low income housing tax credits beyond the basics @dozcpa

TRANSCRIPT

Low Income Housing Tax Credits

Beyond the Basics

@dozcpa

Outline

• Credit Period versus Extended use period• Calculation of Low Income Housing Tax Credits• Tenant File Qualification• Upward and downward adjusters• Section 42 Recapture• Impact of New Repair Regulations on LIHTC• LIHTC Audit Technique Guide

Credit Period vs. Extended Use Period

• Credit Period – Section 42(f)(1) New Construction Acquisition/Rehabilitation – Section 42(f)(5)

• Extended Use Period – Section 42(h)(6)(D) Beginning on the 1st day in the compliance period on which such

building is part of a qualified low-income housing project, and Ending on the later of the date specified by such agency in such

agreement, or the date which is 15 years after the close of the compliance period.

Calculation of Low Income Housing Tax Credits

• High Cost Area (QCT)• Applicable Fraction• 70% P.V 9% Fixed vs. October 2014• Equity Pricing

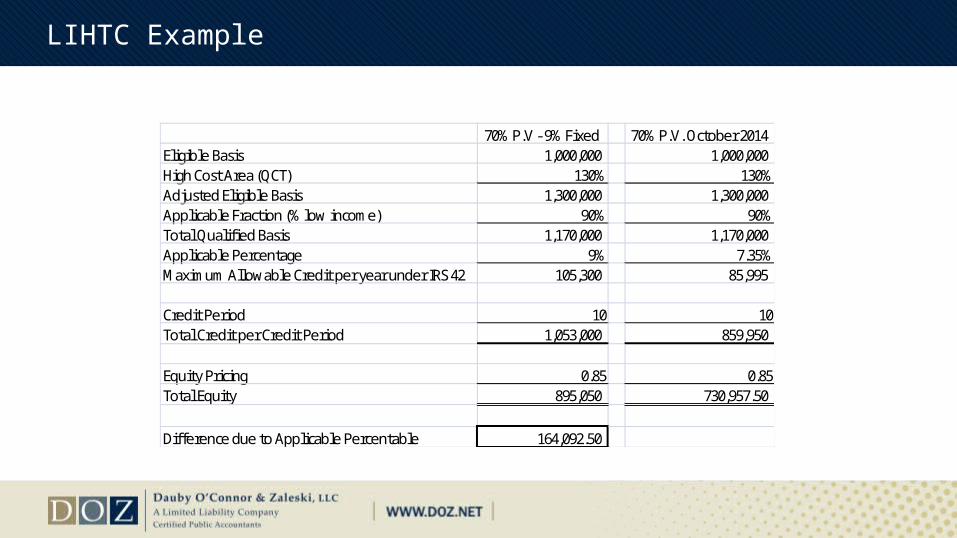

LIHTC Example

70% P.V - 9% Fixed 70% P.V. October 2014 Eligible Basis 1,000,000 1,000,000 High Cost Area (QCT) 130% 130%Adjusted Eligible Basis 1,300,000 1,300,000 Applicable Fraction (% low income) 90% 90%Total Qualified Basis 1,170,000 1,170,000 Applicable Percentage 9% 7.35%Maximum Allowable Credit per year under IRS 42 105,300 85,995

Credit Period 10 10Total Credit per Credit Period 1,053,000 859,950

Equity Pricing 0.85 0.85Total Equity 895,050 730,957.50

Difference due to Applicable Percentable 164,092.50

Tenant File Qualification

• New construction• Rehabilitation

120 day rule

• Initial Tenant File Qualification Report (AUP) Tenant Qualifications Elections

• Multiple Building Election• Credit Period – Section 42(f)(1)

Minimum Set-Aside

Upward and Downward Tax Credit Adjusters

• Causes Difference in eligible basis Timing of tenant move-in/re-certifications

• Impact on Internal Rate of Return

Section 42 - Recapture

• Recapture Qualified basis decrease from one year to the next Disposition of building

• Recapture is on the accelerated portion of the credits• Recapture allocation method• Provisions in Partnership/Operating Agreements

Recapture of accelerated credit - percentage

Tax Credit Recapture-Exceptions

• There are five general exceptions to the recapture rules: Posting a bond

• The Housing Act of 2008 eliminated the bond posting requirement for interest in building disposed of after July 30, 2008.

Originally claiming a reduced credit Receiving no tax benefit for the credit De minimis floor space changes Disposition due to casualty losses

State Reported Noncompliance

• All noncompliance found by the state agency must be reported to the IRS on Form 8823 This is regardless of whether the item was later corrected unless,

• Noncompliance issues were identified and corrected by the owner prior to notification of the upcoming review by the state agency, OR

• Noncompliance issues are related to state requirements that are in excess of the Federal Requirements

December 31st an Important Date

• Under Section 42(f)(1), a building’s credit period is the period of 10 years(120 months) beginning with the first day of the taxable year in which the building is placed in service or the succeeding tax year if the election under Section 42(f)(3)(8) is made.

• Example: a building is damaged by a casualty and fully restored within the same tax year, then there is no recapture and no loss of credits

Impact of New Repair Regulations on LIHTC

New Construction Rehabilitation Allocation of Building into 9 components Partial disposition Elections

LIHTC Audit Technique Guide

• Purpose of Guide• Difference between 8823 Guide and LIHTC Guide• Specific Sections

Questions?

Nancy Morton, [email protected]

Jeff Lathrop, [email protected]

Heather Plake, [email protected]

@dozcpa