professor_mark_blyth__lisbon_december_2013_final (1).pdf

TRANSCRIPT

Austerity: The

History of a

Dangerous Idea

“Does Austerity Kill? Does Austerity Cure?”

IDEFF - Law School of Lisbon University

November 29th 2013

Mark Blyth, Brown University and the Watson Institute for International Studies, USA

So What is Austerity Anyway?

• Austerity is not cutting when you grow. Cutting when you grow is commonly known as ‘sensible economic policy.’

“The Boom, not the slump, is the time for Austerity”

J.M. Keynes, 1933

• Austerity is cutting in a slump, which is turbocharged when everyone does it at the same time and they are all each others trading partners

• ”It is an undisputable fact that excessive state spending has led to unsustainable levels of debt and deficits that now threaten our economic welfare. Piling on more debt now will stunt rather than stimulate growth in the long run. Governments in and beyond the Eurozone need not just to commit to fiscal consolidation and improved competitiveness – they need to start delivering on these now.”

• W. Schauble, 2010

•

So we have to cut the debt – right?

But why then have the countries that have cut spending the most increased their debts the most?

• Greek Debt to GDP • Greek Public Spending

The same is true whether big or small

• Spain’s debt goes down then up • While Spain’s spending goes up then down

The Irish Tiger?

• Ireland looks like Spain • Only its worse

Even the “Poster Child” quadrupled their debt as they cut

• Latvia’s Debt to GDP • And what paid for it

What About Germany?

German debt to GDP

German public spending?

And Portugal?

Portuguese Debt to GDP

Portuguese Debt to GDP

SO WHAT CAUSED THIS?

Two Stories: ECB ‘Credibility’ or ‘the Greatest Moral Hazard Trade in Human History?’

You can’t have Over-Borrowing without Over-Lending

Assets held by banks in Germany, France, and the UK are about double the annual GDP of the entire EU

0

5000000

10000000

15000000

20000000

25000000

30000000

35000000

40000000

45000000

50000000

GDP Bank Assets

Other

UK

Germany

France

• Gross contribution to GDP and Bank Assets in the EU (millions of EUR)

If that goes bad, its game over for the Euro and the core banks

For Comparison – The “too Big to Fail” USA

Bank Assets (millions of USD) Bank Assets (% of GDP)

0

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

12.000.000

14.000.000

16.000.000

18.000.000

20.000.000

Bank Assets GDP

GDP

Other

Wells Fargo

Citigroup

Bank of America

Morgan Stanley

JP Morgan

Goldman

0

20

40

60

80

100

120

140

GDP Top 6 Bank Assets Total Bank Assets

France is the exemplar of the ‘too Big to BAIL’ problem

Bank Assets (millions of EUR) Bank Assets (% of GDP)

0

50

100

150

200

250

300

350

400

450

500

GDP Top 3 Bank Assets Total Bank Assets

0,00

1.000.000,00

2.000.000,00

3.000.000,00

4.000.000,00

5.000.000,00

6.000.000,00

7.000.000,00

8.000.000,00

9.000.000,00

10.000.000,00

Bank Assets GDP

GDP

Other

Societe Generale

Credit Agricole

BNP Paribas

Which is why this is not really a government debt crisis…

…but it is why we have Austerity policies…

Keeping the periphery in at all costs

• Its all about stopping the Bank run round the bond market…

But…

You Can’t Solve a Banking

Problem with Budget Cuts

You Can’t run a Gold Standard in a Democracy (in Theory…)

You can’t all cut at once and expect to grow without increasing your debt

Because you can ‘kick the can down the road’ with unlimited liquidity to keep the banks afloat

• Thanks Mr. Draghi!

• December 2011: Long Term Refinancing Operation (LTRO) (1 trillion Euro)

• March 2012: LTRO 2 (0.529 T Euro)

• June 2012: Emergency Liquidity Assistance (0.4 Euro)

• July 26th 2012: Draghi says he will do “whatever it takes…”

• Italian Ten Year Bond Yields June 2011 – May 2013

So government debts were going down going into the crisis – they went up (massively) during the crisis despite austerity -

and yet yields went down…despite the debt going up!

• And all at a sadly predictable cost…

So why did anyone, especially in Europe, ever

think that Austerity was a good idea?

Liberalism’s Reluctant Embrace of the State

• John Locke’s fifth chapter

• Markets as inequality generators

• States as Policemen

• Don’t trust the state since it will rob you blind

• But you need it to create the markets you want

The Fear of Debt: “Public Credit will Destroy the Nation”

• David Hume

• Money and Merchants

• The Ease of Debt Issuance

• Crowding Out and Easy Money

• Adam Smith

• Parsimony, Inequality and the Necessity of the State

• Taxation?

• Debt perverts parsimony

The Result: The “can’t live with/without it and don’t want to pay for it” problem

Liberalism’s Neuralgia with Debt and the Aspirin of Austerity

This creates two Liberal Stories through 19th Century Economics

• Story One: Can’t live with it and don’t want to pay for it

• Story Two: Accepting the need for it and to pay for it

And then came the Great Depression

Austerity American Style: Liquidationism

• Modern Business Cycle Theory

• Long Run Capital Structure (too much and wrong type)

• Misallocation of capital

• Austerity via Binge and Purge

British Austerity: The Treasury View

• Laissez Faire and crowding out

• Public Spending, Investment, and Taxes

• Lack of Suitable Public Works

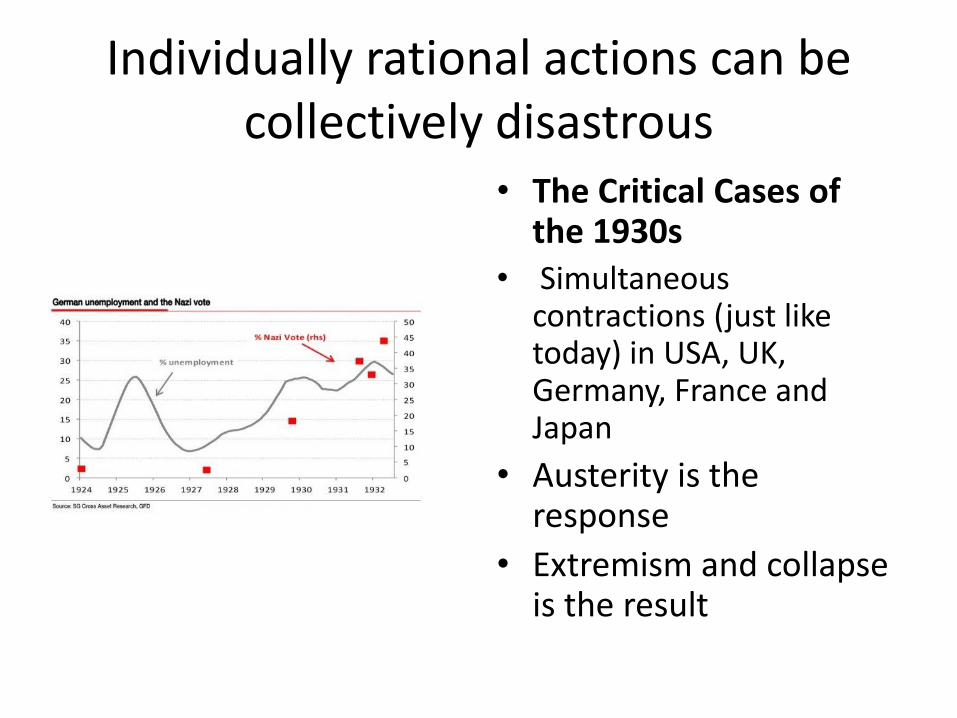

Individually rational actions can be collectively disastrous

• The Critical Cases of the 1930s

• Simultaneous contractions (just like today) in USA, UK, Germany, France and Japan

• Austerity is the response

• Extremism and collapse is the result

SO WHERE DO BAD IDEAS HIBERNATE?

An ‘Ordoliberal’ Home for Austerity

• Late Development and Export Led Growth

• Freiburg and the State

• The economic constitution

• Competition not consumption

• Sound Money and CBI

• Result: Exports Yes, Keynes No.

Generalizing Ordoliberalism

• The Euro as Generalized Ordoliberalism

• Commission > Parliament

• Sound Money > Output considerations

• Rules > Discretion

• Competitiveness > Consumption

• Result: Let’s all be more Competitive

And then came the current crisis, which was not (only) made in America

• Thanks Mr. Trichet!

• “... the idea is to revive the market [for covered bonds], which has been very heavily affected, and all that goes with this revival, including the spreads, the depth and the liquidity of the market. We are not at all embarking on quantitative easing." [italics added] (ECB: May 7th 2009)

The New Bad Old Idea: The Expansionary Austerity Hypothesis

• Credibility and cutting the state

• Spending and future taxes

• The New Cases: Ireland, Sweden, Canada, Denmark, Australia

Is written right into the ECB’s Crisis Response

• Alesina’s Ecofin Brief

• ECB June 2010 Report

• Troika conditionality

• Structure of periphery bailouts (cuts not taxes)

• Result: The Greatest Bait and Switch in Human History

But Reality Bites?

• IMF challenges to EFA hypothesis

• October 2012 IMF WEO and 1.5-1.7 negative multipliers

• 0.3 percent growth Q3 2013 based on NOT doing austerity

• More debt not less

• Emigration of future tax bases

• 12-25-50 percent unemployment in Europe

• 0.1 percent Growth last quarter…

SOME CONCLUSIONS AND CONJECTURES

Where does this all end?

• More of the Same? Problem of different preferences and ideas (Merkel, ECB, EC, IMF)

• Turning Japanese? Perma-Austerity and Perma-low growth?

• Or Worse? If the North runs a Perma-surplus and no corresponding deficit is allowed, the result must be unemployment and bankruptcy

• Gray Swans? Political Unrest? Interest rate spike from global recovery?

• Black Swans? Italy leaves?