a global leader in used equipment sales · pdf filea global leader in used equipment sales ......

TRANSCRIPT

1

A global leader in used equipment salesInvestor overview presentation

September 2016

2

Forward looking statements and non-GAAP measuresCaution Regarding Forward-Looking Statements

This presentation contains forward-looking statements and forward-looking information within the meaning of applicable U.S. and Canadian securities legislation (collectively, “forward-looking statements”), including, in particular, statements regarding the terms and potential benefits of the proposed transaction between Ritchie Bros. and IronPlanet, the terms and conditions of the proposed transaction, the expected timetable for completing the proposed transaction, benefits and synergies of the proposed transaction, future opportunities for the combined businesses of Ritchie Bros. and IronPlanet, future financial and operational results and any other statements regarding events or developments that Ritchie Bros. believes or anticipates will or may occur in the future. Forward-looking statements are statements that are not historical facts and are generally, although not always, identified by words such as “expect”, “plan, “anticipate”, “project”, “target”, “potential”, “schedule”, “forecast”, “budget”, “estimate”, “intend” or “believe” and similar expressions or their negative connotations, or statements that events or conditions “will”, “would”, “may”, “could”, “should” or “might” occur. All such forward-looking statements are based on the opinions and estimates of management as of the date such statements are made. Forward-looking statements necessarily involve assumptions, risks and uncertainties, certain of which are beyond Ritchie Bros.’s control, including risks and uncertainties related to: general economic conditions and conditions affecting the industries in which Ritchie Bros., IronPlanet and Caterpillar operate; obtaining regulatory approvals in connection with the proposed transaction; each of Ritchie Bros.’ andIronPlanet's ability to satisfy the merger agreement conditions and consummate the transaction on the anticipated timetable, or at all; Ritchie Bros.’ ability to successfully integrate IronPlanet's operations and employees with Ritchie Bros.’ existing business; the ability to realize anticipated growth, synergies and cost savings in the proposed transaction; the maintenance of important business relationships; the effects of the IronPlanet transaction on relationships with employees, customers, other business partners or governmental entities; transaction costs; deterioration of or instability in the economy, the markets we serve or the financial markets generally; as well as the risks and uncertainties set forth in Ritchie Bros.’ Annual Report on Form 10-K for the year ended December 31, 2015, which is available on the SEC, SEDAR, and Ritchie Bros.’ website. The foregoing list is not exhaustive of the factors that may affect Ritchie Bros.’ forward-looking statements. There can be no assurance that forward-looking statements will prove to be accurate, and actual results may differ materially from those expressed in, or implied by, these forward-looking statements. Forward-looking statements are made as of the date of this presentation and Ritchie Bros. does not undertake any obligation to update the information contained herein unless required by applicable securities legislation. For the reasons set forth above, you should not place undue reliance on forward-looking statements.

This presentation contains certain non-GAAP financial measures. For a discussion of non-GAAP measures and the most directly comparable GAAP financial measures, see the Appendix to this presentation as well as our earnings release and our Form 10-Q interim report, which are available at: investor.ritchiebros.com. These non-GAAP financial measures are not measures of financial performance in accordance with GAAP and may exclude items that are significant in understand and assessing our financial condition and results. Therefore, these measures should not be considered in isolation or as alternatives to measures of profitability, liquidity or other performance under GAAP. These measures may not be comparable to similarly-titled measures used by other companies.

This presentation also includes certain forward-looking non-GAAP financial measures. We are unable to present a quantitative reconciliation of this forward-looking non-GAAP financial information because management cannot reliably predict all of the necessary components of such measures. Accordingly, investors are cautioned not to place undue reliance on this information.

All figures are in US dollars, unless otherwise noted.

3

Ritchie Bros. overview

The trusted source for buying and selling industrial equipment• Global leader for industrial auctions; unreserved process

» No minimum bid/reserved price. No buy-backs. » Ensures the sale of goods on the day of the auction at global market price

• Cater to the needs of heavy equipment owners» Customers are from the construction, trucking, agricultural & resource sectors

• 345 auctions; $4.25 billion in Gross Auction Proceeds during 2015» Enormous growth opportunity, with a highly fragmented market

• Provide multichannel sales solutions to expand the breadth of services available to equipment sellers:» EquipmentOne launched in 2013» Mascus (equipment sales listing service) acquired in 2016

Strong financial performance • $515.9 million of revenue during fiscal 2015• $121.1 million of adjusted net income¹ during fiscal 2015

Publicly listed on the NYSE and TSX (as RBA)• Market cap of approx. US$3.8 billion

RBA Auction - Circa 1958

RBA Auction - Now

Ritchie Bros. has a strong heritage –selling used equipment since 1958

¹ Net Income attributable to stockholders

4

32%

50%

10%7%

Canada

United States

Europe

Other

Global reach

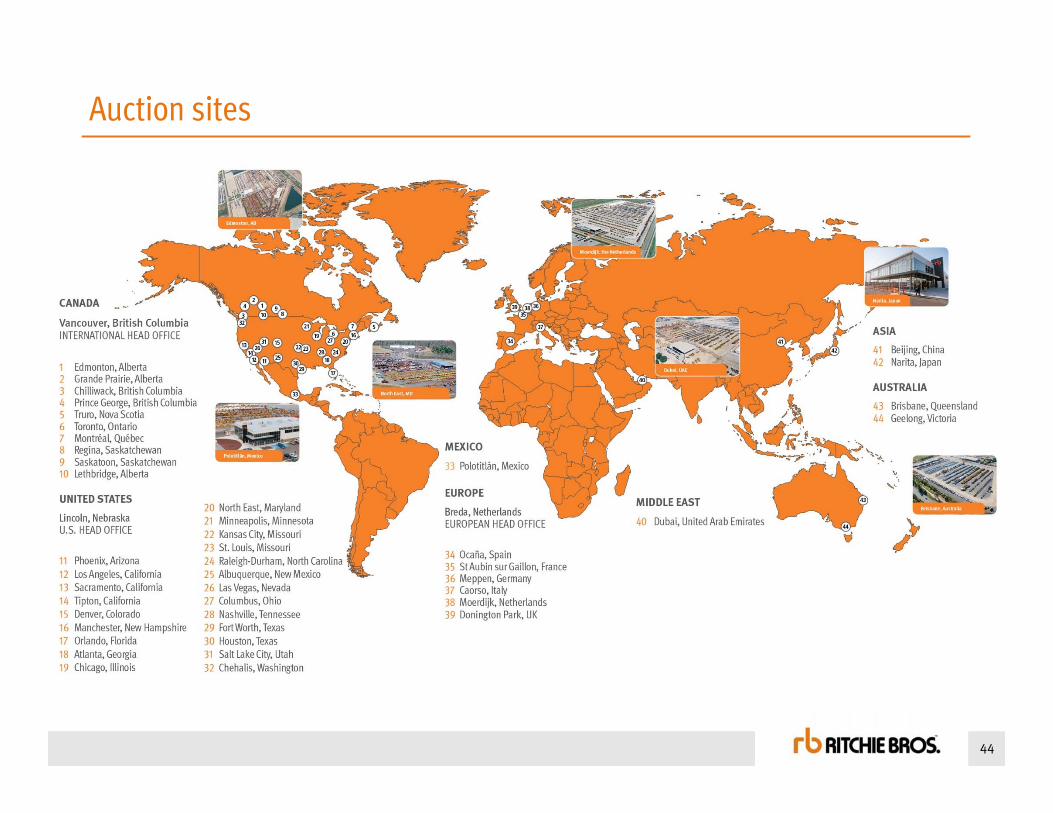

44 auction sites in 14 countries worldwide• More than half of auction purchases are made by bidders from outside

the region of the auction

• Allows RBA to effectively transfer equipment between regions experiencing different economic cycles

• Consignors benefit from global market pricing for their equipment, generated by international demand

• Buyers benefit from a global supply, with an ability to purchase and ship equipment from weak economic regions to areas with stronger growth

32%

47%

12%9%

CanadaUnited StatesEuropeOther

2015 Regional breakdown of revenue(Revenue breakdown - % of 2015 total)

Ritchie Bros.’ online bidding allows customers from around the world to bid on equipment at any of our auctions.

• Real-time information from live auctions available online to registered bidders

$481 Mil

2014 Revenue breakdown - % of 2014 total

$516 Mil

US comprised a greater proportion of revenue in 2015 relative to 2014.

5

Global equipment market size is $360 billion

Ritchie Bros. is a global leader in used equipment sales, with $4.2 billion of equipment sold in 2014However, this represents only 1.2% of a highly fragmented global used equipment exchange market

The US market alone represents over $50 billion, 7x Canada – a key market for growth

Mining

Oil & Gas

Transportation

Agriculture

Construction

Source: Internal estimates; based on historical OEM unit sales, estimates of fleet turnover, and average selling prices at RB auctions. Allocation by geography based on sector GDP.

Mining

Oil & Gas

Transportation

Agriculture

Construction

6

0

100,000

200,000

300,000

400,000

500,000

600,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Registrants

Lots

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Consignors

Buyers

Growing seller and buyer base

5.0% CAGR in consignments over last 10 years

6.4% CAGR in buyers over last 10 years

8.2% CAGR in registrants over last 10 years

5.2% CAGR in Lots over last 10 years

Consignments & buyer base (Metrics are for industrial auctions only)

Auction registrants & lots(Metrics are for industrial auctions only)

7

Growth of Gross Auction Proceeds (GAP)

US$4.25 billion of GAP produced during fiscal 2015

GAP:The aggregate dollar amount transacted through Ritchie Bros. Auctioneers and EquipmentOne

Includes transactions of AssetNation and EquipmentOne online marketplaces in 2012 - 2015

Gross Auction Proceeds (US$ millions)

4,245

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

8

Four external influences on GAP

The pricing environment• A strong pricing environment will enhance market values of equipment sold at auctions• Stable or increasing pricing environment provides consignors with more confidence to sell

equipment through unreserved auctions

The mix of categories of assets sold • RBA sells a wide variety of industrial and agricultural equipment and other products. There is

no consistency to the mix of assets sold, as it varies at each auction held due to regional, seasonal and cyclical factors.

• The proportion of higher-valued items sold at each auction relative to smaller goods impacts the auction proceeds generated

The mix of equipment age• Newer equipment generally has a higher market value compared to older machinery

The number of Lots consigned• Each sale generates proceeds. Increasing the number of Lots sold can bolster gross auction

proceeds

12

34

9

Unreserved auction revenue model

Four main revenue streams support Ritchie Bros.’ unreserved auction business:

Unreserved Auction

Straight Commission

Guaranteed Proceeds (underwritten transaction)

Inventory (underwritten transaction)

Consignors contract to sell their equipment through one of Ritchie Bros. unreserved auctions. A pre-determined percentage of the selling price is provided to RBA as commission.

Consignors are guaranteed to receive a pre-determined amount for their equipment, regardless of the final selling price at the auction. A stepped commission fee is negotiated, accounting for the additional risk being assumed by RBA. (Also known as an ‘at risk’ transaction)

On rare occasions, Ritchie Bros. may choose to purchase equipment outright, obtaining title of the piece to sell at an upcoming auction.

TRANSACTION TYPE REVENUE

Straight Commission fee (% of auction proceeds)

Stepped commission fee (x% of guaranteed proceeds; x+y% for proceeds above guaranteed amount)

Gains on sale

Sellers (Consignors)

Buyers Admin Fees & Value-added Services (VAS) Admin fees and fees from value-added service activities

RBA provides many services to assist with the purchase of equipment, including financing , inspection services, painting etc.

Revenue from other business lines supplement our revenue: EquipmentOne buyer and seller fees; Xcira revenue; Mascus revenue

10

54%

46%

0%

10%

20%

30%

40%

50%

60%

70%

Q1 2012 Q 2 Q 3 Q 4 Q1 2013 Q 2 Q 3 Q 4 Q1 2014 Q 2 Q 3 Q 4 Q1 2015 Q 2 Q 3 Q 4 Q1 2016 Q2

Online

Onsite

Q2 2016: First time more than half of GAP sold online

Online purchases comprised 51% of GAP in Q2 2016, the first time more than half of GAP was generated by online buyers.• Online transactions growing due to changing customer preferences, greater participation from non-

local bidders, the introduction of the Ritchie Bros. app, and growth of E1 • Sold approx. $650 million of assets through online transactions (incl. E1) during Q2 2016, an increase

of 11% from Q2 2015 • 54% of buyers during Q2 2016 participated in our auctions online

*Industrial auction data

Percent of buyers: # of buyers, on site or online

54% of total # of buyers were online(51% of total GAP was sold online)

11

Investing in our digital capabilities

Public launch of Ritchie Bros. App has been highly successful• Officially launched in App stores July 11, 2016• Early reviews in App stores are all 5-stars, demonstrating strong user endorsement• Including the beta testing period in Q1 and Q2 (prior to public launch), the app has

accumulated:• 68 successful winning bids• US$1.35 million of GAP

• Increased promotion of the App (and smartphone enabled bidding) will occur in coming months

Creation of Enterprise Sales Solution direct user portals for key EquipmentOne accounts launched earlier this year• Flexible, end-to-end solution that allows companies to better control asset management • Product includes data integrations, automated process workflows, remarketing solutions,

public and private (e.g. dealer to dealer networks, internal corporate redeployment sites) disposition channels, and detailed reporting capabilities.

• New customers include one of the world’s largest transportation OEM’s and a leading energy companies; interest in the product is aggressively growing

12

Growing our breadth of services through acquisitions

Since November 2015 we have deployed $90 million of capital to grow our sales channels and bolster our core business

Additional $758.5 committed to acquire IronPlanet

• During Q3 2016 (to date) we acquired the remaining 49% stake of Ritchie Bros. Financial Services, a minority investment in Machinio, and the purchase of Petrowsky Auctioneers

• On August 29, 2016 we announced the acquisition of IronPlanet for US$758.5 million (to close before or during H1 2017)

• Continue to evaluate M&A opportunities

Q4 2015 Q1 2016 Q3 2016 (to date)

(75% stake)

(Minority interest)

Recent M&A Activity:

(Announced; to close before or during H1 2017)

13

Multichannel solutions:

• Offers sellers more control over the sales price, time and purchaser; opens up opportunities for RBA to bid on RFPs

• During 2015, EquipmentOne contributed approx. $120 million of GTV (Gross Transaction Value) to GAP; up 13% from 2014

• Operates primarily in the United States; expanded into Canada in Q1 2016

• Website traffic up 11% in 2015, compared to 2014 (average monthly user)

Commercially launched in 2013

Customers of EquipmentOne value having control over the process and price, more than the guarantee of sale. They prefer a negotiated price, over global market value.

The launch of EquipmentOne provided customers with another sales solution – an online equipment marketplace

The seller journey: sellers choose methods based upon needed degree of controlOur vision is to position appropriate solutions at each point of seller journey and connect them

High

Cont

rol t

o Se

ller

LowEffort for Seller

Control over:PriceTime

LocationBuyer

Low

High

Uncertain CertainSome Certainty of Sale

Result: Transacting anyhow, anytime, anywhere

14

Multichannel solutions:

• Acquired during Q1 2016• Provides equipment sellers with a turn-key suite of business tools

and software solutions catering to the needs of OEMs, dealers and large equipment fleet owners• Generates sticky customer relationships

• Mascus generates 3.2 million monthly website visits• Business currently has 360,000+ listings of equipment and other assets for sale• Financial terms: €24.0 million (US$26.6 million)

• Additional cash consideration, totaling no more that €3.4 million (US$3.8 million) may be paid contingent upon certain operating performance targets being achieved over the next 3 years

• Expected to be marginally accretive to RBA’s performance immediately• Performance of Mascus is fully consolidated into RBA’s financial reports

Mascus is a leading global online equipment sales listing serviceGrows our service offering, to offer additional sales solutions to equipment sellers.Expands our buyer audience

Established a large presence in Europe

15

Strategic roadmap

16

PRIORITY DISCUSSION

1. Grow dividends with earnings Highly valued return of cash to shareholders

2. Hold fully-diluted shares flat Offset dilution from management stock options through share buybacks

3. Acquisitions Accelerate top-line growth and leverage the model

4. Share buy-backs Growth initiatives are a higher priority at this time

5. Pay down debt Only if better economic returns are not available

Capital allocation priorities

Consistently make use of cash on our balance sheet to facilitate underwritten transactions;The strength of our balance sheet is a competitive advantage.

(1) Priorities for cash utilization after operating CAPEX needs have been met.

17

0.10

50 0.11

25

0.11

25

0.11

25

0.11

25

0.12

25

0.12

25

0.12

25

0.12

25 0.13

00

0.13

00

0.13

00

0.13

00

0.14

00

0.14

00

0.14

00

0.14

00

0.16

00

0.16

00

0.16

00

0.16

00

0.17

00

0.1000

0.1100

0.1200

0.1300

0.1400

0.1500

0.1600

0.1700

0.1800

Q1/1

1

Q2/1

1

Q3/1

1

Q4/1

1

Q1/1

2

Q2/1

2

Q3/1

2

Q4/1

2

Q1/1

3

Q2/1

3

Q3/1

3

Q4/1

3

Q1/1

4

Q2/1

4

Q3/1

4

Q4/1

4

Q1/1

5

Q2/1

5

Q3/1

5

Q4/1

5

Q1/1

6

Q2/1

6

6.3% increase in quarterly cash dividend

Growing our dividend alongside earnings; announced a 1 cent increase to quarterly cash dividend on August 8, 2016Committed to 55-60% dividend payout, based on earnings trailing 12 months

Dividends declared ($US cash dividends)

7.1% increase

8.9% increase

6.1% increase

7.7% increase

6.3% increase

14.0% increase

18

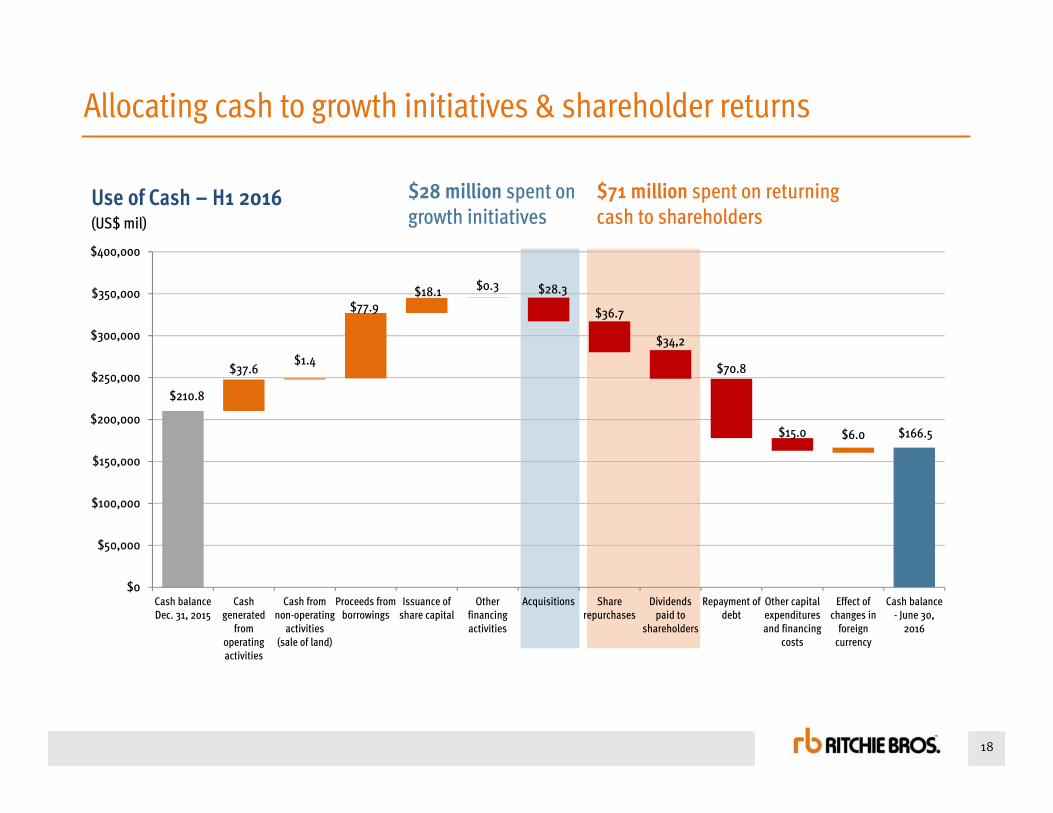

Allocating cash to growth initiatives & shareholder returns

Use of Cash – H1 2016(US$ mil)

$71 million spent on returning cash to shareholders

$28 million spent on growth initiatives

$210.8

$166.5

$37.6$1.4

$77.9$18.1 $0.3 $28.3

$36.7

$34,2

$70.8

$15.0 $6.0

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

Cash balanceDec. 31, 2015

Cashgenerated

fromoperatingactivities

Cash fromnon-operating

activities(sale of land)

Proceeds fromborrowings

Issuance ofshare capital

Otherfinancingactivities

Acquisitions Sharerepurchases

Dividendspaid to

shareholders

Repayment ofdebt

Other capitalexpendituresand financing

costs

Effect ofchanges in

foreigncurrency

Cash balance- June 30,

2016

Acquisition of IronPlanet

19

On August 29, 2016, Ritchie Bros. announced it will acquire IronPlanet

20

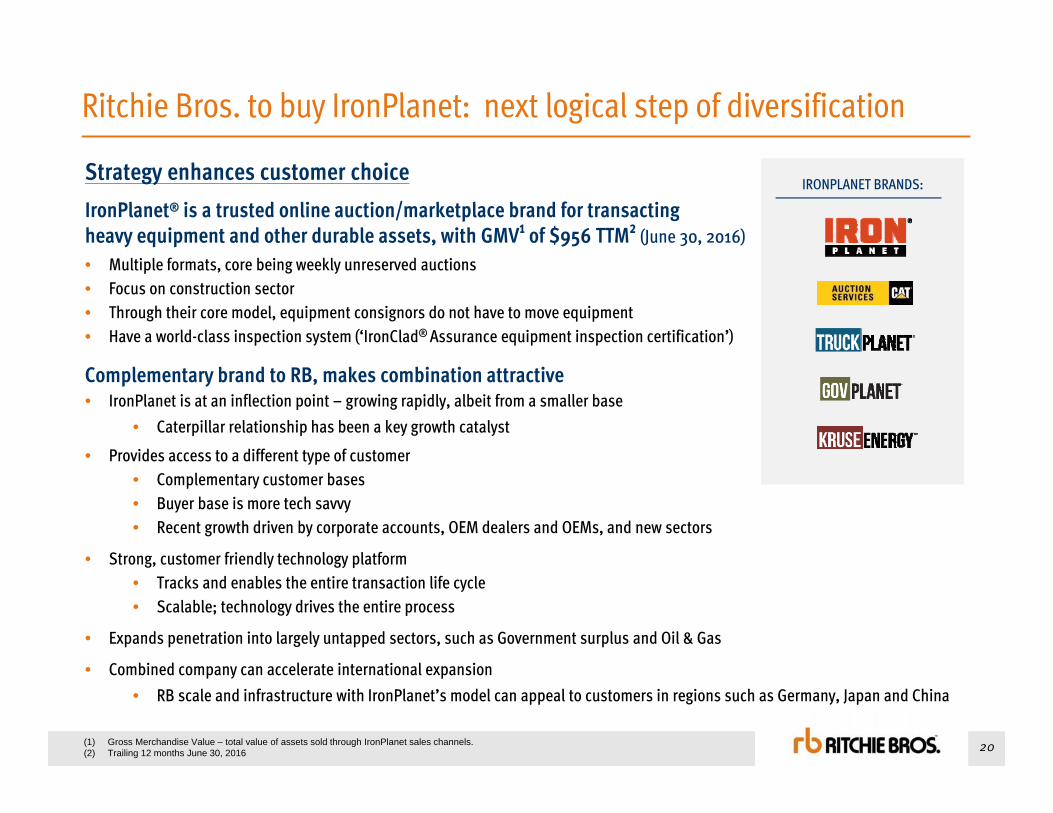

Strategy enhances customer choiceIronPlanet® is a trusted online auction/marketplace brand for transacting heavy equipment and other durable assets, with GMV¹ of $956 TTM² (June 30, 2016)• Multiple formats, core being weekly unreserved auctions• Focus on construction sector• Through their core model, equipment consignors do not have to move equipment• Have a world-class inspection system (‘IronClad® Assurance equipment inspection certification’)

Complementary brand to RB, makes combination attractive• IronPlanet is at an inflection point – growing rapidly, albeit from a smaller base

• Caterpillar relationship has been a key growth catalyst

• Provides access to a different type of customer• Complementary customer bases • Buyer base is more tech savvy • Recent growth driven by corporate accounts, OEM dealers and OEMs, and new sectors

• Strong, customer friendly technology platform• Tracks and enables the entire transaction life cycle• Scalable; technology drives the entire process

• Expands penetration into largely untapped sectors, such as Government surplus and Oil & Gas

• Combined company can accelerate international expansion• RB scale and infrastructure with IronPlanet’s model can appeal to customers in regions such as Germany, Japan and China

Ritchie Bros. to buy IronPlanet: next logical step of diversification

(1) Gross Merchandise Value – total value of assets sold through IronPlanet sales channels.(2) Trailing 12 months June 30, 2016

IRONPLANET BRANDS:

21

Summary of transaction terms

CONSIDERATION• ~US$758.5 million cash transaction¹ • 13.0X multiple of 2017E EBITDA²

EXPECTED FINANCIAL BENEFITS

• The transaction is expected to be earnings accretive within the first year ³• Annual cost synergies of ~$20 million, expected to be achieved by 2018• NPV of tax synergies of ~$100 million• Similar operating leverage model as Ritchie Bros.• Similar cash flow characteristics to Ritchie Bros.

GROWTHIMPLICATIONS

• RB’s revenue growth target4 revised upward to high single to low teens (% growth) post transaction• RB’s EPS growth target4 revised upward to low teens to high teens (% growth)

FINANCING

• Fully committed financing in place• Expect to replace committed facility with mix of pre-payable debt and long-term debt• Utilizes strength of Ritchie Bros. balance sheet• After final financing in place, expect <3.0x net to adjusted EBITDA ratio on closing

(with a target of returning to 2.5x)

CLOSING• Expect closing during or before H1 2017• Transaction is subject to customary closing conditions, including regulatory clearances

Ritchie Bros. has entered into an agreement to acquire 100% of IronPlanet

(1) Consists of US$740 million in cash plus approximately $18.5 million assumption of unvested equity interests, subject to standard closing adjustments(2) Inclusive of $100 million NPV of tax synergies and $20 million in run-rate cost synergies. Based on current tax environment(3) Transaction is expected to be accretive to earnings within the first year, excluding acquisition related costs(4) Growth implications is part of our new evergreen model post transaction; does not represent annual guidance

Provided to help with modeling an average annual basis over a 5 to 7 year period

22

$49

$72

$-

$20

$40

$60

$80

H1 2015 H1 2016

$395

$567

$- $100 $200 $300 $400 $500 $600 $700

H1 2015 H1 2016

IronPlanet brings exciting new opportunities to Ritchie Bros.

About IronPlanet

IronPlanet is the leading online marketplace for used heavy equipment.

US$787 million of GMV¹ (GAP) in 2015• 25.2% CAGR from 2013 – 2015• Most growth occurred in the last year• Strong growth trajectory

Strong collaborative relationship with Caterpillar and equipment dealerships in the Caterpillar network

Holds the U.S. Department of Defense rolling stock surplus contract (DLA contract)

490+ employees worldwide• Majority are based in the United States• ~10% are based in countries other than US

Private company • Current owners include Caterpillar Inc., Caterpillar

dealers, Volvo, venture cap (Kleiner Perkins and AccelPartners) and IP executives & employees

$502 $524

$787

$-

$100

$200

$300 $400

$500

$600

$700

$800

$900

2013 2014 2015

$58$65

$103

$-

$20

$40

$60

$80

$100

$120

2013 2014 2015

GROSS MERCHANDISE VALUE (GMV)(US$ millions)

REVENUE(US$ millions)

Strong growth in 2015 and H1 2016, generated by strategy to focus on major accounts, Caterpillar dealers and government contracts

50% growth 58% growth

44% growth 47% growth

(1) GAP/GMV represents the total proceeds from all items sold at auctions and online marketplaces. It is a measure of operational performance and not a measure of financial performance, liquidity, or revenue. It is not presented in our consolidated financial statements.

23

IP has built a platform for growth based on different value propositionsPR

ODUC

TS

FeaturedMarketplace

• Scheduled public online unreserved auctions held weekly

One-OwnerMarketplace

• Similar to “Featured Marketplace” but targets single-owner, single-event sales

DailyMarketplace

• Equipment pieces listed for sale, with a reserve price, on the website for a defined period of time

PrivateMarketplace

• Available for large industrial, rental companies and OEM equipment sellers who want to offer equipment assets to a select group of potential buyers

SERV

ICES Sellers • Includes equipment pricing & market evaluation, listing

services, inspection services, and funds settlement

Buyers • Offers detailed inspection reports to prospective buyers

SUMMARY OF IRONPLANET OFFERINGS:

IRONPLANET HISTORY

1999:Founded as Federal Sales Corp.

2013:Acquired Asset Appraisal Services (AAS), an inspection, appraisal and online auction services company

November 2014:Acquired Kruse Energy and Equipment Auctioneers, a leader in oilfield equipment auctions

April 2015:Merged with Cat Auction Services, an alliance of Caterpillar and independent Cat dealers

2016:Agrees to be acquired by Ritchie Bros.

More frequent auctions meet the needs of urgent sales. Improves the flow of business

VALUE PROPOSITION & OPPORTUNITY:

White labeled sales solutions to promote the brand and reputation of the selling customer

Reserve model meeting the needs of equipment sellers with minimum pricing restrictions

Private labeled sales solution to meet the ongoing needs of a single seller to a defined group of buyers. (Ensures preferred access to the sale to a pre-approved customer base, such as dealers within a brand family)

Full service sales offering that provides the seller with the option of keeping equipment where it is

IronClad guarantees and detailed inspection reports provide comfort to online buyers who have not inspected the equipment

Multiple formats provide customers with options that meet their specific needs/wantsCustomers that use multiple formats tend to consign more

July 2014:Awarded contract for U.S. Department of Defense rolling stock surplus contract

24

Combining RB and IronPlanet is transformative for our business

Offers a superior customer experience

a) Multiple sales channels for used equipment sellers and buyersb) More diversified, multichannel, multi-format live and digital sales ecosystemc) Equipment buyers and sellers will be able to transact and list when, where and how they want

Accelerates Growth

a) Expedites RB’s stated growth strategies: important gateways for growth in new sectors, regions and customer segments

b) Significantly enhances financial performance, with immediate positive impact to GAP, revenue & earningsc) Logical next step in our transformation – at the right time with a complementary brand

Strengthens relationships with OEMs and Dealers

a) New strategic alliance with Caterpillar is transformational for our business b) As a combined business independent Cat dealers will benefit from industry-leading data intelligence and

global marketing efforts, alongside established auction and online marketplace sales supportc) IronPlanet leadership has developed deep relationships with independent Cat dealers

Builds on the power of our existing

global platform

a) IronPlanet sales formats will benefit from RB’s established global footprint, scale, marketing prowess and brand awareness to drive incremental growth

b) Complementary cultures and talented leadership teams that will continue to drive innovationc) Equally committed to delivering value to our customers

Enhances digital and technology

capabilities

a) Significantly diversifies and expands RB online capabilitiesb) Combined data will drive greater transaction volume and build deeper relationships with OEMs and customersc) EquipmentOne and IronPlanet technology platforms are complementary

1

2

3

4

5

Compelling strategic rationale

25

Live on site and live simulcastonline auctions

Event-based sales of used

construction and heavy equipment

Online sales of used construction and used trucks

and trailers

Online reserve auction and marketplace

Online sales of government

surplus rolling stock

Event-based sales of used oil

and gas equipment

Online advertising

listing service and B2B portals

Confidential, negotiated sales

Providing unprecedented choice to used equipment sellers & buyers

Together, we will offer customers the widest range of sales solutions and selling formats:

Live auction(with online simulcast)

Online-Only Auction

Event-Based Auction

Reserve Price options Buy Now options Single Seller

optionsPrivate-Label

optionsListing service

✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

A MULTITUDE OF SALES CHANNEL OPTIONS, MEETING MORE CUSTOMER NEEDS:

OUR FULL-SERVICE OFFERING WILL CATER TO SPECIFIC NEEDS OF EQUIPMENT CONSIGNORS, WITH DIFFERING NEEDS:

26

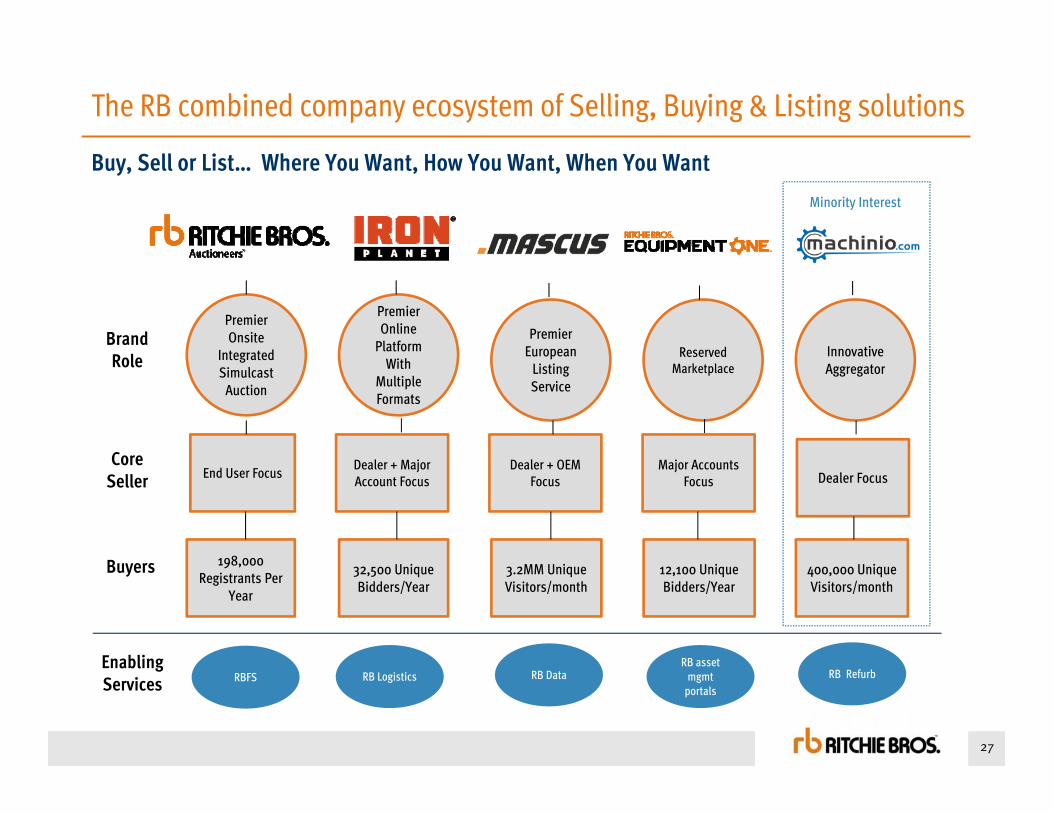

RB AuctionsEquipmentOneIronPlanet

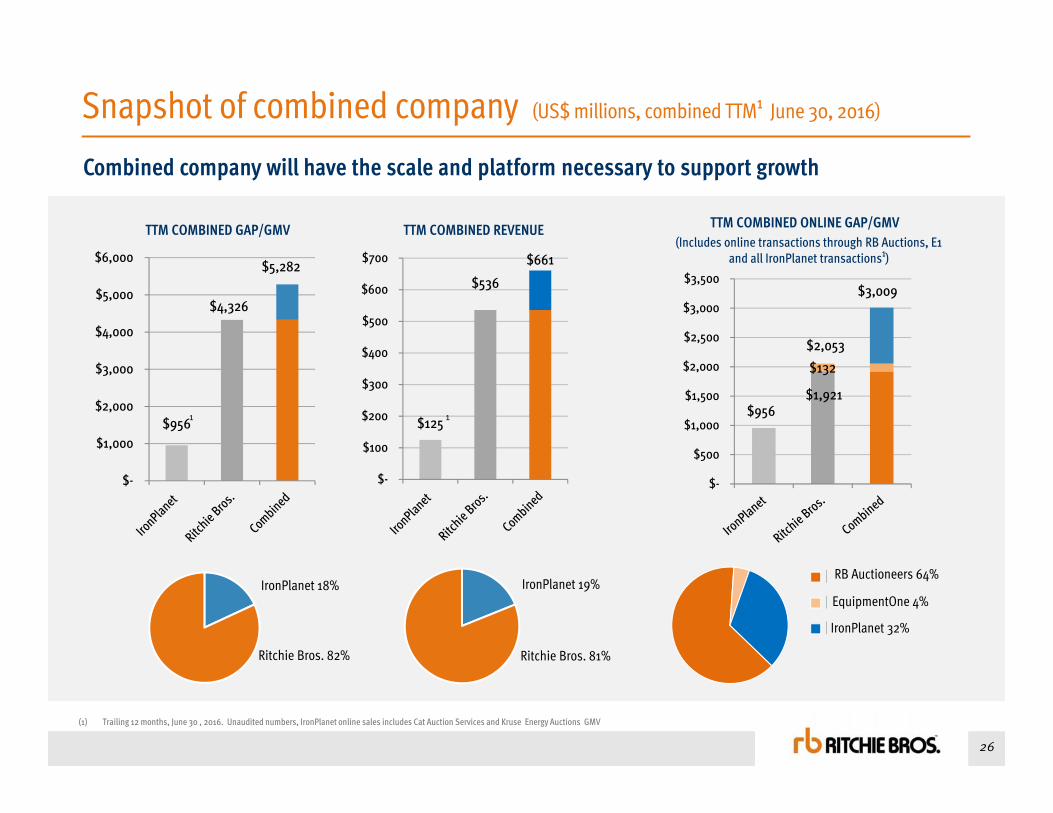

Snapshot of combined company (US$ millions, combined TTM¹ June 30, 2016)

Combined company will have the scale and platform necessary to support growth

TTM COMBINED GAP/GMV(Includes online transactions through RB Auctions, E1

and all IronPlanet transactions¹)

TTM COMBINED REVENUE

IronPlanet 18% IronPlanet 19%

Ritchie Bros. 82% Ritchie Bros. 81%

(1) Trailing 12 months, June 30 , 2016. Unaudited numbers, IronPlanet online sales includes Cat Auction Services and Kruse Energy Auctions GMV

$956

$4,326

$5,282

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$125

$536

$661

$-

$100

$200

$300

$400

$500

$600

$700

IronPlanet 32%

EquipmentOne 4%

RB Auctioneers 64%

$956$1,921

$3,009

$132

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$2,053

TTM COMBINED ONLINE GAP/GMV

¹ ¹

27

The RB combined company ecosystem of Selling, Buying & Listing solutions

Buy, Sell or List… Where You Want, How You Want, When You Want

Premier Onsite

Integrated Simulcast

Auction

Premier Online

Platform With

Multiple Formats

Premier European

Listing Service

Reserved Marketplace

Innovative Aggregator

End User Focus Dealer + Major Account Focus

Dealer + OEM Focus

Major Accounts Focus Dealer Focus

198,000 Registrants Per

Year

32,500 Unique Bidders/Year

3.2MM Unique Visitors/month

12,100 Unique Bidders/Year

400,000 Unique Visitors/month

Brand Role

Core Seller

Buyers

RBFS RB DataRB asset

mgmtportals

Enabling Services

Minority Interest

RB Logistics RB Refurb

28

0.9 0.90.6 0.6 0.6 0.5 0.6 0.7 0.6

3.02.5

0.00.51.01.52.02.53.03.5

FINANCING PLAN AND PRO FORMA CAPITALIZATIONFinancing plan and pro forma capitalization

• RB has secured a financing commitment sufficient to fund the acquisition until permanent capital structure can be put in place

• Permanent structure will consist of short-term and long-term components

» We will work with our existing creditors to evaluate our alternatives for our final, permanent capital structure

• We estimate that $850 million of debt will be outstanding on the closing date of the transaction

» The transaction implies net leverage multiple of 3.0x and the potential for rapid de-levering with abundant free cash flows (evergreen target for net debt to adjusted EBITDA remains at 2.5x)

• Effectively uses the balance sheet while allowing for continued financial flexibility

• Additional cash flows for combined company can be allocated towards:

» de-levering, » investing in organic growth opportunities, » returning cash to shareholders via dividends, and/or» potential bolt-on acquisitions

Sizeable opportunity to deploy under-levered balance sheet to support growthNET-DEBT TO ADJUSTED EBITDA (Historical and projected RB, TTM periods)

Target ratio of <2.5x by 2018

$153

$164

$158

$119

$112

$119

$110

$125

$145

$125

Appr

ox. $

850+

0100200300400500600700800900

1000

Long term debt

Short term debt

DEBT HELD & PROJECTED (US$ millions)

29

Alliance with Caterpillar Inc.

Alliance with Caterpillar will be transformative for our business; Provides RB with a strong foundation to be a trusted partner with the Cat dealer network… building on a strong foundation built by IronPlanet

• Initial 5-year agreement term with Caterpillar Inc. and its wholly owned subsidiaries; focus on long-term evergreen relationship

• Ritchie Bros. becomes their preferred global partner for auction and online marketplace sales services for used equipment upon IP transaction closing

• Caterpillar Inc. and its dealers will be supported through our industry leading data intelligence, sales information and global marketing efforts

• Cat Auction Services will continue to be the brand for auctions on Cat dealer sites

STRATEGIC ALLIANCE

2014 2015

CAT FAMILY VOLUME AT IRONPLANET¹( % of total IronPlanet GMV)

(1) Source: estimates provided by IronPlanet. Gross Merchandise Value: total value of assets sold through IronPlanet channels, comparable to Ritchie Bros. Gross Auction Proceeds

30

PERFORMANCE METRICSBefore transaction:

Avg. Annual Growth Targets

GAP Growth (%) High Single Digit to Low Double Digits

Revenue Growth (%)1 Mid Single Digit to High Single Digit

Operating expense Growth (%) Will grow slower than revenues

Operating Income Margin 50 bps+

EPS Growth2 (%) High Single Digit to Low Double Digits

Capex Intensity3 <10%

OFCF4 % of Net Income >100%

ROIC5 Increase 50 bps+

Dividend Payout Ratio 55% to 60%

Net Debt / Adjusted EBITDA <2.5x

1 Includes Tuck in and Bolt on Acquisitions.2 Variances may occur in certain years based on tax rate that is influenced by geographic revenue mix. 3 Net Capital Spending as % of Revenue.

RB’s updated evergreen financial model (post transaction)

4 Operating Free Cash Flow.5 Return on Invested Capital.

Transaction is expected to bolster growth New Evergreen Model (post transaction)(Average annual expectation over a 5 to 7 year period)

KEY SHAREHOLDER VALUE DRIVERS

Growth targets

GAP & Revenue growth (%) High single digit to low teens

EPS growth (%) Low teens to high teens

OFCF as a % of net income > 100%

Dividend Payout ratio 55%-60%

DRIVERS OF EPS GROWTH- Operating expenses growing slower than revenue- Cost synergies- Tax efficiencies

OTHER KEY METRICS Targets

Net debt to EBITDA <2.5 x

Capex Intensity <8.5%

EBITDA margins of 40%+ by 2018

ROIC returning to current levels by 2020 (15.1%: Q2 2016 TTM)

31

MERGERS AND ACQUISITIONSTuck-Ins and Bolt-Ons

Scale Enhancers & Needle MoversAccretive in Relatively Short Time Frame

GEOGRAPHIESDrive Depth vs Breadth

Focus on the US as #1 priority, grow Middle East and AustraliaOptimize Canada & Europe, turnaround LATAM

Position China for long term

SECTORSLeverage Construction

Grow Agriculture and TransportationPursue Oil & Gas opportunistically

SERVICESScale RBFS, achieve super majority

Pilot logistics

SEGMENTSAccelerate Strategic Accounts

Pilot Private Treaty as a New Vehicle forHighvalue, Specialized Deals

UNDERWRITTEN CONTRACTSUtilize Aggressively, Minimize Volatility

SALES PRODUCTIVITYTerritory Management & Coverage Based on Market Potential

Consistent Go to Market ProcessesImprove Selection, Onboarding & Training of New Hires

Consistently Utilize Sales ToolsReduce TM Turnover

PROCESS & SYSTEMSModernize Legacy Systems

Focus on Customer Relationship Management (CRM)Enable Scaling Business & Leverage Multichannel

Focus on revenue driving Apps

ORG STRUCTURE AND SELLING,GENERAL & ADMINISTRATIVE EXPENSE

Regional Org Structure with Profit & Loss (P&L) Statement and Balance Sheet Accountability

Target SG&A Growth Lower than Revenue Growth

PERFORMANCE METRICSP&L Statement and Balance Sheet Scoreboard

Operational MetricsAccountability at All levels

INCENTIVE COMPENSATIONTie to P&L Statement and Balance Measures

but simplify

CASH FLOWAlign Organization & Incentive

Target OFCF Equal to Net Income

ORGANIC CAPITAL SPENDSTarget Net Capital Spend <10% Revenue

Control Spending on New SitesFocus on IT Systems & Site Maintenance

CAPITAL STRUCTUREReturn Cash Via Ongoing Dividends

Address Option Dilution through Share RepurchaseInvest in Growth-Driven M&A

EXISTING SITE RETURNSHigh, Medium and Low Site Return League Table

Initiatives to Improve Medium and Low Site ReturnsDispose of Excess Assets

GrowRevenue & Earning

1

DriveEfficiencies & Effectiveness

2

OptimizeBalance Sheet

3

IronPlanet transaction meets many stated growth strategies

IronPlanet transaction meets this stated strategic criteria

CHANNELSScale EquipmentOneDrive Multichannel

RITCHIE BROS. LONG-TERM STRATEGY

32

The Ritchie Bros. family of brands

Ritchie Bros. will offer five main sales channels to equipment ownersBusiness units are supported through Ritchie Bros. ownership of Xcira (online auction technology provider) and Ritchie Bros. Financial Services (financial solutions partner for equipment buyers).

75% ownership

100% ownership

Integrated technology platform

Financial intermediary capitalizing on captive customer base to provide an alternative source of capital

Integrated onsite/online auction network¹

Online marketplace

Online listing service

Brokerage channel for highly specialized assets ¹ Includes Petrowsky Auctioneers

and Kruse Energy Auctions:

Online marketplace and online auction

Financial performance

For six and three months ended June 30, 2016, and full year 2015.

33

34

Reported - % Growth Constant Currency - % GrowthVersus Q2 2015 Versus Q2 2015

GAP 1% 3%

Revenue 2% 4%

Operating Income (15)% (13)%

Diluted EPS (12)% n/a

Operating Free Cash Flow (12 month rolling)

(63)% n/a

RONA excl. term loan reclass(12 month rolling)

260 bps n/a

ROIC(12 month rolling)

60 bpsn/a

Q2 2016 financial highlights

Revenue grew modestly on a tough comp versus prior year; maintained strong revenue rate• Costs of Services and SG&A increased disproportionately on account of new businesses, headcount investment in

strategic initiatives, and increased auction volumes; • Cash flow declined due to timing issues, but company remains a strong cash generator

attributable to stockholders

35

Reported - % Growth Constant Currency - % GrowthVersus H1 2015 Versus H1 2015

GAP 4% 6%

Revenue 7% 10%

Operating Income (3)% (2)%

Diluted EPS 2% n/a

Operating Free Cash Flow (12 month rolling)

(63)% n/a

RONA excl. term loan reclass(12 month rolling)

260 bps n/a

ROIC(12 month rolling)

60 bpsn/a

H1 2016 financial highlights

While Q1 generated solid results, first half results for 2016 were proportionately impacted by larger Q2 Foreign exchange continues to have an impact on quarterly comparators

attributable to stockholders

36

Very strong results in 2015

Performance during 2015 demonstrates our commitment to execution, our strategy is gaining traction, and our agility in leveraging market opportunities

Foreign exchange remains a headwind2015 Reported - % Growth 2015 Organic - % Growth

Versus 2014 Versus 2014

GAP 1% 8%

Revenue 7% 16%

Adjusted Operating Income 20% 46%

Diluted Adjusted EPS 22% n/a

Operating Free Cash Flow (12 month rolling)

28% n/a

RONA (12 month rolling)

1100 bps n/a

RONA excluding effects of term loan reclassification

910 bps n/a

attributable to stockholders

37

Income statement scorecard – Q2 2016

3 months trailing ($US Millions except for EPS, %)

June 30, 2016 June 30, 2015 Better / (Worse)

GAP $1,275.7 $1,262.2 1%

Revenues $158.8 $155.5 2%

Revenue Rate 12.45% 12.32% 13 bps

Operating Income $53.6 $62.8 (15)%

Operating Income Margin 33.8% 40.4% (660) bps

EBITDA $64.7 $74.7 (13)%

Diluted EPS $0.37 $0.42 (12)%

Q2 2016 Income statement scorecard

GAP and Revenue Rate increased modestly; Op income and EPS impacted by lower margins than in Q2 2015

attributable to stockholders

38

Balance sheet scorecard – Q2 2016

12 months trailing ($US Millions except for percent figures)

June 30, 2016 June 30, 2015 Better / (Worse)

Operating Free Cash Flow $81.6 $218.1 (63)%

Working Capital Intensity -19.8% -23.9% (410) bps

Capex Intensity 3.6% 3.2% (40) bps

ROIC (Return on Invested Capital) 15.1% 14.5% 60 bps

RONA (Return on Net Assets) 25.4% 25.3% 10 bps

RONA excluding term loan reclassification 25.4% 22.8% 260 bps

Debt / Adjusted EBITDA 0.6x 0.6x no change

Q2 2016 Balance sheet scorecard

39

Income statement scorecard – 2015

12 months trailing ($US Millions except for EPS, %)

Dec. 31, 2015 Dec. 31, 2014 Better / (Worse)

GAP $4,247.6 $4,212.6 1%

Revenues $515.9 $481.1 7%

Revenue Rate 12.14% 11.42% 72 bps

Adjusted Operating Income $166.5 $138.2 20%

Adjusted Operating Income Margin 32.3% 28.7% 360 bps

Diluted EPS $1.27 $0.85 50%

Diluted Adjusted EPS $1.13 $0.93 22%

Full year 2015 Income statement scorecard

Increased Diluted EPS by 50% versus last year – through GAP growth, revenue rate improvement, expense control, excess land sales and tax planning strategies

attributable to stockholders

attributable to stockholders

40

Balance sheet scorecard – 2015

12 months trailing ($US Millions except for percent figures)

Dec. 31, 2015 Dec. 31, 2014 Better / (Worse)

Operating free cash flow $182.2 $141.8 28%

Working Capital Intensity -3.2% -2.3% 90 bps

Capex Intensity 2.8% 6.2% 340 bps

ROIC (Return on Invested Capital) 15.1% 12.0% 310 bps

RONA (Return on Net Assets) 25.7% 14.7% 1100 bps

RONA excluding term loan reclassification 23.8% 14.7% 910 bps

Debt / Adjusted EBITDA 0.5x 0.6x 0.1x

2015 Balance sheet scorecard

41

Focused on generating long-term shareholder value through continued earnings and dividend growth.

A global leader in industrial auctions• Substantial growth opportunity• Focused on growth in the US and in key sectors

Diversifying services to meet broader customer needs• Sales solutions: Ritchie Bros. Auctioneers, EquipmentOne, Mascus• Complementary services: Ritchie Bros. Financial Services, Logistical Services• Supportive business unit: Xcira (online auction technology solutions)

Focused on basics of: • EPS growth • Return on Net Assets• EBITDA margin• Operating free cash flow

Summary

Moerdijk, Netherlands auction

Learn more about Ritchie Bros. auctions through our online videos:

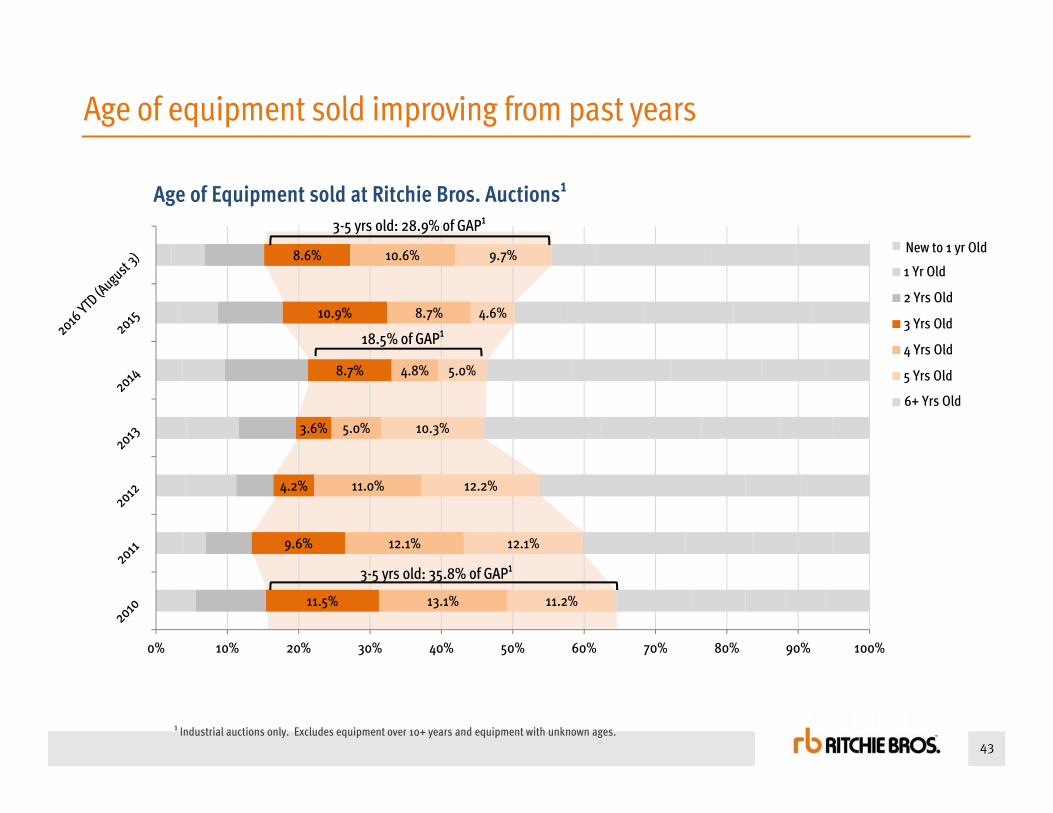

www.youtube.com/ritchiebros

AppendicesAge of equipment sold trendsGlobal auction site network

42

43

11.5%

9.6%

4.2%

3.6%

8.7%

10.9%

8.6%

13.1%

12.1%

11.0%

5.0%

4.8%

8.7%

10.6%

11.2%

12.1%

12.2%

10.3%

5.0%

4.6%

9.7%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

New

1 Yr Old

2 Yrs Old

3 Yrs Old

4 Yrs Old

5 Yrs Old

6 Yrs Old

7 Yrs Old

8 Yrs Old

9 Yrs Old

10 Yrs Old

18.5% of GAP¹

3-5 yrs old: 35.8% of GAP¹

¹ Industrial auctions only. Excludes equipment over 10+ years and equipment with unknown ages.

Age of equipment sold improving from past years

Age of Equipment sold at Ritchie Bros. Auctions¹ 3-5 yrs old: 28.9% of GAP¹

6+ Yrs Old

New to 1 yr Old

44

Auction sites

US GAAP Reconciliation of Non-GAAP measures

Non- GAAP Measures

The following tables reconcile non-GAAP measures referred to in this presentation to the most directly comparable GAAP measure reflected in the Company’s financial statements

45

46

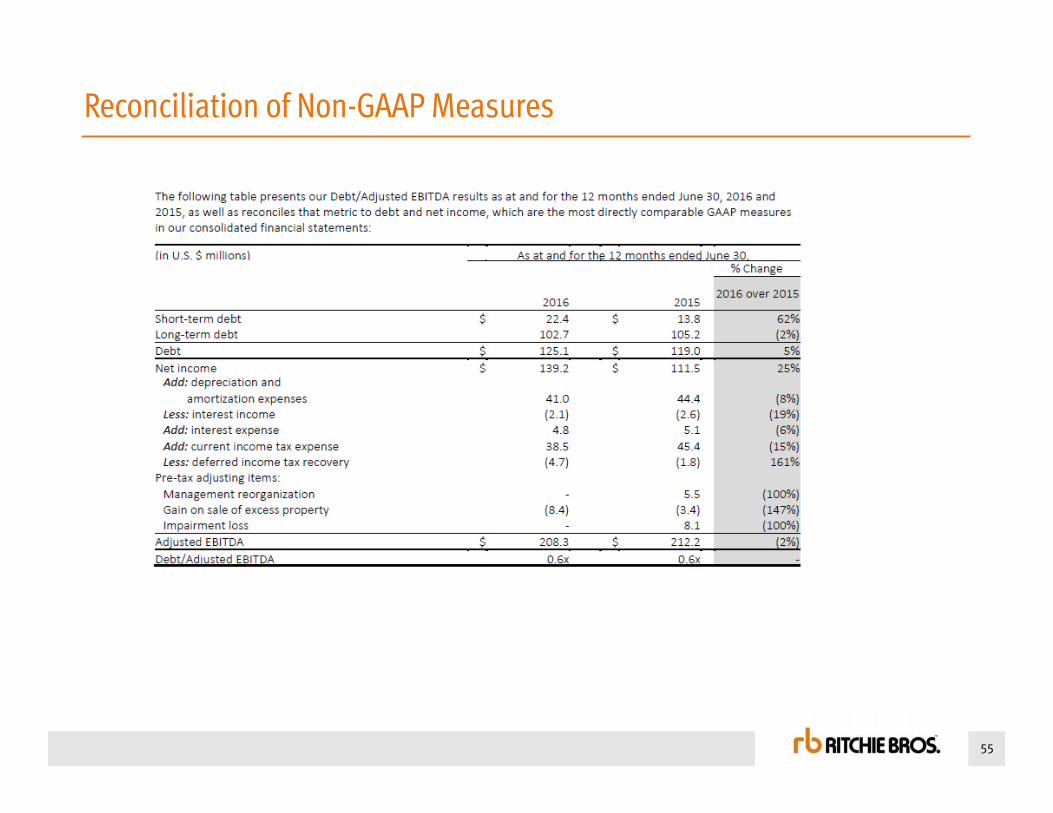

Reconciliation of Ritchie Bros. non-GAAP measuresDebt/Adjusted EBITDAOur balance sheet scorecard includes the performance metric, Debt/Adjusted EBITDA, which is a non-GAAP financial measure. We believe that comparing Debt/Adjusted EBIDTA on a 12-month rolling basis for different financial periods provides useful information about the performance of our operations, and in particular, it is an indicator of the amount of time it would take for us to settle both our short and long-term debt. We do not consider this to be a measure of our liquidity, which is our ability to settle only short-term obligations, but rather a measure of how well we fund liquidity. Measures of liquidity are discussed further below under “liquidity and capital resources”.

We calculate Debt/Adjusted EBITDA by dividing debt by EBITDA excluding the effects of pre-tax adjusting items.

The following table presents our Debt/Adjusted EBITDA results as at and for the years ended December 31, 2015, 2014, and 2013, as well as reconciles that metric to debt and net income, which are the most directly comparable GAAP measures in our consolidated financial statements:

47

Reconciliation of Ritchie Bros. non-GAAP measures

Earnings Before Interest, Taxes, Depreciation and Amortization (“EBITDA”) and EBITDA MarginEBITDA and EBITDA Margin are non-GAAP financial measures that we believe provide useful information about the growth or decline of our net income when compared between different financial periods. EBITDA is also an element of the performance criteria for certain PSUs we granted to our employees and officers in 2013 and 2014. EBITDA is calculated by adding back depreciation and amortization expenses, interest expense, and current income tax expense, and subtracting interest income and deferred income tax recovery from net income. EBITDA Margin presents EBITDA as a multiple of revenues.

The following table presents our EBITDA and EBITDA Margin results for the years ended December 31, 2015, 2014, and 2013, as well as reconciles those metrics to net income and revenues, which are the most directly comparable GAAP measures in our consolidated income statements:

4848

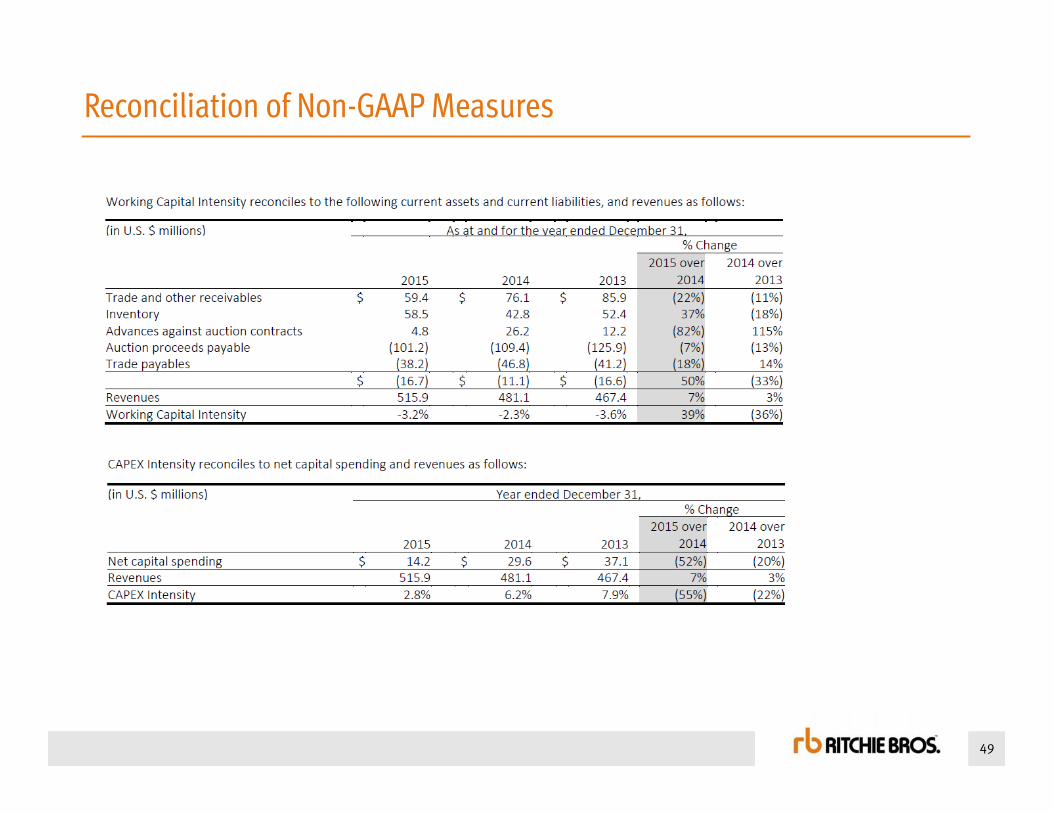

Reconciliation of Non-GAAP Measures

49

Reconciliation of Non-GAAP Measures

50

Reconciliation of Non-GAAP Measures

51

Reconciliation of Non-GAAP Measures

52

Reconciliation of Non-GAAP Measures

53

Reconciliation of Non-GAAP Measures

54

Reconciliation of Non-GAAP Measures

55

Reconciliation of Non-GAAP Measures