might want to instead revoke their S election andtake advantage of the 21 flat tax rate otherwise available for all types of regular C corporationsThis might be especially true if the owners can use the ldquopersonal goodwillrdquoargument to avoiddouble taxation if and when they decide to liquidate the C corporation (and a sale of stock is notavailable) while accumulating some earnings and taking advantage of the Code sect243 dividendreceived deduction

- ldquoService-basedrdquo partnerships might also want to consider converting their business to a regularC corporation if the Sec 199A is not otherwise available due to the partners high taxable incomeson their personal returns In addition the prospect of completely tax-free fringe benefits becomingonce again available with a C corporation could be an attractive side benefit as well

Choice of Entity Most ldquoservice-basedrdquo businesses such as law accounting medicine etc tendto take the profits generated out of the business annually leaving only what is needed for workingcapital purposes If that is the case it probably does not make sense to operate as a C corporationunless substantial sums were instead going to be reinvested back into the business (or within the

10copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

$150000 Code sect531 AET tax limit profits were retained and invested to take advantage of theCode sect243 50 ldquodividend received deductionrdquo) With the double taxation on dividends distributedout of C corporation profits you still face a maximum effective 40 tax rate (ie 21 x $100 ofC corp profits plus 238 x $80 dividend)

LC Corp Electing S Status Allowed Built-In Loss for Bonuses Pegged Against Cash BasisReceivables (PLR 200925005) A cash basis personal service corporation (PSC) that elected S status was permitted to offset thepotential built-in gain from the eventual collection of cash basis receivables with a built-in lossEssentially this took the form of a bonus for services rendered by its professional shareholder (as wellas its nonshareholder employees) that was recorded on the books of the former C corporation during itslast days of existence but which was paid within 2frac12 months after becoming an S corp

Comment Key to the favorable result in this ruling was the fact that the taxpayer would pay to itsshareholderemployees within the first two and one-half months of the recognition period all salaryand wage expenses that were related to the production of accounts receivable that wereoutstanding as of the effective date of the S election

Comment As to the payments made to any nonshareholder employees these could be madeat any point during the 10-year built-in gains period (ie the same time frame as that for any otheraccounts payable or other unpaid payroll expenses)

Background Code sect1374(d)(4) provides that any loss recognized on a disposition of an assetduring the recognition period is recognized built-in loss to the extent the S corporation establishes thatit held the asset on the first day of the recognition period and such loss does not exceed the excess of(i) the adjusted basis of such asset as of the beginning of such first taxable year over (ii) the fair marketvalue of such asset as of such time Code sect1374(d)(5)(B) provides that any item of deduction properlytaken into account during the recognition period but attributable to periods before the first day of therecognition period is recognized built-in loss for the taxable year for which it is allowable as a deductionCode sect1374(d)(5)(C) provides that an S corporations net unrealized built-in gain is properly adjusted foritems of income and deduction that would be recognized built-in gain or loss if taken into account duringthe recognition period Reg sect11374-4(b)(2) provides in relevant part that any item of deductionproperly taken into account during the recognition period is recognized built-in loss if the item would havebeen properly allowed as a deduction against gross income before the beginning of the recognition periodto an accrual method taxpayer Reg sect11374-4(c) limits the treatment under Reg sect11374-4(b)(2) ofitems of deduction properly taken into account during the recognition period as recognized built-in lossThe limitation of Reg sect11374-4(c) applies to items of deduction constituting payments to related partiesand any amount properly deducted during the recognition period under Code sect404(a)(5) (ie relatingto payments for deferred compensation) Reg sect11374-4(c)(1) (relating to regular compensation suchas bonuses paid out of receivables) provides that any payment to a related party properly deducted inthe recognition period under Code sect267(a)(2) will be deductible as recognized built-in loss only if (i) allevents have occurred that establish the fact of the liability to pay the amount and the exact amount ofthe liability can be determined as of the beginning of the recognition period and (ii) the amount is paid(A) within the first two and one-half months of the recognition period or (B) to a related party owning lessthan five percent by voting power and value of the corporationrsquos stock both as of the beginning of therecognition period and when the amount is paid Meanwhile Reg sect11374-4(c)(2) (relating to deferredcompensation payments) provides that any amount properly deducted in the recognition period underCode sect404(a)(5) will be deductible as recognized built-in loss to the extent (i) all events have occurredthat establish the fact of the liability to pay the amount and the exact amount of the liability can be

11copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

determined as of the beginning of the recognition period and (ii) the amount is not paid to a related partyto which Code sect267(a)(2) applies (Code sect1374 BIG Tax)

Comment This is one of the prime considerations when a PSC decides to elect S status Namelyif a cash basis accounts receivable is subject to the built-in gains tax the rate could effectively goas high as 575 (ie 35 x $100 of BIG + (35 x ($100 - 35 BIG tax)) Whereas if S electionhad never been made then the PSC would have simply paid out these receivables as collectedwith the only tax being that paid at the shareholderemployeersquos marginal tax rate (ie at most35) And the IRS has won at least two cases where the planning outlined above was notproperly consummated and the cash basis receivables subsequently collected by the S corp weresubject to the built-in gains tax

- 100 Bonus Depreciation

Comment Since many states must have balanced budgets they often ldquodecouplerdquo from thefederal tax law Therefore provisions such as 100 bonus depreciation and Sec 179 immediateexpensing may not be allowed in determining taxes due at the state or local level So in additionto the federal income tax law prohibitions such as the ldquoat-risk limitations (ie on Form6198) or the Code sect469 passive loss rules there will be the added complexity ofmaintaining distinct bases for depreciable (and perhaps amortizable) assets at the federalv state income tax levels (let alone for book or GAAP purposes)

- Under prior law an additional first-year bonus depreciation deduction was allowed equal to 50of the adjusted basis of qualified property the ldquooriginal userdquo of which began with the taxpayerplaced in service before Jan 1 2020 (Jan 1 2021 for certain property with a ldquolonger productionperiodrdquo) But the 50 allowance was to be phased down to 40 for property placed in servicein 2018 and to 30 for property placed in service in 2019 A first-year depreciation deduction wasalso electively available for certain plants bearing fruit or nuts planted or grafted after 2015 andbefore 2020 Film productions were not eligible for bonus depreciation

- Under the new Tax Act businesses will be able to fully and immediately expense 100 ofthe cost of qualified property acquired and placed in service after Sept 27 2017 and beforeJan 1 2023 (with an additional year for certain qualified property with a longer production period)

Comment Note that the ldquotestrdquo here is conjunctive meaning that the asset must have been bothldquoacquiredrdquo and ldquoplaced in servicerdquo after 92717 Thus assets acquired before 92817 but thenplaced in service after 92717 would result in the ldquooldrdquo 50 bonus depreciation rules applying

- For productions placed in service after Sept 27 2017 qualified property eligible for a 100first-year depreciation allowance now includes qualified film television and live theatricalproductions A production is considered ldquoplaced in servicerdquo at the time of initial release broadcastor live staged performance (ie at the time of the first commercial exhibition broadcast or livestaged performance of a production to an audience)

- For certain plants bearing fruit or nuts planted or grafted after Sept 27 2017 the 100first-year deduction is also available

- The ldquooriginal userdquo requirement has now been eliminated under the new Tax Act It wasproposed that that bonus depreciation would not be available for any property used in a ldquoreal

12copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

property trade or businessrdquo11 But the new Tax Act did not include the exclusion of ldquopropertyused in a real estate trade or businessrdquo (ie as proposed by the House)

Comment Under prior law ldquoqualified propertyrdquo included property acquired by purchase if anothertaxpayer had not previously used the property In other words the property did not have to benew as long as it was not acquired from a related party However under the new Tax Actldquoqualified propertyrdquo does not include property used in a business that is not subject to thenet business interest expense limitation (discussed below) but it does include propertyused in farm business The law also adds a new category for qualified film TV and livetheatrical production property

- Even though bonus depreciation will increase to 100 the effect on the Code sect280Fldquoluxury car capsrdquo is still only an $8000 increase to the first year cap (though the first yearcap will be increasing to $10000 from $3160 starting in 2018 so a total of $18000 mightbe available when bonus depreciation is included)

- The election to accelerate AMT credits in lieu of bonus depreciation is repealed12

Comment For perhaps the sake of simplicity a taxpayer can choose for the first tax yearending after Sept 27 2017 to instead elect to claim 50 bonus first-year depreciation(instead of claiming a 100 first-year depreciation allowance) So for a 2017 calendar-yeartaxpayer 50 bonus depreciation can continue to be used (instead of 100) for otherwisequalifying assets acquired and placed in service after 92717 through 123117

Comment The pre-Act law phase-down of bonus depreciation continues to apply toproperty acquired before Sept 28 2017 In other words otherwise qualifying ldquooriginal userdquoassets placed into service before that date would only be allowed 50 bonus depreciation13 Andif the asset was acquired before Sept 28 2017 but not placed into service until 2018 forexample then the asset would only be eligible for 40 bonus depreciation Furthermore it wouldappear that the ldquooriginal userdquo requirement would also have to be satisfied

Comment And of course unlike Sec 179 immediate expensing which is done on an asset-by-asset basis using Form 4562 bonus depreciation continues to be ldquoautomaticrdquo insomuchas the taxpayer must elect on a MACRS class-by-class basis to not be subject to bonusdepreciation (for each and every tax year that it otherwise applies) And you must elect outon a MACRS class-by-class basis by the extended due date of the return to not be automaticallysubject to this deduction (ie it cannot be done on an amended tax return)

Example ldquoBuying Out Assets at End of Lease - Pre-92817rdquoA taxpayer is leasing a car whose lease expires 92717 at which time he has the option of buyingthe vehicle If the car was new at the beginning of the lease the ldquooriginal userdquo of the vehicle would

11 Keep in mind though that the new Tax Act would now permit Sec 179 immediate expensing for assets

ldquoused in connection with lodgingrdquo even if the rental activity did not involve ldquotransient dwellersrdquo

12 Code Sec 168(k)(4) as amended by Act Sec 12001

13 This statement contained in the final Conference Agreement clarifies that assets purchased before Sept28 2017 but not placed into service until after Sept 27 would receive 50 bonus depreciation (or even be subject tothe 40 or 30 bonus depreciation rules if they were not placed into service until either 2018 and 2019)

13copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

have started with him And with the 50 bonus depreciation rules applying he would be eligible(unless he elected out of bonus depreciation for the MACRS 5-year class) a first-year luxury carcap of $11160 (ie the normal first-year cap of $3160 plus $8000 additional write-off due to the50 bonus depreciation)

Example ldquoBuying Out Assets at End of Lease - Post-92717rdquoSame facts as above except that the vehicle was used as of the beginning of the lease Nowhowever the lease expires one day later on 92817 at which time he decides to buy the car Eventhough the new 100 bonus depreciation rule would now be in effect the impact on the first-yearluxury car cap would be the same Namely it would still only be increased by $8000 (ie to anoverall cap of $11160) Nevertheless bonus depreciation is available even though a ldquousedrdquo assetis being purchased (and the ldquooriginal userdquo of this asset did not begin with this specific taxpayer)

Example ldquoAssets Acquired Before amp After 92717 Effective DaterdquoA taxpayer buys two pieces of equipment one on 92717 and the other on 92817 Although hecan claimed a Sec 179 immediate write-off of up to $510000 he would be limited to 50 bonusdepreciation for the first asset but would have 100 bonus depreciation for the second asset

Comment So for the assets mentioned in the above examples were purchased after 92717it would no longer matter if the ldquooriginal userdquo of them started with the taxpayer In other words theycan be new or used

Comment Obviously with 100 bonus depreciation for the next 5 years it essentially makesSec 179 immediate expensing superfluous along with the fact that there is no overall cap nophaseout rules or the need for ldquotrade or business taxable incomerdquo to claim the deduction Ineffect then bonus depreciation can be used to create or increase an NOL (as opposed to Sec179 write-offs) Nevertheless there will be some situations where Sec 179 should still be electedFor example where a state only allows $25000 for Sec 179 and nothing for bonus depreciationAt least $25000 under Sec 179 should be elected on the federal tax return so that it will also beavailable for the state return as well

LTechnical Correction Needed for ldquoQualified Improvement Propertyrdquo

- ldquoQualified improvement property (QIP)rdquo is any improvement to an interior portion of a buildingthat is nonresidential real property if the improvement is placed in service after the date thebuilding was first placed in service except for any improvement for which the expenditure isattributable to

1 Enlargement of the building

2 Any elevator or escalator or

3 The internal structural framework of the building (Code sect168(e)(6))

- Under the TCJA the statutory language for Code sect168(e)(3)(E) does not include QIP leavingit as nonresidential real property (ie MACRS 39-year commercial real estate) and therefore notsubject to bonus depreciation or some other class of property (eg a property with 15 yearsMACRS) However according to the conference committee QIP was intended to be 15-yearproperty qualifying for bonus depreciation

14copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

- A technical correction is therefore needed to the property class life for QIP so that it would clearlynow be classified as MACRS 15-year property and thus eligible for 100 bonus depreciation

Comment ldquoQualified improvement propertyrdquo was a new category added to the MACRSclassification system as 39-year commercial real property effective for the 2016 tax year (andcarried over for 2017) More importantly it was eligible for 50 bonus depreciation In otherwords tangible personal or real property no longer needed to have a MACRS class of 20 yearsor less to be eligible for bonus depreciation Now for otherwise qualifying assets acquired andplaced into service after 92717 (ie regardless of tax year) 100 bonus depreciation wouldapply even if the ldquooriginal userdquo of the asset did not commence with the taxpayer

Comment With ldquoimprovement propertyrdquo such as QIP this would normally involve assetsconnected with commercial real estate that the taxpayer did not feel comfortable in expensing asa ldquorepairrdquo and therefore ones which they would capitalize as part of the real property As a resultthe question as to whether the ldquooriginal userdquo commenced with the taxpayer would usually be amoot point

- Increased Sec 179 Immediate Expensing Election

- In general ldquoqualifying propertyrdquo is defined as depreciable tangible personal property that ispurchased for use in the active conduct of a trade or business14 and includes off-the-shelfcomputer software and ldquoqualified real propertyrdquo (ie qualified leasehold improvementproperty qualified restaurant property and qualified retail improvement property)

Comment As discussed below in greater detail the TCJA expanded the definition of qualifiedproperty to include ldquoqualified improvement propertyrdquo specified improvements (eg new roofsHVAC along with fire and security alarm systems) to nonresidential real property and assets usedin connection with lodging (eg rugs appliances and FampF)

Comment As explained below the term ldquoqualified real propertyrdquo (with its special ldquotestsrdquo such ashaving to be subject to a lease on a commercial building placed in service gt 3 years previouslyor made to a ldquoqualifying restaurant buildingrdquo under the ldquo50 of square footage testrdquo) has beeneliminated so that Sec 179 will be available regardless of these requirements being metHowever restaurant building property placed in service after December 31 2017 that does notmeet the definition of ldquoqualified improvement propertyrdquo is not eligible for section 179 expensingFurthermore without the special ldquo50 of square footage testrdquo such buildings (ie real property)would now be classified once again as MACRS 39-year commercial real estate

- ldquoQualified improvement propertyrdquo is any improvement to an interior portion of a buildingthat is nonresidential (ie commercial) real property if such improvement is placed inservice after the date such building was first placed in service But qualified improvementproperty does not include any improvement for which the expenditure is attributable to theenlargement of the building any elevator or escalator or the internal structural framework of thebuilding These latter types of fixed assets would be considered as part of the MACRS 39-year

14 Keep in mind that triple net lease situations might not qualify as assets being used in the ldquoactive conductof a trade or businessrdquo Also if a ldquononcorporate lessorrdquo is involved (eg SMLLC or multi-member LLC) then Codesect179(d)(5) will impose a special limitation test during the first 12 months that the asset is being leased

15copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

commercial real property

- Passenger automobiles subject to the Code sect280F limitation continue to be eligible for Codesect179 expensing only to the extent of the Code sect280F dollar limitations (which has now beenincreased to $10000 for the first year placed in service for tax years beginning after 2017) Butfor sport utility vehicles above the 6000 pound weight rating and not more than the 14000 poundweight rating (ie which are therefore not subject to the Code sect280Fcar caps) the maximumcost that may be expensed for any tax year under Code sect179 remains at just $2500015

- Under the House bill the Sec 179 cap would have been increased to $5 million (from the current$510000) and the phase-out amount would have increased to $20 million (from the current$2030000) effective for tax years beginning after 2017 through tax years beginning before 2023The Senate version would have allowed for $1 million in immediate expensing with a phaseoutof $25 million The final Conference bill adopted the Senate version

Comment As mentioned previously with bonus depreciation now 100 (for otherwise qualifyingnew or used assets placed into service after Sept 272017) along with the fact that this write-offis not subject to a cap does not have a phaseout mechanism or the need for ldquotrade or businesstaxable incomerdquo it now makes Sec 179 (at no matter what the overall cap is set at) basicallyredundant in most instances

Comment Once again keep in mind that unlike bonus depreciation (which is ldquoautomaticrdquo unlessthe taxpayer chooses to elect out of that particular MACRS class of assets by the extended duedate of that yearrsquos tax return) Sec 179 immediate expensing can always be revoked or electedon an amended tax return (ie assuming that the tax year in question is still open)

Example ldquoAmending Return to Elect Sec 179Upon being audited by the IRS the taxpayer is informed that they must capitalize certain assetimprovements which had originally been written off as ldquorepairsrdquo Despite the taxpayerrsquos protestsand in order to settle the IRS audit without additional expense the taxpayer capitalizes theldquorepairsrdquo but then chooses to amend the return in question taking Sec 179 immediate expensing(at least to the extent that it is still available to them for that particular tax year)

Example ldquoElecting Sec 179 After Cost Seg StudyrdquoAs a result of a cost segregation study numerous MACRS 5- and 7-year assets are uncoveredFurthermore the tax year in which they were placed into service is still open In this situation thetaxpayer can choose to amend their tax return for that year and immediate expense such newly-found assets (at least to the extent that the overall cap for Sec 179 has not yet been exceeded)Of course if those assets have been acquired and placed into service after Sept 27 2017 aForm 3115 could instead be filed to ldquocatch uprdquo on any depreciation along with 100 bonusdepreciation (even if it were a closed tax year assuming that the taxpayer had not elected out ofthat MACRS classlife for the year that the assets were first placed into service)16

15 For tax years after 2018 this $25000 limit will be indexed for inflation (something that was not done in thepast)

16 Keep in mind that if the taxpayer had merely misclassified an asset (or simply failed to claimed anydepreciation) and only one year had passed with the use of this erroneous method then a ldquomethod of accountingrdquowould not have been ldquoadopted for two or more consecutive yearsrdquo and therefore an amended return could be filed(and Form 3115 would not be necessary)

16copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018

- The definition of section 179 property would now also include ldquoqualified energy efficientheating and air-conditioning propertyrdquo (ie HVAC assets) effective for property acquired andplaced in service after Nov 2 201717

Comment And now it would not matter for purposes of Sec 179 for instance if the air-conditioning equipment was located outside of the building (ie as is the current requirementfor ldquoqualified improvement propertyrdquo to be in the ldquointeriorrdquo of the building under the bonusdepreciation rules)

Comment Such property would be any depreciable Code sect1250 property that is (a) installed aspart of a buildings heating cooling ventilation or hot water system and (b) within the scope ofStandard 901-2007 of the American Society of Heating Refrigerating and Air-ConditioningEngineers and the Illuminating Engineering Society of North America

- The new Tax Act now allows for Sec 179 with regard to assets ldquoused in connection withlodgingrdquo (without regard to the current 30-day ldquotransient dwellerrdquo rule which normally applied tohotels motels and BampBs)

- Example ldquoAssets Used in Connection with Lodging - FampFrdquo In 2017 a taxpayer acquires a condo for rental purposes in FL and proceeds to fully furnish it withrugs furniture appliances etc Sec 179 would not be allowed for immediate write off of theseassets (although 50 bonus depreciation would be since these are MACRS 5-year assetsclassified as ADR 570 ldquoDistributive Trades or Businessesrdquo) Had the condo be acquired (orfurnished) in 2018 Sec 179 (let alone 100 bonus depreciation) could be used

- Example ldquoAssets Used in Connection with Lodging - Other AssetsrdquoA large 250-unit apartment complex has a maintenance shed in the rear of the property in whichare stored riding mowers snow blowers a pick-up truck and other equipment all of which areused to maintain the premises If this equipment and truck were placed in service in 2017 Sec179 would not be available since these assets ldquoare used in connection with lodgingrdquo (although 50bonus depreciation could be claimed) If the assets were instead placed into service after2017 Sec 179 could be used

Comment Of course either 50 or 100 bonus depreciation could be used on such MACRS5-year property depending on when they were acquired and placed into service (ie based onthe change for 92717 for bonus depreciation)

Example ldquoAssets Used in Connection with Lodging - HotelsMotelsrdquoIf these assets were instead being used in connection with a hotel motel or BampB etc then Sec179 would be available regardless of when the assets had been placed into service since theyinvolve real property being rented out to ldquotransient dwellersrdquo (ie whose average stay was 30days or less)

Comment Use of either Sec 179 immediate expensing or bonus depreciation avoids anydepreciation adjustment for AMT purposes since neither is a not a write-off ldquoexpressed in

17 Hopefully this change will clear up the confusion where the PATH Act (121815) stated that Sec 179

was available for HVAC assets but then the IRS came out with Rev Proc 2017-33 and insisted that it was only forldquoportable heaters and air conditioning unitsrdquo Code Sec 179 as amended by Act Sec 13101

17copyTax Educatorsrsquo Network Inc - 2018 Current as of 6142018