april 2017 u.s. employment update and outlook

TRANSCRIPT

National employment situation: March 2017

April 7, 2017

March 2017 U.S. labor market at a glance

2

+98,000(78 consecutive months

of growth)

1-month net change

+2,185,000(+1.5% y-o-y)

12-month change

+795,00010-year average annual growth

4.5%Unemployment rate

5,626,000(-1.5% y-o-y)

Job openings

-50bp12-month change in unemployment

63.0%Labor force participation rate

5,440,000(+6.3% y-o-y)

Hires

3,220,000(+11.3% y-o-y)

Quits

Source: JLL Research, Bureau of Labor Statistics

After two strong months, March disappointsJanuary and February both exceeded the 200,000-job threshold, while March fell well below expectations with only 98,000 net new jobs. A contraction in retail

trade and slowdowns in all major sectors with the exception of professional and business services (PBS) were the primary drivers of this, compounded by

volatility due to tightening and employment growth continuing to exceed the rate of labor-force expansion. Although March’s monthly growth did not meet consensus figures, the broader trend remains positive and future months will dictate whether this is an anomalous month or a broader shift in growth rates.

Unemployment drops, but slack is beginning to run outCounter to job growth, unemployment metrics improved once again, with the unemployment rate dropping by another 20 basis points to a cyclical low of 4.5

percent. Total unemployment fell below the 9.0-percent threshold for the first time since 2007 and now stands at 8.9 percent. With unemployment already low,

the slowing rate of labor-force expansion (0.5 percent annually compared to total non-farm job growth of 1.5 percent) will present a challenge for employers

seeking to increase headcounts, particularly as unemployment for bachelor’s-degree holders remains steady at 2.5 percent.

Confidence is up even as inflation ramps upThe consumer confidence index spiked in March to 125.6 points, its highest figure since 2000. Business confidence metrics have also showed optimism,

indicating further economic growth ahead. The acceleration in inflation to 2.7 percent – now at the same rate as wage growth – may begin to affect consumer

spending, however, but tightening labor-market conditions will likely push wages up further.

March 2017 U.S. labor market highlights

3Source: JLL Research, Bureau of Labor Statistics

360,0

00

226,0

00

243,0

00

96,0

00

110,0

00

88,0

00

106,0

00

122,0

00

221,0

00

183,0

00

164,0

00 196,0

00

360,0

00

226,0

00

243,0

00

96,0

00

110,0

00

88,0

00

160,0

00

150,0

00

161,0

00

225,0

00

203,0

00

214,0

00

197,0

00

280,0

00

141,0

00

203,0

00

199,0

00

201,0

00

149,0

00

202,0

00

164,0

00

237,0

00 2

74,0

00

84,0

00

166,0

00

188,0

00 2

25,0

00

330,0

00

236,0

00

286,0

00

249,0

00

213,0

00 2

50,0

00

221,0

00

423,0

00

329,0

00

221,0

00

265,0

00

84,0

00

251,0

00

273,0

00

228,0

00

277,0

00

150,0

00

149,0

00

295,0

00

280,0

00

262,0

00

168,0

00

233,0

00

186,0

00

277,0

00

24,0

00

271,0

00

252,0

00

176,0

00 208,0

00

135,0

00 164,0

00

155,0

00

216,0

00

219,0

00

98,0

00

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2011 2012 2013 2014 2015 2016 2017

1-m

onth

net ch

an

ge

After a strong start to 2017, March saw only 98,000 net new jobs, while downward revisions hit Jan. and Feb.

Source: JLL Research, Bureau of Labor Statistics 4

0%

2%

4%

6%

8%

10%

12%

-1,000

-800

-600

-400

-200

0

200

400

600

Un

em

plo

ym

ent ra

te (

%)

1-m

onth

net ch

an

ge

(th

ou

san

ds)

1-month net change Unemployment rate

Unemployment fell to its lowest rate this cycle (4.5 percent) on the back of further labor-market tightening

5Source: JLL Research, Bureau of Labor Statistics

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

Jo

b o

pe

nin

gs (

thou

san

ds)

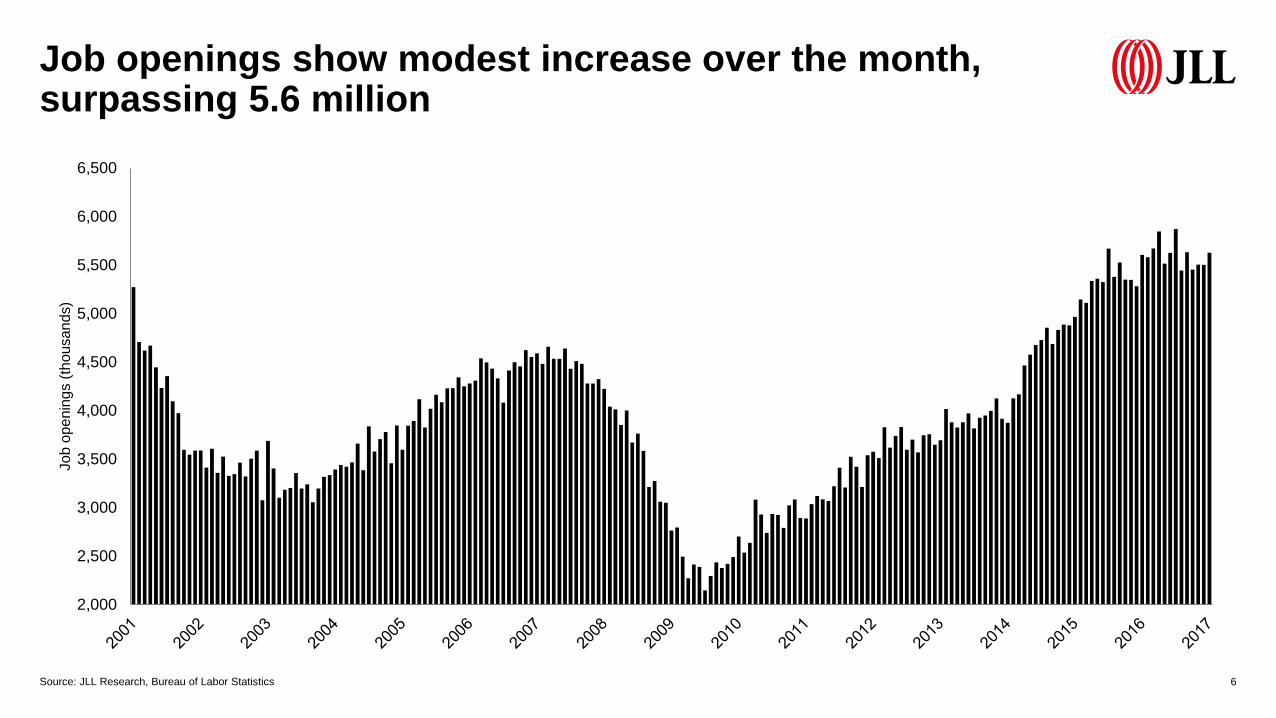

Job openings show modest increase over the month, surpassing 5.6 million

6Source: JLL Research, Bureau of Labor Statistics

2.1%

2.3%

2.9%

3.0%

3.4%

3.9%

4.3%

4.5%

4.7%

5.2%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

Construction

Mining and logging

Manufacturing

Information

Trade, transportation and utilities

Other services

Leisure and hospitality

Financial activities

Education and health

Professional and business services

Job openings rate (%)

The rate of job openings across sectors has remained largely stable, although financial activities has risen

7Source: JLL Research, Bureau of Labor Statistics

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

12-m

onth

% c

han

ge

Wage growth Inflation

Inflation has now caught up with wage growth, which may begin to squeeze consumer spending

8Source: JLL Research, Bureau of Labor Statistics

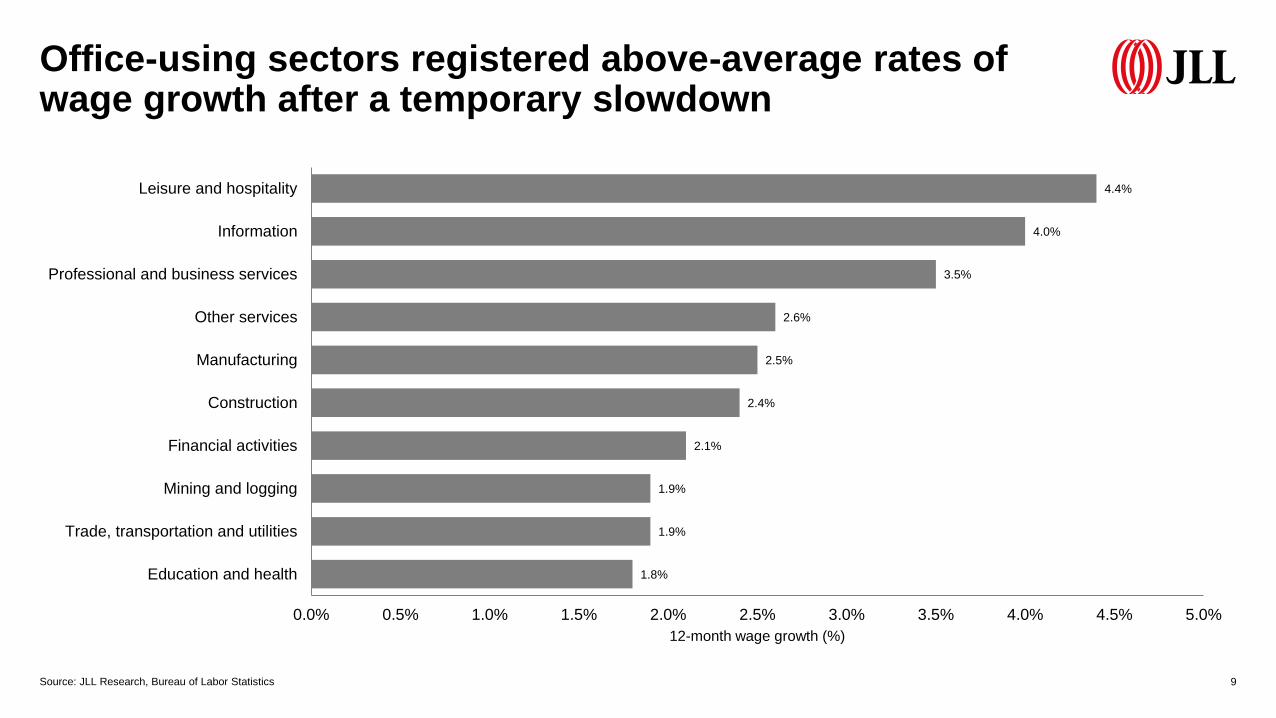

1.8%

1.9%

1.9%

2.1%

2.4%

2.5%

2.6%

3.5%

4.0%

4.4%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% 5.0%

Education and health

Trade, transportation and utilities

Mining and logging

Financial activities

Construction

Manufacturing

Other services

Professional and business services

Information

Leisure and hospitality

12-month wage growth (%)

Office-using sectors registered above-average rates of wage growth after a temporary slowdown

9Source: JLL Research, Bureau of Labor Statistics

62%

63%

63%

64%

64%

65%

65%

66%

66%

67%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

12-m

onth

% c

han

ge

The labor force participation rate showed no sign of change in March at 63.0 percent

10Source: JLL Research, Bureau of Labor Statistics

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

12-m

onth

% c

han

ge

Civilian labor force Employment

The rate of labor force expansion continues to slow, posing further difficulty for employers

11Source: JLL Research, Bureau of Labor Statistics

-29.7

-3.0

-0.7

-0.4

0.0

1.0

3.0

3.5

6.0

9.0

9.0

9.0

10.5

11.0

11.0

11.0

16.0

16.7

56.0

-40 -30 -20 -10 0 10 20 30 40 50 60 70

Retail trade

Information

Utilities

Wholesale trade

Nondurable goods

Other services

Motor vehicles and parts

Transportation and warehousing

Construction

Financial activities

Government

Leisure and hospitality

Temporary help services

Mining and logging

Durable goods

Manufacturing

Education and health services

Health care and social assistance

Professional and business services

1-month net change (thousands)

Professional and business services was the only major sector that did not record a slowdown in March

12Source: JLL Research, Bureau of Labor Statistics

-32.0

-1.5

1.0

3.0

9.3

36.0

37.0

46.4

54.0

58.5

88.7

110.2

152.0

177.0

178.0

258.0

437.0

527.0

639.0

-100 0 100 200 300 400 500 600 700

Information

Utilities

Durable goods

Mining and logging

Motor vehicles and parts

Nondurable goods

Manufacturing

Wholesale trade

Other services

Retail trade

Transportation and warehousing

Temporary help services

Government

Construction

Financial activities

Leisure and hospitality

Health care and social assistance

Education and health services

Professional and business services

12-month net change (thousands)

Mining and logging has returned to growth on an annual basis after a sharp contraction

13Source: JLL Research, Bureau of Labor Statistics

639.0

527.0258.0

178.0

58.5

487.5

PBS Education and health

Leisure and hospitality Financial activities

Retail trade Manufacturing

All other jobs

Core subsectors added 77.7 percent of all

jobs over the past 12 months.

0%

1%

2%

3%

4%

5%

6%

12-m

onth

% c

han

ge

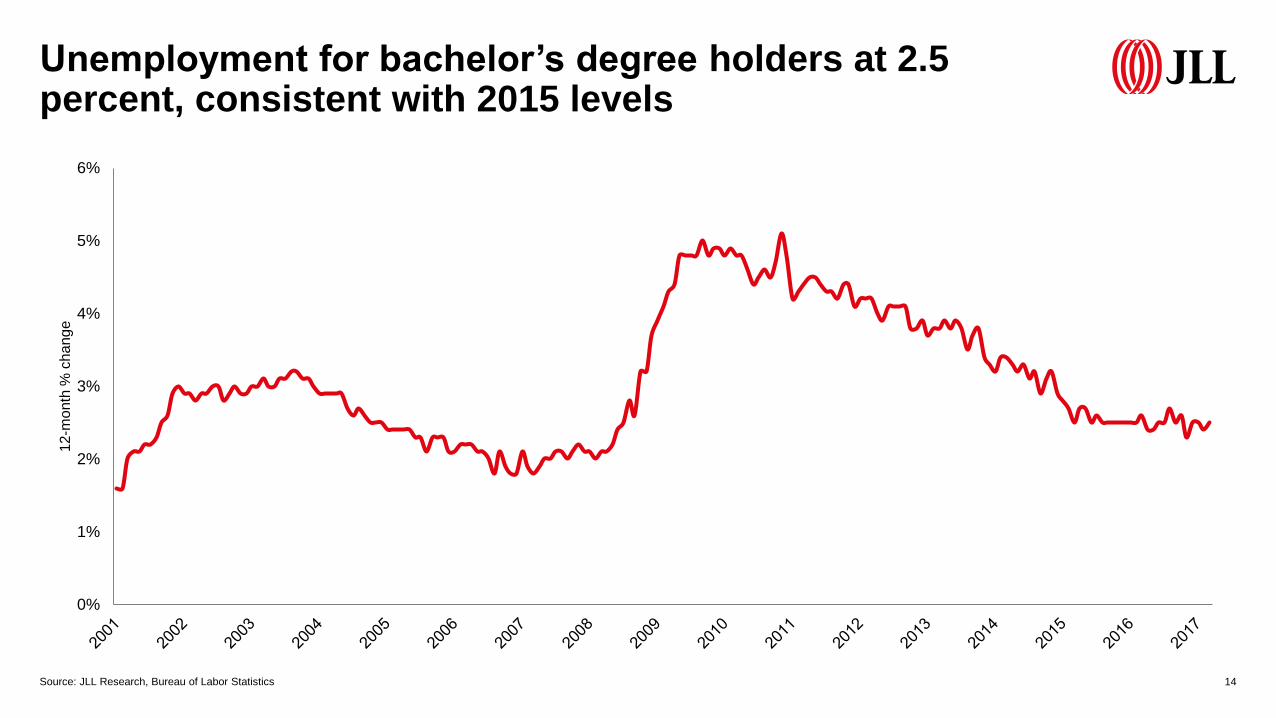

Unemployment for bachelor’s degree holders at 2.5 percent, consistent with 2015 levels

14Source: JLL Research, Bureau of Labor Statistics

-300

-250

-200

-150

-100

-50

0

50

100

150

200

2009 2010 2011 2012 2013 2014 2015 2016 2017

1-m

onth

net ch

an

ge

(th

ou

san

ds)

Professional and business services Financial activities Information

A third consecutive month of contraction in information is beginning to drag down office-using growth

15Source: JLL Research, Bureau of Labor Statistics

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

12-m

onth

% c

han

ge

Tech Energy, mining and utilities Office-using Total non-farm

Tech’s slight bump to 4.9-percent growth held up, but remains below 2015 highs

16Source: JLL Research, Bureau of Labor Statistics

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

Initia

l u

ne

mp

loym

ent cla

ims p

er

we

ek

Intial weekly claims 4-week moving average

Initial unemployment claims remain on a downward trend despite already being at cyclical lows

17Source: JLL Research, U.S. Department of Labor

0

20

40

60

80

100

120

140

Co

nsu

me

r co

nfid

en

ce in

de

xConsumer confidence is soaring even as inflation rises and now strongly exceed their previous peak

18Source: JLL Research, Conference Board

All metro areas exceeding 3.0-percent job growth except for Salt Lake City are in the Sun Belt

19

3.1%

3.2%

3.6%

3.7%

3.9%

3.9%

4.3%

2.5% 3.0% 3.5% 4.0% 4.5%

Salt Lake City

Charlotte

Atlanta

Dallas

Jacksonville

Nashville

Orlando

12-month % change

Source: JLL Research, Bureau of Labor Statistics

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

12-m

onth

% c

han

ge

Total unemployment 10-year average

Total unemployment dropped to 8.9 percent, the first time below 9.0 percent since 2007

20Source: JLL Research, Bureau of Labor Statistics