mckinsey telecoms. recall no. 08, 2009 - high growth

TRANSCRIPT

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 1/64

Telecommunications

Networks

RECALL No8

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 2/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 3/64

3RECALL No 8 – Networks

Welcome ...… to the 8th issue of Recall, a publication for leaders

in the telecommunications industry. Within the overall

operations and technology (O&T) arena, this issue

focuses on networks and extends the McKinsey publication

series on marketing and sales themes, launchedsuccessfully last year.

There is a strong, growing management interest in

O&T topics in the telecommunications industry. Besides

the challenges of stagnating growth and declining

margins in many parts of the world, it has been undergoing

major technological changes – some marking progress

while others have been disruptive.

New entrants and alternative, innovative business

models present ongoing hurdles to established structures.

This has led to a greater focus on management’s part

in delivering services not only efficiently and effectively

but also with maximum service quality in mind – thus

seeking competitive advantages from operations

and technology. Successful operations in this environment

require close senior management involvement in

identifying opportunities and options, to devise optimal

solutions, and to drive mindset changes across the

whole organization.

This publication aims at providing a comprehensive view

of priority operations and technology issues, covering

the range from new network technologies to IT and from

service operations to procurement, discussing bothinnovative technical solutions as well as challenges arising

from operational transformations. In this series,

we’ll “recall” how successful companies manage their

operations and technology base but also offer our

emerging perspect ives and outlooks for the future.

Networks are the backbone of the industry, as they are

one of the main cost elements of telecommunications

operations. Networks are also the primary arena for

ongoing technology innovations.

We begin this issue with an introduction to network

operations and technologies, exploring the ways to

do more with networks – with less money. In the next

article, we discuss the value of fiber networks and follow

that with a look at the challenges of consolidating and

offshoring certain functions within network operations.

An overview of network outsourcing is next on the agenda

and leads to a discussion of wireless business models ,

a look at the exciting new technologies of femtocells and

4G, and the case for alternate spectrum use. We round

out this issue with an interview with Mads Middelboe.

We were very excited to sit down with the CEO of

TDC Mobile and get a firsthand account of operations and

technology issues in telecommunications.

Over the past several years, McKinsey’s Global

Telecommunications Practice – a group of more than

380 dedicated practitioners and over 60 research

analysts – has built extensive capabilities in telecoms

operations and technology. Through our global

practitioner base, we now bring these capabilities to the

service of our clients. The authors of Recall are all

members of this practice, and each of us hopes that you

find this series useful and that it provides insights that

trigger ideas or discussions around the challenges andopportunities you face.

We look forward to your feedback on the articles in this

issue and to your thoughts on topics you would like to

see covered in future issues.

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 4/64

Jürgen Meffert

EMEA Leader of McKinsey’s

Telecommunications Practice

Fabian Blank

Leader of the EMEA Mobile Operations

Service Line and Editor of this RECALL issue

Tomas Calleja

Co-leader of McKinsey’s Operations

and Technology in Telecommunications

Practice

Klemens Hjartar

Co-leader of McKinsey’s Operations

and Technology in Telecommunications

Practice

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 5/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 6/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 7/64

7

Contents01 Introduction to Network Operations and Technologies 9

02 High Fiber Diet: The Value of Next-Generation Access Networks 15

03 Over the Seas of Complexity: Consolidating Mobile Network Functions Offshore 21

04 Off loading the Core: Exploring Network Outsourcing 27

05 Mobile Networks of the Future 35

Building a Sustainable Wireless Carrier Business Model 35

The Value of Femtocells 41

The Rocky Road to 4G 45

The Alternate Spectrum Opportunity 49

06 The Power of Letting Go 53

Appendix

RECALL No 8 – Networks

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 8/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 9/64

9RECALL No 8 – Networks

Introduction to Network Operations and Technologies

01 Introduction to Network Operationsand Technologies

With change quickly becoming an industry watchword,

network operations represent a key telco priority.

Understanding which technologies will transform the

network operating model and their operator-specific

challenges is fundamental to success.

In a rapidly changing industry where players must deal

with fading top-line results and shrinking bottom-line

predictions, fixed-line and mobile operators face the twin

tasks of exploring new business models while becoming

significantly more efficient. Telcos must also confront the

reality that the introduction of new services will do

relatively little to reverse the deceleration in revenue growth

or the outright sales declines. These new services, such as

IPTV for fixed carriers or mobile TV for wireless operators,

will instead bring additional costs, thus placing morepressure on already stretched margins. Operationally

complex services will lead to increased call center volumes,

for example, while new services will generate higher

sales and marketing costs and probably additional invest-

ments in network capacity. Compared to voice, the average

provisioning cost per “gross add” for IPTV is two to three

times as great. Convergence and increased competition

will just make this picture more complex.

The network’s growing role

McKinsey’s research in this context of change indicates

that the network will play an increasingly important

role among both fixed-line and mobile telcos. On the one

hand, new network technologies will enable new

services (e.g., IPTV, mobile broadband, femtocell-based

services, and others). A key telco challenge involves

understanding the commercial possibilities these new

technologies bring, their potential impact on business

models, and the changes they could effect in the

competitive and regulatory landscape. On the other hand,

network operations represent a critical area in which

telco managers must improve in order to compete success-

fully in the industry’s likely less profitable future

environment. By optimizing current network operations

and leveraging new technological possibilities, telcos

can work to keep pace with the increasing demand for

products and services while maintaining or improving

margin levels. In a nutshell, operators need to find ways

to reduce cost in order to finance the new investments.

To this end, operators must ensure transparency of the

cost structure across their operating model.

The current telco operating model incorporates four

major dimensions (Exhibit 1): customer service (“sell”),

product innovation (“innovate and develop”), the

network itself (“access”), and support services (“support”).

Differences arise in terms of where costs occur for fixed

and mobile players. For example, for fixed operators the

network itself, with its hardwired tentacles reaching

out across the market, represents about 60 percent of a

company’s total spend (i.e., operating expenses – opex –

and capital expenditures – capex). Customer service

represents about 20 percent, support serv ices account

for 15 percent, and product innovation holds the smallest

share at 5 percent. Mobile operators, on the other hand,

find most of their costs (50 percent) in customer service,

while the network with its wireless efficiency consumes

only 25 percent, support services represent about 20

percent, and 5 percent is spent on product innovation.

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 10/64

10

Telecoms operators’ costs comprise 4 domains01

Analyzing costs, capex accounts for about a quarter of

a typical fixed-line incumbent’s total cost in Western

Europe, with much of this (about 95 percent) focused on

the network itself. Operating costs make up the remain-

ing three quarters of a fixed operator’s total cost,

with the network requiring about 45 percent. For a mobile

operator in Western Europe, capex makes up about 15

percent of total costs, with much of this (about 80 percent)

concentrated on the network. Opex accounts for the

remaining 85 percent of total costs, with customerservice accounting for about 60 percent followed by the

network at about 20 percent.

Highlighting network costs and leveragepoints

Given the central role network improvement plays in

their value propositions, successful telcos wil l make

this work a priority. Overall, managers can map out

a network’s cost structure based on seven key areas

known as domains: the network’s IT system and

operational support systems (OSS), customer access,

aggregation, transport, platforms, the core IP network

and, for wireless players, the mobile network core.

They can also map costs across five main, high-level

processes: design and planning, implementation/

deployment, provisioning, supervision and main-

tenance, and basic infrastructure. Com bining these

two mapping approaches allows managers to create

a cost matrix that can serve as the basis upon which they

define and prioritize cost reduction levers.

From a network domain perspective, most costs arise

in the customer access domain while, from the viewpoint

of the high-level processes, most of the costs originate

in the supervision and maintenance areas. For the

integrated player in Exhibit 2, the key element of the coststructure involves supervision and maintenance of

the customer access domain.

This matrix will present different cost structures

depending on the type of operations (e.g., fixed, mobile,

integrated) and the level of maturity. For example,

mature operators with no major network rollout invest-

ments should focus on optimizing the supervision

and maintenance processes, whereas growing operators

(e.g., mobile operators in emerging markets) must

work to reduce implementation and deployment costs,

especially regarding capex optimization.

This transparency should allow operators to evaluate

different operational efficiency levers that, for an

integrated operator, can yield cost reductions in the

order of 35 to 40 percent of the total network cost base:

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 11/64

11

The matrix gives the integrated operator perspective on the various elements

of overall network costs02

1. Efficiency levers that are independent of a telco’s

business model, such as the adoption of lean network

operations, network outsourcing, and wireless

network consolidation

2. Levers that depend on a telco’s specific assets,

such as fixed/mobile integration and cross-border

synergies

3. Radical moves that represent major business modelshifts, such as network sharing, structural network

separation, and significant complexity reduction (e.g.,

“no frills”)

4. Technological transformations that can have a potential

impact on the telco’s business model.

Charting a technological networktransormation

New network technologies can enable telcos to take

advantage of the commercial migration toward new,

high-capacity access approaches. They promote

technological renovation, make new, more efficient

operations possible, and simplify and rationalize

the network, eliminating obsolete elements and avoiding

duplications.

One example of such a transformation is t he rollout of

a Next Generation Access Network, both for fixed and

for mobile operators. Fixed operators are exploring – or

already rolling out – alternatives to the traditional copper

access network. The debate over FTTH vs. FTTC

developments is not new, but it has intensified of late as

the cost and performance gaps between the two network

alternatives have narrowed. Most fixed operators in

Western Europe have already made a decision based on

commercial business cases and on the hope that theendgame wil l be a network with a lower opex. Yet the

question for network operations managers remains – to

what extent are fiber developments really reducing

opex, and what is the best way for operators to capture

these potential savings?

In the mobile arena, wireless broadband access networks

open the door to “the next big thing” in terms of

applications and services, as consumer and business

adoption of mobile broadband services starts becoming

a major growth engine for wireless operators. In this

context, several technological options are emerging for

operators to satisfy the increasing bandwidth demands.

Beyond current 3G/WCDMA networks, the 4G race

has already started between technologies such as LTE,

Mobile WiMAX, and UMB, and operators will start

RECALL No 8 – Networks

Introduction to Network Operations and Technologies

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 12/64

12

making their decisions on their migration paths in the

coming years.

Finally, some “hybrid” (fixed/wireless) access network

alternatives are receiving increasing interest from

operators globally. With major infrastructure players

such as Motorola and Ericsson already investing in this

technology, femtocells – i.e., indoor base stations – are

set to cause fundamental changes in the industry if key uncertainties are resolved.

On the backbone side, the main technological transfor-

mation ahead for operators is the switch to an “all-IP”

operation along the aggregation and switching domains.

This would allow a radical reduction in switching/

aggregation equipment and eliminate “service-edge”

hardware, generating savings in the order of about 70

percent. It would also result in reduced network

management costs for load optimization and replace the

public switched telephone network (PSTN) with IMS

(IP Multimedia Subsystem) or soft switches. The newly

converged POTS/data access infrastructure will reduce

the amount of time and effort needed for installations,

and the all-IP approach would eliminate traditional

ATM and SDH transmission approaches in favor of

Gigabit Ethernet aggregation.

In the core network, the shift to all-IP would result

in significant reductions in backbone switching and core

equipment, producing savings in the 40 to 60 percent

range, depending on the specific situation. It would allow

network management centralization and processsimplification, reduce maintenance costs by 40 percent,

and cut space, power, and HVAC costs approximately in half.

* * *

As the traditional industry gives way to new competitors

and new ways of doing business, telecoms players

need to find ways to deliver the profitable growth that

investors require and the products and services that

subscribers demand. Given the central role the network

plays in delivering customer value, incumbents can

explore a multitude of cost-saving technologies and

techniques that will allow them to do a lot more with

their networks with a lot less money.

Duarte Begonha

is a Principal in McKinsey’s Lisbon office.

Javier Gil Gomez

is an Engagement Manager in McKinsey’s

Madrid office.

Hugo del Campo

is a Principal in McKinsey’s Madrid office.

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 13/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 14/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 15/64

15

With few applications requiring its blazing access speeds,

many telcos are still aggressively pursuing fiber.

Holistic modeling ensures the right rollout strategy and

a prof itable investment.

Internet usage continues to expand at phenomenal

speed. Demand for bandwidth has kept pace, creating

a completely new playing field for service and applications

providers in terms of what kinds of services can be

offered through Internet/DSL connections. YouTube

and Akimbo are examples of service providers with

business models that rely on high-speed access. Despite

the fact that – from an application point of view –

no real demand exists for access speeds beyond those

that ADSL2+ can deliver (i.e., 20 to 25 Mbps), most

operators worldwide are mobilizing to transform their

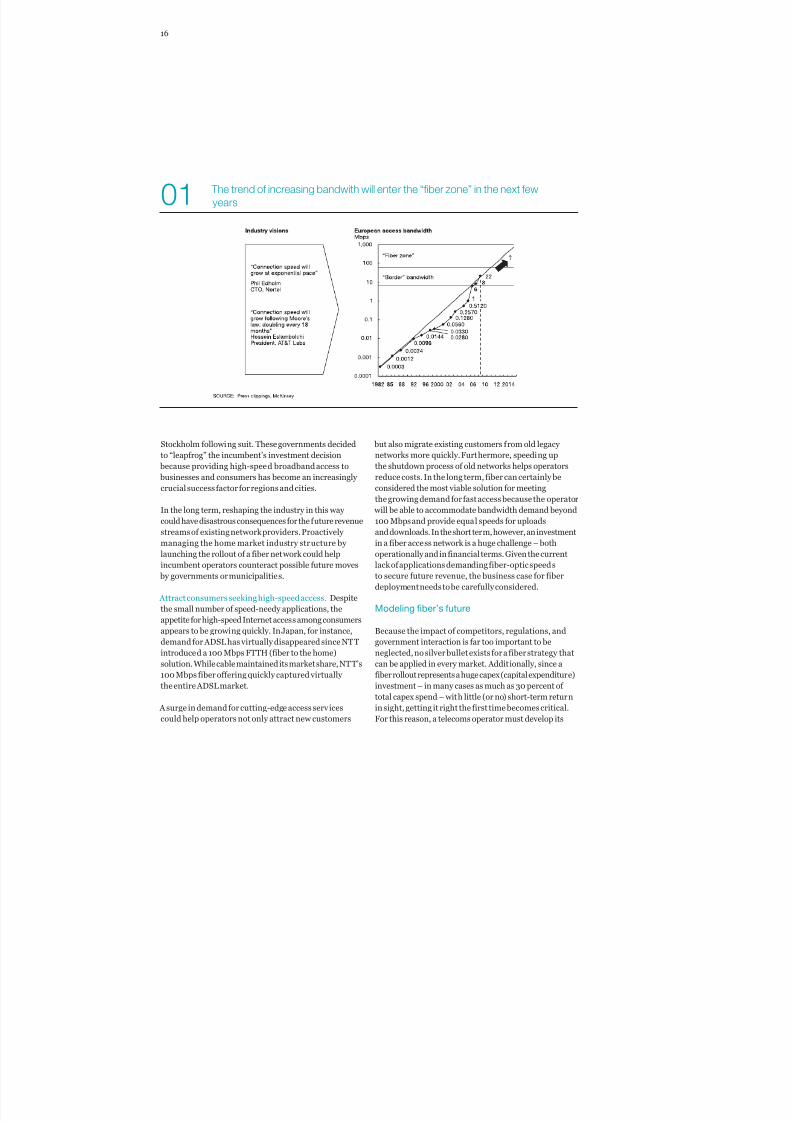

access networks in order to accommodate theever-increasing demand for bandwidth (Exhibit 1).

From among a number of different technology solutions,

deploying pure fiber close to end customers has

emerged as the potential silver bullet for telecoms

operators – one that could suddenly transform 30 Mbps

into a mass-market product. High-speed applications

are seeking new, faster avenues into the home. For

example, standard-definition TV requires only 3 to 4

Mbps per channel, while high-definition TV cal ls for

speeds in the 8 to 10 Mbps range, and multi-feed HDTV

streams would need even higher speeds. Major telecoms

operators have already announced more than EUR 100

billion in fiber investments, accounting for more than

90 rollouts worldwide – a fair amount of money considering

that current applications don’t even need the speed. So,

what is really driving this investment frenzy? McKinsey

research reveals three goals that have whetted the

industry’s appetite for f iber’s high speed.

Defend market share. Competitive pressure continues

to grow as telcos aggressively push triple-play offerings

(i.e., TV, telephony, and high-speed Internet access) and

as cable operators eat into the margins of incumbent

telecoms operators around the world. Cable operators

enjoy an existing network infrastructure that supports

much higher speeds than a telecoms operator’s legacy

access network, which is limited by the “last mile”

connection to the typical customer’s home or business,

usually consisting of lower-speed copper. Furthermore,

upgrading to “fiber speed” (i.e., 100 Mbps+) could

also be done more quickly and at a lesser relative cost by

a cable operator, should the demand arise.

Many cable operators worldwide already provide 20 Mbps+

Internet access services to their high-end customers.

More than a few telcos, however, face a structural

impediment that prevents them from being able to offer

similar speeds. Due to existing local loop lengths in

Europe, for example, without fiber only 30 percent of

EU consumers could be reached with a 15 Mbps product

and only 12 percent would have access to 30 Mbps.

The figure is even lower in the US.

Protect the industry structure. Another reason for the

industry’s switch to fiber has emerged from an unusual

corner. In some markets, government initiatives to fund

fiber rollouts have become serious threats to incumbents.

In Switzerland, for example, local municipalities

decided to fund a fiber rollout across Zurich, with other

large European cities such as Amsterdam and

02 High Fiber Diet: The Value of Next-Generation Access Networks

RECALL No 8 – Networks

High Fiber Diet: The Value of Next-Generation Access Networks

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 16/64

16

Stockholm following suit. These governments decided

to “leapfrog” the incumbent’s investment decision

because providing high-speed broadband access to

businesses and consumers has become an increasingly

crucial success factor for regions and cities.

In the long term, reshaping the industry in this way

could have disastrous consequences for the future revenue

streams of existing network providers. Proactively

managing the home market industry structure by launching the rollout of a fiber network could help

incumbent operators counteract possible future moves

by governments or municipalities.

Attract consumers seeking high-speed access. Despite

the small number of speed-needy applications, the

appetite for high-speed Internet access among consumers

appears to be growing quickly. In Japan, for instance,

demand for ADSL has virtually disappeared since NTT

introduced a 100 Mbps FTTH (fiber to the home)

solution. While cable maintained its market share, NTT’s

100 Mbps fiber offering quickly captured virtually

the entire ADSL market.

A surge in demand for cutting-edge access services

could help operators not only attract new customers

but also migrate existing customers from old legacy

networks more quickly. Furthermore, speeding up

the shutdown process of old networks helps operators

reduce costs. In the long term, fiber can certainly be

considered the most viable solution for meeting

the growing demand for fast access because the operator

will be able to accommodate bandwidth demand beyond

100 Mbps and provide equal speeds for uploads

and downloads. In the short term, however, an investment

in a fiber access network is a huge challenge – bothoperationally and in financial terms. Given the current

lack of applications demanding fiber-optic speeds

to secure future revenue, the business case for fiber

deployment needs to be carefully considered.

Modeling fber’s uture

Because the impact of competitors, regulations, and

government interaction is far too important to be

neglected, no silver bullet exists for a fiber strategy that

can be applied in every market. Additionally, since a

fiber rollout represents a huge capex (capital expenditure)

investment – in many cases as much as 30 percent of

total capex spend – with little (or no) short-term return

in sight, getting it right the first time becomes critical.

For this reason, a telecoms operator must develop its

The trend of increasing bandwith will enter the “fiber zone” in the next few

years01

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 17/64

17

fiber strategy with micro-markets in mind, taking into

consideration all aspects of the specific regional market

conditions the company faces.

McKinsey’s approach to making the telecoms operator’s

business case for the optimal next-generation

access strategy takes a holistic view of the operator’s

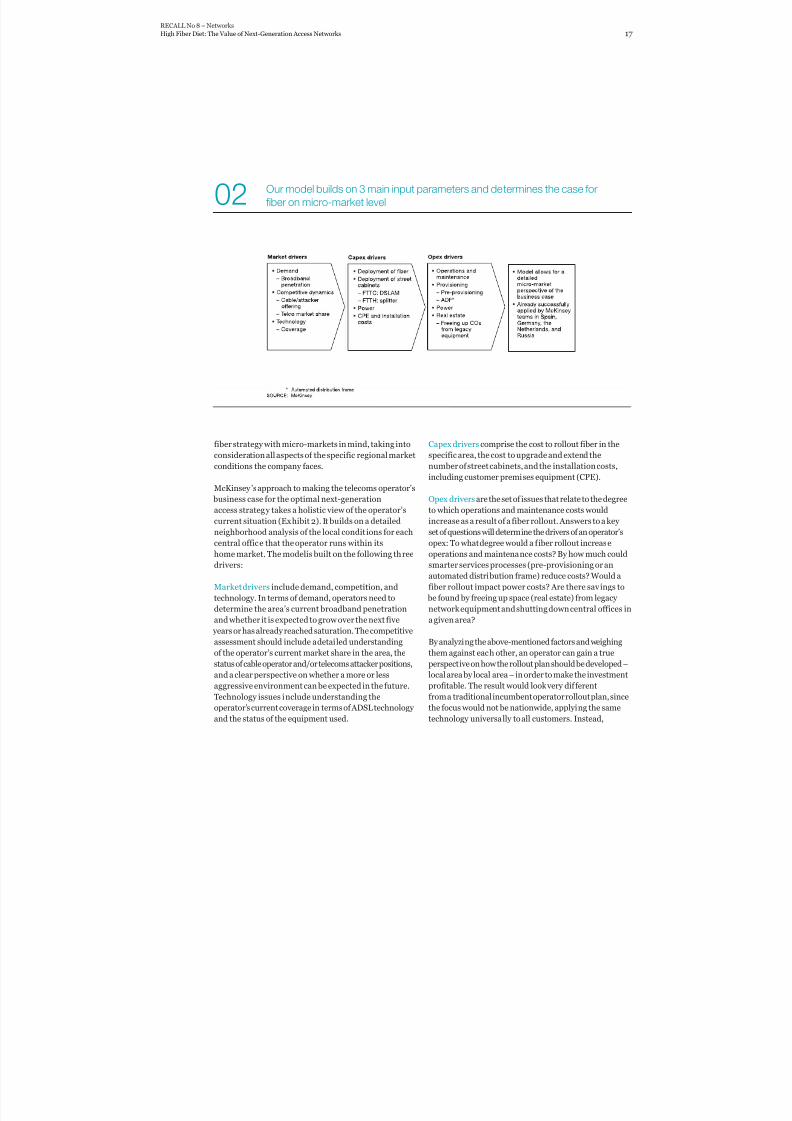

current situation (Exhibit 2). It builds on a detailed

neighborhood analysis of the local condit ions for each

central office that the operator runs within itshome market. The modelis built on the following three

drivers:

Market drivers include demand, competition, and

technology. In terms of demand, operators need to

determine the area’s current broadband penetration

and whether it is expected to grow over the next five

years or has already reached saturation. The competitive

assessment should include a detailed understanding

of the operator’s current market share in the area, the

status of cable operator and/or telecoms attacker positions,

and a clear perspective on whether a more or less

aggressive environment can be expected in the future.

Technology issues include understanding the

operator’s current coverage in terms of ADSL technology

and the status of the equipment used.

Capex drivers comprise the cost to rollout fiber in the

specific area, the cost to upgrade and extend the

number of street cabinets, and the installation costs,

including customer premises equipment (CPE).

Opex drivers are the set of issues that relate to the degree

to which operations and maintenance costs would

increase as a result of a fiber rollout. Answers to a key

set of questions will determine the drivers of an operator’s

opex: To what degree would a fiber rollout increaseoperations and maintenance costs? By how much could

smarter services processes (pre-provisioning or an

automated distribution frame) reduce costs? Would a

fiber rollout impact power costs? Are there savings to

be found by freeing up space (real estate) from legacy

network equipment and shutting down central offices in

a given area?

By analyzing the above-mentioned factors and weighing

them against each other, an operator can gain a true

perspective on how the rollout plan should be developed –

local area by local area – in order to make the investment

profitable. The result would look very different

from a traditional incumbent operator rollout plan, since

the focus would not be nationwide, applying the same

technology universally to all customers. Instead,

Our model builds on 3 main input parameters and determines the case for

fiber on micro-market level02

RECALL No 8 – Networks

High Fiber Diet: The Value of Next-Generation Access Networks

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 18/64

18

The regulatory framework can significantly reduce the profitability

of a fiber investment03

area-specific approaches would be chosen, all depending

on the above-mentioned factors. For example, FTTH

could be the best alternative for densely populated areas

with high broadband penetration rates and high market

shares, while FTTC (fiber to the curb) or DSL may work

best in less densely populated areas that still have a high

demand for broadband. Areas already heavily

penetrated by cable and/or those with very low broadband

penetration might not even justify an investment at all

at this point. In other words, an incumbent mustundergo a complete change in mindset to make a multi-

billion dollar fiber investment successful, abandoning

the old belief that one service fits all and, instead,

incorporating a carefully planned mix of technologies

and implementation strategies for each local market in

which the company is active.

Several specifc challenges ahead

We note a number of operator hurdles to a successful

fiber rollout in the areas of fiber strategy and regulatory

frameworks. An operator’s chosen fiber strategy can

have a far-reaching impact on its operating model. Since

telcos cannot fully reduce complexity until all legacy

networks have been shut down completely, deploying

fiber will more likely increase complexity in the

short to medium term. Fiber access (i.e., FTTH, FT TC,

or both) will be an additional component that

managers must control and maintain within the network,

alongside DSL and other legacy networks.

NTT decided to undertake a complete migration to

FTTx (i.e., FTTH or FTTC) in a single process by leveraging

existing network assets. The company faced specific

challenges, including the need to convince customers of

the value of FTTx, to design a completely new process

to reduce opex, to put operations skills training in place,and to migrate to a brand-new system while reshaping

the existing one. Verizon, by contrast, chose to split the

value chain (i.e., FTTx versus non-FTTx), managing

both oper ations separately. In doing so, Verizon had to

contend with several hurdles, including complexity

management issues in terms of operations and systems

as well as an increase in opex, the duplication of some

systems, and operations skills training.

Operators must also carefully consider the regulatory

framework within their home markets because these

frameworks can significantly reduce the profitability of

a fiber investment (Exhibit 3). Thus far, three different

rollout models have emerged globally.

Protectionist model. Adopted in the US, this model

favors incumbent operators because it does not require

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 19/64

19

network unbundling. It provides the telco with a

competitive advantage against attackers that cannot

provide TV/high speed outside the direct coverage

of the central office area.

Open model. Adopted by many European countries,

this approach obligates operators to unbundle and offer

wholesale services to attackers. This model will likely

result in telco market share erosion, although improvedTV content quality and service/customer experience

performance may change this result.

Subsidy model. Some Asian countries (e.g., South Korea

and Singapore) have chosen this model, whose main

goal is “broadband for everyone.” Under the model,

governments closely involve themselves in the fiber rollout,

either by subsidizing existing players that are investing

in fiber or by driving the rollout process themselves.

* * *

Incumbents have been compelled to pursue high fiber

diets in order to defend their market shares, protect the

industry structure, or attract consumers seeking high-speed access. Our fiber model provides critical insights

regarding the challenges incumbents face in rolling

out these networks. Successful operators will carefully

choose from among several possible fiber rollout strategies

and closely consider the regulatory frameworks under

which the rollout will take place.

Ferry Grijpink

is an Associate Principal in McKinsey’s

Amsterdam office.

Achim Wörner

is an Associate Principal in McKinsey’s

Munich office.

Eric Grob

is a Principal in McKinsey’s Zurich office.

Luis Miguel Santos

is an Associate Principal in McKinsey’s

Madrid office.

RECALL No 8 – Networks

High Fiber Diet: The Value of Next-Generation Access Networks

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 20/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 21/64

21

Mobile players can reduce certain network costs by up

to 30 percent by consolidating and offshoring key network

functions. Assessing the potential and evaluating

management commitment are essential to mak ing the

right choice and ensuring successful relocation.

With profits wilting beneath a one-two combination of

competitive intensity and regulatory pressure,

network-related costs can weigh heavily on a mobile

network operator’s (MNO’s) bottom line. As a result,

most operators are considering their network cost

reduction options, which include applying “lean” principles

to network operations, signing managed services deals

with equipment manufacturers or agreeing to network

sharing arrangements with other operators. The most

common cost reduction options share one characteristic:

they focus on local costs and activities, and rightly so,since network maintenance and operations comprise up

to 85 percent of non-people-related operating expenditure

(opex) – or two thirds of the total network opex. If

considering people costs, however, the picture changes:

up to 75 percent of these costs are incurred by functions

that don’t necessari ly require a presence in the field,

such as network planning.

Attempts to regionalize network functions in order to

cut costs tend to concentrate primarily on workforce

consolidation and offshoring opportunities. Key oppor-

tunities for consolidating jobs lie in network design,

planning and engineering, and network monitoring and

support. As the only sizeable remote network functions,

these three represent the primary areas suitable for

regionalization. Offshoring possibilities also include

network design and remote support for maintenance.

Within network functions, “desk-based” activities offer

the greatest potential for relocation and consolidation

(Exhibit 1). Operators interested in capturing region-

alization value should build two business cases: one for

planning and engineer ing and the other for network

monitoring and support.

Planning and engineering. Areas of interest exist

through-out the network, including transmission, the

network core, the intelligent network layer, value-

added services such as SMS and MMS, and operations

support systems (OSS). In these cases, regionalized

functions don’t require direct access to live infrastructure,

and because they’re primarily office-based, the need

for specialized equipment beyond software is minimal.

Planning and engineering functions that demand

significant access to live infrastructure, such as radioaccess planning and optimization, should remain local.

MNOs can regionalize or offshore all of the other functions,

including the remaining radio planning and engineering,

core architecture/capacity design, and OSS.

Network monitoring and support. Network monitoring

and support activities can be performed from remote

locations (i.e., other countries) using appropriate network

management systems. In addition, it is possible to

redesign processes in order to maintain direct interfaces

with local maintenance suppliers, thus removing the

need to locate a network management center (NMC) in

the country of origin. In many instances, however,

regulatory and security concerns restrict operators from

taking full advantage of these opportunities, since

they are required to retain monitoring capabilities in the

country of origin.

03 Over the Seas of Complexity:Consolidating Mobile Network

Functions Offshore

RECALL No 8 – Networks

Over the Seas of Complexity: Consolidating Mobile Network Functions Offshore

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 22/64

22

Making the case or regionalization

The resulting business cases show that the combination

of regionalization and workforce consolidation can

generate significant run-rate wage savings, albeit from

a small base. One company operating in many European

countries identified savings of about 30 percent of

the addressable cost base, corresponding to a reduction

of about 1 to 2 percent of the operator’s total annual

network costs (i.e., capex plus opex). The operatoridentified economies of scale and scope that brought

the potential for efficiency gains to at least 20 percent

of all addressable FTEs (full-time equivalents) in

the network planning, engineering and monitoring, and

support functions. Managers discovered that labor

cost arbitrage would deliver between 70 and 80 percent

of the savings, while staff consolidation would contribute

the remaining 20 to 30 percent. The comparatively

low savings seen in staff consolidation result from the

tendency of operators to scale up most capacity-

planning functions (e.g., site selection, transmission

planning) based on the amount of network change

taking place, so these actions couldn’t simply be taken

just once across all operating countries.

Likewise, while design functions such as new technology

assessment or systems integration could, in principle,

be addressed once, compared to capacity planning this

phenomenon is less common.

Another impediment involves processes and IT systems,

which tend to differ across operating countries. They

often rely on different vendors and have separate systems

architectures and products/services, thus inhibiting the

potential consolidation of design or monitoring functions.

The significant role of labor cost arbitrage has

valuable implications beyond the multinational realm:mobile operators active in only one country could “match”

80 percent of the savings available to multinational

operators by relocating their remote network functions

to low-cost countries without the need to involve

an outsourcer.

In terms of timing, operators should be aware that

differences in local processes can complicate implemen-

tation. In fact, paral lel implementation of the

regionalization and consolidation programs could take

several years in order to minimize service level disruptions.

As a result, payback can take three to four years, and

recruitment, restructuring, and knowledge transfer will

require significant management commitment.

Operators must put a number of prerequisites in place to

ensure a successful regionalization effort. They need

Relocation and consolidation potential is highest for “desk-based” activities01

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 23/64

23

to establish the right governance model before region-

alization can start and cultivate sufficient focus and

support from both top- and middle-level management

that doesn’t distract from their other local initiatives.

MNOs should make sure that the host country can step

up the pace of recruitment without triggering significant

wage inflation and also determine whether a timeline

of two to three years to complete the ful l transition is

acceptable.

Choosing rom among three network operatingrameworks

For a multinational group, the divide between remote/

regional and local functions implies a choice of three

natural network operating frameworks (Exhibit 2).

1. Stand-alone. Independent operating companies

could deliver up to 80 percent of total identified savings

through the independent offshoring of remote functions

(or more than 80 percent if a network outsourcer of

the right profile and with suff icient scale is used, so that

economies of scale and scope can be achieved as well).

2. Remote functions coordinated. This model divides

network functions between one regional and several

local units. All report primarily to a group network unit

and only secondarily to their country businesses. The

regional funct ions could be consolidated across the

group (with or without the help of an outsourcer),

and the local functions could be optimized independently

on a per-country basis.

3. All functions coordinated.A single group network

function would drive the consolidation of regional

functions and a single, cross-group strategy to optimize

local functions. Outsourcing arrangements could

also be negotiated for regional and local functions on a

cross-group basis.

The model that an operator chooses will depend on

its key beliefs and the opportunities in the local markets

in which it operates. MNOs pursuing the stand-alone

model likely assume that the best way to capture labor

arbitrage savings is for each country to act alone (i.e.,

creating independent near- or of fshore centers). They

probably also believe that consolidation savings from

regionalization will be too small to be worth the cost

in terms of increased management complexity. These

beliefs may be compounded by the need to act in widely

varying markets – possibly in emerging economies

or from incumbent or attacker positions in different

countries.

Companies pursuing the coordinated remote functions

model will consider the group to be sufficiently stable

Potential operating frameworks consider a geographic spread of

responsibilities02

RECALL No 8 – Networks

Over the Seas of Complexity: Consolidating Mobile Network Functions Offshore

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 24/64

24

and similar in priorities. They will probably also view

regionalization savings as being incremental to those

gained on local equipment and functions, consider

a coordinated low-cost hub pref erable to individual

initiatives, and believe that regional management can work due to the flexibility of their management culture. If

they are active in emerging markets, they will probably

favor this option, since talent shortages may not

allow them to replicate network functions in each country.

In addition, these players might view single-vendor

outsourcing as unacceptable due to vendor risk and vary-

ing local conditions. Final ly, groups choosing the

“all functions coordinated” model will likely align with

the coordinated remote functions model in terms of

beliefs, except regarding how to outsource. They will

presumably deem single-vendor outsourcing for

multiple countries acceptable and consider it less expensive

than usingmultiple suppliers.

Operators can implement any of these three models

with outsourcing in mind. Outsourcing can enable network

sharing among competitors, accelerate savings

through vendor financing, lower the level of management

focus needed, and reduce severance costs if the

outsourcer is able to reallocate dismissed staff. It may

also lead to increased savings if lower-cost countries

host the outsourced regional functions and due to theoutsourcer’s potentially greater scale. Additionally,

a growing body of reference cases exists for outsourcing

some or all network functions, so operators need not

fear they are pioneering some new and untried experiment.

That said, a number of drawbacks could also arise,

including the risk of relying on a third party for key network

functions, the probable need for an extra management

layer to interface with the outsourcer, and the risk that

the operator won’t achieve expected service levels and

cost savings.

Extending the benefts o regionalization

Operators may find that while regionalizing and

consolidating network functions provides a positive

business case in terms of opex savings, it addresses

a small portion of overall network costs and requires

as possible. For example, it retained its chief technology

officer and its data centers in Europe and North

America, while centrally locating remote engineer ing

operations in the emerging market region.

The operator maintained only the radio network

and field maintenance functions “in-country.” As a

result, it captured substantial overall savings,

including those gained through the creation of common

processes and standardized technical specifications.

Falling short

Conversely, an MNO consolidated its network

functions from more than 20 countries down to 3,

but, in this case, didn’t capture the expected

synergies due to a lack of coordinated governance

and an over-reliance on the remaining local teams.

Consequently, most of the regionalized functions

were gradually returned to local operating unit

control.

Consolidation around the Globe

Examples from emerging markets

It’s not surprising that a growing number of operators

are looking at relocating some activities off- or near-

shore – or at cross-border consolidation of network

functions in the case of multinationals. But to date,such plans have seen varying degrees of success.

Making the grade

One emerging market operator benefi ted by

establishing regionally shared services among up to

six national operators, gaining economies of scale,

scope, and expertise. It solidified these gains by creating

a number of global best-practice sharing centers,

enabling the pooling of expert ise for each topic area

and providing hands-on coaching for national operators.

Likewise, another emerging market operator

grouped the businesses of its network operations for

15 countries into regions. By dividing functions and

operations between developed and developing

markets, it rationalized its approach as cost-efficiently

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 25/64

a significant multi-year effort that poses implementation

risks. When deciding whether to proceed, a multi-

national operator should also consider more strategic

implications brought on by the needs to rationalize

architectures, processes, and systems, such as capex

sav ings, asset efficiency gains, and quick network/

systems rollout across countries. In the long run, such

benefits will extend to the entire network capex base and

could enable operators to optimize network investments

significantly across countries. This is especially the casein markets with high growt h potential where the

network buildup remains to be completed.

Making it all work

To evaluate a regionalization project’s potential, group-

and country-level chief technology officers must be

open to radically reorganizing their departments and

willing to commit their functional organization managers

to the project. The head of each network function in

every country represented should conduct workshops

to allot FTEs against a common internal process map

and gain consensus on expert estimates of the project’s

overall consolidation and offshoring potential (Exhibit 3).

* * *

Mobile operators seeking new ways to save can jointly

consolidate and regionalize a range of related network functions, reducing addressable costs and capturing

broader benefits in the long term. Whether this strategy

is worth undertaking depends on the operator’s beliefs,

on its market position and prospects in each country,

and on its overall management culture. If undertaken,

making such a play successful requires that operators

choose which one of the three models best fits their

group’s needs and competitive positioning and devote

sufficient management focus over many years.

5 key practices ensure an accurate assessment of regionalization potential03

25

Giorgio Migliarina

is a Principal in McKinsey’s Beijing office.

RECALL No 8 – Networks

Over the Seas of Complexity: Consolidating Mobile Network Functions Offshore

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 26/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 27/64

27

Vise-like market pressure and a growing network

services industry are compelling operators to significantly

reduce their costs. A new approach to outsourcing

is placing many on the path to achieving the savings that

the market demands.

Should established telecoms operators follow the

attackers’ lead and outsource their net works? Facing

top-line challenges, eroding margins, and declining

incumbent market shares, industry veterans continue to

seek new revenue streams and fresh opportunities

to drive far-reaching operational improvements. In a

recent McKinsey study (Future Telecoms Operating

Model), we concluded that incumbent telecoms operators

in mature markets, such as Western Europe, need

to reduce their total opex + capex (operating expenses +

capital expenditures) cost base by 20 to 40 percent. Inaddition to this focus on costs, they need to simultaneously

invest in new services and technologies (e.g., the

full-scale deployment of 3/3.5G access or IPTV) to remain

competitive and meet capital market expectations.

The network domain constitutes a significant share of

total operator opex + capex (up to 30 percent for mobile

players and up to 60 percent for fixed players) and is

an inevitable target for achieving the next wave of perfor-

mance improvement. However, the experience of most

established telecoms operators is that making network

performance improvements and rolling out new services

at the same time is a challenge.

Attacking operators have already signed large outsourcing

deals that are having significant impact. Players in

the United Kingdom, Germany, Scandinavia, Brazil and

elsewhere already have multi-billion dollar agreements

with Ericsson, Nokia Siemens Networks, Alcatel-

Lucent, Huawei and others to deploy, operate, and

maintain fixed and mobile networks.

Operators’ outsourcing options

From an industry point of view, network outsourcing

is still embryonic compared to IT outsourcing, and most

current arrangements focus only on the “out-tasking”

of operations such as network construction and field

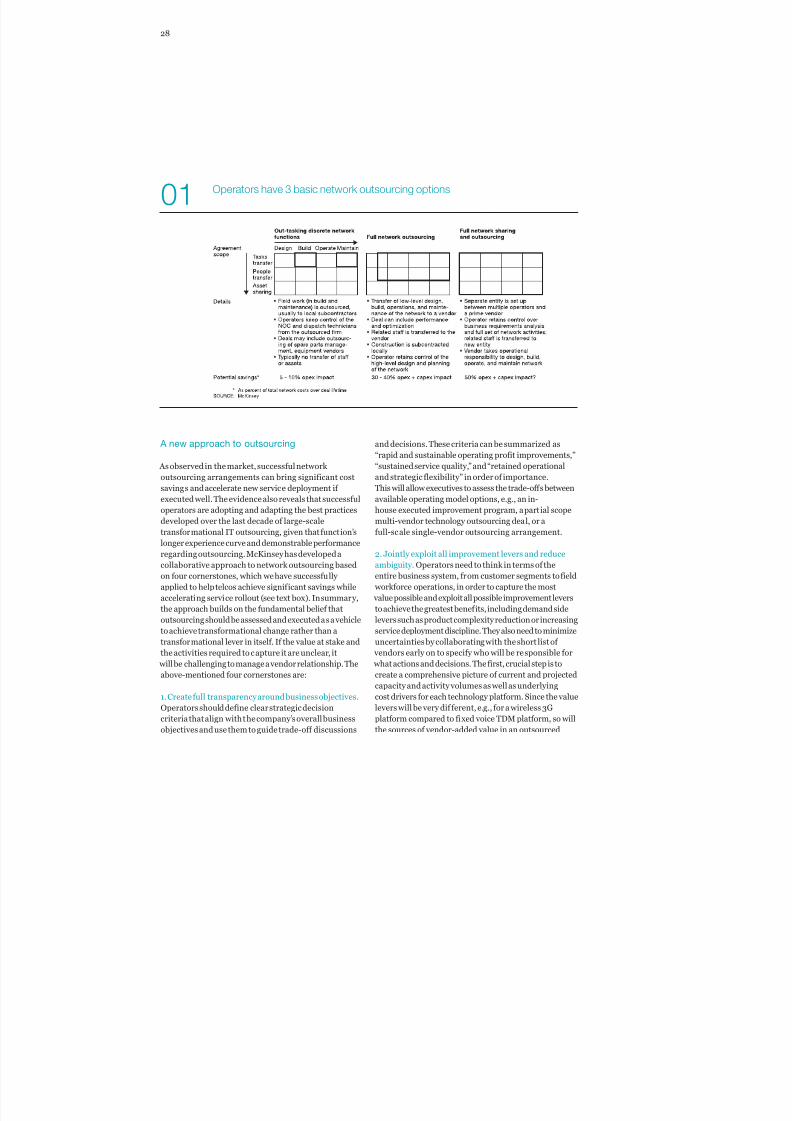

workforce maintenance. We observe three levels of

network outsourcing, beginning with the basic out-tasking

of stable operations, which can deliver savings of 10

to 15 percent through the consolidation of maintenance

contracts and the capture of scale advantages (Exhibit 1).

The second level often involves single-vendor end-to-endoutsourcing and focuses on low-level design, rollout,

and operations, delivering savings in the 30 to 40 percent

range. Finally, operators can choose the extreme of

sharing and outsourcing the entire network. While the

benefits of this approach for established operators

remain to be seen, they will likely be significant.

Attacking mobile network operators have already

embarked on all three levels of outsourcing, but there is

an increasing number of examples of established

operators pursuing full network outsourcing. One mobile

incumbent transferred the full responsibility of rollout

and operations to a single vendor realizing more than

30 percent savings over the lifetime of the deal while

at the same time accelerating the completion of the

3G rollout.

04 Offloading the Core:Exploring Network Outsourcing

RECALL No 8 – Networks

Ofoading the Core: Exploring Network Outsourcing

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 28/64

28

A new approach to outsourcing

As observed in the market, successful network

outsourcing arrangements can bring significant cost

savings and accelerate new service deployment if

executed well. The evidence also reveals that successful

operators are adopting and adapting the best practices

developed over the last decade of large-scale

transformational IT outsourcing, given that function’s

longer experience curve and demonstrable performanceregarding outsourcing. McKinsey has developed a

collaborative approach to network outsourcing based

on four cornerstones, which we have successfully

applied to help telcos achieve significant savings while

accelerating service rollout (see text box). In summary,

the approach builds on the fundamental belief that

outsourcing should be assessed and executed as a vehicle

to achieve transformational change rather than a

transformational lever in itself. If the value at stake and

the activities required to capture it are unclear, it

will be challenging to manage a vendor relationship. The

above-mentioned four cornerstones are:

1. Create full transparency around business objectives.

Operators should define clear strategic decision

criteria that align with the company’s overall business

objectives and use them to guide trade-off discussions

and decisions. These criteria can be summarized as

“rapid and sustainable operating profit improvements,”

“sustained service quality,” and “retained operational

and strategic flexibility” in order of importance.

This will allow executives to assess the trade-offs between

available operating model options, e.g., an in-

house executed improvement program, a part ial scope

multi-vendor technology outsourcing deal, or a

full-scale single-vendor outsourcing arrangement.

2. Jointly exploit all improvement levers and reduce

am biguity. Operators need to think in terms of the

entire business system, from customer segments to field

workforce operations, in order to capture the most

value possible and exploit all possible improvement levers

to achieve the greatest benefits, including demand side

levers such as product complexity reduction or increasing

service deployment discipline. They also need to minimize

uncertainties by collaborating with the short list of

vendors early on to specify who will be responsible for

what actions and decisions. The first, crucial step is to

create a comprehensive picture of current and projected

capacity and activity volumes as well as underlying

cost drivers for each technology platform. Since the value

levers will be very dif ferent, e.g., for a wireless 3G

platform compared to fixed voice TDM platform, so will

the sources of vendor-added value in an outsourced

Operators have 3 basic network outsourcing options01

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 29/64

29

arrangement. As a result, the prerequisites for jointly

capturing that value will be varied as well. As an example,

the biggest source of value in outsourcing a 3G access

network typically lies in single- vendor optimized planning

and the rollout of managed capacity (primarily capex),

whereas for a TDM network, increasing utilization of field

workforce and accelerating the closedown of redundant

sites is often valuable. Exhibit 2 illustrates the logic (wire-

less access platform example) for why operators should

establish clarity concerning their internal ability to improveand the vendor’s ability to incrementally add value.

In our experience, up to half of the value creation in an

outsourced arrangement is subject to the ongoing

participation of the operator. At the very least, the operator

will be involved in the decision making. In wireless,

we have seen as much as 15 to 20 percent in incremental

savings plus accelerated rollout of new capacities

captured via single-vendor outsourcing models using this

approach (Exhibit 3). A typical value creation assessment

should in the end also include a view on internal

management capacity and experience to run an in-house,

large-scale operational transformation program

on top of the business as usual. A common conclusion is

that many of the identified performance improve-

ment initiatives that could be pursued in-house are more

likely to succeed using an outsourced model.

3. Craft a deal that accelerates value capture. Telcos

need to ensure the alignment of key deal mechanisms

and the company’s overall business objectives. Among

these are commercial mechanisms as well as deal

terms. The purpose of the former is to translate the value

realization plan into services, prices, and volumes

and incentivize both the operator and vendor to act in

accordance with the agreed-upon objectives of the deal.

These mechanisms include clear services definitions,

standardized SLAs, capacity-based pricing models, volumeforecast models, and carefully deployed penalty/

reward regimes. Given the industry’s relative lack of

standard definitions of services and SLAs in a managed

service context, it is part icularly important that

telcos invest in getting this right. The purpose of the deal

terms is to minimize the risk of operational disruption

or even dispute should either party divert from the

agreement (with or without proper cause). Operators and

vendors achieve the latter by jointly defining and agreeing

on business principles for how to deal with potential

future issues. Such principles can include HR policies,

deal termination clauses (full and partial), confidentiality

issues, major scope changes, and innovation.

4. Roll out world-class service management and

governance practices. Lastly, operators need to make

sure they have established clear interfaces, roles, and

Jointly negotiating value add minimizes ambiguity of

operator-vendor relationship02

RECALL No 8 – Networks

Ofoading the Core: Exploring Network Outsourcing

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 30/64

30

3. Craft a deal that accelerates value capture

Include clearly defined mechanisms that ensure

realization of strategic objectives, e.g., competitive

pricing, SLAs, continuous improvement

Focus on business impact, not technology,

through negotiations of business principles and

services

4. Roll out world-class service management and

governance practices

Ensure clear interfaces, roles, and responsibilities

for operational, tactical, and strategic issues

Include mechanisms to manage internal demand,

e.g., capacity planning, clear order points, project

prioritization

1. Create full transparency around business objectives

Define clear strategic decision criteria that are

aligned with overall business objectives

Define and detail operating mode options

Evaluate options against business objectives

2. Jointly exploit all improvement levers and reduce

ambiguity

Establish full transparency around prerequisites of

value capture up-front

Understand both parties’ economic models to

define the win-win point

Four Cornerstones of a Collaborative Approach to Outsourcing

Vendor value add can be as much as 20% on top of internal case03

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 31/64

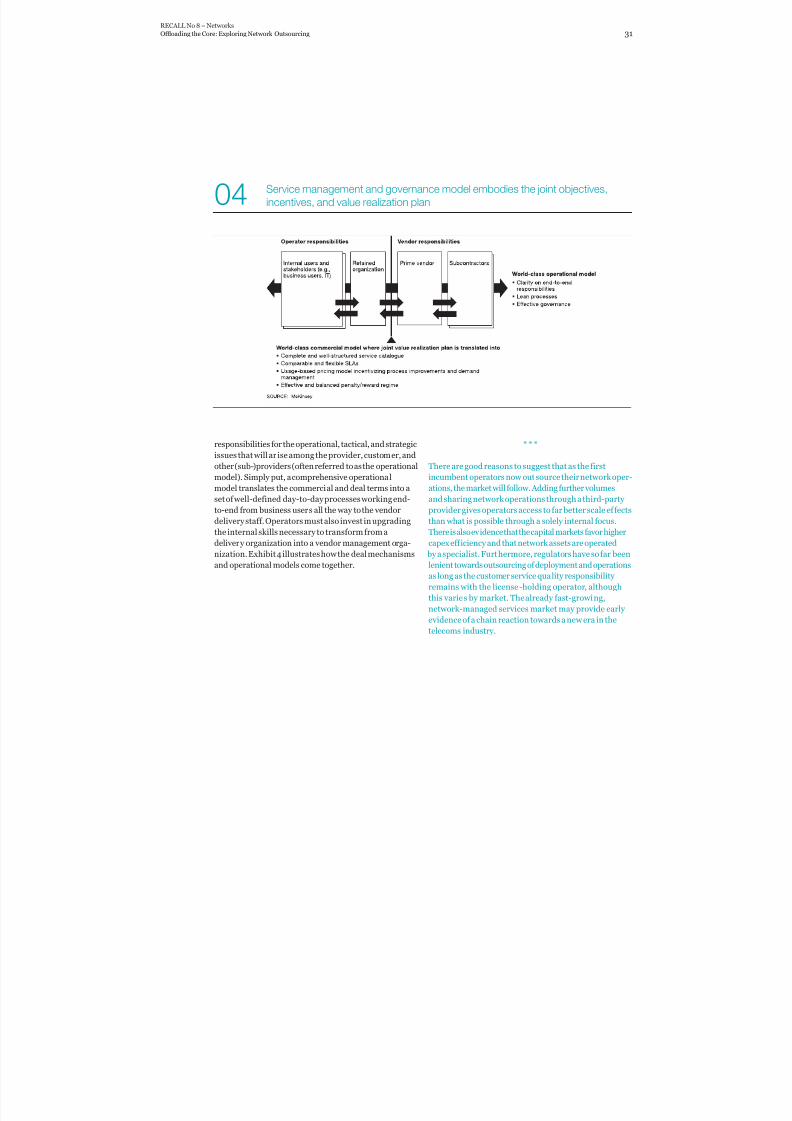

responsibilities for the operational, tactical, and strategic

issues that will ar ise among the provider, customer, and

other (sub-)providers (often referred to as the operational

model). Simply put, a comprehensive operational

model translates the commercial and deal terms into a

set of well-defined day-to-day processes working end-

to-end from business users all the way to the vendor

delivery staff. Operators must also invest in upgrading

the internal skills necessary to transform from a

delivery organization into a vendor management orga-nization. Exhibit 4 illustrates how the deal mechanisms

and operational models come together.

* * *

There are good reasons to suggest that as the first

incumbent operators now outsource their network oper-

ations, the market will follow. Adding further volumes

and sharing network operations through a third-party

provider gives operators access to far better scale effects

than what is possible through a solely internal focus.

There is also evidence that the capital markets favor higher

capex efficiency and that network assets are operated by a specialist. Furthermore, regulators have so far been

lenient towards outsourcing of deployment and operations

as long as the customer service quality responsibility

remains with the license-holding operator, although

this varies by market. The already fast-growing,

network-managed services market may provide early

evidence of a chain reaction towards a new era in the

telecoms industry.

Service management and governance model embodies the joint objectives,

incentives, and value realization plan04

RECALL No 8 – Networks

Ofoading the Core: Exploring Network Outsourcing 31

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 32/64

32

André Christensen

is a Principal in McKinsey’s Toronto office.

Susanne Suhonen

is a Practice Manager in McKinsey’s

London office.

Martin Lundqvist

is an Associate Principal in McKinsey’s

Stockholm office.

Tor Jakob Ramsøy

is a Principal in McKinsey’s Oslo office.

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 33/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 34/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 35/64

35

Driven by lower pricing, higher speeds, and better form

factors, wireless data traffic has f inally taken off. To

cope with this exhilarating demand, mobile operators

must plan significant build-outs of their networks,

in many cases within the next three to five years.

McKinsey’s analysis of wireless trends suggests that

operators will face business model challenges

in the coming years. Competitive pressures have already

led the industry to adopt flat-rate pricing plans

that might starve players of adequate margins.Operators

must now develop innovative approaches to

pricing, revenue generation, and network evolution that

result in cost-effective ways to meet their

customers’ growing need for high-speed mobile

broadband.

Questioning mobile data’s proftability

Demand for high-speed mobile data has seen meteoric

growth since early 2007 (Exhibit 1). Four factors have

ignited this worldwide boom:

1. The introduction of High-Speed Downlink Packet

Access (HSDPA) has led to improved wireless speed

and access time, finally delivering what users expected

nearly a decade ago.

2. New competitors are offering f lat rates as a strategy

to put pressure on mobile data pricing. This, in turn, is

driving down prices across the market. In the UK,

for example, mobile “attackers,” who use f lat-rate plans

to lure customers, drove incremental broadband

price plans down by nearly 90 percent between 2005

and 2007 (Exhibit 2). The same has been seen

in Scandinavia and other European markets.

3. Improved form factors of new handsets lead to

increased data usage – exemplified by Apple’s iPhone

that, when introduced in the US, tripled the carrier’s

mobile data traffic in many major cities.

4. Plummeting prices of UMTS cards make it attractive

for a larger section of society to plug into their laptops,

creating a “wireless DSL” experience.

While backhaul issues are now well researched, we predict

that this seemingly insatiable demand for mobile

broadband will lead to the bottlenecking of access networks

in the next three to five years in highly populated

cities such as Amsterdam, London, and Singapore. Theaccess network problem could accelerate if current

spectral efficiency promises are not kept – historical

wireless performance has, in some cases, undershot

promises by a factor of four. Resulting from fierce com-

petition, mobile operators may be losing the means

to pay for their broadband networks even as they push to

build them out. Research shows that mobile data

premiums over the fixed line continue to erode as many

operators adopt flat-rate fees. In countries such as

the United Kingdom and Austria, operators have currently

priced their broadband mobile plans below fixed-line

DSL alternatives.

Our analysis shows that in cases in which mobile

subscribers exceed usage levels of 1 giga byte per month –

which appears to be quite possible – the incremental

network cost of building capacity alone could exceed the

05 Mobile Networks of the Future:Building a Sustainable Wireless Carrier

Business Model

RECALL No 8 – Networks

Mobile Networks of the Future: Building a Sustainable Wireless Carrier Business Model

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 36/64

36

emerging European flat-rate price (Exhibit 3). In fact,

a significant number of heavy mobile data users may

already be unprofitable – an unsett ling notion,

given that these subscribers have traditionally been the

most profitable for mobile operators. This seems to

be a significant medium-term risk for the industry.

Mobile companies can learn from fixed-lined telcos,

for which the exponential growth of data, driv en by flat-

rate pricing, has already squeezed their economics.For example, the introduction of BBC’s iPlayer has placed

the economics of smaller UK-based ISPs under

pressure, with backhaul cost doubling and resulting in

no ARPU (average revenue per user) increase. This

type of growth can pose an even greater problem for wire-

less networks because the radio access network is

a far more shared and limited resource than the copper

lines for wired networks, with a much higher capex

cost for incremental capacity.

Operator actions

Operators need to star t shaping mobile data usage

immediately to avoid significant profitability issues in

the future. Achieving this change will be diff icult,

given the internal and market pressure to grow data

penetration. It will require operators to take a holistic

view of various customer segments, understanding their

profitability across the portfolio (e.g., in some Asian

markets, data has been a “loss leader” for many years).

We believe that operators need to take three specifications:

1. Consider recasting pricing models to ensure profit-

ability in what is rapidly becoming a “data-heavy” world,

especially on the “access type” UMTS card offerings.

Operators could, for example, better differentiate theirhigh-value customers by offering pricing plans that

pro vide priority access during peak hours. They could

also tighten up and enforce fair-use policies by reducing

traffic allowances or limit/disallow certain data-heavy

applications during peak periods. Other options include

pricing “be yond-limit” minutes at higher rates or promoting

“cache and carry” options, with which the user

downloads fixed-line content onto a mobile device to

use when on the move.

2. MNOs should also invest in exploring the business

model implications of potential shifts in revenue and

profitability towards content and devices, specifically

on applications linked to the mobile phone. This could

include actively shaping traffic, brokering revenue-

sharing content deals with video sites, or opening one’s

own site. Operators can also actively push additional

Wireless data growth is exploding globally01

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 37/64

37

Intense competition has resulted in flat-rate plans ...

... leading to the real risk that margins will come under pressure

02

03

RECALL No 8 – Networks

Mobile Networks of the Future: Building a Sustainable Wireless Carrier Business Model

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 38/64

38

Migration options depend on spectrum availability and the urgency of

operators’ capacity needs04

low-volume applications that carry big margins

(e.g., machine-to-machine applications, location-based

services, low-bandwidth games) or t ime shift down-

loads (e.g., pushing music overnight or offering overnight

phone updates).

3. Operators should also look into building additional

network capacity more cheaply. In principle, the network

solution an operator chooses should depend largely

on spectrum availability and the urgency of the capacity need (Exhibit 4), in combination with operator- and

country-specific characteristics, such as topography,

existing spectrum, existing network investments, and

the wireless/wireline regulations.

* * *

While all three of the elements above are critical

to a sustainable business strategy, the following chapters

will delve more deeply into the third element, network

capacity – given the focus of this publication on technology.

In this area, operators typically have three options

when seek ing to cost-effectively boost wireless capacity:

Use smaller cells and/or more sectors. There is an

economic limit to how small a cell can be and also a

significant cost to taking this approach. The most

interesting recent development is that of femtocells

and the complementary use of wireless LANs (e.g.,

WiFi), which will off-load traff ic from macrocells.

Gain spectral efficiency through 4G. In light of

the current expectations from 4G and their current

3G networks, operators will want to carefully consider their next generation deployment strategy

and all respective trade-offs.

Explore new spectrum. Network, chipset, and CPE

vendors, whose innovations enable network

extensions to multiple spectra and standards, are

helping operators exploit new spectrum. Network

vendors, for example, are providing base stations

that offer flexible frequency and standard support.

Chipset makers continue to move towards multi-mode,

multi-band chipsets, while CPE suppliers offer

high-end phones that combine HSPA, WiMA X, and

WiFi in different bands. The availability of the

current analog TV spectrum within the next two to

three years presents brand-new capacity options.

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 39/64

39

Ferry Grijpink

is an Associate Principal in McKinsey’s

Amsterdam office.

Bart Delmulle

is an Associate Principal in McKinsey’s

Brussels [email protected]

Tanja Vaheri-Delmulle

is a Senior Research Analyst in McKinsey’s

Brussels office.

Suraj Moraje

is a Principal in McKinsey’s Johannesburg

office.

Stagg Newman

is an Advisor to the Global Telecoms

Practices in McKinsey’s Boston office.

RECALL No 8 – Networks

Mobile Networks of the Future: Building a Sustainable Wireless Carrier Business Model

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 40/64

8/2/2019 McKinsey Telecoms. RECALL No. 08, 2009 - High Growth

http://slidepdf.com/reader/full/mckinsey-telecoms-recall-no-08-2009-high-growth 41/64

41

Femtocells have continually grabbed the mobile world’s

headlines for over a year – and for good reason.

They could become the go-to technology for quick and

economical network expansion.

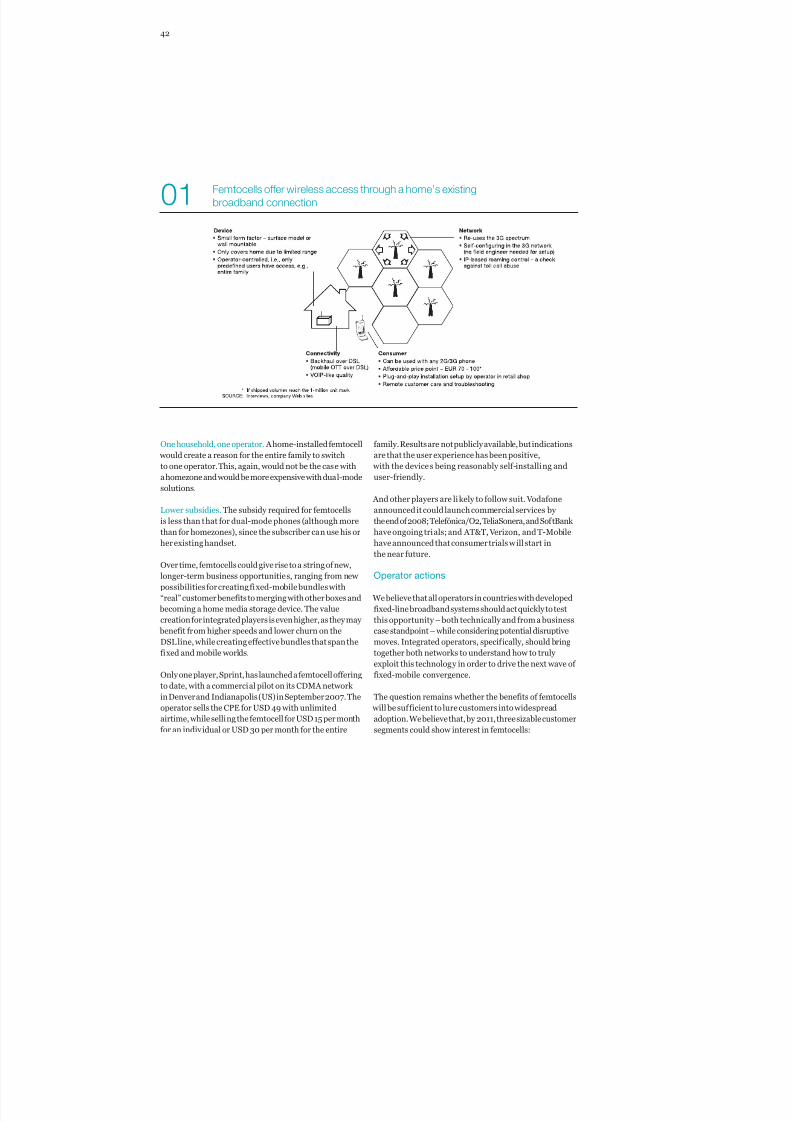

Femtocells, now in advanced field trials and early

commercial deployment, are low-power 2G and 3G home

base-station transceivers (analogous to WiFi hot spots,

but working on licensed spectrum) for consumers, with a

target cost of EUR 70 to 100 (Exhibit 1). They connect

a limited number of pre-defined users as determined by

the operator, using a home’s existing broadband

connection as backhaul to provide a 2G/3G mobile

connectivity directly inside the premises. Femtocells offer

a coverage range of 50 to 200 meters, provide up

to 7 Mbps of bandwidth, and feature plug-and-play

instal lation and remote troubleshooting access. In theideal world, they would be self-configuring within

an operator’s 3G network and capable of operating under

a range of standards.

Therefore, femtocells could feature lower costs and

better coverage than most other home-based technologies

and improve the data usage experience at home.

Furthermore, they can be used with the customer’s current

mobile handset and, therefore, avoid network handover

issues. However, femtocells do require additional customer

premises equipment (CPE), a broadband subscription,

and only offer voice over IP protocol (VoIP) quality

of service (QoS).

With the growing presence of mobile usage in the home

(e.g., almost 50 percent of usage in the US is either at

home or in the office, more than 75 percent of mobile

video usage in Japan is at home), the increased focus

on fixed-mobile convergence, and indoor coverage still

remaining a tough problem to solve, femtocells increasingly

appear to be a potential way forward for the industry.

Operator implications

We believe that from an operator standpoint, femtocells

could significantly improve customer value through

lower churn and higher ARPU, while providing new fixed-

mobile convergence possibilities. Femtocells could

also enable mobile network operators to reduce long-term