2015 kpmg ema tax summit€¦ · retail market rub 60.7 trln rub 45.5 trln rub 30.1 trln by 8%...

TRANSCRIPT

2015 KPMG EMA Tax Summit

Russia’s Changing Economic Environment

Bob WallingfordPartner, Tax and Legal ServicesTax Head of Japan Global Tax Practice KPMG in Russia and CIS

Russia Macro-economic Overview

3© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Macroeconomic overview of the Russian Federation 2015

4© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Macroeconomic overview of the Russian Federation 2015

to 75%

Share of walletfor goods and servicesby

4%

GDP

by 11.3%

Real disposable income in 2012 terms

to 8,3% (Aug 7.8%)

Unemployment

to 23.7%

Food Inflation

RUB 60.3 trln

RUB 18 trln

by 12%

Retail market

RUB 60.7 trln

RUB 45.5 trln

RUB 30.1 trln

by 8%

Household consumption

Sources: Federal State Statistics Bureau, EIU, Bloomberg, Investment banks reports, Ministry of Economic Development, KPMG analysis, pries base period 2012

Takeaway Political an economical issues 2014-2015 drove Russian economy to the recession. What are the perspectives?

5© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Russian GDP forecast

* All following GDP forecasts are given in the prices of base period (2012) unless otherwise specified

Forecast

GDP forecastRUB trln*

Sources: EIU, Bloomberg, KPMG analysis

After the economy shock in 2014/15, Russia is expected to be back to 2014 year level in 2018, following the slow rate recovery starting 2016

63,2

2017

64,2

20202015 2018

65,1

61,9

60,7

63,2

2016 20192014

61,0

- 4% GDP in 2015 (in comparison with 2014)

CAGR2015-2020: 1,4%

GDP RUR: Y2018 = Y2014

Comments

$

Forecast 2015:

61,1 RUR/USDAverage Jan – Jul 2015:

57,4 RUR/USD

Exchangerate

Takeaway

6© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

GDP growth drivers

GDP growth drivers magnitude*, 2015-2020%, RUB trln

Sources: EIU, KPMG analysis

■ Steadily increasing household consumption forecasted to support GDP growth in 2015-2020■ Investments which are hit the most are also expected to recover

2.1

1.1

0.9

0.3

4.4

7.5%

InvestmentsHousehold consumption

23.9%

Total increase

Net export

100%

Government spending

21.4%

47.2%

$

1,4%

2%

1,4%

0,9%

CAGR, 2015-2020

Household consumption

Investments

Government spending

Net export

Comments

* All numbers are given in the prices of base period (2012)

Takeaway

Trends in Consumer Markets Russia

8© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Global retail market attractiveness(a) Comments

Russian vs. Global consumer markets

(6)

(4)

(2)

0

2

4

6

8

10

12

14

16

18

3.5002.0001.000 2.5005000 4.0003.0001.500

YR

etai

l rev

enue

CAG

R,%

, 201

4-20

17

Germany

Russia’15 forecast

Retail sales forecast US$, 2015

Russia “14

US

Japan

Brazil

India

China

Currently Russian consumer market is less attractive to the investors than other BRIC markets

Average cost of capital

to 21st place 2015(from 12th in 2014)

Note: (a) Bubble size represents country’s population Source: Economic Intelligence Unit Forecast. 1Q2015; Bloomberg data; KPMG analysis, A.T. Kearney Global Retail Development Index™

Inflation to 13.9%

Р

%to 18.3%

Global Retail Development Index™

Takeaway

9© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Forecast

Total retail revenue in Russia by segments*RUB trln in the prices of base period (2012)

Comments, 2014-2017

Source: Economic Intelligence Unit forecast, July 2015, Canadean, KPMG analysis

Overall consumption structure will remain untouched due to an increased debt/income ratio of households

Retail market

Debt/income ratio

Home and garden products

by 10%

to 57%

8 %

D I

of sales

61%

10%

18,6

2016

10%

11%

2017

8%8%11%

18,6

10%

10%

61%

10%

9%

11%

10%

+1%-10%

19,0

2015

8%10%

61%

10%

11%

61%

2014

20,7

Apparel and accessoriesFood and grocery Home and garden products

Electrical and electronicsOthers (less than 1 trln RUB)

* All numbers are given in the prices of base period (2012)

Retail Revenue

Takeaway

Russia’s Changing Tax Environment

Evgenia WolfusPartner, International TaxHead of Indirect Tax and Transportation SectorKPMG in Russia

11© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Part of “deoffshorisation” package – Amnesty Law to allow individuals to legalise property located outside Russia

Russian tax concerns – ‘Deoffshorisation’

Russian tax residents were legally able to send funds offshore and then to continue to earn income on those funds, in each case without paying any Russian tax

Deoffshorisation combats tax base erosion and the use of offshore companies by Russian businesses

There are three key goals for Deoffshorisation:

Prevent funds from being sent offshore without tax by:

■ Limiting the use of DTTs through the ‘Beneficial Owner’ concept.

Tax funds which are offshore by:

■ Broadening the Tax Residency rules for companies

■ Enacting Controlled Foreign Company (‘CFC’) rules

Force Russian tax residents to return funds to Russia by:

■ Taxing CFC passive income at the normal corporate income tax rate (20%), rather than at the lower tax rate for dividends (0% or 13%) (‘active’ companies are not CFCs)

■ Requiring the payment of dividends back to Russia to avoid the CFC tax

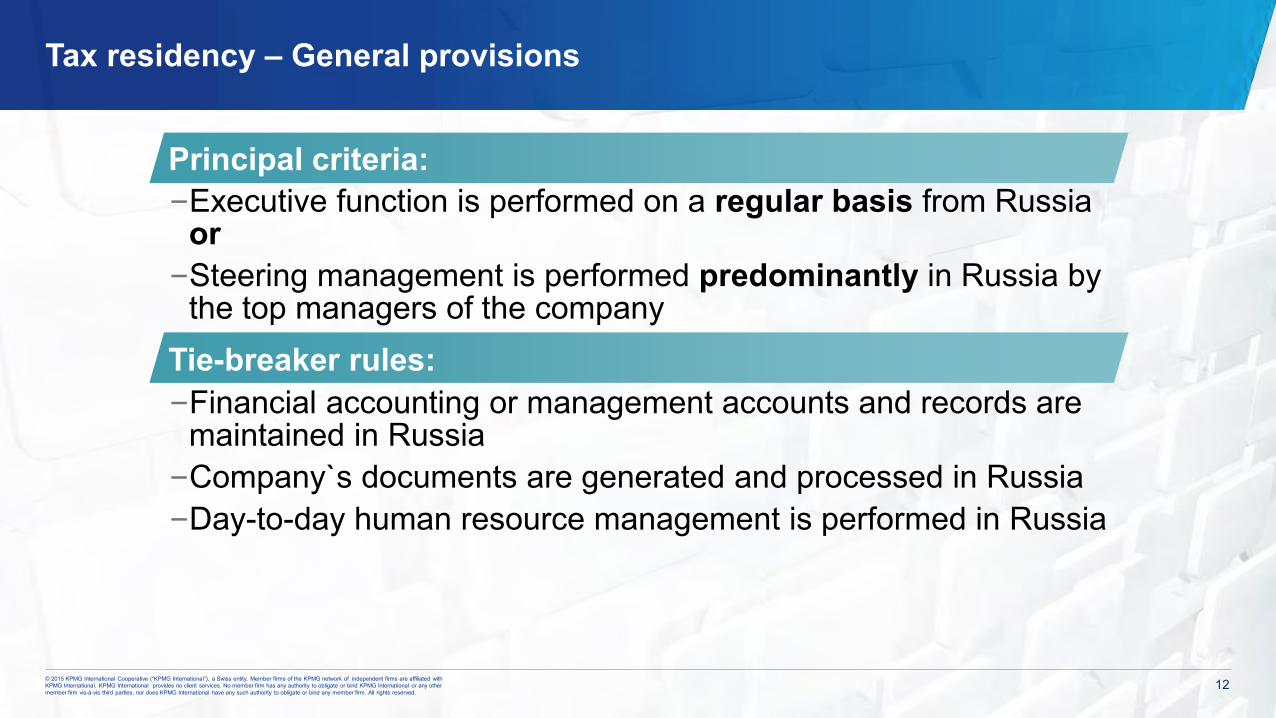

12© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

‒Executive function is performed on a regular basis from Russia or‒Steering management is performed predominantly in Russia by

the top managers of the company

‒Financial accounting or management accounts and records are maintained in Russia‒Company`s documents are generated and processed in Russia‒Day-to-day human resource management is performed in Russia

Tax residency – General provisions

Principal criteria:

Tie-breaker rules:

13© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Tax residency – Implications

■ Russian CIT (20%) is imposed on HoldCo’s profits (or 0%/13% for dividends)■ Recalculation of HoldCo’s profits according to Chapter 25 of the Russian Tax Code■ Russian Withholding Tax (WHT) is imposed on the distribution of profits by HoldCo to

Investors (the tax rates of Russian DTTs are applied if the conditions are met)

Foreign HoldCo’s profit is subject to Russian CIT

Investors

ForeignHoldCo

RusCo

HoldCo considered a Russian tax

resident

Distribution of profits

subject to Russian WHT!

For illustration purposes

14© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Drastic change from a form-based approach to the application of DTT prevalent in Russia before 2015.

Beneficial owner of income paid out of Russia for the purpose of application of DTTs concluded with Russia: ■ An entity who has the right to use income OR■ On whose behalf another entity has the authority to use income

!

NOT a beneficial owner if:■ Limited authority to dispose of income or mere functions of an intermediary with respect to such income.■ No additional functions or risks with respect to the income■ Onwards distribution of income to an entity that is not entitled to benefits under DTT concluded with Russia

‘Look through’ approach specifically set forth in the law if the immediate recipient of income is NOT a beneficial owner:■ Russian beneficial owner: WHT for dividend income at 0% (for companies with qualifying investment) or 13% (in

other cases)■ Foreign beneficial owner: WHT in accordance with DTT between its country and Russia

Beneficial ownership of income – Now explicitly defined in the Russian tax law

15© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Beneficial ownership of income - Example for typical active holding company

Key features of Active Co■ Sufficient level of substance.■ Retention and reinvestment of dividend income

by Active HoldCo.■ Appropriate experience and qualification of the

BoD.■ Confirmation that directors exercise discretion

over the income.

Structuring considerations■ Indirect participation by Active HoldCo equated

with direct participation by Foreign SubHoldCo BUT other conditions for reduced WHT rate also relevant (depending on the treaty).

■ Use of intermediary holding companies minimised.

ActiveHoldCo

ForeignSubHoldCo

RusCo (1) RusCo (2)

Russia

Foreign jurisdiction

Dividends

Dividends

Dividends

Beneficial owner

16© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Beneficial ownership of income – Look through approachExample for investor structure (in the event of low substance)

Waiver of rights of CyprusHoldCo under Russia-Cyprus DTT and declaration of investors as beneficial owners of dividend paid by RusCo■ WHT on distribution of dividends:

– 0% (Russian companies with qualifying investments), or 13% (other Russian investors).

– Rate under applicable DTT rate (for foreign investors).■ Ultimate savings in the amount of 5% WHT in Russia

relating to the part attributable to Russian investors.■ Potential need for a direct shareholding in the capital of

RusCo by a foreign investor wishing to apply a DTT with Russia.

But■ Tax risks for prior periods.■ Lack of clarity on how the Russian tax authorities will

check beneficial ownership or absence thereof.■ It is still unclear how low substance structures will be

affected by the OECD BEPS project.RusCo

CyprusHoldCo

OffshorePE Fund

Not a beneficial

owner

Nota beneficial

owner

Foreign Investor Russian Investor

Beneficial owners

Dividends

Dividends

DividendsWHTunder

DTT with investor’s country

0/13% WHT

Low substance

Low substance

17© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Beneficial ownership of income – Implications for typical financing structures

Possible structureCurrent structure

OffshoreCo

FinCo(DTT)

RusCo

Loan

Loan Interest

Interest

Reduction of tax base by interest payable to OffshoreCo

OffshoreCo

FinCo(DTT)

RusCo

LoanInterest

Reduction of tax base through other mechanisms (e.g. deemed interest deduction)

Transition to more sophisticated structures

Enhancement of substance of FinCo in a foreign jurisdiction

Capital contribution/non-interest-bearing loan

18© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Taxation of indirect sale of Russian real property

Commercial Real Estate Oil and Gas

Company 1 Company 2 Company 3

Foreign Investor’s Consortium –

Cyprus

Russian Oil&GCo

51% 49%

Foreign JV Co

Russian Group Foreign Group

Foreign parent SPV

Russian SPV

Foreign company with Russian

branch

Russian OpCo

Capital gains effectively exempt before 2015 but taxable from 2015

■ No effective mechanism for the payment of tax on foreign to foreign transaction.

■ A few treaties restricting Russian taxing rights (but renegotiation for some in process).

Russia’s Changing Tax Environment

Nina GoulisTax PartnerKPMG in Russia

20© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Legislative trends

Additional attention to expenses deductibility and application of tax incentives

Deoffshorizationlaw

Transfer pricing rules

Thin capitalization rules

Tax incentives Special investment

contracts Partial restriction

of foreign-made products access to the public procurement system

Prevent funds from being sent offshore

Necessity to increase tax budget

Localization and import substitution

21© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Trends in the legislation application

1Active application of «substance over form» approach

2Critical approach to assessment of documents and

economic operations nature

3 Interdependence as a ground for additional scrutiny

4 Active application of all available sources of evidence

5Claims to operations, which are difficult for defense by

taxpayer

22© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Current risk areas of additional tax assessment

1

2Justification of tax incentives application

(e.g., Volkswagen, IKEA, PCM Motors, International paper)

3 PE risks (e.g., Astellas, Berlin-Chemie)

4 Unjustified tax benefit

■ Royalties ■ Interests■ Cost sharing

■ Imputed income

■ Federal and regional tax incentives

■ Additional attention to business structures when goods are sold directly by foreign entity

■ Application to continuing operations■ Blurring of lines between «interdependence» and «affiliation»

Additional attention to all payments outside Russia

(e.g., Oriflame, Suninbev, Ecvant, ADL production)

Russia’s Changing Tax Environment

Victoria SamsonovaDirector, Corporate TaxHead of Healthcare & PharmaceuticalsKPMG in Russia and CIS

24© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Investment climate in Russia – turbulent times

RUB depreciation, decrease of import

Increased “country risk”

Consumer demand shrinking

International sanctions tightening

Rapidly changing domestic legislationLocal production cost reduced

Decrease of competition level

Demand for less expensive commodities

State incentives for investors

Law-making opportunities

25© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Localization and import substitution as economic policy flagships

Russian Government is developing specific action plans for import substitution

The share of imported goods consumed by Russia to be gradually reduced by 2020 in more than 20 industries

Some types of foreign products to be restricted from access to state procurement

Measures to stimulate the manufacturing localization by multinationals are under active elaboration

Priority segments: Industrial Equipment, Hi-Tech Equipment, Chemicals & Petrochemicals, Pharmaceuticals, Medical Devices, Electronics

26© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Localization – ways of market entry

Distribution contract

Sales support office / Trading subsidiary in Russia

■ Direct sales of finished goods to Russia from abroad

■ A representative office / branch / subsidiary engaged in marketing and sales support

■ A Russian subsidiary importing and distributing finished goods in Russia

■ Contracting with a local partner possessing production facilities

Acquiring a local player

■ Including “ready-to-go” and “brownfield” options

Greenfield

■ Investment into construction of a local full-cycle manufacturing site

Contract manufacturing / Assembly

Priority

localization

forms

in terms of the state support

27© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Forms of investors support from the state

Locations for new manufacturing sites, providing land plots with the infrastructure, energy, utilities Subject to certification and expert assessment by a special body A special provider of facility management and support to residents on regulatory / administrative matters No special legal status; tax benefits may be available under regional laws

Industrial Parks and Technoparks

Reduced rates / exemptions for corporate profits tax, property tax, customs duties, social insurance contributions Applies to new construction as well as the existing facilities expanding/modernization An investment agreement to be signed with the regional authorities Could be obtained retro-actively; criteria (the minimal investment volume, payback term) differ per regions

Special legal status, tax and customs benefits Four types: Manufacturing; Technological (Innovation); Touristic (Recreational); Logistic (Port) Support with infrastructure, utilities, administrative work of obtaining residence

Special Economic Zones

Structured incorporation of integrated industrial, scientific, financing, infrastructural entities Operating with state support and aimed at development of a particular industry (group of industries) No special legal status; tax benefits may be available under regional laws

Industrial Clusters

Regional Tax Benefits

28© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Incentives for investors in Russia – examples

Special Economic Zone Industrial Cluster

Industrial Park Regional tax concession

Kaliningrad

PskovMoglino SEZ

St. PetersburgInnovation SEZPharma Cluster

KhabarovskAircraft & Shipbuilding

Innovations ClusterDalEnergoMash Park

VolgogradNikoKhim Park

IrkutskAngarsky Park

Moscow regionStupino Park

Innovation SEZ

KrasnoyarskKrasny Yar Park

Innovations Cluster

KalugaPharma ClusterLyudinovo SEZ

YaroslavlBiopharma ClusterAutomotive Cluster

TatarstanAlabuga SEZ

ChelyabinskStankomash Park

Altaysky regionBiopharma Cluster

BashkortostanPetrochemical Cluster

NovosibirskIT & Medical Cluster For illustration purposes

Russia’s Changing Tax Environment

Bob WallingfordPartner, Tax and Legal ServicesTax Head of Japan Global Tax Practice KPMG in Russia and CIS

30© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Foreign Company

Russian Sales Co• Some profits

Russian Manufacturing Co

• Only losses

Unrelated Shareholder

100%20%

For illustration purposes

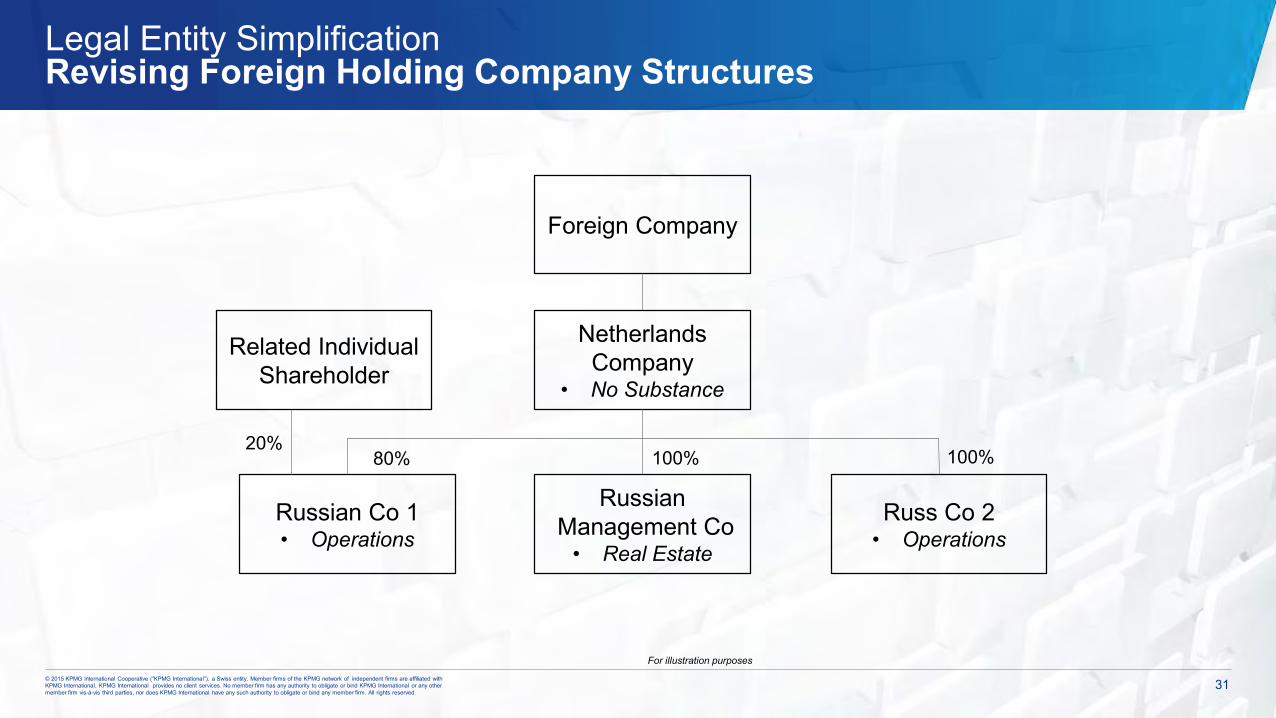

Legal Entity SimplificationRevising Russian Holding Company Structures

31© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Foreign Company

Russian Co 1• Operations

Russ Co 2• Operations

Netherlands Company

• No Substance

RussianManagement Co

• Real Estate

Related Individual Shareholder

100% 100%80%20%

For illustration purposes

Legal Entity SimplificationRevising Foreign Holding Company Structures

32© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Co

mp

any’

s d

ivis

ion

s:

Acc

ou

nti

ng

:

ERP-system:

80% of Russian companies have documents workflow like this:

COSTLY SLOWLY MANY ERRORSNO CONTROL

Man

ual

dat

ain

pu

t

For illustration purposes

Efficiency/OptimizationPaper Documentation

33© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Co

mp

any’

s d

ivis

ion

s:

ERP-system

Au

tom

atic

pro

cess

ing

of

imag

es

Optimized documents workflow will be like this:

Accounting

FAST COST REDUCTIONMINIMUM OF

ERRORS CONTROL

Clie

nt’

s ac

cou

nti

ng

do

cum

ents

Inspection

XML

Electronic archive

Operators of electronic exchange

Analysis of processes

related to documents

workflow

Assistance in

preparation of

requirements for IT

solutions

Assistance in

selection of IT

solutions and

vendors

Quality control

during

implementation of

IT solutions

Development of

recommendations and

assistance in their

implementation

KPMG services

For illustration purposes

Efficiency/OptimizationPaper Documentation

Thank youPresentation by Bob WallingfordEvgenia WolfusNina GoulisVictoria Samsonova

35

© 2015 KPMG International Cooperative ("KPMG International"), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.