Dr. René Kim, Tias van Moorsel and Prof. Ethan B. KapsteinReport 2013

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine

Dr. René Kim, Tias van Moorsel and Prof. Ethan B. KapsteinReport 2013

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 54

A panoramic view of the Ahafo mine

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 76

Table of ContentsABOUT THE AUTHORS 9

EXECUTIVE SUMMARY 10

1. INTRODUCTION AND OBJECTIVES 13 1.1 Introduction 13 1.2 Objectives 13 1.3 Scope 13

2. GHANA’S ECONOMY 15 2.1Nationalandregionaleconomicprofile 15 2.2 The Brong-Ahafo region 17 2.3 The mining sector in Ghana 17 2.4 Newmont Ghana’s operations 19

3. ECONOMIC MODELING & METHODS 21 3.1 Modeling of value added and employment impacts 21 3.2 Household survey 22

4. NGGL’S SOCIO-ECONOMIC IMPACT ON THE NATIONAL LEVEL 24 4.1 NGGL’s expenditures in Ghana 24 4.2 Value added 27 4.3 Employment 31 4.4 Comparison with the 2009 Report 34

5. NGGL’S SOCIO-ECONOMIC IMPACT ON THE BRONG-AHAFO REGION AND ASUTIFI DISTRICT 36

5.1NGGL’sexpendituresinBrong-Ahafo 36 5.2Valueadded 37 5.3Employment 39 5.4ComparisonofNGGL’simpactatthenational,regionalanddistrictlevels 41

6. IMPACT ON THE HOUSEHOLD LEVEL 43 6.1Migration 44 6.2Householdspending 45 6.3Businessactivities 46 6.4Education 48 6.5Accesstowaterandelectricity 50 6.6Overallchange 50

7. CONCLUSIONS AND RECOMMENDATIONS 55 7.1Conclusions 55 7.2Recommendations 55

LITERATURE 57

APPENDIX A: METHODOLOGY BACKGROUND 59 A.1Inputs 59 A.2Output 59 A.3Outcome 62

APPENDIX B: COMPARISON OF RESULTS WITH THE 2009 REPORT 63

APPENDIX C: SECTOR BREAKDOWN 66

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 98

About the AuthorsCompanyProfileStewardRedqueenisastrategyconsultancyfirmthataimstomakebusinessworkforsociety.Asspecialistssince2000,StewardRedqueenfocusesonintegratingsustainability,quantifyingimpact and facilitating change.

Clientsappreciateourrigorousanalysis,ourabilitytosolvecomplexproblems,andbeingaheadofthecurve.Weworkformultinationalcorporations,(development)financialinstitutionsand public sector organizations.

Socio-EconomicImpactAssessments(SEIA)Thecostsandbenefitsofforeigndirectinvestmentareoftencontestedbyvariousstakeholders.Thesedebates,however,arenotalwaysconductedonthebasisofallthefacts.ThepurposeofourSocio-EconomicImpactAssessments(SEIAs)istoprovidestakeholderswithadeeperunderstanding of the ways in which corporate operations contribute to value-added and employment generation in countries around the world. Using the best available modeling and data,weestablishafactualbasisforunderstandingtheimpactsofinvestmentdecisions.

Dr. René KimDr.RenéKimisfounderandpartnerofStewardRedqueen.Hehasworkedwithmanymultinationalcompaniesandprivateequityfundsinbothdevelopedandemergingmarkets.Previously,heworkedforTheBostonConsultingGroupinAmsterdamandasanacademicat the Massachusetts Institute of Technology. He has a PhD cum laude in Hydrology and Meteorology and is the author of many academic articles.

Prof. Ethan B. KapsteinProfessorEthanB.Kapstein,associatepartnerStewardRedqueen,iscurrentlyVisitingFellowat the Center for Global Development; Senior Advisor at the U.S. Institute of Peace; and Senior DirectorforResearchattheMcCainInstituteforInternationalLeadership,aWashington,DCthink-tankassociatedwithArizonaStateUniversity.ThisindependentReport,however,does not represent the views of these organizations. Previously he held the INSEAD Chair in PoliticalEconomyatINSEAD.HehasalsoservedinvariouspositionsatHarvardUniversity,theUniversity of Minnesota and the Organization for Economic Cooperation and Development. A formerinternationalbankerandnavalofficer,Prof.Kapsteinprovideseconomicandstrategyadvice to government agencies and many of the world’s leading multinational corporations. His latestbooksareAIDSDrugsforAll:SocialMovementsandMarketTransformations;EconomicJusticeinanUnfairWorld;andTheFateofYoungDemocracies.

TheauthorswereassistedbyTiasvanMoorsel,MSc,ofStewardRedqueen.ThesupplierandhouseholdsurveyswereconductedbyPABDevelopmentConsultantsLimitedinTema,Ghana.

Socio-EconomicImpactAssessmentTrackRecordSince2006,StewardRedqueenhascompletedmorethan50socio-economicimpactstudiesformultinationalminingcompanies,developmentfinanceinstitutions,multinationalfood&beveragefirms,banksandrecreationalorganizations,inAfrica,Asia,LatinAmericaandEurope.

Formoreinformation,pleasevisit: www.stewardredqueen.comA demonstration of agricultural success in a host community

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 1110

Executive SummaryGoldminingremainsamongthemostsignificanteconomicactivitiesforGhana,acountryonceknownastheGoldCoast.Notonlyistheminingsectorthelargesttaxcontributorofthecountry,italsoaccountsforabout40%ofmechanizedexports,whileattractingUSD780millionofinvestmentin2011andemployingover14,000peopledirectly.

Despitetheseimpressivestatistics,manystakeholdersinGhanastillholdunfavorableopinionsaboutthegoldminingsectoranddonotthinkithasapositiveimpactontheGhanaianeconomy. Some people believe that the sector operates as an “enclave” with few positive “spillover”effects,meaningthatfewwithinGhanabenefitfromgoldmining,whilemostoftheprofitsgooffshore.Unfortunately,thesecontroversiesoverminingareoftendebatedwithoutasolid foundation of empirical research.

Itwaswithinthiscontextthat,in2009,StewardRedqueencarriedoutasocio-economicimpactassessmentofNewmontGhanaGoldLimited’s(NGGL)operationsinGhana(theAhafomine).Makinguseofrigorousacademicmethodsincombinationwithmacro-economicandcompanydata,StewardRedqueenwasabletogenerateestimatesofthemine’seffectsonsuchmacro-economicvariablesasvalueadded(intermsofhouseholdincome,profits&savingsandtaxpayments)andemployment(intermsoffull-timeequivalentjobs).

Subsequently,severalstakeholderswhowereinvolvedinthisstudy,includingthePresident’sOfficeandvariousMinistries,theRegionalGovernment,theAsantehene(AshantiKing),theDistrictChiefExecutivesandGhanaiancivilsocietyorganizations,expressedaninterestinresults that not only captured the impact of the mine on the national but also on the regional level.ThatiswhyfromMarch2012uptoApril2013,StewardRedqueenexecutedthisfollow-up study which focuses on the national and regional impacts of the Ahafo Mine.

The national and regional results presented in this Report were obtained using an economic modelwhichisbasedoninput-outputanalysis,NGGL’s2011financialsandasurveyoflocalsupplierstotheAhafomine.Twoaspectsofeconomicimpactsarecentralinthisreport:valueadded,i.e.thesumofsalaries,profitsandtaxesinGhana,andjobs.Althoughmuchofthe value added and many of the jobs described in this report are to a considerable extent supportedbyNewmont,theyarenotcreatedbyNewmontalone.

Inadditiontothedevelopedeconomic,ahouseholdsurveywasconductedtoassesstheimpacttheminehashadonelementssuchasmigration,housing,income,educationandaccess to utilities for households living in its vicinity.

ThisReportshowsthatNGGLonanationallevel: • SupportsUSD360millionvalueaddedintermsofeconomicactivity(0.95%ofGDPfor

Ghana),ofwhichUSD230millionisdirectlyattributabletoNGGL(0.60%ofGDPforGhana);

• ContributesdirectlyUSD160milliontogovernmenttaxincome(2.56%ofnationaltaxrevenuesofGhana),USD39milliontohouseholdincomesandUSD31millionascarriedinterestincometothegovernment(tobepaidwhendividendsaredeclaredbyNGGL);

• Supports41,000jobs(0.39%ofthetotallaborforceinGhana),ofwhich1,921jobsaredirectlyattributabletoNGGL(0.02%ofthetotallaborforceinGhana);

• Valueaddedhasgrownby135%since2009butthenumberofjobsdeclinedby15%; • FromavisualimpressionofthepathwaysthroughwhichNGGL’sspendingtrickles

throughtheeconomy,weconcludethatforamine,itisrelativelydeeplyconnectedtotheGhanaian economy.

ApartofthiseconomicimpactiscreatedintheBrong-Ahaforegion(theregionwithinwhichtheAhafomineislocated),whichishometo10%oftheGhanaianpopulationandcontributesapproximately10%toGhana’sGDP.ThisReportshowsthatNGGLonaregionallevel: • SupportsUSD31millionvalueadded(0.78%ofregionalGDP),ofwhichUSD15million

isdirectlyattributabletoNGGL(0.38%ofregionalGDP); • Contributes directly USD 3 million in tax payments and USD 12 million in household

incomes in 2011; • Supports8,700jobs(0.86%oftheregionallaborforce).

TheimpactofNGGLintheAsutifidistrictoftheBrong-AhaforegionwheretheAhafoMineislocatedismuchlarger;approximately8%ofthedistrict’s(estimated)GDPand10%of(estimated)employment.TheNewmontAhafoDevelopmentFoundation(NADeF)amplifiesthiseconomiceffectwithanother23%intermsofvalueadded.

ThemainconclusionsregardingNGGL’slocalimpactonhouseholdsare: • NGGL’spresenceanditsneedforskilledlaborhascausedin-migrationofpeoplefrom

outsidetheregioninsearchofworkatthemine,leadingtohigherpricesforproductsand services in the region;

• NGGL’seconomicimpacthastranslatedintohigherdisposableincomeforitsemployees,who spend almost twice as much as people outside NGGL’s catchment area. HouseholdswithoutmembersthatworkdirectlyforNGGL(includingNGGL’scontractors)andwhomresideinthecatchmentareahave11%moretospendthanhouseholdsoutside the catchment area;

• Inevitably,butneverthelesssomewhatworrying,theminehascreatedacertaindependence of people within the catchment area of the mine as they are less engaged in other economic activities than people outside the catchment area;

• A majority of people in the catchment area believe that the overall situation has improved sinceNGGL’sarrival,withpeopleemployedbyNGGLholdingfavorableopinionsbutthepeoplewhowereresettledmostlynegativeones.Toacertainextent,theNewmontAhafoDevelopmentFoundationhascontributedtothisoverallimprovementbydeliveringinfrastructuralandsocialamenitiesincludingcommunitylibraries,teachers’andnurses’quarters,ICTcentersandschoolbuildingsforthecommunities.

ThemainrecommendationsforNGGLarethecontinuation,andwherepossible,intensificationof local sourcing and business activities. Although the low-hanging fruit may already have been picked,wethinktherearestillareaswhereNGGLtogetherwithitssuppliersandcontractorscan bring about positive changes. We also recommend that NGGL conveys its most successful

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 1312

programstotheAkyemmineinordertoreproducethepositiveimpactsthatarecurrentlygenerated at the Ahafo mine.

ConsideringGhana’sincreaseddependencyonresource-relatedincome,werecommendthattheGovernmentdevelopplansforeconomicdiversificationtohelpitprepareforleanertimeswhen commodity prices are lower or resources become depleted. The Government may wish toemphasizetheneedfordiversificationinregionswheredependencyonminingisgreatest.Inmanyminingregions,forexample,agriculturehasalsobeenatraditionaloccupationoflocalresidents.

Investing in increasing the productivity of agricultural lands—including the development of a stronger property rights regime and access to credit and inputs for farmers—could be among the policies that the Government might contemplate.

1. Introduction and Objectives1.1 IntroductionIn2011,NewmontGhanaGoldLimited(NGGL)launcheditssocio-economicimpactstudyoftheAhafominingoperationinGhana’sBrong-AhaforegionandAsutifidistrict.Thekeyfindings,whichwerebasedonNGGL’s2009financialdataalongwiththemostrecenteconomicinformationonGhana(priortotherevisionsofGDPthatweresubsequentlymadebytheGhanaStatisticalService(GSS)),indicatedthat: 1. NGGLisamajorcontributortoGhana’seconomy,generatingnearly10%ofthenation’s

totalexports;4.5%ofitstotalforeigndirectinvestmentand1.3%ofGDP; 2. NGGLdirectlyandindirectlysupportedsome48,000jobsinGhana; 3. NGGLplayedasignificantdevelopmentalroleinthecommunitiesaroundtheAhafoMine

andin2009aloneprovided99regionalcompanieswithnearlyUSD6millionincontracts,supportingmorethan400jobs,notincludingdirectemployment.

Subsequently,severalstakeholderswhowereinvolvedinthisstudy,includingthePresident’sOfficeandvariousMinistries,theRegionalGovernment,theAsantehene(AshantiKing),theDistrictChiefExecutivesandGhanaiancivilsocietyorganizations,expressedaninterestinresults that not only captured the impact of the Mine on the national but also on the regional level.

1.2 ObjectivesNGGL therefore requested this follow-up Report to quantify the economic impact of its activities onGhana,theBrong-AhaforegionandtheAsutifidistrictinwhichitoperatestheAhafomine.ThefollowingquestionsareaddressedinthisReport: • Whatisthetotalsocio-economicimpactofNGGLinGhanaintermsofsalaries,taxes,

profitsandemployment? • HowmuchofthatimpactisachievedintheBrong-AhaforegionandtheAsutifidistrict? • What has changed for the households in the vicinity of the Ahafo mine since the start of

production? • IsGhanamakinggooduseofitsgoldwealthtoaidintheprocessofregional

development? • IsNGGLaneffectivepartnerineconomicdevelopmentintheregionanddistrict?

1.3 ScopeTheReportdistinguishesbetweenthedirect,indirectandinducedsocio-economicimpactofNGGLinGhana.Thesocio-economicimpactiscapturedbyvalueadded(householdincome,profits&savingsandgovernmentincome)intermsofadditionaleconomicactivityandjobssupportedaswellasbasedonmorequalitativefindingsfromthesurveysconducted.Intermsofgeographicfocus,theresultsareshownonthenational(Ghana),regional(Brong-Ahafo)anddistrict(Asutifi)level.

The Ahafo Mine

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 1514

The important question regarding the social and health/environmental impacts of mining is notpartofthisReport.Thisomissionisintentionalasthequantificationoftheseimpactswouldinvolveadifferenttypeofanalysis.Althoughsomeworkhasbeendonetoexpressenvironmentalimpactsinfinancialterms,thesocio-economicandenvironmentalimpactsarenotdirectlycomparable.Yetbothareimportant.ThisReporthoweverfocusesonjobsandeconomicimpactonthenational,regionalanddistrictlevelandnotontheenvironmentalimpacts. In recognition of the importance of the social and health/environmental impacts of the mine,NGGLcommissionedseparateindependentstudiesonthesetwoareasalongsidethisstudy on jobs and economic impact.

ThisReportisdividedintosevensections.Followingthisintroduction,Section2describesGhana’sandBrong-Ahafo’seconomy,theminingsectorandNewmontGhana’soperations.Section 3 summarizes the methodology and economic model used and after that Section 4 focusesonthesocio-economicimpactatthenationallevelandcomparesthefindingswiththepreviousReport.Section5thendescribesNGGL’ssocio-economicimpactontheBrong-AhaforegionwhileSection6outlinesNGGL’simpactsonthehouseholdsresidingintheregionand district where the Ahafo mine is operating. Section 7 concludes this report and gives recommendations.

2. Ghana’s Economy2.1 NationalandRegionalEconomicProfileWithanaverageeconomicgrowthrateof6.9%overthelast10yearsand14.4%in2011,Ghana’s economy has been growing more rapidly than the Sub-Saharan continent as a whole. UnlikemanyotherSub-Saharaneconomiesthatdependheavilyuponasinglecommodity,Ghanaisrelativelydiversifiedamongagriculture,industry,commodities,andservices.Table1showsthat23.9%ofGDPoriginatesfromagriculture,24.1%fromindustriesand45.3%fromservices.The6.3%ofGDPthatstemsfromcrudeoiloftheJubileefieldcouldtilttheeconomicbalance more towards commodities. This is a source of concern as resource dependence can translate into the so-called “resource curse.”

Ghana’stradedeficithasbeenstableataround13%ofGDP(seeExhibit1)asimports,mainlycapitalequipment,petroleumandfoodproducts,increasedasfastasexports.Thisdeficitmaydecreasewhenoilexportsrise,butofcoursethatwillalsobeafunctionofthepriceofcrudeoilonglobalmarkets.Goldcontributesmosttothecountry’sexportsamountingtoUSD4.9billion(almost34%oftotalexports)andwithits2.8%shareofworld-wideproductionGhanaistheworld’s10thlargestgoldproducer.However,duetothepricedeclinein2013,goldwilllikelycontribute less to export revenues.

Inrecentyears,Ghanahastakenimportantstridestoimproveitsbusinessclimate,encouraginggreater foreign direct investment and private sector participation in the economy. The World Bank’s“DoingBusiness2013”rankingputsGhana64th,downonepositionfromlastyear.Whilethissuggeststhatmoreneedstobedonetomakethecountryanattractiveplacetodobusinessonaglobalscale,therecentimprovementshaveplacedthecountryamongAfrica’sleading reformers.

Theincreasingforeigndirectinvestments(FDI),showninExhibit2,confirmthisalthoughmuchoftheFDIwastotheminingandoil&gassectors.Grosscapitalformation,i.e.theinvestmentinfixedassetsownedbyhouseholdsandcompaniesfluctuatesbuttrendsslightlydownward.Considering the current oil boom there is a strong economic rationale for more investment however. Constraints to further development mentioned by companies areaccesstofinanceandelectricity(intermsofavailabilityandreasonableprice).

Aseconomicgrowthoutstrippedpopulationgrowth,GrossNationalIncome(GNI)percapitahassteadilyincreased(Exhibit3)butinequalityislarge.AlthougharelativelybrightspotinSub-SaharanAfrica,Ghana’srankingontheHumanDevelopmentIndex(135outof187)remindsusthatthecountry’ssocialwelfaremustcontinuetoadvanceforthebenefitofallGhanaians.

High rise buildings in a business district in Ghana

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 1716

TABLE1: Key indicators of the Ghanaian economy 20111

GHANA BRONG-AHAFOREGIONA

Population (estimated) 25.3million 2.4 million

Labor force (estimated) 10.6million 1.0 million

Gross Domestic Product USD38.1billion USD 3.9 billion

GDP per capita USD1,507 USD1,653

GDP growth 14.4%

GDP by economic activity:

Agriculture 23.9% 46.1%

Industry 24.1% 15.0%

Mining 1.6%B 3.0%

Oil 6.3% -

Services 45.3% 32.2%

Indirect tax revenue 6.7% 6.7%

GDP by expenditureC:

Household consumption 77.8%

Government consumption 12.5%

Investments 24.5%

Exports 38.4%

Imports 51.7%

Tax Revenue USD6.3billion

Government Budget:

Revenue USD7.5billion

Expenditure USD8.6billion

Ease of doing businessD 64

Human Development IndexE 135outof187

1 GhanaStatisticalServices,BankofGhana,WorldBank,EaseofDoingBusinessIndex,HumanDevelopmentIndex,OxfordPovertyandHumanDevelopmentInitiative.

A Blanksindicatenoregionaldataisavailable.B Thefigureof1.6%appearsverylow.Taxespaidbytheminingsectoralreadyrepresent2.5%ofGDP.When

includingsalariesweestimatethattheGDPcontributionisaround3%insteadofthe1.6%.C ReportedaspercentageofGDP.Thisbreakdowndoesnotaddupduetostatisticaldiscrepanciesreportedby

the Ghana Statistical Service. This is not uncommon with African statistics and does not impact the validity of the results in this Report.

D The Ease of Doing Business Index provides measures of business regulations and their enforcement across 185economiesthatindicateifitiseasytodobusinessinaspecificcountry(http://www.doingbusiness.org/).This is for the year 2013.

E TheHumanDevelopmentIndex(http://hdr.undp.org/en/humandev/)isanindexthatmeasureslong-termprogressinthreebasicdimensions:long/healthylife,accesstoknowledgeanddecentstandardofliving.Thisis for the year 2012.

2.2 The Brong-Ahafo RegionBrong-AhafoissituatedinthemiddleofGhanaandishometo10%ofGhana’spopulation.Theregionformsthetransitionbetweenthewealthier(Southern)andpoorer(Northern)partsofthecountry.ItisnotsurprisingthereforethatTable1showsthatmacro-economically,theregionisnottoodissimilarfromGhanaoverall:GDPpercapitaisslightlyhigher,butsoistheincidenceofpoverty.Themaindifferenceisthattheregion’seconomyrelieson(subsistence)agricultureto a much greater extent than the rest of Ghana.

2.3 The Mining Sector in GhanaAsshowninTable1,theextractiveindustries,oilandmining,makeupabout8%ofGhana’sGDP.2011wasthefirstfullyearinwhichGhanabenefitedfromoilproduction,whichthereforewasresponsibleformostofGhana’seconomicgrowth.Theminingsub-sector,dominatedbygold,grewby14.3%in2011,thehighestgrowthaftertheoilandconstructionsectors.Themain driver of this growth was the average price of gold which increased from on average USD 1,129perouncein2010toUSD1,583perouncein20112. This increase in the price of gold morethanmadeupforthedeclineinproduction,whichfellby2%from2.97millionouncesin2010 to 2.92 million in 2011. Although it is not a measure of the all-in sustaining cost of mining onaperouncebasis,theaveragecashcostofUSD751perouncewasabout17%higherthantheglobalaverageofUSD643,largelyduetoexpensiveelectricpower,laboranddiesel.Nevertheless,investmentintheminingsectorwentupslightlyfromUSD770millionin2010toUSD780millionin2011.

2 Factoid2011,ChamberofMines.

EXHIBIT1:ImportsandexportsofgoodsandservicesandGhana’stradedeficitaspercentageofGDP.Source:WorldBankDatabase80%

60%

40%

20%

0%

-20%

-40%

1995 1997 1999 2001 2003 2005 2009 2011

Imports(%ofGDP) Exports(%ofGDP) TradeDeficit(%ofGDP)

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 1918

In2011,theminingsectormaintaineditspositionasthelargesttaxcontributor,withtotaltaxpaymentsofapproximatelyUSD640million3. Higher gold royalty payments and the fact that more mining companies are now paying corporate income tax has led to a growth in tax payments which will increase in 2012 due to the average increase of gold prices but also due tothedecisionoftheGovernmentofGhanatochangefiscalpoliciesfortheminingindustry,includinganincreaseinthecorporatetaxratefrom25%to35%.

Theminingsectoremploys14,257personsdirectly(ofwhich235areexpatriates)4. Compared to2009,thisisareductionof17.6%,whereasgoldproductionincreasedby0.8%.Notincludedintheabovefiguresaretheillegalandinformalmining(Galamsey)activitiesthatcontinued to grow in 2011. These activities do not only harm other miners who have to protect theirownconcessions,butalsopolluteanddestroypubliclandandwaterbodies.

3 Factoid2011,ChamberofMines.4 Factoid2011,ChamberofMines.

EXHIBIT2:Gross Capital Formation(GCF)andForeignDirectInvestment(FDI)as percentage of GDP. (Source:WorldBankDatabase)

EXHIBIT3:Growth of real Gross National Income(GNI)percapita in current USD.(Source:WorldBankDatabase)

2.4 Newmont Ghana’s OperationsMiningatAhafocommencedin2006andNGGLcurrentlyoperates4openpits.Theminingleasecovers774squarekilometersbuttheactualminingarea,locatedintheAsutifidistrictsouthofSunyani(Exhibit4),coverslessthan2%ofthelease.Inadditiontotheopenpits,NGGL is investigating the viability of a potential underground mine. The process plant consists of a conventional mill and carbon-in-leach circuit. The expansion of the mill is being considered andthecosteffectivenessofbringingtheexpansionforwardiscurrentlybeinginvestigated,but it could be delayed with the current low gold prices. Ahafo’s proven and probable gold reserves,asof31December,2011,wereestimatedat12millionounces.5

In2011,theAhafoMineproduced566,000ouncesofgold,equivalentto19.4%ofGhana’stotalproduction.Thisis21,000ouncesmorethanthepreviousyearand34,000ouncesmorethanin2009.NGGL’srevenueswereUSD869millionor18.8%oftotalgoldrevenueofthecountry.NewmontGhanaemployed2,229peopledirectly,1,729ofwhichworkattheAhafosite,192inAccraand308inAkyem.NGGL’ssistercompany,NewmontGoldenRidgeLimited(NGRL),constructedanopenpitmineinAkyemanditpoureditsfirstgoldinOctober2013.

5 2011ReservesandNon-ReserveMineralization,Disclosesin2011AnnualReportofNewmont

Workers of NGGL at the mine1995 1997 1999 2001 2003 2005 2009 2011

35%

30%

25%

20%

15%

10%

5%

0%

ForeignDirectInvestment,NetInflow(%ofGDP)GrossCapitalFormation(%ofGDP)

1995 1997 1999 2001 2003 2005 2009 2011

2000

1800

1600

1400

1200

1000

800

600

400

200

0

GNIpercapita(currentUSD)GNIpercapita,AtlasMethod(currentUSD)

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 2120

EXHIBIT4:Map of Ghana with the red stars indicatingthelocationsoftheAhafo(nearSunyani)andAkyem(nearKoforidua)Mines.

EXHIBIT5:MapoftheBrong-AhaforegionandtheAsutifidistrictwith the red star indicating the location of the Ahafo Mine.

3. Economic Modeling & Methods3.1 Modeling of Value Added and Employment ImpactsTo assess the socio-economic impact of NGGL’s operations on the national and regional level,wemakeuseofinput-outputmodeling.Simplystated,aninput-outputmodelprovidesa‘roadmap’ofaneconomy,showingtheinter-linkagesbetweenvarioussectors.WedriveNGGL’sfinancialdatathroughthemodelinordertounderstandhowNGGL’srevenuesandexpendituresimpactonothereconomicagents,includingthegovernmentviataxpaymentsand other receipts such as royalties.

EXHIBIT6:Overview of the modeling approach

Company Financials Allocation of P&L items to 13 Economic Sectors

National and Regional Social Accounting Matrix for 13 Sectors (SAM)

Estimated Expenses and Value Added for NGGL on National and Regional Level

Value Added and Employment Multipliers per Sector

Direct and Indirect Effects NGGL on Value

Added and Employment in Ghana and Brong-Ahafo

Employment intensities for 13 Economic Sectors

Supplier Survey

Household Survey

GTAP Data on 57 Economic Sectors

Employment Data for 13 Economic Sectors

INPUT OUTPUT OUTCOME FINAL RESULT

Exhibit6summarizesourapproachinwhichwecombineNGGL’sfinancialswithmacro-economic data to come up with results in terms of value added and employment impact of NGGL on Ghana and Brong-Ahafo. Appendix A discusses the modeling approach in more detail as well as the assumptions made.

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 2322

EXHIBIT 7:Direct,indirectandinducedeffectsonvalueaddedandemploymentdividedintofour rounds

EXHIBIT8:TheAsutifidistrictintheBrong-Ahaforegion(numbersinsidethefiguresindicatethenumberofhouseholdsinterviewed)

Exhibit 7 shows the rounds of impact that we distinguish in this Report. The rounds of impacts are(i)NGGL’sdirectimpact,(ii)thevaluechainimpact(includingsuppliers)and(iii)thetotalimpact(includingimpactsinducedbythere-spendingofsalaries).Withrespecttovalueadded,inducedresultsarenotincludedasitwouldconstituteadoublecounting(i.e.salariesarecountedtwice;oncewhentheyareearnedandoncewhentheyarespent).Inducedemploymentdoesnotsufferfrom double counting and is therefore included throughout this Report.

3.2 Household SurveyAhouseholdsurveywasconductedtoenrichtheeconomicmodelwithmorespecificandreliable household expenditure data as well as to get a more qualitative picture of how the householdsintheregionasawholeandintheAsutifiandTanoNorthdistrictsinparticular,havebeenaffectedbytheAhafoMine.Inco-operationwiththeGhanaianconsultingfirmPABDevelopmentConsultantsLimited(PAB),the survey was structured such that more detailed information about the impact of NGGL’s presence at the household level could be obtained. This was done through interviews with a representativesampleof284householdsinthreesub-groups: • 100householdsthathaveatleast1personworkingforNGGLandthataresituatedin

the catchment area of the Mine; • 94householdswithoutmembersthatworkforNGGL,butwhicharelocatedinthe

catchmentareaoftheMine(ofwhich30wereresettled); • 90householdswithoutmembersthatworkforNGGLandarelocatedoutsidethe

catchment area of the Mine.

Direct (0th Round) Impact - NGGL:Effects directly related to local expenditures of NGGL

Indirect (1st Round) Impact - Direct Suppliers and Trade:Effects arising at suppliers and retailers in the value chain of NGGL.

Indirect (2nd Round) Impact - Suppliers’ suppliers:Effects that come about as suppliers inside the original value chain of NGGL procure goods and services from suppliers outside the original value chain of NGGL.

Indirect (3rd Round) Impact - Re-Spending of Salaries:Effects caused by the re-spending of salaries throughout the economy by employees of NGGL, its trade partners and suppliers’ suppliers whose jobs are directly or indirectly supported by NGGL. The effects of re-spending of salaries are only captured in terms of employment.

Direct

Value Chain

NG

GL’s Total Im

pact

Forpracticalpurposes,thecatchmentareaoftheAhafoMinewasdefinedasthosecommunitiesthataredirectlyaffectedbytheMine,mostofwhicharelocatedtheAsutifiandTanoNorthdistrictsinBrong-Ahafo(Exhibit5).Exhibit8showsthelocationofthehouseholds,how many people have been surveyed and the three distinct groups in order to more clearly delineatetheimpactofNGGL.IncollaborationwithNGGLandPAB,thehouseholdsinthesample were chosen such that they were representative of the population from which they wereselected.Thesizeofthesamplesizeissuchthatwithaconfidencelevelof95%theerrormarginoftheresponsesisplusorminus5%.

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 2524

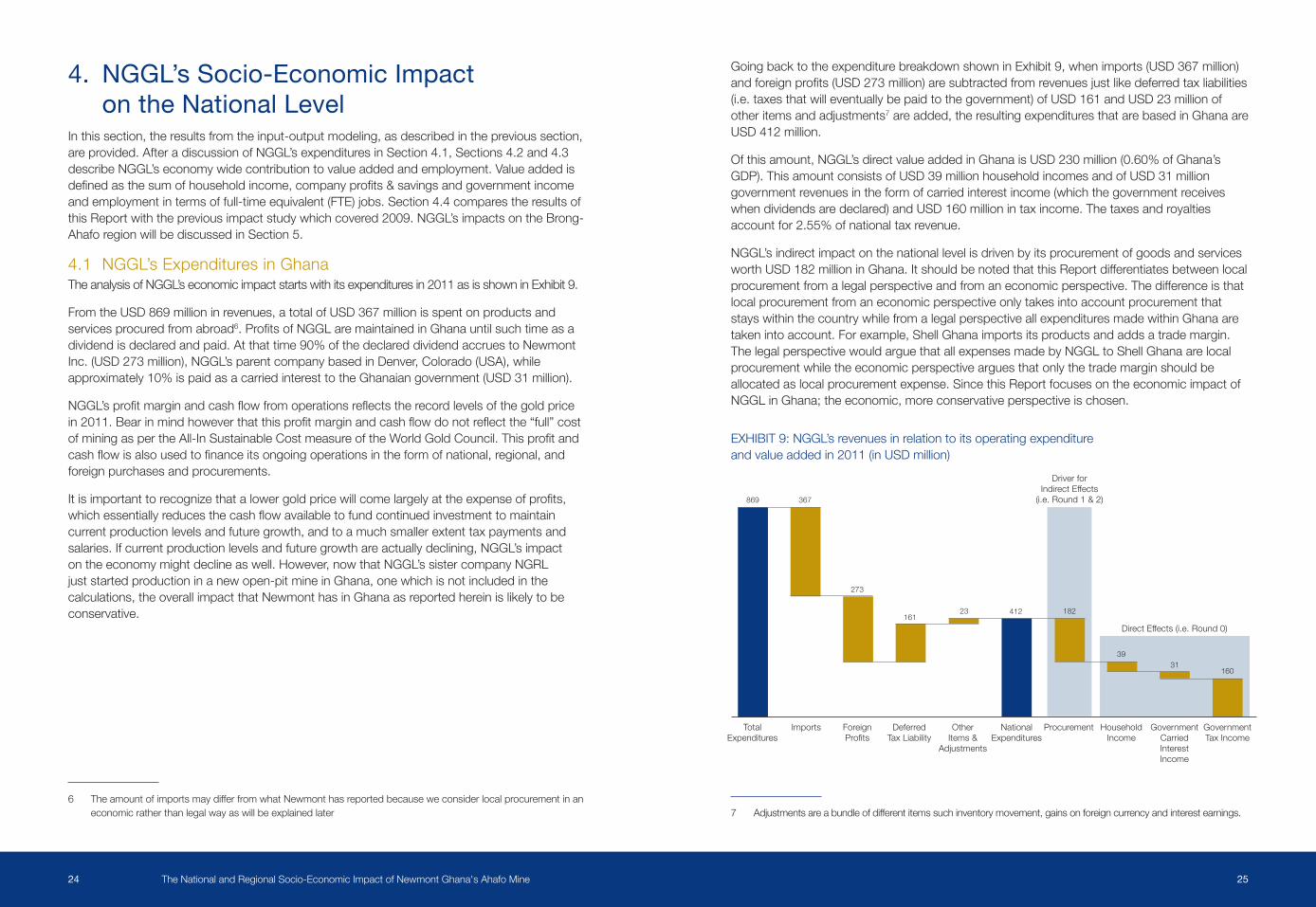

GoingbacktotheexpenditurebreakdownshowninExhibit9,whenimports(USD367million)andforeignprofits(USD273million)aresubtractedfromrevenuesjustlikedeferredtaxliabilities(i.e.taxesthatwilleventuallybepaidtothegovernment)ofUSD161andUSD23millionofother items and adjustments7areadded,theresultingexpendituresthatarebasedinGhanaareUSD 412 million.

Ofthisamount,NGGL’sdirectvalueaddedinGhanaisUSD230million(0.60%ofGhana’sGDP).ThisamountconsistsofUSD39millionhouseholdincomesandofUSD31milliongovernmentrevenuesintheformofcarriedinterestincome(whichthegovernmentreceiveswhendividendsaredeclared)andUSD160millionintaxincome.Thetaxesandroyaltiesaccountfor2.55%ofnationaltaxrevenue.

NGGL’s indirect impact on the national level is driven by its procurement of goods and services worthUSD182millioninGhana.ItshouldbenotedthatthisReportdifferentiatesbetweenlocalprocurementfromalegalperspectiveandfromaneconomicperspective.Thedifferenceisthatlocalprocurementfromaneconomicperspectiveonlytakesintoaccountprocurementthatstays within the country while from a legal perspective all expenditures made within Ghana are takenintoaccount.Forexample,ShellGhanaimportsitsproductsandaddsatrademargin.The legal perspective would argue that all expenses made by NGGL to Shell Ghana are local procurement while the economic perspective argues that only the trade margin should be allocated as local procurement expense. Since this Report focuses on the economic impact of NGGLinGhana;theeconomic,moreconservativeperspectiveischosen.

7 Adjustmentsareabundleofdifferentitemssuchinventorymovement,gainsonforeigncurrencyandinterestearnings.

4. NGGL’s Socio-Economic Impact on the National Level

Inthissection,theresultsfromtheinput-outputmodeling,asdescribedintheprevioussection,areprovided.AfteradiscussionofNGGL’sexpendituresinSection4.1,Sections4.2and4.3describe NGGL’s economy wide contribution to value added and employment. Value added is definedasthesumofhouseholdincome,companyprofits&savingsandgovernmentincomeandemploymentintermsoffull-timeequivalent(FTE)jobs.Section4.4comparestheresultsofthis Report with the previous impact study which covered 2009. NGGL’s impacts on the Brong-AhaforegionwillbediscussedinSection5.

4.1 NGGL’s Expenditures in GhanaThe analysis of NGGL’s economic impact starts with its expenditures in 2011 as is shown in Exhibit 9.

FromtheUSD869millioninrevenues,atotalofUSD367millionisspentonproductsandservices procured from abroad6.ProfitsofNGGLaremaintainedinGhanauntilsuchtimeasadividendisdeclaredandpaid.Atthattime90%ofthedeclareddividendaccruestoNewmontInc.(USD273million),NGGL’sparentcompanybasedinDenver,Colorado(USA),whileapproximately10%ispaidasacarriedinteresttotheGhanaiangovernment(USD31million).

NGGL’sprofitmarginandcashflowfromoperationsreflectstherecordlevelsofthegoldpricein2011.Bearinmindhoweverthatthisprofitmarginandcashflowdonotreflectthe“full”costofminingaspertheAll-InSustainableCostmeasureoftheWorldGoldCouncil.Thisprofitandcashflowisalsousedtofinanceitsongoingoperationsintheformofnational,regional,andforeign purchases and procurements.

Itisimportanttorecognizethatalowergoldpricewillcomelargelyattheexpenseofprofits,whichessentiallyreducesthecashflowavailabletofundcontinuedinvestmenttomaintaincurrentproductionlevelsandfuturegrowth,andtoamuchsmallerextenttaxpaymentsandsalaries.Ifcurrentproductionlevelsandfuturegrowthareactuallydeclining,NGGL’simpactontheeconomymightdeclineaswell.However,nowthatNGGL’ssistercompanyNGRLjuststartedproductioninanewopen-pitmineinGhana,onewhichisnotincludedinthecalculations,theoverallimpactthatNewmonthasinGhanaasreportedhereinislikelytobeconservative.

6 TheamountofimportsmaydifferfromwhatNewmonthasreportedbecauseweconsiderlocalprocurementinaneconomic rather than legal way as will be explained later

EXHIBIT9:NGGL’s revenues in relation to its operating expenditure andvalueaddedin2011(inUSDmillion)

Total Expenditures

Imports Foreign Profits

Deferred Tax Liability

Other Items&

Adjustments

National Expenditures

Procurement Household Income

Government Carried Interest Income

Government Tax Income

869 367

Driver for IndirectEffects

(i.e.Round1&2)

DirectEffects(i.e.Round0)

273

16123 412 182

3931

160

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 2726

4.2 Value AddedExhibit10showsabreakdownoftotalvalueaddedsupportedbyNGGLintheGhanaianeconomy:householdincomes,companyprofits&savingsandgovernmentincome.Together,thesecomponentsadduptoUSD360million8,whichisequalto0.95%ofthetotalGhanaianeconomy.Thisisanincreaseof107%comparedtothe2009totalvalueaddedsupported(formoredetailsseeAppendixB)andadecreaseof6%intermsofcontributiontoGhana’sGDP9. TheUSD208milliongovernmentincome(USD191millionofcarriedinterestincomeandtaxincomepaidbyNGGLdirectlyandUSD18millionpaidbyitssuppliers)constitutesthebiggestvalueaddedcomponent;followedbytheUSD135millionofsalariespaidbyNGGLanditssupplierstoGhanaianhouseholds.Profits&savingsoflocalsuppliersareasmallcomponentwithUSD17million(notethatNGGL’sprofitsaccruetoitsparentcompanyabroad).OftheUSD360milliontotalvalueadded,USD230millionisgenerateddirectlybyNGGL,largelyinthe form of royalties and taxes.

8 Maynotsumupduetorounding.9 ThesignificantincreaseinGhana’sGDP(60%)isthereasonwhyNGGL’srelativecontributiontoGDPdeclined.

ThissignificantincreaseinGhana’sGDPestimateisduetoarevisioninthemethodologythatestimatesGhana’sGDP(SeeJerven&Duncan,2012).

A local signage vendor of NGGL in Ahafo

EXHIBIT10:Directandindirecteffectsonvalueadded(inUSDmillion)

Household Income

Private Sector Profit&Savings

Government Carried Interest Income

Government Tax Income

Total

0.60% of GDP

0.95%of GDP

39

62

33

31

160

47

83

230

13517

31

178 360

2ndRound:Suppliers’Suppliers1stRound:DirectSuppliersandTrade0thRound:NGGL

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 2928

Exhibit 12 shows the sectors where the value added is created. Apart from NGGL’s direct value contribution,mostvalueaddedisfoundintheconstructionsectorduetothenatureofthebusiness which requires the company to hire contractors for construction and maintenance of itsinfrastructure.Withtheexceptionofagriculture,thevalueaddedisfairlyevenlyspreadoverthe other economic sectors. The reason for this is that Newmont procures goods and services fromquiteanumberofdifferentsectorswhichthensourceaportionoftheirsuppliesfromwithinGhana,reflectingtherelativediversifiednatureofGhana’seconomy.

Exhibit11showsadetailedbreakdownoftheUSD178milliontotaltaxpaymentstothegovernment.Thelion’sshareofthesetaxesamountingtoUSD160million,arepaiddirectlybyNGGLitself.AnotherUSD18millionisgeneratedbyNGGL’ssuppliers,ofwhichUSD7millionis actually paid by NGGL as withholding tax. The withholding tax enables the government tomoreeffectivelycollecttaxessinceNGGLiseasytofindincomparisontoallthe(smaller)suppliersofNGGL.ThefactthatNGGLpaysover90%ofthetaxesofitsentirevaluechainunderscoresGhana’srelativelysmalltaxbaseandthedifficultyofcollectingtaxesfrominformalcompanies10.ThetotaltaxpaymentsofNGGL’svaluechainmakeupslightlylessthan3%ofGhana’stotaltaxrevenues.TheUSD160milliontaxespaidbyNGGLalonerepresentabout25%ofthetotaltaxespaidbytheminingsectorinGhana.11

10 NGGLprocuresitsgoodsandservicesfromtheformalsector,butthesuppliersofNGGL’ssuppliershaveahigherprobability of operating in the informal sector and thereby foregoing tax payments.

11 Factoid2011,ChamberofMines.TheChamberofMinesestimatesthataboutGH¢1billionorUSD640millionispaid by the mining sector to the government in the form of taxes.

EXHIBIT12:DirectandindirecteffectsofNGGLonvalueaddedpersector(inUSDmillion)

EXHIBIT11:Directandindirecteffectsontaxes(inUSDmillion)F

F TheNationalFiscalStabilizationLevy(NFSL)isanadditional5%onaccountingprofitsofspecifiedcompaniesandinstitutionsinGhanainordertoreduceGhana’sgrowingdeficit.

2ndRound:Suppliers’Suppliers1stRound:DirectSuppliersandTrade0thRound:NGGL

2.56%ofnational tax

revenue

2.84%ofnational tax

revenue

178737

16092

21

32

12

3

SocialSecurity

Payroll Taxes

Royalties NFSL Income Tax

Total Tax Payments

NGGL

Witholding Tax Paid by NGGL On Behalf of Suppliers

Taxes Paid by

Suppliers

Taxes Paid by

Suppliers’ Suppliers

Total Supported

Tax Payments

2ndRound:Suppliers’Suppliers1stRound:DirectSuppliersandTrade0thRound:NGGL

Agriculture Mining Manufacturing Utilities Construction Services NGGL Transportation Trade Total

412

1914

2819

23016

17 360

47

83

230

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 3130

EXHIBIT13: Pathways through which NGGL’s spending creates value added. Size of the nodes indicatesthetotalvalueaddedgeneratedorreceivedandthelinethicknessindicatesthesizeofaflow.NGGL’sspendingisdarkblue,directandindirectvalueaddedflowstohouseholds,profitsandgovernmentincomearelightblueandintermediarydemandflowsbetweensectorsare green.G

G Forreasonsofinterpretationintra-sectorflowsandflowssmallerthanUSD100,000areexcluded.

4.3 Employment ThissectioncapturesNGGL’simpactonemploymentinfulltimeequivalents(FTE).AsdescribedinSection2,thenumberofjobsthataresupportedbyNGGL’soperationsthroughouttheGhanaian economy have been determined based on government statistics about the labor force per sector.12

AsmentionedinSection2.4,Newmontdirectlyemployed2,229peoplein2011ofwhich1,921are related to the Ahafo Mine13.Takingtheindirectandinducedeffectsintoconsideration,thetotalnumberofjobssupportedis41,000jobs(or0.39%ofthelaborforceinGhana)whichisbrokendownbysectorinExhibit14.Thejobssupportedinthe1stround(9,000)aresubstantiallysmallerthanthejobscreatedbythesuppliersofNGGL’ssuppliers(14,000).ThemainreasonforthisisthatNGGL’sdirectsuppliersarecompaniesthatoperateintheformal,more productive and less labor intensive economy in contrast to the informal sector in which many2ndroundsuppliersoperate.Ontopofthe1stand2ndroundjobssupported,there-spendingofsalaries,whichareearnedbyNGGLemployeesandemployeesofsuppliersinround1and2,supportanadditional16,000jobs.14 This impact that is caused by the re-spending of salaries is only applicable to jobs supported as discussed in Section 3.1.

12 GhanaStatisticalServiceshavepublishedthecensus2010whichcontainsthebreakdownofthelabourforceonthe national and regional level. See Appendix A for more details about our methodology to calculate the number of jobs.

13 Thesumofpeoplethatworkattheminesite(1,729)andthosethatworkattheAccraoffice(192).14 Expendituresonagriculturehavebeenomittedsincethiswillmostlybe“auto-consumption”.Ofthe3,000induced

jobsinmanufacturing,almostallarerelatedtofood&beverageproductioncommensuratewiththefactthatmosthousehold spending is on basic needs.

A large tax payer office in Accra

The exhibits shown so far described the value added results from the economic modeling. A more visual impression of the pathways through which this value added is created as NGGL’s spending travels through the economy is shown in Exhibit 13.

TheexhibitshowsthatthesinglelargestflowisintheformofNGGL’stax,royaltyandcarriedinterest payments to the government of Ghana. NGGL’s considerable expenditures on mining services,construction,utilitiesandmanufacturingareclearlyvisible.Thefactthatminingservicescontributelessvalueaddedthan,say,construction(asindicatedbythesizeofthenodes)despitethelargerinflowofNGGLcashflowisbecausethebulkoftheseservicesrelyonimportsofforeigncapitalgoodsandskillsandrequirerelativelylittle(low-skilled)laborfromwithin Ghana. The construction sector by contrast is more labor intensive and requires fewer skills,allowingittokeepmoreofitsvalueaddedinGhana.Overall,thediagramshowsthatforaminingcompany,NGGLisrelativelydeeplyintegratedintotheGhanaianeconomy.

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 3332

Exhibit15putsemploymentassociatedwithNGGLincontextintermsoftheirquality.Inthisgraph,valueaddedperjobsupportedisusedasanindicatorforthequalityofjobs.15 Although manyjobsareinthetradeandmanufacturingsectors,thesearegenerallylessproductiveor‘lowerqualityjobs’(intheinformalsector).ThequalityofjobswithinNGGLisparticularlyhighwithavalueaddedperjobofUSD119,000,whichis34timeshigherthantheGhanaianaverage.16ThehighcapitalintensityofNGGL’soperationsisthekeydriverhere.Overallonecanconclude that most jobs associated with Newmont’s presence in Ghana are above average in terms of value added.

15 Exhibit15showsthevalueaddedperemployee,whichconsistsofhouseholdincome,profits&savingsandtaxpayments. A direct comparison with the average annual salary therefore does not hold.

16 TheGhanaianaverageisestimatedbydividingGDPbylabourforce;USD38.1billion/10.6million=USD3,578per person in the labour force.

EXHIBIT14:Direct,indirectandinducedeffectsonemploymentpersector(in‘000jobs)

Newmont Ghana is proud to be associated with quality jobs.

H Exhibit15excludestheinducedeffectsonjobssupportedbecausetheinducedeffectisnottakeninto account when calculating the value added.

EXHIBIT15:Valueaddedperdirect&indirectjobsupportedbyNGGL(inUSD‘000)H

0thRound:NGGL1stRound:DirectSuppliersandTrade2ndRound:Suppliers’Suppliers3ndRound:Re-spendingofsalaries

6 1

8 12

72

2

12 41

4

3

3

3

4

7 16

14

9

2

0.39%of labor force0.02%of

labor force

Agriculture Mining Manufacturing Utilities Construction Services NGGL Transportation Trade Total

Jobs (in ‘000)

Value Added per Job (in ‘000 USD)

120,000

118,000

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0 20.0 22.0 24.0 26.0

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

NGGL

Construction

Utilities

TransportationMining

Services

ManufacturingTrade

Ghanaian Average

Agriculture

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 3534

48.2 + 0.2 - 22.4

41.1+15.0

Estimate 2009 DirectEmployment:

More Direct Employment

Correction Labour Productivity

Increase Local Procurement

IndirectEmployment: IndirectEmployment: Estimate 2011

1 2 3

Changes in employment are caused by:1. NGGL directly employing about 200 more people;2. Significantincreaseinlabourproductivityduetotheeconomybeing2.5xlargerwhile

employment increased by just 1.03x since 2009;3. Increaseoflocalprocurement(USD43million)andbetterinsightsinhowthatmoneyis

spentwithintheGhanaianeconomy(duetointerviewinginternationalandlocalcontractors)

4.4 Comparison with the 2009 ReportIn2010,StewardRedqueenperformedasocio-economicimpactassessmentforNGGLbasedonits2009financials.AdetailedcomparisonisincludedinAppendixB.Overall,theresultsatthe national level shown above correspond well with the results of the previous study. The main differencesare: 1. NGGL’srevenueshaveincreasedbyUSD341million(+65%)drivenbythehighergold

price and somewhat higher production volume; 2. Mostofthesehigherrevenuestranslatedintoincreasedprofitsfromoperations;from

USD128milliontoUSD273million.Thiswillultimatelyresultinincreasedincometothegovernment due to its carried interest once dividends are declared;

3. InGhana,procurementincreasedbyUSD43milliontoUSD182million; 4. NGGL’sdirectvalueaddedinGhanaincreasedbyUSD174millionfromUSD56million

to USD 230 million; 5. USD152millionofthishighervalueaddedaccruedtothegovernmentbecausetax

paymentsand(deferred)carriedinterestincomeshareincreasedalmostfivefoldfromUSD39milliontoUSD191million,largelybecauseNGGLstartedtopaytaxesonitsprofits17;

6. HouseholdincomefromsalariespaidbyNGGLrosebyUSD22milliontoUSD39million,reflectingNGGL’slargerworkforceandincreaseofunitlaborcosts.

7. Whenincludingthelargerindirecteffects(comingfromthelargerin-Ghanaprocurement),totalvalueaddedinGhanaincreasedmorethantwicefromUSD153milliontoUSD360million;

8. AsapercentageofGhana’sGDP,NGGL’scontributionissubstantiallysmaller(0.95%comparedto1.30%)astheeconomyin2011wastwoandahalftimeslargerthanin2009becauseoffasteconomicgrowthandtherebasingofGDPmeasurementin2010,whichresultedina60%largereconomy.18

9. The total number of jobs that can be attributed to NGGL’s presence declined by about 7,100(-15%).Exhibit16explainsthesechangesinmoredetail.Thedecreaseinthenumber of jobs supported is solely due to revision of country statistics and has nothing to dowiththemethodologyusedortheperformanceofNGGL(whichactuallyimprovedintermsofdirectemploymentandlocalprocurementexpenditures).

17 ThereasonthatNewmontdidnotpaytaxesonprofitsuntil2010isnotthatminingcompaniesareexemptedduringthefirst5yearsofoperationsasoftenisassumedbutratherthatfavorabledepreciationschemesandthecarryforwardoflossesareallowed.OverthelifeofthemineNewmontthuspaystaxesoverallofitsprofits.Inlieuofsuchafavorableregime,capitalintensiveinvestmentswouldbemuchlessattractive.

18 Jerven.M,&Duncan.M.E.(2012).RevisingGDPestimatesinSub-SaharanAfrica:LessonsfromGhana.AfricanStatisticalJournal,15.

EXHIBIT16: Change in employment supported by NGGL over the period 2009-2011 (in‘000jobs)

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 3736

5. NGGL’s Socio-Economic Impact on the Brong-Ahafo Region and Asutifi District

Inthissection,NGGL’sdirectimpactintermsofvalueadded,i.e.thesumofsalaries,taxesandprofits,andjobsareshownaswellastheindirectimpactthatstemsfromtheprocurementexpenses that are done within Brong-Ahafo. After a discussion of NGGL’s expenditures in Section5.1,Section5.2willdiscussthevalueaddedthatissupportedwithinBrong-Ahafo.Section5.3discussesthejobssupportedandSection5.4comparestheregionalanddistrictimpact with the national impact.

5.1 NGGL’sExpendituresinBrong-AhafoTheanalysisofNGGL’seconomicimpactstartswithitsexpendituresasshowninExhibit17,forwhich the starting point is the USD 412 million in National expenditures from Exhibit 9.

NGGL’snationalexpenditureshavebeenbrokendownintoRestofGhana(RoG)andBrong-Ahafo(BA)procurementandvalueadded.InordertoassessNGGL’simpactonBrong-AhafoonlytheBAprocurement(USD18million)andvalueadded(USD12millionofhouseholdincomes and USD 3 million of government income19)havebeenusedtoestimatetheimpactonthe Brong-Ahafo region.

19 USD 3 million in government income are royalties that accrue to the local government. It is estimated by NGGL’s taxdepartmentthat9%ofroyaltypaymentsaccruetotheAhaforegionofwhich55%goestothedistrictauthorities,25%tolandownersand20%tothelocalchiefs.

EXHIBIT17:NGGL’s revenues in relation to its expenditures and value added in Brong-Ahafo (BA)andtheRestofGhana(RoG)in2011(inUSDmillion) 5.2 ValueAdded

Exhibit18showsabreakdownoftotalvalueaddedwhichissupportedintheBrong-Ahafoeconomy:householdincomes,profits&savingsfordirectandindirectsuppliersandgovernmentincome.ThesesumuptoUSD30.5million,whichrepresents0.78%ofthetotalGDP for the Brong-Ahafo economy. The reason that NGGL’s share of Brong-Ahafo’s GDP (0.38%)islowerthantheshareofnationalGDP(0.60%,seeExhibit10)isthatNGGL’staxand royalty payments largely accrue to the national government.20Inaddition,duetothesimpleandopennatureofBrong-Ahafo’seconomymuchofthemoneyflowsoutoftheregionratherquicklyi.e.justasmallpartofNGGL’sdemandcanactuallybeprocuredregionallyandthereforespillovereffects(round1&2)aresmaller.

TheUSD15.4millionofindirectvalueadded(1stand2ndround)arethespillovereffectsfromtheUSD18millionoflocalspendingdonebyNGGL(seeExhibit17),halfofwhichwaspartoftheAhafoLinkagesProgram21.Exhibit18alsoshowsthatmostoftotalvalueaddedgoesassalaries to households and about half of the value added is generated directly by NGGL.

20 See footnote 30. 21 TheAhafoLinkagesProgramwassetupinconjunctionwiththeInternationalFinanceCorporation.Asan

indication,localpurchasingundertheprogramhasincreasedfromUSD1.7m(with25suppliers)toUSD9.0m(with143suppliers)in2010.

A panoramic view of Ahafo Mine

National Expenditures

RoG Procurement

RoGProfits RoG Household

Income

RoG Government

Income

BA Expenditure BA Procurement BA Household Income

BA Government Income

412

30

164

27157

33 1812 3

Driver for IndirectEffects

(i.e.Round1&2)

DirectEffects(i.e.Round0)

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 3938

EXHIBIT18:Directandindirecteffectsonvalueadded(inUSDmillion)

EXHIBIT19:Directandindirecteffectsonvalueaddedpersector(inUSDmillion)

Exhibit 19 shows in which sectors the value added is created. Apart from NGGL’s direct contribution,mostvalueaddedcanbefoundintheminingsector.Withintheminingsector,USD4.4millionofthetotalUSD4.5millionindirectvalueaddedrelatestocontractorshiredbyNGGL,e.g.fortheconstructionoftheundergroundmine.Inaddition,constructionandotherservices(e.g.thecateringandlodgingservicesprovidedonsite)respectivelyaddUSD3.9million and USD 3.2 million to Brong-Ahafo’s GDP.

NGGL’simpactontheAsutifidistrictisofcoursemanytimeslargerthantheimpactonthewholeBAregion.Itisrealistictoassumethatabout55%oftheUSD27.6million22 Brong-Ahafo householdincomeandprofits&savingsaregeneratedintheAsutifidistrictsinceabout55%oftheNewmontemployeeslivethere.ThisUSD15.2millionvalueaddedinAsutifiisabout8%ofthedistrict'sGDPasitrepresentsabout5%ofBrong-Ahafo’sGDP.

5.3 EmploymentAsmentionedinSection2.4,NGGLemployed2,229peoplein2011inGhana,ofwhich1,729peoplewereemployedinBrong-Ahafo.Whenincludingtheindirectandinducedeffects,thetotalemploymentthatissupportedsumsupto8,700jobswhicharebrokendownbysectorinExhibit20.The1,300jobssupportedbysuppliersinthe1stroundaresmallerinnumberthanthe3,200jobssupportedbythesuppliersofNGGL’ssuppliers.ThemainreasonforthisisthatNGGL’sdirectsuppliersareconsideredtobecompaniesthatoperateintheformal,moreproductive and less labor intensive economy vis-à-vis the informal sector in which many 2nd roundsuppliersoperate.In2011,onaverage,4,139ofNGGL’scontractoremployeesworkedonsitewhichisabout92%ofNGGL’s4,500indirectemployment(1,3001stroundjobsand3,2002ndroundjobs).Ontopoftheindirecteffects(the1stand2ndroundjobssupported),the re-spending of salaries that are earned by NGGL employees and by employees in round 1and2supportanadditional2,400jobs.Mostofthesejobs,arejobsintheagriculturalandtrade sectors.

22 TheregionalgovernmentincomeofUSD2.9millionhasbeenexcludedfromthetotalimpactofUSD30.5millionbecauseitcan’tbeattributedtotheAsutifidistrict,whilehouseholdincomeandprofits&savingscan.

Household Income Profit&Savings Government Income Total

25.7

1.9

2.9 30.5

3.0

2.9 3.8

11.6

15.0

10.6

12.2

2ndRound:Suppliers’Suppliers1stRound:DirectSuppliersandTrade0thRound:NGGL

0.78%of regional GDP

0.38%of regional GDP

Agriculture Mining Manufacturing Utilities Construction Services NGGL Transportation Trade Total

1.4

4.5 0.7 0.1

3.8

2.9

15.0 0.41.6 30.5

1.4

4.4

3.7

2.7

3.8

11.6

15.0

1.62ndRound:Suppliers’Suppliers1stRound:DirectSuppliersandTrade0thRound:NGGL

EXHIBIT20:Direct,indirectandinducedeffectsonemploymentpersector(in‘000jobs)

0thRound:NGGL1stRound:DirectSuppliersandTrade2ndRound:Suppliers’Suppliers3ndRound:Re-spendingofsalaries

1.40.5

0.4 0.00.2

1.1

1.7 0.1

3.3 8.7

0.9

0.5

0.5

2.7

2.5

0.7

2.4

3.2

1.3

1.7

0.5

0.5

0.17%ofregional labor

force

0.86%ofregional labor

force

Agriculture Mining Manufacturing Utilities Construction Services NGGL Transportation Trade Total

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 4140

EXHIBIT21:Valueaddedperdirect/indirectjobsupportedbyNGGL(inUSD‘000)

5.4 ComparisonofNGGL’sImpactattheNational,RegionalandDistrict Levels

NGGL’srelativeeconomicimpactatthenational,regionalanddistrictlevelsasdescribedinSections4and5issummarizedinTable2.NGGL’svalueaddedimpactlargelyaccruesatthenationallevelinabsoluteterms,butinrelativetermstheimpactismoreorlesscomparableatthenationalandregionallevel.BecausethebulkofitsoperationsareintherelativelysmallerAsutifidistrict,itsvalueaddedimpactthereisanorderofmagnitudelarger.Asexpected,NGGL’semploymentimpactislargestinAsutifiandsmallestatthenationallevel.

TABLE2:Summary of NGGL’s direct and total impact on value added and employment at the national,regionalanddistrictlevel

IMPACT GHANA BRONG-AHAFOREGION ASUTIFIDISTRICTDirect Value added 0.60% 0.38% ~4%Total Value Added 0.95% 0.78% ~8%Value Added multiplier 1.6x 2.0x ~ 2xDirect Employment 0.02% 0.17% ~1.5%Total Employment 0.39% 0.86% ~10%Employment multiplier 21x 5x ~6x

A female employee at work at the Ahafo Mine

Jobs (in real terms)

Value Added per Job (in USD)

00 1,000 2,000 3,000 4,000 5,000 6,000

1,0002,0003,0004,0005,0006,0007,0008,0009,000

10,00011,00012,00013,00014,00015,00016,00017,000 Construction

Utilities

MiningNGGL

Transportation

Services

ManufacturingAgriculture

Trade

Brong-Ahafo Average

The8,700jobsinBrong-Ahaforepresent0.86%ofBrong-Ahafo’sworkforce.Giventheassumptionthat55%oftheworkforcelivesintheAsutifidistrict,whichaccountsfor5%ofBrong-Ahafo’spopulation,itfollowsthatabout10%ofAsutifi’semployablepopulationisdirectlyorindirectlyrelatedtoNGGL’spresence.Takingintoaccountthesubstantialunemploymentand underemployment present in Brong-Ahafo23,NGGL’sshareoftheemployedworkforceisprobably much bigger.

Exhibit 21 shows that value added per NGGL employee in Brong-Ahafo is not nearly as high asatthenationallevel(seeExhibit15).ThemainreasonforthisisthatthelargestportionofvalueaddedbyNGGL,namelythetaxpayments,accruesnearlyinitsentiretytothenationalgovernment. The value added per jobs in the other sectors is comparable to the national figures,exceptforthetradesectorwhichisinformaltoamuchgreaterextent.

The reason that value added per job for the construction and mining sector is higher in comparisontoNGGL’svalueaddedperjobisduetothespecifichighvalueaddedservicesthesesectordelivertoNGGL(e.g.undergroundminingservices).Theutilitieshighvalueaddedperjobisacommonfindingasthenatureofthissectoristhatitismorecapitalthanlaborintensive.

23 Unfortunately no reliable data about unemployment is available.

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 4342

Exhibit 22 combines NGGL’s absolute and relative economic impact in one image showing that althoughverylargeattheAsutifidistrictlevel,NGGL’sabsolutevalueaddedisfarlargeratthenational level.

EXHIBIT22:VisualimpressionofNGGL’snational,regionalanddistrictleveleconomicfootprintintermsoftotalvalueadded(Table2).Surfaceareasofthenational,regionalanddistrictlevelsand NGGL’s value added are proportional to GDP and value added

Ghana

Newmont

Asutifi

Brong Ahafo

6. Impact on the Household LevelWhen NGGL signed its investment agreement with the Government of Ghana in December 2003,itwasclearthatalotofcapitalwouldflowintoaregionthatispredominantlyoccupiedwithsubsistenceagriculture.Interestingly,theactualcapitalthatflowedinwasmuchlargerthanoriginallyanticipatedbyNewmontandthegovernment.Thisinflowofcapitaldidnotonlyalterthestructureoftheregionaleconomybutalsoinfluencedthepeople’straditionalwayofliving.Inthissection,weelaborateonwhathasactuallychangedforhouseholdsinthisregionbasedon a household survey that was conducted as part of this assessment.

The households that were interviewed were chosen such that three groups can be distinguished(seealsoSection3.2): • Households within the Ahafo Mine’s economic catchment area24 with at least one

memberworkingforNGGL; • HouseholdswithintheAhafoMine’scatchmentareabutwithoutmembersthatworkfor

NGGL; • HouseholdsoutsidetheAhafoMine’scatchmentareawithoutmembersworkingforNGGL.ThisdivisionallowsustodeterminetheimpactofbeingemployedbyNGGL(firstandsecondgroups)aswellasthemoregeneralimpactsoftheMinebecausethethirdgroupisakindof‘control’ group.

TheresultsfromthissurveyarecomparedwithfindingsfromtheExternalStakeholderPerception Survey 2013 done by the Bureau of Integrated Rural Development of the Kwame NkrumahUniversityofScienceandTechnology(KNUST).Themaindifferencebetweenthetwosurveysisthesampleselection.WhereasthisReportdistinguishesthreesub-groups,KNUSTdoesnotmakeadistinctionbetweenhouseholdsthatareandaren’taffectedbytheAhafoMine.Thisledtosomeopposingfindings,butthesehavebeenaddressedaccordingly.

The results of the household survey carried out for this assessment will be discussed in detail belowbutareheresummarizedasfollows: • ThepresenceoftheMineledtoaninfluxofpeopletotheregion; • The household spending power of NGGL employees in the region is on average twice as

high as the average households in the region; • Households inside the economic catchment area of the Mine are less entrepreneurial

than households outside the catchment area; • Households of NGGL employees are on average better educated than other households

in the region; • AccesstowaterandelectricityhasnotimprovedsignificantlysinceNGGLstartedits

operations; • Households report that their economic situation has improved since NGGL started its

operations.

24 ThecatchmentareaoftheAhafomineisdefinedastheAsutifiandTano-NorthdistrictinBrong-Ahafo.Exhibit8inSection 3.2 shows the location of the households and how many people have been surveyed.

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 4544

6.1 MigrationHouseholdsthatareeconomicallyclosertotheMine(i.e.employedbyNGGLorlivinginthevicinityoftheAhafoMine)aremorelikelytohavemigratedintotheareafromoutside.Table3showsthatfromthehouseholdswithNGGLemployeesonly64%oftheirmemberswerebornwithintheregion.ForhouseholdslivingclosetotheMinethisis82%andforthehouseholdslivingoutsidethecatchmentareathisis87%.

TABLE3:Placeofbirth(%oftotalhouseholdssurveyed)pergroupofhouseholds

BORN IN THE REGIONNGGL Employees 64%

Households inside catchment area 82%

Households outside catchment area 87%

Table4alsoshowsthatNGGLemployeesarelesslikelytoownahouseintheregion.Infact,more NGGL employees still own a house outside the region than inside indicating that they havemigratedintothearea.Otherhouseholdsinsidethecatchmentareaareagainlesslikelytoownahousethanhouseholdsoutsidethecatchmentarea,whichexplainsthehighdemandand consequently the high price for housing.

TABLE4:TheownershipofahouseinsidetheregionorsomewhereelseinGhana(%ofhouseholdssurveyedintheirrespectivegroup)pergroupofhouseholds25

OWNERSHIP OF A HOUSE IN

BRONG-AHAFO

OWNERSHIP OF A HOUSE IN THE REST OF GHANA

NGGL Employees 30% 36%

Households inside catchment area 45% 18%

Households outside catchment area 64% 19%

6.2 HouseholdSpendingItisnotsurprisingthatNGGL’spresencehasledtoaninfluxofpeopleintotheregionconsidering that the Mine’s employees are able to spend on average twice as much as other households in the region. Exhibit 23 shows that the annual spending of NGGL employees isalmostGH¢12,000(approximatelyUSD7,700)whereastheaverageexpendituresofhouseholdsinthecatchmentareaareGH¢6,800(approximatelyUSD4,400).Outsideofthecatchmentarea,theaverageannualfigureisGH¢6,000(approximatelyUSD3,900).ThesefindingsareinagreementwithKNUST’sconclusionthatthecombinationofin-migrationandhigherhouseholdexpendituresleadtolessaffordablegoodsandservicesinthecommunities,especiallythatofhousing.Inadditiontothispriceeffect,peoplelivinginsidethecatchmentareamay have developed a somewhat more expensive lifestyle.

25 Ownership of a house in Brong-Ahafo does not exclude ownership of a house in the Rest of Ghana.

EXHIBIT23:Averagehouseholdexpenditure(inGH¢onannualbasis)pergroupofhouseholds

An aerial view of Ntotroso, a community in Ahafo

11,965

+76%

+12%

6,804

6,065

4,858

3,893

1,727

428

2,143 1,879

1,474

2,350

3,839

1,487

Newmont Employees Inside Catchment Area

OutsideCatchment Area

FoodOther Living ExpensesBusiness ActivitiesEducation

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 4746

6.3BusinessActivitiesExhibit24showsthathouseholdsinsidethecatchmentarea(butwithnomembersemployedbyNGGL)spendabout6%oftheirincomeonbusinessactivitieswhereashouseholdsoutsideofthecatchmentareaspend31%.ApartialexplanationforthisisshowninExhibit25whichshowsthatnon-agriculturalself-employment(e.g.daylabourortrade)asasourceofemployment,issignificantlymoreimportantthanagriculture,whichtypicallyrequiresmoreinputsand(self)financing.26Inthatsense,thepresenceoftheMineseemstohavemadepeopleinsidethecatchmentmoredependentonemploymentbytheMineandtobelessactiveinagriculture,whichisthemainstayoftheeconomyintheregion.Inaddition,KNUSTconcludedthatthecompensationpaymentsmadetothosewholosttheirland,andtherebytheirmainsourceofincome,werenotusedtomakemeaningfulinvestments(inassetsorskills)butinsteaditledtoamore luxurious life style.

KNUSTcontinuedtoconcludethatNGGLprogramsliketheAgriculturalImprovementandLandAccessProgram(AILAP)wereunderutilized.AILAP,setupincooperationbetweentheMinistryofFoodandAgricultureandNGGL,helpstodevelopagricultureinthecommunitiesmostaffectedbyNGGL.From2006until2012,NGGLspentUSD5.4millionontheinputs(seeds,fertilizerandherbicides)andtraining27.Apartfromanincreaseintheamountoflandundercultivation,yieldshaveincreasedby65%forplantainand80%formaize.Inshort,forthosewhomadeuseofit,the program helped achieve substantial improvements but further improvements are possible andinfactneeded.ATS,NGGL’ssupplierofcampandhospitalityservices,isabletosourceonlyabout60%ofitsagriculturalproductslocally.ThemainreasonforthisisthatthedemandfromATSismorediversethanwhatislocallyproduced.Byallreasonablestandards,thediversificationofagriculturalproductionoughttobepossibleinafertileregionlikeBrong-Ahafo.

26 KNUST reports agriculture to be the major source of income for households inside the catchment area and incomefromnon-agriculturalself-employmentasthesecondbiggestsourceofincome.Wethinkbasedonthesurveyresultsthatthereismorenon-agriculturalemploymentinsidethecatchmentareathanoutside.Wecannot,however,concludethatitismoreimportantthanagricultureastheresultsindicate.

27 The fact that NGGL supplies agricultural inputs may also partly explain why households in the catchment area spend less on business activities.

EXHIBIT24:Averagehouseholdexpenditure(%breakdown)pergroupofhouseholds

EXHIBIT25:Sourceofincome(%oftotalhouseholdincome)pergroupofhouseholds

FoodOther Living ExpensesBusiness ActivitiesEducation

100% 100% 100%

12%6% 6%

31%

24%

39%

31%

56%

6%

14%

33%

41%

Newmont Employees Inside Catchment Area

OutsideCatchment Area

Wage IncomeIncome from AgricultureIncome from Non-Agricultural Self-EmploymentOther Income

100% 100% 100%

Newmont Employees Inside Catchment Area

OutsideCatchment Area

8% 11%4%

13%

51%

31%

39%

30%

21%

7%

83%

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 4948

consistent with the fact that the better educated invest more in their children’s education.

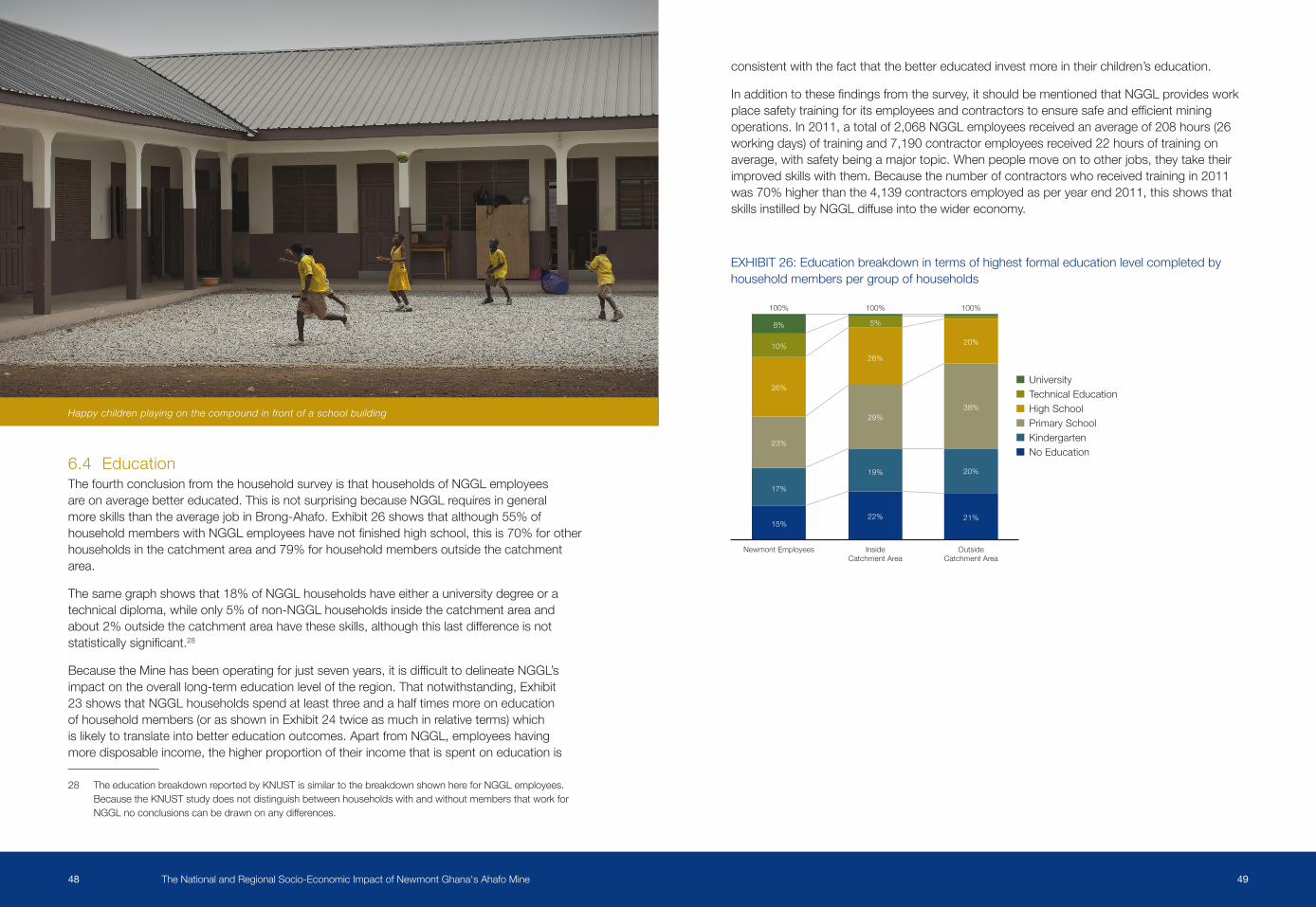

Inadditiontothesefindingsfromthesurvey,itshouldbementionedthatNGGLprovidesworkplacesafetytrainingforitsemployeesandcontractorstoensuresafeandefficientminingoperations.In2011,atotalof2,068NGGLemployeesreceivedanaverageof208hours(26workingdays)oftrainingand7,190contractoremployeesreceived22hoursoftrainingonaverage,withsafetybeingamajortopic.Whenpeoplemoveontootherjobs,theytaketheirimprovedskillswiththem.Becausethenumberofcontractorswhoreceivedtrainingin2011was70%higherthanthe4,139contractorsemployedasperyearend2011,thisshowsthatskillsinstilledbyNGGLdiffuseintothewidereconomy.

EXHIBIT26:Educationbreakdownintermsofhighestformaleducationlevelcompletedbyhousehold members per group of households

6.4 EducationThe fourth conclusion from the household survey is that households of NGGL employees are on average better educated. This is not surprising because NGGL requires in general moreskillsthantheaveragejobinBrong-Ahafo.Exhibit26showsthatalthough55%ofhouseholdmemberswithNGGLemployeeshavenotfinishedhighschool,thisis70%forotherhouseholdsinthecatchmentareaand79%forhouseholdmembersoutsidethecatchmentarea.

Thesamegraphshowsthat18%ofNGGLhouseholdshaveeitherauniversitydegreeoratechnicaldiploma,whileonly5%ofnon-NGGLhouseholdsinsidethecatchmentareaandabout2%outsidethecatchmentareahavetheseskills,althoughthislastdifferenceisnotstatisticallysignificant.28

BecausetheMinehasbeenoperatingforjustsevenyears,itisdifficulttodelineateNGGL’simpactontheoveralllong-termeducationleveloftheregion.Thatnotwithstanding,Exhibit23 shows that NGGL households spend at least three and a half times more on education ofhouseholdmembers(orasshowninExhibit24twiceasmuchinrelativeterms)whichislikelytotranslateintobettereducationoutcomes.ApartfromNGGL,employeeshavingmoredisposableincome,thehigherproportionoftheirincomethatisspentoneducationis

28 TheeducationbreakdownreportedbyKNUSTissimilartothebreakdownshownhereforNGGLemployees.BecausetheKNUSTstudydoesnotdistinguishbetweenhouseholdswithandwithoutmembersthatworkforNGGLnoconclusionscanbedrawnonanydifferences.

Happy children playing on the compound in front of a school building

Newmont Employees Inside Catchment Area

OutsideCatchment Area

100% 100% 100%

8%

10%

26%

23%

17%

15%22%

19%

29%

26%

5%

20%

38%

20%

21%

No EducationKindergartenPrimary SchoolHigh SchoolTechnical EducationUniversity

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 5150

6.5 AccesstoWaterandElectricitySincethestartofminingoperations,thehouseholdsurveyshowsthataccesstowaterhasnotchangedsignificantly.29Surprisingly,howeveristhattheavailabilityofelectricityhasreportedlygottenworse.BeforethestartoftheMine,respectively64%and72%ofthehouseholdsinsideandoutsidethecatchmentareaindicatedthattheywerecutofffromelectricityatleastonceaweek.Now,respectively91%and94%ofthosehouseholdsindicatesuchcuts.The main reason for the worsening situation lies with the mismatch in national demand and supplyofenergyratherthanthepresenceofNGGL,whichinactualfacthasmadesignificantinvestments in the transmission and electricity supply infrastructure in the region and district. National demand for electricity far outweighs actual supply and therefore it is no surprise that electricityshortageshaveledtonationwidepowercutsandblackouts.30

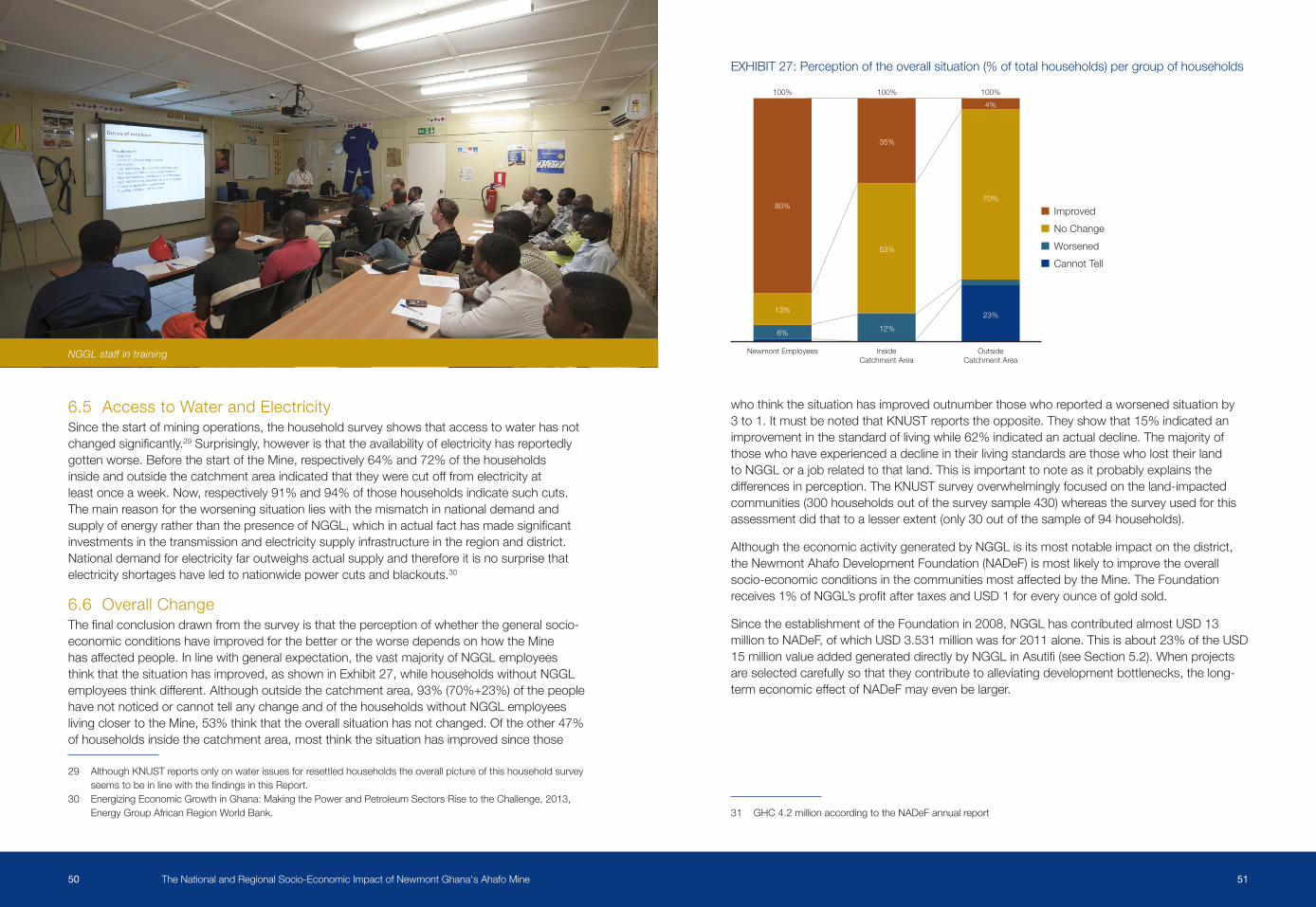

6.6 OverallChangeThefinalconclusiondrawnfromthesurveyisthattheperceptionofwhetherthegeneralsocio-economic conditions have improved for the better or the worse depends on how the Mine hasaffectedpeople.Inlinewithgeneralexpectation,thevastmajorityofNGGLemployeesthinkthatthesituationhasimproved,asshowninExhibit27,whilehouseholdswithoutNGGLemployeesthinkdifferent.Althoughoutsidethecatchmentarea,93%(70%+23%)ofthepeoplehave not noticed or cannot tell any change and of the households without NGGL employees livingclosertotheMine,53%thinkthattheoverallsituationhasnotchanged.Oftheother47%ofhouseholdsinsidethecatchmentarea,mostthinkthesituationhasimprovedsincethose

29 Although KNUST reports only on water issues for resettled households the overall picture of this household survey seemstobeinlinewiththefindingsinthisReport.

30 EnergizingEconomicGrowthinGhana:MakingthePowerandPetroleumSectorsRisetotheChallenge,2013,EnergyGroupAfricanRegionWorldBank.

EXHIBIT27:Perceptionoftheoverallsituation(%oftotalhouseholds)pergroupofhouseholds

whothinkthesituationhasimprovedoutnumberthosewhoreportedaworsenedsituationby3to1.ItmustbenotedthatKNUSTreportstheopposite.Theyshowthat15%indicatedanimprovementinthestandardoflivingwhile62%indicatedanactualdecline.Themajorityofthose who have experienced a decline in their living standards are those who lost their land to NGGL or a job related to that land. This is important to note as it probably explains the differencesinperception.TheKNUSTsurveyoverwhelminglyfocusedontheland-impactedcommunities(300householdsoutofthesurveysample430)whereasthesurveyusedforthisassessmentdidthattoalesserextent(only30outofthesampleof94households).

AlthoughtheeconomicactivitygeneratedbyNGGLisitsmostnotableimpactonthedistrict,theNewmontAhafoDevelopmentFoundation(NADeF)ismostlikelytoimprovetheoverallsocio-economicconditionsinthecommunitiesmostaffectedbytheMine.TheFoundationreceives1%ofNGGL’sprofitaftertaxesandUSD1foreveryounceofgoldsold.

SincetheestablishmentoftheFoundationin2008,NGGLhascontributedalmostUSD13milliontoNADeF,ofwhichUSD3.531millionwasfor2011alone.Thisisabout23%oftheUSD15millionvalueaddedgenerateddirectlybyNGGLinAsutifi(seeSection5.2).Whenprojectsareselectedcarefullysothattheycontributetoalleviatingdevelopmentbottlenecks,thelong-termeconomiceffectofNADeFmayevenbelarger.

31 GHC4.2millionaccordingtotheNADeFannualreport

NGGL staff in training Newmont Employees Inside Catchment Area

OutsideCatchment Area

Cannot TellWorsenedNo ChangeImproved

100% 100% 100%

80%

13%

6% 12%

53%

35%

4%

70%

23%

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 5352

Accordingtoitscharter,NADeFputs10%ofNGGL’scontributionsintoacapitalendowment(currentlyaboutUSD1.2million)andtheremainderisspentonhumanresourcesdevelopment,infrastructure,socialamenities,economicempowerment,naturalresourcemanagement,andculturalheritage&sportactivities32,subjecttoapprovalbytheBoardofTrustees33. So far the foundationhasspentaboutUSD9milliononscholarshipsandprojectslikethebuildingofschools,communityhouses,boreholesandthedeliveryoftoolsandequipment.ThisimpliesthatthefoundationhasspentUSD3millionlessthanintendedduetothelackofsufficientlyrobust projects34,whichincreasesthefoundation’s‘drypowder’forsupportingfutureprojects.

FromapuredevelopmenteconomicsstandpointwewouldarguethatNADeF’scharteristoomuchfocusedon‘oneoff’projectsandthatamoreinvestment-drivenapproachwouldbebetter.Althoughachangeofthecharterwouldneedtobeapprovedbythecommunities,thefoundationisfortunatelymovinginthatdirectionandhas,forexample,setuparevolvingfundforprovidingmicrocredittowomen.Investmentsintonewlivelihoodsources,e.g.agribusinessandtextileprocessing,wouldalsobehighlyrecommendable.

Forexample,NGGLanditscontractorscannotsourcetheirworkclotheslocallybecausethereisnolocaltailorwiththerequiredproductioncapacity.Anotherexampleisthedifficultyof procuring eggs and poultry locally. We would also advocate that the contributions to the endowmentwouldbelargersothatitcanultimatelybeusedasaneconomicshockabsorberwhen the Mine closes.

32 These areas do not have equal share of funds. 33 Theboardoftrusteesconsistofthefollowingpeople:KwameSaarah-Mensah,KojoBedu-Addo,EdwinAllotey-

Acquaye,ImoniAkpofure,RandyBarnes,JacobNtim-Agyei,YawOfosu-Kusi,MaxwellBadu, Joseph Osei Manu

34 TheExternalStakeholderPerceptionSurvey2013mentionsthatcommunitiesexpectthatthefundsthatarenotbeing used should be allocated to those sectors that are in need of infrastructural and social development.

Members of Ahafo Sustainable Development Committee in a meeting

A collage of NADeF projects

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 5554

7 Conclusions and Recommendations 7.1 ConclusionsTheconclusionsthatcanbedrawnfromthiseconomicimpactstudyareasfollows: 1.NGGLiseconomicallyimportantforGhana.Specifically,thecompanysupports0.95%

ofGhana’sGDP,generates2.84%ofthecountry’stotaltaxrevenuesandcreatesemploymentfor0.39%oftheGhanaianworkforce;

2. NGGL’s regional economic impact is somewhat smaller than its national impact on an absolute level due to the fact that taxes and royalties are paid at the national level. Specifically,NGGLgenerates0.78%oftheBrong-AhafoGDPandemploys0.86%oftheregion’sworkforce;

3.NGGL’seconomicfootprintattheAsutifidistrictlevelissignificant,generatingabout8%ofvalueaddedandemployingabout10%oftheworkforce;

4.NGGL’spresenceandneedforskilledlaborhasattractedpeoplefromoutsidetheareatomigratetoBrong-AhafoandtheAsutifidistrict;

5. NGGL’s economic impact has translated into higher disposable income for especially itsemployees,whospendalmosttwiceasmuchaspeopleoutsideNGGL’scatchmentarea.HouseholdswithoutmembersthatworkforNGGLbutthatarelocatedinthecatchmentareaoftheAhafoMinespend11%morethanpeopleoutside;

6. The Mine has created a certain dependence of people not employed by it inside its catchment area. These people are thereby less able to pursue more sustainable means of livelihood;

7. A majority of people in the catchment area believe that the overall situation has improved sinceNGGL’sarrival.TheNewmontAhafoDevelopmentFoundationislikelytohavecontributed to this.

7.2 RecommendationsBasedonthefindingsofthisstudy,ourrecommendationsfocusonthenecessitytocreatealargerandmorevibrantprivatesectorinAsutifiandBrong-Ahafo.WethinkthereareampleopportunitiesforamoreconcertedeffortamongNGGL,itsdevelopmentfoundation,itssuppliersandthe(regionalandnational)government.Specifically: 1.AlthoughtheAhafoLinkagesprogramhascometoanend,wewouldadviseNGGL

tocontinueandifpossibleexpandit.Specifically,NGGLcouldembarkonadetailedassessment of its suppliers’ spending on items that ought to be produced in the district orregion.TogetherwiththeNewmontAhafoDevelopmentFoundation,acoordinatedeffortcanthenbemadetostart(aportfolioof)companiestofillthisneed;

2.AstheremaininglifeoftheMineshortens,thereisaneedfortheprivatesectorinthedistrict and region to diversify economic activities by pursuing alternative livelihoods and gradually but steadily moving away from mining-related activities. The presence of the Mine represents a window of economic opportunity during which private sector activity canbeincubated.Withfinancebeingamajordevelopmentconstraint,NGGLandtheregionalgovernmentcanactivelylookforwaysinwhichthefinancialcontributionsto

Kwasi Asamoah - AILAP Beneficiary and 2011 National Plantain Best Farmer

The National and Regional Socio-Economic Impact of Newmont Ghana's Ahafo Mine 5756

NADeFcancatalyzeother(debt/equity)capital,beitpublicorprivate,toflowtotheregion. This may also help to reduce the dependence on the Mine by households in the catchment area.

3.Similarly,theAgriculturalImprovementandLandAccessProgramandespeciallyAhafoAgribusinessGrowthInitiativeshouldbecontinuedasamoreeffectiveandproductiveagricultural sector is a prerequisite for the private sector to grow. It may be worthwhile that the program explores cooperation with NGGL supplier ATS to substantially increase its local sourcing;

4. NGGL’sabilitytotrainpeopleandhonebusinessskillsremainsimportanttoimprovepeople’sskillsandhelpbusinessprovidehighervalueaddedproductsandservices.AccesstoaneducatedworkforceisanimportantconstraintasmentionedinSection2.1;

5.Accesstopowerisanotherlargebottleneckfortheprivatesectorandoughttobeprovidedbythegovernment.Thehouseholdsurveyresults(seemto)indicatethattheaccess to utilities has not improved since NGGL came to the region. If this is indeed thecase,werecommendNGGLtouseitsinfluencewiththenationalandregionalgovernment to advocate improvement. It may be worthwhile to explore opportunities for retaining more of NGGL’s tax payments within the region;

6.AsNewmontisbuildingasecondmineinAkyemwerecommendthatitreplicatesitssuccessfullinkagesprogram.WhenAkyemproducesatcapacity(andwiththeplannedmillexpansionforAhafo)NewmontwillbethelargestgoldminerinGhanabysomedistance.Inourview,itisimportantthatthislargerscaleenablesitsnationalandlocalsuppliers to scale up as well;

7.ConsideringGhana’sincreaseddependencyonresource-relatedincome,werecommendthattheGovernmentdevelopplansforeconomicdiversificationtohelpitprepareforleaner times when commodity prices are lower or resources become depleted. The Governmentmaywishtoemphasizetheneedfordiversificationinregionswheredependencyonminingisgreatest.Inmanyminingregions,forexample,agriculturehas also been a traditional occupation of local residents. Investing in increasing the productivity of agricultural lands—including the development of a stronger property rights regime and access to credit and inputs for farmers—could be among the policies that the Government might contemplate.

Literature2010PopulationandHousingCensus,GhanaStatisticalOffice.http://www.census-ghana.net/index.html

2011ReservesandNon-ReserveMineralization,Disclosedin2011Annual Report of Newmont. http://www.newmont.com/sites/default/files/u87/NEM_2011%20Attributable%20Reserves%20and%20NRM.PDF

R.Khan(2012).AfricanEconomicOverview&theRoleofthePrivateSector.StandardChartered public presentation.

CIA,TheWorldFactBook.https://www.cia.gov/library/publications/the-world-factbook/geos/gh.html#

EaseofDoingBusiness(2012).“EaseofDoingBusinessinGhana”,EaseofDoingBusinessIndex,IFCandWorldBank.http://www.doingbusiness.org/data/exploreeconomies/ghana/

EnergizingEconomicGrowthinGhana:MakingthePowerandPetroleumSectorsRisetotheChallenge,2013,EnergyGroupAfricanRegionWorldBank.http://documents.worldbank.org/curated/en/2013/06/18027411/energizing-economic-growth-ghana-making-power-petroleum-sectors-rise-challenge

EnterpriseSurveys.“GhanaCountryProfile2007”,EnterpriseSurveys,IFCandWorldBank.http://www.enterprisesurveys.org/~/media/FPDKM/EnterpriseSurveys/Documents/Profiles/English/Ghana-2007

Factoid2011,ChamberofMines.http://ghanachamberofmines.org/en/our-publications.php

Fofana,I.,Lemelin,A.&Cockburn,J.,(2005).BalancingaSocial-AccountingMatrix:Theoryand Application.