thailand strategy

TRANSCRIPT

ed: KK / sa:TP, PY, CS

External risks trump local positives

• Our portfolio outperformed the SET in June and YTD

• The market slump makes current valuations attractive, but

increased volatility in global financial markets could cap near-

term upsides

• Accumulate on dips stock with good fundamentals, reasonable

valuations and generous yields

• Top picks for July are AEONTS, CPN, LH, DIF, and IVL

• Top picks for 2H18 are ADVANC, AEONTS, AMATA, BBL,

CPALL, CPN, DIF, IVL, LH, and STEC.

Stock market slumped in 1H18. The Stock Exchange of

Thailand (SET) hit a peak of 1852 points in February but the index

has since headed downwards to end 1H18 at 1595.58, down

9.0% from end-2017. It underperformed regional peers which

dropped 5.5% during the same period. This was mainly due to

heavy selling by foreign investors.

Accumulate on dips. Our regional equity strategist rates

Thailand as Neutral in 3Q18. After tumbling over 200 points

from its recent peak in February, the Thai stock market is now

trading on a 2018 PE of 14.6x, which is in line with its historical

average. While the domestic economy is now on an upward

momentum, key risks are lingering concerns on; (i) the Thai baht

weakening against the greenback; (ii) the length and depth of

the US-China trade tension and its potential impact on global

growth; (iii) rising interest rate trend and; (iv) potential election

delays. We still prefer domestic plays and recommend investors

to accumulate on dips those strong fundamental stocks with

reasonable valuation and high yields. Among the sectors we like

are Commerce, Tourism, and Residential Property. The REIT

sector should also offers a safe bet amidst rising volatility.

Top picks for July 2018. They are Aeon Thana Sinsap (AEONTS),

Central Pattana (CPN), Land & Houses (LH), Digital Telecom

Infrastructure Fund (DIF) and Indorama Ventures (IVL).

Key themes and top picks for 2H18. We have five themes for

the market in 2H18: (i) Recovering domestic consumption and

elections (AEONTS, CPALL). (ii) EEC theme (AMATA, BBL, STEC),

(iii) Resilient earnings (ADVANC). (iv) High growth with

reasonable valuation (IVL, CPN). (v) Generous yields (DIF, LH).

SET : 1,607.27

Analyst Chanpen SIRITHANARATTANAKUL +662 857 7824 [email protected]

Thailand Research Team +662 658 1222 [email protected]

Key Indices

Current % Chng

SET Index 1607.27 0.73%

SET 100 Index 2339.76 0.82%

SET 50 Index 1058.12 0.62%

Bt/US$ Exchange Rate 33.16 0.36%

Daily Volume (m shrs) 12,098

Daily Turnover (US$m) 1,457

Source: Bloomberg Finance L.P.

Market Key Data

(%) EPS Gth Div Yield

2017F 6.0 3.1

2018F 10.0 3.6

2019F 8.0 3.8

(x) PE EV/EBITDA

2017F 16.1 8.3

2018F 14.6 7.6

2019F 13.5 7.2

DBS Group Research . Equity 3 Jul 2018

Thailand Market Focus

Strategy Refer to important disclosures at the end of this report

STOCKS

12-mth

Price Mkt Cap Target Performance (%)

Bt US$m Bt 3 mth 12 mth Rating

Aeon Thana Sinsap Thailand 168 1,268 208 (6.2) 55.1 BUY Amata Corporation 18.70 604 30.00 (10.1) 6.9 BUY Advanced Info Service 185 16,654 232 (11.1) 4.5 BUY Bangkok Bank 196 11,299 218 (0.8) 6.5 BUY CP ALL 73.50 19,991 95.00 (16.5) 18.1 BUY Central Pattana 69.75 9,478 85.00 (10.6) 3.3 BUY Digital Telecom Infrastructure Fund 14.50 4,231 15.90 (0.7) 0.0 BUY Indorama Ventures 54.75 9,197 71.00 (4.4) 42.2 BUY Land & Houses 11.30 4,089 12.80 7.6 10.8 BUY Sino-Thai Engineering 18.10 836 23.00 (5.2) (35.9) BUY

Source: DBSVTH, Bloomberg Finance L.P.

Closing price as of 29 Jun 2018

Market Focus

External risks trump local positives

Page 2

Our portfolio performance

Our top picks slightly outperformed the market in Jun 2018. The

value of our portfolio dropped 6.7% in Jun 2018, slightly

outperforming the general market which dropped 7.2% during

the same period. This was led by Land & Houses (LH), which

saw its share price increase 0.9% during the period. The stock

managed to stay in positive territory mainly due to Khun Anant

Asavabhokin’s announcement of a tender offer for 10% stakes

in LH at Bt11.80 apiece.

YTD…

The value of our portfolio rose 5.3% in 6M18, outperforming the

general market’s 9.0% loss. This was led by IVL and Aeon Thana

Sinsap (AEONTS).

Our picks slightly outperformed the market in June 2018

Source: DBSTH

Our monthly picks’ performance vs SET Index

Source: DBSTH

…and since end-February 2016. Our portfolio has posted an

impressive 132% price return since end-February 2016 when we

started to track our monthly performance vs the market’s 21%

rise during the same period.

Outperforming the market since we initiated our portfolio

Source: DBSTH

1- J un-18 29- J un-18 Change

AP 9.15 8.15 -10.9%

CK 26.50 23.90 -9.8%

IVL 57.75 54.75 -5.2%

LH 11.20 11.30 0.9%

CPN 76.25 69.75 -8.5%

-6.7%

Index change 1719.82 1595.58 -7.2%

Outperformance 0.5%

Our port folio's price return

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Oct

-17

No

v-1

7

De

c-1

7

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

May

-18

Jun

-18

Market Our portfolio

80

100

120

140

160

180

200

220

240

260

280

Feb

-16

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

De

c-16

Feb

-17

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

De

c-17

Feb

-18

Ap

r-1

8

Jun

-18

Market

Our portfolio

Market Focus

External risks trump local positives

Page 3

Top picks for July 2018

Aeon Thana Sinsap (BUY; TP: Bt208)

We like AEONTS for its strong position in the retail finance

industry and strong balance sheet health. AEONTS is one of the

largest non-bank players in Thailand and commands the largest

share of the personal loan market. It also provides various other

finance services, including credit cards, hire purchase, debt

collection and insurance brokerage. More than half of its

revenue is derived from personal loans, followed by credit cards.

Improving consumer confidence, on the back of promising

economic growth outlook, should translate into stronger retail

spending, which is in turn the key driver for retail loan demand

and AEONTS’s operating performance.

Central Pattana (BUY; TP: Bt85.00)

CPN is Thailand's largest shopping mall developer. We like the

company for its dominant position in the industry, strong

recurring income base from its 32 quality shopping malls across

Thailand, clear expansion plans, solid management team and

strong earnings growth of 26% in 2018 and 13% in 2019. CPN

has a rock-solid balance sheet, with net gearing of only 3.4% at

end-1Q18. Our TP on the stock is Bt85, based on DCF valuation.

Digital Telecommunications Infrastructure Fund (BUY; TP:

Bt15.90)

DIF is one of the top picks under our telecommunications

coverage, thanks to its c.7% yield guaranteed over the long-

term. On 18 May 2018, DIF raised capital with total proceeds of

Bt53.2bn. The capital raised and additional debts of Bt2.0bn

issued were used to purchase Phase II assets (including fibre from

TRUE). With Phase II assets investment, distribution per unit

(DPU) is expected to increase from Bt1.01 in FY18F to Bt1.04 in

FY19F. The weighted average investment contract tenor is

extended from 12 years to 21 years post Phase II assets

acquisition

Indorama Ventures (BUY; TP: Bt71.00)

IVL is a global integrated polyethylene terephthalate/ purified

terephthalic acid (PET/PTA) producer with combined PET, fibre

and PTA capacity of 9.8mtpa. Including capacities for mono-

ethylene glycol (MEG) and other high value-added (HVA)

chemical products, its total capacity is currently 10.7mtpa. The

group operates production facilities in 21 countries, with its sales

footprint covering over 100 countries. We are still very positive

on IVL’s earnings outlook, which could be driven by sales volume

growth, increased contribution from HVA chemical products, as

well as improving margins from a balancing of the PET industry.

Land & Houses (BUY; TP: Bt12.80)

LH is Thailand’s leading residential property developer. The

company has several recurring income assets and investment

portfolio in listed companies such as Quality Houses (QH), Home

Product Center (HMPRO) and Land & Houses Bank (LHBANK).

We see several positive catalysts for LH including; i) potential

jump in pre-sales in 2018 amidst aggressive condominium

launches in 2Q18 and; ii) huge gain from US asset divestment in

2Q18. The tender offer by Khun Anant Asavabhokin for 10% of

its shares at Bt11.80 apiece should provide good support for

share price.

Stock picks for July 2018

Mkt Price Target % PE PBV Div Yield ROE

Bloomberg Cap 29 Jun Price Upside (x) (x) (%) (x)

Code (US$m) (Bt) (Bt) 18F 19F 18F 19F 18F 19F 18F Rcmd

AEONTS TB 1,268 167.50 208.00 24% 12.8 11.3 2.3 2.0 2.2 2.3 19.4 BUY CPN TB 9,479 69.75 85.00 22% 25.1 22.1 4.6 4.1 1.6 1.8 19.2 HOLD DIF TB 4,232 14.50 15.90 10% 14.4 14.0 0.6 0.6 7.0 7.2 6.7 BUY IVL TB 9,198 54.75 71.00 30% 13.3 11.1 2.2 1.9 2.6 3.2 17.2 BUY LH TB 4,089 11.30 12.80 13% 13.8 13.3 1.1 1.1 7.6 7.8 7.7 BUY

Source: Company, DBSVTH

Market Focus

External risks trump local positives

Page 4

Top picks for 2H18

Aeon Thana Sinsap (BUY; TP: Bt208)

We like AEONTS for its strong position in the retail finance

industry and strong balance sheet health. AEONTS is one of the

largest non-bank players in Thailand and commands the largest

share of the personal loan market. It also provides various other

finance services, including credit cards, hire purchase, debt

collection, and insurance brokerage. More than half of its

revenue is derived from personal loans, followed by credit cards.

Improving consumer confidence, on the back of promising

economic growth outlook, should translate into stronger retail

spending, which is in turn the key driver for retail loan demand

and AEONTS’s operating performance.

Amata Corporation (BUY; TP: Bt30)

AMATA should be a prime beneficiary of the Eastern Economic

Corridor (EEC) initiative, thanks to its huge land bank in both

Chonburi and Rayong, both of which are in the EEC area. While

current land sales remain weak, we see positive outlook for

foreign direct investments (FD)I and consequently land sales.

Thailand is having a general election early next year and more

infrastructure projects could be developed in the EEC area.

Advanced Info Service (BUY; TP: Bt232)

ADVANC is Thailand's largest cellular operator with over 40%

market share. We expect the company to show an earnings

turnaround with earnings growth of 13% this year and 10%

next year (after two years of earnings contraction), thanks to the

improving competitive landscape. Its earnings are also quite

resilient against the global economic slowdown. The stock now

offers a decent 2018 yield of 4.3% and 25% upside to our DCF-

based TP of Bt232.

Bangkok Bank (BUY; TP: Bt222)

We believe that the resumption of investments will play a key

role in driving Thailand’s economy and the banking sector in

general in 2018. Big banks should benefit from such

investments, given their large exposure to business loans

(corporate + SME loans), and so far their loan growth

momentum has reflected this. BBL fits into this theme and is our

top pick for the sector. Besides, we believe the recent

bancassurance agreement between BBL and AIA will also help

boost BBL’s fee income in 2018-19. BBL is one of the big banks

that would feel the least impact from the fee waiver scheme. At

Bt195.5, the stock is trading slightly below its book value of

equity per share (BVPS) at Bt201.5. It now offers a moderate

2018 dividend yield of 3.6%. We maintain BUY with a TP of

Bt222, based on the Gordon Growth Model, implying 1.0x

FY18F BV.

CP All (BUY; TP: Bt95)

CPALL is an operator of convenience stores (7-Eleven) in Thailand

with the highest market share. It also operates other related

businesses such as bill payment services, manufacturing and

sales of frozen foods and bakery. We like CPALL for its

dominant position in the industry, defensive nature, business

resilience, visible expansion plans and high return on assets

(ROE). With its strong product strategy and new products, we

expect CPALL to continue delivering healthy profits at a

compounded annual growth rate (CAGR) of 17% in the next

three years. We rate the stock a BUY with a DCF-based TP of

Bt95.

Central Pattana (BUY; TP: Bt85.00)

CPN is Thailand's largest shopping mall developer. We like the

company for its dominant position in the industry, strong

recurring income base from its 32 quality shopping malls across

Thailand, clear expansion plans, solid management team and

strong earnings growth of 26% in 2018 and 13% in 2019. CPN

has a rock-solid balance sheet, with net gearing of only 3.4% at

end-1Q18. Our TP on the stock is Bt85, based on DCF valuation.

Digital Telecommunications Infrastructure Fund (BUY; TP:

Bt15.90)

DIF is one of the top picks under our telecommunications

coverage, thanks to its c.7% yield guaranteed over the long-

term. On 18 May 2018, DIF raised capital with total proceed of

Bt53.2bn. The capital raised and additional debts of Bt2.0bn

issued were used to purchase Phase II assets (including fibre from

TRUE. With Phase II assets investment, DPU is expected to

increase from Bt1.01 in FY18F to Bt1.04 in FY19F. The weighted

average investment contract tenor is extended from 12 years to

21 years post Phase II assets acquisition.

Indorama Ventures (BUY; TP: Bt71.00)

IVL is a global integrated polyethylene terephthalate/ purified

terephthalic acid (PET/PTA) producer with combined PET, fibre

and PTA capacity of 9.8mtpa. Including capacities for mono-

ethylene glycol (MEG) and other high value-added (HVA)

chemical products, its total capacity is currently 10.7mtpa. The

group operates production facilities in 21 countries, with its sales

footprint covering over 100 countries. We are still very positive

on IVL’s earnings outlook, which could be driven by sales volume

growth, increased contribution from HVA chemical products, as

well as improving margins from a balancing of the PET industry.

Market Focus

External risks trump local positives

Page 5

Land & Houses (BUY; TP: Bt12.80)

LH is Thailand’s leading residential property developer. The

company has several recurring income assets and investment

portfolio in listed companies such as Quality Houses (QH), Home

Product Center (HMPRO) and Land & Houses Bank (LHBANK).

We see several positive catalysts for LH including; i) potential

jump in pre-sales in 2018 amidst aggressive condominium

launches in 2Q18 and; ii) huge gain from US asset divestment in

2Q18. The tender offer by Khun Anant Asavabhokin for 10% of

its shares at Bt11.80 apiece should provide good support for

share price.

Sino-Thai Engineering (BUY; TP: Bt23)

One of Thailand’s top four construction contractors, STEC should

be a prime beneficiary of rising infrastructure spending next year.

We like the company for its large backlog of about Bt120bn which

should provide revenue stream for the next 4-5 years, more project

wins next year, strong earnings growth outlook and solid balance

sheet with a net cash position. We believe concerns over losses at

the Parliament House project should have already been priced in.

Our TP on the stock is Bt23, based on 30x and 25x PE for this year

and next, respectively.

Stock picks for 2H18

Mkt Price Target % PE PBV Div Yield ROE

Bloomberg Cap 29 Jun Price Upside (x) (x) (%) (x)

Code (US$m) (Bt) (Bt) 18F 19F 18F 19F 18F 19F 18F Rcmd

AEONTS TB 1,268 167.50 208.00 24% 12.8 11.3 2.3 2.0 2.2 2.3 19.4 BUY AMATA TB 604 18.70 30.00 60% 11.9 9.9 1.5 1.3 3.4 4.0 12.9 BUY ADVANC TB 16,654 185.00 232.00 25% 16.2 14.8 8.9 7.4 4.3 4.7 60.3 BUY BBL TB 11,300 195.50 218.00 12% 10.5 10.0 0.9 0.8 3.6 3.8 8.6 BUY CPALL TB 19,992 73.50 95.00 29% 29.1 25.1 7.5 6.5 1.7 2.0 27.7 BUY CPN TB 9,479 69.75 85.00 22% 25.1 22.1 4.6 4.1 1.6 1.8 19.2 BUY DIF TB 4,232 14.50 15.90 10% 14.4 14.0 0.6 0.6 7.0 7.2 6.7 BUY IVL TB 9,198 54.75 71.00 30% 13.3 11.1 2.2 1.9 2.6 3.2 17.2 BUY LH TB 4,089 11.30 12.80 13% 12.6 13.8 2.6 2.5 6.6 6.1 20.7 BUY STEC TB 836 18.10 23.00 27% 23.7 20.0 2.8 2.6 2.1 2.5 12.2 BUY

Source: Company, DBSVTH

Market Focus

External risks trump local positives

Page 6

Stock Picks

BUY Bt167.50 Forecasts and Valuation

Aeon Thana Sinsap Thailand (AEONTS TB; TP: Bt208.00)

Robust outlook

FY Feb (Btm) 2016A 2017A 2018F 2019F

Pre-prov. Profit 8,140 8,392 9,323 10,545

Net Profit 2,403 2,966 3,277 3,708

Net Pft (Pre Ex.) 2,403 2,966 3,277 3,708

Net Pft Gth (Pre-ex) (%) (7.4) 23.4 10.5 13.1

EPS (Bt) 9.61 11.9 13.1 14.8

EPS Pre Ex. (Bt) 9.61 11.9 13.1 14.8

EPS Gth Pre Ex (%) (7) 23 10 13

Diluted EPS (Bt) 9.61 11.9 13.1 14.8

PE Pre Ex. (X) 17.4 14.1 12.8 11.3

Net DPS (Bt) 3.45 3.85 3.65 3.90

Div Yield (%) 2.1 2.3 2.2 2.3

ROAE Pre Ex. (%) 18.6 20.2 19.4 19.1

ROAE (%) 18.6 20.2 19.4 19.1

ROA (%) 3.3 3.9 3.9 3.9

BV Per Share (Bt) 54.8 62.9 72.2 83.3

P/Book Value (x) 3.1 2.7 2.3 2.0

Source: Company, DBSVTH

▪ AEONTS is one of the largest non-bank players in Thailand

and commands the largest share of the personal loan

market. More than half of its revenues are derived from

personal loans, followed by credit cards

▪ AEONTS’s retail finance businesses, as well as debt

collection (both for itself and others), should see stronger

performance this year in line recovering domestic

economy. Though credit card business will be the key

driver for FY18 top-line growth, AEONTS’s spread should

still be maintained, as the company expects to roll over

some of its long-term debts at lower interest rates

▪ Strong growth prospects remain for its overseas

businesses. Currently, its overseas operations collectively

contribute only 3% to AEONTS’s top-line and 2% to the

bottom-line. AEONTS expects revenue and earnings

contribution from CLM countries to reach 10% by 2020,

driven by a younger population, better yields, and stronger

asset quality in those countries, relative to Thailand’s

▪ Trading at undemanding valuations of 2.3x FY18F P/BV

and 12.7x FY18F PE, with a dividend yield of 2.2%. Our TP

is based on the Gordon Growth Model and implies 2.9x

FY18F P/BV and 15.9x FY18F PE.

BUY Bt18.70 Forecasts and Valuation

Amata Corporation (AMATA TB; TP: Bt30.0)

A key beneficiary of the EEC

FY Dec (Btm) 2016A 2017A 2018F 2019F

Revenue 4,427 4,491 5,169 6,131

EBITDA 2,496 2,563 2,965 3,572

Pre-tax Profit 1,662 2,019 2,352 2,836

Net Profit 1,198 1,409 1,680 2,015

Net Pft (Pre Ex.) 1,438 1,409 1,680 2,015

Net Pft Gth (Pre-ex) (%) 66.3 (2.0) 19.2 20.0

EPS (Bt) 1.12 1.32 1.57 1.89

EPS Pre Ex. (Bt) 1.35 1.32 1.57 1.89

EPS Gth Pre Ex (%) 66 (2) 19 20

Diluted EPS (Bt) 1.12 1.32 1.57 1.89

Net DPS (Bt) 0.45 0.53 0.63 0.76

BV Per Share (Bt) 11.2 11.8 12.7 13.9

PE (X) 16.7 14.2 11.9 9.9

PE Pre Ex. (X) 13.9 14.2 11.9 9.9

P/Cash Flow (X) 12.1 16.9 15.2 14.8

EV/EBITDA (X) 10.7 11.3 10.5 9.4

Net Div Yield (%) 2.4 2.8 3.4 4.0

P/Book Value (X) 1.7 1.6 1.5 1.3

Net Debt/Equity (X) 0.3 0.4 0.5 0.6

ROAE (%) 10.4 11.5 12.9 14.2

Source: Company, DBSVTH

▪ We see Amata among the first key beneficiaries of the EEC

given its huge 13,634 rai (1 rai = 0.4 acre) land bank in

Chonburi and Rayong. Land prices in the area should

continue to rise as more infrastructure projects are

developed.

▪ Increased contribution from its power business should be

another key earnings driver during 2018-2019 and should

help reduce its earnings volatility going forward. Its

megawatt (MW) share by equity will jump by 58% from

165MW currently to 260MW by end-2018, as three new

power plants in Rayong start commercial operations.

▪ Rising contribution from Vietnam. Amata Vietnam, its

subsidiary, has secured three investment certificates to

develop a high-tech industrial park (410ha, 1ha = 6.25 rai),

a service city (107ha) and a township (753ha) in Long

Thanh. The company is now undertaking a land

compensation process for the hi-tech park and expects to

start construction and land sales in late 2018. We

conservatively assume revenue contribution from Long

Thanh to come in from 2019 onwards.

Market Focus

External risks trump local positives

Page 7

BUY Bt185.00 Forecasts and Valuation

Advanced Info Service (ADVANC TB; TP: Bt232.0)

Safer bet on the telecommunications sector

FY Dec (Btm) 2016A 2017F 2018F 2019F

FY Dec (Btm) 2016A 2017A 2018F 2019F

Revenue 152,150 157,722 166,978 176,039

EBITDA 61,263 70,969 77,627 85,618

Pre-tax Profit 35,841 35,916 39,478 43,355

Net Profit 30,667 30,077 33,854 37,096

Net Pft (Pre Ex.) 30,389 29,852 33,854 37,096

Net Pft Gth (Pre-ex) (%) (21.9) (1.8) 13.4 9.6

EPS (Bt) 10.3 10.1 11.4 12.5

EPS Pre Ex. (Bt) 10.2 10.0 11.4 12.5

EPS Gth Pre Ex (%) (22) (2) 13 10

Diluted EPS (Bt) 10.3 10.1 11.4 12.5

Net DPS (Bt) 10.1 7.08 7.97 8.73

BV Per Share (Bt) 14.3 16.9 20.8 24.9

PE (X) 18.6 18.9 16.8 15.3

PE Pre Ex. (X) 18.7 19.1 16.8 15.3

P/Cash Flow (X) 9.5 11.4 7.0 7.2

EV/EBITDA (X) 10.7 9.4 8.6 7.7

Net Div Yield (%) 5.3 3.7 4.2 4.6

P/Book Value (X) 13.4 11.3 9.2 7.7

Net Debt/Equity (X) 2.0 1.9 1.6 1.2

Source: Company, DBSVTH

▪ We expect to see the earnings turnaround in FY18F after

two years of earnings contraction, thanks to the improving

competitive landscape.

▪ Due to more favourable terms of 1800MHz spectrum

auction (9 license with 5MHz bandwidth per license), we

expect ADVANC to participate in the auction to be set on

19 August 2018.

▪ Pending for the official auction rules to be published on

the Royal Gazette on 5 July 2018, there could be a

potential Capex revision in our forecast post the

announcement.

▪ We like ADVANC for the earnings turnarounds story in

FY18F/FY19F, and dividend yield of c.4% over the next

two years. In addition, ADVANC could potentially benefit

from the relaxation of the 1800MHz auction rule. We think

ADVANC will be a safer bet for the telecommunication

sector during this period.

BUY Bt195.00 Forecasts and Valuation

Bangkok Bank (BBL TB; TP: Bt218.0)

Riding the investment cycle

FY Dec (Btm) 2016A 2017A 2018F 2019F

Pre-prov. Profit 55,256 63,315 64,586 68,114

Net Profit 31,815 33,009 35,383 37,352

Net Pft (Pre Ex.) 31,815 33,009 35,383 37,352

Net Pft Gth (Pre-ex) (%) (6.9) 3.8 7.2 5.6

EPS (Bt) 16.7 17.3 18.5 19.6

EPS Pre Ex. (Bt) 16.7 17.3 18.5 19.6

EPS Gth Pre Ex (%) (7) 4 7 6

Diluted EPS (Bt) 16.7 17.3 18.5 19.6

PE Pre Ex. (X) 11.7 11.3 10.5 10.0

Net DPS (Bt) 6.50 6.50 7.00 7.50

Div Yield (%) 3.3 3.3 3.6 3.8

ROAE Pre Ex. (%) 8.6 8.5 8.6 8.6

ROAE (%) 8.6 8.5 8.6 8.6

ROA (%) 1.1 1.1 1.1 1.1

BV Per Share (Bt) 199 210 222 235

P/Book Value (x) 1.0 0.9 0.9 0.8

Source: Company, DBSVTH

▪ With its large exposure to business loans (41% corporate +

30% SME), BBL should be one of the banks to clinch the

opportunity to grow amid a widely expected investment

upcycle that can lead to a loan demand recovery in 2018.

Besides, with the bank’s strong position in international

loans (15% of its total portfolio, the highest among

Thailand banks), BBL stands to seize the opportunities

arising from regionalisation and urbanisation

▪ We believe decent top line growth (+5% y-o-y) and lower

provision expense (-10% y-o-y) will be the key earnings

growth (+11% y-o-y) drivers for BBL in FY18F

▪ BBL targets to grow its loan portfolio by 5-6% in 2018,

driven by infrastructure-related investments, auto-supply

chain investments, investment resumption from property

developers, and energy-related investments. Fee income is

expected to grow in the mid-to-high single digits, with

new bancassurance agreement with AIA to be a fee

income booster from 2H18 going forward.

▪ The bank believes its NPL ratio would be stable from 2017,

while it targets to set aside some Bt20bn provisions in

2018, vs. Bt22bn in 2017.

Market Focus

External risks trump local positives

Page 8

BUY Bt73.50 Forecasts and Valuation

CPALL (CPALL TB; TP: Bt95.00)

A strong player among domestic retailers

FY Dec (Btm) 2016A 2017A 2018F 2019F

Revenue 434,712 471,069 521,283 568,504

EBITDA 36,473 40,788 45,017 49,518

Pre-tax Profit 20,142 23,506 27,585 32,308

Net Profit 16,677 19,908 22,725 26,306

Net Pft (Pre Ex.) 16,599 19,908 22,725 26,306

Net Pft Gth (Pre-ex) (%) 21.3 19.9 14.1 15.8

EPS (Bt) 1.86 2.22 2.53 2.93

EPS Pre Ex. (Bt) 1.85 2.22 2.53 2.93

EPS Gth Pre Ex (%) 21 20 14 16

Diluted EPS (Bt) 1.86 2.22 2.53 2.93

Net DPS (Bt) 0.90 1.00 1.26 1.46

BV Per Share (Bt) 6.14 8.38 9.86 11.3

PE (X) 39.6 33.2 29.1 25.1

PE Pre Ex. (X) 39.8 33.2 29.1 25.1

P/Cash Flow (X) 17.4 14.3 15.9 15.3

EV/EBITDA (X) 22.5 19.7 17.5 15.7

Net Div Yield (%) 1.2 1.4 1.7 2.0

P/Book Value (X) 12.0 8.8 7.5 6.5

Net Debt/Equity (X) 2.6 1.7 1.3 1.0

ROAE (%) 36.0 30.5 27.7 27.6

Source: Company, DBSVTH

▪ We don’t expect SSSG to rebound significantly this year

but should be at least at a low to mid-single-digit pace for

CPALL.

▪ CPALL’s cash-and-carry business might be pressured by the

opening of new stores overseas, which will still contribute

losses to the group.

▪ However, we expect its convenient store business to still be

miles ahead of its competitors and continue to do well

with positive SSSG, with new products and services to

cater customers’ changing demand.

▪ The strong operations of CVS would lead to solid earnings

growth (FY18F earnings growth forecast of 16% y-o-y) for

the whole group.

BUY Bt76.25 Forecasts and Valuation

Central Pattana (CPN, TP: Bt85.00)

More condominium revenue in 2Q and 3Q18

FY Dec (Btm) 2016A 2017A 2018F 2019F

Revenue 27,634 28,785 35,631 39,522

EBITDA 16,762 17,444 21,098 23,656

Pre-tax Profit 11,033 15,464 14,868 16,881

Net Profit 9,244 13,567 12,468 14,136

Net Pft (Pre Ex.) 9,244 9,892 12,468 14,136

Net Pft Gth (Pre-ex) (%) 17.3 7.0 26.0 13.4

EPS (Bt) 2.06 3.02 2.78 3.15

EPS Pre Ex. (Bt) 2.06 2.20 2.78 3.15

EPS Gth Pre Ex (%) 17 7 26 13

Diluted EPS (Bt) 2.06 3.02 2.78 3.15

Net DPS (Bt) 0.83 1.40 1.11 1.26

BV Per Share (Bt) 11.6 13.8 15.1 17.2

PE (X) 33.9 23.1 25.1 22.1

PE Pre Ex. (X) 33.9 31.6 25.1 22.1

P/Cash Flow (X) 21.8 11.8 20.9 18.5

EV/EBITDA (X) 19.6 18.3 15.5 14.0

Net Div Yield (%) 1.2 2.0 1.6 1.8

P/Book Value (X) 6.0 5.1 4.6 4.1

Net Debt/Equity (X) 0.3 0.1 0.2 0.2

ROAE (%) 18.9 23.8 19.2 19.5

Source: Company, DBSVTH

▪ Strong recurring income base from 32 quality shopping

malls across Thailand. These malls enjoyed high average

occupancy rate of 91% at end 1Q18. This should

improve steadily in 4Q18 and 2019, when major

renovation at CentralWorld is completed and tenants

open their shops.

▪ CPN has a clear expansion plan and is targeting to grow

revenue by 13% CAGR during 2018-2022. This will be

achieved via; (i) rental reversion of 3-5% per annum and

improve in occupancies; (ii) asset enhancement; (iii)

opening of 2-3 new malls per annum and; (iv) expansion

into other assets (e.g. residential, office, hotels, etc.) to

complement its mall business.

▪ Strong earnings growth of 26% this year and 13% next

year. Note that residential condominium revenue will

start to kick in this year. In 1Q18, CPN started to realise

Bt216m revenue from its condominiums. We expect

more revenue to be realised in 2Q and 3Q18, as the

company transfers units at three condominium projects to

its buyers.

Market Focus

External risks trump local positives

Page 9

BUY Bt14.50 Forecasts and Valuation

Digital Telecommunications Infrastructure Fund (DIF, TP: Bt15.90)

Lofty yield with secured long-term income streams

FY Dec (Btm) 2016A 2017A 2018F 2019F

Revenue 6,381 6,741 9,755 11,854

EBITDA 6,111 6,477 9,358 11,390

Pre-tax Profit 18,855 11,105 7,786 9,987

Net Profit 18,855 11,105 7,786 9,987

Net Pft (Pre Ex.) 5,370 5,687 7,786 9,987

Net Pft Gth (Pre-ex) (%) 6.4 5.9 36.9 28.3

EPS (Bt) 3.25 1.91 1.01 1.04

EPS Pre Ex. (Bt) 0.92 0.98 1.01 1.04

EPS Gth Pre Ex (%) 6 6 3 3

Diluted EPS (Bt) 3.25 1.91 1.01 1.04

Net DPS (Bt) 0.96 0.98 1.01 1.04

BV Per Share (Bt) 14.6 15.6 24.7 24.7

PE (X) 4.5 7.6 14.4 14.0

PE Pre Ex. (X) 15.7 14.8 14.4 14.0

P/Cash Flow (X) 16.0 13.8 12.2 13.7

EV/EBITDA (X) 15.8 16.8 14.7 14.5

Net Div Yield (%) 6.6 6.7 7.0 7.2

P/Book Value (X) 1.0 0.9 0.6 0.6

Net Debt/Equity (X) 0.1 0.3 0.2 0.2

ROAE (%) 24.1 12.7 6.7 7.0

Source: Company, DBSVTH

▪ DIF raised additional capital of Bt53.2bn on 18 May 2018,

with the final offering price of Bt13.90 per share.

▪ The proceeds from share offering and additional debt

issuance of Bt2.0bn are used to buy new fibre and tower

from TRUE (Phase II assets), worth of Bt55.2bn.

▪ With Phase II asset, DPU is expected to increase from

Bt1.01 in FY18F to Bt1.04 in FY19F. Additionally, the

weighted average rental agreement tenor has been

extended from 12 years to 21 years.

▪ We like DIF for its c.7% yield and its long-term rental

guarantee, which is highly attractive as compared to other

options available in the market.

▪ Our Bt15.90 TP is based on DCF.

BUY Bt54.75 Forecasts and Valuation

Indorama Ventures (IVL, TP: Bt71.00)

Strong growth outlook continues in FY18-FY19

FY Dec (Btm) 2016A 2017A 2018F 2019F

Revenue 254,620 286,332 331,130 358,471

EBITDA 26,951 34,946 45,065 49,570

Pre-tax Profit 18,421 23,218 28,118 32,227

Net Profit 16,197 20,883 21,566 25,903

Net Pft (Pre Ex.) 9,563 16,610 21,566 25,903

Net Pft Gth (Pre-ex) (%) 225.8 73.7 29.8 20.1

EPS (Bt) 3.36 4.19 4.11 4.94

EPS Pre Ex. (Bt) 1.99 3.33 4.11 4.94

EPS Gth Pre Ex (%) 226 68 23 20

Diluted EPS (Bt) 3.36 4.19 4.11 4.94

Net DPS (Bt) 0.66 0.63 1.44 1.73

BV Per Share (Bt) 18.5 22.3 25.4 28.7

PE (X) 16.3 13.1 13.3 11.1

PE Pre Ex. (X) 27.6 16.4 13.3 11.1

P/Cash Flow (X) 10.6 9.4 5.7 7.6

EV/EBITDA (X) 13.3 10.3 8.0 7.0

Net Div Yield (%) 1.2 1.1 2.6 3.2

P/Book Value (X) 3.0 2.5 2.2 1.9

Net Debt/Equity (X) 1.0 0.7 0.5 0.4

ROAE (%) 19.2 20.3 17.2 18.2

Source: Company, DBSVTH

▪ Strong earnings growth of 30% in 2018F to be driven by

sales volume growth from its acquisition and higher

contribution from HVA products

▪ Increase in earnings before interest, taxes, depreciation and

amortisation per tonne (EBITDA/tonne) in 2018 and

beyond, thanks to the wider spread of PET given the global

PET industry rebalancing, anti-dumping investigation of

PET imports in the US and Canada, and import ban on

waste plastic in China effective from Jan 2018

▪ Several acquisitions of HVA products since 2016 have

enhanced its market positioning in specialty chemical

markets, which would be the key factor in stabilising IVL’s

core EBITDA/tonne in the longer term given its steady

margins

▪ Maintain BUY with TP of Bt71, pegged to 17.5x FY18F PE.

Market Focus

External risks trump local positives

Page 10

BUY Bt11.30 Forecasts and Valuation

Land & Houses (LH TB; TP: Bt12.80)

Offering generous yield of 6.6% with low risks FY Dec (Btm) 2016A 2017A 2018F 2019F

Revenue 29,909 34,922 36,781 35,115

EBITDA 10,796 12,465 13,018 13,102

Pre-tax Profit 10,142 11,790 12,331 11,328

Net Profit 8,618 10,463 10,599 9,686

Net Pft (Pre Ex.) 7,997 9,459 9,676 9,686

Net Pft Gth (Pre-ex) (%) 18.5 18.3 2.3 0.1

EPS (Bt) 0.73 0.89 0.90 0.82

EPS Pre Ex. (Bt) 0.68 0.80 0.82 0.82

EPS Gth Pre Ex (%) 18 18 2 0

Diluted EPS (Bt) 0.73 0.89 0.90 0.82

Net DPS (Bt) 0.65 0.75 0.75 0.69

BV Per Share (Bt) 3.98 4.19 4.36 4.47

PE (X) 15.5 12.7 12.6 13.8

PE Pre Ex. (X) 16.7 14.1 13.8 13.8

P/Cash Flow (X) 18.1 13.4 14.7 9.5

EV/EBITDA (X) 16.2 14.3 14.0 13.8

Net Div Yield (%) 5.8 6.6 6.6 6.1

P/Book Value (X) 2.8 2.7 2.6 2.5

Net Debt/Equity (X) 0.8 0.9 0.9 0.9

ROAE (%) 18.6 21.6 20.7 18.4

Source: Company, DBSVTH

▪ Thailand’s leading residential property developer

▪ 2Q18 earnings to be boosted by gain from divestment of

one of its US assets

▪ Planning for aggressive new project launches this year,

which should help boost presales in 2018

▪ Offering generous dividend yield of 6.6% at current price

▪ Downside risk protected near-term, as Khun Anant

Asavabhokhin will make a voluntary partial tender offer to

purchase 10% of LH shares at Bt11.80 apiece. This should

help support LH’s share price near term.

▪ Maintain BUY with Bt12.80 price, based on RNAV

BUY Bt18.10 Forecasts and Valuation

Sino-Thai Engineering & Con. (STEC TB; TP: Bt23.00)

Time to ride the investment cycle

FY Dec (Btm) 2016A 2017A 2018F 2019F

Revenue 17,953 20,075 25,121 30,183

EBITDA 1,515 (1,440) 1,726 2,089

Pre-tax Profit 1,753 (797) 1,446 1,720

Net Profit 1,381 (611) 1,164 1,383

Net Pft (Pre Ex.) 906 (1,390) 1,164 1,383

Net Pft Gth (Pre-ex) (%) (16.0) nm nm 18.8

EPS (Bt) 0.91 (0.4) 0.76 0.91

EPS Pre Ex. (Bt) 0.59 (0.9) 0.76 0.91

EPS Gth Pre Ex (%) (16) nm nm 19

Diluted EPS (Bt) 0.91 (0.4) 0.76 0.91

Net DPS (Bt) 0.26 0.22 0.38 0.45

BV Per Share (Bt) 6.79 6.04 6.44 6.96

PE (X) 20.0 nm 23.7 20.0

PE Pre Ex. (X) 30.5 nm 23.7 20.0

P/Cash Flow (X) 65.6 30.8 15.6 nm

EV/EBITDA (X) 17.5 nm 13.5 11.9

Net Div Yield (%) 1.4 1.2 2.1 2.5

P/Book Value (X) 2.7 3.0 2.8 2.6

Net Debt/Equity (X) CASH CASH CASH CASH

ROAE (%) 14.1 (6.2) 12.2 13.5

Source: Company, DBSVTH

▪ Expect Bt643bn infrastructure to be up for bidding in

FY18F to be a key catalyst to drive up the share price

▪ STEC has already bought the Term Of References (TORs) of

the Bt237bn of the EEC track high-speed railway for 3

international airports, implying its intention to participate

in this PPP project

▪ STEC’s backlog stood at Bt125bn as of 31 Mar 18 (vs

average 5-year backlogs of Bt50bn), implying more than

four years of its revenue

▪ Expect FY19F earnings to turn into positive with a strong

earnings growth (vs its FY17 loss of Bt1.4bn due to the

recorded provision from its construction projects)

▪ Our TP on STEC is Bt23, based on 30x FY18F PE

Market Focus

External risks trump local positives

Page 11

Politics

Coronation before general election

According to Prime Minister Prayut Chan-o-cha, His Majesty King

Maha Vajiralongkorn’s coronation will take place before the

general election next year. His Majesty King ascended the throne

on December 26, 2016, but the date for his coronation has not

been determined yet. It is widely expected that the general

election will be held in February 2019.

Economy

1Q18 GDP rose 4.8% y-o-y, beating consensus estimates

Gross Domestic Product (GDP) rose 4.8% y-o-y in 1Q18, the

highest in 5 years. This was boosted by all economic engines.

Private consumption grew 3.6% y-o-y, due to an expansion in

service items (+4.9%), non-durable (+2.0%) and semi-durable

items (+2.4%). Durable items expanded by 9.4%. Government

consumption increased 1.9% y-o-y. Gross fixed capital formation

rose 3.4% y-o-y. Private investment grew 3.1% due to an

expansion of both construction and machinery items. Public

investment increased 4.0% due mainly to the growth of

investment in machineries while construction dropped slightly.

For the external sector, exports/imports of goods and services

rose by 6.0% and 9.0% respectively. After seasonal adjustments,

the Thai economy expanded by 2.0% q-o-q in 1Q18.

Thailand’s quarterly GDP growth

Source: National Economic and Social Development Board, DBSVTH

Thailand’s GDP breakdown

Source: National Economic and Social Development Board, DBSVTH

Growth momentum continued in April and May 2018

Domestic demand continued to expand, led by private

consumption which increased in all spending categories. Farm

income showed strong improvement, supported by higher

agricultural production.

Private investment also showed encouraging signs. Public

spending expanded in both current and capital spending.

Private consumption index

Source: Bank of Thailand, DBSVTH

Thailand’s nominal farm income

Source: Bank of Thailand, Office of Agricultural Economics, DBSVTH

Export continued its robust performance, rising 12% and 11% y-

o-y in April and May 2018. Growth came mainly from all

markets except the Middle East. In terms of products, products

showing strong export growth in 5M18 included vehicles & parts

+20%, plastic pellets +20%, chemicals +27%, finished oil +37%,

rice +21%, tapioca products +20%, frozen and processed

chicken +14%, etc.

3.1

3.63.2

3.03.3

3.8

4.34.0

4.8

1.0 0.90.5 0.5

1.3 1.41.0

0.5

2.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18

%

GDP (yoy) GDP (q-o-q SA)

(% y-o-y) 4Q17 1Q18

GDP Growth 4.0 4.8

Private consumption 3.4 3.6

Private investment 2.4 3.1

Government consumption 0.2 1.9

Publ ic investment -6.0 4.0

Exports of goods & services 11.6 9.9

Imports of goods & services 14.6 16.3

Headl ine Inflation 0.9 0.6

0%

1%

2%

3%

4%

5%

6%

7%

8%

80

85

90

95

100

105

110

115

120

125

130

Jan-

16

Mar

-16

May

-16

Jul-

16

Sep

-16

No

v-16

Jan-

17

Mar

-17

May

-17

Jul-

17

Sep

-17

No

v-17

Jan-

18

Mar

-18

May

-18

Private Consumption Index YoY Growth (RHS)

-20%

-10%

0%

10%

20%

30%

40%

Jan

-16

Ma

r-16

Ma

y-1

6

Jul-

16

Sep

-16

No

v-1

6

Jan

-17

Ma

r-17

Ma

y-1

7

Jul-

17

Sep

-17

No

v-1

7

Jan

-18

Ma

r-18

Ma

y-1

8

Nominal farm income

Agricultural production

Agricultural price

Market Focus

External risks trump local positives

Page 12

Thailand’s monthly exports

Source: Ministry of Commerce, DBSVTH

Thailand’s export markets are quite diversified. The country does not rely too much on any single market. China and the US are both key export markets, representing 12.0% and 10.7% of the country’s total exports in 5M18.

Thailand’s monthly export by markets

Source: Ministry of Commerce, DBSVTH

Tourist arrivals continued to grow, albeit at a softer rate of 9.4% and 6.4% in Apr and May 2018, respectively. This was down from 15.4% growth in 1Q18. For 5M18, total tourist arrivals to Thailand were 16.5m people, up 12.6% y-o-y.

Thailand’s tourist arrivals

Source: BOT, DBSVTH

Thailand’s tourist arrivals by country of origin

Source: Ministry of Tourism and Sports, DBSVTH

Financial stability

Headline and core inflation increased slightly

Headline inflation accelerated to +1.49% y-o-y in May 2018,

from 1.07% in the previous month. This was due to increased

retail petroleum and liquefied petroleum gas (LPG) prices, as well

as accelerated core inflation +0.80% y-o-y.

For 5M18, headline inflation grew 0.89% y-o-y. Core inflation

(excluding raw food and energy) inched up 0.66% y-o-y, while

energy prices surged 4.28% and raw food eased 0.49%.

-15%

-10%

-5%

0%

5%

10%

15%

20%

10

12

14

16

18

20

22

24

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

US$bn

Exports (US$bn) YoY Growth (RHS)

Expo rt

M ay-18 5M 18 M ay-18 5M 18 M ay-18 5M 18

Total 22,257 104,032 11.4 11.6 100.0 100.0

1.Matured mk t 6,693 31,318 8.2 13.0 30.1 30.1

USA 2,435 11,126 3.9 7.9 10.9 10.7

Japan 2,229 10,430 11.6 20.3 10.0 10.0

EU 15 2,029 9,762 10.0 11.8 9.1 9.4

2.Dy namic mk t 11,462 53,082 13.7 11.1 51.6 51.0

ASEAN 9 5,934 27,059 14.8 13.1 26.7 26.0

ASEAN 5 3,394 15,580 12.9 11.2 15.2 15.0

CLMV 4 2,540 11,479 17.3 15.8 11.4 11.0

China 2,709 12,443 14.8 6.6 12.2 12.0

South Asia 8 996 4,786 24.8 24.7 4.6 4.6

India 725 3,306 31.2 31.0 3.3 3.2

3.Other mk ts 3,750 17,782 8.4 11.9 16.8 17.1

The Australia 25 1,271 5,529 20.9 15.9 5.7 5.3

Middle East 15 734 3,678 -14.1 2.0 3.3 3.5

Russia and CIS 102 557 7.7 32.5 0.5 0.5

Value (US$ m) Gro wth (% y-o -y) C o ntribut io n

Count ry % of

Total 4Q17 1Q18 A pr-18 May -18

China 27.7 67.2 30.2 31.9 14.0

Hong Kong 2.3 24.6 31.2 -5.9 25.7

Malaysia 9.5 -7.6 3.9 -4.4 -7.3

ASEAN exc. Malaysia 16.3 15.7 10.6 6.1 8.6

Asia exc China & Malaysia 29.6 17.5 11.7 5.7 9.2

Russia 3.8 21 26.6 18.5 -13.0

Europe exc. Russia 14.6 2.6 8.2 -6.1 3.6

Middle East 2.2 -5.6 -3.2 -17.8 -31.3

Total 100.0 19.5 15.4 9.4 6.4

% Change y -o-y

Market Focus

External risks trump local positives

Page 13

Headline and core inflation (y-o-y change)

Source: Ministry of Commerce, DBSVTH

Breakdown of headline inflation and growth

Source: Ministry of Commerce, DBSVTH

Unemployment rate remained low at 1.0%

Unemployment rate eased slightly to 1.0% in May 2018, due to

the falling employment rate in the service sector. Nonetheless,

employment rates in the agriculture, manufacturing and

construction sectors increased.

External stability remained strong and resilient

Thailand’s external stability remained strong and should be able

to withstand volatility in global financial markets.

External stability indicators

Source: BOT, DBSVTH

Thailand’s current account balance and as a % of GDP

Source: BOT, DBSVTH

Thailand’s international reserve

Source: BOT, DBSVTH

-1

-0.5

0

0.5

1

1.5

2

Jan

-16

Mar

-16

May

-16

Jul-

16

Sep

-16

Nov

-16

Jan

-17

Mar

-17

Ma

y-1

7

Jul-

17

Sep

-17

Nov

-17

Jan

-18

Ma

r-1

8

May

-18

%

Headline CPI Core CPI

Weight

% Apr-18 May-18 5M18

All commodities 100.0 1.07 1.49 0.89

Food & Non-alcohol beverages 36.1 0.68 0.74 0.31

Meat, poultry and fi sh 6.5 -0.42 -0.45 -1.18

Vegetable & frui ts 4.5 1.48 0.22 0.15

Prepared food - at home 8.7 1.24 1.37 1.25

Food away from home 8.5 0.95 1.31 0.99

Non Food & beverages 63.9 1.31 1.93 1.23

Hous ing & Furnishing 22.8 1.50 1.12 1.34

Transport & Communication 24.3 1.41 3.31 1.33

- Publ ic transportation 2.0 0.47 0.67 0.52

- Fuel 8.1 3.90 9.86 5.51

- Commu. & equipment 4.2 -0.05 -0.06 -0.04

Tobacco & a lcohol beverages 1.6 5.98 5.94 5.94

Core inflation * 72.5 0.64 0.80 0.66

Raw food & energy 27.5 2.27 3.36 1.53

Raw food 15.5 0.49 0.24 -0.49

Energy 12.1 4.69 7.68 4.28

* Inflation exc raw food & energy

Inflation (% Chg y-o-y)

2017 3Q17 4Q17 1Q18

Solve nc y ind ic a tors

Current account/GDP (%) 11.2 12.5 10.2 11.6

Debt/GDP (%) 35.3 35.5 35.3 35.4

Debt/Exports (%) 51.6 51.6 51.6 51.8

Debt service ratio (%) 5.7 8.1 4.5 6.3

Liqu id i ty ind ic a tors

Gross reserves/ST debt 3.2 3.3 3.2 3.4

Gross reserves/imports 9.8 10.0 9.8 10.0

ST debt/total debt (%) 42.1 40.9 42.1 41.2

-6

-4

-2

0

2

4

6

8

10

12

14

-20

-10

0

10

20

30

40

50

60

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

2016

r

2017

r

5M18

% of GDPUS$ bn

Current Account Balance (US$bn) As a % of GDP (RHS)

0

50

100

150

200

250

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

r

2017

r

5M18

US$ bn

Market Focus

External risks trump local positives

Page 14

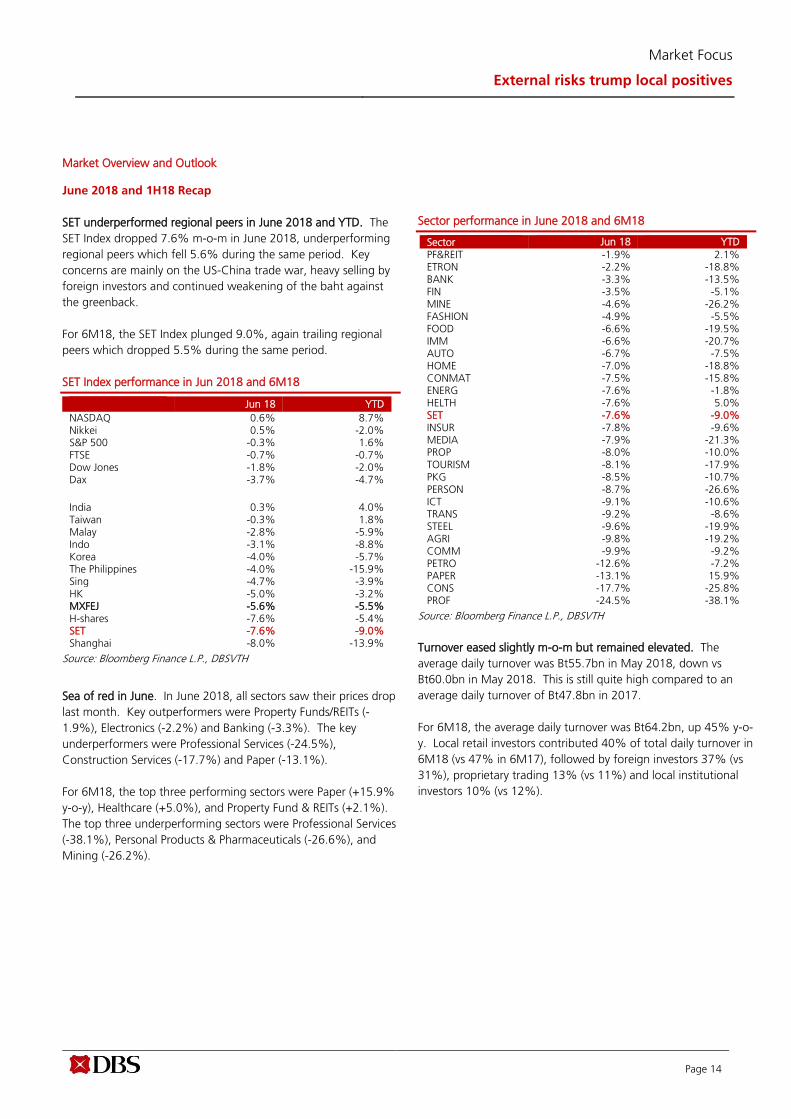

Market Overview and Outlook

June 2018 and 1H18 Recap

SET underperformed regional peers in June 2018 and YTD. The

SET Index dropped 7.6% m-o-m in June 2018, underperforming

regional peers which fell 5.6% during the same period. Key

concerns are mainly on the US-China trade war, heavy selling by

foreign investors and continued weakening of the baht against

the greenback.

For 6M18, the SET Index plunged 9.0%, again trailing regional

peers which dropped 5.5% during the same period.

SET Index performance in Jun 2018 and 6M18

Jun 18 YTD

NASDAQ 0.6% 8.7% Nikkei 0.5% -2.0% S&P 500 -0.3% 1.6% FTSE -0.7% -0.7% Dow Jones -1.8% -2.0% Dax -3.7% -4.7%

India 0.3% 4.0% Taiwan -0.3% 1.8% Malay -2.8% -5.9% Indo -3.1% -8.8% Korea -4.0% -5.7% The Philippines -4.0% -15.9% Sing -4.7% -3.9% HK -5.0% -3.2% MXFEJ -5.6% -5.5% H-shares -7.6% -5.4% SET -7.6% -9.0% Shanghai -8.0% -13.9%

Source: Bloomberg Finance L.P., DBSVTH

Sea of red in June. In June 2018, all sectors saw their prices drop

last month. Key outperformers were Property Funds/REITs (-

1.9%), Electronics (-2.2%) and Banking (-3.3%). The key

underperformers were Professional Services (-24.5%),

Construction Services (-17.7%) and Paper (-13.1%).

For 6M18, the top three performing sectors were Paper (+15.9%

y-o-y), Healthcare (+5.0%), and Property Fund & REITs (+2.1%).

The top three underperforming sectors were Professional Services

(-38.1%), Personal Products & Pharmaceuticals (-26.6%), and

Mining (-26.2%).

Sector performance in June 2018 and 6M18

Sector Jun 18 YTD

PF&REIT -1.9% 2.1% ETRON -2.2% -18.8% BANK -3.3% -13.5% FIN -3.5% -5.1% MINE -4.6% -26.2% FASHION -4.9% -5.5% FOOD -6.6% -19.5% IMM -6.6% -20.7% AUTO -6.7% -7.5% HOME -7.0% -18.8% CONMAT -7.5% -15.8% ENERG -7.6% -1.8% HELTH -7.6% 5.0% SET -7.6% -9.0% INSUR -7.8% -9.6% MEDIA -7.9% -21.3% PROP -8.0% -10.0% TOURISM -8.1% -17.9% PKG -8.5% -10.7% PERSON -8.7% -26.6% ICT -9.1% -10.6% TRANS -9.2% -8.6% STEEL -9.6% -19.9% AGRI -9.8% -19.2% COMM -9.9% -9.2% PETRO -12.6% -7.2% PAPER -13.1% 15.9% CONS -17.7% -25.8% PROF -24.5% -38.1%

Source: Bloomberg Finance L.P., DBSVTH

Turnover eased slightly m-o-m but remained elevated. The

average daily turnover was Bt55.7bn in May 2018, down vs

Bt60.0bn in May 2018. This is still quite high compared to an

average daily turnover of Bt47.8bn in 2017.

For 6M18, the average daily turnover was Bt64.2bn, up 45% y-o-

y. Local retail investors contributed 40% of total daily turnover in

6M18 (vs 47% in 6M17), followed by foreign investors 37% (vs

31%), proprietary trading 13% (vs 11%) and local institutional

investors 10% (vs 12%).

Market Focus

External risks trump local positives

Page 15

Foreign investors were heavy net sellers, with a heavy net sell

position of Bt48.7bn in June 2018. Local brokers’ proprietary

ports were also net sellers, with a net sell position of Bt14.3bn.

Local retail investors and local institutional investors were all net

buyers, with net buy positions of Bt40.8bn and Bt22.2bn

respectively.

For 6M18, foreign investors were heavy net sellers, with a net sell

position of Bt180.1bn. Local brokers’ proprietary ports were also

net sellers, with a net sell position of Bt11.2bn. Local retail

investors and local institutional investors were net buyers with

net buy positions of Bt114.3bn and Bt77.0bn respectively.

Foreign ownership (foreign + NVDR) in Thai stocks has dropped

steadily to 29% in June 2018, down from its peak of 35% in

2012. Most sectors saw declining foreign ownership over the

past few years, except for the Petrochemical sector which has

seen foreign ownership rise steadily to 53% in June 2018 from

about 40% at end 2012.

Foreign net buy/net sell position

Source: Bloomberg Finance L.P., DBSVTH

0

200

400

600

800

1000

1200

1400

1600

1800

2000

(250,000)

(200,000)

(150,000)

(100,000)

(50,000)

0

50,000

100,000

150,000

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Foreign Net Buy-Sell

SET Index (RHS)

Btm SET Index

Market Focus

External risks trump local positives

Page 16

Foreign ownership (%) in Thai stocks

Source: SET, DBSVTH

Foreign ownership (%) in Thai stocks by major sectors

Source: SET, DBSVTH

27

.07

2

6.9

1

26

.82

2

7.2

5

26

.93

2

6.6

7

27

.05

2

6.2

3

26

.15

2

6.7

6

26

.76

2

7.1

6

28

.02

27.5

4

28

.20

27.4

6

27

.00

26.6

8

27

.10

29.2

8

28

.91

29.0

2

28

.10

27.7

9

27

.18

26.9

6

26

.73

2

7.3

3

27

.53

2

7.0

4

27

.68

2

7.1

8

27

.47

2

8.5

3

28

.33

2

8.0

9

28

.08

2

8.2

5

29

.06

2

8.6

6

28

.36

2

7.7

1

26

.74

2

6.9

1

26

.55

2

5.5

5

25

.47

2

5.7

0

25.3

5

24

.97

25.1

0

25

.05

24.9

0

24

.75

24.6

4

24

.65

24.2

9

24

.40

24.6

0

24

.28

24.3

6

24

.17

2

4.1

9

24

.06

2

3.8

2

23

.77

2

3.1

4

22

.60

2

3.1

2

23

.42

2

2.8

2

22

.61

2

2.4

4

22

.47

2

2.6

7

22

.56

2

2.2

6

22

.40

2

2.2

2

22

.22

2

2.1

7

22

.42

2

2.4

5

22.4

6

22

.65

22.7

5

22

.94

22.8

1

22

.96

22.8

8

22

.78

22.8

5

22

.87

22.6

7

22

.62

2

2.3

8

22

.01

2

1.8

2

29

.93

0.2

30

.4 30

.83

0.6

30

.13

0.2

29

.22

9.4

30

.5 30

.93

1.1

32

.031.7

33

.031.8

31

.931.6 32

.134.9

34

.534.4

33

.933.1

31

.830.9

30

.63

2.1 3

2.9

32

.73

3.7

32

.63

3.5

34

.73

4.5

33

.93

3.8

34

.13

5.6

35

.53

5.3

34

.73

4.1

34

.23

3.8

32

.13

2.0

32

.231.8

31

.431.7

31

.631.4

31

.231.2

31

.130.5

30

.630.8

30

.530.6

30

.33

0.3

30

.12

9.8

29

.82

9.2

28

.3 28

.9 29

.32

8.9

28

.72

8.5

28

.5 29

.02

9.0

28

.72

8.7

28

.42

8.4

28

.6 29

.02

8.9

29.0

29

.129.3

29

.529.5 29

.829.8

29

.829.8

29

.829.7

29

.62

9.4

28

.92

8.7

20.0

22.0

24.0

26.0

28.0

30.0

32.0

34.0

36.0

38.0

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

Mar-

14

4-J

un

Jul-14

Sep-1

4

Nov-

14

Jan-1

5

Mar-

15

May-

15

Jul-15

Sep-1

5

Nov-

15

Jan-1

6

Mar-

16

May-

16

Jul-16

Sep-1

6

Nov-

16

Jan-1

7

Mar-

17

May-

17

Jul-17

Sep-1

7

Nov-

17

Jan-1

8

Mar-

18

May-

18

Foreign Holding Foreign Holding+NVDR

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

60.0

1Q02

4Q02

3Q03

2Q04

1Q05

4Q05

3Q06

2Q07

1Q08

4Q08

3Q09

2Q10

1Q11

4Q11

3Q12

2Q13

Mar

-14

Jun-

14Se

p-14

Dec-

14M

ar-1

5Ju

n-15

Sep-

15De

c-15

Mar

-16

Jun-

16Se

p-16

Dec-

16M

ar-1

7Ju

n-17

Sep-

17De

c-17

Mar

-18

Jun-

18Bank Conmat Energy Food ICT Petro Property Steel

Market Focus

External risks trump local positives

Page 17

Foreign investors were net sellers in most regional markets YTD.

In the table below, we can see that foreign investors were net

sellers in most major markets YTD. The net sell positions were

higher in Japan, Taiwan, Thailand and Indonesia.

Regional: Foreign net buy (sell) positions

US$m India Indonesia Japan Malaysia Philippines S. Korea Taiwan Thailand

2005 10,901 (1,737) 113,338 354 (3,549) 23,990 2,947

2006 8,338 1,996 68,885 720 (12,659) 16,962 2,135

2007 18,518 3,141 32,759 1,354 (29,095) 477 1,853

2008 (12,918) 1,801 (66,817) (1,135) (36,742) (16,364) (4,942)

2009 17,639 1,384 (6,513) 420 24,446 15,617 1,137

2010 29,321 2,345 22,926 1,232 19,657 9,577 2,687

2011 (396) 2,853 (1,069) 1,329 (8,584) (9,076) (167)

2012 24,548 1,703 27,733 2,548 15,069 4,907 2,504

2013 19,986 (1,804) 149,920 678 4,855 9,178 (6,211)

2014 16,162 3,766 22,545 (1,849) 1,287 5,967 13,551 (974)

2015 3,274 (1,580) 3,485 (4,989) (1,194) (3,626) 3,322 (4,372)

2016 2,903 1,259 (38,067) (573) 83 10,480 10,956 2,240

2017 10,095 (2,828) 9,384 2,456 1,140 10,234 8,969 (973)

2018 YTD (875) (3,570) (37,776) (1,772) (1,219) (3,702) (8,919) (5,642)

Jan-17 (6) (73) 587 98 6 1,246 1,456 178

Feb-17 1,564 (60) (4,110) 219 (103) 389 1,617 (107)

Mar-17 5,141 759 (14,439) 998 (251) 3,131 2,509 113

Apr-17 (345) 1,050 13,627 597 198 952 1,158 52

May-17 1,542 (48) 6,352 468 173 1,635 1,565 161

Jun-17 610 (325) 274 88 386 1,659 720 (5)

Jul-17 389 (798) 4,237 99 38 (381) 22 (200)

Aug-17 (1,732) (468) (8,110) (48) 50 (1,415) (299) (125)

Sep-17 (1,656) (844) (15,478) (171) 570 (981) (1,910) 211

Oct-17 296 (459) 30,660 (50) 2 2,713 1,724 (220)

Nov-17 2,952 (1,376) (2,797) (6) (28) 418 (1,351) (581)

Dec-17 (739) (319) (7,092) 235 55 (1,097) (1,095) (274)

Jan-18 2,080 132 5,674 868 45 1,967 2,856 (177)

Feb-18 (1,931) (760) (4,401) (277) (296) (2,598) (3,480) (1,310)

Mar-18 2,018 (1,085) (37,497) (18) (371) (449) (2,060) (352)

Apr-18 (943) (750) 10,447 389 (171) (1,213) (2,873) (684)

May-18 (1,427) (460) (1,427) (1,414) (174) (262) (1,064) (1,620)

Jun-18 (630) (647) (10,572) (1,296) (253) (1,148) (2,638) (1,499)

1Q17 6,699 626 (17,962) 1,315 (349) 4,766 5,581 185

2Q17 1,808 678 20,253 1,154 757 4,245 3,442 208

3Q17 (3,000) (2,110) (19,352) (120) 658 (2,777) (2,187) (113)

4Q17 4,588 (2,021) 26,444 1,048 74 4,000 2,133 (1,253)

1Q18 2,167 (1,713) (36,225) 573 (621) (1,080) (2,684) (1,838)

QTD (3,000) (1,857) (1,552) (2,322) (598) (2,622) (6,555) (3,803)

As of 29 Jun 2018

Source: Bloomberg Finance L.P., DBSVTH

Market Focus

External risks trump local positives

Page 18

Strategy

Our regional strategist rates Thailand as Neutral. DBS’ regional

equity strategist believes Asia markets are all likely to be

adversely affected by concerns over peaking growth and strong

US dollar, as well as rising domestic inflation and interest rates.

We rate HK/China and Singapore (relatively safe haven plays) as

Overweight, and India and Taiwan - whose relative resilience so

far poses downside risks and limits rebound upside – as

Underweight. We are Neutral on the rest of the market

including the Philippines, Indonesia, Thailand, and Korea.

DBS Bank’s 3Q18 Asia market recommendations

Source: DBS Bank

Increased volatility in global financial markets could cap near-

term upside. After tumbling over 200 points from its recent

peak in February, the Thai stock market is now trading on 2018

PE of 14.6x, which is in line with its historical average. While the

domestic economy is now on an upward momentum, key risks

remain on; (i) continued selling by foreign investors; (ii) the

weakening of the Thai baht against the greenback; (iii) the

length and depth of the US-China trade tension and its potential

impact on global growth and; (iv) potential election delays.

Corporate earnings to grow 10% in 2018. This represents an

improvement from 6% growth in 2017. Sectors that should

report strong earnings growth in 2018 are Paper, Finance,

Transportation, Tourism, Media, Commerce, and Property

Fund/REIT.

Valuation. The market is now trading at 2018 PE of 14.6x. Our

target SET Index is now 1860, based on 17x PE (+1.0x SD of

historical average).

Accumulate on dips. We recommend investors to accumulate

stocks with solid fundamentals, reasonable valuation, and

decent yields. We still like the Commerce and Tourism, as well

as the Property sectors.

Downgrading Contractor to Neutral. Our hope for more

bidding activities for infrastructure projects in 2H18 has now

faded. It is estimated that the new Financial and Fiscal Discipline

Act 2018, which has been enforced since 19 April 2018, could

result in further delays for these infrastructure projects. Note

that these projects will need to be vetted and approved by the

Monetary and Fiscal Policy Committee.

Among the projects that could see further delays include the 9

routes of dual-track railways phase II worth Bt427bn; the

Orange Line mass transit worth Bt120bn; Purple Line Southern

Part valued at Bt101bn; Nakhon Pathom – Cha Am motorway

worth Bt80.6bn; Bangkok-Wang Manao motorway worth

Bt15bn; Rangsit-Bangpain tollway extension worth Bt30.5bn;

Boromrajchonnanee-Bhuddamonthon Sai 4 extension valued at

Bt7bn; and the motorway toll collection system worth Bt60bn.

Upgrading Property Fund/REIT sector to Overweight. We are

upgrading the Property Fund/REIT sector to Overweight from

Neutral. We believe the sector should offer a safe bet amidst

high market volatility, thanks to its strong recurring income

bases and minimum 90% dividend payout, both of which

should ensure a steady distribution to unitholders. The sector is

now offering a decent distribution yield of 6.3%, which is still

quite attractive compared with the current 10-year Thai

government bond yield of 2.79%.

Key themes and top picks for 2H18. We have five themes for the

market in 2H18: (i) Recovering domestic consumption and

elections (AEONTS, CPALL). (ii) EEC theme (AMATA, BBL, STEC),

(iii) Resilient earnings (ADVANC). (iv) High growth with

reasonable valuation (IVL, CPN). (v) Generous yields (DIF, LH).

SET PE Band

Source: Bloomberg Finance L.P., DBSVTH

Ov erweight Neut ral Underweight

China/Hong Kong The Philippines Taiwan

Singapore Indonesia India

Malaysia Thailand

Korea

China 'A'

4

6

8

10

12

14

16

18

20

22

24

0 08 0 10 11 12 13 1 15 1 1 18

PE (x)

-2 sd

-1 sd

Mean

+1 sd

+2 sd

Market Focus

External risks trump local positives

Page 19

Corporate earnings

Net profit Growth (%) PE (x) YE Dec (Btm) FY18F FY19F FY18F FY19F

Banking 4% 4% 10.4 10.1

Finance 12% 25% 15.9 12.7

Con. Mat. 3% 7% 8.7 8.2

Chemicals 4% 9% 9.8 9.0

Automotive 11% 9% 8.5 7.9

Contractors 117% 8% 23.0 21.3

Paper & Printing Materials 85% 11% 11.8 10.7

Property 9% 10% 12.6 11.5

- Commercial -8% 13% 25.1 22.1

- Residential 16% 8% 9.0 8.3

- Industrial -1% 15% 11.2 9.7

Property Fund 15% 20% 13.2 12.4

Energy 14% 4% 6.4 6.1

Media 0% 8% 18.4 17.0

Commerce 16% 16% 29.0 25.1

Transport 53% 10% 31.9 29.1

Tourism 17% 20% 25.3 21.0

Telecom 13% 16% 17.5 15.0

Electronics -4% 25% 14.7 11.8

Food -13% 10% 18.6 16.8

Health Care Services -1% 14% 36.2 31.8

Total 10% 8% 14.6 13.5

Source: Bloomberg Finance L.P., DBSVTH

Regional Comparison EPS Gth (%) PE (x)

18F 19F 18F 19F

Singapore 15.8 8.2 13.9 12.8

HK HSI 15.4 10.5 11.5 10.4

HK HSCCI (Red) 39.6 13.8 10.3 9.1

HK HSCEI (H) 13.2 10.3 7.6 6.9

CSI300 22.2 15.2 11.8 10.3

SH Comp 27.9 13.5 11.4 10.0

SZ Comp 54.6 22.3 17.7 14.5

Malaysia (0.7) 7.1 16.1 15.0

Thailand 9.6 8.0 14.6 13.5

Indonesia 20.2 10.9 16.0 14.2

Simple Average 21.8 12.0 13.1 11.7

Source: Bloomberg Finance L.P., DBSVTH

SET: Our sector weightings

Source: DBSVTH

Se c tor Re a son Top buys

Ove rwe ight

Commerce Recovering consumption CPALL, HMPRO

Property

- Residential Attractive valuation, with high yield ANAN, LH, ORI

- Commercial Still positive outlook for office and retail properties CPN

PFPOs/REITs Offering stable yields LHHOTEL, QHHR

Tourism Beneficiary of the strong tourism industry AOT, CENTEL

Ne utra l

Bank Beneficiary of recovering economy BBL

Building Materials Supported by high value-added and innovative products SCC

Contractor Beneficiary of rising government infrastructure spending CK, STEC

Electronics Strong baht is hurting margins KCE

Energy Market has factored in oil price recovery assumption PTT

Finance Rising competition and regulatory risks AEONTS

Healthcare Weak earnings outlook and too rich valuation RJH

Industrial Estate Improving outlook supported by EEC AMATA, WHA

Petrochemicals Prefer IVL for volume expansion and improving PET spread IVL

Telecom Improving outlook on easing competition ADVANC, DIF

Transportation A beneficiary of strong tourism industry AAV, BEM

Unde rwe ight

Media Beneficiary of recovering economy, but competition to remain intense VGI

Foods Prolonged challenging environment at both CPF and TU TKN

Market Focus

External risks trump local positives

Page 20

Sector Update

Our Sector View Chart/Table Sector: Commerce Overweight

Top BUY: CP ALL (CPALL; BUY; Bt95.00 TP) Least preferred stock: n.a.

Overall, we don’t expect same-store sales growth (SSSG) to

rebound significantly but should at least improve for most of

the retailers this year. However, this should be driven mostly by

Bangkok, big provinces, and tourist cities which have higher

purchasing power as domestic consumption is still not broad-

based. Many upcountry retailers’ SSSG are still in negative

territory, albeit at a lesser magnitude. On top of a pick-up in

sales revenue growth this year, operating margins should also

improve and drive earnings growth of the retailers under our

coverage to stay at double-digits in FY18F.

We maintain CPALL as one of our favourites as it has been the

market leader in the Convenient Store sector and miles ahead

of its competitors. With its strong product strategy and new

products, we expect CPALL to continue delivering healthy

CAGR of 17% in the next three years. We also like HMPRO,

based on several positive catalysts; i) improving SSSG; ii)

increasing operational efficiency; iii) its ability to anticipate and

adjust to lifestyle changes and; iv) healthy FY18F profit growth

of 16%.

Thailand: Consumer Confidence Index (CCI)

Source: UTCC, DBSVTH

Sector: Tourism Overweight

Top BUYs: The Erawan Group (ERW, BUY, Bt7.70 TP), Asia Aviation (AAV; BUY; Bt7.05 TP )

Least preferred stock: -

The Tourism Authority of Thailand is targeting international

tourist arrivals to reach 37m in 2018 (+4.5% y-o-y). In 4M18,

international tourist arrivals grew 14% y-o-y to 13.7m, driven

by growth of Chinese arrivals that turned positive since May

2017. However, we believe the growth momentum of

international arrivals into Thailand may weaken from May 2018

onwards.

Despite an impressive 1Q18 result, we expect 2Q18 earnings to

drop q-o-q given due to low seasonality, as well as high costs

from the rise in oil price during the period. However,

performance in 2H18 should improve on seasonal factors and

expected lower oil price. On a yearly basis, we believe the sector

will continue growing driven by an increase in number of tourist

arrivals as well as an improving yield due to less domestic

competition.

We like i) CENTEL as it will be beneficiary from strong tourism in Thailand and recovering tourism overseas, and ii) AAV, whose earnings are expected to remain solid, driven by strong tourism growth and efficient cost management.

Thailand: International tourist arrivals

Source: BOT, DBSVTH

40

50

60

70

80

90

100

110

120

2001

2002

2003

200

2005

200

200

2008

200

2010

2011

2012

2013

201

2015

201

201

CCI of Overall economy

CCI of future employment

CCI of future income

600

1,000

1,400

1,800

2,200

2,600

3,000

3,400

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

'000 People

2010 2011 2012 2013 2014

2015 2016 2017 2018

Market Focus

External risks trump local positives

Page 21

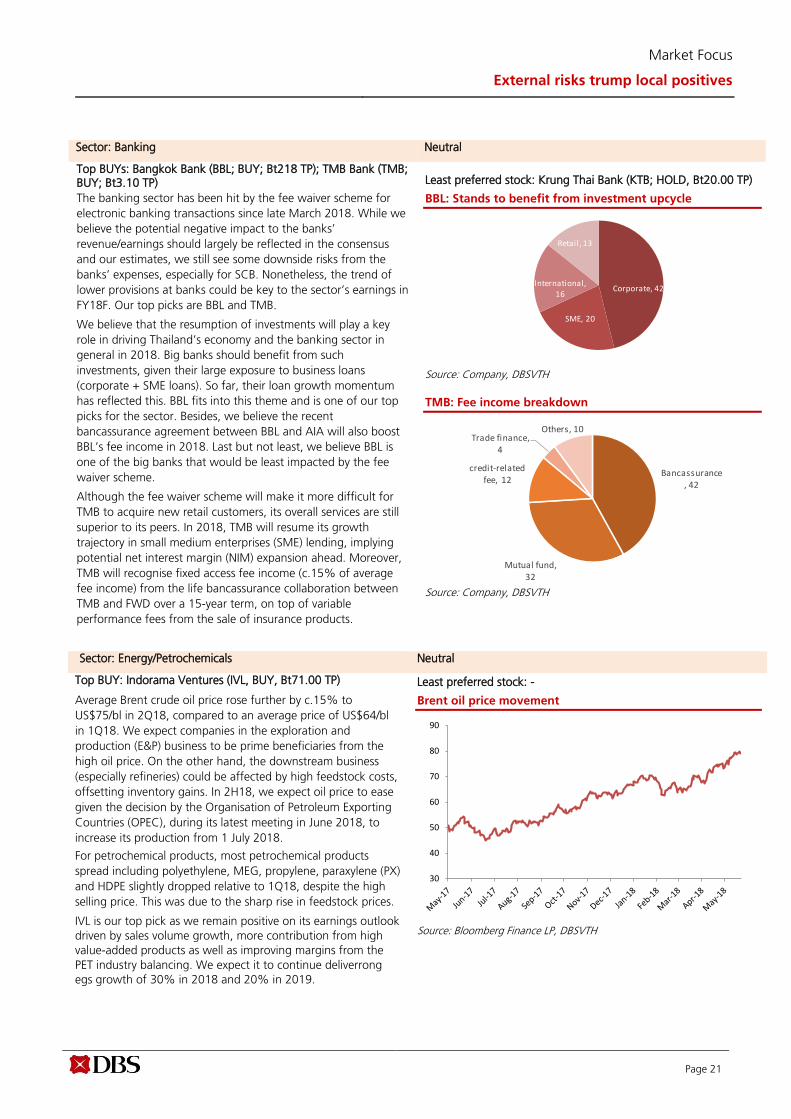

Sector: Banking Neutral

Top BUYs: Bangkok Bank (BBL; BUY; Bt218 TP); TMB Bank (TMB; BUY; Bt3.10 TP) Least preferred stock: Krung Thai Bank (KTB; HOLD, Bt20.00 TP)

The banking sector has been hit by the fee waiver scheme for

electronic banking transactions since late March 2018. While we

believe the potential negative impact to the banks’

revenue/earnings should largely be reflected in the consensus

and our estimates, we still see some downside risks from the

banks’ expenses, especially for SCB. Nonetheless, the trend of

lower provisions at banks could be key to the sector’s earnings in

FY18F. Our top picks are BBL and TMB.

We believe that the resumption of investments will play a key

role in driving Thailand’s economy and the banking sector in

general in 2018. Big banks should benefit from such

investments, given their large exposure to business loans

(corporate + SME loans). So far, their loan growth momentum

has reflected this. BBL fits into this theme and is one of our top

picks for the sector. Besides, we believe the recent

bancassurance agreement between BBL and AIA will also boost

BBL’s fee income in 2018. Last but not least, we believe BBL is

one of the big banks that would be least impacted by the fee

waiver scheme.

Although the fee waiver scheme will make it more difficult for

TMB to acquire new retail customers, its overall services are still

superior to its peers. In 2018, TMB will resume its growth

trajectory in small medium enterprises (SME) lending, implying

potential net interest margin (NIM) expansion ahead. Moreover,

TMB will recognise fixed access fee income (c.15% of average

fee income) from the life bancassurance collaboration between

TMB and FWD over a 15-year term, on top of variable

performance fees from the sale of insurance products.

BBL: Stands to benefit from investment upcycle

Source: Company, DBSVTH

TMB: Fee income breakdown

Source: Company, DBSVTH

Sector: Energy/Petrochemicals Neutral

Top BUY: Indorama Ventures (IVL, BUY, Bt71.00 TP) Least preferred stock: -

Average Brent crude oil price rose further by c.15% to

US$75/bl in 2Q18, compared to an average price of US$64/bl

in 1Q18. We expect companies in the exploration and

production (E&P) business to be prime beneficiaries from the

high oil price. On the other hand, the downstream business

(especially refineries) could be affected by high feedstock costs,

offsetting inventory gains. In 2H18, we expect oil price to ease

given the decision by the Organisation of Petroleum Exporting

Countries (OPEC), during its latest meeting in June 2018, to

increase its production from 1 July 2018.

For petrochemical products, most petrochemical products

spread including polyethylene, MEG, propylene, paraxylene (PX)

and HDPE slightly dropped relative to 1Q18, despite the high

selling price. This was due to the sharp rise in feedstock prices.

IVL is our top pick as we remain positive on its earnings outlook

driven by sales volume growth, more contribution from high

value-added products as well as improving margins from the

PET industry balancing. We expect it to continue deliverrong

egs growth of 30% in 2018 and 20% in 2019.

Brent oil price movement

Source: Bloomberg Finance LP, DBSVTH

Corporate, 42

SME, 20

International, 16

Retail , 13

Bancassurance , 42

Mutual fund, 32

credit-related fee, 12

Trade finance, 4

Others, 10

30

40

50

60

70

80

90

Market Focus

External risks trump local positives

Page 22

Sector: Contractor Neutral

Top BUY: CK, STEC Least preferred stock: -

Our hope for more bidding activities for infrastructure projects

worth Bt780bn to take place in 2H18 has now faded. It is

estimated that the new Financial and Fiscal Discipline Act

2018, which has been enforced since 19 April 2018, could

result in further delays for these infrastructure projects. Note

that these projects will need to be vetted and approved by the

Monetary and Fiscal Policy Committee. We are therefore

downgrading our rating on the sector to Neutral.

The first infrastructure project up for bidding this year should

be the high-speed Railway link 3 international airports, a

Bt237bn public-private-partnership. The project’s Term Of

References (TORs) has been released and we expect the

winning bidder(s) to be announced by 4Q18F.

Other projects to follow suit are the Rama III – Dao Kanong

Expressway valued at Bt31bn, the MRT Purple Line worth

Bt100bn, and the Bt261bn dual-track railway projects (phase II)

in seven routes (from Chira Junction to Nong Khai). Other

projects may be delayed until next year.

Our top picks for the sector are Ch. Karnchang (CK) and Sino-

Thai Engineering and Construction (STEC). Both should stand

to benefit from these planned biddings in 2H18.

Contractor Sector: Projects up for bidding in 2H18F

Projects Project

Value (Btm) Bidding schedule

Rama III - Dao Kanong Expressway 31

To be bidded in

2H18

Fast track: Motorway: Bang Pa In - Nakhon Ratchasima (Construction Part) 7

Fast track: Motorway: Bang Yai - Kanchanaburi (Construction Part) 6

EEC Track: High-Speed Railway link 3 International Airports 237

TORs announced

Fast Track: MRT Purple line (Tao Poon - Ratburana) 101

To be bidded in

2H18

Double Track : Chira Junction - Ubon Ratchathani 36

Double Track : Den Chai - Chiang Mai 60

Double Track : Chumphon - Surat Thani 23

Double Track : Surat Thani - Hat Yai - Songkla 52

Double Track : Hat Yai - Padang Besar 8

Double Track : Paknam Po - Den Chai 56